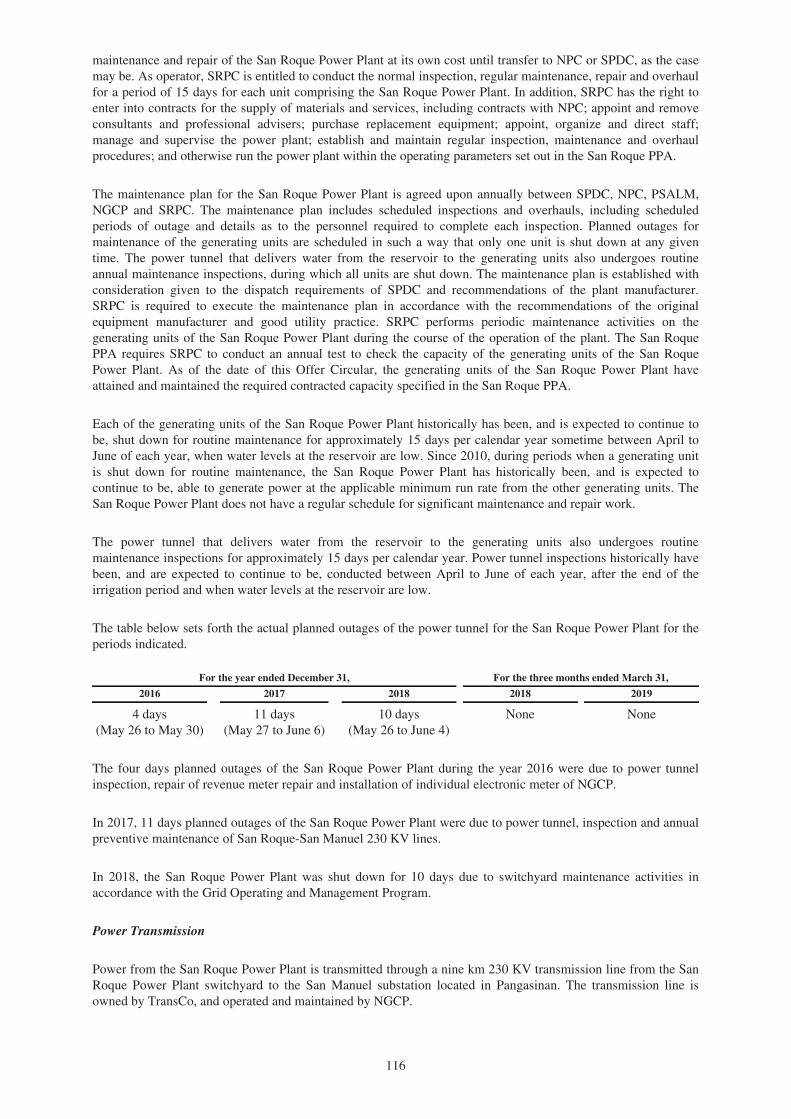

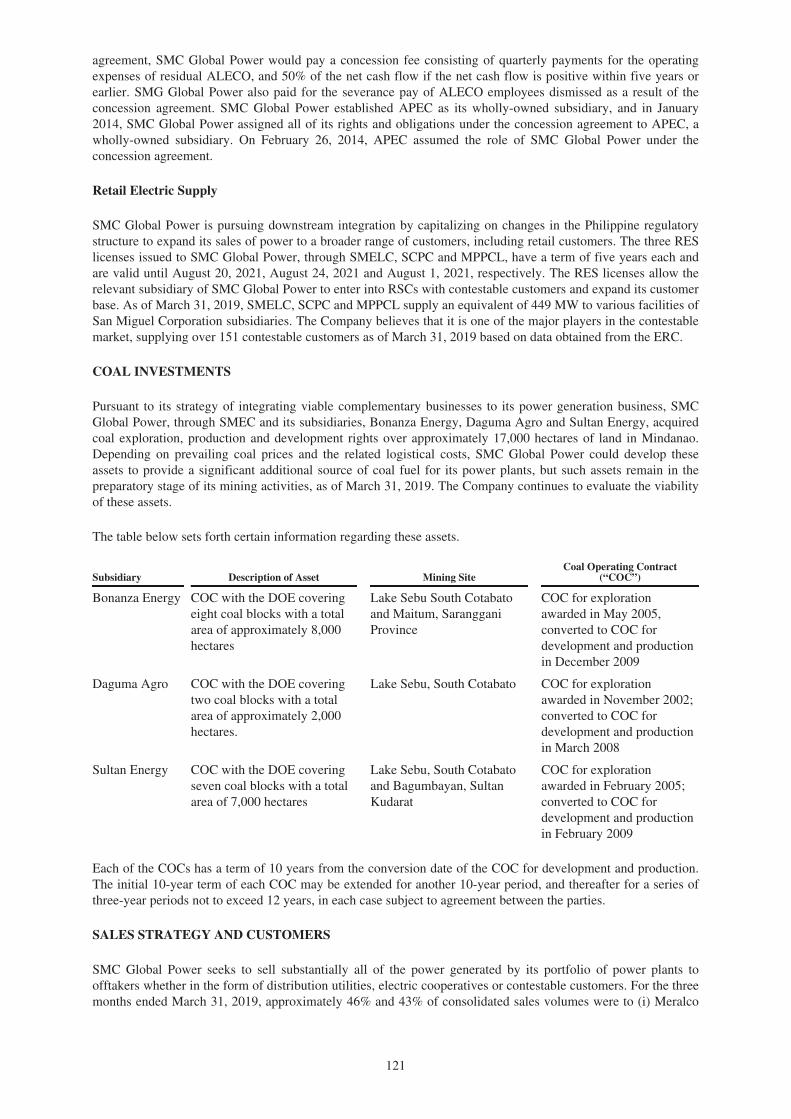

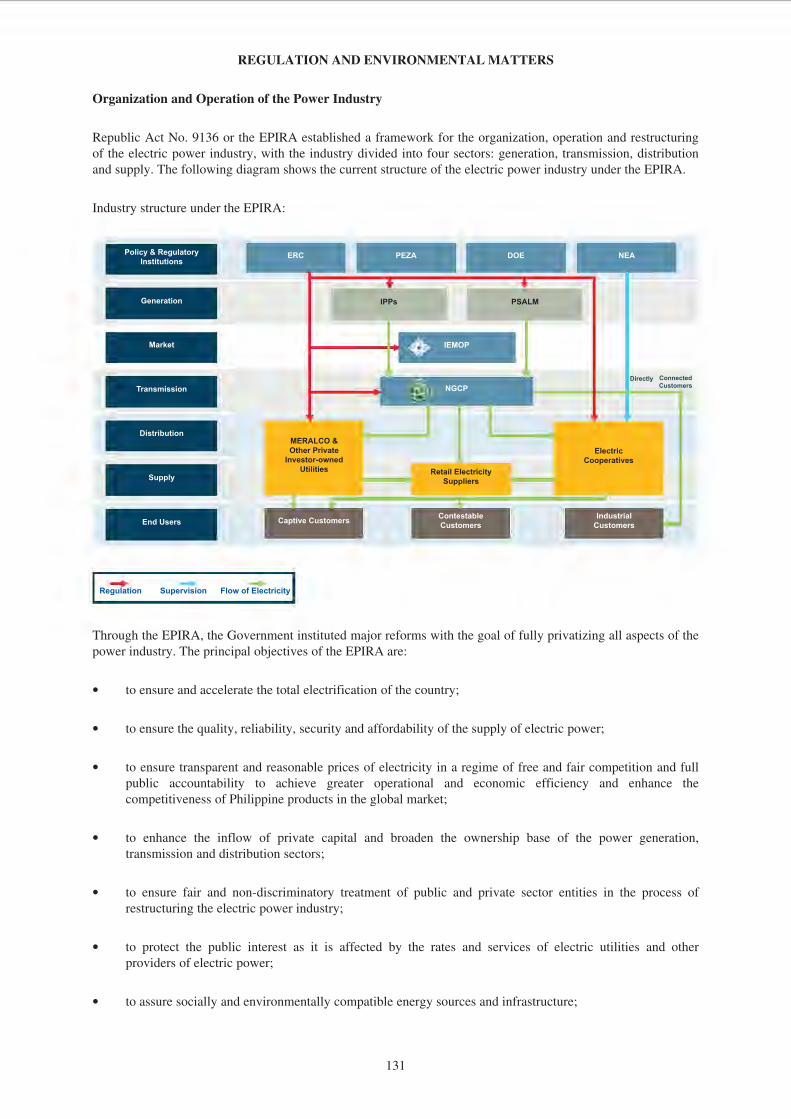

SMC GLOBAL POWER - PDS Group

417

25 June 2019 ii SMC GLOBAL POWER Philippine Dealing & Exchange Corp. 37 th Floor, Tower 1, The Enterprise Center 6766 Ayala Avenue corner Paseo de Roxas Makati City Attention: Atty. Joseph B. Evangelista Head - Issuer Compliance and Disclosure Department Gentlemen: Further to the disclosure of SMC Global Power Holdings Corp. (the "Corporation") dated 25 April 2019, on the issuance of the US$500,000,000.00 Senior Perpetual Capital Securities (the "Original Securities"), we advise that the Board of Directors of the Corporation, on 25 June 2019, authorized the issuance by the Corporation of additional senior perpetual capital securities, in an aggregate principal amount of at least US$200,000,000.00 (the "Additional Securities"), to be consolidated and form a single series with the Original Securities. A copy of the preliminary offering circular for the offer of the Additional Securities is attached herewith as Annex "A". The Additional Securities will be identical in all respects with the Original Securities, other than with respect to the date of issuance and issue price. The net proceeds from the issuance of the Additional Securities will be used and applied by the Corporation for general corporate purposes, investments in power-related assets and repayment of indebtedness. The Additional Securities will be constituted by a Supplemental Trust Deed, which shall supplement the trust deed of the Original Securities, and listed in the Singapore Stock Exchange (SGX-ST). Thank you. Very truly yours, SMC GLOBAL POWER HOLDINGS CORP. By:~ EL,ENITA D. GO Cdrporate Information Officer

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of SMC GLOBAL POWER - PDS Group

25 June 2019

ii ~

SMC GLOBAL POWER

Philippine Dealing & Exchange Corp. 37th Floor, Tower 1, The Enterprise Center 6766 Ayala Avenue corner Paseo de Roxas Makati City

Attention: Atty. Joseph B. Evangelista Head - Issuer Compliance and Disclosure Department

Gentlemen:

Further to the disclosure of SMC Global Power Holdings Corp. (the "Corporation") dated 25 April 2019, on the issuance of the US$500,000,000.00 Senior Perpetual Capital Securities (the "Original Securities"), we advise that the Board of Directors of the Corporation, on 25 June 2019, authorized the issuance by the Corporation of additional senior perpetual capital securities, in an aggregate principal amount of at least US$200,000,000.00 (the "Additional Securities"), to be consolidated and form a single series with the Original Securities. A copy of the preliminary offering circular for the offer of the Additional Securities is attached herewith as Annex "A".

