The U.K. Investment Currency Market1 - IMF eLibrary

53

The U.K. Investment Currency Market 1 PAUL K. WOOLLEY* O VER THE PAST FEW YEARS, there has been considerable discussion of the relative merits of various types of controls over interna- tional capital movements. Controls that have been the subject of the most analysis and empirical investigation are the dual exchange market and the U. S. Interest Equalization Tax. Yet the U. K. investment cur- rency market, which has operated in various forms for the past 30 years and which stems from the embargo on the export of capital by residents, has been largely neglected. 2 In the basic dual exchange market, all capital transactions undertaken by residents and nonresidents take place at the capital exchange rate, and all current transactions take place at the official exchange rate. The United Kingdom's arrangement is a variant of this system in that only certain capital account transactions attributable to U.K. residents are channeled through the investment currency market, while capital and current account transactions undertaken by nonresidents are conducted at the official exchange rate. The U. K. system thus represents an asym- metric version of the dual exchange market in the sense that participa- tion in the financial exchange market is confined to residents. The stock of assets allocated to this market exceeds £7 billion and the premium over the official exchange rate has fluctuated between zero and 88 per cent. The control has survived several devaluations, the move from a fixed parity to a floating pound, and periods in which removal would *Mr. Woolley, economist in the Exchange and Trade Relations Department, received his doctorate from the University of York, England, where he was also a member of the faculty. He has been a member of the U. K. Stock Exchange and a Specialist Adviser to the House of Lords. His contributions to academic and financial journals have been mainly in the field of international finance. 1 The research on which this paper is based was begun while the author was at the University of York, and was then financed by the Esmee Fairbairn Charitable Trust. In addition to colleagues at the Fund, the author is grateful to Heather Hunter for her assistance in preparing this paper. 2 To the best of the author's knowledge, the only previous studies have been Woolley (1974 and 1976), a description of the mechanics of the market published by the Bank of England in 1976 (See "The Investment Currency Market," Bank of England, Quarterly Bulletin, Vol. 16 (September 1976), pp. 314-22.), and an extended reference in Cairncross (1973). 756 ©International Monetary Fund. Not for Redistribution

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of The U.K. Investment Currency Market1 - IMF eLibrary

The U.K. Investment Currency Market1

PAUL K. WOOLLEY*

OVER THE PAST FEW YEARS, there has been considerable discussionof the relative merits of various types of controls over interna-

tional capital movements. Controls that have been the subject of themost analysis and empirical investigation are the dual exchange marketand the U. S. Interest Equalization Tax. Yet the U. K. investment cur-rency market, which has operated in various forms for the past 30years and which stems from the embargo on the export of capital byresidents, has been largely neglected.2

In the basic dual exchange market, all capital transactions undertakenby residents and nonresidents take place at the capital exchange rate,and all current transactions take place at the official exchange rate. TheUnited Kingdom's arrangement is a variant of this system in that onlycertain capital account transactions attributable to U.K. residents arechanneled through the investment currency market, while capital andcurrent account transactions undertaken by nonresidents are conductedat the official exchange rate. The U. K. system thus represents an asym-metric version of the dual exchange market in the sense that participa-tion in the financial exchange market is confined to residents. The stockof assets allocated to this market exceeds £7 billion and the premiumover the official exchange rate has fluctuated between zero and 88 percent. The control has survived several devaluations, the move from afixed parity to a floating pound, and periods in which removal would

*Mr. Woolley, economist in the Exchange and Trade Relations Department,received his doctorate from the University of York, England, where he was alsoa member of the faculty. He has been a member of the U. K. Stock Exchangeand a Specialist Adviser to the House of Lords. His contributions to academic andfinancial journals have been mainly in the field of international finance.

1The research on which this paper is based was begun while the author wasat the University of York, and was then financed by the Esmee FairbairnCharitable Trust. In addition to colleagues at the Fund, the author is grateful toHeather Hunter for her assistance in preparing this paper.

2 To the best of the author's knowledge, the only previous studies have beenWoolley (1974 and 1976), a description of the mechanics of the market publishedby the Bank of England in 1976 (See "The Investment Currency Market," Bankof England, Quarterly Bulletin, Vol. 16 (September 1976), pp. 314-22.), and anextended reference in Cairncross (1973).

756

©International Monetary Fund. Not for Redistribution

U.K. INVESTMENT CURRENCY MARKET 757

probably have had little effect on the balance of payments. With therecovery in prospect for the U. K. balance of payments and with Britain'scommitment to dismantle exchange controls between itself and theEuropean Economic Community (EEC), the present moment is oppor-tune to study the system.

The analysis of the United Kingdom's investment currency market thatfollows would be generally applicable to other countries operating afinancial exchange market for the use of residents only.3 It would not,however, be applicable without modification to countries operatingfinancial exchange markets in which only nonresidents participate.4 Thepaper seeks, in particular, to show the effects of the control on the bal-ance of payments and on domestic interest rate policy, to identify themain influences on the size of the premium, to analyze the premium'simplications for U. K. investors, and to assess some of the major changesthat have been introduced in the regulation and functioning of thesystem.

The discussion proceeds as follows: Section I summarizes the basiccontrols on overseas portfolio investment, identifies the main influenceson the size of the premium, and shows the premium's effects on therisk/return advantages of international diversification by U. K. investors.It goes on to show the significance of the regulation that permits resi-dents to finance overseas portfolio investments by foreign borrowingand the effect of certain direct and property investment flows that havebeen allocated to this market.

Section II reviews the arguments that have been used in the economicliterature to justify capital controls on long-term investment. It thengauges the effectiveness of the U. K. system in fulfilling some of theobjectives that controls are designed to meet. In particular, there is anattempt to show whether or not the system confers a measure of inde-pendence on U. K. interest rate policy. Then, by working through theeffects of abolition of the control, an order of magnitude is given to theoutflow that the control is forestalling.

Section III is devoted to an analysis of several variants of the invest-ment currency market that have been in use at various times. Itexamines the segregation of foreign capital markets and capital flows forexchange control purposes and the multiple premiums to which this

3 France operated a security currency market for residents' transactions invarious foreign securities between 1969 and 1971, and in Norway and Sweden,foreign securities are transferable between residents at a premium, although theforeign exchange itself is not negotiable.

4 South Africa has a securities rand market for nonresidents. Until recently, theNetherlands had an "O-guilder" market for nonresidents investing in Dutch bonds.

©International Monetary Fund. Not for Redistribution

758 INTERNATIONAL MONETARY FUND STAFF PAPERS

gives rise, the parallel operation of an investment currency market fornonresidents, and the possible methods of phasing out controls betweenthe United Kingdom and other member countries of the EEC.

I. Analysis of Present Controls

PREMIUM CURRENCY

The underlying principle of the investment currency market is that aU. K. resident wishing to purchase foreign currency securities must firstobtain the foreign currency from another U. K. resident who is sellingforeign securities. This requirement has the result that the value of allpurchases of foreign securities, in sterling terms, will equal the value ofall sales of foreign securities over any period.5 In consequence, therewill never be an outflow of portfolio investment funds on residents'account. Since nonresidents are not covered by this exchange controlsystem, their transactions will continue to give rise to net inflows oroutflows. Because demand by residents for foreign securities has usuallyexceeded the value of those securities held when they were valued atofficial exchange rates, a premium, known as the "investment currency"or "Dollar" premium, has developed on the currency. Since there is per-fect substitutability of currencies in this market, the premium is the samefor all currencies. All dividends paid on these securities must be repa-triated at the official exchange rate.

There are a number of modifications to this basic principle. The mostimportant is that, while purchasers must acquire all their currencyrequirements at the premium rate, sellers are entitled to dispose of only75 per cent of the proceeds at the premium rate, while the balance mustbe sold at the official exchange rate. This surrender policy results in anet inflow in the balance of payments on resident investors' account, thesize of the inflow depending on the rate of turnover of foreign securities.

