Teaching disciplinary literacy to adolescents: Rethinking content-area literacy

Upload

southdakotaCategory

view

0download

0

PLEASE SCROLL DOWN FOR ARTICLE

This article was downloaded by: [Kindle, Peter A.]On: 5 October 2010Access details: Access Details: [subscription number 927599521]Publisher RoutledgeInforma Ltd Registered in England and Wales Registered Number: 1072954 Registered office: Mortimer House, 37-41 Mortimer Street, London W1T 3JH, UK

Journal of Social Service ResearchPublication details, including instructions for authors and subscription information:http://www.informaworld.com/smpp/title~content=t792306968

Student Perceptions of Financial Literacy: Relevance to PracticePeter A. Kindlea

a Department of Social Work, The University of South Dakota, Sioux Falls, SD

Online publication date: 04 October 2010

To cite this Article Kindle, Peter A.(2010) 'Student Perceptions of Financial Literacy: Relevance to Practice', Journal ofSocial Service Research, 36: 5, 470 — 481To link to this Article: DOI: 10.1080/01488376.2010.510951URL: http://dx.doi.org/10.1080/01488376.2010.510951

Full terms and conditions of use: http://www.informaworld.com/terms-and-conditions-of-access.pdf

This article may be used for research, teaching and private study purposes. Any substantial orsystematic reproduction, re-distribution, re-selling, loan or sub-licensing, systematic supply ordistribution in any form to anyone is expressly forbidden.

The publisher does not give any warranty express or implied or make any representation that the contentswill be complete or accurate or up to date. The accuracy of any instructions, formulae and drug dosesshould be independently verified with primary sources. The publisher shall not be liable for any loss,actions, claims, proceedings, demand or costs or damages whatsoever or howsoever caused arising directlyor indirectly in connection with or arising out of the use of this material.

Journal of Social Service Research, 36:470–481, 2010Copyright c© Taylor & Francis Group, LLCISSN: 0148-8376 print / 1540-7314 onlineDOI: 10.1080/01488376.2010.510951

Student Perceptions of Financial Literacy: Relevance toPractice

Peter A. Kindle

ABSTRACT. The relevance of financial literacy to social work has been framed almost exclusively inthe context of poverty relief, but this study expands this framework to the evidence linking financialstress, not merely poverty, to adverse client outcomes. Using a new 15-item, quantitative instrument,student (N = 1,506) perceptions were collected. Respondents demonstrated a moderate awarenessof the relevance of financial literacy in 11 of 15 problem issues commonly encountered in practice,indicating a moderate receptivity to financial education. Future research should clarify the contours offinancial knowledge that is required to assist clients.

KEYWORDS. Financial literacy, financial stress, poverty, student perceptions

Financial literacy, the most common of avariety of terms to refer to consumer financialacumen, first appeared in the peer-reviewed so-cial work literature in a retirement tribute toKathy Goldman, founder and director of NewYork City’s Community Food Resource Center(J. Mills, 2004). J. Mills credited Goldman withsupporting the extension of financial literacy ser-vices to include tax preparation and Earned In-come Tax Credit eligibility to low-income peo-ple. Beverly and Burkhalter (2005) used the termin an advocacy piece suggesting social workersupport for financial education programs in pri-mary and secondary education as a preventativeintervention against poor financial consequencesthat may negatively impact low-income youthand young adults — a youth-oriented theme thatwas sustained by Johnson and Sherraden (2007)and Scanlon and Adams (2009). The poverty-related focus was extended to social work in-terventions with victims of intimate partner vi-

Peter A. Kindle, PhD, CPA, LMSW, is an Assistant Professor at The University of South Dakota, Depart-ment of Social Work, Sioux Falls, SD.

Address correspondence to: Peter A. Kindle, PhD, CPA, LMSW, Department of Social Work, The Uni-versity of South Dakota, 1400 W. 22nd Street, Sioux Falls, SD 57105 (E-mail: [email protected]).

olence (Sanders, Weaver, & Schnabel, 2007),which tended to substantiate the public healthresearch documenting the beneficial effects ofemployment for women who have been bat-tered (Rothman, Hathaway, & Stidson, 2007).The most comprehensive association of finan-cial literacy with poverty work might be theJuly/September 2007 issue of Families in So-ciety, entitled, “Working, but Poor: Next Stepsfor Social Work Strategies and Collaborations,”that contained three articles explicitly mention-ing financial literacy (S. G. Anderson, Zhan, &Scott, 2007; Gonyea, 2007; Hoffmire, 2007).Most recently, Birkenmaier and Curley (2009)have argued for greater financial literacy amongsocial workers in order to assist clients in need ofadditional financial resources.

To date, the relevance of financial literacyfor social work students and social work edu-cation has been framed almost exclusively in apoverty relief framework (Sherraden, Laux, &

470

Downloaded By: [Kindle, Peter A.] At: 16:51 5 October 2010

Student Perceptions of Financial Literacy 471

Kaufmann, 2007). The contemporary roots ofthis link to poverty work are most likely MichaelSherraden’s (1991) asset-building strategies inwhich Sherraden challenged the prevailing view-point that poverty alleviation focused on in-come supplements. Sherraden’s insight thatpoverty was sustained as well by asset defi-ciencies has had a significant impact on so-cial welfare policies in the United States byencouraging tax-supported and matched sav-ings accounts for people with low incomes.Significant empirical work has been associatedwith the Financial Links for Low-Income Peo-ple (FLLIP) program implemented by the Illi-nois Department of Human Services (S. G.Anderson, Scott, & Zhan, 2004; S. G. An-derson, Zhan, & Scott, 2004, 2005; Zhan,Anderson, & Scott, 2006a, 2006b, 2009). S. G.Anderson and his colleagues have focused onmeasuring the change in financial behaviorsamong people with low incomes as a result offinancial education programs. Perhaps more im-portantly, S. G. Anderson’s team has developedan instrument to assess financial literacy that in-corporates the alternative financial services sec-tor and welfare-to-transition challenges, issueslargely ignored by most research on financialliteracy. Both asset building and the FLLIP pro-gram are initiatives that were led by social workacademics focusing on poverty alleviation.

Framing the relevance of financial literacyto social work in a poverty relief frameworkis rooted in client need. For welfare clientsstruggling with the new work requirements un-der Temporary Assistance for Needy Families(TANF), there is ample evidence that higher lev-els of financial knowledge are required becauseof the complications associated with transition-ing from welfare to work (S. G. Anderson, 2002).The paradigm shift from passive welfare recip-ient to the self-promoting capitalist required bythe welfare-to-work transition (Stoesz, 2007) re-quires substantial knowledge enhancements be-cause the majority of public supports requireself-initiative in order to obtain access (e.g., fed-eral income tax credits), and the TANF leaversmay be inexperienced in understanding and ac-cessing the new private employment benefits forwhich they are eligible (Blank & Schmidt, 2001).TANF leavers need to understand their contin-

uing eligibility for public benefits, but most donot. Acs and Loprest (2004) found that 80% ofleavers did not take advantage of public child-care benefits, and less than 37% even knew thatchildcare was available (S. G. Anderson, 2002).Some have found that the majority (66.7%) knowof continuing food stamp eligibility, but partici-pation in the food stamp program is consistentlyless than half of the eligible leavers (Acs & Lo-prest; Bartlett & Burstein, 2004; National Prior-ities Project, 2007). The only public support forTANF leavers that is well known appears to becontinuing eligibility for Medicaid (S. G. Ander-son, 2002). Ironically, the neediest are the leastlikely to know about and take advantage of thefederal income tax credits (Phillips, 2001) andpublic income supplements (Haskins, 2001).