The Additional Securities will be identical in all respects with the Original Securities, other than with respect to the date of issuance and issue price. The net proceeds from the issuance of the Additional Securities will be used and applied by the Corporation for general corporate purposes, investments in power-related assets and repayment of indebtedness. The Additional Securities will be constituted by a Supplemental Trust Deed, which shall supplement the trust deed of the Original Securities, and listed in the Singapore Stock Exchange (SGX-ST).

Thank you.

Very truly yours,

SMC GLOBAL POWER HOLDINGS CORP.

By:~

EL,ENITA D. GO Cdrporate Information Officer

IMPORTANT NOTICE

NOT FOR DISTRIBUTION TO ANY PERSON OR ADDRESS IN THE UNITED STATES.

Important: You must read the following before continuing. The following applies to the preliminary offeringcircular following this page (the “Offering Circular”), and you are therefore advised to read this carefullybefore reading, accessing or making any other use of this Offering Circular. In accessing the Offering Circular,you agree to be bound by the following terms and conditions, including any modifications to them any time youreceive any information from us as a result of such access.

NOTHING IN THIS ELECTRONIC TRANSMISSION CONSTITUTES AN OFFER OF SECURITIES FORSALE IN THE UNITED STATES OR ANY OTHER JURISDICTION WHERE IT IS UNLAWFUL TO DO SO.THE SECURITIES HAVE NOT BEEN, AND WILL NOT BE, REGISTERED UNDER THEU.S. SECURITIES ACT OF 1933, AS AMENDED (THE “SECURITIES ACT”), OR THE SECURITIESLAWS OF ANY STATE OF THE UNITED STATES OR OTHER JURISDICTION, AND THE SECURITIESMAY NOT BE OFFERED OR SOLD WITHIN THE UNITED STATES, EXCEPT PURSUANT TO ANEXEMPTION FROM, OR IN A TRANSACTION NOT SUBJECT TO, THE REGISTRATIONREQUIREMENTS OF THE SECURITIES ACT AND APPLICABLE STATE OR LOCAL SECURITIESLAWS.

THIS OFFERING CIRCULAR MAY NOT BE FORWARDED OR DISTRIBUTED TO ANY OTHERPERSON AND MAY NOT BE REPRODUCED IN ANY MANNER WHATSOEVER, AND INPARTICULAR, MAY NOT BE FORWARDED TO ANY U.S. ADDRESS. ANY FORWARDING,DISTRIBUTION OR REPRODUCTION OF THIS DOCUMENT IN WHOLE OR IN PART ISUNAUTHORIZED. FAILURE TO COMPLY WITH THIS DIRECTIVE MAY RESULT IN A VIOLATION OFTHE SECURITIES ACT OR THE APPLICABLE LAWS OF OTHER JURISDICTIONS. ANY INVESTMENTDECISION SHOULD BE MADE ON THE BASIS OF THE FINAL TERMS AND CONDITIONS OF THESECURITIES AND THE INFORMATION CONTAINED IN A FINAL OFFERING CIRCULAR THAT WILLBE DISTRIBUTED TO YOU ON OR PRIOR TO THE CLOSING DATE AND NOT ON THE BASIS OF THEATTACHED OFFERING CIRCULAR. IF YOU HAVE GAINED ACCESS TO THIS TRANSMISSIONCONTRARY TO ANY OF THE FOREGOING RESTRICTIONS, YOU ARE NOT AUTHORIZED AND WILLNOT BE ABLE TO PURCHASE ANY OF THE SECURITIES DESCRIBED THEREIN.

Confirmation of the Representation: In order to be eligible to view this Offering Circular or make aninvestment decision with respect to the securities, investors must not be located in the United States. ThisOffering Circular is being sent at your request and, by accepting the electronic mail and accessing this OfferingCircular, you shall be deemed to have represented to us that the electronic mail address that you gave us and towhich this electronic mail has been delivered is not located in the United States and that you consent to deliveryof such Offering Circular by electronic transmission.

You are reminded that this Offering Circular has been delivered to you on the basis that you are a person intowhose possession this Offering Circular may be lawfully delivered in accordance with the laws of jurisdiction inwhich you are located and you may not, nor are you authorized to, deliver this Offering Circular to any otherperson.

The materials relating to any offering of securities to which this Offering Circular relates do not constitute, andmay not be used in connection with, an offer or solicitation in any place where offers or solicitations are notpermitted by law. If a jurisdiction requires that such offering be made by a licensed broker or dealer and theunderwriters or any affiliate of the underwriters is a licensed broker or dealer in that jurisdiction, such offeringshall be deemed to be made by the underwriters or such affiliate on behalf of the Issuer (as defined in theOffering Circular) in such jurisdiction.

This Offering Circular has been sent to you in electronic format. You are reminded that documents transmittedvia this medium may be altered or changed during the process of electronic transmission and consequentlyneither Issuer, the Joint Lead Managers (each as defined in the Offering Circular) nor any person who controlsthe Issuer, a Joint Lead Manager or any director, officer, employee or agent of any of the Issuer, the Joint LeadManagers or affiliate of any such person accepts any liability or responsibility whatsoever in respect of anydifference between this Offering Circular distributed to you in electronic format and the hard copy versionavailable to you on request from the Joint Lead Managers.

You are responsible for protecting against viruses and other destructive items. Your use of this electronic mail isat your own risk and it is your responsibility to take precautions to ensure that it is free from viruses and otheritems of a destructive nature.

ANNEX "A"

The

info

rmat

ion

inth

isPr

elim

inar

yOf

ferin

gCi

rcul

aris

notc

ompl

ete

and

may

bech

ange

d.Th

isPr

elim

inar

yOf

ferin

gCi

rcul

aris

nota

nof

fert

ose

llth

ese

secu

ritie

san

dw

ear

eno

tsol

iciti

ngan

offe

rto

buy

thes

ese

curit

ies

inan

yju

risdi

ctio

nw

here

the

offe

rors

ale

isno

tper

mitt

ed.

Subject to completionPreliminary Offering Circular dated June 25, 2019

CONFIDENTIAL

(incorporated with limited liability in the Republic of the Philippines)

U.S.$[Š] Senior Perpetual Capital Securities(to be consolidated into and form a single series with the

U.S.$500,000,000 Senior Perpetual Capital Securities issued on April 25, 2019)

Issue Price: [Š]% plus an amount corresponding to accrued distributions from (and including)April 25, 2019 to (but excluding) [Š], 2019

The U.S.$[Š] senior perpetual capital securities (the “Additional Securities”) are issued by SMC Global Power Holdings Corp. (“SMC Global Power”, the“Issuer” or the “Company”). The Additional Securities will be issued under a supplemental trust deed dated on or about [Š], 2019 (the “Supplemental TrustDeed”) by and between the Company and Trustee (as defined herein), which shall supplement the trust deed, dated as of April 25, 2019 (the “Original TrustDeed” and, as supplemented by the Supplemental Trust Deed, the “Trust Deed”), by and between the Company and the Trustee, pursuant to which the Companyissued U.S.$500,000,0000 aggregate principal amount of senior perpetual capital securities on April 25, 2019 (the “Original Securities”). The AdditionalSecurities will be consolidated and form a single series with the Original Securities. The Additional Securities are identical in all respects with the OriginalSecurities, other than with respect to the date of issuance and issue price. The Additional Securities will vote on any matter submitted to holders with holders ofthe Original Securities. The Additional Securities will share the ISIN and the Common Code and be fungible with the Original Securities. The Original Securitiesand the Additional Securities are referred to collectively as the “Securities.” Upon issuance of the Additional Securities, the aggregate principal amount of theoutstanding Securities will be U.S.$[Š].

The Securities confer a right to receive distributions (each, a “Distribution”) at the applicable rate described below for the period from and including April 25,2019 or from and including the most recent Distribution Payment Date (as defined below) to, but excluding, the next Distribution Payment Date or anyredemption date. Subject to Condition 4.5 (Optional Deferral of Distributions) of the terms and conditions of the Securities (the “Conditions”), Distributions arepayable semi-annually in arrear on the Distribution Payment Dates in each year. “Distribution Payment Dates” are defined as April 25 and October 25 of eachyear, commencing on October 25, 2019. Unless previously redeemed in accordance with the Conditions and subject to Condition 4.4 (Increase in Rate ofDistribution), Distributions (i) from and including April 25, 2019 to, but excluding, April 25, 2024 (the “Step Up Date”) shall accrue on the outstanding principalamount of the Securities at 6.50% per annum (the “Initial Rate of Distribution”) and (ii) from and including each Reset Date (as defined in the Conditions)(including the Step Up Date) to, but excluding, the immediately following Reset Date, shall accrue on the outstanding principal amount of the Securities at therelevant Reset Rate of Distribution (as defined in the Conditions).

The Issuer may, in its sole and absolute discretion, on any day which is not less than five Business Days (as defined in the Conditions) prior to any DistributionPayment Date, resolve to defer payment of any or all of the Distribution which would otherwise be payable on that Distribution Payment Date unless, during thesix months ending on that scheduled Distribution Payment Date (i) a discretionary dividend, distribution, interest or other payment has been paid or declared on orin respect of any Junior Securities or (except on a pro rata basis) Parity Securities (each as defined in the Conditions) of the Issuer, other than a dividend,distribution or other payment in respect of an employee benefit plan or similar arrangement with or for the benefit of employees, officers, directors andconsultants of the Issuer or (ii) at the discretion of the Issuer, any Junior Securities or (except on a pro rata basis) Parity Securities have been redeemed,repurchased or otherwise acquired by the Issuer or any of its subsidiaries, other than a redemption, repurchase or other acquisition in respect of an employeebenefit plan or similar arrangement with or for the benefit of employees, officers, directors and consultants of the Issuer. Any such deferred Distribution willconstitute “Arrears of Distribution” and will not be due and payable until the relevant Payment Reference Date (as defined in the Conditions). Distributions willaccrue on each Arrears of Distribution for so long as such Arrears of Distribution remains outstanding at the same Rate of Distribution (as defined in theConditions) as the Principal Amount of the Securities bears at such time and will be added to such Arrears of Distribution (and thereafter bear Distributionsaccordingly) on each Distribution Payment Date.

