RBS Ann Review 01-07 - AnnualReports.com

272

Make it happen rbs.com Annual Report and Accounts 2005 Profit before tax up 21% Total income up 14% Adjusted earnings per share up 8% Dividend up 25%

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of RBS Ann Review 01-07 - AnnualReports.com

Make it happenrbs.com

Annual Report and Accounts 2005

Profit beforetax up

21%

Totalincome up

14%

Adjustedearnings pershare up

8%

Dividend up

25%

Make it happen

The Royal Bank of Scotland was

founded in Edinburgh in 1727.

By 1900 it had over 130 branches in Scotland andhad opened its first branch in London. During the1920s and 30s it established a significant presencein England through the acquisition of Glyn, Mills andWilliams Deacon’s. By 1970, having merged with theNational Commercial Bank of Scotland, it was theleading bank in Scotland, with over 700 branches.

During the 1980s RBS diversified its business,pioneering the direct distribution of motor insurancethrough the establishment of Direct Line in 1985,and entering US banking in 1988 with the acquisitionof Citizens Bank of Rhode Island.

In the 1990s RBS re-engineered its retail bankingbusiness, removing processing activities frombranches, and segmenting the Bank’s customersand associated service propositions. Over the sameperiod RBS developed and implemented its multi-brand, multiple channel strategy, launching DirectBanking in 1994, and the UK’s first comprehensiveinternet banking service in 1997, together withfinancial services operations in partnership withVirgin and Tesco in the same year.

In 2000 RBS successfully completed the £21 billionacquisition of NatWest, the biggest takeover inBritish banking history, creating a Group with over 20 million customers, £400 billion assets and 110,000 employees worldwide. The NatWestintegration was completed successfully in February2003, with the original targets for cost savings andrevenue benefits exceeded.

Since the acquisition of NatWest, RBS has continuedto grow the business through the combination ofstrong organic growth and acquisitions. In the US,Citizens’ footprint has been expanded from NewEngland into the Mid-Atlantic states through theacquisition of the Mellon Bank regional franchise,and into the Midwest through the acquisition ofCharter One, completed in 2004. Citizens is nowone of the top ten US commercial bankingorganisations by deposits. In insurance, theacquisition of Churchill broadened the product anddistribution channel capabilities of Direct Line andcreated the second largest general insurer in theUK. In corporate banking, RBS has entered the US,Continental European and Asia Pacific markets.

In August 2005, RBS signed strategic investment and co-operation agreements with Bank of China,the second largest bank in China.

Report and accounts

51 Section 01Operating and financial review

107 Section 02Governance

133 Section 03Financial statements

231 Section 04Additional information

259 Section 05Shareholder information

Gro

up r

evie

wD

ivis

iona

l rev

iew

Cor

pora

tere

spon

sibi

lity

Gov

erna

nce

and

finan

cial

rev

iew

01

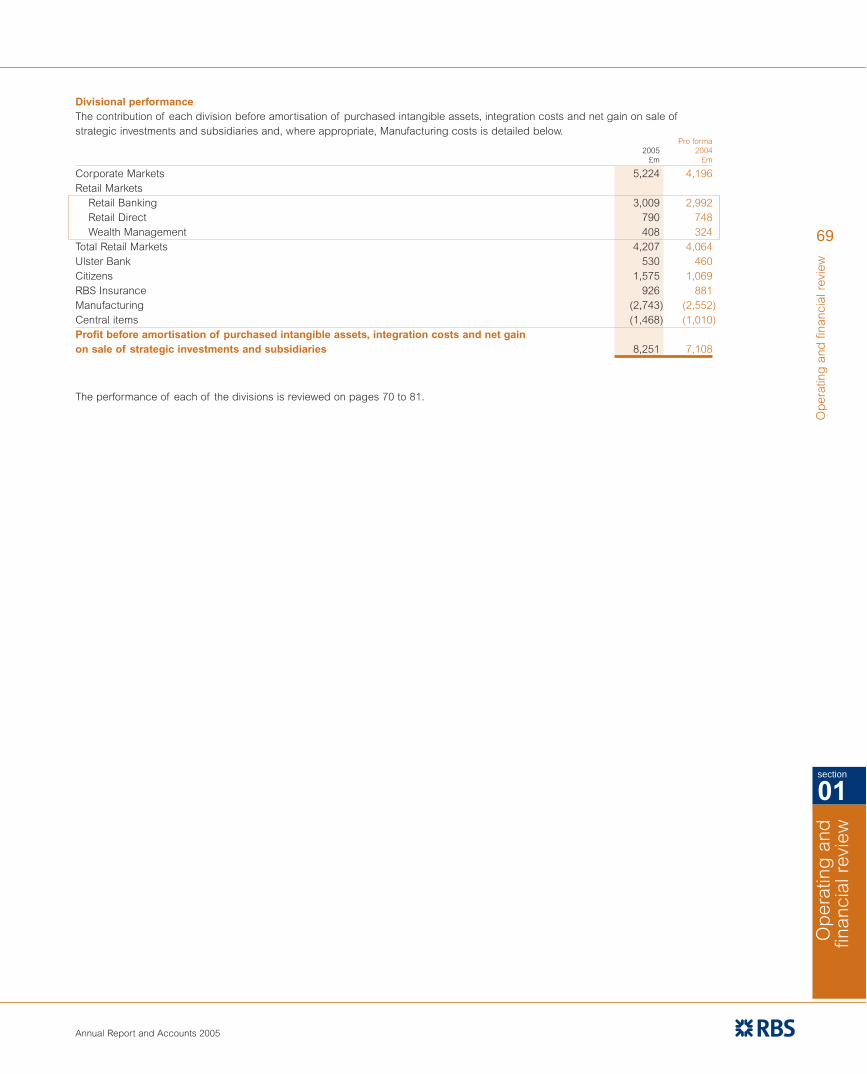

Highlights of 2005

Contents02 Financial highlights

04 Chairman’s statement

06 Group Chief Executive’s review

08 Group profile

10 Divisional profile

Divisional review

14 Corporate Markets

22 Retail Markets

30 Ulster Bank Group

32 Citizens

38 RBS Insurance

42 Manufacturing

Corporate responsibility

46 Corporate responsibility

47 2005 activities

48 Community investment

Annual Report and Accounts 2005

� Group operating profit up 16% to £8.3 billion

� Profit before tax up 21% to £7.9 billion

� Total dividend for the year of 72.5p per share, up 25%

� Share repurchase of up to £1 billion

� Income up 14% to £25.6 billion

� Cost:income ratio, excluding acquisitions,41.8% unchanged from 2004

� Adjusted earnings per ordinary share up 8% to 175.9p

The financial comparisons are with 2004 pro forma results which have been prepared on the basis set out on page 57.

Fin

anci

al h

ighl

ight

sFinancial highlights

Adjusted earnings per share (pence)

The Group’s total income grew by 14% to £25,569 million in 2005.

Group operating profit increased by 16%to £8,251 million in 2005.

Group profit before tax rose by 21%to £7,936 million in 2005.

Profit before tax(£m)

2001 2002 2003 2004

5,778

6,540

7,068

8,101

2001 2002 2003 20042001 2002 2003 2004 2004pro forma

2005

14,558

17,016

19,281

22,754 22,515

25,569

UK GAAP IFRS UK GAAP IFRS UK GAAP IFRS

2004pro forma

2005

7,108

8,251

2004*pro forma

2005*

45.344.2

42.640.8

41.8 41.8

2001 2002 2003 2004

127.9

146.3

157.2

172.5

2001 2002 2003 2004

4,252

4,852

6,076

6,917

UK GAAP IFRS UK GAAP IFRS

2004pro forma

2005

6,543

7,936

2004pro forma

2005

162.6

175.9

2001 2002 2003 2004 2005

38.0

43.7

50.3

58.0

72.5

Income (£m)

Adjusted cost:income ratio(%)

Group operating profit – profit before tax,purchased intangibles amortisation,integration costs and net gain on sale ofstrategic investments and subsidiaries (£m)

Earnings per share increased by 8% to175.9p for 2005, adjusted for purchasedintangibles amortisation, integrationcosts and net gain on sale of strategicinvestments and subsidiaries, and in2001 – 2003 for the AVS dividend.

Dividend per ordinary share (pence)

The directors have recommended a final dividend of 53.1p per ordinaryshare which, when added to the interimdividend of 19.4p, makes a total for 2005of 72.5p, an increase of 25%.

*excluding acquisitions and at constant exchange rates

The Group’s cost:income ratio, excludingacquisitions and at constant exchange rates,was 41.8%. The cost:income ratio is calculatedexcluding purchased intangibles amortisation,integration costs and net gain on sale ofstrategic investments and subsidiaries, andafter netting operating lease depreciationagainst rental income.

