駰rpesSmedyeer menke骸jer yeBke efue. - TJSB Bank

76

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of 駰rpesSmedyeer menke骸jer yeBke efue. - TJSB Bank

11

ìerpesSmedyeer menkeÀejer yeBkeÀ efue.(ceefuì-mìsì Mes[³egu[ yeBkeÀ)

(jefpe.ke´ÀëScedSmedmeerSmed/meerDeej/287/2008 efo.23.10.2008)

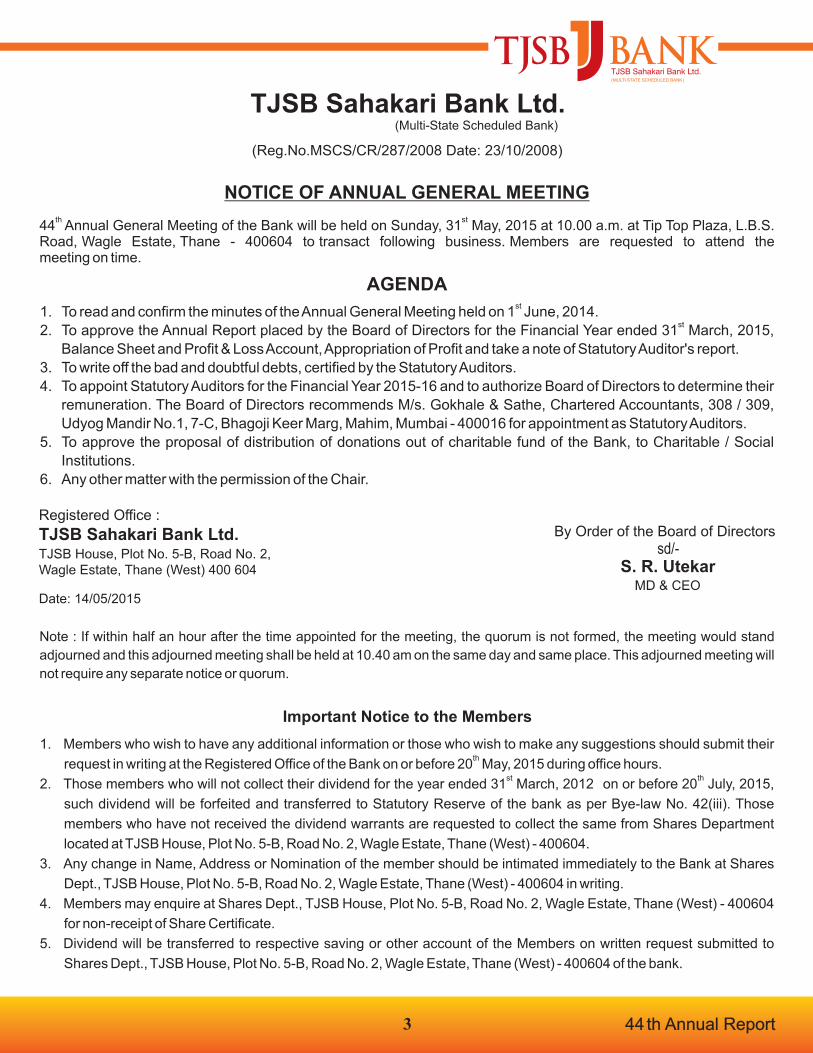

meYeemeoebme Jeeef<e&keÀ meJe&meeOeejCe meYes®eer met®evee

yeBkesÀ®eer 44 Jeer Jeeef<e&keÀ meJe&meeOeejCe meYee, jefJeJeej efoveebkeÀ 31 ces, 2015 jespeer, mekeÀeUer 10 Jeepelee ìerHe ìe@He HueePee, ueeueyeneotj Meeðeer ceeie&, JeeieUs Fmìsì, þeCes – 400 604 ³esLes Heg{erue keÀecekeÀepee®ee efJe®eej keÀjC³eemeeþer YejCeej Deens. lejer meYeemeoebveer JesUsJej GHeefmLele jneJes, ner efJevebleer.

meYesHeg{erue efJe<e³e

1. efo. 1 petve, 2014 jespeer Peeuesu³ee ceeieerue meYes®es FefleJe=lle Jee®etve keÀe³ece keÀjCes.2. meb®eeuekeÀ ceb[Ueves meeoj kesÀuesuee efo. 31 cee®e&, 2015 DeKesj®³ee Je<ee&®ee DenJeeue, leeUsyebo Je veHeÀe leesìe He$ekeÀ cebpetj keÀjÀve veHeÀe JeeìCeer

keÀjCes DeeefCe JewOeeefvekeÀ uesKeeHejer#ekeÀeb®³ee DenJeeuee®eer veeWo IesCes.3. JewOeeefvekeÀ uesKeeHejer#ekeÀebveer He´ceeefCele kesÀu³eevegmeej yeg[erle Je mebMeef³ele keÀpe& Keeleer efveue&sefKele keÀjC³eeme cebpegjer osCes.4. meve 2015-2016 ³ee DeeefLe&keÀ Je<ee&meeþer JewOeeefvekeÀ uesKeeHejer#ekeÀeb®eer vesceCetkeÀ keÀjCes Je l³eeb®es mesJeeMegukeÀ þjefJeC³ee®ee DeefOekeÀej meb®eeuekeÀ

ceb[Ueme osCes. meb®eeuekeÀ ceb[U ces. ieesKeues DeeefCe meeþs ®eeì&[& DekeÀeGÀvìCìmed, 308 / 309, GÐeesie cebefoj veb. 1, 7 - meer, Yeeieespeer keÀerrj ceeie&, ceenerce, cebgbyeF& - 400016 ³eeb®³ee vesceCegkeÀer®eer efMeHeÀejme keÀjerle Deens.

5. Oecee&oe³e/meeJe&peefvekeÀ keÀejCeemeeþer DebMeoeve efveOeerletve mebmLeebvee osCeieer osCesyeeyele He´mleeJeeme ceev³elee osCes. 6. cee. DeO³e#eeb®³ee mebceleerves ³esCeejs Dee³el³ee JesUs®es efJe<e³e.

veeWoCeerke=Àle keÀe³ee&ue³e

ìerpesSmedyeer neTme, Huee@ì veb.5 yeer, jes[ vebb. 2,JeeieUs Fmìsì, þeCes (He) - 400604efoveebkeÀë 14/05/2015

ìerpesSmedyeer menkeÀejer yeBkeÀ efue.meb®eeuekeÀ ceb[Ue®³ee DeeosMeeJejÀve

me. j. GleskeÀjJ³eJemLeeHekeÀer³e meb®eeuekeÀ JecegK³e keÀe³e&keÀejer DeefOekeÀejer

met®evee ë 10 Jeepetve 30 efceefveìebHe³e¥le ieCeHetleea ve Peeu³eeme meYee mLeefiele kesÀueer peeF&ue Je mLeefiele Peeuesueer meYee l³ee®e efþkeÀeCeer l³ee®e efoJeMeer mekeÀeUer 10 Jeepetve 40 efceefveìebveer IesC³eele ³esF&ue. l³ee meYesme ieCeHetleea®eer Je JesieU³ee met®eves®eer DeeJeM³ekeÀlee veener.

meYeemeoebme cenlJee®³ee met®evee ë

1. meYeemeoebvee Jeeef<e&keÀ meJe&meeOeejCe meYesHeg{s keÀener He´Mve/met®evee ceeb[eJe³ee®³ee Demeleerue lej l³eebveer l³ee 20 ces, 2015 He³e¥le keÀecekeÀepee®³ee JesUsle, veeWoCeerke=Àle keÀe³ee&ue³eele uesKeer mJejÀHeele ÐeeJ³eele.

2. yeBkesÀ®³ee Heesìefve³ece ke´À.42(iii) DevJe³ebs p³ee meYeemeoebveer 31 cee®e&, 2012 Je<ee&meeþer®ee ueeYeebMe mJeerkeÀejuee vemesue l³eebveer efo. 20 peguew, 2015 HetJeea ve vesu³eeme l³eeb®³ee ueeYeebMeeb®eer jkeÌkeÀce jeKeerJe efveOeerceO³es pecee keÀjC³eele ³esF&ue. p³ee meYeemeoebvee ueeYeebMe He$ekesÀ efceUeueer vemeleerue l³eebveer leer yeBkesÀ®³ee MesDeme& efJeYeeie, ìerpesSmedyeer neGÀme, Huee@ì veb.5 yeer, jes[ veb.2, JeeieUs Fmìsì, þeCes - 400604 ³esLeerue keÀe³ee&ue³eeletve IesTve peeJeerle.

3. meYeemeoebveer veebJe, Hellee DeLeJee Jeejmeoej yeoueuee Demeu³eeme l³ee®eer MesDeme& efJeYeeie, ìerpesSmedyeer neGÀme, Huee@ì veb. 5 yeer, jes[ veb. 2, JeeieUs Fmìsì, þeCes - 400604 ³esLes veebWo keÀjÀve I³eeJeer.

4. MesDej meìeaefHeÀkesÀìmed efceUeueer vemeu³eeme leer yeBkesÀ®³ee MesDeme& efJeYeeie, ìerpesSmedyeer neGÀme, Huee@ì veb.5 yeer, jes[ veb.2, JeeieUs Fmìsì, þeCes - 400604 ³esLeerue keÀe³ee&ue³eeletve IesTve peeJeerle.

5. ueeYeebMe DeeHeu³ee ye®ele DeLeJee Dev³e Keel³eele pecee keÀjC³eemebyebOeer®es He$e yeBkesÀ®³ee MesDeme& efJeYeeie, ìerpesSmedyeer neGÀme, Huee@ì veb.5 yeer, jes[ veb.2, JeeieUs Fmìsì, þeCes - 400604 ³esLeerue keÀe³ee&ue³eele DeeCetve efou³eeme ueeYeebMee®eer jkeÌkeÀce Keel³eele pecee keÀjlee ³esF&ue.

44 Jee Jeeef<e&keÀ DenJeeue

sd/-

2

meb®eeuekeÀ ceb[U

yeBkesÀ®es Jeefj<þ DeefOekeÀejer

1. Þeer. meer. veboieesHeeue cesveve yeer.S., yeer.peer.Sued. DeO³e#e2. Þeer. He´. o. þeketÀj yeer.keÀe@ced., Sued.Sued.yeer. GHeeO³e#e3. Þeer. efJe. De. JewMebHee³eve Sce.ìskeÀ. (He´e@[keÌMeve), ®eeì&[& FbefpeveerDej meb®eeuekeÀ4. meew. De. je. DeeHeìs yeer.Smed.meer., Sued.Sued.yeer. meb®eeefuekeÀe5. Þeer. j. Keg. DeiejJeeue yeer.Smed.meer. meb®eeuekeÀ6. Þeer. j. Keg. keÀveeveer ef[Hueescee Fve ceske@ÀefvekeÀue FbefpeefveDeefjbie meb®eeuekeÀ7. Þeer. ce. Oe. Keglee[ss meb®eeuekeÀ8. Þeer. vee. o. ceeb[ies Sced.Smed.meer., ef[.S®ed.F&. meb®eeuekeÀ9. Þeer. efJe. ce. HelkeÀer Sced.keÀe@ced., Sued.Sued.yeer., S.Dee³ed.meer.[yuet.S., SHedÀ.meer.S. meb®eeuekeÀ10. kegÀ. keÀ. kesÀ. jeF&uekeÀj yeer.meer.Sced., SHedÀ.meer.S., ef[.Dee³ed.Smed.S. (Dee³e.meer.S.Dee³e) meb®eeefuekeÀe11. Þeer. efo. ³e. megUs ieJnve&cesbì keÀceefMe&Deue ef[Hueescee (peer.meer.ef[.) meb®eeuekeÀ12. Þeer. efJeveesokegÀceej yevmeue SHedÀ.meer.S. mJeerke=Àle meb®eeuekeÀ13. Þeer. me. j. GleskeÀj yeer.keÀe@ced., Sued.Sued.yeer., meer.S.Dee³ed.Dee³ed.yeer-1 J³eJemLeeHekeÀer³e meb®eeuekeÀ Je

cegK³e keÀe³e&keÀejer DeefOekeÀejer

veeWoCeerke=Àle keÀe³ee&ue³e ìerpesSmedyeer neTme, Huee@ì veb.5 yeer, jes[ veb.2, JeeieUs Fmìsì, þeCes -400 604

otjOJeveer – 25878500 He@ÀkeÌme - 25878650

JewOeeefvekeÀ uesKee Hejer#ekeÀieesKeues DeeefCe meeþs ®eeì&[& DekeÀeGÀvìCìmed

1. Þeer. meg. He´. meeþs yeer.keÀe@ced., meer.S.Dee³ed.Dee³ed.yeer., Dee³ed.meer.[yu³eg.S., meer.Smed. cegK³e-mejJ³eJemLeeHekeÀ2. Þeer. meb. meg. keÀecele yeer.Smed.meer, ef[.F.,Sce.meer.Heer, Sce.meer.Sme.F&, meer.Dee³e.Dee³e.Sme.S, mejJ³eJemLeeHekeÀ

