Relationship Between Stock Return, Dividend-Price Ratio, Price Earnings Ratio, Size, Market to book...

50

Waikato Management School Dept of Finance FINA511-13A RESEARCH PAPER Relationship Between Stock Return, Dividend-Price Ratio, Price Earnings Ratio, Size, Market to book Ratio, and Payout Ratio Name :-Niranjan Sant 1 | Page

Transcript of Relationship Between Stock Return, Dividend-Price Ratio, Price Earnings Ratio, Size, Market to book...

Waikato Management School

Dept of Finance

FINA511-13A RESEARCH PAPER

Relationship Between Stock Return,Dividend-Price Ratio, Price

Earnings Ratio, Size, Market tobook Ratio, and Payout Ratio

Name :-Niranjan Sant1 | P a g e

ID :- 1198724

ContentsAbstract..................................................................3

1. Introduction...........................................................42. Literature Review......................................................6

3. Data and Sample........................................................93.1 Banking Sector.....................................................10

3.2 General Industrials................................................103.3 Industrial Engineering.............................................10

3.4 Software and Computer services.....................................114. Methodology...........................................................11

4.1 Dividend Price Ratio...............................................114.2 Price Earnings Ratio...............................................12

4.3 Size...............................................................124.4 Market to Book Ratio...............................................12

4.5 Payout Ratio.......................................................134.6 Stock Return.......................................................13

4.7 Regression Model...................................................145. Empirical Results.....................................................15

5.1 Summary Statistics.................................................155.2 Pearson Correlation Matrix.........................................16

5.3 Regression Result..................................................176. Conclusion............................................................25

References...............................................................28Appendix.................................................................31

2 | P a g e

Abstract

In this paper, I have examined the relationship between stock

returns and five variables, Dividend price ratio, Price Earnings

ratio, Size, Market to book ratio and Payout ratio, by examining

this relationship I have attempted to analyze investors approach

and choice towards investing their money in stock market. I have

also tried to analyze what factors investors do take into

consideration while investing in any particular security or

stock. For this study I have collected the sample of 357 firms

from Indian stock market and divide the sample in four different

sectors Banking Sector, General industrials sector, Industrial

engineering and Software and computer services sector. I have

used OLS regression in this study to study this relationship.

Results and findings of this paper show that, some variables are

statistically significant with stock return for each sector.

Result of each sector is different from each other. Investors

approach is also different in each industry and changes according

to industry. There are different factors in each sector which

3 | P a g e

investors take into consideration, so therefore their strategies

and choices regarding investment differ from one sector to other.

4 | P a g e

1.Introduction

There are many studies in Corporate finance literature who have

focused and examined the relationship between stock return and

other performance variables. In this paper I have attempted to

use Dividend Price ratio, Price Earnings Ratio, Size, Market to

book ratio, and Payout Ratio. Many studies in literature have

focused on developed markets but very few studies have focused on

Indian stock market, which is emerging and developing market.

This study has focused on Indian stock market, I have examined

three major sectors in Indian stock market General Industrial,

Industrial Engineering and Software and computer services. These

three sectors contain major industries in India like Tata Motors,

Infosys, SKF, ABB, Thermax and many others. I have attempted to

analyze these sectors because these three sectors have their

major impact on Indian Stock market as I mentioned earlier, these

three sectors contain major Indian companies.

The main aim of this paper is to examine the predictability and

relationship between stock returns, D/P ratio, Price Earnings

Ratio, Size, Market to book ratio and Payout ratio. This study

also examines the predictability of these ratios to forecast the

future stock returns. I have used the market to book ratio in

this study, this is motivated by findings of Fama and

French(1992) that shows that market to book ratio of individual

5 | P a g e

stock can explain the cross-sectional variation in stock returns.

For determining market prices and earnings of the stocks, book

value and dividend could be very useful for predicting stock

price behavior and behavior of stock returns in future. Due to

this, one can construct very profitable and fruitful strategies

on the basis of dividend, book value and earnings.

According to the mispricing view, P/E effect mentions that stocks

which have low P/E ratio earn significantly higher returns than

that of stocks which have high P/E ratios. Thus according to this

mispricing view, there is inverse relationship between portfolio

return and P/E ratio. By using this approach investor can earn

significantly higher returns by investing in the stocks which

have low P/E ratio. In case of Market to book ratio,MtB effect

states that, stocks with high MtB ratio consistently obtain lower

returns than those securities which have high MtB ratio. Book

value proxy for future cash flow could be the one explanation for

Market to book ratio's ability to predict future stock return.

Coming to Dividend price ratio, High D/P ratio shows that the

market is undervalued. Predictive power of D/P ratio is depends

on role of dividend in capturing some components in price which

are permanent, whereas predictability of P/E is because earnings

is a very good measure of business conditions, which explains the

counter cyclic risk aversion. D/P defines variation in real stock

return in a much better manner on value weighted index. Three

ratios Price to earnings ratio, Market to book ratio, and

dividend price ratio have some same features one of the feature

6 | P a g e

is that all the ratios measure stock prices relative to

fundamentals. So in this respect this study is contributing in

literature by showing the ability of these ratios to predict

stock returns.

With the help of this relationship of Stock return and different

ratios, I will also predict the choices of the investors and the

preferences of the investor regarding all this three sectors,

whether investors are looking for capital gain or they are

looking for Dividend earnings. In case of these three sectors

investors have different approach towards investing in these

sectors, some sectors show that investors are more interested in

capital gain whereas in case of some sectors investors are

holding these stocks for long term basis and looking for Dividend

gains. I have used dividend price ratio and its relationship with

stock return to examine whether investors are looking for long

term investment and looking for Dividend gain. Price earnings

ratio is used to examine whether investors are just looking for

capital gain, Size is used to measure the magnitude of the

company and ultimately of that sector, Size and Stock return

relationship has been used to examine investors approach toward

magnitude of the company and its market capitalization, this has

been used to examine whether investors are looking for high

magnitude stocks and whether size matters for them or not.

So main contribution of this paper is to elaborate the

relationship between stock returns and Dividend price ratio,

7 | P a g e

Price earnings ratio, Size, Market to book ratio, Payout ratio

and examine the predictability of this variables of future stock

returns. And by comparing these variables to stock return I am

also analyzing investors approach towards selecting the stock and

towards their investment choices I have attempted to distinguish

three sectors and investor’s choices towards purchasing stocks

from all these three sectors.

Rest of the paper is the structured as, in section 2 Literature

review and what other papers have examined about stock return and

its relationship with these ratios, section 3 includes Data and

sample used for this study and from where the this data has

obtained, Section 4 has Methodology used to calculate all the

ratios used and the most important stock returns. Section 5

contains Empirical results and last Conclusion of the paper and

future scope of research in the same area.

2. Literature Review

There are many studies in corporate finance literature who have

observed the relationship between stock return and various

financial ratios, but there are very few studies who have

observed this relationship in Indian context in financial crisis

period of 2008 - 2009 hence, my study will be focusing on Indian

markets finding the relationship between stock returns and

various performance variables.

8 | P a g e

According to the Banz(1981), small size firms have higher average

stock returns, but in case of average size and large size firms

this size effect is not consistent. He also mentioned that size

effect exists but it is not clear why this effect exist, he was

not clear with the fact that, size is a factor or it is just a

proxy for one or more true but unknown factors correlated with

size.

Jeffrey Jaffe, Donald B. Keim and Randolph Westerfield(1989),

concluded that, there is significant earning price and size

effects in US market when estimated across all months during the

1951-1986 period. This study also added that, there is difference

between January and the rest of the year as the coefficient on

both E/P and Size are significant in January but in case of other

months, only E/P coefficient is significant outside January.

