Malaysia : Banking Sector Report 2014

18

` ASB 4807 Financial Institutions Strategic Management Malaysia : Banking Sector Report Submitted by: Huzairi bin Zainal Abidin 500355515 January 13 th 2014 Bangor Business School College of Business, Law, Education and Social Sciences Bangor University

Transcript of Malaysia : Banking Sector Report 2014

`

ASB 4807 Financial Institutions Strategic Management

Malaysia : Banking Sector Report

Submitted by:

Huzairi bin Zainal Abidin

500355515

January 13th 2014

Bangor Business School

College of Business, Law, Education and Social Sciences

Bangor University

`

1

Abstract Malaysia is a dynamic country and has one of the best economic records in the world with on average 6.4% growth per year between 1960 and 2012. The banking sector is profitable and as at 30th November 2013, banking system capitalisation is in a robust position with the Common Equity Tier 1 Capital Ratio, Tier 1 Capital Ratio and Total Capital Ratio at 12%, 12.9% and 14.3% respectively. The level of credit profile is improving and banking system is resilient. This paper will report the main characteristics of Malaysian Banking sector and review the literature that examines its performance. It will also deliberate the key environmental factors currently driving bank strategy within that market and an assessment of their likely future impact on bank performance.

`

2

Table of Contents

ABSTRACT .................................................................................................................................... 1

LIST OF FIGURES ........................................................................................................................... 2

APPENDICES ............................................................................................................................ 2

1.0 INTRODUCTION ...................................................................................................................... 3

2.0 MALAYSIAN BANKING SECTOR PROFILE .................................................................................. 3 2.1 THE CENTRAL BANK ........................................................................................................................... 3 2.2 MARKET STRUCTURE .......................................................................................................................... 4 2.3 FINANCIAL SAFETY NET....................................................................................................................... 6

3.0 RECENT PERFORMANCE .......................................................................................................... 6

4.0 COMPETITION AND EFFICIENCY OF MALAYSIAN BANKS ........................................................... 7

5.0 LOOKING AHEAD .................................................................................................................... 9 5.1 ASEAN ECONOMIC COMMUNITY ...................................................................................................... 10 5.2 ISLAMIC FINANCE ............................................................................................................................ 10

6.0 CONCLUSION ........................................................................................................................ 10

REFERENCES .............................................................................................................................. 11

List of Figures

FIGURE 1: STRUCTURE OF THE FINANCIAL SECTOR AS OF END-2011 (BY ASSET SHARE) .................. 4

FIGURE 2: RWCR OF MALAYSIAN BANKING INSTITUTIONS (2006-2011) ......................................... 7

FIGURE 3: NPL RATIOS OF MALAYSIAN BANKING INSTITUTIONS (2006-2011) ................................. 7

FIGURE 4: LOAN GROWTH OF MALAYSIAN BANKING SYSTEM ....................................................... 9

Appendices

APPENDIX A – LIST OF LEGISLATION THAT VESTED POWER TO BANK NEGARA MALAYSIA ............ 13

APPENDIX B – LIST OF LICENSED COMMERCIAL BANKS IN MALAYSIA........................................... 15

APPENDIX C – LIST OF LICENSED ISLAMIC BANKS AND INTERNATIONAL ISLAMIC BANKS IN MALAYSIA ................................................................................................................................. 16

APPENDIX D – LIST OF LICENSED INVESTMENT BANKS AND OTHER FINANCIAL INSTITUTIONS IN MALAYSIA ................................................................................................................................. 17

`

3

1.0 Introduction Malaysia is a dynamic country which has gained independence in 1957. In a relatively short period of

time after independence, Malaysia has transformed from agriculture and primary commodities

nation to an export-driven economy drove by high technology, knowledge-based and capital

intensive industries. From income per capita of merely USD300 in 1960, it has reached USD9,991 in

2012. Moving forward, Malaysian government has laid out a comprehensive Economic

Transformation Programme (ETP) plan to leap the country to a greater height. The government is

hopeful that the ETP will increase the country’s gross national income to USD523 billion; lift per

capita income to at least USD15,000; create 3.3 million new jobs; and enlarge the services sector’s

contribution to the economy to 65% by 2020 (PEMANDU 2010).

In order to achieve that high but achievable ambition, the Financial Sector no doubt plays an

important role. The sector has to be resilient and functioning at its best to support economic growth

of the country. Following the 1997-1998 crisis, Malaysia had put forward a 10 year Financial Sector

Master Plan, which was for the period 2001- 2010 and now has entered the second phase under the

Financial Sector Blueprint which was released in 2011 for the period of 2011-2020. Both master

plans aim to provide the foundation for a balanced, inclusive and sustainable growth of the financial

sector. (BNM 2013b)

This paper will present the profile of Malaysian Banking sector and review the literature that

examines its performance. It will also deliberate the key environmental factors currently driving

bank strategy within that market and asses their likely future impact on bank performance.

