Investor First Name Investor Middle Name Investor Last Name ...

ARTICLE IN PRESS

0301-4215/$ - se

doi:10.1016/j.en

�Tel.: +31-5

E-mail addr

Energy Policy 34 (2006) 461–480

www.elsevier.com/locate/enpol

Support systems for the diffusion of renewable energy technologies—an investor perspective

Valentina Dinica�

Center for Clean Technology and Environmental Policy, University of Twente, P.O. Box 217, 7500 AE, Enschede, The Netherlands

Available online 10 August 2004

Abstract

Concern over climate change impacts and the projected depletion of fossil fuels has urged more governments to adopt policies that

stimulate the diffusion of renewable energy technologies (RET). With an increasingly diverse suite of support instruments, the

question emerges as to which instruments or combinations are able to achieve faster, more substantial diffusion results. Although

various support instruments were extensively addressed in policy studies, there is still no consensus. This is partly because many

policy studies take a policy-maker approach in comparing support instruments, leaving relationships between policy design and

policy results as a black box. This paper proposes an investor-oriented perspective to analyze the diffusion potential of support

systems for RET. The main argument is that it is not the type of support instrument but rather its risk/profitability characteristics

that influence investor behavior and the rate of diffusion. The two instruments most frequently discussed and compared are the feed-

in-tariff and the quota model. The analysis in this paper concludes that policy design is crucial: while often feed-in tariffs are

applauded and quota system feared, feed-in tariffs may also bring about disappointing diffusion results when poorly designed while

quota systems may be also conceived as attractive instruments for independent power producers.

r 2004 Elsevier Ltd. All rights reserved.

Keywords: Renewable energy technologies; Diffusion; Policy risks

1. Introduction

The use of renewable energy resources for electricitygeneration has many advantages compared to fossil fuelor nuclear energy. Renewable resources are indigenous,no/low cost and contribute to the diversification of theenergy resource basis. This significantly increases thesecurity of supply, taking into account the political risksand expected depletion of fossil fuel. Additionally,renewable energy resources reduce environmental andhuman health impacts and are the only types of energycurrently available that respond to the compellingchallenge of sustainable development.

However, currently, the generation of electricity basedon renewable energy technologies (RET) is more

e front matter r 2004 Elsevier Ltd. All rights reserved.

pol.2004.06.014

3-489-4171; fax: +31-53-489-4850.

ess: [email protected] (V. Dinica).

expensive than the conventional technologies usingfossil fuels, large hydropower and nuclear energy. Thereare three main groups of reasons on which the economicand financing obstacles rest. Firstly, the methods usedfor the cost assessment of energy projects are inap-propriate. Awerbuch (1996, 2003a) argues that theaccounting and financial assessment methods used bytraditional engineering economics for electricity projectsare outdated, making renewable energy technologyprojects appear more expensive. The use of standardfinance models accounting would produce differentresults. Engineers and planners use arbitrary discountrates for fuel costs and operating expenses in calculatingthe levelized electricity generating costs, while not takinginto account the financial risks associated with the costsof electricity projects (Awerbuch, 2003a), leading to asystematic overestimation of the costs of renewable-based electricity. Awerbuch (2003b) estimates that usingmarket risk adjusted textbook finance theories results in

ARTICLE IN PRESSV. Dinica / Energy Policy 34 (2006) 461–480462

generation costs for gas-based generation plants in therange of 60–100% higher than currently considered. Heargues that risk-based methods based on the CapitalAsset Pricing Model would produce more realistic costassessments for RET for electricity generation (RET-E),with the consequence of reducing or even eliminating theeconomic obstacle. Another reason why RET-E appearmore expensive is suggested by Wright (2002), arguingthat that for conventional electricity technologies ‘‘theadditional infrastructure costs required for large con-ventional power projects such as transmission anddistribution lines, and pipeline infrastructure for naturalgas, is often not factored into the overall costs’’.However, they are always included in total investmentcosts per kW for RET-E.

Secondly, the failure to internalize the external costsof electricity generation from conventional technologiesis largely responsible for the persistence of the costdifference with RET. The costs of the environmentaland human health impacts of fossil-based and nucleartechnologies are not reflected in the electricity produc-tion costs. There are serious methodological difficultiesin establishing full range and scale of consequences offossil fuels and nuclear energy use. Thirdly, fossil-based,nuclear and large hydropower technologies have beenheavily subsidized for decades. In spite of the privatiza-tion and/or liberalization of electricity industries inmany industrialized countries, fuel subsidies from publicbudgets or from consumers’ bills are still maintained.With the liberalization of electricity industries duringthe 1990s in many industrialized countries, the electricityprice has lowered and is expected to continue to decreasein short-term. This raises the magnitude of the economicobstacle for RET-E. However, governments in manycountries are still interested to support RET-E, in viewof the many benefits it clearly brings in electricityproduction.

However, countries differ both in their levels ofambition for the greening of electricity supply and theirpreferences for support schemes. In the EuropeanUnion, these differences were reflected in the debatepreceding the adoption of the 77/2001 Directive onRenewable Electricity. After years of dialogue, MemberStates could not agree on a common framework forRET support (Lauber, 2002). The 77/2001 Directivestated that due to limited experience with nationalschemes, it would be premature to decide on aCommunity-wide framework regarding supportschemes. The European Council decided to assess thediffusion results of national support schemes at the endof 2005 and eventually propose a common framework.In this context, assessment of RET-E installed capacitypotential represented by various support systems has re-emerged as an important question at the top of theagendas of researchers and policy-makers. This paperaddresses this crucial issue.

This paper argues that current analyses in thepolicy literature of the diffusion potential of varioustypes of support instruments have some short-comings. The description and analysis of supportsystems is not sufficiently helpful for understandingthe consequences for the extent of diffusion. Classifica-tions and analyses of support instruments’ character-istics are mainly made from the perspective ofpolicy-makers. The way financial aspects of supportsystems are described is also not sufficiently suggestivewith regard to attracting potential investors. Policy-makers, analysts and advisers should be askingquestions such as: To what extent are policy instrumentsable to unlock the financial resources of potentialinvestors? Would investors be confident enough tocommission larger plants and elaborate long-terminvestment strategies, which aggregate at industry levelsto create prospects for targeted increases in renewableenergy capacity? Would they rather invest strategicallyin small-size power plants and/or in projects using old-and-tested design technologies, leading to more incre-mental progress in the greening of electricity supply?The paper proposes a different way of analyzinggovernmental support for the market introduction anddiffusion of RET-E, addressing economic and financingbarriers of such technologies. Taking an investorperspective on the analysis of support systems con-tributes to the academic discussion as it helps open theblack box between policy design and policy results. Italso enables policy-makers to perform ex ante analysisof the diffusion potential of policy proposals for RET-Esupport frameworks.

The paper starts with a discussion in Section 2 ofthe analytical perspectives currently dominatingstudies on the diffusion potential of policy instrumentsthat address the economic and financing obstaclesof renewable energy production. In Section 3, I presenta policy analysis approach that uses investors asthe central unit of analysis for diffusion potential.This consists of a combined assessment of the risks facedby investors under the applicable support systems, andthe profitability potential for investments in RET-Eprojects.

Section 4 may be regarded as central to this paper:here I suggest a framework for the risk analysis ofsupport systems. The profitability of investments is avariable that may be straightforwardly assessed withmethods available in economics. The issue of riskassessment is more challenging. This section suggests acode for translating policy language into investorlanguage. In Section 5, I explain the assertion that theanalysis of support instruments from the risk–profit-ability perspective is more fruitful in understanding thechances and rhythm of installed capacity growth ofRET-E. Section 6 concludes this paper with a series ofpolicy recommendations.

ARTICLE IN PRESS

1The report Financing Renewable Energy Systems studied the

financing of five renewable technologies—solar thermal, photovoltaic,

wind, hydropower and biomass systems—in Austria, Denmark,

Germany, Italy, the Netherlands, Spain, Sweden and the United

Kingdom (Langniss, 1999).

