Sources of time-varying exchange rate exposure

76

Int Econ Econ Policy (2010) 7:371–390 DOI 10.1007/s10368-010-0147-y ORIGINAL PAPER Sources of time-varying exchange rate exposure Christian Pierdzioch · Renatas Kizys Published online: 9 March 2010 © Springer-Verlag 2010 Abstract We report evidence of a time-varying link between returns on national stock market indexes and exchange rate returns (exchange rate exposure). We use this evidence to analyze the sources of changes over time in exchange rate exposure. Using monthly data for 14 industrialized countries for the period 1975–2006, we report evidence of a cointegration relation between exchange rate exposure and the industry composition of a country’s imports, and weaker evidence of a cointegration relation between exchange rate exposure and openness to trade. Keywords Stock market returns · Exchange rate exposure · Time-varying parameter model · Cointegration analysis JEL Classifications F31 · F37 · G15 1 Introduction Exchange rate exposure, defined as the link between stock market returns and exchange rate movements, summarizes how exchange rate movements C. Pierdzioch (B ) Department of Economics, Saarland University, P.O. Box 15 11 50, 66041, Saarbruecken, Germany e-mail: [email protected] R. Kizys Departamento de Economia, Instituto Tecnologico y de Estudios Superiores de Monterrey (ITESM), C.P. 64849, Monterrey, Nuevo Leon, Mexico e-mail: [email protected]

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of Sources of time-varying exchange rate exposure

Int Econ Econ Policy (2010) 7:371–390DOI 10.1007/s10368-010-0147-y

ORIGINAL PAPER

Sources of time-varying exchange rate exposure

Christian Pierdzioch · Renatas Kizys

Published online: 9 March 2010© Springer-Verlag 2010

Abstract We report evidence of a time-varying link between returns onnational stock market indexes and exchange rate returns (exchange rateexposure). We use this evidence to analyze the sources of changes over time inexchange rate exposure. Using monthly data for 14 industrialized countriesfor the period 1975–2006, we report evidence of a cointegration relationbetween exchange rate exposure and the industry composition of a country’simports, and weaker evidence of a cointegration relation between exchangerate exposure and openness to trade.

Keywords Stock market returns · Exchange rate exposure ·Time-varying parameter model · Cointegration analysis

JEL Classifications F31 · F37 · G15

1 Introduction

Exchange rate exposure, defined as the link between stock market returnsand exchange rate movements, summarizes how exchange rate movements

C. Pierdzioch (B)Department of Economics, Saarland University, P.O. Box 15 11 50, 66041,Saarbruecken, Germanye-mail: [email protected]

R. KizysDepartamento de Economia,Instituto Tecnologico y de Estudios Superiores de Monterrey (ITESM),C.P. 64849, Monterrey, Nuevo Leon, Mexicoe-mail: [email protected]

372 C. Pierdzioch, R. Kizys

affect the value of firms and the competitiveness of industries. Beginning withAdler and Dumas (1984), much substantial theoretical and empirical researchhas been done to trace out potential sources of exchange rate exposure. Ourresearch contributes to the literature that examines the sources of exchangerate exposure of national stock market indexes (Friberg and Nydahl 1999;Holmes and Magrebi 2002; Kizys and Pierdzioch 2007, to name just a few).

Our first contribution is that we estimated a time-varying parameter modelto trace out how exchange rate exposure has changed over time. Our empiricalmodel measures the link between national stock market returns, the returnson a world stock market index, and exchange rate movements. Keeping withthe standard in the asset pricing literature, we studied monthly data. Ourestimation results, derived using data for 14 industrialized countries for theperiod 1970–2006, indicate that exchange rate exposure substantially changedover time. While exchange rate exposure also showed substantial variationacross countries, when averaged over our cross-section of countries, recurrentupward drifts in exchange rate exposure become visible that lasted untilaround 1995. Thereafter, exchange rate exposure stabilized.

Our second contribution is that we studied the sources of time-varyingexchange rate exposure. First, tests for cointegration revealed that exchangerate exposure, in many of the countries in our sample, shares a commonstochastic trend with the industry composition of imports. We measured theindustry composition of imports in terms of the ratio of the value of importsfrom non-oil exporting countries to imports from oil exporting countries. Wefound that an increase in this ratio brought about a long-run increase inexchange rate exposure. Second, confirming results reported by Friberg andNydahl (1999), we found that exchange rate exposure and a country’s opennessto international trade are correlated. Tests for cointegration, however, do notprovide strong support for a cointegration relation between exchange rateexposure and a country’s openness to trade.

Our third contribution is that we studied the temporal stability of thecointegration relations between exchange rate exposure and its sources. Giventhat our sample period covers the period of time since the introduction ofthe euro in 1999 and, thereby, extends the sample period studied in earlierresearch by Friberg and Nydahl (1999), a detailed analysis of the temporalstability of the cointegration relations is warranted. Because the exact timingof potential changes in the cointegration relations is unknown as marketparticipants may have anticipated the effects of the introduction of the eurolong before 1999, we used a rolling-window-estimation approach to analyzechanges over time in the cointegration relations. We found evidence that thesignificance of the cointegration relations indeed changed over time, whereevidence of cointegration between exchange rate exposure and the industrycomposition of imports is stronger than evidence of cointegration betweenexchange rate exposure and openness to trade.

Exchange rate exposure of national stock markets could be linked toexchange rate pass-through (Friberg and Nydahl 1999; Bodnar et al. 2002).A large body of empirical literature has emerged in which the prevalence, the

Sources of time-varying exchange rate exposure 373

variation over time and the determinants of exchange rate pass-through havebeen analyzed (Yang 1997; Campa and Goldberg 2005; Marazzi and Sheets2007; Sekine 2006). Exchange rate pass-through defines the degree to whichexchange rate movements transmit into goods prices. Limited exchange ratepass-through implies limited price responses in importing countries in the wakeof exchange rate movements. Friberg and Nydahl (1999) have pointed out thatlimited exchange rate pass-through should give rise to a positive correlationbetween exchange rate exposure and a country’s openness to trade. We set upa stylized model based on Floden et al. (2008) to illustrate this argument. Themodel also illustrates the link between the industry composition of imports,exchange rate exposure, and exchange rate pass-through. The model furtherillustrates that the industry composition of imports is likely to be an importantdeterminant of the broad shift towards a larger exchange rate exposure thatwe document for our cross-section of countries.

We organize our analysis as follows. In Section 2, we lay out the time-varyingparameter model we used to analyze the variation over time in exchange rateexposure, we describe our stock market and exchange rate data, and we reportour estimation results. In Section 3, we analyze the sources of exchange rateexposure by means of cointegration tests estimated on the full sample of data.In Section 4, we analyze the sources of exchange rate exposure by means ofrolling-window tests for cointegration. In Section 5, we lay out a stylized modelthat helps to explain why the industry composition of imports can explain time-variation in exchange rate exposure. In Section 6, we offer some concludingremarks.

2 Time-varying exchange rate exposure

We describe, in a first step, the time-varying parameter (TVP) model we usedto measure variation over time in exchange rate exposure. In a second step,we describe the data we used to estimate our TVP model. In a third step, wesummarize our estimation results.

2.1 A time-varying parameter model

We opted for a TVP model to analyze exchange rate exposure becauseempirical evidence suggests that exchange rate exposure has not been stableover time (Allayannis and Ihrig 2001; Williamson 2001). Our TVP model linksnational stock market returns, Ri,t, in country i, to the returns on a world stockmarket index, RW,t, and to exchange rate movements, �Si,t. Our TVP modelis given by the following two equations:

Ri,t = β0,i,t + β1,i,t RW,t + β2,i,t�Si,t + εi,t, (1)

β j,i,t = β j,i,t−1 + u j,i,t, (2)

374 C. Pierdzioch, R. Kizys

where j = 0, 1, 2 and t denotes a time index. The parameter β2,i,t measurestime-varying exchange rate exposure. The disturbance terms, εi,t and u j,i,t, aremutually uncorrelated and independently normally distributed.

The parameters, β j,i,t, have a time index and, thus, can change over time.The time-varying parameters follow a random walk without drift. The randomwalk provides a simple empirical model of the dynamic behavior of regressioncoefficients, is robust to misspecification, and contains constant coefficientsas a special case (Garbade 1977; Engle and Watson 1987). The random walkmodel has been applied in many recent studies to analyze the implications oftime-varying parameters for empirical research in finance (Kim et al. 2001;Kizys and Pierdzioch 2007).

The time-paths of the time-varying parameters can be estimated along withthe variances of the disturbance terms using the Kalman filter (Kim and Nelson2000). To this end, we transformed our TVP model into a state-space form andestimated the model using the maximum likelihood technique. For the sakeof brevity, technical details concerning the Kalman filter and the state-spaceform of the model are not reported, but are available from the authors uponrequest.

When using the Kalman filter to estimate exchange rate exposure, onecan either use filtered or smoothed estimates of the coefficients in orderto estimate exchange rate exposure. The difference between filtered andsmoothed estimates lies in the information set one uses to compute theseestimates. Filtered estimates refer to an estimate of the coefficients based oninformation available up to time t. In contrast, smoothed estimates refer toan estimate of the coefficients based on all available information in the entiresample. The results we report in this paper are based on the filtered estimates,which approximate the information set available to stock market investors inreal time. The results for the smoothed estimates are similar and are availableupon request.

In the context of our TVP model, the time-varying parameter, β2,i,t, mea-sures marginal exchange rate exposure. Marginal exchange rate exposurereflects the link between stock returns and exchange rate movements afterconditioning on movements of “the market” as defined in terms of the returnson the world stock market index. Thus, marginal exposure should reflectchanges in the present value of firms’ and industries’ cash flows causedby exchange rate movements after removing “macroeconomic effects” thattrigger correlated movements in both the world stock market index and theexchange rate.