� Group operating profit up 16%� Profit before tax up 21%� Adjusted earnings per ordinary share up 8% to 175.9p� Total dividend for the year up 25% to 72.5p per share

02

The annual accounts have, for the first time, been prepared in accordance with International Financial Reporting Standards. Certain standards relating to financialinstruments were not adopted until 1 January 2005. As explained on page 58, the Group has provided comparative information on a pro forma basis that includes the estimated effect of these standards for the year ended 31 December 2004.

Gro

up r

evie

w

03

2001 2002 2003 2004 2005

47.8

43.2

48.8

55.6 56.1

Market capitalisation(£bn)

The Group’s market capitalisation at 31 December 2005 was £56.1 billioncompared with £55.6 billion a year earlier.

Geographic analysis of incomedetermined by location of customer

Geographic analysis of operatingprofit determined by location ofcustomer

Geographic analysis:Employees

%

UK 75

US 19

Europe 5

Rest of World 1

75

19

5

1

Geographic analysis:Operating profit

%

UK 58

US 28

Europe 13

Rest of World 1

58

28

13

1

Geographic analysis:Income

%

UK 73

US 18

Europe 8

Rest of World 1

73

18

8

1

0

20

40

60

80

120

100

140

160

FTSE 100RBS

2000 20052004

Source: Datastream

200320022001

Index

Total shareholder return performance

The performance graph illustrates theperformance of the company over the pastfive years in terms of total shareholderreturn compared with that of the companiescomprising the FTSE 100 index. This indexhas been selected because it represents across-section of leading UK companies.The total shareholder return for thecompany and the FTSE 100 have beenrebased to 100 for 2000.

2005

04

Cha

irm

an’s

sta

tem

ent

2005 was another year of excellentperformance by the Group. Increasedearnings and strong capital generationhave enabled us to continue investing for organic growth, as well as raise ourdividend significantly and embark on aprogramme of repurchasing our shares.

Financial performanceIn 2005, Group operating profit increased by 16% to £8,251million (2004 – £7,108 million). Total income grew by 14% to£25,569 million (2004 – £22,515 million), while operating expensesalso grew by 14% to £11,298 million (2004 – £9,871 million).

We have maintained a high level of efficiency across theGroup, reaping the benefits of scale from our Manufacturingoperations while continuing to invest in our businesses.

All acquisition integration benefits are being achieved at orahead of expectations. The integration of Churchill, acquired in September 2003, was completed in September 2005 withbenefits in excess of those forecast at acquisition.

CapitalOur first use of additional capital is to invest in profitablebusiness growth, and we see many opportunities to do soacross the Group. Whilst having no plans for large acquisitions,we will continue to evaluate good opportunities to supplementorganic growth, using strict investment criteria and leveragingour proven integration capabilities. In addition, it has alwaysbeen our plan to be capital generative beyond the developmentneeds of our businesses, and our 2005 results represent animportant milestone in that ambition as we are able to returncapital to shareholders in the form of an increased dividendand share buyback.

Staff profit sharingReflecting the strong financial performance of the Group,we are delighted that our staff are once again sharing in oursuccess with a profit share for the year at 10% of basic salaries.

Board of directorsThe past year has seen significant change for our Board.I am delighted that Sir Tom McKillop agreed to join last year as our Deputy Chairman. Subject to his election, he will takeover from me as Chairman at the Annual General Meeting on28 April 2006. As chief executive of AstraZeneca PLC heenjoyed wide experience of operating successfully in differentinternational markets and his comprehensive understanding of financial services from his previous directorship of a majorbank will be of great value to us.

We bade farewell to Sir Angus Grossart, Lord Vallance, EileenMackay and Iain Robertson as non-executive directors, andFred Watt as Group Finance Director. Their contribution duringa period of dramatic growth and change for RBS has beenhighly appreciated, as has their experience of the economiccycle and its impact on business. On behalf of the Board I would like to pay tribute to their loyal service and express our thanks for the valued contribution they have made.

Over the same period we have welcomed the appointment oftwo new non-executive directors, Janis Kong and, with effectfrom 1 March 2006, Bill Friedrich. I am confident that, with theirdifferent backgrounds and experience across our key markets,both will greatly strengthen the Board as we embark on ournext phase of growth.

On 1 February 2006 Guy Whittaker joined the Board as GroupFinance Director. He is an experienced senior executive of thehighest calibre, with great breadth of international experiencein financial services. On 14 February 2006 the Group was alsovery pleased to announce the appointments of Johnny Cameron,Chief Executive of Corporate Markets, and Mark Fisher, ChiefExecutive of Manufacturing, as executive directors, with effectfrom 1 March 2006.

OutlookLeaving an organisation which has been so important to me for the last 18 years will mark a milestone for me also, but I am pleased to be doing so at a time when the business is in such good shape. We have demonstrated our ability to generate capital consistently from a stable and diverseplatform and I believe we are well placed to take advantage of the many opportunities that lie ahead, for the benefit of ourshareholders, customers and staff.

Sir George Mathewson, Chairman

Chairman’s statement

Gro

up r

evie

w

05

2005

06

Gro

up C

hief

Exe

cutiv

e’s

revi

ewGroup Chief Executive’s review

Gro

up r

evie

w

07

Our results for 2005 demonstrate thestrength and momentum of the Groupand the capabilities of our diversebusiness platform. We increased our total income by 14% and held ourcost:income ratio, before acquisitions,steady at 41.8%. Group operating profitincreased by 16% to £8,251 million.All our divisions increased their incomeand contribution to Group profit.

We are particularly pleased with the geographic mix of ourprofits, 42% of which came from our international operations.Our profits in Europe, outside the UK, have grown to be equalto Citizens’ profits before the acquisition of Charter One. Themajority of this growth is organic. Strong organic incomegrowth has been a recurring theme of our results over recentyears and provided over 70% of our increase in 2005.

During the course of the year we established Retail Markets in order to strengthen the co-ordination and delivery of ourmulti-brand retail strategy. At the beginning of 2006 the formerCorporate Banking & Financial Markets division was renamedCorporate Markets and we reorganised our activities into twobusinesses, UK Corporate Banking and Global Banking &Markets, to enhance our ability to serve the needs of thesedistinct customer segments.

Bank of ChinaIn August 2005 we signed strategic investment and co-operation agreements with Bank of China, the second largestbank in China. Following regulatory approvals, the transaction was completed in December. RBS led a consortium thatinvested $3.1 billion, taking a 10% stake in Bank of China.We have ourselves invested $1.6 billion, financed by the sale of our shares in Banco Santander Central Hispano S.A.We are working closely with Bank of China to develop business co-operation initiatives in areas such as credit cards, wealth management and corporate banking. We arealso supporting Bank of China in key infrastructure areas,including risk and financial management, human resourcesand information technology.

Our customersCustomer numbers increased in all our divisions, with TheRoyal Bank of Scotland securing top position amongst the highstreet banks for personal customer satisfaction and NatWestmoving into joint second position. This result reflects ourinvestment in our branches and our people to support them,and improved access through a wide choice of channels.

Our peopleIn the 2005 Employee Opinion Survey the Group improved itsscore in each of the 14 categories surveyed. At 86%, responseto the 2005 Employee Opinion Survey was even higher thanpreviously. We have launched new initiatives to encourageinnovation and leadership. Our new Business School andprogrammes developed in conjunction with Harvard BusinessSchool are helping to develop the vision and quality ofmanagement that the Group will need in challenging markets in the future.

Our shareholdersStrong earnings and capital generation strengthened our Tier 1 capital ratio to 7.6% at the end of 2005 and our totalcapital ratio to 11.7%. We are committed to capital strengthand efficiency, returning capital to our shareholders boththrough increasing dividends and when appropriate via sharebuybacks. This year the Board proposed a 25% increase in ourdividend to 72.5p per share, representing an increased payoutratio of 41%. In addition, we intend to repurchase up to £1billion of our shares over the next 12 months.

Sir George MathewsonGeorge Mathewson will retire as the Group's Chairman at theAnnual General Meeting. Under his leadership, initially asGroup Chief Executive, RBS has enjoyed an unparalleledperiod of growth and success both at home and internationally.Very few can match his 18-year legacy of consistently increasingvalue generation. Personally and on behalf of his colleagues,I would like to thank George for his outstanding contribution.

OutlookWhilst displaying both opportunities and threats, the economicoutlook for 2006 in all of the major economies in which weoperate would appear to be supportive of the continuedmomentum of the Group. We believe that we have built astrong platform for future growth with a diverse range ofopportunities in a number of geographies, and taken togetherwith our strong capital base, continuing good credit metrics,and firm cost control, we remain optimistic about the futureprospects of the Group.