The effect of the control is to create a pool comprising foreign cur-rency securities, the size of which is determined by the following:

(a) The value of overseas portfolio investments when the exchangecontrol regulations were introduced;

(b) Subsequent changes in the value of securities represented in thepool, owing both to changes in the values of the securities, expressed inthe relevant foreign currencies, and to exchange rate changes;

(c) Subtractions from and additions to the pool as a result of the

5 This is qualified by any changes that may occur in stocks of liquid investmentcurrency held by dealers or investors.

©International Monetary Fund. Not for Redistribution

U.K. INVESTMENT CURRENCY MARKET 759

surrender policy, variations in the countries covered by exchange con-trol, and other administrative policy changes.

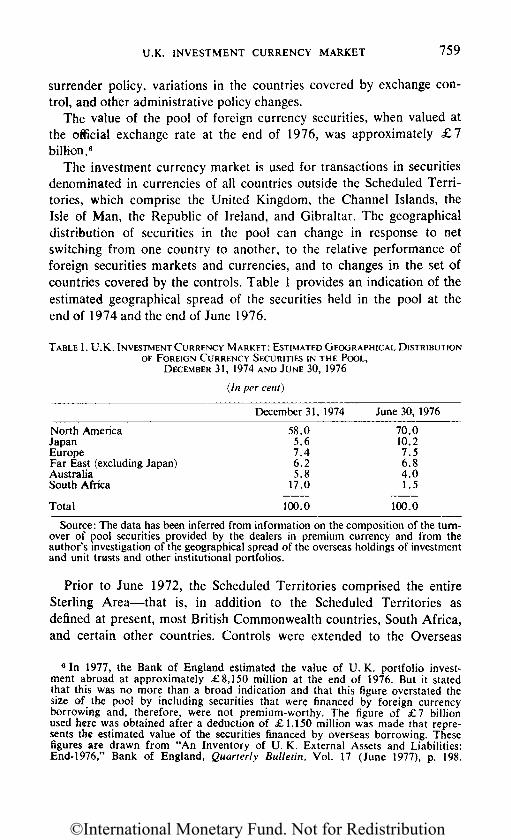

The value of the pool of foreign currency securities, when valued atthe official exchange rate at the end of 1976, was approximately £7bill-io®.6

The investment currency market is used for transactions in securitiesdenominated in currencies of all countries outside the Scheduled Terri-tories, which comprise the United Kingdom, the Channel Islands, theIsle of Man, the Republic of Ireland, and Gibraltar. The geographicaldistribution of securities in the pool can change in response to netswitching from one country to another, to the relative performance offoreigs securities markets and currencies, and to changes in the set ofcountries covered by the controls. Table 1 provides an indication of theestimated geographical spread of the securities held in the pool at theend of 1974 and the end of June 1976.

TABLE 1. U.K. INVESTMENT CURRENCY MARKET: ESTIMATED GEOGRAPHICAL DISTRIBUTIONOF FOREIGN CURRENCY SECURITIES IN THE POOL,

DECEMBER 31, 1974 AND JUNE 30, 1976

(In per cent)

North AmericaJapanEuropeFar East (excluding Japan)AustraliaSouth Africa

Total

December 31, 1974

58.05.67.46.25.8

17.0

100.0

June 30, 1976

70.010.27.56.84.01.5

100.0

Source: The data has been inferred from information on the composition of the turn-over of pool securities provided by the dealers in premium currency and from theauthor's investigation of the geographical spread of the overseas holdings of investmentand unit trusts and other institutional portfolios.

Prior to June 1972, the Scheduled Territories comprised the entireSterling Area—that is, in addition to the Scheduled Territories asdefined at present, most British Commonwealth countries, South Africa,and certain other countries. Controls were extended to the Overseas

6 In 1977, the Bank of England estimated the value of U. K. portfolio invest-ment abroad at approximately £8,150 million at the end of 1976. But it statedthat this was no more than a broad indication and that this figure overstated thesize of the pool by including securities that were financed by foreign currencyborrowing and, therefore, were not premium-worthy. The figure of £7 billionused here was obtained after a deduction of £1,150 million was made that repre-sents the estimated value of the securities financed by overseas borrowing. Thesefigures are drawn from "An Inventory of U. K. External Assets and Liabilities:End-1976," Bank of England, Quarterly Bulletin, Vol. 17 (June 1977), p. 198.

©International Monetary Fund. Not for Redistribution

760 INTERNATIONAL MONETARY FUND STAFF PAPERS

Sterling Area (OSA) in June 1972, and OSA securities became foreigncurrency securities. Since U. K. residents' holdings of securities in thenewly-included countries immediately became eligible for sale throughthe premium market, the pool approximately doubled from its previousvalue of £3 billion.

INFLUENCES ON THE PREMIUM

The size of the premium at any time is determined by the supply of,and demand for, investment currency. The significant relationship istherefore that between the net demand for investment currency by U. K.investors and the available pool of currency. The premium is the pro-portion by which the aggregate desired holdings of foreign securities inthe portfolios of U. K. residents (excluding those financed by means ofoverseas borrowing) exceed the pool of foreign securities when thesesecurities are valued at the ruling official exchange rate.

Aggregate desired holdings of foreign securities(excluding those financed by means of

_ . overseas borrowing) .Premium = ^—=—7-7—= rr. r —,—A . ffi . t -1Pool of foreign securities when valued at official

exchange rates

At the end of 1976, with the pool valued at <£7 billion and with thepremium standing at 45 per cent, U. K. residents were holding investmentcurrency-financed foreign securities with a premium-inclusive marketvalue of <£ 10,150 million.7 It is possible to make an estimate of theaggregate value of U. K. investors' holdings of domestic securities basedon the market capitalization of all quoted U. K. securities, makingdeductions for nonresident holdings. On this basis, premium-worthyforeign securities comprise approximately 15 per cent of the averageU. K. security portfolio.

The aggregate demand for foreign securities depends upon therisk/return opportunities offered by foreign securities relative to thoseavailable on domestic securities, as well as the aggregate value of U. K.residents' portfolios. Ceteris paribus, an increase in the expected returnon foreign securities will lead to switching from domestic to foreignsecurities that will push up the premium. Alternatively, an increase inthe value of U. K. portfolios will, ceteris paribus, increase the demandfor foreign securities and thus will raise the premium as investors seekto hold constant the proportionate composition of their portfolios.

7 This was the replacement value, since it included the full premium, whereasif investors allowed for the 25 per cent surrender, a realizable value of £9,360million was indicated.

©International Monetary Fund. Not for Redistribution

U.K. INVESTMENT CURRENCY MARKET 761

Another positive stimulus will occur if investors attempt to reduce port-folio risk by increasing diversification through raising the foreign com-ponent of their portfolios.

Turning to the denominator, changes in the value of the pool affectthe premium; an increase in the pool will, other things being equal,reduce the premium, and a decrease will raise it. A major cause of varia-tions in the size of the pool are changes in the official rate for sterling,since these affect the values of all securities equally. Thus, a depreciationof sterling will increase the pool in sterling terms and therefore tend toreduce the premium, while an appreciation will have the opposite effect.The size of the pool will also depend upon the price performance of thesecurities held in it; the more successful the international investmentstrategy of U. K. investors, the faster will be its growth. However, thesurrender policy, introduced in 1965 to increase official reserves, hashad the effect of depleting the pool. Since its inception, the surrenderrequirement has applied to sales of all foreign securities, with the excep-tion of former OSA securities between their inclusion in the exchangecontrol net in June 1972 and March 1974. Table 2 shows the annualcontractions in the investment currency pool deriving from the surrenderpolicy. The surrender policy, by reducing the pool, tends to increase thepremium over time.8

TABLE 2. UNITED KINGDOM: ANNUAL CONTRACTIONS IN THE INVESTMENTCURRENCY POOL DERIVING FROM THE SURRENDER POLICY, 1965-76

(In mil/ions of pounds)Year 1965 1966 1967 1968 1969 1970 1971 1972 1973 1974 1975 1976

Amount -53 -70 -88 -104 -109 -87 -128 -138 -158 -265 -179 -176

Source: Bank of England, Quarterly Bulletin, various issues.

The relationship between the pool of investment currency and thedemand for overseas securities can be demonstrated diagrammatically.(See Figure 1.)