V. Dinica / Energy Policy 34 (2006) 461–480 463

2. Configurations of support systems and approaches in

analyzing them

In this paper, I define ‘support system’ as the entirecollection of support instruments applicable to enablethe market introduction and continuous diffusion ofRET-E. This takes place in a certain setting—usually acountry—at a certain time, for the removal of two typesof barriers facing RET-E: the economic barrier (or‘expensiveness’) and financing barriers (or the difficultyof obtaining project finance loans or the interest ofequity investors). A support system may consist of asingle support instrument (e.g. a production subsidy),but most often a support system is made up of severalinstruments. Support systems are often dynamic, asgovernments phase-in and out various instruments dueto changing goals, learning effects or budgetaryconsiderations.

Governments in industrialized countries used a largevariety of support instruments during the 1980s and the1990s to stimulate the adoption of RET-E. Thediversification of instruments increased since the mid-1990s, mainly as result of electricity industries’ liberal-ization and the national policies for climate changemitigation. Configuration diversity poses a significantchallenge for policy analysts, especially regarding theapproach when describing support systems used indifferent countries and/or in different periods of time.While in many cases support systems often have in theirconfiguration a prominent instrument that can beviewed as the backbone of the support system, in somecases an array of support instruments is used, theinteraction of which alters the incentive framework toinvest in RET compared to an incentive embedded inthe ‘core’ instrument alone. So far, researchers andmarket/policy analysts describing or evaluating supportsystems for RET-T implemented in various countrieshave used very different ways of describing andcategorizing them (for a detailed typology see Dinica,2003, pp. 19–33; also Ackermann et al., 2001). One ofthe most frequently used typologies is that differentiat-ing between price-based models—or feed-in-tariffs,versus quota/quantity models of support (e.g. Haaset al., 2004; Hvelplund, 2001; Menanteau et al., 2003;Lauber, 2004; Meyer, 2003; Huber et al., 2002;ECN, 2002b).

Two important comments need to be made regardingmost currently used policy analysis approaches andtypologies. First, they do not incorporate the aspect ofthe extent of financial support offered by the supportinstruments or the configurations of support systemsclassified as such. The extent of price support is at leastequally important for investors as the type of instrumentit comes from. Details on the extent of financial supportare present in numerous country surveys on renewablespolicy and market results. They look at the prices per

kWh guarantees or price ranges possible under thesupport instruments described, as well as at thepercentages of investment subsidies and/or tax reductionapplicable to groups of project owners or types of RET-E plants. But since the quality, availability anddistribution of renewable resources differ among coun-tries, these indicators are not satisfactory in assessingand comparing the extent of financial support indifferent countries. Two countries may offer the sameprice support for a certain type of RET-E. However, dueto differences in the quality of resources—and often alsodifferences in the institutional context with conse-quences for financing and permitting/administrativecosts—the production costs incurred by RET-E gen-erators may be largely different. This would result indifferent diffusion patterns with consequences for thediffusion results in the two countries with the sameextent of price support. It would be more desirable toanalyze the extent of financial support with the help ofan indicator that dispenses of the cost impacts of somany exogenous factors.

Second, there is the issue of risks facing RET-Einvestors, and the relationship between risks andreturns. There is one stream of the policy literature,which addresses—to various extends—the issue of thefinancial risks induced by specific types of supportinstruments (e.g. Lemming, 2003; Rader and Wiser,1999; Wiser and Pickle, 1997; Helm, 2002; Kahn, 1996;Menanteau et al., 2003; KPMG, 1999; Langniss, 1999;Harris and Navarro, 2000; Mitchell, 1994). Many ofthem refer to the risk premiums for project financeloans, attracted by instruments that pose high risks inRET-E projects. However, only rarely do analyseselaborate further on the consequences of supportinstrument’ risks for the investment behavior of devel-opers. Mostly the issue of likelihood of market entry isaddressed, while some studies refer also to the type ofeconomic actors likely to enter the market. Similarly, thetheoretical expectations regarding (changes in) diffusionpotential are vague, whenever considered. Studies thatlooked at and compared the diffusion potential of feed-in and quota models have done so mainly empirically.

Several studies have looked into the issue ofconsequences of various types of risks and levels ofreturn for the diffusion patterns of RET-E. A prominentexample is a research project analyzing the prevailingfinancing schemes, constraints and financing parametersof renewable energy projects in eight European coun-tries, which also looked in the empirical case studies atthe motivation driving project owners (Langniss, 1999).1

ARTICLE IN PRESSV. Dinica / Energy Policy 34 (2006) 461–480464

The study proposes a typology of financing schemesdifferentiating between private finance, corporate fi-nance, project finance, participation finance and third-party finance. In describing the key features of each typeof financing scheme and the main findings regardingtheir use in the eight countries, the report also mentionsthe (range of) motivations that developers using eachfinancing scheme are likely to have. This way, invest-ments were observed to be ‘‘not economical in businessterms’’ or having ‘‘an appearance of environmentalconcern and public acceptability’’, ideologically moti-vated or fostering RET-E through track-record build-ing. This research project highlights empirical findingsregarding the relation between types of financingschemes, project sizes in terms of total investment costsper project, and the legal ownership form of project. Asimilarly interesting study was carried out by Mitchell(1994), who analyses the types of financing schemes,types of project developers and project sizes (also interms of total investment costs) for the United Kingdomunder the first two rounds of the Non-Fossil FuelObligation. A quite similar approach but with a less in-depth treatment was taken in the study in supportinstruments and financing mechanisms of the EnergyTechnology Support Unit of the British Department ofTrade and Industry (ETSU, 1996), covering 24 coun-tries. Such approaches are very fruitful in developinginsights into the likely diffusion potential of varioussupport instruments.

This brings into discussion a second stream of theliterature that contributes to the study of RET-Ediffusion: a series of financial-economics studies regard-ing investment options and strategies for energyprojects. For them the unit of analysis is generally nota support instrument or a particular regulatory frame-work, but an energy project/technology, seen in themany dimensions of the context in which it is developed.Some studies regard energy projects in general (e.g.Hines, 1997; Islas and Jeronimo, 2001; Jechoutek andLamech, 1995; Bond and Carter, 1995; Dunkerley, 1995;Churchill, 1995; David and Wong, 1994), while othersrefer to RET-E projects in particular (e.g. Welp andSchimana, 2002; Awerbuch, 2000, 2003a; Ingersoll et al.,1998; Gish, 1999; Mendis, 1997; Gregory, 1997;Langniss, 1999). They address the financial risks forRET-E projects in general, that is beyond the risksassociated with support instrument(s), and offer pre-cious insight into how investors and project developersanalyze the risks associated with different investmentstrategies. For example, Awerbuch (2000) discusses therisks and costs of investing in photovoltaics and howinvestors make decisions on technology choice andproject size (by means of loan size), as compared toother investment opportunities in the energy field orother fields. He brings to attention the fact that thecurrent use by investors and lenders of traditional

energy valuation models undervalue photovoltaic tech-nology. This technology and other RET-E are capitalintensive but they pose lower risks on costs than fossilfuels. He encourages lenders and investors to use aportfolio cost approach in assessing technology andproject options. This way ‘‘PV, which ‘costs more’ servesto reduce the cost of a fossil-generating portfolio at anygiven level of risk’’ (Awerbuch, 2000, p. 1026).

Merging the insights from the economic-financingstream of the literature with those developed in thepolicy literature stream would be most beneficial forunderstanding what underlies diffusion results and howcould governments design and fine-tune comprehensivepolicy packages—addressing the wide range of obstaclesto RET-E, to support the sustained adoption of RET-Eamong investors.

3. A risk–profitability approach to analyze support

systems

The investment behavior of project developers and theattitude of financing agents toward RET-E investmentsare to large extent shaped by the risks on projects’returns. But they are also influenced by the profitabilityof projects. As most RET-E are more expensive thanconventional electricity generation systems they have tocompete with—due to reasons discussed in Section 1,support instruments are used to enable investments.These should be able to at least cover the cost-gaps, andallow developers to yield some profit on their invest-ment. I propose to describe and analyze the supportsystems addressing the economic and financing barriersof RET-E adoption in terms of two characteristics:

�

aggregated risks on the economic feasibility andprofitability of RET-E projects emerging from thesupport instruments used and their interaction, and�

range of project profitability that emerges from allsupport instruments that investors are eligible to usefor the production of RET-E electricity, next to theeventual income from marketing the generatedelectricity on the market.This approach also has the advantage of parsimony,keeping in mind the diversity and complexity of supportsystems encountered in practice, as well as the countlessconfigurations that could be conceived through thecombination of support instruments.

