STATS ChipPAC Ltd. - iFAST Global Markets

376

OFFERING CIRCULAR STRICTLY CONFIDENTIAL $425,000,000 STATS ChipPAC Ltd. (Company Registration No. 199407932D) 8.5% Senior Secured Notes due 2020 We are offering $425,000,000 aggregate principal amount of our 8.5% senior secured notes due 2020 (the “Notes”). The Notes will mature on 24 November 2020. We will pay interest on the Notes on 24 May and 24 November of each year, commencing on 24 May 2016. Prior to 24 November 2018, we may redeem all or part of the Notes at any time by paying a “make-whole” premium plus accrued and unpaid interest. We may redeem all, but not less than all, of the Notes at any time in the event of certain changes affecting withholding taxes at 100.0% of their principal amount plus accrued and unpaid interest. At any time on or after 24 November 2018, we may redeem all or a part of the Notes at any time at the redemption prices specified under the section entitled “Description of Notes — Optional Redemption” plus accrued and unpaid interest. In addition, prior to 24 November 2018, we may redeem up to 35.0% of the Notes with the net proceeds of certain equity offerings. Upon a Change of Control (as defined below), we will be required to offer to purchase the Notes at 101.0% of their principal amount plus accrued and unpaid interest. The Notes will be our senior secured obligations and will rank at least pari passu in right of payment with all of our existing and future senior indebtedness and senior in right of payment to our existing and future subordinated indebtedness. The Notes will be guaranteed by all of our subsidiaries (except STATS ChipPAC Shanghai Co., Ltd. (“our China subsidiary”) and STATS ChipPAC (Thailand) Limited and STATS ChipPAC Services (Thailand) Limited (“our Thai subsidiaries”), with unconditional guarantees (the “Note Guarantees”) that will be senior to existing and future subordinated debt of those subsidiaries. The Notes and the Note Guarantees will be secured, subject to certain permitted liens, on an equal and rateable basis with all Senior Debt (as defined in “Description of Notes”) including any Additional Pari Passu Debt (as defined in “Description of Notes”) under the terms of the Intercreditor Deed (as defined herein) by first priority liens on the Collateral (as defined in “Description of Notes”), which comprises shares of certain of our subsidiaries and certain of our and our subsidiaries’ assets. See “Description of Notes — Brief Description of the Notes, the Note Guarantees and the Security — Security.” Approval in-principle has been obtained for the listing and quotation of the Notes on the Singapore Exchange Securities Trading Limited (the “SGX-ST”). The SGX-ST assumes no responsibility for the correctness of any of the statements made or opinions expressed or reports contained herein. Approval in-principle for the listing and quotation of the Notes is not to be taken as an indication of the merits of the Notes. Admission to the Official List of the SGX-ST is not to be taken as an indication of the merits of the Notes or our Company. The Notes will be traded on the SGX-ST in a minimum board lot size of $200,000 as long as the Notes are listed on the SGX-ST. The Notes have been provisionally rated “BB-” by Standard & Poor’s Ratings Group (“S&P”), “BB” by Fitch Ratings Inc. (“Fitch”) and “B1” by Moody’s Investor Service (“Moody’s”). The ratings do not constitute recommendations to purchase, hold or sell the Notes inasmuch as such ratings do not comment as to market price or suitability for a particular investor. We cannot assure you that the ratings will remain in effect for any given period or that the ratings will not be revised by such ratings agencies in the future if, in their judgment, circumstances so warrant. Applicable laws may limit the enforceability of the Note Guarantees and the pledge of any Collateral. For more information regarding the Notes, the Note Guarantees, the Collateral and the Intercreditor Deed, see “Description of Notes,” beginning on page 175. Investing in the Notes involves a high degree of risk. See “Risk Factors,” beginning on page 28. We have not registered the Notes under the Securities Act of 1933, as amended (the “Securities Act”), or the securities laws of any other place. The Notes are being offered in the United States only to qualified institutional buyers (within the meaning of Rule 144A under the Securities Act) and to persons outside the United States under Regulation S under the Securities Act. See “Plan of Distribution” and “Transfer Restrictions” for additional information about eligible offerees and transfer restrictions. Issue Price: 100.0% plus accrued interest, if any, from 24 November 2015 The Notes are expected to be delivered to purchasers on or about 24 November 2015. Joint Bookrunners and Joint Lead Managers Barclays DBS Bank Ltd. ING Co-Manager First Gulf Bank PJSC The date of this offering circular is 17 November 2015

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of STATS ChipPAC Ltd. - iFAST Global Markets

OFFERING CIRCULAR STRICTLY CONFIDENTIAL

$425,000,000

STATS ChipPAC Ltd.(Company Registration No. 199407932D)

8.5% Senior Secured Notes due 2020

We are offering $425,000,000 aggregate principal amount of our 8.5% senior secured notes due 2020 (the “Notes”). The Noteswill mature on 24 November 2020. We will pay interest on the Notes on 24 May and 24 November of each year, commencing on24 May 2016.

Prior to 24 November 2018, we may redeem all or part of the Notes at any time by paying a “make-whole” premium plusaccrued and unpaid interest. We may redeem all, but not less than all, of the Notes at any time in the event of certain changesaffecting withholding taxes at 100.0% of their principal amount plus accrued and unpaid interest. At any time on or after24 November 2018, we may redeem all or a part of the Notes at any time at the redemption prices specified under the sectionentitled “Description of Notes — Optional Redemption” plus accrued and unpaid interest. In addition, prior to 24 November 2018,we may redeem up to 35.0% of the Notes with the net proceeds of certain equity offerings. Upon a Change of Control (as definedbelow), we will be required to offer to purchase the Notes at 101.0% of their principal amount plus accrued and unpaid interest.

The Notes will be our senior secured obligations and will rank at least pari passu in right of payment with all of our existingand future senior indebtedness and senior in right of payment to our existing and future subordinated indebtedness. The Notes willbe guaranteed by all of our subsidiaries (except STATS ChipPAC Shanghai Co., Ltd. (“our China subsidiary”) and STATSChipPAC (Thailand) Limited and STATS ChipPAC Services (Thailand) Limited (“our Thai subsidiaries”), with unconditionalguarantees (the “Note Guarantees”) that will be senior to existing and future subordinated debt of those subsidiaries. The Notes andthe Note Guarantees will be secured, subject to certain permitted liens, on an equal and rateable basis with all Senior Debt (asdefined in “Description of Notes”) including any Additional Pari Passu Debt (as defined in “Description of Notes”) under the termsof the Intercreditor Deed (as defined herein) by first priority liens on the Collateral (as defined in “Description of Notes”), whichcomprises shares of certain of our subsidiaries and certain of our and our subsidiaries’ assets. See “Description of Notes — BriefDescription of the Notes, the Note Guarantees and the Security — Security.”

Approval in-principle has been obtained for the listing and quotation of the Notes on the Singapore Exchange SecuritiesTrading Limited (the “SGX-ST”). The SGX-ST assumes no responsibility for the correctness of any of the statements made oropinions expressed or reports contained herein. Approval in-principle for the listing and quotation of the Notes is not to be taken asan indication of the merits of the Notes. Admission to the Official List of the SGX-ST is not to be taken as an indication of themerits of the Notes or our Company. The Notes will be traded on the SGX-ST in a minimum board lot size of $200,000 as long asthe Notes are listed on the SGX-ST.

The Notes have been provisionally rated “BB-” by Standard & Poor’s Ratings Group (“S&P”), “BB” by Fitch Ratings Inc.(“Fitch”) and “B1” by Moody’s Investor Service (“Moody’s”). The ratings do not constitute recommendations to purchase, hold orsell the Notes inasmuch as such ratings do not comment as to market price or suitability for a particular investor. We cannot assureyou that the ratings will remain in effect for any given period or that the ratings will not be revised by such ratings agencies in thefuture if, in their judgment, circumstances so warrant.

Applicable laws may limit the enforceability of the Note Guarantees and the pledge of any Collateral. For more informationregarding the Notes, the Note Guarantees, the Collateral and the Intercreditor Deed, see “Description of Notes,” beginning onpage 175.

Investing in the Notes involves a high degree of risk. See “Risk Factors,” beginning on page 28.

We have not registered the Notes under the Securities Act of 1933, as amended (the “Securities Act”), or the securitieslaws of any other place. The Notes are being offered in the United States only to qualified institutional buyers (within themeaning of Rule 144A under the Securities Act) and to persons outside the United States under Regulation S under theSecurities Act. See “Plan of Distribution” and “Transfer Restrictions” for additional information about eligible offerees andtransfer restrictions.

Issue Price: 100.0%plus accrued interest, if any, from 24 November 2015

The Notes are expected to be delivered to purchasers on or about 24 November 2015.Joint Bookrunners and Joint Lead Managers

Barclays DBS Bank Ltd. INGCo-Manager

First Gulf Bank PJSCThe date of this offering circular is 17 November 2015

INNOVATE • CREATE • DELIVER

TABLE OF CONTENTS

Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Risk Factors . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

The Change of Control and RelatedTransactions . . . . . . . . . . . . . . . . . . . . . . . . . 60

Use of Proceeds . . . . . . . . . . . . . . . . . . . . . . . . . 67

Exchange Rate Information . . . . . . . . . . . . . . . . 68

Capitalisation . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

Unaudited Pro Forma Combined FinancialStatements . . . . . . . . . . . . . . . . . . . . . . . . . . 71

