Telenor ASA

15

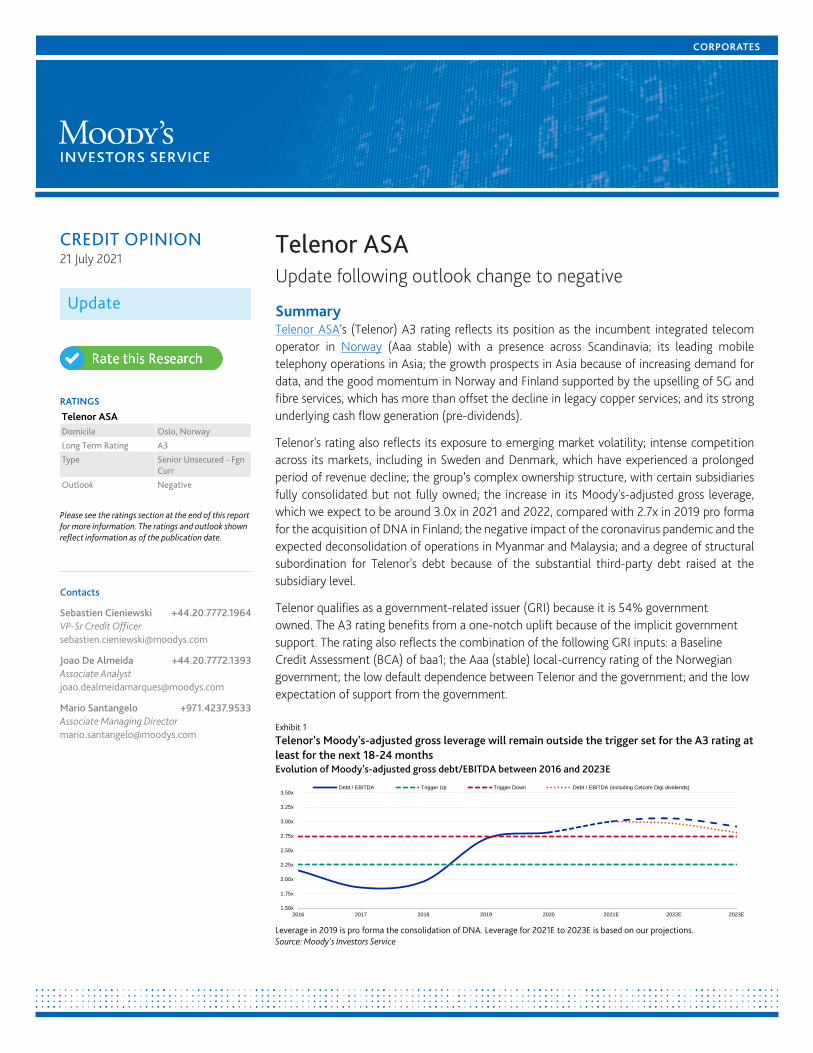

CORPORATES CREDIT OPINION 21 July 2021 Update RATINGS Telenor ASA Domicile Oslo, Norway Long Term Rating A3 Type Senior Unsecured - Fgn Curr Outlook Negative Please see the ratings section at the end of this report for more information. The ratings and outlook shown reflect information as of the publication date. Contacts Sebastien Cieniewski +44.20.7772.1964 VP-Sr Credit Officer [email protected] Joao De Almeida +44.20.7772.1393 Associate Analyst [email protected] Mario Santangelo +971.4237.9533 Associate Managing Director [email protected] Telenor ASA Update following outlook change to negative Summary Telenor ASA 's (Telenor) A3 rating reflects its position as the incumbent integrated telecom operator in Norway (Aaa stable) with a presence across Scandinavia; its leading mobile telephony operations in Asia; the growth prospects in Asia because of increasing demand for data, and the good momentum in Norway and Finland supported by the upselling of 5G and fibre services, which has more than offset the decline in legacy copper services; and its strong underlying cash flow generation (pre-dividends). Telenor's rating also reflects its exposure to emerging market volatility; intense competition across its markets, including in Sweden and Denmark, which have experienced a prolonged period of revenue decline; the group’s complex ownership structure, with certain subsidiaries fully consolidated but not fully owned; the increase in its Moody's-adjusted gross leverage, which we expect to be around 3.0x in 2021 and 2022, compared with 2.7x in 2019 pro forma for the acquisition of DNA in Finland; the negative impact of the coronavirus pandemic and the expected deconsolidation of operations in Myanmar and Malaysia; and a degree of structural subordination for Telenor's debt because of the substantial third-party debt raised at the subsidiary level. Telenor qualifies as a government-related issuer (GRI) because it is 54% government owned. The A3 rating benefits from a one-notch uplift because of the implicit government support. The rating also reflects the combination of the following GRI inputs: a Baseline Credit Assessment (BCA) of baa1; the Aaa (stable) local-currency rating of the Norwegian government; the low default dependence between Telenor and the government; and the low expectation of support from the government. Exhibit 1 Telenor's Moody's-adjusted gross leverage will remain outside the trigger set for the A3 rating at least for the next 18-24 months Evolution of Moody's-adjusted gross debt/EBITDA between 2016 and 2023E 1.50x 1.75x 2.00x 2.25x 2.50x 2.75x 3.00x 3.25x 3.50x 2016 2017 2018 2019 2020 2021E 2022E 2023E Debt / EBITDA Trigger Up Trigger Down Debt / EBITDA (including Celcom Digi dividends) Leverage in 2019 is pro forma the consolidation of DNA. Leverage for 2021E to 2023E is based on our projections. Source: Moody's Investors Service

-

Upload

khangminh22 -

Category

Documents

-

view

5 -

download

0

Transcript of Telenor ASA

CORPORATES

CREDIT OPINION21 July 2021

Update

RATINGS

Telenor ASADomicile Oslo, Norway

Long Term Rating A3

Type Senior Unsecured - FgnCurr

Outlook Negative

Please see the ratings section at the end of this reportfor more information. The ratings and outlook shownreflect information as of the publication date.

