The value of a Brand in the Marketing of Automotve Lubricants ...

185

COPYRIGHT AND CITATION CONSIDERATIONS FOR THIS THESIS/ DISSERTATION o Attribution — You must give appropriate credit, provide a link to the license, and indicate if changes were made. You may do so in any reasonable manner, but not in any way that suggests the licensor endorses you or your use. o NonCommercial — You may not use the material for commercial purposes. o ShareAlike — If you remix, transform, or build upon the material, you must distribute your contributions under the same license as the original. How to cite this thesis Surname, Initial(s). (2012) Title of the thesis or dissertation. PhD. (Chemistry)/ M.Sc. (Physics)/ M.A. (Philosophy)/M.Com. (Finance) etc. [Unpublished]: University of Johannesburg. Retrieved from: https://ujdigispace.uj.ac.za (Accessed: Date).

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of The value of a Brand in the Marketing of Automotve Lubricants ...

COPYRIGHT AND CITATION CONSIDERATIONS FOR THIS THESIS/ DISSERTATION

o Attribution — You must give appropriate credit, provide a link to the license, and indicate if changes were made. You may do so in any reasonable manner, but not in any way that suggests the licensor endorses you or your use.

o NonCommercial — You may not use the material for commercial purposes.

o ShareAlike — If you remix, transform, or build upon the material, you must distribute your contributions under the same license as the original.

How to cite this thesis

Surname, Initial(s). (2012) Title of the thesis or dissertation. PhD. (Chemistry)/ M.Sc. (Physics)/ M.A. (Philosophy)/M.Com. (Finance) etc. [Unpublished]: University of Johannesburg. Retrieved from: https://ujdigispace.uj.ac.za (Accessed: Date).

TilE V L lJ E OF A BR ()

11

II I TII I·. IARKETII ; F T ) H)TI V E L UBlH ~A T

I BILl E "T IlIJ I E ' E IRO

II ' .' )UTII AFRICA

YDER

A r ear It r p rt . . ubmitt d 10 the \ it v t 'r. r nd T hnik n Bu.in

Ii nsc 10 tit' Uni 'r. it f \ I' . in p r i J fullilrn nt of th ' r quir nn mt: for th d r

I 1 I r of Bu in' Adrnini. Irati n

iii

DECLARATION

I declare that this research report is my own, unaided work. It is being submitted in

partial fulfilment of the requirements for the degree of Masterof'Business Administration

at the University of Wales, United Kingdom. It has not been submitted before for any

degree or examination in any other university.

DEDICATIONS

Rob Mahoney

An inspirational manager, who encouraged me

to tackle theunknown.

Joelean Snyder

For the commitment and endless refreshments

that kept me going in difficult times.

Geoff Bick

Supervisor and lecturer, who converted me tothe

Marketing discipline, and who showed meit can be fun.

iv

v

ACKNOVVLEDGEMENTS

John Vevers and the other members of the BP International Lubricants Team. For the

research you made available and your valuable input.

Group H: Duncan, Gary, Marthie and Sara. We made a great team.

Anita, for all her effort, input, hard work, and above all for all the fun we have together.

Rene deConing, BPmarketing research manager. Your input and guidance as well as the

management of theprocess is appreciated.

Justine Snider, Gerhard Smit and Peter Searll from Research International. Thank you

for your patience and professionalism whilst I continuously changed the format, the

presentation of thedata and theassistance afterwards.

All the other team members in DP who gave input, encouragement advice and help. I

could not havedoneit without you. Thank you.

ABSTRACI'

The marketing of lubricants in a business to business environment is facing some tough

challenges. Continuous advances in technology means declining volumes, as the oil lasts

longer and reduces oil drain intervals. During the guarantee/warranty period of the

vehicle, the original equipment manufacturers' specification as to what oil can be used,

plays a critical role, as using unapproved oil can lead to the warranty becoming null and

void. In the market, any number of lubricant manufacturers meet or exceed these

specifications. Once the guarantee period has expired, (OEM) specifications become less

important, and a number ofother variables start influencing the buying decision.

The market in South Africa is highly competitive, with a large number ofplayers capable

of meeting or exceeding OEM specifications. Thus quality alone can not be used as a

competitive advantage. Other variables in the marketing mix must thus be found to

create competitive advantage. In the paper we look at the traditional four P model, the

new four R model, the development of information technology and its role in creating

customer satisfaction. This research seeks to identify what variables in the marketing mix

contribute towards giving a sustainable competitive advantage, ultimately leading to a

strong, reliable and credible Brand.

The research uses the hypothesis that the Brand name plays a role when the decision

making unit has to decide what lubricants to use in their fleet. Market research, based on

the very latest marketing mix thinking investigates this hypotheses, and gives its findings

in a total unbiased, neutral report. Using conjoint analyses, Utility values obtained are

used to make recommendations on how to position the product in the market.

Lastly, based on theresearch, certain conclusions are drawn and recommendations made

on how best to utilise the power of the Orand for creating and sustaining long term

competitive advantage.

TABLE OF CONTENTS

DECLARATION iii

DEDICATIONS iv

ACKNOWLEDGEMENTS v

ABSTRACf vi

TABLE OF CONTENTS vii

LIST OF FIGURES xi

LIST OF TABLES xii

LIST OF ANNEXUR.:S xiii

vii

CHAPTER 1:OVERVIEW/INTRODUCTION

1.1 BACKGROUND

1.2 PROBLEM STATEMENT

1.30BJECfIVES

1.4 HYPOTHESES

1.5 DEFINITIONS, CONCEPTS AND CONSTRUCfS

1.5.1 Additive

1.5.2 Brand

1.6 LIMITATIONS

1.7 VALUE OF RESEARCH

1.8 METHODOLOGYIRESEARCH DESIGN

1.8.1 Research Method

1.8.2 Qualitative or Quantitative

1.8.3 Data Collrction

1.8.4 Da.a Analysis

1.91AYOUT OF RESEARCH REPORT

CHAPTER 2: Tiff; MAKING OF A BRAND

2.1 THEAIM OF CHAPTER

2.2 ADEFINITION OF BRANDING

2.3 COMPONENTS OF TilE BRAND

1

3

3

4

4

4

4

5

6

7

7

7

8

10

10

11

11

12

2.3.1 The Traditional Paradigm

2.3.2 Brand Architecture

2.3.3 Brand Soul

2.4CUSTOMER R.:LATIONSIIIP MANAGEMENT

2.4.1 The New Paradigm

2.4.2 Advertising in Brandbuilding

2.5 BRAND EQUITY

2.6 SUMMARY

CIIAPTER3:

COMMERCIAL MARKETING, LATEST PERSPECTIVES

3.1 TilE AIM OF TilE CHAPTER

3.2 PORTER'S FIVE FORCES MODEL

3.2.1 The Risk of New Entry by Potential Competitors

3.2.2 The Bargaining Power of Suppliers

3.2.3 The Buying Power ofBuyers

3.2.4 The Competitive Forte of Substitute Products

3.2.5 The Degree of Rivalry Among Established Companies

3.3 MARKETING MIX, TIlE FOUR P'S

3.3.1 Product

3.3.2 Price

3.3.3 Place

3.3.4 Promotion

3.4 RELATIONSHIP MARKETING

3.5TilE FOUR R MODEL

3.6 ORGANIZATIONAL BUYING BEHAVIOUR

3.7 ELECTRONIC REPLENISIIMENl'

3.8SUMMARY

CIIAPTER4:

