RICE WEEKLY - S&P Global

10

February 26, 2021 RICE WEEKLY www.platts.com PLATTS WEEKLY RICE ASSESSMENTS ($/mt) Price Change Price Change Price Change Thailand - Long Grain White Rice 100% Grade B LRAAC00 529.00 +7.00 5% Broken LRABB00 519.00 +7.00 10% Broken LRACA00 518.00 +7.00 15% Broken LRADD00 515.00 +7.00 25% Broken LRAEE00 502.00 +5.00 A1 Super 100% Broken LRAFC00 460.00 0.00 Thailand - Long Grain Parboiled Rice Parboiled Milled 100% STX LRAGC00 524.00 +10.00 Parboiled Milled 100% LRAHC00 514.00 +10.00 Parboiled Milled 5% STX LRAIB00 519.00 +10.00 Parboiled Milled 5% LRAJB00 509.00 +10.00 Thailand - Long Grain Fragrant Rice Hom Mali 100% Grade B (FOB FCL) LRAKA00 805.00 -3.00 Hom Mali A1 Super 100% Broken LRALA00 468.00 -2.00 (FOB FCL) Pathumthani Fragrant 100% Grade B LRAMC00 688.00 0.00 (FOB FCL) Thailand - Long Grain Glutinous Rice White Glutinous 10% Broken (FOB FCL) LRANC00 698.00 0.00 Vietnam - Long Grain White Rice 5% Broken LRBAB00 515.00 +5.00 10% Broken LRBBA00 510.00 +5.00 15% Broken LRBCD00 505.00 +5.00 25% Broken LRBDE00 490.00 0.00 100% Broken LRBEC00 450.00 0.00 Vietnam - Long Grain Fragrant Rice Fragrant 5% Broken LRBFA00 520.00 -10.00 Vietnam - Long Grain Glutinous Rice White Glutinous 10% Broken (FOB FCL) LREAB00 519.00 -1.00 Cambodia - Long Grain Fragrant Rice Phka Malis (Wet Season) 5% Broken STX LREFB00 790.00 0.00 (FOB FCL) Sen Kra Ob (Dry Season) 5% Broken STX LREGB00 750.00 0.00 (FOB FCL) Fragrant 100% Broken A1 Super (FOB FCL) LREHC00 450.00 0.00 Myanmar - Long Grain White Rice 5% Broken (FOB FCL) LRHAB00 450.00 0.00 25% Broken LRHBE00 390.00 0.00 B1 & B2 Broken (FOB FCL) LRHCI00 365.00 0.00 Myanmar - Long Grain Parboiled Rice Parboiled Milled 5% STX (FOB FCL) LRHDB00 530.00 0.00 India - Long Grain White Rice 5% Broken LRCAB00 415.00 +10.00 25% Broken LRCBE00 385.00 +5.00 100% Broken LRCCC00 285.00 +10.00 Swarna 5% Broken LRCDB00 390.00 0.00 Sharbati 2% Broken (FOB FCL) LRCEG00 623.00 -8.00 India - Long Grain Parboiled Rice Parboiled Milled 5% STX LRCFG00 385.00 0.00 India - Basmati Rice Traditional White Basmati 2% (FOB FCL) LRCGG00 1328.00 +63.00 Traditional Brown Basmati 2% (FOB FCL) LRCHG00 1130.00 -40.00 Traditional Parboiled Milled Basmati 2% LRCIG00 1170.00 -20.00 (FOB FCL) Pusa White Basmati 2% (FOB FCL) LRCJG00 877.00 -3.00 Pusa Brown Basmati 2% (FOB FCL) LRCKG00 762.00 +2.00 Pusa Parboiled Milled Basmati 2% LRCLG00 794.00 +4.00 (FOB FCL) 1121 White Basmati 2% (FOB FCL) LRCMG00 904.00 -3.00 1121 Parboiled Milled Basmati 2% LRCNB00 760.00 +4.00 (FOB FCL) Pakistan - Long Grain White Rice 5% Broken LRDAB00 443.00 -5.00 10% Broken LRDBA00 440.00 -3.00 15% Broken LRDCD00 437.00 -1.00 25% Broken LRDDE00 398.00 -5.00 100% Broken LRDFG00 358.00 -5.00 386 2% Broken (FOB FCL) LRDEC00 568.00 -22.00 Pakistan - Long Grain Parboiled Rice Parboiled Milled 5% Broken STX LRDGG00 448.00 -10.00 Parboiled Milled 15% Broken STX LRDHG00 443.00 -10.00 Pakistan - Basmati Rice Super Kernel White Basmati 2% (FOB FCL) LRDIG00 825.00 -25.00 Super Kernel Brown Basmati 2% (FOB FCL) LRDJG00 770.00 -20.00 Super Kernel Parboiled Milled Basmati 2% LRDKG00 915.00 -35.00 (FOB FCL) 1121 Steam Basmati 2% (FOB FCL) LRDLB00 875.00 -5.00 1121 Parboiled Milled Basmati 2% LRDMD00 850.00 +5.00 (FOB FCL) US - Gulf Long Grain Rice US #2, 4% Broken, Hard Milled LRIAH00 630.00 0.00 (FOB Lake Charles) US #2, 4% Broken, Hard Milled LRIBH00 525.00 0.00 (FOB Bulk NOLA) US #3, 15% Broken, Hard Milled LRICD00 515.00 0.00 US #5, 20% Broken, Hard Milled LRIDF00 525.00 0.00 US #1, Parboiled Milled 4% Broken LRIEH00 570.00 +5.00 US #2, Paddy, 55/70 Yield LRIFI00 315.00 +3.00 Southern Flour Quality Broken (Ex-works) LRIGI00 457.00 0.00 Southern Pet Food Quality Broken LRIHI00 425.00 0.00 (Ex-works) US - Californian Medium Grain Rice US #1, 4% Broken (FAS FCL Oakland) LRIIH00 925.00 +15.00 US #1, Paddy, 58/69 Yield (Ex-works) LRIJI00 531.00 +11.00 South America - Long Grain White Rice Uruguayan 5% Broken (FOB FCL) LRJAB00 633.00 -2.00 Uruguayan Olímar 5% Broken (FOB FCL) LRJBB00 659.00 -18.00 Argentine 5% Broken (FOB FCL) LRKAB00 610.00 0.00 Brazilian 5% Broken (FOB FCL) LRGAB00 630.00 -10.00 Brazilian 100% Broken (1/2 Grain Brokens) LRGBC00 370.00 +15.00 Paraguayan 5% Broken (FOB FCL) LRLAB00 515.00 0.00 South America - Long Grain Parboiled Rice Brazilian Parboiled Milled 5% Broken STX LRGCB00 630.00 -10.00 (FOB FCL) Uruguayan Parboiled Milled 5% Broken STX LRJCB00 650.00 0.00 (FOB FCL) Egypt - White Rice Medium Grain #2 5% Broken (FOB FCL) LRFAB00 NA NA Medium Grain #3 10% Broken (FOB FCL) LRFBA00 NA NA Round Grain #2 5% Broken (FOB FCL) LRFCB00 NA NA Round Grain #3 10% Broken (FOB FCL) LRFDA00 NA NA 100% Broken Grade 0 (FOB FCL) LRFEC00 NA NA Italy - White Rice (Eur/mt) Indica 5% Broken (Ex-works) LRLBB00 670.00 0.00 Arborio 5% Broken (Ex-works) LRLCB00 850.00 0.00 Basis: FOB bulk vessel, unless otherwise stated.

