Hermawan Kartajaya BANKING COMPETITION IN 2013 IN THE TIME OF REGULATORY TRANSITION

COMPETITION IN THE EUROPEAN BANKING SECTOR

by

Ioannis Samantas

A thesis submitted in partial fulfilment of the requirements for the degree

of Doctor of Philosophy (DPhil)

National and Kapodistrian University of Athens

Department of Economics

2013

ii

I Ioannis Samantas declare that the work presented in this PhD thesis is my own.

ii

Acknowledgments

This thesis is dedicated to Grigoris and Mary, my parents, Kalliopi, my grandmother

and Thanassis, my brother. Had there not been their patience as well as their

emotional and financial support, that thesis would not reach its completion.

I wish to thank my principal supervisor, Prof. Panayotis Alexakis for his

encouragement, guidance and support during my thesis-writing phase. His availability

upon my request for any issues popped up, and sincere interest in my progress are

deeply appreciated. I also owe sincere thanks to the other two members of my thesis

scientific committee, Prof. Yannis Bilias and Prof. Manolis Xanthakis for their

advice.

I also wish to express my gratitude to Bank of Greece and, especially, to Prof. Ioannis

Papadakis, Deputy Governor of Bank of Greece, and Dr. Heather Gibson, Director-

Advisor in the Economic Research department of Bank of Greece, for granting me

with access to bank-specific data of the Bankscope database. Without their assistance,

I could not possibly move on to the econometric analysis of my thesis.

I onw special thanks to the participants of the XXI European Workshop on Efficiency

and Productivity Analysis (EWEPA), the 18th Annual Conference of Multinational

Finance Society, the conference on Advances in Financial and Insurance Risk

Management, the International Conference on Applied Business and Economics and

the 10th Annual Conference of the Hellenic Finance and Accounting Association for

their valuable comments.

Last but not least, I am also indebted to my close friends in Greece and abroad for

being patient and supportive with me, and for making my life emotionally ample and

consistent.

iii

Table of contents

CHAPTER 1 PROLEGOMENA ........................................................................................... 1

1.1. General standpoint .......................................................................................................... 3

1.2. Research questions........................................................................................................... 5

1.3. Contribution of the thesis ................................................................................................ 8

1.4. Structure of the thesis .................................................................................................... 12

CHAPTER 2 COMPETITIVE ISSUES .............................................................................. 17

2.1. Introduction .................................................................................................................... 19

2.2 Institutional perspective .................................................................................................. 20

2.2.1 Efficiency ................................................................................................................... 20

2.2.2 Consolidation .............................................................................................................. 22

2.2.3 Relationship banking .................................................................................................. 24

2.3 Macro finance perspective .............................................................................................. 26

2.3.1 Regulatory developments ........................................................................................... 26

2.3.1.1 International initiatives ....................................................................................... 28

2.3.1.2 Towards a single EU financial market ................................................................ 36

2.3.1.3. Basel III – framework in progress ...................................................................... 42

2.3.1.4. Free banking ....................................................................................................... 46

2.3.2. Integration ................................................................................................................. 47

2.3.3. Financial stability ...................................................................................................... 49

1.4. Conclusion ....................................................................................................................... 52

CHAPTER 3 EMPIRICAL MODELS OF COMPETITION IN THE EUROPEAN

BANKING .............................................................................................................................. 53

3.1. Introduction .................................................................................................................... 55

3.2. Non-formal structural methods ..................................................................................... 55

3.2.1. The Structure – Conduct – Performance (SCP) paradigm - The relative efficiency

(RE) hypothesis ................................................................................................................... 55

3.2.2. Formal structural approaches .................................................................................... 60

3.2.2.1. The HHI in a S – P model ................................................................................... 62

3.2.2.2. The CRk in a S - P model ................................................................................... 65

iv

3.2.3. Concentration ratios................................................................................................... 66

3.2.3.1. The k bank concentration ratio ........................................................................... 68

3.2.3.2. Herfindah - Hirschman Index (HHI) .................................................................. 69

3.2.3.3. The Hall - Tideman Index (HTI) and Rosenbluth Index (RI) .............................. 71

3.2.3.4. The comprehensive industrial concentration measure ....................................... 72

3.2.3.5 The Hannah and Kay index ................................................................................. 73

3.2.3.6. The U index......................................................................................................... 74

3.2.3.7. The Hause indices ............................................................................................... 75

3.2.3.8 Entropy measure .................................................................................................. 77

3.3. Non-structural methods ................................................................................................. 78

3.3.1. The New Empirical Industrial Organisation (NEIO) approach ................................. 78

3.4. Alternative models .......................................................................................................... 83

3.5. Review of empirical analysis .......................................................................................... 91

3.5.1. Panzar – Rosse methodology ..................................................................................... 91

3.5.1.1. Cross-country comparisons ................................................................................ 91

3.5.1.2. Country-specific studies ..................................................................................... 94

3.5.2. Bresnahan-Lau methodology ..................................................................................... 97

3.5.2.1. Cross-country applications................................................................................. 97

3.5.2.2. Country-specific studies ..................................................................................... 97

3.5.3. Lerner index .............................................................................................................. 99

3.6. Conclusion ..................................................................................................................... 100

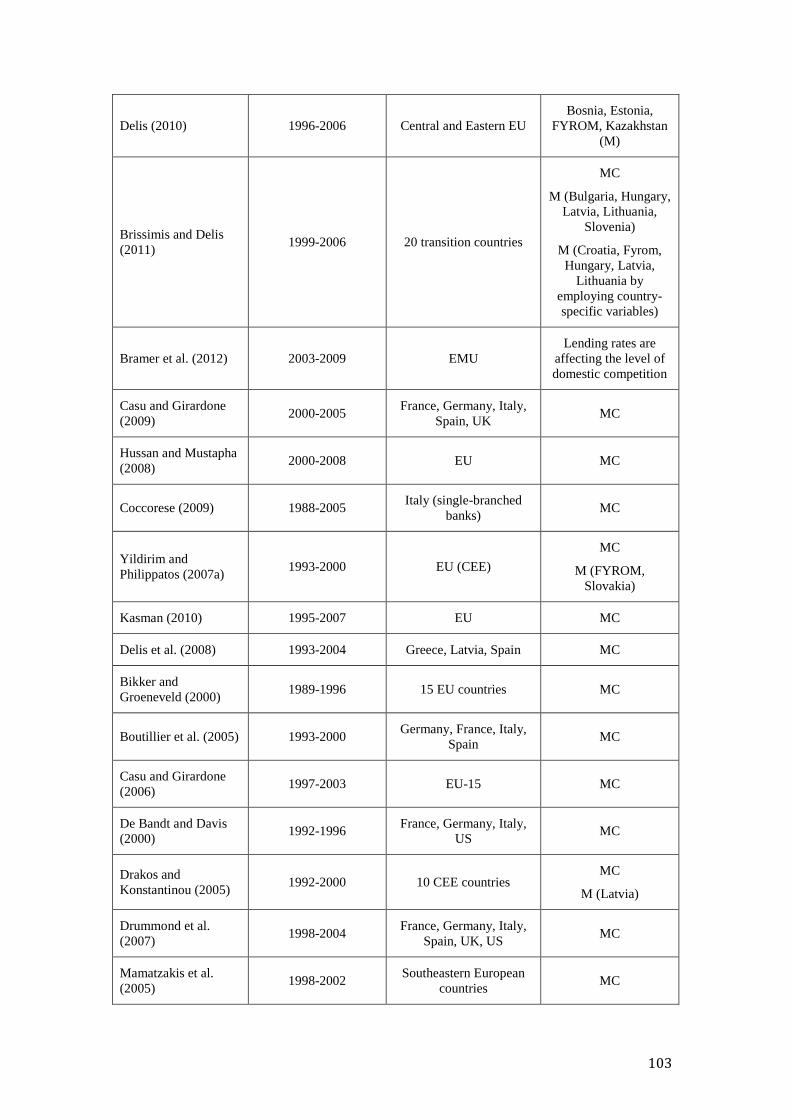

Chapter 3 Appendix ............................................................................................................ 101

CHAPTER 4 A REVIEW OF EFFICIENCY ANALYSIS ............................................. 111

4.1. Introduction .................................................................................................................. 113