TIIESOUTII AFRICAN MARKET AND ENVIRONMENT

4.1 TIlE AIM OF TilE CHAPTER

4.2 LUBRICANTS IN AFRICA

\-iii

lZ

14

17

18

18

21

22

23

25

25

26

27

28

29

29

31

32

33

33

34

35

36

38

44

45

47

47

4.3 TilE SOUTII AFRICAN LUBRICANTS INDUSTRY 48

4.3.1 Lubricants Manuradu~ 49

4.3.1 Distribution and Logistics 51

4.3.3The Automotive Lubricants Industry 51

4.3.4Comparative 1100 Brands 57

4.4 MARKET SEGMENTATION 63

4.5 EFFICIENT CONSUMER RESPONSE 64

4.6 SUMMARY 65

CIIAPTf:R 5: TilE RESEARCH DESIGN

5.1 TilE AIM OF TilE CIIAPTER 67

5.1 QUALITATIVE AND QUANTITATIVE RESEARCH PARADIGMS 67

5.3 PREVIOUS RESEARCH AND NEW RESEARCH REQUIREMENTS 69

5.4 SAMPLE DESIGN 71

5.5 RELIABILITY AND VALIDITY 74

5.6 QUESTIONNAIRE DESIGN 75

5.6.1 The Questionnaire 76

5.6.1 Conjoint Analysis 79

5.7I1YPOTHESIS TESTING 80

5.8 SUMMARY 81

CIIAPTER 6: DATA ANALYSIS AND INTERPRETATION

6.1 TilE AIM OF TilE CIIAPTER 83

6.1 SAMPLE COMPOSITION 83

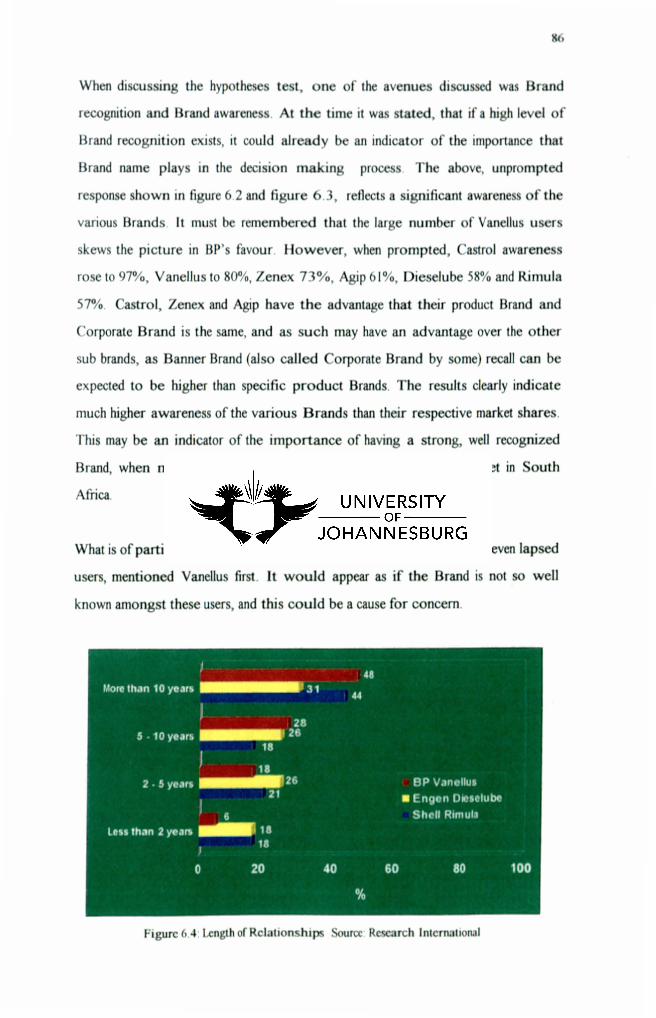

6.3 BRAND AWARENESS 85

6.4 PRICE 88

6.5 PRESENTATION 90

6.6 PROMOTION 90

6.7 CUSTOMf:R Rf:I.ATIONSIIIP MANAGEMENT AND

TECHNOI.OGY 91

6.8 RANKING OF BRAND ATIRIBUTES 93

6.9 CONJOINT VALUEANALYSIS 94

6.10SUMMARY 97

CIIAPTER 7: CONCLUSIONS AND RECOMMENDATIONS

7.1 TilE AIM 0 ..' TilE CIIAPTER 99

7.2 IIYPOTIIESIS TESTING 99

7.2.1 Observed Validity 100

7.2.2 Regression Analysis 100

7.2.3 Conjoint Value Analysis Utility Ranking 101

7.2.4 The Chi-Square Goodness of Fit Test 101

7.3 RESEARCH CONSTRAINTS 104

7.4 CONCLUSIONS AND RECOMMENDATIONS ON BRAND 105

7.5 CONCLUSIONS AND RECOMMENDATIONS ON MARKETING

~U~ 1M

7.5.1 Customer Relationships and Information Technology III

7.5.2 Current Usen 112

7.5.3 Lapsed Users 113

7.5.4 Non-Users 114

7.6 TilE FUTURE 114

7.7 SUMMARY us

BIBLIOGRAPIIY 117

UST OF FIGURES

Figure 1.1: Market Overview

"'igure2.1: The Function of the Brand for Buyen and Sellen

Figure3.1: Porter's Five Forces Model

Figure3.2: Marketing Mil Model

Figure3.3: Comparative Growth of Various Communications Media

Figure4.1: Lubricants Demand in Africa

Figure4.2: Commercial Vehicle Sales

Figure4.3: Lubricants Market Share, Commercial Only

Figure4.4 : Lubricants Market Share, Including Retail

Figure4.5: Diesel Lubricants Positioning Matrix

Figure6.1: Sample Composition by Market Segment

Figure6.2: Spontaneous Brand Awareness, Fint Mention

Figure6.3: Spontaneous Brand Awareness, Total Mention

Figure6.4: Length of Relationships

Figure6.5: Brand ImageVanellus, All Respondents

Figure6.6: The Price Ladder

Figure6.7: Vanellus Price Perceptions

Figure6.8: Packaging Perceptions

Figure6.9: Advertising Awareness

Figure6.10: Current and Preferred Methods of Ordering 1100 Oil

Figure6.11: Current an Preferred Methods ofContact with Supplier

Figure 7.1: Brand Knowledge by Manufacturer

Figure7.2: Areas of Under Performance

Figure7.3: Artas of Under Performance continued

Figure7.4: Reasons for Switching Brands

Figure7.5: Methods ofSourcing Oil

1

13

16

34

44

47

51

55

55

61

84

85

85

86

87

88

89

90

90

91

91

.. 105

107

107

109

110

xi

LIST OF TABLES

Table 2.1: Architecture or Added Value

Table 3.1: Market Share or Lubricants Majors

Table 3.2: Importance or radors in making buying dtcisions

Table 3.3: Influences in the buying decision

Table 3.4: Sources used in keeping up with market trends

Table 4.1: Automotive Lubricants Sales Volumes 1994 to 1998

Table 4.2: IIDD Oils,Comparable Brands

Table S.I: Sample Breakdown, Project Shuttle

Table S.2: Market ShartlElptcted Users in Sample

Table 6.1: Sample Composition in Terms or Users

Table 6.2: Position orDecision Makers

Table 6.3: Brand Attributes Ranked in Order or Importance

Table 6.4: Utility Ranking for Total Market

Table 7.1: Observed Usen or the Brand

Table 7.2: Amended Table of Expected Frequency of Users

Table 7.3: Calculation of the Chi-Square Statistic

15

JO

41

42

42

53

58

73

81

83

84

93

97

102

102

103

xii

· jii

LI T

Turno -r lid olume I'i ur

i nne IIr

/ 1111 IIr 8 :

i 0 Po ilionin Iri

/ nil ure : T hni lOla ih

1111 ur D: lilil Ibn ill

An ne IIr ion Allal

Ann IUt 4 pl in d

ion 7 '() b

ord, indow 9. e ion 7.

QU tionnair

umm

~ () RO 1 ith Qu lionn ir lind II urv R ult

.·0 rl)oinl for indoI) ' lid . ' ho on Findin J

2) Proj hUIII .

) Proj huttl abl

) UP ' Proje t huttl

) Proj . I huttl oplin

I nn ure

CHAPTER 1

OVERVIEW/INTRODUCTION

1.1 BACKGROUND

The research is intended to have a practical application. The student is employed in

South Africa as Automotive Lubricants Marketing Manager by DP Southern

Africa, one of the major global petroleum companies. A substantial amount of

Business Process Re-engincering took place in this company in 1999, and

numerous departments were restructured, downsized and then re-focused on a

sector based approach. Very recently this company also bought the Burmah

Castrol Oil Company, oneof the leading Brands of lubricants in the world.

Prior to the acquisition of Castrol, the company was not seen to be a lubricants

focused organisation, being better known as a major player in the petroleum fuels

industry. Whether this perception is justified or not, the company is very

innovative and in 1999 launched the first application branded lubricants range in

South Africa, namely the Visco range ofautomotive oils. This range is unique, as

it takes the guesswork out of picking the right oil for the consumer's vehicle. The

container clearly shows a picture of the vehicle it is intended for. As such, one gets

on oil for older vehicles, Taxi's, 4 x 4's, Sport vehicles, Diesel vehicles and an oil

for light delivery vehicles. (See Annexure Afor a positioning matrix of this range

ofoils.)

