Resource and Skill Transfers in Subcontractor SME Acquisitions: Influence on the Long-Term...

19

Resource and Skill Transfers in Subcontractor SME Acquisitions: Influence on the Long-Term Performance of Acquired Firms Véronique Favre-Bonté and Catherine Thévenard-Puthod IREGE, Université de Savoie, Annecy-le-Vieux, France This paper investigates the link between resource and skill transfers and the long-term performance of acqui- sitions. Rather than taking the more common acquirer’s perspective, this research emphasizes the point of view of the acquired firm and focuses on a little-studied type of business, namely, small and medium-sized subcontractor firms. Through 14 case studies of subcontractor acquisitions, we show that those acquired firms can improve their long-term performance in terms of turnover, profitability, number of employees and reduced dependency, if they receive certain types of new resources and skills from acquirers. Particularly, post-acquisition performance is more closely related to the transfer of managerial and functional skills than to operational resources. Three factors (e.g., geographical, business and cultural proximity) also help facilitate some types of transfers. However, the degree of post-acquisition integration does not play a key role in those transfers. Keywords: acquisition; resource transfer; skill transfer; small and medium-sized enterprises; subcontractors; performance Introduction Acquisition performance is a recurrent theme in stra- tegic management research (Zollo and Meier, 2008; Haleblian et al., 2009). Yet most studies examine the acquirer’s point of view or combine both firms’ perspec- tives (Capron and Hulland, 1999; Ahuja and Katila, 2001; Capron and Pistre, 2002; Cloodt et al., 2006); the acquirer’s perspective may seem more important, in the sense that being acquired is a signal of weakness or failure (Graebner and Eisenhardt, 2004). Although research has considered a firm’s capacity to choose whether and by whom it will be acquired (Graebner, 2004; Graebner and Eisenhardt, 2004; Dalziel, 2008), few studies have explored the acquired firm’s side of the story (Bandick and Görg, 2010). However, acquirer and acquired firms may differ in their assessments of acqui- sition performance, such that ‘one party could consider an acquisition successful while the other views it as disappointing’ (Graebner et al., 2010: 77). For example, owners who sell their companies are often concerned about their longevity, especially when the companies are family-owned, small and medium-sized enterprises (SMEs). To preserve their employees’ jobs, maintain the know-how and culture of their firm, and nurture good relationships with customers and suppliers (Uzzi, 1997; Dalziel, 2008), they tend to choose an acquirer carefully (Kets de Vries, 1988) and attend to the performance of the firm even after its acquisition (Graebner et al., 2010). The long-term performance of acquired firms has also become a major concern of public institutions in many Western countries, because the demographics of owner- managers 1 and the relatively high failure rate of acqui- sitions raise both economic and social issues (Calogirou et al., 2011). Even when a selling firm no longer exists as an independent legal entity, it can still be analysed as an acquired unit, especially if its post-acquisition integra- tion into the acquirer is low and it retains a high level of autonomy. In such a scenario, we could appraise acquisition performance in terms of the long-term Correspondence: Catherine Thévenard-Puthod, IREGE, Université de Savoie, chemin de Bellevue, BP 80439, 74944 Annecy-le-Vieux Cedex, France. E-mail: [email protected] 1 Each year, business transfers in the EU 27 due to the age of firm owners affect 450,000 firms and 2,000,000 employees (Calogirou et al., 2011). European Management Review, Vol. 10, 117–135 (2013) DOI: 10.1111/emre.12014 © 2013 European Academy of Management

-

Upload

univ-savoie -

Category

Documents

-

view

3 -

download

0

Transcript of Resource and Skill Transfers in Subcontractor SME Acquisitions: Influence on the Long-Term...

Resource and Skill Transfers inSubcontractor SME Acquisitions:

Influence on the Long-Term Performanceof Acquired Firms

Véronique Favre-Bonté and Catherine Thévenard-PuthodIREGE, Université de Savoie, Annecy-le-Vieux, France

This paper investigates the link between resource and skill transfers and the long-term performance of acqui-sitions. Rather than taking the more common acquirer’s perspective, this research emphasizes the point of view ofthe acquired firm and focuses on a little-studied type of business, namely, small and medium-sized subcontractorfirms. Through 14 case studies of subcontractor acquisitions, we show that those acquired firms can improve theirlong-term performance in terms of turnover, profitability, number of employees and reduced dependency, if theyreceive certain types of new resources and skills from acquirers. Particularly, post-acquisition performance ismore closely related to the transfer of managerial and functional skills than to operational resources. Three factors(e.g., geographical, business and cultural proximity) also help facilitate some types of transfers. However, thedegree of post-acquisition integration does not play a key role in those transfers.

Keywords: acquisition; resource transfer; skill transfer; small and medium-sized enterprises; subcontractors;performance

Introduction

Acquisition performance is a recurrent theme in stra-tegic management research (Zollo and Meier, 2008;Haleblian et al., 2009). Yet most studies examine theacquirer’s point of view or combine both firms’ perspec-tives (Capron and Hulland, 1999; Ahuja and Katila,2001; Capron and Pistre, 2002; Cloodt et al., 2006); theacquirer’s perspective may seem more important, in thesense that being acquired is a signal of weakness orfailure (Graebner and Eisenhardt, 2004). Althoughresearch has considered a firm’s capacity to choosewhether and by whom it will be acquired (Graebner,2004; Graebner and Eisenhardt, 2004; Dalziel, 2008),few studies have explored the acquired firm’s side of thestory (Bandick and Görg, 2010). However, acquirer andacquired firms may differ in their assessments of acqui-sition performance, such that ‘one party could consideran acquisition successful while the other views it asdisappointing’ (Graebner et al., 2010: 77). For example,

owners who sell their companies are often concernedabout their longevity, especially when the companies arefamily-owned, small and medium-sized enterprises(SMEs). To preserve their employees’ jobs, maintain theknow-how and culture of their firm, and nurture goodrelationships with customers and suppliers (Uzzi, 1997;Dalziel, 2008), they tend to choose an acquirer carefully(Kets de Vries, 1988) and attend to the performance ofthe firm even after its acquisition (Graebner et al., 2010).The long-term performance of acquired firms has alsobecome a major concern of public institutions in manyWestern countries, because the demographics of owner-managers1 and the relatively high failure rate of acqui-sitions raise both economic and social issues (Calogirouet al., 2011). Even when a selling firm no longer exists asan independent legal entity, it can still be analysed as anacquired unit, especially if its post-acquisition integra-tion into the acquirer is low and it retains a high levelof autonomy. In such a scenario, we could appraiseacquisition performance in terms of the long-term

Correspondence: Catherine Thévenard-Puthod, IREGE, Université deSavoie, chemin de Bellevue, BP 80439, 74944 Annecy-le-Vieux Cedex,France. E-mail: [email protected]

1Each year, business transfers in the EU 27 due to the age of firmowners affect 450,000 firms and 2,000,000 employees(Calogirou et al., 2011).

European Management Review, Vol. 10, 117–135 (2013)DOI: 10.1111/emre.12014

© 2013 European Academy of Management

performance of the previously separate entity (Dalziel,2008).2

Prior research has emphasized the role of resourceand skill transfers in the performance of acquisitions(Haspeslagh and Jemison, 1991; Bresman et al., 1999;Larsson and Finkelstein, 1999; Ranft and Lord, 2002;Stahl and Voigt, 2008), yet sufficient knowledgeabout such transfers is lacking (Haleblian et al., 2009).Empirical work is essential to address the link betweentransfers and post-acquisition performance using non-financial measures and to examine long-term evaluationsand strategic measures (King et al., 2004; Laamanen andKeil, 2008; Haleblian et al., 2009) to reveal firms’ futurepotential (Cording et al., 2010). Consequently, weexplore the impact of resource and skill transfers on theacquired unit’s long-term post-acquisition performance,using a resource-based view of the internal sources of afirm’s sustained competitive advantage (Barney, 1991;Kraaijenbrink et al., 2010). An acquirer can obtain valu-able, rare, inimitable and non-substitutable resourcesfrom an acquired unit (Wernerfelt, 1984; Haspeslaghand Jemison, 1991; De Man and Duysters, 2005); inturn, the resources and skills an acquired firm possessesmight be enhanced during the integration process if itreceives resources and competences from the acquirer(Morosini et al., 1998; Stahl and Voigt, 2008). Thisprediction seems particularly apt for SMEs, especiallysubcontractors,3 which often suffer from a structuraldeficit of resources and skills (Alvarez and Barney,2002). Therefore, we investigate the link betweenresource and skill transfers and the long-term perfor-mance of an acquisition, from the acquired subcontrac-tor firm’s point of view. In particular, we address thefollowing research questions: What resources and/orskills are most important to ensure the long-term perfor-mance of an acquired subcontractor SME, and whichtypes of factors facilitate those transfers?

We focus on small subcontractor firms for four mainreasons. First, it is easier to determine the effects ofresource and skill transfers for smaller firms. Second,these subcontractors often need additional resources andexpertise to improve their competitiveness and managetheir situation of dependence in relation to their princi-pal (Wilson and Gorb, 1983; Radway et al., 2011).Third, subcontractors represent a critical part of theeconomies of many industrialized countries (12% ofvalue added in Portugal, 9% in France, 8% in Germanyand 6% in the United Kingdom; Eurostat, 2009). Fourth,

to our knowledge, few studies have examined thesefirms, even though they are prime targets for acquisitions(Quah and Young, 2005). To explore which types ofresource and skill transfers play a key role in the long-term performance of an acquired subcontractor firm,given the lack of prior theory and empirical work onthese topics, we adopt an exploratory, partially inductiveresearch design, based on a multiple case studyapproach. We analysed 14 acquisition cases of subcon-tractor SMEs in the automotive industry. Unlike moststudies of skill transfers in acquisitions (Capron et al.,1998; Capron and Hulland, 1999), we focus on not onlyhorizontal acquisitions but all types of buyers. That is, asubcontractor can be bought by a competitor, but it alsomight be acquired by a customer, supplier, or companyfrom another industry.

