The IMF is a great force for good in the world, discuss

27

Jan Boltvan C10803971 DT558/4 Malgorzata Mijalska D11125372 DT558/4 Marta Pieklak C10734369 DT558/4 Jelena Rimovica C10716293 DT558/4 Fernando Rodriquez C10712809 DT558/4 International Political Economy The IMF is a great force for good in the world, discuss. 29 th of November 2013 Lecturer: John Hogan

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of The IMF is a great force for good in the world, discuss

Jan Boltvan C10803971 DT558/4

Malgorzata Mijalska D11125372 DT558/4

Marta Pieklak C10734369 DT558/4

Jelena Rimovica C10716293 DT558/4

Fernando Rodriquez C10712809 DT558/4

International Political Economy

The IMF is a great force for good in the world,

discuss.

29th

of November 2013

Lecturer: John Hogan

2

Declaration of ownership

We hereby certify that this material, which we now submit for assessment as a

continuous assessment project in International Political Economy is entirely our own

work and has not been submitted in whole or in part for assessment for any academic

purpose other than in fulfillment for that stated above.

Signed: ……………………….. Date: ……………………………….

Signed: ……………………….. Date: ……………………………….

Signed: ……………………….. Date: ……………………………….

Signed: ……………………….. Date: ……………………………….

Signed: ……………………….. Date: ……………………………….

3

Table of Contents

1. Introduction ......................................................................................................... 4 2. International Monetary Fund .............................................................................. 4 3. Developing Countries ......................................................................................... 6

4. Ireland ................................................................................................................. 8 5. Iceland ............................................................................................................... 13 6. Greece ............................................................................................................... 17 7. Russia ................................................................................................................ 20 8. Conclusions ....................................................................................................... 23

9. References ......................................................................................................... 25

4

1. Introduction

The following project will discuss the role of the International Monetary Fund (IMF)

in the world economy. Our main goal is to examine whether the IMF is a great force

for good in the world. In order to objectively explain the role of the IMF we will

provide multiple examples of countries that have undergone the IMF bailout process

and have received financial support. The countries mentioned in the project (Ireland,

Iceland, Greece, Russia and example developing countries) vary greatly in their

economical, political and sociological aspects, providing us with a base for an

impartial discussion of the IMF subject.

2. International Monetary Fund

The talks for the creation of the IMF began during the Bretton Woods conference that

was held in 1944. However, it was not until December of 1945 that the IMF was

formally created. The main reasons for the formation of the IMF were to create

policies to reduce trade barriers (which were also one of the main reasons for the great

depression) and to help recover European countries following World War II

devastation (Körner, 1987).

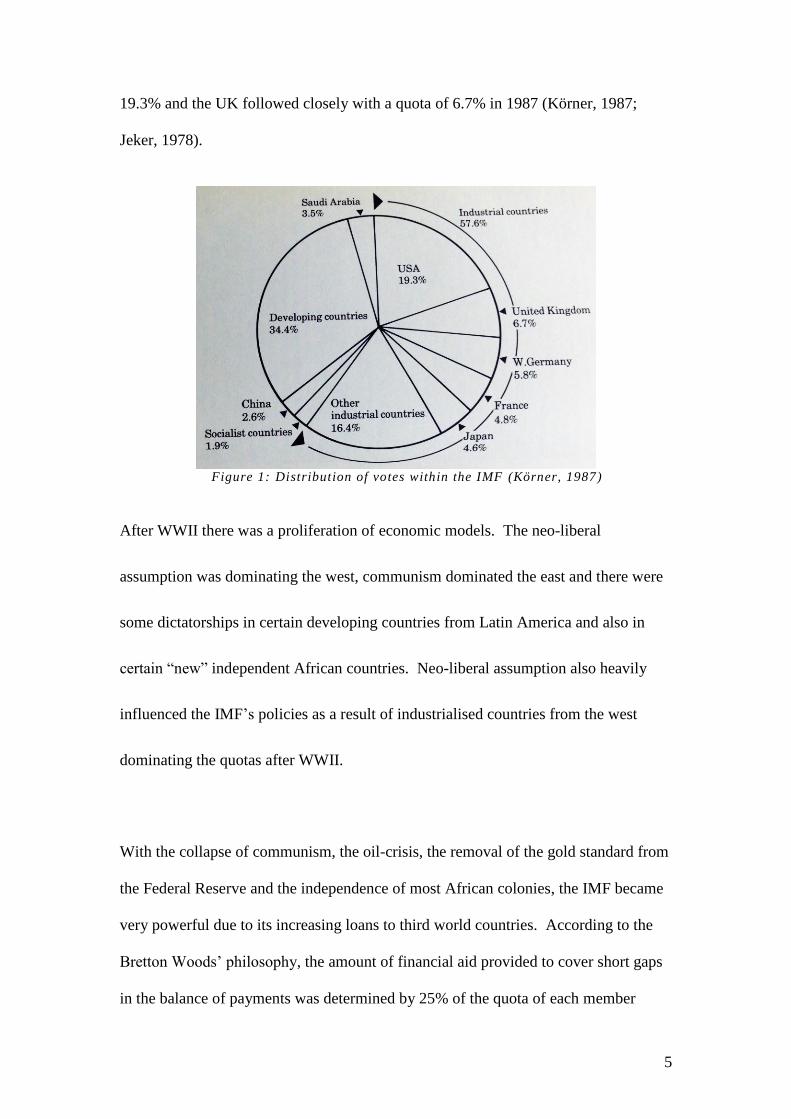

148 countries, mostly developing countries, signed the IMF agreement. Despite the

numerical superiority of the developing countries that signed the IMF agreement, the

developing countries didn‟t have a significant influence on the decision making

process. Instead, quotas that are based on payment obligations, credit facilities and

un-balanced voting rights of members determine the balance of power in the

decisions. Using the unwritten equation $1 equals 1 vote, the US held a quota of

5

19.3% and the UK followed closely with a quota of 6.7% in 1987 (Körner, 1987;

Jeker, 1978).

Figure 1: Distribution of votes within the IMF (Körner, 1987)

After WWII there was a proliferation of economic models. The neo-liberal

assumption was dominating the west, communism dominated the east and there were

some dictatorships in certain developing countries from Latin America and also in

certain “new” independent African countries. Neo-liberal assumption also heavily

influenced the IMF‟s policies as a result of industrialised countries from the west

dominating the quotas after WWII.

