World Bank Document - World Bank Group

256

;;;,-: , .: - . - :- - ~ ~ ~ ~ . - -- -: . , - .~~~~~~~~~~~~~~~~~~~~ . .. .- .:A , Economy - '~ ~ ~ ~ ~ ~ ~~~~~~C s. -- ~~~~- ~ ~ ~:- a~--- :-- K-aNzakOUstaR Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of World Bank Document - World Bank Group

;;;,-: , .: - .- :-- ~ ~ ~ ~ . - -- -: . , -

.~~~~~~~~~~~~~~~~~~~~ . .. .-

.:A , Economy

- '~ ~ ~ ~ ~ ~ ~~~~~~C

s. -- ~~~~- ~ ~ ~:-

a~--- :-- K-aNzakOUstaR

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

A W O R LD B ANK COUNTRY S TU DY

Kazakhs tanThe Transition to a MarketEconomy

The World BankWashington, D.C.

Copyright i 1993The Intemational Bank for Reconstructionand Developmen/TFHwoRLD BANK1818 H Street, N.W.Washington, D.C. 20433, USA.

All rights reservedManufactured in the United States of AmericaFirst printing August 1993

World Bank Country Studies are among the many reports orginally prepared for intemal useas part of the continuing analysis by the Bank of the economic and related conditions of itsdeveloping member countries and of its dialogues with the governmens. Some of the reports arepublished in this series with the Ieast possible delay for the use of govenments and theacademic, business and financial, and development communities. The typescript of this papertherefore has not been prepared in accordance with the procedures appropriate to formal printedtexts, and the World Bank accepts no responsibility for errors.

The World Bank does not guarantee the accuracy of the data included in this pub' cation andaccepts no responsibility whatsoever for any consequence of their use. Any maps that accompanythe text have been prepared solely for the convenience of readers; the designations andresentation of material in them do not imply the expression of any opinion whatsoever on the

part of the World Bank its affiliates, or its Board or member countries concerning the legal statusof any country, territory, city, or area or of the authorities thereof or concerning the delimitationof its boundaries or its national affiliation.

The material in tiis publication is copyrighted. Requests for permission to reproduce portionsof it should be sent to the Office of the Publisher at the address shown in the copyright noticeabove. The World Bank encourages deion of its work and will normally give permissionpromptly and, when the reproduction is for noncommerial purposes, without asking a fee.Permission to copy portions for classroom use is granted trough the Copyright ClearanceCenter, 27 Congress Street, Salem, Massachusetts 01970, U.SA

The complete backlist of publications from the World Bank is shown in the annual Index ofPublicatiom, which contains at alphabetical title list (with full orderng information) and indexesof subjects, authors, and countries and regions. The latest edition is available free of charge frmthe Distribution Unit, Office of the Publisher, The World Bank, 1818 H Street, N.W., Washingtonr,D.C. 20433, U.SA, or from Publications, The World Bank, 66, avenue d'lena, 75116 Paris, France.

FZN.: 0253-2123

Libray of Congress Cataloging-in-Publication Data

Kazakbstan: the transition to a marlket economy.p. ar. - (A World Bank country study, ISSN 0253-2123)

ISBN 0-8213-2644-91. Kazakhstan-Economic conditions. 2. Kazakhstan-Economic

policy. . Intemational Bank for Reconstruction and DevelopmentIL Series.HC420-5.K293 1993338.958'45'-dc2O : 93-32013

CP

Preface iii

PREFACE

Kaakbstan became a memter of dte World Bank on July 23, 1992. This report is basedon the work of two economic missions that visited Kazakhstan in January and April 1992 led by WafilkGrais and Chandrashekar Pant, respectively. The report was discussed with the authorities in October1992 and distributed to the first Consultative Group (CG) meedng for Kazakhstan, which took place onDecember 14, 1992. The staff that prepared this report wishes to thank the authorities in Kazakhstan fortheir excellent support and cooperation.

Country Economic Reports are prepared as part of the normal work of the Bank to meetseveral needs. They provide analysis relevant to the Bank's own lending activities. They are a usefulsource of information for other donors. Ih addition, the analyses and recommendations are an importantinput into the economic dialogue between officials of the country and Bank staff. The report is basedmainly on official data, but where necessary it draws upon independent estimates. Although statisticalmaterial has been prepared with care, the methods and concepts were not always familiar to Bank staff,and the data should be interpreted carefully. The judgements and recommendations in the report areentirely the responsibility of the Bank.

This report was put together by Isabel Guerrero, John Holsen and Keith Lloyd. The maineconomic mission included: Craig Andrews, Homayoon Ansari, Paul Apthorp. Mohinder Berry, JamesBond, Earl Brown, Lily Chu, Patrick Conway, Heinz Henlriks, Ann Ishee, Ernst Lauridsen, ThurvaraS. Nayar, Brian O'Connor, Barbara Ossowicka, Salem Ouahes, Joseph Saba, Ossi Rakhonen, MarcelScoffier, Inderjit Singh, Kuti Somel, Kalanidbi Subbarao, Alfredo Thome, Jacques Toureille, HasanTuluy, Jurgen Voegele. Other staff conibuting to the wrting of the report included Suzanne Barnes,Christina Leijonhufvud, Klaus Lorch, Michael Mills, and Michael Walton. The study was carried outunder the general supervision of Kadir Tanju Yurukoglu, Division Chief and Russell J. Cheedham,Director.

Since the report was distributed to the CG, many reform measures, addressing key areasdiscussed in this report, have been undertaken by the Government. A brief update on key developmentsin recent months is presented below, while the rest of the report remains as it was presented to the CGmeeting. The report therefore reflects the Bank's assessment of Kazakhstan's economy at the end of1992.

Important structural reforms that have been approved since this report was distributed tothe CG include: (i) the adoption by Parliament of a new Constitution in January 1993, which establishesthe legal basis for private ownership; (ii) the design and implementation of an ambitious privatizonprogram. By April 1993, approximately 10 percent of state assets had been privatized. The majority ofthese, were small-scale enterprises-in the trade and services sedors; (iii) the elimination of most legaland institutional barriers to private sector participation in trade and distribution; and (iv) the adoptionby Parliament of new statutes for the National Bank of the Republic of Kazakhs giving it increasedindependence, a law on banking activities and a new foreign currency law.

The Goverment of Kazakhsan has agreed to the elements of an initial stabilizationprogram, allowing Kazakhstan access to the use of the Systemic Transformation Facility with the IMF.The program was presented to and approved by the IM Board on July 23, 1993 and oovers a 12- monthperiod starting in July 1993. The program targets sharp reductions in the rate of inflation to sigle digitmonthly rates by the end of 1993, a contaction in the budget deficit (from 9 percent of GDP in 1992 to6 percent in 1993) and growth of broad money and domestic credit.

kV Abbreviations

GLOSSARY OF ABBREVIATIONS

ACU - Aid Coordination UnitAMC - Anti-Monopoly CommitteeBAC - Bank Advisory CommitteeBOP - Balance of PaymentsCBR - Centra Bank of RussiaCEE - Central and Eastern Europecs - Commonwealth of ndepennt StatesCMEA - Council for Mutual Economic AssistaCPI - Consumer Price IndexEBRD - European Bank for Reconstuction and Developm1tEC - Europem CommunityEA - Enviromental - AmmentERP - Economic Reform ProgramFDI - Foreig Direct InvstmFSU - Former Soviet UnionG-7 - Groutp of Seven ndustrial NationsGDP - Gross Domestic ProductGNP - Gross National ProductGoskmprda - State Committee for Enviromnental ProtectionGoskomstat - State Committee on StatisticsIBRD - Itenational Bank for Reconstruction and DevelopmentICSID - Intenational Centre for Settlement of lIvestment DisputesIDA - hiternational Development AssociationIFI - International Financial InstitionsIMF - Inteational Monetary FundPAE - Miistry of Foreign Ecnowmic RdationsMIGA - Multilateral Inetment Guaantee AgencyMOC - Ministry of CommunicationsMOH - Ministry of HealthMoU - Memorandum of Un ningNAFI - Natioal Agency to Foreign InvesumentNBK - National Bank of KazakhstanNMP - Net Material ProductNGO - NonGovemmental OrganizationOECD - Organization for Economic Cooperation and DevelopmePIP - Public Investment ProgramSB -Savings BankSOE - State Owned EntepriseSPC - State Property CommitteeTA - Technical AssistanceTCP - Tedcnical Cooperation Program-UNEP - United Nations Enviro nt ProgrammeUNICEF - United Nations Children's FundVAT - Value-Added TaxVPF - Voluntary Pension FundWHO - World Health OrganizationWI! - Wholesale Price Index

cunncy Euivaleas v

CUBENCY EOUIVALENTS

Currency Unit = ruble1 ruble = 100 kopecks

I SDR = USS 1.36855US$ I SDR 0.7307

Rubles per US Dollar

Official Ecba e Re(average)

1987 0.62381988 0.60801989 0.62741990 0.58561991 0.5819

MIFCE Rate (averan AIMYAuctiLnRt h

JamWr 1992 110 n.Febiay 1992 103 n.aMarch 1992 93 n.aApril 1992 100 n.a.May 1992 94 n.a.June 1992 90 138July 1992 143 155August 1992 168 164Setmber 1992 220 254October 1992 354 365November 1992 426 441December 1992 415 480Jamnzy 1993 484 S45February 1993 572 704March 1993 665 785April 1993 767 870May 1993 949 949

vi

CONTENTS

EXECUIJ sSUMMAtRY .......................... .. i

PART I: T1E FRAMEWORK 1.

