SBB STEEL MARKETS DAILY

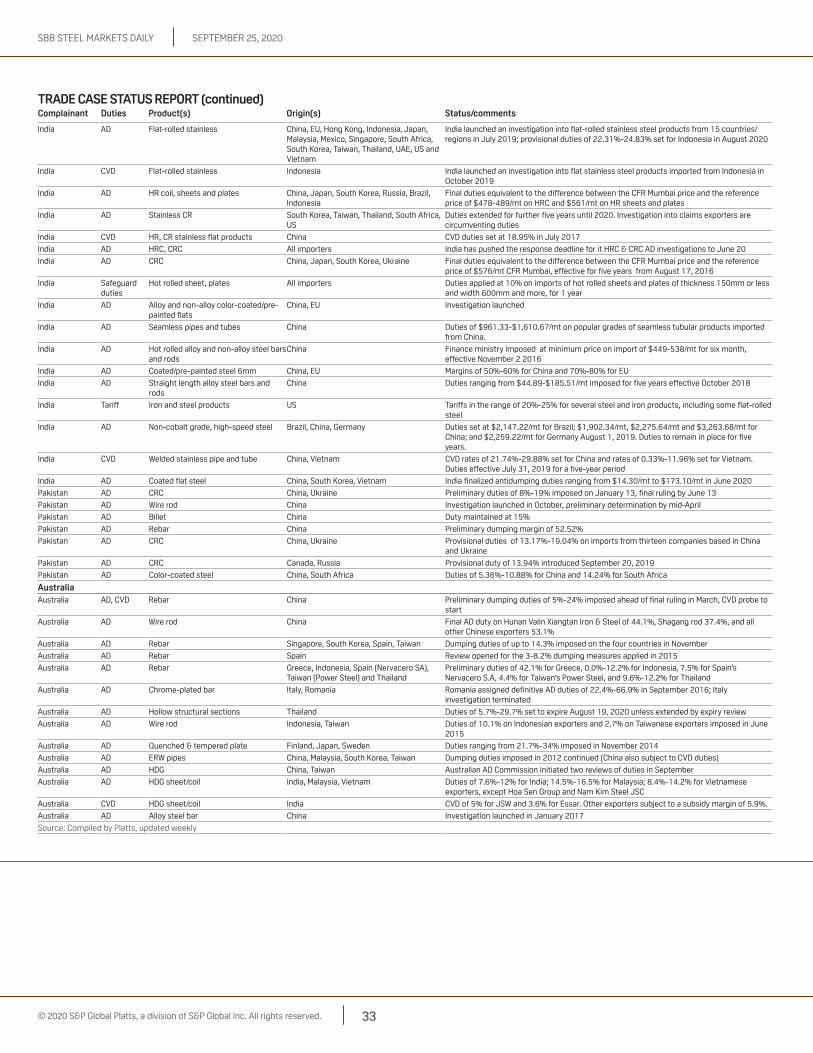

33

Volume 14 / Issue 190 / September 25, 2020 SBB STEEL MARKETS DAILY www.platts.com www.twitter.com/PlattsSteel INSIDE THE ISSUE Iron ore market 2 Coking coal market 3 Scrap market 4 Exchanges 6 Ferroalloys market 6 Other News 6 Americas 7 Freight 8 Subscriber Notes 8 Assessment Rationales 11 Marketplace 12 ASSESSMENTS Platts daily iron ore assessments, September 25 2020 18 Per 1% differentials (Range 60-63.5% Fe, $/dmt) 18 Per 1% differentials (Range 55-60% Fe, $/dmt) 18 Rolling monthly average 18 Platts daily iron ore lump spot assessments 18 Pellet premiums 18 IOPEX: Platts daily port stock iron ore fines assessment, September 25 19 Platts daily iron ore seaborne brand assessments, September 25 19 Freight differentials to major import ports, $/wmt 19 TSI 62% Fe CFR North China derivative forward curve, September 25 19 Iron ore lump premium CFR China derivative forward curve, September 25 19 Platts daily metallurgical coal assessments, September 25 20 Platts daily Asia Pacific metallurgical coal relativities, September 25, 2020 21 Platts weekly metallurgical coal relativities, September 25, 2020 21 Europe and US cold-rolled coil assessments, September 25 21 Metallurgical Coke 22 Platts China PLV, met coke price differentials 22 TSI premium HCC FOB Australia derivative forward curve, September 25 22 Penalties & Premia: Differentials ($/mt) 22 FOB netbacks per route 22 Platts TSI ferrous scrap reference prices 23 HMS 1&2 80:20 CFR Turkey derivative forward curve, September 25 23 Rebar FOB Turkey derivative forward curve, September 25 23 SBB-SMD raw materials reference prices 24 Platts TSI steel industry assessments, September 25 24 Platts TSI steel assessments currency and unit comparisons, September 25 25 Scrap: iron ore ratios 25 Platts Turkey ARC Steel Tracker, September 25, 2020 25 Weekly Ferroalloy Prices 26 Monthly average steel prices: August 2020 27 Monthly average raw materials prices: August 2020 27 Trade Case Status Report 28 PLATTS TSI RAW MATERIAL ASSESSMENTS, SEPTEMBER 25 2020 Symbol Close Change % Chg IODEX Iron ore fines 62% Fe ($/dmt) CFR North China IODBZ00 116.05 0.15 0.13 Please see Platts complete iron price/netbacks table, p.2-3 Coking coal, premium low vol ($/mt) FOB Australia PLVHA00 139.00 3.50 2.58 CFR China PLVHC00 148.50 2.00 1.37 TSI Premium hard, Australian exports (FOB port) TS01034 137.40 1.40 1.03 Please see full metallurgical coal price/freight table, p.4 Ferrous scrap ($/mt) HMS 1/2 80:20 CFR Turkey TS01011 295.50 0.00 0.00 Please see full ferrous scrap price table, p.6 Speculative demand for Nov continues High portside inventories weigh on concentrate Singapore—Seaborne iron ore prices remained largely rangebound at the end of the week to Sept. 25 amid speculative demand for November-loading cargoes. S&P Global Platts assessed the 62% Fe Iron Ore Index at $116.05/ dry mt CFR North China on Sept. 25, up 15 cents from Sept. 24. Front-month October 62% Fe derivatives were up $0.35/dmt from Sept. 24 to $113.2/dmt on Sept. 25. Expectations of a shift in preference for medium grade fines on narrowing discounts for lower grade options supported buying interest for November-loading Pilbara Blend fines, an international trader said. There was also demand for alternative medium grade fines as they were viewed as increasingly more cost efficient than low grade fines, while serving as a cheaper alternative for end-users looking to cut production costs, a Chinese trader said. A tender for two cargoes of PBF loading in November and December was heard to have been concluded around $3.10/dmt CFR Seaborne iron ore prices mostly stable amid continued speculative demand (continued on page 2) US high-vol A met coal firm, Asia-Pacific market strong Market tighter with improved demand Still room for further increases Coke said to be in shorter supply in Europe London—US high-vol A met coal prices rose another $1/mt Sept. 25, pushed higher by continually strong Premium Low Vol prices in the Asia-Pacific market. Atlantic met coal prices have been supported in recent weeks by strong demand and tighter availability. A miner source said high-vol A prices were around $120/mt, adding that it was not easy to get spot out of the US, and particularly at fixed prices. “There is still room for further increases. That would be fresh air for US producers,” the miner said. “I'm not too bullish yet -- despite the increases, prices are not exciting yet. Only once [high-vol A] gets to $130-140/mt can producers start to invest in the future and in operations, keep the situation workable,” S&P Global Platts assessed Premium Low Vol up $3.50/mt Sept. 25 to $139/mt FOB Australia, while the Platts TSI Premium HCC reference price, used for settlement of the Singapore Exchange's coking coal futures, gained $1.40/mt to $137.40/mt FOB Australia.

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of SBB STEEL MARKETS DAILY

Volume 14 / Issue 190 / September 25, 2020

SBB STEEL MARKETS DAILY

www.platts.com www.twitter.com/PlattsSteel

InsIde the IssueIron ore market 2Coking coal market 3Scrap market 4Exchanges 6Ferroalloys market 6Other News 6Americas 7Freight 8Subscriber Notes 8Assessment Rationales 11Marketplace 12

AssessmentsPlatts daily iron ore assessments, September 25 2020 18Per 1% differentials (Range 60-63.5% Fe, $/dmt) 18Per 1% differentials (Range 55-60% Fe, $/dmt) 18Rolling monthly average 18Platts daily iron ore lump spot assessments 18Pellet premiums 18IOPEX: Platts daily port stock iron ore fines assessment, September 25 19Platts daily iron ore seaborne brand assessments, September 25 19Freight differentials to major import ports, $/wmt 19TSI 62% Fe CFR North China derivative forward curve, September 25 19Iron ore lump premium CFR China derivative forward curve, September 25 19Platts daily metallurgical coal assessments, September 25 20Platts daily Asia Pacific metallurgical coal relativities, September 25, 2020 21Platts weekly metallurgical coal relativities, September 25, 2020 21Europe and US cold-rolled coil assessments, September 25 21Metallurgical Coke 22Platts China PLV, met coke price differentials 22TSI premium HCC FOB Australia derivative forward curve, September 25 22Penalties & Premia: Differentials ($/mt) 22FOB netbacks per route 22Platts TSI ferrous scrap reference prices 23HMS 1&2 80:20 CFR Turkey derivative forward curve, September 25 23Rebar FOB Turkey derivative forward curve, September 25 23SBB-SMD raw materials reference prices 24Platts TSI steel industry assessments, September 25 24Platts TSI steel assessments currency and unit comparisons, September 25 25Scrap: iron ore ratios 25Platts Turkey ARC Steel Tracker, September 25, 2020 25Weekly Ferroalloy Prices 26Monthly average steel prices: August 2020 27Monthly average raw materials prices: August 2020 27Trade Case Status Report 28

