The Servicing of Global Insurance Programmes

24

1 The Servicing of Global Insurance Programmes: can insurers overcome the challenge? Mark Randall Fellowship Dissertation

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of The Servicing of Global Insurance Programmes

1

The Servicing of Global Insurance Programmes: can insurers overcome the challenge?

Mark Randall

Fellowship Dissertation

2

Contents

Introduction 3

Part 1: Global Programmes and the Servicing of Global Programmes 4

Part 2: The Challenge of Servicing a Global Programme 7

Part 3: Overcoming the Challenge 9

Proposition A 10

Proposition B 12

Proposition C 14

Conclusion 17

Bibliography 19

3

Introduction

Global insurance programmes (hereafter “global programmes”) are a complex product. By

design they are intended to both sit within, and sit above, multiple jurisdictions. Much has

been written about global programmes for the purpose of marketing their advantages to

buyers; be it the costs saved, the compliance and regulatory standards met or the improved

claims service delivered. (AGCS, 2020)1 (AIG, 2012)2

The literature surrounding global programmes as a product is understandably focused on

the interactions between a ‘tripartite relationship’ of the insurance buyer (usually the head

office of a multinational corporation), their insurance broker, and the insurance company.

(Strategic Risk, 2011)3 However the success of global programmes requires a vast network

of branches, subsidiaries and partners across multiple countries to implement any

agreement made.

In researching this topic it is clear that very little analysis has been undertaken which

specifically focuses on the challenges which arise for those parties who form the

aforementioned network, whose responsibility it is to implement insurance coverage which

has been agreed on their behalf with little to no input themselves. This paper will provide an

analysis of this underexplored area and suggest solutions to the challenges which arise for

specifically one of those parties – the insurance company. This is an area in which I have

worked and have therefore encountered such challenges myself.

While specific detailed literature on this subject is limited, much has been written about

global programmes generally and so this literature will be considered insofar as it furthers

this paper’s analysis.

1 Allianz Global Corporate & Specialty, ‘Allianz Multinational’, https://www.agcs.allianz.com/services/allianz-multinational.html [accessed 16 April 2020] 2 AIG, ‘How to Build a Multinational Program’, https://www.aig.com/content/dam/aig/america-canada/us/documents/brochure/aig-how-to-build-mn-prog-12-21-12-brochure.pdf [accessed 16 April 2020] pages 4 and 5 3 Strategic Risk, ‘Global Programmes’, https://www.strategic-risk-europe.com/download?ac=19856 [accessed 16 April 2020] page 8

4

The first part of this paper will define the relevant concepts and relationships. The second

part will explore why these concepts and relationships give rise to challenges for the insurer.

The third part will offer solutions as to how these challenges can be overcome.

Part 1: Global Programmes and the Servicing of Global Programmes

Global programmes seek to combine the benefits of possessing locally admitted insurance

with the consistency of coverage which a global insurance policy provides. By grouping a

multinational company’s global exposure under one programme, the economies of scale

and buying power of the multinational may allow the leveraging of lower premiums when

compared to each subsidiary purchasing their own insurance locally. The advantages of

global programmes have been further summarised by Chubb as such:

‘A global insurance programme provides for compliance with complex regulatory and

tax regimes, the ability to pay claims locally and efficiently; control over risk

management practices; cost efficiency; consistency of coverage and claims service and

enhanced customer outcomes.’ (Chubb)4

However when surveyed, buyers hold the compliance advantages and consistency of

coverage afforded by global programmes as the two most desired outcomes of the product.

(Airmic)5 It is these two outcomes which shall be of particular importance in this paper

because it is the parties who are not directly involved in negotiating a global programme

who nonetheless serve a fundamental role in delivering these outcomes. Global

programmes and the parties involved in their agreement and implementation will now be

defined and explored.

Global programmes are delivered through the issuance of two types of policy. First the

insurance company issues a master policy to the buyer or their broker. This master policy

provides coverage on a worldwide basis for both the buyer’s parent company and any

overseas subsidiary companies. However to navigate around the issue of non-admitted

insurance, the insurance company will instruct an overseas office present in the same

4 Chubb, ‘Global Insurance Programmes’, https://www.chubb.com/za-en/_assets/documents/global-programmes--what-every-corporate-risk-manager-insurance-buyer-needs-to-know.pdf [accessed 16 April 2020] 5 Airmic, ‘ACE Risk Management Survey: 90% say risk complexity increasing’, https://www.airmic.com/news-story/ace-risk-manager-survey-90-say-risk-complexity-increasing [accessed 16 April 2020]

5

jurisdiction as the buyer’s subsidiary to issue an admitted insurance policy to that

subsidiary. These are called local policies. The master policy will then provide difference in

conditions/difference in limits cover over any coverage afforded under the local policy.

(Strnad, 2009)6

To distinguish between the parties who are in control of the programme and those who

implement what has been agreed, the terms “producing” and “servicing” will be applied

throughout this paper. However other such terms are frequently used, for example servicing

business is often referred to as ‘reverse flow’ business. (London Market Group, 2018)7 It is

the producing underwriter within the insurance company who instructs the servicing

underwriter in one of its overseas offices to issue a local policy to the local subsidiary or

their appointed servicing broker. It is possible for servicing parties to not be part of the

same corporate structure as the producing parties (such as for third party fronting

arrangements) but throughout this paper the assumption will be applied that both parties

are part of the same corporate structure. Insurance companies which compete in offering

global programmes as a product have established vast in-house overseas networks precisely

to provide control over that product and to increase competitive advantage over those who

do not. This has led to a small pool of insurers and brokers who can deliver global

programmes. (FCA, 2019)8 Indeed as Dwyer observes: ‘The pool of carriers and brokers that

can execute a multinational program well is relatively small… even the best methodologies

and technologies can’t deliver without the foundation of ample talent, resources and