Part of the range oflubricants supplied by BP, is a veryspecific range ofdiesel oils,

branded Vanellus. Vanellus is an oil designed for application in heavy duty diesel

(1100) vehicles, from light commercial to extra heavy transporters and off-road

vehicles.

During 1999, the company lost a substantial volume of sales on the Vanellus

range, in excess of 900 000 litrcs, at a substantial loss of contribution to the

company (Sec Annexure B for actual figures).

Th purp • of this r r h i ' th r fold: Firul , t d I rnun thi

10 's of bu in s, lookin riabl s of th III r ·tin rni appr h n

Br nd nd 1 md

nd thirdl , t u

h.th

po itionin J pi

Th pr du t. rc hi hI t hni I, hn i

sp ilk uion , a ' pr s ' rib d b numb r of t stin 1'1 iliti s, th II n n

being th urn In lustry (API) r lin (. ' 1lI1 ' , ur f n

xampl or r hni al sp .cif u ions ).

Over md abov this, th n III :.quipm III M nu f turer ( ~M ' s hay

sp cific r

list th pr dUCI in thoir b

vchicl "

t or ' ,C d in order for th m to

pprov d pr ducts that can be u. d in th ir

omp titi n is fierc , and in uth frica th r ar 7 major who d Jar th rr

figur and about a hundred mall bl nd r. and fill rs of lubricant .

rk t 0 e rv icw U Amoro

.., ' ·. Il - jl,.- --" '-..-

1,,·•• <--_ .". .

- -- ~---::---

i 1

... . - . J

b ll" I I

A, n Ill. r r m in d irtu 11

tatic

d linin

r th I I upl

dr in.

ov r 11 m r

min Ion r th qu lit f lubri nt r

3

continuously improving. A loss of substantial volume is thus of major concern to

any ofthe players in the industry.

This study shall look at the power of the Brand in the decision making process,

consumer behaviour in the commercial context as far as the Brand is concerned,

the traditional 4Pmarketing mix and its role in Brand building, the more recent 4

R marketing mil', the integrated solutions approach and the actual needs and

requirements ofthe commercial consumer ofdiesel automotive lubricants, and how

BP/Castrol can best satisfy those needs and further enhancelbuild these Brands. Of

particular interest would be a question included on a guarantee against engine

breakdown, should the prescribed oil be used, and if this will influence the

purchasing decision and further enhance the Brand.

1.2 PROBLEM STATEMENT

To determine the reason for the volume loss of Vanellus and how this can enhance

the Brand to better meet consumer's needs.

Identify ways and means to improve the Brand proposition, in order to attract

more customer loyalty, enhance its Brand equity in the process, and increase sales

and market share.

I.J OBJECTIVES

• Identify extent and cost ofvolumeand contribution loss tothe company.

• Investigate and analyse the South African commercial lubricants market.

• Determine the key drivers that influence the purchasing decision and that make

up the overall Brand image.

• Make recommendations and reposition the Brand in its optimum position, based

on the research findings.

..

1.4 IIYPOTHESIS

The hypothesis would be that Brand name is a significant criterion in the decision

making process when procuring HOD oils in the business to business environment

in South Africa.

1.5 DEFINITIONS, CONCEPTS AND CONSTRUCTS

1.5.1 Additive

• Additive: Any material added to base stock oils to change its properties,

characteristics or perfonnance.

1.5.2 Brand

• Brand: (Kapferer, 1992: 15 - 20), says the following:

A Brand is both the memory and the future of its products. A Brand

becomes credible through endurance and repetition. By creating satisfaction

and loyalty, the brand enters into avirtual contract binding it to the market.

A Brand is not a product: it is the product's source, its meaning, and its

direction. The primary capital of many businesses are their brands. Brands

are the only truly international language • a business Esperanto.

According to him, it is necessary todefine what the Brand infuses into the

product orservice, and how theBrand transforms it:

• What attributes arc embodied in the productor service ?

• What advantages does it incorporate 1

• What benefits docs it provide?

• What obsessions docs it represent?

• User; The users will be those who respect the product's values. culture.

and personality.

When an audience can visualise all six dimensions ofthe Brand, the Brand

is deep, otherwise it is shallow..

• Brand: (Koller, 1997: 443). says:

A Brand is essentially a seller's promise to consistently deliver a specific set

of features, benefits and services to the buyers. The best Brands convey a

warranty ofquality. But a Brand is even a more complex symbol. A Brand

can convey up to six levels of meaning:

• Attributes

• Benefits

• Values

• Culture

• Personality)

(• (Dickens, 1998: 11), Describes Brand as follows:

