SELECTION AMONG EMPLOYER-SPONSORED PENSION PLANS: THE ROLE OF INDIVIDUAL DIFFERENCES

28

PERSONNEL PSYCHOLOGY m. 53 SELECTION AMONG EMPLOYER-SPONSORED PENSION PLANS: THE ROLE OF INDIVIDUAL DIFFERENCES JAMES H. DULEBOHN Department of Management Georgia State University BRIAN MURRAY Whittemore School of Business and Economics University of New Hampshire MINGHE SUN Division of Management and Marketing University of Rxas at San Antonio Recognizing the explosive growth and increasing importance of al- ternative forms of retirement plans, this study investigated determi- nants of employees’ choice among the three major types of employer- sponsored pension plans: defined benefit, defined contribution, and hybrid cash balance. Using a field survey of 2,400 employees who par- ticipated in a state sponsored retirement system covering 60 participat- ing employers, we tested a general model of public employee pension choice, and examined the roles of plan feature preferences, employee attitudes, and demographics in pension plan participation choices. The results identified primary predictors distinguishing plan selection and indicated that employees’ preferences for plan features explained sig- nificant variation in their selection among pension plans. The results challenged the conventional wisdom regarding the nature of pension plan choice and highlighted the critical role played by individual dif- ferences. Employer-sponsoredpension plans play a number of important roles for both employers and employees. Although employers provide pen- sion plans for a variety of reasons, the overall goal of organizations is to design compensation systems that are consistent with their human re- source policies (Mitchell & Rappaport, 1993). Specific objectives in- clude the attraction and retention of particular employees, the regula- tion of retirement outflow, and the alignment of employee work effort with the company objectives (Gustman, Mitchell, & Steinmeier, 1994). Employees desire employer-sponsored pension plans primarily because Funding for this study was provided by research support from TIM-CREF and is Correspondence and requests for reprints should be addressed to James H. Dulebohn, gratefully acknowledged by the authors. Department of Management, Georgia State University, Atlanta, GA 30303. COPYRIGHT 0 2000 PERSONNEL PSYCHOLOGY, INC. 405

Transcript of SELECTION AMONG EMPLOYER-SPONSORED PENSION PLANS: THE ROLE OF INDIVIDUAL DIFFERENCES

PERSONNEL PSYCHOLOGY m. 53

SELECTION AMONG EMPLOYER-SPONSORED PENSION PLANS: THE ROLE OF INDIVIDUAL DIFFERENCES

JAMES H. DULEBOHN Department of Management

Georgia State University

BRIAN MURRAY Whittemore School of Business and Economics

University of New Hampshire

MINGHE SUN Division of Management and Marketing

University of Rxas at San Antonio

Recognizing the explosive growth and increasing importance of al- ternative forms of retirement plans, this study investigated determi- nants of employees’ choice among the three major types of employer- sponsored pension plans: defined benefit, defined contribution, and hybrid cash balance. Using a field survey of 2,400 employees who par- ticipated in a state sponsored retirement system covering 60 participat- ing employers, we tested a general model of public employee pension choice, and examined the roles of plan feature preferences, employee attitudes, and demographics in pension plan participation choices. The results identified primary predictors distinguishing plan selection and indicated that employees’ preferences for plan features explained sig- nificant variation in their selection among pension plans. The results challenged the conventional wisdom regarding the nature of pension plan choice and highlighted the critical role played by individual dif- ferences.

Employer-sponsored pension plans play a number of important roles for both employers and employees. Although employers provide pen- sion plans for a variety of reasons, the overall goal of organizations is to design compensation systems that are consistent with their human re- source policies (Mitchell & Rappaport, 1993). Specific objectives in- clude the attraction and retention of particular employees, the regula- tion of retirement outflow, and the alignment of employee work effort with the company objectives (Gustman, Mitchell, & Steinmeier, 1994). Employees desire employer-sponsored pension plans primarily because

Funding for this study was provided by research support from TIM-CREF and is

Correspondence and requests for reprints should be addressed to James H. Dulebohn, gratefully acknowledged by the authors.

Department of Management, Georgia State University, Atlanta, GA 30303.

COPYRIGHT 0 2000 PERSONNEL PSYCHOLOGY, INC.

405

406 PERSONNEL PSYCHOLOGY

they are forms of indirect compensation that help them to save for retire- ment, accumulate wealth, and lessen old-age economic insecurity (Gust- man & Mitchell, 1992). The salience of employer-sponsored retirement plans to American employees has grown in recent years as a result of a number of factors including the graying of the labor force and the grow- ing concern regarding the future solvency of Social Security (cf. Boskin, 1986; Goodfellow & Schieber, 1993).

The two major types of pension plans offered by employers are de- fined benefit (DB) plans and defined contribution (DC) plans. DB plans are formula-based pension plans in which employers typically promise to pay their employees a benefit based on the employee’s retirement age, final average salary, and years of service. DCplans are similar to savings plans and provide a benefit based on annual contributions, as a percent- age of pay made on behalf of the employee, and accumulated investment earnings on the employee’s account.

Historically, DB plans have been the most common type of pen- sion plan that employers have provided to their employees (Kotlikoff & Smith, 1983). Recently, however, there has been a growth in the use of DC plans among both private and public employers (Gustman & Stein- meier, 1992; Kruse, 1995; Jankowski, 1997). For example, the number of private sector DC pension plans increased by over 200% between 1975 and 1997 (Quick, 1999). Many employers are providing employees with DC pension plans in addition to, or in replacement of, DB plans (McEn- tee, 1997; Mitchell & Rappaport, 1993; Wisniewski, 1999).

Furthermore, a number of employers have begun offering employees “hybrid” plans combining features of both plan types (Bodie & Merton, 1993; Rothy, 1992). An example is a cash-balance plan, which is a DB plan that provides a DC type lump sum distribution for early leavers, consisting of contributions and interest earnings (Laabs, 1995). Re- cently, at least 325 organizations have converted more than $330 billion of assets into this type of plan (Williamson, 1999). The offering of alter- native pension plans to employees has been driven by employer efforts to reduce pension liability, attract employees who desire DC plans, and provide employees with a choice among pension plans that will best fit their needs (Crane, 1995; Sollinger, 1993).

The choice among these plans is important for employees because typically pension plan choice is an irrevocable decision made once during the employment relationship. With increased job mobility, employees may be faced with this decision more than eight times during their work- ing career (O’Rourke, 2000). The purpose of this study is to test a model of the determinants of employee selection among employer-sponsored retirement plans and to report the results of an exploratory investigation. Using a field survey, we examined public employees’ choice among three

JAMES H. DULEBOHN ET AL. 407

employer-sponsored retirement plans: a DB plan, a DC plan, and a hy- brid plan. The focus of this study was on the role of preferences for pen- sion plan features, employee attitudes, and demographic characteristics in employees’ selection among three pension plans.

Theoretical Rationale and Model of Pension Plan Choice

Although the changes occurring in employer offerings of pension plans have received notable research attention (cf. Clark & McDermed, 1990; Gustman & Steinmeier, 1992; JSruse, 1995), a review of the liter- ature indicates that only one study has investigated employees’ choice among retirement plans. The study by Clark, Harper, and Pitts (1997) examined the direct effects of demographic predictors on a choice be- tween a DC plan and a DB plan among faculty members at a state univer- sity. Their results indicated that age and years of service were positively related to the selection of the DB plan, and salary was positively related to the selection of the DC plan.

This current study goes beyond prior research by building a general model of public employee pension choice and investigating the role plan feature preferences, individual attitudes, and demographic variables play in public employees’ selection among three employer-sponsored pension plans. Specifically, we examined both the direct and mediated effects of these variables on plan selection. Attitude theory served as the theoretical foundation for our model specification, selection of predic- tors of retirement plan choice, and the ordering of the variables in our analysis. Figure 1 presents the model and variables tested in this study.

