Technostructural Intervention of the Tax Ombudsman Unit in ...

Upload

khangminh22Category

view

0download

0

PROCEEDINGS BEFORE THE INSURANCE OMBUDSMAN, GUWAHATI

(UNDER RULE NO: 16(1)/17 of INSURANCE OMBUDSMAN RULES 2017) OMBUDSMAN – K.B. SAHA

CASE OF: : Complainant MR BEDABIT ACHARYA VS THE ORIENTAL INSURANCE CO. LTD. COMPLAINT REF NO: GUW – H-50-2021-0140: Award No:

1. Name & Address of the Complainant

MR BEDABIT ACHARYA REHABARI BILPAR, HOUSE NO.26,GUWAHATI -781008.

2. Policy No: Type of Policy Duration of policy/Policy period

321105/48/2021/349 ,SI Rs 4,00,000/--, Group Mediclaim Tailor made Policy . 1 Year /From 13.07.2020 to 12.07.2021.

3. Name of the insured Name of the policyholder

MR BEDABIT ACHARYA RASHTRIYA GRAMIN VIKASH NIDHI.

4. Name of the insurer THE ORIENTAL INSURANCE CO. LTD.

5. Date OF OCCURANCE OF LOSS/CLAIM

20.10.2020

6. DETAILS OF LOSS The Insured was covered by the Group Mediclaim policy for the period from 13.07.2020 to 12.07.2021. He was admitted to Swagat Super Speciality Surgical Institute, Guwahati on 20.10.2020. He was diagnosed with Calculus Cholecystitis .His Laparoscopic Cholecystectomy was done at hospital on 21.10.2020. Insured lodged a claim of Rs 1,58,055/-to the Insurer.

7. REASON FOR GRIEVANCES Insurer settled his claim bill at Rs 88,332/- on 04.12.2020. Insured was not satisfied with the settlement amount and hence, put up his grievance at this Forum.

8.a 8.b

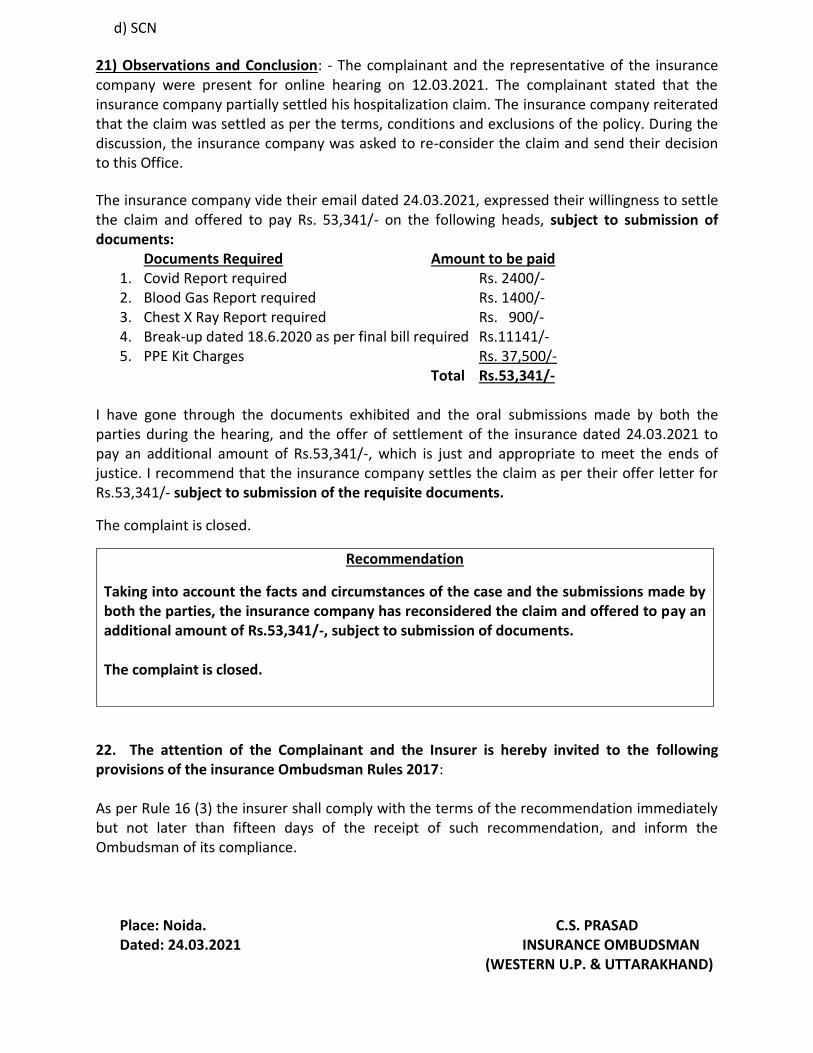

Nature of complaint Date of receipt of the complain

Unsatisfied over his settlement amount. 01.02.2021

9. Amount of Claim Rs 47,500/=. 10. Date & Amount of Partial

Settlement Rs 88,332/- on 04.12.2020.

11 Amount of relief sought Rs 47,500/=

12. Complaint registered under Rules of Ins Ombudsman 2017

13(1)(b)

13. Date of hearing/place 26.02.2020 at O/O Ins Ombudsman Office, Guwahati. 14. Representation at the hearing For the Complainant Mr Bedabit Acharya For the insurer Mr Ranabir Ganguli.

15 Complaint how disposed Through personal hearing and online hearing 16 Date of Award/Order 10.03.2021

17) Brief Facts of the Case: The Insured was admitted to Swagat Speciality Surgical Institute, Guwahati on 20.10.2020 and diagnosed with Calculus Cholecystitis. The doctors performed Laparoscopic Cholecystectomy on 21.20.2020.He was discharged from the Hospital on 24.10.2020. The Insured lodged a claim of Rs 1,58,055/-to the Insurer. The Insurer settled his claim bill at Rs 88,332/- on 04.12.2020. Insured was not satisfied with the settlement of claim and made complaint at this Forum settlement of his balance amount of claim.

18 (a) Complainant’s argument: The Insured stated that Insurer settled his claim bill at Rs 88,332/- on 04.12.2020, which was approx 55% of the total bill. The Insured was not satisfied with the settlement amount. The Insured had alleged that his claim for Rs 2500/- for Covid -19 test , Hospital charge for Rs 5200/- and consumables charge Rs 39,800 for Trocker i.e. total for Rs 47,500/-was illegally deducted by the company. Hence, he had put up his grievance at this Forum for natural justice. 18 (b) Insurers’ argument: The Insurer stated that a renewal Group Mediclaim Tilormade policy bearing no. 321102/48/2021/349 was issued to M/s Rashtriya Gramin Vikash Nidhi covering their employees for the period from 13.07.2020 to 12.07.2021 and the Insured – patient was also covered by the policy. The Insured lodged a claim for Rs 1,58,055/- against which Rs 88,322/- was paid for full and final settlement of the claim. The Insurer stated the Investigation charge related to Covid test for Rs 5200/- is not payable as it is not related to the treatment of the disease. The bed charge amounting Rs 4000/- and nursing charges Rs 1200/- i.e. total Rs 5200/-, is related to Recovery room. A recovery room is a room near the operating or delivery room of a hospital ,used for recovery from anesthesia of a postoperative or obstetrical patient before taking them to a hospital room or ward. The bed charges and the OT charges as levied by the hospital has been paid to the claimant. The recovery room being a part of the Operation Theater, has been already charged in the bill amounting to Rs 8000/- as ‘Operation Theater Charge’ . The equipment used in the treatment of Laparoscopic gallbladder removal surgery has been levied in the bill under procedure charge as Equipment amounting to Rs 10,000/-which is already paid. Trocar and LASER Fiber are tools for easy access in minimal invasive surgeries and are reusable after sterilization. As per the bill , the trocker device has been treated under OT Consumable and not as instrument during operation procedure of gall bladder . Hence, the amount is not admissible. 19) Reason for Registration of Complaint: - Scope of the Insurance Ombudsman Rules 2017 (Rule after proper approval from honorable ombudsman13 (1) (b). 20) The following documents were placed for perusal. a) Complaint letter b) Annexure – VI A c) Copy o the policy d) Annexure VII A e) S C N Result of hearing with both parties (Observations & Conclusion):- Both the parties were called for hearing on 26 .02.2021. The complainant Mr. Bedabit Acharya was present and the insurer was represented by Mr Ranabir Ganguly. DECISION We have taken in to consideration the facts and circumstances of the case from the documentary as well as verbal submission made by the claimant as well as representative of the Insurance company. On perusal of claim papers, policy documents and arguments of Insured and Insurer, it is noted that the Insured was admitted to the hospital for Calculus Cholecystitis and Lacparoscopic Cholecystectomy was done in the hospital. The Insured complained with the Forum against deduction of bill for Covid -19 Rs 2500/- , Recover charge Rs 5200/ and Consumable for Troker Rs39,800/- i.e. total for Rs 47,500/- made by Insurer while processing the claim. It is noted as per the documentary evidence and verbal submission of the Insured and the Insurer’s representative present in the hearing that the Covid -19 test was not related with treated disease, so it is not payable. Only the hospital services was incurred by patient after operation i.e. discharged from OT for recovery, which is a integral part of treatment and is to be treated as applicable room rent. On the other hand, the Consumable charge for Troker i.e. instrument is not payable as per the policy terms and conditions. The trocker device is treated under OT Consumable and not as instrument during operation procedure. Insurer also sent some documents confirming trocker as reusable system through mail on 02/03/2021. Billing of reusable trocker system as OT consumable is surely an unethical practice by the hospital. However, the Insurance Company is not liable to reimburse the same as part of the claim. The complainant may approach an appropriate court of law for resolution of his grievance.

