PROCEEDINGS BEFORE THE INSURANCE OMBUDSMAN ...

253

PROCEEDINGS BEFORE THE INSURANCE OMBUDSMAN, AHMEDABAD State of Gujarat and Union Territories of Dadra & Nagar Haveli, Daman and Diu (Under Rule No: 16 / 17 of The Insurance Ombudsman Rules, 2017) Complaint of: - Mr. Khushal M. Thaker Vs. The New India Assurance Co. Ltd. Complaint No.: AHD-G-049-2122-0055 1 Name & Address of the Complainant Mr. Khushal Thaker 452, Nandbhoomi Appt., Opp. T. N. Rao College, Kerala Park Main Road, Off University Road, Rajkot-360007 Policy No: Type of Policy: Policy period: Sum Insured (IDV) 13130031190300004331 Private Car Enhancement Cover Policy 30.04.2019 to 29.04.2020 Rs.6,50,000/- 3 Name of the insured Name of the policy holder Date of accident Mr. Khushal Thaker Mr. Khushal Thaker 30.07.2019 4 Name of the Insurer The New India Assurance Co. Ltd. 5 Reason for partial settlement As per policy terms and conditions 6 Date of receipt of complaint 19.03.2021 7 Nature of complaint Partial Settlement of Claim 8 Amount of claim Rs.14,52,204/- 9 Date of Consent 24.01.2022 10 Date of receipt of SCN 13.09.2021 11 Amount of relief sought Rs.2,50,000/- 12 Complaint registered under Rule No. Rule 13 (1) (b) of I. O. Rules, 2017 13 Date of hearing / mode 24.02.2022 / Online hearing 14 Representation at the hearing: For the Complainant: For the Insurer: Mr. Khushal Thaker Ms. Varsha Mullick 15 Complaint how disposed Award

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of PROCEEDINGS BEFORE THE INSURANCE OMBUDSMAN ...

PROCEEDINGS BEFORE THE INSURANCE OMBUDSMAN, AHMEDABAD

State of Gujarat and Union Territories of Dadra & Nagar Haveli, Daman and Diu

(Under Rule No: 16 / 17 of The Insurance Ombudsman Rules, 2017)

Complaint of: - Mr. Khushal M. Thaker Vs. The New India Assurance Co. Ltd.

Complaint No.: AHD-G-049-2122-0055

1 Name & Address of the Complainant Mr. Khushal Thaker

452, Nandbhoomi Appt., Opp. T. N. Rao

College, Kerala Park Main Road, Off

University Road, Rajkot-360007

Policy No:

Type of Policy:

Policy period:

Sum Insured (IDV)

13130031190300004331

Private Car Enhancement Cover Policy

30.04.2019 to 29.04.2020

Rs.6,50,000/-

3 Name of the insured

Name of the policy holder

Date of accident

Mr. Khushal Thaker

Mr. Khushal Thaker

30.07.2019

4 Name of the Insurer The New India Assurance Co. Ltd.

5 Reason for partial settlement As per policy terms and conditions

6 Date of receipt of complaint 19.03.2021

7 Nature of complaint Partial Settlement of Claim

8 Amount of claim Rs.14,52,204/-

9 Date of Consent 24.01.2022

10 Date of receipt of SCN 13.09.2021

11 Amount of relief sought Rs.2,50,000/-

12 Complaint registered under Rule No. Rule 13 (1) (b) of I. O. Rules, 2017

13 Date of hearing / mode 24.02.2022 / Online hearing

14 Representation at the

hearing:

For the Complainant:

For the Insurer:

Mr. Khushal Thaker

Ms. Varsha Mullick

15 Complaint how disposed Award

16 Date of Award 24.02.2022

17. Brief History:

The Complainant, Mr. Khushal Thaker’s Tata Nexon car, Reg. No.GJ-32-B-5376, was covered

under the Private Car Enhancement Cover Policy, No. 13130031190300004331 for the period

of 30.04.2019 to 29.04.2020 with IDV of Rs.6,50,000/- issued by The New India Assurance

Co. Ltd. His car met with an accident on 30.07.2019 for which the complainant put up a claim

for Rs.14,52,204/- which was settled by the Company for Rs.4,11,000/- on total loss / Net of

Salvage with RC basis, after deducting a value of Salvage amounting to Rs.2,38,000/- and

Rs.1,000/- as excess by construing the claim as total loss claim. However, unsatisfied with the

decision of the Company, he represented to the Company against the partial settlement, but

of no avail. Aggrieved by the same, the complainant approached this forum.

18. Cause of Complaint:

(A) Complainant’s argument:

The complainant submitted that his car met with an accident on 30.07.2019 and he

immediately intimated the intermediary agent. He stated that the claim was settled by the

respondent insurer for the amount of Rs.6,50,000/-, after a deduction of Rs.2,38,000/- for the

salvage and Rs.1000/- for an excess. He submitted that he got only Rs.65,000/- for the

salvage amount and he should be in receipt of the remaining amount from the respondent

insurer. He submitted that his claim is genuine and should be paid to him in full. He has urged

the Forum to help him in getting his balance claim.

(B) Insurer’s Argument:

The representative of the respondent submitted that, the claim was settled for Rs 4,11,000/-

on Net of Salvage with RC basis, after receiving Insured’s consent, to the financier. The

Insured has retained the salvage with RC.

It was a total loss case as the repair liability exceeds IDV. As per survey report of M/s A. S.

Rathod dated 25.09.2019, salvage of the damaged vehicle can be sold for about Rs

2,38,000/- in as & where condition with RC book subject to immediate disposal (supported by

online quotation attached) and excess was Rs 1,000/-.

Hence the settlement is proper and it is done having taken the insured’s consent.

The grievance regarding the salvage disposal was raised much after receiving the payment,

hence it is an afterthought.

In view of the same, she has prayed before the forum to dismiss the case without any relief to

the insured.

19. Result of hearing with both parties (Observation & Conclusion):

Based on the submission of both the parties and the materials made available to this Forum,

the following points have emerged which are pertinent to decide the case:-

1) The Complainant, Mr. Khushal Thaker’s Tata Nexon car, Reg. No.GJ-32-B-5376, was

covered under the Private Car Enhancement Cover Policy, No.

13130031190300004331 for the period of 30.04.2019 to 29.04.2020 with IDV of

Rs.6,50,000/- issued by The New India Assurance Co. Ltd.

2) His car met with an accident on 30.07.2019 for which the complainant put up a claim

for Rs.14,52,204/- which was settled by the Company for Rs.4,11,000/- on total loss/

Net of Salvage with RC basis, after deducting a value of Salvage amounting to

Rs.2,38,000/- and Rs.1,000/- as excess by considering the claim as total loss claim.

3) It was a total loss case as the repair liability exceeds IDV. As per survey report of M/s

A. S. Rathod dated 25.09.2019, salvage of the damaged vehicle can be sold for about

Rs 2,38,000/- in as & where condition with RC book subject to immediate disposal and

excess was Rs 1,000/-.

4) The forum also took a note of the insured’s consent dated 22.05.2020, whereby he

accepted the settlement for Rs.4,11,000/- on Net of Salvage with RC basis, after

deduction of Salvage amounting to Rs.2,38,000/-. In view of the same, without

going into the merit of the case, the forum finds no infirmity in the decision taken

by the respondent insurer to settle the claim.

5) The deduction of Rs.1,000/- towards excess is in order.

In view of the forgoing facts, the decision of the respondent insurance company to

repudiate the claim is justified, hence the complaint stands dismissed.

20. If the decision of the Forum is not acceptable to the Complainant, he/she is

at liberty to approach any other Forum/Court as per law of the land against the

respondent insurer.

Dated at Ahmedabad on 24th day of February, 2022.

(KULDIP SINGH)

INSURANCE OMBUDSMAN

AWARD

Taking into account the facts & circumstances of the case and the submissions made,

the complaint stands dismissed with no relief to the Insured.

APROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, STATE OF M.P. & C.G.

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

OMBUDSMAN – RAVINDRA MOHAN SINGH

Mr. Ramesh Kumar Patel……..………..…………………..……………….………….…Complainant V/s

Bharti Axa General Insurance Company ..……………….…….……...…………...Respondent

COMPLAINT NO: BHP-G-007-2122-0139 ORDER NO: IO/BHP/A/GI/ 0022 /2021-2022

• Mr. Ramesh Kumar Patel (Complainant) has filed a complaint against Bharti Axa General

Insurance Company (Respondent) alleging Non Settlement of claim by the respondent.

• Brief facts of the Case –

1. Name & Address of the Complainant

Mr. Ramesh Kumar Patel B-Star 305 Royal Villas Ashima Mall Bhopal

2. Policy No: Type of Policy Duration of policy/Policy period

P13/12900497/C3/10/004948 Private Car Policy 18.10.2018 to 17.10.2019

3. Name of the insured Name of the policyholder

Mr. Lalit Patel Mr. Lalit Patel

4. Name of the insurer Bharti Axa General Insurance Company

5. Date of Repudiation/ Rejection 10.02.2021

6. Reason for Repudiation/ Rejection

Non Settlement of claim due to change of Driver

7. Date of receipt of the Complaint 12.04.2021 & 25.01.2022

8. Nature of complaint Repudiation of death claim in Car accident

9. Amount of Claim 24.31 Lakhs

10. Date of Partial Settlement --

11. Amount of relief sought Rs. 7,76,288/- + Charges

12. Complaint registered under Rule Rule No. 13(1)(b) Ins. Ombudsman Rule 2017

13. Date of hearing/place 01.02.2022 at Bhopal

14. Representation at the hearing

a) For the Complainant Mr. Ramesh Kumar Patel over Go To Meet App

b) For the insurer Mr. Ashay Mahajan, Manager over Go To Meet App

15. Complaint how disposed Dismissed and closed

16. Date of Award/Order 01.02.2022

• Contention of the complainant –The Complainant has stated that on 06.08.2019

Policy holder / his brother late Shri Lalit Patel was driving the vehicle and another

person Manish Shukla was sitting beside him, unfortunately accident took place and

Lalit Shukla lost his life. Person with him Mr. Manish Shukla lodged the FIR. According

to FIR Late Lalit Patel was driving the car. One couple on motorcycle came suddenly

on the way and to save them his car was toppled down in valley. The damaged Car

was sent to Police Station. After taking possession through court the vehicle was taken

to repairer and claim was lodged by nominee (complainant) Mr. Ramesh Kumar Patel.