PlAtts tsI rAw mAterIAl Assessments, sePtember 25 2020 symbol Close Change % Chg

IOdeX Iron ore fines 62% Fe ($/dmt)

CFR North China IODBZ00 116.05 0.15 0.13Please see Platts complete iron price/netbacks table, p.2-3

Coking coal, premium low vol ($/mt)

FOB Australia PLVHA00 139.00 3.50 2.58CFR China PLVHC00 148.50 2.00 1.37TSI Premium hard, Australian exports (FOB port) TS01034 137.40 1.40 1.03Please see full metallurgical coal price/freight table, p.4

Ferrous scrap ($/mt)

HMS 1/2 80:20 CFR Turkey TS01011 295.50 0.00 0.00Please see full ferrous scrap price table, p.6

�� speculative demand for nov continues�� high portside inventories weigh on concentrate

Singapore—Seaborne iron ore prices remained largely rangebound at the end of the week to Sept. 25 amid speculative demand for November-loading cargoes.

S&P Global Platts assessed the 62% Fe Iron Ore Index at $116.05/dry mt CFR North China on Sept. 25, up 15 cents from Sept. 24.

Front-month October 62% Fe derivatives were up $0.35/dmt from Sept. 24 to $113.2/dmt on Sept. 25.

Expectations of a shift in preference for medium grade fines on narrowing discounts for lower grade options supported buying interest for November-loading Pilbara Blend fines, an international trader said.

There was also demand for alternative medium grade fines as they were viewed as increasingly more cost efficient than low grade fines, while serving as a cheaper alternative for end-users looking to cut production costs, a Chinese trader said.

A tender for two cargoes of PBF loading in November and December was heard to have been concluded around $3.10/dmt CFR

seaborne iron ore prices mostly stable amid continued speculative demand

(continued on page 2)

us high-vol A met coal firm, Asia-Pacific market strong

�� market tighter with improved demand�� still room for further increases�� Coke said to be in shorter supply in europe

London—US high-vol A met coal prices rose another $1/mt Sept. 25, pushed higher by continually strong Premium Low Vol prices in the Asia-Pacific market.

Atlantic met coal prices have been supported in recent weeks by strong demand and tighter availability.

A miner source said high-vol A prices were around $120/mt, adding that it was not easy to get spot out of the US, and particularly at fixed prices.

“There is still room for further increases. That would be fresh air for US producers,” the miner said. “I'm not too bullish yet -- despite the increases, prices are not exciting yet. Only once [high-vol A] gets to $130-140/mt can producers start to invest in the future and in operations, keep the situation workable,”

S&P Global Platts assessed Premium Low Vol up $3.50/mt Sept. 25 to $139/mt FOB Australia, while the Platts TSI Premium HCC reference price, used for settlement of the Singapore Exchange's coking coal futures, gained $1.40/mt to $137.40/mt FOB Australia.

September 25, 2020Sbb Steel marketS Daily

2© 2020 S&P Global Platts, a division of S&P Global Inc. All rights reserved.

A second miner source said he had heard that coke was in short supply in Europe at moment, due to steel production starting to recover, with both resulting in falling inventories of coking coal.

The first miner source said he would not be surprised if coke stocks in Europe were in short supply, as he had spoken to people who were optimistic for coke prices, meaning it was probably a good market in the short term

“I’m not even sure people in Europe can find all the coal they need in time, so they could buy coke as well,” the first miner said.

The Platts US high-vol A index was assessed $1/mt higher Sept. 25 to $120/mt FOB USEC, based on 32.25% volatile matter, 1.05% reflectance (MMR), 220% dilatation, 7.5% ash, 0.95% sulfur, 30,000 ddpm and CSR typically in the low 60s.

The Platts US high-vol B assessment was steady at $106/mt FOB USEC, based on 36% VM unblended product with 0.95% MMR, 160% dilatation, 8% ash, 1% sulfur, 25,000 ddpm fluidity.

Platts US East Coast low-vol HCC was also stable at $114/mt FOB, based on 58% CSR and 19.25% volatile matter, 8.25% ash and 0.95% sulfur.

The contango in met coal futures came in slightly Sept. 25, with the October contract remaining unchanged at $142.75/mt and November future contracts losing 50 cents/mt to $145.75/mt.

— Jacqueline Holman

IrOn Ore mArket

black sea pig iron softer as Chinese bids fall and us stays flat

�� bids from China come down�� Prices roll over in us sales�� CIs mills reluctant to cut prices

London—CIS-origin merchant pig iron export prices came under pressure from falling Chinese bids, while the US seemed to allow only for a price roll-over rather than further upside, sources said on Sept. 25.

A Russian cargo, 50,000-55,000 mt, November production, was sold in the week starting Sept. 21 at $387/mt CFR Mobil, a couple of industry sources reported. Three other loads from the CIS were sold a week earlier at $385-$388/mt CFR New Orleans.

So far the US market has resisted $390/mt CFR, an exporter said. He believed $390/mt CFR was still a realistic target given that HRC prices in the US have reached the $660/mt mark. Another seller also noted he was reluctant to drop the price for the US market from the previously achieved level.

After months of driving basic pig iron prices up, Chinese demand was no longer there to support further increase in the week, a number of market players said. Earlier sales to China helped CIS mills fill order books and feel more comfortable in resisting the downward pressure at the moment, one seller noted.

At the height of Chinese pig iron demand some CIS offers reached $400/mt CFR and even higher but were never achieved, a merchant commented. Falling iron ore prices, softening Chinese futures and weakening steel demand reversed the upward trend in pig iron. Recent bids coming from the Chinese market were down to $385/mt CFR or $350/mt FOB Black Sea, two sources said.

The highest concluded CIS sale, by traders to end users, was

China over the loading month average of Platts IODEX.There were some expectations of stronger demand for low alumina

fines closer to the winter season and on rising coking costs.Brazilian fines are relatively cost-effective now and some end

users may look to rebalance their sinter feed usage and increase their utilization, a Chinese procurement source said.

However, the tolerance for silica has been declining due to earlier high usage of discounted low alumina high silica fines as well as high silica domestic concentrates, the source said.

seaborne iron ore prices mostly stable amid continued speculative demand ...from page 1

A tender for a 100,000 mt cargo of Standard Sinter Feed Guaiba loaded Sept. 15 was heard to be concluded at a premium of around $3.50/dmt CFR China over the arrival month 62% index.

The total inventory for imported concentrates at 45 Chinese ports climbed to a multi-year high of 11 million mt, according to market sources.

“We have been receiving fresh portside offers for a variety of concentrate options with origins from Ukraine, Chile and Peru; however, with domestic concentrate prices falling along with the overall market, the prices of imported concentrates are still not attractive,” an end user in Hebei said.

Platts assessed the 66% Fe domestic concentrate at Yuan 1,020/dmt on Sept. 18, delivered to mills in Tangshan, down Yuan 15/dmt week on week.

Market sources saw a softening of liquidity for lump at Chinese quayside while the pace of inventory reduction slowed, sources said.

“The recent price rebound for lump have limited its value-in-use and there is no further upside to its blending ratio.” a procurement source said.

S&P Global Platts assessed the spot lump premium at 7.5 cents/dmtu on Sept. 25, flat from Sept. 24.

— Staff

September 25, 2020Sbb Steel marketS Daily

3© 2020 S&P Global Platts, a division of S&P Global Inc. All rights reserved.

reported at $395/mt CFR China. Since then some 30,000 mt was sold by one CIS exporter in during the week ended Sept. 25 at $389/mt CFR China, loading in the Russian Far East, a couple of sources reported.

To sell at the same level from the European part of Russia or Ukraine, CIS mills would need to cut their prices to offset higher freight rates, meaning a $10-$15/mt drop from $365-$368/mt FOB achieved in the latest US bookings.

But CIS merchants were adamant to hastily lower prices for China. They believed that the lower activity was only a phase as China was going into a holiday week. After October 12, the market might rebound again, which put some CIS mills in a wait-and-see mode. November allocation from the CIS is also expected to be shorter than normal, buying CIS exporters time, a few sources noted. In the meantime, pig iron should be under pressure, with a likely small “technical” decrease, according to a sell-side source.

Asking prices in the Italian market were cited at $385/mt CIF Marghera, or $365/mt FOB Black Sea. Buyers were resisting even $380/mt CIF, a market participant said. A trader added that bids from Italian buyers were closer to $370/mt CIF.

— Wojtek Laskowski

COkIng COAl mArket

Coking coal prices to recover notably by year-end: kolmar

London—Russian metallurgical and energy coal mining company Kolmar believes coking coal prices will recover significantly by the year-end; they have already started to rise on both FOB Australia and CFR China basis.

Kolmar expects coking coal prices to get support from the end of the monsoon season in Asia and subsequent revival in construction activity in the region, its spokeswoman told S&P Global Platts.

