proceedings before - the insurance ombudsman, lucknow

188

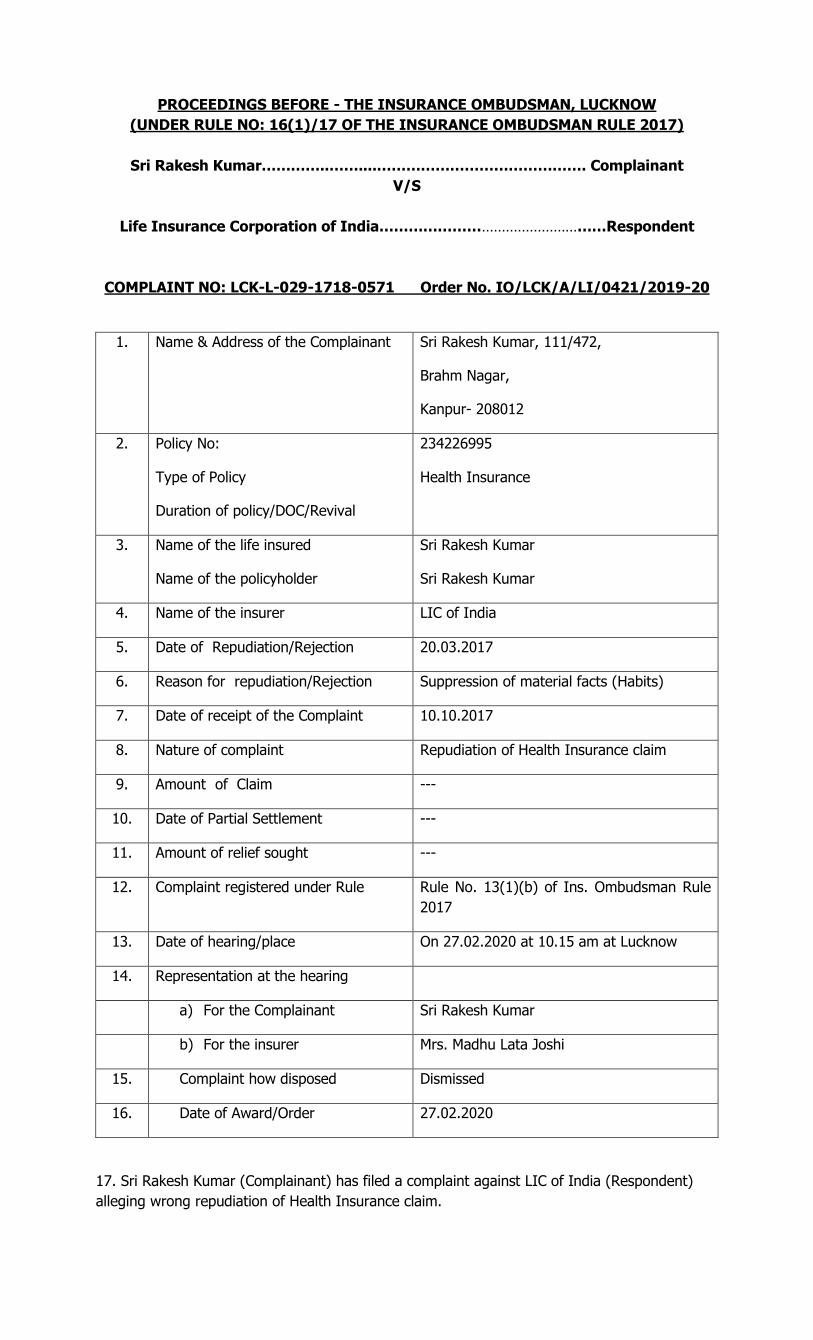

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, LUCKNOW (UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017) Sri Rakesh Kumar…………..……....……………………………………. Complainant V/S Life Insurance Corporation of India……………………………………………Respondent COMPLAINT NO: LCK-L-029-1718-0571 Order No. IO/LCK/A/LI/0421/2019-20 1. Name & Address of the Complainant Sri Rakesh Kumar, 111/472, Brahm Nagar, Kanpur- 208012 2. Policy No: Type of Policy Duration of policy/DOC/Revival 234226995 Health Insurance 3. Name of the life insured Name of the policyholder Sri Rakesh Kumar Sri Rakesh Kumar 4. Name of the insurer LIC of India 5. Date of Repudiation/Rejection 20.03.2017 6. Reason for repudiation/Rejection Suppression of material facts (Habits) 7. Date of receipt of the Complaint 10.10.2017 8. Nature of complaint Repudiation of Health Insurance claim 9. Amount of Claim --- 10. Date of Partial Settlement --- 11. Amount of relief sought --- 12. Complaint registered under Rule Rule No. 13(1)(b) of Ins. Ombudsman Rule 2017 13. Date of hearing/place On 27.02.2020 at 10.15 am at Lucknow 14. Representation at the hearing a) For the Complainant Sri Rakesh Kumar b) For the insurer Mrs. Madhu Lata Joshi 15. Complaint how disposed Dismissed 16. Date of Award/Order 27.02.2020 17. Sri Rakesh Kumar (Complainant) has filed a complaint against LIC of India (Respondent) alleging wrong repudiation of Health Insurance claim.

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of proceedings before - the insurance ombudsman, lucknow

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, LUCKNOW

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

Sri Rakesh Kumar…………..……....……………………………………. Complainant

V/S

Life Insurance Corporation of India……………………………………………Respondent

COMPLAINT NO: LCK-L-029-1718-0571 Order No. IO/LCK/A/LI/0421/2019-20

1. Name & Address of the Complainant Sri Rakesh Kumar, 111/472,

Brahm Nagar,

Kanpur- 208012

2. Policy No:

Type of Policy

Duration of policy/DOC/Revival

234226995

Health Insurance

3. Name of the life insured

Name of the policyholder

Sri Rakesh Kumar

Sri Rakesh Kumar

4. Name of the insurer LIC of India

5. Date of Repudiation/Rejection 20.03.2017

6. Reason for repudiation/Rejection Suppression of material facts (Habits)

7. Date of receipt of the Complaint 10.10.2017

8. Nature of complaint Repudiation of Health Insurance claim

9. Amount of Claim ---

10. Date of Partial Settlement ---

11. Amount of relief sought ---

12. Complaint registered under Rule Rule No. 13(1)(b) of Ins. Ombudsman Rule

2017

13. Date of hearing/place On 27.02.2020 at 10.15 am at Lucknow

14. Representation at the hearing

a) For the Complainant Sri Rakesh Kumar

b) For the insurer Mrs. Madhu Lata Joshi

15. Complaint how disposed Dismissed

16. Date of Award/Order 27.02.2020

17. Sri Rakesh Kumar (Complainant) has filed a complaint against LIC of India (Respondent)

alleging wrong repudiation of Health Insurance claim.

YKS

COMPLAINT NO: LCK-L-029-1718-0571 Order No. IO/LCK/A/LI/ 0421/2019-20

Brief Facts of the Case:-

18. The complainant in his complaint has stated that the policy was purchased by him on

18.03.2008 on yearly premium of Rs. 15000/- and last premium was paid on 14.03.2017. His

grievance is against LIC for wrongful rejection of his health insurance claim and subsequent

cancellation of his policy for the reason of ―preexisting disease‖. He has mentioned that first

detection of illness was noticed about 6-7 months prior to his hospitalization. He has mentioned

that he was not under the habit of tobacco chewing. He has approached this forum for

redressal of his grievance. He has requested to pay the health insurance claim payment and

restoration of his policy.

Written reply/SCN:-

19. In their reply/ SCN dated 27.11.2017, RIC has stated that claim papers were received on

16.08.2016 at DO and were sent to TPA. The claim was for the surgery of Ca Left Buccal

Mucosa. The claim case was rejected by TPA vide letter dated 30.09.2016. The TPA observed in

medical papers that the claimant was having the habit of pan/tobacco chewing since 20 years,

and this material fact was not disclosed in proposal form. The claim was reviewed by DODRC on

09.03.2017 and the decision of TPA was uphold with the cancellation of the policy. Then

decision was communicated on 20.03.2017.

20. The complainant has filed a complaint letter, annexure VI A, correspondence with respondent

while respondent has filed SCN.

21. I have heard the complainant as well as respondent representative and perused the record.

Findings:-

22. Undisputedly insured complainant Rakesh Kumar was covered under the ―LIC Health Plus

Policy- Plan 901‖ since 2008. He was paying the premium of Rs. 15,000/- per annum. He filled

in the proposal form. In the year 2016 he had some problems in his oral cavity. Then he

consulted Jograj Singh Memorial Hospital, Farrukhabad on 11.05.2016 wherein he informed the

Doctor that he is in the habit of Paan chewing for the last 20 years. He was referred to Rajiv

COMPLAINT NO: LCK-L-029-1718-0571 Order No. IO/LCK/A/LI/ 0421 /2019-20

Gandhi Cancer Institute & Research Centre, Delhi where he got registered at CR No. 200992.

He was examined wherein it was mentioned on the OPD card clinical notes that he is chronic

tobacco chewing for the last 40 years. Subsequently he was diagnosed with Carcinoma Left

Buccal Mucosa (CT3N1MO). The consultant Doctor was Dr. A. K Diwan, Director and Senior

Consultant Department of Surgical Oncology.

23. Complainant insured submits the claims which were repudiated by the respondent vide

letter dated 20.03.2017 of Senior Divisional Manager, Division Office, LIC, Kanpur wherein the

cause of repudiation was as under:-

No.

Repudiation

code

Cause of Repudiation with particulars

H01 Insured member having habit of paan chewing/Tobacco since 20 years

from the date of manifest of current illness. This habit (material fact) was

not disclosed in the proposal form at the time of taking up of the policy.

24. Aggrieved by the repudiation of claim, complainant has moved to this forum. Complainant

submits that he was never in the habit of chewing pan or tobacco. He was not suffering from

any disease prior to the taking of the policy. He has not concealed any material information in

the proposal form.

25. Repudiation was made on the basis of non-disclosure and concealment of the habit of

chewing tobacco and paan at the time of the proposal form. In the OPD description of Jograj

Singh Memorial Hospital, Farrukhabad as well as in the OPD card of Rajiv Gandhi Cancer

Institute & Research Centre, Delhi it is mentioned that the insured complainant was in the

habit of chewing paan for the last 20 years and for chewing tobacco for the last 40 years.

26. In order to make a deep scrutiny of the matter respondent LIC was asked to furnish a

certificate of the concerned doctor. In compliance a certificate dated 31.12.2019 of Dr. A. K.

COMPLAINT NO: LCK-L-029-1718-0571 Order No. IO/LCK/A/LI/ 0421 /2019-20

Diwan, Director and Senior Consultant Department of Surgical Oncology of Rajiv Gandhi Cancer

Institute & Research Centre, Delhi is submitted which is as under:-

―This is to certify that Mr. Rakesh Kumar, Cr. No. 200992 came to this hospital on 12/05/2016

with the complaint of growth in left Buccal Mucossa for 6 months duration. As per hospital

record he had history of chronic tobacco chewing for 40 years reformed 1 and half year back,

pan masala 20 yrs left 6 weeks back.‖

27. An opportunity was given to the insured complainant to rebut this document but the

complainant could not file any certificate or material to rebut the certificate of Dr. Diwan. It may

be observed that Rajiv Gandhi Cancer Institute & Research Centre, Delhi is an institute of

national repute. Certificate by the Director of the Surgical Oncology could not be put to

suspicion or any doubt can be raised about it. Certificate was issued on the basis of hospital

record. In such circumstances I do not find any reason to disbelieve the certificate of Dr. Diwan

dated 31.12.2019. Oral statement of the insured complainant to the effect that he was not in

the habit of chewing the tobacco or paan prior to submission of the proposal form could not be

accepted.

