THE APPLICATION OF CUMULATIVE PROSPECT THEORY IN BUILDING OPTIMAL PORTFOLIO IN VIETNAMESE STOCK...

138

1 FOREIGN TRADE UNIVERSITY FACULTY OF BUSINESS ADMINISTRATION ---------***-------- GRADUATION THESIS Major: International Business Administration THE APPLICATION OF CUMULATIVE PROSPECT THEORY IN BUILDING OPTIMAL PORTFOLIO IN VIETNAMESE STOCK MAKRKET Student name: Nguyễn Thị Thu Hằng Student code: 1001020040 Class: A8 Intake: 49

Transcript of THE APPLICATION OF CUMULATIVE PROSPECT THEORY IN BUILDING OPTIMAL PORTFOLIO IN VIETNAMESE STOCK...

1

FOREIGN TRADE UNIVERSITY

FACULTY OF BUSINESS ADMINISTRATION---------***--------

GRADUATION THESISMajor: International Business

Administration

THE APPLICATION OF CUMULATIVE PROSPECT

THEORY IN BUILDING OPTIMAL PORTFOLIO IN

VIETNAMESE STOCK MAKRKET

Student name: Nguyễn Thị Thu

Hằng

Student code: 1001020040

Class: A8

Intake: 49

2

Supervisor: M.Sc. Le Thi Thu

Ha Noi, May 2014

ACKNOWLEDGEMENTS

Firstly, I express my deep sense of gratitude to M.Sc.

Le Thi Thu for her inspiring guidance, scholarly

interpretations and valuable criticisms throughout the

course of my thesis. I am gratefully obliged to the

faculty of Business Administration at Foreign Trade

University, for approving the title and supporting me to

conduct the study. I extend my sincere thanks to Ms Pham

Mai Phuong Linh, Hoang Xuan Huy, Nguyen Viet Phuong, for

their support.

Especially, I also thank my close friends Ngo Bach Thien

Huong, Le Ngoc Hai, Nguyen Tung Minh, Ngo Thi Thu Huong,

Nguyen Lan Anh, Pham Hai Yen and Nguyen Phuong Thanh for

all their encouragement throughout the completion of the

work.

Above all, many thanks to mom, dad, and my younger

brother and sisters who always stimulate and spend all

love for me.

3

Nguyen Thi Thu Hang

Class: A8, Faculty of Business Administration, Intake: 49, Foreign Trade

University

4

CONTENT

CHAPTER 1: INTRODUCTION................................1

1.1.The rationale of the research....................1

1.2.Objectives of the research.......................3

1.3.Scope of the research............................3

1.4.Research methodology.............................3

1.5.Research structure...............................4

CHAPTER 2: CUMULATIVE PROSPECT THEORY..................5

2.1.Introduction to Cumulative Prospect Theory.......5

2.2.Hypotheses of Cumulative Prospect Theory.........6

2.2.1. Three basic hypotheses.............................6

2.2.2. Mathematic form.................................8

2.2.3. Stochastic Dominance approach to test hypotheses........11

2.3.Typical biases explaining for Cumulative Prospect

Theory..............................................18

2.3.1. Loss Aversion...................................19

2.3.2. Anchoring and Adjustment..........................19

2.3.3. Herding Bias....................................20

CHAPTER 3: BUILDING OPTIMAL PORTFOLIO FOR INDIVIDUAL

INVESTORS.............................................22

3.1.Individual investors............................22

3.2.Optimal portfolio...............................23

5

3.2.1. Introduction....................................23

3.2.2. Approaches of portfolio optimization..................24

3.2.3. Processes of portfolio management...................26

3.2.4. Optimization constraints...........................28

3.3.Designing optimal portfolio for individual

investors...........................................29

CHAPTER 4: MODEL OF STATIC PORTFOLIO OPTIMIZATION UNDER

CUMULATIVE PROSPECT THEORY............................31

4.1.Introduction....................................31

4.2.Static Portfolio Choice under Cumulative Prospect

Theory..............................................32

4.2.1. Background....................................32

4.2.2. Content of Static Portfolio Optimization model...........33

4.3.Evaluation of Static Portfolio Optimization Model

36

4.3.1. Advantages.....................................36

4.3.2. Disadvantages..................................37

CHAPTER 5: INTRODUCTION TO VIETNAMESE INDIVIDUAL

INVESTORS.............................................39

5.1.Overview of Vietnamese stock market.............39

5.1.1. A brief history of Vietnamese stock market..............39

5.1.2. Overall movements of Vietnamese stock market during the

period of 2007-2013....................................41

6

5.2.Overview of individual investors................44

5.3.Typical features of individual investor in

designing portfolios................................44

5.3.1. Lack of knowledge................................44

5.3.2. Lack of technological investment tools.................46

5.3.3. Affected by behavioral biases........................47

CHAPTER 6: DATA AND METHODOLOGY.......................52

6.1.Data collection.................................52

6.2.Overview of methodology.........................52

6.3.Research design.................................53

6.3.1. Stochastic Dominance approach.....................53

6.3.2. Questionnaire survey..............................55

6.4.Limitations of the study........................56

CHAPTER 7: EMPIRICAL RESULTS..........................57

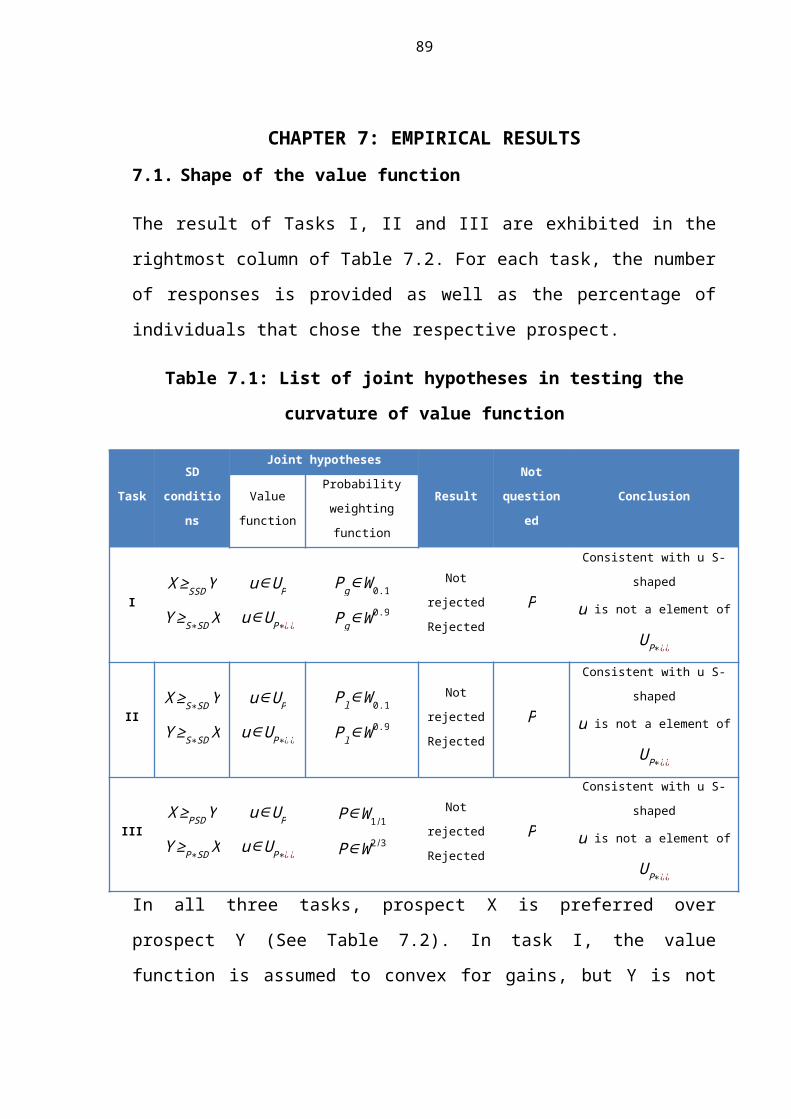

7.1.Shape of the value function.....................57

7.2.Shape of the probability weighting function.....58

7.3.Empirical result................................59

CHAPTER 8 – RECOMMENDATION............................61

8.1.Individual investors............................61

8.1.1. Improve knowledge and skills.......................61

8.1.2. Build up plausible investment strategy.................62

8.1.3. Filter information and experts’ opinions................65

7

8.1.4. Apply models in practical investments..................66

8.1.5. Notations......................................67

8.2.Financial institutions and investment service

suppliers...........................................70

8.2.1. Provide instruments for constituting and managing portfolio.70

8.2.2. Provide biases defense for private clients...............72

CONCLUSION............................................73

REFERENCE.............................................75

APPENDIX A: SURVEY....................................79

APPENDIX B: MATHEMATICAL BACKGROUND...................81

8

LIST OF ABBREVIATIONS

BFT

CPT

EMH

EU

GDP

PT

SD

VN-Index

Behavioral Finance Theory

Cumulative Prospect Theory

Efficient Market Hypothesis

Expected Utility Theory

Gross Domestic Product

Prospect Theory

Stochastic Dominance

Vietnamese Index of Stock Price

9

LIST OF TABLES

Table

5.1

HOSE’s listing summary recorded in April

201440

Table

5.2

HNX’s listing summary recorded in April

201441

Table

5.3

Level of knowledge of individual investors in

2000-2007 in Viet Nam45

Table

6.1c and d 54

Table

7.1

List of joint hypotheses in testing the

curvature of value function57

Table

7.2Result of Tasks I, II and III 58

Table

7.3

List of joint hypotheses in testing the

curvature of probability weighting function59

Table

7.4Result of Tasks IV and V 59

LIST OF EXHIBITS

Exhibit

2.1

The value function assumed by Prospect

Theory7

Exhibit The value function u (x) for different values 9

10

2.2 of α,β∧μ

Exhibit

2.3The probabilities distortion functions,γ=0.61 and δ=0.69

10

Exhibit

2.4

Prospect Theory S-shape function and

Reverse S-shape function15

Exhibit

2.5Schematic depiction of the Wc

dclass of

probability weighting function18

Exhibit

3.1The process of portfolio management 26

Exhibit

5.1VN-index in the period of 2004 to 2014 42

Exhibit

5.2HNX-index in the period of 2004 to 2014 42

Exhibit

5.3

Dow Jones and VN-index from the end of 2008

to the end of 201049

1

CHAPTER 1: INTRODUCTION1.1. The rationale of the research

Individual wealth management, especially individual

optimal portfolio has been relatively new but expanding

field that attract more and more the concern of

financial researchers. Numerous studies regarding this

domain are carried out over the world, including

standard finance models and behavioral finance model.