financial strength.’ (Dwyer, 2019)9

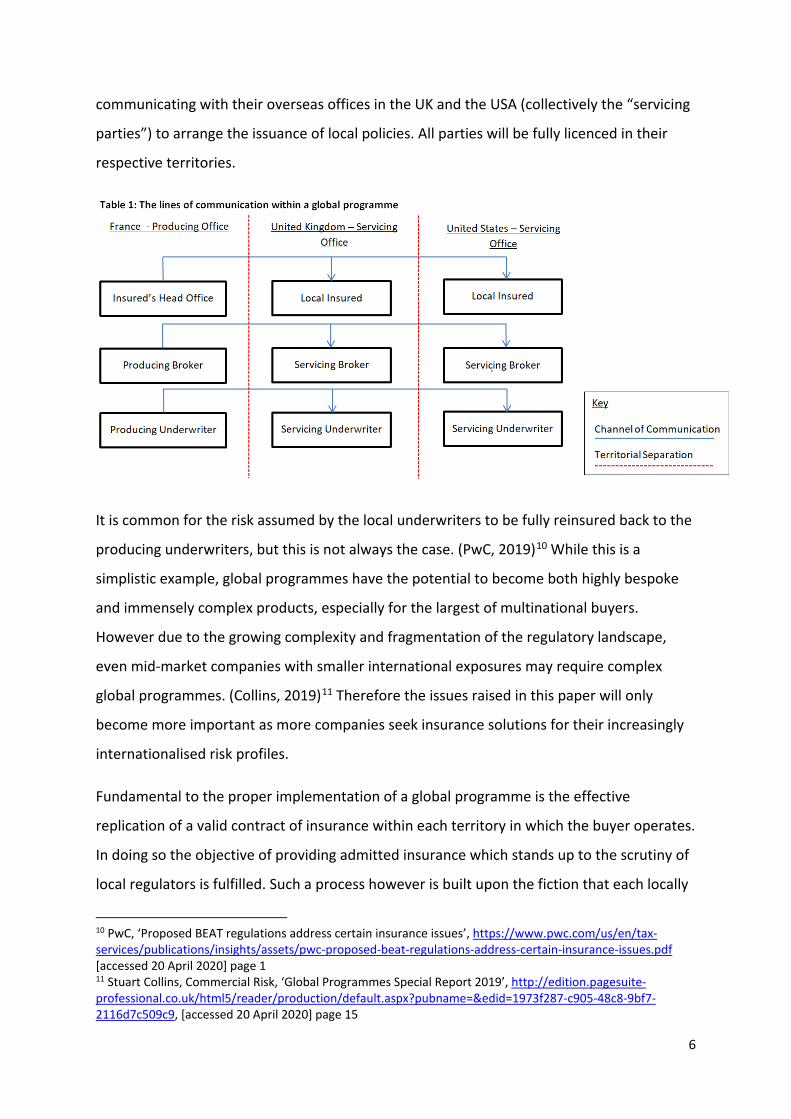

The table below (Table 1) illustrates the relationships and chains of communication

throughout a global programme. This shows a French multinational buyer, along with a

broker and insurer who have operations in France (collectively the “producing parties”),

6 Martin Strnad, International In-house Counsel Journal, ‘International Insurance Programs – Legal Frictions and Solutions’, https://www.iicjlaw.com/subscribersonly/09august/iicj5-internationalinsurance-martinstrnad-zurich-switzerland.pdf [accessed 16 April 2020] page 1,265 7 London Market Group, ‘Global Programme and Reverse Flow Business relating to Brokers and Company (Re)Insurers in the London Market’, https://lmg.london/wp-content/uploads/2019/07/Global-Programme-and-Reverse-Flow-Business-Guidance-September-2018.pdf [accessed 20 April 2020] page 1 8 Financial Conduct Authority, ‘Wholesale Insurance Broker Market Study’, https://www.fca.org.uk/publication/market-studies/ms17-2-2.pdf [accessed 05 June 2020] page 44 9 Katie Dwyer, Risk & Insurance, ‘4 Maddening Global Insurance Challenges and the Expert Solutions to Solve Them’, https://riskandinsurance.com/expert-solutions-for-5-of-the-most-maddening-global-insurance-challenges/ [accessed 02 June 2020]

6

communicating with their overseas offices in the UK and the USA (collectively the “servicing

parties”) to arrange the issuance of local policies. All parties will be fully licenced in their

respective territories.

It is common for the risk assumed by the local underwriters to be fully reinsured back to the

producing underwriters, but this is not always the case. (PwC, 2019)10 While this is a

simplistic example, global programmes have the potential to become both highly bespoke

and immensely complex products, especially for the largest of multinational buyers.

However due to the growing complexity and fragmentation of the regulatory landscape,

even mid-market companies with smaller international exposures may require complex

global programmes. (Collins, 2019)11 Therefore the issues raised in this paper will only

become more important as more companies seek insurance solutions for their increasingly

internationalised risk profiles.

Fundamental to the proper implementation of a global programme is the effective

replication of a valid contract of insurance within each territory in which the buyer operates.

In doing so the objective of providing admitted insurance which stands up to the scrutiny of

local regulators is fulfilled. Such a process however is built upon the fiction that each locally

10 PwC, ‘Proposed BEAT regulations address certain insurance issues’, https://www.pwc.com/us/en/tax-services/publications/insights/assets/pwc-proposed-beat-regulations-address-certain-insurance-issues.pdf [accessed 20 April 2020] page 1 11 Stuart Collins, Commercial Risk, ‘Global Programmes Special Report 2019’, http://edition.pagesuite-professional.co.uk/html5/reader/production/default.aspx?pubname=&edid=1973f287-c905-48c8-9bf7-2116d7c509c9, [accessed 20 April 2020] page 15

7

admitted insurance policy has been individually negotiated between the servicing parties. As

shall be discussed within this paper, the maintenance of this fiction is often the source of

tension between the producing and servicing parties.

The intricacies of how to properly construct a global programme from the perspective of the

producing parties has already been thoroughly explored (see Strnad12, Roberto13 and

Krishnan14) and so this paper will avoid re-exploring this topic. It will instead focus on the

challenges faced by insurance companies in servicing a global programme which, as

previously mentioned, has been underexplored. This will require particular focus on the role

and challenges faced by the servicing underwriter.

Part 2: The Challenge of Servicing a Global Programme

A fundamental gap exists between the theory and practice of how a global programme is

implemented. In theory, the producing underwriter negotiates the global coverage and the

servicing underwriter merely replicates that coverage. However in practice what amounts to

a process of clarification occurs internally between the producing and servicing underwriters

of the insurance company. This involves the servicing underwriter clarifying what insurance

coverage has been agreed on their behalf by the producing underwriter, and considering

how best to implement it. This could also include clarifying the terms and conditions to

apply or the policy form to use (be it standard or manuscript).

