Risk management to sustain development in the banking sector

51

TREAS PREPA FACULTY OF COMMERCE DEPARTMENT OF BANKING SURY MANAGEMENT 11(CBA 2208) COUR ARED BY JONATHAN TEMBO (LECTURER RSE MODULE R)

Transcript of Risk management to sustain development in the banking sector

TREASURY

PREPARED

FACULTY OF COMMERCE

DEPARTMENT OF BANKING

TREASURY MANAGEMENT 11(CBA 2208) COURSE

PREPARED BY JONATHAN TEMBO (LECTURER

COURSE MODULE

(LECTURER)

2

Welcome Note

This module has been prepared for the National University of Science and Technology Banking

Department. Its contents are based on information accessed by the author from authoritative texts,

academic popes, banking practitioners, media publications and personal opinion. The main objective

of the module is to introduce undergraduate students to the basics of treasury management through

a combination of old tried and tested treasury management theoretical concepts , modern

theoretical views and practical knowledge. In this holistic approach reference is made in certain

instances to examples obtained from other fields, be they religious, medical, sociology or any other. It

is against this background that the author hopes that the module will leave the student with a very

vivid picture of treasury management and its importance in present day financial management.

And this our life , exempt from public haunt, finds tongues in trees , books

in the running brooks, sermons in stones, and good in everything.

3

COURSE CONTENT

Study Unit 1: Risk in the Treasury Department

• Market Risk

• Interest rate risk

• Liquidity risk

• Foreign exchange risk

• Counterparty risk

• Credit risk

• Operational risk

Study Unit 2: Risk Management Strategies

• Goals of risk management

• Risk management process

• Strategies for management of:

• Interest rate risk

• Foreign exchange risk

• Liquidity risk

• Operational risk

• Market Risk

Study Unit 3: Asset and Liability Management

• Objectives of asset and liability management

• Asset and liability management strategies

• Role of the asset and liability management committee

• Composition of the asset and liability management committee (ALCO)

• Securitisation Process

Study Unit 4: Fund Management

• Introduction to investment/fund management

• Functions of a fund manager

• Types of funds

• Hedge funds and the risks associated with them.

• Bond portfolio management strategies

• Equity portfolio management strategies

•••• Measures of Performance

4

STUDY UNIT ONE

RISK IN THE TREASURY DEPARTMENT

Risk Defined

Risk is the chance of incurring a loss due to the volatility or variability of expected future returns of

assets, investments, projects, securities etc. Risk differs from uncertainty in that with uncertainty, it

is difficult to estimate either all possible future outcomes or the probability distribution there to.

Financial risk management refers to the controlling of the possibility or chance of suffering a

monetary loss from an asset, investment, security or project.

Activity

Identify the difference between investment, gambling, speculation, and arbitrage?

RISK CATEGORISATION

Credit /Default Risk

This refers to the risk that a loan will be irrecoverable in the case of outright default or the

probability of a delay in the servicing of the loan .Such risk reduces the present value of an asset

thereby undermining the solvency of a banking institution.

Counterparty Risk

This form of risk occurs in the case of traded financial instruments as compared to loans. It is the risk

that the counterparty to a transaction reneges on the terms of the contract for example on an

arranged buyback of Bas or TBs one fails to deliver the financial instruments or securities after

transfer of funds has already been done.

Liquidity and Funding Risk

Liquidity risk is the risk of insufficient liquidity for normal operating requirements ie the ability of the

bank to meet its liabilities when they fall due. The problem arises because of a shortage of liquid

assets or because the bank is unable to raise cash on the retail or wholesale markets. Funding risk is

the risk that a financial institution will be unable to fund its day to day operations.

5

Activity

Since the introduction of the multiple currency regime in 2009 most banking institutions in

Zimbabwe have been facing a liquidity crisis, which they say is not a result of their inability to match

their assets and liabilities .Their argument is that deposits that are being made are for short term

only and very few deposits are for long term .In addition the central bank in Zimbabwe is

incapacitated to play the lender of last resort role thereby making the situation even worse.

Question one

Is this a valid argument?

What other factors are contributing to the liquidity crisis?

Question two

Given the above scenario, is it a noble idea to consider the introduction of a local currency alongside

the available hard currencies?

The House of Rock

Northern Rock was a stable bank until the liquidity crisis of 2007. During the liquidity crisis of 2007,

Northern Rock could not acquire backing from institutional lenders, who themselves were reeling

from the US subprime mortgage meltdown. The Tripartite Authority (The Bank of England, the FSA

and HM Treasury) lent the bank 3 billion pounds on September 12, 2007. After the news broke,

Northern Trust’s stock fell 32%. Depositors ran on the bank. Unlike a classic bank run, which throws

a bank into crisis, this one followed a crisis and compounded a preexisting liquidity problem. On

February 17, 2008, the British government nationalized Northern Rock.

Why do you think Northern rock was nationalized? Compare this with the ZABG story?

Interest Rate Risk

This arises from interest rate mismatches in both volume and maturity of interest

sensitive assets and liabilities.eg a 2 year loan with a rate of 10% funded by a 1 year

deposit with a rate of 9% would earn the bank a spread of 1%.However , if in the

second year, interest rates change and the one year deposit rate becomes 11% , the

bank would have a negative spread of 1% thus by holding on to longer term assets

relative to liabilities , the bank potentially exposes itself to refinancing risk. This is

the risk that the cost of rolling over or reborrowing could be more than the returns

earned on asset investments. Suppose again the bank has a 10 % , 1 year loan funded

by a 9 % , 2 year deposit , and the rates in the second year fall to 8% .The bank would

have a negative spread of 1% in the second year as the asset would earn 8% whilst the

2 year deposit would cost 9%.Thus by holding shorter term assets relative to longer

6

term liabilities the bank exposed itself to reinvestment risk ie the uncertainty about

the rate at which it could reinvest funds borrowed for a longer period.

Activity

There are 4 forms of interest rate risk .These include repricing risk, basis/spread risk, option risk,

yield curve risk. Give an explanation for each of them.

Market or Price Risk

This is the risk that the prices of instruments such as equities or bonds etc move adversely .General

or systematic market risk is caused by a movement in the prices of all market instruments because of

for example changes in macroeconomic policy. Market risk results from changes in the prices of

equity instruments, commodities, money and currencies. Its major components are therefore, equity

position risk, commodities risk, interest rate risk, and currency risk.

Foreign Exchange Risk

This is the risk that arises from adverse exchange rate fluctuations which affect the institution`s

foreign exchange positions taken on its account or on behalf of a client. It can be divided into 3 ie

translation or accounting exposure which occurs when exchange rate changes alter the home

currency value of foreign currency denominated liabilities and assets , transaction exposure which

refers to the net exposure of foreign currency denominated transactions already entered into. Upon

settlement, these transactions may give rise to gains or losses. Economic exposure refers to the

sensitivity of a firm`s assets liabilities and operating cash flows to random changes in exchange rates.

Operational Risk

This refers associated with losses arising from theft or fraud as a result of failure to separate the

front and back office, risk from unauthorised trading, rogue trading, human error, common failures,

and breakdown of control systems.

7

Collapse of Barings Bank

In 1995, Barings PLC was a 233 year old institution (chartered in 1762), that was Britain's oldest

merchant bank. With a stellar history, Barings financed the 1803 Louisiana Purchase which doubled

the land in the United Stated. In addition, the bank helped finance the British government battle

against Napoleon by loaning and raising money to pay soldiers, buy equipment, and maintain the

overall war effort. Barings almost collapsed in 1890 when it sustained enormous losses in Argentina

but the Bank of England bailed it out. Nick Leeson, a 28 year old derivatives trader in the bank`s

Singapore office located in Singapore office lost over $1.4b betting on Nikkei futures, wiping out the

bank's equity capital and making it technically bankrupt.

Settlement/Payment /Herstatt Risk

Is the risk created if one party to a deal pays money or delivers assets before receiving his own cash

or assets’ thereby exposing himself to potential loss .It is more pronounced in international markets

because of time differences eg opening times on the ZSE and closure on Nikkei. The RTGS was

brought about in order to curb this timing difference.

Origins

German regulators seized the ailing Herstatt Bank and forced it to liquidate on June 26, 1974. The

same day, other banks had released Deutsch Mark payments to Herstatt, which was supposed to

exchange those payments for US dollars that would then be sent to New York. Regulators seized the

bank after it received its DM payments, but before the US dollars could be delivered. The time zone

difference meant that the banks sending the money never received their US dollars. This “Herstatt

Debacle” led to a new continuous linked settlement (CLS) protocol, which enables foreign banks to

trade currencies without a settlement risk if one party or the other fails in their obligation.

Legal Risk

The risk of loss arising from uncertainty about the enforceability of contracts. It includes risk arising

from disputes over insufficient documentation, alleged breach of contracts. The risk can also arise

from uncertainty over legal jurisdictions and over prospective changes in the legal and regulatory

systems.

Political and Sovereign Risk

Sovereign risk refers to the risk that a government will default on debt owed to a private entity

.Political risk is the risk of political interference in the operations of a private sector entity. Both are

closely related or similar in nature to country risk.

8

STUDY UNIT TWO

RISK MANAGEMENT STRATEGIES

• Risk management is the framework within which a firm manages and controls the various

types of risk that it faces.

• It is both a set of tools and techniques and processes that are required to implement a

strategy of a financial institution.

Goals of Risk Management

The main objective of risk management is to optimise the risk reward tradeoff by accurately

measuring risk in order to monitor and control optimization of risk

• Optimization refers to the minimisation of risk.