The major characteristics of private investors are small

capital size, lack of technology support and affected by

behavioral biases. Small scale of investments prevents

individual investors from selecting many securities for

their portfolio. The shortage of supporting high-tech

tools poses the problem of how individual practioners

apply optimal portfolio models. Lastly, behavioral

biases are the in-depth reason for investors’ wrong

decisions and mistakes while constituting portfolio. In

three above features, individual behaviors is considered

as the most typical difference, which divides optimal

portfolio models into two approaches: one based on

Standard Finance paradigm, and one based on Behavioral

Finance paradigm.

Standard Finance paradigm proposes Markowitz Portfolio

Theory, which is considered as the best mathematical

2

model for optimizing portfolio. This model of portfolio

optimization bases on the assumption that individual

investors are analytically sophisticated and

knowledgeable about markets. By assumption, private

investors in such these constituted models make optimal

decision in a rational manner. However, MPT is strongly

criticized by behavioral finance scholars. According to

Bernstein (1998), “evidence reveals repeated patterns of

irrationality, inconsistency and incompetency in the

ways human being arrive at decisions and choices when

faced with uncertainty”. Nofsinger (2001) asserts that

assumption of rationality and unbiasedness of economic

participants has been drubbed by psychologist for a long

time.

As the mandatory requirement of financial research,

behavioral finance researchers advance substitute models

of individual portfolio management. The major studies

specializing in portfolio optimization emphasize that

(i) investors are normal (Statman, 2005); (ii) they use

S-shape utility function (Kahneman and Tversky, 1979)

that reflects their attitudes toward risk; (iii)

investors are also affected by their emotions (Lopes,

1987). Derived from these realistic assumptions, a vast

number of researches regarding individual portfolio have

conducted in over the world. The principal contribution

of individual optimal portfolio is with no doubt

3

Cumulative Prospect Theory initiated by Kahneman and

Tversky (1992) – the keystone of Behavioral Finance

Theory.

Moving focus on Vietnamese stock market, due to the

great number of private investors to the financial

market, individual wealth management is still a pivotal

domain. According to the interview result of Tran Dac

Sinh – chairman of HOSE, by the end of the year 2013,

there were 1.3 million trading accounts comprise

1,282,071 accounts of domestic individual investors

compared with 5,081 accounts of domestic institutional

investors, 13,950 accounts of foreign individual

investors and the 1,631 remaining of foreign

institutional investors. In addition, during the

development of the Vietnamese stock market, there is an

increasing number of private investors picking stock and

allocating their portfolio instead of short-term

trading.

Nevertheless, in reality, Vietnamese individual

investors are not equipped by strategic models helping

them to overcome their emotional and cognitive biases.

Many of them simplify portfolio selection process by

using heuristics approach because they find models of

optimal portfolio sophisticate and difficult to apply.

Other individual investors designing portfolio based on

available models are still unable to optimize their

4

wealth because of models’ implausible assumption of

rationality. This status is one of the reasons causing

the speculative bubble crash in 2007, even maybe

threatening the sustainability of Vietnamese stock

market.

Thus, the matter of wrong individual portfolio

investment decisions affecting on the sustainability and

the enhancement of Vietnamese stock market is the

rationale of my thesis “The application of Cumulative

Prospect Theory in building optimal portfolio for

individual investors in Vietnamese stock market”.

1.2. Objectives of the research

Behavioral Finance paradigm is a theoretical and

empirical system that includes numerous sub-theories

such as Heuristics, Prospect Theory, Cumulative Prospect

Theory, behavioral biases, disposition effect, etc. Each

relative theory, which has its mathematic forms, can be

a base constructing models of portfolio optimization.

Due to limited time and a lack of research capacity, my

thesis will only concentrate on Cumulative Prospect

Theory – the keystone of Behavioral Finance Theory, and

the most simple model, which is so-called “Static

Portfolio Optimization model”, with one risky asset and

one free-risk asset in one-period economy.

5

My thesis aims to answer two key research questions. Are

hypotheses of Cumulative Prospect Theory compatible with

Vietnamese individual investors’ characteristics? If the

model is suitable for privately applying, are there any

recommendations to realize the models in practical

investments?

1.3. Scope of the research

Individual investors were picked up for the survey since

they were more likely to have limited knowledge about

application of the Behavioral Finance or Cumulative

Prospect Theory in portfolio construction, hence prone

to make psychological mistakes. The influence has

primarily analyzed in term of whether behavioral factors

affect the portfolio management behavior of individual

investors.

1.4. Research methodology

This study follows the methodology of survey research

design of which data processing was supported by

quantitative approach.

As Holme and Solvang (1996), a quantitative method is

formalized, structured and is characterized by

selectivity as well as a distance from the source of

information. The approach concentrates on numerical

observations and attempts to generalize a phenomenon

6

through formalized analysis of observed data where

statistic indicators are indispensable parts. On the

other hand, a qualitative approach is formalized to a

lesser extent is directed at testing whether the

information is valid. The typical feature of this method

is the use of verbal description instead of purely

numerical data and aims at creating a common

understanding of the subject in research.

In my thesis, by using descriptive survey, primary data

is collected for quantitative and qualitative analyses.

Stochastic Dominance is used to interpret individual

decisions between two options.

1.5. Research structure

Except Introduction, Conclusion and Appendices, the

thesis is structured as follows:

Chapter 2: Cumulative Prospect Theory

Chapter 3: Building Optimal Portfolio for individual

investors

Chapter 4: Static Portfolio Optimization Model Under

Cumulative Prospect Theory

Chapter 5: Introduction to Vietnamese individual

investors in the stock market

Chapter 6: Data and Methodology

7

Chapter 7: Empirical results

Chapter 8: Recommendations

8

CHAPTER 2: CUMULATIVE PROSPECT THEORY 2.1. Introduction to Cumulative Prospect Theory

Cumulative Prospect Theory (Kahneman and Tversky, 1992)

is one of the most important theories of Behavioral

Finance Paradigm. CPT has assistance for behavioral

researchers to understand and explain individual

decision-making process under uncertainty. Hence, CPT

has many important implications in constructing

portfolio.

Cumulative Prospect Theory is the second version of

Prospect Theory (Kahneman and Tversky, 1979). Both of

them are considered as two of the best theories to

explain individual decision under risk. In essence,

there are many such relative theories as Expected Value,

Expected Utility having great contribution to the

financial decision-making process under conditions of

risk, but each of them has its own limitations. Expected

value is calculated by multiplying its payoff with its

probability. This model fails in predicting the final

choice because the value was not always directly related

to its precise monetary worth, but rather dependent on

other psychological factors. Daniel Bernoulli (1738)

releases works discovering this contradiction and

advancing an alternative to the expected value notion.

Throughout his experiments, Bernoulli recognizes that

9

the value a person attaches to an outcome can be

influenced by such factors as the likelihood of winning,

or probability, etc. Expected Utility, however, the

notion of Expected Utility also fails in predicting all-

loss choices.

In 1979, Kahneman and Tversky provided an alternative,

empirically supported theory of choice, so-called

Prospect Theory, one that accurately describes how

people actually go about making their decision. In

short, the theory predicts that individuals tend to be

risk averse in a domain of gains and relatively risk-

seeking in a domain of losses. However, there are some

theoretical problems in PT. The main problem is that the

functional form of PT violates “stochastic dominance”

(Kahneman and Tversky, 1979, pp. 283±284). Stochastic

dominance requires that a shift of probability mass from

bad outcomes to better outcomes leading to an improved

prospect. The theoretical problems have recently been

resolved in a new version of PT, called Cumulative

Prospect Theory (CPT) that was introduced by Tversky and

Kahneman (1992); in particular, CPT satisfies stochastic

dominance.

2.2. Hypotheses of Cumulative Prospect Theory

2.2.1. Three basic hypotheses

10

According to Kahneman and Tversky in their work in 1992,

there are three elements forming the decision making

process of CPT. CPT-investor is defined as an investor

who behaves consistently with Cumulative Prospect

Theory.

Firstly, a CPT –investor will be concerned with the

deviation of his final wealth from a reference level

instead of final value under EU hypothesis. Secondly,

CPT-investor is more sensitive with losses than gains.

Lastly, investors do not evaluate random outcomes using

reasonable probabilities, but base upon distortion by

overestimating low probabilities.

For the first hypothesis, Kahneman and Tversky presented

in their study in 1979 the following experimental

evidence to illustrate that the evaluation of decision

outcomes has to be reference-dependent (“reference” in

this context refers to the current state of wealth), a

principle that is incompatible with Expected Utility. In

this empirical work, experimental participants were

asked to choose between a lottery offering a 25% chance

of winning 3000 and a lottery offering a 20% chance of

4000, 65% of their participants chose the second option

(20%; 4000). On the contrary, when they were asked to

choose between a 100% chance of winning 3000 and an 80%

chance of winning 4000, 80% of them chose the former

(100%, 3000). On contrary to reality, EU predicts that

11

they should not choose different option in both

circumstances as the expected utility in the second

choice is always better than the first one.

To understand this certain situation, consider a gamble:

(x−m,p−m;x−m+1,p−m+1;…;x0,p0;…;xn−1,pn−1;xn,pn )

Where the notation should be understand as “gain xi with

probabilitypi with i=−m,n; where the outcomes are

organized in increasing order, so that xi<xj for i<j, and

where x0 = 0. For instance, a lottery offering a 50%

chance of winning $333 or losing $111 would be

formulated as (−111,12 ;333,12 ). Under EU, a rational

investor valuates the above gamble as:

∑i=−m

npiu(W+xi)

Where: W is the current asset and u(x) is the utility

function that is increasing and concave.

This formulation demonstrates the four key components of

prospect theory: 1) reference – dependence, 2) loss

aversion, 3) diminishing sensitivity, and 4) probability

weighting.