Under the circumstances and in order to ensure fairness to the policy holder, the claim is hereby awarded to be paid by the insurer as under for full and final settlement of the claim: Hospital service charge against Recovery room for 1 day = Rs 4,000/- TOTAL PAYABLE AMOUNT(In addition to earlier payments) = Rs 4,000/- Hence, the complaint is treated as closed. The attention of the Complainant and the Insurer is hereby invited to the following provisions of Insurance Ombudsman Rules, 2017. As per Rule 17(6) of the said rules the Insurer shall comply with the Award within 30 days of the receipt of the Award and intimate the compliance of the same to the Ombudsman. Dated at- Guwahati 10th March. 2021. K.B.Saha INSURANCE OMBUDSMAN

PROCEEDINGS BEFORE

THE INSURANCE OMBUDSMAN, GUWAHATI (UNDER RULE NO: 16(1)/17 of INSURANCE OMBUDSMAN RULES 2017)

OMBUDSMAN – K.B. SAHA CASE OF: : Complainant MR. AVERIL R.J.NONGBET VS UNIVERSAL SOMPO GENERAL INSURANCE CO.LTD

COMPLAINT REF. NO: GUW-G-052-2021-0073: Award No

1. Name & Address of the Complainant MR.AVERIL R.J.NONGBET

2. Policy No:

Type of Policy

Duration of policy/Policy period

3333/59685445/00/000

PERSONAL ACCIDENT POLICY

13/06/2018 TO 13/04/2019,S.I.Rs.10,00000/-

3. Name of the insured

Name of the policyholder

LARRY KUPAR JANA KUPER NONGBET LARRY KUPAR JANA KUPER NONGBET

4. Name of the insurer UNIVERSAL SOMPO GENERAL INSURANCE CO.LTD.

5. Date OF OCCURANCE OF LOSS/CLAIM 30/05/2019

6. DETAILS OF LOSS Rs.1000000/-(S.I.)

7. REASON FOR GRIEVANCES Rules 17(6) of the Insurance ombudsman Rule 2017

8.a

8.b

Nature of complaint

Date of receipt of the complain

REPUDIATION OF THE CLAIM

23/02/2021

9. Amount of Claim AS PER ENTITLEMENT

10. Date & Amount of Partial Settlement NIL

11 Amount of relief sought AS PER ENTITLEMENT

12. Complaint registered under Rules of Insurance Ombudsman 2017

13(1)(b)

13. Date of hearing/place O/o Insurance Ombudsman Guwahati

29/03/2021

14. Representation at the hearing

For the Complainant MR.AVERIL R.J.NONGBET

For the insurer MR.PROSHANT V SHUKLA

15 Complaint how disposed Through personal Hearing

16 Date of Award/Order 29/03/2021

17) Brief Facts of the Case: As stated by the complainant Mr. Averil R.J.Nongbet that his brother (late) Larry Kupar Jana

Nongbet had enrolled for IOB Suraksha (Group Personal Accident Insurance Scheme) on 13/06/2018. Complainant is the

nominee of the policy. On 30/05/2019 at around 21.50 hrs to 22.00 hrs Larry Kuper met with a fatal hit at Shillong Jowai road

near Assam Auto Agency Petrol Pump, Fire Brigade, Shillong and had died on spot. Death Certificate was issued on

28/06/2019 and accordingly Mr. Nongbet had filed the claim with all the documents required.After a long gap & harassment,

on 19/08/2020 he was asked to receive an unsigned rejection letter addressed to the Bank dated 05/06/2019 from Universal

Sompo General Insurance Co. Ltd . The rejection was made under policy clause of requirement of post mortem report. As the

complainant submitted the Post Mortem Exempted Certificate signed by Additional District Magistrate, Khasi Hills, he is not

satisfied with the reason of repudiation of the claim. So he approached us for reconsideration of the claim.

18 a) Complainant’s Argument: - Complainant submitted the approval of exemption of Post Mortem by Additional District

Magistrate of East Khasi Hills District,Shillong dated 31/05/2019. The approval was forwarded by In-Charge Laitumakhrah

Traffic Branch,East Khasi Hills,Shillong against the prayer for exemption from post mortem of the dead body of LA by

complainant.In the forwarding I/C TRAFFIC Branch written that ‘during enquiry it is learnt that the case is purely an accident

case and there is no any foul play found.’

After repeated enquiries at IOB Shillong on 19/08/2020 he was asked to receive an unsigned rejection letter dated

05/06/2019 from insurer that was addressed to IOB. As cause of rejection was non submission of post mortem report the

complainant submitted a request for reconsideration of his claim along with IOB Suraksha Claim Process details which states

Post Mortem Report is not mandatory.

He also stated that the policy number of his brother late Larry Kuper Jana Nongbet mentioned as per this unsigned claimed

Rejection letter is policy no.3333/59685445/00/000 did not tally with the Master policy number in the enrollment form

which is 333/58241289/00/000.

He had also raised his objection to the fact that the IOB, Shillong Branch/Universal that he was made aware of this fact after

a passage of 1 year through the letter of rejection issued by Universal Sompo General Insurance Co. Ltd.

He also stated that the policy number of his brother late Larry Kuper Jana Nongbet mentioned as per this unsigned claimed

Rejection letter is policy no.3333/59685445/00/000 did not tally with the Master policy number in the enrollment form

which is 333/58241289/00/000.

18b) Insurers’ argument: Insurance co. submitted the following points in their SCN-:

1. The plain reading of Group Personal Accident policy terms and conditions clearly spells out “We undertake

that in the event of ‘Accidental’ Bodily injury sustained by the insured person(s) during the policy period, we will

make payment to them or their legal representative/nominee as per the Table of Benefits set forth in the policy

provided that all the terms, conditions and exceptions of this policy in so far as they relate to anything to be

done or complied with by them have been met.

2. After scrutinizing the documents placed in the claim file and after due application of the mind by the officials

of the insurance company, the claim of the complainant was repudiated vide letter dated 05/06/2020 on the

ground of non-submission of post mortem report by the nominee claiming under the policy. Insurance co.

clarified it further that as stated in the complaint that the unsigned letter was sent, the reason for which is that

the nation was reeling under nationwide lockdown and Maharastra (Mumbai) was the worst hit state and they

were prevented to come to their office getting signatures, stamped and scanning. However, Insurance co. had

also informed the IOB vide their email dated August 18, 2020 regarding rejection of the claim of the insured.

3. Insurance co. further stated in their SCN that, following documents shall be required in the event of a

claim(the same has been envisaged under terms and conditions of Group Personel Accident policy.)

For death claim

Duly filled up claim form

Death certificate

Original FIR original panchnama

Post mortem report

4.The concern of the complainant with regard to policy number is changed is that the product under which the

complainant is claiming is a group personal accident & the policy number gets changed every year as the

beneficiaries are added and deleted every year. Hence the policy number gets changed every year.

5. As regards the issue of non-payment of claim under the policy, Insurance co. affirm their stand yet again and

stated that when the post mortem report is not made available to them, their right to verify the fact with regard

to the admissibility of a claim got prejudiced. It is understood that the cause of death along with the

ascertainment of any intoxication/drug abuse cannot be ruled out in absence of a vital and inevitable document

viz-a viz post mortem report for the purpose of analysis of the claim.

6. Insurance co. submitted it further that Group Personal Accident Policy has Death and Disablement benefits.

However, as far as IOB Suraksha Scheme for this group is concerned the policy has been underwritten for

Accidental Deaths only’ for the beneficiaries of the policy.

7. The concern of the Complainant that the word ‘if applicable’ has been mentioned on IOB website is untenable

as a Post Mortem will not be conducted in cases of Disablement. Hence, requirement of Post Mortem will not

arise in case of Disablement.

8.As the complainant is seeking clarification as to why the post mortem exemption accorded under the seal and

signature of a government official namely the Additional District Magistrate East Khasi Hills stating “No foul

play is suspected’ is not a reason for exemption of Post Mortem Report. We would like to submit that the best

known reason for exemption of a post mortem is best known to the applicant making an application to Deputy

Commissioner which has nothing to do with Insurance perspective. The purpose of injury report and Inquest

Report are very much different from the Post Mortem Report. The Insurance is a contract between Insured and

Insurer only; the Insurer has every right to get the claim verified and conditions fulfilled before accepting any

liability. In cases of Death more importantly an accidental death a Post Mortem Report plays a very vital

position in deciding the admissibility of any claim. The insurers right to verify the claim gets prejudiced in

absence of the necessary documents.

19) Reason for Registration of Complaint: -: Scope of the Insurance Ombudsman Rules 2017 (Rule after proper

approval from honorable ombudsman13 (1) (b).

20) The following documents were placed for perusal. a) Complaint letter b) Annexure – VI A c) Copy o the policy d) Annexure VII A e) S C N

Result of hearing with both parties (Observations & Conclusion):- Both the parties were called for hearing on 29/03/2021. The complainant was represented by Mr.Averil R.J. Nongbet himself and the insurer was represented by Mr. PROSHANT V SHUKLA.

DECISION

We have taken into consideration the facts & circumstances of the case from the documentary as well as

verbal submission made by the claimant and representative of Insurance co. We have also gone through the

records.

Insurance co.repudiated the claim on the ground of non-submission of Post Mortem Report. But

complainant submitted the approval of exemption of Post Mortem by Additional District Magistrate of

Khasi Hills District,Shillong dated 31/05/2019.The approval was forwarded by In-charge Laitumukhrah

Traffic Branch,East Khasi Hills,Shillong against the prayer for exemption from post mortem of the dead body

of LA by complainant.In the forwarding letter I/C Traffic Branch had written that ‘during enquiry it is learnt

that the case is purely an accident case and there is no any foul play found’. Moreover,in course of hearing

the complainant clarified that the reason for seeking exemption was basically emotional and religious

consideration.

It is clear from the Investigation report of In-Charge Laitumukhrah Traffic Branch,East Khasi Hills,Shillong

that it is a pure accidental case. Claimant also submitted the sketch map of Accident Site and GR Case

No.115(s) of 2019 of Chief Judicial Magistrate,Shillong of the accident.So,it is clear that,the cause of death

of L/A is accident and as per i.c.,Traffic there was no foul play involved.

