STRATEGIC REPORT FOR WARNER MUSIC GROUP, INC.

31

STRATEGIC REPORT FOR WARNER MUSIC GROUP, INC. ELIHU BOGAN SAMUEL MEEHAN PATRICK FLEMMING April 19, 2007

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of STRATEGIC REPORT FOR WARNER MUSIC GROUP, INC.

STRATEGIC REPORT FOR WARNER MUSIC GROUP, INC.

ELIHU BOGAN

SAMUEL MEEHAN PATRICK FLEMMING

April 19, 2007

2

TTABLE OF ABLE OF CCONTENTSONTENTS

EEXECUTIVE XECUTIVE SSUMMARYUMMARY ................................................................ ........................................ 33

CCOMPANY OMPANY BBACKGROUNDACKGROUND ................................................................ .................................. 44

CCOMPETITIVE OMPETITIVE AANALYSISNALYSIS ................................................................ .................................. 66 IINTERNAL NTERNAL RRIVALRYIVALRY ................................................................ .............................. 66

EENTRYNTRY ................................................................ ............................................................ 1010

SSUBSTITUTESUBSTITUTES AND AND CCOMPLEMENTSOMPLEMENTS .............................................................. 1111

SSUPPLIER UPPLIER PPOWEROWER ................................................................ .................................. 1414

BBUYER UYER PPOWEROWER ................................................................ .......................................... 1515

SWOT ASWOT ANALYSISNALYSIS ................................................................ ................................................ 1616

FFINANCIAL INANCIAL II SSUESSSUES ................................................................ .............................................. 1717

SSTRATEGIC TRATEGIC IISSUESSSUES ................................................................ ............................................ 2020

RRECOMMENDATIONSECOMMENDATIONS ................................................................ .......................................... 2424

3

EEXECUTIVE XECUTIVE SSUMMARYUMMARY

Since its birth as a music publisher in 1929, Warner Music Group (WMG) has

managed and produced a wide-range of successful musicians and performers,

and now boasts a recorded music portfolio of over 38,000 artists. WMG’s artists

include such big names as Led Zeppelin, The Doors, Green Day, and The Red Hot

Chili Peppers, and the company owns the rights to 29 of the top 100 best selling

albums of all time.i WMG’s business consists of two divisions: Recorded Music

and Music Publishing. The Recorded Music business produces revenue through

the marketing, sale and licensing of recorded music in various physical and

digital formats. The Music Publishing business owns and acquires rights to

musical compositions, and markets these compositions and receives royalties or

fees for their use. WMG, along with Universal, Sony BMG, and EMI Music,

competes in a music publishing industry with a small number of major players, as

well as a host of smaller, independent labels. Of the major competitors, all

operate internationally and compete in both traditional music markets and in

new digital enterprises such as tunes. Industry competition is both price and non-

price based, with advertising and marketing playing an important role in

protecting firms’ market share.

WMG was purchased in 2003 in a leveraged buyout led by Edgar Bronfmann, Jr.,

the current Chairman and CEO. In the past two years, WMG has been cutting

costs and seeking out new markets in digital goods as the CD market continues a

seven-year decline, and has established itself as a market leader in providing

content for both MP3 players and 3G-enabled cell phones. WMG and its

comparatively sized rival EMI have repeatedly initiated back-and-forth

acquisition negotiations, however regulatory uncertainty in the EU continues to

stifle progress.

A number of factors affect the performance of WMG, as well as the music

industry as a whole. The declining CD market, widespread digital piracy in the

U.S. and physical piracy abroad, and the growing importance of digital goods are

some of the most important. To date, WMG has been successful in positioning

4

itself aggressively in new markets, offering copyright-protected digital downloads

through legal services such as iTunes, as well as marketing music videos and

ringtones to 3G cell-phone subscribers. To counter the declining CD market,

WMG has engaged in an aggressive cost-cutting initiative, lowering annualized

costs by approximately $250 million in 2005. WMG hopes to continue improving

its balance sheet, income statement and cash flows through a merger with EMI.

Going forward, WMG’s greatest challenge will be to address the changing nature

of the music publishing business, as technological advances have threatened to

erode the traditional rival, excludable nature of music goods.

CCOMPANY OMPANY BBACKGROUNDACKGROUND

The history of WMG Group can be traced all the way back to 1929 through its

publishing arm, Warner Chappell Music. At that time, Jack Warner, president of

Warner Bros. Pictures, Inc., sought to acquire music copyrights as a way of

providing inexpensive scores and music for his films. Additional publishing firms

acquired in the 1920s and 1930s by Warner Bros. were all subsequently sold

within a decade, and WMG’s real roots in Time Warner began with the founding

of Warner Bros. Records as a division of the Warner Bros. movie studio in 1958.

In 1960, Warner Bros. Records signed the world’s first million dollar record

contract with the Everly Brothers.

In 1963 Warner Bros. Records acquired Reprise Records, which was founded by

Frank Sinatra in 1960. In 1967, Warner Bros. became Warner Bros.-Seven Arts,

when Jack Warner sold his stake in the company (and thus control of the group)

to Seven Arts Productions for approximately US$95 million. The same year, the

firm purchased Atlantic Records, which is now WMG’s oldest label. In 1969,

Kinney National, the comics, talent agency, parking lot, cleaning and funeral

parlour conglomerate, acquired the company. Kinney also acquired Elektra

records (founded in 1950) for US$10 million in 1970, and rechristened itself

Warner Communications.

5

WMG has operated internationally through Warner Music International (“WMI”)

since 1970. The current logo of WMG was designed for use by WMI since the

1970s. In 1972, the three major labels were assembled into one group then known

as WEA (Warner-Elektra-Atlantic). Later Warner Communications merged with

Time Inc. to form Time Warner. The company Time Warner remained

fundamentally unchanged until it was acquired by America Online in 2000.

In 2003, Time Warner sold their Warner Music arm to an investment consortium

led by Edgar Bronfman, Jr. (the former head of Universal) for US$2.6bn. The

investor group consisted of Thomas H. Lee Partners L.P., Bain Capital, LLC,

Providence Equity Partners, Inc. and Music Capital Partners L.P. In May 2005,

WMG became the only stand-alone music content company in the U.S. with

publicly traded common stock.

The transition to independent ownership was completed on February 27, 2004.

Since establishment, the group has been downsizing the firm, offloading marginal

or low revenue units such as record production by closing or selling disk-pressing

plants (particularly in the US and the Netherlands). In 2005 WMG sold Warner

Bros. Publications (their sheet music business) to Alfred Publishing, founded in

1922. Miami-based Warner Bros. Publications printed and distributed a broad

selection of sheet music, books, educational material, orchestrations and

arrangements, and tutorials. The sale excluded the print music business of

WMG's Word Music (church hymnals, choral music and associated instrumental

music).

In 2006 EMI and WMG engaged in a bizarre, reciprocal takeover battle with each

rejecting an unwelcome US$4.6bn bid from the other. EMI announced that it had

rejected the first acquisition offer from WMG, its smaller rival, calling the

proposal "wholly unacceptable" and increasing its offer for WMG. That offer was

in turn rebuffed. Also in 2006, WMG acquired Ryko Corporation for US$675m

from an investment group led by J.P. Morgan Partners, and agreed to purchase a

controlling stake in independent label Roadrunner (est. 1980) for US$73.5m. In

6

February 2007, WMG made another offer for EMI for $4.1bn in cash, which was

also rejected, this time due to regulatory uncertainty.

CCOMPETITIVE OMPETITIVE AANALYSISNALYSIS

WMG is classified as SIC Industry 7929, an all-encompassing genre defined as

Bands, Orchestras, Actors, and Other Entertainers and Entertainment Groups.