In Guler Aras and Mustafa Kemal Yilmaz(2008) they examined the

predictability of stock return taking into consideration 12

emerging markets around the world. They have used, price-earnings

ratio, dividend yield and market-to-book ratio as predictable

variables and covered the period of 1997 to 2003. This study

finds variation in their findings, Market to book ratio shows

significant result in predicting stock return for one year period

for most of the emerging countries, But overall investor can

forecast the potential stock market return for one year period

up-to certain extent by using Market to book ratio, partially

9 | P a g e

dividend yield ratio and price earnings ratio. According to the

authors investor can improve their predictability by adding other

variables like, consumer price index which shows the

macroeconomic changes in predicting stock return in the market.

Robert H. Litzenberger and Krishna Ramaswamy(1982) studied the

relationship between dividend yield and stock return. According

to this study,their results show that, there is positive but non-

linear relationship between dividend yield and stock return. But

study also says that significant dividend yield effects cannot

pinned to information content in the prior knowledge that firm

will declare dividend of unknown magnitude.

Keith S. K. Lam(2002) studied the relationship between stock

return and β Size (ME), Leverage, book to market equity ratio and

earning price ratio in Hong Kong stock market, in this study he

has used Fama and French (FF) approach. Result from this study

shows that, three accounting variables book to market, E/P, ratio

and size really captured the cross sectional variation in average

returns over the period. Other variables like book and market

leverage also captured the cross sectional variation but effects

of those variables are dominated by Size, book to market equity

and E/P ratio, Hence those cannot be considered.

Pradosh Simlai(2009), In this paper Author has examined and

reinvestigated the performance of common stock return with two

10 | P a g e

popular variables Size and book to Market Ratio. According to

their findings incorporation of time varying conditional

variance can significantly supports the impact of the three risk

factors, he also concluded that, because of this findings Fama

and French model is successful and unaffected by the

incorporation of time varying investment opportunity set. His

study also finds positive and significant relationship between

size and Stock return.

In the study of Jeffrey Pontiff and Lawrence D. Schall(1995) they

have examined the predictive ability of the book to market ratio

in Dow Jones industrial average. According to their findings,

Dow Jones Industrial average book to market ratio is good

predictor of market return than the other variables like dividend

yield, and interest rates. Author also mention that, their

findings are sample specific where predictive power of book to

market ratio occurs only before 1960. As after 1960 there is no

significant relationship.

Ian McManus, Owain AP Gwilym and Stephen thomas(2004) they

observed the relationship between stock return and dividend yield

in UK stock market, they have introduced the data related to

earning to the asset pricing model in the form of payout ratio.

In this study they have introduced payout ratio and examines the

relationship between payout ratio, dividend yield and stock

11 | P a g e

return. According to the result of this study, payout ratio does

have impact on dividend yield itself in explaining stock return.

Gabriel Perez-Quiros and Allan Timmermann (2000) have observed

difference ofvariation in stock return in different economic

conditions and tried to examine stock returns of both small firms

and large firms. In that study they have considered three factors

firm size, economic and market condition for analyzing and

capturing sensitivity of expected risk and returns. According to

the findings of this paper, Interest rate is the vital factor for

sensitivity of stock return volatility, expected returns of the

firm is also very sensitive to this interest factor. In the

recession phase stock return of small firms are mostly affected,

large firms stock returns also get affected in such situation but

compared to small firms it is less sensitive.

Kee Hong Bae, Jeong-Bon Kim(1998) in their study, they have taken

the sample data of Japanese firms. The main aim of their study

was to examine the usefulness of the two fundamentals, accrual

earnings and book value of equity share for the purpose of

predicting stock returns. According to the result of this study,

both accrual earnings and book value of equity can predict the

stock return and investors and policy makers can build profitable

strategies by using this approach. Paper also mentioned that,

book value captures some aspects of equity value of stock which

are not captured by earnings.

12 | P a g e

Raj AggarwalTakatoHiraki and Ramesh P Rao(1992) examined the

price to book ratio effect in Japanese market. In this study they

have observed that stocks with high price to book value ratio

have earn low returns whereas stocks with low price to book ratio

have high low stock returns. This study has observed inverse

relationship between stock return and price to book ratio in

Japanese market. The result of this study also shows that,

accounting data is useful for deciding trading strategies in

Japanese stock market because investors can actually predict the

stock return by calculating price to book ratio.

JYH-LIN WU, YU-HAU HU and CHINGNUN LEE (2011) this paper tried to

solve the question whether dividend yield can actually predict

the stock return without short rates in UK stock market. For this

study they have collected monthly stock data for the period of

1923 to 2007. According to the findings of this study, dividend

yield can actually be predicted without short rates but only if

the forecast horizon is more than four months.

ChakerAloui, DucKhuong Nguyen and HassenNjeh(2012) in this paper

they have examined the impact of oil prices on Stock return in

emerging stock markets. In this study they have segregated the

countries according to the countries which are the largest

importer of Oil, countries which are moderately depend on oil and

the countries which are largest exporter of oil. In their study

13 | P a g e

they have used data from 25 different countries for the period of

1997 to 2007. According to their findings relevance of oil price

risk is conditional in case of emerging markets, also there is

asymmetry in case of stock return and significant when oil prices

are rising. Their results also show significant relationship

between global market betas and stock returns of emerging stock

markets. But however they have also mentioned that, this

relationship Is negative when world market was falling down.

3. Data and Sample

For this paper I have collected all the data from DataStream

database, I have segregated the data sample in three sectors,

Banking sector, General Industrials, Industrial Engineering,

Software and Computer services. I have collected the data sample

for the period of May 2003 to May 2013. All the ratios which,

used as independent variables have been calculated individually.

All the data which is required to calculate these ratios have

been obtained from DataStream. Three sectors in total constitute

357 firms altogether. This data consists of monthly average of

Dividend price ratio, Price Earnings ratio, Market to book ratio,

Payout ratio and Size from May 2003 to May 2013.

Stock returns are calculated by dividend adjusted approach. For

calculating the return for the month of May 2003, I have

downloaded the data for the month of April 2003 as an Initial

14 | P a g e

price of stock. After calculating all the returns for every

month, I have taken the average of all the returns of all firms

from May 2003 to May 2013.

Sectors Sample Size Banking Sector 33 General Industrials 48 Industrials Engineering 146 Software And ComputerServices 130 Total Sample Size 357

3.1 Banking Sector

In banking sector, I have included all nationalized banks in

Indian stock market. This sector includes some banking giants

like, State bank of India, Punjab National Bank, Bank of India,

and Bank of Baroda. In this sector I have included some major

private banks like ICICI, Indusind Bank, HDFC bank, these private

banks are also have good market cap and these are also some of

the giant banks in India.

3.2 General Industrials

This sector covers some wide variety of data as various

manufacturing companies are included in this sector. This sector

has several companies dealing in different areas of products like

15 | P a g e

construction material, retail goods product, and many others.

This sector also includes some conglomerate like 3M India.

3.3 Industrial Engineering

As name suggests, this sector includes engineering companies and

also some forging companies. This sector includes some major

automobile companies like, Tata Motors, Ashok Leyland, Forbes,

Mahindra and Mahindra, these some companies are major players in

Indian stock market with huge market capitalization and have huge

impact on index movement. Some government owned companies are

also there in this sector like, Bharat heavy electrical, Bharat

Bijlee, BEML, Nelco etc. Forging companies like Bharat forge

which is largest forging company in Asia became world’s second

largest forging company after acquiring Carl Dan Peddinghaus GmbH

(CDP), one of the largest forging companies in Germany, for an

undisclosed sum.

