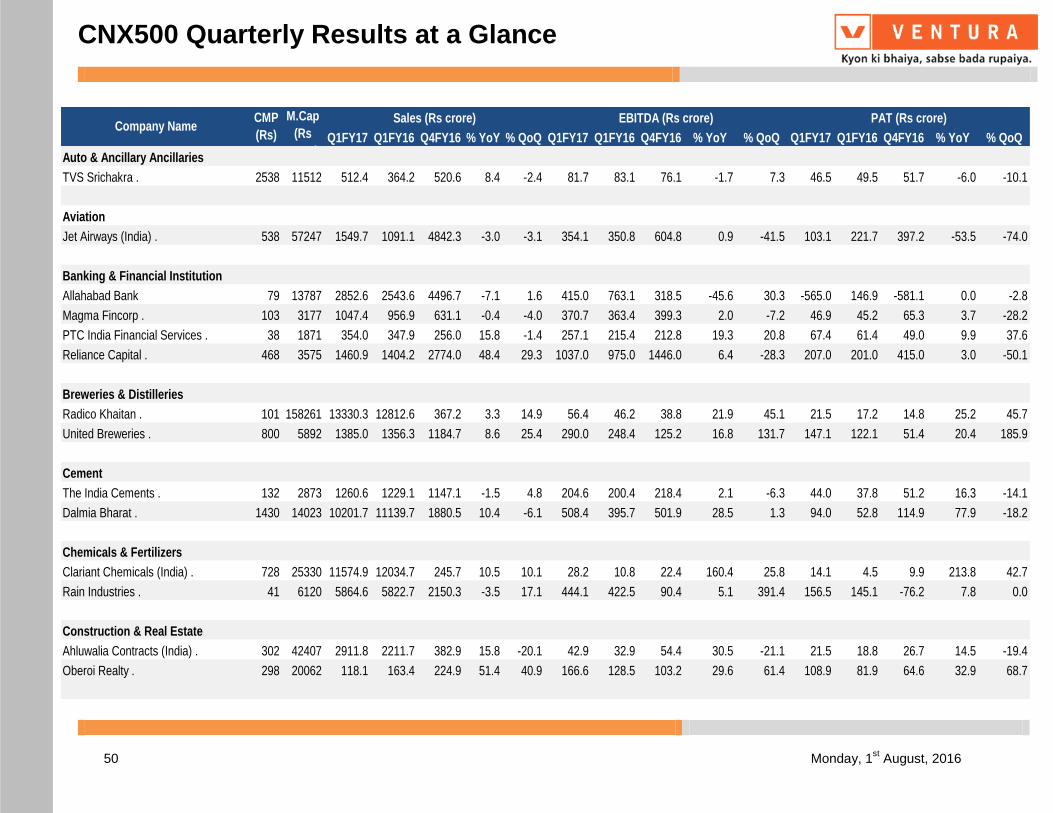

Q1FY17 Performance Summary - Ventura Securities

52

Q1FY17 Performance Summary 1 Monday, 22nd August, 2016 This document is for private circulation, and must be read in conjunction with the disclaimer on the last page. Q1FY17 RESULTS REVIEW Nifty 8,667 Sensex 28,077 The Q1FY17 earnings season continued on a mixed note. SBI’s 1QFY17 asset quality has surprised on the positive side. Lower than expected slippages have helped in reporting better than expected bottom-line. Bank of Baroda’s ratios have increased partly on account of the conscious reduction in the asset base during the year. BOB has reported a drop in net profit on YoY basis, due to higher provisions and lower net interest income. Adani Ports and Special Economic Zone has reported healthy growth in cargo volumes, operational efficiencies and their strategy to increase bulk cargo volumes, other than coal volumes have enabled to report all round growth in financial numbers. For 1QFY2017, Hero Motor Corp posted a good set of numbers. The company has sold 1.74 million units in this quarter. Lupin has reported strong results in Q1FY17. The company’s revenue was high compared to previous year. The company’s net profit also boosted on yearly basis. Bosch Ltd reported good revenue growth for June quarter FY17. Automotive segment grew well, where as non automotive segment had a marginal growth. Power Grid Corporation of India has posted positive topline and bottom-line numbers in Q1FY17. Net revenue had a robust growth. Cipla reported poor numbers for Q1FY17, revenue declined on yearly basis. Grasim Industries’ 1QFY17 EBITDA showed a robust growth, driven by near-peak utilizations, high pricing and lower energy costs. Hindalco has delivered robust operational performance in adverse macroeconomic conditions. Its operational performance was supported by deflationary energy prices. Macroeconomic headwinds will persist and uncertain global macro factors pose challenges. The level of imports continues to impact domestic sales volumes. Sun Pharmaceutical Industries posted growth in net profit for Q1FY17 on a year-on-year basis on the back of growth in its US business. US business accounts for half of Sun Pharma's revenue and the company has reported two successive strong quarters of growth due to 180 day exclusivity in sale of anti leukemia drug Gleevec.

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of Q1FY17 Performance Summary - Ventura Securities

Q1FY17 Performance Summary

1 Monday, 22nd August, 2016

This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Q1F

Y1

7 R

ES

UL

TS

RE

VIE

W

Nifty 8,667 Sensex 28,077 The Q1FY17 earnings season continued on a mixed note. SBI’s 1QFY17 asset quality has surprised on the positive side. Lower than expected slippages have helped in reporting better than expected bottom-line. Bank of Baroda’s ratios have increased partly on account of the conscious reduction in the asset base during the year. BOB has reported a drop in net profit on YoY basis, due to higher provisions and lower net interest income. Adani Ports and Special Economic Zone has reported healthy growth in cargo volumes, operational efficiencies and their strategy to increase bulk cargo volumes, other than coal volumes have enabled to report all round growth in financial numbers. For 1QFY2017, Hero Motor Corp posted a good set of numbers. The company has sold 1.74 million units in this quarter. Lupin has reported strong results in Q1FY17. The company’s revenue was high compared to previous year. The company’s net profit also boosted on yearly basis. Bosch Ltd reported good revenue growth for June quarter FY17. Automotive segment grew well, where as non automotive segment had a marginal growth. Power Grid Corporation of India has posted positive topline and bottom-line numbers in Q1FY17. Net revenue had a robust growth. Cipla reported poor numbers for Q1FY17, revenue declined on yearly basis. Grasim Industries’ 1QFY17 EBITDA showed a robust growth, driven by near-peak utilizations, high pricing and lower energy costs. Hindalco has delivered robust operational performance in adverse macroeconomic conditions. Its operational performance was supported by deflationary energy prices. Macroeconomic headwinds will persist and uncertain global macro factors pose challenges. The level of imports continues to impact domestic sales volumes. Sun Pharmaceutical Industries posted growth in net profit for Q1FY17 on a year-on-year basis on the back of growth in its US business. US business accounts for half of Sun Pharma's revenue and the company has reported two successive strong quarters of growth due to 180 day exclusivity in sale of anti leukemia drug Gleevec.

2 Monday, 22nd August, 2016 This document is for private circulation, and must be read in conjunction with the disclaimer on the last page.

Company Synopsis

Quarterly Result Update

State Bank of India Ltd.

Asset quality deteriorates

- 3 - Monday, 22nd

August, 2016

Defying tough operating environment, State Bank of India put up a relatively better show beginning the FY17 on an upbeat note. Moderate increase in NPAs, declining slippage trends, decreasing credit costs and improving credit off-take summarizes the healthy earnings for the quarter. PAT at INR 25.2 bn stood broadly in-line and almost doubled on sequential basis. While NII stayed muted (down 6% Q-o-Q; up mere 4% Y-o-Y) primarily due to NIM compression (20 bps Y-o-Y) on account of base rate cut, the operating metrics looked better for SBI. The operating profits stood well off for the bank on the back of strong other income performance (in the form of treasury gains, forex and dividend income and cross sell income), tax write-backs and controlled opex (216 bps dip Y-o-Y). NIMs witnessed slight moderation at 2.83% (down both YoY, QoQ). Q1 being seasonally soft quarter for SBI; resultantly the advances looked down Q-o-Q by 3%. That said, on Y-o-Y basis, SBI’s loan book acceleration outpaces peers with loans at 11% growth primarily buoyed by healthy 20% retail loans with greater traction in home, auto and personal loans segments during Q1FY17; clocking significant market share gains in home and auto loans. The non-interest income traction (25.6% Y-o-Y growth) led by 18% Y-o-Y growth in treasury gains (up 212% Y-o-Y), forex (22%) and dividend income (388%) and cross sell fee income (39% Y-o-Y). Also, NIMs witnessed slight moderation at 2.83% (down both YoY, Q-o-Q) but on expected lines primarily on account of base rate cut. That said, margins are expected to stabilize at 2.85-2.9% as cited by the Management. Currently, at the CMP of Rs 256, SBI is valued at 1.3 Adj P/BV on 1 yr forward basis. We recommend a BUY on the stock.

Recommendation (Rs)

CMP 256 Rating BUY

Index Details

Sensex 28,077

Nifty 8,667

Industry Banks

Scrip Details

Mkt Cap (Rs cr) 198,960

Eq Shares O/s (Cr) 776.2

Avg Vol (Lakhs) 45.0

52 Week H/L 268/148

Dividend Yield (%) 2.2

Face Value (Rs) 1.0

Latest shareholding pattern (%)

Promoters 61.3 Public 38.7

Total 100.0

Stock performance (%)

1m 3m 6m

SBI 12.5 49.5 57.0 Nifty 1.62 11.35 20.19

Quarterly Result Update

- 4 - Monday, 22

nd August, 2016

Description Q1FY17 Q1FY16 % Chg. Q1FY17 Q4FY16 % Chg.FY201603FY201503 % Chg.

Interest Earned 55915.1 53746.2 4.0 55915.1 57275.4 -2.4 221854.8 207974.3 6.7

Interest on Advances 39989.7 39040.2 2.4 39989.7 39352.0 1.6 157001.8 153144.6 2.5

% of Total Int. Earned 71.5 72.6 -- 71.5 68.7 -- 70.8 73.6 --

Interest on Balances with RBI 315.8 350.1 -9.8 315.8 200.4 57.6 1186.8 1033.6 14.8

% of Total Int. Earned 0.6 0.7 -- 0.6 0.4 -- 0.5 0.5 --

Income From Investments 14626.2 13392.9 9.2 14626.2 15059.1 -2.9 57922.7 48952.3 18.3

% of Total Int. Earned 26.2 24.9 -- 26.2 26.3 -- 26.1 23.5 --

Others 983.3 963.1 2.1 983.3 2664.1 -63.1 5743.6 4843.9 18.6

% of Total Int. Earned 1.8 1.8 -- 1.8 4.7 -- 2.6 2.3 --

Other Income 13499.7 9418.3 43.3 13499.7 18488.4 -27.0 51016.2 49315.2 3.5

Total Income 69414.8 63164.5 9.9 69414.8 75763.8 -8.4 272871.0 257289.5 6.1

Interest Expended 36366.7 34971.9 4.0 36366.7 36425.8 -0.2 143047.4 133178.6 7.4

Operating Expenses 18498.9 15859.9 16.6 18498.9 21787.8 -15.1 73717.1 73224.2 0.7

Payment to provisions for Employee8196.0 7706.6 6.4 8196.0 8888.2 -7.8 32525.6 31117.6 4.5

% of Opt. Expenses 44.3 48.6 -- 44.3 40.8 -- 44.1 42.5 --

Other Opt. Expenses 10302.8 8153.3 26.4 10302.8 12899.6 -20.1 41191.5 42106.6 -2.2

% of Opt. Expenses 55.7 51.4 -- 55.7 59.2 -- 55.9 57.5 --

Total Expenses 18498.9 15859.9 16.6 18498.9 21787.8 -15.1 73717.1 73224.2 0.7

Operating Profit before prov. & cont.14549.2 12332.7 18.0 14549.2 17550.2 -17.1 56106.6 50886.6 10.3

% of Total Int. Earned 26.0 23.0 -- 26.0 30.6 -- 25.3 24.5 --

Provisions and Contigencies 13130.5 5294.5 148.0 13130.5 16393.6 -19.9 37929.8 25032.1 51.5

PBT 1418.7 7038.3 -79.8 1418.7 1156.7 22.7 18176.8 25854.6 -29.7

% of Total Int. Earned 2.5 13.1 -- 2.5 2.0 -- 8.2 12.4 --

Tax 551.4 2184.7 -74.8 551.4 -203.6 LP 5433.5 8337.2 -34.8

PAT 867.3 4853.6 -82.1 867.3 1360.3 -36.2 12743.3 17517.4 -27.3

% of Total Int. Earned 1.6 9.0 -- 1.6 2.4 -- 5.7 8.4 --

Paid up equity share capital 776.3 756.6 2.6 776.3 776.3 0.0 776.3 746.6 4.0

EPS (Rs.) 1.4 6.2 -78.4 1.4 1.6 -16.7 15.8 22.8 -30.8

Capital Adequacy Ratio - 0.0 0.0 -

NII 19548.4 18774.3 4.1 19548.4 20849.6 -6.2 78807.5 74795.7 5.4

NIM

Gross NPA - 0.0 0.0 -

% of Gross NPA - 0.0 0.0 -

Net NPA - 0.0 0.0 -

% of Net NPA - 0.0 0.0 -

ROA(%) - 0.0 0.0 -

CEPS (Rs.) 168.85 123.15 37.11 168.85 159.48 5.88 539.33 434.38 24.16

Quarterly Result Update

- 5 - Monday, 22

nd August, 2016

Deposits-Advance Growth Revenue Growth (%)

40.0

40.5

41.0

41.5

42.0

42.5

43.0

43.5

44.0

44.5

45.0

0.0

200,000.0

400,000.0

600,000.0

800,000.0

1,000,000.0

1,200,000.0

1,400,000.0

1,600,000.0

1,800,000.0

2,000,000.0

Q3 F

Y14

Q4 F

Y14

Q1 F

Y15

Q2F

Y15

Q3F

Y15

Q4F

Y15

Q1F

Y16

Q2F

Y16

Q3F

Y16

Q4F

Y16

Q1F

Y17

Rs.Crore

Advance Deposit CASA RHS(%)

(%)

-10.0

-5.0

0.0

5.0

10.0

15.0

0.0

2,000.0

4,000.0

6,000.0

8,000.0

10,000.0

12,000.0

14,000.0

16,000.0

18,000.0

Q3 F

Y14

Q4 F

Y14

Q1 F

Y15

Q2F

Y15

Q3F

Y15

Q4F

Y15

Q1F

Y16

Q2F

Y16

Q3F

Y16

Q4F

Y16

Q1F

Y17

Rs.Crore

NII QoQ Growth (%)

(%)

Source: SBI, Ventura Research Source: SBI, Ventura Research

LDR (%) Incremental LDR (%)

76.0

78.0

80.0

82.0

84.0

86.0

88.0

90.0

Q3 F

Y14

Q4 F

Y14

Q1 F

Y15

Q2F

Y15

Q3F

Y15

Q4F

Y15

Q1F

Y16

Q2F

Y16

Q3F

Y16

Q4F

Y16

Q1F

Y17

LDR Ratio (%)

(%)

-150.0

-100.0

-50.0

0.0

50.0

100.0

150.0

200.0

250.0

300.0

Q3 F

Y14

Q4 F

Y14

Q1 F

Y15

Q2 F

Y15

Q3 F

Y15

Q4 F

Y15

Q1F

Y16

Q2F

Y16

Q3F

Y16

Q4F

Y16

Q1F

Y17

Incremental LDR Ratio (%)

(%)

Source: SBI, Ventura Research Source: SBI, Ventura Research

Quarterly Result Update

- 6 - Monday, 22

nd August, 2016

Cost to Income Ratio Asset Quality improves QoQ (%)

Error! N ot a valid l ink.