We did not include potential sources of exchange rate exposure in our TVPmodel. Rather, we opted for a two-stage approach. The first stage consistsof estimation of our TVP model to trace out the variation of exchange rateexposure over time. The second stage consists of a cointegration analysisto trace out the sources of variation over time in exchange rate exposure(Sections 3 and 4). A two-stage approach yields the flexibility necessary toshed light on the economic determinants of exchange rate exposure fromdifferent angles. For example, the two-stage approach makes it easy to run a

Sources of time-varying exchange rate exposure 375

horserace between openness to trade and the industry composition of imports(Table 2). In addition, a two-step approach renders it possible to implementin a straightforward way rolling-window cointegration tests that shed light onpotential changes in cointegration relations over time.

2.2 Stock market and exchange rate data

In order to study time-variation in exchange rate exposure, we collected datafor the period from January 1970 to August 2006 for the following 14 industri-alized countries: Austria, Belgium, Denmark, Finland, France, Germany, Italy,Japan, the Netherlands, Norway, Sweden, Switzerland, the United Kingdom,and the United States. Our sample of countries is the same as the one studiedby Friberg and Nydahl (1999), making it easy to compare our results with theirresults.

In order to measure returns on a national stock market index, we down-loaded monthly MSCI stock market indexes from Thompson Financial Datas-tream and computed continuously compounded monthly returns. We usedthe MSCI index for the U.S. stock market as our proxy of the returns onthe world stock market index. In the case of the United States, we usedthe MSCI world market index excluding the U.S. to measure the returnson the world stock market index. We used national consumer-price indexes,retrieved from the IFS CD-ROM published by the IMF, to transform nominalreturns into real returns. Finally, we used the real effective exchange rateindex constructed and disseminated by the BIS (2006) to measure exchangerate movements. We transformed the BIS data such that an increase in theindex implies a depreciation of the exchange rate, whereas a decrease impliesan appreciation of the exchange rate. Results for nominal returns and nominaleffective exchange rates are similar to the results for real ones and are availablefrom the authors upon request.

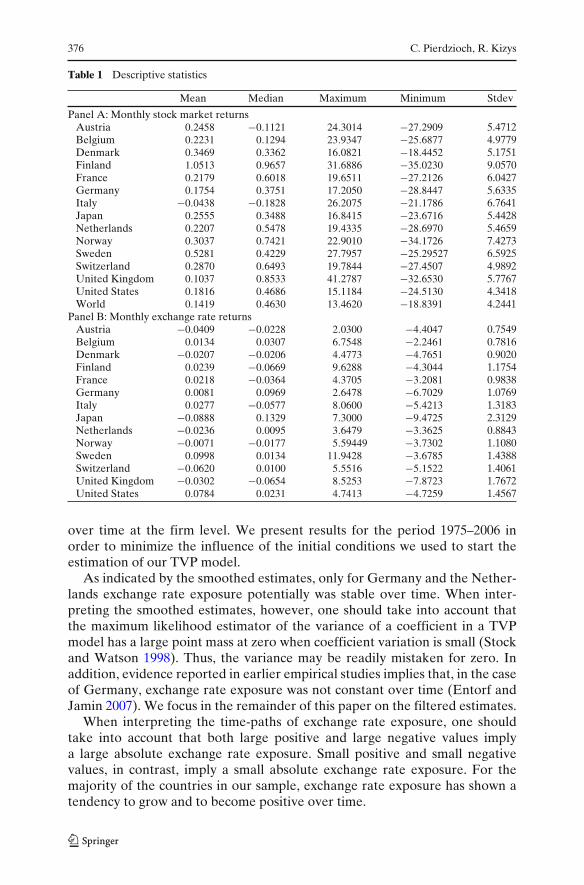

Table 1 summarizes descriptive statistics of monthly stock market returnsand exchange rate movements. Mean returns during our sample period werehighest in Finland and lowest in Italy (Panel A). Stock market returns showedthe highest standard deviation (Stdev) in Finland. As one would have ex-pected, investments in the world stock market portfolio were the least risky.The mean change in the real effective exchange rate (Panel B) was largest(smallest) in Sweden (Japan). Exchange rate movements showed the highest(lowest) standard deviation in the case of Japan (Austria).

2.3 Estimation results

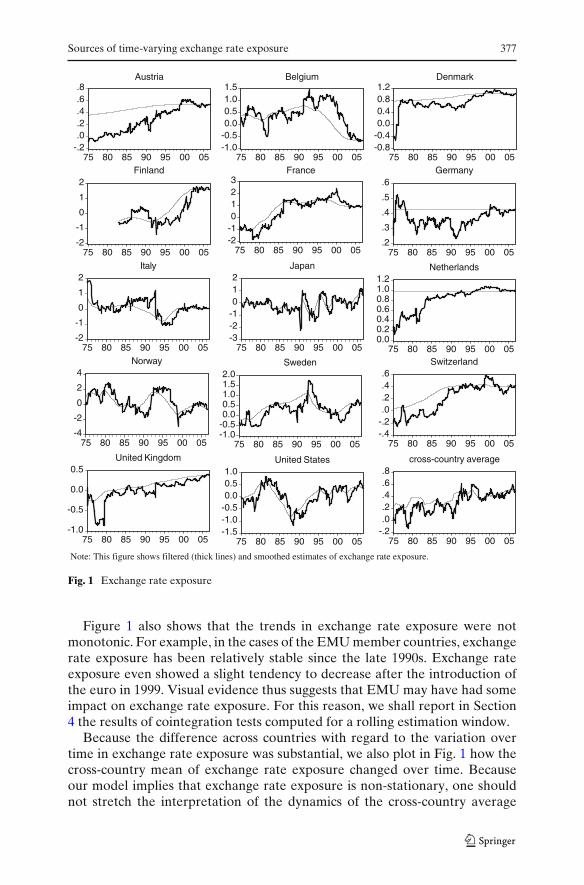

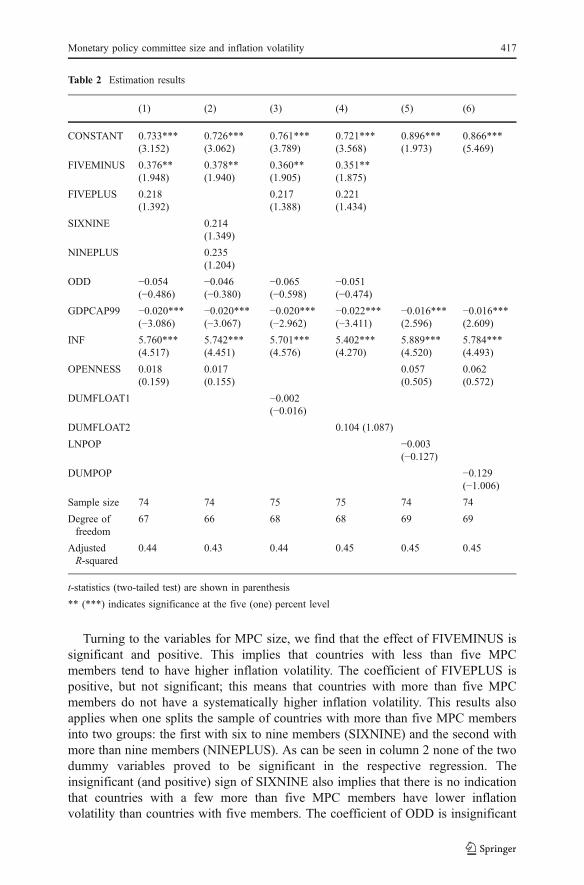

Figure 1 shows how exchange rate exposure changed over time. The resultthat exchange rate exposure changed over time is consistent with evidenceof time-variation in exchange rate exposure reported in the earlier literature(for example, Williamson 2001). Dominguez and Tesar (2006), however, haveargued, for a sample consisting of both OECD and developing countries, thatexchange rate exposure tends to be constant at the country level, and is varying

376 C. Pierdzioch, R. Kizys

Table 1 Descriptive statistics

Mean Median Maximum Minimum Stdev

Panel A: Monthly stock market returnsAustria 0.2458 −0.1121 24.3014 −27.2909 5.4712Belgium 0.2231 0.1294 23.9347 −25.6877 4.9779Denmark 0.3469 0.3362 16.0821 −18.4452 5.1751Finland 1.0513 0.9657 31.6886 −35.0230 9.0570France 0.2179 0.6018 19.6511 −27.2126 6.0427Germany 0.1754 0.3751 17.2050 −28.8447 5.6335Italy −0.0438 −0.1828 26.2075 −21.1786 6.7641Japan 0.2555 0.3488 16.8415 −23.6716 5.4428Netherlands 0.2207 0.5478 19.4335 −28.6970 5.4659Norway 0.3037 0.7421 22.9010 −34.1726 7.4273Sweden 0.5281 0.4229 27.7957 −25.29527 6.5925Switzerland 0.2870 0.6493 19.7844 −27.4507 4.9892United Kingdom 0.1037 0.8533 41.2787 −32.6530 5.7767United States 0.1816 0.4686 15.1184 −24.5130 4.3418World 0.1419 0.4630 13.4620 −18.8391 4.2441

Panel B: Monthly exchange rate returnsAustria −0.0409 −0.0228 2.0300 −4.4047 0.7549Belgium 0.0134 0.0307 6.7548 −2.2461 0.7816Denmark −0.0207 −0.0206 4.4773 −4.7651 0.9020Finland 0.0239 −0.0669 9.6288 −4.3044 1.1754France 0.0218 −0.0364 4.3705 −3.2081 0.9838Germany 0.0081 0.0969 2.6478 −6.7029 1.0769Italy 0.0277 −0.0577 8.0600 −5.4213 1.3183Japan −0.0888 0.1329 7.3000 −9.4725 2.3129Netherlands −0.0236 0.0095 3.6479 −3.3625 0.8843Norway −0.0071 −0.0177 5.59449 −3.7302 1.1080Sweden 0.0998 0.0134 11.9428 −3.6785 1.4388Switzerland −0.0620 0.0100 5.5516 −5.1522 1.4061United Kingdom −0.0302 −0.0654 8.5253 −7.8723 1.7672United States 0.0784 0.0231 4.7413 −4.7259 1.4567

over time at the firm level. We present results for the period 1975–2006 inorder to minimize the influence of the initial conditions we used to start theestimation of our TVP model.