12

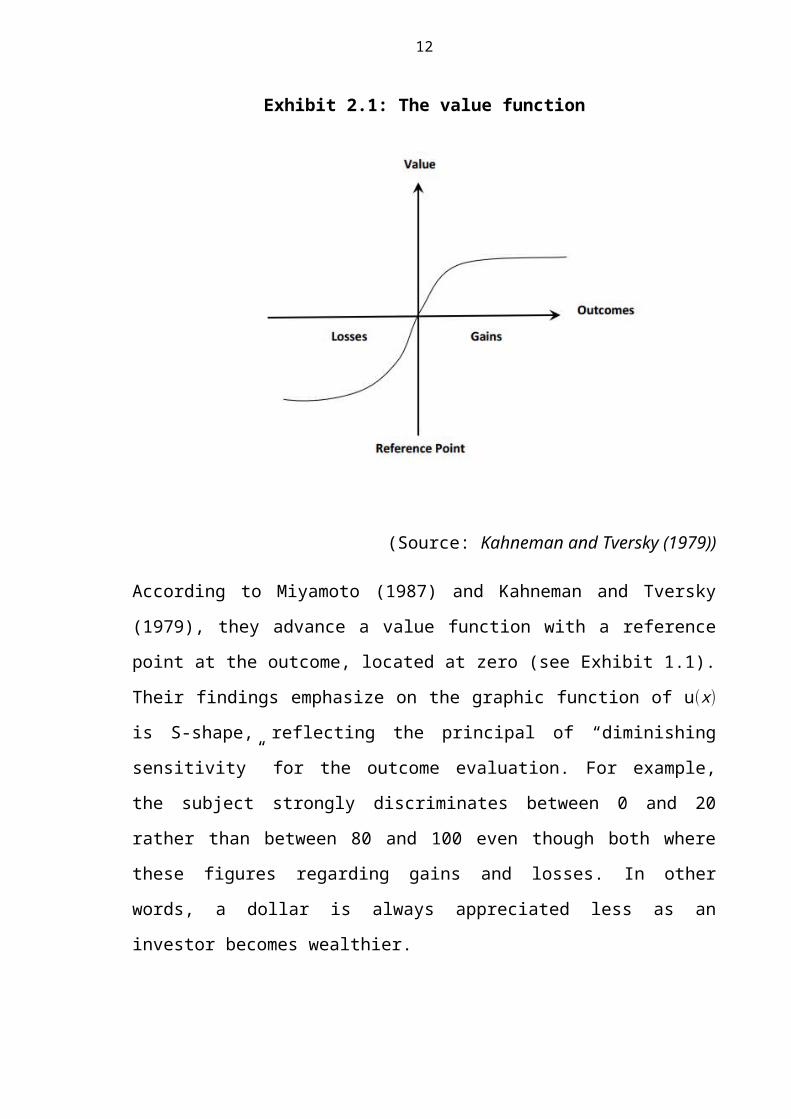

Exhibit 2.1: The value function

(Source: Kahneman and Tversky (1979))

According to Miyamoto (1987) and Kahneman and Tversky

(1979), they advance a value function with a reference

point at the outcome, located at zero (see Exhibit 1.1).

Their findings emphasize on the graphic function of u(x)

is S-shape, reflecting the principal of “diminishing

sensitivity” for the outcome evaluation. For example,

the subject strongly discriminates between 0 and 20

rather than between 80 and 100 even though both where

these figures regarding gains and losses. In other

words, a dollar is always appreciated less as an

investor becomes wealthier.

13

Secondly, it is also found that u(x) is more sensitive to

losses than for gains (loss aversion). Empirical tests

conducted by Kahneman and Tversky (1991) indicate that

losses are weighted about twice as heavily as gains –

losing $1 is about twice as painful as the pleasure of

gaining $1.

Last but not least, Kahneman and Tversky find that

preferences of subjects can be modeled by probability

weighting that amplifies small probabilities and reduces

higher probabilities. Therefore, the weighting function

is definitely sensitive to changes in probability near

the final points 0 and 1 but obviously insensitive to

changes in probability in middle region. As Kahneman and

Tversky (1979), weighting function is an important

hypothesis in supporting explanation for investors’

decision.

2.2.2. Mathematic form

Let W and Wref be the wealth and the reference level at

the end of the period.

Define the deviation D from the reference level as

follows:

D=W−Wref

14

D is the random variable that alters and motivates all

decision because each investor has different reference

level, hence different deviation D.

Let FXand SXbe the cumulative distribution function and

the complementary distribution function, respectively.

FX (x)=P (X≤x ) and SX (x)=1−FX (x)

2.2.2.1. The value function

According to Kahneman and Tversky (1992), the value

functionu (x)is defined as follows:

u (x)=¿

Where: x is random variable D, 0<∝<1,α≤β<1∧μ>1

It can be referred from definition of the value function

that the function g (x)and l (x) are positively homogenous,

increasing, invertible, and twice differentiable.

Parameter ∝ and β demonstrate risk aversion, parameter μ

illustrate loss-aversion. Moreover investors show the

tendency to risk-averse for gains and risk-seeking for

losses, hence it is clear to find that α≤β<1. Kahneman

and Tversky (1979) suggest that ∝=0.8, β=0.88 and μ=2.25

. See Exhibit 2.2

15

Exhibit 2.2: The value function u (x) for different values

of α,β∧μ

(Source: Kahneman and Tversky, 1979)

2.2.2.2. The probability weighting function

The third element forming CPT decision-making process

lies in the systematic distortion of physical

probability measure. The probabilities distortion may be

slightly different in case of gains (D>0) and losses (D<0).

The probability distortions (or probability weighting

functions) are denoted by Pgand Pl. For a random variable

D with cumulative distribution function FX and

decumulative distribution SX, Tversky and Kahneman

(1992) suggest the following two probabilities weighting

16

functions with Pg: [0;1 ]→ [0;1 ] for gains andPl: [0;1 ]→ [0;1 ]for

losses:

Pg (p )= pγ

[pγ+(1−p)γ ]1 /γ with0.28<γ<1

Pl (p )= pδ

[pδ+(1−p)δ ]1 /δ with0.28<δ<1

Where:p=FX(D), γ and δ are both less than 1 as if γ=1or

δ=1, there is no distortion in gain domain or loss

domain, respectively.

It is can be referred from the definition of the

probability weighting function Pgand Plthat they are

differentiable. Remember that investors show the

tendency to risk-averse for gains and risk-seeking for

losses, hence it is clear to find that γ<δ.

Kahneman and Tversky (1992) estimated γ=0.61 and δ=0.69

for a typical investor. (See the Exhibit 2.3)

Exhibit 2.3: The probabilities distortion functions,γ=0.61 and δ=0.69

17

(Source: Kahneman and Tversky, 1992)

Ingersoll (2008) shows that the condition of ( γ,δ>0.28)

ensures that Pgand Pl are increasing. Rieger and Wang

(2004) indicate that the probability weighting function

is not monotone for γ≤0.278.

Prelec (1998) proposes an alternative specification for

the weighting function: P (p )=e−(−lnp)γ, where parameter γis

similar to the one in the function proposed by Kahneman

and Tversky.

2.2.2.3. Objective function (Prospect function)

Bernard and Ghossoub (2009) define the objective

function of the CPT-investor, denoted byO (D), as:

O (D)=∫0

+∞

Pg (SX (x ))dg (x)+∫−∞

0

Pl(FX (x ))dl (x )

Or, the CPT-objective function O (D)also rewrite as:

18

O (D)=∫0

+∞

Pg (SX (x ))dg (x)−∫0

+∞

Pl (FX (x ))dl (x)

Where: FX (x) and SX (x) are cumulative distribution function

and decumulative distribution function, respectively

(see page 8), Pland Pgare probability weighting functions

(see page 10)

In order to ensure that both integrals are finite and

computable, the objective function requires thatα<2min (γ;δ) and β<2min (γ;δ), where αandβ is parameter in

the value function (see page 9), γ∧δ are parameters in

the probability weighting function (see page 10)

2.2.3. Stochastic Dominance approach to test hypotheses

2.2.3.1. Overview of approaches

In order to test features of Prospect Theory, Kahneman

and Tversky (1979) employ the Certainty Effect approach

that also supports for Cumulative Prospect Theory. In

their experiments in 1979 and 1992, they rely upon

comparison of two outcomes, one certain, one uncertain;

hence, probabilities distortion function can be

explainable for their results. Wu and Gonalez (1996)

also apply the Certainty Effect approach on their study

supporting Tversky and Kahneman’s probability weighting

function.

19

Even though Certainty Effect approach has many

applications and implications in decision theory under

uncertainty, it has the well-known drawback, recognized

by Levy and Levy (2001). Many experiments show that the

approach is ineffective in case of more than two

outcomes and each outcome has the same probability (for

instance, gain $1000 with probability of 25%; loss -$200

with probability of 25%; gain $0 with probability of

25%; gain -$300 with probability of 25%). The problem of

Certainty Effect poses the need of alternative

approaches.

In their work, Levy and Levy (2001, 2002a) propose to

employ Stochastic Dominance (SD) criteria to analyze

decisions and implied preference in experimental

research. The prominent advantages of SD approach over

Certainty Effect approach are that SD can compare two

uncertain choices with many outcomes, which can be all

positive, all negative or mixed. According to Levy and

Levy (2002b), Certainty Effect approach is not

explainable for the curvature of the preference with

mixed prospects while SD approach can provide

conclusion. Furthermore, based on SD condition, recent

studies suggest experimental designs that can isolate

elements of CPT without having to estimate all

parameters of functions.

20

In my thesis, the experiment, testing whether investors’

decisions are consistent to CPT, is conducted with the

support of SD approach. Firstly, we consider theoretical

framework of Stochastic Dominance Approach.

2.2.3.2. Stochastic Dominance approach

a. Background

In this section, consider an individual investor who has

investor has investment chances in one of the n

portfolios, where return (per unit invested) in a single

period on portfolio i is Xi (non-negative random

variable). Hence, wealth at the end of the period iswXiwith i=1;n.

Let w and v(x)be the current wealth and utility function

respectively. According to expected utility criterion,

the investor will choose portfolio k if:

E [v (wXk )]=max1≤i≤n

E[v (wXi)]

It is clear that if you determine the distribution of

each wXi(i=1;n) and value function of each option, you

can predict and explain the portfolio preferred to

others.

Notation:

The cumulative distribution function of X: FX (x)=P(X≤x)

21

The complementary or tail distribution function of X:SX (x)=FX (x)=1−FX (x)

Density function: fX (x )=F'X (x )

b. Absolute and First-order Stochastic Dominance

Absolute dominance/ almost-sure dominance: Y is

absolutely dominant over X ifP (X≤Y)=1 and there is at

least one y such that FY (y)<FX (y )

First-order stochastic dominance/ simple stochastic

dominance: Y is first-order stochastically dominant over

X if FY (y)≤FX (y )for all y, and there is at least one y such

thatFY (y)<FX (y ). It can be understood that Y has more

chance than X of being bigger than any given value y.

When Y is first order stochastic dominant over X, this

relationship is defined as Y≥fsdX

And,P (Y≤y )=FY (y )≤P (X≤y )=FX (y ), thus, if Y is absolutely

dominant over X, then Y is also first-order

stochastically dominant over X.