Contacts

Sebastien Cieniewski +44.20.7772.1964VP-Sr Credit [email protected]

Joao De Almeida +44.20.7772.1393Associate [email protected]

Mario Santangelo +971.4237.9533Associate Managing [email protected]

Telenor ASAUpdate following outlook change to negative

SummaryTelenor ASA's (Telenor) A3 rating reflects its position as the incumbent integrated telecomoperator in Norway (Aaa stable) with a presence across Scandinavia; its leading mobiletelephony operations in Asia; the growth prospects in Asia because of increasing demand fordata, and the good momentum in Norway and Finland supported by the upselling of 5G andfibre services, which has more than offset the decline in legacy copper services; and its strongunderlying cash flow generation (pre-dividends).

Telenor's rating also reflects its exposure to emerging market volatility; intense competitionacross its markets, including in Sweden and Denmark, which have experienced a prolongedperiod of revenue decline; the group’s complex ownership structure, with certain subsidiariesfully consolidated but not fully owned; the increase in its Moody's-adjusted gross leverage,which we expect to be around 3.0x in 2021 and 2022, compared with 2.7x in 2019 pro formafor the acquisition of DNA in Finland; the negative impact of the coronavirus pandemic and theexpected deconsolidation of operations in Myanmar and Malaysia; and a degree of structuralsubordination for Telenor's debt because of the substantial third-party debt raised at thesubsidiary level.

Telenor qualifies as a government-related issuer (GRI) because it is 54% governmentowned. The A3 rating benefits from a one-notch uplift because of the implicit governmentsupport. The rating also reflects the combination of the following GRI inputs: a BaselineCredit Assessment (BCA) of baa1; the Aaa (stable) local-currency rating of the Norwegiangovernment; the low default dependence between Telenor and the government; and the lowexpectation of support from the government.

Exhibit 1

Telenor's Moody's-adjusted gross leverage will remain outside the trigger set for the A3 rating atleast for the next 18-24 monthsEvolution of Moody's-adjusted gross debt/EBITDA between 2016 and 2023E

1.50x

1.75x

2.00x

2.25x

2.50x

2.75x

3.00x

3.25x

3.50x

2016 2017 2018 2019 2020 2021E 2022E 2023E

Debt / EBITDA Trigger Up Trigger Down Debt / EBITDA (including Celcom Digi dividends)

Leverage in 2019 is pro forma the consolidation of DNA. Leverage for 2021E to 2023E is based on our projections.Source: Moody's Investors Service

MOODY'S INVESTORS SERVICE CORPORATES

Credit strengths

» Broad geographical diversification

» Leading positions in most of its markets

» Good progress in delivering cost-efficiency measures, which supports its higher-than-peer EBITDA margin

» Publicly stated financial policy to maintain net debt/EBITDA (as reported by the company) within the target range of 1.8x-2.3x(post-IFRS 16)

» Favourable structural trends in Asia, driven by increasing smartphone penetration and data usage, despite the relatively high short-term impact of the pandemic

Credit challenges

» High exposure to emerging market volatility

» Intense competition in most markets

» Spectrum payment needs outside the Nordic region

» Leverage likely to increase over the next two years based on our projections from an already high level for the rating category

» Structural subordination for Telenor's holding company debt

Rating outlookThe negative rating outlook reflects our expectation that Telenor’s metrics will remain outside of the updated leverage and cash flowtarget ranges in 2021 and 2022 with potential improvement from 2023 as the company returns to more significant EBITDA growth.However, the pace of this improvement remains uncertain and will partly depend on the phasing off of the impact of the pandemic andthe future financial policy of the group, including its M&A strategy.

Factors that could lead to an upgradeWe would consider upgrading Telenor's rating if the group's credit metrics improve such that its Moody's adjusted retained cash flow(RCF)/debt increases towards 30% on a sustained basis, and Moody's-adjusted debt/EBITDA falls consistently and comfortably below2.25x. In addition to the factors listed above that affect the company's BCA, the rating could be affected by changes in the rating of thesupporting government or changes in our assessment of default dependence and government support.

Factors that could lead to a downgradeNegative rating pressure could develop if Telenor's Moody's-adjusted RCF/debt remains well below 20% for a prolonged period; itsMoody's-adjusted debt/EBITDA remains above 2.75x, or the company were to adopt a more aggressive financial policy that would leadto sustained negative free cash flow (FCF).

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page onwww.moodys.com for the most updated credit rating action information and rating history.

2 21 July 2021 Telenor ASA: Update following outlook change to negative

MOODY'S INVESTORS SERVICE CORPORATES

Key indicators

Exhibit 2

Telenor ASANOK Millions Dec-15 Dec-16 Dec-17 Dec-18 Dec-19 Dec-20 Mar-21 (LTM) Proj 2021 Proj 2022

Revenue 128,175 125,395 112,069 105,923 113,666 122,811 120,731 110,009 98,435

Debt / EBITDA 2.0x 2.2x 1.9x 2.0x 2.8x 2.8x 2.7x 3.0x 3.1x

RCF / Debt 24.5% 26.4% 31.7% 29.7% 13.2% 18.3% 18.5% 17.3% 16.8%

(EBITDA - CAPEX) / Interest Expense 8.0x 7.1x 8.4x 7.7x 5.2x 7.4x 7.5x 7.0x 6.9x

All figures and ratios are calculated using our estimates and standard adjustments.Periods are financial year end unless indicated. LTM = Last 12 months.The Projections (Proj) are our opinion and do not represent the views of the issuer. Proj 2021 is pro forma for the reclassification of Myanmar operations as assets held for sale while Proj2022 is also pro forma for the deconsolidation of operations in Malaysia. Pro forma for dividends to be received from Celcom Digi we project Moody's adjusted debt/EBITDA at 3.0x in Proj2022.Source: Moody's Investors Service

ProfileTelenor ASA (Telenor) is the incumbent integrated telecommunications provider in Norway. The company delivers a full range of servicesand products, including mobile and fixed-line telephony, broadband and data services for residential and business customers, and a broadrange of wholesale services. In addition, the company is one of the leading international providers of mobile services, with around 182million mobile subscribers worldwide as of December 2020. The company's activities outside its home market include mobile and fixedoperations in Sweden and Denmark, and mobile operations in Thailand (dtac), Malaysia (Digi), Bangladesh, Pakistan, Myanmar and Finland.Telenor is also a leading provider of television and broadcasting services in the Nordic region. The company is majority owned by theNorwegian government, which holds a 54% stake in the company.

