SME CLOUD PROJECT

52

December 2012 Business Model Development for TDP-ERP SME Cloud Product By: Gergely Balazs December 27 2012

-

Upload

independent -

Category

Documents

-

view

4 -

download

0

Transcript of SME CLOUD PROJECT

December 2012

Business Model Development for TDP-ERP

SME Cloud Product

By: Gergely Balazs

December 27 2012

Gergely Balazs

December 2012

Business Model Development for TDP-ERP

SME Cloud Product

The Bachelor Degree in International Sales and Marketing

Author: Gergely Balazs

Assignment: Bachelor Project

Supervisor: Christian Preuthun Pedersen

Characters: 105 480

Submitted: 28 December 2012

Gergely Balazs

December 2012

Table of contents

1 Introduction ................................................................................................................................................1

1.1 Problem formulation ..........................................................................................................................1

1.2 Delimitation ........................................................................................................................................2

1.3 Scientific approach ............................................................................................................................2

1.3.1 Choice of scientific paradigm ...................................................................................................2

1.3.2 Choice of models and methods ...............................................................................................3

1.4 Reflection ............................................................................................................................................4

1.4.1 Quality Assessment and Source Criticism ..............................................................................4

1.4.2 Process Reflection .....................................................................................................................4

2. Product description ..................................................................................................................................5

3 The main characteristics of the SME sector ..........................................................................................6

3.1 SME categories ..................................................................................................................................6

3.2 Size of the SME sector ......................................................................................................................6

3.3 Characteristics of the SME Sector ...................................................................................................7

3.3.1 Political factors of the SME sector (Political)..........................................................................7

3.3.2 The financial situation of the SME sector (Economy) ...........................................................7

3.3.3 Managerial characteristics (Social) .........................................................................................8

3.3.4 ERP systems in the SME sector (Technological) ....................................................................9

3.4 Conclusion of SME sector .................................................................................................................9

4. Bookkeeping and accounting .............................................................................................................. 10

4.1 Internal bookkeeping and accounting ......................................................................................... 10

4.2 External bookkeeping ..................................................................................................................... 10

4.3 The range of provided services ..................................................................................................... 11

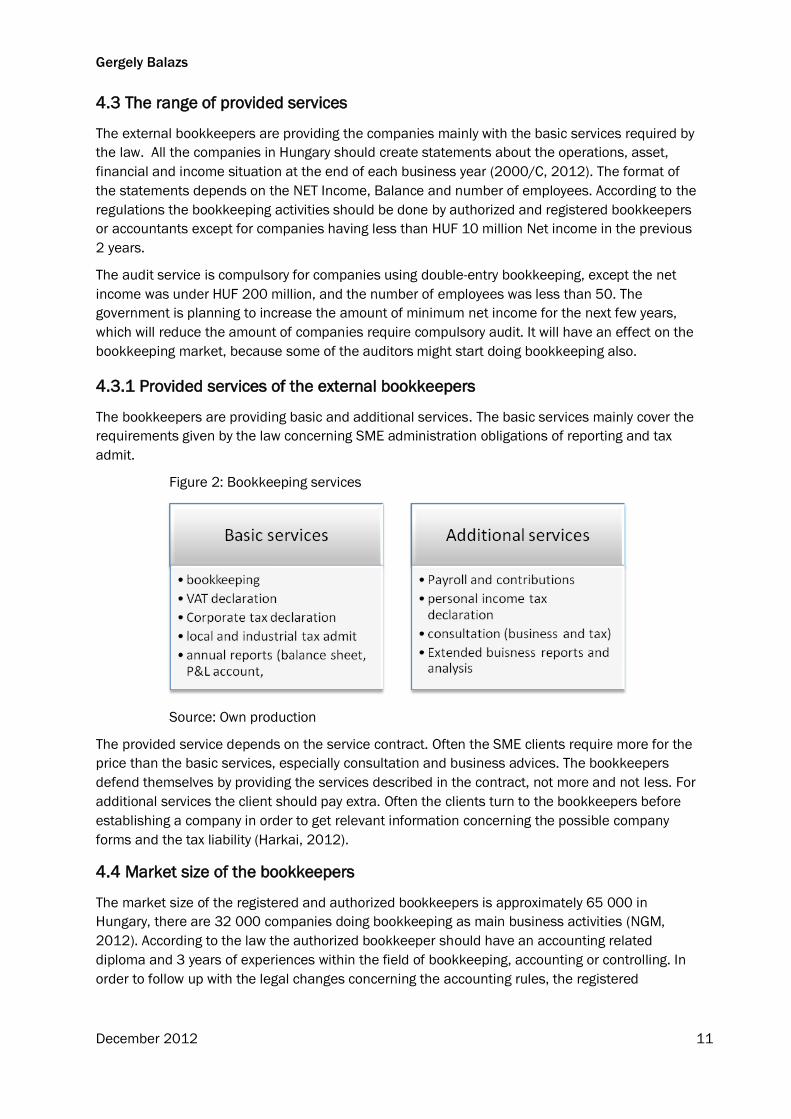

4.3.1 Provided services of the external bookkeepers .................................................................. 11

4.4 Market size of the bookkeepers ................................................................................................... 11

4.5 Pricing strategy ................................................................................................................................ 12

4.6 Relationship and partnership ........................................................................................................ 13

4.7 Competition on the bookkeeper market ...................................................................................... 14

4.7 Conclusion of the bookkeeping sector......................................................................................... 15

5. The characteristics of the Hungarian bank sector ............................................................................ 16

5.1 Strategy of Granit Bank .................................................................................................................. 16

5.2 Pillars of growth Strategy of Granit Bank ..................................................................................... 17

5.3 Sales channels of Granit Bank...................................................................................................... 18

Gergely Balazs

December 2012

5.4 Channel expansion ......................................................................................................................... 18

5.5 Conclusion of the bank sector and Granit Bank ......................................................................... 18

6 IT sector in Hungary ............................................................................................................................... 19

6.1 Financing ERP implementation ..................................................................................................... 19

6.2 Software developers of the SME cloud system .......................................................................... 20

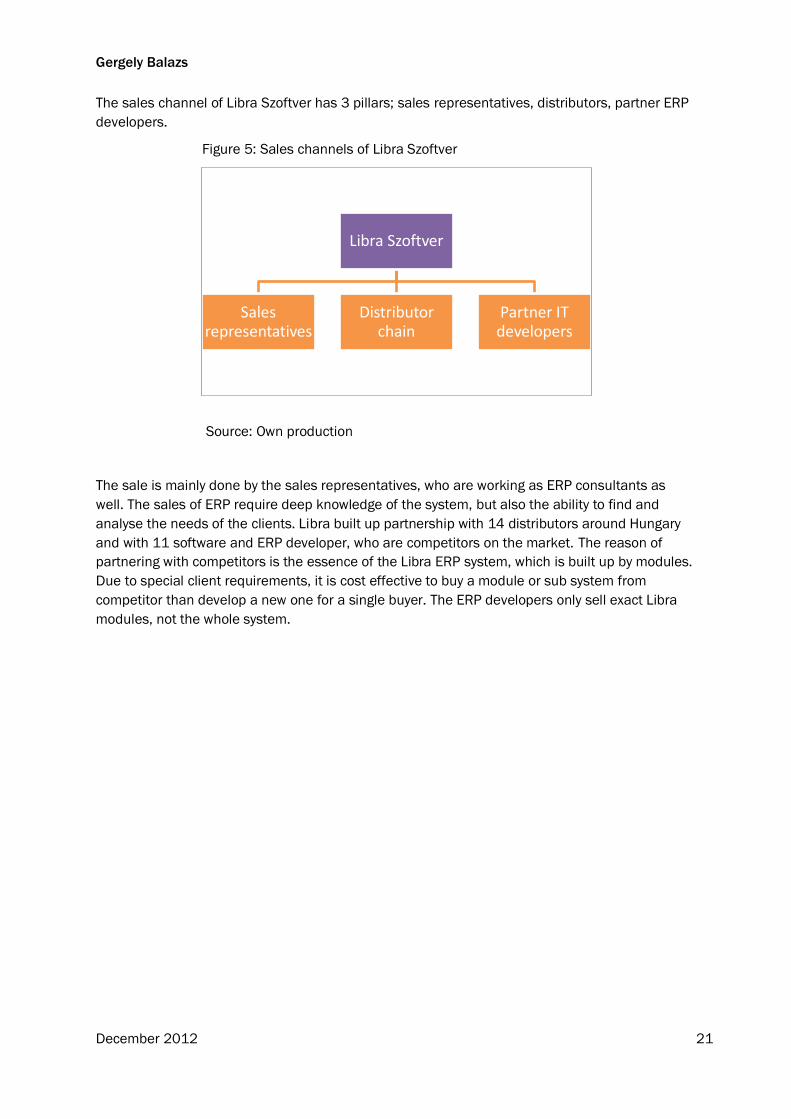

6.2.1 Libra Szoftver ........................................................................................................................... 20