4.2. Definition of bank ......................................................................................................... 113

4.3. Measurement of X – efficiency .................................................................................... 114

4.3.1. Parametric approaches ............................................................................................. 115

4.3.1.1. The Stochastic Frontier Analysis ...................................................................... 115

4.3.1.2. Distribution-free approach ............................................................................... 116

4.3.1.3. Thick frontier approach .................................................................................... 117

4.3.2. Non-parametric approaches ..................................................................................... 120

4.3.2.1. Data Envelopment Analysis .............................................................................. 120

4.3.2.2. The free disposal Hull approach ...................................................................... 122

4.4. Review of empirical applications ................................................................................ 125

4.4.1. International comparisons ....................................................................................... 125

4.4.2. European cross-country comparisons ...................................................................... 129

v

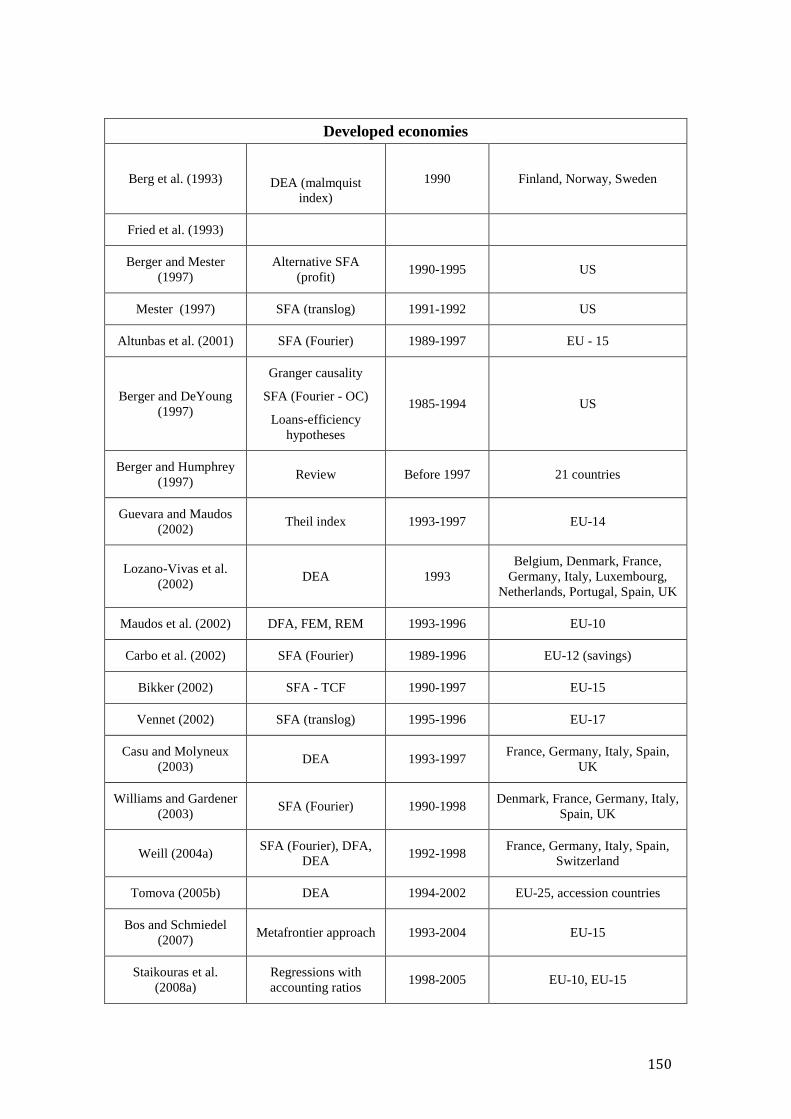

4.4.3. Developed economies .............................................................................................. 133

4.4.4. Transition economies............................................................................................... 137

4.4.5. Country – specific studies ....................................................................................... 141

4.5. Conclusion ..................................................................................................................... 148

Chapter 4 Appendix ............................................................................................................ 149

CHAPTER 5 THE NEXUS BETWEEN BANK COMPETITION AND FINANCIAL

STABILITY ......................................................................................................................... 155

5.1. Introduction .................................................................................................................. 157

5.2. Theory............................................................................................................................ 157

5.3. Empirical review ........................................................................................................... 162

5.4. Conclusion ..................................................................................................................... 167

Chapter appendix..................................................................................................................157

CHAPTER 6 INCOME-SPECIFIC ESTIMATES OF COMPETITION IN EUROPEAN

BANKING ............................................................................................................................ 177

6.1. Introduction .................................................................................................................. 179

6.2. Methodology .................................................................................................................. 180

6.3. Competition determinants ........................................................................................... 183

6.4. Data ................................................................................................................................ 185

6.5. Results............................................................................................................................ 189

6.6. Conclusion ..................................................................................................................... 213

CHAPTER 7 COST AND PROFIT EFFICIENCY IN EUROPEAN BANKING:

COMPARISON OF PARAMETRIC METHODOLOGIES AND CONVERGENCE

DYNAMICS ......................................................................................................................... 217

7.1. Introduction .................................................................................................................. 219

7.2. Methodological issues ................................................................................................... 222

7.3. The model ...................................................................................................................... 225

7.4. Sample - Evidence ........................................................................................................ 228

7.5. Scale economies ............................................................................................................. 240

vi

7.6. Convergence .................................................................................................................. 245

7.7. Other stylized facts ....................................................................................................... 250

7.8. Conclusion ..................................................................................................................... 254

Chapter 7 appendix ............................................................................................................. 256

CHAPTER 8 BANK COMPETITION AND FINANCIAL (IN)STABILITY IN

EUROPE: A SENSITIVITY ANALYSIS ......................................................................... 263

8.1. Introduction .................................................................................................................. 265

8.2. Methodology .................................................................................................................. 266

8.3. The model ...................................................................................................................... 269

8.4. Determinants of stability .............................................................................................. 272

8.4.1. Bank-specific variables ........................................................................................... 272

8.4.2. Macroeconomic variables ........................................................................................ 273

8.4.3. Regulatory environment .......................................................................................... 273

8.5. Data ................................................................................................................................ 275

8.6. Main results ................................................................................................................... 281

8.7. Does the effect of market structure variables alter with the interplay between

regulation and ownership? ................................................................................................. 292

8.8. Are there other governance indicators that enter non-linearly? .............................. 295

8.9. Are the results robust to alternative measures of risk? ............................................ 298

8.10. How market structure variables behave per specialization group? ...................... 303

8.11. Other robustness checks ............................................................................................ 305

8.12. Conclusion ................................................................................................................... 308

Chapter 8 Appendix ............................................................................................................ 311

CHAPTER 9 SYNOPSIS .................................................................................................... 317

9.1. Major findings of the research .................................................................................... 319

9.2. Policy implications of the research ............................................................................. 325

9.3. Limitations of research ................................................................................................ 329

9.4. Suggestions for further research ................................................................................. 331

REFERENCES .................................................................................................................... 333

THESIS APPENDIX ........................................................................................................... 390

vii

List of tables

TABLE 1: NUMBER OF BANKS .............................................................................................................. 186

TABLE 2: SUMMARY STATISTICS OF VARIABLES IN MODEL 6.1 .............................................................. 187

TABLE 3: SUMMARY STATISTICS OF VARIABLES IN MODELS 6.4 AND 6.5 ............................................. 188

TABLE 4: MARGINAL COSTS AND LERNER INDEXES ................................................................................. 190

TABLE 5: REGRESSION OUTPUT (WHOLE SAMPLE) ................................................................................... 191

TABLE 6: REGRESSION OUTPUT PER BANK TYPE ....................................................................................... 196

TABLE 7: SUR FOR COMMERCIAL BANKS ................................................................................................... 200

TABLE 8: SUR FOR COOPERATIVE BANKS .................................................................................................. 204

TABLE 9: SUR FOR SAVINGS BANKS ............................................................................................................. 207

