Stocks of knowledge, simplification and unintended consequences: the persistence of post-war...

21

Management Accounting Research 16 (2005) 59–79 Stocks of knowledge, simplification and unintended consequences: the persistence of post-war accounting practices in UK agriculture Lisa Jack ∗ Department of Accounting, Finance and Management, University of Essex, Wivenhoe Park, Colchester CO4 3SQ, UK Received 8 September 2003; accepted 28 August 2004 Abstract In this paper, agricultural gross margin accounting is examined as an institutionalized practice, within a theoretical framework that embraces Giddens’s theory of structuration and new institutionalism in sociology. An analysis of the transmission and maintenance of the institution suggests that it persists through the dominant advisory group within the industry. The development of private commercial consultancy in the industry and the decline of the university based government advisory schemes in the period from the Second World War led to simplified management accounting practices that are resistant to change. Another factor is the role of accounting education in the agricultural sector in the same period, and the paucity of conventional accounting knowledge in the sector. This study is based on both historical and written data covering the period from 1939 to 2003, and on interviews obtained from industry participants in 2001–2003. It is unusual in that it examines an accounting practice in which participation is voluntary, but that has become embedded and used nationally in the industry for over 40 years. It is also a story of how an academic innovation was diffused, with unintended consequences. © 2004 Elsevier Ltd. All rights reserved. Keywords: Stocks of knowledge; Structuration theory; New institutionalism; Agricultural accounting; Management consultancy 1. Introduction This paper gives an analysis of one particular accounting practice in the UK agricultural industry, the agricultural gross margin, which is so firmly embedded that it is sometimes simply referred to as agricultural accounting. The story of the agricultural gross margin is not widely known outside the ∗ Tel.: +44 1206 872730; fax: +44 1206 873429. E-mail address: [email protected]. 1044-5005/$ – see front matter © 2004 Elsevier Ltd. All rights reserved. doi:10.1016/j.mar.2004.08.003

Transcript of Stocks of knowledge, simplification and unintended consequences: the persistence of post-war...

Management Accounting Research 16 (2005) 59–79

Stocks of knowledge, simplification and unintended consequences:the persistence of post-war accounting practices in UK agriculture

Lisa Jack∗

Department of Accounting, Finance and Management, University of Essex, Wivenhoe Park, Colchester CO4 3SQ, UK

Received 8 September 2003; accepted 28 August 2004

Abstract

In this paper, agricultural gross margin accounting is examined as an institutionalized practice, within a theoreticalframework that embraces Giddens’s theory of structuration and new institutionalism in sociology. An analysis of thetransmission and maintenance of the institution suggests that it persists through the dominant advisory group withinthe industry. The development of private commercial consultancy in the industry and the decline of the universitybased government advisory schemes in the period from the Second World War led to simplified managementaccounting practices that are resistant to change. Another factor is the role of accounting education in the agriculturalsector in the same period, and the paucity of conventional accounting knowledge in the sector. This study is basedon both historical and written data covering the period from 1939 to 2003, and on interviews obtained from industryparticipants in 2001–2003. It is unusual in that it examines an accounting practice in which participation is voluntary,but that has become embedded and used nationally in the industry for over 40 years. It is also a story of how anacademic innovation was diffused, with unintended consequences.© 2004 Elsevier Ltd. All rights reserved.

Keywords:Stocks of knowledge; Structuration theory; New institutionalism; Agricultural accounting; Management consultancy

1. Introduction

This paper gives an analysis of one particular accounting practice in the UK agricultural industry,the agricultural gross margin, which is so firmly embedded that it is sometimes simply referred to asagricultural accounting. The story of the agricultural gross margin is not widely known outside the

∗ Tel.: +44 1206 872730; fax: +44 1206 873429.E-mail address:[email protected].

1044-5005/$ – see front matter © 2004 Elsevier Ltd. All rights reserved.doi:10.1016/j.mar.2004.08.003

60 L. Jack / Management Accounting Research 16 (2005) 59–79

sector, despite its being established for more than 40 years, and having its roots in the radical changesin agriculture that occurred during the Second World War1. Even for those without a specific interestin agriculture, it provides some insights into how an accounting practice developed and introduced byacademics to meet a particular need in the industry at a particular time can persist in spite of fundamentalchanges in the industry itself. From this perspective, the paper builds on and contributes to the growinginstitutionalist literature in accounting (e.g.,Carruthers, 1995; Burns and Scapens, 2000; Modell, 2001;Granlund, 2001; Seal, 2003).

Dirsmith (1998, p. 69) suggests that researchers might ‘probe substantive domains wherein organi-zations are breaking out of their traditional orientations and forms, and within which accounting andaccountants may play different roles’. The agricultural industry in the UK is undergoing fundamental andquite turbulent changes (Markham, 2003); traditional farming is giving way to agri-business and underthe EU Mid Term Review of the Common Agricultural Policy (SPICe, 2002), subsidisation of the industryis being overhauled. There has been an increasing dependence on technology, and a rise in the proportionof overhead expenditure, that is not dissimilar to other industries that have explored new managementaccounting or performance measurement techniques. Yet, there has been no discernible change in theaccounting methods or accounting discourse in the agricultural industry. As one interviewee observed,‘those who are furthest forward in their thinking are further back than you’d have thought’. It is not thatthere are no signs of emergent practices, particularly as individual farm businesses diversify into moreconventional business areas, but that the existing methods – or the people that use them, appear to be highlyresistant to change. This study, then, differs from many other institutional studies in that it attempts tocapture institutionalized practices that could change quite suddenly, and therefore probes the durability ofthose practices. It could be called a ‘verge-of-change’ study: ironically, the author thought that she wouldfind that deinstitutionalization was underway when the study began in 2000. In 2003, signs that could beconstrued as possible precursors of change were just becoming apparent and the study instead took theform of an investigation into persistent practices, following a trail that led back to the Second World War.

Agricultural accounting is an area that is under researched world wide, particularly by those outsidethe industry. As Argiles and Slof have said in a recent paper in European Accounting Review:

Inspite of its relative importance in the economy of many countries and its growing interrelation-ships with other sectors, agriculture has traditionally not received much attention from accountingresearchers, practitioners and standard setters. (2001, p. 361)

The literature – particularly the empirical literature – is sparse (Juchau and Hill, 2000, preface;Argilesand Slof, 2001, p. 361). Agricultural academics tend not to be interested in accounting and accountingresearchers tend to stay clear of agriculture and related industries. Yet, this is one industry that has everysingle person as a stakeholder, relying on it for food and clothing. Identifying practices that are resistantto change should influence policy both at individual business and government level, especially at a timewhen European politicians are concerned with creating a sustainable agricultural industry.

The paper begins by setting out the context in which the agricultural gross margin method of accountingis used, and by clarifying what is meant here by UK agriculture. This is followed by a brief review of both

1 Short et al. (2000, p. 229)state:

‘In the six years of war there came indeed a fundamental and irreversible change to the farming community, such that ithas been argued that the Second World War is of greater significance to the development of British Agriculture than anycomparable period since the Norman Conquest’.

L. Jack / Management Accounting Research 16 (2005) 59–79 61

the institutional literature and the literature related to agricultural accounting. A theoretical frameworkbased on new institutionalism and structuration theory is then set out, which examines the cognitive aspectsof the persistence of the institutionalised practice. The framework is then followed by a brief considerationof the qualitative methods used. The main section of the paper tells the story of the agricultural grossmargin and shows how both the rise of the professional agricultural consultant and the role of farmmanagement academics have ensured the persistence of the institution, supported by government policy.Persistence is related to the reproduction of the accounting practice over time and in particular to thetransmission of the stock of knowledge associated with gross margin accounting. Without suggesting thatany universal points can be made from the qualitative analysis applied, this study may also give someappropriate insights into the role of accounting education in the reproduction of institutionalized practicesin the wider world and in the potential deinstitutionalization of outmoded ones.