3.4 Software and Computer services

In last several years software and IT sector in India has rapidly

grown up and now it is one of the important sector for Indian

Stock market, so I have included this sector in my study to

analyze. Indian IT sector is in boom for last several years and

developing rapidly. In this sector, there are some IT giants like

Infosys, Wipro, Satyam computer services, Zensar Technologies,

16 | P a g e

Rolta India, HCL technologies etc. This sector is one of those

sectors which have huge impact on Indian stock market movements.

4. Methodology

This study shows the relationship between stock return and

various performance variables like, Dividend price ratio, Earning

price ratio, Market to Book Ratio, Payout Ratio and Size. For

calculating stock returns dividend adjusted. I have calculated

each ratio on monthly basis for every company and then took the

average of those ratios for each month for entire sample period.

4.1 Dividend Price Ratio

For calculating this ratio, I have obtained monthly prices for

all of the firms in data sample and dividend per share from

DataStream. Dividend data which is obtained from DataStream is 12

moth rolling basis data.

Dividend Price Ratio = Dividend per Share / Price per

Equity Share

Dividend price Ratio is company's annual gross dividend paid

divided by its market cap or the dividend per share divided by

price per share. This dividend price ratio is typically used by

researchers in finance where the study of variability of this

ratio is main concern.

17 | P a g e

4.2 Price Earnings Ratio

In general, high P/E ratio suggests that investors are expecting

high earning growth in future compared to the companies with low

P/E Ratio. P/E ratio has been calculated by dividing price per

share with the EPS (Earning per share) of that particular share.

P/E ratio also calculated for every single firm in sample and

then average of P/E ratio is calculated. EPS for each firm in the

data sample is obtained from DataStream for 357 firms in all

three sectors.

Price Earnings Ratio has been calculated as:

Price Earnings Ratio = Market Value per Share /

Earning Per Share

4.3 Size

Size which is also known as a market capitalization of the

company. Size represents the magnitude of that company. I have

used size in my study to examine its relationship with stock

returns. I have also examined whether investors make their

investment decisions on the basis of Size or Market Cap of the

company. For calculating Size I have downloaded monthly prices of

the equities and number of outstanding shares from DataStream.

Size is calculated as:

Size = NOSH × Market Price of Equity share

18 | P a g e

Size also represents the total market price of the company.

4.4 Market to Book Ratio

Market to book ratio compares the book value and market value of

the stock. MtB ratio also indicates that whether stock is

undervalued overvalued. Low MtB ratio represents that stock is

undervalued. With the help of this ratio, investors can also

access whether they are paying too much for the stock, if company

goes bankrupt immediately. This Ratio is obtained from DataStream

database, to examine its relationship with stock return. MtB

ratio is also useful to examine the window dressing in stock

market.

Ratio is calculated as:

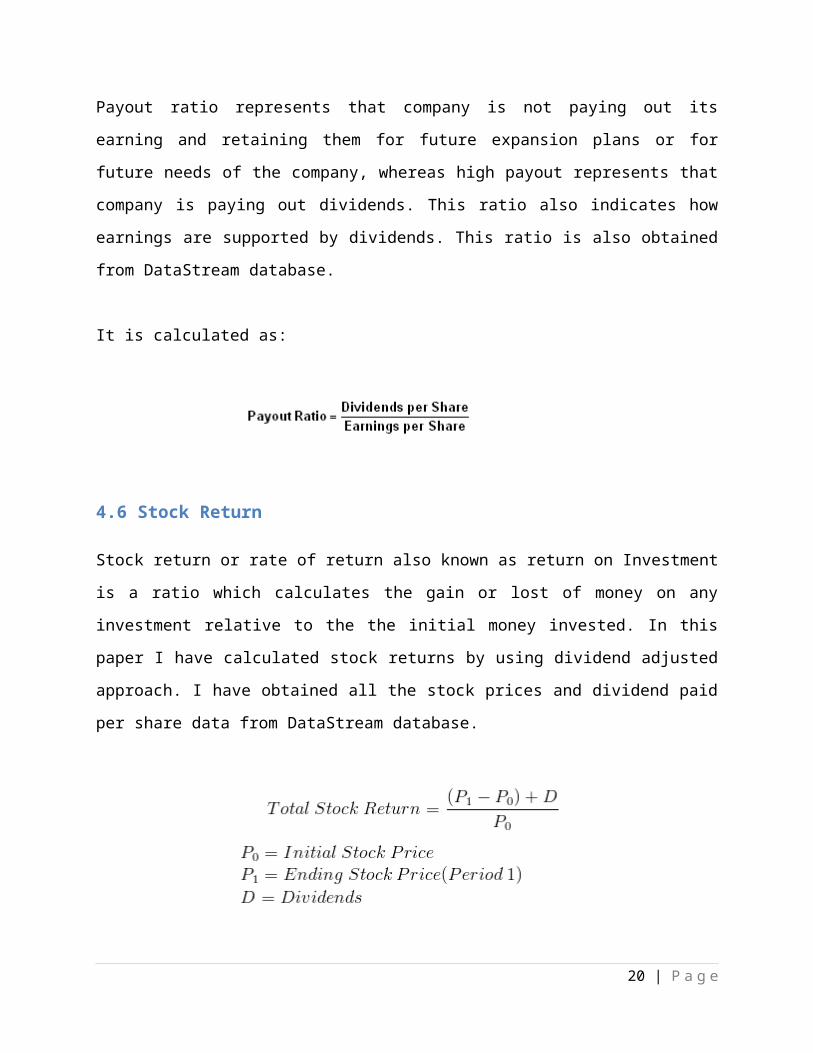

4.5 Payout Ratio

Payout ratio briefly represents the earning paid to the

shareholders of the company. This ratio can be used by investors

to know what company is doing with its earning, whether company

is retaining this earnings or paying out to its shareholders. Low

19 | P a g e

Payout ratio represents that company is not paying out its

earning and retaining them for future expansion plans or for

future needs of the company, whereas high payout represents that

company is paying out dividends. This ratio also indicates how

earnings are supported by dividends. This ratio is also obtained

from DataStream database.

It is calculated as:

4.6 Stock Return

Stock return or rate of return also known as return on Investment

is a ratio which calculates the gain or lost of money on any

investment relative to the the initial money invested. In this

paper I have calculated stock returns by using dividend adjusted

approach. I have obtained all the stock prices and dividend paid

per share data from DataStream database.

20 | P a g e

According to this formula I have calculated stock returns for all

the 357 companies in my dataset for the period of May 2003 to May

2013. This formula calculates appreciation by increase in stock

price plus dividend paid if any, and then divided by initial or

Original also known as Opening stock price of the stock. Main

sources of income for any investor in stock market is the

Increase in a stock price of the company and Dividend paid by the

company on investment, numerator of this formula shows total gain

or loss and dividend earned on investment and denominator shows

initial stock price or opening stock price.

4.7Regression Model

To examine the correlation between stock return and predictive

variables I have used OLS (ordinary least squares) regression.

The regression equation can be expressed as follow:

Y = α + β1X1 + β2X2 + β3X3 + β4 X4 + β5X5

Where,

Y =Dependent variable that is Stock Return.

α =Indicates the value of Y when all the values of

explanatory variables are zero.

21 | P a g e

β =this parameter indicates the average change in

Y that is associated with unit change in

variable X.

X= Independent Variable.

X1 Dividend price ratio, X2 is Price earnings ratio, X3 is Size

Variable, X4 is Market to book ratio and X5 is a payout ratio, as

mentioned before Y is dependent variable that is Stock return.

5. Empirical Results

In this section I have tried to examine the relationship between

stock return and other variables like Dividend Price ratio, Price

earnings Ratio, Size, Market to Book Ratio and Payout ratio. In

this section I examine the correlation between stock return and

predictive variables to analyze their predictive ability. I have

used this correlation to analyze investors approach towards each

sector and whether they invest in those sectors for capital gain

or for Dividend earning.