During the course of hearing Insurance co. also stated that the cause of death along with the ascertainment

of any intoxication/drug abuse cannot be ruled out in absence of a very vital and inevitable document viz

Post Mortem Report for the purpose of analysis of the claim. But they could not produce any proof or

document against their claim.There was no such indication in the investigation report of police also.So,this

point is ignored.

During the course of hearing Insurance co. also had mentioned a point that the claimant submitted the

claim intimation after one month of the incidence. But in his letter claimant alleged that,he submitted the

claim in time and was again harassed by Bank and Insurer before finally accepting the claim documents.It is

also very illogical to question the time frame of claim process as it was a very sad demise.

The exemption of post mortem was approved by state Govt. Officer of the rank of Additional District

Magistrate of East Khasi Hills District,Shillong dated 31/05/2019.The approval was forwarded by In-Charge

Laitumakhrah Traffic Branch,East Khasi Hills,Shillong against the prayer for exemption from post mortem of

the dead body of LA by complainant.In the forwarding I/C Traffic Branch had clearly written that ‘during

enquiry it is learnt that the case is purely an accident case and there is no any foul play found.’It shows that

full official protocol was maintained and it is expected that competent authority has given due deliberations

before approving the exemption of post mortem. The Insurer’s decision is prejudiced with baseless

suspicion and they have taken recourse of purely untenable legalese without any due diligence and

application of mind.

Under the above circumstances & in order to ensure fairness to the insured this forum is in the opinion that

insurance co. had wrongly repudiated the claim & directs the insurance co. to pay full sum insured of

Rs.1000000/- to the nominee of the insured as final settlement of the claim.

Hence the complaint is treated as closed.

The attention of the Complainant and the Insurer is hereby invited to the following provisions of Insurance

Ombudsman Rule 2017.

As per Rule 17(6) of the said rules the Insurer shall comply with the Award within 30 days of the receipt of

the award and shall intimate the compliance of the same to the Ombudsman.

Dated at Guwahati, the 29th Day Of March , 2021

K.B.Saha

Insurance Ombudsman

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, STATE OF M.P. & C.G. (UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

OMBUDSMAN – G S SHRIVASTAVA Mr. K.C.Jain …..……..……………………………..……………….……….….Complainant

V/s United India Insurance Co. Ltd. ………....….………….…….……...…………...Respondent

COMPLAINT NO: BHP-H-051-2021-0260 ORDER NO: IO/BHP/A/HI/0085/2020-2021

Mr K.C.Jain (Complainant) has filed a complaint against United India Insurance Co. Ltd.(Respondent) alleging rejection of claim of child (Amira Jain) of his daughter-in-law.

1. Name & Address of the Complainant

Mr. K.C.Jain 1, Avantika Parisar, Lalghati Bhopal

2. Policy No: Type of Policy Duration of policy/Policy period

021002819P100272169 Group Mediclaim Policy for New India Insurance Co. Ltd 01.04.2019 to 31.03.2020

3. Name of the insured Name of the policyholder

Mr. K.C.Jain- Claim of Amira Jain New India Insurance Co Ltd

4. Name of the insurer United India Insurance Co. Ltd

5. Date of Repudiation/ Rejection 27.10.2020

6. Reason for Repudiation/ Rejection Dependent / Daughter-in-law is not covered under the Policy since 3 years

7. Date of receipt of the Complaint 02.03.2021

8. Nature of complaint Rejection of claim

9. Amount of Claim Rs.1,68,693/-

10. Date of Partial Settlement --

11. Amount of relief sought Rs.1,68,693/-

12. Complaint registered under Rule Rule No. 13(1)(b) Ins. Ombudsman Rule 2017

13. Date of hearing/place On 18.03.2021 at Bhopal

14. Representation at the hearing

For the Complainant Mr K C Jain over Go To Meeting App

For the insurer Ms Shikha Malviya, Administrative Officer, over Go To Meeting App

15. Complaint how disposed Dismissed

16. Date of Award/Order 18.03.2021

Brief facts of the Case –

Contention of the complainant - The Complainant has stated that the claim was repudiated by TPA on 27.10.2020 stating therein as ‘Maternity benefit extended to an independent child or a family member of the dependent / independent child, provided such child or family member has been covered in the policy for 3 years as on date of hospitalization under the maternity cover. But the said dependent / daughter in law is not covered in the policy since 3 years only so claim of new born is also not admissible hence the claim recommended for rejection under the clause 1.2A(f). In this connection he added that his daughter in law gave birth to twins and the same were covered by paying additional premium of Rs.5,148/- covering the risk from Sept.2019 to March 2020. As per clause no. 2.6 sub Clause (h) ( Maternity Expenses and New born Child Cover) it is clearly mentioned that the new born child shall be covered from the day one upto the age of 3 months and expenses incurred for treatment taken in hospital as in patient shall only be payable subject to the full sum insured. He has stated further that initially TPA approved the claim on SMS on 08.10.2020 which respondent repudiated on 27.10.2020.

Contention of respondent- The respondent in their SCN have stated that Mrs.Payal Jain daughter in law of complainant was hospitalized for treatment of SGA/LSCS/IVF/MALE/VLBW/RDS (birth of child) from 18.09.2019 to 10.10.2019. The insured lodged a claim under the said Group Health Policy and Health claim was repudiated for breach of clause no 1.2A (f) of the policy and revised guidelines of Group Medical policy for employees and retirees of GIPSA and as per circular dated 06.03.2017. The clause states that ‘Maternity benefit extended to an independent child or a family member of dependent / independent child provided such child or family member has been covered in the policy at least for 3 years as on date of the hospitalization under maternity cover’. It is further stated that Payal Jain (daughter in law) covered in the policy since 2017 only. Maternity benefit extended to an independent child or a family member of dependent / independent child provided such child or family member has been covered in the policy atleast for 3 years as on date of hospitalization under the maternity cover. But the said dependent / Daughter in law is the not covered in the policy since 3 years only hence claim rejection was done under the clause 1.2 A (f).

The Complainant has filed complaint letter, Annex. VIA and correspondence with respondent while respondent have filed SCN with enclosures.

I have heard both parties over Go To Meeting App at length and perused paper filed on behalf of the complainant as well as the Insurance Company.

Observation and Conclusion : A claim under above policy was lodged by the complainant for the reimbursement of expenses incurred in the treatment of Amira Jain, second baby of his daughter in law, Payal Jain from 18.09.2019 to 10.10.2019 which was repudiated by the respondent under clause 1.2(A)(f) stating maternity benefit is extended only when the dependent (here it refers to Daughter in law) is covered under the policy since 3 years as on date of hospitalisation. Policy clause No.1.2(A)(f) provides that maternity benefit shall be extended to an independent child or a family member of dependent / independent child provided such child or family member has been covered in the policy at least for the last 3 years as on date of the hospitalization under maternity cover. It is admitted fact that daughter in law of the complainant was not covered under the policy for the past three years and was covered only since 2017. Complainant has referred to clause No.2.6 (h) of the policy and has stated that new born child shall be covered from the day one upto the age of 3 months and expenses incurred for treatment taken in hospital as in patient shall only be payable subject to the full sum insured, hence claim is payable. Representative of the respondent opposed the above argument and stated that in this case as the 3 years continuous coverage of mother of new born child was not completed, hence the provision of clause 1.2 (f) shall apply. As the continuous coverage of mother of

the child has not completed three years, hence the rejection of the claim under clause 1.2(f) of policy by respondent is in order. Clause 2.6(h) referred by complainant also pertains to maternity expenses and newborn child cover benefit extension. It is pertinent to mention here that as maternity expenses itself is not covered under 1.2(f) then the question of applicability of clause 2.6(h) does not arise. Complainant in his complaint has stated that the twins delivered by his daughter in law were covered under the policy as he had paid premium of Rs.5,148/- covering their risk from September, 2019 to March 2020 and submitted a receipt dated 04.10.2019. On perusal of receipt dated 04.10.2019 it is seen that the receipt does not specify as to whom, since when and for what coverage / policy, the receipt was issued. Even policy number and date of commencement is not specified on the receipt. Supporting document such as Certificate of Insurance has also not been provided by the complainant. Hence with this receipt it cannot be inferred that the new born child was covered or not (on the date of hospitalisation of the patient for whom claim was filed). Hence the repudiation by respondent is as per policy and needs no interference by this forum. In the result, compliant is liable to be dismissed.

Let copies of the order be given to both the parties. Dated : Mar 18, 2021 (G.S.Shrivastava) Place : Bhopal Insurance Ombudsman

OMBUDSMAN – G S SHRIVASTAVA

Mr. K.C.Jain…..…….……………………..……………….…………….…..….….Complainant V/s

United India Insurance Co. Ltd. ………....….………….…….……...…………...Respondent

COMPLAINT NO: BHP-H-051-2021-0262 ORDER NO: IO/BHP/A/HI/0086/2020-2021

AWARD

The complaint filed by Mr K C Jain stands dismissed herewith.

1. Name & Address of the Complainant

Mr. K.C.Jain 1, Avantika Parisar, Lalghati Bhopal

2. Policy No: Type of Policy Duration of policy/Policy period

021002819P100272169 Group Mediclaim policy for New India Insurance Co.Ltd 01.04.2019 to 31.03.2020

3. Name of the insured Name of the policyholder

Mr. K.C.Jain- Claim of Mr. Amay Jain New India Insurance Co.Ltd.

4. Name of the insurer United India Insurance Co. Ltd

5. Date of Repudiation/ Rejection 27.10.2020

6. Reason for Repudiation/ Rejection Dependent / Daughter-in-law is not covered under the Policy since 3 yeras

7. Date of receipt of the Complaint 01.02.2021

8. Nature of complaint Rejection of claim

9. Amount of Claim Rs.1,76,047/-

Mr K.C.Jain (Complainant) has filed a complaint against United India Insurance Co. Ltd.(Respondent) alleging repudiation of claim of child (Amay Jain) of his daughter-in-law.