The Securities are undated securities in respect of which there is no fixed redemption date. Subject to applicable law, the Issuer may redeem the Securities (inwhole but not in part) on the Step Up Date or any subsequent Distribution Payment Date falling after the Step Up Date at the Redemption Price (as defined in theConditions), on the giving of not less than 30 and not more than 60 calendar days’ irrevocable notice of redemption to the Securityholders in accordance withCondition 12.1 (Notices to Securityholders). The Securities may also be redeemed (in whole but not in part) at the option of the Issuer at the Redemption Priceupon the occurrence of certain changes in Philippine tax law requiring the payment of Additional Amounts (as defined in the Conditions). In addition, theSecurities may be redeemed (in whole but not in part) at the option of the Issuer (A) upon the occurrence of a Change of Control Event (as defined in theConditions) (i) at any time prior to (but excluding) the Step Up Date at the Special Redemption Price (as defined in the Conditions) or (ii) on or at any time afterthe Step Up Date at the Redemption Price, (B) upon the occurrence and continuation of a Reference Indebtedness Default Event (as defined in the Conditions) atany time at the Redemption Price, (C) upon the occurrence and continuation of an Accounting Event (as defined in the Conditions) (i) at any time prior to (butexcluding) the Step Up Date at the Special Redemption Price or (ii) on or at any time after the Step Up Date at the Redemption Price or (D) in the event that theaggregate principal amount of the Securities originally issued that remains outstanding is equal to or less than 25% (i) at any time prior to (but excluding) the StepUp Date at the Special Redemption Price or (ii) on or at any time after the Step Up Date at the Redemption Price, in each case on the giving of not less than 30and not more than 60 calendar days’ irrevocable notice of redemption to the Securityholders in accordance with Condition 12.1 (Notices to Securityholders).

Investing in the Additional Securities involves certain risks. See “Risk Factors” beginning on page 19.THE ADDITIONAL SECURITIES BEING OFFERED OR SOLD HEREIN HAVE NOT BEEN, AND WILL NOT BE, REGISTERED WITH THEPHILIPPINE SECURITIES AND EXCHANGE COMMISSION UNDER THE PHILIPPINE SECURITIES REGULATION CODE (“PHILIPPINESRC”). ANY FUTURE OFFER OR SALE OF THE ADDITIONAL SECURITIES IS SUBJECT TO THE REGISTRATION REQUIREMENTSUNDER THE PHILIPPINE SRC UNLESS SUCH OFFER OR SALE QUALIFIES AS AN EXEMPT TRANSACTION UNDER THE PHILIPPINESRC.

The Additional Securities are being offered only outside the United States in offshore transactions in compliance with Regulation S under the U.S. Securities Actof 1933, as amended (the “Securities Act”). The Additional Securities have not been, and will not be, registered under the Securities Act or the securities laws ofany other jurisdiction. Unless they are so registered, the Additional Securities may be offered only in transactions that are exempt from or not subject toregistration under the Securities Act or the securities laws of any other jurisdiction. For further details, see “Subscription and Sale.”

The Original Securities are listed on the Singapore Exchange Securities Trading Limited (the “SGX-ST”). Application will be made to the SGX-ST for the listingand quotation of the Additional Securities on the SGX-ST.

The SGX-ST assumes no responsibility for the correctness of any of the statements made or opinions or reports contained in this Offering Circular. Admission ofthe Additional Securities to the Official List of the SGX-ST is not to be taken as an indication of the merits of the Securities or SMC Global Power or itssubsidiaries. Investors are advised to read and understand the contents of this Offering Circular before investing. If in doubt, investors should consult theiradvisers.

The Additional Securities will be evidenced by a global certificate (the “Global Certificate”) in registered form, which will be registered in the name of anominee of, and deposited with a common depositary for, Euroclear Bank SA/NV (“Euroclear”) and Clearstream Banking, S.A. (“Clearstream, Luxembourg”).Beneficial interests in the Global Certificate will be shown on, and transfers thereof will be effected only through, records maintained by Euroclear andClearstream, Luxembourg and their respective accountholders. Except in the limited circumstances set out herein, definitive certificates for the Securities will notbe issued in exchange for beneficial interests in the Global Certificate. See “The Global Certificate.” It is expected that delivery of the Global Certificate will bemade on or about [Š], 2019.

Joint Lead Managers(in alphabetical order)

BofA Merrill Lynch Credit Suisse UBSOffering Circular dated [Š], 2019.

I SMC GLOBAL POWER

A SUBSIOIARY OF SAN MIGUEl CORPORATION

TABLE OF CONTENTS

Page

SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

RISK FACTORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

TERMS AND CONDITIONS OF THE SECURITIES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

THE GLOBAL CERTIFICATE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61

EXCHANGE RATES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63

USE OF PROCEEDS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

CAPITALIZATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

SELECTED FINANCIAL INFORMATION AND OTHER DATA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 66

MANAGEMENT’S DISCUSSION AND ANALYSIS OF RESULTS OF OPERATIONS . . . . . . . . . . . . . 71

INDUSTRY OVERVIEW . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79

BUSINESS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 90

REGULATION AND ENVIRONMENTAL MATTERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 131

MANAGEMENT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 147

PRINCIPAL SHAREHOLDER . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 151

RELATED PARTY TRANSACTIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 152

TAXATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 153

CLEARANCE AND SETTLEMENT OF THE SECURITIES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 157

SUBSCRIPTION AND SALE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 159

LEGAL MATTERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 163

INDEPENDENT AUDITORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 164

GLOSSARY OF SELECTED TERMS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 165

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F-1

---

In this Offering Circular, references to “SMC Global Power”, the “Company” and the “Issuer” are to SMCGlobal Power Holdings Corp. or SMC Global Power Holdings Corp. and its subsidiaries, as the context requires.For avoidance of doubt, references to the Company as the independent power producer administrator (“IPPA”)are references to the relevant consolidated subsidiary of the Company which executed the relevant IPPAAgreement for the administration of each of the Sual Power Plant, Ilijan Power Plant and San Roque Power Plant(collectively, the “IPPA Power Plants”) and references to the administration by, or ownership of, the Companyof any other power plant or power generation facility in this Offering Circular should be understood to refer tothe administration or ownership of such plant or facility by the relevant consolidated subsidiary of the Company.References to the “combined installed capacity” in this Offering Circular are to the aggregate of the installedgeneration capacity of (i) the IPPA Power Plants administered by the Company as the IPPA, (ii) the LimayGreenfield Power Plant, (iii) the Davao Greenfield Power Plant, (iv) the Masinloc Power Plant, (v) the Masinlocbattery energy storage system and (vi) the Angat Hydroelectric Power Plant (“AHEPP”), in which the Companyhas a 60.0% ownership interest. References to the total installed generating capacity based on ERC ResolutionNo. 04, Series of 2018 issued in February 2018 (“ERC Resolution on Grid Market Share Limitation”) havebeen adjusted to include (i) 150 MW generating capacity from the commencement of commercial operations ofLimay Greenfield Power Plant Unit 3 and (ii) 14 MW additional generating capacity from the retrofit ofMasinloc Power Plant Unit 2 completed in May 2018.

The term “Joint Lead Managers” refers to Credit Suisse (Hong Kong) Limited, Merrill Lynch (Singapore) Pte.Ltd. and UBS AG Singapore Branch. All references in this Offering Circular to the “Philippines” are to theRepublic of the Philippines. Certain acronyms, technical terms and other abbreviations used are defined in the“Glossary of Selected Terms” of this Offering Circular.

Prospective investors should rely only on the information contained in this Offering Circular. The Issuerand the Joint Lead Managers have not authorized anyone to provide prospective investors withinformation that is different. The information in this document may only be accurate on the date of thisOffering Circular. Nothing in this Offering Circular should be relied upon as a promise or representationas to future results or events, and neither the delivery of this Offering Circular nor any offering or sale ofthe Additional Securities shall under any circumstances imply that there has been no change in the affairsof the Issuer or that the information herein is correct as of any date subsequent to the date hereof.

This Offering Circular is being furnished by the Issuer in connection with an offering exempt from theregistration requirements under the U.S. Securities Act of 1933, as amended (the “Securities Act”) solely for thepurpose of enabling a prospective investor to consider whether to purchase the Additional Securities. Theinformation contained herein has been provided by the Issuer and other sources identified herein. None of theJoint Lead Managers, DB Trustees (Hong Kong) Limited (the “Trustee”) or the Agents (as defined in the termsand conditions of the Securities, the “Conditions”) has independently verified the information contained herein.No representation or warranty, express or implied, is made by the Joint Lead Managers, the Trustee or the Agentsas to the accuracy or completeness of such information, and nothing contained herein is, or may be relied uponas, a promise or representation by the Joint Lead Managers, the Trustee or the Agents as to the past or the future.To the fullest extent permitted by law, none of the Joint Lead Managers, the Trustee or the Agents accepts anyliability in relation to the information contained in this Offering Circular or any other information provided bythe Issuer, or for any other statement made or purported to be made by the Joint Lead Managers, the Trustee orthe Agents or on any of their behalf in connection with the Issuer or in connection with the offering of theAdditional Securities. The Joint Lead Managers, the Trustee and the Agents accordingly disclaim all and anyliability whether arising in tort or contract or otherwise that any of them might otherwise have in respect of thisOffering Circular or any such statement.

The distribution of this Offering Circular and the offering and sale of the Additional Securities in certainjurisdictions may be restricted by law. Persons into whose possession this Offering Circular comes must informthemselves about and observe any such restrictions. There are restrictions on the distribution of this OfferingCircular and the offer and sale of the Additional Securities in certain jurisdictions, including the United States,the United Kingdom, Singapore, Hong Kong, Japan, the European Economic Area (“EEA”) and the Philippines.This Offering Circular does not constitute, and may not be used for or in connection with, an offer or solicitationby anyone in any jurisdiction in any circumstance in which such offer or solicitation is not authorized or to anyperson to whom it is unlawful to make such offer or solicitation.

i

Each person investing in the Additional Securities shall be deemed to acknowledge that:

• it has been afforded an opportunity to request from the Issuer and to review, and has received, alladditional information considered by such person to be necessary to verify the accuracy of, or tosupplement, the information contained herein;

• it has had the opportunity to review all of the documents described herein;

• it has not relied on the Joint Lead Managers, the Trustee, the Agents or any person affiliated with the JointLead Managers, the Trustee or the Agents in connection with its investigation of the accuracy of theinformation contained in the Offering Circular or its investment decision; and

• no person has been authorized to give any information or to make any representation concerning theAdditional Securities other than those contained in this Offering Circular and, if given or made, such otherinformation or representation should not be relied upon as having been authorized by the Issuer, the JointLead Managers, the Trustee or the Agents.

Prospective investors should not construe the contents of this Offering Circular as investment, legal or tax adviceand should consult with their own counsel, accountant and other advisors as to legal, tax, business, financial andrelated aspects of receiving the Additional Securities.