With the collapse of communism, the oil-crisis, the removal of the gold standard from

the Federal Reserve and the independence of most African colonies, the IMF became

very powerful due to its increasing loans to third world countries. According to the

Bretton Woods‟ philosophy, the amount of financial aid provided to cover short gaps

in the balance of payments was determined by 25% of the quota of each member

6

requesting aid. However, in 1974, the IMF created the Extended Fund Facility, which

permitted drawings of up to 140% of the quota if the member country had an

extended arrangement of conditionality with the IMF (Körner, 1987). During the

1970‟s the IMF created the Compensatory Financing Facility, which was designed to

lend capital to financially struggling raw materials exporting countries, whose

financial difficulties were caused by outside forces (e.g.: the drop of oil prices during

the oil crisis in oil exporting countries) (Körner, 1987).

As a result of the IMF‟s newly created lending facilities, the national debt in many

IMF member countries began to rise. There was a notion that if a nation didn‟t hold

any debt, it would indicate that the nation didn‟t hold any valuable assets to back up a

loan application (George, 1988).

3. Developing Countries

There were only two dominant classes in the social structure of the developing

countries: firstly, the bourgeoisie class who owned the factories and banks; and

secondly, the proletariat who worked in the factories of said bourgeoisie (Rodney,

1972). The lack of change in the social structure of the developing countries as well

as the absence of liberation of forces of production led to unproductive usage of debt.

Developing countries were stuck in a cycle of using new loans to service legacy debt.

Consumption increases in developing countries contributed to the increase of their

debt. Between 1979 and 1982, Chile began to borrow to finance imported goods for

its upper middle class discouraging the consumption of nationally made products.

Chile borrowed $11 Billion to finance its increased foreign spending, which resulted

7

in a trade deficit and increased unemployment (George, 1988). The will of

developing countries for industrialisation also help escalate their national debt. In

1974, the sugar boom encouraged many developing countries to build additional sugar

mills and refining factories. The supply of machinery and technology was dominated

by industrialised countries, which supplied services and goods at a higher price

(George, 1988). The flight capital was very common in developing countries. Arms

don‟t produce wealth, and when not manufactured locally, they don‟t create jobs or

inject money into the local economy. However, the IMF constantly demands that its

members reduce civil spending, but leave arms budgets untouched. In 1980,

Ethiopia‟s GDP per capita was $110, the lowest anywhere in the world. Nevertheless,

this did not prevent Ethiopia from spending $13 per head a year on its military to

protect against the liberation struggles in the northern provinces. According to

Stockholm Peace Research Institute, developing countries could have borrowed 20%

less every year between 1972 and 1982 if they did not purchase arms produced by

foreign countries (George, 1988).

During the 1970‟s, borrowers (industrialised countries) didn‟t want the IMF to

intervene in developing countries, as IMF‟s intervention would mean adjustment and

austerity measures and therefore, unprofitable business for the commercial banks.

Between 1974 and 1979 the IMF supplied less than 5% of the finance that developing

countries required. In 1978, oil-producing developing countries repaid $900 million

more in interest to the IMF than they borrowed. However, the second oil-price shock

from 1981 doubled the developing countries‟ deficits from $45 billion in 1979 to $90

billion in 1981 (George, 1988).

8

At the beginning of the 1980‟s, when Mexico, Brazil and other major developing

countries where at the point of default, the IMF created bailout programmes. The

developing countries had to adhere to bailout conditions which included: devaluation

of currency, reduction of government expenditure, privatisation of government

services, reduction of labour wages, restriction of credit and higher taxes to reduce

inflation. The elites from the developing countries were not affected as much as the

lower classes. Unemployment increased due to the IMF adjustments. In Chile, for

example, unemployment rose from 4.8% to 14.5% between 1973 and 1975 (Körner,

1987).

However, transnational firms from developing countries benefited from the IMF

programs. The liberation of payments systems facilitated profit transfers and

devaluation enabled transnational firm to buy uncompetitive domestic companies

cheaply. Therefore, there was a shift of wealth and power to export oriented

companies, which reduced the supply of basic needs to the poor. Increasing

marginalisation of the poor in the developing countries led to continuous violent

protests against the IMF measures. In June of 1981, workers from Casablanca went to

a protest against the cuts on wages imposed by the IMF. The official statistics said

that 66 people were killed; however, unofficial statistics said that 600 people were

killed and 2,000 people were arrested (Körner, 1987).

4. Ireland

The Irish Celtic Tiger years (1994 to 2000) largely consisted of export-led activities.

In 2001 export dependent growth was replaced by debt-financed capital spending with

the cheap credit leading to the property and construction bubble (Kinsella, 2010).

9

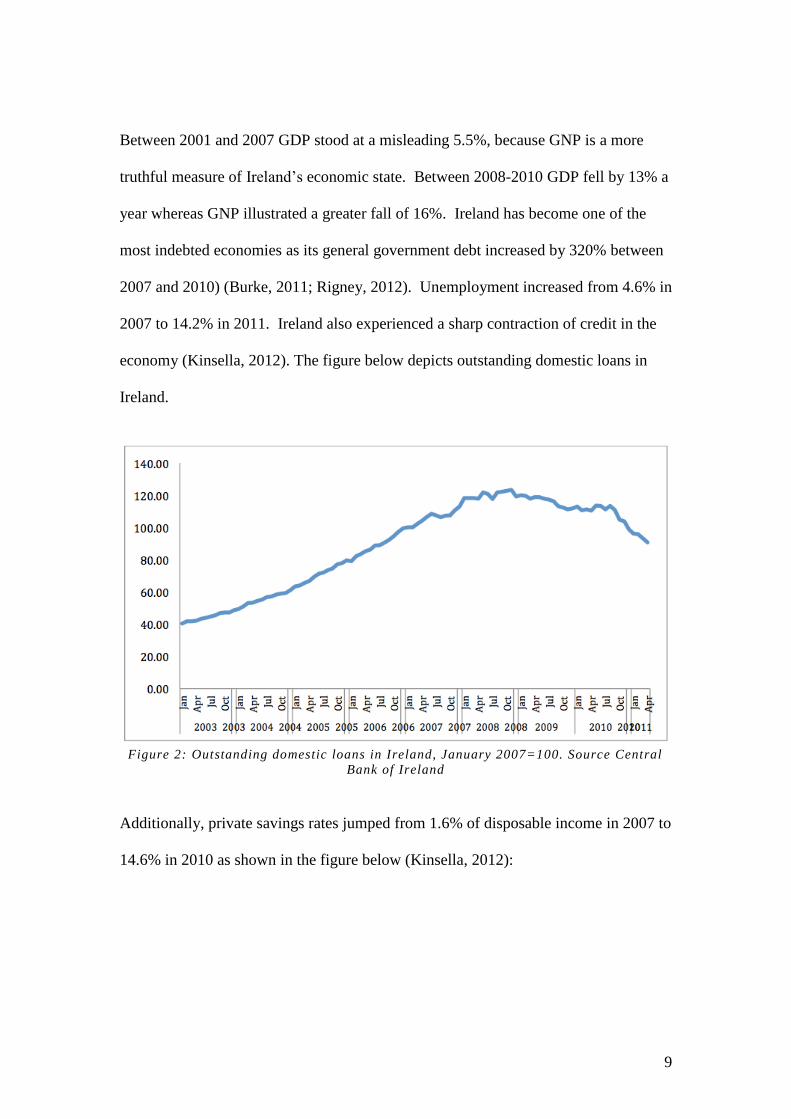

Between 2001 and 2007 GDP stood at a misleading 5.5%, because GNP is a more

truthful measure of Ireland‟s economic state. Between 2008-2010 GDP fell by 13% a