5.1 Summary StatisticsTo begin with, Table 1 Shows summary statistics for all the five

variables used in this study, and also the stock return. This

table also includes the mean and standard deviation for stock

returns and all other independent variables. According to this

table General industrial sector has highest average stock return

and also standard deviation, whereas banking sector has lowest

stock return and standard deviation in all sectors. But in case

22 | P a g e

of Dividend price ratio, Industrial engineering has the highest

D/P ratio and banking sector has the lowest one. Looking at the

Size factor, banking sector is huge in Size compared to any other

sector and also way ahead of all the sectors mentioned. From this

we can conclude that Indian banking sector has huge magnitude

effect on Indian stock market. After banking, software sector

comes at number two in case of Size, IT sector is in boom in

India and its effect is clearly seen on Size and magnitude of

that sector, So after banking, Software sector is the next most

affecting sector in Indian stock market. As i have mentioned

earlier in this paper, I have covered this three sectors because

this sectors constitute the major Indian companies and giants. In

Banking all the nationalized banks and major banks have been

covered like, State bank of India, Punjab National Bank, Bank of

Baroda, Bank of India etc, and in software and computer service

sector I have covered all the major software giants in India like

Wipro, Infosys, etc. Due to this Size factors affects a lot.

Table. 1 Summary Statistics for all Sectors from May2003 to May 2013

23 | P a g e

Sectors M ean SD M ean SD M ean SD M ean SD M ean SD M ean SD

Banking Sector 0.054 0.118 0.029 0.009 9.833 3.349 109803237 6.50E+07 1.199 0.264 17.480 1.288

General Industrials 0.115 0.433 0.043 0.019 17.946 13.861 2052537 1.27E+06 1.443 0.539 17.180 5.708

Industrial Engineering 0.099 0.165 0.054 0.023 22.885 10.410 9518441 6.06E+06 2.263 1.056 19.530 2.264

Software and Com puter Services 0.088 0.246 0.043 0.017 43.780 21.183 16844239 9.27E+06 2.257 1.049 12.111 4.459

Stock Return P/E Ratio Size M tB Payout RatioD/P ratio

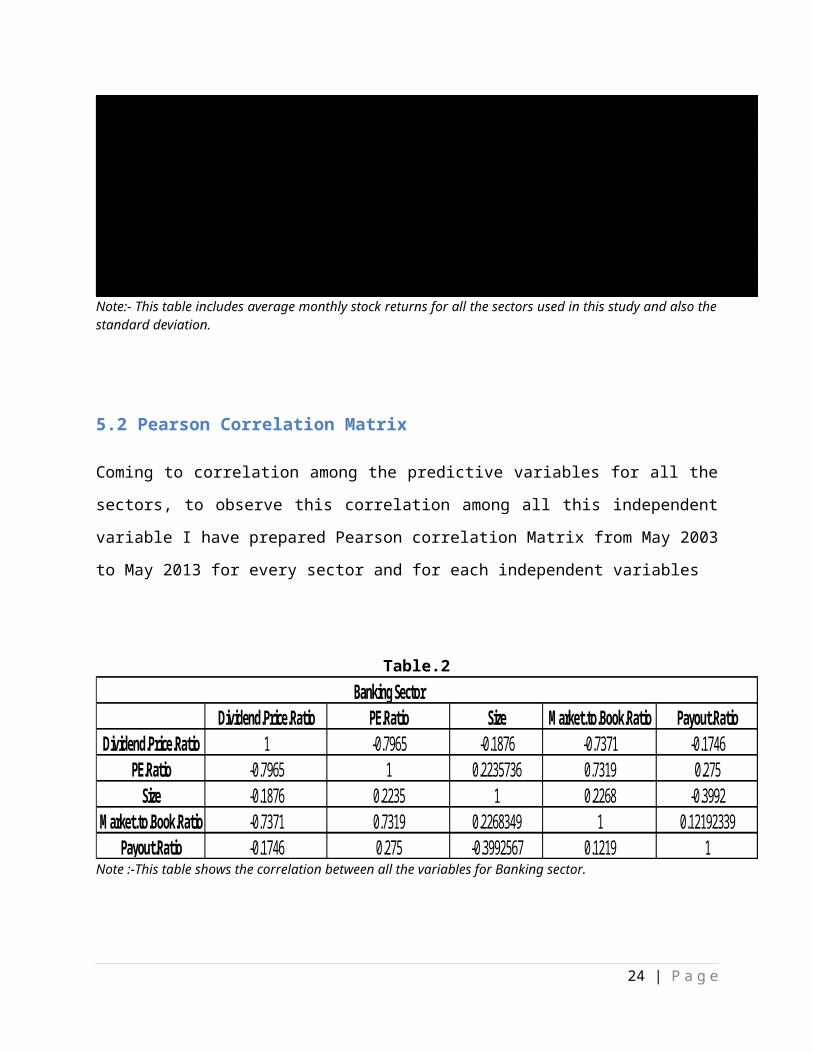

Note:- This table includes average monthly stock returns for all the sectors used in this study and also thestandard deviation.

5.2 Pearson Correlation Matrix

Coming to correlation among the predictive variables for all the

sectors, to observe this correlation among all this independent

variable I have prepared Pearson correlation Matrix from May 2003

to May 2013 for every sector and for each independent variables

Table.2Banking Sector

Dividend.Price.Ratio PE.Ratio Size M arket.to.Book.Ratio Payout.RatioDividend.Price.Ratio 1 -0.7965 -0.1876 -0.7371 -0.1746

PE.Ratio -0.7965 1 0.2235736 0.7319 0.275Size -0.1876 0.2235 1 0.2268 -0.3992

M arket.to.Book.Ratio -0.7371 0.7319 0.2268349 1 0.12192339Payout.Ratio -0.1746 0.275 -0.3992567 0.1219 1

Note :-This table shows the correlation between all the variables for Banking sector.

24 | P a g e

Table.3General Industrials

Dividend.Price PE.Ratio Size M arket.to.Book.Ratio Payout.RatioDividend.Price 1 -0.3121946 -0.7324208 -0.1190192 0.7020803

PE.Ratio -0.3121946 1 0.2526798 0.1715212 -0.1207696Size -0.7324208 0.2526798 1 -0.2570843 -0.7541131

M arket.to.Book.Ratio -0.1190192 0.1715212 -0.2570843 1 0.4097802Payout.Ratio 0.7020803 -0.1207696 -0.7541131 0.4097802 1

Note :- This table shows the correlation between all the variables for General Industrials. Table.4

Industrial EngineeringDividend.Price.Ratio PE.Ratio Size M arket.to.Book.Ratio Payout.Ratio

Dividend.Price.Ratio 1 -0.5439804 -0.8359583 0.004464535 0.5860022PE.Ratio -0.543980408 1 0.248454 0.288080558 -0.2707581Size -0.835958327 0.248454 1 -0.154825759 -0.6504607

M arket.to.Book.Ratio 0.004464535 0.2880806 -0.1548258 1 -0.2460164Payout.Ratio 0.586002176 -0.2707581 -0.6504607 -0.246016406 1

Note :- This table shows the correlation between all the variables for Industrial Engineering.Table.5 5

Software and Com puter ServicesDividend.Price.Ratio PE.Ratio Size M arket.to.Book.Ratio Payout.Ratio

Dividend.Price.Ratio 1 -0.2541287 -0.1269445 -0.3495384 0.1849232PE.Ratio -0.2541287 1 0.3267063 -0.1372427 -0.3347966Size -0.1269445 0.3267063 1 -0.6376264 -0.7559005

M arket.to.Book.Ratio -0.3495384 -0.1372427 -0.6376264 1 0.7246725Payout.Ratio 0.1849232 -0.3347966 -0.7559005 0.7246725 1

Note :- This table shows the correlation between all the variables for Software and Computer Services.