Other registrants under this code include World Wrestling Entertainment, Inc.,

Pro Elite, Inc., AVP Inc., IFSA Strongman, Inc., and Paradise Music &

Entertainment, Inc. As this market classification does not include any of

Warner’s major competitors, we will focus on Warner’s GICS classification,

Consumer Discretionary, specifically the sub-industry classification of Movies &

Entertainment (2540103), which includes rivals Universal, Sony BMG and EMI.

Universal and Sony BMG are significantly larger than WMG, controlling 26% and

22% of world market share, respectively. Universal Music Group is a subsidiary of

the French media conglomerate Vivendi S.A., and Sony BMG is a joint venture

between Sony Corp. and the German firm Bertelsmann A.G. British firm EMI,

with a market cap of $3.5 billion, accounts for another 13% of world market

share. With the inclusion of WMG, with a market cap of $2.54 billion and an 11%

market share, these four firms account for approximately 72% of worldwide

recorded music sales (based on 2004 figures). Each of these companies competes

internationally as well as in the US domestic market. In most markets, WMG and

its major competitors compete to a lesser degree with smaller boutique and mid-

market music publishers. Issues of scale as they relate to the music industry will

be addressed in the Substitutes and Complements section below.

IINTERNAL NTERNAL RRIVALRYIVALRY

Competition between the four major firms occurs on both price and non-price

(i.e. marketing, advertising, recruitment) levels. To maintain market share,

companies seek to recruit and retain popular artists for current music publishing

purposes, and to effectively manage growing portfolios for reissuance and other

7

publishing purposes such as licensing. The music industry as a whole has been

suffering greatly from a seven-year decline in CD sales, and this decline took an

even stronger downturn in the first three months of 2007, falling 20% from a

year earlier.ii CDs still account for 85% of all music sold, and sliding sales are

eclipsing gains in sales of digital downloads. Falls in CD sales are the result of a

number of factors, including consumer substitution, piracy, cross-price

competition with DVD purchases, and the closing of a number of prominent

specialty CD retailers such as Tower Records. In 2006, about 800 music stores

were closed, including Tower’s 89 locations.

As the industry contracts, firms looking to maintain market share often seek to

acquire competitors or merge. The 2005 merger of Sony’s music arm and BMG,

as well as the on-again, off-again negotiations between WMG and EMI, may be

seen as a response to market pressure. Recently accelerated merger activity may

continue in the future as profit margins fall due to piracy, and consolidation of

market power will have a significant impact on both output and pricing.

Demand for WMG’s products is highly elastic, with competition from other media

such as DVDs, satellite radio, and illegal copies of both digital and physical goods.

Consumers have low switching costs, as purchase of one firm’s CD or MP3 does

not preclude purchase of other firms’ products in the future. What brand loyalty

is available to WMG is a direct result of loyalty to artists under contract, and as

such it is important that WMG continue to augment and cultivate its talent pool.

To hedge against unpredictable shifts in consumer taste, WMG has invested in a

wide range of music, including hip-hop, country, jazz and classical.

Internationally, WMG and its competitors are invested in promoting both

Western and local music groups. As each of WMG’s competitors has a similar

portfolio, it is unlikely that WMG can reliably leverage exposure in a particular

genre into increased profits. The value of each music publishing firm is based

primarily on the intangible value of the firm’s music portfolio and retinue of

artists and intellectual property. Firms can to increase the value of their

portfolios through discovery of artists, or through acquisition of current artists

8

through management changes or mergers and acquisition. To illustrate, in 2006

WMG acquired both Ryko Corporation ($675MM) and the Roadrunner music

label ($74MM).

Protecting and increasing market share depends primarily on consumer

purchasing decisions, and therefore successful marketing and advertising is very

important. Advertising and marketing not only increases awareness of the

publishing firm’s artists, but may also lower price elasticity among consumers by

ensuring loyalty among listeners.

The relative strengths of various music firms in the digital marketplace have yet

to be determined. As the volume of CD sales continues to fall, the importance of

digital goods (and digital pricing) will become more important. The distinct

nature of digital goods, as well as lack of any excessive property or equipment

investment, implies that market dominance will not necessarily go to the firm

with the deepest pockets but to those who are able to achieve technological lock-

in first. To achieve this lock-in, firms seek a first-mover advantage, marketing a

superior technology early enough to capture the network size necessary to

discourage competition.

Cooperation between firms directly and through the Recording Industry

Association of America (RIAA) has become increasingly important in the industry

as new standards for digital goods are agreed upon and legal positions are taken

to protect the companies from erosion of intellectual property rights. Currently,

the major firms are taking a united stance against music piracy and are

attempting to resolve the fate of digital rights management (DRM) technology. It

is in the interest of all major firms involved to promote legal sales over illegal

copies or file-sharing.

Time Warner spun off WMG in 2003 because the parent firm was having

difficulty keeping the division profitable. WMG’s new owners have responded to

falling sales volume and downward pressure on prices by aggressive cost-cutting,

a strategy common among its competitors. WMG specifically underwent

9

restructuring initiatives in 2005 and 2006, and reduced annualized operating

costs by $250 million in 2005. Included in these cuts were significant headcount

reductions from consolidation of operations, streamlining corporate and label

overhead, as well as exiting leased facilities to consolidate manufacturing and

physical distribution.

The maturity of the music publishing industry in physical sales implies that

future gains in market share must come at the expense of competitors. Though it

is unlikely that any firm will greatly increase market share by increasing physical

sales of CDs or records, the creation of new products (such as ringtones, online

videos, and other special ‘perks’ such as bundled DVDs) may open new markets.

Additionally, firms may choose to increase their market share through mergers

and acquisitions, though the already high concentration of industry sales implies

that anything short of a high-level merger is unlikely to significantly affect market

shares.

In digital media, the iTunes is the preeminent online retailers of MP3s, although

some competition has emerged from rival firms such as Napster, Rhapsody and

Urge. There also exists an opportunity for music publishers to market their music

directly online (through artists’ websites, for example) as an alternative that

might allay price-pressure from online retailers and perhaps even institute

variable pricing in order to recapture the producer surplus that was common

when sales of “singles” were popular. The price discrimination that major labels

once enjoyed has been lost under Apple’s $.99-per-track system. Continued

growth of legal download services such as iTunes is important to combat piracy,

however consumers are increasingly downloading tracks legally for free from

artists’ MySpace pages from other sources such as MP3 blogs.

Digital sales of individual songs in 2007 have risen 54% from a year earlier to

173.4 million. Concurrently, CD sales fell 20% to 81.5 million units. Overall sales

of music are down 10% this year (physical and digital). Even including sales of

ringtones, subscription services, and other “ancillary” goods, sales are still down

10

9%.iii Going forward, overall market growth will depend on continued expansion

of the digital market.

Possible growth opportunities abroad are being investigated by WMG, driven by

positive sales growth in Japan in 2006. However, most emerging markets have

the drawback of widespread physical piracy and the difficulty of enforcing

property rights makes them an unreliable source of future income. The advantage

of international expansion is that the appeal of American artists abroad may

translate into lower price elasticities and opportunities for higher profit margins.

In the future, CDs may become no more than advertising for more lucrative

ventures such as concert tickets and t-shirts. If the CD or the MP3 becomes more

of a marketing device than a vital source of revenue, it will alter the nature of the

music business completely. Strategies for this contingency are discussed below in

the Recommendations section.

EENTRYNTRY

WMG’s market is characterized by large fixed costs and as such there is little

movement in and out of the top echelon of firms. While there are many mid-sized

and smaller players in the industry (including independent music companies),

their limited size and scope suggests little risk to WMG.