CHAPER 1: Disintegration of the Union .3

CHiAPTElR 2: The Mlacroeconony ............................... ,.... 7Kazakhstan in Perspective . 7Recent Economic Performance . 10

CHAPITER 3: The Refom Program and the Medium Term Outlook . ......... 24The Reform Program: Stabilization and Strucural Adjustment . 24Economic Proepects. 28Extenal Trade Prospects .35The Major Risks .37Alternative Scenarios ......................................... 39

CHAPTER 4: Extenal Flancing and Debt Mna.me.. 41Kazakhstan's Estimated Extnal Financing Requirement .41Deferral and Rescheduling of Debt Service .47External Financing Overview .51Institutional Arrangements Aid Management and Coordination .52

Part U: THE AGENDA FOR STRUCTURAL REFORM

CHIAPTER 5: Establshing Competitive Markets and Facilitating Resource Mobility...... 54The Labor Market .54Microeconomic Functioning .61The Financial Market .62

CHAPTER 6: Private Sedor Development and Privazatin .69The Business Enviromnent of Private Sector Activity .69

CHAPIER 7: The Frmework for Social Protection .92The Social Safety Net ...... 92The Health Sector ........................................... 99

Part HI: THE TRANSFORMATION OF TEE REAL ECONOMY

CHAPTER 8: Energy and Aiing Sectors ............................... 106The Energy Sector .......................................... 106Mining and Metallurgy ................ 125

Contents vii

CAPrr= 9: Agriuen ....................................................... 130

CI1AP`TEI 14k The Infrastructure for Production ....... . . . ......................... . 144Transportation ............................................ 144Te leoo m m u nicatio ns ......................................... 147

CIAFIER 11: Environment .. d ....................... s........ 152The Environmt Prblems .................................... 152Sector Oraizon ........................................... 155

ANNEX 1: Transitional Trade & Payments Arrangemns ......... . . . . * . . . .... . 159

srATrISKCAAPPENDIX ....................... 179

MAP BRD

Tt Tables2.1 Kazakhstan: Mineral Endowmens and Energy Production .. 2.2 Kazakstan . 102.4 Indicators of Output and Exps, 1990.92. .122.5 Trends in Retail Prices and Wages, 1991-92 ........................ 132.6 Goverment Ffinncial Operations, 1988-91 .162.7 Central Govenment Fiscal Opemons in 1992.162.8 Montary Accounts for National Bank and Banking Systen .202.9 Balace of Payments Eimates for 1992.233.1 Kazakhstan Key Economic Projetio - Central Scenario. .284.1 Kazakhstan - Exrnal Fmancg R i nad Disbursemnts for 1993 .... 424.2 Medium-Ten Projections: Kazakhstan Extend Fanci Rq n,

Centrl Adjustmn Scenario, 1995, 1997, 1999 . 434.3 Katan - Projected Committments and Disbuenns for 1993 ..454.4 Medium-Term Projections: Kazakhstan Extemal Financing Requirements,

Low Case Scenario: Slower Reform d Delayed Investmen. .505.1 Changes in Employmet, 1988-92 .586.1 Size Structure of the StaEnteErpris Sector, End 1991 .756.2 The Structure of Industry ................ 7.................... 76.3 Privaizati and Corporadzion untl August 31, 1992 .807.1 Government Exnditrson Cash Benefits Kazakbstan and OECD Countries ... 937.3 Budget of the Pension Fund, 1992 .958.2 ProjectionsforEnergyCowsumpion .1138.3 Energy Trade Balance.1148.4 Energy Trade .1158.5 Kazakhstan Ener Prices. .1189.1 Selected Indicators in Agriculture, 1990.1329.2 Kazakbstan - Distibution and Productivity of Major Crops,

1987-1990 average .13........ . .. 3.9.3 Average Prpni edr costs in Agriculture, 1991 ...... ........... 136

viii

9.3 Average Prices and Direct Costs in Agriculture, 1991 . ................ 136A2. 1 Total and Intraregional Foreign Trade as a Percentage of GNP Former Soviet States,

Eastern Europe CMEA and EC Members ......................... 163

Text Fges4.1 Kastan, Potential Sources of Exteral Financing Requirements .... ....... 455.1 Total State Employment, 1980-92 ............................... 565.2 Non-state Employment 1980-92 ................................ 565.3 Sectoral Employment, 1980-92 ................................ 575.4 Real Wages, 1984-1992 ..................................... 575.5 U.S. in the Great Depression, 1927-1943 .......................... 596.1 Employees by Sector, 5f1992 ................................. 766.2 Book Value of Assets by Sector, 12/1991 .......................... 769.1 Overview of Agricultual Land ............................... 131

Text Boxes2.1 Deregulation of Prices ...................................... 143.1 Public Investment Progrm ................................... 354.1 Inter-republican Debt Agreements and the Current Payments Situation .... .... 465.1 Financial Sector Technical Assistane ............................ 686.1 Core Business Legislation as of 5/1992 ........................... 706.2 Support Services Needed by Private Industry ........................ 736.3 Priority Technical Assistance Needs for Private Sector Development, 1993 .... . 746.4 Methods of Privatization - Lessons from Intenational Experence .... ....... 786.5 Priority Technical Assistance Needs for Privatization and Restuturing, 1993 ... 917.1 Technical Assistance to Improve Social Protection .................... 997.2 Technical Assistance to the Health Sector in Kazakhstan ................ 1048.1 Kazakhstan Energy Sector Technical Assistance ..................... 1249.2 Areas of Technical Assistance ................................ 143

10.1 Main Technical Assistance Requirements in the Transportadon Sector .... ... 1472A.1 Different Types of State Trade ................................ 1652A.2 Interrepublic Oil Subsidies vs. Transfers ......................... 1682A.3 Export Tax vs. Export Licenses ................................ 1712A.4 The Ca for Moderate Transitional Tariffs ........................ 1742A.5 Clearing Unions vs. Payments Union ............................ 1752A.6 Customs Union vs. PTA ................................... 177

EXECUTIVE SUMMARY

Kazakhstan became the 163rd member of the Bank on July 23, 1992, seven months afterbecoming independent as a result of the dissolution of the former Soviet Union. It has a population of17 million inhabitants, and ranks second only to the Russian Federation in size, with 2.7 million squarekldometers. Covering a vast geographical area stretching from the Caspian Sea to China. Despite itslarge territory, Kaakhstan is a land-locked country which depends on its neighbors for access tointrnational markets. The country is endowed with rich natural resources, including oil, gas and non-ferrous metals

By 1993, real output in Kazakhstan will have most probably dropped by over 30 percentas compared to 1990; prices will have increased by over 20 times. The huge contraction in output hasbeen caused by factors mostly beyond Kazakhstan's control. The instability in the trade and paymenesmechanisms that has occurred with the disintegration of the Former Soviet Union (FSU), coupled withthe extem horizontal itegration of the productive sucture with the other republics, has led to apronounced slow down in inter-regional trade and economic activity. A severe drught in 1991, whichhas now ended, aggravated output decline. The massive adjustment in prices was partially a correctionof artificial micro distortions inherited from a price controlled economy, accenuated by the existence ofmonopolies. In addition, the breakdown of the former system of moneary control became a source ofinflation, as budget deficits in the FSU were moneized within the ruble zone.