On the vertical axis is the exchange rate between the pound sterling

8 If there is a turnover of the pool of proportion a per period, then at the endof period /, the pool will have a value St, of

St = Soe-"xt

where So is the value of the pool at t=0. We therefore have the premium at time/ equal to

where 2 denotes the aggregate desired holdings of foreign securities in residents'portfolios.

1 and

Year 1965 1966 1967 1968 1969 1970 1971 1972 1973 1974 1975 1976

Amount -53 -70 -88 -104 -109 -87 -128 -138 -158 -265 -179 -176

©International Monetary Fund. Not for Redistribution

762 INTERNATIONAL MONETARY FUND STAFF PAPERS

FIGURE 1

and the dollar—the dollar being used as the numeraire for all foreigncurrencies. The current official exchange rate is equal to OL. The supplyof foreign securities is fixed in the short run in dollar terms, thus givinga zero elastic supply curve TN. DD represents the U. K. demand forforeign currency securities at different exchange rates. The pool of secu-rities, when valued at official exchange rates, is represented by LRNO,

MLthe demand for foreign securities by MSNO, and the premium by ~^T •

Chart 1 shows the course of the premium since 1965. The premiumis based here on the difference between the investment currency rate andthe concurrent official rate. The premium is frequently quoted in thepress in relation to the last fixed official parity between the dollarand the pound sterling ($2.60571 = <£ 1), thus overstating the truepremium. Chart 2 shows the course of the official exchange rate andthe investment currency rate between the dollar and the pound sterlingsince the floating of the pound.

IMPACT ON INVESTORS

Investors are mainly concerned with the return and riskiness of secu-

©International Monetary Fund. Not for Redistribution

CHART 1. UNITED KINGDOM: INVESTMENT CURRENCY PREMIUM, 1965-77

&L

IJDW

VW A

DN

aaan

o IN

HWXS

HANI

-rn

Source: The Financial Times, various issues.

©International Monetary Fund. Not for Redistribution

764 INTERNATIONAL MONETARY FUND STAFF PAPERS

CHART 2. UNITED KINGDOM: OFFICIAL AND INVESTMENTCURRENCY EXCHANGE RATES, 1972-77

Source: Bank of England, Quarterly Bulletin, various issues.rities, and the investment currency premium affects both.9 The standardportfolio theory definition of the return on a domestic security is thechange in the price of the security between two dates plus accrued divi-dends as a proportion of the price at the beginning of the period (or thepurchase price).10 The return on a foreign currency security if all settle-

9 It is assumed in this paper that investors observe the axioms for portfolioselection first proposed by Markowitz (1959), and that investors' preferences maytherefore be described by an ordinal preference function.

U = U(R, a)where U = an ordinal preference index

R = expected portfolio rate of returna = variance of portfolio rate of return

and where

where Po is the buying price, Pi is the selling price, and d is the dividend payablein the holding period.

©International Monetary Fund. Not for Redistribution

U.K. INVESTMENT CURRENCY MARKET 765

ments took place at the official exchange rate would therefore be thedifference between the prices of the securities at the beginning and atthe end of the period, converted at the ruling official exchange ratesplus the accrued dividends, similarly converted, all as a proportion ofthe price at the beginning of the period.11

Allowing for exchange controls, the return now becomes based on asterling equivalent price at the beginning of the period that incorporatesthe premium and on a price at the end of the period that is inclusive ofthe premium on all but the 25 per cent surrendered at the officialexchange rate.12 Because the dividend is repatriated at the officialexchange rate, the proportionate return is reduced by the premium; thehigher the premium at the time of purchase, the lower the yield. The 25per cent surrender is also a factor tending to reduce the return.13

Over the period from the end of 1961 to the end of 1976, an invest-ment in U. K. equities by a resident would have yielded an annual aver-age return of 6.8 per cent. This compares with an annual average returnof 7.9 per cent available on U. S. equity investment over the sameperiod, had all settlements taken place at the official exchange rate. Ifallowance is made for the premium (but the surrender is excluded), thislast return becomes 11.5 per cent.14 The additional yield from invest-

11

(1)

where Co is the official exchange rate between sterling and the relevant currencyat the time of purchase, Ci is the exchange rate at the end of the period, andthe dividend is converted at Ci.

12

(2)

where TTO and ir\ are the premiums at the time of purchase and sale, respectively,and x is the surrender proportion. The dividend is again assumed to be convertedat the official exchange rate at the end of the period, since it is not eligible forthe premium.

13 This discussion has implicitly assumed that the foreign currency in whichthe securities are denominated has a unitary exchange rate and free convertibility.For certain countries of interest to U. K. residents (e.g., South Africa, Belgium),there are dual exchange markets and other capital controls that must be takeninto account in calculating the return. In order to formulate the expected return,the investor must therefore make estimates not only of Pi, Ci, TTI, and d, togetherwith any possible changes in U. K. exchange controls (such as might, for example,affect r), but must also try to anticipate any relevant changes or developments inregulations or two-tier markets abroad.

14 The returns are based on the U. K. Financial Times—Actuaries 500-shareindex and the U. S. Standard and Poor's 425-share industrial index. U. S. invest-ment is taken as the proxy for overseas investment because of its heavy weightingin the pool. Equity returns, rather than bond returns, have been used, since thepremium penalizes fixed-interest investment and ensures that few foreign bondsare purchased with investment currency.

©International Monetary Fund. Not for Redistribution

766 INTERNATIONAL MONETARY FUND STAFF PAPERS

ment in the United States has therefore been only 1.1 percentage pointsover this period, although investors in U. S. securities have fared muchbetter because of the rise in the premium. One explanation for the cur-rent high level of the premium may be that investors expect the yielddifferential in favor of overseas securities to widen in the future.

In general, foreign securities offer scope for risk reduction throughportfolio diversification. Risk reduction may be obtained because thereturns on foreign securities are less variable over time than those ondomestic securities. But, at a more general level, because foreign secu-rities markets are subject to different sets of prevailing economic andpolitical conditions, the various overseas securities indices display arelatively low correlation, both with the U. K. securities market and witheach other. A U. K. resident's securities portfolio with internationaldiversification will therefore be less risky than one without.15

The existence of a volatile premium can be expected to alter thevariability of the returns on foreign securities and therefore the benefitsof international diversification, but these changes are not necessarilysystematic.16 However, by comparing the variability and correlation ofthe premium-inclusive returns with the hypothetical returns that wouldhave been received had the investments been made at the officialexchange rate, some indication can be gained of this effect in practice.The quarterly returns on investment in the U. K. and U.S. equity indiceswere taken for 1962-69, 1969-75, and for the entire period 1962-75.The findings are, first, that, for all three periods, the variability of U. K.equity returns was greater than that of U. S. equity returns, whether thereturn for the latter was premium-inclusive or calculated at the officialexchange rate; the premium also reduced the variability of U. S. equityreturns to a U. K. investor.17 Second, the correlation between the U. S.and U. K. returns was higher with the premium than without for the firstperiod but lower for the second period, so that the results here wereinconclusive. Third, no systematic change was introduced by thepremium in the correlations of returns on equity investment in differentcountries. The premium was not, therefore, responsible over the periodin question for any significant increase in risk, and the potential bene-fits of international diversification were not noticeably lessened.

15 For a discussion of the potential gains from international diversification, seeGrubel (1968) and Levy and Sarnat (1970).

16 In portfolio theory terms, the effect can be assessed in terms of the changein the variance of the returns on the foreign securities and the covariances betweenthe returns on the various foreign securities and between the returns on foreignand domestic securities.

17 These findings are reported in greater detail in Woolley (1976).

©International Monetary Fund. Not for Redistribution

U.K. INVESTMENT CURRENCY MARKET 767

BORROWING ALTERNATIVE

As an alternative to investment currency financing, investors mayfinance overseas portfolio investment by foreign currency borrowing.Permission to do this must first be granted by the Bank of England;one of the conditions is that asset cover of 115 per cent must be pro-vided for the overseas Joan, with 15 per cent of the amount of the loanbeing purchased with investment currency. In other words, the foreigncurrency value of the premium-paid securities must be at least 15 percent of the foreign currency loan. If a drop in security prices exposesa shortfall in this cover, the purchase of more foreign securities mustbe made with investment currency to restore the position.