6.2.2 Sales channel of Libra Szoftver ............................................................................................. 20

6.2.3 Consortium of TDP-ERP and Global Solution....................................................................... 22

6.2.4 Sales channels of TDP-ERP.................................................................................................... 23

6.3 Conclusion ....................................................................................................................................... 23

7 Establishing partnership ........................................................................................................................ 23

7.1 In depth understanding of the customer`s requirement .......................................................... 24

7.2 In depth understanding of the partner`s requirement .............................................................. 24

7.3 Reduction or elimination of cost of sale ...................................................................................... 25

7.4 Value-added chain .......................................................................................................................... 25

7.1.4 Value addition through partnership to the end users ........................................................ 26

7.5 Conclusion of the partnership ....................................................................................................... 26

8 SWOT analyses ....................................................................................................................................... 27

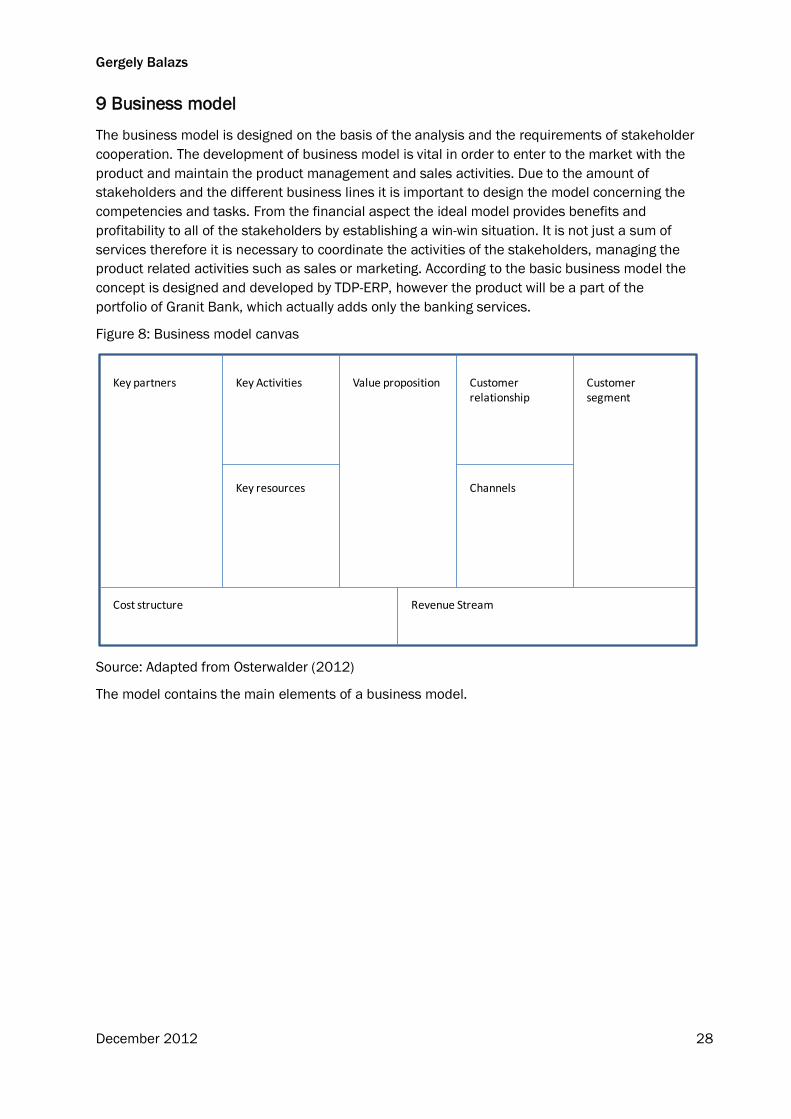

9 Business model ...................................................................................................................................... 28

9.1 Key partners .................................................................................................................................... 29

9.2 Key activities ................................................................................................................................... 29

9.3 Key resources .................................................................................................................................. 31

9.4 Value proposition ............................................................................................................................ 31

9.5 Customer relationship .................................................................................................................... 32

9.6 Channels .......................................................................................................................................... 32

9.7 Customer segment ......................................................................................................................... 33

9.8 Cost structure .................................................................................................................................. 33

9.9 Revenue stream .............................................................................................................................. 34

10 Conclusion ............................................................................................................................................ 34

Bibliography .................................................................................................................................................... i

Appendix 1: Personal interview with Istvan Cieleszky ............................................................................. iv

Appendix 2: Notes from SME Academy Conference ............................................................................... vi

Appendix 3: Personal Interview with Istvan Harkai ................................................................................. vi

Gergely Balazs

December 2012

Executive Summary

The Cloud SME product is developed by the international consortium of TDP-ERP and Global

Solution. The development phase is 13 month; the expected date of product launch is the

beginning of 2014. The project is partly financed by the EUREKA_HU_12 grant offered by the New

Szechenyi Plan. The product provides integrated and complex solution for the SMEs in order to

reduce their resources spent on administration activities. The project has several stakeholders;

Granit Bank provides banking services, Libra Szoftver adds the modular ERP system. The

bookkeeping services are planned to be done by quality partners.

The agreement concerning the collaborative product launch has not been done yet, therefore it is

necessary to evaluate how the partners can benefit from the partnership and create a business

model as a basis of negotiation.

The analysis covers the SME sector in order to find the main characteristics and needs. The

bookkeeping industry is evaluated from the aspect of competition on the market, pricing and the

relationship between the clients. Granit Bank is one of the main stakeholders within the product

launch. The SME cloud product is planned to be the part of the bank`s product range and to be

sold through the existing sales channels. The analysis covers the sales strategy of the bank and

the value creation. The ERP system is developed by Libra Szoftver and the consortium of TDP-ERP

and Global Solution. The main characteristics, core competences and the sales channels are

investigated.

The second part of the analysis is moving from the individual level of companies to the level of

possible long term partnership. The aim is to investigate the additional values and benefits

concerning the product launch in partnership.

The findings clearly shows, that the product launch in a partnership creates more value for the

clients and partners, reduces the cost of sales and increases the sales possibilities. It is also

important from the sales aspect. Granit Bank as a newly established financial institute is still

acquiring clients. The sales channel of the bank is not enough to penetrate the market. The

resources are booked on the regular business activities; therefore it is necessary to use

alternative methods for client acquisition. Targeting the existing clientele of the partners gives the

possibility for sales activities at low cost. It also creates a win-win situation to the partners.

The quality bookkeeping services positively affect the lending activities of Granit Bank, which

evaluates the loan application based on the ledgers, reports and books. The ERP system is

special in a way that some modules can be accessed by the SMEs, and the bookkeeping module

by the bookkeepers. The data is provided from the cloud server base. The bookkeepers can

withdraw the data from the database to the bookkeeping module, which saves time adding those

manually. Libra Szoftver can target the micro and small segments. Other benefits are acquiring

the customer needs from different channels.

The business model should be built on the basis of partnership concerning the sales possibilities

and the required quality of the services. The key partners in the business model are the

consortium of TDP-ERP and Global Solution, Granit Bank, Libra Szoftver and the bookkeeping

companies.