His claim was rejected due to reason that (1) as per claim intimation / claim form the

vehicle was driven by Mr. Lalit Patel and as per respondent’s investigation finding

vehicle was driven by Mr. Manish Shukla. (2) the car hit with pole. Then he

represented that his claim was rejected on the basis of faulty presumptions only. But

respondent has not resolved the grievance nor settled the claim.

• Contention of respondent-The respondent in their SCN have stated that the

complainant had obtained a motor insurance policy for his vehicle no. MP-20CH-6994

.The Insured met an accident on 6th August, 2019 and thereafter lodged a claim with

us. We deputed a surveyor for assessment of damages and an investigator to ascertain

the veracity of the claim. The surveyor submitted his assessment report and assessed

the said damage to ₹ 3,75,000. The Investigator submitted his report wherein a lot of

enumerated discrepancies were found i,e (1) Claimant & Late Insured’s friend did not

confirm the spot of accident. (2) Inward/Outward details and gate pass was denied by

the Workshop. (3) Name and age of Nominee and Claimant are found to be different.

(3) Body of the Insured was found outside the IV; not possible if the Insured would

have been using the Safety Restraint System (seat belt) making it violation of MV Act

as well as negligence under our Policy terms and condition (4) Insured Vehicle was

driven in a rash & negligent manner (also violative of Law & Policy terms and

condition) (5) Manish Shukla (co-passenger) refused to meet the fact finder and did

not coordinate in the fact finding. Given the findings of the Investigator, the claim of

the Insured stands repudiated on the grounds of concealment/misrepresentation of

facts, guilty of negligence and violation of prevailing laws among other. The claim of

the Insured doesn’t falls Policy Terms & Condition. The description of the accident

and the damages as well as the death of the Insured were not correlating.

• The Complainant has filed complaint letter, Annex. VIA and correspondence with

respondent while respondent have filed SCN with enclosures.

• I have heard both parties over Go To Meet App at length and perused paper filed on

behalf of the complainant as well as the Insurance Company.

• Observation and Conclusion :

The case was re-registered in the light of earlier Hearing / Order dated 04.10.2021 of

Ombudsman Lucknow. Wherein, the complainant was directed to file affidavit within 10

days and respondent to settle the PA claim within 30 days and for OD claim, complainant

to submit the desired documents and respondent to settle the claim within 30 days.

Further complainant would be at liberty if he is not satisfied.

In compliance of that respondent has, reported to have, settled the PA claim and

consented to settle the OD claim accordingly to repair bill as per policy terms and

conditions. The complainant approached, again, to this forum and submitted letter dated

09.12.2021, mail dated 25.01.2022. He argued during hearing that Company is liable to

get repaired his vehicle from authorized dealer using genuine auto parts and pay for

parking charges and entire transport charges.

The respondent in his turn argued that Insurance Company does not do any repairing job

of damaged vehicle. It is insured who has to get repaired the vehicle and submit the bills

for settlement of the claim.

I am of the view that Insurance Company is not liable to repair any damaged vehicle itself

as per contract. In compliance of order dated 04.10.2021 he has already consented for

settlement to the Company, on submission of bills / Cash memo, as per policy terms and

condition. The vehicle owner is not expected to keep repairing on hold / pending for

indefinite time and wait for disputes to get resolved. Nothing on the record is available

which shows that respondent has obstructed in repairing the vehicle at any point of time,

infact during the hearing the respondent have confirmed to advance 60% of the claim

amount in order to get the vehicle repaired. During the hearing the complainant has also

claimed for transport and parking charges. In this also I don’t find any substance. The

respondent cannot be held liable if authorized dealer is not available as on date.

The order of earlier Ombudsman, issued earlier, dated 04.10.2021 is just and proper and

need no intervention. Hence the matter is being dismissed and closed with the direction

to complainant to get repaired the vehicle and submit the bills / Cash memos and to

respondent it settle the claim as per policy terms and condition with 30 days of receipt of

documents.

•

• Let copies of the order be given to both the parties.

Place :- Bhopal M.P. ( RAVINDRA MOHAN SINGH )

Date:-21.01.2022 INSURANCE OMBUDSMAN

………………………………………………………………………………………………………………………………………………

…………..

OMBUDSMAN – RAVINDRA MOHAN SINGH

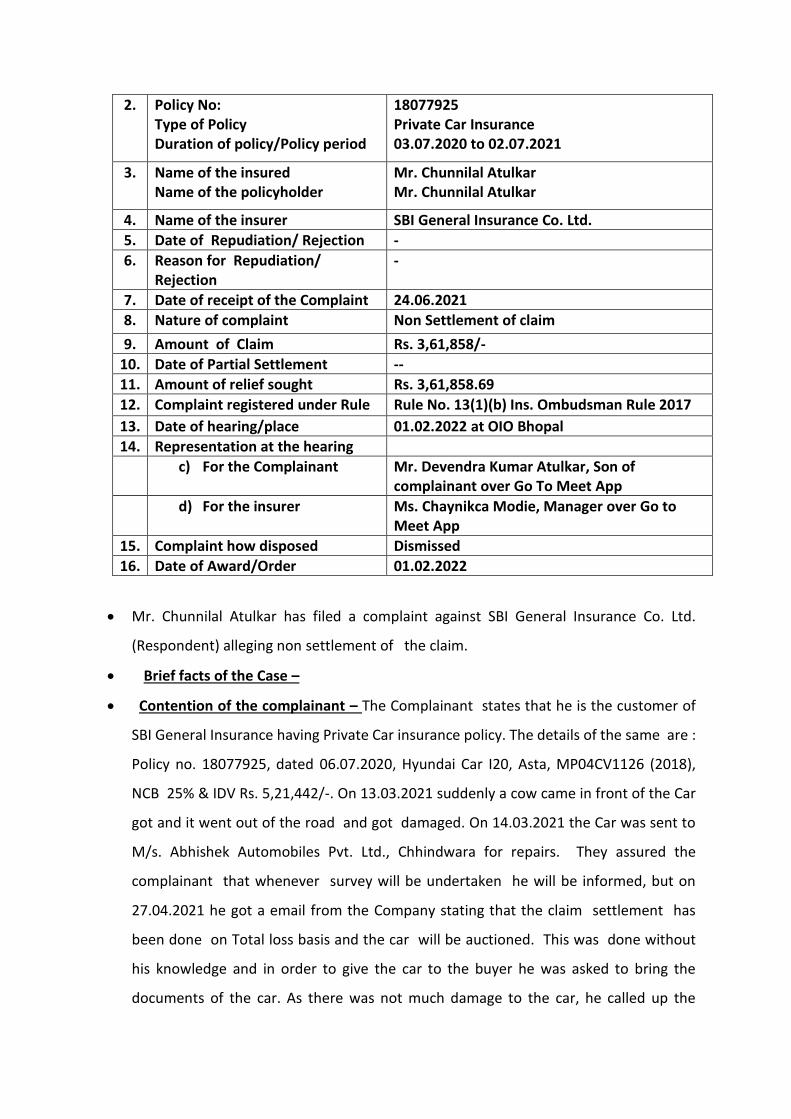

Mr. Chunnilal Atulkar …………..……………...……………..……………….…………………...…Complainant V/s SBI General Insurance Co. Ltd. ……………….. .……………….…….……...………….………...Respondent

COMPLAINT NO: BHP-G-040-2122-0024 ORDER NO: /BHP/A/GI/0008 /2021-2122

AWARD

The order dated 04.10.2021 by the earlier Ombudsman needs no intervention hence the

complainant is directed to get repaired the vehicle and submit the bills / Cash memos to

the respondent and respondent to settle the claim as per policy terms and condition

with 30 days of receipt of documents

1. Name & Address of the Complainant

Mr. Chunnilal Atulkar SUPER E- 1207, MPPGCL Colony, Betul - 460447

• Mr. Chunnilal Atulkar has filed a complaint against SBI General Insurance Co. Ltd.

(Respondent) alleging non settlement of the claim.

