THE ‘DEEPENING’ OF STRATEGIC PARTNERSHIP BETWEEN IRAQ AND IRAN

Upload

independentCategory

view

0download

0

Argentina’s Banking Sector in the

Nineties: From Financial Deepening

to Systemic Crisis

Guillermo Rozenwurcel and Leonardo Bleger

1. INTRODUCTION

THE first important attempt to liberalise financial markets in Argentina tookplace between 1977 and 1981 and ended in a complete failure. Throughout

the eighties the degree of ‘financial repression’ oscillated, but interest ratesremained basically market-determined. However, the financial system continuedto experience significant distortions, mainly due to the extreme volatility of themacroeconomic environment.

The implementation of the Convertibility Plan in March/April 1991 and thedrop in international interest rates gave a decisive thrust to the liberalisationpolicy undertaken in mid-1989, which aimed to restructure the economy alongmarket-friendly guidelines. Also the establishment of a convertibility regime bylaw, requiring the Central Bank to back the whole monetary base with foreignexchange reserves, together with the adoption of a new charter for this institution,drastically limited the scope of monetary policy and the Central Bank’s role aslender of last resort.

While the Convertibility Plan was quite successful at dramatically reducing theinflation rate, it also had other less desirable consequences on economicperformance. On the one hand, it accentuated the economy’s vulnerability toexternal shocks. On the other, it contributed to the fragility of the domesticbanking system. As a result, it greatly amplified the fluctuations of the businesscycle.

ß Blackwell Publishers Ltd 1998, 108 Cowley Road, Oxford OX4 1JF, UKand 350 Main Street, Malden, MA 02148, USA. 369

GUILLERMO ROZENWURCEL is from Centro de Estudios de Estado y Sociedad andUniversidad de Buenos Aires. LEONARDO BLEGER is from Universidad de Buenos Aires andBanco Credicoop, Buenos Aires. An earlier draft of this paper was presented at the 1996 AnnualMeeting of the AAEP (Argentine Economic Association). The authors are grateful for thecomments received there and for those of the anonymous referee. Guillermo Rozenwurcel alsothanks the support received from IDRC (Canada) and Mellon Foundation (USA).

Since the beginning of the Convertibility Plan the Argentine economy hasevolved through two contrasting phases. The first one, lasting until the Mexicancrisis in December 1994, was characterised by a swift growth in GDP which wasfuelled by huge capital inflows. The second phase, triggered by the abruptreversal in capital flows induced by the Tequila effect, plunged the economy intoa deep recession. Despite the remarkably fast normalisation of internationalfinancial markets after the crisis, it took the economy almost a year and a half (upuntil mid-1996) to begin to recover, albeit gradually and with a persistently muchhigher rate of unemployment than during the pre-crisis period.

Taking this background into account, this paper tries to accomplish two maingoals. The first is to analyse the most important consequences of the reformprocess on the structural and institutional features of the Argentine bankingsystem. Based on this analysis, the second goal is to understand why the Tequilaeffect prompted such a deep financial crisis in Argentina, unlike the lesstraumatic effects induced in all other major Latin American economies, and toassess the main repercussions of this crisis.1

In order to acheive these goals, we will focus our analysis on the specific waysin which a Currency-Board arrangement shapes the links between themacroeconomic environment and the financial system. We think that thisperspective is quite relevant for at least two connected reasons. First, thewidespread debate on the opportunity of adopting similar schemes in severalemerging economies currently taking place both at the academic and policylevels. Second, the fact that the Argentine case is crucial to empirically assess thepros and cons of a Currency-Board scheme, because it is actually one of thelargest and most complex economies operating under such an arrangement.

The approach of the paper is basically macroeconomic. We do not thereforediscuss in much detail the micro fundamentals determining the behaviour ofbanks during the liberalisation process and the ensuing financial crisis, though wedo point out some of its most salient features and provide the relevant referencessupporting our assertions.

In our view, the emphasis on the macro side of the process is further justifiedby what we think was the systemic nature of the Tequila crisis, which combinedmassive capital outflows and a sharp monetary contraction triggered by a‘contagion’ effect, with the Central Bank unable to deal with a systemic run onbank deposits due to the constraints imposed on its policy actions by theconvertibility regime and its own 1992 new Charter. The remainder of this paperis therefore structured as follows: Section 2 deals with the recent evolution ofArgentina’s banking system, Section 3 discusses the Tequila effect, and finally,Section 4 concludes.

1 The evolution of Argentina’s monetary aggregates and other key macroeconomic indicators overthe first half of the current decade can be traced in Table 1.

370 ROZENWURCEL AND BLEGER

ß Blackwell Publishers Ltd 1998

2. THE EVOLUTION OF THE BANKING SYSTEM UNDER FINANCIAL

LIBERALISATION

Argentina has not been a typically ‘repressed’ economy since the liberalisationattempt of the late seventies. In fact, although that experience ended in acomplete failure, many of the changes it produced in domestic financial marketsand the banking system proved irreversible. As a result, during the past decadeinterest rates were basically market-determined; credit allocation wasincreasingly decentralised; and the conventional goals of monetary policy weremainly pursued through indirect policy instruments. But still, mostly as a result ofextremely high inflation and severe macroeconomic uncertainty, the economycontinued to experience massive financial distortions throughout the eighties.

The functioning of domestic financial markets, and the credit market inparticular, has changed dramatically since the early nineties because of the jointimpact of the CP and the current new attempt at financial liberalisation.Accordingly, the primary purpose of this section is to analyse the most importantrepercussions which this process had on the structural and institutional features ofthe Argentine banking system, including its legal and regulatory framework, therole of the Central Bank, prudential regulation, and the management of liquidityand solvency problems. In order to do so, we present and discuss below the maininitial conditions and stylised facts of the banking system in the nineties:2

(a) Argentina’s banking system still displays a large number ofinstitutions and is physically oversized when compared with therelatively reduced volume of funds it intermediates. Despite themanifest inefficiency of the banking sector, the system revealed verylittle evidence of structural adjustment during the initialexpansionary phase of the Convertibility Plan.

Demonetisation has been chronic in the Argentine economy since the latefifties and it deepened even further during the debt crisis period. Nevertheless,throughout the CP’s initial expansionary phase there was a sustained recovery inthe monetisation level. As a result, M2* jumped from five percentage points ofGDP in1990 to slightly over 20 per cent in 1994.

However, the level of financial intermediation (compared with the size of theArgentine economy) is still not only well below that of developed countries, but isalso below that of other economies on a comparable level of development. Indeed,all relevant measures of liquidity as a proportion of GDP are currently quite inferiorto those Argentina reached before the financial crisis in the early eighties.

2 See Rozenwurcel and Ferna´ndez (1994) for a more detailed discussion on the workings of theArgentine banking system before the 1995 financial crisis.

ARGENTINA’S BANKING SECTOR IN THE NINETIES 371

ß Blackwell Publishers Ltd 1998

By contrast, the number of financial institutions and their houses functioningin the domestic system is still sizable, despite a steady reduction as from the earlyeighties. In fact, prior to the eruption of the most recent financial crisis in late1994, there were still 205 financial institutions (168 banks plus 37 nonbanks),while the number of branches reached 4,081.

Although the proportion of inhabitants per house is similar to that inindustrialised countries (8,000) it is inconsistent with Argentina’s lower degree ofmonetisation and financial deepening. In effect, despite their important growth,total deposits per branch registered just 11.2 million dollars in late 1994.3 Indeed,the use of banking services by the Argentine population is extremely reducedcompared with that in developed countries, and even with that in similar LatinAmerican countries. Thus, while the ratio of sight deposits over M1 (a plausibleindicator of the level of ‘bankarisation’) is less than 50 per cent in Argentina, it is63 per cent in Brazil and about 70 per cent in Mexico and Chile.