year whereas GNP illustrated a greater fall of 16%. Ireland has become one of the

most indebted economies as its general government debt increased by 320% between

2007 and 2010) (Burke, 2011; Rigney, 2012). Unemployment increased from 4.6% in

2007 to 14.2% in 2011. Ireland also experienced a sharp contraction of credit in the

economy (Kinsella, 2012). The figure below depicts outstanding domestic loans in

Ireland.

Figure 2: Outstanding domestic loans in Ireland, January 2007=100. Source Central

Bank of Ireland

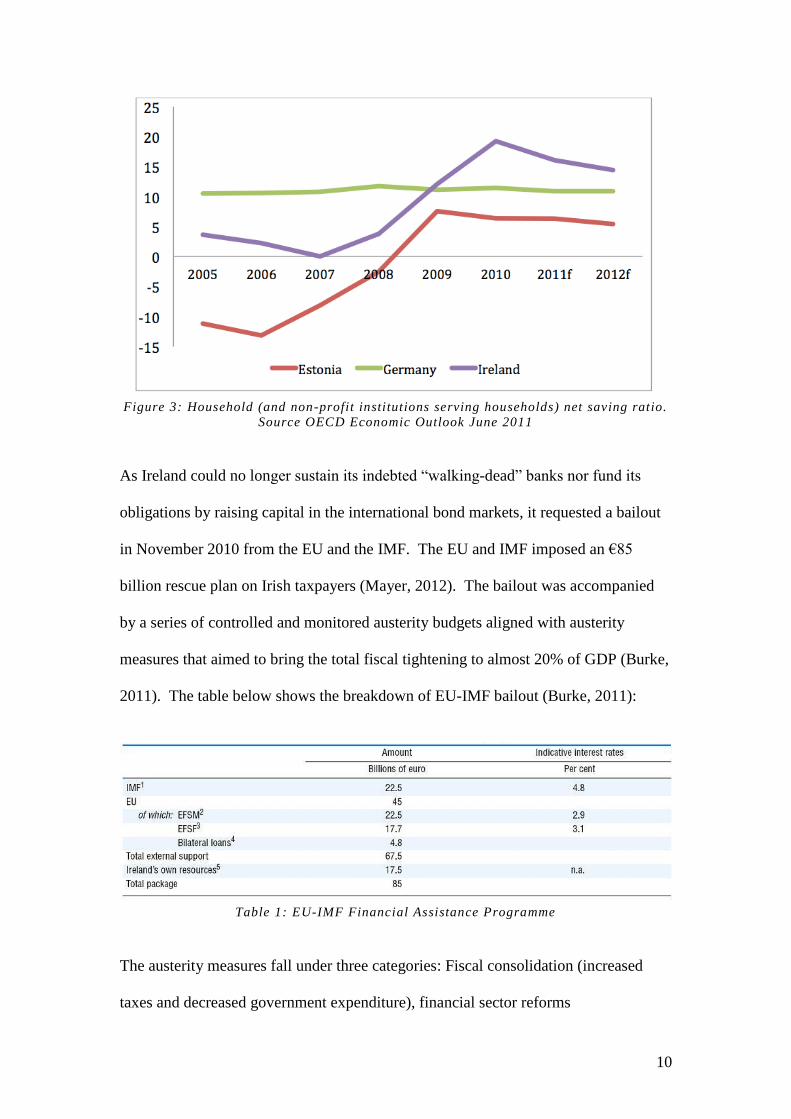

Additionally, private savings rates jumped from 1.6% of disposable income in 2007 to

14.6% in 2010 as shown in the figure below (Kinsella, 2012):

10

Figure 3: Household (and non-profit institutions serving households) net saving ratio.

Source OECD Economic Outlook June 2011

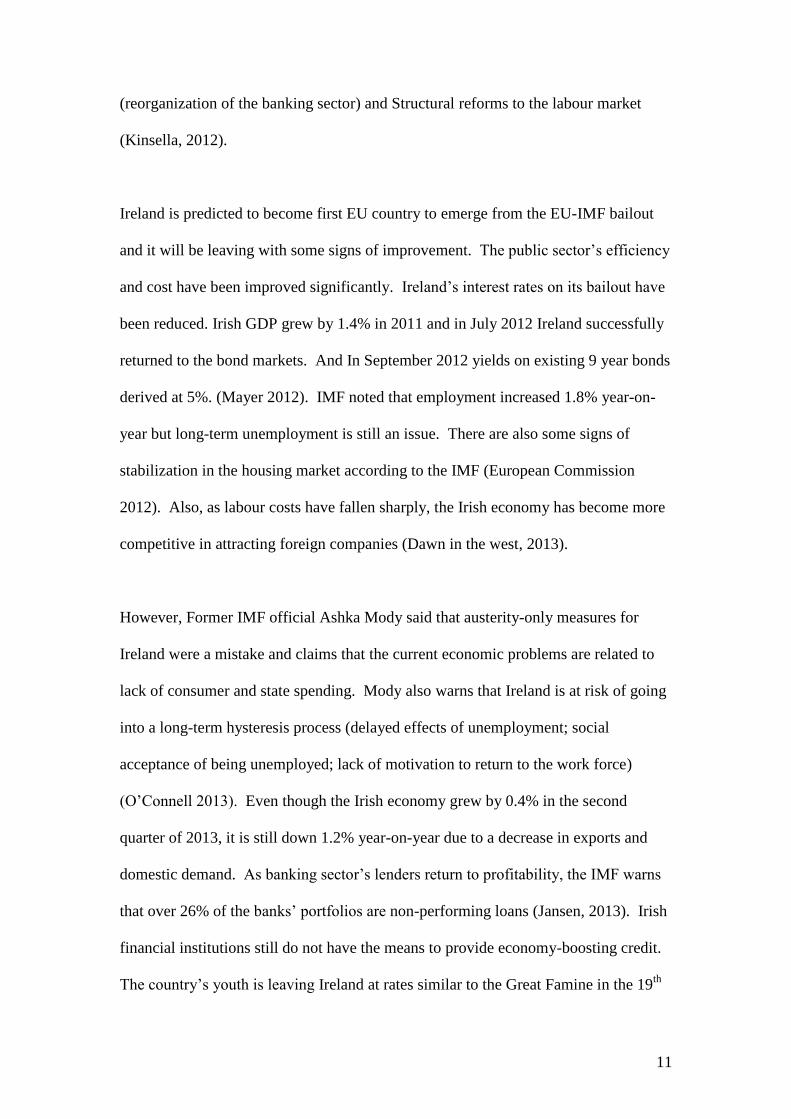

As Ireland could no longer sustain its indebted “walking-dead” banks nor fund its

obligations by raising capital in the international bond markets, it requested a bailout

in November 2010 from the EU and the IMF. The EU and IMF imposed an €85

billion rescue plan on Irish taxpayers (Mayer, 2012). The bailout was accompanied

by a series of controlled and monitored austerity budgets aligned with austerity

measures that aimed to bring the total fiscal tightening to almost 20% of GDP (Burke,