Dependent Construct: Plan Choice

Attitudes have been proposed to be important predictors of individ- uals’ evaluatory thoughts, affective responses, and resulting behavior toward target objects, intentions, or decisions (e.g., Ajzen, 1988, 1991; Ajzen & Fishbein, 1980). Likewise, attitude researchers have found that individuals often demonstrate consistency between their cognitive and affective evaluations of attitude objects and their behavioral re- sponses (Chaiken and Yates, 1985; Kelman, 1974; Schuman & John- son, 1976). This consistency principle upon which we base our devel- opment of a pension choice model is similar to the needs-supplies per- spective of fit as the match between individual preferences and orga- nizational systems (Kristof, 1996). That is, when given a choice among employer sponsored pension plans, an employee will choose the pension plan that matches his or her individual preferences or needs (cf. Cable & Judge, 1994; Caplan, 1987). Accordingly, we expect individuals to

Pers

onal

C

hara

cter

istic

s

Invo

lvem

ent

Self-

Effi c

acy

Risk

Pre

fere

nce

Cur

rent

Pla

n Sa

tisfa

ctio

n A

ge

Yea

rs o

f Ser

vice

In

com

e Jo

b C

ateg

ory

Gen

der

Mar

ital S

tatu

s N

umbe

r of D

epen

dent

s

Plan

Fea

ture

Pr

efer

ence

s

b

Plan

C

hoic

e

Porta

bilit

y Lu

mp

Sum

Dis

tribu

tion

Ben

efit

Det

erm

inat

ion

Inve

stm

ent C

hoic

e Su

rviv

or B

enef

its

.a

0

00

Def

ined

Ben

efit

Plan

Def

ined

Con

tribu

tion

Plan

~

Hyb

rid P

lan

A

Spou

se P

artic

ipat

ion

Oth

er P

lan

Parti

cipa

tion

Oth

er S

avin

gs

Oth

er B

enef

its

I

Figu

re I: M

odel

of P

ensio

n C

hoice

JAMES H. DULEBOHN ET AL. 409

possess and act on attitudes that they have toward their retirement and retirement funding. We also expect that those attitudes will be consis- tent, arising from affective and cognitive responses to personal charac- teristics and the consideration of specific plan features and resulting in behavioral choices among plan options.

As presented in Figure 1, the dependent construct of our model is the individual’s pension plan choice. For our study, the three choices included a DB plan, a hybrid plan, and a DC plan. We expected that the behavioral choice would be a function of the personal characteristics that should drive affective or cognitive responses from the individual, mediated by attitudinal preferences for plan features that are consistent with the personal characteristics.

Mediating Constructs: Artitudinal Plan Feature Preferences

As presented in Figure 1, the second component of the model rep- resents individual attitudinal preferences toward plan features. Pref- erences toward plan features are proximal to plan choice in that the features are embedded in the plans. As indicated above, we expected preferences toward plan features to mediate the personal characteris- tics included as independent predictors in the model.

Our selection of plan feature preferences was informed by functional attitude theory proposed by Katz (1960) who asserted that attitudes de- velop to meet certain needs of the individual and are to be understood according to the functions they serve. One of the functions that Katz pro- posed is the instrumental or utilitarian function, which is based on the behaviorist premise that people are motivated to maximize rewards and minimize punishments from an object. The instrumental function posits that individuals develop positive attitudes toward objects that they asso- ciate with the satisfaction of their needs and negative attitudes toward objects that hinder the satisfaction of their needs (Katz, 1960).

More recently, Herek (1986) refined this approach by defining a neo- functional theory that identified evaluative roles for utilitarian functions. In describing the evaluative function, Herek (1986) wrote: “Positive at- titudes toward an object tend to result when it is perceived as a source of benefit, reward, or pleasure; negative attitudes result from past or anticipated detrimental, unpleasant, or punishing experiences with it” (p. 105). In regard to pension plan feature preferences, following Herek (1986) we approached them as evaluative because an individual expects to reap a net personal benefit in income and because the retirement plan choice is relatively private and projects little social expression. Consis- tent with Shavitt (1990), we also expected them to be single function, utilitarian attitudes because retirement benefits are explicitly defined in

410 PERSONNEL PSYCHOLOGY

terms of reward, can reflect punishment in terms of lost value or oppor- tunity cost, and can be related to behavior that maximizes rewards. Ac- cordingly, we have defined each of the plan feature preferences in terms of the reward generating properties of the object, retirement plan, or the corresponding utility maximizing characteristics, responses, or behaviors of the individual. The following describes the plan feature preferences included as mediators in the model.

Portability and lump sum distribution. DB plans reward long tenure and often have the effect of discouraging employees from changing jobs by imposing a loss in retirement benefits for those who separate from their employer prior to retirement. DB plans are back-loaded and con- sequently benefits accrue disproportionately during later years of em- ployment (Gustman & Steinmeier, 1992). In contrast, a primary reason employers offer DC plans is because of the portability provided by the plans (Roberts & Hanley, 1997). DC plans enable employees to change jobs and take their retirement savings with them, often in the form of a lump sum distribution. This portability aspect of DC plans is seen as a compensation feature to recruit or attract qualified employees who value portability (Crane, 1995). Similarly, a hybrid plan, such as a cash- balance plan, is a DB plan that provides each employee with an indi- vidual account that accumulates interest. If the employee remains until retirement age, he or she receives the defined benefit, otherwise he or she receives the amount in the account. Thus, we expected that indi- viduals who preferred the pension features of portability and lump sum distribution would be more likely to choose a DC plan or hybrid plan over a DB plan.

Benefit determination and investment choice. Two distinct features of employer-sponsored pension plans are whether the final retirement ben- efit is determined by a guaranteed formula or account contributions and investment earnings and whether they provide participants with invest- ment choice. In DB plans the final benefit is determined by a guaranteed formula. In addition, DB plans manage the retirement contributions and do not provide employees with the option to decide where their retire- ment savings are invested. A cash-balance plan is similar to a DB plan and does not provide investment choice. In contrast, in DC plans the retirement benefit is determined by the contribution amount and the in- vestment earnings. These plans often allow employees to select among investment options and to take an active role in managing their retire- ment savings. For the benefit determination, we expected that prefer- ence for a guaranteed formula would be related to the choice of a DB or hybrid plan and preference for a benefit based on investment earnings would be related to the choice of a DC plan. Second, we expected that

JAMES H. DULEBOHN ET AL. 41 1

preference for investment choice would be related to the choice of a DC plan rather than a DB plan or hybrid plan.

Survivor benefits. DB plans generally provide postretirement survivor benefits to a surviving spouse. In contrast, survivor benefits are not typically included in DC plans but have to be purchased separately by the participant. Similarly, in exchange for the portability feature provided by a cash-balance hybrid plan, those who select this type of plan may have to forfeit the postretirement survivor benefit feature. Consequently, we expected that a preference for postretirement survivor benefits would be associated with the choice of a DB plan rather than a hybrid plan or DC plan.

Independent Predictors: Personal Charactektics

Important independent predictors of plan choice are personal char- acteristics that include attitudinal, dispositional, and demographic mea- sures. Although personal characteristics are distal to plan choice, as possible antecedents to plan feature preferences, personal characteris- tics may influence plan choice indirectly through their impact on indi- viduals’ attitudinal preferences for plan features (cf. Eagly & Chaiken, 1993; Triandis, 1971). As presented in Figure 1, the following personal characteristics were included in the first component of the model be- cause of their expected impact on preference development and behav- ioral choice.

Involvement. Participant involvement represents a multifaceted con- struct that has been found to be associated with choices (Lastovicka & Gardner, 1979). One facet of participant involvement is interest (Lau- rent & Kapferer, 1985). As noted, although DB and hybrid plans are managed for the participants, DC plans require participants to take part in managing their retirement savings. Individuals who are interested in being involved in managing their retirement savings may have higher preference for the plan feature of investment choice provided by a DC plan.