In making an investment decision, prospective investors must rely on their own examination of the Issuer and theterms of the Additional Securities, including, without limitation, the merits and risks involved. None of theIssuer, the Joint Lead Managers, the Trustee or the Agents is making any representation to any prospectiveinvestor regarding the legality of an investment in the Additional Securities by such investor under any legalinvestment or similar laws or regulations. The offering of the Additional Securities is being made on the basis ofthis Offering Circular. Any decision to invest in the Additional Securities must be based on the informationcontained in this Offering Circular. Each purchaser of the Additional Securities must comply with all applicablelaws and regulations in force in each jurisdiction in which it purchases, offers or sells such Additional Securitiesor possesses or distributes this Offering Circular and must obtain any consent, approval or permission requiredby it for the purchase, offer or sale by it of such Additional Securities under the laws and regulations in force inany jurisdictions to which it is subject or in which it makes such purchases, offers or sales, and none of theIssuer, the Joint Lead Managers, the Trustee or the Agents shall have any responsibility therefor.

Each person receiving this Offering Circular is advised to read and understand the contents of this OfferingCircular before investing in the Additional Securities. If in doubt, such person should consult his or her advisors.This Offering Circular has been prepared on the basis that all offers of the Additional Securities will be madepursuant to an exemption under the Prospectus Directive (Directive 2003/71/EC, as amended), as implemented inthe member states of the EEA, from the requirement to produce a prospectus for offers of the AdditionalSecurities. Accordingly, any person making or intending to make any offer within the EEA of the AdditionalSecurities which are the subject of the placement contemplated in this Offering Circular should only do so incircumstances in which no obligation arises for the Issuer or any of the Joint Lead Managers to produce aprospectus for the offer. Neither the Issuer nor the Joint Lead Managers have authorized, nor do they authorizethe making of any offer of the Additional Securities through any financial intermediary, other than offers madeby the Joint Lead Managers which constitute the final placement of the Additional Securities contemplated in thisOffering Circular.

PROHIBITION OF SALES TO EEA RETAIL INVESTORS — The Additional Securities are not intended tobe offered, sold or otherwise made available to and should not be offered, sold or otherwise made available toany retail investor in the EEA. For these purposes, a “retail investor” means a person who is one (or more) of:(i) a retail client as defined in point (11) of Article 4(1) of Directive 2014/65/EU (as amended, “MiFID II”); or(ii) a customer within the meaning of Directive 2002/92/EC (as amended, the “Insurance MediationDirective”), where that customer would not qualify as a professional client as defined in point (10) of Article4(1) of MiFID II. Consequently no key information document required by Regulation (EU) No 1286/2014 (asamended, the “PRIIPs Regulation”) for offering or selling the Additional Securities or otherwise making themavailable to retail investors in the EEA has been prepared and therefore offering or selling the AdditionalSecurities or otherwise making them available to any retail investor in the EEA may be unlawful under thePRIIPs Regulation.

ii

This Offering Circular is only being distributed to and is only directed at (i) persons who are outside theUnited Kingdom or (ii) investment professionals falling within Article 19(5) of the Financial Services andMarkets Act 2000 (Financial Promotion) Order 2005 (the “Order”) or (iii) high net worth companies, and otherpersons to whom it may lawfully be communicated, falling within Article 49(2)(a) to (d) of the Order (all suchpersons together being referred to as “relevant persons”). The Additional Securities are only available to, andany invitation, offer or agreement to subscribe, purchase or otherwise acquire such Additional Securities will beengaged in only with, relevant persons. Any person who is not a relevant person should not act or rely on thisOffering Circular or any of its contents.

Notification under Section 309B(1)(c) of the Securities and Futures Act, Chapter 289 of Singapore (the“Securities and Futures Act”) — SMC Global Power has determined, and hereby notifies all relevant persons(as defined in Section 309A(1) of the Securities and Futures Act), that the Additional Securities are prescribedcapital markets products (as defined in the Securities and Futures (Capital Markets Products) Regulations 2018of Singapore) and Excluded Investment Products (as defined in MAS Notice SFA 04-N12: Notice on the Sale ofInvestment Products and MAS Notice FAA-N16: Notice on Recommendations on Investment Products).

The Issuer reserves the right to withdraw this offering of the Additional Securities at any time. The Issuer and theJoint Lead Managers also reserve the right to reject any offer to purchase the Additional Securities in whole or inpart for any reason and to allocate to any prospective investor less than the full amount of Additional Securitiessought by such investor. This Offering Circular does not constitute an offer to sell, or a solicitation of an offer tobuy, any Additional Securities offered hereby in any circumstances in which such offer is unlawful.

The Additional Securities have not been approved or disapproved by the U.S. Securities and ExchangeCommission, any state securities commission in the United States or any other United States, Philippine or otherregulatory authority, nor have any of the foregoing authorities passed upon or endorsed the merits of the offeringof the Additional Securities or the accuracy or adequacy of this Offering Circular. Any representation to thecontrary is a criminal offense in the United States.

The Additional Securities are subject to restrictions on transferability and resale and may not be transferred orresold except as permitted under the Securities Act and other applicable state, Philippine or other securities lawspursuant to registration thereunder or exemption therefrom. See “Subscription and Sale.” Prospective investorsshould thus be aware that they may be required to bear the financial risks of this investment for an indefiniteperiod of time.

FORWARD-LOOKING STATEMENTS

This Offering Circular contains forward-looking statements that are, by their nature, subject to significant risksand uncertainties. These forward-looking statements include, without limitation, statements relating to:

• known and unknown risks;

• uncertainties and other factors that may cause the actual results, performance or achievements of SMCGlobal Power to be materially different from any future results; and

• performance or achievements expressed or implied by forward-looking statements.

Such forward-looking statements are based on numerous assumptions regarding the present and future businessstrategies of SMC Global Power and the environment in which SMC Global Power will operate in the future.Important factors that may cause some or all of the assumptions not to occur or cause actual results, performanceor achievements to differ materially from those in the forward-looking statements include, among other things:

• the ability of SMC Global Power to successfully implement its strategies;

• the ability of SMC Global Power to anticipate and respond to market trends;

iii

• changes in availability and prices of fuel used in the power plants of SMC Global Power;

• unexpected shutdowns of (i) the IPPA Power Plants for which SMC Global Power acts as the IPPA and(ii) the Masinloc Power Plant, the Davao Greenfield Power Plant, the Limay Greenfield Power Plant andthe AHEPP;

• adverse weather patterns and natural disasters;

• the ability of SMC Global Power to successfully manage its growth;

• the ability of SMC Global Power to successfully implement and manage its power portfolio;

• the condition of and changes in, the Philippine, Asian or global economies;

• any political instability in the Philippines;

• the ability of SMC Global Power to secure additional financing;

• changes in interest rates, inflation rates and the value of the Peso against the U.S. dollar and othercurrencies;

• price volatility in the wholesale energy spot market;

• other risks relating to the Philippines, including changes in laws, rules and regulations, including tax lawsand licensing requirements;

• changes in power supply and demand dynamics in the Philippines;

• competition in the Philippine power industry; and

• risks relating to the Securities.

Additional factors that could cause the actual results, performance or achievements of SMC Global Power todiffer materially from forward-looking statements include, but are not limited to, those disclosed under“Risk Factors” and elsewhere in this Offering Circular. These forward-looking statements speak only as of thedate of this Offering Circular. SMC Global Power, the Joint Lead Managers, the Trustee and the Agent expresslydisclaim any obligation or undertaking to release, publicly or otherwise, any updates or revisions to any forward-looking statement contained herein to reflect events or circumstances, or to reflect any change in the expectationsof SMC Global Power with regard thereto or any change in events, conditions, assumptions or circumstances onwhich any statement is based or to reflect that SMC Global Power became aware of any such events orcircumstances, that occur after the date of this Offering Circular. The Issuer, the Joint Lead Managers, theTrustee and the Agents assume no obligation to update any of the forward-looking statements after the date ofthis Offering Circular to conform those statements to actual results, subject to compliance with all applicablelaws.

This Offering Circular includes statements regarding the expectations and projections of the Company for futureoperating performance and business prospects. The words “believe,” “plan,” “expect,” “anticipate,” “estimate,”“project,” “intend,” “will,” “shall,” “should,” “may,” “would” and similar words identify forward-lookingstatements. In addition, all statements other than statements of historical facts included in this Offering Circularare forward-looking statements. Statements in the Offering Circular as to the opinions, beliefs and intentions ofSMC Global Power accurately reflect in all material respects the opinions, beliefs and intentions of itsmanagement as to such matters as of the date of this Offering Circular, although SMC Global Power gives no

iv

assurance that such opinions or beliefs will prove to be correct or that such intentions will not change. ThisOffering Circular discloses, under the section “Risk Factors” and elsewhere, important factors that could causeactual results to differ materially from expectations of the Company. All subsequent written and oral forward-looking statements attributable to SMC Global Power or persons acting on behalf of SMC Global Power areexpressly qualified in their entirety by the above cautionary statements.

Should one or more of such risks and uncertainties materialize, or should any underlying assumptions proveincorrect, actual outcomes may vary materially from those indicated in the applicable forward-lookingstatements. Any forward-looking statement or information contained in this Offering Circular speaks only as ofthe date the statement was made.

All of the forward-looking statements of SMC Global Power made herein and elsewhere are qualified in theirentirety by the risk factors discussed in “Risk Factors” and “Industry Overview”. These risk factors andstatements describe circumstances that could cause actual results to differ materially from those contained in anyforward-looking statement in this Offering Circular.

INDUSTRY AND MARKET DATA

Market data and certain industry forecasts used throughout this Offering Circular were obtained from internalsurveys, market research, publicly available information and industry publications. Industry publicationsgenerally state that the information they contain has been obtained from sources believed to be reliable but thatthe accuracy and completeness of that information are not guaranteed. Similarly, internal surveys, industryforecasts and market research, while believed to be reliable, have not been independently verified, and none ofthe Issuer, the Joint Lead Managers, the Trustee nor the Agents makes any representation as to the accuracy orcompleteness of that information.

Information relating to or obtained from the Business Monitor, Department of Energy (“DOE”), EconomistIntelligence Unit, Energy Regulatory Commission (“ERC”), Manila Electric Company (“Meralco”), NationalGrid Corporation of the Philippines (“NGCP”), National Power Corporation (“NPC”), Philippine StatisticsAuthority, Philippine Electricity Market Corporation (“PEMC”), Power Sector Assets and LiabilitiesManagement Corporation (“PSALM”), National Transmission Corporation (“TransCo”) and WholesaleElectricity Spot Market (“WESM”) set forth in this Offering Circular was obtained from publicly availablesources that are believed to be reliable but such information has not been independently verified. Neither theIssuer nor the Joint Lead Managers makes any representation as to the accuracy of such information regardingthe Business Monitor, DOE, Economist Intelligence Unit, ERC, Meralco, NGCP, NPC, the Philippine StatisticsAuthority, PEMC, PSALM, TransCo or WESM.