2.0 Malaysian Banking Sector Profile

Malaysia maintains both conventional banking system and Islamic banking system which co-exists

and operate in parallel. This strategy is in line with the fact that Malaysia is a trading nation which

has to have integration with the international financial system in its trading activities as well as

working on to meet the demand for Shariah compliance financial products of 60% of its population

who are Muslims. Since it is estimated that almost 24% of world’s population (1.3 billion) are

Muslims (Khan & Bhatti 2008) and the number is expected to double in 2030 (Hannamayj 2011),

Islamic financial system definitely has a lot of growth potential.

2.1 The Central Bank

Both systems fall under the purview of Bank Negara Malaysia (BNM) which serves the function of

the Central Bank of Malaysia. Formed in in 1959, BNM’s primary functions are to:

formulate and conduct monetary policy in Malaysia;

issue currency in Malaysia;

regulate and supervise financial institutions which are subject to the laws enforced by the

Bank;

provide oversight over money and foreign exchange markets;

`

4

exercise oversight over payment systems;

promote a sound, progressive and inclusive financial system;

hold and manage the foreign reserves of Malaysia;

promote an exchange rate regime consistent with the fundamentals of the economy; and

act as financial adviser, banker and financial agent of the Government.

Source: (MIDA 2013)

The objectives of BNM are mainly promoting economic growth with price stability and maintaining

monetary and financial stability. Various laws vested power to BNM to enable the Central Bank to

regulate and supervise the banking institutions and other non-financial intermediaries effectively.

Similar to other developing countries, BNM as the Central Bank plays a significant role in shaping the

financial sector of the country.

2.2 Market Structure Malaysian banking sector is the primary mobiliser of funds and the main source of financing for

economic activities in Malaysia with 50.6% share of Financial Sector’s assets (see Figure 1). It

consists of the conventional commercial banks, investment banks, Islamic banks, International

Islamic Banks and Other Financial Institutions.

Figure 1: Structure of the Financial Sector as of end-2011 (by asset share)

Source: Bank Negara Malaysia

At present, there are 27 commercial banks (constituted by 8 domestics banks and 19 foreign banks-

see Appendix B), 16 Islamic Banks (constituted by 10 domestic banks and 6 foreign owned-banks -

see Appendix C), 5 International Islamic banks (all foreign owned – see Appendix C), 15 investment

banks (all domestic owned-banks – see Appendix D), and 2 other financial institutions (also

domestically owned-banks – see Appendix D).

Commercial banks are the largest and most significant providers of funds in the banking system.

Technically, Commercial Banks refer to banks that are providing retail banking services, trade

financing facilities, cross border payment services, safe deposits, hire-purchase, leasing for

`

5

individuals and businesses as well as treasury services in accordance to conventional financial

principles.

Islamic Banks on the other hand operate similar businesses as commercial banks but in accordance

to Islamic Shariah principles, notably “no application of interest, no uncertainty or speculation, no

financing of companies in certain sectors (e.g., weapons, pork, gambling), sharing of profit and loss

must be shared and requires financial transactions be backed by tangible assets” (Sarah Gearen

2009). The presence and promotion of Islamic banking which has become an increasingly important

component of the financial structure is a distinctive feature of the Malaysian financial system. As at

December 2011, Malaysia’s total Islamic banking assets has reached RM334.9 billion with a market

share of 22.4% and recorded an average annual growth rate of 16.07% for the period 2002 to 2011

(MIDA 2013).

BNM introduced International Islamic Banks (IIB) license in September 2006 under the Islamic

Banking Act 1983 to allow qualified foreign and Malaysian financial institutions to conduct Islamic

banking business in international currencies other than Malaysian ringgit. The license holders are

allowed to conduct wide array of international Islamic banking business with non-residents and

residents. IIB also enjoy full tax exemption accorded under the Income Tax Act 1967 for ten (10)

years beginning from the assessment year of 2007 as they are regarded as a resident (BNM 2006). It

is part of the Government initiative to promote and strengthen Malaysia's position as “a centre of

origination, distribution and trading of Islamic capital market and treasury instruments, Islamic fund

and wealth management, international currency financial services, and takaful and re-takaful

business” (MIFC 2013).

The next category is Investment Banks. BNM issues Investment Banks license to institutions which

main business are facilitating the buying and selling of stocks, bonds and other investments. They

play a role in the short-term money market and capital raising activities including financing,

specialising in syndication, corporate finance and management advisory services, arranging for the

issue and listing of shares, as well as investment portfolio management.