Brief facts of the Case – a) Contention of the complainant - The Complainant has stated that the claim was repudiated by TPA on 27.10.2020 stating therein as ‘Maternity benefit extended to an independent child or a family member of the dependent / independent child, provided such child or family member has been covered in the policy for 3 years as on date of hospitalization under the maternity cover. But the said dependent / daughter in law is not covered in the policy since 3 years only so claim of new born is also not admissible hence the claim recommended for rejection under the clause of 1.2A(f). In this connection he added that his daughter in law gave birth to twins and the same were covered by paying additional premium of Rs.5,148/- on dated 04.10.2019 for covering the risk from Sept.2019 to March 2020. As per clause no. 2.6 sub Clause (h)( Maternity Expenses and New born Child Cover) it is clearly mentioned that the new born child shall be covered from the day one upto the age of 3 months and expenses incurred for treatment taken in hospital as in patient shall only be payable subject to the full sum insured. He stated, further, that initially TPA approved the claim on SMS on 08.10.20 which respondent repudiated on 27.10.2020.

Contention of respondent- The respondent in their SCN have stated that Mrs Payal Jain daughter-in-law of Insured was hospitalized for treatment of SGA/LSCS/IVF/MALE/VLBW/RDS (birth of child) from 18.09.2019 to 10.10.2019. The insured lodged a claim under the said Group Health Policy and Health Claim was repudiated for breach of clause no 1.2A (f) of the policy and revised guidelines of Group Medical policy for employees and retirees of GIPSA and as per circular dated 06.03.2017. The clause states that ‘Maternity benefit extended to an independent child or a family member of dependent / independent child provided such child or family member has been covered in the policy at least for 3 years as on date of date of the hospitalization under maternity cover’. It is further stated that Payal Jain (daughter in law) covered in the policy since 2017 only. Maternity benefit extended to an independent child or a family member of dependent / independent child has been covered in the policy after 3 years as on date of hospitalization under the maternity cover. But the said dependent / Daughter in law is the not covered in the policy since since 3 years only. Hence claim rejection was done under the clause 1.2 A (f).

The Complainant has filed complaint letter, Annex. VIA and correspondence with respondent while respondent have filed SCN with enclosures.

I have heard both parties over Go To Meeting App at length and perused paper filed on behalf of the complainant as well as the Insurance Company.

Observation and Conclusion : A claim under above policy was lodged by the complainant for the reimbursement of expenses incurred in the treatment of Amay Jain, first baby of his daughter in law, Payal Jain from 18.09.2019 to 10.10.2019 which was

10. Date of Partial Settlement --

11. Amount of relief sought Rs.1,76,047/-

12. Complaint registered under Rule Rule No. 13(1)(b) Ins. Ombudsman Rule 2017

13. Date of hearing/place On 18.03.2021 at Bhopal

14. Representation at the hearing

For the Complainant Mr K C Jain over Go To Meeting App

For the insurer Ms Shikha Malviya, Administrative Officer over Go To Meeting App

15. Complaint how disposed Dismissed

16. Date of Award/Order 18.03.2021

repudiated by the respondent under clause 1.2(A)(f) stating maternity benefit is extended only when the dependent (here it refers to Daughter in law) is covered under the policy since 3 years as on date of hospitalisation. Policy clause No.1.2(A)(f) provides that maternity benefit shall be extended to an independent child or a family member of dependent / independent child provided such child or family member has been covered in the policy at least for the last 3 years as on date of the hospitalization under maternity cover. It is admitted fact that daughter in law of the complainant was not covered under the policy for the past three years and was covered only since 2017. Complainant has referred to clause No.2.6 (h) of the policy and has stated that new born child shall be covered from the day one upto the age of 3 months and expenses incurred for treatment taken in hospital as in patient shall only be payable subject to the full sum insured, hence claim is payable. Representative of the respondent opposed the above argument and stated that in this case as the 3 years continuous coverage of mother of new born child was not completed, hence the provision of clause 1.2 (f) shall apply. As the continuous coverage of mother of the child has not completed three years, hence the rejection of the claim under clause 1.2(f) of policy by respondent is in order. Clause 2.6(h) referred by complainant also pertains to maternity expenses and newborn child cover benefit extension. It is pertinent to mention here that as maternity expenses itself is not covered under 1.2(f) then the question of applicability of clause 2.6(h) does not arise. Complainant in his complaint has stated that the twins delivered by his daughter in law were covered under the policy as he had paid premium of Rs.5,148/- covering their risk from September, 2019 to March 2020 and submitted a receipt dated 04.10.2019. On perusal of receipt dated 04.10.2019 it is seen that the receipt does not specify as to whom, since when and for what coverage / policy, the receipt was issued. Even policy number and date of commencement is not specified on the receipt. Supporting document such as Certificate of Insurance has also not been provided by the complainant. Hence with this receipt it cannot be inferred that the new born child was covered or not (on the date of hospitalisation of the patient for whom claim was filed). Hence the repudiation by respondent is as per policy and needs no interference by this forum. In the result, compliant is liable to be dismissed.

Let copies of the order be given to both the parties. Dated : Mar 18, 2021 (G.S.Shrivastava) Place : Bhopal Insurance Ombudsman

AWARD

The complaint filed by Mr K C Jain stands dismissed herewith.

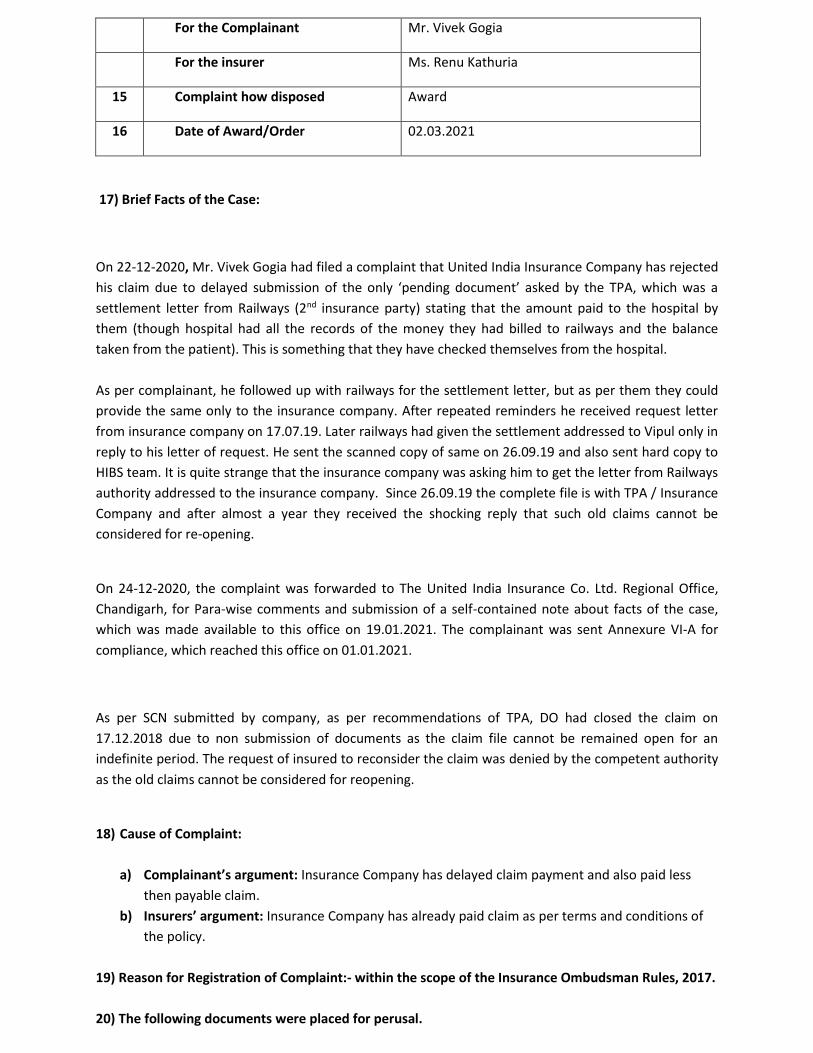

PROCEEDINGS BEFORETHE INSURANCE OMBUDSMAN, CHANDIGARH (UNDER INSURANCE OMBUDSMAN RULES, 2017)

INSURANCE OMBUDSMAN- Dr. D.K. VERMA

Case of Mr. Vivek Gogia V/S The United India Insurance Co. Ltd.

COMPLAINT REF. NO: CHD-H-051-2021-0492

1. Name & Address of the Complainant Mr. Vivek Gogia

E-3/3, Ground Floor, DLF Valley,

Panchkula, Haryana- 134107

Mobile No.- 8283883322

2. Policy No:

Type of Policy

Duration of policy/Policy period

0407002818P116956099

Group Health Policy

01.01.2018 to 31.12.2018

3. Name of the insured

Name of the policyholder

Mr.Vivek Gogia

M/s Pearson India Educ. Services Pvt Ltd.

4. Name of the insurer The United India Insurance Co. Ltd.

5. Date of Repudiation 17.12.18

6. Reason for repudiation Non submission of documents.

7. Date of receipt of the Complaint 22-12-2020

8. Nature of complaint Non settlement of claim

9. Amount of Claim Approx. 3.4 lacs

10. Date of Partial Settlement NA

11. Amount of relief sought Nil

12. Complaint registered under

Rule no: Insurance Ombudsman Rules,

2017

Rule 13 (1)(b) – any partial or total repudiation

of claim by an insurer

13. Date of hearing/place 23.02.2021/ Chandigarh/Through VC

14. Representation at the hearing

For the Complainant Mr. Vivek Gogia

For the insurer Ms. Renu Kathuria

15 Complaint how disposed Award

16 Date of Award/Order 02.03.2021

17) Brief Facts of the Case:

On 22-12-2020, Mr. Vivek Gogia had filed a complaint that United India Insurance Company has rejected

his claim due to delayed submission of the only ‘pending document’ asked by the TPA, which was a

settlement letter from Railways (2nd insurance party) stating that the amount paid to the hospital by

them (though hospital had all the records of the money they had billed to railways and the balance

taken from the patient). This is something that they have checked themselves from the hospital.