We begin by presenting our analysis framework,developed from a resource-based view of acquisitions,together with our case study methodology. We thendescribe the types of resources and skills transferred tothe subcontractor SMEs in our sample after acquisitionand their effects on the firms’ long-term post-acquisitionperformance. Despite their loss of autonomy, acquiredfirms can benefit from acquisition, provided they receivenew resources and skills from their acquirers. Althoughpost-acquisition performance may be linked to theamount of resources and skills transferred, it also mayrelate to the types of transfer, such as functional andmanagerial skills rather than operational resources.Finally, we discuss key facilitators of resource or skilltransfers.

Literature review: analysis framework

Performance of acquisitions, from the acquired firm’spoint of view

Unlike large companies, in which management andownership are separated, many SMEs belong to singleowner-managers or families with a controlling stake inthe company that may have founded or inherited thefirm.4 This connection influences their corporate objec-tives, which are often confused with the personal goalsof the firms’ leaders or families. Acquisition in thissetting is nearly always a process of mutual agreementbetween a potential acquirer and a seller,5 rather than a

2Indirectly, the performance of the acquired entity also affectsthat of the acquirer.3Subcontractors differ from first-tier supplier or equipmentmanufacturer. An equipment manufacturer is commercially andtechnically responsible for its products. The subcontractor isitself a contractor; its activity is subordinate to that of the prin-cipal, and it must meet the technical specifications required bythe principal.

4Family businesses are the dominant form of organizationsworldwide (Churchill and Hatten, 1987; Shanker and Astrachan,1996). In 2003, they represented 93% of companies in Italy,80% in Greece, 70% in Belgium and 60% each in France andGermany (IFERA, 2003). In the United States, they represented90% of companies (Ibrahim and Ellis, 1994).5We use the term ‘seller’ to refer to the owner-manager of theSME; it becomes an ‘acquired firm’ or ‘acquired unit’ after thedeal is concluded.

118 V. Favre-Bonté and C. Thévenard-Puthod

© 2013 European Academy of Management

hostile transaction directed by the acquirer (Wang andZajac, 2007). Owners can adopt a proactive approachtoward acquisition (Graebner and Eisenhardt, 2004) andactively seek an acquirer when their firms confrontstrategic hurdles (e.g., strategic gaps, sales ramp-up,funding search). In this case, an acquisition secures asuitable partner for firms to overcome weak financialperformance or achieve renewal or growth (Teerikangas,2010), particularly in the case of small subcontractors inmature industries (e.g., forestry, textile, automotive, air-craft; Amesse et al., 2001; Kilduff, 2005). For example,in the automotive industry, it has long been difficult forsmall subcontractors that use a traditional economicmodel based on the sale of ‘human hours’ to demonstratetheir added value to primary contractors. They haveadopted various strategies to achieve a status of ‘partner’or ‘preferred supplier’ (Turnbull et al., 1992), whichhelps ensure their long-term survival (Lyons et al.,1990), including investing in efficient production toolsto increase productivity and resist aggressive competi-tion or improving their technical expertise and innovat-ing to meet complex client requirements in internationalsettings (Hyun, 1994; De Toni and Nassimbeni, 1996;Holmlund and Kock, 1996; Ali et al., 1997). To satisfysuch requirements, those SMEs face two main cumula-tive handicaps – their small size (lack of resources andskills) and their symbiotic dependency (Pfeffer andSalancik, 1978) on primary contractors that seek lowprices – which lead to a ‘pincer movement effect’. Thatis, to keep abreast of developments in the industrialenvironment, they must make changes that demand sig-nificant investments (Presutti, 1991), but they often lackthe financial capacities to realize such changes (e.g.,insufficient profitability to self-finance investments,inability to obtain traditional loans due to their insuffi-cient profitability and uncertain activities; EuropeanCommission, 2012). The more they wait to make invest-ments though, the more they risk losing their competi-tiveness, creating a vicious cycle of declining financialresources. These difficulties can be exacerbated for SMEowners who have reached retirement age and thusare less motivated to engage in ambitious projects,accept stress or work long hours. Selling the firm to anacquirer offers a solution that can alleviate both environ-mental constraints (reduced vulnerability, complemen-tary resources and skills, access to new markets) andpersonal challenges (e.g., desire to abandon stressfulmanagerial responsibilities).

However, SME owners might not opt for the highestbidder or the acquirer that offers the most attractivepositions in the combined structure. Rather, theyendeavour to find an acquirer that can ensure thelong-term survival of their firm (Graebner andEisenhardt, 2004) and help it prosper in a positive post-acquisition environment. They seek similarities andcomplementarities that create synergy or diversification,

not just a financial transaction to maximize their ownprofit. They favour buyers who possess the resourcesneeded to make the target successful in the long term(Graebner et al., 2010). In this sense, their assessment ofacquisition performance differs from the acquirer’s,such as in relation to long-term performance. Thisassessment also could reflect social considerations(Uzzi, 1997). For example, Dalziel (2008) shows thatsellers consider an acquisition successful when theiremployees benefit from it. First, they may want to ensurethat the people associated with the past success of theSME are rewarded for their contributions. Second,employees may be critical to ensuring their firms’ long-term survival objective. Third, though manager turnoveris high after acquisitions (Siehl et al., 1990; Krug andNigh, 2001), some owner-managers stay on as execu-tives in the combined structure for many years(Graebner, 2004).

Benefits of resource and skill transfers tosubcontractor SMEs

Acquisitions are usually seen as a means for the acquirerto obtain access to the valuable resources and capabil-ities (e.g., technology) of the acquired firm (Larsson andFinkelstein, 1999; Birkinshaw et al., 2000; Ahujaand Katila, 2001; Vermeulen and Barkema, 2001; Ranftand Lord, 2002; Björkman et al., 2007; Stahl and Voigt,2008). However, the acquired firm can also benefit fromthe redeployment of the acquirer’s resources and skills(Haspeslagh and Jemison, 1991; Capron et al., 1998;Bresman et al., 1999).

Because the resource-based view does not clearlydefine resources and competences (Kraaijenbrink et al.,2010), we use Grant’s (1991) and Haspeslagh andJemison’s (1991) approaches to distinguish three typesof transfers (see Table 1).

The first type refers to operational resources, suchthat the acquirer can bring physical assets (buildings,manufacturing facilities, distribution channels), humanresources (technical employees, sales force), immaterialassets (brands), or financial resources to the acquiredfirm. In general, SMEs have fewer resources than otherfirms (Alvarez and Barney, 2002; Street and Cameron,2007), such as a lack of qualified personnel or equityshortages (Chatterjee, 1986; Palepu, 1986). Only largerfirms or those that possess technological expertise gainaccess to capital markets; others must rely on their owncash reserves or bank loans. Subcontractors’ commer-cial dependence also increases those financial chal-lenges, because their weaker negotiation power relativeto primary contractors allows the latter to impose pricecuts (Wilson and Gorb, 1983; Holmlund and Kock,1996; Donada, 2002; Kilduff, 2005), which result in lowprofits (profits of 1.8% vs. 3.8% for the rest of theindustry in France in 2001; commercial profitability of

Skills Transfers and Acquired Firm’s Performance 119

© 2013 European Academy of Management

0.8% in 2007, according to the French Department ofStudies and Industrial Statistics6). This lack of financialresources represents a significant obstacle to effectiveinvestments in the human and material resourcesrequired to enhance subcontractor firms’ status in theindustry or to diversify. The structural deficits suggestthat resource transfers from an acquirer would bebeneficial.

The acquirer firm can also transfer functional skillsthrough horizontal interactions between the managers ofboth firms (Haspeslagh and Jemison, 1991), suchas those related to research and development (R&D)(technological skills, development of new products),

human resource management (HRM), or finance andmarketing skills (distribution network, customer rela-tionship management, reputation). These skills can beuseful for subcontractors, which typically are not highlystructured. With their situation of symbiotic dependency(Pfeffer and Salancik, 1978), these firms sell productsdesigned by the primary contractor. Although they likelycontain manufacturing and purchasing departments,they do not possess research or marketing structures.This lack of functional skills can be an obstacle tochange. Moreover, contractors often interfere in theirsubcontractors’ management processes, such as produc-tion, HRM, or quality (Kamath and Liker, 1990; Hanet al., 1993; Rutherford et al., 1995). Thus, the transferof skills from an acquirer might offer an opportunity tobecome less dependent on a particular client and repo-sition itself within the competitive marketplace (Furlanet al., 2007).

Finally, the acquirer can transfer managerial skills,granting the acquired company more general skills, suchas leadership, strategic planning, and the use of businessintelligence, as well as other administrative skills (e.g.,resource allocation). These transfers can occur throughcoaching, direct involvement, or the imposition ofsystems (Haspeslagh and Jemison, 1991), which usuallyrequire vertical interactions at general managementlevels between the acquiring and acquired firms. Suchskills also benefit subcontractors that lack a strategicorientation (Lehtinen, 1999); for example, owner-managers might follow tradition, struggle with change,engage in reactive tactics, or suffer from short-sightedness. In general, subcontractor owners have abetter grasp of technical aspects and concentrate on theoperational side of the business or short-term efficiency,while relegating strategy to the background. Finally,dependency does not favour entrepreneurship (Lyonset al., 1990), so the subcontractor owner tends to nurturea relationship with the primary contractor but neglectgrowth or development (Wilson and Gorb, 1983;Radway et al., 2011).

