The Southern Gas Corridor and The EU Gas Security of Supply: What's Next?

14

THE SOUTHERN GAS CORRIDOR AND THE EU GAS SECURITY OF SUPPLY: WHAT’S NEXT? MANFRED HAFNER JOHNS HOPKINS UNIVERSITY SAIS-EUROPE AND SCIENCES-PO PARIS SIMONE TAGLIAPIETRA 20 MANFRED HAFNER

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of The Southern Gas Corridor and The EU Gas Security of Supply: What's Next?

THE SOUTHERN GAS CORRIDOR AND THE EU

GAS SECURITY OF SUPPLY: WHAT’S NEXT?

MANFRED HAFNER

JOHNS HOPKINS UNIVERSITY SAIS-EUROPE AND SCIENCES-PO PARIS SIMONE TAGLIAPIETRA

20

MAN

FRED

HAF

NER

Because of the decreasing trend of the EU domestic gas production, the EU gas

import requirements have increased rapidly over the last decade.

THE GENESIS OF THE SOUTHERN GAS CORRIDOR

Gas is an essential component of the energy mix of the European Union (EU), constituting one quarter of pri-mary energy supply and contribut-ing mainly to electricity generation, heating, feedstock for industry and fuel for transportation.

Because of the decreasing trend of the EU domestic gas production (particularly due the United King-dom), the EU gas import require-ments have increased rapidly over the last decade, leading to higher levels of import dependence and ultimately outlying the need to ad-dress the issue of security of gas sup-ply at the EU level.

This need unexpectedly became tangible in January 2006, when af-ter a long-lasting disagreement on gas prices, Russia cut off supplies to Ukraine for 3 days, Ukraine diverted volumes destined to Europe, and as a consequence gas supply to some Cen-tral European countries fell briefly.1

As a response to the energy security concerns emerged after this Rus-sian-Ukrainian-European gas cri-sis, the European Commission (EC) launched in 2008 a double strategy, aimed at enhancing the EU gas se-curity of supply architecture. On the one hand, the EC targeted to en-hance the EU internal energy market in order to foster gas flows between EU Member States. On the other hand, it aimed at enhancing gas sources diversification, including building LNG receiving terminals in Central and South-East Europe and pursuing the 4th corridor (generally known as Southern Gas Corridor) in order to bring gas from Caspian and Middle Eastern producing countries to the EU.

The implementation of this strategy -and particularly of the Southern Gas Corridor- was accelerated after another major natural gas crisis be-tween Russia and Ukraine occurred in January 2009. In fact, this crisis re-sulted to be even worse than the pre-vious one, as the transit of Russian gas through Ukraine was completely cut for two weeks, which resulted in

1. As Pirani, Stern and Yafimava underline natural gas conflicts between Russia and Ukraine go back to the immediate aftermath of the independence of the two countries. Regular transit conflicts emerged as transit usually became a part of the price dispute on the Russian gas price for the Ukrainian domestic market. In fact, no separation between the transit gas network and the domestic gas network exists in Ukraine and Ukrainian customers usually served themselves from the transit volumes which Russia called theft of gas through the transit system. See: Pirani, S., Stern, J. and Yafimava, K. (2009), The Russo-Ukrainian Gas Dispute of January 2009: A Comprehensive Assessment, OIES paper: NG27, Oxford Institute for Energy Studies.

21

CASPIAN REPORT, FALL 2014

22

MAN

FRED

HAF

NER

23

CASPIAN REPORT, FALL 2014

humanitarian crises in several Cen-tral and Eastern European countries that were strongly dependent on Russian gas supplies across Ukraine. This dispute has resulted in long-term economic consequences and affected the reputation of Russia as a reliable supplier and of Ukraine as a reliable transit country.

The official document on which the Southern Gas Corridor is rooted is thus represented by the Com-munication delivered in 2008 by the EC: the “Second Strategic En-ergy Review – An EU Energy Secu-rity and Solidarity Action Plan.”2

The document recognized in the Southern Gas Corridor one of the EU’s highest energy security pri-orities, outlying the need of a joint work between the EC, EU Member States and the countries concerned (Azerbaijan and Turkmenistan, Iraq and Mashreq countries) with the ob-jective of rapidly securing firm com-mitments for the supply of natural gas and the construction of the pipe-lines necessary for all stages of its development. Uzbekistan and Iran were also mentioned in the Commu-nication as potential partners, albeit only in a long-term scenario.

After the release of this document, the EC invited representatives of the countries concerned to a Ministe-rial level meeting aimed at securing concrete progress of the initiative in May 2009. The summit, held in Prague and named “Southern Cor-

ridor - New Silk Road”, served to express the political support to the realization of the Southern Gas Cor-ridor as an important and mutually beneficial initiative, aimed at pro-moting the common prosperity, sta-bility and security of all countries in-volved. The countries participating at the summit declared to consider the Southern Gas Corridor concept as a modern Silk Road interconnect-ing countries and people from dif-ferent regions and establishing the adequate framework, necessary for encouraging trade, multidirectional exchange of know-how, technologies and experience.