2011). The table below shows the breakdown of EU-IMF bailout (Burke, 2011):

Table 1: EU-IMF Financial Assistance Programme

The austerity measures fall under three categories: Fiscal consolidation (increased

taxes and decreased government expenditure), financial sector reforms

11

(reorganization of the banking sector) and Structural reforms to the labour market

(Kinsella, 2012).

Ireland is predicted to become first EU country to emerge from the EU-IMF bailout

and it will be leaving with some signs of improvement. The public sector‟s efficiency

and cost have been improved significantly. Ireland‟s interest rates on its bailout have

been reduced. Irish GDP grew by 1.4% in 2011 and in July 2012 Ireland successfully

returned to the bond markets. And In September 2012 yields on existing 9 year bonds

derived at 5%. (Mayer 2012). IMF noted that employment increased 1.8% year-on-

year but long-term unemployment is still an issue. There are also some signs of

stabilization in the housing market according to the IMF (European Commission

2012). Also, as labour costs have fallen sharply, the Irish economy has become more

competitive in attracting foreign companies (Dawn in the west, 2013).

However, Former IMF official Ashka Mody said that austerity-only measures for

Ireland were a mistake and claims that the current economic problems are related to

lack of consumer and state spending. Mody also warns that Ireland is at risk of going

into a long-term hysteresis process (delayed effects of unemployment; social

acceptance of being unemployed; lack of motivation to return to the work force)

(O‟Connell 2013). Even though the Irish economy grew by 0.4% in the second

quarter of 2013, it is still down 1.2% year-on-year due to a decrease in exports and

domestic demand. As banking sector‟s lenders return to profitability, the IMF warns

that over 26% of the banks‟ portfolios are non-performing loans (Jansen, 2013). Irish

financial institutions still do not have the means to provide economy-boosting credit.

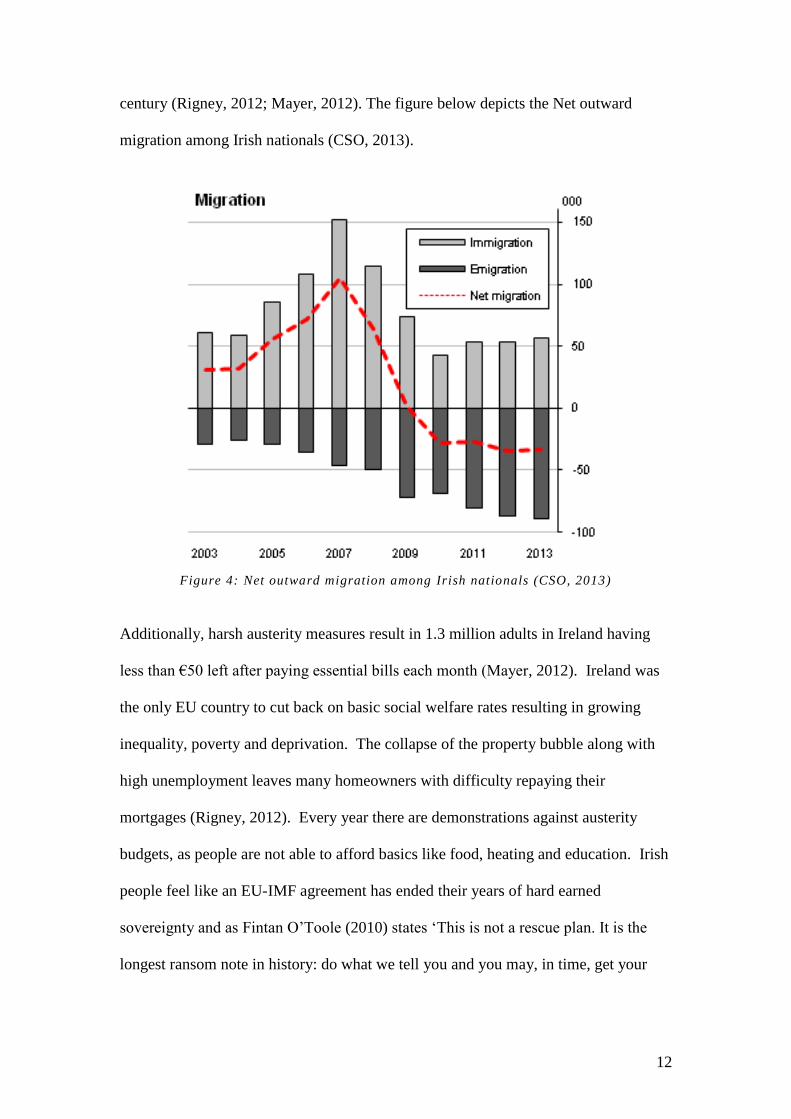

The country‟s youth is leaving Ireland at rates similar to the Great Famine in the 19th

12

century (Rigney, 2012; Mayer, 2012). The figure below depicts the Net outward

migration among Irish nationals (CSO, 2013).

Figure 4: Net outward migration among Irish nationals (CSO, 2013)

Additionally, harsh austerity measures result in 1.3 million adults in Ireland having

less than €50 left after paying essential bills each month (Mayer, 2012). Ireland was

the only EU country to cut back on basic social welfare rates resulting in growing

inequality, poverty and deprivation. The collapse of the property bubble along with

high unemployment leaves many homeowners with difficulty repaying their

mortgages (Rigney, 2012). Every year there are demonstrations against austerity

budgets, as people are not able to afford basics like food, heating and education. Irish

people feel like an EU-IMF agreement has ended their years of hard earned

sovereignty and as Fintan O‟Toole (2010) states „This is not a rescue plan. It is the

longest ransom note in history: do what we tell you and you may, in time, get your

13

country back‟ (Brown, 2010). The budget deficit remains high at 7.5% of GDP and

public debt is reaching 124% in 2013.

