THE CAPITAL BUDGETING MANUAL - DiVA portal

27

THE CAPITAL BUDGETING MANUAL bY Esbj örn Segelod

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of THE CAPITAL BUDGETING MANUAL - DiVA portal

THE CAPITAL BUDGETING MANUAL

bY

Esbj örn Segelod

Abstract

There has been very many postal surveys of capital budgeting practice, but almost no studies of the writtenroutines that fix the practice of those groups that use a capital budgeting manual. This article tills this vacuum bydescribmg and analysing the capital budgeting manuals used by major Swediih groups, most of whom aremultinationals. Changes in the manuals during the last 30 years are studied using hvo earlier Swedish studies ofmanuals from the 60’s and 70’s. Comparisons are made with studies of capital budgeting practice from Anglo-Saxon countries.

1. IntroductionCompanies with a large volume of capital investment generally have a capital budgetingmanual. How these companies process and evaluate investments, i.e. specify the initial outlayand cash flow, use IRR or NPV, etc., is stipulated in the capita1 budgeting manual of theCompany.

The purpose of this article is to describe and analyse the tontent of capital budgetingmanuals used by groups of companies with their head office in Sweden.

An objection against a study of this kind might be that the results may orrly be valid forSwedish companies. However, that is not the case. Sweden has unusually many multination-als, some with several hundred companies and investments in a hundred different countries.The group language is English and the same manual is valid for all companies in the group. Itsets the rules of the game and provides the group with a tommon language with regard toinvestment issues. That also means that a multinational cannot deviate to much from standardpractice in Europe, the US. and other parts of the world. Those using the manual must be ableto understand it regardless of cultural background. They who have developed the manualshave therefore studied manuals from other European and American groups, and according tothem these groups have by and large had similar manuals, although tailored to the needs ofthese groups.

The structure of the article is as follows. First, we will survey earlier studies of capitalbudgeting practice by large firms, and give an account of the research methodology. Part 3 to8 Will describe the formal decision process as described in the manuals and, part 9 to 12, Willshow how investments are classitled, cash flow defined, the tut-off rate is fixed and whichprofitability criteria are used. Finally, we Will end the article by analysing the development ofthe capital budgeting manual during the last 30 years and state a few conclusions concemingthe use and role of capita1 budgeting manuals.

2. Earlier research on capital budgeting practiceMost large groups have written administrative routines for capital investment matters. Themost commonly used term for this document is perhaps the capital budgeting manual,although both American (Mukherjee, 1988) and Swedish groups use many different terms forthis document as well as for other topics treated in the manual. There is considerableterminologital tonfusion. Even the term capital can be a little misleading as many companies

1

use the manual also for expenses and intangible investments. In these cases investmentmanual might be a more correct term.

Pike and Wolfe (1988) found “that 84 per cent of respondents claim to have an up-to-date investment manual” (p. 44). In 1975 that figure had been 65 per cent (Pike, 1982; Pikeand Wolfe, 1988). Mills (1988) and Mills and Herbert (Mills and Herbert, 1987) could in theirpostal questionnaire and interview study conclude that

[flurthermore, these interviews revealed that the techniques required to be used and theimportante assigned to them were usually specified within the capital budgeting manual.(Mills and Herbert, 1987, p. 77)

Strangely enough there are very few studies of written routmes for capital budgeting. Instead,there are a great many postal surveys of capital budgeting routines. For a few recent examplesfrom Australia see (Lilleyrnarr, 1984; Freeman and Hobbs, 1991), from Canada (Blazouske,Carlin and Rim, 1988), from New Zealand (Patterson, 1989), from Sweden (Yard, 1987;Andersson, 1988), from the U.K. (Scapens and Sale, 1981; Scapens, Sale and Tikkas, 1982;Jones, 1986; Mills and Herbert, 1987; Pike, 1982; Pike and Wolfe, 1988), from the U.S.(Oblak and Helm, 1980; Rosenblatt, 1980; Bavishi, 1981; Hendricks, 1981; Moore andReichert, 1983; Kim, Crick and Farragher, 1984; Stanley and Block, 1984; Farragher, 1986;Reichert, Moore and Byler, 1988; Cooper, Comick and Redmon, 1992). For a few recentreviews of surveys of practice see (Gumami, 1984; Klammer and Walker, 1984; Scott andPetty, 1984; Canada and Miller, 1985; Mukherjee, 1987; Mukherjee and Henderson, 1987).

There are also some interview studies, but these have been fewer, especially during thelast two decades. For a few recent British examples see (Mills and Herbert, 1987; Wilson,1988), for an American example (Ross, 1986) and for Swedish examples (Gandemo, 1983;1992; Arwidi and Yard, 1985; 1992; Segelod, 1986). A minority of studies have as (Segelod,1986; Mills and Herbert, 1987; Yard, 1987) combined postal questionnaires and interviews.Furthermore, there are case studies of investment processes. See, for instance, (Aharoni,1966; Ackerman, 1970; Bower, 1970; 1972; Carter, 1971a; b; Ring, 1975; Lumijärvi, 1991a;b; Sahlin-Andersson, 1992) that show how capital investments are championed and evaluatedin companies and groups.

Turning to the capital budgeting manual the amhor has only been able to identify foursuch studies, two American and two Swedish ones. The fiist was conducted by Istvan (1959;1961a; b) more then 30 years ago. He interviewed finantial executives and studied capitalbudgeting manuals in forty-eight large American companies.

A more recent study has been made by Mukherjee (1988). He sent a request to Fortune500 companies ‘to send documents pertaining to their capita1 investment policies and proced-ures’, but he only received sixty complete manuals. Provided that all 500 companies had amanual that means a response rate of 12 per cent.

2

Turning to the Swedish language area there are two major studies of capital budgetingmanuals of Swedish companies. The furst one was carried out by Renck (1966), who in 1964collected manuals from twenty-eight larger Swedish companies. In 1977 this study wasreplicated by Tel1 (1978) who collected manuals from thirty large companies of which twentyhad been included in Renck’s initial study. For a review of Swedish empiri& research oncapital investment see Segelod and Hägg (1992).

Besides these four studies Weaver (1974) has presented the capital budgeting manual ofICI United States and other researchers (Istvan, 1961a; Renck, 1966; Bower, 1972; Tell,1978; Claesson and Hiller, 1982; Mukherjee, 1988; Wilson, 1988) examples of projectevaluation forms, and Marshuetz (1985) the administrative routines of American Can forallocating capital. Marshuetz description accords fairly well with many of the groups studiedin this study, while Weaver’s manual belongs to a Company with large staff units, somethingthat is rare in present-day Swedish groups. Another kind of studies that should be mentionedin this connection is Eliasson’s (1976), Goold’s and Campbell’s (1987) and Lorange’s (1993)studies of administrative routines in large companies for plantting and control.

3. Research methodologySwedish industry has through acquisitions and divestments been considerably restructuredduring the last fifteen years. Of Renck’s (1966) twenty-eight groups twenty remained in 1977,and Tel1 (1987) was therefore obliged to supplement Renck’s population of companies withten new large groups. In 1990 only ftiteen groups remained of which several had been greatlyrestructured. It was therefore considered better to study a cross-section sample of largerSwedish groups quoted on the Stockholm Stock Exchange in 1990, than to concentrate on theoriginal groups.