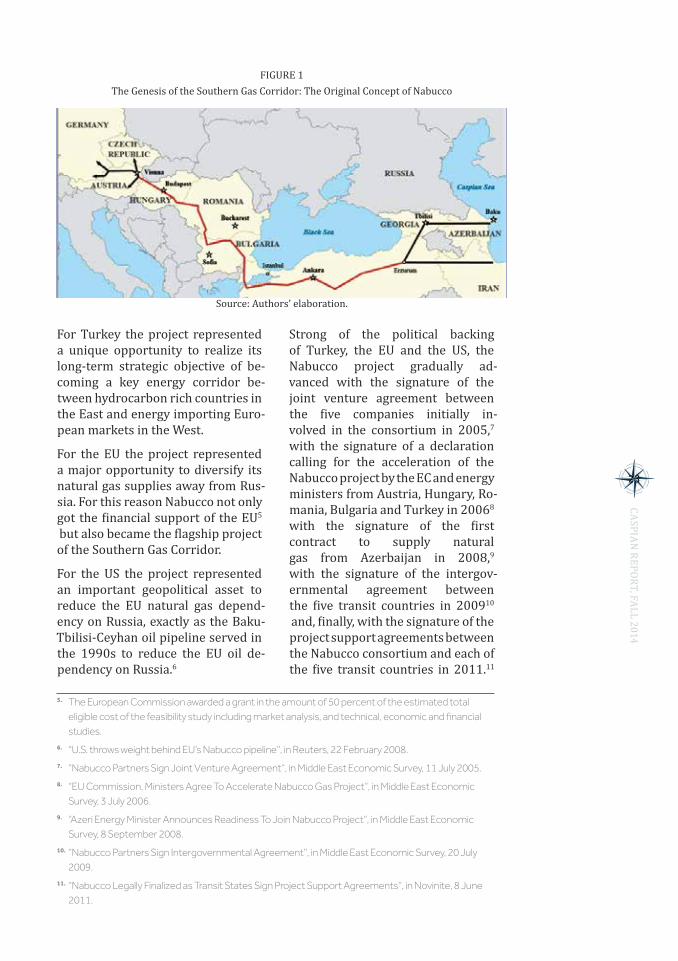

Furthermore, the countries partici-pating at the summit also agreed to give necessary political support and, where possible, technical and finan-cial assistance to the development of a project already launched in 2002 by a consortium composed by OMV of Austria, MOL Group of Hungary, Bulgargaz of Bulgaria, Transgaz of Romania and BOTAŞ of Turkey:3 Nabucco.

THE RISE AND FALL OF NABUCCO

In fact, in 2002 the five-company consortium agreed to cooperate on the development of Nabucco, a pro-jected 3,800 kilometers (km) long pipeline with a capacity of 31 billion cubic metres per year (bcm/year) designed to carry natural gas ex-tracted in Azerbaijan, Turkmenistan, Iraq, Iran and Egypt to Southeast and Central Europe via Turkey.4

The Nabucco project immediately got an unprecedented political sup-port from Turkey, the EU and the United States (US).

THE DOCUMENT RECOGNIZED IN THE SOUTHERN

GAS CORRIDOR ONE OF THE EU’S HIGHEST ENERGY

SECURITY PRIORITIES.

2. European Commission, Second Strategic Energy Review – An EU Energy Security and Solidarity Action Plan. COM(2008) 781 final, 13 November 2008.

3. The consortium was successively extended to RWE of Germany in 2008.4. Gas flows from these producing countries would have reached the Turkish border as follow: via the

South Caucasus Pipeline in the case of Azerbaijan; via Iran or the planned Trans-Caspian Pipeline in the case of Turkmenistan; via the planned extension of the Arab Gas Pipeline in the case of Iraq; via the Arab Gas Pipeline in the case of Egypt.

22

MAN

FRED

HAF

NER

23

CASPIAN REPORT, FALL 2014

For Turkey the project represented a unique opportunity to realize its long-term strategic objective of be-coming a key energy corridor be-tween hydrocarbon rich countries in the East and energy importing Euro-pean markets in the West.

For the EU the project represented a major opportunity to diversify its natural gas supplies away from Rus-sia. For this reason Nabucco not only got the financial support of the EU5 but also became the flagship project of the Southern Gas Corridor.

For the US the project represented an important geopolitical asset to reduce the EU natural gas depend-ency on Russia, exactly as the Baku-Tbilisi-Ceyhan oil pipeline served in the 1990s to reduce the EU oil de-pendency on Russia.6

Strong of the political backing of Turkey, the EU and the US, the Nabucco project gradually ad-vanced with the signature of the joint venture agreement between the five companies initially in-volved in the consortium in 2005,7

with the signature of a declaration calling for the acceleration of the Nabucco project by the EC and energy ministers from Austria, Hungary, Ro-mania, Bulgaria and Turkey in 20068 with the signature of the first contract to supply natural gas from Azerbaijan in 2008,9 with the signature of the intergov-ernmental agreement between the five transit countries in 200910

and, finally, with the signature of the project support agreements between the Nabucco consortium and each of the five transit countries in 2011.11

5. The European Commission awarded a grant in the amount of 50 percent of the estimated total eligible cost of the feasibility study including market analysis, and technical, economic and financial studies.

6. “U.S. throws weight behind EU’s Nabucco pipeline”, in Reuters, 22 February 2008.7. “Nabucco Partners Sign Joint Venture Agreement”, in Middle East Economic Survey, 11 July 2005.8. “EU Commission, Ministers Agree To Accelerate Nabucco Gas Project”, in Middle East Economic

Survey, 3 July 2006.9. “Azeri Energy Minister Announces Readiness To Join Nabucco Project”, in Middle East Economic

Survey, 8 September 2008.10. “Nabucco Partners Sign Intergovernmental Agreement”, in Middle East Economic Survey, 20 July

2009.11. “Nabucco Legally Finalized as Transit States Sign Project Support Agreements”, in Novinite, 8 June

2011.