Those various types of resource and skill transfersmight help the subcontractor SME face changes in itsenvironment and the resulting constraints. However,several studies have shown that the transfer of resourcesand skills depends on strategic and organizational fitbetween the acquirer and acquired firms (Hagedoorn andDuysters, 2002). Among them, factors such as businessproximity (Finkelstein and Haleblian, 2002), geographi-cal proximity (Bresman et al., 1999), or cultural prox-imity (Buono and Bowditch, 1989; Björkman et al.,2007) between the two firms are likely facilitators. Thenature of the resource and skill portfolio of each firmand their motivations for the acquisition/sale are alsotaken into account. Acquirers must also find adequateways to manage the post-acquisition integration phase(Shrivastava, 1986) to enable resource and skill transfers

6See www.insee.fr/fr/ppp/bases-de-donnees/donnees. . ./midest_09.pdf.

Table 1 Types of resources and skills

Type of transfers Examples

Operational resources(adapted from Grant,1991)

• Human resources: staff• Physical resources (land,

machinery, stocks, industrialequipment, distribution networks)

• Intangible resources (brand,patents, licences, reputation)

• Financial resources• Organizational resources

(information and managementsystems)

Functional skills(adapted from Haspeslaghand Jemison, 1991)

• Marketing and commercial skills(understanding client’s needs,sales administration, sellingproducts, managing distributionnetworks, communicating withclients, pricing)

• R&D (technical & technologicalskills, project management, newproduct development)

• Logistics & procurement skills(receiving, storing, stock control,warehousing, transport, acquisitionof various inputs)

• Financial skills (planning &budget, cash management,forecasting)

• HRM (recruiting, training,developing, rewarding people)

• Operational skills (qualityimprovement, productivityimprovement, management ofproduction costs or deadlines)

Managerial skills(adapted from Haspeslaghand Jemison, 1991)

• Leadership• Strategic planning• Use of business intelligence tools• Use of management tools• Resource allocations• Defining a growth strategy or

refining an existing strategy• Organizing the firm (choice of a

structure)

120 V. Favre-Bonté and C. Thévenard-Puthod

© 2013 European Academy of Management

(Puranam et al., 2003; Quah and Young, 2005). Theymust assess the acquired firm’s organizational autonomy(Puranam et al., 2009), because interdependencies candisturb the boundaries of the acquired firm (Haspeslaghand Jemison, 1991; Krug and Nigh, 2001; Björkmanet al., 2007).

Figure 1 summarizes the analysis framework and thetwo main research questions that guided this work (Whatresources and/or skills are most important to ensure thelong-term performance of an acquired subcontractorSME, and which types of factors facilitate those trans-fers?). On these bases, we designed our empiricalresearch.

Multiple case study methodology

No prior research has addressed the long-term perfor-mance of acquired subcontractor firms. In the post-acquisition phase, it is important to understandprocesses as they occur in their natural context ratherthan in an artificially constructed setting (e.g., Yin,1994; Langley, 1999). To account for all facets of theproblem, a qualitative methodology is more appropriatefor gaining insights (Teerikangas and Very, 2006;Meglio and Risberg, 2010). To provide an initial assess-ment of how resource and skill transfers affect acquiredsubcontractor firms’ long-term performance, we need toconsider the context in which these transfers take place,such as the profiles and motivations of firms (acquirersand acquired), assessment of their resources and skillsportfolio, and the factors that may interfere with thetransfer. From this perspective, we adopted a multiplecase study approach (Yin, 1994; Piekkari et al., 2009).

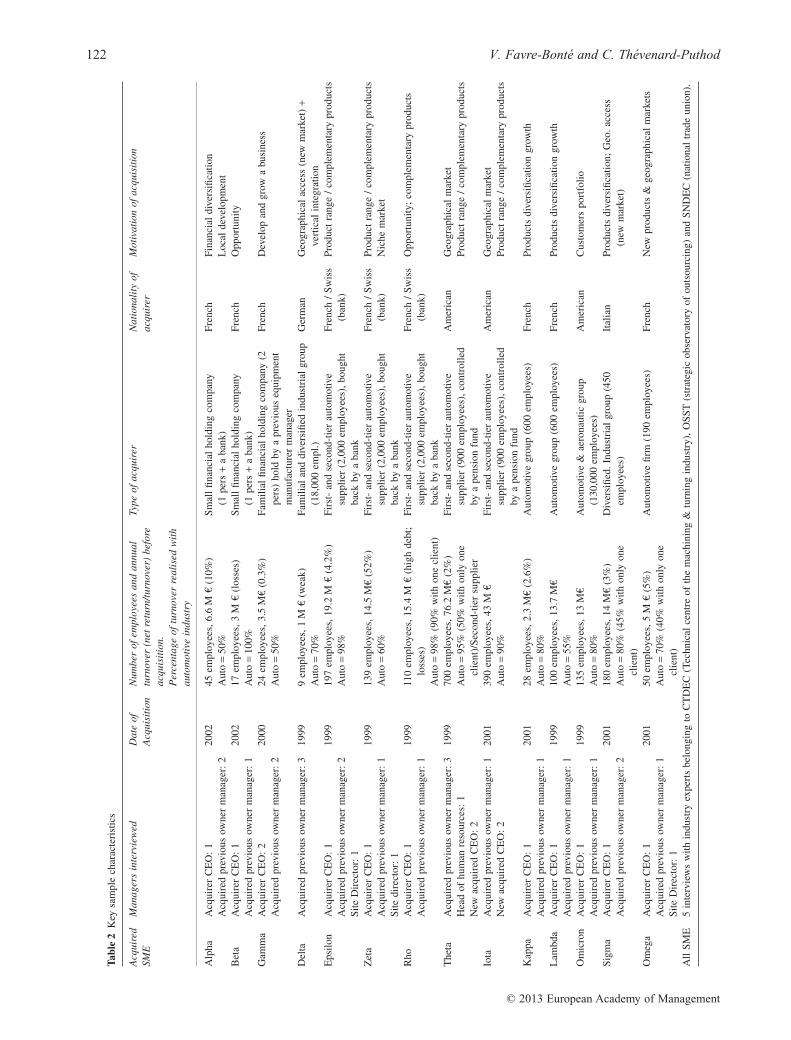

Case selection

Selected cases constituted the theoretical sample (Glaserand Strauss, 1967; Eisenhardt, 1989). The sample char-acteristics appear in Table 2. We took great care to selectcases that shared common characteristics (same indus-try, geographical location and period of analysis) to

ensure homogeneity for comparison purposes. There-fore, we selected 14 automobile subcontractors that werethird-tier and sometimes second-tier suppliers, not thefirst tier (i.e., they are not equipment manufacturers).7

We focused on the automotive industry for two reasons.First, it represents a critical part of the economies ofmany industrialized countries.8 Many subcontractorsdepend on the automotive industry, one of the first indus-tries to outsource activities (Rutherford et al., 1995).Second, automotive subcontractors have been primeacquisition targets in the past 10 years,9 due to their lackof structural resources and the highly competitive envi-ronment (Quah and Young, 2005). All the acquiredcompanies were French and located in the same geo-graphical area, which helped us control for the potential

7The value chain of the automotive industry includes four groupsof actors at different levels: automotive manufacturers (majorautomotive brands), which often assemble components made byfirst-tier suppliers, first-tier companies, or equipment manufac-turer (which manufacture equipment or modules for vehiclesand generally have made significant internationalization andinnovation efforts to support manufacturers), second-tier com-panies (specialty or capacity subcontractors dependent on theautomotive industry) and third-tier companies (both capacitysubcontractors and subcontractors of components that are thenassembled by second-tier subcontractors, which depend heavilyon first- and second-tier suppliers and must comply with allconstraints imposed by upstream manufacturers, so they absorball the pressures of the industry).8In Europe, the automotive industry is a structuring activity forthe economy. It represents around 12 million direct and indirectjobs and delivers a sizeable positive contribution to the EU tradebalance (growing over the last few years and reaching €90billion in 2011; European Commission, 2012). The world’sautomotive industry in 2005 produced more than 66 millioncars, vans, trucks and buses, a level of output equivalent to aglobal turnover (gross revenue) of almost €2 trillion. Building 66million vehicles requires the employment of approximately 9million people directly, or more than 5% of the world’s totalmanufacturing employment. Each direct auto job supports anestimated five more indirect jobs in the community, resulting inmore than 50 million jobs from the auto industry (InternationalOrganization of Motor Vehicle Manufacturers, www.OICA.net).9There were 532 deals in 2009, representing worth than $121.9billion (PriceWaterhouseCoopers, 2010).

ACQUIRER:• Motivations• Geographic

location• Resources and

skills portfolio

LONG-TERM PERFORMANCE OF

ACQUIREDSUBCONTRACTOR

RESOURCE AND SKILL TRANSFERS:

• Type (resources, functional skills, managerial skills)?

• Extent?

Role of influencingfactors?

Figure 1 Analysis framework

Skills Transfers and Acquired Firm’s Performance 121

© 2013 European Academy of Management

Tabl

e2

Key

sam

ple

char

acte

rist

ics

Acq

uire

dSM

EM

anag

ers

inte

rvie

wed

Dat

eof

Acq

uisi

tion

Num

ber

ofem

ploy

ees

and

annu

altu

rnov

er(n

etre

turn

/tur

nove

r)be

fore

acqu

isit

ion.

Per

cent

age

oftu

rnov

erre

alis

edw

ith

auto

mot

ive

indu

stry

Type

ofac

quir

erN

atio

nali

tyof

acqu

irer

Mot

ivat

ion

ofac

quis

itio

n

Alp

haA

cqui

rer

CE

O:

1A

cqui

red

prev

ious

owne

rm

anag

er:

220

0245

empl

oyee

s,6.