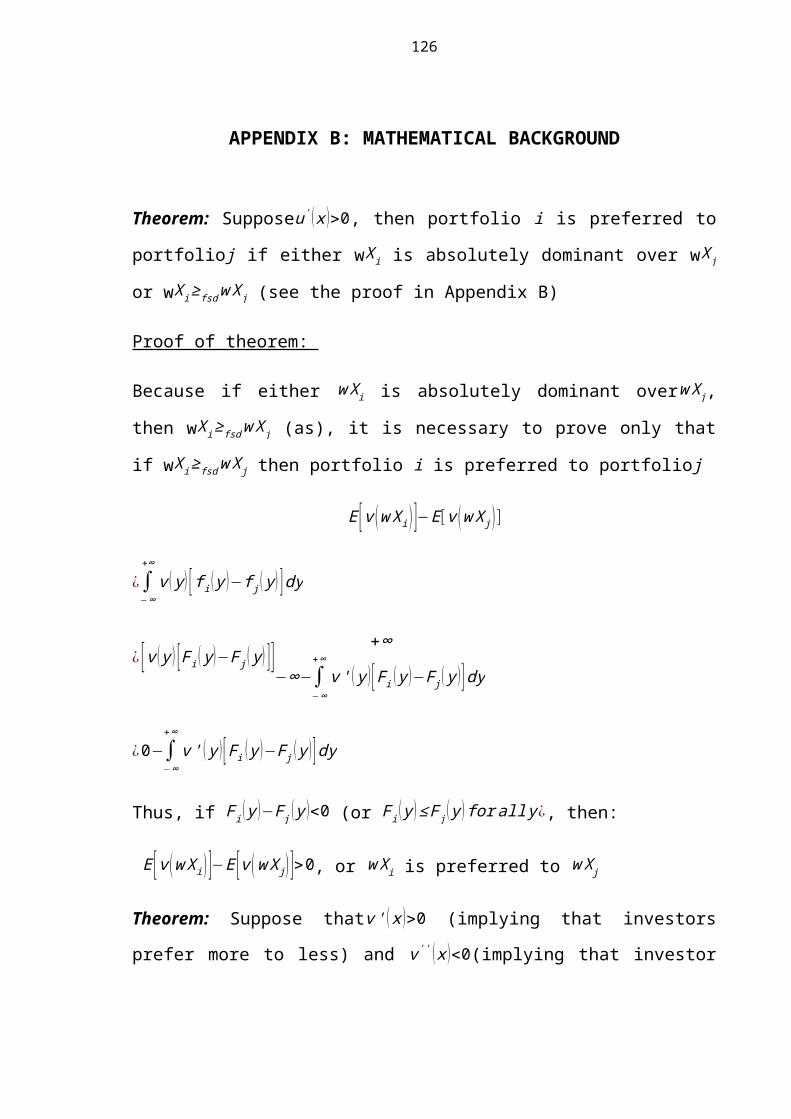

Theorem: Supposeu' (x )>0, then portfolio i is preferred to

portfolioj if either wXi is absolutely dominant over wXj

or wXi≥fsdwXj (See the proof in Appendix B)

c. Second-Order Stochastic Dominance

22

Second-order stochastic dominance: Y is second-order

stochastically dominant over X if ∫−∞

x

FY (y )dy≤∫−∞

x

FX (y )dy for

all x, and there is at least one x, for which the above

inequality is strict. When Y is second-order stochastic

dominant over X, this relationship is defined as Y≥ssdX

Theorem: Suppose thatv' (x )>0 (implying that investors

prefer more to less) and v'' (x )<0(implying that investor

is risk averse), WXi is preferred to wXj if wXi is second

- order stochastically dominant overwXj, or:

∫−∞

x

Fi (y )dy≤∫−∞

x

Fj (y )dy

(See the proof in Appendix B)

d. Prospect Stochastic Dominance

Prospect stochastic dominance: Y is prospect

stochastically dominant over X (v'>0,v''>0for x<0 , and

u''<0forx>0) if and only if

{∫y0

FY (x )−FX (x )dx≥0forallx≤0

∫0

x

FY (x )−FX (x )dx≥0forallx≥0

With at least one strict inequality.

2.2.3.3. Applying Stochastic Dominance approach to test

hypotheses of CPT

23

Investors are assumed to abide by the framework of CPT.

It implies that investors are compatible with three

basic hypotheses of CPT (See page 6)

The value function is u (x) where x is defined as the

deviation of wealth in comparison with a determined

reference point) (See page 9)

u (x)=¿

The probability function is Pg(FX (x )) for non-negative

outcomes and Pl (FX (x )) for negative outcomes, with

P (0 )=0,P (1)=1, where FX (x) is the cumulative distribution

function of X. (See page 10)

Pg (p )= pγ

[pγ+(1−p)γ ]1 /γ with0.28<γ<1

Pl (p )= pδ

[pδ+(1−p)δ ]1 /δ with0.28<δ<1

Exhibit 2.4: Prospect Theory S-shape function and

Reverse S-shape function

24

(Source: Levy and Levy (2002a))

Denote UP the set of prospect value functions containingu (x) that are convex for x<0 and concave for x≥0

Denote UP∗¿¿ the set of inverse prospect value functions

containing u (x) that are convex for x<0 and concave forx≥0

Denote Uconvex the set of prospect value functions

containing u (x) that convex for all x

Denote Uconcave the set of inverse prospect value functions

containing u (x) that are concave for all x

In essence, to test the value function or the

probability weighting function, it is advised that

researchers will test the curvature of graphic curves of

both functions. If u (x) that convex for x<0 and concave

25

for x≥0, then u (x) is an element of the set of prospect

value functions. Similarly, if the probability functionP(p) has the reserve S-shape, then P(p) is also a

probability weighting function of Cumulative Prospect

Theory.

Stochastic Dominance Approach relies on comparison of

two outcomes. By analyzing choice results, scholars are

able to predict the shape of the value function and

probability weighting function.

1.3.3.1. Applying Stochastic Dominance to test the value

function

Consider two prospects X and Y:

E [u (X ) ]−E [u (Y )]

¿∫a

b

u (x ) [fX (x )−fY (x) ]dx

¿ [u (x ) [FX (x )−FY (x )] ]b

a−∫a

bu' (x ) [FX (x )−FY (x )]dx

¿−∫a

b

u' (x ) [FX (x)−FY (x) ]dx=∫a

b

u' (x) [FY (x )−FX (x )]dx

Consider the function: h (x)=∫a

x

[FY (y )−FX (y )]dy

26

Let A=[a0,a1 ] and B=[b0,b1 ] be intervals such that

A∪B=[a,b ]. Given prospects X and Y, h (x)=∫a

x

[FY (y )−FX (y )]dy.

Then,

h (x)≤h (a1)fora0≤x<a1, and

h (x)≥h (b0)forb0≤x<b1

Both inequalities hold if and only if X is preferred to

Y for all function u (x), that are convex in A and concave

in B

X dominates Y according to Prospect theory (See page

14), denoted byX≥PY, if and only ifh (x)≤h (0)fora≤x<0, andh (x)≥h (0)for0≤x<b. Remember that X≥PY if and only if X is

preferred to Y according to Prospect Theory or u∈UP

Denote X≥P∗¿ Y ¿ when X dominates Y according to Inverse

Prospect Theory, if and only ifh (x)≥h (a)fora≤x≤0, andh (x)≤h (b)for0≤x≤b. And, X≥P∗¿Y¿ if and only if X is

preferred to Y according to Inverse Prospect Theory for

all u∈UP∗¿ ¿

Denote X≥ssdY when X dominates Y according to second-

order stochastic dominance (see page 18), if and only ifh (x)≥h (a)fora≤x≤b. And, X≥ssdY if and only if X is

preferred to Y according to second-order stochastic

dominance for all u∈Uconvex

27

Denote X≥s∗sdY when X dominates Y according to inverse

second-order stochastic dominance, if and only ifh (x)≤h (b)fora≤x≤b. And, X≥convexY if and only if X is

preferred to Y for all u∈Uconvex

1.3.3.2. Test the probability weighting function

We assume that the decision maker abides by Cumulative

Prospect Theory, we have:

Pg (FX (x ))= Fγ (x)

[Fγ (x)+Sγ (x )]1γ

with0.28<γ<1

Pl (FX (x ))= Fδ (x)

[Fδ (x)+Sδ (x )]1δ

with0.28<δ<1

The empirical researches show that probability weighting

function is “shallow in the open interval and changes

abruptly near the end-points where P (0 )=0,P (1)=1” (Tversky

and Kahneman, 1992). More specifically, an inverse S-

shape probability weighting function will be concave

first, then convex.

Consider the probability distortion functions that are

concave in ¿ and convex in ¿, for given values of d, c

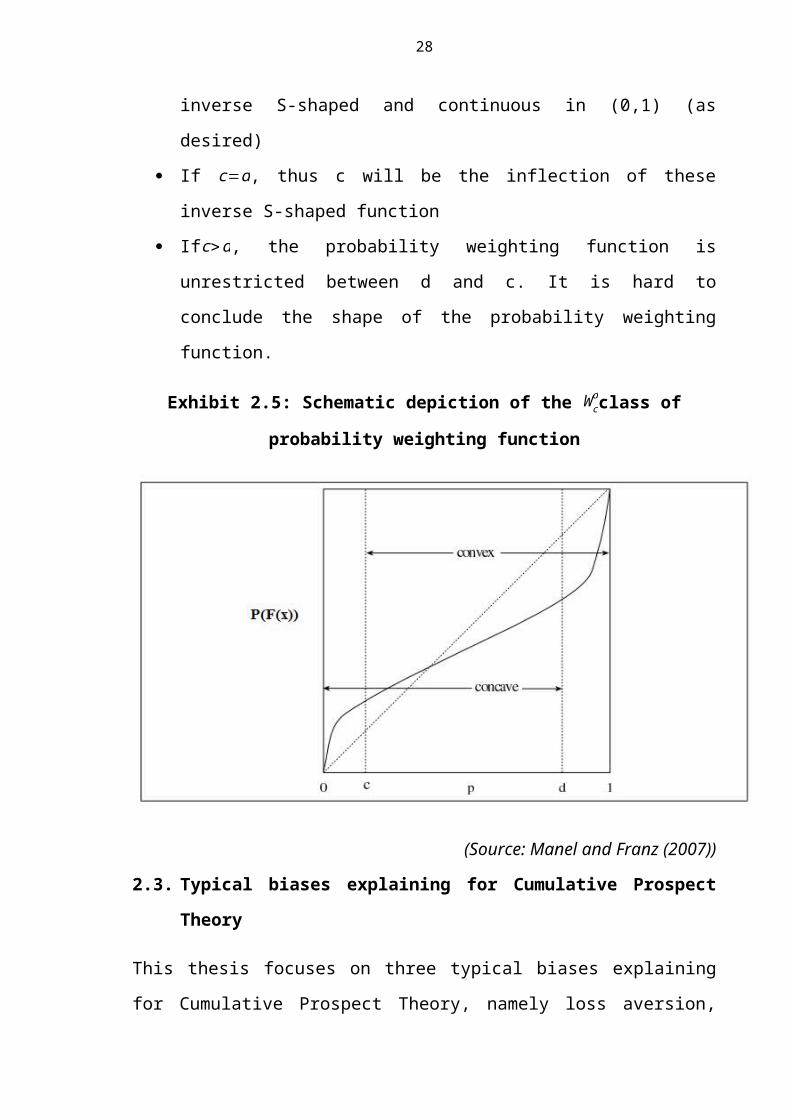

in [0,1]. Denote this class by Wcd (See Exhibit 2.5)

If c<d, then the segment between c and d is nearly

linear, then the probability weighting function is

28

inverse S-shaped and continuous in (0,1) (as

desired)

If c=d, thus c will be the inflection of these

inverse S-shaped function

Ifc>d, the probability weighting function is

unrestricted between d and c. It is hard to

conclude the shape of the probability weighting

function.