On an FOB Australia basis, coking coal prices have gained $7/mt over the last seven days, rising to $136/mt on Sept. 24. The CFR China price moved up to $147/mt from $138/mt a week ago, according to Platts data.

The market was also buoyed by recent data on the manufacturing sector in India, whose Purchasing Managers' Index passed 50, signaling a more confident outlook for the industry. “Demand in the spot market outside of China is gradually picking up,” said the spokeswoman, adding steel mills have started to blow in blast furnaces suspended during the coronavirus pandemic’s first wave.

What also brings relief is a possible easing of quotas at the ports of China. There has been talk about it more and more and consumers are no longer afraid to start closing the gap between prices for local Chinese coal and imports, according to Kolmar.

The miner said prices would also gain from some tightness on the supply side, which is possible should the current weather forecasts for Australia come true.

According to the Australian Bureau of Meteorology, there is a 70% probability cyclone La Nina will form in the coming months with October-November likely to see precipitation above average levels.

The rain will primarily affect Queensland. So, Chinese consumers may encounter disruption in coking coal supply after the Golden Week holidays (Oct. 1-7).

“Looking further ahead, we have an upbeat view for China’s 13th and 14th five-year development cycles. The infrastructure plans they contain should boost coking coal prices from their current extremely low level,” said the spokeswoman.

What could adversely affect the coal market in the short term is the second wave of the pandemic currently gathering pace in a few regions, she said. Also, strong iron ore prices could be a factor, reducing steelmakers’ profitability and keeping coke prices in check.

Excessive inventories at mills and limited resources to finance public construction projects, for instance in India, are also factors not helping the market to recover at a faster pace.

Yet Kolmar hopes the bullish events will outweigh and prices will recover significantly by year-end.

The company recently launched the first stage of its new coking coal mine Inaglinskaya, and new coking coal washing plant Inaglinskaya-2, both in the Neryungri district of the Sakha Republic (Yakutia).

Inaglinskaya is expected to deliver 1.4 million mt of coal by the end of December, while the company targets 7.57 million mt output this year with the total comprised of both metallurgical and thermal coal.

— Ekaterina Bouckley

Asia met coal prices continue to rally on firm demand

�� higher PlV bid fails to draw offers�� Firm buying interest seen in spot market

Singapore—Asia-Pacific metallurgical coal prices continued the upward momentum on firm buying interest and positive outlook amid spot demand.

S&P Global Platts assessed Premium Low Vol up $3.50/mt at $139/mt FOB Australia Sept. 25, and PLV CFR China was up $2/mt at $148.50/mt CFR China.

The spot market saw continued strength in prices with higher firm bids for Premium Low Vol coals failing to draw firm offers from the market. Market sources said the outlook remains firm as spot demand is expected from India and China.

In China, the market saw thin trading activity as market participants adopted a wait-and-see mode, as both the sell and buy sides need some time to re-assess their expectations following the strength seen in the spot market, sources said.

“Many buyers stepped back from the market simply because the price moved up too fast in the past weeks. I think more demand will emerge after buyers come back from the Golden Week holiday,” a Chinese trader said.

Meanwhile, some also said that while strength in prices could be supported on firm buying interest, the pace of the price uptick could be mild in the near term as arbitrage narrows.

“Expectation on prices is firm, but we think price movements might be less dramatic as compared to previous two weeks, as buyers

September 25, 2020Sbb Steel marketS Daily

4© 2020 S&P Global Platts, a division of S&P Global Inc. All rights reserved.

become more cautious now,” a Chinese end-user said.Still in China, at Jingtang port, sources said that port stock

availability was moving lower as traders still face difficulties with port clearance. Platts assessed PLV ex-stock Jingtang up Yuan 10/mt at Yuan 1,440/mt on Sept. 25, equivalent to $182.52/mt CFR Jingtang, and HCC 64 Mid Vol ex-stock Jingtang up Yuan 10/mt at Yuan 1,310/mt, equivalent to $165.63/mt CFR Jingtang.

The market outside China saw thin liquidity as well, but the expectation on spot demand remains positive. In India, sources said the market continued to see inquires on spot cargoes as end-users plan to take October-November laycan cargoes to meet their restocking needs.

— Jessie Li, Yi-Le Weng

sCrAP mArket

China’s shagang cuts ferrous scrap prices by another Yuan 50/mt, high product inventory

Singapore—Eastern China’s largest scrap buyer Jiangsu Shagang Group has cut its bid for local ferrous scrap again Sept. 25, a day after its previous cut, amid high rebar and scrap inventories, a source from the mill said.

The company’s bid, effective Sept. 25, for scrap with minimum thickness of 6 mm, was Yuan 2,640 ($387/mt), down Yuan 50/mt from the last adjustment Sept. 24, and including 13% value added tax.

“The season for good sales is gone, and rebar inventories now remain on the higher side,” the source said. “Likewise for scrap inventories as well, so there’s no need to be paying premium prices in this situation.”

The Sept. 25 cut came immediately after a similar Yuan 50/mt cut on Sept. 24, and since entering the month of September, prices were down by a total of Yuan 160/mt.

Meanwhile, in the nearby actively traded Hangzhou market, rebar transacted prices fell another Yuan 10/mt on the day, and heard at Yuan 3,630/mt Sept. 25. This marked a total decrease of Yuan 130/mt since the beginning of the month.

Sentiment too continues to be weighted down by bearish movements within the futures market. Prices for January 2021 marked a Yuan 30/mt fall on the day, or a total of Yuan 252/mt since entering September.

— Samuel Chin, Analyst Chelsea Ye

taiwan containerized scrap prices slip as buyers in wait-and-see mode

�� hms I/II 80:20 offers down $5-$10/mt�� downside potential cited limited on better expected Q4 demand

Singapore—Containerized scrap prices to Taiwan slipped further during the trading week of Sept. 25, as buyers remained in wait-and-see mode, sources said.

The S&P Global Platts daily TSI HMS I/II 80:20 containerized scrap

spot price was assessed at $274/mt CFR Taiwan on Sept. 25, down $6/mt week on week.

Offers for USWC HMS I/II 80:20 cargoes to Taiwan were lower at $275/mt CFR on Sept. 25, from $280-$285/mt the week prior, with sellers saying they were seeing no interested takers even after the downward adjustment. Workable values, however, were cited in a range of $272-$275/mt CFR.

Trading continued to be lackluster throughout the week, with a 3,000 mt deal at $280/mt CFR on Sept. 22, prior to the mid-week retraction of interest from mill as they expected weaker prices after a cut in Taiwan’s domestic scrap prices.

"Buyers don't want to bid now while prices are still declining," a Taiwanese mill source said. "We will wait for subsequent weeks until levels are more stable."

Japanese H1:H2 50:50 offers to Taiwan similarly fell to $290-$295/mt CFR, down from $299-$303/mt the week before, with buyers also heard to be awaiting more competitive levels.

Despite recent weaker Asian indications and sentiments, some traders said the recent bearishness may only be short lived, as most saw better demand to come for Taiwanese mills begin in mid-October.

“I don't think the downside potential is a big one," a Taiwanese trader said. “Buyers are seeing a possible increase of production in the fourth quarter as the monsoon season wraps up, while electricity prices return to normal. Perhaps after the mid-autumn holidays [the first week of October], we might see some better construction demand as they rush to complete projects. So there could be more scrap demand returning."

— Marcus Ong, Samuel Chin

turkish import scrap stable, near-term sentiment mixed

�� bearish factors include lower euro-us dollar rate, soft finished steel market�� bullish factors include firm expected October scrap settlements in eu and us

London—Deepsea Turkish import scrap prices were stable Sept. 25 amid split sentiment toward the near-term price direction, sources said.

S&P Global Platts assessed Turkish imports of premium heavy melting scrap 1/2 (80:20) at $295.50/mt CFR, unchanged on the day.

“There is a stalemate in the market and I think we will see some movement next week,” a Turkish mill source said. He cited a tradable value for premium HMS 1/2 (80:20) at $290-$295/mt CFR and noting that confidential deals could have already been booked at this lower range.

A Turkish trading source also said $290-$295/mt CFR was likely to be workable for Baltic-origin material, while US sellers were still firm at $300/mt CFR.

“There are lots of scrap offers in the market and the Turkish domestic market is not so strong,” the trading source said. “Most mills were pushing for $290/mt CFR and they won’t follow the latest Samsun deals higher and start bidding at $295-$296/mt CFR, so the

September 25, 2020Sbb Steel marketS Daily

5© 2020 S&P Global Platts, a division of S&P Global Inc. All rights reserved.

market is silent and sellers are all stepping back.”Two Baltic-origin cargoes totaling around 52,500 mt were booked

on Sept 23 by a Samsun mill, The deals saw HMS 1/2 (80:20) calculated at $295.50/mt CFR, including a 50 cent/mt downward adjustment to reflect freight to Samsun, in line with Platts methodology.

The trader estimated that a further four-five cargoes are still required for end-October shipment from EU or Baltic sellers, while a Turkish agent source said around 7-8 cargoes are likely to be booked for the same shipment date.

Agents eye lower pricesA second Turkish agent source said $290/mt CFR maximum was

possible for EU-origin HMS 1/2 (80:20), and $293-$294/mt CFR for US- or Baltic-origin material, should recyclers decide to sell.

Baltic recyclers were expected to attempt to push HMS collection prices down to a $290/mt CFR no margin-equivalent, once September loading shipments are fulfilled, sources said. HMS collection prices in the St. Petersburg region were cited at around $297-298/mt CFR Turkey equivalent, down from $302/mt CFR earlier in the week.