With some knowledge about which groups could be expected to use a capita1 budgetingmanual, a request for a copy was sent to all fifty-four groups classified as engineeringindustry (including the electro-engineering and metal industries), chemical industry(including the pharmaceutical industry), forest industry and the category remainingcompanies (conglomerates and other groups difficult to classify). The sample excludedsmaller groups in these lines of business listed on the over-the-counter list.

The letter was addressed to the chief finantial executive of the group, and in accordancewith practice developed by Renck (1966) and Tel1 (1978) participsting companies werepromised anonymity. Those finantial executives who had not answered the setond letter wereall contacted by telephone whereby the response rate could be increased three times.

Thirty-four of the fifty-four groups used a group manual, although three were underdevelopment and still not approved. Another five had abandoned the group manual andallowed the divisions to develop their own manuals. Three of these groups supplied themanuals of their core business. Altogether, twenty-nine manuals were received.

3

This means that the study is based on 74 per cent of those groups that use a manual; 8 1per cent if we only take into consideration those groups that had an approved manual at thetime of the request. The most important reason for some groups not wanting to participate inthe study was that the finantial executive of the group did not want to supply an outsider withthis internal document. In spite of the restructuring of Swedish industry the manuals have asimilar division on lines of business as in the earlier studies, so also the non respondents (seeTable 1).

Table 1. Manuals dividedon line of business

1964 1977 1990 None responses

Engineering industry 15 18 15 X3)Chemical industry 2 2 3 l(l)Forest industry 3 3 5 l(1)Remaining companies 5 7 6 3~2)

All manuals 28 30 29 lO(7)

Note: Ten groups did not want to participate in the study. However, orrly seven of these tengroups had an approved manual at the time of the request.

The analysis of manuals was followed up by interviews in ninteen of the tifty-fourgroups, fourteen of which used a manual. These groups were selected by random numberfrom a list of the fifty-four groups stratified with regard to the market value of the groups.The interviews were conducted with the chief financial executive of the group, the corporatecontroller or another person responsible for the capita1 budgeting routines of the group. In1993 shorter interviews were held with the same people that had been interviewed earlier toinvestigate developments during the recession 1990-1993.

To be able to place the manual in a wider tontext additional interviews were conductedat corporate leve1 with finantial executives of fifteen groups in lines of business where capita1budgeting manuals are not necessarily used, as for instance, banks, shipping, trading, softwareand tonsulting fiis, and groups listed on the over-the-counter list. All interviews were taped,transcribed, and sent to the interviewees for tomments.

4. Which groups have capital budgeting manuals?Capital appropriation requests or investment requests are made in almost all companies, butfar from all companies have put these administrative routmes on paper and developed acapital budgeting manual. However, with some knowledge about the business areas of

4

Swedish industry it is not altogether difficult to guess which companies use a manual, andwhich do not. All larger groups with a large volume of fixed investment and many fixedinvestments have a manual, that is, the engineering, electro-engineering, chemical andpharmaceutical, forest, steel and metal, and power industries have such a manual, as well assome conglomerates and some of the construction and building groups.

Shipping companies are an exception. The reason being that all purchases and sales ofships are handled at corporate level. Consequently, there is no need for written routines thatmake it possible to decentrahse such decisions. Furthermore, some small independant groupsand companies of the above mentioned lirtes of business also lack a capital budgeting manual.

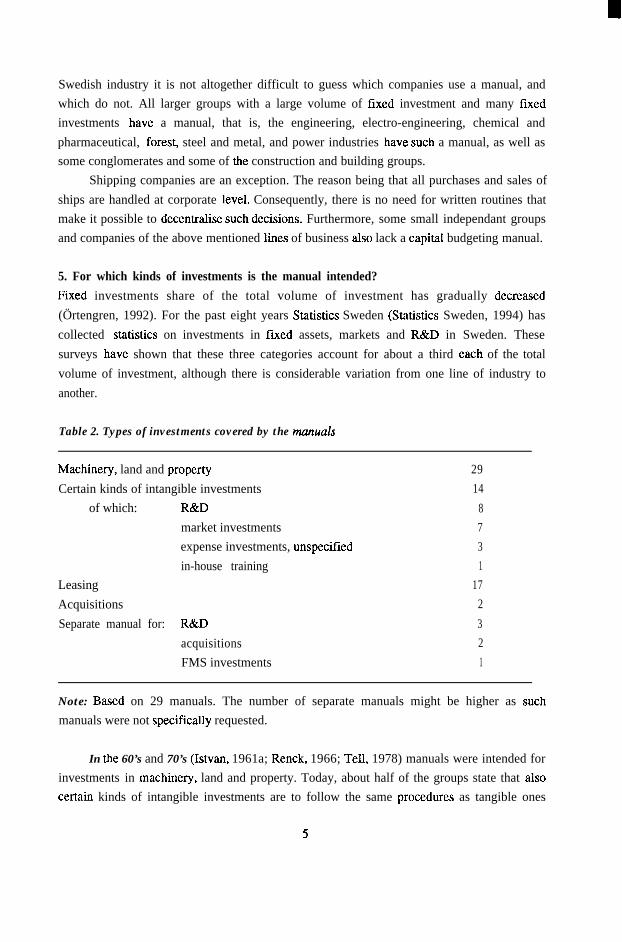

5. For which kinds of investments is the manual intended?Fixed investments share of the total volume of investment has gradually decreased(Örtengren, 1992). For the past eight years Statistics Sweden (Statistics Sweden, 1994) hascollected statistics on investments in fixed assets, markets and R&D in Sweden. Thesesurveys have shown that these three categories account for about a third each of the totalvolume of investment, although there is considerable variation from one line of industry toanother.

Table 2. Types of investments covered by the manuals

Machinery, land and property 29Certain kinds of intangible investments 14

of which: R&D 8market investments 7expense investments, unspecified 3in-house training 1

Leasing 17Acquisitions 2Separate manual for: R&D 3

acquisitions 2FMS investments 1

Note: Based on 29 manuals. The number of separate manuals might be higher as suchmanuals were not specifically requested.

In tie 60’s and 70’s (Istvan, 1961a; Renck, 1966; Te& 1978) manuals were intended forinvestments in machinery, land and property. Today, about half of the groups state that alsocertain kinds of intangible investments are to follow the same procedures as tangible ones

5

(see Table 2). Whether investment requests are also made for market investments and otherexpense investments is another issue. The interviewees have not seen many such requestscoming to them at group level.

Large groups with large investments in R&D have often developed manuals for suchinvestments. Moreover, some groups that have grown through acquisitions and havedecentralized the evaluation of acquisition candidates have developed manuals for thatpurpose. Thus, companies that regularly carry out a certain kind of investment tend to developwritten routines forthat type of investment.

6. Different routhes for different types of investmentsDepending on the size and character of the investment different decision procedures apply.Every group has several such routmes. Exactly how many depends on how one defines anindependent routine and whether business areas and divisions have developed separateroutines.

Most investments are small and medium-sized. They concem replacement of existingequipment, usually combined with technical improvements, cost reduction or capacityexpansion. Requests conceming major investments and investments in new lieids of businessare far less frequent.

All groups put higher demands on a capita1 budgeting request for a major investment,than for a minor one. They have one routine for small investments and one for large invest-ments, and often also one for medium-sized investments.