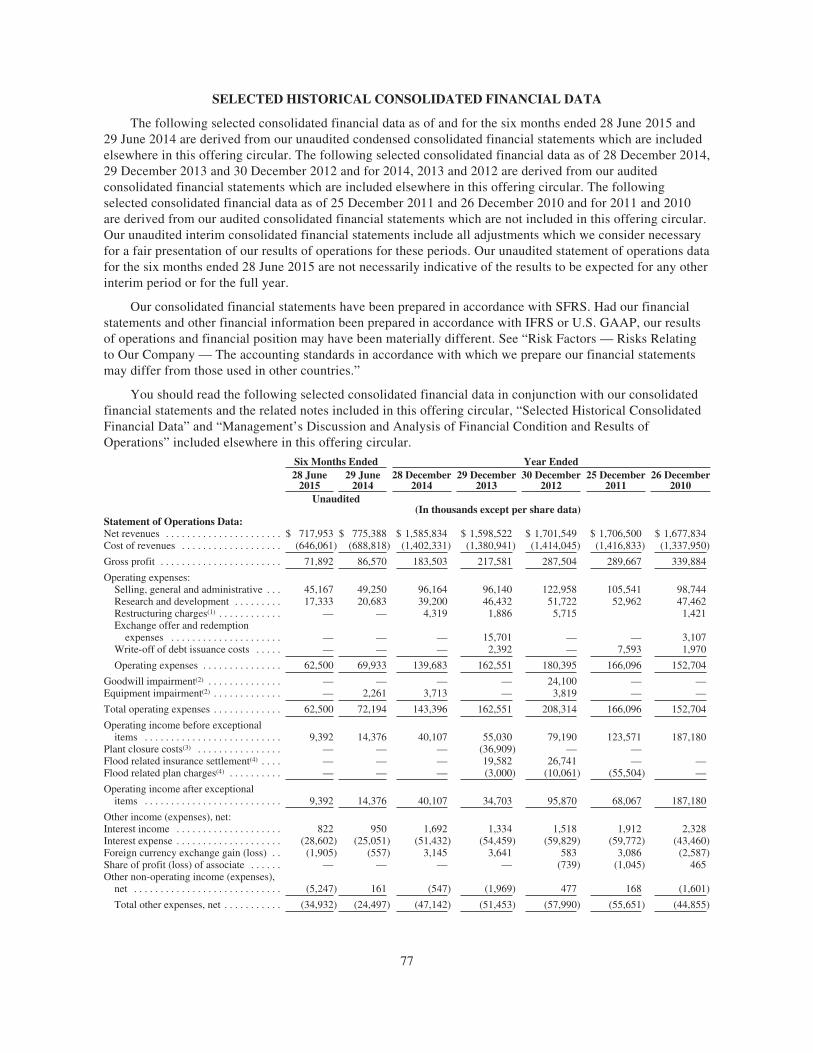

Selected Historical Consolidated FinancialData . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

Management’s Discussion and Analysis ofFinancial Condition and Results ofOperations . . . . . . . . . . . . . . . . . . . . . . . . . . . 81

Business . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 115

Management . . . . . . . . . . . . . . . . . . . . . . . . . . . 154

Principal Shareholders and Related PartyTransactions . . . . . . . . . . . . . . . . . . . . . . . . . 162

Description of Indebtedness and OtherMaterial Contracts . . . . . . . . . . . . . . . . . . . . . 164

Description of Notes . . . . . . . . . . . . . . . . . . . . . 175

Taxation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 235

Plan of Distribution . . . . . . . . . . . . . . . . . . . . . . 242

Transfer Restrictions . . . . . . . . . . . . . . . . . . . . . 248

Enforcement of Judgments . . . . . . . . . . . . . . . . 251

Validity and Enforceability of the NoteGuarantees and the Security . . . . . . . . . . . . . 254

Legal Matters . . . . . . . . . . . . . . . . . . . . . . . . . . . 262

Independent Auditor . . . . . . . . . . . . . . . . . . . . . 263

Index to Financial Statements . . . . . . . . . . . . . . F-1

THIS CONFIDENTIAL OFFERING CIRCULAR DOES NOT CONSTITUTE AN OFFER TOSELL, OR A SOLICITATION OF AN OFFER TO BUY, ANY NOTE OFFERED HEREBY BY ANYPERSON IN ANY JURISDICTION IN WHICH IT IS UNLAWFUL TO MAKE SUCH AN OFFER,SOLICITATION OR SALE. NEITHER THE DELIVERY OF THIS OFFERING CIRCULAR NORANY SALE MADE HEREUNDER SHALL UNDER ANY CIRCUMSTANCES IMPLY THAT THEREHAS BEEN NO CHANGE IN THE AFFAIRS OF OUR COMPANY OR OUR SUBSIDIARIES ORTHAT THE INFORMATION SET FORTH IN THIS OFFERING CIRCULAR IS CORRECT AS OFANY DATE SUBSEQUENT TO THE DATE HEREOF.

You should rely only on the information contained in this offering circular. Neither we, the initialpurchasers, nor The Bank of New York Mellon as trustee (the “Trustee”), as paying agent and transfer agent(the “Paying Agent”) and as registrar (the “Registrar” and, together with the Paying Agent, collectivelyreferred to as the “Agents”) has authorised any other person to provide you with different information. Ifanyone provides you with different or inconsistent information, you should not rely on it.

Information in this offering circular with respect to Jiangsu Changjiang Electronics Technology Co., Ltd.(“JCET”), JCET-SC (Singapore) Pte. Ltd. ( “JCET-SC”), the National Integrated Circuit Industry InvestmentFund Co., Ltd. (the “IC Fund”), SilTech Semiconductor (Shanghai) Corporation Limited (“SSSC”),Semiconductor Manufacturing International Corporation (“SMIC”), the Consortium (as defined below) andany arrangements described herein between any members of the Consortium has been primarily extracted fromor is based on documents issued by, or on behalf of, JCET-SC in connection with the JCET Offer that are filedwith the SGX-ST. JCET, the IC Fund and SSSC are collectively referred to herein as the “Consortium.”Neither we, the initial purchasers, the Trustee nor the Agents have made any investigation or enquiry withrespect to such publicly available documents and information. Neither we, the initial purchasers, the Trusteenor the Agents make any representation or accept any responsibility with respect to the accuracy,completeness or sufficiency of such information relating to any of JCET, JCET-SC, the IC Fund, SSSC,SMIC, the Consortium and any arrangements described herein between any members of the Consortium. Inparticular, the information provided is primarily extracted from or is based on historical documents issued by,or on behalf of, JCET-SC in connection with the JCET Offer and may have changed.

We are relying on an exemption from registration under the Securities Act for offers and sales ofsecurities in the United States that do not involve a public offering. The Notes offered hereby have not beenregistered under the Securities Act or under any other securities laws. Unless they are registered, the Notesmay be offered only in transactions that are exempt from these securities laws. By purchasing the Notes, you

i

will be deemed to have made the acknowledgements, representations, warranties and agreements describedunder the heading “Transfer Restrictions” in this offering circular. You should understand that you may berequired to bear the financial risks of your investment for an indefinite period of time.

This offering circular contains information provided by other sources that we believe are reliable. Wecannot assure you that this information is accurate or complete. This offering circular summarises certaindocuments and other information and we refer you to them for a more complete understanding of what wediscuss in this offering circular. In making an investment decision, you must rely on your own examination ofour Company and the terms of the offering and the Notes, including the merits and risks involved.

We are not making any representation to any purchaser of the Notes regarding the legality of aninvestment in the Notes by such purchaser under any legal investment or similar laws or regulations. Youshould not consider any information in this offering circular to be legal, business or tax advice. You shouldconsult your own attorney, business advisor and tax advisor for legal, business and tax advice regarding aninvestment in the Notes.

This offering circular is highly confidential and has been prepared by us solely for use in connection withthe proposed private placement of the Notes described herein. We and the initial purchasers reserve the rightto reject any offer to purchase, in whole or in part, for any reason, or to sell less than the amount of the Notesoffered hereby. This offering circular is personal to each offeree and does not constitute an offer to any otherperson or to the public generally to subscribe for or otherwise acquire the Notes. Distribution of this offeringcircular to any person other than the offeree and those persons, if any, retained to advise such offeree withrespect thereto is unauthorised, and any disclosure of any of its contents, without prior written consent, isprohibited. This offering circular may not be copied or reproduced in whole or in part. Each prospectivepurchaser, by accepting delivery of this offering circular, agrees to the foregoing. See “Transfer Restrictions.”

You must comply with all laws that apply to you in any place in which you buy, offer or sell any notes orpossess this offering circular. You must also obtain any consents or approvals that you need in order topurchase the Notes. Neither we nor the initial purchasers are responsible for your compliance with these legalrequirements.

The Notes will be issued in fully registered book-entry form and will be represented by one or morepermanent global certificates, deposited with a custodian for, and registered in the name of a nominee of, TheDepository Trust Company (“DTC”) in New York, New York. Beneficial interests in any such global securitywill be shown on, and transfers thereof will be effected only through, records maintained by DTC and itsdirect and indirect participants, and any such interest may not be exchanged for certification notes, except inlimited circumstances described in this offering circular.

The Notes have not been approved or disapproved by the U.S. Securities and Exchange Commission (the“SEC”), any state securities commission in the United States or any other U.S. regulatory authority, nor haveany of the foregoing authorities passed upon or endorsed the merits of this offering or the accuracy oradequacy of this offering circular. Any representation to the contrary is a criminal offence in the United States.

IN CONNECTION WITH THIS ISSUE, BARCLAYS BANK PLC, SINGAPORE BRANCH (THE“STABILISING AGENT”) MAY, TO THE EXTENT PERMITTED BY APPLICABLE LAWS ANDREGULATIONS, OVER-ALLOT THE NOTES OR EFFECT TRANSACTIONS WITH A VIEW TOSUPPORTING THE MARKET PRICE OF THE NOTES AT A LEVEL HIGHER THAN THATWHICH MIGHT OTHERWISE PREVAIL. HOWEVER, THERE IS NO ASSURANCE THAT THESTABILISING AGENT WILL UNDERTAKE ANY STABILISATION ACTION. ANYSTABILISATION ACTION MAY BEGIN ON OR AFTER THE DATE ON WHICH ADEQUATEPUBLIC DISCLOSURE OF THE OFFER OF THE NOTES IS MADE AND, IF BEGUN, MAY BEENDED AT ANY TIME, BUT MUST END NO LATER THAN THE EARLIER OF 30 DAYS AFTERTHE ISSUE DATE OF THE NOTES AND 60 DAYS AFTER THE ALLOTMENT OF THE NOTES.

ii

NOTICE TO NEW HAMPSHIRE RESIDENTS

NEITHER THE FACT THAT A REGISTRATION STATEMENT OR AN APPLICATION FOR ALICENSE HAS BEEN FILED UNDER CHAPTER 421-B OF THE NEW HAMPSHIRE REVISEDSTATUTES WITH THE STATE OF NEW HAMPSHIRE NOR THE FACT THAT A SECURITY ISEFFECTIVELY REGISTERED OR A PERSON IS LICENSED IN THE STATE OF NEWHAMPSHIRE CONSTITUTES A FINDING BY THE SECRETARY OF STATE THAT ANYDOCUMENT FILED UNDER RSA 421-B IS TRUE, COMPLETE AND NOT MISLEADING.NEITHER ANY SUCH FACT NOR THE FACT THAT AN EXEMPTION OR EXCEPTION ISAVAILABLE FOR A SECURITY OR A TRANSACTION MEANS THAT THE SECRETARY OFSTATE HAS PASSED IN ANY WAY UPON THE MERITS OR QUALIFICATIONS OF, ORRECOMMENDED OR GIVEN APPROVAL TO, ANY PERSON, SECURITY, OR TRANSACTION. ITIS UNLAWFUL TO MAKE, OR CAUSE TO BE MADE, TO ANY PROSPECTIVE PURCHASER,CUSTOMER, OR CLIENT ANY REPRESENTATION INCONSISTENT WITH THE PROVISIONSOF THIS PARAGRAPH.