FIGURE 1The Genesis of the Southern Gas Corridor: The Original Concept of Nabucco

Source: Authors’ elaboration.

24

MAN

FRED

HAF

NER

25

CASPIAN REPORT, FALL 2014

Notwithstanding the strong political commitment of the five transit coun-tries and the unprecedented politi-cal support of the EU and the US, the Nabucco project ultimately failed, mainly because of commercial and financial reasons: a very large scale pipeline project combined with a hugely uncertain demand outlook and the potential competition of South Stream. Moreover, the project promoters were mainly mid-size companies who have to rely on pro-ject finance and bank loans, and the banks ask for guarantees and long term ship or pay contracts which the market could not deliver. Fur-thermore, another major element of uncertainty for the Nabucco project was related to the fact that -with the only exception of Azerbaijan- all the potential suppliers were facing ma-jor difficulties to materialize their willingness to evacuate gas to Eu-rope via Turkey.

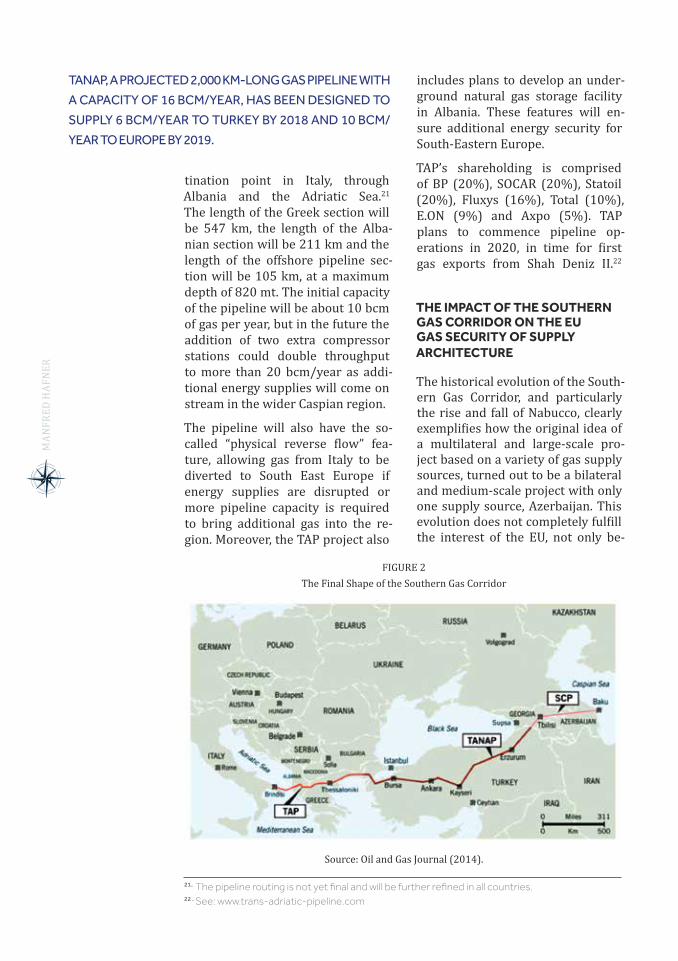

THE EVOLUTION OF THE SOUTHERN GAS CORRIDOR BEYOND NABUCCO: TANAP AND TAP

Taking into consideration the in-surmountable commercial and fi-nancial barriers that the Nabucco project was facing, Azerbaijan

-clearly the gas producing country most interested on the develop-ment of the Southern Gas Corridor12

- completely reshaped the Southern Gas Corridor game in 2011 by rap-idly conceptualizing its own infra-structure project to evacuate future gas flows from Shah Deniz Phase II to Turkey: the Trans Anatolian Natu-ral Gas Pipeline (TANAP).

TANAP, a projected 2,000 km-long gas pipeline with a capacity of 16 bcm/year, has been designed to sup-ply 6 bcm/year to Turkey by 2018 and 10 bcm/year to Europe by 2019. TANAP will run from the Georgian-Turkish border to the Turkish-Greek border, but the exact route of the pipeline is not clear yet. TANAP will receive its gas from the South Cau-casus Pipeline (SCP), a pipeline al-ready evacuating gas from the Azer-baijani Shah Deniz field to Turkey, which will be expanded in order to accommodate the new volumes of gas coming from Shah Deniz Phase II and going to TANAP.

On the contrary of Nabucco, TAN-AP was not born as a multilateral project but rather as a producer driven bilateral project between Azerbaijan and Turkey. The initial act of the project -occurred in De-cember 2011- was the signature of a Memorandum of Understand-ing (MoU) between Azerbaijan and Turkey establishing a consortium to build and operate the pipeline.13

This initial step was then followed by the signature of a binding inter-governmental agreement on TANAP made by Azerbaijan’s President Ali-yev and Turkey’s (at the time) Prime Minister Erdoğan in June 2012.14

Of course this bilateral relation was not symmetric, but rather unbal-anced in favour of Azerbaijan. In fact, the State Oil Company of Azerbaijan (SOCAR) was initially set to hold an 80 percent stake in the project, leav-ing only the remaining 20 percent to the Turkish partners (15 percent to BOTAŞ and 5 percent to TPAO).

12. Not only because of the investments already made on its Shah Deniz natural gas field, but also because of the need to reach a final investment decision for Shah Deniz Phase II (a decision that finally arrived on December 17, 2013).

13. “Turkey and Azerbaijan Sign MoU for TANAP Pipeline”, in Middle East Economic Survey, 9 January 2012.