A Brand is a name, Brand equity ist~that name. Brand loyalty is

"- ----built onquality, price, image and service. all elements that constitute value.

~~~~ the value in and ~f a brand. Brands and Intellectual

Properties are intrinsically linked. Without Brands, a company is nameless,

without a name a company has no equity. without equity you can not build

customer loyalty. Nobody knows your quality; one cannot assess your

value. You have no image and can offer no service..

1.6 LIMITATIONS

BP Vanellus users are spread throughout South Africa, over a wide geographic

area as well as over a wide variety of segments. These segments include

workshops, fleet operators. construction, mining. agriculture, marine. forecourt

top-up, resellers, high street retailers, do-it-yourself mechanics and original

equipment manufacturers.

6

As set out in the research design section that follows later, the survey covered

large, medium and small fleets in thethree major geographic areas of Cape Town,

Durban and Johannesburg.

By the very nature of the complexity of the interviews, the potential sample size

and the geographic area, there were serious financial constraints.. The cost of this

survey was capped atR 120000.00

1.7 VALUE OFRESEARCH

Leedy (1997: 189), says that causal comparative research describes relationships

between something that occurred in the past and subsequent responses. The intent

isto uncover possible cause-and-effect relationships among these phenomena.

These variables, which include amongst others, quality, specifications, economy,

preventive maintenance qualities and technical performance, also include "soft"

variables like relationships between businesses, service provided, risk aversion,

references and reassurances, and realised performance.

The research has also investigated all the latest thinking in terms of commercial

marketing, investigated the available models and highlighted relevance to the study

undertaken.

By making use of the survey findings and conjoint analysis, it was possible to re

position Vanellus in its optimum marketing position.

In conjunction with all of the above, it was also possible to make very positive

recommendations to overcome existing weaknesses, to meet consumer needs and

to recapture lost sales volumes and market share.

7

Ultimately the research , survey and recommendations can be incorporated in a

fuUy fledged Marketing Plan for np Vanellus. That does, however, faU outside tho

scopeofthis research document.

1.8 METIIODOLOGV/RESEARCII DESIGN

1.8.1 Researeh Method

As this research isbased on known variables that can beapplied in different ways

in tho market place, the research can be classified as applied research. Its findings

wiU be used to manage the Brand and range of products better, to re-position the

Orand and to formulate a new marketing plan. AU of this puts it in the applied

research category, in contrast to basic research which is abstract and is used in

subjects like mathematics, chemistryand physics.

1.8.2 QUllitativeor Qu.ntUative

Quantitative research consists of thosestudies in which the data concerned can be

analysed in teons of numbers. Quantitative research is based morc din:ctJy on its

original plans and its results are more readily analysed and interpreted (Dm and

Kahn, 1989: 89·90 in Blaxteret aJ., 1996).

The questionnaire is designed in such. way that the findings can be expressed

numerically, thus making statistical analysis possible. As it is also dealing with a

Orand, an intln8lblc, some open ended questions will be included, questions that

will have to be analysed through personal judgement by experts in the panicular

field (ChisnaJl, 1981: 170).

As • whole, the research design is more quantitative than qualitative, no one-to

one discussions, group discussions, psychometric - or psychological testing wu

conducted.

8

1.8.3 Data Colltction

A personal interview was held with respondents, using a customised and pro

tested questionnalre. This primary data was then analysed and presented in figure

and table form, with conclusions drawn from it.

As far as researching the South African Market and environment is concerned,

desk research using secondary data was conducted. Books, trade journals, the

Internet, company records and internal data sources were utilised.

1.8.3.1 Population and sampling techniques.

The universe is all businesses in South Africa that operate vehicles powered by

diesel engines.

Sample sizeplanned is 2S0 respondents.

BP has comparative customer records ofall customers who purchased Vanellus for

1998 and 1999. The sample population will be 100 current customers taken from

this list, 7S lapsed users and 7S companies who do not appear on this list, that is,

fall in one of the required segments, butare not currently BP Vanellus users

The initial selection criterion for the users will be according tovolumes used.

Less than 1000 litre per annum: small user.

Between 1000 and SOOO litreper annum: medium user.

More than SOOO litre per annum: large user.

From this, thefollowing stratification ofthe population will be done:

Long distance haulien, heavy dutylJight vehicles.

Short distance haulien, heavy dutylJight vehicles

Workshops for the above.

Agricultural Co-operatives

9

Mining

Construction

The sample will beweighted to include 60010 larger customers/users. 200.10 medium

usersand 20% small companies.

Over and above mining and agriculture, that has to be sampled at geographic

locations nonnaJly outside cities. research will be concentrated around Cape Town,

Durban and Johannesburg for ease of data collection.

Chisnall (1981: III), states that stratification of population in sample design

involves stratification or division of the population to be surveyed into groups

with characteristics identified as relevant to the needs of the particular survey.

From these strata and the known non-users of the product, a quota will be

selected for interviewing.

Quota sampling is a form of judgementsampling in which the biases arising from

the nonprobability method of selection are controlled by some extent by

stratification and thesetting ofquotas for each stratum (Chisnall, 1981: 81).

1.8.3.2 Datacollection techniques

Ultimately primary data was collected through personal interviews with 233

respondents using a customised. pilot tested questionnaire. The interviews were

done by trained professionals, employed by a bona fide research company of note.

This ensured impartiality and neutrality. It also greatly enhanced the validity of the

research, as the same format and fonnula can be used again in future and it should

produce similar results. It is intended to set a benchmark through this survey as far

as brand tracking and brand recognition is concerned, so that future efforts can be

measured against this base. Telephone screening was conducted and appointments

made for the interviews with bona fide decision makersin the company.

10

1.8.4 Oata Analysis

Statistical measures were used to test the hypotheses and certain other variables.

but in the main lhe research results are more descriptive, expressed in graphs of a

comparative naiure and showing correlations between the major players in the

market. Finally, conjoint analyses is used toshow the best possible positioning for

BP Vanellus, laking all the variables into consideration.

1.9 LAYOUT OFTilE RESEARCH REPORT

Sec Index and Tables ofContent.

11

CHAPTER 2

THE MAKINGOF A BRAND

2.1 TilE AIM OF TilE CIIAPTER

This chapter, the first of the literature review section, reviews what has previously

been published about Brands. It will consider all the attributes ascribed to Brands,

objective and subjective perceptions about Branding, its various components and

the role it plays in adding value to the prOduct and the company. It is extremely--important to understand exactly all the meanings and connotations of the Branding

. _..~.~. -- -- .~ ._,--...-_., .. ~-_. _._--~.--_._- ....

concept, ifoneis to study its importancein the buying scenario......,._. - ". ~ ..,.~._ ... _.

2.2 A DEFINITION OF BRANDING

I Hankinson and Cowking (1993: I), define a Brand as a product or service made

distinctive by its positioning relative to the competition and by its personality. Its

positioning defines a Brand's point of reference with respect to the competition

whilst the Brand's personality consists of a unique combination of functional

attributes ~~s;~~~~ Collectively, the positioning and Brand--personality

are termed the Brand proposition. This constitutes the starting point for Brand

managers charged with the responsibility ofdeveloping and/or maintaining a Brand

in the marketplace.

Also see 1.5.2: 4 for more definitionsof Branding.

In developing and maintaining a Brand, you need to have a simple proposition._-_._---_._----._--------which is easy to understand. Brand propositions which are complicated or

inconsistent, will have little chance of success ( Davidson, 1987 ).

Wilson (1999:3), states that Branding and the strength of brand-person relations

may be one of the last domains of sustainable competitive advantage for firms. It is

12

hard to replicate another brand's personality and copy the traits and meaning

developed over time from a successful Brand relationship. Once a Brand

~ relationship isestablished, it is very hard totake away: if you don't believe it, try to

~0( change your grandparent's political beliefs. He continues: Trends, such as

~:'\' ~~, increasing product and service diversity, increasing global competition, accelerated

~ '\:'f' (" product life cycles, converging product quality, increased technological parity and

~)" the escalation ofbuyer power, have helped contribute towards shifting the focus

towards branding issues.

From the above it isalready clear that a Brand is a very complex issue. It is not

merely made up from a number of product attributes, a name, logo and slogan; it- '-'-----"'-

also contains "soft" elements like a personality and values, and this personality is

made up by emotional and self-expressive benefits.

2.3 COMPONENTS OF THE BRAND

N 2.3.1 The Traditional Paradigm(l\

Pitt (1998: 95), states that the quintessential function of Branding is to create-----_ ... _- .---

differences between entities with a similar potential forneed satisfaction. From this._",---- --, "-"-' - --_.- _.._._~ --,-----_._---

primary distinction a series of utilities or benefits emerge for both buyers and~._---" _._- ----_._.- ....__ . ------------._-_..._---------- -,-

sellers. He uses the figure2.1 below to summarise the benefits for both parties. For

buyers it performs the function of reduction. It reduces search costs, it reduces the~ _.- - -~ .-.. ----- -

buyers perceived risk, and interestingly, the buyer is considered to receive certain

psychological rewards by purchasing Brands which symbolise status and prestige,

thereby reducing the social and psychological risks associated with owning and

using the wrong product.