As per complainant, he followed up with railways for the settlement letter, but as per them they could

provide the same only to the insurance company. After repeated reminders he received request letter

from insurance company on 17.07.19. Later railways had given the settlement addressed to Vipul only in

reply to his letter of request. He sent the scanned copy of same on 26.09.19 and also sent hard copy to

HIBS team. It is quite strange that the insurance company was asking him to get the letter from Railways

authority addressed to the insurance company. Since 26.09.19 the complete file is with TPA / Insurance

Company and after almost a year they received the shocking reply that such old claims cannot be

considered for re-opening.

On 24-12-2020, the complaint was forwarded to The United India Insurance Co. Ltd. Regional Office,

Chandigarh, for Para-wise comments and submission of a self-contained note about facts of the case,

which was made available to this office on 19.01.2021. The complainant was sent Annexure VI-A for

compliance, which reached this office on 01.01.2021.

As per SCN submitted by company, as per recommendations of TPA, DO had closed the claim on

17.12.2018 due to non submission of documents as the claim file cannot be remained open for an

indefinite period. The request of insured to reconsider the claim was denied by the competent authority

as the old claims cannot be considered for reopening.

18) Cause of Complaint:

a) Complainant’s argument: Insurance Company has delayed claim payment and also paid less

then payable claim.

b) Insurers’ argument: Insurance Company has already paid claim as per terms and conditions of

the policy.

19) Reason for Registration of Complaint:- within the scope of the Insurance Ombudsman Rules, 2017.

20) The following documents were placed for perusal.

a) Complaint to the Company b) Copy of Policy Document

c) Annexure VI-A d) Reply of the Insurance Company

21) Result of Personal hearing with both parties(Observations & Conclusion)

On perusal of various documents and submissions made by both parties during hearing held through

video conferencing it has been observed that health claim of patient Mrs. Shanta Gogia was closed by

insurance company vide letter dt. 17.12.2018 for non compliance of queries/documents which includes

settlement letter of already paid claim by Railways. The said settlement letter is issued by Medical

director, N.Rly. Central Hospital, New Delhi vide their letter dt. 23.09.19. Insurance company vide letter

dt. 18.11.2020 denied the request for reopening of closed file of complainant. After the complaint was

lodged with this office, insurance company has paid the said claim. Insurance company vide e-mail dt.

26.02.2021 informed that out of total billed amount of Rs. 995318/-, Rs. 653677/- was paid by railway,

Rs. 57010 is deducted for co-pay, Rs.4000/- deducted for face mask. After making initial payment of Rs.

228042/- insurance company has paid Rs. 42071, (Rs.52589 – 20% co-pay) on 25.02.2021 in the matter.

Complainant during hearing admitted receipt of claim of Rs. 228042/- paid by company. Further,

complainant vides e-mail dt.26.02.2021 informed that he received the balance deducted amount of Rs.

42000/- from the company and his claim has now been settled. Although he also requested for

compensation for the expenses incurred in travelling, mental stress, physical and mental harassment

along with bonafide interest on the delayed payment. I have seen all the relevant documents carefully

and it is evident that there has been a delay in settlement of claim by insurance company after receipt

of all documents from complainant tantamounting to deficiency in service. As such, insurance company

is directed to pay a lump sum amount of Rs. 8000/- as interest for delaying the claim payment of

complainant, within 30 days of receipt of award copy.

AWARD

Taking into account the facts & circumstances of the case and the submissions made by both the

parties during the course of on line hearing, Rs. 8000/- is hereby awarded to be paid by the

Insurer to the Insured as interest, for delaying the claim payment of complainant.

Hence, the complaint is treated as closed.

Dated at Chandigarh on 2nd day of March, 2021.

D.K. VERMA

INSURANCE OMBUDSMAN

PROCEEDINGS BEFORETHE INSURANCE OMBUDSMAN, CHANDIGARH (UNDER INSURANCE OMBUDSMAN RULES, 2017)

INSURANCE OMBUDSMAN- Dr. D.K. VERMA

Case of Mr. Harbhajan Singh V/S Cholamandalam MS Gen. Insurance Co. Ltd.

COMPLAINT REF. NO: CHD-G-012-2021-0655

1. Name & Address of the Complainant Mr. Harbhajan Singh

# 1410, Street No.-14,

Guru Nanak Nagar, Patiala, Punjab-0

Mobile No.- 9815937870

2. Policy No:

Type of Policy

Duration of policy/Policy period

2876/00044619/000043/000/01

Group Health Insurance

31.01.19 to 30.01.20

3. Name of the insured

Name of the policyholder

Mr. Inderjeet Singh/Ms. Rajinder Kaur

Mr. Harbhajan Singh

4. Name of the insurer Cholamandalam MS Gen. Insurance Co. Ltd.

5. Date of Repudiation 23.10.20

6. Reason for repudiation Inpatient admission not required

7. Date of receipt of the Complaint 16-02-2021

8. Nature of complaint Repudiation of claim

9. Amount of Claim Rs.2,06,985/-

10. Date of Partial Settlement NA

11. Amount of relief sought Rs.2,06,985/-

12. Complaint registered under

Rule no: Insurance Ombudsman Rules,

2017

Rule 13 (1)(b) – any partial or total repudiation

of claim by an insurer

13. Date of hearing/place 12.03.2021/ Chandigarh/Through VC

14. Representation at the hearing

For the Complainant Mr.Harbhajan Singh

For the insurer Dr.Manish

15 Complaint how disposed Award

16 Date of Award/Order 15.03.2021

17) Brief Facts of the Case:

On 16-02-2021, Mr. Harbhajan Singh had filed a complaint vide which he informed that his son

Inderjeet Singh and wife Rajinder Kaur has been admitted to hospital Vardhman Mahaveer health care

at Patiala with the diagnosis of COVID positive on 22 Sept 2020. He applied for claim to insurance

company, but they have declined his genuine claim of Rs.2,06,985/- of reimbursement.

On 19-02-2021, the complaint was forwarded to Cholamandalam MS Gen. Insurance Co. Ltd. Regional

Office, New Delhi, for Para-wise comments and submission of a self-contained note about facts of the

case, which was made available to this office on 09.03.2021. The complainant was sent Annexure VI-A

for compliance, which reached this office On 25.02.2021.

As per SCN submitted by insurance company, against the subject policy two claims were reported.

i) The claim of Smt. Rajinder Kaur bearing claim no. 2876022590 for reimbursement of hospitalization expenses at Vardhman Mahaveer Health Care Hospital for the period 22.09.20 to 30.09.20.

ii) The Claim of Mr.Inderjeet Singh bearing claim no. 2876022589 for reimbursement of hospitalization expenses at Vardhman Mhaveer Health Care Hospital for the period 22.09.2020 to 30.09.2020.

On perusal of both the claim documents, it was observed that the patients were stable, and as per the

MOHFW; CLINIICAL MANAGEMENT PROTOCOL : COVID 19(copy attached) such patient does not require

hospitalization and the treatment can be done in home quarantine. Further as per the policy, no

indemnity is available or payable for the claims beyond scope of policy coverage, Part B Section 1

(necessity of hospitalization). The hospitalization records of the patients reveal that the vitals were

stable. Hence as per the Govt. guidelines, hospitalization is not warranted for such patients, thus the

claim for hospitalization for the patients is clearly beyond the policy scope. Therefore the claim was

rightly repudiated by the insurer.

18) Cause of Complaint:

a) Complainant’s argument: Insurance company has not paid health claim related to COVID-19 of

his wife and son on flimsy grounds.

b) Insurers’ argument: Claims were repudiated as per terms and conditions of the policy.

19) Reason for Registration of Complaint:- within the scope of the Insurance Ombudsman Rules, 2017.

20) The following documents were placed for perusal.

a) Complaint to the Company b) Copy of Policy Document

c) Annexure VI-A d) Reply of the Insurance Company

21) Result of Personal hearing with both parties(Observations & Conclusion)

On perusal of various documents and considering submissions made by both the parties during online

hearing it has been observed that health claims related to COVID-19 of Mrs. Rajinder Kaur &

Mr.Inderjeet Singh have not been paid by insurance company. Mrs. Rajinder Kaur, wife & Mr.Inderjeet

Singh, son of complainant, after being COVID-positive hospitalized in Vardhman Mahaveer Health Care,

Patiala from 22.09.20 to 30.09.20. As per company, they observed that the treatment given during the

hospitalization period doesn’t warrant inpatient admission and that can be treated in outpatient

department, which is outside scope of policy coverage under clause Part B Section 1. They added that

related documents suggest that vitals of all the members were stable and as per MOHFW guidelines

member did not require hospitalization and treatment could have been done under home quarantine,

hence claim has been denied. Complainant argued that the admissions were made as per advice of

treating doctors. Clinical management protocol for COVID -19 is advisories from government in specific

circumstances. Final call on requirement of hospitalization has to be made by treating doctor on the

basis of present condition, previous history, age of patient and other factors of the case. In current case,

patient Mrs. Rajinder Kaur has history of appendicitis. Moreover, treating doctor vide certificates

dt.11.11.20 has confirmed the necessity of hospitalization for both patients. In my opinion, being

layman, in the present scenario due to COVID-19, patients have not much option but to follow

instructions from treating doctor, which has been done in present case also. As such, admission of both

patients in hospital in above said case is very much justified and decision of insurance company to

repudiate their claims is unjustified. Accordingly, insurance company is directed to pay admissible claim

of Mrs. Rajinder Kaur & Mr. Inderjeet Singh to insured as per terms and conditions of the policy within

30 days of receipt of award copy.