In light of these practicalities a question should be posed – why is this required at all? Surely

what the producing underwriter agrees must be implemented without question, otherwise

the primary purpose of organising the buyer’s insurance into a centralised global

programme is lost? Such an opinion is understandable because that is how global

programmes are marketed. (AGCS, 2020)15 However the insurance market globally is highly

12 Martin Strnad, International In-house Counsel Journal, ‘International Insurance Programs – Legal Frictions and Solutions’, https://www.iicjlaw.com/subscribersonly/09august/iicj5-internationalinsurance-martinstrnad-zurich-switzerland.pdf [accessed 16 April 2020] 13 Joanna Roberto, Insurance Law, ‘The Rise of Global Insurance Policies’, https://media.goldbergsegalla.com/uploads/jmr-forthedefense-may2016.pdf [accessed 16 April 2020] page 21 14 Suresh Krishnan and James Potts, ‘Structuring Multinational Insurance Programmes: Challenges and Solutions for International Companies with US Exposures’, https://d18b3k73pw7q78.cloudfront.net/app/uploads/2013/09/AM-Chubb-Insurance-Programmes-US-2013.pdf [ accessed 16 April 2020] 15 Allianz Global Corporate & Specialty, ‘Allianz Multinational’, https://www.agcs.allianz.com/services/allianz-multinational.html [accessed 16 April 2020]

8

fragmented, not just between nations but within the devolved institutions of those nations.

(Canamero, 2014)16 (NIAC, 2011)17 The result is that, when the producing parties negotiate

a global insurance programme which is informed by the laws, practices, customs and

language of their own market, that agreement can become undone when it comes into

contact with those same features of another market. (Skinner, 2008)18 (Fomchenko, 2006)19

The servicing underwriter must take the producing underwriter’s instructions, which contain

the skeleton coverage and pricing negotiated, and transform them into a fully compliant

local policy. The role of a servicing underwriter must therefore be less focused on the strict

implementation of any instructions received and instead focus on interpreting and adapting

those instructions to fit the local market. This process does give rise to a fundamental

challenge. If it is accepted that a servicing underwriter must interpret and adapt any

instructions received from the producing underwriter, then it follows that the servicing

underwriter’s role is different from that propagated by insurers themselves (being that

servicing underwriters merely implement the instructions received). By necessity, servicing

underwriters need to amend the coverage agreed.

This necessity is borne out of the aforementioned fragmented nature of the regulatory

landscape. Because the servicing underwriter is operating within a different jurisdiction,

they must consider the interests of the local insurance company who employs them in

addition to owing the local insured the duty of care mandated by local laws and by the local

regulator. As was highlighted earlier, a key outcome of a global programme is its ability to

maintain the fiction that each local transaction was negotiated between the servicing

parties of that jurisdiction, and hence stand up to the scrutiny of local regulators. To act

otherwise would be to remove the admitted insurance element of the programme and

16 Maria Canamero, Moody’s Analytics, ‘Regulatory Radar for Insurance: Emerging Regulations are Reshaping the Global Insurance Industry’, https://www.moodysanalytics.com/risk-perspectives-magazine/managing-insurance-risk/insurance-regulatory-spotlight/emerging-regulations-are-reshaping-the-global-insurance-industry [accessed 12 June 2020] 17 National Association of Insurance Commissioners, ‘State Insurance Regulation’, https://www.naic.org/documents/topics_white_paper_hist_ins_reg.pdf [accessed 12 June 2020] page 1 18 Nathan Skinner, Strategic Risk, ‘Are you breaking the law?’, https://www.strategic-risk-europe.com/are-you-breaking-the-law/1375136.article [accessed 05 June 2020] 19 Steven Fomchenko and Peter Smithdale, ‘International Property Coverage: thinking globally acting locally’, https://www.thefreelibrary.com/International+property+coverage%3A+thinking+globally+acting+locally.-a0141048569 [accessed 01 May 2020]

9

would jeopardise the key feature which differentiates a global programme from non-

admitted solutions.

Therefore, it has been revealed that the practicalities of servicing a global programme give

rise to a significant departure from the theory behind it. Servicing underwriters, due to the

necessities of the markets and jurisdictions in which they operate, cannot simply implement

the coverage agreed on their behalf by the producing underwriters. They must take into

account the interests and requirements of the local insurer as well as those of the local

insured, especially when the consideration of such interests is required by local laws and

regulations. This is the fundamental challenge of servicing a global programme. As a result

of this challenge, servicing underwriters often find themselves in a position of balancing the

competing interests of multiple parties. Because this reality is not acknowledged by

insurers, servicing underwriters have to overcome challenges on an ad hoc basis.

This paper will now propose solutions to resolve this fundamental challenge. To do this, and

to better understand the competing interests which a servicing underwriter must balance,

this paper will proceed with defining a new concept: that of a servicing underwriter’s

“mandate”.

Part 3: Overcoming the Challenge

A servicing underwriter does not possess an underwriting authority in the traditional sense

because they cannot make unilateral underwriting decisions. To allow such decisions would

go against the purpose of a global programme. Despite this, the exposures which servicing

underwriters bind the local insurer to can far exceed the underwriting authority of any

individual within the local insurance company. This is because the local policy may also act

as fronting documentation on behalf of an entire panel of co-insurers in the producing

territory, thus the coverage afforded under it can accommodate vast exposures. This

arrangement is also utilised where the local policy is fronting on behalf of a captive.

(Wohrmann, 2018)20 While the potentially large exposures are reinsured, the local policies

are nonetheless valid and enforceable contracts as perceived by the local authorities.