The sceptic may say that this does not apply in commercial procurement, but as

will be evident later in the research, more than sixty percent ofthe buying decision

is ultimately made by one person, and then psychological factors can come into

play

1101101nd,

- -- - ---- ..- -

l"i UN 2.1 : I"uSou 101

lSu)"Q and SelInAppra8dI U'. P

lEC

Pitt ( I ), I I that th r nd p rfonn Ih fun

t n d 10 b P rf rm d,

2 I) il fi ili t I

fimili IN I th m) , nd

n b n blin th

Dr nd It

t m r up,

rt ntl , Br nd f ilit t pr mium

r lu th

c h r nt m

ih m Dr nd i.

pri in b

pr du I r m b

parti ul rl imp rt nt in pr du t

14

buying behaviour. He sees the Brand as a symbol around which both parties can

establish a relationship.

His viewsstill hold true, but other authors expand quite considerably on this basic

paradigm. Some ofthis thinking is reflected below.

2.3.2 Brand Architecture

Architectural thinking on Branding as a core value adding process suspends

judgements onmany conventional rules ofthumb which applied when Brands were

operated as separate empires within a corporation. Architecture links Brand

identities - for example corporate Brand and product sub-brand - so that both

endorse each other, and play different leading roles in fonning stakeholder

relationships and earning customer loyalty.

2.3.2. I Business Wide Brands

Uncles (1995: I), has some very interesting insight into this. He proposes that the

number of standalone Brands must be reduced and moreequity must be invested in

business-wide Brands and less in products. "We need to re-learn what Brand

marketing is all about and we need to elevate marketing to ensure that there is

widespread participation in the process of adding value." The organisational

implications orthis are dramatic and challenging (www.b).

Table 2.1 clearly points out that Branding should no longer be product focused,

but should reach far wider, encompassing the total organisation and all its people,

with everyone focused towards a common goal, that of adding value to the total

business through service and support to the customer. Brands should also be

leveraged to maximise goodwill between linked Brands. Permanent double-branded

linkages between different levels of Brands should be developed so that over time

both Brandsgain from the other's goodwill.

T bl • _. I: r .hite ture of Add V ilu • Melnet, 6

2..2.2 Lea lJ'S of Brandin

Th ne t cone pi entail ari u league of Branding. gue of Br ndin II u

the purp whieh a particular Br nd i aiming 10 fulfil. The tru tur I c n i

of h. rt 'ring i de ign d to

wor In n the me goal . Th ide of Brand lea u

Br nd' ult in

ppo it d

• if

d

• Ih

nd I I, on 111 di nl

• th Br ndin

• th

di iplin d

(

16

2.3.2.3 Brand Architecture at Work

Aaker (1999: 3), at a Brand Summit had the following to say about Brand

architecture: "There are three mistakes that companies make when it comes to

Brand architecture.

The first is the 'Brand is an island' trap. A stand alone Brand is a wasted

opportunity. By launching sub-brands and endorsed-brands, a company increases

its presence in the market while eliminating any chances of cannibalisation". Aaker

(1993), proposes that the value entry ismade as distinct from the master Brand as

possible.

The second Brand identity trap is the external perspective trap. When a company is

intent on selling to external customers, it forgets all about creating a clear Brand

identity within the organisation. As a result, the staff are not able to identify, and

communicate, the heart of the Brand.

The third trap is the company's fixation with the product attributes. Companies

should expand the value proposition and bring emotional and self-expressive

benefits into playas well. Features can be matched by the opposition every day.

There are four ways of projecting a Brand: as product, organisation, person or

symbol. While product attributes can be matched, intangible benefits can not

(www.d).

2.3.2.4 Human Characteristics of the Brand

Americar car marketer Saturn is a Brand that derives its image from the values of

its organisation. Then there are a whole slew of Brands that come across as a ~ ..

bundle of human characteristics: Harley-Davidson (macho, male, freedom),

Anderson Consulting (competent, confident), Virgin (meteor-like, underdog, but

energetic) and many more. Turning to symbols, there is the Michelin man, the Nike

Swoosh and so on.

17

Aaker (1999), summed up byadvising the audience to look for emotional and self

expressive benefits. They make for a much stronger relationship with the customer.

Mike Lipkin, a well known South African Motivator, propagates that people make----_.

decisions on emotional grounds. then justify them withlogic.-~ ~- _..- -~--

In an unpublished paper. Prashun Dutt (1998), says that the role of familiar

Brands in reducing uncertainty may be salient with customers seeking security.

This aspect will be addressed under the new marketing variables of risk aversion

and realised performance in the next chapter.

2.3.3 Brand Soul

Wickens Tutt Southgate, a London based Brand agency. are evolving a manifesto

for a radical new approach to Brand marketing. Their approach of Brand Soul

questions whether the Brand fully realises the concerns of marketing to literate

consumers. They integrate visions. values and passions as a necessary condition in

organising campaigns for real Brands. This represents a synthesis ofmany schools

of thought about people. drawing particularly on the work of pioneers such as

Carl Jung (Man and his Symbols), Stephen R Covey (Principle Centred

Leadership), and Gary Zukav (the Seatofthe Soul) (www.cc).

The sourcesof Brand Soul arc threefold: Culture. Context and People.

• Values draw on historical company Culture

• Vision draw on future Context (Consumers, Customers, Competitors)

• Passion draws on the present-day team ofPeople

The company culture within which the Brand is managed gives a Brand its noons,

rules and paradigms, in other words, its values. The passions of the people

currently involved with the brand (all of them, not just those in the marketing

department), represent the drives and energies behind the Brand. Finally. the

IS

marketplace context (in terms of consumers, customers and competitors), give rise

to the Brand'sdrive in defining and constantly updating itsvision.

The aim is no longer to build Brands however the consumer wants them. but to

build Brandswhich truly live up to their full potential. This potential will always be

far greater than customers would ever have imagined. It involves a completely

new. and much more inspirational. set ofstrategic planning techniques (www.a).

The article continues by stating that the next step is about Brand Realisation.

Brand Realisation isconcerned with the "reality" of the Brand - with the Brand as

the customersees it, touches it. uses it and interacts with it. It is about creating and

developing the living embodiment of the Brand's Soul through the reality of

products. services, packaging. 3D environments and everything else by which the

Brand is made physically manifest. It is Brand building at its most holistic

(www.a).

This concept is gaming ground. specifically in qualitative research, where

respondents in focus groups are often asked how they perceive the product or

company as a person. often with interesting results.

2.4 CUSTOMER RELATIONSHIP MANAGEMENT

2.4.1 The New Paradigm

Two outstanding features highlighted so far are the need for emotional appeal to

the customer's own aspirations towards self-aetualisation and the absolute

necessity of impeccable service. In America service is part of the paradigm; in

South Africa it is still sadly lacking. The latest developments in information

technology can help to overcome this. as to a large extent it eliminates the people

factor, and ineffective people can seriously harm the Brand. Through electronic

data interchange and seamless just-in-time supply streams. customers can be tied in

with their suppliers. thus raising barriers to exit and cementing relationships.

19

Moore, (1996: 2- 3), quotes the following real life example:

Part of the genius of Wal-Mart's ecosystem was also its unprecedented

involvement and entanglement in the affairs of its suppliers. By 1984 Wal-Mart

began exerting heavy pressure on suppliers to keep their prices down. Moreover,

Wal-Mart compelled its suppliers to set up cross-company infonnation systems to

obtain maximum manufacturing and distribution efficiency. In 1987, Wal-Mart and

Proctor and Gamble reached an unprecedented partnership that involved extensive

electronic ordering and information sharing between the companies,

2.4.11 Just in Time Concept

Rexha (1998: 2), explains the just-in-time concept very well. Based on strong

functional links between big Brand owners and their suppliers in a system of

networked organisations, the Japanese developed highly efficient collaborative

buyer-seller relationships, highlighted by the just-in-time manufacturing system and

earlier supplier involvement in customer innovation efforts (Blenkorn and Noori,

1990~ Dion, et al, 1990; Turnbull, et al, 1992). Aiming to follow this path, Western

firms are increasingly interested in the Japanese model of buyer-seller co-operative

relationships and they make efforts to implement them in their own environment.

2.4.1.2 Information Technology

Towards this, information technology is playing an ever increasing role. McCann

(1995: 18), explains: "Brand managers spend their time studying consumers and

working with advertising agencies to find and communicate the right image for

their Brand". Since advertising is a means of establishing a strategic competitive

advantage, marketing managers make sure they understand how it works and how

they can usc it to their advantage. The target of the majority ofa Brand's budget is

usually the customer, not the consumer, When the target shifts to the

retailer/reseller, the usc of information to enhance the product becomes even more

important. But this time, the advertising agency is not the key partner in product

enhancement, it is the IT professional. Marketing programmes aimed at the

20

customer are becoming computer dependent becausethe computer is the means by

which information is attached to the product. In Computerworld (1994: 133), a

marketing manager describes how he was able to achieve Brand growth by being

tops at delivering actionable data. In the eyes of the customer, the Brand is clearly

enhanced when marketing managers can provide information on how the customer

can use the Brand to increase profits. This inevitably raises the issue of the Internet

and its roleas a channel to market and a medium to build the Brand.

2.4.1.3 The Internet

Lindstrom (2000: 3), sees the Brand as the gateway to the Internet. He says that

for many users, Brands will act as a trusted consumer guide to the Internet, a

development that will make greater demands of the online Brand. And this might

