Country Study Report on “Banking Sector Analysis of Sri Lanka”

680

1| Page A GLOBAL / COUNTRY STUDY REPORT ON “Banking Sector Analysis of Sri Lanka” Submitted to Gujarat Technological University IN PARTIAL FULFILLMENT OF THE REQUIREMENT OF THE AWARD FOR THE DEGREE OF MASTER OF BUSINESS ADMINISTRATION UNDER THE GUIDANCE OF Project Guide Asst. Prof. Nilesh Ankleshvariya SUBMITED BY Mahipal Zala, Tejas Khakhkher, Chirag Kapadia, Trupti Vansajaliya, Dipika Trivedi (C. C. Gardi Institute of Management) [Batch: 2011-13] MBA SEMESTER III/IV MBA PROGRAMME Affiliated to Gujarat Technological University Ahmadabad

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Country Study Report on “Banking Sector Analysis of Sri Lanka”

1 | P a g e

A

GLOBAL / COUNTRY STUDY REPORT

ON

“Banking Sector Analysis of Sri Lanka”

Submitted to

Gujarat Technological University

IN PARTIAL FULFILLMENT OF THE REQUIREMENT

OF THE AWARD FOR THE DEGREE OF

MASTER OF BUSINESS ADMINISTRATION

UNDER THE GUIDANCE OF

Project Guide

Asst. Prof. Nilesh Ankleshvariya

SUBMITED BY

Mahipal Zala, Tejas Khakhkher, Chirag Kapadia,

Trupti Vansajaliya, Dipika Trivedi

(C. C. Gardi Institute of Management)

[Batch: 2011-13]

MBA SEMESTER III/IV

MBA PROGRAMME

Affiliated to

Gujarat Technological University

Ahmadabad

2 | P a g e

STUDENT’S DECLARATION

We,MahipalZala(117880592001),ChiragKapadia(117880592002),Trupti Vansajaliya(117880592003),

Dipika Trivedi(117880592004),Tejas Khakher(117880592005) are students of C.C. Gardi Institution

of Management, hereby declare that the report for Global/ Country Study Report entitled

“GLOBAL / COUNTRY STUDY REPORT ON BANKING SECTOR ANALYSIS” in SRI

LANKA is a result of our own work and our indebtedness to other work publications,

references, if any, have been duly acknowledged.

Place: ……..

(Signature)

Date:

(Name of Student) - Mahipal Zala

- Chirag Kapadia

- Trupti Vansajaliya

- Dipika Trivedi

- Tejas Khakher

3 | P a g e

PREFACE

Today we are at the door step of 21st century. The world is widening without having a

New and new developments are coming these days in all fields all over India to make

the people life more comfortable and luxurious. The industries are growing so fast in

India in order to satisfy all the needs of people. Similarly Gov. has supported to these

companies for their development and progress of private companies.

Thus in order to survive in the market one should have theoretical as well as Practical

knowledge about all different fields prevailing in market. For this we have chosen SRI

LANKA country for Global country report.

4 | P a g e

ACKNOWLEDGEMENT

We feel pleasure to submit this report, which includes the practical aspect of study. We

are very happy to express our deepest gratitude to all the persons who spared their

valuable time & helped us in preparation of this Global Country Report.We might like to

thank our project guides Asst. Prof. Pratik Gandhi, Prof. Nilesh Anklesvariya for our

moral support & guidance.

DATE:

PLACE: Rajkot

Signature of Student

5 | P a g e

6 | P a g e

EXECUTIVE SUMMARY

Today in course like MBA, project is very important with the theoretical knowledge. The importance of project work has greater role in business world. Combination of practical knowledge with theoretical knowledge makes student perfect in his work. we have prepared our global country report on “BANKING SECTOR ANALYSIS OF SRI LANKA”.

Sri Lanka is a country of the southern coast of the Indian subcontinent. Known until

1972 as Ceylon, Sri Lanka is an island surrounded by the Indian Ocean, the Gulf of

Mannar and the Palk Strait, and lies in the vicinity of India and the Maldives. It is part of

South Asia.

The Official Name of Sri Lanka Democratic Socialist republic of Sri Lanka and its capital

is Sri Jayewardenapura Kotte. And Colombo, the former capital is the commercial

capital and largest city of Sri Lanka.

Sri Lanka and India trade relations with existing business volume for various products

Lanka. India, Sri Lanka, the nearest neighbor. The relationship between these 2

countries for more than 2,500 years old, and both sides of the intellectual, cultural,

religious and linguistic intercourse is built on a legacy.

India and Sri Lanka Sri Lanka bilateral trade in the last decade and a leading Indian

private sector investment and a rapidly growing number of companies establishing a

presence in the country with a vibrant and growing economic and commercial

partnership, enjoy. Sri Lanka is India's largest trading partner in SAARC. 19.52% and

5.69% respectively in 2012, India's share of global imports and exports in Sri Lanka.

India's exports to Sri Lanka in 2012 largely reduced excise duty on imported vehicles

twice a steep rise in the year 2012 that a serious competitive advantage enjoyed by

Indian auto companies and affected the entire volume of the imposition of imported

vehicles in India in 2012 50-60% declining In India, the largest in the whole of Sri Lanka

(nine months as above) $ 210 million on U.S. emerged as the investor with investments

7 | P a g e

In this global country report, we have include five banks of India as well as Sri Lanka

from that we make comparisons of Interest income, Interest expense, Net interest

income, Net profit, Equity Dividend (%) from profit and loss account and Equity Share

Capital, Reserves, Net worth, Deposits, Borrowings, Total Debt, Balance with RBI/

banks, Investments and Total Assets from balance sheet.

Other than that we have include in Sri Lankan banking sector, licensing policies &

standards, Licensing procedures, exporting and importing policies etc. we also include

rules and regulation of banking sector of both the countries.

In such a way, we completed our Global Country Report. Almost all of our faculties,

colleagues and our friends given us good co-operation and help us to collect various

types of information too.

8 | P a g e

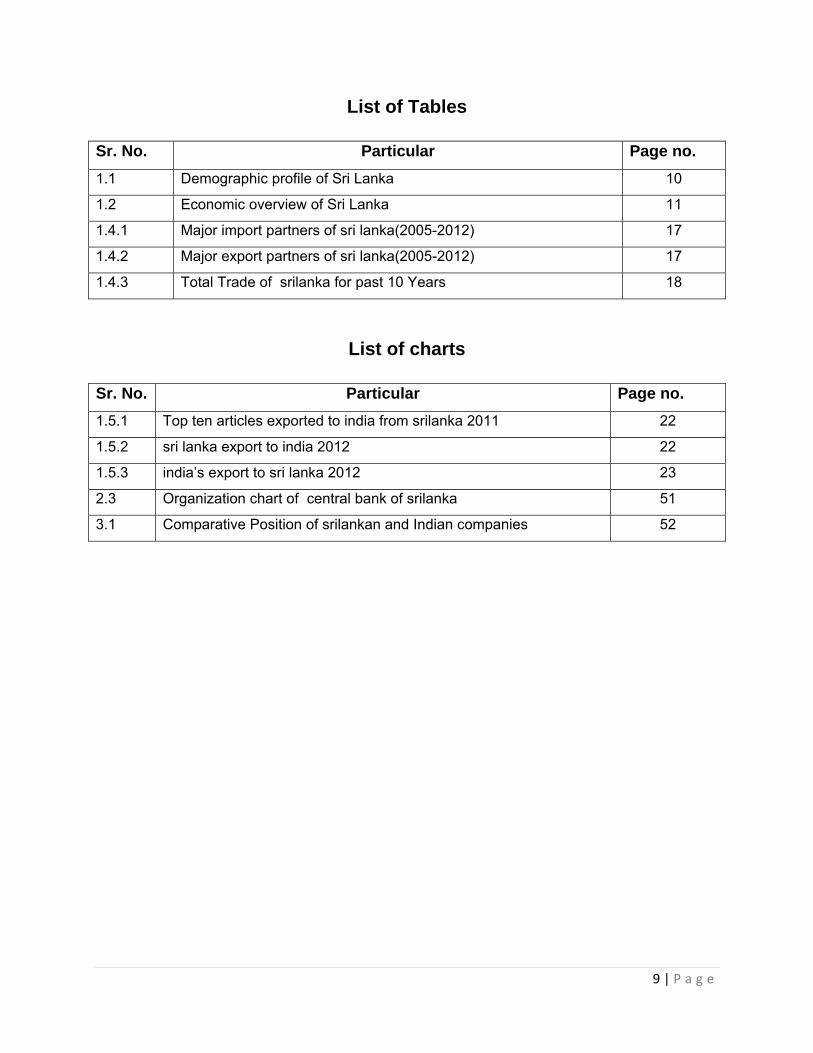

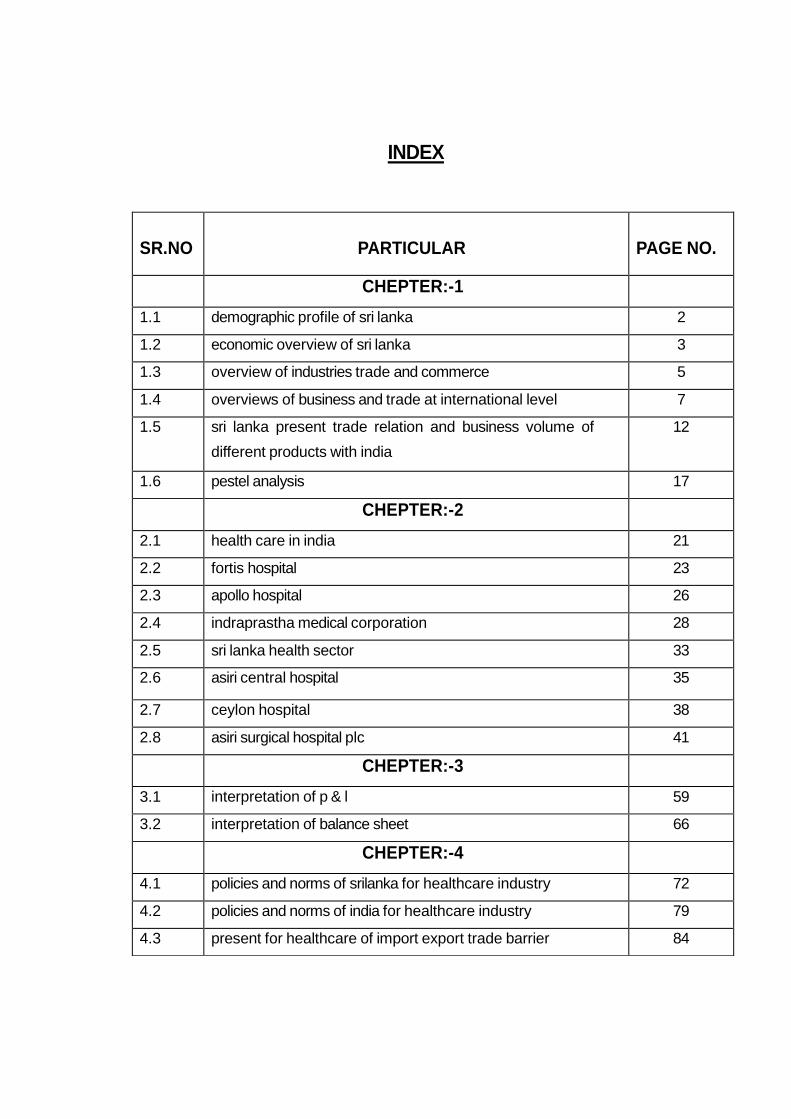

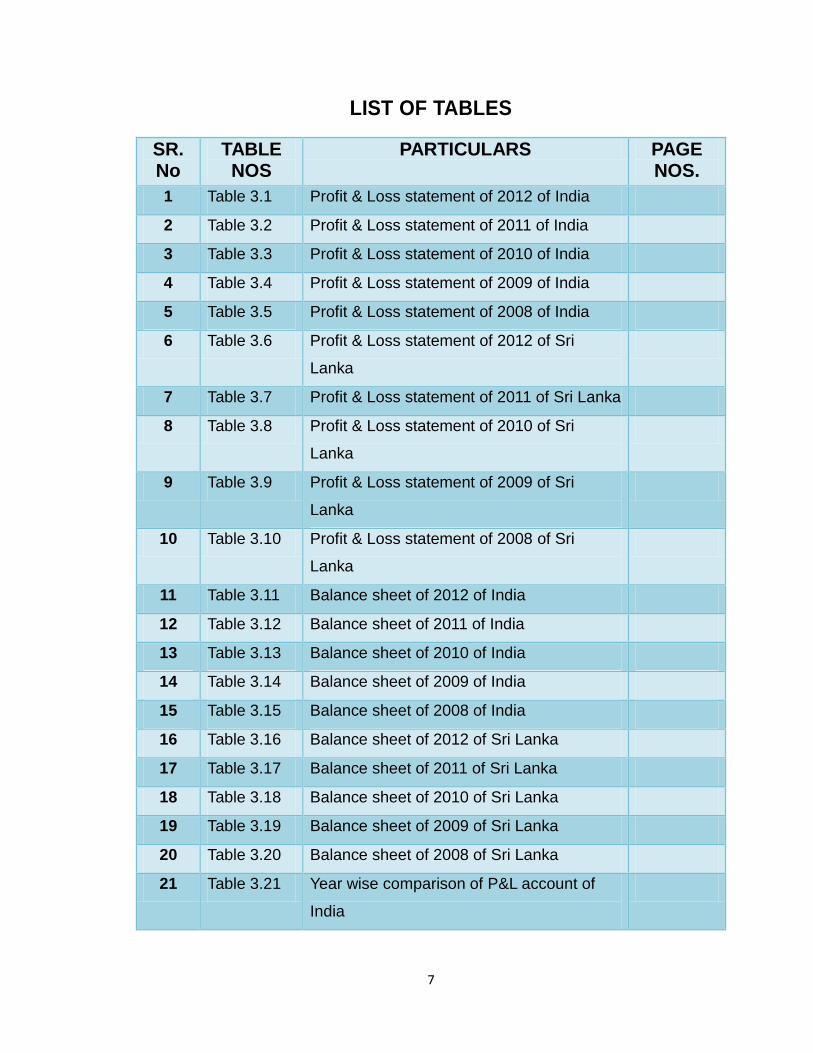

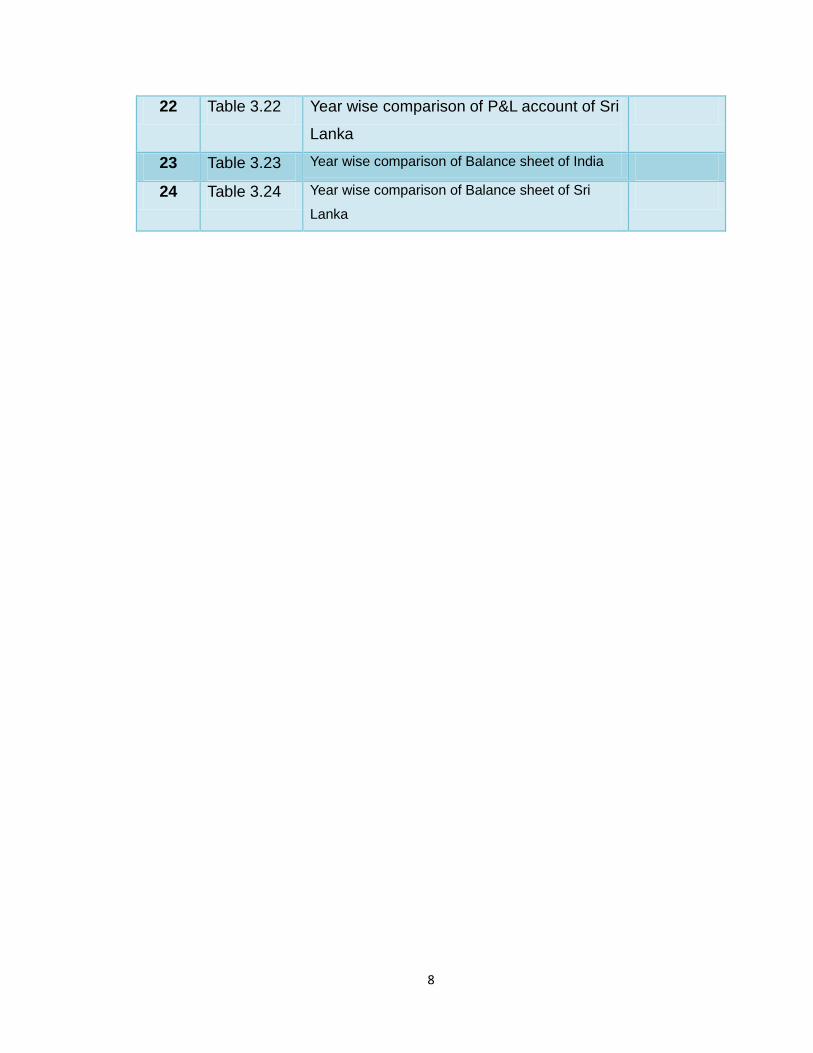

Table of contents

Sr. No. Particular Page no.

CH-1 1.1 Demographic profile of Sri Lanka 10

1.2 Economic overview of Sri Lanka 11

1.3 Overview Different economic sectors of srilanka 13

1.4 Overview of srilankan business and trade at international level 17

1.4.1 Major import partners of sri lanka(2005-2012) 17

1.4.2 Major export partners of sri lanka(2005-2012) 17

1.4.3 Total Trade of srilanka for past 10 Years 18

1.5 Present Trade Relations and Business Volume of different products of srilanka

with India

19

1.5.1 top ten articles exported to india from srilanka 2011 22

1.5.2 sri lanka export to india 2012 22

1.5.3 india’s export to sri lanka 2012 23

1.6 PESTEL Analysis 24

CH-2 2.1 Introduction of selected Indian and srilankan companies of banking sector 26

2.1.1Indian bank 26

2.1.2 Srilankan bank 37

2. 2 objective and function of banking industry 49

2.3 Organization chart of central bank of srilanka 51

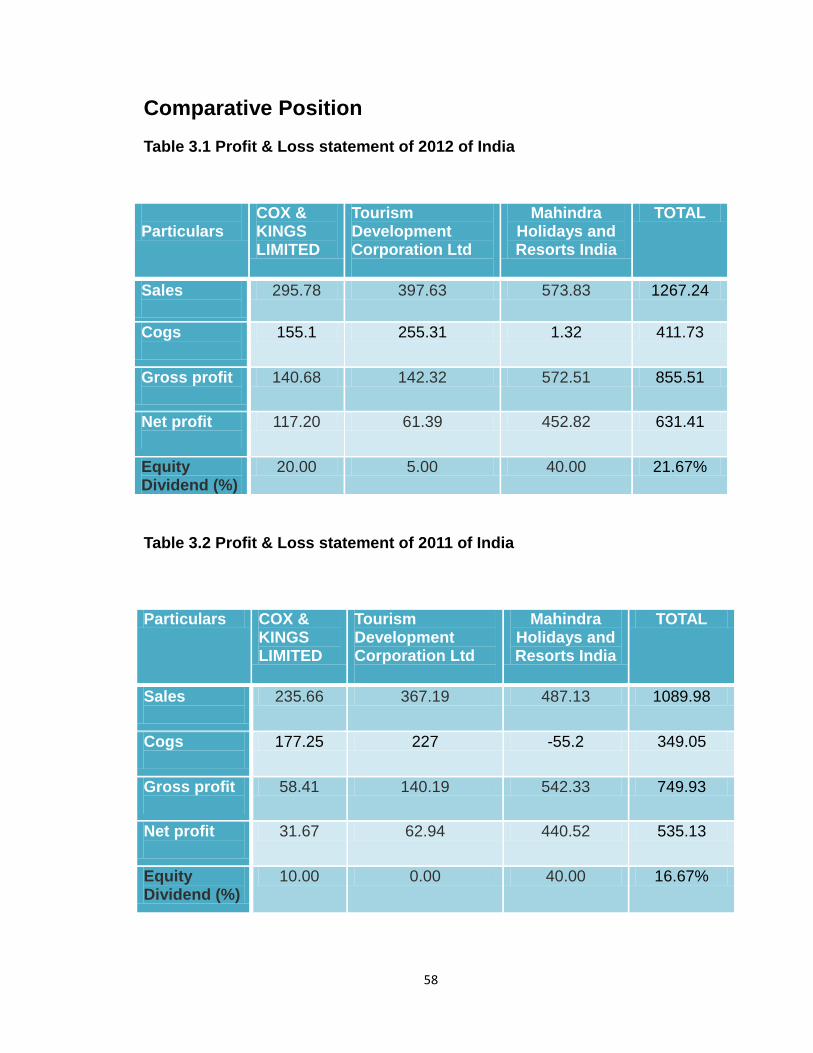

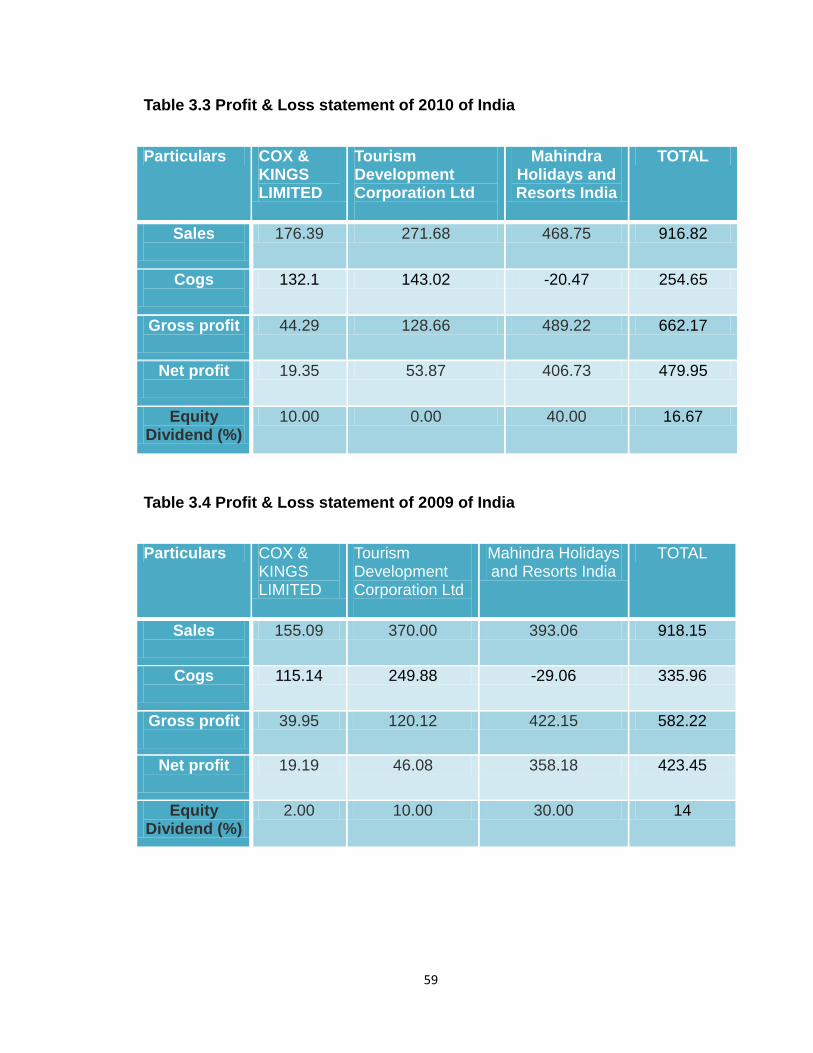

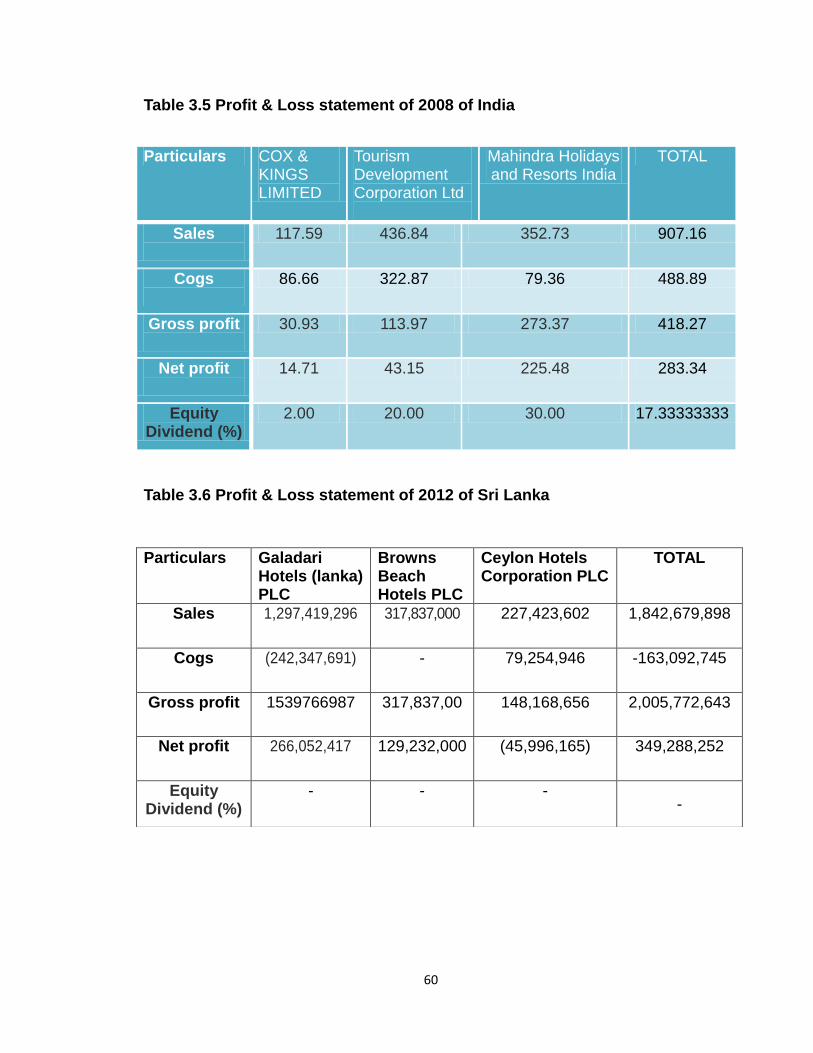

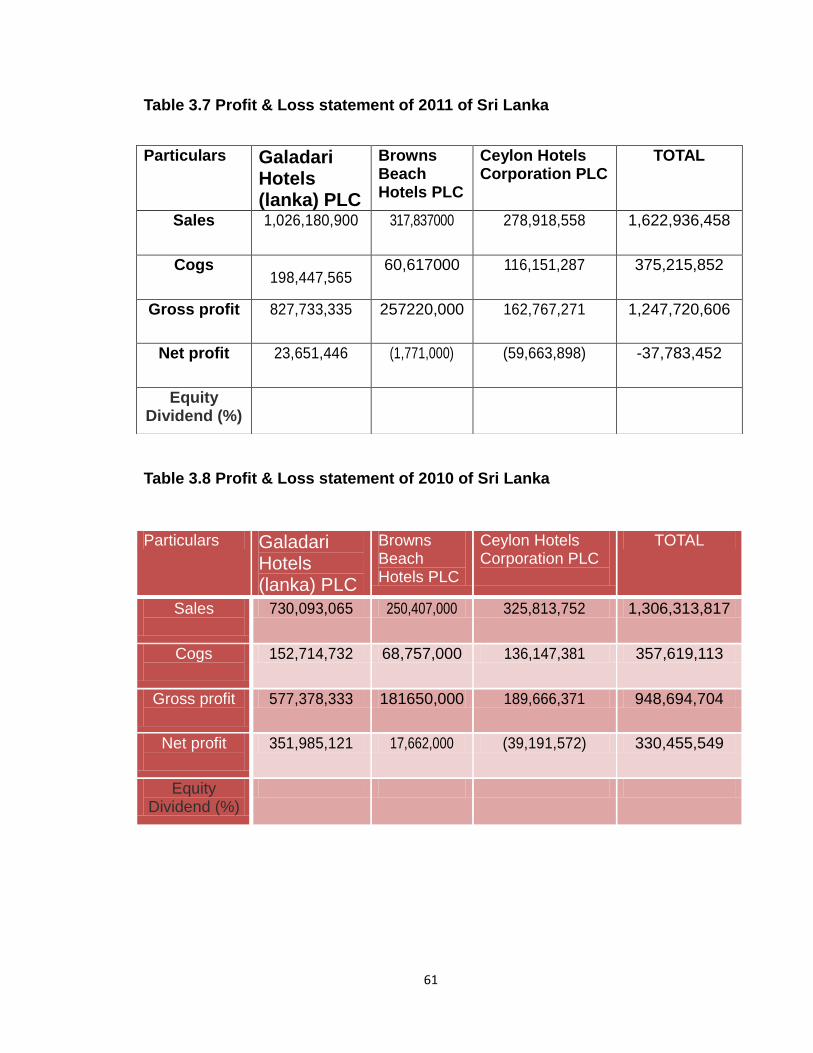

CH-3 3.1 Comparative Position of srilankan and Indian companies 52

3.2 Present Position of Indian bank in srilanka 69

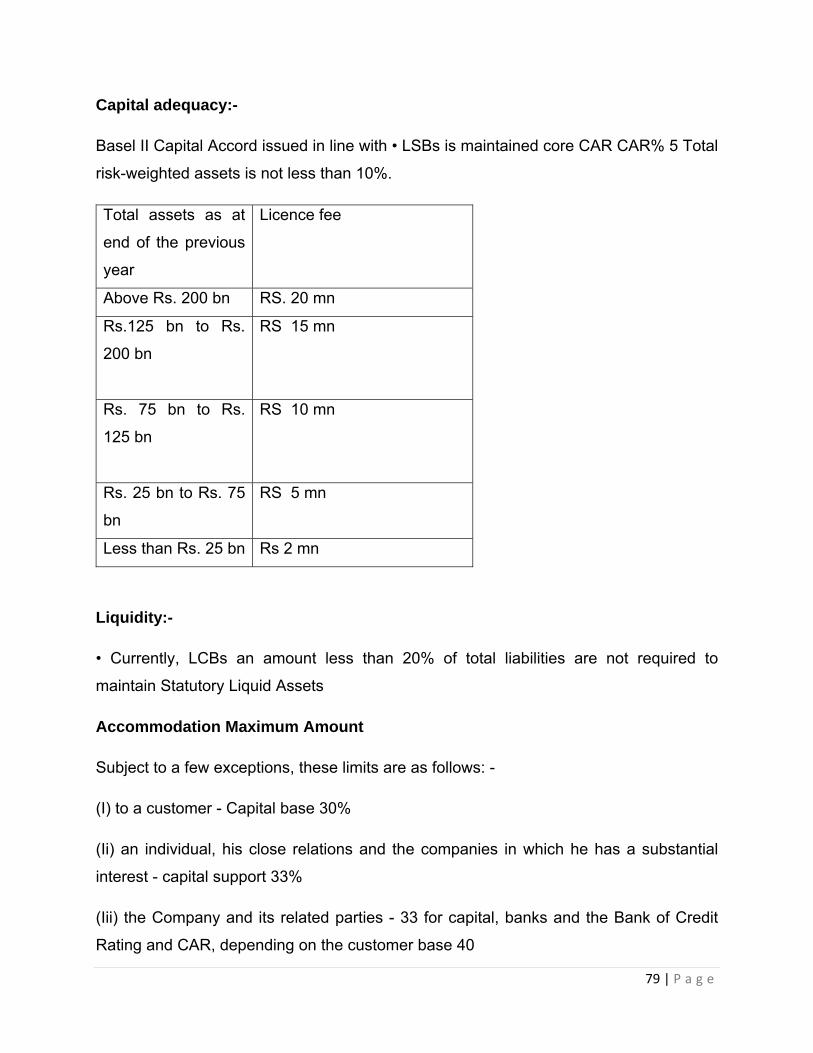

CH-4 4.1 Sri Lankan banking sector’s licensing policies & standards 72

4.2 Regulatory authorities of the Central Bank of Sri Lanka 74

4.3 Licensing procedures for opening a bank in Sri Lanka 76

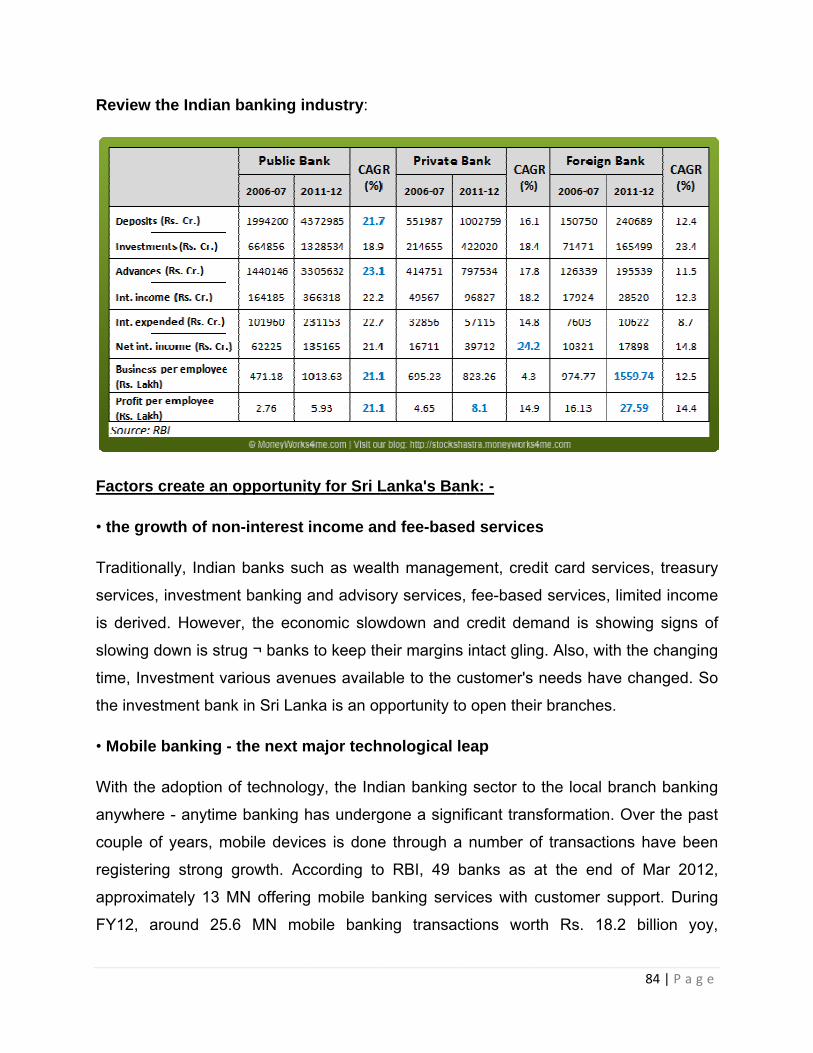

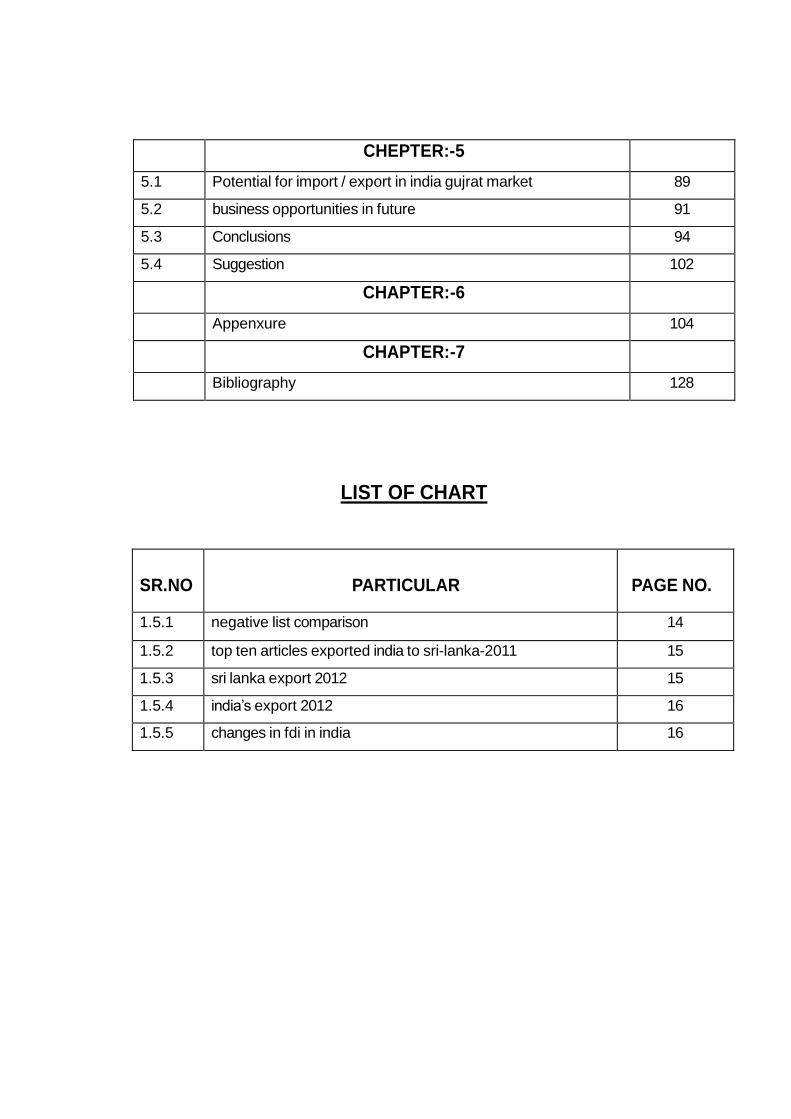

CH- 5 5.1 Business opportunities for srilankan banks in india 83

5.2 conclusion and suggestions 87

Reference an bibliography 90

Appendix 91

9 | P a g e

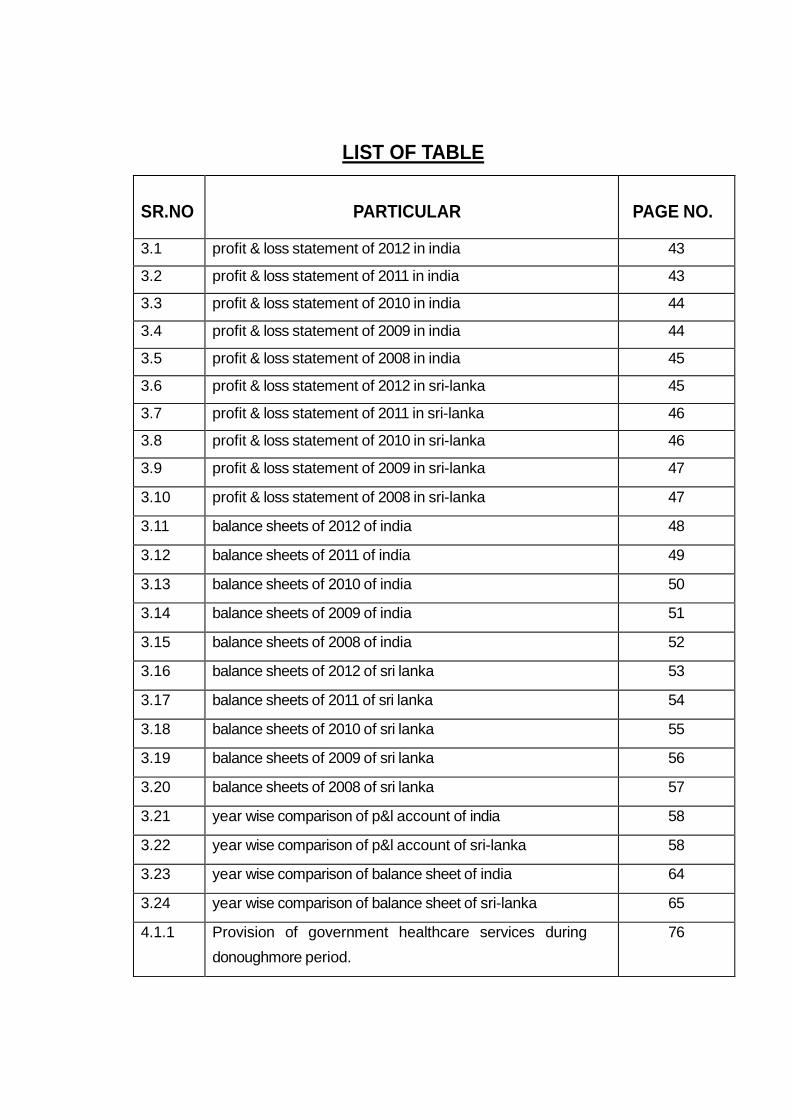

List of Tables

Sr. No. Particular Page no.

1.1 Demographic profile of Sri Lanka 10

1.2 Economic overview of Sri Lanka 11

1.4.1 Major import partners of sri lanka(2005-2012) 17

1.4.2 Major export partners of sri lanka(2005-2012) 17

1.4.3 Total Trade of srilanka for past 10 Years 18

List of charts

Sr. No. Particular Page no.