Some evidence exists in the literature to sug-gest that a poverty relief framework may be in-sufficient to motivate social work students tomaster the financial skills needed to meet clientneeds. In the few cases in which social work stu-dents or social workers have been asked aboutinterests that could be considered associated insome fashion with financial literacy, researchersgenerally consider the attitudes expressed or in-ferred by student and/or social worker as defi-cient. Most recently, Eamon and Zhang (2006)found that graduate social work students wereinadequately sensitive to the economic con-straints and obstacles that clients faced in a ran-dom assignment vignette study. Earlier work in-cludes that by Grinnell and Kyte (1975), whonoted, ironically, that inadequate financial re-sources were rarely noted as a presenting prob-lem in the records of a public welfare office.Despite the fact that client reports of present-ing problems often identify the need for con-crete financial assistance as more important thantherapy (Chafin, Bonner, & Hill, 2001; Cook,Freedman, Freedman, Arick, & Miller, 1996;McGuire, Bikson, & Blue-Howells, 2005; Spaid,Lewis, & Pecora, 1991), the few researcherswho have addressed the discrepancy betweenclient and practitioner assessments have foundthat social workers and/or social work studentsare more closely attuned to intrapersonal prob-lems than to environmental (e.g., financial) con-straints (Monkman, 1991; Rosen, 1993; Rosen &Livne, 1992). This study intentionally expands

Downloaded By: [Kindle, Peter A.] At: 16:51 5 October 2010

472 P. A. Kindle

the framework for the relevance of financial liter-acy to social work by reference to the substantialevidence linking financial stress and strain, notmerely poverty, to adverse client outcomes.

A NEW FINANCIAL LITERACYFRAMEWORK: FINANCIAL STRESS

AND FINANCIAL STRAIN

Financial stress has been associated with el-evated levels of parental conflict (Conger, Ge,Elder, & Lorenz, 1994; Henry & Miller, 2004;Parke et al., 2004; Tse, 2007; Vosler, 1996),parental dysphoria (Conger et al., 2004; Parkeet al., 2004), and higher rates of divorce (J.D. Anderson, 2005). Adverse financial circum-stances have been associated with an elevatedoccurrence of intimate partner violence (Jewkes,2002; Tse, 2007) and child abuse (Cadzow, Arm-strong, & Fraser, 1999; Vosler, 1996). These neg-ative effects have been confirmed with a varietyof ethnicities and cultures (Cutrona et al., 2003;Tse, 2007). In contrast, basic needs provision hasbeen associated with increased marital survivalrates (Chafin et al., 2001).

Poor psychological well-being has often beenassociated with financial stress (R. J. Mills,Grasmick, Morgan, & Wenk, 1992). Depression(Kahn & Pearlin, 2006; Kraaij, Arensman, &Spinhoven, 2002; Kraaij, Kremers, & Arens-man, 1997; Lincoln, Chatters, & Taylor, 2005;Lynch, Kaplan, & Shema, 1997; Parke et al.,2004; Price, Choi, & Vinokur, 2002; Rantakeisu& Jonsson, 2003; Vinokur, Price, & Caplan,1996), anxiety (Rantakeisu & Jonsson, 2003;Westman, Etzion, & Horovitz, 2004), hostility(Lynch et al., 1997; Parke et al., 2004), lack ofoptimism (Lynch et al., 1997), and lower cog-nitive functioning (Lynch et al., 1997) have allbeen linked in some manner to financial stress,unemployment, or other disadvantageous eco-nomic events. Risk of suicide, in particular, isstrongly associated with unemployment (Brown,Beck, Steer, & Grisham, 2000; Duberstein, Con-well, Conner, Eberly, & Caine, 2004). These ef-fects have been generalized across ethnicities(Lincoln et al., 2005) and cultures (Westman,et al., 2004) with increasing cumulative effectsover time (Kraaij et al., 2002; Lynch et al., 1997).

The efficacy of social support, often identified ashaving a positive buffering mental health effect,can be effectively undermined by financial strain(Lincoln et al., 2005).

Children are particularly vulnerable in fami-lies encountering financial pressure. Whether thenegative impact of financial strain on children ismediated by low parental involvement with thechild (Newman & Chen, 2007; Simons, Lorenz,Conger, & Wu, 1992), low quality parenting(Hilton & Desrochres, 2000; Parke et al., 2004),adverse mental health issues among parents asnoted above, or the deleterious influence oflow-income neighborhoods (Newman & Chen,2007), adverse child outcomes are the result.Even children who escape the higher risk of childabuse are unlikely to escape higher incidents ofadverse internalizing emotions and externaliz-ing behaviors by adolescence (Conger et al.,1994; Gutman & McLoyd, 2005). High child-hood economic stress and poverty have beenassociated with lower adult educational levels,lower occupational prestige, lower income, andmultiple marriages (Hill, Ross, Mudd, & Blow,1997). Holzer, Schanzenbach, Duncan, and Lud-wig (2007) conducted a systematic review of theliterature confirming Hill et al. and also find-ing a lifelong increased risk of involvement inthe criminal justice system and impaired health.Even Emery, Otto, and O’Donohue (2006), ina systematic assessment of child custody eval-uations for Psychological Science in the Pub-lic Interest, were critical of what they term thepsychologizing of child custody decisions. Theyfound that half of the negative academic effectcommon in children following divorce or separa-tion is due to income variance in the restructuredhousehold. They placed economic security justbehind good parental relationship and minimalparental conflict as a predictor of child adjust-ment.

High debt levels have been associated withpoor measures of physical health and lowself-reports of physical well-being (Drentea &Lavrakas, 2000; O’Neill, Sorhaindo, Xiao, &Garman, 2005), and financial stress/strain hasbeen associated with impaired health and highermortality (Angel, Frisco, Angel, & Chiriboga,2003; Kahn & Pearlin, 2006; Lynch et al., 1997;Vosler, 1996). Debtors participating in debtor

Downloaded By: [Kindle, Peter A.] At: 16:51 5 October 2010

Student Perceptions of Financial Literacy 473

counseling reported improved health followingadoption of improved financial practices and re-duction in debt (O’Neill et al., 2005), and evenblood pressure and cortisol levels improved af-ter alleviation of financial stressors (Steptoe,Brydon, & Kunz-Ebrecht, 2005).

The association of poverty relief efforts witharguments for the relevance of financial liter-acy is quite appropriate because people with lowincomes may be particularly vulnerable tothe negative consequences of financial strain;however, the transfer of financial risk from gov-ernments and corporations in the last 30 years(Gosselin, 2008; Hacker, 2006) and the stressassociated with high debt levels (Drentea &Lavrakas, 2000; O’Neill et al., 2005; Phillips,2008) affect a significant proportion of everyeconomic class in America (Manning, 2000;Wheary, Shapiro, & Draut, 2007). The nega-tive outcome on clients that accrues from thepresence of financial stress and financial strainimpacts the entire family and social systemregardless of the level of income or earningpotential of the client. Accordingly, financialstress and financial strain point to the relevanceof financial literacy to social work practice.