As indicated by the smoothed estimates, only for Germany and the Nether-lands exchange rate exposure potentially was stable over time. When inter-preting the smoothed estimates, however, one should take into account thatthe maximum likelihood estimator of the variance of a coefficient in a TVPmodel has a large point mass at zero when coefficient variation is small (Stockand Watson 1998). Thus, the variance may be readily mistaken for zero. Inaddition, evidence reported in earlier empirical studies implies that, in the caseof Germany, exchange rate exposure was not constant over time (Entorf andJamin 2007). We focus in the remainder of this paper on the filtered estimates.

When interpreting the time-paths of exchange rate exposure, one shouldtake into account that both large positive and large negative values implya large absolute exchange rate exposure. Small positive and small negativevalues, in contrast, imply a small absolute exchange rate exposure. For themajority of the countries in our sample, exchange rate exposure has shown atendency to grow and to become positive over time.

Sources of time-varying exchange rate exposure 377

-.2.0.2.4.6.8

75 80 85 90 95 00 05

Austria

-1.0-0.50.00.51.01.5

75 80 85 90 95 00 05

Belgium

-0.8-0.40.00.40.81.2

75 80 85 90 95 00 05

Denmark

-2

-1

0

1

2

75 80 85 90 95 00 05

Finland

-2-10123

75 80 85 90 95 00 05

France

.2

.3

.4

.5

.6

75 80 85 90 95 00 05

Germany

-2

-1

0

1

2

75 80 85 90 95 00 05

Italy

-3-2-1012

75 80 85 90 95 00 05

Japan

0.00.20.40.60.81.01.2

75 80 85 90 95 00 05

Netherlands

-4

-2

0

2

4

75 80 85 90 95 00 05

Norway

-1.0-0.50.00.51.01.52.0

75 80 85 90 95 00 05

Sweden

-.4-.2.0.2.4.6

75 80 85 90 95 00 05

Switzerland

-1.0

-0.5

0.0

0.5

75 80 85 90 95 00 05

United Kingdom

-1.5-1.0-0.50.00.51.0

75 80 85 90 95 00 05

United States

-.2.0.2.4.6.8

75 80 85 90 95 00 05

cross-country average

Note: This figure shows filtered (thick lines) and smoothed estimates of exchange rate exposure.

Fig. 1 Exchange rate exposure

Figure 1 also shows that the trends in exchange rate exposure were notmonotonic. For example, in the cases of the EMU member countries, exchangerate exposure has been relatively stable since the late 1990s. Exchange rateexposure even showed a slight tendency to decrease after the introduction ofthe euro in 1999. Visual evidence thus suggests that EMU may have had someimpact on exchange rate exposure. For this reason, we shall report in Section4 the results of cointegration tests computed for a rolling estimation window.

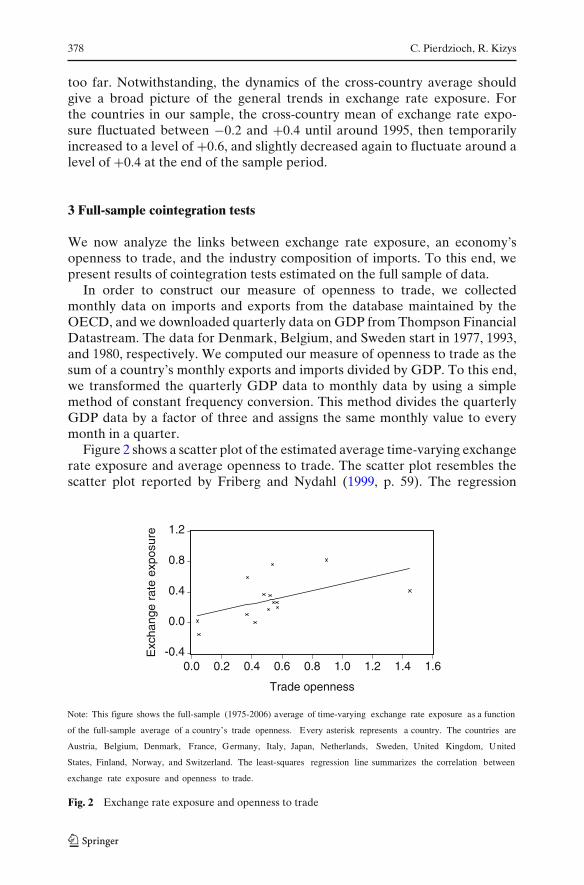

Because the difference across countries with regard to the variation overtime in exchange rate exposure was substantial, we also plot in Fig. 1 how thecross-country mean of exchange rate exposure changed over time. Becauseour model implies that exchange rate exposure is non-stationary, one shouldnot stretch the interpretation of the dynamics of the cross-country average

378 C. Pierdzioch, R. Kizys

too far. Notwithstanding, the dynamics of the cross-country average shouldgive a broad picture of the general trends in exchange rate exposure. Forthe countries in our sample, the cross-country mean of exchange rate expo-sure fluctuated between −0.2 and +0.4 until around 1995, then temporarilyincreased to a level of +0.6, and slightly decreased again to fluctuate around alevel of +0.4 at the end of the sample period.

3 Full-sample cointegration tests

We now analyze the links between exchange rate exposure, an economy’sopenness to trade, and the industry composition of imports. To this end, wepresent results of cointegration tests estimated on the full sample of data.

In order to construct our measure of openness to trade, we collectedmonthly data on imports and exports from the database maintained by theOECD, and we downloaded quarterly data on GDP from Thompson FinancialDatastream. The data for Denmark, Belgium, and Sweden start in 1977, 1993,and 1980, respectively. We computed our measure of openness to trade as thesum of a country’s monthly exports and imports divided by GDP. To this end,we transformed the quarterly GDP data to monthly data by using a simplemethod of constant frequency conversion. This method divides the quarterlyGDP data by a factor of three and assigns the same monthly value to everymonth in a quarter.

Figure 2 shows a scatter plot of the estimated average time-varying exchangerate exposure and average openness to trade. The scatter plot resembles thescatter plot reported by Friberg and Nydahl (1999, p. 59). The regression

-0.4

0.0

0.4

0.8

1.2

0.0 0.2 0.4 0.6 0.8 1.0 1.2 1.4 1.6

Trade openness

Exc

hang

e ra

te e

xpos

ure

Note: This figure shows the full-sample (1975-2006) average of time-varying exchange rate exposure as a function

of the full-sample average of a country’s trade openness. Every asterisk represents a country. The countries are

Austria, Belgium, Denmark, France, Germany, Italy, Japan, Netherlands, Sweden, United Kingdom, United

States, Finland, Norway, and Switzerland. The least-squares regression line summarizes the correlation between

exchange rate exposure and openness to trade.

Fig. 2 Exchange rate exposure and openness to trade

Sources of time-varying exchange rate exposure 379

line also shown in the scatter plot captures the positive correlation betweenexchange rate exposure and openness to trade. In the context of our empiricalmodel, however, a comparison of the full-sample averages of exchange rateexposure and openness to trade could be problematic. Our TVP model impliesthat exchange rate exposure follows a random walk and, by construction,has a stochastic trend. Similarly, because international trade has substantiallyincreased over time, it is not surprising that the results of unit root tests shownin panel A of Fig. 3 indicate that openness to trade also may feature a stochastictrend.

Imported inputs and the industry composition of imports may matter forexchange rate exposure (see, for example, Allayannis and Ihrig 2001). In orderto measure the industry composition of a country’s imports, we computed theratio of imports from non-oil exporting countries to imports from oil exportingcountries. The data on imports are from Thompson Financial Datastream.The data for Belgium start in 1997. The results of unit root tests suggest that,with few exceptions, the industry composition of imports may be integrated oforder one (panel B of Fig. 3). Because the industry composition of importsmay be integrated and thus may feature a stochastic trend, it is interestingto analyze whether time-varying exchange rate exposure shared the samestochastic trend.

In order to test for a common stochastic trend, we implemented Johansen’s(1988) approach to test for cointegration. For the sake of brevity, we report the

Panel A: Openness to trade

0.0

0.2

0.4

0.6

0.8

1.0

1 2 3 4 5 6 7 8 9 10 11 12 13 14

Panel A: Industry composition of imports

.0

.2

.4

.6

.8

1 2 3 4 5 6 7 8 9 10 11 12 13 14

Note: Panel A shows p-values of Augmented Dickey-Fuller (ADF) tests for a unit root in trade openness. Panel

B shows p-values of ADF tests for a unit root in the industry composition of imports. The numbers shown at the

horizontal axis represent the countries in our sample, where 1 = Austria, 2 = Belgium, 3 = Denmark, 4 = France,

5 = Germany, 6 = Italy, 7 = Japan, 8 = Netherlands, 9 = Sweden, 10 = United Kingdom, 11 = United States, 12 =

Finland, 13 = Norway, and 14 = Switzerland. We used data for the period 1975-2006 to implement the tests. The

solid (dashed) horizontal line denotes the 5 (10) percent level of significance.