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of RICE WEEKLY - S&P Global

February 26, 2021

RICE WEEKLY

www.platts.com

Platts Weekly Rice assessments ($/mt) Price Change Price Change Price Change

thailand - long Grain White Rice100% Grade B LRAAC00 529.00 +7.005% Broken LRABB00 519.00 +7.0010% Broken LRACA00 518.00 +7.0015% Broken LRADD00 515.00 +7.0025% Broken LRAEE00 502.00 +5.00A1 Super 100% Broken LRAFC00 460.00 0.00

thailand - long Grain Parboiled RiceParboiled Milled 100% STX LRAGC00 524.00 +10.00Parboiled Milled 100% LRAHC00 514.00 +10.00Parboiled Milled 5% STX LRAIB00 519.00 +10.00Parboiled Milled 5% LRAJB00 509.00 +10.00

thailand - long Grain Fragrant RiceHom Mali 100% Grade B (FOB FCL) LRAKA00 805.00 -3.00Hom Mali A1 Super 100% Broken LRALA00 468.00 -2.00(FOB FCL)Pathumthani Fragrant 100% Grade B LRAMC00 688.00 0.00(FOB FCL)

thailand - long Grain Glutinous RiceWhite Glutinous 10% Broken (FOB FCL) LRANC00 698.00 0.00

Vietnam - long Grain White Rice5% Broken LRBAB00 515.00 +5.0010% Broken LRBBA00 510.00 +5.0015% Broken LRBCD00 505.00 +5.0025% Broken LRBDE00 490.00 0.00100% Broken LRBEC00 450.00 0.00

Vietnam - long Grain Fragrant RiceFragrant 5% Broken LRBFA00 520.00 -10.00

Vietnam - long Grain Glutinous RiceWhite Glutinous 10% Broken (FOB FCL) LREAB00 519.00 -1.00

cambodia - long Grain Fragrant RicePhka Malis (Wet Season) 5% Broken STX LREFB00 790.00 0.00(FOB FCL)Sen Kra Ob (Dry Season) 5% Broken STX LREGB00 750.00 0.00(FOB FCL)Fragrant 100% Broken A1 Super (FOB FCL) LREHC00 450.00 0.00

myanmar - long Grain White Rice5% Broken (FOB FCL) LRHAB00 450.00 0.0025% Broken LRHBE00 390.00 0.00B1 & B2 Broken (FOB FCL) LRHCI00 365.00 0.00

myanmar - long Grain Parboiled RiceParboiled Milled 5% STX (FOB FCL) LRHDB00 530.00 0.00

india - long Grain White Rice5% Broken LRCAB00 415.00 +10.0025% Broken LRCBE00 385.00 +5.00100% Broken LRCCC00 285.00 +10.00Swarna 5% Broken LRCDB00 390.00 0.00Sharbati 2% Broken (FOB FCL) LRCEG00 623.00 -8.00

india - long Grain Parboiled RiceParboiled Milled 5% STX LRCFG00 385.00 0.00

india - Basmati RiceTraditional White Basmati 2% (FOB FCL) LRCGG00 1328.00 +63.00Traditional Brown Basmati 2% (FOB FCL) LRCHG00 1130.00 -40.00Traditional Parboiled Milled Basmati 2% LRCIG00 1170.00 -20.00(FOB FCL)Pusa White Basmati 2% (FOB FCL) LRCJG00 877.00 -3.00Pusa Brown Basmati 2% (FOB FCL) LRCKG00 762.00 +2.00Pusa Parboiled Milled Basmati 2% LRCLG00 794.00 +4.00(FOB FCL)1121 White Basmati 2% (FOB FCL) LRCMG00 904.00 -3.001121 Parboiled Milled Basmati 2% LRCNB00 760.00 +4.00(FOB FCL)

Pakistan - long Grain White Rice5% Broken LRDAB00 443.00 -5.0010% Broken LRDBA00 440.00 -3.0015% Broken LRDCD00 437.00 -1.0025% Broken LRDDE00 398.00 -5.00100% Broken LRDFG00 358.00 -5.00386 2% Broken (FOB FCL) LRDEC00 568.00 -22.00

Pakistan - long Grain Parboiled RiceParboiled Milled 5% Broken STX LRDGG00 448.00 -10.00Parboiled Milled 15% Broken STX LRDHG00 443.00 -10.00

Pakistan - Basmati RiceSuper Kernel White Basmati 2% (FOB FCL) LRDIG00 825.00 -25.00Super Kernel Brown Basmati 2% (FOB FCL) LRDJG00 770.00 -20.00Super Kernel Parboiled Milled Basmati 2% LRDKG00 915.00 -35.00(FOB FCL)1121 Steam Basmati 2% (FOB FCL) LRDLB00 875.00 -5.001121 Parboiled Milled Basmati 2% LRDMD00 850.00 +5.00(FOB FCL)

Us - Gulf long Grain RiceUS #2, 4% Broken, Hard Milled LRIAH00 630.00 0.00(FOB Lake Charles)US #2, 4% Broken, Hard Milled LRIBH00 525.00 0.00(FOB Bulk NOLA)US #3, 15% Broken, Hard Milled LRICD00 515.00 0.00US #5, 20% Broken, Hard Milled LRIDF00 525.00 0.00US #1, Parboiled Milled 4% Broken LRIEH00 570.00 +5.00US #2, Paddy, 55/70 Yield LRIFI00 315.00 +3.00Southern Flour Quality Broken (Ex-works) LRIGI00 457.00 0.00Southern Pet Food Quality Broken LRIHI00 425.00 0.00(Ex-works)

Us - californian medium Grain RiceUS #1, 4% Broken (FAS FCL Oakland) LRIIH00 925.00 +15.00US #1, Paddy, 58/69 Yield (Ex-works) LRIJI00 531.00 +11.00

south america - long Grain White RiceUruguayan 5% Broken (FOB FCL) LRJAB00 633.00 -2.00Uruguayan Olímar 5% Broken (FOB FCL) LRJBB00 659.00 -18.00Argentine 5% Broken (FOB FCL) LRKAB00 610.00 0.00Brazilian 5% Broken (FOB FCL) LRGAB00 630.00 -10.00Brazilian 100% Broken (1/2 Grain Brokens) LRGBC00 370.00 +15.00Paraguayan 5% Broken (FOB FCL) LRLAB00 515.00 0.00

south america - long Grain Parboiled RiceBrazilian Parboiled Milled 5% Broken STX LRGCB00 630.00 -10.00(FOB FCL)Uruguayan Parboiled Milled 5% Broken STX LRJCB00 650.00 0.00(FOB FCL)

egypt - White RiceMedium Grain #2 5% Broken (FOB FCL) LRFAB00 NA NAMedium Grain #3 10% Broken (FOB FCL) LRFBA00 NA NARound Grain #2 5% Broken (FOB FCL) LRFCB00 NA NARound Grain #3 10% Broken (FOB FCL) LRFDA00 NA NA100% Broken Grade 0 (FOB FCL) LRFEC00 NA NA

italy - White Rice (eur/mt)Indica 5% Broken (Ex-works) LRLBB00 670.00 0.00Arborio 5% Broken (Ex-works) LRLCB00 850.00 0.00

Basis: FOB bulk vessel, unless otherwise stated.