1.1. Context

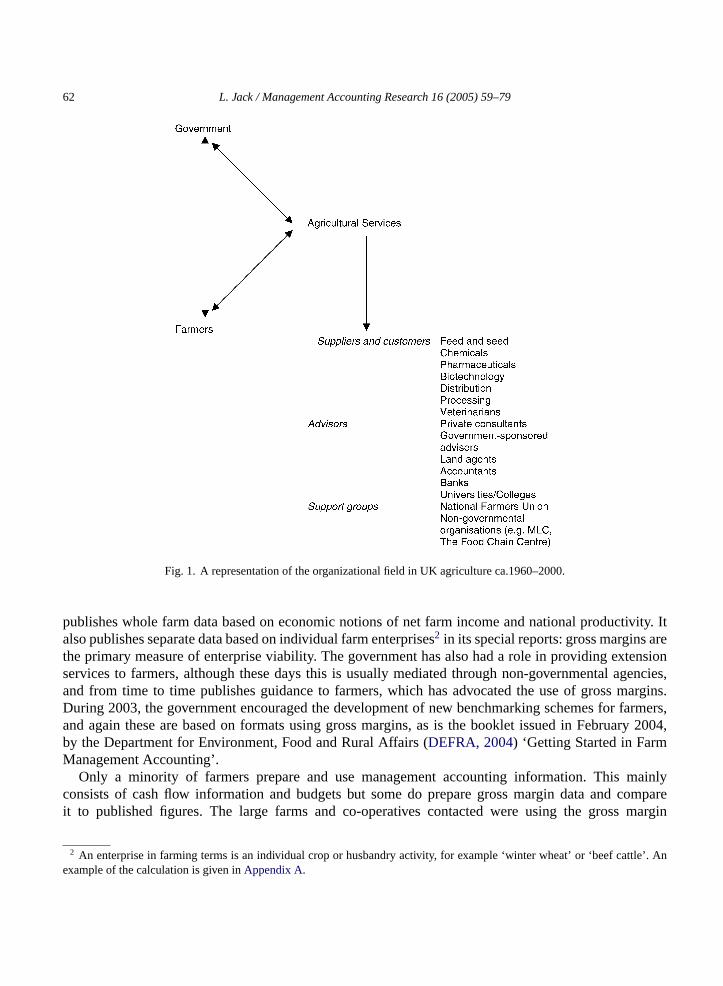

Adopting the term introduced byDiMaggio and Powell (1983), the agricultural industry in the UKcan be seen as an organizational field that consists of the Government, farmers and agricultural serviceorganisations. The industry is primarily concerned with the efficient cultivation of land for arable cropsand with rearing animals in order to feed the whole population, and to create a surplus for trade purposes,although this view of agriculture has persisted since the Second World War. Recent developments in theUK and Europe have indicated that the industry model is changing towards one where farmers are partof agri-food business supply chains, such as those that dominate the US market: the so-called ‘plough toplate’ or ‘farm to fork’ model. In the UK, however, this transition is in its early stages.

During the Second World War, the Government took over control of agricultural production, andalthough this control was mediated through local farmer groups and ended with the end of the war, it seta precedent of government setting production policy that is still apparent in the workings of CommonAgricultural Policy of the European Union (CAP). Around 70% of UK farms are owner-occupied, withthe remainder being tenancies and managed estates. Over the last 50 years, a service sector has grownthat dominates the industry (Fig. 1). To begin with, the suppliers, advisors and support groups were thereto provide services to the farmer, who had a real status as one who was increasing production of food tomake Britain self sufficient once more following the disasters of war. Gradually, over the years, a pointhas been reached where the farmers feel that they are serving the agricultural industry, made up of theprocessors, distributors, service providers and large landowners. A number of the farmers interviewedfelt alienated from the industry, and no longer central to it. In government terms, however, small farmersare still considered part of the industry and CAP is still framed in terms of support for small and mediumsized farmers. Co-operatives, where the farmers sit on the board, are still rare in the UK and the big foodmanufacturers are mainly separate corporations. In this study, the definition of the agricultural industrydoes not include food processing or manufacturing. This is incidentally in line with the definitions usedin IAS41 Agriculture, which covers biological assets and agricultural produce but not processed foods oryarns.

1.2. The significance of the agricultural gross margin

Within this organizational field of government policy makers, farmers and service organizations, theagricultural gross margin is used as one of the main tools of analysis. The government collects and

62 L. Jack / Management Accounting Research 16 (2005) 59–79

Fig. 1. A representation of the organizational field in UK agriculture ca.1960–2000.

publishes whole farm data based on economic notions of net farm income and national productivity. Italso publishes separate data based on individual farm enterprises2 in its special reports: gross margins arethe primary measure of enterprise viability. The government has also had a role in providing extensionservices to farmers, although these days this is usually mediated through non-governmental agencies,and from time to time publishes guidance to farmers, which has advocated the use of gross margins.During 2003, the government encouraged the development of new benchmarking schemes for farmers,and again these are based on formats using gross margins, as is the booklet issued in February 2004,by the Department for Environment, Food and Rural Affairs (DEFRA, 2004) ‘Getting Started in FarmManagement Accounting’.

Only a minority of farmers prepare and use management accounting information. This mainlyconsists of cash flow information and budgets but some do prepare gross margin data and compareit to published figures. The large farms and co-operatives contacted were using the gross margin

2 An enterprise in farming terms is an individual crop or husbandry activity, for example ‘winter wheat’ or ‘beef cattle’. Anexample of the calculation is given inAppendix A.

L. Jack / Management Accounting Research 16 (2005) 59–79 63

as their main accounting tool. All farm-based software packages incorporate gross margin calcula-tions.

The main users of gross margins are accountants, consultants and teachers. Banks however tend torequest profit and loss accounts, balance sheets and cash flow – basic business plan information – anduse their gross margin software to analyse ‘the difficult cases’, as one bank manager put it. As the banksand the tax authorities are the primary reason for farmers to do any accounting, the fact that they do notrequest other management accounting reports is one reason why so many farmers do not prepare thosereports. In addition, a number of books of standard gross margin data are published annually by colleges,banks and agencies. Gross margin figures are quoted frequently in the relevant press, such as the ‘Farmer’sWeekly’ and the ‘Farmer’s Guardian’. Even those consultants spoken to, who expressed dissatisfactionwith the technique as an analytical tool, admitted that their explorations of alternative techniques were intheir early stages. There is some evidence that when farms become part of longer supply chains, such asthose involving supermarkets, then individual farm accounting practices are modified as ‘suppliers haveto demonstrate their ability to fit in with supermarket business processes’ (Frances and Garnsey, 1996, p.609). But, there is no evidence that the industry as a whole, to date, has adopted practices imported frommore conventional businesses.

Therefore, the institutionalized practice of agricultural gross margin accounting has a number ofpeculiarities that sets this study apart from other studies of institutional practice and change. Firstly, theuse of the method is entirely voluntary. Secondly, it is recognised across the entire industry despite thefact that the industry is composed of several hundred individual businesses and organisations. Thirdly, itis more or less only used in the UK as a generally accepted accounting method but there are no writtenstandards, only textbooks. Even more interestingly, at this point in time, the relationship between advisorsand farmers is poised at the position described byGiddens (1991, p. 31)below in the context of agrariansocieties:3

In modern social life,farmersmay be able to get along for periods of time by mixing establishedhabits with consultation of specific experts for ‘general repairs’ and for unexpected contingencies.Experts themselves. . . may proceed within their technical work by means of a resolute concentrationon a narrow specialist area, paying little attention to broader consequences or implications. In suchcircumstances, risk assessment is fairly well ‘buried’ within more or less firmly established ways ofdoing things.But at any point these practices might become suddenly obsolete or subject to quitethoroughgoing transformation (my italics).

1.3. A brief overview of the literature

The critical literature covering performance measurement in agriculture is not extensive and empiricalstudies are scarcer still (Juchau and Hill, 2000, preface). The papers and texts that have appeared over thelast century have been almost exclusively written by agricultural economists or more recently by thosewith a farm management background who were themselves taught by agricultural economists. Thesepapers form part of the story of the gross margin and are therefore covered in the next section. Therehave been a small number of papers concerning the related subject of business objective setting anddecision-making that take a more sociological approach (for example,Robinson, 2000; Willock et al.,

3 “Individuals” in the original text but the previous lines use farming as a metaphor.

64 L. Jack / Management Accounting Research 16 (2005) 59–79

1999; Schucksmith, 1993). Again, these emanate from agricultural colleges and university departmentsthat have a bias towards agricultural economics. Therefore, there is an opportunity to take a fresh look atthe subject from an accounting and sociological point of view.

