SW P1 1 1 - World Bank Documents and Reports

82

This paper is prepared for staff use and is not for publication. The views CAtAL0O No. 156 expressed are those o.' the author and not necessarily those of the Bank. INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT INTERNATIONAL DEVELOPMENT ASSOCIATION INTl Economic Staff Working Paper No. 111 SW P1 1 1 July 26, 1971 R RECONM* v: gn. N U1 VLPEWT WASIIINGTQN, D.C. 20161 The Economics of International Trade in Cotton-Type Textiles This paper examines the major elements of comparative advantage which presently favor the development of the textile industry in developing countries and account for developing countries' success in exporting cotton ard cotton-type textiles to industrialized countries. It then seeks to assess whether technological changes which are now taking place, or which are soon likely to take place, will lead to an erosion of such comparative advantage. Policy options for both the developing and the industrialized countries are then discussed. Mr. Shepherd is completing a thesis on textiles at the Centre for Contemporary European Studies, University of Sussex. He wrote this paper while attached to the Industrialization Division of the Economics Department in the summer of 1970. He will be joining the Young Professional Program in September 1971. Economics of Industry Division Prepared by: Geoffrey Shepherd Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

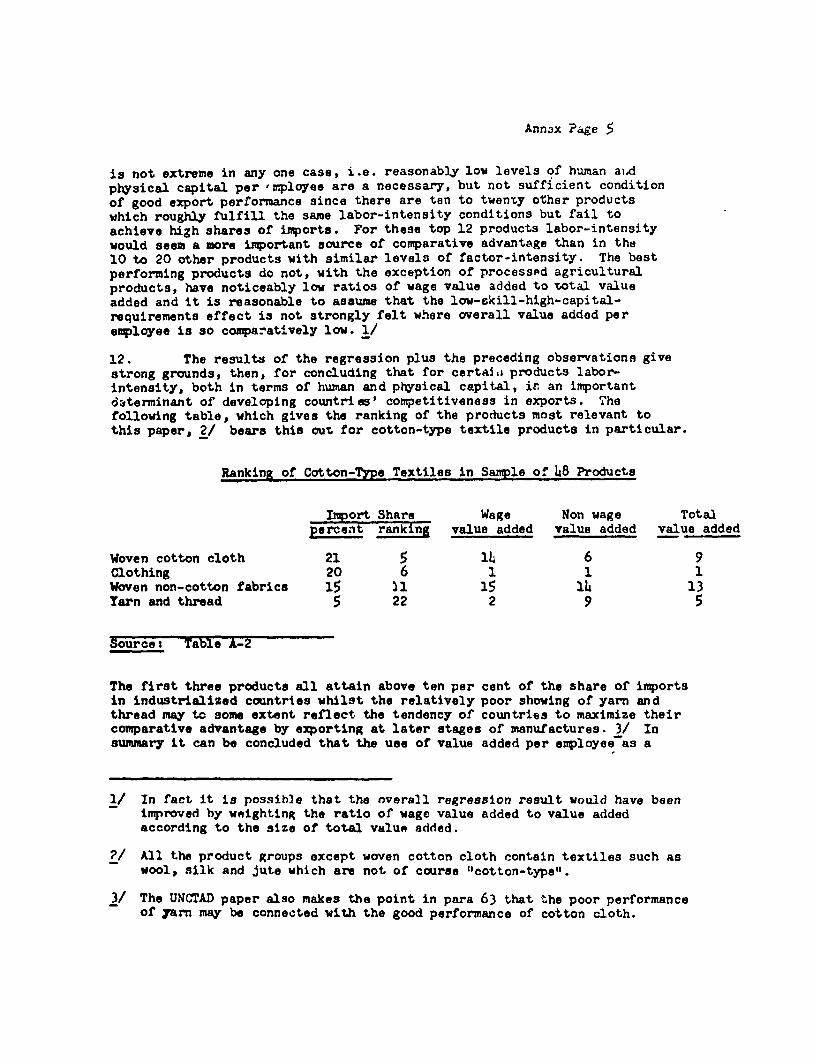

download

0

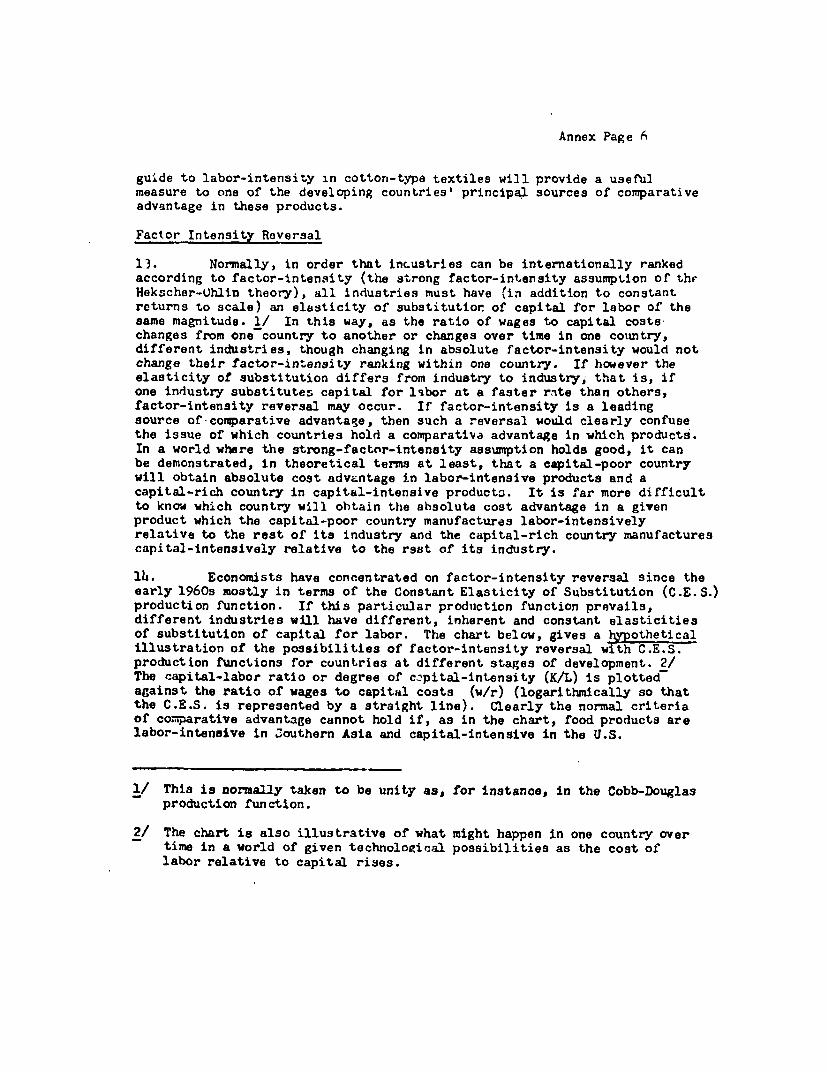

Transcript of SW P1 1 1 - World Bank Documents and Reports

This paper is prepared forstaff use and is not forpublication. The views

CAtAL0O No. 156 expressed are those o.'the author and notnecessarily those ofthe Bank.

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

INTERNATIONAL DEVELOPMENT ASSOCIATIONINTl

Economic Staff Working Paper No. 111 SW P1 1 1July 26, 1971 R

RECONM* v: gn. N U1 VLPEWTWASIIINGTQN, D.C. 20161

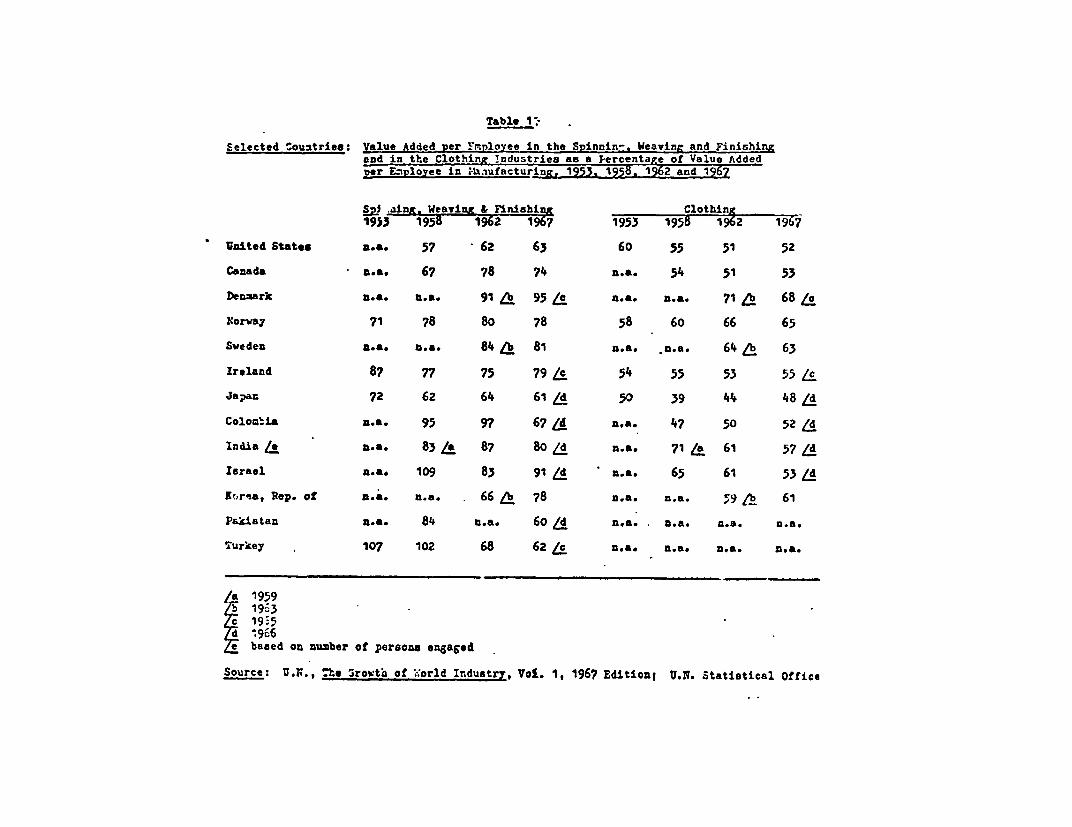

The Economics of International Trade in Cotton-Type Textiles

This paper examines the major elementsof comparative advantage which presentlyfavor the development of the textileindustry in developing countries and accountfor developing countries' success inexporting cotton ard cotton-type textiles toindustrialized countries. It then seeks toassess whether technological changes whichare now taking place, or which are soonlikely to take place, will lead to an erosionof such comparative advantage. Policy optionsfor both the developing and the industrializedcountries are then discussed.

Mr. Shepherd is completing a thesis on textilesat the Centre for Contemporary European Studies,University of Sussex. He wrote this paper whileattached to the Industrialization Division ofthe Economics Department in the summer of 1970.He will be joining the Young Professional Programin September 1971.