Sir Fred Goodwin, Group Chief Executive

2005

08

Gro

up p

rofil

eGroup profile

Corporate Markets

Citizens

Corporate Markets

Retail Markets

Ulster Bank Group

RBS Insurance

Manufacturing

United Kingdom US

2005

Income (£bn) 18.8

Operating profit (£bn) 4.8

Loans to customers (£bn) 281

Deposits by customers (£bn) 235

Employees 103,000

2005

Income (£bn) 4.6

Operating profit (£bn) 2.3

Loans to customers (£bn) 90

Deposits by customers (£bn) 85

Employees 26,000

Geographic analysis of income and operating profit determined by location of customer

Gro

up r

evie

w

09

2005

Corporate Markets

Retail Markets

Ulster Bank Group

RBS Insurance

Manufacturing

Corporate Markets

Retail Markets

Europe Asia Pacific

2005

Income (£bn) 2.0

Operating profit (£bn) 1.1

Loans to customers (£bn) 42

Deposits by customers (£bn) 18

Employees 7,000

2005

Income (£bn) 0.2

Operating profit (£bn) 0.1

Loans to customers (£bn) 4

Deposits by customers (£bn) 5

Employees 1,000

TOTAL 2005

Income (£bn) 25.6

Operating profit (£bn) 8.3

Loans to customers (£bn) 417

Deposits by customers (£bn) 343

Employees (full time equivalent basis) 137,000

10

Div

isio

nal p

rofil

eDivisional profile

Corporate Markets

Chief ExecutiveJohnny Cameron

UK Corporate BankingGeographical spreadUK

Global Banking & MarketsGeographical spreadUK, Europe, US and Asia

Market data

�No.1 UK corporate and commercialrelationship bank

�No.1 for UK payments

�No.1 for card transaction processing

�No.1 for deposits

�No.1 for lending

�No.1 for asset finance

�No.1 for invoice finance

�No.1 for foreign exchange

�No.1 for sterling interest ratederivatives

Market data

�Serves over 95% of the FTSE 100

�Serves over 80% of Fortune 100companies in the US

�Banking relationships with over 90%of the Dow Jones Eurostoxx 50

�Top 10 globally for total debtissuance

�No.2 securitisation house globally

�No.1 project finance bank globally

�No.3 commercial aircraft financierglobally

�Top 5 globally for foreign exchange

Market data

�No.1 for structured syndicated loans in Europe

�No.1 leveraged finance house in Europe

�No.1 train operating lessor inEurope

�No.1 bookrunner of Agencycommercial mortgage-backedsecurities

�No.1 in US government sales for liquid products

Corporate Markets (formerly Corporate Banking & Financial Markets) is a leading provider of banking services and integrated financial solutions to corporate customers in the UKand major corporates and financial institutions globally.

Since the start of 2006 we have organised Corporate Markets into two distinct businesses:UK Corporate Banking, which focuses on the needs of UK domestic and internationalcorporate and commercial customers, and Global Banking & Markets, which supports therequirements of large international corporates and financial institutions around the world.

Gro

up r

evie

w

11

2005

Retail Markets

Chief ExecutiveGordon Pell

Retail BankingGeographical spreadUK

Retail DirectGeographical spreadUK and Europe

Wealth ManagementGeographical spreadUK, Europe, Asia and offshore locations

Retail Markets has the largest network of bank branches and ATMs in the UK; it has leadingpositions in the UK in credit card issuing, merchant acquiring, consumer finance andsupermarket banking; and it provides services to clients through premier brands in UKprivate banking and UK offshore banking. It offers a wide range of banking, financial,insurance, life assurance, pension, credit card and charge card products and client servicesfor private, corporate, expatriate and offshore customers.

Retail Markets brands include The Royal Bank of Scotland and NatWest in retail banking and credit cards. MINT and Tesco Personal Finance also offer cards, and a range ofproducts and services are available through The One account, First Active UK, Direct LineFinancial Services, Lombard Direct and other brands. Through Streamline and InternationalMerchant Services, which includes WorldPay and Bibit, we are the leading merchantacquirer in Europe. Wealth Management brands include Coutts Group, Adam & Company,Royal Bank of Scotland International and NatWest Offshore.

Market data

�Largest retail network in the UK

�2,274 branches

�Largest ATM network in the UK

�Over 14 million personal customers

�Largest provider of banking servicesto small and medium sizedenterprises (SMEs) in the UK

�Over 1.1 million business customers

Market data

�Over 17.5 million customer accounts

�Over 11 million credit card andstorecard accounts in the UK

�Over 2 million customer accounts in Europe

Market data

�Coutts – premier UK private bankingbrand

�Over 100,000 private bankingcustomers

�Third largest foreign-owned privatebank in Switzerland

�160,000 offshore customers

Ulster Bank Group

Chief ExecutiveCormac McCarthy

Geographical spreadIsland of Ireland

Ulster Bank Group operates across the island of Irelandproviding a full range of banking and financial products and services for personal customers and corporates viabranches, telephone and the internet. Ulster Bank Grouphas the largest share of personal banking customers in Northern Ireland and is the third largest bank in theRepublic of Ireland. In 2005 Ulster Bank Group launchedmarket-leading mortgage and current account products and a new brand identity with the RBS logo.

Market data

�Largest share of personal bankingcustomers in Northern Ireland

�Third largest bank in the Republic of Ireland

�1.6 million personal and businesscustomers across the island of Ireland

�304 branches and business outlets

12

Div

isio

nal p

rofil

eDivisional profile continued

Citizens is the eighth largest commercial bankingorganisation in the US, based on deposits. The Charter Oneacquisition in August 2004 enabled it to expand into sixadjacent states in the northeastern and midwestern US.Citizens offers personal banking, residential mortgages,home equity loans, credit cards and merchant cardservices, and a wide variety of commercial bankingservices through its extensive, convenient network of citycentre, local and supermarket branches.

Market data

�Eighth largest commercial bankingorganisation in the US by deposits

�Second largest supermarket banker in the US

�4.6 million personal customers,450,000 business customers and 1.6 million retail credit card customeraccounts

�Retail branch footprint extends to 13states and 30% of the US consumerpopulation

�With credit cards and our partnershipwith Kroger our total retail andcorporate presence stretches across40 states

�Over 1,100 traditional bank branches

�Over 520 in-store branches

�More than 3,800 ATMs

Citizens

Chairman and Chief Executive OfficerLarry Fish

Geographical spreadNew England, Mid-Atlantic andMidwest regions of the US

Gro

up r

evie

w

13

2005

Manufacturing

Chief ExecutiveMark Fisher

Geographical spreadUK and Europe

RBS Insurance

Chief ExecutiveAnnette Court

Geographical spreadUK and Europe

Manufacturing’s diverse range of services supports the customer-facing operations of the Group’s multiplebrands. It provides customer support via telephony,account management, lending, mortgage processing and money transmission.

Group Technology develops and maintains the infrastructureand technology that supports the branches, ATMs andinternet banking for customers of Corporate Markets,Retail Markets and RBS Insurance.

Purchasing is responsible for the vast majority of purchasingundertaken by the Group, leveraging its scale to maximisecost efficiencies.

The Group’s property portfolio is managed, maintained and refurbished by Manufacturing, which also oversees the property investment programme.

Market data

�No.1 in the UK for cheque payments

�No.1 in the UK for Bank AutomatedClearing System (BACS) transactions

�No.1 in the UK for Clearing HouseAutomated Payment System (CHAPS)transactions

�Runs the UK’s largest ATM network

RBS Insurance is the second largest general insurer in theUK and a growing provider of general insurance in Spain,Italy and Germany. It sells and underwrites insurance via the telephone, the internet, partnerships and a network ofbrokers. Its brands, including Direct Line, Churchill, Privilege,Green Flag and NIG, are some of the best known in the UK.

Market data

�Second largest general insurer in the UK

�No.1 for UK car insurance

�No.2 for UK home insurance

�25.9 million in-force policies

�8.7 million UK car policies

�4.6 million UK home policies

�Largest tele-direct insurer in Spain

�1.9 million international car policies

14

Cor

pora

te B

anki

ng &

Fin

anci

al M

arke

tsCorporate Markets

14

Cor

pora

te M

arke

ts

Make it happen

� Profit contribution £5,224 million (2004 – £4,196 million)� Total income up 17%� Profit up 24%

Kew Gardens has an international reputation.In 2005 they selected RBS for the quality ofonline banking data we offered alongside a verycompetitive and flexible interest bearing account.RBS is UK market leader in the provision ofbanking services to the charitable sector.

Div

isio

nal r

evie

w

15

Corporate Markets is focused onthe provision of financial services to commercial and corporatecustomers in the UK and to large corporates and financialinstitutions around the world. In2005 Corporate Markets increasedincome by 17% to £8,815 million.

��� The former Corporate Banking & FinancialMarkets division was renamed Corporate Marketson 1 January 2006, when we reorganised ouractivities into two businesses, UK CorporateBanking and Global Banking & Markets, in order toenhance our focus on the distinct needs of thesetwo customer segments.