14. “TANAP Project, the Silk Road of Energy, Has Been Signed”, http://www.tanap.com, 26 June 2012.

24

MAN

FRED

HAF

NER

25

CASPIAN REPORT, FALL 2014

This figure has changed over time, to a more balanced structure entail-ing a share of 58 percent for SOCAR, 25 percent for BOTAŞ, 5 percent for TPAO and 12 percent for BP.15

Notwithstanding this realignment of shares, SOCAR is set to continue to retain a controlling share of TANAP and operatorship of the line in the future. In fact, TANAP is crucially important for the Azerbaijani state owned company, as it will have a key role in the delivery of gas from its Shah Deniz field further down the supply chain to Europe, rather than selling at its border.

Among other factors, a key element of strength of the TANAP project relates to its financing: because of the considerable oil revenues pro-vided by the exports through the Baku-Tbilisi-Ceyhan pipeline, Azer-baijan is able to directly ensure the financing of the infrastructure. In fact, the cost of TANAP is esti-mated about USD 7-10 billion,16

an amount that Azerbaijan could easily finance just by making use of its sovereign wealth fund, the State Oil Fund, which currently retains about USD 34 billion in assets under management.17

The entrance of TANAP into the Southern Gas Corridor race in De-

cember 2011 gave the “coup de grace” to the already moribund Nabucco project. For this reason the Nabucco consortium tried to reinvent itself in 2012, by propos-ing a new -and smaller- version of the project: Nabucco West.18

This pipeline was designed to carry the TANAP 10 bcm/year destined to Europe from the Turkish-Euro-pean border to Austria via Bulgaria, Romania and Hungary. This pro-ject -again supported by the EU19

- ultimately failed like its predecessor, as the Shah Deniz consortium select-ed in June 2013 the Trans Adriatic Pipeline (TAP) to provide the miss-ing link between TANAP and the Eu-ropean market.20

TAP is an 870 km-long projected gas pipeline designed to provide the missing link for gas transpor-tation from Kipoi, on the border of Turkey and Greece (connection point with TANAP), to Brindisi, des-

NOTWITHSTANDING THE STRONG POLITICAL

COMMITMENT OF THE FIVE TRANSIT COUNTRIES

AND THE UNPRECEDENTED POLITICAL

SUPPORT OF THE EU AND THE US, THE NABUCCO

PROJECT ULTIMATELY FAILED, MAINLY BECAUSE

OF COMMERCIAL AND FINANCIAL REASONS.

15. “Turkish Companies Increase Their Shares in TANAP Up To 30%”, Azeri News Agency, 2 June 2014.

16. “BP Agrees to Join Tanap Gas Pipeline Project by Taking 12% Stake”, in Bloomberg, 23 January 2013.

17. Sovereign Wealth Fund Institute.18. “Nabucco-West: Abridged Pipeline Project Officially Submitted to Shah Deniz Consortium”, in

Eurasia Daily Monitor, Vol. 9, Issue 98, 23 May 2012.19. European Commission, Commissioner Oettinger welcomes decision on “Nabucco West”

pipeline, Press Release, 28 June 2012. The Nabucco West project was also supported by British Petroleum (BP), the operator of Shah Deniz Phase II. In fact, in order to support Nabucco West, in June 2012 BP ceased the development of its South East Europe Pipeline (SEEP), a project launched in September 2011 to carry the TANAP 10 bcm/year destined to Europe from the Turkish-European border to Austria.

20. “Shah Deniz consortium chooses TAP to carry Azeri gas to Europe”, in Reuters, 28 June 2013. Nabucco West also had the support of British Petroleum. In September 2011 British Petroleum also proposed a pipeline project, the so-called South East Europe Pipeline (SEEP), to carry the TANAP 10 bcm/year destined to Europe from the Turkish-European border to Austria. Albeit designed by the operator of Shah Deniz Phase II .

26

MAN

FRED

HAF

NER

27

CASPIAN REPORT, FALL 2014

tination point in Italy, through Albania and the Adriatic Sea.21

The length of the Greek section will be 547 km, the length of the Alba-nian section will be 211 km and the length of the offshore pipeline sec-tion will be 105 km, at a maximum depth of 820 mt. The initial capacity of the pipeline will be about 10 bcm of gas per year, but in the future the addition of two extra compressor stations could double throughput to more than 20 bcm/year as addi-tional energy supplies will come on stream in the wider Caspian region.

The pipeline will also have the so-called “physical reverse flow” fea-ture, allowing gas from Italy to be diverted to South East Europe if energy supplies are disrupted or more pipeline capacity is required to bring additional gas into the re-gion. Moreover, the TAP project also

includes plans to develop an under-ground natural gas storage facility in Albania. These features will en-sure additional energy security for South-Eastern Europe.

TAP’s shareholding is comprised of BP (20%), SOCAR (20%), Statoil (20%), Fluxys (16%), Total (10%), E.ON (9%) and Axpo (5%). TAP plans to commence pipeline op-erations in 2020, in time for first gas exports from Shah Deniz II.22

THE IMPACT OF THE SOUTHERN GAS CORRIDOR ON THE EU GAS SECURITY OF SUPPLY ARCHITECTURE

The historical evolution of the South-ern Gas Corridor, and particularly the rise and fall of Nabucco, clearly exemplifies how the original idea of a multilateral and large-scale pro-ject based on a variety of gas supply sources, turned out to be a bilateral and medium-scale project with only one supply source, Azerbaijan. This evolution does not completely fulfill the interest of the EU, not only be-

TANAP, A PROJECTED 2,000 KM-LONG GAS PIPELINE WITH

A CAPACITY OF 16 BCM/YEAR, HAS BEEN DESIGNED TO

SUPPLY 6 BCM/YEAR TO TURKEY BY 2018 AND 10 BCM/

YEAR TO EUROPE BY 2019.