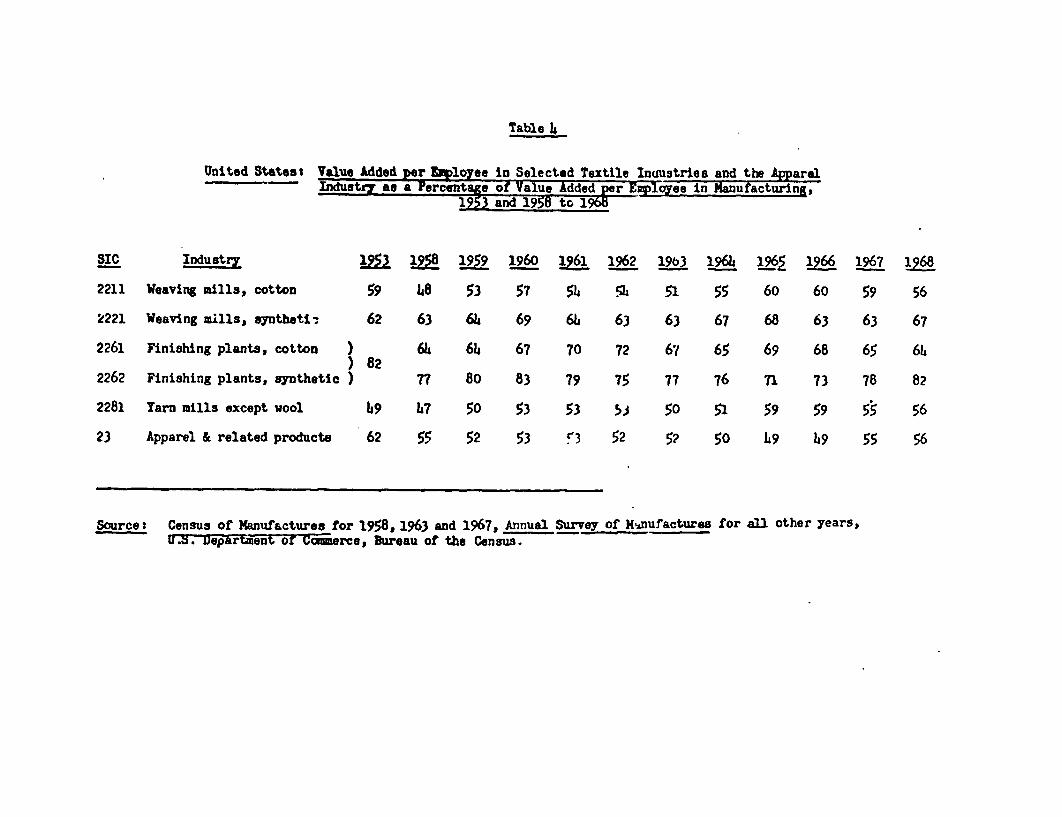

Economics of Industry Division

Prepared by: Geoffrey Shepherd

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

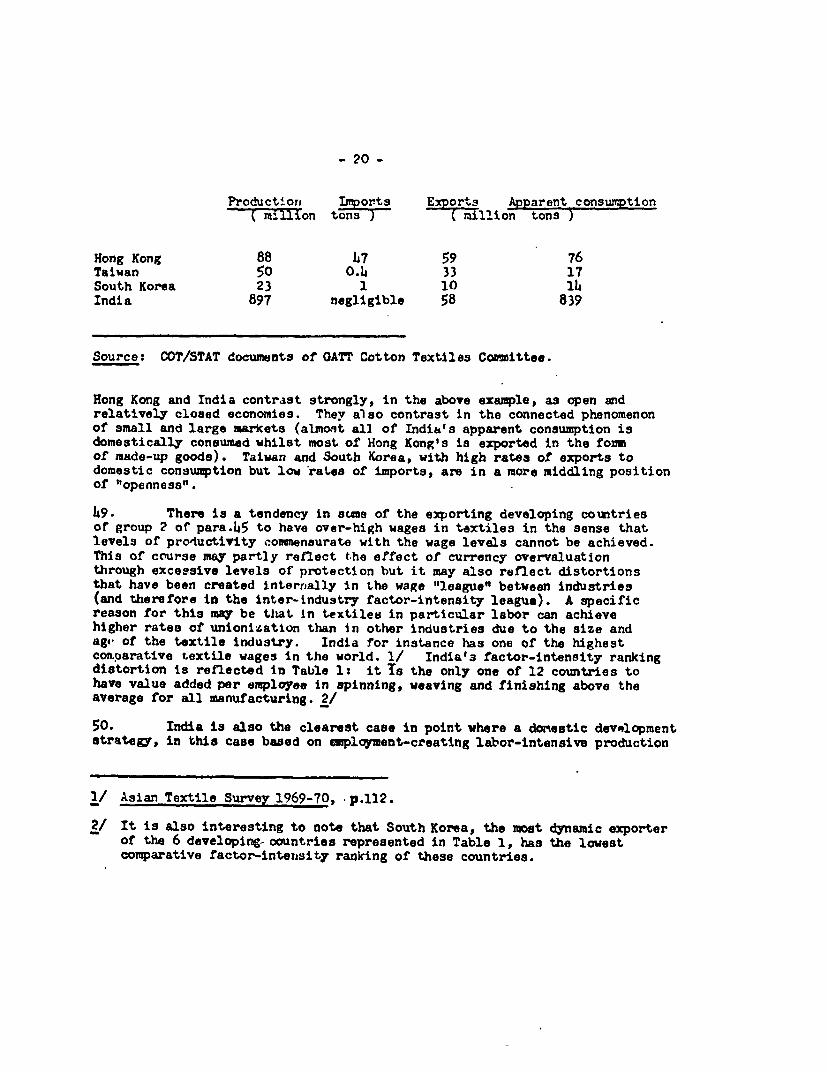

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

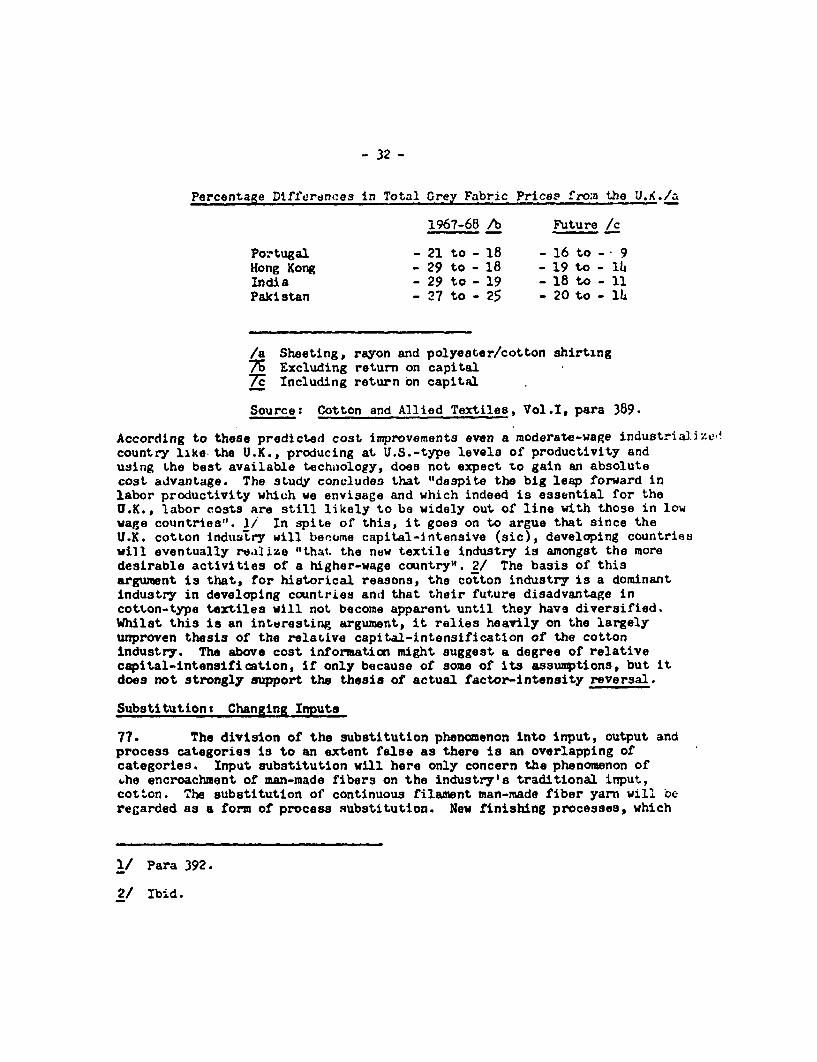

lic D

iscl

osur

e A

utho

rized

TABLS OF CONIT&Sr

Introduction

1

I Comparative Advantage in the Present and Recent Past 4

II Comparative Advantage in the Future 23

III Policy Options for Developing and Industrialized

Countries 42

Annex: Factor Intensity and Comparative Advantage 1 - 8

List of Tables

INTRODMCTION

1. The problems of international trade in cotton-type textiles arewell known. Some developing countries have capitalized on comparativeadvantages to make cotton textiles one of their msst successful manufacturedexports to industrialized countries whilst the latter have set up an arrayof restrictions to protect their own cotton industries. International tradein cotton textiles between industrialized and developing countries continuesto be controlled, in a departure from G.A.T.T. free trade princip2es, bythe Long Term Arrangement for International Trade in Cotton Textiles.Pres.sure is now building up, notably in the Unit.ad States, for a similararrangement, whether at the national or international level, covering man-made fiber and wool textiles. I/ Textiles are a major problem in inter-nation.a trade threatening repercussions in other branches. This paperaims to examine the economics of international trade in cotton-type textilesin order to clarify some of the issues involved in this departure from free-trade assumptions.

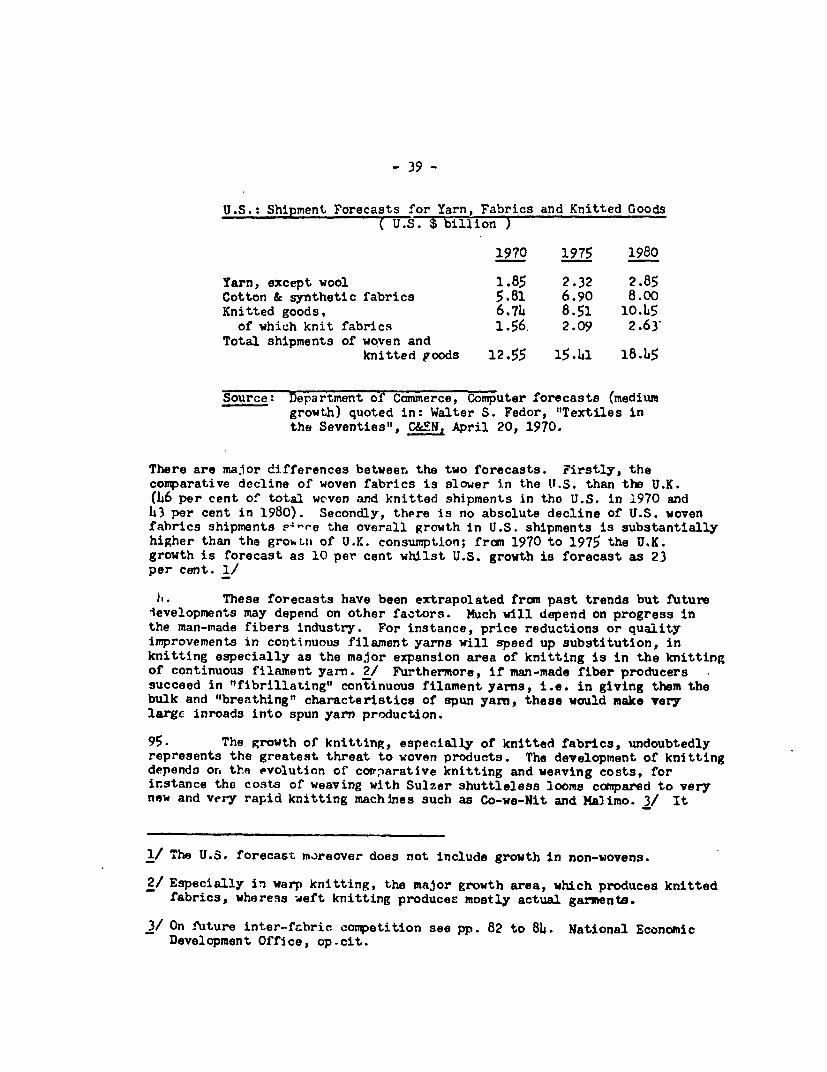

2. Thn main reasons for the successful ir4Oinntation and exportactivity of cotton industries in some developingt *.ounlries are well known.There may be some grouncis - mo.tly the chainging technology of the industry -for industrialized countries niaiming that. this comparative advantage isnot applicable to .ae future. Many industrialt7e1 countries seek to protecttheir cotton industries not only on these grounds" hut also on the groundsthat the adjustment implied in acceding to a changing international divisionof labor would cause too many domestic problems.