Fig. 3 Unit-root tests

380 C. Pierdzioch, R. Kizys

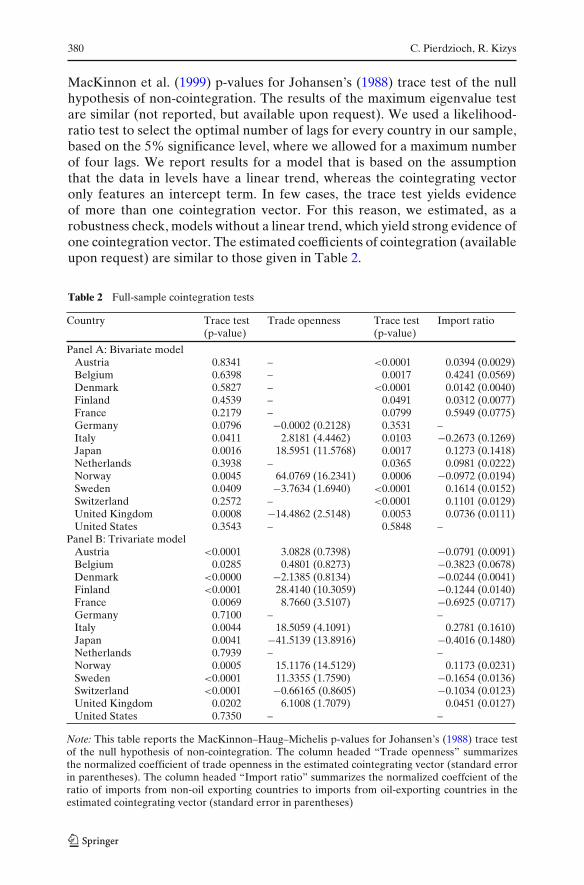

MacKinnon et al. (1999) p-values for Johansen’s (1988) trace test of the nullhypothesis of non-cointegration. The results of the maximum eigenvalue testare similar (not reported, but available upon request). We used a likelihood-ratio test to select the optimal number of lags for every country in our sample,based on the 5% significance level, where we allowed for a maximum numberof four lags. We report results for a model that is based on the assumptionthat the data in levels have a linear trend, whereas the cointegrating vectoronly features an intercept term. In few cases, the trace test yields evidenceof more than one cointegration vector. For this reason, we estimated, as arobustness check, models without a linear trend, which yield strong evidence ofone cointegration vector. The estimated coefficients of cointegration (availableupon request) are similar to those given in Table 2.

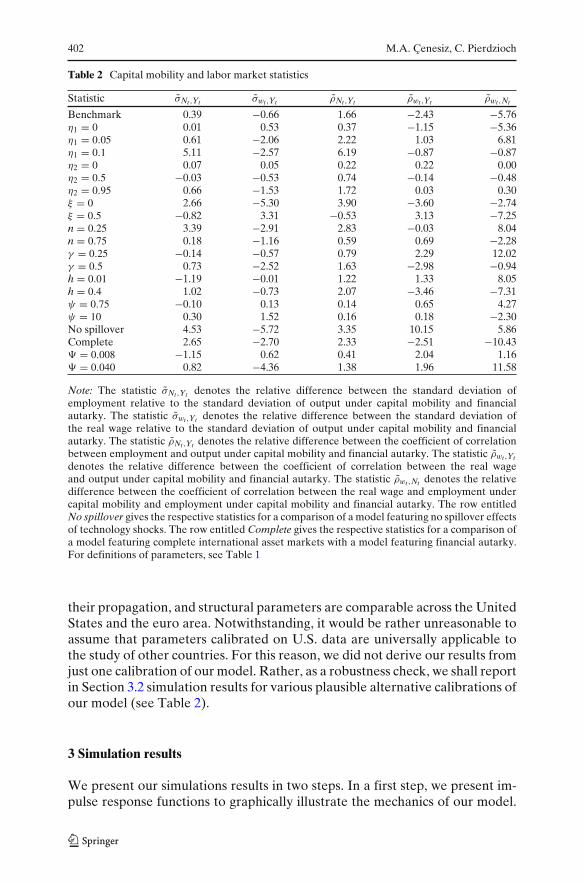

Table 2 Full-sample cointegration tests

Country Trace test Trade openness Trace test Import ratio(p-value) (p-value)

Panel A: Bivariate modelAustria 0.8341 – <0.0001 0.0394 (0.0029)Belgium 0.6398 – 0.0017 0.4241 (0.0569)Denmark 0.5827 – <0.0001 0.0142 (0.0040)Finland 0.4539 – 0.0491 0.0312 (0.0077)France 0.2179 – 0.0799 0.5949 (0.0775)Germany 0.0796 −0.0002 (0.2128) 0.3531 –Italy 0.0411 2.8181 (4.4462) 0.0103 −0.2673 (0.1269)Japan 0.0016 18.5951 (11.5768) 0.0017 0.1273 (0.1418)Netherlands 0.3938 – 0.0365 0.0981 (0.0222)Norway 0.0045 64.0769 (16.2341) 0.0006 −0.0972 (0.0194)Sweden 0.0409 −3.7634 (1.6940) <0.0001 0.1614 (0.0152)Switzerland 0.2572 – <0.0001 0.1101 (0.0129)United Kingdom 0.0008 −14.4862 (2.5148) 0.0053 0.0736 (0.0111)United States 0.3543 – 0.5848 –

Panel B: Trivariate modelAustria <0.0001 3.0828 (0.7398) −0.0791 (0.0091)Belgium 0.0285 0.4801 (0.8273) −0.3823 (0.0678)Denmark <0.0000 −2.1385 (0.8134) −0.0244 (0.0041)Finland <0.0001 28.4140 (10.3059) −0.1244 (0.0140)France 0.0069 8.7660 (3.5107) −0.6925 (0.0717)Germany 0.7100 – –Italy 0.0044 18.5059 (4.1091) 0.2781 (0.1610)Japan 0.0041 −41.5139 (13.8916) −0.4016 (0.1480)Netherlands 0.7939 – –Norway 0.0005 15.1176 (14.5129) 0.1173 (0.0231)Sweden <0.0001 11.3355 (1.7590) −0.1654 (0.0136)Switzerland <0.0001 −0.66165 (0.8605) −0.1034 (0.0123)United Kingdom 0.0202 6.1008 (1.7079) 0.0451 (0.0127)United States 0.7350 – –

Note: This table reports the MacKinnon–Haug–Michelis p-values for Johansen’s (1988) trace testof the null hypothesis of non-cointegration. The column headed “Trade openness” summarizesthe normalized coefficient of trade openness in the estimated cointegrating vector (standard errorin parentheses). The column headed “Import ratio” summarizes the normalized coeffcient of theratio of imports from non-oil exporting countries to imports from oil-exporting countries in theestimated cointegrating vector (standard error in parentheses)

Sources of time-varying exchange rate exposure 381

The results summarized in Table 2 indicate that, in a bivariate model,there is strong evidence of cointegration between exchange rate exposure andthe industry composition of imports. In contrast, evidence of cointegrationbetween exchange rate exposure and openness to trade is weak. The resultsfor a trivariate model indicate that, for the majority of countries, there is acommon stochastic trend among exchange rate exposure, openness to trade,and the industry composition of imports. Germany, the Netherlands, andthe United States are exceptions. For some countries, Johansen’s trace testindicates cointegration between trade openness and the industry compositionof imports (results not reported).

The coefficient that captures the effect of the industry composition ofimports on exchange rate exposure is positive in the majority of countries. Itfollows that an increase in the ratio of imports from non-oil exporting countriesto imports from oil-exporting countries led to a long-run increase in exchangerate exposure. Given the positive correlation between average time-varyingexchange rate exposure and openness to trade reported in Fig. 2, it is somewhatunexpected in economic terms that the coefficient of openness to trade often isnegative in the trivariate model. A negative coefficient implies that an increasein a country’s openness to trade in many cases led to a decrease in long-runexchange rate exposure. A negative coefficient, however, is consistent with theview that exchange rate exposure is linked to imported input factors and, morespecifically, the industry structure of imports rather than to openness to tradeper se.

4 Rolling-window cointegration tests

Because the cointegration relations between exchange rate exposure and itssources may have changed over time, we implemented rolling-window tests forcointegration. We used bivariate models to estimate the cointegration relationbetween exchange rate exposure and openness to trade and between exchangerate exposure and the industry composition of imports. We excluded Belgiumand Finland from the analysis because data start relatively late in the sampleperiod.

We used a rolling estimation window of length 10 years to compute Jo-hansen’s trace eigenvalue test for cointegration. Concerning the number oflags in the error correction model, we varied the number of lags between oneand four and selected, in every estimation, the lag length based on a likelihoodratio test. In order to assess the statistical significance of our results, we formedthe ratio of the trace eigenvalue statistic to the respective 95% critical value. Ifthe ratio exceeds one, the null hypothesis of non-cointegration can be rejected.

The cointegration analysis in Section 3 yielded the result that in the longrun the industry composition of imports may be a more important source ofchanges over time in exchange rate exposure than a country’s openness totrade. The results of the rolling-window cointegration tests summarized inFigs. 4 and 5 corroborate this result. In the case of the industry composition

382 C. Pierdzioch, R. Kizys

0.0

0.4

0.8

1.2

1.6

1985 1990 1995 2000 2005

Austria

0.0

0.5

1.0

1.5

2.0

2.5

1985 1990 1995 2000 2005

Denmark

0.0

0.5

1.0

1.5

2.0

2.5

1985 1990 1995 2000 2005

France

0.4

0.8

1.2

1.6

2.0

2.4

1985 1990 1995 2000 2005

Germany

0

1

2

3

4

1985 1990 1995 2000 2005

Italy

0.0

0.5

1.0

1.5

2.0

2.5

1985 1990 1995 2000 2005

Japan

0.0

0.5

1.0

1.5

2.0

2.5

1985 1990 1995 2000 2005

Netherlands

0.0

0.5

1.0

1.5

2.0

2.5

1985 1990 1995 2000 2005

Norway

0

1

2

3

4

5

1985 1990 1995 2000 2005

Sweden

0.0

0.4

0.8

1.2

1.6

2.0

1985 1990 1995 2000 2005

Switzerland

0

1

2

3

4

5

1985 1990 1995 2000 2005

United Kingdom

0.0

0.4

0.8

1.2

1.6

2.0

1985 1990 1995 2000 2005

United States

Note: The tests for cointegration are based on models that feature exchange rate exposure and openness to

trade. The rolling estimation window has a length of ten years. This figure summarizes results for Johansen’s

trace eigenvalue statistic scaled by its critical value (thick line). Whenever the scaled statistic exceeds unity, the

null hypothesis of non-cointegration is rejected.

Fig. 4 Rolling-window cointegration tests (openness to trade)

of imports, the trace eigenvalue test clearly exceeds its critical value in themajority of cases. The only clear-cut exception is Germany. In contrast, thetrace eigenvalue test is often smaller than its critical value in the case ofopenness to trade. The evidence of cointegration between exchange rateexposure and openness to trade is strongest for Denmark, Norway, Sweden,and the United Kingdom. In the cases of the other countries in our sample, thetrace eigenvalue test only becomes significant occasionally.