6M

€(1

0%)

Aut

o=

50%

Smal

lfin

anci

alho

ldin

gco

mpa

ny(1

pers

+a

bank

)Fr

ench

Fina

ncia

ldi

vers

ifica

tion

Loc

alde

velo

pmen

tB

eta

Acq

uire

rC

EO

:1

Acq

uire

dpr

evio

usow

ner

man

ager

:1

2002

17em

ploy

ees,

3M

€(l

osse

s)A

uto

=10

0%Sm

all

finan

cial

hold

ing

com

pany

(1pe

rs+

aba

nk)

Fren

chO

ppor

tuni

ty

Gam

ma

Acq

uire

rC

EO

:2

Acq

uire

dpr

evio

usow

ner

man

ager

:2

2000

24em

ploy

ees,

3.5

M€

(0.3

%)

Aut

o=

50%

Fam

ilial

finan

cial

hold

ing

com

pany

(2pe

rs)

hold

bya

prev

ious

equi

pmen

tm

anuf

actu

rer

man

ager

Fren

chD

evel

opan

dgr

owa

busi

ness

Del

taA

cqui

red

prev

ious

owne

rm

anag

er:

319

999

empl

oyee

s,1

M€

(wea

k)A

uto

=70

%Fa

mili

alan

ddi

vers

ified

indu

stri

algr

oup

(18,

000

empl

.)G

erm

anG

eogr

aphi

cal

acce

ss(n

ewm

arke

t)+

vert

ical

inte

grat

ion

Eps

ilon

Acq

uire

rC

EO

:1

Acq

uire

dpr

evio

usow

ner

man

ager

:2

Site

Dir

ecto

r:1

1999

197

empl

oyee

s,19

.2M

€(4

.2%

)A

uto

=98

%Fi

rst-

and

seco

nd-t

ier

auto

mot

ive

supp

lier

(2,0

00em

ploy

ees)

,bou

ght

back

bya

bank

Fren

ch/

Swis

s(b

ank)

Prod

uct

rang

e/

com

plem

enta

rypr

oduc

ts

Zet

aA

cqui

rer

CE

O:

1A

cqui

red

prev

ious

owne

rm

anag

er:

1Si

tedi

rect

or:

1

1999

139

empl

oyee

s,14

.5M

€(5

2%)

Aut

o=

60%

Firs

t-an

dse

cond

-tie

rau

tom

otiv

esu

pplie

r(2

,000

empl

oyee

s),b

ough

tba

ckby

aba

nk

Fren

ch/

Swis

s(b

ank)

Prod

uct

rang

e/

com

plem

enta

rypr

oduc

tsN

iche

mar

ket

Rho

Acq

uire

rC

EO

:1

Acq

uire

dpr

evio

usow

ner

man

ager

:1

1999

110

empl

oyee

s,15

.4M

€(h

igh

debt

;lo

sses

)A

uto

=98

%(9

0%w

ithon

ecl

ient

)

Firs

t-an

dse

cond

-tie

rau

tom

otiv

esu

pplie

r(2

,000

empl

oyee

s),b

ough

tba

ckby

aba

nk

Fren

ch/

Swis

s(b

ank)

Opp

ortu

nity

;co

mpl

emen

tary

prod

ucts

The

taA

cqui

red

prev

ious

owne

rm

anag

er:

3H

ead

ofhu

man

reso

urce

s:1

New

acqu

ired

CE

O:

2

1999

700

empl

oyee

s,76

.2M

€(2

%)

Aut

o=

95%

(50%

with

only

one

clie

nt)/

Seco

nd-t

ier

supp

lier

Firs

t-an

dse

cond

-tie

rau

tom

otiv

esu

pplie

r(9

00em

ploy

ees)

,con

trol

led

bya

pens

ion

fund

Am

eric

anG

eogr

aphi

cal

mar

ket

Prod

uct

rang

e/

com

plem

enta

rypr

oduc

ts

Iota

Acq

uire

dpr

evio

usow

ner

man

ager

:1

New

acqu

ired

CE

O:

220

0139

0em

ploy

ees,

43M

€A

uto

=90

%Fi

rst-

and

seco

nd-t

ier

auto

mot

ive

supp

lier

(900

empl

oyee

s),c

ontr

olle

dby

ape

nsio

nfu

nd

Am

eric

anG

eogr

aphi

cal

mar

ket

Prod

uct

rang

e/

com

plem

enta

rypr

oduc

ts

Kap

paA

cqui

rer

CE

O:

1A

cqui

red

prev

ious

owne

rm

anag

er:

120

0128

empl

oyee

s,2.

3M

€(2

.6%

)A

uto

=80

%A

utom

otiv

egr

oup

(600

empl

oyee

s)Fr

ench

Prod

ucts

dive

rsifi

catio

ngr

owth

Lam

bda

Acq

uire

rC

EO

:1

Acq

uire

dpr

evio

usow

ner

man

ager

:1

1999

100

empl

oyee

s,13

.7M

€A

uto

=55

%A

utom

otiv

egr

oup

(600

empl

oyee

s)Fr

ench

Prod

ucts

dive

rsifi

catio

ngr

owth

Om

icro

nA

cqui

rer

CE

O:

1A

cqui

red

prev

ious

owne

rm

anag

er:

119

9913

5em

ploy

ees,

13M

€A

uto

=80

%A

utom

otiv

e&

aero

naut

icgr

oup

(130

,000

empl

oyee

s)A

mer

ican

Cus

tom

ers

port

folio

Sigm

aA

cqui

rer

CE

O:

1A

cqui

red

prev

ious

owne

rm

anag

er:

220

0118

0em

ploy

ees,

14M

€(3

%)

Aut

o=

80%

(45%

with

only

one

clie

nt)

Div

ersi

fied.

Indu

stri

algr

oup

(450

empl

oyee

s)It

alia

nPr

oduc

tsdi

vers

ifica

tion;

Geo

.acc

ess

(new

mar

ket)

Om

ega

Acq

uire

rC

EO

:1

Acq

uire

dpr

evio

usow

ner

man

ager

:1

Site

Dir

ecto

r:1

2001

50em

ploy

ees,

5M

€(5

%)

Aut

o=

70%

(40%

with

only

one

clie

nt)

Aut

omot

ive

firm

(190

empl

oyee

s)Fr

ench

New

prod

ucts

&ge

ogra

phic

alm

arke

ts

All

SME

5in

terv

iew

sw

ithin

dust

ryex

pert

sbe

long

ing

toC

TD

EC

(Tec

hnic

alce

ntre

ofth

em

achi

ning

&tu

rnin

gin

dust

ry),

OSS

T(s

trat

egic

obse

rvat

ory

ofou

tsou

rcin

g)an

dSN

DE

C(n

atio

nal

trad

eun

ion)

.

122 V. Favre-Bonté and C. Thévenard-Puthod

© 2013 European Academy of Management

influence of environmental factors. To reduce biasrelated to drastically different economic conditions, thefirms were acquired within the same period (between1999 and 2002). However, they still exhibited some dif-ferences, such as various automotive subcontractingactivities, different sizes and varied acquirer types (interms of activity, motivations and nationality).

Following Eisenhardt (1989), we aimed initially toanalyse 10 cases of acquired companies, but severalgroups acquired multiple firms in the same territory.Thus, we needed to include all acquisitions in thesample, because their existence could influence the inte-gration process of subsidiaries of the same group(Barkema and Schijven, 2008). For example, weincluded Theta in the sample, even though its size ishigher than commonly accepted for SMEs (500employees in Canada and the United States, 250 inEurope), because we first selected and studied Iota(acquired by the same firm as Theta).

Because value creation does not take place immedi-ately but only during a later post-acquisition phase(Larsson and Finkelstein, 1999), we chose acquisitionsthat took place two to five years before the data collec-tion of the study, which started in 2004. This processprovided sufficient time for the resources and skills to betransferred (Morosini et al., 1998).10

Data collection and analysis

We used many different data sources to analyse cases indepth, and we developed insights through a comparativelogic. We conducted 42 semi-directive interviews(average length of two to three hours) with at least twomanagers involved in the operation, including ownersand managers from the acquired company and theacquirer. We also interviewed five industry experts inthe institutional environment, such as trade unionrepresentatives or strategic observatory members (seeTable 2), to obtain a more objective view on the acqui-sitions progress and accurate information about theindustry and its evolution. To create the interview guide,we used the previously described analysis frameworkand structured it chronologically to follow the acquisi-tion process: the context of the SME before the acquisi-tion (history, key figures, strategy, lack of resources andskill, environmental constraints, other difficulties), thetype of acquirer and its motivations, how the operationtook place, the integration process (degree of autonomyleft with the SME, changes after the acquisition, internaland external difficulties), the types of resources and

skills transferred, and the post-acquisition performanceassessment. Each interview was transcribed, resulting innearly 300 pages in total. To mitigate retrospectivebiases and achieve triangulation in our informationsources (Yin, 1994), we also collected vast amounts ofsecondary data, such as sector-based notes, internalpresentations/notes written by companies at the time oftheir acquisition and press articles. Finally, we engagedin passive observation (visits to factories and offices) togain familiarity with the immediate environment, thework atmosphere and the changes implemented.