28. Clause 22 (xii) of the policy bond provides as under:-

―Xii

If any of the insured or the claimant shall make or advance any claim knowing the same to be

false or fraudulent as regard amount or otherwise, this policy shall immediately become void

and all claims or payments in respect of all the Insured under this policy shall be forfeited. Non-

disclosure of any health event or ailment/condition/sickness/Surgery which occurred prior to the

taking of this policy, whether such condition is relevant or not to the ailment/disease/ Surgery

for which the insured is admitted/ treated shall also constitute Fraud.‖

29. In the proposal form insured complainant in column no. 1 has mentioned that neither he

smokes nor consumed any form of tobacco or alcohol. This relates to the health event of the

insured which is covered under the definition of fraud in the policy bond. Accordingly claim was

COMPLAINT NO: LCK-L-029-1718-0571 Order No. IO/LCK/A/LI/ 0421/2019-20

repudiated on the ground of concealment of material fact which amounts to fraud and the

policy was cancelled.

30. On the basis of discussion made above I am of the view that claim of the complainant

insured has rightly been repudiated by the respondent which did not call for any interference.

Order:-

31. Complaint is dismissed.

32. Let the copy of award be given to both the parties.

Date: 27.02.2020 (Justice Anil Kumar Srivastava)

Place: Lucknow Insurance Ombudsman

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, STATE OF UP

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

Mr. Rais Aalam…………. ………………..……....…………………..………. Complainant

V/S

Life Insurance Corp. of India …….…..…....…………………………….………Respondent

COMPLAINT NO: LCK-L-029-1819-0499 Order No. IO/LCK/A/LI/ 0379/2019-20

1. Name & Address of the Complainant Mr. Rais Aalam

Ansar Nagar

Kanpur

2. Policy No:

Type of Policy

Duration of policy/DOC

234018389

Jeevan Tarang

21.11.2007

3. Name of the insured

Name of the policyholder

Mr. Rais Aalam

Mr. Rais Aalam

4. Name of the insurer Life Insurance Corp. of India

5. Date of Repudiation/Rejection -

6. Reason for repudiation/Rejection -

7. Date of receipt of the Complaint 06.12.2018

8. Nature of complaint Amount less paid on surrender

9. Amount of Claim

10. Date of Partial Settlement

11. Amount of relief sought

12. Complaint registered under Rule Rule No. 13(1)(b) of Ins. Ombudsman Rule

2017

13. Date of hearing/place On 18.02.2020 , 10.30 am at Lucknow

14. Representation at the hearing

a) For the Complainant Absent

b) For the insurer Sri. Harinath Kumar

15. Complaint how disposed Allowed

16. Date of Award/Order 18.02.2020

17. Mr. Rais Aalam (Complainant) has filed a complaint against Life Insurance Corp. of India

(Respondent) alleging payment of less amount on Surrender of policy.

MS

COMPLAINT NO: LCK-L-029-1819-0499 Order No. IO/LCK/A/LI/ 0379/2019-20

Brief Facts of the Case:-

18. Mr. Rais Aalam has lodged his complaint on 06.12.2018 stating that less amount was paid

by the Life Ins. Corp. of India on surrender of his policy. The complainant has stated that he

was in need of money so he surrendered his policy before maturity of the policy. In branch

office the complainant submitted surrender forms and there he got surrender value quotation

showing amount as Rs.2,59,295/=. The complainant has stated that when he received

surrender value in his account, it was Rs. 1,80,000/= which was a Less Rs. 79,295/= from

original surrender quotation. He has written to branch for payment of remaining amount

repeatedly, as well as Divisional Office but with no result. Being aggrieved he has approached

this forum for the redressal of his grievance.

Written Reply/SCN:-

19. In their SCN/reply, the RIC has stated that due to technical problem, this happened. The

RIC has made payment of Rs.79,295/= through NEFT on 29.03.2019.

20. The complainant has filed a complaint letter, annexure VI A, correspondence with

respondent while respondent has filed SCN with enclosures.

21. Despite notice complainant is not present. I have heard the respondent representative and

perused the record.

Findings:-

22. Main concern of the complainant is that an amount of Rs. 79295/- was not paid to him

when he surrendered his policy. As per the SCN of the respondent the amount of Rs. 79295/-

has been paid to the complainant in his account through NEFT. An amount of Rs. 1,80,000/-

was paid to the complainant on 20.11.2017. Difference amount Rs. 79295/- was paid on

29.03.2019. Why payment was delayed and if delay was made then the complainant insured is

entitled for penal interest. It is not a sweet will of LIC to withhold the payment and make the

payment subsequently.

COMPLAINT NO: LCK-L-029-1819-0499 Order No. IO/LCK/A/LI/ 0379/2019-20

23. In such circumstances although the complainant has received the payment of Rs. 79295/-

but he is entitled for penal interest at the rate of 8.25 percent per annum from 20.11.2017 to

29.03.2019.

Order:-

24. Complaint is partially allowed to the extent that the respondent would make the payment of

penal interest at the rate of 8.25 percent per annum on an amount of Rs. 79295/- from

20.11.2017 to 29.03.2019 within 30 days to the complainant.

25. Let the copy of award be given to both the parties.

Date: 18.02.2020 (Justice Anil Kumar Srivastava)

Place: Lucknow Insurance Ombudsman

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, STATE OF UP

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

Sri Ram Narayain Misra…………. ………………..……....………………. Complainant

V/S

Life Insurance Corp. of India…………………....…....…………………………Respondent

COMPLAINT NO: LCK-L-029-1819-0574 Order No. IO/LCK/A/LI/0355 /2019-20

1. Name & Address of the Complainant Sri Ram Narayain Misra

Vill. Bhadaipur, Post Dikauli

Distt. Shravasti

2. Policy No:

Type of Policy

Duration of policy/DOC

236648105, 226653904

Wealth Plus

31.03.2010, 08.05.2010

3. Name of the insured

Name of the policyholder

Sri Ram Narayain Misra

Sri Ram Narayain Misra

4. Name of the insurer Life Insurance Corp. of India

5. Date of Repudiation/Rejection -

6. Reason for repudiation/Rejection -

7. Date of receipt of the Complaint 25.01.2019

8. Nature of complaint Surrender Amount less paid

9. Amount of Claim

10. Date of Partial Settlement

11. Amount of relief sought

12. Complaint registered under Rule Rule No. 13(1)(b) of Ins. Ombudsman Rule

2017

13. Date of hearing/place On 14.02.2020 , 10.30 am at Lucknow

14. Representation at the hearing

a) For the Complainant Sri Ram Narayain Misra

b) For the insurer Mr. Heera Singh

15. Complaint how disposed Dismissed

16. Date of Award/Order 14.02.2020

17. Sri Ram Narayain Misra (Complainant) has filed a complaint against SBI Life Insurance

Co. Ltd. (Respondent) alleging that less amount was paid on surrender.

MS

COMPLAINT NO: LCK-L-029-1819-0574 Order No. IO/LCK/A/LI/0355 /2019-20

Brief Facts of the Case:-

18. Sri Ram Narayain Misra has lodged his complaint on 25.01.2019 stating that less amount

was paid by the company Life Ins. Corp. of India on surrender of his policies. The complainant

has stated that he deposited total 3 premium of Rs.60000/= under both the policies. On

surrender of these policies he received only Rs.27,799 /= and Rs. 31,710/=respectively for his

policies.He has further stated that on 12.09.2013 value of his policies was Rs.37,139.49 and

Rs.39,294.65.On surrender he was paid less than 50% of his deposit amount. He received

surrender value amount after two month 26/28 days late so delayed interest was also claimed

by the complainant. The complainant has raised his dis-satisfaction on working method of the

corporation that even branch manager and responsible employee does not know what is to be

done and assured him that correspondence with higher office is continued and arrear with

interest will be paid . He approached RIC`s divisional office but nothing was heard from them.

The complainant was not satisfied. Being aggrieved he has approached this forum for the

redressal of his grievance.

Written reply/SCN:-

19. In their SCN/reply, the RIC has stated that as per policies terms and conditions under policy

nos.236648105 surrender value of Rs.27799/= was paid on 26.06.2018. In Policy

No.236653904 surrender value of Rs.31710/= was paid on 06.08.2018 to the policy holder. At

the time of proposal the age of insured was 65 years and risk premium, other charges and

charges for extended risk cover was deducted as per rules. RTI application and complaint letter

was duly replied by the RIC. Copy of terms and condition of the policy and NAV chart for both

the policies was also enclosed with SCN. As per respondent letter dated 31.01.2020 they have

paid penal interest of Rs. 548/= and Rs. 645/= under both policies due to late payment.

20. The complainant has filed a complaint letter, annexure VI A, correspondence with

respondent while respondent has filed SCN with enclosures.

21. I have heard the complainant as well as respondent representative and perused the record.

COMPLAINT NO: LCK-L-029-1819-0574 Order No. IO/LCK/A/LI/0355 /2019-20

Findings:-

22. Policies were taken under the plan TT 801-08 Wealth Plus. An amount of Rs. 60,000/- was

deposited under both policies but on maturity after 8 years insured received Rs. 27799/- and

Rs. 31710/- only. Main concern of the complainant is that he got less amount.

23. It was the policy under ‗Wealth Plus Plan‘ where the maturity value was paid in accordance

with the terms and conditions of the policy bond. Highest NAV during the last 7 years or on the

date of maturity was to be paid. Charges under the head of administration and mortality were

deducted by the insurer. Hence the maturity amount was paid in accordance with the terms and

conditions of the policy bond. Complaint lacks merit and liable to be dismissed.

Order:-

24. Complaint is dismissed.

25. Let the copies of award be given to both the parties.

Date: 14.02.2020 (Justice Anil Kumar Srivastava)

Place: Lucknow Insurance Ombudsman

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, LUCKNOW

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

Mr. Ashok Kumar Singh………………………………....……....………………. Complainant

VS

Life Insurance Corporation of India………………………………….………...Respondent

COMPLAINT NO: LCK-L-029-1819-0259 Order No. IO/LCK/A/LI/ 0350/2019-20

1. Name & Address of the Complainant Mr. Ashok Kumar

Vill. & Post- Khanpur

Dist. Mirzapur - 231306

2. Policy No:

Type of Policy

DOC /DOR

DOD

Duration of policy

286635868

Endowment Plan Table-48

28.04.2009

N/A

10 years

3. Name of the insured /

Name of the policyholder

Mrs. Chandrawati Singh

Mrs. Chandrawati Singh

4. Name of the insurer Life Insurance Corporation of India

5. Date of Repudiation/Rejection N/A

6. Reason for repudiation/Rejection N/A

7. Date of receipt of the Complaint 31.07.2018

8. Nature of complaint Surrender Value not paid

9. Amount of Claim 500000/-

10. Date of Partial Settlement

11. Amount of relief sought Surrender Value is not paid

12. Complaint registered under Rule Rule No.13(1)(f)of Insurance Ombudsman

Rule 2017

13. Date of hearing/place 13.02.2020 at 10.15 A.M.

14. Representation at the hearing

a) For the Complainant Absent

b) For the insurer Mr. Shri Prakash

15. Complaint how disposed Dismissed as settled

16. Date of Award/Order 13.02.2020

17. Mr. Ashok Kumar Singh (Complainant) has filed a complaint against Life Insurance

Corporation of India. (Respondent) alleging Surrender Value has not been made.