• Risk management supports the financial institution through:

• Assisting in the implementation of business strategy ie in forecasting of future outcomes

and returns.

• It is an aid to decision making. An effective risk management system is developed to the

level where it aids the decision making ie reporting and hedging of risk and influencing the

decision making process before the decisions are made.

• It also affects pricing decisions, on how we come up with the price , the price must be a

function of risk.

• It assists the development of competitive advantage. Controlling future costs as much as

currents costs is a contribution to income both in the present and the future. Therefore,

risk control is a key factor of profitability and competitive advantage.

The current trend is that most risk management programmes are implemented at the corporate

level rather than the divisional level. Various factors influence the level at which risk management is

going to be implemented. These include the expertise in the various divisions, availability of

information, transaction costs of risk hedging, motivation for risk hedging etc

Activity

Should risk management operate out of the firm`s treasury department?

9

Risk Management Process

This is a sequential and continuous risk management activity. The life cycle of the management

process involves the identification, measurement, planning, monitoring, control, and feedback.

Communication takes place in every stage of the model.

Identification

• It involves the searching for and location of risks before they become problems

• An organisation should have a procedure to review the risks it faces and identify what they

are.

• Risk changes over time hence risk reviews should be regular.

Measurement

• Risk data is transformed into decision making information. The measurement of risk also

encompasses

• Evaluation of risk impact

• Evaluation of probability and time frame

• Classification of risk

• Risk prioritization ie which form f risk should be of the highest priority

Planning

It involves the translation of risk information into decision making and mitigating actions as well as

implementation of those actions

Monitoring

This involves monitoring of risk indicators as well as mitigation actions

Control

This is the correction of deviations from the risk mitigation plans .Risk control is not just a system of

controls being put in place also involves proper application of the system controls and regular check

by management.

Communication

10

This refers to the provision of information and feedback to internal and external operations,

management and the board on risk activities .Communication is centrally paced within the risk

management process as it occurs throughout all the functions of the risk management process.

Management of interest rate risk

Interest rate risk is the potential for loss arising from changes in interest rates. It is the exposure of a

bank`s current or future earnings and capital to interest rate changes. Every well managed financial

institution should have a process that enables it to identify and measure interest rate risk in a timely

and comprehensive manner.

Interest rate risk measurement

Any system adopted by a bank or financial institution to measure interest rate risk should provide a

meaningful measure of the bank`s interest rate exposure and should be capable of identifying any

excessive exposures that may arise. The following are the techniques used to measure interest rate

risk:

1 Gap Analysis /Static Repricing gap

This approach was common in the 1980s and 90s .Its aim is to allocate interest sensitive assets and

liabilities to maturity buckets, defined according to their repricing characteristics and to measure the

gap at each maturity point.

Steps taken to develop a gap analysis

• Establish a series of time intervals or buckets for allocating interest sensitive assets and

liabilities.

• Group the assets and liabilities into appropriate buckets.

• Calculate the gap for each bucket.

• Interpret the gap and identify the interest rate risk.

• Develop strategies to minimise or hedge against the interest rate risk.

11

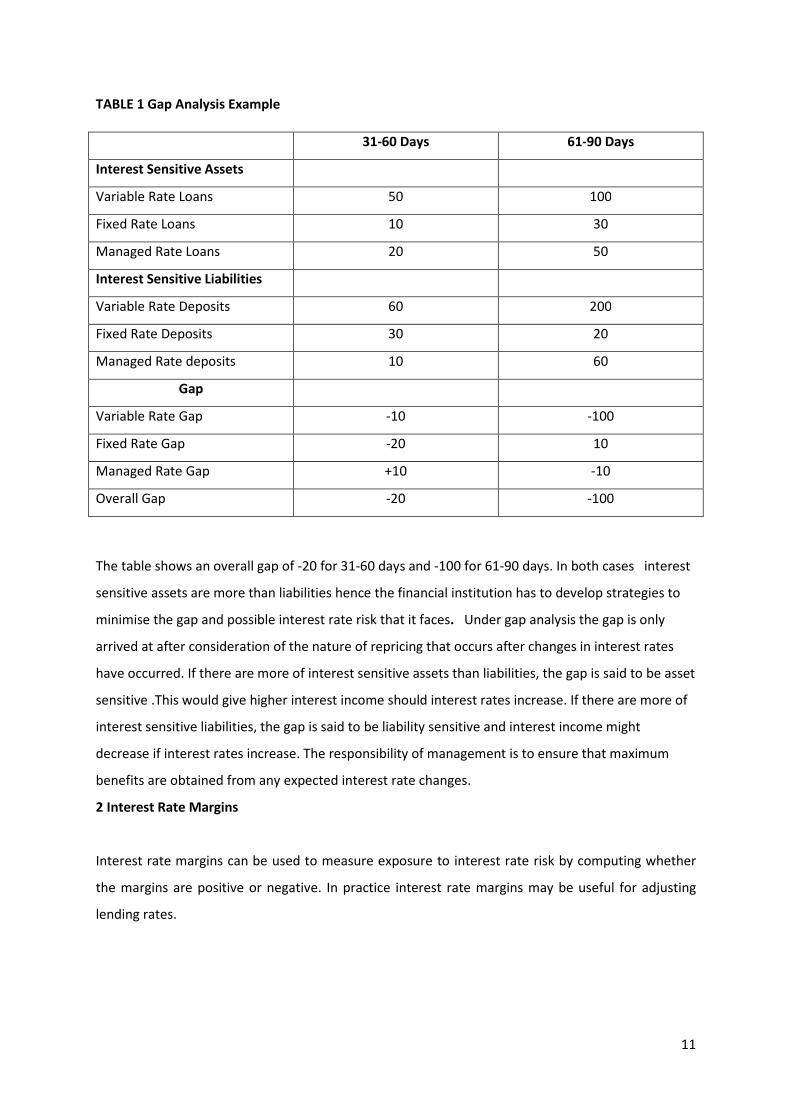

TABLE 1 Gap Analysis Example

The table shows an overall gap of -20 for 31-60 days and -100 for 61-90 days. In both cases interest

sensitive assets are more than liabilities hence the financial institution has to develop strategies to

minimise the gap and possible interest rate risk that it faces. Under gap analysis the gap is only

arrived at after consideration of the nature of repricing that occurs after changes in interest rates

have occurred. If there are more of interest sensitive assets than liabilities, the gap is said to be asset

sensitive .This would give higher interest income should interest rates increase. If there are more of

interest sensitive liabilities, the gap is said to be liability sensitive and interest income might

decrease if interest rates increase. The responsibility of management is to ensure that maximum

benefits are obtained from any expected interest rate changes.

2 Interest Rate Margins

Interest rate margins can be used to measure exposure to interest rate risk by computing whether

the margins are positive or negative. In practice interest rate margins may be useful for adjusting

lending rates.

31-60 Days 61-90 Days

Interest Sensitive Assets

Variable Rate Loans 50 100

Fixed Rate Loans 10 30

Managed Rate Loans 20 50

Interest Sensitive Liabilities

Variable Rate Deposits 60 200

Fixed Rate Deposits 30 20

Managed Rate deposits 10 60

Gap

Variable Rate Gap -10 -100

Fixed Rate Gap -20 10

Managed Rate Gap +10 -10

Overall Gap -20 -100

12

3 Scenario Analysis/ Stress Testing/ Simulation

This is a forward looking method of estimating risk exposure .To implement the method, managers

need to be focused on earnings/ cash flow for a variety of factor realisations e.g. A war will specify a

range of scenarios and under each scenario estimate profits or cash flows that would occur under

each scenario are generated within the confines of certain assumptions.(Read on Value at Risk VaR

and Compare. VaR calculates the worst possible loss under normal market conditions for a given

time period .Note VaR is not examinable) .

4 Duration Analysis

Macaulay Duration

It was developed in 1938 by Frederick Macaulay. The Macaulay Duration represents the weighted

average time to maturity (or weighted average life) on an instrument using the present value of the

cash flows as the weights .It may also be considered as the time required to recover the initial

investment on a loan and is measured in years. It is used as a tool to balance and hedge bond

portfolios against the risk associated with changes in bond portfolios since it measures risk and how

much cash flows from bonds fluctuate overtime.

Characteristics of Duration

• The larger the numerical value of duration, the more sensitive the price of the asset or

liability to interest rate changes.