However, it should be acknowledged that there is academic activity in the field of agricultural accountingoutside the UK. Juchau and Hill (2000, s.1.5) comments that the 1990s have been a ‘dramatic periodfor agricultural accounting’, culminating in the development of IAS41 Agriculture effective from 2003.This work is exclusively in Canada, Australia and New Zealand, countries that have largely abandonedsubsidisation of farming. There have been no papers in the UK and very few articles in the press regardingIAS41, nor any other reference to the work of these overseas researchers. Juchau also notes that a voluntarygroup in the US, the Farm Financial Standards Council has researched and produced financial guidelinesfor agricultural producers. This scope of this study is strictly within the UK but it is worth mentioningtwo observations in recent papers from Australia. The first is byMalcolm (1990, s.2.70)who in reviewingthe work of farm management academics and advisors in Australia in the period 1940–1990, concludedthat:

The resilience of the appeal of farm recording and comparative analysis after the productioneconomists’ early critique was closely tied in with the development of the capability for com-puterised collection and analysis of data which occurred in the 1960s, and the potential this wasperceived to hold for the standardisation of the accounting process.

Ronan and Cleary (2000)claim that this appeal and the use of comparative analysis have not yetdisappeared from the Australian scene. They comment that current moves in Australia to popularisebenchmarking in farming (a trend also seen in the UK during 2003) have led some contemporary agricul-tural economists to comment that they ‘are unable to distinguish ‘benchmarking’ from the much-criticisedcomparative analysis of the 1960s’. Both papers argue that the appeal of standardisation, computerisationand simplification of processes, along with the absence of a ‘whole-farm’ approach, are significant factorsin the persistence of accounting practices in agriculture.

1.4. Theoretical framework

Initially, the framework adopted byBurns and Scapens (2000)to analyse management accountingfrom an institutional perspective was considered. This framework uses Giddens structuration theory asits basis (as doMacintosh and Scapens, 1990; Barley and Tolbert, 1997) and allies it to old institu-tionalism in economics (OIE). An analysis of institutions and their underlying structures are based ondichotomies of formal versus informal change, revolutionary versus evolutionary change and regressiveversus progressive change is developed from this theoretical background.

This approach would have provided a robust and in many ways relevant framework for the subjectof performance measurement in agriculture, particularly considering the historical role of governmentinstitutions in agriculture since the middle of the twentieth century. However, the problem of inertia,as perceived here, actually lay in the way that the accounting method was understood and perceivedin practice. In other words, the cognitive element of the institution was highly significant, as was thegrouping of the various actors within the industry. The possibility of using sociological rather thaneconomic theories of institutionalism was then examined.

Summarising briefly, economic institutionalism interests itself mainly in the economic and legalinstitutions of society – governments, large corporations and markets (Rutherford, 1994, pp. 1–4).

L. Jack / Management Accounting Research 16 (2005) 59–79 65

Institutionalism in sociology interests itself more in organisations and collectives of actors. Generallyspeaking, economic institutionalists subscribe to either behaviourist or rational choice models to explainprocesses of institutionalisation and resistance to change by institutions, whereas sociological institu-tionalists are sceptical about rational-actor models of organization (Powell and DiMaggio, 1991, pp.11–14). In both disciplines, the ‘old’ schools of thought are centred on the norms, values and attitudesembedded in the institutions and the conflicts of interest that pre-figure change. ‘New’ institutionalistsplace more of a structural emphasis on their analyses of institutions and examine why institutions persist.Within the sociological tradition, old institutionalists ‘describe organizations that are embedded in localcommunities’ whereas new institutionalists look at non-local environments, organizational fields such asa national agricultural industry. The data available when this study was planned suggested strongly thatnew institutionalism in sociology was the most sympathetic of the institutional theories for the material,and would provide the richest analysis. It was decided to use a theoretical framework based on newinstitutionalism in sociology, incorporating Giddens structuration model. A number of recent studies inmanagement accounting have taken a similar approach (Burns and Vaivio, 2001, p. 398;Modell, 2001;Granlund, 2001; Seal, 2003).

The use of structuration theory enables the institution to be examined in terms of processes rather thanproperties (Scott, 2001, p. 92), the structures being reproduced chronically by actors. It is, as Giddenshimself claimed, a sensitising device, rather than a universal framework (1984, p. 326). The recent studiescited above tend to take a specific management accounting system change, and examine the resistance tothat change (Granlund, 2001) or the implications for legitimacy and power relations (Collier, 2001; Ahrensand Chapman, 2002; Seal, 2003). This paper examines the structures from another perspective, by lookingat the cognitive process itself. There are similarities in the findings of the study with those ofAnsari andEuske (1987), whose study of the use a management accounting in the US Department of Defence foundthat ‘what started as a ritual of rationality and a political symbol of influence is today viewed as a technicalsystem and is institutionalized’ (p. 564). This technical-rational perspective of accounting informationwas intertwined with socio-political and institutional perspectives, whichMacintosh and Scapens (1991,p. 142)suggest could be further reinterpreted using structuration theory. The signification processes canbe separated for ‘analytical purposes only’ (ibid., p. 141), yet that separation is sometimes necessary todraw out the depth and detail involved in the structure of the institution.

1.5. Stocks of knowledge, simplification and unintended consequences

Giddens (1984, p. 29)termed the dimensions of the duality of structure that characterise structurationtheory, signification, legitimation and domination (Macintosh and Scapens, 1990, 1991). Structures aredefined as ‘rules and resources, or sets of transformation relations, organized as properties of socialsystems’ (Giddens, 1984, p. 25). Crucially, they exist across time and space. In their interactions witheach other, actors (knowledgeable agents) reproduce these structures over time, routinely drawing onthe modalities and reconstituting the structures over and over again (ibid., p. 28). Each structure andits form of interaction and modality may be separated for analytical purposes but in reality interaction‘implies the interlacing of meaning, normative elements and power’ (p. 28). This paper concentrateson the signification structure, but recognises that, as Giddens says, ‘structures of signification alwayshave to be grasped in connection with domination and legitimation’ (p. 31). One of Giddens’ other basictenets states that ‘the knowledgeability of actors is always bounded on the one hand by the unconsciousand on the other by unacknowledged conditions/unintended consequences’ (p. 282). Social activities are

66 L. Jack / Management Accounting Research 16 (2005) 59–79

acted out through purposive action that leads to unintended consequences (p. 294). Here it is arguedthat teaching and advising became routinized and the unintended consequence was that a detailed andtheoretically supported analysis and planning method became a set of formats, definitions and devises.Unintended consequences condition social reproduction, and are largely operate ‘behind the backs ofsocial agents’ (Knorr-Cetina, 1988, p. 35). These influences cannot be found in micro-situations but thesimplified conditions of micro-sociological situations give us evidence of their existence. Within theunconscious are the ‘basic existential parameters of self and social identity’ (Giddens, 1984, p. 375):somewhere in the persistence of ‘agricultural accounting’ is the need of actors to retain the identity ofbeing part of agriculture and farming.

Giddens (1984, p. 29)defines interpretative schemes as ‘the modes of typification incorporated withinactors’ stocks of knowledge’. In the context of performance measurement, stocks of knowledge encompassthe accounting methods and underlying theories used to produce and support the measures, as well astheir accepted interpretations. It also encompasses the history of the measure’s development and use,and understanding of why and when the measure is used, who should carry out the calculations, andwho should make use of them. AsBerger and Luckmann (1967, pp. 94–96)comment: ‘a society’s stockof knowledge is structured in terms of what is generally relevant and what is relevant only to specificroles’. Generally relevant knowledge may concern acknowledged facts, methods and procedures. Rolespecific knowledge is both concrete: for example, a practising accountant should know about accountingtechniques, GAAP and other areas as well as about norms, values and emotions appropriate to thatspecialist role. Generally relevant knowledge includes a typology of who these experts are and wherethey fit into the scheme of things. Knowledge is thus ‘socially distributed’ and, furthermore, it can beassumed that ‘role-specific knowledge will grow at a faster rate than generally relevant and accessibleknowledge’.

