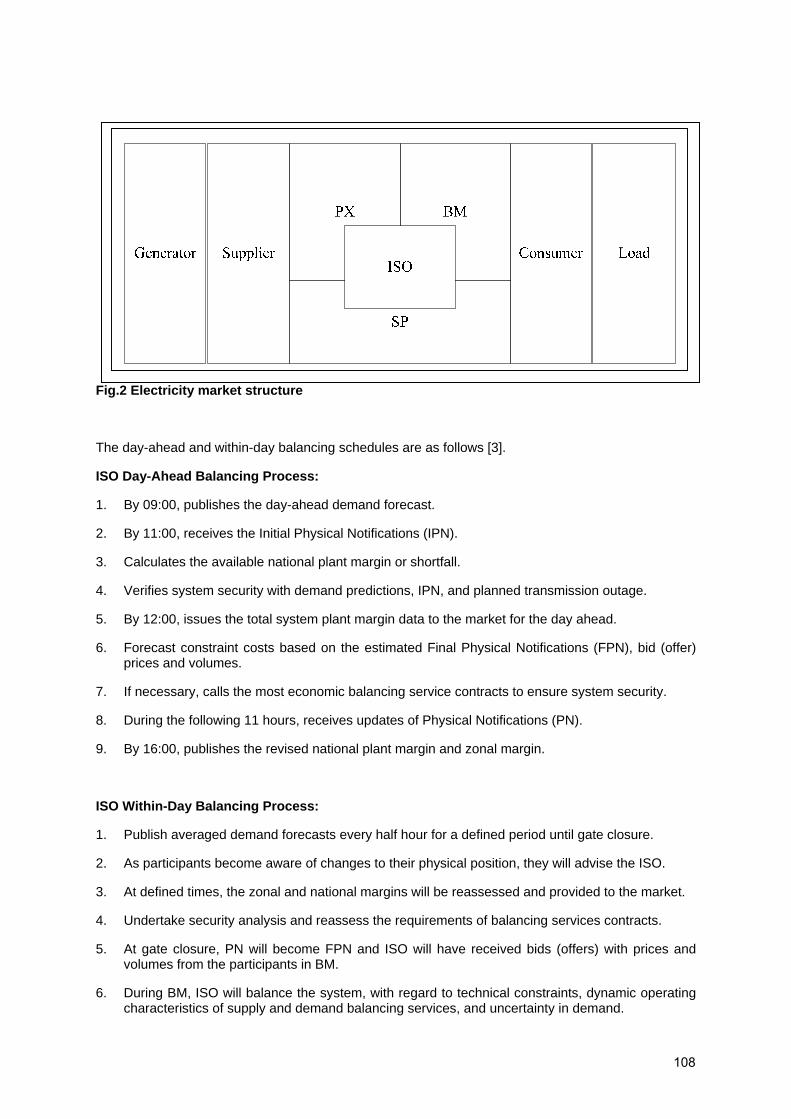

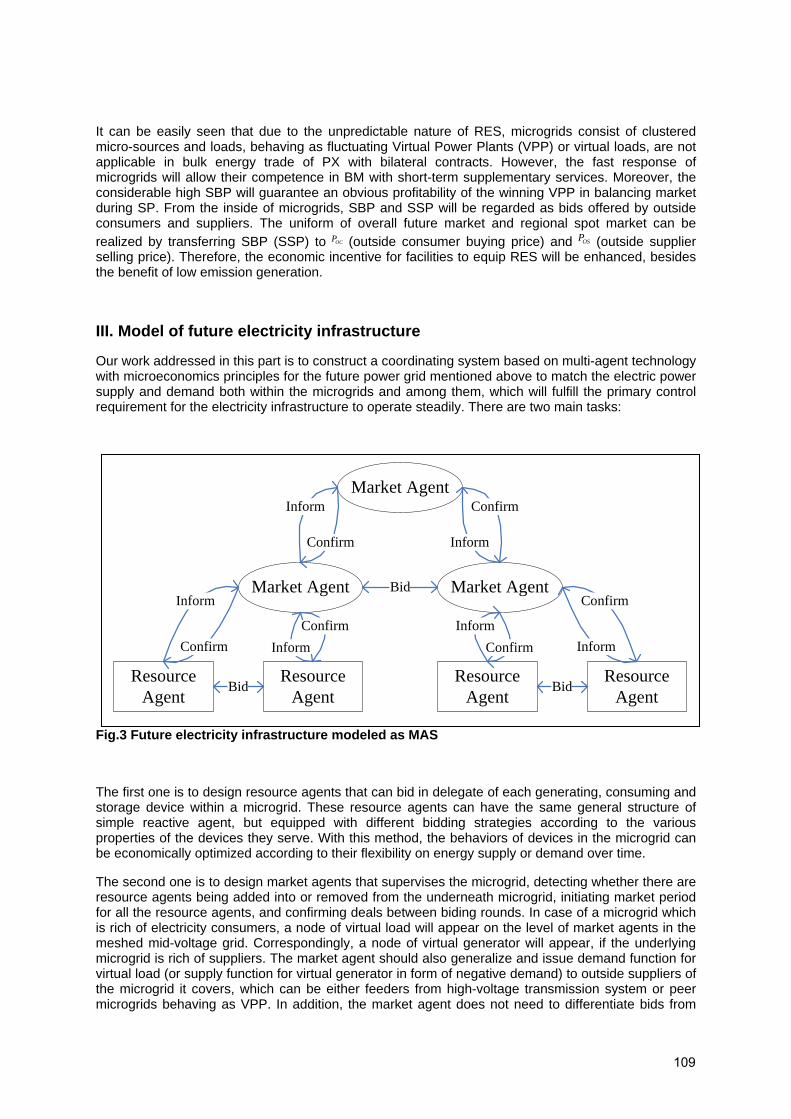

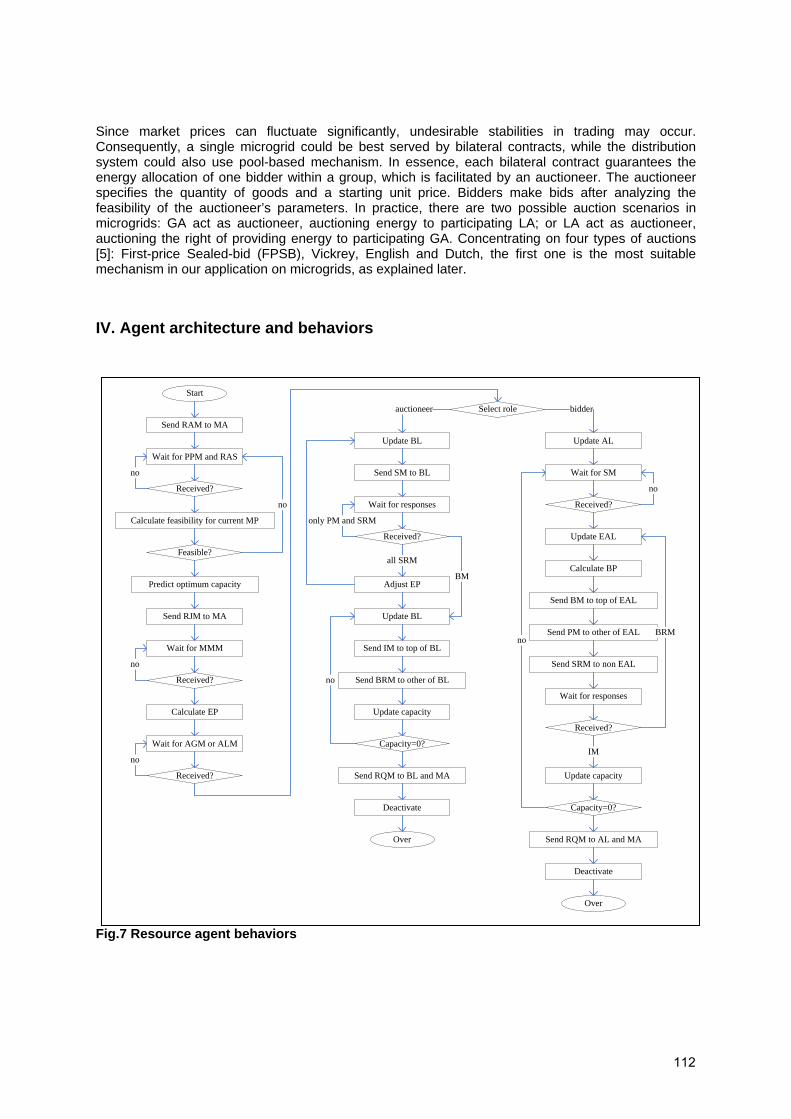

Title (Use “Title” style here) - JRC Publications Repository

456

EUR 24139 EN/1 - 2010 ENERGY EFFICIENCY IN DOMESTIC APPLIANCES AND LIGHTING Proceedings of the 5th International Conference EEDAL'09 16-18 June, Berlin, Germany VOLUME 1 Editors: Paolo BERTOLDI, Rita WERLE

-

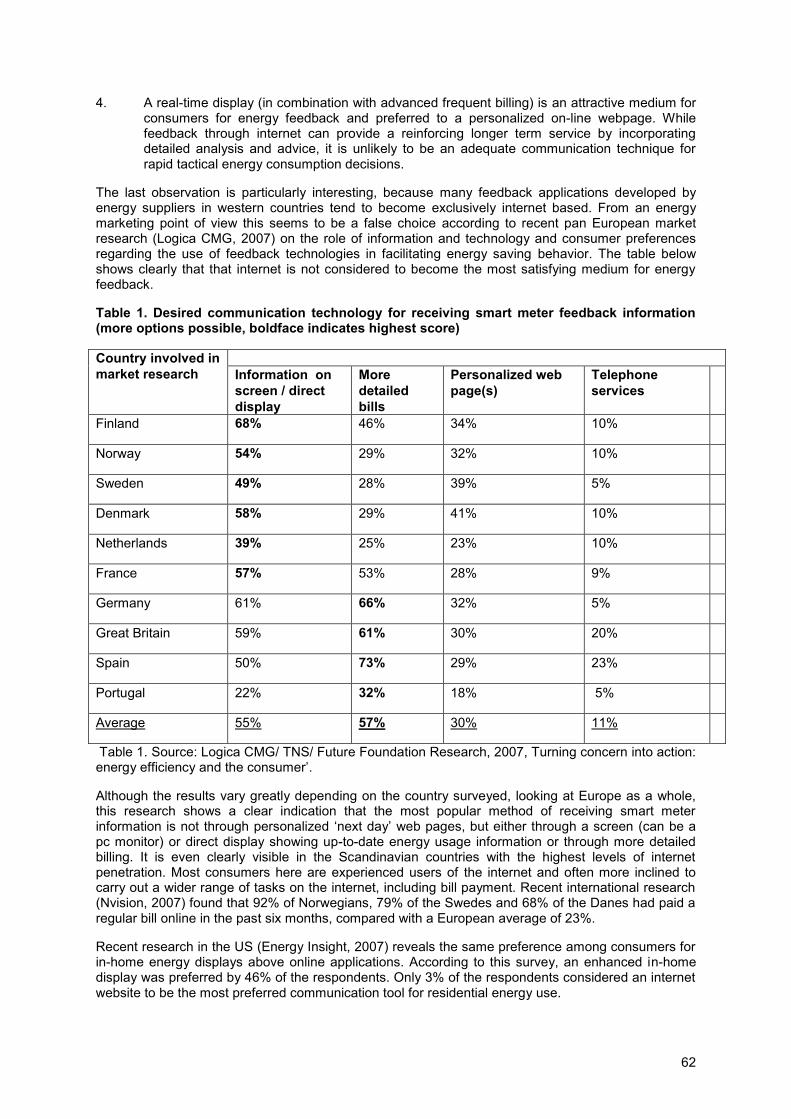

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Title (Use “Title” style here) - JRC Publications Repository

EUR 24139 EN/1 - 2010

ENERGY EFFICIENCY IN DOMESTIC APPLIANCES AND LIGHTING

Proceedings of the 5th International Conference EEDAL'09 16-18 June, Berlin, Germany

VOLUME 1

Editors: Paolo BERTOLDI, Rita WERLE

The mission of the JRC-IE is to provide support to Community policies related to both nuclear and non-nuclear energy in order to ensure sustainable, secure and efficient energy production, distribution and use. European Commission Joint Research Centre Institute for Energy Contact information Address: Via E. Fermi, 2749, I-21027 Ispra (VA), ITALY E-mail: [email protected] Tel.: +39 (0)332 78 9299 Fax: +39 (0)332 78 9992 http://ie.jrc.ec.europa.eu/ http://www.jrc.ec.europa.eu/ http://re.jrc.ec.europa.eu/energyefficiency/

Legal Notice Neither the European Commission nor any person acting on behalf of the Commission is responsible for the use which might be made of this publication.

Europe Direct is a service to help you find answers to your questions about the European Union

Freephone number (*):

00 800 6 7 8 9 10 11

(*) Certain mobile telephone operators do not allow access to 00 800 numbers or these calls may be billed.

A great deal of additional information on the European Union is available on the Internet. It can be accessed through the Europa server http://europa.eu/ JRC 56066 EUR 24139 EN/1 ISBN 978-92-79-14836-1 ISSN 1018-5593 DOI 10.2788/54535 Luxembourg: Office for Official Publications of the European Communities © European Communities, 2010 Reproduction is authorised provided the source is acknowledged Printed in Italy

ENERGY EFFICIENCY IN DOMESTIC APPLIANCES AND LIGHTING

Proceedings of the 5th International Conference EEDAL'09

16-18 June, Berlin, Germany

VOLUME 1

Editors: Paolo BERTOLDI, Rita WERLE

ii

EEDAL‘09 ProceedingsContents

VOLUME 1

Metering and Smart Appliances 1

Smart Metering – a means to promote sustainable energy consumption? Socio-technical research and development on feedback systemsSebastian Gölz, Fraunhofer-Institut für Solare Energiesysteme ISE, GermanyKonrad Götz, Jutta Deffner, Institute for social-ecological Research ISOE, Frankfurt/Main, Germany

3

‘Nice to Know’ - metering and informative feedbackEllen Christiansen, University of Southern Denmark & Aalborg University, Denmark

14

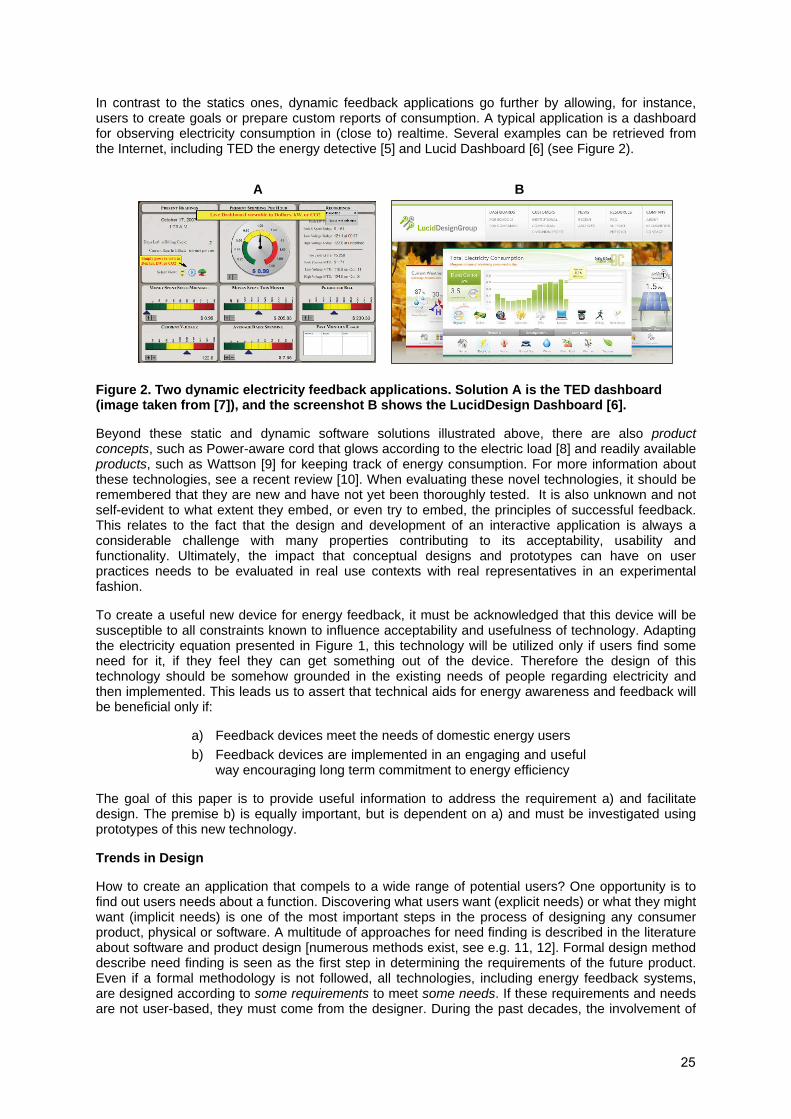

Extreme-user approach and the design of energy feedback systemsLassi A. Liikkanen, Helsinki Institute for Information Technology HIIT, Finland