Are social work students aware of the rele-vance of financial literacy to their future prac-tice? Although Sherraden et al. (2007) reporteda moderately positive response to an electivefinancial management course for undergraduateand graduate social work students, the smallnumber of student enrolled (N = 18) precludesgeneralizing their findings. Using a new 15-iteminstrument designed to capture student percep-tions, this study attempts to measure undergrad-uate and graduate student awareness of the rel-evance of financial literacy to specific problemissues encountered in practice. Student percep-tions provide not only a contemporary snapshotof emerging professionals but also, by implica-tion, a potential window through which to assessacademic receptivity to the potential relevanceof financial literacy to the social work practice.

METHOD

Participants

The population of interest included all un-dergraduate and graduate social work students

in the United States during the 2008–2009 aca-demic year. Release of the Council of SocialWork Education’s Annual Program Statistics forthis academic year is still pending; however,there were 32,457 undergraduate, 39,566 mas-ter’s of social work students, and 2,554 doc-toral social works students in 2006 (Council onSocial Work Education [CSWE], 2007b). Afterapproval by the applicable institutional reviewboard, which ensured the protection of humansubjects, the survey questionnaire was set up onSurveyMonkey.com. The first page of the sur-vey questionnaire contained the informed con-sent, and respondent agreement to participate inthe study was indicated by completing the ques-tionnaire. Participants were solicited by e-mailsdistributed through the listservs of the NationalAssociation of Deans and Directors, the Groupfor the Advancement of Graduate Education, andthe Baccalaureate Program Directors on January26, 2009. One follow-up e-mail was distributedon February 9, 2009. Additional follow-up wasnot warranted because a priori power analy-sis using G*Power 3 (Faul, Erdfelder, Lang, &Buchner, 2007) required a sample size of only1,302 respondents with alpha, power, and effectsize set at .05, .95, and .10, respectively.

None of the listservs were fully comprehen-sive of all accredited social work programs, andnone precluded participation by people outsideof the United States. Accordingly, it was nec-essary to exclude respondents who did not con-firm that they were students currently enrolledin the United States and missing data resultedin list-wise deletion of cases. Recruitment ofrespondents resulted in a nonrandom, self-selected sample of 1,506 useful responses.

Instrumentation

Demographic information comparable to thatcollected and reported by the CSWE (2007a,2007b) was collected from respondents to fa-cilitate post-hoc analysis of surface similaritybetween the sample and population. As mightbe expected using a statistical test designed forsmall sample sizes, the chi-square tests indicatedthat the distribution of respondents in the sampleis statistically different from the proxy popula-tion on every demographic variable. However,with the exception of racial or ethnic identity,

Downloaded By: [Kindle, Peter A.] At: 16:51 5 October 2010

474 P. A. Kindle

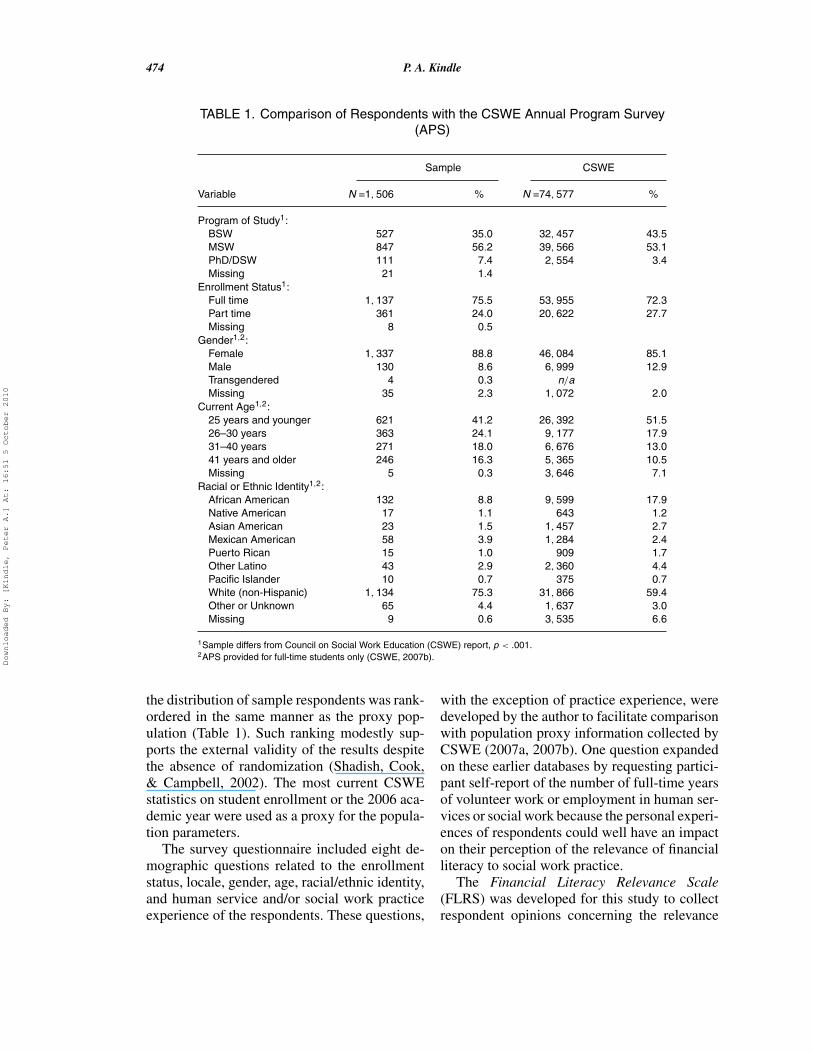

TABLE 1. Comparison of Respondents with the CSWE Annual Program Survey(APS)

Sample CSWE

Variable N =1, 506 % N =74, 577 %

Program of Study1:BSW 527 35.0 32, 457 43.5MSW 847 56.2 39, 566 53.1PhD/DSW 111 7.4 2, 554 3.4Missing 21 1.4

Enrollment Status1:Full time 1, 137 75.5 53, 955 72.3Part time 361 24.0 20, 622 27.7Missing 8 0.5

Gender1,2:Female 1, 337 88.8 46, 084 85.1Male 130 8.6 6, 999 12.9Transgendered 4 0.3 n/aMissing 35 2.3 1, 072 2.0

Current Age1,2:25 years and younger 621 41.2 26, 392 51.526–30 years 363 24.1 9, 177 17.931–40 years 271 18.0 6, 676 13.041 years and older 246 16.3 5, 365 10.5Missing 5 0.3 3, 646 7.1

Racial or Ethnic Identity1,2:African American 132 8.8 9, 599 17.9Native American 17 1.1 643 1.2Asian American 23 1.5 1, 457 2.7Mexican American 58 3.9 1, 284 2.4Puerto Rican 15 1.0 909 1.7Other Latino 43 2.9 2, 360 4.4Pacific Islander 10 0.7 375 0.7White (non-Hispanic) 1, 134 75.3 31, 866 59.4Other or Unknown 65 4.4 1, 637 3.0Missing 9 0.6 3, 535 6.6

1Sample differs from Council on Social Work Education (CSWE) report, p < .001.2APS provided for full-time students only (CSWE, 2007b).

the distribution of sample respondents was rank-ordered in the same manner as the proxy pop-ulation (Table 1). Such ranking modestly sup-ports the external validity of the results despitethe absence of randomization (Shadish, Cook,& Campbell, 2002). The most current CSWEstatistics on student enrollment or the 2006 aca-demic year were used as a proxy for the popula-tion parameters.