meer.Dee³e.Sme.Heer., mee³eyej uee@ (ef[Hueescee)3. Þeer. mebb. efJe. HeeþkeÀ yeer.keÀe@ced., meer.S.Dee³ed.Dee³ed.yeer., yeer.peer.Sued., meer.SHedÀ.S.- Fbìj. GHe-mejJ³eJemLeeHekeÀ4. Þeer. iees. De. ieebieue yeer.keÀe@ced., pes.S.Dee³ed.Dee³ed.yeer. GHe-mejJ³eJemLeeHekeÀ5. Þeer. me. n. keÀesjevves yeer.keÀe@ced., Sued.Sued.yeer., meer.S.Dee³ed.Dee³ed.yeer. GHe-mejJ³eJemLeeHekeÀ6. Þeer. efve. veb. DeejskeÀj yeer.keÀe@ced., meer.S.Dee³ed.Dee³ed.yeer. GHe-mejJ³eJemLeeHekeÀ7. Þeer. mJe. ue. peebYeUs yeer.F&. (Dee³e.ìer.) GHe-mejJ³eJemLeeHekeÀ8. Þeer. ce. cee. HeÀ[kesÀ yeer.keÀe@ced., Sued.Sued.yeer., meer.S.Dee³ed.Dee³ed.yeer., meer.Smed.-Fbìj GHe-mejJ³eJemLeeHekeÀ9. Þeer. ce. Heeb. iees[mes yeer.keÀe@ced., meer.S.Dee³ed.Dee³ed.yeer. GHe-mejJ³eJemLeeHekeÀ10. Þeer. n. vee. kegÀuekeÀCeea yeer.keÀe@ced. mene.mejJ³eJemLeeHekeÀ11. Þeer. efJe. ie. veJejs yeer.keÀe@ced., meer.S.Dee³ed.Dee³ed.yeer. mene.mejJ³eJemLeeHekeÀ12. Þeer. meg. ce. ce³eskeÀj yeer.keÀe@ced., meer.S.Dee³ed.Dee³ed.yeer. mene.mejJ³eJemLeeHekeÀ13. Þeer. J³eb. ®eb. cegodiesjerkeÀj yeer.F&.(ceske@ÀefvekeÀue),Heer.peer.[er.Sced.,meer.Dee³ed.Smed.S,meer.Dee³e.S,ISO 27000 LA mene.mejJ³eJemLeeHekeÀ14. Þeer. ns. j. yeeHeì yeer.Smed.meer., meer.S.Dee³ed.Dee³ed.yeer., Sued.Sued.yeer., mene.mejJ³eJemLeeHekeÀ15. meew. mJee. keÀew. keÀUkesÀ yeer.keÀe@ced., meer.S., meer.Smed.Fbìj (ie´gHe-1), meer.S.Dee³ed.Dee³ed.yeer. mene.mejJ³eJemLeeefHekeÀe16. Þeer. Oe. ue. kegÀuekeÀCeea yeer.keÀe@ced., pes.S.Dee³ed.Dee³ed.yeer., Deesj@keÀue mene.mejJ³eJemLeeHekeÀ17. Þeer. efJe. o. efoef#ele yeer.keÀe@ced., meer.S.Dee³ed.Dee³ed.yeer. mene.mejJ³eJemLeeHekeÀ18. Þeer. efJe. ie. ieesjs yeer.keÀe@ced., pes.S.Dee³ed.Dee³ed.yeer. mene.mejJ³eJemLeeHekeÀ 19. meew. De. efve. megUs yeer.keÀe@ced., pes.S.Dee³ed.Dee³ed.yeer., Sued.Sued.yeer., peer.ef[.meer.S. mene.mejJ³eJemLeeHekeÀ20. Þeer. He´. Heeb. Hebef[le yeer.keÀe@ced., meer.S.Dee³ed.Dee³ed.yeer., peer.ef[.meer.S. mene.mejJ³eJemLeeHekeÀ21. Þeer. efJe. Jee. iee[ieerU yeer.keÀe@ced., meer.S.Dee³ed.Dee³ed.yeer. mene.mejJ³eJemLeeHekeÀ

Website : www.tjsb.co.in E-mail : [email protected]

44 Jee Jeeef<e&keÀ DenJeeue

TJSB Sahakari Bank Ltd. (Multi-State Scheduled Bank)

(Reg.No.MSCS/CR/287/2008 Date: 23/10/2008)

NOTICE OF ANNUAL GENERAL MEETING

th st 44 Annual General Meeting of the Bank will be held on Sunday, 31 May, 2015 at 10.00 a.m. at Tip Top Plaza, L.B.S. Road, Wagle Estate, Thane - 400604 to transact following business. Members are requested to attend the meeting on time.

AGENDAst

1. To read and confirm the minutes of the Annual General Meeting held on 1 June, 2014.st

2. To approve the Annual Report placed by the Board of Directors for the Financial Year ended 31 March, 2015,

Balance Sheet and Profit & Loss Account, Appropriation of Profit and take a note of Statutory Auditor's report.

3. To write off the bad and doubtful debts, certified by the Statutory Auditors.

4. To appoint Statutory Auditors for the Financial Year 2015-16 and to authorize Board of Directors to determine their

remuneration. The Board of Directors recommends M/s. Gokhale & Sathe, Chartered Accountants, 308 / 309,

Udyog Mandir No.1, 7-C, Bhagoji Keer Marg, Mahim, Mumbai - 400016 for appointment as Statutory Auditors.

5. To approve the proposal of distribution of donations out of charitable fund of the Bank, to Charitable / Social

Institutions.

6. Any other matter with the permission of the Chair.

Registered Office :

TJSB Sahakari Bank Ltd.TJSB House, Plot No. 5-B, Road No. 2,Wagle Estate, Thane (West) 400 604

Date: 14/05/2015

By Order of the Board of Directors

S. R. UtekarMD & CEO

Note : If within half an hour after the time appointed for the meeting, the quorum is not formed, the meeting would stand

adjourned and this adjourned meeting shall be held at 10.40 am on the same day and same place. This adjourned meeting will

not require any separate notice or quorum.

1. Members who wish to have any additional information or those who wish to make any suggestions should submit their th

request in writing at the Registered Office of the Bank on or before 20 May, 2015 during office hours.st th

2. Those members who will not collect their dividend for the year ended 31 March, 2012 on or before 20 July, 2015,

such dividend will be forfeited and transferred to Statutory Reserve of the bank as per Bye-law No. 42(iii). Those

members who have not received the dividend warrants are requested to collect the same from Shares Department

located at TJSB House, Plot No. 5-B, Road No. 2, Wagle Estate, Thane (West) - 400604.

3. Any change in Name, Address or Nomination of the member should be intimated immediately to the Bank at Shares

Dept., TJSB House, Plot No. 5-B, Road No. 2, Wagle Estate, Thane (West) - 400604 in writing.

4. Members may enquire at Shares Dept., TJSB House, Plot No. 5-B, Road No. 2, Wagle Estate, Thane (West) - 400604

for non-receipt of Share Certificate.

5. Dividend will be transferred to respective saving or other account of the Members on written request submitted to

Shares Dept., TJSB House, Plot No. 5-B, Road No. 2, Wagle Estate, Thane (West) - 400604 of the bank.

Important Notice to the Members

3

sd/-

44 th Annual Report

444 th Annual Report

Website : www.tjsb.co.in E-mail : [email protected]

BOARD OF DIRECTORS1.

2. SHRI. P. D. THAKUR B.Com., LLB VICE-CHAIRMAN

3. SHRI. V. A. VAISHAMPAYAN M.TECH. (PRODUCTION), Chartered Engineer DIRECTOR

4. MRS. A. R. APTE B.Sc., LLB DIRECTOR

5. SHRI. R. K. AGARWAL B.Sc. DIRECTOR

6. SHRI. R. K. KANANI Diploma in Mech. Engg. DIRECTOR

7. SHRI. M. D. KHUTADE DIRECTOR

8. SHRI. N. D. MANDGE M.Sc., DHE DIRECTOR

9. SHRI. V. M. PATKI M.Com., LLB, AICWA, FCA DIRECTOR

10. MISS. K. K. RAILKAR BCM, FCA, DISA (ICAI) DIRECTOR

11. SHRI. D. Y. SULE Government Commercial Diploma (GCD) DIRECTOR

12. SHRI. VINODKUMAR BANSAL FCA CO-OPTED DIRECTOR

13. SHRI. S. R. UTEKAR B.Com., LLB, CAIIB-I MANAGING DIRECTOR

& CHIEF EXECUTIVE

OFFICER

SHRI. C. N. MENON B.A., BGL CHAIRMAN

SENIOR EXECUTIVES

Registered Office:TJSB House, Plot No. 5-B, Road No. 2,

Wagle Industrial Estate, Thane (W) – 400 604Phone – 25878500 Fax – 25878650

Statutory Auditors:Gokhale & Sathe

Chartered Accountants

1. SHRI. S. P. SATHE B.Com., CAIIB, ICWA, CS CHIEF GENERAL MANAGER

2. SHRI. S. S. KAMAT B.Sc., DE, MCP, MCSE, CIISA, CISP GENERAL MANAGER

DIPLOMA IN CYBER LAW

3. SHRI. S. V. PATHAK B.Com., CAIIB, BGL, CFA-Inter DY. GENERAL MANAGER

4. SHRI. G. A. GANGAL B.Com., JAIIB DY. GENERAL MANAGER

5. SHRI. S. H. KORANNE B.Com., LLB, CAIIB DY. GENERAL MANAGER

6. SHRI. N. N. AREKAR B.Com., CAIIB DY. GENERAL MANAGER

7. SHRI. S. L. JAMBHALE B.E.(IT) DY. GENERAL MANAGER

8. SHRI. M. M. PHADKE B.Com., LLB, CAIIB, CS-Inter DY. GENERAL MANAGER

9. SHRI. M. P. GODSE B.Com., CAIIB DY. GENERAL MANAGER

10. SHRI. H. N. KULKARNI B.Com ASST. GENERAL MANAGER

11. SHRI. V. G. NAVARE B.Com., CAIIB ASST. GENERAL MANAGER

12. SHRI. S. M. MAYEKAR B.Com., CAIIB ASST. GENERAL MANAGER

13. SHRI. V. C. MUDGERIKAR B.E.(MECH)PGDM,CISA,CIA,ISO 27000LA ASST. GENERAL MANAGER

14. SHRI. H. R. BAPAT B.Sc., CAIIB, LLB ASST. GENERAL MANAGER

15. MRS. S. K. KALKE B.Com., C.A., CS INTER (GR-I), CAIIB ASST. GENERAL MANAGER

16. SHRI. D. L. KULKARNI B.Com., JAIIB ASST. GENERAL MANAGER

17. SHRI. V. D. DIXIT B.Com., CAIIB ASST. GENERAL MANAGER

18. SHRI. V. G. GORE B.Com., JAIIB ASST. GENERAL MANAGER

19. MRS. A. N. SULE B.Com., JAIIB, LLB, GDCA ASST. GENERAL MANAGER

20. SHRI. P. P. PANDIT B.Com., CAIIB, GDCA ASST. GENERAL MANAGER

21. SHRI. V. V. GADGIL B.Com., CAIIB ASST. GENERAL MANAGER

5 44 Jee Jeeef<e&keÀ DenJeeue

44 Jee Jeeef<e&keÀ DenJeeue 2014-15

mevceeveveer³e meYeemeo yebOeg-Yeefieveerbvees,

yeBkesÀ®³ee 44 J³ee Jeeef<e&keÀ meJe&meeOeejCe meYesceO³es meb®eeuekeÀ ceb[Ue®³ee Jeleerves ceer

DeeHeues neefo&keÀ mJeeiele keÀjlees. 31 cee®e& 2015 jespeer mebHeuesu³ee DeeefLe&keÀ

Je<ee&®ee uesKeeHejeref#ele leeUsyebo Je Jeeef<e&keÀ DenJeeue ³ee meYesHeg{s þsJeleevee ceuee

efJeMes<e Deevebo nesle Deens.

ìerpesSmeyeer yeBkeÀ n³ee GppJeue keÀejkeÀero& Demeuesu³ee mebmLes®ee DeO³e#e ³ee veel³eeves

ceer Demes meebiet Fef®ílees keÀer DeeHeCee meJee¥®³ee YejerJe HeeþeRy³eecegUs yeBkeÀ DenJeeue

Je<ee&lener GÊece keÀeceefiejer keÀjC³eele ³eMemJeer þjueer Deens.

ceer DeefYeceeveHetJe&keÀ veceto keÀjlees keÀer ₹ 10000 keÀesìeR®ee ìHHee ielemeeueer Heej

kesÀu³eeveblej yeBkesÀves ₹ 100 keÀesìeR®ee efveJJeU veHeÀe Je 100 MeeKeeb®ee

SsefleneefmekeÀ ìHHee DenJeeue Je<ee&le Deesueeb[uee Deens.

meb®eeuekeÀ ceb[Ue®eer efveJe[CetkeÀ ë

ceuìermìsì keÀ[email protected]³eìer keÀe³eoe 2002 ®³ee keÀuece 45 DevJe³es

meb®eeuekeÀ ceb[Ue®³ee efveJe[CegkeÀer®eer He´efke´À³ee efo. 9.12.2014 les

25.12.2014 ³ee keÀeueeJeOeerceO³es HetCe& keÀjC³eele Deeueer. meoj

keÀe³eÐeeleerue lejlegoebrvegmeej meb®eeuekeÀ ceb[Ueves efveJe[CetkeÀ efveCe&³e DeefOekeÀejer

cnCetve Þeer. meboerHe ceeUJeer Ghee³egkeÌle, þeCes ceneveiejHeeefuekeÀe, þeCes ³eeb®eer vesceCetkeÀ

kesÀueer Je lemes cee. keWÀêer³e efveyebOekeÀ ³eebvee keÀUefJeC³eele Deeues. meoj efveJe[CetkeÀ

ceuìermìsì keÀes. Dee@He. meesmee³eìer keÀe³eoe 2002®³ee efve³ece ke´À.19 Debleie&le

veceto kesÀuesu³ee He´efke´À³esvegmeej IesC³eele Deeueer.

efJeÐeceeve meb®eeuekeÀ ceb[Ueme efyeveefJejesOe efveJe[tve efou³eeyeÎue ceer meJe&

meYeemeoeb®ee ceveëHetJe&keÀ DeeYeejer Deens.

meve 2014-15 ®³ee keÀeceefiejer®ee DenJeeue DeeHeu³eemeceesj þsJeC³eeHetJeer&

mebHetCe& yeBkeÀeRie J³eJemee³eeJej HeefjCeece keÀjCeeN³ee DeLe&J³eJemLesleerue Ie[ecees[eR®ee

HejeceMe& IesCes Gef®ele þjsue.