AWARD

Taking into account the facts & circumstances of the case and the submissions made by both the

parties during the course of online hearing, admissible claims of Mrs. Rajinder Kaur & Mr. Inderjeet

Singh is hereby awarded to be paid by the Insurer to the Insured as per policy terms and

conditions, towards full and final settlement of the claim.

Hence, the complaint is treated as closed.

Dated at Chandigarh on 15th day of March, 2021.

D.K. VERMA

INSURANCE OMBUDSMAN

PROCEEDINGS BEFORETHE INSURANCE OMBUDSMAN, CHANDIGARH (UNDER INSURANCE OMBUDSMAN RULES, 2017)

INSURANCE OMBUDSMAN- Dr. D.K. VERMA

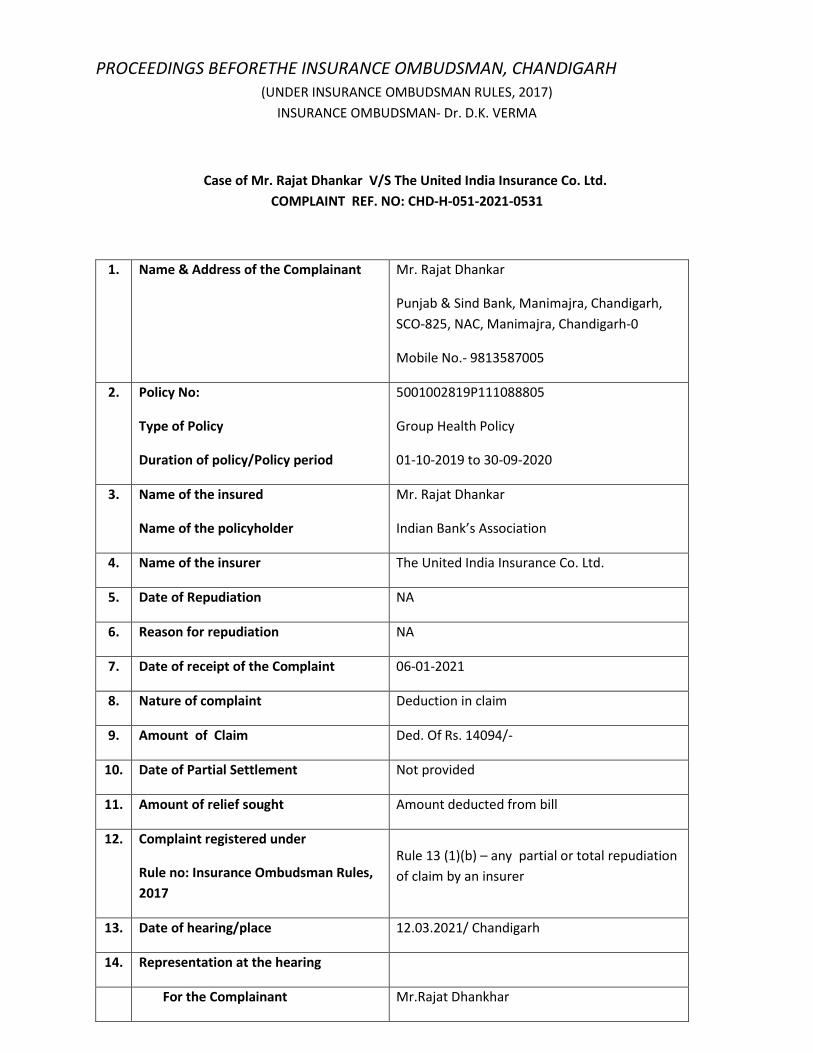

Case of Mr. Rajat Dhankar V/S The United India Insurance Co. Ltd.

COMPLAINT REF. NO: CHD-H-051-2021-0531

1. Name & Address of the Complainant Mr. Rajat Dhankar

Punjab & Sind Bank, Manimajra, Chandigarh,

SCO-825, NAC, Manimajra, Chandigarh-0

Mobile No.- 9813587005

2. Policy No:

Type of Policy

Duration of policy/Policy period

5001002819P111088805

Group Health Policy

01-10-2019 to 30-09-2020

3. Name of the insured

Name of the policyholder

Mr. Rajat Dhankar

Indian Bank’s Association

4. Name of the insurer The United India Insurance Co. Ltd.

5. Date of Repudiation NA

6. Reason for repudiation NA

7. Date of receipt of the Complaint 06-01-2021

8. Nature of complaint Deduction in claim

9. Amount of Claim Ded. Of Rs. 14094/-

10. Date of Partial Settlement Not provided

11. Amount of relief sought Amount deducted from bill

12. Complaint registered under

Rule no: Insurance Ombudsman Rules,

2017

Rule 13 (1)(b) – any partial or total repudiation

of claim by an insurer

13. Date of hearing/place 12.03.2021/ Chandigarh

14. Representation at the hearing

For the Complainant Mr.Rajat Dhankhar

For the insurer Ms.Pamela Pinto

15 Complaint how disposed Award

16 Date of Award/Order 15.03.2021

17) Brief Facts of the Case:

On 06-01-2021, Mr. Rajat Dhankar had filed a complaint against United India Insurance Company Ltd.

regarding unjustified deduction from claimed bill. He submitted his claim documents in first week of

December at ZO Punjab and Sind Bank. After various mail and telephone call they settled the claim on

07.03.2020. Complainant asked for payment of deduction made of Rs. 14094/- plus penalty and late

settlement of claim.

On 11-01-2021, the complaint was forwarded to The United India Insurance Co. Ltd. Regional Office,

Chandigarh, for Para-wise comments and submission of a self-contained note about facts of the case,

which was made available to this office on 09.03.2021. The complainant was sent Annexure VI-A for

compliance, which reached this office on 18-01-2021.

As per SCN submitted by insurance company, they have issued a Group Mediclaim Policy to IBA –Punjab

and Sind Bank covering their employees alongwith their dependent member for the period 01.10.2019

to 30.09.2020. Sh.Rajat Dhankar alongwith dependent member Mrs. Richa (spouse) are included in the

above policy for S.I. of Rs. 400000 subject to LSCS Maternity limit of Rs. 75000/-. Company settled

G2P1L1 Pregnancy claim of Smt. Richa Dhama for Rs. 63690/- against claimed amount of Rs. 77784/-.

Deduction of Rs.14094/- has been made as under:

Item Head Deducted

Amount

Reason for deduction

Pre-post Natal Expenses 6107 Under Clause 3.5(ii) of policy terms and conditions

Consultation 600 Consultation Notes not submitted

US –Emergency charges 2400 Ref bill no.009307 dt.03.11.19 not payable as per

terms and conditions of the policy

150 Calculation error

Chemist Bill 3285 Chemist Bill dt.16.11.19 does not have GST Number as

required under clause 4.12 of policy

Chemist Bill 1552 Chemist Bill dt.16.11.19 does not have GST Number as

required under clause 4.12 of policy

Total 14094

18) Cause of Complaint:

a) Complainant’s argument: Insurance Company has wrongly deducted claim amount from

hospitalization claim of her wife.

b) Insurer’s argument: Deduction has made from claim as per terms and conditions of the policy.

19) Reason for Registration of Complaint: - within the scope of the Insurance Ombudsman Rules, 2017.

20) The following documents were placed for perusal.

a) Complaint to the Company b) Copy of Policy Document

c) Annexure VI-A d) Reply of the Insurance Company

21) Result of Personal hearing with both parties (Observations & Conclusion)

On perusal of various documents and considering submissions made by both the parties during online

hearing it has been observed that in maternity claim of Mrs. Richa Dhama, insurance company has made

payment of Rs. 63,690/- against claimed amount of Rs. 77784/- after deduction of Rs.14094/- for which

complainant has made this complaint. I have seen the relevant documents and observed that Insurance

company rightly deducted for pre/post natal expenses under clause 3.5 (ii) of policy terms and

conditions which states that pre/post natal charges in respect of maternity benefit are covered under

the policy only if the same requires hospitalization. On careful examination of all deductions, it is seen

that insurance company has made deductions as per policy terms and conditions of the policy except

deduction of Rs.3285/- and Rs. 1552/- made due to non availability of GST number on chemist bill. These

bills relates to pharmacy shop within the Paras hospital where patient was hospitalized. Complainant

provided copy of GST registration certificate of Paras Health Care Pvt. Ltd. Moreover, as hospitalization

bill of same hospital has already been settled by company, their stand of deduction is not justified.

Accordingly insurance company is directed to pay balance claim amount of Rs. 4837/-(3285+1552) to

insured in above said claim as per policy terms and conditions within 30 days of receipt of award copy.

AWARD

Taking into account the facts & circumstances of the case and the submissions made by both the

parties during the course of personal hearing, balance claim amount of Rs.4837/- is hereby

awarded to be paid by the Insurer to the Insured, towards full and final settlement of the claim.

Hence, the complaint is treated as closed.

Dated at Chandigarh on 15th day of March, 2021.

D.K. VERMA

INSURANCE OMBUDSMAN

PROCEEDINGS BEFORETHE INSURANCE OMBUDSMAN, CHANDIGARH (UNDER INSURANCE OMBUDSMAN RULES, 2017)

INSURANCE OMBUDSMAN- Dr. D.K. VERMA

Case of Mr. Surinder Kumar Khanduja V/S The United India Insurance Co. Ltd.