In practice, most investors borrowing abroad already hold a portfolioof foreign securities financed by the premium; they merely earmarkpart of this as the extra backing for the loan. If, on final sale of thesecurities, the proceeds are insufficient to repay the loan in full, thebalance must be repaid with investment currency, whereas any profitremaining after repayment may be sold for the benefit of the premium,subject to the surrender. Any shortfall between the dividends on thesecurities and the interest payable on the loan must also be made goodwith investment currency. Switching of securities financed by overseasborrowing is not subject to the 25 per cent surrender.

The above provisions ensure that the borrowing option does not giverise to any loss to the balance of payments. If a profit is realized onthe securities, the capital account benefits to the extent of the proportionsurrendered at the official rate, and the size of the pool is increased bythe balance of the profit. If there is a loss, this is made good through apurchase of premium currency, which reduces the size of the pool buthas no effect on the capital account.

Prior to 1970, there had been only moderate use of overseas borrow-ing. As shown in Table 3, it developed strongly in 1972 and 1973, buthas since fallen back to lower levels. If it is assumed that there wasoutstanding borrowing of £200 million at the beginning of 1970, andthat there were no net currency gains or losses, the total outstandingborrowing was £1,040 million at the end of 1975. Approximatelyone tenth of overseas portfolio investment was therefore financed byborrowing at the end of 1975.

The investor's choice between financing by investment currency oroverseas borrowing will hinge on which offers the more attractive risk/return prospects. The principal difference is that overseas borrowinglargely insulates investors from fluctuations in the official exchange

©International Monetary Fund. Not for Redistribution

768 INTERNATIONAL MONETARY FUND STAFF PAPERS

TABLE 3. UNITED KINGDOM: PRIVATE PORTFOLIO INVESTMENT UNDERTAKENWITH FOREIGN BORROWING, 1970-75

(In millions of pounds}

Repayments

Year

197019711972197319741975

Foreign CurrencyBorrowing

48.7111.9696.7373.5167.0276.0

Using proceeds ofsales of foreign

currency securities

3.97.5

37.6186.1216.1129.2

Using investmentcurrency l

35.6148.465.1

Source: U. K. Treasury.1 Repayments with investment currency are generally made when, because of a fall

in the value of the securities, the sale proceeds are by themselves insufficient to meetthe full cost of loan repayment.

rate and the premium. If the borrowing takes place in the same currencyas the investment, changes in the official exchange rate or the premiumduring the holding period will only alter by a scale factor the capitalloss or gain from the transaction. Investors will therefore have apreference for overseas borrowing, other things being equal, when theyexpect a fall in the premium or a rise in the official exchange rate or,because of the freedom from the surrender penalty on switches underthe borrowing option, when they anticipate frequent switching.

A further consideration is that, the larger the amount of overseasborrowing in the financing mix, the higher is the leverage in theoverseas investment. Leverage from this source is eliminated if theinvestor makes a sterling deposit equal to the initial sterling value ofthe loan. Such combinations of loan and collateral deposit (knownas back-to-back loans) are frequently employed and are required bylaw for investment and unit trusts.

Because expectations about the movements of the relevant variablesare not held with certainty, a portfolio of foreign securities will usuallybe financed by a combination of the two methods, with premium-financed securities providing cover, well in excess of the stipulatedminimum of 115 per cent, for the foreign loan.18

18 The capital return on securities purchased with investment currency is:

This is the same as the overall return except that it omits the dividendelement, which is considered separately below. The capital return, assuming that

©International Monetary Fund. Not for Redistribution

U.K. INVESTMENT CURRENCY MARKET 769

Use of the borrowing option has a number of consequences for thesize of the pool and the premium. First, the bypass reduces the demandfor investment currency and therefore lessens the premium. Some ideaof the reduction in demand can be obtained from the data for foreigncurrency borrowing in Table 3. Second, if foreign securities prices fall,there will be asset cover shortfalls that have to be made good withpurchases of investment currency. Falling securities prices have alreadybeen associated with a contracting pool and a rising premium, andthese are similarly the consequences of the restoration of asset cover.Conversely, rising securities prices are associated with an enlargementof the pool and a falling premium. Rising prices will result in profitsfrom overseas borrowing activities that will also serve to enlarge thepool and to lower the premium. The borrowing option will thereforetend to accentuate the effect on the premium of fluctuating foreignsecurities prices.

These relationships are well illustrated by what happened in 1974.In the preceding two years, there had been a heavy buildup of overseasborrowing, most of it undertaken to finance investment in securitiesdenominated in other currencies. Investors were tending to pay more

the borrowing and the investment are in the same currency and that a back-to-back loan is employed, is

If Pi - PQ < 0, x = 0, whereas if Pi - P0 > 0, x = 0.25.Where the investment takes place in a different currency from the borrowing,

the capital return is

where Co and Ci are the official exchange rates between the currency in whichthe securities are denominated and sterling at the time of purchase and sale,respectively; Fo and Fi are the official exchange rates between the currency inwhich the borrowing is denominated and sterling at the time of purchase andsale, respectively. The conclusions regarding changes in the premium are thesame as when the currencies are matched, but, in this case, a change in either ofthe two official exchange rates can alter the sign of the overall return.

The income return on currency-financed investment is

where Y is the annual dividend yield on the securities. The income return,assuming a back-to-back loan, is

where /•« is the servicing cost of the overseas loan and ruK is the return on thedeposit in the United Kingdom. Of the variables in this expression, Ci, in, and Yare expected future values; ra and ruK are known or expected, depending uponthe length of the loan and the corresponding deposit.

©International Monetary Fund. Not for Redistribution

770 INTERNATIONAL MONETARY FUND STAFF PAPERS

regard to interest charges than to exchange risk, and there was exten-sive borrowing in deutsche mark and Swiss francs in order to investin dollar securities. The subsequent capital losses had to be madegood with investment currency, and these covering purchases werelargely responsible for the rise in the premium from 30 per cent to88 per cent in the 12 months ended in June 1975.

DIRECT AND PROPERTY INVESTMENT

While the investment currency market was originally designed tocover portfolio investment, the authorities have extended its use overthe past 15 years to include certain flows of direct and property invest-ment funds owned by U.K. residents. The conditions under whichoutward flows of direct and property investment are required to passthrough the investment currency market and under which returninginflows are permitted to pass through it have varied from time totime, primarily according to the pressure on the balance of payments.For overseas direct investment by firms, the greater the pressure onthe balance of payments, the fewer are the projects that have beeneligible to be financed at the official exchange rate and that have hadto be financed with either premium currency or foreign borrowing. Thecontrols at the end of 1976 were as tight as they ever have been; theonly direct investment eligible to pass through the official market wasthat which met the "supercriterion," which is defined as a benefit to thebalance of payments equal to the initial outflow within 18 months andcontinuing thereafter. Profits accruing from all direct investment abroad,together with the proceeds of any disposal of assets, could only berepatriated at the official rate, whereas until March 1974 the liquidationproceeds of direct investment made outside the Overseas Sterling Areaand the European Economic Community had been eligible for repatria-tion through the premium market.

As the premium is not recoverable, it resembles a tax on overseasdirect investment.19 The deterrent effect of the premium thereforeensures that only a very small portion of overseas direct investment isfinanced in this way, since firms find that overseas profit retentionand foreign borrowing are lower-cost alternatives. The bias against

19 The return on direct investment collapses to

Where PO denotes the initial foreign currency outlay, d denotes the accrued profits,and Pi denotes any proceeds from the liquidation or sale of the investment.