21. The pipeline routing is not yet final and will be further refined in all countries.22 . See: www.trans-adriatic-pipeline.com

FIGURE 2The Final Shape of the Southern Gas Corridor

Source: Oil and Gas Journal (2014).

26

MAN

FRED

HAF

NER

27

CASPIAN REPORT, FALL 2014

cause of the different market struc-ture (both in terms of volumes and supply sources) but also because of the different legal structure of the two projects.

In fact, Nabucco was a project com-pletely under EU law; this signifies that the pipeline was to be regu-lated by rules such as third party access and unbundling through-out its entire length. The intergov-ernmental agreement signed by the five transit countries in 2009 provided a legal framework for 50 years, confirming that 50 percent of the pipeline’s capacity was to be reserved for the shareholders of the project and the remaining 50 per-cent was to be offered to third-party shippers on the basis of a regula-tory transit regime under EU law.23

The situation of TANAP is clearly very different. In fact, considering that Turkey has not yet adopted the EU energy acquis on its legislation, Azerbaijan -with a major stake in the project- will practically have the control of the pipeline and of the gas transit through it. Moreover, consid-ering both Turkey’s reluctance to enter the Energy Community and the difficulties related to the open-ing of the energy chapter of Turkey’s EU accession process, this situation will unlikely change in the foresee-able future. Albeit Azerbaijan could eventually have an interest in having some volumes of non-Azerbaijani gas into TANAP temporarily in the short term (in order to make the project more bankable), it will un-likely have the interest of doing so in the longer term, as the development of Shah Deniz and other fields will continue and additional volumes of Azerbaijani gas will thus be ready to be evacuated to Turkey and the EU via TANAP.

However, beyond all these issues, the pipeline-tandem TANAP-TAP certainly represent the first, histori-cal, concretization of what often ap-peared to be the “never-ending od-yssey” of the Southern Gas Corridor. Thanks to the development of TANAP and TAP we are now in the position to add 10 bcm/year to the EU gas security of supply architecture from 2020. This volume will certainly not radically change the overall EU gas security of supply architecture, as it will basically represent less than 3% of the EU gas import requirements, but it will represent an important el-ement for the South-East European gas security of supply.

TAP will connect to the Italian natu-ral gas grid operated by Snam Rete Gas, from which all Italian gas exit points to European destinations can be reached. Furthermore, TAP will provide a new source of gas to Bulgaria, by linking to existing and planned pipeline infrastructure, in-cluding reverse flow through an interconnector to the Kula-Sidi-rokastro line, and/or a proposed connection with the planned Inter-connector Greece-Bulgaria (IGB) pipeline. Finally, as far as the wider South-East European region is con-cerned, Caspian gas could be flowing also to growing markets in the Bal-kans that are currently dependent on a single gas supplier: Russia. In fact, TAP is already cooperating with the developers of the planned Ion-ian Adriatic Pipeline (IAP) to discuss connection possibilities to markets without gas in Southern Croatia, Al-bania, Montenegro, and Bosnia and Herzegovina.

According to the 25-year sales agree-ments announced in December 2013

23. “Nabucco: Delivering Diversification to the European Gas Market”, in Natural Gas Europe, 23 May 2013.

28

MAN

FRED

HAF

NER

29

CASPIAN REPORT, FALL 2014

by the Shah Deniz consortium,24

of the total 10 bcm/year destined to reach the European market via TANAP and TAP, around 1 bcm/year will go to buyers intending to supply to each of Bulgaria and Greece and the rest will go to buyers intending to supply Italy and “adjacent market hubs”. This last part of the sentence

seems to be particularly important, principally considering that among the nine companies that will pur-chase this gas in Italy, Greece and

Bulgaria (Axpo Trading AG, Bulgar-gaz EAD, DEPA Public Gas Corpora-tion of Greece S.A., Enel Trade SpA, E.ON Global Commodities SE, Gas Natural Aprovisionamientos SDG SA, GDF SUEZ S.A., Hera Trading srl and Shell Energy Europe Limited) there are some with important activities in Central and North West European countries.

In this framework, part of the gas ar-riving from TAP could well be evacu-ated also to Central and North-West European markets, notably Aus-tria, Germany, Switzerland, France and the United Kingdom (UK). This eventuality is reinforced by the fact that the TAP design offers various connection options to a number of existing and proposed pipelines along its route. This would enable

THE PIPELINE-TANDEM TANAP-TAP CERTAINLY

REPRESENT THE FIRST, HISTORICAL, CONCRETIZATION

OF WHAT OFTEN APPEARED TO BE THE “NEVER-

ENDING ODYSSEY” OF THE SOUTHERN GAS

CORRIDOR.