“We all prefer the market to go down today, but with other sellers dropping the market, and then we can collect cheaper,” the second Turkish agent source said.

Market sources also cited the softer euro against the US dollar, which could put downward pressure on the US-dollar denominated CFR Turkey price. The euro was trading at $1.16203 as of 5 pm London time on Sept. 25, down from $1.18407 one week earlier.

Other bearish indicators pointed to by sources were lower iron ore prices ahead of the China mid-autumn holiday over Oct. 1-8. Platts assessed the 62% Fe Iron Ore Index at $116.05/dry mt CFR North China on Sept. 25, up 15 cents from Sept. 24, but down from $125.20/dmt one week earlier on Sept. 18.

This meant the Platts Turkey Scrap-Iron ore daily ratio was at 2.55 on Sept. 25, down slightly from 2.56 on Sept. 23, but hovering at its highest level since June 29.

However, other sell-side sources cited higher workable levels following the Samsun deals booked on Sept. 23.

The first Turkish agent cited a Baltic recycler target at $298-$299/mt CFR, while an EU trading source said $296-$298/mt CFR was workable for US- or Baltic-origin material.

“I believe sellers are firmer based on tighter than expected scrap availability and the [October] domestic settlement in the EU and USA are pointing upwards,” the EU trader said. “Plus, the Turks have to still finish their October buying and completely cover November.”

Early indications for US domestic October scrap settlements were heard to be sideways or up $10/lt on average across grades, while EU sellers are targeting Eur5-10/mt increases compared to September levels.

Another Turkish agent source said $297/mt CFR was workable for premium HMS 1/2 (80:20).

A UK trading source cited a near-term tradable value for premium material at closer to $300/mt CFR, while a US trader cited an offer for Venezuela-origin material at above $295/mt CFR, with US-origin material at $299-$300/mt CFR.

The Turkish longs melting margin -- the spread between Turkish export rebar and import scrap -- was assessed at $157/mt Sept. 25, down $1.50/mt on day.

— Viral Shah

India import shredded scrap prices soften, slack buying

�� weak demand and wider market sentiment keep buyers away�� Pound sterling and euro continue to soften against the dollar

London—Workable Indian import prices for containerized shredded scrap continued to soften over the week ending Sept. 25, as mills held back amid mixed sentiment over wider market direction.

S&P Global Platts assessed India import containerized shredded scrap at $312/mt CFR Nava Sheva Sept. 25, down $3 on the week.

“The market is very quiet and the wider sentiment is negative with buyers anticipating a big fall in prices so activity into Nava Sheva has totally halted,” an Indian trading source said.

A midweek softening in the benchmark Turkish import scrap price, coupled with weak buyer demand, affected sentiment in the Indian import shredded scrap market, a second trading source said.

Platts’ assessment of the benchmark Turkish import premium HMS 1/2 (80:20) had softened to $293/mt CFR on Sept. 23, before recovering to $295.50/mt CFR on Sept 24, following news of two fresh Baltic-origin deals.

Market sources cited tradable values ranging $310-$315/mt CFR Nava Sheva, with a majority of sources citing around $312/mt CFR as representative of market value. Indicative bids were cited around $300-$305/mt CFR Nava Sheva.

While the Indian import market was quiet, sources cited multiple deals at around similar levels into Pakistan.

A deal booked on Sept. 22 was cited at $315/mt CFR Port Qasim, while a UK-origin sale for 1,000 mt was booked at $312/mt CFR Qasim on Sept. 24. The same UK trader had also booked a deal at $310/mt CFR for 500 mt on Sept 24.

Following news of the rebound in the Turkish import scrap market, prices also firmed into Pakistan, with an EU-origin cargo totaling 1,000 mt heard booked at $312/mt CFR on Sept. 25.

Pound sterling also saw a sharp drop against the US dollar over the week ending Sept. 25, putting further downward pressure on the US-dollar denominated CFR price. Sterling was trading at $1.27501 at 5 pm London time on Sept. 25. This was down from $1.29194 on Sept. 18.

Similarly, the euro, also saw softening on week, trading at

Analytics

Visit spglobal.com/analytics-insight

Integrated, innovative. Across geography and across commodity.

September 25, 2020Sbb Steel marketS Daily

6© 2020 S&P Global Platts, a division of S&P Global Inc. All rights reserved.

$1.16203 as of 5 pm London time on Sept. 25, down from $1.18407 one week earlier.

New daily coronavirus cases totaled 85,919 on Sept. 24, down on week from 96,793 on Sept. 17, with total cases around 5.84 million mark.

— Viral Shah

eXChAnges

Futures wrAP: lme scrap, rebar contracts soften further on market uncertainty

London—The scrap and rebar forward curves on the London Metal Exchange both saw losses over the week to Sept. 24, amid mixed sentiment over near-term physical market direction.

The scrap forward curve moved lower, maintaining a backwardated structure, with losses apparent over September to December contracts.

September LME scrap futures were down $3.50/mt week on week at $295.50/mt on Sept. 24. The October contract dropped $5/mt over the week to $291.50/mt.The later-dated November contract fell $6/mt to $290/mt, while the December contract fell $5/mt week on week to $289.50/mt.

However, the Turkish import scrap market recovered on the day, following fresh ex-Baltic deals heard late on Sept. 24, which is likely to shift sentiment on near-term price direction. Spot prices for physical imports of premium heavy melting scrap 1/2 (80:20) were assessed at $295.50/mt CFR Turkey on Sept. 24, up $2.50/mt on the day, and up 50 cents/mt from Sept. 17.

Market participants pointed to a firm US domestic scrap market, and the hike in the Turkish benchmark interest rate, which could lower domestic lira-based rebar prices, and thus improve domestic rebar demand, which in turn could support scrap prices.

However, sources also pointed to the euro and pound sterling softening against the dollar, which could put downward pressure on US dollar-denominated CFR Turkey scrap prices. In addition, iron ore prices have also fallen week on week, while sentiment in China has turned bearish with futures.

The most actively traded January 2021 rebar futures contract on the Shanghai Futures Exchange closed at Yuan 3,522/mt on Sept. 25, down from Yuan 3,603/mt on Sept. 18.

Scrap futures trading volumes over the week to Sept. 24 sat at 90,740 mt, a sharp increase from 19,070 mt recorded last week, making it the highest weekly trading volume since late May. Scrap trading volumes over the year to date now total 3.96 million mt, the highest volume over a January-September period since the contract’s launch in late 2015.

The rebar forward curve on the London Metal Exchange shifted into backwardation over the week to Sept. 24, from a completely flat forward curve one week earlier.

The September contract rose $2/mt to $455.50/mt while the October contract fell $3/mt to $450.50/mt. The November rebar contract was assessed at $449.50/mt, dropping $4/mt week on week, and the December contract fell $6/mt to $447.50/mt on Sept. 24.

Platts assessment of Turkish exported rebar was down $1/mt over the week at $454/mt FOB Turkey Sept. 24, as some mills were heard to

consider lower workable levels in search for export demand.Rebar futures weekly trading volumes this week on the LME totaled

7,600 mt, down from 10,350 mt recorded last week.The Turkish longs melting margin -- the spread between Turkish

exported rebar and import scrap -- was down $1.50/mt week on week at $158.50/mt Sept. 24.

— Viral Shah

FerrOAllOYs mArket

molybdenum oxide slides as holidays near in China

�� market eyes next support level for molybdenum�� european ferromolybdenum testing $20/kg resistance

London—Molybdenum prices continued to slide Sept. 25 with market participants noting that buying interest was picking up as prices declined.

The Platts Daily Dealer Molybdenum Oxide assessment was at $8-$8.20/lb, from $8.10-$8.35/lb on Sept. 24.

“There were more inquiries in the afternoon," one Asian trader said. "European traders are restocking.”

Others said they had received lots of bids at $8-$8.10/lb in Asia but did not want to sell and preferred to wait while a second Asian trader said it was “not a good time to buy.”

In Europe, deals were concluded at $8/lb and $8.05/lb, which one European trader noting that sellers who had rejected low bids in the market on the previous day had come back in at lower levels.

With China’s autumn holidays approaching, market participants said they were not surprised that prices had continued to slip along with buying interest.

“Holidays are coming in Asia -- everyone anticipated the cooling off,” a second European trader said.

European ferromolybdenum prices, meanwhile, also felt pressure as deals to a mill in Austria were heard at $20.15/kg DDP and offers in Rotterdam at $20/kg.

Sources said while there were bids in Europe below $20/kg there were no keen sellers at this level.

— Jitendra Gill

Other news

Japan's August steel output climbs on month amid rise in demand: JIsF

�� Crude steel output up 6.6% on month�� Product output up 18.3% on month

Singapore—Japan’s crude steel production rose 6.6% on the month in August to reach 6.45 million mt, but was down 20.6% year on year, latest figures from the Japan Iron & Steel Federation showed Sept. 24.

September 25, 2020Sbb Steel marketS Daily

7© 2020 S&P Global Platts, a division of S&P Global Inc. All rights reserved.

1935-7354

SBB STEEL MARKETS DAILY

The names “S&P Global Platts” and “Platts” and the S&P Global Platts logo are trademarks of S&P Global Inc. Permission for any commercial use of the S&P Global Platts logo must be granted in writing by S&P Global Inc.