TABLE 1Main Macroeconomic Indicators

1990 1991 1992 1993 1994 1995 1996

GDP at market prices (3) 141.4 189.6 228.8 257.7 281.6 285.0 301.6Real GDP growth (%) 0.1 8.9 8.7 6.0 7.4 ÿ4.6 4.4Annual Inflation (CPI) 1343.9 84.0 17.5 7.4 3.9 1.6 0.1Gross domestic investment (1) 14.0 14.6 16.7 18.2 19.9 18.1 19.1National savings (1) 17.7 14.9 14.1 15.9 17.0 17.3 17.8Real exchange rate (2) 100.0 75.0 61.3 56.2 54.5 54.6 55.7Current account (3) 4.8 ÿ0.7 ÿ6.7 ÿ7.6 ÿ10.2 ÿ2.4 -3.5Capital account (3) ÿ1.3 1.6 10.4 14.8 10.4 ÿ0.4 7.1Trade account (3) 8.2 3.7 ÿ2.6 ÿ3.7 ÿ5.9 2.2 -3.7Exports (3) 12.2 12.0 12.2 13.1 15.8 21.0 23.5Imports (3) 4.0 8.3 14.9 16.8 21.6 18.7 21.9Reserves (3) 4.6 8.0 11.0 15.3 16.0 15.9 19.7M1/GDP (%) 2.1 4.3 5.2 6.0 6.1 6.7 7.7M2/GDP (%) 3.8 7.4 9.5 11.8 11.9 11.1 13.0M2*/GDP (%) (4) 5.0 11.1 14.4 19.0 20.0 19.5 23.1Total external debt (3) 62.2 65.4 67.6 70.7 77.0 82.1 85.1(6)Non-financ. public sectordeficit (1) 2.7 1.3 0.7 ÿ1.0 0.1 1.1 1.7

Primary deficit (1) ÿ1.4 ÿ1.7 ÿ2.2 ÿ2.2 ÿ1.0 0.5 0.3Unemployment rate (5) 6.3 6.0 7.0 9.3 12.2 16.6 17.3

Notes:(1) % of GDP – (2) WPI USA/CPI Arg – (3) bns. of US dollars – (4) includes dollar deposits – (5) in Octobereach year – (6) Sept.96.

Source: Based on data from the Central Bank and the Ministry of the Economy.

3 Total deposits per employee were quite modest as well: they amounted to barely 374,000 dollarsat the same date.

372 ROZENWURCEL AND BLEGER

ß Blackwell Publishers Ltd 1998

TABLE 2Number of Institutions and Houses

Dec. 1980 Dec. 1991 Dec. 1994 Aug. 1995 Nov. 1996Type of Institutions Inst. Houses Inst. Houses Inst. Houses Inst. Houses Inst. Houses

National Public Banks 4 695 6 931 6 907 4 594 3 553Provincial and Municipal Public Banks 31 1.145 29 916 27 752 29 1.012 21 920

Total Public Banks 35 1.840 35 1.847 33 1.659 33 1.606 24 1.473

Nat. Private Banks 57 1.090 66 1.198 59 1.467 59 1.807Foreign Banks 27 215 31 322 31 360 31 405 28 375Cooperative Banks 44 799 38 842 12 524 8 350

Total Private Banks 179 1.999 132 2.211 135 2.400 102 2.396 95 2.532

Total Banks 214 3.839 167 4.058 168 4.059 135 4.002 119 1.005

Total Nonbanking Inst. 255 280 47 28 37 22 31 51 26 44

Total in the System 469 4.119 214 4.086 205 4.081 166 4.053 144 4.049

Source: ‘Indicadores del Sistema Financiero’ and ‘Estados Contables de las Entidades Financieras’, Central Bank.

All this suggests that low productivity and inefficiency are still criticalproblems in Argentina’s financial system. The combination of economic stabilityand financial liberalisation brought about by the CP and the market-friendlyreforms did not propel the banking sector’s structural adjustment any further.Given the still prevalent inefficencies in the system, this was somewhatunexpected, at least for the policy makers.4

The failure of the banking sector to take advantage of such favourablecircumstances to endogenously start to reorganise, a step which was broadlyacknowledged as inevitable, strongly suggests that when it comes to restructuringthe financial system, market incentives alone may sometimes provide the wrongsignals, and that an active CB policy inducing mergers and takeovers may benecessary.

Indeed, despite a strikingly fast growth in bank lending, originating both in therapid evolution of their deposits and their renewed access to foreign credit lines,the initial economic boom prompted by the CP generated a massive excessdemand for loans.5 This excess demand, in turn, pushed the real lending rates upto quite high levels and allowed banks to record significant profits in their booksthough, as we will discuss later, it was probably at the cost of underestimating theprospective burden of bad debts.

In sum, as is usually the case during credit booms, while the expansion in bothdeposits and loans in that period was far from selective (illustrating once againthe importance of informational asymmetries and moral hazard issues in financialmarkets), problem banks did not face major liquidity constraints and could easilyoverlook their solvency problems. This probably helps to explain the persistenceof many poorly managed domestic banks before the crisis.6

(b) The traditionally tight constraints imposed by the domestic bankingsystem on prospective small customers clearly persisted after thelaunching of the CP.

Limited access to bank credit and other financial services can seriously hindereconomic performance and even more so during a period of structural reform. Anexcessive concentration of bank loans among borrowers is a clear symptom ofsuch a limitation. This was traditionally the case in Argentina, and it hasremained so since the beginning of the CP, despite the simultaneous rise observedin total credit. As a result, over the last five years, the so-called ‘principal

4 See Machinea (1996).5 As a matter of fact, from the beginning of the CP to the end of 1994, total bank credit grew at anaverage annual rate of 31 per cent, while the average annual growth in bank loans to the privatesector was almost 40 per cent over the same period.6 Stiglitz (1993), among others, underlines the distinct significance of widespread informationproblems in underdeveloped financial markets.

374 ROZENWURCEL AND BLEGER

ß Blackwell Publishers Ltd 1998

debtors’ of the system (that is, debtors with loans that surpassed 250,000 dollarsor who made up the list of 50 major debtors of any single financial institution)concentrated on average over 60 per cent of total bank lending.

As was already discussed in (a), financial liberalisation, at least in the way itwas implemented in Argentina in the early nineties, failed to improve theefficiency of the banking system. According to the available information, it alsoproved insufficient to weaken the longstanding market segmentation betweenlarge and small borrowers regarding both loan conditions and access to otherfinancial services.7

(c) Public banking retains a key position in the domestic financialsystem.

Public banks played a decisive role in the period of import-substitutionindustrialisation (ISI), replacing the virtually nonexistent domestic capitalmarkets as suppliers of long-term financing. Since the collapse of the ISI inthe mid-seventies, they have been immersed in a deep crisis. When the CP wasimplemented, the smallest provincial public banks, in particular, had probablyalready been technically bankrupt for quite some time. Most of them have sincebeen privatised, and the rest will soon follow suit. However, public banks stillplay a very significant role in Argentina’s financial system. In effect, four of theten most important banks are public, including the largest two in the system.

A direct consequence of the weight public banks maintain in domesticfinancial markets is that their problems strongly affect the overall financialconditions in the real economy. On the other hand, the stability of Argentina’s

TABLE 3Share of Different Types of Institutions in Deposits and Loans (In percentages)

Type of Institutions November 94 July 95 October 96Deposits Loans Deposits Loans Deposits Loans

National Public Banks 14.5 18.1 16.3 20.5 14.5 19.1Provincial and MunicipalPublic Banks 24.3 23.5 24.6 22.7 22.4 19.0

Private Banks 33.4 32.4 33.0 32.5 39.3 38.8Foreign Banks 16.1 16.2 19.7 17.9 19.0 18.6Cooperative Banks 10.4 8.2 5.7 5.3 4.1 3.3Nonbanking Institutions 1.3 1.6 0.7 1.1 0.7 1.2TOTAL 100.0 100.0 100.0 100.0 100.0 100.0

Source: Own calculations based on data from ‘Estados Contables de las Entidades Financieras’, Central Bank.

7 Market segmentation and the difficulties faced by small bank customers, in particular by small-and medium-sized firms, in the domestic financial system are discussed in detail by Rozenwurceland Ferna´ndez (1994).

ARGENTINA’S BANKING SECTOR IN THE NINETIES 375

ß Blackwell Publishers Ltd 1998

immature and volatile financial markets, as well as the financial needs of certainactivities and regions with very limited access to the private banking system, isstill likely to require some degree of public-sector participation in the domesticfinancial markets.

The need for an active government involvement in the financial markets iswidely acknowledged in the literature. At present, there is hardly any dispute onthe importance of prudential regulations and the supervision of financialinstitutions, though the extent and nature of other more direct ways of publicintervention is still higly controversial.

Given the distinctive nature of developing economies we think (together withsome authors such as Stiglitz, 1993) that when the human capital and aninstitutional setting providing adequate incentives are available, the presence of afew public banks in the financial system can improve the outcome of theintermediation process. This may well be the case in Argentina where, at least inprinciple, these conditions apply, and where financial liberalisation alone provednot enough to face the challenges posed by sharp macroeconomic fluctuations,the almost absolute lack of long-term financial markets, and the extremesegmentation of existing ones.

(d) The new monetary regime sharply narrowed CB powers regardingboth the conduct of monetary policy and its capacity to deal withpotentially destabilising shocks. As a result, the financial systembecame much more vulnerable to systemic risk.