The Govemment's immediate response to the crisis has been to emphasize stabilizafionefforts. Having chosen to remain within the ruble zone, it has implemented a strong contraction in creditin real terms. It has also implemented budget deficit reduction measures, in order to pardy compensatefor the elimination of the large transfers (9 percent of GDP in 1988-90) it used to receive from the Union.The Government has liberalized nearly all prices since January 1992, leaving only a small list of essentialgoods under price controls.

The top leadeship of the country is committed to a market-based and externally orienteddevelopment strategy, and has begum pursuing the dual objectives of economic stabilization and tiz designand implemenation of systemic reforms. The large output contraction and the unprecedented changesin relative prices, have exps more deep-seated pmblems relating to the structure of Kazakhstan'seconomy - a legacy of seventy years of central planning and a rigid command economy. Despite therapid progress in reform that the authorities have already made, the transition to a strong, market onentedeconomy is likely to take several years.

Although the agenda and the challenge of reform is enormous, the country has majoradvantages: significant oil and natural reserves that bave already attracted foreign investment,comparatively low debt ratios, and a reasonably well educated workforce. These advantages, coupledwith a leadership which is commited to a strong reform agenda, will probably result in a faster transitionthan that of the other republics of the FSU. Indeed, increased exploitaton of the oil reserves is expectedto underpin investm and output growth over the mid-to late 1990s. In addition, there are significantreserves of minerals, copper, lead, and gold. Furthermore, Kazakhstan is practically self sufficient infood. In per capita term, tis resourc endowment is even larger, since this is one of the most under-populated countries in the world. In the medium-term, foreign investment may bnng about substantialincreases in both exports and fiscal revenue, and the country is expected to have, maybe even substantial,terms of trade gains.

ii Executive Summary

Kakhstan has recently bcen at the forefront of foreign investment agreements in theFSU, following the announcent of three significant deals since the middle of the year. In May anagreement was finalized with Chevron to develop Kazakhstan's Tengiz oilfield, with recoverable reservesranking along side some of the bigger fields in Saudi Arabia. In June, British Gas and Agip wonexclusive negotiating rights to develop the Karachaganak field with 20 trillion cubic feet of gas and 2billion barrels of oil and condensate. The field is one of the biggest in the world, four times the size ofthe UR's largest gas field. Moreover, th-e estimates of oil reserves probably represent a minimum, basedon curent extraction technology. A third deal, concluded with a Turkish group involves developinganother large oil field in exchange for the construction of increased electricity production capacity.

In spite of its favorable resource endowment, the reasons to move ahead rapidly withsystemic reform are compelling. First, without systemic reforms airned at increasing the flexibility ofthe economy, the expansion in the oil and gas sector could result in the development of an "oil-eonomy"with stmctral dutch disease problems. The development of a broad export base, reduces the economy'svulnerability to large terms of trade shocks arising from fluctations in the intional mieral andcommodity prices. Second, the economic structure emergig from the systemic reform should ensurethat rents arising from natural resource exploitation are efficiendy reallocated. The example of some oil-produig counties vividly illustrates how resource surpluses may be wasted sustaining extraordinarilyiefficient state enterprise production that both fails to meet the short-run employment requirements ofthe pop;:!ation. and the long-run growth requimn of the economy.

A FEASIBLE SCENARIO

Prospects for output growth are low for the nex tbree to four years. Like many otherreforming former Eastern block economnies it will take some time to adjust to the huge relative price shiftsoccurring in the reform process and for resources to be mobilized towards areas of comparativeadvantage. Since resonrces need to be reallocated from a massive state enterprise sector to a new, muchsmaller private sector, even spectacular growth in the private sector is unlikely to compensate for thedecline in state enterprises in the short-term.

The strongest output response in UtD short run is expected to come from the energy sector.Industrial output is expected to decline by around 20 percent in real terms in 1993, given the restructuringneeds of the sector. Agricultural output may revert to downward trends in yields following the 1992reboud from the drought. It could decline by up to 5 percent in 1993 as traditional supply anddistribution channels are disrupted. Merchant trade in the scrvice sector, however, is epected to growin the short term and cushion some of the industrial output decline.

A marked acceleration of growth could come in the second half of the nineties from threesources. First, the country's natal resources specially minerals, oil and gas, could serve as a base forsustainable growth in both exports and fiscal revenues. Second, rapid growth could be generated throughthe privauization of small scale businesses, trade and commerce and the promotion of private sectordevelopment. Although the private sector is small, it could be an important source of growth for the laterpart of the decade. Third, moderate growth could be expected in agriculture provided reforms areimplemeited and no major droughts disrupt production.

Executive S&nmary iii

The construction of a new economic structure also involves the destruction of an oldsystem, wvhich will imply heavy dislocation costs in the transition. A substa decline in industry isinevitable and it should be phased over several years. This may bring about an initial rise inunemployment up to 10 or 20 percent of the labor force in 1993 and 1994, gradually decining therafter.Inflation should drop but is expected to remain high in 1993; any lower forecast would be unrealistic.Finally, the reform process will inevitably bring about a rise in inequality and poverty. An appropriatesafety net will be able to moderate the reduction in welfare of the most vunerable groups throughbudgetary transfers.

HOW TO ACHIEVE 1T?

Although the reform agenda is more extensive, this summary focusses on the most urgentmeasures that need to be undetake in dte next eighteen months. The Govemment of Kazakbstan facestwo critical issues: the stabilization of the economy and structural adjustment to provide the basis for arapid supply response in the productive sectors.

Structurl Reforms

An important element of the systemic reform program is the redeJfinion of the role ofthe Governmue. The Goverment has inherited a structre designed for a centrally planned economy,and moreover, one directed from Moscow rather than from Alma-Ata. The Government will need temanage a program that enis the progressive privatzation of virtually the entire productive econwmy,reasserting state property rights, re-ordering public expenditure priorities, maintaining essential services,and providing an acceptable social safety net. In addition, the Government needs to ensure that externalresources provided in support of the reform program are efficiently utilized and coordinated. This willinvolve building that capacity as well as linking the management of extnal assistance to econonmic policymaking and day-to-day management, and the development of a procurement capacity to ensure theefficient use of those resources.

The Govermnent faces the enornaiiis &Utige of putting in place a legalfwework thatis representative of the country's new philosophy and principles. While Parliament is to review a newconstitution this year, a number of laws have either, been passed (eg. privatization law) or, are in theprocess of being drafted. The emerging legal system will need to be coherent, and frame the enormoustransfonnation process that the country has embarked upon. Urgent legislation requring immediateattention to underpin and promote private sector activity are; (i) commercial codes and laws that recognizeprivate sector property, deregulate entry and ent, define bankruptcy procedures, and provide aframework for legal remedy in the event of contract failure; (ii) a banking law which provides the CentalBank with adequate control over the soundness of the fnancial sector; (iii) petroleum and mining lawsthat ensure an adequate common framework for all new exploration and developments, (some of whichhave already started); (iv) a legislative framework to promote privatization and com alion of theeconomy; and, (v) the amendment, of existing laws to clarify the regulation of foreign capital and profitflows. While the govenmment's objective of attracting foreign investment is commendable, special taxholidays or exemptions for foreign investor tha are not equally available to domestic investors shouldbe avoided. A stable binding legal framework and a consistent set of macro and micro economic policiesare more effective at attracting foreign investment compatible with the long-run growth objectives of aneconomy than fiscal incentives.

iv Executive Summary

Adoption of a coherent legal firamework is not sufficient. Without the appropriateinstiudonal sd-up for enforcement, the laws on paper have very litdte maning. It will be important torevamp the judicial system so that the new legislation underpinning the reform program can be enforced.Bankruptcy and contract laws are only effective when there is a court system which can litigate disputes.Similarly, adoption of commercial code and accounting standards are effective only when there aretrained and qualified accountn who can apply these sta.ndards in the corporate sector. Unless there areuniform accouning standards, the functioning of a stock market, one of the key elements in theprivatization process, will be in question.

In addition to the legal framework, the minimum requirements for an appropriateincentive system in the short run is the completion of price lTeralirai-n and the implemenation of atradefwnework where there are no quantitative restictions on exports nor imports. Less than completeeconomv-wide liberalization has the danger of creating distortions in relative prices which might affectthe short-term viability of certain activities which might otherwise have been profitable, or even have acomparative advantage. The Government's plans to liberalize all prices, wih the exception of rents,passenger transport, and some public utilities such as household heating and electricity does reflect anapproprite transitional response to current crmsances.