The last category is ‘Other Financial Institutions’ which currently consists of 2 special purpose

company set up by the government namely ERF Sdn. Bhd. and Pengurusan Danaharta Berhad for

facilitating participation of SME Program and managed Non Performing Loan recovery mission

during the Asian financial crisis respectively.

It is worth to note that the Malaysian Banking sector has undergone considerable consolidation

exercises through merger and acquisition following the Asian financial crisis. As a result, the number

of domestic commercial banking groups has been reduced from 31 commercial banks (of which 14

are fully foreign owned), 19 finance companies, 12 merchant banks and 7 discount houses in the

Malaysian financial system at the end of 2000 (Hon et al. 2011) to the present figures in order to

improve the resilient of the domestic banks as well as to gain greater scale and capacity. “Finance

companies were merged into commercial banking groups while discount houses, securities firms and

merchant banks were consolidated into investment banks”(IMF 2013b). In terms of outreach, there

are more than 2,000 bank branches across the country, which covers all the 13 states and Federal

Territories in Malaysia.

`

6

Despite the sizeable present of foreign banks, domestic banking groups remain dominant in the

Malaysian banking sector. The domestic banking groups’ combined market share of total banking

system assets and deposits are stable at 73.3% and 73.8% respectively (BNM 2013c) while six of

them have presence in 19 countries through branches, representative offices, subsidiaries, equity

participation and joint ventures (MIDA 2013).

The 27% market share of foreign banks in Malaysian Banking sector in a way “acknowledged

Malaysia’s growth potential and connectivity with other economies” (BNM 2013a) and re-affirmed

the Government’s approach towards liberation and welcome foreign banks as long as they

contributed to a more efficient and competitive market while enhancing the breadth and depth of

the financial sector.

In terms of concentration, top 10 anchor commercial banks holds 90% of total assets share while in

the Islamic sector, the percentage stood at 89.28% as end September 2013 (see Appendix B & C for

detailed breakdown of asset size). This fact may suggest that the market is of monopolistic in

character however the strong presence of Central Bank with regulatory framework may absorb the

downside of monopolistic market.

2.3 Financial Safety Net

In order to preserve the reliability and confidence in the banking sector, Malaysia has established

BNM as the lender-of-last-resort and incorporated Perbadanan Insurans Deposit Malaysia which

protects depositors’ deposit in the bank up to the maximum limit of RM250,000 per depositor per

member institution. Each bank is also required to have their own Contingency Funding Plan as a

preparation for any adverse event.

3.0 Recent Performance

The recent performance of the banking sector is remarkable. Financial Sector Assessment Program

undertaken by IMF has found that Malaysia’s financial system is resilient; proven by its success in

overcoming the recent global financial crisis. The recipe is due to “a well-developed supervisory and

regulatory regime, and a well-capitalized banking system”(IMF 2013b).

