Sources of Innovation and Ideas in ICT Firms in Australia

13

© 2006 The Authors Journal compilation © 2006 Blackwell Publishing 182 CREATIVITY AND INNOVATION MANAGEMENT Volume 15 Number 2 2006 doi:10.1111/j.1467-8691.2006.00378.x Sources of Innovation and Ideas in ICT Firms in Australia Paul W. Hyland, Jane Marceau and Terry R. Sloan This paper examines a sample of Information and Communication Technology (ICT) firms in Australia drawn from a wide range of product and service providers in the Sydney region. It researches the sources of information and ideas that firms utilize to sustain their competitive position through innovation. While the firms in the survey varied in size in terms of turnover, number of employees and level of business activity, most see themselves as innovative. Not all firms utilized the same sources of innovation-related knowledge and most used research and technology organizations (RTOs) or other publicly funded sources of information for help with ‘technical’ (standards etc) or trade issues. While ICT firms are often regarded as leading- edge developers of new ideas, this research indicated that ICT firms still see their sales force, customers and suppliers as the most important sources of innovation knowledge and ideas. Introduction ost observers think of the ICT sector as one that most characterizes the ‘new’ economy and one that lives off successfully innovating new products and services. Most organizations and sectors are part of, or are aligned with, the information sector or infor- mation economy in the sense that IT plays a major part in their operational activities. The study of ICT firms reported here was part of a larger project examining the growth of research and technology organizations (RTOs) in Australia, and the utilization and funding of these organizations by local firms. This article examines the innovation trajectories of a small sample of ICT firms that are producing new products and services for the Australian market, with a view to examining the nature of the innovation processes undertaken and the sources of innovation-related information used by these ‘hi tech’ companies to gain their innovation ideas and related knowledge. We also examine their use of publicly funded innovation services. In this examination we consider the firms use of exploitative and explorative trajectories to acquire innovative ideas and information. In the main, firms seek ideas for new products from customers, com- petitors, and in a few cases, research bodies such as universities. Sources of information that can lead to exploitative new products M include government authorities, universities, technical colleges, industry bodies and RTOs. For example, in 2005 the Australian Meat and Livestock Association (MLA) set up a mandatory system for tagging cattle using radio frequency identification (RFID) tags. The introduction of this RFID system has the potential to produce a demand for new prod- ucts for farmers wishing to maximize the ben- efits of the tracking and tagging system. This mandatory system was announced in 2004, so ICT companies could use that information in their new product development planning. Government policies in Australia and Europe are increasingly encouraging businesses to work with RTOs and universities to tap into the knowledge, skills and expertise resident in these organizations. Moreover, governments not only want industry to tap into and use the expertise that exists in these publicly funded institutions, they also want industry to pay for the expertise and to provide a commercial focus for research carried out in the RTOs. Where this policy focus has been successful, RTOs can be seen as having moved to a ’hybrid’ position, part public and part private, both in orientation and in funding sources, compared with the homogeneous and sepa- rate modes of public and private operation that prevailed in previous periods of public administration and funding. RTO perfor- mance measures, such as the only recently

-

Upload

westernsydney -

Category

Documents

-

view

0 -

download

0

Transcript of Sources of Innovation and Ideas in ICT Firms in Australia

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing

182

CREATIVITY AND INNOVATION MANAGEMENT

Volume 15 Number 2 2006

doi:10.1111/j.1467-8691.2006.00378.x

Sources of Innovation and Ideas in ICT Firms in Australia

Paul W. Hyland, Jane Marceau and Terry R. Sloan

This paper examines a sample of Information and Communication Technology (ICT) firms inAustralia drawn from a wide range of product and service providers in the Sydney region. Itresearches the sources of information and ideas that firms utilize to sustain their competitiveposition through innovation. While the firms in the survey varied in size in terms of turnover,number of employees and level of business activity, most see themselves as innovative. Notall firms utilized the same sources of innovation-related knowledge and most used researchand technology organizations (RTOs) or other publicly funded sources of information for helpwith ‘technical’ (standards etc) or trade issues. While ICT firms are often regarded as leading-edge developers of new ideas, this research indicated that ICT firms still see their sales force,customers and suppliers as the most important sources of innovation knowledge and ideas.

Introduction

ost observers think of the ICT sector asone that most characterizes the ‘new’

economy and one that lives off successfullyinnovating new products and services. Mostorganizations and sectors are part of, or arealigned with, the information sector or infor-mation economy in the sense that IT plays amajor part in their operational activities. Thestudy of ICT firms reported here was partof a larger project examining the growth ofresearch and technology organizations (RTOs)in Australia, and the utilization and funding ofthese organizations by local firms. This articleexamines the innovation trajectories of a smallsample of ICT firms that are producing newproducts and services for the Australianmarket, with a view to examining the natureof the innovation processes undertaken andthe sources of innovation-related informationused by these ‘hi tech’ companies to gain theirinnovation ideas and related knowledge. Wealso examine their use of publicly fundedinnovation services. In this examination weconsider the firms use of exploitative andexplorative trajectories to acquire innovativeideas and information. In the main, firms seekideas for new products from customers, com-petitors, and in a few cases, research bodiessuch as universities. Sources of informationthat can lead to exploitative new products

M

include government authorities, universities,technical colleges, industry bodies and RTOs.For example, in 2005 the Australian Meatand Livestock Association (MLA) set up amandatory system for tagging cattle usingradio frequency identification (RFID) tags. Theintroduction of this RFID system has thepotential to produce a demand for new prod-ucts for farmers wishing to maximize the ben-efits of the tracking and tagging system. Thismandatory system was announced in 2004, soICT companies could use that information intheir new product development planning.Government policies in Australia and Europeare increasingly encouraging businesses towork with RTOs and universities to tap intothe knowledge, skills and expertise resident inthese organizations. Moreover, governmentsnot only want industry to tap into and use theexpertise that exists in these publicly fundedinstitutions, they also want industry to pay forthe expertise and to provide a commercialfocus for research carried out in the RTOs.

Where this policy focus has been successful,RTOs can be seen as having moved to a’hybrid’ position, part public and part private,both in orientation and in funding sources,compared with the homogeneous and sepa-rate modes of public and private operationthat prevailed in previous periods of publicadministration and funding. RTO perfor-mance measures, such as the only recently

INNOVATION AND IDEAS IN AUSTRALIAN ICT FIRMS

183

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing

Volume 15 Number 2 2006

modified requirement for CSIRO (Australia’speak science research organization) to gen-erate 30 percent of its revenue externally,increasingly require them to trade in servicesand generate revenue and commercial valuein addition to their traditional output activ-ities such as educating professionals andpublishing research results in the scientificand professional literature. Innovation-relatedknowledge is thus now widely available in thelocal areas in which most ICT and other firmsoperate. The question remains however: areICT firms utilizing and accessing this expertiseand putting money into these hybrid RTOs, orare they using more market-focused and inparticular more client-focused sources?