23

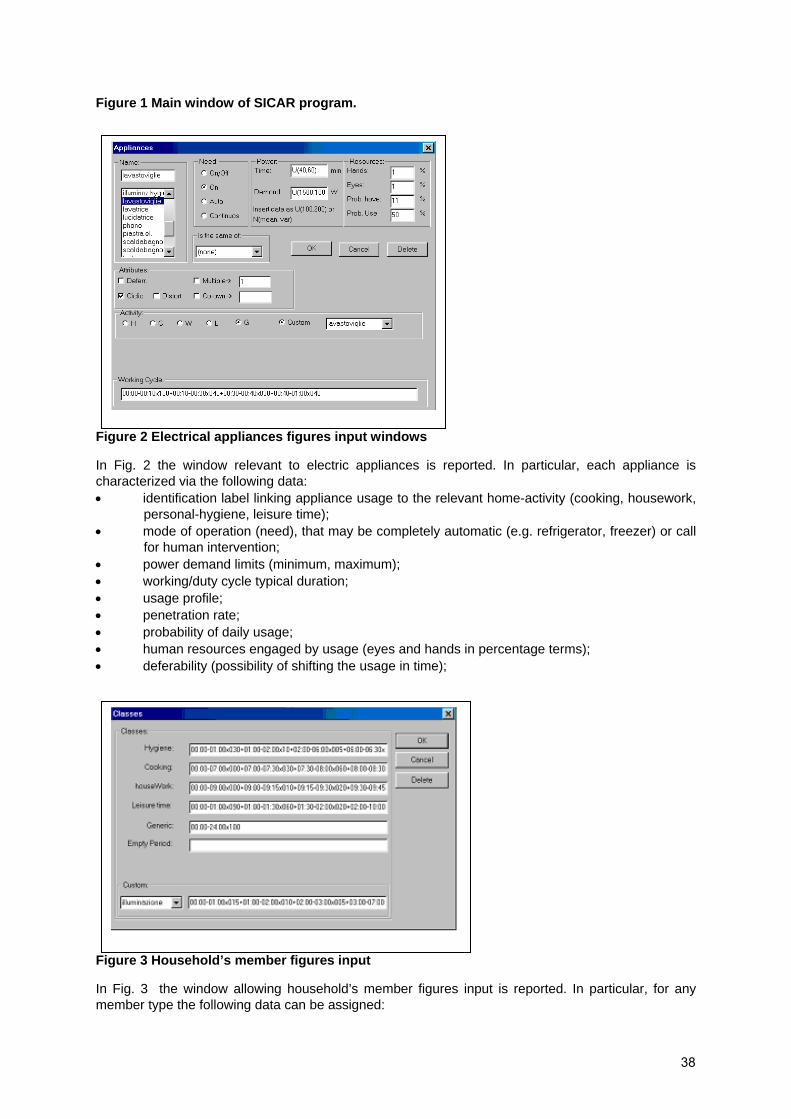

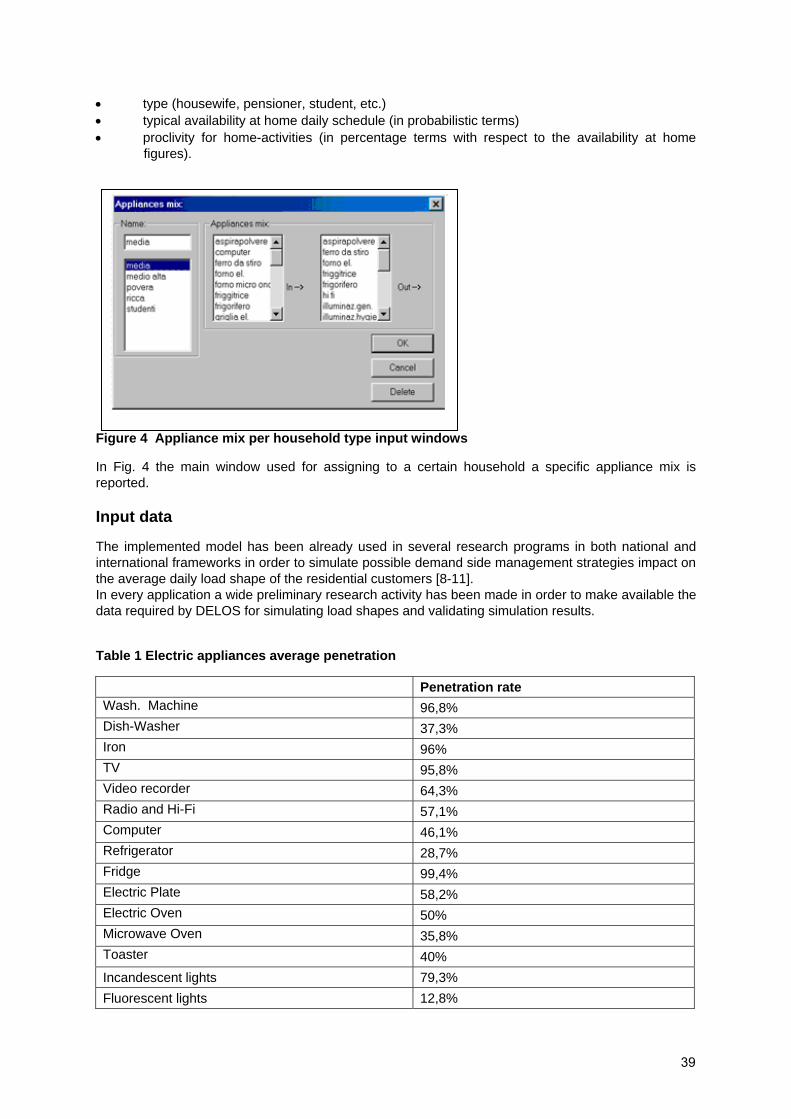

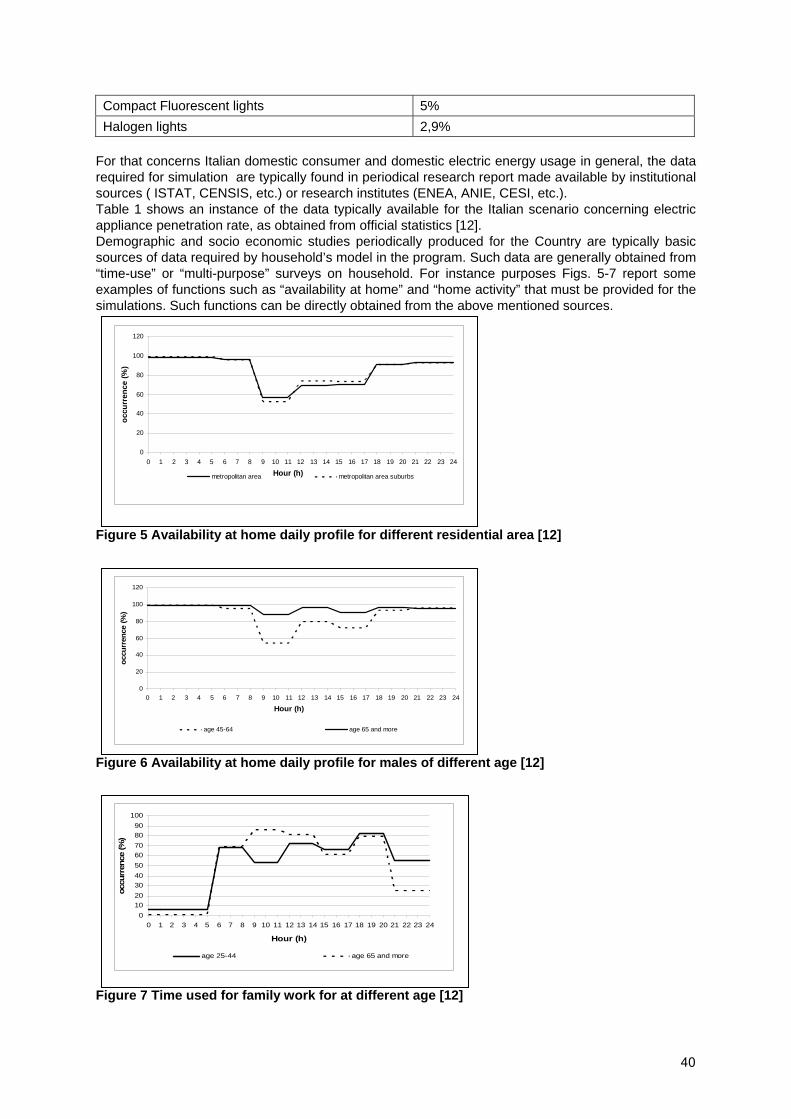

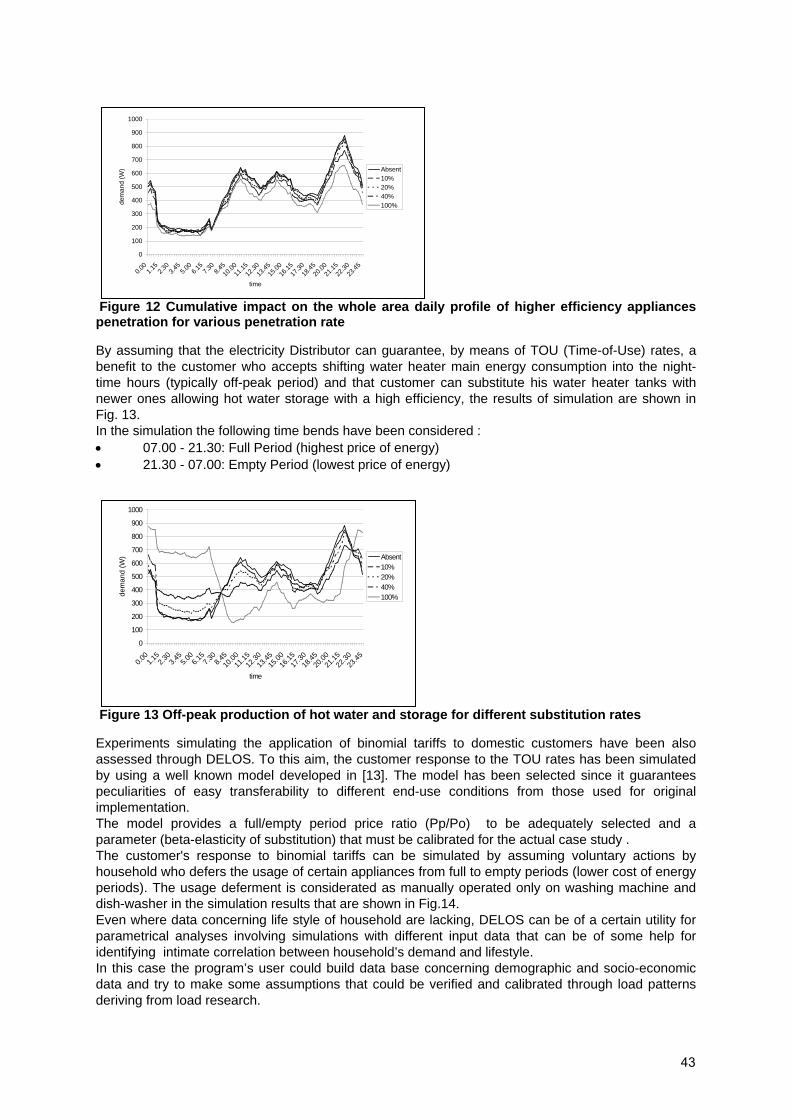

A Residential Electric Load Simulator to Support Demand Management Strategies in Competitive Electricity MarketsAlberto Prudenzi, University of L’Aquila, Italy & 2nd University of Rome “Tor Vergata”, Italy

36

PowerCentsDC Program – Demand and Conservation Effect of Pricing and Advanced FeedbackChris King, eMeter Strategic Consulting, USA

46

Encouraging public support for smart metering via appealing and enabling in-home energy feedback devicesHenk van Elburg, European Smart Metering Alliance (ESMA), United Kingdom

57

My Home – the interactive and “intelligent” way to save energyGöran Wilke, The Danish Electricity Saving Trust, DenmarkAnders Hjort Jensen, The Danish Electricity Saving Trust, Denmark

65

E-mail and SMS as a tool for electricity savings in households, report from a field experimentAnders Larsen, Institute for Society and Globalisation, Roskilde University, Denmark

78

Metering and Smart Grid 90

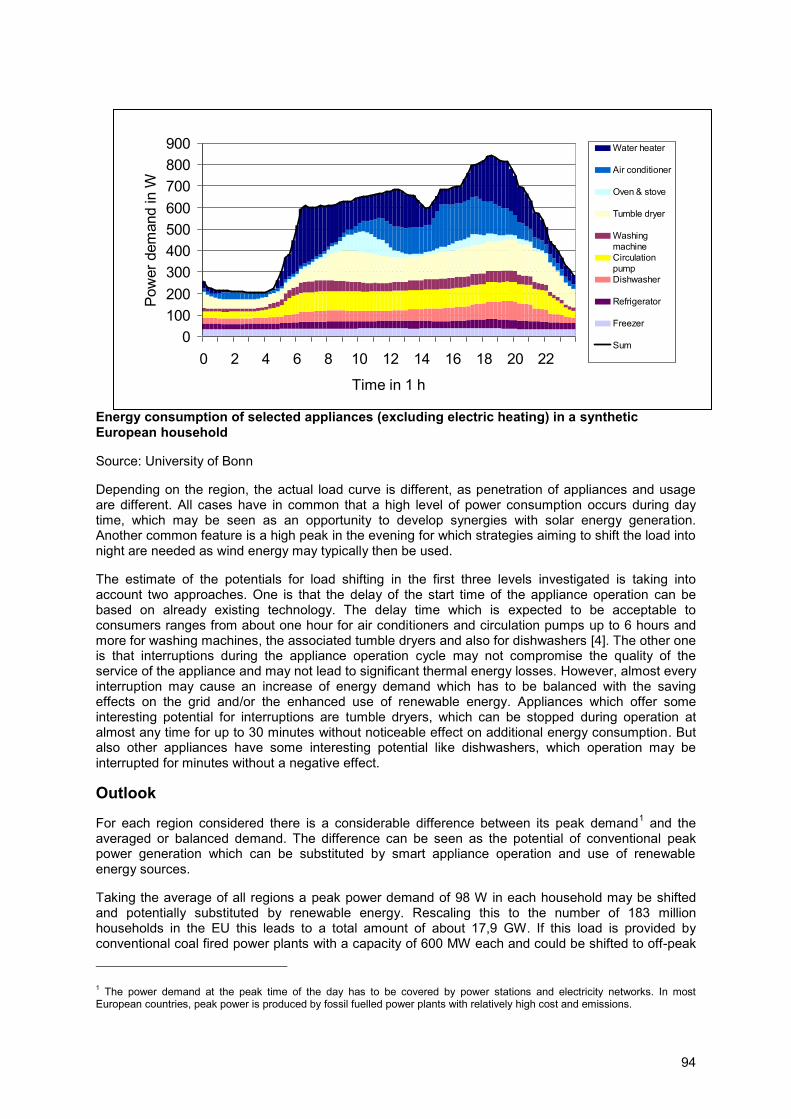

Smart use of domestic appliances in renewable energy systemsRainer Stamminger, University of Bonn, Germany

92

Simulation of high-resolution domestic electricity demand based on a building occupancy model and its applicability to the study of demand side managementMurray Thomson, Graeme Hodgson, Ian Richardson, Centre for Renewable Energy Systems Technology at Loughborough University, United Kingdom

97

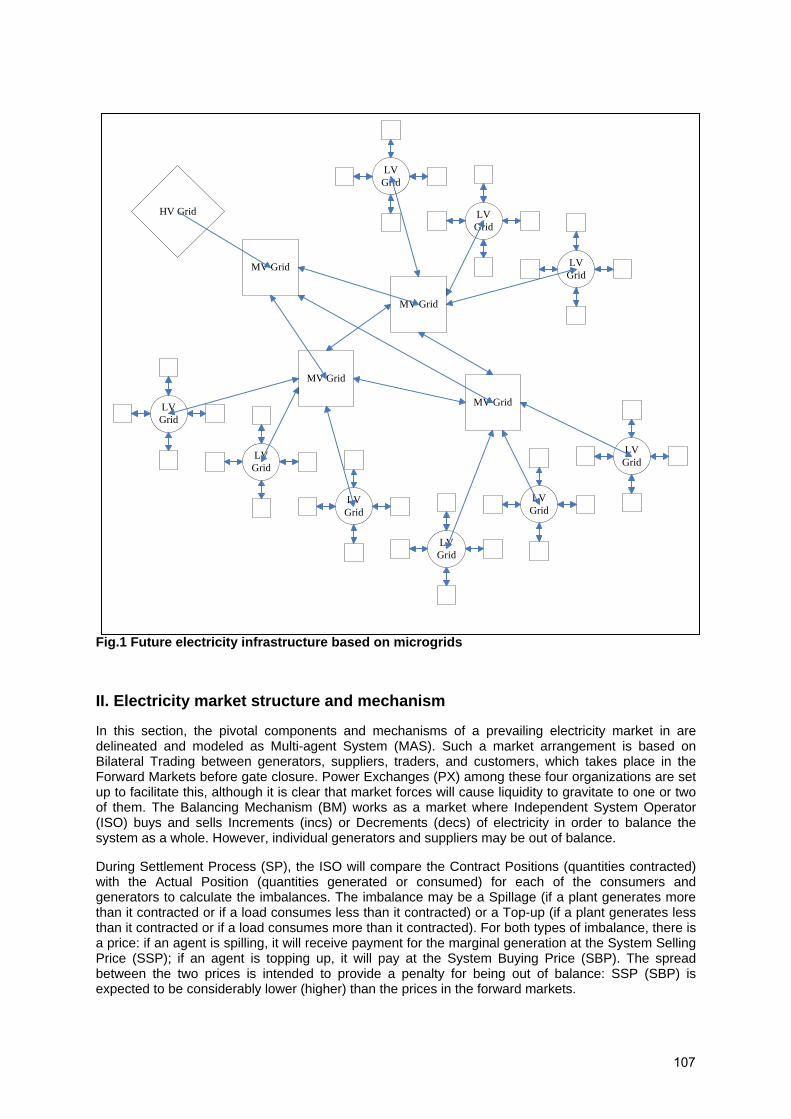

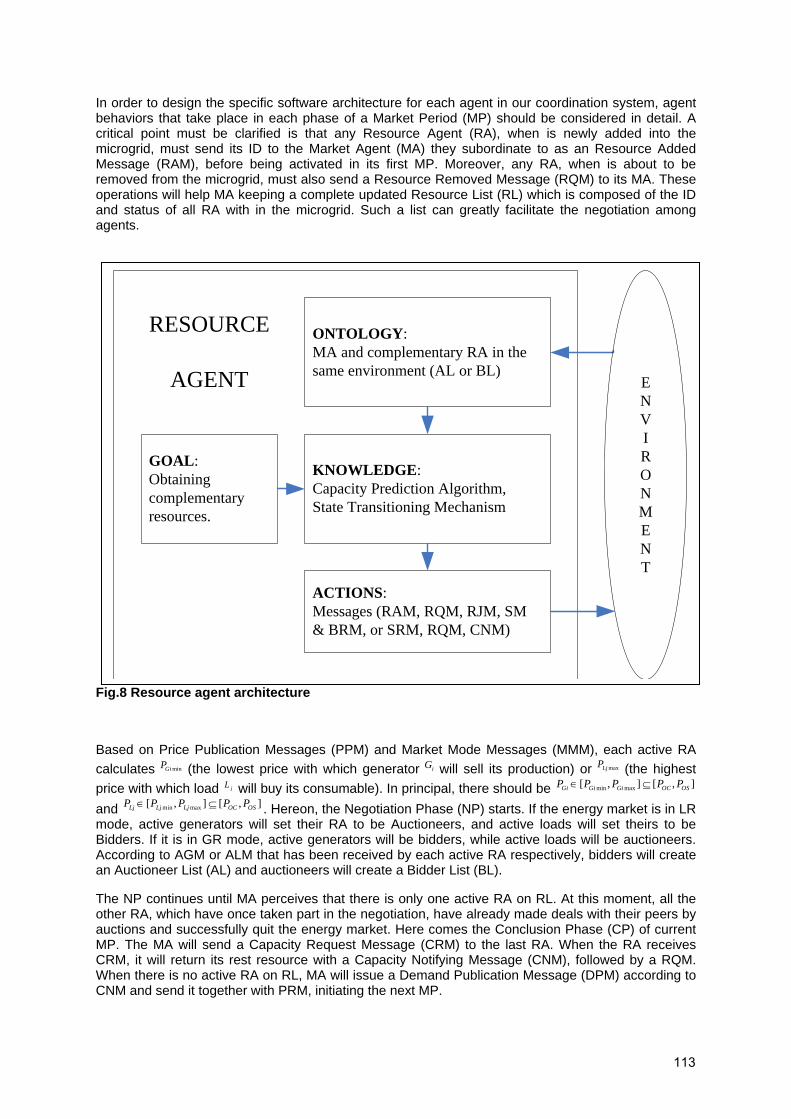

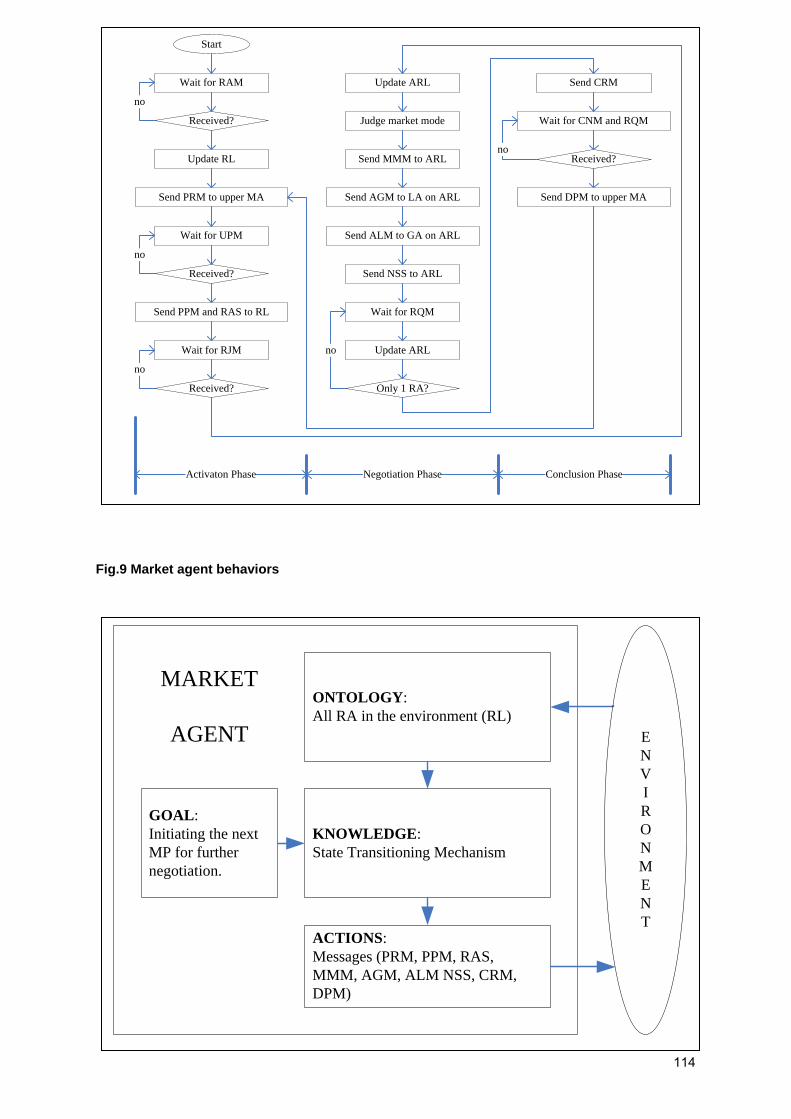

Microgrid with Agents: the DSM Mechanism of a Promising Model for Future Electricity InfrastructureRui Duan, Katholieke Universiteit Leuven, Belgium

106

How Smart Domestic Appliances Can Support the Integration of Renewable Energy in Local and National Energy SystemsChristof Timpe, Öko-Institut e.V. - Institute for Applied Ecology, GermanyChristian Möllering, enervision GmbH, Germany

117

Evaluation 129

Best Practices and Issues for Attributing Effects to Energy Efficiency and Behavioural Programs – Discussion of Net-to-Gross (NTG) and Non-Energy Benefits (NEBs)Lisa Skumatz, Skumatz Economic Research Associates, Inc. (SERA Inc.), USA

131

Domestic information, communication and entertainment (ICE) appliance monitoring: A practical perspective and implications for inter-disciplinary researchMichael Coleman, The Institute of Energy and Sustainable Development (IESD), De Montfort University, United Kingdom

142

A “Bottom Up” Model For Estimating Australian Residential Energy UseLloyd Harrington, Energy Efficient Strategies, Australia

154

How Long Do Program Savings Last? Issues in Measure Lifetimes and Retention of 166

iii

Savings and BehavioursLisa Skumatz, Skumatz Economic Research Associates, Inc. (SERA Inc.), USAMeasuring Market Transformation in U.S. Appliance and Lighting MarketsKenneth Tiedemann, BC Hydro, Canada

176

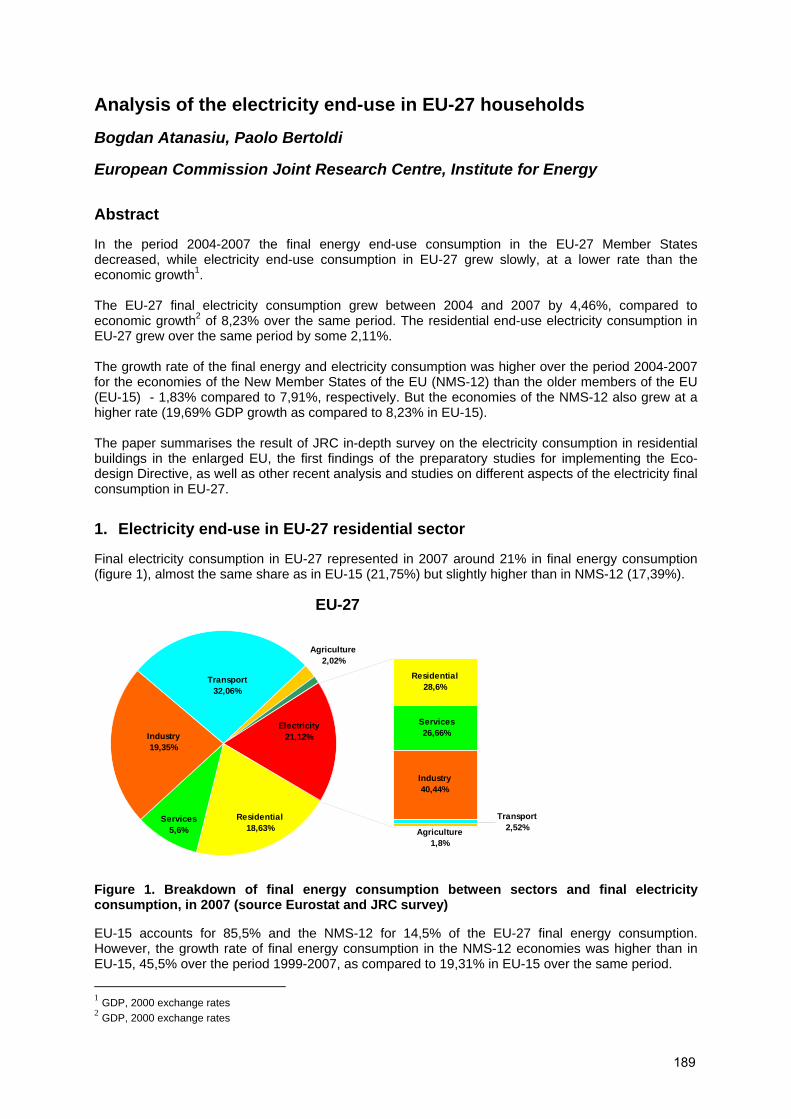

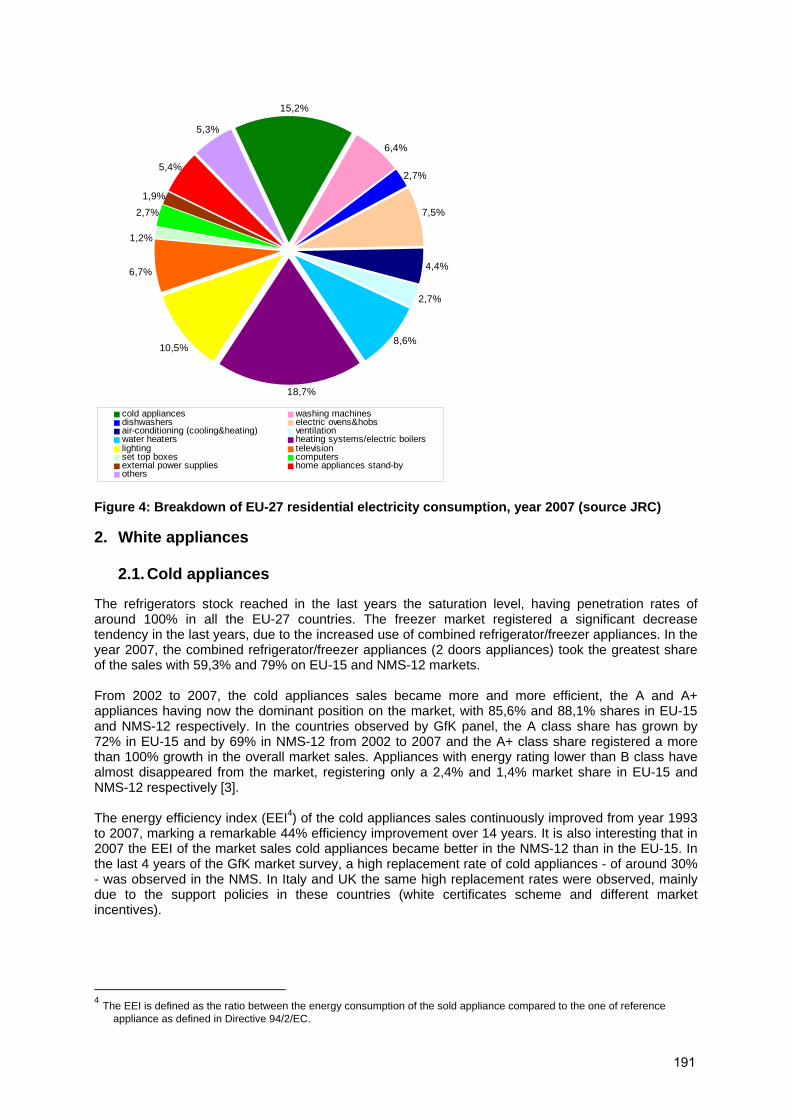

Analysis of the electricity end-use in EU-27 householdsBogdan Atanasiu, Joint Research Centre, Directorate-General of the European Commission