Exhibit 2.5: Schematic depiction of the Wcdclass of

probability weighting function

(Source: Manel and Franz (2007))

2.3. Typical biases explaining for Cumulative Prospect

Theory

This thesis focuses on three typical biases explaining

for Cumulative Prospect Theory, namely loss aversion,

29

anchoring - adjustment and herding. Loss aversion is a

pivotal part of risk attitude influencing investment

choices. Analyzed cognitive bias is anchoring –

adjustment, which forms the reference lever, stemming

from faulty reasoning. In addition, emotional biases

such as herding originating from impulsive feelings or

intuition, rather than conscious reasoning and are

hardly possible to be adjusted to traditional

rationality.

2.3.1. Loss Aversion

Kahneman and Tversky (1979, 1992) advanced Prospect

Theory and Cumulative Prospect Theory that describe how

decision-makers actually behave when confronted with

choice under uncertainty. The value function shows the

asymmetry between the values people treat between gains

and losses. This theory hypothesizes that prior losses

increase risk-seeking, while prior gains reduce it. This

asymmetry is called loss aversion.

Empirical tests conducted by Kahneman and Tversky (1991)

indicate that losses are weighted about twice as heavily

as gains – losing $1 is about twice as painful as the

pleasure of gaining $1. In other words, people tend to

hold on losses in the hope that prices will eventually

go back up. It can be explained on the basis of the

Cumulative Prospect Theory, that value function is

30

upward sloping for wealth levers under each individual’s

reference point. In additional, investors are predicted

to be risk averse in gains. Shefrin and Statman (1985)

called this occurrence, stemmed from loss aversion, of

“selling winners too early and riding losers too long”

as disposition effect.

Loss aversion is one of three components of risk

attitude under the lenses of behavioral finance.

Numerous studies resolving the problem of portfolio

optimization derive from the base assumption of risk,

particularly, loss aversion, there can be Static

portfolio optimization model and Multi-stock portfolio

optimization under Prospect Theory for instances.

2.3.2. Anchoring and Adjustment

As proposed by Tversky and Kahneman (1974), Anchoring

and Adjustment heuristic is one strategy for estimating

unknown magnitude by starting from information that is

adjusted to yield the acceptable value. A vast number of

studies demonstrate that regardless of how the initial

anchors were selected, people have the tendency to

adjust their anchors inefficiently, leaving final

estimates too close to the original anchor,

consequently, irrationally. In other words, people are

generally better at relative comparison than absolute

numbers.

31

In his survey carried out in 2006, Pompian require

participants to estimate a good buy price for a share.

Investors are likely to start by using an initial value

as an anchor which can be the 52-week price of stock for

instance. People, then adjust their information by using

their analysis and interpretation which are indicated as

inefficient approach. It is undeniable that investors

anchor their thoughts to a logically irrelevant

reference point while making portfolio investment

decision.

Andersen (2010) presents the involvement of anchoring in

investment decision of market participants by using an

existing arbitraging algorithm. He applies the algorithm

for practical date of Dow Jones Industrial average,

providing evidence that anchoring plays an indispensable

part in the weekly price fixing of the Dow Jones

Industrial Index.

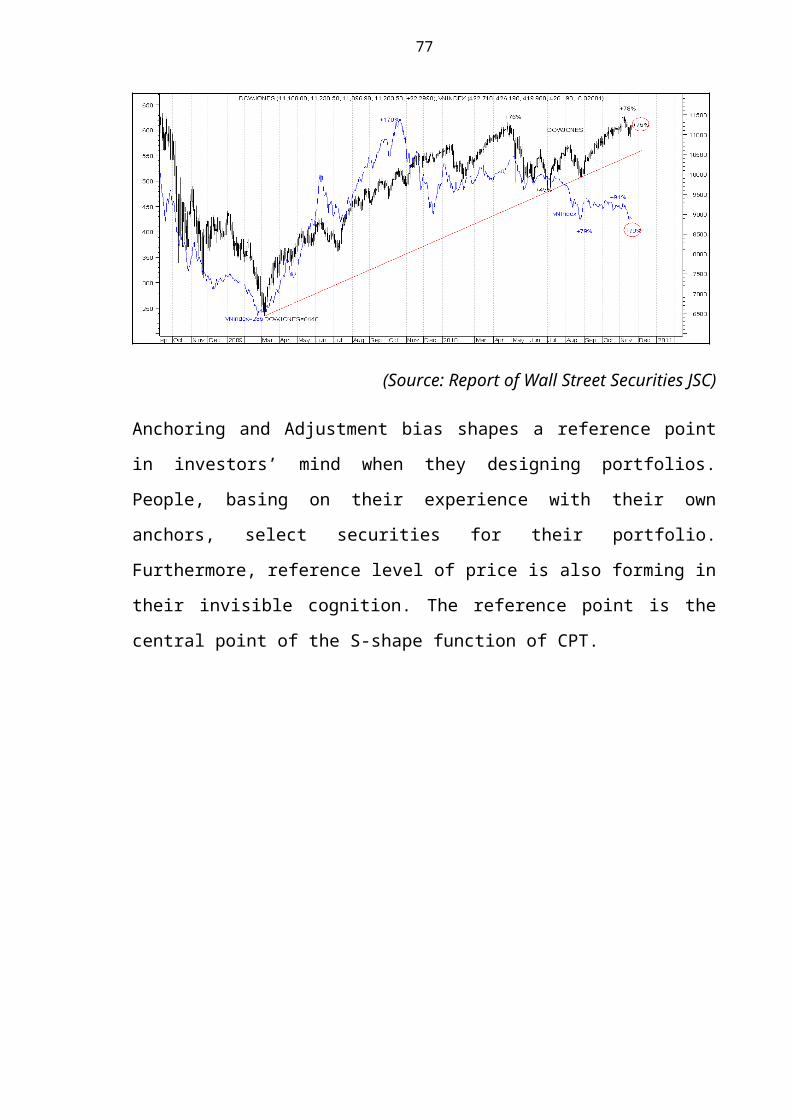

Anchoring and Adjustment bias shapes a reference point

in investors’ mind when they designing portfolios.

People, basing on their experience with their own

anchors, select securities for their portfolio.

Furthermore, reference level of price is also forming in

their invisible cognition. The reference point is the

central point of the S-shape function of the Cumulative

Prospect Theory.

32

2.3.3. Herding Bias

“Herding behavior is an alternative explanation of the

way that investment choices are made by investors”

(Demirer and Kutan, 2006, Ferruz at al., 2008).

Hirshleifer and Teoh (2003) define herding in financial

markets as mutual imitation leading to a convergence of

action. In other words, herding is a fundamental

tendency of human society that people follow the

investment decisions taken by majority. That is why

people tend to alter their “wrong” answer when they are

confronted with the judgment of large group of people.

Popular analysts have considerable influence on private

investors‘ decisions. However, even completely rational

professionals can deal with herding bias when they take

into account other’s viewpoints, even if they know

people react in a herd like manner. One reason is

originating from the past when our ancestors used to

live sociably and generally tend to seek the allowance

from the crowd rather than being a stand-out.

Furthermore, they believe when a large number of people

are unanimous in its judgments, they are certainly right

due to their illusion that the crowd may know something

they do not.

Word of mouth is a pivotal importance of herding.

Investors generally trust their relatives, colleagues,

33

friends instead of credible institutions or media

(printed newspaper, television, radio). Talking to

others seems rapid and effective information - spreading

approach that no means of communication can surpass. In

their study, Shiller and Pound (1986b) with their

intensive survey in investor’s behavior, only six

percent of the respondents specified newspapers and

periodicals.

The existence of herding may have implications for

asset-pricing models because its behavioral affects on

stock price movement. The assumption of EMH is totally

incorrect because in the real world, people, instead be

rationally valuate the stock price, they react in herd-

like manner.

In spite of the fact that herding bias is not a

component of CPT-investor, this important bias provides

a proof that it is not plausible to apply models of

portfolio optimization of which assumption is investors’

rationality and independence.

34

CHAPTER 3: BUILDING OPTIMAL PORTFOLIO FOR INDIVIDUAL

INVESTORS 3.1. Individual investors

An individual investor is a person who buys and sells

securities for their personal account, and not for

another company or organization. Private investors play

an indispensable part in stock market from the developed

stock markets such as USA’s to the emerging financial

market such as Viet Nam’s.

Standard Finance Paradigm assumes that individual

investors are analytically sophisticated and

knowledgeable about markets. By assumption, private

investors in such these constituted models make optimal

decision in a rational manner. However, numerous studies

criticizing the notion of rationality, pointing out that

individual investors are affected by irrational nature

of buying and selling behaviors. According to Bernstein

(1998), “evidence reveals repeated patterns of

irrationality, inconsistency and incompetency in the

ways human being arrive at decisions and choices when

faced with uncertainty”. Nofsinger (2001) asserts that

assumption of rationality and unbiasedness of economic

participants has been drubbed by psychologist for a long

time.

35

The irrationality of individual investors is discovered

during the decision-making process because this process

is a cognitive process resulting in the choice of a

course of action among several alternatives. In this

process, the emphasis is on thinking based on weighting

the outcomes and alternative prior to the last decision.

During this process, individual investors are under the

influence of numerous biases that drive them to wrong

decisions and mistakes.

Regularly, individual investors are irrational while

they have to make buying and selling decisions in the

stock market. In reality, private investors are under

the lack of abilities, knowledge and technology,

therefore, they decide to manage their asset through

investing in an investment trust. The investment trust

is just cognized inside, not the rational entity in the

market. Pompian (2006) lists more than twenty biases

appearing in the decision-making process, which alter

and motivate all decisions of individual investors.

In light of the above discussion, individual investors

are irrational and biased during the process of making

decision or process of buying and selling. Private

investors manage their assets on the basis of investment

trusts instead of investment analyses. Thus, it is

advisable that individual investors should have

36

different investment instruments from institutional

investors.

3.2. Optimal portfolio

3.2.1. Introduction

Wealth management and especially the portfolio choice,

one important bloc of the financial literature, have

developed substantially over several decades, utilizing

the enormous advancement under power of mathematics and

calculus science.

For the start, my thesis provides definitions of

portfolio and optimal portfolio. A portfolio is defined

as a grouping of financial assets such as stocks, bonds

and cash equivalents, as well as their mutual, exchange

– traded and closed-fund counterparts. Optimal portfolio

is a set of portfolios that offers the highest expected

return rate for a particular investor’s acceptable level

of risk or the lowest risk for a given level of expected

return.

Portfolio construction is designed based on underlying

principle of the notion that risk can be diversified by

adding other assets that allow the portfolio to achieve

a better outcome per each risk unit. From an investor’s

perspective, portfolios are to be constructed taking

into account risk return preference of investors with

optimal portfolios lying on the efficient frontier. With

37

each intensive objective either minimizing risk or

maximizing return, more models of portfolio choice are

proposed.