YKS

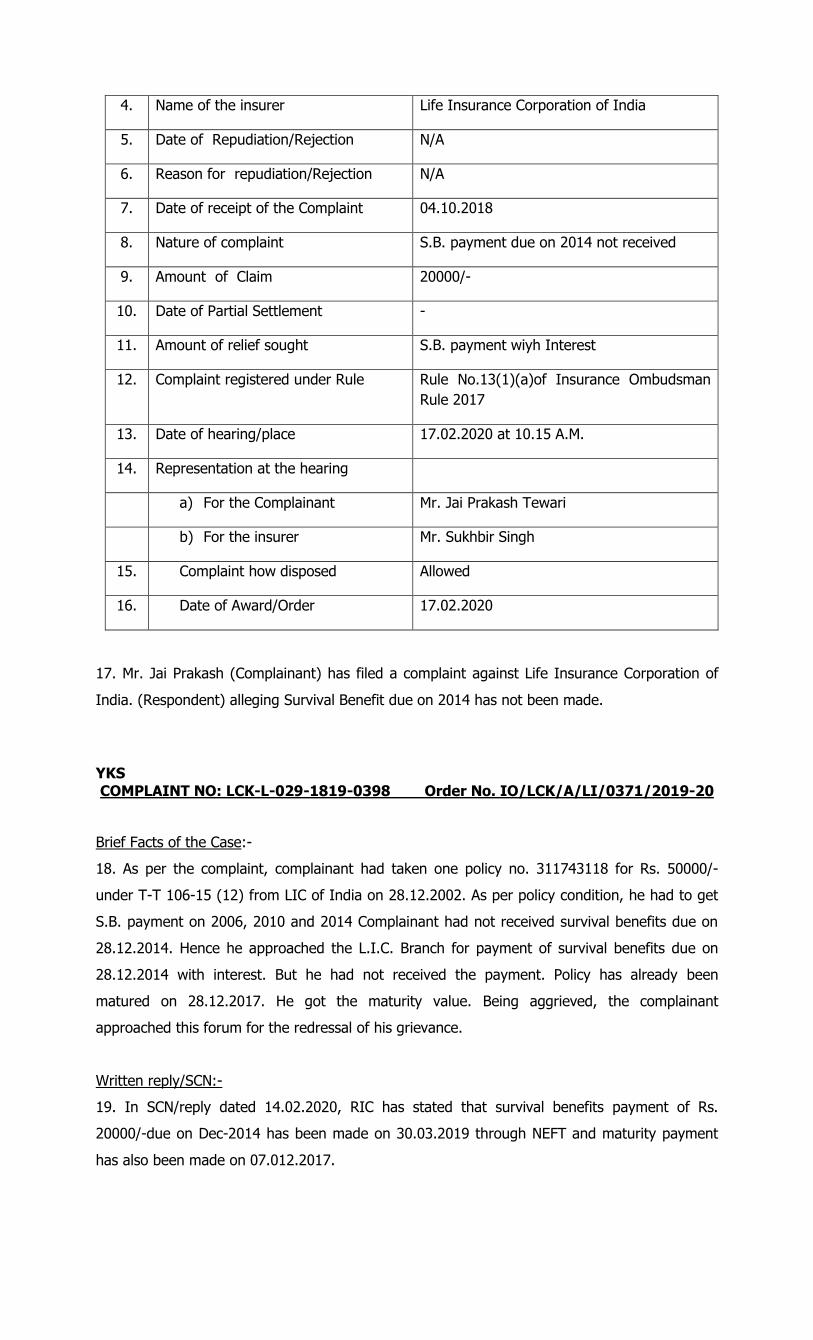

COMPLAINT NO: LCK-L-029-1819-0259 Order No. IO/LCK/A/LI/0350 /2019-20

Brief Facts of the Case:-

18. As per the complaint, complainant had taken one policy no. 286635868 on the life of his

wife Smt. Chandrawati Singh for Rs. 500000/- under Single Premium mode for 10 years on

28.04.2009 from LIC of India. As per policy condition, Life assured had applied for Loan on

30.10.2017,but she had not received Loan amount. Hence she approached the L.I.C. Branch

where they have informed that the loan of Rs. 365000/- has paid on 07.02.2013 but it has been

reversed on 09.03.2013 due to NEFT rejection. After that he had not received this amount.

Being aggrieved, the complainant approached this forum for the redressal of his grievance.

Written reply/SCN:-

19. In SCN/reply dated 22.01.2020, RIC has stated that aforesaid policy no. 286635868 was

issued under T-T 18-10(1) ON 28.04.2009 on the life of Ashok Kumar Singh. Policy holder has

deposited Rs.415525/- and status of the policy was ‗FORECLOSED‘. Policy holder has applied for

surrender and the surrender value was Rs. 434974/- . As the policy was Auto Foreclosed, hence

payment could not be made. Policy became matured on 28.04.2019 and maturity value was Rs.

663730/- was paid to policy holder.

20. The complainants have filed a complaint letter along with other relevant papers while

respondent has filed SCN without enclosures. But Annexure VI A is not enclosed.

21. Despite notice complainant is not present. I have heard the respondent representative and

perused the record.

Findings:-

22. Complainant had taken the policy under ‗Single Premium Plan‘ in the name of his wife, he

wanted to surrender the same on the value which was not being paid by the insurance

company. In the SCN submitted it is mentioned that the policy was in foreclosed stage.

However on maturity of the policy an amount of Rs. 6,63,730/- has been paid to the

complainant. Accordingly complaint become infructous and is disposed off.

COMPLAINT NO: LCK-L-029-1819-0259 Order No. IO/LCK/A/LI/0350/2019-20

Order:-

23. Complaint is disposed off.

24. Let copy of award be given to both the parties.

Date: 13.02.2020 (Justice Anil Kumar Srivastava)

Place: Lucknow Insurance Ombudsman

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, LUCKNOW

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

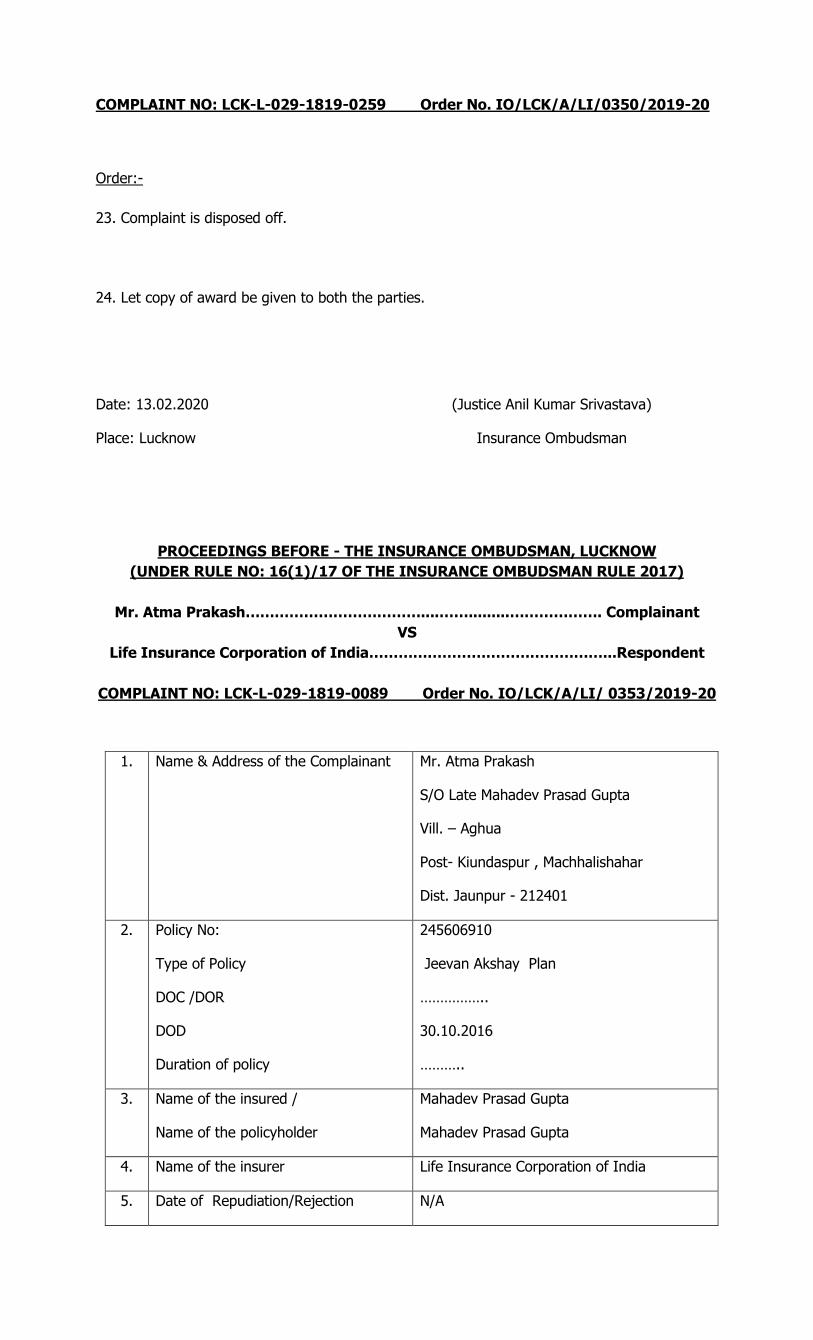

Mr. Atma Prakash………………………………....…….........………………. Complainant

VS

Life Insurance Corporation of India…………………………………………...Respondent

COMPLAINT NO: LCK-L-029-1819-0089 Order No. IO/LCK/A/LI/ 0353/2019-20

1. Name & Address of the Complainant Mr. Atma Prakash

S/O Late Mahadev Prasad Gupta

Vill. – Aghua

Post- Kiundaspur , Machhalishahar

Dist. Jaunpur - 212401

2. Policy No:

Type of Policy

DOC /DOR

DOD

Duration of policy

245606910

Jeevan Akshay Plan

……………..

30.10.2016

………..

3. Name of the insured /

Name of the policyholder

Mahadev Prasad Gupta

Mahadev Prasad Gupta

4. Name of the insurer Life Insurance Corporation of India

5. Date of Repudiation/Rejection N/A

6. Reason for repudiation/Rejection N/A

7. Date of receipt of the Complaint 16.03.2018

8. Nature of complaint Interest on Claim amount

9. Amount of Claim ……….

10. Date of Partial Settlement …………..

11. Amount of relief sought Interest on Claim amount

12. Complaint registered under Rule Rule No.13(1)(f)of Insurance Ombudsman

Rule 2017

13. Date of hearing/place 13.02.2020 at 10.15 A.M.

14. Representation at the hearing

a) For the Complainant Mr. Atma Prakash

b) For the insurer Mr. Dileep Kumar Tiwari

15. Complaint how disposed Allowed

16. Date of Award/Order 13.02.2020

17. Mr. Atma Prakash (Complainant) has filed a complaint against Life Insurance Corporation of

India. (Respondent) alleging that interest on delayed payment was not made.

YKS

COMPLAINT NO: LCK-L-029-1819-0089 Order No. IO/LCK/A/LI/ 0353/2019-20

Brief Facts of the Case:-

18. As per the complaint, complainant‘s father had taken one policy no.245606910 on the life

under Pension Plan and opted option ‗F‘ .His father expired on 30.10.2016 and he was the

nominee under the policy. He submitted claim form to the branch on 31.01.2017. But he had

not received the claim amount. LIC has informed him that wrong option was feeded under the

policy and the matter is referred to the higher office. After a long time he received only claim

amount without interest. Being aggrieved, the complainant approached this forum for the

redressal of his grievance.