• Brief facts of the Case –

• Contention of the complainant – The Complainant states that he is the customer of

SBI General Insurance having Private Car insurance policy. The details of the same are :

Policy no. 18077925, dated 06.07.2020, Hyundai Car I20, Asta, MP04CV1126 (2018),

NCB 25% & IDV Rs. 5,21,442/-. On 13.03.2021 suddenly a cow came in front of the Car

got and it went out of the road and got damaged. On 14.03.2021 the Car was sent to

M/s. Abhishek Automobiles Pvt. Ltd., Chhindwara for repairs. They assured the

complainant that whenever survey will be undertaken he will be informed, but on

27.04.2021 he got a email from the Company stating that the claim settlement has

been done on Total loss basis and the car will be auctioned. This was done without

his knowledge and in order to give the car to the buyer he was asked to bring the

documents of the car. As there was not much damage to the car, he called up the

2. Policy No: Type of Policy Duration of policy/Policy period

18077925 Private Car Insurance 03.07.2020 to 02.07.2021

3. Name of the insured Name of the policyholder

Mr. Chunnilal Atulkar Mr. Chunnilal Atulkar

4. Name of the insurer SBI General Insurance Co. Ltd.

5. Date of Repudiation/ Rejection -

6. Reason for Repudiation/ Rejection

-

7. Date of receipt of the Complaint 24.06.2021

8. Nature of complaint Non Settlement of claim

9. Amount of Claim Rs. 3,61,858/-

10. Date of Partial Settlement --

11. Amount of relief sought Rs. 3,61,858.69

12. Complaint registered under Rule Rule No. 13(1)(b) Ins. Ombudsman Rule 2017

13. Date of hearing/place 01.02.2022 at OIO Bhopal

14. Representation at the hearing

c) For the Complainant Mr. Devendra Kumar Atulkar, Son of complainant over Go To Meet App

d) For the insurer Ms. Chaynikca Modie, Manager over Go to Meet App

15. Complaint how disposed Dismissed

16. Date of Award/Order 01.02.2022

insurance Company and the workshop he demanded the estimate but both of them did

not provide the details but stated that it is now lock down time. The vehicle was jointly

insptected with the representative of M/s. Abhishek Hyundai the repairing cost with tax

came to Rs. 3,61,858/-. The complainant asks how it is then Total Loss. The earlier

estimate done by the Insurance Company and M/s. Abhisheh Hyundai was for Rs.

6,93,266.59. It was due to inclusion of the full assembly instead of individual parts. On

26.05.2021 he received the estimate of Rs.3,61,858/-. On 28.05.2021 he took up the

matter with the Insurance Co. and on 01.06.2021 he also informed the surveyor. But no

satisfactory reply was given. Hence on 03.06.2021 he informed the grievance officer of

the Insurance Company. A resurvey was done on 11.06.2021 jointly by surveyor and

Abhishek Hyundai ‘s representative. As per resurvey the estimate of the parts + labour

cost came to Rs. 2.8 lakhs only. This shows their collusion for declaring the vehicle as

total loss. Due to this reason the SBI team (Surveyor) & M/s. Abhishek Hyundai

representative did not give estimate. He also asked for the copy of joint survey dated

11.06.2021, but the same was not given to him. Again through a mal dated 12.06.2021

the copy of estimate was asked but the same was again not given. On 21.06.2021 the

GRO sent a mail stating that his claim will be settled on total loss basis. There is not

much damage to his car and can be repaired, But declaring it as total loss and being

auctioned is for avoiding paying money to repairer.

• Contention of respondent- The respondent in their SCN have stated that Complaint has

been lodged by Complainant with foremost prayer to allow repair mode of

indemnification. Claim of the complainant has already been assessed through an IRDA

Licensed independent Surveyor having prescribed skillset and knowledge. Further, as

per the findings of the Surveyor vis-a-vis policy terms and conditions, it was observed

that the Loss assessed is 104.69% higher than the IDV of the vehicle and thus the

Company as per terms and conditions of the policy has offered to settle the claim

through a Constructive Total Loss mode of settlement. Alternatively, the Complainant

was also offered the option to retain the vehicle in the same wreck value as received in

Online Auction and receive the rest of the offered settlement amount. However despite

receiving the Offer of settlement and its repeated reminders, the complainant did not

agree with either of the option given or shared any of the required documents till date.

Hence, the said claim is pending for lack of cooperation from Insured. The same is

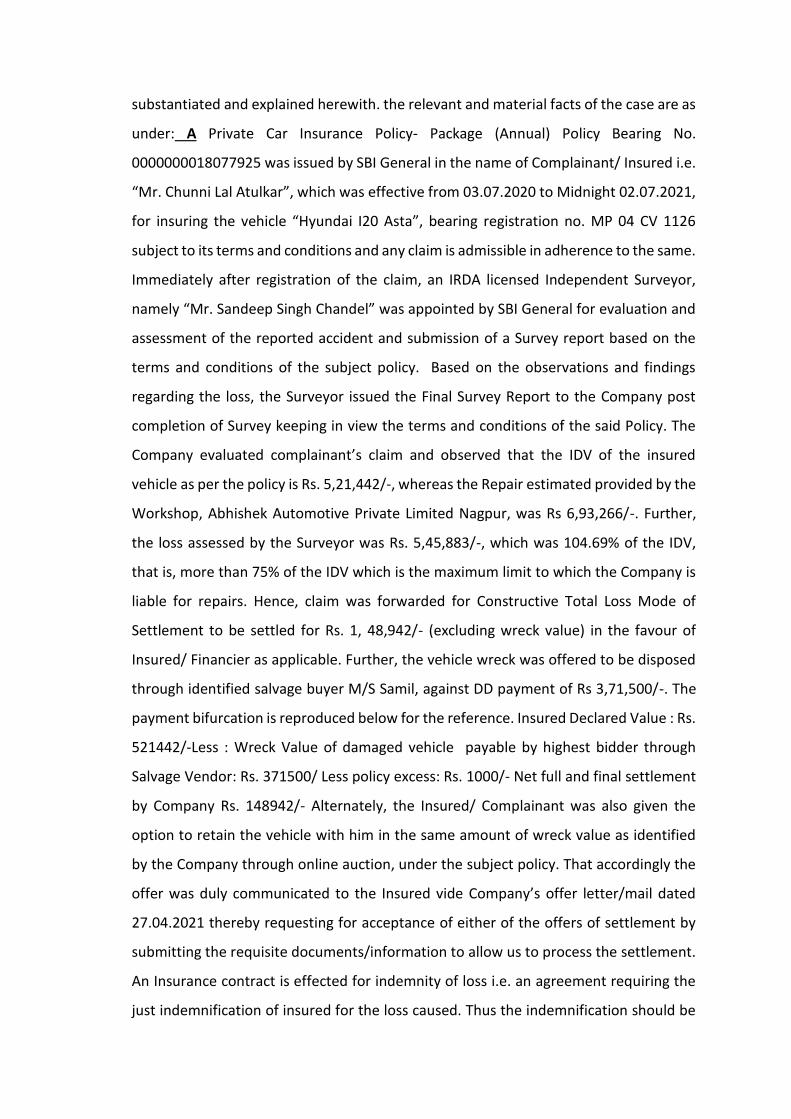

substantiated and explained herewith. the relevant and material facts of the case are as

under: A Private Car Insurance Policy- Package (Annual) Policy Bearing No.

0000000018077925 was issued by SBI General in the name of Complainant/ Insured i.e.

“Mr. Chunni Lal Atulkar”, which was effective from 03.07.2020 to Midnight 02.07.2021,

for insuring the vehicle “Hyundai I20 Asta”, bearing registration no. MP 04 CV 1126

subject to its terms and conditions and any claim is admissible in adherence to the same.

Immediately after registration of the claim, an IRDA licensed Independent Surveyor,

namely “Mr. Sandeep Singh Chandel” was appointed by SBI General for evaluation and

assessment of the reported accident and submission of a Survey report based on the

terms and conditions of the subject policy. Based on the observations and findings

regarding the loss, the Surveyor issued the Final Survey Report to the Company post

completion of Survey keeping in view the terms and conditions of the said Policy. The

Company evaluated complainant’s claim and observed that the IDV of the insured

vehicle as per the policy is Rs. 5,21,442/-, whereas the Repair estimated provided by the

Workshop, Abhishek Automotive Private Limited Nagpur, was Rs 6,93,266/-. Further,

the loss assessed by the Surveyor was Rs. 5,45,883/-, which was 104.69% of the IDV,

that is, more than 75% of the IDV which is the maximum limit to which the Company is

liable for repairs. Hence, claim was forwarded for Constructive Total Loss Mode of

Settlement to be settled for Rs. 1, 48,942/- (excluding wreck value) in the favour of

Insured/ Financier as applicable. Further, the vehicle wreck was offered to be disposed

through identified salvage buyer M/S Samil, against DD payment of Rs 3,71,500/-. The

payment bifurcation is reproduced below for the reference. Insured Declared Value : Rs.

521442/-Less : Wreck Value of damaged vehicle payable by highest bidder through

Salvage Vendor: Rs. 371500/ Less policy excess: Rs. 1000/- Net full and final settlement

by Company Rs. 148942/- Alternately, the Insured/ Complainant was also given the

option to retain the vehicle with him in the same amount of wreck value as identified

by the Company through online auction, under the subject policy. That accordingly the

offer was duly communicated to the Insured vide Company’s offer letter/mail dated

27.04.2021 thereby requesting for acceptance of either of the offers of settlement by

submitting the requisite documents/information to allow us to process the settlement.

An Insurance contract is effected for indemnity of loss i.e. an agreement requiring the

just indemnification of insured for the loss caused. Thus the indemnification should be

appropriately done to bar any unjust enrichment or gratuitous profit beyond the pale of

indemnity. It is further submitted that it is the prerogative of the Company to decide

whether to repair, replace or settle the claim on total loss basis under Condition 3 of the

subject Policy and the offer of settlement made to the Complainant was done in

conformity with all the aforesaid principles and policy condition 3 in order to accurately

indemnify him of his loss. In view of the above, the relevant extracts of the policy are

reproduced hereunder for ready reference: SUM INSURED- INSURED’S DECLARED

VALUE (IDV): The insured vehicle shall be treated as a CTL if the aggregate cost of

retrieval and / or repair of the vehicle, subject to terms and conditions of the Policy,

exceeds 75% of the IDV of the vehicle. CONDITION: 3. The Company may at its own

option repair reinstate or replace the vehicle or part thereof and/or its accessories or

may pay in cash the amount of the loss or damage and the liability of the Company shall

not exceed: (a) For total loss / constructive total loss of the vehicle - the Insured's

Declared Value (IDV) of the vehicle (including accessories thereon) as specified in the

Schedule less the value of the wreck. (b) For partial losses, i.e. losses other than Total

Loss/Constructive Total Loss of the vehicle - actual and reasonable costs of repair and/or

replacement of parts lost/damaged subject to depreciation as per limits specified.