Recent developmentsOn 8 July 2021, Telenor announced that it had entered into an agreement to sell 100% of its mobile operations in Myanmar toM1 Group for $105 million (around NOK900 million), of which $55 million (around NOK470 million) is deferred over five years.The company's decision was driven by the deterioration of the economic and political situation in the country as well as increasingconstraints imposed on telecom operators. On 4 May 2021, Telenor announced that it had fully written off its Myanmar operationsfollowing the military coup in the country on 1 February 2021, which worsened the economic and business environment outlook in thecountry with no prospects of improvement. Myanmar’s authorities have repeatedly blocked internet access, with mobile data accessrestricted across much of the country since 15 March 2021, significantly hurting Telenor's results. The company generated NOK7.1billion of total revenue and NOK4.2 billion of EBITDA (as reported by the company) in Myanmar, or 6% and 7% of total group revenueand EBITDA in 2020, respectively.

On 21 June 2021, Axiata Group Berhad (Axiata, Baa2 stable) and Telenor announced that they had signed an agreement regarding theproposed merger of the Malaysian mobile operations, Celcom Axiata Berhad and Digi (49% owned by Telenor). Axiata and Telenor willbe equal partners with each having a 33.1% ownership stake in the merged entity, which will assume Digi’s listing on Bursa Malaysia.At completion, the merger of Celcom and Digi will result in Axiata receiving newly issued shares of Digi representing 33.1% of theenlarged issued share capital of Digi, and cash of around $470 million, of which $400 million will come from Digi as debt in the mergedentity and around $70 million from Telenor as part of an ownership equalisation under the terms of the merger. The completion of thetransaction, expected by the second quarter of 2022, will be subject to the approval of both Axiata and Digi shareholders, regulatoryapprovals, and other customary terms and conditions.

3 21 July 2021 Telenor ASA: Update following outlook change to negative

MOODY'S INVESTORS SERVICE CORPORATES

Exhibit 3

Norway and Thailand are the largest contributors to Telenor'srevenueRevenue breakdown by geography for 2020

Exhibit 4

Pro forma for the disposal of Myanmar and the deconsolidation ofMalaysia, Telenor's Scandinavian operations accounted for morethan 50% of revenues in 2020Pro forma revenue breakdown by geography in 2020 (pro forma for disposalof Myanmar and deconsolidation of Digi in Malaysia)

Denmark4% Myanmar

5% Pakistan5%

Other units6%

DNA - Finland8%

Sweden10%

DiGi - Malaysia11%

Grameenphone -Bangladesh12%

dtac - Thailand18%

Norway21%

Before eliminations.Source: Company reports

Denmark5% Pakistan

6%

Other units7%

DNA - Finland9%

Sweden12%

Grameenphone -Bangladesh14%

dtac - Thailand22%

Norway25%

Before eliminations.Source: Company reports

Detailed credit considerationsDespite its moderate scale, Telenor has high geographical diversificationWhile Telenor’s scale is moderate with revenue of NOK123 billion in 2020 (or NOK116 billion pro forma for the disposal of TelenorMyanmar), the company has above-average geographical diversification compared with that of its telecom peers.

Telenor is the incumbent telecom operator in Norway with a 55% revenue market share in the mobile segment and 2.8 millionsubscriptions as of year-end 2020. However, Telenor’s operations in its domestic market only accounted for 21% of total revenue(before eliminations) in 2020 (23% pro forma for the disposal of Telenor Myanmar). This relatively low proportion of domestic revenuereflects the company’s high geographical diversification.

In addition to Norway, the company has operations in other Nordic countries, including Sweden and Denmark, and the companyrecently entered Finland with the closing of the acquisition of DNA in 2019. We positively view Telenor’s expansion into Finlandbecause this gives the company exposure to a growing mobile market that complements its existing operations in the Nordic region.

The company has also expanded into Asia. Telenor splits its operations in the region between developed Asia (31% of 2020 totalrevenue), including Malaysia and Thailand, and emerging Asia (23%), including Bangladesh and Pakistan. With the exit from Myanmar,Telenor's proportion of revenue generated from the Nordics and developed Asia will increase. To enhance governance, Telenorestablished two hubs in Norway and Singapore in 2020 to oversee its operations in the Nordics and Asia, respectively. While expansioninto Asia has historically provided Telenor with exposure to higher-growth markets relative to the more mature Nordic region, it hasalso brought increased revenue and earnings volatility, including from the appreciation and depreciation of the local currencies versusthe Norwegian krone, Telenor group’s reporting currency. Thus, the disposal of Telenor Myanmar is likely to contribute to increasing theproportion of revenue generated from the Nordics and developed Asia, and potentially contribute to reducing the revenue and earningsvolatility of the group.

Telenor is the largest or second-largest mobile operator in all the countries in the Nordics and Asia where it operates, except forThailand and Finland where it ranks number three.

4 21 July 2021 Telenor ASA: Update following outlook change to negative

MOODY'S INVESTORS SERVICE CORPORATES

Exhibit 5

Telenor has a dominant position in its domestic mobile marketNorwegian mobile market share based on subscribers

Exhibit 6

Telenor has a dominant position in its domestic fixed-broadbandmarketNorwegian fixed-broadband market share based on subscribers

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

Telenor

Telia

Ice

Fjordkraft

Lycamobile

Chili mobil

Other

Data as of H1 2020.Source: Norwegian Communications Authority

0% 5% 10% 15% 20% 25% 30% 35% 40%

Telenor

Altibox

Telia

NextGenTel

Global Connect

Tafjord Marked

Other

Data as of H1 2020.Source: Norwegian Communications Authority

Higher negative impact of the pandemic on Telenor’s Asian operations than in the Nordics; timing of recovery in Asiaremains uncertainAlthough the telecom sector has been resilient to the pandemic compared with other sectors, it has not been fully immune to theshock created by it. Telenor experienced a 2.3% decline in total organic revenue and a 1.9% decline in organic subscription and trafficrevenue in 2020 compared with the year earlier. Subscription and traffic revenue further declined by 4.0% in Q1 2021 compared withthe year earlier (or -2.9% excluding Myanmar, which has been suffering from restrictions on mobile internet usage from March 2021).Subscription and traffic revenue returned to a 2% organic growth in Q2 2021.