COMPLAINT REF. NO: CHD-H-051-2021-0533

1. Name & Address of the Complainant Mr. Surinder Kumar Khanduja

Tower-B-3, Flat No.- 104, Surya Tower,

VIP Road, Zirakpur, Punjab- 140603

Mobile No.- 9876079213

2. Policy No:

Type of Policy

Duration of policy/Policy period

5001002819P112942762

Group Mediclaim Policy

01-11-2019 tom 31-10-2020

3. Name of the insured

Name of the policyholder

Mr.Surinder Kumar Khanduja

Indian Bank’s Association a/c UCO Bank

4. Name of the insurer The United India Insurance Co. Ltd.

5. Date of Repudiation NA

6. Reason for repudiation NA

7. Date of receipt of the Complaint 07-01-2021

8. Nature of complaint Deduction in claim

9. Amount of Claim Rs. 52361/- (Partially paid)

10. Date of Partial Settlement Not provided

11. Amount of relief sought Rs.18000/-

12. Complaint registered under

Rule no: Insurance Ombudsman Rules,

2017

Rule 13 (1)(b) – any partial or total repudiation

of claim by an insurer

13. Date of hearing/place 12.03.2021/ Chandigarh/Through VC

14. Representation at the hearing

For the Complainant Mr.Surinder Kumar Khanduja

For the insurer Ms.Pamela Pinto

15 Complaint how disposed Award

16 Date of Award/Order 18.03.2021

17) Brief Facts of the Case:

On 07-01-2021, Mr. Surinder Kumar Khanduja had filed a complaint vide which he informed that his

wife underwent for cataract surgery on 21.08.2020 and accordingly a reimbursement claim of Rs.

52361/- was lodged. The bills consists of hospitalization bill of Rs. 42000/-, Pre hospitalization bill of Rs.

7308/- and pharmacy bill of Rs. 3053/-. The TPA had settled the bill for Rs. 34361/- and made arbitrary

deduction of Rs. 18000/-. Despite his repeated requests the TPA has not provided him item wise

breakup of the amount approved and also not given satisfactory reply for deductions. He requested for

balance payment of Rs. 18000/-.

On 11-01-2021, the complaint was forwarded to The United India Insurance Co. Ltd. Regional Office,

Chandigarh, for Para-wise comments and submission of a self-contained note about facts of the case,

which was made available to this office on 09.03.2021. The complainant was sent Annexure VI-A for

compliance, which reached this office on 15-01-2021.

As per SCN submitted by insurance company, Group Medical Policy was issued to IBA-UCO bank

covering their retired employees alongwith their dependent members for the period 01.11.2019 to

31.10.2019 with sum insured of Rs. 400000/-. Company has received claim for payment of

hospitalization at Laser Eye Clinic, Chandigarh for right eye cataract surgery with MICS. Against claimed

amount of Rs. 52361/- + Rs.1532 (per/post Hosp.), claim settled for Rs. 34361/- + Rs. 1532/- with

deduction of Rs. 18000/-. Company deducted Rs. 18000/- from bill for Rs. 42000/- as per prevailing PPN

rates for MICS cataract surgery in same geographical area. Hence the deductions are made as per

definition 2.44 of the policy which defines reasonable and customary charges as the charges for services

or supplies, which are the standard charges for the specific provider and consistent with the prevailing

charges in the geographical area for identical or similar services, taking into account the nature of

illness/injury involved. Claim has been settled as per Ahmadabad Municipal Corporation rates within the

sub limits specified in the terms and conditions of the policy.

18) Cause of Complaint:

a) Complainant’s argument: Insurance Company has made deduction in health claim of her wife

on wrong grounds.

b) Insurers’ argument: Deduction has been made as per terms and conditions of the policy.

19) Reason for Registration of Complaint:- within the scope of the Insurance Ombudsman Rules, 2017.

20) The following documents were placed for perusal.

a) Complaint to the Company b) Copy of Policy Document

c) Annexure VI-A d) Reply of the Insurance Company

21) Result of Personal hearing with both parties (Observations & Conclusion)

After examining documents submitted by both parties and considering submissions made by

complainant as well as representative of insurance company during online hearing, it has been observed

that in health claim of right eye cataract surgery of Mrs. Kiran Khanduja insurance company made

payment of Rs. 34561/- against claimed Rs. 52361/-. Deduction of Rs. 18000/- has been made by

company as per 2.44 of policy related with reasonable and customary charges. Insurance company

argued that Rs. 18000/- is deducted as per prevailing PPN rates for MICS cataract surgery in the same

geographical area. But company has not provided any proof of charges prevailing in that geographical

area in such type of treatment. Moreover PPN rates have not been specified for various ailment diseases

in the policy for different locations, as such insurance company cannot take the plea that the claim

amount being more than the PPN rate has to be deducted in this case. Insurance company arbitrarily

makes deductions, as rates of different hospitals may vary with infrastructure, locations and status of

treating doctors etc. As such decision of insurance company to make deduction on the basis of

reasonable and customary charges clause in above said claim is incorrect. Hence, company is directed to

pay balance admissible claim to insured as per terms and conditions of the policy within 30 days of

receipt of award copy.

AWARD

Taking into account the facts & circumstances of the case and the submissions made by both the

parties during the course of personal hearing, balance admissible claim is hereby awarded to be

paid by the Insurer to the Insured, towards full and final settlement of the claim.

Hence, the complaint is treated as closed.

Dated at Chandigarh on 18th day of March, 2021.

D.K. VERMA

INSURANCE OMBUDSMAN

PROCEEDINGS BEFORETHE INSURANCE OMBUDSMAN, CHANDIGARH (UNDER INSURANCE OMBUDSMAN RULES, 2017)

INSURANCE OMBUDSMAN- Dr. D.K. VERMA

Case of Mr. Gaurav Gupta V/S Cholamandalam MS Gen. Insurance Co. Ltd.

COMPLAINT REF. NO: CHD-H-012-2021-0656

1. Name & Address of the Complainant Mr. Gaurav Gupta

# 4515, I-Block, Darshan Vihar,

Sec-68,Mohali, Punjab-160062

Mobile No.- 9041833322

2. Policy No:

Type of Policy

Duration of policy/Policy period

2876/00021838/000002/000/01

Group Health Insurance

07-09-2020 To 06-09-2021

3. Name of the insured

Name of the policyholder

Mr. Gaurav Gupta & Ms.Shail Gupta

Mr. Gaurav Gupta

4. Name of the insurer Cholamandalam MS Gen. Insurance Co. Ltd.

5. Date of Repudiation 23.11.20

6. Reason for repudiation Non disclosure of facts

7. Date of receipt of the Complaint 16-02-2021

8. Nature of complaint Repudiation of claim

9. Amount of Claim Rs. 5.0 Lacs

10. Date of Partial Settlement NA

11. Amount of relief sought Rs. 5.0 Lacs

12. Complaint registered under

Rule no: Insurance Ombudsman Rules,

2017

Rule 13 (1)(b) – any partial or total repudiation

of claim by an insurer

13. Date of hearing/place 12.03.21/ Chandigarh/Through VC

14. Representation at the hearing

For the Complainant Mr.Gaurav Gupta

For the insurer Dr.Manish Bata

15 Complaint how disposed Award

16 Date of Award/Order 22.03.2021

17) Brief Facts of the Case:

On 16-02-2021, Mr. Gaurav Gupta had filed a complaint that insurance company has wrongfully denied

his mediclaim for treatment of Covid-19 of his mother, Mrs. Shail Gupta. This is the second year of his

policy and there is an error on the company’s part. As per complainant all the necessary details were

provided to the company at the time of buying the policy but the company is now saying that they have

not disclosed the facts, which is incorrect rather the company had not shared the duly signed proposal

form at the time of taking the policy. Even now company sent across an unsigned document. Further in

the e-mail dt. 28.01.2021, the company official has claimed that word ‘NIL’ is mentioned under PED

column on the policy certificate. However in the document sent across to him, word ‘NA’ is mentioned

and NIL is not mentioned anywhere. Furthermore the company is relying on policy T & C to inform him

that the policy is null and void however the same too was never shared with him. Due to company’

negligence, he left out to bear the medical expenses of approx. Rs.10 lacs at his own.

On 19-02-2021, the complaint was forwarded to Cholamandalam MS Gen. Insurance Co. Ltd. Regional

Office, New Delhi, for Para-wise comments and submission of a self-contained note about facts of the

case, which was made available to this office on 09.03.2021. The complainant was sent Annexure VI-A

for compliance, which reached this office on 23.02.2021.

As per SCN submitted by company, one claim was reported with claim no. 2876025741 for pre

authorization request for cashless. The claim was repudiated on the ground of non disclosure of the

material information. On perusal of the documents, it is observed that the insured is a known case of

hypertension since 18 years as per history recorded in the discharge summary. The information is not

disclosed in the proposal form while proposing for insurance. In view of the non disclosure of material

information as per policy wording, the contract of insurance become void and no claim was payable

under the policy. Further, insured never come before the company for request of reimbursement of the

claim. Company also informed that policy was issued under Group Health Insurance and declaration of

proposal was received by the company in excel sheet. The column of pre-existing disease was blank in

the same. Company also refer a court judgment and claimed that claim of complainant was rightly

repudiated by the company.

18) Cause of Complaint:

a) Complainant’s argument: Insurance company has not paid health claim of her mother on the

basis of false grounds of misrepresentation of facts.

b) Insurers’ argument: Insurance Company has denied the claim as per terms and conditions of the

policy.

19) Reason for Registration of Complaint:- within the scope of the Insurance Ombudsman Rules, 2017.

20) The following documents were placed for perusal.

a) Complaint to the Company b) Copy of Policy Document

c) Annexure VI-A d) Reply of the Insurance Company

21) Result of Personal hearing with both parties (Observations & Conclusion):

As per discharge summary of hospital Chandigarh healthcare Pvt. Ltd., patient Ms. Shail Gupta remained

hospitalized from 18.11.2020 to 20.11.2020 with diagnosis as COVID 19 POSITIVE. Insurance company

denied cashless request for her health claim due to non-disclosure of facts. As per insurance company,

insured is a known case of hypertension since 18 years as per history recorded in discharge summary,

which is not disclosed in the proposal form while proposing for insurance. Accordingly through letter dt.