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

Our consolidated financial statements are prepared in accordance with Singapore Financial ReportingStandards (“SFRS”), which differ in certain respects from International Financial Reporting Standards(“IFRS”) and generally accepted accounting principles in the United States (“U.S. GAAP”). As a result, ourconsolidated financial statements and reported earnings could be different from those which would be reportedunder IFRS or U.S. GAAP. Such differences may be material. This offering circular does not contain areconciliation of our consolidated financial statements to IFRS or U.S. GAAP nor does it include anyinformation in relation to the differences between SFRS and IFRS or U.S. GAAP. Had our financialstatements and other financial information been prepared in accordance with IFRS or U.S. GAAP, the resultsof operations and financial position may have been materially different. In making an investment decision,investors must rely upon their own examination of our Company, the terms of the offering and the financialinformation. Potential investors should consult their own professional advisors for an understanding of thedifferences between SFRS and IFRS or U.S. GAAP, and how such differences might affect the financialinformation contained herein. See “Risk Factors — Risks Relating to Our Company — The accountingstandards in accordance with which we prepare our financial statements may differ from those used in othercountries.”

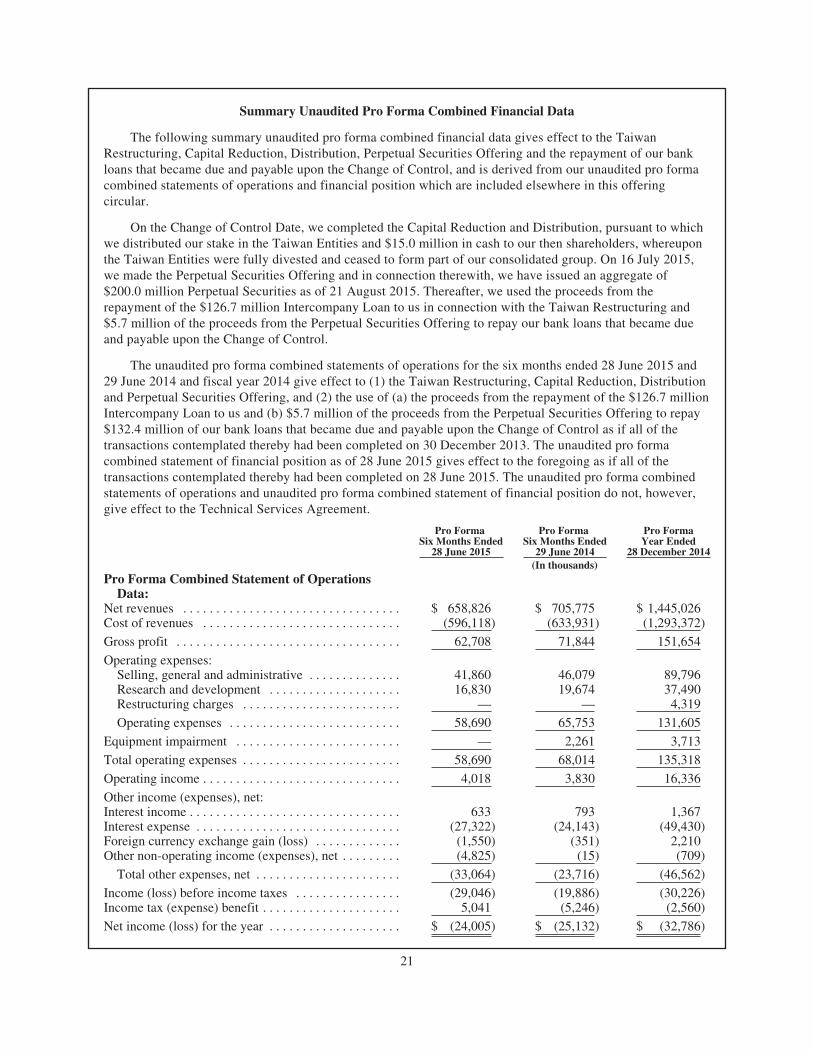

This offering circular includes our unaudited pro forma combined statements of operations for the sixmonths ended 28 June 2015 and 29 June 2014 and fiscal year 2014, which give effect to (1) the TaiwanRestructuring, Capital Reduction, Distribution and Perpetual Securities Offering (each as defined herein), and(2) the use of (a) the proceeds from the repayment of the $126.7 million Intercompany Loan (as describedunder “The Change of Control and Related Transactions — Taiwan Restructuring”) to us and (b) $5.7 millionof the $200.0 million of proceeds from the Perpetual Securities Offering to repay $132.4 million of our bankloans that became due and payable upon the Change of Control (as defined herein), as if all of the transactionscontemplated thereby had been completed on 30 December 2013, and our unaudited pro forma combinedstatement of financial position as of 28 June 2015, which gives effect to the foregoing as if they had beencompleted on 28 June 2015. Our unaudited pro forma combined statements of operations and unauditedpro forma combined statement of financial position do not, however, give effect to the Technical ServicesAgreement (as defined herein). See “The Change of Control and Related Transactions” and “UnauditedPro Forma Combined Financial Statements.” References to our results of operations or financial position“pro forma for the Taiwan Restructuring, Capital Reduction, Distribution and Perpetual Securities Offering”or “our pro forma” results of operations or financial statements refer to these pro forma financial statements.

References to “U.S. dollar” or “$” in this offering circular mean United States dollars, the legal currencyof the United States of America. References to “Singapore dollars” or “S$” mean Singapore dollars, the legalcurrency of the Republic of Singapore. References to “South Korean Won” mean Korean Republic Won, thelegal currency of the Republic of Korea. References to “Chinese Renminbi” or “RMB” mean ChineseRenminbi, the legal currency of the People’s Republic of China. References to “Malaysian Ringgit” mean

iii

Malaysian Ringgit, the legal currency of Malaysia. References to “Thai Baht” mean Thai Baht, the legalcurrency of Thailand. References to “New Taiwan dollar” or “NT$” mean New Taiwan dollars, the legalcurrency of Taiwan. References to “Japanese Yen” mean Japanese Yen, the legal currency of Japan. Theclosing rate appearing on Reuters on 28 June 2015 was S$1.3496 per $1.00 for Singapore dollars, NT$30.9840per $1.00 for New Taiwan dollars and RMB6.2080 per $1.00 for Chinese Renminbi. For your convenience,unless otherwise indicated, certain amounts in these currencies have been translated into U.S. dollars based onthese exchange rates. Certain amounts (including percentage amounts) have been rounded for convenience; asa result, certain figures may not sum to total amounts or equal quotients.

No representation is made that the U.S. dollar, Singapore dollar, South Korean Won, Chinese Renminbi,Malaysian Ringgit, Thai Baht, New Taiwan dollar or Japanese Yen amounts shown in this offering circularcould have been or could be converted at such rate or at any other rate.

References to the “PRC” or “China” are to the People’s Republic of China. References to “Korea” or“South Korea” in this offering circular means the Republic of Korea.

In this offering circular, unless otherwise specified or the context requires, the terms “we,” “our,” and“us” refer to STATS ChipPAC Ltd., a Singapore company, and its consolidated subsidiaries, “our Company”refers to STATS ChipPAC Ltd. and its consolidated subsidiaries or to STATS ChipPAC Ltd. as the contextrequires and “STATS ChipPAC” refers to STATS ChipPAC Ltd.

Prior to the Change of Control, up to and including our fiscal second quarter ended 28 June 2015, our52-53 week fiscal year ended on the Sunday nearest and prior to 31 December and our fiscal quarters ended ona Sunday and were generally thirteen weeks in length. Following the Change of Control, commencing fromthe fiscal third quarter of fiscal year 2015, we adopted a fiscal calendar year with interim fiscal quartersending on 31 March, 30 June, 30 September and 31 December to align with the financial reporting period ofour parent company, JCET. Our first, second and third quarters of 2015 ended on 29 March, 28 June and30 September, respectively. Our first, second and third quarters of 2014 ended on 30 March, 29 June and28 September, respectively and our fourth quarter and fiscal year 2014 ended on 28 December. Our thirdquarter of 2013 ended on 29 September, and our fourth quarter and fiscal year 2013 ended on 29 December.Our fiscal years 2012, 2011 and 2010 ended on 30 December, 25 December and 26 December, respectively.Unless otherwise stated, all years and dates refer to our fiscal years.

This offering circular incorporates by reference the audit report for our consolidated financial statementsas of and for our fiscal year ended 30 December 2012, which appears on page 37 of our annual report for 2012that was uploaded to the SGX-ST on 9 April 2013. No other portion of such annual report is incorporated byreference in this offering circular.