The optimal portfolio literature can be reviewed as

being in two major parts according to the approaches.

The first is Markowitz mean – variance model which is

well-known as “Modern portfolio theory”, which developed

on the premise of expected utility theory by Markowitz

(1952b, 1959) and Tobin (1958, 1965). Each security is

modeled by two parameters: mean and variance of its

return rate. Parameter “mean” is representative for

expected return concept, while “variance” is

representative for risk concept. The key insight of the

model is the expected return is combination weighted

average return of each individual security, but variance

of portfolio is not. Thus, rational investors focus on

the subset of portfolios lying on “efficient frontier”

which achieve the maximum value for a given variance or

the minimum risk for each expected return rate. The

investor’s ultimate decision is on the basis of their

preference along the efficient frontier.

Although the mean-variance model seems attractive and

useful, there is a variety of problems for

practitioners. As Michaud (1989), the principal problems

are stemming from optimization procedure that leads to

concentrated portfolios, corner solutions, the shortage

38

of robustness and especially requirement of much input

data, hence it is unsuitable for private investors. The

model is also strongly criticized by psychologists

because it is built in terms of investors’ rationality.

The underlying assumption of Modern portfolio theory

prevents MPT from applying in reality.

The second approach is developed under the advancement

of behavioral finance that proposes better understanding

of portfolio management behavior as well as decision-

making process. When people confront with risk and gain,

they are affected of invisible biases deriving from

psychology (Kahneman and Tversky, 1979, 1991) and

emotions (Lopes 1987). Furthermore, investors have more

accurate security assessment in long-time rather than

within one year.

Portfolio construction based on behavioral finance

assumes that investors are irrational. Each behavioral

model introduced in this domain concentrates on several

major psychological concepts such as risk asymmetry,

emotions, behavioral biases, the prospect theory, mental

accounting etc. Within this thesis, my concentration is

on the model designed on Cumulative Prospect Theory

base.

3.2.2. Approaches of portfolio optimization

39

The expected utility theory, developed by Von Neumann

and Morgenstern (1947), originates from early working

paper of Bernoulli (1738), providing an idealized,

normative economic model of rational decision under

uncertainty. Complying with the theory, investors

maximize their utility through aggregating the weighted

outcomes. Utilities, formulated in a utility function,

are graphed nonlinearly related to monetary amounts.

In their study in 2005, Copeland, Weston and Shastri

witness that expected utility rests on a set of axioms,

such as comparability or completeness, transitivity and

invariance. Comparability means that agents know exactly

their preference, hence can select the most desired

outcomes. Transitivity implies that people have

consistent preferences that are unable to be altered.

Invariance can be understood that preferences are framed

independently. Based on these assumptions, models of

portfolio optimization, asset allocation and valuation

are constructed. The expected utility model, as with all

theoretical models, is not without its limitations. One

is that the theory considers uncertainty as objective

risk. It is obviously unacceptable to plan for

probabilities of events.

Despite its limitations, EU assumption is irreplaceable

until the occurrence of psychological concept in

finance. Each behavioral concept, such as risk

40

asymmetry, emotions, behavioral biases, prospect theory,

mental accounting, can be added into a model of

portfolio optimization. Nevertheless, Prospect Theory

and Cumulative Prospect Theory are two most popular

approaches to resolve the problem of optimization under

lenses of behavioral finance.

The Prospect Theory is similar in character to that of

utility function, but the major difference between two

theories is the reference point. While EU is the key

background for construction of mean-variance portfolio

theory, PT is an essential premise for models of

portfolio choice in behavioral finance. However, many

researches show the limitation of PT that the theory can

be only applied to gambles with at most two nonzero

outcomes; it predicts that people sometimes choose

dominated gambles.

In modified version published in 1992, the theory known

as “Cumulative Prospect Theory” is popularly accepted

and typically used in both academic and practical

worlds. Empirical research has been testing CPT and

providing evidence of its relevance for models of

investment decision than original version. The

theoretical and empirical studies, proposed by Tversky

and Kahneman (1979), are a striking proof in support of

the CPT when CPT is accessible to resolve some

limitations of Prospect Theory.

41

To conclude, different assumptions shape different

models of portfolio optimization. The Expected Utility

Theory is the key motivation for traditional

mathematical model while PT and CPT are indispensable

parts of the enhancement of optimal portfolio models

accounting for behavioral biases.

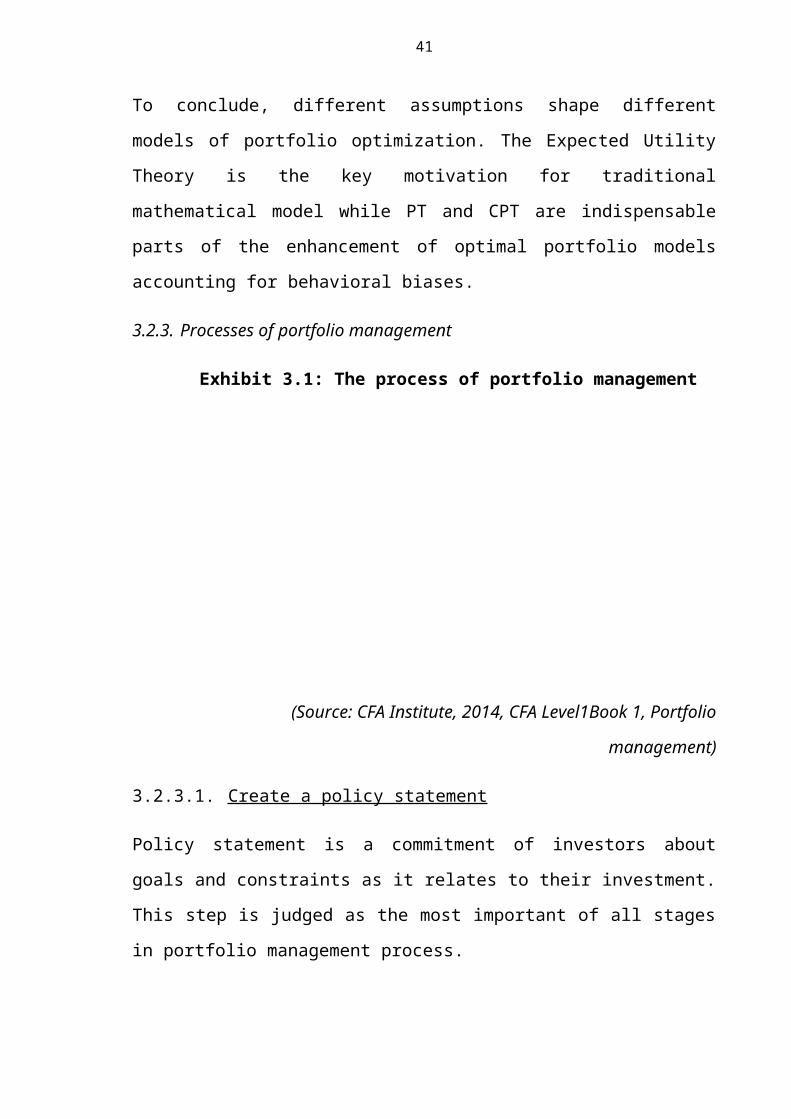

3.2.3. Processes of portfolio management

Exhibit 3.1: The process of portfolio management

(Source: CFA Institute, 2014, CFA Level1Book 1, Portfolio

management)

3.2.3.1. Create a policy statement

Policy statement is a commitment of investors about

goals and constraints as it relates to their investment.

This step is judged as the most important of all stages

in portfolio management process.

Create a policy statementDevelop an investment strategyPortfolio selectionAsset allocationMonitor and update portfolios

42

It is requisite for an investor to understand his true

financial needs both in short-run and long-run. Based on

this good understanding, the investor will manage his

portfolio to meet his needs. When there is market

volatility or a change in his private needs, the policy

statement will guide him to make necessary adjustments

in a disciplined manner.

Prior to design a policy statement plan, it is of

pivotal importance for an investor to express his

investment objectives in terms of risk and return.

It is undeniable that return objectives play great roles

in investment decision-making process as they help to

focus investors on reaching financial goal. However,

level of risk tolerance are far more important than

expected return rate. With each risk level, the

requirement of return rate is distinct. Furthermore,

despite the need for a high return, an investor may be

uncomfortable with the risk that is attached to that

higher return portfolio. As such, it is important to

consider not only return, but the risk of the investor

in a policy statement.

3.2.3.2. Develop an investment strategy

Strategic investment plan is the strategy combining

investors’ goals and objectives with current financial

market and economic conditions.

43

Before investment decision, investors should spend time

on researching and analyzing the macroeconomic

situation. There is no one denying the dependence

between the development of stock market upon the

sustainability of national economy and the stability of

manufacturing environment.

Actual experiences show that stock and other asset

prices are important parts of the driving forces to

economic growth. For example, the rise of stock prices

has positive effects to the increased investment of

enterprises (excluding too high speculation and

imperfect information). Stock prices also have effects

to the wealth of the households and their spending.

3.2.3.3. Select securities

Portfolio selection is the process that investors decide

to pick securities for their portfolio. In this stage,

the investor will choose securities including foreign

exchange, gold, stocks, bonds, etc. Portfolio selection

is an indispensable step in portfolio management

process. Based on policy statement, investment strategy

and private screening systems, assets are add in to list

of portfolio.

There are many approaches to pick stock or securities.

Many fundamental investors prefer huge companies that

generate more profit with sustainable growth rates.

44

While some individual investors select technical tools

to pick growing stocks based on market performance

rather than the company’s fundamental factors. Types of

preference lead to the different selection of stocks,

bond or cash.

3.2.3.4. Allocate assets

After having a list of securities, investors jump into

the next stage, allocation. The major objective of this

step is to distribute total original monetary wealth

into different investments. In other words, they have to

answer the following questions: how proportion of cash

should an investor maintain? How much proportion of

asset X should be purchased? In my thesis, the model

Static Portfolio Optimization model, designed on the

basis of Cumulative Prospect Theory, aims to help

investors to answer these questions in real world.

In reality, with the support of such models as Capital

Asset Pricing Model, Fama French Three Factors,

Discounted Cash Flow model, Dividend Discounted Model,

etc, investors are equipped with many screening system

allowing to shorten choosing process.

3.2.3.5. Monitor and update portfolios

The last stage of portfolio management process requires

investors to adjust when both markets and investors’

45

needs change. It is necessary for investors to monitor

for these changes as they occur and update the plan as

soon as the market changes has big influence on

portfolio performance in the foreseeable future.

3.2.4. Optimization constraints

3.2.4.1. Regulation and taxes

Regulation and taxes are constraints imposed on the

optimization process. Investors may be forbidden by law

to hold some assets because in some cases, unconstrained

portfolio optimization would lead to short-selling of

some assets while short-selling can be forbidden in

several countries. Additionally, it is impractical to

hold an asset due to too high associated tax cost.