It is interesting to note that the introduction of the euro in 1999 did not leadto a discernible change in the cointegration relation between exchange rateexposure of EMU member countries and the industry composition of imports.In contrast, cointegration between exchange rate exposure and opennessto trade temporarily peaked after the introduction of the euro, but lost insignificance again at the very end of the sample period.

5 An illustrative model

In order to illustrate why openness to trade and the industry compositionof imports may matter for exchange rate exposure, we consider a stylized

Sources of time-varying exchange rate exposure 383

0

5

10

15

20

1985 1990 1995 2000 2005

Austria

0

2

4

6

8

1985 1990 1995 2000 2005

Denmark

0.0

0.5

1.0

1.5

2.0

1985 1990 1995 2000 2005

France

0.0

0.4

0.8

1.2

1.6

1985 1990 1995 2000 2005

Germany

0

1

2

3

4

1985 1990 1995 2000 2005

Italy

0.0

0.5

1.0

1.5

2.0

1985 1990 1995 2000 2005

Japan

0

1

2

3

4

1985 1990 1995 2000 2005

Netherlands

0

1

2

3

4

1985 1990 1995 2000 2005

Norway

0

2

4

6

8

10

1985 1990 1995 2000 2005

Sweden

0.5

1.0

1.5

2.0

2.5

3.0

1985 1990 1995 2000 2005

Switzerland

0

1

2

3

4

5

1985 1990 1995 2000 2005

United Kingdom

0.0

0.4

0.8

1.2

1.6

1985 1990 1995 2000 2005

United States

Note: The tests for cointegration are based on models that feature exchange rate exposure and the industry

composition of imports. The rolling estimation window has a length of ten years. This figure summarizes results

for Johansen’s trace eigenvalue statistic scaled by its critical value (thick line). Whenever the scaled statistic

exceeds unity, the null hypothesis of non-cointegration is rejected.

Fig. 5 Rolling-window cointegration tests (industry composition of imports)

monopolistic-competition model based on Floden et al. (2008). For a oligopolyversion of the model, see Bodnar et al. (2002). We consider a model thatdeliberately leaves many aspects important for the study of exchange rateexposure unexplored, but it illustrates the theoretical foundation of our mainresults. We then move on to study the effect of large multinational firms onexchange rate exposure. Finally, we consider the effect of the introduction ofthe euro on exchange rate exposure.

5.1 The model

The model features a firm that sells a good at home and abroad at prices pand p∗, where foreign sales account for a proportion 0 ≤ α ≤ 1 of total sales.The firm combines domestic and imported raw materials for producing thegood, where the proportion of domestic raw materials used in production isgiven by 0 ≤ μ ≤ 1. The price of foreign raw materials is denominated in termsof foreign currency. We assume that both the price of domestic inputs andthe foreign currency price of foreign raw materials are constant and scaled toassume the value unity. When q (q∗) denotes the quantity of the good sold at

384 C. Pierdzioch, R. Kizys

home (abroad) and S denotes the exchange rate (the price of a unit of foreigncurrency in terms of units of domestic currency), the profits, �, of the firm canbe written as

� = αSp∗q∗ + (1 − α)pq − [μ + S(1 − μ)][αq∗ + (1 − α)q] (3)

The firm operates under monopolistic competition, where the demand curveat home is q = (p)

− 11−ρ , where 0 < ρ < 1. The demand curve abroad is given

by q∗ = (p∗)−1

1−ρ .A firm that uses imported raw materials for producing its good and sells this

good only in the home market (α = 0), maximizes profits by setting the priceof its good to p = μ+S(1−μ)

ρ. Upon defining exchange rate pass-through for this

firm as ηp,S = ∂p∂S

Sp , it follows

ηp,S ={

1, if μ = 00, if μ = 1

. (4)

In the first of the considered two polar cases, the importing firm only usesimported raw materials as input factors. In the second polar case, the firm usesno imported raw materials as input factors. It follows that, for an importingfirm, exchange rate pass-through decreases as the importance of imported rawmaterials as input factors decreases.

Upon defining exchange rate exposure for the importing firm as η�,S =∂�∂S

S�

, standard calculations show that

η�,S ={

− ρ

1−ρ, if μ = 0

0, if μ = 1. (5)

In words, exchange rate exposure decreases in absolute value if the proportionof imported raw materials decreases.

Similarly, the profit-maximizing price for an exporting firm that sells all itsgood abroad (α = 1) is given by p∗ = μ+S(1−μ)

ρS . Upon defining exchange rate

pass-through for this exporting firm as ηp∗,S = − ∂p∗∂S

Sp∗ , it follows

ηp∗,S ={

0, if μ = 01, if μ = 1

. (6)

Exchange rate exposure for an exporting firm is given by

η�,S ={

1, if μ = 01

1−ρ, if μ = 1

. (7)

Sources of time-varying exchange rate exposure 385

In the case of an exporting firm acting under monopolistic competition,exchange rate pass-through and exchange rate exposure increase as the pro-portion of imported raw materials decreases.

Because a national stock market index comprises both importing andexporting firms, the model shows that, when one neglects imported rawmaterials, a country’s trade openness should have a positive effect on exchangerate exposure (Friberg and Nydahl 1999). As μ approaches unity, the exchangerate exposure of the exporting firm clearly is larger than the exchange rateexposure of the importing firm.

When the proportion of imported raw materials decreases, exchange rateexposure of the importing firm decreases (in absolute terms) and exchangerate exposure of the exporting firm increases. Because the price of oil isdenominated in terms of dollars, exchange rate exposure should increase andbecome more positive at the aggregate level as the industry composition ofimports shifts from imports from oil-exporting countries to imports from non-oil-exporting countries. In line with the largely positive signs of the estimatedcointegration coefficients summarized in Table 2, Fig. 6 illustrates that this isexactly what may have happened in our cross-section of countries.

The model further illustrates that changes in the industry composition ofimports should result in changes in exchange rate pass-through. Exchangerate pass-through should decrease for importing firms and it should increasefor exporting firms. Because the industry composition of imports also causesvariation over time in exchange rate exposure, changes in exchange ratepass-through and changes in exchange rate exposure may have a commonsource.

In fact, Campa and Goldberg (2005) have argued that the degree of ex-change rate pass-through crucially depends on the industry composition of acountry’s imports. Specifically, a shift from imports with a large pass-throughelasticity (such as energy) to imports with a small pass-through elasticity

-.2

.0

.2

.4

.6

.8

0

4

8

12

16

20

1975 1980 1985 1990 1995 2000 2005

Exchange rate exposureIndustry composition of imports

Note: This figure shows exchange rate exposure (left axis) and the import composition of imports (right axis).

Fig. 6 Exchange rate exposure versus industry composition of imports

386 C. Pierdzioch, R. Kizys

(such as manufacturing) should result in a decrease of exchange rate pass-through into import prices. Using data for 25 OECD countries, Campa andGoldberg (2005) have found that an increase in the ratio of imports from non-oil exporting countries to imports from oil exporting countries indeed loweredthe degree of exchange rate pass-through into import prices.

Our stock-market-based evidence of a cointegration relation between theindustry composition of imports and exchange rate exposure, thus, lendssupport to the result reported by Campa and Goldberg (2005) that the industrycomposition of a country’s imports is an important determinant of exchangerate pass-through. Moreover, because changes in exchange rate pass-throughand changes in exchange rate exposure may have a common source, thenon-monotonic variation over time in exchange rate exposure documented inSection 2.3 may explain why some authors have reported that exchange ratepass-through has declined in the past decade (Marazzi and Sheets 2007), whileother authors have reported mixed evidence of such a decline (Campa andGoldberg 2005).

Finally, we only mention very briefly that evidence of time-varying ex-change rate pass-through is important for macroeconomic modeling. Recentresearch on micro-founded dynamic general equilibrium modeling showsthat the welfare effects of, for example, monetary policy in open economiescrucially depend on the degree of exchange rate pass-through (Betts andDevereux 2000). The fact that our stock-market-based evidence of time-varying exchange rate exposure can be linked to time-varying exchange ratepass-through, thus, may provide insights useful for macroeconomic modelingof open economies.

5.2 Large multinational firms

Yet another aspect that is worth mentioning is that large multinational firmsaccount for a considerable weight in MSCI stock market indexes, which weused to calculate stock returns for our sample of countries. Multinational firmsmay account for a substantial proportion of total stock market capitalizationin small countries. The model shows that large multinational firms withproduction facilities abroad may have a substantial effect on exchange rateexposure. In terms of the model, multinational firms with production facilitiesabroad may fall into the category of a firm with revenues and costs mainlydenominated in terms of foreign currency (α = 1, μ = 0).

The growing importance of multinational firms may, thus, account for thestabilization of average exchange rate exposure in the second half of the 1990s.On the one hand side, an ongoing shift away from imported raw materialsmay have caused exchange rate exposure to increase. On the other hand,the growing importance of multinational firms may have countered the effectof this shift on exchange rate exposure because, when cast in terms of themodel, the exchange rate exposure of multinational firms with production

Sources of time-varying exchange rate exposure 387

facilities abroad may be more appropriately described by the case α = 1, μ = 0,η�,S = 1 than by the case α = 1, μ = 1, η�,S = 1

1−ρ.

As regards empirical evidence concerning exchange rate exposure of multi-national firms, the results of recent research by Williamson (2001) suggestthat exchange rate exposure of automotive firms from the United Statesand Japan changed over time, and that exchange rate exposure is positivelylinked to the ratio of foreign sales to total sales. Gao (2000) has found thata depreciation of the dollar has a significant positive effect on the returnsof stocks of U.S. multinational firms through foreign sales, and a significantnegative effect through foreign production. Crabb (2002) has documentedevidence that some previous findings of insignificant exchange rate exposure ofU.S. multinational firms may be due in part to hedging activities undertaken bythese firms. As for Japan, He and Ng (1998) have argued that highly leveragedJapanese multinational firms tend to have smaller exchange rate exposure, buta firm’s foreign involvement is positively linked to the degree of exchangeexposure.