Correction of relative prices in the economy needs to be supported by trade reform andthe rationalization of the vast array of implicit and explicit subsidies and taxes in the existing system.These take the form of inteest rate and foreign exchange subsidies, extra-budgetary funds, andconsumption and input subsidies. The system needs to be rationalized with two objectives in mind: (i)a reduction in the waste of fiscal resources through targeting; and (ii) trsparency. Trade protectionshould be uniform and tramsparent. An import tariff in the range of 25 to 15 percent should be the maininstrment of protection.

Becase of political constraints, or development objectives, the Govermment wishes touse some subsidies to soften the social costs of adjustment. This should be done explicitly through thebudget, and not through the banking system or the foreign exhange market, and should be targeted atvery specific objectives. -Towards this end, the Goverinment has ak-eady moved to a one-rate foreignexchange market. Furthermore, positive real interest rates sbould be maintained, subsidies through thebanking system should be eliminated, and all extra-budgetary finids should be integrated into the budgetof the central government.

For the successful completion of price liberalization, state orders need to be elininated,including the elimination of import and export state orders. The market, not state order, should provideproducers and suppliers with the inputs they need, and consumers vith the flaai goods they demand.Experience with state orders has shown that they are likely to become a source of rents and corruptionand that they do not provide appropriate inceives to increase productivity. Government's ownprocenment of goods and services should be undertaken through competitive bidding and at marketpnces.

The overall succe3s of the refbrm program will depend on the country's ability tocounteract the inevitable output drop in industry with a positive supply response in other sectors of theecono-my. Three key sectors of the Kazakhstan economy will shape the nature of the supply response -energy and mining, agriculture, and restrctured industry sectors.

Executve Summary v

Across all sectors, the supply response will heavily depend on the removal of obstaclesto the development of the privatc sector. In 1991, the registration of a new business required ninedifferent signatures from govenal agencies, which was a daunting task Recent legislationeliminated many steps and fees, and suppressed bureaucratic inference. Nevertheless, registrationremains a lengthy task in several oblasts and Alma Ata. Chikent, by contast, has established anexensive data base and a one- stop model that has allowed over 3,500 registrations. The Chimkent modelshould be reviewed, strngthened, and used as a model for a country-wide registration system.Difficulties in access to physical space for business facilities, lack of competition, state domination ofdistibution structures, and lack of know-how on technology, management, finance, quality control, andmarketing are the oJier main obstacles to private sector development.

The rich e,er and mineral resources of the country are the largest source of potentialoutput and export growth. In this area, there are three supportive policy msum that need to beImplemented in the next eighteen monts. First is the need to increase domestic energy prices to their

true economic value. Although steps have been taken to raise energy prics during 1992, inflation hasoffset most of this increase, and domestic energy prices remain at only a fraction of world market pricingand domestic economic costs of supply. Energy consumption is also far too high m relation to economicoutput and must be reduced. Domestic oil pnces, wbich have been leading the energy pricig policyshould be raised to reflect the cost of interrpublican oil imports. At a minimum domestic oil pricesshould be incrased to 50% of equivalent world market prices by December 1992, and to 100% by March1994, and should not fall below domestic prices in Russia Second, it will be imortant for theGovernment to develop the capacity to coordinate the large foreign invesmet iflows into the oil sector,including ensuring the construction of an oil export pipeline with non-discriminatory access and stndardiernational tariffs. Third, it is importa that the Governmen establish a clear legal and regulatoryframework m the petoleun sector, and implement a profit based petroleum taxation system to widen theGovenmment's ta base in a neutral manner.

Although less dratic than enrgy, the supply response in aqicdtre could be veiyimportant. Kmkbstan is already self-sufficient in food. However, productivity and crop yields are lowand fertdlir utilizaon is excessive. While measures designed to increase productvity and reduceunnecessary fertili application may be expected to yield results over the longrW-te, sigificant short-run supply gains may still be achieved if famers are given approprate pnce and profit icentves. Thissupply response will not eventuate if increased ral retuns are absorbed by trading and distibuionmonopolies. It will be a dcallenge for the Govenment to manage the transition so that inefficiencies arerapidly eliminated while at the same time availabilty of food to the low income population is assured.As a first step towards achieving the desired supply response, state control should be immditlyreduced, production quotas should be eliminated, the private sector given commeril access to storage,distribution, and marketing activities and all producers both pnvate and state given equal access to inmputs,services, and financing. The second important measure is the eiminaton of input and output subsidies.A short to medium term program of phasing out subsidies should be implemented, with any remainingsubsidies going explicitly through the budget. The third crucial action is the privatization of land.

Some output and employment loss is inevitable in industry. However, rapid rss Aa cragand privatifion will speed the supply response and avoid unnecessay disruption. The eastern euopeanexperience shows that one of the biggest losses of reform have resulted frm the confused ownership andincentive system under which SOE's were operating. Early privatzaion and introduction of corporate

vi Executive Summary

govemance should avoid these type of unnecessary costs. In Septmber 1992, a joint World Bank,EBRD. and USAED mission working in close cooperation with the State Property Committee and variousother agencies proposed a detailed program of privatiaon in Kazakhstan

Under the proposed program pnvatizon would be cared out in three components.First, small isism would be auctioned off against cash and unused housing vouchers. Second, mostmedium and large enteprises would be sold against 'invesme points in a mass privatization programthe complexity of which is mduced through the central role of investment finds. Finally, most yv lagg.eerflMpjL (more than 5.000 employees) and special enterprises - natural monopolies and firms with non-commercial functions or exploitng non-renewable natural resources - would be sold on a case-by-casebasis, ohfen with prior sector studies, regultoy work, and some restrucring.

The early privaion of small scale enterprises can yield rapid benefits in terms ofimproved servie and availability of goods, and hence also popular support for economic reform. Theproposed approach reflects the successful implementation experiences of a growing number of cities inCzechoslovakia, Poland and Dow Russia. The enterprises would be liquidated and their business spacesold in open auctions; the equipment and inventory would then be offered to the winning bidder at pre-announced prices, or auctioned off separately for both cash and housing vouchers.

In order to avoid a crisis in the i diat futre and to support the supply response inthe- productive sectors the financial sector will need to be revamped. Ina te next eighteen months,implemention of policy measures in two areas are urgently required. First, stronger control over thefinancial system is needed if a financial crisis is to be avoided. Currenty, the Central Bank has litdecontrol over the banking system. Like m the rest of the FSU, most of the newly created banks are ownedby SOE's. High exosure levels to one client, or to the owner, are currenty impossible to control andbanks will not exercise prudent lending practices under these conditions. A more stringent legal andsupervisoxylregulatory framwork needs to be put in place as soon as possible in line with interationalnorms. Second, the Central Bank shodd mpose direct credit controls during the transition, while theinstitutional and finandal market fiamework is developed, before moving to a more indirect form ofmonetary control. Significant institutional sting and training will be required for both theNational Bank of Kmkhstan and commercial banks. Finally, privatization of banks should be phasedin gradually only after sound prdential regulations are in place.

Managing the Social of the Reform Program

Lauoe market policies need to ensure that dte lack of labor mobility does not generateunnessary frictional umployment duinng the transition to a new productive structure. Workers needto have full fireedom to move both between geograpbical locations and betweenjobs when enterprises areconfronted with employmen retrenchment. To allow this, the residence requirement to get a job("propisla") should be eliminatd as soon as possible. Housing policies, to both increase supply andencourage the development of a rental market, are also priority measures. Allowing the private sector intothe construion industry is another important measure which would generate employment.

Unemployment increases shoud be moderated through the management of copleymacro and trade policies. Altiough expected to subsially increase in the next two years, too largeunemployment would have high political and socidal costs and could jeopardize the attainability of fiscalstability. This constrint should be taken into account when designing the structure anspeed of trade

Executive Summary vii

reform: some activities might need some transitional protection during the next two years. In addition,to control inflation and avoid excessive unemployment over the next eighteen months there should bemoderation in benefit levels, and tax-based wage controls in the context of an overall incomes policy.

Adequate resources should be avaiablefor essentiad socia needs. The reform processis expected to lead in the short run to large increases in frictional unemployment; already the real valueof fixed incomes is falling as a result of continued inflation; and social services are beginnming to beundermined as a result of expenditure cutbacks. An adequate social safety net is, therefore, critical toensure that the vulnerable population is protected. Given the large number of households which will needto be covered and the scarcity of fiscal resources, targeig of social spending is particularly important.In Kazakbstan the most vulnerable groups identified so far are pensioners and large families. Theexperience in other countries shows that in times of adjustment there are additional groups which arevulnerable: the children and the unemployed. In order to identify the poor more accurately, it is necessaryto define a minimum consumption basket, further analyze existing data, and organize monitoring systems.