The survey questionnaire included eight de-mographic questions related to the enrollmentstatus, locale, gender, age, racial/ethnic identity,and human service and/or social work practiceexperience of the respondents. These questions,

with the exception of practice experience, weredeveloped by the author to facilitate comparisonwith population proxy information collected byCSWE (2007a, 2007b). One question expandedon these earlier databases by requesting partici-pant self-report of the number of full-time yearsof volunteer work or employment in human ser-vices or social work because the personal experi-ences of respondents could well have an impacton their perception of the relevance of financialliteracy to social work practice.

The Financial Literacy Relevance Scale(FLRS) was developed for this study to collectrespondent opinions concerning the relevance

Downloaded By: [Kindle, Peter A.] At: 16:51 5 October 2010

Student Perceptions of Financial Literacy 475

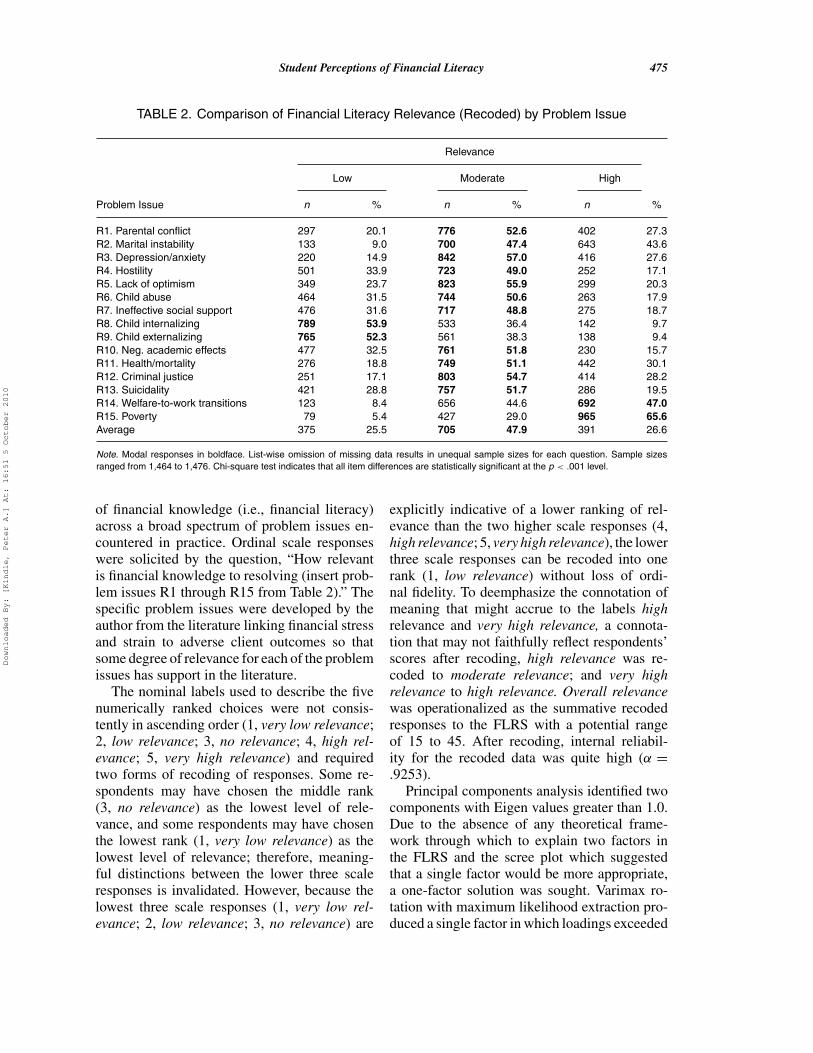

TABLE 2. Comparison of Financial Literacy Relevance (Recoded) by Problem Issue

Relevance

Low Moderate High

Problem Issue n % n % n %

R1. Parental conflict 297 20.1 776 52.6 402 27.3R2. Marital instability 133 9.0 700 47.4 643 43.6R3. Depression/anxiety 220 14.9 842 57.0 416 27.6R4. Hostility 501 33.9 723 49.0 252 17.1R5. Lack of optimism 349 23.7 823 55.9 299 20.3R6. Child abuse 464 31.5 744 50.6 263 17.9R7. Ineffective social support 476 31.6 717 48.8 275 18.7R8. Child internalizing 789 53.9 533 36.4 142 9.7R9. Child externalizing 765 52.3 561 38.3 138 9.4R10. Neg. academic effects 477 32.5 761 51.8 230 15.7R11. Health/mortality 276 18.8 749 51.1 442 30.1R12. Criminal justice 251 17.1 803 54.7 414 28.2R13. Suicidality 421 28.8 757 51.7 286 19.5R14. Welfare-to-work transitions 123 8.4 656 44.6 692 47.0R15. Poverty 79 5.4 427 29.0 965 65.6Average 375 25.5 705 47.9 391 26.6

Note. Modal responses in boldface. List-wise omission of missing data results in unequal sample sizes for each question. Sample sizesranged from 1,464 to 1,476. Chi-square test indicates that all item differences are statistically significant at the p < .001 level.

of financial knowledge (i.e., financial literacy)across a broad spectrum of problem issues en-countered in practice. Ordinal scale responseswere solicited by the question, “How relevantis financial knowledge to resolving (insert prob-lem issues R1 through R15 from Table 2).” Thespecific problem issues were developed by theauthor from the literature linking financial stressand strain to adverse client outcomes so thatsome degree of relevance for each of the problemissues has support in the literature.

The nominal labels used to describe the fivenumerically ranked choices were not consis-tently in ascending order (1, very low relevance;2, low relevance; 3, no relevance; 4, high rel-evance; 5, very high relevance) and requiredtwo forms of recoding of responses. Some re-spondents may have chosen the middle rank(3, no relevance) as the lowest level of rele-vance, and some respondents may have chosenthe lowest rank (1, very low relevance) as thelowest level of relevance; therefore, meaning-ful distinctions between the lower three scaleresponses is invalidated. However, because thelowest three scale responses (1, very low rel-evance; 2, low relevance; 3, no relevance) are

explicitly indicative of a lower ranking of rel-evance than the two higher scale responses (4,high relevance; 5, very high relevance), the lowerthree scale responses can be recoded into onerank (1, low relevance) without loss of ordi-nal fidelity. To deemphasize the connotation ofmeaning that might accrue to the labels highrelevance and very high relevance, a connota-tion that may not faithfully reflect respondents’scores after recoding, high relevance was re-coded to moderate relevance; and very highrelevance to high relevance. Overall relevancewas operationalized as the summative recodedresponses to the FLRS with a potential rangeof 15 to 45. After recoding, internal reliabil-ity for the recoded data was quite high (α =.9253).