The Irish exit from the enormous bailout at the end of 2013 will be perceived as a big

success. But in reality Ireland will be faced with economic and fiscal vulnerabilities.

If global growth weakens, Ireland will be greatly affected, as it relies strongly on its

export market. The history of countries trying to resolve fiscal crisis shows that

exports alone will not be enough to stabilize the country‟s economy (Rigney, 2012).

Conscious of its weakness, Ireland wants its borrowing to be shielded from bond

vigilantes by the ECB. This will only be allowed if the country signs up for a

precautionary program with the Eurozone‟s rescue fund. Additionally, the ECB said

that the IMF should be involved in the rescue fund which means that Ireland will

enter a second bailout program shortly after leaving the first one (What Angela isn‟t

saying, 2013).

Note: As of 14th

of November Ireland will not be applying for a precautionary credit

line (Kinsella, 2013).

5. Iceland

Iceland is a small, but well developed economy that was led by a centre right coalition

government consisting of two Parties: The Independence Party and the Progressive

Party from 1995 to 2007. For over a decade the country enjoyed growth and

prosperity, with both inflation and unemployment at very low levels. The ruling

coalition achieved popularity by pursuing the policy of limiting the involvement of

the State in the economy. The Government‟s agenda was to privatize all state-owned

enterprises including: Telekom companies and banks (Country Watch Incorporated,

14

2013). Unfortunately economic freedom came at a very high price, and in 2008

Iceland needed the assistance of the IMF bailout program.

The new owners of the privatised Icelandic banks took advantage of low interest rates

and rising property prices and borrowed money from foreign capital markets to lend it

later to themselves or other related parties. Loans were used to buy shares in foreign

firms and stakes in foreign commercial real estate. Due to the borrowing, banks were

very much exposed to the financial crisis that started in the summer of 2007. They

were heavily reliant on loans from foreign money markets to meet their obligations,

and their assets were vulnerable to any volatility in the stock market. Additionally

there were doubts that the Icelandic Government would be able to rescue the

country‟s banks. In October 2008 Glitnir bank defaulted and in doing so exposed the

vulnerability of other banks. On the 6th

of October the Parliament passed the

Emergency Act which led to the creation of new nationalized banks. The emergency

act didn‟t provide a bailout program for the indebted banks resulting in them

defaulting on their loans (Organisation for Economic Cooperation and Development,

2011).

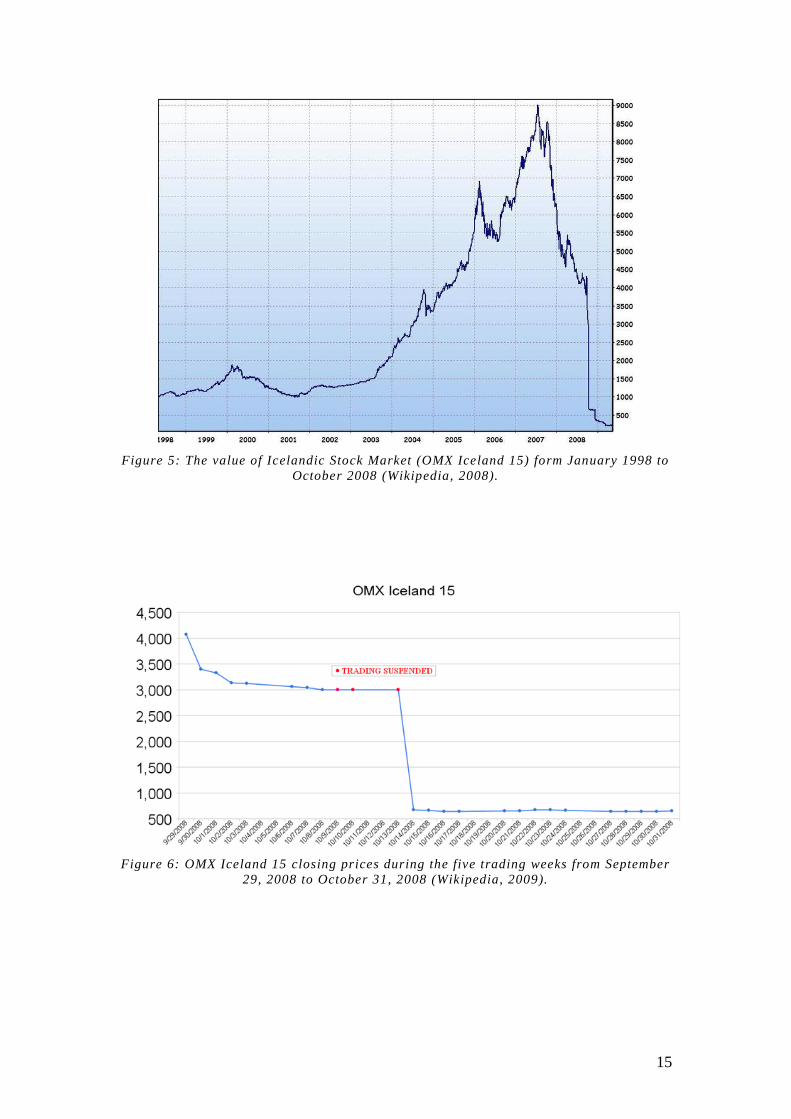

15

Figure 5: The value of Icelandic Stock Market (OMX Iceland 15) form January 1998 to

October 2008 (Wikipedia, 2008).

Figure 6: OMX Iceland 15 closing prices during the five trading weeks from September

29, 2008 to October 31, 2008 (Wikipedia, 2009).