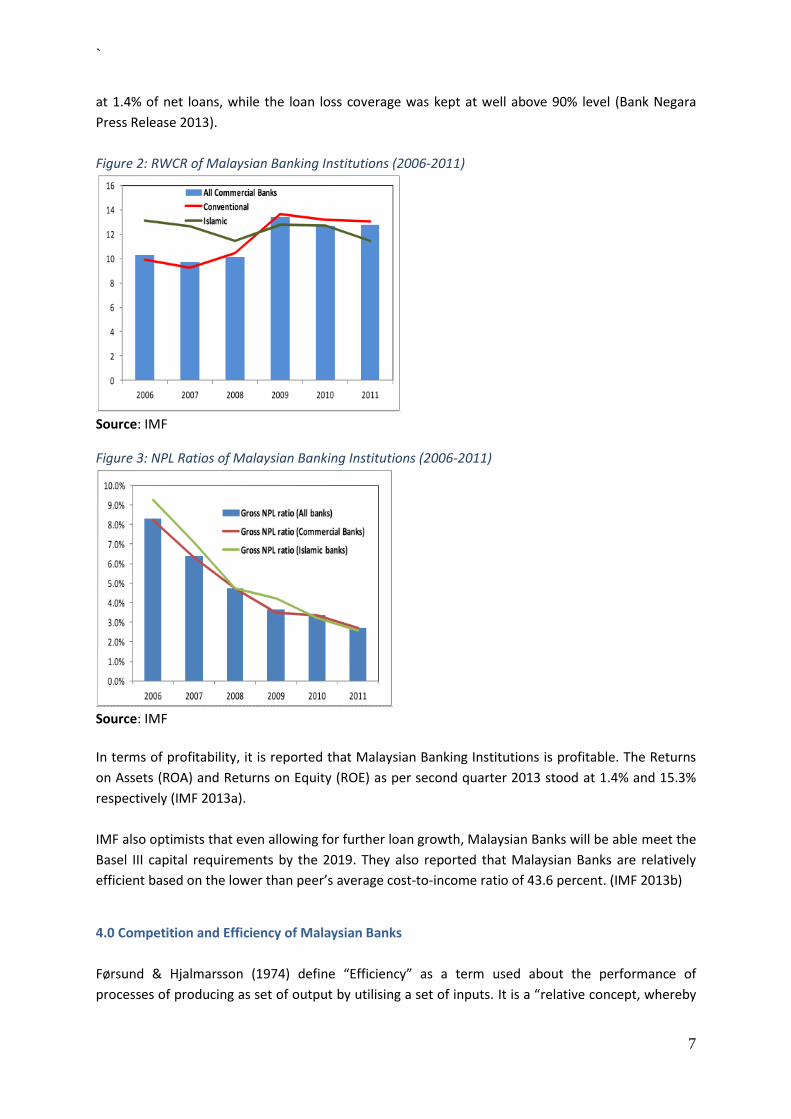

IMF also reported that Malaysian banking institutions as whole (both conventional and Islamic) are

well capitalized and there has been a significant improve in the asset quality. The banking sector risk-

weighted capital adequacy ratio (RWCR) had improved to 15.1 percent in 2011 (Figure 2) while the

gross Non-Performing Loans has declined to below 2.7% in 2011 (Figure 3). On the same positive

score, the loan loss coverage was 99.6% indicating the soundness of the system.

Recent figures by Bank Negara showed that banking system capitalisation as at 30th November 2013

remains in strong position with the Common Equity Tier 1 Capital Ratio, Tier 1 Capital Ratio and Total

Capital Ratio at 12%, 12.9% and 14.3% respectively. The level of net impaired loans remained stable

`

7

at 1.4% of net loans, while the loan loss coverage was kept at well above 90% level (Bank Negara

Press Release 2013).

Figure 2: RWCR of Malaysian Banking Institutions (2006-2011)

Source: IMF

Figure 3: NPL Ratios of Malaysian Banking Institutions (2006-2011)

Source: IMF

In terms of profitability, it is reported that Malaysian Banking Institutions is profitable. The Returns

on Assets (ROA) and Returns on Equity (ROE) as per second quarter 2013 stood at 1.4% and 15.3%

respectively (IMF 2013a).

IMF also optimists that even allowing for further loan growth, Malaysian Banks will be able meet the

Basel III capital requirements by the 2019. They also reported that Malaysian Banks are relatively

efficient based on the lower than peer’s average cost-to-income ratio of 43.6 percent. (IMF 2013b)

4.0 Competition and Efficiency of Malaysian Banks

Førsund & Hjalmarsson (1974) define “Efficiency” as a term used about the performance of

processes of producing as set of output by utilising a set of inputs. It is a “relative concept, whereby

`

8

the performance of an economic unit is compared against a standard unit” as further clarified by

(Hon et al. 2011).

In line with Berger et al. (1993) finding that most studies of efficiencies are concentrated in

industrialized countries, studies on banking efficiency in the Malaysian context are rare. Among the

few is the study by Dogan & Fausten (2003) which found that Malaysian banks experienced a decline

in productivity from 1989 to 1998 using Malmquist indices. Despite the introduction of technological

innovation and a more liberal approach in the sector during that period, the intended increase in

productivity did not materialized. The reason suggested was because it was too early for both

initiatives to bear positive results as it was the initial phase of implementation. They also suggested

that by imposing restrictions on the operations of foreign banks in the country, Malaysian Banking

sector was insulated by foreign competitive. However, the moving away from facing foreign

competition is not conducive to productivity growth of the sector.

Krishnasamy. G. et al. (2003) used DEA method and Malmquist total factor productivity index to

study on the productivity change of Malaysian banks from 2000 to 2001 and found that Malaysian

banks’ overall productivity increased over the period. The analysis showed that the growth was

attributed to technological rather than technical efficiency change. They also found that Malaysian

banks achieved a total factor productivity change of 5.1 per cent in the post-merger period of 2000–

01. They found that 80% of the banks regressed in terms of scale efficiency while 20% exhibited

positive result. Although some banks experienced regression in technological change the net

technology change post-merger hovered around 5 per cent to 16.8 per cent.

Another study is by Sufian & Ibrahim (2005) on the effects of including off balance sheet items (OBS)

in the output definition for the total factor productivity change indexes by applying the Malmquist

Productivity Index to a sample of post- merger Malaysian banks over the years 2001–03. They found

that the estimated productivity levels for all banks under study showed and increase with the

inclusion of OBS items.

A more recent study is by (Hon et al. 2011) that utilizes DEA efficiency scores and the Malmquist

indices in investigating the efficiency of domestic anchor banks following the implementation of the

Financial Sector Master Plan. They uses the data of 10 anchor banks from 2001-2005 and found that

if Malaysian banks were fully efficient, the productivity level can be improved further by on average

11 per cent to 24 per cent. The banking system seemed to encounter problem of poor management,

skill issues and the inability to leverage fully on technology to improve their performance which are

the culprits for pure technical inefficiency in the system.