In the more broadly defined entertainment market, the role of WMG as a media

distributor may be eroded in the long run as the proliferation of decentralized

music sharing programs continues and consumers choose to purchase other

forms of media, such as DVDs.

A new entrant to the industry would have to offer the same level of quality as

existing firms, and given the value of reputation in the business, along with the

positive cross-market benefits of signing with a firm that has a proven track

record of successful marketing, it is unlikely that new firms will appear to

challenge WMG. New competitors would also have to spend a disproportionate

amount of money on marketing and advertising to entice artists to switch labels.

11

There are significant benefits due to economies of scale and scope, as digital

music sales feed off of radio airtime and CD sales, and vice versa.

Economies of scale also exist in production, marketing and distribution. Lastly,

potential entrants would almost immediately face acquisition by the major firms,

which has been the manner in which the big four firms have managed to

maintain such a large consolidated market share. Threat of entry by another

major player is low. Entry by smaller players is a lesser threat due to the option of

acquisition by larger firms.

While consumers may not choose music by the artists’ label, artist look for labels

that have established successful reputations at marketing and promotion through

radio deals and music videos, for example, and thus there is an inherent

advantage in reputation in discovery and acquisition of new talent. The major

players have also established a system of recruitment that is designed to acquire

not only the best talent, but also the best talent scouts, and this makes it even less

likely that a smaller entrant will be able to compete successfully with the larger

firms in the long run.

SSUBSTITUTES AND UBSTITUTES AND CCOMPLEMENTSOMPLEMENTS

The threat of substitutes is significant for WMG, and for the music publishing

industry in general. Illegal piracy produces almost identical products at zero

marginal cost, and as such poses a serious threat to the valuation of industry’s

intellectual property portfolios.

The cost of illegal copying is expected to grow in both the short and long-term, as

the quality of illegal copies increases and converges to that of legal goods sold.

This poses a problem because they are direct substitutes, and as such can put

downward pressure on the prices that labels can charge without alienating their

customer base. A number of economic models exist which contend that producers

can incorporate the value of future copies into the original sale price of a digital

good, thus capturing the costs of illegal copies, however given the growing price

12

elasticity of demand among consumers it is unlikely that producers will try this

tactic anytime soon.iv This growing elasticity implies that the negative affect on

volume sold will outweigh the positive effect of increased price per unit.

Internationally, piracy issues exist on a wider scale. Though digital piracy online

may not be as widespread in countries with less developed high-speed internet

and data networks, less effective copyright enforcement abroad, especially in

Asia, has led to a proliferation of illegal pirated copies of CDs and other physical

goods. To maintain prices and distinguish their products from illegal copies, the

major labels have acted in concert and through the RIAA to launch marketing

campaigns emphasizing the negative effect of piracy on artists’ incomes, and

stressing the legal ramifications of copyright violations.

In the United States, the majority of industry effort to deter piracy has been

concentrated in pursuing legal and regulatory measures, as well as employing

technological barriers to piracy. WMG in particular has instituted a campaign to

educate potential copyright violators about the unambiguous illegality of their

actions. Though WMG cites the success of this campaign over the years 2005-

2006, any reduction in reported abuse based on survey data might be merely the

result of increased reticence on the part of survey-takers to admit any

wrongdoing. The success of WMG’s legal battles depends ultimately on the

deterrent effect or secondary, word-of-mouth influence that lawsuits have on

consumers. In 2006, one billion songs were traded monthly on illegal file-sharing

networks, compared to the 173.4 million songs purchased legally during the

entire year.v

The use of DRM technology has been somewhat effective in curbing individual

file-sharing, though a number of consumer complaints have arisen due to

incompatibility between different firms’ DRM technology and various MP3

players. In April 2007, EMI announced that it would begin selling unprotected

MP3 files on iTunes for $1.29 per track, explicitly to avoid these compatibility

issues, as well as to offer higher quality music with the same file size. The high

likelihood that the other firms will follow suit makes future innovation or

13

cooperation in DRM technology uncertain, at least for the type of music files

currently in use.

Another main substitute that has been cited by some as the cause of the recent

CD sales decline is the growth of DVD sales over the same period. DVDs are an

imperfect substitute for CDs, however the two markets do affect each other by

occupying similar spaces in consumer budgeting. Music labels have responded by

researching new CD formats that would offer music enthusiasts new compelling

features (such as including videos of live performances). With technologies such

as DualDisc, DVD-Audio and SACD, labels are offering better-than-CD quality

stereo audio and high-quality surround sound, as well as promoting free digital

music downloads with a physical purchase. These features are also being touted

to address competition with satellite radio, another substitute for CD and MP3

sales.

Demand for music is not only dependent on incomes, but also depends on radio

penetration, access to music clubs, movies, etc. For example, movie soundtrack

sales are directly linked to the popularity of the movie.

There are a number of complementary markets for music. The success of 3G cell

phone networks in the US will determine how many ringtones and music

downloads Warner is able to sell to potential customers. WMG currently has a

partnership with Motorola to provide content for the “MOTO Experience Pack.”

Motorola’s revenue grew 21.6% in 2006, and gross profits grew 11.36%. Motorola

is expanding aggressively, and through its partnership WMG will benefit from

increased market exposure. The profitability of legal online music providers like

iTunes and Napster is also important for ensuring a legal alternative to piracy

continues to exist. Websites such as YouTube that offer free access to music

videos on demand can also spur demand through network effects.

14

SSUPPLIER UPPLIER PPOWEROWER

Labels offer a fair amount of value added through production, remastering,

packaging, tours, music video and ring-tone production, and therefore should

continue to maintain consistent margins. However, as they operate in a superstar

business, some artists may have localized effects through negotiation of

contracts, royalties, and album advances. As the revenue expected from CD sales

continues to fall, contract renegotiation with artists may become a bigger issue.

WMG’s physical music business relies almost entirely on contracts with Cinram,

a compact disc manufacturer that was also spun-off from Time Warner when

WMG was sold to Bronfman. Previously, Time Warner’s CD production was all

in-house, and therefore was not subject to the same market effects that WMG

deals with today. Contracts with Cinram begin to expire in 2007 vi and it is

unclear at this point what effect price negotiations will have on operating costs.

The market for physical inputs is competitive and market determined, and given

the declining importance of the CD medium it is unlikely that Cinram or other

suppliers will be able to hold WMG “hostage” through contract negotiation. As

WMG continues to look for cost-cutting opportunities to compensate for volume

losses, future contracts with suppliers will no doubt be targeted. Unless mass

production of music DVDs become commonplace, there are few if any substitutes

for CDs. Digital goods can be produced in-house for the most part, and thus the

growing importance of digital sales will decrease the risk of supplier power.

Negotiations with artists can often lead to unexpected costs, and artist advances

account for a significant amount of operating expenses. Although firms can be at

the mercy of new, popular artists who may threaten to change labels, the longer a

musician is under contract with a firm, the more of the artists’ catalog is owned

by the firm and thus greater leverage is available to the firm. Up-and-coming

artists have little bargaining power and increased firm leverage, as well as

personal relationships, is responsible for a fair amount of artist loyalty later in

their careers.

15

There is little threat of forward integration of suppliers into the product market,

due to the differences between the two businesses, as well as the barriers to entry

mentioned earlier.

BBUYER UYER PPOWEROWER

The effects of buyer power are becoming more important as WMG’s distributors

become increasingly concentrated in both the CD and MP3 industries. As CD

sales are in an increasingly concentrated number of retail stores such as Wal-

Mart and Target, these “big box” retailers have leveraged that power to drive

down prices. Growing buyer power has put increased pressure of WMG’s

operating margins. A merger with EMI might help to alleviate the problem. Wal-

Mart has significant power to control the prices of products it purchases for

resale, and can pull products or give preferential treatment to competitors if a

company is unwilling to cooperate. A merger with EMI may help to alleviate this

problem to the extent that Wal-Mart would have fewer alternatives with which to

threaten WMG.