16

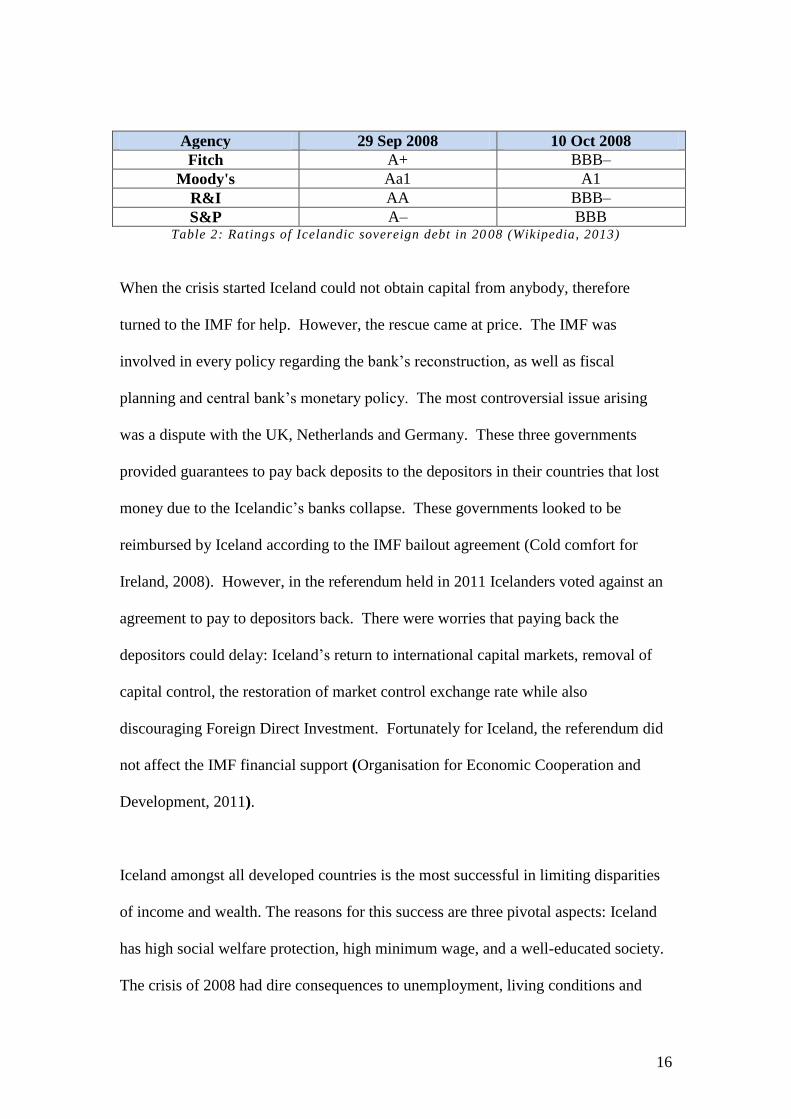

Agency 29 Sep 2008 10 Oct 2008

Fitch A+ BBB–

Moody's Aa1 A1

R&I AA BBB–

S&P A– BBB Table 2: Ratings of Icelandic sovereign debt in 20 08 (Wikipedia, 2013)

When the crisis started Iceland could not obtain capital from anybody, therefore

turned to the IMF for help. However, the rescue came at price. The IMF was

involved in every policy regarding the bank‟s reconstruction, as well as fiscal

planning and central bank‟s monetary policy. The most controversial issue arising

was a dispute with the UK, Netherlands and Germany. These three governments

provided guarantees to pay back deposits to the depositors in their countries that lost

money due to the Icelandic‟s banks collapse. These governments looked to be

reimbursed by Iceland according to the IMF bailout agreement (Cold comfort for

Ireland, 2008). However, in the referendum held in 2011 Icelanders voted against an

agreement to pay to depositors back. There were worries that paying back the

depositors could delay: Iceland‟s return to international capital markets, removal of

capital control, the restoration of market control exchange rate while also

discouraging Foreign Direct Investment. Fortunately for Iceland, the referendum did

not affect the IMF financial support (Organisation for Economic Cooperation and

Development, 2011).

Iceland amongst all developed countries is the most successful in limiting disparities

of income and wealth. The reasons for this success are three pivotal aspects: Iceland

has high social welfare protection, high minimum wage, and a well-educated society.

The crisis of 2008 had dire consequences to unemployment, living conditions and

17

provided uncertainty about the future but these results were mitigated in a short time

(Khan, 1999).

In 2008 Iceland lunched criminal investigations which led to convictions of several

prominent figures of the political and business sectors. The change on political scene

was significant; centre right government was replaced with centre left coalition.

However, in 2013 election centre right coalition returned to power.

Since mid-2012 Iceland is the IMF‟s success story. The country has two years of

economic growth, the rate of unemployment is down to 6 % and exports became more

competitive due to currency devaluation. In 2013 Iceland won disputes with the UK

and the Netherlands. The EFTA Surveillance Authority cleared Iceland from the

obligations of repaying disputed deposits. Without the IMF‟s help and international

cooperation, the country would not be able to restore its economy in such a short time.

6. Greece

In order to bring Greece‟s public finance under control a 110 billion rescue package

was introduced by the IMF, European Union (EU) and the European Central Bank

(ECB) in 2010. Austerity measures included cuts in in the form of: education, income,

health care, public services, accompanied by an increase in direct and indirect taxes

(Matsaganis, et al. 2010). Standard VAT went up from 19% to 23% and VAT on fuel

increased by 30%. Lower pension benefits were also established with the retirement

age increasing to 65 years. Greece has lost 25% of its GDP since the bailout.

18

The austerity measures have created more unemployment in certain regions and

people have been forced to move to bigger cities in search of jobs. Moreover, many

people had no choice but to move from private healthcare into the public domain,

which had already suffered 40% cuts due to restrictions imposed by the troika.

(Kentikelenis, et al. 2011). The cuts and unbalanced redistribution of resources in

Greece have widened the inequalities between the classes, decreasing living standards

in certain classes (Venieris 2013).

The Greek example shows that social policies have failed, and inequalities have

become the highest in the history of the country. Venieris (2013) claims that the

problems in Greek society are streaming from the promotion of individualism over

collectivism. The promotion of individualism has hugely influenced the lives of the

poorest and most vulnerable in society who are basically being victimized by right

wing economies supported by the IMF and the „troika‟. The group agrees with

Culpitt (1999) who stated „However, it is the economic liberalism of the radical right

that has generated the risk to society in order to consolidate its own ideological

hegemony by defeating the concepts and values of the classic welfare era‟. Moreover,

Hogg & Baines (2011) noticed that expanding responsibilities for welfare services

reflect tension arising in the most developed economies in Europe.

The following statement shows that the austerity measures enforced were not

correctly explored: „Crisis‟s social policy in Greece is defined by market imperatives

and EU/IMF directives, which neglect or appear to have little understanding of

reality‟ (Venieris, 2013, p.41). Matsaganis (2012) stated that „the need for social

protection is now much greater than any before‟ because it prevents demographic

shrinking and brain. Additionally social protection prevents child poverty and

19

supports women‟s participation in the labour market in order to escape household

poverty (Venieris 2013). However, as a result of the bailout process, many collective

bargaining laws have changed in order to “increase” flexibility, and competitiveness

of labour at the cost of decentralization of the welfare state.

Even though some attempts were made to introduce benefits to vulnerable people by

the Greek government, EU-IMF pressure soon interrupted the process in early 2010

(Venieris, 2013). The research conducted by Manos Matsaganis (2013) stated that the

poorest households lost 8.7% of their income, the middle class households 9.5% and

upper class households between 10.1% - 11.6%. Nonetheless, the impact of these

measures does not affect the poor equally to the upper class, as the poorer had to give

up a higher proportion of their income pushing them closer to poverty. Moreover, the

labour market creates diminishing rights for employees whilst giving employers more

rights (Venieris, 2013).