They also found that the efficiency scores showed a declined over the five-period of FSMP,

particularly in terms of scale efficiency. This adverse result came as a setback to the objectives of

FSMP and some possible reasons could be attributed to fact that many banks have become too large

to be efficient, at least in the initial period after the merger. Pure technical efficiency has also

regressed during 2001-2005 signalling that there are still clear efficiency gaps between the best

practice banks and the rest of the pack in the banking industry.

`

9

The comparison made between the banks indicated that smaller- sized banks scored better scale

efficiency and thus were on average more efficient than larger ones. The result prompted for

reassessment on the whether the mergers and acquisitions strategy to increase the size of the banks

did in fact contribute to increase the efficiency of banks or gain better the returns from having larger

markets and greater outreach. They also found that smaller and niche banks (such as Southern Bank

Berhad and AmBank Berhad) were consistently more efficient than its larger counterparts mainly

due to the bank strategies. Maybank Berhad was the only exception which is large in terms of size

and at the same time having the edge in terms of efficiency. The exceptional performance of

Maybank Berhad was attributed to its constant proactive strategy of being at the leading of utilising

technological innovations in its operation.

Hon et al. (2011) concluded the study by highlighting that the stimulus of the FSMP initiative had

improved efficiency for technological innovations but “still lagging in terms of improvements in scale

and technical efficiency”. Further consolidation of banks could continue to be promoted but the

acquiring banks must have a clear idea of their intended strategy and how the acquiree bank will

complement their strategies to reap the benefits of bigger size and greater access.

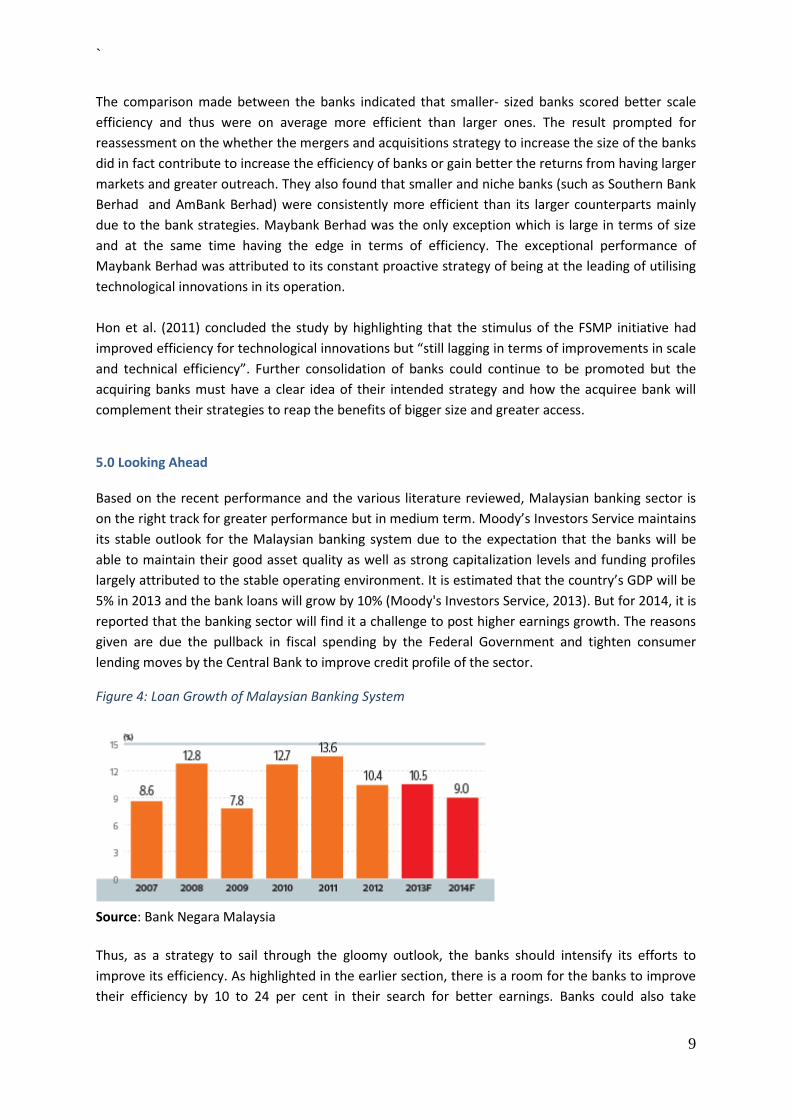

5.0 Looking Ahead Based on the recent performance and the various literature reviewed, Malaysian banking sector is

on the right track for greater performance but in medium term. Moody’s Investors Service maintains

its stable outlook for the Malaysian banking system due to the expectation that the banks will be

able to maintain their good asset quality as well as strong capitalization levels and funding profiles

largely attributed to the stable operating environment. It is estimated that the country’s GDP will be

5% in 2013 and the bank loans will grow by 10% (Moody's Investors Service, 2013). But for 2014, it is

reported that the banking sector will find it a challenge to post higher earnings growth. The reasons

given are due the pullback in fiscal spending by the Federal Government and tighten consumer

lending moves by the Central Bank to improve credit profile of the sector.