In deciding on innovation trajectories firmscan explore new technologies or radically newideas for products that are high risk, if success-ful are high return, can have uncertain andwidespread effects on existing products andhave a high uncertainty of market acceptance.Such a trajectory would mean that a firm hasthe capacity and capabilities needed to searchfor and identify new technologies or ideasthat can be potentially commercialized. Whilemany firms set out on an exploratory trajec-tory, many fail for a variety of reasons, includ-ing lack of capital and poor commercializationcapabilities. Firms on an exploratory trajectorywould be expected to be scanning for ideas ina network that includes RTOs and universityresearch centres as well as start-ups, and usingtheir own R&D staff for highly speculativeresearch. The other innovation trajectory is anexploitative trajectory in which firms seek toexploit existing skills and technologies tomaintain or improve their competitive posi-tion in the market. An exploitative trajectory isrelatively low risk, and the products devel-oped can provide good short-term returns andhave a fairly certain acceptance and outcomein the market. In exploratory trajectories firmsare more likely to working with customers andsuppliers in their supply chain and scanningcompetitors ideas rather than looking for rad-ical ideas. Firms set on an exploitative trajec-tory will be maintaining an existing networkthat includes supply-chain partners, industryassociations, government bodies and stan-dards associations. They will use their net-work to gain short-term market advantagesover competitors rather than seeking high risklong-term advantages through radical ideas.Many firms attempt to maintain both anexploratory and an exploitative trajectory sothat they can ensure both long and short-termreturns and maintain primacy in the market,but as March (1991) points out, it is difficult tobalance exploration and exploitation in anorganizational setting.

Innovation and Sources of Ideas

Product/service, process or organizationalinnovation is widely recognized as a cumula-tive process that includes idea generation, ideaevaluation and product development, andmethods for best implementing new ideas.Idea generation is critical to new productdevelopment (Troy, Szymanski & Varadarajan,2001), although the majority of ideas gener-ated often turn out not to make sense in com-mercial terms (see e.g. Stasch, Lonsdale &LaVenka, 1992). The development of a new orinnovative product is expensive and its suc-cess is uncertain, even if the idea is perceivedas ‘good’.

In an attempt to improve the success of theprocess from new idea generation to commer-cialization, in order to reduce market failures,firms are continually seeking new sources ofideas and advice. In recent years research andtechnology organizations (RTOs) and univer-sities have been encouraged to become sourcesof commercial ideas and knowledge for busi-nesses seeking to commercialize innovations.Not all universities and RTOs have beenequally successful in these endeavours,however.

University researchers are often regarded ascentres of excellence in exploring and deli-vering new knowledge, which may result innew concepts and product ideas (Logar et al.,2001). From a public-sector perspective, work-ing with firms enables academics to developalliances with the private sector to commer-cialize research outputs, while private-sectororganizations can align themselves with aca-demic institutions using the research outputsof these organizations to enhance new productdevelopment. This mutual interest offers pri-vate-sector organizations a potentially signifi-cant avenue of new product ideas (Logar et al.,2001). Firms that scan academic research maycome across ideas for new products, or thefindings of the research can stimulate newideas that are then sold to firms (Peterson,1988). The potential role of the public sector asa source of product exploratory ideas andinnovations is often overlooked in practice,however, even by ‘science-intensive’ firms thatare exploratory in their product performance.

Not all innovations involve completely newproducts or services and many innovationsemerge from the need for the extension of aproduct line or from an existing product fam-ily. The stakes are too high in today’s corporateworld for companies to depend on a stagnantproduct line so the exploitation of line exten-sion concepts need new ideas. Major sourcesinclude user input and feedback on existingproducts, scanning competitors’ product

184

CREATIVITY AND INNOVATION MANAGEMENT

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing

Volume 15 Number 2 2006

strategies and emerging consumer trends.The ongoing search for product improvementfrom consumer perceptions and measures toenhance manufacturing efficiency and prod-uct or service delivery can also themselveslead to successful line extensions (Katz, 1993).The needs and ideas of suppliers, competitorsand customers all need to be considered, whileother external environmental factors, includ-ing economic, regulatory, social, political andecological variables can also provide sourcesof novel ideas (Connell et al., 2001). The regu-latory environment may, for example, provideopportunities for customized products to meetregulatory requirements in areas such as pol-lution and emission control, or indicate theneed for new services to assist businesses tomeet regulatory requirements.

Innovation Trajectories: Exploration or Exploitation

In his work on organizational learning, March(1991, p. 71) maintains that exploration hascome to include activities encapsulated interms such as ‘search, variation, risk taking,experimentation, play, flexibility, discovery,innovation’, while exploitation includes termssuch as ‘refinement, choice, production, effi-ciency, selection implementation, execution’.In subsequent work, Levinthal and March(1993, p. 105) clarified the concepts definingexploration as ‘the pursuit of knowledge, ofthings that might come to be known’, andexploitation as ‘the use and development ofthings already known’. In March’s (1991)research, he points out that exploration has ahigh level of uncertainty, requires longer time-frames and has more diffuse effects thanexploitation activities. Many firms are morecomfortable focusing on exploitation as itallows for ‘the refinement and extension ofexisting competences, technologies and para-digms’ and from a performance perspectivethe returns are ‘positive, proximate and pred-icable’ (March, 1991, p. 85). On the other handexploration is more likely to have uncertainand negative returns. In most cases March(1991, p. 85) argues that firms seeking to beglobally competitive and to ‘finish near thetop’ place an emphasis on exploitation, whilethose firms with little or nothing to loose canemphasize exploration. So, depending on thestrategic positioning of a firm they will selectan innovation trajectory that may be onlyexploitation or exploration, or a combinationof both, but as March (1991, p. 74) observed,when firms seek to be dominant in a mar-ket they will experience difficulties in ‘defin-ing and arranging an appropriate balance

between exploration and exploitation’. Severalauthors have recently used the explore/exploit dichotomy to investigate R&D activi-ties, innovation processes and the impact ofalliances on product development.

So different players in an industry playdifferent roles in relation to product devel-opment, and select different innovationtrajectories, as might be expected. Some play-ers generate new and novel ideas and con-cepts, while other players exploit existingideas and extend product lines rather thanexplore the possibilities of entirely new prod-ucts that are radically different. Thus, forinstance, information on competitors’ prod-ucts is usually gathered to gain ideas andexploit existing, new technological innova-tions or to support a market positioning deci-sion (Azzone & Pozza, 2003), while analysingthe product successes and failures of othercompanies can indicate broadly what consum-ers are looking for. It is often the job of thesales force to provide consumer feedback, par-ticularly in the highly competitive ICT sectorwhere the sales force is an especially impor-tant interface between consumers and sup-pliers. Rather than providing specific newproduct ideas, monitoring of competitors’activities in sales, marketing, distribution andpublic relations provides broader informationon what works and what is less successful, andwhat can be exploited or avoided (Katz, 1993).

Other researchers, such as Rothaermel andDeeds (2004), have linked the exploration-exploitation framework of organizationallearning to strategic alliances and argue thatthe relationship between the businesses in alli-ances and their new product development tra-jectory depends on the type of the alliance.From their perspective a product developmenttrajectory begins with exploration alliancesinvolving products in a phase, then involveexploitation alliances, and lastly exploitationalliances that see products launched onto themarket. As a business grows and developscore capabilities, it tends to reduce thisproduct development trajectory to discover,develop and commercialize product exten-sions through vertical integration. Koza andLewin (1998) applied March’s (1991) model oforganizational learning to a firm’s strategicalliances and they argue that a firm’s decisionto enter an alliance depends upon the decisionto exploit an existing capability or to explorefor new opportunities’ (Koza & Lewin, 1998,p. 256). Similarly, Rothaermel (2001) has usedan exploration/exploitation dichotomy toexamine inter-firm co-operation. Rothaermel(2001, p. 690) argues that firms motivated by aneed for organizational learning will enter intoexploration partnerships within networks,

INNOVATION AND IDEAS IN AUSTRALIAN ICT FIRMS

185

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing

Volume 15 Number 2 2006

while firms wishing to access complimentarycompetences or capabilities will enter intoexploitation partnerships within supply-chainnetworks.