These all table show high level of correlation among all the

independent variables used in this study, also these variables

are statistically significant.

25 | P a g e

5.3 Regression Result

After examining the correlation between all the independent

variables now I can go for regression result. I have used OLS

regression for this study, where stock return is my Dependent

variable (Y), and I have used five independent variables namely,

Dividend Price ratio, Price earnings ratio, Size, Market to book

ratio, and Payout ratio to examine the relationship between these

variables and stock returns for all the sectors from the period

May 2003 to May 2013.

Table.6Regression results for VariablesSector Constant PE D/P Size MtB Payout Ratio R Squared Adj R Squared F-Statistics N

Banking Sector 0.055 0.348 0.840 0.036 0.838 0.053 0.050 0.009 1.222 121[1.937359] [0.9434] [-0.202609][-2.121051][-0.204389] [-1.956304]

General Industrials 0.013 0.202 0.000 0.129 0.208 0.431 0.17 0.14 4.768 121[-2.518] [1.281] [3.837] [1.528] [1.265] [-0.789]

Industrial Engineering 0.446 0.012 0.051 0.975 0.390 0.969 0.14 0.11 3.832 121[-0.764] [2.561] [1.974] [0.031] [0.862] [0.039]

Software and Com puter Services 0.490 0.001 0.694 0.499 0.670 0.962 0.11 0.07 2.826 121[-0.693] [3.607] [0.394] [-0.678] [0.427] [0.047]

Note :- In this table coefficients in parenthesis show the P values. Figures in Bracket show the t-statistics

value for each variabl. This table represents the result for average stock returns, D/P, P/E, Size, MtB,

Payout ratio for four sectors for the period of 2003 to 2013.

Table 6 shows the result of my regression test which constitutes

four major sectors in Indian market and five variables.

Banking Sector

26 | P a g e

Starting with banking sector, Size is statistically significant

with P value of 0.036, so according to the result Size has

positive significant relationship with stock return. So size or

magnitude of the company has positive and significant impact on

stock return. So this results actually supporting the results of

PradoshSimlai(2009) as in his study on US market he found

positive relationship between Stock return and Size variable. So

from this result I can say that in Indian market Size is very

important factor for investors when they are investing in a stock

from Banking Sector. This result shows that Indian investors look

for market value when investing in Banking sector rather than

other things.

Another Significant variable is payout ratio in case of banking

sector, which represents positive and statistically significant

relationship among stock returns and Payout ratio. Higher the

Payout ratio better is for the earnings from earning means when

Payout ratio it indicates that company is paying dividend rather

than retaining it. In banking sector significant payout ratio

shows that Investors can predict future stock returns using this

variable, and accordingly they could decide their strategies for

investment in this particular sector. Positive and significant

payout ratio also indicates that investors are more concern about

dividend payout by banks while investing in this sector, as this

ratio represents how much dividend company is paying and how much

27 | P a g e

earnings company is retaining. Investors are looking for Dividend

earnings while investing in this sector.

Other variable like P/E ratio which shows positive but

insignificant relationship with stock return, According to Guler

Aras and Mustafa Kemal Yilmaz(2008)P/E ratio can predict the

stock return for the period of 1 year in four emerging markets,

but markets which have been targeted in that study are not big

markets and those markets are not liquid like Indian market.

Indian market is also an developing market but size wise Indian

market is way bigger than those emerging markets targeted in that

study. BSE which is the 10th largest stock exchange in the world

in terms of Market capitalization, So results in Indian context

is different. P/E ratio does not seem to predict stock return in

Indian stock market particularly in case of banking sector. From

the investor’s perspective, P/E ratio shows that Investors are

not looking for capital gain on banking stock rather they are

going for Long term investment and dividend earning is more

important for them than that of Capital gain. Market to book

ratio which is also highly insignificant in case of banking

sector shows that, MtB cannot predict stock returns in Banking

sector, also Investors are not concern with book value of the

banking stock, Market value is more important factor for them

while investing in this sector.

General Industrials

28 | P a g e

In case of General Industrials, Dividend price ratio is highly

significant with t-statistics value of 3.837, this shows positive

and statistically significant relationship between stock return

and dividend price ratio. According to the result, Dividend price

ratio can predict the stock return for general industrials stocks

as there is positive and highly significant relationship between

stock return and this ratio, this findings are supporting the

view of Robert H. Litzenberger and Krishna Ramaswamy(1982) as in

their study as well they find significant relationship between

stock return and dividend yield. Dividend price ratio helps

investor to know how much effective return he is going to get on

his investment in future, In this case positive and significant

D/P ratio shows that investors while investing in this sector are

more likely looking for dividends and returns on their investment

through dividends.

Another significant variable in this sector is Size with t-

statistics value of1.528. It is significant and positive which

shows positive and significant relationship between stock return

and Size. Size is the magnitude of the company or market value of

the company, Size is another important factor for investors while

investing in these stocks. Company size is total market

capitalization of the company and results shows that for

investors Size is very important factor.

29 | P a g e

But in this sector Payout ratio is not significant as well as

Market to book ratio. Price earnings ratio which is also

insignificant in case of this sector. This result represents

that, Payout Ratio, Market to book ratio and price earnings ratio

have no significant relationship with stock return and cannot

predict stock return. But this result of Market to book ratio is

contradictory to the findings of Raj AggarwalTakatoHiraki and

Ramesh P Rao(1992), in their study on Japanese stock market they

found positive and significant relationship between price to

book ratio and stock return, they have also mentioned that

investors can build their strategies according to their findings.

But in Indian market, particularly about General industrial

sector MtB ratio does not seem significant. Raj

AggarwalTakatoHiraki and Ramesh P Rao(1992) have considered the

whole Japanese stock market, whereas my result is for particular

sector hence results could be different in case of Indian

context.

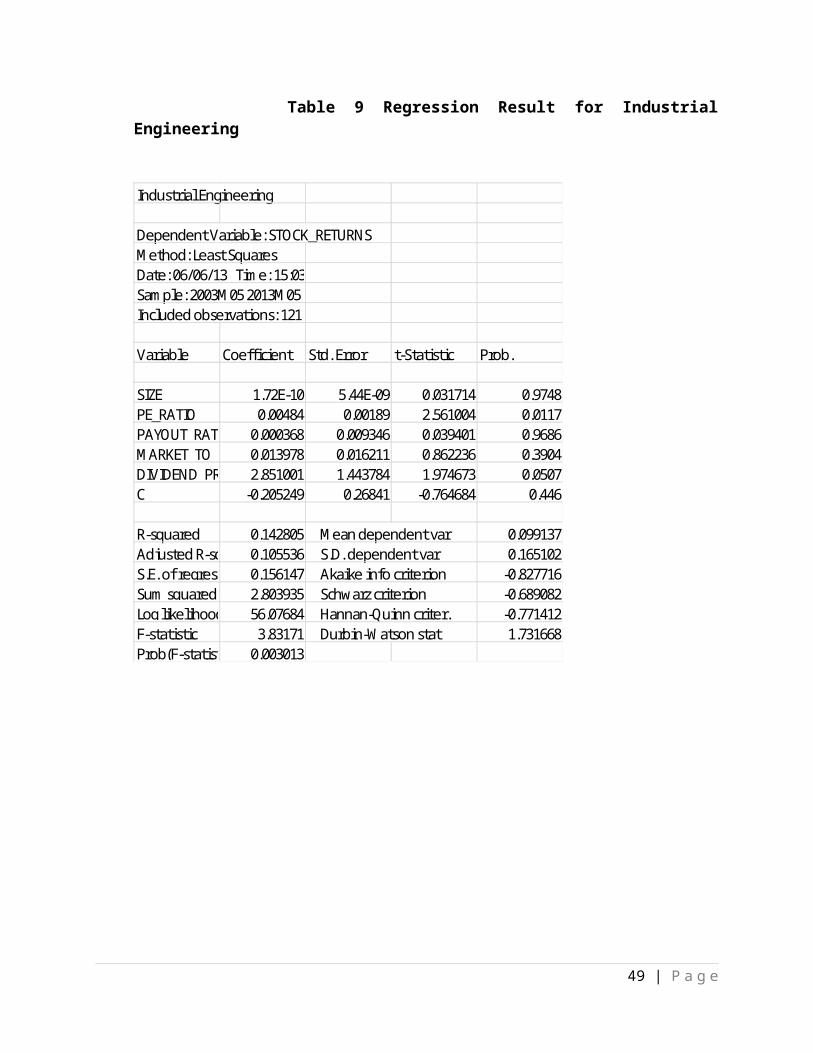

Industrial Engineering

Industrial Engineering is next sector in my regression result.