��� Corporate Markets’ extensive product range includes cash and liquidity management and comprehensive debt, risk management andtreasury services. Debt services include overdraft,bilateral and syndicated lending; primary bondissuance; trade finance; asset finance; andstructured finance solutions for property, acquisitionfinance, project finance and infrastructure finance(including PPP/PFI). Risk management and treasuryservices include trading of corporate, institutionaland public sector debt; futures brokerage; foreignexchange; and money markets, currency derivativeand interest rate risk management services.

UK Corporate Banking provides customers with a fullsuite of banking products and specialist services tomeet domestic and international needs. We continueto be the UK’s No.1 corporate and commercialrelationship bank and market leader in the UK inpayments, card transaction processing, deposits,lending, asset finance, invoice finance, foreignexchange and sterling interest rate derivatives.

��� Our corporate and commercial bankingbusiness has 86,000 customers supported by 1,500 dedicated relationship and businessdevelopment managers operating out of170 corporate centres spread across the UK.

��� We differentiate ourselves through thestrength of our long-term relationships with ourcustomers. Service is delivered by a network ofexperienced and highly trained relationshipmanagers operating in their local communities.Acting as a single point of contact, they workproactively with our product teams to deliver theright solutions for their customers’ needs. Qualityoperational service is provided by specialistcustomer service teams who are also closelyaligned with our relationship managers.

��� In addition to our core banking offering oflending, payments, deposits and internationalservices, our specialist businesses offer a full rangeof financing solutions to UK customers. Lombard isthe market-leading provider of asset financing andmanagement services from traditional hire purchase,leasing and contract hire through to bespokesolutions. RBS Invoice Finance’s services includefactoring, invoice discounting, asset-backed lending,trade cycle finance and bad debt protection.Lombard and RBS Invoice Finance have 400 sales staff working out of 53 offices, and over100,000 customers.

2005

Make it happen

Delivery

16

Cor

pora

te M

arke

ts

Make it happen

Corporate Markets continued

2005 successes include:��� RBS jointly underwrote and syndicated a £1.2 billion funding package to enable TravisPerkins to acquire Wickes, creating one of thelargest building supply businesses in the UK. Wethen acted as sole adviser on the raising of $400million of debt in the US Private Placement market,Travis Perkins’ first such transaction. As a leadbanker to the enlarged group we also provideclearing services, interest rate hedging and Lettersof Credit to support its international business.

��� We acted as an Underwriter and Bookrunnerfor Premier Foods, one of the largest suppliers of grocery products in the UK, in a £780 millionfinancing package to support the acquisition ofMarlow Foods Limited, owner of the Quorn brand,the UK’s leading meat alternative.

��� Our relationship team, working with FinancialMarkets’ colleagues, provided South Yorkshirebased Castings Technology International withfunding for new flagship premises, allowing thecompany to grow its business and create 48 newjobs in the region.

��� A strong relationship with Icelandic ready-prepared foods group Bakkavör resulted in RBSbeing mandated to structure and jointly arrange a £500 million facility to enable Bakkavör to acquirethe entire share capital of Geest and refinance its debt.

��� As the leading UK clearing bank for TNT, weprovide a comprehensive range of payment andcheque reconciliation services, including integratedIT systems and secure e-mail communication withour service centre. Our close relationship enablesus to integrate product delivery and enhance ourcustomer service.

��� Lombard provided a funding package to support the installation of a revolutionary new ‘G-Force’ rollercoaster ride at Drayton Manor Theme Park in Staffordshire.

��� RBS Invoice Finance delivered a committed£16.5 million stock and debtor funding package for Hargreaves Group, a leading bulk haulage andaggregates business. This allowed the customer to complete the acquisition of Monckton Coke &Chemical Co whilst refinancing existing credit lines.

��� We helped Joy Mining Machinery to managethe payment risks associated with exporting to theFar East, Russia and North Africa. Our Letter ofCredit processing expertise enabled the companyto trade safely in these countries.

Global Banking & Markets is a leading bankingpartner to major corporates and financial institutionsaround the world, specialising in providing thesecustomers with a full range of debt financing, riskmanagement and investment services.

��� We serve our Global Banking & Marketscustomers from offices in 20 countries, with a leadingposition in the UK, established and strongly-growingpositions in the US and continental Europe and an increasing capability in Asia-Pacific. Thesesophisticated customers benefit from our sectoralexpertise, product excellence and access to markets.

��� A focus on long-term relationships backedby our strong balance sheet and suite of value-added product capabilities is at the heart of ourapproach to our customers. This approach enabledexcellent growth across the full range of productsand markets that Global Banking & Markets serves.We have relationships with the overwhelming majorityof the members of each of the FTSE 100 index,the Fortune 100 list and the Dow Jones Eurostoxx50 index.

��� The integration of our banking operations inthe US with RBS Greenwich Capital, our industry-leading US government bonds and asset-backedsecurities business, has delivered excellent resultsduring 2005, with strong growth in new corporaterelationships, corporate loan syndications andinterest rate derivative volumes.

RBS, through UK Corporate Banking, is the UK’s No.1 relationship bank.

Div

isio

nal r

evie

w

17

2005

Fondo ImmobiliPubblici.RBS Italy led three banksin the underwriting of thefirst closed-end real estatefund for the €3.3 billiontransfer of property fromthe Italian Ministry ofEconomy and Finance tothe newly created FIP.

��

Open University.RBS has a long standingrelationship with TheOpen University, Britain’sfirst university dedicatedto distance learning.In 2005 the OpenUniversity consolidated its loan facilities with RBSas sole lender.

� � BloomsburyPublishing is one ofBritain’s most successfulpublishing houses. It isbest known for titles suchas Harry Potter and thePru Leith Cookery booksand is a long-standing UK Corporate Bankingcustomer.

��

18

Cor

pora

te B

anki

ng &

Fin

anci

al M

arke

tsCorporate Markets continued

18

Cor

pora

te M

arke

ts

Our focus on long-term relationships backed by value-adding solutions has won Global Banking& Markets major corporate and institutional customers around the world. We have relationshipswith over 95% of the FTSE 100, over 80% of Fortune 100 companies in the US and over 90% ofthe Dow Jones Eurostoxx 50.

Make it happen

Pernod Ricard.In April 2005 Pernod Ricard completed theacquisition of Allied Domecq. RBS was one offour Bookrunners for the €9.2 billion facilityoffering specialist expertise in €/£ foreignexchange hedging and structured loans.

Div

isio

nal r

evie

w

19

2005

��� A controlled expansion of our franchise overthe last five years across France, Germany, Spain,Italy and the Nordic region has enabled us tocapture and develop major client relationships incontinental Europe. We now provide a full range of products to customers in these countries.

��� In the Asia Pacific region we have selectivelybuilt up our presence, particularly where we haveidentified opportunities to leverage our expertise indelivering financial markets products to financialinstitutions. We continue to achieve impressiveresults from the region, where we now employ 500 people. In Australia our wide range of productshas been particularly successful with both corporateand institutional customers.

��� Our worldwide team of structured financeprofessionals provides specialised financing solutionsfor acquisitions, property, projects, infrastructureand commercial equipment including aircraft, shipsand trains. In Europe we have a long-standingmarket-leading position in leveraged finance as a preferred partner to financial sponsors. Globallywe are the No.1 project finance bank and No.3commercial aircraft financier.

��� Our financial markets activities benefit fromour established platform and the real scale that wehave developed. We are able to provide a full rangeof solutions that deliver against different customerrequirements, from rapid access to electronicplatforms, to high quality advice and excellentexecution by highly skilled sales people.

2005 successes include:��� RBS arranged and underwrote £1.7 billionof debt facilities to finance Gala Group’sacquisition of Coral Eurobet in the UK. Thistransaction was one of the largest-ever sterlingleveraged transactions (awarded Domestic Deal of the Year by Acquisitions Monthly).

��� We were awarded the role of Sole LeadArranger on the €470 million debt refinancing of

the api Energia Power Project in Italy due to ourlong-term relationship, structuring expertise andmarket-leading position. api Energia is one of threeintegrated gasification combined cycle plants inEurope showcasing an environmentally friendlygasification process which converts refinery residueto electrical power. This transaction and our ongoingsupport have enabled the api Group to continuewith its development plans and long-term growthobjectives.

��� RBS was instrumental in the largest PublicTender Offer ever made by a privately ownedcompany in Germany, when it served as the exclusivefinancial arranger to Spohn Cement GmbH in itsacquisition of Heidelberg Cement AG. RBS wasmandated as Sole Bookrunner to underwrite andarrange the financing needs of the bid, including theprovision of acquisition facilities totalling €3.1 billion.

��� When RBS co-arranged the US$1.2 billionprivate placement for Wolseley, the world’s largestdistributor of heating and plumbing products, it set a market record for private placements.