You may view or otherwise use the information, prices, indices, assessments and other related information, graphs, tables and images (“Data”) in this publication only for your personal use or, if you or your company has a license for the Data from S&P Global Platts and you are an authorized user, for your company’s internal business use only. You may not publish, reproduce, extract, distribute, retransmit, resell, create any derivative work from and/or otherwise provide access to the Data or any portion thereof to any person (either within or outside your company, including as part of or via any internal electronic system or intranet), firm or entity, including any subsidiary, parent, or other entity that is affiliated with your company, without S&P Global Platts’ prior written consent or as otherwise authorized under license from S&P Global Platts. Any use or distribution of the Data beyond the express uses authorized in this paragraph above is subject to the payment of additional fees to S&P Global Platts.

S&P Global Platts, its affiliates and all of their third-party licensors disclaim any and all warranties, express or implied, including, but not limited to, any warranties of merchantability or fitness for a

particular purpose or use as to the Data, or the results obtained by its use or as to the performance thereof. Data in this publication includes independent and verifiable data collected from actual market participants. Any user of the Data should not rely on any information and/or assessment contained therein in making any investment, trading, risk management or other decision. S&P Global Platts, its affiliates and their third-party licensors do not guarantee the adequacy, accuracy, timeliness and/or completeness of the Data or any component thereof or any communications (whether written, oral, electronic or in other format), and shall not be subject to any damages or liability, including but not limited to any indirect, special, incidental, punitive or consequential damages (including but not limited to, loss of profits, trading losses and loss of goodwill).

ICE index data and NYMEX futures data used herein are provided under S&P Global Platts’ commercial licensing agreements with ICE and with NYMEX. You acknowledge that the ICE index data and NYMEX futures data herein are confidential and are proprietary trade secrets and data of ICE and NYMEX or its licensors/suppliers, and you shall use best efforts to prevent the unauthorized publication, disclosure or copying of the ICE index data and/or NYMEX futures data.

Permission is granted for those registered with the Copyright Clearance Center (CCC) to copy material herein for internal reference or personal use only, provided that appropriate payment is made to the CCC, 222 Rosewood Drive, Danvers, MA 01923, phone 1-978-750-8400. Reproduction in any other form, or for any other purpose, is forbidden without the express prior permission of S&P Global Inc. For article reprints contact: The YGS Group, phone 1-717-505-9701 x105 (800-501-9571 from the U.S.).

For all other queries or requests pursuant to this notice, please contact S&P Global Inc. via email at [email protected].

SBB Steel Markets Daily is published daily by Platts, a division of S&P Global, registered office: 55 Water Street, 37th Floor, New York, N.Y. 10038.

Contact Platts support: [email protected]; Americas: 1-800-752-8878; Europe & Middle East: 44-20-7176-6111; Asia Pacific: 65-6530-6430

Australia:

Senior Managing EditorPaul Bartholomew (61 3963 12096)

London:

Editor-in-ChiefDiana Kinch (44 207 176 8390)

Senior Editor, Raw materials, analysisHector Forster (44 207 176 6285)

Senior Pricing Specialist, Ferrous ScrapViral Shah

Senior EditorBen Kilbey

Markets EditorJitendra Gill

Pittsburgh:

Senior EditorTom Balcerek (1 412 916 8476)

News and Markets EditorsJustine Coyne; Joe Eckelman; Michael Fitzgerald

Singapore:

Markets EditorsYoko Manabe; Weng Yi Le; Niki Wang; Lu Han; Jun Kai Heng; Samuel Chin; Marcus Ong

Shanghai:

Senior Managing Editor, Steel & Raw MaterialsKeith Tan (86 21 5110 5478)

Platts PresidentMartin Fraenkel

AdvertisingTel: 1-720-264-6618

Manager, Advertisement SalesBob Botelho

Officers of the Corporation: Charles E. Haldeman, Jr., Non-Executive Chairman; Doug Peterson, President and Chief Executive Officer; Ewout Steenbergen, Executive Vice President, Chief Financial Officer; Steve Kemps, Executive Vice President, General Counsel

© 2020 S&P Global Platts, a division of S&P Global Inc. All rights reserved.

Regional Pricing Director, Metals – Asia (Singapore)Julien Hall (65 6530 6531)

Associate Regional Pricing Director, EMEA – Metals (London)Scott Yarham (44 20 7176 8390)

Regional Pricing Director, Metals – Americas (Pittsburgh)Christopher Davis (1 412 431 0398)

Global Content Director, Metals and Agriculture (London)Ian Dudden (44 20 7176 6772)

Head of Pricing & Market InsightDave Ernsberger

ISSN:

Production in the first eight months of 2020 amounted to 54.72 million mt, down 19%.

Blast furnace output in August amounted to 4.89 million mt, up 10.9% from July, but down 22.9% from a year ago. On the other hand, production via electric furnaces in August was at 1.55 million mt, down 4.9% from July and down 12.2% year on year.

The August crude steel output rise on the month came as the Japanese economy made efforts to overcome the lingering effects of the COVID-19 pandemic.

The third-quarter outlook was expected to record a better performance than the previous quarter, as overall market activity was to see automakers and machinery manufacturers gear up from the easing of previous production cuts in the second quarter.

The au Jibun Bank Manufacturing Purchasing Managers' Index's reading for August stood at a seasonally adjusted 47.2, up from 45.2 in July.

Meanwhile, September is expected to be stable as the flash au Jibun Bank PMI for the month stood at 47.3, relatively sideways from August, IHS Markit said Sept. 23.

In terms of August steel product output, the hot-rolled sheet and plates category saw a month-on-month increase of 12.7% to 3.5 million mt, while the wire rod category was up 4.8% at 71,500 mt. Sections and bars, meanwhile, contracted on the month by 7.8% and 7.4%, respectively, to 378,900 mt and 653,100 mt.

Overall, supporting the August increase in demand for steel were new export orders for ships, which amounted to 579,400 gross tons, or nine vessels. This figure was up from 469,750 GT in July, or eight

vessels then, and a year-on-year improvement of 4.6%, Japan Ship Exporters’ Association data showed.

However, according to the Shipbuilders' Association of Japan, steel demand is projected to still see bearish figures this year of about 2.66 million mt, down from 3.34 million mt in 2019.

In terms of steel demand from vehicles, new car sales performance remained sluggish and totaled 326,436 units in August, down from 396,346 units in July and also lower from 388,600 units in August 2019, data from the Japan Automobile Manufacturers Association showed.

— Clement Choo, Samuel Chin

AmerICAs

steel scrap price expectations remain firm for us October buy

�� most expect up $10/lt on obsoletes in October�� Primes expected to be firmer

Pittsburgh—Market sources expect sideways to stronger pricing as the October buy week approaches in the US.

Most expect primes to be firmer than obsolete grades, as the material is still heard to be tight in the Midwest and the spread

September 25, 2020Sbb Steel marketS Daily

8© 2020 S&P Global Platts, a division of S&P Global Inc. All rights reserved.

between shredded scrap and the premium material remains historically narrow. Since October 2017 the average spread between prime scrap and shredded has been $42/lt. Prices on the two products currently sit at approximately half that spread.

"The market feels very firm, demand is strong it's just a matter of what kind of uptick we'll get on obsoletes, maybe more on primes," said one Midwest supplier.

"Prime has more upside chance because pig iron is so strong," said another Midwest supplier.

Many project shred will be sideways to up $10/lt, and up $20/lt at most.

"I think increases will be capped at $20/lt," said one Ohio Valley supplier. "I'm not sure we get up $20/lt, but it can’t go higher than that. I think mills are eager buyers at sideways," he added.

"I feel October is sideways at worst," said one Ohio Valley supplier who believed cut grades could be up $10 next month. "I would almost bet you my savings that $20 isn't in the playbook," he added.

"I'm not feeling it, I think this market has slipped. I think we're sideways," said a more pessimistic source. He added that one major mill buying group was heard to be trying to talk the market down. "Primes – there's a little bit more momentum there – but I think the [finished] steel price increase announcements are the tale wagging the dog a little bit."

"[The mill buying group] may try to put a lid on the market," agreed the first Midwest supplier.

— Joe Eckelman

FreIght

Capesize market takes a break after bustling week

�� Atlantic market muted before weekend amid standoff�� Pacific market cools off with freight rates edging down

The Capesize market took a breather on Sept. 25 after witnessing momentum since Sept. 18. The strong uptrend in the week to Sept. 25 was the second big jump in 2020 since the first one in June, a Europe-based shipbroker said.

A shipbroker said that it is unlikely Platts Cape T4 Index rates for

Capesize will exceed the year's high of $31,901/d reached on July 6.Trading activities cooled off before the weekend due to a subtle

sentiment change, starting from a softening freight derivative market. Ballast interest has been well-supported by the decent time charter equivalent returns on the key Brazil routes.

“The Capesize market is unpredictable, but personally I believe that next week maybe more upside,” a Chinese-ship operating source said.

The bunker market saw prices edging up, but failed to make waves in such a volatile freight market.

Atlantic marketDriven by the strong sentiment on the Brazil route, the short

term market outlook in Atlantic remained rosy. On the key Tubarao to Qingdao route, the trading day was sluggish without much activity. Fixture-wise, miner Vale was heard fixing a few ships late Sept. 24 for mid-October laycans, with freight rates at around $20/wmt. The freight indicated on the Brazil to China route was in the $19/wmt to $20.50/wmt range.