2.8

2.9

3.0

3.1

3.2

3.3

3.4

3.5

3.6

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Q3 F

Y14

Q4 F

Y14

Q1 F

Y15

Q2F

Y15

Q3F

Y15

Q4F

Y15

Q1F

Y16

Q2F

Y16

Q3F

Y16

Q4F

Y16

Q1F

Y17

Yield on Advance Cost of Deposits NIM (RHS)

(%) (%)

Error! N ot a valid l ink.

Source: SBI, Ventura Research Source: SBI, Ventura Research

0.4

10.4

20.4

30.4

40.4

50.4

60.4

Q3 F

Y14

Q4 F

Y14

Q1 F

Y15

Q2 F

Y15

Q3 F

Y15

Q4 F

Y15

Q1 F

Y16

Q2 F

Y16

Q3 F

Y16

Q4F

Y16

Q1F

Y17

Cost to Income …

(%)

Fee income to Advances (%) Yield on Advance , NIM & Cost of Deposits

0.0

0.1

0.2

0.3

0.4

Q1 F

Y14

Q2 F

Y14

Q3 F

Y14

Q4 F

Y14

Q1 F

Y15

Q2F

Y15

Q3F

Y15

Q4F

Y15

Q1F

Y16

Q2F

Y16

Q3F

Y16

Fee Income as % of Advances

(%)

2.8

2.9

3.0

3.1

3.2

3.3

3.4

3.5

3.6

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Q3 F

Y14

Q4 F

Y14

Q1 F

Y15

Q2F

Y15

Q3F

Y15

Q4F

Y15

Q1F

Y16

Q2F

Y16

Q3F

Y16

Q4F

Y16

Q1F

Y17

Yield on Advance Cost of Deposits NIM (RHS)

(%) (%)

Source: SBI, Ventura Research Source: SBI, Ventura Research

Quarterly Result Update

- 7 - Monday, 22

nd August, 2016

ROA vs ROE (%) Capital Adequacy Ratio (%)

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

3.0

5.0

7.0

9.0

11.0

13.0

15.0

Q3 F

Y14

Q4 F

Y14

Q1 F

Y15

Q2F

Y15

Q3F

Y15

Q4F

Y15

Q1F

Y16

Q2F

Y16

Q3F

Y16

Q4F

Y16

Q1F

Y17

ROE ROA (RHS)

(%) (%)

Source: SBI, Ventura Research Source: SBI, Ventura Research

10.5

11.0

11.5

12.0

12.5

13.0

13.5

14.0

14.5

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

Q3 F

Y14

Q4 F

Y14

Q1 F

Y15

Q2F

Y15

Q3F

Y15

Q4F

Y15

Q1F

Y16

Q2F

Y16

Q3F

Y16

Q4F

Y16

Q1F

Y17

Tier I Capital Tier II Capital

(%) (%)

1 Yr Forward P/E 1 Yr Forward P/BV

0

50

100

150

200

250

300

350

400

Sep-03 Sep-06 Sep-09 Sep-12 Sep-15

CMP 4.75X 6.93X 9.1X 11.28X 13.46X

0

50

100

150

200

250

300

350

400

450

Sep-03 Sep-06 Sep-09 Sep-12 Sep-15

CMP 0.8X 1.05X 1.3X 1.55X 1.8X

Source: SBI, Ventura Research Source: SBI, Ventura Research

Quarterly Result Update

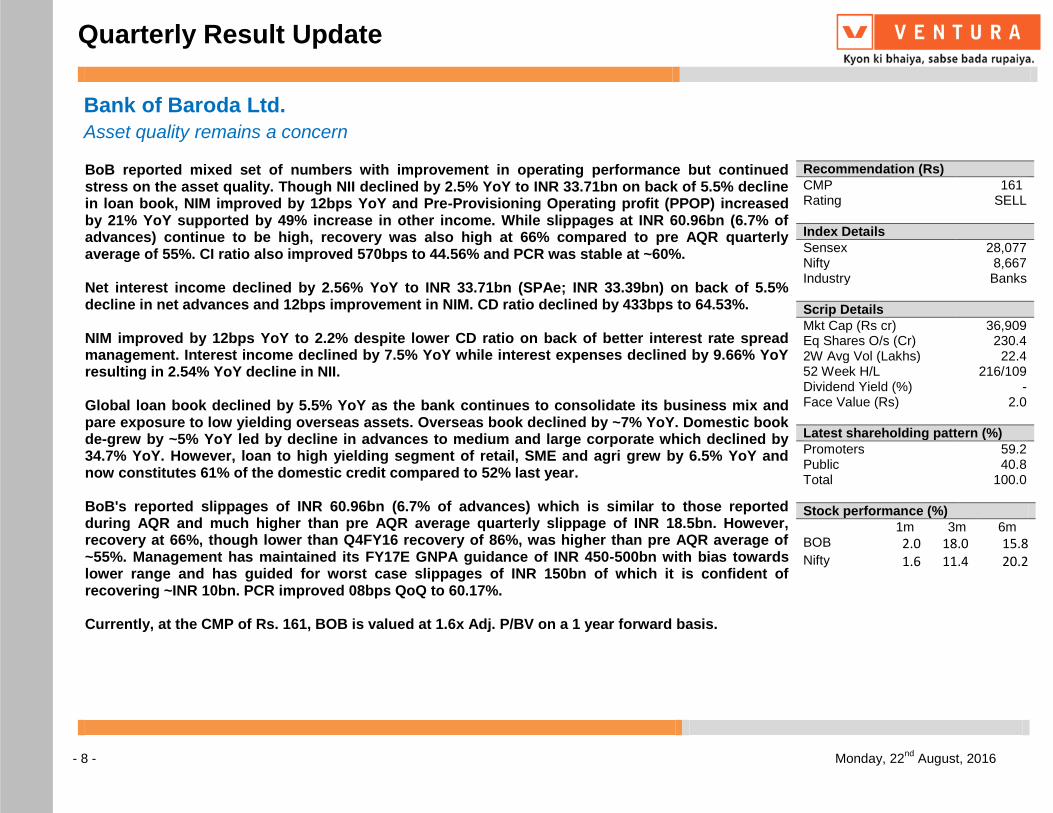

Bank of Baroda Ltd.

Asset quality remains a concern

- 8 - Monday, 22nd

August, 2016

BoB reported mixed set of numbers with improvement in operating performance but continued stress on the asset quality. Though NII declined by 2.5% YoY to INR 33.71bn on back of 5.5% decline in loan book, NIM improved by 12bps YoY and Pre-Provisioning Operating profit (PPOP) increased by 21% YoY supported by 49% increase in other income. While slippages at INR 60.96bn (6.7% of advances) continue to be high, recovery was also high at 66% compared to pre AQR quarterly average of 55%. CI ratio also improved 570bps to 44.56% and PCR was stable at ~60%. Net interest income declined by 2.56% YoY to INR 33.71bn (SPAe; INR 33.39bn) on back of 5.5% decline in net advances and 12bps improvement in NIM. CD ratio declined by 433bps to 64.53%. NIM improved by 12bps YoY to 2.2% despite lower CD ratio on back of better interest rate spread management. Interest income declined by 7.5% YoY while interest expenses declined by 9.66% YoY resulting in 2.54% YoY decline in NII. Global loan book declined by 5.5% YoY as the bank continues to consolidate its business mix and pare exposure to low yielding overseas assets. Overseas book declined by ~7% YoY. Domestic book de-grew by ~5% YoY led by decline in advances to medium and large corporate which declined by 34.7% YoY. However, loan to high yielding segment of retail, SME and agri grew by 6.5% YoY and now constitutes 61% of the domestic credit compared to 52% last year. BoB's reported slippages of INR 60.96bn (6.7% of advances) which is similar to those reported during AQR and much higher than pre AQR average quarterly slippage of INR 18.5bn. However, recovery at 66%, though lower than Q4FY16 recovery of 86%, was higher than pre AQR average of ~55%. Management has maintained its FY17E GNPA guidance of INR 450-500bn with bias towards lower range and has guided for worst case slippages of INR 150bn of which it is confident of recovering ~INR 10bn. PCR improved 08bps QoQ to 60.17%. Currently, at the CMP of Rs. 161, BOB is valued at 1.6x Adj. P/BV on a 1 year forward basis.

Recommendation (Rs)

CMP 161 Rating SELL

Index Details

Sensex 28,077 Nifty 8,667 Industry Banks

Scrip Details

Mkt Cap (Rs cr) 36,909 Eq Shares O/s (Cr) 230.4 2W Avg Vol (Lakhs) 22.4 52 Week H/L 216/109 Dividend Yield (%) - Face Value (Rs) 2.0

Latest shareholding pattern (%)

Promoters 59.2 Public 40.8 Total 100.0

Stock performance (%)

1m 3m 6m BOB 2.0 18.0 15.8 Nifty 1.6 11.4 20.2

Quarterly Result Update

- 9 - Monday, 22

nd August, 2016

Description Q1FY17 Q1FY16 % Chg. Q1FY17 Q4FY16 % Chg. FY201603 FY201503 % Chg.

Interest Earned 10433.5 11276.5 -7.5 10433.5 11014.4 -5.3 44061.3 42963.6 2.6

Interest on Advances 7162.1 8032.7 -10.8 7162.1 6882.3 4.1 29796.2 30802.7 -3.3

% of Total Int. Earned 68.6 71.2 -- 68.6 62.5 -- 67.6 71.7 --

Interest on Balances with RBI 324.9 296.1 9.8 324.9 365.3 -11.1 1305.9 1549.8 -15.7

% of Total Int. Earned 3.1 2.6 -- 3.1 3.3 -- 3.0 3.6 --

Income From Investments 2495.0 2558.7 -2.5 2495.0 2689.4 -7.2 10673.2 9431.0 13.2

% of Total Int. Earned 23.9 22.7 -- 23.9 24.4 -- 24.2 22.0 --

Others 451.6 389.1 16.1 451.6 1077.4 -58.1 2285.9 1180.1 93.7

% of Total Int. Earned 4.3 3.5 -- 4.3 9.8 -- 5.2 2.8 --

Other Income 1444.4 967.2 49.3 1444.4 1774.7 -18.6 4998.9 4402.0 13.6

Total Income 11877.9 12243.7 -3.0 11877.9 12789.1 -7.1 49060.1 47365.6 3.6

Interest Expended 7062.4 7816.9 -9.7 7062.4 7684.0 -8.1 31321.4 29776.3 5.2

Operating Expenses 2146.0 2224.9 -3.6 2146.0 2532.6 -15.3 8923.1 7674.1 16.3

Payment to provisions for Employee 1108.1 1345.1 -17.6 1108.1 1434.2 -22.7 4978.0 4261.4 16.8

% of Opt. Expenses 51.6 60.5 -- 51.6 56.6 -- 55.8 55.5 --

Other Opt. Expenses 1037.9 879.8 18.0 1037.9 1098.5 -5.5 3945.1 3412.8 15.6

% of Opt. Expenses 48.4 39.5 -- 48.4 43.4 -- 44.2 44.5 --

Total Expenses 2146.0 2224.9 -3.6 2146.0 2532.6 -15.3 8923.1 7674.1 16.3

Operating Profit before prov. & cont. 2669.5 2202.0 21.2 2669.5 2572.5 3.8 8815.6 9915.1 -11.1

% of Total Int. Earned 25.6 19.5 -- 25.6 23.4 -- 20.0 23.1 --

Provisions and Contigencies 2004.1 599.7 234.2 2004.1 6857.7 -70.8 15513.7 4494.5 245.2