��� RBS jointly led the £18 billion acquisition ofUK mobile operator 02 by Telefónica, underwriting£6.1 billion. This was one of the largest acquisitionsin the telecom sector and the largest ever singleacquisition made by a Spanish company (awardedMost Impressive Loan and Best Western EuropeanLoan by Euroweek).

��� The UK Debt Management Office and HerMajesty’s Treasury mandated RBS to act as one offour Bookrunners in the UK Government’s first eversyndicated offering in sterling bonds and the first50 year inflation bond in the world.

��� Through long-standing relationships with bothof the UK’s leading cable companies, deep sectorknowledge and tactical use of our balance sheet wehelped to pave the way for the merger between NTLand Telewest, thereby consolidating our position as atop-tier partner bank to this customer.

20

Cor

pora

te B

anki

ng &

Fin

anci

al M

arke

tsCorporate Markets continued

20

Cor

pora

te M

arke

ts

We’ve been the fastest growing debt issuance bank globally over the last four years.

��� RBS was the only bank to be awarded bothBookrunner and Mandated Lead Arranger roles infunding each of the three deals to acquire stakes in France's leading motorway companies from theFrench government. This was achieved through thecombined strength of our multi-product platform,infrastructure sector expertise and local corporaterelationships. Our teams led the underwriting ofinnovative and competitive financing packagestotalling some €17.5 billion in support of the €21.3 billion-worth of acquisitions.

��� As Joint Mandated Lead Arranger andUnderwriter, via our offices in France and Spain,RBS provided an innovative financing structure for€532 million of debt to fund the €1.1 billion highspeed rail link concession to be built through thePyrenees between Perpignan and Figueras(awarded EMEA Infrastructure Deal of the Year, PFIAwards, and EMEA Rail Transport Deal of the Yearby Project Finance Magazine).

��� RBS Greenwich Capital acted as JointBookrunner for the US$750 million 10-year GlobalNotes offering for Harrah’s operating company,Harrah’s Entertainment Inc. Harrah’s is a leadingentertainment and casino group and is the onlyinvestment grade gaming company in the world. Bytaking advantage of an attractive financing windowthe transaction was twice over-subscribed.

��� In Australia we completed our first leveragedfinance transaction as Joint Mandated Lead Arrangerand Bookrunner for the US$1.7 billion acquisition ofDyno Nobel, a leading global supplier of commercialexplosives, by a consortium of investors.

��� RBS acted as Joint Arranger of a cross-border securitisation for SC First Bank (previouslyKorea First Bank) raising €500 million in triple-Arated notes. The issue was more than 2.5 timesover-subscribed with more than 30 institutionalinvestors and was structurally innovative, marking

the first instance an amortising junior note wasintroduced for a Korean cross-border mortgage-backed securitisation.

��� RBS Aviation Capital, working closely withour Shanghai Branch, completed a major JapaneseOperating Lease financing with China SouthernAirlines. The deal comprised an initial US$93 millionbridge loan financing of three Boeing 737-700aircraft from RBS Shanghai which wassubsequently restructured into a JapaneseOperating Lease financed through RBS Tokyo.

Selected Awards:��� Best UK Bank

Euromoney Awards for Excellence 2005

��� European Loan House of the Year

IFR

��� European ABS Arranger of the Year 2005

ISR Awards

��� Securitisation House of the Year - Europe

The Banker

��� Top Bank for European Leveraged Finance

Financial News

��� Mezzanine Debt provider of the year

European Venture Capital (& Private Equity) Journal

��� EMEA Bank of the Year – Project Finance

PFI awards

��� Best Bank in Foreign Exchange in London

FX Week

��� Best Bank in Asian Prime Brokerage

AsiaMoney FX Survey

Make it happen

Hyatt Corporation.The international hotelgroup, headquartered in Chicago, embarked on a significant hotelinvestment in 2005. RBSin New York was joint leadarranger for the US$1 billionloan facility.

��

Adidas. We acted asagent on a US$1 billionprivate placement forAdidas, a global leader in the sporting goodsindustry. It was the largestsuch placement in the USout of Germany. Thefunding will largely be usedto finance their acquisitionof Reebok in the US.

� � Monro Muffler.RBS Securities and CharterOne in Chicago joinedforces as Lead Arranger and Sole Bookrunner forMonro Muffler, which runs a network for automotiverepairs, showing thestrength of the RBSplatform in the US.

��

Div

isio

nal r

evie

w

21

2005

22

Ret

ail M

arke

ts

RBS – Child Trust Fund.RBS was one of the first banks to offer a Child Trust Fund in response to theGovernment’s commitment to give £250 to each child born after September 2002.RBS has matched the £250 with discountedretail vouchers and created a newstakeholder product to capitalise on the value the child will receive at 18.

Retail Markets

� Profit contribution £4,207 million (2004 – £4,064 million)� Total income up 7%� Profit up 4%

Make it happen

Div

isio

nal r

evie

w

23

2005

Retail Markets was established in June 2005 to strengthen co-ordination and delivery ofour full range of retail servicesthrough all our brands andchannels. It has brought togetherthe three businesses – RetailBanking, Retail Direct and WealthManagement – which focus on the interests of our personal and small business customers.In a challenging market, RetailMarkets increased total income by 7% to £8,213 million.

��� The number of personal Retail Bankingcustomers increased by 274,000 (2%), with personalcurrent accounts up 275,000 (2%); Retail Directincreased its total customer accounts by 734,000(4%); and Wealth Management increased its clientbase with Coutts UK personal customers up 7%and Adam & Company up 11%.

��� In Retail Banking, average loans andadvances to customers grew by 11%, with averagemortgage balances up 12%, personal lending up10% and small business lending up 9%. In RetailDirect, average loans to customers grew by 15%,personal loan balances grew by 11% andmortgage lending grew by 34%. In WealthManagement, average loans to clients grew by20%, while average client deposits grew by 11%.

Retail Banking has the largest network of bankbranches and ATMs in the UK and is the leading bankfor small business customers. In 2005 Retail Bankingincreased its total income by 5% to £5,433 million.

��� In 2005 our measures to improve customerservice were rewarded when The Royal Bank ofScotland secured top position amongst the high streetbanks, and NatWest moved into joint second position,for customers who rate themselves “extremelysatisfied” with their main current account provider.Source: Gfk Financial Research Survey, 12 months to November2005; high street banks defined as RBS, NatWest, Barclays, LloydsTSB, HSBC and HBOS.

��� We added nearly 800 people to our Royal Bank of Scotland and NatWest branch networksand telephony service, improved personal accessfor customers by opening new branches andcontinuing our refurbishment programme, increasedthe number of branches open on Saturdays andextended our mobile banking service.

��� Our quality of service has also beenenhanced by our new Customer Service Review/Personal Service Review, which enables our peopleto run a comprehensive financial health checktailored to a customer’s individual circumstances.The Review offers recommendations to meet thecustomer’s immediate and future needs. Ourrevised Customer Account Opening system enablesour customers to open additional accounts withinminutes, whether they use our branches, telephoneservice or the internet.

��� Continued emphasis on long-term savings,assisted by excellent salesforce recruitment andretention, resulted in an increase of 25% in sales inour joint venture for life assurance and investments.The second half of 2005 saw record sales volumes,up 52% on the same period in 2004. Our team ofFinancial Planning Managers continues to grow, withmore of them located in our branches to broaden theservices we can offer through the network. The launchof new investment products enabled us to provide ourcustomers with more choice and better value.

Make it happen

Passion

24

Ret

ail M

arke

tsRetail Markets continued

Retail Banking provides customers with a choice of when and how they do their banking through access to branches, a 24-hour telephone banking service, a network of ATMs and a full internet banking service.

��� The Royal Bank of Scotland and NatWestattracted more than 135,000 new Stakeholder Child Trust Funds during 2005, making us one of the key providers of this product.

��� Partly through its network of 54 campusbranches, NatWest yet again achieved No.1 statusfor student accounts. Of first-year students inEngland and Wales, 44% chose to open a studentaccount with us.

��� The Royal Bank of Scotland launched FirstHome Saver, a new savings account designed tohelp customers get onto the property ladder byencouraging them to save regularly for the deposit,and by giving a tax-free bonus on taking out aRoyal Bank of Scotland mortgage.

��� In September 2005, Royal Bank of ScotlandBusiness was voted No.1 for service to small businesscustomers in Scotland.

��� Mentor, our Business Advice Service forEmployment Law, Health & Safety and Tax, reachedmore than 15,000 customers last year. It is thefastest-growing service of its type in the UK andincreased income by 18% whilst delivering significantimprovements to our proposition, including trainingin Health & Safety and Employment Law.

��� Loans to our small business customers were up 9% in 2005. Deposits by small businesscustomers, taking advantage of our competitiverange of products, grew by 4%.