Principal components analysis identified twocomponents with Eigen values greater than 1.0.Due to the absence of any theoretical frame-work through which to explain two factors inthe FLRS and the scree plot which suggestedthat a single factor would be more appropriate,a one-factor solution was sought. Varimax ro-tation with maximum likelihood extraction pro-duced a single factor in which loadings exceeded

Downloaded By: [Kindle, Peter A.] At: 16:51 5 October 2010

476 P. A. Kindle

.40 for all items while explaining 45.53% of thevariance.

RESULTS

This study attempted to measure undergrad-uate and graduate student awareness of the as-sociation of financial knowledge with a varietyof client problem issues encountered in prac-tice. Student respondents were most likely to re-port a moderate level of relevance for each prob-lem issue (Table 2). Moderate relevance was themodal response in 11 of the 15 problem issuesincluded on the instrument, indicating that socialwork students were aware of the association be-tween financial stressors and relationship prob-lems (R1, R2, and R7), parenting issues (R1,R6, and R10), mental health (R3, R4, R5, andR13), physical health (R11), and involvementwith the criminal justice system (R12). As mightbe expected from the emphasis on a povertyrelief framework in the social work literature,respondents identified welfare-to-work transi-tions (R14) and poverty (R15) as highly rele-vant. Only adverse child internalizing behaviors(R8) and adverse child externalizing behaviors(R9) had low relevance as modal, indicating thatsocial work students are less inclined to relatechildhood behaviors with financial stress in thelarger family environment. Chi-square tests indi-cated that the distribution of responses for everyproblem issue was statistically significant at thep < .001 level.

Respondents were reluctant to report finan-cial education as highly relevant to any ofthe problem issues identified in the literatureas associated with financial stress and finan-cial strain. Only marital instability (43.7%),impaired health/mortality (30.1%), welfare-to-work transitions (47.0%), and poverty (65.6%)had more than 30% of the respondents indi-cate high relevance. Alternatively, respondentswere somewhat more likely to report low rele-vance, with more than 30% of respondents as-sessing hostility (33.9%), child abuse (31.5%),ineffective social support (31.6%), adverse childinternalizing behaviors (53.9%), adverse childexternalizing behaviors (52.3%), and negativeacademic effects (32.5%) as low.

Summative recoding of all responses on theFLRS (N = 1,425) resulted in ratio scaling foran overall relevance score ranging from 15 to45. Most respondents (54.8%) reported total rel-evance raw scores between 26 and 34 with amean of 30.24 (SD = 6.98). A small number ofrespondents (n = 35; 2.5% of sample) reportedlow relevance for all problem issues. A largernumber (n = 88; 6.2% of sample) reported highrelevance for all problem issues.

The overall moderate level of relevance as-cribed to financial literacy by respondents sup-ports the conclusion that there is a moderate levelof awareness by social work students of the rel-evance of financial literacy to practice contextswhen presented within a broad-based frameworkthat includes financial stressors. Additional sta-tistical analysis was conducted to determine ifstudent responses could be predicted from thedemographic variables collected in this study.

Analyses of variance did not reveal significantdifferences in students’ perceptions of relevancebased on program of study, enrollment status,gender, or race and ethnic identity, whether as-sessed as reported by respondents or bifurcatedinto White and non-White categories. Students’perceptions of the relevance of financial liter-acy were not significantly associated with yearsof reported work and volunteer experience (r =.051; p = .054); however, there was a small rela-tionship between age ranges and relevance (rs =.058; p = .029).

Linear regression was attempted to determinedemographic effects on student perceptions ofrelevance. Although 9 of 15 correlations be-tween program of study (0, undergraduate; 1,graduate), gender (0, female; 1, male), race (0,White; 1, non-White), work and volunteer expe-rience (in years), enrollment status (0, full time;1, part time), and age range (1, under 26 years;2, 26 to 30 years; 3, 31 to 40 years; 4, 41 yearsand older) were statistically significant at thep < .05 level, none of the correlations were suf-ficiently strong as to present a multicollinearityproblem. Work and volunteer experience (M =7.96 years, SD = 7.57) did require trimming (alltotals more than 34 years were recoded as 34years) to reduce the positive skew of this vari-able from 2.719 to 1.573 to comply with theassumption of normality. In the resulting linear

Downloaded By: [Kindle, Peter A.] At: 16:51 5 October 2010

Student Perceptions of Financial Literacy 477

TABLE 3. Individual Linear Regressions ofPotential Predictor Variables on Overall

Relevance

Predictor Variables β SE Significance R2

Program of study –.195 .313 .617 .000Gender –.271 .642 .673 .000Race –.036 .434 .933 .000Work and volunteer .048 .025 .054 .003

experienceEnrollment status .025 .431 .953 .000Age range .350 .166 .035 .003

regression, which did not produce a statisticallysignificant result, none of the potential predic-tor variables were statistically significant, andthe overall variance explained in the regressionwas only one-half of 1% (R2 = .005). Regress-ing each predictor individually against overallrelevance identified age range as statisticallysignificant, and work and volunteer experienceapproached significance (see Table 3); accord-ingly, future research should take care to includethese measures.

IMPLICATIONS

For the first time, this study attempted to di-rectly assess social work student perceptionsof the relevance of financial literacy for theirfuture social work practice using a frameworkfor relevance that extended beyond the narrowassociation of financial literacy to poverty. Ex-pectations were modest because the few priorstudies associated with student and/or socialworker attitudes toward client financial issuesmight be interpreted as suggesting a degree ofdisinterest (Chafin et al., 2001; Cook et al., 1996;Eamon & Zhang, 2006; Grinnell & Kyte, 1975;McGuire et al., 2005; Spaid et al., 1991). De-spite modest expectations related to student per-ceptions of relevance, the findings in this studywere encouraging. Ranking of responses in low-,moderate-, and high-relevance categories re-sulted in modal moderate responses on 11 of 15problem issues indicating some degree of aware-ness by social work students on all program lev-els that financial stressors contribute to a broad

spectrum of client problems. Modal responsesfor two problem issues (poverty and welfare-to-work transitions) were high as might be expectedfrom the near-universal association of financialliteracy with poverty in earlier research. Modalresponses for two problem issues (adverse childinternalizing and externalizing) were low, possi-bly indicating that social work students underes-timate the environmental impact financial stresshas on children.