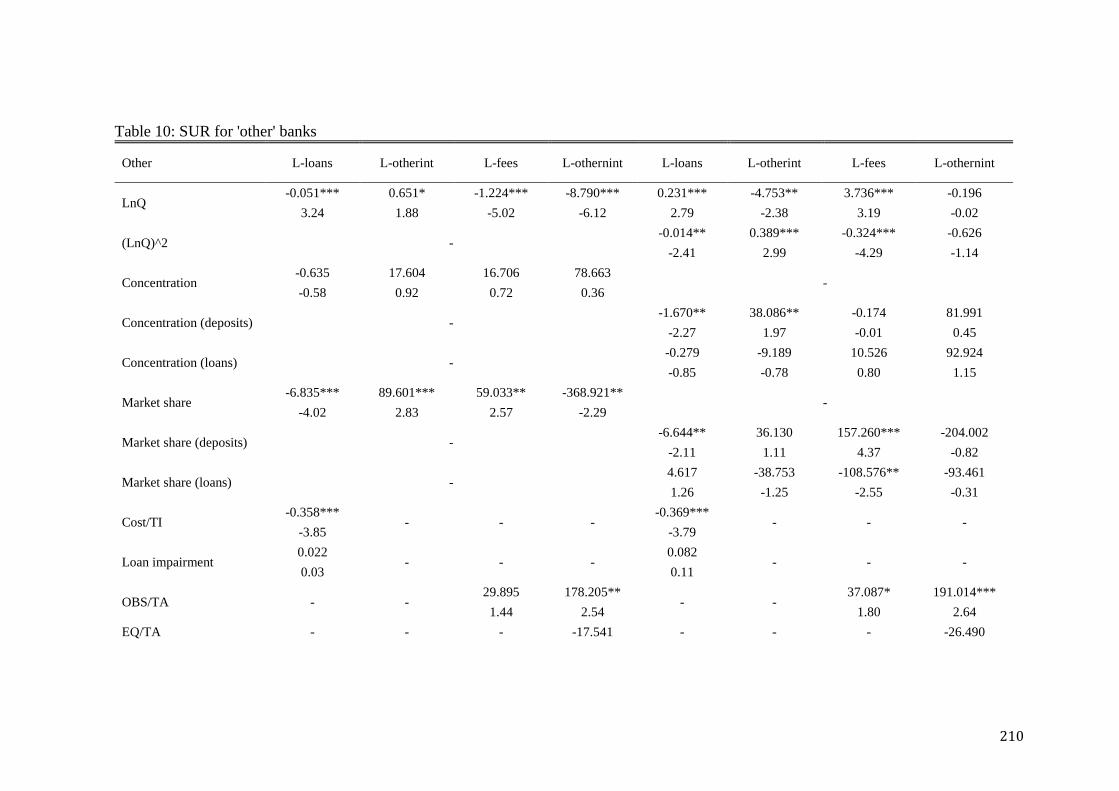

TABLE 10: SUR FOR 'OTHER' BANKS ........................................................................................................... 210

TABLE 11: NUMBER OF BANKS ...................................................................................................................... 229

TABLE 12: COST EFFICIENCY (INTERMEDIATION APPROACH) ............................................................... 231

TABLE 13: COST EFFICIENCY (VALUE-ADDED APPROACH) ..................................................................... 233

TABLE 14: PROFIT EFFICIENCY (INTERMEDIATION APPROACH) ........................................................... 235

TABLE 15: PROFIT EFFICIENCY (VALUE-ADDED APPROACH) ................................................................. 237

TABLE 16: COST/PROFIT EFFICIENCY BY PRODUCTIVE SPECIALISATION AND ASSET CLASS ............ 239

TABLE 17: SCALE ECONOMIES BY COUNTRY .............................................................................................. 241

TABLE 18: SCALE ECONOMIES BY BANK TYPE AND ASSET CLASS .......................................................... 244

TABLE 19: Β-CONVERGENCE AND Σ-CONVERGENCE OF COST EFFICIENCY .......................................... 248

TABLE 20: Β-CONVERGENCE AND Σ-CONVERGENCE OF PROFIT EFFICIENCY ...................................... 249

TABLE 21: DISTRIBUTION OF COST/PROFIT EFFICIENCY ......................................................................... 253

TABLE 22: DESCRITIVE STATISTICS OF KEY VARIABLES ......................................................................... 277

TABLE 23: CORRELATION BETWEEN COUNTRY-LEVEL VARIABLES ...................................................... 280

TABLE 24: REGRESSION OUTPUT OF MODEL 8.1 ........................................................................................ 283

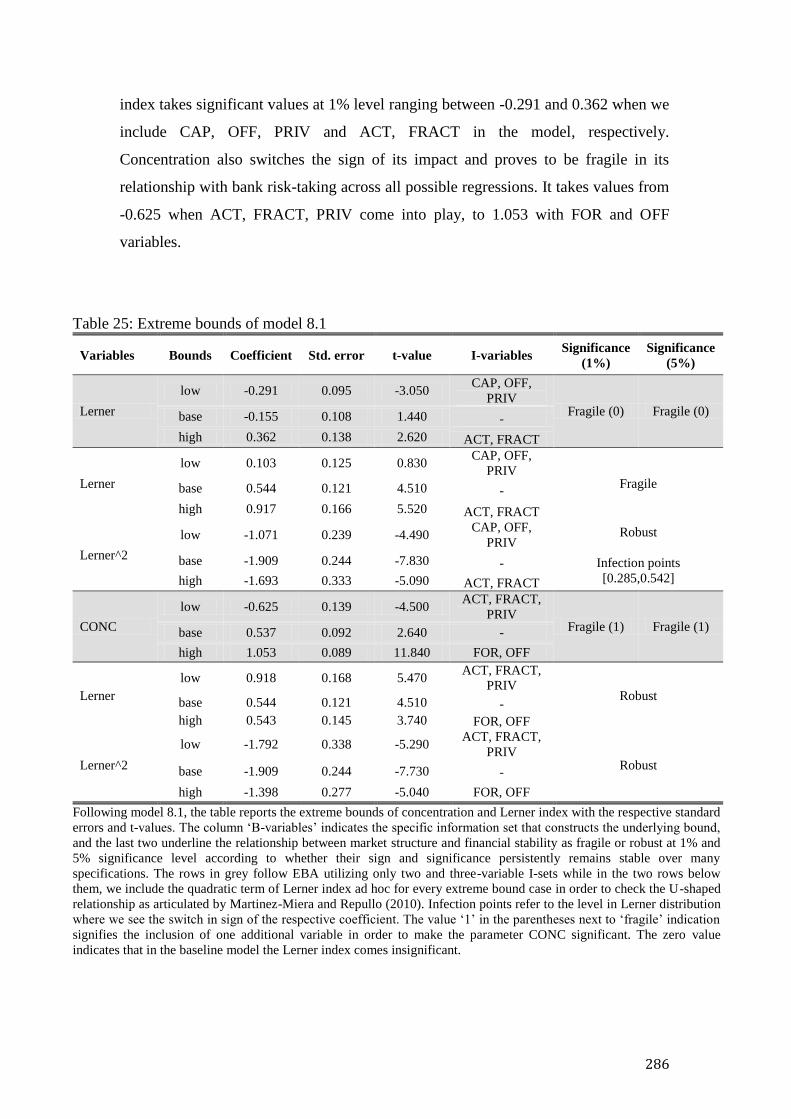

TABLE 25: EXTREME BOUNDS OF MODEL 8.1 ............................................................................................. 286

TABLE 26: REGRESSION OUTPUT OF MODEL 8.2 ........................................................................................ 288

TABLE 27: EXTREME BOUNDS OF MODEL 8.2 ............................................................................................. 291

TABLE 28: SENSITIVITY ANALYSIS OF MODEL 8.7 ..................................................................................... 294

TABLE 29: SENSITIVITY ANALYSIS OF MODEL 8.8 ..................................................................................... 297

TABLE 30: SENSITIVITY ANALYSIS OF MODEL 8.9 ..................................................................................... 299

TABLE 31: SENSITIVITY ANALYSIS WITH ALTERNATIVE MEASURES OF STABILITY ............................ 302

TABLE 32: MODEL 8.1 OUTPUT PER BANK TYPE ........................................................................................ 304

TABLE 33: FURTHER EBA OF MODEL 8.1 ................................................................................................... 306

TABLE 34: FURTHER EBA OF MODEL 8.2 ................................................................................................... 308

viii

Abstract

The aim of the thesis is to investigate the structure of banking sectors in the European

Union during the period 2002-2010. It encompasses the theoretical premises of bank

competition and how it is interrelated to contemporary issues in European banking.