February 26, 2021rice Weekly

© 2021 S&P Global Platts, a division of S&P Global inc. all rights reserved. 2

estimated Volatility index (12-months) Value Value Value

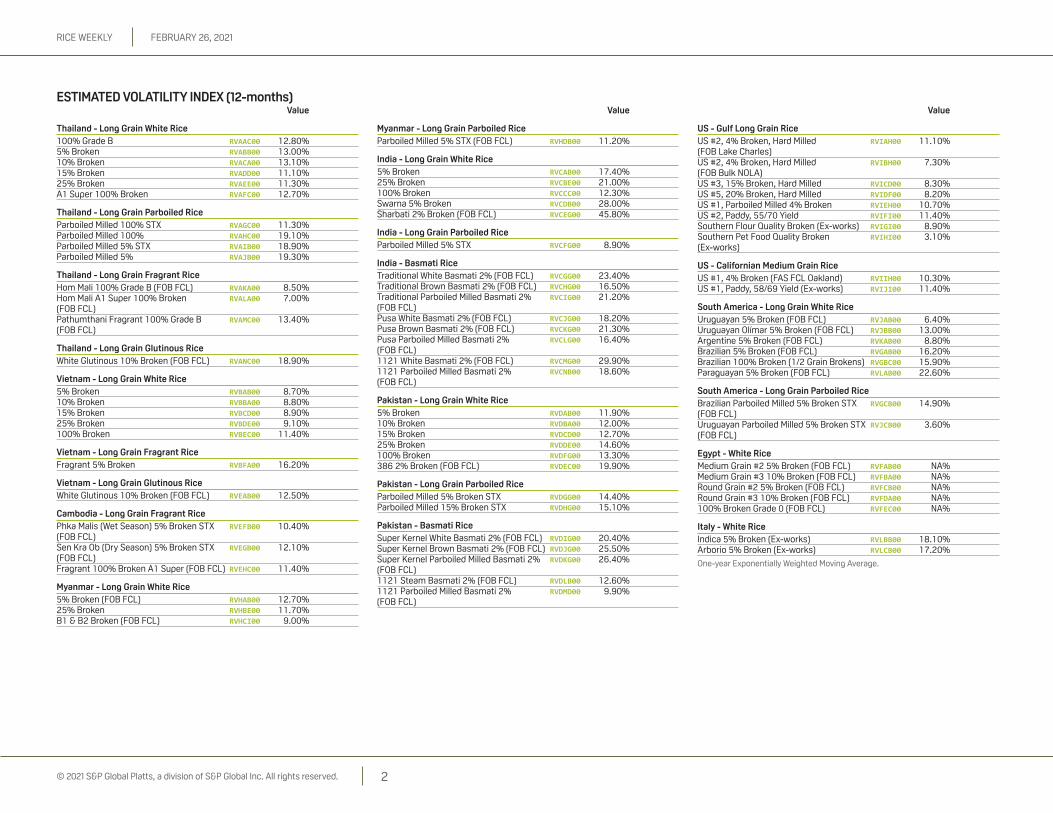

thailand - long Grain White Rice100% Grade B RVAAC00 12.80%5% Broken RVABB00 13.00%10% Broken RVACA00 13.10%15% Broken RVADD00 11.10%25% Broken RVAEE00 11.30%A1 Super 100% Broken RVAFC00 12.70%

thailand - long Grain Parboiled RiceParboiled Milled 100% STX RVAGC00 11.30%Parboiled Milled 100% RVAHC00 19.10%Parboiled Milled 5% STX RVAIB00 18.90%Parboiled Milled 5% RVAJB00 19.30%

thailand - long Grain Fragrant RiceHom Mali 100% Grade B (FOB FCL) RVAKA00 8.50%Hom Mali A1 Super 100% Broken RVALA00 7.00%(FOB FCL)Pathumthani Fragrant 100% Grade B RVAMC00 13.40%(FOB FCL)

thailand - long Grain Glutinous RiceWhite Glutinous 10% Broken (FOB FCL) RVANC00 18.90%

Vietnam - long Grain White Rice5% Broken RVBAB00 8.70%10% Broken RVBBA00 8.80%15% Broken RVBCD00 8.90%25% Broken RVBDE00 9.10%100% Broken RVBEC00 11.40%

Vietnam - long Grain Fragrant RiceFragrant 5% Broken RVBFA00 16.20%

Vietnam - long Grain Glutinous RiceWhite Glutinous 10% Broken (FOB FCL) RVEAB00 12.50%

cambodia - long Grain Fragrant RicePhka Malis (Wet Season) 5% Broken STX RVEFB00 10.40%(FOB FCL)Sen Kra Ob (Dry Season) 5% Broken STX RVEGB00 12.10%(FOB FCL)Fragrant 100% Broken A1 Super (FOB FCL) RVEHC00 11.40%

myanmar - long Grain White Rice5% Broken (FOB FCL) RVHAB00 12.70%25% Broken RVHBE00 11.70%B1 & B2 Broken (FOB FCL) RVHCI00 9.00%

myanmar - long Grain Parboiled RiceParboiled Milled 5% STX (FOB FCL) RVHDB00 11.20%

india - long Grain White Rice5% Broken RVCAB00 17.40%25% Broken RVCBE00 21.00%100% Broken RVCCC00 12.30%Swarna 5% Broken RVCDB00 28.00%Sharbati 2% Broken (FOB FCL) RVCEG00 45.80%

india - long Grain Parboiled RiceParboiled Milled 5% STX RVCFG00 8.90%

india - Basmati RiceTraditional White Basmati 2% (FOB FCL) RVCGG00 23.40%Traditional Brown Basmati 2% (FOB FCL) RVCHG00 16.50%Traditional Parboiled Milled Basmati 2% RVCIG00 21.20%(FOB FCL)Pusa White Basmati 2% (FOB FCL) RVCJG00 18.20%Pusa Brown Basmati 2% (FOB FCL) RVCKG00 21.30%Pusa Parboiled Milled Basmati 2% RVCLG00 16.40%(FOB FCL)1121 White Basmati 2% (FOB FCL) RVCMG00 29.90%1121 Parboiled Milled Basmati 2% RVCNB00 18.60%(FOB FCL)

Pakistan - long Grain White Rice5% Broken RVDAB00 11.90%10% Broken RVDBA00 12.00%15% Broken RVDCD00 12.70%25% Broken RVDDE00 14.60%100% Broken RVDFG00 13.30%386 2% Broken (FOB FCL) RVDEC00 19.90%