Written reply/SCN:-

19. In SCN/reply dated 06.02.2020, RIC has stated that aforesaid policy was issued by their

Mungrabadshahpur Branch under Varanasi Division. But by mistake option ‗J‘ was captured in

place of option ‗F‘ at the time of data capturing. This information was also delivered to claimant

on 10.03.2018 in reply of RTI. Now the case is referred to SDC, we will made the payment to

claimant.

20. The complainants have filed a complaint letter, Annexure VI A along with other relevant

papers while respondent has not filed SCN with enclosures.

21. I have heard the complainant as well as respondent representative and perused the record.

Findings:-

22. At the very outset it is clear that the policy was taken by Shri Madhav Prasad. Admittedly

option ‗F‘ was claimed by the insured but option ‗J‘ was feeded in the system inadvertently but

till date even after the lapse of about 2 years correction is not made by LIC. Consequently

payment is also not made to the complainant who is the nominee of insured.

23. It is a case of gross negligence on the part of officers of LIC, Varanasi, Division Varanasi.

The most revealing fact is that when the mistake came to their knowledge even then they did

not correct the same. In such circumstances I have no option but to allow the complaint with a

direction to the insurance company to correct the option and make the payment within 30 days.

COMPLAINT NO: LCK-L-029-1819-0089 Order No. IO/LCK/A/LI/ 0353 /2019-20

Order:-

24. Complaint is allowed. Respondents are directed to make the payment of claim under the

policy within 30 days positively.

25. Let copy of award be given to both the parties.

Date: 13.02.2020 (Justice Anil Kumar Srivastava)

Place: Lucknow Insurance Ombudsman

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, STATE OF UP

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

Mr. IFTIKHAR ASHRAF SIDDIQUE.…….…….....……………………………. Complainant

V/S

SBI Life Insurance Co. Ltd...……………………………………….……………..…Respondent

COMPLAINT NO: LCK-L-041-1819-0431 Order No. IO/LCK/A/LI/ 0396/2019-20

1.

Name & Address of the Complainant Mr. Iftikhar Ashraf Siddque

Moh.- Kaziyara

Post- Khairabad

Sitapur- 261131

2. Policy No:

Type of Policy

DOC

Duration of policy

22000922105

Annuity Plus Plan

29.03.2013

11 years

3. Name of the insured

Name of the policyholder

Mr. Iftikhar Ashraf Siddque

Mr. Iftikhar Ashraf Siddque

4. Name of the insurer SBI Life Insurance Co. Ltd

5. Date of Repudiation/Rejection -

6. Reason for repudiation/Rejection -

7. Date of receipt of the Complaint 23.10.2018

8. Nature of complaint Mis-selling

9. Amount of Claim 500000/-

10. Date of Partial Settlement Pension Rs.2935/- P.M.

11. Amount of relief sought Refund of Amount

12. Complaint registered under Rule Rule No. 13(1)(f) of Ins. Ombudsman Rule

2017

13. Date of hearing/place 24.02.2020 at 10.15 am

14. Representation at the hearing

a) For the Complainant Absent

b) For the insurer Mohd. Tarique Khan

15. Complaint how disposed Dismissed

16. Date of Award/Order 24.02.2020

17. Mr. Iftikhar Ashraf Siddque (Complainant) has filed a complaint against SBI Life Insurance

Co. Ltd. (Respondent) alleging mis-selling of policy.

YKS

COMPLAINT NO: LCK-L-041-1819-0431 Order No. IO/LCK/A/LI/ 0396 /2019-20

Brief Facts of the Case:-

18. As per the complaint, complainant had taken an Annuity Policy no.22000922105 of Rs. 5.00

lac on 29.03.2014 from SBI Binaura branch. Claimant is getting annuity of Rs.2935/- per month.

But due to some business problem, he was in need of money. Hence he has surrendered the

policy. But company denied to pay the amount by informing that the amount will be refunded

only after his death. Being aggrieved, the complainant approached this forum for the redressal

of his grievance.

Written reply/SCN:-

19. In their SCN/reply dated 13.1.2018 RIC has stated that policy was issued on the basis of

duly signed proposal form for Insurance from the policyholder .The policy is issued under

Annuity Plan and annuity is being paid to complainant. Further they stated that once the

annuity started, it could not be surrendered. Even Loan is also not available under this plan.

20. The complainant has filed a complaint letter & correspondence with respondent and copy of

policy document while respondent has filed SCN with enclosures. Annexure VI A NOT

ENCLOSED.

21. Despite notice complainant is not present. I have heard the respondent representative

and perused the record.

Findings:-

22. Undisputedly the complainant has taken ―Annuity Plus Plan‖ with date of

commencement as 28.03.2014. One time premium of Rs. 5 lakhs was deposited wherein

annuity of Rs. 2935/- per month is being paid to the complainant. Complainant contention

is that he wants to get back his amount. As per the terms and conditions of the policy bond

complainant is entitled for annuity for the terms of the policy which is being regularly paid

to him. In case of any mis-happening nominee would be entitled for the capital refund.

COMPLAINT NO: LCK-L-041-1819-0431 Order No. IO/LCK/A/LI/ 0396/2019-20

Policy was issued as per the terms and conditions of the policy bond accordingly payment is

being made to the complainant. Complaint is devoid off merit and is liable to be dismissed.

Order:-

23. Complaint is dismissed.

24. Let the copy of award be given to both the parties.

Date: 24.02.2020 (Justice Anil Kumar Srivastava)

Place: Lucknow Insurance Ombudsman

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, LUCKNOW

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

Mr. Jai Prakash Tewari……………....……..…....………………..…………. Complainant

VS

Life Insurance Corporation of India…………………………………………...Respondent

COMPLAINT NO: LCK-L-029-1819-0398 Order No. IO/LCK/A/LI/ 0371/2019-20

1. Name & Address of the Complainant Mr. Jai Prakash Tewari

VILL.- Oauha

Post- Belasain(Machhali Sahar)

Jaunpur -222143 (U.P.)

2. Policy No:

Type of Policy

DOC /DOR

DOD

Duration of policy

311743118

Money Back Plan

28.12.2002

N/A

15 years

3. Name of the insured /

Name of the policyholder

Mr. Jai Prakash Tewari

Mr. Jai Prakash Tewari

4. Name of the insurer Life Insurance Corporation of India

5. Date of Repudiation/Rejection N/A

6. Reason for repudiation/Rejection N/A

7. Date of receipt of the Complaint 04.10.2018

8. Nature of complaint S.B. payment due on 2014 not received

9. Amount of Claim 20000/-

10. Date of Partial Settlement -

11. Amount of relief sought S.B. payment wiyh Interest

12. Complaint registered under Rule Rule No.13(1)(a)of Insurance Ombudsman

Rule 2017

13. Date of hearing/place 17.02.2020 at 10.15 A.M.

14. Representation at the hearing

a) For the Complainant Mr. Jai Prakash Tewari

b) For the insurer Mr. Sukhbir Singh

15. Complaint how disposed Allowed

16. Date of Award/Order 17.02.2020

17. Mr. Jai Prakash (Complainant) has filed a complaint against Life Insurance Corporation of

India. (Respondent) alleging Survival Benefit due on 2014 has not been made.

YKS COMPLAINT NO: LCK-L-029-1819-0398 Order No. IO/LCK/A/LI/0371/2019-20

Brief Facts of the Case:-

18. As per the complaint, complainant had taken one policy no. 311743118 for Rs. 50000/-

under T-T 106-15 (12) from LIC of India on 28.12.2002. As per policy condition, he had to get

S.B. payment on 2006, 2010 and 2014 Complainant had not received survival benefits due on

28.12.2014. Hence he approached the L.I.C. Branch for payment of survival benefits due on

28.12.2014 with interest. But he had not received the payment. Policy has already been

matured on 28.12.2017. He got the maturity value. Being aggrieved, the complainant

approached this forum for the redressal of his grievance.

Written reply/SCN:-

19. In SCN/reply dated 14.02.2020, RIC has stated that survival benefits payment of Rs.

20000/-due on Dec-2014 has been made on 30.03.2019 through NEFT and maturity payment

has also been made on 07.012.2017.

20. The complainant has filed a complaint letter, ANNEXYRE VI A along with other relevant

papers and respondent has filed SCN.

21. I have heard the complainant as well as respondent representative and perused the record.

Findings:-

22. The complainant is the policy holder of a plan ‗Jeevan Surabhi‘ with profits. Undisputedly

survival benefits were to be paid to him in 2006 and 2010. Insured received the survival benefits.

But the survival benefits of the 2014 were not paid to him. Then he made a representation but of

no avail. In the SCN the only fact mentioned is that the Branch Office CBO 3, Allahabad has made

the payment of survival benefits due in December, 2014 on 30.03.2019.Maturity amount is also

paid on 07.12.2017. It means that the payment was made with a long delay. LIC has not

compensated the insured for the delayed payment. It is to be looked into by the LIC Officers as to

why delayed payment was made. However interest of the insured has to be protected. Accordingly

he is entitled for the penal interest for the delayed payment. Accordingly complaint is liable to be

allowed.

COMPLAINT NO: LCK-L-029-1819-0398 Order No. IO/LCK/A/LI/ 0371 /2019-20

Order:-

23. Complaint is allowed. Respondents are directed to pay the penal interest at the rate of 8.25

percent per annum at Rs. 20,000/- with an effect from December, 2014 till 30.03.2019 within 30

days. Let a copy of order be sent to the Senior Divisional Manager, Allahabad for information and

necessary action.

24. Let the copy of award be given to both the parties.

Date: 17.02.2020 (Justice Anil Kumar Srivastava)