��� 13,000 customers have opened a FlexibleBusiness Loan, our market-leading product thatenables business customers to customise theirloan. They can choose from a range of options at

the start of their loan, and can then update theirchoices if their circumstances alter. We alsolaunched Client Money Services, a unique productthat enables our business customers to managetheir client funds simply and easily.

Retail Direct has leading positions in the UK in credit card issuing, merchant acquiring,consumer finance and supermarket banking.In 2005 Retail Direct increased its total income by 11% to £1,966 million.

��� Retail Direct’s Credit Cards business is one of Europe’s leading issuers of personal andcommercial credit cards, as well as one of themajor global merchant acquirers.

��� The personal cards issuing business issuespersonal credit cards to customers of The RoyalBank of Scotland and NatWest primarily throughbranches, and also to non-banked customers usingthe MINT brand through direct channels.

��� During 2005, we introduced an enhancedcredit card offer for The Royal Bank of Scotlandand NatWest brand cards, with preferential pricingfor current account holders. In addition, the MINTbrand continued to improve the quality and breadthof service it offers to customers by launching motorand home insurance.

��� The commercial cards business hasmaintained its leading position in the UK. It offers arange of corporate cards, purchasing cards andtravel solutions to a broad range of businesses. Itenhanced its services by including ‘Smart dataonline’ as part of the onecard package. This allowsbusiness customers to receive and analyse alltransaction data centrally.

Make it happen

NatWest BusinessManagers. In 2005NatWest re-introducedlocal business managerscovering 180 keybranches. In FarehamChris Jack meets NickBowes of Airport Bodyshopon his premises.

��

Google.Retailer Card Servicesprovides Google with a multi-currency capability,which enables theprocessing and settlementof credit card transactionsin a wide choice of majorinternational currencies.

��

NatWest MobileBank. Last year NatWestlaunched a new mobilebank in Cornwall bringingbanking services to 13local communities weekly,travelling around 20,000miles per year. Here it isseen on the Cornish coast.

� �

Div

isio

nal r

evie

w

25

2005

26

Ret

ail M

arke

tsRetail Markets continued

Retail Direct offers a full range of financial services products through a number ofbrands and a variety of convenient channels in the UK and continental Europe.

Tesco Personal Finance in Hungary.Our joint venture with Tesco isdeveloping its presence in Europe.Financial services products are nowavailable through Tesco PersonalFinance in Hungary.

Make it happen

Div

isio

nal r

evie

w

27

2005

��� Our merchant acquiring business is thefourth-largest merchant acquirer globally. Thebusiness enhanced its product range during 2005,enabling retailers to offer customers the ability totop up their mobile phones through point-of-saleterminals. The business is now European leader inonline merchant acquiring.

��� Retail Direct has worked closely with theGroup’s Irish mortgage business, First Active,to launch the brand in the UK. First Active hasestablished itself as one of the fastest-growing UKmortgage lenders with total gross lending of £3.9billion in 2005, and has expanded its product rangewith the launch of a buy-to-let mortgage product.

��� RBS’s mortgage intermediary business wasbrought under the stewardship of Retail Directduring 2005, in order to co-ordinate the Group’smortgage brand offer in the growing intermediarymarketplace.

��� During the year the number of customeraccounts at Tesco Personal Finance exceeded fivemillion. First Active supported the launch of twonew TPF mortgage products, making TPF the onlysupermarket bank to offer mortgages. Retail Directalso continued to support the development ofTesco’s financial services operations in CentralEurope and Asia.

��� Elsewhere in Europe our relationship withTchibo, a major German retailer, has grownsuccessfully, with the offer of consumer loans nowextended across the store network in Germany and online.

Wealth Management provides private banking andinvestment services to its global clients through anumber of leading UK and overseas private bankingsubsidiaries and offshore banking businesses.It has a network of more than 50 offices globally.In 2005 Wealth Management increased its totalincome by 10% to £814 million.

��� Investment assets under managementincreased by 18%. Investment programmes withinWealth Management have grown by 18% to US$27billion and continue to perform competitivelyagainst industry benchmarks. Coutts is a significantinvestor in multi-manager hedge funds with morethan US$7 billion invested.

��� Adam & Company continued its eleven yearrecord of double-digit profit growth, and opened anew office in Aberdeen.

��� The Offshore Bank grew income by 7% and launched a Spanish Mortgage productavailable across the Group to all customers.Offshore mortgage balances increased by 35%and Royal Bank of Scotland International is a leading provider in the UK offshore islands of electronic banking services.

��� Coutts continued to enhance its position asthe leading private bank in the UK and increased itsclient base by 7%. A philanthropy service waslaunched in 2005, which won Coutts the title of BestProvider of Philanthropy Services. Coutts alsolaunched its Family Business Service, offeringspecialist advice as well as education andnetworking forums for family business owners.In parallel, Coutts created its family prize andsponsored the Guide to Giving. Internationally,Coutts celebrated 10 years in Singapore in 2005.

Make it happen

28

Ret

ail M

arke

tsRetail Markets continued

Wealth Management provides private banking and investment services to its global clients through anumber of leading UK and overseas private banking subsidiaries and offshore banking businesses.

Selected Awards��� The Royal Bank of Scotland – Best forOverall Customer Service category

2005 Personal Finance and Savings Readership Awards

��� NatWest Kirkham Branch – Customer ServiceTeam of the Year Financial Services Award

National Customer Service Awards 2005

��� The Royal Bank of Scotland – Best DirectBanking for the fifth year in a row

Your Money Direct Awards 2005

��� The Royal Bank of Scotland – Best OnlineBusiness Banking Provider for the second year in a row

Your Money Direct Awards 2005

��� Lombard – Best Online Loan Provider

Your Money Direct Awards 2005

��� NatWest Mortgages Direct – Best Mortgage Provider

Your Money Direct Awards 2005

��� Tesco Personal Finance – Best Overall Provider

Your Money Direct Awards 2005

��� NatWest Mortgages – Best Bank, Best LargeLoans and Highly Commended Remortgage Lender

Your Mortgage Awards

��� The Royal Bank of Scotland – Best Business Bank

Start Your Business Magazine

��� First Active – Best Mortgage Lender of theYear and Innovator of the Year

Mortgage Strategy Awards

��� First Active – Best Remortgage Lender

Mortgage Magazine Awards and Mortgage Advisor

& Homebuyer Awards

��� The One account – Best Current Account Mortgage Lender

Your Mortgage Magazine

��� Direct Line – Best Personal Loan Provider

MoneyFacts

��� Streamline – Best Merchant Acquirer 2005 – Europe

Lafferty Group

��� MINT – Best Credit Card Direct Mail,Peoples Choice award

Tank!/Direct Marketing Association

��� Commercial Cards – Best Business Charge Card Provider

Business Moneyfacts

��� Coutts – Best Private Bank in the UK

Euromoney

��� Coutts – Best Private Bank for super-affluentindividuals (US$500k to US$1m)

Euromoney

��� Coutts – Best Private Bank for high net worth individuals (US$1m to US$10m)

Euromoney

��� Coutts – Best provider of services to artists and entertainers

Euromoney

��� Coutts – Best provider of services to sports players

Euromoney

Div

isio

nal r

evie

w

29

2005

Stella McCartney isone of the most successfulof Britain’s young fashiondesigners with a now wellrecognised luxury brand.Stella and Coutts have a fruitful commercialrelationship includingexclusive customer eventsfor Coutts clients.

��

The One account.“One Day” as theadvertisements say… I’llhave my own music studio.Mark Young transferred his mortgage to The Oneaccount three years ago and saved enough toconvert one of the bed-rooms in the family home.

��

First Active.For Jill Hewitt and her nineyear old son Jack, value formoney is important. LastMay after consolidatingher mortgage and a homeimprovement loan into afixed rate mortgage withFirst Active, she savedover £100 a month.

� �

30

Uls

ter

Ban

k G

roup

Ulster Bank Group

� Profit contribution £530 million (2004 – £460 million)� Total income increased 15%� Profit up 15%

University of Limerick.Ulster Bank and University of Limerick share a passion for innovation and high standards.A 10-year agreement has underlined UlsterBank’s commitment to the education sectornationally and to the Munster region where theuniversity is located – covering the University’sown banking and on-campus banking forstudents, staff and local businesses.

Make it happen

Div

isio

nal r

evie

w

31

2005

Ulster Bank Group saw sustainedgrowth in 2005 and the launch of market-leading mortgage and current account products.A branch improvement programmeand a new Ulster Bank brandidentity moved us towards ourvision of becoming the best bankon the island of Ireland. UlsterBank Group’s total incomeincreased by 15% to £858 million.

��� Ulster Bank Group ended 2005 with 1.6million personal and business customers across theisland of Ireland.

��� Product development has been a key factorin Ulster Bank Group’s success. In November 2005we launched a radical overhaul of personal currentaccounts in Northern Ireland to provide free bankingto all personal customers.