Pakistan - long Grain Parboiled RiceParboiled Milled 5% Broken STX RVDGG00 14.40%Parboiled Milled 15% Broken STX RVDHG00 15.10%

Pakistan - Basmati RiceSuper Kernel White Basmati 2% (FOB FCL) RVDIG00 20.40%Super Kernel Brown Basmati 2% (FOB FCL) RVDJG00 25.50%Super Kernel Parboiled Milled Basmati 2% RVDKG00 26.40%(FOB FCL)1121 Steam Basmati 2% (FOB FCL) RVDLB00 12.60%1121 Parboiled Milled Basmati 2% RVDMD00 9.90%(FOB FCL)

Us - Gulf long Grain RiceUS #2, 4% Broken, Hard Milled RVIAH00 11.10%(FOB Lake Charles)US #2, 4% Broken, Hard Milled RVIBH00 7.30%(FOB Bulk NOLA)US #3, 15% Broken, Hard Milled RVICD00 8.30%US #5, 20% Broken, Hard Milled RVIDF00 8.20%US #1, Parboiled Milled 4% Broken RVIEH00 10.70%US #2, Paddy, 55/70 Yield RVIFI00 11.40%Southern Flour Quality Broken (Ex-works) RVIGI00 8.90%Southern Pet Food Quality Broken RVIHI00 3.10%(Ex-works)

Us - californian medium Grain RiceUS #1, 4% Broken (FAS FCL Oakland) RVIIH00 10.30%US #1, Paddy, 58/69 Yield (Ex-works) RVIJI00 11.40%

south america - long Grain White RiceUruguayan 5% Broken (FOB FCL) RVJAB00 6.40%Uruguayan Olímar 5% Broken (FOB FCL) RVJBB00 13.00%Argentine 5% Broken (FOB FCL) RVKAB00 8.80%Brazilian 5% Broken (FOB FCL) RVGAB00 16.20%Brazilian 100% Broken (1/2 Grain Brokens) RVGBC00 15.90%Paraguayan 5% Broken (FOB FCL) RVLAB00 22.60%

south america - long Grain Parboiled RiceBrazilian Parboiled Milled 5% Broken STX RVGCB00 14.90%(FOB FCL)Uruguayan Parboiled Milled 5% Broken STX RVJCB00 3.60%(FOB FCL)

egypt - White RiceMedium Grain #2 5% Broken (FOB FCL) RVFAB00 NA%Medium Grain #3 10% Broken (FOB FCL) RVFBA00 NA%Round Grain #2 5% Broken (FOB FCL) RVFCB00 NA%Round Grain #3 10% Broken (FOB FCL) RVFDA00 NA%100% Broken Grade 0 (FOB FCL) RVFEC00 NA%

italy - White RiceIndica 5% Broken (Ex-works) RVLBB00 18.10%Arborio 5% Broken (Ex-works) RVLCB00 17.20%

One-year Exponentially Weighted Moving Average.

February 26, 2021rice Weekly

© 2021 S&P Global Platts, a division of S&P Global inc. all rights reserved. 3

Rice Weekly

The names “S&P Global Platts” and “Platts” and the S&P Global Platts logo are trademarks of S&P Global Inc. Permission for any commercial use of the S&P Global Platts logo must be granted in writing by S&P Global Inc.

guarantee the adequacy, accuracy, timeliness and/or completeness of the Data or any component thereof or any communications (whether written, oral, electronic or in other format), and shall not be subject to any damages or liability, including but not limited to any indirect, special, incidental, punitive or consequential damages (including but not limited to, loss of profits, trading losses and loss of goodwill).

ICE index data and NYMEX futures data used herein are provided under S&P Global Platts’ commercial licensing agreements with ICE and with NYMEX. You acknowledge that the ICE index data and NYMEX futures data herein are confidential and are proprietary trade secrets and data of ICE and NYMEX or its licensors/suppliers, and you shall use best efforts to prevent the unauthorized publication, disclosure or copying of the ICE index data and/or NYMEX futures data.

Permission is granted for those registered with the Copyright Clearance Center (CCC) to copy material herein for internal reference or personal use only, provided that appropriate payment is made to the CCC, 222 Rosewood Drive, Danvers, MA 01923, phone +1-978-750-8400. Reproduction in any other form, or for any other purpose, is forbidden without the express prior permission of S&P Global Inc. For article reprints contact: The YGS Group, phone +1-717-505-9701 x105 (800-501-9571 from the U.S.).

For all other queries or requests pursuant to this notice, please contact S&P Global Inc. via email at [email protected].

You may view or otherwise use the information, prices, indices, assessments and other related information, graphs, tables and images (“Data”) in this publication only for your personal use or, if you or your company has a license for the Data from S&P Global Platts and you are an authorized user, for your company’s internal business use only. You may not publish, reproduce, extract, distribute, retransmit, resell, create any derivative work from and/or otherwise provide access to the Data or any portion thereof to any person (either within or outside your company, including as part of or via any internal electronic system or intranet), firm or entity, including any subsidiary, parent, or other entity that is affiliated with your company, without S&P Global Platts’ prior written consent or as otherwise authorized under license from S&P Global Platts. Any use or distribution of the Data beyond the express uses authorized in this paragraph above is subject to the payment of additional fees to S&P Global Platts.

S&P Global Platts, its affiliates and all of their third-party licensors disclaim any and all warranties, express or implied, including, but not limited to, any warranties of merchantability or fitness for a particular purpose or use as to the Data, or the results obtained by its use or as to the performance thereof. Data in this publication includes independent and verifiable data collected from actual market participants. Any user of the Data should not rely on any information and/or assessment contained therein in making any investment, trading, risk management or other decision. S&P Global Platts, its affiliates and their third-party licensors do not

editorial: Charlotte James (Managing Editor), Peter Storey, Maude Desmarescaux, William Bland

contact Platts support: [email protected]; Americas: +1-800-752-8878; Europe & Middle East: +44-20-7176-6111; Asia Pacific: +65-6530-6430

© 2021 S&P Global Platts, a division of S&P Global Inc. All rights reserved.

maRket commentaRy

Platts thailand Rice Weekly commentary■■ long grain market reopens with much firmer undertone■■ Private white rice demand remains “extremely quiet”■■ exports in January down by 12% on month: ministry of

commerce

The Thai white and parboiled rice markets opened the week ending Feb. 26 much firmer due to covering of sales to Asian destinations on Feb. 19.

Multiple sources reported that Malaysia’s Bernas entered the market at this point to purchase a significant volume. While being a widespread talking point, details such as the volume purchased remain unclear.

One exporter, typically involved in Bernas tenders, said that no tender had been announced and that Bernas must have purchased directly from an exporter. “Some people are adamant that the recent domestic buying is for Bernas”, the exporter added. Bernas did not respond to a request for comment.

Exporters also cited recent tender sales to Japan, in addition to an indirect sale to Iran, as potential reasons for the abrupt reversal to the increasingly bearish momentum. Thai 5% broken white rice closed the week assessed up at $519/mt FOB. However, white rice demand from private buyers remained illiquid, with one major exporter reporting that the market is “extremely quiet” and that some exporters may be forced to leave the market until liquidity returns.