PBT 665.4 1602.2 -58.5 665.4 -4285.2 LP -6698.1 5420.6 PL

% of Total Int. Earned 6.4 14.2 -- 6.4 -38.9 -- -15.2 12.6 --

Tax 241.8 550.1 -56.0 241.8 -1055.1 LP -1302.5 2022.2 PL

PAT 423.6 1052.2 -59.7 423.6 -3230.1 LP -5395.6 3398.4 PL

% of Total Int. Earned 4.1 9.3 -- 4.1 -29.3 -- -12.3 7.9 --

Paid up equity share capital 462.1 443.6 4.2 462.1 462.1 0.0 462.1 443.6 4.2

EPS (Rs.) 1.8 4.7 -61.4 1.8 -14.0 LP -23.4 15.3 PL

Capital Adequacy Ratio 14.1 12.7 135.0 14.1 14.2 -11.0 14.2 13.3 87.0

NII 3371.1 3459.6 -2.6 3371.1 3330.4 1.2 12739.8 13187.2 -3.4

NIM

Gross NPA 42991.7 17274.0 148.9 42991.7 40521.0 6.1 40521.0 16261.5 149.2

% of Gross NPA 11.2 4.1 702.0 11.2 10.0 116.0 10.0 3.7 627.0

Net NPA 20783.8 8470.0 145.4 20783.8 19406.5 7.1 19406.5 8069.5 140.5

% of Net NPA 5.7 2.1 366.0 5.7 5.1 67.0 5.1 1.9 317.0

ROA(%) 0.3 0.6 -35.0 0.3 -1.9 215.0 -0.8 0.5 PL

Quarterly Result Update

- 10 - Monday, 22

nd August, 2016

Deposits-Advance Growth Incremental LDR (%)

Error

27.0

28.0

29.0

30.0

31.0

32.0

33.0

34.0

35.0

0.0

100,000.0

200,000.0

300,000.0

400,000.0

500,000.0

600,000.0

700,000.0

Q3

FY14

Q4

FY14

Q1

FY15

Q2

FY15

Q3

FY15

Q4

FY15

Q1

FY16

Q2

FY16

Q3

FY16

Q4

FY16

Q1

FY17

Rs.Crore

Advance Deposit CASA RHS(%)

(%)

-400.0

-300.0

-200.0

-100.0

0.0

100.0

200.0

Q3 FY14 Q1 FY15 Q3 FY15 Q1 FY16 Q3 FY16 Q1FY17

Incremental LDR Ratio (%)

(%)

Source: BOB, Ventura Research Source: BOB, Ventura Research

LDR (%)

62.0

63.0

64.0

65.0

66.0

67.0

68.0

69.0

70.0

71.0

72.0

Q3

FY14

Q4

FY14

Q1

FY15

Q2

FY15

Q3

FY15

Q4

FY15

Q1

FY16

Q2

FY16

Q3

FY16

Q4

FY16

Q1

FY17

LDR Ratio (%)

(%)

Source: BOB, Ventura Research

Quarterly Result Update

- 11 - Monday, 22

nd August, 2016

Cost to Income Ratio (%) Asset Quality under pressure Error! N ot a valid l ink.

50.0

55.0

60.0

65.0

70.0

75.0

80.0

85.0

90.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Q3

FY14

Q4

FY14

Q1

FY15

Q2

FY15

Q3

FY15

Q4

FY15

Q1

FY16

Q2

FY16

Q3

FY16

Q4

FY16

Q1

FY17

(%)

Gross NPA Net NPA PCR (RHS)

(%)

Source: BOB, Ventura Research Source: BOB, Ventura Research

30.0

35.0

40.0

45.0

50.0

55.0

60.0

Q3 FY14 Q1 FY15 Q3 FY15 Q1 FY16 Q3 FY16 Q1 FY17

(%)

Cost to Income Ratio …

Fee Income as a % of Advances NIM, Cost of deposit & Yield on Advances

0.0

0.1

0.2

Q2 FY14

Q3 FY14

Q4 FY14

Q1 FY15

Q2 FY15

Q3 FY15

Q4 FY15

Q1 FY16

Q2 FY16

Q3 FY16

Q4 FY16

Fee Income as % of Advances

(%)

Source: BOB, Ventura Research Source: BOB, Ventura Research

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Q3 FY14 Q1 FY15 Q3 FY15 Q1 FY16 Q3 FY16 Q1FY17

NIM Yield on Advance Cost of Deposits

(%)

Quarterly Result Update

- 12 - Monday, 22

nd August, 2016

1 Yr Forward PE 1 Yr Forward P/BV

0

50

100

150

200

250

Sep-03 Sep-05 Sep-07 Sep-09 Sep-11 Sep-13 Sep-15

CMP 4X 5.2X 6.4X 7.6X 8.8X

0

50

100

150

200

250

Sep-03 Sep-05 Sep-07 Sep-09 Sep-11 Sep-13 Sep-15

CMP 0.6X 0.75X 0.9X 1.05X 1.2X

Source: BOB, Ventura Research Source: BOB, Ventura Research

Net Interest Income & Growth (%) Capital Adequacy Ratio (%)

Source: BOB, Ventura Research Source: BOB, Ventura Research

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

0.0

500.0

1,000.0

1,500.0

2,000.0

2,500.0

3,000.0

3,500.0

4,000.0

Q2 FY14

Q4 FY14

Q2 FY15

Q4 FY15

Q2 FY16

Q4 FY16

Rs.Crore

NII

(

11.0

11.5

12.0

12.5

13.0

13.5

14.0

14.5

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

Q3 FY14 Q2 FY15 Q1 FY16 Q4 FY16

Tier I Capital Tier II Capital

( (

Quarterly Result Update

Adani Ports and Special Economic Zone Ltd

Strong container volume

- 13 - Monday, 22nd

August, 2016

Q1FY17 consolidated income came at Rs18.2 bn up by 6.3% YoY led by higher volumes at 42.3 mn

MT which increased at 7% YoY with stable realizations, there was no significant SEZ revenue

during the quarter. Port income reported a rise of 10% YOY at Rs16.33 bn, Port EBITDA went up by

10% Rs11.56 bn YoY as Port EBITDA margin came higher at 70.8%. The company continues its

focus on container and other cargo business as well as coastal cargo movement in its strategy to

replace lower coal volumes which is starting to gradually play out as seen by the Q1FY17 volume

growth drivers.

Net profit came at Rs8.36 bn growth of 30.8% YoY on higher operational profitability and other

income which grew by 63% YoY at Rs2.67 bn. Interest cost was Rs2.67 bn decline of 19.5% YoY.

Effective tax rate came lower at 6.6% against 9.1% in same quarter last year.

The management has highlighted that they will be targeting to reduce Loans & Advances to related

parties by as much as Rs10 bn by September, 2016. The company maintains its guidance for

consolidated volume growth of 10-15% for FY17E.

At the CMP of Rs 272, the stock is trading at 17.8x and 15.9x its FY17E and FY18E earnings,

respectively, and we recommend HOLD on the stock.

Recommendation (Rs)

CMP 272

Rating HOLD

Index Details

Sensex 28,077

Nifty 8,667

Industry Port

Scrip Details

Mkt Cap (Rs cr) 56,495

Eq Shares O/s (Cr) 207.1

Avg Vol (Lakhs) 7.0

52 Week H/L 374/169

Dividend Yield (%) 0.4

Face Value (Rs) 2.0

Latest shareholding pattern (%)

Promoters 56.7

Public 43.3

Total 100.0

Stock performance (%)

1m 3m 6m

APSEZ 23.9 58.9 30.8 Nifty 1.6 11.4 20.2

Quarterly Result Update

- 14 - Monday, 22nd

August, 2016

Description Q1FY17 Q1FY16 % Chg. Q1FY17 Q4FY16 % Chg.FY201603FY201503 % Chg.

Net Sales 1817.2 1708.9 6.3 1817.2 1859.7 -2.3 6968.8 5836.2 19.4

Other operational Income 9.4 5.9 58.5 9.4 87.5 -89.3 287.0 315.8 -9.1

Total Oper. Income(TOI) 1826.6 1714.8 6.5 1826.6 1947.2 -6.2 7255.7 6152.0 17.9

Raw Materials Cons.- - - 0.0 0.0 0.0

% to TOI -- -- 0.0 0.0 --

Stock adj. (-)Inc / (+)Dec- - - 0.0 0.0 0.0

% to TOI -- -- 0.0 0.0 --

Net Raw Mat adj. for stock 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

% to TOI 0.0 0.0 -- 0.0 0.0 -- 0.0 0.0 --

Other expenses 532.2 516.0 3.1 532.2 622.3 -14.5 2218.1 1940.3 14.3

% to TOI 29.1 30.1 -- 29.1 32.0 -- 32.0 32.7 --

Contribution Net_Sales 1247.1 1179.3 5.8 1247.1 1295.5 -3.7 4932.7 4139.5 19.2

Personnel 77.4 62.3 24.1 77.4 70.7 9.5 282.2 237.2 19.0

% to TOI 4.2 3.6 -- 4.2 3.6 -- 3.9 3.9 --

Total expenditure 609.5 578.4 5.4 609.5 692.9 -12.0 2500.3 2177.4 14.8

Operating Profit 1217.1 1136.4 7.1 1217.1 1254.3 -3.0 4755.5 3974.6 19.7

% to TOI 66.6 66.3 -- 66.6 64.4 -- 64.1 63.4 --

Non-Operating Income 257.1 157.6 63.2 257.1 353.2 -27.2 810.0 754.8 7.3

Interest 267.2 332.1 -19.6 267.2 278.1 -3.9 1224.2 1244.2 -1.6

Exceptional Items 47.3 19.5 142.9 47.3 29.4 60.7 104.9 72.3 45.3

Gross Profit 1159.7 942.5 23.1 1159.7 1300.0 -10.8 4236.3 3412.9 24.1

Depreciation 281.0 253.0 11.1 281.0 255.5 10.0 1079.4 911.7 18.4

PBT before Extra-ord 878.7 689.5 27.5 878.7 1044.5 -15.9 3156.9 2501.2 26.2

% to TOI 48.1 40.2 -- 48.1 53.6 -- 43.5 40.7 --

Extraordinary Items - - 0.0 0.0 0.0

PBT 878.7 689.5 27.5 878.7 1044.5 -15.9 3156.9 2501.2 26.2

Tax Rate 6.9 9.3 -25.5 6.9 13.0 -46.6 10.4 7.1 46.6

Prov. for Tax 61.0 64.2 -5.1 61.0 135.8 -55.1 326.9 176.7 85.0

% to TOI 3.3 3.8 -- 3.3 7.0 -- 4.5 2.9 --

Profit after Tax 817.8 625.2 30.8 817.8 908.7 -10.0 2829.9 2324.5 21.7

% to TOI 44.8 36.5 -- 44.8 46.7 -- 39.0 37.8 --

Minority Interest 2.4 9.0 -73.6 2.4 9.3 -74.4 42.1 -10.2 LP

PAT (adj. For MI) 835.7 638.9 30.8 835.7 914.1 -8.6 2867.4 2314.3 23.9

Face Value 2.0 2.0 -- 2.0 2.0 -- 2.0 2.0 --

Equity Share capital 414.2 414.2 -- 414.2 414.2 -- 414.2 414.0 --

EPS (Rs.) 4.0 3.0 30.8 4.0 4.4 -10.0 13.7 11.2 21.7

CEPS (Rs.) 5.3 4.2 25.1 5.3 5.6 -5.5 18.9 15.6 20.8

Quarterly Result Update

- 15 - Monday, 22nd

August, 2016

APSEZ’s Consolidated Cargo Volume Trend Cargo Volume Trend at Mundra Port

-5

0

5

10

15

20

25

30

35

0

5

10

15

20

25

30

35

40

45

Q2F

Y15

Q3F

Y15

Q4F

Y15

Q1F

Y16

Q2F

Y16

Q3F

Y16

Q4F

Y16

Q1F

Y17

Cargo Volume YoY growth (RHS)

MMT (%)

-10

-8

-6

-4

-2

0

2

4

6

8

10

23

24

25

26

27

28

29

30

31

Q2F

Y15

Q3F

Y15

Q4F

Y15

Q1F

Y16

Q2F

Y16

Q3F

Y16

Q4F

Y16

Q1F

Y17

Cargo Volume YoY growth (RHS)

MMT (%)

Source: APSEZ, Ventura Research Source: APSEZ, Ventura Research

1 Yr Forward PE 1 Yr Forward P/BV

0

100

200

300

400

500

600

Sep-09 Sep-11 Sep-13 Sep-15

CMP 22X 27.7X 33.4X 39.1X 44.8X

0

50

100

150

200

250

300

350

400

450

500

Sep-09 Sep-11 Sep-13 Sep-15

CMP 4.5X 5.3X 6.1X 6.9X 7.7X

Source: APSEZ, Ventura Research

Source: APSEZ, Ventura Research

Quarterly Result Update

- 16 - Monday, 22nd

August, 2016

1 Yr Forward EV/EBITDA

0

20000

40000

60000

80000

100000

120000

140000

160000

Sep-09 Sep-11 Sep-13 Sep-15

EV 11X 15.95X 20.9X 25.85X 30.8X

Source: APSEZ, Ventura Research

Quarterly Result Update

Hero MotoCorp Ltd.