20 Paul Wohrmann, Global Programmes 2018, Captive Review, ‘The Changing Insurance Market’ via AIG UK, https://www.aig.co.uk/content/dam/aig/emea/united-kingdom/documents/Insights/ct-global-programmes.pdf [accessed 05 June 2020] page 15

10

Therefore any mistake, miscommunication or misapprehension between the producing and

servicing parties as to what the local policy should or should not cover may still be

enforceable against the local insurer if implemented into the policy document. This is

because insurance policies, like all contracts, are interpreted on an objective basis. (Clarke,

2014)21 This issue is especially acute considering how subjective the interpretation of

insurance terminology can be, let alone insurance terminology utilised between different

jurisdictions. (Fomchenko, 2006)22

From these observations, it must follow therefore that the “mandate” a servicing

underwriter has to bind the local insurer to potentially vast liabilities must be derived from a

clear source with clear guidelines. This is not the case. There are multiple sources of

authority from which a servicing underwriter derives their mandate to bind the local insurer;

some express, some implied, and some out of necessity. This paper will now proceed by

analysing these sources of authority and how useful they may be in terms of validating the

servicing underwriter’s actions. To distinguish the authority of a servicing underwriter to

bind the local insurer from that conferred upon a traditional underwriter, the term

“mandate” will be applied henceforth in order to avoid any suggestion of equivalence

between the two.

This paper proposes three sources from which a servicing underwriter’s mandate could be

derived. These proposed sources are A) from the producing underwriter, B) from the local

insurer and C) between the servicing parties.

Proposition A: The mandate is derived from the producing underwriter

The primary responsibility of a servicing underwriter is to issue a local policy in accordance

with the instructions which they receive from the producing underwriter. Often these

instructions are near replications of the master coverage. (Roberto, 2016)23 It would seem

appropriate therefore that a servicing underwriter should implement these instructions

21 Malcolm A Clarke, Routledge, ‘The Law of Liability Insurance’, section 6.2 22 Steven Fomchenko and Peter Smithdale, ‘International Property Coverage: thinking globally acting locally’, https://www.thefreelibrary.com/International+property+coverage%3A+thinking+globally+acting+locally.-a0141048569 [accessed 01 May 2020] 23 Joanna Roberto, Insurance Law, ‘The Rise of Global Insurance Policies’, https://media.goldbergsegalla.com/uploads/jmr-forthedefense-may2016.pdf [accessed 16 April 2020] page 23

11

because they represent the agreement made between the producing parties. Indeed, if one

of the primary advantages of a global programme is the avoidance of the need for

individually negotiated local policies, then it follows that servicing underwriters should not

seek to amend or otherwise re-underwrite the terms negotiated and subsequently

memorialised within the instructions received. Furthermore the existence of reinsurance

behind the local policy suggests that the servicing underwriter need not be concerned with

the consequences of implementing those instructions. Therefore the mandate of a servicing

underwriter to bind the local insurer is conferred by the producing underwriter, with each

individual instruction to be considered an individual mandate.

However this argument has some fundamental problems. To equate the mandate of a

servicing underwriter within a global programme as tantamount to a “rubber stamp” is to

misinterpret their role in addition to misunderstanding what the local policy’s function is in

delivering the outcomes which a global programme seeks to deliver. A good local policy

should not just implement the instructions of the producing underwriter, but should

conform to the regulations and customs of its market. The alternative would be to issue

local policies which may technically count as “admitted” policies but which would not stand

up to scrutiny should their content be challenged. Therefore such local policies would act

contrary to their intended function within the programme by increasing legal risk, since

ambiguous contracts when subjected to the interpretation of the courts can result in

unintended outcomes. (Clarke, 2014)24 Furthermore local policies that seek to participate in

local pools may also be challenged by the authorities that govern those pools should the

rules of participation be contravened. Two examples can be offered to illustrate this fallacy:

1. A UK servicing underwriter, upon receipt of instructions from a French producing

underwriter, issues a property damage policy implementing instructions requesting

tenants and neighbours liability cover. This is duly documented in the policy

schedule, even though such coverage on a property damage policy is only standard

in Napoleonic Code jurisdictions. (Greenwald, 2019)25 No accompanying clause is

contained in the policy wording fully defining the scope of coverage. Hence

24 Malcolm A Clarke, Routledge, ‘The Law of Liability Insurance’, section 6.7 25 Judy Greenwald, Business Insurance, ‘Napoleonic code does not apply to Chubb coverage dispute: Court’, https://www.businessinsurance.com/article/20190722/NEWS06/912329725/Napoleonic-code-does-not-apply-to-Chubb-coverage-dispute-Court [accessed 19 June 2020]

12

ambiguity is created because the cover is neither market standard nor adequately

defined.

2. A UK servicing underwriter, whose local insurer is a member of Pool Reinsurance

Company Limited (Pool Re)26 only covers the local insured’s central London buildings

against terrorism under the scheme as requested in the instructions received. This is

in breach of Pool Re’s adverse selection rules and therefore places at risk the viability

of the coverage. (Willis Ltd, 2014)27

Therefore, despite what may appear to be the prima facie case that the mandate of a

servicing underwriter is to simply follow the instructions of a producing underwriter, this

does not stand up to scrutiny. However there must be some truth to this proposition. If the

producing parties were not fundamentally in control of the global programme, and the

global insurance operation mandated the rejection of instructions over the implementation

of those instructions, the desired outcome of a global programme where the local policies

reflected the cover agreed by the producing parties would be defeated. The product would

therefore be unsustainable and competitive advantage lost.

In summary, while the mandate of the servicing underwriter must involve following the

producing underwriter’s instructions this mandate cannot be considered to be derived

wholly from those instructions where to follow them would create uncertainty and legal

risk.

Proposition B: The mandate is derived from the local insurer

The opposite of proposition A, this proposition places the mandate of the servicing

underwriter to bind the local insurer as arising from within the local insurer itself. Since local

policies are issued by the locally licenced insurer it would seem correct for the servicing

underwriter, in issuing that local policy, to be mandated to place the interests of the local

insurer above that of the producing underwriter. Those interests would include compliance

with local laws, regulations and customs.