Online, iTunes is responsible for the vast majority of WMG’s online sales, and as

such has a significant amount of power over determining track pricing. As online

music sales continue to grow in popularity, it is possible that more alternatives to

iTunes may become available, including the marketing and sale of MP3s by the

labels themselves on their own or artists’ websites. This would significantly

decrease the amount of buyer power online. Songs purchased on iTunes use

Apple’s propriety version of DRM, known as “FairPlay,” which makes songs

purchased from rival online stores using different DRM technologies

incompatible with iPods. After the recent announcement that EMI will be selling

DRM-free MP3 downloads through iTunes, it is unlikely that iTunes will be able

to exploit its monopoly on iTunes-compatible DRM for much longer.

The ability to buyers to recognize weakness on the part of music publishers

depends in part on how the industry reacts to falling CD sales volumes. If it

becomes apparent that the industry may move away from physical formats, then

16

there is less opportunity for suppliers to benefit, but if the industry recommits to

CD sales and promotion, then buyers may negotiate harder.

SWOT ASWOT ANALYSISNALYSIS

Strengths

• Large firm, diversified labels (Atlantic, Elektra, Rhino)

• Strong artist portfolio in a number of genres

• Aggressive positioning vis-à-vis the digital music business and related new

markets

• Successfully restructuring to cut costs

• Low threat of entry by new firms

• High value added

• Growing exposure to worldwide markets (also a negative)

Weaknesses

• Declining CD retail environment, low growth opportunities

• Main product is becoming non-rival, non-excludable.

• Must make strategic acquisitions for growth

• Low switching costs for consumers

• Costly legal and regulatory issues

• Highly leveraged ($2.26b in debt)

• Pricing issues with iTunes and Wal-Mart

• Subject to unpredictable changes in consumer preference

Opportunities

• Recorded Music digital revenue may offset declines in Recorded Music

physical revenue.

• Room for international growth

• Development of new digital markets, new technologies

• Streaming media, paid for by advertising

17

• CDs can be unbundled into ringtones, video downloads, etc. allowing for

more variable pricing

Threats

• Illegal copying, both physical (developing countries) and digital (US and

Europe)

• Increased ease of piracy given ubiquity of computer technology and the

Internet, as well as P2P services.

• No room for increased leverage

• Challenges from DVD industry and other non-music substitutes

• Unpredictable cash flow

• Growth is contingent on complementary markets (3G phones, YouTube,

iTunes, etc.)

• Unfavorable litigation outcomes, high legal fees.

FF INANINANCIAL CIAL IISSUESSSUES

The Recorded Music business consists of the discovery and development of

artists and the related marketing, distribution and licensing of recorded music

produced by such artists. In addition to the more traditional methods of

discovering and developing artists, firms often grow their music portfolios by

acquiring competitors and smaller labels that cater to niche markets. Below we

will look at some of WMG’s most recent performance data, then address the

financial issues surrounding it’s large debt levels and a potential merger with

EMI.

Warner’s market capitalization, at $2.54 billion, is significantly below that of

Universal and Sony BMG, both of which benefit from parent companies that

dwarf WMG in size (Sony Corp. currently has a market cap of $55.5 billion).

Warner is also relatively smaller than rival EMI, which has a market cap of $3.5

billion as of March this year. Warner’s smaller size is a liability when attempting

to negotiate future partnerships with mobile phone companies, music retailers,

18

and internet groups. Potential strategic partners, in search of stability, may look

to WMG’s larger competitors for more lucrative contracts.

Warner’s price-to-earnings ratio, at 279.8, is extremely high, and may reflect high

expected growth in the future. More likely, this is the result of takeover

expectations, or is due to the recent drop in earnings, which lowered the

denominator sharply. Such a high P/E ratio may also account for the steadily

declining share price observed recently.

First quarter performance was disappointing in 2007, as profits fell 74% due to

fewer albums released during the period and soft domestic and European sales.

The importance of first quarter performance cannot be understated, as it

represents holiday sales and typically accounts for 32% of all sales. Net income

declined to $18 million, or 12 cents per share, from $69 million, or 46 cents per

share, during the same period a year ago. Such a drop in profit margins may

abate as cost-cutting efforts come into effect, or as digital revenues begin to pick

up later in the year. Total revenue fell 11% to $928 million from $1.04 billion

during the prior-year period. WMG announced that 2007 results would be

weighted to the back end of the year.

Digital revenue of $100 million in 2006 grew 45% from $69 million in the prior-

year quarter, but slid 4% from $104 million in the fourth quarter of 2006. Digital

revenue was 11% of total revenue and 17% of total domestic recorded music

revenue. Revenue for WMG's recorded music business decreased 13% to $800

million on softer domestic and European sales. On a positive note, CEO

Bronfman also noted that Warner gained market share during the quarter.

This digital shortfall may cause some analysts to reconsider their future revenue

estimate. "Our valuation model assumes continued deterioration in physical

sales, but a much higher future growth rate for digital sales," said Morningstar

analyst Jonathan Schrader after the 1Q results. "Given this, we'll be revisiting our

growth assumptions and probably lowering our fair value estimate."vii Other

reports predict that earnings will climb for the remainder of the fiscal year, and

19

physical sales will deteriorate to a much lesser extent than in the December

period. These optimistic reports assume much-improved sales figures due to the

release of numerous CDs and DVDs during the March quarter, so second-quarter

results should be valuable for predicting the rest of the year’s performance.

WMG’s continued expansion into new music on mobile phone and online formats

should further enhance sales. Analysts are relying on growth in digital sales to

fuel improved results, and margin expansion should also benefit from a

heightened level of digital sales. This will be offset partly by price declines on

CDs.