Telenor’s performance in 2020 was uneven though, with stronger resilience in the Nordic region than in Asia. The company continuedto experience year-over-year subscription and traffic revenue growth in its domestic Norwegian market at 2% in 2020, an accelerationcompared with 2019 when these revenue increased by only 1% year over year. This performance is remarkable in a market that weconsider mature and demonstrates management’s ability to cross-sell value-added services to its customers, which mainly refer tosecurity and insurance services, and account for around two-thirds of the mobile average revenue per user growth (ARPU) in thecountry. Other drivers for growth in Norway include the successful penetration of fibre-to-the-home (FTTH) and fixed wireless access(FWA) services that are being adopted by a large percentage of existing customers, who are switching from copper. In Q1 2021, organicsubscription and traffic revenue in Norway recorded a moderate decline of 0.9% as the acceleration in the switch from copper andweak roaming more than offset the growth in fibre, FWA and 5G but then stabilised in Q2 2021. In Finland, the continued quarter-on-quarter subscription and traffic revenue growth in 2020 has been driven mainly by the solid momentum in the upselling of 5G servicesto its existing customer base at a premium to 4G services. This strong performance in Norway and Finland has more than offset theprolonged decline in the highly competitive Swedish and Danish markets where ARPU continued to decline by 11% and 3% on a year-on-year basis in Q4 2020, respectively. However, these two markets have been improving. Subscription and traffic revenue in Swedenstabilised during Q2 2021 while Denmark experienced its second consecutive quarter of subscription and traffic revenue growth in Q22021 after a long period of decline.

After strong subscription and traffic revenue growth in January and February of 2020, performance in both developed Asia andemerging Asia was strained for the rest of the year. The decline was most pronounced in developed Asia, including Thailand andMalaysia, where fewer tourists and migrant workers arrived because of pandemic-related travel restrictions, contributing to the year-on-year decline in Telenor’s subscriber base to 182 million as of year-end 2020 from 186 million as of year-end 2019. The temporarylockdown of physical retail channels hurt sales, especially in Asian prepaid markets. There have been new waves of COVID-19 infectionsin Q4 2020 in several markets, including in Myanmar and Pakistan, while the number of daily new COVID-19 cases in Bangladesh

5 21 July 2021 Telenor ASA: Update following outlook change to negative

MOODY'S INVESTORS SERVICE CORPORATES

has been stable. In Thailand and Malaysia, the number of daily new cases continued to increase into 2021. To face the new waves ofinfections, many countries in Asia have reinstated local lockdowns.

Based on the high level of uncertainty and the significant disruption caused by the pandemic, particularly in the first half of theyear, Telenor expects organic subscription and traffic revenue to grow at between 0% to 1% in 2021. Q1 2021 was the last quarterwhen the company faced a year-on-year decline in roaming revenue because of the pandemic and Q2 2021 experienced a positivesubscription and traffic revenue growth supported by strong momentum in Finland and Denmark, and a strong revenue developmentin Bangladesh and Pakistan from data and subscription growth. At the same time subscription and traffic revenue growth benefittedfrom a stabilisation in Sweden, Thailand and Malaysia in Q2 2021. On a reported basis, we expect total revenue to decline by up to5% based on our assumption that the Norwegian krone will stabilise although at a higher level than the 2020 average against most ofthe currencies in the Nordic and Asian countries where it operates. Beyond 2021, we project Telenor to return to more robust revenuegrowth of around 2% per year, supported by its continued strong performance in Norway and Finland, less negative trends in Swedenand Denmark, and recovery in Asia, including a recovery in roaming revenue. Asia will benefit from positive structural trends, includingincreasing demand for data as smartphone penetration continues to grow. In 2020, data revenue grew by 5% in Bangladesh and 30%in Pakistan.

Exhibit 7

Higher negative impact from COVID-19 on Asian operations relative to Scandinavia in 2020Organic subscriber and traffic revenue growth by region (Q1 2020-Q2 2021)

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Norway Sweden Denmark Finland Thailand Malaysia Bangladesh Pakistan Myanmar

Q1 20 Q2 20 Q3 20 Q4 20 Q1 21 Q2 21

No quarterly statistics were available for Finland in Q1 2020 and Q2 2020 and for Myanmar in Q2 2021.Source: Company reports

Strong track record in delivering cost efficiencies have enabled Telenor to deliver strong EBITDA growthTelenor has maintained an ambitious cost-saving programme that aims to reduce operating expenses by 1%-3% yearly between 2020and 2022; this follows a similar plan implemented for 2018-20. Improved cost efficiency will come from workforce reductions, as thecompany shifts its customer service to digital channels; lower marketing and sales spending; optimisation of tower and infrastructureoperations; and lower operating spending from network and IT modernisation, including copper decommissioning in Norway.Management estimates that such initiatives will generate NOK3 billion-NOK4 billion of gross savings across the projected period.

Telenor has demonstrated its ability to deliver on its cost-saving programme, having reduced operating expenses by a significant 6%in 2020 (excluding DNA and adjusted for foreign exchange), of which around 60% was driven by structural initiatives (equivalent toaround NOK1.5 billion of operating expense savings realised in 2020). The remaining cost reductions realised in 2020 were mainlytemporary savings related to the pandemic, including travel costs, sales and marketing costs. Previously, Telenor had already reducedits costs by 3% and 1% in 2018 and 2019, respectively.

The good progress in delivering cost savings contributed to Telenor generating 2% organic EBITDA growth in 2020 despite the above-mentioned strain on total organic revenue, organic subscription and traffic revenue during the year. Reported EBITDA before otherincome and other expenses increased by 11% in 2020 compared with the year earlier because of the full-year consolidation of DNAand positive foreign-exchange movements. The strain on revenue in certain countries in 2020 directly translated into an EBITDAdecline, including in Thailand (1% year-on-year decline in organic EBITDA in 2020), Denmark (1%), Sweden (6%) and Malaysia (6%).