26 Pool Reinsurance Company Limited, https://www.poolre.co.uk/ [accessed 01 May 2020] 27 Willis Ltd, ’Terrorism Insurance – The Pool Re Adverse Selection Rule Explained’, http://www.willis.com/Documents/Publications/Industries/Property_Investors/20140728_Terrorism_Adverse_Selection_JULY_2014_FINAL.pdf [accessed 01 May 2020]

13

Because the local insurer has a stake in ensuring its good reputation in the local market, to

issue poor quality or even non-compliant local policies would damage its reputation and

even its regulatory status. Poorly drafted policies containing unfamiliar and non-standard

coverage may also lead to protracted and contested claims, and would therefore negate the

efficiency in local claims handling which the local policy was intended to facilitate. (Hassett,

2014)28 For example, a producing underwriter may instruct a UK servicing underwriter to

issue an employers’ liability policy on their behalf, knowing that it is a legal requirement in

the UK. However, the instructions may request that a limit of indemnity of £5,000,000 in the

annual aggregate be applied. There are two aspects of this to consider. First, the Employers’

Liability (Compulsory Insurance) Regulations 199829 prevents aggregated limits of indemnity

being applied on employers’ liability policies. Second, the application of a £5,000,000 limit of

indemnity is contrary to market practice, though not contrary to law. (Willis Ltd, 2011)30 The

dichotomy between the two warrants further consideration.

The servicing underwriter should reject the aggregation of the limit of indemnity on the

basis that it conflicts with local laws. If the mandate of the servicing underwriter is to ensure

that their local insurer’s regulatory status and reputation is not damaged, on the basis that

without that status the local insurer will be unable to issue local policies, then it follows that

considerations of legality must take precedence over the producing underwriter’s

instructions. The issuance of “illegal admitted” policies is a self-defeating concept and

contrary to the local policy’s function as part of a global programme. While it is easy for

local policies to be an afterthought, they represent a cornerstone of the insured’s risk

management strategy and should be perceived as a fundamental aspect of the insurer’s

product. As one publication states: ‘Implementing best practices and a consistent loss

prevention philosophy must take place within the context of local conditions and respect

the requirements of local jurisdictions.’ (Advisen, 2014)31 This therefore supports the

28 Clive Hassett, Commercial Risk, ‘Why local is best’, https://www.commercialriskonline.com/why-local-is-best-clive-hassett-ace/ [accessed 05 June 2020] 29 Section 3 Employers’ Liability (Compulsory Insurance) Regulations 1998, http://www.legislation.gov.uk/uksi/1998/2573/made [accessed 02 June 2020] 30 Willis Ltd, ‘UK Employers’ Liability’ – A Guide, https://www.willis.com/Documents/Publications/Services/International/2011/UK_Intl_Alert_0911_v3.pdf [accessed 02 June 2020] page 2 31 Advisen, ‘Managing a Globally Compliant Insurance Progam’, https://www.advisenltd.com/wp-content/uploads/managing-globally-compliant-insurance-program-white-paper-2014-11-10.pdf [accessed 05 June 2020] page 6

14

proposition that the servicing underwriter’s mandate is to apply local considerations first,

over the requirements of the producing parties.

However the same cannot be said for customs. Acting contrary to standard market practice

is not the same as illegality because those local policies would still be perceived as valid by

local regulators and enforceable in court. Furthermore the practical realities of servicing

global programmes demand that servicing underwriters pursue the path of least resistance.

If every instruction were to become a drawn out negotiation between producing and

servicing underwriters then the legitimate expectations of the buyer, that the programme

would be seamlessly implemented upon the finalisation of terms by the producing parties,

would not be delivered. Therefore the argument that the mandate of the servicing

underwriter can be drawn from the customs of the market in which they operate would

seem inappropriate in this context.

Therefore the mandate of the servicing underwriter is to enforce the standards of the

market insofar as they amount to legal standards, not customary standards. This conclusion

remains consistent with the desired outcomes of a global programme and the function of a

local policy within that programme.

Proposition C: The mandate is derived from ensuring the transaction between the servicing

parties follows reasonable underwriting principles

Global programmes are built upon the fiction that each local policy is individually negotiated

between the servicing parties. This means that, when perceived out of the context of the

wider global programme, the local transaction should follow reasonable underwriting

principles on the basis that local regulators would view the transaction from just a local

perspective. The maintenance of this fiction is important because multiple taxation and

regulatory issues would result should this fiction be compromised. However the current

practice by the producing parties of considering the needs of the servicing parties ‘almost as

an afterthought’ (Hall, 2001)32 threatens this fiction because it produces local transactions

which do not adhere to reasonable underwriting principles. Therefore should it be the

32 Robert Hall, ‘Fronting: Business Considerations, Regulatory Concerns, Legislative Reactions and Related Case Law’, https://debrahalljd.files.wordpress.com/2018/02/fronting-business-considerations-reguatory-concerns-legislative-reactions-and-related-caselaw.pdf [accessed 05 June 2020] page 2

15

mandate of the servicing underwriter to ensure that the transaction follows reasonable

underwriting principles in order to avoid the legal and regulatory risks which may result

from deviating from those principles?

First however, it should be clarified what reasonable underwriting principles constitute. It

should be noted that the concept of following reasonable underwriting principles as a proxy

for ensuring regulatory compliance has already been suggested by Sharma, albeit

specifically in the context of premium allocation. (Sharma, 2009)33 In this same context

Skinner equated reasonable underwriting principles with the terms which the local market

would demand. (Skinner, 2008)34 However such an approach would ignore the economies of

scale which global programmes can leverage, and also does not consider the business

decisions underwriters make in choosing to write desirable risks cheaply to win them from

competitors. Therefore a servicing underwriter should not seek to re-underwrite the local

risk. Instead their mandate should merely be to ensure that the local transaction does not

constitute a gross deviation from reasonable underwriting principles. Such a standard

should therefore only seek to target wholly unreasonable and unjustifiable local

transactions.

There are two ways in which a servicing underwriter should be mandated to ensure the

local transaction follows reasonable underwriting principles in order to avoid legal and

regulatory risk: ensuring a sufficiency of capacity and a sufficiency of premium. Each shall be

explored in turn.