BothBerger and Luckmann (1967)andGiddens (1984)draw on the work of Alfred Schutz when dis-cussing the nature of knowledge.Berger and Luckmann (1967, p. 27)credit Schutz with the fundamentalinsight that ‘the sociology of knowledge must concern itself with the social construction of reality’.Schutz talked about the ‘typifications of common sense thinking’ (the stock of knowledge), which areboth taken-for-granted and socially approved. ‘Their structure determines among other things the socialdistribution of knowledge and its relativity and relevance to the concrete social environment of a con-crete group in a concrete historical situation’ (Schutz, 1962, p. 149). Schutz (in this discussion on theearlier work of Husserl and elsewhere) also refers to ‘stocks of knowledge at hand’, describing these as‘the sedimentation of previous experiencing acts together with their generalizations, formalizations andidealizations’ (ibid., p. 146).

Berger and Luckmann also make use of the term ‘formulae’, and link the creation of formulae (suchas the format of a gross margin) to simplification:

‘Since human beings are frequently stupid, institutional meanings tend to become simplified in theprocess of transmission, so that the given collection of institutional ‘formulae’ can be readily learnedand memorized by successive generations’ (1967, p. 87)

Sedimentation, they point out, involves routinization and trivialization (ibid., p. 88).Simplification is also identified as a phenomenon by functional sociologists and social systems analysts

(Douglas, 1986; Cicourel, 1973). The rational and natural reaction to a complex idea is to simplify and toextract the working solution. Functionalists emphasize the scarcity of attention and the overload of infor-mation: it is impossible to act unless one reduces information to something usable for decision-making.

L. Jack / Management Accounting Research 16 (2005) 59–79 67

1.6. Transmission and persistence

Zucker (1977, p. 104)identifies institutionalization as a continuous process rather than a state andanalyses three cognitive processes measuring the creation of institutional effects and cultural persistence,largely unchanged, over time. FollowingBerger and Luckmann (1967, p. 111)she identifies transmis-sion from one generation to the next as an element of institutionalization and therefore of persistence.Transmission is followed by maintenance and resistance-to-change. ‘For highly institutionalized acts’she says, ‘it is sufficient for one person to tell another that this is how things are done’ for the institutionto persist (p. 83).

The change in the understanding and use of gross margins occurred in the initial stages of the in-stitutionalization process.Berger and Luckmann (1967, p. 78)saw institutionalisation as a dialecticalprocess of externalisation, objectification and internalisation. The origins of an institution are in the mo-ment of externalisation: any change must have occurred through the objectification and internalizationphases of the institutionalization, during the diffusion of the innovation to the agricultural community.The application of diffusion processes to institutionalism is underdeveloped (DiMaggio, 1991, p. 268;Chua and Petty, 1999). Fligstein (1991, p. 335)comments that the functioning of organizational fields isnot well understood and that ’one main issue concerns the way diffusion processes work and the role ofnetworks as a source of diffusion’. However, diffusion and institutionalization have been linked in studiesof other areas of social science – education, social policy and law (for example,Edelmann et al., 1999) –and in organizational studies:Yin (1979)notes that diffusion is characterised by three phases: initiation,implementation and routinization or institutionalization. Diffusion models help the understanding of theprocess of habitualization, where an idea or technology spreads and is repeated until it becomes routineand then taken-for-granted.

Against this backdrop, the paper examines the initiation, diffusion and routinization of the grossmargin technique, setting the innovation (which occurred around 1960) in context of government post-war extensionism programmes, and seeks to understand why the practice still persists, albeit in a simplifiedand unintended form.

2. Methods and data collection

The discussion in this paper draws on two sources of data: firstly, a review of the historical literaturesurrounding performance measurement in agriculture in Britain since the Second World War and secondly,interviews with a number of different figures in the industry. At the start of the project, informal interviewswere sought and obtained with some key figures in the industry that had expressed views on the currentstate of agricultural accounting and the industry. These included interviews with the agricultural partnerof a top ten accounting firm, three well-known academic writers and a large farming co-operative. Theprimary purpose of the interviews was to establish whether or not the ideas that I was forming as an outsiderto the industry were sustainable and to speculate about the feasibility the proposed research. Some of thetypical comments have been incorporated into this discussion, as examples of the conclusions drawn.

Field data were collected using semi-structured interviews with farmers, farm secretaries, bank man-agers and the Department for the Environment, Food and Rural Affairs (DEFRA). Farmers were selectedand approached through contacts at one of the agricultural colleges. It was important that the farmers se-lected had some external pressure that may have caused them to modify accounting and business practices.

68 L. Jack / Management Accounting Research 16 (2005) 59–79

In particular, farms where diversification had taken place, where one or more members of the farmworked off the farm or where the farm management had been contracted out were sought, these being thekey areas of income generation that are not easily incorporated into current performance measures in theindustry. Of the farmers quoted in this paper, Farmer A had successfully run two diversification projectsin the 1980s and 1990s, had then contracted out the management of his farm and returned to collegeto complete his degree. He is now employed by a government agency running training programmes forfarmers but still owns the farm in partnership with his father and aunt, the latter being the bookkeeper in thebusiness. Farmer B is part of a family business, run as a small group of limited liability companies, whichhas diversified very successfully into largely tourism-based activities. Farmer C runs a dairy productbusiness with her spouse on their dairy farm: previously, she had worked off the farm as a farm secretary.

3. Results and discussion

3.1. The story of the agricultural gross margin

The Second World War brought an increased level of government involvement in the agricultural in-dustry. Through mapping processes, the instigation of the Farm Management Survey and the introductionof income tax for farmers, the government had far more information about the economic workings of theindustry than it had before. It also had a post-war policy: never to let Britain become dependent on othercountries for food again. As in other industries, a production ethos was established and as part of this drivefor production, the government took over the running of the pre-war Provincial Agricultural EconomicsService. Before the war, university and civil service economists had been both theorists and advisors,collecting data and developing costing schemes. In the post-war period, realising that the industry wouldneed many more advisors to achieve new efficiencies and growth in the industry, the government estab-lished the National Agricultural Advisory Service (NAAS). The advisory service was separate from theacademic agricultural economists who became largely responsible in the university Farm Business Unitsfor collecting data for the Farm Management Survey and for carrying out research (Lloyd, 1970, p. 22).

It was soon realised that the two services needed to work together: the NAAS advisors needed to betrained and the university economists needed the data and practical feedback. The government respondedat the beginning of the 1950s by creating the post of Farm Management Liaison Officer (FMLO) ineach region, to act between the two groups (Giles and James, 1993). Blagburn, the FMLO at ReadingUniversity, developed a package of efficiency measures, known as yardsticks, which could be used asa basis for diagnosing farm economic problems. Developed on the ground and making practical useof both tax accounts and government statistics, NAAS advisors could collect the data, calculate themeasures and call on the economists to provide a sound interpretation. The technique was known aswhole farm comparative economic analysis. Although initially successful, the method proved to be verytime consuming, and other academics were sceptical about the validity of the methods used.

By the late 1950s, a simpler method was sought (Lloyd, 1970, p. 102;Giles, 1986, p. 146). A researcherin northern Ireland, Liversage, resurrected an idea first put forward in 1928 by King but ignored, of usingvariable and fixed costs to work out gross profits on individual enterprises within a farm.Liversagepublished his article in 1956 in the Journal of Agricultural Economics and the idea itself was taken upand developed by another FMLO, David Wallace of Cambridge University. The method was ideal forworking out marginal effects of arable crops, and he developed the method, with colleagues, into a form

L. Jack / Management Accounting Research 16 (2005) 59–79 69

of marginal costing. Agricultural marginal costing was not the same as the more conventional marginalcosting being developed in other industries at the same time, where the marginal cost of increasing outputby one more unit is calculated. Agricultural marginal costs are based on inputs, rather than outputs, andwork on the output that can be achieved from one more unit of input. The law of diminishing returns canbe applied to calculate the optimum output for the input given and from that alternative plans to maximisegross profits across the farm enterprises can be developed.

Wallace termed his method gross profit analysis and planning and set about converting his colleaguesat Cambridge and in the eastern Region of NAAS. In 1960, the method was aired as ‘new’ in the annualfarm report from Cambridge and by 1964, it was accepted but under a slightly different title: farmers inthe eastern region objected to the use of the term ‘gross profit’ in a farming context and wanted it changedto gross margin, which was accepted. It is, in fact, a measure of contribution to fixed costs and not profitas such. By 1970, gross margins were in almost universal use (Nix, 1979, p. 284) and every textbookand every handbook since views gross margin accounting as the costing and benchmarking method inthe industry. The reason for its rapid uptake was largely due to the enthusiasm and persuasiveness ofDavid Wallace himself, using BBC television and pamphlets to spread the method (Giles, 1986; Sellyand Wallace, 1961; Wallace and Burr, 1963). It became institutionalized as a practice and internalized asa discourse of accounting, though not in its original form. The sector, having embraced gross margins,has proved to be highly resistant to change. This paper examines the one aspect of the stock of knowledgeconcerning the theory and application of the agricultural gross margin and considers why it persists,despite fundamental changes in the industry since its inception.