• A zero coupon bond has a duration equal to its maturity

• Duration is always less than or equal to maturity

• In comparing bonds of equal maturity , the bond with a higher coupon rate will have a lower

duration

• Duration is a better approximation for small changes in interest rates than for larger changes

Modified duration

The Macaulay duration does not precisely give the sensitivity of a bond to changes in interest rates

.A derivation of the Macaulay duration called the modified duration allows us to determine the

percentage change in the price of a bond for a 1 percentage change in the yield. The formula is

given as follows:

Modified Duration = Macaulay Duration/ (1+r/t)

Where r is the yield to maturity

13

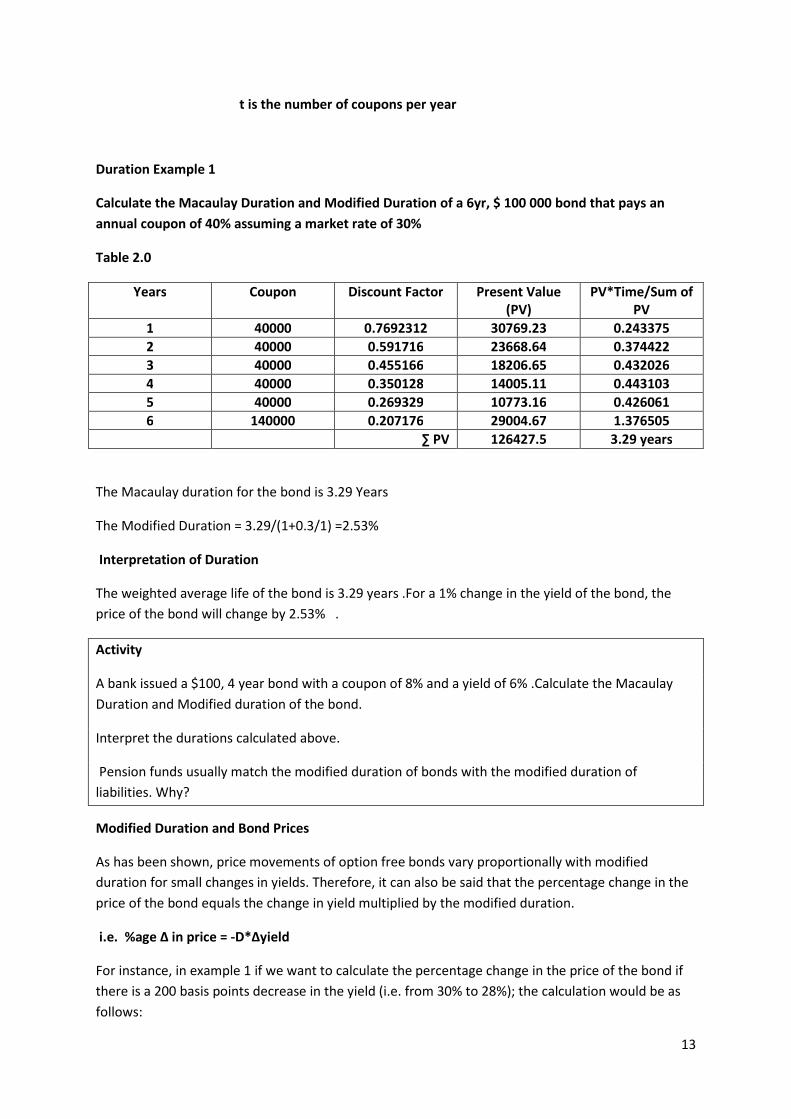

t is the number of coupons per year

Duration Example 1

Calculate the Macaulay Duration and Modified Duration of a 6yr, $ 100 000 bond that pays an

annual coupon of 40% assuming a market rate of 30%

Table 2.0

Years Coupon Discount Factor Present Value

(PV)

PV*Time/Sum of

PV

1 40000 0.7692312 30769.23 0.243375

2 40000 0.591716 23668.64 0.374422

3 40000 0.455166 18206.65 0.432026

4 40000 0.350128 14005.11 0.443103

5 40000 0.269329 10773.16 0.426061

6 140000 0.207176 29004.67 1.376505

∑ PV 126427.5 3.29 years

The Macaulay duration for the bond is 3.29 Years

The Modified Duration = 3.29/(1+0.3/1) =2.53%

Interpretation of Duration

The weighted average life of the bond is 3.29 years .For a 1% change in the yield of the bond, the

price of the bond will change by 2.53% .

Activity

A bank issued a $100, 4 year bond with a coupon of 8% and a yield of 6% .Calculate the Macaulay

Duration and Modified duration of the bond.

Interpret the durations calculated above.

Pension funds usually match the modified duration of bonds with the modified duration of

liabilities. Why?

Modified Duration and Bond Prices

As has been shown, price movements of option free bonds vary proportionally with modified

duration for small changes in yields. Therefore, it can also be said that the percentage change in the

price of the bond equals the change in yield multiplied by the modified duration.

i.e. %age ∆ in price = -D*∆yield

For instance, in example 1 if we want to calculate the percentage change in the price of the bond if

there is a 200 basis points decrease in the yield (i.e. from 30% to 28%); the calculation would be as

follows:

14

%age ∆ in price = -D*∆yield

%age ∆ in price = - 2.53* -(200/100)

%age ∆ in price =-2.53*2

= 5.06% change in the price of the bond

Now, since we already know that there is an inverse relationship between the price and yield of a

bond , it means the 5.06 % change is an increase in the price of the bond by the calculated

percentage .Therefore , if the price of the bond was $100 , it means now it will be

100(1.0506)=$105.06

Assuming that instead of a 200 basis points decrease, we have an increase, the percentage change in

the price of the bond would be calculated as follows:

%age ∆in price = -2.53*(200/100)

=-2.53*2

=-5.06%

This means the price of the bond would decline by 5.06%.Therefore the new price of the bond would

be $100(0.9494) = $ 94.94

N.B A basis point is equal to 1/100th of 1% (1 basis point is 0.01%) and is used to denote the change

in a financial instrument.1% therefore is equal to 100 basis points.

Activity

Use of the Macaulay and Modified duration models is now limited since the introduction of Effective

and Empirical Duration models.

What are the weaknesses of the Macaulay and Modified Duration models?

Interest Rate Risk Management Practices

The bank`s complexity and risk profile should determine the formality and sophistication of its

interest rate risk management programs. Although there are many methodologies to guide interest

rate risk management, the following base elements should be addressed.

• Appropriate board and senior management

15

The board has ultimate responsibility for understanding the nature and level of risk taken by the

bank. The board must ensure that management effectively identifies, monitors, measures and

controls interest rate risk .The board should ensure that there are policies, procedures and systems

that can be used to achieve the above goals.

• Senior Management Oversight

Senior management is responsible for day to day interest rate risk management .Senior

management should:

1. Develop and implement procedures and practices that translate the board`s policies with

clear operating standards.

2. Maintain adequate systems and standards for identifying, measurement, and monitoring of

interest rate risk.

3. Establish internal controls over the interest rate risk management process. The

responsibility for establishing specific interest rate policies and procedures is usually

delegated to the ALCO.ALCO usually delegates day to day operating responsibility to the

treasury department.

• Adequate Risk Management Policies and Procedures

There should be adequate risk management policies and procedures. Duties pertaining to key

elements of the risk management process should be adequately separated to avoid potential

conflicts of interest i.e. a bank`s monitoring and control functions should be sufficiently independent

from its risk taking functions. Complex or larger banks should have independent units for the design

and administration of balance sheet management , including interest rate risk .given today`s

widespread innovation in banking and the new dynamics of markets, banks should identify risks

inherent in new products or services before they are introduced.

• Comprehensive Internal Controls

Banks should have an adequate system of internal control to oversee the interest rate risk

management process .A fundamental component of such a system is regular , independent review

and evaluation to ensure the system`s effectiveness and when appropriate to recommend revisions

or enhancements.

16

LIDUIDITY RISK MANAGEMENT

Liquidity Risk

Liquidity risk is usually defined as the inability of a bank to meet its obligations as they fall due.

Causes of liquidity problems

• Unexpected withdrawals

• Excessive lending commitments

• Failure of assets to mature

• Poor asset quality(Bad Loan book)

• Decrease in asset values

• Poor Earnings

• Deposit Concentration

• Damage to reputation

Liquidity Management

For effective liquidity management banks and other financial institutions should:

• Maintain a proper system for managing cash flows

• Maintain a stock of liquid assets

• Develop / Maintain borrowing capacity

• Observe liquidity standards and limits

• Have liquidity contingent plans

Managing Cash flows

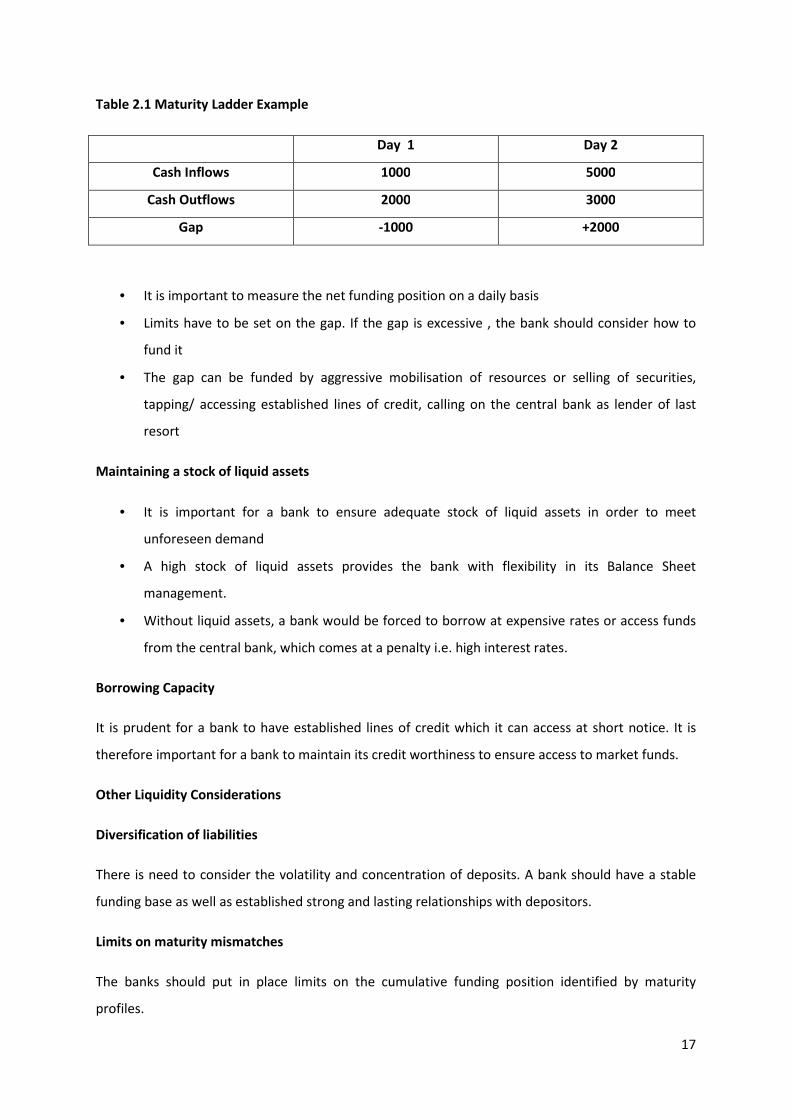

On managing cash flows, there is need to use a maturity ladder to identify the net funding position

or its nature. The maturity ladder measures outgoing commitments compared to inflows of funds.