1.5.1 Top ten articles exported to india from srilanka 2011 22

1.5.2 sri lanka export to india 2012 22

1.5.3 india’s export to sri lanka 2012 23

2.3 Organization chart of central bank of srilanka 51

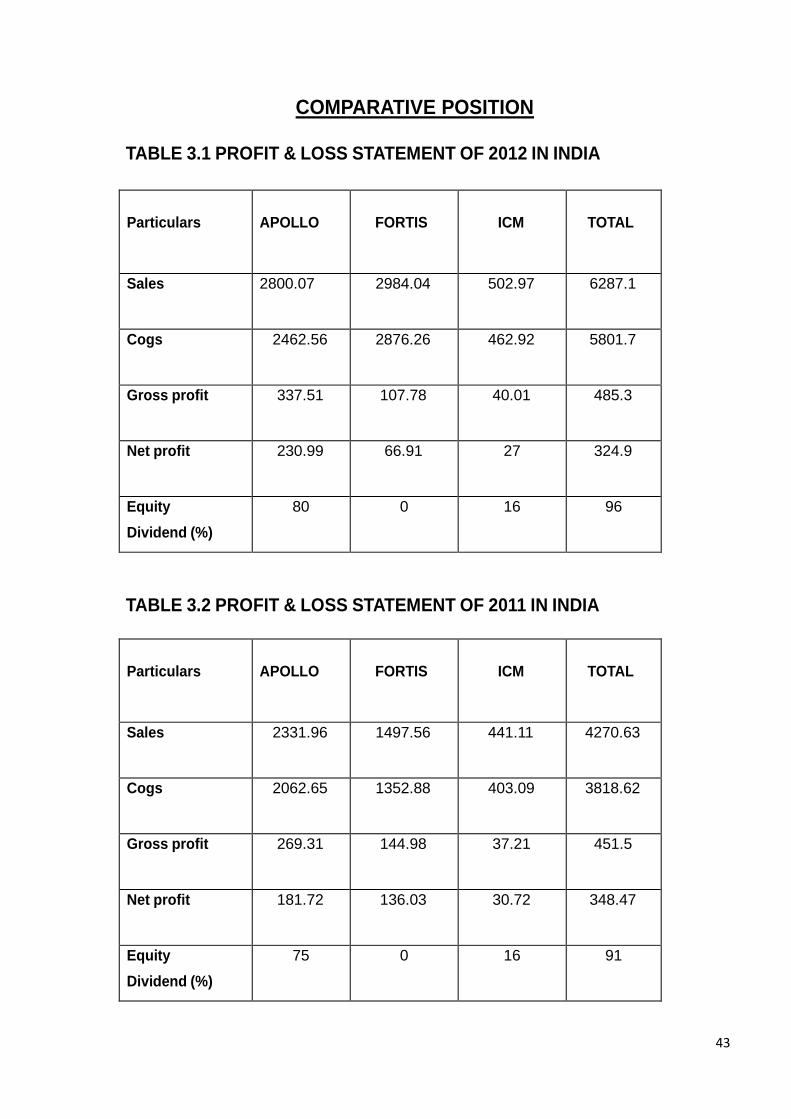

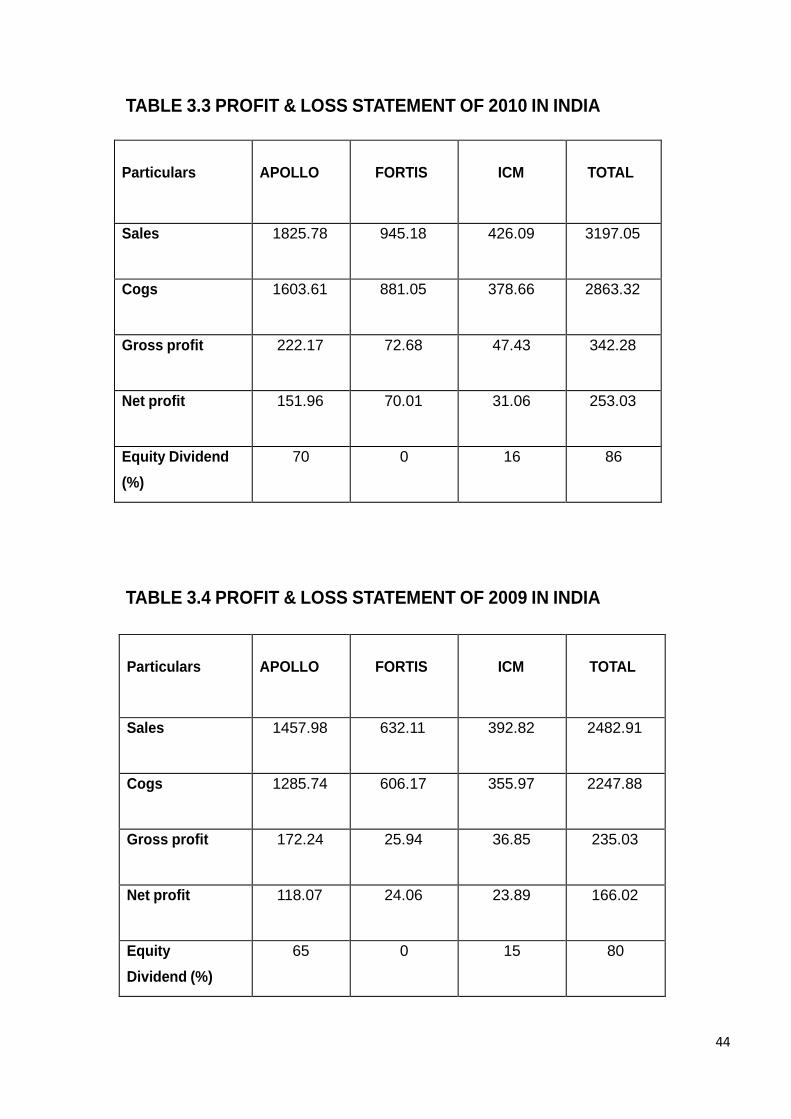

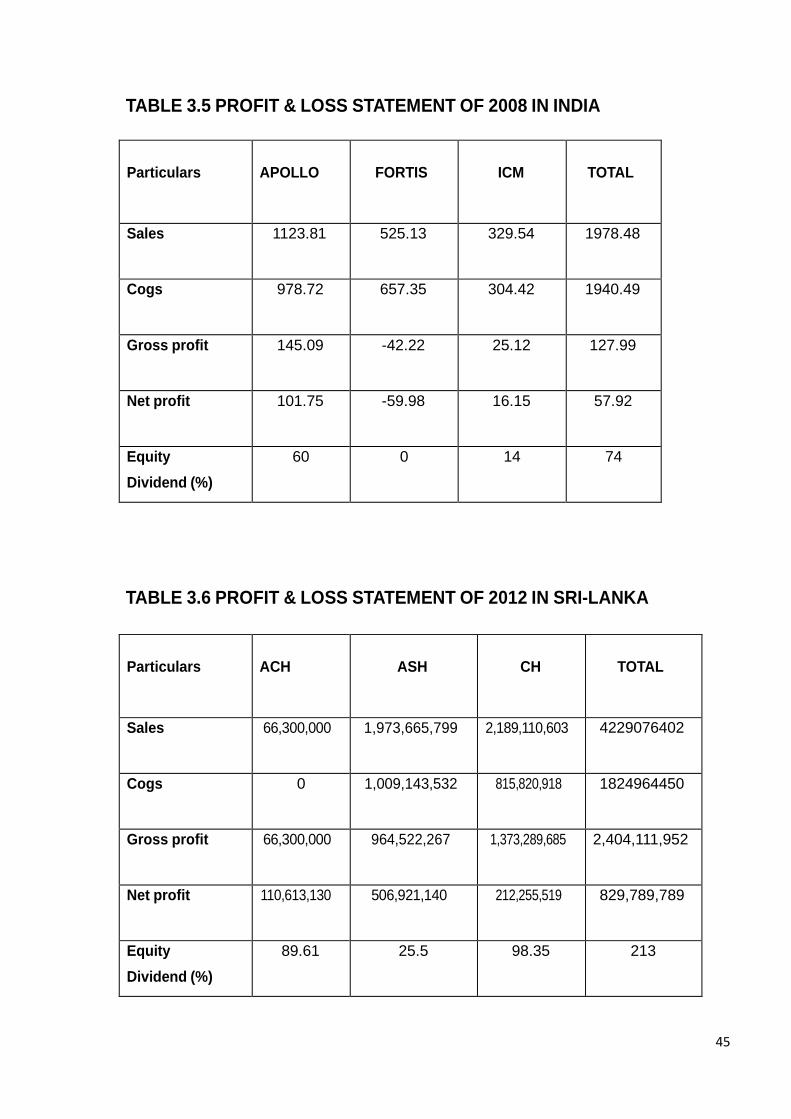

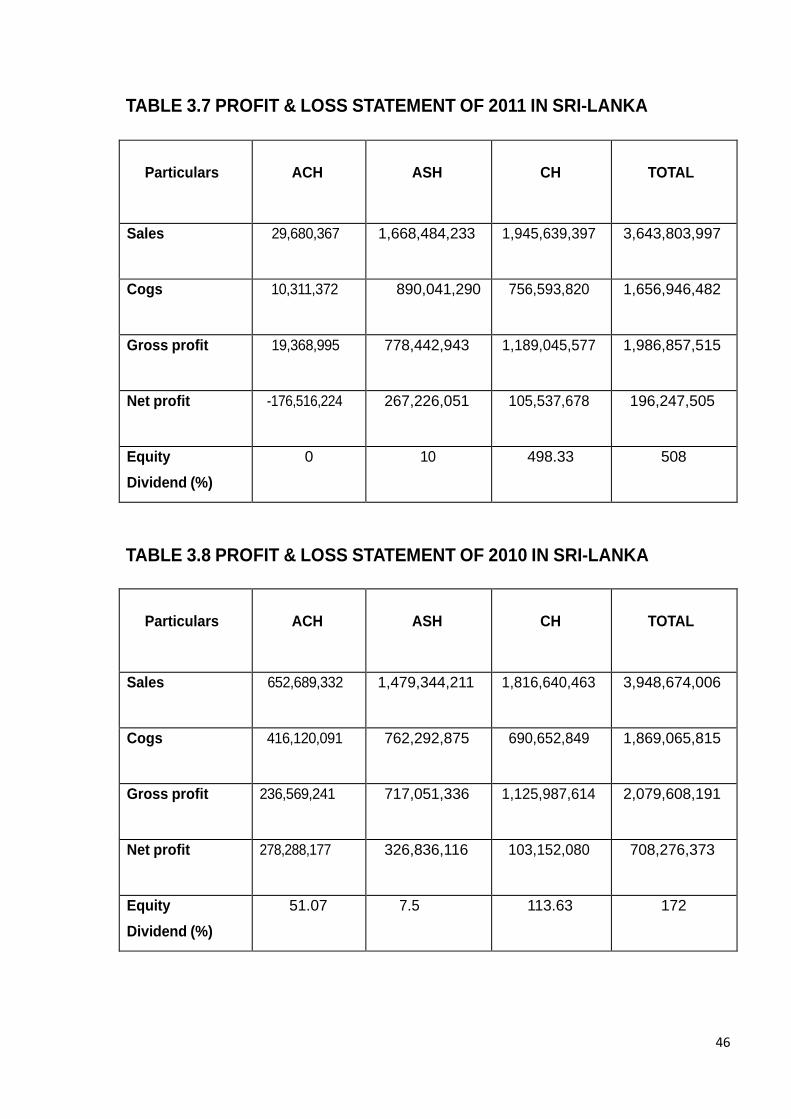

3.1 Comparative Position of srilankan and Indian companies 52

10 | P a g e

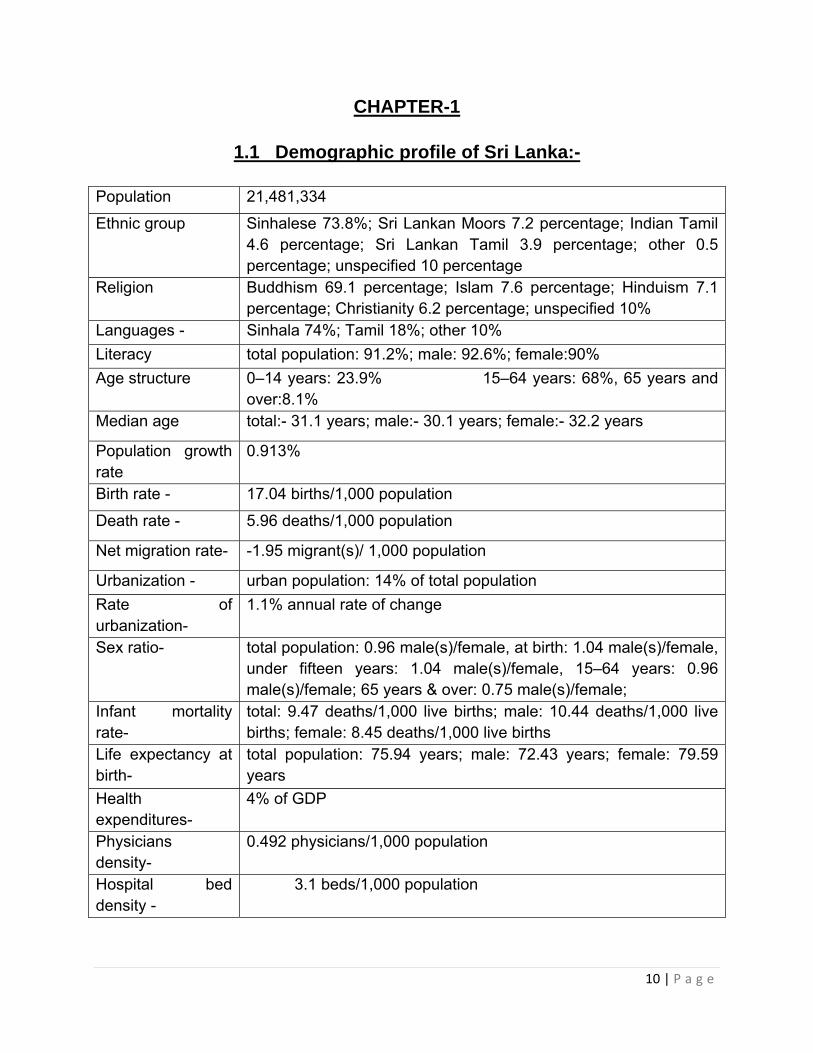

CHAPTER-1

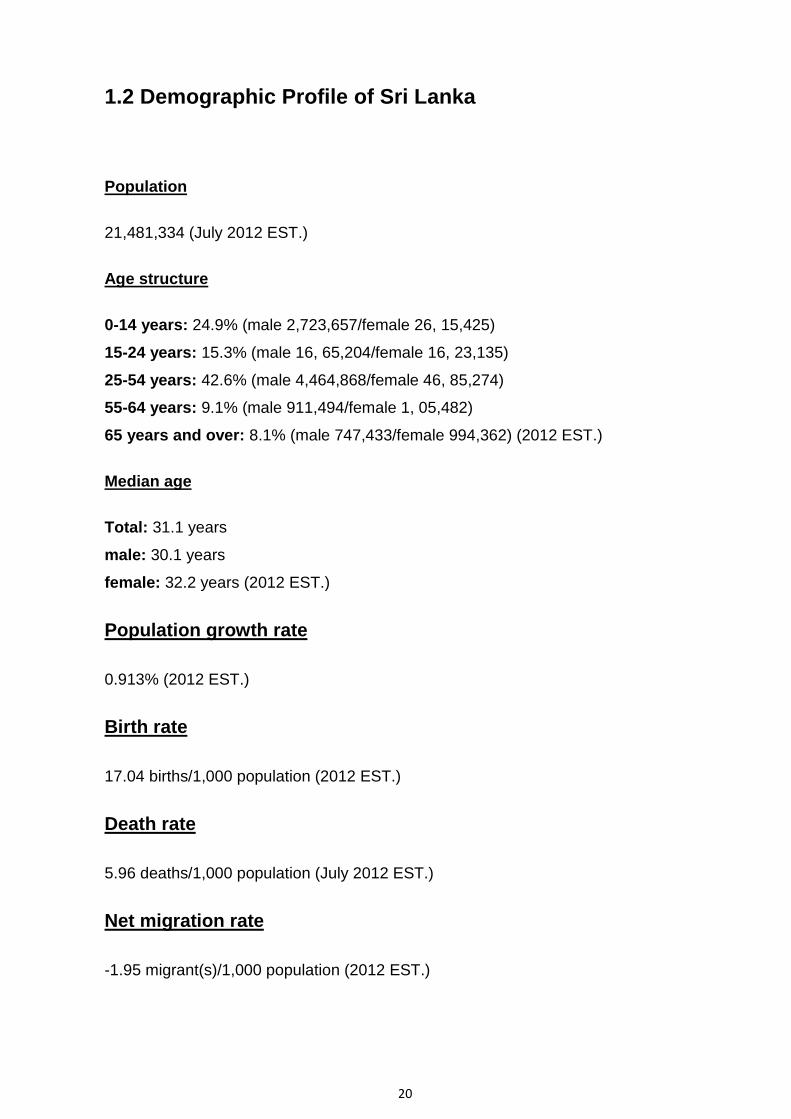

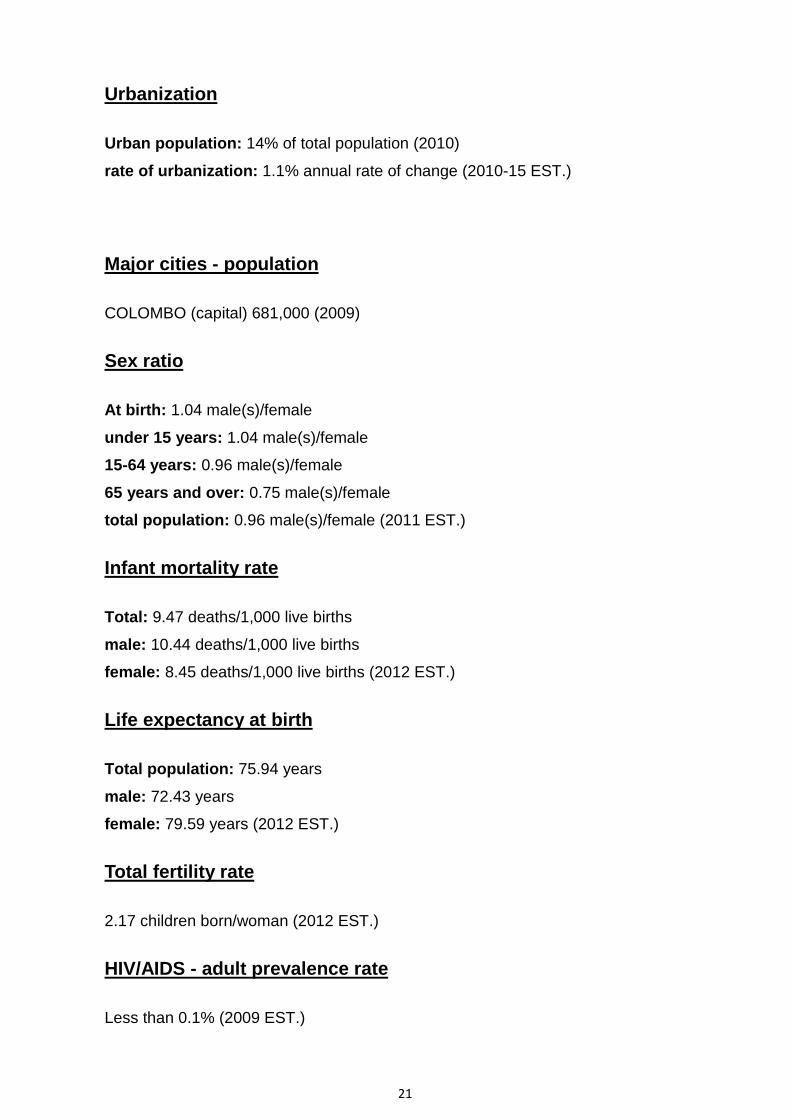

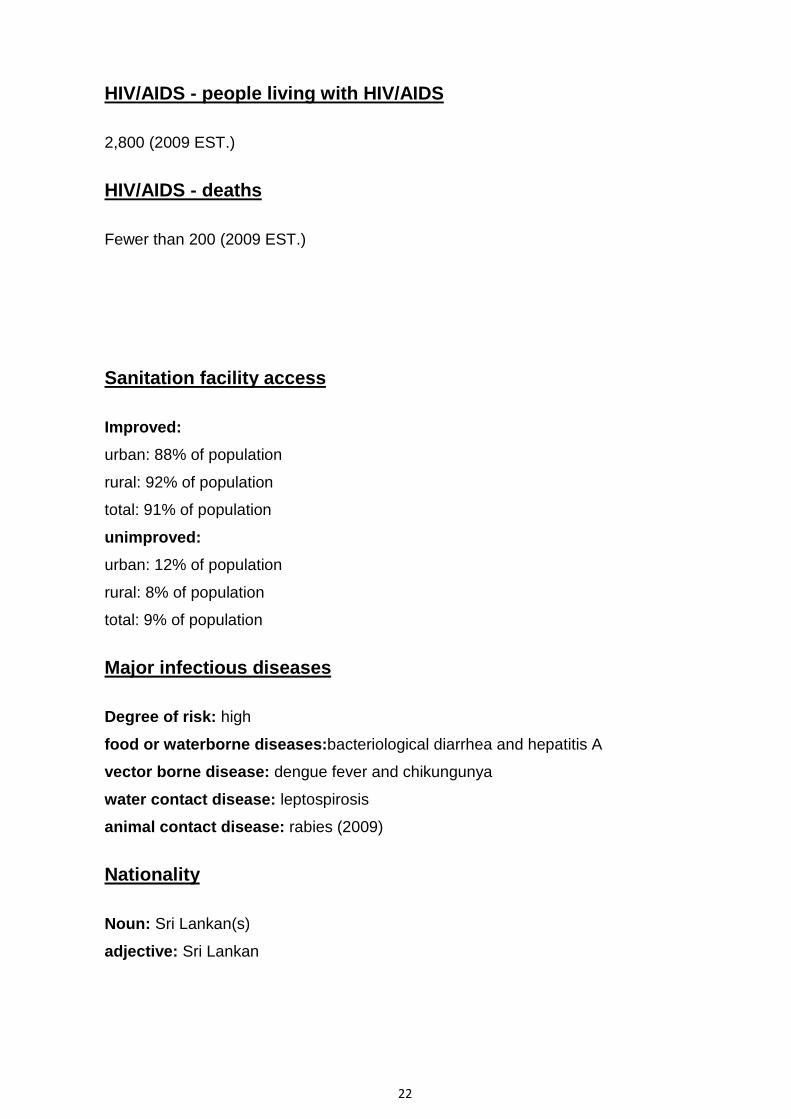

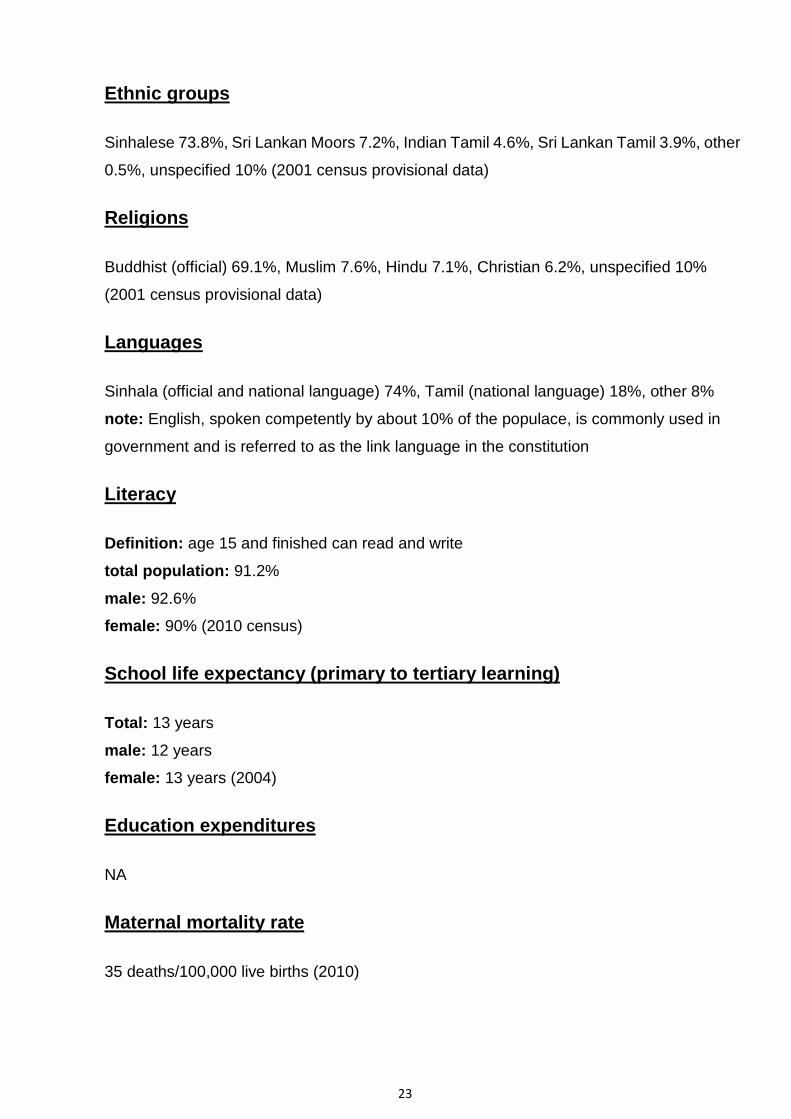

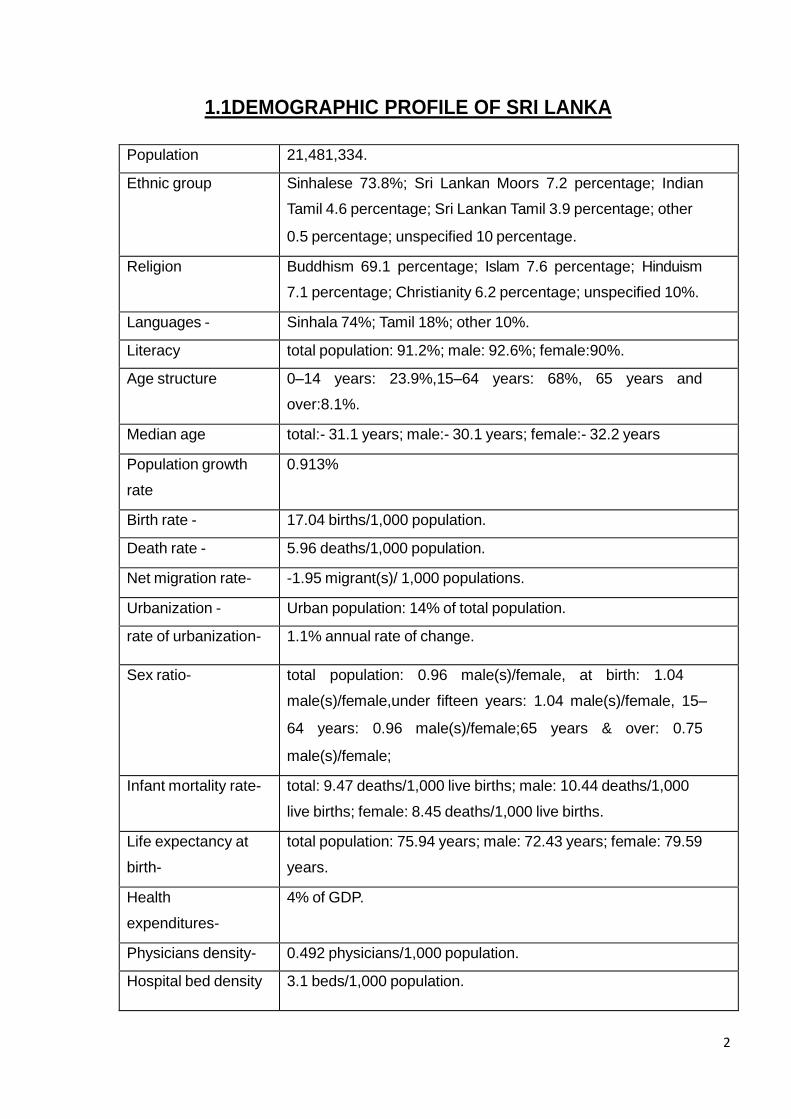

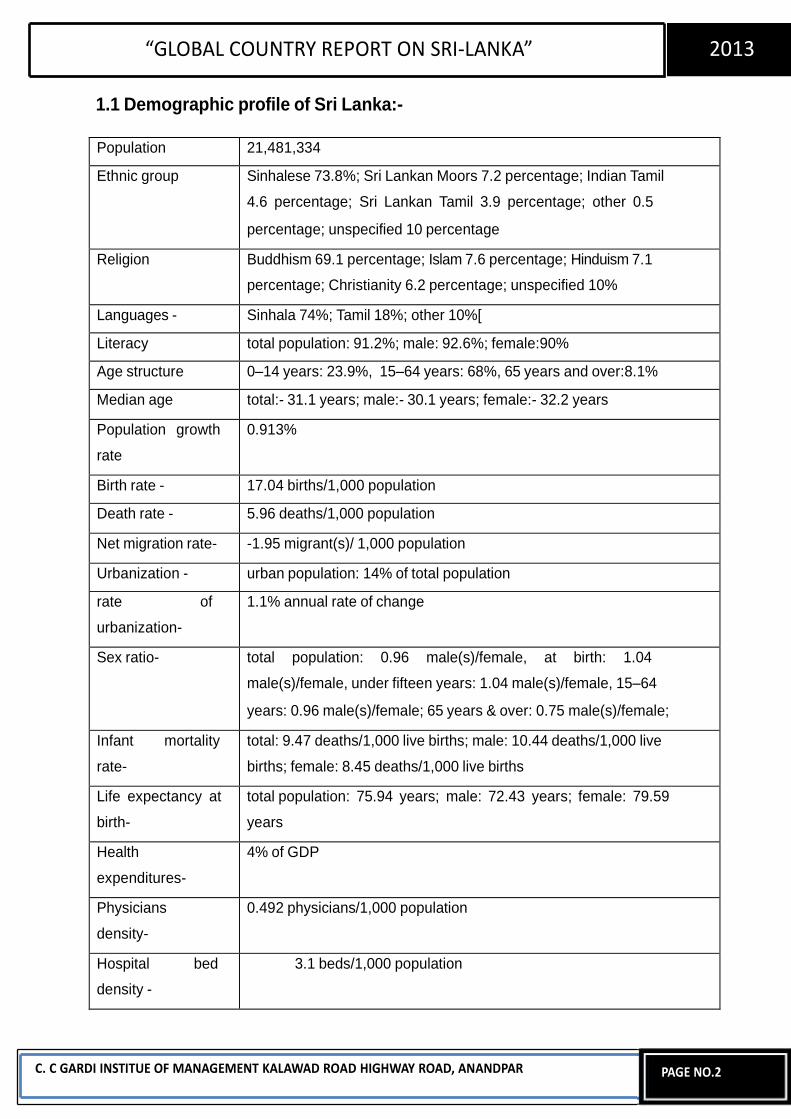

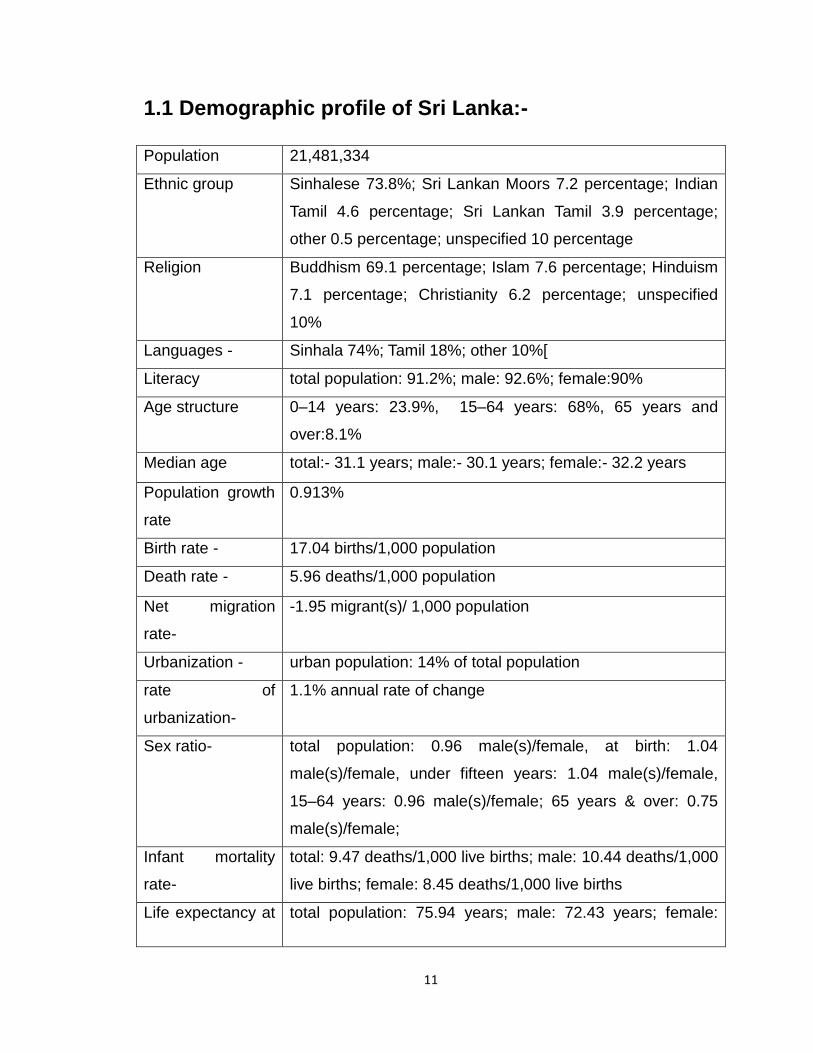

1.1 Demographic profile of Sri Lanka:-

Population 21,481,334

Ethnic group Sinhalese 73.8%; Sri Lankan Moors 7.2 percentage; Indian Tamil 4.6 percentage; Sri Lankan Tamil 3.9 percentage; other 0.5 percentage; unspecified 10 percentage

Religion Buddhism 69.1 percentage; Islam 7.6 percentage; Hinduism 7.1 percentage; Christianity 6.2 percentage; unspecified 10%

Languages - Sinhala 74%; Tamil 18%; other 10%

Literacy total population: 91.2%; male: 92.6%; female:90%

Age structure 0–14 years: 23.9% 15–64 years: 68%, 65 years and over:8.1%

Median age total:- 31.1 years; male:- 30.1 years; female:- 32.2 years

Population growth rate

0.913%

Birth rate - 17.04 births/1,000 population

Death rate - 5.96 deaths/1,000 population

Net migration rate- -1.95 migrant(s)/ 1,000 population

Urbanization - urban population: 14% of total population

Rate of urbanization-

1.1% annual rate of change

Sex ratio- total population: 0.96 male(s)/female, at birth: 1.04 male(s)/female, under fifteen years: 1.04 male(s)/female, 15–64 years: 0.96 male(s)/female; 65 years & over: 0.75 male(s)/female;

Infant mortality rate-

total: 9.47 deaths/1,000 live births; male: 10.44 deaths/1,000 live births; female: 8.45 deaths/1,000 live births

Life expectancy at birth-

total population: 75.94 years; male: 72.43 years; female: 79.59 years

Health expenditures-

4% of GDP

Physicians density-

0.492 physicians/1,000 population

Hospital bed density -

3.1 beds/1,000 population

11 | P a g e

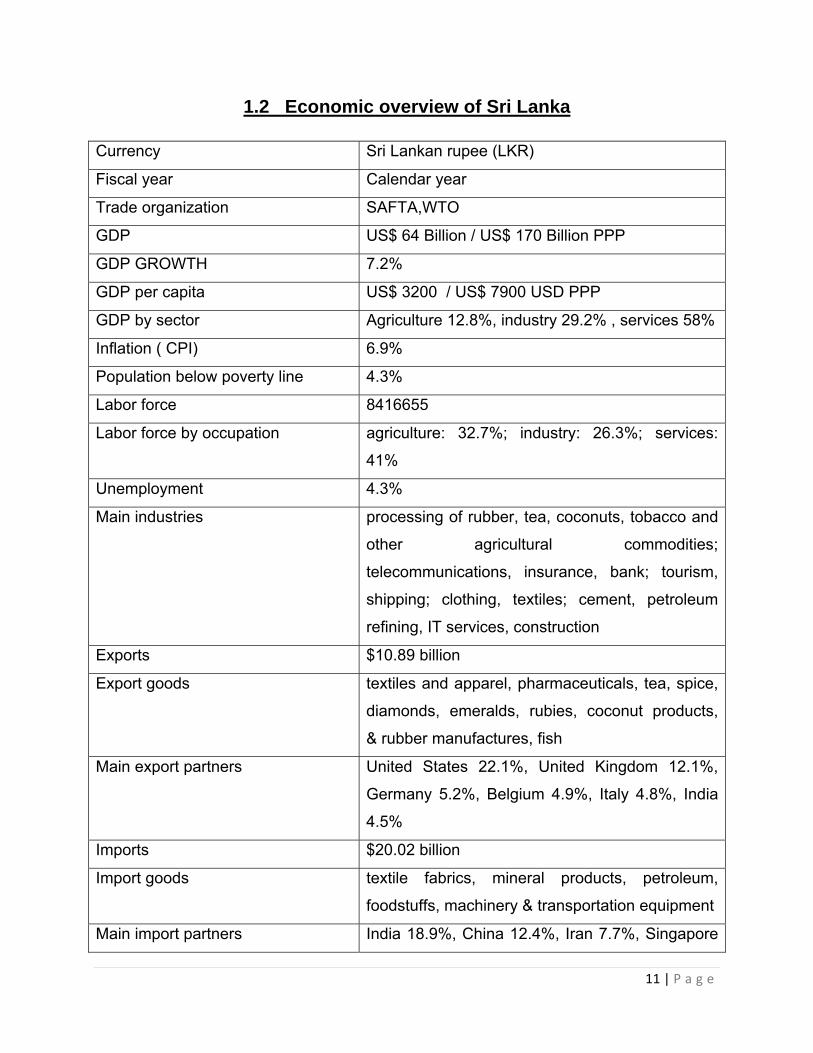

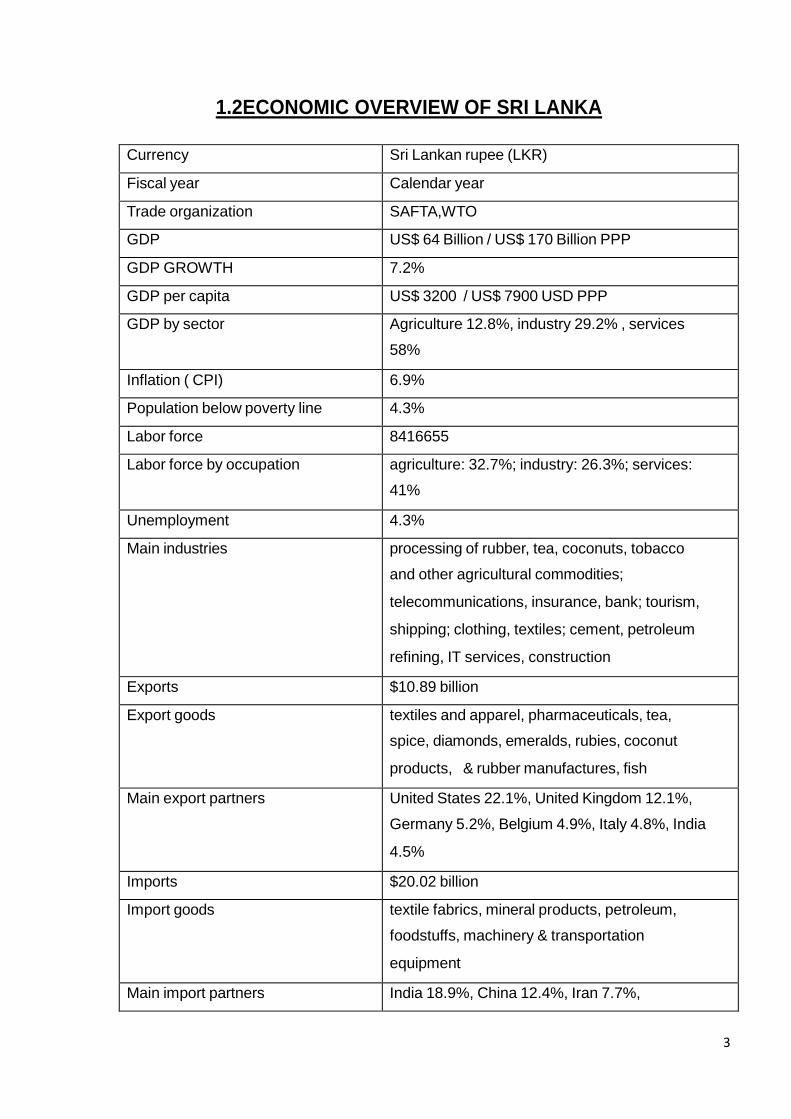

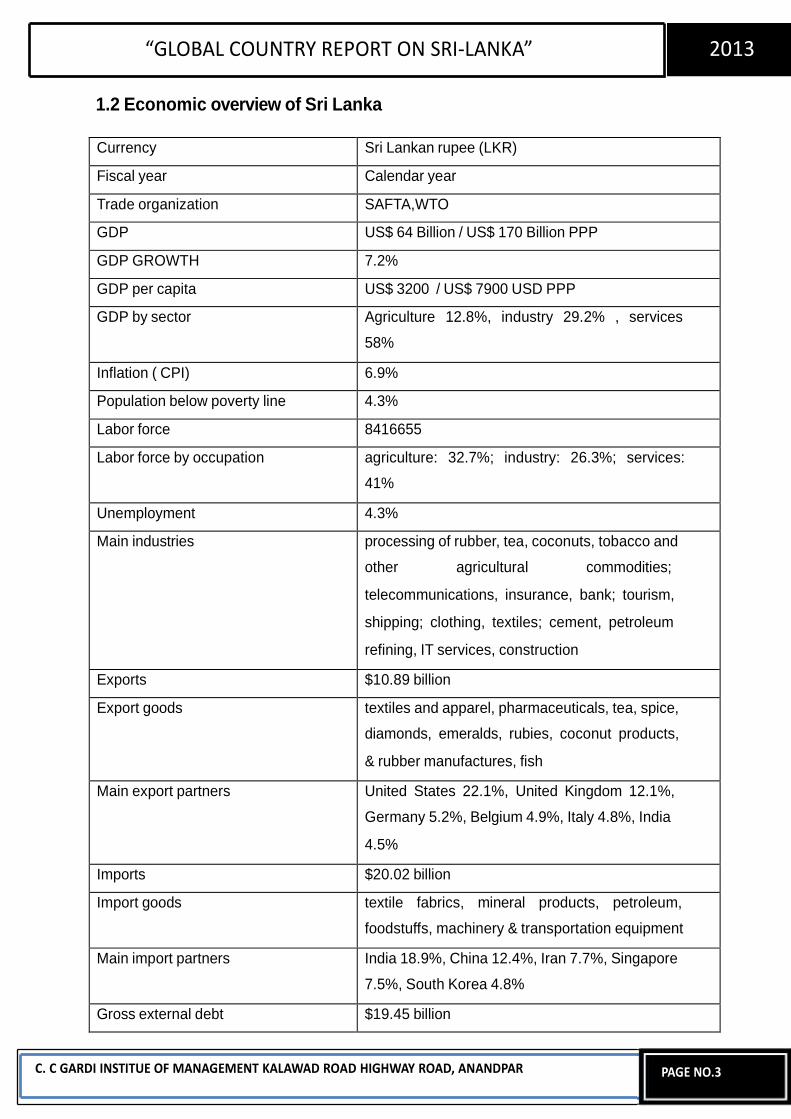

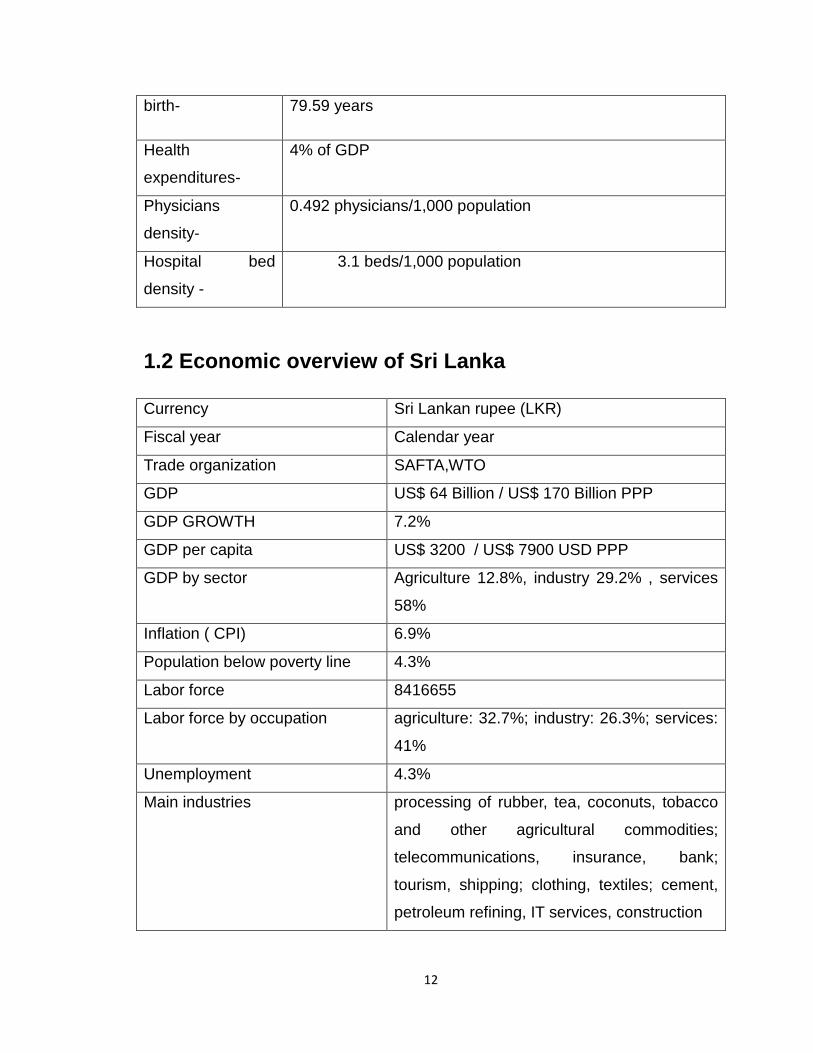

1.2 Economic overview of Sri Lanka

Currency Sri Lankan rupee (LKR)