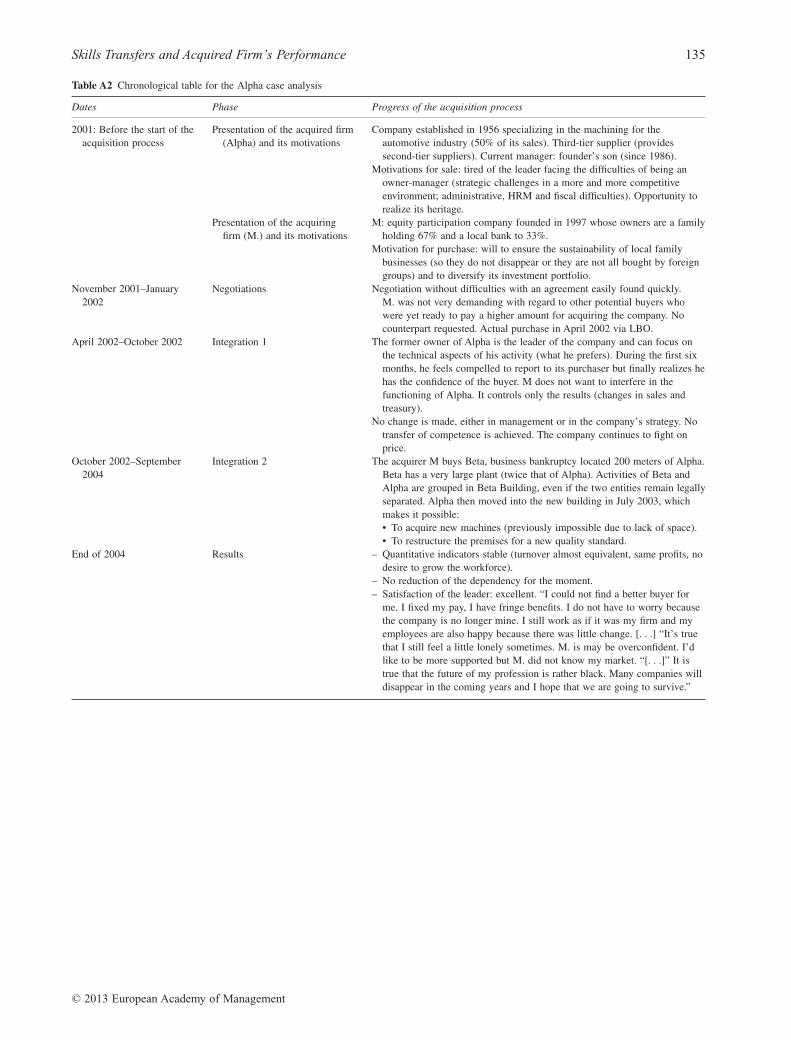

To code the data, we used content analysis procedures(Strauss, 1987). During within-firm analysis, we codedall data into categories, according to our theoreticalmodel. For example, each type of resource or skill trans-ferred was codified, along with the variables that influ-enced the nature of these transfers (e.g., type of acquirer,geographical and cultural distance, integration difficul-ties). For the first 10 interviews, we used a double-coding check by two researchers to ensure consistencyin the classification. In parallel, we traced the wholeacquisition history of each case. We developed tablesand timelines of historical events (two examples appearin the Appendix), to summarize key facts about theprocess, identify emerging predictors of post-acquisitionperformance of acquired companies and determine theinfluence factors of resource and skill transfers (Milesand Huberman, 1994). We then used cross-case analysisto find patterns across multiple cases and to determinethe relationship between the type of transfer and post-acquisition performance. We draw several meta-matricesto facilitate the case comparisons (Miles and Huberman,1994). To increase the validity of our results, we pre-sented our analysis to the five industry experts alreadymentioned, which helped strengthen our interpretations.

No consensus exists on how to measure acquisitionperformance (Zollo and Meier, 2008; Cording et al.,2010; Papadakis and Thanos, 2010); various availableindicators include stock market–based measures (abnor-mal returns; Capron and Pistre, 2002; accountingmetrics, such as return on assets or investment and cashflows; Haleblian et al., 2009), strategic-based measures(market share, innovation capability; Ahuja and Katila,2001; Puranam et al., 2003; Cloodt et al., 2006),organization-based measures (management turnover;Krug and Aguilera, 2005) or more subjective measuressuch as managers’ assessments of the materialization ofpre-acquisition objectives (Vaara, 2002; Schoenberg,2006). These measures are of interest for different typesof stakeholders. Because the performance measureshould be temporally proximal to our research objective(King et al., 2004; Cording et al., 2010) and because asingle-dimensional approach can lead to controversialresults (Papadakis and Thanos, 2010), we retained fourobjective and one subjective strategic management andaccounting indicators. Objective measures reflected the

10Acquisition research does not agree about when integration iscomplete. The process of combination may take a two-yearperiod after the acquisition, after which the results of integrationefforts can be measured effectively (Morosini et al., 1998), butother researchers claim the need for a longer period (Birkinshawet al., 2000; Quah and Young, 2005).

Skills Transfers and Acquired Firm’s Performance 123

© 2013 European Academy of Management

evolution of the acquired firm’s turnover11 (growth insales compared with the industry average), profitability,number of employees and dependency. We measureddependency with two criteria: commercial dependencyand industrial dependency. Commercial dependency isthe portion of turnover realized with the three mainclients, and industrial dependency is the portion of turn-over realized with the automotive industry specifically.The idea was to observe an evolution in dependence. Forcommercially dependent firms, we sought to determineif they managed to diversify their customer base withinthe automotive sector. For those firms dependent on theautomotive industry, but not in any one or two clients,we wanted to know if they were able to diversify theirmarkets outside the automotive sector. These measuresindicate the future potential of the acquired firm(Cording et al., 2010). The subjective measure capturedthe satisfaction of the acquired firm’s previous ownerwith the acquisition (comprehensive measure of whetheracquisition outcomes met expectations).

Findings

In general, the subcontractor SMEs we studied experi-enced greater negotiation power after their acquisitionand also enjoyed a better image in the market (i.e., theircustomers appeared more confident). Beyond theseinitial benefits, the acquirers contributed resources totheir acquired companies. However, the enrichment offunctional or managerial skills was not always system-atic, and the latter type of transfer primarily affected thelong-term performance of the acquired unit.

Description of resource and skill transfers

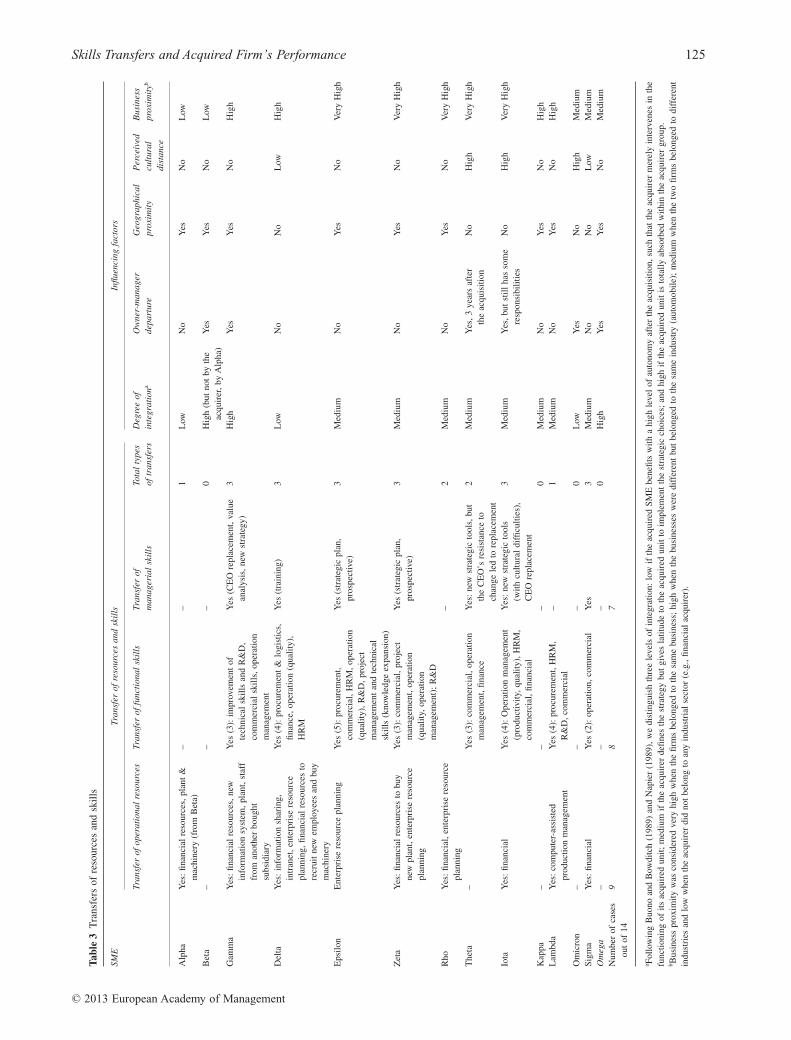

The acquisitions mostly occurred for strategic reasons,such as to enter a new geographic market (France orEurope) or to extend the product range. In this context,almost all the acquisitions we studied involved the trans-fer of new resources and skills to the acquired company(10 of 14 cases), regardless of the degree of integration(only three were highly integrated: Beta, Gamma andOmega). Table 3 presents the type of transfers involvedin each case and the influence factors we studied.

Regarding the types of resources or skills transferred,only two firms benefited solely from new resources(Alpha and Rho). For Alpha, the acquirer came fromanother industry and did not intend (or have the skills) toinvest anything other than financial resources. Rho’s

acquirer represented the same industry but did not wantto transfer anything except financing. The remainder ofthe acquired firms received at least two of the three typesof transfers. Theta benefited from functional and mana-gerial skills, Lambda gained resources and functionalskills and six firms benefited from global packages of allthree transfers (Gamma, Delta, Epsilon, Sigma, Zeta andIota). Therefore, in most cases (8 of 14), the acquirerintended to develop the acquired firm and endeavouredto transfer as many skills and resources as possible.Time did not seem to influence transfer extent; we foundno more transfers in the SME acquired five years previ-ously than in the firm acquired only two years previ-ously. Therefore, transfers, if they occurred, took placeearly in the post-acquisition process.