STANDARDS FOR OPERATING STATISTICS

The power plant operating statistics included in this Offering Circular are based on the power plant operatingdata that have been provided by the independent power producer of the relevant power plant and grid systemoperators. SMC Global Power believes these have been measured in accordance with internationally recognizedpower plant operation standards set by the American Society of Mechanical Engineers, Power Test Code,Institute of Electrical and Electronics Engineering, Energy Power Research Institute or equivalentinternationally-accepted standards, as applicable. SMC Global Power has not independently verified the powerplant operating data provided by the independent power producers and grid system operators. Neither SMCGlobal Power nor any of the Joint Lead Managers makes any representation as to the accuracy of suchinformation provided by the independent power producers and grid system operators.

PRESENTATION OF FINANCIAL INFORMATION

The consolidated financial statements of SMC Global Power are reported in Pesos and are prepared based on itsaccounting policies, which are in accordance with the Philippine Financial Reporting Standards (“PFRS”) issuedby the Financial Reporting Standards Council of the Philippines (“FRSC”). PFRS include statements namedPFRS and Philippine Accounting Standards, and Philippine Interpretations from International FinancialReporting Interpretations Committee.

v

Unless otherwise stated, all financial information relating to SMC Global Power contained herein is stated inaccordance with PFRS.

Figures in this Offering Circular have been subject to rounding adjustments. Accordingly, figures shown in thesame item of information may vary, and figures which are totals may not be an arithmetic aggregate of theircomponents.

References to “U.S.$” and “U.S. dollars” in this Offering Circular are to United States dollars, the lawfulcurrency of the United States of America, references to “P”, “Philippine Peso” and “Peso” are to the lawfulcurrency of the Philippines. The Issuer publishes its financial statements in Philippine Pesos. This OfferingCircular contains translations of certain amounts into U.S. Dollars at specified rates solely for the convenience ofthe reader. These translations should not be construed as representations that the Philippine Peso amountsrepresent such U.S. dollar amounts or could be, or could have been, converted into U.S. dollars at the ratesindicated or at all. Unless otherwise indicated, all translations from Philippine Pesos to U.S. dollars have beenmade at a rate of P52.50 = U.S.$1.00, being the closing rate on March 29, 2019 (the last date in March 2019 thatsuch rate was published) for the purchase of U.S. dollars with Philippine Pesos under the Bankers’ Association ofthe Philippines (“BAP”). On June 21, 2019, the closing spot rate quoted on the BAP was P51.56 = U.S.$1.00.See “Exchange Rates” for further information regarding the rates of exchange between the Philippine Peso andthe U.S. dollar.

The financial information included in this Offering Circular has been derived from the consolidated financialstatements of SMC Global Power and its subsidiaries. Unless otherwise indicated, the description of the businessactivities of the Issuer in this Offering Circular is presented on a consolidated basis.

NON-PFRS FINANCIAL MEASURES

This Offering Circular contains references to EBITDA. EBITDA is a supplemental measure of the performanceand liquidity of the Company that is not required by, or presented in accordance with, PFRS. Further, EBITDA isnot a measurement of the financial performance or liquidity of the Company under PFRS and should not beconsidered as an alternative to net income, gross revenues or any other performance measure derived inaccordance with PFRS or as an alternative to cash flow from operations or as a measure of the liquidity of theCompany. The Company calculates EBITDA as the sum of net income (excluding items between any or all of theCompany and its subsidiaries), income tax expense (benefit), finance cost (less interest income) and depreciation,in each case excluding amounts attributable to ring-fenced subsidiaries, less foreign exchange gain (loss), gain onsale of investment, and aggregate fixed payments made to PSALM. The calculation of EBITDA by SMC GlobalPower may be different from the calculations used by other companies, and, as a result, the EBITDA of SMCGlobal Power may not be comparable to other similarly titled measures of other companies.

The Company believes that EBITDA facilitates operating performance comparisons from period to period andfrom company to company by eliminating potential differences caused by variations in capital structures, taxpositions and the age and book depreciation of tangible assets. The Company presents EBITDA because itbelieves it is frequently used by securities analysts and investors in the evaluation of companies in its industry.

ENFORCEABILITY OF CIVIL LIABILITIES

SMC Global Power is established in the Philippines and all or a substantial portion of its operating assets arelocated in the Philippines. Substantially all of its directors and senior management reside in the Philippines. TheCompany has been advised by its Philippine legal counsel, Picazo Buyco Tan Fider & Santos, that a final andconclusive judgment on the merits rendered against the Company and these persons by courts outside thePhilippines obtained in an action predicated upon the civil liability provisions of laws other than Philippine lawswould be recognized and enforced by the courts in the Philippines through an independent action filed to enforcesuch judgment, and without re-trial or re-examination of the issues, provided the following conditions aresatisfied, namely: (i) the court rendering such judgment had jurisdiction in accordance with its jurisdictionalrules, (ii) such persons had notice of the proceedings, (iii) such judgment was not obtained by collusion or fraudor based on a clear mistake of law or fact and (iv) such judgment was not contrary to public policy, law, moralsor good customs in the Philippines.

vi

SUMMARY

The following summary is qualified in its entirety by, and is subject to, the more detailed information and theconsolidated financial statements of SMC Global Power that appear elsewhere in this Offering Circular. Themeaning of terms not defined in this summary can be found elsewhere in this Offering Circular.

OVERVIEW

SMC Global Power, together with its subsidiaries, associates and joint ventures, is one of the largest powercompanies in the Philippines, controlling 4,197 MW of combined capacity as of March 31, 2019 and benefitsfrom a portfolio of diversified fuel sources, including natural gas, coal, hydroelectric power and more recently,battery energy storage systems. Based on the total installed generating capacities reported in ERC ResolutionNo. 04, Series of 2018 (the “ERC Resolution on Grid Market Share Limitation”), the Company believes thatits combined installed capacity comprises approximately 19% of the National Grid, 25% of the Luzon Grid and9% of the Mindanao Grid, in each case as of March 31, 2019.

San Miguel Corporation entered the power industry in 2009 following the acquisition of rights to administer theoutput produced by IPPs in privatization auctions conducted by the Government through PSALM. The followingcompanies under the San Miguel Corporation group became the IPPA of the following plants: (1) San MiguelEnergy Corporation (“SMEC”) became the IPPA for the Sual Power Plant, a coal-fired thermal power plantlocated in Sual, Pangasinan, in November 2009; (2) Strategic Power Devt. Corp. (“SPDC”) became the IPPA forthe San Roque Power Plant, a hydroelectric power plant located in San Manuel, Pangasinan in January 2010; and(3) South Premiere Power Corp. (“SPPC”) became the IPPA for the Ilijan Power Plant, a natural gas-firedcombined cycle power plant located in Ilijan, Batangas in June 2010 (the Ilijan Power Plant, Sual Power Plantand San Roque Power Plant are collectively referred to as the IPPA Power Plants).

An IPPA under the relevant IPPA agreement has the right to sell electricity generated by the power plants ownedand operated by the relevant IPPs without having to bear any of the large upfront capital expenditures for powerplant construction or maintenance. As an IPPA, each of SMEC, SPDC and SPPC also has the ability to manageboth market and price risks by entering into bilateral contracts with offtakers while capturing potential upsidefrom the sale of excess capacity through the WESM.

In September 2010, San Miguel Corporation consolidated its power generation business through the transfer ofits equity interests in SMEC, SPDC and SPPC to SMC Global Power. SMC Global Power also became a wholly-owned subsidiary of San Miguel Corporation. Since then, SMC Global Power has controlled the 2,545 MWcombined contracted capacity of the IPPA Power Plants through the IPPA agreements executed by SMEC, SPDCand SPPC, respectively.

Building on its experience as an IPPA since San Miguel Corporation’s transfer of interests in SMEC, SPDC andSPPC, SMC Global Power embarked on the development of its own greenfield power projects. In 2013, SMCGlobal Power initiated two greenfield power projects, namely, the construction of the 2 x 150 MW DavaoGreenfield Power Plant which is owned by San Miguel Consolidated Power Corporation (“SMCPC”), itswholly-owned subsidiary, and the 4 x 150 MW Limay Greenfield Power Plant which is owned by SMCConsolidated Power Corporation (“SCPC”), another wholly-owned subsidiary. Units 1, 2 and 3 of the LimayGreenfield Power Plant commenced commercial operations in May 2017, September 2017 and March 2018,respectively, while Unit 4 has completed testing and commissioning and is expected to commence commercialoperations in the third quarter of 2019 once the ERC issues the certificate of compliance. Units 1 and 2 of theDavao Greenfield Power Plant commenced commercial operations in July 2017 and February 2018, respectively.

SMC Global Power also pursued strategic acquisitions to increase its energy portfolio. In November 2014, SMCGlobal Power, through its subsidiary PowerOne Ventures Energy Inc. (“PVEI”), acquired a 60% stake in AngatHydropower Corporation (“AHC”), the owner and operator of the 218 MW Angat Hydroelectric Power Plant(the “AHEPP”). More recently, on March 20, 2018, SMC Global Power acquired 51% and 49% of the equityinterests in SMCGP Masin Pte. Ltd. (“SMCGP Masin”, formerly Masin-AES Pte. Ltd) from AES Phil

1

Investment Pte. Ltd. (“AES Phil”) and Gen Plus B.V., respectively. SMCGP Masin indirectly owns, through itssubsidiaries, Masinloc Power Partners Co. Ltd. (“MPPCL”) and SMCGP Philippines Energy Storage Co. Ltd(“SMCGP Philippines Energy”, formerly, AES Philippine Energy Storage Co. Ltd.). On September 19, 2018,Prime Electric Generation Corporation (“PEGC”), a wholly-owned subsidiary of SMC Global Power, andOceantech Power Generation Corporation (“OPGC”) purchased the entire partnership interests in SMCGPPhilippines Energy from subsidiaries of SMCGP Masin. MPPCL owns, operates and maintains the 1 x 330 MW(Unit 1), 1 x 344 MW (Unit 2) coal-fired power plant and 335 MW (Unit 3) expansion project under construction(together, the “Masinloc Power Plant”), and the 10 MW battery energy storage system project (the “MasinlocBESS”), all located in Masinloc, Zambales, while SMCGP Philippines Energy has commenced pre-constructionof a 20 MW battery energy storage system facility in Kabankalan, Negros Occidental (the “KabankalanBESS”).