Fiscal year Calendar year

Trade organization SAFTA,WTO

GDP US$ 64 Billion / US$ 170 Billion PPP

GDP GROWTH 7.2%

GDP per capita US$ 3200 / US$ 7900 USD PPP

GDP by sector Agriculture 12.8%, industry 29.2% , services 58%

Inflation ( CPI) 6.9%

Population below poverty line 4.3%

Labor force 8416655

Labor force by occupation agriculture: 32.7%; industry: 26.3%; services:

41%

Unemployment 4.3%

Main industries processing of rubber, tea, coconuts, tobacco and

other agricultural commodities;

telecommunications, insurance, bank; tourism,

shipping; clothing, textiles; cement, petroleum

refining, IT services, construction

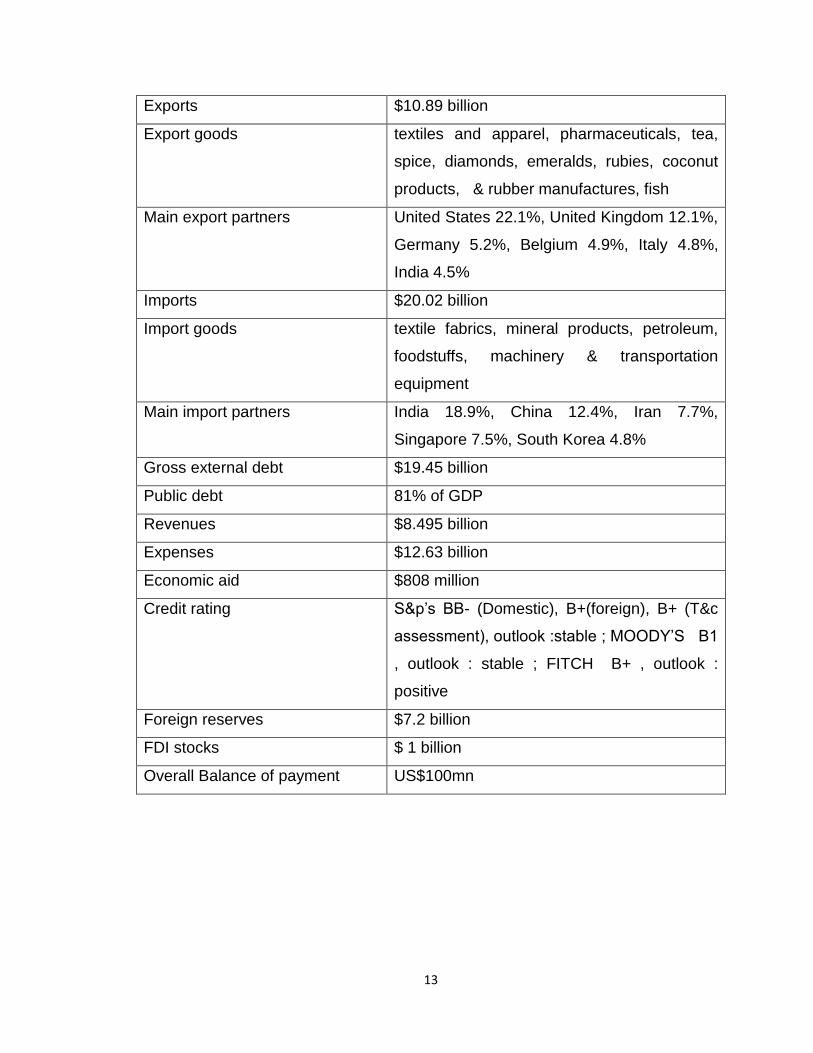

Exports $10.89 billion

Export goods textiles and apparel, pharmaceuticals, tea, spice,

diamonds, emeralds, rubies, coconut products,

& rubber manufactures, fish

Main export partners United States 22.1%, United Kingdom 12.1%,

Germany 5.2%, Belgium 4.9%, Italy 4.8%, India

4.5%

Imports $20.02 billion

Import goods textile fabrics, mineral products, petroleum,

foodstuffs, machinery & transportation equipment

Main import partners India 18.9%, China 12.4%, Iran 7.7%, Singapore

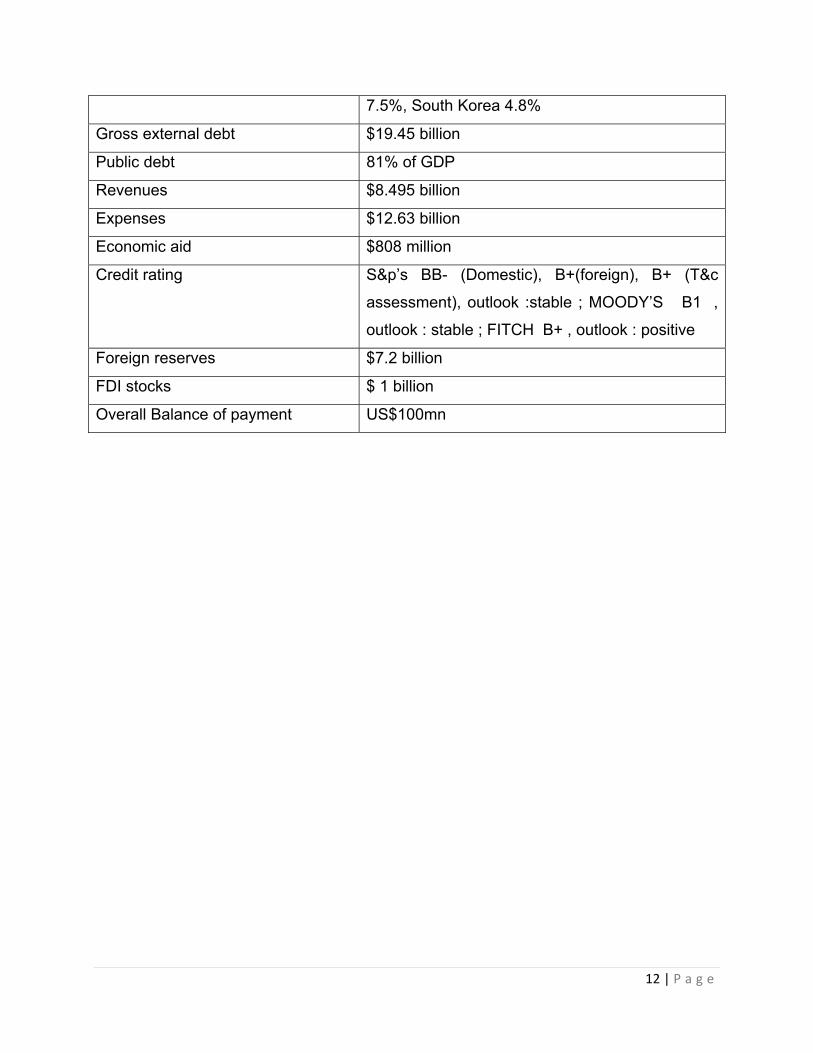

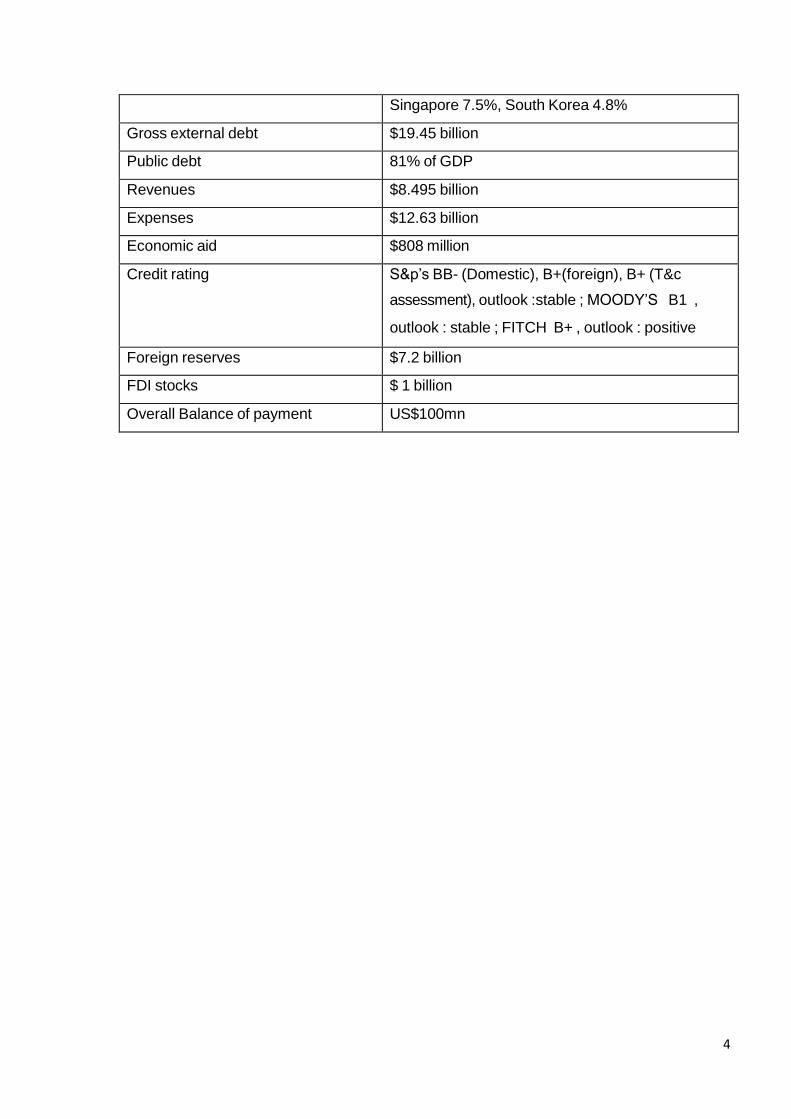

12 | P a g e

7.5%, South Korea 4.8%

Gross external debt $19.45 billion

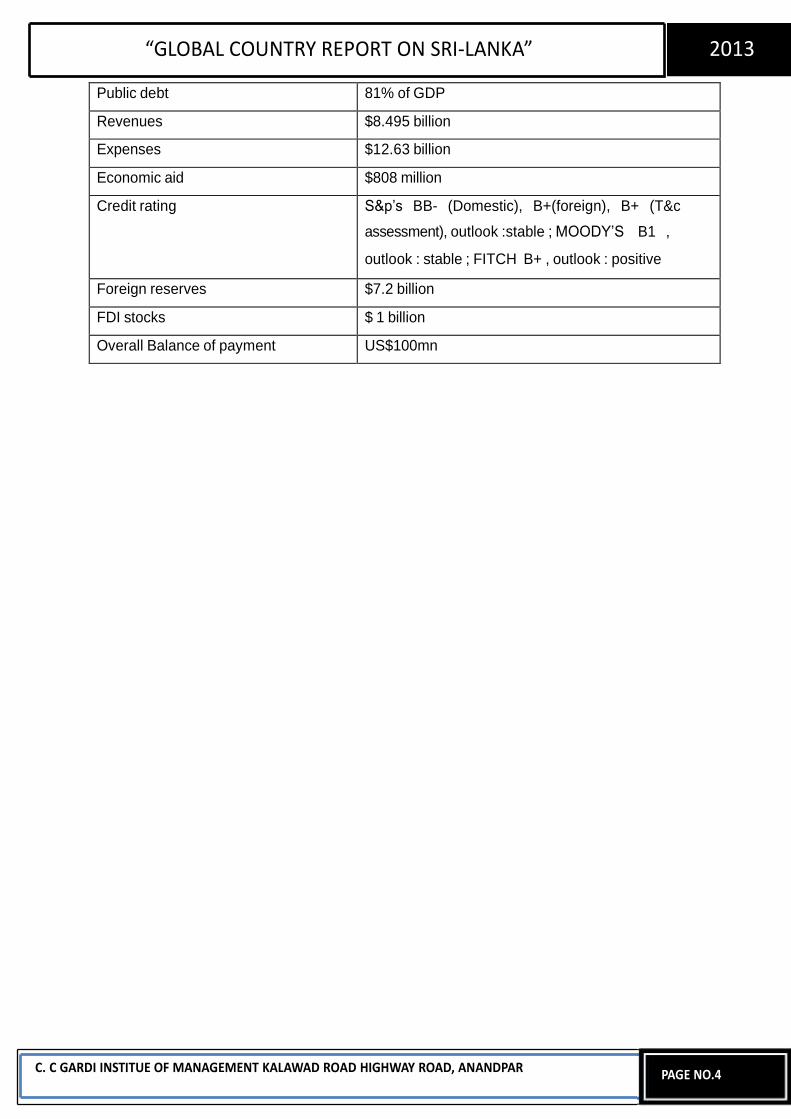

Public debt 81% of GDP

Revenues $8.495 billion

Expenses $12.63 billion

Economic aid $808 million

Credit rating S&p’s BB- (Domestic), B+(foreign), B+ (T&c

assessment), outlook :stable ; MOODY’S B1 ,

outlook : stable ; FITCH B+ , outlook : positive

Foreign reserves $7.2 billion

FDI stocks $ 1 billion

Overall Balance of payment US$100mn

13 | P a g e

1.3 Overview Different economic sectors of Sri-lanka

• Tourism:-

Tourism is a major industry in Sri Lanka. The main tourist attraction is the famous

southern islands and mountainous regions of the country and the ancient heritage of the

country and country resort is located in the eastern parts of the interior is sites is located

about warning the coast. Rubies and sapphires were also frequently found in the

Ratnapura and its nearby areas, such as mined precious stones, they are a major

tourist attraction.

2004 Indian Ocean tsunami and the advent of tourism has declined in the past civil war,

however, the number of tourists visiting the new increase, starting in early 2008. 8.6%

by March 2008 and Sri Lanka in 2012, 1,003,000 tourists, according to the Central Bank

of Sri Lanka 2013 roadmap. 2012 one billion ($ U.S.) and 16% increase in earnings for

2011 compare to year. The Sri Lankan government is key to growth is to attract guests

to 2.5 million by 2016, with an ambitious target for the development of post-conflict area

known as the tourism sector.

Significant growth in this industry, the most important travel magazines around the

world, and the world leading travel guide "Lonely Planet" book, a digital media publisher

in mind, Sri Lanka is ranked as the best country to visit in 2013. The main advantage of

Sri Lanka as a tourist destination and is currently engaged in a variety of accessible

infrastructure development under the government's accessible attraction.

14 | P a g e

• Tea industry:-

Tea industry, operating under the Ministry of Public Estate Management and

Development, one of the main industries in Sri Lanka. A 23% share of the global tea

exports, which Kenya with more than 22% share of the world's leading exporter in 1995

to become. The country's central highlands of the year and the annual rainfall and

moisture levels are suitable for growing tea in the low-temperature climate. The industry

in 1867, James Taylor, the British planter who entered the country in 1852 was by

inwards.

Recently, Sri Lanka is a fair trade tea in the UK, and additional countries in exporting

countries. It is believed that such a project can reduce rural poverty.

• Apparel and textile industry:-

The Sri Lanka apparel industry primarily in the United States and Europe of exports. Sri

Europe due to the high cost of labor in Europe ever more dependent on textiles. There

are countries, such as Pierre Cardin Liz Claiborne, Nike, Gap and Tommy Hilfiger

serving around 900 factories of the company.

The apparel sector is the most industrial employment generator and the largest foreign

swap film. The field for the year 2011 the amount of 39.6% of the export revenue was

USD 4.2Bn $.24% year on year growth of exports in 2011. These allows the output

exporters of apparels locally to dispose of 40% of all comprehensive tax payment Sri

Lankan rupees (Rs) 25 and are restricted for sale to the general corporate income tax of

12% per Piece tax is subject to 28%.

Find employment increased by 283,000 in 2011. Originally, the industry savanna

(contract manufacturer) offered by the operator and textile USA and the EU as a quota

based on the start and now it is converted into a full apparel solution provider.

15 | P a g e

• Agriculture:-

The country's agricultural sector is mostly mostly for local consumption and export to

rare coconut rice, and grain products. Agriculture sector contributes 11% of the

country's GDP, total export earnings 23.9% and 32.9% in 2011 year national

employment.

The three main traditional export crops of tea from Sri Lanka in the Rubber and

Coconut. Because these industries are already well established, BOI's central focal

point increase local value addition to agricultural crops has increased, especially in

terms of another. Particular type of technology to advance the efficiency levels of

government, to improve access to global markets for investment looks, quality seeds

and planting material use and overall value adding recover. Some of the opportunities

include:

Horticulture

Fisheries

livestock

• Knowledge Services:-

The knowledge of the services sector in the IT software development, knowledge

process processing / outsourcing business include the outsourcing industry, and it

enabled services and information technology training center, it is possible to hold a key

growth area appears as Sri Lanka. Students, English and literacy height, and looking at

the quality of its proximity to India, Sri Lanka is ideal for high value added IT / KPO

services, supplier development mode.

ITEs and software development:-

There are 100 on the software development work in Sri Lanka which provides both

independent and captive markets. Sri Lankan companies are internationally recognized

in their own software products that they have been able to build.

16 | P a g e

B / KPO BPO industry:-

The industry / KPO BPO is an emerging area of Sri Lanka. Still a nascent industry, its

small history since 2000 within / KPO BPO sector is a significant difference in the world

/ BPO KPO to attract some of the giants. Sri Lanka state financial and other

professional services, transaction processing and document management specialist

areas is increasing, and high literacy rate (about 92%) rate and a growing pool of

accounting graduates, call center services for credit.

IT Training Center:-

The education industry is a knowledge services in key areas have been identified as

one of the Sri Lanka government is trying to develop the Sri Lanka. Continuing the work

force flow in order to ensure that the needs of the growing knowledge of the service

industry personnel, information technology and training have been individually identified

and given priority. There are about 20 IT training center under the BOI.

• Infrastructure:-

Progress in infrastructure development in the medium and long term to support the

country's drive to a higher and sustainable growth is expected to maintain. To help

improve economic efficiency for the timely development of the economic structure of the

economy will expand production capacity, increase efficiency and reduce the regional

differences

Construction cost by 14.2% compared to 9.3% in 2010, significantly expanding field

conditions added in 2011. Construction activity increased 8.6% during the year by the

goods to domestic production growth. Cement availability of 21.5 per cent in 2011 to

18.9% in 2010, compared with a contraction. Construction in the private sector

increased by 15.8% during the year for the purpose of private sector credit growth was

reflected by.

17 | P a g e

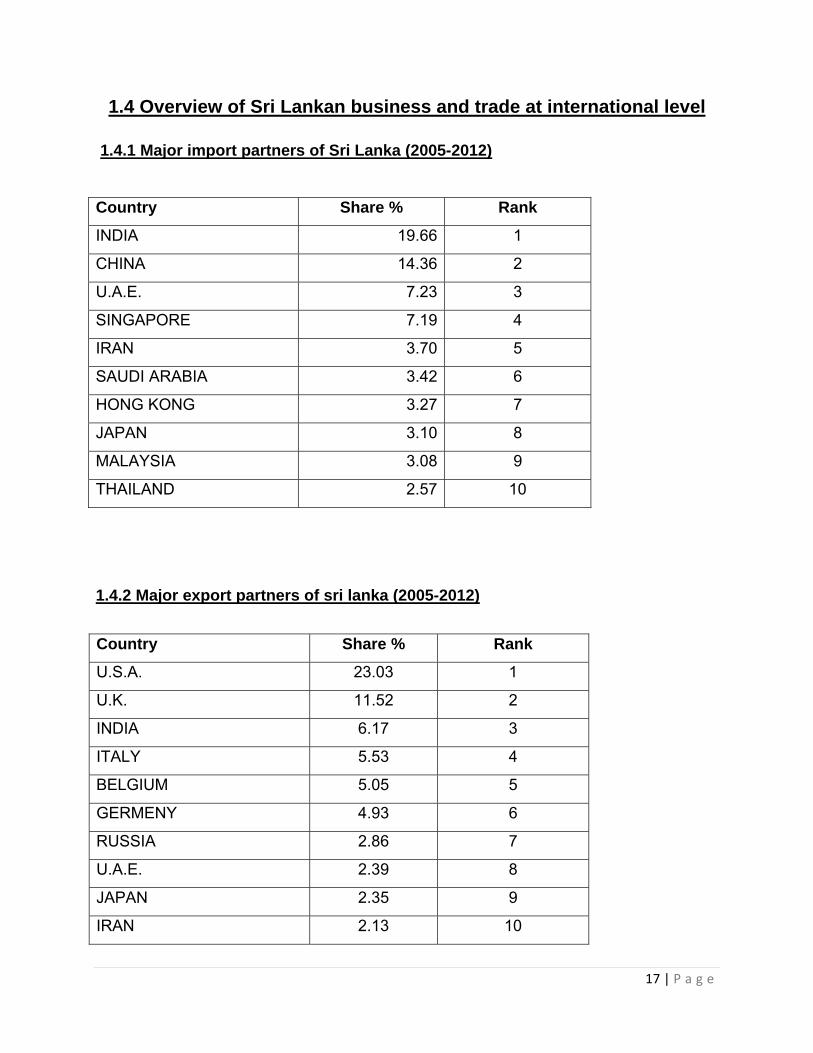

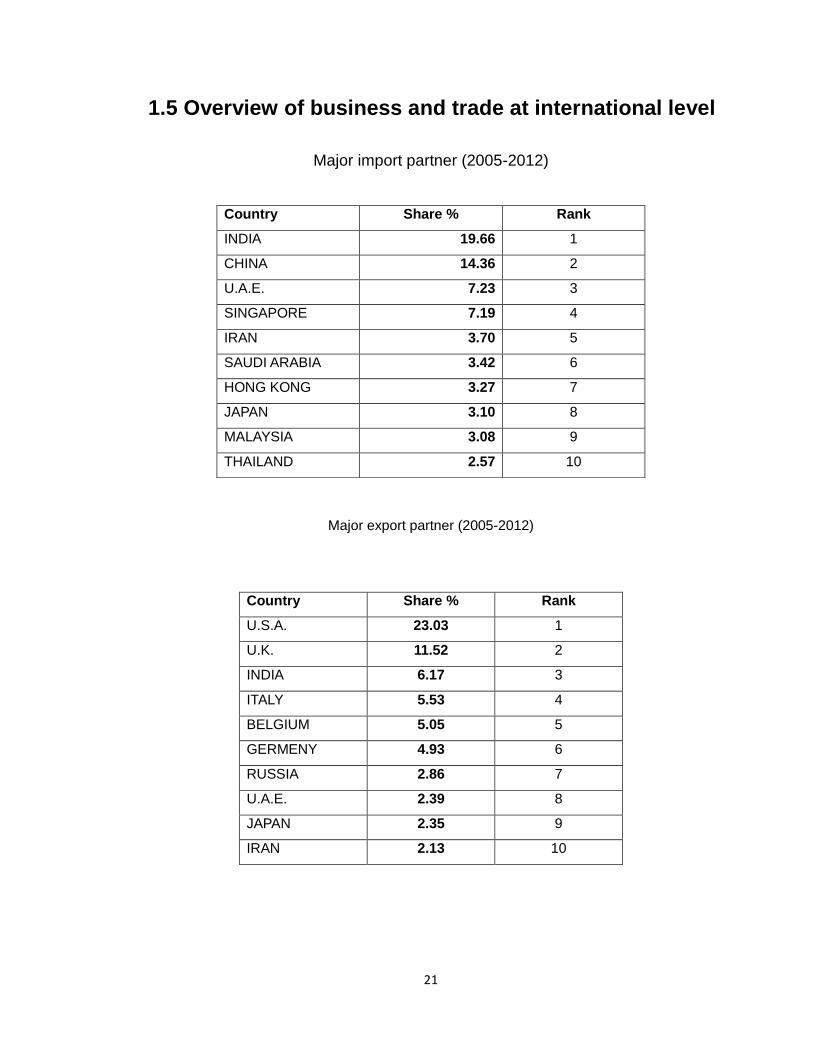

1.4 Overview of Sri Lankan business and trade at international level

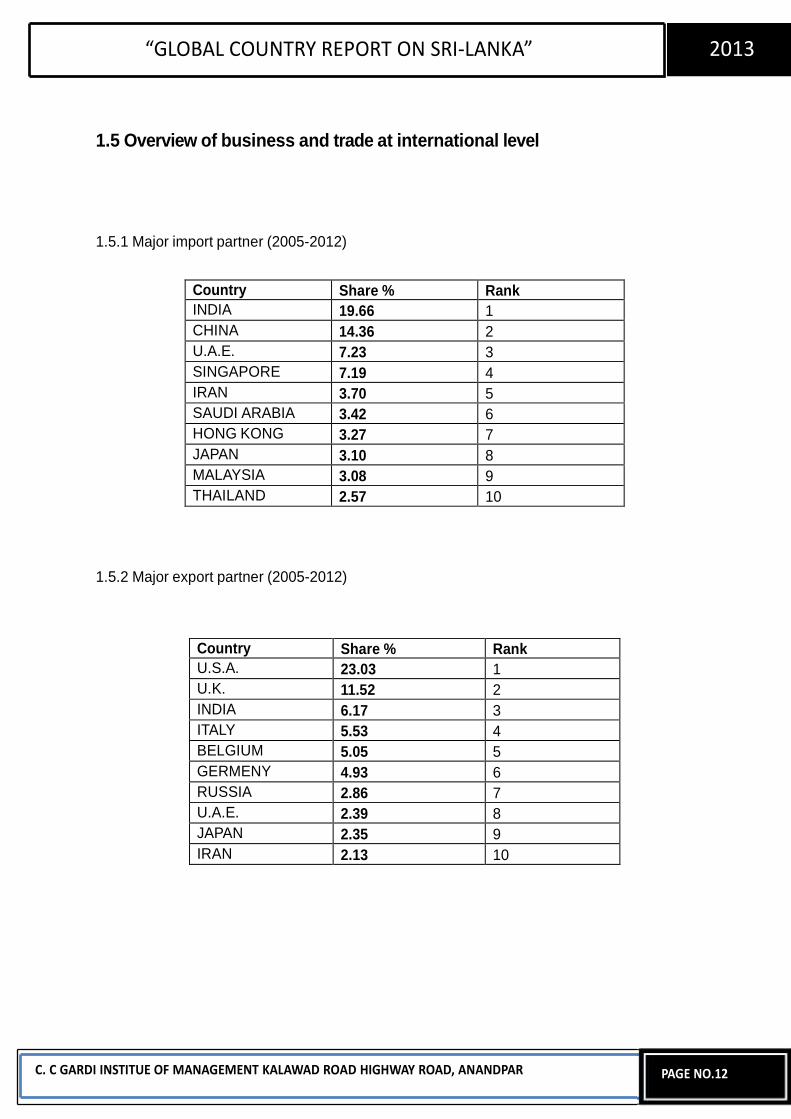

1.4.1 Major import partners of Sri Lanka (2005-2012)

1.4.2 Major export partners of sri lanka (2005-2012)

Country Share % Rank

INDIA 19.66 1

CHINA 14.36 2

U.A.E. 7.23 3

SINGAPORE 7.19 4

IRAN 3.70 5

SAUDI ARABIA 3.42 6

HONG KONG 3.27 7

JAPAN 3.10 8

MALAYSIA 3.08 9

THAILAND 2.57 10

Country Share % Rank

U.S.A. 23.03 1

U.K. 11.52 2

INDIA 6.17 3

ITALY 5.53 4

BELGIUM 5.05 5

GERMENY 4.93 6

RUSSIA 2.86 7

U.A.E. 2.39 8

JAPAN 2.35 9

IRAN 2.13 10

18 | P a g e

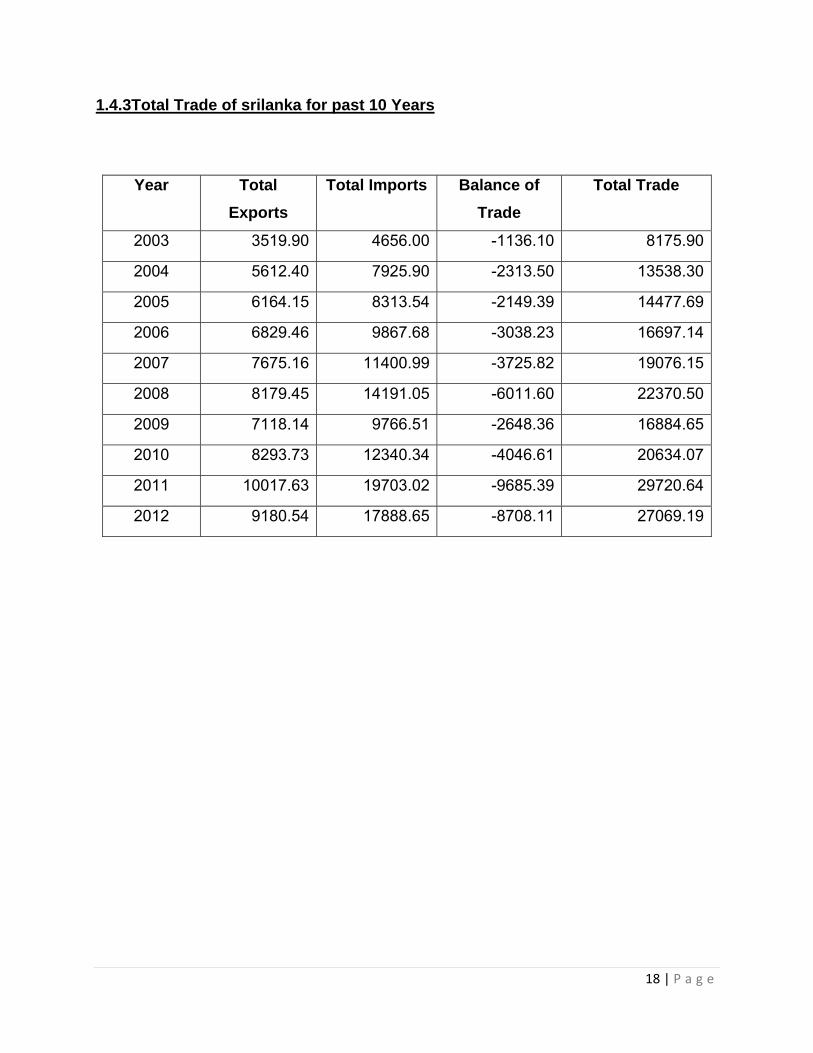

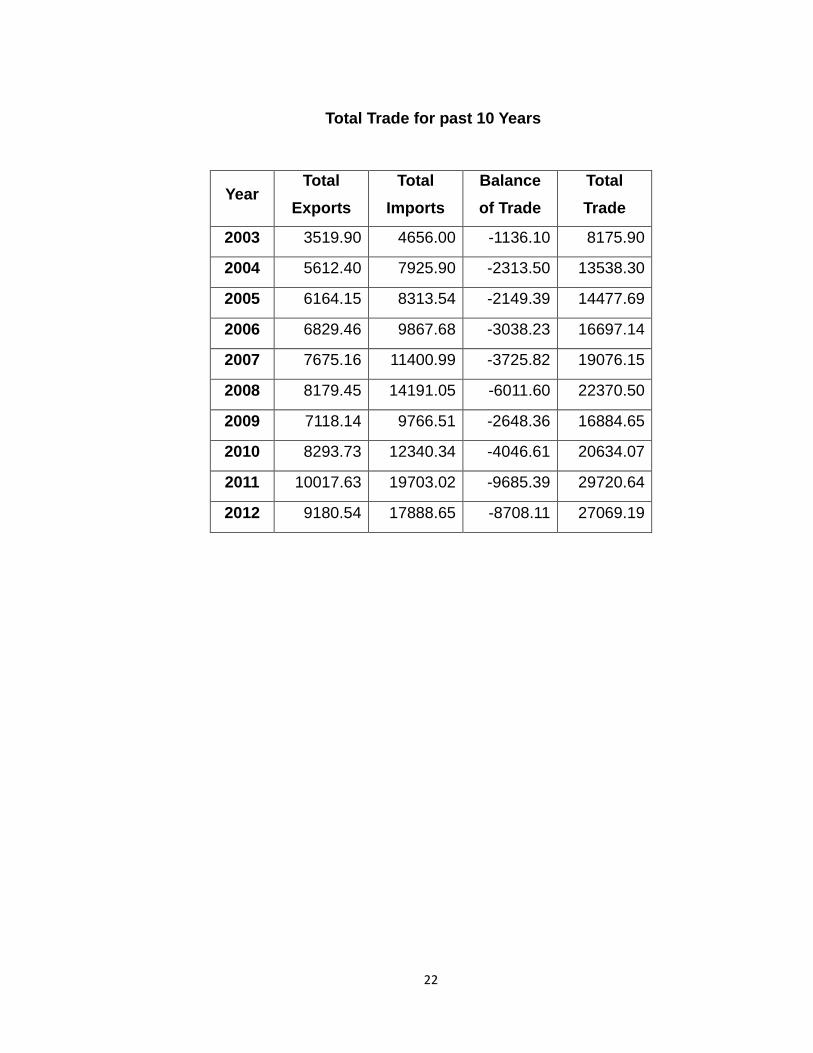

1.4.3Total Trade of srilanka for past 10 Years

Year Total

Exports

Total Imports Balance of

Trade

Total Trade

2003 3519.90 4656.00 -1136.10 8175.90

2004 5612.40 7925.90 -2313.50 13538.30

2005 6164.15 8313.54 -2149.39 14477.69

2006 6829.46 9867.68 -3038.23 16697.14

2007 7675.16 11400.99 -3725.82 19076.15

2008 8179.45 14191.05 -6011.60 22370.50

2009 7118.14 9766.51 -2648.36 16884.65

2010 8293.73 12340.34 -4046.61 20634.07

2011 10017.63 19703.02 -9685.39 29720.64

2012 9180.54 17888.65 -8708.11 27069.19

19 | P a g e

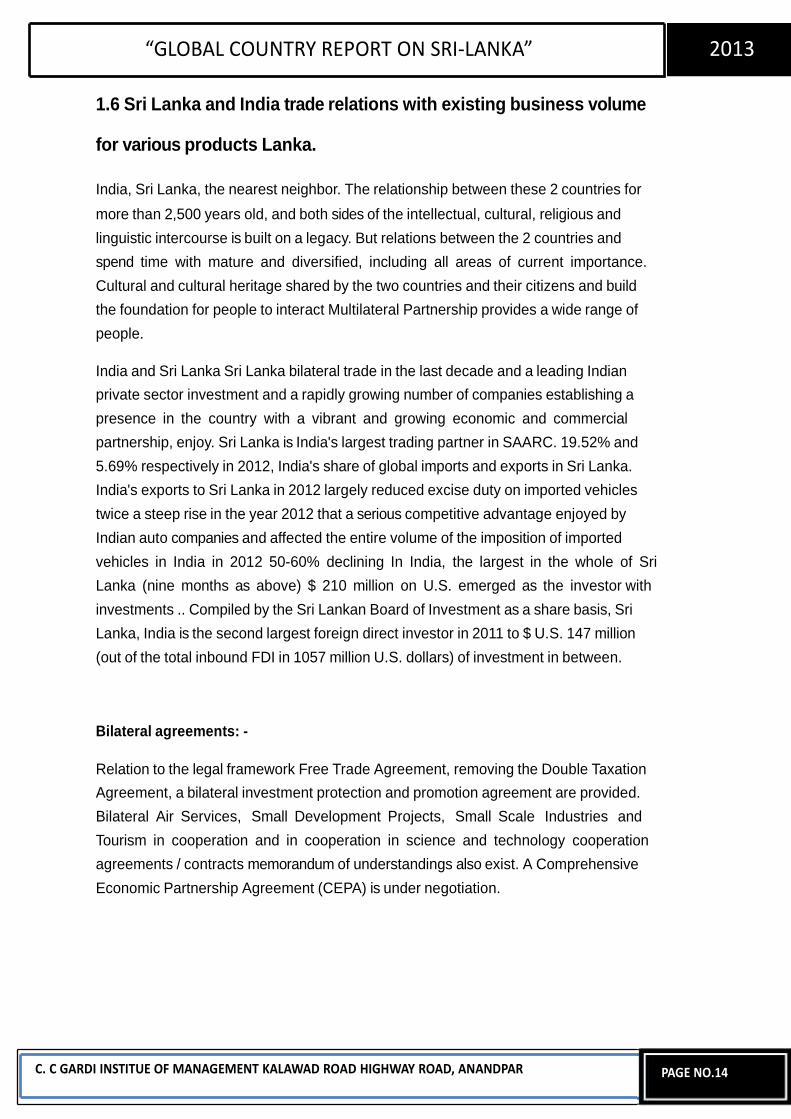

1.5 Present Trade Relations and Business Volume of different products of srilanka with India.

India, Sri Lanka, the nearest neighbor. The relationship between these 2 countries for

more than 2,500 years old, and both sides of the intellectual, cultural, religious and

linguistic intercourse is built on a legacy. But relations between the 2 countries and

spend time with mature and diversified, including all areas of current importance.

Cultural and cultural heritage shared by the two countries and their citizens and build

the foundation for people to interact Multilateral Partnership provides a wide range of

people.

India and Sri Lanka Sri Lanka bilateral trade in the last decade and a leading Indian

private sector investment and a rapidly growing number of companies establishing a

presence in the country with a vibrant and growing economic and commercial

partnership, enjoy. Sri Lanka is India's largest trading partner in SAARC. 19.52% and

5.69% respectively in 2012, India's share of global imports and exports in Sri Lanka.

India's exports to Sri Lanka in 2012 largely reduced excise duty on imported vehicles

twice a steep rise in the year 2012 that a serious competitive advantage enjoyed by

Indian auto companies and affected the entire volume of the imposition of imported

vehicles in India in 2012 50-60% declining In India, the largest in the whole of Sri Lanka

(nine months as above) $ 210 million on U.S. emerged as the investor with investments

. Compiled by the Sri Lankan Board of Investment as a share basis, Sri Lanka, India is

the second largest foreign direct investor in 2011 to $ U.S. 147 million (out of the total

inbound FDI in 1057 million U.S. dollars) of investment in between.

Bilateral agreements: -

Relation to the legal framework Free Trade Agreement, removing the Double Taxation

Agreement, a bilateral investment protection and promotion agreement are provided.

Bilateral Air Services, Small Development Projects, Small Scale Industries and Tourism

in cooperation and in cooperation in science and technology cooperation agreements /

contracts memorandum of understanding also exist. A Comprehensive Economic

Partnership Agreement (CEPA) is under negotiation.

20 | P a g e

India Sri Lanka Free Trade (ISFTA) contract: -

The main framework for bilateral trade in India, Sri Lanka Free Trade (ISFTA) contract

that was in 1998 and entered into force in March 2000 has been through. ISFTA As a

result, 4150 is currently the Indian tariff lines of Sri Lanka's exports to India has been a

zero duty. Similarly, the 3932 tariff lines, Indian exports to Sri Lanka has been to provide

a zero duty.

South Asian Free Trade (SAFTA) Area: -

South Asian Free Trade Area (SAFTA) Agreement on 1 January, has been operational

since 2006. India, Pakistan and Sri Lanka non-least developed contracting (NLDCS

States) and Bangladesh, Bhutan, the Maldives are classified as, Afghanistan and Nepal

as the least agreement States (eladisio) are classified as Developed. Article 7 of the

SAFTA agreement phased tariff liberalization (TLP) in which a programmer, 2 years,

NLDC recession brought a 20% tariff, while eladisio will bring them down to 30%

provides. After 5 years, 20% are from non eladisio 0-5% tariff (Sri Lanka 6 years) will,

when will eladisio so 8 years.