The choice to characterize support systems in terms oflevel of risks for the economic feasibility and profit-ability of RET-E projects is motivated by the impor-tance of knowing what types of economic actors asupport system is likely to attract and whether tradi-tional financing agents in the country in question wouldbe willing to support the sustained diffusion of RET-E.

ARTICLE IN PRESS

3‘‘Equity’’ is a term used in financing literature to refer to the cash

payments made by project developers, while ‘loan’ or ‘debt’ are the

terms referred for the payments made by financing agents—commer-

cial banks, saving banks/funds, pension funds, insurance companies.

This does not exclude financing agents providing equity to finance

projects.4In addition to the internal rate of return on projects, both

theoretical and empirical studies discuss the internal rate of return

for equity investors. In order to avoid confusion, we use the terms

V. Dinica / Energy Policy 34 (2006) 461–480 465

Different types of economic actors have differentrequirements with regard to risk on project returns.Some are more flexible than others, but higher riskinvestment contexts require higher profits. Traditionalfinancing agents—such as commercial banks, pensionfunds, saving funds and so on—also have specific risklevel requirements. Generally they tend to be more riskadverse than project developers.

Support instruments could, intently or not, pose riskson project returns, which could discourage certain typesof economic and financing actors from the business ofRET-E electricity production. But risks on projectreturns are also influenced by other variables as well.Guidelines and empirical literature for power plantinvestment advise developers of electricity generationprojects to carefully scrutinize the following types ofrisks before taking the decision to invest: resourcequality, availability and cost risks, technology risks,construction risks, planning approval risks, environ-mental impact risks (i.e. impacts or pollution beyondthat permitted by competent authorities), interest raterisks, currency exchange risks, operation risks, institu-tional and other regulatory risks2 (Ingersoll et al., 1998;Pollio, 1998; Bond and Carter, 1995; Hines, 1997,pp. 189–209; Welp and Schimana, 2002; Jechoutekand Lamech, 1995; Rose et al., 1997; Islas andJeronimo, 2001).

Financing agents look at a range of risks thatencompasses that of project developers. This rangeincludes the credit worthiness of project developers,to the extent to which their financial reserves andmarket-valuable assets are sufficient for the reimburse-ment of loans when project returns decrease belowthe limit of economic viability. In addition to projectrisks and company characteristics, financing agentsalso look at industry characteristics such asindustry structure, economics, maturity and stability(Finnerty, 1996). Industry characteristics also influenceboth the timing of project developers to enter themarket and its detailed investment plans. Although theexistence and reliability of a contract for electricitypurchase and price risks are at the core of the investmentdecisions, these other risks and considerations men-tioned significantly influence the decision to invest andthe particularities of project development plans. I arguethat support system risks are important bridges avail-able for understanding the relationship between supportsystem design and investors’ decisions to finance RET-Eprojects.

Regarding the second characteristic—the range ofprojects’ profitability—its selection is motivated by theneed to measure the extent of financial backing offered

2In this category, Langniss (1999) mention among others: generally

applicable tax regulations, environmental, economic and energy

policies, aspects of administrative culture.

by support systems. With this, comparisons can be madebetween countries and, even at the same time, acrosstypes of renewable technologies. This characteristicoffers a second bridge between the design of supportsystems and investors’ decisions to finance RET-Eprojects. This indicator is suggestive for the attractive-ness of support systems for project developers andfinancing agents. Project profitability is an economicindicator for power plants that incorporates both theinterest rate required by the financing agent (when loansare used) and the profits of project owners/developers,referred to in the financing literature as returns onequity.3

I label ‘project profitability’ what in the financing andeconomic literature is often referred to as the ‘internalrate of return’ of projects.4 Projects’ returns have toallow for the payment of debt to the financing agent, therecovery of equity investments by project developer/owner, the payment of operation and maintenance costs,fuel costs (when necessary), taxes and other fees such asland rents and insurance. They also have to allow for thepayment of interest rates on debt to financing agents andfor equity returns to project owners. These last twovariables constitute the basis for calculating project’sprofitability in the form of a rate.5 Very roughly therelationship between project returns and project gainscan be represented as below.

project returns ¼ ðdebt reimbursement payments

þ equity recovery paymentÞ

ðþoperating=maintenance costs

þ fuel costsþ taxes

þ other regular fees=expensesÞ

þ project gains: (1)

Project gains are understood here as representing thesum of the total amount to be paid in the form ofinterest rates to loan financiers and the total amount tobe paid in the form of equity returns to the equityinvestors of the project.

project gains ¼ total amount paid as interest rate

þ total amount paid as returns on equity: (2)

‘project profitability’ and ‘equity returns’.5See Hadley et al. (1993) for a more detailed discussion on

profitability with specifications for renewable power investments in

the USA by different types of economic actors, with different tax

obligations.

ARTICLE IN PRESSV. Dinica / Energy Policy 34 (2006) 461–480466

By arranging different types of financing schemes,project developers may end up with different possiblelevels of project gains. Project profitability is not anamount but a rate. In the financial structure of theproject, loan will contribute with a share of Y% onwhich the loan financier requires a certain interest rate,and equity will contribute with a share of Z% of totalproject costs on which investors will require a certainequity return. When no bank loans are used to financethe project (Z ¼ 100%), then the project profitability isthe same with the return on equity, since the projectowner is the only financing agent. Simply stated

project profitability ¼ ½Y% of total project costs�

�½interest rate in %�

þ ½Z% of total project costs�

�½equity returns in %� ð%Þ: (3)

The financial structure of projects, the interest ratelevel and the equity returns requirement are stronglyinfluenced by the risks to which the RET-E project isexposed, including risks associated with the supportsystem.

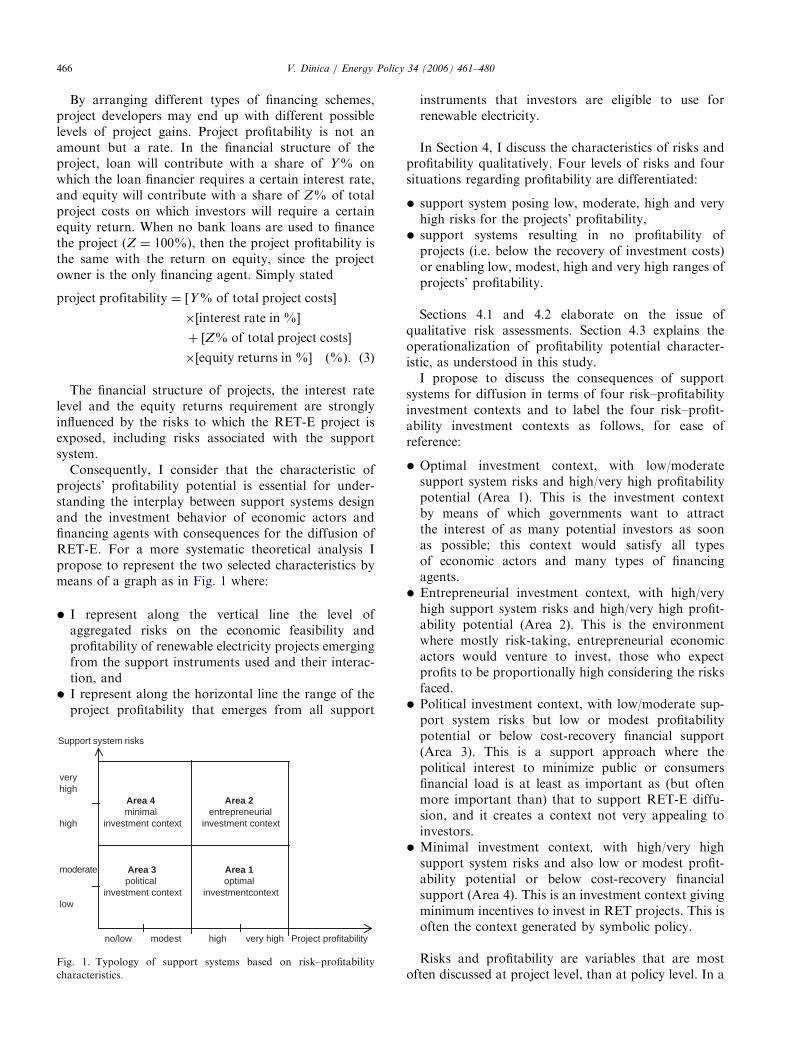

Consequently, I consider that the characteristic ofprojects’ profitability potential is essential for under-standing the interplay between support systems designand the investment behavior of economic actors andfinancing agents with consequences for the diffusion ofRET-E. For a more systematic theoretical analysis Ipropose to represent the two selected characteristics bymeans of a graph as in Fig. 1 where:

�

Su

vehi

hi

m

lo

Fig

ch

I represent along the vertical line the level ofaggregated risks on the economic feasibility andprofitability of renewable electricity projects emergingfrom the support instruments used and their interac-tion, and

�

I represent along the horizontal line the range of theproject profitability that emerges from all supportpport system risks

rygh

Area 4 Area 2minimal entrepreneurial

gh investment context investment context

oderate Area 3 Area 1political optimal

investment context investmentcontextw

no/low modest high very high Project profitability

. 1. Typology of support systems based on risk–profitability

aracteristics.

instruments that investors are eligible to use forrenewable electricity.

In Section 4, I discuss the characteristics of risks andprofitability qualitatively. Four levels of risks and foursituations regarding profitability are differentiated:

�

support system posing low, moderate, high and veryhigh risks for the projects’ profitability,�

support systems resulting in no profitability ofprojects (i.e. below the recovery of investment costs)or enabling low, modest, high and very high ranges ofprojects’ profitability.Sections 4.1 and 4.2 elaborate on the issue ofqualitative risk assessments. Section 4.3 explains theoperationalization of profitability potential character-istic, as understood in this study.

I propose to discuss the consequences of supportsystems for diffusion in terms of four risk–profitabilityinvestment contexts and to label the four risk–profit-ability investment contexts as follows, for ease ofreference:

�

Optimal investment context, with low/moderatesupport system risks and high/very high profitabilitypotential (Area 1). This is the investment contextby means of which governments want to attractthe interest of as many potential investors as soonas possible; this context would satisfy all typesof economic actors and many types of financingagents.�

Entrepreneurial investment context, with high/veryhigh support system risks and high/very high profit-ability potential (Area 2). This is the environmentwhere mostly risk-taking, entrepreneurial economicactors would venture to invest, those who expectprofits to be proportionally high considering the risksfaced.�

Political investment context, with low/moderate sup-port system risks but low or modest profitabilitypotential or below cost-recovery financial support(Area 3). This is a support approach where thepolitical interest to minimize public or consumersfinancial load is at least as important as (but oftenmore important than) that to support RET-E diffu-sion, and it creates a context not very appealing toinvestors.�

Minimal investment context, with high/very highsupport system risks and also low or modest profit-ability potential or below cost-recovery financialsupport (Area 4). This is an investment context givingminimum incentives to invest in RET projects. This isoften the context generated by symbolic policy.Risks and profitability are variables that are mostoften discussed at project level, than at policy level. In a

ARTICLE IN PRESSV. Dinica / Energy Policy 34 (2006) 461–480 467

certain national investment context, individual projectsmay be able to yield different levels of profitability (e.g.due to differences resource quality, permitting costs, inthe financing arrangements such as interest rates anddebt-to-equity ratio), while the specific aspects sur-rounding a project (such as resource environmentalregulations, technological design used, etc.) may exposeprojects to different overall investment risks. The policyanalysis approach proposed here acknowledges thatsome individual projects may have substantial differ-ences in risk–profitability profiles. Nevertheless, itmaintains that at national level it could be able to tracea range of investment risks associated with the supportsystem and a range of project profitability that arerepresentative for the majority of projects commissionedand/or potential investors.

Support system risk is one of the many types ofrisks investors take into account when deciding theextent of their (financial) commitment to the RET-Eindustry and the particularities of their investmentplans—project size, nature of projects: strategic/commercial/self-generation, choice of technologicaldesign innovativeness and type of financing scheme.However, there are indications in empirical studiesdocumenting investment decisions—available in thespecialized national and international (renewable)energy journals—that both instrument risks and theextent of price support hold powerful explanatorypower for the diffusion patterns and results. Section 4proposes a framework for the analysis of risksassociated with the support instruments used toencourage RET-E adoption.

6The label ‘strategic instruments’ is used here simply to refer to all

policy instruments that are not included in the direct arrangements for

the trade of electricity from renewable energy resources—meant as

physical streams of electricity and/or the ‘greenness’ of RET-E by

means of tradable green certificates. These instruments can have

consequences for trade patterns and power purchase price indirectly by

means of: direct financial support, improving the accessibility to

financing resources and/or improving the market position of RET-E.

However, it is analytically very useful to differentiate between two

components of support systems, as done in Table 1, in order to more

systematically investigate where the various types of risks on investors,

where they originate and how they interact. The labels themselves are

here not as important as the purpose they serve for analysis.

4. Analysis of support system from the risk perspective

This section proposes a framework for the analysis ofthe risks for investors, emerging from the design ofsupport systems. Support systems pose risks to inves-tors, which are ultimately political risks, in thatinstruments or their details could change duringprojects’ economic lifetime, lowering the profitabilitypotential, or making them no longer economicallyfeasible. But to some extent they can be also marketrisks when certain price or trade aspects are left fornegotiations between buyers and sellers of RET-Eelectricity. I adopt the view on risks of Megill (1988),who argues that risk refers to an opportunity of loss.From the perspective of support systems, risks can beseen as the likelihood of not getting a certain targetedprofitability on projects. Under the theoretical assump-tion that no other risks affect the project except forthose associated with the support system, the overallpossibility of failing to receive the targeted projectprofitability for a RET-E project could be qualitativelydescribed as outcome of a series of possibilities, each

representing a design element in the support system. Forexample:

�

the possibility of failing to ensure demand for RET-Eelectricity purchase;�

the possibility of failing to have the purchase contractrenewed, or to find contracts on the free market at all,when no governmental guarantee on demand isoffered;�

the possibility that the price per kWh in the tradearrangements will change (more than expected at themoment of investment);�

the possibility that the application of each (addi-tional) support instrument—next to the protectedtrade arrangements—will be prematurely terminatedor substantially reduce the financial support offered.The overall chance of success for a project can be thenapproximated as the product of the underlying negativepossibilities taken into account.

I propose to analyze support systems’ risks bydistinguishing between the trade component and thestrategic-instruments component6 of support systems.The elements proposed for the analysis of the twocomponents are shown in Table 1. The trade componentrefers to the forms of support that directly concern tradearrangements for RET-E electricity or tradable greencertificates (TGCs). Trade could rely on governmentallyguaranteed demand for RET-E electricity. In this case,regulations are usually rooted in the legal framework forthe organization and functioning of the electricitysector—the electricity law and/or accompanying gov-ernmental or ministerial regulations. The regulatoryframework specifies one or more of the followingelements: how much electricity will be purchased fromeach RET-E generator and/or at company level and/orindustry level, for how long, at what prices, and how theprices are calculated and changed. The availability andtype of governmentally guaranteed purchase of RET-Eelectricity, the availability of a contract for electricitypurchase, the length and reliability of that contract(whenever contracts are also regulated), as well as thepredictability and reliability of the price for purchase areall crucial factors for the decision of economic and

ARTICLE IN PRESS

Table 1

Risk analysis of support systems

Trade arrangements

Elements Characteristics/forms

Type of demand for purchase of RET-E electricity Guaranteed purchase for individual RET-E plants:

Unlimited purchase

Limited purchase

Quota purchase at industry level. Trade flexibility:

With tradable green certificates

Without tradable green certificates

Contractual relations for ‘Guaranteed purchase for individual RET-E

plants’

Contract duration

Availability of options for extension of purchase after termination of

contract

Quantity

Price design for ‘Guaranteed purchase for individual RET-E plants’ Price components

Method of price calculation

Price types

Decisions mechanism

Strategic instruments

Target Types

Direct financial/price support Investment subsidies

Production subsidies

Direct fiscal incentives

Financing accessibility Soft loans

Governmental guarantee on project loan

Project aggregation programs

Third party financing

Improved market position Indirect fiscal incentives

V. Dinica / Energy Policy 34 (2006) 461–480468

financing actors to invest in RET-E projects. I proposeto describe trade arrangements in terms of threeelements: type of demand, contractual parameters, whenalso part of instrument design, and price. The analysis ofthe forms of these elements leads to the assessment ofdemand risks, contract risks and price risks associatedwith trade arrangements. Together they form the traderisks of the support system.