The freight rate for a Capesize ship to move 170,000 mt (plus/ minus 10%) of iron ore from Tubarao to Qingdao was assessed at $20.50/wmt, flat day on day.

Nothing fresh was heard out of South Africa. Some coal shipment from Richards Bay to India were heard to be split from Capesize to Panamax due to the current high Cape TCE rates, a ship-operating source said.

Freight rate for a Capesize ship to move 170,000 mt (plus/ minus 10%) of iron ore from Saldanha Bay to Qingdao was assessed at $15.40/wmt, unchanged from Sept. 24.

Pacific marketFreight rates inched down amid scant trading activities after a

slew of trades concluded in the previous days. In general, the shipping demand in Pacific remained healthy and constant while the port congestion in China ports was easing slowly. Among fixtures, miner Rio Tinto was heard to have fixed a ship for moving iron ore from west Australia to Qingdao for the Oct. 11-13 laycan at $8.70/wmt. The indicative freight heard on the west coast Australia to Qingdao route was in the $8.50/wmt to $9/ wmt range.

The freight rate for a Capesize ship to move 170,000 mt (plus/minus 10%) of iron ore on the Port Hedland-Qingdao route was assessed at $8.70/wmt, down 20 cents/wmt from Sept. 24.

— Carina Li

subsCrIber nOtes

Platts to merge tsI and Platts Premium hard Coking Coal Price seriesFollowing industry feedback, S&P Global Platts has decided to merge the TSI Premium Hard Coking Coal FOB East Coast Australia index (TS01034) and the Platts Premium Low Vol HCC FOB Australia assessment (PLVHA00), effective April 1, 2021.

The decision follows market feedback received for a first proposal published May 22 (http://plts.co/CzN430qVcSJ), and a second updated proposal published July 7 (https://bit.ly/3hzEU7Z).

The majority of feedback received from market participants was supportive of the proposed merger of the TSI PHCC and Platts PLV indices, which aims to simplify Platts suite of premium coking coal assessments, and further reinforce the robustness of the TSI PHCC index in times of market illiquidity.

Aligning the methodologies will mean that the TSI PHCC and Platts PLV HCC price series will be published as two identical values from April 1, 2021. This will have the added benefit of eliminating the basis risk for market participants looking to hedge their PLV HCC-linked physical coking coal exposure via derivatives contracts settling against the TSI PHCC index. Platts received widespread feedback from all segments of the market and geographies, including during open webinars run for the purpose of explaining the proposal.

dAtA treAtment: The newly merged assessments, which will follow Platts Market-on-Close principles, will reflect repeatable market value at the close of the assessment process, after incremental market testing. Platts tracks market price evolution during the entire day, and publishes a

September 25, 2020Sbb Steel marketS Daily

9© 2020 S&P Global Platts, a division of S&P Global Inc. All rights reserved.

wide range of data relating to market value, including firm bids and offers, transactions and indicative values Transparent data is prioritized in the assessment process, because it is available to the entire market for testing. The full description of the Platts assessments methodology and data hierarchy can be found here: https://www.spglobal.com/platts/plattscontent/_assets/_files/en/our-methodology/methodology-specifications/platts-assessments-methodology-guide.pdf

Affected price series: TSI Premium Hard Coking Coal Australia Export FOB East Coast Port (TS01034).

tImestAmP: To align the TSI PHCC index with other assessments across metallurgical coal and the ferrous value chain, including iron ore, steel and ferroalloys, the index after alignment will represent an end-day value with a timestamp of 5:30 pm Singapore time (0930 GMT). At present, the TSI PHCC index takes into account data reported until 6 pm Singapore time and is calculated as a volume-weighted average. Affected price series: TSI Premium Hard Coking Coal Australia Export FOB East Coast Port (TS01034).

QuAlItY: Platts will revise the specifications of its merged assessments to better align them with the current specifications of premium low-vol hard coking coals in the physical market. These changes can be seen in the table below. Based on Platts evaluation, the new specifications do not amount to any meaningful value difference for the assessment relative to its previous specifications or relative to the major premium hard coking coal brands trading in the physical market. All premium mid-vol hard coking coals will continue to be assessed and normalized to the Platts defined PLV benchmark specification.

Csr Vm ad tm ar Ash ad s ad P ad Fluidity Vit %

Platts PLV 71 21.5 9.7 9.3 0.5 0.045 500 65

TSI PHCC 71 21 10 10 0.45 0.05 600 68

Proposed 70 20 10 10.5 0.65 0.04 300 67 Specifications

Affected price series: TSI PHCC index, the PLV HCC assessment, and other seaborne and port stock assessments that are related to the PLV HCC assessment. The list of affected price series is as follows:

description symbol

TSI Premium Hard Coking Coal Australia Export FOB East Coast Port TS01034

TSI Prem JM25 Coking Coal China Imports CFR Jingtang Por TS01044

Premium Low Vol HCC FOB Australia PLVHA00

Prem Low Vol HCC FOB Australia (China netback) PLVHD00

Premium Low Vol HCC CFR China PLVHC00

Premium Low Vol HCC CFR India PLVHI00

Prem Low Vol Ex-Stock Jingtang AAWZN00

Prem Low Vol CFR Jingtang Equivalent AAWZO00

Met Coal Prem Low Vol Import-Port Stock CFR China Differential PLVHL04

tImIng: The timing specification of the Platts PLV FOB Australia assessment will be adjusted to represent cargoes loading 7-60 days forward from the current 7-45 days forward, in line with the current loading window of the TSI PHCC index. As is the case in Platts methodology, where a time structure is observed in the physical market, cargoes loading within this loading window are normalized to the mid-window day, in this case the 33rd day forward. The change will better align with typical loading timings in the physical spot market and increase overall liquidity eligible for inclusion in the assessment. Affected price series: Premium Low Vol HCC FOB Australia (PLVHA00) and Prem Low Vol HCC FOB Australia (China Netback) (PLVHD00) assessments. Platts will also change the delivery timing for the assessments with CFR incoterms to delivery in 20-75 days, from the current delivery in 20-60 days. Affected price series: Premium Low Vol HCC CFR China (PLVHC00) and Premium Low Vol HCC CFR India (PLVHI00).

QuAntItY: The volume basis of the TSI PHCC assessment will be set at minimum 10,000 mt, in line with the Platts PLV HCC specification, from the present minimum 15,000 mt. Affected price series: TSI Premium Hard Coking Coal Australia Export FOB East Coast Port (TS01034).

lOCAtIOn: Platts will define the location basis for the TSI PHCC index as FOB Hay Point, Australia, in line with the existing Platts PLV HCC assessment. The port of Hay Point includes the two terminals of HPCT and DBCT. Cargoes loading from other ports will continue to be reflected, but will be normalized to the stated basis location. Affected price series: TSI Premium Hard Coking Coal Australia Export FOB East Coast Port (TS01034)

PremIum mId VOl: Following market feedback, Platts has decided not to launch a new premium mid-vol assessment at this point. Platts currently publishes daily assessments of a number of mid-vol brands, namely Goonyella, Illawarra, Moranbah North, Goonyella C, Peak Downs North and Riverside. According to market participants, these existing brand assessments (also known as relativities) already serve as an accurate and transparent price reference for the premium mid-vol segment of the market. Platts remains open to market feedback and continues to review the relevance of any additional mid-vol assessments.

The realigned assessments will be published in SBB Steel Markets Daily, Coal Trader International, on the real-time Platts Metals Alert on fixed pages 1064, 205, 1051, 1062, and in the Platts price database under the symbols mentioned above.

Please send any feedback, comments or questions to [email protected], [email protected] and [email protected].

For written comments, please provide a clear indication if comments are not intended for publication by Platts for public viewing. Platts will consider all comments received and will make comments not marked as confidential available upon request.

Platts to launch 65% Fe CFr China iron ore forward curve, update spot specFollowing a proposal period, S&P Global Platts has decided to update the specifications of its 65% Fe CFR China iron ore fines spot assessment effective Jan. 4, 2021, and to start assessing a respective derivative forward curve, effective Nov. 2, 2020.

Platts launched a formal proposal on Aug. 12, 2020, in a subscriber note available here: https://www.spglobal.com/platts/en/our-methodology/subscriber-notes/081220-platts-proposes-to-launch-65-fe-cfr-china-iron-ore-forward-curve-update-spot-spec

sPeCIFICAtIOn ChAnge: Effective Jan. 4, 2021, Platts will amend the specifications of the 65% Fe iron ore fines assessment (IOPRM00) to 1.4% alumina, 2% silica and 0.065% phosphorus, from current 1% alumina, 3.5% silica and 0.075% phosphorus. The change will bring this assessment in line with the latest specifications seen in the high grade fines segment of the market. The affected assessment is published on the fixed page 1105 of the real-time Platts Steel Alert and Platts Metals Alert, on page 16 of SBB Steel Markets Daily, in Platts Market Center and in the Platts price database.