Figure 4: Loan Growth of Malaysian Banking System

Source: Bank Negara Malaysia

Thus, as a strategy to sail through the gloomy outlook, the banks should intensify its efforts to

improve its efficiency. As highlighted in the earlier section, there is a room for the banks to improve

their efficiency by 10 to 24 per cent in their search for better earnings. Banks could also take

`

10

advantage of the technology advancement to reduce their operating costs in addition to better

management and skill enhancement initiatives.

For longer term however, apart from the opportunities offered in the Malaysian Government’s

Economic Transformation Program and Financial Sector Blueprint, it is worth to take into account

the potential of the following ASEAN Economic Community and Islamic Banking as the key factors

that could drive the current and future strategy of the banks:

5.1 ASEAN Economic Community

Malaysia is an ASEAN member country and in 2007, the leaders of ASEAN has pledged their

commitment to transform ASEAN into a region with free movement of goods, services, investment,

skilled labour and capital known as ASEAN Economic Community (EAC) by the end of 2015. Even

though the dateline seems too idealistic, at least the work towards it has already started. The

diversity between the ten ASEAN countries is expected to create positive synergies for AEC with

McKinsey back in 2003 estimated of at least 10% increase in regional GDP or USD50 billion as a result

of integration while operational cost is expected to cut down by up to 20% (Anna 2013). Thus, banks

operating in Malaysia will have bigger market access when AEC kick-off and foreign banks may find

Malaysia as the strategic hub for their entrance to the AEC market considering its economic and

financial sector stability. It is therefore recommended for local banks to prepare themselves to face

the competition from the other regional banks as well as non-ASEAN banks in the bigger market.

5.2 Islamic Finance

Malaysia has positioned itself as one of the key players in Islamic finance and is moving towards

establishing as the global centre for Islamic Finance. The Malaysian Islamic banking assets have been

experiencing annual growth of 18-20% since 2007 with a lot of potential of untapped market. With

coercive efforts laid down in the BNM published Financial Sector Blueprint, Securities Commission’s

Capital Market Masterplan 2 and Corporate Governance Blueprints, the regional integration and

internationalisation of Islamic finance is believed to be the factor that the banks should look in. The

wave would force the structural change in the market once the few issues with regards to

differences in the applications and consistency across jurisdictions are resolved (Sarah Gearen 2009).

As a Muslim country and member of OIC, Malaysia is well positioned to act as a gateway to facilitate

and enhance greater international linkages and market integration in Islamic finance as well as

providing access to 1.3 billion Muslims in the world.

6.0 Conclusion

In conclusion, Malaysian Banking sector has a lot to offer. With impressive economic records as well

as comprehensive plans to move forward, investing in Malaysian Banking sector particularly related

to Islamic Financial services would be a wise decision. The Government is supportive; the vision is

clear; the policies are on the right track; the political climate is stable; the infrastructure is at par

with the advanced countries and as ASEAN Economic Community is near reality, the general long-

term outlook for Malaysian Banking sector even is bright and rosy.

`

11

References

Anna, P., 2013. Assessing the AEC. Banking Insight, 2013(December), pp.14–19.

Berger, A.N., Hunter, W.C. & Timme, S.G., 1993. The efficiency of financial institutions: A review and preview of research past, present and future. Journal of Banking and Finance, 17, pp.221–49.

BNM, 2013a. BNM Annual Report 2012, Kuala Lumpur.

BNM, 2013b. Financial Sector Development. Available at: http://www.bnm.gov.my/index.php?ch=en_fsd&pg=en_fsd_intro&ac=737&lang=en.

BNM, 2006. Guidelines on International Islamic Bank.

BNM, 2013c. The Financial Stability and Payment Systems Report 2012, Kuala Lumpur.

Dogan, E. & Fausten, D.K., 2003. Productivity and Technical Change in Malaysian Banks, 1989–1998. Asia Pacific Financial Markets, 10, pp.205–37.

Førsund, F.R. & Hjalmarsson, L., 1974. On the measurement of productive efficiency. Swedish Journal of Economics, (7), pp.141–54.

Hannamayj, 2011. 2.2 Billion: World’s Muslim Population Doubles. Time Newsfeed. Available at: http://newsfeed.time.com/2011/01/27/2-2-billion-worlds-muslim-population-doubles/.