Price earnings ratio for this sector is highly significant, Price

earnings representthe expectations of the investors regarding the

earnings from the stock, high P/E ratio represents that investors

are expecting higher earnings growth. According to the result

there is positive and statistically significant relationship

between stock returns and price earnings ratio. So in case of

30 | P a g e

this sector Price earnings ratio can predict the future stock

returns. Each industry sectors have different growth prospects,

and according to these prospects investors invest their money in

particular industry. This significant Price earnings ratio shows

that investor are looking for capital gain when they are

investing in the stocks from this sector of Industrial

engineering.

This Industrial engineering sector has included with some of the

major companies in Indian stock market, which are giant in their

particular field, some of the companies from this sector are ABB,

Bharat Forge, Bharat Heavy electrical, Mahindra and Mahindra,

Nelco, SKF India, Tata Motors and Thermax. ABB is Zurich,

Switzerland based multinational company operating in robotics and

mainly automation and power areas, It is one of the largest

engineering company in the world with presence in more than 100

companies. Price earnings ratio of ABB was consistently very high

starting from 14.60 in 2003, It was highest in 2011, whereas in

2008 due to recession and bad market condition Price earnings

ratio falls down as expected, In recession investors become

pessimistic about growth prospect of the company and it had

clearly reflected on company's Price earnings ratio in the period

of 2007 - 2008 where Price earnings ratio of this company had

hampered badly. But otherwise Price earnings ratio was

consistently high showing investors are expecting significantly

high returns from the company's stock. Bharat forge which is also

31 | P a g e

in this sector, this is also another Giant in the field of

forging industry. Forbes has rated Bharat Forge as the best

forging company in Asia, Price earnings ratio for this company

was consistently high except in recession phase. Bharat heavy

electrical is government owned company and another big company in

Indian stock market, Tata Motors is another example from this

industry with high Price earnings ratio.

This consistent high price earnings ratio shows that investors

are expecting high returns from these stocks, this represents

that investors are looking for capital gain on their investments

in this sector. Result for price earning from my regression

result is somehow supporting the findings of Guler Aras and

Mustafa Kemal Yilmaz(2008), because in their research also they

found significant price earnings ratio in case of most of the

stock markets, where P/E ratio is positively and statistically

significant with stock return and can predict the stock return.

Dividend price ratio is another significant variable in this

sector. Result for this sector shows positive and statistically

significant relationship among dividend price ratio and stock

return, Dividend price ratio is another variable which can

predict the stock return for this particular sector. D/P is

significant with t-statistic value of 1.97, which show that

investors can use this variable as predictive variable for stock

return, Price earnings ratio is another predictive variable in

32 | P a g e

case of this sector. D/P ratio represents how much company pays

out earnings as dividend each year relative to its share price.

Positive and significant dividend price ratio shows that,

Investors are looking for dividend earnings from the stocks in

this sector, while investing in this sector investors are more

concern about dividends they will be getting from their

investments.

Overall in this sector investors are looking for capital gains as

well as dividend earnings while investing in this sector as Price

earnings ratio and Dividend price ratio both show positive and

statistically significant relationship with stock returns. Other

three variables like Size, Market to Book ratio and Payout ratio

which are statistically insignificant in case of this sectors

shows that, there is not relationship among these variables and

stock return, hence MtB, Size and Payout ratio cannot predict

stock return for this particular sector. Insignificant MtB ratio

shows that investors are not concern about whether stock is

overvalued or undervalued compared to its book value. They are

just looking for Capital gains and dividend earnings out of their

investment in this particular sector as P/E and D/P ratios are

positive and statistically significant. Size also insignificant

and cannot predict stock return for this sector, result is same

in case of payout ratio for this sector.

Software and Computer Services

33 | P a g e

Taking Software and Computer services Sector into consideration,

only price earnings ratio is the significant variable out of all

five variables used in this study. Price earnings ratio is

significant with t-statistic value of 3.607, this shows that only

P/E ratio can predict the stock return for Software and computer

services sector. This significant P/E ratio shows that, investors

are just looking for capital gains from software stocks, they are

just concern about the earnings through the increase in the price

of stock. While investing in this sector investors are not

concern about book value of the stock as market to book ratio is

insignificant, they are just concern about market price of the

stocks, hence stocks from this sectors are mostly inflated than

its book value. Dividend price ratio is insignificant and shows

no relationship with stock return,

Unlike industrial engineering in this sector dividend price ratio

is insignificant therefore investors are not concern about

dividend earning in this sector, they are looking for capital

gain on their investment. As investors are looking for capital

gain most of the stocks from this sector are very volatile and

show sudden ups and downs in their prices. Stocks like Infosys,

Wipro which are highly efficient and flexible to new information

and new events in the market. Ups and downs of the prices of

these stocks are totally depend on the favorable and unfavorable

information hitting stock market time to time. Due to this

approach of investors who are just looking for capital gain from

34 | P a g e

the stocks, these stock prices are very volatile. Dividend price

ratio which is highly insignificant in case of software industry

which shows that, there is not relationship between stock returns

and D/P ratio for this sector, and ultimately this D/P ratio

cannot be used as predicable variable for stock return or for

predicting stock return. Dividend price ratio is used by

investors to assess how much returns they are getting in form of

dividend from their investment in that stock by comparing the

returns to the actual stock price, D/P ratio is nothing but

comparing stock returns in the form of dividend to the market

price of the stock. From this ratio investors can actually

evaluate the returns they are getting out of their investment. My

regression results show insignificant D/P ratio and insignificant

relationship among D/P and stock return which means this variable

cannot predict the stock returns for Software sector.

This insignificant relationship between D/P and stock return also

shows that investors are not worried and concern about the

returns or dividends while investing in this particular sector,

they are only looking for capital gains or gains from increase in

stock price as the price earnings ratio is significant. Size,

Market to book ratio, and Payout ratio all these variable seem

insignificant according to my regression result and show no

relationship of these variables with stock return, So in this

software sector these variables like MtB, Size, and Payout ratio

cannot predict stock returns. From the investors prospective as

35 | P a g e

well, Investors don't look for Book value, size or payout ratio

of any company while investing their money in this sector and

findings regarding this three variables are not supporting the

findings of Kee Hong Bae, Jeong-Bon Kim(1998), the main reason

for this contradictory results could be different markets

altogether, My study is focused on Indian stock market and this

particular result is only for one particular sector that is

Software and Computer services sector whereas Kee Hong Bae,

Jeong-Bon Kim(1998) have focused on Japanese stock market and

that too they have focused on whole market. Japanese market is

developed stock market and is way different than Indian stock

market in case of regulations and governance matter, hence this

possibility cannot be neglected and hence result from one sector

of Indian stock market is different than Japanese stock market.