5.3 The introduction of the euro

The model can be used to illustrate the implications of the introduction of theeuro for exchange rate exposure. As concerns the eurozone, the introductionof the euro should have reduced exchange rate exposure stemming from intra-eurozone trade. In terms of the model, firms that are involved mainly in intra-eurozone trade may be described in terms of an importing firm that sells itsgood in the euro area, but that still imports raw materials. A comparison ofEqs. 5 and 7 then shows that, for a given openness to trade and a given industrycomposition of imports, the introduction of the euro should have led to areduction in exchange rate exposure. It follows that the introduction of theeuro in 1999 may also help to explain, at least with respect to EMU membercountries, why average exchange rate exposure stabilized in the second half ofthe 1990s.

The introduction of the euro also may explain in part why we found onlyweak evidence of a common stochastic trend of exchange rate exposure andopenness to trade. Only an extra-eurozone measure of openness to tradeshould matter for exchange rate exposure of the eurozone countries (Hutsonand O’Driscoll 2009). However, the introduction of the euro does not explainwhy our rolling-window cointegration tests often yield insignificant results inthe case of openness to trade even before the introduction of the euro. In anycase, the introduction of the euro reinforces our main result that the industrycomposition of imports should be a more important source of exchange rateexposure than openness to trade.

Available empirical evidence suggests that the introduction of the euro hashad a significant effect on exchange rate exposure in EMU member countries.For example, Bartram and Karolyi (2006) have reported that the introductionof the euro led to a reduction in exchange rate exposure of euro-area firms and

388 C. Pierdzioch, R. Kizys

of non-euro firms with a high proportion of foreign sales or assets in Europe.Furthermore, they have found that exchange rate exposure of firms withpositive (negative) exchange rate exposure decreased (increased) after theintroduction of the euro. In another empirical study, Hutson and O’Driscoll(2009) have found that the introduction of the euro was followed by an increasein firm-specific exchange-rate exposure. Hutson and O’Driscoll (2009) havealso reported that the introduction of the euro was followed by a reduction inmarket-level exchange rate exposure.

6 Concluding remarks

We have reported evidence of time-varying exchange rate exposure sharing acommon stochastic trend with the industry composition of a country’s imports.Evidence of a common stochastic trend of exchange rate exposure with acountry’s openness to trade, in contrast, is weaker than in the case of theindustry composition of imports. We have also implemented rolling-windowcointegration tests to account for changes in cointegration relations over timethat were caused, for example, by the introduction of the euro. While tradeopenness has received considerable attention as a potential source of exchangerate exposure in the earlier empirical literature (Friberg and Nydahl 1999;Hutson and O’Driscoll 2009), the role played by the industry composition ofimports has received less attention in the empirical literature (see, for example,Allayannis and Ihrig 2001 for the US). Our evidence sheds some light on thevariation over time in exchange rate exposure, and on the sources of thisvariation, but more research needs to be done to better understand time-variation of exchange rate exposure.

First, the evidence we have reported mainly describes the sources of long-run trends in exchange rate exposure. A natural challenge is to identifyfactors that help to explain the variation in exchange rate exposure over shorthorizons. Second, we have assumed that the link between stock market returnsand exchange rate movements is linear. Because some authors have studiednonlinearities in exchange rate exposure (Holmes and Magrebi 2002; Kizys andPierdzioch 2007), it is interesting to complement our analysis in future researchby taking into account such nonlinearities. Third, we have been concernedwith the variation over time in the exchange rate exposure of national stockmarket indexes. In future research, one could extend our analysis to the levelof individual industries or individual firms. Such an analysis may have thepotential to link the research on exchange rate exposure with the micro-oriented research on the determinants of exchange rate pass-through. Fourth,apart from the industry composition of imports, another potentially importanteconomic determinant of exchange rate exposure is the well-known “balance-sheet effect”. In case of a depreciation, firms balance-sheets deteriorate incase firms debt is denominated in terms of foreign currency. While beyondthe scope of this paper, it would be interesting to study in future research thebalance-sheet effect in more detail.

Sources of time-varying exchange rate exposure 389

Acknowledgements Part of this paper was written during a visit of Renatas Kizys at SaarlandUniversity. The hospitality of Saarland University is gratefully acknowledged. We thank threeanonymous referees for helpful comments. We also thank participants of a seminar at theFraunhofer-Institut für Techno- und Wirtschaftsmathematik, Kaiserslautern, for helpful com-ments. The usual disclaimer applies.

References

Adler M, Dumas B (1984) Exposure to currency risk: definition and measurement. Financ Manage3:41–50

Allayannis G, Ihrig J (2001) Exposure and markups. Rev Financ Stud 14(3):805–835Bartram SM, Karolyi GA (2006) The impact of the introduction of the Euro on foreign exchange

rate risk exposures. J Empir Finance 13:519–549Betts C, Devereux MB (2000) Exchange rate dynamics in a model of pricing-to-market. J Int Econ

50:215–244BIS (2006) BIS effective exchange rate indices. Data available from the internet page of the BIS

at http://www.bis.org/statistics/eer/index.htmBodnar GM, Dumas B, Marston RC (2002) Pass-through and exposure. J Finance 57:199–231Campa J, Goldberg L (2005) Exchange rate pass-through into import prices. Rev Econ Stat

87:679–690Crabb, PC (2002) Multinational corporations and hedging exchange rate exposure. Int Rev Econ

Finance 11:299–314Dominguez KME, Tesar LL (2006) Exchange rate exposure. J Int Econ 68:188–218Engle RF, Watson M (1987) Kalman filter: applications to forecasting and rational-expectation

models. In: Bewley T (ed) Advances in econometrics, fifth world congress. Cambridge Uni-versity Press, Cambridge

Entorf H, Jamin G (2007) German exchange rate exposure at DAT and aggregate levels, interna-tional trade and the role of exchange rate adjustment costs. Ger Econ Rev 8:344–374

Floden M, Simbanegavi W, Wilander, W (2008) When Is a lower exchange Rate pass-throughassociated with greater exchange rate exposure? J Int Money Finance 27:124–139

Friberg R, Nydahl S (1999) Openness and the exchange rate exposure of national stock markets.Int J Financ Econ 4:55–62

Gao, T (2000) Exchange rate movements and the profitability of U.S. multinationals. J Int MoneyFinance 19:117–134

Garbade K (1977) Two methods for examining the stability of regression coefficients. J Am StatAssoc 72:54–63

He J, Ng LK (1998) The foreign exchange exposure of Japanese multinational corporations. JFinance 53:733–753

Holmes MJ, Magrebi N (2002) Non-linearities, regime switching, and the relationship betweenAsian equity and foreign exchange markets. Int Econ J 16:121–139

Hutson E, O’Driscoll A (2009) Firm-level exchange rate exposure in the Eurozone. Int Bus Rev(in press)

Johansen S (1988) Statistical analysis of cointegration vectors. J Econ Dyn Control 12:231–254Kim CJ, Nelson CR (2000) State-space models with regime switching. MIT, CambridgeKim CJ, Morley MC, Nelson CR (2001) Does an intertemporal tradeoff between risk and return

explain mean reversion in stock prices? J Empir Finance 8:403–426Kizys R, Pierdzioch C (2007) Time-varying nonlinear exchange rate exposure. Applied Financial

Economics Letters 3:385–389Marazzi M, Sheets N (2007) Declining exchange rate pass-through to U.S. import prices: the

potential role of global factors. J Int Money Finance 26:924–947MacKinnon JG, Haug AA, Michelis L (1999) Numerical distribution functions of likelihood ratio

tests for cointegration. J Appl Econ 14:563–577Sekine T (2006) Time-varying exchange rate pass-through: experiences of some industrialized

countries. BIS working papers 202. Bank for International Settlements, Basel

390 C. Pierdzioch, R. Kizys

Stock JH, Watson MW (1998) Median unbiased estimation of coefficient variance in a time-varying parameter model. J Am Stat Assoc 93:349–358

Williamson R (2001) Exchange rate exposure and competition: evidence from the automotiveindustry. J Financ Econ 59:441–475

Yang J (1997) Exchange rate pass-through into U.S. manufacturing industries. Rev Econ Stat79:95–104

Int Econ Econ Policy (2010) 7:391–409DOI 10.1007/s10368-010-0146-z

ORIGINAL PAPER

Capital mobility and labor market volatility

M. Alper Çenesiz · Christian Pierdzioch

Published online: 12 February 2010© Springer-Verlag 2010

Abstract We used a dynamic two-country optimizing model featuringefficiency wages to analyze the implications of capital mobility for labor mar-ket volatility. Capital mobility magnifies the short-run effects of productivityshocks and monetary shocks on employment and the real wage, but dampensthe medium-run effects. The overall effects of capital mobility on the volatilityand the cyclical properties of employment and the real wage are moderate.

Keywords Capital mobility · Efficiency wages · Labor market volatility

JEL Classification E44 · F36 · F41

1 Introduction

A question widely discussed among academics and politicians is whether theincrease in capital mobility that has taken place since the mid-1980s has givenrise to more labor market volatility and job uncertainty (Scheve and Slaughter2004). This question is of central importance because the burden of adjustmentthat labor has to bear in the wake of macroeconomic fluctuations shouldincrease when capital is internationally highly mobile while labor is not. Inconsequence, the recent increases in capital mobility may have resulted in an

M. A. Çenesiz (B)FEP, CEF.UP, University of Porto, R. Roberto Frias, 4200-464 Porto, Portugale-mail: [email protected]

C. PierdziochDepartment of Economics, Saarland University, P.O. Box 15 11 50,66041, Saarbruecken, Germanye-mail: [email protected]

392 M.A. Çenesiz, C. Pierdzioch

asymmetric distribution of the benefits and losses from globalization amongmobile capital and immobile labor. Inflexibilities and frictions in labor marketsthat are beleaguered by structural unemployment have the power to reinforcethis asymmetric distribution of the benefits and losses from globalization. Inconsequence, the potentially complex interaction of capital mobility and labormarket frictions is likely to be one key determinant of the extent to whichpeople are willing to accept the economic and social changes brought about bythe globalization of the world’s economy.