In terms of resources, equity capital occurred in halfthe cases (Alpha, Gamma, Delta, Rho, Zeta, Iota andSigma), which is less than in other studies; for example,Capron et al. (1998) find that 88% of acquirers providefinancial resources. The additional financial resourcesenabled the smallest firms to purchase new machines orlarger facilities and to recruit staff to grow or extend intonew markets. Thus, the acquisitions were springboardsfor growth. As the previous owner of Alpha stated:

With the acquisition of the company Beta, six monthsafter that of my company, we could move to a largerbuilding. The financial contribution of M [theacquirer] also allowed us to invest in new machineryand to meet the demands for new markets. Previously,the surface saturation limited investments . . . Andthe new financial resources will soon allow us torearrange our premises and thus seek a new standardthat few of our competitors have. If we get it, we willreach the second-tier level. Of course, after that, wewill have to find customers.

For other companies, new financial resources enabledthem to pull through a crisis. Six acquired firms thatjoined groups also benefited from new information andmanagement systems (e.g., intranet access, enterpriseresource planning, computer-assisted production man-agement), installed to facilitate data exchanges with thehead office or other subsidiaries (which also enabledinternal benchmarking). Thus, the resources providedmainly related to the industrial production function,which is a strategic element for automotive suppliers.

The transfer of functional skills to the acquired firm ineight cases (Delta, Epsilon, Zeta, Sigma, Theta, Iota,Gamma and Lambda) was effective almost from the startof the post-acquisition phase as a means to structurethe organization rapidly. This transfer took place witheither the acquirers’ headquarters or other subsidiariesif they represented the same industry. Various types offunctional skill transfers occurred. The most frequentskill entailed operation management (7 cases); manyfactories were reorganized to increase productivity. The

11When the acquired entity is fully integrated into the group andbecomes a simple plant, it is sometimes difficult to measure itsperformance. However, in our study, our acquirers implemented‘internal billing’, which enabled us to identify measures such asturnover and profit rate.

124 V. Favre-Bonté and C. Thévenard-Puthod

© 2013 European Academy of Management

Tabl

e3

Tra

nsfe

rsof

reso

urce

san

dsk

ills

SME

Tran

sfer

ofre

sour

ces

and

skil

lsIn

fluen

cing

fact

ors

Tran

sfer

ofop

erat

iona

lre

sour

ces

Tran

sfer

offu

ncti

onal

skil

lsTr

ansf

erof

man

ager

ial

skil

lsTo

tal

type

sof

tran

sfer

sD

egre

eof

inte

grat

iona

Ow

ner-

man

ager

depa

rtur

eG

eogr

aphi

cal

prox

imit

yP

erce

ived

cult

ural

dist

ance

Bus

ines

spr

oxim

ityb

Alp

haY

es:

finan

cial

reso

urce

s,pl

ant

&m

achi

nery

(fro

mB

eta)

––

1L

owN

oY

esN

oL

ow

Bet

a–

––

0H

igh

(but

not

byth

eac

quir

er,b

yA

lpha

)Y

esY

esN

oL

ow

Gam

ma

Yes

:fin

anci

alre

sour

ces,

new

info

rmat

ion

syst

em,p

lant

,sta

fffr

oman

othe

rbo

ught

subs

idia

ry

Yes

(3):

impr

ovem

ent

ofte

chni

cal

skill

san

dR

&D

,co

mm

erci

alsk

ills,

oper

atio

nm

anag

emen

t

Yes

(CE

Ore

plac

emen

t,va

lue

anal

ysis

,new

stra

tegy

)3

Hig

hY

esY

esN

oH

igh

Del

taY

es:

info

rmat

ion

shar

ing,

intr

anet

,ent

erpr

ise

reso

urce

plan

ning

,fina

ncia

lre

sour

ces

tore

crui

tne

wem

ploy

ees

and

buy

mac

hine

ry

Yes

(4):

proc

urem

ent

&lo

gist

ics,

finan

ce,o

pera

tion

(qua

lity)

,H

RM

Yes

(tra

inin

g)3

Low

No

No

Low

Hig

h

Eps

ilon

Ent

erpr

ise

reso

urce

plan

ning

Yes

(5):

proc

urem

ent,

com

mer

cial

,HR

M,o

pera

tion

(qua

lity)

,R&

D,p

roje

ctm

anag

emen

tan

dte

chni

cal

skill

s(k

now

ledg

eex

pans

ion)

Yes

(str

ateg

icpl

an,

pros

pect

ive)

3M

ediu

mN

oY

esN

oV

ery

Hig

h

Zet

aY

es:

finan

cial

reso

urce

sto

buy

new

plan

t,en

terp

rise

reso

urce

plan

ning

Yes

(3):

com

mer

cial

,pro

ject

man

agem

ent,

oper

atio

n(q

ualit

y,op

erat

ion

man

agem

ent)

;R

&D

Yes

(str

ateg

icpl

an,

pros

pect

ive)

3M

ediu

mN

oY

esN

oV

ery

Hig

h

Rho

Yes

:fin

anci

al,e

nter

pris

ere

sour

cepl

anni

ng–

2M

ediu

mN

oY

esN

oV

ery

Hig

h

The

ta–

Yes

(3):

com

mer

cial

,ope

ratio

nm

anag

emen

t,fin

ance

Yes

:ne

wst

rate

gic

tool

s,bu

tth

eC

EO

’sre

sist

ance

toch

ange

led

tore

plac

emen

t

2M

ediu

mY

es,3

year

saf

ter

the

acqu

isiti

onN

oH

igh

Ver

yH

igh

Iota

Yes

:fin

anci

alY

es(4

):O

pera

tion

man

agem

ent

(pro

duct

ivity

,qua

lity)

,HR

M,

com

mer

cial

,fina

ncia

l

Yes

:ne

wst

rate

gic

tool

s(w

ithcu

ltura

ldi

fficu

lties

),C

EO

repl

acem

ent

3M

ediu

mY

es,b

utst

illha

sso

me

resp

onsi

bilit

ies

No

Hig

hV

ery

Hig

h

Kap

pa–

––

0M

ediu

mN

oY

esN

oH

igh

Lam

bda

Yes

:co

mpu

ter-

assi

sted

prod

uctio

nm

anag

emen

tY

es(4

):pr

ocur

emen

t,H

RM

,R

&D

,com

mer

cial

–1

Med

ium

No

Yes

No

Hig

h

Om

icro

n–

––

0L

owY

esN

oH

igh

Med

ium

Sigm

aY

es:

finan

cial

Yes

(2):

oper

atio

n,co

mm

erci

alY

es3

Med

ium

No

No

Low

Med

ium

Om

ega

––

–0

Hig

hY

esY

esN

oM

ediu

mN

umbe

rof

case

sou

tof

149

87

a Follo

win

gB

uono

and

Bow

ditc

h(1

989)

and

Nap

ier

(198

9),w

edi

stin

guis

hth

ree

leve

lsof

inte

grat

ion:

low

ifth

eac

quir

edSM

Ebe

nefit

sw

itha

high

leve

lof

auto

nom

yaf

ter

the

acqu

isiti

on,s

uch

that

the

acqu

irer

mer

ely

inte

rven

esin

the

func

tioni

ngof

itsac

quir

edun

it;m

ediu

mif

the

acqu

irer

defin

esth

est

rate

gybu

tgi

ves

latit

ude

toth

eac

quir

edun

itto

impl

emen

tth

est

rate

gic

choi

ces;

and

high

ifth

eac

quir

edun

itis

tota

llyab

sorb

edw

ithin

the

acqu

irer

grou

p.b B

usin

ess

prox

imity

was

cons

ider

edve

ryhi

ghw

hen

the

firm

sbe

long

edto

the

sam

ebu

sine

ss;

high

whe

nth

ebu

sine

sses

wer

edi

ffer

ent

but

belo

nged

toth

esa

me

indu

stry

(aut

omob

ile);

med

ium

whe

nth

etw

ofir

ms

belo

nged

todi

ffer

ent

indu

stri

esan

dlo

ww

hen

the

acqu

irer

did

not

belo

ngto

any

indu

stri

alse

ctor

(e.g

.,fin

anci

alac

quir

er).

Skills Transfers and Acquired Firm’s Performance 125

© 2013 European Academy of Management

introduction of quality skills and procedures alsoincreased the levels of qualification required in the auto-motive industry. Such transfers are not surprising, con-sidering the requirements of the industry in terms ofquality, costs and deadlines.

We noted significant strengthening of the commercialfunction (seven cases). For example, Gamma’s commer-cial practices changed completely, through the introduc-tion of more proposals for customers (e.g., search forproduct improvements, anticipation of price cuts). OtherSMEs (Lambda, Zeta, Epsilon, Sigma, Theta and Iota)implemented new, more centralized sales policies, withsales conducted on a group basis to achieve the benefitsof a larger sales force and a global offering. The salesforces of these firms benefited from additional trainingon how to sell all the products available in the combinedstructure.

Other contributions pertained to HRM (4 cases) orlogistics/procurement (3 cases). As Gamma’s managernoted, ‘The acquisition made it possible to introduce aprofit sharing agreement for the staff, resulting in highermotivation’. Furthermore, Delta’s manager reported,‘Our logistics were strengthened after the acquisition.This was a necessary step considering the foreign originof the major part of our purchases of raw material, thesupply chain to be managed (several hundred tonnes)and delivery deadlines imposed by our clients’. For theseskill transfers, geographical distance was not a problem;the acquired units received the transfers even when theiracquirers were not in France.