DeeefLe&keÀ efmLeleer ë

meve 2014-15 ceO³es Yeejleer³e DeLe&J³eJemLes®eer megOeejCeskeÀ[s Jeeì®eeue nesle

Demeu³ee®es mebkesÀle efceUle nesles. SkeÀe yeepetme {esyeU je<ì^er³e GlHeeoveele Jee{ nesle

nesleer Je ogmejerkeÀ[s ceneieeF& efveoxMeebkeÀ, ®eeuet Keel³eeJejerue letì Je efJelleer³e letì

³eele Ieì nesle nesleer. ³ee Je<ee&le Yeejleer³e jÀHe³ee®es cetu³eosKeerue yengleebMeer efmLej

jeefnues.

efjPeJn& yeBkesÀves HeleOeesjCeeÜejs kesÀuesu³ee Ghee³e³eespeveebcegUs efkeÀjkeÀesU ceneieeF&

efveoxMeebkeÀ 8.31 … Je©ve meve 2014-15®³ee DeKesjerme 5.17 … He³e¥le

Keeueer Deeuee. meve 2014-15 ceO³es efjPeJn& yeBkeÀ Dee@HeÀ Fbef[³ee Je Yeejle

mejkeÀej ³eebceO³es HeleOeesjCeemeboYee&le keÀjej nesTve efjPeJn& yeBkeÀssves efkeÀjkeÀesU

efveoxMeebkeÀ keÀceer keÀjC³eeJej Yej osC³ee®es þjefJeues Je l³eevegmeej ne efveoxMeebkeÀ

peevesJeejer 2016 He³e¥le 6 …He³e¥le lej meve 2017-18 ®³ee MesJeìer 4 …

He³e&ble Keeueer DeeCeC³ee®es GÎer<ì þjJeC³eele Deeuess.

meve 2013-14 ®³ee leguevesle meve 2014-15 ceO³es Yeejleer³e ©He³ee®es

cetu³e efmLej jeefnues. ³ee Je<ee&le ©He³ee®es cetu³e DecesefjkeÀve [e@uej®³ee leguevesle

₹ 58 les 64 ³ee ojc³eeve jeefnues. Yeejlee®³ee HejkeÀer³e ®euevee®ee meeþe

344 efyeueer³eve [e@ueme& ³ee efJeke´Àceer mlejeJej Hees®eu³eecegUs Yeejlee®³ee HejkeÀer³e

®euevee®³ee efmLeleerle iesu³ee 18 ceefnv³eeb®³ee leguevesle ceesþ³ee He´ceeCeeJej megOeejCee

Peeueer Deens.

meve 2014-15 ceO³es DeesHeskeÀ cenemebIe, DecesefjkeÀe Je jefMe³ee ³eebceO³es keÀ®®³ee

lesuee®es ceesþ³ee He´ceeCeele GlHeeove Peeu³eecegUs keÀ®®³ee lesuee®ee YeeJe 115

[@euej He´leer ye@jue JejÀve 45 [e@uej He´leer ye@jueHe³e¥le Iemejuee. ®eerve®³ee DeeefLe&keÀ

J³eJemLes®eer ceboeJeuesueer ieleer ns osKeerue keÀ®®³ee lesuee®³ee IemejCeer®es DebMeleë

keÀejCe jeefnues. Yeejlee®³ee Dee³eeleerleerue 70… FlekeÀe ceesþe efnmmee keÀ®®³ee

lesuee®ee Demeu³eecegUs Deeblejje<ì^er³e yeepeejele keÀesmeUCeeN³ee keÀ®®³ee lesuee®³ee

efkebÀceleer®ee Yeejleeme ceesþ³ee He´ceeCeeJej ueeYe Peeuee Je Yeejlee®eer ®eeuet

Keel³eeJejerue letì ceesþ³ee He´ceeCeele keÀceer nesTve leer {esyeU je<ì^er³e GlHeeovee®³ee

1.3… Keeueer ³esC³ee®eer DeHes#ee Deens. lemes®e Deeblejje<ì^er³e yeepeejele keÀceer

nesCeeN³ee lesuee®³ee efkebÀceleercegUs Yeejle mejkeÀejves ef[Pesue®eer efkebÀcele osKeerue

efve³eb$eCecegkeÌle keÀjC³ee®ee cenÊJee®ee efveCe&³e Iesleuee.

meve 2014-15 ceO³es {esyeU je<ì^er³e GlHeeove 7.5… veerr Jee{u³ee®ee Deboepe

Demetve meve 2015-16 ceO³es DeLe&J³eJemLes®ee Jesie 8… les 8.50…

₹

6

jenC³ee®eer DeHes#ee DeLe&ceb$³eebveer J³ekeÌle kesÀueer Deens. DeLe&J³eJemLes®³ee Jee{CeeN³ee

JesieecegUs osMeele DeefOekeÀeefOekeÀ jespeieej efvecee&Ce nesC³eeme ceole nesF&ue.

meve 2014 -15 ceO³es DeLe&J³eJemLesle keÀener He´ceeCeele megOeejCee efomeueer

lejer iesu³ee DeveskeÀ ceefnv³eebHeemetve ®eeuet Demeuesu³ee ceboer®³ee JeeleeJejCeecegUs

GÐeesieOebÐeeleerue He´keÀuHe HetCe& nesC³eeme DeHes#esHes#ee DeefOekeÀ keÀeueeJeOeer ueeieuee Je

HeefjCeeceer yeBkeÀeb®³ee keÀpee¥®³ee HejleHesÀ[er®ee keÀeueeJeOeer osKeerue keÀener He´ceeCeele

ueebyeuee iesuee. ³eecegUs yeBkeÀeRie #es$eemeceesj DeeJneveelcekeÀ HeefjefmLeleer efvecee&Ce

nesTve yeBkeÀeRie®³ee Je=Ooer®ee Jesie lej ceboeJeuee®e Je yeBkeÀebvee DeveglHeeokeÀ keÀpee¥®es

He´ceeCe ce³ee&efole jeKeC³eekeÀjlee osKeerue yejer®e keÀmejle keÀjeJeer ueeieueer. ³ee

Je<ee&le yeBkeÀeb®³ee þsJeerle 11.4 … lej keÀpee&le 9.5… Je=Ooer Peeueer.

³ee meJe& HeefjefmLeleerle DeeHeu³ee yeBkesÀ®eer meve 2014-15 ceO³es DeeefLe&keÀ

keÀeceefiejer GÊece jeefnueer Demetve l³ee®ee efJemle=le Dee{eJee Heg{s Iesleuee Deens.

YeefJe<³ee®ee JesOe ë

He´iele osMeebleerue megOeejCeejer DeeefLe&keÀ ieleer Je Ieìle Demeuesu³ee Keefvepe lesue,

keÀesUmee Fl³eeoerb®³ee efkebÀceleerbcegUs peeieeflekeÀ DeLe&J³eJemLes®³ee Jee{er®eer ieleer meve

2016 ceO³es megOeejC³ee®es mebkesÀle Deensle. ®eerve®³ee DeLe&J³eJemLes®ee ceboeJeuesuee

Jesie, keÀ®®³ee lesuee®³ee efkebÀceleerb®eer meeMebkeÀlee lemes®e HejkeÀer³e ®eueve DeeefCe

J³eeHeejer Je Mesleceeuee®³ee efkebÀceleeb rleerue ®e{Gleej ner peeieeflekeÀ

DeLe&J³eJemLesHeg{erue DeeJneves Deensle.

DecesefjkeÀve [e@uej®³ee cetu³eele Peeuesu³ee Je=OoercegUs DecesefjkesÀ®³ee DeLe&J³eJemLes®eer

ieleer He´Lece DeOe&Je<ee&le ceboeJeC³ee®eer Meke̳elee Demetve ogmeN³ee DeOe&Je<ee&le cee$e

DeLe&J³eJemLee megOeejC³ee®es mebkesÀle Deensle. ³egjesefHe³eve ceO³eJeleea yeBkeÀebveer ke=Àef$ece

®eueve efveefce&leerÜejs kesÀuesu³ee Ghee³e³eespevee Je keÀ®®³ee lesuee®³ee Iemejuesu³ee

efkebÀceleerbcegUs SketÀCe ceeieCeerle Peeuesueer Jee{ ³eecegUs ³egjesefHe³eve osMeeb®eer

DeLe&J³eJemLeeosKeerue keÀener He´ceeCeele megOeejC³ee®eer DeHes#ee Demetve ®eerve®³ee

DeLe&J³eJemLes®eer ieleer ceboeJeC³ee®eer He´efke´À³ee cee$e meg©®e jenC³ee®es mebkesÀle Deensle.

DecesefjkesÀleerue J³eepeoj Jee{ Heg{s {keÀueueer iesu³eecegUs peeieeflekeÀ DeLe&yeepeejele

Glmeene®es JeeleeJejCe nesles. ³ee®e keÀeUele Flej He´iele Je He´ieleerMeerue osMeebleerue

ceO³eJeleea yeBkeÀebveer DeeefLe&keÀ ieleer®ee Jesie Jee{C³eekeÀefjlee J³eepeojele keÀHeele

kesÀueer. veefpekeÀ®³ee keÀeUele DecesefjkesÀleerue J³eepeojeleerue DeHesef#ele Jee{ ne

cenlJee®ee cegÎe þjCeej Demetve peeieeflekeÀ DeLe&J³eJemLee Je He´ecegK³eeves He´ieleerMeerue

osMeebJej ³ee®ee ceesþ³ee He´ceeCeeJej HeefjCeece nesC³ee®eer Meke̳elee Deens.

Yeejleeleerue meÐeefmLeleer ë

meve 2014 ceO³es YeejleeceO³es cenlJee®ee jepekeÀer³e yeoue Ie[uee Je 25

Je<ee¥veblej He´Lece®e Yeejleele mebHetCe& yengcele Demeuesues mejkeÀej He´mLeeefHele Peeues.

veJeerve mejkeÀejves oerIe& keÀeueeJeOeer®³ee DeeefLe&keÀ megOeejCeeb®ee keÀe³e&ke´Àce efveefM®ele

kesÀuee Demetve Yeejleele ³ee®es DevegketÀue HeefjCeece YeefJe<³eele efveefM®ele®e efomet

ueeieleerue.

meve 2015-16®³ee DeLe&mebkeÀuHee®³ee ceeO³eceeletve Yeejle mejkeÀejves efJeÊeer³e

OeesjCee®eer efoMee megefveefM®ele kesÀueer Demetve meyeefme[er®es He´ceeCe meve 2014-

15ceOeerue {esyeU je<ì^er³e GlHeeovee®³ee 2.1… JejÀve meve 2015-16

ceO³es {esyeU je<ì^er³e GlHeeovee®³ee 1.7 … He³e¥le keÀceer keÀsues Deens. ³ee®eyejesyej

osMeeleerue Hee³eeYetle megefJeOeebJejerue Ke®ee&®es He´ceeCe cee$e meve 2014-15ceOeerue

1.5 … ®³ee leguevesle meve 2015-16 ceO³es 1.7 … He³e&le Jee{C³ee®es

He´mleeefJele kesÀues Deens. efJelleer³e Dee³eesiee®³ee efMeHeÀejmeervegmeej efJelleer³e legìer®es

He´mleeefJele He´ceeCe {esyeU je<ì^er³e GlHeeovee®³ee 3.6 … Demetve DeLe&ceb$³eebveer cee$e

JeemleJee®³ee DeeOeejs legìer®es ns He´ceeCe meve 2015-16 ceO³es 3.9…

jeKeC³ee®es He´mleeefJele kesÀues Deens. keWÀêmejkeÀej®³ee SketÀCe JeeìHe³eesi³e

keÀjmebkeÀueveeleerue jep³ee®³ee efnMM³eele 32 … JejÀve 42 … FlekeÀer Jee{

DeLe&mebkeÀuHeele He´mleeefJele kesÀueer iesueer Deens.

mejkeÀej®³ee Hee³eeYetle megefJeOeebJej DemeCeeje Yej Je l³eemeeþer jmles, jsuJes, Jeerpe Je

ie´eceerCe efJekeÀeme ³eemeeþer kesÀu³ee iesuesu³ee lejlegoeRcegUs Yeejleer³e DeLe&J³eJemLes®³ee

ieleerle Jee{ efveefM®ele®e DeHesef#ele Deens. SketÀCe®e DeLe&mebkeÀuHeeletve mejkeÀej®³ee

megefveefM®ele Je oerIe&keÀeueerve DeeefLe&keÀ OeesjCee®ee He´l³e³e ³esle Deens.

³ee DeLe&mebkeÀuHeele kebÀHeveer keÀjele keÀHeele kesÀueer iesueer Demetve l³ee®eyejesyej efJeefJeOe

GÐeesieOebÐeebmeeþer Demeuesu³ee meJeueleer osKeerue jÎ kesÀu³ee Deensle. SketÀCe®e

keÀjHe´Meemeve meesHes Je megMeeefmele keÀjC³ee®ee mejkeÀej®ee ceeveme ³eeletve He´ecegK³eeves

peeCeJelees.

mejHesÀmeer keÀe³eoe Je veJeerve yeBkeÀjHìdmeer keÀes[ ³eeDebleie&le efyeiej yeBkeÀeRie efJelleer³e

mebmLeeb®ee DebleYee&Je keÀjC³eele Deeuee Demetve ³ee®ee HeÀe³eoe HeefjCeecekeÀejkeÀ Jemegueer

keÀjÀve DeveglHeeokeÀ keÀpex keÀceer keÀjC³eekeÀjlee efveefM®ele nesT MekesÀue. mejkeÀejer

yeBkeÀebkeÀjlee mebHetCe& mJee³eÊelee Demeuesu³ee efJeMes<e ceb[Ue®eer mLeeHevee kesÀueer iesueer

44 Jee Jeeef<e&keÀ DenJeeue

7 44 Jee Jeeef<e&keÀ DenJeeue

Demetve ³ee yeBkeÀebvee owvebefove J³eJenejele mebHetCe& mJee³eÊelee efceUC³ee®eer DeHes#ee Deens.