Hon, L.Y., Tuck, C.E. & Lin Yu, K., 2011. Efficiency in the Malaysian Banking Industry. Asean Economic Bulletin, 28(1), p.16. Available at: https://bookshop.iseas.edu.sg/publication/65 [Accessed January 7, 2014].

IMF, 2013a. Financial Soundness Indicators. Available at: http://fsi.imf.org/ [Accessed January 1, 2014].

IMF, 2013b. Malaysia : Financial Sector Stability Assessment International Monetary Fund Prepared by the Monetary and Capital Markets and Asia Pacific Departments Approved by José Viñals and Anoop Singh. International Monetary Fund, (13).

Khan, M.M. & Bhatti, M.I., 2008. Islamic banking and finance: on its way to globalization. Managerial Finance, 34(10), pp.708–725. Available at: http://www.emeraldinsight.com/10.1108/03074350810891029 [Accessed December 23, 2013].

Krishnasamy. G., Ridzwa, A.H. & Perumal, V., 2003. Malaysian Post Merger Bank’s Productivity: Application of Malmquist Productivity Index. Managerial Finance, 30(4), pp.63–74.

MIDA, 2013. Banking, Finance and Exchange Administration. Invest in Malaysia. Available at: http://www.mida.gov.my/env3/index.php?page=banking-system.

MIFC, 2013. International Islamic Bank Licenses. Available at: http://www.mifc.com/index.php?ch=ch_kc_framework&pg=pg_kcfm_regulatory&ac=200.

`

12

PEMANDU, 2010. Chapter 1: New Economic Model of Malaysia. In Economic Transformation Programme : A Roadmap For Malaysia. pp. 57–120.

Sarah Gearen, 2009. Islamic Finance: Malaysia’s Growing Role,

Service, M.I., 2013. Announcement : Moody“ s maintains stable outlook on Malaysia”s banking system,

Sufian, F. & Ibrahim, S., 2005. An analysis of the relevance of off-balance sheet items in examining productivity change in post-merger bank performance: Evidence from Malaysia. Management Research News, 28, pp.74–92.

`

13

APPENDIX A

Appendix A – List of Legislation that vested power to Bank Negara Malaysia

1. Central Bank of Malaysia Act 2009

An Act to provide for the continued existence of the Central Bank of Malaysia and for

the administration, objects, functions and powers of the Bank, for consequential or

incidental matters. Incorporating Latest Amendments up to Act A1443/2013 cif 8 Feb

2013

2. Insurance Act 1996

An Act to provide new laws for the licensing and regulation of insurance business,

insurance broking business, adjusting business and financial advisory business and

for other related purposes. Incorporating Latest Amendments up to Act A1247/2005

- cif : 1 Jan. 1997

3. Development Financial Institutions Act 2002 (Act 618)

The DFIA which came into force on 15 February 2002 focuses on promoting the

development of effective and efficient development financial institutions (DFIs) to

ensure that the roles, objectives and activities of the DFIs are consistent with the

Government policies and that the mandated roles are effectively and efficiently

implemented. DFIA also emphasises on efficient management and effective

corporate governance, provides a comprehensive supervision mechanism and

mechanism to strengthen the financial position of DFIs through the specification of

prudential requirements. Incorporating Latest Amendments up to PU(A)285/2007 -

cif : 31 August 2007

4. Anti-Money Laundering and Anti-Terrorism Financing Act 2001 (Act 613)

This renamed and revised Act which came into force on 15 January 2002, is to

provide for the offence of money laundering, the measures to be taken for the

prevention of money laundering and terrorism financing offences and to provide for

the forfeiture of terrorist property and property involved in, or derived from, money

laundering and terrorism financing offences, and for matters incidental thereto and

connected therewith. Incorporating Latest Amendments up to PUA 144/2012 cif : 18

May 2012 gazetted: 17 May 2012

5. Money Services Business Act 2011

An Act to provide for the licensing, regulation and supervision of money services

business and to provide for related matters.

6. Government Funding Act 1983

An Act to provide for the raising of funds by the Government of Malaysia in

accordance with the Syariah principles and to provide for matters incidental thereto

or connected therewith.

`

14

7. Financial Services Act 2013

An Act to provide for the regulation and supervision of financial institutions,

payment systems and other relevant entities and the oversight of the money market

and foreign exchange market to promote financial stability and for related,

consequential or incidental matters.

Date come into force: 30 June 2013, except section 129 and Schedule 9, see [P.U.(B)

276/2013]

8. Islamic Financial Services Act 2013

An Act to provide for the regulation and supervision of Islamic financial institutions,

payment systems and other relevant entities and the oversight of the Islamic money

market and Islamic foreign exchange market to promote financial stability and

compliance with Shariah and for related, consequential or incidental matters.