3.2.4.2. Transaction costs

Transaction costs are the costs of trading in order to

change the portfolio weights. Since the optimal

portfolio changes with time, there is a financial

incentive to optimize again frequently. However, too

frequent trading will lead to too-frequent transactions

costs; hence, the optimal strategy is to find the

frequency of re-optimization and trading that balance

between transaction costs and up-to-date optimal

portfolios.

46

3.3. Designing optimal portfolio for individual

investors

Each individual investor is affected by different types

of cognitive and emotional biases. These biases

influence on purchasing and selling decisions, hence

have great impacts on selection and allocation stages

(See Exhibit 3.1).

Selection stage is the stage when individual investors

choose stocks, bonds and cash for their portfolio. The

choices can deviate from the initial investment policy

and strategy due to herding and anchoring for instances.

Therefore, investors should take advantage of screening

system to isolate them from the craziness of the stock

market.

Allocation is the process of optimization, thus it is of

critical importance to apply suitable models to allocate

portfolios. For example, if one of the most obvious

biases is loss aversion, the investor should apply the

model of portfolio optimization based on loss aversion

index or loss aversion function. Another examples, when

an investor abide by Cumulative Prospect Theory, he

should use models based on theoretical framework of CPT.

To summarize, designing individual portfolio is

different from financial institutions because of

investors’ irrationality. Each investor requires a

47

private model benefiting them in order to optimize their

portfolio. These models should be based on the most

clear biases affecting on them.

48

CHAPTER 4: MODEL OF STATIC PORTFOLIO OPTIMIZATION

UNDER CUMULATIVE PROSPECT THEORY4.1. Introduction

Cumulative Prospect Theory has been emerging as the best

financial premises for constructing optimal portfolio in

comparison with Expected Utility Hypothesis and Prospect

Theory; hence, some theoretical optimization models have

been designed under CPT.

Pirvu and Schulze (2012), in their working paper No.

742, propose advance model of multi-stock portfolio

optimization under CPT. The model is developed on the

basis of Static portfolio optimization of Bernard and

Ghossoub (2009). They consider a CPT-investor in one-

period economy with one riskless bond and multiple risky

stocks, which follow a multivariate elliptical

distribution. The key contribution of their work is a a

two-separation between the riskless bond and a mean-

variance-portfolio. Based on their finding, they resolve

the optimization problem by imposing a regulatory risk

constraint.

He and Zhou (2011) resolve the static problem in the

presence of n risky choices, corresponding to a multi-

stock financial market. They introduce a new measure of

loss aversion for large payoffs, known as large-loss

49

aversion degree (the LLAD), which is proved to be a

pivotal determinant of the model. The problem of

maximizing the prospect value is explicitly demonstrated

for the cases when the reference level is the risk-free

return and when it is not. They compose the LLAD, the

reference point and the curvature of of the probability

distortion within their statics of optimal risky

portfolio.

Gomes (2003) in “Portfolio Choice and Trading Volume

with Loss-Averse Investors” presents a model of

portfolio selection and security trading volume in case

of loss aversion bias. The demand function of model is

discontinuous and non-monotonic risky assets. Loss-

averse investors complying with disposition effect will

not hold stocks unless the equity return rate is quite

high. Gomes provides the cogent proof of that elasticity

of the aggregate demand curve fluctuate considerably,

depending upon the distribution of wealth.

Within the thesis, my principal objective is to

introduce Static portfolio optimization model holding in

a risky asset and a risk- free asset under Cumulative

prospect Theory, in a one-period economy. This model

valid in case of the assumption of CPT-investor is

reasonable.

50

4.2. Static Portfolio Choice under Cumulative Prospect

Theory

4.2.1. Background

Consider the portfolio choice problem in case of one-

period economy with one risk-free asset (return rate p

over the period) and one risky asset (return rate q over

period).

Denote W0 to be the investor’s initial wealth. An amountK (withK>0) is invested in the risky asset and the

remaining (W¿¿0−K)¿ is invested in the risk-free asset.

Assume that short-selling is forbidden.

The final wealth at the end of the period is given by:

W=(W0−K ) (1+p)+K (1+q)=W0 (1+p)+K(q−p)

Define y as the excess return rate on the risky asset

over the risk-free rate:

y=q−p

Define Wref, the reference level of wealth at the end of

period as:

Wref=W0 (1+r )

Wrefis the amount the individual would have receive at

the end of period if he invested all his initial W0 in

the risk-free asset (for example: bank account or

Treasury bills).

51

It is clear to see that:

W=Wref+Ky

The deviation from the reference level is defined as:

D (K)=W−Wref=Ky

4.2.2. Content of Static Portfolio Optimization model

The objective function of the CPT – investor, O(x), is

given by:

O (D)=∫0

+∞

Pg (S (x ))dg (x )−∫0

+∞

Pl (F (−x ))dl(x) (See page 11)

F and S is the cumulative distribution functions and

decumulative distribution functions of risky asset and

risk-free asset, respectively.

Lettingy=xK, in order to x=Ky anddx=Kdy.

Thus, S (x)=S (Ky ) andF (x)=F (Ky ). Then, obtain:

O (D (K ))=∫0

+∞

Pg (S (Ky) )dg(Ky)−∫0

+∞

Pl (F (−Ky ))dl (Ky)

¿∫0

+∞

∝(Ky)∝−1Pg (S (y ))Kdy−∫0

+∞

μβ (Ky )β−1Pl (F (−y ))Kd(y)

¿K∝∫0

+∞

Pg (S (y ))dg (y )−Kβ∫0

+∞

Pl (F (−y))dl(y)

To simplify, rewrite the formulation as follows:

O (D (K ))=G (y )−L (y ) (¿)

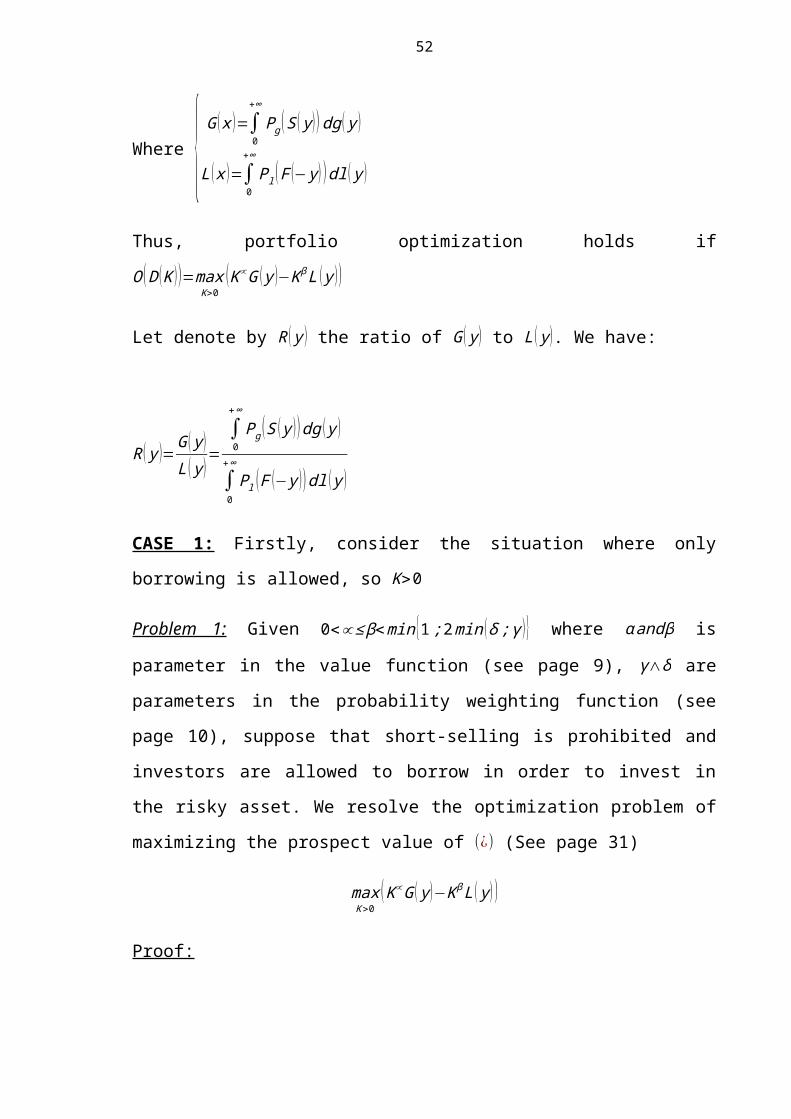

52

Where { G (x )=∫0

+∞

Pg (S (y))dg(y )

L (x )=∫0

+∞

Pl (F (−y) )dl(y )

Thus, portfolio optimization holds ifO (D (K ))=max

K>0(K∝G (y )−KβL (y ))

Let denote by R (y ) the ratio of G (y) to L (y). We have:

R (y )=G (y)L (y)

=∫0

+∞

Pg (S (y ))dg (y )

∫0

+∞Pl (F (−y ))dl (y )

CASE 1: Firstly, consider the situation where only

borrowing is allowed, so K>0

Problem 1: Given 0<∝≤β<min {1;2min (δ;γ )} where αandβ is

parameter in the value function (see page 9), γ∧δ are

parameters in the probability weighting function (see

page 10), suppose that short-selling is prohibited and

investors are allowed to borrow in order to invest in

the risky asset. We resolve the optimization problem of

maximizing the prospect value of (¿) (See page 31)

maxK>0

(K∝G (y)−KβL (y) )

Proof:

53

If ∝=β, then we can write O (D)=K∝O (y ), then we consider 3

cases as follows:

- If O (y)=0, any holding in the risky asset is

optimal. The prospect value is constant and equal

to 0

- If O (y)>0, the borrowing finite amount to invest in

the risky asset optimize the portfolio. The

prospect value is equal to +∞.

- If O (y)<0, the optimal amount K to invest in the

risky asset is equal to 0.