The capital budgeting manual is normally designed primarily for medium-sized invest-ments. It is for this category of investments that the manual is the most detailed, and somefirms have two forms; a project request form that summarizes the appraisal and a profitabilitycalculation form.

At least nine of the twenty-nine groups have supplemented their manual with a verysimple form of manual which in one to three pages specifies how and which informationshould be presented when a decision has to be made on the appropriation request by the groupboard. These instructions or models for group board requests apply for major investments andinvestment programmes, and it gives more room for qualitative data, then the traditionalforms used for minor and medium-sized investments. Istvan (1961a) terms tbis kind of form afree form, and the traditional one a fixed form. In some groups this free form is used for allrequests decided by the group board, in one group for all decisions made by Company boardsand business boards of the group, and in other groups to all investments above a certain limitof authorisation and in a few of the groups this limit is higher than the limit for decision bythe group board.

6

Already Renck (1966) noticed that additional manuals may exist at lower levels butneither he nor Tel1 (1978) mention anything about free forms, why the free forms seem tohave been introduced, or more correctly, reintroduced during the last fifteen years.

Thirteen of the manuals specifies a lower limit for when requests shah be made. Thatlimit varies between 2,000 and 100,000 SEK (10 SEK is approximately equivalent to 0). Inother cases this decision has been delegated to the divisions.

Five groups have different evaluation forms for replacement and expansioninvestments. The form for mplacement investments considers only costs and cost differentesbetween the new and the old machine.

The growing heterogene@ of some of the multinational groups has affected the invest-ment routines. Some groups have made the manual so general that it can be applied to allcompanies in the group and given the business areas or divisions right to develop their ownmanuals and capital appropriation procedures. The group manual then creates a frameworkfor manuals at lower levels of the group.

Three of the twenty-nine groups have taken yet another step and abolished the groupmanual altogether. In these three cases we are studying the manual of the core business areaof these three groups.

7. The purpose of the capital budgeting manualWhen Renck (1966) made his study Swedish companies had just introduced or started tointroduce capital budgeting manuals. Several of his interviewees pointed out that the proposerearlier was free to make the assumptions and choose the form of evaluation that he or shefound best. Guiding principles were therefore issued to guarantee that the requests containedthe factors considered important for an investment decision by the management. In this waythe request became more reliable as an instrument of decision support, and it also becamepossible to rank investments. When Tel1 (1978) replicated Renck’s surdy the motives werestill the same, i.e. uniform requests to support decisions on individual investments, andpossibly also to rank them.

Today the picture has changed (see Table 3). Twenty-two of the twenty-nine groupsstate the aim of the capita1 budgeting manual in the manual, and thirteen of these groups referto the same purpose as Renck and Tel1 observed. Almost equally many, or eleven manuals,say that the manual is important for strategic planning and control, four state that it isimportant for finantial planning and three for creating a tommon language within the groupwith regard to investments.

These changes became even more obvious in the interviews. The respondents atcorporate leve1 have especially stressed the importante of the manuals for finantial planning,strategic control and a unified language and system of rules for investments within the group.The last communicative purpose has especially been emphasised in those groups that have

7

grown through international acquisitions and in this way have become more heterogeneous.One should remember that some of the groups studied tonsist of several hundred companiesand can have investment requests from up to a hundred different countries. In such heteroge-neous groups written routines become important.

Table 3. Purposes of the capita1 budgeting manual

Unitary principles for evaluatingand ranking investments

Finaxial planningStrategic planning and controlCreate a tommon group language

136

113

Note: Based on twenty-two manuals. A manual can state more than one purpose.

The changes mentioned reflect, among other things, the transition from a functional to amultidivisional organisation. During the 60’s and 70’s many Swedish companies havedivisionahsed and decentralised their organisation. This is a process of decentralisation thathas taken place gradually over a longer period of time (Edgren, Rhenman and Skarvad, 1983),and a process that has continued during the 80’s. Former technical group staff units have beendecentralised to business areas or divisions, transformed into group companies or abolished.Today, only one of the larger companies has a functional organisation. In the other groups thecompanies have been organised in divisions and in the larger groups the divisions in businessareas.

In this connection it should be noticed that the manual fulfils different roles at differentlevels of a group. The manual is developed by somebody at corporate leve1 and written foruse at lower levels. ConsequentIy, it can be seen as an instrument of decentralisation andcontrol of decisions on investments.

Proposals of investments in buildings, vehicles, machinery and equipment are normallyinitiated by engineers at business leve1 (see e.g. Bower, 1972). Often, together with thecontroller of the Company, the engineer develops a capital appropriation request according towhat is stated in the capital budgeting manual. If the investment outlay is above the authoris-ation leve1 of the managing director of the Company, then he or she has to request forapproval by signing the request and sending it upwards for appropriation. During this processof selling the investment idea the request Will be scrutinized by staff units and decisionmakers at different levels which all have different interests to look after. A request thatrequires approval at corporate leve1 Will therefore in most groups have been scrutinizedseveral times.

8

The profitability of a capital investment is seldom appraised at corporate leve1 at leastnot in Swedish groups. It is assumed that the profitability has been evaluated at lower levels.More emphasis is placed on the total volume of investment, evaluating and controlling thestrategic direction of the investments and companies of the group, and coordinating invest-ments within the group to realise synergies. Not the least coordination seems to take up a lotof the time of many corporate managers responsible for investments.

8. The tontent of the capital budgeting manualThe manual statts how investments should be evaluated and a request designed, and containsone or several different investment requests, profitability calculations and follow-up forms.Almost all manuals also contain something about the formal decision process and delineationof amhormes, and seventeen of the twenty-nine manuals contain instructions on how thefigures requested should be worked out and forms filled in, and in a lesser number of casescheck-lists. The number of pages in the manual varies from three to sixty-four, with a medianof eighteen pages.

In the manuals from 1964 there was comprehensive material on how cash flowcalculations should be made, what distinguishes a new investment from a reinvestment, howdifferent profitability criteria should be calculated and the assumptions that they rest on.Thirteen years later this material had almost completely disappeared. Today, such material isonly to be found in a few of the earliest dated manuals. The manuals of today assume that theuser knows how to discount, and calculate the PBP, net present value (NPV), internal rate ofinterest (IRR), etc.

Twenty-five of the twenty-nine manuals were dated, and the median age of thesemanuals was one year. When Tel1 (1978) made the same control he recorded a median age offour years. The reason seems to be that most companies today update their decision processannually. Completely new manuals seem to be rare.

The capital budgeting manual is today often a part of the accounting, fmancial or thefinante and administration manual of the group. The American manuals that Mukherjee(1988) collected seem to have been detailed on the capital budgeting process. That isgenerally not the case with Swedish manuals. Such information is often found in the part ofthe finantial manual dealing with the budgetary control process.

All groups handle investment requests within the framework of the annual budgetarycontrol process. The interviews revealed that 68 per cent of the groups interviewed at groupleve1 only had a one year capita1 expenditure budget including several well-knownmultinationals. Three had a three year capita1 spending plan and three a five year plan.Studies of U.K. (Scapens and Sale, 1981; Scapens, Sale and Tikkas; 1982; Mills and Herbert,1987; Pike and Wolfe, 1988; see also Goold and Campbell, 1987) and U.S. (Hendricks, 1981;Scapens and Sale, 1981; Scapens, Sale and Tikkas, 1982) show that 80-85 per cent of major

9

U.K. and U.S. groups have a capital budget lortger than orre year, although the budget isdetailed orrly for the first year in about 85 per cent of these groups (Scapens and Sale, 1981;Scapens, Sale and Tikkas, 1982; Mills and Herbert, 1987). Thus, long term capital budgetsseem to be more tommon in the U.K. and U.S., than in Swedish and Japanese groups (Hameland Prahalad, 1986; Goold and Campbell, 1987).