Although some resources will come from additional budget allocations, given the likelymagnitade of safety net requirements, some re-allocation of expenditures from existng social services willneed to be implemented. Savings may be adieved by protecting the pensions of only the lowest incomegroups against the worsening of inflation; tightening up eligibility requirmnets for receiving a pension;reducing unemployment benefits for certain kinds of beneficiaries (such as reentrants, or those that weretrained and are employed); and requiring employers to pay for at least the first 20 days of sick leave.The existing health system should be prevented from collapsing. In the very short-term foreign exchangeis needed to finance the imporaion of critical drugs and vaccines to avoid a health emergency.

The Macroeconomic Framework and External FIancing Req ents

All these strucural measures will not be effective if they are not undertaken within amacro framework which ensures the sustainability of the new system. Moreover, Kazakhstan has to takemeasures to adapt to the loss of the large transfers it was receiving from the union, both to the budgetand the balance of payments. The country will need financial support from the international communityin the initial transition. Otherwise, even sharper drops in output and consumption will take place,endangering the susainabiity of the reform program.

In the short term, Kazakbstan has only limited control over macroeconomicdevelopments. As long as it remains in the ruble zone, monetary and exchange rate policies will dependon the policies of the Cetral Bank of Russia. Theoretically, clear rles could be adopted that wouldenable credit policy within the zone to fumntion effectively. However, this is far from being achieved atthe moment. This has increased the incentives to enter into barter arrangements, increase inter-enterprisearrears, and turn to other means of non-monetary financing. This further erodes the National Bank ofKazakhstan's control over the monetary and banking system. Furthermore, within a non-regulated rublezone dtere is little incentive to attain lower budget deficits than other countries in the zone.

If monetary instability confinues in the rest of the ruble zone, and in particular, in Russia,Kazakhstan will need to consider the negative impact this will have on their attempts to stabilize over thenext 18 months to two years. Given the importance of long-run p:ice stability, the authorities may needto consider establishing their own currency as a means of regaining monetary control, and achieving pricestabilization. If, because of inflationary expectations and speculative demand, the exchange rate continues

viii Executive Summary

to seriolusly undervalue the ruble, then the otherwise desirable open economic policies could lead tosubstantial imported inflation. The principal benefit of a separate national currency is the ability topursue an independent monetary and exchange rate policy, and thus have direct influence over thenational inflation rate.

Currency reform, however, would only be effective if it is accompanied by appropriatelyfirm macroeconomic policies that help build confidence in the new currency and stabilize its value.First, the goverrnent would need to maintain appropriate control over fiscal policy. Continued fiscaladjustment and restraint would be critical to the overall success of the stabilization and reform program.The government would therefore need to focus on linmiting budgetary deficit financing from the monetarysystem to a level consistent with achieving the inflationary control objectives. Confidence would bediminished, and the value of the new currency eroded if the government finances budget deficits byprinting money- This could potentially lead to capital flight out of the new currency back into the ruble-

Secondly, monetary policy would need to focus on reducing inflation. Therefore it shouldbe designed to limit the expansion of net domestic credit to a rate consistent with a convergence ofKazakhstan's rate of inflation over time to that prevailing internationally. Interest rate policy would needto be consistent with exchange rate policy under either a fixed or flexible exchange rate regime. Fiscalpolicy would need to be controlled tightly in order to support the new currency and avoid the need forinflationary financing. For post-currency reform credibility, it would be important that priceliberalization, the removal of subsidies, and other relative price adjustments be nearly complete by thetime of the introduction of the new currency. If not, the job of monetary policy would be much moredifficult in the presence oi future adverse price adjustments. Furthermore, it would be extremelyimportant that the National Bank has the technical ability to successfully operatz monetary policy withthe new currency. In particular, it would be essential that the National Bank possess the skills andinstruments necessary to analyze economic developments, formulate appropriate monetary policies, andimplement them.

The medium-term outlook for the economy of Kazakbstan depends critically on thesuccess of the stabilization and systemic reforn program, and on the support of the international financialcommunity. If the key elements of the reform program begin to take root, the decline in output may berestricted to 5-7 percent in 1993, after a decline of around 14 percent in 1992. To achieve this, however,significant amounts of external assistance need to be mobilized over the next eighteen months, since thecurrent account deficits corresponding to these levels of activity are estimated at around US$950 andUS$890 million for 1992 and 1993 respectively.

First, the technical assistance requirements to implement these reforms are large. Thetransformation of institutions from the old Soviet system to a system compatible with a market-basedeconomy will require a massive restructuring of the political and institutional framework. Newinstitutions and functions that did not exist under the old system will have to be created. A significantelement of the technical assistance will need to take the form of training. Specific needs are addressedin each of the chapters of this report. Second, balance of payments financing will be crucial to arrestfurther declines in output and consumption. Imports are required not only to complement limiteddomestic supplies, but also to ensure that inputs and intermediate goods for domestic production areavailable. Third, projectfinancing wil be needed for import requirements of cntical investment projectsin basic infastucture and public services. Investment requirements in the oil sector, in particular, willbe relatively large in the next few years in order to develop new oil and gas fields and to ensure that

Executive Summary ix

sufficient export pipeline capacity exists to transport the new production. There is a large scope for directforeign investment in these areas. The telecommunication agency has very little resources available forthe capital development required to support the desired economic growth. Capacity utilization ofavailable lines is extremely high (98 percent) and the average age of the network is 25 years. Inagriculture, projects supporting decentralization of agricultural marketing and input distribution,rehabilitation of irrigation systems, and research and extension to support land privatization will alsorequire large external assistance.

The external financing requirements, including Kazakhstan's debt service obligations forits share of the external debt of the FSU, reserve build-up and clearing of arrears, are estimated atbetween US$2.2 and US$2.4 billion in 1993, and is expected to be between US$1.7 and US$2.0 billionin 1995. Whether or not FSU debt repayments are deferred, the interational financial community,including multilaterals, will need to finance between US$l.5 and US$1.7 billion in 1993.

Mobilizing these levels of external resources will reqiire a major effort on the part of theGovernment, the Il's and the donor community, including possibly debt relief. The role of directforeign investment, estimated to rise from between US$380 and US$580 million a year in 1993 to justunder a billion in 1995, will be particularly important in the energy sector. However, foreign directinvestment will not be en important source of net inflows in the short run (large imports are associatedwith these flows), unless it is used for purchasing assets that are being privatized. The remainderfinacing of the gap will need to come from multilateral sources, bilateral programs, export creditagencies, and commercial creditors. Technical assistance requirements, estimated at $60 million - $70million a year are expected to be mostly met with grant type financing. Some concessionality, forbalance of payments and project financing, should be secured at least for the initial years of the transition.

The medium-tern creditworthiness of Kazakhstan depends on both the success of theoverall reform program and a timely increase in oil exports - The Government of Kazakhstan w1il needto develop a track record of unwavering reform effort. Moreover, if existing energy sector developmentsoccur as envisaged, the additional oil exports should be capable of financing Kazakhstan's developmentin the medum-term. The Government of Kazakbstan must therefore manage this process carefully, andensure that existing commitments made to joint-venture partners are met, within budget and on time. ForKazakbstan's full potential to be reached, the international financial community will need to provideconcessional support in the short-term. This will underpin the adjustment program and provide criticalsupport during the difficult early stages of transition. With international support in the initial stages,Kazakhstan has a real possibility of moving to a sustainable growth path which does not require on-goingextemal financial assistance.

Kazakhstan's inidal stock of extermal debt, which corresponds in around 30 to 45 percentof GDP, is comparatively low by international standards. With principal debt deferral over the periodto in 1995, the debt service ratio is expected to remain under 15 percent. Provided that new oilproduction can be brought on stream for export over the next three to four years, Kazakhstan's foreignexchange earning capacity is expected to be sufficient to meet future debt servicing obligations arisingfrom the financing of the projected external gaps. If Kakhstan agrees with Russia to exchange its claimon FSU foreign assets for its share of FSU debt (and obligations), then Kazakhstan's creditworthiness willbe significantly improved, and the economy would be able to sustain a higher level of imports over thetransition period.

x Executive Summary

Condcsion

Failure to resolve outstanding issues on the ground rules and operation of the ruble zone,lack of solution to the collapse of the inter-republican payments system, slow progress on structural andinstitional reform, slippage on the fiscal front, restricted access to foreign exchange and the inabilityto bring to fruition plamned investments in the energy sector, would jeopardize the success of the reformprogram. The success of the program also hinges upon the building up of the institutional capacity toimplement it.