Comprehensive Economic Partnership (CEPA) Agreement:-

Following the positive results of the FTA and FTA of success emboldened by

governments, felt that more action was needed to loose our bilateral economic

relationship, full of potential. CEPA to build on the momentum generated by the FTA

and further integration of the two economies in the direction of trade in goods and fresh

impetus to bilateral economic interaction and wanted to give Synergy. Discussion on

CEPA began in December 2010.

21 | P a g e

Major Indian Investments in:-

1) Lanka IOC PLC

2) Bharti Airtel Lanka

3) Piramal Glass Ceylon

4) Taj Hotels

5) UltraTech Cement

6) JVGokal Ceylon Pvt Ltd.

7) Tata Communications Ltd. Lanka

8) From India Banks

9) Asian Paints Ltd. (Lanka)

10) Ceat - Kelani Associated Holdings Ltd. (Pvt)

Other economic functions:-

1) Civil Aviation Agreement

2) S & T cooperation

3) On the ferry service contract

4) Agriculture Agreement

5) agreements on telecommunication...

22 | P a g e

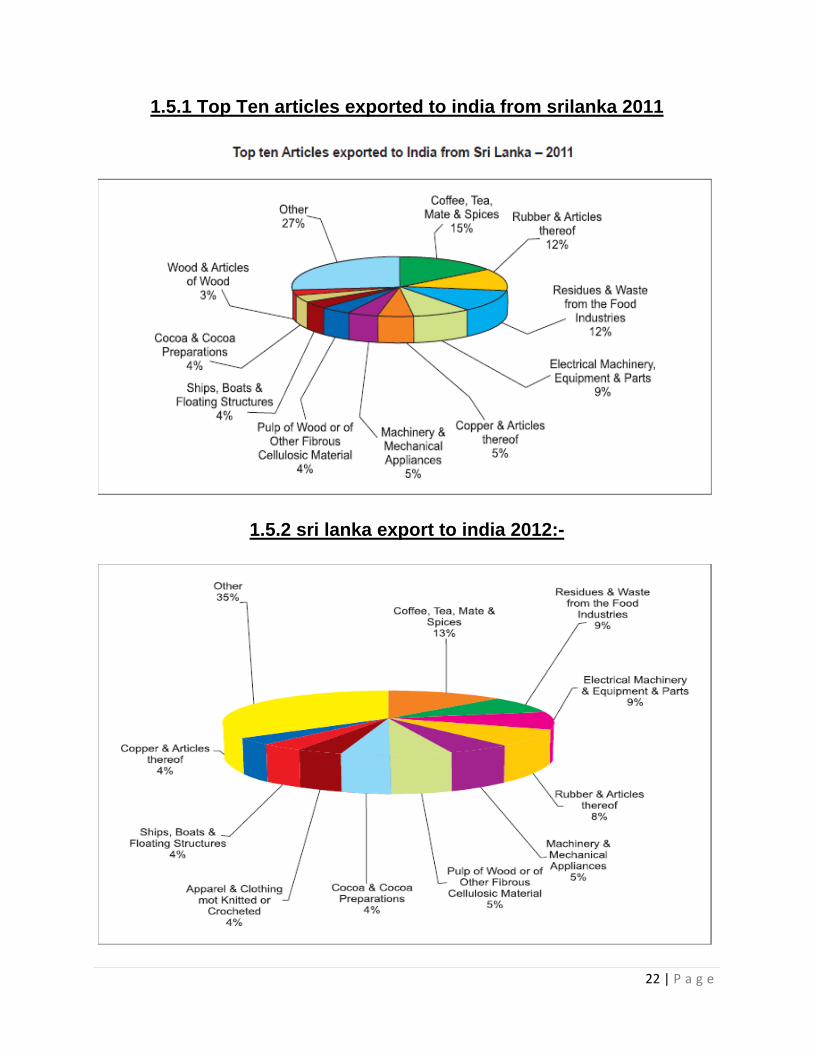

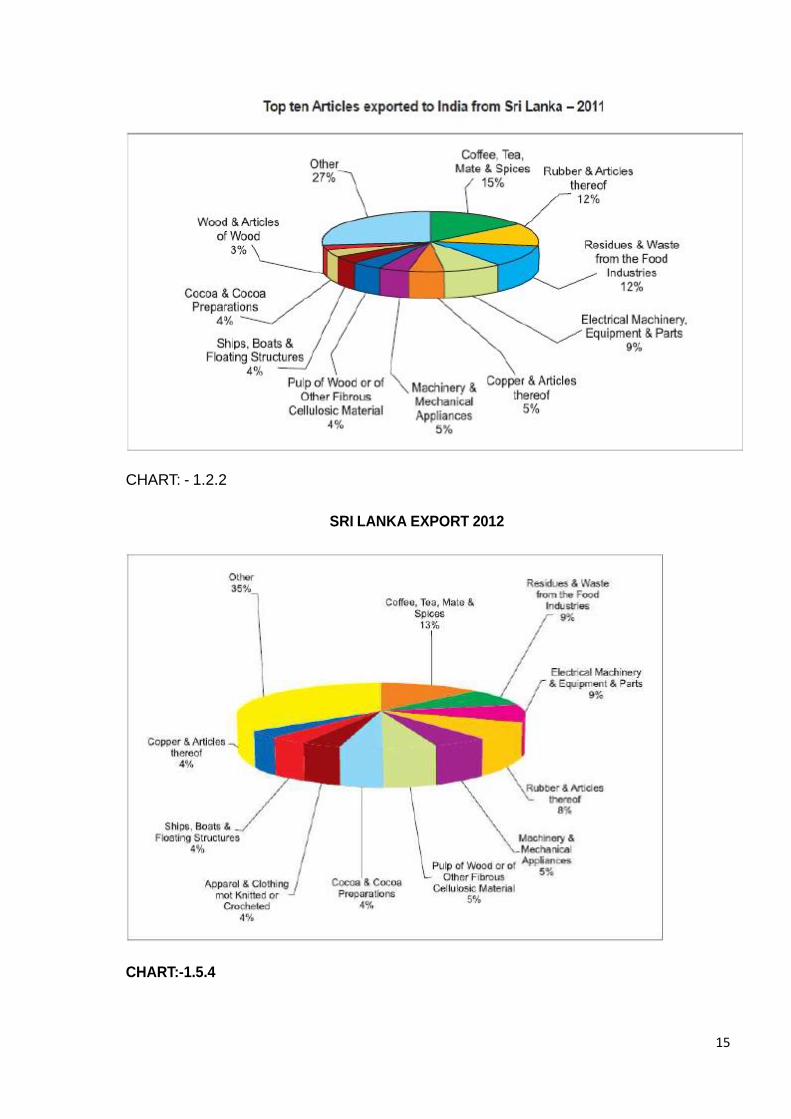

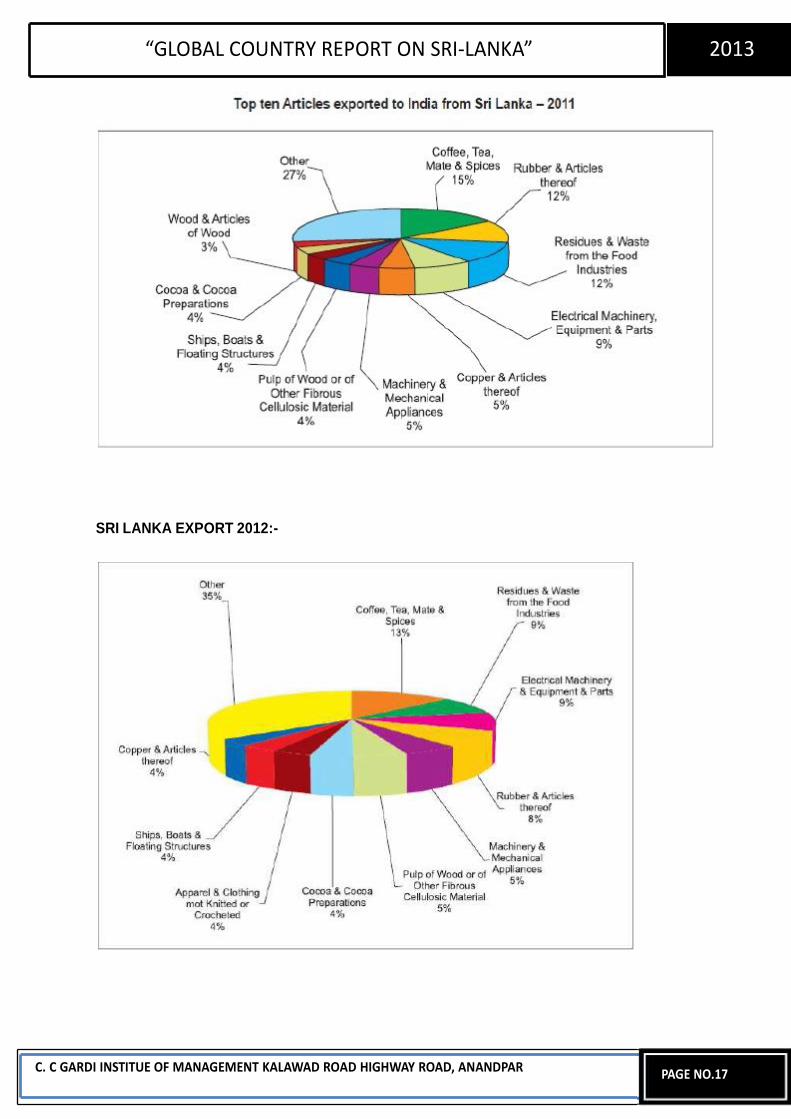

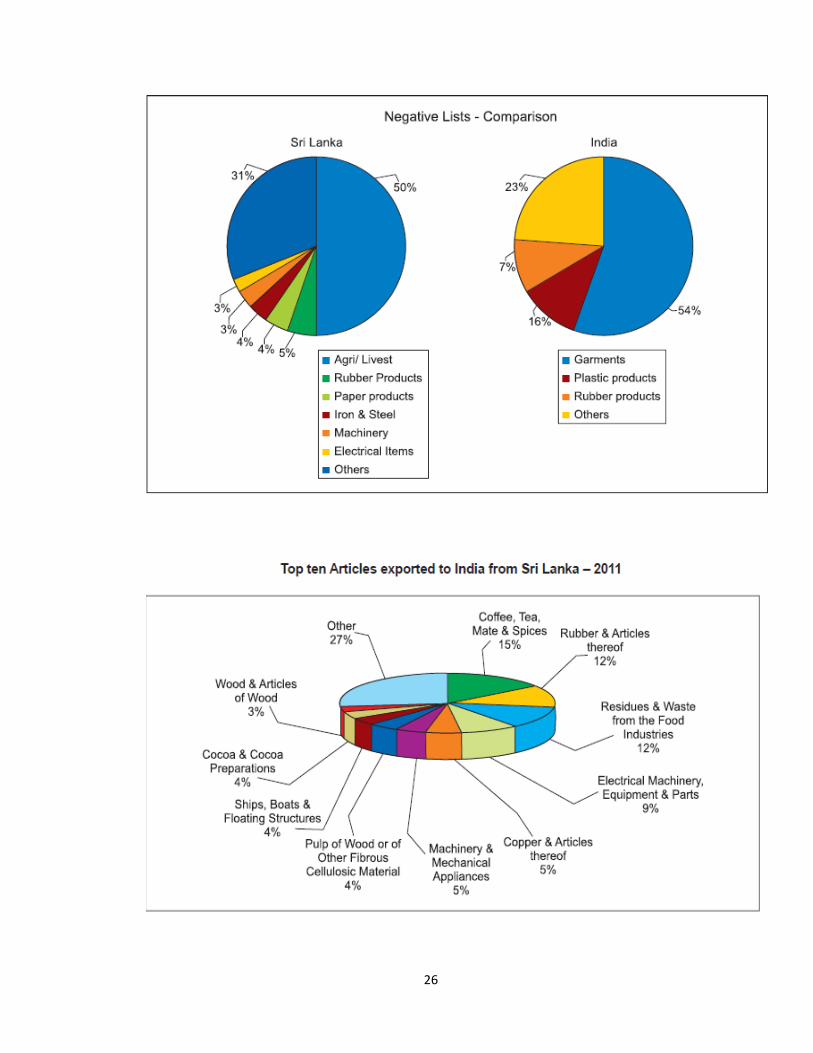

1.5.1 Top Ten articles exported to india from srilanka 2011

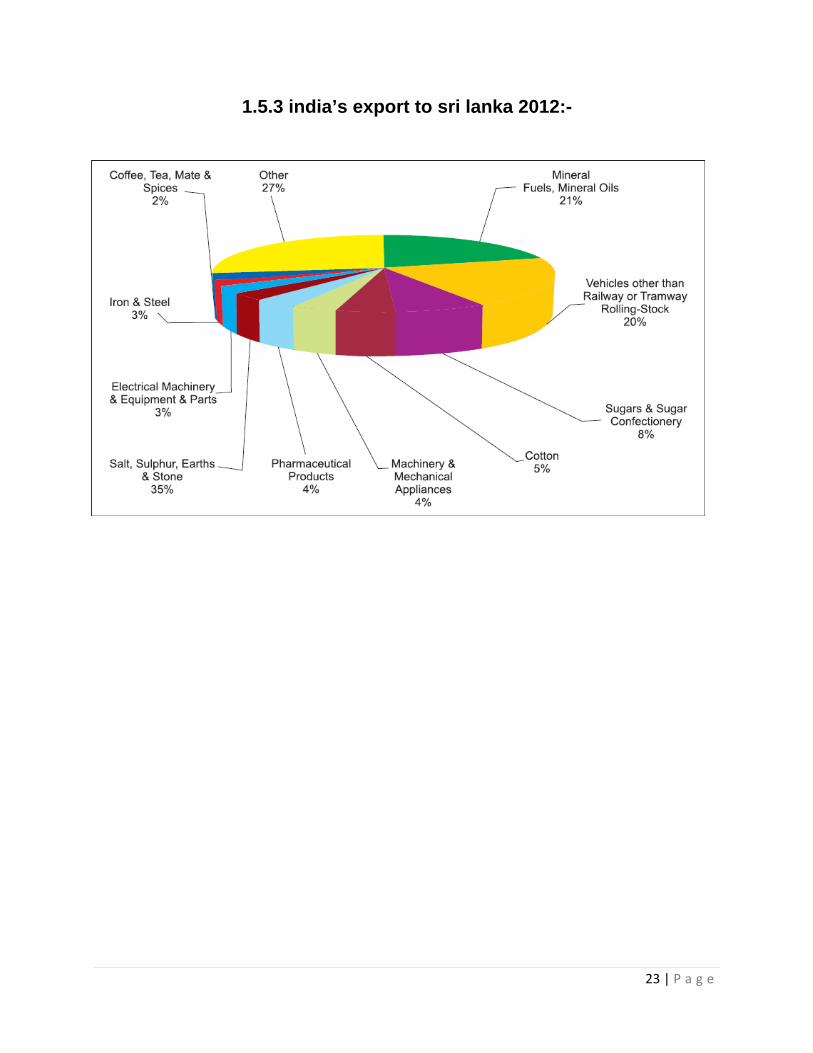

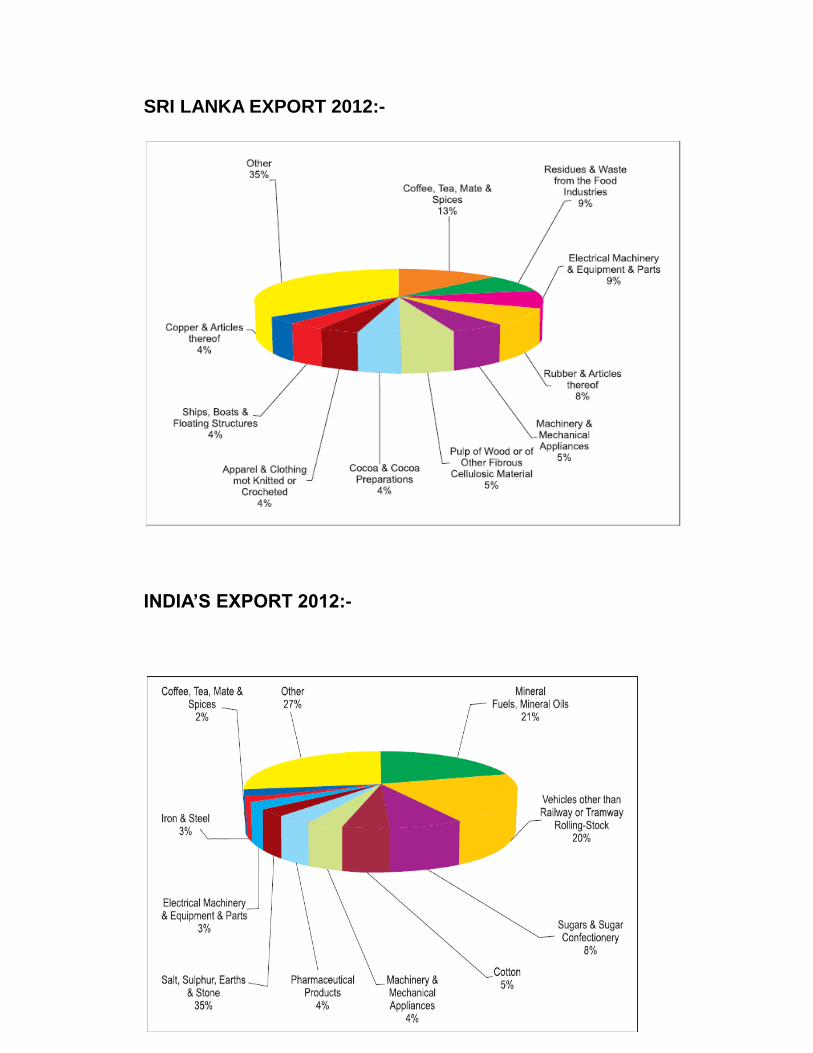

1.5.2 sri lanka export to india 2012:-

23 | P a g e

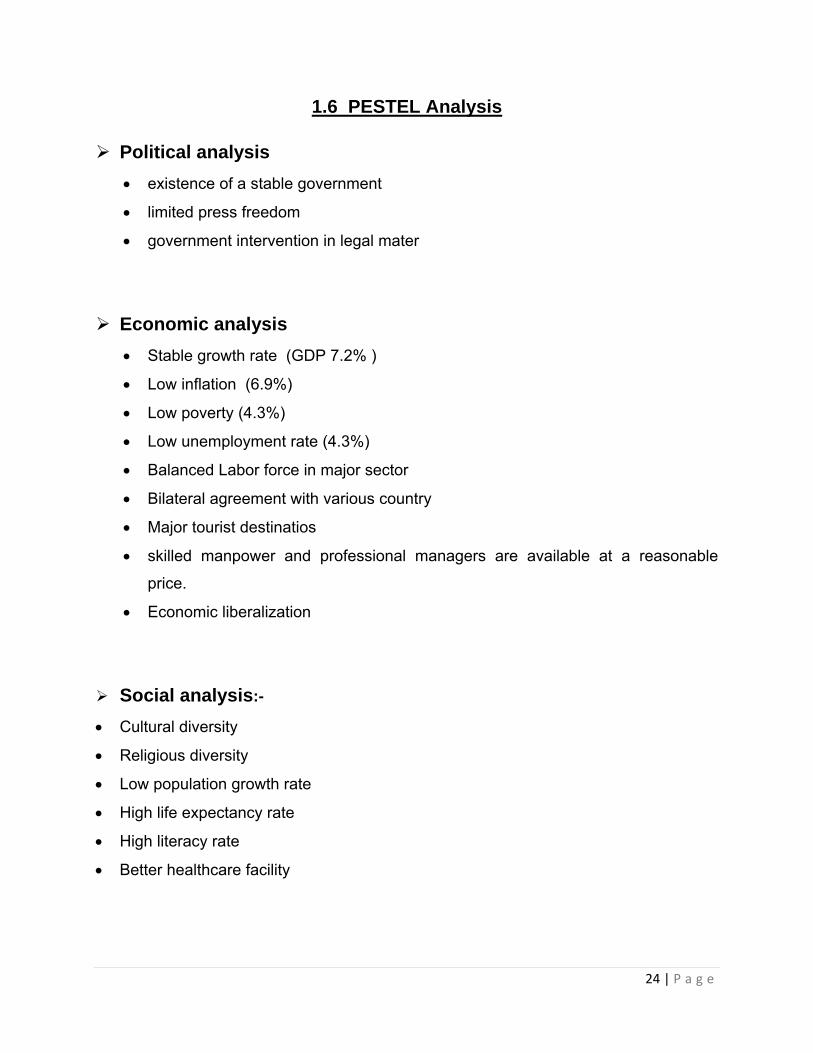

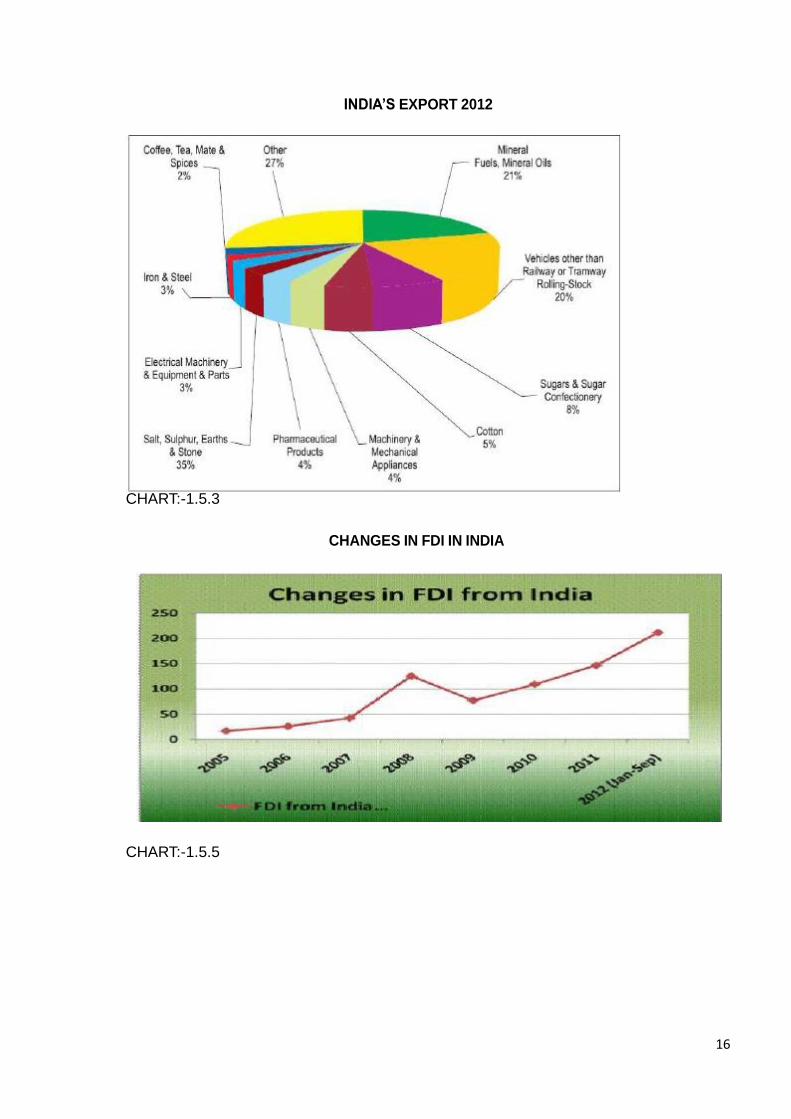

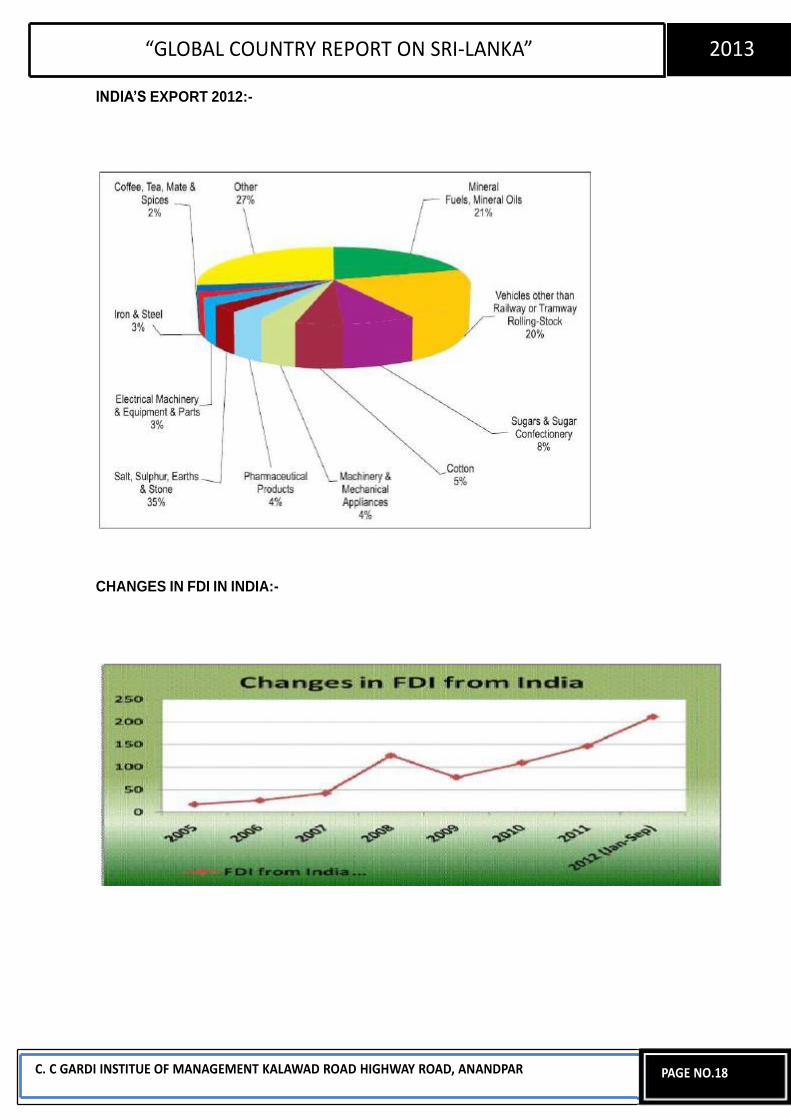

1.5.3 india’s export to sri lanka 2012:-

24 | P a g e

1.6 PESTEL Analysis

Political analysis

existence of a stable government

limited press freedom

government intervention in legal mater

Economic analysis

Stable growth rate (GDP 7.2% )

Low inflation (6.9%)

Low poverty (4.3%)

Low unemployment rate (4.3%)

Balanced Labor force in major sector

Bilateral agreement with various country

Major tourist destinatios

skilled manpower and professional managers are available at a reasonable

price.

Economic liberalization

Social analysis:-

Cultural diversity

Religious diversity

Low population growth rate

High life expectancy rate

High literacy rate

Better healthcare facility

25 | P a g e

Technological Analysis:-

better communication facility

Growing IT market at 10% CAGR

Government support towards infrastructure facility

Enviromental Analysis:-

Low rate of urbanization

Most of industry depends upon agriculture sector

Legal Analysis:-

The legastrict labour laws

Existence of corruption

morePolitical intervention

Existence of Various regulatory body

26 | P a g e

CHAPTER -2

2.1 Introduction of selected Indian and srilankan companies of

banking sector

2.1.1Indian bank

Bank of Baroda

History:-

Vision and enterprise.It a saga in 25 countries throughout nearly a century has been a

long and eventful journey. Baroda small increase in the HI-high-tech Baroda Corporate

Centre in Mumbai building new and starting in 1908, a veteran of vision, enterprise,

financial prudence and corporate governance.

It is a story scripted in corporate wisdom and social pride. It is a private capital, princely

patronage and state ownership crafted story. It is common for bankers and their

corporate spectacle of Bank of Baroda's extraordinary contribution in the ascent on the

towering height of a story. Customers, stakeholders, employees and the public at large -

who in ample measure, have contributed to building an organization that is a story that

needs to be shared with all the people in the millions.

532134 Maharaja Sayajirao Gaekwad and at its headquarters in Vadodara, India,

established in1908 by: Bob Banking Financial Services in BSE traded as a public

company. The area served Worldwide. Who is the chairman and managing director SS

Mundra their key people. Its products, credit cards, consumer banking, corporate

banking, finance and insurance, investment banking, mortgage loans, private banking,

private equity, wealth management. Bob revenue 345.88 billion ($ 6.3 U.S.) (2012), and

its net income 52.48 billion (U.S. $ 955.14 million) (2012). Total assets 4.574 trillion

(U.S. $ 83.25 billion) (2012), the

27 | P a g e

Our Mission Statement:-

Care is a top international concern, and through the ability of 'holding value of

augmenting ranking National Bank is committed to standards.

Our logo:-

Our new logo is a unique representation of a universal symbol. It has dual 'B' letterforms

that the rays of the rising sun. We call this the Baroda Sun.

Achievement:-

Bank of Baroda Bank award for best PSU

Award for Excellence in Financial Reporting.

Bank of Baroda Bank award for the best public sector.

bag Baroda Bank of The Sunday Standard FINWIZ 2012 Awards.

Baroda for the prestigious Indira Gandhi Rajbhasha Shield Bag of Bank.

HDFC Bank

Background:-

Housing Development Finance Corporation Limited (HDFC) was in 1977 and in 1981

introduced its first retail deposit product. In 1996, HDFC its first international office

opened in Dubai. HDFC mainly associated with housing loans.

Profile:-

HDFC Bank was announced in August 1994 and is currently a nationwide network of

branches and ATMs of Indian towns and cities.

28 | P a g e

HDFC's product range of home loans, home improvement loans, home extension loans

short-term bridge loans, home equity loans and land purchase loans among others are

included. HDFC distribution network of 250 outlets across the country in 2400 on

chavayelo and provides customer locations. It also project management services,

investment consultancy and property related services are provided. During FY08, the

company worth Rs 425.200 MN loans approved, representing a 28% increase yoy.

During FY08, HDFC 16 lowincome and community micro-finance for the EWS housing

schemes approved for a new loan. 31 2008 Mar on, the company said CAR 16.8% and

gross NPAs at 0.77% as against 0.68% in the previous year. During FY08, HDFC

HDFC Chubb General Insurance Ltd and 100% of the 26% stake in the company and

also International AG, Germany, with the joint venture was entered in the insurance

business.

HDFC Bank traded as a public type and BSE: 500180, NSE: HDFCBANK, NYSE: HDB,

BSE Sensex included. And their Industries Banking, Financial 1994And in Mumbai,

Maharashtra, India is headquartered established services in August. Worldwide service

and their key people in the area, Mr Aditya Puri (MD) of the products, credit cards,

consumer banking, corporate banking, finance and insurance, investment banking,

mortgage loans, private banking, private equity, wealth management .. The RevenueUS

6,487 billion (2012), operating income of 1.451 billion USD (2012), Profit 978.3 million

dollars U.S. (2012), the total of $ 70.17 billion assetsUS (2012), and his total of $ 7.793

billion equityUS (2012). They are up employment 66,76 (2012) is.

Business focus:-

HDFC Bank deals with three major business segments. - Wholesale banking services,

retail banking services, treasury. The working capital finance, trade services, corporate

finance, and merchant banking to provide 50 top companies of the banking consortia

entered. It also foreign exchange and derivatives, money markets and debt trading and

equity research in the field of providing sophisticated product structures.

29 | P a g e

Award:-

Euromoney Poll India 2012 - Best Super Affluent Private Bank.

Best Performing Bank - UTI MF and CNBC TV18 Financial Advisor Awards 2011

by private.

best year for the 2011 Asian Banker Excellence in Retail Financial Services

Awards 2012 by the International Bancassurance provider.

Euromoney Poll India 2011 - Best Super Affluent Private Bank.

The Banker and Professional Wealth Management (PWM), the Financial Times

Publications, Global Private Banking Awards 2010 - Best Private Bank in 2010.

Property Forum Advisor Awards 2010

• Highest Net Sales - Income Statement

• AUM highest increase (non-hybrid +)

• Highest Live cusakio

• Highest Live Investor Folios

• Highest AUM (Non Hybrid +)

Career and Corporate Governance:-

India's leading private sector bank that won accolades from top national and

international magazines, join the workforce, opportunities and explore the world. HDFC

Bank's corporate governance policy is to consider suitability for all participants, as well

as the importance of maintaining organizational efficiency has been achieved.

30 | P a g e

Shareholding in Bank:-

Our well as browse through the entire previous allotment of shares detailed records.

ICICI Bank

Background

Profile:-

ICICI Bank, the retail banking, corporate banking, international banking, project finance

SME financing, rural and ICICI Bank Limited (ICICI Bank) in 1994 and was promoted in

2001 by ICICI Limited, the business acquired Bank of Madura and ICICI Ltd. in 2002

and its subsidiaries engaged in retail lending, has been merged with the Bank. In 2007,

ICICI Bank, The Sangli Bank Ltd. The business acquired

Agricultural banking business and treasury operations. Under the deposit and loan

accounts in the retail banking and wealth management services are provided. Corporate

banking, cash management and structured finance, including such services. ICICI Bank

also mutual such products, life insurance and general insurance distribution of. In

addition, the bank money transfer, loans under the NRI segment, international banking

and property solutions for clients such as providing banking services. 31 2008 Mar on,

the bank had a total business of Rs. 4,700.5 billion and 10% yoy growth. For FY08, the

priority sector advances for RNBC at 50.3%, while 17% were RNBC for agricultural

lending. 31, 2008 1,249 3,881 bank branches and ATMs in a network.

ICICI Bank is the bank of a public nature and traded as BSE: 532174, NSE: ICICIBANK,

NYSE: IBN, BSE Sensex included. The Corporate Banking, Financial Services that is

established in1954 and its Mumbai, Maharashtra, India, the headquarters is located.

Area served Worldwide Key people and Chanda Kochhar (MD & CEO) is. Their

products, credit cards, consumer banking, corporate banking, finance and insurance,

investment banking, mortgage loans, private banking, wealth management.their $ 13.52

billion in revenue U. (2012), operating income of 2.117 billion USD (2012), Yu profit of

1.597 billion (2012), $ U.S. 98.99 billion (2012) announced their total equity billion USD

12.62 (2012) total assets. His 81,254 Employment (2012).

31 | P a g e

Objective:-

ICICI Bank's Green initiatives in the organization of a healthy environment;

interpersonal skills to build and customer understanding between an organization's

employees amongs.

The ICICI broad goals:

(A) the creation, expansion and modernization of private affairs to help;

(B) internal and external capital took part in the promotion of private matters;

(C) to promote industrial investment in private ownership

Awards and achievements:-

For the third consecutive year

ICICI Bank by Businessworld BW Quote 500 in "India's 50 Biggest Financial

Companies" in figured.

ICICI Prudential Insurance Domain Series, All India (AIMA) Management and

Delhi Management Association (DMA) 2012 by 2 G. Shared Services

Excellence Awards, and won the recognition.

ICICI Bank tops the list of most fans and global social media study conducted

by Ketchum Sampark in connection to Facebook ranks fifth among financial

institutions.

Airtel, the top 100 global brands, ICICI between.

Polaris Financial Technology Banking Awards –

ICICI Bank Best Global Business Development, Rural Reach Dun & Bradstreet

and SME lending by banks to the private sector categories.

ICICI Lombard series 'Creating Shared Value', the famous 'Porter Prize' was

awarded. Porter Prize, the most prestigious award in the field of strategy and

competitiveness. Competitiveness of the Indian Institute Professor Michael E.

32 | P a g e

Porter, named for the award by the gift and economically weaker sections of

society are responsible for mass and micro-insurance sector in achieving

economic success of ICICI Lombard recognizes the efforts.

Punjab National Bank

Background:-

Punjab National Bank (PNB) 1895 was established in 1969, and was subsequently

nationalized bank. The bank primarily operates in the banking and corporate, retail and

treasury space.

Business Profile:-

PNB individual, corporate, social, international and business banking services are

provided. Its personal banking services, savings accounts, and credit schemes among

others include fixed deposit schemes. PNB corporate banking services provided by the

EXIM finance, cash management services, etc., and the business sector, including

services, including trade and finance to SSIs. Provide for its social banking services to

farmers and women. On 31 Mar, 2008 the bank had a total business of Rs. 2859.6

billion, registering a growth of 20% yoy. For FY08, priority sector advances bank ANBC,

where as only 18% of agricultural credit constituted of 44% above formed. During FY08,

PNB 150 322 31 new branches opened in the 2008, including extension counters, 4,589

offices, taking its total branch network. The bank also has three foreign branches.

Fired by the spirit of nationalism and founded on the idea that Indians should own a

National Bank, Punjab National Bank Ltd. far-sighted visionaries and patriotic, between

the efforts of those were the result of individuals like Lala Lajpat Rai, Mr. EC Jessawala,

Babu 1882 Article VI of the Act Prasono under Roy, Lala Harkishan Lal and Sardar Dyal

Singh Majithia.Incorporated Kali, the Indian Act companies, 2 r, with an authorized total

capital on April 12, 1895 in Lahore, on the bank commencedoperations, million and

20,000 r of workingcapital. Prophetically, bank telegraphic address as its "stability"

select, as proved in the course of events in the future - in the form of Bank of India

33 | P a g e

Partition trauma when the bank was closed 92 offices (33% of the financial crisis,

including withstood West Pakistan) and its deposits 40% whichconstituted and 15 of its

staff for the victims of the typhoon. All registered office in Delhi wasshifted and bank

deposit base ofwhatever there is little evidence they honored produce.Subsequently,

Bank impressiveperformance can register and also on the increase in the strength of

the refugee claim.

Awards and RECOGNIZITION:-

2011 the year of the "Golden Peacock Award for Corporate Social Responsibility"

Instituteof Directors (IOD).

"CSRE xcellence a Ward 2 0 1 0" by Assocham.

Wind Power 2011 Awards - Second India

By World Institute of Sustainable Energy � "Best Wind PowerProject Financier" under

the category Prize in 2011.

"RRBs computer" to SKOCH 2010 Award.

SKOCH Financial Inclusion Award 2010.

500Indian companies ranked among the top 24 best as per Economic Times

Company.

2010 for the 3rd and 5th Best Big Bank FastestGrowing Bank Ranked by

Business World.

2010 14 Most Valuable announced today by the Business Ranked

SectorCompany.

34 | P a g e

State bank of india

Background:-

In 1959, the State Bank of India (Subsidiary Banks) Act was passed by Parliament in its

subsidiary SBI associated banks as are the eight former state. Today, SBI extensive

administrative structure to oversee the largest network of branches in India and abroad.

State Bank of Saurashtra, State Bank of India FY09 feet, a wholly-owned associate

acquired.

Business Profile:-

SBI Banking services are provided by default unless it ventured into many new

industries such. Pension funds, general insurance, custodial services, private equity,

mobile banking, point of sale merchant acquisition, advisory services, structured

products and many more. SBI personal banking products and services segment, which

deposit scheme such as term deposits, recurring deposits include bank also collected a

wide range of government debt and pension payments, e railway freight payment,

online storage, such as a state government business in the 31 Mar 2009, government

receipts, etc., the bank's total business in the previous year's growth of 23.38% as

against 34.63% in yoy growth. 31 Mar 2009 11,448 branches and 8,581 ATMs, the

Bank had a network.

SBI Bank is traded as a public type NSE: sbin, BSE: 500112, LSE: SBID BSE Sensex

included. Industry, banking, financial services by 1 July 1955 and established its

headquarters in Mumbai, Maharashtra, India is situated. Worldwide service in their area

and their key people isPratip (Chairman), Chaudhry their products. Credit cards,

consumer banking, corporate banking, finance and insurance, investment banking,

mortgage loans, private banking, wealth management.their revenue 36.950 billion USD

(2012), the profit 3.202 billion USD (2012), total 359.237 billion USD (2012) Assets,

Total Equity USD 20.854 billion (2012). India and their 292.215 Employibility their owner

(s) Government (2012).

35 | P a g e

State Bank of India, the Frankfurt office as a representative in 1965 and completed in

1974 as a branch was started. We are also part of the Indo-German trade with India as

a part of the European trade in the purchase. Our representative liabilities Scandinavian

countries and some of the Eastern European States. SBI Frankfurt, we also Milan,

Italy.In a representative office in Germany to support the independent Bank of status.

We are individual, institutional and corporate attractive interest rate deposit products

offered. Under the German Deposit Insurance our customer deposits are covered up to

61.7 million per customer.

The associate banks with SBI:-

• State Bank of Bikaner and Jaipur

• State Bank Hyderabad

• State Bank Mysore

• State Bank of Patiala

• State Bank of Travancore

Logo and slogan:-

The bank's business in the middle of - • India State Bank of logos at the bottom of the

completion of the common man and small man with a small cut in the blue circle.

"The common man a bank", "every Indian Banker", "U on the nation's banks" "Pure

Banking, nothing else", "All the Way With You": • sources.

Recent awards and honors:-

Best Online Banking Award, Best Customer Initiative Award & IBA Banking

Technology Award 2010 by the Best Risk Management Award (runner-up).

year, Bank of 2009, India The Banker magazine (won the second year in a row).

Best Bank - Business Bank Awards 2009 by the largest and most socially

responsible bank.

Best Bank 2009 by Business India

36 | P a g e

Most Trusted Brand 2009 The Economic Times.

The most favorite and most preferred home loan provider by CNBC Bank.

by FINO financial benefit of the Visionaries.

IBA Banking Technology Award of the Year by Technology Bank.

Virtual Corporation SKOCH 2010 category awards for its payment solution e.

37 | P a g e

2.1.2 Srilankan bank

Seylan Bank PLC

History:-

Seylan Bank PLC was established in 1987, and its doors opened for business on 24 th

March 1988, Colombo, Sri Lanka's largest city is Fort traditional banking district.

Originally named Seylan Trust Bank Limited was appointed a licensed commercial bank

and the shareholders as a publicly traded company with a comprehensive support

structure .. It was established to, a new organization companies in the Ceylinco Group,

one of the main industries in a large variety of Sri Lankan group operating divisions.

Bank founder Chairman Dr. Lalith Kotelawala, the more welcome retail customers, and

the general disciplined banking culture which is usually, but this was seen as a bit

austere provide an alternative service was friendly. Initially to, Seylan Bank itself

aelastic, selection offered as a customer friendly gatherings - the service formula that

was soon corrected in consideration of potential customers agree: 'One Heart with a

bank.