Selfeficacy. Self-efficacy refers to the judgments an individual makes about his or her abilities to mobilize the cognitive resources, motivation, and courses of action needed to engage in performance on a specific task (Gist & Mitchell, 1992). It is reasonable to expect self-efficacy to influence choice among pension plans (cf. Bandura, 1982). Specifically, individuals who have low self-efficacy with respect to effectively man- aging their retirement savings and making investment choices would be expected to choose a DB or hybrid plan while those who have high self- efficacy may be more likely to choose a DC plan.

412 PERSONNEL PSYCHOLOGY

Riskpreference. Risk preference has been described as a dispositional characteristic; individuals who enjoy the challenge that risks entail are often more likely to undertake risky actions than those who do not (Sitkin & Pablo, 1992). Risk involves the choice among two or more alternatives where at least one of the alternatives exposes the individual to the PO- tential of loss (MacCrimmon & Wehrung, 1986). Because DB or hybrid plans provide a guaranteed retirement benefit, they represent a lower risk option than DC plans that expose individuals to the potential of in- vestment loss. consequently, we expected individuals’ risk preference to have an impact on their preference for the plan features of benefit determination and to be associated with plan choice, that is, higher risk preference level toward DC plan choice and lower risk preference level toward DB plan or hybrid plan choice.

Current plan satisfaction. A fourth personal characteristic that we expected to be related to plan choice is satisfaction with one’s current retirement plan. As noted by Hirschman (1970), individuals can respond to dissatisfying situations in three ways: exit, voice, or loyalty. Exit refers to withdraw or separation. It is to be expected that individuals who are dissatisfied with their current employer-sponsored pension plan (e.g., typically a DB plan) would be more likely to choose to exit the plan by choosing another plan (i.e., DC plan or hybrid plan).

Demographic variables. We first included the demographic variables age, years of service, and income, which, as noted above, were found to be significant by Clark and Pitts (1999) in pension plan choice. We expected these variables to have an impact on employee preference for plan fea- tures including benefit determination, lump sum distribution, and porta- bility and to be associated with plan choice. Second, we included job categoy (professional and academic vs. staff‘), which represented a pri- mary distinction in the population we surveyed. Because of the typically higher level of education and mobility of professional and academic em- ployees, we expected this group to differ from staff in its preferences. Third, we includedgender based on Clark and McDermed’s (1989) study that indicated the importance of gender on retirement choice. Fourth, we included marital status, number of dependents, and spouse participa- tion in a pension plan because, as noted by Clark and Pitts (1999), these variables influence the mobility of employees and may affect their pref- erence for pension portability and preference for survivor benefits.

Finally, we included otherplanparticipation, which indicated whether the employee participated in any other DC pension plans; other savings, which indicated whether the employee voluntarily saved for retirement through participation in an IRA or pre-tax deferred annuity; and other benefits, which indicated whether the employee expected to receive re- tirement benefits from other retirement plans than the one in which

JAMES H. DULEBOHN ET AL. 413

they currently participated. These variables represent indicators of re- tirement plan experience and other future retirement income streams and may affect preference for pension plan features such as investment choice, benefit determination, and survivor benefits.

Methods

Sample and Procedures

Surveys were administered to a stratified random sample of active participants of a major state sponsored retirement system. This sys- tem administered a DB plan pension program that covered over 80,000 employees and included 60 participating employer organizations. The participating employer organizations included community colleges, state colleges and universities, and university hospitals. Participation in the pension program was mandatory for employees. Due to changes in state legislation, the organization was required to provide to employees the choice of two new retirement plans, in addition to the traditional DB plan offering: a hybrid cash-balance plan and a DC plan. Current em- ployees were given an opportunity to make an irrevocable choice among the three retirement plans. We administered our survey prior to the open enrollment periods for the new plans.

The study used response rates based on years of service, age, and job categories from a survey conducted during the prior year to esti- mate the number of surveys needed to be sent out in order to generate a sufficient sample for particular groups. The sampling procedure in- volved oversampling younger employees and employees who were not vested (service less than 5 years) because prior surveys had found that this group had a very low response rate. Surveys were mailed to 14,000 active members. Prior to mailing, the surveys were coded in order to match the survey respondents with data in the pension plan’s database.

The survey was prefaced by an explanatory cover letter from the retirement system’s director. The survey booklet was 10 pages in length. The survey was ordered such that individuals reported their attitudes and preferences first; subsequently, they chose among plan options.

The sample consisted of 2,410 useable responses, representing a re- sponse rate of 17%. Analysis indicated that the sample distribution was representative of the population distribution in terms of age, gender, and years of service. The average age of the respondents was 43.3 years (SD = 11.2) while the average age of the population was 42 years; fe- males constituted 46.4% of the sample compared to 46% of the pop- ulation. The average accumulated years of service with the employer- sponsored pension plan for the respondents was 7.4 years (SD = 7.1)

414 PERSONNEL PSYCHOLOGY

compared to 7.4 years for the population. Professional and academic employees accounted for 53% of the respondents compared to 47% of the population. Professional and academic jobs included faculty mem- bers, administrators, and academic professionals, and staff jobs include all support staff, maintenance workers, police and firefighters, house- keepers, and others.

Dependent Variable: Plan Choice

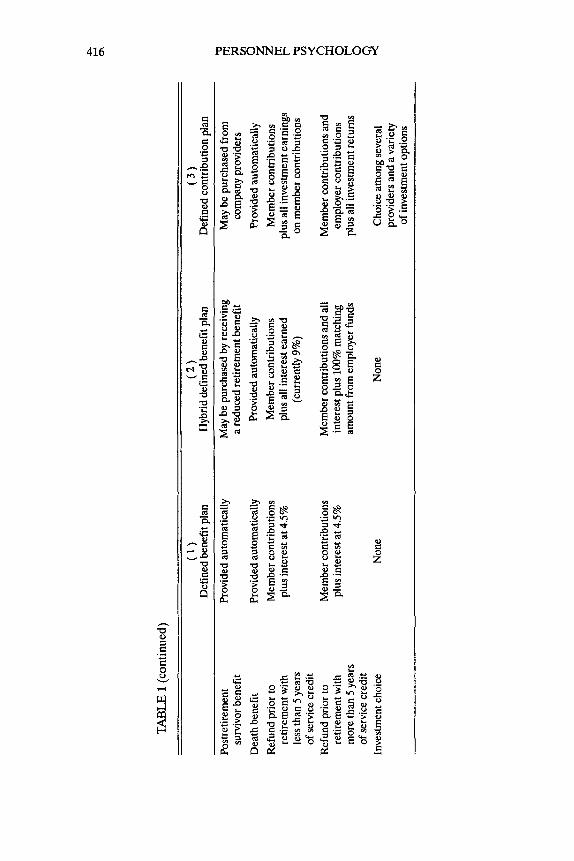

The survey presented respondents with a comparative description of the three employer-sponsored pension plans that were being offered to the employees (see Table 1). As presented in Table 1, the first plan was the DB pension plan that had been offered by the system since its inception. The second plan was the hybrid pension plan. Similar to a cash-balance plan, this plan provided greater pension portability to participants than the DB plan by its provision of a larger refund prior to retirement (i.e., it included a refund of employer contributions and interest), at the cost of not automatically providing a postretirement survivor benefit. The third plan was the DC pension plan. This plan was markedly different from the other two in its provision of investment choice. In addition to being presented with this comparison of plan features, survey participants were provided with text descriptions of the differences among plans. Respondents were asked to indicate which plan they would choose. Their intended choice response served as the dependent variable.'

Mediating Attitudinal Preference Measures

Benefit determination. Respondents answered a dichotomous ques- tion that asked if they preferred a retirement benefit based on invest- ment earnings (= 0) or a guaranteed defined benefit formula (= 1).

Distribution preference. Respondents answered a dichotomous ques- tion that asked if they preferred an indexed monthly retirement benefit (= 0) or a lump sum distribution (= 1).