The bank must determine acceptable mismatches or cumulative gaps.

17

Table 2.1 Maturity Ladder Example

Day 1 Day 2

Cash Inflows 1000 5000

Cash Outflows 2000 3000

Gap -1000 +2000

• It is important to measure the net funding position on a daily basis

• Limits have to be set on the gap. If the gap is excessive , the bank should consider how to

fund it

• The gap can be funded by aggressive mobilisation of resources or selling of securities,

tapping/ accessing established lines of credit, calling on the central bank as lender of last

resort

Maintaining a stock of liquid assets

• It is important for a bank to ensure adequate stock of liquid assets in order to meet

unforeseen demand

• A high stock of liquid assets provides the bank with flexibility in its Balance Sheet

management.

• Without liquid assets, a bank would be forced to borrow at expensive rates or access funds

from the central bank, which comes at a penalty i.e. high interest rates.

Borrowing Capacity

It is prudent for a bank to have established lines of credit which it can access at short notice. It is

therefore important for a bank to maintain its credit worthiness to ensure access to market funds.

Other Liquidity Considerations

Diversification of liabilities

There is need to consider the volatility and concentration of deposits. A bank should have a stable

funding base as well as established strong and lasting relationships with depositors.

Limits on maturity mismatches

The banks should put in place limits on the cumulative funding position identified by maturity

profiles.

18

Contingency Liquidity Planning

A bank should put in place a formal liquidity plan approved by its board of directors for dealing with

major liquidity problems. The plan should outline course of action for alternative assets and

liabilities strategies e.g. plans to market more aggressively, raise deposits etc. Liquidity management

is usually delegated to ALCO.ALCO is responsible for coming up with appropriate strategies to

manage the bank`s mix of assets and liabilities.

19

MARKET RISK MANAGEMENT

Market risk is the risk that a bank may experience loss due to unfavourable movements in market

prices .Such activities may result from proprietary trading(speculative positions) or dealer

activities(bank`s market making).

Sources of market risk

Market risk results from changes in the prices of equity instruments, commodities, currencies, .Its

major components are therefore equity position risk, commodities risk, interest rate risk and

currency risk. It is important to note that each component of risk includes a general market risk

aspect.

Market Risk Measurement

Given the increasing involvement of banks in investment and trading activities and the high volatility

of the market environment, the timely and accurate measurement of market risk is a necessity. In

measuring market risk, the following market risk factors should be taken into account.

• Interest Rate Risk i.e. positions in fixed income securities and their derivatives.

• Equity Risk i.e. risk which relates to holding trading book positions in equities or instruments

that display equity like behaviour e.g. convertible securities and their derivatives eg futures

and options

• Commodity Risk i.e. Holding or taking positions in exchange traded commodities e.g. gold

futures, oil futures

• Currency risk –Refers to proprietary trading positions in currencies and gold.

Methods of measuring market risk

There are different methods of measuring market risk. These include advanced techniques like VAR,

Stress Testing as well as the net open position (market factor sensitivity model)

Net Open Position/Market Factor Sensitivity

This is a method which calculates the net open position of a bank. The net book value of assets is the

starting point in calculating the position. Afterwards all forward and unsettled transactions are taken

into account to give a final position at book value. This book value is converted to market value using

a common denominator representing the equivalent position in the cash markets. This will give the

net open position before derivative transactions. Afterwards derivative transactions are taken into

account to give the net open position after derivatives .Based on the net open position after

20

derivatives; one can estimate the potential earnings or capital at risk by multiplying the net open

position (market risk factor sensitivity) by the price volatility. A simplistic net open position

calculation table is given in Table 2.2 below

Table 2.2

Position Commodities Fixed Income Equities Currencies

NBV of assets per

balance sheet

Forward Transactions

Position @ book value

Position @ mkt value

before derivatives

Position in derivatives

Net effective open

position after

derivatives

Possible mvmnts in

mkt prices(price

volatility

Impact on

earnings/capital

Management of market risk

Market risk management policies should specifically state a bank`s objectives and the related policy

guidelines that have been established to protect capital from the negative impact of unfavourable

market price movements. The following policies are identifiable with most banks:

Marking to Market

This refers to the repricing of a bank`s portfolio to reflect changes in asset prices due to market

price movements .The volume and nature of the activities in which a bank engages generally

determine the prudent frequency of pricing. Pricing in a trading portfolio should be evaluated and

marked to market at least once per day. Risk management policy should stipulate that prices be

determined and marking to market be executed by officers who are independent of the respective

dealer or trader and his managers.

21

Position Limits

A market risk management policy should provide for limits on positions bearing in mind the

liquidity risk that could arise on execution of unrealised transaction e.g. commitment to purchase/

sell securities/option contracts .Such positions should be related to the capital available to cover

market risk. Banks are also expected to set limits on the level of risk taken by individual dealers or

traders.

Stop Loss Provisions

Market risk management policy should also include stop loss sell or consultation requirements that

relate to a predetermined loss exposure limit. The stop loss exposure limit should be determined

with regard to a bank`s capital structure and earnings trends as well as to its overall risk profile.

Limits to new market presence

There should be a policy which provides limits related to a new market presence because investment

in a new market involves a special kind of risk for an instrument whose return and variance may not

have been tested.

Basel Committee Standards for Market Risk

The Basel Committee on Banking Supervision`s capital adequacy standard for market risk specifies a

set of qualitative criteria for market risk: These include:

• An independent risk control unit responsible for the design and implementation of the

bank`s market risk management system.

• Board and senior management who are actively involved in the risk control process and

who regard risk control as an essential aspect of business.

• A market risk measurement system that is closely integrated into the daily risk

management process of a bank.

• A routine and rigorous program of stress testing to supplement the risk analysis provided

by the risk measurement model.

• A process to ensure compliance with a documented set of bank policies , controls and

procedures concerning then trading activities and the operation of the risk measurement

system.

22

FOREIGN EXCHANGE RISK MANAGEMENT

Foreign exchange risk is the risk that results from changes in exchange rates between a bank`s

currency and other currencies .It originates from mismatches between the values of assets and

liabilities denominated in different currencies e.g. differences between foreign receivables and

payables. Forms of foreign exchange risk include:

Transaction Risk

This is the price based impact of exchange rate changes on foreign receivables and any foreign

payables i.e. The difference in price at which they are collected or paid and the price at which they

are recognised in local currency in the financial statements of a bank.

Economic/Business Risk

This is related to the impact of exchange rate changes on a country`s long term or a company`s

competitive position e.g. a depreciation in the local currency may cause a decline in imports and

increase in exports which might in turn benefit an exporting company and hurt an importing

company.

Revaluation/Translation/Accounting Exposure

This arises when a bank`s foreign currency positions are revalued in domestic currency or when a

parent institution conducts financial reporting or periodic consolidation of financial statements and

has to revalue the foreign currency denominated assets and liabilities on its balance sheet at current

exchange rates.

Foreign Exchange Risk Management Practices

• The bank`s board of directors should establish objectives and principles of foreign currency risk

management.

• The principles should include setting limits to the risk taken by the bank in its foreign exchange

business.

• Policies should also specify the frequency of revaluing foreign currency positions for accounting

and risk management policies.

• There should be a distinction between foreign currency exposure from trading and dealing

operations and exposure due to more traditional banking business.

• Banks should determine the foreign currency net open position , which is a reflection of a bank`s

total foreign currency position.

23

• Limits should also be set on risk exposure to specific currencies.

• Banks should have stop loss provisions .When losses reach their stop loss limits, open positions

should automatically be covered.

OPERATIONAL RISK MANAGEMENT

Operational risk is the risk that deficiencies in information systems or internal controls will result in

Unexpected losses. It is associated with human error, system failures, and inadequate procedures

and controls.

Operational Risk Management Practices

• The board of directors of the bank and senior management should ensure the proper

dedication of resources i.e. financial and personnel to support operations and systems

development and maintenance.

• The operations unit for derivative activities and other investment activities should report to

an independent unit and should be managed independently of the business unit

• Systems support and operational capacity should be adequate to accommodate the

activities in which the institution engages.

• Segregation of operational duties is also critical to proper internal control.

• Proper internal control should be provided over the entry of transactions into the database,

numbering, date confirmation and settlement processes.

• Monitoring should be done between the terms of a transaction as they were agreed upon

and the terms as they were subsequently confirmed.

• The operations department should be responsible for ensuring proper reconciliation of front

and back office databases on a regular basis.

• There should be periodic review procedures , documentation requirements, data processing

systems, operational practices etc

Measurement of Operational Risk

Operational risk is difficult to quantify but can be evaluated by examining a series of “worst case” or

“what if” scenarios e.g. what if a power outage occurs, what if transaction volumes double.