189

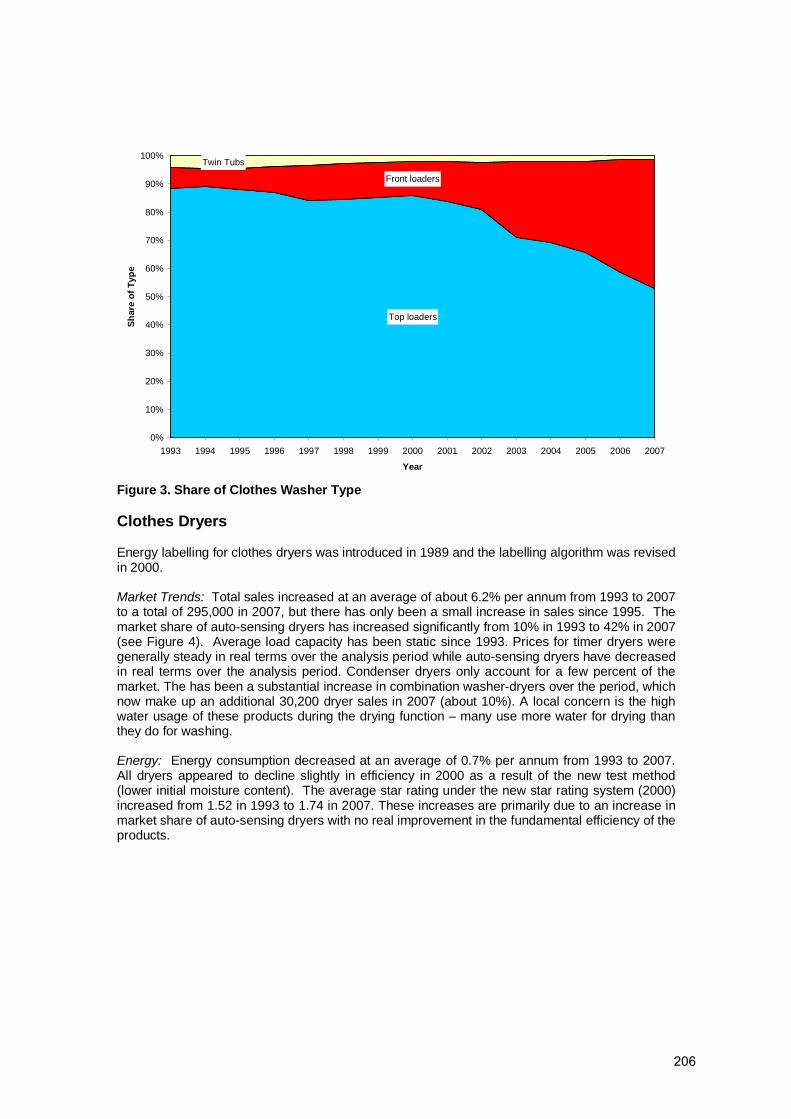

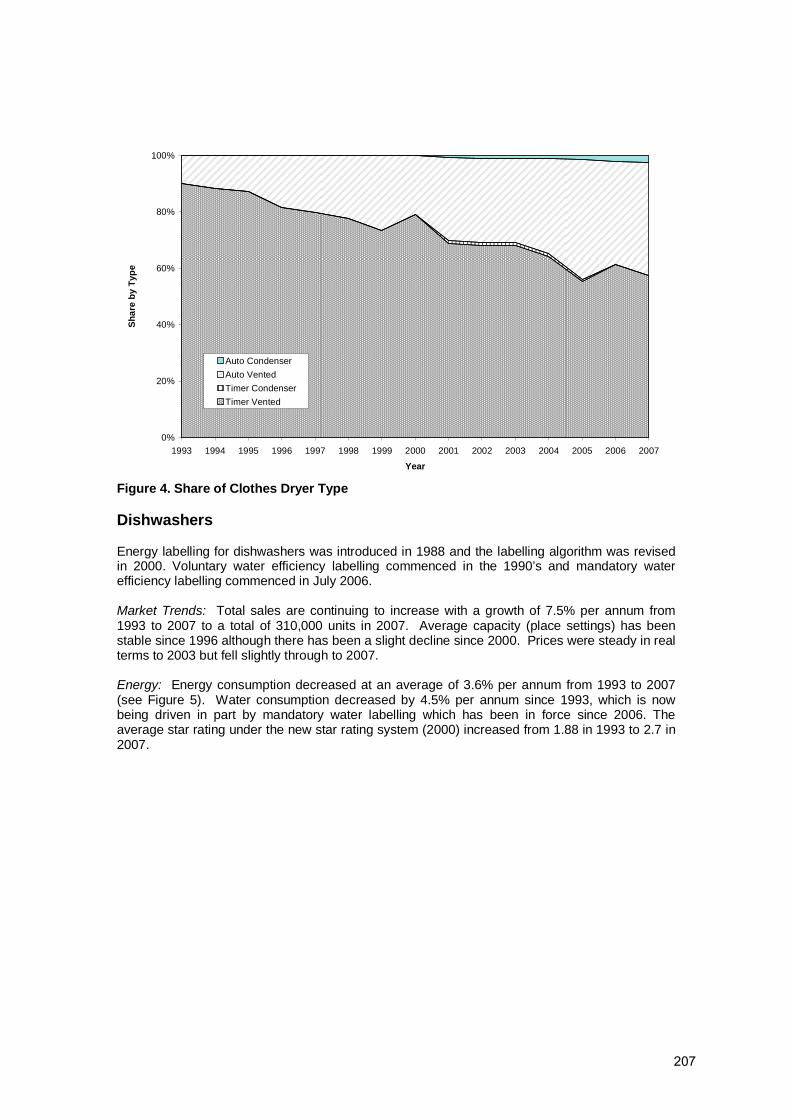

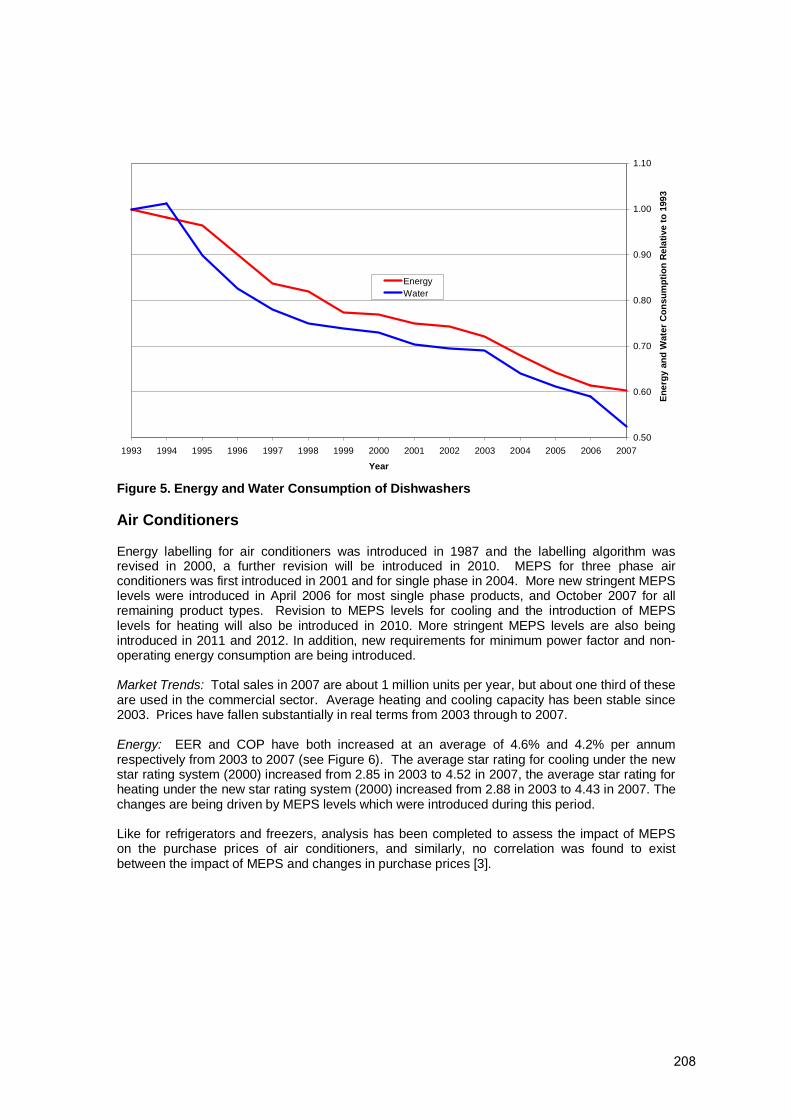

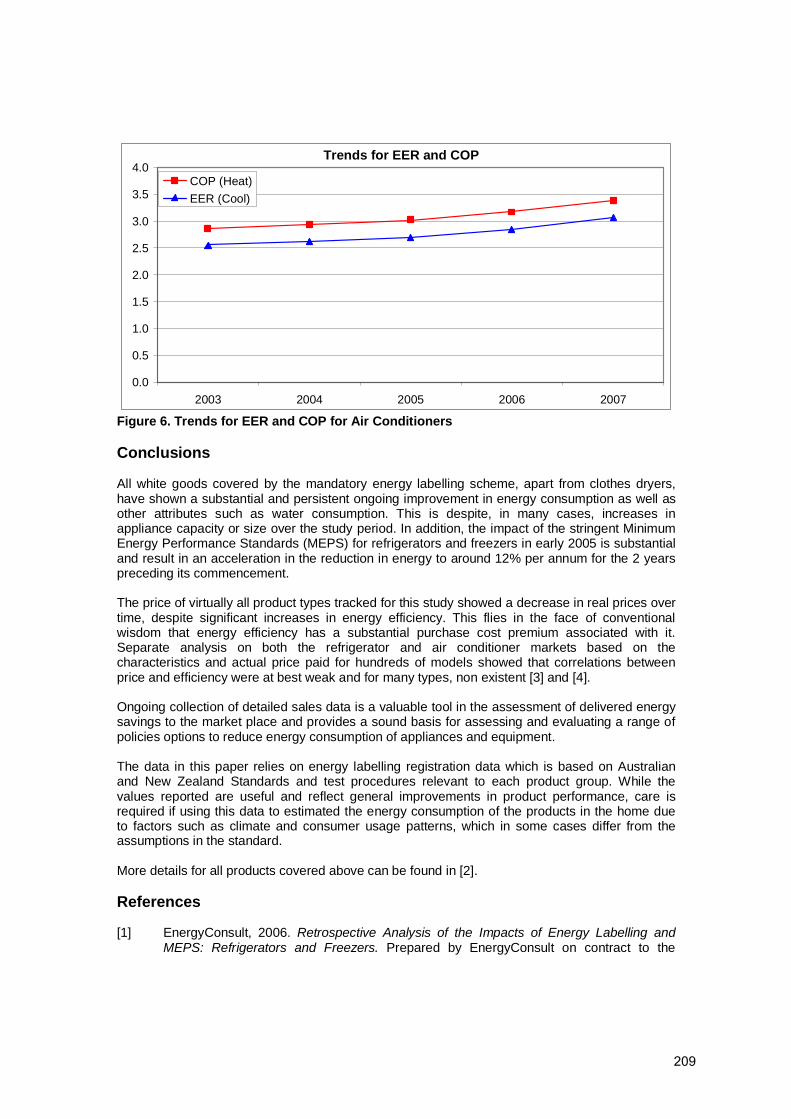

Energy consumption of whitegoods - what is improving and what is not: analysis of 15 years of data in AustraliaLloyd Harrington, Energy Efficient Strategies, Australia

202

Monitoring and evaluation of energy savings from domestic appliances for the EU’s Energy Service DirectiveStefan Thomas, Wuppertal Institut für Klima, Umwelt, Energie GmbH, Germany

211

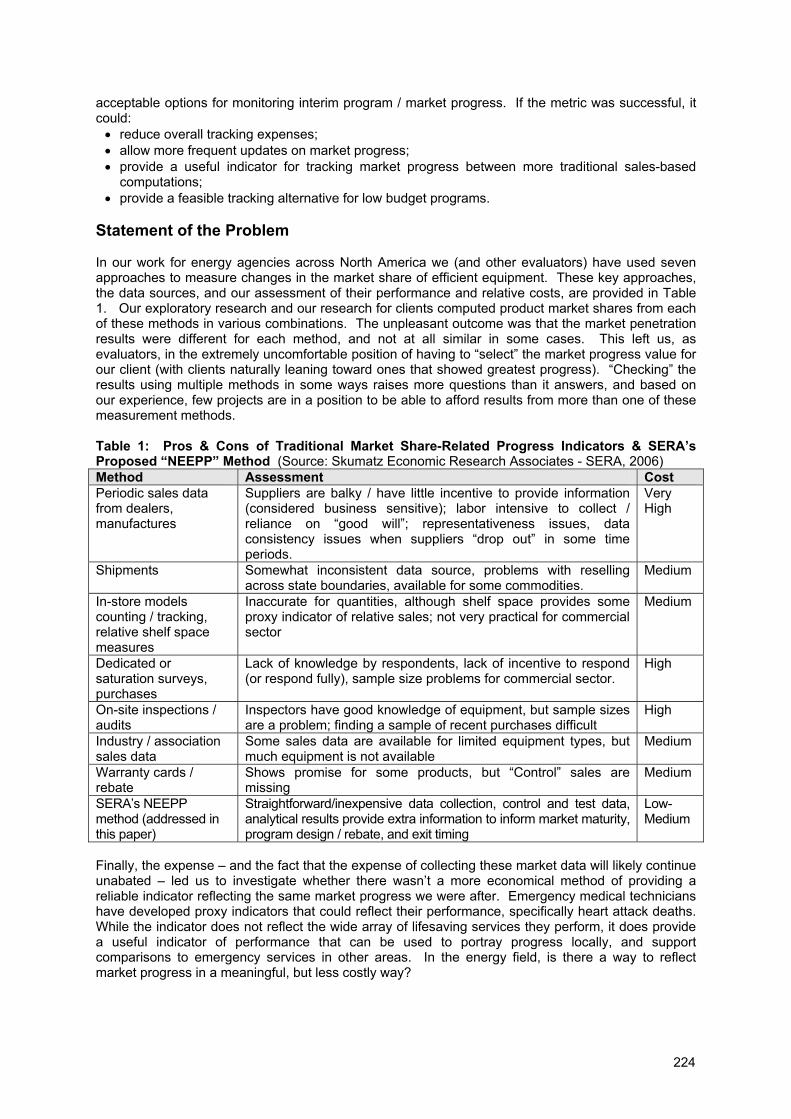

Tracking Market Progress – Alternatives to Market Share Methods to Better Identify “Market Effects” and Program Exit InformationLisa A. Skumatz, Skumatz Economic Research Associates, Inc. (SERA Inc.), USA

223

Policies and Programmes 232

An analysis of the global carbon impacts of energy-using productsChris Evans, Bilyana Chobanova, Market Transformation Programme, UK, Klinckenberg Consultants

234

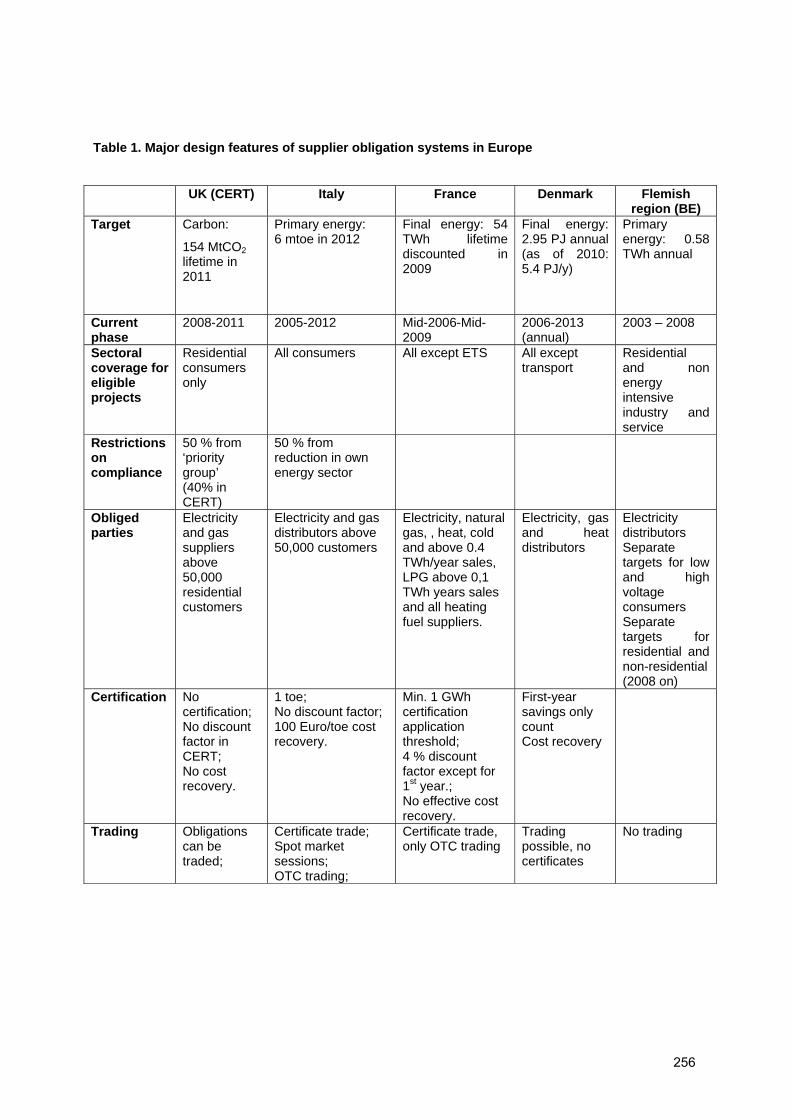

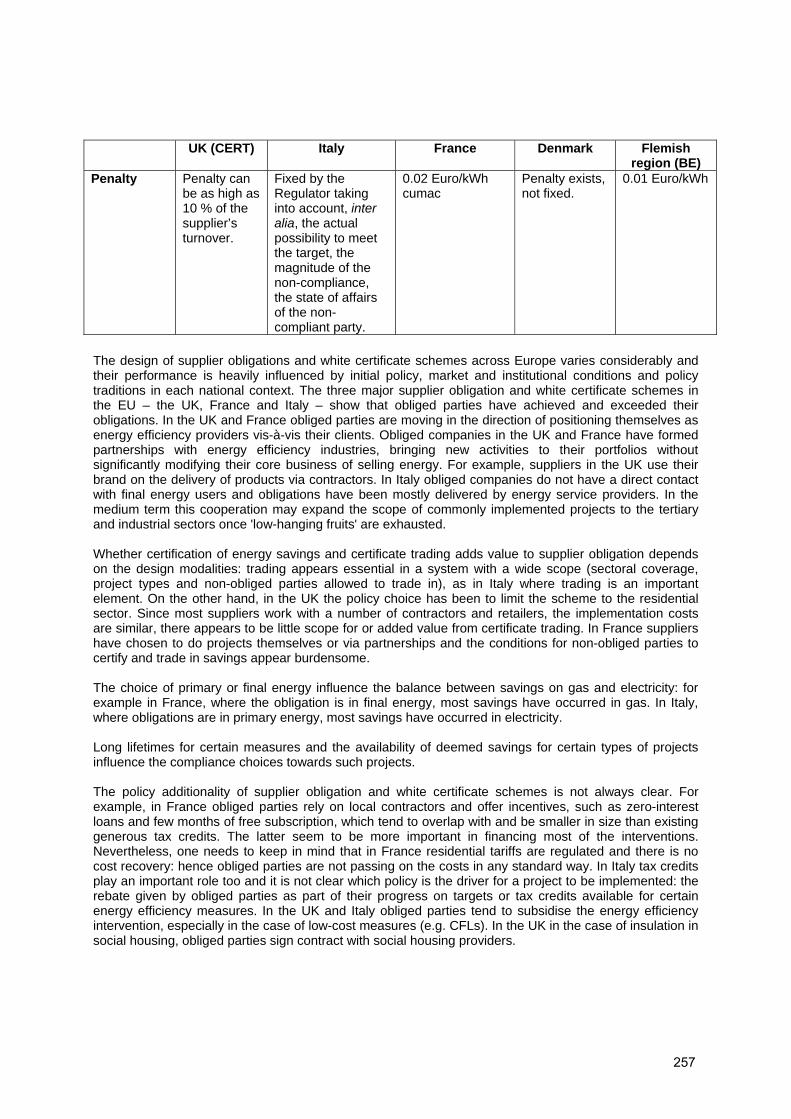

Assessment of Supplier Obligations and White Certificate Schemes in Improving Residential Energy EfficiencyPaolo Bertoldi, Joint Research Centre, Directorate-General of the European Commission

245

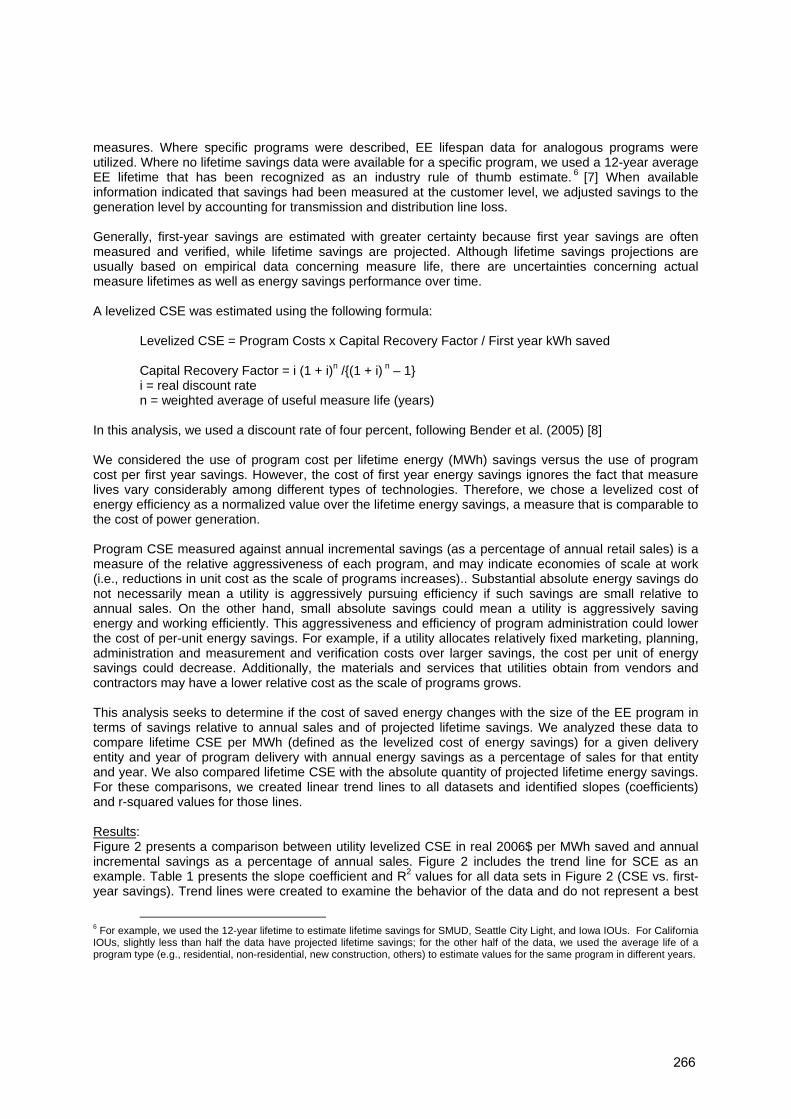

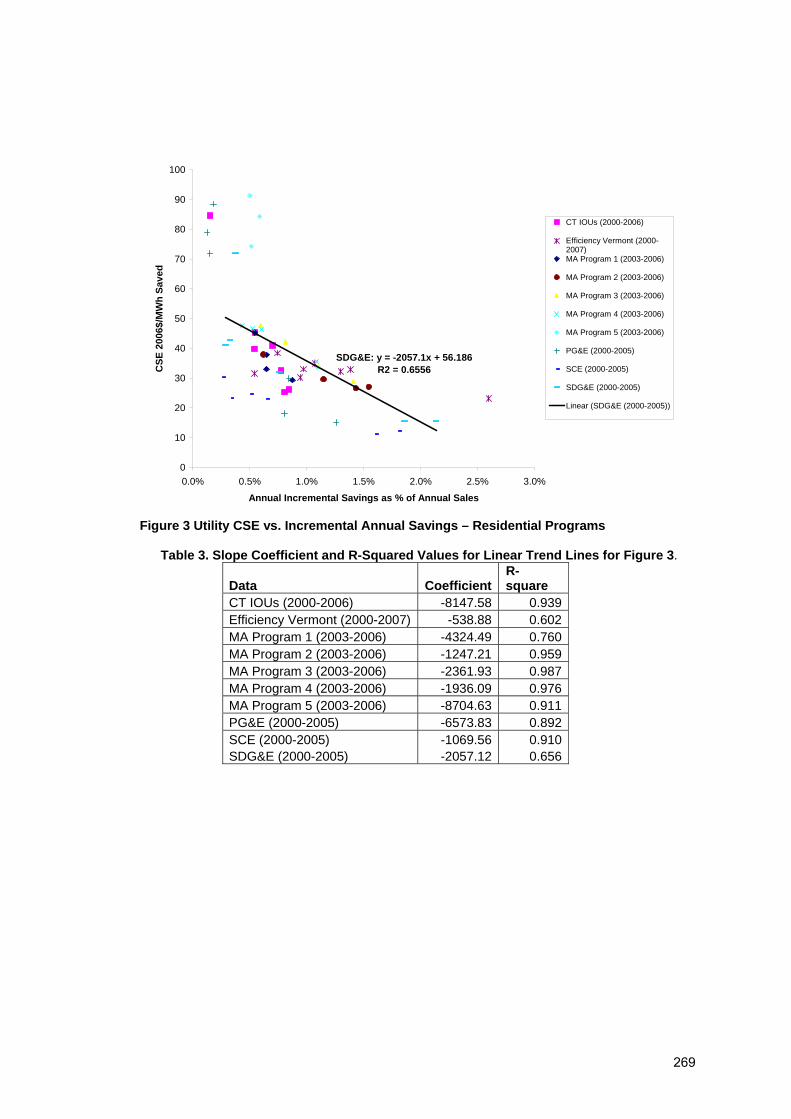

The Costs of Increasing Electricity Savings through Utility Efficiency Programs: Evidence from US ExperienceKenji Takahashi, Synapse Energy Economics, Inc., USA