In September 1992 a new CB Charter established the institution’s autonomyfrom the Executive Power. It also granted the CB full responsibility for theadministration of monetary policy and the supervision of the financial system. Inpractice, however, the government’s radical approach to stabilisation-cum-structural reform sharply narrowed the scope of monetary instruments and theinstitution’s ability to set up a proper safety net against unexpected shocks.

Specifically, the new regime stipulated that the CB should maintain freelyavailable reserves in gold and foreign currency to the equivalent of 100 per centof its monetary base. During the administration of the first CB Board a 20 percent maximum of these reserves could be made up of dollar-denominated publicbonds valued at market prices. As from the administration of the second Board,which has since been appointed, this proportion was raised to 33 per cent.8

Consequently, in order to prevent the monetary base from growing without acorresponding expansion in foreign reserves, the CB was only allowed to finance

8 However, for the time being it seems unlikely that the CB might actually approach the new ceilingwithout severely impairing private expectations. In fact, even at the peak of the recent financialcrisis the authorities never let the backing of the monetary base with public bonds surpass 20 percent.

376 ROZENWURCEL AND BLEGER

ß Blackwell Publishers Ltd 1998

the national government through the purchase of Treasury bonds at market prices,and to provide funding to financial institutions exclusively in situations oftransitory illiquidity and for very reduced amounts. Another step in the samedirection was the virtual elimination of deposit insurance.

The authorities claimed that this was the proper approach in dealing withmoral hazard problems and meant a step forward in the process of financialderegulation. In fact, the absence of both a working deposit insurance scheme anda lender of last resort left the financial system with no safety net and no doubtcontributed to propagating the Tequila crisis in Argentina, since it increased thesystem’s vulnerability to systemic risk.9

(e) No matter how significant the improvement in the prudentialregulatory framework had been, banking supervision prior to thecrisis was still weak in Argentina.

While the convertibility regime certainly limited the CB’s regulatory powers,the optimism prompted by the favourable international situation and the progressof structural reform in the early nineties may have led to a somewhat lightapproach to supervision and enforcement of banking prudential regulation priorto the Tequila crisis. Thus, given that systemic financial turmoil seemed highlyunlikely, the monitoring and enforcement capacities of the supervisory authoritieswere not strengthened as was required by the new policy regime.10

To be sure, the problem had very little to do with the suitability of theregulatory framework itself. To the contrary, in 1992 a Supervisory Board ofFinancial Institutions reporting directly to the CB president was created, andstricter norms concerning capital adequacy, diversification of credit risks,provisions for bad loans, and minimum auditing standards were adopted. Inaddition, legal reserves were set at high levels.

Moreover, in some cases these norms became even harsher than those definedin the original version of the Basle Accords.11 Thus, in the case of solvencyprovisions, besides taking into account banks’ risk-weighted assets, as wasestablished by Basle I standards, additional capital requirements were imposedaccording to their level of immobilisations and that of their lending interest rates(penalising riskier strategies based on excessively high loan rates).

As a result, in December 1994 the stated capital/assets ratio in the Argentinebanking system was on average 16 per cent. This meant a far lower leverage than9 For a theoretical analysis of safety nets in financial systems, see Dewatripont and Tirole (1994),Larraın (1994) and Aglietta (1995).10 This was certainly not an exclusively Argentine peculiarity. The same expectation confusionarose in Mexico before the crisis. The issue is discussed in Frenkel (1995) and Dornbusch et al.(1995) among others.11 For a detailed description and critical assessment of the Basle Accords, see Davies (1995) andDewatripont and Tirole (1994).

ARGENTINA’S BANKING SECTOR IN THE NINETIES 377

ß Blackwell Publishers Ltd 1998

that found in most other countries, either developed or underdeveloped, and was acost at least partly associated with the rigidity of the policy regime, particularlywith the lack of a lender of last resort.12

Some improvements were also made regarding the disclosure of more detailedbalance-sheet information by banks.13 However, in late 1994, more than threeyears after the CB became independent and despite the improvements made in theprudential regulatory framework, the supervisory authorities were not yet readyto carry out full scale regular inspections in financial institutions according tomodern international standards.

As the crisis showed, a significant number of banks had been taking advantageof this weakness not to fulfil even the most basic prudential regulations, nor toaccurately report their real situation to the CB. In this regard, some analysts havesuggested that the stated capital of many banks may actually be overestimated,because an important fraction is likely to be eroded by provisions and write-offsof bad loans currently in their portfolios.14

(f) The memories of protracted high inflation and the more recenthyperinflation episodes imposed severe constraints on the financialsystem’s performance.

In effect, past history matters a great deal to present performance. This isreflected in at least four issues: monetary hysteresis, dollarisation, preference forflexibility and portfolio diversification. After five years of increasing pricestability, demand for domestic financial assets and other banking services inArgentina is still significantly lower than the pre-high inflation period and muchlower than in most other countries with comparable inflation levels. This showsthe existence of monetary hysteresis. At the same time, since the beginning ofconvertibility the banking system has become even more dollarised than in thepast. Both developments tend to accentuate the vulnerability of the financialsystem to macroeconomic shocks, and particularly to volatile capital flows.15

Other evidence of the inadequate development of the financial system is thelow average term-maturity of deposits. Although there has been a minorimprovement in this regard, time deposits are on average slightly longer than 30days. Depositors are still strongly risk-averse, and consequently choose to keepvery flexible financial positions.

12 Since the Tequila crisis, the CB has even begun to take the necessary steps to include some ofthe more recent Basle proposals regarding interest rate, liquidity and other market risks in capitalrequirements.13 On the importance of disclosure provisions, and also on the disincentives and difficulties facedby small depositors to benefit from them, see Stiglitz (1993).14 Based on this conjecture, Corrigan (1996) argues that a banking crisis was probably in themaking in Argentina even before the Tequila effect.15 Calvo (1995) stresses this vulnerability as an important factor behind the 1994 collapse inMexico.

378 ROZENWURCEL AND BLEGER

ß Blackwell Publishers Ltd 1998

And finally, the massive capital flight caused by the turbulent macroeconomicenvironment of the eighties had a permanent impact on the financial behaviour ofdomestic agents, leading to a much higher international diversification ofdomestic portfolios. Thus, it de facto integrated domestic financial markets withinternational ones, drastically limiting the room for autonomy in monetary policyby strongly increasing the sensitivity of portfolio choices to differentials inexpected returns between domestic and foreign assets.16

(g) Exchange-rate overvaluation plus a swift financial liberalisation ledto overindebtedness and financial vulnerability.

During the first stage of the CP, economic activity followed the typical courseobserved in most stabilisation attempts based on fixed exchange rates. The successof the plan, coupled with the steady progress in structural reform, induced a boomin domestic absorption and a sharp rise in output, given the initial low level ofcapacity utilisation. On the other hand, owing to price inertia, disinflation was notinstantaneous, thereby producing a significant exchange-rate overvaluation. This,together with the swift implementation of trade and financial liberalisation, led togrowing trade and current account deficits.17 Both the expansion in absorption andthe external deficit were primarily financed by massive capital inflows, whichwere channelled through domestic credit and capital markets, thereforecontributing to a fast build-up in private and public indebtedness.

As was the case with many other attempts at rapid financial liberalisation, likethe Southern Cone experiences in the late seventies, the mix of aggressive banklending with lax prudential supervision once again resulted in a dangerousaccumulation of bad loans and growing fragility in the financial system. Thisprocess began well before the Tequila crisis. In fact, the incidence ofnonperforming loans in total credit for the whole convertibility period presentswide discrepancies between different types of institutions.

In any case, after the Tequila crisis the share of bad loans in bank portfoliosgrew considerably for all groups of institutions, and particularly so for the publicand private provincial banks (Table 4). Moreover, the figures most probablyconceal the full extent of the problem. Indeed, there are strong presumptions thatbank books systematically underestimated the incidence of bad loans.18

16 Calvo (1995) offers a similar argument, but referred to the behaviour of foreign institutionalinvestors to explain the swift porfolio change in the Mexican case.17 See, among many others, Frenkel (1995) and Dornbusch et al. (1995).18 In effect, even allowing for the severity of the recent crisis, the incidence of problem loans couldnot have reached its 1996 levels in just twelve months. Moreover, credit costs for the pre-crisisperiod strongly suggest a pre-crisis build-up in problem loans, while impressions gained throughinformal discussions with individual banks point to the same conclusion (Corrigan, 1996).