For this purpose, the thesis comprises two parts; the former refers to the literature

review of theoretical and empirical analysis and, the latter, to the econometric

analysis.

The first aspect of this thesis is the measurement of the degree of competition in the

developed sub-group of European Union since the advent of Euro. We, therefore,

estimate the marginal cost out of a translog cost function and then investigate

potential correlates of income-specific estimates of market power for commercial,

cooperative and savings banks as well as other financial institutions.

We next compare parametric methodologies widely employed in the literature in

order to estimate cost and profit efficiency scores of financial institutions. In so doing,

we juxtapose the results from different definitions of bank outputs/inputs, namely the

intermediation and value-added approach. Other section reports time-varying

estimates of scale economies per banking market, bank type and asset class, while the

analysis concludes with the investigation of beta and sigma convergence of cost/profit

efficiency along with equality and other distribution issues.

The final part of the thesis deals with the competition-stability nexus; that is, whether

and to what extent bank competition and concentration drive to systemic stability or

fragility. We conduct sensitivity analysis of the underlying relationship subject to

different informational sets so as to construct the extreme bounds of their beta

coefficients and draw remarks on their statistical and sign persistence. The analysis

allows for non-linearities between competition and controls of regulation, ownership,

various governance indicators for robustness-checking reasons.

CHAPTER 1

Prolegomena

2

3

1.1. General standpoint

The operation of banks in the wake of a single currency system has had a considerable

impetus to the economic growth and financial stability of the European banking

sector. Social welfare is theoretically accomplished by the competitive conduct and

high economic efficiency of profit-maximising financial institutions. All firms and

consumers take advantage of the broad supply of banking services at low prices

within a context of fast-developing financial markets that eventually foster economic

development.

From a policy perspective, there exists a number of banking issues that have

embarked the academic debate and a series of international initiatives in order to

„unfreeze‟ the potential of financial system. To this end, structural reforms have taken

place since the „80s culminating in the advent of Euro and until the onset of current

financial crisis. In particular, banks increased the range of their products in response

to free trade of foreign-owned banks in domestic markets bringing about the

classification of the financial institutions with respect to their productive

specialisation. Hence, high competitive pressures have made banks engage in lower

costs, efficient risk management, new corporate governance structures and alternative

non-traditional income activities.

That dynamic tendency of integration comes under the Financial Service Action Plan,

which seeks to alleviate centrifugal forces that undermine the harmonisation in retail

and wholesale markets; European Commission (2002) identifies heterogeneous

consumer protection schemes, regulation, costly asset allocation and payment in

cross–border banking, among others. The premises of Basel Accord constitute a new

regime that imposes requirements on capital reserves with asymmetric implications on

competition and efficiency. In fact, capital requirements enable banks in the form of

better risk management to price competitively and thereby eschewing from cross-

subsidising practices followed in an unsystematic and unsophisticated way. In

contrast, it might be the case of banks aiming not at market shares but implementing

high prices to preserve their profit margins. Although pillar II sets out some degree of

supervisory discretion, which dismantles a level-playing field for all banking markets,

4

the estimation of capital requirements pertains to a portion of non-banking firms

through standard as well as sophisticated methods of quantifying risk.

The motivation towards greater consolidation is traced to the importance of the

aforementioned techniques. Standard methodology is preferable to smaller sized

banks, as it is less cumbersome and expensive than more advanced techniques, albeit

the estimated capital requirements in the former case constitute a greater burden than

that of the latter. Thus, mergers and acquisitions are motivated by the superior

structure of large banks to afford more expensive but effectively economising capital

reserves.

The ongoing financial crisis since 2008 has rendered the mandate of further reforms,

since in perfect hindsight we are able to cast doubt on traditional tenets in finance. For

example, the risk-free asset allocations on Treasury bills and other bonds turn out to

withhold a considerable risk once the exacerbation of country spreads (due to

speculation in fixed-income markets), institutional shortcomings and investment

shortage have put additional risks on banks‟ solvency. By the time politics and

banking go one step further to restructure the Euro zone, the institutional reform

seems to be advancing previous policies that have already been proved inadequate to

armour financial institutions in times of bank crises. Accordingly, the most

contemporary act of Basel Accord III expected to take place in 2013 builds upon the

premises of previous initiatives to strengthen banks by requiring more fraction of

common equity, Tier 1 capital and additional buffers in periods of high credit growth.

In a nutshell, competition constitutes a multidimensional concept of bank behaviour

and operation in a context of efficiently regulated financial system. If regulatory

initiatives do not effectively account of the importance of shadow banking system

along with financial innovation (derivatives) and off-balance sheet practices, negative

externalities are bound to expose the rickety financial apparatus vis-à-vis potential

shocks.

5

1.2. Research questions

The general purpose of this thesis is to shed some light on banking issues related to

competition. To this end, we assess the level of competition, efficiency and financial

stability and their interconnections amongst them as well as with contemporary

concepts of regulation and supervision, bank-level specificities and other

macroeconomic conditions. We classify the research questions into three groups

according to the three chapters (6, 7, 8) of the empirical part, which are theoretically

and empirically reviewed in chapters 3, 4 and 5. In particular, we provide answers to

the following research questions.

1. What is the level of competition in Europe? Are there any determinants of

competition with respect to specific sources of banking income? What does

the analysis tell us about the pricing conduct of differently specialized

financial institutions?

2. What is the level of cost and profit efficiency in European banking according

to different parametric methodologies and definitions of bank outputs/inputs?

Are relative rankings of banking markets, bank types and asset classes stable

across all specifications? What pattern has the evolution of scale economies

followed since 2003? Do we experience beta and sigma convergence of cost

and profit efficiency even after allowing for dynamic effects?

3. Does market structure variables drive to financial stability and to what extent?

Which are the bounds that their respective coefficients lie within? Is this

tendency persistent and robustly significant? Are there non-linearities among

competition, regulation, ownership and other governance indicators that

determine bank soundness? Are alternative measures of stability explained by

similar model specifications? Which banks are affected the most by market

structure?

6

Research question 1

This question highlights a new endeavour of investigating competitive conditions in

the European banking industry. Since the vast literature of competition modeling has

produced mixed results, the proposed methodology goes one step further De Guevara

et al. (2005), Bolt and Humphrey (2010) and Carbo et al. (2009) in order to produce

income-specific competition indicators providing the intensity of their key effects on

bank competition breaking further down the subsets of bank activities.

We therefore employ the translog cost function of Ariss (2010b) that omits the price

of borrowed funds as input price, since it may capture some degree of monopoly

power of incumbent banks in the deposit markets. Next, we construct Lerner indexes

with respect to total income as well as income on loans, other interest income, fees

and commissions and other non-interest income. As such indexes reflect unobserved

bank pricing on relative products, we employ Seemingly Unrelated Regression (SUR)

framework to run regressions concurrently and account thereby of the within error

correlation across the models.

The sample comprises nine of the most developed banking markets in the European

region during the period 2002-2010. In so doing, we draw remarks over the

explanatory power of traditional collusion, relative market power, efficiency and other

key controls on bank pricing conduct.

Research question 2

We aim to shed light on the comparison of different parametric methodologies in

measuring cost and profit efficiency in European banking. We therefore employ

REM, DEA their truncated versions at 1%, 5% and 10% of each distribution tail,

along with the TFA producing averaged efficiency scores at the bank level and its

time-varying specification. The analysis follows alternative definitions of bank

inputs/outputs, which seem to be widely applied in the literature, namely under the

intermediation and value-added approach. We report time-varying country averages to

conclude on relative rankings and their persistence across different specifications. We

next estimate economies of scale to see whether and to what extent they are evolving

through time per banking market, bank type and asset size class.

7

We also employ OLS and ADL specifications to verify the significance of „catching-

up effect‟ and dispersion of cost and profit efficiency according to IA and VA

approaches. We conclude on how the efficiency distribution shifted in terms of

skewness and kurtosis from 2003 to 2008, apart from the mean and standard deviation

of EU-15 and EU-12 European regions. We also observe whether the evolution of

cost and profit efficiency scores make banks more equal in the distribution of the

employed European sample.