Yeejle mejkeÀej DeeHeu³ee DeeefLe&keÀ megOeejCeeb®ee keÀe³e&ke´Àce Keeueerue He´keÀuHeebÜejs

He´ecegK³eeves jeyeefJele Deens.

· ceskeÀ Fve Fbef[³ee

· Hee³eeYetle megefJeOeeb®eer efveefce&leer

· He´Oeeveceb$eer peve Oeve ³eespevee

· mceeì& efmeìerpe®eer efveefce&leer

· mJe®í Yeejle DeefYe³eeve

³ee®eyejesyej Yeejle mejkeÀejves keÀesUmee, efJecee, peer.Smed.ìer. Je peceerve DeefOeie´nCe

³ee #es$eeble osKeerue OeesjCeelcekeÀ megOeejCee kesÀu³ee Deensle. vegkeÀleer®e keÀesUmee

KeeCeeR®³ee efueueeJee®eer He´efke´À³ee ³eMemJeer Je HeejoMe&keÀHeCes Heej He[ueer Demetve

mejkeÀejves efJecee #es$eeleerue HejkeÀer³e Lesì iegbleJeCegkeÀer®³ee ce³ee&osle osKeerue Jee{

kesÀueer Deens. peer.Smed.ìer. meboYee&leerue efJeOes³ekeÀ vegkeÀles®e ueeskeÀmeYesves cebpetj kesÀues

Demetve ueJekeÀj®e peceerve DeefOeie´nCeemebyebefOele efJeOes³ekeÀ osKeerue ueeskeÀmeYee Je

jep³emeYesle cebpetj nesF&ue.

cee. HebleHe´Oeeveebveer osKeerue HejkeÀer³e iegbleJeCetkeÀoejeb®ee YeejleeJejerue efJeMJeeme ¢{

keÀjC³eekeÀefjlee Yeejlee®eer He´eflecee Gb®eeJeC³ee®³ee ¢<ìerves Hejje<ì^er³e OeesjCe

DeJeuebefyeues Deens. Yeejlee®³ee DeeefLe&keÀ efJekeÀemee®³ee ¢<ìerves ns OeesjCe Heg{erue

keÀeUele DeefleMe³e cenllJee®es þjCeej Deens.

Jejerue veceto kesÀuesu³ee meJe& DeeefLe&keÀ megOeejCee mejkeÀej®³ee efJekeÀemeeleerue

iegbleJeCegkeÀer®³ee He´³elveeb®es ÐeeslekeÀ Deensle. DeeefLe&keÀ efJekeÀemeeuee ieleer osCeejer ner

OeesjCes DeeefLe&keÀ #es$eemeeþer Heg{erue keÀeUele DeveskeÀ He´keÀej®³ee mebOeer efvecee&Ce

keÀjleerue. Hejbleg nJeeceeveele nesCeejs DeJekeÀeUer yeoue Je mejemejerHes#ee keÀceer

HeeJemee®ee Deboepe ner veefpekeÀ®³ee keÀeUele mejkeÀej meceesjerue ceesþer DeeJneves

DemeCeej Deensle.

meve 2014-15 ceOeerue yeBkesÀ®³ee J³eJeneje®eer þUkeÀ JewefMe<ì³esë

ceuee veceto keÀjC³eeme Deevebo nesle Deens keÀer , yeBkesÀ®ee SketÀCe J³eJenej

meve 2014-15 ceO³es ₹ 11600 keÀesìer SJe{e Deens DeeefCe efveJJeU

veHeÀe ₹ 101.20 keÀesìer FlekeÀe Peeuee Deens.

þsJeer ë

meve 2014-15 ceO³es SketÀCe þsJeeRceO³es peJeUHeeme 1000 keÀesìeR®eer Jee{

Peeueer Demetve ner Jee{ 16… veeWoefJeueer Deens. yeBkesÀJej efJeMJeeme oeKeJeCeeN³ee meJe&

YeeieOeejkeÀeb®es Je þsJeeroejeb®es Deecner DeeYeejer Deenesle. DeeOeer veceto kesÀu³eeHe´ceeCes

efjPeJn& yeBkesÀ®³ee DeeefLe&keÀ OeesjCee®es keWÀêmLeeve ceneieeF& efve³ebef$ele keÀjCes ns nesles,

HeefjCeeceer J³eepeoj ®e{s jeefnues. l³eecegUs ie´enkeÀebveer ®eeuet/ye®ele Keel³eebceO³es Hewmes

þsJeC³eeHes#ee cegoleþsJeeRceO³es iegbleJeCetkeÀ keÀjCes Hemeble kesÀues. l³eecegUs ®eeuet/ye®ele

Keel³eeb®³ee þsJeeRceO³es IemejCe Peeueer. yeBkesÀves efJeÐeeLeea, ceefnuee Je

meJe&meeceev³eebkeÀefjlee DeveskeÀ ³eespevee jeyeefJeu³ee Deensle. lemes®e DeeOegefvekeÀ

mees³eeRmen Fbìjvesì yeBkeÀeRie®eer megefJeOee meJe& ®eeuet/ye®ele Keel³eebkeÀefjlee osC³eele

Deeueer Deens.

þsJeeR®ee leHeMeerue KeeueerueHe´ceeCes ë

keÀpe& ë

DenJeeue Je<ee&le keÀpe& J³eJenej 8.21… cnCepes ₹ 334.46 keÀesìeRveer

Jee{uee Deens. ieleJe<eea keÀpe& Je þsJeeR®es 65.77… Demeuesues He´ceeCe DenJeeue

Je<ee&le 61.40… Peeues Deens.

yeBkesÀves mJeerkeÀejuesues O³es³e ieeþC³eekeÀefjlee ie´enkeÀ mesJesle megOeejCee kesÀu³ee Deensle.

yeBkesÀ®ee meO³ee®ee MeeKee efJemleej ue#eele Ieslee YeewieesefuekeÀ HeefjefmLeleeruee DevegmejÀve

yeBkesÀves efJeYeeieer³e mlejeJej keÀpe&He´efke´À³ee megueYe Je ieefleceeve nesC³eekeÀefjlee

efJeMues<ekeÀeb®eer vesceCetkeÀ kesÀueer Deens. efjPeJn& yeBkesÀ®³ee He´®eefuele OeesjCeeb®ee efJe®eej

₹

31.03.2015 31.03.2014 … Jee{ / (Ieì)leHeMeerue

SketÀCe Guee{eue 11588.85 10268.01 12.86

þsJeer 7180.38 6194.00 15.92

keÀpes& 4408.47 4074.01 8.21

{esyeU veHeÀe 162.06 146.39 10.70

efveJJeU veHeÀe 101.20 93.52 8.21

mJeefveOeer 754.89 667.19 13.14

{esyeU DeveglHeeokeÀ keÀpes& 4.02 … 3.58 … 0.44

efveJJeU DeveglHeeokeÀ keÀpes& 0.00 … 0.40 … (0.40)

Hegbpeer He³ee&Hlelee 14.96 … 15.05 … (0.09)

( ₹ keÀesìerbceO³es )

( ₹ keÀesìerbceO³es )

þsJeer®ee He´keÀej 2014-15 … 2013-14 …

®eeuet 352.77 4.91 316.29 5.11

ye®ele 1309.58 18.24 1205.30 19.46

cegole 5518.03 76.85 4672.42 75.43

SketÀCe 7180.38 100.00 6194.01 100.00

8

keÀjÀve yeBkesÀves keÀpe&cebpegjer He´efke´À³ee megueYe Je meelel³eHetCe& jeKeC³ee®es OeesjCe

mJeerkeÀejues Deens. lemes®e peesKeerceeb®es efJekeWÀêerkeÀjCe keÀjC³eekeÀefjlee yeBkesÀves efJeefJeOe

#es$eebvee keÀpe& cebpetj kesÀues Deens.

Jej veceto kesÀu³eeHe´ceeCes DeeefLe&keÀ ceboercegUs osKeerue keÀpe& Jee{erJej HeefjCeece Peeuee

Deens.

meJe& He´keÀej®³ee ³eespeveeb®ee DeJeuebye keÀjÀvener yeouel³ee peeieeflekeÀ HeefjefmLeleer®ee

keÀpe&oejeb®³ee J³eJemee³eeJej HeefjCeece Peeu³eeves keÀener keÀpex DeveglHeeokeÀ Peeueer.

DeveglHeeokeÀ keÀpee¥®ee leHeMeerue KeeueerueHe´ceeCes ë

meve 2014-15 keÀefjlee yeBkesÀves veHe̳eeletve DeveglHeeokeÀ keÀpee&bkeÀefjlee 100…

lejleto kesÀueer Deens. l³eecegUs yeBkesÀ®eer efveJJeU DeveglHeeokeÀ keÀpex Metv³e Deensle.

iegbleJeCetkeÀ ë

ieleJe<eea®³ee ₹ 2267.87 keÀesìeR®³ee leguevesle cee®e& 2015 He³e¥le iegbleJeCetkeÀ

5.16… ves Jee{tve ₹ 2385.02 keÀesìer Peeueer Deens. DenJeeue Je<ee&le efjPeJn&

yeBkesÀ®³ee efvekeÀ<eevegmeej jesKelee Je iegbleJeCegkeÀer®es He´ceeCe Je vee@ve Smed.Sued.Deej.

iegbleJeCegkeÀer®es He´ceeCe ³eesi³e jeKeues Deens. mejkeÀejer jesKes GlHevve ns ieleJe<eea®³ee

8.80… JejÀve 7.74… FlekesÀ Iemejues Deensle. peeieeflekeÀ yeepeejele ceneieeF&

Je keÀ®®³ee lesuee®³ee efkebÀceleerle IemejCe Peeu³eecegUs yeeB[ Je mejkeÀejer jesKes ³eeb®³ee

efkebÀceleerle cesU meeOeuee iesuee. iegbleJeCegkeÀerJejerue oerIe&keÀeueerve HejleeJ³eeuee yeeOee

³esT ve oslee DenJeeue Je<ee&le Kejsoer efJeke´ÀerÜejs ₹ 7.55 keÀesìer GlHevve efceUefJeues.

þsJeeRJejerue mejemejer J³eepeojeHes#ee iegbleJeCegkeÀerJej efceUeuesu³ee DeefOekeÀ

J³eepeojecegUs yeBkesÀuee peeoe J³eepe GlHevve keÀe³ece jeKelee Deeues Deens.

31.3.2015 jespeer iegbleJeCetkeÀ Heesì&HeÀesefueDeesceO³es ₹ 70 keÀesìeR®eer

cetu³eJe=Ooer Peeueer Deens.

Deeblejje<ì^er³e J³eJemee³e ë

efjPeJn& yeBkesÀves efouesu³ee efJeosMe efJeefvece³e J³eJeneje®³ee HejJeeveieer Debleie&le 19

peguew 2010 Heemetve yeBkeÀ DeefOeke=Àle [eruej cnCetve keÀe³e&jle Deens. meO³ee yeBkesÀ®es

`De' ÞesCeer®es SkeÀ keWÀê cegK³e keÀe³ee&ue³eele Demetve `ye' ÞesCeer®eer keWÀês Devegke´Àces

veewHee[e-þeCes, DebOesjer, veeefMekeÀ Je HegCes ³esLes keÀe³e&jle Deensle. DenJeeue Je<ee&le

Deeblejje<ì^er³e J³eJemee³e efJeYeeieeves SketÀCe ₹ 1546.06 keÀesìeR®ee J³eeHeejer

J³eJenej kesÀuee Demetve ₹ 7.03 keÀesìer FlekeÀe efveJJeU veHeÀe efceUefJeuee Deens. ³ee

meboYee&leueer DeeblejyeBkeÀ J³eJenej ₹ 1477.48 keÀesìer FlekeÀe Peeuee Deens.

ieleJe<eea®³ee leguevesle J³eeHeejer J³eJenejeleerue SketÀCe Jee{ 16.52… Deens. ̀ De'

ÞesCeer®³ee keWÀêeceOetve DeeblejyeBkeÀ J³eJenej lemes®e Dee³eele efve³ee&le efJe<e³ekeÀ J³eJenej

kesÀues peeleele. DenJeeue Je<ee&le ³ee meJe& keWÀo´ebveer ue#eCeer³e keÀeceefiejer kesÀueer Deens.

`keÀ' ÞesCeer®³ee SketÀCe 38 keWÀo´ebceOetve HejosMeer ®eueveefJe<e³ekeÀ J³eJenej kesÀues

peeleele.

DeeefLe&keÀ Je<e& 2014-15 ns Yeejleer³e ®eueveemeeþer ueeYeoe³ekeÀ þjues Deens.