In Swedish groups the investment budget is followed up three to twelve times a year atcorporate level, and the reviews have become more frequent in many groups during the lastfew years of recession. In fatt, today many large groups review their investment budget on amonthly basis.

In four groups the budgetary control process is preceded by a planning process in whichmajor investments and strategic initiatives are decided. The purpose is to improve strategiccontrol of the investments of the group.

Another group with large fiied investments has an investment committee that worksdirectly with the divisions on assessing the investment requests thereby giving corporatemanagement a tool for influencing their choices and for coordinating investments. Goold andCampbell (1987) would term three of these groups strategic planners. However, today mostlarge Swedish groups seem to emphases strategic control.

9. Delineation of authoritiesThe practice of delegating capital budgeting decisions below a certain sum is older than themanual itself (Heller, 1951; Renck, 1966; Faulhaber and Baumol, 1988). Most manualscontain information on such limits of authorisation, when a number of staff has to becontacted, and sometimes also on who is rcsponsible for what in the definition andimplementation of the investment. The larger investment expenditure that is requested, thehigher up the request needs to gain support. A detailed example from one of the manualsreads:

Investment amount Approval< 1 MSEK Subsidiary President1-5 MSEK Business Area President5-10 MSEK Chief Executive Officer> 10 MSEK Group Board of Directors

Twenty-four of the manuals state that the group has limits of authorisation and twenty-onestate the actual limit, that means that at least 83 per cent, or all but a few, of the groups setlimits. This is in line with statistics obtained for U.K. groups which have shown frequenciesof 85 per cent (Scapens, Sale and Tikkas, 1982) and 77 per cent (Mills and Herbert, 1987) andfor U.S. groups of 75 per cent (Istvan, 1961a) and 89 per cent (Scapens, Sale and Tikkas,1982).

The limit for when an investment needs a decision by the group board varies from 1 to50 MSEK (10 MSEK is approximately equivalent to £l M), and for the multinationals in the

10

sample from 5 to 50 MSEK. One group has tied the limit to the volume of investment and hastherefore a considerably higher limit. Many groups only specify when a request needsapproval from corporate leve1 or the group board, and delegates to lower levels to decide theirown limits and decision rules within the framework of the manual; “Limits for Business AreaMangers are set by the CEO.”

When Gandemo (1983) surveyed limits in fourteen major Swedish groups with largecapital expenditures the limit for divisional leve1 was on average 0.5 MSEK and for corporateleve1 3 MSEK. A little less than ten years later these limits were 5 and 16 MSEK respectively.It is only partly the same groups in both the studies but limits have no doubt been heavilyraised during the economic boom of the 80’s. The follow up interviews during 1993 showedthat this wave of decentralisation had ceased during the recession of 1990-1993. In fatt somegroups have found it necessary to tighten up their capital budgeting rommes.

Sale and Scapens (1982) found that “[o]n the whole, although ceilings increase withcorporate size, they do not vary with the nature of the project or the size or focus of thedivision” (p. 26). In especiaIly the Swedish engineering industry the opposite is usually true.

Most groups require all acquisitions to be decided by the group board, in some groupsonly acquisitions above a certain limit, and in some other groups also development projectsthat can alter the strategic direction of an individual business, the latter being an exceptionalso in many U.S. groups according to Mukherjee (1988). The reason for these exceptions isthat they do not want to delegate completely decisions on the strategic direction of thecompanies of the group, their business idea. They want to exercise strategic control.

Thirteen of the twenty-four groups that supplied information about their lirnits ofauthorisation have different limits for different kinds of investments or companies/divisions.And as most larger groups seem to allow their divisions to develop their own rules thenumber of groups with varying limits should be greater. It is especially the engineeringindustry that has lower limits for computer and telecommunication equipment. In additionmany manuals stipulate that a staff unit is to be contacted when investing in computers andtelecommunications, land and properbes, leasing, and finante of large investments, and in afew groups also types of investments specific to the line of business of the group.

It should also be mentioned that six groups have special routines for investmentprogrammes. Large investments and investment programmes must not be divided into sub-projects. The reason is that the board does not want to commit itself to contingentinvestments. However, only two manuals point out that investments must not be designed tohave a short payback at the cost of a short life and high cost of operation and maintenance, atrade-off that is very important to the economy of an investment (Segelod, 1986; 1992; Dixonand Duffey, 1990).

Istvan (1961a), Eliasson (1976), Scapens and Sale (1981), Scapens, Sale and Tikkas(1982), Gandemo (1983) and Mills and Herbert (1987) have noticed that not all companies

11

have fixed authorization limits. The interviews revealed one large multinational group thathas abolished its authorization limits.

Group executives are regularly informed about all major projects under investigation,among other things, by being represented on the business area boards, which are in tumrepresented on the Company boards. Therefore, the boards can decide which request needs tobe examened at a higher level. In this group it has been decided that a capital investmentdecision need not be referred upwards as long as the investment docs not alter the businessidea and strategies agreed on for the Company and the Company can finante the investmentitself. Therefore, a major investment need not necessarily be decided by the corporate boardeven if it is a billion SEK investment. On the other hand, it may be tbc case that smallinvestment expenditures for ventums in new areas have to be sent to the corporate board fordecision.

As should have been clear from this brief account, capital appropriation procedures arequite specific to the group. There are not two groups that have exactly the same routines. Themost complex routines are to be found in the engineering and electro-engineering industries.One reason is that these groups often invest more in markens or R&D than in machinery andbuildings. Another is that group staffs have been decentralised to such an extent that there isonly finante and accounting staff left and therefore in general no time to make separateappraisals. The issue is which decisions can be decentralized, and which require centralcoordination.

As a result of tbis process of decentralisation tbc more decentralized groups have placedmore emphasis on responsibility for the request and investment project. Some manualscontain detailed lists of who is responsible for what in the project definition, impetus andcontrol processes. Others urge all responsible decision makers to sign the request to take on apersonal responsibility for the decision and the request.

10. Classifying capkal investmentsAlready Dean (1951a; b) observed that companies classified investments and discussed indetail different classification systems. Classification systems are rarely discussed by theoretic-al economists, but more often by practitioners. However, there does not seem to be anyagreement on the basis for such a classification system. Piper (1980) who surveyed classifi-cation systems proposed in the literature found thirteen different bases for the various systemsproposed.

Tell (1978) found that the average manual classified investments into four classes.Today, twenty-four of the manuals classify investments and there are on average eight classesper manual: the median being six. It is unclear why the number of classes has doubled, but itilluminates the popularity of this practice difficult to justify from a theoretical point of view.

12

It is difficult to general& about classification systems as no group uses exactly thesame system. However, there seem to be two different bases for classification, and one reasonfor the number of classes being so many is that some groups combine these two bases.

First, we have the distinction between, on the one hand, replacement or upholdinginvestments, and, on the other hand, investments in new capacity, products and markens.Already Istvan (1961a) noticed this division and found that most companies used it. Allclassification systems express this distinction in one way or another, between what could beternred operative and strategic decisions.