Margins impress

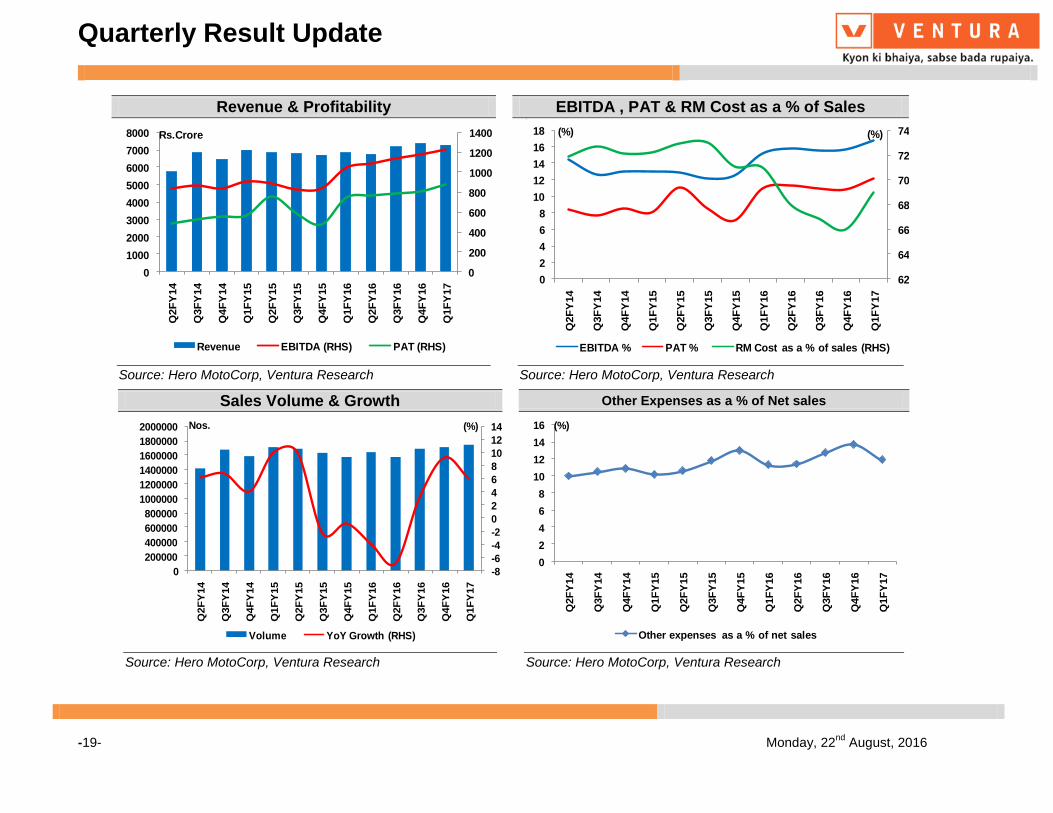

Hero Motocorp Ltd. revenue surged by 7.74% to Rs 8,010 cr from Rs 7,435Cr in the corresponding quarter of previous year, it has achieved highest ever quarterly volumes of 17.45 Lakhs units rising by 6.05% on YoY basis and 1.40% on Q-o-Q basis. Hero’s strong point is the executive segment in the motorcycle market, but this is also the category that is increasingly being cannibalized by scooters, owing to similar price points. Still, the company’s two recent Products—Maestro Edge and Duet—have helped it overtake TVS Motor Co. Ltd in the last quarter, even as it increases capacity. Despite higher cost of materials, Operating EBITDA margins increased by 150 bps to 16.6% on YoY basis which is higher than our expectation and EBITDA for the quarter stood at Rs 1,230 cr, margins improved due to reduction in other expenses and robust volume growth in scooters and motorcycles segments during the quarter. Q1 profit surged by 17.7% to Rs.883 crore on YoY. Due to control on other expenses and higher sales volumes helped Hero Motocorp to post higher profit. The growth trajectory has been the 125cc segment where the company now commands well over 50% market share which is contributed by Glamour and Super Splendor. In Q1FY17, Glamour grew by 32% and Super Splendor grew by 29% over the corresponding quarter in the previous fiscal. Recently launched the all new splendour ismart 110- the first motorcycle to have been completely designed and developed by in -house R&D team at Jaipur, and the initial response from customers have been positive. At the CMP of Rs 3370, Hero is trading at 18.3x and 15.2x its estimated earnings for FY17E and FY18E, respectively, and we recommend a HOLD on the stock.

Recommendation (Rs)

CMP 3370 Rating HOLD

Index Details

Sensex 28,077

Nifty 8,667

Industry Automobile

Scrip Details

Mkt Cap (Rs Cr) 67,276

Eq Shares O/s (Cr) 20.0

Avg Vol (Lakhs) 0.5

52 Week H/L 3556/2257

Dividend Yield (%) 1.7

Face Value (Rs) 2.0

Latest shareholding pattern (%)

Promoters 34.6 Public 65.4

Total 100.0

Stock performance (%)

1m 3m 6m

HeroMoto 4.0 16.2 24.2 Nifty 1.6 11.4 20.2

-17- Monday, 22

nd August, 2016

Quarterly Result Update

Description Q1FY17 Q1FY16 % Chg. Q1FY17 Q4FY16 % Chg. FY201603 FY201503 % Chg.

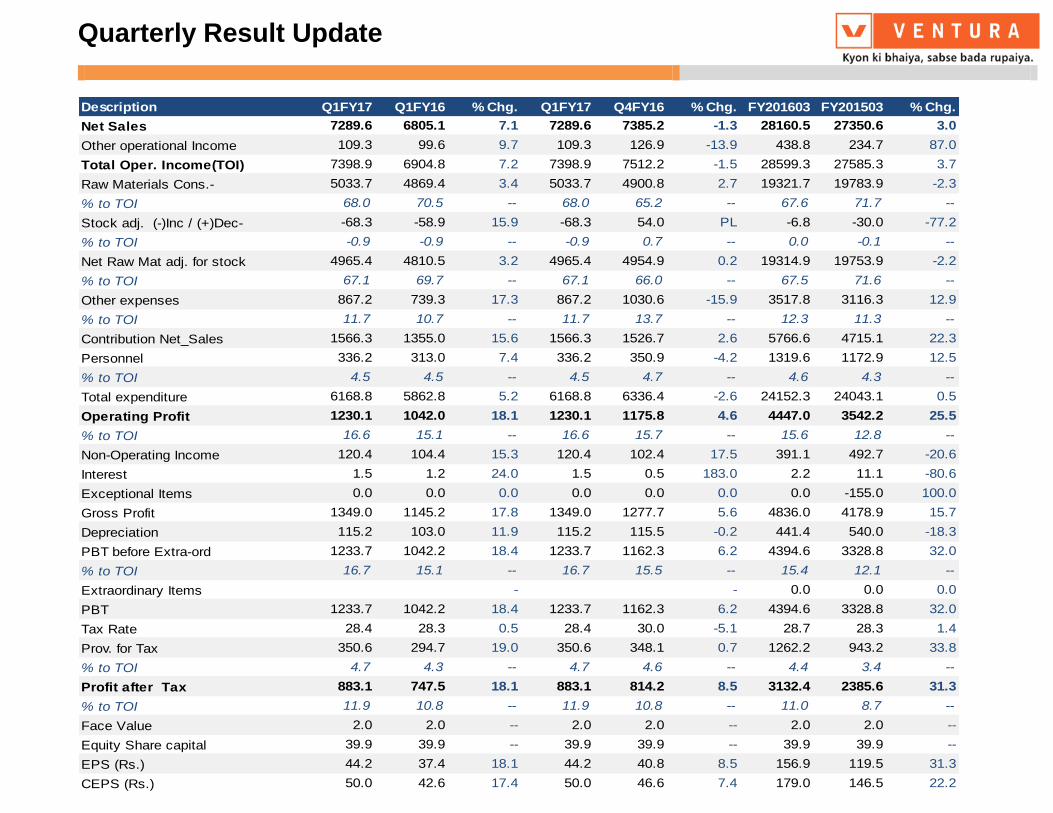

Net Sales 7289.6 6805.1 7.1 7289.6 7385.2 -1.3 28160.5 27350.6 3.0

Other operational Income 109.3 99.6 9.7 109.3 126.9 -13.9 438.8 234.7 87.0

Total Oper. Income(TOI) 7398.9 6904.8 7.2 7398.9 7512.2 -1.5 28599.3 27585.3 3.7

Raw Materials Cons.- 5033.7 4869.4 3.4 5033.7 4900.8 2.7 19321.7 19783.9 -2.3

% to TOI 68.0 70.5 -- 68.0 65.2 -- 67.6 71.7 --

Stock adj. (-)Inc / (+)Dec- -68.3 -58.9 15.9 -68.3 54.0 PL -6.8 -30.0 -77.2

% to TOI -0.9 -0.9 -- -0.9 0.7 -- 0.0 -0.1 --

Net Raw Mat adj. for stock 4965.4 4810.5 3.2 4965.4 4954.9 0.2 19314.9 19753.9 -2.2

% to TOI 67.1 69.7 -- 67.1 66.0 -- 67.5 71.6 --

Other expenses 867.2 739.3 17.3 867.2 1030.6 -15.9 3517.8 3116.3 12.9

% to TOI 11.7 10.7 -- 11.7 13.7 -- 12.3 11.3 --

Contribution Net_Sales 1566.3 1355.0 15.6 1566.3 1526.7 2.6 5766.6 4715.1 22.3

Personnel 336.2 313.0 7.4 336.2 350.9 -4.2 1319.6 1172.9 12.5

% to TOI 4.5 4.5 -- 4.5 4.7 -- 4.6 4.3 --

Total expenditure 6168.8 5862.8 5.2 6168.8 6336.4 -2.6 24152.3 24043.1 0.5

Operating Profit 1230.1 1042.0 18.1 1230.1 1175.8 4.6 4447.0 3542.2 25.5

% to TOI 16.6 15.1 -- 16.6 15.7 -- 15.6 12.8 --

Non-Operating Income 120.4 104.4 15.3 120.4 102.4 17.5 391.1 492.7 -20.6

Interest 1.5 1.2 24.0 1.5 0.5 183.0 2.2 11.1 -80.6

Exceptional Items 0.0 0.0 0.0 0.0 0.0 0.0 0.0 -155.0 100.0

Gross Profit 1349.0 1145.2 17.8 1349.0 1277.7 5.6 4836.0 4178.9 15.7

Depreciation 115.2 103.0 11.9 115.2 115.5 -0.2 441.4 540.0 -18.3

PBT before Extra-ord 1233.7 1042.2 18.4 1233.7 1162.3 6.2 4394.6 3328.8 32.0

% to TOI 16.7 15.1 -- 16.7 15.5 -- 15.4 12.1 --

Extraordinary Items - - 0.0 0.0 0.0

PBT 1233.7 1042.2 18.4 1233.7 1162.3 6.2 4394.6 3328.8 32.0

Tax Rate 28.4 28.3 0.5 28.4 30.0 -5.1 28.7 28.3 1.4

Prov. for Tax 350.6 294.7 19.0 350.6 348.1 0.7 1262.2 943.2 33.8

% to TOI 4.7 4.3 -- 4.7 4.6 -- 4.4 3.4 --

Profit after Tax 883.1 747.5 18.1 883.1 814.2 8.5 3132.4 2385.6 31.3

% to TOI 11.9 10.8 -- 11.9 10.8 -- 11.0 8.7 --

Face Value 2.0 2.0 -- 2.0 2.0 -- 2.0 2.0 --

Equity Share capital 39.9 39.9 -- 39.9 39.9 -- 39.9 39.9 --

EPS (Rs.) 44.2 37.4 18.1 44.2 40.8 8.5 156.9 119.5 31.3

CEPS (Rs.) 50.0 42.6 17.4 50.0 46.6 7.4 179.0 146.5 22.2

Quarterly Result Update

-19- Monday, 22

nd August, 2016

Revenue & Profitability EBITDA , PAT & RM Cost as a % of Sales

0

200

400

600

800

1000

1200

1400

0

1000

2000

3000

4000

5000

6000

7000

8000

Q2F

Y14

Q3F

Y14

Q4F

Y14

Q1F

Y15

Q2F

Y15

Q3F

Y15

Q4F

Y15

Q1F

Y16

Q2F

Y16

Q3F

Y16

Q4F

Y16

Q1F

Y17

Rs.Crore

Revenue EBITDA (RHS) PAT (RHS)

es

62

64

66

68

70

72

74

0

2

4

6

8

10

12

14

16

18

Q2F

Y14

Q3F

Y14

Q4F

Y14

Q1F

Y15

Q2F

Y15

Q3F

Y15

Q4F

Y15

Q1F

Y16

Q2F

Y16

Q3F

Y16

Q4F

Y16

Q1F

Y17

EBITDA % PAT % RM Cost as a % of sales (RHS)

(%) (%)

Source: Hero MotoCorp, Ventura Research

Source: Hero MotoCorp, Ventura Research

Sales Volume & Growth Other Expenses as a % of Net sales

-8

-6

-4

-2

0

2

4

6

8

10

12

14

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

1800000

2000000

Q2F

Y14

Q3F

Y14

Q4F

Y14

Q1F

Y15

Q2F

Y15

Q3F

Y15

Q4F

Y15

Q1F

Y16

Q2F

Y16

Q3F

Y16

Q4F

Y16

Q1F

Y17

Nos.

Volume YoY Growth (RHS)

(%)

0

2

4

6

8

10

12

14

16

Q2F

Y14

Q3F

Y14

Q4F

Y14

Q1F

Y15

Q2F

Y15

Q3F

Y15

Q4F

Y15

Q1F

Y16

Q2F

Y16

Q3F

Y16

Q4F

Y16

Q1F

Y17

Other expenses as a % of net sales

(%)

Source: Hero MotoCorp, Ventura Research

Source: Hero MotoCorp, Ventura Research

Quarterly Result Update

-20- Monday, 22

nd August, 2016

1 Yr Forward P/E 1 Yr Forward P/BV

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Sep-09 Sep-10 Sep-11 Sep-12 Sep-13 Sep-14 Sep-15

CMP 7X 10.1X 13.2X 16.3X 19.4X

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Sep-03 Sep-05 Sep-07 Sep-09 Sep-11 Sep-13 Sep-15

CMP 4X 5.45X 6.9X 8.35X 9.8X

Source: Hero MotoCorp, Ventura Research

Source: Hero MotoCorp, Ventura Research

Quarterly Result Update

Lupin Ltd.

Robust quarter

- 22 - Monday, 22nd

August, 2016

Revenues grew 40.7% YoY to Rs 4439.4 crore mainly due to 83.8% growth in US sales to Rs 2188.6

crore. Strong US sales were due to Gavis consolidation, robust sales in Metformin (anti-diabetic).

Domestic sales grew 5.2% YoY to Rs 931.3 crore. EBITDA margins improved 333 bps YoY to 29.5%

mainly on account of a strong gross margin performance. EBITDA grew 58.6% YoY to Rs 1308.0

crore. Net profit grew 55.1% YoY to Rs 882.0 crore owing to a strong operational performance

Lupin’s US business is witnessing a shift from branded to generics with a slowdown in the

branded space and emergence of generics. Post the acquisition of US based Gavis, the company

now owns one of the strongest ANDA pipeline comprising 336 filed ANDAs and 149 pending

approvals including 45 FTFs. This acquisition will strengthen its position in dermatology,

controlled substance products and other high value niche generics segments besides its maiden

foray into US institutional business.