As part of the purchase relating to the Masinloc power assets, SMC Global Power also acquired SMCGPTranspower Pte. Ltd. (“SMCGP Transpower”, formerly, AES Transpower Private Ltd.), and SMCGPPhilippines Inc. (“SPHI”, formerly, AES Philippines Inc.). SMCGP Transpower was a subsidiary of The AESCorporation, which provides corporate support services to MPPCL through its Philippine regional operatingheadquarters, while SPHI was a wholly-owned subsidiary of AES Phil and provides energy marketing services toMPPCL.

In July 2018, PEGC acquired the entire equity interest of ALCO Steam Energy Corporation in Alpha WaterRealty & Services Corp. (“Alpha Water”), representing 60% of the outstanding capital stock of Alpha Water. Asa result, SMC Global Power now effectively owns 100% of Alpha Water through its subsidiaries, PEGC andMPPCL. Alpha Water is the owner of the land on which the current site of the Masinloc Power Plant in ZambalesProvince is located.

In September 2018, PEGC and OPGC, another wholly-owned subsidiary of SMC Global Power, purchased theentire partnership interests in SMCGP Philippines Energy from subsidiaries of SMCGP Masin.

SMC Global Power, through its subsidiaries SMEC, SPDC, SPPC, AHC, SCPC, SMCPC, SMELC and MPPCL,sells power through offtake agreements directly to customers, including Meralco and other distribution utilities,electric cooperatives and industrial customers, or through the WESM. The majority of the consolidated sales ofSMC Global Power are through long-term take-or-pay offtake contracts most of which have provisions forpassing on fuel costs, foreign exchange differentials and certain other fixed costs.

SMC Global Power is also engaged in distribution and retail electricity services. In 2013, SMC Global Powerentered into a concession agreement for the operation and maintenance of Albay Electric Cooperative, Inc.(“ALECO”), which is the franchise holder for the distribution of electricity in the province of Albay in Luzon.SMC Global Power has also expanded its sale of power to a broader range of customers, including retailcustomers. The three retail electricity supplier (“RES”) licenses issued to SMC Global Power, through SanMiguel Electric Corp. (“SMELC”), SCPC and MPPCL, allowed it to enter into contracts with contestablecustomers and expand its customer base.

SMC Global Power, through SMEC and its subsidiaries, Bonanza Energy, Daguma Agro and Sultan Energy, alsoowns coal exploration, production and development rights over approximately 17,000 hectares of land inMindanao. While the Company does not intend to develop these sites imminently, depending on prevailingglobal coal prices and the related logistical costs, it may consider eventually tapping these sites to serve as asignificant additional source of coal fuel for its planned and existing greenfield coal-fired power plants.

SMC Global Power is a wholly-owned subsidiary of San Miguel Corporation, one of the largest and mostdiversified conglomerates in the Philippines, founded in 1890 that is listed in the Philippine Stock Exchange, Inc.(the “PSE”). San Miguel Corporation has market-leading businesses in various sectors, including beverages,food, packaging, fuel and oil, energy, infrastructure and property, and investments in car distributorship andbanking services. The Company believes that its relationship with San Miguel Corporation allows it to draw onthe extensive business networks, local business knowledge, relationships and expertise of San MiguelCorporation and its key executive officers.

2

For the years ended December 31, 2016, 2017 and 2018 and the three months ended March 31, 2018 and 2019,SMC Global Power sold 15,758 GWh, 15,707 GWh, 20,273 GWh, 4,330 GWh and 6,098 GWh of powerpursuant to bilateral offtake agreements and 1,588 GWh, 1,520 GWh, 3,590 GWh, 462 GWh and 727 GWh ofpower through the WESM, respectively. For the years ended December 31, 2016, 2017 and 2018 and the threemonths ended March 31, 2018 and 2019, SMC Global Power purchased 767 GWh, 684 GWh, 1,144 GWh,213 GWh and 279 GWh of power from the WESM, respectively.

For the year ended December 31, 2018, the total consolidated revenue, net income and EBITDA of SMC GlobalPower was P120,102.8 million (U.S.$2,287.7million), P8,300.1 million (U.S.$158.1 million) andP10,716.9 million (U.S.$204.1 million), respectively. For the three months ended March 31, 2019, the totalconsolidated revenue, net income and EBITDA of SMC Global Power was P34,675.9 million(U.S.$660.5 million), P3,578.5 million (U.S.$68.2 million) and P3,036.8 million (U.S.$57.8 million),respectively. As of March 31, 2019, SMC Global Power had total consolidated assets of P499,288.8 million(U.S.$9,510.3 million).

STRENGTHS

SMC Global Power believes it has the following competitive strengths:

• Industry leader with a strong growth platform.

• Well-positioned to capture future demand growth.

• Stable and predictable cash flows.

• Flexible and diversified power portfolio.

• Established relationships with world class partners.

• A member of the San Miguel Corporation group of companies.

• Experienced and highly competent management team.

• Strong commitment to stringent environmental policies and pollution controls.

STRATEGIES

The principal business strategies of SMC Global Power are set out below:

• Optimize the installed capacity of its power portfolio and strategically contract capacity to enhancemargins.

• Continue to grow its power portfolio through the development of greenfield power projects and acquisitionof power generation capacity in line with regulatory and infrastructure developments.

• Vertically integrate complementary businesses in order to diversify its energy portfolio.

• Continue to pursue and develop measures to reduce gas emissions and operate power plants within andbelow applicable environmental compliance standards.

• Leverage operational synergies with San Miguel Corporation group of companies.

3

RECENT DEVELOPMENTS

On January 25, 2019, the Company subscribed to 18,314,898 common shares of MPGC, increasing its ownershipfrom 49% to 73.58% of the total issued and outstanding capital stock of MPGC. The subscription was a result ofthe waiver by MPGC’s other shareholders of their right to contribute additional equity pursuant to the capital callapproved by MPGC. On the same date, the Company subscribed to an additional 28,929,347 common shares tobe issued out of the proposed increase in the authorized capital stock of MPGC, which is subject to the SEC’sapproval. As of March 31, 2019, MPGC’s application for the increase in authorized capital stock is pending.

On March 28, 2019, the Company priced three series of Philippine Peso fixed-rate bonds in an aggregate amountof P25 billion with an oversubscription option of up to P5 billion. The Philippine Peso fixed-rate bonds in theaggregate amount of P30 billion were issued and listed on the Philippine Dealing and Exchange Corp onApril 24, 2019.

On April 25, 2019, the Company issued the Original Securities, which were listed on the SGX-ST on April 26,2019.

CORPORATE INFORMATION

SMC Global Power is incorporated under the laws of the Philippines. The registered office and principal place ofbusiness of SMC Global Power is located at SMC Global Power Holdings Corp., 155 EDSA, Wack-Wack,Mandaluyong City, Philippines. The telephone number of SMC Global Power is +632-702-4500.

The investor relations officer of SMC Global Power is Reyna-Beth De Guzman, who can be reached [email protected].

4

SUMMARY FINANCIAL INFORMATION AND OTHER DATA

The summary historical consolidated statement of financial position data as of December 31, 2016,December 31, 2017 and December 31, 2018, and summary historical consolidated statement of income and cashflow data for the years ended December 31, 2016, December 31, 2017 and December 31, 2018 set forth below,have been derived from, and should be read in conjunction with, the audited consolidated financial statements ofSMC Global Power, including the notes thereto, included elsewhere in this Offering Circular. The summaryhistorical consolidated statement of financial position data as of March 31, 2019 and summary historicalconsolidated statement of income and cash flow data for the three months ended March 31, 2018 and March 31,2019, respectively set forth below, have been derived from, and should be read in conjunction with, the unauditedinterim condensed consolidated financial statements of SMC Global Power, including the notes thereto, includedelsewhere in this Offering Circular.

The consolidated financial statements of SMC Global Power as of and for the years ended December 31, 2016,2017 and 2018 were audited by KPMG. The consolidated financial statements of SMC Global Power as of andfor the three months ended March 31, 2018 and 2019 were reviewed by KPMG.

Unless otherwise stated, SMC Global Power has presented its consolidated financial results under PFRS.

Potential investors should read the following data together with the more detailed information contained in“Management’s Discussion and Analysis of Results of Operations” and the consolidated financial statementsand related notes included elsewhere in this Offering Circular. The following data is qualified in its entirety byreference to all of that information.

Translations from Philippine Pesos to U.S. dollars for the convenience of the reader have been made at the BAPclosing rate on March 29, 2019 of p52.50 to U.S.$1.00.

5

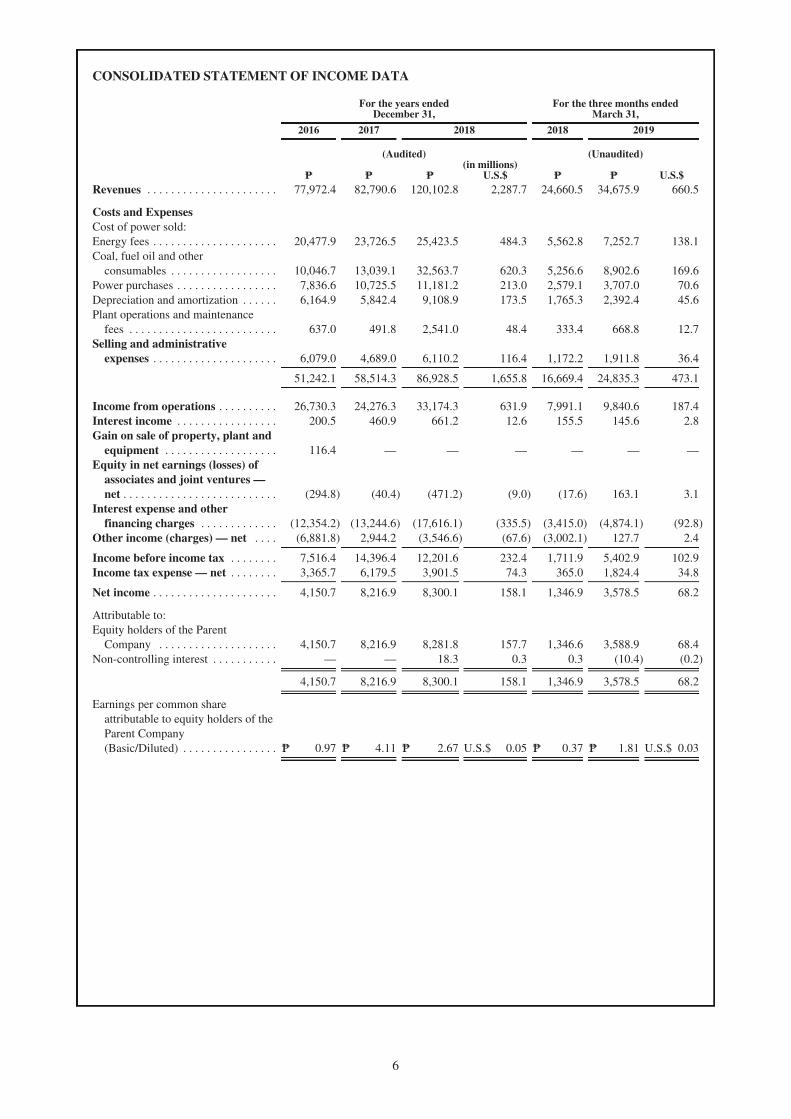

CONSOLIDATED STATEMENT OF INCOME DATA

For the years endedDecember 31,

For the three months endedMarch 31,

2016 2017 2018 2018 2019

(Audited) (Unaudited)(in millions)