FORWARD-LOOKING STATEMENTS

Certain of the statements in this offering circular are forward-looking statements that are based onmanagement’s current views and assumptions and involve a number of risks and uncertainties which couldcause actual results to differ materially. These include statements regarding our financial condition and resultsof operations, cash flows, financing plans, business strategies, operating efficiencies and synergies, impact ofthe Change of Control Transaction (as defined below) (including potential benefits from synergies with JCET)and the Taiwan Restructuring (as defined below), budget, capacity utilisation, capital and other expenditures,competitive positions, growth opportunities for existing products, benefits from new technology, plans orobjectives of management, outcome of litigation, industry growth, the impact of regulatory initiatives, marketsfor our securities and other statements on underlying assumptions, other than statements of historical fact,including but not limited to those that are identified by the use of words such as “anticipates,” “believes,”“estimates,” “expects,” “intends,” “plans,” “predicts,” “projects,” “will,” “may,” “seeks” and similarexpressions.

These forward-looking statements, wherever they occur in this offering circular, are estimates reflectingthe best judgment of our management. These forward-looking statements involve a number of risks anduncertainties that could cause actual results to differ materially from those suggested by the forward-looking

iv

statements. Forward-looking statements should, therefore, be considered in light of various important factors,including those set forth in this offering circular.

Factors that could cause actual results to differ include, but are not limited to, general business andeconomic conditions and the state of the semiconductor industry; prevailing market conditions; demand forend-use applications products such as communications equipment, consumer and multi-applications andpersonal computers; decisions by customers to discontinue outsourcing of test and packaging services; level ofcompetition; our reliance on a small group of principal customers; our continued success in technologicalinnovations; pricing pressures, including declines in average selling prices; intellectual property rightsdisputes and litigation; our ability to control operating expenses; our substantial level of indebtedness andaccess to credit markets; potential impairment charges; availability of financing; changes in our product mix;our capacity utilisation; delays in acquiring or installing new equipment; limitations imposed by our financingarrangements which may limit our ability to maintain and grow our business; returns from research anddevelopment investments; changes in customer order patterns; customer credit risks; disruption of ouroperations; shortages in supply of key components and disruption in supply chains; disruption of ouroperations and other difficulties related to the relocation of our China operations; loss of directors, keymanagement or other personnel; defects or malfunctions in our testing equipment or packages; rescheduling orcancelling of customer orders; adverse tax and other financial consequences if the taxing authorities do notagree with our interpretation of the applicable tax laws; our ability to develop and protect our intellectualproperty; changes in environmental laws and regulations; exchange rate fluctuations; regulatory approvals forfurther investments in our subsidiaries; beneficial ownership by JCET of all of our ordinary shares that mayresult in conflicting interests with other holders of our securities; our inability to capture all or any of thebenefits from acquisitions and investments in other companies and businesses or from the acquisition of us byJCET; loss of customers or failure to compete effectively with the Taiwan Entities; labour union problems inSouth Korea; uncertainties of conducting business in China and changes in laws; currency policy and politicalinstability in other countries in Asia; natural calamities and disasters, including outbreaks of epidemics andcommunicable diseases; the delisting of our ordinary shares from the SGX-ST; and other risks described in“Risk Factors.”

All forward looking statements attributable to us or persons acting on our behalf are expressly qualified intheir entirety by the cautionary statements set forth above. You should not unduly rely on such forward-looking statements, which speak only as of the date of this offering circular.

We do not intend, and do not assume any obligation, to update any industry information or forward-looking statements to reflect subsequent events or circumstances. In light of these risks, uncertainties andassumptions, any of the events anticipated in these forward-looking statements might not occur.

AVAILABLE INFORMATION

We have agreed that, for so long as any Notes are “restricted securities” within the meaning ofRule 144(a)(3) under the Securities Act, we will, during any period in which we are neither subject toSection 13 or 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), nor exemptfrom reporting pursuant to Rule 12g3-2(b) thereunder, provide to any holder or beneficial owner of suchrestricted securities or to any prospective purchaser of such restricted securities designated by such holder orbeneficial owner for delivery to such holder, beneficial owner or prospective purchaser, in each case upon therequest of such holder, beneficial owner or prospective purchaser, the information required to be provided byRule 144A(d)(4) under the Securities Act.

ENFORCEABILITY OF CIVIL LIABILITIES

Our Company is a limited liability company incorporated under the laws of Singapore. Many of thesubsidiary guarantors are incorporated under the laws of countries other than the United States, includingBarbados, the British Virgin Islands, Malaysia and South Korea. Most of our directors, the directors of thesubsidiary guarantors and our senior management reside outside the United States. In addition, a majority of

v

our assets, the assets of the subsidiary guarantors and the assets of those persons are located outside the UnitedStates. As a result, it may be difficult for holders of the Notes to effect service of process within the UnitedStates upon these persons or to enforce in courts outside the United States any judgment obtained in theUnited States against us, the subsidiary guarantors, or any of these persons, including judgments based uponthe civil liability provisions of the laws of the United States, including federal securities laws. In addition, inoriginal actions brought in courts in jurisdictions located outside the United States, it may be difficult forholders of the Notes to enforce liabilities based upon United States federal securities laws. We have beenadvised that judgments of U.S. courts based on the civil liability provisions of the federal securities laws of theUnited States may not be enforceable in Singapore courts. We have also been advised that there is doubt as towhether Singapore, Malaysia and South Korea courts will enter judgments in original actions brought inSingapore, Malaysia, or South Korea courts, respectively, based solely upon the civil liability provisions of thefederal securities laws of the United States.

In addition to the foregoing, a final judgment in respect of the subsidiary guarantees in respect of anylegal suit or proceeding relating to a subsidiary guarantee obtained against a subsidiary guarantor in onejurisdiction may not be enforceable in another jurisdiction without further review of the merits unless thecourts of the jurisdiction in which enforcement is sought are satisfied that certain conditions are met, whichmay include (non-exhaustive) one or more of the following:

• the court that rendered the judgment had jurisdiction over the subject matter according to the laws ofthe court in which enforcement is sought;

• the judgment and the court procedure resulting in the judgment are not contrary to the public policy orpublic order or good morals of the jurisdiction in which enforcement is sought;

• there was proper service of process in the relevant jurisdiction;

• the judgment is final and conclusive. Finality of a default judgment is tested by its effect under the lawof the originating jurisdiction, so that it is necessary to determine the effect of the default judgmentunder foreign law; and

• judgment of the court in which enforcement is sought is recognised in the court rendering the judgmenton a reciprocal basis.

See “Enforcement of Judgments.”

INDUSTRY AND MARKET DATA

This offering circular includes information regarding the semiconductor industry, semiconductorpackaging and test services industry and various markets in which we compete. Where possible, thisinformation is derived from third party sources that we believe are reliable, including Gartner, Inc.(“Gartner”), IC Insights, Inc.: The McLean Report 2015 (“IC Insights”), Yole Développement: Fan-Out andEmbedded Die: Technologies and Market Trends 2015 (“Yole Développement”), IEE Global SemiconductorPatent Scorecard 2014 and International Business Strategies, Inc.: Global Systems IC Industry Service Report:Chinese Electronics and Semiconductor Industry, April 2015 (“IBS”). Certain information is also based onestimates made by our management, based on their industry and market knowledge, which we believe to bereasonable. However, this data is subject to change and cannot be verified with complete certainty due tolimits on the availability and reliability of raw data, the voluntary nature of the data gathering process andother limitations and uncertainties inherent in any statistical survey. As a result, you should be aware thatindustry projections, market share, ranking, retention, turnover and other similar data set forth herein, andestimates and beliefs based on such data, should not be unduly relied upon. We do not have any obligation toannounce or otherwise make publicly available updates or revisions to these forecasts.

The information attributed to Gartner described herein represent data, research opinion or viewpointspublished, as part of a syndicated subscription service, by Gartner, and are not representations of fact. EachGartner report speaks as of its original publication date (and not as of the date of this offering circular) and theopinions expressed in the Gartner reports are subject to change without notice.

vi

SUMMARY

This summary highlights information contained elsewhere in this offering circular. It is not complete andmay not contain all of the information that you should consider before investing in the Notes. This offeringcircular contains a description of the Notes, as well as information about our business and detailed financialdata. You should read this offering circular in its entirety, including the information presented under theheading “Risk Factors” and the more detailed information in the historical financial statements and relatednotes appearing elsewhere in this offering circular. For a more complete description of our business, see the“Business” section of this offering circular.

Our Company

We are a leading service provider of semiconductor packaging design, bump, probe, assembly, test anddistribution solutions. We have the scale to provide a comprehensive range of semiconductor packaging andtest solutions to a diversified global customer base servicing the computing, communications and consumermarkets. Our services include:

• Advanced packaging and wirebond packaging services: providing advanced integrated circuit (“IC”)packaging technology such as wafer bump, redistribution layer design and fabrication, flip-chipinterconnect, fan-out wafer level package (“FOWLP”) or embedded wafer level ball grid array(“eWLB”), wafer level chip-scale package (“WLCSP”), Through Silicon Via (“TSV”), integratedpassive devices (“IPD”), and wirebond IC packages such as leaded, laminate and memory card tocustomers for a wide variety of electronics applications. As part of our full turnkey packaging services,we offer package design; electrical, mechanical and thermal simulation; measurement and design ofleadframes and laminate substrates; and wafer processing and bumping on 200 millimetre (“mm”) and300mm wafers with options for wafer repassivation, redistribution and IPD layers;

• Test services: including wafer probe and final testing on a diverse selection of test equipment coveringthe major test platforms in the industry. We have expertise in testing a broad variety of semiconductors,especially mixed-signal, radio frequency (“RF”), analog and high-performance digital devices. We alsooffer test-related services such as burn-in process support, reliability testing, thermal and electricalcharacterisation, dry pack, and tape and reel; and

• Pre-production and post-production services: such as package development, test software and relatedhardware development, warehousing and drop shipment services.