Assessment 65% Fe CFR North China 65% Fe CFR North China

Code IOPRM00 IOPRM00

Status New Current

Iron Content 65% 65%

Alumina 1.4% 1%

Silica 2% 3.5%

Phosphorus 0.065% 0.075%

FOrwArd CurVe: Effective Nov. 2, 2020, Platts will launch a new daily assessment of 65% Fe Fines CFR China Derivative Forward Curve, in response to the growing liquidity in this segment of the iron ore derivatives

September 25, 2020Sbb Steel marketS Daily

10© 2020 S&P Global Platts, a division of S&P Global Inc. All rights reserved.

market. The assessments will reflect the daily values at 5:30 pm Singapore time for 65% Fe iron ore fines derivative contracts, on a CFR China basis, normalized to a minimum volume of 5,000 mt, in line with the standard industry practice. Platts will publish derivatives assessments for current month (Mo0), month one (Mo01), second month (Mo02) and third month (Mo03) strips, which roll on the first day of the month. Platts will collect trade information from active market participants and forward curves from brokers. Derivative bids/offers and trades will continue to be published in real time throughout the day on the Platts electronic information service and Platts Metals Alert (PMA), along with information in the physical market. The new assessments will be published on the fixed page 1113 of the real-time Platts Steel Alert and Platts Metals Alert, on page 17 of SBB Steel Markets Daily, in Platts Market Center and in the Platts price database.

Please send all comments, feedback and questions to [email protected] and [email protected].

For written comments, please provide a clear indication if comments are not intended for publication by Platts for public viewing.

Platts will consider all comments received and will make comments not marked as confidential available upon request.

Platts invites feedback on iron ore and metallurgical coal assessmentsAs part of its commitment to open and transparent pricing and product specifications, S&P Global Platts would like to invite feedback on its global iron ore and metallurgical coal assessments.

Platts reviews all methodologies and specifications annually to ensure they continue to reflect the physical markets. Platts regularly assesses the relevance of methodologies through continuous contact with the market. Feedback on methodologies is always welcomed by Platts.

Platts is committed to providing advance notice in a clear time frame that gives users sufficient opportunity to analyze and comment on the impact of such proposed changes. Time frames vary depending on Platts analysis of the overall circumstances of a particular change. Methodology changes that materially alter assessments and indices and require an update to the methodology specification are preceded by extensive bilateral discussions with market stakeholders and open public forums. Routine changes or clarifications, generally do not materially alter an assessment/index.

Platts holds open public forums in which material methodology changes and feedback are presented, and at which further feedback may be given.

Please send all comments, feedback and questions to [email protected] and [email protected]. For written comments, please provide a clear indication if comments are not intended for publication by Platts for public viewing. Platts will consider all comments received and will make comments not marked as confidential available upon request.

Platts proposes to rename hCC 64 mid Vol assessments to low Vol hCCS&P Global Platts proposes to rename the HCC 64 Mid Vol (also known as Hard Coking Coal) assessments to Low Vol HCC, effective April 1, 2021.

The purpose of the proposal is for the assessment names to better align with the underlying specifications defined in Platts methodology, which were changed in 2018. On June 1, 2018, specifications of HCC 64 Mid Vol (also known as Hard Coking Coal) FOB Australia (HCCAU00), CFR China (HCCCH00) and CFR India (HCCIN00) assessments were adjusted to: 62% coke strength after reaction, 21.5% volatile matter, 10.5% total moisture, 8% ash, 0.45% sulfur, 0.06% phosphorus, 100 ddpm max fluidity, 52% vitrinite. The subscriber note can be viewed at https://bit.ly/2CLzbfT.

The proposal does not affect the assessment methodology itself, or the qualities of coals whose pricing information is considered in those assessments.

Some of these assessments are globally-referenced benchmarks for generic (non-premium) hard coking coals. This prolonged notice period is to provide sufficient time for market participants who are using these assessments to make any necessary adjustments in their contracts.

The change would affect the following assessments and all their averages:

Current description Proposed description symbol

HCC 64 Mid Vol FOB Australia Low Vol HCC FOB Australia HCCAU00

HCC 64 Mid Vol CFR China Low Vol HCC CFR China HCCCH00

HCC 64 Mid Vol CFR India Low Vol HCC CFR India HCCIN00

HCC 64 Mid Vol Ex-Stock Low Vol HCC Ex-Stock AAWZP00 Jingtang Jingtang

HCC 64 Mid Vol CFR Jingtang Low Vol HCC CFR Jingtang AAWZQ00 Equivalent Equivalent

The affected prices are published in SBB Steel Markets Daily, Coal Trader International, on the real-time Platts Metals Alert and Platts Steel, Raw Materials Alert on fixed pages 1064, 205, and 1062 and in the Platts price database under the symbol mentioned above.

Please send comments, questions and other feedback on this proposal by October 9, 2020 to [email protected] and [email protected].

For written comments, please provide a clear indication if comments are not intended for publication by Platts for public viewing. Platts will consider all comments received and will make comments not marked as confidential available upon request.

s&P global Platts amends 58%-Fe iron ore CFr China specificationsEffective May 4, 2020 and as part of an overall revision of its iron ore coverage, S&P Global Platts has amended the specifications of the 58% iron ore fines assessment (IODFE00) to align them with the major Australian brands and reflect the average specification of global brands in this segment of the iron ore market.

The assessment now reflects material with 2.9% alumina, 6% silica and 0.06% phosphorus.

Platts first published the proposal on January 31, 2020 in a subscriber note available here: https://www.spglobal.com/platts/en/our-methodology/subscriber-notes/013120-sampp-global-platts-proposes-changes-to-its-58-fe-iron-ore-coverage. Market participants across the supply chain stated the amendments would be more reflective of current iron ore brands with iron content below 60% in the market, and that the change would allow for liquidity in this segment of the market to be pooled together around a single assessment.

Under the new specifications, all iron ore fines with iron content below 60% will be considered under the 58% iron ore fines CFR China index and normalized according to Value-in-Use (VIU) assessments and observed brand relativities. This includes the brands that currently fall under the assessment for 58% low-alumina iron ore fines CFR China index (IONC580 & TS01047). Going forward, Platts may consider spreads and dynamics in the Chinese portside market as indicative factors to help calibrate VIU adjustments for seaborne 58% iron ore fines assessment as well as changes to brand relativities.

As part of this change, Platts now also reflects the new specification in its 58% iron ore West India netback price (IODFA00). This price continues to be automatically calculated by deducting the assessed freight rate between West coast India and Qingdao for a 50,000 mt (Supramax) iron ore cargo from the 58% Fe iron ore fines CFR China assessment.

Separately, effective October 1, 2020, Platts will discontinue the Platts & TSI IO Fines 58% Fe low-alumina iron ore fines CFR China assessments

September 25, 2020Sbb Steel marketS Daily

11© 2020 S&P Global Platts, a division of S&P Global Inc. All rights reserved.

(IONC580 & TS01047) and respective averages to further consolidate the coverage of the iron ore fines with iron content below 60%. Platts will publish a separate subscriber note on the day of discontinuation to inform market participants of the change.

Assessment 58% 58% 58% Low-Alumina

Code IODFE00 IODFE00 IONC580, TS01047

Status Effective May 4 Before May 4 To discontinue on Oct 1

Iron content 58% 58% 58%

Alumina 2.9% 4% 1.5%

Silica 6% 5% 5.5%

Phosphorus 0.06% 0.05% 0.05%

The affected assessments are published on the fixed page PMA1105 and PMA1106 of the real-time Platts Metals Alert, on page 2 and 6 of the Steel Markets Daily, in the Platts Market Center and in the Platts price database.

Please send all comments, feedback and questions to [email protected] and [email protected].

For written comments, please provide a clear indication if comments are not intended for publication by Platts for public viewing. Platts will consider all comments received and will make comments not marked as confidential available upon request.

Platts clarifies us steel specifications following annual reviewAs part of its annual review of the ferrous metals specifications guide, S&P Global Platts wishes to clarify certain specification details for its US steel products and ferrous scrap assessments.

hOt-rOlled COIl: Platts TSI US HRC index (STHRI00) and all its conversions reflect a shipment window of three to eight weeks from the date of publication, while US HRC DDP Houston (STHRG00) import assessment and all its conversions reflect delivery eight to 14 weeks forward.

COld-rOlled COIl: Platts TSI US CRC index (STRRI00) and all its conversions reflect a shipment window of four to 12 weeks from the date of publication, while US CRC DDP Houston (STRRG00) import assessment and all its conversions reflect delivery 10-16 weeks forward.

hOt-dIP gAlVAnIZed COIl: Platts TSI US HDG index (ATSIA00) and US HDG (incl. G90) calculation (SB01123) reflect a shipment window of four to 12 weeks forward. The US HDG DDP Houston import assessment reflects 500-1,500 st clips delivered 12-18 weeks from the date of publication and payment within 30 days after delivery.

PlAte: All US plate prices reflect material conforming to ASTM A36/A36M or equivalent with the following parameters: width to 96 inches, thickness 0.375-2 inches, length to 240 inches. The Platts TSI US plate index (STPRI00) and its conversions reflect shipments four to 12 weeks forward in minimum 20-st clips shipped. The US plate DDP Houston import assessment (STPRG00) and its conversions represent deliveries eight to 14 weeks forward. Platts clarified the names of currency and UOM conversions to align them with the names of the main index and assessment.

sCrAP: All US scrap assessments, indexes and calculations (shredded FEMWD00, 10-day average TS11003, HMS ½ SB01135, plate and structural SB01174, #1 busheling SB01001) on a delivered basis reflect deliveries to the US Midwest mill within 30 days from the date of publication. FOB East Coast scrap assessments (shredded FEECD00 and HMS FEECH00) reflect deliveries five to 45 days forward and payment terms LC at sight. US HMS assessments reflect material conforming to ISRI 200-206 quality; plate and structural assessment - ISRI 231-232 quality, and #1 busheling assessment - ISRI 207 quality.

metAllICs: The US pig iron price (MMPNO04) was specified to be CIF New Orleans with a delivery window of five to 10 weeks. REBAR: US rebar assessments on EXW Southeast (STCBC00) and Midwest (SB01202) bases reflect a shipment window of four to 12 weeks forward, while the DDP Houston assessment (STCBG00) and all its conversions reflect deliveries eight to 14 weeks forward. WIRE ROD: US wire rod mesh quality assessment (SB01249) reflects a shipment window of four to 12 weeks forward. PIPE: The US OCTG ex-works domestic assessment (SB01253) reflects shipments two to eight weeks from the date of publication, while the DDP Houston import assessment (SB01254) reflects deliveries six to 12 weeks forward.