However the insured did not give his consent to either of the modes for settlement, and

maintained that the damage to his car is less than the loss assessed by the Surveyor.

That in line with the Company’s policy of fair, just and transparent assessment of claims,

the Company scheduled another Survey with the workshop manager and Surveyor, in

the presence of the Insured/ Complainant. Further, in the said joint inspection, the

Surveyor and Workshop manager had explained the loss on damaged parts to the

insured. It is also relevant to mention here that the Survey Report was not shared with

the Insured/Complainant as the Company did not receive any requirement from the

Insured for the same. Often when a claim is filed, there could be differences between

what an insurer and the insured believe the actual loss in a particular situation to be.

Hence, Insurance Regulatory and Development Authority (IRDA) under Section 64UM of

The Insurance Act, 1938, authorizes independent entities/individuals (called Surveyor &

Loss Assessors) to act as a professional link between the insured and the insurer. A

surveyor and loss assessor for motor insurance possess mandatory qualifications in

mechanical or automobile engineering. Further, the surveyor and loss assessors

evaluate the damage and submit their report which is independent of the insurer and

the insured’s view. Accordingly, the aforesaid claim was approved as per the surveyor’s

independent and professional view vide the Surveyor’s report submitted to the

Company. Thereafter, the complainant was again reminded about the aforesaid offer of

claim settlement and required documents vide the Company’s letters/Mails dated

17.06.2021 and 25.06.2021.By denying each and every allegation as mentioned in the

said complaint under the present reply (SCN), SBI General states that the contents of

the complaint, wherever admitted, are a matter of record. Further, the said settlement

offer was just, lawful as per the policy terms and conditions, It is thus submitted that

Complainant’s Ombudsman Complaint is misconceived and is liable to be dismissed.

• The Complainant has filed complaint letter, Annex. VIA and correspondence with

respondent while respondent have filed SCN with enclosures.

• I have heard both parties at length and perused paper filed on behalf of the complainant

as

well as the Insurance Company.

• Observation and Conclusion : The case was re-registered in the light of earlier Hearing

/ Order dated 06.10.2021 of Hon’ble Ombudsman. Wherein, the respondent were

directed to appoint a surveyor under the guidelines and get the Survey report within 15

days and respondent shall decide the claim within a period of 30 days. If complainant is

aggrieved with the decision, he would be at liberty to approach this forum again.

In compliance of that complainant has approached this forum and submitted a letter

dated 24.12.2021 stating that Co has arranged the survey again and provided a copy of

report to him on dated 10.12.2021. The insurance Co has offered Total Loss settlement

again. He submitted and argued during the hearing again that the surveyor has assessed

for some of affected parts which need not to be replaced for his accidented vehicle.

Whereas he wants to get it repaired and the vehicle is very much repairable. The

respondent argued further that the cost of repair shall be well within the 75 % of the

IDV and he is ready to bear the difference over that cost.

The respondent in his turn argued that insurance Co has complied with the Ombudsman

Order dated 06.10.2021. In compliance of that Co has arranged for the 2nd Surveyor,

provided the copy of report and offered the settlement as per assessment of surveyor.

The complainant cannot put his condition to get the claim settled. Claim settlement shall

be as per policy terms / condition only. Respondent argued further that insured cannot

challenge the assessment of professionally qualified and duly licensed Surveyor. The

respondent further submitted that from their side they have done everything to resolve

the complainant’s grievance.

I have heard both the parties and have carefully examined the documents on record.

I am of the considered opinion that respondent has already complied with the

Ombudsman’s Order and offered for claim settlement of claim as per Second Surveyor

assessment. As per policy condition no 3 ‘Co may its own option repair, reinstate or

replace the vehicle..’ So insured cannot insist to go for settlement as per his choice. The

policy states that Vehicle shall be treated as Constructive Total Loss if the aggregate

cost of retrieval and / repair of the vehicle exceeds 75% of the IDV of the vehicle. So

respondent’s action / offer of settlement is in accordance with the terms and condition

of the policy. There cannot be any other option of settlement of the claim beyond

method specified in the policy.

The order of earlier Hon’ble Ombudsman, issued earlier, dated 06.10.2021 is just and

proper and need no intervention. The complaint filed for review, is dismissed with the

direction to insured / complainant to proceed as per settlement initiated by respondent

Co in compliance of Ombudsman’s order passed on dated 06.10.2021.

AWARD

The revised complaint of Mr. Chunnilal Atulkar is herewith dismissed and earlier

award of Hon’ble Ombudsman is upheld.

• Let copies of the order be given to both the parties. Compliance shall be intimated to this

forum.

Place : Bhopal (RAVINDRA MOHAN

SINGH)

Date : 01.02.2022 INSURANCE

OMBUDSMAN

PROCEEDINGS BEFORE THE INSURANCE OMBUDSMAN, STATE OF ODISHA, BHUBANESWAR

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULES, 2017) OMBUDSMAN – Shri Suresh Chandra Panda

CASE OF MR. SRIKANTA KUMAR BRAHMA Vrs. THE NEW INDIA ASSURANCE COMPANY

LIMITED COMPLAINT REF: NO: BHU-G-049-2122-0181

AWARD NO: IO/BHU/A/GI/ /2021-22

1. Name & Address of the Complainant

Mr.Srikanta Kumar Brahma, Biju Pattnaik Chhak, Tulsipur, Cuttck, Odisha.Pin-753008 Cell no.9437011500

2. Policy No: Type of Policy Duration of policy/Policy period

55010531150100003610 Two wheeler package policy-Honda Aviator OD-05-AD-7847- 2008 Model-IDV-Rs.19,500/- 12 months-20/12/2015 to 19/12/2016, D.O.L.-11/06/2016

3. Name of the insured Name of the policyholder

Mr.Srikanta Kumar Brahma Mr.Srikanta Kumar Brahma

4. Name of the insurer The New India Assurance Company Limited

5. Date of Repudiation Neither repudiated nor settled Not applicable 6. Reason for repudiation

7. Dt of receipt of the Complaint

26/11/2021

8. Nature of complaint Non settlement of claim

9. Amount of Claim Rs.19,500/-

10. Date of Partial Settlement Neither repudiated nor settled

11. Amount of relief sought Rs.22,230/-

12. Complaint registered under Rule no: of IO rules

13(1)b

13. Date of hearing/place 04/02/2022, Bhubaneswar

14. Representation at the hearing

a) For the Complainant Self through VC

b) For the insurer Mr. MAQ Baig, Asst. Manager through VC

15 Complaint how disposed U/R 17 of the Insurance Ombudsman Rules, 2017

16 Date of Award/Order 04/02/2022

17. a. Brief Facts of the Case/ Cause of Complaint: -The complainant had insured his 2008 Model Honda Aviator bearing Registration no.OD-05-AD-7847 for an IDV-Rs.19,500/- for the period 20/12/2015 to 19/12/2016 with The New India Assurance Company Limited. On 11/06/2016, Mr Nirakar Swain had parked the said vehicle in front of their office at Plot no.841, Keshab Complex, Cuttack Puri Road and around 3.30 pm did not found the vehicle

where it was parked. The matter was intimated to Sahid Nagar Police by Mr Nirakar Swain who had registered the case vide vide FIR no.403 dated 18/07/2016. The intimation regarding theft was informed to Insurer on 13/06/2016 by complainant. Mr Manoj Kumar Sahoo was deputed by Insurer for investigation who submitted his report to Insurer on 03/07/2017. Investigator opined that theft claim should be settled subject to submission of Final Police report and other documents from Insured. Complainant has submitted zerox copy of FIR, final form which was submitted by investigation officer vide FF no.398 dated 30/09/2016, Form no.35 (1) and (5) to this forum. Final form does not contain any documentary evidence as to whether the same has been accepted by court or not. Insured has submitted a copy of representation dated 01/10/2021 without his signature addressed to Sr D.M. Bhubaneswar D.O.1 with a copy to Claim hub at Alok Bharati Tower, Saheed Nagar. The letter does not speak on any acknowledgment from Insurer’s office. Insurer has not submitted any letter issued by them to Insured for compliance of documents required for processing and settlement of claim. Being not satisfied on settlement of the claim complainant has approached this forum for redressal of his grievance. b. The insurer, in its self-contained note, has admitted insurance of the vehicle and receipt of claim intimation letter, FIR, Claim form from complainant. They have also submitted investigator’s report submitted by Mr Manoj Kumar Sahoo. They have further stated that insured is yet to submit required documents like Original Policy, FIR and Final Report accepted by court, Original RC, certified copy of RC with theft endorsement, keys in duplicate, letter of subrogation/Indemnity, Form 29, 30, 35 from RTO, proof of intimation to NCRB by registered post, Pan, Aadhar/Voter ID copy, Bank details with pre-printed cancelled cheque for processing and settlement of claim. 18. a. Complainant’s Argument: - He had lodged the FIR on 11/06/2016 and submitted police final investigation report to Insurer zerox copy of which has been sent to us. In spite of several request and last letter sent on 01/10/2021 to Insurer, the claim has not been settled for which he is entitled for getting claim proceeds. b.Insurer’s Argument: - Insured is yet to submit required documents like Original Policy, FIR and Final Report accepted by court, Original RC, certified copy of RC with theft endorsement, keys in duplicate, letter of subrogation/Indemnity, Form 29, 30, 35 from RTO, proof of intimation to NCRB by registered post, Pan, Aadhar/Voter ID copy, Bank details with pre-printed cancelled cheque for which claim is pending for processing and settlement.