6 21 July 2021 Telenor ASA: Update following outlook change to negative

MOODY'S INVESTORS SERVICE CORPORATES

However, this decline was more than offset by EBITDA growth in Norway (4%), Finland (8%) and Myanmar (12%). The company'sMyanmar business recorded strong performance in the first nine months of 2020 driven by revenue growth and cost savings beforedeclining in Q4 2020, hurt by a 7% decrease in subscription and traffic revenue during the quarter as a result of a decline in pricesand the number of customers following the implementation of a SIM registration process. In Q1 2021, the relatively large decline inrevenue, partly driven by the company's performance in Myanmar, was not fully offset by the year-over-year reduction in operatingexpenses of 7%, and resulted in an organic EBITDA decline of 2% during the quarter. However EBITDA returned to a 4% organicrevenue growth in Q2 2021 supported mainly by the stronger subscription and traffic revenue trend and a 1% reduction in operatingexpenses during the quarter.

In line with the flat to modest organic subscription and traffic revenue projected by management over 2021, Telenor forecasts organicEBITDA to grow by 0% to 2% during the year (pro forma for the disposal of the Myanmar business, which has experienced higherprofitability than the group) as the continued realisation of cost savings will be partly offset by additional costs driven by the recoveryin activity, particularly in Asia, during H2 2021. Assuming such a recovery takes place, Telenor will likely increase spending on certaincost items, including sales and marketing, which were subdued in 2020. Beyond 2021, the revenue recovery and continued focus oncost efficiencies are likely to drive solid growth in EBITDA in line with the growth in revenue.

Exhibit 8

Telenor's cost-saving programme drives EBITDA margin expansionEBITDA (before other income and other expenses) margin evolution

38.1%

41.0%

42.9%

37.7%

42.4%

41.7%

45.6%

37.4%

44.8%

43.8%

45.7%

42.2%

45.6%

46.4%

48.6%

43.7%

45.1%

45.5%

45.1%45.5%

34%

36%

38%

40%

42%

44%

46%

48%

50%

Q1 17 Q2 17 Q3 17 Q4 17 Q1 18 Q2 18 Q3 18 Q4 18 Q1 19 Q2 19 Q3 19 Q4 19 Q1 20 Q2 20 Q3 20 Q4 20 Q1 21 Q2 21 Next 12-18months

Margins in 2019 are pro forma the consolidation of DNA for 2019. Q2 2021 data excludes Myanmar. Next 12-18 months reflects our projections excluding Myanmar.Source: Company reports

Increasing competition in Asia in particular may lead to consolidation in the regionAsian markets where Telenor operates have experienced greater competition over the last two years, which is reflected in the strain onARPU or subscriber losses.

The merger of Telenor's and Axiata's operations in Malaysia will marginally weaken Telenor's credit profile because the company'sstake in the combined group will be diluted to 33.1% compared with its current 49% ownership of Digi on a standalone basis. Thus,Telenor's Malaysian operations will be deconsolidated as Digi-Celcom and will be treated as an associate entity. At the same time, thedeconsolidation of Digi will lead to a modest increase in Telenor's leverage. However, the transaction reflects the increased focus onconsolidation in the region. The reduction in the number of mobile network operators as a result of the merger of Digi and Celcom mayalleviate the competitive pressure that has been increasing in the country, which has partly been driven by new entrants. In addition,the increased scale and capacity to innovate will allow Celcom-Digi to mitigate the negative impact from the Malaysian government'saim to deploy 5G infrastructure across the country through a state-owned special-purpose vehicle, Digital Nasional Berhad. Weexpect such an initiative to increase competition in the mobile market as mobile operators will solely compete on services and notinfrastructure, which will be shared by all operators.

We expect Telenor to execute deals in the medium term because the company has publicly stated its intention to participate in theconsolidation of the telecom industry in Asia.

7 21 July 2021 Telenor ASA: Update following outlook change to negative

MOODY'S INVESTORS SERVICE CORPORATES

Telenor may also consider consolidation in the Nordics, including in Denmark, where there are currently four mobile network operators.Telenor and Telia Company AB (Baa1 stable) failed to consolidate their operations in the country in 2015.

We expect Telenor's Moody's-adjusted gross leverage to increase over the next two years from an already high level in2020Telenor's Moody's-adjusted gross leverage was 2.7x for 12 months that ended Q1 2021, slightly below 2.8x as of year-end 2020. Weexpect an increase in the company’s adjusted gross leverage to around 3.0x in 2021 and 2022. The increase in leverage in 2021 willbe driven by the negative impact on EBITDA from the appreciation of the Norwegian krone and the classification of the company’soperations in Myanmar as assets held for sale.

Despite the likely moderate recovery in EBITDA in 2022, we expect a further negative effect on leverage because of the deconsolidationof Digi, its 49%-owned fully consolidated operations in Malaysia, following the expected closing of the merger with Celcom AxiataBhd (a subsidiary of Axiata) in Q2 2022. The deconsolidation of both Telenor’s Myanmar and Malaysian operations will have a negativeeffect on the company’s Moody’s-adjusted gross leverage of around 0.3x (or 0.2x including dividends to be received from Celcom Digi,as estimated by us) because of the subsidiaries’ relatively low leverage compared with the group average. For example, the Malaysianoperations accounted for only around 8% of Telenor's consolidated debt (including lease and spectrum licence liabilities) and 13% ofgroup EBITDA in 2020.

Exhibit 9

Disposal of Telenor Myanmar and deconsolidation of Digi in Malaysia have a moderately negative impact on group leveragePro forma impact on leverage of the deconsolidation of Telenor Myanmar and Digi from Telenor's accounts (FY 2020) FY2020

Moody's Àdjusted EBITDA 54,223

Digi reported EBITDA 6,938

Myanmar reported EBITDA 4,055

Moody's Adjusted EBITDA (exc. Digi and Myanmar) 43,230

Moody's Adjusted Debt 153,553

Digi reported Debt (incl. capitalised leases) 11,606

Myanmar reported Debt (inc. capitalised leases) 5,587

Moody's Adjusted Debt (exc. Digi and Myanmar) 136,360

Moody's Adjusted Debt/EBITDA 2.83x

Moody's Adjusted Debt/EBITDA (exc. Digi) 3.00x

Moody's Adjusted Debt/EBITDA (exc. Myanmar) 2.95x

Debt/EBITDA (exc. Digi and Myanmar) 3.15x

Digi and Myanmar's EBITDA as provided in the company's annual accounts. Debt includes capitalised leases.Source: Company reports and Moody's Investors Service

Previously, Telenor's Moody's-adjusted gross leverage ratio had increased significantly to 2.7x in 2019 (pro forma for the acquisitionof DNA) from 2.0x a year earlier, mainly because of the debt-funded acquisition of DNA and the implementation of IFRS 16. Theapplication of the new accounting standard resulted in a 0.2x increase in its Moody's-adjusted gross leverage as lease liabilities underIFRS 16 were higher than capitalised leases under our operating lease adjustment based on IAS 17 disclosure. Net debt/EBITDA, asreported by the company, was 1.8x as of 31 March 2021 — towards the lower end of Telenor's revised target range. To reflect theimpact of IFRS 16 on its metrics, Telenor revised its target net leverage range in 2019 to 1.8x-2.3x from 1.5x-2.0x previously.