262

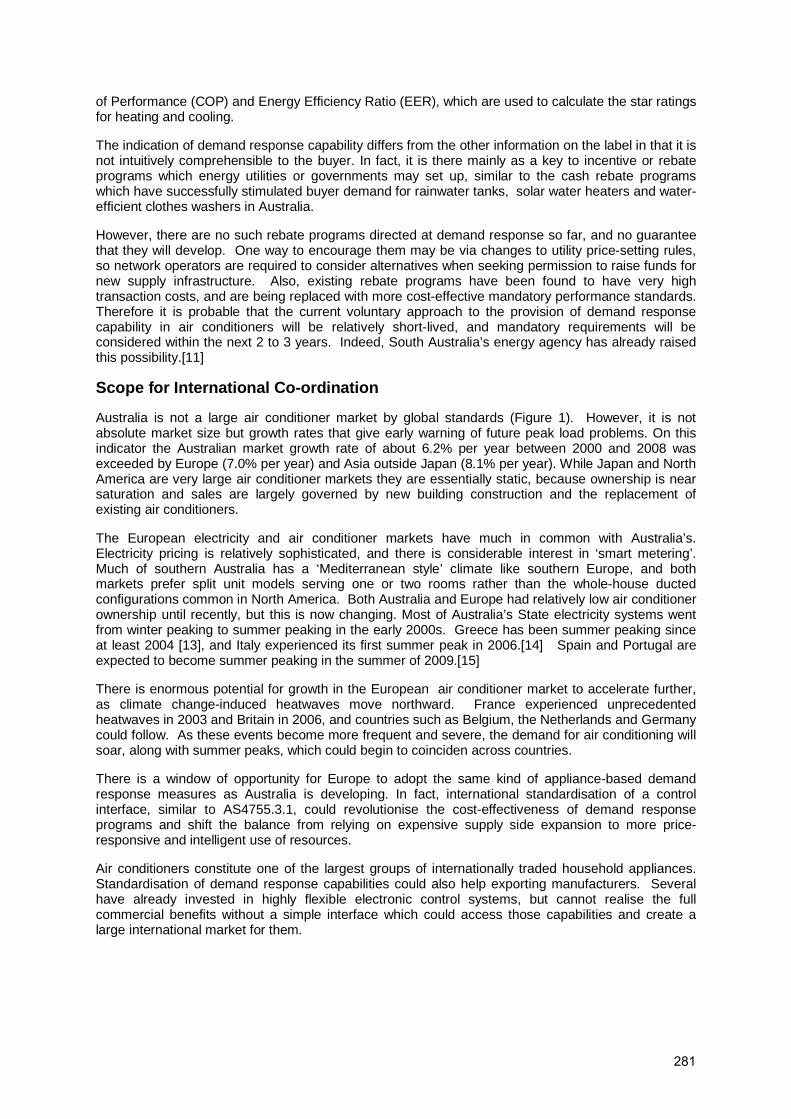

Making demand response standard for household air conditioners: the Australian experienceGeorge Wilkenfeld, George Wilkenfeld and Associates, Australia

274

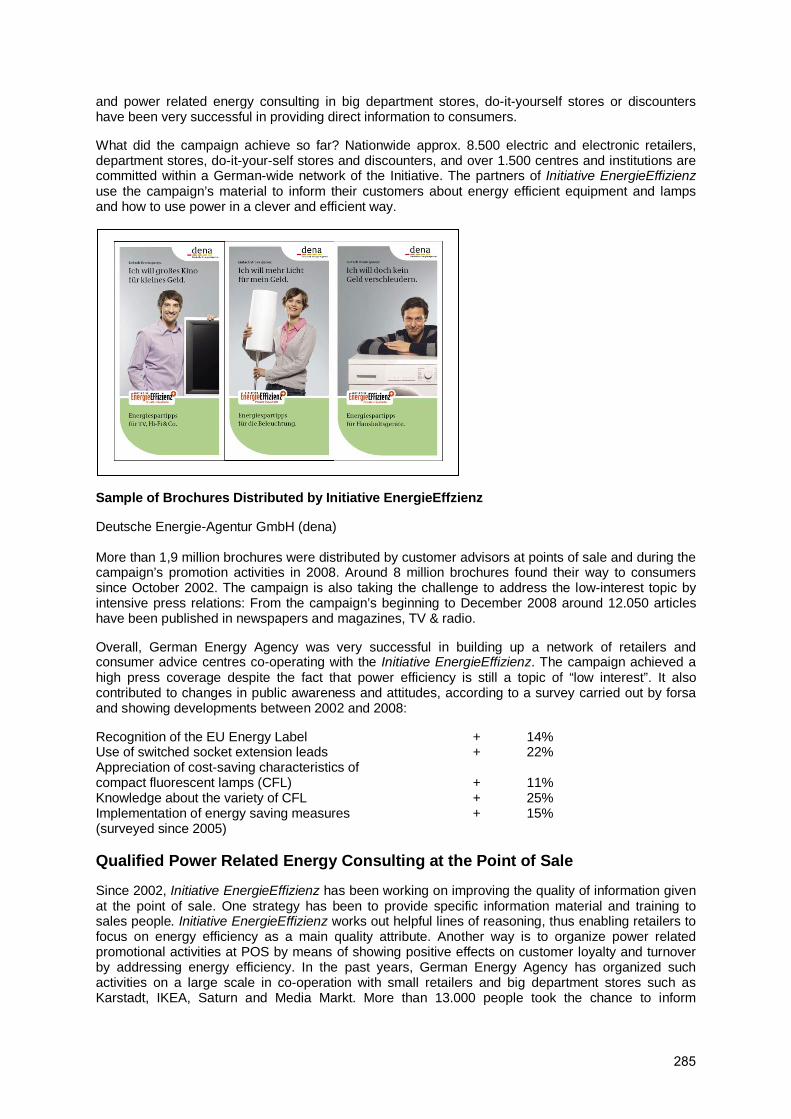

Standardization of Power Related Energy ConsultingMonika Löber, Deutsche Energie-Agentur GmbH (dena) – German Energy Agency, Germany

284

Working with retailers to push beyond EuP compliance: Some different approaches used, and options for international strengtheningJeremy Tait, Tait Consulting Limited, United Kingdom

290

IEA Mapping and Benchmarking Annex: Informing Sustainable Product Policy Decision MakingDavide Minotti, Defra & Market Transformation Programme UK, United Kingdom

302

Raising energy efficiency through the Intelligent Energy Europe programme: first results from ten projects on domestic appliancesChristophe Coudun, Executive Agency for Competitiveness and Innovation (EACI), EU

310

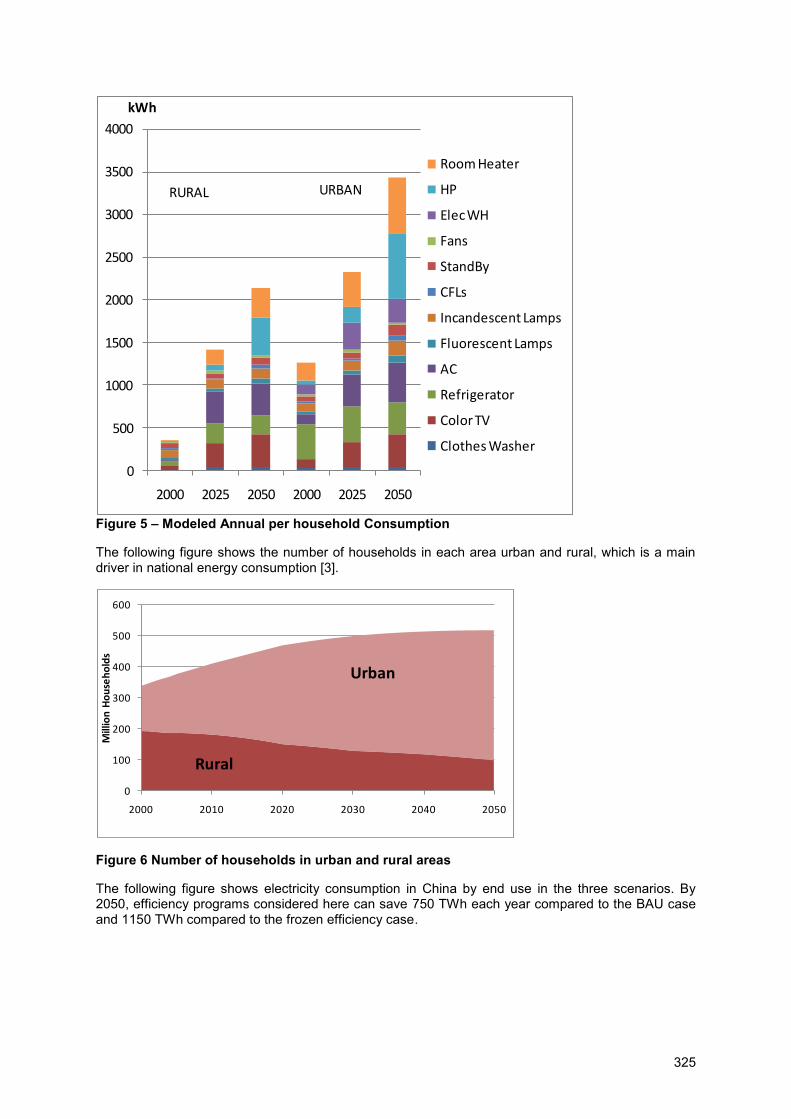

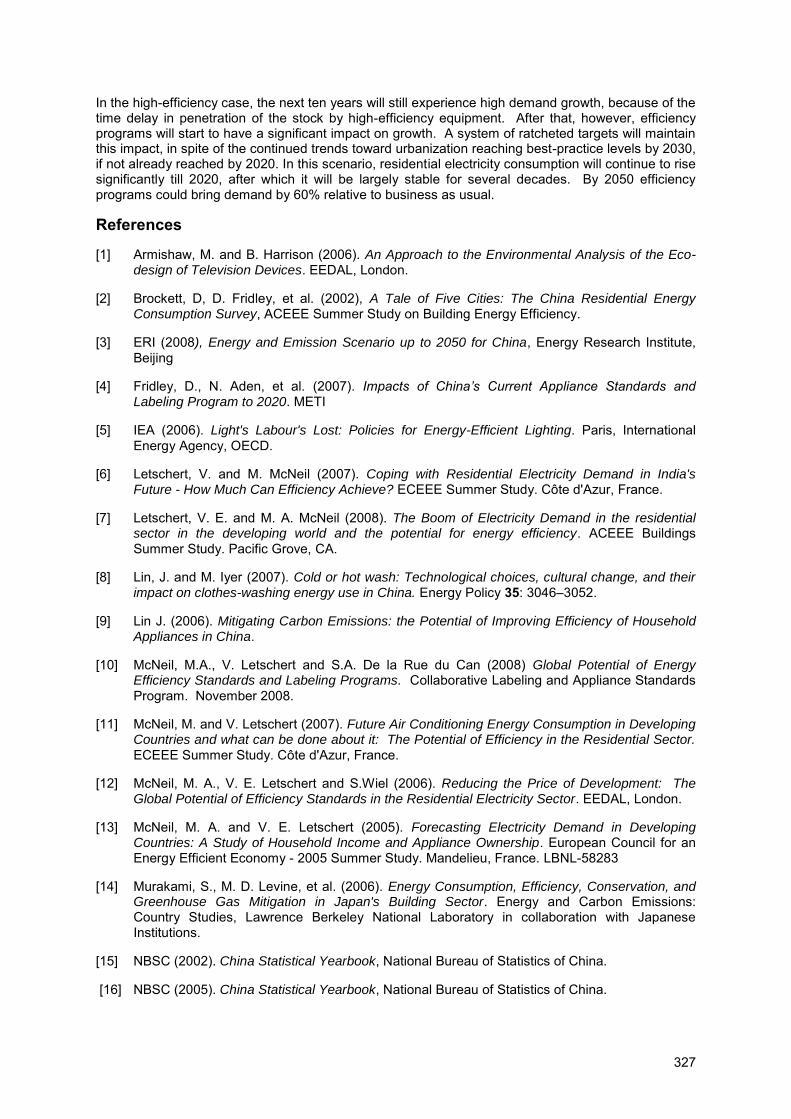

Residential Electricity Demand in China – Can Efficiency Reverse the Growth?Virginie E. Letschert, Ernest Orlando Lawrence Berkeley National Laboratory, USA

318

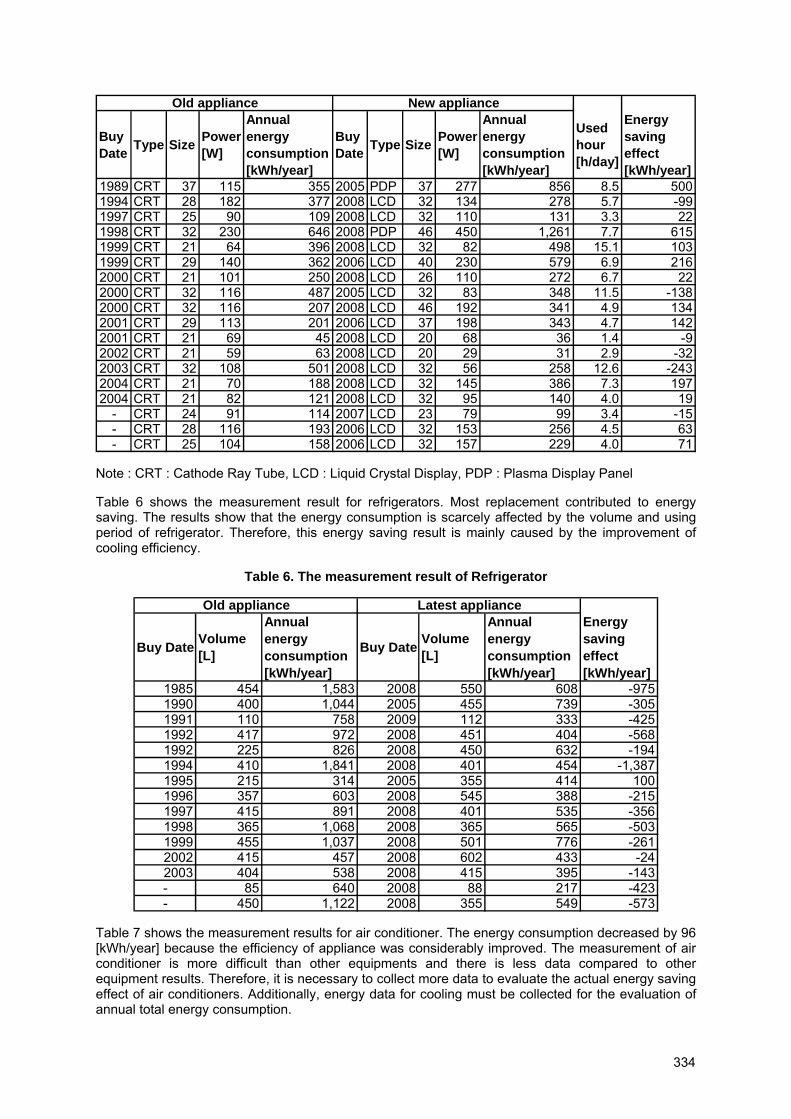

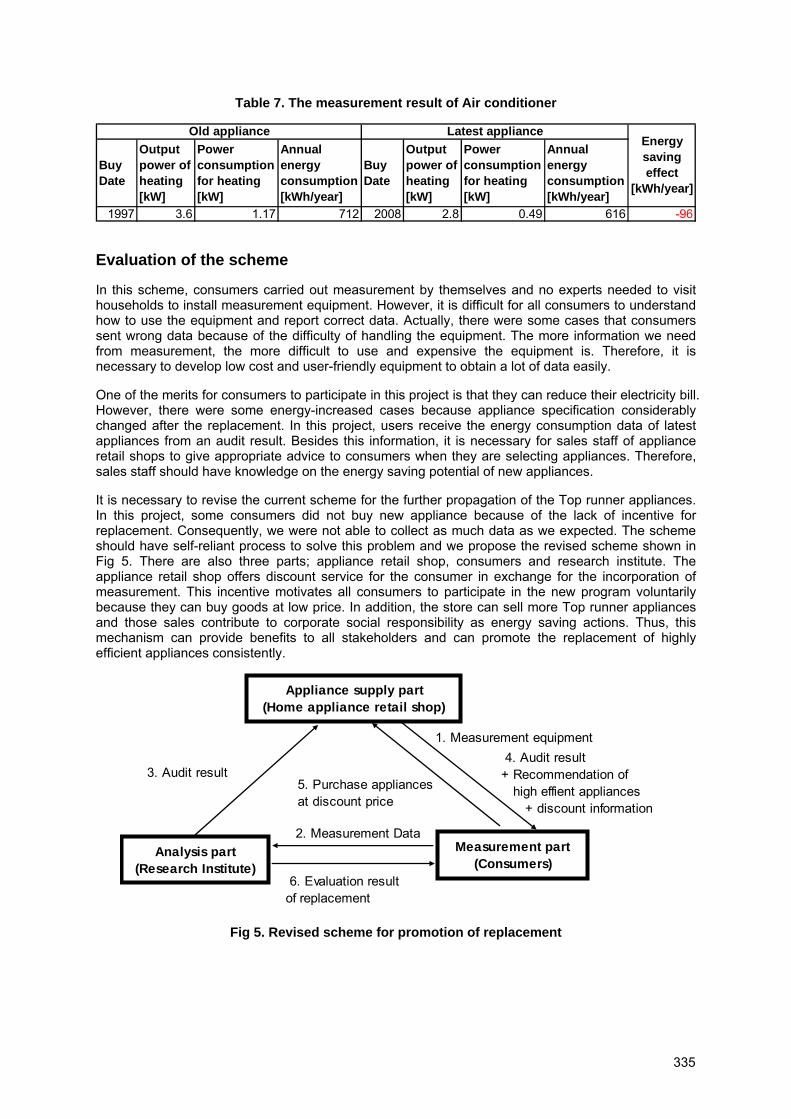

Demonstration of the new promotion scheme for high-efficiency home appliances and evaluation of its energy saving effectShinichi Kishida, Jyukankyo Research Institute, Japan

329

Indicator-Benchmark-System: A cost-effective and market-based method for quantitative verification of energy efficiency improvementsDr. Jan Witt, Jörg Zöllner, HEA – Fachgemeinschaft für Energieeffizienz e.V. – Berlin, Germany

337

National campaigns transforming the marketGunnar Pautzke, CECED (European Committee of Domestic Equipment Manufacturers), Belgium

343

iv

Replacing outdated household appliances saves energy and improves performance –A national initiativeClaudia Oberascher, HEA – Fachgemeinschaft für effiziente Energieanwendung e.V., Germany