24. “http://www.bp.com/en_az/caspian/press/pressreleases/Shah-Deniz-sales-agreements- European-purchasers.html

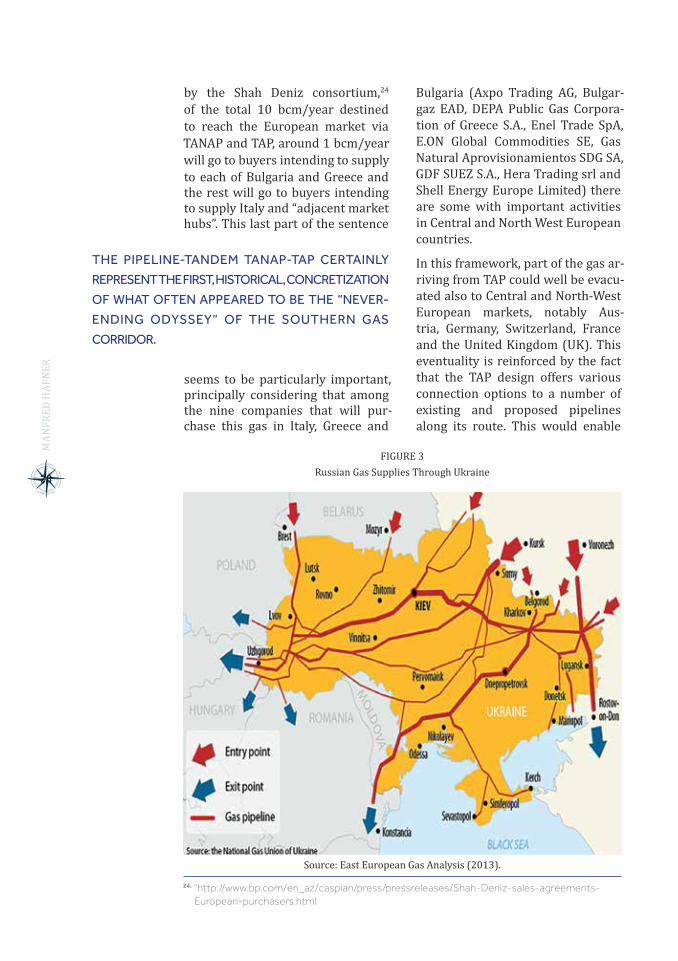

FIGURE 3Russian Gas Supplies Through Ukraine

Source: East European Gas Analysis (2013).

28

MAN

FRED

HAF

NER

29

CASPIAN REPORT, FALL 2014

the possible delivery of Caspian gas to destinations such as:

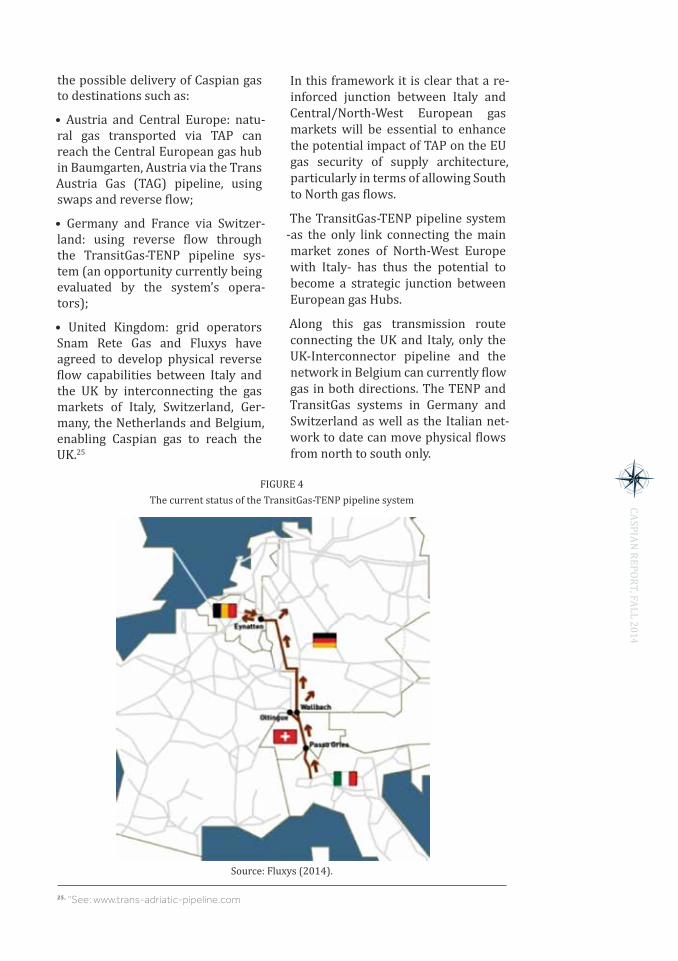

• Austria and Central Europe: natu-ral gas transported via TAP can reach the Central European gas hub in Baumgarten, Austria via the Trans Austria Gas (TAG) pipeline, using swaps and reverse flow;

• Germany and France via Switzer-land: using reverse flow through the TransitGas-TENP pipeline sys-tem (an opportunity currently being evaluated by the system’s opera-tors);

• United Kingdom: grid operators Snam Rete Gas and Fluxys have agreed to develop physical reverse flow capabilities between Italy and the UK by interconnecting the gas markets of Italy, Switzerland, Ger-many, the Netherlands and Belgium, enabling Caspian gas to reach the UK.25

In this framework it is clear that a re-inforced junction between Italy and Central/North-West European gas markets will be essential to enhance the potential impact of TAP on the EU gas security of supply architecture, particularly in terms of allowing South to North gas flows.

The TransitGas-TENP pipeline system -as the only link connecting the main market zones of North-West Europe with Italy- has thus the potential to become a strategic junction between European gas Hubs.

Along this gas transmission route connecting the UK and Italy, only the UK-Interconnector pipeline and the network in Belgium can currently flow gas in both directions. The TENP and TransitGas systems in Germany and Switzerland as well as the Italian net-work to date can move physical flows from north to south only.