The change of outlook to negative from stable on Telenor's ratings in July 2021 reflects the fact that we expect metrics to remainoutside of the triggers set for the A3 rating over the next 18 months. Therefore, Telenor's rating will remain weakly positioned duringthis period. Similarly, Telenor's adjusted RCF/debt remained weak at 18% in 2020 — below the trigger set for the A3 rating at above20% — and is projected to be around 17% in both 2021 and 2022.

Despite the deterioration in credit metrics since 2019, Telenor has historically followed a balanced financial policy betweenshareholders and creditors. The group's capital allocation priorities have been to maintain a solid balance sheet and aim for annual

8 21 July 2021 Telenor ASA: Update following outlook change to negative

MOODY'S INVESTORS SERVICE CORPORATES

growth in dividend per share. The company has announced its intention to pay a dividend of NOK9 per share for 2019 (NOK12.6billion), to be paid in two tranches in June 2021 and October 2021. This represents a 3% increase in ordinary dividend per sharecompared with the year earlier (NOK12.4 billion payout in 2019). However, the fact that Telenor has not announced any new sharebuyback programme for 2021 is a positive.

Lower capital spending intensity to support cash flowTelenor's reported capital spending, excluding leases, licences and spectrum, amounted to NOK16.4 billion in 2020, a NOK1.0 billiondecrease from the year earlier. Capital spending in 2020 was mainly driven by network modernisation in several markets, including thefibre and 5G rollout in Norway, the 5G rollout in Finland, and network capacity and coverage expansion in Thailand. Capital spendingfor spectrum and licences amounted to NOK5.1 billion in 2020 and was primarily in Thailand, Denmark and Finland. Capital spendingas a proportion of revenue, excluding licences and spectrum, was 13% in 2020 compared with 15% in the year earlier because of lowerinvestments in its Asian subsidiaries, as well as high comparables in Thailand in 2019 and import restrictions in Bangladesh at thebeginning of the year.

Telenor now projects capital spending as a percentage of revenue to increase to 15%-16% in 2021 (excluding Myanmar), in line withits medium-term guidance of 15% average annual spend for 2020-22. This reflects continued strong investment in Norway's fibre and5G networks. Telenor has started modernising its network in Norway to migrate all customers on its copper network by 2023. Capitalspending will also support the strong growth in data usage from a relatively low level across its Asian operations.

In Thailand, at the spectrum auction in February 2020, dtac decided not to participate in the 2.6 gigahertz (GHz) bidding and onlyacquired 200 megahertz of 26 GHz spectra because dtac could get the 3.5 GHz spectra (currently in use by Thaicom) on better terms.The company faces risks related to the uncertainty surrounding the timing of the 3.5 GHz auction, and this will result in increasedcompetition for dtac because its competitors are starting to offer 5G services.

Based on our EBITDA, capital spending and dividend assumptions, we project Telenor will generate Moody's-adjusted FCF (afterdividends and leases) of around NOK3 billion per year over the next two years, representing FCF/Moody's-adjusted debt of 2% peryear.

Exhibit 10

Capital spending is likely to bounce back in 2021 and 2022, in line with the 2020-22 planCapital spending (excluding spectrum, in NOK millions), and capital spending/sales evolution, 2018-22E

15.8%

15.0%

13.3%

12.0%

12.5%

13.0%

13.5%

14.0%

14.5%

15.0%

15.5%

16.0%

12,000

13,000

14,000

15,000

16,000

17,000

18,000

19,000

2018 2019 2020 2021E 2022E

NO

K m

illio

ns

Capex excluding spectrum (LHS) Capex / Revenue (RHS)

Data for 2019 is pro forma the consolidation of DNA for 2019. 2021E is pro forma for the reclassification of Myanmar operations as assets held for sale while 2022E is also pro forma for thedeconsolidation of operations in Malaysia.Source: Company reports

ESG considerationsFrom a corporate governance perspective, Telenor is a public company, majority-owned by the Kingdom of Norway. We take intoconsideration the fact that Telenor has a clearly defined financial policy, including a target leverage ratio.

Social considerations were a key driver for the change of outlook to negative from stable in July 2021. While we positively viewTelenor’s exposure to a growing population and relatively underpenetrated markets for mobile data consumption through its presence

9 21 July 2021 Telenor ASA: Update following outlook change to negative

MOODY'S INVESTORS SERVICE CORPORATES

in developed and emerging Asian countries, the change of outlook was partly driven by political unrest in Myanmar. Following themilitary coup in Myanmar, the authorities ordered a nationwide mobile data network shutdown from 15 March 2021. This order,alongside the worsening economic and business environment, had a negative impact on Telenor's financial results and eventually led tothe company deciding to completely write off its Myanmar operations and sell the business.

In terms of environmental and social risks, Telenor’s exposure is in line with that of the overall industry. While telecom operators havelow direct business exposure to environmental risks, data security and data privacy issues are prominent in the sector.

Liquidity analysisTelenor benefits from its good liquidity position. As of 30 June 2021, the company had NOK19.7 billion in cash and cash equivalents aswell as full availability under its €2.0 billion committed revolving credit facility maturing in April 2024, with options for extension untilApril 2025 on certain terms. Additionally, despite the large dividend distributions, we project that Telenor will continue to generatepositive FCF.