ARGENTINA’S BANKING SECTOR IN THE NINETIES 379

ß Blackwell Publishers Ltd 1998

TABLE 4Nonperforming Loans as a Proportion of Total Financing (In percentages)

Type of Institutions March 91 June 91 Dec. 91 June 92 Dec. 92 June 93 Dec. 93 June 94 Dec. 94 April 95 Sept. 96

National Public Banks 28.71 53.65 56.38 44.60 33.17 34.63 22.37 23.64 21.87 22.16 25.90Provincial and MunicipalPublic Banks 43.69 39.93 42.16 39.88 36.33 36.81 37.23 38.46 37.55 44.19 33.20

Private Banks in the FederalCapital 9.32 6.77 5.34 4.76 5.62 6.36 6.53 5.89 6.26 8.15 11.60 (*)

Private Banks in the Interior 13.43 10.69 12.04 12.30 12.73 11.87 11.29 10.88 11.41 15.93Foreign Banks 5.60 5.74 4.78 3.76 4.68 5.56 7.60 6.89 6.76 7.18 7.20Nonbanking Institutions 8.09 6.96 6.43 7.36 10.61 13.36 9.75 8.91 8.44 14.72 16.90Total in the System 25.16 36.95 37.29 27.97 22.69 21.73 17.28 17.06 16.05 18.53 18.20

Note:As from June 1994 the figures include loans in categories 3 to 5 of the new loan rating adopted that month. (*) Private Banks (Total).Source: Own calculation based on data from ‘Indicadores del sistema financiero’, Central Bank.

380R

OZ

EN

WU

RC

EL

AN

DB

LEG

ER

ßB

lackwell

Publishers

Ltd1998

(h) High operational unit costs and significant credit risks lie behind thecoexistence of wide spreads and low profits.

The sustained high level of country risk is one of the key variables explainingthe persistence of an appreciable spread between domestic and internationalinterest rates. On the other hand, convertibility has been truly effective atproducing a marked fall in expected devaluation (Table 5).19 In any case, theTequila crisis interrupted the declining trend in domestic borrowing rates andprompted a substantial rise in both peso and dollar rates, which extendedthroughout the first half of 1995.

Borrowing rates exceeding international ones and declining intermediationspreads that still remained extremely large resulted in excessively high domestic

TABLE 5Interest, Country Risk, and Expected Devaluation Rates (In percentages, in annual terms)

Domestic IRR Libor Estimated ExpectedRate Bonex 89 Rate Country Risk Devaluation(1) Rate Rate

1990 December 94.49 25.99 7.56 17.14 54.361991 March 207.74 19.58 6.50 12.29 157.34

December 19.83 10.17 4.38 5.55 8.771992 December 25.31 12.68 3.63 8.74 11.211993 December 8.67 6.33 3.50 2.73 2.201994 March 7.03 9.13 4.25 4.68 ÿ1.92

June 8.08 9.31 5.25 3.86 ÿ1.12September 8.33 8.66 5.75 2.75 ÿ0.30December 9.55 9.67 7.00 2.32 ÿ1.09

1995 January 10.65 11.09 6.63 4.19 ÿ0.40February 11.64 14.89 6.44 7.94 ÿ2.83March 19.38 13.81 6.44 6.93 4.89April 19.07 12.50 6.31 5.82 5.84May 15.54 9.91 6.06 3.63 5.12June 10.83 9.93 5.88 3.83 0.82July 10.24 10.12 5.88 4.01 1.09August 9.16 9.73 5.88 3.64 ÿ0.52September 9.22 10.47 6.25 3.97 ÿ1.13December 9.17 8.92 5.53 3.21 0.23

1996 March 7.27 8.79 5.50 3.19 ÿ1.40June 6.58 9.80 5.80 3.78 ÿ2.96September 7.80 8.84 5.75 2.92 ÿ1.00December 7.60 7.41 5.63 1.68 0.18

Notes:(1) Interest rate on 30-day term deposits.Source: Own calculation based on data from the Central Bank and ‘Carta Econo´mica’.

19 We take the difference between the IRR of Bonex (a dollar-denominated public bond) and theLIBOR rate as proxy for country risk, and the spread between the average rate of peso deposits andthe IRR of Bonex as proxy for expected devaluation.

ARGENTINA’S BANKING SECTOR IN THE NINETIES 381

ß Blackwell Publishers Ltd 1998

lending rates, especially in real terms.20 Wide intermediation spreads basicallyoriginate in two factors: first, the high operational unit costs associated with thephysical oversize of the financial system, in relation to the low level ofmonetisation and bankarisation of the economy; and second, the significant creditrisks connected with the heavy burden of bad loans in bank portfolios.21 It isprecisely because of the same factors, and despite the above-mentioned widemargins, that average long-term profitability in the bank system is astonishinglylow.

3. SYSTEMIC RISK AND THE MACROECONOMIC IMPACT OF THE BANKING CRISIS

a. The Unfolding of the Crisis

The outbreak of the Mexican crisis in December 1994 had deep repercussionson Argentina’s economy and financial system and it unleashed one of the mostserious financial crises in the history of the country. During the second quarterof 1994, the decision taken by the Fed to raise short-term interest rates at thestart of that year had already produced a decline in capital inflows, harmingArgentina’s economic and financial performance. Additionally, the govern-ment’s inability to fulfil the fiscal guidelines set in the Extended FacilitiesAgreement with the IMF led the Government to discontinue the deal beforeacceding to the final tranche of the loan. This decision had a negative impact onthe expectations of both local and foreign investors and placed Argentina in anextremely vulnerable position.

In such a context, the Mexican devaluation was quickly felt across the localfinancial system. The crisis was triggered by an initial massive withdrawal ofpeso deposits in domestic wholesale banks.22 The fragility of these institutionsturned markedly worse with the interruption of the credit lines open to them in theinterbanking call market. This concentration of deposits in 30-day terms made itpossible for the run to proceed quite quickly. Investors feared that Argentinawould follow in Mexico’s footsteps and devalue the domestic currency. Thiswould have affected the dollar value of their peso deposits which were stillconsiderable.

20 It is worth noting, however, that the cost of credit exhibits strong disparities linked, among otherthings, to the size and geographical location of borrowers. The most adversely affected are thesmall- and medium-sized firms excluded from international financial markets. The large economicgroups, of course, are far less affected because of their access to foreign credit and, to a lesserextent, to the local capital market.21 Of course, exceedingly high real lending rates themselves have lately developed into one of thecauses of the growing weight of problem loans.22 Most of the domestic wholesale banks had fluid contacts abroad but were potentially quite fragilebecause of their relatively high leverage ratios.

382 ROZENWURCEL AND BLEGER

ß Blackwell Publishers Ltd 1998

Meanwhile, the mistrust that arose in response to the default of somewholesale institutions spread to other segments in the market, particularly thesmallest public and private provincial banks. A repercussion of this mistrust wasthe virtual disappearance of the interbanking market which was reduced to thetransactions of only a small group of leading banks. At the same time, thehardening of international capital market conditions compelled large firms toseek out financing in the local market. As a consequence, the access of small- andmedium-sized companies to bank credit was further rationed.

The CB’s initial reaction to the liquidity crisis included the following measures:a significant cutback in reserve requirements; the granting of rediscounts and short-term swaps backed with public bonds by the Central Bank (within the strict limitsimposed by its Charter); and the hurried creation of an emergency safety net toassist the institutions with liquidity problems.23 In addition, institutions undergoingdifficulties were induced to agree to a takeover by more solid banks so as to avoidliquidation and the consequent losses for its investors.

The national government responded just as quickly. In the first days of Marchsome aspects of the CB Charter were changed. These changes, providing themonetary authority with more tools to confront the crisis, empowered the CB togrant rediscounts and advances in larger amounts and longer terms in situationsof systemic crisis, and extended the maximum term of suspension of financialinstitutions. They also authorised the bank to relinquish, transfer or sell the assetsit had acquired from the entities with liquidity problems.

At the same time, the monetary authorities tacitly allowed the forced rolloverof deposits by several institutions. While this step certainly undermined theinvestors’ confidence in the system, it at least made it possible to restrict thesuspensions or liquidations of institutions, preventing the crisis from becomingtotally uncontrollable. However, these measures alone were not enough and onlyserved to lessen the run on deposits temporarily. In the first fortnight of Marchthere was an escalation in withdrawals which affected the majority of theinstitutions, including some of the leading and most prestigious banks.

This time the change in private portfolios was not exclusively fuelled byexchange-rate expectations but also by the risk of default on bank deposits, be itfor liquidity or solvency problems of individual institutions, or for the possibilityof an overall refinancing of bank liabilities, as had happened in 1989 under theBonex Plan. A series of rather untimely announcements by some top publicofficials only increased investors’ fears.