Date come into force: 30 June 2013, except paragraphs 1 to 10 of Schedule 9 and

paragraphs 13 to 19 of Schedule 9, see [P.U.(B) 277/2013]

`

15

APPENDIX B

Appendix B – List of Licensed Commercial Banks in Malaysia

Commercial Banks

No. Name Ownership Assets Size

USD mil

1 Affin Bank Berhad L 17,037

2 Alliance Bank Malaysia Berhad L 14,134

3 AmBank (M) Berhad L 27,243

4 BNP Paribas Malaysia Berhad F 627

5 Bangkok Bank Berhad F 1,057

6 Bank of America Malaysia Berhad F 735

7 Bank of China (Malaysia) Berhad F 1,496

8 Bank of Tokyo-Mitsubishi UFJ (Malaysia) Berhad F 3,451

9 CIMB Bank Berhad L 87,109

10 Citibank Berhad F 12,573

11 Deutsche Bank (Malaysia) Berhad F 3,507

12 HSBC Bank Malaysia Berhad F 25,055

13 Hong Leong Bank Berhad L 51,466

14 India International Bank (Malaysia) Berhad F 116

15 Industrial and Commercial Bank of China (Malaysia) Berhad F 1,031

16 J.P. Morgan Chase Bank Berhad F 1,905

17 Malayan Banking Berhad L 161,811

18 Mizuho Bank (Malaysia) Berhad F 355

19 National Bank of Abu Dhabi Malaysia Berhad F 101

20 OCBC Bank (Malaysia) Berhad F 23,828

21 Public Bank Berhad L 89,797

22 RHB Bank Berhad L 55,474

23 Standard Chartered Bank Malaysia Berhad F 16,891

24 Sumitomo Mitsui Banking Corporation Malaysia Berhad F 838

25 The Bank of Nova Scotia Berhad F 1,375

26 The Royal Bank of Scotland Berhad F 1,499

27 United Overseas Bank (Malaysia) Bhd. F 26,301

Source : Bank Negara Malaysia and Bankscope as at September 2013

`

16

APPENDIX C

Appendix C – List of Licensed Islamic Banks and International Islamic Banks in Malaysia

Source : Bank Negara Malaysia and Bankscope as at September 2013

International Islamic Bank

No. Name Ownership

1 Al Rajhi Banking & Investment Corporation F

2 Alkhair International Islamic Bank Bhd F

3 Deutsche Bank Aktiengesellschaft F

4 Elaf Bank B.S.C. (c) F

5 PT. Bank Syariah Muamalat Indonesia, Tbk F

Source : Bank Negara Malaysia

Islamic Banks

No. Name Ownership Assets Size

USD mil

1 Affin Islamic Bank Berhad L 3,834

2 Al Rajhi Banking & Investment Corporation (Malaysia) Berhad

F 2,287

3 Alliance Islamic Bank Berhad L 2,210

4 AmIslamic Bank Berhad L 10,525

5 Asian Finance Bank Berhad F 919

6 Bank Islam Malaysia Berhad L 12,237

7 Bank Muamalat Malaysia Berhad L 6,823

8 CIMB Islamic Bank Berhad L 16,750

9 HSBC Amanah Malaysia Berhad F 3,972

10 Hong Leong Islamic Bank Berhad L 6,836

11 Kuwait Finance House (Malaysia) Berhad F 2,974

12 Maybank Islamic Berhad L 29,896

13 OCBC Al-Amin Bank Berhad F 2,276

14 Public Islamic Bank Berhad L 9,580

15 RHB Islamic Bank Berhad L 8,374

16 Standard Chartered Saadiq Berhad F 2,397

`

17

APPENDIX D

Appendix D – List of Licensed Investment Banks and Other Financial Institutions in Malaysia

Investment Banks

No. Name Ownership

1 Affin Investment Bank Berhad L

2 Alliance Investment Bank Berhad L

3 AmInvestment Bank Berhad L

4 CIMB Investment Bank Berhad L

5 ECM Libra Investment Bank Berhad L

6 Hong Leong Investment Bank Berhad L

7 HwangDBS Investment Bank Berhad L

8 KAF Investment Bank Berhad L

9 Kenanga Investment Bank Berhad L

10 MIDF Amanah Investment Bank Berhad L

11 MIMB Investment Bank Berhad L

12 Maybank Investment Bank Berhad L

13 OSK Investment Bank Berhad L

14 Public Investment Bank Berhad L

15 RHB Investment Bank Berhad L

Other Financial Institutions

No. Name Ownership

1 ERF Sdn. Bhd. L

2 Pengurusan Danaharta Nasional Berhad (now managed under Prokhas Sdn. Bhd.)

L

Source : Bank Negara Malaysia