The key activities contain individual and centralized activities. Due to the core competences the

partners should deal with tasks concerning the services they provide, such as help and support

Gergely Balazs

December 2012

function. The partnership should be managed by TDP-ERP. The centralized activities are similar to

the tasks of project management, it has defining and organizing part which is creating the overall

strategy and objectives. It is done by consensus of the partners. Within the planning the tasks

should be broken down to the individual level. The controlling function is done by TDP-ERP, which

is responsible for comparing the targets with actual results, and make action in case of deviation.

The overall quality should be measured also by collecting feedbacks from the end users.

The key resources at the beginning of the product launch are mainly provided by the partners. The

cost of sales and marketing activities is planned to be covered by part of the revenue of sales.

This is the reason why in the first stage of the sales the existing sales channels should be used

targeting the clientele of the partners.

The product provides several values to the clients such as cost savings, increasing

competitiveness of the SME, quality bookkeeping and online banking services. The cloud system

enables the managers to have a real time access to the company results everywhere at any time

requiring only an internet connection. The partnership creates values for the partners concerning

the increased sales, R&D activities or strengthening the client relationship with extended

services.

The partners have already established relationship between the clients. In order to strengthen the

relationship with the end users, communication channels are established. It is necessary also to

collect the client feedbacks and develop the services offered to them.

The sales are done through the channels of the partners targeting existing clients. The strongest

relationship exists between the bookkeepers and their clientele. This is the reason why it is

important to increase the amount of bookkeeper partners. The trust is the basis of relationship

selling, which enables increased sales activities through the bookkeepers.

The targeted customer segment of the TDP-ERP cloud concept is micro small and medium sized

enterprises which do not have ERP system and using the services of external bookkeepers.

The main costs of the partnership after the product development phase are the management,

marketing and sales activities. The establishment of agreements with bookkeeping companies

also requires additional costs. For better control over the costs budgets should be created

according to the common strategic objectives.

The revenue is the sum of the sales price, which contains the fee of basic banking services, the

bookkeeping and the ERP license. TDP-ERP receives royalty on the basis of the sales price. The

royalty also covers the cost of centralized activities.

Gergely Balazs

December 2012 1

1 Introduction

The consortium of TDP-ERP and Global Solution started to develop an innovative product concept

targeting small and medium sized enterprises (hereinafter referred to as SME). The project is

carried out within the EUREKA, which is an international organization aiming for raising the

productivity and competitiveness by supporting the R&D activities. The purpose is to get closer

the companies and research institutes from the member countries, and initiate partnerships

between them. The TDP-ERP SME Cloud project is financed by own resources and 45 percent of

the development costs expected to be funded by the New Széchenyi Plan within the

EUREKA_HU_12 grant. The development phase of the project has been started in November

2012. The expected date of market launch will be in 2014 depending on the outcome.

The background of the project idea is the need discovery of the SME sector. The research

covered the main business activities and processes and the incurred costs. As a result the SMEs

are spending way too much covering their administration tasks, which contains regular business

processes such as billing, invoicing. The other administrative expenses concern the costs of

banking services and meeting the taxation and reporting requirements settled by the legislation.

The high administration expenses reduces the competitiveness of the sector, because the

companies need to spend a lot on administration instead of developing new products and

services or investing in marketing activities.

The main characteristics of the activities are the multiply, repetitive processes, where a single

data added and used multiply times during the business. Without an ERP system the managers

and other employees of the SMEs have no up-to-date knowledge about the performance, liquidity

and other relevant information, which are required for decision making and daily business

management. In order to be competitive on the market, they need to have a better control over

the costs. Based on the aforementioned characteristics, it is assumed that the SME sector

requires a cheap and innovative solution for business activities, such as accounting, sales or

purchase transaction processing, controlling or payroll.

The research involved the banks and bookkeepers as well. They are facing problems concerning

the SME sector. The bookkeepers need to do repetitive tasks due to the paper or excel based

SME administration. Almost all the transaction related processes done within a company should

be done again by the bookkeeper, which results a repetitive processing of the same data. It

increases the internal costs due to the time consumption, in the other hand the SMEs need to

pay more for the service and due to the price sensitivity do not buy other services from the

bookkeeper.

In the banking sector the aim is to decrease the costs concerning the financial transactions.

Instead of personal administration their aim is to increase the use of online banking services.

The banks are important elements of the SMEs daily business by handling their daily financial

flows and activities like transfers, cash, credit, investment management, and the data from the

bank are used for financial forecasting and parts of the bookkeeping.

1.1 Problem formulation

The project is expected to be partly financed by the EUREKA_HU_12 grant established by the

New Széchenyi Plan. The requirement concerning the application is a publication about the

project in an optional topic. The purpose is to fulfil the aforementioned requirement. The other

purpose of the project is settling down the main elements of the business model of the TDP-ERP

Gergely Balazs

December 2012 2

SME Cloud product launch. The complex product involves services provided by several partners;

therefore the planning of the model is important before entering to the market. The goal is to

evaluate the possibilities and create a basis for further agreements with the partners.

During the development phase the bank agreed with the concept, but the final decision has not

been made. There is no agreement with bookkeeping firms, and there is only verbal agreement

with Libra Software about the ERP system, which indicates the requirement of creating a basic

business model as a starting point of the agreements.

In order to fulfil the purpose of the project, the following problems should be answered:

What are the main values and benefits of a possible partnership?

How should be the business model of the TDP-ERP SME Cloud product?

1.2 Delimitation

The background of the project is a product development. The concept contains an ERP system,

as one of the most innovative part of a package offered by a bank. Deep description of the ERP

features is not a part of the project, since it is obvious nowadays in a business life. The features

and the advantages of the ERP is well known, the project is focusing on how the complex product

and its services can create value over the values of the single elements.

Within the pre-development phase focus group interviews has been made to develop the product

concept and measure the willingness of the bookkeepers participation. The analysis had positive

results, therefore the high level of willingness and interest are assumed in the project without

further analysis.

The developed product is planned to be sold on the Hungarian market. However the Consortium

contains the Polish Global Solution, the company is irrelevant in the product launch activities in

the domestic market concerning the sales activities. There is an agreement to develop and

launch the product on the Polish market based on the Hungarian results. This future plan is not

part of the project. Global Solution is introduced in the project as key partner within the

partnership as appreciating their quality and hard work in the product development.

1.3 Scientific approach

1.3.1 Choice of scientific paradigm

The chosen scientific paradigm is the social constructivism in the project. The explanation of the

main reason in a simplified way is first to understand the reality, and in the second part of the

project try to re-construct. The development of the business model first requires understanding

the status of the SME sector, the specification of Granit Banks’, the ERP developer’s and the

bookkeeper’s business. On the ontological level the reality is social construction. The aim during

the project is to know the reality, especially the areas for providing benefits not just to the clients

but also to the partners in order to create the model with the purpose of establishing win-win

situation. On the epistemological level the reality is acquired through the researcher, which is

therefore relative. Through the research methods and techniques the researcher should gather

enough information in order to understand the interests of the involved parties creating a basis

for the recommendations.

Gergely Balazs

December 2012 3

1.3.2 Choice of models and methods

The basis of the project is desk research supplemented by personal interviews and internal

communications. During the project the main research method is the qualitative, however for a

better understanding quantitative data are used as well. The reason of the interviews is the

reinforcement of the information gathered during the desk research.

The business model development requires focusing on value creation, individual strength of the

partners and their sales potential, especially the sales channel and the relationship between

their clients.

The analysis is structured as it follows in order to solve the problem:

1. Analysis of the SME sector

The importance of the SME analysis is to find out the market size of the sector using

segmentation and identifying the characteristics applying the PEST analysis. In order to find out

the needs of the SME sector the analysis is done concerning the following research question:

What is the size of the market?

What are the main characteristics of the SME sector?

2. Analysis of the bookkeeping sector

Within the product concept it is necessary to find the main characteristics of the sector. The

analysis covers the relationship between the clients and service providers, the range of offered

services and the elements of the sales strategy such as pricing and sales channels. During the

analysis the theories of relationship management and Porter`s Five forces model is used to

evaluate the competition. The research questions in this part are the following:

How is the competition in the bookkeeping market?

How is the relationship between the clients and bookkeepers?

3. Analysis of Granit Bank

The complex product will be a part of the product portfolio of Granit Bank. It is necessary to

analyze the strategy and the way of customer acquisition in order to find out if Granit Bank has

the established sales channel for selling the product. The research questions in this part are the

following:

What is Granit bank sales strategy?