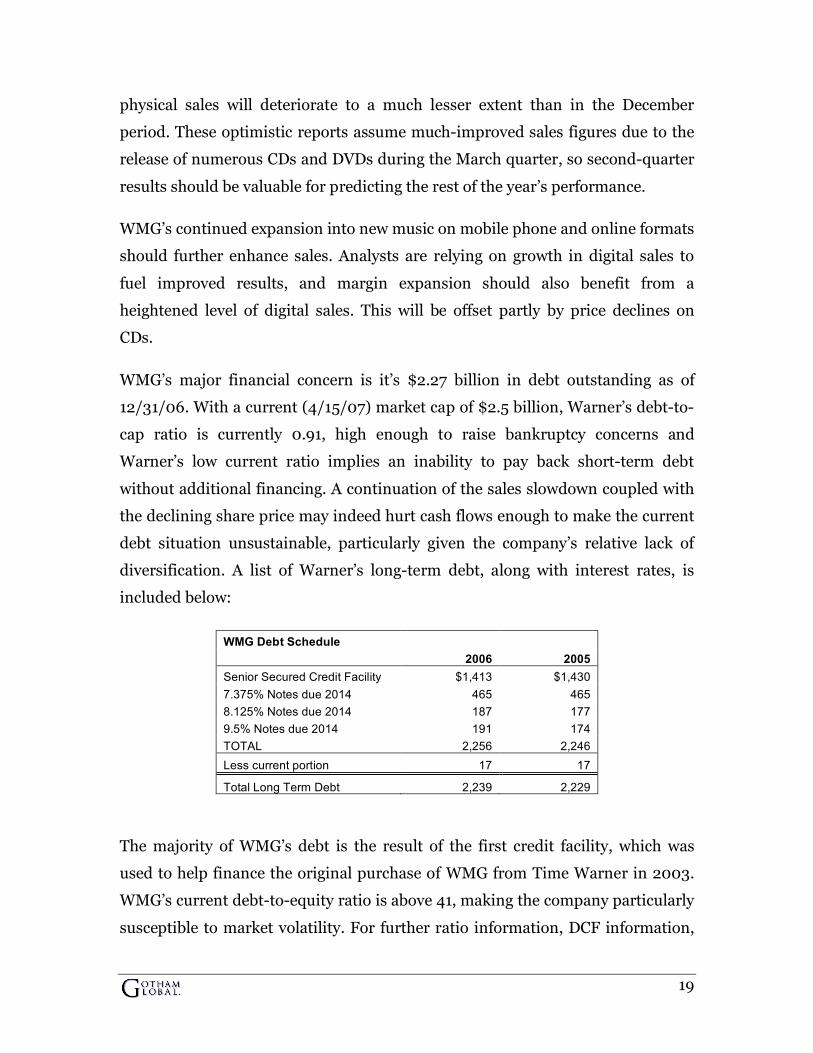

WMG’s major financial concern is it’s $2.27 billion in debt outstanding as of

12/31/06. With a current (4/15/07) market cap of $2.5 billion, Warner’s debt-to-

cap ratio is currently 0.91, high enough to raise bankruptcy concerns and

Warner’s low current ratio implies an inability to pay back short-term debt

without additional financing. A continuation of the sales slowdown coupled with

the declining share price may indeed hurt cash flows enough to make the current

debt situation unsustainable, particularly given the company’s relative lack of

diversification. A list of Warner’s long-term debt, along with interest rates, is

included below:

WMG Debt Schedule 2006 2005 Senior Secured Credit Facility $1,413 $1,430 7.375% Notes due 2014 465 465 8.125% Notes due 2014 187 177 9.5% Notes due 2014 191 174 TOTAL 2,256 2,246 Less current portion 17 17

Total Long Term Debt 2,239 2,229

The majority of WMG’s debt is the result of the first credit facility, which was

used to help finance the original purchase of WMG from Time Warner in 2003.

WMG’s current debt-to-equity ratio is above 41, making the company particularly

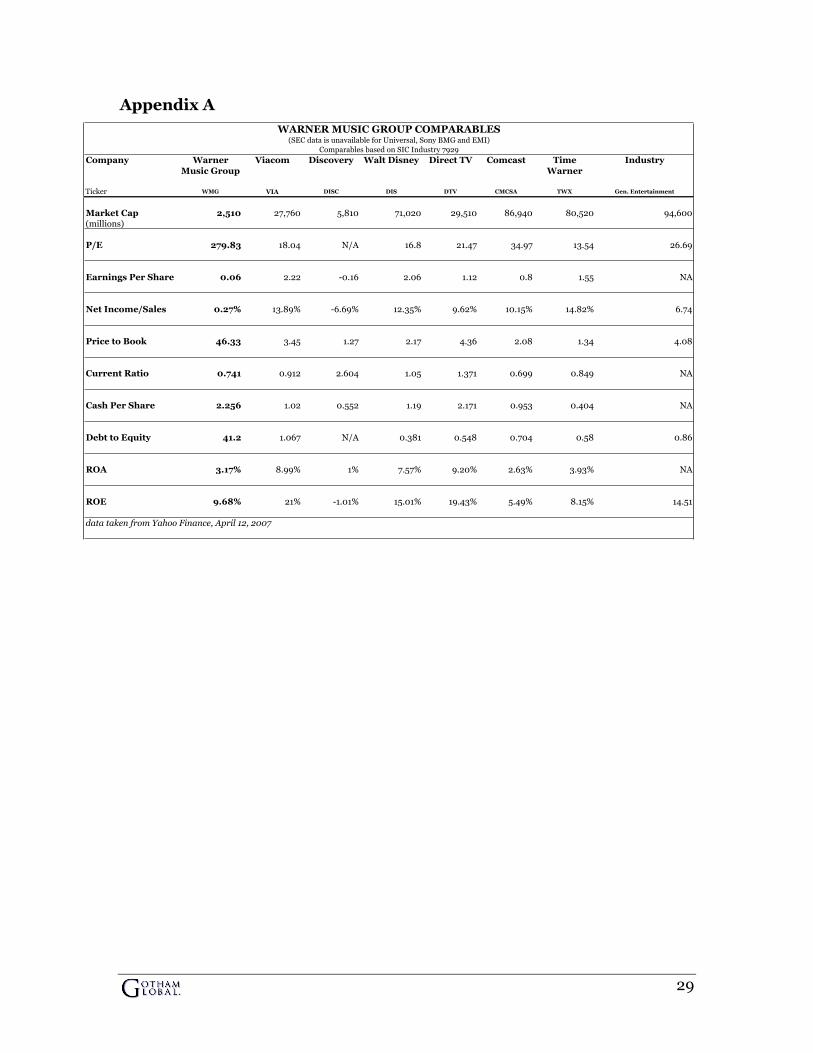

susceptible to market volatility. For further ratio information, DCF information,

20

and comparables with other US-based companies registered under SIC 7929,

please refer to Appendix A.

WMG’s S&P corporate credit rating of ‘BB-‘ was put on S&P’s CreditWatch with

negative implications following the announcement of the potential acquisition of

EMI in February. Despite analysts’ opinions that the synergies from such a

merger would exceed $150 million per year, the question of how Warner would

finance such a deal overshadowed future benefits. Warner’s most recent offer of

$4.1 billion in cash would most likely have required the company to not only take

on more debt but also to sell off some of its assets to raise the necessary funds.

Though WMG is again beginning to make operating profits (EBITDA), interest

expense is incredibly high. In 2006, interest expense was $180 million, down

from $182 million in 2005. With a reported $337 million in cash, Warner is

spending over half of it on interest payments.

Investment interest in WMG may be generated by speculation on the potential

sale of the company, given that growth prospects are not particularly strong and

previous results have been unsatisfactory. Digital sales may well increase to about

25% of industry sales by the 2009-2010 timeframe, however, and successful

positioning may make WMG a stronger company in the future than it is now. viii

SSTRATEGIC TRATEGIC IISSUESSSUES

WMG has been seen increasingly as an inadequate stand-alone company that

would benefit immensely from either acquiring EMI or being acquired itself.

WMG has twice entered negotiations with EMI, with a $4.7 billion dollar offer in

2005 and a $4.1 billion dollar offer in February this year. Though both offers

were rejected, the regulatory uncertainty that was given as a reason will likely be

cleared up by the end of the year and new merger negotiations may be more

successful.

The viability of the merger hinges on the outcome of the European Commission’s

investigation of the 2004 merger between Sony and BMG. EU courts threw out

21

regulators’ approval of the merger that created Sony BMG in 2004, saying the

European Commission, the EU’s antitrust regulator, had only carried out “an

extremely cursory examination” of the effects of the merger.ix The court ordered

the regulator to review the case again, and to present findings on March 1, 2007.

WMG’s second offer to EMI was made before the committee’s expected ruling on

March 1st, but was rejected when the committee postponed its ruling until July 1,

2007. In the process of courting EMI in 2007, Warner gained the support of the

Independent Music Publishers and Labels Association (IMPALA), an influential

group representing over 3500 independent music publishers. This blessing came

after Warner’s promise to divest “certain recorded music assets” and promising

to fund a digital rights management system for independent recording labels.x

The regulatory risk of a possible merger will be much clearer following the EU

review of Sony BMG, though the profitability of such a merger must not take into

consideration not only cost-savings but also the effects of any promised

divestitures. xi There has been some concern that the “distraction” of a potential

merger has been having a negative effect on management’s ability to handle day-

to-day operations.