The ‘strategic-instruments’ component of supportsystems may include instruments such as those men-tioned in Table 1. They refer to the forms of interventionthat:

�

improve the economics of RET-E projects; instru-ments such as, investment subsidies, productionsubsidies not incorporated in trade arrangements,and direct fiscal incentives, could be introduced eitherin parallel with some form of governmentallyguaranteed trade arrangement for RET-E electricity,or as unique instruments to enable the profitability ofRET-E projects;�

contribute directly to the reduction of financingbarriers; such instruments are soft loan schemes,governmental guarantees on project loans, third-party financing by a public agency, project ag-gregation programs whereby the government pro-cures a large loan that is subsequently dividedamong small investors; further, instruments can beused that;

�

improve the market position of RET-E, in terms ofinvestors and/or consumer choice between renewableand conventional energy technologies; examples hereare the indirect fiscal incentives such as electricityconsumption taxes, or taxes on the carbon content ofenergy resources.4.1. Design of governmentally supported trade

arrangements

4.1.1. Types of demand and demand risks

I differentiate among two commonly used typesof demand for RET-E electricity purchase, fromthe perspective of potential investors, as mentioned inTable 1. The first type is that of governmentally

guaranteed purchase for individual RET-E plants.This can be designed in the forms of unlimited purchaseguarantee or limited purchase guarantee. In thefirst case, regulations oblige electricity companies tobuy RET-E electricity from any generator locatedin its region of licensed operation. The purchaseobligation holds for unlimited amounts of electricityproduced by eligible RET-E plants. When such a

ARTICLE IN PRESS

7For an interesting analysis of contractual prices and price risks see

Comnes et al. (1995, pp. 15–28).

V. Dinica / Energy Policy 34 (2006) 461–480 469

type of demand is guaranteed in the law, demand risksare low.

The limited purchase guarantee for individual RET-Eplants can be implemented as an obligation to buy onlya limited volume of electricity from each generationplant (e.g. the electricity produced in the first 20,000hours of plant operation). Investments under this typeof demand are attractive mainly for the types ofdevelopers, technologies and sites where the costs andrequired profitability can be recovered through theelectricity volumes with a guaranteed purchase. Anotherscheme that has been used is to guarantee RET-Eelectricity purchase for a specified contract duration, forexample 8 years as it was practiced in Italy based onLaw No. 9/91 of January 1991 jointly with CIPProvision No. 6/92 of April 1992, or 5 years as it hasbeen so far in Spain based on Royal Decrees 2366/1994and 2818/1998. Under this type of demand, the analysisof demand risks basically merges with the analysis ofcontract risks (see below). For technologies usingintermittent resources, the risks under such type ofguarantee may be higher, the shorter contracts arebecause of the possibility of insufficient electricityproduction during the respective period to recover theinvestment costs. This is due to poor predictability ofsome intermittent sources (such as wind and small-hydropower resources). Consequently, there is the riskthat project returns received on the base of thesecontracts cannot cover investment costs, variable costsand still ensure minimum levels of profitability in theperiod available. However, under both forms of limitedpurchase guarantee it is possible that after the termina-tion of the guaranteed purchase, even if returns lower,projects still have an overall profitability that satisfiesthe owners.

The second type of demand is very different from theprevious ones and refers to quota purchase guarantee atindustry level. It assumes that certain electricitycompanies or consumers must provide evidence by acertain deadline that they bought or consumed specifiedvolumes of RET-E electricity. The quota type ofdemand is discussed in Section 4.1.2.

When governmentally guaranteed trade arrangementsoffer the type of demand ‘guaranteed purchase forindividual RET-E plants’, the assessment of contractrisks and price risks is also necessary, as proposed in thefollowing two sub-sections. Section 4.4 illustrates therisk analysis of governmentally guaranteed purchase forindividual RET-E plants’ (commonly referred to as‘feed-in-tariff’ support), in interaction with two othersupport instruments that were used in Spain.

4.1.1.1. Contract risks. The literature on power plantinvestment indicates the importance of securing a long-term and fixed-price electricity purchase contract beforethe plant is constructed (David and Wong, 1994;

Ingersoll et al., 1998; Gish, 1999; Hines, 1997; Joskow,1995; Burr, 1999; Murray, 1998; Sidak and Spulber,1998; Woo et al., 2001). The shorter the contract and/orthe more vague the legal framework referring tocontractual aspects, the higher contract risks are (Gish,1999; Hines, 1997). The core characteristics of contrac-tual relations that can be considered in analyzingcontract risks are: duration, the options for contractextension after termination, quantity; next to them thereis also the aspect of contractual purchase price whichcan be analyzed in the context of the price design as setin the legal framework.

4.1.1.2. Price risks. Price risks may come from twosources: the legal framework and from the details forcontractual purchase price. The legal framework mayallow for different degrees of freedom for buyers andsellers of RET-E electricity to set contractual prices. Thegovernment may prescribe tariffs that apply for thetrade of RET-E electricity. This may be set throughunilateral decision by the government or one of itsministries/agencies, or it may be taken based onconsultations with the industry. But governments mayprefer to give various kinds of guidelines for price designby contractual parties, such as the price components tobe taken into account, the frequency of price update,and set price floor and/or price ceiling that have to beobserved by buyers and sellers. As regards pricecomponents, legal provisions may for example prescribeor suggest the voluntary inclusion in contractual price ofa premium for the environmental benefits of RET-Eand/or premium for the contribution of RET-T tosecurity of supply in the system.

Price risks are related to the extent to which, and theforms in which, the following aspects are regulated: howthe price for RET-E electricity should be calculated andwhat are the included price components, whether thepurchase price should take specific levels, how often isthe price reviewed, who decides on these price aspectsand how.7 Consequently, I propose to describe the pricedesign aspect based on the following characteristics:

�

price components: prescribed, suggested, not indi-cated;�

price types: tariffs, ceilings, floors, no limits indicated; � frequency of updating: no updating, annual, severalyears;

� decision system: directive, consultation.4.1.2. Quota guaranteed purchase at industry level

This type of governmentally guaranteed trade ar-rangement can take a large variety of forms dependingon: the level in the value chain of electricity supply

ARTICLE IN PRESS

Table 2

Quota design variables for the assessment of demand risks and price risks

Assessment of demand risks Assessment of price risks

Who are the obligees, if they have the right to own renewable plants,

and if banking/borrowing is allowed

The cost-discharge mechanism; and the presence of price floors and

ceilings

Which cost-discharge mechanism applies and what is the penalty for

non-compliance

The lifetime of certificates and the frequency of compliance proof

The time horizon of the obligation/duration RET project eligibility Type of penalty for non-compliance and the destination of penalty

funds

The split of the obligation in technological bands

V. Dinica / Energy Policy 34 (2006) 461–480470

where the obligation is placed, whether obligees have theright to comply with the obligation by investing in RET-E projects or only by means of purchasing from othercompanies, and whether the obligation can be fulfilledby means of TGCs or only through the purchase ofphysical streams of electricity.

The risks for non-obligee investors under a quota typeof demand depend on the extent to which certain aspectsare addressed in the obligation design. The key designaspects and the forms they can take are mentioned inTable 2. Under quota types of demand, regulations donot cover the aspects of contractual relations becauseobligees need to have the opportunity to look for thelowest cost option of complying. Regarding pricedesign, the aim in principle is to minimize governmentalintervention. However, because investors need to have areference for the assessment of the economic viabilityand profitability of the plants they intend to build, undersome regulatory approaches certain aspects of quotaobligations are designed in such a way as to offeracceptable levels of price risks. Hence, under the quotatype of demand, investors can make assessmentsregarding only demand and price risks. I suggest thatthis is evident in the interaction of the forms of certainquota design variables in Table 2.