Place: Lucknow Insurance Ombudsman

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, LUCKNOW

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

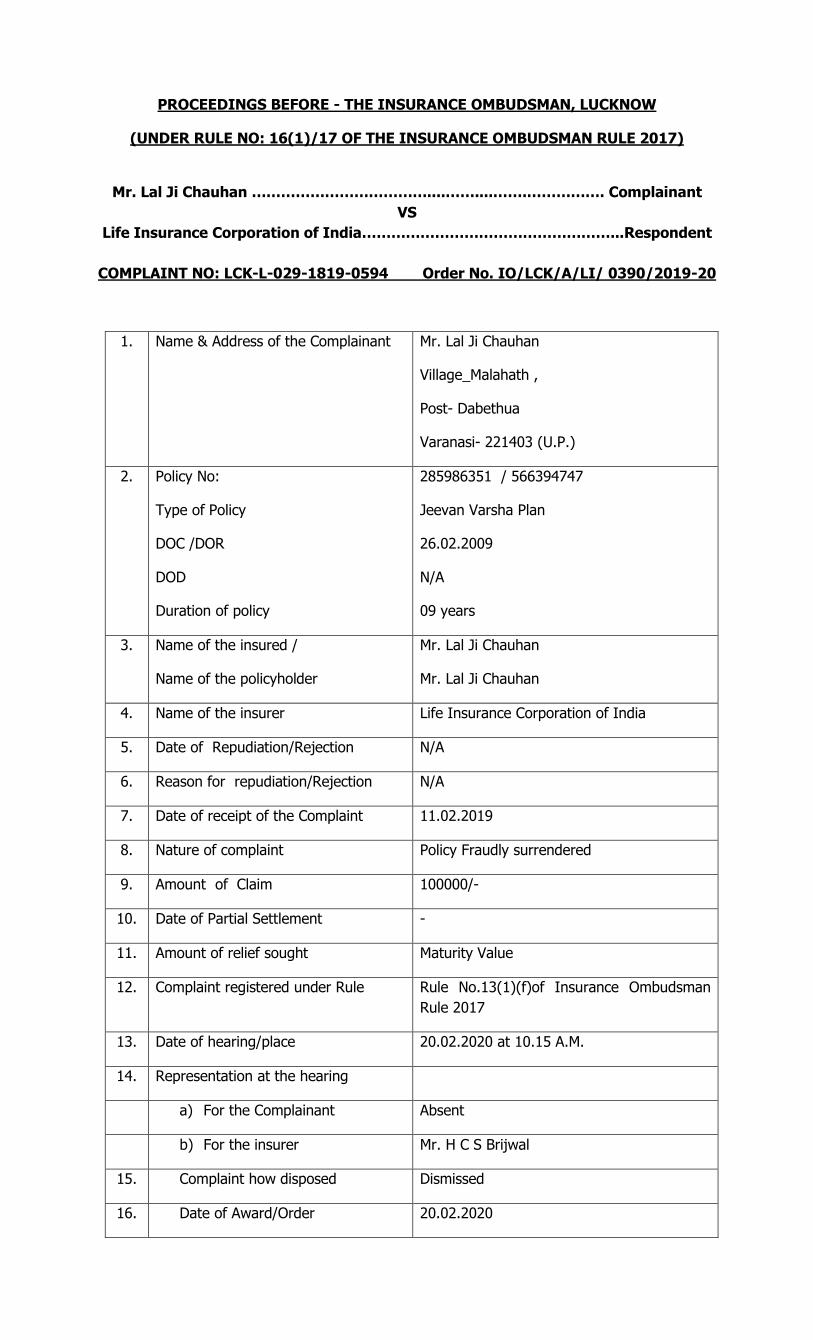

Mr. Lal Ji Chauhan ………………………………....……....…….……………. Complainant

VS

Life Insurance Corporation of India……………………………………………...Respondent

COMPLAINT NO: LCK-L-029-1819-0594 Order No. IO/LCK/A/LI/ 0390/2019-20

1. Name & Address of the Complainant Mr. Lal Ji Chauhan

Village_Malahath ,

Post- Dabethua

Varanasi- 221403 (U.P.)

2. Policy No:

Type of Policy

DOC /DOR

DOD

Duration of policy

285986351 / 566394747

Jeevan Varsha Plan

26.02.2009

N/A

09 years

3. Name of the insured /

Name of the policyholder

Mr. Lal Ji Chauhan

Mr. Lal Ji Chauhan

4. Name of the insurer Life Insurance Corporation of India

5. Date of Repudiation/Rejection N/A

6. Reason for repudiation/Rejection N/A

7. Date of receipt of the Complaint 11.02.2019

8. Nature of complaint Policy Fraudly surrendered

9. Amount of Claim 100000/-

10. Date of Partial Settlement -

11. Amount of relief sought Maturity Value

12. Complaint registered under Rule Rule No.13(1)(f)of Insurance Ombudsman

Rule 2017

13. Date of hearing/place 20.02.2020 at 10.15 A.M.

14. Representation at the hearing

a) For the Complainant Absent

b) For the insurer Mr. H C S Brijwal

15. Complaint how disposed Dismissed

16. Date of Award/Order 20.02.2020

17. Mr. Ram Prakash (Complainant) has filed a complaint against Life Insurance Corporation of

India. (Respondent) alleging that his policy was fraudulently surrendered and amount was

adjusted in third party policy.

YKS

COMPLAINT NO: LCK-L-029-1819-0594 Order No. IO/LCK/A/LI/0390/2019-20

Brief Facts of the Case:-

18. As per the complaint, complainant had taken from LIC of India one policy no. 285986351

under ―Jeevan Varsha plan‖ for Rs. 100000/- with half yearly premium of Rs.8295/- for 09 years

term on 26.02.2009. Policy was due to mature on 26.02.2018, hence he has given Original

Policy bond with other relevant papers to LIC agent Mr. Ramapati Srivastava. But he did not get

the maturity amount. After vigorous follow-up, complainant came to know that the maturity

amount of Rs. 1,22,239/- of this policy has already been transferred in the policy no.

566394747 of Mr. Akhilesh Kumar. Complainant has further stated that he has never given any

request for transfer of his policy money to another policy than how LIC at his own used his

money for new business of another person. Being aggrieved, the complainant approached this

forum for the redressal of his grievance.

19. In SCN/reply dated 11.02.2020, RIC has stated that policy no. 285986351 was matured on

26.02.2018 and maturity amount of Rs.129500/- was due for payment. But policyholder has

given a request letter to recycle this amount and accordingly the amount was adjusted in new

policy no. 566394747 of his son Mr. Akhillesh Kumar. Later on Mr. Akhilesh Kumar has

requested to cancel the policy during Free Look Period. Hence the policy no.566394747 was

cancelled and amount refunded to Mr. Akhilesh Kumar.

20. The complainants have filed a complaint letter along with other relevant papers while

respondent has filed SCN with enclosures. Annexure VI A is also not enclosed.

21. Despite notice complainant is not present. I have heard the respondent representative

and perused the record.

Findings:-

22. Complainant Lal Ji Chauhan was the policy holder of the policy no. 285986351 which got

matured and the maturity amount was recycled for purchase of a new policy no. 566394747 in

the name of his son Akhilesh Kumar on the request of complainant. Subsequently Akhilesh

Kumar exercises his right for cooling off and an amount of Rs. 127601/- was refunded to

COMPLAINT NO: LCK-L-029-1819-0594 Order No. IO/LCK/A/LI/0390/2019-20

to Akhilesh Kumar. Policy was issued in the name of Akhilesh Kumar on his proposal from.

Amount was recycled on the request of Complainant Lal Ji Chauhan. Akhilesh Kumar exercised

his right for withdrawl of amount during cooling off period. Accordingly the complainant is

devoid of any merit and is liable to be dismissed.

Order:-

23. Complaint is dismissed.

24. Let the copy of award be given to both the parties.

Date: 20.02.2020 (Justice Anil Kumar Srivastava)

Place: Lucknow Insurance Ombudsman

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, STATE OF UP

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

Mr. Moti Lal Prajapati.…….…….....…………………………………………. Complainant

V/S

SBI Life Insurance Co. Ltd...……………………………………………..………Respondent

COMPLAINT NO: LCK-L-041-1819-0387 Order No. IO/LCK/A/LI/ 0398/2019-20

1. Name & Address of the Complainant Mr. Moti Lal Prajapati

E-5(A), New Defence Colony

Utethia

Raebareli Road

LDA Colony

Lucknow- 226012

2. Policy No:

Type of Policy

DOC

Duration of policy

56012474203

Flexi Smart Plan

31.03.2012

10 years

3. Name of the insured

Name of the policyholder

Mr. Moti Lal Prajapati

Mr. Moti Lal Prajapati

4. Name of the insurer SBI Life Insurance Co. Ltd

5. Date of Repudiation/Rejection -

6. Reason for repudiation/Rejection -

7. Date of receipt of the Complaint 26.09.2018

8. Nature of complaint Policy wrongly terminated by company

9. Amount of Claim -

10. Date of Partial Settlement -

11. Amount of relief sought Revive the policy

12. Complaint registered under Rule Rule No. 13(1)(f) of Ins. Ombudsman Rule

2017

13. Date of hearing/place 24.02.2020 at 10.15 am

14. Representation at the hearing

a) For the Complainant Mr. Moti Lal Prajapati

b) For the insurer Mohd. Tarique Khan

15. Complaint how disposed Dismissed

16. Date of Award/Order 24.02.2020

17. Mr. Moti Lal Prajapati (Complainant) has filed a complaint against SBI Life Insurance Co.

Ltd. (Respondent) alleging that company has wrongly terminated his policy.

YKS

COMPLAINT NO: LCK-L-041-1819-0387 Order No. IO/LCK/A/LI/ 0398/2019-20

Brief Facts of the Case:-

18. As per the complaint, complainant had taken a policy no.56012474203 with monthly

premium of Rs. 10000/- on 31.03.2012 from SBI Life Insurance Co. Ltd. Claimant has further

stated that the policy was issued under ECS mode and the premiums were deducted from his

account from April-2012 to December 2016 without interruption. In January 2017, complainant

has received a message that premium for the month of Jan-2017 is not deposited due to

insufficient amount in the account. Complainant has informed that this is his salary account and

this month salary was credited on 31.01.2017, but this time cheque was floated on 25.01.2017

and again on 31.01.2017. Claimant was ready to deposit the said premium with interest. Hence

he submitted all required papers for revival, but it was not accepted by the company and they

have refunded Rs. 556381.28 only. Being aggrieved, the complainant approached this forum for

the redressal of his grievance.

Written reply/SCN:-

19. In their SCN/reply dated 24.10.2018, RIC has stated that above policy was issued on the

basis of duly signed proposal form for Insurance from the policyholder .The policy is issued

under ― Flexi Smart Plan.‖ Policy bond was dispatched at the registered address of the policy

holder. Terms and conditions of the policy and the benefits payable under the policy were

clearly mentioned in the policy document issued to the complainant. Premium was deducted

through ECS on 31st of every month. But the premium due on 31.01.2017 was not received due

to insufficient amount in the account. Hence the policy became lapsed and was not revived

within 12 months. Thereafter company has refunded the lapsed terminated amount of Rs.

556351.81 to the complainant on 06.04.2018.

20. The complainant has filed a complaint letter Annexure VI A & correspondence with

respondent and copy of policy document while respondent has filed SCN with enclosures.

21. I have heard the complainant as well as respondent representative and perused the record.

COMPLAINT NO: LCK-L-041-1819-0387 Order No. IO/LCK/A/LI/0398 /2019-20

Findings:-

22. Undisputedly complainant was insured with the respondent with a monthly premium of Rs.

10,000/-. He was paying the premium since March 2012. Premium was to be deducted from his

bank account through ECS Mode. In January, 2017 premium could not be debited from his bank

account due to inefficient funds. Complainant received a message on his mobile. Therefore, the

policy got in a lapse mode. After the lapse of a period of 12 months i.e. January, 2018 the

company refunded the value lapsed terminated amount of Rs. 5,56,351.81/- to the complainant

on 06.04.2018.

23. Complainant submits that he contacted the official of respondent in July, 2017 for revival of

policy but the same was not done. Even the revival proposal was not received. He received the

amount of Rs. 5,56,351.81/- in April, 2018 which was even lower than the actual amount

deposited by him.

24. Undisputedly premium due in January, 2017 was not debited in the account of complainant

due to inefficienct fund. Grace period was 30 days after which policy got lapsed. In the

condition no. 8 of the policy bond revival procedure is given wherein the relevant portion is as

under:-

―You can revive your policy during its revival period of 12 months from the due date of the

earliest premium not paid. Such revivals are subject to all the following:-

8.8 You cannot revive after the revival period.‖

25. When the revival period had lapsed then the surrender value was deposited in the account

of complainant.

26. The complainant did not avail the facility of grace period to deposit the premium amount or

the revival period for the policy. Accordingly the surrender value was paid in accordance with

the terms and conditions of the policy bond which did not require any interference. Complainant

is liable to be dismissed.