Seylan Bank, for the first time in history, records 2 billion rupees profit post tax

Seylan Bank 12 31 months ended December 2012 report to the pre-tax profit of 3.18

billion rupees, published on Friday, according to the bank results, but in a historical

profit post tax.

"Post-tax profit of Rs. Was surpassed. Billion footage of its history. 1 Lee-time, 2. 2.049

billion, which is 208% of the 665 million rupees / SLFRS LKAS reported under

accounting standards adopted this year, compared to an increase of the bank statement

issued by the Media , "he said.

Interest margins on lending and pressure control industry, despite the huge growth, net

interest income by 4.76% Rs 9 billion for the period under review, more value was the

result of advances in selective growth.

38 | P a g e

During the period under review, the bank said it had focused its considerable overhead

cost control. Many buildings in and around Colombo such functions were moved to a

central location. Hard work on humanizing cost efficiency improvements result directly

as a result of specified end of this year, it said.

The bank's deposits and Rs 22.7 billion and Rs 18.3 billion increase in net advances

portfolio basis, respectively deposits and a rising interest rate environment, competitive

despite anger. The bank said it also focused, consistent and effective reform efforts

through its asset quality has been able to improve every time since 2009. By Nihal

Jayamanne Bank chairman, said, "These results prove that the desired results of our

strategy and we started bright idea of sustainable development for the platform

provided".

During 2012, 15 new bank branches / appropriate centers opened, fully 17 branches /

appropriate centers, refurbish and more customer-friendly places in many other

branches of science.

Preparing for the future growth of the Bank in February, despite a successful debenture

issue was that the difference between the funds collected over subscribed. "Over the

next year, the bank identified the key areas of the bank's new product expansion,

branch expansion, increase service quality, staff guidance and strategy for future

growth, including expansion and IT infrastructure in line with the intent to invest," he

said.

Achievement:-

Seylan Bank Slim brand of excellence on the 'Brand of the Year turns around

with a gold cover "

01 October 2010, his winning streak, Seylan Bank continues, the prestigious

"brand that is most beneficial to the bottom of a recession or crisis as" Slim

Brand Excellence Awards at "The Year of the brand around a turn," won the Gold

Award.

Slim brand quality brand conservators for now the single most important measure

of quality in event marketing helpfulness.

39 | P a g e

Bank with a Heart

Bank or Just Farr, and reliable

Vision Statement:-

Sri Lanka has become the most important source of financial services - we are

recognized by all stake holders.

Mission Statement:-

We provide financial services that are of value, pricing flexibility, and terms of service

for our customers, providing them with needed

We do Seylan Bank, which is also known as a team and the results will be satisfied with

the direction

We will ensure that our hard work at the same time the prospect of our shareholders, as

interpreted by the always reliable for meeting performance as corporate citizens

Values:-

High ethical and professional behavior

Brilliancy for the exorcism

Editing balanced Heroic

Steady growth

General praise and trust

Creating a permanent deal

Milestones:-

In 1988, our parent Deshamanya Dr. Lalith Kotelawala, chairman began a mission to Sri

Lanka for a really long felt requirement for commercial banks. Its foundation to, bank

customer service attention and now offers a variety of appropriate banking services.

The total number of service centers in Sri Lanka is now one of the one hundred leading

role in the financial sector increased.

40 | P a g e

The bank is going to state technology-based goods and services marketing. Seylan

Bank's social responsibility and the obligation has grown significantly. Bank of benefit

programs such projects and the promotion of sport, festivals, and those who

participated in the service project a major role in group...

Hatton national Bank

History:-

Hatton of Hill Station in 1888 saw the Bank of origin; tea plantations in Ceylon then

contained by its rapidly growing population of the first. Properly named Hatton Bank, the

Bank became a lifeline for thousands of plantation workers.

Great disappointment of 1930 as a result of two world wars and by the damage, Ceylon

desire to free colonization began. Realising that Ceylon will soon become an

independent country, Brown and Company, Edmund J. Cooray, Chairman of visionary

business opportunity, he began laying the foundation for the self-conception of the post.

Hatton Bank's owners, RD Banks and AT Aitkin, after discussions with the success,

Brown & Company Bank acquired and 'Ceylonisation' process that permeated the entire

management and operations began.

Kandy, Nuwara Eliya and the nationalization process in 1970, the National Bank of

branches acquired Grindlays Bank saw, Hatton National Bank name change heralding,

as it is known today. Only one year later, HNB Gampola 1 branch opened its continued

and extended branches Pussellawa and Maskeliya. The expansion is still in Sri Lanka

HNB's largest network of branches among private commercial banks, continues.

Acquisition that will increase its presence and business, was adopted in 1974, the main

office and the Mercantile Bank of Pettah Branch acquisition and long before, both

Emirates International Bank and banque Indosuez of Colombo branches. In 1983, the

Bank de mail Mawatha, 3 spacious locale of its main office in Colombo are encouraged.

In mid-1980, HNB service that prevails throughout the country for the banking distorted.

1993 saw the most successful product innovate HNB, HNB Pathum Vimana, an

41 | P a g e

incentive-based savings product savings habit instilled in the population and encourage

savers idle money in the banking system to create economic growth through the

channel. These awards are presented to a large bank Rs 1 billion until 2009, the

country's largest banking history, perhaps with the prize money.

HNB its product portfolio in the country's first Housing Finance Scheme for peace, which

they distributed to LKR 15 billion and 154 banking centers on the student, including the

establishment undermines a number, arrangement continued. To 1980 and a large

population of Sri Lankan expatriates in the Middle East saw the creation of employment

reported HNB Pathum Udanaya The savings and advanced economic development

award scheme which impel immigrants satisfaction.

Various communities in the country Gami Pubuduwa (Village Awakening) was

introduced to serve the rural Sri Lanka and HNB social stability for the World Bank from

liability to income in respect of more than 50,000 families create a livelihood for some

250,000 people.

Award:-

Awards bank navajya Recognition

In Sri Lanka 'Bank of the Year 2012' for the Bracken Award.

Retail Bank in Sri Lanka for a great performance in 2011.

Our Target

Our Vision;-

Choose a well-known leader and partner in providing financial solutions that inspire

people.

Our mission:-

People and leading-edge technology, continuous stakeholder power to go forward with

the entrepreneurial energy mix of the future.

42 | P a g e

Our Values:-

Wealth of professional and personal honesty at all times

All communication demonstrates our mutual respect Passionate in all

weCommitted to being customer centric Courage to change the challenge, and

varies Displays various solidarity.

Sampath Bank PLC

History:-

Bank Origin "Investment and Credit Bank Ltd." in 1987 became chairman of the bank at

the same time as Mr.'s Jayawardhana was integrated. Bank popular way, "Sampath"

became known. In 1988, Sampath Bank Automated Teller Machines in the country for

the 1st time (ATM) network for multi-point work and the service "Sampath Electronic

Taylor" or "set" became popular. After the popularity of ATM Banking (1989),

MasterCard, PBU (Personal Banking Unit) and University - to enter the banking system.

Bank Introduction to South Asia, "debit card" for the first time in 1997 and was the

opening of Sri Lanka's first account was issued a debit card immediately. Sri Lanka in

the first Cheque Imaging and truncated site (CIT) was in 2004 by Sampath Bank. Since

2009, the bank's largest private sector bank in Sri Lanka is the third in terms of total

assets. London, the second successive year and the "National Business Excellence

Awards 2010" for - Recently, Sampath Bank Financial Times Limited, "The Banker" by

the "Bank of the Year" award.

Company Description:-

Sampath Bank PLC, together with its subsidiaries, Sri Lanka, and related financial

services to its customers provides various commercial banking. The company also

engages in accepting deposits, trade finance, banking to shore resident and non-

resident foreign currency operations related services, corporate and retail lending,

import and export financing, project financing, lease, financing, pawning, local and

international debit cards issued travel and credit card, chip card, telebanking facilities,

43 | P a g e

Company analysis:-

According to the Consolidated - Audited Financial Statements for the year 2011 was

11.48%, with an increase in total net operating income, LKR 9.839.820 10,969,444 for

hundreds of thousands of LKR. Operating result LKR 4.794.208 hundreds of thousands

of LKR 5.983.518, which means an increase of 24.81% change. Results for the period

increased 19.12% as against LKR 3.484.466 hundreds of thousands of reach LKR

4.150.618 at the end of last year. Equity (Net / Income Total Equity) went back to

2293.98% and 6928.44%, return on asset (net gain / income total asset), 1.85% to

1.67% and net profit margin (net income / net sales) in from 37.84% to 35.41% when

compared to the same period last year

Our Vision:-

"Growing Force in Sri Lankan Financial Services"

Our Values:-

• a learning culture that encourages personal and organizational development as well as

to promote and create value for customers reform.

• All internal and external customers are treated like how we behave.

• All aspects of behavior, encourage and promote teamwork.

• Open the response and enthusiasm of individual development.

• Monitor and the results show an impressive responsibility.

• inflexible moral and professional standards of behavior.

Award:-

1996: 1996 Year by "Asiamoney" "Best Commercial Bank"

1997: by "Asia Banking Digest" "Best in South Asia Small Cap Bank"

44 | P a g e

1997: 1997, the Year by "Asiamoney" "Best Commercial Bank"

1998: the year 1998 by "Asiamoney" "Best Commercial Bank"

1998: by "Asia Banking Digest" "Outstanding New Business Venture Project in 1998"

1999: by "Forbes Global" under the "300 World's Best Small Companies" List

2000: "The 2000 Year Bank of" "The Banker" ("Financial Times group" by the Sri

Lankan Bank award for the first event) by

2004: National HRM Awards 2004 in the "Best Service Category in HR Practice"

2005: "by the South Asian Federation of Accountants (SAFS)" Best Presented

Accounts Award Runner-up "

2005: "Annual 2004 reports Excellence Award", "Chartered Accounts Institute of Sri

Lanka" by

2005: "Best Corporate Citizen"

2006: "The best economic performance for the year 2005"

2005: by "Chartered Accounts Institute of Sri Lanka" "Best Financial Application"

2005: by "Chartered Accounts Institute of Sri Lanka" "Gold Award in the financial

category"

2005: Sri Lanka National Chamber of Commerce's "Business Excellence, second

runner-up for the banking sector"

2008: by "the Ceylon Chamber of Commerce," Sri Lanka between the 4th

consecutive year, "The Top Ten Best Corporate Citizens" put

2008: "National Business Excellence Award" for "Best Performance Management

Practice Excellence" Sri Lanka National Chamber of Commerce by

2008: by "Asia Brand Congress, Mumbai, India" "Brand Leadership Award"

45 | P a g e

2009: "National Business Excellence Silver Award for the overall competition"

2009: Excellence in Business and Financial Performance Award Winner

2009: "Financial Times - London of The Banker" by the "Bank of the Year 2009"

2009: 2009 for Corporate Responsibility Award (Best Corporate 2009 Citizen)

2010: "Bank of the Year 2010" by the "Financial Times of The Banker - London"

2011: ARC Awards - Sampath Bank Annual 2010 report "National Banks" under the

category 25 th "ARC Awards Ceremony" held in New York a "Gold Award" won.

2012: World Finance Award - Sampath Bank in the prestigious World Finance

magazine's Best of Sri Lanka in 2012, the Banking Group awarded the accolade

achieved...

Growth:-

Sampath and later in 1997 Wijewardhana Mawatha, 10 is the Bank's first office in

Colombo, the Sir James Peiris Mawatha, 02 Colombo, Sri Lanka It was enthused. On

the end of the first year, 94 members of staff.

Powered by First Bank ATM was installed in 1986 and the year 2007 marks the end of

the 150 islands and 220 ATMs operating exceeded the bank.

In 1996, the Bank "Tele-Banking" facility was introduced. Internet Banking in July 2000

launched the facility - this has motivated IT 1998 "SampathNet" re-engineering was in

banking technology.

The 209 bank branches and 260 ATMs, including a total of 8 to site ATM operates.

Technology:-

Sri Lanka Sampath Bank was the first bank is fully computerized and its birth in 1986

was to work with database technologies.

46 | P a g e

Sampath Bank for "Automated Teller Machine" Mr. "set", MasterCard, personal banking

unit facility, Uni banking system and debit cards (Maestro and Cirrus and Visa begin

with) was the first brand to enter Lanka. Major re-engineering of its IT banking

technology inspired by the work for the bank after Bank Internet Banking, Internet

payment gateways and mobile banking services with the launch of the on-line 24x7.

First of all check for Bank of Sri Lanka "One day clearing" any Sampath Bank branch on

the dimmer, the islan collected by any commercial bank in Sri Lanka Automated

Clearing House (SLACH) is presented.

Cheque in Sri Lanka was first conceived and truncated (CIT) site was made by the Bank

in October 2004.

Sampath Bank National "Credit Approval System" (CAS) and "Electronic Money

Transfer" (EMTS) best quality software for in-house application development category

at the Awards 2008 Gold and Merit Award.

It is also a "local Developed New Technologies", which has been successfully marketing

/ product "Sampath Payment System" for lead generation service category prizes

awarded to the National Science and Technology 2008.

South Asia's first - Cheque Deposit ATM was launched online in real time.

ATMs are able to access nearly 1,500 islands - the country's largest ATM (iConnect)

network operated.

Financial Highlights:-

At the end of 2011

4.1bn GROUP profit (18.5% growth tax notice)

Advances in 34.9% growth (31.9%, surpassing the industry growth)

Deposit growth of 27.3% (18.7% increase across the industry)

Assets 32.2% growth (19.5% of the growth in cross-industry)

47 | P a g e

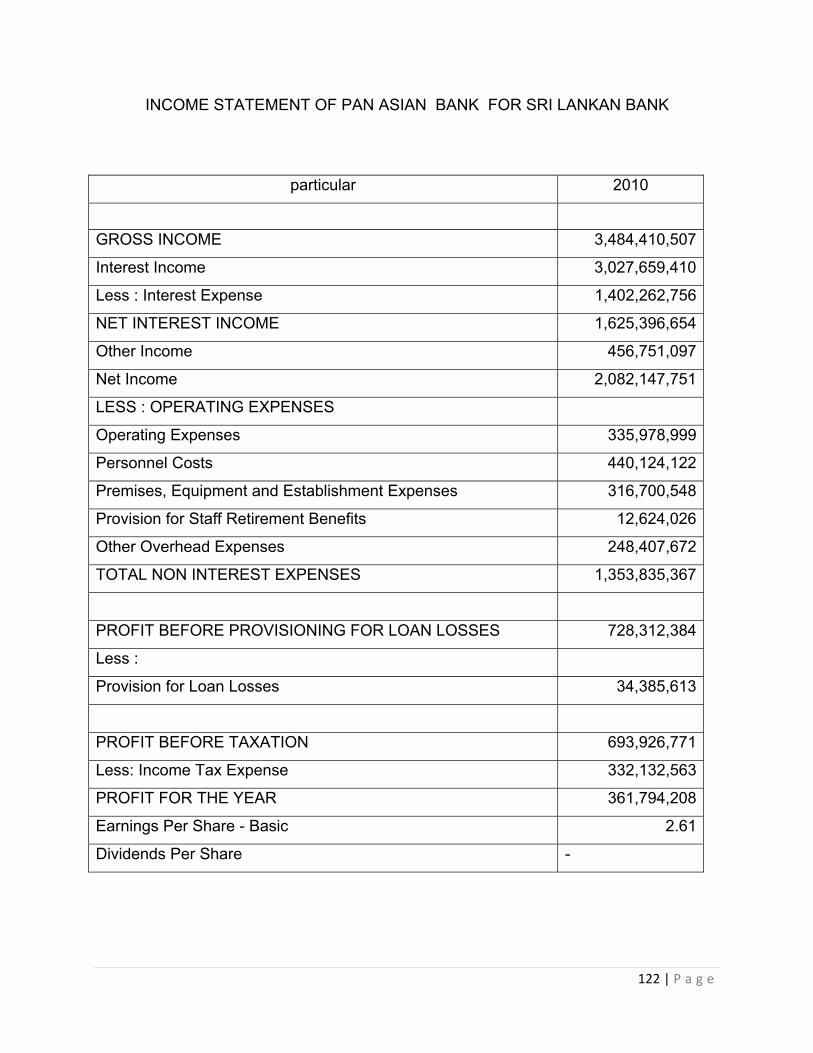

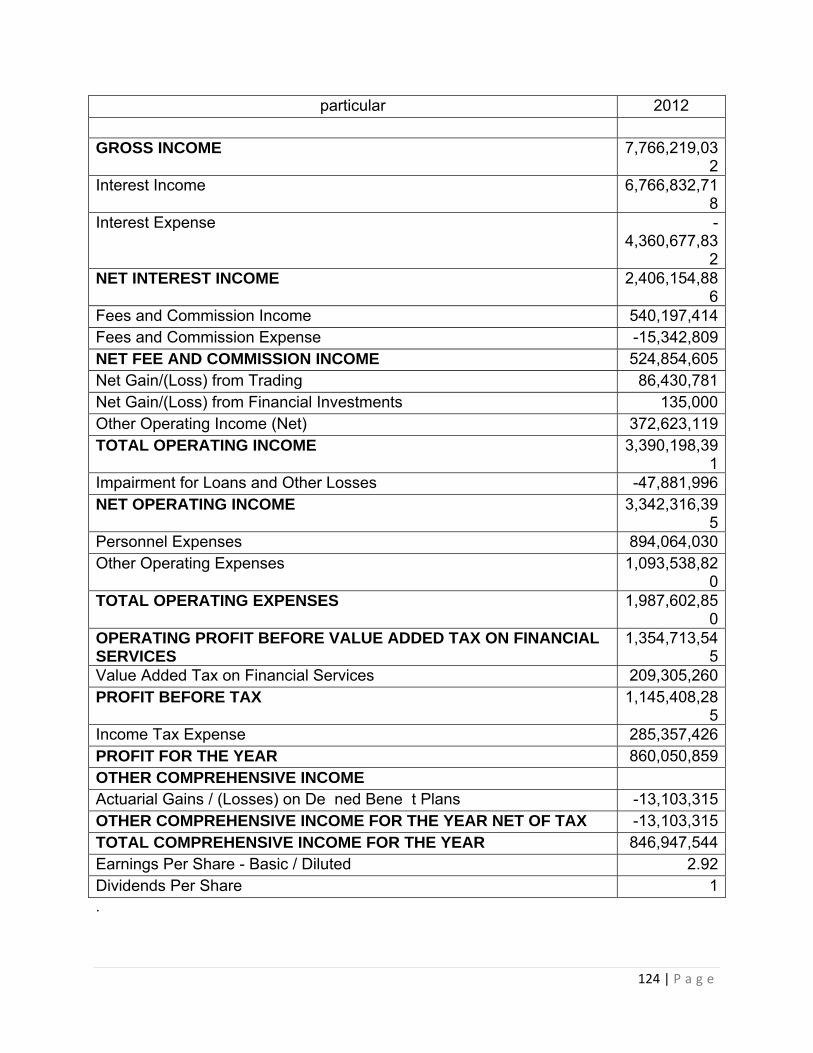

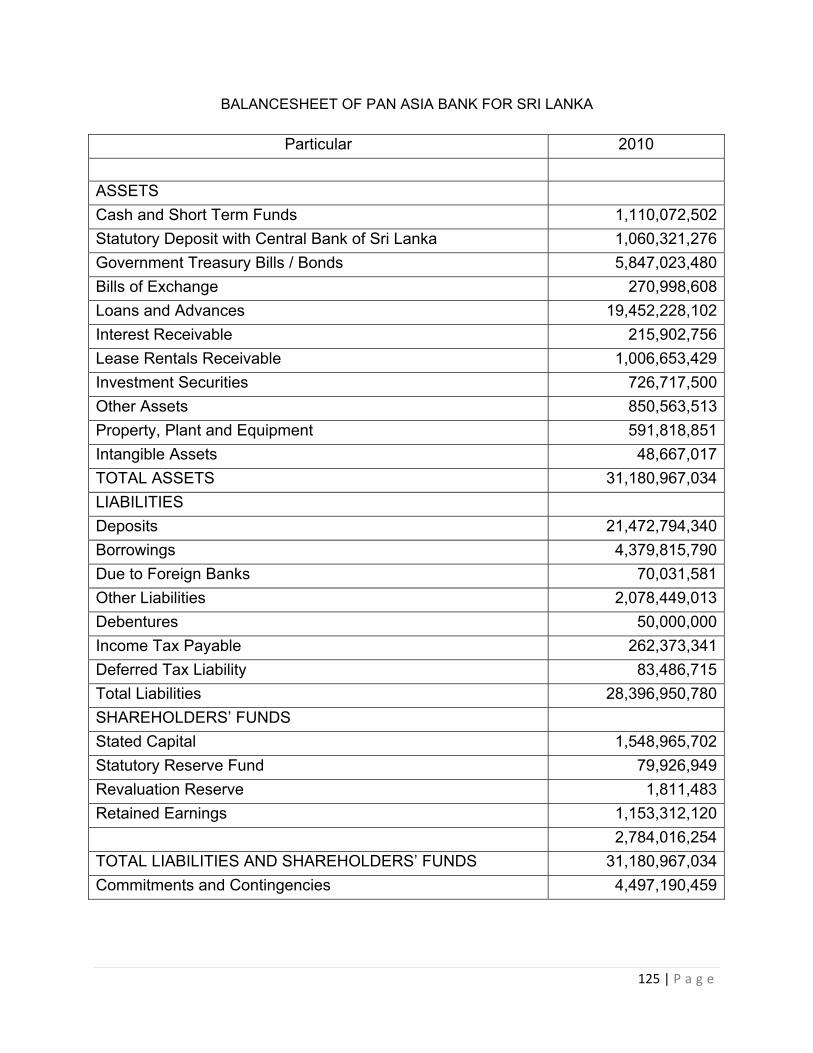

Pan Asia Banking Corporation

Company Description:-

Pan Asia Banking Corporation PLC commercial banking and related financial services

in Sri Lanka provides. Various accounts of the company, the individual current and

savings accounts, small accounts, Nonresident and resident foreign currency accounts,

foreign currency accounts of non-resident, Security investment accounts, especially

foreign investment deposit accounts, share investment external rupee accounts, rupee

accounts include it offers Nonresident Sri investment, treasury investment consortium

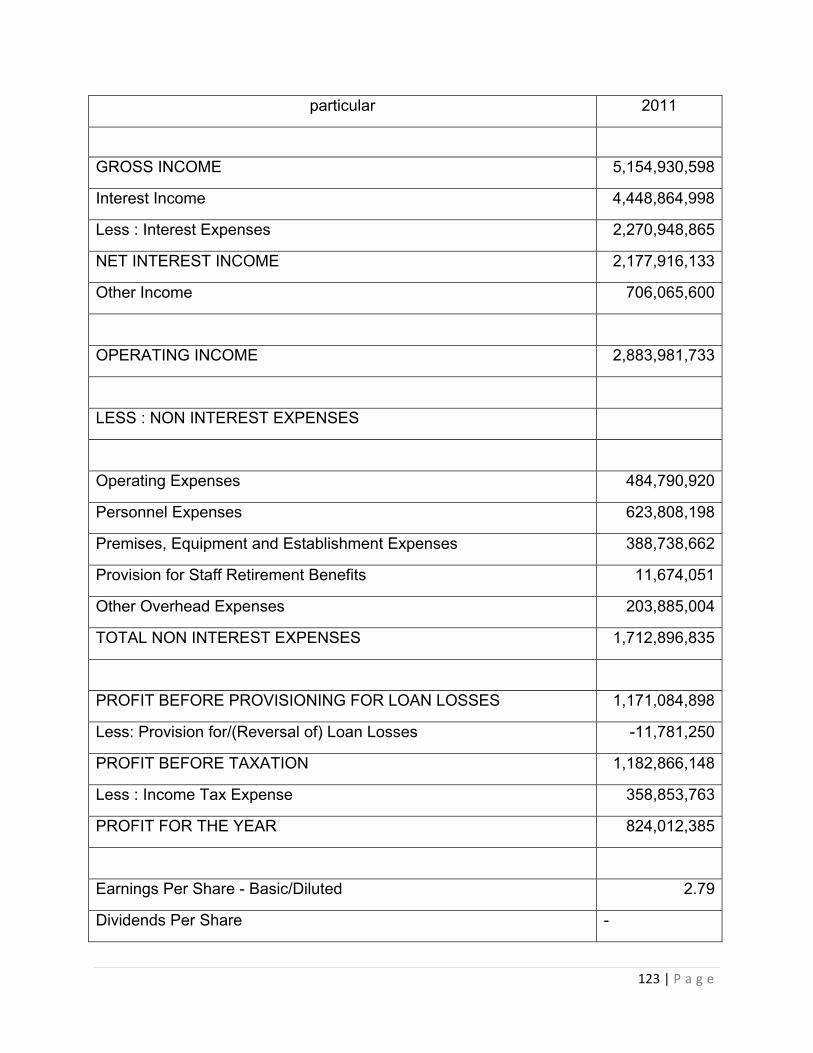

Company analysis:-

According to the Consolidated - Audited Financial Statements for the year 2011 was

39.75%, with an increase in total net operating income, LKR 1.708.342 2,387,442 for

hundreds of thousands of LKR. Operating result LKR 693.927 hundreds of thousands of

LKR 1.182.866 change means an increase of 70.46%. Results for this period of time

against LKR 361.794 thousand at the end of last year, an increase of 127.76% success

LKR 824.012 thousand. Equity (Net / Income Total Equity) went up 0.00% from 0.00%

return, return on asset (net gain / income total asset), 1.16% from 1.75% and net profit

margin (net income / Net Sales) went up from 21.18 % 34.51% when compared to the

same period last year.

Mission and Vision:-

Our Vision:-

"Sri Lanka's largest commercial bank to become a preferred customer"

Our Mission:-

"We are professional, personal, safe, quality banking and financial services are

provided, using modern technology and innovative products to create the most satisfied

customer base., We delight our customers, employees and partners to create a better

future price increase "

48 | P a g e

Nations Trust Bank

History:-

Nations Trust Bank was established in July 1999 when it acquired Overseas Bank Trust

Ltd. Colombo branch of the initial public offering (IPO) of oversubscription admission

considerable emphasis in our market.

Since then, we have gone from strength to strength, with a client base quickly

expanding our portfolio in our following strategic acquisitions. Waldock Mackenzie Ltd.

Acquisition Standard Chartered Bank of candy Branch Acquisition Deutsche Bank's

private banking portfolio of acquisition The commercial banking business and foreign

exchange of business acquisition Colombo, American Express, Bank of Mercantile

Leasing Company with the merger in January 2006 In September 2007, Fitch Ratings

Lanka Ltd. A (lka) or the issuer issues a firm in another country qualify for the credit risk

rating assigned to the dictates of the bank confirmed.

Mission and Vision:-

Our Vision:-

Making life simple by being the benchmark of convenience

Our Mission:-

Try innovative customer centric solutions continues to grow in our team is constantly

trying to loose market share of the best talent in the industry to grow and by 2015 the

most profitable and respected in Sri Lanka, try to let the bank.

49 | P a g e

2. 2 objective and function of banking industry

Objectives Banking industry :-

The Central Bank has two main goals:

1. Maintaining Economic and price stability:-

Price constancy safeguards the value of the currency in terms of what it will buy at

home and in terms of other currencies. Price constancy or stable prices means low

price raises. Experience has revealed that the economy performs better when inflation

is low and is probable to be low. Interest rates are too low in this situation. Such an

situation allow an nation to attain its development prospective and foster high

employment opportunities. Free from the disrupting effects of high and changeable

inflation, both customers and producers make financial decisions with self-confidence.

Low inflation or price stability fosters sustainable long-term financial growth and

employment opportunities. The Central Bank uses monetary guidelines measures to

manage inflation.

Financial system stability:-

A stable economic structure creates a positive atmosphere for depositors and investor,

encourages competent monetary intermediation and the efficient operation of markets,

and therefore, promotes investment and economic expansion. Financial system

steadiness means the efficient functioning of the financial system (economic institutions

and markets) and the deficiency of banking, currency and balance of payments crisis.

Financial unsteadiness is caused by bank failures, too much asset price instability, and

fall down of market liquidity or a disturbance to the payments system. Financial system

stability requires a stable macro-economic atmosphere, efficient authoritarian structure,

well prepared financial markets, sound financial organizations and secure and healthy

payments infrastructure. The maintenance of financial stability entail the avoidance,

recognition and lessening of fear to the financial system as a whole, through the

observation of markets and financial organizations, oversight of the payments system

and crisis declaration.

50 | P a g e

Functions of banks:-

The CBSL, so as to achieve its core objectives and discharge its responsibilities as a

financial advisor and banker.