Setondly, we have systems that categorise investments with regard to functions as, forinstance, computers, land and property, machinery, training, etc. Most groups emphases thatonly orre alternative can be marked with a cross, a few that several can be crossed.

Only one of the manuals give a reason for classifying investments and it stams that thesystem Will ‘provide Group Management and the Board of Directors with a uniform basis fordecisions’ and ‘also provide possibilities of assessing risk and uncertainty and a better basisfor ranking of priorities’. However, the interviews reveal that their are no statistics on howmuch the group as a whole invests in the different classes.

If categories are not budgeted, at least not on corporate level, it seems probable that animportant purpose of classification systems is to communicate information about investments.Management knows the categories of the form and that helps them in fornring an opinionabout the strategic direction and significance of these investment& that is, to exercise strategicand finantial control when budget tuts have to be made. One should also remember that suchsystems are used for small and medium-sized investments, investments that are summarizedon one piece of paper. Requests for large investments are in many groups presented on a freeform without such a system of classification.

11. Definition of cash flowFremgen (1973), Gitman and Forrester (1977) and Patterson (1989) could conclude that

[t]he respondents also indicated that the most difficult and most important stage of theprocess involves the definition and estimation of cash flows. (Gitman and Forrester, 1977,p. 70)

The initial outlay is for most types of investments much smaller than the discounted costsduring the life of an investment. The estimation of cash flow is therefore of key importantebut this is also the area in which the manuals are most vague and varying.

According to theory the appraisal should rest on payments and receipts. In reality.twelve out of twenty-nine groups state mat the proposer should consider costs and revenues,equally many are vague on this point, and only in the forms of ten of the manuals arepayments and receipts treated separately. Six of these manuals also present a list of items matshould be considered. Fourteen only ask for the payments minus receipts and the additional

13

five do not specify the items of the cash flow at all. However, thirteen manuals emphases thatall assumptions made have to be made explicit.

Initial outlay is in all manuals, in one way or another, defined as expenditures related tothe project, that is, also certain expenses should be considered as investment expenditures,which varies from manual to manual. This is a change from earlier studies (Istvan, 1961a;Renck, 1966) when investments by most fnms were detined in accounting terms.

Twenty-two of the manuals take working capital into consideration. Twelve of thesemanuals consider these payments in the estimation of initial outlay and salvage value, eighttreats them as yearly payments, and two as a rent.

Twenty-three groups use economic life, commonly determined by practice andguidelines for depreciation. A smaller number of groups have specified a period ofcalculation, but orrly ten calculate a salvage value.

Many manuals am, contrary to what Mukherjee (1988) found, very brief when theydescribe how the cash flow should be estimated, and some are also vague and ambiguous. Themanuals of today are couched in more general terms then those manuals Renck (1966) andTel1 (1978) analysed. One explanation can be that many decisions related to the capitalbudgeting process have been delegated, and in many groups business areas and divisionsallowed to fix their own procedures. In these groups the group manuals are meant to serve asa framework for investments of various kinds and in different businesses and for manuals onlower levels of the group.

12. Profitability criteriaThe most researched issue within empirital research on capital budgeting is the use ofdifferent protitability criteria. Table 4 shows our contribution to this tradition.

Table 4 shows that ninety-three per cent of the groups, that is twenty-seven out oftwenty-nine, use either an IRR or capital value (CV) based method for some of theirinvestments. Two smaller domestic market based machinery groups did not use a DCFtechnique.

There have been certain changes. The NPV criterion has become increasingly popular,although not as popular as the table may give an impression of. Some of the groups that usethe IRR use the NPV or the profitability index to interpolate the correct IRR. Both criteria arerequested an their forms, but one can suspect that the IRR is the important criterion for thesegroups.

Another criterion that according to the table has become more popular is the PBP.However, it may also be the case that the payback criterion earlier has been used without thatbeing stated in the manual. Today, the criterion is used both as the only criterion forinvestments below a certain limit, and for medium-sized and major investments as asupplement to another criterion.

14

Table 4. Frequency of difSerent projitability criteria

1964 1977 1990191

Payback 7 9 87 100

Simple payback 4 6 60 7 9Discounted payback 32 27 28Simple payback only n.a. 7 7

IRR or capital value methods 62 93 93

IRR methods 5 4 53 45

IRR 50 50 45True IRR 4 3 0

Capital value methods 68 n.a. 7 2

NPV 11 33 55Terminal value 0 0 3Profitability index 14 20 21Annuity 25 10 14

Annuity index 7 10 7MAPI 11 10 3

ARR 4 3 0

Break even analysis 0 0 3

No specific criterion mentioned 0 0 3

Note: Based on Renck (1966), Tel1 (1978) and the forms and manuals of 29 groups. The totalpercentage sum is larger than one hundred because most groups demand different criteria fordifferent kinds of investments and more than one criterion to be presented.

The user frequency for DCF techniques is high compared to most studies from Anglo-Saxon countries. That is especially true for the figures from 1964 and 1977. Does this meanthat Swedish groups use more advanced investment criteria. Probably not because these areall groups that use an capital budgeting manual.

15

Setondly, it can be observed that the average rate of return (ARR), which is one of themost frequently used criterion in all Arrglo-Saxon countries (regarding Australia see (e.g.Freeman and Hobbes, 1991), Canada (Blazouske, Carlin and Kim, 1988), New Zealand(Patterson, 1989), the U.K. (Pike and Wolfe, 1988), and the U.S. (Rosenblatt and Jucker,1979; Klammer and Walker, 1984; Canada and Miller, 1985), is rare as an investmentcriterion in Swedish groups.

13. Profitability requirementsThirteen of the manuals specify how the cost of capital or tut-off rate should be calculated.None of them uses exactly the same formula, although the formulas reveal one distinctdifferente between multinationals and the less multinational groups.

Theory advocates (Copeland and Weston, 1979) firms to use tbc weighted average costof capital (WACC), and multinationals to differentiate their hurdle rate with regard to country(Shapiro, 1988). Seven of the more multinational groups also use different rams of interest forcompanies in different countries. However, they all use an interest rate determined by the costof borrowing in lotal currency and four of the companies add a risk premium. Two havetaken still another step by calculating a weighted average cost of capital. In 1977 only one ofeight groups used different rates for different companies. At this time about 50 per cent of tbcU.S. multinationals used differentiated rams (Hendricks, 1981; Oblak and Helm, 1980).

The less multinational groups all use a unitary rate for the whole group calculated as anaccounting-based weighted average cost of capital. However, as said before, none of them useexactly the same formula. The weighted average cost of capital is the most tommon measurein the U.S. (Oblak and Helm, 1980; Hendricks, 1981; Gitman and Mercurio, 1982), and thenumber of ways in which it is calculated are many also there (Gitman and Mercurio, 1982).

The interviews showed that a further four multinational groups had abandoned thegroup rate, however, without issuing any guidelines on how the rate was to be calculated. Thereason for these groups not to fix a rate was claimed to be that preconditions changed sorapidly, that group management did not want to fix the rate for requests that needed groupleve1 decision. How the rate of interest should be calculated and which rate to use was left tolower levels to decide.