'We compared intended choice and actual choice for 1,007 of the 2,410 sample respon- dents. The Spearman nonparametric correlation coefficient between the intended and actual choices for the 1,007 respondents was strong and positive ( T = .91; p < 401). The result of a nonparametric chi-square goodness-of-fit test was insignificant (xz = 1.58, n.s.) indicating no significant difference between the proportions of values for actual choice and intended choice frequencies for each plan choice category. We used intended plan choice as the dependent variable for this study because the respondent demographic char- acteristics more closely reflected the population. In addition, respondents' status may have changed between the survey and end of the open enrollment period (e.g., promotion with tenure or dependent change), that would have introduced error into the analysis or neces- sitated re-surveying to update the individuals' reported characteristics.

TABL

E 1

Des

crip

tion

of Pl

an F

eatu

res P

rovi

ded

to R

espo

nden

ts

(1)

(2)

(3)

Def

ined

ben

efit

plan

H

ybrid

def

ined

ben

efit

plan

D

efin

ed c

ontri

butio

n pl

an

Empl

oyee

cont

ribut

ion

rate

Em

ploy

er co

ntrib

utio

n ra

te

Type

of r

etire

men

t ben

efit

Ret

irem

ent b

enef

it am

ount

Post

retir

emen

t

Dis

abili

ty be

nefit

Pr

eret

irem

ent

surv

ivor

bene

fit

bene

fit in

crea

ses

8.0%

9.

1%

Life

time

mon

thly

annu

ity

Dep

ende

nt o

n se

rvic

e an

d sa

lary

; max

imum

ben

efit

is 8

0% of

fin

al sa

lary

A

utom

atic

3%

ann

ual

retir

emen

t ben

efit

incr

ease

Pr

ovid

ed a

utom

atic

ally

Pr

ovid

ed a

utom

atic

ally

8.0%

9.

1%

Life

time

mon

thly

annu

ity

Dep

ende

nt o

n se

rvic

e an

d sa

lary

; max

imum

ben

efit

is 80

% of

fin

al sa

lary

A

utom

atic

3% a

nnua

l re

tirem

ent b

enef

it in

crea

se

Prov

ided

aut

omat

ical

ly

Prov

ided

aut

omat

ical

ly

8.0%

7.

6%

1) M

onth

ly a

nnui

ty; o

r 2)

Lum

p su

m d

istri

butio

n at

tim

e of

ret

irem

ent

Det

erm

ined

by

empl

oyee

an

d em

ploy

er c

ontri

butio

ns

and

inve

stm

ent e

arni

ngs

Det

erm

ined

by in

vest

- m

ent p

erfo

rman

ce

Prov

ided

aut

omat

ical

ly

May

be

purc

hase

d fr

om

com

pany

pro

vide

rs

F t v,

TAB

LE 1

(con

tinue

d)

__

__

__

~

~_

__

__

__

__

_

_

.~

(2)

(3)

Hyb

rid d

efin

ed b

enef

it pl

an

Def

ined

con

tribu

tion

plan

(1

) D

efin

ed b

enef

it pl

an

Post

retir

emen

t Pr

ovid

ed a

utom

atic

ally

M

ay b

e pu

rcha

sed

by re

ceiv

ing

May

be

purc

hase

d fr

om

% E Pr

ovid

ed a

utom

atic

ally

i?

surv

ivor

bene

fit

a re

duce

d re

tirem

ent b

enef

it co

mpa

ny p

rovi

ders

D

eath

ben

efit

Prov

ided

aut

omat

ical

ly

Prov

ided

aut

omat

ical

ly

Ref

und

prio

r to

Mem

ber c

ontri

butio

ns

retir

emen

t with

le

ss th

an 5

yea

rs

of se

rvic

e cre

dit

plus

inte

rest

at 4

.5%

M

embe

r con

tribu

tions

pl

us a

ll in

tere

st e

arne

d (c

urre

ntly

9%

)

z m

plus

all i

nves

tmen

t ear

ning

s r

Mem

ber c

ontri

butio

ns

on m

embe

r con

tribu

tions

Ref

und

prio

r to

Mem

ber c

ontri

butio

ns

Mem

ber c

ontri

butio

ns an

d al

l M

embe

r con

tribu

tions

and

re

tirem

ent w

ith

plus

inte

rest

at 4

.5%

in

tere

st p

lus

100%

mat

chin

g em

ploy

er c

ontri

butio

ns

mor

e th

an 5

yea

rs

plus

all i

nves

tmen

t ret

urns

of

ser

vice

cred

it 8

amou

nt fr

om e

mpl

oyer

fund

s

Inve

stm

ent c

hoic

e N

one

Non

e C

hoic

e am

ong

seve

ral

prov

ider

s and

a va

riety

of

inve

stm

ent o

ptio

ns

JAMES H. DULEBOHN ET AL. 417

Investment choice. Respondents’ preference for investment choice was assessed using three items created for this study. An example of an item was: “How important is it to you to have a retirement plan that provides you with the ability to choose how your money is invested?” Responses for the items were assessed using a 5-point Likert-type scale anchored by not at all important to crucial. The coefficient alpha relia- bility estimate was 34.

Survivor benefit. Respondents answered a dichotomous question that asked if they preferred a retirement plan that automatically provided and financed postretirement survivor benefits (= 1) or a plan that provided a larger account refund prior to retirement but did not automatically provide survivor benefits during retirement (= 0).

Portabilifypreference. Respondents’ preference for portability was as- sessed using two items created for this study. An example of an item was: “How important is it to you to have a retirement plan that is portable-one allowing you to take the full value of your account with you from one employer to another?” Responses for the items were as- sessed using a 5-point Likert-type scale anchored by nor at all important to crucial. The coefficient alpha reliability estimate was .74.

Independent Variable Measures

Most of the demographic measures used were objective choice items. Income was classified into the following six categories: less than $15,000

(= 3), $50,001-$75,000 (= 4), and over $75,000 (= 5). The coding for other categorical demographic variables is given in Table 2.

Self-eficacy. Respondents’ self efficacy was assessed using three items created for the study following Judge and Martocchio (1996). One of the items was: “Making investment decisions is probably something I will never be good at.” Responses for the items were assessed using a 5-point Likert-type scale anchored by “strongly disagree” to “strongly agree.” The coefficient alpha reliability estimate was .78.

Risk preference. Respondents’ risk preference was assessed using one item developed by Fidelity Investments (Fidelity, 1998). The question stated: “When thinking about your retirement plan, where would you place yourself on the following scale?” Respondents chose from three options representing different levels of risk preference (1 = low; 2 = moderate; 3 = high).

Currentplan satisfaction. Respondents’ satisfaction with their current pension plan was assessed using one item that stated: “How satisfied are you with your current retirement plan?” Responses for the items were

(= 0), $15,001-$25,000 (= l), $25,001-$35,000 (= 2), $35,001-$50,000

TABL

E 2

Corr

elat

ions

and

Des

crip

tive

Stat

istic

s for A

ll Va

riabl

es

e. W

M

SD

1 2

3 4

5 6

7 8

9 10

11

12

13

14

15

16

17

18

19

20

21

22

1.

.4

1 .4

9 2.

.44

SO -

.56

4. .2

6 .4

4 .2

7 .OO

-.28

3.

.16

.36

-.43

-.51

5. .3

1 .4

6 -.2

8 -.

07

.37

-.25

6.

7.99

1.

66 -

.21

-.14

.37

-34

.27

7.

.57

SO

.40

-.16

-.23

.22

-.27

-.I7

8.

6.68

2.

11 -

.41

.18

.23

-.27

.26

.37

-.52

% 9.

.47

SO

.22

-.08

-.14

.05

-.09

.01

.15

-.16

9 10

. 3.

19

1.40

-.1

2 .0

3 .1

0 -.0

3 .0

1 -.0

4 -.

lo

-.05

-.41

11.