One of Warner’s major handicaps is the lack of diversification in its product

portfolio. While competitors Universal and Sony BMG offer a wide range of

products that allows for cross-subsidization through other media formats such as

movies and video games, the lack of transfer-pricing opportunities and over-

weighted exposure to a volatile music market is troublesome. Because of the

importance of quickly increasing network exposure in capturing rents from music

that is current in vogue, Warner must rely on other companies to help it market

its contemporary music portfolio effectively. Time Warner, the parent company

of WMG before its sale in 2003, no longer holds an equity stake in the company,

and thus it is unlikely that Warner will benefit from any better-than-market

offers for services to Time Warner’s television or film divisions. Transitioning from a focus on CD sales to digital media sales will be a tricky issue

for WMG. Compact discs were originally rival, excludable goods, and as such it

22

was a simple matter for their provision to the market. With the advent of new

technologies, both CDs and MP3s can be reproduced at zero marginal cost by end

users, and thus the good has become non-rival and non-excludable (in short, a

public good). WMG will need to address this issue when determining pricing in

the years to come. Strategically speaking, WMG’s objective is to maintain the

excludability of their music goods, and market them as an artificially scarce good.

To achieve this, WMG has considered technological, legal, and educational

solutions.

One method of technological exclusion has been through the utilization of DRM

software designed to impede potential copyright violations, but a lack of

cooperation between the various firms involved (Sony, Microsoft, Apple, and

WMG’s major competitors) has led to an ineffective and unpopular system of

incompatible file formats (see Apple CEO Steve Jobs’ “Thoughts on Music” from

Februaryxii). The creation of a uniform, mutually compatible DRM system may be

the most effective short-term solution for dealing with MP3 sales issues. WMG’s

CEO has reaffirmed WMG’s commitment to DRM technologies multiple times in

the last few weeks. Bronfmann also insists that music deserves the same anti-

piracy protections as software, TV, broadcasts, video games and other forms of

intellectual property. Despite what music may “deserve,” however, market

realities may force WMG to act.

These market forces appeared on April 2, 2007, when WMG rival EMI

announced that the company would begin offering DRM-free music downloads

online through iTunes. Citing market research that downloads of non-DRM

tracks are more popular than their DRM counterparts by a factor of ten, EMI

plans to release music that not only offers unrestricted personal copies, but also

improved quality, as file size previously reserved for DRM software has been

appropriated to improving the audio bitrate, a proxy for audio quality. Most

importantly, the elimination of DRM from EMI’s music downloads will eliminate

compatibility issues between music players, making EMI’s music files more

desirable for consumers concerned with playing their music on multiple players

23

of different brands. This radical step will force a response on the parts of EMI’s

competitors, including WMG. For more discussion of WMG’s options regarding

DRM technology, refer to the Recommendations section below.

WMG is relatively well positioned in the digital music market today, and was the

only major music publishing firm with a higher digital album share above

physical album share in 2006. WMG’s digital sales doubled in 2006.

Legal options to control piracy are also available. Traditionally, music publishing

companies have limited themselves to lawsuits against providers of illegal

software that enables or benefits users engaged in music piracy. In 2005 WMG

received $19 million as part of an out-of-court settlement with Kazaa, Inc.

(“Kazaa”) and will likely continue to pursue legal avenues against other providers

of file-sharing programs such as LimeWire, BitTorrent, and also apply pressure

to colleges and universities that do not tightly regulate internal file-sharing. As of

writing, WMG is also involved in litigation regarding radio promotion activities

and pricing of digital music downloads, but these do not seem to pose a large

operating risk.

More recently, WMG, along with its competitors and the RIAA, has begun suing

individual users of peer-to-peer (P2P) networks who violate music copyright

issues. The difficulties of suing individual users, as well as the lower value of

settlements imply that the marginal benefit of these lawsuits may be less than the

cost of legal fees associated with them. Even suing the program providers has

proved difficult, as the companies are registered off-shore and use servers based

in countries with particularly lax digital property laws such as the Netherlands.

Lastly, WMG has used marketing and educational campaigns to deter would-be

music pirates by stressing the impact on future artists and the serious legal

consequences of piracy. Though WMG reports success in deterring piracy based

on poll data taken between 2005 and 2006, it is unclear whether this is a result of

an actual reduction in piracy or merely a lower reporting rate due to increased

awareness of those same legal ramifications.

24

Lastly, it is not clear whether or not WMG will be able to maintain current prices

while dealing with an increasingly consolidated distribution network in both

physical and digital goods. Buyer power on the part of Wal-Mart will continue to

limit the ability of WMG to sell popular artists’ releases for a premium, and

Apple’s restrictive $.99 cent track restriction on iTunes has caused the RIAA to

protest publishing companies’ inability to use differential pricing for popular

artists, albums and songs. This limits the firms’ ability to capture the greater

consumer surplus associated with newer releases.

RRECOMMENDATIONSECOMMENDATIONS

First and foremost, WMG must address its current competitive situation vis-à-vis

its major competitors. Takeovers of rivals and smaller labels are not uncommon

in this market, and WMG’s overtures to EMI are grounded in solid economics.

WMG’s smaller size and heavy debt load, however, make it unclear whether it will

acquire EMI or vice versa. It is clear, however, that no major mergers or

acquisitions will occur until after the European Commission reaches its

regulatory decision on Sony BMG in July of this year. Assuming that regulators

do not attempt to unravel two years’ worth of cooperation between Sony and

Bertelsmann, we recommend that WMG again attempt to acquire or set itself up

for acquisition by EMI. Should performance in the second quarter exceed

expectations, it may be possible for WMG to acquire EMI, though it will require

the divestment of significant assets on Warner’s part. Such a merger will be

beneficial to both companies, with synergies estimated at $150 million.xiii Also

important is the increased bargaining power that a combined firm will have with

major retailers. By not competing with each other, a combined firm should be

better able to compete with Universal and Sony BMG, and will improve profit

margins through stronger negotiations with iTunes and Wal-Mart as well as

improved cross-marketing for each firm’s top artists.

It is important that WMG continue to maintain strong relationships with major

retailers, particularly Wal-Mart and Target. Early consumer exposure is crucial to

25

protecting market share, and being squeezed out of the retail market would be

fatal to Warner’s physical CD sales. Unlike Sony or Universal, Warner does not

have alternative in-house avenues to promote its music such as movies and video

games. Going forward financially, it is paramount that WMG continue to increase

revenue growth rates while reining in cost growth. To do this, partnerships with

international firms such as Motorola will also help to shield WMG from volatility

in domestic markets.

Warner is the only stand-alone music publishing company publicly traded in the

United States. The prestige of such specialization is short-lived, however, and

WMG’s lack of diversification in different media such as movies and video games

is a liability, as WMG is unable to exploit transfer pricing opportunities or use

other outlets to promote its music portfolio. Although it would be premature to

suggest that WMG look to acquiring alternative media companies, we

recommend the company redouble its efforts to establish relationships with film

companies as well as with internet and entertainment firms (Microsoft,

Nintendo, iTunes alternatives). After a merger with EMI, we also recommend

continued product diversification, as well as possibly establishing joint ventures

with other media companies.

The key to WMG’s success in the next few years is going to be its ability to capture

a larger share of the faster growing sectors of digital music goods, particularly

MP3s and ringtones. There are still a number of competing business models

online, from paid downloads such as iTunes offers to free download services that

only require a user watch paid advertising. Universal is cooperating with

Spiralfrog.com to offer one of the latter services, and ABC.com has been using

such a model successfully with its television programming.