350

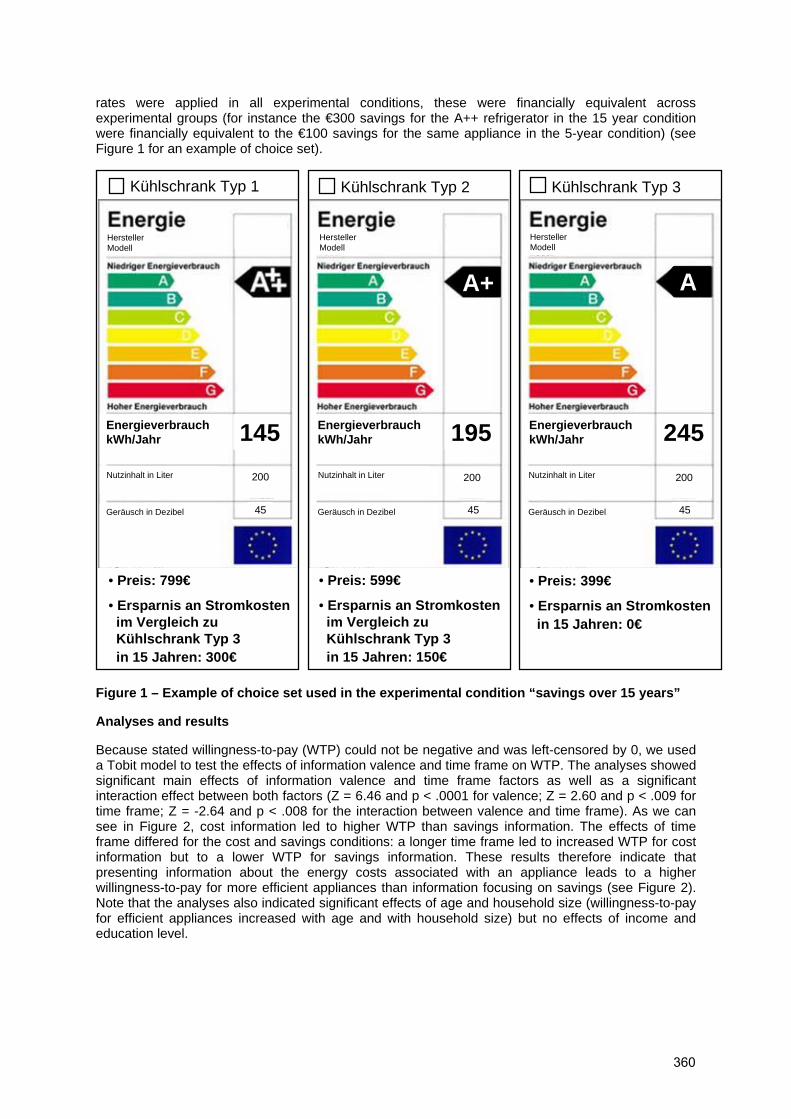

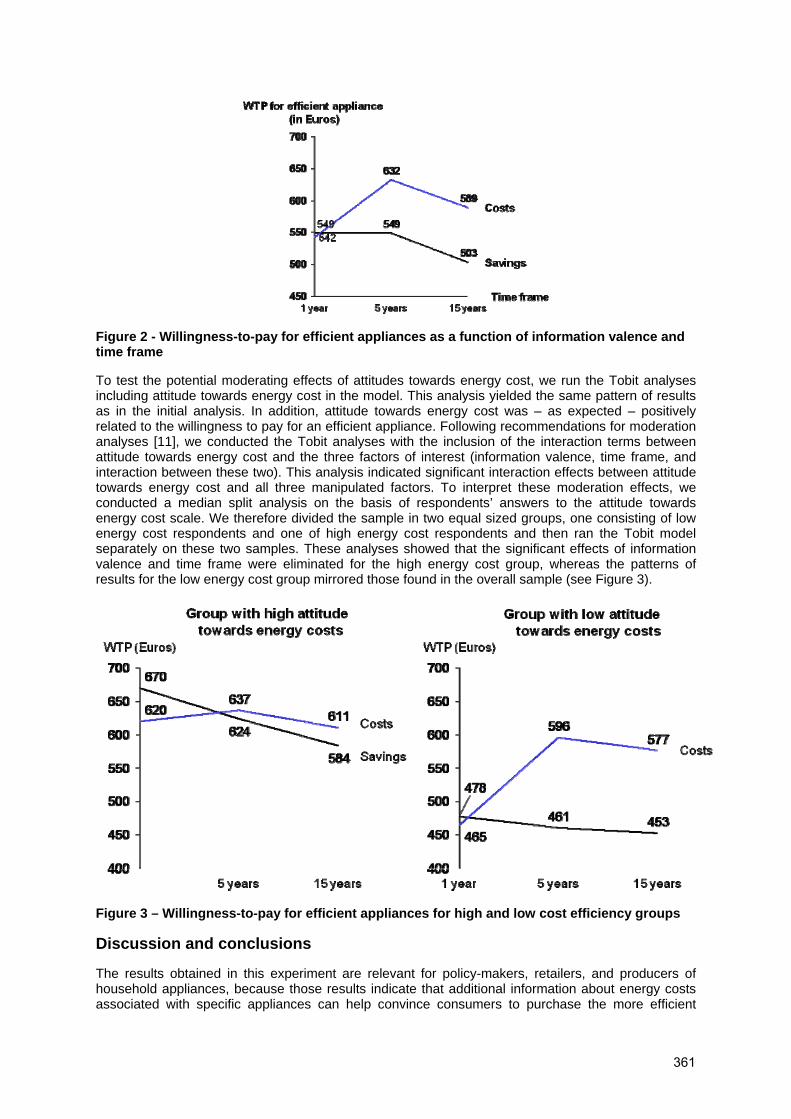

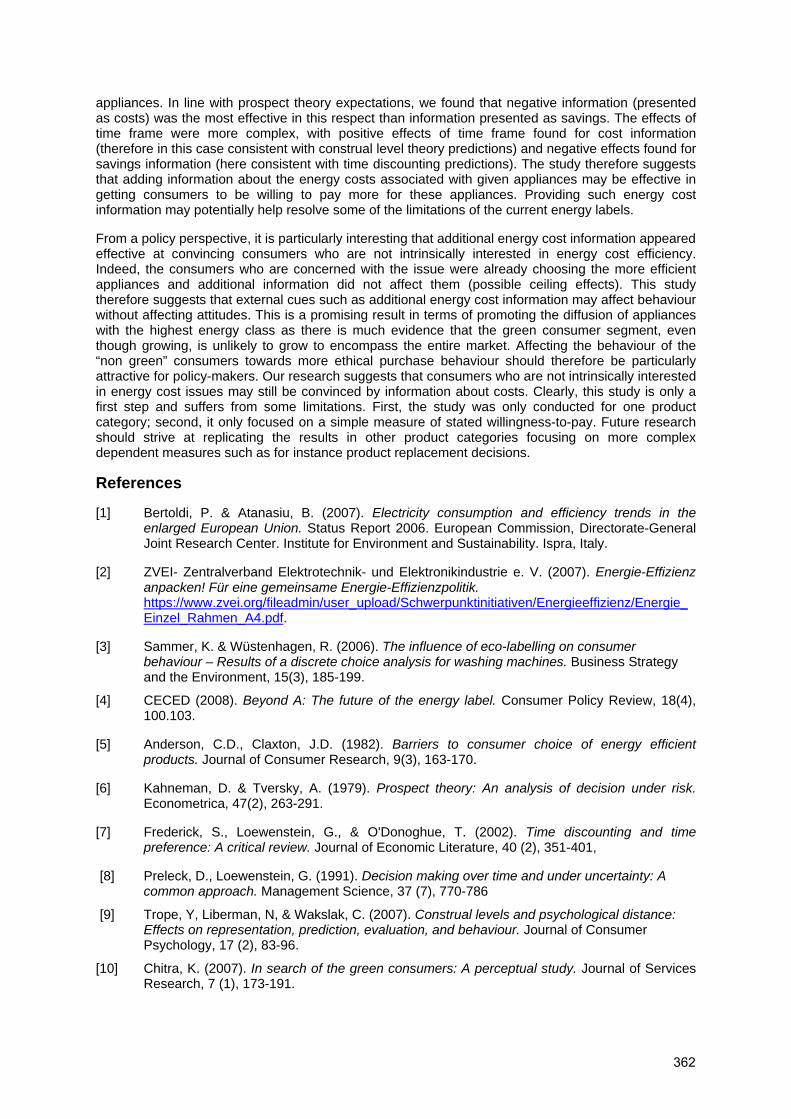

Effective presentation of energy cost information in conjunction with EU-energy labels: An experimental study with refrigerating appliances in GermanyCorinne Faure, Goethe-Universität Frankfurt, Germany

357

Refrigerator Replacement Programs in BrazilGilberto De Martino Jannuzzi, University of Campinas – UNICAMP, and International Energy Initiative – IEI, Latin American Office, Brazil

364

Household Energy Efficiency – always the bridesmaid?Jo Grugeon, Rachel Ollivier, Lara Olsen, Cool nrg International, Australia

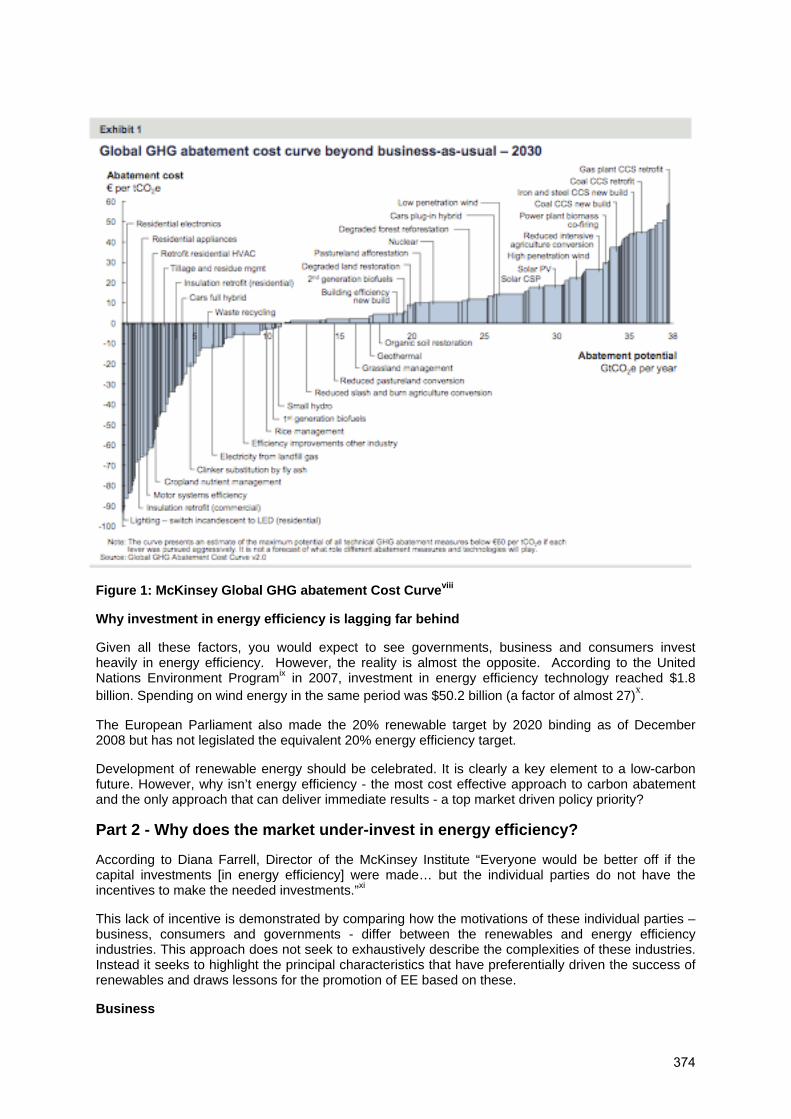

373

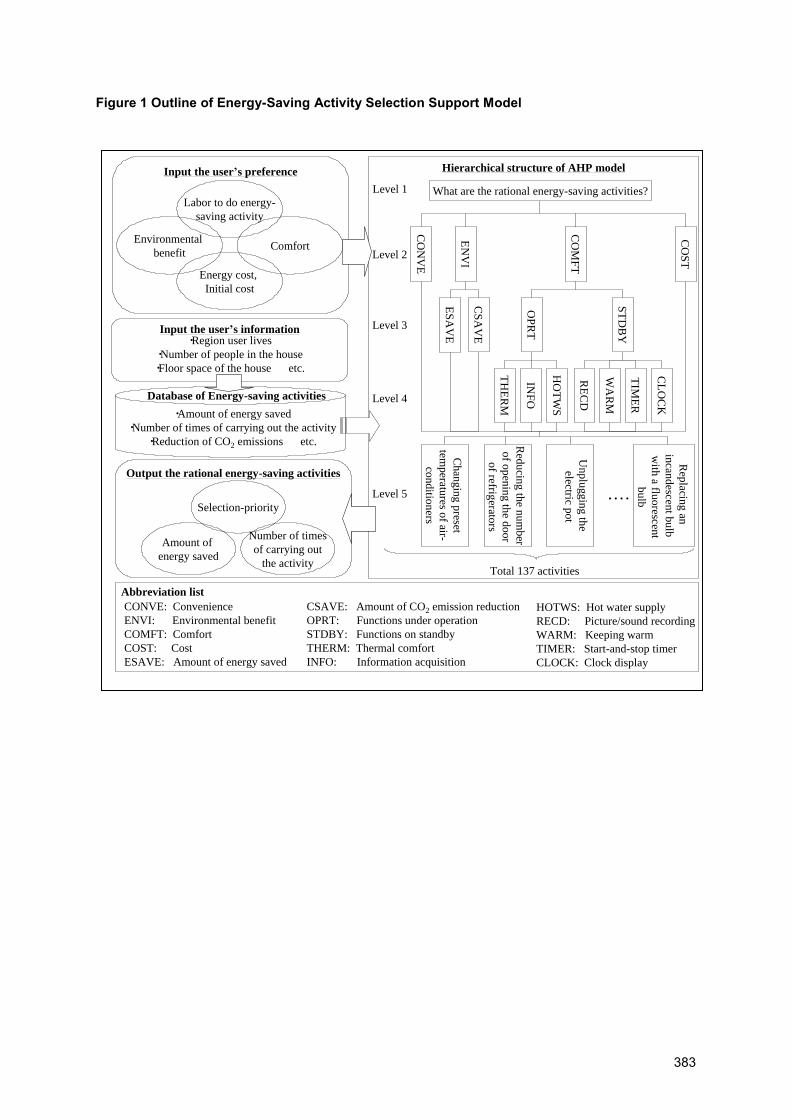

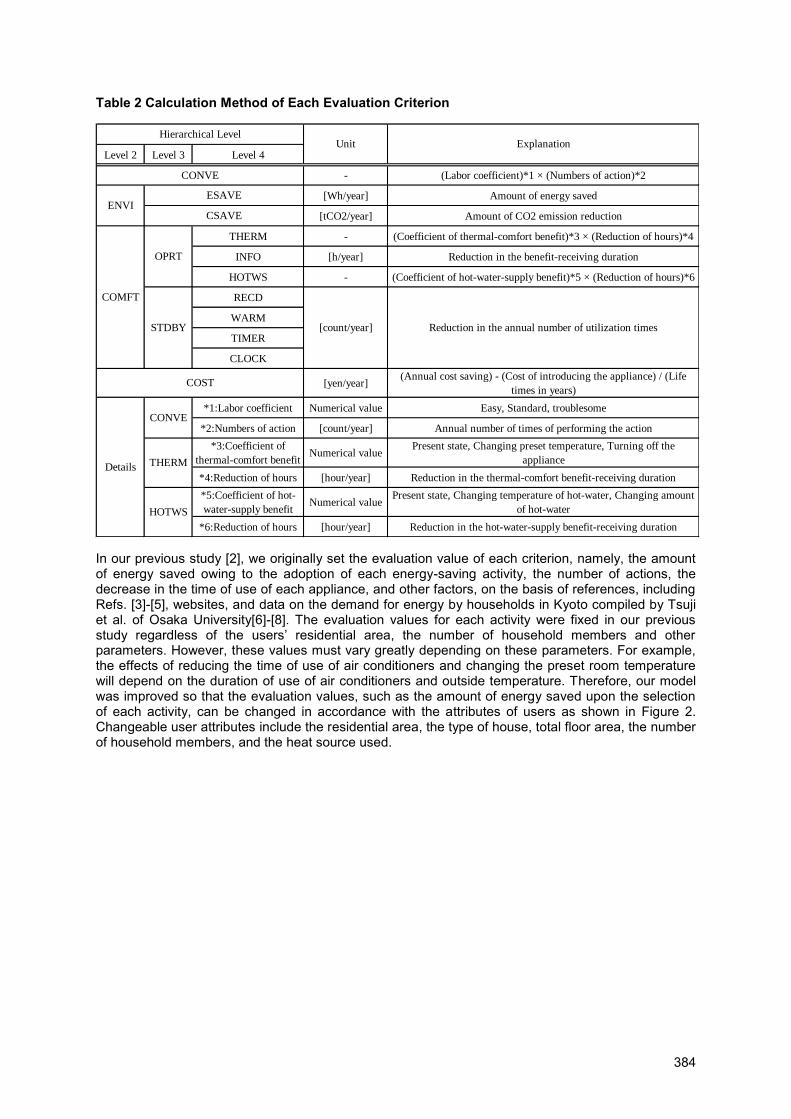

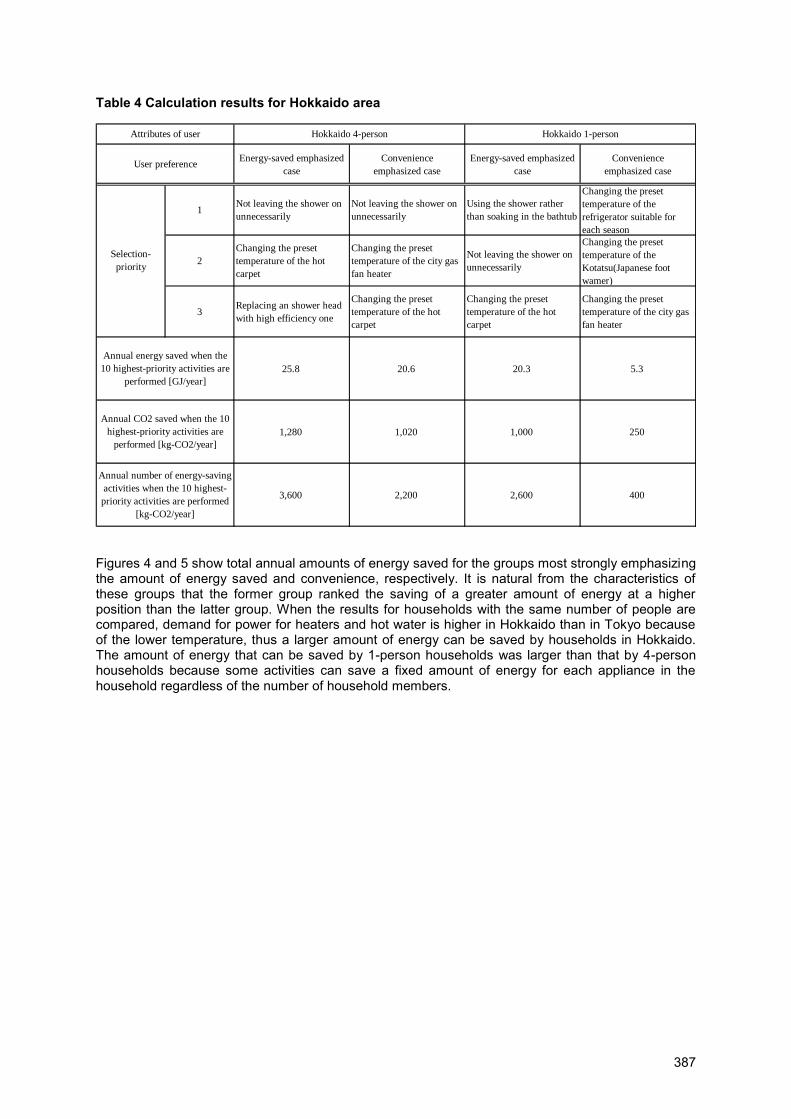

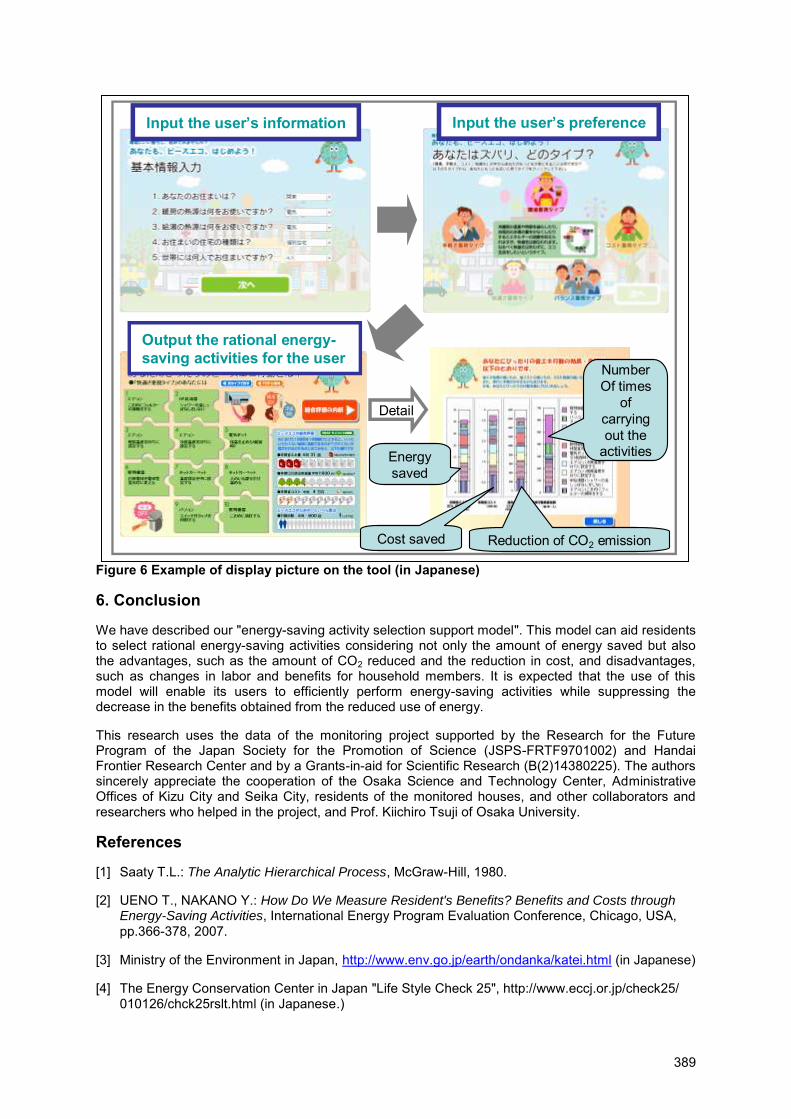

How Can We Rank Energy-Saving Activities? -Development of an Energy-Saving Activity Selection Tool Considering Residents Preferences-Tsuyoshi Ueno and Yukio Nakano, Central Research Institute of Electric Power Industry, Japan

381

Policies and Behaviour 391

What's driving sustainable energy consumption - a survey of the empirical literatureKlaus Rennings, Centre for European Economic Research (ZEW GmbH), Germany

393

Analysis of the Hungarian residential energy consumption and influence of the end-user behaviour on energy consumption patternsViktoryia Novikava, Center for Climate Change and Sustainable Energy Policy (3CSEP), Central European University, Hungary

410

The Impact of Price on the Residential Demand for Electricity, Natural Gas and WaterLarry Dale, Lawrence Berkeley National Laboratory, USA

422

VOLUME 2

Monitoring 436

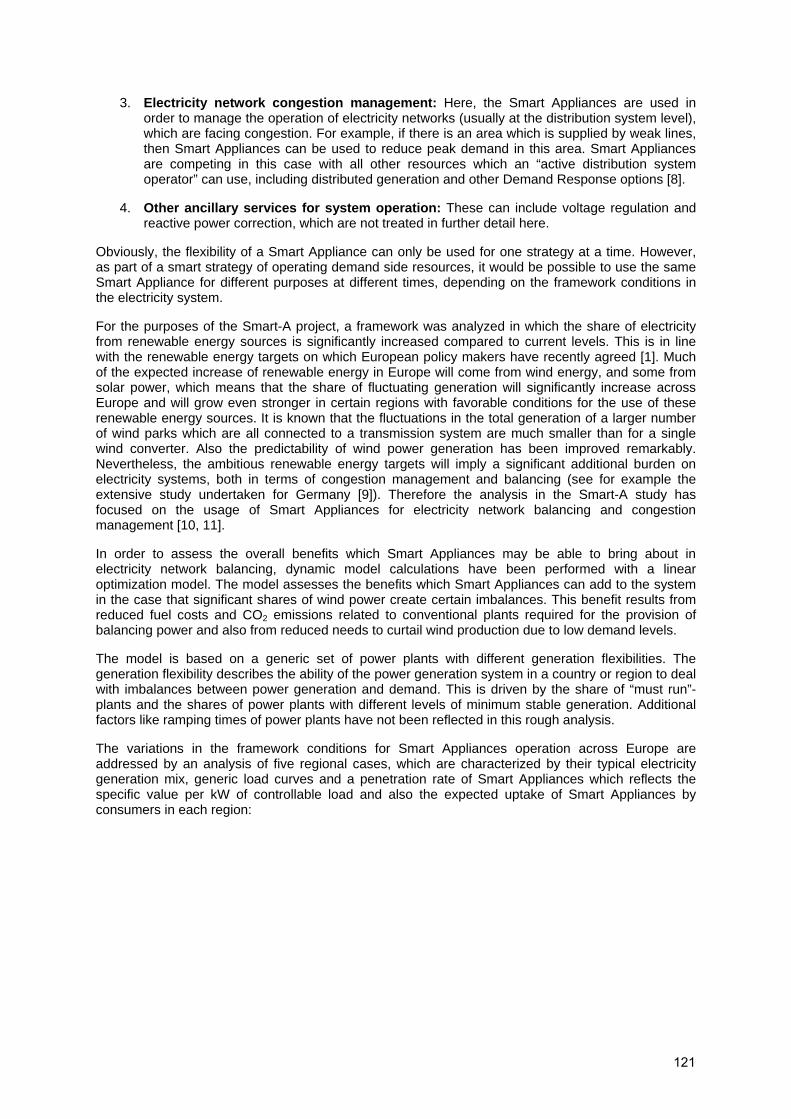

Decomposing Electricity Use of Finnish Households to Appliance CategoriesRouhiainen Virve, Adato Energia Oy, Finland

438

Characterization of the Household Electricity Consumption in the EU, Potential Energy Savings and Specific Policy RecommendationsAníbal De Almeida, ISR - University of Coimbra, PortugalNicolai Feilberg, SINTEF Energy Research, NorwayHervé Lefebvre, ADEME, French Energy Agency, France

456

Energy demand for white goods, what influences? – Answer from in-depth metering of electricity demand in 400 Swedish householdsPeter Bennich, Egil Öfverholm, Zinaida Kadic, The Swedish Energy Agency, Switzerland

477

Residential End-Use Electricity Consumption Pattern in Chennai CityB. P. Chandramohan, Presidency College, Chennai, India

492

Potential 512

Potential for CO2 mitigation in the Hungarian residential buildingsAleksandra Novikova, Central European University, Hungary

514

Predictions for the contribution of residential lighting to the carbon emissions of the UK to 2050Daniel Curtis, Environmental Change Institute, University of Oxford, United Kingdom

529

Energy savings potential in the use of residential lightingMats Bladh, Linköping University, Sweden

538

EcoTopTen scenarios for sustainable consumption – reduction potentials due to the use of energy efficient productsDietlinde Quack, Öko-Institut e.V. Institute for Applied Ecology, Germany

547

Developing Countries 558

Positive impacts of energy efficiency on the electricity services to the urban and peri-urban poor

560

v

John R. Mollet, International Copper Association (ICA), USASolar Water Heating in South AfricaNico Beute, Cape Peninsula University of Technology, South Africa

572

On-line use rate meters for solar cookers and “Hot Box” heat retention cookers in Developing Countries: Concept, tests, verification of output data and field test methodologyMichael Grupp, Synopsis, France & Institute for Energy and Environment, GermanyMarlett Balmer, ProBEC, South Africa