Regulators are becoming increasingly concerned at the industry standard practice of issuing

local policies carrying low limits of indemnity. From the insurer’s perspective, this avoids

accumulation issues should a large claim event trigger multiple local policies. (Strnad,

2009)35 However the issuance of a local policy does not automatically eliminate all

compliance considerations. As Strnad states, ‘For most jurisdictions, the existence of a local

33 Praveen Sharma, Strategic Risk, ‘Taxing Issues’, https://www.strategic-risk-europe.com/taxing-issues/1380337.article [accessed 05 June 2020] 34 Nathan Skinner, Strategic Risk, ‘Are you breaking the law?’, https://www.strategic-risk-europe.com/are-you-breaking-the-law/1375136.article [accessed 05 June 2020] 35 Martin Strnad, International In-house Counsel Journal, ‘International Insurance Programs – Legal Frictions and Solutions’, https://www.iicjlaw.com/subscribersonly/09august/iicj5-internationalinsurance-martinstrnad-zurich-switzerland.pdf [accessed 16/04/2020] page 1,265

16

policy does not in any way alter the fact that the producing country insurer is transacting

insurance business directly in the [servicing] country if DIL or DIC insures a risk located in the

[servicing] country.’ (Strnad, 2009)36 Therefore, if the local policy limits are easily exhausted

then reverting to the master cover does not negate the issue of non-admitted insurance.

This means that the regular considerations on the payment of claims from non-admitted

policies, such as the repatriation of the claims payment to the local entity, taxation issues,

regulatory issues and loss adjusting issues would still apply. (Willis Ltd, 2011)37 (Barton,

2018)38 (Roberto, 2016)39 (Advisen, 2014)40 Indeed having to navigate around such issues

may not even be anticipated by the insured, since their legitimate expectation would be

that the issuance of a local policy would specifically protect against such problems.

Therefore such an approach should be avoided, especially in the circumstances where the

local insured’s operation is very large. For example a large manufacturing operation may be

provided with a local public and products liability policy carrying a £1,000,000 limit of

indemnity, which would be inappropriately low for the local insured’s needs. While it is

possible that a servicing broker may raise similar issues with the producing broker, it cannot

be guaranteed that the producing broker would have even appointed a servicing broker.

Therefore it should be the mandate of the servicing underwriter to challenge such an

approach in a constructive way to make the local transaction follow reasonable

underwriting principles. A simple solution would be to increase the capacity of the local

policy, though not necessarily to the equivalent limit as the master policy, in order to

mitigate against the aforementioned accumulation issues.

36 Martin Strnad, International In-house Counsel Journal, ‘International Insurance Programs – Legal Frictions and Solutions’, https://www.iicjlaw.com/subscribersonly/09august/iicj5-internationalinsurance-martinstrnad-zurich-switzerland.pdf [accessed 16/04/2020] page 1,267 37 Willis Ltd, ‘Non-Admitted Coverage and Premium Taxes: No Standard Solution’, https://www.willis.com/Documents/Publications/Services/International/2011/Intl_Alert-_Non_Admitted_0611_v6.pdf [accessed 08 June 2020] page 3 38 Carol Barton, Global Programmes 2018, Captive Review, ‘Global Programmes: Raising the Bar’ via AIG UK, https://www.aig.co.uk/content/dam/aig/emea/united-kingdom/documents/Insights/ct-global-programmes.pdf [accessed 05 June 2020] page 16 39 Joanna Roberto, Insurance Law, ‘The Rise of Global Insurance Policies’, https://media.goldbergsegalla.com/uploads/jmr-forthedefense-may2016.pdf [accessed 16 April 2020] page 22 40 Advisen, ‘Managing a Globally Compliant Insurance Progam’, https://www.advisenltd.com/wp-content/uploads/managing-globally-compliant-insurance-program-white-paper-2014-11-10.pdf [accessed 05 June 2020] page 5

17

Legal and regulatory issues may also arise if local policies carry insufficient premiums. This is

because any tax levied upon that premium would be comparatively lower than if reasonable

underwriting principles were followed and an appropriate premium charged on the local

policy. As one publication states, ‘Regulators may be alerted if a corporation is buying what

could be perceived as an unrealistically low amount of cover for its local operations and

paying a matching amount of insurance premium tax.’ (Strategic Risk, 2011)41 Yet because

the premium of a global programme is often allocated between territories in proportion to

each territory’s share of the economic measure (sums insured, turnover etc.) as standard

practice, the situation can arise where local policies which consistently carry large claims

only demand a low local premium in return. This may cause local regulators to argue that

tax is being avoided, and no defence could be posited that the transaction is reasonable.

Considering that the servicing underwriter will have the details of those claims reported

against the local policy (though they may not have sight of any DIC/DIL claims made against

the master policy), it would be practical for them to raise such issues with the producing

underwriter and seek a proportionately larger allocation of the global premium, especially

before renewal discussions between the producing parties begin. This is where servicing

underwriters must be proactive in ensuring compliance. Since they possess the local

expertise it would be incorrect to attempt to delegate all issues of compliance to the

producing underwriter who cannot be expected to have sight over all aspects of the global

programme. (Norris, 2019)42 Given that any breaches of local compliance issues would be

held against the local insurer, this argument is consistent with the conclusions of

Proposition B.

It can therefore be proposed that the mandate of a servicing underwriter, in co-ordination

with the producing underwriter, should be to ensure that the local transaction follows

reasonable underwriting principles. This would mitigate the legal and regulatory risks of

issuing local policies carrying insufficient capacity and premiums. To go against this notion

41 Strategic Risk, ‘Global programmes’, https://www.strategic-risk-europe.com/download?ac=19856 [accessed 05 June 2020] page 9 42 Ben Norris, Commercial Risk, ‘Global Programmes Special Report 2019’, http://edition.pagesuite-professional.co.uk/html5/reader/production/default.aspx?pubname=&edid=1973f287-c905-48c8-9bf7-2116d7c509c9, [accessed 20 April 2020] page 22

18

would put at risk the fiction which global programmes seek to uphold and would therefore

threaten the viability of the product as a whole.

Conclusion

This paper has established that servicing underwriters, by necessity, serve a purpose greater

than merely “rubber stamping” the insurance coverage agreed by the producing parties.

This necessity is borne out of the need to give effect to the very outcomes which global

programmes are designed to deliver. Therefore the perceived truism that the servicing

underwriter merely implements the entire coverage as agreed by the producing parties has

been revealed as false. Accepting and managing this state of affairs is the fundamental

challenge of servicing a global programme.