Evaluation of the consequences of these “what if” events is then used as a guideline in estimating

the level of operational risk if such an event occurs.

24

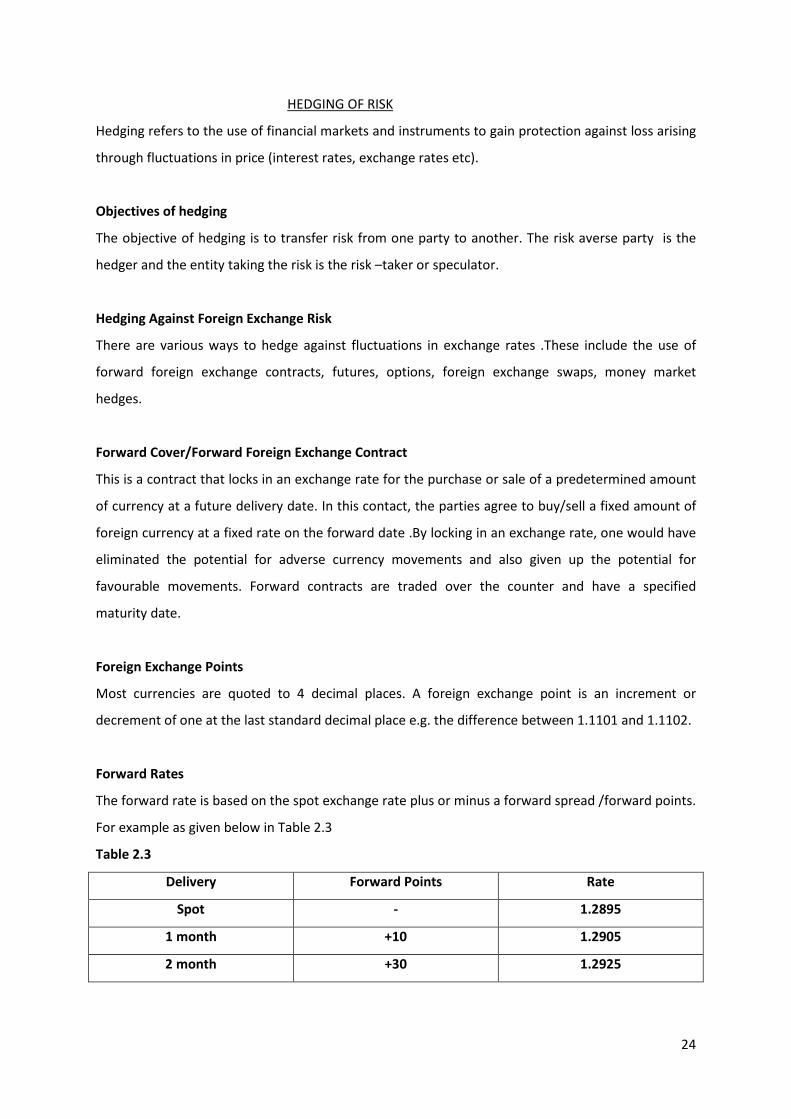

HEDGING OF RISK

Hedging refers to the use of financial markets and instruments to gain protection against loss arising

through fluctuations in price (interest rates, exchange rates etc).

Objectives of hedging

The objective of hedging is to transfer risk from one party to another. The risk averse party is the

hedger and the entity taking the risk is the risk –taker or speculator.

Hedging Against Foreign Exchange Risk

There are various ways to hedge against fluctuations in exchange rates .These include the use of

forward foreign exchange contracts, futures, options, foreign exchange swaps, money market

hedges.

Forward Cover/Forward Foreign Exchange Contract

This is a contract that locks in an exchange rate for the purchase or sale of a predetermined amount

of currency at a future delivery date. In this contact, the parties agree to buy/sell a fixed amount of

foreign currency at a fixed rate on the forward date .By locking in an exchange rate, one would have

eliminated the potential for adverse currency movements and also given up the potential for

favourable movements. Forward contracts are traded over the counter and have a specified

maturity date.

Foreign Exchange Points

Most currencies are quoted to 4 decimal places. A foreign exchange point is an increment or

decrement of one at the last standard decimal place e.g. the difference between 1.1101 and 1.1102.

Forward Rates

The forward rate is based on the spot exchange rate plus or minus a forward spread /forward points.

For example as given below in Table 2.3

Table 2.3

Delivery Forward Points Rate

Spot - 1.2895

1 month +10 1.2905

2 month +30 1.2925

25

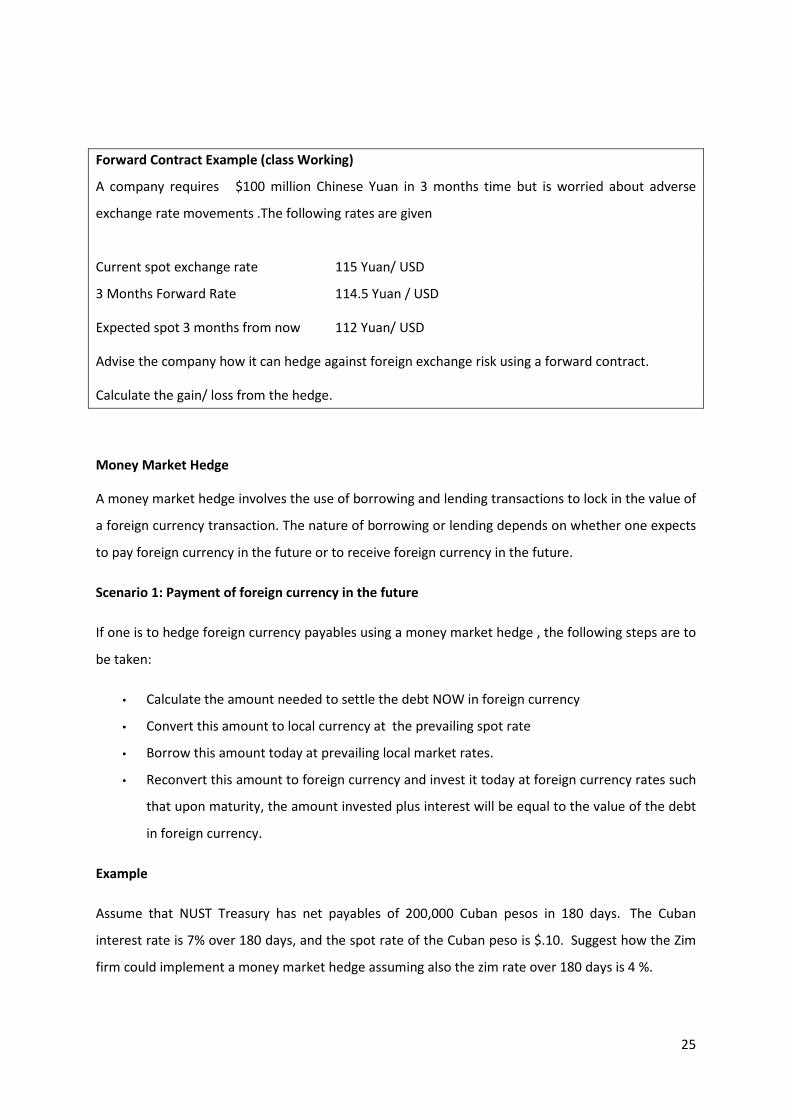

Forward Contract Example (class Working)

A company requires $100 million Chinese Yuan in 3 months time but is worried about adverse

exchange rate movements .The following rates are given

Current spot exchange rate 115 Yuan/ USD

3 Months Forward Rate 114.5 Yuan / USD

Expected spot 3 months from now 112 Yuan/ USD

Advise the company how it can hedge against foreign exchange risk using a forward contract.

Calculate the gain/ loss from the hedge.

Money Market Hedge

A money market hedge involves the use of borrowing and lending transactions to lock in the value of

a foreign currency transaction. The nature of borrowing or lending depends on whether one expects

to pay foreign currency in the future or to receive foreign currency in the future.

Scenario 1: Payment of foreign currency in the future

If one is to hedge foreign currency payables using a money market hedge , the following steps are to

be taken:

• Calculate the amount needed to settle the debt NOW in foreign currency

• Convert this amount to local currency at the prevailing spot rate

• Borrow this amount today at prevailing local market rates.

• Reconvert this amount to foreign currency and invest it today at foreign currency rates such

that upon maturity, the amount invested plus interest will be equal to the value of the debt

in foreign currency.

Example

Assume that NUST Treasury has net payables of 200,000 Cuban pesos in 180 days. The Cuban

interest rate is 7% over 180 days, and the spot rate of the Cuban peso is $.10. Suggest how the Zim

firm could implement a money market hedge assuming also the zim rate over 180 days is 4 %.

26

• Amount needed now

200 000/1.07 =186 915.9 Pesos

• Convert to local currency

186 915.9*0.10 =USD18 691.5

• Borrow this amount at local rates today

Amt to be repaid in 180 days = 18 691.5(1.04) =19439.16(cost of the hedge)

• Reconvert the borrowed USD18691.5 to Pesos and Invest this amount at foreign currency

rates today.

Reconverted = 186 915 .when invested for 180 days at Cuban rates , the amt invested plus principal

will give 200 000 Pesos thus hedging effectively against foreign exchange risk.

Example 2 Class Working

ABC corporation , a Zim company, has net payables of ZAR 500 000 due in 90 days.If South African

interest rates are 9 % , Zim interest rates 10 % and the spot rate of the South African Rand is $0.50

.Show how ABC can hedge this net payables using a money market hedge.