19. Reason for Registration of Complaint: Scope of the Insurance Ombudsman Rules, 2017. 20. The following documents are placed in the file:- Photocopies of Policy, Investigation report, claim intimation, claim form, FIR submitted by Insurer, Photocopies of form 35(1) and (5), intimation letter, representation dated 01/10/2021 sent to Insurer, RC book, Final form submitted by complainant 21. Result of hearing with both parties (Observations & Conclusion): - This Forum has carefully gone through all the documents relating the complaint and heard both the parties. The complainant stated that he submitted all required documents except policy copy in original and the Final Report copy from Court. He stated that he did not collect the final report

from court as he did not challenge the police final report, but he has already submitted the Police Final Report. He further stated that the insurer has not yet settled the claim in spite of their receiving all other documents. The insurer claimed that the complainant has not submitted any document and therefore, they are not in a position to settle the claim. 22. The attention of the Complainant and the Insurer is hereby invited to the following

provisions of Insurance Ombudsman Rules, 2017: a. According to Rule 17(6) of Insurance Ombudsman Rules,2017, the Insurer shall

comply with the award within 30 days of the receipt of the award and shall intimate the compliance of the same to the Ombudsman.

b. As per Rule 17(8) of the said rules and award of the Insurance Ombudsman shall be binding on the Insurers.

Dated at Bhubaneswar on the 4th day of February, 2022 INSURANCE OMBUDSMAN

FOR THE STATE OF ODISHA

PROCEEDINGS BEFORE

THE INSURANCE OMBUDSMAN, STATE OF ODISHA, BHUBANESWAR (UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULES, 2017)

OMBUDSMAN – Shri Suresh Chandra Panda CASE OF MR DEBASHIS OJHA Vrs. BAJAJ ALLIANZ GENERAL INSURANCE COMPANY LIMITED

COMPLAINT REF: NO: BHU-G-005-2122-0164

AWARD

Taking into account the facts and circumstances of the case and submissions made by both

the parties during the course of hearing, the Forum finds that the insurer has submitted

xerox copies of all necessary documents to this office and believes that he has submitted

the documents to the insurer except the Policy copy and final report from the court. The

Forum observes that since Police Final report is already submitted and the complainant is

not against the Police findings, the Final Report from Court may not be a necessary

document. Therefore, the complainant is advised to submit the original policy copy to the

insurer within a week from the date of receipt of the order and the insurer is directed to

pay the complainant the full IDV subject to deduction of policy excess, on receipt of the

original policy document as full and final disposal of the complaint. Accordingly, the

complaint is allowed.

AWARD NO: IO/BHU/A/GI/ /2021-22

1. Name & Address of the Complainant

Mr. Debashis Ojha, C/o Sri Ramesh Chandra Ojha, At-Balianta Patna, PO/PS-Balianta, Dist-Khordha, Odisha. Pin-752101. Cell no.7735146472

2. Policy No: Type of Policy Duration of policy/Policy period

OG-2024031802-00000970, Two-wheeler package policy 12 months-23/08/2019 to 22/08/2020 Pulser-180 Regd no. OD-33Q-7691 IDV-Rs.59,336/- DOL-30/08/2019

3. Name of the insured Name of the policyholder

Mr Sunil Kumar Moharana Mr Sunil Kumar Moharana

4. Name of the insurer Bajaj Allianz General Insurance Company Limited

5. Date of Repudiation 21/10/2019 & 28/10/2019 No insurable interest 6. Reason for repudiation

7. Dt of receipt of the Complaint

11/10/2021

8. Nature of complaint Non settlement of claim

9. Amount of Claim Full insured value

10. Date of Partial Settlement Not applicable

11. Amount of relief sought Full insured value

12. Complaint registered under Rule no: of IO rules

13(1)b

13. Date of hearing/place 04/02/2022, Bhubaneswar

14. Representation at the hearing

a) For the Complainant Self through VC and phone

b) For the insurer Mr. Prateek Harichandan, Executive through VC

15 Complaint how disposed U/R 17 of the Insurance Ombudsman Rules, 2017

16 Date of Award/Order 04/02/2022

17. a. Brief Facts of the Case/ Cause of Complaint: - Mr Sunil Kumar Moharana had insured his Pulser-180 Motorcycle bearing Regd no. OD-33Q-7691with Bajaj Allianz General Insurance Company Limited against Package cover for an IDV-Rs.59,336/- vide policy no. OG-2024031802-00000970 for the period 23/08/2019 to 22/08/2020. Mr Debashis Ojha as usual used to keep the said Motorcycle with chain lock, disk lock, handle lock outside of his house. On 30/08/2019 Mr Debashis Ojha kept the motorcycle in the said place and on 31/08/2019 could not find the vehicle. He intimated the matter to Dhauli PS which was registered vide FIR no. 0120 on 31/08/2019. Theft matter was intimated to the insurer by Debashis Ojha online which was registered vide claim no. OC-20-2403-1802-00000114 wherein he was asked to submit policy copy and Panchanam/FIR in nearby claim location of Insurer’s office. Complainant had submitted transfer fees receipt of Rs.200/- deposited at office of RTA II vide receipt no. OR-33R19100000898/OR19101018638775 wherein transfer date has been mentioned as 27/08/2019 and accordingly RC was issued in favour of Mr Debashis Ojha. On 20/07/2019 complainant had intimated Insurer that after receipt of policy bond Mr Sunil Kumar Moharana and complaint had been to Finance company for obtaining No due certificate and submitted papers at RTO for change of ownership on 28/08/2019. No proof

has been submitted by complainant as to when he had intimated for the first time for transfer of policy in his name though after theft i.e. on 31/08/2019 he has intimated Insurer on theft of the vehicle. Police had final report as “Final Report true but No Clue u/s 379 of IPC vide vide no.53 dated 10/03/2021 which was accepted by Hon’ble SDJM Bhubaneswar. On 19/07/2021 Insured Mr Sunil Kumar Moharana informed Insurer that he had sold the motorcycle to Mr Debashis Ojha which was stolen on 30/08/2019. Though documents were submitted for transfer of ownership the same was affected in October 2019. However, he has no objection if the insurance amount is paid to Mr Debashis Ojha. b. The insurer, in its self-contained note, has admitted insurance of the vehicle No. OG-20-2403-1802-00000970 in favour of Mr Sunil Kumar Moharana for the period 23/08/2019 to 22/08/2020. On receipt of theft intimation investigator was deputed for investigation of loss and based on the same claim was closed as insurance was not transferred to Mr Debashis Ojha. Neither the complainant nor Sunil Ku mar Moharana intimated them for change of ownership nor provided any written intimation to change name of insured which is a gross violation of GR 17 of Indian Motor Tariff. As per GR 17 on transfer of ownership, the Liability only cover either under liability only policy or under a package policy is deemed to have been transferred in favour of the person to whom the motor vehicle is transferred with effect from the date of transfer. The transferee shall apply within fourteen days from the date of transfer in writing under recorded delivery to the insurer who has insured the vehicle with the details of registration number of vehicle and the insurance policy for making necessary changes in record the issue fresh certificate of insurance. For effecting transfer, a fresh proposal form duly completed must be obtained in respect of both liability only and package policies on payment of Rs.50/- along with refund of NCB if any. The old certificate is required to be surrendered and if not submitted a proper declaration to that effect is to be taken from the transferee before a new certificate of Insurance is issued. As the insurance was not transferred in the name of complainant there is no insurable interest for which the claim was rightfully repudiated on which they have no deficiency. 18. a. Complainant’s Argument: - Though he had purchased the motorcycle prior to theft and submitted papers to RTO office II Bhubaneswar for transfer of vehicle in his name same could not be done due to rush due to implementation of new MVI policy and insurance was made prior to theft for the period 23/08/2019 to 22/08/2020 he is entitled to get the claim towards theft loss of captioned Motorcycle which occurred on 30/08/2019. b.Insurer’s Argument: - As neither the complainant nor insured had intimated them for change of ownership it was a gross violation of GR 17 of Indian Motor Tariff. The transferee shall have to apply within 14 days from the date of transfer and submit a fresh proposal form and Rs.50/- for issuance of fresh certificate. As the same was not complied and vehicle was not transferred to Debashis Ojha he has no insurance interest for which the claim was repudiated an communicated to the complainant. 19. Reason for Registration of Complaint: Scope of the Insurance Ombudsman Rules, 2017. 20. The following documents are placed in the file:- Photocopies of Policy, & policy wordings, note sheet for repudiation, repudiation letter submitted by Insurer, Photocopies of FIR, Final

report, money receipt towards deposit of transfer fees in RTO Bhubaneswar, representation by Insured and complaint for settlement of claim submitted by complainant. 21. Result of hearing with both parties (Observations & Conclusion): - This Forum has carefully gone through all the documents relating the complaint and heard both the parties. The complainant stated that he had purchased the vehicle and had already changed the registration with RTO to his name but he had not received the transferred registration certificate before theft of the vehicle and therefore, he could not change the insurance to his name. He further stated that since it is a process and he is the registered owner, he should be paid the compensation. The insurer stated that as per the Motor Tariff, there is a process of transfer of insurance and it is necessary to get the insurance transferred to his name but any loss to the vehicle in between is not covered. The insurer stated that the complainant is not a policy-holder and is not entitled for the claim. Dated at Bhubaneswar on the 4th day of February 2022 INSURANCE OMBUDSMAN

FOR THE STATE OF ODISHA

PROCEEDINGS BEFORE THE INSURANCE OMBUDSMAN, STATE OF ODISHA, BHUBANESWAR

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULES, 2017) OMBUDSMAN – Shri Suresh Chandra Panda

CASE OF MR PRASANTA KUMAR JENA Vrs. HDFC ERGO GENERAL INSURANCE COMPANY

LIMITED COMPLAINT REF: NO: BHU-G-018-2122-0170

AWARD NO: IO/BHU/A/GI/0060 /2021-22

1. Name & Address of the Complainant

Mr. Prasanta Kumar Jena, At-Bhatapada, Po-Debidola, Dist Jagatsoinghpur Mobile-9438182447

2. Policy No: 2311203135743201000, Private Car Package Policy

AWARD

Taking into account the facts and circumstances of the case and submissions made by both

the parties during the course of hearing, the Forum finds that the insurance is not

transferred to the complainant’s name before the loss and therefore there is no insurance

contract exists between the insurer and the complainant, hence the complainant is not

entitled to get compensation for the theft of the vehicle in question. Accordingly, the

complaint stands dismissed.