By mid-March, the propagation of the crisis had already depleted the funds setaside by the CB to support the financial system and forced the government toannounce a new Financial Programme expressly destined to obtain foreign

23 This instrument, to be managed by the BNA (Banco Nacio´n), was intended to buy loan portfoliosof the troubled institutions.

ARGENTINA’S BANKING SECTOR IN THE NINETIES 383

ß Blackwell Publishers Ltd 1998

funding and counteract the expectations of default by the public sector and thefinancial system. This programme contained a renewal and extension of theprevious Extended Facilities Programme for an additional year, which meantfresh money for the government to the amount of 2.4 billion dollars. Loans for atotal of 2.6 billion dollars from the World Bank and the IDB were alsoannounced, as well as the commitment of foreign and local investors to subscribeto a new public bond (‘Bono Argentina’) for 2 billion dollars. The external loans,together with the projected fiscal surplus, would be devoted to increasing foreignreserves, to servicing the principal of the public debt due in 1995, and toconstituting two funds – the Trust Fund for Banking Capitalisation and the TrustFund for Provincial Development – to finance the restructuring of private andprovincial public banks, respectively.

TABLE 6Interest Rates and Financial Spread

Annual Interest Rates on 30-day Peso Deposits and Loans (In percentages)

Nominal Nominal Real Real FinancialLending Borrowing Lending Borrowing Spread

(prime rate) (1) (1)

1989 December 443.31 394.71 ÿ53.56 ÿ55.53 48.601990 December 274.25 124.68 ÿ39.49 ÿ63.67 149.571991 March 196.07 135.14 ÿ15.37 ÿ32.79 60.93

December 85.76 52.97 3.27 ÿ16.02 32.791992 December 32.12 11.62 11.14 ÿ6.05 20.501993 December 24.65 10.17 15.89 2.23 14.481994 March 20.80 7.06 17.23 5.78 13.74

June 24.21 8.12 20.59 4.97 16.09September 25.68 8.35 21.20 4.48 17.33December 26.80 9.55 22.04 5.44 17.25

1995 January 30.15 10.65 23.95 5.38 19.50February 30.01 11.64 23.82 6.32 18.37March 38.43 19.38 32.60 14.35 19.05April 34.27 19.07 28.37 13.83 15.20May 28.63 15.54 23.33 10.78 13.09June 24.30 10.83 19.86 6.88 13.47July 18.41 10.24 14.74 6.82 8.17August 17.45 9.17 14.36 6.30 8.28September 19.64 9.21 17.06 6.86 10.43December 13.90 9.16 12.11 7.44 4.74

1996 March 11.39 7.27 11.17 7.06 4.12June 10.81 6.55 10.92 6.66 4.26September 13.21 7.76 12.98 7.54 5.45November 11.84 7.53 11.39 7.10 4.31

Notes:(1) deflated by the CPI.

Source: Own calculations based on data from the Central Bank and ‘Carta Econo´mica’.

384 ROZENWURCEL AND BLEGER

ß Blackwell Publishers Ltd 1998

The announcements had an important influence on expectations, especially oflarge investors. This could be seen in the considerable deceleration in the run ondeposits. In order to boost the confidence of small investors, a partial butcompulsory deposit insurance to be financed by the institutions themselves wasalso established. However, because of the persistence of an acute uncertainty atthe political level, a full reversion of the downward trend in deposits could not beachieved until after the presidential elections in the second half of May.24 By theend of 1995 the most dramatic effects of the crisis had receded. In December1995 the domestic financial system had already recovered almost all the depositslost during the bank run.

b. Stylised Facts and Main Outcomes

The previous section described the domestic financial crisis, stressing its short-run impact on the evolution of monetary aggregates and interest rates, as well asthe behaviour of market participants and the monetary authorities during thatperiod. This section focuses on the crisis from a more analytical perspective,trying to highlight its main causes, features, and consequences (both short- andlong-term). The following points develop this analysis in a stylised fashion:

(a) The crisis was basically the result of a macroeconomic external shock– namely the Tequila effect – hitting an economy already exhibitingweak fundamentals, including a particularly fragile banking system.

Even the most casual analysis would suffice to show that the crisis was notsimply a sectorial event which originated in the wrongdoings of some individualbanks. Rather, both the timing and depth of the crisis strongly suggest that it arosefrom a macroeconomic external shock – namely the Tequila effect. The actualmotives for the investors’ panic before the shock, however, are a bit morecontroversial. Was the bank run exclusively as a self-fulfilling prophecy, in norelevant way connected with economic fundamentals as some authors wouldargue, or were there some deeper reasons behind it?25 It is certainly true that asizable contagion effect was felt in several emerging markets, in particular in LatinAmerica, immediately after the Mexican devaluation in late 1994.26 However, inalmost all the cases these effects tended to dissipate relatively fast. By contrast, theimpact of the Mexican shock in Argentina was much deeper and long-lived.

All this suggests that in the Argentine case, no matter how important thecontagion effect may have been, there were most probably some additional

24 A more detailed account of the crisis can be found in Broda and Secco (1996).25 Calvo (1995) can be taken as a good example of the first position, and Sachs et al. (1996) as agood example of the second.26 See, for instance, Calvo and Reinhart (1996).

ARGENTINA’S BANKING SECTOR IN THE NINETIES 385

ß Blackwell Publishers Ltd 1998

factors behind the crisis as well. According to our previous analysis, these factorsappeared to stem mainly from the weaknesses of both the country’smacroeconomic environment and its economic fundamentals. The former hadto do basically with the unsustainable combination of the economy’s growthperformance with a steadily accelerating current account deficit, while the latterwere primarily attached to the sizable distortions prevalent in the relative-pricestructure (especially the exchange-rate overvaluation) and the conspicuousfragility of the banking system.

In fact, it is rather easy to show in a simple macromodel admitting multipleequilibria that, after an exogenous shock increasing the expectations of adevaluation, an economy operating under a pegged exchange-rate regime wouldundergo a currency crisis and adjust to a ‘bad’ equilibrium if, and only if, it hadweak fundamentals (be it either exchange-rate overvaluation, a fragile bankingsystem, or both) in addition to insufficient foreign reserves.27 Argentina wasprecisly in that predicament when the Tequila crisis erupted.28 On the other hand,if the economy had strong fundamentals, then such a shock would produce nopermanent effect.

(b) The pervasiveness of the banking system’s fragility in the eightieswas a predictable outcome of high inflation and extreme uncertainty.What economic reformers in the nineties did not anticipate, however,was that financial deregulation and liberalisation would notautomatically cure this problem but, if anything, would worsen thesystem’s fragility.

We have already discussed in Section 2 the damaging implications that theprocess of demonetisation, dollarisation and short-termism had, from theviewpoint of fragility and systemic risk, for Argentina’s banking sector duringthe eighties. While the early nineties’ process of financial liberalisation andderegulation did not significantly alter the previous trends regarding eitherdollarisation or short-termism, it did produce a dramatic reversal in the evolutionof monetary and credit aggregates. Although it may seem paradoxical, the veryspeed with which the process of remonetisation and credit expansion proceededonly increased the banks’ vulnerability to systemic risk.

On the one hand, the financial boom that took place in the first three years ofthe CP allowed banks both to attract an ever growing flow of funds and to displayhuge profits in their books, thereby delaying a much needed restructuring. Among

27 See, for instance, Sachs et al. (1996).28 In fact, not only was the Argentine peso significantly appreciated and its financial system ratherwobbly, but the backing of the money supply (as measured by M2*) with liquid foreign reserves inthe CB and the commercial banks had sharply diminished, from 37.6 per cent in March 1991 to 25.1per cent in November 1994.

386 ROZENWURCEL AND BLEGER

ß Blackwell Publishers Ltd 1998

other things, this delay prevented them from improving their competence in sometraditional banking functions such as screening, monitoring or hedging, whichwere becoming more crucial for risk management as the economy was leavingbehind the prolonged period of high inflation. On the other hand, the newinstitutional scenario brought about by the quasi-Currency Board regime, the1992 Central Bank Charter and the modifications introduced into the Law ofFinancial Institutions that same year undoubtedly accentuated the inherentdangers of the myopic approach to adjustment which the banks chose. In fact, aswe have already argued in Section 2, some of the regulatory reforms introducedin the nineties significantly increased the system’s fragility. The extremelimitation of the CB’s lender of last resort functions (well beyond that imposed bythe Convertibility Law), the absolute absence of discretionary powers to assistproblem banks, and the elimination of the deposit guarantee were among the mostnotable examples of this circumstance. A similar case can be made regarding thesomewhat loose attitude adopted by the CB towards banking supervision and theenforcement of prudential regulation.