COMPLAINT NO: LCK-L-041-1819-0387 Order No. IO/LCK/A/LI/ 0398/2019-20

Order:-

27. Complaint is dismissed.

28. Let the copy of award be given to both the parties.

Date: 24.02.2020 (Justice Anil Kumar Srivastava)

Place: Lucknow Insurance Ombudsman

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, STATE OF UP

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

Mr. Om Prakash Tripathi .…….……..............................………………. Complainant

V/S

SBI Life Insurance Co. Ltd...…………………………………………….………Respondent

COMPLAINT NO: LCK-L-041-1819-0502 Order No. IO/LCK/A/LI/0397/2019-20

1. Name & Address of the Complainant Mr.Om Prakash Tripathi

CH B- 206,

Sunrise Appartment

Mansarovar Yojna, Kanpur Road

Lucknow- 227817

2. Policy No:

Type of Policy

DOC

Duration of policy

32934374003

Group Credit Insurance Plan

29.04.2013

11 years

3. Name of the insured

Name of the policyholder

Mr. Om Prakash Tripathi

Mr. Om Prakash Tripathi

4. Name of the insurer SBI Life Insurance Co. Ltd

5. Date of Repudiation/Rejection -

6. Reason for repudiation/Rejection -

7. Date of receipt of the Complaint 14.12.2018

8. Nature of complaint Refund the Extra premiums deducted

9. Amount of Claim 26020/- with interest

10. Date of Partial Settlement --

11. Amount of relief sought

Refund of Extra premiums.

12. Complaint registered under Rule Rule No. 13(1)(f) of Ins. Ombudsman Rule

2017

13. Date of hearing/place 24.02.2020 at 10.15 am

14. Representation at the hearing

a) For the Complainant Mr. Om Prakash Tripathi

b) For the insurer Mohd. Tarique Khan

15. Complaint how disposed Dismissed

16. Date of Award/Order 24.02.2020

17. Mr. Om Prakash Tripathi (Complainant) has filed a complaint against SBI Life Insurance Co.

Ltd. (Respondent) alleging poor servicing of the company.

YKS

COMPLAINT NO: LCK-L-041-1819-0502 Order No. IO/LCK/A/LI/0397/2019-20

Brief Facts of the Case:-

18. As per the complaint, complainant had taken a housing loan of Rs. 7.00 lakh on 29.04.2013

from SBI Jagdishpur branch. Bank in order to secure the housing loan, issued an insurance

policy (SBI Raksha) with a premium of Rs. 13010/-. Claimant has repaid the total housing loan

on 05.05.2014, but bank continued to debit insurance premium from account till 2016.On

persuasion, Bank has refunded only one premium of Rs.13010/- but excess two premiums has

yet to be refunded. Being aggrieved, the complainant approached this forum for the redressal

of his grievance.

Written reply/SCN:-

19. In their SCN/reply dated 25.01.2018,2018, RIC has stated that above policy was issued on

the basis of duly signed proposal form for Insurance from the policyholder .Renewal premium

deducted as per auto debit mandated form and deactivation request was not received. On

receipt of surrender request, surrender value of Rs.13244/-was paid as per terms and condition

of the Master Policy.

20. The complainant has filed a complaint letter Annexure VI A & correspondence with

respondent and copy of policy document while respondent has filed SCN with enclosures.

21. I have heard the complainant as well as respondent representative and perused the record.

Findings:-

22. Undisputedly complainant had taken a loan of Rs. 7 Lakhs for house building from the SBI,

Jagadishpur Branch on 29.04.2013. As a collateral security loan was insured to the respondent

and the policy no. 32934374003 was issued. As per complainant he deposited the EMI‘s of loan

regularly and paid the remaining amount in lump-sum in 2014. Controversy arose when the

respondent continue to receive the premiums of insurance cover till 2016 when the complainant

gave an application for surrender on 24.10.2016. A surrender value of Rs.13244/- was paid to

the complainant.

COMPLAINT NO: LCK-L-041-1819-0502 Order No. IO/LCK/A/LI/0397 /2019-20

23. Complainant submits that since he has already re-paid the loan he premium debited by the

respondent be refunded.

24. Clause 10.3 of the policy bond related to pre closure of loan which reads as under:-

―Pr-closure of Loan

If a member repays entire loan outstanding before the policy term, any one of the following will

happen:

10.3.1. Member may continue member policy as per the death benefit as mentioned in COI.

10.3.2 Member may surrender member policy and avail surrender benefit as applicable.‖

25. No intimation was provided either by the complainant or by bank to respondents for

surrender of the policy. It is note-worthy that the life of the insured was covered under the

policy bond. As soon as the intimation was received by the respondent, surrender value was

paid in account of the complainant. Complainant himself was the person assured under the

policy bond. It was his duty to inform the respondent about closure of the loan account. Hence

if the complainant himself has not communicated to the respondents regarding closure of the

loan account respondent could not be held responsible in any manner. As soon as they received

the information they refunded the surrender value in accordance with the terms and conditions

of the policy bond which did not require any interference. Accordingly complainant is liable to

be dismissed.

Order:-

26. Complaint is dismissed.

27. Let the copy of award be given to both the parties.

Date: 24.02.2020 (Justice Anil Kumar Srivastava)

Place: Lucknow Insurance Ombudsman

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, LUCKNOW

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

Mr. Salik Ram………………………………...............……....………………. Complainant

VS

Life Insurance Corporation of India……………………………………………...Respondent

COMPLAINT NO: LCK-L-029-1819-0483 Order No. IO/LCK/A/LI/0373/2019-20

1. Name & Address of the Complainant Mr. Salik Ram

S/O Late Ram Kuber

Vill. – Sarai Lili URF Khojapur

Tehsil- Phoolpur

Dist. Allahabad - 212402

2. Policy No:

Type of Policy

DOC /DOR

DOD

Duration of policy

316292151

Jeevan Akshay Plan

11.09.2017

---

-

3. Name of the insured /

Name of the policyholder

Mr. Salik Ram

Mr. Salik Ram

4. Name of the insurer Life Insurance Corporation of India

5. Date of Repudiation/Rejection N/A

6. Reason for repudiation/Rejection N/A

7. Date of receipt of the Complaint 30.11.2018

8. Nature of complaint Surrender of policy

9. Amount of Claim 2000000/-

10. Date of Partial Settlement

11. Amount of relief sought 2000000/-

12. Complaint registered under Rule Rule No.13(1)(f)of Insurance Ombudsman

Rule 2017

13. Date of hearing/place 17.02.2020 at 10.15 A.M.

14. Representation at the hearing

a) For the Complainant Mr. Sanjay Kumar Pal

b) For the insurer Mr. Sukhbir Kumar

15. Complaint how disposed Allowed

16. Date of Award/Order 17.02.2020

17. Mr. Ashok Kumar (Complainant) has filed a complaint against Life Insurance Corporation of

India. (Respondent) alleging mis-selling of policy.

COMPLAINT NO: LCK-L-029-1819-0483 Order No. IO/LCK/A/LI/0373 /2019-20

Brief Facts of the Case:-

18. As per the complaint, complainant had taken one policy no.316292151 on the life under

‗Jeevan Akshay Plan‘ under Single premium mode for Rs.20,00,000/- with option ‗F‘ on

11.09.2007.Claimant has further stated that agent has told him that it is a Pension plan and can

be surrendered any time. Unfortunately his wife became ill. Hence he approached LIC to

surrender his policy but they have informed him that this money can only be refunded after his

death. Being aggrieved, the complainant approached this forum for the redressal of his

grievance.

Written reply/SCN:-

19. In SCN/reply 14.02.2020, RIC has stated that they have not received any request for

surrender of his policy from complainant. Quarterly Pension of Rs. 33825/- is being paid

regularly to complainant from 01.10.2017. Complainant has opted option ‗F‘, hence he can

surrender his policy only in case of critical illness.

20. The complainants have filed a complaint letter along with other relevant papers while

respondent has filed SCN with enclosures. Annexure VI A not received.

21. I have heard the complainant as well as respondent representative and perused the record.

Findings:-

22. Complainant Mr. Salik Ram has taken a single premium policy under ‗LIC Jeevan Akshay- VI‘

on 11.09.2017 with deposit of Rs. 20 Lakhs. Unfortunately he felt ill and got paralytic attack. He

was treated in Priti nursing Home, Allahabad. He applied for the surrender of the policy on

02.11.2018. But the policy was not allowed to be surrendered and a pension of Rs. 33825/- on

quarterly basis is being paid to him. It is a case which shows clearly negligence on the part of

officers of the LIC, Branch, Phoopur as well as Divisional office, Allahabad. A reminder was also

sent by the complainant insured by speed post to Divisional Office, Allahabad on 30.11.2018 but

of no consequence.

COMPLAINT NO: LCK-L-029-1819-0483 Order No. IO/LCK/A/LI/ 0373 /2019-20

23. Even the SCN submitted in this case is nothing but waste paper. In the complaint itself it is

mentioned that insured is suffering from paralysis. Copy of letter written by insured to the

branch office, Phoolpur, Allahabad is also annexed but no reply is given in the SCN regarding

the ailments as well as application moved by the insured complainant rather it is stated in the

SCN that if the complainant would move the application it would be dealt with. It shows that

with ulterior motive the concerned officers of the LIC have withheld the matter. No response

was given to the insured on his application. Why it was done? It is a matter of enquiry to the

undertaken by the Competent Authority but it is a case wherein the punishment should be

awarded against the concerned officers. Today the copy of medical papers was provided by the

insured which are provided to the respondent representative. Complainant is suffering from

paralysis. It is a fit case where respondents should allow the complainant for surrender of his

policy.

24. Having considered the ailment as well as the delay the complaint is allowed with a direction

to the respondent to decide the complainant application for surrender within 15 days.

Order:-

25. Complaint is allowed. Respondent are hereby directed to decide the insured application for

surrender of policy within a period of 15 days after giving an opportunity of hearing to the

insured. If the insured is not satisfied with the decision of the respondent he would be at liberty

to move again in accordance with rules.

26. Let the copy of award be given to both the parties.

Date: 17.02.2020 (Justice Anil Kumar Srivastava)

Place: Lucknow Insurance Ombudsman

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, LUCKNOW

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

Mrs. Varsha Gupta………………..……....…………………………….…………. Complainant

V/S

L.I.C. of India……..…...……………..………..…………………………..………...Respondent

COMPLAINT NO: LCK-L-029-1819-0151 Order No. IO/LCK/A/LI/ 0368 /2019-20

1. Name & Address of the Complainant Mrs. Varsha Gupta

W/O Late Sudhir Gupta

67 , Nyaya Nagar Colony

Jhunsi

Dist.- Allahabad- 211019

2. Policy No:

Type of Policy

DOC /DOR

DOD

Duration of policy

315974677

Jeevan Tarun Plan

31.08.2015

14.09.2016

01y & 13 days

3. Name of the insured

Name of the policyholder

Manaansh Gupta

Sudhir Gupta

4. Name of the insurer L.I.C. of India

5. Date of Repudiation/Rejection 30.11.2017

6. Reason for repudiation/Rejection Illness of Proposer prior to proposal

7. Date of receipt of the Complaint 07.06.2018

8. Nature of complaint P.W.B. Disallowed

9. Amount of Claim 200000/-

10. Date of Partial Settlement -

11. Amount of relief sought Allow P.W.B. under the policy

12. Complaint registered under Rule Rule No.13(1)(b)of Insurance Ombudsman Rule

2017

13. Date of hearing/place 17.02.2020 at 10.15 A.M.

14. Representation at the hearing

c) For the Complainant Mr. Rajendra Prasad Gupta

d) For the insurer Mr. Sukhbir Gupta

15. Complaint how disposed Dismissed

16. Date of Award/Order 17.02.2020

17. Mrs. Varsh Gupta (Complainant) has filed a complaint against LIC of India (Respondent)

alleging that P.W.B. of insured Manaansh Gupta was allowed after her husband‘s death.