581

Promotions of Compact Fluorescent Lamps (CFLs) by Utility-Bill-Payback Scheme in VietnamYoshiaki Shibata, Jyukankyo Research Institute, Japan

592

A Breath of Fresh air: protos the plant-oil stoveSamuel N. Shiroff, BSH Bosch und Siemens Hausgeräte GmbH, Germany

602

Lighting 610

Do new types of Energy Saving Lamps change the markets?Michael Bross, GfK Retail and Technology GmbH, Germany

612

The EuP preparatory study for the eco-design of domestic lightingPaul Van Tichelen, VITO & BIO IS & Energy piano & Kreios, Belgium

622

CFLs in the USA – Market and Technical Status ReportChristopher Granda, Vermont Energy Investment Corporation, USAStephen Bickel, D&R International, USA

636

Really bright- the lighting campaignChristiane Egger, O.Oe. Energiesparverband, Austria

649

ENBW Lighting Expert - Showing the difference in lighting installationsHans Lang, EnBW Vertriebs- und Servicegesellschaft mbH, GermanySimon Wössner, Jan de Boer, Fraunhofer-Institute of Building Physics, Germany

655

Energy-Saving Experiment in Moscow Residential SectorJulian Aizenberg, GC «Topservice» & Light House, Moscow, Russia

664

Lighting efficiency in dwellings: a case studyBenoit Roisin, Université Catholique de Louvain (UCL), BelgiumMagali Bodart, Belgian Building Research Institute (BBRI), Belgium

666

The development trend of China's Green LightingZhao Yuejin, CNIS, China

678

Off-Grid-Lighting solutions for least developed countriesReinhard Weitzel, OSRAM GmbH, Germany

686

Transforming the Market for Efficient Lighting, RussiaJulian Aizenberg, Russian Lighting Research Institute (VNISI), Russia

692

Be aware of CFLs: our experience in the implementation of the energy saving lamps’ usePatrizia Pistochini, ENEA, Italian National Agency for New technology, Energy and the Environment, ItalyGeorges Zissis, Université de Toulouse; UPS, INPT; LAPLACE (Laboratoire Plasma et Conversion d'Energie), France

699

Tubular daylight guidance systems - Energy Saving Potential in Residential Buildings in RomaniaC•lin CIUGUDEANU, Florin POP, Lighting Engineering Center UTC-N, Technical University of Cluj-Napoca, Romania

713

Labelling & Standards 725

Progress towards Managing Residential Electricity Demand: Impacts of Standards and Labeling for Refrigerators and Air Conditioners in IndiaMichael A. McNeil, Ernest Orlando Lawrence Berkeley National Laboratory, USA

727

CECED encourages fair competition among all appliance manufacturersGerhard Fuchs, CECED (European Committee of Domestic Equipment Manufacturers),Belgium

739

UK Government Standards Process for Energy-using productsFrank Klinckenberg, Klinckenberg consultants & AEA Energy & Environment, the Netherlands

743

vi

Energy labeling in White Goods WorldwideAnton Eckl, GfK Retail and Technology GmbH, Germany

749

Opportunities for Energy Standards and Labels in CIS countriesFrank Klinckenberg, Klinckenberg Consultants, the Netherlands

767

Review on Chinese Energy Efficiency Standards and Energy Label SystemGeng Wang, China National Institute of Standardization, China

777

Standards and labels for promoting energy efficiency in RussiaNataly Olofinskaya, United Nations Development Programme (UNDP), RussiaGennady Smaga, United Nations Development Programme (UNDP)/Global Environment Facility (GEF) project, Russia

784

New developments in enforcing compliance with Standards and Labels in the UKDaniel Kapadia, Defra, United KingdomChris Evans, Market Transformation Programme, United Kingdom

794

Label It and They Will Buy? The Case of Energy Efficient Class-A AppliancesJoachim Schleich, Fraunhofer Institute for Systems and Innovation Research (ISI), Karlsruhe, Germany & Virginia Polytechnic Institute and State University, Blacksburg, USA

802

Design of an Endorsement Labeling Program for Economies in Transition - a case from IndiaAmit Khare, ICF International, USA

812

Results of a recent survey of compliance with Directive 92/75/EEC (Energy Labelling) in all EU Member StatesBarbara Schlomann, Fraunhofer Institute for Systems and Innovation Research (Fraunhofer ISI), Germany

825

The impact of Ecodesign measures on household electricity consumption in the Netherlands: even more savings are possibleHans-Paul Siderius, SenterNovem, the Netherlands

837

Pro-poor Standard and Labelling programmes? Results of a survey on S&L for domestic appliances in Southern Mediterranean countries Sylvaine Herold, European Institute for Energy Research (EIFER), Germany

848

Beyond A: the future of the energy labelPaolo Falcioni, CECED (European Committee of Domestic Equipment Manufacturers), Belgium

861

The Evaluation Methods of China Monitor Energy Efficiency StandardGuanglei Du, 3M China Limited, ChinaXin Zhang, Haihong Chen, China National Institute of Standardization, China

865

Heating 870

Reducing the Carbon Footprint of Existing Domestic Heating: A Non-Disruptive ApproachMartin O’Hara, Danfoss Randall Limited, United Kingdom

872

Raising the Efficiency of Boiler Installations (BOILeff)Guenter R. Simader, Austrian Energy Agency, AustriaNúria Quince, CREVER - Group of Applied Thermal Engineering, Universitat Rovira i Virgili, Spain

881

Policies for reducing environmental impacts and improving energy efficiency: the case of solid fuel small combustion installationsShailendra Mudgal, BIO Intelligence Service S.A.S., France

890

VOLUME 3

Heating/Water Heating and CHP 897

Energy Services for Domestic Heating – Special Aspects of the Domestic Heating Oil MarketChristian Küchen, Institut für wirtschaftliche Ölheizung e.V. (IWO), Germany

899

The use of heat pumps in the renovation of buildingsKai Schiefelbein, Norbet Markus, Stiebel Eltron GmbH & Co. KG, Germany

909

Policy Instruments to Support Uptake and Appropriate Application of Micro-CHPAdam Hawkes, Centre for Energy Policy and Technology (ICEPT), Imperial College

919

vii

London, United KingdomCalifornia’s Solar Water Heating Program: Scaling Up to Install 200,000 Systems by 2020Robert Mowris, Verified, Inc. USA

932

Heating, Ventilating and Air Conditioning (HVAC) 942

Dynamics of the AC Markets WorldwideTanja Heidingsfelder, Tobias Kupczyk, GfK Retail and Technology GmbH, Germany

944

Energy consumption of European residential comfort fansJerome Adnot, Center for Energy and Processes, Mines Paristech, France

951

Energy Efficiency Standards for Residential Air Conditioning and Heating Equipment –The U.S. ExperienceKarim Amrane, Air-Conditioning, Heating, and Refrigeration Institute, USA

961

Energy Efficiency Labelling of Ceiling Fans in India: Challenges and the Way ForwardAlvin Jose, Bureau of Energy Efficiency, Ministry of Power, Government of India, India

970

Analyses of the energy consumption of complex HVAC systems in residential buildings taking into account the thermal comfortJoachim Seifert, Technical University of Dresden & Viessmann Werke & Institute of Building energy systems, Dresden, Germany

978

Sustainable Building 989

Sustainable Building Operation – Experiences from Danish Housing EstatesJesper Ole Jensen, Danish Building Research Institute, Denmark

991

Dynamic Analysis Methodologies Applied to Energy Management in Residential BuildingsHans Bloem, Joint Research Centre, Directorate-General of the European Commission

1003

Beyond Solar Decathlon – Germany’s contribution to the international competition in energy efficient residential building design and residential appliancesHannes Guddat, TU Darmstadt, FB15, Energy Efficient Building Design GroupMichael Keller, TU Darmstadt, FB15, Energy Efficient Building Design GroupChristoph Thim, BSH Bosch und Siemens Hausgeräte GmbH

1012

Set Top Boxes 1032

Energy efficiency trends in STBsRobert Turner, Pace plc, United Kingdom

1034

Policies for reducing environmental impacts and improving energy efficiency: the case of complex set-top boxesSanaée Iyama, BIO Intelligence Service S.A.S., France

1040

The international effort to develop a new IEC measuring method for Set Top Boxes (STBs)Keith Jones, Digital CEnergy Australia, Australia

1052

Information and Communications Technology (ICT) 1065

Energy Consumption for Information and Communication Technologies in German households – present state and future trendsBarbara Schlomann, Fraunhofer Institute for Systems and Innovation Research (Fraunhofer ISI), Germany

1067

Energy and environmental efficiency for broadband deployment and multi-services implementationDominique Roche, FT/NSM/TECHNOLOGIES, FranceLuca Giacomello, Telecom Italia, Italy

1079

Network connectivity and low-power mode energy consumptionBruce Nordman, Lawrence Berkeley National Laboratory, USA

1091

Graphics and Microprocessor Technology for More Sustainable Media-Rich ComputingDonna Sadowy, AMD - Advanced Micro Devices, Inc., USA

1102

viii

Consumer Electronics 1110

Gadgets and GigawattsMark Ellis, Mark Ellis and Associates, Australia

1112

How compatible are Consumer Electronics and sustainability?Heribert Tippenhauer, GfK Retail and Technology GmbH, Germany

1123

Difficulties in the Energy Efficiency Standards Program for Consumer Electronics, by the Case of Set-Top BoxesLi Pengcheng, China National Institute of Standardization, China

1132

Domestic Appliances Standby Power Losses: The Case of Eleven Suburbs in the Greater JohannesburgMercy V. Shuma-Iwisi, University Of Witwatersrand, South Africa

1139

Televisions and Consumer Electronics 1151

The IEC 62087 TV Testing Methodology Review – A Template for International Stakeholder Cooperation in Developing Harmonised Testing StandardsRobert Harrison, UK Government Market Transformation Programme, United KingdomKeith Jones, Department of Environment, Water, Heritage and the Arts (DEWHA) Australian Government, Australia

1153

Standby Labeling and Procel Seal on TVs – The Brazilian ExperienceHamilton Pollis, PROCEL – Brazilian National Program of Electric Energy Conservation, ELETROBRAS – Centrais Elétricas BrasileirasAlexandre Novgorodcev, PBE – Brazilian Labeling Program - INMETRO – National Institute of Metrology, Standardization and Industrial Quality, Brazil

1159

Potential energy savings for televisions due to the application of labelling and MEPS in Australia Keith Jones, Digital CEnergy Australia, Australia

1172

The Research of China FPD TV Energy Efficiency Standard MethodologyZhang Xin, China National Institute of Standardization, China

1184

Washing and Drying 1192

Ecodesign requirements on spinning speed for washing machines? An analysis of the trade-off with the penetration and use of tumble dryers in EuropeMilena Presutto, Italian National Agency for New Technologies, Energy and the Environment (ENEA), Italy

1194

Energy Efficiency of washing machines – A harmonized standard for a diversified marketGundula Czyzewski, BSH Bosch und Siemens Hausgeräte GmbH, GermanyTom Hilgers, wfk Institutes and Test Materials, Germany

1206

Promotion of energy-efficient heat pump driersJürg Nipkow, Swiss Agency for Efficient Energy Use (S.A.F.E.), Switzerland

1215

Large Energy Savings by Sorption-assisted DishwasherHeinz Heißler, BSH Bosch und Siemens Hausgeräte GmbH, Germany

1226

Cold Appliances 1229

Relevance of consumer real life behaviour in cold storage on energy consumptionJasmin Geppert, University of Bonn, Germany

1231

Cool Carbon - BSH Refrigerator Exchange Program with the Carbon CertificatesSamuel N. Shiroff, BSH Bosch und Siemens Hausgeräte GmbH, GermanyDr. Thomas Grammig, Proklima, Germany

1242

A New Global Test Procedure for Household RefrigeratorsLloyd Harrington, Energy Efficient Strategies, Australia

1251

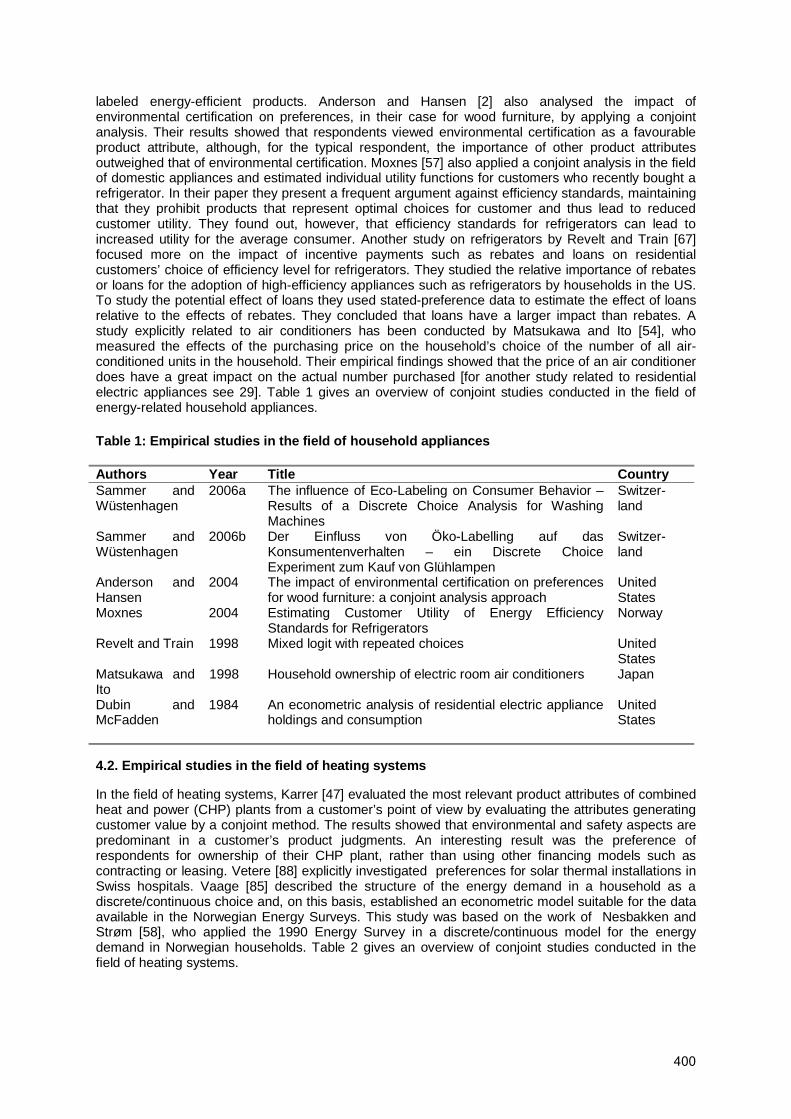

Highest energy efficiency in household refrigerating appliancesThomas Ertel, Liebherr-Hausgeräte Ochsenhausen GmbH, Germany

1265

Advances in Environmentally Sustainable Refrigerants and Blowing AgentsJ. M. Bowman, Honeywell International, USA

1271

Preliminary measurement of energy consumption for residential refrigerators and refrigerator-freezersBudihardjo, Refrigeration and Air Conditioning Laboratory, University of Indonesia,

1279

ix

IndonesiaImproving Energy Efficiency of Product Use: An Exploration of Environmental Impacts of Household Cold Appliance Usage PatternsTang Tang, Loughborough University, United Kingdom

1286

Other Appliances 1298

Strategies to Enhance Energy Efficiency of Coffee MachinesEric Bush, Topten International Group, Switzerland

1300

Energy Implications of Appliances in CarsAlan Meier, Lawrence Berkeley National Laboratory, USA

1308

Energy savings potentials in domestic ventilation products and the necessary technologiesR. Volkmar Uebele, BSH Bosch und Siemens Hausgeräte GmbH, Germany Energy

1315

Labelling and Standards for Domestic Gas Cooking Appliances in Brazil – Improving Energy Efficiency and SafetyClaudio Guimarães Alzuguir, CONPET – Programa Nacional da Racionalização do Uso dos Derivados do Petróleo e do Gás Natural & PETROBRAS – Petróleo Brasileiro S.A., Brazil

1327

Topten.info: Market Pull for High Efficiency ProductsEric Bush, Topten International Group, Switzerland

1339

x

Introduction

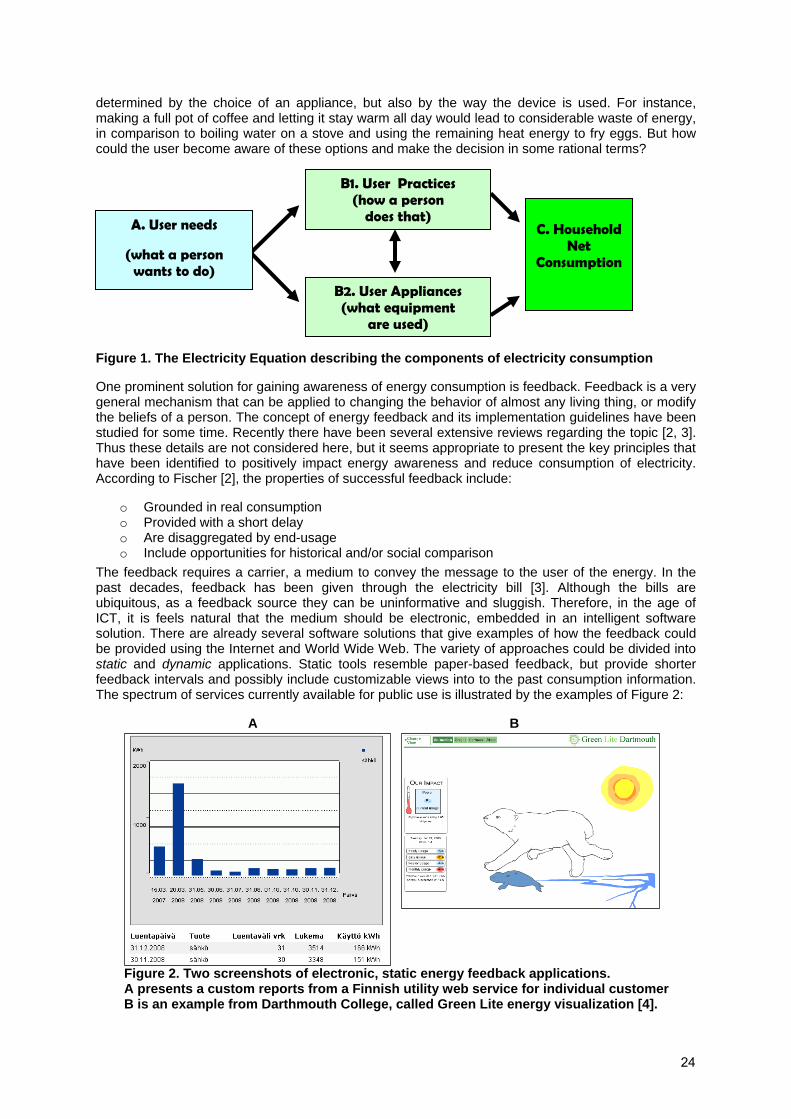

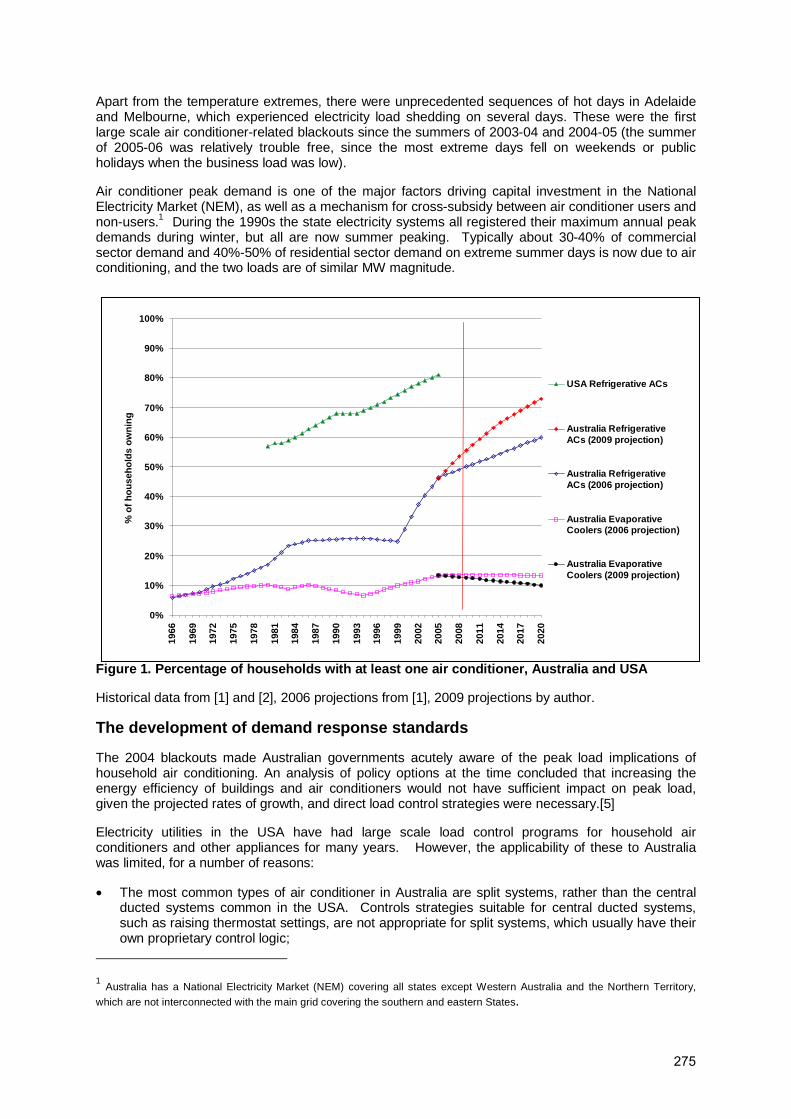

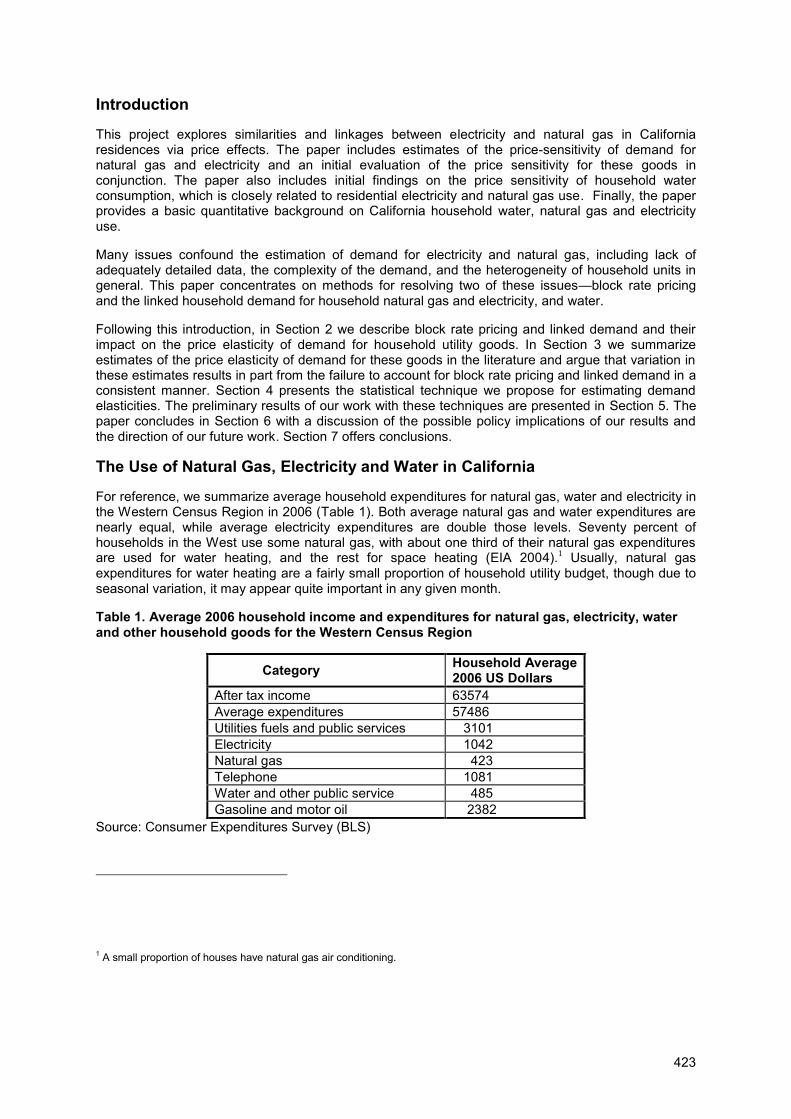

The residential sector is responsible for a large and increasing share of energy and electricity consumption and the related emissions into the atmosphere. Residential energy demand is also rapidly increasing putting a strain on the available finances and infrastructures of several developed and developing countries. Although recent progress in energy efficiency of major domestic appliances and lighting equipment, new and larger appliances are continuouslyadded to the existing stock. Recently the rapid introduction and expansion of ICT and consumer electronics has contributed to the additional power request from the domestic sector, together with the request for more comfort and large dwellings. This has resulted not only in additional CO2 emissions, but also in a larger strain on the electricity network, contributing to electricity blackouts and other electricity supply problems mainly in developing countries.