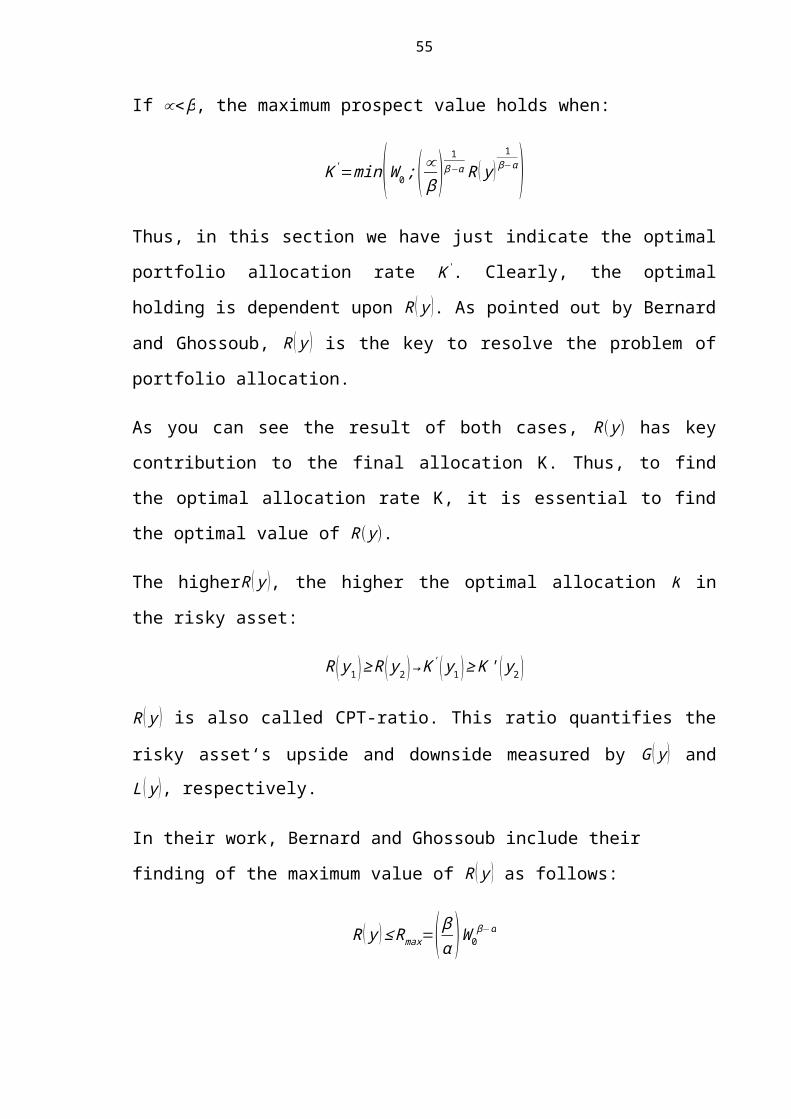

If ∝≠β, the maximum prospect value holds when:

d (K∝G (y )−KβL (y ))dK

=0

According to Bernard and Ghossoub (2009), the equality

yields the only root:

K'=(βL (y )αG (y ))

1α−β=(∝β )

1β−α R (y)

1β−α

In order to K' is the optimal point for the equality, it

leads to the requirement as follows:

d2 (K∝G (y)−KβL (y) )d2K

<0

↔ (α−1 )Kα−2<K'α−β (β−1)Kβ−2

54

When K=K', then (α−1)K'∝−2<K'α−2 (β−1 )↔α<β (as desired).

Thus, K' is the optimal allocation when borrowing is

allowed.

CASE 2: Consider the condition where both short-selling

and borrowing constraints are imposed. This leads toK∈ [0;W0 ]

Problem 2: Given 0<∝≤β<min {1;2min (δ;γ )}, where αandβ is

parameter in the value function (see page 9), γ∧δ are

parameters in the probability weighting function (see

page 10), suppose that both short-selling and borrowing

are not allowed, we resolve the optimization problem of

maximizing the prospect value of ( ¿ ) (See page 31)

maxK>0

(K∝G (y)−KβL (y) )

Proof:

If ∝=β, then we can write O (D)=K∝O (y ), then we consider 3

cases as follows:

- If O (y)=0, any holding in the risky asset is

optimal. The prospect value is constant and equal

to 0

- If O (y)>0, It is optimal to invest W0in the risky

asset optimize the portfolio.

- If O (y)<0, the optimal amount K to invest in the

risky asset is equal to 0.

55

If ∝<β, the maximum prospect value holds when:

K'=min(W0;(∝β )1

β−α R (y)1

β−α)Thus, in this section we have just indicate the optimal

portfolio allocation rate K'. Clearly, the optimal

holding is dependent upon R (y ). As pointed out by Bernard

and Ghossoub, R (y ) is the key to resolve the problem of

portfolio allocation.

As you can see the result of both cases, R(y) has key

contribution to the final allocation K. Thus, to find

the optimal allocation rate K, it is essential to find

the optimal value of R(y).

The higherR (y ), the higher the optimal allocation K in

the risky asset:

R (y1 )≥R (y2 )→K' (y1 )≥K' (y2 )

R (y ) is also called CPT-ratio. This ratio quantifies the

risky asset‘s upside and downside measured by G (y) andL (y), respectively.

In their work, Bernard and Ghossoub include their

finding of the maximum value of R (y ) as follows:

R (y )≤Rmax=(βα )W0β−α

56

To summarize: ∝<β (See the detailed proof in page 32, 33

when ∝=β)

Case 1: consider the situation where only borrowing is

allowed, so K>0

Koptimal=(∝β )1

β−αR (y )1

β−α

Case 2: Consider the condition where both short-selling

and borrowing constraints are imposed. This leads toK∈ [0;W0 ]

Koptimal=min(W0;(∝β )1

β−αR (y )1

β−α)Where:

R (y )≤Rmax=(βα )W0β−α

4.3. Evaluation of Static Portfolio Optimization Model

4.3.1. Advantages

Static Portfolio Optimization model is the simplest

model resolving the problem of maximizing the prospect

value in one period economy with one risky asset and one

risk-free asset for CPT-investor. The model is

constructed on the basis of Cumulative Prospect Theory,

hence it is applicable for investors who are loss-

averse, anchoring in the reference level and

overweighting small probabilities. Furthermore, this

57

model is easy to understand and apply in practical

world.

To academics, Bernard and Ghossoub introduce a new

approach to resolve the problem of optimization under

the lens of CPT. Based on their working paper, more

researches are conducted with more complex and

sophisticated scenarios.

4.3.2. Disadvantages

4.3.2.1. Violate Loss Aversion Index

Risk attitude consists of three components: (i) the

basis utility; (ii) probability distortion, and (iii)

loss aversion known as “behavioral concept” measured

through LA index. Numerous academics point out that

there are many different alternative measures of

behavioral criterion of loss aversion in the literature

with their own advantages and disadvantages. As

Kobberling and Wakker, loss aversion is illustrated by

an index defined as follows:

LAkw= limx→0−¿l'(x)

limx→0+¿g' (x )

¿ ¿

¿¿

The gist of the formulation is to consider foundations

of risk attitude outside marginal utility by using a

“probabilistic risk attitude” resulting from model of

rank-dependent utility. As Schmidt and Zank (2007), this

58

idea is inherited from Prospect Theory introduced by

Kahneman and Tversky (1979), and Expected Utility

Theory, but is inaccessible to apply under Cumulative

Prospect Theory because it ignore rank dependence. In

their work, Schmidt and Zank (2005) propose an

alternative quantitative approach to define loss

aversion in terms of both the value function and

probabilities distortion.

Consider the Objective function:

For x>0 is a fixed real number, then

Og (d )=∫0

+∞

Pg (S (x))dg(x)=∫0

+∞

Pg¿¿¿

¿∫0

+∞

Pg ¿¿

Similarly, Ol (x)=l (x ) withx>0. Hence, for any x>0, we have

O (x)=g (x)=xα and |O (−x )|=|−l (x)|=μxβ. Consequently, loss

aversion holds when xα<μxβ or μ>xα−β

Obviously, when ∝=βand μ>1, loss aversion holds.

When ∝<β, the model violates the accepted measure of

loss aversion proposed by Kobberling and Wakker in a

neighborhood of the reference point, namely for:

0<x<ε=μ1

α−β

59

However, the violation with loss aversion index

suggested by Kobberling and Wakker is not a serious

matter as some recent experimental studies show that

individuals’ decision sometime violate loss aversion,

Bleichrodt and Pinto’s work of “An Experimental Test of

Loss Aversion and Scale Compatibility” in 1995 is a

typical example.

Thus, in their model of Static portfolio optimization,

Bernard and Mario (2009) consider loss aversion as the

behavioral phenomenon that “losses loom larger than

gains” (Kahneman and Tversky) that do not concern where

loss aversion deriving from, the utility function or

from the probability weighting function or from both.

4.3.2.2. Ignore diversification benefits

It is undeniable that the model is too simple with only

one risky asset and one risk-free asset, which cannot

reach the portfolio diversification. Investors who

desire to invest more types of asset do not take

advantage of the Static portfolio optimization model.

However, this difficulty is surmountable with the

evolutionary model of Pirvu and Schulze (2012) with

multi-stock portfolio optimization under CPT.

60

CHAPTER 5: INTRODUCTION TO VIETNAMESE INDIVIDUAL

INVESTORS5.1. Overview of Vietnamese stock market

5.1.1. A brief history of Vietnamese stock market

On July 2000, Viet Nam took a major step towards

establishing a more robust market and forming a new

channel of capital mobilization for enterprises by

opening Securities Trading Centre in Ho Chi Minh. On the

first day of trading, only two individual stocks with

total market capitalization of VND 444,000 million

(about USD 27.95 million) were transacted on the market.

After four years of preparation and a vast number of

delays, the Government of Viet Nam ultimately fulfilled

its commitment to the opening of Vietnamese stock

market. After 13 years of the enhancement, Vietnamese

stock market has been evolving with significant

contribution to the national economy sustainable

development.

5.1.1.1. HOSE

Due to the rapid growth of the securities market, the

economic innovation and the business restructure, Prime

Minister approved Decision No.599/QĐ-TTg to transform Ho

Chi Minh Trading Centre into Ho Chi Minh Stock Exchange

61

(HOSE), which is current accounting for about 89% of

aggressive capitalization.

Thirteen years after the foundation of the Vietnamese

stock market, at the end of June 2013, the market had

309 listed companies in Ho Chi Minh with capitalization

worth almost USD 40 billion, an increase of 480% in

comparison with year 2000. Especially, the average

trading volume per day during June 2013 reached about

65.69 million shares, equivalent to about USD 51 million

per a trading session. The amazing turnover rate was

42.05% during the first six-month period in 2013.

The products traded on HOSE consist of stock, corporate

bonds, municipal bonds and fund certificates. There are

currently also two types of fund certificates, 38 bonds

listed on HOSE with the volumes of about 30.3 billion

shares, 70 million bonds and 45 million fund

certificates, respectively.

Table 5.1: HOSE’s listing summary recorded in April 2014

ALL STOCK

INVESTMENT

FUND

CERTIFICATE

BOND

Total listed

shares (1

share)

342 302 2 38,00

Percent (%) 100,00 88.30 0.58 11.11

62

Listed

Volume (1000

shares)

30,314,902

.9

30,199,292

.145,417.53 70,092.3

Percentage

(%)100,00 99.62 0.15 0.23

Listed Value

(VND

million)

309,457,33

4.2

301,993,93

0.9454,175.30

7,009,22

8.0

Percentage

(%)100,00 97.59 0.15 2.27

(Source: www.hsx.vn, the official website of Ho Chi Minh Stock

Exchange)

5.1.1.2. HNX

Ha Noi Stock Exchange was established in accordance with

Decision No.01/2009/QDD-TTg by Prime Minister on the

basis of transforming and restructuring Ha Noi

Securities Trading Center.