What kind of channels the bank is using in order to acquire new clients?

4. Analysis of the ERP developers

The analysis covers the characteristics of the ERP developers with a strong focus on the sales

activities. It is important to find out whether the companies have sales channel and good

customer base. The research questions are the following:

What are the characteristics of the developers form the sales aspect?

5. Evaluation of relationship

The final part is built upon the result of the analysis of the stakeholders from the aspect of

relationship management. In this section it is necessary to analyse how the concept can be

improved by an established partnership. In this part Brennan`s partnership approach is used to

Gergely Balazs

December 2012 4

determine the values, benefits and the essence of the establishment. The research questions are

the following:

How the partners can create values and benefits by establishing partnership?

What are the required activities in order to sustain and improve the partnership?

1.4 Reflection

1.4.1 Quality Assessment and Source Criticism

Methods and models assessment

The analysis contains two main elements; it starts with investigating the individual level of the

stakeholders. The second part is the analysis of the possible partnership. The first part is

descriptive. The aim is to understand the main characteristics of the SME sector and business of

Granit Bank, TDP-ERP, Libra Szoftver and the bookkeeping industry. In the first part segmentation

is used to analyze the market potential regardless of industry. The SME sector is investigated

also from the managerial behaviour in order to get a clear picture. The analysis concerning the

bookkeeping industry focuses mainly on the relationship and the competition using Porter`s Five

Forces model.

Granit Bank is analyzed form the aspect of the growth strategy and the sales organization, while

TDP-ERP and Libra from the core competences and sales activities.

In the second part Brennans` partnership approach is used in order to analyze the values and

benefits of the possible partnership. The approach is ideal to find out how the partnership

creates values for both the partners and the customers. The findings are collected within a SWOT

table.

The applied models resulted enough information in order to understand the reality and based on

it reconstruct the business model.

Source assessment

The sources for the analysis are gathered via desk research and interviews. The used online

materials are from official entrusted sites such as KSH (Central Statistic Office), HFSA (Hungarian

Financial Supervisory Authority) or other company websites (K&H, Granit Bank). There is no

available statistical data concerning the competition on the IT market, which is a weakness of the

project. The interviews were done with two acknowledged person from the bookkeeping industry.

The credibility of their words is high. During the research and analysis in the online articles and

projects the author found the same statements than during the interviews. It strengthened both

the data and information gathered from online materials and from the interviews.

Validity and reliability

The research is mainly qualitative rather than quantitative. The results are valid; those answer

the question on a high extent. The research provides a good basis for collecting the findings and

makes the recommendation on a basis of those.

1.4.2 Process Reflection

At the beginning of the project it was hard to find relevant topic concerning the SME Cloud

Project, which can be useful for the company as well. The business model creation seemed to be

a good choice, but due to the business secret it was not allowed to use lot of the previously

gathered information. During the analysis I tried to use only relevant theories instead of adding

Gergely Balazs

December 2012 5

too much which are irrelevant concerning the main problem. The value creation of partnership

part was added only in the middle of the analysis into the problem statement, because I realized,

that the business model cannot stand without it. After all the final result is close to my

expectation, which was creating a business model as a basis for further agreement with the

partners. The time management of the project was definitely wrong, the project was finalized

more than 7 days after the planned deadline.

2. Product description

The product is developed by the consortium of the Hungarian TDP-ERP and the Polish Global

Solution. The product concept contains an ERP cloud system which includes online bank services

provided by Granit Bank and bookkeeping services offered by external bookkeepers. The basis of

the ERP system is the Libra S3 owned by Libra Szoftver designed for small and medium

enterprises. The system has a modular architecture which enables the clients to get a

customized product due to the requirements and company specifications. The TDP-ERP Cloud

system is planned to have only the most important modules, the billing, invoicing, cash register,

banking and stock modules. The speciality of the system is that the bookkeeping module can be

accessed by the bookkeepers and the reporting and features of controlling by both, the client and

bookkeeper. The implementation of the system does not require huge investments from the

clients such as internal server. The ERP is running on cloud system giving the ability to the

owners and managers to have access regardless of place. The only requirement is having a

computer, tablet or iPhone with internet connection.

The concept is linking together the elements, and provides a common online user web interface

for the different services, which makes easier solving the tasks of the company, and providing

good control and knowledge about the actual results, and business performance. As an

assumption in the complex, integrated product the users should only add a data once to the

system, which will be processed in different modules of the ERP. During the business activities

the added data can be viewed any time, and it will be used and modified during the processes.

The data required for bookkeeping will be withdrawn from the database and from the bank to

finalize bookkeeping, balance sheet, profit and loss account, income statement, VAT registry etc.

The bank provides the relevant data and sheets to both the ERP system for reporting and to the

bookkeeping firms. This solution reduces the process time, the costs, and gives a better control

to the managers over the company.

Gergely Balazs

December 2012 6

3 The main characteristics of the SME sector

3.1 SME categories

According to European Law “ The category of micro, small and medium –sized enterprises (SMEs)

is made up of enterprises which employ fewer than 250 persons and which have an annual

turnover not exceeding EUR 50 million and/or an annual balance sheet total not exceeding 43

million“ (2003/361/EC). The quoted definition is the general description of the SMEs. Within the

recommendation the micro, small and medium sized businesses are defined by the number of

employees and the turnover or balance sheet total:

Table 1: Displaying SME Categories

Category Employees Turnover Total Balance

Medium 50-249 ≤ EUR 50 m ≤ EUR 43 m

Small 10-49 ≤ EUR 10 m ≤ EUR 10 m

Micro 0-9 ≤ EUR 2 m ≤ EUR 2 m

Source: Adapted from 2003/361/EC

The used categorization in the Commission Recommendation was implemented by the Hungarian

legislation as well.

3.2 Size of the SME sector

During the analysis it is important to differentiate and calculate the amount of the registered and

the active companies. At the end of 2011 the number of the registered companies were 1,79

million (KSH, 2012). This amount contains both the sole proprietorships and joint ventures. In

2012 the number of sole companies were 1,06 million and the joint companies were almost 0,6

million. The amount of the joint ventures started to grow compared to the sole proprietorship

from the end of 2007 as a result of the reduction of minimum foundation capital from HUF 3

million to HUF 0,5 million concerning the limited liability company (Llc.) and from HUF 20 million

to HUF 5 million concerning the companies limited by shares (Plc.). The ratio of the registered

and active companies is approximately 30% of the sole and 66% of the joint companies. It results

approximately 317 000 active sole and 395 000 active joint ventures.

Table 2: Table Displaying the SME Sector in Hungary

2012 Sole Proprietorship Joint Ventures

SUM 317 000 395 000

Micro (%) 95,5 % 92 %

Micro (nr.) 315 415 363 400

Small (%) 0,5 % 6,6 %

Small (nr.) 1 585 26 070

Medium (%) 0,001 % 1,3 %

Medium (nr.) 25-30 5 135

Source: Own production

Gergely Balazs

December 2012 7

From the aspect of establishment, closure and bankruptcy the sector shows stagnation in the

last 7 years regardless the effects of the economical crisis (European Commission, 2012). This

result does not mean, that the Hungarian economy responded in a positive way for the crisis. The

number of the companies was stagnating before the crisis and during the last 5 years the

government made several actions in order to keep the number of the companies such as

maximizing the administration time for company establishment. After the regulation the

establishment could have been done within 1 hour. At the beginning of 2012 this rule has been

changed by requiring the prior control of the National Tax Authority in order to filter the founders

who had previously tax debt or whose activities were against the law. This action has a positive

effect on the sector; however it will decrease the amount of the established companies.

3.3 Characteristics of the SME Sector

The support and development of the Hungarian SME sector is a never ending story in the politics.

There have been many different attempts to improve reducing the competitive disadvantages of

the sector without breakthrough results. The sector is facing several problems, such as low

capitalization, lack of funding, circular debt and low efficiency and productivity. Often dealing with

administration tasks, which exceeds their resources (KSH, 2011). The analysis of characteristics

includes the political, economical, social aspects.