Rothaermel and Deeds (2004) have usedMarch’s (1991) exploration-exploitationframework to characterize the type of ideaseeking and type of alliances that businessesengage in at differing stages of the productdevelopment process. This work built onRothaermel’s (2001) earlier work on networks,alliances or partnering relationships in bio-technology, which argued that inter-firm rela-tionships can assist existing dominant firms toaccess emerging technologies, and can make itpossible for start-ups to successfully commer-cialize exploratory technologies and opportu-nities. A firm’s choice of the type of alliancecan be determined by the decision to eitherexplore for new fields or exploit existing tech-nologies and products (Koza & Lewin, 1998).Holmqvist (2004) argues that this interplay ofexploitation and exploration takes place bothwithin and between businesses. Beckman,Haunschild and Phillips (2004) maintain thatexpanding to new network partners is similarto the concepts of exploration, while extendingthe relationships with existing partners is sim-ilar to exploitation. Therefore, firms that scanoutside their normal supply-chain networksare more likely to be exploring for innovationsthan firms who are attempting to exploit exist-ing opportunities and ideas. In their research,Beckman, Haunschild and Phillips (2004) rec-ognized that Pfeffer and Salancik (1978) wereamongst the earliest researchers to identifythat firms expand their networks by engagingwith new actors in an effort to reduce theuncertainty and constraint that is generatedwhen actors in a network become dependenton one another. Others, such as Kogut (1988),and Powell, Koput and Smith-Doerr (1996),have noted that actors expand their networksto explore new practices and technologies.According to Beckman, Haunschild andPhillips (2004), firms are attempting to reducefirm specific uncertainty through new rela-tionships within new networks. This is anexploration trajectory because the firms areseeking to diversify their information sourcesand the new relationships are more likely toprovide new and different information thanexisting relationships. Furthermore they main-tain that firms will pursue an exploitative tra-jectory and reinforce their networks whenthere is market uncertainty; in these situationsfirms build additional interactions with exist-ing alliance partners.

In their work on industrial R&D Cesaroni,Di Minin and Piccaluga (2005) see exploita-tion and exploration as outcomes of strategic

choices. They propose that in exploitationtrajectories firms either leverage their R&Dinvestments within their main operations orfirms with a dominant, emerging design canleverage their leading position through strate-gic alliance, so securing complimentary assets.Cesaroni, Di Minin and Piccaluga (2005) arguethat an explorative trajectory is needed whenold complementary assets are no longer suffi-cient to maintain a leadership position. Thismeans that, as March (1991, p. 72) suggests, tosurvive firms must effectively select amongforms, routines or practices, and success andsurvival are also dependent on the ‘generationof new alternative practices’. Scanning theexisting environment and existing networksand alliances for alternatives and looking atwhat competitors are doing provides potentialalternative practices and ideas. The future,however, is also important. Here, one criticalgroup of exploratory, idea generators thatlooks to the future is lead users. Lead userscombine two characteristics: they aremotivated to innovate because they wantinnovation-related benefits from a solution totheir needs and they are the first to see theneed for an innovation. According to Lilienet al. (2002), lead users live in the future rela-tive to other target-market users, experiencingtoday what other users will experience later.Lilien and colleagues found that lead users’ideas are significantly more novel than areideas generated by non-lead users. They havegreater potential to develop ideas into anentire product line, while non-lead user ideasmainly produced ideas for product improve-ments and extensions to existing product lines(Lilien et al., 2002).

Methodology

The study reported on here was small andwas considered exploratory in this field inAustralia as there has been no previous exam-ination in Australia of the nature of interactionbetween RTOs and innovative firms. Datawere collected using a self-administered ques-tionnaire, sent by post to a sample of firmsselected from a listing of ICT product and ser-vice providers listed on the Kompass data-base. Selection of firms sampled was limited tothose in the greater Sydney region as thisregion had the greatest concentration of ICTfirms in Australia. A sample of 120 organiza-tions received the questionnaire and, aftertelephone follow-up, 45 respondents returnedcompleted questionnaires. In some casesrespondents did not answer all questions, andthe number of respondents to each question isindicated in each figure or table.

186

CREATIVITY AND INNOVATION MANAGEMENT

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing

Volume 15 Number 2 2006

The ICT industry is only loosely heldtogether by the idea that they are involved incomputing and telecommunication technolo-gies. There is no clear product focus, and manyIT and micro-chip technologies are used in awide range of applications across sectors suchas finance and manufacturing. ICT suppliersand component suppliers were identified bycreating a dataset of products, services andbundled products and services that are eitherused by ICT firms or supplied by ICT firms totheir customers. The suppliers of these prod-ucts and services are then identified from acommercial dataset (Kompass) and this pro-vides a population frame that enables theidentification of firms across the ICT supplychain. This also provides a wider definition ofICT firms as it includes more dimensions ofthe supply chain. In this study we include sup-pliers and users of ICT products and servicessuch as plastics products for the electricaland electronics industries, telecommunicationtransmission equipment, electrical and elec-tronic instruments and apparatus for mea-suring, electronic data-processing services,telecommunication network services, andfrom sectors including high-end users in theleisure and entertainment industry, such ascasinos.

The Australian ICT Sector

According to the OECD (2001), by the late1990s the ICT sector remained a relativelysmall part of the Australian economy, and itsshare in the total business sector in 1998–1999was 4.1 percent for value added and 2.6percent for employment. In 2000–2001 theindustry was overwhelmingly composed ofsmall and small-medium size firms (almost 80percent employing 1–4 people). In the sameyear, less than 1 percent of firms employed 100or more people, but these accounted for 55percent of employment and 72 percent ofincome (Department of CommunicationsInformation Technology and the Arts, 2003).The ICT sector was only a modest contributorto business sector GDP growth between 1992and 1999 (from 5 percent to 8 percent on aver-age, according to the period considered) butthe potential for innovation and collaborationwith RTOs seems considerable, as R&D inten-sity in the ICT sector (ratio of R&D to valueadded) in 2000–2001 was about 4.6 percent,more than six times as large as for the econ-omy as a whole, and R&D expenditure grewby 50 percent between 1996–1997 and 2000–2001. Most of that expenditure (83 percent)was by private-sector firms (ABS, 2004;DCITA, 2003). In terms of value added, tele-

communications services were the largestcomponent (almost 52 percent) of the sector.Other ICT services contributed over 40 per-cent, and manufacturing only 8 percent. Interms of employment, wages, salaries andproduction, the significance of the telecom-munications services sector was somewhatdiminished, with ‘other’ ICT services contrib-uting 50 percent of overall ICT employmentand production, and more than 57 percent forwages and salaries. Australia remains veryhighly dependent on imports of manufacturedICT goods to meet domestic demand.