Lupin ranks fifth in domestic formulations with a market share of 3.7%. The acute: chronic: sub-

chronic ratio for the company is at 27:37:36. In terms of MR productivity, at Rs 61.67 lakh per MR it

has one of the best MR productivity among large cap peers. Recent tie-ups with Eli Lilly and

Boehringer for anti-diabetics and with MSD for pneumonia vaccines are some of the steps to

bolster the domestic franchise.

Lupin is bearing the fruits of geographical diversification for broad based growth. It has

established a significant presence in the US by focusing on limited competition/FTF opportunities,

concentration on niche therapies such as oral contraceptives, dermatology, ophthalmology,

respiratory, etc, and acquiring small but profitable brands at the right price. It is slowly but surely

establishing itself in other geographies such as Japan and Australia. Higher growth on a fairly

consistent basis, a strong balance sheet (despite Gavis acquisition) and high return ratios are

some of the differentiators for Lupin besides management pedigree.

At the CMP of Rs 1,589 Lupin is trading at 24.6x and 21.1x its FY17E and FY18E consensus

earnings, respectively. We recommend a HOLD on the stock.

Recommendation (Rs)

CMP 1,589 Rating HOLD

Index Details

Sensex 28,077

Nifty 8,667

Industry Pharma

Scrip Details

Mkt Cap (Rs cr) 71,737

Eq Shares O/s (Cr) 45.0

Avg Vol (Lakhs) 2.27

52 Week H/L 2129/1280

Dividend Yield (%) 0.5

Face Value (Rs) 2.0

Latest shareholding pattern (%)

Promoters 46.8 Public 53.2

Total 100.0

Stock performance (%)

1m 3m 6m

Lupin -6.7 -4.7 -11.5 Nifty 1.6 11.4 20.2

Quarterly Result Update

- 23 - Monday, 22

nd August, 2016

Description Q1FY17 Q1FY16 % Chg. Q1FY17 Q4FY16 % Chg.FY201603FY201503 % Chg.

Net Sales 4313.6 3080.9 40.0 4313.6 4091.3 5.4 13701.6 12599.7 8.8

Other operational Income 125.9 75.2 67.4 125.9 89.8 40.1 506.9 170.3 197.7

Total Oper. Income(TOI) 4439.4 3156.1 40.7 4439.4 4181.2 6.2 14208.5 12770.0 11.3

Raw Materials Cons.- 772.7 689.4 12.1 772.7 671.3 15.1 2765.6 2519.4 9.8

% to TOI 17.4 21.8 -- 17.4 16.1 -- 19.5 19.7 --

Stock adj. (-)Inc / (+)Dec- -45.1 -200.9 -77.5 -45.1 -91.6 -50.7 -476.0 -145.7 226.7

% to TOI -1.0 -6.4 -- -1.0 -2.2 -- -3.4 -1.1 --

Net Raw Mat adj. for stock 727.6 488.5 49.0 727.6 579.8 25.5 2289.6 2373.7 -3.5

% to TOI 16.4 15.5 -- 16.4 13.9 -- 16.1 18.6 --

Other expenses 1697.9 1345.5 26.2 1697.9 1664.9 2.0 6057.7 5029.4 20.5

% to TOI 38.3 42.6 -- 38.3 39.8 -- 42.6 39.4 --

Contribution Net_Sales 2013.9 1322.1 52.3 2013.9 1936.5 4.0 5861.1 5366.9 9.2

Personnel 705.9 497.3 42.0 705.9 569.1 24.0 2107.7 1747.3 20.6

% to TOI 15.9 15.8 -- 15.9 13.6 -- 14.8 13.7 --

Total expenditure 3131.4 2331.2 34.3 3131.4 2813.8 11.3 10455.0 9150.4 14.3

Operating Profit 1308.0 824.8 58.6 1308.0 1367.4 -4.3 3753.5 3619.6 3.7

% to TOI 29.5 26.1 -- 29.5 32.7 -- 26.4 28.3 --

Non-Operating Income 82.6 75.7 9.2 82.6 25.4 224.9 187.7 239.8 -21.7

Interest 32.0 7.0 355.6 32.0 22.9 39.8 44.6 9.8 354.8

Exceptional Items 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Gross Profit 1358.7 893.5 52.1 1358.7 1370.0 -0.8 3896.5 3849.5 1.2

Depreciation 202.7 101.4 100.0 202.7 144.6 40.2 463.5 434.7 6.6

PBT before Extra-ord 1156.0 792.1 45.9 1156.0 1225.4 -5.7 3433.0 3414.8 0.5

% to TOI 26.0 25.1 -- 26.0 29.3 -- 24.2 26.7 --

Extraordinary Items - - 0.0 0.0 0.0

PBT 1156.0 792.1 45.9 1156.0 1225.4 -5.7 3433.0 3414.8 0.5

Tax Rate 23.7 28.5 -17.0 23.7 33.7 -29.9 33.6 28.4 18.3

Prov. for Tax 273.4 225.8 21.1 273.4 413.2 -33.8 1153.6 970.4 18.9

% to TOI 6.2 7.2 -- 6.2 9.9 -- 8.1 7.6 --

Profit after Tax 882.6 566.3 55.8 882.6 812.2 8.7 2279.5 2444.4 -6.8

% to TOI 19.9 17.9 -- 19.9 19.4 -- 16.0 19.1 --

Minority Interest -0.6 0.3 PL -0.6 -5.1 -87.9 -8.8 -41.2 -78.7

PAT (adj. For MI) 882.0 568.6 55.1 882.0 807.1 9.3 2270.7 2403.2 -5.5

Face Value 2.0 2.0 -- 2.0 2.0 -- 2.0 2.0 --

Equity Share capital 90.2 90.0 -- 90.2 90.1 -- 90.1 89.9 --

EPS (Rs.) 19.6 12.6 55.5 19.6 18.0 8.5 50.6 54.4 -7.0

CEPS (Rs.) 24.07 14.84 62.19 24.07 21.23 13.38 60.87 64.05 -4.96

Quarterly Result Update

- 24 - Monday, 22

nd August, 2016

Revenue Mix- Geography wise Revenue & Profitability Trend

0

20

40

60

80

100

120

Q2

FY

14

Q3

FY

14

Q4

FY

14

Q1

FY

15

Q2

FY

15

Q3

FY

15

Q4

FY

15

Q1

FY

16

Q2

FY

16

Q3

FY

16

Q4

FY

16

Q1

FY

17

India US EuropeJapan South Arica Emerging MarketAPI

(%)

0

5

10

15

20

25

30

35

40

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Q2

FY

14

Q3

FY

14

Q4

FY

14

Q1

FY

15

Q2

FY

15

Q3

FY

15

Q4

FY

15

Q1

FY

16

Q2

FY

16

Q3

FY

16

Q4

FY

16

Q1

FY

17

Rs.Crore

Revenue EBITDA Margin (RHS) PAT Margin (RHS)

(%)

Source: Lupin, Ventura Research Source: Lupin, Ventura Research

1 Yr Forward PE 1 Yr Forward P/BV

0

500

1000

1500

2000

2500

Dec-03 Dec-05 Dec-07 Dec-09 Dec-11 Dec-13 Dec-15

CMP 13X 19.5X 26X 32.5X 39X

0

500

1000

1500

2000

2500

Dec-03 Dec-05 Dec-07 Dec-09 Dec-11 Dec-13 Dec-15

CMP 4.2X 5.4X 6.6X 7.8X 9X

Source: Lupin, Ventura Research Source: Lupin, Ventura Research

Quarterly Result Update

- 25 - Monday, 22

nd August, 2016

1 Yr Forward EV/EBITDA

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

100000

Dec-03 Dec-05 Dec-07 Dec-09 Dec-11 Dec-13 Dec-15

EV 10.25X 13X 15.75X 18.5X 21.25X

Source: Lupin, Ventura Research

Quarterly Result Update

Bosch Ltd.

Strong quarter…

- 26 - Monday, 22nd

August, 2016

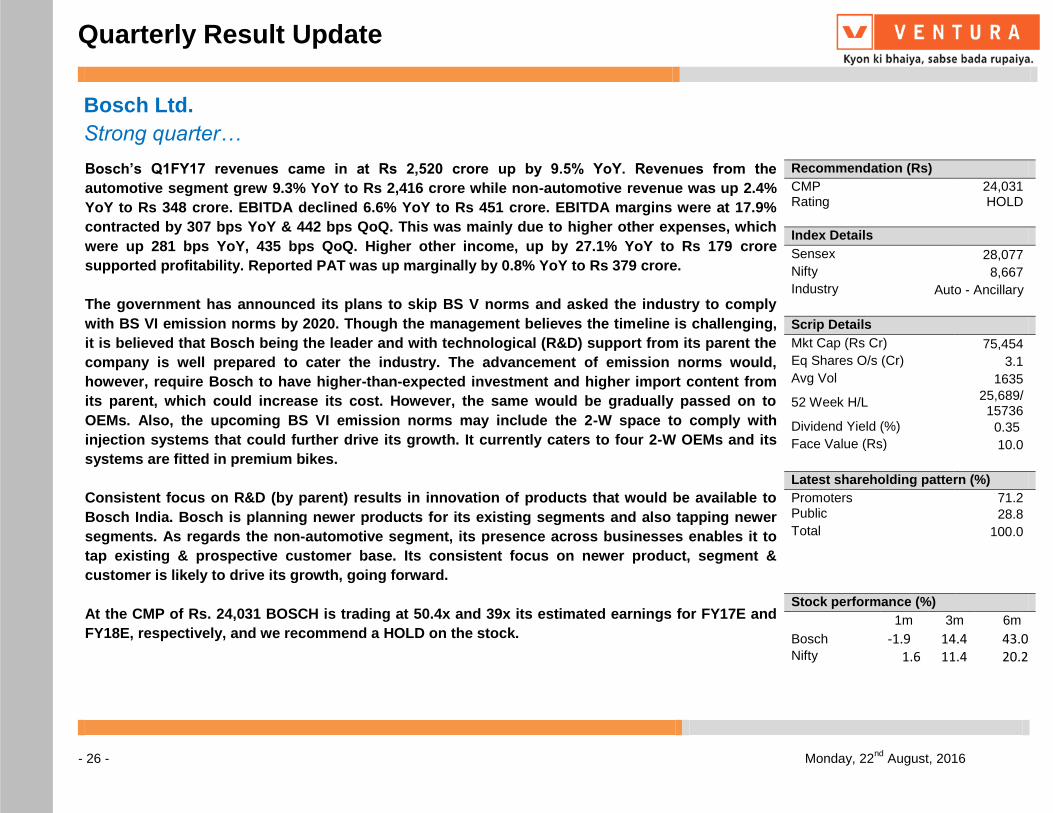

Bosch’s Q1FY17 revenues came in at Rs 2,520 crore up by 9.5% YoY. Revenues from the

automotive segment grew 9.3% YoY to Rs 2,416 crore while non-automotive revenue was up 2.4%

YoY to Rs 348 crore. EBITDA declined 6.6% YoY to Rs 451 crore. EBITDA margins were at 17.9%

contracted by 307 bps YoY & 442 bps QoQ. This was mainly due to higher other expenses, which

were up 281 bps YoY, 435 bps QoQ. Higher other income, up by 27.1% YoY to Rs 179 crore

supported profitability. Reported PAT was up marginally by 0.8% YoY to Rs 379 crore.

The government has announced its plans to skip BS V norms and asked the industry to comply

with BS VI emission norms by 2020. Though the management believes the timeline is challenging,

it is believed that Bosch being the leader and with technological (R&D) support from its parent the

company is well prepared to cater the industry. The advancement of emission norms would,

however, require Bosch to have higher-than-expected investment and higher import content from

its parent, which could increase its cost. However, the same would be gradually passed on to

OEMs. Also, the upcoming BS VI emission norms may include the 2-W space to comply with

injection systems that could further drive its growth. It currently caters to four 2-W OEMs and its

systems are fitted in premium bikes.

Consistent focus on R&D (by parent) results in innovation of products that would be available to

Bosch India. Bosch is planning newer products for its existing segments and also tapping newer

segments. As regards the non-automotive segment, its presence across businesses enables it to

tap existing & prospective customer base. Its consistent focus on newer product, segment &

customer is likely to drive its growth, going forward.

At the CMP of Rs. 24,031 BOSCH is trading at 50.4x and 39x its estimated earnings for FY17E and

FY18E, respectively, and we recommend a HOLD on the stock.

Recommendation (Rs)

CMP 24,031 Rating HOLD

Index Details

Sensex 28,077

Nifty 8,667

Industry Auto - Ancillary

Scrip Details

Mkt Cap (Rs Cr) 75,454

Eq Shares O/s (Cr) 3.1

Avg Vol 1635

52 Week H/L 25,689/ 15736

Dividend Yield (%) 0.35

Face Value (Rs) 10.0

Latest shareholding pattern (%)

Promoters 71.2 Public 28.8

Total 100.0

Stock performance (%)

1m 3m 6m

Bosch -1.9 14.4 43.0 Nifty 1.6 11.4 20.2

Quarterly Result Update

- 27 - Monday, 22

nd August, 2016

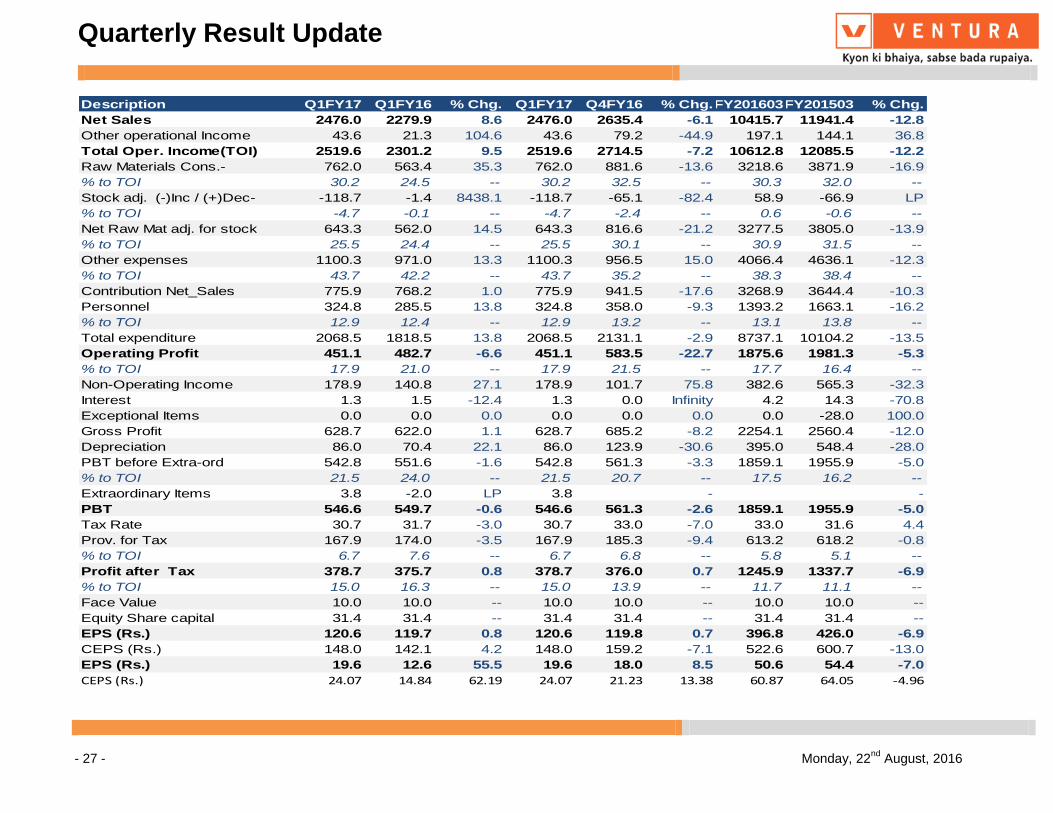

Description Q1FY17 Q1FY16 % Chg. Q1FY17 Q4FY16 % Chg.FY201603FY201503 % Chg.