Demand for parboiled rice from South African buyers improved as the week progressed and Parboiled 100% STX closed the week assessed up to $524/mt FOB. The monthly breakbulk shipment to South Africa is due in Thailand to be

loaded on March 10, according to one source. The source added that while approximately 30,000 mt of the cargo will comprise parboiled rice destined for Durban, around 15,000 mt of capacity will be discharged in Maputo, Mozambique – an unusually large portion of the shipment.

South Korea’s Agro-Fisheries and Food Trade Corporation awarded Thai exporters a total of 1,500 mt of rice on Feb. 24, including 1,400 mt of long grain and 100 mt of Hom Mali (see Tenders). While the tender was held on Jan. 22, testing issues delayed the announcement of awards.

Asian demand for Hom Mali and Glutinous rice remained thin following Lunar New Year on Feb. 12, with minimal activity reported and Hom Mali 100% Grade B closed the week assessed down to $805/mt FOB FCL. West African demand also remained subdued for Hom Mali A1 Super 100% broken, which was assessed down at $468/mt FOB FCL. One trader for the region viewed offers at $470/mt FOB FCL as “too high for our markets.” Pathumthani market activity also remained subdued, although it is expected to pick up in the coming weeks with the harvesting of the off-season crop.

The Thai market was closed on Feb. 26 for a public holiday.Thai rice exports totaled 421,477 mt in January, down

12% on the month and 23% on the year, according to the

UnoFFicial and PReliminaRy thai Rice exPoRts (exclUdinG hom mali FRaGRant Rice)Week ending Weekly exports exports since y-o-y change (mt) January 1, 2021 (%) (mt)03-Jan 20,915 140 -9810-Jan 68,472 68,612 -2317-Jan 55,362 123,973 -3224-Jan 82,204 206,178 -2531-Jan 96,775 302,953 -1607-Feb 89,267 392,220 -1414-Feb 45,926 438,146 -8

Source: USDA

February 26, 2021rice Weekly

© 2021 S&P Global Platts, a division of S&P Global inc. all rights reserved. 4

Ministry of Commerce. Milled rice exports are estimated at 375,803 mt. Of this volume, 54,666 mt were exported to Cameroon, 48,596 mt to the US and 46,188 mt to South Africa. Broken rice exports are estimated at 40,999 mt. Of this volume, 9,630 mt were exported to Senegal, 7,553 mt to Cameroon and 6,991 mt to Ghana. Brown rice exports are estimated at 4,675 mt. Of this volume, 935 mt were exported to the UK, 756 mt were exported to the US and 474 mt were exported to Singapore.

Platts Vietnam Rice Weekly commentary■■ White rice prices stable as domestic demand limits

exports■■ Vietnamese traders inquire about importing 5% broken

white rice from india■■ Fragrant rice price falls as new harvest approaches

Despite the imminent arrival of the new crop, Vietnamese white rice prices were stable, underlining the effect of many farmers' decision to grow other, less commoditized varieties of rice instead, especially Fragrant rice.

This reallocation of land away from IR 50404 long grain rice has weighed on prices of Fragrant rice and supported white rice prices, reducing the premium for Fragrant rice over white rice to just $5/mt, its lowest level since S&P Global Platts assessments began in 2011. Vietnamese 5% broken white rice closed the week assessed up at $515/mt FOB as lower offers were no longer available.

"It's likely that white rice will set the floor for how low DT8 could drop," said one trader.

Growers preference for more niche varieties has also made Vietnamese white rice prices much higher than other origins. Traders say that there have even been inquiries about importing 5% broken rice from India, where prices are currently $100/mt lower.

Vietnam bought around 70,000 mt of broken rice from India late in 2020, according to a Reuters report in January, and most traders said those purchases would mostly be used for animal feed and brewing.

When that news was announced, officials in Vietnam were quick to dismiss the idea that Vietnam might face any shortage of white rice. News website Vietnam.net quoted an official from the Ministry of Agriculture and Rural Development saying "for sure there will be abundant rice for export." However, the official did not specify whether that would include the variety knows as IR 50404, which is typically the most widely exported white rice variety thanks to demand from Cuba and Africa.

One trader said that while they did not know of any confirmed Vietnamese purchases of 5% brokens from India, there had been interest in offers on a CFR basis.

Fragrant 5% broken closed the week assessed down at $520/mt FOB, with Philippine buyers unwilling to trade at the higher levels seen earlier in February.

One market source speaking early in the week said that ex-warehouse prices for DT8 in Vietnam were the equivalent of around $540/mt FOB, and that the lower export offers came from traders speculating on an upcoming fall.

"The price of DT8 has come down already, but buyers have also lowered their target prices," said one source

shortly afterward, pointing to the change in sentiment as more new crop becomes available.

Another seller of DT8 said they had also received inquiries from African buyers, adding that typically interest for the Fragrant variety comes from Ghana, Ivory Coast and Mozambique.

White Glutinous 10% broken was assessed down slightly to $519/mt FOB FCL, and renewed interest from China was reported by one trader who had lowered their indication for the variety.

Vietnamese exporter Trung An Hi-tech Farming is expecting the value of country's rice exports in 2021 to exceed the 2020 total of $3.07 billion, the state-owned Vietnam News Agency reported, quoting the company's General Director Pham Thai Binh, who highlighted that Vietnam's rice sector has restructured to focus on quality over quantity.

Platts cambodia Rice Weekly commentary■■ strong demand supports sen kra ob price■■ 5451 long grain harvesting fully underway■■ Q1 2021 exports expected to decrease on year: cRF

Strong demand from multiple destinations continued to support the price of Cambodian Sen Kra Ob 5% broken STX.

S&P Global Platts’ assessment of this variety was unchanged at $750/mt FOB FCL based on bids and offers, with bids from Chinese buyers reported at around $720/mt FOB FCL.

While one exporter believed that Chinese buyers would accept offers of Sen Kra Ob at $740/mt FOB FCL, it would only create a very small profit margin for exporters due to high Sen Kra Ob paddy prices and they decided instead to focus on covering previous sales.

Competitively priced Thai Hom Mali continued to put pressure on the price of Phka Malis 5% broken STX. However, Platts’ assessment of this grade was also unchanged at $790/mt FOB FCL, as exporters resisted lowering their offers due to tightening supplies. Fragrant

February 26, 2021rice Weekly

© 2021 S&P Global Platts, a division of S&P Global inc. all rights reserved. 5

100% broken A1 Super was assessed unchanged at $450/mt FOB FCL as exporters maintained their offers.

Harvesting of the 5451 long grain crop progressed in the week ended Feb. 26, with significant volumes harvested in most provinces, according to one exporter. This exporter also reported that Vietnamese cross-border demand for 5451 paddy has slowed amid COVID-19 related issues at the countries’ borders. Sales of 5451 5% broken white rice to China continued to be reported at around $575-$580/mt FOB FCL, although one exporter speculated that declining paddy prices could weigh on the price next week.

According to Cambodia Rice Federation President Song Saran, as reported by news website Khmer Times, Cambodian exports in Q1 2021 are expected to decrease on the year. Global shipping issues were cited as the principal reason for the anticipated decline, with shipping dubbed “the main challenge for the sector currently”. A shortage of containers and space on pre-courier transport from Sihanoukville Port to ships have affected sales to Europe, which declined by almost 60% year on year in January.