The finding that social work students perceivefinancial literacy as relevant to a broad spectrumof problem issues facing social work clients sug-gests a degree of receptivity among social workstudents to the inclusion of financial educationin the social work curriculum which tends toconfirm the results obtained by Sherraden et al.(2007). Care, however, should be taken by so-cial work educators in addressing issues relatedto financial literacy because rigorous research inthis area is scant. Adequately reliable and validinstruments have yet to be developed to satis-factorily assess financial literacy, and accord-ingly, little is known about the existing level offinancial knowledge among social work students(Kindle, 2009). Many financial education curric-ula are extant (Frederichs, Rohrke, & Robinson,2002; Vitt et al., 2000); however, almost all ofthese curricula suffer substantial inadequacies ifassessed from the perspective of people with lowincomes. For example, the Federal Deposit In-surance Corporation’s MoneySmart curriculumprovides virtually no information on managingaccess to credit equivalents in the alternativefinancial services sector or in navigating the dif-ficult transition from welfare to work. Findingsthat indicate modest or no indication of behav-ioral change following financial education pro-grams (Birkenmaier & Tyuse, 2005; Braucher,2001; Caskey, 2006; Edmiston & Gillett-Fisher,2006) suggest that the content and/or pedagogyassociated with the educational program may bedeemed irrelevant to the lived experiences of theparticipants. Furthermore, although the associa-tion of financial stressors with a broad spectrumof client problems is well established, evidencethat financial education programs effectively re-solve financial stress remains largely untested.At this point, it may be premature to assumethat financial knowledge alone buffers against

Downloaded By: [Kindle, Peter A.] At: 16:51 5 October 2010

478 P. A. Kindle

financial stress without modification of financialbehaviors.

The findings of this study imply a reasonablelevel of awareness among social work studentsthat finances have an important impact on thelives of their clients; however, the research baseis currently inadequate to clarify the nature offinancial knowledge, skills, or behaviors neces-sary to buffer against financial stress and strain.To the extent that people with low incomes havea degree of restricted access to credit and asset-building mechanisms available to the middleclass, there is little justification of a presumptionthat one size fits all when it comes to financialeducation. A level of financial knowledge andskill that is sufficient to protect a middle-classconsumer from participation in the high-cost al-ternative financial services sector may be woe-fully inadequate for a person with low incomewhose only access to credit is in this sector. Anawareness that finances have import to clientsis, at the present time, a call for more researchrather than a call for an educational focus on fi-nancial education. Until the inadequacies of ex-isting pedagogy related to financial education areaddressed through future research and until spe-cific educational interventions have been shownto be effective at relieving financial stress, so-cial work educators may be wise to satisfy theirstudents’ need for financial education throughexisting community-based programs rather thanby expanding the existing social work curricu-lum to include financial education.

LIMITATIONS

Generalization of results from a self-selectedsample should always be taken with care, evenwhen the sample is broad based and the de-mographics of the sample somewhat resemblea proxy for the population. Furthermore, socialwork student responses for this study were col-lected during January and February 2009, morethan a year after the start of what has beencalled the Great Recession that began in De-cember 2007. Media coverage of the bursting ofthe housing bubble, the bankruptcy of LehmanBrothers in September 2008, the Troubled AssetRelief Program passed during the waning days

of the Bush administration in October 2008, andthe ever-growing unemployment rates may havecreated an increased sensitivity on the part of so-cial work students to financial issues. The extentto which the economic news had an impact onrespondents’ perceptions is unknown.

CONCLUSION

Social work students are not, of course, pro-fessional social workers. However, prior re-search seems to indicate, rather convincingly,that financial stress has a potentially damag-ing impact on whoever suffers its effects. So-cial work students appear to be somewhat awareof this connection, and social work educatorsmight be advised to begin the process of infusingan awareness of this connection throughout theexisting curriculum. Those who are already pro-fessional social work practitioners may be ad-vised to anticipate accelerating levels of financialstrain among an economically diverse clienteleas the impact of the changing global economy re-verberates throughout the American workplace.Although it remains largely untested, elevatedlevels of financial literacy may contribute toimproved client outcomes. How the professionwill choose to address the challenges associatedwith the changing financial and economic en-vironment, by infusing financial education intothe social work curriculum or by strengthen-ing referral networks to existing financial ex-perts, has yet to be determined. That the financialenvironment impacts the social work client, thesocial work student, and the social work practi-tioner is a conclusion that is unavoidable.

REFERENCES

Acs, G., & Loprest, P. (2004). Leaving welfare: Employ-ment and well-being of families that left welfare in thepost-entitlement era. Kalamazoo, MI: W. E. Upjohn In-stitute for Employment Research.

Anderson, J. D. (2005). Financial problems and divorce:Do demographic characteristics strengthen the relation-ship? Journal of Divorce & Remarriage, 43(1/2), 149–161. doi:10.1300/J087v43n01 08

Anderson, S. G. (2002). Ensuring the stability of welfareto work exits: The importance of recipient knowledgeabout work incentives. Social Work, 47, 162–170.

Downloaded By: [Kindle, Peter A.] At: 16:51 5 October 2010

Student Perceptions of Financial Literacy 479

Anderson, S. G., Scott, J., & Zhan, M. (2004, June).Financial links for low-income people (FLLIP):Final evaluation report. Retrieved from the Sar-gent Shriver National Center on Poverty Law Website: http://www.povertylaw.org/advocacy/publications/2004-06-fllip-evaluation.pdf

Anderson, S. G., Zhan, M., & Scott, J. (2004). Targeting fi-nancial management training at low-income audiences.Journal of Consumer Affairs, 38, 167–177.

Anderson, S. G., Zhan, M., & Scott, J. (2005). Developingfinancial management training in low-income commu-nities: Assessing needs and community practice impli-cations. Journal of Community Practice, 13(4), 31–49.doi:10.1300/J125v13n04 03

Anderson, S. G., Zhan, M., & Scott, J. (2007). Improv-ing the knowledge and attitudes of low-income fam-ilies about banking and predatory financial practices.Families in Society, 88, 443–452. doi:10.1606/1044-3894.3654

Angel, R. J., Frisco, M., Angel, J. L., & Chiriboga, D.A. (2003). Financial strain and health among elderlyMexican-origin individuals. Journal of Health and So-cial Behavior, 44, 536–551. doi:10.2307/1519798

Bartlett, S., & Burstein, N. (2004, May). Foodstamp access study: Eligible nonparticipants. Eco-nomic Research Service (E-FAN No. 03-013-2).Retrieved from the U.S. Department of Agricul-ture Web site: http://www.ers.usda.gov/publications/efan03013/efan03013-2/efan03013-2.pdf

Beverly, S. G., & Burkhalter, E. K. (2005). Improving thefinancial literacy and practices of youths. Children &Schools, 27, 121–124.

Birkenmaier, J., & Curley, J. (2009). Financial credit:Social work’s role in empowering low-income fam-ilies. Journal of Community Practice, 17, 251–268.doi:10.1080/10705420903117973

Birkenmaier, J., & Tyuse, S. W. (2005). Does home owner-ship education and counseling (HEC) help credit scores?Journal of Social Service Research, 32(2), 81–103.doi:10.1300/J079v32n02 05

Blank, R. M., & Schmidt, L. (2001). Work, wages, andwelfare. In R. Blank & R. Haskins (Eds.), The new worldof welfare (pp. 70–102). Washington, DC: BrookingsInstitute Press.

Braucher, J. (2001). An empirical study of debtor educationin bankruptcy: Impact on chapter 13 completion notshown. American Bankruptcy Institute Law Review, 9,557–592.

Brown, G. K., Beck, A. T., Steer, R. A., & Grisham,G. R. (2000). Risk factors for suicide in psychi-atric outpatients: A 20-year prospective study. Jour-nal of Consulting & Clinical Psychology, 68, 371–377.doi:10.1037//0022-006X.68.3.371

Cadzow, S. P., Armstrong, K. L., & Fraser, J. A. (1999).Stressed parents with infants: Reassessing physicalabuse risk factors. Child Abuse & Neglect, 23, 845–853.