Type of Policy Duration of policy/Policy period

21/11/2020 to 20/11/2021 Vehicle no. OD-02-AG-5356 Mahindra Scorpio -2016 Model IDV-9,00,000/- DOL-21/03/2021

3. Name of the insured Name of the policyholder

Mr Prasanta Kumar Nanda Mr Prasanta Kumar Nanda

4. Name of the insurer HDFC ERGO General Insurance Company Limited

5. Date of Repudiation 22/07/2021 Misrepresentation 6. Reason for repudiation

7. Dt of receipt of the Complaint

03/09/2021

8. Nature of complaint Non settlement of claim

9. Amount of Claim Rs.8,45,805/-

10. Date of Partial Settlement Claim repudiated

11. Amount of relief sought Rs.9,00,000/-

12. Complaint registered under Rule no: of IO rules

13(1)b

13. Date of hearing/place 04/02/2022, Bhubaneswar

14. Representation at the hearing

c) For the Complainant Self through phone

d) For the insurer Ms. Saswata Banerjee, Executive through VC

15 Complaint how disposed U/R 17 of the Insurance Ombudsman Rules, 2017

16 Date of Award/Order 04/02/20222

17. a. Brief Facts of the Case/ Cause of Complaint: -The complaint had insured his 2016 Model Mahindra Scorpio Vehicle no. OD-02-AG-5356 for the period 21/11/2020 to 20/11/2021 for an IDV of Rs.9,00,000/-. The vehicle was hypothecated to Syndicate Bank, Salajangha branch, Jagatsinghpur. As per the claim form on 21/03/2021 some unknown persons set fire to front portion of the car as a result of which vehicle was burnt totally. The matter was intimated by complainant to Baripada Sadar PS which was registered vide SD entry no.07 dated 04/05/2021. As per SD entry while the vehicle was standing on left side of his house, it caught fire due to short circuit of internal system. After getting the loss intimation by complainant on 22/03/2021 Er Suvendu Kumar Jena was engaged to assess the loss. Er Jena had assessed the loss for Rs.6,14,956/- after deduction of depreciation, policy excess and salvage. As there were two different reasons mentioned in two different documents i.e. claim form and FIR the insurer repudiated the claim on the ground of misrepresentation. After repudiation, the policy was cancelled and premium amounting to Rs.7539/- was refunded on 29/07/2021. The Fire Incident Report and FIR record the same reason of short-circuit. Being aggrieved by repudiation, the complainant has approached this forum for redressal of his grievance. b. The insurer, in its self-contained note, has admitted insurance of vehicle and loss within policy period. They have admitted that surveyor had assessed the loss for Rs.6,14.956/-. They have stated that as per claim form submitted by complaint vehicle was set fire by unknown persons whereas in the SD entry filed by complainant cause of loss was mentioned as short circuit. As there was discrepancy in the manner of loss and since such discrepancy was material fact, the claim was denied on the ground of suppression of material fact and

misrepresentation to them for getting insurance claim somehow. As per principle of General insurance “If there is non-disclosure or misrepresentation with fraudulent intention, the insurance contract becomes void. Avoid contract has no legal effect or validity. In fact, it is not contract at all. If the duty is broken in any other way, the contract voidable, which means, the Insurer will have the option to avoid the contract and reject it”. Moreover, as the vehicle was a case of CTL/total loss and hence required RC cancellation has not been undertaken by complainant. They have also cancelled the policy wef 20/03/2021 and premium amount for Rs.7539/- was refunded to complainant. In view of misrepresentation, they have repudiated the claim on valid and legal grounds and there is no deficiency of service or unfair trade practice. 18. a. Complainant’s Argument: - As during the effective period of insurance vehicle was burnt, he is entitled to get the claim proceeds from Insurer. The complainant states that the surveyor himself did not attend the case but his office staff named Basanta (9853164119) verified the vehicle at spot, who guided complainant’s person to fill in the claim form which he found later on to be incorrect. b.Insurer’s Argument: - As there was suppression of material fact, and two different reasons was mentioned on cause of in claim form and station diary they had repudiated the claim on valid and legal ground and cancelled the insurance after which premium amounting to Rs.7539/- was refunded to complainant. 19. Reason for Registration of Complaint: Scope of the Insurance Ombudsman Rules, 2017. 20. The following documents are placed in the file:- Photocopies of Policy, & policy wordings, survey report, claim form, station diary, cancellation endorsement submitted by insurer, Photocopies of vehicular documents, confirmation of receipt of refund amount of premium to the tune of Rs.7539/- submitted by complainant 21. Result of hearing with both parties (Observations & Conclusion): - This Forum has carefully gone through all the documents relating the complaint and heard both the parties. The complainant stated that he found the vehicle was lost due to fire, which is covered under the policy but the insurer has denied the claim. The Forum examined the claim form details and found the complainant has mentioned that the loss has taken place due to some unknown persons put fire on the vehicle. The complainant has further stated that he was not exactly sure as to how the fire took place but he guessed some unknown persons might have caused the loss. The insurer informed that the vehicle got burnt due to electrical short-circuit as per the Police Record and the Fire-Brigade report. Since the complainant has given mis-information about the cause of loss, the insurer declined the claim under Mis-representation clause and also cancelled the policy by refunding the premium.

AWARD

Taking into account the facts and circumstances of the case and submissions made by both

the parties during the course of hearing, the Forum has examined the Fire incident

certificate of the Fire Station and the SD entry of the Police and found that the loss has

taken place due to short circuit of internal electric system. The Forum also examined the

claim form, where the complainant alleged the loss to have happened due to fire being put

by some unknown persons. The insured, during hearing, stated that he was not sure about

the exact cause of loss, but out of guess he mentioned the loss to be caused by unknown

persons. Under the above circumstances, the insurer could have taken into confidence the

Police record and the Fire station record which are authentic in nature and accordingly

22. The attention of the Complainant and the Insurer is hereby invited to the following

provisions of Insurance Ombudsman Rules, 2017: a) According to Rule 17(6) of Insurance Ombudsman Rules,2017, the Insurer shall comply with the award within 30 days of the receipt of the award and shall intimate the compliance of the same to the Ombudsman. b) As per Rule 17(8) of the said rules and award of the Insurance Ombudsman shall be binding on the Insurers. Dated at Bhubaneswar on the 4thnd day of February 2022 INSURANCE OMBUDSMAN

FOR THE STATE OF ODISHA

PROCEEDINGS BEFORE

THE INSURANCE OMBUDSMAN, STATE OF ODISHA, BHUBANESWAR (UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULES, 2017)

OMBUDSMAN – Shri Suresh Chandra Panda

CASE OF MR. TRILOCHAN SAHOO Vrs. FUTURE GENERALI INDIA INSURANCECOMPANY NLIMITED

COMPLAINT REF: NO: BHU-G-016-2122-0185 AWARD NO: IO/BHU/A/GI/ /2021-22

1. Name & Address of the Complainant

Mr. Trilochan Sahoo, S/o Somanath Sahoo, C/o Prahallad Sahoo, At/Po/Ps-Daspalla, Dist Nayagarh, Odisha. Cell no.6371078873

2. Policy No: Type of Policy Duration of policy/Policy period

HFB21261, Private Car Package Policy Hyundai Xcent-2015 12 months 11/04/2015 to 10/04/2016, Model-OD-12-7677 IDV-Rs.6,42,686/- DOL-09/06/2015 as per plaint and 07/06/2015 as per survey report and claim form