Platts myanmar Rice Weekly commentary■■ Political unrest disrupts rice supply chain■■ exporters refrain from offering amid high uncertainty■■ January milled rice exports forecast at 260,000 mt:

Usda

Myanmar exporters continued to face significant hurdles in the week ending Feb. 26 due to the political turmoil which ensued from the Feb. 1 military coup.

Government departments remained closed, resulting in participants’ inability to obtain documents required for exports, including phytosanitary licenses. Large protests, as well as a general strike, were also reported across the country, resulting in further disruptions along the rice supply chain.

According to sources, cargo transportation from production areas to ports is complicated. In this context, exporters prioritized loading previously agreed sales, while refraining from offering fresh volumes due to the uncertainty

underpinning export logistics for the foreseeable future.One participant said that while shipments had resumed

in the week ending Feb. 19, they had come to a halt again. In this context, fresh offers were unavailable and prices remained largely nominal, as a result.

Myanmar 5% and 25% broken white rice were assessed unchanged at $450/mt FOB FCL and $390/mt FOB, respectively. B1 & B2 broken rice and Parboiled 5% STX were also assessed unchanged at $365/mt FOB FCL and $530/mt FOB FCL respectively, amid extremely limited liquidity.

The US Department of Agriculture, or USDA, has forecast exports in January at 260,000 mt (milled equivalent), down by 9.3% month on month but up by 18% year on year. The month-on-month decline was attributed to high domestic prices and Chinese buyers not having received import licenses for whole grain rice. However, broken rice sales to China were boosted by greater demand ahead of Lunar New Year (Feb. 12).

The USDA forecast main crop and off-season crop planted area at 6.1 million hectares and 1 million hectares, respectively. The main crop harvest was nearly 99% complete by late January, while planting of the off-season crop was estimated to be 45% complete. Inadequate rainfall is expected to result in reduced field yields. Reduced production, strong broken rice demand from China and delays caused by social unrest were expected to support higher domestic prices in February.

Platts india Rice Weekly commentary■■ Rising freight rates, tightening container availability

constrain fresh trade■■ 2020-21 milled rice production forecast at record 120

million mt■■ slow end-consumer demand weighs on Basmati prices■■ exports total 1.6 million mt in January, up by 78% on

year: dGcis

The Indian non-Basmati market developed a firm undertone in the week ending Feb. 26, supported by strong offshore

demand, as importers favored competitively priced Indian rice over other origins.

However, participants deplored rising freight rates which, coupled with tightening vessel space and container availability, were said to be damaging export economics. One trader attributed the increase in freight rates to increased demand from Indonesia, East African

February 26, 2021rice Weekly

© 2021 S&P Global Platts, a division of S&P Global inc. all rights reserved. 6

destinations and the Middle East ahead of Ramadan (April 12-May 12).

Indian 5% and 25% broken white rice closed the week assessed up at $415/mt FOB and $385/mt FOB, respectively, amid tight current crop availability and demand from Vietnam and China. Old crop demand from African destinations was also reported. Parboiled 5% STX closed the week assessed unchanged at $385/mt FOB, with fundamentals balancing between tight supply and relatively slow demand.

Sources also noted strong demand for 100% broken white rice, which closed the week assessed up at $285/mt FOB, as exporters raised their offers. “No one is willing to short sell anymore,” one participant said. The recent uptick in prices and prospects of tightening stocks -- both at origin and destination -- prompted West African buyers to seek fresh volumes. Importers also aimed to secure rice ahead of Ramadan. However, one participant noted that cargo being loaded this week ran the risk of missing the expected delivery window.

In contrast, Basmati demand remained moribund. Ramadan requirements have already been covered, according to one major exporter, who reported slow end-consumer demand and no prospects of improvement in the short term. “Most of the Arab world is in lockdown, nobody goes to the retailers for buying groceries,” the exporter said. Pusa White Basmati 2% broken and 1121 White Basmati 2% broken were assessed down at $877/mt FOB FCL and $904/mt FOB FCL, respectively.

The US Department of Agriculture, or USDA, has maintained its forecast for India’s milled rice production in the 2020-21 marketing year (October-September) at a record 120 million mt, up by 1.3% on the year. The production increase is driven by higher kharif crop production in October-December 2020 and is further supported by expectations of a healthy rabi crop harvest.

While late precipitation is causing planting of the rabi crop to lag 2020 levels at present, the USDA anticipates that it will recover over the next few weeks. Total planted

area is forecast to expand by 1.6% on year to 44.5 million hectares. The Indian government’s Second Advance Estimates also shows 2020-21 production at a record 120 million mt, which is 7% higher than average production over the past five years.

Government procurement remains well above last year’s levels. Expectations of record production and relatively low prices underpinned this, as well as the government’s efforts to show support to farmers amid protests against new farm laws. According to the Ministry of Consumer Affairs, Food and Public Distribution, paddy procurement totaled 65.9 million mt as of Feb. 22, up nearly 17% on the year. Punjab alone procured 20.3 million mt, or approximately 31% of the total volume.

Finally, the USDA forecast that milled equivalent exports will increase by 11% on year to 14 million mt due to abundant production and competitive prices compared with other origins. Milled equivalent ending stocks are anticipated to be steady on year at 29.7 million mt, with higher exports forecast to offset production increases.

Indian rice exports totaled 1.6 million mt in January, up by 78% on the year, according to the Directorate General of Commercial Intelligence and Statistics. Non-Basmati exports rose by 174% on the year to 1.2 million mt while Basmati exports decreased by 17% to 380,014 mt.

Platts Pakistan Rice Weekly commentary■■ iRRi-6 prices soften amid reduced trade■■ Prices anticipated to rise again if china returns to the

market■■ lack of iranian sales weigh on super kernel White

Basmati price

Pakistani IRRI-6 white and parboiled rice prices softened amid a steady decline in local prices and very slow offshore demand.

While some exporters reported that Chinese buyers had received their 2021 import quotas, others reported that buyers were not expecting them until March, with minimal

activity anticipated until they are obtained. While exporters lowered their offers to attract fresh buying interest, one major exporter stated that even “small demand” would cause prices to rise again.

Similarly, a trader described the market as a “mini rollercoaster” that moved according to the volume of Chinese demand. As this demand had not materialized, 5% broken white rice closed the week assessed down to $443/mt FOB as lower offers were available. One exporter said that a 25,000-30,000 mt sale of 5% broken white rice was concluded in the week ended Feb. 19 at around $435/mt FOB for March shipment to West Africa. However, fresh demand from African destinations was minimal, with buyers described as “silent”.

Pakistani 100% broken white rice closed the week assessed down at $358/mt FOB as lower offers were available, although a slowdown in white rice milling is expected to support the market in the coming days. Sales of premium specification broken rice to China were reported at $395-$400/mt CFR Chinese ports on Feb. 26. Lower offers were also available for Parboiled 5% STX, which closed the week assessed down to $448/mt FOB.