©International Monetary Fund. Not for Redistribution

U.K. INVESTMENT CURRENCY MARKET 771

direct investment as opposed to portfolio investment is contrary to therelative stringency of controls usually accorded to the two types ofcapital flow by most countries and, indeed, by past policy in theUnited Kingdom.20

Private property purchases by U. K. residents must also be madewith investment currency, but in contrast to the rules for direct invest-ment, 100 per cent of the proceeds of sales may normally be sold forthe benefit of the premium. Confining the initial transactions for directand property investment abroad to the investment currency marketensures that there is no loss to the balance of payments. The purchaseof investment currency by a U. K. firm making a direct investmentabroad will be matched by a sale of foreign securities or property byanother U. K. resident. However, the difference in the consequencesfor the balance of payments between the use of the investment currencymarket for direct or portfolio investment is that, whereas 75 per centof the proceeds of a sale of securities is eligible for the premium, noneof the proceeds of a sale of a direct investment are eligible. Since theentire return on direct investment is transmitted at the official rate,the balance of payments will generally benefit more from direct invest-ment than from portfolio investment. The value of the pool will alsobe reduced by the full amount of any direct investment transactedthrough the investment currency market.

Because both purchases and sales of private property are channeledthrough the premium market, consistent analytical treatment requiresthat U. K. residents' holdings of private property abroad, valued atofficial rates, be added to the value of foreign securities to arrive atthe full value of the pool. However, the value of these holdings is notknown. Also, the use of the market for property fund flows in eitherdirection is small, relative to portfolio investment flows, and they aretherefore commensurately less significant in the determination of thepremium. In the circumstances, it is probably best to regard propertyfund flows as giving rise to changes in the size of the pool over time—negative changes for purchases and positive changes for sales.

20 The usual argument in favor of lighter controls on direct investment outflowsis that the investing companies retain control over the investment, trading, financ-ing, and profit distribution policies of their overseas subsidiaries and branches, andthese policies can still be influenced by the authorities of the capital-exportingcountries in a way that is impossible when minority shareholdings are purchasedin overseas firms. In addition, it is felt, rightly or wrongly, that the return ondirect investment is both quicker and higher, and thus more useful for the bal-ances of payments, than that on portfolio investment.

©International Monetary Fund. Not for Redistribution

772 INTERNATIONAL MONETARY FUND STAFF PAPERS

II. Evaluation

CAPITAL CONTROLS AS POLICY INSTRUMENTS

Countries usually impose controls on outflows of long-term privateinvestment for one or more of the following reasons:

(a) to reduce the pressure on the balance of payments;(b) to extend the freedom of maneuver for the monetary authorities;(c) to increase the amount of domestic investment in preference to

overseas investment;(d) to influence the composition and destination of outward invest-

ment.As a palliative for balance of payments disequilibrium, the imposition

of capital controls may be regarded principally as an alternative toexchange rate adjustment. The choice will depend on how responsivethe current account balance is to the corrective measures available tothe authorities, the likely impact and effectiveness of the capital con-trols, and how important it is to insulate the current account frompressures deriving from capital flows that may prove to be episodicand without any real root in the normal structure of trade and pay-ments.21 For example, the current account may respond feebly or withan unacceptably long delay to an exchange rate depreciation. Theaction taken will be influenced by the expected duration of the imbal-ance; the authorities may not wish to depreciate if they anticipate thatthe balance of payments pressure is a short-run phenomenon.

Capital controls can be erected with relative ease and, if effectivelypoliced, their immediate consequences are more predictable and quanti-fiable than those of exchange rate variation. There is a danger, how-ever, that restrictions on the outflow of capital may have a perverseeffect on capital inflows or give rise to retaliation abroad. Controlsalso have a habit of remaining long after the grounds for their incep-tion have disappeared. This observed longevity may be self-defeating,since the capital controls of today may prevent an improvement inthe balance of payments in a year or two when the rewards of theoverseas investment would have been reaped. Finally, the choice ofpolicy will depend upon the distributional consequences, the inter-national setting, political expediency, and so forth.

The more that freedom of maneuver is sought for monetary policyand the more that fluctuations in exchange rates are limited, thegreater is likely to be the need for controls on capital movements.

21 See Cairncross (1973) and various papers in Swoboda (1976).

©International Monetary Fund. Not for Redistribution

U.K. INVESTMENT CURRENCY MARKET 773

Conversely, the case for capital controls is weaker, the more readilyone contemplates floating exchange rates or the abandonment ofmonetary instruments for domestic purposes. In principle, controls oncapital outflows will enable a country to sustain a lower rate of interestthan that prevailing in the rest of the world. Nevertheless, there aremany linkages between economies that will tend to undermine anautonomous interest rate policy, however tough the capital controls.For instance, leads and lags, export credits, and overseas borrowingwill all tend to bring a country's real interest rate into line with pre-vailing international rates. Short-term capital movements are moreresponsive than long-term ones to interest rate differentials, so thatcontrols on long-term capital movements are less relevant if the targetis an independent monetary policy. However, such distinctions dependupon the substitutability between the two types of capital flow, and itmay be felt that substitutability is sufficiently high at the margin towarrant the extension of controls to both or that to distinguish betweenthe two would give rise to unacceptable distortions.

A recurrent argument for restricting outflows is based on the viewthat real capital formation at home does more for productivity, employ-ment, and long-run growth than does investment abroad. Thus, eventhough the private returns are equal, the social return from investmentat home is greater. It is also argued that, despite the equality of theprivate returns, the social returns will be higher at home because, wheninvestment is made abroad, the taxation accrues to the overseas govern-ment. Even the existence of tax treaties fails to compensate the domesticexchequer for the forfeited revenue.

Given the decision to impose capital controls, the questions will thenbe which type to adopt, to which categories of investment it shouldapply, and whether to cover residents or nonresidents or both. Thechoices between symmetric and asymmetric two-tier exchange markets,taxation, quantitative controls, etc. will be based on how much restric-tion is sought and on which control is the most efficient in exerting thedesired influence on the target variable.22 It will also depend uponwhether one method rather than another gives rise to any especiallyunpalatable side effects, such as the loss of international financial inter-mediation or undue losses or windfall gains to residents or nonresidents.There will also be the fundamental issue of enforceability—can the dualmarkets be effectively separated or can the control be policed withoutexcessive cost?

22 See Snider (1964) for an appraisal of the efficiency of the U.S. InterestEqualization Tax.

©International Monetary Fund. Not for Redistribution

774 INTERNATIONAL MONETARY FUND STAFF PAPERS

INTEREST RATE DIFFERENTIAL

The U. K. investment currency market can now be evaluated in thelight of this summary of the general case for capital controls. Considerfirst the effects of the investment currency controls on the relativereturns to portfolio and direct investment available in the United King-dom and the rest of the world (RoW). In the absence of controls overflows of direct investment between the United Kingdom and RoW—and given the satisfaction of the usual competitive conditions—theexpected real returns on long-term real investment will be equated (ateach level of risk) despite the existence of exchange rate fluctuations.If portfolio investment funds can flow freely between the UnitedKingdom and RoW, then, under the same set of ideal conditions, theexpected real returns to investment in bonds and equities will also beequated. If exchange controls are imposed by either the United Kingdomor RoW, whether on inflows or outflows of both direct and portfolioinvestment, capital flows may be prevented from exercising their equal-izing influence. The disparity in expected real returns will depend uponthe type and the stringency of the controls.

If controls are imposed by either the United Kingdom or RoW on theflows of portfolio investment, but not on the flows of direct investment,the returns on direct investment will be equated; however, the equaliza-tion of the returns on portfolio investment depends upon the degree ofsubstitutability between direct and portfolio investment in theUnited Kingdom and RoW. If there is anything less than perfect sub-stitutability, the returns on portfolio investment will not, in general, beequated. Assume that the only restriction on the free flow of capitalbetween the United Kingdom and RoW is the U. K. investment currencycontrol and that it relates exclusively to portfolio investment flows. Theinvestment currency market will prevent any flows of portfolio invest-ment funds into or out of RoW by U. K. residents. If direct and portfolioinvestment are perfect substitutes in both areas, there will be no obsta-cles to the equalization of the returns on both direct and portfolio invest-ment between the United Kingdom and RoW. If there is not completesubstitutability, then the portfolio investment funds of U.K. residentscannot be used as an instrument of equalization of returns on portfolioinvestment. However, if the residents of RoW are free to allocate theirfunds between the two areas, their portfolio investment fund flows will,in general, act as an instrument of equalization. The same is true evenif the investment currency market extends to full or partial coverage ofdirect investment.