Core functions:-

1.Economic and price stability

2. Financial system stability

The core functions related to:-

Currency issuance and management

agency functions:-

1. Employees' Provident Fund Management

2. Foreign Exchange Management

3. Public debt management

4. Regional development

5. Financial Intelligence

6. Provincial Office Monitoring

51 | P a g e

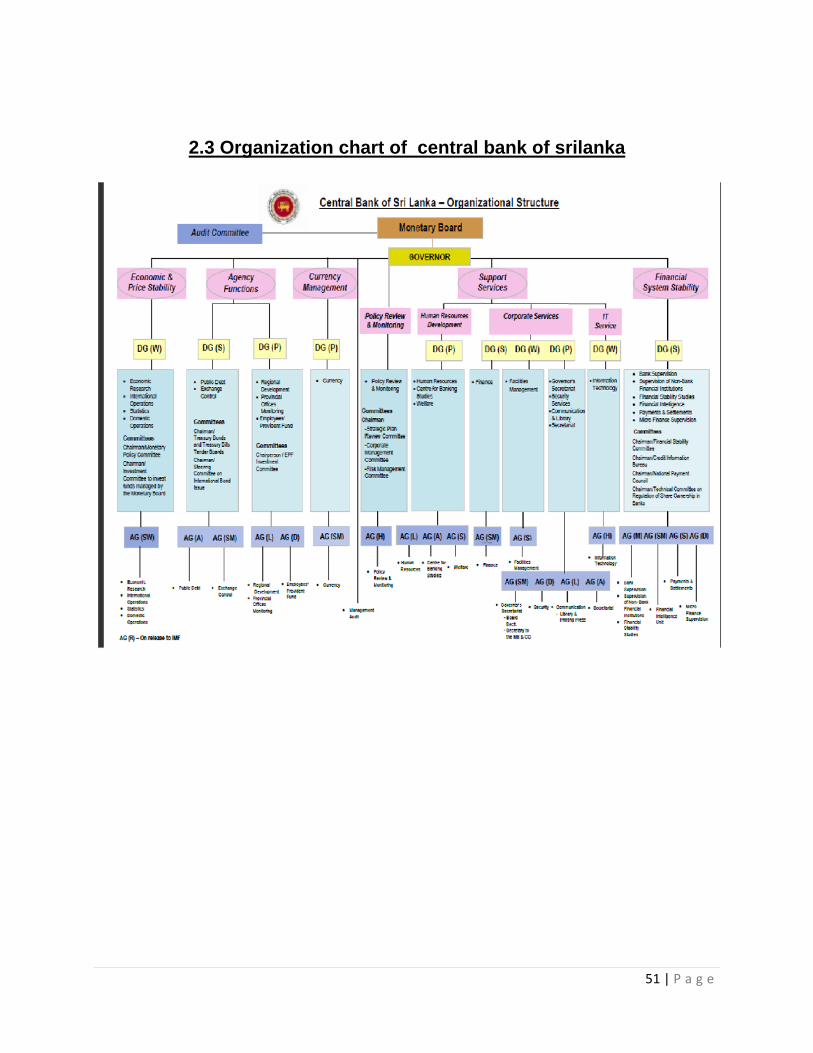

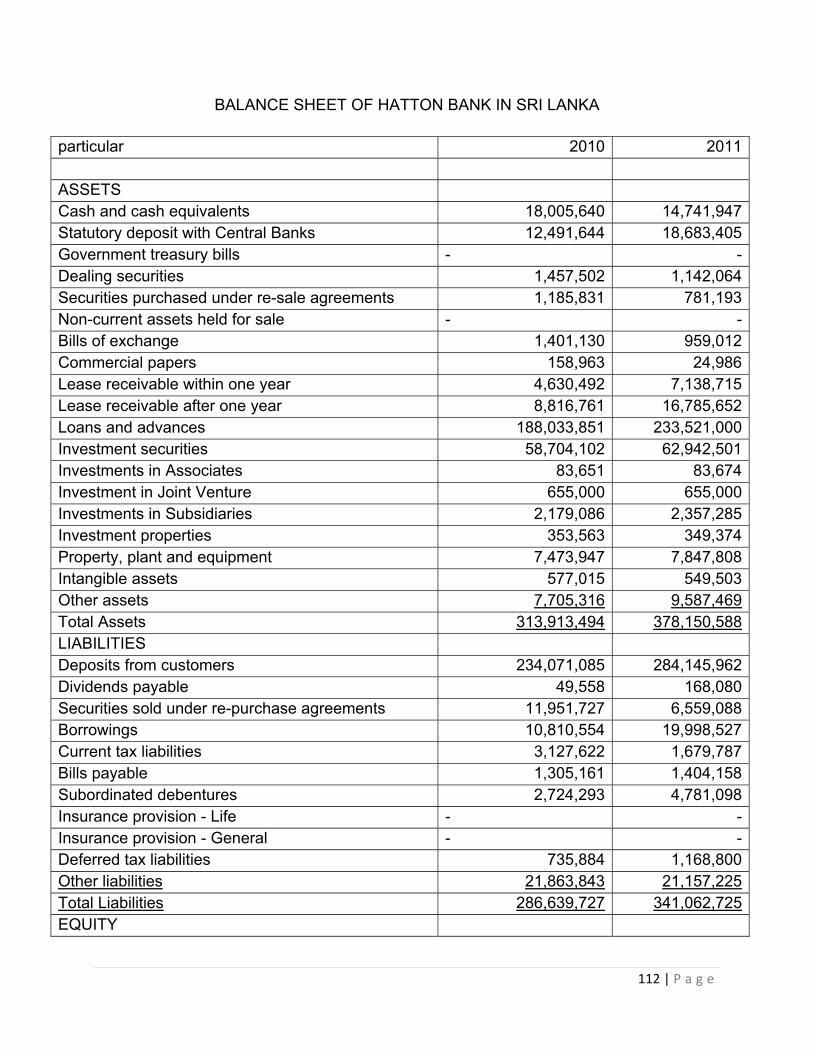

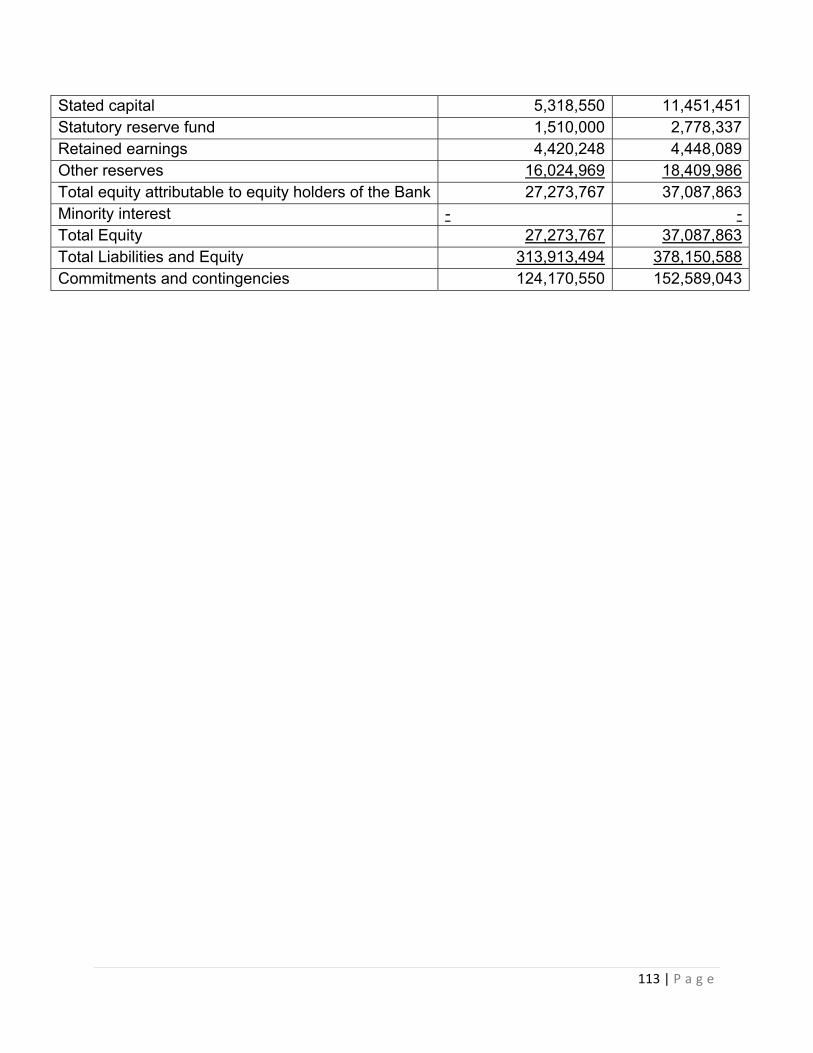

2.3 Organization chart of central bank of srilanka

52 | P a g e

CHAPTER -3

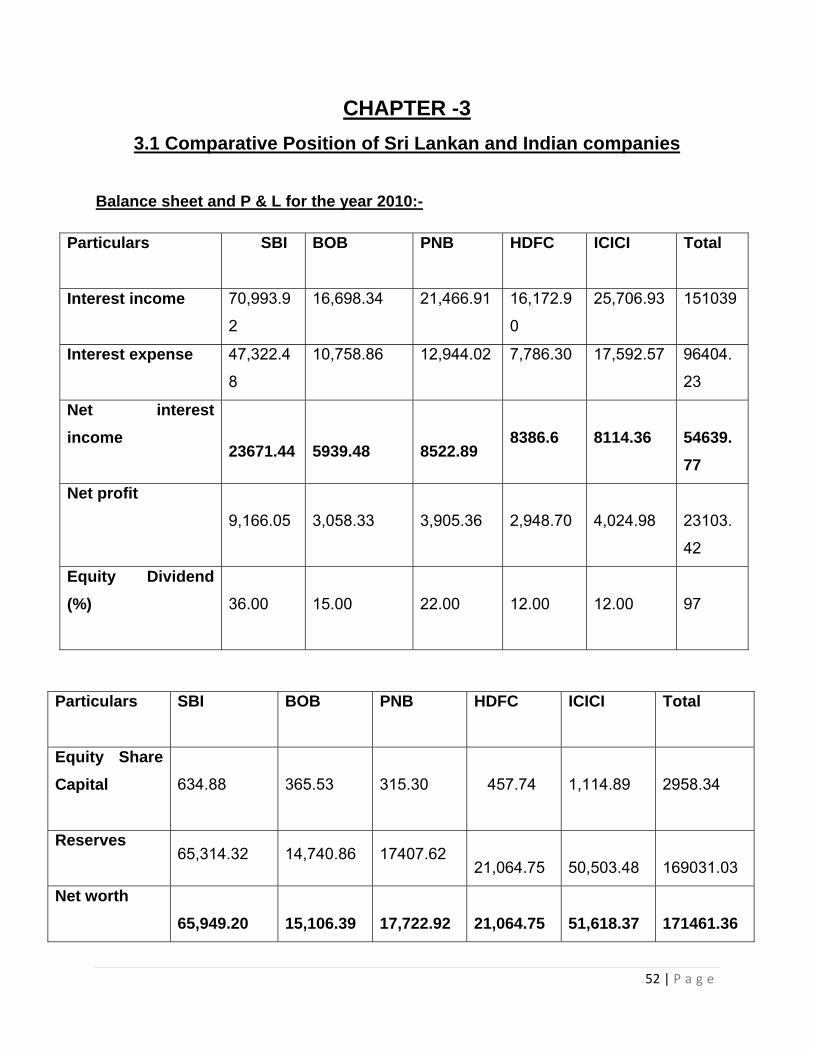

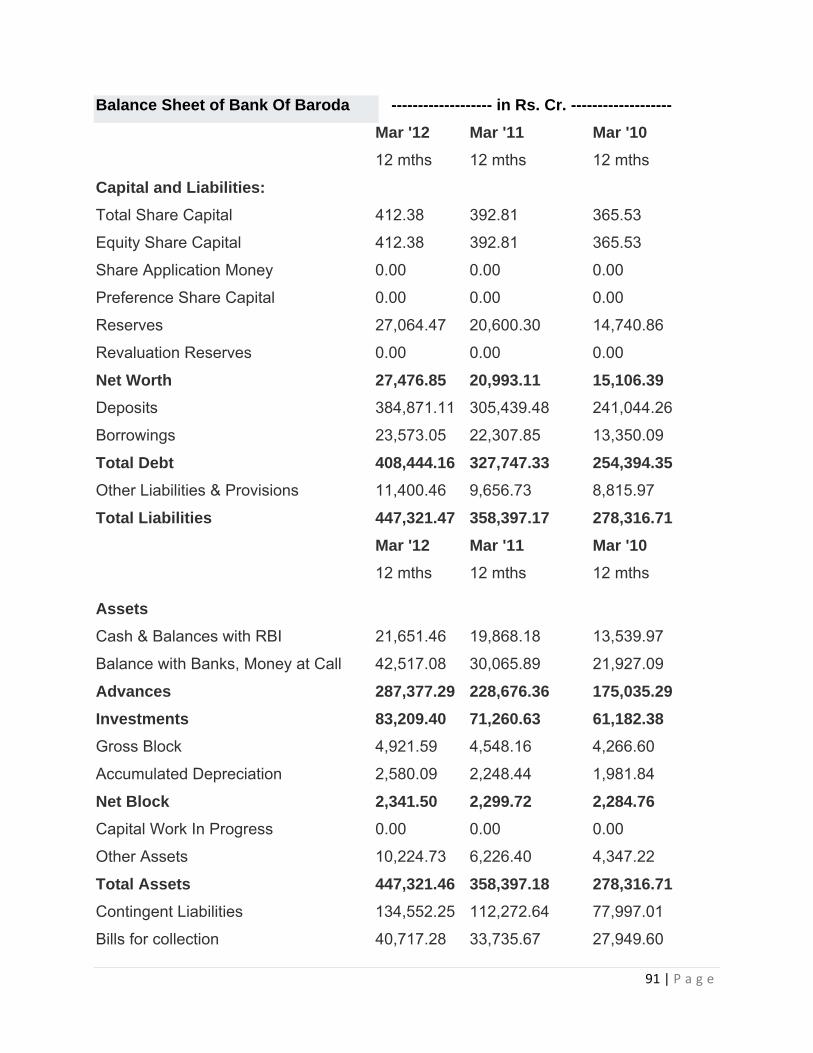

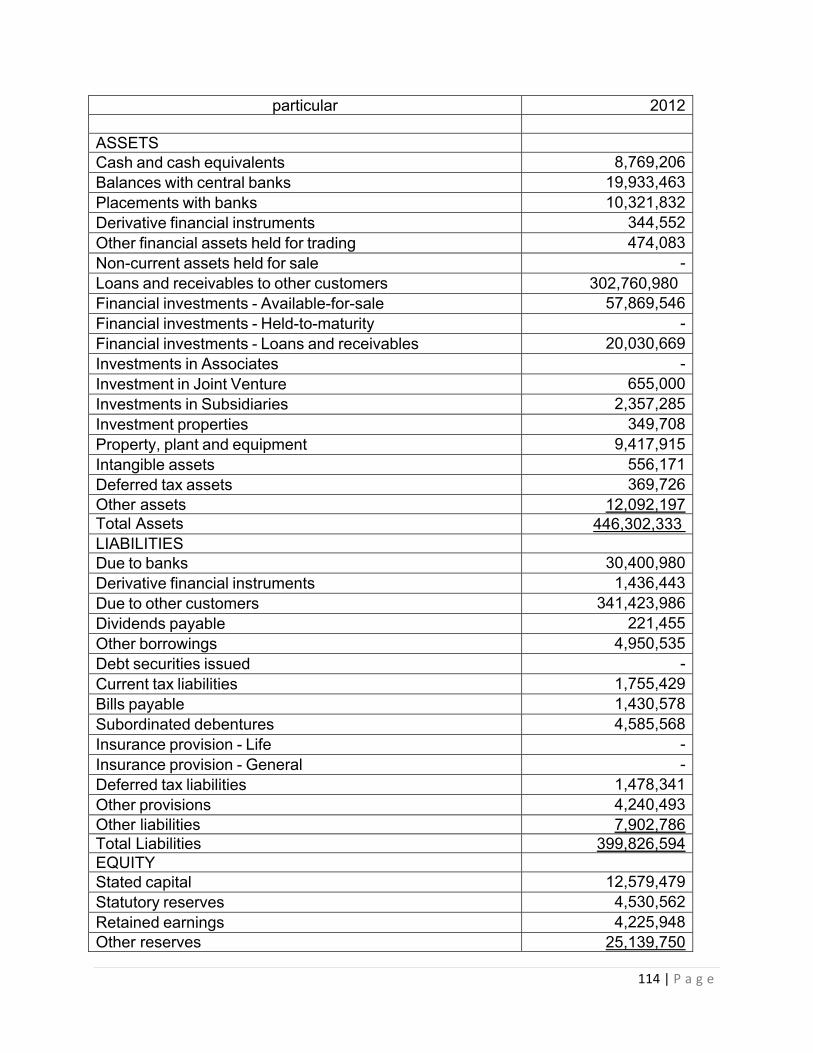

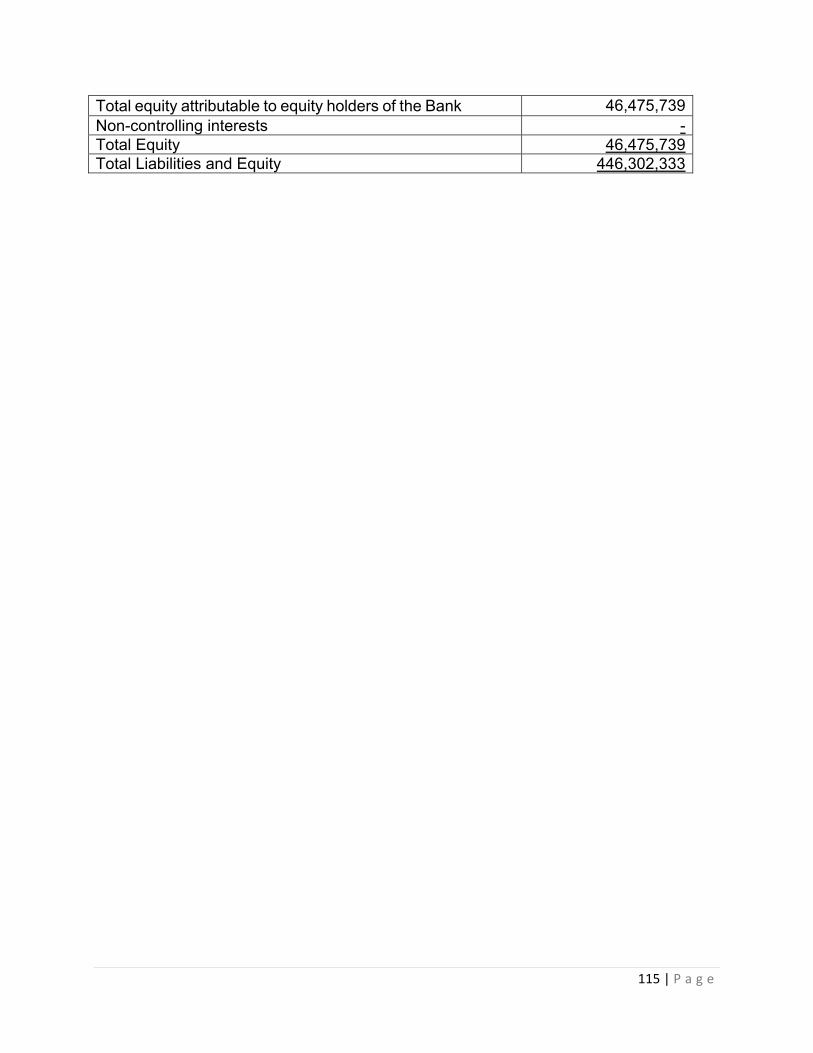

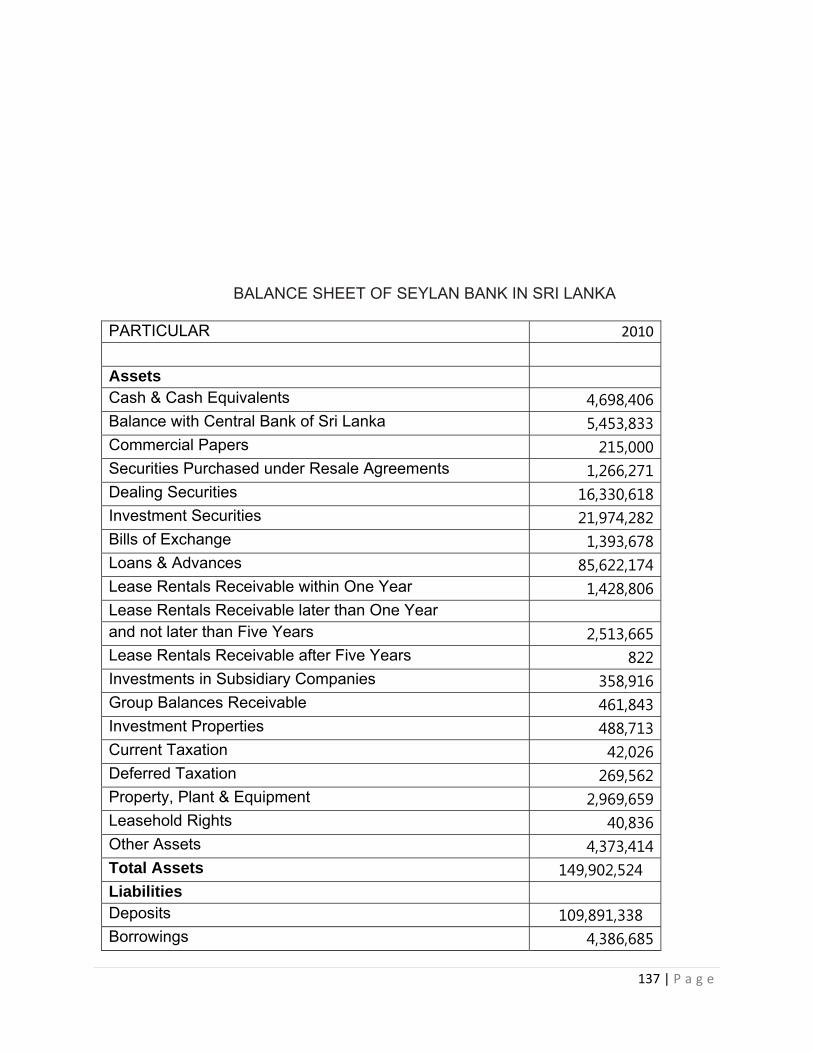

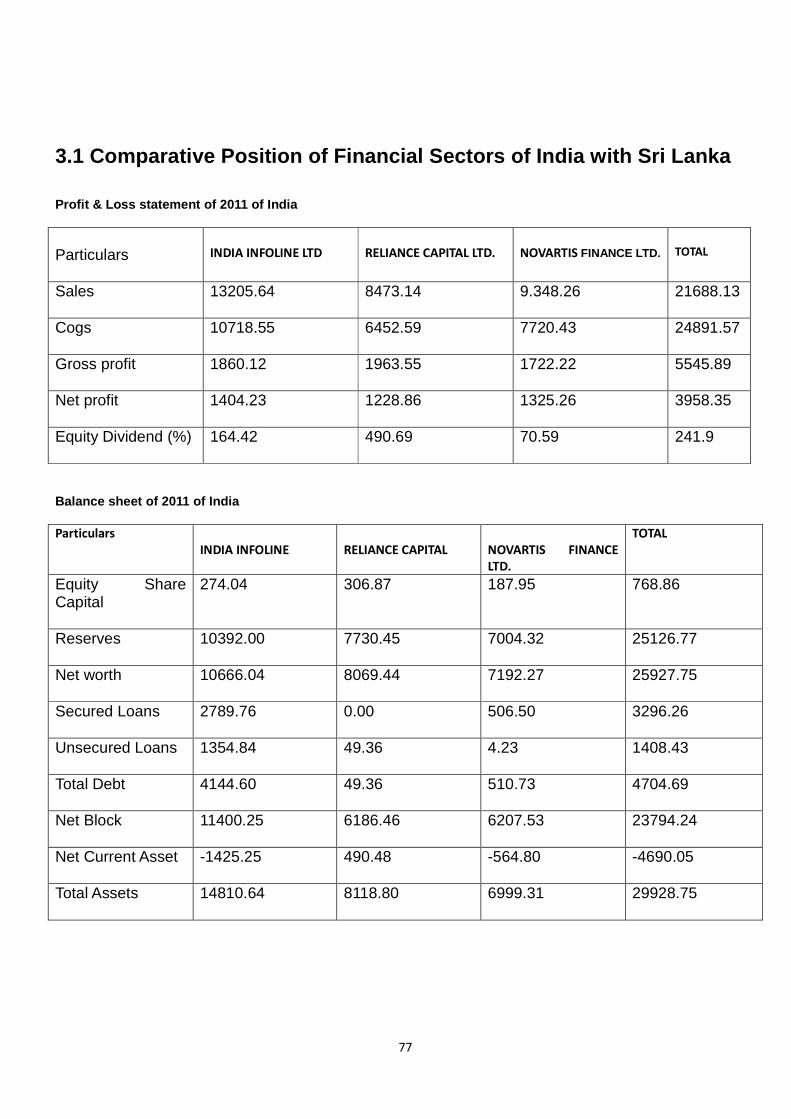

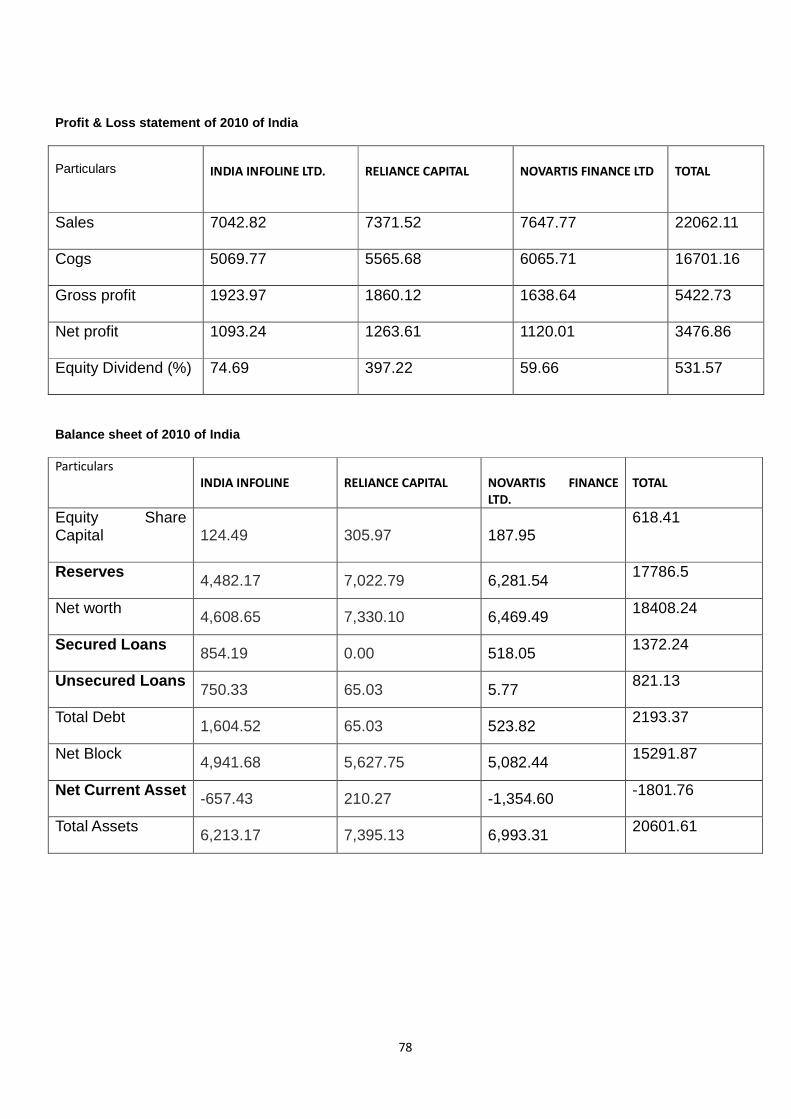

3.1 Comparative Position of Sri Lankan and Indian companies

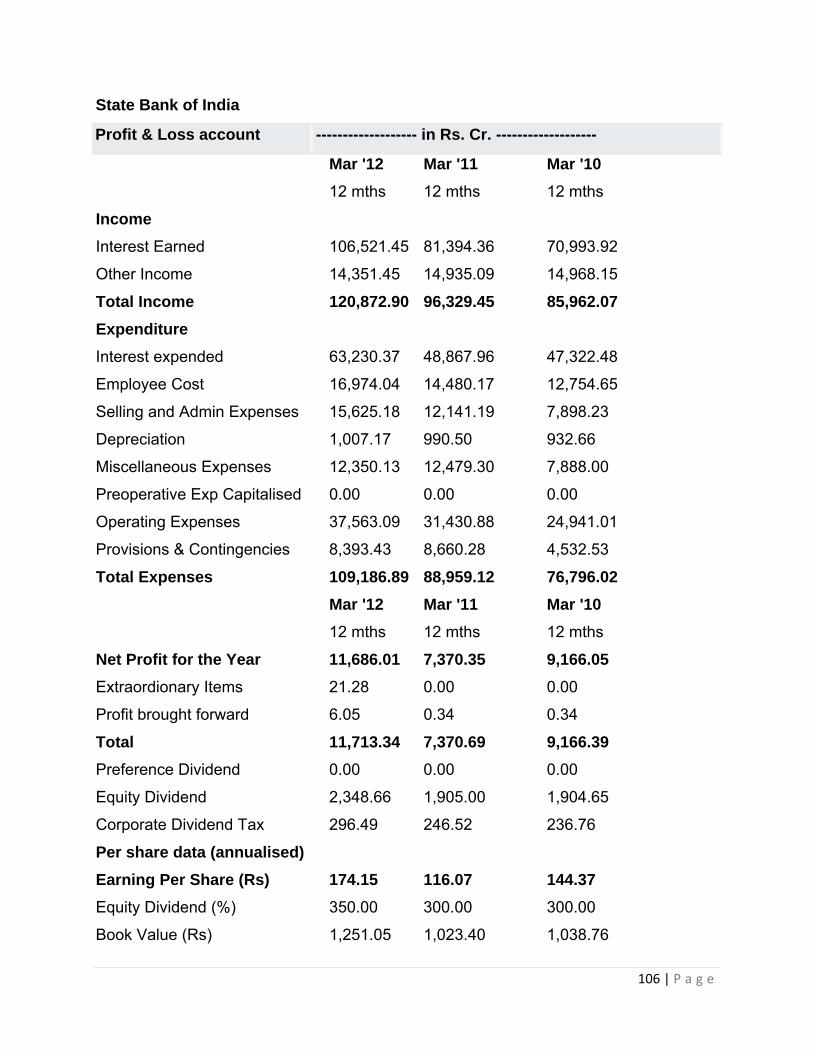

Balance sheet and P & L for the year 2010:-

Particulars

SBI BOB PNB HDFC ICICI Total

Interest income 70,993.9

2

16,698.34 21,466.91 16,172.9

0

25,706.93 151039

Interest expense 47,322.4

8

10,758.86 12,944.02 7,786.30 17,592.57 96404.

23

Net interest

income

23671.44

5939.48

8522.89

8386.6

8114.36

54639.

77

Net profit

9,166.05 3,058.33 3,905.36

2,948.70

4,024.98

23103.

42

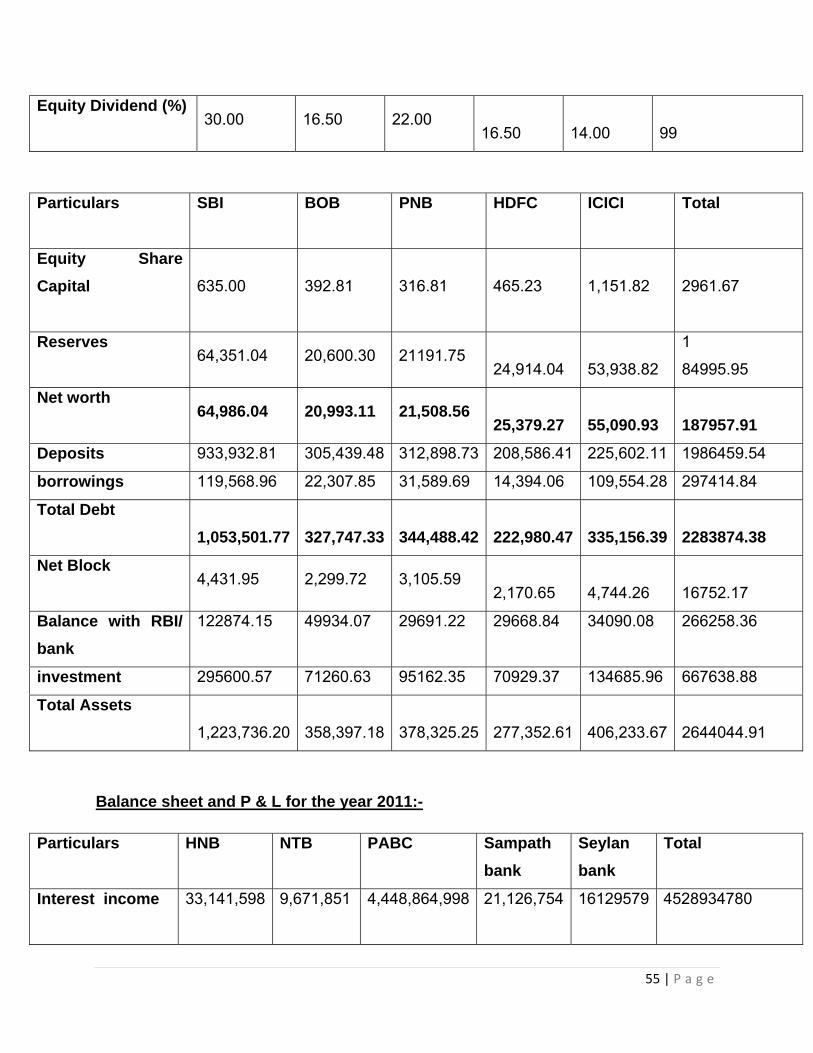

Equity Dividend

(%)

36.00 15.00 22.00

12.00

12.00

97

Particulars

SBI BOB PNB HDFC ICICI Total

Equity Share

Capital

634.88 365.53 315.30

457.74

1,114.89

2958.34

Reserves

65,314.32 14,740.86 17407.62

21,064.75

50,503.48

169031.03

Net worth

65,949.20

15,106.39

17,722.92

21,064.75

51,618.37

171461.36

53 | P a g e

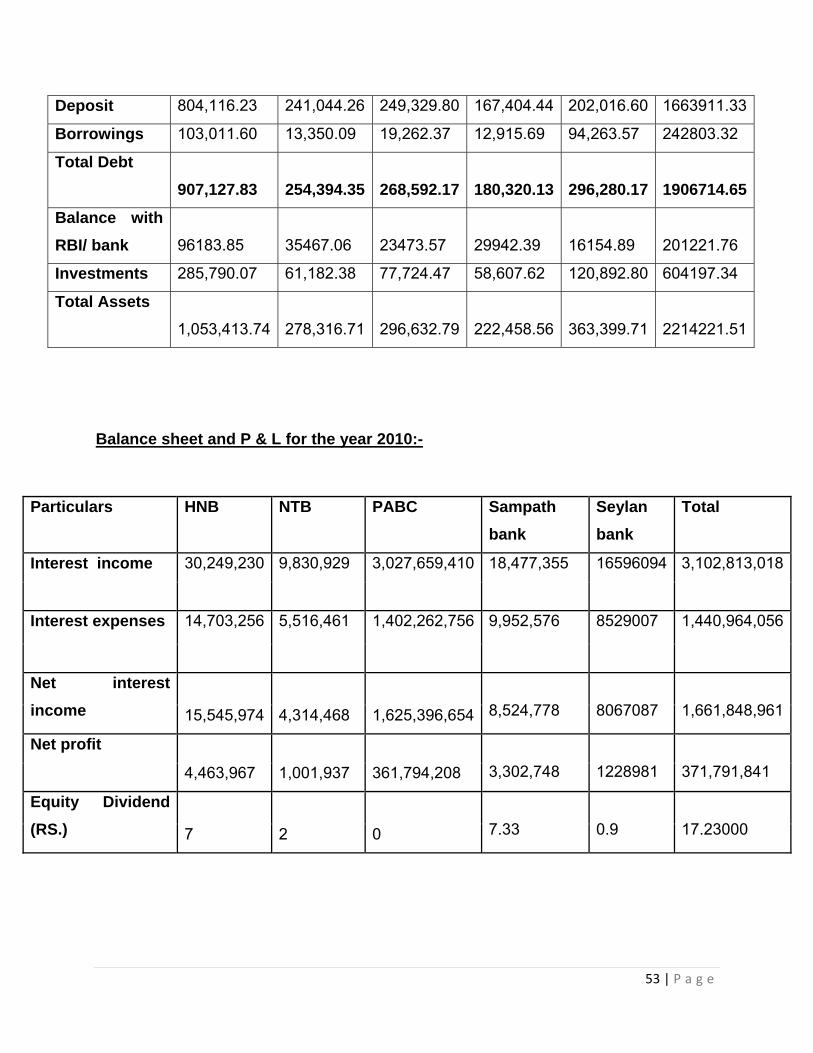

Deposit 804,116.23 241,044.26 249,329.80 167,404.44 202,016.60 1663911.33

Borrowings 103,011.60 13,350.09 19,262.37 12,915.69 94,263.57 242803.32

Total Debt

907,127.83

254,394.35

268,592.17

180,320.13

296,280.17

1906714.65

Balance with

RBI/ bank

96183.85

35467.06

23473.57

29942.39

16154.89

201221.76

Investments 285,790.07 61,182.38 77,724.47 58,607.62 120,892.80 604197.34

Total Assets

1,053,413.74

278,316.71

296,632.79

222,458.56

363,399.71

2214221.51

Balance sheet and P & L for the year 2010:-

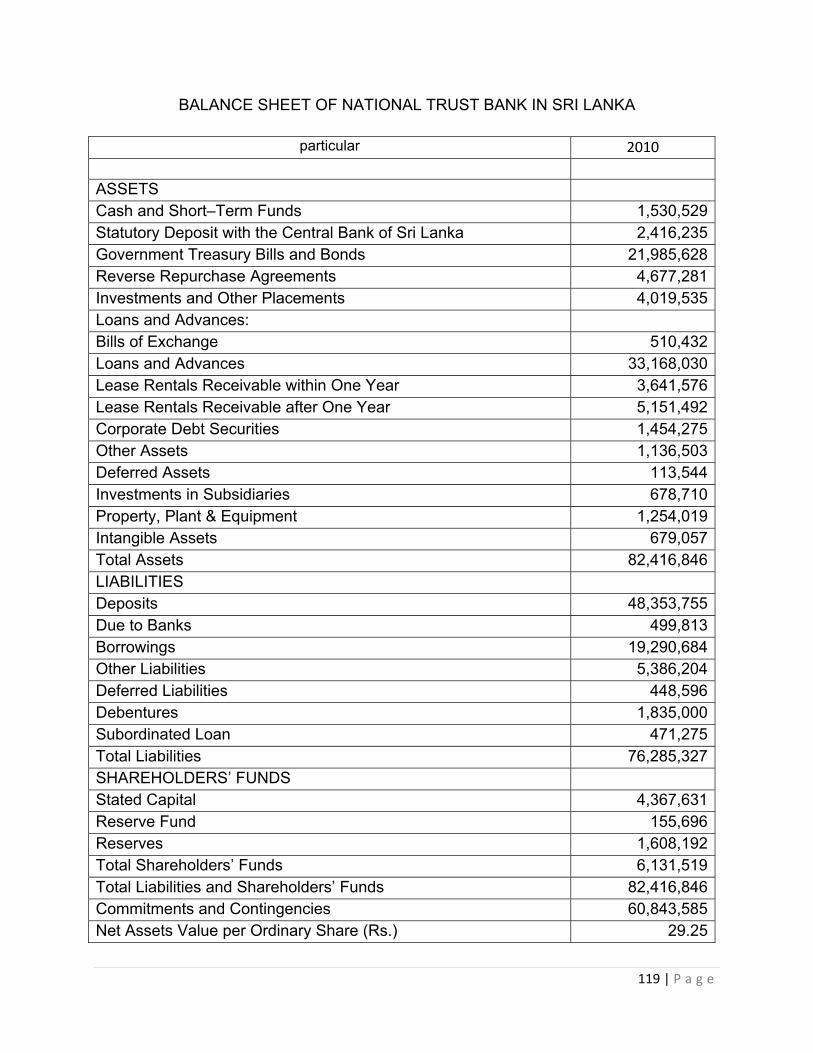

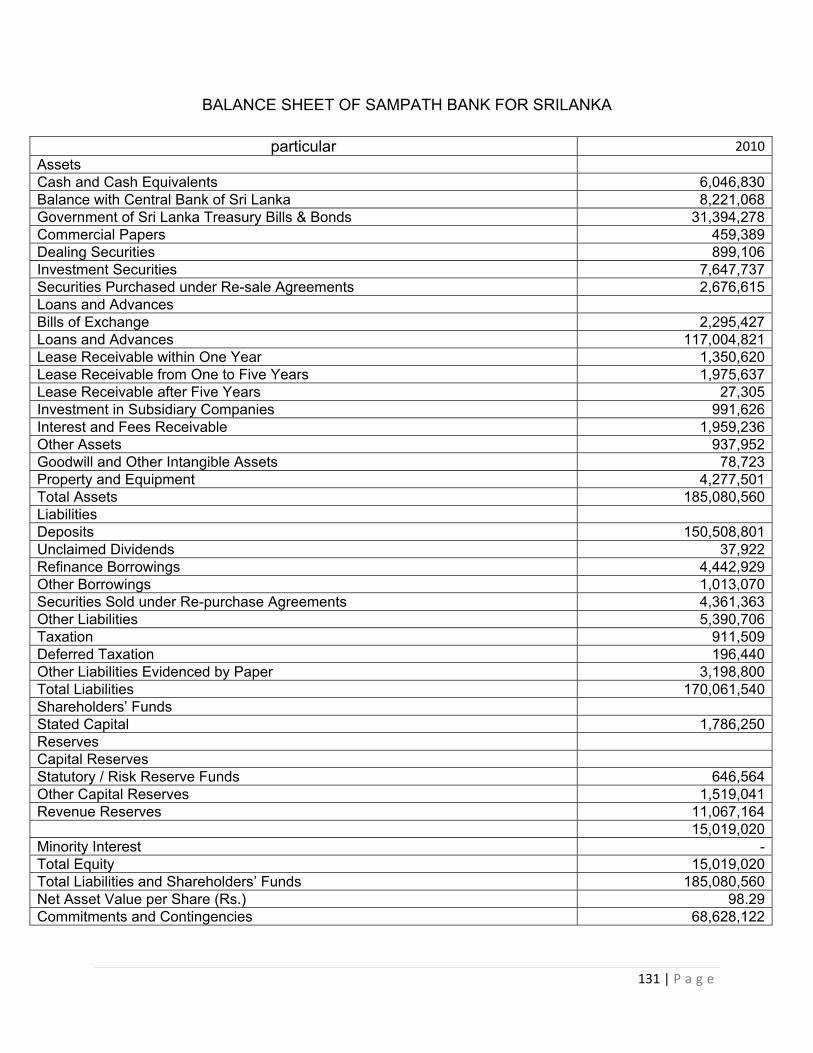

Particulars HNB NTB PABC Sampath

bank

Seylan

bank

Total

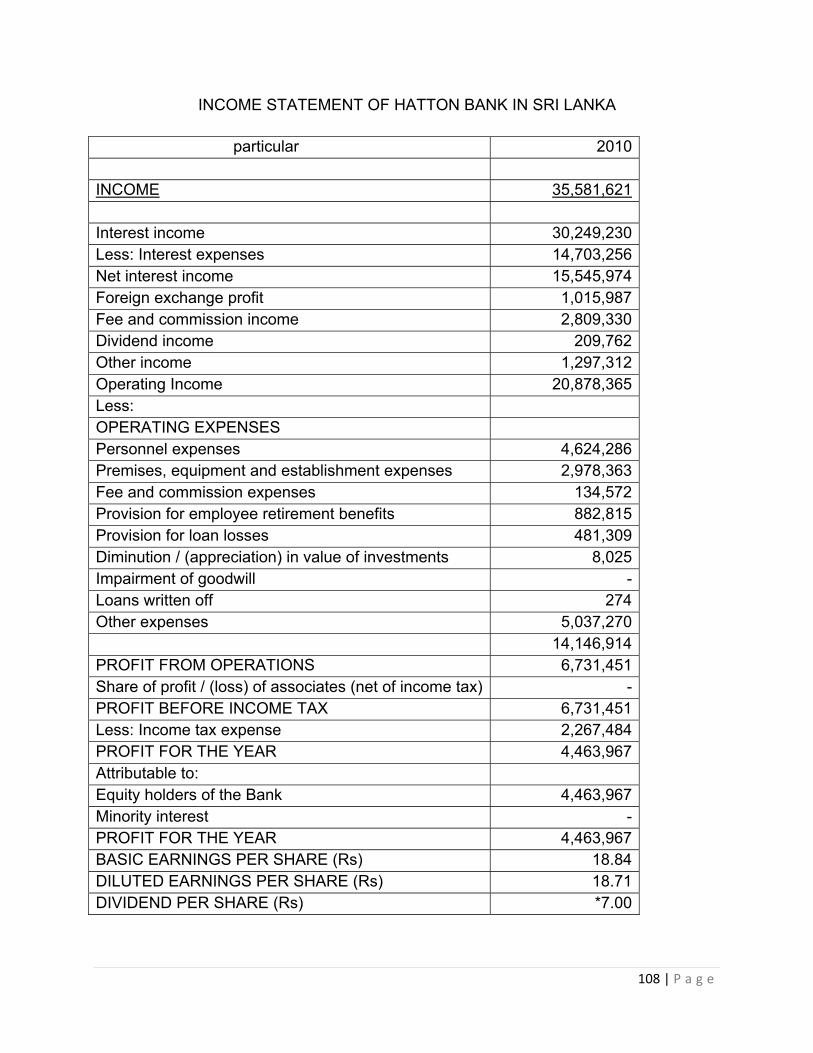

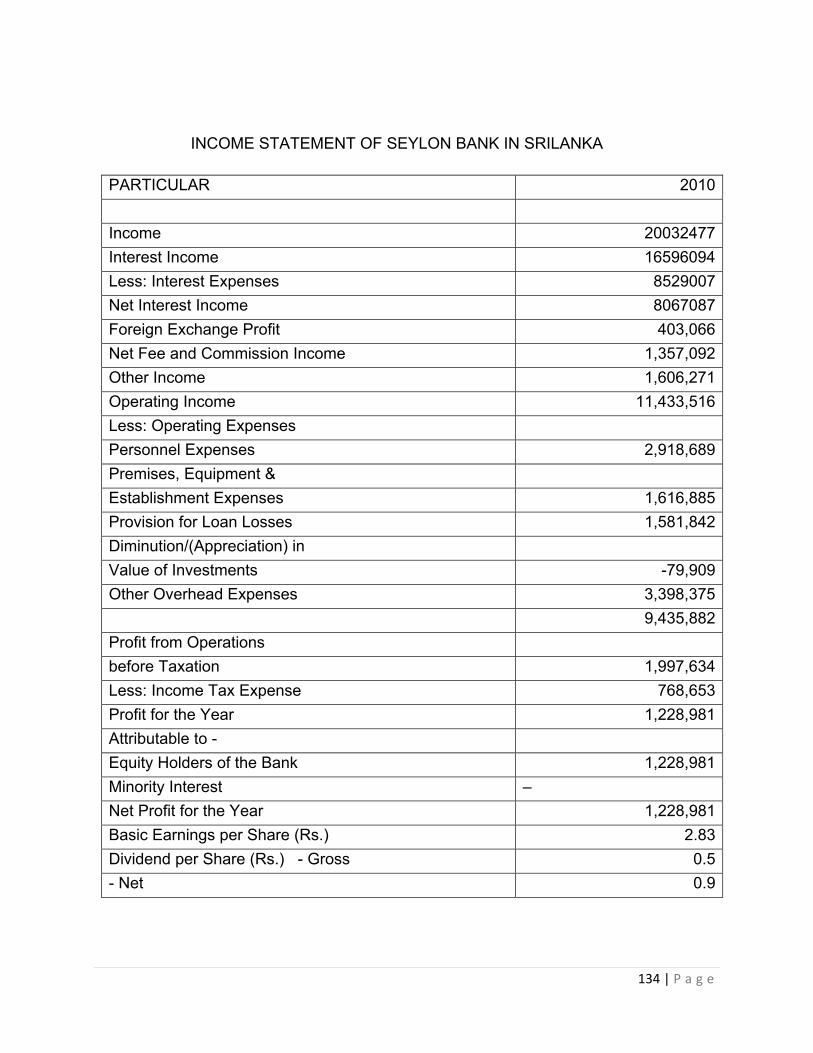

Interest income 30,249,230 9,830,929 3,027,659,410 18,477,355 16596094 3,102,813,018

Interest expenses 14,703,256 5,516,461 1,402,262,756 9,952,576 8529007 1,440,964,056

Net interest

income 15,545,974 4,314,468

1,625,396,654

8,524,778

8067087

1,661,848,961

Net profit

4,463,967 1,001,937 361,794,208

3,302,748

1228981

371,791,841

Equity Dividend

(RS.) 7 2 0

7.33

0.9

17.23000

54 | P a g e

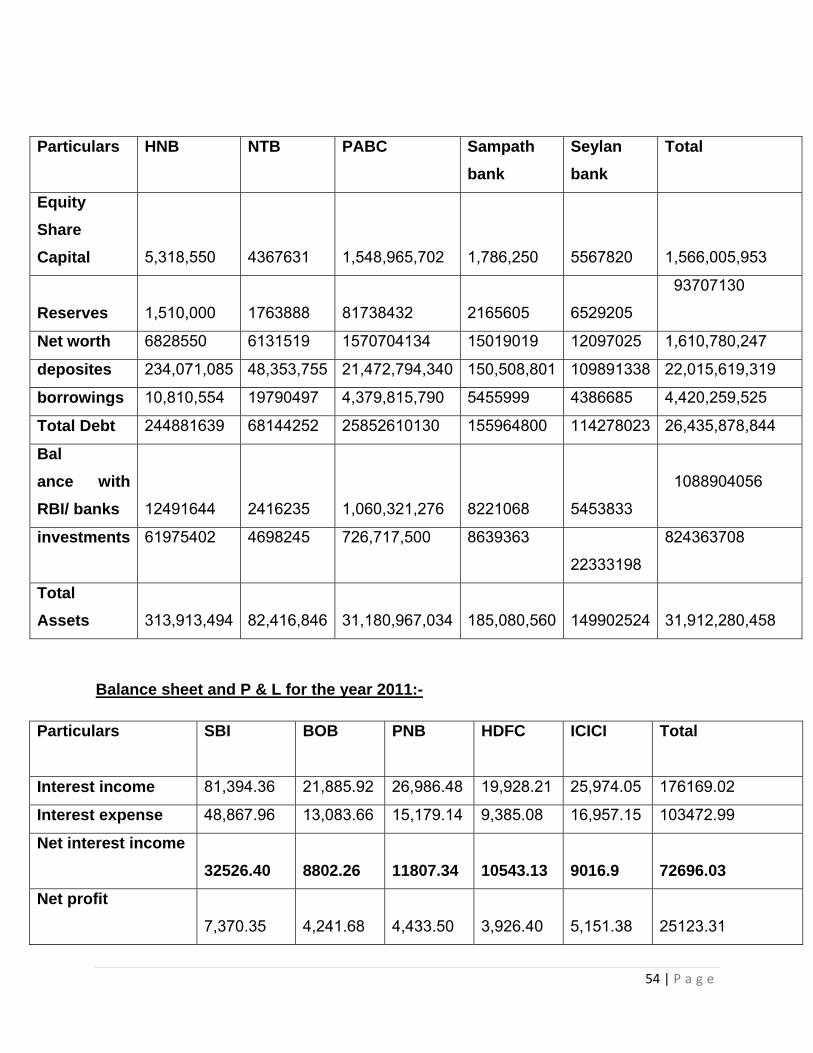

Particulars HNB NTB PABC Sampath

bank

Seylan

bank

Total

Equity

Share

Capital 5,318,550 4367631 1,548,965,702

1,786,250

5567820

1,566,005,953

Reserves 1,510,000 1763888 81738432

2165605

6529205

93707130

Net worth 6828550 6131519 1570704134 15019019 12097025 1,610,780,247

deposites 234,071,085 48,353,755 21,472,794,340 150,508,801 109891338 22,015,619,319

borrowings 10,810,554 19790497 4,379,815,790 5455999 4386685 4,420,259,525

Total Debt 244881639 68144252 25852610130 155964800 114278023 26,435,878,844

Bal

ance with

RBI/ banks 12491644 2416235 1,060,321,276

8221068 5453833

1088904056

investments 61975402 4698245 726,717,500 8639363

22333198

824363708

Total

Assets 313,913,494 82,416,846 31,180,967,034 185,080,560

149902524

31,912,280,458

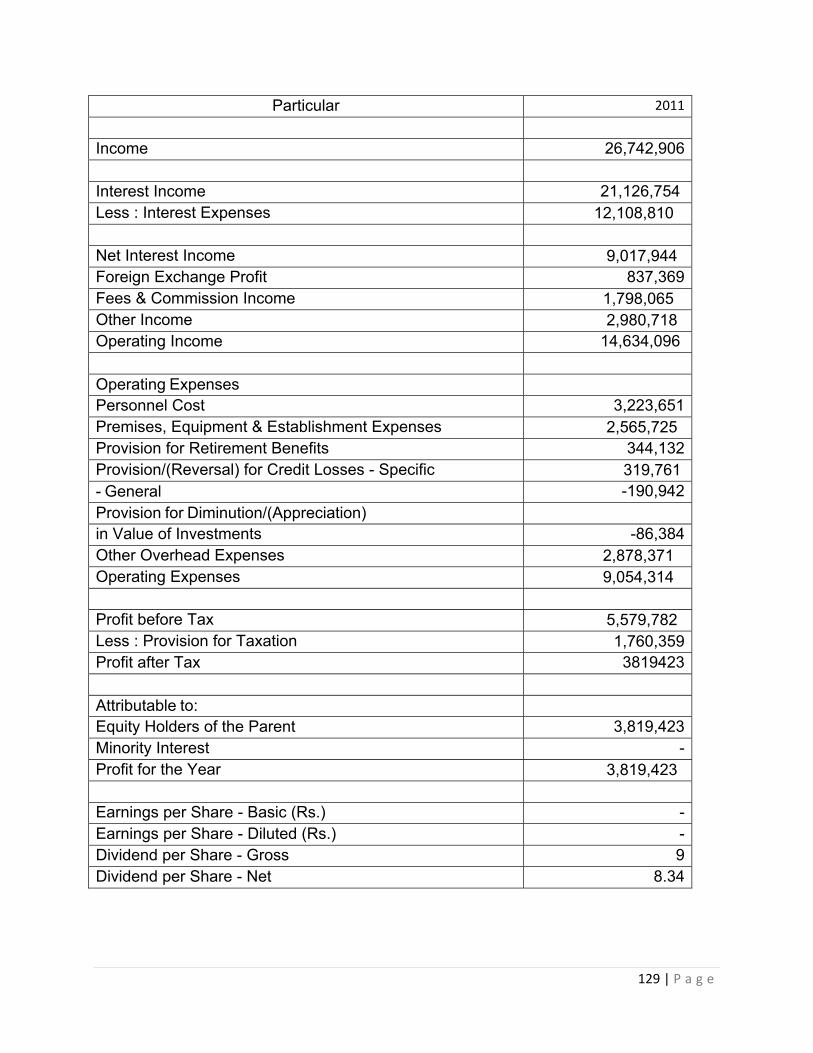

Balance sheet and P & L for the year 2011:-

Particulars

SBI BOB PNB HDFC ICICI Total

Interest income 81,394.36 21,885.92 26,986.48 19,928.21 25,974.05 176169.02

Interest expense 48,867.96 13,083.66 15,179.14 9,385.08 16,957.15 103472.99

Net interest income

32526.40

8802.26

11807.34

10543.13

9016.9

72696.03

Net profit

7,370.35

4,241.68

4,433.50

3,926.40

5,151.38

25123.31

55 | P a g e

Equity Dividend (%)