3.3.1 Political factors of the SME sector (Political)

The government is aware of the importance of the SME sector. It actively supports the sector by

establishing guarantee funds in order to bear the risks with the banks in case the SME cannot

repay the loan. Another funding alternative is the grant, which contain European and Hungarian

sources. Generally the SMEs can apply for grants with support intensity vary from 20 up to 100 %

for innovation, research and development, organization development, market entry etc… The

positive aspect of the grants are that the investment is only partly financed by own resources.

3.3.2 The financial situation of the SME sector (Economy)

In the Hungarian market, as general in the other European countries, the strongest player is the

SME sector. On the labour market 74 % of the 2, 7 million people are employed by SMEs. The

micro sized companies are dominating in the employment rate covering 51-54 % of the overall

employment, followed by the small and medium sized enterprises with 21-24 % (KSH, 2011). The

SME sector is important concerning the Hungarian Gross Value Added (GVA) with its 56% of the

overall output. The difference between the sole proprietorship and the joint ventures in the sector

can be shown by the revenue; the joint ventures resulted HUF 41 600 billion, while the sole

companies only HUF 2 065 billion.

Governmental intervention concerning the consumer debt in foreign currency hit negatively the

SME sector in 2012. In the previous years the Hungarian banks offered CFH based loans to

households with lower interest rate than the HUF loans. The crisis affected negatively the

economy and increased the risks of repayment. “The financial crisis in the euro zone led to

increased sovereign risks, which in turn brought significant growth risk premiums and

contributed to the major appreciation of the CFH against the euro”( Hungarian Financial

Supervisory Authority, 2012).

The amount of the debt dramatically increased, many households could not pay the loan. The

government set the CFH-HUF exchange rate below the real market rate and let the households

Gergely Balazs

December 2012 8

repay the loan on the basis of the fixed rate. Another regulation allowed the change of CFH loans

to HUF loans using the above mentioned rates. The intervention had two results; first of all the

bank sector suffered losses, second the households used their savings in order to pay the debt,

which decreased the demand for goods on the market. The SME sector as suppliers is still

suffering from the bad market environment and conditions.

In the SME sector the capital supply is low, the companies are often underfinanced. In many

cases the efficiency and productivity are low. Of course in the financial situation the mentioned

lack of managerial business knowledge has also a negative impact. The Hungarian companies

are producing mainly to the domestic market; therefore the unstable economy has also a bad

impact on the sector. The SMEs are normally financing themselves internally by reinvesting the

yearly profit, because it is hard for them to get a bank loan. Due the negative market conditions

and concerning the size and management knowledge of the micro and small companies, the

banks evaluate the lending as high risk activity (KSH, 2011).

3.3.3 Managerial characteristics (Social)

In the SME sector it is common that the owner cannot differentiate the company interest with the

own interest. The company income often viewed as a personal. It means that running a business

is always self-interest; the goal is to increase the personal income instead of the revenue of the

company. It affects negatively the basic financial management knowledge by lack of

differentiating the accounting and financial approach. The main objective of the owners is to

increase the expenses and reduce the invoiced revenue in order to pay less tax and increase the

“grey income” (Harkai, 2012). This management attitude has a negative impact on the economy

by strengthening the black market. The mentioned behaviour also affects the performance

measurement and results companies with limited or zero profits.

The background of the problem is the lack of managerial and business knowledge in the sector.

Normally a company is viewed as temporary cash cow without long run planning and strategies.

In the business life a common mindset to optimize the resources and decrease the costs,

however in the Hungarian SME sector, especially in the micro segment the aim is to increase the

costs in order to reduce the tax to be paid.

Some of the SMEs are running without strategic or financial plans. Often it is experienced that

managers and owners have a limited knowledge of the actual business performance of the

company. This affects negatively the planning, managing and decision making activities

(Demcsak & Harkai, 2012). The lack of business knowledge also negatively affects the liquidity of

the companies, which often ends up with insolvency or bankruptcy. This is one of the main

reasons of the circular debt in the economy.

According to the theories of management planning and control systems, one of the main

problems within the SME sector can be demonstrated. The main purpose of the management

control systems to use the resources and assets in an effective and efficient way. The control

activities are only small parts of the overall system. First of all the managers should know the

company, its capabilities and resources, which gives a basis for strategic planning. Of course a

good strategy requires knowledge about both; the external and internal characteristics and

elements. Some of the Hungarian companies, especially the micro and small enterprises are

already failing at the first step by having limited knowledge of the company (Balazs & Guangyu,

2012).

The business strategy is always designed on the basis of actual or present status of the

organization, however the contents of the strategy is always something predicted or forecasted; a

Gergely Balazs

December 2012 9

wanted future direction and status. In order to increase the effectiveness of the strategy,

managers often add objectives and targets, which can be measured during the period of the

strategy. Those can be budgets, forecasted or targeted results etc... The essence of the control

system is measuring the results, evaluating those according to the planned and initiating actions

in order to react due to the variance between the actual and the planned. It is more than obvious

that the strategic planning and management control activities require elementary business

knowledge or intelligence, which is not really common in the Hungarian SME sector.

3.3.4 ERP systems in the SME sector (Technological)

Within the segment of large firms, the ERP usage is covered 100%, in the SME sector it is only

40% (Toth, 2009). The ERP penetration is approximately 68 % in the medium, 21 % in the small,

and 4% in the micro sized enterprises sub-sectors.

Figure 1: Frequency of ERP usage within the SME sector

Source: Own production

It can be assumed the frequency of using ERP system is increasing by the size of the enterprises.

The cause is related to the growth of the organization and the internal characteristics such as

financial background or the amount of different business processes. A small or micro companies

cannot afford and do not require complex ERP solutions. In the medium sized sub-sector the

companies are using integrated solutions for covering 5-6 processes, in the small sized sub-

sector the result is only 1-2 (Fekete, 2009).

3.4 Conclusion of SME sector

The SME sector has a strong economic power in the Hungary. There are more than 600 000

active SMEs, which gives a big market potential. In the last few years the financial crisis affected

negatively the sector. The SMEs are producing mainly for the domestic market. The private sector

used their savings for paying back the loan which result a decrease in the market demand. The

government tried to intervene in order to strengthen the competitiveness of the sector with

insignificant success. The sector depends on the bank loans and different EU funding schemes in

order to finance the investments. The managers are lacking business knowledge in the SME

Micro enterprises

Small Enterprises

Medium Enterprises

Gergely Balazs

December 2012 10

sector especially in the subsector of micro sized companies. The ERP penetration within the

micro and small sub-sector is relatively low, which is definitely positive concerning the SME cloud

project.

4. Bookkeeping and accounting

The difference between the meaning of bookkeeping and accounting should be described in

order to have a better understanding. From the side of the activities, basically there are four

entities:

Data register: Person who adds and registers the data in the bookkeeping system

concerning the transactions of the companies.

Bookkeeper: The bookkeeper is responsible mainly for making reports, books and ledgers

according to the Act C of 2000 on Accounting.

Accountant: The accountant has wider tasks and responsibilities than the bookkeeper.

The accountant is analysing and evaluating the financial data and creates information

from those. In a medium size company the accountant deals with financial strategies,

costing systems or controlling.

Auditor: The auditor is examining the accounting system and the outputs from the

aspects of validity, reliability of the information and the activities from a legal point of

view.

In the Hungarian system there are internal and external bookkeepers and accountants. It

requires the differentiation and explanation of the two systems.

4.1 Internal bookkeeping and accounting

The internal bookkeeping contains all the activities concerning data registry, accounting and

bookkeeping within the company. Depending on the size of the organization the tasks of data

registry, bookkeeping and accounting might be done by a single or several persons. On the

Hungarian market these kinds of companies are mainly using ERP system in order to reduce the

cost and other resources of administration activities. The internal bookkeeping and accounting is

not relevant for the introduced SME product.

4.2 External bookkeeping

The micro and small sized enterprises mainly outsource the bookkeeping to external

bookkeepers. The data registry and accounting is done internally, and the reports, books, ledgers

are created by the external bookkeeper according to the legal requirements. As a matter of fact

within the sub sector of micro and small enterprises the spread of ERP systems are very low; only

approximately 4-5% of the active companies are using those (Toth, 2009 p.1). It has a negative

impact on the administration processes, because first the invoices, bills are manually (paper

based) registered within the company, and the transactions registered again at the external

bookkeepers in order to create the reports, books and ledgers. The accounting related activities

are mainly done by the manager or owner of the SME, but as it has been written due to the low

level of business and managerial knowledge the main activities such as financial planning or

control are basically undone.