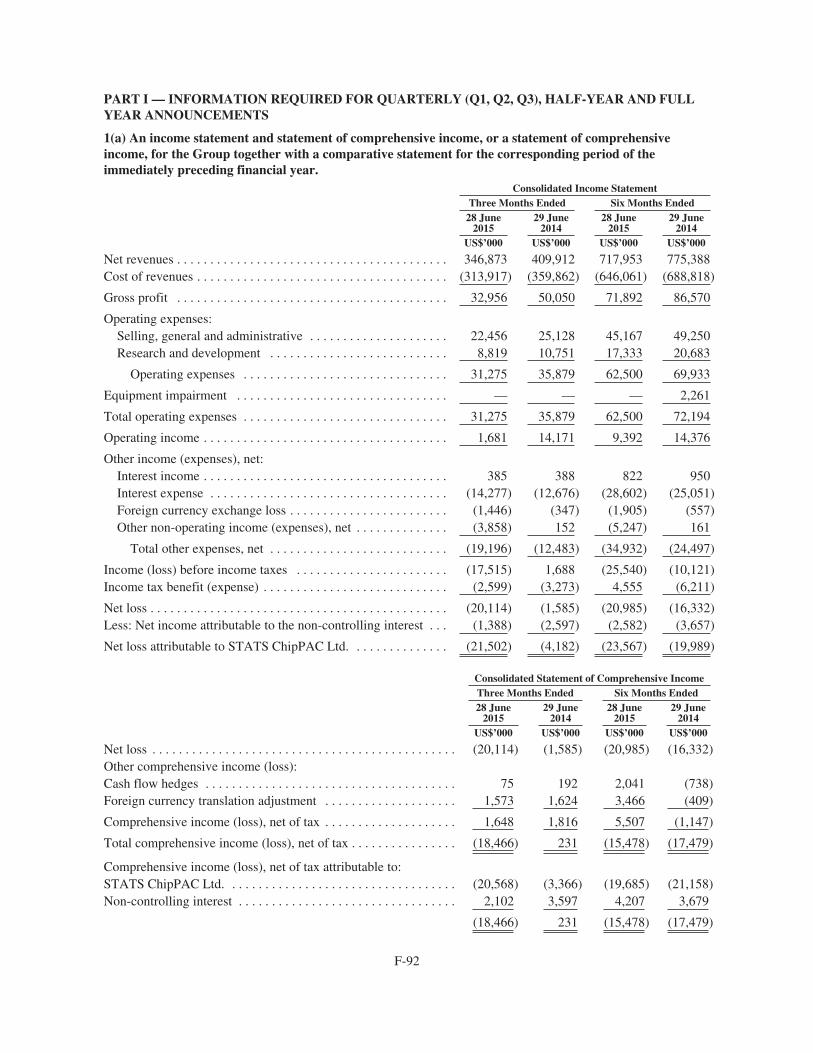

In the six months ended 28 June 2015, our net revenues were $718.0 million compared to $775.4 millionin the six months ended 29 June 2014. In 2014, 2013 and 2012, our net revenues were $1,585.8 million,$1,598.5 million and $1,701.5 million, respectively.

In the six months ended 28 June 2015 and the six months ended 29 June 2014, our net loss attributable toshareholders of STATS ChipPAC was $23.6 million and $20.0 million, respectively. In 2014, 2013 and 2012,our net income / (loss) attributable to shareholders of STATS ChipPAC was $(21.8) million, $(47.5) millionand $16.6 million, respectively.

In the six months ended 28 June 2015, 50.7% of our net revenues were derived from advanced packaging,25.7% of our net revenues were derived from wirebond packaging and 23.6% of our net revenues were derivedfrom test services. In 2014, 48.2% of our net revenues were derived from advanced packaging, 29.4% of ournet revenues were derived from wirebond packaging and 22.4% of our net revenues were derived from testservices. In 2013, 46.9% of our net revenues were derived from advanced packaging, 30.8% of our netrevenues were derived from wirebond packaging and 22.3% of our net revenues were derived from testservices. In 2012, 44.7% of our net revenues were derived from advanced packaging, 35.2% of our netrevenues were derived from wirebond packaging and 20.1% of our net revenues were derived from testservices.

We are one of the four leading outsourced semiconductor assembly and test (“OSAT”) companies in theOSAT industry. We are among the leaders in providing advanced packaging technology, such as flip-chip,

1

wafer level packaging and services (including TSV mid-end and back-end processes), die and packagestacking, System-in-Package and 3-dimension (“3D”) integration. We are also among the leaders in testingmixed-signal, RF semiconductors or semiconductors combining the use of analog and digital circuits in a chip.Mixed-signal and RF semiconductors are used extensively in fast-growing communications and consumerapplications. We have strong expertise in testing a wide range of high-performance digital devices in System-on-Chip (“SoC”).

We have been successful in attracting new customers with our packaging and test capabilities and thenexpanding our relationship with such customers to provide full turnkey solutions tailored to their individualneeds.

We are headquartered in Singapore and our manufacturing facilities are strategically located in SouthKorea, Singapore and China. We market our services through our direct sales force in the United States, SouthKorea, China, Singapore, Taiwan and Switzerland. With an established presence in the countries wherestrategic semiconductor industries are located, we are in close proximity to the major hubs of wafer fabricationwhich allows us to provide customers with fully-integrated, multi-site, end-to-end packaging and test services.

JCET beneficially owns all of our ordinary shares. JCET is an electronics packaging service provider inChina and has been listed on the Shanghai Stock Exchange since 2003. JCET has five manufacturing facilitiesin Jiangsu and Anhui provinces in China. See “The Change of Control and Related Transactions.”

Our Strengths and Strategy

Our goal is to strengthen our position as a leading global provider of a full range of semiconductorpackaging and test services. The key elements of our strengths and strategy include the following:

Leverage our technology capabilities and leadership position

We focus on being a leader in our industry by developing innovative technologies and collaborating withindustry leaders in strategic partnerships. We are a supplier to a large number of semiconductor industryleaders, many of whom support end customers that are major participants in the evolving technology sector. Inparticular, we have a strong market position in the large, high-growth segments of converged mobile devices(such as smartphones, tablets and other mobile computing devices). Market research indicates that theseconverged segments of the semiconductor market, as well as the industrial and automotive (in particularintegrated infotainment) markets, are poised for strong growth in the medium to long-term. We believe thatour installed manufacturing capacity, which can be configured to support growth for these segments, ourtechnology base and technical capabilities and our broad and diversified customer base will present us withsignificant opportunities to support our growth.

We have focused our development efforts on advanced technologies, including (i) improved eWLBtechnology that utilises innovative fan-out wafer level packaging and higher integration to reduce cost andsize; (ii) development of a manufacturing line that can process multiple silicon wafer diameters, includingwafers of up to 450mm, and produce both fan-in and fan-out wafer level packages on the same manufacturingline; and (iii) development of encapsulated wafer level chip scale package (“eWLCSP™”) which provideshigher quality and lower cost fan-in wafer level packages for space constrained mobile devices and newapplications such as wearable technologies. We have achieved high volume eWLB manufacturing as well ashigher efficiencies and economies of scale via our proprietary FlexLine™ manufacturing process to provide amore cost effective solution, which we believe positions us well to achieve design wins and new productintroductions in the next generation of devices. FlexLine™ is an innovative approach to wafer levelmanufacturing that processes multiple silicon wafer diameters in the same manufacturing line, deliveringflexibility in producing both fan-out and fan-in packages. FlexLine™ also provides the ability to scale adevice to larger panel sizes at a lower cost compared to conventional wafer level packaging methods. Webelieve that these proprietary technologies position us well for any future growth opportunities arising fromevolving end market trends such as mobile convergence, wearable electronics, and the Internet of Things.

2

In 2014, we were ranked for the fourth consecutive year among the world’s top 20 semiconductormanufacturing companies in the 2014 Patent Power Scorecard published by IEEE Spectrum, the flagshipmagazine of the Institute of Electrical and Electronics Engineers (“IEEE”), a professional association for theadvancement of technology, and 1790 Analytics, an intellectual property evaluation firm. We were the onlyOSAT service provider ranked among the top 20 companies in the semiconductor manufacturing category. Inaddition, our leadership in innovation is demonstrated by the fact that we had more patents granted andapplications filed with the United States Patent and Trademark Office than any other OSAT provider as of30 June 2015. Of these granted patents, a substantial number were related to advanced wafer level and flip-chip technology. Our strong intellectual property portfolio and research and development teams enable closecollaboration with such industry leaders at the early stages of product development, which we believeenhances our long-term customer loyalty. As of 28 June 2015, we had 239 employees in our research anddevelopment department, which focuses on developing advanced technologies to meet our customers’ needs.

We intend to continue to strengthen our core technical capabilities in advanced technologies and protectour position as an innovator and technology leader to enable us to capture potential opportunities andaccelerate our growth.

Deepen our market penetration in China

We believe that our acquisition by JCET provides us with access to JCET’s broad Asian, and inparticular, growing Chinese customer base, which we have historically not enjoyed because our customer baseto date has been predominantly American and European. We believe this access is timely as growth rates ofthe fabless semiconductor market and the OSAT market in China have significantly exceeded those in otherparts of the world in recent years. The PRC government has in recent years provided funding and promulgatedfavourable policies with a view to encouraging this growth and to aid in the development of internationallycompetitive enterprises across the semiconductor value chain. For example, JCET, the largest electronicspackaging service provider in China by revenue in 2014, has benefited from tax rebates and other governmentconcessions, such as funds provided for research and development.

In addition, we believe that our acquisition by JCET will allow us to provide products across the fullvalue spectrum, which we believe will allow us to widen our customer base. We intend to leverage ouradvanced technology platform and access to JCET’s broader resources and network of strong relationships inChina to meet the growing demand for advanced packaging in China, particularly in the mobile device marketas well as in the analogue, automotive and infotainment market segments. As the mid-tier and entry levelsegments of the mobile device market also continue to grow in China, we expect to broaden our portfoliospectrum and mitigate our exposure to the volatility in the higher-end segment of the mobile device market.

We also expect that our acquisition by JCET will enable us to benefit from research and developmentefficiencies by giving us access to JCET’s research and development resources in wirebonding and othertechnologies, thereby allowing us to continue to focus our investments on advanced packaging and fan outtechnology.

Strengthen our global customer relationships by providing integrated, turnkey solutions

We believe that offering high-quality customer service and an integrated supply chain solution is criticalto attracting and retaining leading semiconductor companies as our customers. We focus on developing anddelivering to our customers semiconductor devices that are designed, packaged, tested and delivered on timeand as specified to any of their global locations. In particular, through our acquisition by JCET, we expect tobroaden and deepen our relationships with global semiconductor companies as we are now well positioned tosupport their plans for expansion into China.