25. “See: www.trans-adriatic-pipeline.com

FIGURE 4The current status of the TransitGas-TENP pipeline system

Source: Fluxys (2014).

30

MAN

FRED

HAF

NER

31

CASPIAN REPORT, FALL 2014

Snam Rete Gas has already begun in-vestments in the Italian network to enable substantial physical south to north flows at the Italian-Swiss bor-der at Passo Gries. For the TENP and Transitgas systems, investments to make the infrastructure bi-direc-tional are in the planning stage and

would create not only physical south to north capacity but also additional capacity from Germany to Belgium.

In December 2012, Fluxys Belgium, Fluxys TENP, FluxSwiss and Snam Rete Gas launched a coordinated market process for interested ship-pers to book long-term gas trans-mission capacity from the Italian trading point PSV through Switzer-land to the NCG and GASPOOL trad-ing points and/or the ZTP trading point in Belgium.

The joint approach of the four TSOs resulted from the Memorandum of Understanding agreed between parent companies Snam and Fluxys in August 2012 for developing and marketing reverse flow capacities from south to north between Italy and the UK.

Though shippers showed strong interest in south to north capacity they were uncomfortable with mak-ing binding commitments as it was not clear when a few remaining out-standing issues would be resolved.

The potential of South to North gas flows could represent a tool to ena-ble Southern suppliers -such as per-spective TAP suppliers- to compete with Northern suppliers (mainly

Russia and Norway) in the wider EU gas market. Just as in the past Italy’s Eni imported more expensive (in relation to Russian prices) gas from Norway and the Netherlands for di-versification and therefore security of supply reasons, it is possible to imagine that operators North of the Alps will import gas from Italy (and beyond) for diversification of supply reasons.

For this reason the development of TAP could have a positive impact on the development of reverse-flow ca-pacity on the TransitGas-TENP pipe-line system, as supply diversification is expected to be the main rational for reverse flows of this system. The recent events in Crimea and Ukraine and the reaction in Europe where many officials push for a reduced dependency on Russian gas, could further favor such a diversification policy.

With a future gas demand North of the Alps of around 300 bcm/year, a reverse flow of 10 bcm represents just a 3% diversification and a re-verse flow of 15 bcm represents a 5% diversification. Large wholesal-ers/operators/clients active North of the Alps with a large gas demand might be willing to pay a certain price premium for additional supply diversification in their supply port-folio and therefore increasing their supply security.

It is understood that the gas vol-umes that will reach Italy via TAP are being priced in view to be able to compete also North of the Alps. In fact, large wholesalers like E.ON or GDF Suez might want to diversify their gas supply portfolio directly with the producers from the Caspian basin (in addition to North Africa), while industrial and other clients will most likely diversify by buying from wholesalers South of the Alps (e.g. Eni) which have a different sup-

SNAM RETE GAS HAS ALREADY BEGUN INVESTMENTS

IN THE ITALIAN NETWORK TO ENABLE SUBSTANTIAL

PHYSICAL SOUTH TO NORTH FLOWS AT THE ITALIAN-

SWISS BORDER AT PASSO GRIES.

30

MAN

FRED

HAF

NER

31

CASPIAN REPORT, FALL 2014

ply portfolio compared to the main wholesalers North of the Alps.

Due to the limited volume of 8-9 bcm/year (depending on how much TAP gas will finally remain in Greece) from 2020, this intra-Euro-pean flows will of course not radi-cally change the EU gas landscape. However, the importance of TAP for both South-East and Central/North-West European gas markets could well rise in the future as new gas supplies will be accessible and ready to justify an expansion of TAP.

THE SOUTHERN GAS CORRIDOR AFTER THE 2014 UKRAINE CRISIS: WHAT’S NEXT?

As previously mentioned, in the fu-ture the addition of two extra com-pressor stations could double the capacity of TAP to more than 20 bcm. This opportunity, to be positioned in the post-2020 horizon, could radi-cally augment the relevance of TAP and the overall Southern Gas Corri-dor for the EU gas security of supply architecture, particularly consider-ing the new market and political re-alities emerging in Europe.

In particular, the unprecedented po-litical standoff between the Western world and Russia resulted by the 2014 Ukraine crisis might reinvigor-ate the EU’s quest to diversify its gas supply portfolio.

In fact, in the aftermath of the an-nexation of Crimea to the Russian Federation, the European Commis-sion decided to postpone talks with Russia over the legal status of the planned South Stream pipeline and full capacity utilization of the exist-

ing Nord Stream line. Both issues re-quire a compromise to move forward, but the EU Energy Commissioner Gunther Oettinger declared that he will not advance talks about pipelines such as South Stream for the time be-ing.26 The European Commission has also delayed a decision on exempting the Opal pipeline from Germany to the Czech Republic from the EU’s third-party access rules. This means the 55 bcm/year Nord Stream pipeline, built under the Baltic Sea to supply Russian gas to Europe, will have to continue running below full capacity.27 South Stream, a projected pipeline aimed at delivering 63 bcm/year of Russian gas to Europe under the Black Sea, repre-sents -together with Nord Stream- the cornerstone of Russia’s strategy to evacuate natural gas to Europe by-passing Ukraine.

Furthermore, the European Council of March 2014 concluded that “efforts to reduce Europe’s high gas energy de-pendency rates should be intensified, especially for the most dependent Member States”28 and the EU leaders tasked the European Commission to elaborate a plan for reducing energy dependence from Russia.