Many participants attended Gulfood (Feb. 21-25) and while some sources said that the exhibition had gone “well”, others stated that there was “very little turnover”, with limited representation from countries including

February 26, 2021rice Weekly

© 2021 S&P Global Platts, a division of S&P Global inc. all rights reserved. 7

Vietnam, China and Singapore due to COVID-19 travel restrictions.

The Basmati market had a softer undertone due to competitive Indian prices and as anticipated Iranian sales failed to materialize. Demand for Super Kernel White and 1121 Parboiled and Steam Basmati from other destinations was limited to small volumes, with buyers asking for lower prices, according to one exporter.

Super Kernel White Basmati 2% broken and 1121 Steam Basmati 2% broken were assessed down at $825/mt FOB FCL and $875/mt FOB FCL, respectively, based on fresh market information. Strong local demand supported the price of 1121 Parboiled Basmati 2% broken, which was assessed up to $850/mt FOB FCL. While European buyers continued to inquire for Super Kernel Brown Basmati, buyers’ bid well below exporters’ offers. Super Kernel Brown Basmati 2% broken was assessed down at $770/mt FOB FCL based on bids and offers. Pakistani 386 2% broken was also assessed down at $568/mt FOB FCL as lower offers were available.

Platts Us Rice Weekly commentary■■ southern paddy price bottoms out■■ southern mills resume operations■■ calrose paddy price firms on supply concerns

US Southern mills resumed operations following unexpected shutdowns caused by adverse weather and restrictions on energy usage in the week ended Feb. 19.

Participants talked of a “changing mood” in the market and said prices had likely bottomed out. Farmers were in no rush to conclude new sales and participants reported signs of improving demand.

“The down time really has put milling time at a premium,” one source said. “There have also been issues with availability of transportation, so it has even affected the market more. […] Demand shouldn’t be an issue for several week, if not longer.”

One trader speculated that the price of paddy had already hit its lowest level this year and anticipated an extended rally on the back of competition for acreage due to higher corn and soy prices. The trader noted that there was “no urgency from farmers to load barges like before” and that regular trade to Mexico and Central America provided further support to the paddy market.

The US Department of Agriculture reported a 76% year-on-year increase in the value of US rice exports to the Dominican Republic in 2020, to $22.8 million. US #2 Paddy, 55/70 Yield closed the week assessed up at $315/mt FOB bulk NOLA as lower offers were no longer available. Bids at around $310-$312/mt FOB bulk NOLA were also reported.

However, US #2, 4% broken white rice closed the week assessed unchanged at $525/mt FOB bulk NOLA and was assessed unchanged at $630/mt FOB Lake Charles as exporters maintained their offers. Broken rice supply remained tight due to recently slow milling activity.

The US Kansas City Commodity Office will hold a domestic tender for 200 mt US #5, 20% broken fortified long grain rice on March 2. Shipment is required in May. According to market sources, Taiwan’s Bank Corp. purchased the full 20,652 mt of US rice in its Feb. 25 re-tender, with prices ranging from $458.94-$550.16/mt delivered government warehouse.

The Calrose market also maintained a firm undertone, amid reports of strong domestic and international demand.

US #1 Paddy, 58/69 Yield and US #1, 4% broken white rice closed the week assessed up at $531/mt ($17/cwt over loan) ex-works and $925/mt FAS FCL Oakland, respectively, as lower offers were no longer available. While participants reported limited trade activity on milled rice aside from Japan’s tenders, they argued that higher paddy prices commanded an increase in the price of finished product.

According to sources, ADM secured the three lots of US rice awarded in South Korea's Agro-Fisheries and Food Trade Corp.’s, or KAFFTC, Jan. 22 Minimum Market Access tender (see Tenders). In total, KAFFTC awarded 45,944 mt to US exporters but is due to hold a re-tender for the unawarded US lot on Mar. 4.

US exportS highlightS from febrUary 12-18country Volume (mt)Venezuela 27,500Japan 13,400Haiti 4,500Mexico 3,600Jordan 3,400

Source: USDA

US net SaleS highlightS from febrUary 12-18country Volume (mt)Japan 48,700Venezuela 18,300Dominican Republic 10,000Haiti 7,100Panama 1,300

Source: USDA

Usa cBot RoUGh Rice FUtURes ($) ——————————— cwt ————————————— ———————————— mt —————————————month February 25 net change net change February 25 net change net change close price from February 24 from February 18 close price from February 24 from February 18Mar-21 12.81 -0.06 0.07 282.30 -1.43 1.65May-21 13.11 -0.06 0.10 288.92 -1.43 2.09Jul-21 13.36 -0.05 0.16 294.43 -1.10 3.53Sep-21 12.74 -0.09 -0.02 280.76 -1.87 -0.33Nov-21 12.74 -0.08 -0.02 280.87 -1.87 -0.33Jan-22 12.88 -0.09 -0.02 283.85 -1.87 -0.33Mar-22 12.88 -0.09 -0.02 283.85 -1.87 -0.33

All figures rounded to two decimal places.

Source: CME

February 26, 2021rice Weekly

© 2021 S&P Global Platts, a division of S&P Global inc. all rights reserved. 8

Platts south america Rice Weekly commentary■■ Real’s depreciation against dollar weighs on Brazilian

prices■■ Brazilian harvest 1.3% complete: irga■■ Uruguayan prices stable as traders await clarity on new

crop

One source said that the US Department of Agriculture’s annual Agricultural Outlook Forum has been “mildly bullish” for export prices from South America because the department raised the possibility of an 11% contraction in US rice planted area in the 2021-22 marketing year (August-July), which would leave a supply gap in Mexico and Central America that could be filled from Mercosur. Despite this, Brazilian prices fell in dollar terms after President Jair Bolsonaro moved to replace the head of the country’s largest company, Petrobras, fuelling concerns about political instability and a weakening of the real against the US currency.

The volatility came just as the harvest was beginning in some areas, and one trader quoted two different prices – one for each possible exchange rate. “It’s softening a little these days, but it’s very difficult to put a single number on it,” said another source.

“The market is very weak this week...the market is

preparing for harvest time,” agreed a third, adding that offers for long grain white rice might be as low as $610/mt FOB FCL but the situation would not be clear for another two weeks.

Brazilian Parboiled 5% STX and 5% broken white rice both closed the week assessed down at $630/mt FOB FCL, as lower offers were available. Brazilian 100% broken white rice closed the week assessed up at $370/mt FOB on limited availability. “The start of the harvest will be staggered across the country until the second half of March and in most provinces it won’t be complete until well into May,” said one source.

According to news website Canal Rural, 12,467 hectares had been harvested as of Feb. 22, representing 1.3% of the total sown area of 944,841 hectares. The website cited data from Rio Grandense do Arroz Instituto (Irga).

Brazilian news portal DBO reported that harvesting in the country’s second largest rice producing state, Santa Catarina, has started, with 1.18 million mt of paddy expected to be produced. Based on the most recent estimates for the 2020-21 marketing year (April 2021-March 2022), Santa Catarina would account for 11% of the country’s total paddy production.