We believe our manufacturing model allows us to better address periodic, product-specific capacityconstraints that negatively affect smaller players. We have implemented IT platforms to enable a high level ofintegration of our customers’ systems within ours, to enable them to obtain real-time information on theirworks-in-progress and thereby facilitate their production planning processes. We intend to continue fostering aservice-oriented and customer-focused environment.

3

We have taken a selective and disciplined approach to investment in order to leverage our researchcapabilities and capital resources while aligning our overall development framework with the needs of ourcustomers. Because of the capital-intensive nature of semiconductor packaging and test operations, we believethat many of our customers are looking for turnkey packaging and test solutions. We seek to structure ourcapital investments in a manner that permits us to offer such turnkey services to our customers to leverage onour capabilities, technology and existing equipment base where appropriate so as to maximise the operationalimpact of our investments. We believe we currently offer one of the broadest portfolios of comprehensive end-to-end packaging and test services in the semiconductor industry.

Focus on operational excellence, cost competitiveness and financial discipline

We continually seek out opportunities to streamline our procurement, supply chain management,manufacturing and organisational structure in a way that enables us to maximise cost efficiencies whilemaintaining our excellent operational track record. We have reorganised our product developmentorganisation to increase our focus on the greater China region in order to accelerate revenue growth and takeadvantage of emerging market opportunities. We continually seek to achieve additional supply chainefficiencies through a global approach to materials procurement and the offering of optimised materialssources and specifications for our customers. We intend to leverage JCET’s equipment and materialsprocurement sources, as well as combine JCET’s and our procurement orders where appropriate to improveour procurement efficiency and effectiveness. We also intend to jointly develop new materials processes andjointly evaluate new materials performance with suppliers in order to achieve alternative low cost solutions.

Further, we also seek to maintain a lean manufacturing profile by seeking out labour and overheadefficiencies, deployment of lean manufacturing techniques and improving our responsiveness to customers.For example, we have consolidated our operations into three manufacturing plants, each with the scale tobenefit from operational efficiency. We have also restructured operation of our manufacturing plants todevolve, to a large extent, responsibility for the management of labour and overhead costs to each of thembased on their specific needs and operate them as separate business units.

We also expect to be able to rationalise our capital expenditures and enhance our operational performancewith our acquisition by JCET. For example, we and JCET have established collaboration mechanisms,including the allocation of customer engagements to be serviced by one of ours or JCET’s manufacturingfacilities, depending on the customer’s needs, and vice versa. We believe that these collaboration mechanismsenable us to increase capacity utilisation as well as improve our operational efficiencies. Since we focus onadvanced technologies while JCET focuses on wirebonding and other lower-end and mainstream technologies,our Company and JCET benefit from little overlap between our and JCET’s product offerings and customerbases, which we believe will increase the likelihood of optimising capacity utilisation and improvingoperational efficiencies.

4

Corporate Structure

The diagram below summarises our corporate structure. We may, from time to time, make acquisitionsof, or investments in, other companies or businesses. STATS ChipPAC Ltd., the entity at the top of thestructure, will be the issuer of the Notes, with the guarantors of the Notes represented by shaded boxes. OurChina subsidiary and our Thai subsidiaries, although not guarantors of the Notes, will be restrictedsubsidiaries.

STATS ChipPAC Ltd.(Singapore)

STATS ChipPAC(Thailand) Limited

(Thailand)(1)

STATS ChipPAC Services(Thailand) Limited

(Thailand)

STATS ChipPAC, Inc.(Delaware, United States)

STATS ChipPAC (Barbados)Ltd.

(Barbados)

ChipPAC InternationalCompany Limited

(British Virgin Island)

STATS ChipPAC (BVI)Limited

(British Virgin Islands)

STATS ChipPAC Shanghai Co.,Ltd.

(China)

STATS ChipPAC Korea Ltd.(Korea)

100% 100% 100%

100% 100%

100%

100% 100% 99.9% 0.1%

STATS ChipPAC Malaysia Sdn.Bhd.

(Malaysia)(2)

Notes:

(1) Ceased operations in October 2011.

(2) Ceased operations in September 2014.

We were incorporated under the laws of Singapore as a limited liability company on 31 October 1994. Ourregistered office and principal executive offices are located at 10 Ang Mo Kio Street 65, #04-08/09 Techpoint,Singapore 569059, Republic of Singapore, and our telephone and facsimile numbers at that address are(65) 6824-7777 and (65) 6720-7826, respectively. Our website address is www.statschippac.com. Informationcontained on our website does not constitute a part of this offering circular.

5

Recent Developments

Change of Control Transaction

On 26 June 2015, JCET-SC, a subsidiary of JCET, announced a voluntary conditional cash offer (the“JCET Offer”) for all the ordinary shares of our Company (excluding shares held by JCET-SC and partiesacting in concert with it) at S$0.46577 per share. The JCET Offer was conditional upon (1) JCET-SC havingreceived valid acceptances of the JCET Offer in respect of more than 50% of the ordinary shares of ourCompany, (2) our Company making the Perpetual Securities Offering described below and (3) the completionof the Taiwan Restructuring, Capital Reduction and Distribution described below.

We made the Perpetual Securities Offering on 16 July 2015 and, following the acceptance of the JCETOffer by Singapore Technologies Semiconductors Pte Ltd (“STSPL”), a wholly-owned subsidiary of TemasekHoldings (Private) Limited (“Temasek”), the first two conditions were satisfied. Temasek, a private limitedcompany incorporated in Singapore, is wholly-owned by the Minister for Finance, a body corporateconstituted by the Minister for Finance (Incorporation) Act (Cap. 183). On 5 August 2015, we completed theTaiwan Restructuring, the Capital Reduction and the Distribution and accordingly, the JCET Offer wasdeclared unconditional in all respects and we became beneficially majority-owned by JCET (the “Change ofControl” and such transaction, the “Change of Control Transaction”). We refer to 5 August 2015, being thedate on which the JCET Offer was declared unconditional in all respects, in this offering circular as theChange of Control Date. The JCET Offer closed on 27 August 2015 and JCET-SC announced that it hadreceived acceptances in respect of 97.26% of our ordinary shares as of that date.

As JCET-SC had acquired more than 90% of our ordinary shares, JCET-SC was entitled, pursuant to theCompanies Act, Chapter 50 of Singapore, to exercise the right to compulsorily acquire all the remainingordinary shares of shareholders who had not accepted the JCET Offer. On 15 October 2015, JCET-SCcompleted the compulsory acquisition of all of our remaining ordinary shares and became our soleshareholder. On 19 October 2015, our ordinary shares were delisted from the Official List of the SGX-ST.

See “The Change of Control and Related Transactions — Change of Control” for more details on theChange of Control Transaction.

Our Capital Reduction and Distribution

Prior to the Capital Reduction and the Distribution, we owned 51.9% of STATS ChipPAC TaiwanSemiconductor Corporation (“STATS Taiwan Semiconductor”) and 100.0% of STATS ChipPAC Taiwan Co.,Ltd. (“STATS Taiwan”), each a Taiwan corporation (collectively, the “Taiwan Entities”). The Taiwan Entitiesfell outside the scope of the JCET Offer. Accordingly, we undertook an internal restructuring described under“The Change of Control and Related Transactions — Taiwan Restructuring” (the “Taiwan Restructuring”) anddistributed our stake in the Taiwan Entities and $15 million in cash to our shareholders by way of a capitalreduction (such capital reduction, the “Capital Reduction” and such distribution, the “Distribution”). TheCapital Reduction and the Distribution were completed on the Change of Control Date, whereupon the TaiwanEntities were fully divested and ceased to form part of our consolidated group.

See “The Change of Control and Related Transactions — Capital Reduction and Distribution” for moredetails on the Taiwan Restructuring, Capital Reduction and Distribution.

Perpetual Securities Offering

On 16 July 2015, we commenced an offering of $200.0 million of our 4% perpetual securities (the“Perpetual Securities” and such offering, the “Perpetual Securities Offering”) to our then shareholders by wayof a non-renounceable rights offering to strengthen our financial position. The Perpetual Securities Offeringclosed on 21 August 2015. STSPL had, subject to certain conditions, undertaken to subscribe for its 83.7%pro rata share of the Perpetual Securities and all other Perpetual Securities not subscribed by our other thenshareholders. Pursuant to the undertaking, STSPL has subscribed for $199.8 million of the PerpetualSecurities. On the Change of Control Date, we issued $167.4 million of the Perpetual Securities subscribed bythat date. We issued the balance $32.6 million of the Perpetual Securities on 21 August 2015.

6

The Perpetual Securities constitute our direct, senior and unsecured obligations and rank pari passu withall our other outstanding senior and unsecured and unsubordinated obligations, except our ContractuallySenior Obligations (as defined in “Description of Indebtedness and Other Material Contracts — Description ofCertain Indebtedness and Perpetual Securities — Perpetual Securities”). The Perpetual Securities rank juniorto the Contractually Senior Obligations.

The Perpetual Securities have no maturity date. Under the terms and conditions of the PerpetualSecurities, we may at any time (including upon the occurrence of the Step Up Date or a Step Up Event (asdefined in “Description of Indebtedness and Other Material Contracts — Description of Certain Indebtednessand Perpetual Securities — Perpetual Securities”)) redeem all but not some of the Perpetual Securities at theprincipal amount of the Perpetual Securities plus any accrued but unpaid distributions (the “Perps RedemptionPrice”).

We are subject to certain covenants under the terms and conditions of the Perpetual Securities. The termsand conditions of the Perpetual Securities require us, among others, to use commercially reasonable efforts toredeem the Perpetual Securities at the time of refinancing the Bridge Loan Facility (as defined below),although our failure to effect such redemption would not be a breach of the terms and conditions of thePerpetual Securities nor constitute a Step Up Event (as defined thereunder).