be the off-line Brand's survival kit. One of the emerging problems of today's

Internet world is the lack of trust consumers have in web sites and online Brands.

One cannot buy goodwill and trust - you earn it over time. This means that trusted

Brands have a free ticket to consumer trust on the web while the online market is

still immature. It isnot surprising that online consumers tend to visit their preferred

main Brands on the Internet within a relatively short period of time, because they

already have a positive relationship with the product in the off-line world. Creating

a Brand is now easier than it ever has been. However, committing Brand suicide is

even easier, due to the inability to adapt tothe rapidly changing technology.

2.4.1.4 Off-line Brands

Off-line Brands lack interactivity. They are passive. Off-line Brands can only

communicate one way via television, print and radio. Online Brands 'listen' to the

consumer, learn from them and react based on the consumer's needs. This new

skill - this interactivity - is an online Brand's strongest asset. It enables the Brand

owner to fonn aone-to-one relationship with the customer hum-.dd).

21

2.4.1.5 Summary

The web's power to drive awareness, interest and action, give it attributes of both

an advertising medium and a sales channel. Customers may never visit a brick-and

mortar store, talk to a company or have physical contact with a particular product,

yet Brand preferences and choices have been made. In such scenario's, the Web

experience isthe complete Brand experience.

Lou Gerstner (www.e), from IBM warned that the new dot com companies (like

Amazon. com, Netscape. com) arc fireflies before the storm· all stirred up,

throwing ofTsparks. The storm that's arriving - the real disturbance in the force - is

when thousands and thousands of institutions that exist today seize the power of

this global computing and communications infrastructure and use it to transform

themselves.

2.4.2 Advertising in Brandbuilding

Rosenshine (1999), in a debate with Freeling, sees the situation asset out below.

Branding will move beyond traditional advertising to embrace a slew of media. In

other words, customer relationship management (CRM) is the future. This is where

agencies have a crucial role to play. Creating relationships is an area where

agencies hold the edge. It will take creative people thinking about consumers'

hearts and minds to dev~~p.J!!C? Brand images. And you will not find the creative

people at the consulting companies or at the dot-corns, one will find them at the

advertising agencies.

Freeling (1999), in the same article, sees it differently.

There are four new rules of Branding.

• The first is that, increasingly. there is little functional difference between---_.,~,,_._-~-_._._~----------

products. To surmount this. companies will have to co~e on functional... __ .,.~. -- .._---~.- .._.-

22

benefits (product attributes), process benefits (ease of purchase, servicing_.~ --_.~ .•. ----------

benefits), and relationship benefits.-• Two, a company will have to deliver the key touch points - basically, identify

the mo~~nts ~~e.~ the ~u:!~~_~r _r~quires assistance, and spring into action.

• Third, surround the customer with the Brand. Take greater recourse to non-._-->_._------~.- ..._--- ~_..-._ ..-._----_._,--_.__.__ ._-----

traditional -mcdill~~ Brand building. As the media fragments, trust in

advertising falls, and the Net takes eyeballs away from television, non

traditional media will come to playan important role in Brand building.

• Finally, there is permission marketing, where companies will forsake intrusive

marketing inorder to build a dialogue with the customer.

CRM focuses the Brand image on the current customer, who is more likely to

purchase any given product tomorrow. It is only a matter of time before marketers

will create the necessary databases that will fonn the basis for their Customer

Relationship Marketing exercises.

~ • Z.5 BRAND EQUIT\'

\,j \

Brand is called an intellectual asset in the management field and called an intangible

asset in the accounting field. Brands represent a certain quality and image

acknowledged in the market. The power ofa Brand derives from the fact that. as

soon as a customer perceives a Brand, it reminds customers of its quality and

image, and this fact gives rise to loyalty to a certain Brand or company (Gale,. -- . _. --------------------

1994). The essence of a Brand can be regarded as a source of an excess return

because oftheBrand 10~a1~JOkada, 1998: 2).

Cullman, stated as far back as 1982, that in today's environment, building strong.-._-- _.• _.-._--, ------

Brands and establishing Brand equity is becoming more and more challenging.

Increased pressures to compete on price, increased competition through product---

introductions and the fragmentation of advertising and market segments arc just a

2)

5ADlDhLQfthe preuures being faced by companies in today's highly competitive"-._"~'_._-_ .._~._.~.--._----

envirC?nm~t_ (www g)

The most important asscts of any busin~~~_ ar~i!'tan~~le - including its base of

loyal customers, brands, symbols and slogans - and the Brand's underlying image,--- - - ._. ...

personality, identity, auitudes. familiarity, associations and name awareness. These

assets· along with patents, trademarks and channel relationships - comprise Brand

equity, and arcaprimary source of competitive ad~a..!1tatte an~ f~!~r~.~rnings.

At least five general approaches to asscssing the value of Brand equity have been

proposed.

• Price premium that the name can support

• Impact of the name on customer preference

• Stock market valuation (in BP's Annual Report of 1999, net auets are given as

about $44 billion, yet Market Capitalisation exceeds $ 1SO billion)

• Replacement value ofthe Brand

• Earning power of the Brand

• The set of consumer associations and behaviours that permits the Brand to earn

greater volume or margins than it could without the Brand name (www.h).

Cravens and Guilding (1999:61), states that ultimately the success of any brand

valuation method depends on the firm's ability to use the measure to help improve

financial performance. Some suggest that the measurement of intangibles such as

brand value, human capital, and innovation power should take precedence over the

measurement of profits It is these longer-lasting assets of an organisation that will

traMlate to sustainable long term profits

1.6 SUMMARY

Thi, charter point, out that a nrand is made up of • "lUI mJmber of variables.

some tangible, but even more that arc intAngible A Urand is normall)' auoaatcd

with a name, symbol or slogan, but this purely serves to identify a product

24

Companies are trying to appeal to psychological motivators to establish an

association with the Brand. a sense of belonging. This is done by positioning the

product correctly according to its attributes. but also by giving it a Brand

personality. This personality stands for the values and norms. not only of the

product. but also of the company and its people. If this image is favourable. and

compatible with the customers aspirations, the purchase of the product is made

much more readily.

Products can be differentiated. even when considered to be an everyday

commodity. bygiving it a Brand soul. This allows for a premium price to be asked.

Even when the customer believes that he/she isdealing with technical products that

are all similar. subconsciously he/she will have a preference, a Brand hclshe best

associates with. And even in business-to-business marketing. sixty percent of

decisions aretaken by one individual.

Numerous ways exist to build Brand equity. but the latest focus ison relationship

building and the role information technology will play in growing and advancing

the Brand.especially as the Web develops as a newchannel to market products.

2S

CHAPTER 3

COMMERCIAL MARKETING, LATEST PERSPECTIVES

3.1 TilE AIM OFTilE CIIAPTER

In Chapter I thecomposition of a Brand was discussed. It was clearly shown that a

Brand does not simply consist of a product or range of products with certain

attributes, a name and an icon to identify it. Ogilvie and Mather, the global

advertising agency, uses the concept of three hundred and sixty degrees branding.

This simply means that the total presentation and communication of the Brand

must be consistent and be based on the Brand print or DNA of the Brand as they

call it. It is the unique set of values, personality, perceptions and resources that

makes up the customer's perception of the overall or so called corporate or banner

Brand (Makin, 2000).

It would thus make sense to look at and analyze all the levers that make up a

Brand strategy in order tounderstand fully how far the integration process must go

and to make meaningful recommendations at the end of this study. This will be

done by looking at the accepted marketing models, reflecting the latest thoughts

on these models and adding the impact of infonnation technology. Finally, The

study looks at buying behavior in the commercial environment, asopposed to retail

consumer buying. This need to be understood, as the traditional belief is that

Brand plays a lesser role in business-to-business procurement.

2.1 PORTER'S FIVE FORCES MODEL

Ifill and Jones(1998: 123), says that the Sforces that shape the competition in an

industry influence profits of the established companies in that industry. If we refer

to Porter's model in figure 3.1, one finds that these forces are: The risk of new

entry by potential competitors, the bargaining power of suppliers, the bargaining

..pm I' () bu I' • th rnp titi f ub titut pI' du I nd th

din , th

infl u /I III rk etin in th comrn rei I lubri nt

induu in • outh fri will b an ti t d.

comp 'Iit rs i bra rd 'I' til /I wh t

KOII-r, (I 7' 229), . th I th r /I of tu I nd P t nti I

lik -I

10 b· outdo n . b it. III rgin

comp niror s

rnp -tit I' or n w t hn ie. th n b it. urr nt

The t5 ForelS Driving Comp tlon:

Thr I of oowII' 11

I TRYCOMPETlTORS

8 8

Th t ofproducts ex

Fizu 3.1'

uuv d\ nt c:

. I ncr

3.2,1 'I , R ' of l e ./11 b t nli 1 , mp til

In . t imp rt nt pI' int til III I' I

reh h uld pr

I' h it d

th I'

thi. I'

rnrn rei I lubri nt '

Th purpo.

Dr ndin in th

I' n thi

27

Kotler (1997:230), describes this as Brand Competition. i.e. offering a similar

product and services to the same customers at similar prices. Following on this

definition, existing competitors would be: Shell, Castrol, Mobil, Caltex, Engen,

Zenex, Sasol, Total, Agip and Elf These would be the Industry Competitors in

figure 3.1.

Kotler (1999), also mentions industry competition which occurs when a company

sees its competitors as all companies making the same product or class of

products. In South Africa there are almost a hundred small fillers and blenders

servicing mostly niche markets. The barriers to entry arc low, especially if the