S&P Global Platts continued new crop transitions for Uruguayan 5% broken white rice and Parboiled 5% STX, which closed the week down at $633/mt FOB FCL and unchanged at $650/mt FOB FCL, respectively. Platts continued its new crop transition for Olimar 5% broken white rice, which was assessed down at $659/mt FOB FCL on the sixth day of the 10-day transition. “There aren’t firm offers for the new crop so everyone is pushing to keep the old crop prices,” said one trader in the country.

“I haven’t seen changes this week. The harvest is delayed, prices are firm and aren’t starting to fall yet…. they’ll certainly go down but it hasn’t happened yet,” said another source, explaining that the delay is due to the drought across Mercosur last year.

Argentine 5% broken white rice closed the week assessed unchanged at $610/mt FOB FCL, following S&P Global Platts transition to new crop pricing.

Paraguayan 5% broken white rice was also unchanged at $515/mt FOB FCL with no significant trades reported.

Platts italy Rice Weekly commentary■■ mills still looking for march orders, but demand remains

weak■■ Paddy prices remain broadly unchanged on week■■ indica buyers looking to asia and south america,

despite logistical issues

The Italian market remained sedate during the week ending Feb. 26, with little market activity reported.

eU and Uk cUmUlatiVe Rice imPoRts, September 1, 2020 - febrUary 23, 2021country Volume (mt)Austria 2,557Belgium 20,590Bulgaria 6,632Croatia 0Cyprus 1,750Czech Republic 14,348Denmark 4,236Estonia 32Finland 1,115France 83,938Germany 35,671Greece 3,103Hungary 4,409Ireland 2,417Italy 53,505Latvia 530Lithuania 10,992Luxembourg 20Malta 530Netherlands 86,872Poland 37,623Portugal 26,393Romania 4,792Slovakia 5,869Slovenia 1Spain 36,842Sweden 11,188United Kingdom 80,355EU + UK 536,309

Source: European Commission’s D.G. of Agriculture

February 26, 2021rice Weekly

© 2021 S&P Global Platts, a division of S&P Global inc. all rights reserved. 9

Demand was described by one source as “regular” but “slow”, with mills still looking to fill their March milling schedules. A broker said that mills are complaining that “nothing is happening” and that they are approximately half as busy as they were at this point last year. The same broker said that some parboiling plants – which are typically

run continuously for efficiency purposes – are closing on weekends due to the slowdown in demand. A second broker said that the reduced milling activity is perpetuating the “crazy” broken rice shortage in Europe.

While Indica prices have spiked in recent weeks on reduced production and the global container shortage, most buyers appear willing to risk delays and are snubbing Italian long grain. One such buyer remarked that it still made much more sense to buy from Asia and South America. Indica 5% broken white rice was assessed unchanged at Eur670/mt ex-works. Indica parboiled rice was indicated by two sources at Eur730-740/mt ex-works.

Although some mills were willing to discount prices for small volume sales, generally resolute paddy prices were hindering mills from lowering prices for substantial volumes, with most farmers in a strong financial position. Arborio 5% broken white rice was also assessed unchanged at Eur850/mt ex-works.

One broker said a small week-on-week decrease in the price of Carnaroli paddy to Eur500/mt ex-works, while the Vercelli Chamber of Commerce reported a Eur10/mt increase in the price of Selenio paddy (see table). Another source was perplexed by the higher Selenio paddy price due to extremely slow demand for round grain rice.

The source speculated that it could be that thin liquidity in the round grain market is producing erratic price moves.

tendeRs

south korea awards 69,666 mt of rice in Jan 22 mma tender: kaFFtcSouth Korea’s Agro-Fisheries and Food Trade Corporation (KAFFTC) has awarded 69,666 mt out of a possible 113,555 mt in its Jan. 22 Minimum Market Access tender (see table).

This is KAFFTC’s third purchase of US rice this season, its second purchase of Chinese rice and its first purchase of Thai rice since June 2020.

In total, it awarded 45,944 mt to US exporters, 22,222 mt to Chinese exporters and 1,500 mt to Thai exporters.

According to US sources, official results were delayed due to issues testing Chinese and Thai samples, with “unofficial” results circulating in the Californian market in early February which correspond to KAFFTC’s official results.

In its previous MMA tender on Dec. 8, KAFFTC awarded the full 45,458 mt of US and Vietnamese rice.

south korea to hold brown rice re-tender on march 4: kaFFtc

South Korea’s Agro-Fisheries and Food Trade Corp, or KAFFTC, will hold a re-tender on March 4 for two of the

italian paddy and broken rice priceS - FeBRUaRy 23, 2021ex-Vercelli, italy (eur/mt ex-market)Variety ‘maximum’ Previous ‘maximum’ price priceBalilla, Centauro and similar 330 330Sole CL 310 310Selenio and similar 350 340Ribe 330 330Loto and similar 371 371Augusto 361 361S. Andrea and similar 435 435Roma and similar 385 385Baldo and similar 435 435Arborio and Volano 455 455Carnaroli and similar 485 485Thaibonnet and similar 375 375

Broken

Corpetto 440 430Mezzangrana 430 420

Source: Vercelli Chamber of Commerce

italian milled priceS - febrUary 23, 2021ex-Vercelli, italy (eur/mt ex-market)Variety ‘minimum’ Previous ‘minimum’ price priceOriginario 640 640Selenio 780 780S. Andrea 900 900Roma 850 850Baldo 900 900Ribe 680 680Augusto 710 710Arborio 1040 1040Carnaroli 1050 1050Thaibonnet 680 680

Parboiled

Ribe 770 770Baldo 980 980Thaibonnet 760 760

Source: Vercelli Chamber of Commerce

kaFFtc’s Jan. 22 mma tendeR ResUltsVariety Volume (mt) awarded origin awarded awarded price Port of arrival arrival date companies ($/mt ciP)Non-glutinous brown MG 22,222 US NA - Donghae 30-JunNon-glutinous brown MG 22,222 US Fina Line Co. $918.24 Incheon 30-JunNon-glutinous brown MG 22,222 US Fina Line Co. $912.34 Gunsan 31-JulNon-glutinous milled MG 1,500 US Fina Line Co. $997.64 Busan 30-JunNon-glutinous milled LG 1,400 Thailand Jupiter Agricultural Co. $620.00 Busan 31-MayNon-glutinous milled LG (Hom Mali) 100 Thailand Hyorim International $1,176.66 Busan 31-MayNon-glutinous brown SG 22,222 China POSCO Intl. $927.00 Incheon 30-AprNon-glutinous brown SG 16,667 China NA - Masan 30-JunGlutinous milled SG 5,000 China NA - Busan 1-May - 30-JunTotal awarded 69,666

Source: KAFFTC

February 26, 2021rice Weekly

© 2021 S&P Global Platts, a division of S&P Global inc. all rights reserved. 10

three lots not awarded in its Jan. 22 Minimum Market Access tender. KAFFTC will re-tender for 22,222 mt of US

specific non-glutinous brown medium grain rice and 16,667 mt of Chinese specific non-glutinous brown short grain rice.

Offers are to be submitted on a CIP Donghae and CIP Masan basis for Sept. 30 and June 30 arrival, respectively.