Q Q Q U.S.$ Q Q U.S.$Revenues . . . . . . . . . . . . . . . . . . . . . . 77,972.4 82,790.6 120,102.8 2,287.7 24,660.5 34,675.9 660.5

Costs and ExpensesCost of power sold:Energy fees . . . . . . . . . . . . . . . . . . . . . 20,477.9 23,726.5 25,423.5 484.3 5,562.8 7,252.7 138.1Coal, fuel oil and other

consumables . . . . . . . . . . . . . . . . . . 10,046.7 13,039.1 32,563.7 620.3 5,256.6 8,902.6 169.6Power purchases . . . . . . . . . . . . . . . . . 7,836.6 10,725.5 11,181.2 213.0 2,579.1 3,707.0 70.6Depreciation and amortization . . . . . . 6,164.9 5,842.4 9,108.9 173.5 1,765.3 2,392.4 45.6Plant operations and maintenance

fees . . . . . . . . . . . . . . . . . . . . . . . . . 637.0 491.8 2,541.0 48.4 333.4 668.8 12.7Selling and administrative

expenses . . . . . . . . . . . . . . . . . . . . . 6,079.0 4,689.0 6,110.2 116.4 1,172.2 1,911.8 36.4

51,242.1 58,514.3 86,928.5 1,655.8 16,669.4 24,835.3 473.1

Income from operations . . . . . . . . . . 26,730.3 24,276.3 33,174.3 631.9 7,991.1 9,840.6 187.4Interest income . . . . . . . . . . . . . . . . . 200.5 460.9 661.2 12.6 155.5 145.6 2.8Gain on sale of property, plant and

equipment . . . . . . . . . . . . . . . . . . . 116.4 — — — — — —Equity in net earnings (losses) of

associates and joint ventures —net . . . . . . . . . . . . . . . . . . . . . . . . . . (294.8) (40.4) (471.2) (9.0) (17.6) 163.1 3.1

Interest expense and otherfinancing charges . . . . . . . . . . . . . (12,354.2) (13,244.6) (17,616.1) (335.5) (3,415.0) (4,874.1) (92.8)

Other income (charges) — net . . . . (6,881.8) 2,944.2 (3,546.6) (67.6) (3,002.1) 127.7 2.4

Income before income tax . . . . . . . . 7,516.4 14,396.4 12,201.6 232.4 1,711.9 5,402.9 102.9Income tax expense — net . . . . . . . . 3,365.7 6,179.5 3,901.5 74.3 365.0 1,824.4 34.8

Net income . . . . . . . . . . . . . . . . . . . . . 4,150.7 8,216.9 8,300.1 158.1 1,346.9 3,578.5 68.2

Attributable to:Equity holders of the Parent

Company . . . . . . . . . . . . . . . . . . . . 4,150.7 8,216.9 8,281.8 157.7 1,346.6 3,588.9 68.4Non-controlling interest . . . . . . . . . . . — — 18.3 0.3 0.3 (10.4) (0.2)

4,150.7 8,216.9 8,300.1 158.1 1,346.9 3,578.5 68.2

Earnings per common shareattributable to equity holders of theParent Company(Basic/Diluted) . . . . . . . . . . . . . . . . P 0.97 P 4.11 P 2.67 U.S.$ 0.05 P 0.37 P 1.81 U.S.$ 0.03

6

CONSOLIDATED STATEMENT OF FINANCIAL POSITION DATA

As of December 31, As of March 31,

2016 2017 2018 2018 2019

(Audited) (Unaudited)(in millions)

P P P U.S.$ P P U.S.$ASSETSCurrent AssetsCash and cash equivalents . . . . . . . . . . . . . . . 21,491.4 28,655.4 28,511.9 543.1 32,465.7 23,144.2 440.8Trade and other receivables — net . . . . . . . . . 22,342.9 20,435.1 33,046.7 629.5 26,906.3 37,000.0 704.8Inventories . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,272.3 3,147.7 5,294.6 100.8 5,383.4 4,801.7 91.4Prepaid expenses and other current assets . . . 17,683.0 17,791.8 21,761.7 414.5 20,377.3 21,843.1 416.1Assets held for sale . . . . . . . . . . . . . . . . . . . . . 184.3 — — — — — —

Total Current Assets . . . . . . . . . . . . . . . . . . . 63,973.9 70,030.0 88,614.9 1,687.9 85,132.7 86,789.0 1,653.1

Noncurrent AssetsInvestments and advances — net . . . . . . . . . . 16,245.4 16,621.1 12,149.0 231.4 16,884.2 11,375.7 216.7Property, plant and equipment — net . . . . . . . 246,488.0 250,961.3 312,315.4 5,948.9 312,707.2 144,602.0 2,754.3Right-of-use assets —net . . . . . . . . . . . . . . . . — — — — — 168,375.2 3,207.1Deferred exploration and development

costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 693.4 699.0 705.5 13.4 700.0 706.5 13.5Intangible assets and goodwill — net . . . . . . . 2,572.1 2,594.2 72,613.4 1,383.1 72,587.1 72,617.1 1,383.2Deferred tax assets . . . . . . . . . . . . . . . . . . . . . 2,955.6 1,316.9 1,137.6 21.7 1,633.8 1,156.5 22.0Other noncurrent assets — net . . . . . . . . . . . . 1,020.8 7,950.5 6,314.4 120.3 10,277.0 13,666.8 260.3

Total Noncurrent Assets . . . . . . . . . . . . . . . . 269,975.3 280,143.0 405,235.3 7,718.8 414,789.3 412,499.8 7,857.1

333,949.2 350,173.0 493,850.2 9,406.7 499,922.0 499,288.8 9,510.3

LIABILITIES AND EQUITYCurrent LiabilitiesLoans payable . . . . . . . . . . . . . . . . . . . . . . . . . — 5,930.0 8,675.7 165.2 8,277.2 8,662.5 165.0Accounts payable and accrued . . . . . . . . . . . . 37,729.4 31,074.8 31,109.9 592.6 41,192.4 33,830.7 644.4Finance lease liabilities — current portion . . . 16,344.3 16,844.4 19,659.6 374.5 17,824.4 20,898.1 398.1Income tax payable . . . . . . . . . . . . . . . . . . . . . 127.2 151.9 310.9 5.9 525.4 637.8 12.1Current maturities of long term debt — net of

debt issue costs . . . . . . . . . . . . . . . . . . . . . . 1,040.7 1,139.6 4,939.5 94.1 3,121.7 4,976.9 94.8

Total Current Liabilities . . . . . . . . . . . . . . . 55,241.6 55,140.7 64,695.6 1,232.3 70,941.1 69,006.0 1,314.4

Noncurrent LiabilitiesLong-term debt — net of current maturities

and debt issue costs . . . . . . . . . . . . . . . . . . . 65,283.0 89,589.1 202,025.8 3,848.1 182,851.2 203,244.9 3,871.3Deferred tax liabilities . . . . . . . . . . . . . . . . . . 4,785.2 7,324.1 8,180.1 155.8 7,468.6 9,233.1 175.9Finance lease liabilities — net of current

portion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 153,745.3 137,949.3 122,347.4 2,330.4 136,568.8 117,679.1 2,241.5Other noncurrent liabilities — net of current

portion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 223.5 404.3 843.6 16.1 8,451.1 821.6 15.6

Total Noncurrent Liabilities . . . . . . . . . . . . 224,037.0 235,266.8 333,396.9 6,350.4 335,339.7 330,978.7 6,304.4

Total Liabilities . . . . . . . . . . . . . . . . . . . . . . . 279,278.6 290,407.5 398,092.5 7,582.7 406,280.8 399,984.8 7,618.8

EquityCapital stock . . . . . . . . . . . . . . . . . . . . . . . . . . 1,062.5 1,062.5 1,062.5 20.2 1,062.5 1,062.5 20.2Additional paid-in capital . . . . . . . . . . . . . . . . 2,490.0 2,490.0 2,490.0 47.4 2,490.0 2,490.0 47.4Redeemable perpetual securities . . . . . . . . . . . — — 32,751.6 623.8 33,127.7 32,751.6 623.8Undated subordinated capital securities . . . . . 26,933.6 26,933.6 26,933.6 513.0 26,933.6 26,933.6 513.0Equity reserves . . . . . . . . . . . . . . . . . . . . . . . . 758.9 761.6 618.3 11.8 796.1 595.1 11.3Retained earnings . . . . . . . . . . . . . . . . . . . . . . 23,425.6 28,517.8 31,901.7 607.7 29,033.0 34,493.8 657.0

54,670.6 59,765.5 95,757.7 1,824.0 93,442.9 98,326.6 1,872.9Non-controlling interest . . . . . . . . . . . . . . . . . — — — — 198.4 977.4 18.6

Total Equity . . . . . . . . . . . . . . . . . . . . . . . . . . 54,670.6 59,765.5 95,757.7 1,824.0 93,641.2 99,304.0 1,891.5