To overcome this challenge, this paper has sought to rationalise the priorities and

responsibilities of a servicing underwriter through proposing the concept of an underwriting

mandate. This seeks to clearly delineate which interests of the various parties should take

precedence when those interests are placed in opposition. The parties in question are the

producing underwriter, the local insurance company and the local insured. This paper has

explored the roles and responsibilities of a servicing underwriter vis-à-vis these parties and

in doing so can propose a clear hierarchy of priorities which should form the servicing

underwriter’s mandate. By following this mandate, the challenge of servicing a global

programme can be overcome. Procedures could be established throughout the insurance

company’s network to give effect to this mandate.

This paper can conclude the proposed mandate as such: a servicing underwriter should

follow the instructions of the producing underwriter but only insofar as they do not create

legal and regulatory risk. What constitutes legal and regulatory risk should be construed

narrowly to give the greatest scope for the agreement made by the producing parties to be

implemented. For example, servicing underwriters should not seek to enforce the

customary standards of the local market because customary standards are not tantamount

to legal standards. However, they should ensure that the transaction follows reasonable

underwriting principles because to not follow them has been demonstrated as constituting

a legal and regulatory risk. To act otherwise would threaten the capability of the insurer to

19

issue a local policy in the territory, and hence place at risk the insurer’s ability to provide

global programmes as a solution to the needs of multinational buyers.

This paper has sought to limit the scope of its analysis to that of the challenges faced by the

insurance company. Considering the complexity involved in servicing global programmes,

further analysis should be undertaken focusing on the challenges faced by the servicing

broker and local insured. In doing so, this previously underexplored yet complex area of

insurance can be given the degree of analysis which is warranted.

Word Count: 4,985

Bibliography

Articles

Advisen, ‘Managing a Globally Compliant Insurance Program’,

https://www.advisenltd.com/wp-content/uploads/managing-globally-compliant-insurance-

program-white-paper-2014-11-10.pdf [accessed 05 June 2020]

AIG, ‘How to Build a Multinational Program’,

https://www.aig.com/content/dam/aig/america-canada/us/documents/brochure/aig-how-

to-build-mn-prog-12-21-12-brochure.pdf [accessed 16 April 2020]

AIG, ‘Multinational Insurance Programmes fit for the future’, https://www-

409.aig.co.uk/insights/multinational-insurance-programmes-fit-for-the-future [accessed 08

July 2020]

Airmic, ‘ACE Risk Management Survey: 90% say risk complexity increasing’,

https://www.airmic.com/news-story/ace-risk-manager-survey-90-say-risk-complexity-

increasing [accessed 16 April 2020]

Allianz Global Corporate & Specialty, ‘Allianz Multinational’,

https://www.agcs.allianz.com/services/allianz-multinational.html [accessed 16 April 2020]

20

Ben Norris, Commercial Risk, ‘Global Programmes Special Report 2019’,

http://edition.pagesuite-

professional.co.uk/html5/reader/production/default.aspx?pubname=&edid=1973f287-

c905-48c8-9bf7-2116d7c509c9, [accessed 20 April 2020]

Carol Barton, Global Programmes 2018, Captive Review, ‘Global Programmes: Raising the

Bar’ via AIG UK, https://www.aig.co.uk/content/dam/aig/emea/united-

kingdom/documents/Insights/ct-global-programmes.pdf [accessed 05 June 2020]

Chubb, ‘Global Insurance Programmes’, https://www.chubb.com/za-

en/_assets/documents/global-programmes--what-every-corporate-risk-manager-insurance-

buyer-needs-to-know.pdf [accessed 16 April 2020]

Clive Hassett, Commercial Risk, ‘Why local is best’,

https://www.commercialriskonline.com/why-local-is-best-clive-hassett-ace/ [accessed 05

June 2020]

CMS, ‘Global Insurance Programmes: the interplay between local and master policies’,

https://www.cms-lawnow.com/ealerts/2009/06/global-insurance-programmes-the-

interplay-between-local-and-master-policies?sc_lang=en [accessed 08 July 2020]

Financial Conduct Authority, ‘Wholesale Insurance Broker Market Study’,

https://www.fca.org.uk/publication/market-studies/ms17-2-2.pdf [accessed 05 June 2020]

Joanna Roberto, Insurance Law, ‘The Rise of Global Insurance Policies’,

https://media.goldbergsegalla.com/uploads/jmr-forthedefense-may2016.pdf [accessed 16

April 2020]

Judy Greenwald, Business Insurance, ‘Napoleonic code does not apply to Chubb coverage

dispute: Court’,

https://www.businessinsurance.com/article/20190722/NEWS06/912329725/Napoleonic-

code-does-not-apply-to-Chubb-coverage-dispute-Court [accessed 19 June 2020]

Katie Dwyer, Risk & Insurance, ‘4 Maddening Global Insurance Challenges and the Expert

Solutions to Solve Them’, https://riskandinsurance.com/expert-solutions-for-5-of-the-most-

maddening-global-insurance-challenges/ [accessed 02 June 2020]

21

Kennedys, ‘Claims payments under global insurance programmes’,

https://www.lexology.com/library/detail.aspx?g=963109f5-e56b-49d2-b79e-1685844976e2

[accessed 08 July 2020]

Kennedys, ‘Foresight may provide the best risk insight in a multinational programme’,

https://www.kennedyslaw.com/thought-leadership/article/ [accessed 08 July 2020]

Leader’s Edge, ‘Sense Less’, https://www.leadersedge.com/industry/sense-less [accessed 08

July 2020]

London Market Group, ‘Global Programme and Reverse Flow Business relating to Brokers

and Company (Re)Insurers in the London Market’, https://lmg.london/wp-

content/uploads/2019/07/Global-Programme-and-Reverse-Flow-Business-Guidance-

September-2018.pdf [accessed 20 April 2020]

Maria Canamero, Moody’s Analytics, ‘Regulatory Radar for Insurance: Emerging Regulations

are Reshaping the Global Insurance Industry’, https://www.moodysanalytics.com/risk-

perspectives-magazine/managing-insurance-risk/insurance-regulatory-spotlight/emerging-

regulations-are-reshaping-the-global-insurance-industry [accessed 12 June 2020]

Martin Strnad, International In-house Counsel Journal, ‘International Insurance Programs –

Legal Frictions and Solutions’, https://www.iicjlaw.com/subscribersonly/09august/iicj5-

internationalinsurance-martinstrnad-zurich-switzerland.pdf [accessed 16 April 2020]