Results

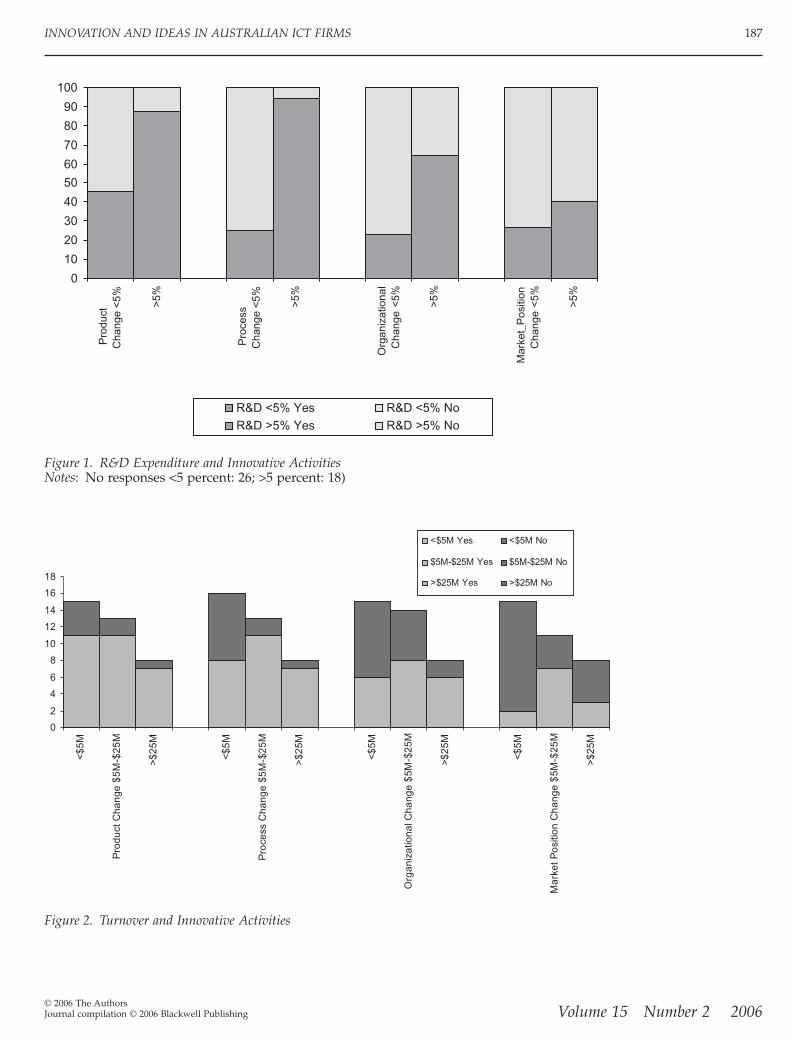

The level of spending on research and devel-opment has been widely used as an indicatorof a firm’s propensity to innovate and itsinvestment in innovation. Figure 1 shows thedistribution of firms by their spending inR&D, and an indication of the types of inno-vative activities they intended to engage in inthe future, and shows that spending on R&D isunevenly spread throughout the sample offirms in this exploratory study.

The respondents reported in Figure 1 thusengaged in a range of innovative activities,including process and organizational change,and some were investing considerable per-centages of their turnover in R&D. Given thisinvestment, it is interesting to note that morefirms spending less than 5 percent on R&Dindicated that they were not undergoing prod-uct or process change or changes in work orga-nization and coordination. A similar numberof firms were involved in changes in the firmspositioning, although the percentage was nothigh in either category. The change with thehighest relative response rate was processchange in firms investing in excess of 5 percentof turnover in R&D. Firms investing in processchanges are more likely to be interestedin enhancing and exploiting operationaleffectiveness by improving their processesinternally and building on existing processskills than investing in explorative productdevelopment.

When examining the nature of innovationactivities by the turnover of firms (seeFigure 2) an interesting pattern emerges, withfirms of all sizes being involved significantlyin product and process innovations. But interms of organizational changes and marketrepositioning, small firms are less active inthese areas than medium-sized firms and largefirms. In this sample it would appear thatmedium-sized firms (with a turnover of $5–$25 million) are able to invest in a wider rangeof innovative activities.

INNOVATION AND IDEAS IN AUSTRALIAN ICT FIRMS

187

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing

Volume 15 Number 2 2006

Figure 2. Turnover and Innovative Activities

0

2

4

6

8

10

12

14

16

18

<$

5M

Pro

du

ct C

ha

ng

e $

5M

-$2

5M

>$

25

M

<$

5M

Pro

cess

Ch

an

ge

$5

M-$

25

M

>$

25

M

<$

5M

Org

an

iza

tion

al C

ha

ng

e $

5M

-$2

5M

>$

25

M

<$

5M

Ma

rke

t P

osi

tion

Ch

an

ge

$5

M-$

25

M

>$

25

M

<$5M Yes <$5M No

$5M-$25M Yes $5M-$25M No

>$25M Yes >$25M No

Figure 1. R&D Expenditure and Innovative ActivitiesNotes

: No responses

<

5 percent: 26;

>

5 percent: 18)

0

10

20

30

40

50

60

70

80

90

100P

rodu

ct

C

hang

e <

5% >5%

Pro

cess

Cha

nge

<5% >5%

Org

aniz

atio

nal

Cha

nge

<5%

>5%

Mar

ket_

Pos

ition

Cha

nge

<5%

>5%

R&D <5% Yes R&D <5% No

R&D >5% Yes R&D >5% No

188

CREATIVITY AND INNOVATION MANAGEMENT

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing

Volume 15 Number 2 2006

Firms were asked to indicate their level ofagreement with several statements concerningtheir competitive positioning. These state-ments included: ‘It is hard to improve ourcompetitive position through product or pro-cess change’; ‘Competitors can easily imitateour changes’; ‘Our products or services are allcustomized’; ‘In our business, doing thingswell is much more important than doing newand different things’; ‘We do not have the R&Dresources needed to introduce changes’; and‘In our business, radical change is too risky’.The responses are presented in Figure 3.

The data in Figure 3 considers two group-ings of firms, there were 18 firms with anexpenditure of less than 5 percent on R&D and15 firms that had more than 5 percent of turn-over spent on R&D. The results indicate that inthis sample more firms spending in excess of 5percent on R&D agreed competitors can easilyimitate the changes the firms have made, andthe same group indicated that in their businessdoing things well (exploiting) is much moreimportant than doing new and different things(exploring).

Sources of Innovation-Related Knowledge

The study suggested that a very large propor-tion (82.1 percent) of the respondents had usedsome form of publicly funded services duringthe previous three years. Respondents over-whelmingly used publicly funded services tosource information, knowledge, skills, tech-

nology and other non-financial inputs to inno-vation. Publicly funded services were definedin the survey as those that provide informa-tion, knowledge, skills, technology and othernon-financial inputs to innovation on a no-costor subsidised basis to the user firm. Examplesof these services include: guides; summaries;analyses; reports; seminars or workshopspublished or promoted by publicly fundedorganizations or government; informationpublished on websites; services and schemesdelivered via public agencies offering subsi-dized or free consultancy, advice, training andawareness updates; and human-resource ser-vices including recruitment, training and skillsupdates.