Net Sales 2476.0 2279.9 8.6 2476.0 2635.4 -6.1 10415.7 11941.4 -12.8

Other operational Income 43.6 21.3 104.6 43.6 79.2 -44.9 197.1 144.1 36.8

Total Oper. Income(TOI) 2519.6 2301.2 9.5 2519.6 2714.5 -7.2 10612.8 12085.5 -12.2

Raw Materials Cons.- 762.0 563.4 35.3 762.0 881.6 -13.6 3218.6 3871.9 -16.9

% to TOI 30.2 24.5 -- 30.2 32.5 -- 30.3 32.0 --

Stock adj. (-)Inc / (+)Dec- -118.7 -1.4 8438.1 -118.7 -65.1 -82.4 58.9 -66.9 LP

% to TOI -4.7 -0.1 -- -4.7 -2.4 -- 0.6 -0.6 --

Net Raw Mat adj. for stock 643.3 562.0 14.5 643.3 816.6 -21.2 3277.5 3805.0 -13.9

% to TOI 25.5 24.4 -- 25.5 30.1 -- 30.9 31.5 --

Other expenses 1100.3 971.0 13.3 1100.3 956.5 15.0 4066.4 4636.1 -12.3

% to TOI 43.7 42.2 -- 43.7 35.2 -- 38.3 38.4 --

Contribution Net_Sales 775.9 768.2 1.0 775.9 941.5 -17.6 3268.9 3644.4 -10.3

Personnel 324.8 285.5 13.8 324.8 358.0 -9.3 1393.2 1663.1 -16.2

% to TOI 12.9 12.4 -- 12.9 13.2 -- 13.1 13.8 --

Total expenditure 2068.5 1818.5 13.8 2068.5 2131.1 -2.9 8737.1 10104.2 -13.5

Operating Profit 451.1 482.7 -6.6 451.1 583.5 -22.7 1875.6 1981.3 -5.3

% to TOI 17.9 21.0 -- 17.9 21.5 -- 17.7 16.4 --

Non-Operating Income 178.9 140.8 27.1 178.9 101.7 75.8 382.6 565.3 -32.3

Interest 1.3 1.5 -12.4 1.3 0.0 Infinity 4.2 14.3 -70.8

Exceptional Items 0.0 0.0 0.0 0.0 0.0 0.0 0.0 -28.0 100.0

Gross Profit 628.7 622.0 1.1 628.7 685.2 -8.2 2254.1 2560.4 -12.0

Depreciation 86.0 70.4 22.1 86.0 123.9 -30.6 395.0 548.4 -28.0

PBT before Extra-ord 542.8 551.6 -1.6 542.8 561.3 -3.3 1859.1 1955.9 -5.0

% to TOI 21.5 24.0 -- 21.5 20.7 -- 17.5 16.2 --

Extraordinary Items 3.8 -2.0 LP 3.8 - -

PBT 546.6 549.7 -0.6 546.6 561.3 -2.6 1859.1 1955.9 -5.0

Tax Rate 30.7 31.7 -3.0 30.7 33.0 -7.0 33.0 31.6 4.4

Prov. for Tax 167.9 174.0 -3.5 167.9 185.3 -9.4 613.2 618.2 -0.8

% to TOI 6.7 7.6 -- 6.7 6.8 -- 5.8 5.1 --

Profit after Tax 378.7 375.7 0.8 378.7 376.0 0.7 1245.9 1337.7 -6.9

% to TOI 15.0 16.3 -- 15.0 13.9 -- 11.7 11.1 --

Face Value 10.0 10.0 -- 10.0 10.0 -- 10.0 10.0 --

Equity Share capital 31.4 31.4 -- 31.4 31.4 -- 31.4 31.4 --

EPS (Rs.) 120.6 119.7 0.8 120.6 119.8 0.7 396.8 426.0 -6.9

CEPS (Rs.) 148.0 142.1 4.2 148.0 159.2 -7.1 522.6 600.7 -13.0

EPS (Rs.) 19.6 12.6 55.5 19.6 18.0 8.5 50.6 54.4 -7.0

CEPS (Rs.) 24.07 14.84 62.19 24.07 21.23 13.38 60.87 64.05 -4.96

Quarterly Result Update

- 28 - Monday, 22

nd August, 2016

Revenue Trend Profitability Trend

2,200

2,300

2,400

2,500

2,600

2,700

2,800

Q4

FY

14

Q1

FY

15

Q2

FY

15

Q3

FY

15

Q4

FY

15

Q1

FY

16

Q2

FY

16

Q3

FY

16

Q4

FY

16

Q1

FY

17

Revenue

Rs. Crore

0

5

10

15

20

25

Q4

FY

14

Q1

FY

15

Q2

FY

15

Q3

FY

15

Q4

FY

15

Q1

FY

16

Q2

FY

16

Q3

FY

16

Q4

FY

16

Q1

FY

17

EBITDA Margin PAT Margin

(%)

Source: Bosch, Ventura Research

Source: Bosch, Ventura Research

1 Yr Forward P/E 1 Yr Forward P/BV

0

5000

10000

15000

20000

25000

30000

Sep-11 Sep-12 Sep-13 Sep-14 Sep-15

CMP 20X 26.1X 32.2X 38.3X 44.4X

0

5000

10000

15000

20000

25000

30000

Sep-11 Sep-12 Sep-13 Sep-14 Sep-15

CMP 4X 4.9X 5.8X 6.7X 7.6X

Source: Bosch, Ventura Research

Source: Bosch, Ventura Research

Quarterly Result Update

- 29 - Monday, 22

nd August, 2016

1 Yr Forward EV/EBITDA

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

Sep-11 Sep-12 Sep-13 Sep-14 Sep-15

EV 12X 16.85X 21.7X 26.55X 31.4X

Source: Bosch, Ventura Research

Quarterly Result Update

Power Grid Corporation of India Ltd.

Strong quarter

- 30 - Monday, 22nd

August, 2016

Power Grid’s (PGCIL) Q1FY17 result sprung a positive surprise as net income at Rs 6069 jumped

33% YoY and 12.7% QoQ mainly aided by robust growth in income from telecom and transmission

business. EBIDTA stood at Rs 5368.8, while EBIDAT margin went up by 76 bps YoY to 88.46% and

PAT stood at Rs 2284.

PGCIL reported 33% increase in profit despite capitalising only Rs 25bn worth of projects during the

quarter (capex incurred was Rs 55.9bn). This was partly aided by healthy incentive income of Rs

770mn (Rs 1.27bn for FY16) and higher other operating income owing to interest income booked on

receiving final tariff orders from CERC. The capitalisation pace is set to pick up in ensuing quarters

as some of the larger projects get operational during the year. Management reiterated its

commissioning target of RS280-300bn higher than the planned capex outlay of RS225bn for FY17

At the CMP of Rs 182, the stock is currently trading at a P/E multiple of 12.8x and 10.8x for FY17E

and FY18E on consensus earnings estimates, respectively. We recommend a HOLD on the stock.

Recommendation (Rs)

CMP 182 Rating HOLD

Index Details

Sensex 28,077

Nifty 8,667

Industry Power

Scrip Details

Mkt Cap (Rs cr) 94,377

Eq Shares O/s (Cr) 523.1

Avg Vol (Lakhs) 3.8

52 Week H/L 183/120

Dividend Yield (%) 1.1

Face Value (Rs) 10.0

Latest shareholding pattern (%)

Promoters 57.9 Public 42.1

Total 100.0

Stock performance (%)

1m 3m 6m

Power Grid 8.7 25.7 28.3 Nifty 1.6 11.4 20.2

Quarterly Result Update

- 31 - Monday, 22nd

August, 2016

Description Q1FY17 Q1FY16 % Chg. Q1FY17 Q4FY16 % Chg.FY201603FY201503 % Chg.

Net Sales 6069.1 4689.3 29.4 6069.1 5753.6 5.5 20802.2 17177.2 21.1

Other operational Income 50.8 0.5 9307.4 50.8 6.5 686.4 0.0 0.0 0.0

Total Oper. Income(TOI) 6119.9 4689.9 30.5 6119.9 5760.1 6.3 20802.2 17177.2 21.1

Raw Materials Cons.- - - -

% to TOI -- -- --

Stock adj. (-)Inc / (+)Dec- - - -

% to TOI -- -- --

Net Raw Mat adj. for stock 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

% to TOI 0.0 0.0 -- 0.0 0.0 -- 0.0 0.0 --

Other expenses 428.8 321.7 33.3 428.8 399.8 7.3 1476.1 1402.3 5.3

% to TOI 7.0 6.9 -- 7.0 6.9 -- 7.1 8.2 --

Contribution Net_Sales 5691.1 4368.2 30.3 5691.1 5360.3 6.2 19326.1 15775.0 22.5

Personnel 271.4 233.6 16.2 271.4 266.5 1.9 980.5 1023.7 -4.2

% to TOI 4.4 5.0 -- 4.4 4.6 -- 4.7 6.0 --

Total expenditure 700.2 555.3 26.1 700.2 666.3 5.1 2456.7 2425.9 1.3

Operating Profit 5419.6 4134.5 31.1 5419.6 5093.8 6.4 18345.6 14751.3 24.4

% to TOI 88.6 88.2 -- 88.6 88.4 -- 88.2 85.9 --

Non-Operating Income 139.4 102.5 36.0 139.4 201.4 -30.8 479.0 602.8 -20.6

Interest 1517.8 1141.6 33.0 1517.8 1477.3 2.7 5023.0 3979.3 26.2

Exceptional Items -0.4 0.0 0.0 -0.4 0.0 #NAME? -0.1 0.0 0.0

Gross Profit 4041.7 3095.4 30.6 4041.7 3817.9 5.9 13801.6 11374.8 21.3

Depreciation 1757.3 1377.9 27.5 1757.3 1784.7 -1.5 6182.8 5085.4 21.6

PBT before Extra-ord 2283.6 1717.5 33.0 2283.6 2033.2 12.3 7618.7 6289.4 21.1

% to TOI 37.3 36.6 -- 37.3 35.3 -- 36.6 36.6 --

Extraordinary Items - - -

PBT 2283.6 1717.5 33.0 2283.6 2033.2 12.3 7618.7 6289.4 21.1

Tax Rate 21.1 21.1 0.1 21.1 21.4 -1.2 20.9 20.8 0.3

Prov. for Tax 481.9 361.9 33.2 481.9 434.1 11.0 1592.0 1310.2 21.5

% to TOI 7.9 7.7 -- 7.9 7.5 -- 7.7 7.6 --

Profit after Tax 1801.8 1355.6 32.9 1801.8 1599.1 12.7 6026.7 4979.2 21.0

% to TOI 29.4 28.9 -- 29.4 27.8 -- 29.0 29.0 --

Face Value 10.0 10.0 -- 10.0 10.0 -- 10.0 10.0 --

Equity Share capital 5231.6 5231.6 -- 5231.6 5231.6 -- 5231.6 5231.6 --

EPS (Rs.) 3.4 2.6 32.9 3.4 3.1 12.4 11.5 9.5 21.0

CEPS (Rs.) 6.8 5.2 30.2 6.8 6.5 5.1 23.3 19.2 21.3

EPS (Rs.) 19.6 12.6 55.5 19.6 18.0 8.5 50.6 54.4 -7.0

CEPS (Rs.) 24.07 14.84 62.19 24.07 21.23 13.38 60.87 64.05 -4.96

Quarterly Result Update

- 32 - Monday, 22nd

August, 2016

Transmission Revenue & Growth (%) Telecom Revenue & Growth (%)

0

5

10

15

20

25

30

35

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Q3F

Y14

Q4F

Y14

Q1F

Y15

Q2F

Y15

Q3F

Y15

Q4F

Y15

Q1F

Y16

Q2F

Y16

Q3F

Y16

Q4F

Y16

Q1F

Y17

Rs.Crore

Transmission Y-o-Y Growth (%)

(%)

-20

-10

0

10

20

30

40

50

60

70

0

20

40

60

80

100

120

140

Q3F

Y14

Q4F

Y14

Q1F

Y15

Q2F

Y15

Q3F

Y15

Q4F

Y15

Q1F

Y16

Q2F

Y16

Q3F

Y16

Q4F

Y16

Q1F

Y17

Rs.Crore

Telecom Y-o-Y Growth (%)

(%)

Source: Power Grid Corp, Ventura Research Source: Power Grid Corp, Ventura Research

Consultancy Revenue Growth (%) Revenue Profitability Quarterly Trend

-100

-50

0

50

100

150

0

20

40

60

80

100

120

140

160

180

200

Q3F

Y14

Q4F

Y14

Q1F

Y15

Q2F

Y15

Q3F

Y15

Q4F

Y15

Q1F

Y16

Q2F

Y16

Q3F

Y16

Q4F

Y16

Q1F

Y17

Rs.Crore

Consultancy Y-o-Y Growth (%)

(%)

0

10

20

30

40

50

60

70

80

90

100

0

1000

2000

3000

4000

5000

6000

7000

Q3F

Y14

Q4F

Y14

Q1F

Y15

Q2F

Y15

Q3F

Y15

Q4F

Y15

Q1F

Y16

Q2F

Y16

Q3F

Y16

Q4F

Y16

Q1F

Y17

Rs.Crore

Revenue EBITDA (RHS) PAT (RHS)

(%)

Source: Power Grid Corp, Ventura Research Source: Power Grid Corp, Ventura Research

Quarterly Result Update

- 33 - Monday, 22nd

August, 2016

1 Yr Forward PE 1 Yr Forward P/BV

0

50

100

150

200

250

300

350

400

Dec-09 Dec-11 Dec-13 Dec-15

CMP 10X 14.5X 19X 23.5X 28X

0

50

100

150

200

250

300

Dec-09 Dec-11 Dec-13 Dec-15

CMP 1.5X 1.95X 2.4X 2.85X 3.3X

Source: Power Grid Corp, Ventura Research Source: Power Grid Corp, Ventura Research

1 Yr Forward EV/EBITDA

30000

60000

90000

120000

150000

180000

210000

240000

Dec-09 Dec-11 Dec-13 Dec-15

EV 9X 10X 11X 12X 13X

Source: Power Grid Corp, Ventura Research

Quarterly Result Update

Cipla Ltd.