Also the payback criterion is used flexibly. Three factors have especially been pointedout in manuals and interviews; economic life, country and strategy. If the investment isexpected to have a long life or is central to a strategy then a longer payback can be accepted.Seven to eight years have sometimes been accepted for major investments, although one and ahalf to three years is normal for small and medium-sized investments, shorter in times ofcapital shortage. It is tommon to demand shorter payback for investments in polititallyunstable countries. Longest payback is accepted for investments in Japan, North America and

16

Western Europe. However, if a subsidiary wishes to invest in a country affected by a civil warthe Company must present a very good reason.

14. The evolution of the capkal budgeting manualFirms have always invested, but it is only during the last thirty to forty years that DCFcalculations have been used with some regularity. Still the technique of discounting has beendescribed as early as 1319 (Faulhaber and Baumol, 1988) and its use as a tool for evaluatinginvestments developed in the mid 19th century by German forest economists (see e.g.Faustman, 1849). Industry long regarded DCF as of only theoretical interest and Heller (1951)described managers’ hesitation to introduce the simple PBP instead of subjective judgements.

Some type of formal cost-savings or payoff calculation is increasingly used by the TwinCities firms. . . .

Yet some managements resist these ‘fancy formulas as a basis for their decisions,giving such reasons as: ‘We rely on the judgment of the operating people,’ or ‘There are somany intangibles that the computation is misleading,’ or ‘We don’t have enough funds to domore than replace the machines that are obviously ready for the scrap heap.’ (Heller, 1951,p. 100-101)

Firms that wanted to be still more sophisticated introduced DCF methods in the mid-to-late50’s (Ashton, 1962; Canada and Miller, 1985), and it was probably also then the furstcompanies developed capital budgeting manuals (Renck, 1966). Early Swedish and U.S.(Canada and Miller, 1985) adapters of the DCF technique have often chosen the IRR, lateadapters the NPV. Thus who found this to be a too large step to take made a detour viadiscounted PBP. However, the ARR has never been popular in Swedish groups.

Today, many companies have different routines for small, medium-sized and largeinvestments or investment programmes. For small investments it is enough to calculate thePBP. Medium-sized investments demands a more detailed request. The requirements are PBPplus discounted PBP or IRR or a capital value method. It is these requests that are mostformalised and one can claim that the manuals in many lines of business are primarily writtenfor medium-sized investments. The request is usually summed up on one form and piece ofpaper and the calculations sometimes on another form. In addition, some companies havedifferent forms for replacement and expansion investments. When deciding on replacementinvestments only the cost side is compared. In a few groups special forms also exist for buy ormake, buy or lease, land and property, computer and communication equipment, research anddevelopment, and acquisition.

Large investments and investment programmes demand the PBP plus IRR or NPV to becalculated. Several groups have developed special routmes and free forms for theseinvestments, instructions mat stress qualitative data. In some groups the same principles ofevaluation apply for these investments, others have developed partly different requirements or

17

leave much of this to the investigator and allow him or her to adjust the request to thecharacter of the investment decision.

Preconditions are often different for investments in different business areas. Somegroups have chosen to meet this challenge by making the manual less specific and aframework for possible administrative procedures and manuals that individual business areasand divisions choose to develop. A smaller number have taken a further step and abandonedthe group manual. As could be seen this also applied to the determination of the cost ofcapital or tut-off rate.

’ When comparing manuals from different lines of business those from forest and steelgroups reveal many similarities. These companies often invest 10 per cent of sales in newmachinery and buildings, and their manuals are fornred to fit those large investment projectsthat these companies regularly carry out.

The manuals from the engineering and electro-engineering industries are different. Theyinvest perhaps 5 per cent in capital investments and often equally much or even more inR&D, as well as, in market investments. Some groups have met this development byinstructions specifying that the rules of the manuals also apply to the kinds of intangibleinvestments important for the group, introduced special forms for these intangibleinvestments, review procedures and levels of authorization, and in a few groups specialmanuals for investments in R&D. The many different kinds of investments handled by theengineering industry has made their manuals and capita1 appropriation routines the mostcomplex ones.

15. Conclusions concerning the use and design of manualsHaving surveyed the tontent of the capital budgeting manuals used by Swedish groups weshah end by formulating a few conclusions and hypotheses conceming the use and role ofsuch manuals.

(Hl) Large firms with a large number of substantial investments in production equipmenthave a capita1 budgeting manual, if the evaluation of investments is decentralized.

When the evaluation of capital investments is not decentralized there is no need for writtenrommes. However, when there is a long distance between the evaluator and the decisionmaker as in large divisionalized groups and the group invest more than say 5 per cent of salesin fixed investments there is a manual. The manual makes decentralisation possible andbecomes an instrument of communication.

(H2) If intangible investments are more important than tangible ones then the importantattached to the manual decreases.

18

Some groups, as for instance pharmaceutical and hi-tech groups, have very large R&Dbudgets compared to the capital investment budget. In such groups the results from the R&Dprojects decide which capital investments Will be made. The R&D manual and procedures forevaluating the progress of the R&D projects become central also to the allocation of capitalfor fixed investments, and this reduces the importante of the capital budgeting manual. Asimilar situation may often be said to exist in groups with large market investments, as forinstance service groups that lack a capita1 budgeting manual; Market investments induce fixedinvestments and thereby reduce the importante of the capital budgeting manual as aninstrument in the capital allocation process of the group.

(H3) Firms with large immaterial investments in R&D, markets, software development,competence development, have in general developed special routines for suchinvestments.

When a firm has a large volume of investment in software development, R&D, markets orcompetence development, they tend to develop special routines for that kind of investment. Atommon solution is to create an investment committee for that specific kind of investment.Furthermore, if the evaluation of such investments is decentrahsed written routines aresometimes also developed.

(H4) Decentralisation presupposes simple evaluation techniques.

Almost all managers interviewed have emphasised the necessity of keeping the manualsimple. The rules of the game must be understood by everybody when decisions oninvestment are decentralised. This is especially true for the large multinational groups. Thisdemand for simplicity is emphasised when different kinds of investments and investmentsfrom companies in different countries and cultural areas have to be compared. The manualsets the rules of the game and gives the participants a tommon language to communicate anddistuss capital budgeting issues.

The demand for simplicity has led to standardisation. Renck (1966), for instance, foundten different formulas for calculating simple and discounted payback, which defined thepayments of the numerator and the denominator differently or approximated the discountedpayback. Today, only two formulas are given in those few manuals that give a formula at all.In the same way there is today no group calculating the true IRR or growth rate, previouslyused by two different groups in the earlier studies, advocated by among others Baldwin(1959) and given a theoretical basis by Henke (1973. Thus the use of capital budgetingmanuals have contributed to creating a tommon practice not only in individual fiis, but alsoin the industry and through the multinationals internationally.

(H5) The capital budgeting manual creates unitary principles conceming capital budgeting.

19

Many Swedish groups do not have a manual. For instance, shipping companies, certainsmaller engineering groups, banks, trading firms, tonsulting firms, and various other servicegroups with a small volume of capital investments. When making investment requests thePBP is reported to be used, sometimes supplemented with a DCF calculation. But, as there isno investment manual practice is less well fixed and the design of the request and choice ofcriteria much more up to the proposer to decide.