Research question 3

We attempt to address the question of causality of bank soundness from market

structure variables in a sample of banks headquartering within the enlarged European

Union for the period 2002-2008. We utilize concentration and competition in a

sensitivity analysis that determine bank risk subject to different information sets of

regulatory, macroeconomic and bank specific factors. Due to our heterogeneous

sample, we employ Random Effects (RE) methodology to the baseline models that

allow for (non-) linearities between regulatory/supervisory factors and bank

competition. Thus, we implement extreme bound analysis of the values that the

Lerner and Herfindahl indexes can take across all the possible combinations of key

deterministic factors. Furthermore, we implement ad hoc regressions employing the

quadratic term of competition to verify whether it is the case of U-shaped relationship.

We also extend the analysis allowing for non-linear relationships between regulatory

and foreign ownership variables to see if market structure variables lie in the

estimated bounds. As a next step, interactions of competition and governance

indicators retrieved from the World Bank come into play for more robust results. And

last, we decompose the explanatory power of independent variables on alternative

measures of financial stability and systemic risk.

Last section of chapter 8 replicates the analysis for commercial, cooperative, savings

and „other‟ banks of the sample and provides support to the model fit that is

representatively attributed to certain bank specialisation groups.

8

1.3. Contribution of the thesis

The thesis pertains to the field of studying the level of bank-level competition and its

potential correlates in European banking. It investigates sample of 9 out of the most

developed banking markets since the advent of Euro whereas other papers deal with

the previous decade since the first years of Euro zone. Hence, it might be the case of

structural break around the year 2002 and even if it is econometrically feasible to

account of such institutional events, it does not make sense when comparing periods

before and after 2002, and from a policy perspective to verify how competition

evolves within the Euro system in conjunction with other competitive issues.

The per se fact that there is no extensive literature for the period 2002-2010 over a

heterogeneous European sample is attributed to the fact that Bankscope database has

no available data for European countries especially after 2005. Our attempt is to adapt

the methodology of cost and profit function to include the most available variables not

at the expense of model fit. We rely on the work of Ariss (2010b), who omits the

price of borrowed funds as input price in a version of the cost function as it could

capture some degree of monopoly power of large banks in the deposit markets. That

enables us to come up with competition-adjusted measures of marginal cost that is

subsequently employed to measure competition at the bank level (Lerner index).

Paper 1 updates the analysis of De Guevara et al. (2005) adding some other potential

correlates of competition, like credit risk, income diversification, equity capital,

liquidity, efficacy of regulatory laws and cyclicality with respect to price and

population effects. What seems totally new to the empirical literature is the estimation

of income-specific estimates of market power although it has no merit of cross-

country comparison. Our aim is to investigate how the aforementioned effects

determine simultaneously the pricing behaviour of certain banking products and to

what extent. In so doing, we replicate the analysis for every productive specialisation

group across different specifications allowing for sample asymmetries and

unobserved bank specificities. Thus, it is the first time that we can explain, at least

partially, differences on relative market power at the income level although the

mechanisms lying underneath are not a priori known.

9

Paper 2 contributes more on the literature that studies cross-country comparison of

efficiency in the European region, with a particular focus on various parametric

approaches. Non-parametric methodologies have produced quite divergent results and

given that data shortage brings about bias in the analysis, we opt to report even more

detailed evidence with truncated versions of random effects methodology (REM),

distribution free approach (DFA) and thich frontier approach (TFA). The problematic

application of SFA, failing to accomplish curvature conditions in the maximum

likelihood technique, advocates to our employed methoology.

We also extend the literature that applies both profit and cost functions and compares

the results across various regions or countries. The underlying juxtaposition of

efficiency scores is facilitated by the employment of different definitions of bank

outputs, which is addressed scarcely in a handful of studies. Scale economies come

out of the employed cost models and draw remarks on their evolution since 2002; in

contrast, almost all relevant studies seem outdated published before 2003 and

generally in the „90s. Last, convergence analysis for bank efficiency is a new area of

research and our application aims at contributing to this accumulating knowledge.

Paper 3 contributes to the literature by extending the limited number of studies

investigating the competition-stability nexus over a European sample rather than on

specific countries or sub-regions. We also provide support of the U-shaped

relationship between competition and bank soundness, as proposed by Martinez-

Miera and Repullo (2010), on top of the applications of Berger et al. (2009) and Beck

et al. (2012).

By means of extreme bound analysis, which has not been applied in the banking

literature so far, we observe how the effects of competition and concentration take

shape along with different informational sets and specifications. The latter consists in

regulation and supervision variables, governance indicators and ideas about non-linear

effects of competition and bank ownership, among others. We, thus, produce various

robustness checks coming up with remarks on collateral banking issues.

The findings of the above research are presented on the synopsis chapter and mainly

refer to the significant:

10

1) negative relationship between asset size and market power in cooperative,

savings and „other‟ banks. In more detail, higher size drives to low prices on

loans (cooperative, „other‟ banks), other interest products (commercial,

cooperative banks) and other non-interest bearing activities (commercial,

cooperative, „other‟ banks); however, higher scale operation comes in line with

higher (lower) fees in cooperative (savings and „other‟) banks. Non-linearities

imply positive bearing of size on market power switching to negative in savings

and „other‟ banks (of higher levels of total assets). We also see this inverse U-

shaped (positive-negative) pattern in loans (commercial, cooperative, „other‟

banks), fees and commissions (cooperative, savings, „other‟ banks) and other

interest income (savings banks) whereas a U-shaped (negative-positive) path is

traced in loans of savings banks, other interest-bearing activities in „other‟ banks

and other non-interest products in commercial, cooperative and „other‟ banks.

2) SCP doctrine with the persistent effect of market concentration on banks‟

monopolistic pricing (especially in the case of savings banks). In particular,

commercial (savings) banks seem to enjoy higher fees (other interest income)

whereas cooperative banks exploit collusion in the deposits (loans) market

through lower (higher) loan rates. „Other‟ banks respond to the monopolistic

structure of deposit markets through competitive loan rates and high prices on

other interest activities.

3) relative market power in „other‟ banks and cooperative banks of relatively large

market share. Higher market share is associated with lower fees (in commercial

and cooperative banks), other interest charges (in cooperative and savings banks)

and other non-interest rates (savings banks) while „other‟ banks tend to compete

in loans and other non-interest products and act monopolistically for the

remainder. Higher shares in the deposit markets induce banks to compete each

other for loan rates and „other‟ banks to charge higher fees. In contrast, higher

loan prices (of commercial and cooperative banks) and lower fees (for

commercial and cooperative banks) are evident once share is considerable in

loans markets.

4) relative efficiency hypothesis, according to which lower costs enable banks to

impose low prices on their products systematically across all specifications.

11

5) differences in cost and profit efficiency across various parametric methodologies

and definitions of bank outputs. However, they converge in levels if we assess

their truncated levels (TFA though is much lower due to negative efficiency

scores) and seem to produce almost identical country rankings.

6) discrepancies in yearly scale economies with the intermediation approach

demonstrating diminishing pattern from diseconomies of scale whereas the

production approach comes from below unity towards their full exploitation.

7) catching-up effect and converging dispersion of cost and profit efficiency insofar

as dynamic effects are employed. Above unity coefficient (in cost efficiency

under VA) has no economic sense due to the oscillation of negative values to

positive and back, albeit the lagged dependent variable operates in a

counterbalancing manner.

8) inequality amongst the cost efficiency scores within their frequency distribution,

while IA (VA) approach shows increasing (decreasing) path until 2006 and

exacerbates (ameliorates) thereafter.

9) fragile relationship between market power and systemic stability even after

accounting for interaction terms with country-specific factors of regulation,

supervision and macroeconomic conditions.

10) U-shaped relationship between competition and stability since the quadratic term

appears significant in the extreme bounds of the Lerner and Herfindahl-

Hirschman index. The devastating turn of market power effect coming at the

expense of stability lie at the point of 28.5%.

11) positive - albeit of marginal fragility in persistence - impact of concentration on

bank soundness and even higher slopes in markets of monopolistic conduct.