.46

SO -

.06

-.03

.09

.OO

.05

.03

-.02

-.02

-.19

.31

12.

7.38

7.05

.2

0 -.0

6 -.1

5 .1

4 -.1

6 -.2

2 .1

7 -.4

4 -.0

1 .2

8 .0

3 13

. .6

9 .46

-.02

-.03

.06

-.01

.02

.01

.05

-.11

-.06

.10

.13

.04

15.

1.16

.9

6 -.0

1 -.0

2 .0

3 -.0

2 .OO

.0

5 .0

6 -.0

8 -.0

1 .1

3 .1

4 .0

4 .5

3 -.0

1 'd

17.

.74

.44

-.03

.01

.02

-.06

.06

.08

-.04

.07

.OO

-.03

.04

-.22

.OO

.18

.02

-.03

18.

.52

SO -

.12

-.02

.15

-.12

.09

.13

-.11

.14

-.14

.ll

.11

-.15

.04

.12

-.02

.26

.13

20.

8.76

2.

50 -

.27

-.07

.36

-.21

.29

.43

-.21

.23

-.16

.ll

.17

-.12

.09

-.08

.04

.21

.05

.17

.16

21.

4.70

1.

54 -

.32

.OO

.33

-.21

.21

.26

-.25

.20

-.29

.28

.ll

-.08

.15

.OO

.05

.46

.03

.26

.45

.40

23.

9.26

3.

00 -

.28

-.09

.38

-.26

.30

.54

-.22

.25

-.09

.08

.18

-.13

.07

-.02

.03

.20

.06

.19

.17

.77

.37

-.05

m 14

. 43

.30

11.2

3 .1

3 -.

lo

-.02

.ll

-.05

-.15

.06

-.40

-.08

.I1

.10

.32

.13

r

16.

.51

SO -

.15

-.04

.20

-.07

.06

.12

-.13

.02

-.20

.31

.09

.06

.07

.15

.01

2 2 $ 19

. .6

3 .4

8 -.1

4 -.0

1 .1

5 -.0

5 .0

4 .0

9 -.

lo

-.01

-.21

.25

.10

.08

.13

.26

.OO

.52

-.O1

.40

22.

3.19

3

3

.17

.OO

-.18

.ll

-.15

-.18

.14

-.26

.06

.OO .

03

.16

.OO

.02

-.04

.01

-.11

.O1

.08 -.06

-.07

Not

e: 1

. =

def

ined

ben

efit

choi

ce (

1 =

DB

); 2.

= h

ybrid

def

ined

ben

efit

choi

ce (1

= h

ybrid

); 3.

= d

efin

ed c

ontri

butio

n (1

= D

C);

4.

= b

enef

it de

term

inat

ion

(0 =

ear

ning

s, 1

= g

uara

ntee

d);

5. =

dis

tribu

tion

pref

eren

ce (

0 =

mon

thly

, 1 =

lum

p su

m);

6. =

inve

stm

ent (

scal

e) c

hoic

e; 7

. =

su

rviv

or be

nefit

s (1

= a

utom

atic

, fin

ance

d su

rviv

or be

nefit

); 8.

= p

orta

bilit

y pr

efer

ence

(sca

le);

9. =

job

cata

gory

(0 =

aca

dem

ic a

nd/o

r pro

fess

iona

l, 1

= s

taff

); 10

. = in

com

e (3

= $

25,00

1-35

,OO

O);

11. =

gen

der (

1 =

fem

ale,

0 =

mal

e); 1

2. =

yea

rs o

f ser

vice

; 13.

= m

arita

l sta

tus (

1 =

mar

ried,

0 =

no

t mar

ried)

; 14

. = a

ge; 1

5. =

dep

ende

nts

(0 =

non

e, 1

= o

ne, 2

= tw

o-th

ree,

3 =

> th

ree)

; 16.

= o

ther

pla

n pa

rtici

patio

n (0

= n

o, 1

= y

es);

17. =

sp

ouse

par

ticip

atio

n (

0 =

no,

1 =

yes

); 18

. = o

ther

ben

efits

(0 =

no,

1 =

yes

); 19

. = o

ther

savi

ngs (

0 =

no,

1 =

yes

); 20

. =

sel

f-ef

ficac

y; 21

. =

risk

pr

efer

ence

; 22.

= c

urre

nt p

lan

satif

actio

n; 2

3. =

invo

lvem

ent p

refe

renc

e.

.06

< T

< .1

O,p

< .01

.05

< T

< .0

6,p <

.05

**

r >

.11,

p <

.OO1

T

< .0

5, n

.s.

JAMES H. DULEBOHN ET AL. 419

assessed using a 5-point Likert-type scale anchored by very dissatisfied to very satisfied.

Involvement preference. Respondents’ preference for involvement with their retirement plan was assessed using three items following Lau- rent and Kapferer (1985). One of the items was: “If my retirement plan required me to manage my retirement savings, I feel that I would have the time to evaluate and monitor investment choices I might make.” Re- sponses for the items were assessed using a 5-point Likert-type scale an- chored by strongly disagree to strongly agree. The coefficient alpha relia- bility estimate was .69.

Results

Descriptive statistics and correlations are listed in Table 2. For the outcome choice variables, approximately 41% of the survey participants chose the DB plan, 44% the hybrid plan, and 16% the DC plan. Of the plan features, 26% of the respondents preferred a guaranteed pen- sion benefit to one based on contribution and investment earnings, and about 31% preferred a lump sum payment to an indexed monthly dis- tribution. Over half of the sample (57%) preferred automatic, financed survivor benefits to a plan that provided a larger account refund prior to retirement but did not automatically provide survivor benefits during retirement.

Procedure

For the analysis of the research questions, we first created dichoto- mous splits of a single plan choice compared to the other two for each of the three retirement options. We chose this approach because it reflected the choice faced by each individual; for example, “Would I choose this plan over the other plans?” Second, we split the whole sam- ple by approximately half into test and hold-out samples. Third, using only the test sample, we completed the procedure outlined by Baron and Kenny (1986) to test for direct and mediated predictors of plan choice. We chose this method over structural equations modeling because the categorical dependent variable required the use of logistic regression.

Fourth, we examined the results to identify significant predictors of plan choice, and then included these variables in reduced models. Fifth, we repeated the Baron and Kenny (1986) procedure using the reduced model variables and calculated the odds of making a choice based on the antecedent variables. Sixth, to examine the stability of the results, we fit the same reduced models for the hold-out sample and compared the results with those obtained with the test sample. Seventh, to fur-

420 PERSONNEL PSYCHOLOGY

ther validate the logistic regression results, we resampled the whole sam- ple using an approach similar to bootstrapping (Efron, 1982, 1987). In our resampling process, we split the original sample into two samples, without replacement, and obtained statistics on classification rates. Fi- nally, we summarized those antecedents that consistently predicted plan choice across all analyses.

We also completed multinomial logistic and discriminant analyses. For a 3-category limited dependent variable, the multinomial analysis required us to choose an omitted category and fit two equations for the remaining two categories. It differed from the approach we reported above by the question it answered. For example it asked, “What deter- mines the choice of the hybrid plan or the DC plan over the DB plan?” Though we found comparable but not identical results, we chose not to pursue this method because we preferred to answer the question of choosing one plan over both others rather than over an omitted plan. Al- though the discriminant analysis allowed us to identify important predic- tors and to calculate classification rates, it was not useful for estimating the effect sizes. As expected, we found comparable classification rates to those from the logistic analysis.

Full Model Results

Following the method described by Baron and Kenny (1986), we first examined the regression outcomes of the mediating variables on the independent variables using the test sample. We found significant relationships between each of the five mediators and years of service, risk preference, current plan satisfaction, and involvement preference. In addition, job category was a significant predictor of investment choice, survivor benefit, and portability preference.