Caskey, J. P. (2006, March). Can personal financialmanagement education promote asset accumulationby the poor? (Networks Financial Institute 2006-PB-06). Retrieved from Social Science Research Networkat http://papers.ssrn.com/sol3/papers.cfm?abstract id=923565

Chafin, M., Bonner, B. L., & Hill, R. F. (2001). Fam-ily preservation and family support programs: Childmaltreatment outcomes across client risk levels andprogram types. Child Abuse & Neglect, 25, 1269–1289.

Conger, R. D., Ge, X., Elder, G. H., & Lorenz, F. O. (1994).Economic stress, coercive family processes, and devel-opmental problems of adolescents. Child Development,65, 541–561.

Cook, C. A. L., Freedman, J. A., Freedman, L. D., Arick,R. K., & Miller, M. E. (1996). Screening for social andenvironmental problems in a VA primary care setting.Health & Social Work, 96, 41–47.

Council on Social Work Education. (2007a, August 13).Statistics on social work education in the United States2006: A summary. Alexandria, VA: Author.

Council on Social Work Education. (2007b, October 1).2006 annual survey of social work programs. Alexan-dria, VA: Author.

Cutrona, C. E., Russell, D. W., Abraham, W. T., Gardner,K. A., Melby, J. M., Bryant, C., & Conger, R. D. (2003).Neighborhood context and financial strain as predictorsof marital quality in African American couples. Per-sonal Relationships, 10, 389–409. doi:10.1111/1475-6811.00056

Drentea, P., & Lavrakas, P. J. (2000). Over the limit: Theassociation among health status, race, and debt. SocialScience & Medicine, 50, 517–529.

Duberstein, P. R., Conwell, Y., Conner, K. R., Eberly, S.,& Caine, E. D. (2004). Suicide at 50 years of age andolder: Perceived physical illness, family discord, andfinancial strain. Psychological Medicine, 34, 137–146.doi:10.1017/S0033291703008584

Eamon, M. K., & Zhang, S. (2006). Do social work stu-dents address and assess economic barriers to clientsimplementing agreed tasks? Journal of Social Work Ed-ucation, 42, 525–542.

Edmiston, K. D., & Gillett-Fisher, M. C. (2006, July).Financial education at the workplace (CommunityAffairs Working Paper No. 06-02). Retrieved fromthe Federal Reserve Bank of Kansas City Web site:http://www.kansascityfed.org

Emery, R. E., Otto, R. K., & O’Donohue, W. T. (2006). Acritical assessment of child custody evaluations: Lim-ited science and a flawed system. Psychological Sciencein the Public Interest, 6, 1–29.

Faul, F., Erdfelder, E., Lang, A. G., & Buchner, A. (2007).G*Power 3: A flexible statistical power analysis pro-gram for the social, behavioral, and biomedical sciences.Behavior Research Methods, 39, 175–191.

Downloaded By: [Kindle, Peter A.] At: 16:51 5 October 2010

480 P. A. Kindle

Frederichs, M., Rohrke, A., & Robinson, L. (2002,April). Guide to financial literacy resources. Retrievedfrom Federal Reserve Bank of San Francisco Website: http://www.frbsf.org/community/webresources/bankersguide.pdf

Gonyea, J. G. (2007). Improving the retirement prospectsof low-wage workers in a defined-contribution world.Families in Society, 88, 453–462. doi:10.1606/1044-3894.3655

Gosselin, P. (2008). High wire: The precarious financiallives of American families. New York: Basic Books.

Grinnell, R. M., Jr., & Kyte, N. S. (1975). Delivering con-crete environmental services in a public welfare agency.Journal of Social Welfare, 2, 69–82.

Gutman, L. M., & McLoyd, V. C. (2005). Financial strain,neighborhood stress, parental behaviors, and adoles-cent adjustment in urban African American families.Journal of Research on Adolescence, 15, 425–449.doi:10.1111/j.1532-7795.2005.00106.x

Hacker, J. S. (2006). The great risk shift: The assault onAmerican jobs, families, health care, and retirement andhow you can fight back. New York: Oxford UniversityPress.

Haskins, R. (2001). Effects of welfare reform on familyincome and poverty. In R. Blank & R. Haskins (Eds.),The new world of welfare (pp. 103–136). Washington,DC: Brookings Institute Press.

Henry, R. G., & Miller, R. B. (2004). Marital problemsoccurring in midlife: Implications for couples therapists.The American Journal of Family Therapy, 32, 405–417.doi:10.1080/01926180490455204

Hill, E. M., Ross, L. T., Mudd, S. A., & Blow, F. C. (1997).Adult functioning: The joint effects of parental alco-holism, gender, and childhood socioeconomic stress.Addiction, 92, 583–596.

Hilton, J. M., & Desrochres, S. (2000). The influence ofeconomic strain, coping with roles, and parental controlon the parenting of custodial single mothers and custo-dial single fathers. Journal of Divorce & Remarriage,33(3/4), 55–76.

Hoffmire, J. S. (2007). Promising practices in the devel-opment and distribution of asset-building products andprograms. Families in Society, 88, 472–474.

Holzer, H. J., Schanzenbach, D. W., Duncan, G. J., &Ludwig, J. (2007, April). The economic costs of povertyin the United States: Subsequent effects of childrengrowing up poor (Discussion Paper No. 1327-07). Re-trieved from the Institute for Research on Poverty Website: http://www.irp.wisc.edu/publications/dps/pdfs/dp132707.pdf

Jewkes, R. (2002). Intimate partner violence: Causes andprevention. Lancet, 359, 1423–1429.

Johnson, E., & Sherraden, M. S. (2007). From financialliteracy to financial capability among youth. Journal ofSociology & Social Welfare, 34(3), 119–146.

Kahn, J. R., & Pearlin, L. I. (2006). Financial strainover the life course and health among older adults.

Journal of Health and Social Behavior, 47, 17–31.doi:10.1177/002214650604700102

Kindle, P. A. (2009). Financial literacy and social work:Questions of competence and relevance (Doctoral dis-sertation, University of Houston, 2009). ProQuest UMIDissertation Publishing, AAT 3361457.

Kraaij, V., Arensman, E., & Spinhoven, P. (2002). Neg-ative life events and depression in elderly persons:A meta-analysis. Journals of Gerontology Series B:Psychological Sciences & Social Sciences, 57B, 87–94.

Kraaij, V., Kremers, I., & Arensman, E. (1997). The rela-tionship between stressful and traumatic life events inthe elderly and depression. Crisis, 18, 86–88.

Lincoln, K. D., Chatters, L. M., & Taylor, R. J. (2005).Social support, traumatic events, and depressive symp-toms among African Americans. Journal of Mar-riage and Family, 67, 754–766. doi:10.1111/j.1741-3737.2005.00167.x

Lynch, J. W., Kaplan, G. A., & Shema, S. J. (1997). Cu-mulative impact of sustained economic hardship onphysical, cognitive, psychological, and social function-ing. New England Journal of Medicine, 337, 1889–1895.