3.2. The transmission of stocks of knowledge

It is the reproduction of the stock of knowledge that is fundamental to our understanding the natureof the institution of gross margin accounting. A particular phenomenon can be observed from the storygiven at the start of the paper: what is understood and used in practice today does not appear to be whatwas put forward by the originators of the method. This phenomenon is not unusual. It has been analysedby a number of researchers and in institutional theory can be associated with phenomena of simplificationand unintended consequences. Here, what began as a tool for consultancy, with a detailed and pragmaticstock of knowledge appears to have been reduced to a small set of definitions, a format or accountingmodel and a set of benchmarks. It is this smaller stock of knowledge that is sedimented, to adoptSchutz’(1962)phrase, and given the title ‘agricultural accounting’.

Zucker’s (1977)model is useful when considering the transmission of gross margin accounting since1970. In 1979, John Nix reported that there had been ‘no significant change in farm management account-ing and analysis procedures for many years’ and that gross margins are ’in widespread (almost universal)use’ (Nix, 1979, pp. 282–284). A description of farm management accounting in 2003 would be verysimilar to his 1979 description. In 1990, Nix gave a presidential address to the Agricultural EconomicsSociety that indicated that there had been no significant further developments, despite obvious changes inthe rural and farming environment (Nix, 1990). In 1998, Martyn Warren of the Seale-Hayne Faculty at theUniversity of Plymouth and the author of a widely recommended textbook on farm financial management,attempted to start a debate through the journal of the Institute of Agricultural Managers. He suggestedthat it was time to abandon ‘traditional’ methods and terminology (in other words, agricultural grossmargins and their cost definitions) and come in line with conventional accounting (Warren, 1998b, p. 75).One or two brusque responses ensued but no further debate or changes. It appears that the sedimentation

70 L. Jack / Management Accounting Research 16 (2005) 59–79

of gross margin accounting knowledge – the definitions and the formats – occurred in the late 1960s andhas been transmitted and maintained in this form to this date, with obvious resistance to change.

3.3. Applying the theoretical model to the historical story

The question that needs to be addressed is, “what happened in the period between the innovation beingintroduced and being taken-for-granted as the way agricultural accounting is done”. The innovation wasdiffused, around the period 1958–1959 (inSturrock and James, 1959/60, Foreword, p. 10ff).4

From the original story it is known that the method spread very quickly and was implemented byNAAS advisors in the field and taught in colleges within a couple of years. By 1964, gross margin was anaccepted term in the Journal of Agricultural Economics and articles for and against it fizzled out aroundthis time. The next academic development was the use of linear programming to assist in the production ofthe production mix plans and the budgets that gross margins were designed to provide. The most detailedexposition of these methods is inBarnard and Nix (1979), originally published in 1967. In the mid-sixties,however, the use of the gross margin was altered. The innovation was spread through academics as wellas through advisors. David Wallace, as a liaison officer, worked with both groups. The academic side isrelatively straightforward and could be seen as those courses that were taught by John Nix at Wye andthose that were taught based on John Nix’s textbook. Later textbooks by other authors dispensed with thelinear programming aspects but retained a basic pattern: book-keeping (usually single entry), physicalrecord keeping, production of enterprise gross margins, whole farm accounts based on gross margins andforecasting and budgeting. These topics, along with business plans, remain the core subjects on nearlyall agriculture courses. A practical approach is adopted on what are, after all, vocational degree courses.

The diffusion through advisors is more complex.Lloyd (1970, p. 103)andGiles (1986, p. 136)statethat the method was taken up very quickly as standard practice in east Anglia and then across the countryby NAAS advisors. There was one practical problem however. These same advisors had been originallytrained in the methods of comparative whole farm economic analysis that gross margins replaced. Usingthat method, measures generated from farm level data were compared against standard measures derivedfrom survey data. In gross margin accounting and planning, no standard data were available and, in theoryat least, none were required: the advisors could use their own judgement to assess the relative merits ofthe alternative plans generated using the method. But as Lloyd puts it, ‘very few advisors trusted theirown judgement’ (Lloyd, 1970, p. 108) and there was felt to be a need for standard gross margin data. Inresponse, John Nix compiled and published his ‘Farm Management Pocketbook’ in 1966 and crucially,it was widely available to farmers as well as advisors. Previous books of data had been felt to be onlysafely used by agricultural economists and the advisors that they supported (Lloyd, 1970, p. 29) or wereonly available in local areas covered by the Farm Management (now Business) Survey. In his originalForeword (republished every year since) Nix stated that:

‘The material contained is based on the sort of information which the author finds himself frequentlyhaving to look up in his twin roles as an advisor and teacher’. (Nix and Hill, 2002, p. iii)

4 The fact that King had originally postulated the idea of gross profits, variable and fixed costs in 1928, is irrelevant to thisanalysis. AsRogers (1995, p. 11)says:

An innovationis an idea, practice, or object that is perceived as new by an individual or other unit of adoption. It matterslittle, so far as human behaviour is concerned, whether or not an idea is objectively new as measured by the lapse of timesince its first use or discovery.

L. Jack / Management Accounting Research 16 (2005) 59–79 71

The figures in the pocketbook (which is very comprehensive) are forward estimates – they are intendedfor budgeting purposes, and every book comes with the warning that the figures need to be adjusted forcomparative use. Nevertheless the book set out the formula and layout of the gross margin in a standardisedform and so encouraged the use of per hectare/acre and per livestock unit calculations. In Barnard andNix, these unit measures are regarded as a weaker use of the data to measure farm efficiency and measuressuch as cost per labour or machine hour were preferred (1973, p. 490ff). Yet the physical data for the latterare not often recorded in practice, despite being widely advocated (Fedie, 1997; Warren, 1998a). Nix(personal communication, 2002) is adamant that the measures shown in the handbook are not benchmarksagainst which to assess past performance but aids to producing forecast figures for budgeting purposes.

3.4. Evidence concerning current practice in the industry

None of the farmers interviewed to date made use of the data in Nix, although everyone had heard ofthe book and had owned at least one copy at some point. The head office of the farm co-operative visitedin the initial phase of the project had a number of handbooks, including Nix, but some considerablescepticism was expressed over their usefulness in practice. Everyone interviewed received derivativehandbooks from their bank (‘Budget Books’). One farm interviewee (Farmer A) was a contributor to theFarm Business Survey5 (FBS) and received data on an annual basis from the Cambridge University FarmBusiness Unit. Another farm interviewee (Farmer C) had received dairy benchmarks from a consultantin the past but no longer carried out the comparative calculations.

Both farmers used the figures to check that they were ‘doing alright’ in comparison to other farmers,and were pleased to have that reassurance but that no further use was made of the figures. Neither showedany indication that they used the figures of top performing farms as targets, as Blagburn suggested wouldhappen in the 1950s (Lloyd, 1970, p. 29) and as the agricultural partner in the accounting firm interviewedhoped would happen with their Client Database benchmarks, issued as a value added item with each setof prepared or audited accounts. The farmer involved in the FBS did analyse the regional figures but morein his capacity as an team co-ordinator within a government sponsored advisory scheme (Farmer A hademployed a full-time farm manager in order to work off the farm). Farmer C expressed the opinion thatin reality they were a small business, and their information needs were smaller than their advisors hadadvocated. This farmer was unusual in having a background in farm accounting and bookkeeping, and sospoke as someone who had tested and understood the methods used. In addition, the farm had followed theadvice given by their consultant, that they should increase marginal yields but had satisfactory results. Thehigher capital and fixed costs associated with purchasing animals, higher grade feed and milk quota, plusthe lack of a market for their milk (the farm has recently diversified by setting up its own dairy-productsunit) had led to disillusionment with the advice they were given and the use of comparative data. As shecommented: ‘we’re not like any other dairy farm now’.