The dual challenge of stabilization and structural reform that Kazakstan, along with theother FSU countries, is facing is historically unprecedented. The Govermment has moved decisively andadopted an ambitious program to achieve both objectives. As output and consumption contracts, therewill be pressures to move away from the fiscal austerity dtat stabilization requires. Further pressure toderail the refonr program will come from those who have a vested interest in maintaing the status quo.It is critical to maintain the political support and the momentam of the reform program. Populistspending policies to address discontent are likely to destabilize the economy and breed uncertainty. Thepath that the Goverment has embarked on has a lot of rislk, yet the most critical risk is to waver.

PART I

THE FRAMEWORK

Part I of the report discusses the political and macroeconomic conditions under whicheconomic reform in Kazakhstan has begun (chapters I and 2), and then considers the adjustment path andexterial financing requirements of the economy over the medium term (chapters 3 cnd 4).

Although the existing economic structure, which is orientated toward the supply of rawmaterials and intermediate goods, will make adjustment to market conditions a much less painfulexperience for Kazakhstan than for other former Soviet Union (FSU) countries, macroeconomicstabilization and extensive structural reform are essential if Kazakhstan is to adjust quickly to the realitiesof a market economy. The dissolution of the Union has come at some cost for Kazakhstan, as it hasdisrupted pre-existing trade within the FSU and has cut off fiscal support from the center. Priceliberalization has accentuated the existence of monopolies in the short run, and the ruble zonearrangements have heightened the need for fiscal discipline. The medium-term outlook may be promnisingif the reform program can be implemented successfully, and Kazakhstan is able to develop its rich energyand mineral resources. Adjustment will not be easy, and Kazakhstan will need the assistance of theinternational financial community over the next three to four years to smooth its transition to a marketeconomy.

CHAPTER 1

THE DISINTEGRATION OF THE UNION'

In December 1990, the International Monetary Fund (IMF), the World Bank, theOrganization for Economic Cooperation and Development (OECD), and the European Bank forReconstruction Development (EBRD) published The Economy of the USSR: Summary andRecommendations. This study (known as the Joint Study of the Soviet Economy, or JSSE) made specificreconmuendations for economic reform in the USSR and suggested a framework within which Westernassistance could be rendered; it was the first comprehensive study of the USSR economy in which theWorld Bank participated. Yet the timing of the JSSE coincided with the beginnings of a dual system ofgovernment authority, and, consequently, with divergent tracks of economic reform. This chapteroutlines the political sources of that divergence and its ultimate impact on the economic reform processin the Soviet Union from mid-1990 to the end of 1991.

Hopes for a single reform. process in the Soviet Union could not be sustained muchbeyond mid-1990. The first democratic competitive elections at local and republican levels ofGovermnent in the Soviet Union were held in March 1990. While the openness of the elections did notprevent communists from gaining a majority of seats in many institutions (as they had in the March 1989elections to the Union legislature), the 12-month time lag between the Union and republican-levelelections led to a situation in which most republican legislatures were significantly more reformist thanthe Union Supreme Soviet. This in turn meant that the more committed refonners conceived theirpolicies and programs in a republican, rather than a Union, context. Thus, while it was not necessarilyeven the reforners' original intention to dismantle the Union, the republican structure in which thesereformers were operating conflicted with the imperatives driving the Union Government to maintain itsinstruments of power for the very purpose of conducting reforms. The eventual emergence of multiple'tracks" of reform was inevitable.

Thus by September 1990 two competing programs were under active discussion: theUnion "Ryzhkov" Plan (named after the Union Prime Minister at the time, Nikolai Ryzhkov), and the"Shatalin" Plan (named after its primary author, Academician Stanislav Shatalin). The Shatalin Plan wasin many ways a challenge from the Russian leadership to the Union authorities' claim to be the arbitersof economic reformn. Although its authors were drawn from both the Union (President's) and Russian(President's) groups of advisers, the plan had initially been presented to the Russian Supreme Sovietrather than the Union Supreme Soviet. The Ryzhkov Plan, formulated shortly thereafter, was the Union'sresponse to that challenge.

Not unexpectedly, the Shatalin Plan gave greater freedom of decision making to therepublics, and in many ways was more radical than the Ry-Nrkov Plan. The Shatalin Plan was also calledthe "500-Day Plan" because it envisaged a very specific timetable of reforms-particularly regardingprivatization and price liberalization. It also assigned primary taxing authority to the republics, with theUnion budget to be funded through negotiated shares of the republic budgets. The Ryzhkov Plan, bycontrast, advocated a slower pace of reforms and did not cede significant powers to the republics.

This chapter is taken frinm World Bank, Russian Econonzc Refonn, World Bank Country Study, 1992, Chapter 1.

4 Chapter 1

The so-called Presidential Guidelines issued in the fall of 1990 represented the fairlynarrow field of consensus between these two programs. That consensus, however, was limited to somegeneralized goals and failed to specify a timetable for achieving these goals. In p-ticular, the Guidelinesgranted republics considerable freedom over the pace of reform and the formation of republican fiscalpolicies-without political agreement as to how or whether republican actions could be limited when suchactions threatened the Union reform program. Meanwhile, the economic situation in 1990 had beenmarked by strikes, inter-ethnic strife, the collapse of the Union-wide market owing to the raising ofrepublican and even local barriers to trade, and a breakdown of the system of state orders. As the partyapparatus-the core mechanism of informal coordination and management in a planned economy-beganto be deliberately weaned from its central role in the economy, the inflexibility within the Soviet economybecame apparent through the first decline in output in the peacetime history of the Soviet Union.

Significantly, none of the alternative recommendations for economic reform advocatedfinding a "third way,' or a "controlled market," as a solution to the USSR's economic ills. The RyzhkovPlan, the Shatalin Plan, and the Presidential Guidelines differed, not on the need to achieve financialstabilization, price reform, or privatization, but on the ways in which (and at what pace) these goalswould be achieved. Although the JSSE was critical of the gradual pace of reform envisaged in thePresidential Guidelines, it recognized the fact that the Guidelines did not seek a half-way approach toreform. As it tumed out, however, the critical difference between the Shatalin and Ryzhkov programswas that the Shatalin Plan proposed to resolve the general govermnent deficit by curtailing the Union'sindependent revenue-raising capacities while the Ryzhkov Plan foresaw no such devolution of fiscalcontrol. It was a difference that the Presidential Guidelines could not bridge, and this failure eventuallymanifested itself in the bankruptcy of the Union budget. Moreover, the Guidelines could not reconcilethe allocation of fiscal revenues and responsibilities between the Union and the republics-not so muchbecause such a compromise was economically infeasible, but because the center's political power andauthority to resolve that contradiction and enforce an effective compromise was being continuously erodedin 1990 and 1991.

By the latter half of 1990, republican unrest had increased considerably, and PresidentMikhail Gorbachev was widely viewed as being susceptible to increased pressure from conservatives.The crackdown in the Baltics confirmed these suspicions and served to flrther fuel separatist tendencies.In tune with these political and military measures, the economic policies of the Government took aconservative turn; in October 1990 the Govermnent decreed that all enterprise ties were to be frozen, andin January 1991 the Government authorized police and state security agencies to investigate businessesfor violations of state laws and regulations.

Thus, even as some of the objectives outlined in the Presidential Guidelines of 1990 werepassed as laws in t991, general economic, political, and legal disarray precluded their implementation.Economic relations between the Union and the republics for 1991 had been agreed upon in April 1990(and confirmed in January 1991), but the republics avoided implementation of the law by signing treatiesand economic cooperation agreements with each other anc by withholding tax revenues due to the Unionbudget. A so-called War of Laws began in which republican authorities began drafting and enactinglegislation in areas which were also the subject of Union legislation. In Russia, the same Shamalin Planthat had ultimately been rejected by the Union legislature had been approved by the republican legislature.Of greater consequence was the fact that the tax laws of the Union began to be defied as the Russianrepublic began issuing independent republican tax regulations. For example, the Union tax lawestablished a profit tax rate of 45 percent, but the Russian Federation offered enterprises a 38 percent

The Disintegration of the Union 5

rate. In the process the Russian Federation also undertook to retain a greater share of that tax than hadbeen agreed to with the Union in 1990. By 1991 it was clear that the republics' blatant disregard of theUnion's attempts to achieve macroeconomic stability had the`r basis in political desires for independencerather than in any differences of economic thinking.