Exhibit 11

Telenor's debt maturity profile over the next 12-18 months is well covered by its existing liquidity sourcesDebt maturity profile as of 30 June 2021

4.41.4 3.1 3.8 4.7

7.42.8

5.15.1

10.6 6.6

45.7

0

10

20

30

40

50

60

2021 2022 2023 2024 2025 2026 and Beyond

NO

K b

illio

ns

Subsidiaries Telenor ASA

Source: Company reports

10 21 July 2021 Telenor ASA: Update following outlook change to negative

MOODY'S INVESTORS SERVICE CORPORATES

Methodology and scorecardThe following table shows Telenor's scorecard-indicated outcome using our Telecommunications Service Providers rating methodology,with data as of 31 March 2021, and on a forward-looking basis. The assigned rating is one notch above the scorecard-indicatedoutcome, reflecting the one-notch uplift for potential government support for the baa1 BCA.

Exhibit 12

Rating FactorsTelenor ASA

Telecommunications Service Providers Industry Scorecard [1][2]

Factor 1 : Scale (12.5%) Measure Score Measure Score

a) Revenue (USD Billion) $13.2 Baa 11.6-13 Ba

Factor 2 : Business Profile (27.5%)

a) Business Model, Competitive Environment and Technical Positioning Aa Aa Aa Aa

b) Regulatory Environment Ba Ba Ba Ba

c) Market Share A A A A

Factor 3 : Profitability and Efficiency (10%)

a) Revenue Trend and Margin Sustainability A A A A

Factor 4 : Leverage and Coverage (35%)

a) Debt / EBITDA 2.7x Baa 2.9x - 3.1x Ba

b) RCF / Debt 18.5% B 16.8% - 17.3% B

c) (EBITDA - CAPEX) / Interest Expense 7.5x Aa 6.9x - 7x Aa

Factor 5 : Financial Policy (15%)

a) Financial Policy A A A A

Rating:

a) Scorecard-Indicated Outcome Baa1 Baa1

b) Actual Rating Assigned A3

Government-Related Issuer Factor

a) Baseline Credit Assessment baa1

b) Government Local Currency Rating Aaa

c) Default Dependence Low

d) Support Low

e) Actual Rating Assigned A3

Current

LTM 3/31/2021

Moody's 12-18 Month Forward View

As of 7/14/2021 [3]

[1] All ratios are based on 'Adjusted' financial data and incorporate our Global Standard Adjustments for Non-Financial Corporations. [2] As of 12/31/2020. [3] This represents our forwardview, not the view of the issuer, and reflects the disposal of Telenor Myanmar and the deconsolidation of Digi in Malaysia.Source: Moody's Investors Service

11 21 July 2021 Telenor ASA: Update following outlook change to negative

MOODY'S INVESTORS SERVICE CORPORATES

Telenor's status as a Government-Related Issuer (GRI)Telenor qualifies as a GRI under our methodology because it is 54% government owned. Our A3 rating for the company reflects thecombination of the following GRI inputs: a BCA of baa1, the Aaa (stable) local-currency rating of the Norwegian government, the lowdefault dependence between Telenor and the government, and the likelihood that the government will provide a low level of supportto the company if needed.

The low level of default dependence between Telenor and the government reflects the weak correlation between the company's creditprofile and the economic trends in Norway, which is mainly a result of the group's strong liquidity and increasing market diversification.More specifically, our assessment that there is a low level of default dependence between Telenor and the government is based onthe lack of financial and operational links between the two. Telecom operators generally have a fairly low level of correlation with thesovereign. In particular, direct and indirect fiscal transfers and government telecom spending represent a low proportion of Telenor'srevenue. More generally, the company and the government are not exposed to the same revenue base and do not share the samecredit risks as demonstrated by the fact that 79% of Telenor's revenue in 2020 was generated outside Norway.

Our assessment of a low level of government support available to Telenor in the event of stress is based on the following observations:there is no explicit support from the government, we are not aware of any formal verbal or written confirmation that the governmentwill support the company in the event of a default on its financial debt and the company does not have any special legal status thatwould suggest a closer link with the state or an implicit form of support.

The government's 54% ownership of Telenor and its willingness to act as a rational shareholder suggest that the government wouldnot be the sole provider of support in a stress scenario. Instead, the government would likely only consider providing support jointlywith other shareholders in the form of a capital increase. The state's rationale for its ownership of Telenor is to maintain a leadingtechnological and industrial company with head office functions in Norway.

The Norwegian government is noninterventionist, despite holding significant ownership stakes in several companies. In our view, itis unlikely that the government's solid reputation would be damaged in the event of default by Telenor. The company's economicand social importance in Norway has diminished over the recent years. This reduction is a result of the increasing presence of viable,privately owned competitors with significant market shares and the group's presence in emerging markets.

12 21 July 2021 Telenor ASA: Update following outlook change to negative

MOODY'S INVESTORS SERVICE CORPORATES

Ratings

Exhibit 13

Category Moody's RatingTELENOR ASA

Outlook NegativeSenior Unsecured A3Commercial Paper P-2

Source: Moody's Investors Service

13 21 July 2021 Telenor ASA: Update following outlook change to negative

MOODY'S INVESTORS SERVICE CORPORATES

Appendix

Exhibit 14

Moody's-adjusted debt reconciliation for Telenor ASA

in NOK millionsFYE

Dec-2016FYE

Dec-2017FYE

Dec-2018FYE

Dec-2019FYE

Dec-2020LTM

Mar-2021As Reported Debt 86,361.0 74,297.0 71,666.0 140,045.0 150,806.0 139,072.0

Non-Standard Public Adjustments 2,061.0 3,002.0 2,144.0 708.0 0.0 0.0Pensions 2,585.0 2,565.0 2,819.0 2,386.0 2,747.0 2,747.0Leases 13,978.3 15,132.9 14,955.1 0.0 0.0 0.0

Moody's-Adjusted Debt 104,985.3 94,996.9 91,584.1 143,139.0 153,553.0 141,819.0All figures are calculated using our estimates and standard adjustments.Periods are financial year end unless indicated. LTM = Last 12 months.Source: Moody's Financial MetricsTM

Exhibit 15

Moody's-adjusted EBITDA reconciliation for Telenor ASA

in NOK millionsFYE

Dec-2016FYE

Dec-2017FYE

Dec-2018FYE

Dec-2019FYE

Dec-2020LTM

Mar-2021As Moody's-Reported EBITDA 42,459.0 42,659.0 39,926.0 50,103.0 58,675.0 61,164.0