Pursuant to a deed poll undertaking and guarantee (the “Deed Poll Undertaking and Guarantee”) in favourof the holders of the Perpetual Securities, JCET has unconditionally and irrevocably agreed to procure andensure that we exercise our right to redeem all of the Perpetual Securities upon the Step Up Date or a Step UpEvent (that occurs after the Step Up Date). In addition, pursuant to the Deed Poll Undertaking and Guarantee,in the event that we do not redeem all of the Perpetual Securities in accordance with the terms and conditionsof the Perpetual Securities and by the time specified for a redemption in connection with a Step Up Date or aStep Up Event (that occurs after the Step Up Date), each holder of the Perpetual Securities will have the rightto require (i) JCET to purchase all of the Perpetual Securities held by the holder at the Perps Redemption Priceor (ii) JCET, pursuant to a guarantee, to pay to the holder, with respect to the Perpetual Securities held by suchholder, the Perps Redemption Price on our behalf. Jiangsu Xinchao Technology Group Co., Ltd. (“Xinchao”),a substantial shareholder of JCET, has, in turn, unconditionally and irrevocably pursuant to the Deed PollUndertaking and Guarantee, undertaken to procure the performance of, and has guaranteed the obligations andpayments by, JCET under the Deed Poll Undertaking and Guarantee.

In addition, JCET has agreed in a deed of undertaking dated 6 August 2015 with Citicorp InternationalLimited, as common security agent under the Intercreditor Deed (as defined below), for the benefit of holdersof the Notes and certain other senior creditors, to (and to cause us to) cause (1) the Perpetual Securities to beamended so that they become subordinated to certain senior debt of our Company, including the Bridge LoanFacility, the Existing Notes, the Notes, the Take-Out Facilities, certain hedging obligations and other debt aspermitted under the Intercreditor Deed and the indenture governing the Notes, and (2) the holders (or trustee)of the Perpetual Securities to accede to the Intercreditor Deed as unsecured, subordinated creditor(s), in eachcase, within six months of the third anniversary of the first issue date of the Perpetual Securities. The firstissue date of the Perpetual Securities was the Change of Control Date. See “Description of Indebtedness andOther Material Contracts — Description of Certain Indebtedness and Perpetual Securities — PerpetualSecurities” for more details on this deed of undertaking.

We used $5.7 million of the proceeds from the Perpetual Securities Offering, together with proceeds fromthe repayment of the $126.7 million Intercompany Loan to us, to repay $132.4 million of our bank loans thatbecame due and payable upon the Change of Control. We used the balance of $194.3 million remaining fromthe proceeds from the Perpetual Securities Offering, together with borrowings of $538.0 million under theBridge Loan Facility, to fund the Tender Offer and Consent Solicitation (each as defined below) in respect ofthe Existing Notes (as defined below) and the Change of Control Offer (as defined below). See “Description ofIndebtedness and Other Material Contracts — Description of Certain Indebtedness and Perpetual Securities —Perpetual Securities” for more details on the Perpetual Securities.

7

Bridge Loan Facility

On 6 August 2015, we entered into a senior bridge loan facility agreement with DBS Bank Ltd. for a loanfacility of up to $890.0 million (as amended by an amendment consent and waiver request letter dated1 October 2015 and as further amended by a deed of amendment dated 17 November 2015, the “Bridge LoanFacility Agreement” and such facility, the “Bridge Loan Facility”). The purpose of the Bridge Loan Facility isto refinance certain of our outstanding debt. We have drawn down $538.0 million from this facility to fund,together with the balance of $194.3 million remaining from the proceeds from the Perpetual SecuritiesOffering, the Tender Offer and Consent Solicitation in respect of our then outstanding $200.0 million of5.375% senior notes due 2016 (the “2016 Notes”) and our then outstanding $611.2 million of 4.5% seniornotes due 2018 (the “2018 Notes” and, together with the 2016 Notes, the “Existing Notes”) and the Change ofControl Offer, each as described below. Pursuant to the deed of amendment dated 17 November 2015, theamount available under the Bridge Facility Agreement has been reduced to $120.0 million, which we may use,together with cash on hand, if necessary, to redeem outstanding Existing Notes.

All amounts borrowed under the Bridge Loan Facility and accrued interest thereon are due on the datefalling six months from the date of the Bridge Loan Facility Agreement, which may (subject to certainrequirements) be extended twice with the second extension’s maturity date falling 12 months from the date ofthe Bridge Loan Facility Agreement. The interest payable will range from 1.50% plus LIBOR (up to andincluding the original maturity date prior to any extensions) to 2.40% plus LIBOR (from the first extension’smaturity date to second extension’s maturity date) per annum. Interest is payable on interest periods elected byus. We are also paying a customary commitment fee from the date of the Bridge Loan Facility Agreement tothe end of the availability period under the Bridge Loan Facility Agreement.

The Bridge Loan Facility is guaranteed by all of our subsidiaries except our China subsidiary and ourThai subsidiaries. The Bridge Loan Facility is also secured by the Initial Collateral (as defined in “Descriptionof Notes”) and will be secured by the Additional Bridge Collateral (as defined in “Description of Notes”). TheInitial Collateral, the Additional Bridge Collateral and the Korea Collateral (as defined in “Description ofNotes”) are collectively defined herein as the “Collateral.” The Collateral will also secure the Notes offered inthis offering, and certain other senior debt, on an equal and rateable basis pursuant to the security sharingarrangements provided in the Intercreditor Deed. For details on the Collateral, see “Description ofNotes — Brief Description of the Notes, the Note Guarantees and the Security — Security.”

We are required to prepay amounts outstanding under the Bridge Loan Facility Agreement with the netproceeds of any debt issuance, equity issuance, disposal of certain assets and any insurance claim, subject tocertain exclusions. Such net proceeds are, pursuant to the terms of the deed of amendment to the Bridge LoanFacility Agreement dated 17 November 2015, required to prepay any amounts borrowed under the facility and,solely with respect to net proceeds under this offering, thereafter be applied to reduce the amount of availablefunds under the Bridge Loan Facility Agreement.

See “Description of Indebtedness and Other Material Contracts — Description of Certain Indebtednessand Perpetual Securities — Bridge Loan Facility” for more details on the Bridge Loan Facility and“Description of Indebtedness and Other Material Contracts — Other Material Contracts — Intercreditor Deed”for more details on the Intercreditor Deed.

Take-Out Facilities

We have entered into a commitment letter (the “Take-Out Commitment Letter”) with DBS Bank Ltd.,Barclays Bank PLC and ING Bank N.V (together, the “MLABs”), dated 4 September 2015, pursuant to whichthe MLABs have agreed, subject to certain conditions, to make available to us up to $500 million in seniorsecured credit facilities comprising a term loan facility (the “Term Loan Facility”) of $425 million and arevolving credit facility (the “Revolving Credit Facility” and, together with the Term Loan Facility, the “Take-Out Facilities”) of $75 million, on the terms and conditions set out in a term sheet appended thereto. Weintend to use amounts borrowed under the Take-Out Facilities to refinance a portion of the borrowings underthe Bridge Loan Facility and certain other debt facilities of our Company and certain of our subsidiaries.

8

Following the repayment of this indebtedness, we intend to use amounts borrowed under the Revolving CreditFacility for working capital requirements of our Company and our subsidiaries.

The MLABs’ obligation to provide the Take-Out Facilities is subject to the execution of final definitivedocuments by no later than 180 days from the date of the commitment letter (or such later date as agreed bythe parties thereto). Such definitive documents will include conditions customary for financings ofsuch nature.

The conditions precedent to draw down under the Take-Out Facilities will include the successful raisingby us of additional debt financing (which may take the form of either an issuance of new senior secured notesand/or other alternative financing subject to certain conditions as set out in the Take-Out Commitment Letter)in an aggregate amount of at least $400 million. Draw down under the Take-Out Facilities is subject to otherconditions customary for financings of such nature.

The Term Loan Facility will be available for five drawdowns during a period of three months from thedate of execution of the agreement for the Take-Out Facilities (such agreement, the “Take-Out FacilitiesAgreement” and the date of execution of such agreement, the “Agreement Date”). The Revolving CreditFacility will be available for draw down on a revolving basis up to one month prior to the final maturity dateof the Take-Out Facilities. The final maturity date of the Take-Out Facilities will be five years from theAgreement Date (the “Take-Out Maturity Date”).

The Term Loan Facility is repayable in accordance with an amortising repayment schedule commencing15 months from the Agreement Date and the Revolving Credit Facility is repayable on the Take-Out MaturityDate. The interest payable for the Term Loan Facility will be 3.70% (the “Applicable Margin”) plus LIBORper annum. An upfront fee of 3.20% of the total principal amount of the Take-Out Facilities will also bepayable. A commitment fee of 40% of the Applicable Margin will also be payable with respect to theRevolving Credit Facility.

The obligations of our Company under the Take-Out Facilities will be secured and guaranteed by all ofour subsidiaries, except our China subsidiary and our Thai subsidiaries. Further, the obligations of ourCompany under the Take-Out Facilities will be secured by the Collateral, on a pari passu basis, with certainhedging obligations and the Notes.

The foregoing description of the proposed up to $500 million Take-Out Facilities is based upon theTake-Out Commitment Letter and related term sheet. We have not yet negotiated the Take-Out FacilitiesAgreement and related documents, and the final terms of the Take-Out Facilities are subject to final definitivedocumentation. Such documentation may contain terms which are in addition to, or different from, the termsset forth above. See “Description of Indebtedness and Other Material Contracts — Description of CertainIndebtedness and Perpetual Securities — Take-Out Facilities” for more details on the Take-Out Facilities.

Intercreditor Deed

Prior to completion of the Consent Solicitation, each of the indentures governing the Existing Notescontained a limitation on liens covenant that restricted us from granting liens over our assets above andbeyond the permitted liens specified therein, unless we secured the Existing Notes on an equal and rateablebasis. In compliance with these indentures, concurrently with entering into the Bridge Loan FacilityAgreement, on 6 August 2015, STATS ChipPAC and certain of our subsidiaries entered into supplementalindentures and an intercreditor deed (the “Intercreditor Deed”) with DBS Bank Ltd., as facility agent for theBridge Loan Facility, Citicorp International Limited, as common security agent (the “Common SecurityAgent”), and Citibank Korea Inc., as Korean security agent (the “Korean Security Agent”), to effect the grantof equal and rateable security over the Initial Collateral, and the rest of the Collateral as and when available, infavour of holders of the Existing Notes and the lender under the Bridge Loan Facility.