By April 1991 the Union budget had already reached the projected deficit lvel for thewhole year, and was, in practice, bankrupt. The "Anti-Crisis" program, based on the agreement of ninerepublics, sought "the unconditional fulfillment [of obligations of Union bodies and republics outlined inthe economic agreement of 1991] primarily as regards budgets and the formation of extra-budgetaryfunds." It also sought to carry out a tough anti-inflationary monetary policy, to further liberalize prices,to take various measures to halt output drop. and to secure the social safety net. Although in some casesthe program made expedient concessions to political pressures-such as its willingness to consider wageindexation-this program was understood to be necessary to sustain economic reform, politically as wellas economically. The agreement of the nine republics could nu: be sustained; the "Anti-Crisis" programwas almost immediately preempted by other arrangements arrived at in the course of negotiations towarda Union Treaty between April and August of 1991.

Thus, by the spring of 1991, a crisis of governance began to supersede the economicreform program in the Soviet Union. There was no clear authority left in the Union to implement anyprogram of reform, however promising. One of the last Union plans for economic reform was drawnup in May 1991-the "Window of Opportunity,' better known as the Aliison-Yavlinsky Plan, after itsmam authors, Graham Allison and Grigory Yavlinsky. This program acknowledged the crisis ingovernance by positing that political restabilization was a prerequisite to economic reform. To that endit recognized the impossibility of achieving economic reform without the explicit consent of republicanauthorities; it proposed basing economic reform on a "Nine-Plus-One" agreement, and incorporated thesigning of a Union Treaty and the adoption of a new constitution as an integral part of an economicreform program. In addition, it detailed stages and scales of Western economic assistance to the Union.The drawback, nf course, was that the plan proposed to delay many economic reforms until after thestabilization of a new political union.

The very process of drafting a new political basis for the Union consolidated theopposition of the conservative forces. The opposition's coup attempt of August 1991 succeeded indestroying the very thing the coup had set out to preserve-the Union. The political authority of theUnion and of President Gorbachev himself were seriously undermined by the coup; in tum, only BorisYeltsin, who had been elected to the newly created presidency of the Russian republic two months earlier,emerged as the defender of democracy and the Russian republic. The two-mont hiatus that followed wasmarked by enfeeoled union Treaty negotiations and some puzzling inactivity on the part of the Russianleadership. While the Russian republic continued its policy of bankrupting the Union Government, theleadership did not appear as opposed to the Union Treaty as was the Republic of Ukraine.

In November 1991, the Russian leadership announced the appointment of a newGovernment, and oudined its commitment to radical economic reforn. The program included: (i) priceand wage liberalization by end-1991; (ii) commitment to a tight monetary policy, fiscal reform, and rublestabilization; (iii) privatization of up to 50 percent of all small- and medium-size enterprises within threemonths; (iv) the halting of the funding of defense, foreign economic aid, and 73 all-Union ministries andcommittees; (v) the supplementing of the social safety net; and (vi) a qualified commitment to an inter-republic Central Bank. Of these objectives, only the fourth was implemented without delay, thus

6 Chapter 1

completing the process of extending Russian Govermnent control over Union government functionsdtrough their forced dependence on the Russian Government for funds.

The Soviet Union was declared dissolved on December 8 by the signatories to the MinskAccord (Belarus, Ukraine, and Russia). The dissolution was finalized upon the resignation of Gorbachevas President of the USSR on December 25, 1991.

CHAPTER 2

THE MACROECONOMY

KAZAHSTAN IN PERSPECTIVE

Kazakhstan's Parliament declared independence on December 16, 1991. PresidentNursultan Nazarbayev was re-elected President of the Republic as a result of the general ballotpresidential elections. The current Parliament, whose term expires in 1994, is preparing a newconstitution for the republic. The President publicly endorsed the Government's intention to design andimplement a refonn program in order to transforn the economy of Kazakhstan into a market-basedsystem. Since independence, the President and the Government have been strong proponents of theprinciple of maintaining economic ties with the other republics of the former Soviet Union (FSU).Kazakhstan applied for membership in the IMF and the World Bank Group in January 1992, and becamea member of the IMF, IBRD, IDA, MIGA, and ICSID in July 1992.

The first part of this chapter provides a brief overview of Kazakchstan: its people,geography, and economic character. The latter part provides an assessment of macroeconomicdevelopments during 1991 and 1992.

Geography and Demography

Kazakhstan has the second largest land mass in the FSU. With a 1991 population of 16.7million, or 6.1 per square kilometer, it is one of the most sparsely populated regions in the world. Thisrelatively small population lives on a proportionately large share of FSU arable land, as wel' as on largeendowments of precious minerals. Its landmass is five times that of France, but with only one-third ofF*rance's population.

This land is full of contrasts: fertile valleys border on dry and barren endless steppes.There are high mountains and depths that reach below sea level. The climate is sharply continental withthe difference between the coldest and the hottest day of the year at times reaching 162 degreesFahrenheit.

The largest ethnic group, the Kazakhs, draws roots from the Mongols, who conqueredthese lands in the thirteenth century and mixed with the various local tribes of nomads. Before theOctober 1917 revolution, the Kazakhs were nomads. Animal husbandry was their main occupation.There were neither schools nor books, since the Kazakhs did not have a written language of their own.Today, more than a hundred nationalities live in Kazakhstan. Kazakhs and Slavs constitute the two mostimportant ethnic groups. Significant German and Korean conununities are setded in the Republic as well.Currently Kazakhs rTepresent slightly more than 40 percent of the population and Russians slightly lessthan 40 percent with the remaining 20 percent distributed over the other nationalities.

The country borders Turkinenistan, Uzbeldstan, and Kyrgyzstan in the south, and isbounded by the Volga River, the Ural Mountains and the west Siberian regions of Russia in the north.Kazakbstan has a common border in the east with the Xinjiang Province of China and reaches as far westas the Caspian Sea.

8 Chapter 2

Economic Structre

Kazakhstan is richly endowed with natural resources. It is an important producer of gold,iron ore, and coal, copper, chrome, wolfram, and zinc. Although Kazakhstan has only 6 percent of theFSU total population, it has 90 percent of the total reserves of chromium, and close to half of the totalreserves of lead, wolfram, copper, and zinc. It has about r percent of the FSU iron ore reserves (Table2.1). In 1989 it produced about one-fifth of the FSU gold and coal. Other mineral resources found inexploitable amounts within the economy are oil, natuiral gas, nickel, titanium, tungsten, molybdenum,lead, zinc, manganese, and aluminum.

The countryTable 2.1: KAZAKESTAN: MINERAL ENDOWMENTS AND is a producer and net

ENERGY PRODUCTION exporter of oil and gas..__ __ ___ __ __ ___ __ ___ __ __ ___ __ ___ __ _ Recoverable oil reserves are

Cenual estimated at 12 billionAsian KAZ/ barrels. The current level of

Kazakhstan Republics* Russia FSU production is 470,000

Gold Production 69.0 43 344 20% bbl/day. Kazakhstan ranks(Metric Tons, 1980) second in oil production after

Russia. Although it accountsIon Ore Reserves 7.6 0 45.5 17.5% for only 6 percent of FSU(billion r-ons, 1990) production, its petroleum

OR Producuion 1989 34.0 6 607 6% potential is considered(mil. metric tons. 1989) exceptional by the

Natural Gas, 1989 7.0 131 796 1% international petroleum(billion cubic meters) industry. Production isCoal, 1989 130 18 740 19% located in the westem part ofCnilion m. tons) the republic while most of its

population and the two* Kyrghyzstan, Tadjikistan, Turkmenismn, and Uzbekisrn largest refineries are located

in the eastern part. Themajority of the country's production is, therefore, exported to western Russia, while crude oil for itsrefineries is imported from central Siberia. Much higher production levels are expected as newsupergiant oil fields are brought on stream by international petroleum companies.

Industry which accounted for about 40 percent of GDP in 1991, it is dominated by miningand processing activities, largely geared to exploiting the rich natural resource base. There are processingplants for both ferrous and nonferrous metals, especially in the northern and eastern sections of theeconomy close to the mineral deposits. Local industries produce heavy machinery and tools. Refineriesand petrochemical plants also take advantage of the existing hydrocarbon resources. Besides theseindustries, Kazakhstan has a variety of agro-processing industries, including meat and fish canneries,wineries, and footwear and textile manufacture.