Second, we individually regressed each of the plan choice indicators on the independent variables. Service years and risk level were signifi- cant predictors of each of the plan choices. Job category was a significant predictor of the DB and hybrid plan choices. Current plan satisfaction and involvement preference were significant predictors of the DB and DC plan choices.

Third, we individually regressed each of the plan choice indicators on both the independent and mediating variables. Of the mediating vari- ables, benefit determination and portability preference were significant predictors of all plan choices. Distribution preference was a significant predictor of DB and DC plan choices. Investment choice preference was a significant predictor of hybrid and DC plan choices. Survivor benefit preference was a significant predictor of defined benefit and hybrid plan choices.

JAMES H. DULEBOHN ET AL. 421

Reduced Model Results

To test a reduced model of plan choice, we retained each of the above noted significant predictors. We again repeated the testing procedure for the test sample using these variables. n b l e 3 reports the results for the first series of regressions, and n b l e 4 reports the results for the second and third series of regressions.

The results were comparable to those found in the full model. Be- cause of the significant relationships found in the first and second, but not third, series of regressions, we concluded that the years of service, risk level preference, and current plan satisfaction were fully mediated predictors of hybrid plan choice, and involvement preference was a fully mediated predictor of DB plan choice.

Alternatively, because significant relationships were found in all three series of regressions, we concluded that each of the independent vari- ables, except involvement preference, were partly mediated predictors of DB plan choice. Likewise, all except job category were partly me- diated predictors of DC plan choice, and job category and involvement preference were partly mediated predictors of hybrid plan choice.

Of the mediating variables, all were predictors of hybrid plan choice. All, except investment choice preference, were predictors of DB plan choice. Benefit determination, distribution, and investment choice pref- erences were predictors of DC plan choice.

To test the consistency of the results, we repeated the procedure for the hold-out validation sample of data. We found similar variables to be significant predictors and the pattern of relationships to be comparable. In the first series of regressions, no differences in the pattern of rela- tionships were found. In the second series, a difference was that current plan satisfaction and involvement preference were predictors of hybrid plan choice, although risk level preference was not. In the third series of regressions, the first difference was that distribution preference was not a predictor of DB plan choice. Second, benefit determination pref- erence was not a predictor of hybrid plan choice, and job category was. Third, portability preference, current plan satisfaction, and involvement preference were not predictors of DC plan preference.

Resampling Results

To validate our final logistic regression results, we resampled to test our reduced model. After excluding those cases with missing values, we had the whole sample to serve as our “population” for resampling. Each time, we once again randomly split the whole sample into a test sample and a hold-out sample stratified on the plan choices; that is, we

P

h)

h)

TABL

E 3

OLS

Reg

ress

ion

of M

edia

ting P

refe

renc

e on

Inde

pend

ent I

/aria

bles

a ~ ~~

Bene

fit d

eter

min

atio

n D

istri

butio

n pr

efer

ence

In

vest

men

t cho

ice

Surv

ivor

ben

efit

Port

abili

w p

refe

renc

e St

anda

rdiz

ed

Stan

dard

ized

St

anda

rdiz

ed

Stan

dard

ized

St

anda

rdiz

ed

Var

iabl

e p

coef

ficie

nt

p co

effic

ient

p c

oeff

icie

nt

p co

effic

ient

p

coef

ficie

nt

Job

cate

gory

Se

rvic

e yea

rs

Risk

pre

fere

nce

Plan

satis

fact

ion

Invo

lvem

ent p

refe

renc

e F RZ

N

.013

.M

8*

-. 16

3. * *

,0

81"

-.171

***

24.7

84**

* .0

94

1,14

2

-.018

-.1

04**

* .1

04**

-.1

07**

* .2

49**

* 34

.746

* **

.128

1,

153

.093

***

-.134

***

.189

***

-. 14

3* * *

.4

43**

* 12

5.56

6***

.3

54

1,13

8

.108

***

.095

**

-. 17

5** *

.087

**

-.155

***

33.2

23**

* .1

24

1,13

4

-.105

***

-.406

* **

.1

33* *

* -.1

55**

* .0

92**

* 98

.023

' **

.293

1,

174

0 9

a Th

e ref

eren

ce c

ateg

ory f

or c

ateg

oric

al in

depe

nden

t var

iabl

es is

the o

ne w

ith th

e low

est c

ode

num

ber.

*

p <

.05

**p <

.01

***p

< ,0

01

TAB

LE 4

O

dds C

oeffi

cien

ts Fro

m L

ogist

ic R

egre

ssio

n of

Pla

n C

hoic

e on

Inde

pend

ent K

zria

bles

an

d In

depe

nden

t and

Med

iatin

g Pre

fere

nce K

zria

bles

a

Def

ined

ben

efit

plan

H

ybrid

pla

n D

efin

ed c

ontri

butio

n pl

an

Job

cate

gory

1.

843*

**

1.56

4* *

0.68

0**

0.83

7 0.

845

0.78

8 Se

rvic

e yea

rs

1.07

0* * +

1.03

4* *

0.97

3**

1.00

3 0.

806*

**

0.79

3; *

* Ri

sk p

refe

renc

e 0.

525*

* * 0.

706*

* 1.

271*

1.

066

2.15

9** *

1.

677*

* Pl

an s

atisf

actio

n 1.

510'

**

1.30

6**

0.92

1 1.

027

0.58

5 * * *

0.

706*

* In

volv

emen

t pre

fere

nce

0.89

4***

0.

981

0.96

9 0.

954

1.32

5' **

1.

124.

0.

179'

* Be

nefit

det

erm

inat

ion

2.12

4*+ *

0.56

9**

Dist

ribut

ion

pref

eren

ce

0.63

1.

0.74

1 2.

837'

* *

Inve

stmen

t cho

ice

0.99

8 0.

891;

' 1.

488*

* Su

rviv

or be

nefit

3.

757.

*

0.39

1***

0.

884

Porta

bilit

y pr

efer

ence

0.

752*

**

1.33

8***

0.

859'

-2 L

og li

kelih

ood

1244

.39

1062

.38

1422

.79

1302

.97

631.

50

554.

56

Goo

dnes

s of f

it 10

70.9

3 11

06.5

5 10

58.9

4 10

59.5

5 12

68.2

8 11

07.4

4 co

x LQ

Sn

ell

~2

~

.179

,3

08

,030

.1

33

,192

,2

55

Nag

elke

rke

RZ

b

,240

,4

13

,040

.1

79

,346

.4

61

Mod

el X

* 20

9.89

7***

39

1.91

0***

31

.856

' *

151.

666'

* *

226.

168.

* 31

3.10

7. *

* Cl

assif

icat

ion

rate

%

69.7

0%

77.1

1%

58.0

6%

65.7

9%

87.7

6%

N 1,

066

1,06

1 1,

061

Var

iabl

e EX

P (B

) EX

P (8

) Ex

p (B

) EX

P (B)

EXP

(B)

EXP

(B)

CI 3: E 8 Y F U

C m

0

88.5

1%

a T

he re

fere

nce

cate

gory

for c

ateg

oric

al in

depe

nden

t var

iabl

es is

the

one w

ith th

e lo

wes

t cod

e nu

mbe

r. A

logi

stic r

egre

ssio

n R

a is

a lik

elih

ood

ratio

inde

x an

d sh

ould

not

be

inte

rpre

ted

as an

OLS

coef

ficie

nt o

f det

erm

inat

ion.