According to the conclusions of the EU Council: “The plan should reflect the fact that the EU needs to acceler-ate further diversification of its energy supply, increase its bargaining power and energy efficiency, continue to de-velop renewable and other indigenous energy sources and coordinate the development of the infrastructure to support this diversification in a sus-tainable manner, including through the development of interconnections. Such interconnections should also

26. “EU Postpones Talks on Russian Gas Pipelines”, in Energy Intelligence, 13 March 2014.27. Although Nord Stream had been construed before the Third Energy Package was introduced, the

commission has so far refused to exempt Opal from the third-party access demands required by the new rules. As a result, Gazprom has been able to use only 50% of Opal’s 36 Bcm/yr capacity, leaving Nord Stream underutilized.

28. European Council, Conclusions, EUCO 7/1/14 REV1, 29/21 March 2014, p. 10.

32

MAN

FRED

HAF

NER

33

CASPIAN REPORT, FALL 2014

include the Iberian peninsula and the Mediterranean area. Where rel-evant, interconnections should also be developed with third countries. Member States will show solidarity in case of sudden disruptions of en-ergy supply in one or several Mem-ber States. In addition, further ac-

tion should be taken to support the development of the Southern Cor-ridor, including further spur routes through Eastern Europe, to examine ways to facilitate natural gas ex-ports from North America to the EU and consider how this may best be reflected in TTIP, and increase the transparency of Intergovernmental Agreements in the field of energy.”29

The European Commission pub-lished its plan for reducing energy dependence from Russia on May, 26 with the Communication “European Energy Security Strategy.”30 With this document the European Com-mission outlines once more the need to reinforce the EU’s energy security, particularly in terms of natural gas supplies. The strategy proposed is structured on eight key pillars aimed at promoting closer coopera-tion among Member States in light of the principle of solidarity, while respecting national energy choices:

“i) Immediate actions aimed at in-creasing the EU’s capacity to over-come a major disruption during the

winter 2014/2015; ii) Strengthen-ing emergency/solidarity mecha-nisms including coordination of risk assessment and contingency plans; iii) Moderating energy demand; iv) Building a well-functioning and fully integrated internal market; v) Increasing energy production in the EU; vi) Further developing energy technologies; vii) Diversifying exter-nal supplies and related infrastruc-ture; viii) Improving coordination of national energy policies and speak-ing with one voice in external energy policy.”31

As far as the diversification of ex-ternal natural gas supplies is con-cerned, the strategy designed by the European Commission outlines that

“beyond strengthening our [EU’] re-lationship with existing suppliers, a EU policy goal should also be to open the way for new sources. The establishment of the Southern Cor-ridor and the identified projects of common interest is an important element in this respect, as it pre-pares the ground for supplies from the Caspian region and beyond. Pur-suing an active trade agenda in this region is crucial to ensure market access but also for the development of critical infrastructure, the viabil-ity of which depends on access to sufficient export volumes. In a first phase it is expected that by 2020 10 bcm/y of natural gas produced in Azerbaijan will reach the European market through the Southern Gas Corridor. Moreover, this new pipe-line connection is vital in providing a connection to the Middle East. The currently envisaged infrastructure in Turkey could accommodate up to 25 bcm/y for the European market.

THE ESTABLISHMENT OF THE SOUTHERN CORRIDOR

AND THE IDENTIFIED PROJECTS OF COMMON

INTEREST IS AN IMPORTANT ELEMENT IN THIS RESPECT,

AS IT PREPARES THE GROUND FOR SUPPLIES FROM THE

CASPIAN REGION AND BEYOND.

29. Ibidem, p. 10.30. European Commission, European Energy Security Strategy, COM(2014) 330 final, 28 May 2014.

This official document is accompanied by a major study on the state of the European energy security: European Commission, In depth study of European Energy Security, SWD(2014) 330 final, 28 May 2014.

31. European Commission, European Energy Security Strategy, op. cit., p. 3.

32

MAN

FRED

HAF

NER

33

CASPIAN REPORT, FALL 2014

In the longer term perspective, oth-er countries such as Turkmenistan, Iraq and Iran, if conditions are met to lift the sanctions regime, could also significantly contribute to the enlargement of the Southern Gas Corridor.”32

Of course this strategy will likely not have the impossible target of reducing by 100 percent the EU de-pendence on Russian gas, but it will certainly target a substantial reduc-tion. If so, this strategy will not be very different from the one adopted by the EU in 2008 with the Commu-nication “Second Strategic Energy Review - An EU Energy Security and Solidarity Action Plan”,33 the one launching the Southern Gas Corri-dor. However, as far as the Southern Gas Corridor is concerned, this time the situation could well turn out to be different from 2008, not only be-cause of the reinvigorated quest of the EU towards the diversification

of its gas supply portfolio after the Ukraine crisis, but also because of the availability of major natural gas re-serves in the Kurdistan Region of Iraq and in offshore Israel on the supply side.

These most recent developments seem to suggest that, despite all the long development described in this article -from the genesis of Nabucco to the rise of TAP- the Southern Gas Cor-ridor remains a story still to be largely written. On the basis of the past expe-rience we can expect this story to be complicated, under certain perspec-tives even byzantine, but certainly also fascinating and full of twists.

33. European Commission, European Energy Security Strategy, op. cit., p. 16.33. European Commission, Second Strategic Energy Review – An EU Energy Security and Solidarity

Action Plan (COM(2008) 781 final), 13 November 2008.