Respondents were asked to rate the impor-tance of different publicly funded organiza-tions, and all firms rated research institutesand co-operative research centres (CRCs) asleast important to their product innovation, atleast as sources of ideas, where as almost aquarter (23 percent) of globally competitivefirms and 30 percent of nationally competi-tive firms saw universities, TAFE, and otherhigher- and further-education organizationsas important sources of ideas. This suggeststhat public-sector organizations such asTechnical and Further Education (TAFE) anduniversities may be relatively more importantsources of knowledge, or may simply be moreaccessible to firms that regard themselves asnationally or globally competitive. This aspectof innovation of the more competitive enter-prises may in turn be related to a firm’s strat-egies involving more radical changes in

Figure 3. R&D Expenditure and Competitive Position

0

20

40

60

80

100

Impr

ovem

ent

hard

<5% >

5%

Com

petit

ors

imita

te <

5%

>5%

Cus

tom

ised

Pro

duct

s <

5%

>5%

Con

solid

ate

<5%

>5%

Lack

R&

DR

esou

rces

<5%

>5%

Rad

ical

Cha

nge

is R

isky

5% >5%

R&D <5% Strongly Disagree R&D <5% R&D <5% R&D <5% R&D <5% Strongly Agree

R&D <5% Strongly AgreeR&D >5% Strongly Disagree R&D >5% R&D >5% R&D >5%

INNOVATION AND IDEAS IN AUSTRALIAN ICT FIRMS

189

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing

Volume 15 Number 2 2006

product, and hence to a greater need for test-ing where products are totally untried.

ICT firms in Australia are dominated by afew large multi-national firms, but there is asubstantial number of smaller firms involvedin the sector. While the sample is dominatedby firms with a turnover of less than $25 mil-lion, firms of all sizes as defined by turnoveraccessed publicly funded services, as can beseen in Figure 4. In this study firms that had asmall turnover and fewer than 50 employeesthe respondents did not access any form ofpublic services.

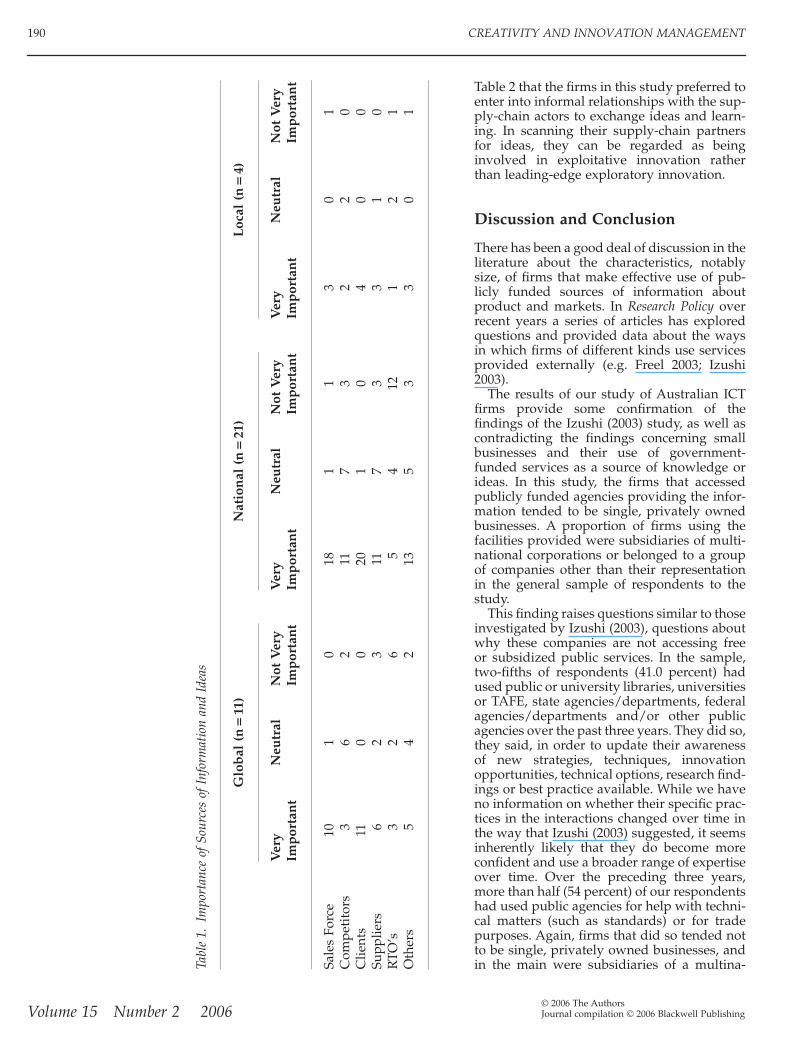

Firms were also asked how they rated theimportance of different actors and organisa-tions as sources of ideas, information, knowl-edge and skills for their organisations. As canbe seen in Table 1, in both nationally and glo-bally competitive businesses clients and theirsales forces are reported as the most importantsources of ideas for innovation. In response tothis question, nine firms did not rank them-selves as competitive at a local, national or glo-bal level.

The predominance of this source of productideas confirms much international work onthe sources of innovation, including that ofvon Hippel (1994) and Marceau (1999). Thisalso indicates that the firms in this study wereinvolved in exploiting activities within thesupply chain network rather than exploringsignificantly new opportunities with networkpartners in RTOs and other organizations.

Networking Activities

Firms engage in many innovation-relatedactivities and, as Rothaermel (2001) suggested,networks, alliances or partnering relationshipscan assist incumbent firms to access emergingtechnologies and can assist start-ups tocommercialize exploratory technologies and

opportunities. There has been an increasingemphasis in the innovation literature on net-working as a source of knowledge and learn-ing (e.g. Beckman, Haunschild & Phillips 2004;Florén & Tell 2004) and, as research has shown,informal activities associated with geographi-cal co-location can enhance firms’ innovativecapabilities.