©International Monetary Fund. Not for Redistribution

U.K. INVESTMENT CURRENCY MARKET 775

The conclusion is thus that the asymmetric investment currency mar-ket will not necessarily prevent the equalization of expected real returnsin the United Kingdom and RoW, since nonresident capital will be ableto perform the equalizing role. Of course, if rUK < rRoW, residents inRoW may not have sufficient funds already invested in theUnited Kingdom to repatriate and so promote the equalization. On theother hand, as stated in the preceding section, there are other ways inwhich interest rates tend to be drawn together between countries, evenin the absence of capital flows.

The preceding analysis has shown that the U. K. investment currencymarket, when it relates to portfolio investment flows alone, does little toassist the authorities in the pursuit of an independent monetary policy.The flows of direct investment funds owned by U. K. residents and flowsof all categories of nonresident capital will result in an equalization ofthe expected real rates of return in the United Kingdom and RoW.Rather more scope for autonomy is conferred when the investment cur-rency market is extended to direct investment. There may also be scopefor a lower real interest rate in the United Kingdom if nonresident assetholding in the United Kingdom is relatively small.

The prediction of this analysis is borne out by the evidence of thepast 15 years. The annual average return to U. K. investors in domesticgovernment bonds over the period 1962-76 was 7.0 per cent perannum, whereas the return available to them on U. S. Governmentbonds, allowing for changes in the official exchange rate, would havebeen 7.4 per cent. The evidence on the return from equities has alreadyshown that the differential was a mere 1.1 per cent per annum in favorof the United States.

In the light of the preceding analysis, why would a premium everdevelop on investment currency? In other words, would U. K. residentsever wish to invest abroad if it involved a penalty in the form of a lowerreal return on investment than that available in the United Kingdom?On the basis of the assumptions that have been made, they would not,and, consequently, no premium (or, for that matter, no discount) wouldever develop on investment currency. If some of the assumptions arerelaxed, however, we see that a premium may arise.

In the first place, expectations about the return and the riskiness ofportfolio investment in the United Kingdom and RoW on the part ofresidents in both areas may differ, so that the expected return mayappear equalized to residents in one area but not to residents in theother. In this event, a premium may develop on investment currencyso as to equalize the expected returns as perceived by U. K. residents.

©International Monetary Fund. Not for Redistribution

776 INTERNATIONAL MONETARY FUND STAFF PAPERS

Second, the U. K. investment currency market will not usually be theonly control in operation between the United Kingdom and RoW. Non-resident capital may be prevented from performing its equalizing func-tion by deterrents to capital inflows into the United Kingdom otherthan those of an exchange control nature,23 or there may be capital con-trols operated in RoW. Third, exchange rates do not, in general, adjustin such a manner as to offset price level differentials exactly. If adjust-ment is delayed or jerky, there will be incentives for short-term pur-chases of foreign currency assets by U. K. residents.

OUTFLOW PREVENTED BY THE CONTROL

Some idea of the balance of payments significance of the investmentcurrency market can be gained by working through the consequences ofabolition. By appealing to comparative static analysis of the mean-variance approach to portfolio theory, it is possible to make some tenta-tive statements about the possible capital outflow for the general case ofabolition and, by inserting the current figures, to get an indication of thepossible outflow if abolition occurred now.

Let the observed pre-abolition value of the aggregate desired holdingsof foreign securities, when valued to include the premium, be 20 andthe post-abolition value of desired holdings be S^ The lifting of controlswould cause the premium to disappear, and investors would be leftholding foreign securities amounting to the value of the pool, S. Assume,for the moment, that the elimination of the premium rate does not affectthe official exchange rate, so that S remains unchanged following aboli-tion. As investors sought to build up their holdings to the desired post-abolition level, the capital outflow would be (2,1 — S).

I0 would not necessarily be equal to ̂ because the disappearanceof the premium will change the risk/return characteristics of foreignsecurities and the value of U. K. residents' portfolios. Following aboli-tion, the proportionate return on foreign securities will increase becauseboth dividends and capital will now be channeled through the officialmarket and the surrender penalty will disappear.24 This increase inreturn will be greater, the higher the premium prior to abolition. InSection I, it was reported that the variance of return on overseas invest-ment might be reduced by the existence of the premium, but that therewas no systematic change in the covariance between the returns on U. K.and U. S. investment or between the returns on equity investment in

23 Such deterrents may be of a fiscal, legal, or political nature.24 The increase in return will be equal to the difference between equation (1) in

footnote 11 and equation (2) in footnote 12.

©International Monetary Fund. Not for Redistribution

U.K. INVESTMENT CURRENCY MARKET 777

different countries. Comparative static analysis of the mean-varianceapproach to portfolio theory seeks to determine how the optimal weightsof an individual's portfolio will respond to changes in the expectedreturn and risk.

Royama and Hamada (1967) found that, while a decrease in thevariance of the return of a particular security led to an unambiguousincrease in the proportion in which that security was held, changes inboth the expected return and the covariance between returns on thatsecurity and any other had essentially indeterminate effects. This inde-terminacy arises from the possibility that the wealth effect may be posi-tive or negative. By adopting somewhat more restrictive assumptionsconcerning the portfolio holder's preference function, Jones-Lee (1971)was able to derive the prediction that an increase in the return on thesecurity led to an increase in the proportion in which that security washeld. Abolition, therefore, increases the return, which, in turn, impliesan increase in the desired holdings of foreign securities (2i > 20).

The change in risk and its impact on demand is not clear-cut. Aboli-tion may increase the risk according to past evidence on thevariances/covariances; this implies a negative effect on demand.Variance/covariance evidence, however, does not capture the risk ofabolition that will invariably be on investors' minds, so this should beincluded as one of the risks of holding premium-financed securities. Thehigher the premium, the greater the risk of loss from abolition; but alsothe higher the premium, the less probable abolition becomes because ofits cost to the balance of payments. If the effect of risk on demand isdeemed more or less neutral, we are left with ^ > 20 based on theincrease in return.

The sudden loss of the premium reduces the aggregate value of U. K.investors'portfolios by (20 - S) or (1 - *)(20 ~~ ^) if investors valuetheir holdings at realizable, rather than replacement, value. It may seemparadoxical that a move toward greater freedom in capital mobilityactually involves a cost to investors. However, those investors who heldforeign securities when these exchange controls were introduced back in1947 have received a benefit, and the loss now would be the counterpartof this benefit. Exchange control was an alternative to the devaluationof sterling, and both strategies would have increased the value of foreignsecurity portfolios. If investors were to hold constant the proportionatecomposition of their portfolios, the proportion of total U. K. portfoliosthat the previously mentioned loss represented would be an indicationof the proportionate fall in demand for foreign securities owing to thewealth effect.

©International Monetary Fund. Not for Redistribution

778 INTERNATIONAL MONETARY FUND STAFF PAPERS

Drawing together the risk/return effect and the wealth effect, with itsnegative impact on demand, it seems unlikely that 2^ would differ greatlyfrom 20, implying that, as investors adjust their portfolios followingabolition, the outflow would be (S0 - S).

In Figure 1, the demand curve shifts from DD to D'D' owing to thewealth effect, and the outflow in sterling terms is RUVN, which wouldbe approximately equal to MSRL. It has so far been assumed that theofficial rate will remain constant at OL. In practice, the outflow wouldprobably cause the rate to fall, which, in turn, would choke off some ofthe outflow. Moreover, the inflow of funds into countries overseas couldlead to a rise in foreign securities prices, thus providing a further offset.The conclusion is that, in general, the higher the premium, the greaterthe outflow that is prevented. Based on the above analysis, with thepremium at 45 per cent and the pool valued at <£7 billion, abolitionwould result in an immediate outflow of £3,150 million as investorsadjusted their portfolios. After the initial outflow, there would be ebbsand flows, depending upon the expectations of relative money rates ofreturn and exchange rate changes in the United Kingdom and elsewhere.