By improving energy efficiency of domestic appliances and lighting countries can afford to maintain the present level of comfort, and at the same time avoid large investments in the energy and electricity infrastructure, and even more important avoid an irreversible impact on the environment. Domestic appliances and lighting offers a large untapped energy efficiency potential, which in most cases is cost-effective for the users, as well for the society as a whole.

Energy efficiency improvements in residential appliances and lighting can play a key role in assuring a sustainable energy future and socio-economic development, and at the same time mitigate climate change. Energy efficiency measures related to residential appliances and lighting are among the most cost-effective CO2 emission reduction actions, and offer the best opportunity to increase the security and reliability of energy supply. In developing countries efficient residential appliances and lighting are vital to improve living conditions and reduce local pollution.

However market, policy, trade and information barriers impede the further penetration of energy efficient residential appliances and lighting, resulting in a missed opportunity for climate change mitigation and socio-economic development.

The International Energy Efficiency in Domestic Appliances and Lighting (EEDAL) conference started in 1997 in Florence, filling a gap: there was no energy efficiency conference was dedicated entirely to residential appliances and lighting. The EEDAL conference has established itself as an influential and recognised international event where participants can discuss the latest developments and build international partnerships among stakeholders.

The fifth EEDAL conference was organised in Berlin on 16 to 18 June 2006. EEDAL’09 was of the most successful conference in the series with over 300 participants coming from all continents, representing 26 countries.

The EEDAL’09 conference have been very successful in attracting an international audience, representing a wide variety of stakeholders involved in policy implementation and development, research and programme implementation, manufacturing and promotion of energy efficient residential appliances and lighting.

EEDAL'09 has provided a unique forum to discuss and debate the latest developments in energy and environmental impact of residential appliances and installed equipment, and lighting. The presentations were made by the leading experts coming from all continents. The presentations covered the policies and programmes adopted and planned in several geographical areas and countries, as well as the technical and commercial advances in the dissemination and penetration of energy efficient residential appliances and lighting.

The three-day conference included plenary sessions where key representatives of governments and international organisations and manufacturers presented their views and programmes to advance energy efficiency in residential appliances and lighting. Concurrent

xi

sessions on specific themes, dealing both with technologies, socio-economic issues and policies, allowed in-depth discussions among participants.

The conference presentations highlighted the available technologies to improve efficiency, as well the numerous programmes and policies adopted by developed and developing countries. Among them it emerged that standards and labels are essential component of any country policy set, and these two instruments have delivered remarkable results in a very cost-effective manner. Other market transformation programmes such as procurements, increased information, and smart meters are as well important and more efforts in this area have started. The often forgotten components of the energy demand, the consumer behaviours and the usage patterns, is still a topic of research, and it demands more attention both from policy makers as well as programme design and managers. Energy efficiency in the residential sector is an important component of climate change and sustainable development policies and as such it should be further supported, including financing support and an adequate legislative and organisational framework, by national and international organisation.

This year’s conference focussed on how to improve the energy efficiency of appliances and lighting products traded around the world, through improved technology, better information for consumers, and effective product standards and policies, posing two basic questions:

In all parallel sessions a combination of technologies, programmes and policies were presented.

From the presentations emerged that:• In most countries residential energy consumption, and in particular electricity, is still

growing;• There is still a large, cost-effective saving potential in developed and developing

countries, despite the several policies and programmes implemented (a lot of work in front of us). This saving potential is among the most cost-effective option to reduce CO2.

• Lighting is of particular importance, and it offers a fast solution (CFLs), many countries have started the process if phasing out incandescent lighting, and LED are now a new available technology. Standby is still increasing and needs more attention (could become the largest electricity use, including on-mode of CE and ITC). Coldappliances are still predominant in residential electricity consumption. HVAC and water heating still need attention. Cooking is important for developing countries.

• The need for more data collection on the installed equipment, user, real technical options to better quantify the large saving achieved through programme evaluation, and the remaining.

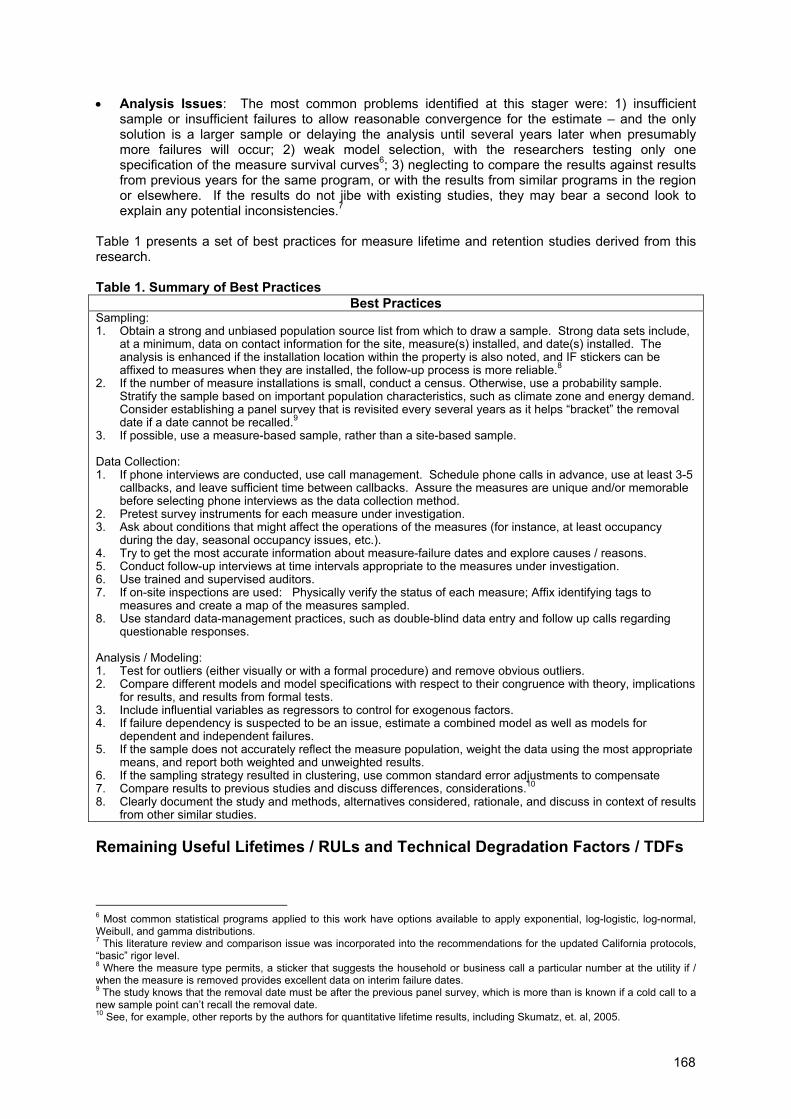

Among the policy options there is been in many sessions a call for:

• more aggressive and progressive efficiency standards, more use of labels on more equipment, and a stronger enforcement;

• Market based policies to support energy services in the residential sector and rebalancing investments between supply and demand (including distributed generation). This may include white certificates and ‘personal’ carbon allowances.

• More attention to metering, demand response, billing, and consumer feedback.• International Collaborations and partnerships on test methods, efficiency levels and

quality levels, labels • The need to build a strong case for energy efficiency (including carbon and financial

benefits), to assure policy makers on the real saving potential, and bring private investors money.

The book contains the papers presented in the concurrent sessions.

It is hoped that the availability of this book will enable a large audience to benefit from the presentations made at the conference. Potential readers who may benefit from this book

xii

include energy and environment researchers, engineers and equipment manufacturers, policy makers, energy agencies and energy efficiency programme managers, energy supply companies, energy regulatory authorities.

The EEDAL'09 conference was organised by DENA, the German Energy Agency and the European Commission Directorate General Joint Research Centre.

Metering and Smart Appliances

1

2

Smart Metering – a means to promote sustainable energy consumption? Socio-technical research and development on feedback systems

Sebastian Gölz 1; Konrad Götz, Jutta Deffner 2

1 Fraunhofer-Institut für Solare Energiesysteme ISE,

2 Institute for social-ecological Research ISOE, Frankfurt/Main

Abstract

Technical innovation with metering technologies and the possibility of continuous consumption feedback and demand response programs for private homes provide optimism that so-called Smart Metering could contribute significantly to sustainable energy consumption.

The project consortium of Intelliekon funded by the German Ministry for Education and Research focuses on the hypothesis that not only the operation of the technology but also the associated interaction within the socio-technical system contributes to energy conservation in the exemplary field of electricity. Knowledge – provided and specifically displayed by the feedback-system –leads to action by households only if the information can socially and cognitively be integrated into the everyday routines of the recipients.

The ambitious goal of Intelliekon is overcoming obstacles and integrating everyday routines of household members with the perspectives of nine participating utilities and a system provider of smart metering. Transdisciplinarity starts with developing feedback systems by integrating perspectives of social sciences and with those of utilities.

The conclusion from an exploratory study is that it does not make sense to bombard people with real-time data, because it is barely possible to interpret the data. Means of relating and comparing data at manageable intervals are more attractive and helpful as a kind of benchmarking. Visualisation in graphs and the information in general must help consumers to make practical changes in their household habits. It makes sense to give a few but carefully selected and well-designed data views. Along with the conclusions derived from the study, two feedback instruments have been defined and developed and will be operated in a field test at numerous sites.

Introduction: The project “Intelliekon”

Is it reasonable to believe that feedback based on Smart Metering technology stimulates the dissemination of knowledge and motivates more efficient use of household and electronic appliances? Is the use of such feedback instruments so much fun that people will integrate them as an additional feature in their daily routines? Or, do we have to acknowledge the limitation of this innovation due to its current lack of standardisation and have to face a - technically and social scientifically spoken – flash in the pan. These are some of the major questions the project consortium of Intelliekon1 focuses on. The three-year cooperative project is the largest in the German-speaking region area in terms of scope and partners. Its orientation toward practical results renders it specifically promising. Three research institutes (Fraunhofer ISE, ISOE and Fraunhofer ISI), a smart metering system provider (EVB Energie AG), nine German utilities (Energieversorgung Oelde, Stadtwerke Hassfurt, Stadtwerke Muenster, Stadtwerke Schwerte, Stadtwerke Ulm, SVO Energie, Celle, swb, Bremen, SWK SETEC, Krefeld, Technische Werke Kaiserslautern) and an Austrian utility (Linz AG) are working together to test and evaluate jointly developed feedback instruments in a one-year field test with several thousand households. 1 funded by the German Ministry for Education and Research under the Contract 01 UV0804A

3

The project has three phases: 1. Development phase (year 1): for the socio-technical definition and development of feedback

instruments that match household needs and preferences in regard to energy consumption and saving.

2. Field test phase (year 2): using the same feedback instruments in all sites, measuring and documenting energy consumption and use of feedback data, with three scientific surveys of all participating households.

3. Analyze and dissemination phase (year 3): final assessment of the C02 impact of the achieved consumption effects and development of conclusions on the effect of feedback features.

Detailed research questions are presented below, with further information available at www.intelliekon.de.

Smart Metering and sustainable energy consumption

“Smart Metering“ is the advanced intelligent metering of energy consumption with electronic recording of the consumption in small temporal intervals and having bidirectional communication that also allows automated or indirect management of loads according to economic or other criteria. Additionally following functions for energy services can be provided as well [1].

Smart Metering permits [2]:

1. Automated and remote metering reading

2. Information (feedback) for the consumer (also possible for different energy sources, e.g. multi-utility metering) on consumption, costs, CO2 emissions, historical, and current data, including comparisons

3. Remote connection and disconnection

4. Energy management of automated loads and appliances

5. Quality assurance by ongoing power quality monitoring, with identification of voltage sages and power outages

6. Services for local energy feed-in

Technical innovation in metering technologies and the possibility of continuous consumption feedback and demand response programs for private homes provide optimism that Smart Metering could contribute significantly to sustainable energy consumption.

By using digital meters – which will serve customers all over Europe in the future – to monitor the energy consumption of private households at all times, new possibilities will arise to obtain detailed and up-to-date data. This will not only simplify billing for the utilities, but also provide consumers precise data feedback on their energy consumption patterns through visualisation and reporting. Many stakeholders share the expectation that, based on this information feedback, it will be possible for households and small and medium businesses to learn how to save energy in the future.

The technical innovations

At present various technical concepts for Smart Metering are being tested and investigated all over Germany. Here we can only give a very short description on components and possible systems [3]: A digital meter collects energy consumption data and replaces the mechanical Ferraris meter. A data concentrator can be placed in the household to collect data from different energy sources or can be situated near a local transformer to collect the data from several hundred households. Data processing is normally offered by the service provider, i.e. the utility or a metering company.

To be marketable, smart meter communications systems must offer reliable bidirectional communications along all positions of the distribution line. The communication infrastructure often

4

must be adapted to local conditions and turned out to be the most failure prone element in the system. Additionally communication between components of different suppliers often is not possible as standards are not (yet) defined, and many suppliers use proprietary protocols.

The most common communications medium between meters, data concentrator and the data processing center is power line carrier (PLC). In these cases, the data concentrator is usually in the nearest substation; from there the information is – due to the technical limitations of PLC – transferred via mobile phone lines / radio (GSM/GPRS) or a wire-based medium (i.e. DSL) to the data processing center [4].

The political frameworks

The target of the EU directive on energy end-use efficiency and energy services 2006/32/EG [5] is energy savings of 9% in each EU-member state by the year 2015. This directive and the German federal laws concerning the liberalisation of the energy market and the metering service companies promote the dissemination of the technology.

In German Federal legislation, the amendment of the Energy Economy Law (EnWG) [6] has established the rapid liberalisation of meter reading services. According to the law, beginning in 2010, it is obligatory for metering service companies to install meters which collect actual consumption and time of use. This will stimulate the wide-spread installation of Smart Meters in households.

State of the art

The importance of sustainable energy consumption is increasing because of both environmental concerns and also rising electricity costs. Though households report an interest in saving energy [7], use of new appliances and the continued operation of old appliances in parallel lead to the so called rebound effect [8] - meaning the saving effects of the new appliances are neutralized. Psychological studies show that feedback promotes a decrease in energy consumption. The effects of feedback on electricity consumption are summarized in three review papers.

Fischer [9] screened 26 studies on feedback from 11 countries in the years 1987 until 2007. She concentrated on studies which focused directly on feedback. According to her findings feedback led to energy savings between 5% and 12%.

Darby [10] reports energy savings between 5% and 15% for direct feedback, i.e. display of actual consumption on the meter or a screen. Between 0% und 10% savings have been attained with indirect feedback, which is processed information, mostly the electricity bill.

Abrahamse und Steg [8] reviewed 38 papers from 1977 through 2004 with several interventions promoting energy saving in households. In the case of feedback they confirm its effectiveness, which is stronger if it is provided frequently. The effects differ between households with low and high consumption. No difference is reported for the feedback of costs or environmental impacts, as well as for individual feedback or social comparisons.

Most studies deal with effects of feedback and some with factors which influence the scale of effects [8]. Virtually none of the studies describes the mechanisms which lead to the effectiveness of feedback. Wilhite und Ling [11] support compatibility in the way feedback is displayed and the way consumers analyze their consumption and make decisions about alternative consumption patterns. More insight into these psychological processes could help to optimize the technical part of the feedback system and develop it adequately to meet consumers’ needs – eventually including specific differences for different target groups.

The project Intelliekon is investigating the way that households use the feedback implemented via smart metering. Both the preferences for information provided as well as the reasons that motivate behaviour that comes into play from the feedback will be analyzed, and their role in causing changes in the use of electrical appliances (and household consumption) will be assessed.

5

Methods of the research

On the one hand, the empirical project is be based on the concept of household functions meaning that the use of feedback systems has to be compatible with everyday life routines like washing, cleaning, cooking, raising children, information management, household organization, entertainment, etc. On the other hand, it is assumed that societal mores as well as personal goals, attitudes and orientation will influence energy consumption and the acceptance of feedback information.

Within a qualitative and quantitative empirical approach two problems are addressed: the societal problem of unsustainable energy use at the household level and the everyday problem of the fact that households do not yet have direct access to data about their energy consumption which could have an effect on energy use. So the questions arising from this focus on the following:

- Do consumers use information feedback information provided in the field test? Is the use of feedback systems compatible with everyday life routines of the users and their household members?

- How are socio-demographic aspects (like household size, gender, income, and age) related to power consumption on the one hand and the use of feedback systems on the other? Is there a relationship between individual preferences and motivations and the use of feedback instruments?

- How does use of feedback instruments correlate with electricity consumption? And what is the result if the effects are projected for the whole country’s population?

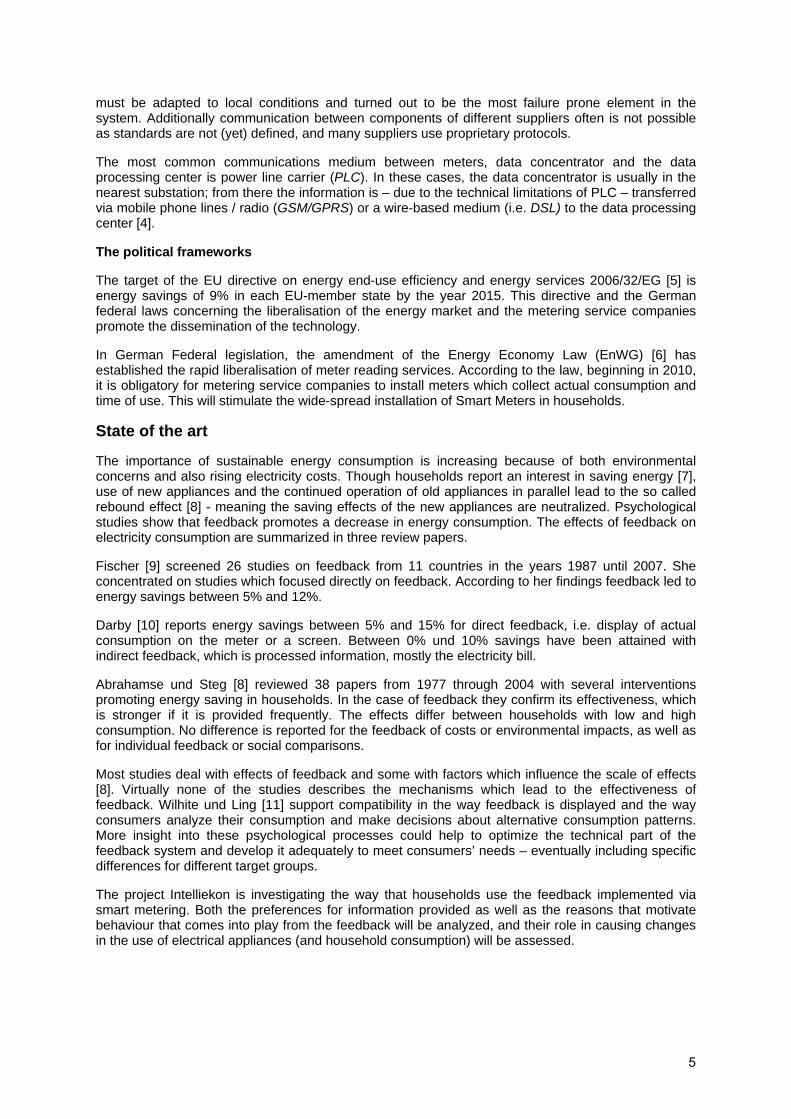

To find answers to these questions, the empirical design of the project consists of a qualitative explorative phase (already finished) and a one-year field test of feedback options with a panel survey in the service area of the nine utilities (cities). Figure 1 shows the schedule of the empirical steps and deliverables.

Figure 1: Schedule of the empirical research

The explorative phase was conducted in spring 2008 (see section on results) with 76 interviews with individual household members in three of the nine pilot cities. The panel survey starts in May 2009 with approximately 2,500 to 3,000 participating households. Both steps are described in the following:

6

Explorative pilot study

The function of the qualitative empirical step was to gather initial evidence on different feedback options in different social groups, especially on the valuation of the subjects’ electricity and their motives for saving energy. A second aim was to gather initial reactions on continuous feedback of electricity use in households. Thirdly it was to explore the needs of the users/consumers regarding the feedback instruments. The whole design should contribute to developing research hypotheses and good phrasing for the standardised questionnaire design.

A qualitative study was the optimal design, as it enabled interviewees to express themselves in everyday language. This is important for understanding the subjects’ contexts and daily routines and for being able to interpret motivations [12]. In four of the pilot cities (Bremen, Kaiserslautern, Muenster, Schwerte) a total of 76 in-depth interviews were conducted [13] in spring 2008. The sample was socio-demographically distributed by age, gender, social status, household size, and households with and without children. The aim of this sample scheme was to form a sample which represents as much as possible relevant and typical combinations of attributes and attitudes. The interviews lasted between 60 and 90 minutes and were digitally recorded. The analysis was done after transcription by computer assisted qualitative data analysis (caqda) and coding referring to content analysis [14]. The analysis allows vertical (analyzing one case) and horizontal (analyzing one topic over all cases) interpretation. The topics of the prepared interview guideline were the basis of the data analysis. Among the topics of the interview guidelines were:

- socio-structural, and cultural background: household description, internet usage, and appliance holdings of the household

- Feedback visualisation and functionality: discussion of six feedback visualisations

- Handling feedback systems in three concrete options: informative overview of paper via mail, an energy display, and a web-based energy portal

Panel survey

During a one-year pilot phase, households will be surveyed in the partner utilities’ service areas regarding different feedback instruments. The objectives of the panel study are to specify the relationships between electricity consumption, household size and formation, appliance holding of households, social structure, attitudes on energy consumption and saving, and attitudes toward , as well as to evaluate the feedback options. With this data in combination with the continuous data on energy consumption, a projection will be developed on the saving potential of feedback systems in the context of Germany via computational modelling.

To achieve this, a treatment and control group design was chosen. The basic concept is that all treatment participants will be testing two basic feedback instruments (informative electricity mail and web portal) over a six-month time span. After this time period, the participants will be able to chose an additional (basic package is ongoing) option for a time span of another six months. The expected options will be personal energy consultations, energy displays, and tariff options offered by the utilities.

To monitor the use and effects of the feedback instruments, a panel survey with three interview periods will be conducted. The first will be in May 2009, the second at the end of testing the basic feedback option, and the third during testing of the additional options (beginning of 2010). To be able to compare the behaviour and opinions of feedback users and non feedback users, the study design includes a control group. The control group guarantees that external effects that may influence behaviour concerning energy consumption (increasing energy prices, framing by media etc.) are accounted for. The control group will also have digital electricity counters but no access to the feedback instruments. The relationship in sample size between the treatment and control groups will be 2/3 to 1/3. The approximate sample size in total will be between 2,500 and 3,000 participants (households) from the service areas of the nine utilities. The survey will be conducted as CATI (computer assisted telephone interview): The control group will be surveyed at the beginning and during the final questionnaire period. The selection of households which are equipped with new smart metering technology by the utilities is not representative of the total population. Thus it is necessary to describe and evaluate the sub samples concerning representative distribution in the different cities by

7

Fun / hands-on approach to technology

Fun / hands-on approach to technology

Economy and control

Economy and control

Challenge, efficiency

orientation

Challenge, efficiency

orientation Socialisation Upbringing

Socialisation Upbringing

No benefit / no point

Disinterest / inability

No benefit / no point

No benefit / no point

Disinterest / inability

Disinterest / inability

Existential economy

Economy mentality

Existential economy

Existential economy

Economy mentality Economy mentality

Environmental protection /

reducing CO2

Environmental protection /

reducing CO2

Problem of data privacyProblem of

data privacy

inte

rest

in a

nd a

ccep

tanc

eof

feed

back

info

rmat

ion

high

low

comparing it with data from the micro census2.Data analysis will be done using social science statistical software. The dependent variables in the statistical analyses will be the current electricity usage and the use of the feedback instruments. Beside univariate analysis of data and descriptive results on the acceptance of feedback and energy consumption, there will be testing of hypotheses via correlation analysis and inter correlation analysis (e.g. multivariate analyses, multiple regressions); factor analyses and cluster analyses will be conducted to develop target group models.