The most lasting impression of Table 4 is the small changes that have taken placeduring the last three decades. It may be of interest to note that seven relatively unrestructuredgroups are present in all three studies. One of these groups uses the same criterion today, asthey did in 1977 and 1964. Four of the groups have introduced a new criterion between 1964and 1977 and two between 1977 and 1990. What has happened is that four of the six haveabandoned discounted payback and introduced a more advanced criterion. If these groups arerepresentative for companies in general then the introduction of a new criterion is a rather rareevent, and the existence of different kinds of criterion a rather stable phenomenon. Onereason for this stabilny seems to be that the need for evaluation techniques that can be used byall proposers in multinational groups and the existing capita1 budgeting manual counteract theintroduction of new and more advanced methods of evaluation.

(H6) The capital budgeting manual preserve existing capital budgeting routines.

Another example of this is the choice of protitability criteria. Early adapter of the DCFtechnique, in the U.S. and Sweden, chose the IRR, late adapter have tended to choose theNPV criterion (Canada and Miller, 1985). However, those that once introduced the IRRcriterion have not abandoned it for the more theoretically correct NPV criterion.

This and earlier studies of capital budgeting manuals by Renck (1966) and Tel1 (1978)have shown that formal capital budgeting routines can be studied through capital budgetingmanuals. As large firms demand the capital appropriation request to be designed the way themanual stipulate this approach avoids some of the biases associated witb postal questionnairesurveys. Furthermore, the problem that practice is less well tixed in companies not using amanual.

Further studies are needed to find out whether the manuals of groups with their headoffice omside Sweden are different.

AcknowledgementsThis research has been made possible by generous grants from the Swedish Council forResearch in the Humanities and Social Sciences. The amhor wishes to thank Roger Johanssonand a elass of master students for carrying out some of the interviews, and docent IngemundHägg for supervising the elass together with the amhor.

20

ReferencesAckerman, R. W., 1970, “Influence ofintegration and diversny on the investment process”,Administrative Science Quarterly, 15, pp. 341-351.

Aharoni, Y., 1966, The Foreign Investment Decision Process, Boston, Mass.: HarvardUniversity.

Andersson, B., 1988, Kapitalkostnader och avkastningskrav, Stockholm: Statens Energiverk.

Arwidi, 0. and Yard, S., 1985, ‘Investment plattning in some Swedish companies - criteriaand uses”, Scandinavian Journal of Management Studies, May, pp. 27 1-96.

Arwidi, 0. and Yard, S.. 1992, “Investment plantring in some Swedish companies - criteriaand uses”, in Hägg, 1. and Segelod, E., eds., Zssues in Empirital Investment Research,Amsterdam: North-Holland, pp. 83-105.

Ashton, A. S., 1962, “Investment plantring by private enterprise”, Lloyds Bank Review, 66,Oct, pp. 23-29.

Baldwin, R. H., 1959, “How to assess investment proposals”, Harvard Business Review, 37,No. 3, pp. 98-104.

Bavishi, V. B., 1981, “Capital budgeting practice at multinationals”, ManagementAccounting, Aug, pp. 32-35.

Blazouske, 3. D., Carlin, I. and Kim, S. H., 1988, “Current capita1 budgeting practices inCanada”, CMA Magazine, 62, No. 2, pp. 51-54.

Bower, J. L., 1970, Managing the Resource Allocation Process, Division of Research,Graduate School of Business Administration, Harvard University, Boston.

Bower, J. L., 1972, Managing the Resource Allocation Process, Homewood, 111.: Richard DIrwin, Inc.

Canada, J. R. and Miller, N. P., 1985, “Review of surveys on use of capita1 investmentevaluation techniques”, The Engineering Economist, 30, No. 2, pp. 193-199.

Carter, E. E., 1971a, “The behavioral theory of the firm and top-leve1 corporate decisions”,Administrative Science Quarterly, 16, pp. 413-428.

Carter, E. E., 1971, “Project evaluations and firm decisions”, Journal of Management Studies,8, Oct, pp. 253-279.

Claesson, K. and Hiller. P., 1982, Investeringsprocessen i några svenska verkstadsföretag,Stockholm: EFI.

Cooper, W. D., Comick, M. F. and Redmon, A., 1992, “Capital budgeting: a 1990 study ofFortune 500 Company practice”, Journal ofApplied Business Research, 8, NO. 3, pp. 20-23.

Copeland, T. E. and Weston, J. F., 1979, Finantial Theory and Corporate Policy, Reeding,Addison-Wesley.

Dean, J., 1951a, Capita1 Budgeting, New York, Columbia University Press.

Dean. J., 1951b, Managerial Economics, New York: Prentice-Hall, Inc.

21

Dixon, J. R., and Duffey, M. R., 1990, “The neglect of engineering design”, CaliforniaManagement Review, 32, No. 2, pp. 9-23.

Edgren, J., Rhenman, E. and Skarvad, P. H., 1983, Divisionalisering och därefter, Stockholm:Management Media.

Eliasson, G., 1976, Business Economic Planning, New York: Wiley.

Farragher, E. J., 1986, “Capital budgeting practice of non-industrial fis”, The EngineeringEconomist, 31, No. 4, pp. 293-302.

Faulhaber, G. R. and Baumol, W. J., 1988, “Economists as innovators: practical products oftheoretical research”, Journal of Economic Literature, XXVI, June, pp. 577-600.

Faustman, M., 1849, “Berechnung des Werthes, welchen Waldboden, sowie noch nichthaubare Holzbestände fur die Waldwirthschaft besitzen”, Allgemeine Forst- und Jagd-Zeitung, 15 Dec, pp. 441-455.

Freeman, M. and Hobbes, G., 1991, “Capital budgeting: theory versus practice”, AustralianAccountant, 61, No. 8, pp. 36-41.

Fremgen, J. M., 1973, “Capital budgeting practices: a survey”, Management Accounting, 54,No. 11, pp. 19-25.

Gandemo, B., 1983, Investeringar i företag, SIND 1983:5, Stockholm: Liber.

Gandemo, B., 1992, “Capita1 investment behaviour - results from some Swedish studies”, inHägg, 1. and Segelod, E. ,eds., Zssues in Empirital Investment Research, Amsterdam: North-Holland, pp. 39-59.

Ginnarr, L. J. and Forrester, J. R., 1977, “A survey of capital budgeting techniques used bymajor U.S. fiis”, Finantial Management, VI, No. 3, pp. 66-71.

Gitman, L. J. and Mercurio, V. A., 1982, “Cost of capital techniques used by major U.S.fiis: survey and analysis of Fortune’s lOOO”, Finantial Management, 11, NO. 4, pp. 21-29.

Goold, M. and Campbell, A., 1987, Strategies and Styles, Oxford: Basil Blackwell Ltd.

Gumami, C., 1984, “Capital budgeting: theory and practice,” The Engineering Economist, 30,No. 1, pp. 19-46.

Hamel, G. and Prahalad, C. K., 1986, “Unexplored routes to competitive revitalization”,Centre for Business Strategy, London Business School working paper, No 14.

Heller, W. W., 1951, “The anatomy of investment decisions”, Harvard Business Review,XXIX, No. 2, pp. 95- 103.

Hendricks, J. A., 1981, “Capital budgeting practice including adjustments: a survey”,Managerial PZanning, Jan-Feb, pp. 22-28.

Henke, M., 1973, “Vermögensrentabilität - ein einfaches dynamisches Investitionskalkul”,Zeitschriffir Betriebswirtschaft, No. 3, pp. 177-198.