Manning, R. C. (2000). Credit card nation: The conse-quences of America’s addiction to credit. New York:Basic Books.

McGuire, J., Bikson, K., & Blue-Howells, J. (2005). Howmany social workers are needed in primary care? Apatient-based needs assessment example. Health & So-cial Work, 30, 305–313.

Mills, J. (2004). Dignity, financial literacy, and food, glo-rious food! The legacy of Kathy Goldman. Affilia, 19,317–321. doi:10.1177/0886109904265789

Mills, R. J., Grasmick, H. G., Morgan C. S., & Wenk, D.(1992). The effects of gender, family satisfaction, andeconomic strain on psychological well-being. FamilyRelations, 41, 440–445.

Monkman, M. M. (1991). Outcome objectives in socialwork practice: Person and environment. Social Work,36, 253–258.

National Priorities Project. (2007). Half of low-income people not receiving food stamps. Retrievedfrom http://www.nationalpriorities.org/images/stories/nationalprioritiesprojectfoodstampsaugust2007.pdf

Newman, K. S., & Chen, V. T. (2007). The missing class:Portraits of the near poor in America. Boston: BeaconPress.

O’Neill, B., Sorhaindo, B., Xiao, J. J., & Garman, E. T.(2005). Financially distressed consumers: Their finan-cial practices, financial well-being, and health. Finan-cial Planning and Counseling, 16(1), 73–87.

Parke, R. D., Coltrane, S., Buriel, R., Dennis, J., Powers, J.,French, S., & Widaman, K. F. (2004). Economic stress,parenting, and child adjustment in Mexican Americanand European American families. Child Development,75, 1632–1656. doi:10.1111/j.1467-8624.2004.00807.x

Downloaded By: [Kindle, Peter A.] At: 16:51 5 October 2010

Student Perceptions of Financial Literacy 481

Phillips, K. R. (2001). The earned income tax credit:Knowledge is money. Political Science Quarterly, 116,413–424.

Phillips, K. R. (2008). Bad money: Reckless finance, failedpolitics, and the global crisis of American capitalism.New York: Viking.

Price, R. H., Choi, J. N., & Vinokur, A. D. (2002). Linksin the chain of adversity following job loss: How fi-nancial strain and loss of personal control lead to de-pression, impaired functioning, and poor health. Jour-nal of Occupational Health Psychology, 7, 302–312.doi:10.1037//1076-8998.7.4.302

Rantakeisu, U., & Jonsson, L. R. (2003). Unemploy-ment and mental health among white-collar workers:A question of work involvement and financial situa-tion? International Journal of Social Welfare, 12, 31–41. doi:10.1111/1468-2397.00004

Rosen, A. (1993). Correction of workers’ personal ver-sus environmental bias in formulation of client prob-lems [Electronic version]. Social Work Research andAbstracts, 29(4), 12–17.

Rosen, A., & Livne, S. (1992). Personal versus envi-ronmental emphases in social workers’ perceptionsof client problems. Social Service Review, 66, 85–96.

Rothman, E. F., Hathaway, J., & Stidson, A. (2007). Howemployment helps female victims of intimate partnerviolence: A qualitative study. Journal of OccupationalHealth Psychology, 12, 136–143. doi:10.1037/1076-8998.12.2.136

Sanders, C. K., Weaver, T. L., & Schnabel, M.(2007). Economic education for battered women:An evaluation of outcomes. Affilia, 22, 240–254.doi:10.1177/0886109907302261

Scanlon, E., & Adams, D. (2009). Do assets affect well-being? Perceptions of youth in a matched savings pro-gram. Journal of Social Service Research, 35(1), 33–46.doi:10.1080/01488370802477048

Shadish, W. R., Cook, T. D., & Campbell, D. T. (2002). Ex-perimental and quasi-experimental designs for general-ized causal inference. Boston: Houghton Mifflin Com-pany.

Sherraden, M. W. (1991). Assets and the poor: A new Amer-ican welfare policy. Armonk, NY: M. E. Sharpe.

Sherraden, M. W., Laux, S., & Kaufmann, C. (2007). Finan-cial education for social workers. Journal of CommunityPractice, 15, 9–36. doi:10.1300/J125v15n03 02

Simons, R. L., Lorenz, F. O., Conger, R. D., & Wu,C. (1992). Support from spouse as mediator andmoderator of the disruptive influence of economicstrain on parenting. Child Development, 63, 1282–1301.

Spaid, W. M., Lewis, R. E., & Pecora, P. J. (1991). Factorsassociated with success and failure in family-based andintensive family preservation services. In M. W. Faser,P. J. Pecora, & D. A. Haapala (Eds.), Families in crisis:The impact of intensive family preservation services (pp.49–58). New York: Walter de Gruyter.

Steptoe, A., Brydon, L., & Kunz-Ebrecht, S. (2005).Changes in financial strain over 3 years, ambu-latory blood pressure, and cortisol responses toawakening. Psychosomatic Medicine, 67, 281–287.doi:10.1097/01.psy.0000156932.96261.d2

Stoesz, D. (2007). Bootstrap capitalism: Sequel towelfare reform. Families in Society, 88, 375–388.doi:10.1606/1044-3894,3646

Tse, S. (2007). Family violence in Asian communities,combining research and community development. So-cial Policy Journal of New Zealand, 31, 170–194.

Vinokur, A. D., Price, R. H., & Caplan, R. D. (1996). Hardtimes and hurtful partners: How financial strain affectsdepression and relationship satisfaction of unemployedpersons and their spouses. Journal of Personality andSocial Psychology, 71, 166–179.

Vitt, L. A., Anderson, C., Kent, J., Lyter, D. M.,Siegenthaler, J. K., & Ward, J. (2000). Personal fi-nance and the rush to competence: Financial lit-eracy education in the U.S. Washington, DC: In-stitute for Socio-Financial Studies. Retrieved fromhttp://www.isfs.org/documents-pdfs/rep-finliteracy.pdf

Vosler, N. R. (1996). New approaches to family prac-tice: Confronting economic stress. Thousand Oaks, CA:Sage.

Westman, M., Etzion, D., & Horovitz, S. (2004).The toll of unemployment does not stop withthe unemployed. Human Relations, 57, 823–844.doi:10.1177/0018726704045767

Wheary, J., Shapiro, T. M., & Draut, T. (2007). Bya thread: The new experience of America’s mid-dle class. Retrieved from The Institute on Assetsand Social Policy at Brandeis University’s Web site:http://iasp.brandeis.edu/pdfs/byathreadlatino.pdf

Zhan, M., Anderson, S. G., & Scott, J. (2006a). Finan-cial knowledge of low-income population: Effects ofa financial education program. Journal of Sociology &Social Welfare, 33, 53–74.

Zhan, M., Anderson, S. G., & Scott, J. (2006b). Finan-cial management knowledge of low-income popula-tion. Journal of Social Service Research, 33, 93–106.doi:10.1300/J079v33n01 09

Zhan, M., Anderson, S. G., & Scott, J. (2009). Bankingknowledge and attitudes of immigrants: Effects of afinancial education program. Social Development Is-sues, 31(3), 15–32.

Downloaded By: [Kindle, Peter A.] At: 16:51 5 October 2010

Copyright © 2022 FDOKUMEN