30.00 16.50 22.00

16.50

14.00

99

Particulars

SBI BOB PNB HDFC ICICI Total

Equity Share

Capital

635.00 392.81 316.81

465.23

1,151.82

2961.67

Reserves

64,351.04 20,600.30 21191.75

24,914.04

53,938.82

1

84995.95

Net worth

64,986.04 20,993.11 21,508.56

25,379.27

55,090.93

187957.91

Deposits 933,932.81 305,439.48 312,898.73 208,586.41 225,602.11 1986459.54

borrowings 119,568.96 22,307.85 31,589.69 14,394.06 109,554.28 297414.84

Total Debt

1,053,501.77

327,747.33

344,488.42

222,980.47

335,156.39

2283874.38

Net Block

4,431.95 2,299.72 3,105.59

2,170.65

4,744.26

16752.17

Balance with RBI/

bank

122874.15 49934.07 29691.22 29668.84 34090.08 266258.36

investment 295600.57 71260.63 95162.35 70929.37 134685.96 667638.88

Total Assets

1,223,736.20

358,397.18

378,325.25

277,352.61

406,233.67

2644044.91

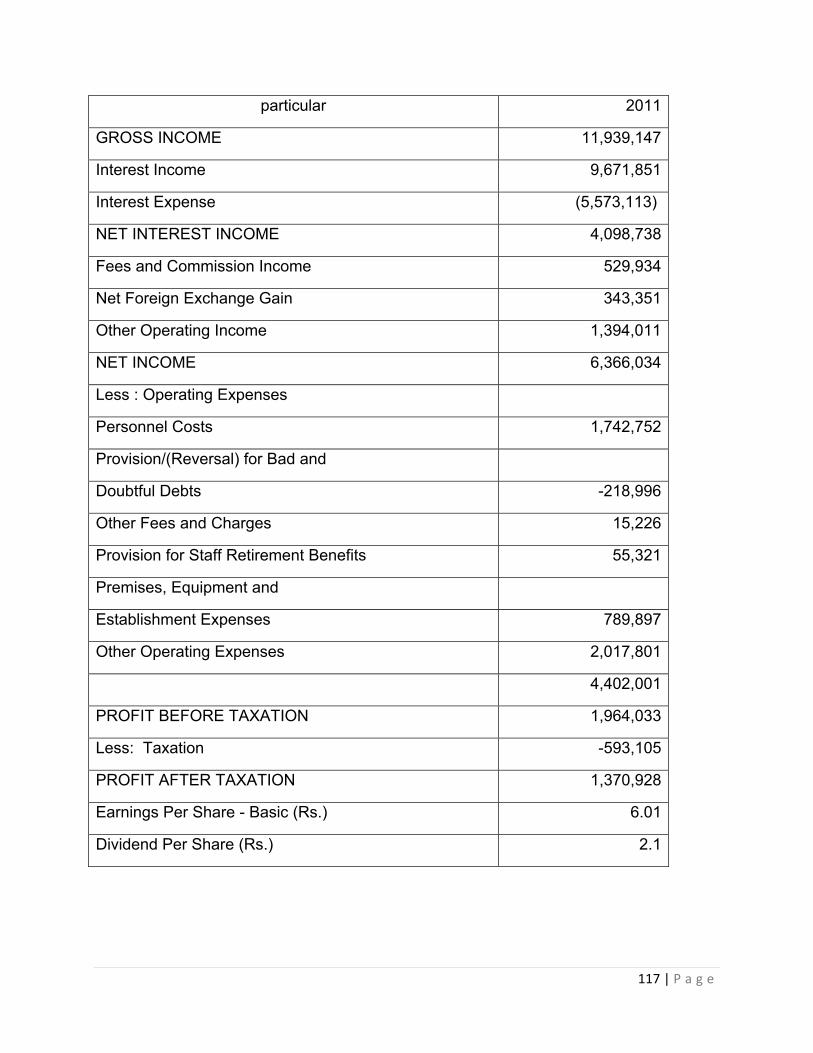

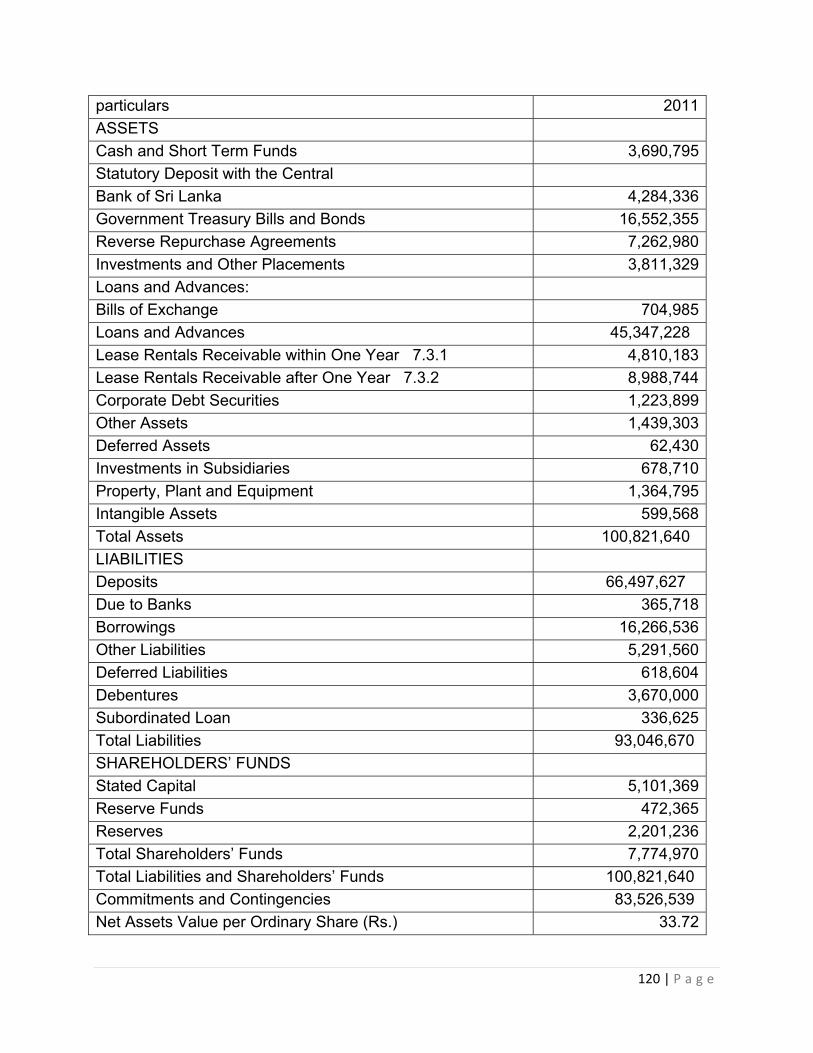

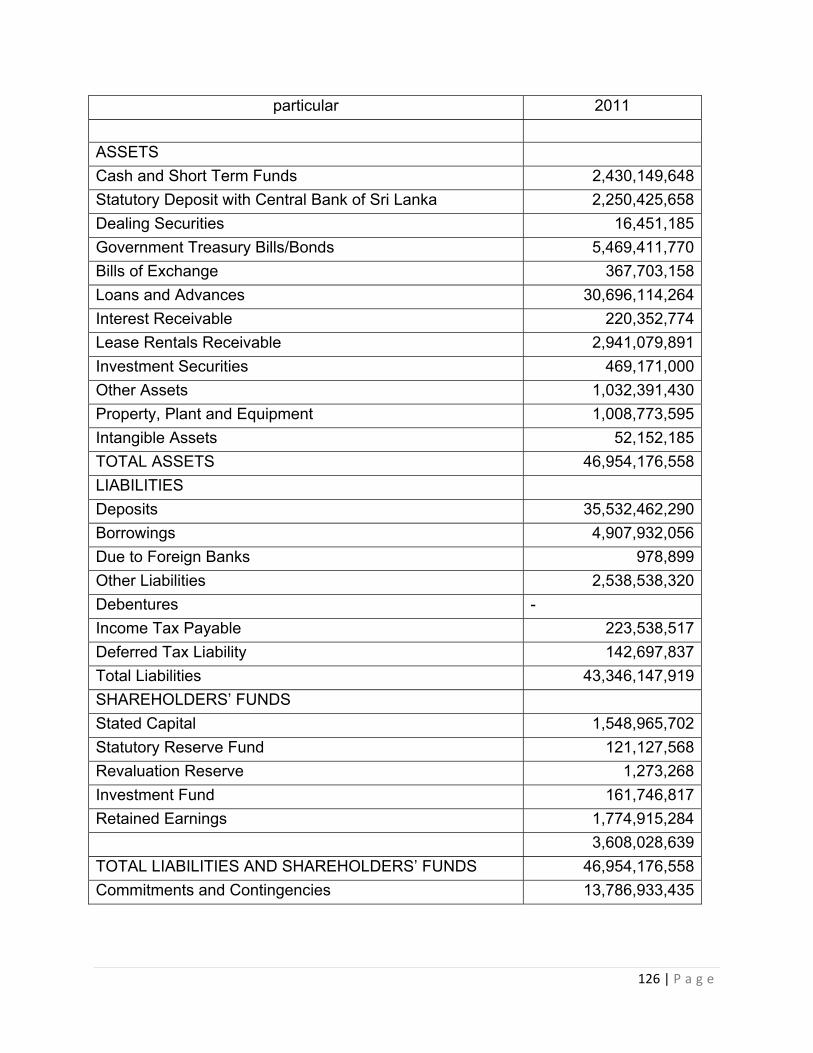

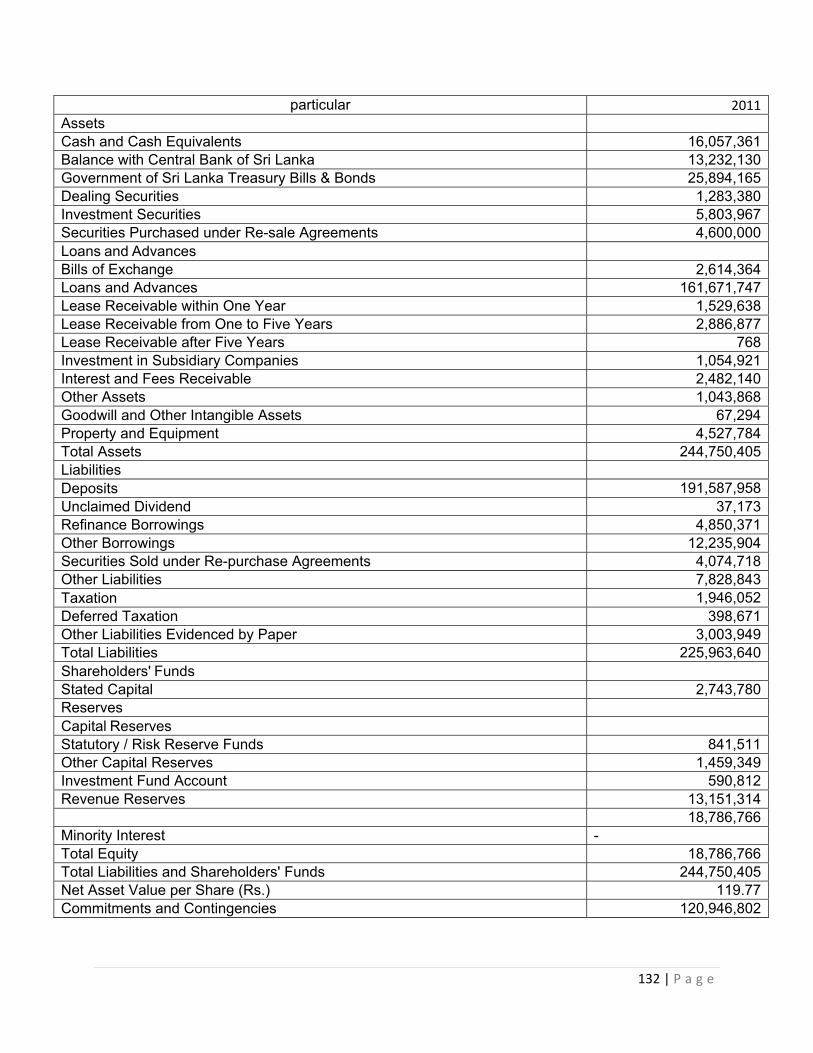

Balance sheet and P & L for the year 2011:-

Particulars

HNB NTB PABC Sampath

bank

Seylan

bank

Total

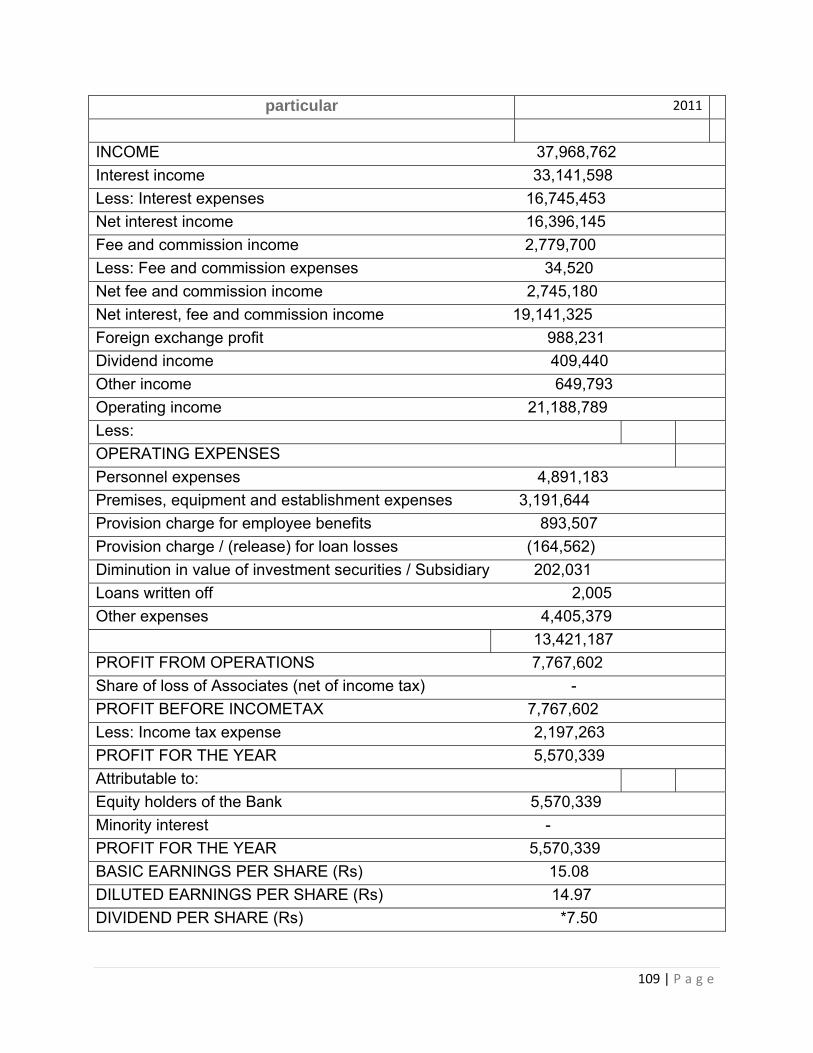

Interest income

33,141,598 9,671,851 4,448,864,998 21,126,754 16129579 4528934780

56 | P a g e

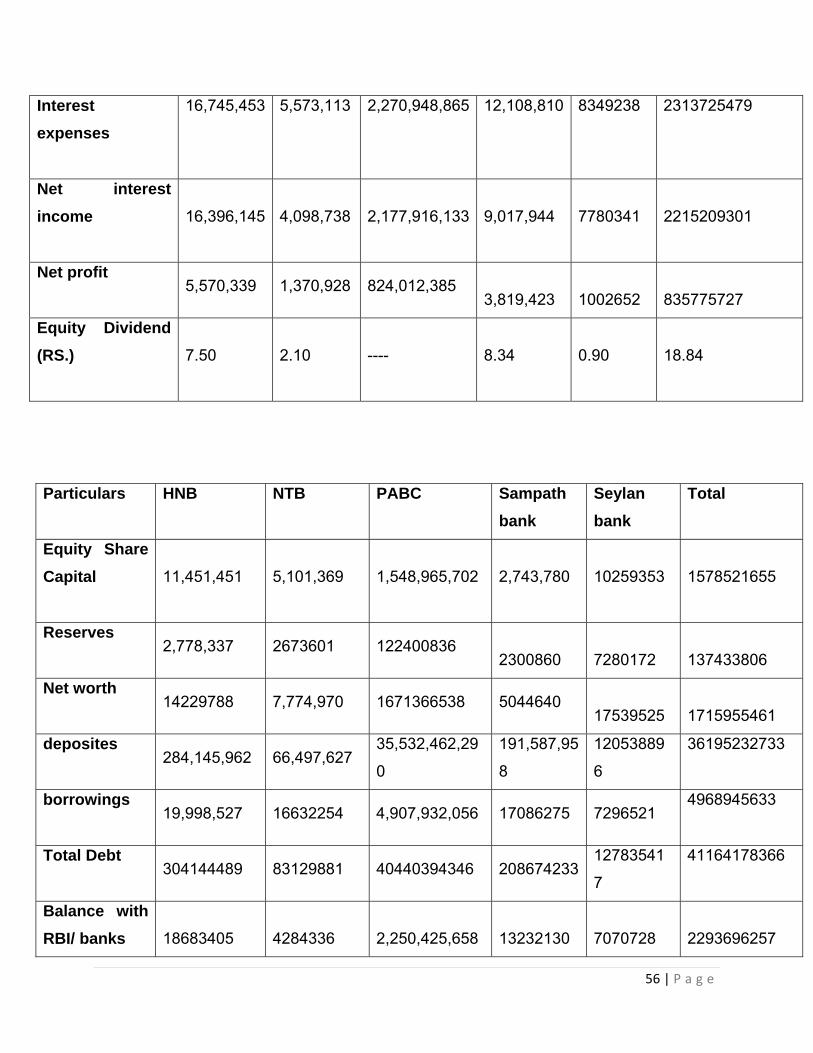

Interest

expenses

16,745,453 5,573,113 2,270,948,865 12,108,810 8349238 2313725479

Net interest

income

16,396,145 4,098,738 2,177,916,133

9,017,944

7780341

2215209301

Net profit

5,570,339 1,370,928 824,012,385

3,819,423

1002652

835775727

Equity Dividend

(RS.)

7.50 2.10 ----

8.34

0.90

18.84

Particulars

HNB NTB PABC Sampath

bank

Seylan

bank

Total

Equity Share

Capital

11,451,451 5,101,369 1,548,965,702

2,743,780

10259353

1578521655

Reserves

2,778,337 2673601 122400836

2300860

7280172

137433806

Net worth

14229788 7,774,970 1671366538 5044640

17539525

1715955461

deposites

284,145,962 66,497,627

35,532,462,29

0

191,587,95

8

12053889

6

36195232733

borrowings

19,998,527 16632254 4,907,932,056 17086275 7296521

4968945633

Total Debt

304144489 83129881 40440394346 208674233

12783541

7

41164178366

Balance with

RBI/ banks

18683405

4284336

2,250,425,658

13232130

7070728

2293696257

57 | P a g e

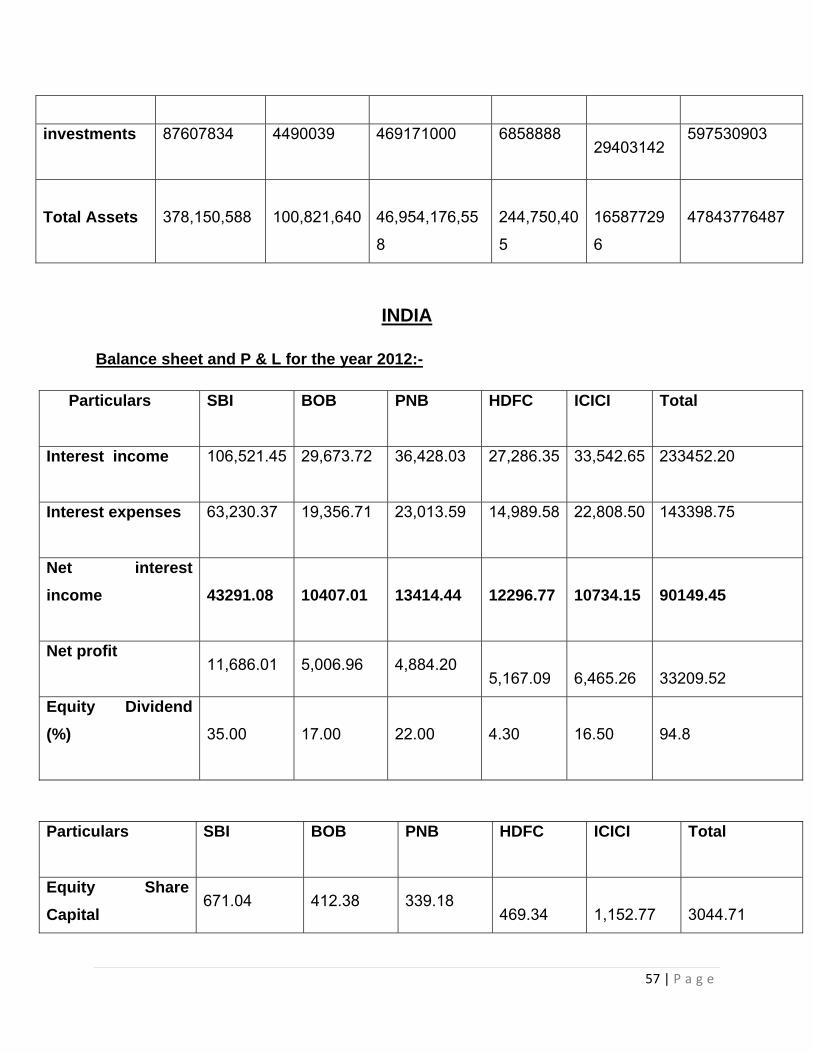

investments 87607834 4490039 469171000 6858888 29403142

597530903

Total Assets

378,150,588 100,821,640

46,954,176,55

8

244,750,40

5

16587729

6

47843776487

INDIA

Balance sheet and P & L for the year 2012:-

Particulars

SBI BOB PNB HDFC ICICI Total

Interest income

106,521.45

29,673.72 36,428.03 27,286.35 33,542.65 233452.20

Interest expenses

63,230.37 19,356.71 23,013.59 14,989.58 22,808.50

143398.75

Net interest

income

43291.08 10407.01 13414.44

12296.77

10734.15

90149.45

Net profit

11,686.01 5,006.96 4,884.20

5,167.09

6,465.26

33209.52

Equity Dividend

(%)