Scenario : Receiving foreign currency in the future

If one is to hedge foreign currency receivables using a money market hedge, the following steps are

to be taken:

• Borrow an amount in foreign currency today, which when interest and principal are added

will give the total amount to received.

• Convert the borrowed amount to local currency.

• Invest the borrowed amount at local rates and calculate the receipts thereon.

NB: The amount borrowed plus principal will be set off by the amount to be received in the future.

Example

Assume that you are the treasury manager of a bank which is to receive 500 000 pounds in 90 days

time.UK 90day interest rates are 2% and local 90 day interest rates are 10%.The spot rate of the

Pound is $1.57.The Bank wants to hedge these receivables using a money market hedge. Advise

• Borrow an amount which when interest and principal are added gives 500 000 pounds

500 000/1.02= 490 196.10 pounds

• Convert the borrowed amount to US

490 196.10*1.57 =769 607.80

27

• Invest the borrowed amount at local rates

769 607.8(1.1)=846 568.60

Example: Class Working

Assume the following information:

180-day U.S. interest rate = 8%

180-day British interest rate = 9%

180-day forward rate of British pound = $1.50

Spot rate of British pound = $1.48

Assume that Riverside Corp. from the United States will receive 400,000 pounds in 180 days. Would

it be better off using a forward hedge or a money market hedge? Substantiate your answer with

estimated revenue for each type of hedge

Currency Swap

A currency swap enables swap counterparties to exchange payments in different currencies. At the

beginning, the parties to the swap /exchange the principal amounts e.g. loan of a currency for the

equivalent of another currency. By so doing the 2 will have exchanged their interest obligations as

well thus providing the hedge against currency movements.

Currency Futures

These are exchange traded contracts to buy or sell a predetermined amount of currency on a future

delivery date. Contract size, expiry date and trading are standardised by the exchange on which the

parties trade. The futures contract allows a currency buyer or seller to lock in an exchange rate for

future delivery, thus removing the uncertainty of exchange rate fluctuations.

Decision whether to buy or sell

One`s exposure in a situation determines whether one should buy (take a long position) or sell ( take

a short position).If you expect to pay foreign currency, you will have to buy foreign currency futures

and vice versa.

28

Foreign Currency Options

A foreign currency option is a contract that gives the holder the right but not the obligation to buy or

sell foreign currency at a specific price at a specified future date. The purchase of options can reduce

the risk of adverse currency movements whilst maintaining the ability to benefit from favourable

movements. A foreign currency call option gives the right but not the obligation to buy foreign

currency whilst a put option gives the right but not the obligation to sell foreign sell foreign

currency.

Hedging against interest rate risk

There are various methods used to hedge against interest rate risk. These include the use of forward

rate agreements, interest rate futures, interest rate options, and interest rate swaps. However, for

this study focus will be placed on forward rate agreements and interest rate swaps.

Forward Rate Agreement (FRA)

This is an OTC agreement between two parties to lock in an interest rate for a short period of time.

The period is usually one month or three months, beginning at a future date. A borrower buys a

forward FRA to protect against rising interest rates, while a lender sells a FRA to protect against

declining interest rates. The idea behind the FRA is that the lender will lock in a rate at which he/ she

lends and the borrower will lock in a rate at which he/she borrows for the specified period.

However, at the beginning or end of the period covered by the FRA, the reference (benchmark) rate

is compared to the FRA rate .If the reference rate is higher; the FRA seller makes a compensating

payment (settlement amount) to the FRA buyer. If the reference rate is lower, the FRA buyer pays

the FRA seller. The notional contract amount is used for calculating the settlement amount but is not

exchanged.

N.B After entering into the agreement both the borrower and the seller will borrow and lend using

the normal channels i .e. in the market .However at the beginning of the FRA, if the reference rate( i.

e market or benchmark rate) at which the borrower accesses his funds is higher than the FRA rate,

he is entitled to compensation from the other party in the FRA i. e the lender and vice versa. (its

like taking a bet on the movements of interest rates) eg Assume we have 2 parties a borrower and a

lender. The borrower wants to borrow in 3 months time but is not sure about the movement of

interest rates in 3 months time .The lender also is unsure about the movement of lending rates in 3

months time. Both decide to enter into a 3 months FRA at 10% . If at the beginning of the FRA, the

FRA rate is 10 % and reference rate is 12 % the seller of the FRA will compensate the buyer for the 2

% difference in interest rate hence in this case the FRA buyer will have effectively locked in an

29

interest rate of 10 % and so will the lender because the compensation he pays is based on the

difference between the 2 rates..

Calculation of compensation or settlement proceeds

The settlement proceeds are given by the following formula

[ ( L- R )*D*N ]/ [ (D*L) + (B*100)]

Where N = Nominal FRA Amount

R= Fixed or FRA rate or contract rate in absolute terms

L= The reference or benchmarks rate in absolute terms

D= The tenor of the FRA in days

B= Day Base or number of days in a year

Example 1

Calculate the compensation proceeds of a FRA with the following variables: Nominal Amount $ 10

Million, FRA rate 4 %, Reference rate 5%, Tenor of 90 days , Day base 360 days

Class working Answer $24 691, 36 .In this case the reference rate is greater than the FRA rate

hence the compensation of $ 24 691 .36 will go be paid to the buyer of the FRA.

Example 2

Calculate the settlement proceeds of a FRA contract described below:

Nominal Amount $ 1 million , FRA rate 15 %, Reference rate 18 %, Term in days 91 days, day base

365 days

Class working Answer $ 7 158, 21 .Who will be paid this amount?

Interest Rate Swap

This is an agreement between two parties to exchange their respective cash flows. It mainly refers to

companies exchanging fixed rate and floating rate interest payments .The two parties can then swap

their interest rate payments enabling both to achieve the type of interest each prefers.

Two companies face the following costs in their respective markets

30

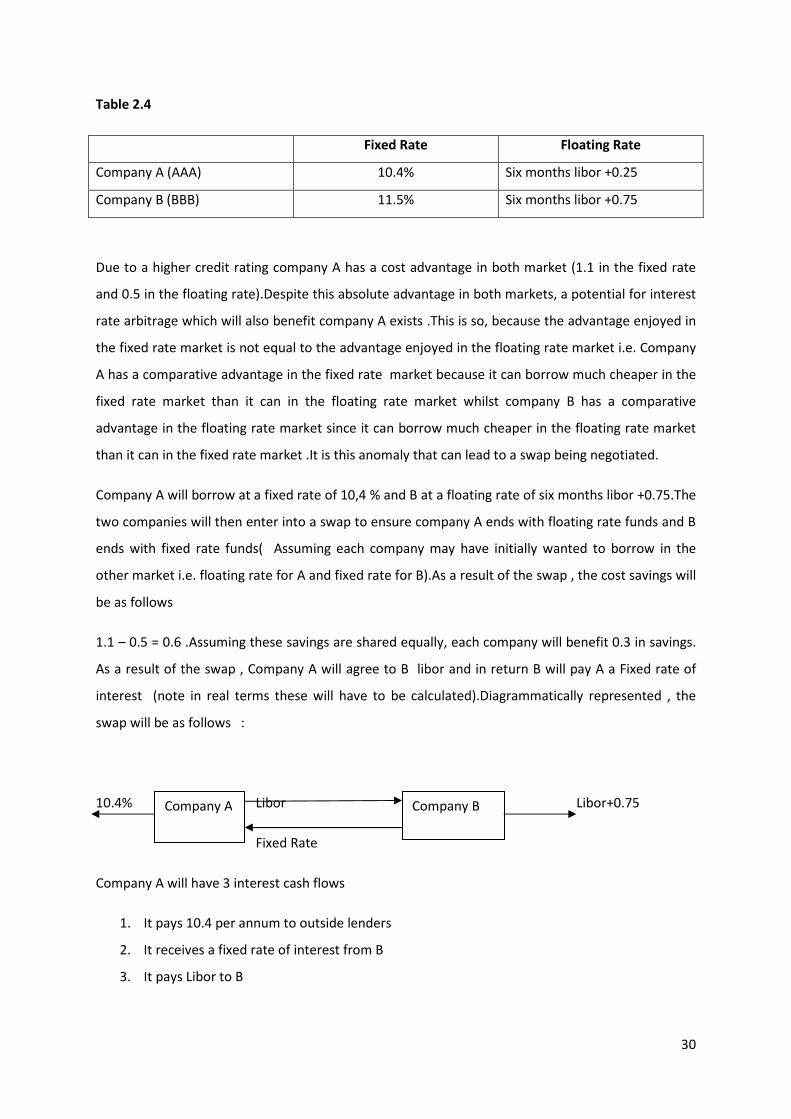

Table 2.4

Fixed Rate Floating Rate

Company A (AAA) 10.4% Six months libor +0.25

Company B (BBB) 11.5% Six months libor +0.75

Due to a higher credit rating company A has a cost advantage in both market (1.1 in the fixed rate

and 0.5 in the floating rate).Despite this absolute advantage in both markets, a potential for interest

rate arbitrage which will also benefit company A exists .This is so, because the advantage enjoyed in

the fixed rate market is not equal to the advantage enjoyed in the floating rate market i.e. Company

A has a comparative advantage in the fixed rate market because it can borrow much cheaper in the

fixed rate market than it can in the floating rate market whilst company B has a comparative

advantage in the floating rate market since it can borrow much cheaper in the floating rate market

than it can in the fixed rate market .It is this anomaly that can lead to a swap being negotiated.