YKS

COMPLAINT NO: LCK-L-029-1819-0151 Order No. IO/LCK/A/LI/ 0368 /2019-20

Brief Facts of the Case: -

18. The complainant has stated that her husband had taken a policy no.315974677 on the life

of his son Manaansh Gupta from LIC of India on 28.08.2015 with Premium Waiver Benefits.

Unfortunately her husband expired on14.09.2016. She had submitted all claim papers but L.I.C.

has disallowed P.W.B. under the policy. After that she had also appealed before Zonal Manager

of LIC who also upheld the previous decision. Being aggrieved, the complainant approached this

forum for the redressal of her grievance.

Written reply/SCN:-

19. In SCN/reply dated 13.07.2018, RIC has stated that Proposer Late Sudhir Gupta had taken

a policy no.315974677 on the life of his son with P.W.B on 28.08.2015.Under PWB, premium is

waived after the death of proposer till assured attains the age of 18 years. In this policy

proposer died but claim was repudiated by LIC on the ground of wrong declaration of good

health statement submitted by proposer. As per P.D. Hinduja National Hospital & Medical

Research Center Certificate dated 06.10.2014, proposer was suffering from Cancer. But these

facts were not disclosed in proposal forms. Had this fact been mentioned in proposal form, LIC

would not have accepted the proposal with PWB. Hence P.W.B was disallowed under the policy.

20. The complainants have filed a complaint letter Annexure VI A, along with other relevant

papers while respondent has filed SCN with enclosures.

21. I have heard the complainant as well as respondent representative and perused the record.

Findings:-

22. Deceased life assured had taken the policy on 28.08.2015 while he died on 14.09.2016.

Claim was repudiated on the ground that he was suffering from ailments of lung cancer but this

fact was not disclosed in the proposal form. Accordingly the claim was repudiated and PWB

claim was also repudiated.

COMPLAINT NO: LCK-L-029-1819-0151 Order No. IO/LCK/A/LI/ 0368 /2019-20

23. It is not in dispute that the DLA had taken the policy in the name of his son Mannansh. DLA

expired due to cancer. He was suffering prior to the commencement of policy. Accordingly his

claim was repudiated with PWB repudiation.

24. Having considered the fact and circumstances I am of the view that claim has rightly been

repudiated which need not require any interference. Accordingly complaint is liable to be

dismissed.

Order:-

25. Complaint is dismissed.

26. Let the copy of award be given to both the parties.

Date: 17.02.2020 (Justice Anil Kumar Srivastava)

Place: Lucknow Insurance Ombudsman

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, LUCKNOW

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

Mr. Vijay Yadav………………………………....……………….…..………………. Complainant

VS

Life Insurance Corporation of India…………………………..…………………...Respondent

COMPLAINT NO: LCK-L-029-1819-0626 Order No. IO/LCK/A/LI/0393/2019-20

1. Name & Address of the Complainant Mr. Vijay Yadav

5/141 , Vilpul Khand

Gomti Nagar

Lucknow - 226010

2. Policy No:

Type of Policy

DOC /DOR

DOD

Duration of policy

212579018

Jeevan Suraksha Plan

28.04.2000

N/A

18 Years

3. Name of the insured /

Name of the policyholder

Mr. Vijay Yadav

Mr. Vijay Yadav

4. Name of the insurer Life Insurance Corporation of India

5. Date of Repudiation/Rejection N/A

6. Reason for repudiation/Rejection N/A

7. Date of receipt of the Complaint 28.02.2019

8. Nature of complaint Less amount of Pension

9. Amount of Claim 781/- Per Month since 28.02.2018

10. Date of Partial Settlement Pension of Rs. 2990/- Per Month

11. Amount of relief sought 781/- Per Month since 28.02.2018

12. Complaint registered under Rule Rule No.13(1)(f)of Insurance Ombudsman

Rule 2017

13. Date of hearing/place 20.02.2020 at 10.15 A.M.

14. Representation at the hearing

a) For the Complainant Mr. Vijay Yadav

b) For the insurer Mr. Rishi Misra

15. Complaint how disposed Allowed

16. Date of Award/Order 20.02.2020

17. Mr. Vijay Yadav (Complainant) has filed a complaint against Life Insurance Corporation of

India. (Respondent) alleging that he is getting less pension of Rs.781/- per month since

28.05.2018.

YKS

COMPLAINT NO: LCK-L-029-1819-0626 Order No. IO/LCK/A/LI/ 0393/2019-20

Brief Facts of the Case:- 18. As per the complaint, complainant had taken one policy no.212579018 on 28.04.2000 on

his life under ―Pension Plan‖ and opted option ‗F‘ with monthly mode of pension without

commutation (But in the policy bond, option ‗E‘ is printed). In the option letter provided by LIC,

it is clearly mentioned there that under option ‘F‘, monthly pension would be Rs. 3771/- per

month. But he is getting pension Rs.2990/- per month .Claimant has further stated that in

another case, LIC is paying high pension of Rs. 5731/-per month under policy no. 232130946 to

someone else. Claimant has written many letters to Sr. Divisional Manager LIC Lucknow but he

did not respond to all his notices. Being aggrieved, the complainant approached this forum for

the redressal of his grievance.

Written reply/SCN:-

19. In SCN/reply dated 19.02.2020, RIC has stated that under this policy, proposal date was

30.12.2000 and proposal was completed on 10.01.2001 with date backing as

28.04.2000.Notional cash option was Rs. 3,99,500/-.Annuity amount of Rs. 2990/- is being

released by IPP Cell with the detail calculation as follows—

Date of birth (LA) 01.05.1957

Date if commencement 28.04.2000

Deferred Period 18 YEARS

Age at vesting 60years

Annuity rates per annum 83.60 (Per 1000 of cash option_

Incentive rate under high cash option 89.80

NCO 399500/-

Hence Annuity per month 89.80 x 399500

1000 x 12

= Rs.2990/-

20. The complainants have filed a complaint letter, Annexure VI A along with other relevant

papers while respondent has not filed SCN with enclosures.

21. I have heard the complainant as well as respondent representative and perused the record.

COMPLAINT NO: LCK-L-029-1819-0626 Order No. IO/LCK/A/LI/0393 /2019-20

Findings:-

22. Undisputedly complainant insured had taken ―Jeevan Suraksh (Endowment Funding) policy‖

with guaranteed conditions at the age of 42 years. Date of proposal was 30.12.2000. It was

back dated and the commencement date was 28.04.2000. Date of start of the annuity was

28.04.2018. Notional cash option value was Rs. 3,99,500/- which was also the purchase price.

The instalment was 10037/- per annum with a sum assured Rs. 1,70,000/-. Table no. 122 E

was applicable with a default annuity option ‗E‘, an amount of Rs. 3452/- is mentioned in the

policy bond. In the policy bond there was a provision for exercising the option for annuity which

was to be exercised at least 6 months before the vesting date. All these facts are undisputed

but the whole problem arose when the option was sought from the insured by the branch of

respondent. Initially the option was sought vide an e-mail 14.11.2017 and 21.08.2018. In both

these communications table for exercising the option was attached wherein the option ‗F‘

monthly annuity was shown as Rs. 3771/- per month as annuity. It is further submitted that this

amount was shown in both the letters sent by the respondent hence there is no occasion of any

mistake. Complainant is getting Rs. 2990/- per month only while he should receive Rs. 3771/-

per month.

23. Respondent representative submits that the annuity is in accordance with table and the

chart which is feeded in the master computer. No change in the annuity amount can be made

manually. If any amount other than this amount is mentioned in the letters it a manual mistake

but the master computer system would not accept any other calculation done manually. It is

further submitted that if no response is given by the branch it is mistake on the part of LIC for

which respondent‘s LIC is submitting its apology.

24. In the SCN chart is attached for calculation:-

―ANNUITY RATES PER ANNUM PAYABLE FOR THE ANNUITY OPTION –F- ANNUITY PAYABLE

FOR LIFE WITH RETURN OF PURCHASE PRICE ON DEATH OF THE ANNUITANT FOR CASH

OPTION OF RS. 1000 WHERE DEFEREMNT PERIOD IS 11 YEARS AND ABOVE ONLY‖

According to it at the age of 60 years in monthly annuity the amount would be Rs.83.60/- per

thousand coupled with it an incentive at the rate of Rs. 6.20/- is added as high cash option

COMPLAINT NO: LCK-L-029-1819-0626 Order No. IO/LCK/A/LI/0393 /2019-20

accordingly the total amount comes to Rs. 89.80/- per thousand. On the amount of cash option

that is Rs. 3,99,500/- the annual annuity would be Rs. 2989.58/- or round off Rs. 2990/-.

25. I have also gone through the charts coupled with the policy bond. Option ‗F‘ was exercised

by the complainant. The charges and the calculation submitted by the respondent LIC clearly

shows that the annuity would be Rs. 2990./- .However in the letter sent to the complainant the

amount of monthly annuity is shown as Rs. 3771/- only It is serious mistake. It is recommended

that the Senior Divisional Manager, Lucknow should hold an enquiry for fixing the liability for

the lapse so that such type of lapses may not occur in future.

26. Complainant submits that a certificate of maturity of the policy may be issued to him so that

in future he may not face similar type of problems. Let a copy of this award be sent to Senior

Divisional Manager, LIC, Lucknow for information and necessary action.

Order:-

27. Complaint is disposed off. A certificate of maturity along with the sum which the

complainant or his nominee (as the case may be) would be entitled be provided to the insured

at his registered address within a period of 30 days.

28. Let the copy of award be given to both the parties.

Date: 20.02.2020 (Justice Anil Kumar Srivastava)

Place: Lucknow Insurance Ombudsman

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, STATE OF UP

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

Sri Ram Narayain Misra…………. ………………..……....………………. Complainant

V/S

Life Insurance Corp. of India…………………....…....…………………………Respondent

COMPLAINT NO: LCK-L-029-1819-0574 Order No. IO/LCK/A/LI/0355 /2019-20

1. Name & Address of the Complainant Sri Ram Narayain Misra

Vill. Bhadaipur, Post Dikauli

Distt. Shravasti

2. Policy No:

Type of Policy

Duration of policy/DOC

236648105, 226653904

Wealth Plus

31.03.2010, 08.05.2010

3. Name of the insured

Name of the policyholder

Sri Ram Narayain Misra

Sri Ram Narayain Misra

4. Name of the insurer Life Insurance Corp. of India

5. Date of Repudiation/Rejection -

6. Reason for repudiation/Rejection -

7. Date of receipt of the Complaint 25.01.2019

8. Nature of complaint Surrender Amount less paid

9. Amount of Claim

10. Date of Partial Settlement

11. Amount of relief sought

12. Complaint registered under Rule Rule No. 13(1)(b) of Ins. Ombudsman Rule

2017

13. Date of hearing/place On 14.02.2020 , 10.30 am at Lucknow

14. Representation at the hearing

a) For the Complainant Sri Ram Narayain Misra

b) For the insurer Mr. Heera Singh

15. Complaint how disposed Dismissed

16. Date of Award/Order 14.02.2020

17. Sri Ram Narayain Misra (Complainant) has filed a complaint against SBI Life Insurance

Co. Ltd. (Respondent) alleging that less amount was paid on surrender.