We used a dynamic general equilibrium model to analyze whether and, if so,to which extent capital mobility increases labor market volatility. Our dynamicgeneral equilibrium model builds on the two-country general equilibriummodels developed by Obstfeld and Rogoff (1995) and Betts and Devereux(2000, 2001), which have become the prototype models for analyzing macro-economic dynamics in open economies. Their models feature a Walrasianlabor market in which wages adjust rapidly, households are always on theirlabor supply schedule, and structural unemployment is absent. To accountfor the stylized facts of real-world labor markets, we developed an extendedmodel that features a non-Walrasian labor market. Our extended model canexplain important stylized facts of labor markets like the existence of structuralunemployment, the moderate procyclical dynamics of real wages, the lowcorrelation between real wages and employment, and the high volatility ofemployment relative to that of real wages.

In order to model a non-Walrasian labor market, we extended our dynamicgeneral equilibrium model to incorporate efficiency wages. The analysis ofthe implications of efficiency wages for the properties of dynamic generalequilibrium models has a long tradition in macroeconomic research (Danthineand Donaldson 1990). Our approach to introduce efficiency wages into ourdynamic general equilibrium model builds on the recent contributions ofCollard and de la Croix (2000) and Danthine and Kurmann (2004). Theyextend dynamic general equilibrium models to incorporate the so-called “giftexchange” efficiency-wage theory that traces back to the work of Akerlof(1982). The “gift exchange” efficiency-wage theory stipulates that workersdislike effort. Workers are willing to provide effort beyond some referencelevel of effort (the gift of workers) if they feel that their firm treats them well.Firms, in turn, seek to motivate workers by offering a wage above the market-clearing wage (the gift of the firm). The optimizing behavior of workers andfirms results in structural unemployment.

We found that, in a model featuring efficiency wages, capital mobilitymagnifies the response of employment and the real wage in the immediate af-termath of productivity shocks and monetary shocks. At the same time capitalmobility dampens the medium run effects of productivity shocks and monetaryshocks on employment and the real wage. As a result, the overall effect ofcapital mobility on the volatility of employment and the real wage, and on theircyclical properties, is moderate. Our results regarding the effects of capital

Capital mobility and labor market volatility 393

mobility on the volatilities of key macroeconomic variables is reminiscent of afamous result derived by Cole and Obstfeld (1991), who show that allocationsin an endowment economy may be identical under complete markets andfinancial autarky.

Much significant research has been done in recent years to explore the linkbetween financial openness and macroeconomic volatility. Razin and Rose(1994), who study common and country-specific shocks as well as transitoryand persistent shocks in a large panel of countries, find no clear linkagebetween measures of goods and capital mobility and volatility (Page 71). Theyattribute their result to the prevalence of shocks that are common acrosscountries (Page 73). Using a search-theoretic model, Aziarides and Pissarides(2007) report that capital mobility may result in a substantial increase in labormarket volatility. Buch and Pierdzioch (2005) and Buch et al. (2005) reportthat the link between capital mobility and macroeconomic volatility in OECDcountries has changed over time and may depend on the nature of shockshitting an economy. Similarly, Kose et al. (2003) find that capital mobility maybe associated with an increase in the ratio of consumption volatility to incomevolatility, but that this effect turns negative if the volume of gross capitalflows crosses a particular threshold. Recent empirical evidence, thus, showsthat capital mobility need not necessarily increase macroeconomic volatility.This result is consistent with the observation that in the United States andother Western countries business-cycle volatility and employment volatilityhave tended to decrease since the mid 1980s (Stock and Watson 2002; Carlinoet al. 2003).

We organize the remainder of this paper as follows. In Section 2, we layout the dynamic general equilibrium model we used to derive our results. Thebasic structure of our model resembles the structures of the models developedby Obstfeld and Rogoff (1995) and Betts and Devereux (2000, 2001), so thatour discussion can be relatively brief. In Section 3, we report the results ofnumerical simulations of our model. In Section 4, we offer some concludingremarks.

2 The model

The world consists of two countries. Both countries are populated by a con-tinuum of infinitely lived households. Households form rational expectations.Domestic and foreign households have identical preferences. Households areinternationally immobile. Households own the firms of the country in whichthey reside. Firms sell the differentiated goods they produce in a monopolisti-cally competitive goods market. Some firms set the prices of their goods in thecurrency of the country in which they reside. Other firms set the prices of theirgoods in the currency of their customers. We call the latter a pricing-to-market

394 M.A. Çenesiz, C. Pierdzioch

(PTM) firms (Betts and Devereux 2000, 2001). In addition to households andfirms, every country is populated by a government.

2.1 Households’ preferences

Each household consists of a large number of household members of totalmeasure unity. Some members of households are unemployed, while the oth-ers are employed. Following Alexopoulos (2004) and Danthine and Kurmann(2004), employment is randomly allocated across workers. The proportion ofunemployed household members is the same across households. Householdsmake all intertemporal decisions, and redistribute consumption equally amongtheir members. Each household inelastically supplies one unit of time for work.At the household level, fluctuations in employment can, thus, be interpretedas fluctuations in hours worked. Each household has preferences definedover consumption, real balances, and effort. The expected discounted lifetimeutility of a representative household is given by

E0

∞∑

t=0

β t

⎡

⎣log(C jt − X j

t ) + χ

1 − σ

(M j

t

Pt

)1−σ

− N jt G(e j

t )

⎤

⎦ , (1)

with j being a household index and 0 < β < 1, χ > 0, and σ > 0. Et denotesthe conditional expectations operator, Nt denotes the proportion of householdmembers working, G(et) denotes the disutility of effort, Mt/Pt denotes realmoney holdings, and Ct denotes a real consumption index. This consumption

index, Ct =[∫ 1

0 ct(z)θ−1θ dz

] θθ−1

, is defined as a constant elasticity of substitutionindex of differentiated goods, ct(z), z ∈ [0, 1], where the elasticity of substi-tution is given by θ > 1 . The consumer price index, Pt, is defined as theminimum expenditure required to buy one unit of Ct. The consumer priceindex is defined as

Pt =[∫ n

0pt(z)1−θdz +

∫ n+(1−n)ξ

nqt(z∗)1−θdz +

∫ 1

n+(1−n)ξ

(St p∗(z∗)1−θdz] 1

1−θ

,

(2)

where n ∈ (0, 1) denotes the size of the domestic country, pt(z) denotes thedomestic currency price of a domestically produced good, qt(z∗) denotes thedomestic currency price of a foreign PTM good, St denotes the nominalexchange rate, and p∗

t (z∗) denotes the foreign currency price of a foreign non-

PTM good. The parameter ξ denotes the proportion of PTM firms.Households do not only derive utility from consuming the consumption

index, C jt , but also derive disutility from the variable X j

t . This variable capturesa “catching-up with the Joneses” effect in households’ preferences and isdefined as

X jt = hCA

t−1, (3)

Capital mobility and labor market volatility 395

where 0 < h < 1, and CAt = denotes aggregate (per capita) consumption. An

increase in the level of aggregate consumption results in a decrease in thelevel of utility a household attains, and in an increase in the marginal utilitya household derives from consumption, implying that households try to “catchup with the Joneses”.

The disutility a household derives from effort is determined by an effortfunction, G(e j

t ). Four considerations matter for the specification of the effortfunction (Collard and de la Croix 2000; Danthine and Kurmann 2004). First,if a firm pays a higher real wage, households are motivated and work harder.For this reason, their reference level of effort is an increasing function of theindividual households’ current real wage, w

jt . Second, if the aggregate level

of employment is high, households realize that they can easily find a newemployment opportunity in case they lose their job. Hence, the reference levelof effort is a decreasing function of the aggregate level of employment, Nt.Third, if the real wage received by a household does not change when theaggregate real wage increases, individual households’ relative compensationdecreases. Because households perceive this to be unfair, they decrease thelevel of effort they provide. This implies that the reference level of effort isa decreasing function of the aggregate real wage, wt. Fourth, if householdsobserve changes in real wages from one period to the next, they adjust theirreference level of effort. This captures the empirical finding reported byBewley (1998) that changes in wages rather than wage levels are an importantdeterminant of effort. Accordingly, the reference level of effort is a decreasingfunction of an individual households’ past wage, w

jt−1. Assuming that the

past wage affects effort resolves the problem documented by Danthine andDonaldson (1990) that effort functions which only feature contemporaneousvariables do not give rise to rigid and sluggish equilibrium wage dynamics (seealso Danthine and Kurmann 2004). Taken together, these four considerationsimply that the effort function is of the format

G(e jt ) =

[e j

t −(φ0 + φ1 log w

jt + φ2 ln Nt + φ3 log wt + φ4 log w

jt−1

)]2, (4)

where φ1 > 1, φ2 < 0, φ3 < 0, and φ4 < 0.

2.2 Budget constraint and first-order conditions

Households maximize their expected discounted lifetime utility subject totheir budget constraint. According to households’ budget constraint, the totalincome received by households consists of the yield on their holdings inbonds, the profit income yielded by their ownership of domestic firms, theirlabor income, and their income from renting capital to domestic firms. Giventheir total income, households determine their optimal consumption, effort,investment, and next period’s capital stock. Households also decide on their

396 M.A. Çenesiz, C. Pierdzioch

preferred holdings in domestic money and bonds. The individual households’budget constraint is given by

D jt = Rt−1 D j

t−1 + M jt−1 + w

jt N j

t Pt + Rkt k j

t Pt

−PtCjt − Pt I

jt − Pt AC j

t + �t + PtTt, (5)

where Dt denotes the quantity of domestic nominal riskless one-period bonds,Rt denotes the gross nominal interest rate on bonds, Rk

t denotes the realrental rate of capital, Tt denotes real lump-sum transfers received from thegovernment, It denotes real investment, ACt is the real adjustment costhouseholds incur when adjusting their capital stock, and �t denotes the profitincome the household receives from domestic firms. The law of motion ofhouseholds’ capital stock, k j

t , is given by

I jt = k j

t+1 − (1 − δ)k jt , (6)

where 0 < δ < 1 denotes the depreciation rate. The investment good, I jt , is

constructed in the same way as the consumption index, C jt . The adjustment

cost households incur when adjusting their capital stock are given by

AC jt = ψ

2(k j

t+1 − k jt )

2

k jt

, (7)

where ψ ≥ 0.The first-order conditions that describe the solution to an individual house-

holds’ utility-maximization problem are given by

C jt − X j

t = λt Pt, (8)

χ

(M j

t

Pt

)−σ

= λt Pt − β Pt Etλt+1, (9)

λt = β Rt Etλt+1, (10)

e jt = φ0 + φ1 log w

jt + φ2 ln Nt + φ3 log wt + φ4 log w

jt−1, (11)

λt Pt + β(1 − δ)Etλt+1 Pt+1 + βEt Rkt+1λt+1 Pt+1 − ψλt Pt

k jt+1 − k j

t

k jt

+ ψ

2βEtλt+1 Pt+1

(k jt+2)

2 − (k jt+1)

2

(k jt+1)

2= 0 (12)

where λt denotes the Lagrange multiplier on the households’ budget con-straint.