(c) The run on deposits triggered by the Tequila effect was clearlycrucial in the deterioration of the banks’ balance sheets, stronglysuggesting that the crisis was mainly of a liquidity nature. Its rapidpropagation, on the other hand, turned it into a systemic event.

It is often very hard to distinguish liquidity from solvency problems in thefinancial position of fragile banks, especially as these problems are so closelyintertwined. Nevertheless, and despite the steady growth in the share of bad loansin banks’ assets during the pre-crisis period, average solvency ratios were stillacceptable at the end of 1994. There is little doubt, therefore, that the 1995 crisiswould not have been activated had it not been for the massive depositwithdrawals triggered by the Tequila effect.

The view that the crisis was originally of a liquidity nature is also supported bythe fact that the more solid small wholesale banks were able to outlive it bygradually selling their positions in public bonds and high-grade corporatesecurities. Sure enough, with the progression of the crisis the solvency of thehardest hit banks began to deteriorate swiftly. On the other hand, despite the crisisoriginating in the most vulnerable segment of the market (wholesale andprovincial banks), by March 1995 it had already spilled over into the rest of thesystem, thereby turning into a systemic event.

(d) In order to face the crisis the economic and monetary authoritieswere forced to introduce major changes in the credit and financialpolicies applied during the first half of the nineties.

ARGENTINA’S BANKING SECTOR IN THE NINETIES 387

ß Blackwell Publishers Ltd 1998

With the escalation of the financial crisis, the entire monetary and financialscheme set up in the early nineties was put to the test. Reality quickly showed thatsome of the basic traits of the new scheme could not adequately handle a systemiccrisis. Consequently, major modifications had to be made in the regulatoryframework in order to at least restore a minimum safety net with which to supportthe banking system. This net included broader CB powers to finance troubledinstitutions and to deal with problem banks, as well as a new deposit insurancemechanism. The early nineties’ arrangements practically deprived the CB of itsfaculties as lender of last resort. Accordingly, they extended a key role to legalreserve requirements for the provision of liquidity in the face of a potential crisis.

Although the existence of high bank reserves prior to the crisis helped theinstitutions to face its most immediate repercussions, it soon became clear thatthey did not suffice to cover the increasing liquidity needs generated by thespreading of the bank run. As a result, the authorities decided that the CB wouldassist the financial system with all the funds available from the excess of itsforeign-currency reserves above the monetary base (including dollar-denominated public bonds up to the limit allowed by the Convertibility Law),thereby re-establishing its function as lender of last resort, though on a limitedscale. In order to do so, Congress sanctioned a modification in the CB charterwhich broadened the bank’s power to grant rediscounts and advances in bothamounts and terms, as long as this did not affect the functioning of theconvertibility regime.

Neither did the provisions incorporated into the Law of Financial Institutionsin 1992 contemplate any official action to support the rehabilitation of problembanks. In fact, they only specified that any entity facing solvency problems,deficient liquid reserves or any other difficulty that would affect its functioninghad to undertake a regularisation plan, subject to CB approval. Its nonfulfilmentimplied automatic liquidation of the institution.29

The strict application of these norms would have forced the liquidation of amajor number of entities and would have made it impossible for the monetaryauthorities to handle the crisis. Thus, the charter was modified so as to extend thesuspension term of an institution: after the first thirty days have expired, thesuspension can be renewed for up to ninety days.

The Law of Financial Institutions was also revised in the chapter on bankrestructuring. In the event that an entity experiences severe solvencydifficulties, these modifications would give the CB the power to act in orderto protect the interests of both bank depositors and borrowers, either throughtakeover of the floundering institution or by inducing the sale of a portion of its

29 In fact, there were no solid theoretical arguments in favour of this stance, which also ran againstmost of the accumulated international experience in the field. On this issue see, for instance,Dewatripont and Tirole (1994).

388 ROZENWURCEL AND BLEGER

ß Blackwell Publishers Ltd 1998

assets and liabilities to a more solid institution in the system. The healthierinstitutions’ interest in participating in the rehabilitation process was enhancedby the CB’s decision to forbid the opening of new bank branches. With regardto deposit insurance, there is little doubt that, to some extent, the absence ofsuch a scheme contributed to propagating the Tequila crisis in Argentina.Therefore, to rectify the government’s previous mistake and recover theconfidence of small depositors, Congress was urged to enact a law creating anew deposit insurance.

As a result, a Deposit Guarantee Fund was created, to be administrated bySedesa, a corporation made up by the banking sector under the supervision of theCB. The funding of the insurance would originate in monthly payments by allbanks, proportional to the amount of their deposits. The coverage extended to alldeposits in domestic or foreign currency up to 10,000 pesos for checking andsavings accounts and for term deposits of under 90 days, and up to 20,000 pesosfor longer terms.

As an indirect regulatory mechanism of borrowing rates, designed to limit themoral hazard inherent in any deposit guarantee regime, it was also establishedthat the deposits whose interest rates exceeded that determined by the BNA forthe same type of deposit by two percentage points would not be insured.30

Despite its low ceiling by international standards, the new scheme formallycovered 74 per cent of the deposit certificates in pesos and 55 per cent of thecertificates in dollars, positively affecting the confidence of small investors.31

(e) There is little doubt, however, that overcoming the crisis would havebeen even more costly had it not been for the foreign rescue packagepromptly set up under the coordination of the IMF.

The recovered CB powers to assist distressed banks, though certainlynecessary, arrived too late and were too modest to stop the crisis, only helpingto lessen the run on deposits temporarily. By mid-March, the propagation of thecrisis pushed the government to quickly devise a more comprehensive FinancialProgramme expressly destined to obtain foreign funding and counteract theexpectations of default by the public sector and the banking system. The foreignassistance and, in particular, the Fund’s active involvement were not incidentalfactors in the resolution of the crisis. Instead, they were decisive in limiting theharm it provoked.

30 On this issue, see Glaessner and Mas (1995) and Dewatripont and Tirole (1994).31 It is interesting to note, however, that real possibilities of coverage were initially virtually nilgiven the meagreness of the Guarantee Fund. In fact, the scheme stipulated that when theaccumulated resources could not cover the commitments, reimbursements would be made on a prorata basis from the available funds.

ARGENTINA’S BANKING SECTOR IN THE NINETIES 389

ß Blackwell Publishers Ltd 1998

(f) The liquidity squeeze was almost fully reversed at the end of 1995. Theextent of the crisis, nonetheless, fostered a sharp acceleration in marketconcentration and a full-scale restructuring in the banking system.

Even though the crisis had subsided significantly by the end of 1995, it hadlasting repercussions on the structural and institutional configuration of thefinancial system. The number of financial entities was reduced from 205 to 166between December 1994 and August 1995. This reduction was due principally tomergers and takeovers since only nine financial institutions were liquidatedduring the crisis. This explains why total branches only diminished from 4,081 to4,053 during that period (Table 2).

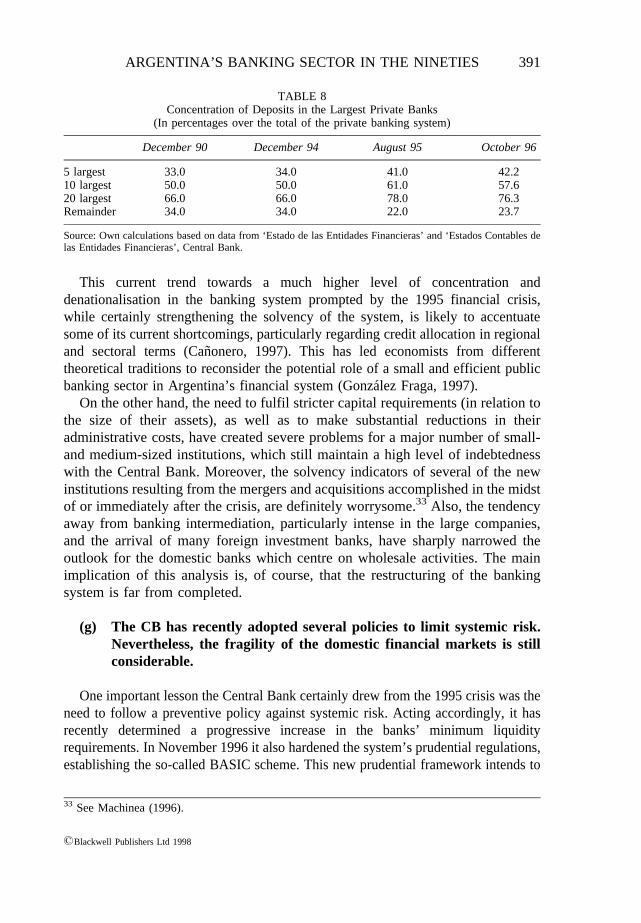

Considering the distribution of deposits by type of institution, the mostsignificant changes were the growth in national public banks and foreigninstitutions, and the fall in cooperative banks (Table 3). Likewise, the share oftotal deposits in the largest banks evidenced a huge jump (Table 7). This trendwas even more striking in the private banking segment (Table 8). As a result,banking concentration accentuated abruptly.