MS

COMPLAINT NO: LCK-L-029-1819-0574 Order No. IO/LCK/A/LI/0355 /2019-20

Brief Facts of the Case:-

18. Sri Ram Narayain Misra has lodged his complaint on 25.01.2019 stating that less amount

was paid by the company Life Ins. Corp. of India on surrender of his policies. The complainant

has stated that he deposited total 3 premium of Rs.60000/= under both the policies. On

surrender of these policies he received only Rs.27,799 /= and Rs. 31,710/=respectively for his

policies.He has further stated that on 12.09.2013 value of his policies was Rs.37,139.49 and

Rs.39,294.65.On surrender he was paid less than 50% of his deposit amount. He received

surrender value amount after two month 26/28 days late so delayed interest was also claimed

by the complainant. The complainant has raised his dis-satisfaction on working method of the

corporation that even branch manager and responsible employee does not know what is to be

done and assured him that correspondence with higher office is continued and arrear with

interest will be paid . He approached RIC`s divisional office but nothing was heard from them.

The complainant was not satisfied. Being aggrieved he has approached this forum for the

redressal of his grievance.

Written reply/SCN:-

19. In their SCN/reply, the RIC has stated that as per policies terms and conditions under policy

nos.236648105 surrender value of Rs.27799/= was paid on 26.06.2018. In Policy

No.236653904 surrender value of Rs.31710/= was paid on 06.08.2018 to the policy holder. At

the time of proposal the age of insured was 65 years and risk premium, other charges and

charges for extended risk cover was deducted as per rules. RTI application and complaint letter

was duly replied by the RIC. Copy of terms and condition of the policy and NAV chart for both

the policies was also enclosed with SCN. As per respondent letter dated 31.01.2020 they have

paid penal interest of Rs. 548/= and Rs. 645/= under both policies due to late payment.

20. The complainant has filed a complaint letter, annexure VI A, correspondence with

respondent while respondent has filed SCN with enclosures.

21. I have heard the complainant as well as respondent representative and perused the record.

COMPLAINT NO: LCK-L-029-1819-0574 Order No. IO/LCK/A/LI/0355 /2019-20

Findings:-

22. Policies were taken under the plan TT 801-08 Wealth Plus. An amount of Rs. 60,000/- was

deposited under both policies but on maturity after 8 years insured received Rs. 27799/- and

Rs. 31710/- only. Main concern of the complainant is that he got less amount.

23. It was the policy under ‗Wealth Plus Plan‘ where the maturity value was paid in accordance

with the terms and conditions of the policy bond. Highest NAV during the last 7 years or on the

date of maturity was to be paid. Charges under the head of administration and mortality were

deducted by the insurer. Hence the maturity amount was paid in accordance with the terms and

conditions of the policy bond. Complaint lacks merit and liable to be dismissed.

Order:-

24. Complaint is dismissed.

25. Let the copies of award be given to both the parties.

Date: 14.02.2020 (Justice Anil Kumar Srivastava)

Place: Lucknow Insurance Ombudsman

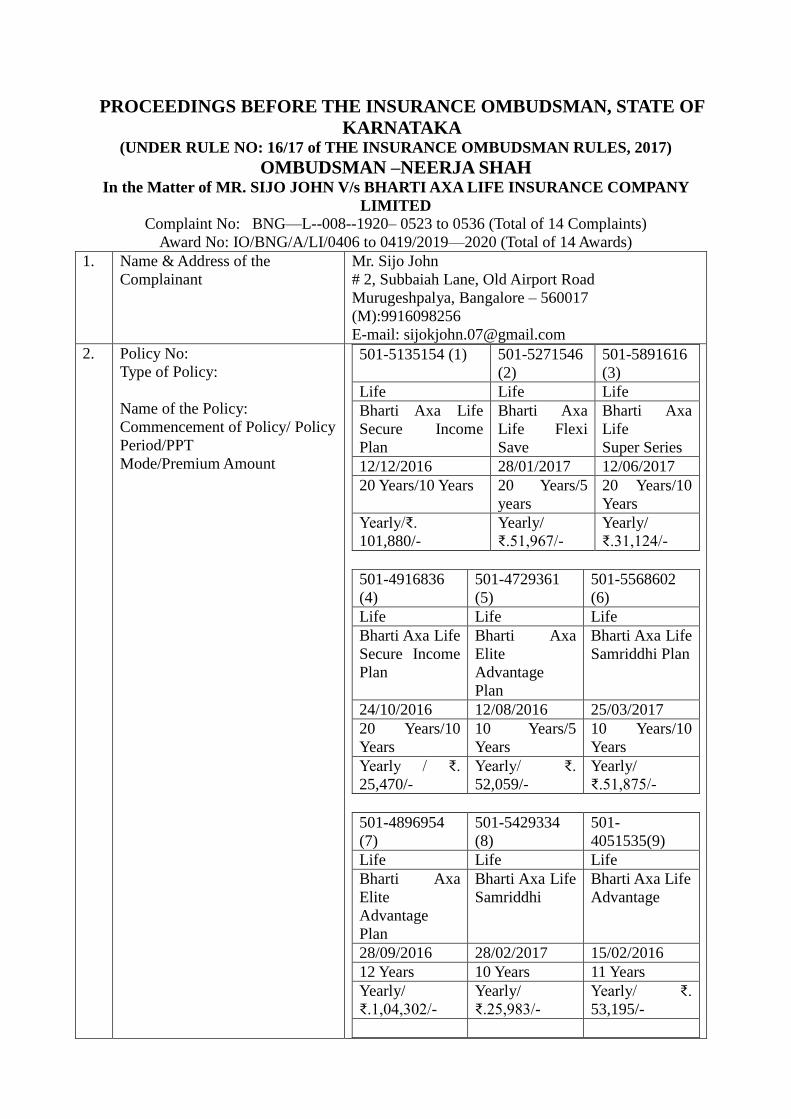

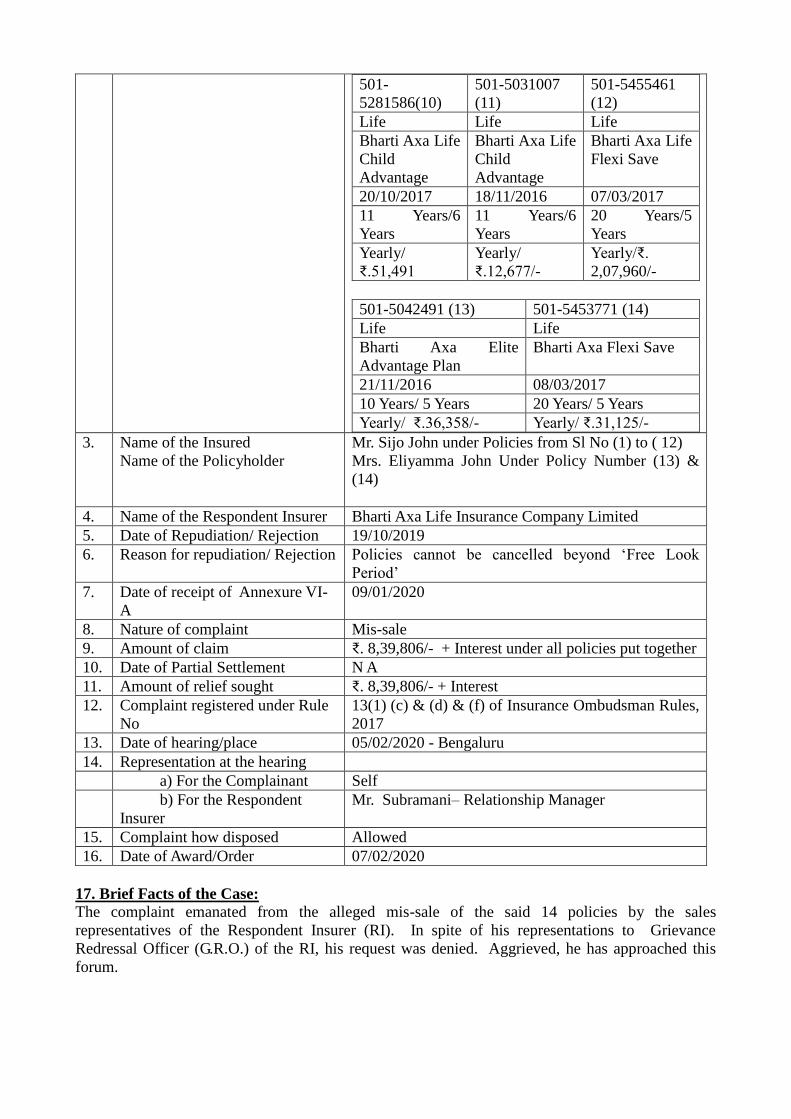

PROCEEDINGS BEFORE

THE INSURANCE OMBUDSMAN, STATE OF WESTERN U.P. AND UTTARAKHAND

UNDER INSURANCE OMBUDSMAN RULES 2017

OMBUDSMAN – SH. C.S.PRASAD

CASE OF MRS. SANJU DEVI V/S LIFE INSURANCE CORPORATION OF INDIA

COMPLAINT REF: NO: NOI-L-029-1920-0236

AWARD NO:

1. Name & Address of the Complainant

Smt. Sanju Devi W/O Sh. Gyan Prakash Pandey P.O. Shiromani Nagar, Tehsil.- Shahbad Hardoi, Uttar Pradesh, 241124

2. Policy No: Type of Policy Duration of policy/Policy period

222842801 Life Plan 20/20

3. Name of the insured Name of the policyholder

Smt. Sanju Devi Smt. Sanju Devi

4. Name of the insurer Life Insurance corporation of India

5. Date of Repudiation NA

6. Reason for repudiation NA

7. Date of receipt of the Complaint 10.7.2019

8. Nature of complaint Non-Receipt of Survival Benefit Payment due on 14.12.2017

9. Amount of Claim Rs.10,000/-

10. Date of Partial Settlement NIL

11. Amount of relief sought Rs.10,000/-

12. Complaint registered under IOB rules

13 (1) (b)

13. Date of hearing/place 13.12.2019 at Noida

14. Representation at the hearing

c) For the Complainant Absent on both days

d) For the insurer Sh. Sunit Kumar, AO

15 Complaint how disposed Award

16 Date of Award/Order 26.2.2020

17)Brief Facts of case:- This complaint is filed by Smt. Sanju Devi against the decision of LIC of India relating to non payment of survival benefit payment under policy no.222842801 issued on her own life.

18)Cause of Complaint:- Non-Receipt of Survival Benefit Payment.

a) Complainants argument :- The complainant stated that she had taken a Money Back policy from LIC of India on 14.12.2007 with policy term of 20 years. She further stated that she has not received second survival benefit payment which was due on 14.12.2017. The complainant had written to the insurer and had visited Branch office but till date she had not received the due payment.

b)Insurers’ argument:- The insurer stated that Policy no. 222842801 was issued on the life of Smt. Sanju Devi under plan and term 75/20 on 14.12.2007. As per terms and conditions of policy 2nd survival benefit payment which was due on 14.12.2017 has been paid through NEFT in her bank account A/C no. 025110410005807 with Avadh Gramin bank. The complainant had submitted NEFT mandate alongwith copy of pass book of Avadh Gramin Bank to the insurer on 18.12.2012 and survival benefit payment has been made to the mentioned account.When the complainant approached insurer with correct account number , the insurer wrote a letter to the Bank manager on 7.4.2018 for recovery of amount from the concerned account holder and credit the amount to the complainants account.

19) Reason for Registration of Complaint: Scope of the Insurance Ombudsman Rules 2017.