Please submit any feedback, comments or questions about this notice to: PL_Americas_Metal and pricegroup. For written comments, please provide a clear indication if comments are not intended for publication by Platts for public viewing. Platts will consider all comments received and will make comments not marked as confidential available upon request.

Assessment rAtIOnAles

Platts Asia Iron Ore IOdeX daily rationale & exclusionsS&P Global Platts assessed the 62% Fe Iron Ore Index at $116.05/dry mt CFR North China on Sept. 25, up 15 cents from Sept. 24, in line with a Pilbara Blend Fines (PBF) trade and supported by tradable values.

At 4.30 pm Singapore time, Rio Tinto sold a 170,000-mt cargo of PBF at a premium of $4.30/dmt over the November average of IODEX CFR Qingdao basis 62% Fe, on COREX, loading Oct. 28 to Nov. 6.

Taking into account the impurity adjustments, timing and the November swaps at $109.65/dmt around the trade timestamp, the PBF trade normalized to $116.05/dmt CFR China on IODEX specifications.

Industry sources said Pilbara Blend fines arriving between late October and early November was tradeable at $115-$116.5/dmt basis 62% Fe, which normalized to a range of $115.35-$116.85/dmt on IODEX basis, after accounting for impurity adjustments.

Platts used a physical backwardation structure of $3.3/dmt based on the physical structure between October and November.

The above rationale applies to Platts 62% FE IODEX & TSI Iron Ore Fines 62% CFR China with the associated data code: IODBZ00, TS01021Exclusions: No market data was excluded from the assessment process on Sept. 25.

Platts China Iron Ore lump Premium daily rationale & exclusionsS&P Global Platts assessed the spot lump premium at 7.5 cents/dmtu on Sept. 25, flat from Sept. 24, in line with tradable levels.

Industry sources said that the spot lump premium was tradable at around 7 to 8.25 cents/dmtu over the Platts 2-8 week delivery window on a CFR China basis.

Platts used a contango physical structure for lump premium between October and November based on the swaps structure.

No market data was excluded from the assessment process.

The above rationale applies to market data code: <IOCLP00>Exclusions: No market data was excluded from the Sept. 25 Platts Market on Close assessment process.

Platts CFr north China Iron Ore 65% Fe low Al Assessment rationaleS&P Global Platts assessed the 65% Fe North China Index at $127.40/dry mt CFR North China on Sept. 25, stable from Sept. 24, narrowing the spread between 65% Fe and 62% Fe iron ore indexes to $11.35/dmt.

Industry sources said the tradable spread between 65%-Fe and 62%-Fe iron ore indexes was around $11-$12/dmt.

No market data was excluded from the assessment process on Sept. 25.

This assessment rationale applies to the following market data codes: 65% Fe CFR North China: IOPRM00

September 25, 2020Sbb Steel marketS Daily

12© 2020 S&P Global Platts, a division of S&P Global Inc. All rights reserved.

Platts CFr north China Iron Ore 58% Fe low Al Assessment rationaleSingapore—S&P Global Platts assessed the 58% Fe Iron Ore Index at $108.65/dry mt CFR North China on Sept. 25, up 20 cents from Sept. 24, narrowing the spread between 58% Fe and 62% Fe iron ore index to $7.4/dmt.

No market data was excluded from the assessment process on Sept. 25.

The above rationale applies to Platts Iron Ore 58% Fe low Al CFR North China & TSI 58% Fe Fines, 1.5% Al, CFR Qingdao port, with the associated market data codes: IONC580; TS01047

Platts hard Coking Coal Premium low Vol CFr China daily rationaleSingapore—S&P Global Platts assessed Premium Low-Vol HCC up $2/mt on the day at $148.50/mt CFR China on Sept. 25.

The highest bid was indicated between $136-$137/mt CFR China for an Australian Premium Low Vol Saraji coal cargo assessed at parity to Platts PLV CFR China.

No data was excluded from the assessment.

The above rationale applies to Platts premium low vol CFR China assessment (PLVHC00) & TSI Prem JM25 CFR Jingtang (TS01044)

Platts hard Coking Coal Premium low Vol FOb Australia daily rationaleSingapore—S&P Global Platts assessed Premium Low-Vol HCC up $3.50/mt at $139/mt FOB Australia on Sept. 25.

The highest firm bid was heard at $138/mt FOB Australia for an 85,000-mt cargo of globalCOAL HCCLV Saraji, with October laycan, assessed at parity to Platts PLV FOB Australia.

A firm bid at $139/mt FOB Australia for an 85,000-mt cargo of globalCOAL HCCLV Saraji coal, with October laycan, was not considered for the Sept. 25 assessment process as it was reported to Platts after the Market On Close timestamp of 5:.30 pm Singapore time.

The above rationale applies to Platts premium low vol FOB Australia assessment, with the associated data code: PLVHA00

Platts emeA turkish Ferrous scrap daily rationaleLondon—S&P Global Platts assessed Turkish imports of premium heavy melting scrap 1/2 (80:20) at $295.50/mt CFR on Sept. 25, unchanged on the day.

Market sentiment was split, with one Turkish mill source citing a tradable value for premium HMS 1/2 (80:20) at $290-$295/mt CFR, and a trading

source citing the same level as workable for Baltic-origin material, while US sellers were still firm at $300/mt CFR.

A Turkish agent said $290/mt CFR maximum was possible for EU-origin HMS 1/2 (80:20), and $293-$294/mt CFR for US- or Baltic-origin material, should recyclers decide to sell.

A second Turkish agent cited a Baltic recycler target at $298-$299/mt CFR, while an EU trading source said $296-$298/mt CFR was workable for US- or Baltic-origin material. Another Turkish agent source said $297/mt CFR was workable for premium HMS 1/2 (80:20).

A UK trading source cited a near-term tradable value for premium material at closer to $300/mt CFR, while a US trader cited an offer for Venezuela-origin material at above $295/mt CFR, with US-origin material at $299-$300/mt CFR.

A Baltic-origin cargo booked on Sept. 23 by a Samsun mill, was heard late on Sept 24, with 12,000 mt HMS 1/2 (80:20), 10,000/mt shred, 1,000 mt bonus scrap, and 1,000 mt busheling scrap at a cargo average price of $299/mt. The deal was calculated at $295.50/mt CFR for HMS 1/2 (80:20), including a 50 cent adjustment to reflect freight to Samsun, in line with Platts methodology.

No data were excluded from the assessment.

The above rationale applies to Platts-TSI assessment of Turkish premium deep sea HMS 1/2 (80:20) imports, with the associated market data code: TS01011

us shredded scrap midwest daily rationalePittsburgh—The S&P Global Platts US shredded scrap index was calculated at $286/lt delivered Midwest Sept. 25, up $6.50 from Sept.18.

An Ohio Valley supplier indicated tradable value of up $10-$20/lt on obsolete grades from September pricing for October delivery in the Midwest. A Midwest supplier expected tradable value up $10-$20/lt on shredded scrap from September pricing for October delivery. Another Midwest supplier indicated tradable value up $10/lt on all grades from September pricing for October delivery, and a third Midwest supplier indicated tradable value for shredded scrap sideways from September pricing. Another Ohio Valley supplier indicated tradable value of up $10/lt from September pricing for October delivery in the Midwest. The above rationale applies to the daily Platts shredded scrap, delivered US Midwest index, with the associated market data code: FEMWD00.

mArketPlACe

Iron oretrade�■ Platts Iron Ore: 62.00% Fe Australian Jimblebar Fines trade reported done at Platts & Mysteel 62% Fe -$1.95/dmt CFR China 1-30 Nov Avg pricing on 25 Sep, on globalORE, sold by BHP, from Port Hedland delivery 1-30 Nov to Qingdao, 90,000 mt, traded at 3:45pm Singapore time.�■ Updated: Platts Iron Ore: 57.00% Fe Australian Yandi Fines trade reported done at Platts & Mysteel 62% Fe $1.80/dmt CFR China 1-30 Nov Avg pricing on 25 Sep, on COREX, sold by BHP, from Port Hedland delivery 1-30 Nov to Qingdao, 90,000 mt, traded at 3:51pm Singapore time.�■ Updated: Platts Iron Ore: 62.00% Fe Australian Pilbara Blend Fines trade reported done at IODEX 62% $4.30/dmt CFR China 1-30 Nov Avg pricing on 25 Sep, on COREX, sold by Rio Tinto, loading 28 Oct - 6 Nov from Dampier to Qingdao, 170,000 mt, trade concluded at 4:30pm Singapore time.�■ Platts Iron Ore: 62.00% Fe Australian Jimblebar Fines trade reported done at Platts & Mysteel 62% Fe -$1.70/dmt CFR China 1-30 Nov Avg