3. Several long-term issues appear to be involved. Their analysisseems relevant not only for textiles but also for any other export industrieswhich developing countries might eventually move into as a group. Fortextiles industrialized countries may have to think in terms of three broadfuture possibilities. If it is decided that 1hb advantages of pursuing Lheinternational division of labor are outweighe1 oy the costs of adjustment,industrializnd countries might continue to protect their uncompetitiveindustries. The two broad alternatives to t.'" are for the cotton industriesof industrialized countries to become internationally competitive or forindustrialized countries to abandon, partially at least, activity in thecotton industry in favor of an industrial activity more suited to theirendowments, real wage rates and investment policies.

4. This paper seeks to maXe some contribut'on to such a long-term lookat the cotton industry by diecussing three related issues. In Part I thebases of the comparative advan+goe %h1ih developing countries presently enjoyin cotton textile production are discussed. tar LI treats the possibilitiesof reversal or erosion of this comparative advantage. This might come about

1/ See parit.i Of Exports of Cot.ton Textiles fromn Develoning Countries to theEuropean Economic Communitz and the Jnited_Kin do -9-197, EconomicsDepartment Working Paper No. 52.

through rapid technological 1evelopoents in the cotton infdstry which wouldrender it relatively capital-Intensive and more suited to thc economicposition of lndustriliyied couritrie3. it might happen through changingpatterns of consuiptioii in theae countrios favoring textile products which,again, were more suited to production in industrialized countries. InPart III the conclusions to this examiriation of possiblo changes lead intoa discussion of the various policy tecnniques and opportunities open toindustrialized and developing countries. 1/

5. Although initially _oncerned with prospects for developing countrLes'exports of manufacturei to industria2ized countries, this paper concentrateson the problem from the point of view or tndustriaaized countries. Develop-ments in these countrie3 determine market prospects for developing countries.However, a modicum of discussion from a developing country viewpoint isinevitable as all devolnpingr *: ntries are not equally competitive in cotton-type textiles. Discu:;: -.:n cf e.niparative aovantage deriving from differentfactor endowments has tradltlioa,..ly iLuen conceived of in terms of two-countrymodels uid, partly by exlensi,n, in terms of two homogeneous groups,industrialized and ,' vur!a,: couintries, but this degree of simplification isunrealistic in a stuty o. int,brn.otxona. trade for a specific product. Thereis a continuuim of levels of 'l.-velopment as well as a multitude of combinationsof factors and conditionn of p,roduction which means that certain developingcountries are better placed t-han othere to compete in world markets. Whilstthe term develorping cr)untr2ea will be considered -.n this paper as a more orless homogeneous natpgory in the more general discussion of comparativeadvantage 2/ it will !be ne-essary in a suhsequently more precise discussionof the locaLion of comparative advantage t. distinguish between tha mor3advanced of these, the so-called vemi-industrialized countries, 3/ and theless advanced.

6. Data is mainly taken from industrialized countries though someinformation on production costs will come from some developing countries.Data will be derived from censuses and surveys of manufactures which, sincethere is a relative paucity of up-to-date historical series, will be supportedwith more qualitative material. Much of it comes from three countries only -the United States, Canada anrl the United Kingdom - because census and otherdata about changes in the cotton industry seem more readily available than

I/ In this paper comparative advantage is generally equated with realizedcomparative advantage (or cost competitiveness). The section on thelocation of compara.ive advantage is in a sense a discussion of underwhat conditions potential becomes realized comparative advantage.

2/ Developing countries cover U.N. Economic Class II together with theSouthern European countries excluding Italy. See para. 8 of EconomicsDepartment Working Paper No. 52.

3/ Japan, though an industrialized country, has sufficient in common withsemi-industrialized countries, relatively low wages and high productivityand consequently large textile.exports, to be discu3sed in conjunctionwith these countries.

from other industrialized countries. 1/ It was felt particularly importantto review developments in the U.S. and Canada, the highest wage countries,whilst the U.K. provides a useful contrast in that its cotton industry 2/is to acne extent typical of those of Western Europe (and different fromthose of North America).

7. Although the exports of developing countries have been traditionallybased on cotton, man-made fiber textiles are becoming an increasingly importantpart of international trade in textiles. Alt.hough the cotton industry inindustrialized countries is increasingly losing its icentity within an over-all textile industry, it is felt justified to continue to talk of aseparate cotton industry. The cotton industry sLill does have some id3ntityin industrialized countries. Moreover, it has a clear identity and tenidscompletely to dominate other textiles in devaloping countries; this isreflected in the predominance of cotton-type textiles in the developingcountries' textile exports. A discussion of the cotton industry cannotafford to ignore developments in two related industries, man-made fibers a3a supplier industry and apparel as a customer industry. These will bediscussed, albeit in more general terms, along with the cotton industry.

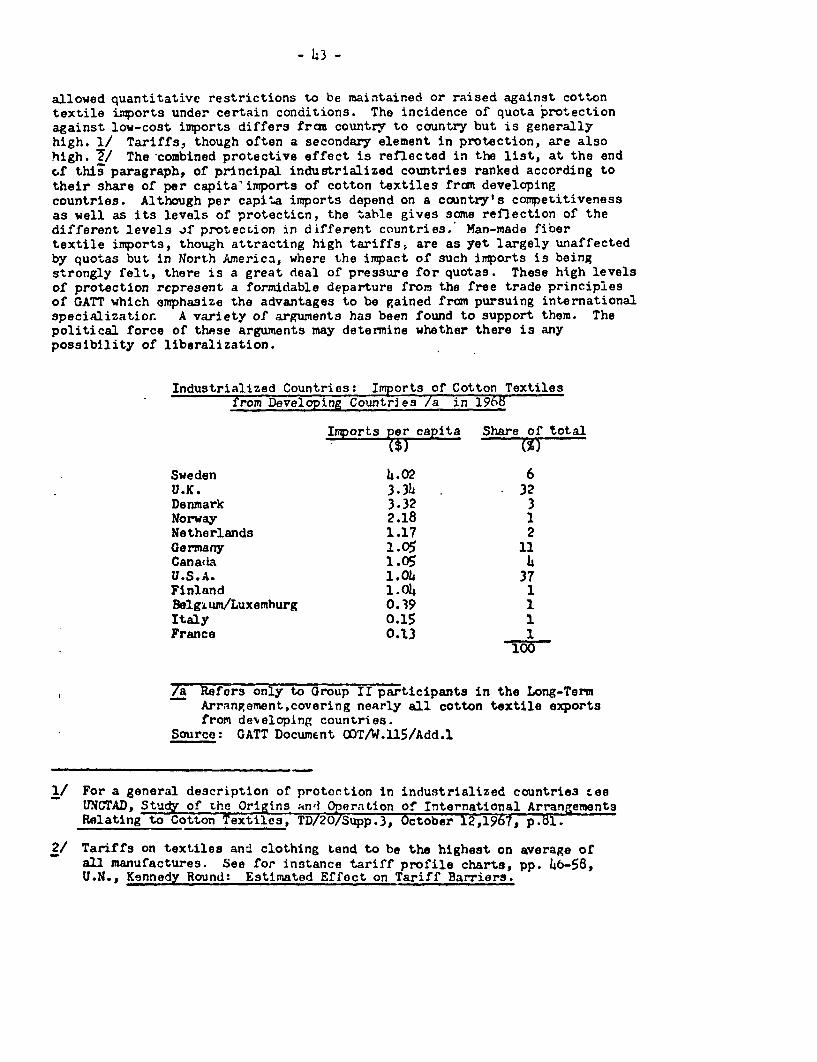

8. Finally two assumptions concerning economie development indeveloping countries underly this paper. First, exports of manufacturesfrom developing to industrialized countrles can be beneficial to bothparties. This ib often being called Into question more frequently by theformer and intra-developing couintry trade is prpoennd as an alternative. Y6tthey are not mutually exclusive. It is assnimnd thnat exports of manufactureshave an important role to play in earning foreign exchange to permit the,)urchase of goods and know-how only available from more advanced industrialeconomies.

9. The second assumption is that the ;tt.ttg .,p of an industry forexport such as the cotton textilo iriduntry which is typically labor-intensivedoes lot run counter to development strategie.5 whicfth may ror instance bebased on capital-intensive indlintries. Now. tho'e is a very real danger ofdomestic development strateg5es n'vprsely affecting nn industry's capacityto export but it is felt thAt the two rdevelopment pathnt are not necessarilymutually exclusive. Moreover, a ttellinp, argument. is that the cotton industryis alreadty in place in many developing countries and .as proved to be botha "natural" import substitution and export industry.

1/ The U.K. is relatively rich in published informttion on the textile industrywhilst published information from North America was supplemonted byinformation sought directly from texti3e eom .n.es and other textileinterests.

2/ In this paper the cotton -_y.Lonm processing indu:.r.ry will be referred to,irrespective of the fiber processed, as the cotton industry.

I. COMPARATIVE ADVAZ'TAGE IN TiE PRESWNT AND RECENT PAST

10. This part of the paper will seek to establish the major elementsexplaining the general export success that certain developing countries haveachieved today in cotton-type (mostly cotton) textiles. This will beessentially a static view of intornational competitiveness whilst Part IIwill be a drnamic view, looking at the same trade determinants and askingwhether any changes in international competitiveness can be predicted.

11. The elements of comparative advantage are that bundle of factorswhich give certain countries absolute cost advantages in certain products.Comparative advantage, baesd on many - and not all measurable - factorsbecomes translated into absolate advantage by means of the exchange rate. 1/Part I will firstly discuss the most important elements of comparativeadvantage and, where possible, attach some measure to them. Its approachwill be very general in that countries will be regarded in the two broadgroups of industrialized and developing countries. Secondly, a discussionof the available cost information will seek not only to confirm the findingsof the earlier discussion, but also to locate comparative advantage moreprecisely, to see for instance which developing countries have the greatestcomparative advantage ,;nd to offer some reasons for this.

The Sources of Co2merative Advantage

12. The theory of internal.ional trade determination is at present anarea of great dispute. It is not the intentJor here to discuss this theoryin depth, but, in brief, in the last few years the theory of comparativeadvantage stemming from different factor endowments (principally labor andcapital endowment,), which huas been the prinelpa) theory of trade determinationfor much of the c -tury, has increasingly come under fire because it did notseem to correspcld to the real internationa] trade eituation. For instancethe fastest groith in internwitional trade has been observed to occur betweenindustrialized countries with similar factor endowmonts, instead of betweenindustrialized and developing countries where 1raditional comparativeadvantage theory might have suggested 'he greatest benefits from trade,thanks to the widely different factor endowments of the two groups. As aresult new theories of trade determination have been advanced. Many of thesetend to have supplemented, qualified or simply redefined the traditionaltheory rather than to have replaced it. For instance the traditional viewof comparative advantage in terms of two homogeneouxs inputs, labor and capital,has been criticized as an oversimplification and further factors have beensuggested such as natural reaources, technological capital and entrepreneurahip.

1/ See para. 33. The best measure of comparative advantage, though notnecessarily an indicator of the sources or this advantage, would beabsolute costs over the whole range of internationally traded productsbut these are not of course available.