12) positive association of stability with capital regulation and market discipline as

well as negative one with low activity restrictions, supervisory intervention and

foreign ownership especially in cases of well-developed governance.

13) risk-taking tendency in markets with high degree of foreign ownership if coupled

with official intervention, considerable capital regulation, granted market entry

applications and information requirements.

12

1.4. Structure of the thesis

To fulfil the aim of providing answers to the aforementioned research questions, the

structure of my thesis takes the following form:

Chapter 2 refers to contemporary banking issues that are closely related to bank

competition. In fact, by „competition‟ we do not imply several models that have been

proposed in the literature for the measurement of its level, but particularly delineate

policy-relevant concepts in an institutional and macro finance perspective. The former

comprises efficiency (section 2.2.1), - some of its standard constituents, namely X-

efficiency, allocative efficiency, economies of scale and scope, synergies and

technological change -consolidation (section 2.2.2) - expressed by means of mergers

and acquisitions, the motivation behind such practices and cross-border activity – and

relationship banking (section 2.2.3) along with its definition, motivation, benefits and

primary costs.

On the other hand, the latter points out the importance of macroprudential regulation

(section 2.3.1) and the evolution of international initiatives (Basel I, II, III) since the

„80s. Integration (section 2.3.2) follows, which is literally a broader concept that

consolidation since it is also expressed by the organic growth of branches and

subsidiaries and the cross-border provision of financial services. Last, we investigate

the theoretical underpinnings of financial stability (section 2.3.3) and the implications

of potential empirical evidence on bank competitiveness. Section 2.4 summarizes the

analysis on competitive issues.

Chapter 3 deals with the empirical models of competition proposed in the literature

and the applications based upon their premises. It covers the structural approach that

engulfs the whole range of concentration ratios and their empirical importance on

bank performance. That link is firmly grounded on the Relative efficiency (RE) and

Structure-Conduct-Performance (SCP) paradigms (section 3.2) and the empirical

models implemented in the literature to verify their significance.

The New Empirical Industrial Organisation (NEIO) approach (section 3.3) is then

analysed as the alternative empirical literature, which defines market competition in

terms of the pricing conduct of banks. We therefore adduce the non-structural

13

methods of Iwata (1974), Bresnahan (1982), Lau (1982) and Panzar and Rosse

(1987), coupled with the notion of contestability, the practice of incumbent banks to

impose competitive prices in fear of policies against abnormal profits through „hit-

and-run‟ market entries.

We last report some alternative models (section 3.4) that propose a non-systematic

methodology of measuring competition intensity. In particular, some examples are the

generalized linear pricing model of Hefernan (2002), the so-called Boone indicator of

Leuvensteijn et al. (2011), the error-specification model of Carbo et al. (2009), the

empirical model of Delis and Tsionas (2009) that simultaneously estimate market

power and operating efficiency, and the attempt of Bolt and Humphrey (2010) to

measure competition efficiency along the lines of efficiency-related standard

methodology (DFA). Section 3.5 sums up the theoretical and empirical review on

competition.

Chapter 4 lays down alternative definitions of bank output/inputs (section 4.2),

namely the production and intermediation approach (among others), before it comes

to the measurement of X-efficiency based on various parametric (section 4.3.1) and

non-parametric approaches (section 4.3.2). The former comprises the Stochastic

Frontier Analysis (SFA) of Aigner et al. (1977) and Meeusen and Van de Broeck

(1977), the Distribution-free approach of Bauer et al. (1992) and the Thick frontier

approach of Berger and Humphrey (1991). On the other hand, the latter includes the

linear programming method of Data Envelope Analysis (DEA) first proposed by

Charnes et al. (1978) and the free disposal Hull approach (FDH) of Deprins et al.

(1984).

Section 4.4 presents a thorough review of empirical applications conducting

international comparisons of efficiency estimates, European cross-country

comparisons, developed economies, transition economies and country-specific

studies. Conclusion is offered in the last section (section 4.5).

Chapter 5 makes reference to the relationship between bank competition and

financial stability. In other words, there are two strands of the literature (section 5.3)

that endorse whether competitive conduct of banks is a conducive channel-through of

systemic risk in international and European samples. On the one hand, we report the

so-called „franchise (charter) value‟ paradigm of Keeley (1990), which appears to

14

trace in a competitive market banks eager to recoup their squeezed profit margins by

engaging in risky projects. On the other hand, Stiglitz and Weiss (1981) put ‟blame‟

on incumbent banks for imposing high prices and exacerbating thereby their risk

profile due to potential defaults. Along the lines of both theories, we review the whole

argumentation stemming from theoretical papers to establish the underlying

relationship (section 5.2).

We also document the proposition of Martinez-Miera and Repullo (2010), who concur

that the two contending theories need not be mutually exclusive as a U-shaped

relationship may unify them if occurring at markets of different bank competition.

Section 5.3 offers some concluding remarks.

Chapter 6 initiates the empirical analysis of the thesis investigating the intensity of

competitive conditions in nine of the most developed European banking industries.

Section 6.2 refers to the methodology followed with respect to the translog cost

function in order to estimate the marginal cost. We then end up with estimates of

competition through the Lerner index referring to the overall banking income and to

its decomposition into loans, other interest income, fees and commission and other

non-interest operating income. We also propose a model of potential correlates of

market power for commercial, cooperative, savings and „other‟ banks as well as to the

whole sample.

The analysis in section 6.3 makes a brief description of competition determinants that

proxy for bank-specific, industry-specific and macroeconomic variables along with

time and country fixed effects. In section 6.4 we delineate descriptive statistics of the

employed variables and the way each banking market represents the sample

represents over the whole period. Section 6.5 shows the results of empirical modeling

the (income-specific) estimates of competition, and section 6.6 summarizes the

analysis.

Chapter 7 documents some methodological issues (section 7.2) regarding alternative

definitions of bank outputs/inputs, specifications of the cost function and the reasons

beneath our decision to apply specific methodologies. Section 7.3 presents the

employed model the results from the comparison of various parametric methodologies

(REM, DFA, TFA) that estimate cost and profit efficiency scores under alternative

definitions of bank outputs/inputs. We come up with relative rankings of country

15

rankings as well as rankings of different productive specialisations and asset size

classes. We next measure economies of scale (section 7.4) through the partial

derivative of total costs with respect to total assets and observe how they have

evolved since 2003 under both IA and VA approaches.

Section 7.5 investigates the beta and sigma convergence dynamics of cost and profit

efficiency scores. We apply the models for all cases along the lines of standard linear

modeling and dynamic specifications. Last, section 7.6 draws remarks on the

evidence.

Chapter 8 shows a sensitivity analysis of the causal effect of market structure

variables, namely concentration and market power, on bank soundness. In so doing, in

section 8.2 we present the methodology of extreme bound analysis as set out by

Leamer (1983; 1985) and Leamer and Leonard (1983) as well as the methodological

issues of modeling the underlying relationship. Section 8.3 lays down the employed

cost function and the formulas to estimate the marginal cost and the Lerner index in

the first place. Next, in section 8.4 we make reference to the determinants of

competition with regard to regulation and supervision alongside other controls of

bank specificities and economic development. Section 8.5 displays descriptive

statistics correlation matrices between key variables and section 8.6 provides full

account of the empirical evidence stemming from the baseline models.

We also investigate in section 8.7 how the impact of competition takes shape in

response to the interplay between regulation and foreign ownership. The analysis goes

one step further allowing for non-linear relationship between competition and

indicators of institutional development (section 8.8), such as corruption, government

effectiveness, dissemination of credit information, among others. Section 8.9 allows

for the constituents of Z-score to be used as dependent variables in order to verify

which aspects of bank soundness are explained by the model. Section 8.10

investigates how market structure variables behave for commercial, cooperative,

savings and „other‟ banks of the market, and section 8.11 makes a synopsis of the

results.

Chapter 9 provides the concluding remarks (section 9.1) of the empirical analysis

and pertinent policy implications (section 9.2), coupled with methodological

limitations (section 9.3) and some suggestions for further research (section 9.4).