18.11.2020, cashless request is denied by company under general condition no. 11. Complainant denied

any misrepresentation and informed that neither he filed any proposal form, nor signed any such form. I

have seen all the relevant documents and observed that first of all hospitalization was due to COVID

Positive, which has no relation with hypertension. Treating doctor also in writing confirmed that this is a

case of COVID-19 which is not due to Hypertension. Further insurance company has failed to submit any

duly signed proposal form of the relevant policy to confirm misrepresentation on part of insured.

Moreover, copy of unsigned excel sheet submitted by insurance company as part of proposal form is

showing no data under column pre existing disease, which cannot be taken as misrepresentation on part

of insured. Keeping in view the facts of the case and above discussion decision of insurance company to

deny the claim is incorrect. Accordingly insurance company is directed to pay the admissible claim

amount to insured as per terms and conditions of the policy within 30 days of receipt of award copy in

above said case. Company is also directed to reinstate the said policy, if cancelled subject to submission

of due premium by insured.

AWARD

Taking into account the facts & circumstances of the case and the submissions made by both the

parties during the course of online hearing, admissible claim is hereby awarded to be paid by the

Insurer to the Insured, towards full and final settlement of the claim along with reinstatement of

policy, if cancelled.

Hence, the complaint is treated as closed.

Dated at Chandigarh on 22nd day of March, 2021.

D.K. VERMA

INSURANCE OMBUDSMAN

PROCEEDINGS BEFORETHE INSURANCE OMBUDSMAN, CHANDIGARH (UNDER INSURANCE OMBUDSMAN RULES, 2017)

INSURANCE OMBUDSMAN- Dr. D.K. VERMA

Case of Mr. Sita Ram V/S Tata AIG General Insurance Co. Ltd.

COMPLAINT REF. NO: CHD-H-047-2021-0516

1. Name & Address of the Complainant Mr. Sita Ram

H. No.- 3104, Sector-25-D,

Chandigarh

Mobile No.- 9988202804

2. Policy No:

Type of Policy

Duration of policy/Policy period

0237868334041857

Group Medicare

29-10-2020 To 28-10-2021

3. Name of the insured

Name of the policyholder

Mr. Sita Ram

Axis Bank Limited

4. Name of the insurer HDFC ERGO General Insurance Co. Ltd.

5. Date of Repudiation 28.12.2020

6. Reason for repudiation Not payable due to two years waiting period.

7. Date of receipt of the Complaint 01-01-2021

8. Nature of complaint Denial of Hospitalization Expenses

9. Amount of Claim Rs. 58590/-

10. Date of Partial Settlement N.A

11. Amount of relief sought Rs.58590/-

12. Complaint registered under

Rule no: Insurance Ombudsman Rules,

2017

Rule 13 (1)(b) – any partial or total repudiation

of claims by an insurer

13. Date of hearing/place 15.03.2021/ online

14. Representation at the hearing

For the Complainant Mr. Sanjay Kumar(Son)

For the insurer Mr. Dhiraj Mhatre

15. Complaint how disposed Dismissed

16. Date of Award/Order 18.03.2021

17). Brief Facts of the Case:

On 01-01-2021, Mr. Sita Ram had filed a complaint against HDFC ERGO General Insurance Co.

Ltd. for rejection of his mediclaim and submitted that complainant is holding the policy with the

insurer since Oct. 2019 and no claim has been claimed till now. Despite paying the regular

premium insurance company has rejected his claim for the wrong reason. The complainant

stated that he fell down at home at 10 days ago and there was injury in lower part of his body in

the ass hole. On examination doctor found trauma at ass hole and operated and removed the

infection from complainant’s body because of emergency. The Doctor also confirmed that

infection and trauma was caused due to fall at home as it was emergency surgery with the case

of accident but still the company rejected the claim with the reason of waiting period of 24

months. The complainant further stated that as it was emergency surgery with cause of accident

then how it would be under waiting period of 24 months. The complainant requested for

resolution of grievance against insurer regarding reimbursement of expenses amounting to

Rs.60000/- incurred by him on treatment.

On 07-01-2021, the complaint was forwarded to Tata AIG General Insurance Co. Ltd. Regional

Office, Noida, for Para-wise comments and submission of a self-contained note about facts of

the case, which was made available to this office on 25-01-2021.As per the SCN, the

complainant Mr. Sita Ram had obtained a tailor made Group Medicare Policy for sum insured of

Rs. 5 Lac for the period 29.10.2019 to 28.10.2020. This policy is tailor made for the customers of

axis bank with specific coverage as required by the bank and the policy was renewed for the

period 29.10.2020 to 28.10 2021 along with specific exclusion under section 3(ii) which is

relevant to the claim and is reproduced below;

Section 3- General Exclusions

Exclusions with waiting periods

ii) A waiting period of 24 months from the first policy commencement date will be applicable to

the medical and surgical treatment of illness, disease, or surgical procedures mentioned below,

unless necessitated due to cancer:

a. ……… n. Fissure/fistula in anus, hemorrhoids, pilonidal sinus

r. Perineal Abscesses

s. Perineal/Anal Abscesses

Insurer submitted that they had received a preauthorization request on 10th December 2020

indicating that Mr. Sita Ram had complaints of pain in anal region for 5-6 days with poor oral

intake and history of constipation. He was diagnosed as a case of Perianal Abscess with Fistula in

Ano for which he underwent Incision and Drainage with Fistulotomy.

Since Perianal abscess falls under2 years waiting period, insurer rejected the pre-authorization

vide letter dated 10th December 2020. Insurance company received the claim documents from

insured on 25.10.2020 with a diagnosis of ‘Perianal Abscess with Fistula in Ano’. Since Perianal

Abscess and Fistula in Ano surgery is not payable within first two years of policy inception, the

claim was rejected by insurer vide letter dated 28th December 2020. The customer produced a

document indicating that the Perianal Abscess and Fistula were related to an injury. Insurer

further stated that they highlighted to the complainant that the exclusion for Fissure and fistula

apply in case of injury. Insurer stated that History of trauma is an afterthought as neither the

preauthorization documents, emergency department initial assessment nor indoor case papers

of the hospital indicate any history of trauma. This was highlighted only after preauthorization

was denied and not any time prior. Also just a fall at the back does not generally cause Anal

fissure and fistula, trauma in the context of Fissure/Fistula is more common in the context of:

- Passage of hard stool - Repeated diarrhea - Anorectal surgery - In rare cases, it is due to Anoreceptive intercourse/ foreign body insertion. In the Para-wise reply the insurer submitted;

1. It is submitted that in preauthorization documents received, there was no where mentioned that insured has history of trauma or injury. Had the patient was really suffering from injury prior to admission treating doctor would have mentioned vigorously about date/time/place/nature of injury in the preauthorization form no 2 against question no K & L. Even if we were to consider the history of trauma/injury, it has no bearing on the case as the exclusion applies irrespective of the cause

2. It is submitted that in claim documents viz. discharge summary, indoor case papers it was nowhere that said ailment was attributed due to trauma. This was after thought from the insured that the said ailment was attributed due to trauma. The same has been evident from the reimbursement claim form page no. 2 against question “Hospitalization due to” there were 3 options viz. injury/illness/maternity, insured himself ticked on ‘illness’. He has not ticked against the “injury”. It suggests that insured never had any injury. Even in reimbursement claim form, on page 5, against question “Hospitalization due to injury” there were two options viz. Yes/No. treating doctor himself ticked on “No”. Hence it is evident that insured never had any trauma/injury.

3. It is submitted that complainant has presented a certificate from the treating doctor indicating that the indurations and infection could be due to an alleged fall. This neither mentioned in the, emergency department initial assessment nor in the indoor case papers of the hospital nor in the pre-authorization request or discharge summary. Even if we take this document into consideration, the claim would still not be admissible under the policy as the two years exclusions apply even in case of injury as per the tailor made policy issued to the Axis Bank.

4. It is submitted that even they were to consider the injury, Fistula in Anus are never an acute problem but due to long standing infection. The treating doctor has now clarified that the earlier certificate issued was based on the patient’s declaration of history of fall which was not given at the time of pre-authorization but later came up with this history. This letter is marked as Annexure 7. There are no external injuries which are noted in the critical documents viz. discharge summary and indoor case papers.

5. It is evident from the mail dated 29.12.2020 where he mentioned fall /injury was 3-4 days back from the date of admission & complainant letter submitted to Ombudsman by the complainant where he mentioned fall was 10 days back, this clearly shows that complainant is twisting facts and giving contradictory statements. The insurance company has sought dismissal of complaint as the claim falls under the

specific exclusion highlighted above even if this is due to an injury/trauma.

The complainant was sent Annexure VI-A for compliance, which reached this office on 22-01-

2021

18) Cause of Complaint:

a) Complainant’s argument: The denial of claim for Perianal Abscess with Fistula in Ano due to

24 months waiting period is not justified as emergency surgery was necessitated due to

accidental fall.

b) Insurers’ argument: The claim is not admissible due to specific exclusion under section

3(1)(ii) of the policy which is related with waiting period of 24 months from the first policy

inception.

19) Reason for Registration of Complaint: Within the scope of the Insurance Ombudsman Rules,

2017.

20) The following documents were placed for perusal.

a) Complaint to the Company b) Copy of Policy Document

c) Annexure VI-A d) Reply of the Insurance Company

21) Result of Personal hearing with both parties (Observations & Conclusion):

On perusal of the various documents available in the file including the copy of the complaint,

SCN of the insurance company, discharge summary and submission made by both the

complainant and the insurance company during on line hearing, it has been observed that

complainant’s reimbursement claim under Mediclaim policy, for hospitalization at Max Super

Speciality Hospital from 09.12.2020 to 12.12.2020 for treatment of perianal abscess fistula in

ano, has been repudiated by the insurer under section 3)1)ii of the policy as the treatment falls