The theory has also been criticised as being too static and not allowing forchanges in comparative advantage. 1/

13. For the purpose of this paper it will be postulated that thedeterminants of international trade aro many and often complicated, thoughsome are clearly more important than others. If this is an "ad hoc"approach to theory, it reflects the current, confused state of the theory.Essentially it postulates that the theory of comparative advantage, whichemphasizes the relative scarcity of capital and 3abor in different countries,is very relevant in certain prod'cts, including cotton-type textiles, thatare traded between industrialized and developed countries 2/; at the same timeadr4.tionnl, qualifying theories of trade determination are reflected in theadditional important elements of comparative advantage which are set outbelow. Many of these additional determinants result from modifications ofthe implicit assumption of traditional comparative advantage theory that thereis free trade: this theory tends to ignore barriers to trade arising fromcommercial policy (of importing and exporting countries), psychologicalattitudes and costs of transport and communications. 3/

314. The following are postulated to he, the major overall determinants(in terms of industrialized and developing countries as groups) of comparativeadvantage in internationally traded manufactures and to specifically accountfor cmparative a'4 wantage in cotton-type textiles: 4/

i. Fac.or-intensity in tnerms of lhuman (lahor and entrepreneurship)and physical (innorporating technological) capital: traditionally the cottonindustry has required comparatively low levels of capital intensity.

ii. The supply conditions or inputs: the cotton industries ofdeveloping countries have in the past either been partly resource-based orat least obtained inputs at world prices.

iii. The nature of the product, determining both the size of theoverall market and the product's suitabilit.y for international trade: cottontextiles have been, frma the point of view of patterns of demand at lowincome levels, a prime candidate for early import substitution in developingcountries and they arm, from the point of view of foreign demand mostly ahighly standardized, hence tradeable, product.

iv. The scale factor: although most countries (includJng manyindustrialized countries ) have failed to achieve optimal scales of production

1/ See para.l of Annex, Factor-Intensity and Cor.orativa Advantage, which liststhe major restrictive assumptions of traditional comparative advantage theory.See also H.G. Johnson, Comparative Coat and Commercial Policy ThnorY fora Developing World Econony, Wick-r;tu Stockholm, 1968, for a reviewof the current state of international trade theory.

2/ See Annex, paras. 6-12, for a justification of this approach.

3/ In some waya the theory would seem to bo of more value in a normative thana positive context.

hi/ The ranking implies no order of importance.

in the cotton InjuotLry, 3ac hiats not proven a specially . -Fdvantageousfeature to doveloping countries in establishing cotton industries andexpor 4 ing their prodSuct.

v. The structure of the industry in terms of the factor-intensitycompatibility of its component parts anid the effect of the physical structure(the horizontal versus the vertical organiz.atien of the industry) cn exportand import prospects: not only have some of the cotton industries ofdeveloping countries been able to profit from the labor-intensity of agparelindustry and thus maximize their comparative advantage, they have alsobeen able to profit fromn a tendency for horizontal organization in the cottonindustry, its customer industries and related chains of distribution toencourage imports in preference to domestic 3upplies.

vi. Monopoly: neither scale, terhnological factors nor supplyconditions of inputs have ereated monopolistic conditions in the cottonindustry which might have been exploited by industrialized countries. 1/

vii. International factor movexments: these have been comparativelysmall in the cotton industry.

viii. Protectiun: thia has tended to be higher for cotton-typetextiles In indust-riali ed countries than tor other manufactures and hasclearly inhibited exrorts from developing countries. However, it is a clearconsequence of the overall comparative advantage enjoyed by developingcountries. 2/

15. It is proposed to pay particular attention to the first element ofcomparative advantage, factor-intensity since this is demonstrably a veryimportant element and to make some detailed assessments of labor-inten3ityin cotton-type textiles. Following this, some of the remaining elements ofcomparative advantage will be discussed, perforce in qualitative terms.

Factor-intensity in the Cotton Industry

16. The annex to this paper, Factor-intensity and Comparative Advantagesfirstly establishes through the work of Hal B. Lary, the use of value addedper e- yee as a measure of the value of human and capital servicesrequii.. -i different indus,;ries and therefore as a useful guide to themeasur',1.i,".t of factor-intensity in manufacturing industry. 3/ Secondly, itestablishes, on the basis of some empirical work by UNCTAD, the importanceof f%ctor-intensity aB a determinant of the export success of developing

I/ The advent of man-made fibers has changed both the supply conditions ofinputs and the monopoly aspects of international trade in cotton-typetextiles but such changes are considered in Part II since the presentstatic view of comparative advantage mostly concerns deve'loping countries'export success in cotton textiles.

2/ This aspect of comparative advantage has been covered in the EconomicsDepartment Papers on U.K., E.E.C. and U.S. imports of cotton-type textilesbut will again be referred to in Part III.

i/ See Annex, paras. 3 to 5.

- 7 -

countries in certain manufactures amongst which were cotton fabrics, clothingand non-cotton fabrics. 1/

17. The measurement of factor intensity with value added data shouldbe qualified in the case of textiles. Possibly lower-than-average rates ofunionization (or of union activity), employment of a high proportion offemale labor and the tendency of textile industries to be situated in areaslacking alternative employment prospects may help to depress wage valnieadded. 2/ Low profit levels, low levels of advertising and R & D expenditaremay have a similar effect on non-wage value added. On the other hand level,of protection, which are generally higher than in other industries, may havean opposite effect. 3/ In spite of these qualifications, value added figuresprovide the best available source of information on comparative factor-intensity in the cotton industry. [L

18. The proposed measurement of factor intensity is simple. Valueadded per employee iTn the relevant textile branches will be expressed as apercentage of average value added per employee in all manufacturing. Itshould be stressed that this approach cannot give the precisest of indicationsof the location of comparative advantage, not on'y ior reasons of theinaccuracies inherent in value added figures bu%. Lor two other main reasons.Firstly, it is insufficient to assume that an industry in an industrializedcountry which is loss capital-intensive than the average (i.e. 100 per cent)will, all other thirngs being equal, cede a comparative advantage to developingcountries. The "cut-off" point may have to be as low as 60 par cent of theaverage before the effects of labor-intensity can be strongly felt; but thiswill differ over time and fram industrialized country to industrialized

1/ Ibid., paras 6 to 12. This evidence is reinforced by attitudes pruvalentin the cotton industries of industrialized countries: it is felt that,since the labor-intensity of the industry is at present the greatestdisadvantage facing these industries in industrialized countries, asuccessful attempt to make the industry relatively capital-intensivewould solve the problem of imports in industrialized countries.

2/ In som European countries imwigrant labor is employed in the cottonindustry at rates above the national average, probably with similareffects.

3/ It has been held that the general downward price movement of textileproducts may have depressed textile value added but such movements caneither affect profit levels - in any case low in the cotton industry -or themselves be the result of productivity gatrjs or falling input prices.

is Since moreover the qualifications tend not to have become more pronouncedover time, they will not vastly upset a view of changing factor intensityin the cotton indistry as measured by value added data over time.

country, and will depend upon the st-ate of industrialization of developingcountries. Secondly, the inclusion of all manufactures in, an attempt tomeasure comparative advantage tbased on factor intensity is strictlyunrealistic because of the "ailings of tls factor intensity theory.Measurement would be improved, for ins;ance, by excluding resource-basedindustries and possibly non-standardized goods industries, if this could beaccurately done. 1/

19. Value added figures are derived from censuses and surveys ofmanufactures; the former are generally more accurate than the latter as theyare carried out on a complete enumeration, as opposed to a sample, basis butthe accuracy of either will vary from country to country. It is proposedfirstly to present the data in an internationally comparable fornm and second2yto present the data that Is available from industrialized countries in areasonably detailed form.

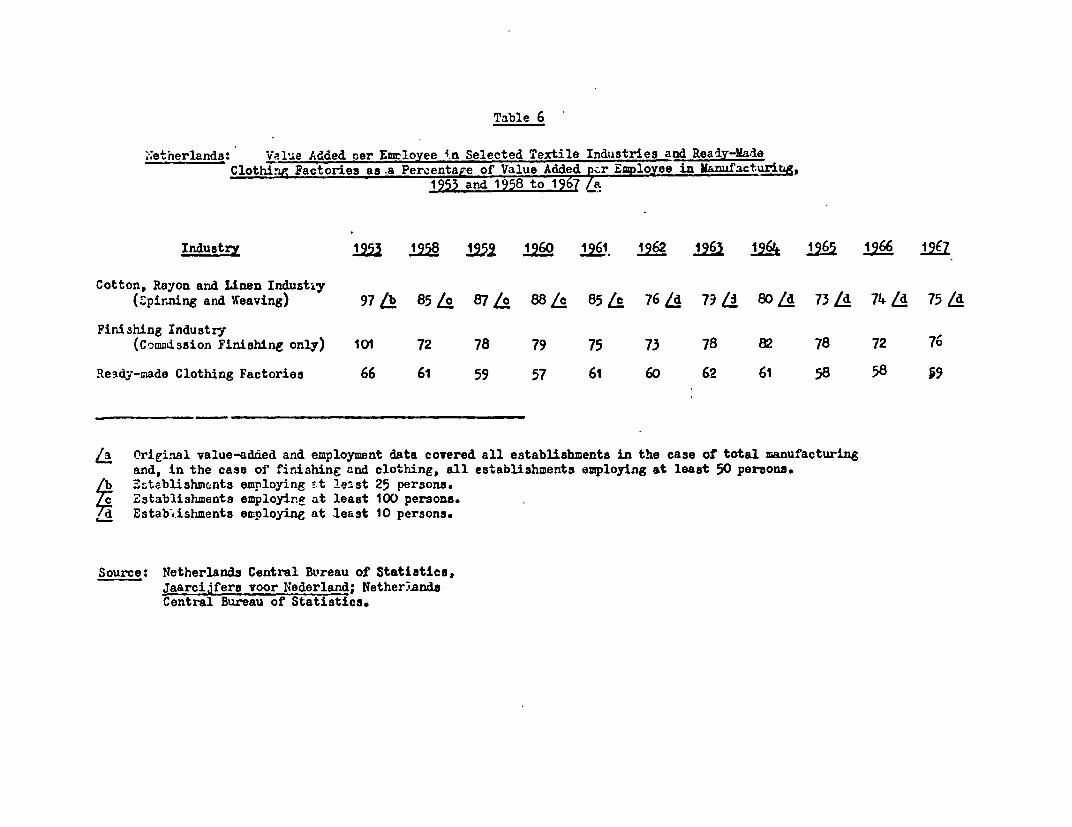

20. The only large scale exercise in the presentation of internationallycomparaole census data is provided by the U.N. in its Growth of World Industryseries. Table 1 is drawn from this source and gives the value added peremployee ratio for spinning, weaving, finishing, 2/ and for the clothingindustry for selected years from 1953 to 1967 for-somo of the countries,industrialized and developing, most concerned in international trade intextiles. The major conclusions to be drawn from the table are that, ingeneral hoth apinning, weaving, finishing and clothing are well belowaverag ._iels of capita.L-intensity in manufacturing, more markedly in thecase of Industrialized than developing countriee, 3/ and more markedly inthe case of clothing than spinning, weaving, and finishing. What the tabledoes not show is which other industries might come lower in the factor-inten3ity league. Hal B. Lary's comparison of 13 major manufacturing industrygroups for nine countries showed textiles and apparel to be the two lowestranked industries in industrialized countries whil t in developing countriesthey tended to dispute bottom place with furniture tid leather. 4/

1 It could be even further argued that certain internationally tradedservices should be included.

2/ This aggregates 3 processes and gives data for the whole textile industry,but given * i- -- 'rities of, say, wool and cotton weaving this shouldnot over- Fe rosult.

3/ The facto ty of textiles in developing countries is nearer theaverage pr ,..1l due to the greater weight of labor-intensive industries,especially textiles, in total manufacturing.

h1 Hal B. Lary; Imports of Manufactures from Less Developed Countries, 1968,see charts 8, 9 and 10, pp. 67-69.

- 9 -

21. Navionally published censuses provide more detailed informationconcerning the factor-intensity "league". Information is presented forthree industrialized countries with large cotton industries, the U.K., theU.S. and Canada, which have detailed, historical and up-to-date censusinformation and it is hopes that, along with the U.N. figures, these willsuffice to establish a valid picture for other industrialized countries.