3. Name of the insured Name of the policyholder

Mr Trilochan Sahoo Mr Trilochan sahoo

4. Name of the insurer Future Generali India Insurance Company Limited

5. Date of Repudiation 29/03/2016 Not applicable 6. Reason for repudiation

7. Dt of receipt of the Complaint

08/11/2021

8. Nature of complaint Non settlement of balance amount

9. Amount of Claim Rs.73,756/- Plus Interest

10. Date of Partial Settlement 29/03/2016

11. Amount of relief sought Rs.73,756/- Plus Interest

12. Complaint registered under Rule no: of IO rules

13(1)b

13. Date of hearing/place 11/02/2022, Bhubaneswar

14. Representation at the hearing

a) For the Complainant Not appeared

b) For the insurer Mr. Debidutta Mohanty through phone

15 Complaint how disposed U/R 17 of the Insurance Ombudsman Rules, 2017

16 Date of Award/Order 11/02/2022

17. a. Brief Facts of the Case/ Cause of Complaint: -The complaint had insured his Hyundai Xcent-2015 Model Private Car bearing Registration no. OD-12-7677 with Future Generali India Insurance Company Limited for the period 11/04/2015 to 10/04/2016 vide Private Car Package policy no. HFB21261 for an IDV of Rs.6,42,686/-. The vehicle was registered on 05/05/2015 and met with an accident on 07/06/2015 while going from Bhubaneswar to Phlulbani. On receipt of intimation from complainant Insurer had engaged Er Dharanidhar Das for assessment of loss. Er Das assessed the loss for Rs.1,89,000/- after inspection of vehicle at the authorized workshop of M/s Aditya Car Care Pvt Ltd after deduction of depreciation, salvage and policy excess. On receipt of discharge voucher for Rs.1,89,000/- the amount was paid to workshop as it was a cash less settlement. Being aggrieved on less settlement of claim the complaint had approached Hon’ble High Court vide WP(c) No.28867 of 2021 who had disposed the case on 22/09/2021 with a direction to dispose the representation of petitioner in accordance with law within a period of 3 months from the date of receipt of certified copy of the order by passing a reasoned order. b. The insurer, in its self-contained note, has admitted insurance of vehicle and loss within policy period. On receipt of intimation, they had engaged and independent IRDA approved insurance surveyor and loss assessor Er Dharanidhar Das. After inspection the car minutely the surveyor, had taken photographs of the car as proof of loss as per norms. After considering the loss associated with the incident in question and as per insurance byelaws and in consultation with the said workshop surveyor had assessed the loss for Rs.1,89,000/- out of total repaired bills of Rs.2,55,546/-. They had further stated that manufacturing year of car is of 2015 and policy is a normal comprehensive policy without any zero-depreciation cover. On receipt of discharge voucher duly signed by complainant the amount of Rs.1,89,000/- was paid on 29/03/2016 vide NEFT reference no.4440U16090011633 to Aditya

Car Care Pvt Ltd as it was a cashless settlement. As the present complaint is based on false and misleading grounds it should be dismissed. 18. a. Complainant’s Argument: - Though the vehicle met with an accident within policy period, and he has got less amount to the tune of Rs.73,756/- he is entitled to get the said amount. b.Insurer’s Argument: - They had processed the claim as per surveyor’s report and after getting loss voucher discharged by complainant had paid Rs.1,89,000/- to Aditya Car Care Pvt Ltd and there was no deficiency on their part. 19. Reason for Registration of Complaint: Scope of the Insurance Ombudsman Rules, 2017. 20. The following documents are placed in the file. Photocopies of Policy, & policy wordings, RC book, Survey report, claim form, discharge voucher submitted by Insurer and Photocopies of Hon’ble High court order submitted by complainant. 21. Result of hearing with both parties (Observations & Conclusion): - This Forum has carefully gone through all the documents relating the complaint and heard the party/ies present during the hearing. The complainant was sent a notice vide letter dated 12.01.2022 under speed post to attend the hearing. It is verified from postal tracking and found that the notice is delivered to the complainant on 15.01.2022. He was informed by the office over phone at 10.40 AM today requesting him to attend the hearing. Since the complainant did not appear the hearing, an attempt was taken to contact the complainant through phone, but his mobile was switched off at the time of hearing, therefore, non-appearance of the complainant is recorded. The insurer informed that they have settled the claim as per surveyor’s report, where the depreciation is deducted as per policy terms and conditions. The insurer further stated that the amount preferred under this forum is related to depreciation, policy excess and salvages, which are not payable under the policy.

AWARD

Taking into account the facts and circumstances of the case and submissions made by

party/ies present during the course of hearing, it is recorded that the complainant is given

reasonable opportunity to place his case before the forum, but he failed to avail the

opportunity. The Forum examined the complaint and related documents filed by both the

parties. The Forum also examined the surveyor’s assessment and found that the insurer has

deducted the claim towards depreciation on plastic, rubber and fibre parts, which are as

per policy terms and conditions. Accordingly, the Forum does not consider any merit in the

complaint and therefore, the complainant is not entitled for his claim under this complaint.

Accordingly, the complaint stands dismissed.

Dated at Bhubaneswar on the 11th day of February 2022 INSURANCE OMBUDSMAN

FOR THE STATE OF ODISHA

PROCEEDINGS BEFORE THE INSURANCE OMBUDSMAN, CHANDIGARH

(Under Rule 13 r/w 16/17 of the Insurance Ombudsman Rules, 2017)

Insurance Ombudsman: Shir Atul Jerath

Case of Ved Parkash V/S Magma HDI General Insurance Co. Ltd.

Complaint Ref. NO: CHD-G-030-2122-0133

1. Name & Address of the Complainant

Shri Ved Parkash

S/o Sh. Ram Kumar, H. No.- 43, Gali No.- 11,

Jawahar Nagar, Hisar, Haryana-125001

2. Policy No:

Type of Policy

Duration of policy/Policy period

P0020400002/4107/106410

Motor Insurance

23-07-2019 to 22-07-2020

3. Name of the insured

Name of the policyholder

Ved Parkash

Ved Parkash

4. Name of the insurer Magma HDI General Insurance Co. Ltd.

5. Date of Repudiation 29.09.2020

6. Reason for repudiation Misrepresentation and non-registration of

vehicle.

7. Date of receipt of the Complaint 02-08-2021

8. Nature of complaint Incorrect denial of claim

9. Amount of Claim Rs.23,18,000/-

10. Date of Partial Settlement N.A

11. Amount of relief sought Claim amount + interest

12. Complaint registered under

Rule no: Insurance Ombudsman Rules,

2017

Rule 13 (1)(b) – any partial or total repudiation

of claims by an insurer

13. Date of hearing/place 13.01.2022/Online hearing

14. Representation at the hearing

For the Complainant Shri Ved Parkash, the complainant

For the insurer Shri Anirudh Devraj

15 Complaint how disposed Award under Rule 17

16 Date of Award/Order 07.02.2022

17. Brief Facts of the Case: Shri Ved Parkash (hereinafter, the complainant) has filed this complaint

against Magma HDI General Insurance Co. Ltd. (hereinafter, the insurers) alleging incorrect denial of

claim.

18. Cause of Complaint:

a) Complainant’s argument: He timely submitted all the claim documents with the company and had handed over the two keys of the vehicle to the surveyor but the insurance company still rejected the claim. The complainant further sought the intervention of this forum for payment of claim along with interest.

b) Insurer’s Argument: In the SCN, insurance company stated that vehicle number HR17B2980 got theft on 15-09-2019. FIR number 32908 dated15.09.2019 was registered at PS Shalimar Bagh, Delhi. Matter was assigned for investigation to M/s Triple Tracer & investigation on basis of investigation report claim has been repudiated on the grounds of non registration of vehicle in accordance with section 39 motor vehicle Act, 1988 and on ground of misrepresentation of Actual Facts. As per the available details and investigation carried out it was revealed that last user cum driver Umesh Kumar was not present at loss location as he was unable to answer the route, toll tax details etc during this entire journey from Hisar to Delhi. Narration of alleged incident and date of loss as per statement of both insured and driver are different. Insured driver inspite of many requests did not come forward to narrate the loss, route, toll plaza details coming on his way during the journey. The claim through investigator PLH Solution and services. During the same period M/s PLH Solution and services were investigating one more case of motor theft of insured Sakir assigned to them by the insurer M/s Magma HDI GIC Ltd. During the course of investigation, they received information that the said vehicle (Truck bearing registration number HR55X1947) of the insured Mr. Sakir, has been recovered by the IGIS Crime Branch New Delhi.

As per the information received from IGIS Crime branch, they had arrested 4 persons including the

insured Mr. Sakir and had recovered the insured vehicle bearing registration number HR55X1947

from them. On interrogating the accused they informed that they had tampered the vehicle

number, engine number and chassis number and sold the vehicle. Currently the vehicle was playing

on RJ11GB5483 number. Post selling the vehicle they lodged the FIR with the PS Dwarka North.

New Delhi U/s 028444/2020 on dted 11/08/2019. When they retrieved the copy of the FARD it was

known that the accused Sakir had other 3 accused were involved in such activites of tampering the

vehicle. Engine and chassis number and selling the vehicles and subsequently lodging the fake FIR’s

or helping others to lodge fake FIR’s against money. Insured Mr. Sakir informed police that he along

with one of his acquaintance Mr. Khurshid and his known Mr. Ved Prakash who is resident of

Bhiwani, Haryana had lodged fake FIR about theft of JCB( HR 171090) of Mr. Ved Prakash with the

Shalimar Bagh Police Station. Mr. Sakir informed that Mr. Khurshid had sold the JCB in Mewat. Mr.

Sakir futher stated that he can help police in arresting Mr. Khurshid.

19. Reason for Registration of Complaint: Incorrect denial of claims and cancellation of policy.

20. The following documents were placed for perusal:

a) Complaint to the Company b) Copy of Policy Document

c) Annexure VI-A d) Reply of the Insurance Company

21. Result of Personal hearing with both parties (Observations & Conclusion): Case called for

hearing, both the parties are present and recall their arguments as noted in Para 18 above.

The complainant stated that despite submission of all the documents insurers denied the theft claim

of his JCB on the ground of non-registration of vehicle. He further submitted that fee for registration

of vehicle was timely submitted to the dealer.