There are a number of ways in which the asymmetric two-tier marketcan be designed to yield a result other than a zero net flow of funds.The authorities might, for example, intervene by making purchases inthe investment currency market so as to decrease the pool and to swellthe official reserves.25 However, this policy would be costly and, giventhat the pool is finite, the scope for making compensatory purchases tooffset a large and persistent current account deficit is limited. The U. K.authorities do not intervene in the market for this or, indeed, for anyother purpose, although through the surrender policy, they do ensurethat the investment currency market yields a net inflow.26 There are,however, a number of problems created by the surrender policy. First, itcauses the premium to be higher than it would be in the absence ofsuch a policy; the higher premium leads to policing problems and con-

25 See Day (1976).26 The reverse of the surrender policy might be an arrangement requiring inves-

tors to acquire only part of the foreign currency for purchases of securities at thepremium rate and enabling them to acquire the balance at the official exchangerate while permitting the whole of the proceeds of sales of securities to be trans-mitted through the premium currency market. Such a policy would, at first sight,appear appropriate if the overall balance of payments position improved suffi-ciently to countenance a small net outflow in place of the small net inflow yieldedby the present policy. The scheme would, however, be unworkable, since it wouldbe profitable for investors to purchase foreign currency securities and immediatelyresell them so as to gain the premium on that part that had not borne the pre-mium when purchased. This process would be repeated until, in a short time, thepremium disappeared and the outflow through the official market would be thesame as if the exchange restrictions had been lifted entirely.

©International Monetary Fund. Not for Redistribution

U.K. INVESTMENT CURRENCY MARKET 779

notes weakness in sterling as well. Nonresidents, observing the premiumU. K. residents are prepared to pay to invest outside the domestic mar-ket, might feel disinclined to buy U. K. securities. To the extent that thisis true, then the balance of payments saving indicated earlier would bereduced by the amount of the inflow that is deterred.

Second, the surrender penalty inhibits switching, since utility maxi-mizing investors will fail to switch from one foreign security to another(equally risky) foreign security offering a higher expected return unlessthe expected return on the alternative exceeds that on the existing hold-ing by a margin that will compensate them for their surrendered pre-mium. So long as investors' expectations concerning the relative returnsare fulfilled, the balance of payments will suffer from the surrender pol-icy because investors will not necessarily be holding securities offeringthe highest returns. The third drawback is that the surrender inhibitsspeculation in the premium market. Speculation has the merit of increas-ing the rate of turnover, thereby making the market less narrow andreducing dealing margins. The consensus of the literature on speculationis that it may also have the effect of stabilizing the rate.

All dual exchange markets confront the problem of market separa-tion, although the symmetric two-tier exchange market is almost cer-tainly subject to greater leakages than the investment currency marketbecause of nonresident participation and because the financial marketrate usually covers a wider range of capital transactions than does theU. K. scheme.27 The divergence of the investment currency rate and theofficial exchange rate in the past is testimony to the widespread observ-ance of the present U. K. controls. Nevertheless, evasion is known tooccur and can take two forms: (a) the export of capital at the officialexchange rate that should have been channeled through the premiummarket; (b) the selling of foreign currency investments for the benefit ofthe premium when they have not borne it at the time of purchase.

The effect of (a) is to reduce the demand for investment currency,although probably by a good deal less than the amount of the illegallyconverted funds because of the higher exchange cost involved. Themajor effect comes from (b), since these sales increase the size of thepool and therefore tend to depress the premium.

SOME FURTHER CONSIDERATIONS

The investment currency market has survived for 30 years, yet during

27 Lanyi (1975) has provided examples of linkages between the financial andofficial markets in the symmetric two-tier system.

©International Monetary Fund. Not for Redistribution

780 INTERNATIONAL MONETARY FUND STAFF PAPERS

this time there have been a number of occasions when the authoritiesmight reasonably have considered abolition. These included the periodin the early 1960s when the premium almost disappeared, the devalua-tion of the pound in 1967, and the move from a fixed parity to a floatingpound in 1972. The strength of the case perceived by the authorities forthe market's retention at any time will depend upon prevailingconditions.

Against the balance of payments benefit of the system must be set thecosts. The costs imposed on investors stem from the restriction on theexport of capital for portfolio investment.28 The premium to which thisrestriction gives rise reduces the return on overseas securities whilethe surrender compounds this effect. The overseas borrowing optiongives investors scope to augment their holdings of foreign securitiesbut not to increase their net foreign position. The borrowing arrange-ment therefore serves to reduce only partially the loss of utility imposedby the control.

The cost of the control to the community as a whole includes theresources devoted to its administration and some loss of internationalarbitrage business. For example, following the extension of controls toSouth African securities in 1972 and the imposition of the surrenderon former Overseas Sterling Area securities in 1974, the London StockExchange has lost international arbitrage business in South Africansecurities to stock exchanges in New York and elsewhere. Even morerecently, the London Stock Exchange has failed to make progress withplans for a Chicago-style options market in major European equities, inno small measure owing to the complexities introduced by the invest-ment currency premium. This has left the field open to the Dutch, whoare planning to start trading in options next year.

With the major improvement that has already occurred and thefavorable prospect for the U. K. balance of payments in the next yearor two, consideration will almost certainly be given to the lifting ofrestrictions on overseas portfolio investment. A major stumbling blockis the capital loss that would be incurred by existing investors. Theauthorities will feel bound to weigh this carefully, since investors com-prise mainly investment and unit trusts, insurance companies, pensionfunds, and other institutional investors. The impact of lifting restric-tions would be substantial and widespread, and, unlike, say, a fall indomestic security prices that will often be temporary, it would haveto be regarded as an irrevocable loss.

28 See Richard Caves, "The Welfare Economics of Controls on Capital Move-ments," in Swoboda (1976), pp. 31-46.

©International Monetary Fund. Not for Redistribution

U.K. INVESTMENT CURRENCY MARKET 781

III. Alternative Arrangements

This section examines some of the variants of the investment currencymarket that have been adopted in the past 30 years. It also considersa major policy change to which the authorities are committed in thefuture.

DUAL POOL SYSTEM

From the passing of the Exchange Control Act of 1947 until 1954,U. K. residents were not permitted to switch between securities quotedin different non-sterling area currencies.29 In 1954, there was a relaxationthat sanctioned switching by U. K. residents of securities quoted inany of the non-sterling area countries excluding the United States andCanada. Since no new funds could be exported and since the proceedsof sales of these securities could be transferred between residents, apremium, known as the "soft dollar" premium, developed on this cur-rency. At the same time, switching between securities quoted in theUnited States and Canada was permitted, and this gave rise to the"hard dollar" premium. There were thus two pools of investment cur-rency, the size of each being determined by the value of U. K. resi-dents' portfolio investments in the area at the time of the institutionof exchange control and by subsequent changes in the value of thesecurities represented in each pool over time. The main feature of thetwo-pool arrangement was that it ensured that the net flows of portfolioinvestment funds between the United Kingdom and both sets of coun-tries were zero, whereas the one-pool system simply ensures that the netflows between the United Kingdom and the rest of the world as a wholeis zero. The markets were merged in 1962, when the two premiumsdiverged little and both were close to the official parity.

The authorities' objective in imposing restrictions on the switchingof securities between currencies and sets of currencies was probably toensure that there was no net withdrawal of funds by U. K. residentsfrom the respective countries lest it provoke a rundown of sterlingbalances. The cost of the segmentation policy was that investors in theaggregate were restricted in their freedom to vary the distribution oftheir portfolios among foreign currencies. The premiums in the two-pool version could adjust to reflect the perceived attractions of the twocurrency groups, but the size of the underlying pools was unresponsiveto switching by investors.

29 See "The U.K. Exchange Control: A Short History," Bank of England,Quarterly Bulletin, Vol. 7 (September 1967), pp. 245-60.

©International Monetary Fund. Not for Redistribution

782 INTERNATIONAL MONETARY FUND STAFF PAPERS

As a general rule, investor utility is lessened if transferability betweenresidents of foreign currency for security purchases is restricted or ifthe geographical composition of overseas investments is constrained.The evolution of the U. K. exchange controls and the emergence of asingle pool and full transferability between residents has thereforebenefited investors.