Capital mobility and labor market volatility 397

2.3 Financial markets

As regards the structure of international financial markets, we consideredtwo polar cases. First, we considered the case of a world economy in whichagents can trade in integrated financial markets for riskless one-period nom-inal bonds. For simplicity, we assume that domestic households invest ina home-currency denominated nominal bond, and that foreign householdsinvest in a foreign-currency denominated nominal bond and a home-currencydenominated nominal bond. This assumption implies that, in the case of anintegrated international bond market, the condition of uncovered interest-rate parity holds. Second, we considered the case of a world economy inwhich markets for trade in international assets do not exist (Cole and Obstfeld1991; Heathcote and Perri 2002). In this case, home households invest in ahome-currency denominated nominal bond, and foreign households invest ina foreign-currency denominated nominal bond. The market-clearing conditionfor the home-currency denominated nominal bond in the case of an integratedinternational bond market is given by

∫

jD j

t d j +∫

jD j∗

t d j = 0 (13)

and the market-clearing conditions in the case of financial autarky are givenby

∫

jD j

t d j = 0 (14)

and∫

jF j∗

t d j = 0 (15)

where F j∗t denotes the foreign-currency denominated bond.

2.4 Firms

Each firm consists of a production and a price-setting unit. The production unitproduces the good, z, according to the production function

yt(z) = Atkt(z)α[et(z)Nt(z)]1−α, (16)

where At denotes an aggregate productivity shock. Given the level of effortprovided by households, the production unit determines the real wage andchooses the level of capital and employment in order to minimize totalproduction costs. Following Danthine and Kurmann (2004), we assume thatthe production unit replaces the individual households’ past wage, w

jt−1, with

the aggregate past wage wt−1 in the effort function when minimizing totalproduction costs. Because firms treat wt−1 as exogenous when minimizing

398 M.A. Çenesiz, C. Pierdzioch

total production costs, they do not account for the consequences of offeringa higher wage today for the future effort of households. In technical terms,this assumption implies that the production unit solves a static wage-settingproblem. Hence, the production unit does not have to store informationon the distribution of past wages of its employees. In economic terms, thisassumption implies that, in a symmetric equilibrium, all firms will pay identicalwages. Using wt−1 in the effort function, the first-order conditions for the cost-minimization problem are given by

wt(z) = (1 − α)mct(z)yt(z)

nt(z), (17)

nt(z) = (1 − α)mct(z)φ1 yt(z)

et(z)wt(z), (18)

Rkt (z) = αmct(z)

yt(z)

kt(z), (19)

where mct(z) denotes real marginal costs. The first-order conditions implyet(z) = φ1, a condition known as the Solow (1979) condition.

Because of monopolistic competition in the goods market, the price-settingunit can set the price of the good produced by the production unit in order tomaximize profits. We let q∗

t (z) denote the foreign-currency price of a domesticPTM good, and yD

t (z) and yFt (z) denote the demand at home and abroad. The

demand functions are given by

yDt (z) = (pt(z)/Pt)

−θ Qt, (20)

yFt (z) = (

q∗t (z)/P∗

t

)−θQ∗

t , (21)

Qt = n(Ct + It + ACt) and Q∗t = (1 − n)(C∗

t + I∗t + AC∗

t ). The price-settingunit sets the price of the good subject to a discrete time version of the price-setting mechanism developed by Calvo (1983). With probability 0 < γ < 1, theprice-setting unit cannot revise the price of its good in any given period oftime. Therefore, the price-setting unit of a PTM firm sets the current domestic-currency and foreign-currency prices of the product, pt(z) and q∗

t (z), so as tomaximize the expected discounted present value of profits. The solutions tothis maximization problem are

pt(z) = θ

θ − 1Et

∑∞s=t γ

s−t Rt,s(Qs/P−θs )mcs

Et∑∞

s=t γs−t Rt,s(Qs/P1−θ

s ), (22)

q∗t (z) = θ

θ − 1Et

∑∞s=t γ

s−t Rt,s(Q∗s /P∗−θ

s )mcs

Et∑∞

s=t γs−t Rt,s(Q∗

s /P∗−θs )Ss/Ps

, (23)

Capital mobility and labor market volatility 399

where Rt,s ≡ ∏tj=s R−1

t is the market discount factor. Similar expressions canbe derived for the profit-maximizing prices, qt(z∗) and p∗

t (z∗), set by the price-

setting unit of a foreign PTM firm, and for the profit-maximizing price setby the price-setting unit of a non-PTM firm. The latter set a single domesticcurrency denominated price for both the domestic and the foreign goodsmarket.

2.5 The government sector

The government sector consists of a single central bank and a fiscal authority.The central bank controls the money supply. The budget constraint of the fiscalauthority is given by

PtTt = Mt − Mt−1. (24)

2.6 Solution and calibration of the model

We log-linearized our model around a symmetric flexible-price steady state inwhich bond holdings in the domestic and foreign country are zero. We thensimulated the calibrated model using the algorithm developed by McCallum(1998, 2001) and Klein (2000). The calibrated parameter values are summa-rized in Table 1.

We calibrated the model to match quarterly data. We assumed that thedomestic and foreign countries are of equal size (n = 0.5). With regard tohouseholds’ preferences, we assumed β = 0.99, implying an annual real in-terest rate of approximately 4.1%. We followed Sutherland (1996) and Senay(1998) in assuming σ = 9, an assumption consistent with the calibration usedby Hairault and Portier (1993). As regards the parameter that captures the“catching-up with the Joneses” effect in households’ preferences, we used thenumerical values used by Ljungqvist and Uhlig (2000) and set h = 0.8. Thiscalibration of the parameter h is consistent with the estimates reported byFuhrer (2000) for U.S. data. Smets and Wouters (2005) report a somewhat

Table 1 Calibratedparameters

Country size: n = 0.5Discount factor: β = 1.041−1/4

Semi elasticity of money demand: σ = 9Degree of habit formation: h = 0.8Demand elasticity: θ = 11Depreciation rate: δ = 0.024Capital share: α = 0.36Reset probability: 1 − γ = 0.25Capital adjustment costs: ψ = 21.5Proportion of PTM firms: ξ = 0.95Elasticity of real wage w.r.t.

a) Employment: η1 ≡ −φ2/(φ1 + φ3)=0.03b) Past real wage: η2 ≡ −φ4/(φ1 + φ3)=0.99

Risk premium: � = 0.004

400 M.A. Çenesiz, C. Pierdzioch

lower parameter of h = 0.59 for the euro area and h = 0.69 for U.S. data.In Section 3.2 we, therefore, shall report results for alternative calibrationsof the parameter that captures the “catching-up with the Joneses” effect inhouseholds’ preferences.

With regard to the elasticity of substitution between differentiated goods,we assumed θ = 11, which is common in the literature. The value we chosefor θ implies a steady-state markup of prices over marginal costs of 10%. Asregards the depreciation rate, we assumed δ = 0.024, implying an annual de-preciation rate of 10%. The capital share parameter in the production functionassumes the value α = 0.36. We calibrated the Calvo-pricing parameter suchthat the average delay between price adjustments is four periods (γ = 0.75),a value roughly the same as the one in Danthine and Kurmann (2004). Weresorted to the empirical estimates that have recently been reported by Bergin(2006) to calibrate the adjustment costs households’ incur when adjustingtheir capital stock. Accordingly, we assumed ψ = 21.5. Following again Bergin(2006), we assumed that the proportion of firms that follow a PTM price-setting strategy is relatively large. We set ξ = 0.95.

In order to calibrate the parameters of the effort function, we first derivedthe efficiency-wage function. The efficiency-wage function obtains when theSolow condition, et = φ1, is used in the effort function. Apart from a constant,the efficiency-wage function, in a symmetric equilibrium, is given by

log wt = η1 log Nt + η2 log wt−1, (25)

where η1 = −φ2/(φ1 + φ3) and η2 = −φ4/(φ1 + φ3). Danthine and Kurmann(2004) report the estimates η1 = 0.0348 and η2 = 0.9912 for the United States.Given significant cross-country differences with regard to labor-market in-stitutions and labor-market rigidities, it is interesting to ask whether thiscalibration is also valid when one studies, for example, a European or Asiancountry. In order to explore this question, we collected quarterly data fromthe International Financial Statistics CD-ROM published by the IMF onemployment, wages, and the GDP deflator for Germany and Japan. Using datafor the sample period 1991:1−2004:4 and applying the two-stage least squaresestimation technique described in detail by Danthine and Kurmann (2004),we estimated the parameters, η1 and η2, of the efficiency-wage function. ForGermany, we found η1 = 0.05 and η2 = 0.75. For Japan, we estimated η2 =0.02 and η2 = 0.90. As one would have expected, the estimation results suggestthat, with regard to labor-market related variables, there are in fact interestingdifferences between Germany and Japan, on the one hand side, and the UnitedStates, on the other hand side. Because the parameters of the efficiency-wage function are key parameters of our model, we shall present in Section 3simulation results that we obtained when we used alternative numerical valuesfor the parameters of the efficiency-wage function to calibrate our model.

Capital mobility and labor market volatility 401