Gergely Balazs

December 2012 11

4.3 The range of provided services

The external bookkeepers are providing the companies mainly with the basic services required by

the law. All the companies in Hungary should create statements about the operations, asset,

financial and income situation at the end of each business year (2000/C, 2012). The format of

the statements depends on the NET Income, Balance and number of employees. According to the

regulations the bookkeeping activities should be done by authorized and registered bookkeepers

or accountants except for companies having less than HUF 10 million Net income in the previous

2 years.

The audit service is compulsory for companies using double-entry bookkeeping, except the net

income was under HUF 200 million, and the number of employees was less than 50. The

government is planning to increase the amount of minimum net income for the next few years,

which will reduce the amount of companies require compulsory audit. It will have an effect on the

bookkeeping market, because some of the auditors might start doing bookkeeping also.

4.3.1 Provided services of the external bookkeepers

The bookkeepers are providing basic and additional services. The basic services mainly cover the

requirements given by the law concerning SME administration obligations of reporting and tax

admit.

Figure 2: Bookkeeping services

Source: Own production

The provided service depends on the service contract. Often the SME clients require more for the

price than the basic services, especially consultation and business advices. The bookkeepers

defend themselves by providing the services described in the contract, not more and not less. For

additional services the client should pay extra. Often the clients turn to the bookkeepers before

establishing a company in order to get relevant information concerning the possible company

forms and the tax liability (Harkai, 2012).

4.4 Market size of the bookkeepers

The market size of the registered and authorized bookkeepers is approximately 65 000 in

Hungary, there are 32 000 companies doing bookkeeping as main business activities (NGM,

2012). According to the law the authorized bookkeeper should have an accounting related

diploma and 3 years of experiences within the field of bookkeeping, accounting or controlling. In

order to follow up with the legal changes concerning the accounting rules, the registered

Gergely Balazs

December 2012 12

members should participate on a compulsory accounting course once a year (200/C, 2012). The

registration of the bookkeepers is done by the Ministry of National Economy.

According to the amount of active companies and the bookkeeping firms, there are

approximately 20 companies for a bookkeeping company in average. This result however does

not show the clear picture of the market, because there are many unregistered bookkeepers

working on the Hungarian market (Harkai, 2012). The result was calculated from the number of

active companies, which contains the enterprises with less than HUF 10 million net income.

These companies, at it has been written before, does not require registered and authorized

bookkeeping services, often the owner or one of the employees is dealing with the bookkeeping

and other administration related tasks. It can be concluded that less than on average a

bookkeeper has less than 10 clients in average. In practice the number of clients depends on

many factors like type or size of the company, financial details, number of employees, number of

invoices, recipes etc... (Cieleszky,2012).

4.5 Pricing strategy

Before the analysis of the pricing it is important to differentiate the two most common types of

bookkeeping companies. On the Hungarian market according to the bookkeepers there are

“dabblers” and bookkeepers. (Harkai, 2012) The first one is registering the transactions into the

book, and simply withdraws the different reports from the bookkeeping software. The aim is to

reduce the time spent on the bookkeeping activities for the companies, regardless the quality.

The real bookkeepers are doing quality bookkeeping; the transaction registering is only the basis

of the real task. The aim is always to reduce the amount of tax obligation, and provide the

authorities and the owner with correct reports according to the legal requirements. This is why it

is often said that the business performance of a company always depends on who is doing the

bookkeeping. The theoretical and practical knowledge concerning the accounting law is

important within the bookkeeping business.

The bookkeeping companies are using special pricing. The main factors affecting the price is the

time spent on the service activities and the sympathy of the owner (Harkai, 2012). Of course

other factors are also relevant such as receiving the data on paper base or by ERP system, but

normally these are the matters of time consumption. The sympathy is an uncommon specialty

compared to other businesses. The reason is basically the establishment of partnership between

the company and the bookkeeping firms, which will be described in the next section.

There are two main price setting strategies in the industry; the “dabblers” or low-price companies

mainly try to keep the price as low as possible. They are using fixed, menu-based pricing

depending on the company form, number of invoices, recipes per month. These kinds of

companies are taking strong online marketing effort in order to acquire clients (Cieleszky, 2012).

The price of the basic bookkeeping service starts from HUF 5 000, which implies that high quality

cannot be expected. In order to keep the price low, the companies are reducing their costs and

the time spent on the activities. The bookkeeping due to the saving has a low quality and it is

more transaction recording then a classical bookkeeping. Often the office is placed at the private

residence or in a garage in order to reduce the costs (Harkai, 2012).

The other type of bookkeeping companies provides high quality services to the clients. The basic

monthly fee depends on the financial results, size, form and industrial category of the SME. The

price is not fixed; the bookkeeper is arbitrary setting the price by considering the required time

consumption of the service. The behaviour and sympathy of manager or owner of the company

has a huge impact on the final price. Often the bookkeeper is overpricing the service in case of

Gergely Balazs

December 2012 13

lacking sympathy (Harkai, 2012). This is a method of customer relationship management, where

as a starting point it is important to find the right customers.

These kind of bookkeeping firms do not spent huge marketing effort in order to acquire new

clients. Normally the satisfied clients recommend the service to other businesses; which enables

the bookkeeping firms acquire new clients in a way of word by mouth marketing.

4.6 Relationship and partnership

The typical client bookkeeper relationship is built up on trust, which is also the basis of the long

term commitment. Often it is said, that the main reason of the close relationship is that the

bookkeeper knows all the financial details and “tricks” done for the client concerning the reports,

books, ledgers or tax admit, therefore the owner does not want to take the risk by leaving the

bookkeeper (Herczeg et al. 2012). The clients are cancelling the service contract in case of

mistakes in the bookkeeping, lack of communication and consultancy, bad overall quality of the

service and loss of trust (Demcsák & Harkai, 2012). Due to a research 95 % of the SME owners

would change the bookkeeper in case of loss of trust, which clearly shows the most important

element of the relationship (Herczeg et al., 2012).

The other reason of the long term relationship is the aspect of quality. There is no basis for

comparing the services on a basis of quality. Until the SME is not charged by the tax authority

because of mistakes in the reports or late delivery, the bookkeeper is assumed to provide a good

service, even if there are quality differences concerning the outputs (Harkai, 2012). The practical

and theoretical knowledge of the bookkeeper affects the quality of the output and the amount of

taxation. In this manner an SME can save a lot finding the ideal bookkeeper. There is no basis for

measuring the quality on quantitative data, which is the reason why the SMEs are finding the

bookkeepers by word-by-mouth (recommendation of business partners).

The relationship between the SMEs and the bookkeepers is strong with the aim to create

partnership. The companies rely on the work of the bookkeepers and their advices concerning

taxation, legal or financial problems. The knowledge of the bookkeepers is useful for

compensating the lack of business and managerial intelligence of the owners and leaders of the

SMEs. The described partnership is not that simple as it has been described. There is a

misunderstanding concerning the pricing and provided services between the SME and the

bookkeeper. The owners and managers expect consultancy and advices for the price they are

paying for the bookkeeping; however those are additional services, which are not part of the

basic price. The service contract clearly states what the price covers, but still the owners require

more services. This is one of the weaknesses of the partnership.

According to theory of creating customer relationship management the bookkeeping companies

are trying to select the most valuable customers. The evaluation is done basically on the financial

aspects such as profitability or the cost of serve the clients (Huth&Speh, 2010). In this manner

the bookkeepers often decide not just on financial aspect but also on the subjective personality

as it have been described at the pricing strategy. However it sounds a bit strange, by thinking it

over the bookkeepers would like to establish long term relationship between the clients. The long

term commitment increase the potential future benefits for both of the parties, therefore it is

reasonable to eliminate those clients who are unable to fit into the requirements of cooperation.