35.00 17.00 22.00

4.30

16.50

94.8

Particulars

SBI BOB PNB HDFC ICICI Total

Equity Share

Capital 671.04 412.38 339.18

469.34

1,152.77

3044.71

58 | P a g e

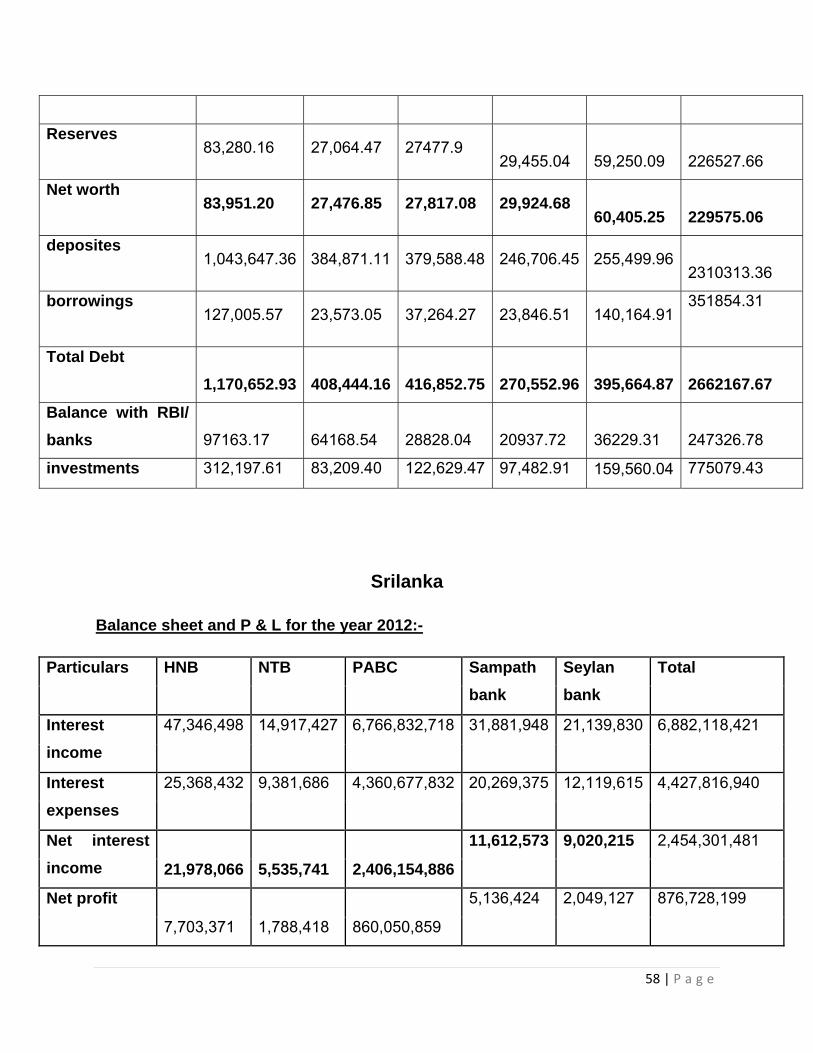

Reserves

83,280.16 27,064.47 27477.9

29,455.04

59,250.09

226527.66

Net worth

83,951.20 27,476.85 27,817.08 29,924.68

60,405.25

229575.06

deposites

1,043,647.36 384,871.11 379,588.48 246,706.45 255,499.96

2310313.36

borrowings

127,005.57 23,573.05 37,264.27 23,846.51 140,164.91

351854.31

Total Debt

1,170,652.93

408,444.16

416,852.75

270,552.96

395,664.87

2662167.67

Balance with RBI/

banks

97163.17

64168.54

28828.04

20937.72

36229.31

247326.78

investments 312,197.61 83,209.40 122,629.47 97,482.91 159,560.04 775079.43

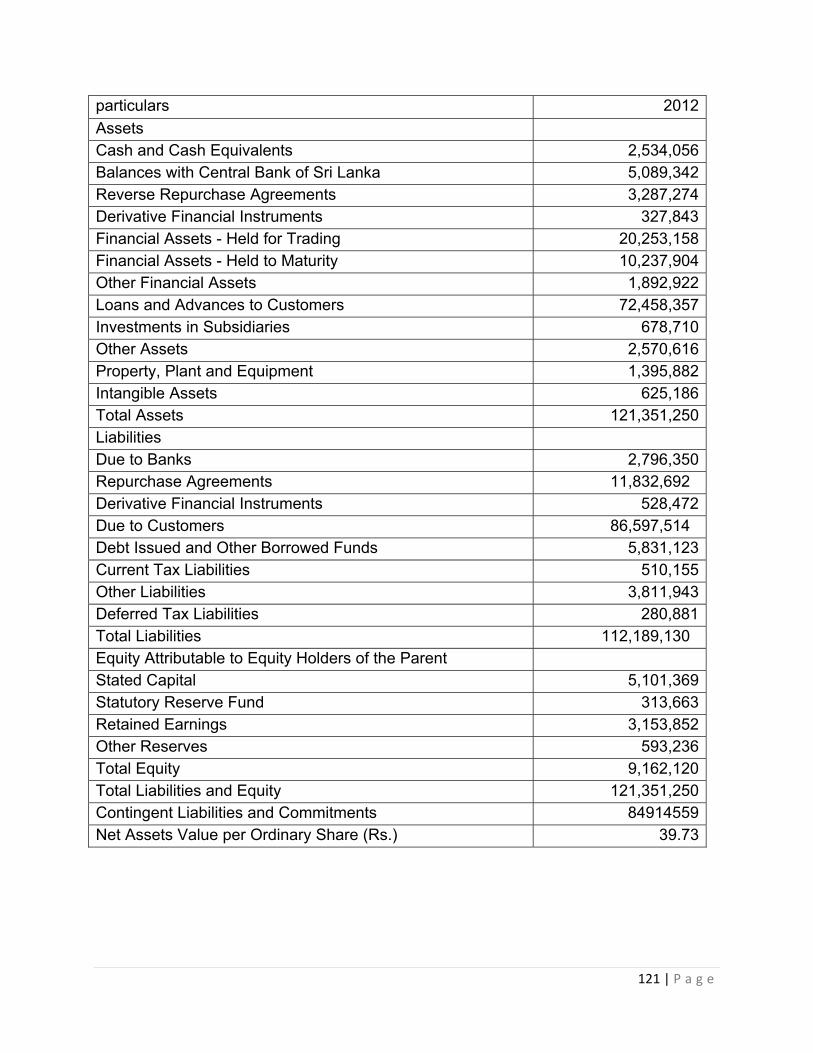

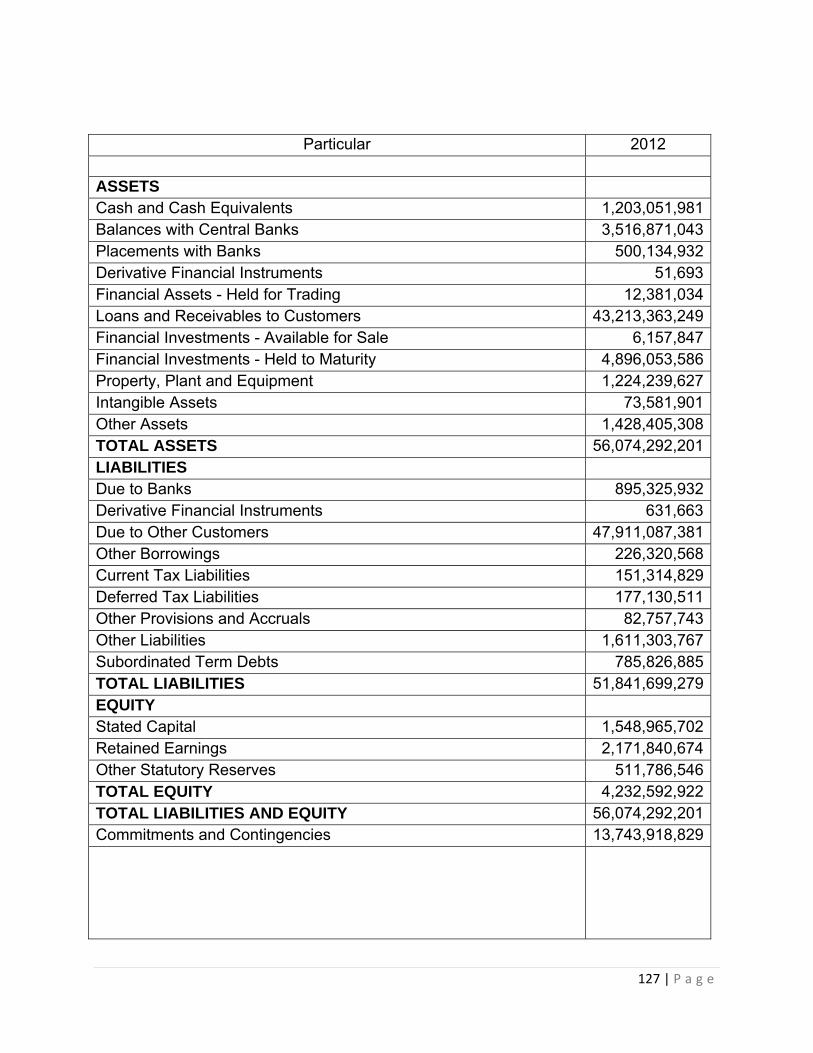

Srilanka

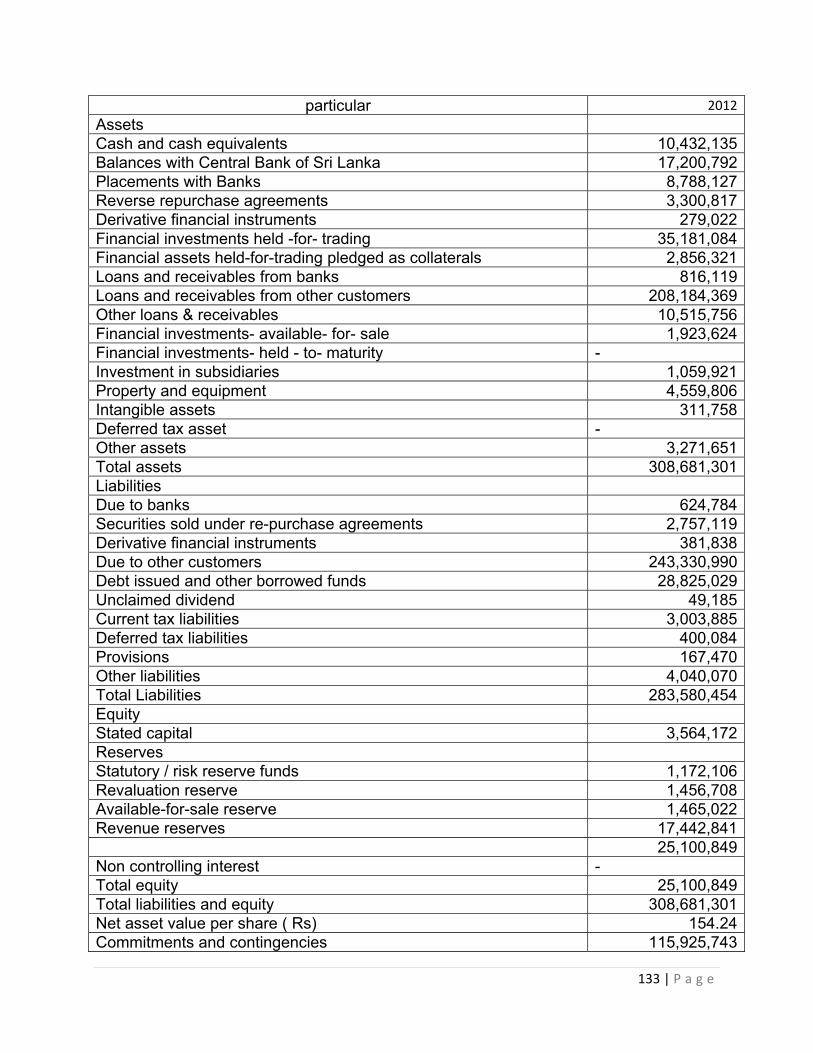

Balance sheet and P & L for the year 2012:-

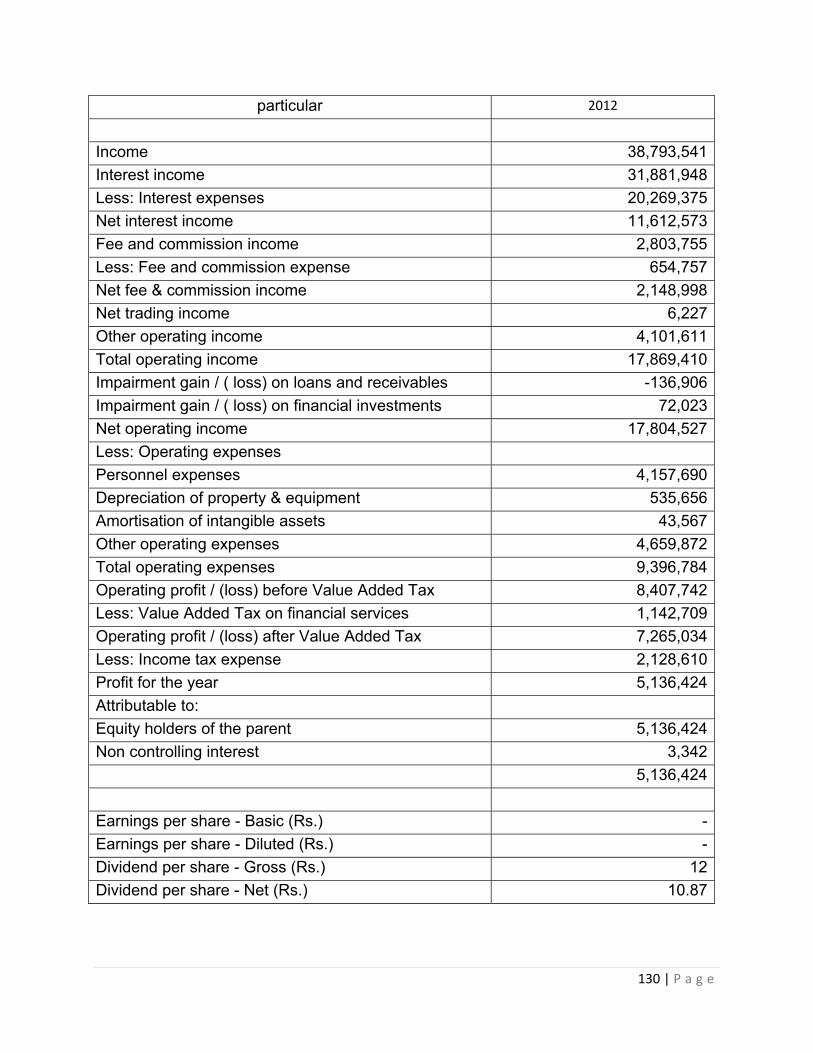

Particulars HNB NTB PABC Sampath

bank

Seylan

bank

Total

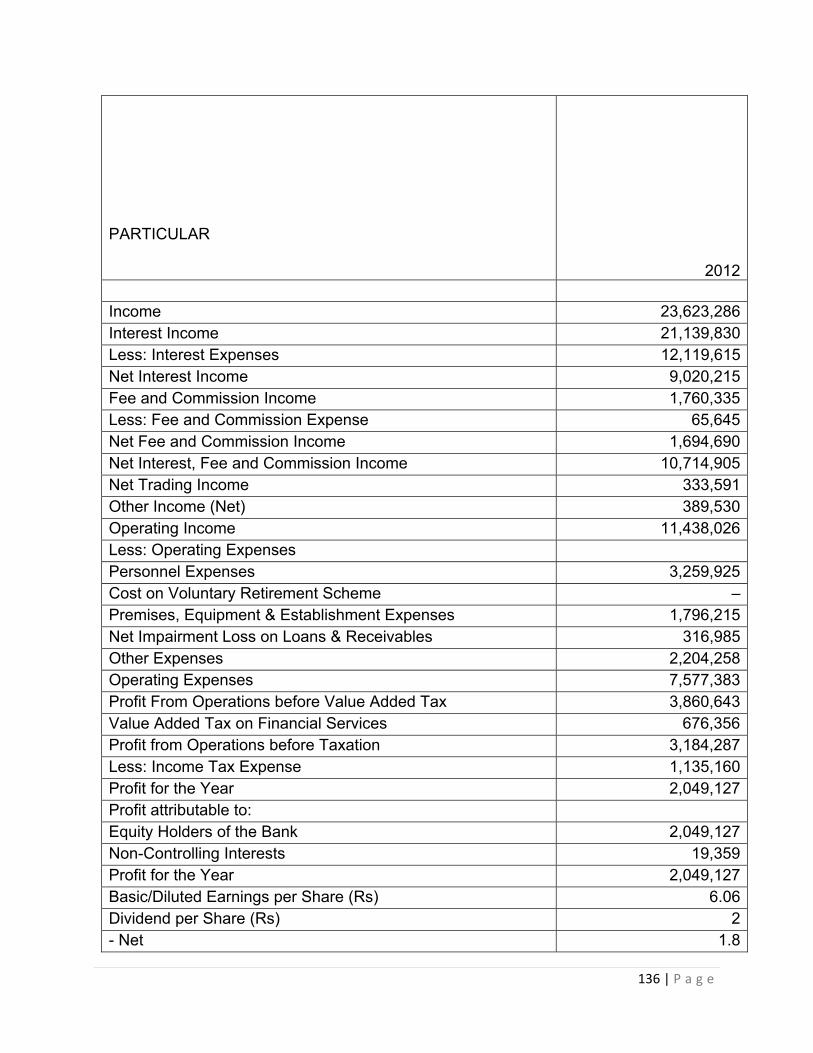

Interest

income

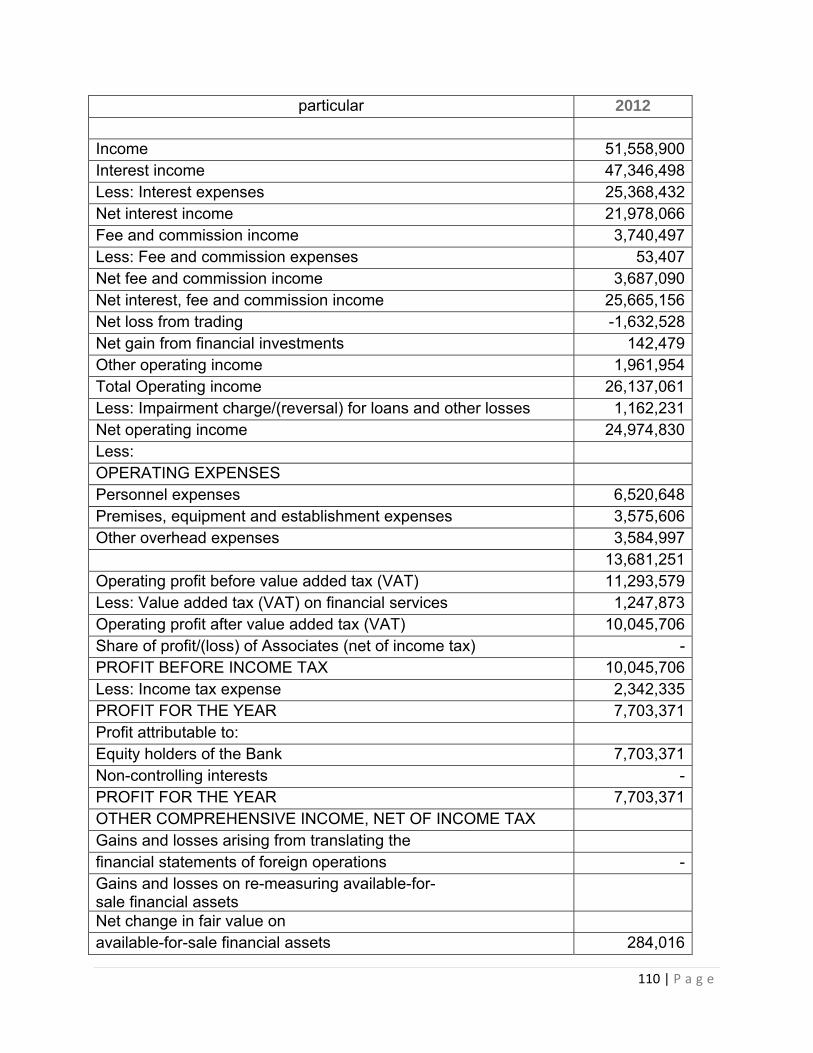

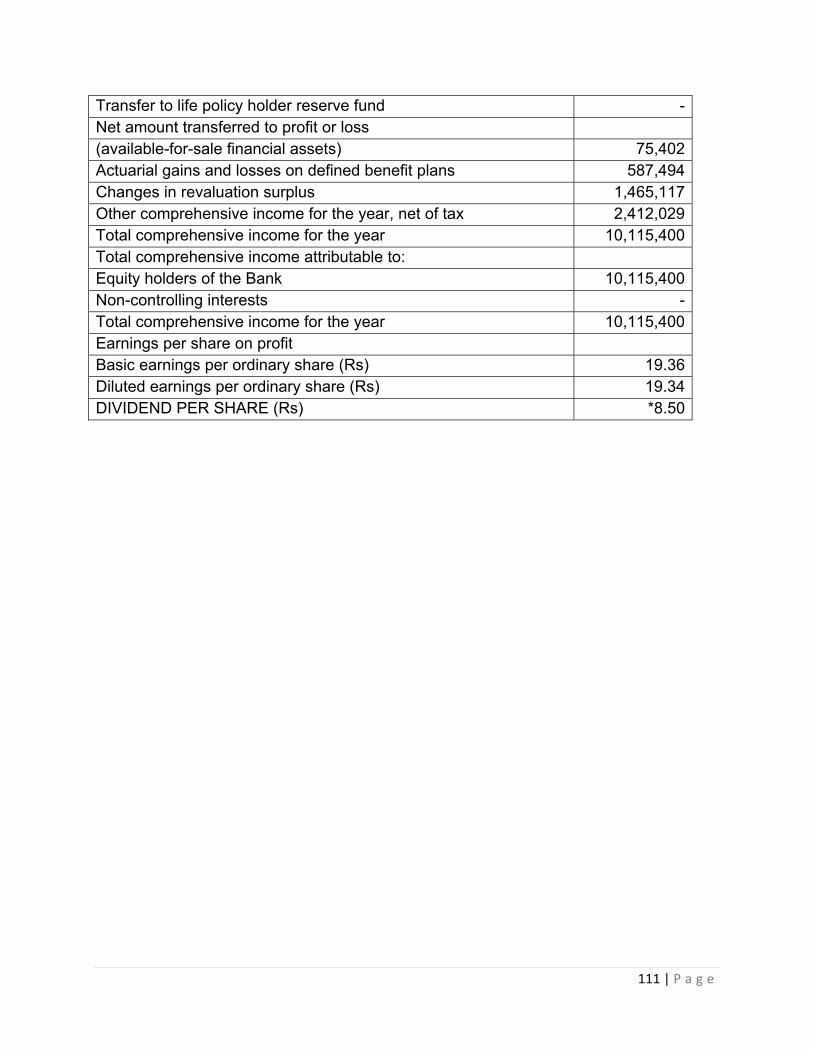

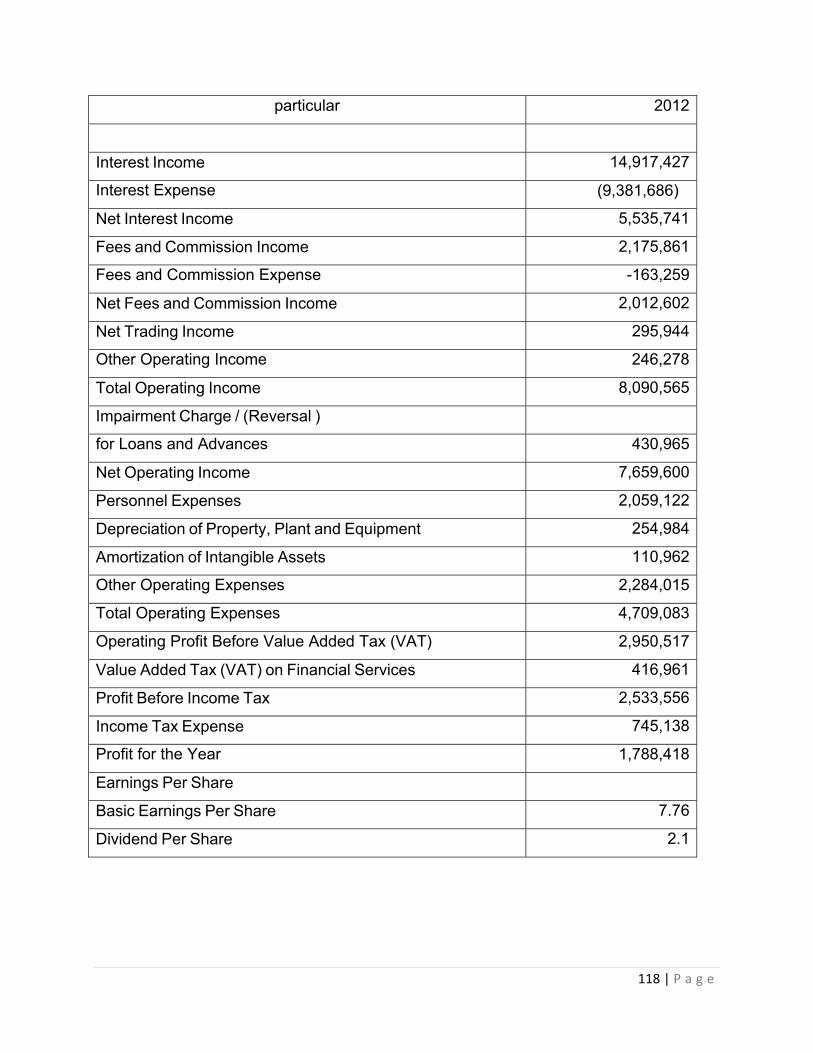

47,346,498 14,917,427 6,766,832,718 31,881,948 21,139,830 6,882,118,421

Interest

expenses

25,368,432 9,381,686 4,360,677,832 20,269,375 12,119,615 4,427,816,940

Net interest

income 21,978,066 5,535,741 2,406,154,886

11,612,573 9,020,215 2,454,301,481

Net profit

7,703,371 1,788,418 860,050,859

5,136,424 2,049,127 876,728,199

59 | P a g e

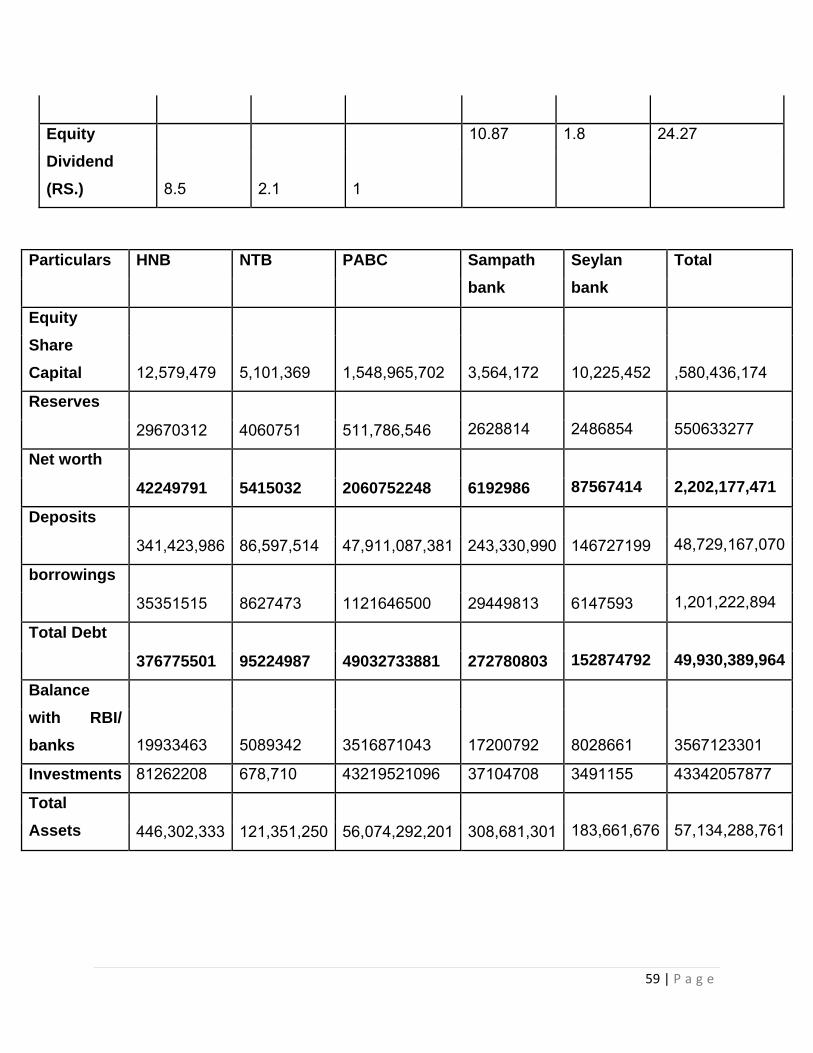

Equity

Dividend

(RS.) 8.5 2.1 1

10.87 1.8 24.27

Particulars HNB NTB PABC Sampath

bank

Seylan

bank

Total

Equity

Share

Capital 12,579,479 5,101,369 1,548,965,702

3,564,172

10,225,452

,580,436,174

Reserves

29670312 4060751 511,786,546

2628814

2486854

550633277

Net worth

42249791 5415032 2060752248 6192986

87567414

2,202,177,471

Deposits

341,423,986 86,597,514 47,911,087,381 243,330,990 146727199

48,729,167,070

borrowings

35351515 8627473 1121646500 29449813 6147593

1,201,222,894

Total Debt

376775501 95224987 49032733881 272780803

152874792

49,930,389,964

Balance

with RBI/

banks 19933463 5089342 3516871043

17200792 8028661

3567123301

Investments 81262208 678,710 43219521096 37104708 3491155 43342057877

Total

Assets 446,302,333 121,351,250 56,074,292,201 308,681,301

183,661,676

57,134,288,761

60 | P a g e

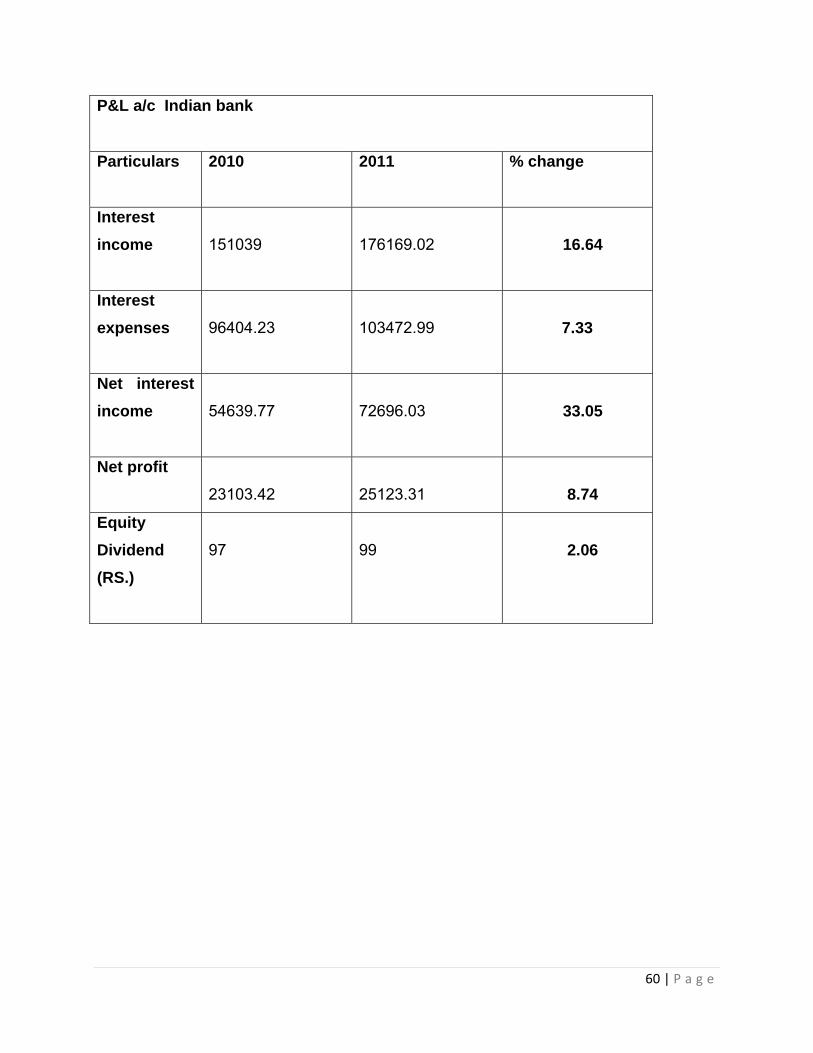

P&L a/c Indian bank

Particulars

2010 2011 % change

Interest

income

151039

176169.02

16.64

Interest

expenses

96404.23

103472.99

7.33

Net interest

income

54639.77

72696.03

33.05

Net profit

23103.42

25123.31

8.74

Equity

Dividend

(RS.)

97

99

2.06

61 | P a g e

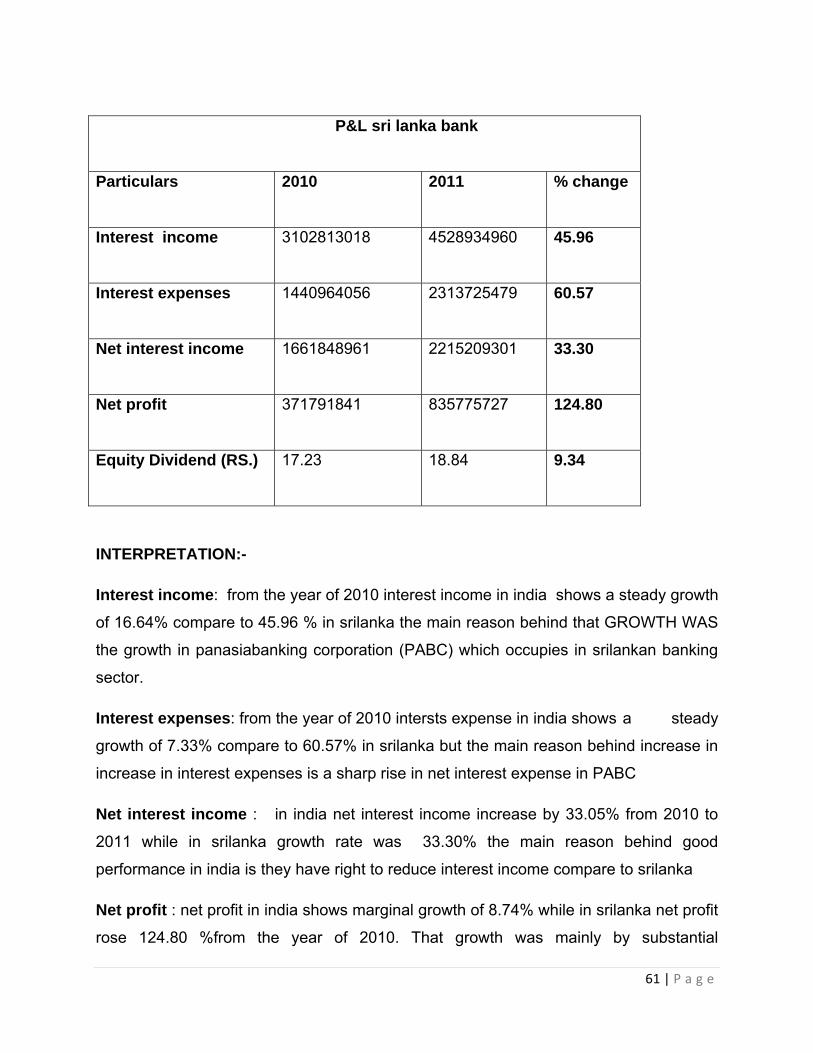

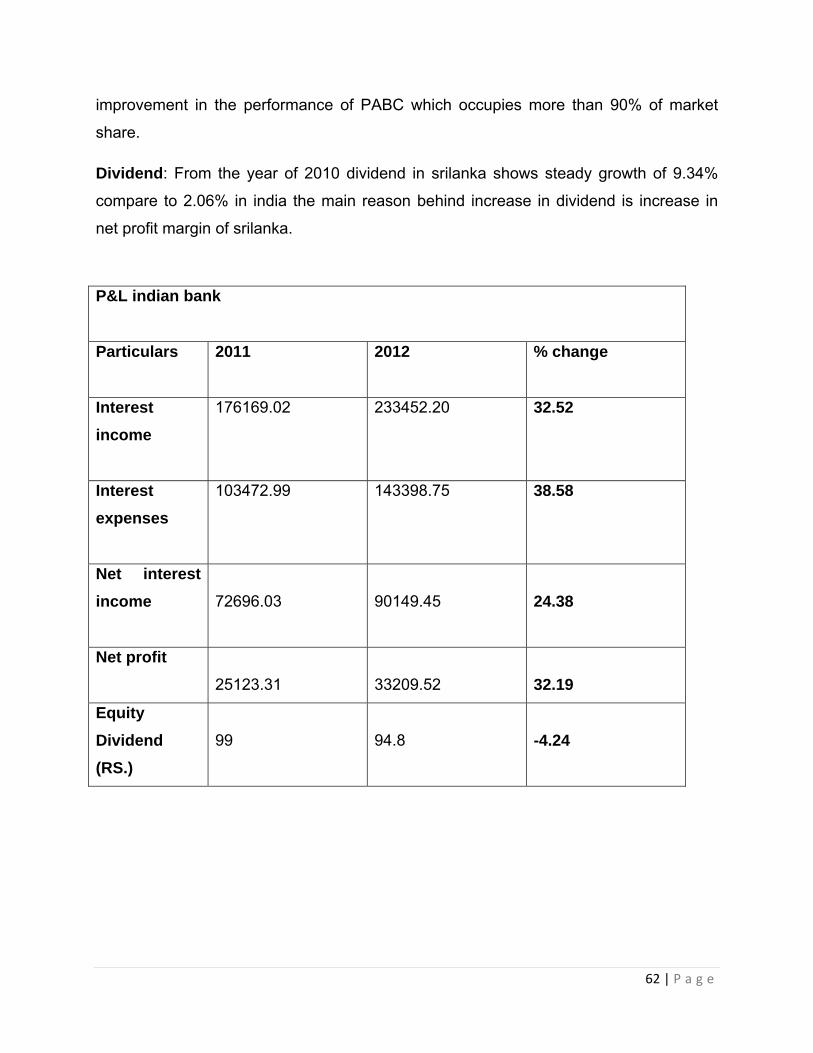

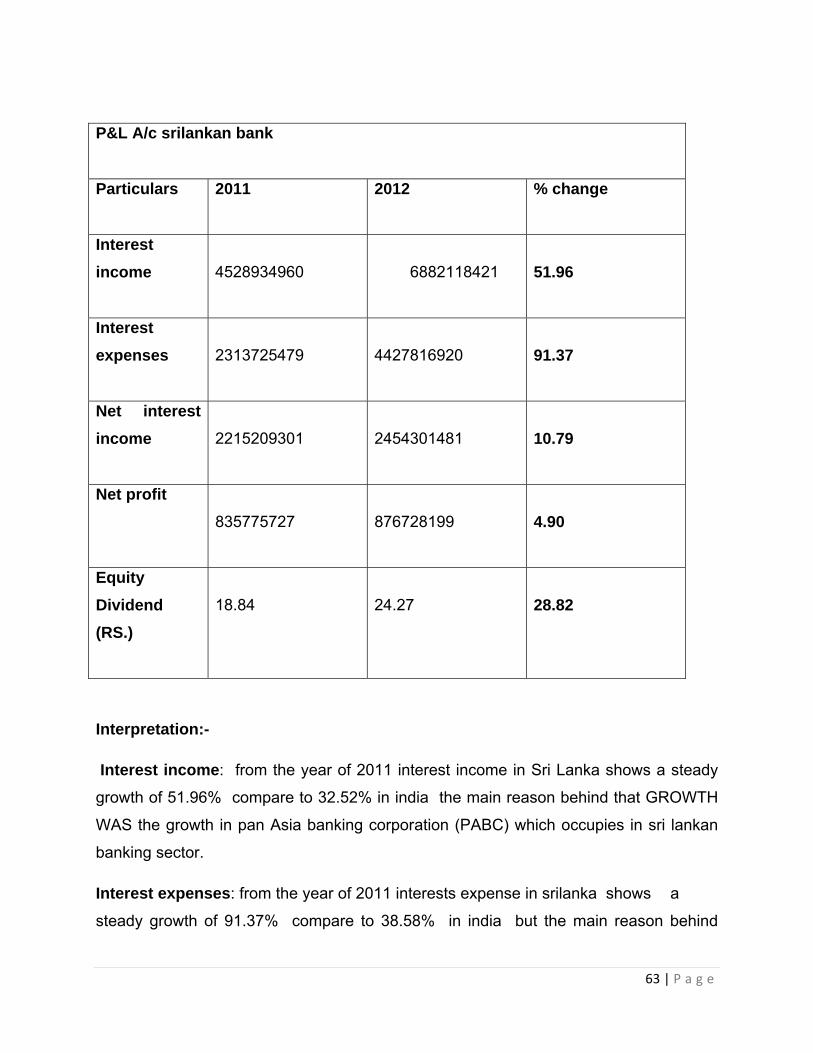

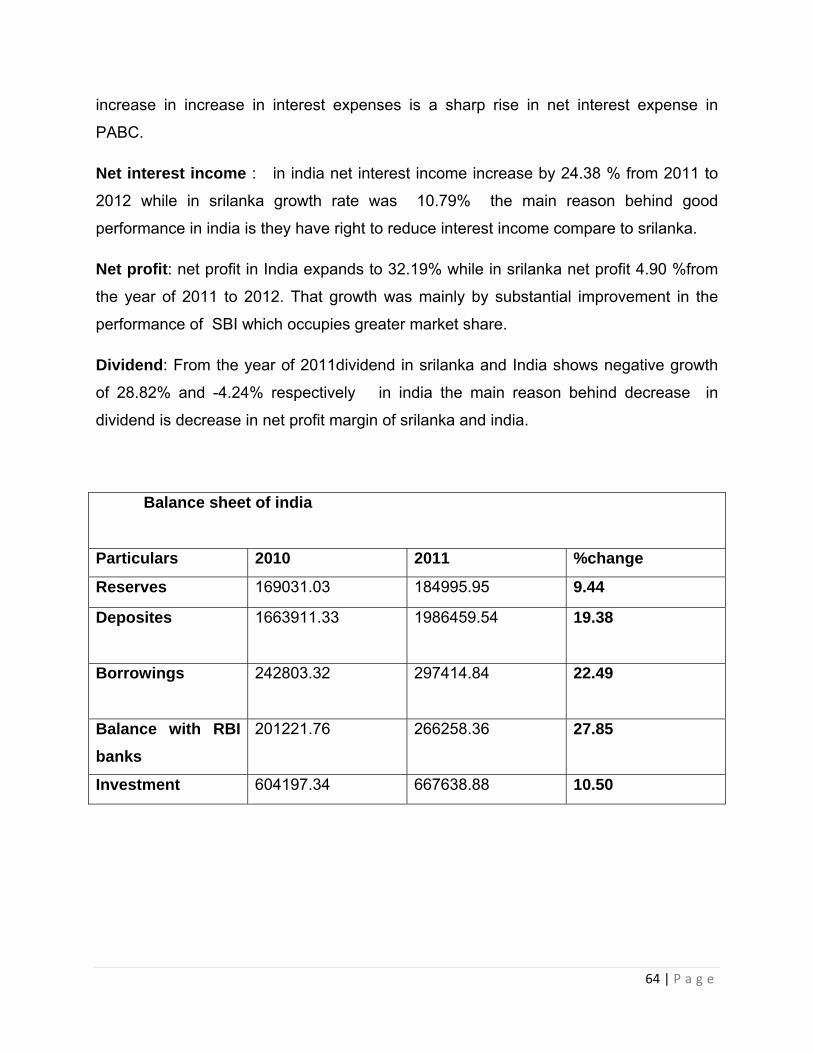

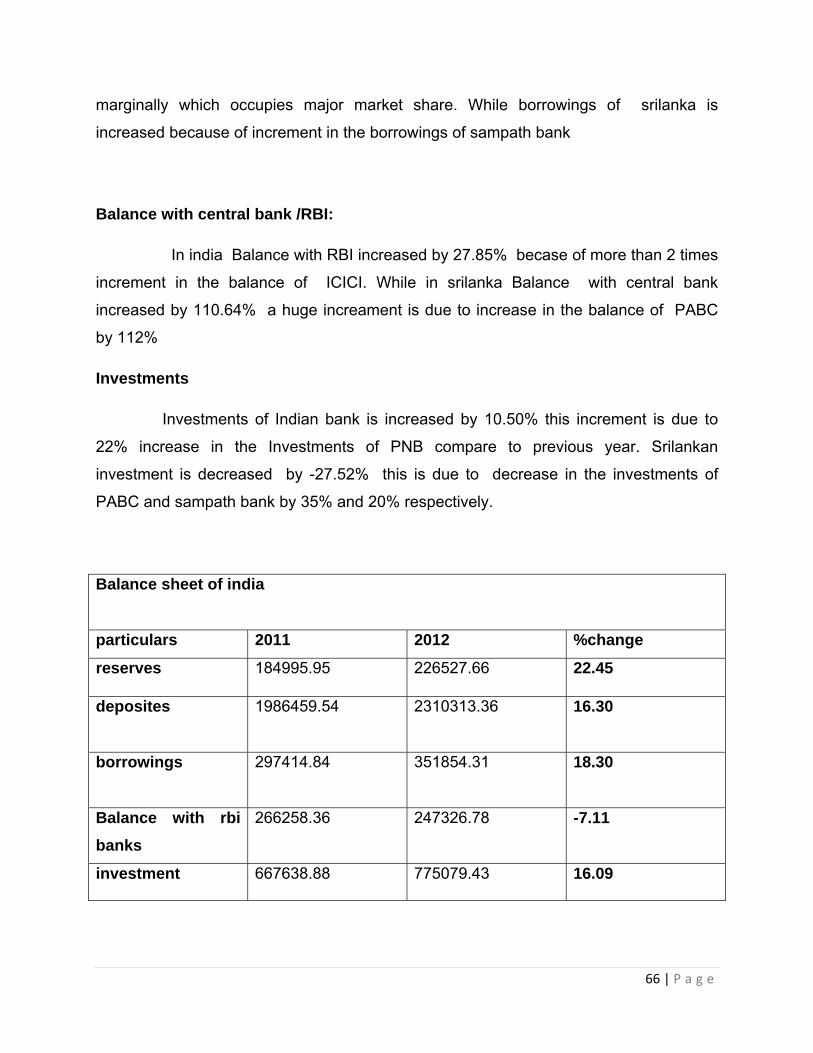

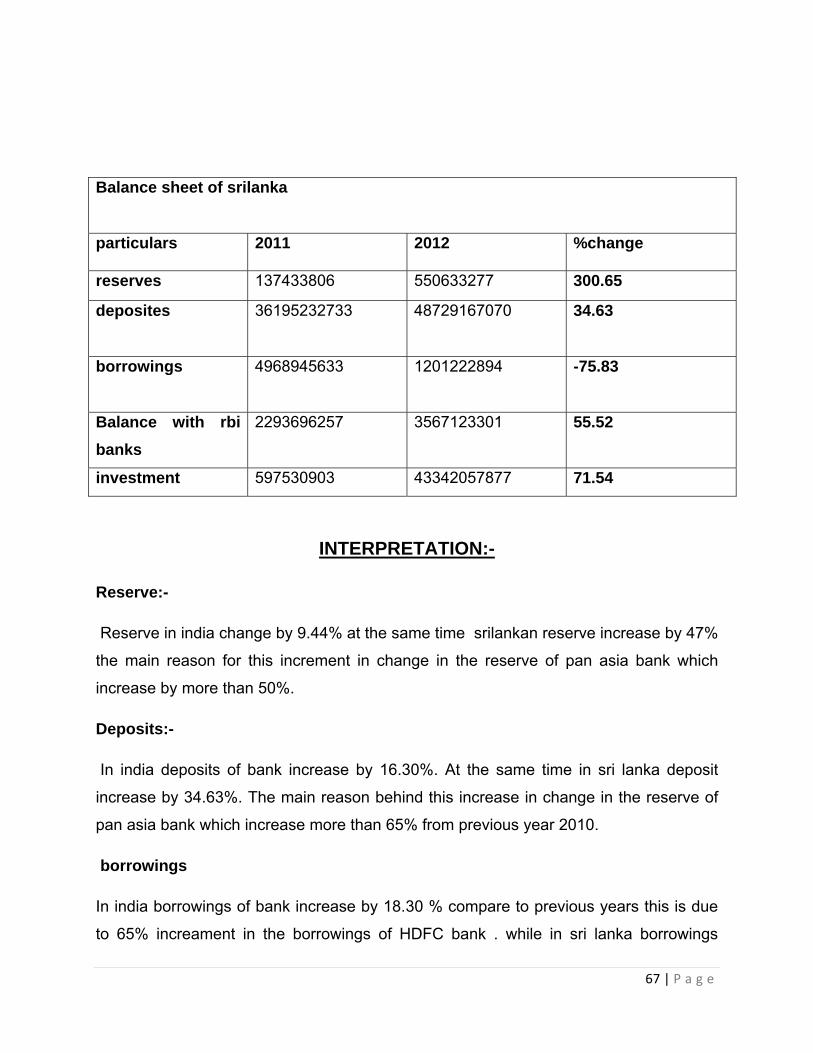

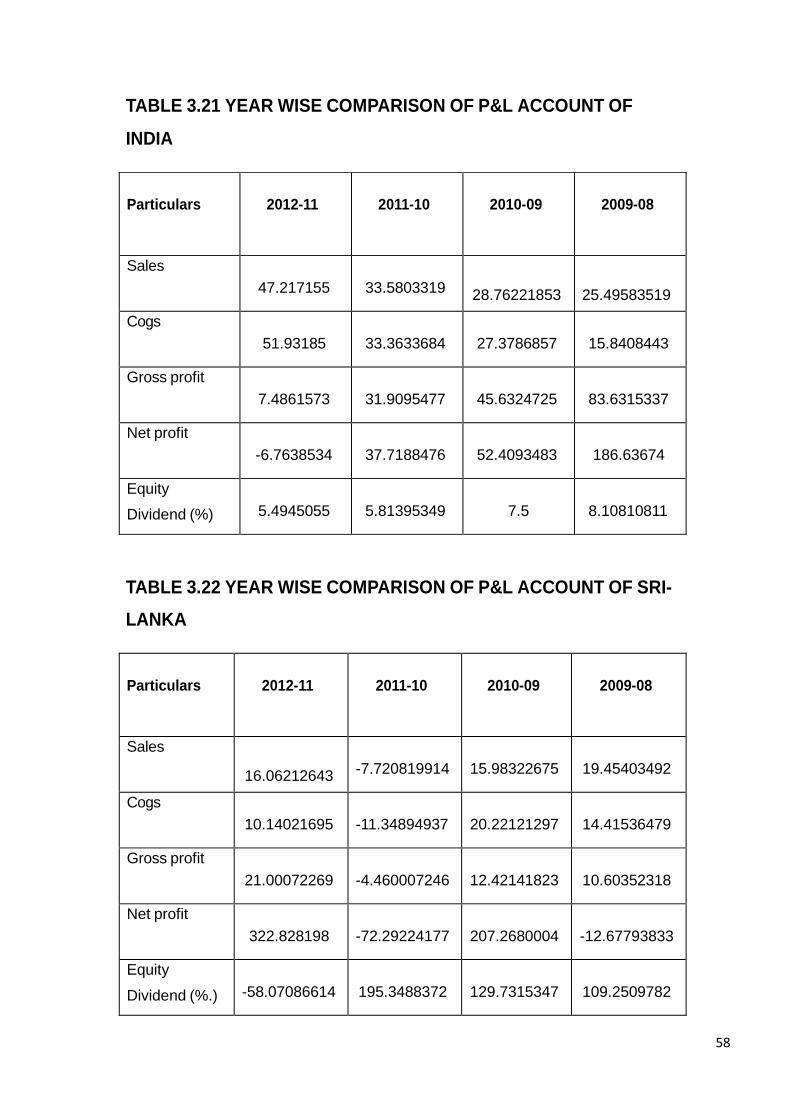

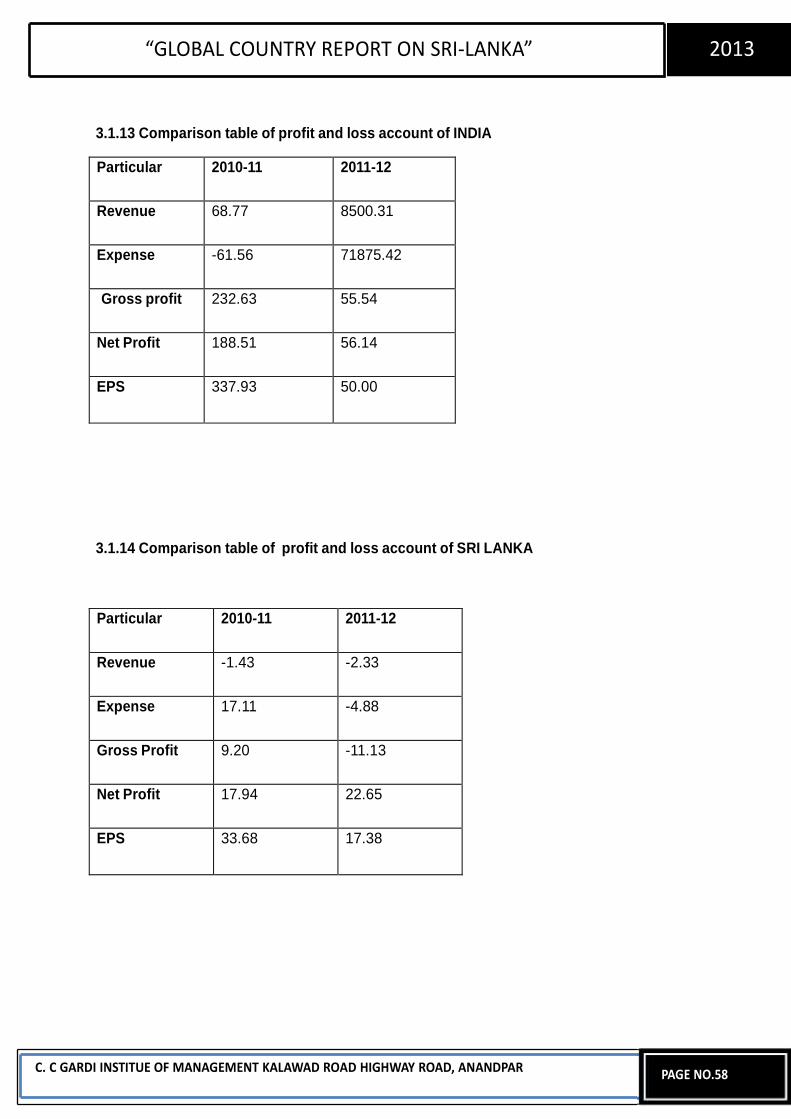

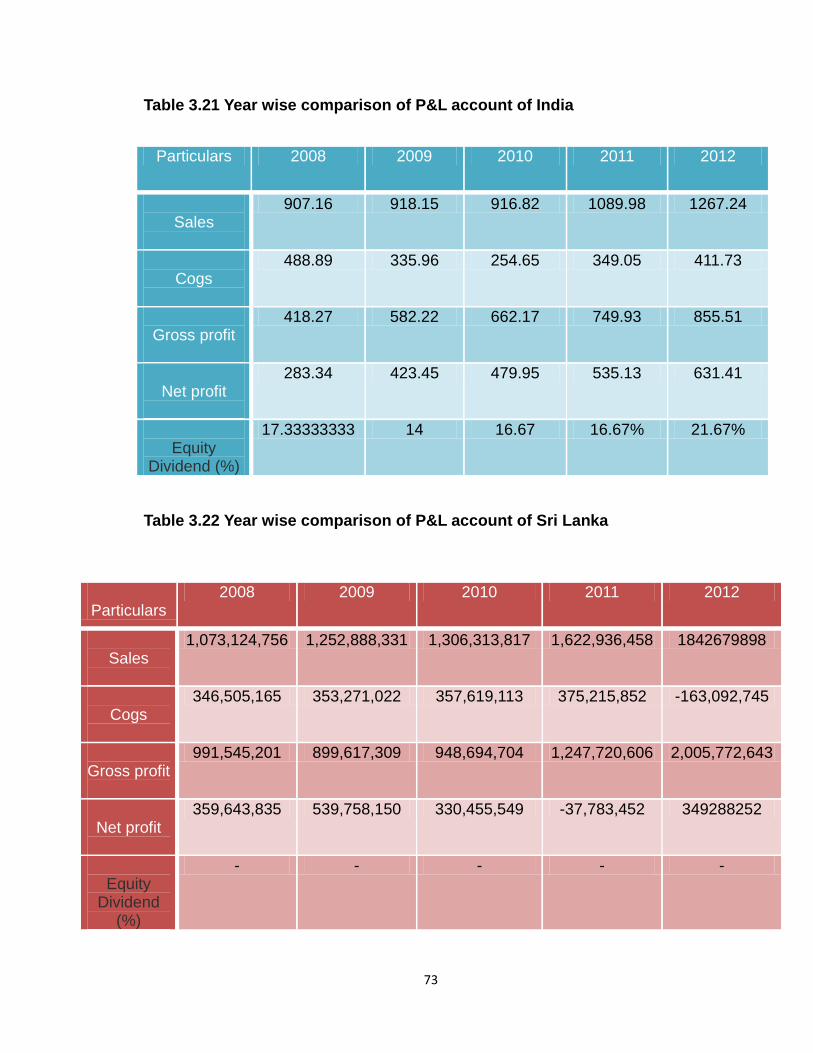

INTERPRETATION:-

Interest income: from the year of 2010 interest income in india shows a steady growth

of 16.64% compare to 45.96 % in srilanka the main reason behind that GROWTH WAS

the growth in panasiabanking corporation (PABC) which occupies in srilankan banking

sector.

Interest expenses: from the year of 2010 intersts expense in india shows a steady

growth of 7.33% compare to 60.57% in srilanka but the main reason behind increase in

increase in interest expenses is a sharp rise in net interest expense in PABC

Net interest income : in india net interest income increase by 33.05% from 2010 to

2011 while in srilanka growth rate was 33.30% the main reason behind good

performance in india is they have right to reduce interest income compare to srilanka

Net profit : net profit in india shows marginal growth of 8.74% while in srilanka net profit

rose 124.80 %from the year of 2010. That growth was mainly by substantial

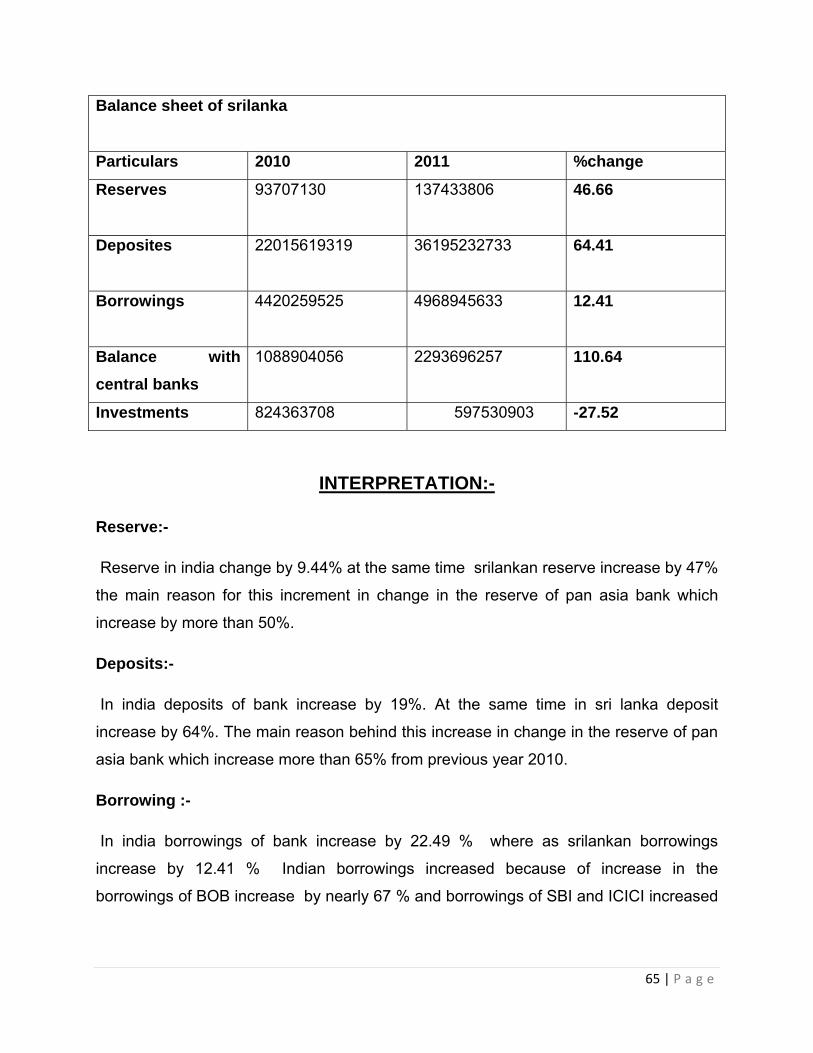

P&L sri lanka bank

Particulars

2010 2011 % change

Interest income

3102813018 4528934960

45.96

Interest expenses