��� First Active introduced the Republic ofIreland’s first 100% First Time Buyers’ Mortgageconfirming First Active’s reputation for innovativeproducts. These include the Current AccountMortgage and Elevator savings account.

��� Ulster Bank also led as the first clearing bankto extend its 100% mortgage to first-time buyersacross the island. The Switcher Mortgage packagehas made it easy for customers to switch to us.

��� Ulster Bank Group’s Corporate Banking and Financial Markets (CBFM) division continued to experience strong lending growth to its corporatecustomers. Average lending grew by 29% in 2005 –26% in Northern Ireland and 30% in the Republic of Ireland.

��� Important transactions completed during theyear included the banking business of United DairyFarmers, a leading dairy producer; funding theconstruction of major shopping centres in Essexand Dundalk, and working with the RBS SpecialistHealthcare team to win the mandate to funddevelopment of Beacon Hospital, a major newprivate hospital in Dublin.

��� 89 branches were overhauled as part of our improvement to the Ulster Bank branchnetwork, with work planned on a further 57 during2006. The Ulster Bank and First Active branchestogether create a network of 272 branches.

��� 2005 was also significant for the visibility of our brands. The Ulster Bank brand adopted the RBS logo in November, enhancing its identity as a member of the RBS Group, while First Activecontinued its targeted focus on the mortgage sector.

Awards��� Corporate Banking Excellence Award

KPMG’s Financial Services Excellence Awards

��� Best practice in recruitment andemployment of people with disabilities

02 Ability Award

��� Aimhigher programme – Northern IrelandBig Tick Award for Business in the CommunityExcellence and Chambers of Commerce in IrelandPresident’s Awards Commendation

Make it happen

Potential

Citizens

32

Citi

zens

� Profit contribution £1,575 million (2004 – £1,069 million)� Total income up 43%� Profit up 47%

Make it happen

K-Sea Transportation has been a businesscustomer with Citizens for over 3 years.It builds ferries, tugs and barges, one ofwhich is seen here on the famous StatenIsland crossing. To help fund furtherinvestment in its business K-Sea looked toCitizens Bank for a US$37 million SeniorCredit Facility, US$34 million in equipmentleases, and foreign exchange services.

2005

Div

isio

nal r

evie

w

33

Citizens ranks as the eighth largestcommercial banking organisationin the US by deposits. Last yearwas Citizens’ 13th consecutiveyear of record profits, achievedthrough the integration of CharterOne and strong organic growth.In 2005 Citizens increased itsincome by 42% to US$5,940 million.

��� Through Citizens Bank and Charter OneBank, Citizens’ network of retail and corporatebanking covers Connecticut, Delaware, Illinois,Indiana, Massachusetts, Michigan, New Hampshire,New Jersey, New York state, Ohio, Pennsylvania,Rhode Island and Vermont. Citizens has a retailand corporate presence in about 40 states.

��� The systems and account integration for 3 million customer accounts and around 8,000colleagues of the former Charter One Financial, Inc.,the company’s largest US acquisition, was completedin July 2005, five months ahead of schedule.

��� In 2005, all Citizens Bank and Charter Onebranches and facilities were re-branded, with morethan 70,000 new signs and ATM surrounds usingthe RBS logo, a new font for the bank name and thedistinctive Citizens green.

��� Citizens made more than 900,000 newconsumer loans totalling US$22 billion during 2005and processed more than 1.5 million credit

applications. Its Consumer Finance division is theNo.2 bank auto lender in the US and a top homeequity lender. The Consumer Finance divisionintroduced two new business lines: IndirectRecreational Vehicle and National Home Equity.Both new initiatives contributed operating profit intheir first year of operation.

��� Citizens’ “Switch Support” programme with automated concierge service has smoothedthe transition of customers switching to Citizensand Charter One from other banks.

��� Our supermarket banking programmecontinued its momentum during 2005, adding 34 branches in strategic locations with our primarypartners. With around 520 Citizens Bank andCharter One in-store branches, Citizens is now thesecond-largest supermarket banker in the US.

��� Building on this momentum, in January 2006 Citizens announced the opening of 75 branchesin Stop & Shop Supermarkets over the next threeyears, expanding its supermarket banking franchise into New York’s Hudson Valley, Rocklandand Westchester Counties and Long Island. Thepartnership with Stop & Shop began in the NewEngland franchise in 2001, where it has grown to125 stores.

��� RBS National Bank, now part of Citizens’ UScredit cards division, launched the Circle RewardsMasterCard that can be issued automatically when a qualifying customer opens an account at a Citizens Bank or Charter One branch.

Make it happen

Drive

Citizens continued

34

Citi

zens

Citizens was the No.2 US Small Business Administration lender in the US for the fourth consecutive year.

Citizens’ International Cash Management collaboration with Corporate Markets resulted in 300 new Citizens accounts with existing RBS customers.

Make it happen

Ryerson, Inc., based in Chicago, is NorthAmerica’s leading processor and distributorof metals. Our ability to meet the complexneeds of large commercial customers isdemonstrated in the partnership betweenRBS Corporate Markets, which providedRyerson with credit facilities, and CharterOne, which was able to offer treasurymanagement services.

2005

Div

isio

nal r

evie

w

35

��� Kroger Personal Finance, a joint venturebetween Citizens’ cards division and Kroger Co.,the second largest supermarket chain in the US,is offering KPF credit cards in nearly 2,200 storesand is branching out into other products.We launched seven different branded cardprogrammes in 2005 for Kroger customers,launched a MasterCard-branded gift card andstarted installing RBS Lynk-supported ATMs into a number of Kroger locations.

��� Citizens was the No.1 US Small BusinessAdministration (SBA) lender in the Mid-Atlantic,Midwest and New England regions in 2005, and the No.2 lender in the US for the fourth consecutiveyear. We made over 10,000 SBA-backed loans,totalling more than US$416 million, whichrepresented a 79% increase in volume over 2004.

��� In its first year of Citizens ownership,Charter One’s new Business Banking team grew its SBA lending to No.1 in the Midwest in both thenumber of loans written and total dollars loanedduring 2005. Charter One became top SBA lenderin Illinois, Indiana, Michigan and Ohio.

��� Also in Ohio, Charter One is sponsoring the new Charter One Global Enterprise Center inCleveland to fuel economic growth by maximisingnortheast Ohio’s international businessdevelopment potential.

��� In addition to lending at the communitybanking, middle market and large corporate levels, Citizens Corporate Banking services hasworked effectively in partnership with RBSCorporate Markets. This provides additional expertiseand flexibility to meet the needs of larger customersand craft complex financings. Services include

interest rate protection, foreign exchange, cashmanagement, asset finance and administration,asset-based lending and private equity capital.

��� The management and business of RBSAsset Finance, Inc. has been transferred from RBS Corporate Markets to Citizens. This integrationcombined the existing Citizens asset financecompany, Citizens Leasing, with Charter One’s ICX Corporation and the group formerly known as RBS Lombard to form RBS Asset Finance.The combined company is the eighth largest bank-affiliated leasing company in the US.

��� During 2005, RBS transferred to Citizens the operating control of the electronic processingprovider RBS Lynk. RBS Lynk began cross-sellingmerchant services to small business customersthrough Citizens and Charter One branches andtheir business bankers.

��� In late 2004, Citizens established newInternational Cash Management services withCorporate Markets for companies doing business in the US and the EU, resulting in nearly 300 newcustomer accounts at Citizens during 2005 forexisting RBS customers. These customers use anextensive array of cash management services, andhave brought in more than US$80 million of newcore deposits.

��� Since it began in 2004, Citizens’ Job Bankoffered US$144 million in loan funds at below-market rates to 11 companies that agreed to createan estimated 4,536 jobs. Citizens’ Housing Bankoffered US$167 million in low-interest loan funds tonon-profit housing developers to create 2,286affordable housing units in New England and Ohio.Both programmes will be extended in 2006.

36

Citi

zens

Citizens continued

Citizens is among the top 10 rankings in deposits among US commercial banking organisations.It ranks seventh in branches and ninth in ATMs.

Citizens was one of just two companies in 2005 to receive the US Chamber of Commerce Corporate Stewardship Award.

Make it happen

��� Citizens’ support for the community isextensive. Examples include a comprehensive,multi-million dollar investment plan to increase homeownership, strengthen commercial retail districts,and create an education district in Albany, New York;a new innovative product for low/moderate-incomehomebuyers introduced by CCO Mortgage Corp intraditionally under-served areas; a strong partnershipwith the Chicago Urban League on housing andfinancial literacy; US$700,000 of help with heating costsfor more than 345 homeless shelters in eight statesthrough the “Shelter Heating Assistance Campaign”;and assistance through our Champions in ActionSM

programme for close to 70 small, non-profit agenciesdedicated to a range of housing, health and youthissues in New England, Pennsylvania and Ohio.