On 7 October 2015, after receipt of the requisite consents from holders of Existing Notes of both seriestendered in the Tender Offer and Consent Solicitation and payment therefor, the rights of holders of theExisting Notes in the Collateral were released.

9

The Trustee is expected to accede to the Intercreditor Deed upon the closing of this offering, to effect thegrant of equal and rateable security over the Collateral in favour of holders of the Notes.

See “Description of Indebtedness and Other Material Contracts — Other Material Contracts —Intercreditor Deed” for more details on the security arrangements.

Tender Offer and Consent Solicitation in respect of the Existing Notes

On 4 September 2015, we commenced a cash tender offer pursuant to an offer to purchase and consentsolicitation statement dated 4 September 2015 to repurchase any and all of the Existing Notes (the “TenderOffer”). In conjunction with the Tender Offer, we also solicited consents of holders of the Existing Notes (the“Consent Solicitation”) to release the rights of holders of the Existing Notes in the Initial Collateral and toadopt proposed amendments to the indentures governing the Existing Notes that would eliminate or modifysubstantially all of the restrictive covenants, certain reporting obligations, certain events of default and certainother provisions under the indentures. The purpose of the Tender Offer was to acquire any and all outstandingExisting Notes and the purpose of the Consent Solicitation was to release the rights of holders of the ExistingNotes in the Initial Collateral and to adopt the proposed amendments to eliminate or modify substantially allof the restrictive covenants in the indentures governing the Existing Notes.

Holders of the Existing Notes who tendered prior to the early tender date on 25 September 2015 receivedthe early participation consideration, of $1,012.50 per $1,000 principal amount of the 2016 Notes and the 2018Notes. Holders who tendered on or prior to the early tender date were deemed to have delivered their consentsto release the rights of holders of the Existing Notes in the Initial Collateral and to certain proposedamendments. Holders who tendered after the early tender date but prior to the expiration of the Tender Offerreceived only the tender consideration, which consisted of the early participation consideration minus the earlyparticipation premium of $12.50 per $1,000 principal amount of the 2016 Notes and the 2018 Notes. Holdersalso received accrued interest up to, but not including, the applicable settlement date. The Tender Offerexpired on 9 October 2015 and was completed on 16 October 2015.

We repurchased $663.0 million in principal amount of the Existing Notes (comprising $152.6 million ofthe 2016 Notes, representing 76.3% of the 2016 Notes, and $510.4 million of the 2018 Notes, representing83.5% of the 2018 Notes) for a total consideration (including accrued interest and premium) of $672.4 million(comprising $154.6 million for the 2016 Notes and $517.7 million for the 2018 Notes) in the Tender Offer.We used the balance of $194.3 million remaining from the proceeds from the Perpetual Securities Offering,together with borrowings of $538.0 million under the Bridge Loan Facility, to fund the Tender Offer andConsent Solicitation in respect of the Existing Notes and the Change of Control Offer as described below.

Following completion of the Tender Offer and Change of Control Offer, $115.9 million in principalamount of the Existing Notes (comprising $41.4 million of the 2016 Notes and $74.5 million of the 2018Notes) remain outstanding.

Change of Control Offer

On 4 September 2015, we commenced an offer (the “Change of Control Offer”) pursuant to a notice ofchange of control and offer to purchase dated 4 September 2015 to purchase all outstanding Existing Notes ata purchase price equal to 101.0% of the aggregate principal amount of the Existing Notes repurchased, plusaccrued interest up to, but not including, the date of purchase (the “Change of Control Payment Date”). On theChange of Control Date, we became beneficially majority-owned by JCET, which constituted a Change ofControl as defined in the indentures governing the Existing Notes. Pursuant to the terms of the indenturesgoverning the Existing Notes, we were required to make the Change of Control Offer. The Change of ControlOffer expired on 13 October 2015 and the Change of Control Payment Date was on 16 October 2015.

We repurchased $32.3 million in principal amount of the Existing Notes (comprising $6.0 million of the2016 Notes, representing 3.0% of the 2016 Notes, and $26.3 million of the 2018 Notes, representing 4.3% ofthe 2018 Notes) for a total consideration (including accrued interest and premium) of $32.7 million(comprising $6.1 million for the 2016 Notes and $26.6 million for the 2018 Notes) in the Change of Control

10

Offer. We used the balance of $194.3 million remaining from the proceeds from the Perpetual SecuritiesOffering, together with borrowings of $538.0 million under the Bridge Loan Facility, to fund the Change ofControl Offer and the Tender Offer and Consent Solicitation in respect of the Existing Notes as describedabove.

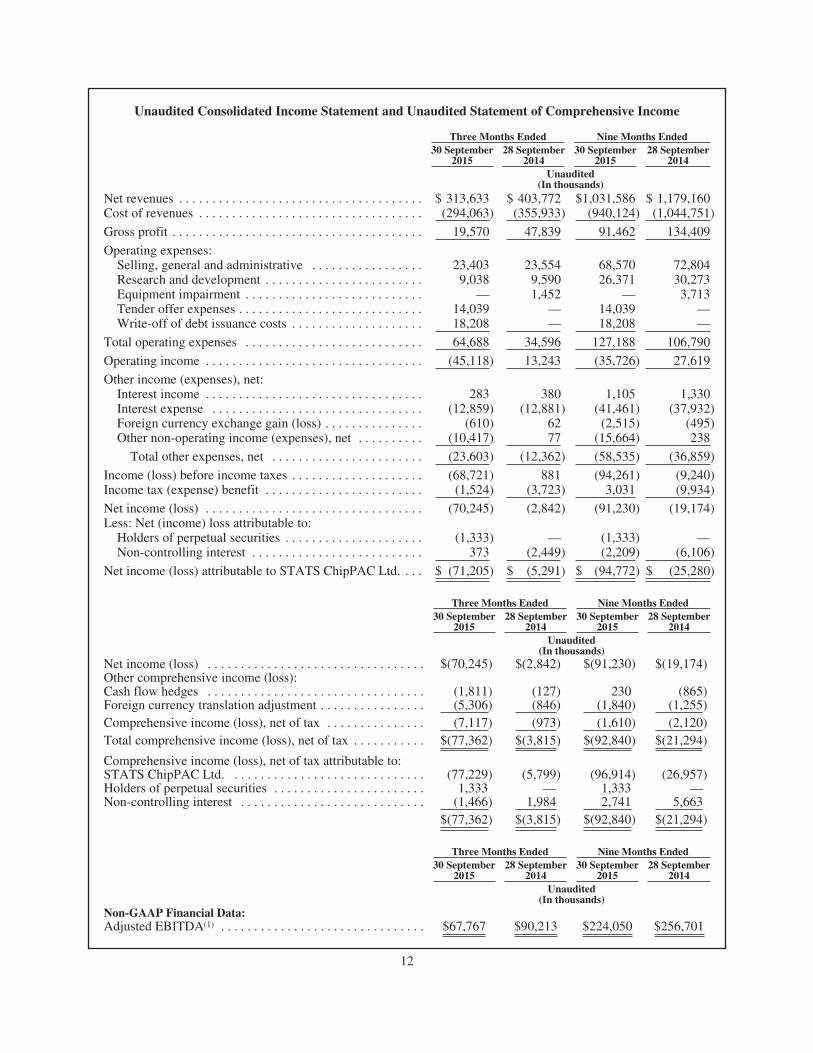

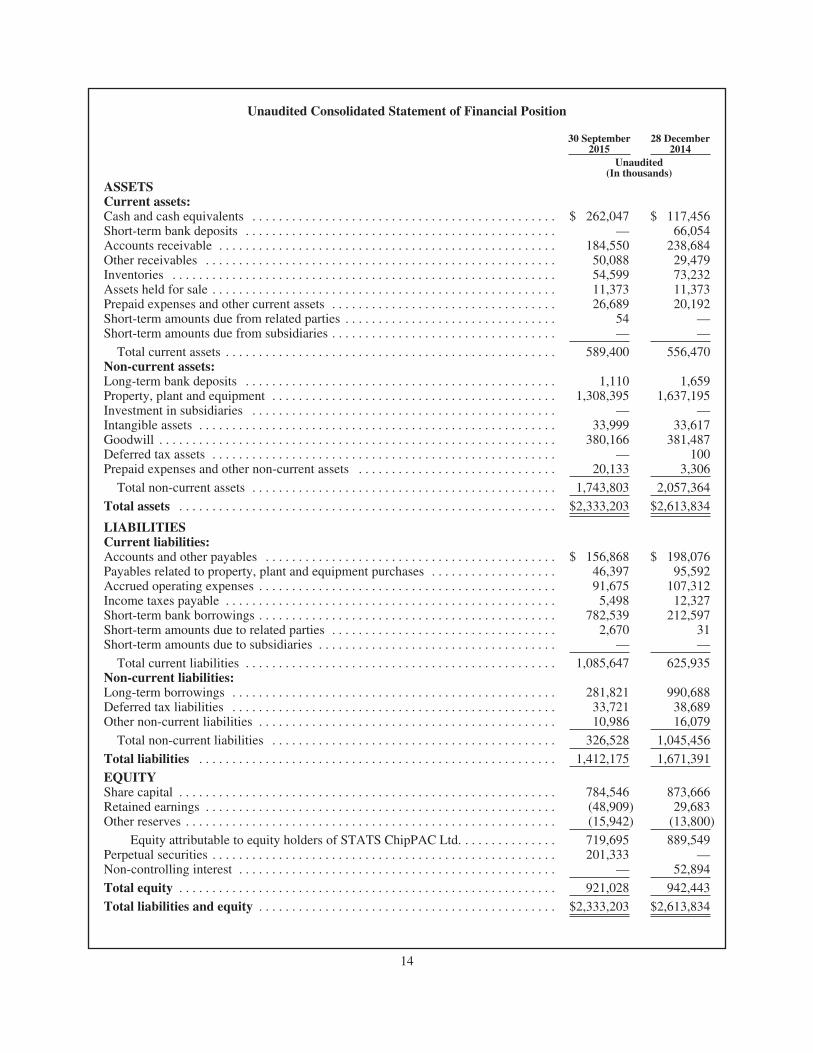

Financial results for three months and nine months ended 30 September 2015