EMI’s recent decision to offer unprotected music downloads is the most pressing

strategic issue for WMG. If EMI’s marketing data is correct and sales of

unprotected songs will increase dramatically, it may become impossible for WMG

to compete online through iTunes without following suit and abandoning DRM

technologies, or at least offering two-part pricing for DRM and non-DRM

26

versions of the same songs. The previous possibility of a universal DRM for all

publishing companies is no longer a viable solution for resolving compatibility

issues with MP3 players. If WMG chooses not to abandon DRM, they may also

suffer the marketing risk of being singled out as a music company that only offers

lower quality music downloads. EMI’s new pricing strategy will go into effect in

May 2007, and we recommend WMG enter into negotiations with Apple as soon

as possible so that WMG will be able to follow suit if EMI’s strategy is successful.

It is unclear what the effect of the price increases (from $.99 to $1.29) will be.

Some economic theorists argues that the price of an unprotected MP3 reflects the

present value of all future copies that end-users will ultimately make, however

this is extremely simplified. It is more probable that users are willing to pay a

higher price to ensure that there will be no compatibility issues with their MP3

players. One should appreciate the irony that the best strategic response for a

firm selling an artificially scarce good would be to make it even more susceptible

to piracy. This unlikely result is due to the rational realization of the major music

labels that DRM-protected MP3s represent a very small share of the entire MP3

market, and that correcting compatibility issues is important for ensuring

network growth.

While CD sales will continue to make up the majority of WMG’s revenue, it is

possible that the market is in terminal decline. While some argue that the nature

of the CD has changed fundamentally to one of advertising for more profitable

music concerts and ancillary merchandise sales, it is important that WMG

maintain its cash flow from CD sales for as long as possible. It will not hurt,

however, to begin thinking beyond the CD as a major revenue source to how it

can be used most effectively as an advertising tool.

To promote Warner’s music portfolio, we also recommend that Warner work with

Apple to sell iPods with selected artists’ music pre-downloaded. A similar strategy

was followed by popular band U2 with the release of the iPod U2 Special Edition.

The advantage of this strategy is that early exposure to a limited set of WMG’s

artists with a user’s purchase of an iPod will increase the chances that users will

27

pay for downloads through iTunes. Additionally, WMG could provide a few tracks

of select artists for free, and offer iPod users discounted prices for full album

downloads through iTunes. Like cooperating with big box retailers, it would be

wise for WMG to ally itself with successful online music providers.

The strategic benefits of continued litigation are unclear. A cursory cost-benefit

analysis of the current strategy of ‘shotgun’ lawsuits against heavy users of

pirated music on college networks and at home shows that the legal fees and

negative publicity being generated by the lawsuits far outweighs the actual

benefits. Given the continuing minute probability that music pirates will actually

be caught, the perceived risk is so low that these lawsuits do not provide an

adequate deterrent effect.

Despite the ineffectiveness of lawsuits against individual users, we do

recommend that WMG, either unilaterally or through the RIAA, attempt to work

with larger communities such as universities and offices to better regulate their

internet traffic. As it stands, most universities do not monitor file-sharing on

campus intranets, where most piracy occurs. An interesting precedent is being set

by Napster, which has signed exclusive deals with a number of universities to

provide free music download service to students, paid for by the university. This

may be a cost-effective way of weaning students and other high-risk groups from

illegal file-sharing. We recommend that WMG abandon or seek swift resolution

of outstanding individual lawsuits, while concentrating efforts on major user

networks where a greater impact can be had at equal or lesser cost.

Other attempts to internalize the cost of music piracy have been less successful.

The RIAA has attempted to recover the cost of illegal downloads by requiring

buyers of audio hardware such as MP3 players and CD burners to pay a royalty

fee. However, this tactic seems unlikely to be successful in major markets, and

has met with regulatory disapproval in Europe.

WMG should also investigate alternative models of music sharing. Innovative

digital distribution may allow Warner to capture a larger digital market share

28

than its competitors, regardless of their current market capitalization. To save the

music industry, companies must find a successful business model that allows

companies to maintain profitability while encouraging more consumers to

eschew piracy for legal downloads. Some other formats, such as ad-supported

music videos on artist websites or revenue-sharing plans with user-generated

media content providers such as YouTube or MySpace may also be profitable

ventures.

Lastly, international expansion is becoming an increasingly pressing issue.

Although Warner’s international labels have been performing relatively well,

there are a number of factors that will affect the extent to which the company

should expand internationally. In developed markets such as Europe and Japan,

the maturity of the 3G cell-phone market makes competition fierce. We

recommend that Warner ally itself with industry leaders in relatively advanced

markets to promote its portfolio, but we do not recommend any major unilateral

investment. In the most promising developing countries such as China and India,

profitability is contingent on the strength of intellectual property rights

protection. We recommend that major expansion into developing countries be

taken on a case-by-case basis, after ensuring that stability and enforceability of

digital property rights has been established. The importance of capturing market

share in developing economies cannot be underemphasized for ensuring long-

term growth.

29

Appendix A

Company Warner

Music Group

Viacom Discovery Walt Disney Direct TV Comcast Time

Warner

Industry

Ticker WMG VIA DISC DIS DTV CMCSA TWX Gen. Entertainment

Market Cap 2,510 27,760 5,810 71,020 29,510 86,940 80,520 94,600(millions)

P/E 279.83 18.04 N/A 16.8 21.47 34.97 13.54 26.69

Earnings Per Share 0.06 2.22 -0.16 2.06 1.12 0.8 1.55 NA

Net Income/Sales 0.27% 13.89% -6.69% 12.35% 9.62% 10.15% 14.82% 6.74

Price to Book 46.33 3.45 1.27 2.17 4.36 2.08 1.34 4.08

Current Ratio 0.741 0.912 2.604 1.05 1.371 0.699 0.849 NA

Cash Per Share 2.256 1.02 0.552 1.19 2.171 0.953 0.404 NA

Debt to Equity 41.2 1.067 N/A 0.381 0.548 0.704 0.58 0.86

ROA 3.17% 8.99% 1% 7.57% 9.20% 2.63% 3.93% NA

ROE 9.68% 21% -1.01% 15.01% 19.43% 5.49% 8.15% 14.51

data taken from Yahoo Finance, April 12, 2007

WARNER MUSIC GROUP COMPARABLES

Comparables based on SIC Industry 7929

(SEC data is unavailable for Universal, Sony BMG and EMI)