Michael J Moody, ‘New concerns for international insurance programs, Jurisdictions looking

for tax revenue may go after local affiliates’,

http://roughnotes.com/rnmagazine/2012/june2012/2012_06p078.htm [accessed 08 June

2020]

Nathan Skinner, Strategic Risk, ‘Are you breaking the law?’, https://www.strategic-risk-

europe.com/are-you-breaking-the-law/1375136.article [accessed 05 June 2020]

National Association of Insurance Commissioners, ‘State Insurance Regulation’,

https://www.naic.org/documents/topics_white_paper_hist_ins_reg.pdf [accessed 12 June

2020]

22

Paul Wohrmann, Global Programmes 2018, Captive Review, ‘The Changing Insurance

Market’ via AIG UK, https://www.aig.co.uk/content/dam/aig/emea/united-

kingdom/documents/Insights/ct-global-programmes.pdf [accessed 05 June 2020]

Pinsent Masons, ‘Flexsys v XL’, https://www.pinsentmasons.com/out-law/guides/flexsys-v-xl

[accessed 08 July 2020]

Pool Reinsurance Company Limited, https://www.poolre.co.uk/ [accessed 01 May 2020]

Praveen Sharma, Strategic Risk, ‘Taxing Issues’, https://www.strategic-risk-

europe.com/taxing-issues/1380337.article [accessed 05 June 2020]

PwC, ‘Proposed BEAT regulations address certain insurance issues’,

https://www.pwc.com/us/en/tax-services/publications/insights/assets/pwc-proposed-beat-

regulations-address-certain-insurance-issues.pdf [accessed 20 April 2020]

Robert Hall, ‘Fronting: Business Considerations, Regulatory Concerns, Legislative Reactions

and Related Case Law’, https://debrahalljd.files.wordpress.com/2018/02/fronting-business-

considerations-reguatory-concerns-legislative-reactions-and-related-caselaw.pdf [accessed

05 June 2020]

Robert Klein, ‘Principles for Insurance Regulation: An Evaluation of Current Practices and

Potential Reforms’, https://link.springer.com/content/pdf/10.1057%2Fgpp.2011.9.pdf

[accessed 08 July 2020]

Steven Fomchenko and Peter Smithdale, ‘International Property Coverage: thinking globally

acting locally’,

https://www.thefreelibrary.com/International+property+coverage%3A+thinking+globally+a

cting+locally.-a0141048569 [accessed 01 May 2020]

Strategic Risk, ‘A Guide To: Global Insurance Regulations’, https://www.strategic-risk-

europe.com/download?ac=21888 [accessed 08 July 2020]

Strategic Risk, ‘Complex compliance requirements puts global businesses at risk’,

https://www.strategic-risk-europe.com/complex-compliance-requirements-puts-global-

businesses-at-risk/1416472.article [accessed 08 July 2020]

23

Strategic Risk, ‘Compliance hot spots of international programmes’, https://www.strategic-

risk-europe.com/compliance-hot-spots-of-international-programmes-/1420600.article

[accessed 08 July 2020]

Strategic Risk, ‘Global Programmes’, https://www.strategic-risk-

europe.com/download?ac=19856 [accessed 16 April 2020]

Strategic Risk, ‘Guide To: Multinational Risks’ https://www.strategic-risk-

europe.com/download?ac=39126 [accessed 08 July 2020]

Strategic Risk, ‘Q&A: Multinational insurance programmes fit for the future’

https://www.strategic-risk-europe.com/qanda-multinational-insurance-programmes-fit-for-

the-future/1427376.article [accessed 08 July 2020]

Stuart Collins, Commercial Risk, ‘Global Programmes Special Report 2019’,

http://edition.pagesuite-

professional.co.uk/html5/reader/production/default.aspx?pubname=&edid=1973f287-

c905-48c8-9bf7-2116d7c509c9 [accessed 20 April 2020]

Stuart Collins, Commercial Risk, ‘Growing demand for multinational insurance despite

headwinds, https://www.commercialriskonline.com/growing-demand-multinational-

insurance-despite-headwinds/ [accessed 08 July 2020]

Suresh Krishnan and James Potts, ‘Structuring Multinational Insurance Programmes:

Challenges and Solutions for International Companies with US Exposures’,

https://d18b3k73pw7q78.cloudfront.net/app/uploads/2013/09/AM-Chubb-Insurance-

Programmes-US-2013.pdf [accessed 16 April 2020]

Swiss Re Corporate Solutions, ‘An international insurance programme proposition built

‘from scratch’ delivers speed and accuracy’,

https://corporatesolutions.swissre.com/insights/knowledge/an-international-insurance-

programme-proposition-built-from-scratch-delivers-speed-and-accuracy.html [accessed 08

July 2020]

24

Tony Dowding, Commercial Risk, ‘Ten factors in claims handling for global programmes’,

https://www.commercialriskonline.com/ten-factors-in-claims-handling-for-global-

programmes/ [accessed 08 July 2020]

Willis Ltd, ‘Navigating the risks of a global insurance marketplace in transition’,

https://www.willistowerswatson.com/en-AE/Insights/2019/04/navigating-the-risks-of-a-

global-marketplace-in-transition [accessed 08 July 2020]

Willis Ltd, ‘Non-Admitted Coverage and Premium Taxes: No Standard Solution’,

https://www.willis.com/Documents/Publications/Services/International/2011/Intl_Alert-

_Non_Admitted_0611_v6.pdf [accessed 08 June 2020]

Willis Ltd, ’Terrorism Insurance – The Pool Re Adverse Selection Rule Explained’,

http://www.willis.com/Documents/Publications/Industries/Property_Investors/20140728_T

errorism_Adverse_Selection_JULY_2014_FINAL.pdf [accessed 01 May 2020]

Willis Ltd, ‘UK Employers’ Liability – A Guide’,

https://www.willis.com/Documents/Publications/Services/International/2011/UK_Intl_Alert

_0911_v3.pdf [accessed 02 June 2020]

Books

Malcolm A Clarke, Routledge, ‘The Law of Liability Insurance’ (2014)

Legislation

Section 3 Employers’ Liability (Compulsory Insurance) Regulations 1998,

http://www.legislation.gov.uk/uksi/1998/2573/made [accessed 02 June 2020]