Overall, my results are supporting some previous studies in case

of some sectors and in case of some variables but not completely.

This difference in result is observed due to different phases

each market is experiencing, Indian market is emerging market and

need to develop in many ways. Developed markets are well

regulated and well governed but in case of emerging market these

factors differ, Indian market is big and huge in terms of market

capitalization but they are many aspects which need to be

improved in Indian market like, Regulation, Governance mechanism

and many other regulatory aspects. Due to this differences

36 | P a g e

results from Indian stock market are somewhat different from

other developed markets like Japan, UK, and US.

Another aspect is Indian stock market is very efficient and

flexible to new information and new events in global market, you

can observe immediate effect of any unfavorable or favorable news

or events on Indian stock market. Major markets around the world

like New York Stock Exchange, American Stock Exchange, London

stock exchange have significant impact on Indian stock market, It

shows fluctuation according to these major markets so taking into

consideration all these effects and impacts of global markets it

is very difficult to examine why exactly some results and

findings from this paper is not supporting other literatures and

studies in finance based on other market. Due to this sensitivity

of the Stock market sometimes it experiences bullish or bearish

movements depending on favorable or unfavorable information.

Satyam computer services scandal which actually did hamper a

stock market a lot that too in a period of global financial

crisis. Due to this scandal investors become more pessimistic and

feel insecure about their investments in the stock market and

pulled out all of their money invested out of stock market which

cause major stock market crash and Sensex closed at 8,160.40

lowest close since 2nd November 2005. Satyam computers scandal

was biggest scandal in IT industry in India, On 7th January 2009

company's CEO RamalingaRaju had resigned and confessed that he

37 | P a g e

had manipulated the accounts by $1.47 billion. The whole global

and corporate community was shattered because of this scandal and

this scandal hampered Indian stock market badly. Such unfavorable

events make the stock market unstable and therefore it is very

difficult to find consistency in results for all the stock

exchanges around the world.

6. Conclusion

In this study I have observed the relationship between stock

returns and five different variables namely Dividend price ratio,

Price earnings ratio, Size, Market to Book ratio, and payout

ratio. I have collected the total data sample of 357 firms in

total from four different sectors, I have observed this

relationship according to the sector. Paper also tried to examine

the investors choice and approach towards investment and how and

what variables do matter for them while investing in any

particular stock.

According to the findings some variables are significant and show

significant positive relationship with stock return, on the other

hand some variables from some sectors are highly insignificant

and show no relationship with stock return. In case of banking

sector Size and payout ratio are positive and significant which

show positive and significant relationship between stock return

and these variables. Investors who are investing in banking

38 | P a g e

sector would be concern about these variables while investing in

this particular sector, other variables like, D/P, MtB, and P/E

ratio are insignificant and do not show any significant

relationship with stock return. I have also examined the general

industrial sector, this sector constitutes all the major

manufacturing industries in India like, 3M India, Sharp

Industries. Result for this sector shows that D/P ratio is highly

significant and have positive significant relationship with stock

return, which represents that D/P ratio can actually predict the

stock returns for the stocks from this sectors. Another variable

which is significant for this particular sector is Size, which is

also shows positive significant relationship with stock return.

Investors while investing in this general industrial sector

would be looking for Dividend earning and the returns from the

stocks in which they have invested, another important factor for

investors would be Size while investing in this Sector, other

variables like P/E ratio, MtB ratio, and Payout ratio for General

Industrials are not significant and therefore show no

relationship with stock return, this result also shows that

investors while investing in this sector are not concern about

capital gain or increase in stock price they are looking for

Dividend and want to hold the stock for long term period,

insignificant MtB ratio shows that investors are not concern

about book value of the stocks particularly for this sector.

These finding for General industrial sector are supporting the

view of Robert H. Litzenberger and Krishna Ramaswamy(1982).

39 | P a g e

In case of Industrial engineering sector, P/E and D/P ratios are

positive and significant which show positive and significant

relationship with stock return, these two variables can predict

the stock return for this sector. By using these variables

investors can decide their investment strategies. Results

regarding Price earnings ratio for Industrial Engineering are

supporting the results of Guler Aras and Mustafa Kemal

Yilmaz(2008), in their study as well they found significant

relationship between P/E ratio and Stock return.

According to the results of Software and Computer services sector

I found only Price earnings ratio as a significant variable out

of five variables used. This is mainly because IT sector is

continuously and rapidly growing which has increased the

expectations of investors regarding their investments and

therefore price earnings ratio is positively significant, high

P/E ratio shows that investors are expectin higher growth from

stock and ultimately capital gain. From this result it is clear

that, investors who are investing in software industry are

investing money in stock just to take the advantage of stock

price increase.

Overall my study contributes to the corporate finance literature

by examining the relationship between all five variables and

stock return of four different sectors of Indian stock market. I

have also examined the investors choices and approaches towards

investing in these four sectors. In case of some sectors like

40 | P a g e

Software and computer services sector and Industrial Engineering

sector investors are looking for capital gain and only concern

about the increase in a price of stock, which is supported by my

findings regarding P/E ratio, where In both the sectors namely

Software and Industrial Engineering P/E ratio is positive and

statistically significant. But in Banking sector investors are

concern about magnitude of the company that is Size variable

hence, Size variable can predict stock return for banking

industry. For General Industrial D/P ratio is significant

variable which can predict stock return for this industry and

also investors which are investing in this industry are concern

about dividend and returns from their investments. In this study

I have analyzed five variables and four different major sectors

of Indian stock market. Some of the findings from this paper are

supporting literature and some findings are not supporting. In

these four sectors, for each sectors some variables Which I found

significant and some insignificant which do not have any

relationship with stock return.

Further research could be done on the same topic by adding some

more variables and by covering some more data period. Further

research study could include some new variables like Leverage,

book to market ratio etc. In this paper I have not covered the

impact of other major stock markets on Indian stock market in

detail, so in further research this point could be of more focus

and one can analyze and examine the detail effect of other stock

exchanges on Indian stock market. This paper also not covered the

41 | P a g e

impact of regional and local events on stock market such as

scandals, changes in Interest rates, Changes in Government

policies etc which could be covered in further research. Such

events news and new information make the stock market unstable

for some time and because of such instabilities sometimes

research result could be bias and cannot evaluate and find the

actual results and findings.

References

42 | P a g e

Robert H Litzenberger and Krishna Ramaswamy.(1982).The effects of

Dividends on common stock prices Tax effects or Information

Effects ? . Journal Of Finance. Retrieved From

http://www.jstor.org.ezproxy.waikato.ac.nz/stable/2327346

Guler Aras and Mustafa Kemal Yilmaz.(2008). Price-Earnings Ratio,

Dividend Yield, and Market to Book Ratio to predict return

on stock Market: Evidence from the emerging markets. Journal

of Global Business and Technology, Volume. 4, Number 1. Retrieved From

http://search.proquest.com.ezproxy.waikato.ac.nz/docview/

216940328?accountid=17287

Keith S.K. Lam .(2002). The relationship between Size, book to

market equity ratio, earning Price ratio, and return for

the Hong Kong Stock market. Global Finance Journal 13. Retrieved

from

http://www.sciencedirect.com/science/article/pii/

S1044028302000492

Rolf W. Banz.(1980). The relationship between return and market

value of common stock.Journal of Financial economics 9.Retrieved

from

http://www.sciencedirect.com.ezproxy.waikato.ac.nz/science/

article/pii/0304405X81900180

43 | P a g e

JaffreJafffe, Donald B Keim, and Randolph Westerfield.(1989).