Farmer A and B had used the pocket books during their agriculture and business management degreestudies, to provide hypothetical data for business plan assignments. This was also common practice atthe agricultural college that I taught in myself. This observation re-enforces the suggestion that the roleof the handbooks is educative and designed to promote the use of management accounting techniquesin farming, whichWarren (1998b, p. 79)acknowledges was successful at least in showing that farmmanagement accounting was both possible and accessible.

5 Farm Management Survey was renamed the Farm Business Survey (FBS) in 1986/87.

72 L. Jack / Management Accounting Research 16 (2005) 59–79

In sum, this seems to be a paradoxical situation. Each year a mass of meticulous calculation and datacollection produces a number of published handbooks, some of which are purchased (such as Nix or theScottish agricultural colleges handbook) and many more are distributed free of charge to customers andcontributors by banks, land agents, accountants and the Farm Business Units. In practice, these are onlyused for budgeting purposes by a small number of farmers. Their main use appears to be by studentsand as once a year reading by farmers. Large accountancy firms, land agencies and consultancies suchas ADAS Management Consulting make use of their own Client Database compiled over 12 years toprovide comparative information, although there is some evidence that they also make use of governmentstatistics and other published benchmarking data.

3.5. Theoretical and technical knowledge

The existence of the handbooks appears to be taken-for-granted by the sector and appears to reinforcethe way in which farm management accounting is done. The evidence from the colleges and their ex-students is that the most useful thing that they learned was how to put together a business plan. Taking thedefinition of stocks of knowledge supplied by Schutz, then it would appear that the stock of knowledgerelating to gross margin accounting can be split into the theoretical and the technical. The stock oftheoretical knowledge resides in the surviving academics from the early 1960s (now in their seventies)who were the second generation FMLOs. The transmission of the technical knowledge has been throughtextbooks and through use in the field.

Over time, the farm management textbooks have concentrated on passing on the techniques of grossmargin accounting, particularly the analysis of variable costs and fixed costs using the definitions peculiarto agriculture and the need to keep cash books and physical records. Planning and budgeting is based onthese analyses backed up with handbook data. The particular practice of using gross margins as part of aproduct mix calculation has dropped out of the textbooks but its use as a budgetary tool is retained (as intwo most widely recommended texts,Turner and Taylor, 1998; Warren, 1998). Although full costing iscovered for completeness, it is rarely recommended for practical use (despite evidence that some farmersare using full cost methods). These publications provide evidence that the technique and the understandingrequired by students of the method has been simplified for everyday use by farmers/teachers, to providea workable method of management accounting. Evidence so far suggests that mechanistic approach toteaching accounting (or financial management, which is the preferred term in most colleges for bookkeeping and rudimentary accounting practice). There is an emphasis on the practical and vocational, withan underpinning message that this is what farmers ought to be doing. It may also be an extension of theperennial problem of ‘getting farmers to do their books’, the subject of many eighteenth and nineteenthcentury tracts and one that only really got a response when farmers became subject to income tax in1941(Lloyd, 1970, p. 15).

In practice, farmers find that the method offers limited information for decision-making purposes butappears to have some benefit in promoting variable cost reductions. Initially, David Wallace and hiscolleagues found that gross margins could be improved by initiating cost reduction exercises (at this pointof course, agricultural prices were fixed). In 2001, the partner in the Top Ten Firm commented that, therewas still great scope in the industry for cutting costs, a point that will be returned to in the discussionabout the role of consultants. Problems arise when costs have been cut as far as possible. The answerwould then appear to be to increase yields – but the increase in yields eventually leads, asBody (1990, p.104)clearly shows, to lower farm incomes. In the late sixties, as price support mechanisms were replaced

L. Jack / Management Accounting Research 16 (2005) 59–79 73

by production subsidies, the question farmers asked was, ‘which are my profitable enterprises?’ (Giles,1986, p. 143) which led to the leap of logic that the least profitable enterprises should be cut out. Thisleap of logic involved one fallacy: it assumed that by comparing the gross margins one could compareone enterprise on a farm to another enterprise on the same farm. The originators of the method wereclear that enterprises could only be compared with the same enterprise on another, or standard, farm.They were also clear that the gross margins, either intra-farm or standard, could not be used as a measureof viability without considering the whole farm position and in particular, fixed costs. However, thereis some evidence that these misconceptions persisted: Farmer A claimed that he knew of farms whichhad abandoned enterprises that provided fodder, on the grounds that the gross margin consisted only ofamounts transferred out to other enterprises. Theoretically, this left only the profitable enterprises butof course, now the farmer had to buy in commercial feed and the aggregate gross margin of the farmwas decreased, not increased. Another ex-farmer claimed that gross margins would be difficult to replacebecause they provided a simple means of seeing which enterprise was most successful and that was thereason they were well regarded by farmers.

One of the few empirical findings in this field holds that educated farmers are more likely to keeprecords and employ more complex accounting procedures (Norman, 1986, pp. 54, 71;Schnitkey et al.,1991, pp. 4, 33).Read (1986, p. 21)also concluded that the higher the level of education of the farmer,the more likely they were to seek consultancy advice. Three of the farmers interviewed in this study havesaid that they only discovered gross margins at agricultural college, which reinforces the suggestion thatcolleges are instrumental in maintaining the institution.

Giles (1986, p. 147)in advocating the use of net margins rather than gross margins (output less variableplus relevant fixed costs) also recognised the dangers of using gross margins to make anything other thanmarginal decisions. What is less clear is how farmers actually internalised this simple understanding ofgross margins as benchmarks. It seems most likely that the handbooks produced initially by academicteachers and advisors, and imitated (and simplified) by consultants and other advisory groups, codifiedthe knowledge concerning gross margins in such a way that they conveyed a different meaning to thosereading them. Blagburn had feared this (Lloyd, 1970, p. 28): he felt that only trained economists shouldhave access to standard data and the calculations involved, for fear of misinterpretation.

Therefore, what appears to have arisen is a situation in which theoretical knowledge resides with agroup of academics, a number of whom (such as Nix and Giles) stopped working as NAAS advisors inthe field by 1970. Those who were protective of the method through their early involvement with thepractice taught the next generation of farm management teachers and academics. There was a laudabledesire amongst these academics to train farmers in these techniques to both understand their advisors andto perform their own accounting and record keeping tasks.

3.6. Government and private consultants

The other group involved is consultants and here, very little empirical evidence is available. Privatecommercial agricultural consultants began to appear in the 1950s, as an alternative to the governmentbased NAAS advisors (Knight, 1989, p. 47). The British Institute of Agricultural Consultants was formedin 1957, but, it was not until the seventies, when the free government advisory scheme was effectivelyrun down, that private commercial consultants appear to have become firmly established and acceptedas part of the industry. In addition, agricultural feed and chemical companies began to offer costing andbenchmarking services to their regular customers, and to issue booklets on farm accounting based on

74 L. Jack / Management Accounting Research 16 (2005) 59–79

gross margins. Accountancy firms and land agents followed into the farm business advisory game inaddition to providing taxation accounting services.

Whilst commercial advisors were challenging the role government advisors, agricultural economistsand farm management accountants appear to have decided that ‘the job of farm management was done’(Nix, 1979, p. 289). Economists, no longer supported by the government to be directly involved ineither the collection of farm data (that was left to technical officers based in the FBU and still is) or inadvisory work (given to ADAS), turned to other research areas such as overseas development, the EECand the macro-economic aspects of agriculture. There are very few articles on the subject of performancemeasurement or farm accounting after 1970. However, there has been an explosion in the numbers ofcommercial advisors working in the industry. Body has commented that:

‘fewer people are engaged on the farm itself all the year round but many more are engaged insupplying or servicing agriculture’ (1991, p. 109)

MacDonald (1995, p. 167)draws onAbbot, 1988to provide an explanation for these scenarios. Theestablishment of the BIAC in 1957 could be seen as an attempt to establish a professional project,similar to the role of the accountancy professional bodies where membership is regarded as necessary forthe genuine practice of the profession (Knight, 1989, p. 47). There was a market for the services in theknowledge developed by the economists, and by scientific researchers. Financial advice is usually offeredalongside advice on husbandry or agronomy, or as part of a whole business plan. There is no separateprofession in agricultural management accounting: it is regarded as one tool of the farm business advisor.An opportunity arises, then, for a professional project but as MacDonald says, commercial and industrialentrepreneurs appeared on the scene:

‘Who might find the opportunity to provide the same services as the professional in organizationalform, or develop the technology to offer it in commodity form’.It is also open to the state to provideknowledge-based services for its citizens (my italics)(p. 171).