For the mitigation of demand and price risks, RET-Egenerators may search to conclude private contracts.Intuitively, investors are more likely to be interested inlong-term contracts, while obligees may rather beinterested in short-term contracts. But experience andresearch so far suggests that the incentives of generatorsand obligees to engage in short or long terms contractsemerge from the design of the quota obligation.8 From

8For example, the Renewable Portfolio Standard implemented in

Texas since 1999 has given the incentive of obligated electricity

suppliers to conclude many long-term contracts of 10–25 years (see

Langniss and Wiser, 2003, p. 530). However, in Italy long-term

contracts are less common, as quota design does not give obligees the

incentive for long-term fixed-price purchase, although this would have

been desired by generators. For an insightful analysis of forward

contracts, prices and financial risks for RET-E investors under the

proposed system of tradable green certificates see Lemming (2003).

Lemming (2003) argues that quota design may give incentives to RET-

E generators to avoid forward fixed-price contracts when there are

higher-return prospects for spot-market trade of certificates.

the investor standpoint: when the perceived demand ishigh, or assessed as sufficient to justify investment,power plants are also built in conditions of having onlya short-term contract, or not having a contract availableyet—i.e. having to rely on the spot exchange in powerpools. Such power plants are referred to as ‘merchantplants’. Section 4.1.3 makes a theoretical discussion fortwo example of quota design, in order to illustrate how arisk analysis could be conducted based on the approachproposed in Table 2.

4.1.3. Analysis of two possible designs of quota type of

demand at industry level

In Table 3, I proposed for illustration two configura-tions of quota obligation design and TGC systems.Variables were given forms so as to result in differentsupport risk circumstances for non-obligee investorsinterested to invest in a specific type of RET-T. Incontrast to governmentally guaranteed purchase con-tracts for individual RET-T projects, the quota type ofdemand may introduce an additional risk for investors,related to the competition among RET-T, unless thequota obligation is split per technological bands. Forboth examples the obligation assumes a gradual increasein quota level. It is assumed that for Configuration 1,RET-E projects may receive TGC during the first 10years of production.

Configuration 1 is an example low support instrumentrisks. This comes from the assessment of low demandrisks and low-modest price risks. The forms of itsvariables create a framework of demand risks that canbe assessed as low because of several reasons. Firstly,the obligees—distribution companies—cannot own gen-eration plants. As they can only be buyers of RET-Eelectricity or green certificates, potential investors arespared of the uncertainties related to the investmentstrategies versus purchase strategies of obligees torespond to their quota requirements. Similarly, theuncertainties related to the obligees strategies ofborrowing and banking are removed. Secondly, whendistributors comply with their obligations they candischarge the TGC costs on a general levy fund (madeup of levies paid by all electricity consumers), while ifthey do not comply they have to pay the average price of

ARTICLE IN PRESS

Table 3

Theoretical examples of configurations of TGC-based quota

Variables in the design of quota obligation Configuration 1 Configuration 2

1. The obligee Distribution firms Suppliers

2. Cost discharge Limited levy fund on all consumers Own customers of obligee

3. Right of obligee to own generation plants No Yes

4. Price ceiling Yes Yes

5. Price floor Yes No

6. Penalty for non-compliance Pay average price from own financial

resources

Pay price ceiling from own financial resources

7. Recycling of financial penalty To generators with unsold TGC Among compliant obligees

8. Lifetime of certificates 1 year 4 years

9. Frequency of compliance proof 3 year 2 years

10. Banking No Yes

11. Borrowing No No

12. Split of obligation in technology bands Yes No

13. Time horizon obligation Large—20 years Short—8 years

V. Dinica / Energy Policy 34 (2006) 461–480 471

TGC for each missing certificate from their quota, fromthe company’s own financial resources. This combina-tion is able to boost confidence in demand for RET-Einvestors, since obligees will have a strong incentive tobuy green electricity/certificates. Thirdly, the long-termhorizon of obligation increases confidence in investmentcosts recovery, even when investments are done at alater time after obligation start, in order to have a betterunderstanding of how the market works. Fourthly,when the quota obligation is split among technologybands, both demand and price risks are reduced,eliminating competition with other RET-T technologies.

Further, price risks can also be assessed as low inConfiguration 1 based on the following signals. Firstly,price ceiling and floors exist, which enables investorsderive some expectations regarding project returns.Besides, the fact the obligees can discharge costs on anall-consumers levy fund leads to the assumption that,under pressure to comply, there might be a willingnessto accept price proposals close to the legal ceiling.Secondly, non-compliant obligees have to pay penalties,and the penalty fund is distributed among generatorswith unsold certificates. This assures generators thateven when they cannot sell (all) green certificates, theywould still have income from the support instrument.However, one attractive aspect may be that the lifetimeof certificates is shorter than the time interval whenobligees have to prove compliance. This does not allowgenerators the flexibility to wait and search for attractiveTGC prices. They might have to accept lower pricesbefore deadline, while obligees are in the position topostpone buying closer to the compliance deadline.When the supply is larger than the demand, generatorswith unsold certificates will not receive any income fortheir TGC as long as all obligees comply with theirobligation. Overall price risks may be assessed asbetween low and modest. However having in view thatRET-T projects may get TGC for the first 10 years of

production, while the obligation assumes a gradualincrease in quota level, and on the background of lowdemand risks, the overall support instrument risks canbe assessed as low.

Configuration 2 is an example of high risks quotadesign for non-obligee investors. This comes from theassessment of high demand risks and modest–high pricerisks. Demand risks for potential investors who are notquota obligees can be assessed as high. Firstly, theobligees have the right to own RET-E plants. Un-certainties on the demand size that non-obligees couldserve emerge because of lack of information regardingthe buying versus investment strategies of obligees, aswell as the possibility that obliges are banking the self-produced certificates. Secondly, an obligation timehorizon of only 8 years would enable the recovery—with more certainty—of investment costs only wheninvestments are done in the first years of the obligation.Thirdly, the fact that the quota obligation is not split intechnological bands increases both demand and pricerisks.

Price risks can be assessed as between modest andhigh. On the one hand, the lifetime of certificates islonger than the compliance frequency. This enablesgenerators to search longer for prices are correspond totheir expectations. But on the other hand, the recyclingof financial penalties is directed toward compliantobligees. This represents a possible price risk for non-obligee investors, as they will get nothing for the unsoldTGC, while the time horizon of the obligation is short.Besides, there are no price floors that investors couldtake as orientation for estimating project returns, whilethe cost-discharge mechanism assumes that expenses areborn by own customers of obliges. In contrast to thesituation when quota expenses could be discarded on thegeneral levy fund on all consumers, in this case obligeeshave a strong incentive to buy TGC as cheaply aspossible. Therefore, only when supply is low compared

ARTICLE IN PRESSV. Dinica / Energy Policy 34 (2006) 461–480472

to quota level, can the design aspect of having thelifetime of certificates longer than the frequency ofcompliance can lead to modest price risks for non-obligee investors. However, on the background of highdemand risks, the overall risks of the instrument can beassessed as high for non-obligees. However, this quotadesign may still generate good diffusion results since it isattractive for obligees to invest—as long as they can doit at costs lower than those incurred by competingsuppliers to comply with their quota (this quota designplaces obligees in competition compared to the preced-ing example where the cost-discharge mechanism wascompetition neutral).

Two conclusions may be drawn from these twotheoretical examples. Firstly, whenever the quota designallows for obligees to comply by owning RET-Tgeneration capacity, the instrument creates two groupsof developers, and the risk–profitability characteristicsof the instrument have to be assessed for both in orderto get insight in the likely diffusion patterns and results.Secondly, quota obligations may be designed in waysthat pose both low risks and high risks on non-obligeeRET-T investors. Given different ranges of projectprofitability potential, the quota type of governmentallyprotected trade arrangements may result in any of thefour types of investment contexts differentiated in Fig. 1.