The representative of the insurance company submitted that at the time of accident the vehicle was

not registered in accordance with section 39 of Motor Vehicle Act, 1988 and due to misrepresentation

of actual facts the claim was repudiated vide their letter dated 29.09.2020. He further informed that

in some other theft case, the company procured a document from IGIS Crime Branch Delhi in context

to a claim which was lodged by the owner of an insured vehicle viz. Mr. Sakir, S/o Naseer, residing at

Mewat, Haryana. In the confessional statement made by the Sakir, Mr. Ved Parkash filed a false FIR

and insured vehicle was sold at Mewat.

During online hearing, the complainant was advised to submit the proof of payment for registration

of the vehicle. Further insurers were advised to submit the documents in support of their contentions.

In response, the complainant vide mail dated 13.01.2022 has placed on record the receipt dated

24.07.2019 for Rs,156,100/- issued by the State Transport Department which shows that necessary

fee for Registration of vehicle was paid him on 24.07.2019 though as per R.C its registration date is

31.12.2019. Insurers have also placed on record a copy of letter dated 14.01.2022 sent to the Joint

Commissioner of Police, Delhi on 17.01.2022. In the captioned complaint to police, insurers stated

that during investigation in some other theft case, they procured a document vide DD no 08 dated

06.11.2020 from IGIS Crime Branch Delhi in context to a claim which was lodged by the owner of that

insured vehicle viz. Mr. Sakir. In the confessional statement made by Sakir, Mr. Ved Prakash had filed

a false FIR and the insured vehicle was sold at Mewat. On the basis of confessional statement,

insurance company has prayed to police for reinvestigation for the offences committed by the accused

Mr. Ved Parkash, who with an illegal intention has committed a fraud on the complainant company.

In view of the representation made by the insurers for reinvestigating the case, the complainant is

pre-mature for decision on merits. Therefore, complainant is rejected and no relief is granted.

Award

Considering the facts & circumstances of the case and the submissions made by both the

parties during the course of hearing, the complaint is hereby rejected being devoid of merits.

( Atul Jerath )

Insurance Ombudsman

7th February, 2022

PROCEEDINGS BEFORE THE INSURANCE OMBUDSMAN, CHANDIGARH

(Under Rule 13 r/w 16/17 of the Insurance Ombudsman Rules, 2017)

Insurance Ombudsman: Shir Atul Jerath

Case of Ashok Kumar Chadha V/S The United India Insurance Co. Ltd.

Complaint Ref. NO: CHD-G-051-2122-0134

1. Name & Address of the Complainant

Shri Ashok Kumar Chadha

S/o Lt. Sh. Sat Dev Chadha, H. No.- 731,

Sector-12, Panchkula, Haryana

2. Policy No:

Type of Policy

Duration of policy/Policy period

1122003115P105458070

Motor Policy

07-08-2015 To 06-08-2016

3. Name of the insured

Name of the policyholder

Ashok Kumar Chadha

Ashok Kumar Chadha

4. Name of the insurer The United India Insurance Co. Ltd.

5. Date of Repudiation 17.05.2018

6. Reason for repudiation Non submission of cancelled R.C

7. Date of receipt of the Complaint 30-07-2021

8. Nature of complaint Incorrect closure of claim

9. Amount of Claim Rs.246919/- on net of salvage basis without R.C

10. Date of Partial Settlement N. A

11. Amount of relief sought IDV Rs.3,50,000/- less Rs.1000/- + Interest +

compensation for harassment

12. Complaint registered under

Rule no: Insurance Ombudsman Rules,

2017

Rule 13 (1)(b) – any partial or total repudiation

of claims by an insurer

13. Date of hearing/place 13.01.2022/Online Hearing

14. Representation at the hearing

For the Complainant Shri Ashok Kumar Chadha, the complainant

For the insurer Shri Nipun Khurana

15 Complaint how disposed Award under Rule 17

16 Date of Award/Order 07.02.2022

17. Brief Facts of the Case: Shri Ashok Kumar Chadha (hereinafter, the complainant) has filed this

complaint against The United India Insurance Co. Ltd. (hereinafter, the insurers) alleging incorrect

denial of claim.

18. Cause of Complaint:

a) Complainant’s argument: An own damage claim of Tata Manja Car bearing Regd. No. HR26 F-0020 filed with the insurers was approved and asked to get the Registration Certificate of the vehicle cancelled for settlement of claim. Insurers vide letter dated 17.05.2018 communicated that R.C may be cancelled from RTO otherwise; the claim of the said car shall be closed as No Claim. The complainant could not comply with the requirement due to peculiar unavoidable family circumstances. The complainant approached Registration Authority where it was told that in case the registration certificate of the car in question viz. HR26F-0020 was got cancelled, he will not be able to retain the said special number which is paid/VIP number, therefore when he purchased a new Hundai i20 car, he got the said RC Number HR26F-0020 reassigned to the said new car by getting a substituted number HR-70D-0198 allotted to the said Tata Manja Car qua which the claim was pending .The complainant sent a letter dated 20.04.2021 of the Registration Certificate of the newly assigned Registration Numbers of Tata Manja Car as well as Hundai i20 car to the insurance company requesting them to issue a fresh letter for cancellation of registration number HR70D-0198 without which cancellation of R.C is not possible. The insurance company is neither issuing the requisite letter nor making payment of claim of complainant. The insurance company has closed the claim wrongly and has caused wrongful gain to themselves In the peculiar circumstances stated above, it is necessary that the insurance company may be

directed to issue the necessary letter for cancellation of R.C number HR-70D-0198 now assigned

to the said Tata Manja car to enable applicant to get the RC cancelled and direction to the

company for payment of claim with interest upon compliance of the said condition by

complainant.

b) Insurer’s Argument: The vehicle bearing Registration Number HR-26-F-0020 covered under motor policy valid from 07.08.2015 to 06.08.2016 had met with an accident on 21.06.2016. The claim had been approved by the competent authority on 23.08.2016 for an amount of Rs. 246919/- on net of salvage basis. The insured had been conveyed the decision regarding the approval of claim vide their letter No. MDO/CHD/2016 dt.23.08.2016 originally addressed to RTO, Haryana State, Chandigarh and endorsing a copy of the same to the insured inter-alia advising him for cancellation of R.C of the said vehicle to enable them to proceed further in the matter. The insured had again been reminded vide their letter No. MDO/CHD/2016/12576 dated 07.02.2016 for compliance of formalities already conveyed vide their letter dated 23.08.2016. Since they had no response from the insured the claim in question had been closed/ repudiated on 29.06.2017 after giving sufficient opportunity to the insured for compliance. After a elapse of approximately four years they had again received a representation dated 22.04.2021 from the insured narrating therein the circumstances leading to non-compliance of said formalities. It is pertinent to mention here that by this time inspite of their communication vide various letters to get the R.C cancelled, the insured had informed that he has got the Registration Number i.e HR-26-F-0020 shifted to new vehicle and had acquired new Regd. Number HR-70-D-0198 for the ill-fated vehicle insured with them with Regd. No HR-26-F-0020. Further no such vehicle with Regd. Number HR-70-D-0198 is insured with them, hence the letter for cancellation of the said registration certificate cannot be issued. Moreover, they are surprised to receive a copy of letter dated 17.05.2018 from the insured alleged to have been written by them to him, but as per insurer’s record no such letter has been issued by them and seems to be an act of malafide intention to turn the dice in his favour. In view of the circumstances narrated it is evident that the insured had been given ample opportunity to get the needful done i.e Cancellation of R.C. And submit proof thereof to enable insurers to proceed further in the matter, yet insured failed to comply with the formalities and did not respond for approx. four years rendering the claim time barred. Hence the claim decision of the competent authority to repudiate the claim in question is correct and justified.

19. Reason for Registration of Complaint: Incorrect closure of claim.

20. The following documents were placed for perusal:

a) Complaint to the Company b) Copy of Policy Document

c) Annexure VI-A d) Reply of the Insurance Company

21. Result of Personal hearing with both parties (Observations & Conclusion): Case called for

hearing, both the parties are present and recall their arguments as noted in Para 18 above. The

complainant stated that claim for his Tata Manja Car bearing Registration No HR-26-F-0020 was

approved by the insurance company but he could not get the R.C cancelled due to family

circumstances. He got the said RC Number HR26F-0020 reassigned to a new car by getting a

substituted number HR-70D-0198 and requested insurance company to issue a fresh letter for

cancellation of registration number HR70D-0198 without which cancellation of R.C is not possible. The

representative of the insurance company submitted that complainant has approached them after five

years and is asking for cancellation of new registration number HR70D-0198 which is not insured under

the policy. It has been observed that complainant’s vehicle bearing Regd. No HR26F-0020 insured

under motor policy had met with an accident 21.01.2016. The claim was approved on net of salvage

basis without R.C. The company wrote letters dated 23.11.2016 / 07.12.2016 to the insured informing

approval of claim and completion of formalities. The insured was requested to get the R.C of the said

vehicle cancelled from the RTO and submit the cancellation certificate within 7 days and incase the

same is not done, file would be closed as no claim. The insurers also sent another letter dated

17.05.2018 on the same lines as per their earlier letters. The complainant the vide his letter dated

20.04.2021 informed the insurers that he has transferred the old R.C No HR 26 F -0020 on his new

purchased vehicle i20 sports model 2021 and RTO has issued new R.C number HR 70 D 0198 and

requested for a new letter for cancellation of R.C of HR70 D 0198. In the captioned case, the

complainant was duly informed by the insurance company vide their letters dated 23.11.2016,

07.12.2016 & 17.05.2018 for cancellation of R.C. The complainant himself did not act and comply with

the requirements of the approved claim in spite of reminders since 23.11.2016. No case is made out

against the insurers as they had approved the claim as per policy terms and had duly informed the

complainant for compliance of formalities. Therefore, complaint is rejected being devoid of merits and

no relief is granted.

Award