DeeefLe&keÀ Je<e& 2013-14 ceOeerue ©He³ee®³ee melele®³ee DeJecetu³eveeveblej,

©He³ee DenJeeue Je<ee&le efmLejeJeuee DeeefCe ns DeJecetu³eve DecesefjkeÀve [e@uej®³ee

efkeÀbceleer®³ee leguevesle 4.3… He³e¥le ce³ee&efole jeefnues. ³eeJe<eea DecesefjkeÀve [e@uej

keÀener ®eueveeb®³ee leguevesle He´YeeJeer þjuee Deens, cee$e Yeejleer³e, ef®eveer Je LeeF& ®eueve

efmLej jeefnues. meO³ee ©He³ee He´efle [e@uej 62.90 les 63.50 ³ee ce³ee&osle

Deens.

meO³ee yeBkeÀ DecesefjkeÀve [e@uej, ³egjes, HeeTb[, pe@Heefvepe ³esve, Dee@mì^sefue³eve

[e@uej, efmebieeHetj [e@uej, ke@Àves[er³eve [e@uej Je efmJeme He´BÀkeÀ DeMee Deeþ ®eueveeble

J³eJenej keÀjle Deens. mebHetCe& peieYejeleerue 168 Hes#ee peemle yeBkeÀebMeer

J³eeJemeeef³ekeÀ mebyebOe yeBkesÀves He´mLeeefHele kesÀues Deensle. DenJeeue Je<ee&le yeBkesÀves

Dee³eele HeleHe$e, yee³eme& ke´sÀ[erì, HejkeÀer³e ®eueveele keÀpe& Je HejkeÀer³e ®eueveele

efve³ee&le keÀpe& HegjJeþe DeMee DeveskeÀ megefJeOee Keelesoejebvee GheueyOe keÀ©ve efou³ee

Deensle. lemes®e, yeBkesÀves S®ed[erSHedÀmeer yeBkesÀ®³ee menkeÀe³ee&ves HejkeÀer³e ®eueveeleerue

He´erHes[ [sefyeì keÀe[& GheueyOe keÀ©ve efoueer Deensle. l³ee®eyejesyej ®eueve

nmleeblejCeemeeþer Jesmìve& ³egefve³eve ceveer ì^evmeHeÀj DeeefCe ceveerie´ece n³ee mesJee yeBkeÀ

osle Deens. DeeefLe&keÀ Je<e& 2013-14 keÀjerlee ye@bkesÀuee keÀe@ce&Ped ye@bkeÀ S.peer.,

pece&veer ³eebpekeÀ[tve `yesmì efjuesMeveefMeHe' HegjmkeÀejeves mevceeefvele keÀjC³eele Deeues

Deens.

yeBke@ÀMegjvme ë

yeBke@ÀMegjvme, c³eg®³egDeue HebÀ[ iegbleJeCetkeÀ mesJee, ef[ce@ì mesJee, He@vekeÀe[& efJelejCe

mesJee DeMee Flej mesJeebJejosKeerue yeBkesÀves DeeHeues ue#e keWÀefêle kesÀues Deens.

ueJekeÀj®e ASBA DeeefCe MesDej ì^s[eRie Hue@ìHeÀe@ce&Jejerue Flej megefJeOee osKeerue

GHeueyOe keÀjÀve osC³eele ³esleerue. ASBA cnCepes Application

‘

( ₹ keÀesìerbceO³es )

leHeMeerue 2014-15 … 2013-14 …

{esyeU DeveglHeeokeÀ keÀpes& 177.23 4.02 145.92 3.58

efveJJeU DeveglHeeokeÀ keÀpes& 0.00 0.00 15.73 0.40

SketÀCe keÀpes& 4408.47 4074.01

44 Jee Jeeef<e&keÀ DenJeeue

9 44 Jee Jeeef<e&keÀ DenJeeue

Supported by Blocked Amount . ASBA ner megefJeOee Yeejleer³e

MesDej yeepeeje®es efve³eecekeÀ ceb[U Demeuesu³ee mesyeerves efJekeÀefmele kesÀueer Deens.

ASBA ³ee He´efke´À³esDebleie&le Depe&oeje®³ee Keel³eele YeeieKejsoermeeþer kesÀuesu³ee

Depee&®eer jkeÌkeÀce jeKetve þsJeC³eele ³esles DeeefCe Depe&oeje®³ee veeJes MesDeme&

efJelejCeeveblej leer jkeÌkeÀce meojnt kebÀHeveerme Deoe kesÀueer peeles. ie´enkeÀebvee SkeÀe®e

efþkeÀeCeer meJe& DeeefLe&keÀ megefJeOee GHeueyiOe keÀ©ve osC³eemeeþer yeBkeÀ He´³elveMeerue

Deens.

yeBkeÀ osle Demeuesu³ee ef[ce@ì mesJesueener Gllece He´eflemeeo efceUle Deens. Jej GuuesKe

kesÀu³eeHe´ceeCes efjPeJn& yeBkesÀ®³ee HejJeeveieerves ie´enkeÀeuee MesDeme& J³eJeneje®eer megefJeOee

GHeueyOe keÀ©ve osC³ee®ee yeBkesÀ®ee ceeveme Deens. ceer meJe& YeeieOeejkeÀebvee DeeJeenve

keÀjlees keÀer l³eebveer ef[ce@ì Keeles megjÀ keÀjeJes Je DeeHeu³ee iegbleJeCetkeÀ J³eJenejemeeþer

³ee megefJeOeeb®ee ueeYe I³eeJee.

³eg ìer Dee³e ìskeÌvee@uee@peer meefJn&mesme®³ee ceoleerves He@vekeÀe[& efJelejCee®eer megefJeOee

yeBkeÀ GHeueyOe keÀjÀve osles. DeepeJej DeveskeÀ Keelesoejebveer ³ee mesJes®ee ueeYe Iesleuee

Deens.

Flej J³eJemee³e - efme[keÀes He´keÀuHe ë

n³ee HetJeea ye@bkesÀves efme[keÀes®es DeveskeÀ ie=nefvecee&Ce He´keÀuHe ³eMemJeerefjl³ee neleeUues

Deensle. lees®e efJeMJeeme keÀe³ece þsJetve efme[keÀesves KeejIej, meskeÌìj 36, veJeer cegbyeF&

³esLeerue mJeHveHetleea ie=nefvecee&Ce He´keÀuHee®eer peyeeyeoejer yeBkesÀkeÀ[s meesHeefJeueer. ³ee

³eespevesuee Gob[ He´eflemeeo efceUeuee Je SketÀCe 155482 Depee&b®eer efJeke´Àer

Peeueer. l³eeHewkeÀer Depe&oejebveer Ye©ve efouesues 65674 Depe& efme[keÀeskeÀ[s megHeto&

keÀjC³eele Deeues. yeBkesÀves efve³eespeveyeOo He×leerves ne He´keÀuHe ³eMemJeerHeCes

neleeUuee.

veHeÀe ë

leerJe´ mHeOee& Je keÀþerCe DeeefLe&keÀ JeeleeJejCeelener yeBkesÀves ₹ 101.20 keÀesìeR®ee

efveJJeU veHeÀe 2014-15 ceO³es efceUefJeuee Deens. DenJeeue Je<ee&le yeBkesÀves

8.21… FlekeÀer Jee{ efveJJeU veHe̳eele kesÀueer Deens.

’ DeeefLe&keÀ Je<e& 2006-07 Heemetve menkeÀejer yeBkeÀebvee Dee³ekeÀj ueeiet keÀjC³eele

Deeuee. efo. 12.07.2009 jespeer Peeuesu³ee meJe&meeOeejCe meYesle mebMeef³ele Je

yeg[erle keÀpe& Keeleer efveuexefKele keÀjC³eeyeeyele®es OeesjCe meYeemeoebvee efJe<eo keÀjC³eele

Deeues nesles. J³eeJemeeef³ekeÀ OeesjCeeb®es DeJeuebyeve keÀjleevee Dee³ekeÀje®es efve³eespeve Je

leeUsyeboe®es J³eJemLeeHeve yeejkeÀeF&ves keÀjCes DeeJeM³ekeÀ Demeles. ³eemeeþer Jemegueer®ee

nkeÌkeÀ DeyeeefOele jeKetve mebMeef³ele Je yeg[erle keÀpe& Keeleer efveuexefKele keÀjC³ee®es

OeesjCe DeeKeCes Gef®ele þjles.

DeefuekeÀ[erue keÀeUele yeBkesÀ®ee J³eJemee³e-efJemleej DeveskeÀ HeìeRveer Jee{le Deens.

cnCetve®e meb®eeuekeÀ ceb[Ueves DeJeuebyeve kesÀuesu³ee mebMeef³ele Je yeg[erle keÀpe& Keeleer

efveuexefKele keÀjCes ³ee OeesjCeevegmeej DeMeer keÀpe& Keeleer efveuexefKele keÀjC³eeme cebpegjer

osCes HeÀe³eosMeerj þjles.

ceuìermìsì keÀes. [email protected]³eìer keÀe³eoe 2002 DevJe³es, meb®eeuekeÀ ceb[Ueme

mebMeef³ele Je yeg[erle Keeleer efveuexefKele keÀjC³eemeeþer®es OeesjCe DeeKeC³ee®es DeefOekeÀej

osC³eele Deeues Deensle. lemes®e, ³ee keÀe³eÐeeleerue lejlegoeRvegmeej n³ee OeesjCeeuee

Devegmeªve DeMeer keÀpe& Keeleer efveuexefKele keÀjC³ee®ee DeefOekeÀejner meb®eeuekeÀ

ceb[Ueme osC³eele Deeuee Deens.

PeHeeìîeeves Jee{Ceeje J³eJemee³e lemes®e Dee³ekeÀj-efve³eespeve Je leeUsyeboe®es

J³eJemLeeHeve keÀjC³eemeeþer ns meb®eeuekeÀ ceb[U mebMeef³ele Je yeg[erle keÀpe& Keeleer

efveuexefKele keÀjC³eemeeþer ³ee DeeefLe&keÀ Je<ee&Heemetve cebpegjer osF&ue.

ueeYeebMe ë

YeeieOeejkeÀebvee ³eesi³e HejleeJee osle Demeleevee®e veHe̳ee®eer Hegve&iegbleJeCetkeÀ keÀ©ve

Hegbpeer He³ee&Hlelee He´ceeCe me#ece jeKeCes ns OeesjCe yeBkesÀvess jeKeues Deens. l³eevegmeej

meve 2014-15 ceO³es 15… ueeYeebMee®eer efMeHeÀejme keÀjleevee meb®eeuekeÀ

ceb[Ueme Deevebo nesle Deens.

veHeÀe efJeYeeieCeer - 2014-15 ë

meYeemeoebvee jeKeerJe efveOeer DeeefCe Flej iebieepeUer ³eeb®es mel³e Je ³eesi³e cetu³eebkeÀve

mecepeeJes cnCetve ³eeJe<eea®eer veHeÀe efJeYeeieCeer ¿ee®e Je<eea®³ee leeUsyeboele Deble&Yetle

kesÀueer Demetve l³eeme meYeemeoeb®eer cebpegjer DeHesef#ele Deens. leHeMeerueJeej efJeYeeieCeer

He=<þ ke´À.24 Jej osC³eele Deeueer Deens.

Hebgpeer He³ee&Hlelee ë

yeBkesÀ®eer Hebgpeer He³ee&Hlelee ceeieerue Je<eea®³ee 15.05… ®³ee leguevesle efkebÀef®ele keÀceer

keÀj Je lejlegoerbHetJeer&®ee veHeÀe 162.06 146.39

keÀj Je lejlegoerbveblej®ee veHeÀe 101.20 93.52

leHeMeerue 2014-15 2013-14

( ₹ keÀesìerbceO³es )

10

nesTve DenJeeue Je<ee&le 14.96 Peeueer Deens. Hejbleg meoj He´ceeCe efjPeJn& yeBkesÀves

efkeÀceeve He´ceeefCele kesÀuesu³ee 12… HeeleUerHes#ee peemle Deens. ³eeleerue

Yeeb[Jeuee®es He´ceeCe 76.25… FlekesÀ ue#eCeer³e Deens. veeiejer menkeÀejer

yeBkeÀebmeeþer pej Basel-ll efkebÀJee Basel-lll ®³ee efMeHeÀejmeer ueeiet keÀjC³eele

Deeu³ee lej meoj Tier – I Yeeb[Jeuee®eer ner G®®e ìkeÌkesÀJeejer yeBkesÀ®eer l³eemeeþer

meppelee oMe&efJeles.

efjPeJn& yeBkesÀ®³ee ceeie&oMe&keÀ leÊJeebvegmeej Tier – II Yeeb[Jeue DemeCeeN³ee

oerIe&keÀeueerve (Subordinated) cegoleþsJeeR®eer jkeÌkeÀce Hegbpeer He³ee&Hlelee

ceespeC³eemeeþer ₹ 80 keÀesìer FlekeÀer®e Iesleueer Deens. ieleJe<eea meoj jkeÌkeÀce

₹ 100 keÀesìer nesleer.

J³eJemee³e efJemleej ë

ceuee meebieC³eeme Deevebo neslees keÀer yeBkesÀ®³ee Jeeì®eeueerle cenÊJeHetCe& Je mebmcejCeer³e

ìHHee Demeuesu³ee 100 J³ee MeeKes®es GodIeeìve efo. 2 Dee@iemì 2014 jespeer

þeC³eeleerue {eskeÀeUer Heefjmejele keWÀêer³e jmlesJeenletkeÀ DeeefCe ceneceeie&, efMeHeeRie

Keel³ee®es ceb$eer cee. Þeer. efveleervepeer ie[keÀjer ³eeb®³ee MegYenmles keÀjC³eele Deeues.