16

17

CHAPTER 2

Competitive issues

18

19

2.1. Introduction

European banking has undergone a state of structural reforming either in an

institutional or macro finance perspective. The evolving financial engineering along

with regulatory initiatives and advanced information technology have contributed to

bank disintermediation as more and more funds are transferred away to insurance

corporations, pensions or investments funds. Firms often use capital markets as a

means of portfolio diversification and debt financing while households are keen on

equity investments to reap high returns in buoyant periods.

Advocate to this trend has been the impact of information technology on the

internationalisation of capital and money markets. The integration of European

financial markets was intensified in the aftermath of the Euro adoption fostering

higher levels of competitive conduct. In addition, bank assets are reported roughly

over 15% to be in hands of foreign owners, especially subsidiaries (branches

secondarily) in Southeastern union to procyclically anticipate and, therefore, affect

economic growth in this region. Further evidence is derived in the significant external

position of European banks in terms of cross-border asset/liability holding and income

geography.

However, the by-product of nonbank competition does not imply a modest role in the

provision of financial services. The driving force of large-scale R&D and allocative

efficiency, potential market entries or market structure impinges on interest rate

margins and bank profitability over time and across different sectors and size classes.

As such continuous process is unfolding, the implications on stability is a matter of

economic theorising and empirical application. On the one hand, Stiglitz and Weiss

(1981) allege that monopolistic markets tend to adopt higher interest rate margins and

thereby inducing potential defaults, whereas Keeley (1990) attributes financial

instability to competition when banks in an attempt to recoup returns carry on riskier

projects.

Before moving onto the literature review of empirical competition models, it is

necessary to define every single issue involved and the way they are related to each

other.

20

2.2 Institutional perspective

2.2.1 Efficiency

Considerable empirical research has been conducted on the X – efficiency of European

Banks. It is measured in terms of costs and profits to highlight the ability of specific

sectors to control costs or revenues with better management and/or technological

advancement. A profit-maximising bank is intended to be close to or right on the

efficiency frontier and, therefore, to eliminate expense preference behaviour of

managers when not acting to the best interests of shareholders. Above and beyond that

threshold, only technological changes can bring about further efficiency levels.

Two measures here are related to X – efficiency: scale and scope economies; that is,

the marginal (negative) change of unit costs in response to the employment of the

total volume of production or range of products, respectively. Possible allocative

inefficiencies are attributed to administrative costs or insufficient management and

staff productivity. In other words, efficiency can be accomplished by the optimal

allocation – and the efficient utilisation, therefore - of the input mix.

However, the fact of whether there is such thing in banking as scale economies has

occupied an extensive part of banking literature. Strictly speaking, it underlines the

possibility of altering the production level on the grounds of varying all factor inputs.

Some problems may arise here; it is quite hard to allege that all inputs are totally

variable and even if we do so, the risk profile of a bank may be at odds with the

maximisation of the shareholders utility. For example, how is it possible to triple the

deposit accounts? And is that action worth taking given that the prospective provision

of loans implies higher portfolio risk? Besides, the problem of indivisibilities rules out

any change of an input unit by a fraction; there is no way of adding one-third of an

ATM machine or so. Last, the range of financial services worldwide makes it hard to

quantify multiple outputs and empirically verify the extent to which scale economies

do exist.

On the other hand, the concept of scope economies stands out in cost minimisation

when it comes to evaluate the positive effects of a merger or acquisition. As a

causatum, it is not always obvious, if at all possible, that a joint production is bound

21

to plunge costs through intermediation. They can apply when supposing, for instance,

the core banking activity of intermediation, whereby a predetermined fraction of

deposits is loaned out to borrowers. However, the payments service system in Europe

is quite fragmented, comparatively to USA, and that constitutes a hindrance to exploit

cost complementarities. Correspondent and custody services as well as payments

through debit/credit charges are not sufficiently spread out in European countries to

be conducive to cost reductions.

The business term of economies of scope is synergy, through capturing a more

dynamic process. It consists in the blend-up of skilful employees and exertion of a

considerable influence on suppliers for further reduction in input prices, among

others. In banking, this concept often proves to be costly in cases where innovation

forces fall short of mixing different cultures or inspiring the entrepreneurial spirit of

small financial boutiques. Consequently, the extent to which scale/scope economies

and synergies exist in European banking is indispensable for strategic decision-

making. However tough it is to come up with such measures, empirical evidence

gives mixed results whether large and multiproduct banks have a comparative cost

advantage over smaller types.

Technological change is the other important component of the efficiency compound.

Irrespectively whether it is applied in either cost or profit equations, it is estimated by

taking the partial derivative of the already cost/profit function with respect to the time

trend. It seems quite possible to draw some lines regarding the constituents of

technological innovation (Baltagi and Griffin, 1988); that is, the pure technological

progress – the effect of time trend depicting knowledge advancement - the non-

neutral change - the elasticity of cost/profit to variation in input prices - the scale

augmenting change - the sensitivity of cost/profit to changes in bank outputs - and

quasi-fixed factor augmenting change – cost reduction attributed to changes in fixed

factors. Empirical evidence has shown that technological change improves profits to

make up for the foregone technology investment up to a point where everything is

diffused and decreasing revenues are offset by greater costs.

It appears to be a hidden trade-off between reductions in costs and profitability,

though not verified on the whole. In countries where big banks endeavoured to taper

costs by increasing ATMs or closing branches faced a much poorer quality in services

22

thereby incurring a considerable profit plummeting. Only commercial banks have

accomplished greater profitability as they utilized innovation for better services and

risk management purposes. However, smaller commercial banks have been subject to

diminishing revenues and smaller cost reductions, probably sticking to reap the

benefits of innovative forces over non-cost channels.

2.2.2 Consolidation

In the European landscape, the consolidation of banks and financial firms is expressed

either by the merger of two independent banks or by the acquisition; the former turns

out to establish a single unit and the latter refers to the control of the acquired bank

through holding the majority of its shares. In such a case, the assets are not integrated

and by no means constitute any form of combination of the two firms. Strategic

alliances can also lead to monopolistic power when tacit agreements come into play

thereby exerting a considerable influence on the other banks‟ competitive stance.

In reality, academics may be up against consultants when they are called to articulate

a word about an imminent merger. There is not always a clear-cut answer whether the

deal is worthwhile as no one is able to back it up with convincing evidence. After all,

both can be right if, for example, bankers are focusing on the cost cuts in the post-

merger phase and at the same time economists observe no efficiency gains in cases

where revenues are moving downwards in line with costs (Rhoades, 1994).

M&As could actually take place for several reasons. In case of expecting efficiency

gains, either stemming from scale/scope economies or cost/profit X – efficiencies

from better organisation and management, the resulting market power of the new

entity may end up to higher pricing and value-added for the shareholders. Moreover,

it might be the case of managerial selfish ego the intimate motive of a merger in a

way to maintain and even enhance their personal power. In addition, structural

changes in the European banking sector have rendered M&As to be imperative and

intensified their operation in off-balance sheet activities (bancassurance) and other

non-interest income sources (commission, fees). By and large, the latter occupies a

large proportion of the income of European banks and keeps on escalating up to 50%

particularly in larger diversified banks (Laeven and Levine, 2007).

23

The empirical literature has been testing the effects of M&As by applying the event

study method – whether and to what extent abnormal returns of stock market shares

are created when announcements about an imminent merger make agents form

relative expectations – and comparing efficiency and performance ratios before and

after the time of a merger/acquisition.

In general, European bank merging has experienced great abnormal returns when the

announcements of deals involved domestic banks and insurance companies for

product differentiation purposes (Cybo-Ottone and Murgia, 2000). In fact, Campa and

Hernando (2006) conclude that only the target banks enjoyed positive market

expectations around the time of the announcement and, on average, improvements in

performance and efficiency; the latter remains put, according to Vennet (1996), but

especially in cases of equal-sized domestic banks and cross-border acquisitions. For a

strategic standpoint, Figueira and Nellis (2007) found consolidation to have incurred

more efficient gains than alternative development strategies from other large banking

entities. However, higher performance has been evidently feasible by domestic banks

of equal balance sheet structure, and cross-border deals that drive similar loan

portfolios, risk management strategies, and capital - cost structures (Altunbas and

Marques, 2008).