22. Of these three countries the information provided by the U.K. isthe most detailed (see Tables 2 and 3). Table 2 establishes, from thebreakdown of about 100 U.K. industries, which of these are at comparablelevels with, or lower levels than, the f;ctor intensity of the relevantbranches of textiles ai.d clothing. It will be seen that te2tiles, andclothing even more so, are very near the bottom of the factcr-intensityleague. 1/ Moreover, inasmuch as total value added in 1968 (last column)is a guide to the size of domestic markets for given products 2/, it wouldseem that the size of markets of labor-intensive industries outside textilesand clothing is limited. The exceptions are bread and flour confectionery,which, by its nature, is not a candidate for significant international trade,and biscuits, footwear and pottery.

23. The U.K. additionally breaks down cereits data into finer detailthan at the three-digit industrial classification of Table 2. Table 3 givesthis breakdown for the principal activities of the cotton industry accordingto process and fiber input. 3/ Table h and 5 give comparable, if lessdetailed, information for the :. 'ted States and Canada. Both these sets ofdata are more complete, in terms .- annual coverage, than the U.K. data. V/

,h. From these three sources a general picture of relative factorintensities emerges. The clothing industry is clearly the most labor-intensive of the industries under consideration. The U.K. censua also putshousehold textiles in the same area. 5/ Spinning and weaving are slightly

1/ Of course if th6 industry breakdown were even more Ietailed according tocomponent processes in any one industry, such processes as assembly maywell come to be very labor-intensive.

2/ The value added figu.-e understates the domestic market weaving wherethere is a very large unfavorable trade balance.

3/ Detailed figures from the 1968 census are not yet available.

1* For Canada there is an annual census of manufactures and ror the U.S.there is an annual survey and quinquennial cor..;us of manufactures.

5/ In North America, and to - ..;-ge extent Europe, the household textilesindustry does not have .. ;c-ntity separate from that of the cottonindustry since the r3la-.vely simple cutting and hemming operations canbe conveniently carried out in cotton mills.

more capital intensive but at leve's Compa-hble with each other. Finishing,though less capital-intenmive than the -.nulf'aturing average, comes outclearly as the cotton inrdustry's most cau- :.i;-nt.ensive operation.

25. The cotton industry'3 processiiug of man-made fibers ter.ds to bemore capital-intensive thar. that of cotton. The U.S. data suggests that thisis most marked t.. fiii 'hing. This wc,uld seem reasonable because differentfibers r7quire definite modi"ications in this process. However, at thespinninr and weaving sLdges the processes are ulmost identical and thedifferences in capital-intensity are probaLly more apparent than real. 1/One reason for this maiy be that the monopoly aspects of man-made fibersupply, together with the continuing large-scale practice of fiber brandadverti:oing have combined to lend a monopoly aspect to man-made fibertex iles. Another reason may be that since man-made fibers have generallybeen more expensive than cotton, they have tended to be used in higherquality textiles requiring greater skills in production and more complicatedequipment.

Other Determinants of CULInP.WAL: ve Advantage

26. In several developing countries, principally Mexico, U.A.R., Turkey,India, Pakistan and Brazil, the cotton industry is a partly resource-basedindustry in the sense t.hat these countries grow cotton in quantity. Whilstthe resource-base may have been irstrwnental in the establishment of theindustry, there is little reason to suppose that it play3 an important positiverole in internatiopal competitiveness in cotton textile3. For instancesuccessful exporting developing countries of SouthoasG Asia, do not growtheir own cotton. In fact a rt Airce-base might prove a liability, eitherwhere a country cannot produce cotton at world prices or where the existenceof cotton growing might lead to protective barriers against imports of man-made fibers for textile processing and re-export.

27. A barrier to international trade which has interedted economistsin recent years is that caused by dirferent patterns of demand in differentcountries. In fact it has been suggested that similaritie3 in patterns ofdemand between industrialized countries account for the faster growth of tradebetween these countries than that between industrialized and developingcountries. This particular barrier would seem to be less of an obstacleto exports from developing countries in textiles than ir. other products sincedemand for textiles is a primary demand felt even at comparatively low incomelevels. It is of course true that low-income demand may be for coarse,

1/ A sma2-. part of the explanation may lie in the fact that man-made fibersor blends (e.g. polyester-cotton) require slightly more air-conditioningor slightly more sophisticated blending equipment than cotton alone. Orthe other hand man-made fibers are generaL,y sulbject to fever breakagesthan cotton and are less costly to ,lean.

- li -

stannardized textiles whilst high-incomo demand miay h-. -.or high-quality,

fashion textile's but the axistence cf a textilo ,n_us.ty to satisfy the

form2er needs creates the possibility of an expcrt :r..- . at least

itl standardizsd goods. As in the case of resource-cnre.y.r.ent. exp rting

on the basis of a home mark-3t is not an unqualified advantage. Itnilst the

home market may be very important in the initial establishment oi the

industry, it by no means necessarily centributes to the industry's ability

to corn-te internationally.

21. One can expect developing co;:ntries to export standardized goods

more easily than non-standardized goods to markets whnrri di-stance, sophisticated

tastes and great nroduct differentiation might require certain additional

market. research skills of exporters i.e. where there is a high cost of entry

into new m.arkets: cotton-type textiles, especially in the yarn and grey

cloth stare and in some cases in the finiehed cloth aid made-up stage, are

highly standardized, either in the sense that tb-ra ir a mtall number of

very in:prortant, product types or in the sense th2t. proc-Jet types are nasily

and precisely specifiable. This featurs of the product nas undoubtedly

contributed to the export success of dGvel.oping countries: for instance

st.randardi%a4 nn has allowed importing agenciese n some industrialized

c:-irtries 1/ to seek out new sources e^ textile imports and there has been

no cost of entry for new suppliers. However, thp f'nshion (anc rat+inna. taste)

element which is rore or less present in much of finish-3d clot-., and made-

up goods sets cer.. n limitat.ions to the advantages of standardiz-.tion;

although certain lines in these products are standardized, for instance many

household textiles and lower-end-of-the-market clothing, trade barriers auch

a:; the cost of communication and entry into new markets reassert themselves.

29. There is in the cotton induistry, especially 5.n finishing, a certain

scale of production which developing comtries, and indeod most industrialized

countries, do not lways ach.ieve. 2/ A typical optimal scale is quoted

today as being foi- spinning 30,OOO7to hO,ooo spindles and for weaving

standardized goods up to 500 conventional modern looms. A finishing unit,

1/ Princip.ally cloth converters and importers and, large retail purchasing

groups such as department stores.

P/ The work on compar-ative advantage in the Annex, based on UNCTAD work,

includnd a test for the effect of a scale factor (value added par establish-

ment). It was concluded that the smaller the optimal. scale of an industry,

the botter a developing country's performance. however, ths result was

fairly weak, both in terms of the size of the regression coefficient and

of the estimated sLanuiard error. In any cajc, ..no subse.nuent exclusion,

from the sample of 57 products, of nine clearly resoirrce-based products

weakened the regression coefficient (see Table A-i).

- 12 -

however, might require the output of up to four optimally sized weavingsheds 1/. In spinning and weaving there is little to suggest that thefailure to achieve optimal scale of production significantly erodes thecomparative advantage of developing countries. However, it may well bethat the higher optimal scale of finishing, together with the high capital-intensity of the process relative to spinning and weaving, and the natureof the market for finishcsd cloth, contributes to the lack of competitivenessof many developing countries in cloth finishing. There is one clear instancewhere this failure may be important: the cotton industry of North Americagenerally operates at optimal scales and this is one of the important reason3why it can to some extent compensate for its large disadvantages stemmingfrom high wages. However, whilst North America can to some extent overcomeits wage disadvantages vis-a-vis Western Europe, it is unable to do so vis-a-vis the most competitive developing countries.

30. Apart from the general effect that various natural ind imposedbarriers have on overall levels of trade, there is probably a secondaryeffect on the structure of trade. It would seem reasonable to suppose thatsuch barriers tend to encourago trade later rather than earlier in thevertical stages of production of a final product. In this way, for instance,transport and foreign selling costs per unit of value added could be minimized.This would suggest that compatibility in the factor-intensities of verticallyrelated production processes might increase overall comparative advantage.In the case of textiles there is a strong compattbility in the major processes.The following table gives a typical value added breakdown and factor intensityranking for the various stages of making a finished item of clothing in anindustrialized country (the figures should be taken as very broad indications): ?

Share in total Value added per employeevalue added (manufacturing 100)

Spinning 15 60Weaving 20 60Finishing 25 75Making-up h0 55

-aigu 62 (average weightedby share of valueadded)

1/ Textile Council, Cotton and Allied Textiles, Vol.I, 1969, paras 335 and 336.In spinning and weaving optimal size tends to reflect managerialconsiderations whereas in finishing it tends to reflect technicalindivisibilities.

2/ Based on orders of magnitude suggested by cost studies (see for instanceTables 6 to 8) for fabrics in industrialized Western European countriesand for apparel making-up in similar countries ;from Profiles ofManufacturing Establibhments, Vol.II, U.N., 1968). Finishing costs varygreatly according to the finish: compared to total value added by spinningand weaving, a print finish can cost as much or more, a dyed finish cancost one half to as mucz, and a plain white finish (e.g. sheets) mig:ntcos' about one-third.

- 13 -

F'inishing is clearly the most capital-intensive operation and accounts forabout one-quarter of value added (but could according to the type of finishaccount for up to one-third). It is clearly the "weak link in the chain" offactor-intensity compatibility, but very labor-intensive; making-up on theother hand accounts for a substantial proportion of total value added and bringathe weighted average of value added per employee down to a low level. Thusthe factor-intensity structure of textile production would seem to suggestthat developing countries can maximize their comparative advantage byexporting as finished a product as possible; it provides a cogent explanationof why developing country cotton-type textile exports are concentrated inthe grey cloth and clothing categories, the two points of maximizedcomparative advantage in the vertical production process. In connectionwith this observation on factor-intensity compatibility, there is a prevalentattitude in the U.S. cotton industry that, even if the U.S. were competitivewith imports at the fabric stage, the developing countries' advantages inmaking-up would more than compensate and the U.S. iports problem wouldremain.

31. Traditionally the production, distribution and retailing oftextiles have been organized along predominantly vertical lines inindustrialized countries; hence one stage in the production process hasbeen able to freely seek its inputs from the cheapest supplier, in manycases foreign. If would be wrong to exaggerate the importance of this asa positive factor which particularly encourages textile imports sincesimilar situations prevail in other industries. However, in certain cases,most notably that of the U.K., the excessively horizontal organization ofthe industry has been attributed with a propensity to encourage importsmore than might otherwise be the case. 1/ Moreover, any moves towa-dsvertical organization may have a discouraging effect on imports, not ofcourse because the simple existence of a vertical firm would force certainstages of production to use uncompetitive domestic inputs, but becausecertain savinge such as reduced selling costs and, more importantly,increased control of production, quality and delivery dates would makedomestic products more competitive.

32. Neither monopolistic tendencies nor international factor movezuntsseem to havo had a great effect on international competitiveness in cotton-type textiles. Cotton industries, usually consisting of marn firms and oftensubject to comparatively high levels of importsp have not tended to acnopoly.

1/ In particular U.K. converters (merchants with little or no producingfunction) account for a larger (if falling) proportion of grey clothimports than merchants in other countries. IL has often been felt thattheir role in importing has aggravated the market disruption problem.See, for inatance, p. 83 of Caroline Miles, Lancashire Textiles: aCase Study of Industrial Change, 1968 for a description of their Fole.

International factor movements have also been comparatively small as regardsthese industries but two phonomena are worthy of note. There is a tendencyfor some European cotton industries to tlse large amounts of immigrant labor(often at higher than average national rates): this buttresses thecompetitive position of such industries which often suffer acute laborshortage problems, especially on the night shift. 1/ On tVe other handthe tendency for international movements of capital has been for industr alized(or relatively industrialized countries such as Hong Kong) to invest in low-wage countries: this has as yet only been an ip ortant phenomenon in itscontribution (mostly through Japanese investment) to the establishment ofcotton industries in Southeast Asia.