30

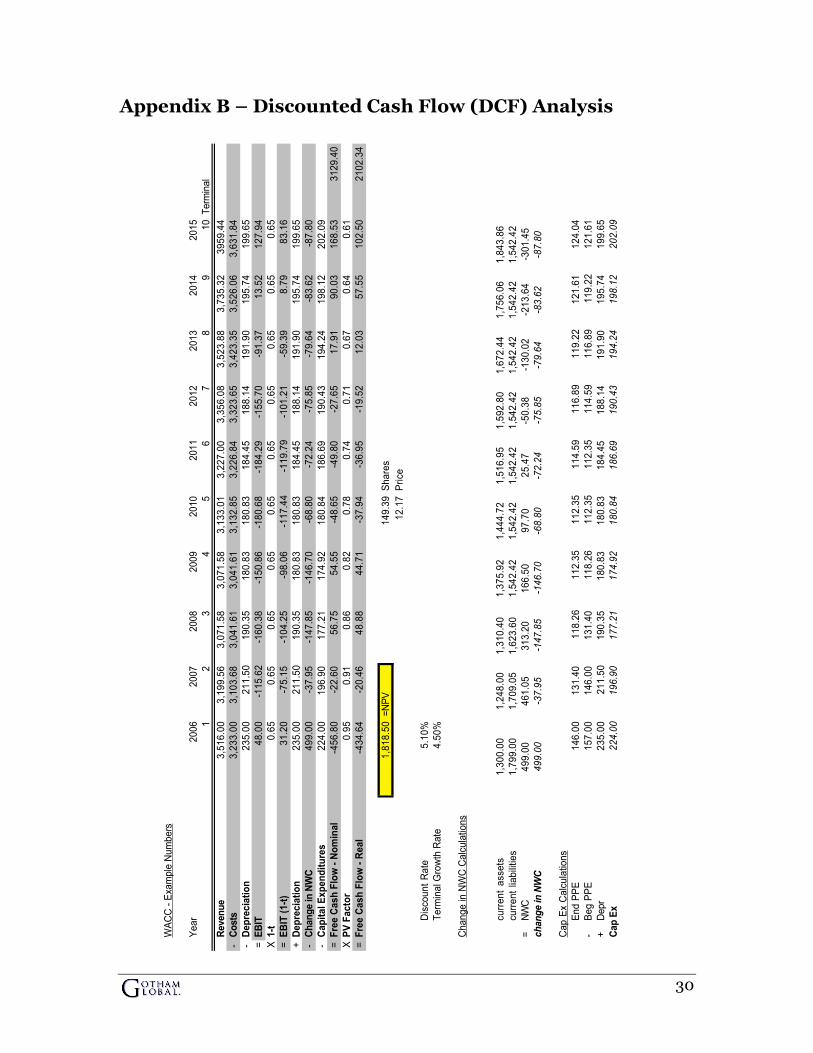

Appendix B – Discounted Cash Flow (DCF) Analysis

WA

CC

- E

xam

ple

Num

bers

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

12

34

56

78

91

0T

erm

inal

3,5

16

.00

3,1

99

.56

3,0

71

.58

3,0

71

.58

3,1

33

.01

3,2

27

.00

3,3

56

.08

3,5

23

.88

3,7

35

.32

39

59

.44

-3

,23

3.0

03

,10

3.6

83

,04

1.6

13

,04

1.6

13

,13

2.8

53

,22

6.8

43

,32

3.6

53

,42

3.3

53

,52

6.0

63

,63

1.8

4

-2

35

.00

21

1.5

01

90

.35

18

0.8

31

80

.83

18

4.4

51

88

.14

19

1.9

01

95

.74

19

9.6

5

=4

8.0

0-1

15

.62

-16

0.3

8-1

50

.86

-18

0.6

8-1

84

.29

-15

5.7

0-9

1.3

71

3.5

21

27

.94

X0

.65

0.6

50

.65

0.6

50

.65

0.6

50

.65

0.6

50

.65

0.6

5

=3

1.2

0-7

5.1

5-1

04

.25

-98

.06

-11

7.4

4-1

19

.79

-10

1.2

1-5

9.3

98

.79

83

.16

+2

35

.00

21

1.5

01

90

.35

18

0.8

31

80

.83

18

4.4

51

88

.14

19

1.9

01

95

.74

19

9.6

5

-4

99

.00

-37

.95

-14

7.8

5-1

46

.70

-68

.80

-72

.24

-75

.85

-79

.64

-83

.62

-87

.80

-2

24

.00

19

6.9

01

77

.21

17

4.9

21

80

.84

18

6.6

91

90

.43

19

4.2

41

98

.12

20

2.0

9

=-4

56

.80

-22

.60

56

.75

54

.55

-48

.65

-49

.80

-27

.65

17

.91

90

.03

16

8.5

33

12

9.4

0

X0

.95

0.9

10

.86

0.8

20

.78

0.7

40

.71

0.6

70

.64

0.6

1

=-4

34

.64

-20

.46

48

.88

44

.71

-37

.94

-36

.95

-19

.52

12

.03

57

.55

10

2.5

02

10

2.3

4

1,8

18

.50

=N

PV

14

9.3

9S

ha

res

12

.17

Pri

ce

Dis

cou

nt

Ra

te5

.10

%

Te

rmin

al G

row

th R

ate

4.5

0%

Ch

an

ge

in N

WC

Ca

lcu

latio

ns

cu

rre

nt

asse

ts1

,30

0.0

01

,24

8.0

01

,31

0.4

01

,37

5.9

21

,44

4.7

21

,51

6.9

51

,59

2.8

01

,67

2.4

41

,75

6.0

61

,84

3.8

6

curr

en

t lia

bili

tie

s1

,79

9.0

01

,70

9.0

51

,62

3.6

01

,54

2.4

21

,54

2.4

21

,54

2.4

21

,54

2.4

21

,54

2.4

21

,54

2.4

21

,54

2.4

2

=N

WC

49

9.0

04

61

.05

31

3.2

01

66

.50

97

.70

25

.47

-50

.38

-13

0.0

2-2

13

.64

-30

1.4

5

ch

an

ge in

NW

C499.00

-37.95

-147.85

-146.70

-68.80

-72.24

-75.85

-79.64

-83.62

-87.80

Ca

p E

x C

alc

ula

tion

s

En

d P

PE

14

6.0

01

31

.40

11

8.2

61

12

.35

11

2.3

51

14

.59

11

6.8

91

19

.22

12

1.6

11

24

.04

-B

eg

PP

E1

57

.00

14

6.0

01

31

.40

11

8.2

61

12

.35

11

2.3

51

14

.59

11

6.8

91

19

.22

12

1.6

1

+D

epr

23

5.0

02

11

.50

19

0.3

51

80

.83

18

0.8

31

84

.45

18

8.1

41

91

.90

19

5.7

41

99

.65

224.00

196.90

177.21

174.92

180.84

186.69

190.43

194.24

198.12

202.09

Fre

e C

as

h F

low

- R

ea

l

Cap

Ex

Ch

an

ge in

NW

C

Cap

ital E

xp

en

dit

ure

s

Fre

e C

as

h F

low

- N

om

ina

l

PV

Fa

cto

r

EB

IT

1-t

EB

IT (

1-t

)

Dep

recia

tio

n

Ye

ar

Reven

ue

Co

sts

Dep

recia

tio

n

31

WAAC Calculations WAAC 5.10% Total Debt 2,256.00 Total Equity 58.00 Total Value 2,314.00 % Debt 97.49% % Equity 2.51% Corporate Tax Rate 35.00% kd 7.50% ke 13.78% ke Calculations 13.78% Risk Free Rate 5.00% Risk Premium 7.50% Beta 1.17

i 2006 10-K. All statistics, unless otherwise cited, are drawn from this report. ii “Sales of Music, Long in Decline, Plunge Sharply.” Wall Street Journal Online, March 21, 2007. 4http://online.wsj.com/article_email/article_print/SB117444575607043728-lMyQjAxMDE3NzI0MTQyNDE1Wj.html iii Pali Research Report, March 2007. iv Boldrin, Michele and David Levine. “The Case against Intellectual Property.” AER 2002, pp. 209-212. v BigChampagne, LLC. vi 10-K, p.28 vii “WMG profit plunges 74% in first quarter.” Associated Press. February 9, 2007. viii Value Line, February 16, 2007. ix http://www.iht.com/articles/2007/02/22/business/sonybmg.php x http://www.wmg.com/news/article/?id=8a0af81210c2b40b0110df66b1ed2939 xi Aisha Phoenix, “Warner Music Approaches Rival EMI on an Acquisition.” 20 February, 2007. http://www.bloomberg.com/apps/news?pid=20601087&sid=at0xjRZlJEkM&refer=worldwide xii http://www.apple.com/hotnews/thoughtsonmusic/ xiii Pali Research Report, March 2007.