However, there were relatively few R&D transfers(four cases). In large entities, project management skillsmoved to the acquired firm (Zeta and Epsilon). In addi-tion, some transfers of technical skills helped expand theknowledge of the acquired unit (Gamma, Lambda), aswell as R&D cooperation between engineers in the newcombined structure (Epsilon and Zeta). In all R&D skilltransfers though, the acquirer (or its subsidiaries) waslocated relatively nearby the acquired units. Accordingto the managers interviewed, it has facilitated thosetypes of transfers (many plants or labs visits and engi-neers meetings).

The sample included three cases of financial skilltransfers (Theta, Iota and Delta). The acquirer of bothTheta and Iota was owned by a pension fund, so thesetransfers were critical to re-structure the acquired units.For Delta, the transfer improved its problematic cashmanagement practices.

In more than half the cases (Sigma, Delta, Gamma,Zeta, Epsilon, Theta and Iota), a change in ownershipcreated changes in managerial skills, regardless of thegeographical or the business distances between theacquirer and the acquired units. The acquisition alteredthe company structure, including implementations ofmore rigorous, formalized management (e.g., dash-boards, value analysis). In one scenario, former owner-

managers remained in place and took advantage oftraining in the strategy and management tools used by theacquirer (Delta, Epsilon, Zeta, Sigma, Theta and Iota),which indicated a real transfer of skills. In another sce-nario, the owners were replaced by a manager, chosen bythe acquirer, who already had the required skills(Gamma). This new strategic vision of the business, theskills to be mastered, the industry and its growth perspec-tives resulted in a more proactive approach. For example,it created motivation to offer customers solutions insteadof waiting for requests and to conquer new markets orobtain new labels. Some acquired units pursued ambi-tious projects, including setting up small manufacturingunits around the world, close to clients’ plants and con-nected via a digital bridge to the French headquarterswhere the products were designed (Gamma).

However, other transfers of managerial skills weredisrupted by cultural differences. For example, thestrong financial vision of the US acquirer of Theta andIota was not always appreciated by the former owner-managers (these two owner-managers remained in placeafter the acquisition for a transitional period of up tothree years and then left the firm). Theta’s former ownerdid not hesitate to disparage the new management direc-tion taken by the acquired firm:

Now the engineers and technicians spend too muchtime filling out charts and participating in meetings tojustify any investment. They do not spend enoughtime in the plants and have less time to find solutionsto technical problems and even less to develop inno-vations. It’s dangerous for the company!

This remark illustrated the subcontractors’ general focuson the technical aspects of the job, as well as the diffi-culties some French firms face in adapting to US man-agement methods, which focus mainly on profitability.They consider such methods too short-term oriented,with likely negative long-term impacts. Cultural differ-ence was less prominent in the acquisitions realized byEuropean acquirers (Italian and German).

Only four companies (Beta, Kappa, Omega andOmicron) benefited from neither resources nor skills. Inthree (Beta, Kappa and Omega), the objective of theacquirer was only to acquire a particular resource orskill. For example, Beta had a large and geographicallywell-located factory. Its acquisition enabled the acquirerto recover this asset and install another unit of its groupthere. Kappa possessed specific knowledge, a specificwork organization and a highly flexible production tool.Thus, the transfer operated in the other direction: skillswere transferred to the acquirer, in a case of valuecapture rather than value creation. For its acquirer,Omega possessed complementary geographical markets(Europe vs. the United States), customers and technol-ogies (welding skills). Although these activities wereperceived by the acquirer as too different to support a

126 V. Favre-Bonté and C. Thévenard-Puthod

© 2013 European Academy of Management

transfer of resources or expertise, Omega’s previousowner believed that the transfer of financial resources ormanagerial skills could have been realized by theacquirer. Finally, due to misunderstandings related tooperating practices (very different cultures) and eco-nomical rationalization reasons, its acquirer did notprovide any resources to Omicron; rather, the acquisitionoccurred as a result of contracts signed by Omicron withan important client. As its manager reported:

The acquirer had a misguided vision of this activity [itbelieved Omicron was a profitable business], so theyacquired our company at a too high price. The resultof this overvaluation is a too high profitability demandfrom the shareholders at the expense of future growth.This leads to freezing investments and downsizing theworkforce (from 130 to 45).

This situation offers another case of value capture,which often occurs when an acquirer uses a leveragedbuyout to finance its operation. Beyond the reasonsgiven by acquirers to justify the lack of transfer ofresources or skills, such a situation tends to harmacquired companies. We address this harm in the nextsection, in which we attempt to draw links betweentransfers and acquired firm performance.

Relationship between skill transfers and long-termperformance of acquired subcontractors

Table 4 provides the acquired firms’ performance afteracquisition, according to five criteria. Overall ‘objectiveperformance’ improved in eight of 14 cases, though theindicators are not always in the same direction. For

example, turnover increased the most after acquisitions(8 positive, 4 neutral and 2 negative turnover cases). Theshifts in the firms’ profit rates and dependence werealmost equally distributed (6 positive, 6 neutral and 2negative). Conversely, the change in the number ofemployees was less favourable (5 positive, 4 neutral and5 negative), in line with the previous findings (Walsh,1989; Cannella and Hambrick, 1993; Barkema andSchijven, 2008).

More than half the acquired SMEs experienced a posi-tive global change in their objective performance afterthe acquisition (Gamma, Delta, Epsilon, Zeta, Theta,Iota, Kappa and Lambda); three SMEs greatly benefited,with positive results for all four performance criteria(Gamma, Delta and Epsilon). The other firms stagnatedor declined. In our attempt to connect acquired unitperformance with the extent of resources and skillstransferred, we find that the companies that progressedmost were those that benefited from an important trans-fer of skills. Table 5 shows a link between the nature ofthe resources and skills transferred and the degree ofpost-acquisition performance by the acquired firm. Thebest performers (Gamma, Delta, Epsilon, Zeta and Iota)obtained all three types of resources and skills throughtransfers, and the good performers (Theta and Lambda)received two types (functional + managerial skills orresources + functional skills). When no transfer tookplace or the transfers involved only resources, perfor-mance suffered, as in the cases of Alpha, Beta, Rho,Omega and Omicron. Therefore, resource transfersappear insufficient to ensure the long-term performanceof an acquired firm; functional or managerial skills arealso required.

Table 4 Post-acquisition performance

SME Health of the firm before acquisitionregarding sector average

Years afteracquisition

Turnover Profitrate

Staff Dependence Result of objectiveperformanceassessment

Satisfactionof the seller

Alpha Good but in a deteriorating situation 2 0 0 0 0 0 +Beta Losses. Financial problems 2 + 0 − − − 0Gamma Profitability problems 4 + + + + +++++ +Delta Improvement after previous crisis 5 + + + + +++++ +Epsilon More than average 5 + + + + +++++ +Zeta Very good 5 + − + + ++ +Rho Financial problems 5 − + 0 − − 0Theta Growth but weak profitability 5 + + − 0 + 0Iota Correct but excessive debt 3 + + 0 0 ++ +Kappa Average 3 + 0 + 0 ++ +Lambda Average 3 0 0 0 + + +Omicron Average 5 − 0 − 0 − 0Sigma Good 3 0 − − + − +Omega Problem of competitiveness /

financial mismanagement3 0 0 − − − 0

+: positive evolution−: negative evolution0: no evolution.

Skills Transfers and Acquired Firm’s Performance 127

© 2013 European Academy of Management

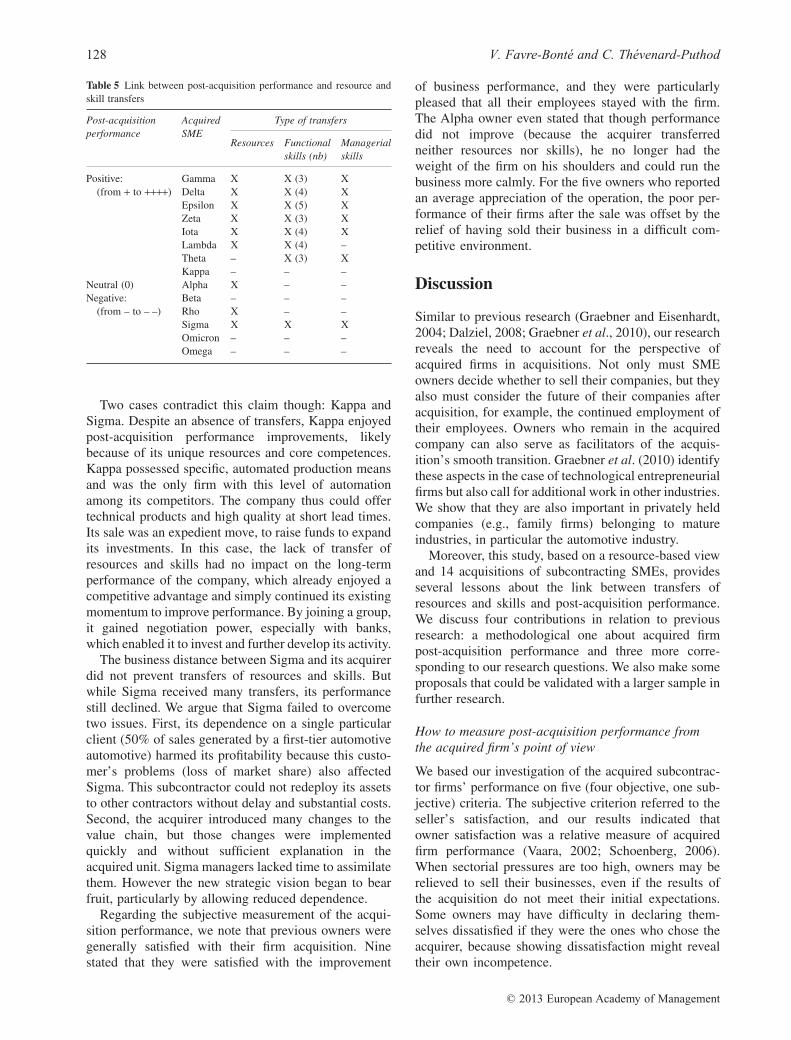

Two cases contradict this claim though: Kappa andSigma. Despite an absence of transfers, Kappa enjoyedpost-acquisition performance improvements, likelybecause of its unique resources and core competences.Kappa possessed specific, automated production meansand was the only firm with this level of automationamong its competitors. The company thus could offertechnical products and high quality at short lead times.Its sale was an expedient move, to raise funds to expandits investments. In this case, the lack of transfer ofresources and skills had no impact on the long-termperformance of the company, which already enjoyed acompetitive advantage and simply continued its existingmomentum to improve performance. By joining a group,it gained negotiation power, especially with banks,which enabled it to invest and further develop its activity.