One-offs impact performance

- 34 - Monday, 22nd

August, 2016

Cipla’s Q1FY17 revenues declining 7% YoY to Rs 35bn, EBITDA declined 42% to Rs 6bn on

account of higher contribution from gNexium in the corresponding quarter of the previous year as

compared to nil revenues booked from gNexium. EBITDA margins for the quarter stood at 17%.

PAT was down 44% YoY to Rs 3.7bn. Domestic formulations sales were up by a moderate 5% YoY

to Rs 14.5bn with a weak export formulations during the quarter which declined by 14% to Rs

20.5bn.

Domestic business demonstrated moderate performance of 5% YoY growth on account of NLEM

and FDC ban resulting in channel disruptions and lower off take. Key therapies of Respiratory and

Anti-Infective posted robust coupled with double digit growth witnessed in Cipla’s Derma &

Urology portfolio.

The company is awaiting approval for gSeretide MDI in UK markets, as the management has

highlighted that they have responded to all the queries raised by UK MHRA. The file is under active

review. The company has ~15% market share in inhaler space in smaller European markets which

can ramp up to 30% in next 18-24 months. Major boost will come when the company will launch in

UK where market size is around ~USD 400mn. Mylan and Sandoz are present in the market. We

believe gAdvair MDI space will be a low competition market with other players Sandoz, Orien,

Chiesi & Mylan. The company has 10 combination inhalers in pipeline targeted for US and EU

launches.

At the CMP of Rs. 557, the stock is currently trading at 25.3x and 19.4x its FY17E and FY18E

earnings. We recommend a HOLD on the stock.

Recommendation (Rs)

CMP 519 Rating HOLD

Index Details

Sensex 28,077

Nifty 8,667

Industry Pharma

Scrip Details

Mkt Cap (Rs cr) 44,801

Eq Shares O/s (Cr) 80.3

Avg Vol (Lakhs) 3.1

52 Week H/L 708/457

Dividend Yield (%) 0.4

Face Value (Rs) 2.0

Latest shareholding pattern (%)

Promoters 37.5 Public 62.5

Total 100.0

Stock performance (%)

1m 3m 6m

Cipla 9.9 8.4 6.2 Nifty 1.6 11.4 20.2

Quarterly Result Update

- 35 - Monday, 22

nd August, 2016

Description Q1FY17 Q1FY16 % Chg. Q1FY17 Q4FY16 % Chg.FY201603FY201503 % Chg.

Net Sales 3499.8 3761.0 -6.9 3499.8 3206.7 9.1 13372.5 10882.4 22.9

Other operational Income 93.9 77.5 21.3 93.9 59.9 56.8 305.8 463.0 -34.0

Total Oper. Income(TOI) 3593.7 3838.5 -6.4 3593.7 3266.5 10.0 13678.3 11345.4 20.6

Raw Materials Cons.- 929.3 1187.7 -21.8 929.3 981.0 -5.3 4178.1 3740.2 11.7

% to TOI 25.9 30.9 -- 25.9 30.0 -- 30.6 33.0 --

Stock adj. (-)Inc / (+)Dec- 179.1 -161.9 LP 179.1 141.9 26.2 63.6 -344.2 LP

% to TOI 5.0 -4.2 -- 5.0 4.3 -- 0.5 -3.0 --

Net Raw Mat adj. for stock 1108.3 1025.8 8.0 1108.3 1122.9 -1.3 4241.7 3396.0 24.9

% to TOI 30.8 26.7 -- 30.8 34.4 -- 31.0 29.9 --

Other expenses 1187.9 1141.9 4.0 1187.9 1265.5 -6.1 4488.5 3820.0 17.5

% to TOI 33.1 29.8 -- 33.1 38.7 -- 32.8 33.7 --

Contribution Net_Sales 1297.5 1670.7 -22.3 1297.5 878.1 47.8 4948.1 4129.4 19.8

Personnel 686.6 616.2 11.4 686.6 659.1 4.2 2447.1 1967.7 24.4

% to TOI 19.1 16.1 -- 19.1 20.2 -- 17.9 17.3 --

Total expenditure 2982.8 2783.9 7.1 2982.8 3047.6 -2.1 11177.2 9183.7 21.7

Operating Profit 611.0 1054.5 -42.1 611.0 219.0 179.0 2501.1 2161.7 15.7

% to TOI 17.0 27.5 -- 17.0 6.7 -- 18.3 19.1 --

Non-Operating Income 25.2 50.5 -50.1 25.2 54.7 -54.0 208.9 165.6 26.2

Interest 31.3 63.9 -50.9 31.3 36.8 -14.7 161.3 168.3 -4.1

Exceptional Items 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Gross Profit 604.8 1041.2 -41.9 604.8 236.9 155.3 2548.6 2159.0 18.1

Depreciation 160.8 149.4 7.6 160.8 141.4 13.7 541.7 504.7 7.3

PBT before Extra-ord 444.0 891.7 -50.2 444.0 95.5 364.9 2007.0 1654.3 21.3

% to TOI 12.4 23.2 -- 12.4 2.9 -- 14.7 14.6 --

Extraordinary Items - - 0.0 0.0 0.0

PBT 444.0 891.7 -50.2 444.0 95.5 364.9 2007.0 1654.3 21.3

Tax Rate 16.0 27.1 -41.2 16.0 -4.1 LP 21.9 24.2 -9.4

Prov. for Tax 70.8 241.8 -70.7 70.8 -3.9 LP 439.6 400.0 9.9

% to TOI 2.0 6.3 -- 2.0 -0.1 -- 3.2 3.5 --

Profit after Tax 373.2 650.0 -42.6 373.2 99.4 275.4 1567.4 1254.2 25.0

% to TOI 10.4 16.9 -- 10.4 3.0 -- 11.5 11.1 --

Minority Interest -5.9 -0.5 1200.0 -5.9 -13.2 -55.6 -49.4 -48.2 2.7

PAT (adj. For MI) 365.2 649.2 -43.7 365.2 80.9 351.6 1505.9 1180.8 27.5

Face Value 2.0 2.0 -- 2.0 2.0 -- 2.0 2.0 --

Equity Share capital 160.7 160.6 -- 160.7 160.7 -- 160.7 160.6 --

EPS (Rs.) 4.6 8.1 -42.6 4.6 1.2 274.2 19.5 15.6 24.9

CEPS (Rs.) 6.65 9.95 -33.24 6.65 3 121.67 26.25 21.91 19.84

Quarterly Result Update

- 36 - Monday, 22

nd August, 2016

Domestic Sales improved significantly Formulations continue to contribute 90%+

0

500

1000

1500

2000

2500

Q2F

Y14

Q3F

Y14

Q4F

Y14

Q1F

Y15

Q2F

Y15

Q3F

Y15

Q4F

Y15

Q1F

Y16

Q2F

Y16

Q3F

Y16

Q4F

Y16

Q1F

Y17

Rs.Crore

India Outside India

86

88

90

92

94

96

98

100

102

Q2F

Y14

Q3F

Y14

Q4F

Y14

Q1F

Y15

Q2F

Y15

Q3F

Y15

Q4F

Y15

Q1F

Y16

Q2F

Y16

Q3F

Y16

Q4F

Y16

Q1F

Y17

Formulations APIs

(%)

Source: Cipla, Ventura Research Source: Cipla, Ventura Research

Revenues and Profitability trend (Quarterly)

0

5

10

15

20

25

30

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Q2F

Y14

Q3F

Y14

Q4F

Y14

Q1F

Y15

Q2F

Y15

Q3F

Y15

Q4F

Y15

Q1F

Y16

Q2F

Y16

Q3F

Y16

Q4F

Y16

Q1F

Y17

Rs.Crore

Sales EBITDA Margin (%) PAT Margin (%)

(%)