Istvan, D. F., 1959, The Capital-Expenditure Decision-Making Process in Forty-Eight LargeCorporations, Bloomington, Ind., D.B.A. dissertation, Indiana University.

22

Istvan, D.F., 1961a, Capita1 Expenditure Decisions: how they are made in lurge torporations,Bloomington, Ind.: Indiana University, Indiana Business Report, No 33.

Istvan, D. F. (1961b) “The economic evaluation of capital expenditures”, Z%e Journal ofBusiness, XXXIV, No. 1, pp. 45-51.

Jones, C. J., 1986, “Finantial planning and control practices in U.K. companies: alongitudinal study”, Journal of Business Finante & Accounting, 13, No. 2, pp. 161-185.

Kim, S. H., Crick, T. and Farragher, E. J., 1984, “Foreign capital budgeting practice used bythe U.S. and non-US. multinational companies”,207-215.

The Engineering Economist, 29, No. 3, pp.

King, P., 1975, “Is the emphasis of capital budgeting theory misplaced?“, Journal of BusinessFinante & Accounting, 2, NO. 1, pp. 69-82.

Klammer, T. P., and Walker, M. C., 1984, “The continuing increase in the use ofsophisticated capital budgeting techniques”, California Management Review, XXVII, No. 1,pp. 137-148.

Lilleyman, P., 1984, “CapitaJ budgeting: current practices of Australian organisations”,Australian Accountant, 54, March, pp. 130-133.

Lorange, P., 1993, Strategic Planning and Control: Zssues in the Strategy Process, Oxford:Blackwell.

Lumijärvi, 0. P., 1991a, “Gameplaying in capital budgeting,” LiiketaloudellinenAikakauskirja, 40, No. 2, pp. 194-200.

Lumijärvi, 0. P., 1991b, “Selling of capital investments to top management,” ManagementAccounting Research, 2, pp. 171-188.

Marshuetz, R. J., 1985, “How American Can allocates capital”, Harvard Business Review, 85,No. 1, pp. 82-91.

Mills, R. W., 1988, “Measuring the use of capital budgeting techniques with the postalquestionnaire: a UK perspective”, Znterfuces, 18, No. 5, pp. 81-87.

Mills, R. W. and Herbert, P. J. A., 1987, Corporate and Divisional Znfluence in Capita1Budgeting, London: The Chartemd Institute of Management Accountants.

Moore, J. S. and Reichert, A. K., 1983, “An analysis of the finantial management techniquescurrently employed by large U.S torporations”, Journal of Business Finante & Accounting,10, No. 2, pp. 623-645.

Mukherjee, T. K., 1987, “Capital-budgeting survey: the past and the future”, Review ofBusiness & Economic Research, 22, No. 2, pp. 37-56.

Mukherjee, T. K., 1988, “The capital budgeting process of large U.S. firms: an analysis ofcapital budgeting manuals”, Managerial Finante, 14, No. 213, pp. 28-35.

Mukherjee, T. K. and Henderson, G. V., 1987, “The capital budgeting process: theory andpractice”, Interfaces, 17, No. 2, pp. 78-90.

Oblak, D. J. and Helm, R. J., 1980, “Survey and analysis of capital budgeting methods usedby multinationals”, Finantial Management, Winter, pp. 37-41.

23

Örtengren, J., 1992, “CapitaI formation in Swedish industry during the post-war period”, inHägg, 1. and E. Segelod, eds., Issues in Empirkal Investment Research, Amsterdam: North-Holland, pp. 15-37.

Patterson, C. S., 1989, “Investment decision criteria used by listed New Zealand companies”,Accounting and Finante, 29, No. 2, pp. 73-89.

Pike, R. H., 1982, Capita1 Budgeting in the 198Os, London: The Chartered Institute ofManagement Accounting.

Pike, R. and Wolfe, M. B., 1988, Capita1 budgeting for the 199O’s, London: The CharteredInstitute of Management Accountants.

Piper, J. A., 1980, “Classifying capital projects for top management decision-making”, L.ongRange Planning, 13, No. 3, pp. 45-56.

Reichert A. K., Moore, J. S. and Byler, E., 1988, “Finantial analysis among large U.S.torporations: recent trends and the impact of the personal computer”, Journal of BusinessFinante & Accounting, 15, No. 4, pp. 469-485.

Renck, O., 1966,Znvesteringsbea&nning i nbgra svenska företag, Stockholm: Stockholm.

Rosenblatt, M., 1980, “A survey and analysis of capital budgeting decision process inmultidivision firms”, The Enginering Economist, 25, No.4, pp. 259-273.

Rosenblatt, M. J., and Jucker, J. V., 1979, “Capital expenditure decision/making: some toolsand trends,” Inte$aces, 9, No. 2, pp. 63-69.

Ross, M., 1986, “Capita1 budgeting practice of twelve large manufacturers”, FinantialManagement, Winter, pp. 15-22.

Sablin-Andersson, K., 1992, “The use of ambiguity,” in Hägg, 1. and Segelod, E., eds., Issuesin Empirital Investment Research, Amsterdam: North-Holland, pp. 143-158.

Sale, J. T. and Scapens, R. W., 1982, “The contxol of capita1 investment in divisionalizedcompanies”, ManagementAccounting, 64, No. 4, pp. 24-29.

Scapens, R. W. and Sale, J. T., 1981, “Performance measurement and formal capita1expenditure controls in divisionalised companies”, Journal of Business Finante &Accounting, 8, No. 3, pp. 389-419.

Scapens, R. W., Sale, J. T. and Tikkas, P. A., 1982, Finantial Control of Divisional Capita1Investment, London: The Institute of Cost and Management Accounts.

Scott, D. F. and Petty, J. W., 1984, “CapitaI budgeting practices in large American fiis: aretrospective analysis and analyses”, The Financial Review, 19, pp. 111-123.

Segelod, E., 1986, Kalkylering och avvikelser, Malmö: Liber.

Segelod, E., 1992, “Project design is an important part of the capital budgeting decision”, inHägg I. and Segelod, E., eds., Issues in Empirital Investment Research, Amsterdam: North-Holland, pp. 159-7 1.

Segelod, E. and Hägg, I., 1992, “Swedish empirital research on capital investments,” in Hägg,1. and Segelod, E. eds., Issues in Empirital Investment Research, Amsterdam: North-Holland,pp. 1-12.

2 4

Shapiro, A. C., 1988, “International capital budgeting”, in Stern, J. M. and Chew, D. H., eds.,New Devebpments in Intemationol Finunce, Oxford: Basil Blackwell, pp. 165-180.

Stanley, M. T. and Block, S. B., 1984, “A survey of multinational capital budgeting”, TheFinantial Review, 19, March, pp. 36-54.

Statistics Sweden, 1994, Statistiska meddelanden, F 13 SM 9302, Stockholm.

Tell, B., 1978, Znvesteringskalkylering ipruktiken, Lund: Studentlitteratur.

Weaver, J. B., 1974, “Organizing and maintaining a capital expenditure program”, Z%eEngineering Economist, 20, No. 1, pp. 1-35.

Wilson, M., 1988. Capita1 Budgeting for Foreign Direct Investment, London: The CharteredInstitute of Management Accountants.

Yard, S., 1987, Kulkyllogik och kulkylkrav, Lund: Lund University Press.

25