focus is on a small niche market. The major oil companies do however have

absolute cost advantages due to their integrated supply chain, infrastructure and

economies of scale. The lubricants business, contrary to petrol, is not regulated, so

this does not create a barrier to entry.

Black Economic Empowerment poses the biggest threat to existing oil companies,

as the market has traditionally been dominated by multinational oil giants. Under

the new dispensation in South Africa. it is the Government's intent, through

employment equity and redistribution of wealth to, rectify this situation. Every

lubricants business will be well advised to remember this and include it in their

strategic plan, especially as the main stream customer of the future will be Black.

This has serious but interesting repercussions on future Brand personality.

(Source: In-house minutes, 1999).

3.2.1 The Bargaining Power of Supplien

Because the supply chains of all the majors are almost fully integrated, very few

suppliers exert any influence over the big multinationals. They all have their own

upstream and downstream resources. It is vinually only the chemical additives

companies that supply any other components to the product, and theoil industry is

their lifeblood. The result is that there is parity on this attribute of the product, and

no competitive advantage can be obtained from this (fig 3.1).

28

An anomaly exists though in that the oil companies actually supply base oil to the

small nichemarket players at prices that allen allow them to undercut the powerful

big players, inorder to maximise production at the upstream refinery and to obtain

benefits ofscale (Reynolds, 2000).

With the addition of Castrol to the fold of DP, it will be interesting to see if the

company is now going to exert its power as a supplier, 8S it now has sufficient

market share to utilize full production capacity.

3.2.3 The Buying Power of Buyen (Figure 3.1)

The main buyers of lubricants in the industrial sector are original equipment

manufacturers, factories, mining, agriculture, marine and transport fleets.

According to Hill and Jones (1998), buyers will be powerful when they are few and

large in size, suppliers are many and small, buyers purchase in large quantities, they

can switch cost-effectively between companies or they can threaten to implement

vertical integration. Of all of these, the cost effective switch between companies

creates by far thebiggest threat. The market isextremely price sensitive and highly

competitive with all suppliers adopting a pragmatic approach to gain market share

(Reynolds, 2000).

The product is also very easy to compare, as it has to show technical

specifications, approvals and endorsements of OEM's. In most instances price,

and to a lesser extent Brand and support. become the differentiators. This

highlights the need of finding a more substantial differcntiator that will provide a

sustainable competitive advantage. Only CastroI seems to have established a

significant Orand presence that allows them to charge a premium price for their

product (Source: E-mirg, 1999).

29

3.2.4 The Competitive Force or Substitute Products (Figure 3.1)

There is no threat of substitute products at this stage. It is foreseen that

hydrocarbons will be with us for the foreseeable future. Products are continuously

improved and enhanced, but there are noother products that can perform a similar

function.

3.2.5 The Degree of Rivalry Among Established Companies (Figure 3.1)

The University of Oregon (www.i) gives a very comprehensive framework of

factors to be considered here. Amongst these are : The industry competitive

structure, demand conditions, exit barriers, high fixed costs, access to distribution

channels and a number more, all of which have to some extent, been covered

above. Some of the above do merit individual discussion.

The competitive structure of the industry is such that there is no interdependence.

Each has its own very elaborate, very expensive infrastructure. There is no

collaboration or collusion, the industry operates under total free market conditions.

Each of the majors are backed by enormous multinationals with substantial

resources, andall have as their objective tocapture market share.

Exit barriers to the majors are extremely high, as huge capital investment has been

made in refineries, tanks, blending and filling plants, pipelines, transport facilities,

distribution depots and other infrastructure. The Black Economic Empowennent

companies are looking at importing as much as possible rcady made product, but

the deterioration in the value of South Africa's currency makes this a somewhat

unviable proposition. The majors, who have an integrated supply stream, benefit

from upstream operations when the price ofcrude oil is high, as they can then sell

the unrefined product at high margins. Should the price of crude drop, they benefit

in the downstream operations as margins then increase on the refined lubricants

sold to the commercial market. The more efficient the logistical supply chain of

the oil majors, the more competitive they can become. As a result of the heavy

investment in infrastructure, all the companies have high fixed costs and they all

o

hav- I ' • 10 and u . th - un - d i tribution h nn I , 11 hould be ob u th t 11

th - lubri 11I1 companic need rn nhin 'Is ' 10 ti e th nu I comp 'Iili

(Rc nol ds, 20 0)

T ibl - , I: [arket h ire Lubri 1111 ijor " our " : UP 10 omp n

Sep.99 Oet,99 Nov-99 Dec-99 Jan·oo Feb-OOBP 1U1 13.11 11.93 14.60 14.23 15.38CALTEX 18.90 18.59 19.05 18.45 19.36 19.54CASTROL 10.40 9 .95 10.06 9.20 9.55 8.48ENGEN 22,57 23.66 25.25 24.89 24.77 23.81SHELL '23.29 23.61 23.28 21 .76 21.32 21.56TOTAL 9.48 10.18 9.13 10.19 9.64 10.06ZENEX 0.94 0 .90 1.30 1.11 1.13 1.18Total Market 100.00 100.00 100.00 100.00 100 .00 100.00

Dnnand conditions arc . u h, th t d pile a . Ii ht rowth in th gro dorn Ii

product, th overall demand i d rca. ing due 10 improvement in th qu lit of

lubricants and mbsequent Ion 'r dr ining interval "

A. n b een from tabl . I, although fluctuating within a p rccnl or . 0, th r

arc n i nificant change. in mar -t harc of th major if taken over a p ri d f

time,

Th obj hould thu b to in a long term u t inabl advanta . r . ult

of thi , th r arc devclopm nt III th markcl thr I ar n I covered b r '

model. Puri I rna rgue Ih I it ill fa ll und r

camp tit rs, \ hil I oth r III

ch n

add d I nt

Ih nd III u. f I hn

r I lion. hips, i. r ut I n to obt in nd III int III

mp titiv ad nu

Thi r liz d nd n d 10 form n int rip rt of n fiuur ( r nd

n.hip mark lin nd I hnolo \ ill di. u: din m r d pth in

31

the marketing mix in the next section. A major shill in the perception of the

fundamentals of marketing is taking place. The shifl is so dramatic that it can, no

doubt, be described as a paradigm shill (Kuhn: 1962). Marketing researchers have

been passionately convinced about the paradigmatic nature of marketing mix

management and the four P model as the basic foundation for all marketing

thinking and to challenge it has been as heretic as it was for Copernicus to proclaim

that the Earth moved (Kuhn, 1970: 149-1 SO).

3.3 MARKETING MIX, TilE FOUR P'S

Marketing, the way most textbooks treat it today was introduced around 1960.

The concept of the marketing mix and the Four P's of marketing - product, price,

place and promotion - entered the marketing textbooks at that time (McCarthy,

1960). It quickly it became the unchallenged basic model of marketing, totally

overpowering previous models and approaches. Other P's have from time to time

been suggested as additions. like people, physical evidence and processes, such as

the & P's model used particularly for services marketing (Booms and Bittner,

1982), and Kotler (1999), in the context ofmegamarketing, added public relations

and politics.

Lauterbom (1990:26), suggested that place becomes convenience, price becomes

cost to user, promotion becomes communication and product becomes customer

needs and wants. Although this has widened the scope of themodel, itwas evident

in chapter two that a Brand needs more than these attributes in order to create a

distinct identity, create brand equity and give it a sustainable competitive

advantage.

This section shall cover the attributes, but also substantially expand on the whole

marketing mix concept to include a number ofnew variables believed to be crucial

in the Brand architecture in order to achieve a strategic advantage.

32

In the market survey questionnaire respondents are asked to rank the importance

ofthe product attributes of the traditional four P model as well as new variables

such as relationships, risk management, references and realized performance,

For this reason, it is important that the product attributes that can contribute

towards the perception ofthe Orand, bediscussed and understood.

3.3.1 Product

The following product attributes are included in the questionnaire:

3.3.1.1 All season application (or viscosity)

This is an attribute easily met by opposition

3.3.).2Quality

This can be subjective or objective, objective in that the product must display

technical specifications and approvals, but effective Brand building. like Castrol, do

lead to certainsubjective preferences.

3.3.1.3 Engine protection

Increased power and performance, quality base oils, prevents breakdowns, protects

against rust and fouling of injectors, reduction of friction and wear, superior

lubrication. These arc all very basic attributes ofall lubricants, but once again there

are perceptions that certain oils pcrfonn better than others, and that is why it is

included. In Brand building perception isasgood as reality.

The following attributes arc measurable and quantifiable, and as such can provide

proofof being a superior product, therefore they are included:

• Extended engine life (in kms)

33

• Fast oil circulation (kinematic viscosity)

• Fuel savings (liters per kilometers)

• Minimum oil consumption (reducing number of top-ups)

• Reduces drain intervals (more kilometers traveled between oil changes)

• OEM specified (dealer approved oilchart),

Aseparate, detailed question then deals with packaging and labeling, its look and

feel, practicality, identification and ease of use, It tests thecustomer perception on

Drand presentation, the visible expressionofwhat the Brand stands for.

3.3.2 Price

Price can either be the initial price paid for the product, or it can bederived savings

as the result of the usage of a superior product. For this reason a number of

questions have been included on price: How important is it to be the best (initial)

priced oil ? Or a1tcrnatively have long term savings through the prevention of

breakdowns, by being reasonably priced or by being good value for money ?

These questions are intended to measure the awareness of thecustomer to the long

term benefits of using a superior product, rather than a short term trade-off on