An increase in poverty and inequality rates has reached a level unseen since 1945

(Toxo and Mendez, 2013). From the upheavals that occurred in Greece it seems that

stability packages work in only one direction, where societies are suppressed by the

attacks of financial capitalism that undermine the welfare state. From this we can

conclude that the political risks continue to pose a threat to democracy.

Unfortunately, the current situation in Greece is far does not pose remedies to tackle

inequalities and prevent increased poverty in the future (Papadopolous and

Roumpakis, 2012). ”So far, the Greek government´s response has been inadequate

(Matsaganis 2011). If social change will not be in major focus, Greece can be

brought back to Balkan misery with deepening economic upheaval that can transform

into a far deeper social crisis (Venieris, 2013).

20

7. Russia

During the last years of the Soviet Union it became obvious that the country was in

need of deep economic and political reforms. Its foreign debt reached approximately

$150 billion and the Soviet government applied for IMF membership. However, the

IMF didn‟t grant Russia full membership because it was obvious that the country

would heavily use the organisation‟s resources.

In 1991, with the break-up of the Soviet Union, Russia was granted “associated

membership” of the IMF on the basis that they would receive advice and technical

support (without the facility of IMF credit). This period in Russia was characterized

with massive unemployment, corruption and crime. Centralized distribution of

material recourses was broken to the point that it led to a food supply crisis. The

budget deficit was approximately 30% of GDP, inflation rate reached 90% and so the

only source the Russian government had to cover the deficit was IMF‟s and World

Bank‟s funds. The IMF implemented a radical program in Russia which included tax

increases, spending cuts, the privatization of state-owned enterprises and the

preservation of common ruble zone. As Gaidar (1997) claims in his article “The IMF

and Russia”, the attempt to maintain the ruble zone in the Post-Soviet zone was

biggest mistake made by the IMF during its work with Russia, as the lack of

coordination between former Soviet Republic banks was evident (Gaidar, 1997).

Finally, 6 months after the reform was implemented the IMF started lending to Russia

($1 billion). However, domestic, political and technical conditions for stabilisation

were ruined at that point and reforms were put under threat (Gould-Davies, Nigel and

Woods, Ngairi, 1999).

21

In 1992, there were some signs of stabilization of the budget. In certain months the

fiscal deficit was less than the recommended 5% of GDP. Moreover, at times there

was a slight decline in inflation: in October 1992 inflation fell to 40% (however in

November increased to 66%). During this same period a new class emerged

(oligarchs) that had a close relationship with President Yeltsin and hence had a great

influence over him. The oligarchs conflicted with parliament, as they strongly

opposed the reforms, as well with the idea of tax increases (Gould-Davies, Nigel and

Woods, Ngairi, 1999).

In 1993, the IMF urged Russia to fight inflation and cut subsidies for state-owned

enterprises. Russia failed to reduce inflation; however, Russia received the first

tranche of so-called Systemic Transformation Facility (STF) valued at $1.5 billion.

The STF was a new experiment for the IMF and, unlike other facilities, had no

standard conditionality.

In 1994, the IMF complained to Russia for its loose monetary policy and did not want

to provide more credit. However, G75 countries and especially the United States,

advised to issue the loan and Russia received the second tranche of the STF payments,

this time $1.5 billion.

In 1995 Russia received $5.5 billion of stand-by credit with the condition of

decreasing inflation by 1% monthly with a view to reduce inflation to 6.5%.

Although Russia was not able to reduce inflation as it was planned, the deficit was

reduced to 4% in 1996, 3% in 1997 and to 2% in 1998. The IMF was satisfied with

the results and was issued credit every year following. Then Russia, in turn, began to

22

repay the debts and in 1996 returned $0.5 billion (Gould-Davies, Nigel and Woods,

Ngairi, 1999).

However, the political and economic conditions in the country were still severe. There

was particularly unfair privatization of enterprises and tax avoidance by the group of

oligarchs eventually led to a financial crisis in 1998. Up to this point Russia amassed

loans of $6.2 billion from the IMF and had re-paid just $0.9 billion. Its foreign debt

amounted 146% of GDP.

In 1999, the IMF discussed the possibility of overcoming the crisis and Russia

received new credit of $640 million. Shortly after this, The G7 decided to stop

providing credit to Russia (Gould-Davies, Nigel and Woods, Ngairi, 1999).

During 2004-2008, due to an increase in revenue from Russia's oil exports, the

improvement of tax legislation and an increase in world prices for raw materials, the

national debt rapidly declined.

In 2006 Russia repaid all debts to the IMF before the appointed time. According to the

World Bank and the IMF‟s report, there was no serious threat to Russia‟s

macroeconomic stability. Russia‟s total foreign debt in 2013 equals $50 billion, or 5-

10% of GDP - one of the lowest in Europe.

23

8. Conclusions

The IMFs current structure prevents developing countries from having any significant

influence in the decision-making process, which results in undemocratic rule

throughout the organization. In Ireland, the IMF loan agreement is based on

expenditure cuts rather than job creation and economic stimulus. In Greece stability

packages undermine the welfare state with political risks posing a threat to

democracy. It can be commonly seen that when IMF‟s austerity measures are

imposed, the poor are more affected than the rich further widening the gap between

the classes. In Russia on the other hand, the IMF was too slow in offering assistance

and it failed to foresee the dangers of a common ruble zone.

Regardless of the negatives mentioned above, the group believes that the International

Monetary Fund is a force for good in the world and with some policy re-adjustments

has the potential to be a great one. The IMF through its lending, surveillance and

assistance is able to play a vital role in the world, but its structure and policies need to

be updated in order to target/help each country individually and implement custom

measures.

Reforms into how the fund‟s quotas are calculated should be the top priority if the

IMF wants to be seen as trustful and respected organization. Emerging economies

should be given more influence on the fund‟s decisions. Rich economies should be

prepared to give up some power in order to unify with developing countries.

The IMF should be a force of good that is fair in its actions. This unfortunately has

not always been the case. In 1981 the US had a greater wealth than any other nation

24

($140 Billion in foreign assets). However, the US began to spend more than it had

and by 1990 its national debt increased to $1.23 Trillion (Burau of the Public Debt,

2012). The Federal Reserve System (fed) began to print money to cover the US‟s

deficit and devaluated its currency in order to increase exports. In normal

circumstances the IMF aids countries with balance of payments problems. However,

the IMF would not prepare an adjustment plan for the US as the IMF itself is an

instrument of the G5 which is led by the US. Therefore an adjustment plan to the

world‟s largest debtor (US) would lead to the international financial system‟s

destabilisation.