It s

houl

d be

inte

rpre

ted

as a

pro

porti

on of

the

mod

el lo

g lik

elih

ood

to th

e lo

g lik

elih

ood

of a

cons

tant

term

-onl

y m

odel

(se

e Hos

mer

& L

emes

how

, 198

9; G

reen

e, 1

993)

. *

p <

.05

**

p <

.01

**

*p

< .0

01

P !2

424 PERSONNEL PSYCHOLOGY

TABLE 5 Summary of Consistent Determinants of Plan Choice

DB plan Hybrid plan DC plan

4- Benefit determination - Benefit determination + Distribution preference - Investment choice + Investment choice

+ Portability preference + Survivor benefits - Survivor benefits - Portability preference + Job category + Service years - Serviceyears - Risk preference + Current plan satisfaction

+ Risk preference

put 50% of the respondents of each plan choice into the test sample and the other 50% into the hold-out sample. Both the test sample and the hold-out sample were used to fit the same reduced logistic regression model identified above for each plan choice. Each fitted model was then used to classify the cases used to fit the same model (in-model) and to classify the cases not used to fit the model (out-model). 'Ltvo pairs of classification rates were obtained, one pair for in-model classification rates and the other for out-model classification rates. The resampling process was repeated 30 times.

The 30 pairs of classification rates for each plan choice were then used to conduct two paired t-tests, one for the in-model pairs and the other for the out-model pairs, to see if there were any significant differ- ences in classification rates. These results did not show any significant differences in classification rates at any reasonable significance level (all p > .lo), further supporting the validity of the identified reduced mod- els.

Summary of Plan Choice Predictors

Table 5 summarizes the predictors that were significant across both the test and hold-out samples. From the analyses, key distinguishing fea- tures for a choice of the DB and DC plans included the benefit deter- mination, years of service, and risk preference. Each of these variables reported opposite coefficients between choices. Based on the sizes of the odds ratios, benefit determination by a guaranteed formula had both a strong positive effect on the choice of the DB plan, the odds of which were more than twice as great, and a strong negative effect on the choice of the DC plan, the odds of which were less than .20. Alternatively, ad- ditional years of service had a stronger negative effect on the odds of choosing the DC plan than the positive effect it had on choosing the DB

JAMES H. DULEBOHN ET AL. 425

plan. The direct effect on the former was an odds of choice less than 30, while for the latter the odds were only 1.03 times greater than having no effect. Risk preference had a comparable magnitude of effect on either choice: The odds were 1.67 greater for DC choice and were only slightly more than .70 as great for DB choice.

Key distinguishing features for a choice of the DB plan and the hybrid plan were survivor benefits and portability preference. Both of these predictors included a trade-off of portability. Individuals who preferred survivor benefits strongly favored the DB plan, with an odds of choice 3.75 times greater, and individuals who were not willing to surrender portability for survivor benefits or who had a strong portability prefer- ence favored the hybrid plan, with a 1.33 times greater odds of choice. The key distinguishing feature for a choice of the hybrid plan and DC plan was investment choice. Individuals who preferred choice favored the DC plan at 1.48 times greater odds, and declined the hybrid plan with .89 times the odds of choice.

Discussion

Although previous research has focused on demographic variables as determinants of retirement plan choice, the results of this exploratory study suggest that preferences for specific plan features best predict plan choice. Only a limited number of demographic and attitudinal variables were significant predictors, and these primarily were mediated by prefer- ences for specific plan features. It may be instructive, then, to ask which more easily observed variables or other characteristics determine these preferences, and which preferences discriminate among plan choices.

Our discussion of the results proceeds by first addressing the com- ponents of our model. Second, we consider the practical implications of the results. Third, we discuss some of the limitations of our approach to studying this issue. Fourth, we make recommendations regarding av- enues for future research in this area.

Plan Feature Preferences

We examined a cross-section of the important features of retirement benefits that tend to differ among types of plans. Interestingly, each one was important, but was idiosyncratic to specific plans. No one feature was an important predictor of choosing any one of all three types of plans over the others. With the exception of distribution preference, however, each of the features did play a role in at least two of the plan decisions. The direction of the effect for each was as expected. Retirement ben- efits determined by a guaranteed or mandated formula indicated DB

426 PERSONNEL PSYCHOLOGY

choice, while those determined by contribution and investment earnings predicted DC choice. Portability preference kept individuals away from the traditional DB plan and steered them toward the hybrid plan. A preference for investment choice predicted DC plan choice, and lower preference drove individuals toward the hybrid plan choice.

Because the study included three employer-sponsored pension plan options, it yielded some interesting results that probably would not have been evident from a typical study of the DB/DC tradeoff. We expected that investment choice preference would be a negative predictor of DB choice, and portability would be a positive predictor of DC choice. How- ever, there seems to be a third group of employees, the high portabil- ity/low investment choice preference group, who preferred an option that allowed them to be mobile but did not require them to take on the responsibility and risk of investment choice. Consequently, this supports the appropriateness of the current trend among employers to provide hybrid plans, and calls into question the conventional wisdom that DC plans necessarily address the desires or needs of more mobile workers.

In conclusion, plan feature preferences are important to choice. The direction and strength of their effects differ, however, by the type of plan chosen. Individuals who choose DB, or alternatively DC, do not con- sider the same factors nor weigh the factors identically in their choice. Furthermore, the traditional DBDC tradeoff ignores a significant pop- ulation of employees whose decision is optimized only by a hybrid plan choice.

Personal Characteristics

Demographics. Although an important area of discussion in the eco- nomics literature, demographic variables played only a small part in pre- dicting plan choice. In fact, only two variables, job category and years of service, were found to be consistently significant across the analy- ses. Moreover, only years of service played a role in both the DB and DC plan selection decisions. As years of service increased, people were more strongly drawn toward the DB plan which rewarded them for their longer participation. Individuals with less tenure, however, favored the DC plan. These results imply that plan administrators cannot gener- alize by, and must look beyond, the readily available information like gender, income, and age when making decisions based on forecasts of plan choice.

Artitudes and dispositions. Based on the large and growing literatures that have linked attitudes and dispositions to behaviors and choices, we expected to see characteristics like self-efficacy, risk preference, current plan satisfaction, and involvement preference play an important role in

JAMES H. DULEBOHN ET AL. 427

retirement plan choice. The results, however, indicated otherwise; only risk preference played a decisive role in both the DB and DC choices. On the other hand, attitudes and dispositions were important predictors of specific plan feature preferences, and through these preferences they may determine plan choice.

These findings give rise to a number of implications for plan man- agement. First, individuals differ in their retirement risk preference, therefore gathering population statistics about risk preference is impor- tant for forecasting plan choice. Second, because risk preference might not be a salient characteristic for every individual, some counseling re- garding risk and risk preference during the enrollment period may help employees to make optimal retirement choices. Third, for those organi- zations supplementing their existing DB plans with new DC plans, sur- veying current plan satisfaction is useful for forecasting the number of employees who will continue in the existing plan.

Implications for Practice

The results of this study offer several points that should affect the way that human resource managers approach the administration, restructur- ing, or augmentation of their retirement benefits. First, and most impor- tant, asking the common question of which retirement plan to choose, DB or DC, may be a naive and less effective approach to managing ben- efits. Based on our findings, the better question to ask might be how to develop plans that allow employees to have choices among plan features or levels of features. From an attitudinal perspective, allowing employ- ees to have options to tailor features in a manner consistent with personal characteristics should lead to greater satisfaction. Ultimately, we then would expect the tailored plan to be a more effective tool for attraction and retention.

Second, as organizations continue to adopt DC plans, we offer sev- eral dimensions on which to evaluate them. Does the plan offer ade- quate opportunity to choose among several, varied investment options? Our results indicated that to those who select this type of plan, being able to choose among and control the distribution of money among in- vestment opportunities is important. Further, does the plan include mul- tiple risk levels among the choices? Our results showed that the choice of a DC plan is determined by a preference for risky choices. The plan should then provide multiple levels of risk among investment opportu- nities allowing the individual to tailor to his or her preference.

Third, information from this study aids in the costing of a DC plan and in predicting migration to the plan from existing DB plans. Though the demographics were not consistent predictors of choice, we were able

428 PERSONNEL PSYCHOLOGY

to identify the effect sizes of plan feature preferences and attitudes to- ward plan choice. Surveying these dimensions, organizations can con- trast alternative plans against one another based on a predicted propen- sity toward selecting a plan with particular features.