Results from the explorative study

As the project will start its core phase, the field testing of feedback instruments, only in May 2009, the main results so far are from the qualitative study and the development of the feedback instruments. These results are described in the following sections

The objective was to provide initial pointers on options for feedback systems desired by different social groups. As already mentioned, the initial question was to find out about the relevance of electricity and electricity-saving issue in different social groups. Secondly we looked for initial reactions to the idea of regular feedback to inform people of their own electricity consumption. Thirdly we did an analysis of desired configurations based on the example of three feedback options and seven forms of presenting the data.

The results focus on general reactions towards the feedback and on selected reactions towards the three specific feedback instruments (informative overview, display, web portal).

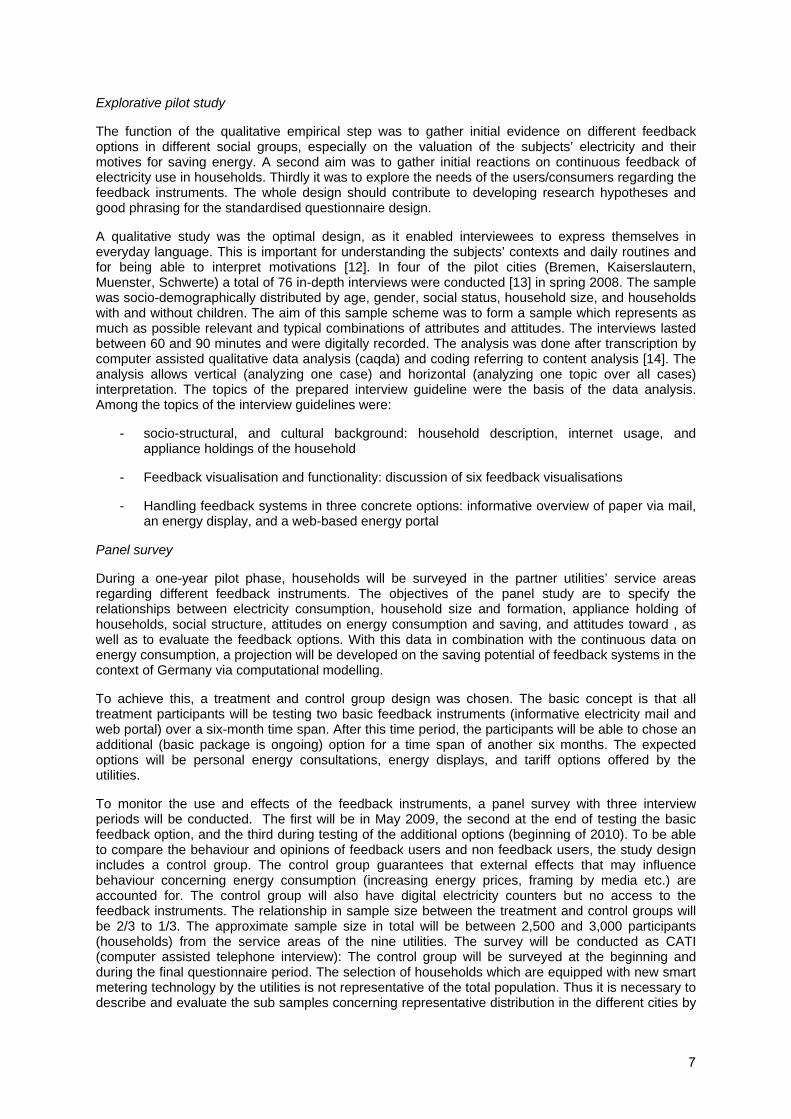

General opinions on feedback information

In the majority of cases, people show interest and take a positive view of receiving feedback and draw practical conclusions from this. But also there are three reluctant or negative sub-groups. One large sub-group is open-minded to the idea of saving energy, but sees no way of cutting down consumption any further. A second, small sub-group wholly rejects the idea of feedback or is indifferent to it. This was expressed by a feeling that one’s behaviour is under surveillance or that the feeling was one of scepticism or pointlessness. A third sub-group is physically, cognitively or socially incapable of adequately processing the information and drawing conclusions from it.

2 The micro census is a statistical census by the Federal Statistical Office, in which selected – along specific criteria - households participate. The number of households is set to secure representativness of results. The micro census is used to control data from population census in repeated(shorter) periods of time and correct it if necessary.

8

An overview of the different reactions towards the feedback given is shown in fig. 2.Figure 2: Overview of reactions towards feedback – overlapping boxes indicate a possible connection between motivations (motivational-alliances)

Key motivations in favour of feedback

The first and most important positive motivation is economy and control. In the first instance, this is a practical, economic orientation based on traditional values. From this perspective energy saving must not, however, restrict living standards and lifestyle. It is more to the contrary: it should be a chance to save money to be spent on something else. In the second instance, control means survival amongst households in precarious circumstances, a must for surviving on the financial means available.

A second motivation to vote for feedback is competitiveness and a modern efficiency orientation. Energy savings is seen as a sporting challenge for an efficient and intelligent approach to energy as part of the rational everyday operation of a modern household. The third motivator we found is social responsibility and upbringing. It is seen in family households as a chance for communication within the family, as an instrument to educate children to save, and as a basis for discussion of energy-saving behaviour. Last but not least, there is the motive of environmental protection/CO2 reduction. It is an intrinsic motivator for those of an ecological persuasion. For others the climate change phenomenon is seen as a rational motive for assessing one's own electricity consumption.

Occasionally a motive is visible on a different level: a fun and hands-on approach to technology. Some interviewees found interesting the offer of technical feedback which sparks curiosity and interest in trying it out in a hands-on way. Technical features of this kind can have a symbolic meaning as a prestigious gadget.

Key attitudes against feedback

Some of the respondents are against feedback instruments because of the problem of data privacy. They expressed concerns about lack of data privacy or protection of personality rights. They realise that a large amount of household-related data will be generated, which could end up in the wrong hands and so they see the risk of a too-transparent customer.

There is also an important group which shows strong indifference: these interviewees do not see any benefit and no point because of disinterest in or rejection of the technology. In this group there is a general dislike of the topic, being uninformed about it. They are questioning the benefit, being convinced that they are already using very little electricity.

There is a third subgroup that is totally disinterested or shows an inability to use a feedback system. On the one hand, for elderly people, there is an age-related focus on just coping from day to day. The second inability is due to social disintegration like language barriers or a lack of cognitive logic.

Reactions towards proposed three feedback options

Feedback option “Informative consumption overview in writing with graphs”

The rejection of this feedback information results mainly from modern internet users, which have become the majority. Information in writing via mail seems to be an anachronistic way of getting information. Besides that, it is presumed that additional costs are produced to make the overview available for the consumers (mailing costs). This lessens the acceptance.

Support for this option is expressed by a minor group for whom feedback on paper is a conventional and familiar medium. From this perspective this option seems to be convenient information without having to become active. The information in writing is welcomed above all by elderly people and those without internet access or any affinity for the internet. Because of this clear segment it seems to be meaningful for selected target groups as basic information in appropriate intervals, e.g. on a monthly basis.

9

Feedback option of a in-home display, so called “Energy Box”

The Energy Box is small display which is able to show current (15 min interval) power consumption in the household in numbers. The display can be used in any room of the house, either cordlessly or plugged into a power socket.

There is limited interest in this option. For potential users it seems to have not much direct benefit and there are doubts about its effectiveness. There arise questions like this: Is there any graphic information? Is there any possibility of memory-based comparison of weeks, days, months? If not, the box gets even more unattractive. Besides this, the Energy Box creates a feeling of surveillance and potential for conflicts. One participant of the study noted, “If I have to monitor consumption every day, it will take away somewhat from my quality of life.” Additional there is fear of additional costs (for the box) and an expectation for being interested only for a limited period: “A nice toy for a week, then you lose interest.” Some foresee even practical restrictions, like the limited number of available power sockets at an easily viewable visual height.

The option of the Energy Box sparks spontaneous curiosity in some: “fascinating, interesting”. The real-time representation of current electricity consumption enhances a direct learning process and seems to motivate some of the respondents to investigate unnecessary sources of consumption, to avoid peak loads, and to identify the base load. Also it is apparent that the box could develop symbolic qualities like an ‘on-board computer’ in a car and can become a topic of discussion in the family and among friends.

Feedback option “Web Portal”

There is broad approval of the web portal as a contemporary feedback medium offering lots of interesting options: it seems possible to individualize representation of data, allows fast and flexible access to information, and invites hands-on, creative use. There are attractive additional functions (e.g. energy-saving tips), and it is perceived to be free of charge. This option seems to be a general source of feedback which is viable for the future.

Those rejecting this option either have an aversion towards the internet (too alien, too virtual) – most of them have no internet access at home – or they shy away from the effort of logging in (the problem of increasingly difficult to remember login data arose often). From the perspective of some respondents, the internet solution is considered to be time consuming and impossible to integrate naturally into daily routines, particularly for busy women with multiple responsibilities (job/mother/household).

Conclusion from the exploratory study

Useful feedback instruments have to take several items into consideration. It does not make sense to bombard people with just-in-time data, because it is barely possible to interpret them. Means of relating and comparing data at manageable intervals are attractive and helpful as a kind of benchmarking. The visualisation in graphs and the information in general must help consumers to make practical changes in their household situation. It makes sense to give a few but carefully selected and well-designed and informative displays.

From our point of view it is recommended that the web portal be introduced as a general feedback instrument, with the possibility of interactive features. Within this, internet users can chose their favourite charts on for a year (comparison of the months), half a year (comparison of the weeks), a month (comparison of the days), a week (days), or a day (hours). It should be possible to choose between graphs (bar charts), tables and a combination of tables and charts.

As an additional option it makes sense to offer a printed informative consumption overview with one or two graphs/bar diagrams for customers without internet access as mandatory for the disinterested. Concerning the Energy Box, it should be possible to lease displays at the utility’s customer care centre for a low fee or to purchase it by those interested. Further it is an indispensable precondition for efficacy to have the option of a personal electricity consultation and assistance in interpreting the feedback, along with pointers for possible action and energy-saving tips (energy-related advisory service).

10

Development of the feedback systems

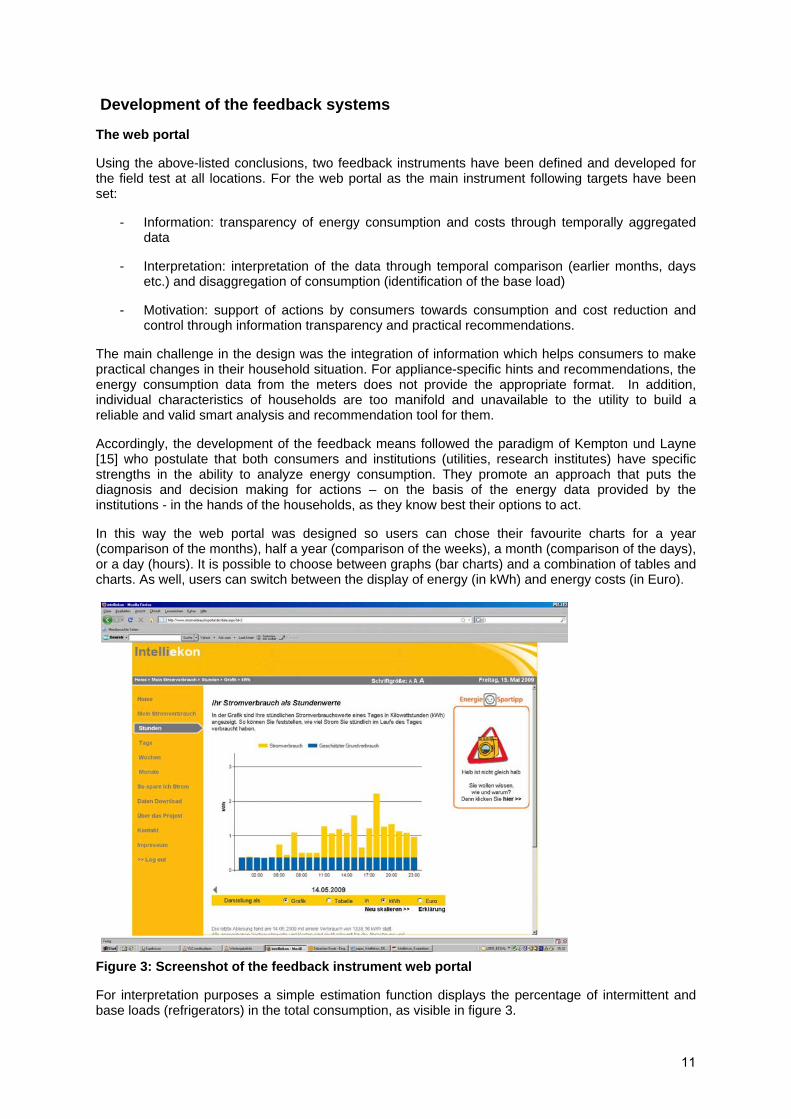

The web portal

Using the above-listed conclusions, two feedback instruments have been defined and developed for the field test at all locations. For the web portal as the main instrument following targets have been set:

- Information: transparency of energy consumption and costs through temporally aggregated data

- Interpretation: interpretation of the data through temporal comparison (earlier months, days etc.) and disaggregation of consumption (identification of the base load)

- Motivation: support of actions by consumers towards consumption and cost reduction and control through information transparency and practical recommendations.

The main challenge in the design was the integration of information which helps consumers to make practical changes in their household situation. For appliance-specific hints and recommendations, the energy consumption data from the meters does not provide the appropriate format. In addition, individual characteristics of households are too manifold and unavailable to the utility to build a reliable and valid smart analysis and recommendation tool for them.

Accordingly, the development of the feedback means followed the paradigm of Kempton und Layne [15] who postulate that both consumers and institutions (utilities, research institutes) have specific strengths in the ability to analyze energy consumption. They promote an approach that puts the diagnosis and decision making for actions – on the basis of the energy data provided by the institutions - in the hands of the households, as they know best their options to act.

In this way the web portal was designed so users can chose their favourite charts for a year (comparison of the months), half a year (comparison of the weeks), a month (comparison of the days), or a day (hours). It is possible to choose between graphs (bar charts) and a combination of tables and charts. As well, users can switch between the display of energy (in kWh) and energy costs (in Euro).

Figure 3: Screenshot of the feedback instrument web portal

For interpretation purposes a simple estimation function displays the percentage of intermittent and base loads (refrigerators) in the total consumption, as visible in figure 3.

11

Several components have been introduced to increase the motivation to undertake and practical knowledge of energy saving measures. The screen in the web portal was divided into several areas to serve for navigation, consumption data presentation and to provide a link to the energy saving recommendations – which was done via a graphical teaser to attract the user’s attention to practical knowledge quickly. For the teasers, adapted traffic signs are expected to provoke surprise and curiosity. In addition a systematic approach through the navigation permits a game to increase motivation for energy saving and to finalise the game as “energy saving king / queen”. For a more analytic approach, energy saving hints are structured along the different rooms and according to the appliances of German households. Last but not least, more curious individuals can browse additional information on energy saving under the category “Do you know …?”. A data download function and contact possibilities for inquiries are also included.

Monthly consumption information

The monthly printed consumption information will use graphs, tables and energy saving recommendations from the web portal and adopt the graphical design. It will comprise not more than two pages, will be printed in colour and sent via paper mail. This feedback instrument will fulfill the legal obligation of utilities from 2010 onwards to provide on request a monthly bill.

Discussion and way forward

The development of the feedback instruments has to acknowledge technical and also legal limitations. These concerns range from the collection and transmission of more frequent metering readings to providing more detailed analysis tools. Here the main concern is the disturbance of the privacy and data security. The planned use of hourly consumption data seems a practical compromise between consumers’ expectation and reasonable systems design and operation costs of the communication technologies.

Nevertheless it can be stated, based upon the previous results, that a rather broad interest exists in different household segments in feedback based on smart metering, , as well as different motives for its use. This confirms the overall research strategy to undertake a socially-differentiated analysis. Here the size of the final sample is the crucial issue and can vary due to the voluntary participation of households. With a population about 6,000 households a large sample can still be achieved that will allow the scientifically-ambitious comparison study with the control group.

The empirical design was approved by all of the industrial partners, so it can be run effectively. Regarding the achievement of the intended project goals, the current status has to be assessed highly positively. The expectation is to be able to report the results of the panel study a year after this publication in the same or similar publications.

12

References

[1] DRAM (2008): Definitions. Demand Response and Advanced Metering Coalition (DRAM). Can be downloaded at: http://www.dramcoalition.org/id19.htm

[2] IEA (2007): DSM Spotlight - DSM on the Rise. IEA Demand-Side Management Executive Commitee. Can be downloaded at: http://www.ieadsm.org/Files/Exco%20File%20Library/Annual%20Reports/IEA%20DSM%20Annual%20Report%202007.pdf

[3] Fraunhofer ISE (2007): AP 2.1 Internationale Feldstudien und AP2.2 Potentialstudien. Internal unpubished research report in the project „E-Box“. Fraunhofer Institut für Solare Energiesysteme (ISE), Freiburg.

[4] Noeren, D. (2008). Entwurf zur soziotechnischen Begleitforschung im Feldversuch eines Smart-Metering-Systems. Unpublished Master thesis, Fraunhofer Institut für Solare Energiesysteme (ISE), Freiburg.

[5] EU (2006): Directive 2006/32/EG of the European Parlament and of the Council. European Union. Can be downloaded at: http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2006:114:0064:0085:EN:PDF

[6] German Bundestag (28.02.2008): Entwurf eines Gesetzes zur Öffnung des Messwesens bei Strom und Gas für Wettbewerb. Drucksache 16/8306.

[7] Mansouri, I., Newborough, M., Probert, D. (1996). Energy Consumption in UK Households: Impact of Domestic Electrical Appliances. Applied Energy, 54 (3), 211- 285.

[8] Abrahamse, W., Steg, L. (2005). A review of intervention studies aimed at household energy conservation. Journal of Environmental Psychology, 25, 273–291.

[9] Fischer, C. (2007). Influencing Electricity Consumption via Consumer Feedback. A Review of Experience, TIPS Discussion Paper 8. Verfügbar unter: http://www.tips-project.de [7.11.2008]

[10] Darby, S. (2006). The effectiveness of feedback on energy consumption. A review for DEFRA of the literature on metering, billing and direct displays. Can be downloaded at: http://www.defra.gov.uk/environment/energy/research/pdf/energyconsump-feedback.pdf

[11] Wilhite, H., Ling, R. (1995). Measured energy savings from a more informative energy bill. Energy and Buildings, 22, 145-155.

[12] Giddens, Anthony (1984): Interpretative Soziologie. Frankfurt a. M. (in German)

[13] Witzel, Andreas (2000). Das problemzentrierte Interview [26 Absätze]. Forum Qualitative Sozialforschung / Forum: Qualitative Social Research [On-line Journal], 1(1). Can be downloaded at: http://www.qualitativeresearch.net/fqs-texte/1-00/1-00witzel-d.htm (in German)

[14] Mayring (1995): Qualitative Inhaltsanalyse. In: Flick, Uwe; Ernst von Kardorff; Heiner Keupp; Lutz von Rosenstiel; Stephan Wolff (1995): Handbuch qualitative Sozialforschung. Weinheim (in German)

[15] Kempton, W., Layne, L. (1994). The consumer’s energy analysis environment. Energy Policy, 22 (10), 857-866

13

“Nice to Know” - metering and informative feedback

Ellen Christiansen* & Anne Marie Kanstrup**

*University of Southern Denmark, **Aalborg University

Abstract

The appropriate information to the customer at the appropriate time is a recipe for influencing consumers to conserve electricity. The Feedback project, from which this paper reports, is a case in point. The idea is to exploit the information possibilities afforded by online metering. This information can be fed back to the consumer, thereby raising awareness of electricity consumption, which may lead to conservation behavior. In connection with a larger experiment with new forms of feedback, we conducted qualitative interviews with 22 families about their one-year experience with receiving feedback via SMS and/or e-mail, to understand how they experienced the feedback. Here we present an analysis of narratives derived from these interviews. We identify three levels of sense-making in which a relationship is established between stimulation and interpretation: (a) the recall of the potential action space, (b) a sense of identity of being an acting electricity consumer, which may or may not spill over to (c) choices when buying appliances, educating children etc. The paper puts this insight into a design perspective, suggesting that design of feedback about metering and billing should consider the practices in which this information plays a role, such as careful housekeeping, storytelling to friends and family, and education of children. Taking customer practice as point of departure could lead to development of a new type of services, which in turn can support conservation behavior. Introduction

Electricity consumption in private households makes up a significant part of the total consumption of electricity both in industrial and developing countries [1]. In Denmark, where this research was conducted, households stand for 1/3 of the total electricity consumption [2]. Initiatives toward electricity savings in private households include technological development of online feedback and automatic controls, and behavior change through feedback and information service, as well as the development of low energy appliances for households, control management and automation. In Denmark it is estimated that use and innovation of present and future control systems can reduce electricity consumption with up to 30% (www.danskenergi.dk). Effort is put into developing intelligent houses and equally effort is put into campaigns for motivating households to change to electricity-conscious behavior. It is estimated that households can make a 26-33% savings on their electricity consumption by behavioral change only [3], provided households’ difficulty in seeing the effect of their contribution to electricity saving is overcome. Initiatives such as Google’s 2009 launch of a ‘power-meter’ http://www.google.org/powermeter/howitworks.html indicates that there are more savings to be harvested by involving web 2.0 activities.

Studies of household electricity consumption point to households being units of varying stability, values and habits. Background variables such as family type, income, education, and the size of the house explain 40% or more of variations in electricity consumption in private households [5]. However, studies also show that feedback for motivating electricity conservation is a quite complex task where personal values, attitudes and social norms regarding environmental behavior play only a minor role compared to structural conditions, such as home size and family size. In other words: green attitudes and electricity consumption are not closely related. One of the reasons for this is the invisible nature of electricity consumption. Additionally, a pronounced reduction in electricity consumption may compromise comfort in the everyday life and may have a disturbing effect on daily routines [4]. As elaborated by Kuehn [5], electricity consumption is a direct or indirect consequence of other fields of consumption. This, and the invisible nature of electricity, means that its consumption is often an un-reflected part of everyday life.

Naturally, making electricity consumption visible has significant influence, and experiences with electronic feedback have measurable effects. There are experiments with electricity meters, monitors and PC-applications [1, 6]. On the basis of a review on metering, billing, and direct displays Darby concludes that “Monitors would be most useful if they showed instantaneous usage, expenditure and

14

historic feedback as a minimum, with the potential for displaying information in microgeneration, tariffs and carbon emissions” [6, p. 17]. However, consumer behavior research related to motivation psychology stresses that making electricity consumption visible is not enough, hence a call for empowerment of consumers. It is pointed out, that “limited abilities and restricted opportunities ... make it difficult even for highly motivated individual to do anything radical to improve the sustainability of their lifestyle” [7, p. 167]. Empowerment involves competence, relatedness, and autonomy [7]. Similar results are found in recent design experiments like ‘222b Lee High Road’ where RED (http://www.reduk.net/) worked on how to strengthen policy towards domestic energy use starting from a householder centered design approach. Design leads from this work are: the importance of making energy visible, design for control, appealing to multiple motivations and collaboration [8].

Generally, the literature can be read as a warning of underestimating the complexity of human behavior in design of feedback. As stressed by Costanzo et al. [9] often used and too simple theories on conservation behavior are ‘the attitude model’ and ‘the rational-economic model’, which, however, turn out to have limited explanatory power when confronted with empirical data.

In this paper we present an analysis of 22 qualitative interviews with households about their experience of receiving feedback about electricity consumption via SMS or e-mail for a year. After accounting for method and data we report our findings and their bearings on design of feedback.

Method and Data