Company A will borrow at a fixed rate of 10,4 % and B at a floating rate of six months libor +0.75.The

two companies will then enter into a swap to ensure company A ends with floating rate funds and B

ends with fixed rate funds( Assuming each company may have initially wanted to borrow in the

other market i.e. floating rate for A and fixed rate for B).As a result of the swap , the cost savings will

be as follows

1.1 – 0.5 = 0.6 .Assuming these savings are shared equally, each company will benefit 0.3 in savings.

As a result of the swap , Company A will agree to B libor and in return B will pay A a Fixed rate of

interest (note in real terms these will have to be calculated).Diagrammatically represented , the

swap will be as follows :

10.4% Libor Libor+0.75

Fixed Rate

Company A will have 3 interest cash flows

1. It pays 10.4 per annum to outside lenders

2. It receives a fixed rate of interest from B

3. It pays Libor to B

Company A Company B

31

Company B will also have 3 sets of cash flows:

1. It pays Libor + 0.75 to outside lenders

2. It receives libor from A

3. It pays a fixed rate to A

32

STUDY UNIT THREE

ASSET AND LIABILITY MANAGEMENT

This is the proactive management of both sides of the Balance Sheet, with a special emphasis on

management of interest rate and liquidity risk. The objective of liquidity risk management is to avoid

a situation where the net liquid assets are negative i. e. to ensure the returns on assets are not less

than the returns on liabilities. ALM involves the pairing or matching of assets i.e. customer loans and

mortgages and liabilities i.e. customer deposits so that changes in interest rates do not adversely

impact the organisation.ALM should guarantee payment of future cash flows.

Asset and Liability Management Policy

This is a recommended asset and liability management plan including a strategy for the management

of interest rate risk, liquidity risk and all other risks. It should state the goals of asset and liability

management, composition of the ALCO committee, duties of the ALCO, reporting requirements of

the ALCO, and provisions for risk weighted capital for all risks identified.

The Asset and Liabilities Committee

Banks have a committee comprising of senior management of the bank to make important decisions

related to the bank. This committee is typically referred to as the Asset and Liability Committee

(ALCO). The specific functions of ALCO are as follows:

• To receive and review reports on all risks and capital management.

• To identify balance sheet management issues like balance sheet gaps, interest rate gaps or

profiles that are leading to underperformance.

• To review deposit pricing strategy for the local market.

• To review contingency plans for the bank.

• To review changes in the money market.

• To monitor, measure and manage interest rate and all forms of risk.

• To review pricing of loan products.

• Discuss the introduction of new products

• To review the financial institution`s or the bank`s reputation in the market

33

Composition of the ALCO

In most financial institutions, the treasury department is responsible for asset and liability

management .Ideally the Treasurer or the CEO is the chairman of the ALCO committee. The

committee may also consist of the following key personnel in the bank:

• Chief Executive Officer or Managing Director

• Head of Treasury

• Head of Corporate Finance

• Head of Corporate Banking

• Head of Consumer Bank

• Head of Information Technology

• Head of Research & Development

• Head of Human Resources

Asset and Liability Management Strategies

Asset and liabilities management strategies include the following

• Gap Analysis ( Already covered )

• Duration Analysis ( Already covered)

• Spread Management ( Already covered)

• Loan Deposit Ratio Analysis

The loan deposit ratio is the most common way used to see a bank`s liquidity position. A bank has to

ensure that its loan to deposit ratio is not too high as excessive lending ( High Loan Deposit Ratio )

may expose the bank to liquidity and interest rate risk.

• Immunisation

This is a technique in which the one purchases a portfolio of securities /bonds whose weighted

average duration is equal to the horizon date of his/ her liabilities. E. g if you have pension

obligations with a horizon date of 3.55 years, you purchase bonds of the same duration such that in

the end the future horizon dates will be immunised.

• Cash flow Matching

This is a technique which involves finding the lowest cost portfolio that generates a pattern of cash

flows which exactly match the pattern of a future liability .The idea is to match the cash flow of the

portfolio with the cash flow of the liabilities.

34

Asset Securitization

Securitization is the transformation of illiquid assets into a security i. e. an instrument that can be

traded on the capital market. Assets that have been transformed in this manner include residential

mortgages, car loans, credit card receivables, leases and utility payments. The term asset-backed

security (ABS) is generally applied to issues backed by non-mortgage assets. Asset securitization

techniques are being embraced in countries the world over, seeking to promote home ownership, to

finance infrastructure growth, and to develop their domestic capital markets.

The securitization Process

In a typical structure, asset securitization works as follows:

• A lender such as a bank, finance company or corporation, originates loans e.g. hire purchase

loans, instalment loans, leases, or credit card receivables. Typically, the financial institution

wishes to expand, but finds that its capital and the term financing available to it are

insufficient to support the desired expansion of its business.

• The securitization structure is developed. A new legal entity is created, a special purpose

vehicle (SPV), purely for the purpose of holding and financing the assets to be securitized.

The originator will sell or assign certain assets, such as its car loan receivables, to the SPV.

The nature of the transfer and the legal status of the SPV vary from issue to issue and

require careful design.

• The assets to be securitised are chosen and are designed to obtain a higher credit rating

from a major credit rating agency and then the SPV sells securities backed by these assets to

investors, promising to pay a given interest rate. Credit Enhancement can be done through

any of the following (1) Employing a prudent criteria in screening assets (2) Credit

improvement at the SPV level, where the SPV is designed such that it is bankruptcy remote

i.e. , anticipated cash flows from the assets exceed the scheduled principal and interest

payment (3 ) Third-party credit enhancement, such as a guarantee purchase from a

specialized financial guarantee company, which itself has a top credit rating. The SPV issues

one or more classes of securities paying defined interest rates, and gives the money it

receives from investors to the seller of the assets.

• Over time, the payments from borrowers to the originator are processed by a servicer

(typically the originating institution itself). The servicer passes the interest, principal and fee

payments from the borrowers, less servicing fees, to the SPV. The SPV in turn pays a

predefined interest rate to the investors, plus any principal repayments, according to the

35

terms of the ABS. The seller/servicer may also accrue excess servicing income, i.e. the

difference between the assets’ revenues and all costs.

• When all principal payments have been made and the securities have accordingly matured,

the SPV is extinguished and any remaining assets (including cash) are returned to the

originating bank or firm.

When is it necessary to securitize?

The brief answer is that it makes sense to securitize when assets can be transformed and clarified , a

process that makes them more valuable to investors outside a company than they are to the

company itself. However, if the debt market is efficient and investors know the company’s condition

with and without the assets, securitization may not, in fact, lower its cost of capital. Nonetheless, it

is frequently the case that even if a company sells its best assets, the cost of the remainder of its

debt is unaffected. Capital requirements and mandatory reserves give financial institutions an

incentive to fund assets at a lower cost and free up their capital. On this basis, securitization has

been adopted by many banks and savings institutions as a means of reducing regulatory capital

requirements without noticeably raising their cost of capital. Where investors have poor information

about the issuing company, or do not like its management, or where the capital market suffers other

imperfections, asset securitization can be a technique that benefits both issuer and investor.

How originators benefit from securitization

Originators gain from securitization by obtaining many of the benefits of high credit-quality financing

without retaining the debt on their books and without foregoing profitable aspects of the assets,

including origination, servicing, expansion of business, and retention of excess spread. The price paid

is that the technique can be complex and may require a significant initial investment of managerial

and financial resources. For those companies willing to make this investment, there can be

significant and permanent advantages from having access to the asset-backed market. These include

the following:

Assets removed from the balance sheet. If structured as a sale, securitization can allow the issuer to

reduce its assets and its debt, thereby increasing its scope for borrowing. In effect, securitization

allows a bank or business to achieve greater leverage.

Retention of servicing revenues. The seller normally continues as servicer, retaining the servicing

fees, the excess of the SPV’s revenue over costs, and surplus collateral once the ABS are redeemed

36

Lower financing costs. Well-regarded pools of assets owned by a company or bank can be used to

structure a security of higher credit quality and, therefore, of lower market cost than the corporate

entity could issue itself.

Reduction in required capital. For a bank or finance company that faces regulatory capital

requirements, a securitization transaction that qualifies as a sale of assets for bank-regulatory

purposes reduces the need for equity financing. The latter may be costly and hard to obtain, and it

may dilute control.

Retention of competitive advantage. Securitization allows for a reduction in assets without the sale

of a business franchise and often with the retention of much of the earning power of the assets.

Nondisclosure. For privately held companies, securitization can offer a means of raising public debt

without extensive disclosure of proprietary information. Instead, disclosure is confined to the

characteristics of the assets being securitized and, perhaps, the servicing capabilities of the

originator.

Recognition of gains (or losses). Depending on accounting rules, a securitization structured as a sale

of assets may allow a seller to recognize an accounting gain (or loss) equal in the aggregate to the

present value of any expected future cash flows payable to the seller that will be derived from the

assets.

Improved asset/liability management. Securitization of assets allows the selling institution to

arrange debt issues to fund assets whose payments are perfectly matched to the cash flows on the

assets. This transfers the funding-mismatch risk to those more willing or able to bear it, such as

those who have an opposite mismatch.

How Investors Benefit

Superior return. The main benefit from the investor's viewpoint is a higher return or spread than is

generally available on corporate or sovereign debt of a similar rating.

Liquidity. The securitization structure offers far greater liquidity than do the individual loans backing

the transaction.

Diversification. Investors gain an opportunity to diversify their portfolios by participating in a

different class of assets.

37

Mitigation of event risk. Unlike similar, high-rated corporate bonds, asset-backed securities are

largely immune from event risk. The latter results from takeovers, restructurings and other events

that effectively alter the credit status of senior unsecured corporate obligations.