Too often it seems that the IMF has little knowledge of the country it‟s focused on

and acts as creditor/bank. The IMF should look at a country as a collection of

individual people with different needs rather than focusing on dehumanized methods

of country debt reformation. Each country in need of assistance from the IMF should

be examined socially, politically and economically with the regards to the country‟s

history, demographics and mentality. The IMF‟s system should focus on healthcare,

education and housing and have view of tightening the inequalities between classes.

25

9. References

Brada, J., Kutan, A. and Vuksic, G. (2011) The costs of moving money across borders

and the volume of capital flight: the case of Russia and other CIS countries. Review

of World Economics, 717-743.

Brown, B. (2010) „From free state to failed state‟. New Statesman, 30-33, Available:

http://www.newstatesman.com/economy/2010/12/ireland-state-irish-party [Accessed

27 October 2013].

Bureau of the Public Debt (2012) „Government – Historical debt outstanding‟.

Available: http://www.treasurydirect.gov/govt/reports/pd/histdebt/histdebt.htm

[Accessed 6 November 2013]

Burke, M. (2011) „An insecure future: Who benefits from the crisis in Ireland?‟

Soundings, Issue 47, 130-142.

Central Statistics Office (2013) „Population and Migration Estimates‟, Available:

http://www.cso.ie/en/releasesandpublications/er/pme/populationandmigrationestimate

sapril2013/ [Accessed 10 November 2013].

„Cold comfort for Iceland‟ (2008) The Economist, 21 November. Available:

http://www.economist.com/node/12666594 [Accessed 18 October 2013].

Country Watch Incorporated (2013) Iceland Country Review, Political Conditions, 1-

15.

„Dawn in the west‟. (2013) The Economist, 6 January. Available:

http://www.economist.com/news/leaders/21569034-why-irish-deserve-helping-hand-

leave-their-bail-out-programme-dawn-west [Accessed 28 October 2013].

European Commission. (2012) „Ireland‟s economic crisis: how did it happen and what

is being done about it?‟ Available:

http://ec.europa.eu/ireland/economy/irelands_economic_crisis/index_en.htm

[Accessed 29 October 2013].

Forbes, S. (1998) „Fact and Comment‟. Forbes, 21 September, 162(6), 31-32.

Gaidar, Y. (2002). The IMF and Russia. The American Economic Review, 87(2), 13-

16.

George, S. (1988) A fate worse than debt. England. Pelican Books.

Gould-Davies, N. and Woods, N. (1999) Russia and the IMF. International Affairs

(Royal Institute of International Affairs 1944-), 75(1), 1-21.

Grozelier, M.A., Hacker, B., Kowalsky, W., Machnig, J., Henning, M. and Unger,

B.(eds) (2013) Social Europe Report. October 2013.

26

IMF. (2013) Russia Rebounds. Available:

http://www.imf.org/external/pubs/nft/2003/russia/ [Accessed 4 November].

Jansen, J. (2013) „IMF gives Ireland mixed review in latest report card‟. World News,

Available: http://www.breakingnews.ie/ireland/imf-gives-ireland-mixed-review-in-

latest-report-card-608133.html [Accessed 30 October 2013].

Khan, S. R. (1999) Do World Bank and IMF Policies Work? New York.

Iceland Country Profile (2013) Social Landscape. Market Line, a Data monitor

business. 53-58.

Kinsella, S (2012) Is Ireland really the role model for austerity? Cambridge Journal

of Economics, 36(1), 223-235.

Kinsella, S. (2010) Understanding Ireland’s Economic crisis. Prospects for recovery.

Blackhall Publishing.

Körner, P., Maass, G., Siebold, T. and Tetzlaff, R. (1987) The IMF and the debt

crisis. Germany. Zed Books.

Matsaganis, M. et al. (2010) Modeling the distributional effects of austerity measures:

The challenges of a comparative perspective. Athens University of Economics and

Business, ISER University of Essex. Research note 8/2010, 5.

Mayer, C (2012) The Irish Answer. Time International (Atlantic Edition), 180(16),

22-27. Available:

http://content.time.com/time/magazine/article/0,9171,2126069,00.html [Accessed 28

October 2013].

Monastiriotis, V. (2011) The Greek crisis in focus: Austerity, Hellenic Observatory

Papers on Greece and Southeast Europe, Recession and paths to Recovery. Special

Issue, July 2011, 8.

O‟Connell, H. (2013) „Ex-IMF mission chief: Ireland needs a new jolt of growth‟.

Business ETC, Available: http://businessetc.thejournal.ie/imf-ashoka-mody-austerity-

growth-budget-1099404-Sep2013/ [Accessed 30 October 2013].

Organisation for Economic Cooperation & Development 2011) OECD Economic

Surveys: Iceland, Assessment and Recommendations, 13-44.

Organisation for Economic Cooperation & Development (2011) OECD Economic

Surveys: Iceland, Restoring the financial sector to health, (22) 45-66.

Rigney, P. (2012) „The Impact of Anti-crisis measures and the social and employment

situation in Ireland.‟ European Economic and Social Committee Workers‟ Group.

Irish Congress of Trade Unions.

Rodney, W. (1972) How Europe underdeveloped Africa. England. Bogie-L‟Ouerture

Publications.

27

Torres, R., Rani, U., Curci, F. and Pelin, S.R. (2012) „Better jobs for a better

economy, World of Work Report‟. 34.

Toxo, I. F. and Mendez, C (2013) „The Social and Political Scope of EU Reform

Policy‟. Social Europe Journal, Available: http://www.social-europe.eu/2013/05/the-

social-and-political-scope-of-the-eu-reform-policy/ [Accessed 8 November 2013].

Venieris, D. (2013) „Crisis Social Policy and Social Justice: the case for Greece,

Hellenic Observatory Papers on Greece and Southeast Europe‟. April 2013, Paper

No.69, 6-36.

„What Angela isn‟t saying‟. (2013) The Economist, 10 August. Available:

http://www.economist.com/news/finance-and-economics/21583257-euro-zone-

rescues-have-left-sovereign-debt-too-high-be-sustainable-what-angela [Accessed 28

October 2013].

Wikipedia (2008) „OMX Iceland 15, The value of the OMX Iceland 15 from

January 1998 to October 2008‟. Available:

http://en.wikipedia.org/wiki/File:OMXI15.jpg [Accessed 5 November 2013].

Wikipedia (2009) „OMX Iceland 15 closing prices during the five trading weeks from

September 29, 2008 to October 31 2008‟. Available:

http://en.wikipedia.org/wiki/File:OMX_Iceland_15_SEP-OCT_2008.png

[Accessed 5 November 2013].

Wikipedia (2013) „Ratings of Icelandic sovereign debt (long-term foreign currency‟.

Available:

http://en.wikipedia.org/wiki/2008%E2%80%9311_Icelandic_financial_crisis

[Accessed 5 November 2013]