The business distance between Sigma and its acquirerdid not prevent transfers of resources and skills. Butwhile Sigma received many transfers, its performancestill declined. We argue that Sigma failed to overcometwo issues. First, its dependence on a single particularclient (50% of sales generated by a first-tier automotiveautomotive) harmed its profitability because this custo-mer’s problems (loss of market share) also affectedSigma. This subcontractor could not redeploy its assetsto other contractors without delay and substantial costs.Second, the acquirer introduced many changes to thevalue chain, but those changes were implementedquickly and without sufficient explanation in theacquired unit. Sigma managers lacked time to assimilatethem. However the new strategic vision began to bearfruit, particularly by allowing reduced dependence.

Regarding the subjective measurement of the acqui-sition performance, we note that previous owners weregenerally satisfied with their firm acquisition. Ninestated that they were satisfied with the improvement

of business performance, and they were particularlypleased that all their employees stayed with the firm.The Alpha owner even stated that though performancedid not improve (because the acquirer transferredneither resources nor skills), he no longer had theweight of the firm on his shoulders and could run thebusiness more calmly. For the five owners who reportedan average appreciation of the operation, the poor per-formance of their firms after the sale was offset by therelief of having sold their business in a difficult com-petitive environment.

Discussion

Similar to previous research (Graebner and Eisenhardt,2004; Dalziel, 2008; Graebner et al., 2010), our researchreveals the need to account for the perspective ofacquired firms in acquisitions. Not only must SMEowners decide whether to sell their companies, but theyalso must consider the future of their companies afteracquisition, for example, the continued employment oftheir employees. Owners who remain in the acquiredcompany can also serve as facilitators of the acquis-ition’s smooth transition. Graebner et al. (2010) identifythese aspects in the case of technological entrepreneurialfirms but also call for additional work in other industries.We show that they are also important in privately heldcompanies (e.g., family firms) belonging to matureindustries, in particular the automotive industry.

Moreover, this study, based on a resource-based viewand 14 acquisitions of subcontracting SMEs, providesseveral lessons about the link between transfers ofresources and skills and post-acquisition performance.We discuss four contributions in relation to previousresearch: a methodological one about acquired firmpost-acquisition performance and three more corre-sponding to our research questions. We also make someproposals that could be validated with a larger sample infurther research.

How to measure post-acquisition performance fromthe acquired firm’s point of view

We based our investigation of the acquired subcontrac-tor firms’ performance on five (four objective, one sub-jective) criteria. The subjective criterion referred to theseller’s satisfaction, and our results indicated thatowner satisfaction was a relative measure of acquiredfirm performance (Vaara, 2002; Schoenberg, 2006).When sectorial pressures are too high, owners may berelieved to sell their businesses, even if the results ofthe acquisition do not meet their initial expectations.Some owners may have difficulty in declaring them-selves dissatisfied if they were the ones who chose theacquirer, because showing dissatisfaction might revealtheir own incompetence.

Table 5 Link between post-acquisition performance and resource andskill transfers

Post-acquisitionperformance

AcquiredSME

Type of transfers

Resources Functionalskills (nb)

Managerialskills

Positive:(from + to ++++)

Gamma X X (3) XDelta X X (4) XEpsilon X X (5) XZeta X X (3) XIota X X (4) XLambda X X (4) –Theta – X (3) XKappa – – –

Neutral (0) Alpha X – –Negative:

(from – to – –)Beta – – –Rho X – –Sigma X X XOmicron – – –Omega – – –

128 V. Favre-Bonté and C. Thévenard-Puthod

© 2013 European Academy of Management

Thus post-acquisition performance can be evaluatedfrom the acquired firm’s point of view (Dalziel, 2008)using objective criteria, such as the evolution of keyfigures (e.g., turnover, profit, staff). We also highlight theimportance of a criterion specific to subcontractor firmsthat has not appeared in prior acquisitions research(Ahuja and Katila, 2001; Puranam et al., 2003; Cloodtet al., 2006), namely, the reduction of commercial andindustry dependence. This criterion is a relevant indica-tor of long-term performance in the specific case ofsubcontracting firms.

Transfers of resources and skills andlong-term performance

From a resource-based perspective, our research showsthat transfers of resources and skills from acquirers sig-nificantly benefit subcontractor SMEs; in our study, theirperformance improved in both the medium term (turn-over and profitability growth) and the longer term, asthey reduced their symbiotic dependence on clients. Thislink between the extent of transferred resources andcompetences and acquisition performance is in line withprior research (Haspeslagh and Jemison, 1991; Capronet al., 1998), though in contrast with these studies, ourfindings place greater emphasis on long-term perfor-mance and acquired firm performance. In addition, wedo not focus solely on horizontal acquisitions, as domany studies of resource and skill transfers (Capronet al., 1998; Capron and Hulland, 1999). As we detailsubsequently, acquirers can transfer resources and skillsto the acquired firm, even when they do not perform thesame activity.

Types of skill transfers most important for long-termperformance of acquired subcontractors

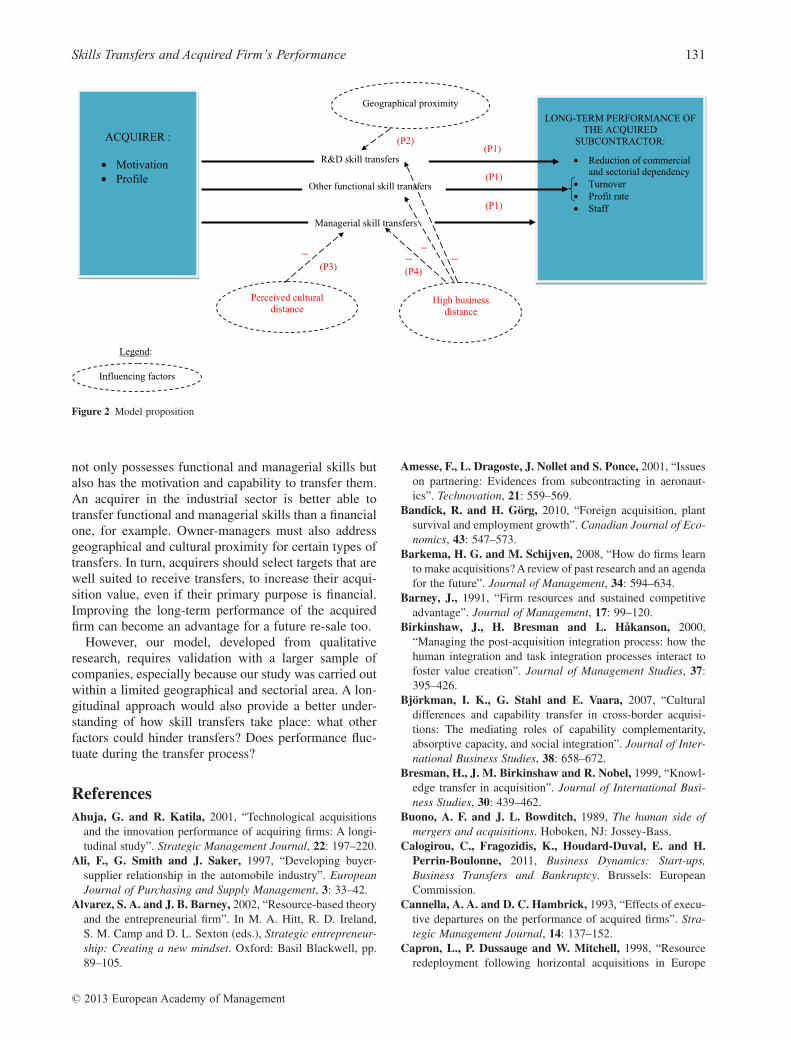

Our research documents the specific resource and skillneeds of subcontractors, a type of business hitherto littlestudied, even if these companies strongly demandresource and skill inputs, given their high level ofdependency. Thus, if the transfer of resources is benefi-cial to the subcontractor, it is not sufficient to ensure thesustainability of the acquired firm. We highlight theimportance of functional and managerial skills forthe performance of the acquired subcontractor firms(Haspeslagh and Jemison, 1991). Subcontractors oftenlack such skills, because they tend to focus exclusivelyon the technical aspects of the business and are stronglyoriented toward operational issues. Thus, they cangreatly benefit from new parent firm skills, suchas commercial/marketing competences (Capron andHulland, 1999) and R&D transfers. A more systematicmanagement approach also is highly effective (Cooke,2006). Previous research has verified the importance forsubcontractors in many industries to gain managerial,

dynamic skills (O’Guin, 1995). The transfer of mana-gerial skills enables acquired firms to adopt a more pro-active vision of their strategy, embrace new markets andreduce their dependency on contractors, which reducesthe profitability of subcontractors. This discussion leadsus to formulate our first proposition:

Proposition 1: In subcontractor SME acquisitions,the simultaneous transfer of resources, functionalskills, and managerial skills are required for greaterlong-term performance; any sole transfer of resourcesis not sufficient.

Facilitating factors of resource and skill transfers