Cross-border activity is supposed to be conducive to the integration of European

banking sector. Barros et al. (2005) point out that the tendency towards the creation of

subsidiaries and not branches constitute a hindrance that deters full integration or even

geographic diversification and deregulation enforcement. In the case of horizontal

product differentiation and exogenously determined sunk costs, the banking sector

becomes more fragmented and deconcentrated the greater the market size (Sutton,

1991). If customers acknowledge different quality in financial products (vertical

differentiation), and incumbent banks are able to endogenously affect sunk cost

expenditures, they are highly motivated to operate in a higher efficient scale by

financially and technologically innovating and branch networking. Discretionary sunk

cost competition is, therefore, focused on fixed costs and take several forms, most

inclined with propagating effects to advertising and, primarily, to information

technology (Vives, 2001). On the other hand, competition on variable costs is

profoundly the typical strategy if concentration is negatively associated to market

24

size; in the „80s, Gual (1999) empirically came up with an ongoing deconcentrated

landscape in European banking with the same patterns.

2.2.3 Relationship banking

The role of relationship banking lies in the definition of the bank‟s raison d‟être. In a

typical balance sheet, bank liabilities (e.g. deposits) are liquid since anyone can

withdraw on demand while assets (e.g. loans) are not marketable due to informational

frictions. The latter includes both asymmetric and proprietary information that needs

to be developed when the provision and pricing of loans requires ruthless screening of

the potential borrowers. The qualitative transformation of assets in the contemporary

financial intermediation theory consists in the way banks are able to serve long-term

loans with short-term deposits, guaranteeing at the same time the liquidity of savings

and inevitably undertaking credit and liquidity risks.

Hence, relationship banking is called to provide specific (proprietary) information for

every customer and evaluate whether the repeated provision of financial services

across time is profitable (Elyasiani and Goldberg (2004). The key thing here is that

banks obtain information when screening and monitoring services in the lending case

(Allen, 1990; Winton, 1995). As Berger (1999) puts it, relationship banking holds if

there is something more to be obtained than the readily available information, it is

confidential and a product out of many repetitive interactions with the customer over

a range of financial products. However, relationship banking is present in nonbank

intermediation and involves other financial services like deposits, check clearing and

so forth.

Now securitization comes into play, being an ongoing funding development in the

contemporary banking finance. Although it seconds more transaction-oriented rather

than relationship-oriented interactions, the so-called credit enhancement is facilitated

by lots of collaterals and letters of credit. The bank, on the other hand, is now more

cautious to price its assets credibly and keep on monitoring collaterals so as to acquire

the necessary proprietary information that abridges default risk; even so, the bank

should be able to preserve accountability in reports and internalise a portion of the

incurred cost.

25

The benefits of relationship banking seem quite obvious once we cerebrate that

bilateral exchangeability is maximized between borrowers and banks when they are

both more willing to reveal exclusive information. The social welfare is positively

affected by long-term agreements that allow for more discretion, – flexibility and

negotiation of contract terms - contractual covenants, - adaptive to the underlying

information set after negotiation takes place as being more effective in loans (Berlin

and Mester, 1992) – collaterals, - mitigating adverse selection and moral hazard

problems (Stiglitz and Weiss, 1981) on the grounds it is monitored closely as far as

relationship banking makes it possible - and time – bearing losses in the short term but

then recouped as relationship has been established. These losses may include

subsidies to new borrowers without which, they would be condemned due to adverse

selection and moral hazard problems. Before moving to the costs of relationship

banking it should not be overlooked that bank provision of loans constitutes a

credential of financial soundness and the quality of the borrower when being

monitored seems to complement capital market funding.

The primary costs of relationship banking are the soft-budget problem and the hold-up

constraint. The former pertains to the lack of bank credible threat (Dewatripont and

Maskin, 1995) to enforce the credit terms since the bank is bound to extend the loaned

money to avert borrower‟s default. It seems quite obvious that the borrower may

demonstrate inadequate endeavour to survive on its own unless the seniority of bank‟s

debt structure renders the threat credible and the overall value insensitive to the claim.

The hold-up problem pertains to the monopoly power a bank has gained from

proprietary information. Borrowers run the risk of getting charged higher interest rates

and trammelled to carry on thus forfeiting valuable investments (Rajan, 1992).

However, multiple bank relationships could disperse the burden of credit at the

expense of less valuable information to be obtained and greater competition, which is

reluctant to lend to young firms. The only way out, as put forward by Von Thadden

(1995), is the long-term contracting and continuation of it upon performance. In other

words, poor projects may be terminated or get compensated depending on some

parameters or alternatively, refinanced at prespecified terms. Therefore, ex post

bargaining power of banks is circumscribed and firms are induced to keep up valuable

projects with single bank relationships.

26

It is quite ambiguous whether competition is negatively correlated with relationship

banking. One strand of argumentation falls in the competitive environment that

enables customers to switch to other banks; that is deemed to imply negative

repercussions relative to reduced and shorter relationship-intense investments

inhibiting costly proprietary information and so forth. However, Degryse and Ongena

(2008) have emphasised the importance of switching costs – e.g. search and shoe-

leather costs, that is time and effort to open/close accounts, transfer funds, etc. – that

amplifies the development of relationship banking. In such case, screening becomes

an integral part of the relationship though it may end up inefficient for borrowers,

whose assets are dominantly intangible (Houston and James, 2001). It could be much

worse for new firms that need to be subsidised in the first place as loan rates may

escalate intertemporally to offset the prospect of no retrievalibility of bank rents.

On the other hand, Boot and Thakor (2000) emphasise that relationship banking may

be part of a bank‟s competitive advantage increasing the welfare of the some. Tailor-

made services render the bank unique in the eyes of borrowers even amid fierce

interbank competition. However, capital market competition is expected to downplay

relationships and the per se lending orientation. In contradistinction, Dell‟ Ariccia

(2000) argues exactly the opposite, that there is a potential trade-off between market

share and relationship banking. As competition heats up, banks are aware of fewer

borrowers (adverse selection problem) and have therefore an incentive to screen.

However, the more banks are competing each other, the higher is the motive to switch

into transaction-oriented mode and grasp greater market share. Empirical evidence

has showed that single bank relationship has resulted in more value-added than

multiple schemes, the less the duration of such relationship, the greater is the distance

between bank and firm and less is that between bank and its competitors (Farinha and

Santos, 2002; Degryse and Ongena, 2001; 2005).

2.3 Macro finance perspective

2.3.1 Regulatory developments

Before delving into the regulatory directives put forth to the unification of the

European countries, we should have a look at the rationale of the purpose of

27

regulating banking markets. To the best interests of any investor, regulation applies

for his protection by providing sufficient information for hidden risks of traded

financial products. Even in cases of law breach, illegal activities, like tax evasion,

money laundering, find their way to judicial prosecution and investors are alarmed for

not engaging in. In addition, the abuse of potential oligopolistic markets make

authorities keep a vigilant eye on mergers and acquisitions to verify whether such

restructurings will have a considerable impact on market shares and product pricing.

Along the lines, negative market externalities might otherwise undermine financial

stability and the viability of intermediation.

Prudential regulation at the microeconomic level is indispensable once the

repercussions of a bank run can have a detrimental effect at the macroeconomic level;

that emanates from the banks operation in a homogenous product market and thus

their exposure to the same kind of risk. However, the reputation of a bank, if exists,

compensates for the prohibitive costs of acquiring information, the transparent

activities as depicted in the balance sheets, among others. A bank failure is

susceptible to the variable confidence of investors, which may then metastasize to

other banks as investors herd to withdraw their deposits before their bank liquidate

their assets. The underlying contagion is exacerbated by the systemic risk possibly

disturbing wholesale and retail markets and, in the extreme, the collapse of bank

intermediation, shortage of liquidity services and problematic resource allocation.

Therefore, social costs are quite severe to be overlooked given that the aggregate

consequences of potential bank runs in the European union render the

macroprundential regulation of primary concern (Borio, 2003, 2006; Acharya, 2009).

On the other hand, if banks are secured in view of upcoming runs on deposits, moral

hazard problems may arise. Banks may be willing to undertake risky investments if

deposits are protected by some insurance scheme or the state treat banks as being too-

big-to-fail institutions. The looting hypothesis as first articulated by Akerlof and