��� Citizens’ support for its own people includesthe Home Buyer Assistance Programme, whichsince 2002 has helped more than 2,000 colleaguespurchase primary residences – often their firsthomes – with forgivable loans totalling more thanUS$10 million. The military leave policy, which bridgespay and benefits to cover the duration of militaryleave, has benefited more than 190 colleagues, andover 70 employees with serving family membershave been given time off with pay, air fares andhelp with travel expenses to visit their loved ones.

��� Since June 2005 Citizens has promotedlocal volunteering through the “Join Us” campaignand its associated website, which also providesinformation on the Champions in Action programmeand enables visitors to let Citizens know about localnon-profit organisations that they feel deserve thebank’s attention. Citizens created a special TsunamiSabbatical to send a colleague to Indonesia forthree months to help with relief and rebuildingefforts through Plan International. Citizens also

matched colleague donations for Hurricane Katrinarelief efforts, added its own corporate contribution,and collected customer donations to The RedCross and The Salvation Army through its networkof more than 1,600 branches.

��� Charter One secured the naming rights to thepreviously designated Lakefront Pavilion, a summerconcert performance centre on Northerly Island,between Lake Michigan and the Chicago skyline.

Awards��� Citizens was one of just two companies inthe United States to be awarded the US Chamberof Commerce Corporate Stewardship Award. Thisrecognition was for the company’s total performanceand contribution to economic, community andsocial progress. It noted Citizens’ Champions inAction, the Citizens Job Bank, and the company’sHome Buyer Assistance Programme.

��� Citizens Bank of Pennsylvania received the2005 Good Government Award from the League ofWomen Voters for its Citizens Job Bank initiative togrow new jobs during 2004 and 2005.

��� Citizens Financial Group received the 2005Secretary of Defense Employer Support FreedomAward, the US government’s highest honour forsupport of the Guard and Reserve for policies and programmes that support colleagues on activeduty well beyond US legal requirement.

��� Citizens received the Alfred P. Sloan Awardfor Business Excellence in Workplace Flexibilityfrom the Families and Work Institute, U.S. Chamberof Commerce’s Center for Workforce Preparationand the Center for Emerging Futures in recognitionof its many programmes to support employees.

2005

Div

isio

nal r

evie

w

37The Chicago

Defender is one of theoldest newspapers inAmerica serving the Afro-American community.Charter One built on itsSBA lending successoffering capital to innercity businesses like TheChicago Defender.

��

Circle Rewards.RBS National Bank, whichsells credit cards in the US, is now offering these to Citizens’ customers.In 2005 we launched Circle Rewards, a loyaltyprogramme with discountsfor air travel, hotels andbranded merchandise.

� � Fence America.RBS Lynk, based in Atlanta,offers a range of paymentsystems for retail andbusiness customers. FenceAmerica is one of the firstto use the innovative newproduct Treo, which allowscredit card payments to bemade via mobile phones.

��

RBS Insurance

38

RB

S I

nsur

ance

� Profit contribution £926 million (2004 – £881 million)� Total income up 8%� Profit up 5%

Churchill Home Insurance.David and Catherine Barton switched toChurchill Home Insurance last year.They loved the brand, saved £200 andfound the quality of service excellent.

Make it happen

Div

isio

nal r

evie

w

39

2005

RBS Insurance is the secondlargest general insurer in the UK.It sells and underwrites insurancevia the telephone, the internet,partnerships and a network ofbrokers. Its brands, includingDirect Line, Churchill, Privilege,Green Flag and NIG, are some ofthe best known in the UK. In 2005RBS Insurance increased its totalincome by 8% to £5,489 million.

��� The integration of the Direct Line andChurchill businesses was completed at the start ofSeptember 2005, within two years, ahead of timeand within budget. The combined businesses nowhave close to 20,000 employees.

��� We celebrated the 20th anniversary of theDirect Line red telephone in 2005. When it firstopened for business in April 1985, Direct Lineemployed just 63 people. Today it employs around6,500 people and handles an average of 12,000 carquotes every day.

��� Across its range of brands and products,RBS Insurance increased its total policies in-forceby 1.6 million to 25.9 million. Within this, total carpolicies increased by 5.7% to 10.6 million acrossthe UK and continental Europe.

��� In the United Kingdom, RBS Insurance isthe No.1 car insurer, with 8.7 million policies, andthe No.2 home insurer, with 4.6 million policies.

��� RBS Insurance now has over 4.9 million carrescue policies sold through Direct Line, Churchill,Green Flag, Privilege and many partners undertheir brands.

��� In continental Europe, RBS Insuranceincreased its car insurance policies by 14% to 1.9 million.

��� RBS Insurance is the No.2 travel insuranceprovider with 2.3 million policies; its pet policiesincreased by 20% to 0.6 million.

��� Direct Line launched several majorenhancements to its car product, including a NoClaims Discount (NCD) for named drivers on a Direct Line policy, multi-car discounts, matchedNCD and an NCD earned on company cars andmotorbikes.

��� Línea Directa became Spain’s sixth largestmotor insurer this year with 1.2 million in-forcepolicies and is now selling breakdown cover directto customers. Direct Line in Germany launchedmotor legal protection.

��� Since the re-launch of Privilege in August 2004, the ‘you don’t have to be posh to beprivileged’ campaign has delivered excellent brandrecognition and sales, with in-force car policiesincreasing by 50% and breakdown policies by 43% respectively.

Make it happen

Focus

RBS Insurance continued

40

RB

S I

nsur

ance

RBS Insurance is the strength behind some of the UK’s biggest and best known insurance brands offering customers more choice and better products.

��� Churchill launched its new travel product inJune, with customers now able to tailor cover totheir individual travel needs.

��� TRACKER, which specialises in recoveringstolen vehicles, was acquired in 2005. TRACKERtraced and recovered more than £36 million worth ofstolen cars and plant equipment over the year. In onecase, a vehicle was recovered in just 21 minutes.

��� NIG held six SME Business Academyroadshows throughout the country. The keyobjective of these events was to build NIG’s profile in the regions and forge close links with brokersand SME customers.

��� NIG joined imarket, the industry e-commerceinitiative designed to make it easier for brokers totransact commercial business electronically.

��� Continuing their consumer champion roles,Direct Line and Green Flag were again the headlinesponsors of Road Safety Week. Organised by roadsafety charity Brake each November to highlightroad safety issues, the 2005 theme was childpedestrian safety.

��� Direct Line partnered Durham Police in ahigh profile campaign to tackle the problem ofuninsured driving. By the end of 2005, more than1,000 uninsured vehicles, which Direct Lineestimates would have caused up to 2,000accidents, had been removed from the streets of Durham County.

Awards��� Direct Line – Car Insurer of the YearPersonal Finance Magazine

��� Direct Line – Best Motor Insurance ProviderYour Money Magazine

��� Direct Line – Best Online Motor InsuranceProviderYour Money Magazine

��� Direct Line – Best Household InsurerYour Mortgage Magazine

��� Direct Line – Special Achievement AwardSuperbrands

��� Churchill – Best Home and ContentsInsurance ProviderYour Money Direct Awards

��� Churchill – Travel Insurer of the YearInternational Travel Insurance Journal Awards

��� Churchill – Customer Service ComplaintsTeam of the YearThe National Customer Service Awards

��� Green Flag – Best Breakdown ProviderYour Money Magazine

��� Green Flag – Best Online Breakdown ProviderYour Money Magazine

��� Green Flag – UK Roadside AssistanceCompany of 2005Institute of Transport Management Awards

��� NIG – Risk Management Product of the Year(for All Risk Management (ARM))European Risk Management Awards

Make it happen

Div

isio

nal r

evie

w

41

2005

TRACKER hasprovided Balfour BeattyPower Networks with theability to track its vehicles24:7 via data on the internet.It has greatly improvedvehicle management,efficiency, flexibility anddriver safety and reducedinsurance premiums.

��

NIG. For the brokermarket, quick and accurateonline quotations are animportant part of theircompetitive offering. NIG’sCommercial Quotes systemis regularly accessed bybrokers such as SaffronInsurance to providecommercial insurance fortheir customers.

��

Direct Line.Over 1,000 uninsured carshave been taken off theroads as part of a jointinitiative between DurhamPolice and Direct Line.Drivers who can't provideevidence of insurancewithin 14 days have theircars crushed.

� �

42

Man

ufac

turin

gManufacturing

Manufacturing is the backbone of RBS, supplying IT, processing, telephone, property andpurchasing support for the Group’s customer-facing divisions.

Gogarburn. On 14 September 2005,Her Majesty The Queen and His RoyalHighness The Duke of Edinburgh formallyopened the new RBS headquarters inEdinburgh. It provides a superb workingenvironment, together with fitness, nurseryand conference facilities.

Make it happen

Div

isio

nal r

evie

w

43

2005