This redistribution of deposits from the smallest cooperative and provincialpublic banks to the largest private institutions, especially the foreign ones, and tothe national public banks suggests that, when deciding which banks still deservedtheir trust, investors cared much more about size or ownership than aboutoperational efficiency. Though rational from their viewpoint, this reaction isprobably reinforcing the already extreme segmentation of the domestic financialmarket and the insufficient credit support received by small- and medium-sizedborrowers, given that the large private banks, particularly the foreign ones,earmark a proportion of their financing that far surpasses the average in thesystem to large companies.32

TABLE 7Concentration of Deposits in the Largest Banks

(In percentages over the total of the banking system)

Dec.79 Dec.85 Dec.90 Dec.94 March 95 July 95 Oct.96

5 largest 27.7 42.5 41.2 37.0 39.9 42.7 38.410 largest 40.2 54.6 54.1 50.6 54.5 58.1 58.420 largest 56.6 66.7 67.8 65.3 69.4 72.8 75.0Remainder 43.5 33.4 32.2 34.7 30.6 27.2 25.0

Source: Own calculations based on data from ‘Estado de las Entidades Financieras’ and ‘Estados Contables delas Entidades Financieras’, Central Bank.

32 In fact, the figures for August 1996 show that while the total bank credit outstanding wasdistributed among 3,716,058 loans, more than one-third of that total was channelled through only1,458 loans which received four million dollars or more each, and about a half was channelledthrough 6,357 loans which obtained one million dollars or more each.

390 ROZENWURCEL AND BLEGER

ß Blackwell Publishers Ltd 1998

This current trend towards a much higher level of concentration anddenationalisation in the banking system prompted by the 1995 financial crisis,while certainly strengthening the solvency of the system, is likely to accentuatesome of its current shortcomings, particularly regarding credit allocation in regionaland sectoral terms (Can˜onero, 1997). This has led economists from differenttheoretical traditions to reconsider the potential role of a small and efficient publicbanking sector in Argentina’s financial system (Gonza´lez Fraga, 1997).

On the other hand, the need to fulfil stricter capital requirements (in relation tothe size of their assets), as well as to make substantial reductions in theiradministrative costs, have created severe problems for a major number of small-and medium-sized institutions, which still maintain a high level of indebtednesswith the Central Bank. Moreover, the solvency indicators of several of the newinstitutions resulting from the mergers and acquisitions accomplished in the midstof or immediately after the crisis, are definitely worrysome.33 Also, the tendencyaway from banking intermediation, particularly intense in the large companies,and the arrival of many foreign investment banks, have sharply narrowed theoutlook for the domestic banks which centre on wholesale activities. The mainimplication of this analysis is, of course, that the restructuring of the bankingsystem is far from completed.

(g) The CB has recently adopted several policies to limit systemic risk.Nevertheless, the fragility of the domestic financial markets is stillconsiderable.

One important lesson the Central Bank certainly drew from the 1995 crisis was theneed to follow a preventive policy against systemic risk. Acting accordingly, it hasrecently determined a progressive increase in the banks’ minimum liquidityrequirements. In November 1996 it also hardened the system’s prudential regulations,establishing the so-called BASIC scheme. This new prudential framework intends to

TABLE 8Concentration of Deposits in the Largest Private Banks

(In percentages over the total of the private banking system)

December 90 December 94 August 95 October 96

5 largest 33.0 34.0 41.0 42.210 largest 50.0 50.0 61.0 57.620 largest 66.0 66.0 78.0 76.3Remainder 34.0 34.0 22.0 23.7

Source: Own calculations based on data from ‘Estado de las Entidades Financieras’ and ‘Estados Contables delas Entidades Financieras’, Central Bank.

33 See Machinea (1996).

ARGENTINA’S BANKING SECTOR IN THE NINETIES 391

ß Blackwell Publishers Ltd 1998

complement the CB’s traditional regulatory functions with some market mechanisms.In order to do so, besides reinforcing the CB’s supervisory powers and includingstricter controls on the banks’ external auditing firms, the new framework plans tooffer the public more complete information on the banks’ performance, and it alsodemands that the banks be rated by an accredited private rating agency. Furthermore,according to the new scheme, the banks will have to issue and float its own bonds as away to have a continuous market evaluation about their prospects.

On the other hand, in December 1996 the CB signed an innovative swapagreement with thirteen large international banks which will operate as aninsurance mechanism against speculative attacks. The arrangement lasts two tofive years according to the individual deals reached with the different banks, andit allows the CB to raise up to six billion dollars (about ten per cent of totaldeposits in the domestic banking system) by selling public bonds, subject to arepurchase agreement, to the banks involved. The swift recovery in the CB’sliquid foreign reserves and the resulting improvement in the backing of themoney supply, initially prompted by the implementation of the foreign rescuepackage and later sustained by the favourable evolution of the world financialmarkets, also contributed to limiting systemic risk.

Despite these policy actions and the ongoing structural changes in the domesticcredit markets, certain indicators suggest that the system’s fragility remainssignificant. In the first place, the sharp recession induced by the crisis provoked asizable increase in bad loans, clearly indicating that the solvency of manyinstitutions had further deteriorated. Although the share of problem loans hassomewhat diminished since the recovery initiated in the second half of 1996, it isstill too high, especially in the weakest banks.34 In the second place, the riskposed by the maturity mismatches in banks’ assets and liabilities is still rampant.

The same judgement is valid for the far-reaching dollarisation of financialintermediation, even though in this case the risk does not necessarily emerge as aresult of a mismatch in the currency denomination of deposits and loans. Instead,it basically arises from the distinct possibility of an unexpected divergence in theevolution of the incomes of a significant proportion of bank borrowers and theexchange rate. In fact, such a possibility could materialise not only as aconsequence of an unanticipated nominal devaluation, but also as an outcome ofprice deflation. In any case, the resulting real devaluation would certainly

34 In September 1996 the aggregate ratio of bad loans to total credit in Argentina’s financial systemwas 18.2 per cent. The ratio was somewhat lower but nonetheless quite impressive in the nationalprivate banks’ segment: 11.6 per cent (Table 4). On the other hand, according to Dick (1996), inDecember 1995 the same ratio was 5.8 per cent for Argentina’s ten largest banks, while it was only0.8 per cent in Chile (for the entire system) and also in the US (41 largest banks), 1.5 per cent inCanada (5 largest banks), 1.9 per cent in Germany (3 largest banks) and 4.2 per cent in the UK (8largest banks). The only case in the sample where the ratio was higher than in Argentina’s tenlargest banks was in Spain’s seven largest institutions (6.3 per cent).

392 ROZENWURCEL AND BLEGER

ß Blackwell Publishers Ltd 1998

increase the debt burden of bank borrowers and, if the shock is deep enough, itwould also impair the solvency of the creditor banks. In the third place, despitethe fact that a deposit insurance is in effect, the Guarantee Fund counts with analmost insignificant volume of resources, which makes the efficacy of theinstrument somewhat doubtful should it be necessary.

Moreover, from a more general perspective, it remains true that under thecurrent monetary regime the CB retains very limited available instruments withwhich to confront a systemic banking crisis.35

Finally, the possibility of further assistance from the multilateral financialinstitutions, at least in the near future, is very restricted, given the profuse use ofthese resources during the recent crisis. On the other hand, even though a newIMF facility to deal with financial crises in emerging countries is currently underdiscussion, it is not at all clear if and when it will be approved.

4. CONCLUSIONS AND POLICY LESSONS

The early-nineties’ liberalisation process has led to significant structuraltransformations in the domestic financial markets and the banking system. Themost positive developments were an important increase in monetisation andfinancial intermediation, the reversal in capital flight and the lifting of the foreigncredit rationing faced by Argentina in the eighties.