Fourth, organizations faced with the mandate, rather than the choice, to move to a DC plan can use these results to mitigate resistance by employees. For example, because risk preference is such an important discriminator between the two types, the DC plan should address it by including less risky options, like guaranteed annuities. In addition, be- cause years with the organization or service level was found to be im- portant, organizations may consider some form of lump-sum rollover amount from the DB to the DC plan prorated by seniority with the orga- nization, being careful not to jeopardize the qualified status of the DC plan. In this way, the playing field would be leveled among greater and lesser tenured employees in the opportunity to accumulate a total sav- ings amount.

Fifth, because benefits play a role in attraction and retention of em- ployees, managers should understand the potential effect of retirement plan on employee characteristics. Our results indicate that those who would be drawn toward a DB environment are probably less risky, have more invested in their current employer, and are nonmovers. On the other hand, we surmise that those attracted to a DC environment prob- ably have a greater preference for risk, are not necessarily more mobile, and prefer increased options for control over their money.

Finally, for those organizations considering a hybrid plan, the key feature seems to be portability. Our results suggested that individuals who are drawn toward the DB environment may still value the portabil- ity of the DC plan, but not want to take on the investment responsibil- ities it brings with it or the risk of totally eliminating the possibility of receiving a defined benefit if they remain with the organization. Fur- thermore, in light of point three above, the move to this hybrid plan may be unnecessary, or at least preliminary to moving to a DC plan, if the DC plan includes a guaranteed annuity option and addresses the points noted above.

Limitations

As with any study, there are limitations and constraints on our con- clusions based on the methodology we chose. First, our study developed and tested a general model of public employee pension plan choice and therefore one should take care when generalizing to the private sector population. Although the expected relationships among the determi- nants, mediators and plan choices were suggested based on theory and

JAMES H. DULEBOHN ET AL. 429

logic, outside the bounds of a designated population, and the measures chosen and the results obtained supported the generalized expectations, differences exist among private and public sector organizations that may limit the generalizability of the findings. For example, employment sta- bility and employee loyalty may be lower in many private organizations, compared to public organizations, and variables such as these would be expected to affect preference for pension portability. Consequently, whether our results would completely generalize to the broader popula- tion of private sector employers represents a research question.

Second and related, our results are difficult to generalize to the ex- tent that other retirement plans, both public and private, may include different options or combinations of features. This study, however, ad- dressed this point by including major features that tend to be found across a variety of employer-sponsored retirement plans. In addition, although some private sector organizations may offer a choice among pension plans to their employees similar to a number of public sector organizations, private sector employers often mandate participation in one type of plan or the other, or alternatively offer the DC option as a supplement to an existing DB plan (Kruse, 1995).

Third, although we measured risk in terms of preference for invest- ment risk, researchers have identified other dimensions of risk (Mac- Crimmon & Wehrung, 1986). For example, a facet of risk is opportunity loss that may result from choosing one plan over another (e.g., a DB plan over a DC plan) and not remaining with the sponsoring employer until retirement. Therefore, future research should examine multiple definitions of risk and their effects on plan choice.

Fourth, the reliabilities for scale items were not all above the .80 level recommended from laboratory studies. Field studies, however, often find lower reliabilities and we do not expect that the results to be significantly changed by the addition of more variables. With greater reliability, current plan satisfaction and involvement preference may rise to being consistent predictors. There is no evidence, though, to look toward self-efficacy as a potential predictor even with greater reliability.

Future Research

The survey method we used was useful for gaining insight into the choices that current public employees would make. This study did not address the question about choices that will be made by new organiza- tional members or entrants to the labor force. Consequently, additional research is needed that examines the choices made by new employees as well as current incumbents.

430 PERSONNEL PSYCH0LOC;Y

Future researchers with access to private sector samples should build upon this initial work and extend this study's model into this other do- main. An effort should be made to include any additional plan features that may characterize the particular employer-sponsored plan offerings that were not included in this study, such as provisions for early retire- ment, postretirement health benefits, and preretirement survivor bene- fits, In addition to the inclusion of relevant plan features, future research also should examine the role of other personal characteristics that may influence plan feature preference and plan choice such as job satisfac- tion, organization commitment, and general pay satisfaction, which may account for variance not explained in this study.

The Future of Retirement Plans

The growing salience of employer-sponsored retirement plans and the trend of organizations to offer DC plans, hybrid plans, and even mul- tiple pension plans to their employees underscores the need for research in this area. Importantly, the frequency of DC plan and hybrid plan adoption by both private and public employers is only expected to grow in the future (Clark, McDermed, & Trawick, 1993; Jankowski, 1997; Land- strom & Bainbridge, 1996). This study contributes important informa- tion by identifying determinants of plan choice across the spectrum of types of employer-sponsored pension plans that are actually in use.

REFERENCES

Ajzen I. (1988). Attitudes, personality, and behavior. Chicago: Dorsey Press. Ajzen I. (1991). The theory of planned behavior. Organizational Behavior and Human

Ajzen i, Fishbein M. (1980). Understanding attitudes andpredictingsocial behavior. Engle- Decision Processes, 50, 179-21 1.

wood Cliffs, NJ: Prentice-Hall. * Bandura A. (1982). Self-efficacy mechanism in human agency. American Psychologist, 37,

122-147. Baron RM, Kenny DA. (1986). The moderator-mediator variable distinction in social psy-

chological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psycholoa, 51, 1173-1 182.

Bodie Z, Merton RC. (1993). Pension benefit guarantees: A functional analysis. In Schmitt R (Ed.), Thefuture ofpensions in fhe United States (pp. 194-234). Philadel- phia: University of Pennsylvania.

Boskin MJ. (1986). Too manypromises: The icncertainfuture ofSocialSecun'ty. Homewood, IL: Dow Jones-Irwin.

Cable D, Judge TA. (1994). Pay preferences and job search decisions: A person-organiza- tion fit perspective. PERSONNEL PSYCHOLOGY, 47,317-348.

Caplan RD. (1987). Person-environment fit theory and organizations: Commensurate dimensions, time perspectives, and mechanisms. Journal of Vocational Behaviq 31, 248-267.

JAMES H. DULEBOHN ET AL. 43 1

Chaiken S, Yates SM. (1985). Affective-cognitive consistency and thought-induced atti- tude polarization. Journal of Personality and Social Pvchology, 49,1470-1481.

Clark RL, McDermed A. (1989). Determinants of retirement by married women. Social Security Bulletin, 52( l), 33-35.

Clark RL, McDermed A. (1990). The choice of pension plans in a changing regulatory environment. Washington, DC: American Enterprise Institute.

Clark RL, Pitts MM. (1999). Faculty choice of a pension plan: Defined benefit versus defined contribution. Industrial Relations, 38( l), 1845.

Clark RL, McDermed A, 'Ifawick MW. (1993). Firm choice of type of pension plan: Trends and determinants. In Schmitt R (Ed.), The future ofpensions in the United States (pp. 115-125). Philadelphia: University of Pennsylvania.

Crane RB. (1995). DC Plans offer benefits to public plans, participants. Pension Manage- ment, 3I(5), 56-58.

Eagly AH, Chaiken S. (1993). The psychology of attitudes. New York: Harcourt Brace Jovanovich.

Efron B. (1982). The jackknye, the bootstrap, and other resamplingplans. Philadelphia: Society for Industrial and Applied Mathematics.

Efron B. (1987). Better bootstrap confidence intervals. Journal of the American Statistical Association, 82,171-200.

Fidelity Investments, Inc. (1998). Investorprofile questionnaire. Boston: Author. Gist ME, Mitchell TR. (1992). Self-efficacy: Implications for organization behavior and

human resource management. Academy of Management Review, 12,472485. Greene WH. (1993). Econometric analysis (2nd ed.). New York Macmillan. Goodfellow GP, Schieber SJ. (1993). Death and taxes: Can we fund for retirement be-