Non-Standard Public Adjustments -1,517.0 -531.0 81.0 955.0 0.0 0.0Unusual Items - Income Stmt 3,378.0 4,427.0 2,260.0 -652.0 -4,438.0 -7,825.0Pensions 64.0 52.0 65.0 71.0 -14.0 -14.0Leases 4,378.0 4,344.0 4,207.0 0.0 0.0 0.0

Moody's-Adjusted EBITDA 48,762.0 50,951.0 46,539.0 50,477.0 54,223.0 53,325.0All figures are calculated using our estimates and standard adjustments.Periods are financial year end unless indicated. LTM = Last 12 months.Source: Moody's Financial MetricsTM

Exhibit 16

Peer comparison

FYE FYE LTM FYE FYE LTM FYE FYE LTM FYE FYE LTM FYE FYE LTM

Dec-19 Dec-20 Mar-21 Dec-19 Dec-20 Mar-21 Dec-19 Dec-20 Mar-21 Dec-19 Dec-20 Mar-21 Dec-19 Dec-20 Mar-21

Revenue 12,926 13,090 13,207 11,526 11,835 12,105 9,098 9,718 9,993 2,064 2,162 2,226 5,935 5,764 5,808

EBITDA 5,740 5,779 5,833 4,412 4,654 4,808 3,348 3,743 3,802 739 790 812 2,639 2,563 2,640

Total Debt 16,289 17,934 16,614 11,035 11,013 10,456 12,021 12,365 11,816 1,445 1,757 1,701 6,302 6,845 6,544

Cash & Cash Equivalents 1,641 2,382 2,647 339 385 557 659 985 985 58 269 322 1,001 1,764 1,580

EBITDA margin % 44.4% 44.2% 44.2% 38.3% 39.3% 39.7% 36.8% 38.5% 38.0% 35.8% 36.5% 36.5% 44.5% 44.5% 45.4%

(EBITDA - Capex) / Interest Expense 5.2x 7.4x 7.5x 12.7x 13.2x 13.3x 4.7x 5.0x 4.8x 17.7x 23.5x 26.1x 1.4x 2.5x 2.6x

Debt / EBITDA 2.8x 2.8x 2.7x 2.4x 2.2x 2.2x 3.6x 3.0x 3.1x 1.9x 2.1x 2.1x 2.4x 2.6x 2.5x

FCF / Debt -5.8% 2.6% 2.3% 3.5% 4.7% 5.4% 0.8% 1.9% 2.4% 1.6% 2.4% 1.5% -1.3% -0.2% -1.9%

RCF / Debt 13.2% 18.3% 18.5% 26.2% 28.3% 27.2% 15.9% 19.1% 18.4% 22.2% 20.1% 20.3% 32.9% 30.3% 31.8%

(in USD million)

A3 Negative A2 Stable Baa1 Stable Baa2 Stable Baa2 Stable

Telenor ASA Swisscom AG Telia Company AB Elisa Corporation Axiata Group Berhad

All figures and ratios are calculated using our estimates and standard adjustments.FYE = Financial year end. LTM = Last 12 months. RUR* = Ratings under review, where UPG = for upgrade and DNG = for downgrade.Source: Moody's Financial MetricsTM

14 21 July 2021 Telenor ASA: Update following outlook change to negative

MOODY'S INVESTORS SERVICE CORPORATES

© 2021 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S CREDIT RATINGS AFFILIATES ARE THEIR CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDITCOMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MATERIALS, PRODUCTS, SERVICES AND INFORMATION PUBLISHED BY MOODY’S (COLLECTIVELY,“PUBLICATIONS”) MAY INCLUDE SUCH CURRENT OPINIONS. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUALFINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT OR IMPAIRMENT. SEE APPLICABLE MOODY’SRATING SYMBOLS AND DEFINITIONS PUBLICATION FOR INFORMATION ON THE TYPES OF CONTRACTUAL FINANCIAL OBLIGATIONS ADDRESSED BY MOODY’SCREDIT RATINGS. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICEVOLATILITY. CREDIT RATINGS, NON-CREDIT ASSESSMENTS (“ASSESSMENTS”), AND OTHER OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOTSTATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK ANDRELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. AND/OR ITS AFFILIATES. MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHEROPINIONS AND PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHEROPINIONS AND PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. MOODY’S CREDITRATINGS, ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS DO NOT COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR.MOODY’S ISSUES ITS CREDIT RATINGS, ASSESSMENTS AND OTHER OPINIONS AND PUBLISHES ITS PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDINGTHAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE,HOLDING, OR SALE.

MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS, AND PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESSAND INAPPROPRIATE FOR RETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS OR PUBLICATIONS WHEN MAKING AN INVESTMENTDECISION. IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER.ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIEDOR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USEFOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTENCONSENT.MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS ARE NOT INTENDED FOR USE BY ANY PERSON AS A BENCHMARK AS THAT TERM ISDEFINED FOR REGULATORY PURPOSES AND MUST NOT BE USED IN ANY WAY THAT COULD RESULT IN THEM BEING CONSIDERED A BENCHMARK.All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as wellas other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information ituses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing its Publications.To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for anyindirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use anysuch information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses ordamages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of aparticular credit rating assigned by MOODY’S.To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatorylosses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for theavoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents,representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY CREDITRATING, ASSESSMENT, OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (includingcorporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any credit rating,agreed to pay to Moody’s Investors Service, Inc. for credit ratings opinions and services rendered by it fees ranging from $1,000 to approximately $5,000,000. MCO and Moody’sInvestors Service also maintain policies and procedures to address the independence of Moody’s Investors Service credit ratings and credit rating processes. Information regardingcertain affiliations that may exist between directors of MCO and rated entities, and between entities who hold credit ratings from Moody’s Investors Service and have also publiclyreported to the SEC an ownership interest in MCO of more than 5%, is posted annually at www.moodys.com under the heading “Investor Relations — Corporate Governance —Director and Shareholder Affiliation Policy.”Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s InvestorsService Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intendedto be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, yourepresent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly orindirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion as tothe creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors.Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’sOverseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a NationallyRecognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by anentity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registeredwith the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferredstock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any credit rating, agreed to pay to MJKK or MSFJ (as applicable) for credit ratings opinions and servicesrendered by it fees ranging from JPY125,000 to approximately JPY550,000,000.MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

REPORT NUMBER 1294765

15 21 July 2021 Telenor ASA: Update following outlook change to negative