"SECURITY STERLING" AND "PROPERTY CURRENCY"

Running parallel with controls on residents were those on nonresi-dents. From March 1953, blocked sterling balances were allowed to betransferred between residents of the same country or monetary area,and from September 1953, transfer was permitted between all nonresi-dents. Blocked sterling, or security sterling as it came to be known,could be invested in any U. K.-quoted security denominated in a sterlingarea currency. Markets in security sterling developed in foreign centers,and the rate of exchange invariably stood at a discount to the officialrate. Purchases and sales of securities by nonresidents continued to bechanneled through the security sterling market until April 1967, whenrestrictions on nonresidents were lifted.

For several years there were, in effect, two back-to-back investmentcurrency markets yielding, in principle, a zero net flow of portfolioinvestment funds for residents and nonresidents, both separately andcombined. The arrangement may be contrasted to the fully symmetrictwo-tier exchange market.30 The latter ensures a zero net flow onlyof resident and nonresident funds combined. Thus, in the symmetricversion, residents may augment their holdings of overseas assets if thereis a corresponding increase in nonresident's holdings of domestic assets.Furthermore, the premium confronting residents would be equivalentto the discount facing nonresidents, whereas in the U. K. version, thepremium and discount were independent. There would also be a largerturnover in the unified financial exchange market of the full two-tiersystem, and the scope for intervention by the authorities to influencethe overall balance of payments would be much enhanced.

From April 1965, U. K. residents were no longer allowed to buyprivate property outside the sterling area with investment currency, asthey had been permitted to do since April -1964. Instead, they wererequired to buy the property for sterling from another resident or topurchase foreign currency in the "property currency" market at the

30 For the basic analysis of the dual exchange market, see Fleming (1971and 1974) and Barattieri and Ragazzi (1971).

©International Monetary Fund. Not for Redistribution

U.K. INVESTMENT CURRENCY MARKET 783

prevailing premium. This experiment in segregating the markets accord-ing to category of capital flow was short-lived. The market turned outto be lumpy and narrow, and three years later it was merged againwith the investment currency market. In part, the failure occurredbecause it was more difficult to police residents who were often buyingproperty with the intention of taking up permanent residence overseas.

PHASING OUT FOR THE EEC

A significant change in the coverage of U. K. exchange controls is inprospect in the next few years. One of the conditions of the UnitedKingdom's entry into the EEC was that the U. K. Government agreedto adjust its exchange control regulations so as to conform to theprovisions of Community directives on capital movements and tocomplete such adjustments over a transitional period of five years afteraccession in 1973. Each category of capital flow between the UnitedKingdom and other EEC countries was allocated a terminal date bywhich it had to be freed from exchange controls. U. K. portfolioinvestment in the EEC was the final category in the phased programof liberalization, with a terminal date of December 31, 1977. TheUnited Kingdom has sought and obtained postponements of its accu-mulated liberalization commitments on balance of payments groundsin each of the past three years. It will undoubtedly be more difficult toobtain further postponements if the balance of payments recoverycontinues.

No indication has been given of how the liberalization of portfolioinvestment would be conducted. There are a number of possibilities,and each has rather different implications for the balance of payments.One is that, overnight, and without prior warning, U. K. residentsmight be required to use the official exchange rate for all subsequentpurchases and sales of EEC securities. Investors would lose thepremium on these holdings, and the pool would be reduced accord-ingly. The cost to the balance of payments would amount to the rela-tively small outflow prompted by investors seeking to restore the pro-portionate composition of EEC securities in their portfolios that hadbeen depleted by the loss of the premium. A second possibility is thatadvance warning of abolition might be provided. If an early date weregiven, investors would sell all their premium-worthy EEC securitiesbefore the due date, the size of the pool would decline only by theamount of the surrender, and the subsequent outflow would be greaterthan in the first option as investors would have to build up their entireEEC holdings again through the official exchange market.

©International Monetary Fund. Not for Redistribution

784 INTERNATIONAL MONETARY FUND STAFF PAPERS

A third alternative is that the pool might be divided into two—onepool for non-EEC securities and a second, and smaller, pool for EECsecurities—with the decision on final abolition deferred for severalyears. Using this method, liberalization could be introduced more grad-ually, the cost to the balance of payments kept to a minimum, andsudden short-term losses to investors avoided.

With the eventual removal of controls between the United Kingdomand the EEC, a major problem presents itself (assuming there are stillcontrols for non-EEC countries), namely, the leakage of U. K.-ownedcapital through the EEC into non-EEC countries. This could only becured by a uniform, equally well-patrolled fence of capital controlsround the Community as a whole.

IV. Summary and Conclusions

A justification often used for capital controls is that they confer ameasure of independence on monetary policy. One of the criteriaof independence is the extent to which domestic real interest rates canbe differentiated from those prevailing abroad. The above analysis hasshown that, since the investment currency market ensures a zero netoutflow of U. K. residents' funds but leaves nonresidents' funds unregu-lated, the latter can perform the function of rate equalization. Infact, the return differential between U. K. and U. S. bonds, allowingfor changes in the official exchange rate, was less than one half of apercentage point per annum between 1962 and 1976; on equities, itwas only one percentage point per annum.

Another closely allied justification for capital controls is the balanceof payments saving that they ensure. Even though interest rates may bemore or less equalized by nonresidents, there will still be a balanceof payments saving represented by the suppressed demand for interna-tional portfolio diversification from U. K. investors. This is borne outhistorically by the size of the premium, despite the very modest improve-ment in return offered by overseas investment. The analysis showedthe balance of payments saving by working through the effects ofabolition and indicated that, on the basis of the assumptions adopted,the initial outflow, with the premium at 45 per cent and the poolpresently standing at approximately £7 billion, would probably bein the region of <£ 3 billion.

The cost of the controls is represented by the loss of utility to inves-tors stemming from the restriction on the export of capital and thepenalty of the consequent premium. Since the overseas borrowing

©International Monetary Fund. Not for Redistribution

U.K. INVESTMENT CURRENCY MARKET 785

option fails to give investors scope to augment their net foreign posi-tion, it only partially offsets their welfare loss. A further cost of thesystem is some loss of international arbitrage business.

There is no official intervention in the premium market, but thesurrender policy ensures a tendency toward a depletion of the pooland an addition to official reserves. The surrender has the drawbackthat it tends to push up the premium, thus aggravating policingproblems, as well as acting as a deterrent to switching of securitiesby investors.

One of the conditions of the United Kingdom's entry into the EECin 1973 was that there would be a progressive liberalization of capitalcontrols between the United Kingdom and other member countries.Portfolio investment was scheduled for liberalization by the end of1977, but deferment of this obligation has been granted on balanceof payments grounds in each of the last three years. Further defermentmay be difficult to obtain if the current and capital accounts of thebalance of payments continue to improve. If the premium no longerapplied to EEC securities but controls were retained for the rest of theworld, policing problems would be greatly aggravated by the abundantscope for capital diversion. However, it is mainly in the context of therecovery in the balance of payments that consideration may be givenby the authorities to the lifting of restrictions and to the abolition ofthe investment currency market.

REFERENCES

Barattieri, Vittorio, and Giorgio Ragazzi, "An Analysis of the Two-Tier ForeignExchange Market," Banca Nazionale del Lavoro, Quarterly Review (December1971), pp. 354-72.

Cairncross, Sir Alexander K., Control of Long-Term International Capital Move-ments (Brookings Institution, 1973).

Day, William H.L., "Dual Exchange Markets Versus Exclusive Forward ExchangeRate Support," Staff Papers, Vol. 23 (July 1976), pp. 349-74.

Fleming, J. Marcus (1971), "Dual Exchange Rates for Current and Capital Trans-actions: A Theoretical Examination," Ch. 12 in his book, Essays in Interna-tional Economics (Harvard University Press, 1971), pp. 296-325.

(1974), "Dual Exchange Markets and Other Remedies for DisruptiveCapital Flows," Staff Papers, Vol. 21 (March 1974), pp. 1-27.

Grubel, Herbert G., "Internationally Diversified Portfolios: Welfare Gains andCapital Flows," American Economic Review, Vol. 58 (December 1968),pp. 1299-1314.