þeCes Menjele®e 100Jeer MeeKee meg© keÀjC³ee®es HetJe&efve³eespeve meb®eeuekeÀ ceb[Ueves

kesÀues nesles. meebieC³eeme Deevebo neslees keÀer meoj MeeKesves þeCeskeÀjeb®³ee DeYetleHetJe&

He´eflemeeoeves Heefnu³ee®e efoJeMeer ₹ 120 keÀesìerbHes#ee peemle J³eJemee³e keÀ©ve

yeBkeÀeRie #es$eeleerue efJeke´Àce He´mLeeefHele kesÀuee. meb®eeuekeÀ ceb[Ue®³ee Jeleerves

YeeieOeejkeÀeb®³ee Je Keelesoejeb®³ee YejerJe He´eflemeeoeyeÎue ceer ke=Àle%elee J³ekeÌle

keÀjlees.

yeBkesÀ®³ee SketÀCe 110 MeeKee keÀe³e&jle Deensle. DeeefLe&keÀ Je<e& 2014-15

ceO³es þeCes, HegCes, iegpejele, keÀvee&ìkeÀ DeeefCe ceneje<ì^eleerue Flej Yeeieeble SketÀCe

19 MeeKee megjÀ keÀjC³eele Deeu³ee. lemes®e HegC³eeleerue efJemleeefjle keÀ#ee®es

MeeKesle jÀHeeblej keÀjC³eele Deeues. ³esl³ee DeeefLe&keÀ Je<ee&le iegpejeleceO³es JeeHeer

DeeefCe veeefMekeÀ ³esLeerue efmevvej ³ee efþkeÀeCeer veJeerve MeeKee megjÀ nesle Deensle.

peesKeerce J³eJemLeeHeve ë

J³eJemee³ee®eer Jee{ Je efmLejlee ³eebmeeþer peesKeerce J³eJemLeeHeve cenlJee®es þjles.

yeBkeÀeRie J³eJemee³eele ke´sÀ[erì efjmkeÀ, ceekexÀì efjmkeÀ, He´eF&me efjmkeÀ, Dee@HejsMeveue

efjmkeÀ DeMee efvejefvejeU³ee peesKeerceebvee meeceesjs peeJes ueeieles. peesKeerces®eer ceeefnleer,

ceespeceeHe, J³eJemLeeHeve DeeefCe osKejsKe ns cenÊJee®es Demeles. yeBkesÀ®³ee ke´sÀ[erì

efjmkeÀ J³eJemLeeHevesmeeþer megHe´ceeefCele ³eespevee DeeefCe efve³eceeJeueer keÀe³ee&efvJele

…

Tier – I

Deensle. efjPeJn& yeBkesÀ®³ee efve³eceeJeueerb®eer Hetle&lee keÀ©ve DeeefCe yeBkesÀ®ee J³eJemee³e

ue#eele IesTve keÀe³e&jle Demeuesu³ee peesKeerce J³eJemLeeHevee®ee meb®eeuekeÀ

ceb[UekeÀ[tve JesUesJesUer Dee{eJee Iesleuee peelees.

ceeveJe mebmeeOeve ë

yeBkesÀ®³ee ceeveJe mebmeeOeve efJekeÀemee®es He´cegKe GÎer<ì keÀce&®eeN³eeb®³ee keÀeceefiejer®eer

He´le meelel³eeves keÀMeer Gb®eeJelee ³esF&ue ns HeenC³ee®es Deens. ns GÎer<ì ieeþleevee

keÀce&®eeN³eeuee keÀewMeu³e, #ecelee, ceeefnleer DeMee efJeefJeOe He´keÀejeb®es He´efMe#eCe osCes

iejpes®es Demeles. lemes®e l³eeb®³ee He´efMe#eCe Je efJekeÀemeemeeþer efve³eespeve keÀjCesner

DeeJeM³ekeÀ Demeles.

yeBkesÀves keÀce&®eeN³eeb®eer keÀewMeu³es Je meeceev³e%eeve efJekeÀefmele keÀjC³eemeeþer efJeefJeOe

He´keÀej®³ee He´efMe#eCeeb®es Dee³eespeve kesÀues. ³eeceO³es Debleie&le He´efMe#eCe, veeceebefkeÀle

DeeefLe&keÀ mebmLeebveer Je yeBkeÀebveer Dee³eesefpele kesÀuesueer He´efMe#eCes, F&-ueefve¥ie Fl³eeoeR®ee

Deble&YeeJe Deens.

yeBkesÀves oerveo³eeU YeJeve, þeCes ³esLes mJeleë®es ogcepeueer He´efMe#eCe keWÀê megjÀ kesÀues

Deens. lemes®e He´efMe#eCeeLeea Je keÀefve<þ DeefOekeÀeN³eebmeeþer F&-ueefve¥ie He´efMe#eCe megjÀ

kesÀues Deens. ns He´efMe#eCe meelel³eeves megjÀ jenerue ³eekeÀ[s yeBkesÀ®es ue#e Demeles.

meve 2014-15 ceO³es SketÀCe 620 keÀce&®eeN³eebvee 55 He´efMe#eCe

keÀe³e&ke´ÀceebÜejs 9443 leeme He´efMe#eCe osC³eele Deeues. ³eeceO³es He´ecegK³eeves

vesle=lJeiegCe Je vesle=lJe-efJekeÀeme, ie´enkeÀmesJee, efJeke´ÀerMeeðe, keÀpe&efve³eceve Je

cetu³eebkeÀve, uesKeeHejer#eCe, efJeosMe efJeefvece³e DeMee efJeefJeOe efJe<e³eeb®ee meceeJesMe

Deens. megj#ee j#ekeÀebmeeþerner He´efMe#eCe Dee³eesefpele keÀjC³eele Deeues.

yeBkeÀ ³eesi³e OeesjCe Je efJeefJeOe keÀe³e&ke´Àceeb®es Dee³eespeve keÀ©ve keÀce&®eeN³eeb®es Je

DeefOekeÀeN³eeb®es keÀewMeu³e efJekeÀefmele keÀjC³eemeeþer meelel³eeves He´³elveMeerue

Demeles.

DeeOegefvekeÀ leb$e%eeve ë

leb$e%eeveecegUs meeceev³e ceeCemeebvee yeBkesÀves HegjefJeuesu³ee efJelleer³e mesJee ³ee keÀceer

JesUele Je keÀceer Ke®ee&le DeefOekeÀ keÀe³e&#ecelesves Je kegÀþtvener GHeueyOe Peeu³ee

Deensle. lemes®e yeBkeÀeRie #es$eeleerue ceesþ³ee He´ceeCeele Demeuesues keÀeieoesHe$eer J³eJenej

keÀceer Peeues Demetve l³ee®es ©Heeblej Flej keÀener leebef$ekeÀ He×leerle keÀjC³eele Deeues

Deensle.

44 Jee Jeeef<e&keÀ DenJeeue

11 44 Jee Jeeef<e&keÀ DenJeeue

DeeHeueer yeBkeÀ ie´enkeÀebme F&-yeBkeÀeRie mesJee GHeueyOe keÀ©ve osle Deens. lemes®e,

ie´enkeÀebme efJnmee Je [sefyeìkeÀe[&, Dee³e.Sced.Heer.Smed. ceesyeeF&ue yeBkeÀeRie, F& HeemeyegkeÀ

DeeefCe veJ³eeves ®eeuet kesÀuesu³ee Fbìjvesì yeBkeÀeRie Fl³eeoer mesJee GHeueyOe keÀ©ve efou³ee

Deensle. DeeHeueer yeBkeÀ mevceeveveer³e ie´enkeÀebme l³eeb®³ee owvebefove peerJeveeleerue

DeeJeM³ekeÀ efyeueYejCee keÀjC³eemeeþer ueJekeÀj®e Utility Payment

Module GHeueyOe ke˩ve osCeej Deens.

DeeOeej keÀe[e&meeþer DeeJeM³ekeÀ Demeuesueer E-KYC He´Ceeueer Keelesoejebvee

2014-15 ceO³es GHeueyOe keÀ©ve efou³eecegUs ie´enkeÀeb®³ee DeesUKeHe$ee®eer

He[leeUCeer leeye[leesye keÀjCes Meke̳e Peeues Deens Je l³eecegUs ie´enkeÀebme ieefleceeve

mesJee efceUeueer Deens. DeeHeu³ee yeBkesÀves ie´enkeÀebme DBTL (Direct Benefit

Transfer of LPG) Devegoevee®eer mees³e keÀ©ve efoueer Deens.

J³eeJemeeef³ekeÀ DevegMeemeve ë

DeeefLe&keÀ J³eJenejebleerue HeejoMe&keÀlee DeeefCe meYeemeoeb®es efnle peHeCes ns

J³eeJemeeef³ekeÀ DevegMeemevee®es iegCeOece& Deensle. YeeieOeejkeÀeb®³ee Je ie´enkeÀeb®³ee

efnlee®eer peHeCetkeÀ DeeefCe l³eeb®³ee iegbleJeCegkeÀer®eer cetu³eJe=Ooer nesC³eemeeþer megefJeefnle

³eespevee jeyeefJeC³eele ³esles.

meom³e mebK³ee ë

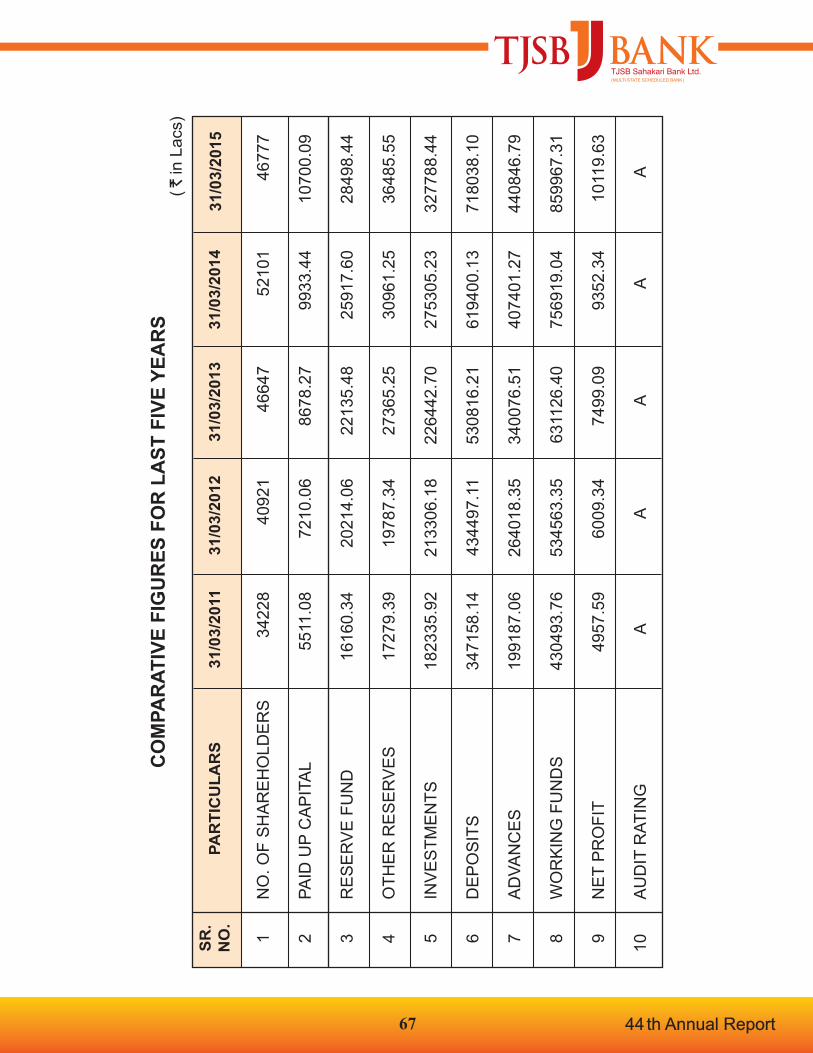

31.03.2015 jespeer yeBkesÀ®eer meom³e mebK³ee 46777 Deens.

uesKeeHejer#ekeÀeb®eer vesceCetkeÀ ë

meve 2015-16 ³ee DeeefLe&keÀ Je<ee&meeþer JewOeeefvekeÀ uesKeeHejer#ekeÀ cnCetve

ces.ieesKeues DeeefCe meeþs, ®eeì&[& DekeÀeTbìbìdme ³eeb®eer efve³egkeÌleer keÀjC³eeyeeyele

meb®eeuekeÀ ceb[U efMeHeÀejme keÀjerle Deens. JewOeeefvekeÀ uesKeeHejer#ekeÀ cnCetve keÀece

keÀjC³eeme ces. ieesKeues DeeefCe meeþs ³eebveer mebceleer efoueer Deens. ³ee vesceCegkeÀeryeeyele®ee

þjeJe efJe<e³e Heef$ekesÀJejerue efJe<e³e ke´À. 4 DevJe³es ceeb[C³eele Deeuee Deens.

meeceeefpekeÀ peyeeyeoejer ë

J³eeJemeeef³ekeÀ mlejeJej He´YeeJeer keÀeceefiejer keÀjle Demeleevee®e ìerpesSmedyeerves DeeHeues

meeceeefpekeÀ Gllejoeef³elJe mJeerkeÀejues Deens Je DeeHeu³ee efveJJeU veHe̳eeleerue

keÀener Yeeie meeceeefpekeÀ mebmLeebvee Devegoeve ©Heeves osle Deens. He³ee&JejCe mebyebOeeleerue

keÀener meeceeefpekeÀ HewuetbMeer yeBkeÀ mebueive jentve keÀece keÀjle Deens. DeeefLe&keÀ Je<e&

2014-15 ceO³es yeBkesÀves SketÀCe 63 mebmLeebvee ₹ 93.40 ueeKe Devegoeve

©Heeves efJeleefjle kesÀues Deensle.

ÞeOoebpeueer ë

DenJeeue Je<ee&le efveOeve HeeJeuesues ye@bkeÀs®es ceepeer meb®eeuekeÀ Þeer. He´YeekeÀj efJe.

kegÀuekeÀCeer& lemes®e DenJeeue Je<ee&le efveOeve HeeJeuesues meYeemeo, Keelesoej Je

efnleef®eblekeÀ ³eebvee efJevece´ ÞeOoebpeueer.