Absolute Costs

33. V It hardly needs to be said that businessmen do business on thebasis of absolute prices and costs rather than on the basis of comparativecosts. What needs to be made clear is the relation between the two. Thefollowing is a very simplified explanation of the relationship. 2/ In orderthat two countries can enter into international trade with each other, theymust in theory fix a currency exchange rate lying somewhere between theextreme points of the countries' comparative advantage and disadvantage inthe products to be traded. This means in theory that a country will alwayshave an absolute cost advantage where it has a comparative cost advantage.Thus the absolute cost advantage over industrialized countries that developingcountries might enjoy in saveral cotton textile products would reflecttheir comparative advantage 'n these products. A shift in the location ofcomparative advantage over time would be reflected either in cheaper costsin the country profiting from this shift, or in adjustment in exchange rates.This simple relationship may of course be largely distorted by elementswhich isolate economies from the world economy such as protection and multiple(and over-valued) exchange rates, etc.

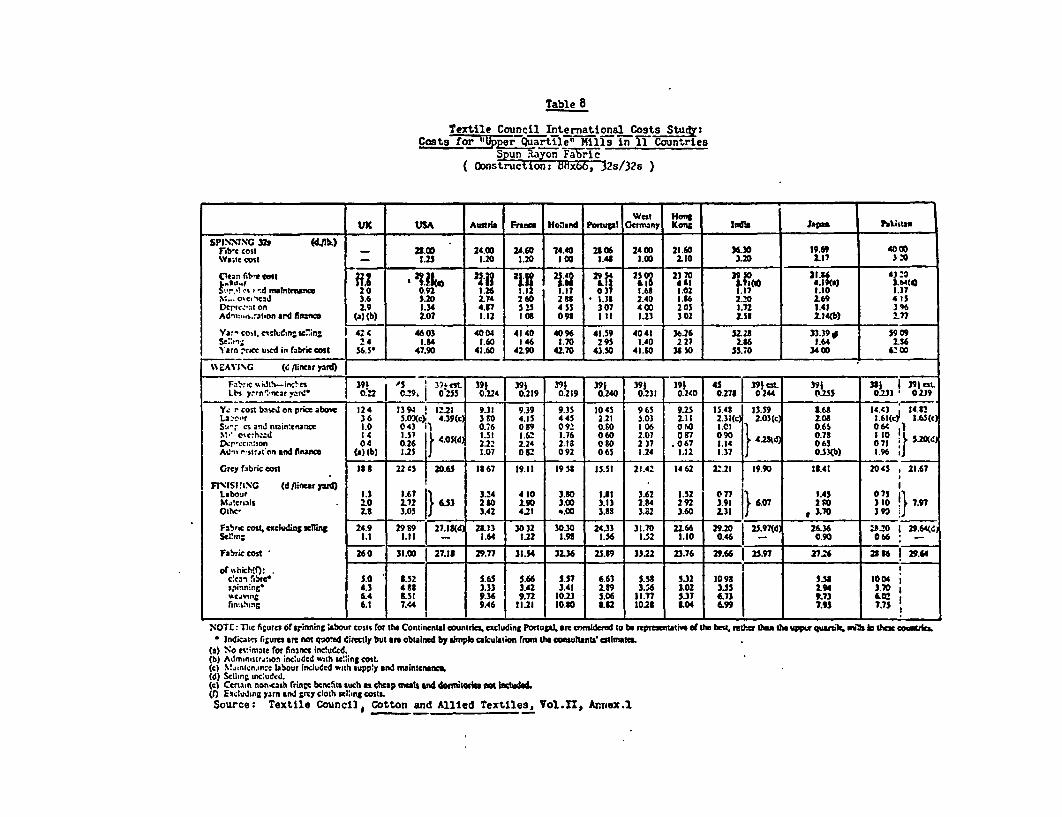

34. Although businessmen trade according to prices, price informationin cotton-type textiles is often unreliable and in some cases can be criticizedas not reflecting real (long term) costs which are of course more closelyrelated to comparative advantage. Informati c on costs is rare. The onlyrecently published source of such information is by the U.K. Textile Councilwhich commissioned a study on international costs from Wierner Associates, Inc.of New York. Werner's study provided production costs for "upper quartile"mills (i.e. mills having lower total costs than three-quarters of the industry)in 10 countries for 4 yarns and 3 fabrics which were important in inter-nat'onal trads whilst the Textile Council Productiv.ty Center undertook theDams. exercise for tsie U.K. The data reflect costs in October/November 1967.

1/ For the U.K. see Appendix XXVI, "A sample survey of the labor force inspinning and weaving" in Textile Council, Cotton and Allied Textiles, Vol.I.

2/ For a fuller explanation see G. Haberler, The Theory or InternationalTrade with its Application to Commercial Policy, 1936, p. 131.

- 15 -

35. The Textile Council published the cost data in two forms. Itpresented the princ-pal Werner findings without alteration in an annex toits 1969 survey of the problems of the U.K. cotton industry. 1/ It tookthese same findings and modified them, principally by up-dating andstandardizing raw material prices, standardizing for each fabric the weightof yarn consumed per yard, and standardizing depreciation charges. Thesemodified costs were incorporated into the main body of the study and servedas the basis of calculation for some of the study's recommendations. 2/Given the difficulties and possiele errors involved in modification o? costfigures, it has been felt preferable to use the cost figures as supplied byWerner for this paper.

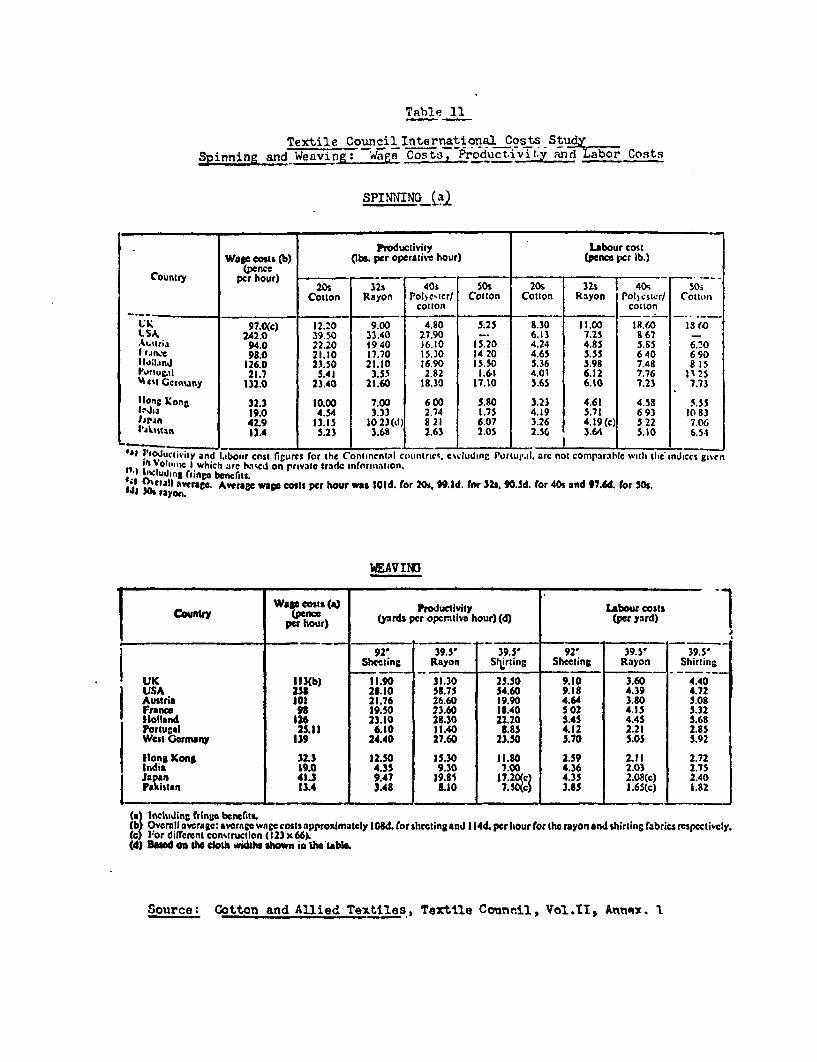

36. Tables 6 and 9 reproduce the figures supplied by Werner (and theTextile Council Productivity Centre) as set out in the Annex to Cotton andAllied Textiles. They are of course subject to the usual warnings aboutaccuracy, etc. 3/ Table 10 reproduces two additional tables from the studywhich relate overall costs to wage costs and productivity. Table 11reassembles the cost information of Tables 6 and 9 on an index basis for thesake of comparability. h/ On the whole the cost information gives a moreconfusing picture than census information. In particular it becomes clearthat the "expected" comparative advantage of tieveloping countries doies notmanifest itself in every case. However, a comparative advantage of developingcountries in spinning and weaving, more so the latter, is generallydemonstrable and t..rtain evident trends can be pointed out.

37. Clean fiber costs in Table 11 approximately represent the price ofinputs in the cotton industry. 5,' Even in cotton there are sometimes

1/ Textile Council, Cotton and Allied Textiles, Vol.I, Annex 1.

2/ For the modified costs see Chapter 5, "International Costs", of Cottonand Allied Textiles, Vol.1

3/ The opinion has been expressed that JApanese costs are particularly lowand may reflect export pricing more than domestic cost. The Indian cottonindustry ;.as felt that its costs should have been higher whilst othersources have felt that they should have been lower. Doubt has also beenexpressed about the comparability of Werner coats with U.K. ProductivityCentre costs.

W/ In this table Germany is used as the basis of the index since, of all thocountries under comparison it is one of the highest wage rountries. TheU.S. would have provided a better index basis exc'pt that width variationsin some of the U.S. fabrics make the cost information slightly moresuspect.

5/ But the clean fiber cost includes a small amount of preparatory processing.Also other inputs which "all under "supplies and maintenance" are notincluded.

- 16 -

surprising variations in th3s figure. GCnerrlly more labor-intensiveprocesses in low-labor countries a3low :;lightly lower quality cotton tobe processed but the saving is small. Houever, in two particular caseshigh-priced cotton inputs render the end-product uncompetitive. One..case is Portugal which is obliged to buy short staple cotton from its Africancolonies at high prices. The other case is India which pays way aboveworld pricus for lorng-staple cotton: thi:b helps make it uncacpetitive incombed cotton yarn.

38. In the same way India and Pakistan (and to a 16sser extent Portugal)are made uncompetitive in man-made fiber goods because of the high pricesthey pay for rayon and very high prices they pay for polyester. Thisreflects the disadvantage that can be incurred in protecting domestic man-made fiber industries.

39. In spinning the competitiveness of the developing countries in thecost study tends to worsen in higher counts. This might be expected since,the higher the count, the slightly more capital-intensive the spinningprocess. Also those developing cour,tries catering for a large home markettend to specialize in lower counts. Even at the lower of the four counts(20s and 32s) the developing countries' advantages would not seem to beoutstanding except in the case of Hong Kong. The information of Table 12throws some light on this since Hong Kong clearly combines low (though notthe lowest) wages wit.h 'iiglh productivity. This is generally true also ofJapan whose wage levels are njearer to the developing than the industrializedcountries of the cost co:nparison. rTh very low wages prevailing in Portugal,India and Pakistan are insuificient to offset their low productivity vis-a-vis Hong Kong and Japan. 1/

4SO. In weaving the developing countries an the whole show costadvantages, more strongly in the rayon and polyester/cotton fabrics thanin sheeting. 2/ Moreover, the developing countries other than Hong Kong tendto perform better in weaving than spinning. Except in sheeting thy clearlyhave lower costs than almost all the industrialized countries except Japan.

1,1. The picture in finishing is less clear, partly due to the comparative.paucity of information, (cost data on two finishes only) and the non-homogeneityof finishing processes. 3/ The developing countries except Hong Kong seem

1/ It is also interesting to note that the U.K. does very badly due tocomparatively kigh wage costs and low productivity whilst the U.S. alsodoes badly since very high productivity cannot offset very high wages.