Agricultural consultants appear to have adopted the techniques used by NAAS in the 1950s, namelywhole farm comparative economic analysis using ratios and benchmarks, and then to have adopted thegross margin benchmarking format. Recent evidence suggests that net margins are being used by privateconsultants, having been aired in the 1980s byGiles, 1986. They did not, however, adopt the farm planningtechniques based on agricultural gross margin analysis and its linear programming tools advocated by theuniversity-based economists. The main evidence for this is one of the few articles written by an agriculturalconsultant to appear in the agricultural literature in the UK. The Journal of Agricultural Economics printedboth Gould’s talk to the Agricultural Economics Society and the subsequent discussion, which includedacademics such as Nix and Reid, and NAAS advisors (Gould, 1973). In this discussion, it becomes clearthat consultants respect the work of the university economists and NAAS, but feel the tools advocated bythese groups are too theoretical for their needs.

However, consultants carry out most of the performance measurement and management accounting inthe industry. They seem to be the guardians of the technical but not the theoretical stock of knowledge andthat this technical knowledge differs from that given by the agricultural college courses. The latter attemptto equip their students with simple devises (a term used in correspondence by Warren) to run their smallbusinesses, using accounting models based largely on gross margin accounting. In contrast, the consultantssell a more sophisticated technique, but which is standardised and packaged in the causes of efficiencyand economy. The former are attempting to provide tools that will obviate the need to employ expensive

L. Jack / Management Accounting Research 16 (2005) 59–79 75

consultants and accounting practitioners to carry out accounting tasks, the latter need to convince farmersof the technical difficulty of doing this for themselves (and interpreting the information correctly) in orderto maintain profitable consultancy businesses. Teachers and academics have no incentive to develop newtechniques and theories based on conventional accounting, because they could lose their unique role,and agriculture could lose its ‘own’ accounting method. An analysis of the roles of legitimation anddomination in maintaining the institution is required, but that is outside the scope of this paper.

3.7. Theoretical implications

In both cases (teaching and consultancy), the original intention of the innovators has been forgotten.Burns and Scapens (2000, p. 11), following Berger and Luckmann (1967, p. 87)define an institution asbeing something for which the historical reasons (for the institution) have been lost. The reasons werelost as the material became encoded, as Burns and Scapens (2000, p. 9) term it and frequently, routinesemerge which have ‘deviated from the original rules’. In this case, there has been simplification. Hence,teachers on vocational agricultural degrees emphasise the method and ‘devises’ that ought to be used byfarmers. Consultants emphasise standardised methods and interpretations. Benchmarks provide a codifiedversion of both, and reduce the need for students and users to assimilate theoretical or complete stocksof knowledge.

Yet it could be said that Giddens seems to approach the phenomenon from the other way round.The interpretative scheme that is part of the signification structure may appear to be simple but oneof his basic concepts of structuration is that ‘all human beings are knowledgeable agents: knowledgeis embedded in our day-to-day lives and isextraordinarily complex (my italics)’ (Giddens, 1984, p.281). In objectifying knowledge – as a functional approach does in designating something as ‘simple’is to miss its innate complexity. In the case of gross margin accounting, the techniques employed areundoubtedly simpler versions of the original method and the theoretical understanding transmitted byvocational training and standardisation is a weaker version of the original. However, the underlyingknowledge of how farmers work and the values and norms (who does what with the practice and why thatis accepted) is complex. Much of their knowledge is tacit (Berger and Luckmann, 1967, p. 158). Moreimportantly, knowledgeability includes, as said before, an understanding of the roles each player has inthe reproduction of the institution.

Unintended consequences can be seen in the development of gross margin accounting. Gross marginanalysis and planning was a tool, a technical aid. In carrying out the task of analysing farm data, com-parative data was called for. The codification of gross margin data, in the form of handbooks, promptedteachers, students and advisors to standardise and routinise their procedures but it seems to have had theunintended consequence that the gross margin and its attendant definitions and formats became reifiedas agricultural accounting. In the discourse of the industry, the gross margin, agricultural variable costs,output and other aspects became objects and the whole package (in its more usable form) became taken-for-granted as the way in which agricultural accounting is done, or at least ought to be done. In talking tomembers of the industry, there are suggestions that gross margins exist independently and that the farmeror other user has to pin them down and understand them; in some cases, it is almost as if the measuresused had platonic forms. The accounting method is describing a reality but the reality is one that has beenconstructed (Armstrong, 2002, p. 281).

The corollary of this discourse is, of course, that farmers do not need conventional accounting. There issome evidence to suggest that the understanding of conventional accounting by those in the industry is this

76 L. Jack / Management Accounting Research 16 (2005) 59–79

simple. Farmers associated accounting with tax (Newby, 1979, pp. 50–51), and tax accounts are acceptedas a regrettable necessity. Agricultural economists have tended to dismiss accounting as simplistic (Nix,1990, p. 271). It is also taken-for-granted that accountants do not understand farming (yet according tothe Lloyds TSB 2001 ‘Focus on Farming’ survey, 9 out of 10 farmers see their accountant as their mainsource of advice).Warren (1998b, p. 75)puts it more plainly:

‘people like me have been able to make a reasonable living over the years out of teaching andwriting about the idiosyncrasies of farm management accounting. . . and we do like to feel differentin agriculture, especially when we can browbeat the new accountant, weaned on the books of moreconventional industries. But it also has its downside, in the form of wasted time, frustration, theneed for specialist computer packages and the creation of barriers to effective communication’.

3.8. Practical Implications and conclusions

The industry itself does not have the management accounting expertise to innovate new costing andperformance measurement systems: net margins and costs per unit are extensions of gross margin ac-counting and based on the same theoretical and technical stock of knowledge. However, the accountingprofession, which could bring new ideas and concepts into the industry, appears to keep its expertiseor interest in agriculture separate from its other activities and has not has not significantly added to thestocks of knowledge in the industry. Accounting academics, asArgiles and Slof (2001)pointed out in thequote given at the start of this paper, appear to have had no interest in analyzing a fundamental industrythat effects everyone through consumption and taxation.

Giddens, in discussing what he means by ‘mutual knowledge’ (similar to, but not the same as commonsense), outlines a number of reasons why new knowledge fails to become accepted or institutionalized.One reason is that the ‘conduct in question depends on motives and reasons which are not altered when newinformation becomes available’ (1984, p. 342) and another is that new information may simply ‘sustainexisting circumstances’. The relationships involved here may be complex and technical developments inaccounting may be halted by the need, here, to be different, to be ‘agricultural’.

Another reason for failure of new knowledge to be institutionalized maybe that those who seek to applyit ‘are not in a position to do so effectively’. Warren has commented that his discussion paper ‘Banishingvariable and fixed costs’ (1998) and other similar papers (albeit few and far between) are put aside as thework of individuals (and eccentric individuals at that). There appear to be no viable networks, such as theone David Wallace was able to motivate in the early sixties. A strong network, either within a segment ofthe industry or across the segments, where both theoretical and practical stocks of knowledge could begenerated by groups of actors should provide the position needed for new knowledge to be accepted.