$eÝCeefveoxMe ë

yeBkesÀJej oeKeefJeuesu³ee efJeMJeemeeHe´leer Je meJee¥ieerCe He´ieleeruee meowJe Heeefþbyee

osCeeN³ee YeeieOeejkeÀeb®ee ceer $eÝCeer Deens. yeBkesÀ®³ee He´ieleerceO³es meelel³eeves menkeÀe³e&

keÀjCeeN³ee Keelesoejeb®³ee He´leer ceer ke=Àle%elee J³ekeÌle keÀjlees.

yeBkesÀuee meelel³eeves He´ieleerHeLeeJej þsJeC³eeme yeBkesÀleerue meJe& keÀce&®eejerJe=boe®es ueeYele

Demeuesues ³eesieoeve DeeJneveelcekeÀ HeefjefmLeleerle cenlJee®es þjles. yeBkesÀ®³ee

He´ieleermeeþer melele keÀe³e&jle DemeCeeN³ee meJe& keÀce&®eejer Jeiee&®es meb®eeuekeÀ

ceb[Ue®³ee Jeleerves ceer ceveëHetJe&keÀ DeefYevebove keÀjlees.

Yeejleer³e efjPeJn& yeBkeÀ, keWÀêer³e menkeÀej Keeles, efouueer, menkeÀej Keeles, ceneje<ì^

jep³e ³eeb®³ee JesUesJesUer efceUCeeN³ee ceeie&oMe&veeyeÎue meb®eeuekeÀ ceb[U l³eeb®es

ke=Àle%e Deens.

yeBkesÀ®es Debleie&le uesKeeHejer#ekeÀ, JewOeeefvekeÀ uesKeeHejer#ekeÀ Je keÀe³eosMeerj

meuueeieej ³eeb®³ee ceeie&oMe&vee®ee yeBkesÀuee melele HeÀe³eoe Peeuesuee Deens. Deecner

l³eeb®es Del³eble DeeYeejer Deenesle.

yeBkesÀuee meelel³eeves He´ieleerHeLeeJej Deie´smej þsJeC³eemeeþer meb®eeuekeÀ ceb[Ueleerue

meYeemeoebveer efouesu³ee JesUs®³ee Je ceeie&oMe&vee®³ee yengcetu³e ³eesieoevee®ee ceer

ke=Àle%eleeHetJe&keÀ GuuesKe keÀjlees.

DeeHeuee,

meb®eeuekeÀ ceb[Ue®³ee Jeleerves,

meer. veboieesHeeue cesveve

DeO³e#e

efoë 09.05.2015

sd/-

12

th44 Annual Report 2014 - 2015

Dear Members,

On behalf of the Board of Directors, I extend a warm th

welcome to all of you at the 44 Annual General Meeting of

the Bank. As the Chairman of this great institution with a

prosperous legacy, I would like to put on record that because

of your generous support, your Bank has continued

achieving business targets during F.Y. 2014-15.

I am proud to inform you that after crossing milestone of

business mix of ₹ 10000 Crores during last financial year,

the Bank has achieved historical landmark of crossing ₹ 100

Crores of Net Profit and 100 branches in the financial year

under reporting.

Election of the Members of the Board of Directors :

In terms of Section 45 of Multi-State Co-operative Societies

Act, 2002, election of the Members of the Board was th th

conducted during 9 December, 2014 to 25 December,

2014. As empowered under the said section, the Board of

Director appointed Mr. Sandeep Malvi, Dy. Commissioner,

Thane Municipal Corporation, Thane as Returning Officer

to conduct election of the Members of the Board. The

Central Registrar was intimated accordingly. The process of

election of the Members of the Board was carried out as per

procedure laid down under Rule 19 of the said Act.

I take this opportunity to thank all the shareholders for

electing the present Board of Director, unopposed.

Before I update you on the financial performance of your

Bank, it is relevant to take a quick look at economic scenario

under which we conducted the banking business.

Economic Scenario :

Indian economy witnessed signs of improvement in F.Y.

2014-15. On one hand, country’s economic growth

improved in terms of GDP and on the other hand, inflation,

Current Account Deficit (CAD), fiscal deficit decreased

during financial year. Local currency also remained stable

during financial year.

RBI’s monetary policy measures helped CPI inflation

coming down to 5.17% in March 2015 which was 8.31% at

the beginning of the F. Y. 2014-15. According to the

Monetary Policy Framework Agreement signed by the

Reserve Bank of India and the Government of India, the

Reserve Bank will stay focused on CPI inflation with a

target of 6 % by January 2016 and 4 % by the end of F. Y.

2017-18.

Indian rupee remained stable in F.Y. 2014-15 as compared

to the previous financial year. During the year, broad range

of exchange rate was ₹ 58 to ₹ 64 against US dollar. In last

18 months, India has positioned itself far more better than in

the past, with Country’s foreign exchange reserves reaching

at an all-time peak of US $ 344 billion.

In the last financial year, crude oil prices fell sharply in the

international markets and Brent crude price came down to

$45 per barrel from its peak of $115 per barrel due to

oversupply from OPEC countries, USA and Russia. Falling

economic growth in China also partly led to fall in oil prices.

India has been the biggest gainer of this price fall, as oil

constitutes almost 70 % of Indian imports. It has also helped

a lot to shape India’s Current Account Deficit (CAD), which

is expected to remain at 1.3% of GDP. The falling crude oil

prices has enabled the government to take forward one of

the key and much pending reforms, namely, diesel price

decontrol.

GDP for F.Y. 2014-15 is estimated to be around 7.5% on the

basis of the changed calculation methodology and also the

changed base year. For F.Y. 2015-16, it is projected to

44 th Annual Report

13

increase in the range of 8% - 8.5%. Increase in GDP will

create new employment in the country.

Although the economy has shown signs of improvement,

slowdown in the same carried on since past several months

resulted in delaying payments and deferment of projects of

the business houses. It created challenges for the banking

sector in managing top-line growth and maintaining asset

quality. Growth in banking sector remained subdued during

F. Y. 2014-15. In this year, deposits grew at 11.4% while the

credit recorded growth of 9.5%.

In the above circumstances, your bank has continued to

register sustainable performance during F. Y. 2014-15.

Detailed performance analysis is given here under :

Way Ahead :

Global growth is likely to firm up in 2016, supported by

stronger recovery in the advanced economies and soft

energy prices. Downside risks mainly radiate from the

slowdown in China, geopolitical risks surrounding oil

prices and the uneven effects of currency and commodity

price movements.

Growth in the United States is likely to be weak in the first

half of the year because of US dollar appreciation, but is

expected to improve in the later part. The Euro area has

started to show modest improvement, supported by a boost

to demand from lower crude prices as well as easing

financial and credit conditions following the

commencement of quantitative easing. Growth continues to

be slow in China amidst financial fragilities and

macroeconomic imbalances. This will have regional and

global consequences, although the softness in international

commodity prices is providing some relief to importers

while adversely impacting exporters.

Global financial markets have been boosted by expectations

of normalisation of US monetary policy being pushed back

into late 2015. Monetary policy stance turned highly

accommodative in other Advanced Economies and several

Emerging Market Economies by easing policy rates to

address growth concerns. Going forward, interest rate hike

in US and its timing would be very crucial as it might have

huge impact on Global economy and more particularly on

the Emerging Market Economies.

Indian Scenario :

There was a radical political change in the country in May

2014 and for the first time in the last 25 years, a Government

was formed in the centre with a clear mandate. The present

Government has initiated action plan to take forward the

agenda of economic reforms with a long term economic

road map for the Country.

The Union Budget presented for F. Y. 2015-16 appears to be

credible one as it is clearly seen as the path of fiscal

consolidation. As far as quality of fiscal consolidation is

concerned, subsidies are estimated to reduce significantly

to 1.7% of GDP in F. Y. 2015-16 as against 2.1% of GDP in

F. Y. 2014-15. At the same time, capital expenditure would

rise from 1.5% to 1.7%. Government’s focus on

infrastructure is evident with the total targeted spending in

F. Y. 2015-16, almost double the revised estimates of F. Y.

2014-15. The Government has stuck to a realistic target of

fiscal deficit at 3.9% of GDP for F. Y. 2015-16 as against

Finance Commission’s recommendation of 3.6%. The

Government has raised State’s share in total divisible pool

of tax revenue to 42% from 32%.

The Budget lays focus on public investment, which will

have large spill-overs on economic growth. Despite

pressure on fiscal consolidation, enough room has been

created for infrastructure spending on sectors like roads,

railways, power and rural development. Overall, the budget

gives clear indication of strategic long term plan for growth.

In line with the Finance Minister’s stated philosophy, the

budget has provided a path towards lowering of corporate

tax rate and simultaneously doing away with multiple

exemptions to simplify the tax administration and reduce

disputes.

44 th Annual Report

14

Inclusion of NBFCs under SARFAESI Act and new

bankruptcy code will provide a boost to recovery efforts and

help rein in asset quality problems over the long run.

Setting-up of autonomous bank board bureau for public

sector banks is expected to provide greater functional

autonomy and pave way for bank holding company

structure which will optimise Government’s capital

contribution.

Government is taking forward its agenda of economic

growth through various projects like:

· Make in India

· Infrastructure Development

· Pradhan Mantri Jan Dhan Yojana

· Smart Cities Development

· Swachh Bharat Abhiyan

Further, the Government has also initiated various policy

reforms under sectors like Coal, Insurance, GST and Land

Acquisition. The Government has successfully completed

process of Coal block auction with a great transparency. It

has also increased percentage of FDI investment under

insurance. The bill related to GST has already been passed

by the Lok Sabha and Land Acquisition bill will be passed

by the parliamentary houses sooner or later.

Hon’ble Prime Minister has also taken initiatives in external

affairs to build up Country’s image in the outside world

which will help in increasing confidence of the Global

investors in India. Success of Government under all these

missions would be a key factor in future as far as country’s

economic growth is concerned.

All the reforms and initiatives taken by the Government

clearly suggest that it is inclined to invest in growth. The

growth momentum policies and strategies will hopefully

bring great opportunities for financial sector in the years to

come. However, uneven weather conditions and less than

normal monsoon projected this year are going to be

challenges before the Government.

Type of Deposits 2014-15 % 2013-14 %

Current 352.77 4.91 316.29 5.11

Savings 1309.58 18.24 1205.30 19.46

Term 5518.03 76.85 4672.42 75.43

Total 7180.38 100.00 6194.01 100.00

( ₹ in Crores)

Performance Highlight of the Bank for the F. Y.

2014- 15 :

I am happy to mention that your Bank recorded sustainable

performance during the year. While your Bank’s business

mix touched ₹ 11600 Crores the net profit of your Bank

surged to reach to ₹ 101.20 Crores.

Financial Highlights :

Deposits :

During the financial year, total deposits of the bank

increased by almost ₹ 1000 Crores registering growth of

nearly 16%. We are thankful to the shareholders and the

depositors for the confidence posed in the bank.

As mentioned earlier, the RBI’s Monetary Policy was

focused towards controlling inflationary pressure and

resulted in interest rate remaining on higher side. On this

background, the customers have preferred to invest in term

deposits rather than in CASA deposits. This has resulted in

slight fall in the composition of CASA deposits in total

deposits. However, Bank has promoted various schemes for

students, women and general public and launched Internet

Banking facility for the customers with added features to

augment the share of CASA deposits.

31.03.2015 31.03.2014 % Increase/(Decrease)Particulars

Business Mix 11588.85 10268.01 12.86

Deposits 7180.38 6194.00 15.92

Advances 4408.47 4074.01 8.21

Gross Profit 162.06 146.39 10.70

Net Profit 101.20 93.52 8.21

Owned Funds 754.89 667.19 13.14

Gross N.P.A. 4.02 % 3.58 % 0.44

Net N.P.A. 0.00 % 0.40 % (0.40)

C.R.A.R. 14.96 % 15.05 % (0.09)

( ₹ in Crores)

44 th Annual Report

15

Advances :

The advances portfolio has increased by ₹ 334.46 Crores

registering growth of 8.21%. The Credit Deposit Ratio

stood at 61.40% which was 65.77% at the beginning of the

year.

The Bank has refurbished its products & appraisal strategies

giving thrust on qualitative achievement of adopted goals.

Established Analyst teams at various geographical

locations, ensure judicious analysis of credit proposals

alongwith the identification of demographical risk imbibed

in it. Ongoing process of streamlining the credit appraisal

process has been adopted to ensure that Bank’s code of

analysis corresponds with the laid guidelines of RBI.

Bank’s credit portfolio entails diversified sectors thereby

averting concentration risk.

As stated above, the slowdown in the economy has affected

credit growth and also aggressive stance for qualitative

credit deployment strategy.

There was an overall sluggishness observed throughout

various industries affecting the businesses of the Borrowers

during F.Y. 2014-15 on this backdrop, the occasions of

default marginally rose during current F.Y. 2014-15.

In the F. Y. 2014-15, Bank has provided to the extent of

100% for NPAs out of the profit. This has enabled the Bank

to maintain net NPAs at zero.

Investments :

Aggregate investment of your Bank as on March 2015

increased to ₹ 2385.02 Crores from ₹ 2267.87 Crores,

registering growth of 5.16 %. Your Bank has maintained

adequate CRR and SLR as stipulated by RBI during

F.Y.2014-15. Your Bank has also maintained non SLR

investment within the prescribed limit set by RBI.

Ten year benchmark Government Security yield fell to st

7.74% on 31 March 2015 as compared to 8.80%, which

was at the end of previous financial year. The rally in Bond

and Government Security prices was mainly led by the fall

in inflation and a sharp fall in crude oil prices in

international market. Treasury management was efficiently

done with changing yield curve and while building up of

best yielding portfolio with long term strategy, trading

income of ₹ 7.55 Crores was generated during F.Y.2014-15.

Besides, the higher interest income on investment has given

significant amount of positive carry over the cost of deposit

which has helped your bank to post higher net interest st

income. On 31 March 2015, there was an appreciation of

more than ₹ 70 Crores to the Investment portfolio which

amply demonstrates its intrinsic value.