2/ This is evidencc that developing countries do not have a lesser comparativeadvantage in the processing of man-made fibers than in the processing ofcotton (see para. 25).

3/ See para. 176 of Cotton and Allied Textiles, Vol.;. It is also true thatsome finishing in some developing countries is qualitatively inferior.There have, for .nstance, been complaints in the U.K. about the qualityof both Spanish and Indian finishes, although both countries are believedto be reasoi.ably competitive in actual finishing costs.

- 17 -

ciearly less competitive in the finishing of sheeting but achieve averagecosts in the printing of the rayon fabric.

42. In addition to this published information sane (unpublishn;) costinformation has been prepared for the World Bank cn the cottor industry ofMorocco, using the Werner data as a basis of comparison. 1/ Aoroccan costscome out high compared to most of the Werner countries, though not too highto preclude all possibilities of Moroccan exports to the E.E.C., one of itsmajor markets where it has preferential access. Morocco occupies a positionin the cost "league" similar to, but lower than, that of India, Pakistan andPorTugal, i.e. in the low-wage/low productivity group. Its low positioneven in this group reflects to some extent its wage costs at 31 pence perhour in spinning and 36 pence per hour in weaving which are by far thehighest in this group and indeed ccmparable with those of Hong Kong andJapan (see Table 10).

W3. A further large-scale international cost study, commissionedfrom another consultant and as yet unpublished, was also carried out forseveral cotton-type textile products for mills of similar levels ofcoupetitiveness (upper quartile) to those in the Werner study and at roughlythe same time (1967). Detailed results from tii.; study are not available butcertain broad trends in costs may throw same light on the information fromWerner. Firstly, in value added by spinning and weaving a clear hierarchyof competitiveness .er several products emerges for the six principalcountries compared. The order from lowest to highest cost, is: Hong Ko;,g,India, Japan, Portugal, U.K. and Germany; moreover, the first four countries,the low-wage countries, have very clear cost advantages over the two high-s- re countries: costs in the former are typically one-half to two-thirds ofzosts in the latter. However, it should be remembered from the Werner datathat the U.K. and Germany, the former more than the latter, are amongst thehighest-cost countries. In spite of this the study suggests greater absolutecost advantages for developing countries than Werner and, unlike Werner. itsuggests that India is competitive enough to oust Japan from second placein the ranking. Whilst trade trends have not seemed to bear out thisparticular conclusion, there is some broad concordance in this and the Wernerspinning/weaving cost data. 2/ This study has more detail than Werner onfinishing costs: it suggests that in fact neither high-wage nor low-wagecountries possess clear cost advantages over each other.

h4t. Overall the cost data suggest a general absolute advantage for low-wage countries in spinning and weaving, though not by any means for all products

1/ Some caution should be exercised as Moroccan costs were from May, 1970and Werner costs from October, 1967.

2/ The differences in detail between the two studies emphasize the need toapproach all cost data with caution.

and for all low-wage countries. In nj.' ng low-wage countries are lerscompetitive, although acrording to cost, .;lone they are not necessarilyuncompetitive. When costs .re t.ranlalLerl nto prices, it must be rememberedthat low-wage countries.are compelirg w.th high-wage countries on the latter'sdomestic markets and thei atainrnent of ftijual or only slightly lower costiby exporting countries will not betoken competitiveness once transport andmarket entry coste and qua)ity/ftashio:n consideritions, not to mentionprotective barriers, are taKen rtio accuivut. On the other hand it may betree that whereas exporL pricbzs are set by the most competitive (e.g. upperquartile) mills, domestic prices may reflect average levels of competitiveness. 1/

The Location of Comparative Advantage Amongst Develocing Countries

I5. Although th- cost information suggests a general correlation betweenlowest costs and lowe:t wages (as predicted by fact.or-intensity and comparativeadvantage), the most competJtive -o.antries, whilst they are lou-wage, do notnecessar-ly have the )owes! w,t!... / Whilst it is relatively easy toideitify which are the most. cuuupetitive countries and the technical reasonsfor their cost advdntagd, it it mune dif'ficult to establish the underlyingeconomic causation. The cost information, bearing out evidence from tradetrends, 3/ snlggest.s a general cost league Ir cotton-type textiles in thefo2lowing broad groups of 3atbrnationally trading countries:

Low wage countries: i. .3t@mi-industrial ized countries and Japan: low wagesanid quite high productivity.

ii. Other exporting developing countries: low wagesand low productivity.

High wage countries: i. European industrialized countries: high wages andhigh productivity.

ii. North Amierica: highest wages and highestproductivity.

1/ Inasmuch as export prices often reflect marginal pricing and domesticprices have to bear the corresponding burden of this, a similar situationobtains.

2/ Hong Kong and Japan have the highest wages in the low wage group ofcountries whilst Taiwan and South Korea, also leading exporters, havefar lower wages. An American Textile Manufacturers' Institute 1968wages survey (quoted in Far Eastern Economic Review, Asian Textile Survey,1969-70, p.82) gives the following hourly textile wage rates in U.S.cents: Japan 36; Hong Kong 25, ?akistan 14, India IL, Taiwan 13, SouthKorea 8.

3/ See the general conclusions of the Economics Depart.ment Working Paperson E.E.C., U.K. and U.S. imports of cotton-type textiles.

- 19-

Whilst the cost information concludes that low wages (reflecting labor-intensity; c.f. the earlier comparative advantage information) are anecessary condition of competitiveness, it also underlines the importanceof a certain level of productivity. Since productivity raflects theavailability of capital in both human and physical form, the "shorthand"explanation of the export success of certain Southeast Asian developingcountries 1/ is to say that they are semi-industrialized, i.e. the mostadvanced developing countries. This however, begs the question to someextent: it is difficult to define semi-industrialization and certain suchcountries may for instance, have a less broad industrial base than othercountries ostensibly at earlier stages of development.

h6. This is not to dery that the absolute lev6l of development doesnot play an important part in export competitiveness in cotton-type textilesin particular and labor-intensive manufactures in general. Only a smallnumber of developing countries export manufactures in significant amountswhilst most developing countries seem to be capable of exporting .:'imaryproducts only (where their comparative Advantage often largely resides innatural resource endowment). This is to suggest that. several developingcountries have a sufficiently solid industrial 1--; and siifficicnt resourcesof capital and labor to be potentially compPtiti.j, in iott.on-type textiles.The failure to achieve competitiveness reflects as much domestic policieswhich have the effect of isolating these countries from international tradeas their absolute .dvel of development.

47. In many such countries high levels of protection, either throughquantitative restrictions or through tariffs, virtually shut off domestic- c'ducers from the competition of imports and inefficiency is fostered.Protection may be made possible by markets which are large enough to supportan industry producing for the home r.Arket only, even at relatively inefficientlevels. If exporting takes place under such conditions, it is often amarginal activity and the inefficiencies of domestic production are of coursereflected in export prices.

4s8. However, if the semi-industrialized economies are comparatively open,they are not, with the important exception of Hong Kong, open in a veryclear sense because they also prot-ect, if to a lesser degree, their domesticmarket:;. They are open economies in that they tend to be small countrieswhich have to depend on foreign trade; exporting cannot therefore be a marginalactivity. The following comparison of product.ion, apparent consumption andtrade in cotton cloth for four developing countries illustrates this point:

1/ Specifically Hong Kong, Taiwan, South Korea bui Japan also reflectssimilar characteristics.

- 20 -

Productiort Imports Exports9 Apparent consumption- mTllion tons

Hong Kong 88 597 76Taiwan 50 O.4 33 17South Korea 23 1 10 l4India 897 negligible 58 839

Source: OOT/STAT documents of OATT Cotton Textiles Coaittee.

Hong Kong and India contrast strongly, in the above example, as open andrelatively closed economies. They also contrast in the connected phenomenonof small and large markets (almoet all of India's apparent consumption isdomestically consumed whilst most of Hong Kong's is exported in the fornof made-up goods). Taiwan and South Korea, with high ratea of exports todomestic consumption but low rates of imports, are in a more middling positionof "openness".

W9. There is a tendency in acne of the exporting developing countriesof group 2 of para.45 to have over-high wages in textiles in the sense thatlevels of productivity commenaurate with the wage levels cannot be achieved.This of course may partly reflect the effect of currency overvaluationthrough excessive levels of protection but it may also reflect distortionsthat have been created internally in the wage "league" between industries(and therefore in the inter-industry factor-intensity leagus). A specificreason for this may be that in textiles in particular labor can achievehigher rates of unionization than in other industries due to the size andage' of the textile industry. India for instance has one of the highestcon.oarative textile wages in the world. 1/ India's factor-intensity rankingdistortion is reflected in Table 1: it Is the only one of 12 countries tohave value added per employee in spinning, weaving and finishing above theaverage for all manufacturing. 2/

50. India is also the clearest case in point where a donestic developmentstrategy, in this case based on enplcyment-creating labor-intensive production

1/ Asian Textile Survey 1969-70, p.112.

2/ It is also interesting to note that South Korea, the most dynamic exporterof the 6 developing- oountries represented in Table 1, has the lowestcomparative factor-intensity ranking of these countries.

_ 21 -

methods, runs counter to export competitiveness. For instance, India, witha similar textile wage rate to that of Taiwan, had in 1967 only 17 per centof its looms automatic as against 70 per cent in Taiwan. South Korea, witha wage rate half that of India, achieved 32 per cent automatic looms. 1/

51. It would be wrong to see the advantages of semi-industrializedcountries in terms of productivity and the openness of the economy alone.Table 10 shows for instance that once high Hong Kong productivity combineswith its high (relative to other developing countries).wage rate to give unitlabor costs, it does not consistently achieve the lowest labor costs.Moreover its rates of machine productivity in terms of machine output peryear, which together hith the cost off capital, deturmines unit depreciationcosts, are not a great deal better than those of some developing countries. 2/A significant key to the advantage of tle semi-industrialized countries mayin fact lie in the relatively easy availabil4ty of capital which reflectscertain chance factors. 3/ The first of these, a historical factor, was thebenefit that Hong Kong and Taiwan derived from the emigration of mainlandChinese entrepreneurs (some bringing their equipment with them) in 1908. Thesecond, or geographical factor, has been the investment of Japan and, on asmaller scale, Hong Kong in textiles (among other products) in neighboringlow-wage countries. W/

Comparative Advantage: Conclusions

52. Of all the trade determinants discuissed there are several reasonsfor citing labor-intensity as the mos1. important; but, if it is the mostimportant, it is largely by virtue of the absence of other inhibiting factorsrch as product differentiation (non-stanv)ardizatitn) or monopoly conditions.The question of whether the labor-intensity advantage of developing co'.ntriescan be sustained in the future concerns not only changes in the relativefactor-intensity of cotton-type textile production, but also the developmentof possible inhibiting factors together with, or even alternatively to,the pure factor-intensity determinant.

53. On the one hand the cost data generally mirrored census data inasmuchas developing countries were seen to possess greater advantages in spinningand weaving than in finishing. On the other hand it showed that comparative

1/ Statisttcs on auLtomatic looms from GATT document OOT/W11l5/add.3, statisticssupplied to the Cotton Textiles Committee by the International Federationof' Cotton and Allied Textiles Tndlstries. Automatic looms are those loomswhich automatically rcplenish the yarn supply to the shuttle; this is doneby hand with non-automatic looms.

2/ Sec Cotton and Alliei ITxtiles, Vol.II, Annex A, tables 9 and lb for machineproductivity in the Werier~oosts study.

3/ It is the sense of the availability of capital that these countries canperhaps most clearly be defined as semi-industrialized.

4/ See for instance an account of curren'. Japanese ovorseas textil.e invest-ment in Asian Text.ile Survey, 1969-70, p.l43.

advantage was not an automat.Ic result of low wages but also required acertain level of produetivity whLch is lpsn likely to be achieved the morea country is isolated .rom the effects of international trade and cannot.mobilize its potential comparative advantage.