However, other developments have not been all that favourable. First, whilethe process of remonetisation and financial deepening has been truly fast, thedemand for domestic financial assets and other banking services is still muchlower than in the period prior to the high-inflation seventies and eighties. Second,dollarisation and its related risks have also deepened. Third, there has been nosignificant lengthening in the term maturity of the banks’ liabilities. Fourth, thesystem’s operational inefficiencies, largely accountable for the wide spreads andcommissions charged by the banks, still determine the persistence of quite highreal lending rates.36 Lastly, the small- and medium-sized firms, with almost noaccess to foreign credit markets, continue to face a tight credit rationing in thedomestic markets too.

35 In fact, even though the Trust Funds are currently in force, they cannot be used to face liquidityproblems since, in principle, they are specifically destined either to the privatisation of public banksor the capitalisation and restructuring of private institutions.36 A recent Banco Central (1997) paper estimates as 12.4 per cent the annual average spread inArgentina’s banking system at the end of 1996, much higher than that calculated for the US, whichwas 5.2 per cent. The paper finds that the main factors behind such a huge difference wereArgentina’s higher operational costs (which explained 4.3 points of the spread in that countryagainst 1.1 points in the US), larger provisions (explaining 5.5 points of the spread in Argentina and2.1 points in the US), and higher taxes (1.9 points and 1.1 points respectively).

ARGENTINA’S BANKING SECTOR IN THE NINETIES 393

ß Blackwell Publishers Ltd 1998

Moreover, the combination of a completely unrestricted financial opening witha quasi-Currency Board regime threatened the stability of the banking system. Infact, while it first served to stimulate capital inflow and boost domestic activity, itlater facilitated the swift capital flight which accompanied the run on depositsonce the financial crisis had been unleashed as a result of the Mexicandevaluation. The recent crisis also illustrated the rigidity of the current exchange-rate regime to absorb external shocks, the fragility of the domestic financialsystem and the lack of a suitable safety net with which to confront a bank run.

Following the same logic that had led to the implementation of convertibility,the government was convinced that legally preventing discretionary monetarypolicies would have such favourable consequences on investor expectations andmoral hazard that no policy tools would be necessary to face a potential systemiccrisis. The eruption of the financial crisis clearly proved how weak this logic wasand forced the government to make urgent modifications to recover the policyinstruments available within the narrow confines of convertibility.

It is worth stressing, incidentally, that all regulatory changes took place in anevironment where the full autonomy of the CB as established in the new Charterwas sharply reduced, since the depth of the crisis forced the Ministry of theEconomy to take charge. At any rate, despite the fact that the anti-crisisinstruments were recovered and utilised with a certain degree of efficacy, it wasthe external support, achieved with the crucial backing of the IMF, that finallymade it possible to fully overcome the crisis by decisively improvingexpectations on the maintenance of convertibility, the fiscal balance and thesoundness of the financial system. The crisis also hastened the ongoing structuralchanges in the banking system, acting as a catalyst for the inevitable restructuringof the financial institutions. As we have already seen, however, this process is farfrom completed.

Therefore, while it is true that the system’s stance is more solid than before thecrisis, it would not be wise to completely dismiss the possibility of furthersystemic complications. Both the multilateral institutions and the nationalgovernment seem to have recognised this point. In order to face it, and accordingto the currently prevailing mainstream international consensus, the Central Bankhas recently hardened the system’s prudential regulations.37 On the other hand, inDecember 1996 the CB signed a swap agreement with thirteen internationalbanks which will operate as a privately funded safety net. At the same time, the

37 Morris Goldstein from the Institute for International Economics, for instance, has recentlysuggested that Central Banks in emerging economies should adjust prudential regulations to the lowlevel of development of their financial markets and institutions. This means, among other things,setting a minimum 12 per cent capital-adequacy ratio, much higher than that established by theBasle Accords, adopting stricter criteria for the identification of bad loans and their provisioning,and stipulating that the performance of each bank be periodically evaluated by an internationallycredited rating agency.

394 ROZENWURCEL AND BLEGER

ß Blackwell Publishers Ltd 1998

CB is actively promoting a second round in the process of mergers andacquisitions, with the explicit purpose that this time the resulting new institutionsbe positively solvent.

In any case, within the tight limits imposed by the convertibility regime, a lessvulnerable financial system is likely to require not only very high bank reservesand a much stricter regulatory framework, but also fewer and larger institutionsand a greater participation of foreign banks.38 This is particularly the caseconsidering that so far the proposals to widen the functions of the IMF, so that itcan systematically play the role of lender of last resort before a financial crisis inan emerging country, do not seem to have attained the support of theindustrialised world.

There are some signs that the financial system may already be heading in thatdirection. While such a trend will hopefully reduce systemic fragility, the risk thatit will further strengthen the market segmentation and restrict the access to bankcredit is certainly high. Therefore, the relevant question of how to ensure that thissystem is also consistent with a sustained and equitable economic growth remainsopen.

REFERENCES

Aglietta, M. (1995), ‘Globalizacio´n financiera, riesgo sistema´tico y control monetario en los paı´sesde la OCDE’,Pensamiento Iberoamericano, No. 27.

Banco Central (1997), ‘Presentacio´n sobre la coyuntura del Sistema Financiero’ (Mimeo, BuenosAires).

Broda, M. and L. Secco (1996), ‘Caja de Conversio´n pura o un Banco Central con lı´mites estrictos?Las ventajas de la flexibilidad durante la crisis del primer trimestre de 1995’ (Anales de laXXXI Reunion Anual, AAEP-UNS, Salta).

Calvo, G. (1995), ‘Capital Flows and Macroeconomic Management, Tequila Lessons’ (Mimeo,presented at the Seminar on Implications of International Capital Flows for Macroeconomic andFinancial Policies, IMF, Washington, DC).

Calvo, G., L. Leiderman and C. Reinhart (1992), ‘Capital Inflows and Real Exchange RateAppreciation in Latin America: The Role of External Factors’,IMF Working Paper 92/62(IMF,Washington, DC).

Canonero, G. (1997), ‘Bank Concentration and the Supply of Credit in Argentina’,IMF WorkingPaper (IMF, Washington, DC).

Corrigan, G. (1996), ‘Building a Progressive and Profitable National Banking System in Argentina’(Report to the Ministry of the Economy).

Davis, P. (1995),Debt, Financial Fragility and Systemic Risk(Clarendon Press, Oxford).Dewatripont, D. and J. Tirole (1994),The Prudential Regulation of Banks(The MIT Press,

Cambridge, Mass).Dick, A. (1996), ‘Costos y eficiencia bancaria en la Argentina’ (Mimeo, presented at the Jornadas

de Economı´a Monetaria y Sector Externo, Central Bank, Buenos Aires).Dornbusch, D., I. Goldfajn and R. Valde´s (1995), ‘Currency Crises and Collapses’,Brookings

Paper on Economic Activity, 2.

38 In fact, these are some of the recommendations proposed in Calvo (1995).

ARGENTINA’S BANKING SECTOR IN THE NINETIES 395

ß Blackwell Publishers Ltd 1998

Frenkel, R. (1995), ‘Macroeconomic Sustainability and Development Prospects: Latin AmericanPerformance in the 1990s’,Discussion Paper 100(UNCTAD, Geneva).

Glaessner, T. and I. Mas (1995), ‘Incentives and the Resolution of Bank Distress’,ResearchObserver(The World Bank, Washington, DC).

Gonzalez Fraga, J. (1997), ‘La Privatizacio´n del Banco de la Nacion Argentina’,La Nacion(Buenos Aires).

Larraın, C. (1994), ‘Modernizacio´n de la Supervisio´n Bancaria’,Revista de la Cepal 54(CEPAL,Santiago de Chile).

Machinea, J. (1996), ‘La crisis financiera argentina de 1995: causas, caracterı´sticas y lecciones’(Mimeo, Buenos Aires).

Rozenwurcel, G. and R. Ferna´ndez (1994), ‘Strengthening the Financial Sector in the AdjustmentProcess: The Case of Argentina’, in R. Frenkel (ed.),Strengthening the Financial Sector in theAdjustment Process(IDB- The Johns Hopkins University Press, Washington, DC).

Sachs, J., A. Tornell and A. Velasco (1996), ‘Financial Crises in Emerging Markets: The Lessonsfrom 1995’,Brookings Papers on Economic Activity, 1.

Stiglitz, J. (1993), ‘The Role of the State in Financial Markets’ (Mimeo, presented at the AnnualBank Conference on Development Economics, The World Bank, Washington, DC).

396 ROZENWURCEL AND BLEGER

ß Blackwell Publishers Ltd 1998

Copyright © 2022 FDOKUMEN