Gergely Balazs

December 2012 14

4.7 Competition on the bookkeeper market

The competition on the market is analysed using Porter’s Five forces model. The competition in

the industry is affected by potential entrants, bargain power of the buyers and suppliers and

substitute services. The model is useful to demonstrate the specialities of the bookkeeping

market.

Figure 3: Competition in the market

Source: Adapted from Porter (2008)

Force 1: Barriers to entry

The entry is easy and requires low resources. According to the law in order to work as a

registered and authorized bookkeeper the requirement is accounting related education and 3

years of experience. From the cost aspects at the beginning the office can be located at the

home residence of the bookkeeper. The biggest expense is buying the accounting software,

which consists of basic entry fee and monthly payment for the licence. As a summary entering to

the market is quiet easy and does not require large investments. The loyalty of the clients is high;

therefore starting a bookkeeping company is done by penetration pricing strategy offering the

services at fixed low prices or by taking the existing clientele from the previous bookkeeping firm.

Due to the mentioned main characteristic; the relationship is strong between the bookkeeper

and the client who are following the person in case of opening a new company.

Force 2: Threat of substitute service

The offered main services of the bookkeepers are the same. Those differs only on the basis of

price and quality, however the last one is hard to measure. The bookkeeping firm is bearing the

switching cost in case the client is changing the service provider. In practice it is easier for the

bookkeeper to redo the books, reports and ledgers in the middle of the financial year than

continue the work of the previously contracted company.

Force 3: Bargaining power of the clients

The clients are looking for quality or price. The low price bookkeeping companies are mainly

providing services to micro sized enterprises, while the quality is important for the small and

Competition within the Industry

Potential Entrants

BuyersSuppliers

Substitute services

Gergely Balazs

December 2012 15

medium sized businesses. The price is only fixed at the low price bookkeeping firms, while the

other service providers evaluating the price based on different aspects. The clients by evaluating

the competitors often ask for recommendations from the business partners in order to find the

ideal bookkeeper and to be sure concerning the quality. The clients do not change often

bookkeeping company, because of the built up trust and also evaluating the risks of changing for

lower quality service. The client migration is not common in the industry.

Force 4: Bargaining power of the suppliers

On the market the bargaining power of the suppliers is strong; the bookkeeping companies can

afford to evaluate the client and pricing the service on a basis of client behaviour. However there

are more than 60 000 registered bookkeepers and 32 000 registered bookkeeping firms in

Hungary, and the offered services are the same the bargaining power is strong. This is a

deviation from the other industries. As it has been written before, even if there are other

companies offering the same service, due to the recommendation from business partners the

SME does not want to take the risk to try an unknown bookkeeping company. There are attempts

to somehow measure and improve the bookkeeping companies from the aspect of quality. The

Association of High Quality Bookkeepers continuously makes success by providing trainings,

education and newsletter in order to increase the quality of the member companies. The

association has more than 120 registered members. This number rapidly increases month by

month (Harkai, 2012).

Force 5: Competition within the industry

The competition within the industry is specific; there are lots of companies providing standard

services which make strong rivalry between them. Within the industry there is no clear

differentiation strategy in a manner of differentiating the services from the others. The aim of the

quality bookkeepers is to increase the client satisfaction. Some of the bookkeeping firms does

not even have a website, and do not spend on marketing (Cieleszky, 2012). The word-by-mouth is

enough marketing for them in order to acquire new clients. The companies are put efforts on

keeping the existing clients, however on the other side the clients are rarely changing the

bookkeeping firm.

4.7 Conclusion of the bookkeeping sector

The bookkeeping is an important element of the SME administration activities. Due to the legal

requirements there are services can only be provided by the bookkeepers such as making

reports, books, and ledgers. The sector offers other services as well, since they are financial

experts. However they offer the same services, those differ by price and quality. The competition

in the market is strong. Some of the bookkeeping companies try to differentiate themselves by

the quality of the service; however it is hard to measure it. The companies take huge effort to

have a good reputation, because rest of the new clients are acquired based on the

recommendation of the existing ones. There is normally a strong relationship between the

bookkeeper and the SME, switching service provider happens only in case of strong

dissatisfaction. In general the SMEs do not want to take the risk of finding a new bookkeeper,

since the quality is unknown; therefore there is a risk to change the bookkeeper for another one

with lower quality. There is a need in the sector for differentiation and a potential to offer

extended services such as consultancy.

Gergely Balazs

December 2012 16

5. The characteristics of the Hungarian bank sector

The economic crisis affected the banking sector also. In the past 13 years 2011 was the year,

when the sector suffered first time losses. The reason of the negative performance was the

repayments of foreign mortgage loans on a fixed HUF-CFH exchange rate, the rising of bad loan

provisions and the implemented industry taxes. The banking sector reacted on the market

changes in different ways. Some of the banks decided to reduce the costs by closing branches,

and started to follow the trends and focus more on developing the online banking solutions. Due

to the fact that only approximately 8,9 per cent of the Hungarian bank system is owned by the

Hungarians, it is obvious that the foreign owners like UniCredit Group SpA, Intesa Sao Paolo SpA,

Raiffeisen Bank International AG or Erste Group Bank AG are more cautious investing or

developing radical new solutions and services in Hungary (Bloomberg, 2012).

The decline in the Hungarian economy hinders the demand for financial products, and in this way

affects negatively the profitability, quality of the portfolios of the banks, and making the financing

possibilities more limited and expensive. As a matter of fact it has a negative impact on financing

especially lending to the SME sector. In the private sector the result of the crisis, especially the

repayment of the bank loans, and due to the decreasing real income by the inflation decreasing

the consumption on the market. The effect of this in the bank and SME sector is the decreasing

SME investment activities which results decreasing lending activities for the banks (HFSA, 2012).

As a result of the declining lending services it is important for the banks to find new services and

acquire customers or reduce the internal costs in order to maintain the profitability or at least

reduce the losses. Within the industry the banks follows the international trend of providing

online banking solutions, and in a way switching from personal administration to online. This way

is definitely reduces the overhead costs of the banks by requiring less branches. All the banks in

the Hungarian market offer e-banking solutions for private and business clients. For the larger

enterprises using SAP, Oracle or Microsoft ERP system it is possible to connect directly to the

banking interface and execute the transactions. The rest of the SME sector is still managing and

executing the transactions manually.

5.1 Strategy of Granit Bank

Granit Bank is a fully Hungarian owned bank placed in Budapest. The bank is part of the Demjan

Group of Companies. In 2010 the Magyar Tőketársaság Zrt. (Hungarian Capital Company cPlc)

bought the Milton Bank. The new management implemented new strategy with a main focus on

the SME and private sector. The bank has only one branch; however it built up partner

relationships with companies like Brokernet, KPMG, Hungarian Development Bank Plc. which are

acting on the market as banking agents (Granit Bank, 2012b). The main reason of having one

branch is a cost saving decision and the overall philosophy which says; provide the clients with

more service cheaper than the competitors. According to the “one-branch-strategy” it is quiet

important to improve the online solutions, and implement better or cheaper services to be

competitive with the other banks in Hungary.

The bank is focusing on acquiring customers; the applied pricing strategy is the penetration

pricing. The charges and fees of the banking services are the lowest on the Hungarian market.

The prices might be raised when the bank gained enough market shares. Granit Bank tries to

differentiate the products and services and focus on innovation. It was the first bank

implementing real time virtual customer support using web-cameras. The strategy is continuously

focusing on IT development, and creating new services for the customers and clients.