Earning Yields, Market Value, and Stock return. Journal Of

Finance. Retrieved from

http://onlinelibrary.wiley.com/doi/10.1111/j.1540-

6261.1989.tb02408.x/abstract

PradoshSimlai.(2009). Stock Return, Size, and book to market

equity. Journal of Economies and Finance Vol 26.Retrieved from

http://www.emeraldinsight.com.ezproxy.waikato.ac.nz/journals.htm?

articleid=1801391&show=abstract

Jeffrey Pontiff and Lawrence D. Schall.(1997). Book to market

ratios as predictors of market returns.Journal of Financial

Economics 49. Retrieved From

http://www.sciencedirect.com.ezproxy.waikato.ac.nz/science/

article/pii/S0304405X98000208

Ian McManus, Owain AP Gwilym and Stephen Thomas.(2004). The role

of payout ratio in the relationship between stock return

and dividend yield.Journal of Business and Accounting 31(9)&(10).

Retrieved from

http://onlinelibrary.wiley.com.ezproxy.waikato.ac.nz/doi/

10.1111/j.0306-686X.2004.00577.x/abstract

44 | P a g e

Gabriel Perez-Quiros and Allan Timmermann .(2000). Firm size and

cyclical variations in stock return. The Journal of Finance Vol.

LV, No 3.Retrieved from

http://www.jstor.org.ezproxy.waikato.ac.nz/stable/222451

Kee Hong Bae, Jeong-Bon Kim.(1998). The usefulness of earnings

versus book value for predicting stock returns and cross

corporate ownership in Japan.Japan and the World Economy 10 (1998)

467-485. Retrieved from

http://www.sciencedirect.com.ezproxy.waikato.ac.nz/science/

article/pii/S0922142598000292

Raj AggarwalTakatoHiraki and Ramesh P Rao.(1992). Price/book

value ratios and equity returns on the Tokyo stock

exchange: Empirical evidence of an Anomalous Regularities.

The Financial Review Vol 27 No. 4.Retrieved from

http://search.proquest.com.ezproxy.waikato.ac.nz/docview/20

8182720

JYH-LIN WU, YU-HAU HU and CHINGNUN LEE .(2011). Can dividend

yields out predict UK stock return without short rates. The

Manchester School Vol 29 No. 6 1179-1196. Retrieved From

http://onlinelibrary.wiley.com.ezproxy.waikato.ac.nz/doi/

10.1111/j.1467-9957.2010.02218.x/abstract

45 | P a g e

ChakerAloui, DucKhuong Nguyen and HassenNjeh.(2012). Assessing

the impacts of oil price fluctuations on stock returns in

emerging markets.Economic Modeling 29(2012) 2686-2695. Retrieved

from

http://www.sciencedirect.com.ezproxy.waikato.ac.nz/science/

article/pii/S0264999312003963

46 | P a g e

Appendix

Table. 7 Regression Result For Banking Sector

Banking Sector

Dependent Variable: STOCK_RETURNM ethod: Least SquaresDate: 06/07/13 Tim e: 19:41Sam ple: 2003M 05 2013M 05Included observations: 121

Variable Coefficient Std. Error t-Statistic Prob.

SIZE -4.13E-10 1.95E-10 -2.121051 0.0361PE_RATIO 5.66E-03 6.00E-03 0.9434 0.3475PAYOUT_RATIO -1.96E-02 1.00E-02 -1.956304 0.0529M ARKET_TO_BOOK_RATIO-1.32E-02 6.48E-02 -0.204389 0.8384DIVIDEND_PRICE_RATIO-4.42E-01 2.18E+00 -2.03E-01 0.8398C 4.14E-01 2.14E-01 1.937359 0.0552

R-squared 0.050446 M ean dependent var 0.053825Adjusted R-squared0.009161 S.D. dependent var 0.118069S.E. of regression 1.18E-01 Akaike info criterion -1.395982Sum squared resid 1.59E+00 Schwarz criterion -1.257348Log likelihood 90.45692 Hannan-Quinn criter. -1.339678F-statistic 1.22E+00 Durbin-W atson stat 1.807331Prob(F-statistic) 0.303345

47 | P a g e

Table. 8 Regression Result for General Industrials

General Industrials

Dependent Variable: STOCK_RETURNM ethod: Least SquaresDate: 06/06/13 Tim e: 14:57Sam ple: 2003M 05 2013M 05Included observations: 121

Variable Coefficient Std. Error t-Statistic Prob.

SIZE 7.86E-08 5.14E-08 1.528731 0.1291PE_RATIO 0.003659 0.002854 1.281938 0.2024PAYOUT_RATIO -0.010273 0.01301 -0.789656 0.4314M ARKET_TO_BOOK_RATIO0.126357 0.099817 1.265887 0.2081DIVIDEND_PRICE 15.48725 4.036018 3.83726 0.0002C -0.786248 0.312132 -2.518957 0.0131

R-squared 0.171712 M ean dependent var 0.114726Adjusted R-squared0.135699 S.D. dependent var 0.432677S.E. of regression 0.40225 Akaike info criterion 1.064828Sum squared resid18.60756 Schwarz criterion 1.203462Log likelihood -58.4221 Hannan-Quinn criter. 1.121133F-statistic 4.768116 Durbin-W atson stat 1.109891Prob(F-statistic) 0.000537

48 | P a g e

Table 9 Regression Result for IndustrialEngineering

Industrial Engineering

Dependent Variable: STOCK_RETURNSM ethod: Least SquaresDate: 06/06/13 Tim e: 15:03Sam ple: 2003M 05 2013M 05Included observations: 121

Variable Coefficient Std. Error t-Statistic Prob.

SIZE 1.72E-10 5.44E-09 0.031714 0.9748PE_RATIO 0.00484 0.00189 2.561004 0.0117PAYOUT_RATIO 0.000368 0.009346 0.039401 0.9686M ARKET_TO_BOOK_RATIO0.013978 0.016211 0.862236 0.3904DIVIDEND_PRICE_RATIO2.851001 1.443784 1.974673 0.0507C -0.205249 0.26841 -0.764684 0.446

R-squared 0.142805 M ean dependent var 0.099137Adjusted R-squared0.105536 S.D. dependent var 0.165102S.E. of regression 0.156147 Akaike info criterion -0.827716Sum squared resid2.803935 Schwarz criterion -0.689082Log likelihood 56.07684 Hannan-Quinn criter. -0.771412F-statistic 3.83171 Durbin-W atson stat 1.731668Prob(F-statistic) 0.003013

49 | P a g e

Table 10 Regression Result for Software and Computer Services

Software and Com puter Services

Dependent Variable: STOCK_RETURNM ethod: Least SquaresDate: 06/06/13 Tim e: 15:11Sam ple: 2003M 05 2013M 05Included observations: 121

Variable Coefficient Std. Error t-Statistic Prob.

SIZE -2.53E-09 3.73E-09 -0.678082 0.4991PE_RATIO 0.004034 0.001118 3.607497 0.0005PAYOUT_RATIO 0.00049 0.010307 0.047496 0.9622M ARKET_TO_BOOK_RATIO0.018982 0.044363 0.427871 0.6695DIVIDEND_PRICE_RATIO7.45E-01 1.89E+00 0.394984 0.6936C -0.127423 0.183819 -0.6932 0.4896

R-squared 0.109412 M ean dependent var 0.087699Adjusted R-squared0.070691 S.D. dependent var 0.245729S.E. of regression0.236884 Akaike info criterion 0.005823Sum squared resid6.453116 Schwarz criterion 0.144457Log likelihood 5.647695 Hannan-Quinn criter. 0.062128F-statistic 2.825633 Durbin-W atson stat 1.45394Prob(F-statistic)0.019143

50 | P a g e