II. COMPARATIVE ADNVANYTAGE IN TTz FUiTUI.!

54. In Part II it is proposed to look at changes in the cotLon industrywhich are taking place or might take place and which might alter the balanceof comparative advantage. The cotton industries . irAustr 4 alized countrieshave claimed such changes, specifically in two areas. Fir,_'-, they havemaintained that technological advances are resulting in a capital-intensification of the cotton industry relative to other industries with theresult that, from the point of view of factor-intensity, cotton-type textileproduction is becoming an activity more suited to the factor endowments ofindustrialized countries. Secondly, there may be different forms of sub-stitution in the industry, in inputs processes and end-products. This mayalso damage the competitive position of developing countries,-either becausethe latter are uncompetitive in new types of inputs or processes or becausethe end-product is becoming more de-standardized (and increaoingly fashion-oriented). 1/

Factor-Intensity Reversal: The Claims of Cotton I-.dustries of IndustrializedCountries

55. Given the importance of lahor-intensity as a source of comparativeadvantage .n cotton-type textiles, ehinges in the technology of the cottonindustry, making it an industry with relatively high capital requirements perworker, woulA clearly threaten the competitive position of developing countries.In the Annex there is a brief disrussion of factor-intensity reversal fromthe general viewpoint of economists. 2/ They have not on the whole come toe.itnimous conclusions: the most prevalent opinion is that there is not much

evidence of factor-intensity reversa1, except in some cases in agriculturewhere the importance of resource endowment partly invalidates a view offactor-intensity simply in terms of labor and capital.

56. In spite of this, the claims of certain cotton industries, notablyin industrialized countries in Western Europe', are insistent enough for thepossibility of factor-intensity reversal to be seriously examined. Morerapid technojogical advance in the cotton industry than in others is all themore feasible since the effect of price competition, a phenomenon moreuniversal and sustained in the cotton industry than in others, may well havebeen to incite a "competitive responae" lin some industrialized countries. 3/

1/ Changes in the trade determinants listed in para.l1 will in fact be examinedbut not in the same order.

2/ Annex, parao. 13 to 16.

3/ Hal B. Lary in a section of ilis study, "Technical advance and factor-intensities: the rase of cotton textiles", p.81, op.cit., suggests sucha competitive response. His approach to the problem of factor-intensityreversal, in particular his challenging of the eotton industry's claims,provided a starting point for the present discussion.

As was noted in para 15 of the Annex, rela.ive capital-intensification(this time in the sense Oa increased output per worker rather than asuperior technology) ray aJso result from improved efficiency. In WesternEurope, average levels of efficiency in the cotton industry seem lowerthan in other industries and there is ample room for improvement which mightlead to sore rise in the industry's ranking in the factc:-intensity "league".ImprovAment from this source does not, however, contain the poter,tial forlarge-scale factor-intensity reversal of technological advance. 1/

57. The evidence for capital-intersification in the cotton industry hasmost frequently been presented by means Of capital-labor ratios comparingthe most recent investment figure per workplace (or per worker) required ina new mill with earlier such figures The best known example of this is the0.E.C.L 's study, Modern .utton Industry - A Capital-Intensive Indtustry,which in 1965 could concludd that the cotton industry was no longercomparatively labor-intensive siimply by pointing out the industry's growinginvestment requirements (whiich in isulation undoubtedly look impressive). 2/In the following y'jar GATT'.s A Study oz} Cotton Textiles was able to state:"A modern cotton industry is r.z;.r;i'.: as heing among the most highly capital.-intensive of the manufacturing industries" on the basis of similar evidence. 3/A recent article by Dr. W. Linn',uann, id which is one of thc most authoritativepresentations of the cotton industry 37case, quotes typical investmentfigures per p.faical workplace for a new integrated spinning and weaving millas follows:

1958: $ 20,000 ) from) OECD

1963:. $ 60,000 - 80,000 ) sources

1969: $ 100,000 (Linneman's estimate)

These approaches to the measurement of increasing capital-intensity havesuffered the drawbacks of simply comparing present with part performance and

1/ The clothirg industry in industrialized countries has not on the whole madesimilar claims of factor-intensity reversal.

2,' See Part II, Chapter II of the study. The evidence thus presented ofcapital-intensification then indirectly becomes tLe junLification of highlevels of protection in industrializdd countries; see pp. 131-133.

3/ GATT, 1966, p. 55.

" Consequences of the Increasing Capital Intensity cf the Cotton TextileIndustry", Cotton and Allied Textile Industries, Vol.10, 1969, InternationalFederation of Cotton and Allied Textile industries.

- 25 -

not comparing performance with the rest of industry. 1/ Where corparisonshave been made with the rest of industry, they have tended to be based oncomparisons, for instance, of optimal investment levels in the cotton industryand average investment levels in industry as a whole. 2/ Clearly, it cannotbe denied that capital-intensification has occurred inJthe cotton industry,but the point is often lost that this is a necessary condition of maintainingcompetitiveness where wage costs arc rising. Capital-intensification has tobe looked at relatively, i.e. in terms of the rest of manufacturing'industry.A further criticism of sone of the quoted capital-lahor ratios is that theyhave tended to be expressed in terms of investment per workplace whereas,since most new plants are run on three shifts; investment per employee wouldmore accurately reflect capital costs.

58. A second approach to measurement of technological change in thecottci industry has been provided by the evolution of gross investment peremployee over time in the cotton industry compared to the rest of the industry.This exercise provides more comparability than the former and has lent someweight to the thesis of capital intensification. Linnemann quotes a morethan two-fold increase in the capital-intensity of the German cotton industrysince 1950 according to this criterion, as compArof' to a two-third increasein the capital goods industry was way below the 'ndnistry average in the early1950s and has now grown very near to that average. The following figures forthe U.S. are reasonably representative of most industrialized countries:

Investment per Employee in the Cotton industry(Manufacturing - 100)

1953 1958 1962 1967

Cotton weaving ) 6 32 79 75Synthotic weaving) 30 62 93Yarn, except wool n.a. 37 93 109

Source: U.S. Censuses & Surveys of Manufactures

Investment figures are very cyclical and can at best only provide generaltrends but there has been in the 1950s and 1960s an undeniably increasingtrend in investment per employee compared to the national average. This is

1/ As well as Hal B. Lary, p.85, op.cit, the Economist has pointed out thatsuch a demonstration of capital-intennifiration m,;st be on a comparativebasis with the rest Of industry ("Textiles not just for the Poor",pp. 68-69, November 22, 1969).

2/ In Para 351 of Cotton and AlliAd TextAles, Vol.I, for instance, a best-practice present (196T-69) or near-future value added per employeefi-gurefor the cotton industry is compared with an average value added peremployee figure for manufacturing in 1967.

- 26 _

discussed later in para 64.

59. It is important to note that the claims that have been made forcapital-intensification generally concern an ongoing process, not a developmentthat has yet to manifest itself. Already in 1965 Modern Cotton Industry wasable to say that capital-intensification was "practically complete in theUnited States and Japan, but still slowly proceeding in Europe". 1/

Factor-Intensity Reversal: The Evidence of Census Data

60. It is proposed once more to use value added per employee figures,on this occasion over time, ds a measure of changes in capital-intensity onthe grounds that the value-added figure represents the best availableapproximation to the services of physical and human capital. The reservationswhich qualify these figures should be recalled. Moraover, with copa2risonover time there is an additional problem >f distortions from cyclicalfluctuations but the fluctuations in valut. added would not seem to be sogreat as to seriously impair the vLlue Of the figures. 2/

61. The data is limited to the same census figures as those used forthe static picture of comparative advantage. in view of the claim of themid-1960s that the capital-intensification of the industry was almost completein the U.S. and since the U.S. has the highest ratio of wage to capitalcosts in the world, the U.S. data is amongst the most important from industrializedcountries. Canada is also a very high wage country. The U.K. is a lower-wagecountry with a less rationalized cotton industry and, since big efforts havebeen made in the 1960s to rationalize, any capital-intensification may tendto reflect this to some degree. Whilst the U.K. and Canada are relativelyliberal importers from low-cost sources, the U.S. is in a middling position.It is difficult to say how levels of protection might affect capital-intensification: whilst it might be thought that low levels of protectionwere a spur to capital-intensification and high levels precluded the need forcapital intensification, the cotton industry has tended to argue the oppositeeffect. 3/

62. Table 1, giving broad information froa 12 countries, shows almostno discernible trends towards mounting capital-intensity in spinning, weaving,finishing, except in the case of the U.S. and Canada. This is generally true

1/ O.E.C.D. op.cit.

2/ Tne U.S. and Canadian data suggest that, in years where the cotton industry'sbusiness cycle is at odds with that of industry in general, value addedper employee is not distorted by more than about 5 percentage points.For the U.K. all the censuses since 195L have reflected comparable, goodtrading conditions in textiles and in all manufacturing except for 1958when cwparable, bad conditions prevailed for both.

3/ I cora.rable census time series were available for some of the moreprotectionist European countr:es, this point could be better pursued.It is 'tcrn up again in para 107.

- 27 -

of clothing too. The more detailed country tables 'Tables 2 to 5) are moredifficult to interpret: while there has been no ma.or capital-intensification,there may have been some minor cases or indeed incipient trends.

63. In the case of the U.K. there seems to have been a substantialupward movement in value added per employee in cotton spinning in the fouryears preceding 1968, but there is not a marked upward trend elsewhere. l/In the U.S. there is no clear trend towards capital-intensity jxcept, takenover the whole period, in yarn mi]ls. However, at the very end of theperiod there is an upward movement in synthetic weaving and finishing whichmay constitute a trend. On the other hand this movement may simply be eithercyclicai, or, inasmuch as it corresponds to a downward trend In cottonweaving and finishing, might betoken short-term gains (i.e. higher profits)in synthetics at the expense of cott.on due lo the recent U.S. boom insynthetic fiber fabrics. In all three countries the figures suggest thatduring the late 1950s the cotton industry rell in the faotor intensity"league" compared to its position in the early 1950s and that it capital-intensified relatively until about the early 1960s to regain its earlierposition and has since hardly moved up the league. The clothing industry bycontrast has tended to show a consistently declining position in the "league"from the early 1950s onwards. 2/

6l. The vague indications of the "curve" in the cotton industrymentioned above ta-.y to some extent with investment data. Investment peremployee has had (as noted in para 58) a tendenny to move towards the averagefor manufacturing by the mid 1960s. This may correspond to the cottonindustry's recovery of earlier levels of capital-intensity. It wculd seemin this case that large increases in investment per employee (when expressedin terms of the average for manufacturing) are associated with small increasesin capital-intensity.

65. In summar4- capital-intensificatior in the cotton industry is farfrom proven. If the phenomenon exists, it is certainly not as far advancedas the OECD maintained in 1965 (see para 59) and there can as yet be no talkof actual factor-intensity reversal: only in the case of Canadian synthetictextile mills does spinning and iuenving approach the average value added peremployee for all manufacturing. Factor-intensity reversal would seem at

1/ The large lump in U.K spinning value added per employee may he partlyaccounted for by the fact that Minimum List Heading U12 (Spinning anddoubling in the cotton and flax system) includes the treatment of continuousfilament yarn (texturizing and bulking, etc.) which has by far the highestlevels of value added per employee and is by r;: the fastest growingsub-division in MLH 412.

2/ The cotton industry has usually maintained that technical change in theindustry was labor saving in the sense that the share Of labor in totalcosts was diminishing. The evidence of value added doe's not support this.There has been some small reduction over time of wage value added intotal value added but this has hardly differed from a similar trend inall man-afactures.

best to be an incipiunt phenomenon 1/ and the next two sections will atteMp.to examine whether this is so, firsTly l,hrough d more qualitative approachto rapital-intensification and the industry's expectations of it and secondlyby presenting some evidenee on future coat: from Cotton and Allied Textiles.