4.2. Risks associated with other support instruments

In Table 1, I labeled as ‘strategic instruments’ all theother schemes that governments may use to supportRET-E overpass the economic and financing barriers.They could help by means of: direct additional financialsupport, improving the accessibility of financing re-sources or improving the market position of RET-E vis-a-vis conventional electricity. I suggest that the risksfrom such instruments can be analyzed in terms of:

(a)

the timing of their application: before the entry ofthe operation of the power plant, or during part orthe entire economic lifetime of the plant;(b)

its position in the regulatory hierarchy, that isparliamentary law, governmental decision or minis-terial order;(c)

the context in which policy support mechanisms areused;(d)

the preferred policy style of economic actors in thecountry.As regards the timing of their application, one candistinguish instruments posing low/no risks because theyare implemented in the phase of project preparation orconstruction. For example, the following instrumentscan be considered as posing low risks: third-partyfinancing, project aggregation programs for governmen-tally negotiated large project finance loans, governmen-

tal guarantee on project loans and investment subsidies.Once these forms of support have been implemented, theprofitability or viability of projects during the operationphase is not exposed to risks if the instrument iswithdrawn, because withdrawal would affect only plantsto be built in future. When the implementation ofinstruments takes place during part or the entireeconomic lifetime of the plant, risk analysis needs tocombine the other three criteria mentioned above. Thisis the case of production subsidies and fiscal incentives—both direct and indirect. Many debates so far focused onthe desirability of fiscal incentives versus productionsubsidies.

In some countries (potential), RET-E generatorsmight tend to consider fiscal incentives less desirablethan production subsidies (e.g. in Spain), because theyare often complex and the eligibility of various types ofeconomic actors/legal status of the company is notalways clear. Besides, more public authorities are ofteninvolved in the implementation of fiscal incentives and,when regulations are not clear enough or leaving toomuch scope for the interpretation of fiscal authorities orlocal agencies, this is perceived to put the economics ofRET-E projects at risk. The perception that productionsubsidies are less risky than fiscal instruments isstrengthened when developers have confidence in thepolitical commitment for RET-E support, and whenother environmental policy goals were achieved withreliable production subsidies schemes in the past.Besides, when production subsidies help indirectly othernational or local goals such as electricity supply inpoorly/no electrified regions or the creation of jobs andindustrial basis in economically depressed areas, the riskperception can also improve.

In other countries, fiscal incentives may be viewed bydevelopers as less risky. The argument used is that theycannot be attacked by the lobby of conventional powerindustry as easily as production subsidies, because theyare compatible with market principles and do not distortcompetition. In some countries, where there is atradition of operating with fiscal instruments to achievepublic goals, the use of fiscal instruments can moreeasily be accepted as low risk support instruments thanin countries which are just experimenting with it.Consequently, the risks of support instruments can beperceived differently in different national contexts andempirical research should take into account suchpossible ‘cultural biases’.

4.3. Representing support systems in the risk/profitability

matrix

In terms of the analytical process for risk assessment,qualitative assessments can be made on a scale with fourlevels: low, moderate, high and very high. Assessmentson this scale can be made in a first step separately for

ARTICLE IN PRESSV. Dinica / Energy Policy 34 (2006) 461–480 473

demand risks, contract risks and price risks, as resultingfrom the governmentally guaranteed trade arrangementswith obligees. In the second step, their interactionshould be interpreted from the perspective of how couldlong-term risks affect projects’ returns (see Section 4.4).This would result in the assessment, on the same four-scale level, of the trade arrangements’ risks. After that, ifother support instruments are simultaneously appliedfor the same type of RET-E, the analysis can becontinued with the risk assessment of individualinstruments, as suggested in Section 4.2. Finally, theinteraction of all instruments and trade arrangements(governmentally guaranteed as well as market trade) canbe studied in terms of overall risks they pose and howthey contribute to the profitability potential of projects.Section 4.1.3 has given an example of high-risk quotaguarantees purchase for independent power producersusing RET-E. Section 4.4. gives an example of a high-risk support system that includes governmentallyguaranteed purchase from individual RET-E projects,investment subsidies and third-party financing by agovernmental agency.

As regards the project profitability characteristic, inprevious empirical analyses I conducted based on thisanalytical approach to support systems, I operationa-lized it as follows: low, up to 4%; modest, 4–8%; high,8–12%; very high, 412%. This operationalization wasdeveloped based interviews with more than 60 projectdevelopers and market analysts from Spain, UnitedKingdom and the Netherlands (see Dinica, 2003, pp.633–636), as well as analyses of a rich diversity ofempirical material on the issue of RET-E projects’economics and financing. In empirical research, profit-ability can be assessed by using one of the followingapproaches: (1) direct profitability data from developers,market experts and available empirical material such asgovernmental documents, journal articles or conferencepapers; and (2) qualitative assessments from developerswhen data are treated as confidential, combined withcomparisons of production costs and extent of price/financial support, using information from developers,market experts and empirical material.

4.4. Support system in Spain, 1980–1994

Altough the Spanish system of RET-E support basedon the 1997/8 regulatory framework has been largelydiscussed in the literature for the success of the so-called‘feed-in tariff’ on wind energy use, little has beenpublished about what happened in an earlier periodbased on the same type of instrument. Between 1980 and1994, the market introduction of RET-E in Spain wassupported by:

9The RET-E generators were however specifically required ‘‘to

abstain from selling the excess electricity to third-party’’ as the

� electricity industry was still organized based on monopoly principles.governmentally guaranteed purchase for individualRET-E projects, defined in the 82/1980 Energy

Conservation Law as: right to grid connection;contracts for the sale of surplus electricity to thelocal energy utility;9 guaranteed fixed-price deter-mined by Ministry of Industry and Energy; only aspecified target group could benefit of guaranteedpurchase; many RET-E projects also benefited of:J third-party financing;J investment subsidies.

According to the legal text, the target group forgovernmentally guaranteed contracts was formed byself-generators having surplus RET-E electricity, de-monstration projects and small-hydropower (o5MW)commercial generators (except for projects developed bydistribution companies). In practice, a series of com-mercial projects based of non-hydro renewable re-sources were nevertheless also developed. Theirnumber increased after 1990, becoming dominant atthe end of the first diffusion period in 1994. One maywonder: Why does it make sense to look at the risksincurred by developers that are not in the legally definedtarget group? The 1991–2000 Spanish Plan for EnergySaving and Efficiency set targets of 168MW windcapacity by 2000, and 779MW new small-hydropowerplants—among other technologies, and expected theirachievement solely through (partly) self-generationprojects. That is why the 82/1980 Law was also targetedat self-generators’ support. But because the interest inself-generation projects proved very low, commercialprojects started to be accepted for contracts with localenergy utilities, in order to reach the policy targets(Ocharan de la Camara, 2001). From here, one canimply that—although accepted, looking from a legalperspective, demand risks were basically very high forcommercial non-hydro renewable plants, since they werenot specifically mentioned in the target group. However,there were no demand risks for small-hydropower plants(o5MW) and for (partly) self-generation and demon-stration non-hydro RET-E projects.

As regards the duration of purchase contracts, therewas no legal provision mentioning this (also not in thegovernmental documents issued in the implementationof the law), or the criteria for contract extension, in caseonly short-term contract, were given by local energyutilities, or how much would be considered as ‘surpluselectricity’. Empirical research revealed that contractduration varied widely between 2 years and projectlifetime, depending on who were the project developersor equity investors (Dinica, 2003, pp. 188–192). Forwind energy most of the grid-connected projectscommissioned in this period had the financial involve-ment of the purchasing energy utilities, the govern-mental renewables agency—Institute for Energy Saving

ARTICLE IN PRESSV. Dinica / Energy Policy 34 (2006) 461–480474

and Diversification (IDAE)—and manufacturers.10 Inthese cases, there were long-term or project lifetimecontracts. Therefore, for some projects developers couldhedge against instrument-related contract risks bychoosing the investment partners strategically or simplybecause they were key actors in the decision-makingprocess for approving RET-E projects. But, seen atindustry level, the phrasing of the ‘governmentallyguarantee’ posed very high contract risks. The absenceof legal provisions on minimum contract length andcontract extension prospects had the consequence ofcreating financing obstacles for many developers,blocking the access to ‘project finance’ loans. Contractrisks weighted heavy in the risk analysis of financingagents, as lenders pointed out many times during thenational workshops for renewables promotion orga-nized during the 1990s by IDAE.