In the context of the existing studies of institutionalized accounting practices,Granlund (2001, p. 144)commented that stability in management accounting systems had previously been approached in twoways. The first is a ‘factors’ approach, which suffers from the inherent complexity of the relationshipsinvolved between actors with the accounting practice and often fails, in his view, to actually explainstability. The second is a more hermeneutic approach, looking at stability, or failure to change, in termsof political resistance or failure to secure legitimacy for a new method. Granlund noted that, in the end,human factors prevented the change of the interpretative scheme in the case studied. This study acceptsthat, and is limited in that it has not explored the issues of power and legitimation, or the external pressureson the institutional structures. This study focussed on the stock of knowledge and how it has been shaped

L. Jack / Management Accounting Research 16 (2005) 59–79 77

both by the actors and by unintended outcomes of their actions. Instead of exploring failed change, orchange in progress (Burns and Vaivio, 2001, p. 393), it captures an accounting practice that could change,but has not yet changed. The persistence, or durability of the method, owes something the breakdown ofnetworks that enabled diffusion in the first place and something to the security it offers to actors: a uniquemethod of accounting for an industry in which the actors want to maintain their unique identity. It isknown that change in the interpretative scheme can be illusory: structures, norms and actors themselvescan remain unchanged (ibid.). This study suggests that maybe stability of practice – and the securityit affords, is also illusory, a construction achieved by simplification and unintended consequences, thatin fact could change quite suddenly. Researchers need to keep taken-for-granted traditional methodsunder observation as well as those that are new, in order to understand both stability and change. Thestory of the agricultural gross margin could be taken as a cautionary tale: where there is innovationand a deliberate attempt at institutionalization, it is likely that there will also be simplification andunintended consequences for the stocks of knowledge and methods proposed. There are possibly lessonstoo, for those tempted to impose single accounting solutions on what are, in reality, diverse and variedbusinesses.

Acknowledgements

I am grateful for the comments of participants following the presentation of earlier versions of thispaper at the BAA Accounting Education SIG, the ACIPFAL and IPA YSC conferences, in particularAnn Loft and Jane Broadbent. I would also like to thank Willie Seal, Sean McCartney, Martin Collisonand colleagues at Writtle College, and the two anonymous referees for their invaluable comments andhelp.

Appendix A. Example of the basic gross margin calculation

An arable cropAverage yield (tones per hectare) 5.5

Price per tonne (£65)Sale value (£) 358Area payment (£) 225Output (£) 583

Variable costsSeed 50Fertilizer 55Sprays 60Total variable costs 165Gross margin per hectare 418

Variable costs must be (a) specific to the enterprise and (b) vary in proportion to the size of the enterprise (Nix, 2002, p. 1).Fixed costs (i.e., all non-variable costs) are subtracted from the aggregate gross margins of all enterprises on the farm and notallocated to individual enterprises.

78 L. Jack / Management Accounting Research 16 (2005) 59–79

References

Abbot, A., 1988. The System of Professions: An Essay on the Division of Expert Labor. University of Chicago Press, Chicago.Ahrens, T., Chapman, C., 2002. The structuration of legitimate performance measures and management: day-to-day contests of

accountability in a U.K. restaurant chain. Manage. Acc. Res. 13, 151–171.Ansari, S., Euske, K.J., 1987. Rational, rationalizing and reifying uses of accounting data in organizations. Acc. Organ. Society

12 (6), 549–570.Argiles, J.M., Slof, E.J., 2001. New opportunities for farm accounting. Europ. Acc. Rev. 10 (2), 361–383.Armstrong, P., 2002. Management, image and management accounting. Critic. Perspect. Acc. 13, 281–295.Barley, S.R., Tolbert, P.S., 1997. Institutionalization and structuration: studying the links between action and institution. Organ.

Stud. 18 (1), 93–117.Barnard, C.S., Nix, J.S., 1979. Farm Planning and Control, 2nd ed. Cambridge University Press Ltd., Cambridge.Berger, P., Luckmann, T., 1967. The Social Construction of Reality. Penguin Books, London.Body, R., 1991. Our Food, Our Land. Why Contemporary Farming Practices Must Change. Rider, London.Burns, J., Scapens, R.W., 2000. Conceptualizing management accounting change: an institutional framework. Manage. Acc.

Res. 11, 3–25.Burns, J., Vaivio, J., 2001. Management accounting change. Manage. Acc. Res. 12, 389–402.Carruthers, B.G., 1995. Accounting, ambiguity and the new institutionalism. Acc. Organ. Society 20 (4), 313–328.Chua, W.F., Petty, R., 1999. Mimicry, director interlocks, and the interorganizational diffusion of a quality strategy: a note. J.

Manage. Acc. Res. 11.Cicourel, A., 1973. Cognitive Sociology. Penguin, Education, Middlesex.Collier, P.M., 2001. The power of accounting: a field study of local financial management in a police force. Manage. Acc. Res.

12, 465–486.DEFRA, 2004. Figures for a Farming Future—Getting Started in Farm Management Accounting, London, DEFRA Publications.DiMaggio, P.J., 1991. Constructing an organizational field. In: Powell, W.W., DiMaggio, P.J. (Eds.), The New Institutionalism

in Organisational Analysis. University of Chicago Press, London.DiMaggio, P.J., Powell, W.W., 1983. The iron cage revisited: institutional isomorphism and collective rationality in organizational

fields. Amer. Soc. Rev. 48, 147–160.Douglas, M., 1986. How Institutions Think. Routledge and Kegan Paul, London.Edelmann, L.B., Uggen, C., Erlanger, H.S., 1999. The endogeneity of legal regulation: grievance procedures as rational myth.

Amer. J. Soc. 105 (2), 406–454.Fedie, D.M., 1997. How to Farm for Profit: Practical Enterprise Analysis. Iowa State University Press, Iowa.Fligstein, N., 1991. The structural transformation of american industry. In: Powell, W.W., DiMaggio, P.J. (Eds.), The New

Institutionalism in Organisational Analysis. University of Chicago Press, London.Frances, J., Garnsey, E., 1996. Supermarkets and suppliers in the United Kingdom: system integration, information and control.

Acc. Organ. Society 21 (6), 591–610.Giddens, A., 1984. The Constitution of Society. University of California Press, US.Giddens, A., 1991. Modernity and Self-identity. Polity Press, Cambridge.Giles, A.K., 1986. Net Margins and All That—An Essay in Management Accounting in Agriculture, Reading, College of Estate

Management, University of Reading Press. Reprinted in Windows on Agricultural Economics and Farm Management, 1993.Giles, A.K., James, P.J., 1993. Farm Management Liaison—A Unique Era, Reprinted in Windows on Agricultural Economics

and Farm Management, 1993. Reading, College of Estate Management, University of Reading.Granlund, M., 2001. Towards explaining stability in and around management accounting systems. Manage.Acc. Res. 12, 141–166.Gould, L., 1973. Agricultural consultancy—a twentieth century profession. J. Agr. Econ. XXIV (1), 23–35.Juchau, R., Hill, P., 2000. Agricultural Accounting: Perspectives and Issues, 2nd ed. University of London, Wye College, Wye.Knight, D.J., 1989. Private consultancy in agriculture. Farm Manage. 7 (1), 47–52.Knorr-Cetina, K., 1988. In: Field, N.G. (Ed.), The Micro-Social Order, Actions and Structure: Research Methods and Social

Theory. Sage Publications, London.Liversage, V., 1956. Accounting for farm planning. J. Agr. Econ. XI (4), 472–476.Lloyd, D.H., 1970. The Development of Farm Business Analysis and Planning in Britain: A Methodological Review and

Appraisal, Reading, University of Reading, Department of Agriculture, Study No. 6.

L. Jack / Management Accounting Research 16 (2005) 59–79 79

MacDonald, K.M., 1995. The Sociology of the Professions. Sage Publications, London.MacIntosh, N.B., Scapens, R.W., 1990. Structuration theory in management accounting. Acc. Organ. Society 15 (5), 455–477.MacIntosh, N.B., Scapens, R.W., 1991. Management accounting and control systems: a structuration theory analysis. J. Manage.

Acc. Res. 3, 131–158.Malcolm, L.R., 1990. Fifty years of farm management in Australia’, review of marketing and agricultural economics. In: Juchau,

R., Hill, P. (Eds.), Agricultural Accounting: Perspectives and Issues, 2nd ed. University of London, Wye.Markham, G., 2003. Accounting for turbulent times. Accountancy, 40–41.Modell, S., 2001. Performance measurement and institutional processes: a study of managerial responses to public sector reform.

Manage. Acc. Res. 12, 437–464.Newby, H., 1979. Green and Pleasant Land—Social Change in Rural England. Hutchinson and Co., Middlesex.Nix, J., 1979. Farm management: the state of the art, or science. J. Agr. Econ. 30 (3), 277–291.Nix, J., 1990. Aspects of profitability: an outmoded concept. J. Agr. Econ. 41 (3), 266–287.Nix, J., Hill, P., 2003. Farm Management Pocketbook, 33rd ed. Wye College Press, Kent.Norman, L., 1986. Managing Farms: What Farmers and Managers Actually Do!. CMA/Hampshire College of Agriculture,