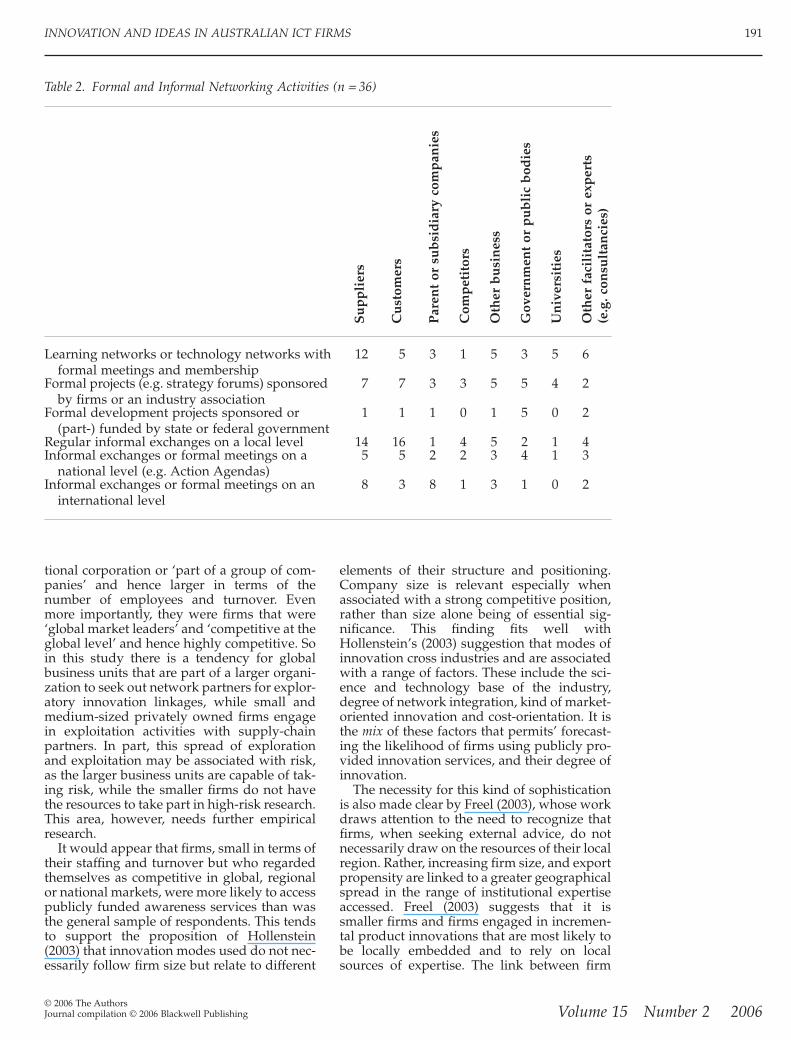

Our study suggested that even in thishi-tech industry the most important of theseactivities involve interaction with customersand suppliers within supply-chain networks.Both formal and informal activities carried outinternally and networking across organiza-tions increase the range of sources of knowl-edge and ideas that are available to firms.In the study, firms were asked if they hadengaged within the previous three years informal and informal innovation and learningactivities. They were also asked to indicate thetypes of parties, such as customers, suppliersand competitors, that they engaged with. Theresponses of the 36 firms answering thisquestion are presented in Table 2, and againit is evident that customers and suppliers areimportant to firms engaged in learning andinnovation activities within these partnershipnetworks. Universities and government mayalso be influential in areas such as learningnetworks and formal projects involving indus-try associations.

As Florén and Tell (2004) argue, when tak-ing part in networked learning, actors need tobe able to take on new perspectives, and to dothis they need to view artefacts and processesfrom the points of view of other actors. Theyalso argue that learning is enabled throughreciprocity, so it is hardly surprising that firmsengaged in learning networks with their sup-pliers. Often the reciprocity is transactional,that is, it results in lower costs or in cost shar-ing between suppliers and customers, but itcan also result in learning. It can also be seen in

Figure 4. Turnover or Sales for the Local Company in 2000–2001(n

=

35)

42%37%

3%11%

5% 3%

32%42%

3%13%

7% 3%

0%10%20%30%40%50%

Less than$5m

$5m - $25m $26m -$50m

$51m -$99m

$100m -$999m

More than$1,000m

Turnover/sales for 2000-2001

Per

cen

tag

e

All sample Accessed publc services sample

190

CREATIVITY AND INNOVATION MANAGEMENT

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing

Volume 15 Number 2 2006

Table 2 that the firms in this study preferred toenter into informal relationships with the sup-ply-chain actors to exchange ideas and learn-ing. In scanning their supply-chain partnersfor ideas, they can be regarded as beinginvolved in exploitative innovation ratherthan leading-edge exploratory innovation.

Discussion and Conclusion

There has been a good deal of discussion in theliterature about the characteristics, notablysize, of firms that make effective use of pub-licly funded sources of information aboutproduct and markets. In

Research Policy

overrecent years a series of articles has exploredquestions and provided data about the waysin which firms of different kinds use servicesprovided externally (e.g. Freel 2003; Izushi2003).

The results of our study of Australian ICTfirms provide some confirmation of thefindings of the Izushi (2003) study, as well ascontradicting the findings concerning smallbusinesses and their use of government-funded services as a source of knowledge orideas. In this study, the firms that accessedpublicly funded agencies providing the infor-mation tended to be single, privately ownedbusinesses. A proportion of firms using thefacilities provided were subsidiaries of multi-national corporations or belonged to a groupof companies other than their representationin the general sample of respondents to thestudy.

This finding raises questions similar to thoseinvestigated by Izushi (2003), questions aboutwhy these companies are not accessing freeor subsidized public services. In the sample,two-fifths of respondents (41.0 percent) hadused public or university libraries, universitiesor TAFE, state agencies/departments, federalagencies/departments and/or other publicagencies over the past three years. They did so,they said, in order to update their awarenessof new strategies, techniques, innovationopportunities, technical options, research find-ings or best practice available. While we haveno information on whether their specific prac-tices in the interactions changed over time inthe way that Izushi (2003) suggested, it seemsinherently likely that they do become moreconfident and use a broader range of expertiseover time. Over the preceding three years,more than half (54 percent) of our respondentshad used public agencies for help with techni-cal matters (such as standards) or for tradepurposes. Again, firms that did so tended notto be single, privately owned businesses, andin the main were subsidiaries of a multina-

Tabl

e 1.

Impo

rtan

ce o

f Sou

rces

of I

nfor

mat

ion

and

Idea

s

Glo

bal

(n

=

11)

Nat

ion

al (

n

=

21)

Loc

al (

n

=

4)

Ver

yIm

por

tan

tN

eutr

alN

ot V

ery

Imp

orta

nt

Ver

yIm

por

tan

tN

eutr

alN

ot V

ery

Imp

orta

nt

Ver

yIm

por

tan

tN

eutr

alN

ot V

ery

Imp

orta

nt

Sale

s Fo

rce

101

018

11

30

1C

ompe

tito

rs3

62

117

32

20

Clie

nts

110

020

10

40

0Su

pplie

rs6

23

117

33

10

RTO

’s3

26

54

121

21

Oth

ers

54

213

53

30

1

INNOVATION AND IDEAS IN AUSTRALIAN ICT FIRMS

191

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing

Volume 15 Number 2 2006

tional corporation or ‘part of a group of com-panies’ and hence larger in terms of thenumber of employees and turnover. Evenmore importantly, they were firms that were‘global market leaders’ and ‘competitive at theglobal level’ and hence highly competitive. Soin this study there is a tendency for globalbusiness units that are part of a larger organi-zation to seek out network partners for explor-atory innovation linkages, while small andmedium-sized privately owned firms engagein exploitation activities with supply-chainpartners. In part, this spread of explorationand exploitation may be associated with risk,as the larger business units are capable of tak-ing risk, while the smaller firms do not havethe resources to take part in high-risk research.This area, however, needs further empiricalresearch.

It would appear that firms, small in terms oftheir staffing and turnover but who regardedthemselves as competitive in global, regionalor national markets, were more likely to accesspublicly funded awareness services than wasthe general sample of respondents. This tendsto support the proposition of Hollenstein(2003) that innovation modes used do not nec-essarily follow firm size but relate to different

elements of their structure and positioning.Company size is relevant especially whenassociated with a strong competitive position,rather than size alone being of essential sig-nificance. This finding fits well withHollenstein’s (2003) suggestion that modes ofinnovation cross industries and are associatedwith a range of factors. These include the sci-ence and technology base of the industry,degree of network integration, kind of market-oriented innovation and cost-orientation. It isthe

mix

of these factors that permits’ forecast-ing the likelihood of firms using publicly pro-vided innovation services, and their degree ofinnovation.