The Temirtau Karaganda Metallurgical Combine, which operates a number of blastfirnaces and steel mills, is the republic's largest industrial enterprise in terms of output value. In 1989it had 28,200 employees and its output was valued at over US$2.0 billion. In terms of number ofworkers, however, it is much smaller than the Karaganda Ugol anthracite coal mines (with 65,200

The Macroeconomy 9

workers). There are five other large enterprises, each with more than 10,000 workers, in mining andminerals (copper, lead, zinc, iron ore, and coal). In the machinery and equipment subsector, the largestsingle enterprise is the Paviodar Tractor Works (20,000 employees and a 1989 output valued at close toUS$1.0 billion).

Kazakhstan has about 20 percent of the arable land of the FSU. This vast area supportsa wide variety of rainfed and irrigated agriculture and the country is a significant producer and exporterof agricultural products. Livestock husbandry is the traditional industry of the indigenous population,based on the extensive opportunities for grazing. Agricultural production constituted about 34 percentof GDP in 1991. The most important agricultural products include wheat, maize for fodder, livestockproducts, cotton, and wool. Agro-industries exploit the production of cotton and sugar beets in the southas well as the fruits and vegetables grown throughout the economy.

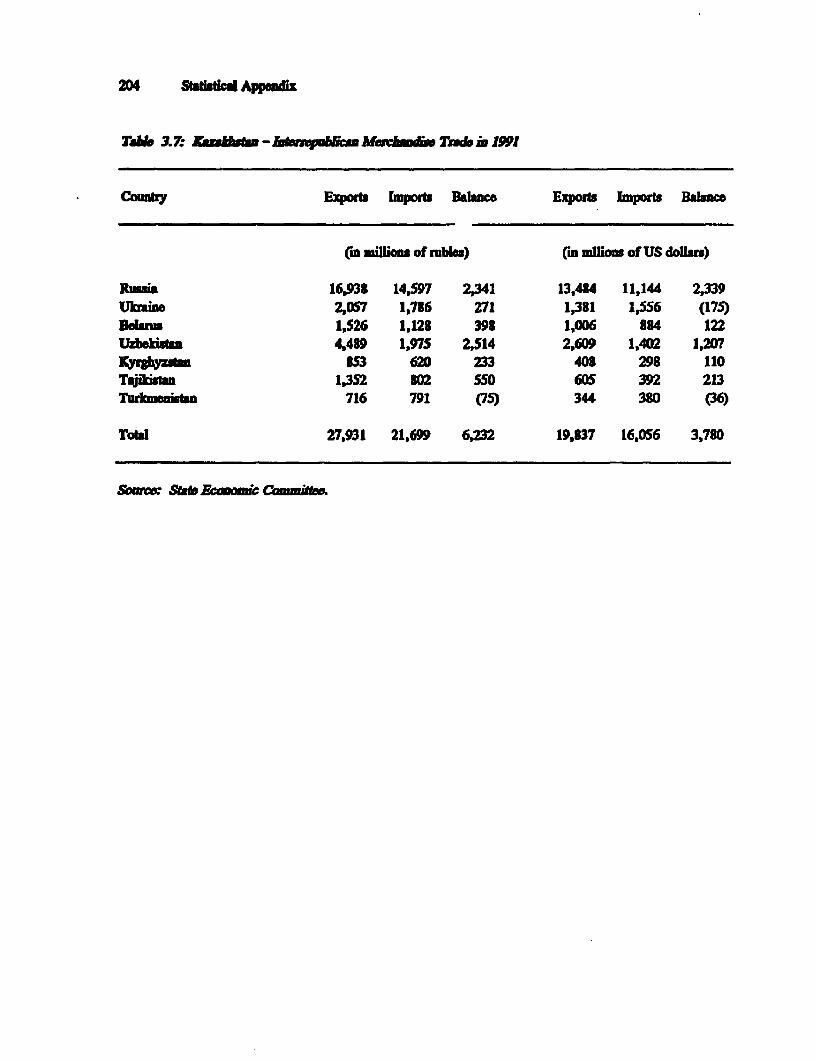

As with other FSU republics, Kazakhstan's economy is closely linked with the economiesof other FSU republics, especially Russia. Exports to Russia comprised about 60 percent of total exports,while imports from Russia accounted for over two-thirds of total imports in the late 1980s. About lbpercent of exports, and 12 percent of imnports, were to countries outside the Commonwealth ofIndependent States (CIS) in 1991. China has been the largest of these trading partners, followed by someEastern European countries.

The traditionally close economic ties with other FSU republics is reflected in therepublic's infrastructure, which is largely geared to serving the economy of the CIS without regard torepublican borders. The transmission/distribution networks for electricity in the north and south ofKazakhstan are not connected for exchanging electric energy, although the southern network is connectedto the Russian grid and the northern network to the grid of the southern republics. The transport andcommunications system connects Kazakbstan with Russia, rather than with points within Kazakhstan.

Kazakhstan within the FSU in the 1980s

Kazakhstan's NM growth rate during 1986-89 averaged 1.9 percent per annum, lowerthan that for Russia and lower than the average for the Central Asian Republics (Table 2.2).Kazakhstan's per capita NMP grew at 0.9 percent during 1986-89, compared with an average of 1.8percent during 1971-85.

As can be suggested by its relatively constant share of total FSU population and economicactivity, Kazakhstan's economic structure changed little during the 1980s (Table 2.3). Citizens receivedincome and amenities that were about average for the Soviet Union. although slightly below those ofRussia. The comparable wages for Russians were 1.052, 1.059, and 1.08 of the Union average in 1980,1985 and 1990 respectively. The corresponding wages and amenities for citizens of the Central AsianRepublics were less than those for Kazakhstan. The average monthly wages for Uzbekistan, for example,were 0.92, 0.86 and 0.78 of the Union average for the respective three years.

Social indicators are high by Western standards and compared with the rest of CentralAsia. However, they are slightly lower than the average for the FSU (Tab,- 2.2). Infant mortality is

10 Chapter 2

26 per 1,000, lower than in Europe (30per 1,000), but higher than in Russia Table 2.2 KAZAKISTANa n d t h e _FSU'. Life expectancy is 69 years, CARwhich is similar to the average in upper Kazakhstan & KAZ. Russia FSUmiddle income countries, is higher thanEast Asia, and is one year lower tan in hvesmenrt/GDP (1989) 29% 26% 30% tr305)Russia and the FSU. Adult literacy is Average growth (198-89) 1.9% 2.8% 2.5% 2.7%comparable with that in economies with Populaton Growth (197949) 1.2 2.4 0.7 0.9per capita GDP above US$6,000 in Infan Mortality (per 1000)1988. (1989) 25.9 38.7 17.8 22.7

Uft Expectancy (years. 1989) 68.7 68.2 69.6 69.5Because of the country's Km of Railways(thousand kIn)

size and low population density, its (1988) 5.4 4F/ 5.1 6.5infrastructure per 1,000 square Hard surface roadkilometers is similar to that of Russia, (per thousand bms. 1988) 38 57.8F1 36.3 58but is lower than that for thfe rest of the Land area (million sq. kn) 2,717 3,994 17,075 22,402FSU, including Central Asia. There are Populaton (millions. 1989) 16.5 49.3 147.4 2895.4 kilometers of railways per 1,000 F= Averagesquare kilometers, and 38 kilometers ofhard surfaced road per 1,000 square Kyrghyzstan, Tadjikismn, Turkmenistn, Uzbekistnkilometers (while Central Asia has anaverage of 57.8). However, when multiplied by the country's total area, this network is very substantive.For example, within the FSU, Kazakhsran Railways is the third largest railway system after Russia andthe Ukraine in terms of traffic volume and rolling stock.

RECENT ECONOMIC PERFORMANCE

Kazakhstan's transition to a market economy began in 1991 with tentative privatizationand institutional measures. The reform gathered momentum in January 1992 with extensive priceliberalization. The process has been sustained during 1992, with a number of initiatives across all areasof state involvement in the economy. Price liberalization brought about a massive adjustment in relativeprices, partially correcting the distortions inherited from the previous price controlled economy.However, the monopolistic structure of many economic activities seemns to have accentuated the priceincreases which followed the January price liberalization. In addition, as a member of the ruble zone,Kamzkhstan shared the effects of the monetization of the large budget deficits that have occurred in otherruble zone republics.

The main macroeconomic trends, discussed in greater detail in the following pages, canbe briefly summarized as follows: GDP in real terms is expected to decline by 14 percent in 1992. Thisbrings the cumulative decline since 1990 to about 21 percent. While this is smaller than the declines inin Russia and some other republics, it still means a significcnt decline in consumption and investmentlevels. Retail prices jumped by 235 percent in January 1992 when most prices were liberalized.

I WDR 1992, Tablc 28.

The Macroeconomy 11