333,949.2 350,173.0 493,850.2 9,406.7 499,922.0 499,288.8 9,510.3

7

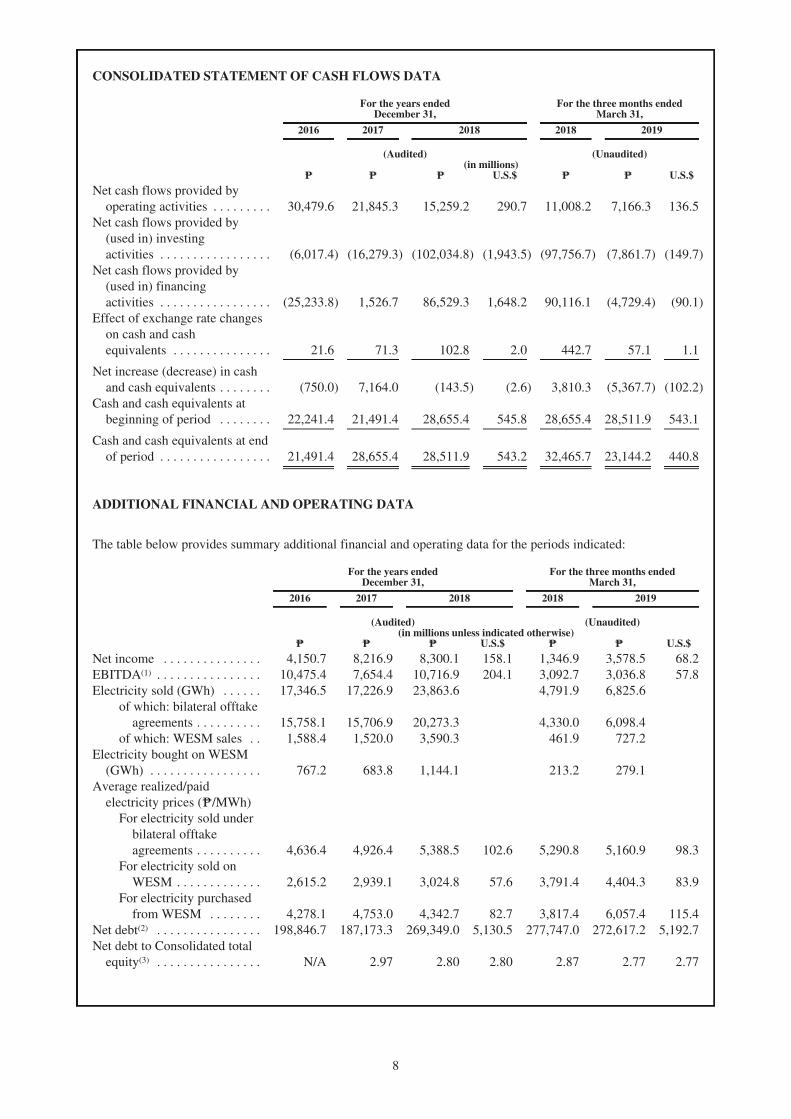

CONSOLIDATED STATEMENT OF CASH FLOWS DATA

For the years endedDecember 31,

For the three months endedMarch 31,

2016 2017 2018 2018 2019

(Audited) (Unaudited)(in millions)

Q Q Q U.S.$ Q Q U.S.$

Net cash flows provided byoperating activities . . . . . . . . . 30,479.6 21,845.3 15,259.2 290.7 11,008.2 7,166.3 136.5

Net cash flows provided by(used in) investingactivities . . . . . . . . . . . . . . . . . (6,017.4) (16,279.3) (102,034.8) (1,943.5) (97,756.7) (7,861.7) (149.7)

Net cash flows provided by(used in) financingactivities . . . . . . . . . . . . . . . . . (25,233.8) 1,526.7 86,529.3 1,648.2 90,116.1 (4,729.4) (90.1)

Effect of exchange rate changeson cash and cashequivalents . . . . . . . . . . . . . . . 21.6 71.3 102.8 2.0 442.7 57.1 1.1

Net increase (decrease) in cashand cash equivalents . . . . . . . . (750.0) 7,164.0 (143.5) (2.6) 3,810.3 (5,367.7) (102.2)

Cash and cash equivalents atbeginning of period . . . . . . . . 22,241.4 21,491.4 28,655.4 545.8 28,655.4 28,511.9 543.1

Cash and cash equivalents at endof period . . . . . . . . . . . . . . . . . 21,491.4 28,655.4 28,511.9 543.2 32,465.7 23,144.2 440.8

ADDITIONAL FINANCIAL AND OPERATING DATA

The table below provides summary additional financial and operating data for the periods indicated:

For the years endedDecember 31,

For the three months endedMarch 31,

2016 2017 2018 2018 2019

(Audited) (Unaudited)(in millions unless indicated otherwise)

Q Q Q U.S.$ Q Q U.S.$

Net income . . . . . . . . . . . . . . . 4,150.7 8,216.9 8,300.1 158.1 1,346.9 3,578.5 68.2EBITDA(1) . . . . . . . . . . . . . . . . 10,475.4 7,654.4 10,716.9 204.1 3,092.7 3,036.8 57.8Electricity sold (GWh) . . . . . . 17,346.5 17,226.9 23,863.6 4,791.9 6,825.6

of which: bilateral offtakeagreements . . . . . . . . . . 15,758.1 15,706.9 20,273.3 4,330.0 6,098.4

of which: WESM sales . . 1,588.4 1,520.0 3,590.3 461.9 727.2Electricity bought on WESM

(GWh) . . . . . . . . . . . . . . . . . 767.2 683.8 1,144.1 213.2 279.1Average realized/paid

electricity prices (P/MWh)For electricity sold under

bilateral offtakeagreements . . . . . . . . . . 4,636.4 4,926.4 5,388.5 102.6 5,290.8 5,160.9 98.3

For electricity sold onWESM . . . . . . . . . . . . . 2,615.2 2,939.1 3,024.8 57.6 3,791.4 4,404.3 83.9

For electricity purchasedfrom WESM . . . . . . . . 4,278.1 4,753.0 4,342.7 82.7 3,817.4 6,057.4 115.4

Net debt(2) . . . . . . . . . . . . . . . . 198,846.7 187,173.3 269,349.0 5,130.5 277,747.0 272,617.2 5,192.7Net debt to Consolidated total

equity(3) . . . . . . . . . . . . . . . . N/A 2.97 2.80 2.80 2.87 2.77 2.77

8

Notes:

(1) Calculated as (a) net income (excluding items between any or all of the Company and its subsidiaries) plus (b) income tax expense(benefit), finance cost (less interest income) and depreciation, in each case excluding amounts attributable to ring-fenced subsidiariesless (c) foreign exchange gain (loss), gain on sale of investment and aggregate fixed payments made to PSALM. EBITDA should not beviewed in isolation or as an alternative to financial measures calculated in accordance with PFRS. See “Presentation of FinancialInformation” and “Non-PFRS Financial Measures.”

(2) Net debt represents the consolidated debt of the Company and its subsidiaries — net of debt issue costs less cash and cash equivalentsand including PSALM finance lease liabilities, in each case, excluding amounts attributable to ring-fenced subsidiaries’ projectfinance debt. The ring-fenced subsidiaries are SCPC, SMCPC and PVEI.

(3) The Company maintains a Net debt to Consolidated total equity ratio of not more than 3.25x. The Net debt to Consolidated total equityratio is computed by dividing Net debt over Consolidated total equity. Consolidated total equity is Equity as adjusted to excludeRetained earnings (deficit) of ring-fenced subsidiaries.

CALCULATION OF EBITDA

The following table presents a reconciliation of EBITDA(1) to net income for each of the periods indicated.

For the years endedDecember 31,

For the three months endedMarch 31,

2016 2017 2018 2018 2019

(Audited) (Unaudited)(in millions)

P P P U.S.$ Q Q U.S.$

Net income(1) . . . . . . . . . . . . . . . . . . . . . . . 5,390.7 9,215.1 5,094.5 97.0 1,295.1 2,363.8 45.0Add:

Income tax expense . . . . . . . . . . . . . 3,677.9 5,352.4 4,638.2 88.3 355.0 1,829.5 34.8Finance cost . . . . . . . . . . . . . . . . . . . 12,342.3 11,747.7 14,919.7 284.2 3,074.3 3,917.8 74.6Interest income . . . . . . . . . . . . . . . . . (196.6) (368.5) (463.5) (8.8) (104.5) (105.8) (2.0)Depreciation . . . . . . . . . . . . . . . . . . . 6,338.7 5,607.7 6,898.6 131.4 1,565.7 1,743.2 33.2

Less:Foreign exchange gains (loss) . . . . . (6,910.1) (975.0) (5,345.0) (101.8) (3,226.1) 27.3 0.5Aggregate fixed payments made to

PSALM(2) . . . . . . . . . . . . . . . . . . . 23,873.3 24,875.0 25,715.6 489.8 6,319.0 6,684.4 127.3Gain on Sale of Investment . . . . . . . 114.4 — — — — — —

EBITDA . . . . . . . . . . . . . . . . . . . . . . . . . . 10,475.4 7,654.4 10,716.9 204.1 3,092.7 3,036.8 57.8

Notes:

(1) Amounts exclude items attributable to ring-fenced subsidiaries. Subsidiaries with project debts were nominated as ring-fencedsubsidiaries. If the amounts from the ring-fenced subsidiaries were to be included, the EBITDA would amount to p10,099.4 million,p9,013.8 million and p18,108.2 million (U.S.$344.9 million) for the years ended December 31, 2016, December 31, 2017 andDecember 31, 2018, and p3,912.2 million and p5,861.0 million (U.S.$111.6 million) for the three months ended March 31, 2018 andMarch 31, 2019, respectively.

(2) Aggregate fixed payments made to PSALM is reflected in the Statement of Cash Flows as Payments of Finance Lease Liabilities.

9

SUMMARY OF THE OFFERING

The following is a brief summary of the offering. For a more complete description of the terms of the Securities,see “Terms and Conditions of the Securities.” Capitalized terms not otherwise defined herein shall have themeanings set forth under “Terms and Conditions of the Securities.”

Issuer . . . . . . . . . . . . . . . . . . . . . . . . . . . . SMC Global Power Holdings Corp., a company incorporated withlimited liability under the laws of the Republic of the Philippines.

Securities Offered . . . . . . . . . . . . . . . . . . U.S.$[Š] senior perpetual capital securities (“Additional Securities”)to be consolidated into and form a single series with theU.S.$500,000,000 senior perpetual capital securities issued by theIssuer on April 25, 2019 (the “Original Securities”, and togetherwith the Additional Securities, the “Securities”).

Status of the Securities . . . . . . . . . . . . . . The Securities constitute direct, unconditional, unsecured andunsubordinated obligations of the Issuer and will at all times rank paripassu without any preference among themselves and at least paripassu with all other present and future unconditional, unsecured andunsubordinated obligations of the Issuer (including the OriginalSecurities), but, in the event of insolvency, only to the extentpermitted by applicable laws relating to creditors’ rights.

The claims of the holders, in respect of the Securities, including inrespect of any claim to Arrears in Distribution, will, in the event ofthe Winding-Up of the Issuer (subject to and to the extent permittedby applicable law), rank at least pari passu with each other and withall other present and future unconditional, unsecured andunsubordinated obligations of the Issuer.

No Set-off . . . . . . . . . . . . . . . . . . . . . . . . To the extent and in the manner permitted by applicable law, noSecurityholder may exercise, claim or plead any right of set-off,counterclaim, compensation or retention in respect of any amountowed to it by the Issuer in respect of, or arising from, the Securitiesand each Securityholder will, by virtue of his holding of any Security,be deemed to have waived all such rights of set-off, counterclaim,compensation or retention.

Initial Rate of Distribution . . . . . . . . . . . 6.50% per annum plus any increase pursuant to Condition 4.4(Increase in Rate of Distribution).