The necessity for this kind of sophisticationis also made clear by Freel (2003), whose workdraws attention to the need to recognize thatfirms, when seeking external advice, do notnecessarily draw on the resources of their localregion. Rather, increasing firm size, and exportpropensity are linked to a greater geographicalspread in the range of institutional expertiseaccessed. Freel (2003) suggests that it issmaller firms and firms engaged in incremen-tal product innovations that are most likely tobe locally embedded and to rely on localsources of expertise. The link between firm

Table 2. Formal and Informal Networking Activities (n

=

36)

Su

pp

lier

s

Cu

stom

ers

Par

ent

or s

ub

sid

iary

com

pan

ies

Com

pet

itor

s

Oth

er b

usi

nes

s

Gov

ern

men

t or

pu

bli

c b

odie

s

Un

iver

siti

es

Oth

er f

acil

itat

ors

or e

xper

ts(e

.g. c

onsu

ltan

cies

)

Learning networks or technology networks withformal meetings and membership

12 5 3 1 5 3 5 6

Formal projects (e.g. strategy forums) sponsored by firms or an industry association

7 7 3 3 5 5 4 2

Formal development projects sponsored or (part-) funded by state or federal government

1 1 1 0 1 5 0 2

Regular informal exchanges on a local level 14 16 1 4 5 2 1 4Informal exchanges or formal meetings on a

national level (e.g. Action Agendas)5 5 2 2 3 4 1 3

Informal exchanges or formal meetings on an international level

8 3 8 1 3 1 0 2

192

CREATIVITY AND INNOVATION MANAGEMENT

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing

Volume 15 Number 2 2006

size, export propensity and the radical orincremental nature of innovations undertakenthus also suggests again that it is competitivestrategies, rather than any one variable such asfirm size, that are critical in determiningwhether firms use external sources of informa-tion, and the types of sources on which theyrely most. Freel (2003) says that there is no cor-relation between networking and innovationin most industries: nearly a third of the 597northern-English firms in his sample had noexternal linkages at all. It is clear, Freel (2003)says, that clients matter most and that mostsuccessful networking occurs along the valuechain. He also refers to an earlier study byKaufmann and Todtling (2000) that showedthat in most industries the lion’s share of inno-vative effort is made by the firms themselvesand occurs within firms themselves, andreminds us that innovation is primarily a pro-cess built on internal capabilities.

It was equally clear that universities andother RTOs were also sources of informationand advice but few, if any, of the firms in thisexploratory study were scanning universitiesas a source of innovative ideas. More specifi-cally, no respondents in this study, includingcompanies that considered themselves to beglobally competitive, indicated that they hadattempted to access international universitiesor research and technology organizations. Theparticular lack of involvement with CRCs mayindicate that, in this sample at least, firms didnot regard the substantial investment of timeand cash required by many CRCs to be a gooduse of scarce resources, or at least not to be asgood an investment as working with custom-ers and suppliers. Given the link betweencompetitive level and propensity to use pub-licly funded sources of external expertise, wesuggest that further studies should focus onthe dynamics of this link as the basis for betterunderstanding the dynamics of different sec-tions of the ICT industry, especially wheregovernments are seeking to target innovationassistance.

While some firms are using both public andprivate service providers, it is evident from thedata gathered in this research that for mostrespondents, supply-chain actors such as cli-ents, their customers, their sales force andtheir suppliers are viewed as their mostimportant sources of innovation ideas and,more particularly, for the development of newproducts, services or product-service pack-ages. However, while this work has significantlimitations because of the small sample size,the work is useful in exploring the linkagesand alliances between organizations and givesan indication of their innovation trajectories.The findings apply to these firms in this study,

and further work is needed both within theICT sector and across other sectors to confirmthese initial findings. This exploratory studywas used to develop a framework for furtherresearch into the food, renewable energy andmining technologies services sectors. This sup-ports the work of Rothaermel and Deeds(2004) and Beckman, Haunschild and Phillips(2004) that, in their view, firms work withinexisting networks such as supply chains whenthey are able to exploit existing technologies.Public-sector organizations are importantsources of advice to most of our firms, butessentially their help is sought on mattersrelating to technical matters, to regulationsand standards, rather than questions concern-ing exploratory innovation

per se

. Furtherwork is needed to better understand why andhow RTOs can better engage with industrypartners.

A significant number of firms (66 percent) inthis study were making substantial invest-ments in R&D and were involved in extensive,ongoing and deliberate changes to their prod-ucts, processes and organizations. Most ofthese ICT firms thus have the characteristicsusually considered by analysts to be those ofinnovative firms, but they nevertheless stillsee their supply chains as key sources of ideasand important drivers of innovation. Manywere involved in exploitative learning net-works, as were the biotechnology firms inRothaermel’s (2001) work and in formal andinformal exchanges of information and knowl-edge, and they recognized the importance ofan awareness of cutting-edge knowledge asthe underpinning of their competitive posi-tions. While March (1991) argued that firmswishing to be globally competitive need toemphasize exploitation, most of the globallycompetitive firms in this study appear to besourcing information or ideas in ways that areexploitative, so that ICT firms in the Austra-lian context appear to be involved in exploit-ative learning within their supply chainnetworks. While some firms may select aninnovation trajectory that is a combination ofboth exploratory and exploitative learning,those seeking to be dominant in a market willexperience difficulties in ‘defining and arrang-ing and appropriate balance between explora-tion and exploitation’ March (1991, p. 74). Inthis study, few firms were scanning outsidetheir normal supply-chain networks and mostare likely to be attempting to exploit existingopportunities and ideas. Respondents in thisstudy appear to have made little effort toexpand their networks by engaging with newactors in an effort to reduce the uncertaintyand constraint that are generated when actorsin a network become dependent on one

INNOVATION AND IDEAS IN AUSTRALIAN ICT FIRMS

193

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing

Volume 15 Number 2 2006

another (Beckman, Haunschild & Phillips,2004). In entering into a network or alliancethe respondents in this research appear moreoften to exploit an existing capability byimproving operational processes rather thanexploring for new opportunities outside oftheir existing supply chain (Koza & Lewin,1998).

Public-sector knowledge organizations stillhave a long way to go to persuade such inno-vative firms of their relevance as sources ofideas. There is clearly a barrier between theideas (technological and other) generated byuniversities and RTOs and the uptake of whatis on offer to companies. For the barrier to beovercome, both private-sector firms and pub-licly funded organizations seeking to assistthem in the development of their innovationtrajectories, need to work on much betterunderstanding the reasons that lead firms toseek assistance as well as their ability to absorbspecific assistance provided. It is clear thatmany firms operate innovation trajectoriesthat need only occasional and specific inputsof assistance. This means that policy makersseeking to encourage better crossing of thisinnovation divide need far better understand-ing of the differences between firms bothwithin the same and in different industry sec-tors, including those in manufacturing, theincreasing number in manufacturing and ser-vices combined and those in services. It seemsto be time to recognize that innovation

modes

rather than industry location or firm size arecritical dimensions of the issue and that on theground, policy makers need to see the place oftarget firms in a complex matrix if they are todeliver the development drivers in question.