initial savings on an inferior product.

3.3.3Place

In the commercial market this plays a much smaller role than in retail marketing

where visibility and availability is critical. Goods are often ordered unseen,

especially re-order merchandise, and these goods can be supplied from virtually

anywhere in thecountry, as a lead time normally fonns part of the supply contract.

For this reason one question was included on place, and that measures how

important availability is to the customer.....

3.3.4 Promotl n

n nd dv rti in . n - n

r B nd .

pI t nn f

n b m ur d.

i bliv d t b

nd

in Iud d to m

in t which futur Br nd building ff rt

lIinon

qu

Any mar tin PI di m h uld b w 11

notion th t th firm i be t off y d ining nd dir tin it tiviti ace rdin t

One can ily rgu that th f ur P ' of th m rk tin nux are not w 11 bl t

fulfi ll th r quir m nt of th mar ting can pt . Di on and Bioi :4 ).

explain : " Inde d, it would n

with a cu tom r' int ~ t (i. . m b dy for whom om thing i don), th

implicit in the Four P approach that the cu tomer i om body to wh m

om thing i don !" Although Mc arthy (1960), r cogniz the interactiv n tur

of th P' , th model it Ifdo not includ any interactiv I m nt . Furth rm r ,

it do not indicate th natur and

" 1I~ ......

, .It , ,

. .. . .. .. . Io.h ' .. . .. H'

Fi re .2:

u : Pri W Ier

Mi. 1.

Mnn:JgJcmcnl.(1 9:I )

R fI rrin t fi ur 3. 2, it i cI

of th our P m d I, th IT

th t n in thi m d m nd upd t d r i n

till pint in on dir tion, 1m impl in

35

unilateral action taking place. This model, designed by one of the leading

consultancies in the world, implies exactly the opposite, bringing into the process

loyalty and relationship management. According to PricewaterhouseCoopers

(1999: 14 - 16): "In some mature industries, or in markets in which many

competitors operate loyalty programs, Relationship.based solutions may be the

final available pathway to sustainable competitive advantage. Customer solutions

often need to be made to fit and they usually require an extensive exchange of

information between customers and value providers. This basically supports an

automatic interest for both parties in maintaining constructive and intimate

relationships".

The right hand side of the model (figure 3.2) , focuses on value driven activities

that aim to optimize the total consumption experience. This involves the

establishment of value-adding relationships with customers and the integration of

products andservices delivered through multiple channels.

In strategic terms, the left hand side of the model is about maximizing the

companies' customer share of wallet, whereas the right-hand side focuses on

achieving maximum customer share oflife.

This serves as the introduction to a new school of thinking, namely that of

relationship marketing.

3.4 RELATIONSIllPMARKETING

The concept of relationship marketing has emerged within the field of services

marketing and industrial marketing (Jackson, 1985: 120 - 128). The phenomenon

described by this concept is strongly supported by on-going trends. Gronroos

(1990: 18), in his book defines relationship marketing as ''marketing to establish,

maintain and enhance relationships with customers and other partners, at a profit,

so that the objectives of the parties are met". This is achieved by a mutual

exchange and fulfillment ofpromises.

36

Relationship marketing is still in its infancy as a mainstream marketing concept,

although it has established itself as an underlying paradigm in modem industrial

marketing. Kotler (1992: I). concludes that companies must move from a short

tenn transaction oriented goal to a long-term relationship building goal.

3.5 TilE FOUR RMODEL

Groundbreaking work was done by the Wits Business School in South Africa by

Abratt, Spence and Bendixen (1997). indeveloping a model that can explore new

marketing frontiers. adopting the relationship based approach, but also taking it

further. They postulate that knowledge products. that is products where a lot of

infonnation is required to understand properly. is not adequately provided for by

the FourP model. They suggested a new model. namely the4P • 4R framework.

While the traditional 4P's in the marketing mix can be seen to cover the

characteristics ofgoods and services relatively thoroughly. the same is not true for

knowledge products. Instead. 4R's appear to emerge as being the relevant

variables ofthemarketing mix. Abratt et al. (1997). propose the following:

• Risk management - to overcome customer's feelings of anxiety and minimize

the consequences ofmaking a wrong choice. This is specifically focused on the

customer and does not relateto reducing risk for the seller.

• Recommendations and references - endorsements by knowledgeable persons

because of the credence qualities of a product. This tends to hold much more

sway than traditional advertising.

• Rdationships - provision of long-term support through networks, alliances and

partnerships. This essentially involves the development of trust and

interdepency between thesupplier and the client.

37

• Realization of perfonnance - to ensure and re-inforce that the product has in

fact met its purpose. The essential element here is setting. managing and

meeting the expectations oftargeted customers.

Products that arc in essence goods or services rather than knowledgc products may

display the characteristics of knowledge products over some period of time. This

results from the fact that there is a knowledge gap between provider and user, the

former having a great deal more knowledgc about the nature and use of the

product thanthe latter.

Enough support for this model exists to justifY the inclusion of these factors as

cause-and-effect variables in the market survey. Questions on the importance of

these variables have been included in the marketing mix section of the

questionnaire, and their importance will be rated against that of the traditional

attributes. The questions cover amongst others risk management and realized

performance by offering a guarantee against engine failure if the product is used

correctly. It also explores the importance of customer/supplier relationships,

including preferred way of communication and order placing, even making

provision for totally electronic relationships, where all interaction takes place via

computers, versus the traditional one-on-one selling.

Calonius (1988: 86 - 103), sees the promise concept as an integral element of the

relationship marketing approach. A finn that is preoccupied with making promises

may attract new customers and initially build relationships. However, if promises

arc not kept, the evolving relationship cannot be maintained and enhanced.

Promises should be mutually given and fulfilled. This ties in very well with the

concept of realized perfonnance above. Promised performance will either be

realized or not after a certain period of timc hu elapsed, and fulfilling promises

that have been given is equally important as means of achieving customer

satisfaction, retention of the customer base and long term profitability. It is all

about credibility, a very important requirement ofa successful Brand.

38

Another key element is trust. The resources of the seller - personnel, technology

and systems· have to be used in such a manner that the customer's trust in the

resources involved, and thus in the firm itself, is maintained and strengthened

(Gronroos, 1990: 3·12). This ties up well with the risk management aspect of the

4Rmodel.

Moorman et aI. (1993: 3), define trust as a willingness to rely on an exchange

partner in whom one has confidence. If a customer believes in his supplier and his

products, he will also believe that risk will be minimized by his supplier·s

recommendations and products.

In support of the argument of 360 degree branding and the role of relationship

marketing in building the Brand. Wilson (1995: 335 - 345),has the final say: By

reviewing available literature studying factors determining success or failures of

relationships. Wilson selected twelve constructs that have both theoretical and

empirical support as focal variables. These relationship variables are: commitment.

trust. cooperation. mutual goals. interdependence and power, performance

satisfaction. structural bonds. comparison level ofthe alternatives, adaptation. non

retrievable investments. shared technology and social bonds. The constructs have

both an active time phase where they are very influential to the relationship and a

latent phase where they are still important but not under active consideration in

relationship interaction. The five stages characterizing the buyer-seller relationship

development process are; I) partner selection. 2) defining purpose. 3) setting

relationship boundaries, 4) creating relationship value. and S) relationship

management. The logical progression from here is to look at industrial buying

behaviour.

3.6 ORGANIZATIONAL BUYING BEIIAVIOVR

Alarge body of research indicates the importance of the buying center or decision

making unit. as it isalso called. in the vendor selection decision-making process.

Since the classic studies of the 1970·5 the buying center has been a focus for

39

examining vendor selection decisions (Webster and Wind, 1972~ Speckman and

Stem, 1979). However, even the early proponents of buying center decision

making point outthat many vendor selection decisions may be made by individuals

alone (Sheth, 1977), and Webster and Wind (1992), also stated earlier on that it is

the specific individual who is the target of the marketing effort, not the abstract

organization (Webster and Wind, 1972).

The question asked in this research is if the power of the Brand plays a role in the

decision making process of the decision making unit, or of the individual who

ultimately places the order. In today's society, every person fulfills multiple roles,

and inevitably that person will be exposed to the Brand outside the work

environment. If this happens, the person is bound to have some perceptions about

the Brand, and this, even if subconsciously, may have an effect when a buying

decision has to bemade at work. If enough individuals are empowered to make a

buying decision, this can have major influence on how commercial lubricants

should be Branded and marketed in South Africa.

Patton III (1995), in a research paper sets out how he conducted research with

431 industrial buyers in the United States. He found that 65.4% of these make

decisions as individuals, 19.3% make decisions jointly with the department and

15.3% makedecisions jointly with peopleoutside the department. The proportions

in each cluster, or decision style group, substantially match the results from

previous research that suggested that approximately two-thirds ofvendor selection

decisions are made by individuals (patton et al., 1986). After refining the date, he

amended the figures so that 56.90.Ic. ofall the vendor selections involved were made