Source: Cipla, Ventura Research

Quarterly Result Update

- 37 - Monday, 22

nd August, 2016

1 Yr Forward EV/EBITDA

0

10000

20000

30000

40000

50000

60000

70000

Sep-03 Sep-05 Sep-07 Sep-09 Sep-11 Sep-13 Sep-15

EV 12X 14.25X 16.5X 18.75X 21X

Source: Cipla, Ventura Research

1 Yr Forward P/E 1 Yr Forward P/BV

Source: Cipla, Ventura Research Source: Cipla, Ventura Research

0

100

200

300

400

500

600

700

800

Sep-03 Sep-05 Sep-07 Sep-09 Sep-11 Sep-13 Sep-15

CMP 13X 18.5X 24X 29.5X 35X

0

200

400

600

800

1000

1200

Sep-03 Sep-05 Sep-07 Sep-09 Sep-11 Sep-13 Sep-15

CMP 2.8X 3.8X 4.8X 5.8X 6.8X

Quarterly Result Update

Grasim Industries Ltd

Robust performance

- 38 - Monday, 22nd

August, 2016

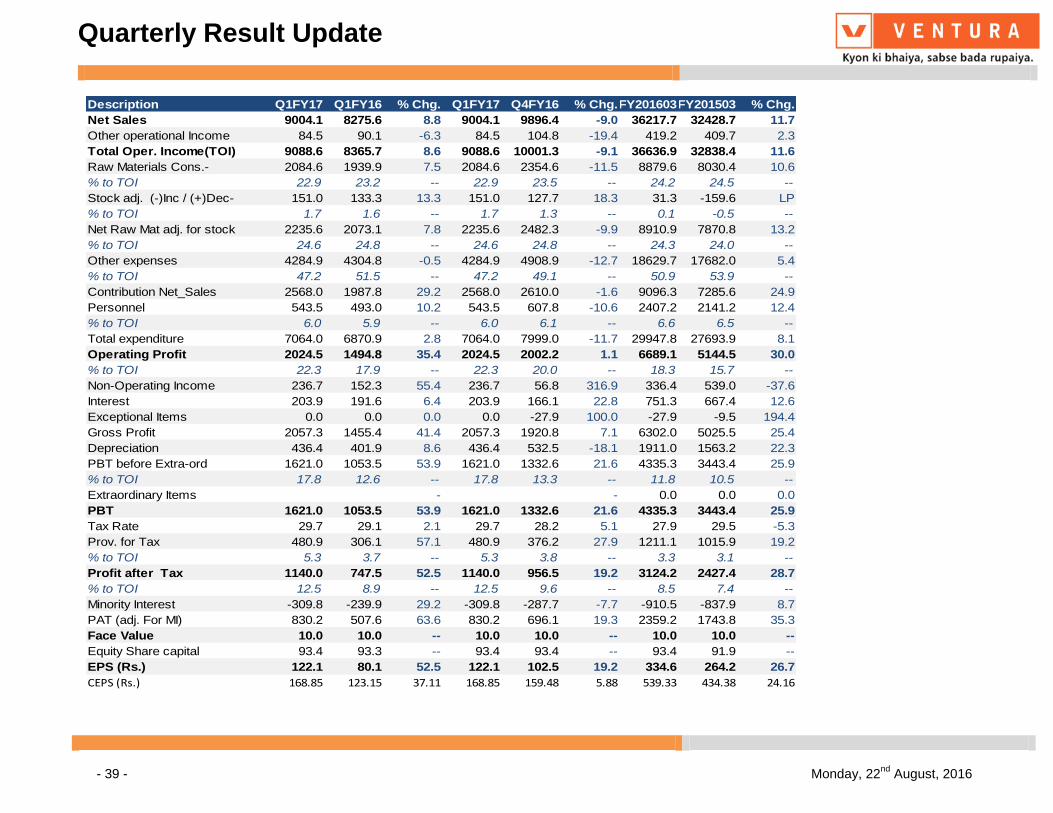

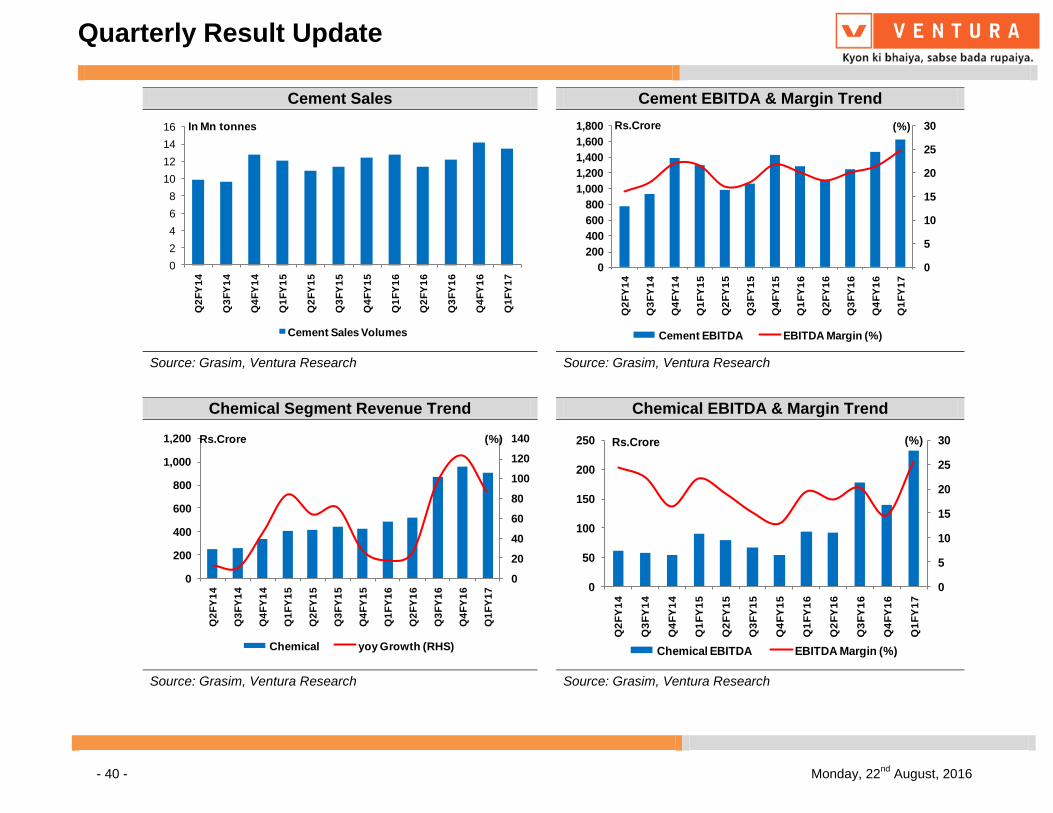

Grasim Industries’ standalone 1QFY17 EBITDA rose 90% YoY (+18% QoQ) to RS 5.1bn, driven by

near-peak utilizations, high pricing and lower energy costs. Revenues grew 25% YoY to RS 24bn,

while PAT stood at RS 3.2bn (2.5x YoY) led by better margins.

VFS revenues grew 32% YoY to RS 16.5bn, led by volume growth of 17% YoY and realizations

boost of 13% YoY, which translated into margins of 19% (v/s 11% in 1QFY16) and RoCE of high-

teens. Realizations boost was attributable to uptrend in prices and depreciation of INR. With

commendable ramp-up at the Vilayat plant, overall utilizations stood at 97%.

Chemicals revenues stood at Rs 9bn (+18% YoY), with utilization at 100%. Margins improved to

35% from 22% in 1QFY16, led by higher volumes.

The Cement business sales volumes stood at 13.6 mt. Revenue for the quarter stood at Rs. 6,590

crores compared to Rs. 6,432 crores in Q1FY16. EBITDA was up by 4% at Rs. 1,626 crores

At the CMP of Rs 4630, Grasim is trading at a PE multiple of 12.2x and 9.8x its estimated earnings

for FY17E and FY18E. We recommend investors to BUY.

Recommendation (Rs)

CMP 4,630 Rating BUY

Index Details

Sensex 28,077

Nifty 8.667

Industry Diversified

Scrip Details

Mkt Cap (Rs cr) 43,245

Eq Shares O/s (Cr) 9.2

Avg Vol (Lakhs) 0.4

52 Week H/L 5361/3233

Dividend Yield (%) 0.4

Face Value (Rs) 10.0

Latest shareholding pattern (%)

Promoters 31.3 Public 68.7

Total 100.0

Stock performance (%)

1m 3m 6m

Grasim -3.2 8.9 34.8 Nifty 1.6 11.4 20.2

Quarterly Result Update

- 39 - Monday, 22nd

August, 2016

Description Q1FY17 Q1FY16 % Chg. Q1FY17 Q4FY16 % Chg.FY201603FY201503 % Chg.

Net Sales 9004.1 8275.6 8.8 9004.1 9896.4 -9.0 36217.7 32428.7 11.7

Other operational Income 84.5 90.1 -6.3 84.5 104.8 -19.4 419.2 409.7 2.3

Total Oper. Income(TOI) 9088.6 8365.7 8.6 9088.6 10001.3 -9.1 36636.9 32838.4 11.6

Raw Materials Cons.- 2084.6 1939.9 7.5 2084.6 2354.6 -11.5 8879.6 8030.4 10.6

% to TOI 22.9 23.2 -- 22.9 23.5 -- 24.2 24.5 --

Stock adj. (-)Inc / (+)Dec- 151.0 133.3 13.3 151.0 127.7 18.3 31.3 -159.6 LP

% to TOI 1.7 1.6 -- 1.7 1.3 -- 0.1 -0.5 --

Net Raw Mat adj. for stock 2235.6 2073.1 7.8 2235.6 2482.3 -9.9 8910.9 7870.8 13.2

% to TOI 24.6 24.8 -- 24.6 24.8 -- 24.3 24.0 --

Other expenses 4284.9 4304.8 -0.5 4284.9 4908.9 -12.7 18629.7 17682.0 5.4

% to TOI 47.2 51.5 -- 47.2 49.1 -- 50.9 53.9 --

Contribution Net_Sales 2568.0 1987.8 29.2 2568.0 2610.0 -1.6 9096.3 7285.6 24.9

Personnel 543.5 493.0 10.2 543.5 607.8 -10.6 2407.2 2141.2 12.4

% to TOI 6.0 5.9 -- 6.0 6.1 -- 6.6 6.5 --

Total expenditure 7064.0 6870.9 2.8 7064.0 7999.0 -11.7 29947.8 27693.9 8.1

Operating Profit 2024.5 1494.8 35.4 2024.5 2002.2 1.1 6689.1 5144.5 30.0

% to TOI 22.3 17.9 -- 22.3 20.0 -- 18.3 15.7 --

Non-Operating Income 236.7 152.3 55.4 236.7 56.8 316.9 336.4 539.0 -37.6

Interest 203.9 191.6 6.4 203.9 166.1 22.8 751.3 667.4 12.6

Exceptional Items 0.0 0.0 0.0 0.0 -27.9 100.0 -27.9 -9.5 194.4

Gross Profit 2057.3 1455.4 41.4 2057.3 1920.8 7.1 6302.0 5025.5 25.4

Depreciation 436.4 401.9 8.6 436.4 532.5 -18.1 1911.0 1563.2 22.3

PBT before Extra-ord 1621.0 1053.5 53.9 1621.0 1332.6 21.6 4335.3 3443.4 25.9

% to TOI 17.8 12.6 -- 17.8 13.3 -- 11.8 10.5 --

Extraordinary Items - - 0.0 0.0 0.0

PBT 1621.0 1053.5 53.9 1621.0 1332.6 21.6 4335.3 3443.4 25.9

Tax Rate 29.7 29.1 2.1 29.7 28.2 5.1 27.9 29.5 -5.3

Prov. for Tax 480.9 306.1 57.1 480.9 376.2 27.9 1211.1 1015.9 19.2

% to TOI 5.3 3.7 -- 5.3 3.8 -- 3.3 3.1 --

Profit after Tax 1140.0 747.5 52.5 1140.0 956.5 19.2 3124.2 2427.4 28.7

% to TOI 12.5 8.9 -- 12.5 9.6 -- 8.5 7.4 --

Minority Interest -309.8 -239.9 29.2 -309.8 -287.7 -7.7 -910.5 -837.9 8.7

PAT (adj. For MI) 830.2 507.6 63.6 830.2 696.1 19.3 2359.2 1743.8 35.3

Face Value 10.0 10.0 -- 10.0 10.0 -- 10.0 10.0 --

Equity Share capital 93.4 93.3 -- 93.4 93.4 -- 93.4 91.9 --

EPS (Rs.) 122.1 80.1 52.5 122.1 102.5 19.2 334.6 264.2 26.7

CEPS (Rs.) 168.85 123.15 37.11 168.85 159.48 5.88 539.33 434.38 24.16

Quarterly Result Update

- 40 - Monday, 22nd

August, 2016

Cement Sales Cement EBITDA & Margin Trend

0

2

4

6

8

10

12

14

16

Q2

FY

14

Q3

FY

14

Q4

FY

14

Q1

FY

15

Q2

FY

15

Q3

FY

15

Q4

FY

15

Q1

FY

16

Q2

FY

16

Q3

FY

16

Q4

FY

16

Q1

FY

17

Cement Sales Volumes

In Mn tonnes

0

5

10

15

20

25

30

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Q2

FY

14

Q3

FY

14

Q4

FY

14

Q1

FY

15

Q2

FY

15

Q3

FY

15

Q4

FY

15

Q1

FY

16

Q2

FY

16

Q3

FY

16

Q4

FY

16

Q1

FY

17

Rs.Crore

Cement EBITDA EBITDA Margin (%)

(%)

Source: Grasim, Ventura Research Source: Grasim, Ventura Research

Chemical Segment Revenue Trend Chemical EBITDA & Margin Trend

0

20

40

60

80

100

120

140

0

200

400

600

800

1,000

1,200

Q2

FY

14

Q3

FY

14

Q4

FY

14

Q1

FY

15

Q2

FY

15

Q3

FY

15

Q4

FY

15

Q1

FY

16

Q2

FY

16

Q3

FY

16

Q4

FY

16

Q1

FY

17

Rs.Crore

Chemical yoy Growth (RHS)

(%)

0

5

10

15

20

25

30

0

50

100

150

200

250

Q2

FY

14

Q3

FY

14

Q4

FY

14

Q1

FY

15

Q2

FY

15

Q3

FY

15

Q4

FY

15

Q1

FY

16

Q2

FY

16

Q3

FY

16

Q4

FY

16

Q1

FY

17

Rs.Crore

Chemical EBITDA EBITDA Margin (%)

(%)

Source: Grasim, Ventura Research Source: Grasim, Ventura Research

Quarterly Result Update

- 41 - Monday, 22nd

August, 2016

1 Yr Forward PE 1 Yr Forward P/BV

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

Dec-03 Dec-05 Dec-07 Dec-09 Dec-11 Dec-13 Dec-15

CMP 5X 7X 9X 11X 13X

0

1000

2000

3000

4000

5000

6000

7000

Dec-03 Dec-05 Dec-07 Dec-09 Dec-11 Dec-13 Dec-15

CMP 1X 1.35X 1.7X 2.05X 2.4X

Source: Grasim, Ventura Research Source: Grasim, Ventura Research

1 Yr Forward EV/EBITDA

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Dec-03 Dec-05 Dec-07 Dec-09 Dec-11 Dec-13 Dec-15

EV 2X 3.9X 5.8X 7.7X 9.6X

Source: Grasim, Ventura Research

Quarterly Result Update

Hindalco Industries Ltd

Aluminium volume surprises

- 42 - Monday, 22nd

August, 2016

Hindalco reported a good set of Q1FY17 numbers, revenues came in at Rs 7597.3 crore which was

down by 11.4%. Revenues from the aluminum segment grew 7.5% YoY to Rs 4263.3 crore while

revenue from the copper segment declined 27.7% YoY to Rs 3336.3 crore. The decline in copper

revenues was primarily on account of lower volumes. Copper production was lower owing to the

planned annual maintenance shutdown. EBITDA was at Rs 1132.5 crore which grew by 30.4% YoY,

while EBIDTA Margin was at 10.1%. Lower cost of raw materials, especially energy inputs aided

margin expansion during the quarter. Subsequently, reported PAT was up 381.3% YoY to Rs 294.1

crore.

As all the three projects Utkal, Aditya and Mahan are currently operating close to their peak

capacity, domestic aluminum operations have reached closer to optimum capacity utilisation

levels. Consequently CoP has witnessed a declining trend over last couple of years due to

economies of scale and decline prices of key raw materials viz coal and crude oil. However, going

forward, part of the benefit is likely to wind down with the recent firming up of crude oil prices.

Novelis reported a good set of Q1FY17 numbers. While total rolled product shipments came in at

755 KT EBITDA/tonne came in at US$363/tonne. The ensuing EBITDA was at US$274 million.

Currently, at the CMP of Rs 158, Hindalco is trading at 13.4x and 12.3x its estimated earnings for

FY17E and FY18E, respectively. We recommend HOLDING the stock.

Recommendation (Rs)

CMP 158 Rating HOLD

Index Details

Sensex 28,077

Nifty 8.667

Industry Metals

Scrip Details

Mkt Cap (Rs cr) 32,720

Eq Shares O/s (Cr) 190.3

Avg Vol (Lakhs) 15.9

52 Week H/L 159/59

Dividend Yield (%) 0.6

Face Value (Rs) 1.0

Latest shareholding pattern (%)

Promoters 37.7 Public 62.3

Total 100.0

Stock performance (%)

1m 3m 6m

Hindalco 14.9 82.0 129.3 Nifty 1.6 11.4 20.2

Quarterly Result Update

- 43 - Monday, 22

nd August, 2016

Description Q1FY17 Q1FY16 % Chg. Q1FY17 Q4FY16 % Chg. FY201603 FY201503 % Chg.

Net Sales 7501.4 8517.3 -11.9 7501.4 8542.7 -12.2 33922.0 34094.4 -0.5

Other operational Income 96.0 58.0 65.5 96.0 124.9 -23.2 395.6 430.6 -8.1

Total Oper. Income(TOI) 7597.3 8575.3 -11.4 7597.3 8667.5 -12.4 34317.7 34525.0 -0.6

Raw Materials Cons.- 3973.2 5230.9 -24.0 3973.2 4522.4 -12.1 19209.5 21056.3 -8.8

% to TOI 52.3 61.0 -- 52.3 52.2 -- 56.0 61.0 --