Foreign Exchange Business :

The International Business Division of your Bank is in th

operation since 19 July 2010, after receiving Authorised

Dealer Category – 1 License from RBI. Presently your

Bank is having “A” category center at its Corporate Office

and “B” category centres at Naupada, Nashik, Andheri and

Pune. During the year under report IBD has achieved the

merchant turnover of ₹ 1546.06 Crores, from all its centres.

IBD has earned net profit of ₹ 7.03 Crores during the

period under report. The Interbank turnover during the

period under report is of around ₹ 1477.48 Crores. The

merchant turnover has increased by nearly 16.52% over the

last year. At “A” category centre, along with the Trade

Finance activities, Interbank Dealing also takes place. The

“B” category centres handle only Trade Finance activities.

All the centres have shown a remarkable performance

during the year. There are 38 centres working as “C”

category which handle the money changing business.

F. Y. 2014-15 was a comeback year for the Indian Rupee.

( in Crores)

Particulars 2014-15 % 2013-14 %

Gross NPA 177.23 4.02 145.92 3.58

Net NPA 0.00 0.00 15.73 0.40

Total Advances 4408.47 4074.01

44 th Annual Report

16

After having been one of the poor performing currencies

during most of F. Y. 2013-14, Rupee managed to limit the

loss to 4.3% of value against the US Dollar. A year, when US

Dollar gained significantly against most currencies

globally, Rupee along with Chinese Yuan and Thai Baht

managed to hold out. Presently rupee is moving in the range

of 62.90 to 63.50 per dollar.

Presently bank is dealing in 8 major currencies viz. USD,

EURO, GBP, JPY, AUD, CHF, CAD & SGD. Separate

Nostro accounts have been opened with various

correspondents. The overall correspondent relationship

with more than 168 Banks across the world has been

established which enables the Bank to handle the business

effectively for its clients. During the year under report,

Bank has handled all types of forex products viz. Import

L/Cs, Buyer’s Credit, Foreign Currency Term Loans, export

finance in Foreign Currency etc. The Bank has made

arrangement for the pre-paid multi-currency cards in

association with HDFC Bank Ltd. for its customers. Your

Bank is also having correspondent arrangement for money

transfer services with Western Union Money Transfer and

Moneygram.

During the year, your Bank has been honoured with ‘Best

Relationship Bank award for 2013-14’ by Commerz Bank

A.G., Germany.

Strategic Business :

The Bank has concentrated on the other business services

like BANKASSURANCE, Mutual Fund services, Demat,

PAN services.

BANKASSUARANCE is emerging as good contributors to

bank’s profit. Sooner TJSB would start ASBA and Trading

account platform as an additional service facilities. ASBA

means “Applications Supported by Blocked Amount”.

ASBA is process developed by the India’s Stock Market

Regulator SEBI for applying to Initial Public Offer (IPO).

In ASBA, an IPO Applicant’s account does not get debited

until shares are allotted to them. The Bank is aimed at

providing the financial services to TJSB customers under

one roof.

The Bank is also extending Demat services to its customers

which is receiving good response. As mentioned above the

bank is planning to offer trading facility with RBI approval

and hence I appeal to all stakeholders to open Demat

Account with the bank which will facilitate you to do

trading of your investment portfolio in secondary market

with ease.

PAN services : The Bank provides PAN issuance service

through UTI Technology services and many Customers

have opted for this service.

Other Business – Project of CIDCO (City and Industrial

Development Corporation of Maharashtra) :

Based on the earlier satisfactory experience of handling

booking projects, CIDCO reposed the same confidence in

the Bank and allotted tenement booking project of

Swapnapurti Housing Scheme at Kharghar, Sector -36,

Navi Mumbai during F. Y. 2014-15.

There was overwhelming response and total 155482

application forms were sold of which 65674 applications

were received. The project was well managed by the Bank

to the satisfaction of CIDCO.

Profitability :

In spite of non conducive economic condition, your Bank

earned net profit of ₹ 101.20 Crores during F. Y. 2014-15.

Your Bank’s Net Profit registered an year-on-year growth

of 8.21%.

From the F. Y. 2006-07, the profits of the co-operative banks

are attracting the Income Tax provisions. The General Body

was appraised about the write-off of Bad and Doubtful Debt

Profit before Tax & Provisions 162.06 146.39

Profit after Tax & Provisions 101.20 93.52

Particulars 2014 - 15 2013 - 14

( ₹ in Crores)

44 th Annual Report

17

Policy in its meeting held on 12/07/2009. As a matter of

Business Policy it is necessary to keep an eye on Tax

Planning and Balance Sheet Management and hence it

becomes prudent business policy to write-off Bad and

Doubtful Debts without affecting our Right of Recovery.

Now Bank’s Business size is increasing multifold and hence

it would be advantageous if we write-off Bad and Doubtful

Debts as a process of Business operations within the

framework of Write-off policy adopted by the Board.

As per the provisions of Multi State Co-operative Societies

Act, 2002, the Board of Directors are empowered to frame

Policy of Write-off and is also empowered to write- off such

advances which are identified as Bad & Doubtful for

Recovery as per the Policy.

Considering increased volumes of Business and from the

point of view of Tax Planning and Balance Sheet

Management, the Board proposes to approve write-off of

Bad and Doubtful Debts from this Financial Year.

Dividend :

Your Board is pleased to recommend dividend @ 15% on

pro-rata basis for the F. Y. 2014-15 after ploughing back

sufficient profit for maintaining a healthy Capital Adequacy

Ratio and supporting future growth.

Appropriation of Profit for F.Y. 2014-15 :

To provide to the shareholders a true and fair value of

reserves, other funds and liabilities as on the date of Balance

Sheet, the Bank has given effect to the appropriation of

profits for the current year in the financial statements for the st

year ended 31 March, 2015 itself, subject to approval at the

Annual General Meeting. (Refer to Page No. 38)

Capital Adequacy :

As compared to last year the Capital to Risk Weighted

Assets Ratio (CRAR) has marginally reduced from 15.05%

to 14.96%. However, it is well above the minimum

requirement of 12% as stipulated by RBI. It is worth noting

that Tier I Capital contributes 76.25% to CRAR. Higher

percentage of Tier I Capital indicates that your bank is well

prepared to withstand with Basel I I or I I I

Recommendations, if made applicable to Urban Co-

operative Banks.

As per RBI guidelines, the Long Term Deposit fund

available for Tier II Capital has been reduced to ₹ 80 Crores

as against ₹ 100 Crores during previous year.

Expansion :

thI am proud to inform that your bank has crossed 100 branch

ndhistoric milestone as on 2 August, 2014 by opening branch

at Dhokali, Thane, at the auspicious hands of Mr. Nitin

Gadkari, Honorable Minister of Road Transport and

Highways and Shipping, Government of India. Your Board th

had strategically planned opening of 100 Branch in Thane

city. I am happy to mention that Thaneites have st

overwhelmingly responded with 1 day business figure

crossing ₹ 120 Crores which became the history in the

Banking World. On behalf of Board of Directors I express

my gratitude to all the stakeholders.

The network of the Bank has reached to total 110 branches.

During the F. Y. 2014-15, Bank has opened 19 branches in

all the regions viz., Thane, Pune, Gujrat, Karnatak, and Rest

of Maharashtra. The prevailing Extension counter at Narhe,

Pune has been converted to Branch.

The process of opening of 2 branches at Vapi (Gujarat) and

Sinnar (Nashik) is under progress and they will be

functional during F. Y. 2015-16.

Risk Management :

Managing and mitigating risk plays a crucial role in

achieving long term financial stability and success.

Banks are generally exposed to various risks such as Credit

risk, Market risk (which includes Liquidity risk and Price

risk) and Operational risk. The identification, measurement,

monitoring and management of risks accordingly remain a

44 th Annual Report

18

key focus area for the Bank.

The Bank has in place well defined credit policy with

explicit rules and instructions pertaining to grant of credit

which aims at following the sound lending practices.

The Bank places great emphasis on compliance with the

ongoing requirements as per RBI directives. The Bank has

put in place a set of best practices in risk management

appropriate to the size and business and the same are

reviewed from time to time by the Board of Directors.

Human Resource :

Human Resource is a function in organization designed to

maximize employee performance by developing their

personal and organizational skills, knowledge & abilities

through a set of systematic and planned activities like

Training & Development, Performance Appraisal System

etc.

Your Bank has taken various initiatives to empower its

employees with required knowledge and skills. These

initiatives include in-house and external training, e-

learning, development of standard operating systems etc.

Bank has started a new well equipped training centre in its

own premises at Deen Dayal Bhavan in Thane.

Bank organizes various training sessions for staff members

at all levels at Bank’s Training Centre. They are also

deputed on various training programmes, workshops &

seminars conducted by renowned organizations and

institutions in banking & financial sector. Bank has also

started E-Learning Module for the Junior Officers &

Trainee Officers which has enabled covering more

employees at a time. Also, employees have continuous

learning experience in various areas of banking.

During this year, 620 participants were trained in 55 training

programmes for 9443 man-hours. Different types of

training programmes were conducted such as Leadership

Development, Training for Security Guards, Customer

Service & Marketing, Credit Appraisal, Programme on

Information System Security & Audit, Programme on

Treasury Management, Programme on Computation of Net

worth and Calculation of CRAR for Officers of UCBs,

Programme on Foreign Exchange Risk Management,

Modelling for Operational Risk Management, Programme

on Leadership, Motivation and Team Building and many

more.

Bank effectively and strategically manages people in a

collaborative manner to boost retention, improve quality &

maximize the productivity of employees.

Technological Advancement :

Technology has changed the way people obtain financial

services by saving time and money by allowing people to

conduct banking efficiently and from anywhere.

Technology has helped banking transformation from bulk

paper and waste to paperless communication and means of

transferring funds.

We at TJSB are striving to get the true experience of

E Banking to our customers. We have the VISA & RUPAY

Debit Cards, IMPS Mobile Banking, E passbook and the

newly launched Internet Banking with Funds transfer. We

shall be launching the Utility payments module shortly

which will help our esteemed customers manage all their

bill payments.

Launching of the AADHAR based E-KYC norms for its

customers during F. Y. 2014-15 has helped in identifying a

customer through his AADHAR credentials in real time and

has made verification procedures simpler and faster. Bank

has also provided the facility of DBTL (Direct Benefit

Transfer of LPG) Subsidy to its customers.

Corporate Governance :

The Bank believes in ensuring transparency in financial

statements and protecting shareholders’ interest as the key

attributes of good Corporate Governance. Adherence to

44 th Annual Report

19

those attributes ensures transparency of banking

transactions and minimizes the chance of fraud and

malpractices.

The strategy is being executed within a sound governance

framework that seeks to balance the interests of all

stakeholders to ensure sustainable value creation.

Membership :

The total number of members of the Bank as on 31.03.2015

stood at 46777.

Appointment of Statutory Auditor :

The Board of Directors recommends to the General

Body, appointment of M/s. Gokhale & Sathe

Chartered Accountants for the financial year 2015 - 16.

M/s. Gokhale & Sathe have consented to be appointed

as Statutory Auditor. The resolutions for their

appointment will be moved under agenda item no. 4 of

the notice.

Corporate Social Responsibility :

TJSB acknowledges its social responsibility by donating a

part amount of its net profit to social organisations. Bank is

actively associated with socially relevant environmental

issues. Your Bank during F.Y. 2014-15 donated an amount

of ₹ 93.40 lacs to 63 social organizations.

Obituary :

We deeply mourn the death of Shri Prabhakar V. Kulkarni,

Ex-Director of the Bank and members of the bank,

customers and well wishers who passed away during the

year under report.

Acknowledgement :

I would like to thank all shareholders for the confidence

reposed in us and in supporting us to scale greater heights in

performance. Our growing customers add strength to our

growth and progress and I would like to express my

gratitude to them.

The Board is grateful to The Reserve Bank of India, Central

Registrar of Co-operative Societies New Delhi,

Commissioner of Co-operation and Registrar of Co-

operative Societies, Maharashtra State for their support and

guidance.

The Bank has been immensely benefited by the contribution

made by its Auditors, Legal advisors and correspondents

and I am grateful to all of them.

I would like to take this opportunity to thank my colleagues

on the Board for the valuable guidance, support and prudent

counsel.

On behalf of the Board of Directors, I would like to place on

record my deep sense of appreciation for the dedicated and

committed services made by all staff members for the

overall growth development and excellent performance of

the Bank in very challenging times.

On Behalf of Board of Directors

C. Nandagopal Menon

Chairman

09.05.2015

44 th Annual Report

sd/-

20

31 cee®e& 2015 DeKesjKe®e& 31 cee®e& 2014

Je<e& DeKesjerme31 cee®e& 2015

Je<e& DeKesjerme

1) þsJeerbJejerue

2) keÀpee&Jejerue J³eepe 19,15,76 13,77,91

3) veeskeÀj Jeiee&®ee Heieej, Yelles 61,53,22 50,16,87

4) keÀjej Ke®e& 1,80,21 1,20,77

5) DeeGÀì meesefme&bie Ke®e& 1,50,52 1,28,88

6) meb®eeuekeÀeb®es ceeveOeve 8,15 7,01

7) Yee[s, keÀj, efJecee Je Jeerpe 31,62,94 23,68,89

8) keÀe³eoe Je J³eeJemeeef³ekeÀ le%eeb®es MegukeÀ 2,28,53 1,45,25

9) ìHeeue, leej Je ìsefueHeÀesve Ke®e& 4,85,72 3,49,02

10) He´Jeeme Ke®e& 2,24,26 2,20,70

11) efnMesye leHeemeCeer MegukeÀ 1,68,68 1,48,75

12) ogjÀmleer Je osKeYeeue 5,54,82 5,65,16

13) ceeuecellesJejerue Iemeeje 16,03,17 15,16,90

14) leejCe He$eebJejerue keÀceer kesÀuesues DeefOecetu³e 2,59,10 3,13,32