Coping with Constraints. Many institutional investors are constrained to purchase only investment

grade securities, and some are limited to triple-A paper. Both requirements can be met in the ABS

market.

Effects on the National Economy

Effects of securitization on the national economy include:

• Capital market development, as more high-quality securities are added to the fixed-income

market.

• A source of funds for rapidly growing, capital-constrained, banks, finance companies and

industrial companies whose expansion depends on the extension of credit to their

customers.

• An expanded source of financing for residential home ownership.

• The potential for financing of infrastructure projects, such as toll roads, that produce

reliable revenue streams capable of being contractually assigned to a separate legal entity.

38

Study Unit Four

Investment /Fund Management

For the kingdom of heaven is as a man travelling into a far country, who called his own servants, and

delivered unto them his goods. And unto one he gave five talents, to another two, and to another

one; to every man according to his several ability; and straightway took his journey. Then he that had

received the five talents went and traded with the same, and made them other five talents. And

likewise he that had received two, he also gained other two. But he that had received one went and

digged in the earth, and hid his lord's money. After a long time the lord of those servants cometh,

and reckoneth with them. And so he that had received five talents came and brought other five

talents, saying, Lord, thou deliveredst unto me five talents: behold, I have gained beside them five

talents more. His lord said unto him, well done, thou good and faithful servant: thou hast been

faithful over a few things, I will make thee ruler over many things: enter thou into the joy of thy lord.

He also that had received two talents came and said, Lord, thou deliveredst unto me two talents:

behold, I have gained two other talents beside them. His lord said unto him, well done, good and

faithful servant; thou hast been faithful over a few things, I will make thee ruler over many things:

enter thou into the joy of thy lord. Then he which had received the one talent came and said, Lord, I

knew thee that thou art a hard man, reaping where thou hast not sown, and gathering where thou

hast not strewed: And I was afraid, and went and hid thy talent in the earth: lo, there thou hast that

is thine.

From the paragraph above, it is clear that the history of investment/ fund management dates back

to centuries and its fundamentals have always been the same over time. An investor (the master),

makes an investment into a wide range of assets/ investment companies (the servants) for a given

time period, at the end of which/ he / she expects a holding period return (HPR). The HPR for the

first servant is 100% , so is that of the second servant and 0 % for the last servant .As is the case

with modern day investment, in medieval times ,a good investment manager was rewarded , in the

parable, the first servant gained the joy of the Lord, and so did the second .Again as is the case with

modern times, in medieval times the unprofitable investment manager would be discarded by

investors , as is the case with the third servant , sent into outer darkness , where there shall be

weeping and gnashing of teeth .

Investment / Fund Management Defined

Investment or fund management refers to the collection of funds from individual investors and

investing these funds in a potentially wide range of securities or other assets. Pooling of assets is the

key behind investment management. Each investor therefore has a claim to the portfolio established

by the investment company in proportion to the amount invested.

Functions of a fund/ investment company

Investment companies perform the following functions for their investors:

39

• Record Keeping and Administration

Investment companies issue periodic status reports, keeping track of capital gains distributions,

dividends, investments and redemptions.

• Diversification and Divisibility

By pooling their money, investment companies enable investors to hold fractional shares of many

different securities.

• Professional Management

Fund managers / investment companies always attempt to achieve superior investment results for

their investors.

• Lower Transaction Costs

Because they trade large blocks of securities, investment companies can achieve substantial savings

on brokerage fees and commissions

The Net Asset Value (NAV)

While investment companies pool assets of individual investors , they also need to divide claims to

those assets among those investors .Investors buy shares in investment companies and ownership is

proportional to the number of shares purchased. The value of each share is the Net Asset Value ,

which is calculated as follows:

NAV= Market Value of Assets less Liabilities / Shares Outstanding

Example : Class Working

Consider a mutual fund that manages a portfolio of securities worth $ 120 million. Suppose the fund

owes $4 million to its investment advisers and another $1 million for rent and wages and that the

fund has 5 million shareholders. Calculate the fund`s net asset value. Answer $23 / share

Types of Investment Companies/ Funds

Unit Investment Trusts (Unmanaged Trusts)

These are pools of money invested in a portfolio that is fixed for the life of the fund. To form a unit

investment trust, a sponsor e.g. brokerage firm buys a portfolio of securities which are deposited

into a trust. It then sells to the pubic shares or units in the trust. All income and payments of

principal from the portfolio are paid out by the fund`s trustee e.g. a bank or trust company to the

40

shareholders. Most unit trusts invest in stocks and fixed investment securities. Unit investment

trusts earn their profit by selling shares in the trust at a premium to the cost of acquiring the

underlying asset.

Managed Investment Companies

Managed investment companies are of two types, closed end and open end funds. In both cases the

fund`s board of directors, which is elected by shareholders hire a management company to manage

the portfolio for an annual fee.

Open End Funds

These stand ready to redeem or issue shares at the net asset value i.e. when investors wish to cash

out, they sell shares back to the fund at net asset value.

Closed End Funds

Investors in closed end funds who wish to cash out must sell their shares to other investors’ .Shares

of close -end funds are traded on organised exchanges and can be purchased through brokers just

like other common stock, therefore their price can differ from the net asset value. Closed end funds

are again sold at a premium but are actively managed i.e. the composition of the funds is actively

managed.

Other Investment Funds

Commingled Funds

Commingled funds are partnerships of investors that pool their funds. The management firm that

manages the partnership e.g. a bank or insurance company manages the funds for a fee. Examples of

commingles funds might be trust accounts which have portfolios that are larger than those of most

individual investors but are too small to warrant managing on a separate basis. Commingled funds

are similar in form to open –end funds but instead of shares the fund offers units which are bought

or sold at net asset value. A bank or insurance may offer an array of different types of commingled

funds e.g. money market funds, bond funds, common stock funds.

41

Mutual Funds

This is the common name for open –end investment funds. Each mutual fund has a specified

investment policy which is described in the fund`s prospectus. They can be classified by investment

policy e.g.

Equity funds

These invest in equities

Money market funds

These invest in money market securities

Fixed income funds

These invest in fixed income securities

Balanced income funds

These hold both equities and fixed income securities in stable proportions

Asset Allocation funds

These are funds which invest in stocks and bonds but may vary the proportions allocated to each

market in accordance with the portfolio manager`s forecast of the relative performance of each

sector.

Index Funds

These are funds that try to match the performance of a broad market index. The fund buys shares in

securities included in a particular index in proportion to each security`s representation in that index

e.g. Vanguard`s 500 mutual index replicates the S&P 500.

Specialised Sector Funds

These concentrate on a particular industry.

Real Investment Trusts

These invest in real estate .They can be of 2 types. Equity and mortgage Trusts. Equity trusts invest in

real estate stocks whereas mortgage trusts invest in mortgage and construction loans.

Investment Fees on Mutual Funds

There are four general classes of fees

• Front End-Load Fees

This is a commission charge paid when one purchases shares

42

• Back – end Load Fees

This is a redemption or exit fee incurred when you sell shares

• Operating Expenses

These are costs incurred by the fund in operating the portfolio

• Other Charges

These include commissions, advertisements, promotional literature for the fund

Exchange Traded Funds (ETFs)

These are offshoots of mutual funds that allow the investor to trade index portfolios in the same

way as trading stock. An ETF tracks an underlying index i.e. they are designed to replicate an

index performance. Unlike mutual funds which can only be sold at the end of the day when NAV

is calculated, ETFs can be traded throughout the day. Also, unlike in mutual funds where

redemption of funds by large investors can lead to the mutual fund selling the underlying

security, in ETFs investors who want to redeem their funds simply sell their shares to other

traders , with no need to sell the underlying portfolio. ETFs, just like stock also have a price at

which they trade and are traded on exchanges just kike stocks. An ETF might consist of various

stocks which are held in the fund .Investors invest in these funds through buying shares within

the fund. The fund`s composition is set up to replicate an underlying index. E.gs include SPDR

which tracks the S&P 500, WEBS by Barclays which tracks MSCI country indices, DOW Diamonds

which track the Dow Jones, NASDAQ QQQQ which replicate the NASDAQ-100.

Hedge Funds

There is no general definition for hedge funds .However; they can be defined as according to the

general characteristics that are common with most hedge funds .Hedge funds can hence be

defined as an aggressively managed portfolio of investment that uses advanced investment

strategies and derivative positions in both domestic and international markets with the goal of

generating high returns (supernormal returns). Previously hedge funds were loosely regulated,

but as a result of the role played by hedge funds in leading to the global financial crisis that

gripped the world in 2008, there were calls for more strict regulation of hedge funds and

eventually legislation around global financial markets was changed to curb some of the negative

effects hedge funds have on the financial markets. Hedge funds are mainly set up as private

partnerships that are open to a limited number of investors and require a very large initial

deposit.

43

Characteristics of Hedge Funds

• Hedge funds are loosely regulated as compared to other funds within financial markets.

• They require a large initial deposit.

• They are usually open to a limited number of people.

• Investment in these funds is illiquid as funds are tied up for a minimum of one year

• The aim of hedge funds is to get extremely high returns.

• Hedge funds face many risks since they invest in all financial instruments but are overally

less risky because of the element of diversification .

• They have a limited liability element in that investors have no liability for losses beyond

their initial investment.

• Hedge funds usually use leverage in excess of their capital to take long and short positions in

financial markets.

• Hedge funds charge substantial incentive and management fees.

Contrasting Mutual Funds with Hedge Funds

• Fees

Most mutual funds charge management fees but not incentive fees. The management fees charged