The price for trade arrangements can be assessed fromthe standpoint of legal text analysis as posing very highrisks because. Although a purchase price was guaran-teed in the law, no level or details on the design of pricewere specified in the law. The price level was set in theform of a feed-in tariff, by Order of Minister of Energyand Industry. The Ministry was given all competences asto what positive aspects of renewables generation wereto be taken into account and to what extent would theybe financially valued. There were no consultations with(potential) project developers regarding the price com-ponents to be taken into account, price type and level.Setting tariffs assumed a ‘directive’ type of decision-making. In addition, decisions at ministerial level wereseen by economic actors potentially more politicallyunstable than decisions at governmental and parliamen-tary level, especially when tariffs have to be annuallyrevised.11 The law also did not offer any price floors thatdevelopers could take as orientation in making theirbusiness plans. Having in view these considerations, theprice risks associated with the governmentally guaran-teed trade arrangements can be assessed as very high.Besides, the feed-in tariff was quite small. Scatteredinformation indicates an average price for electricityfrom small-hydropower plants of 6.3 Ec/kWh, while forwind electricity it varied between 6.1 and 7.2 Ec/kWh.For biomass electricity the feed-in tariff was not evenregulated in ministerial orders but negotiated betweenindividually between the few producers and energyutilities (Dinica, 2003, pp. 194–195).

Looking at the legal framework during 1980–1994 therisks associated with trade arrangements were different

10Small-hydropower projects had a more diverse ownership, while

biomass electricity projects were very scarce because the extent of price

support was not enough to make them profitable.11Manuel Delas, the President of the Association of Renewable

Energy Producers in Spain, ‘‘Position paper’’ 2001 available at the

association’s website: http://www.appa.es; also interview with Manuel

Bustos, public relations officer of the same association, April 2001.

for commercial non-hydro projects (hence includingwind and biomass) than for the rest of RET-E projects.The risks associated with trade arrangements can beassessed as high for all types of small-hydropowerprojects, and for self-generation and demonstrationrenewable wind and biomass projects. This comes fromthe assessed low demand risks for the target group, butvery high contract risks and very high price risks.However, for commercial generators using wind orbiomass resources, demand risks were very high sincethey were not specifically mentioned in the target group.This makes the overall risks associated with tradearrangements for such projects as very high. Interviewedproject developers and market analysts have alsoassessed this support instrument as posing (very) highrisks (Dinica, 2003, pp. 189–195, 225–226). This isreflected by the fact that—with few exceptions—it wasvery difficult to obtain project finance loans for any typeof RET-E projects during these years.

Since the mid-1980s, another scheme was alsointroduced: third-party financing by IDAE. This wasused in order to build confidence in RET-E amongpotential investors and it also aimed to help those whowould have liked to invest but lacked access to financialresources. This scheme does not change the risk–profit-ability profile of the governmentally regulated tradearrangements at industry level. The scheme transfers allproject risks from the project initiator to the third-partyfinancier, who is exposed to the same risks as the otherproject developers in the industry.

Next to this instrument, investment subsidies werealso used during those years. The 1983, 1986 and 1991energy policy plans set various levels of investmentsubsidies for wind and small-hydropower technologies.Investment subsidies were given mostly on a case-by-case basis, depending on the needs and particularities ofthe projects for which applications were made. Subsidiescould cover at maximum 60% during the 1980s of totaleligible investment costs, and maximum 50% up to1994. Some wind demonstration projects and manysmall-hydropower projects also used investment sub-sidies from the European Union. The use of investmentsubsidies did not change the support system related risksof projects. When the government cancels or interruptsthe application of such instrument, this cannot endangerthe economic feasibility or profitability of already builtprojects.

Investment subsidies made the difference betweeneconomically not feasible and (very) high profitabilityproject for wind and biomass electricity technologies.Between 1980 and 1994, the least financial supportwas given for biomass technology because it wasconsidered as not ready for considerable diffusion. Forwind technology, investment subsidies enabled projectprofitability levels in the range of 10–20%, depending onresource location and quality, and also due to variations

ARTICLE IN PRESSV. Dinica / Energy Policy 34 (2006) 461–480 475

in the level of subsidies among projects (Dinica, 2003,pp. 228–229). This placed wind technology in anentrepreneurial investment context (see Fig. 1). Withoutthe use of investment subsidies, the support system forwind technology using the so-called feed-in-tariff modelwould have been of ‘minimal investment context’ type.The same holds for small-hydropower plants, whichbenefited of entrepreneurial investment contexts up to1994. Adding to the modest price support per kWh,investment subsidies enabled high (8–12%) and veryhigh (412%) profitability for most projects built(Dinica, 2003, pp. 234–235). However, for biomasselectricity technologies the lack of widespread invest-ment subsidies left projects unprofitable. Confrontingthe same levels of (very) high risks, developers ofbiomass projects had to operate in a minimal investmentcontexts where only projects mainly aiming at self-generation and demonstration were interesting.

Being able to specify the risk–profitability of theinvestment context is very helpful in deriving expecta-tions on the diffusion potential. Section 5 formulatessome theoretical expectations on the diffusion patters ofRET-T projects and the likely short–medium termdiffusion potential for the four types of investmentcontexts differentiated. Having in view the constrains onthe size of this paper, the analysis in Section 5 appliesonly to support systems that include the type of demand‘governmentally guaranteed purchase for individualRET-T plants’ or support systems that only use one ormore combinations of ‘strategic instruments’ as men-tioned in Table 1. Looking at the diffusion potential ofsuch support systems (as dependent variable) impliesthat the capacity increase at industry level is not known.

5. Diffusion potential of support systems

The analysis of support systems for RET-E electricityfrom the perspective of potential investors is morehelpful than the incumbent approaches in policy studies,as it facilitates the development of expectations regard-ing the likely rate of market growth. In this section, Iexplain how such expectations can be derived.12 Themain assumptions used in this analysis are that:

�

except for the financing and economic obstacles, noother obstacles impede the diffusion of RET-E, suchas environmental and administrative opposition; thisassumption is necessary whenever one wishes tounderstand the ‘investment appetite’ created bysupport systems aimed at the economic and financingaspects of RET-E plants alone;�

there are no restrictions on the market entry for thebusiness of RET-E electricity;12For an in-depth study see Dinica (2003).

�

generation, in terms of type of project owner; � there is sufficient availability of technically exploitablerenewable resources that would enable a significantcontribution of the respective RET-E in the nationalelectricity supply.

The theoretical argument is that the risk–profitabilityprofile of a support system influences the marketdiffusion patterns of the respective technology. In theirturn, diffusion patterns influence the results of thesupport system. In this paper, I discuss the likely resultsin short–medium term—expressed as the level ofinstalled capacity increase in a period of 5–10 years.The relationships are represented in Fig. 2.

In order to analyze diffusion, five indicators fordiffusion patterns can be seen as suitable analytical linksfor understanding the investment appetite under thefour types of support configurations:

�

What kinds of (economic actors) developers would beinterested to invest and which is their financialstrength?�

What are the main reasons motivating their invest-ments: commercial, strategic or self-generation inter-ests?�

What kinds of financing arrangements are they ableto make or willing to use? and�

What could be the size of projects in which they arewilling to invest?I believe these indicators are very significant whenquantifying the speed of renewable technology marketgrowth.

Considering what forms these indicators may take inthe four types of risk–profitability investment contexts,one can hypothesize that diffusion patterns can beconsiderably different. This has consequences for therate of market growth. In addition, the effectiveness of asupport system is influenced by factors specific to thenational context. An in-depth study on the diffusion ofwind electricity technology in the Netherlands, Spainand the United Kingdom (Dinica, 2003) revealed thatthe most important contextual factors are: the businessculture (especially in terms of technology perception andrisk-flexibility) and minimal business requirements (interms of interest rates and equity returns) of thedomestic economic actors and financing agents.