Gergely Balazs

December 2012 17

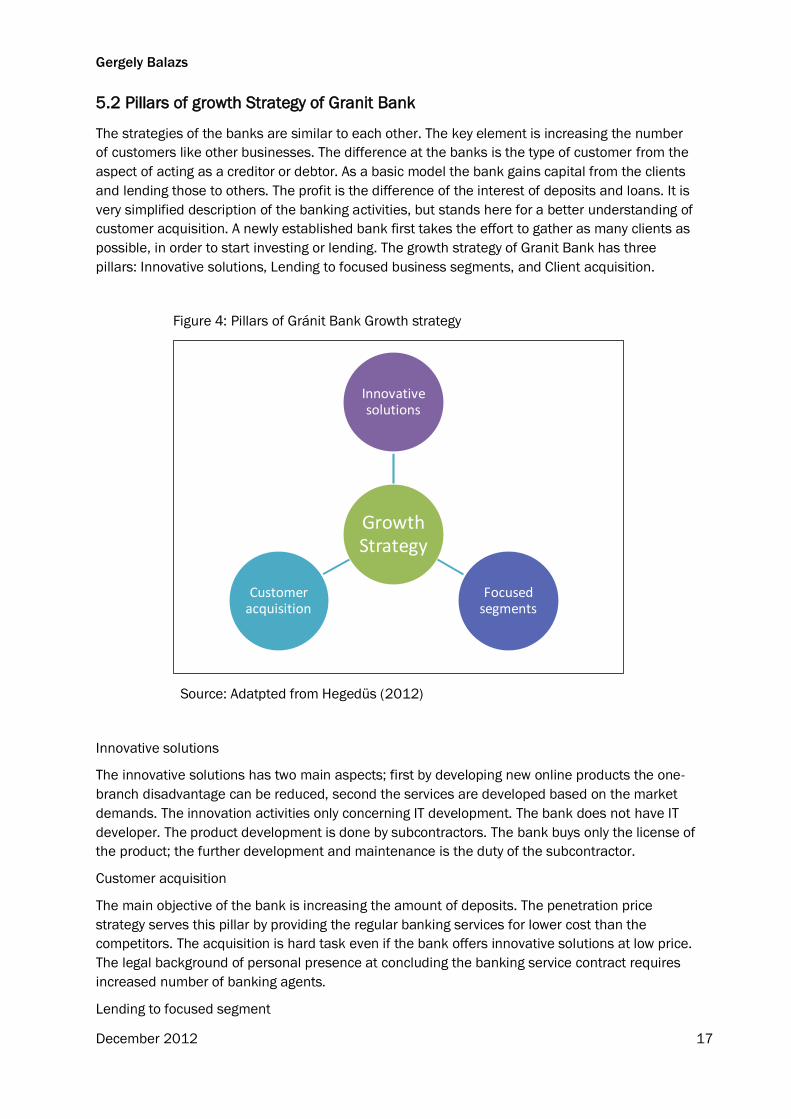

5.2 Pillars of growth Strategy of Granit Bank

The strategies of the banks are similar to each other. The key element is increasing the number

of customers like other businesses. The difference at the banks is the type of customer from the

aspect of acting as a creditor or debtor. As a basic model the bank gains capital from the clients

and lending those to others. The profit is the difference of the interest of deposits and loans. It is

very simplified description of the banking activities, but stands here for a better understanding of

customer acquisition. A newly established bank first takes the effort to gather as many clients as

possible, in order to start investing or lending. The growth strategy of Granit Bank has three

pillars: Innovative solutions, Lending to focused business segments, and Client acquisition.

Figure 4: Pillars of Gránit Bank Growth strategy

Source: Adatpted from Hegedüs (2012)

Innovative solutions

The innovative solutions has two main aspects; first by developing new online products the one-

branch disadvantage can be reduced, second the services are developed based on the market

demands. The innovation activities only concerning IT development. The bank does not have IT

developer. The product development is done by subcontractors. The bank buys only the license of

the product; the further development and maintenance is the duty of the subcontractor.

Customer acquisition

The main objective of the bank is increasing the amount of deposits. The penetration price

strategy serves this pillar by providing the regular banking services for lower cost than the

competitors. The acquisition is hard task even if the bank offers innovative solutions at low price.

The legal background of personal presence at concluding the banking service contract requires

increased number of banking agents.

Lending to focused segment

Growth Strategy

Innovative solutions

Focused segments

Customer acquisition

Gergely Balazs

December 2012 18

In order to keep the high quality of the lending portfolio the bank targets reliable SMEs, and

stable large sized organizations with governmental guarantee. The lending as it has been written

requires a careful evaluation of the clients. The present status of the SME is evaluated on the

basis of different financial ratios from books, reports and ledgers made by the bookkeepers.

5.3 Sales channels of Granit Bank

The bank acquires customers through different sales channels. First of all Granit Bank has one

branch which also works as headquarter. In November 2012 a new customer centre was opened

in the WestEnd City Centre. The features of the centre are limited and not similar to a regular

branch; it does not offer cash related and other classic banking services. The future client can

get information about the services, and conclude banking agreement within few minutes. The

other sales channels are the contracted companies which are acting on the market as banking

agents such as Brokernet or KPMG. The client visiting the office of the previously mentioned

companies and getting information or can conclude banking agreement. The partner businesses

are receiving fixed commission after each new client. The final channel is acquiring clients by

phone call or online application. In these cases a bank representative is visiting the future client

at his/her workplace or home in order to conclude the contract (Granit Bank, 2012).

Due to the law it requires personal presence and verification for opening a bank account and

establishing the agreement. This is the main barrier of the fully online expansion and customer

acquisition strategy of Granit Bank and other banks. The bigger banks such as OTP, Raiffeisen,

Unicredit, K&H or GE have the infrastructure for acquiring new customers by local branches at

several geographic locations in Hungary. K&H bank has more than 200 (K&H, 2012) while OTP

has more than 400 (OTP, 2012) branches in Hungary compared to Granit Bank, which has only

one.

5.4 Channel expansion

According to the Act on Credit Institutions and Financial enterprises, there are two types of

activities. The first group contains financial services, which can be provided only by financial

institutions. The second is the supplementary services including the banking agents. There are

two types of banking agents:

a, The agent acts on behalf of the bank. The bank is liable for the activities of the agent, who is

providing financial and supplementary services.

b, The agent is promoting the financial and supplementary services provided by the bank. The

bank in this case is not liable for the activities of the agent.

The main purpose of using agents in the bank sector is to increase the financial related activities

and give the possibilities to the bank to acquire more clients.

5.5 Conclusion of the bank sector and Granit Bank

The Hungarian bank sector was hit by the economic crisis. The banks acted in different ways on

the effects of the negative market atmosphere, but for all of them the cost reductions became an

important element. Granit Bank is relatively new on the market. The main objective of the bank is

to acquire new clients; however it has only one branch. The bank offers innovative online

solutions to the targeted segments and low prices due to the penetration pricing strategy. The

customer acquisition is done by online advertisements, internal sales representatives and

banking agents allowed by the law. The bank does not have extended sales channels, which is a

Gergely Balazs

December 2012 19

weakness concerning the fact, that the SME Cloud product is planned to be a part of the Granit

Bank portfolio.

6 IT sector in Hungary

On the Hungarian market both the international and national ERP developers sell products. The

large international IT companies such as Oracle, Microsoft and SAP covers the ERP market in the

large sized companies sub-sector. The key players in the SME sector are SAP, Progen, Microsoft,

Epicor, Libra Szoftver, Infor, QAD (Fekete, 2009).

Due to the fact of the amount of micro and small firms there is a good market potential within the

SME sector for small ERP systems with modular architecture. The IT industry has a good sales

perspective in Hungary. Approximately 68% of the companies within the SME sector are planning

development investments in 2013. Concerning the intention of the investments the IT

developments are on the first place since about 30% of the SMEs are planning such an

investment (K&H, 2012b).

6.1 Financing ERP implementation

The main barrier of the ERP implementation in the SME sector is the price. The sector is price

sensitive concerning the costs of developing the IT infrastructure. A regular ERP system requires

additional costs such as hardware costs (servers), additional wages (IT developers), and the

expenses concerning the training of employees. In Hungary the IT implementations are financed

mainly by three different sources:

own source

loans

EU/Governmental grants

The most popular of the sources is the EU/Governmental grants offered within the New

Széchenyi Plan (hereinafter referred to as NSZP). The action plan is ending in 2013. The main

purpose of NSZP is strengthening the economy and increasing the employment. Within the plan

several grants were established concerning the development of business environment. The SMEs

can apply for grants covering from 25% to 70% of the overall expenses depending on the

company size, financial background and the expected increase of employee rate and revenue.

Companies prefer the grants compared to the bank loans and -due to the liquidity matters within

the sector- to own sources.

The micro and small sized enterprises do not require the implementation of expensive ERP

systems. Even if they choose the grants to finance the implementation, they can use only limited