Acknowledgements

The authors wish to acknowledge that theresearch informing this article was supportedthrough Australian Research Council LargeGrant A00106313 (2001–2003) ‘Investigation ofthe changing role of Research and Technologyand Technology organizations and knowledgeintensive business in fostering innovation’.

References

ABS (2004)

Information and Communication Technol-ogy

: Australia. Canberra: ABS.Azzone, G. and Pozza, I. (2003) An integrated strat-

egy for launching a new product in the biotechindustry,

Management Decision

, 41(9), 832–43.Beckman, P.M., Haunschild, R. and Phillips, D.J.

(2004) Friends or Strangers? Firm-SpecificUncertainty, Market Uncertainty, and Network

Partner Selection.

Organization Science

, 15(3),259–76.

Cesaroni, F., Di Minin, A. and Piccaluga, A. (2005)Exploration and Exploitation Strategies in Indus-trial R&D.

Creativity and Innovation Management

,14(3), 222–32.

Connell, J., Edgar, G.C., Olex, B., Scholl, R.,Shulman, T. and Tietjen, R. (2001) Troubling suc-cesses and good failures: Successful new productdevelopment requires five critical factors,

Engi-neering Management Journal

, 13(4), 35–39.DCITA (2003)

An Overview of the Australian ICTIndustry and Innovation Base

. Canberra: DCITA.Freel, M. (2003) Sectoral patterns of small firm inno-

vation, networking and proximity,

Research Pol-icy

, 32(9), 751–70.Florén, H. and Tell, J. (2004) The emergent prereq-

uisites of managerial learning in small firm net-works,

Leadership & Organization DevelopmentJournal

, 25(3), 292–307.Hollenstein, H. (2003) Innovation modes in the

Swiss service sector: a cluster analysis based onfirm level data,

Research Policy

, 32(9), 845–63.Holmqvist, M. (2004) Experiential Learning Pro-

cesses of Exploitation and Exploration Withinand Between Organizations: An Empirical Studyof Product Development.

Organization Science

,15(1), 70–82.

Izushi, H. (2003) Impact of the length of relation-ships upon the use of research institutes bySMEs’.

Research Policy

, 32(9), 771–88.Katz, P.H. (1993) Scoring big in product develop-

ment: Four steps to building a strong team forquick successful launches.

Food Processing

, 54(11),53–7.

Kaufmann, A. and Todtling, F. (2000) Systems ofinnovation in traditional industrial regions: thecase of Styria in comparative perspective.

Regional Studies

, 34, 29–40.Kogut, B. (1988) Joint Ventures: Theoretical and

empirical perspectives.

Strategic ManagementJournal

, 9, 319–32.Koza, M.P. and Lewin, A.Y. (1998) The co-evolution

of strategic alliances.

Organization Science

, 9, 255–64.

Levinthal, D.A. and March, J.G. (1993) The myopiaof learning.

Strategic Management Journal

, WinterSpecial Issue 14, 95–112.

Lilien, G.L., Morrison, P.D., Searls, K., Sonnack, M.and von Hippel, E. (2002) Performance assess-ment of the lead user idea-generation process fornew product development,

Management Science

,48(8), 1042–59.

Logar, C., Ponzurick, T., Spears, J. and France, K.(2001) Commercializing intellectual property: Auniversity-industry alliance for new productdevelopment.

Journal of Product and Brand Man-agement

, 10(4/5), 206–17.Marceau, J., (1999) Networks of innovation, net-

works of production and networks of marketing:collaboration and competition in the biomedicaland toolmaking industries in Australia.

Creativityand Innovation Management

, 8(1 March), 20–7.March J.G. (1991) Exploration and exploitation in

organizational learning.

Organization Science

, 2,71–87.

OECD (2001)

Measuring the ICT Sector

. Paris: OECD.

194

CREATIVITY AND INNOVATION MANAGEMENT

© 2006 The AuthorsJournal compilation © 2006 Blackwell Publishing

Volume 15 Number 2 2006

Peterson, R.T. (1988) An analysis of new productideas in small business.

Journal of Small BusinessManagement

, 26(2), 25–31.Pfeffer, J. and Salancik, G. (1978)

The External Con-trol of Organizations: A Resource Dependence Per-spective

. Harper & Row, New York.Powell, W.W., Koput, K.W. and Smith-Doerr, L.

(1996) Interorganizational collaboration and thelocus of innovation: Networks of learning in bio-technology.

Administrative Science Quarterly

, 41,116–45.

Rothaermel, F.T. (2001) Incumbent’s AdvantageThrough Exploiting Complementary Assets ViaInterfirm Cooperation,

Strategic Management Jour-nal

22(Jun/July), 687–99.Rothaermel, F.T. and Deeds, D.L. (2004) Exploration

And Exploitation Alliances In Biotechnology: ASystem Of New Product Development.

StrategicManagement Journal

, 25(3), 201.Smith, K. (2002)

Assessing the Economic Impacts ofICT

. STEP: Oslo.Stasch, S.F., Lonsdale, R.T. and LaVenka, N.M.

(1992) Developing a framework for sources ofnew-product ideas.

Journal of Consumer Market-ing

, 9(2), 5–15.Troy, L.C., Szymanski, D.M. and Varadarajan, R.P.

(2001) Generating new product ideas: An initialinvestigation of the role of market informationand organizational characteristics.

Academy ofMarketing Science

, 29(1), 89–101.Von Hippel, E. (1994)

The Sources of Innovation

.Oxford University Press, New York.

Professor Paul Hyland ([email protected]) is professor of management in theFaculty of Business and Informatics at Cen-tral Queensland University. He is active inand a Board member of CINet (the Contin-uous Innovation Network), a global net-work set up to bring together researchersand industrialists working in the area ofcontinuous innovation. CINet disseminatesa new way of thinking about managementand the organisation of work. Paul Hylandis the international coordinator of a globalproject surveying continuous improvementactivities in Europe, Australia and SE Asia.He has published over 40 refereed journalarticles, four book chapters and over 100international conference papers.

Dr Terry Sloan ([email protected]) isan Associate Professor in the School of Man-agement of the College of Business, Univer-sity of Western Sydney, Australia. He is theschool’s postgraduate research studentdirector and his current research interestsinclude continuous innovation, knowledgemanagement and logistics. He is an activemember of CINet and has extensive experi-ence in applied business research.

Dr Jane Marceau (j.marceau@uws. edu.au) is an Adjunct Professor at University ofTechnology Sydney in the Centre forInnovative Collaborations, Alliances andNetworks (ICAN). She is a frequent con-sultant and policy advisor to governmentsand business in Australia. She has writtenmany reports for governments and busi-ness associations in Australia on a widerange of industries (from toolmaking tohealth, from building and construction toprocessed food) and science and technologypolicies that could aid in their develop-ment. Since 1998 she has led the develop-ment of the innovative ‘product system’approach to understanding the dynamics ofindustry development and innovation, anapproach that provided much of theinspiration for the federal government’sAction Agenda (industry development)programme. She is presently a Member ofthe Greater Sydney Metropolitan StrategyReference Panel advising on the futuredevelopment of Sydney. She has specialresponsibility for technology, industry andemployment.