Public-Boards-2019.pdf - Ghana Audit Service

1134

REPUBLIC OF GHANA REPORT OF THE AUDITOR GENERAL ON THE PUBLIC ACCOUNTS OF GHANA: PUBLIC BOARDS, CORPORATIONS AND OTHER STATUTORY INSTITUTIONS FOR THE PERIOD ENDED 31 DECEMBER 2019 Our Vision To become a world-class Supreme Audit Institution, delivering professional, excellent, and cost effective auditing Service.

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Public-Boards-2019.pdf - Ghana Audit Service

REPUBLIC OF GHANA

REPORT OF THE AUDITOR GENERAL

ON THE PUBLIC ACCOUNTS OF GHANA:

PUBLIC BOARDS, CORPORATIONS AND

OTHER STATUTORY INSTITUTIONS

FOR THE PERIOD ENDED

31 DECEMBER 2019

Our VisionTo become a wor ld-c lass Supreme Audit Institution, d e l i v e r i n g p r o f e s s i o n a l , excellent, and cost effective auditing Service.

This report has been prepared under Section 14of the Audit Service Act, 2000 for presentationto Parliament in accordance withSection 20 of the Act.

Johnson Akuamoah AsieduActing Auditor GeneralGhana Audit Service22 October 2020

This report can be found on the Ghana Audit Service website: www.ghaudit.org

For further information about the Ghana Audit Service, please contact:

The Director, Communication Unit Ghana Audit Service Headquarters Post Office Box MB 96, Accra.

Tel: 0302 664928/29/20 Fax: 0302 662493/675496 E-mail: [email protected]: Ministries Block 'O'

© Ghana Audit Service 2020

i Report of the Auditor General on the Public Accounts of Ghana – Public Boards, Corporations and Other Statutory Institutions for the year ended 31 December 2019

TABLE OF CONTENT

Para(s) Page (s) Transmittal letter iii-iv

Contributors v

Introduction 1-4 1-2

PART I

Summary of significant findings and recommendations 5-22 3-10

Audit opinion 23-29 10-11

PART II

Summary of findings and recommendations by

Ministries 30-305 12-105

PART III

Details of Findings and Recommendation

No. Departments

1. Ministry of Energy 351-666 106-177

2. Ministry of Finance 667-862 178-224

3. Ministry of Health 863-898 225-238

4. Ministry of Lands and Natural Resources 899-1029 239-269

5. Ministry of Education 1030-2046 270-645

6. Ministry of Agriculture 2047-2132 646-673

7. Ministry of Justice and Attorney-General’s 2133-2186 674-685

8. Department

8. Ministry of Communication 2187-2327 686-734

9. Ministry of Tourism & Creative Arts 2328-2379 735-744

10. Ministry of Interior 2380-2416 745-754

11. Ministry of Youth and Sports 2417-2550 755-800

12. Ministry of Employment and Labour Relations 2551-2813 801-895

ii Report of the Auditor General on the Public Accounts of Ghana – Public Boards, Corporations and Other Statutory Institutions for the year ended 31 December 2019

13. Ministry of Transport 2814-2883 896-908

14. Ministry of Trade and Industry 2884-3376 909-1045

15. Ministry of Information 3377-3477 1046-1074

16. Ministry of Works and Housing 3478-3577 1075-1095

17. Ministry of Sanitation and Water Resources 3578-3641 1096-1109

18. Extra Ministerial Agencies 3642-3710 1110-1126

iii Report of the Auditor General on the Public Accounts of Ghana – Public Boards, Corporations and Other Statutory Institutions for the year ended 31 December 2019

TRANSMITTAL LETTER

Ref. No. AG.01/109/Vol.2/145

Office of the Auditor-General

Ministries Block ‘O’

P O Box MB96

Accra

GA/110/8787

Tel. (0302) 662493

Fax (0302) 675496

22 October 2020

Right Honourable Speaker

REPORT OF THE AUDITOR GENERAL ON THE ACCOUNTS

OF GHANA: PUBLIC BOARDS, CORPORATIONS AND OTHER

STATUTORY INSTITUTIONS FOR THE PERIOD

ENDED 31 DECEMBER 2019

I have the honour to submit my audit report on the Public Accounts of Ghana-

Public Boards, Corporations and other Statutory Intuitions to you to be tabled

in the House pursuant to Article 187 (5) of the 1992 Constitution.

2. The report has been structured into three parts. Part I provides an

overall summary of significant findings and recommendations; Part II is a

summary of findings and recommendations in respect of each Sector

Ministry and their respective Public Boards, Corporations and other

Statutory Instructions, while Parts III gives the full details of my findings

and recommendations.

iv Report of the Auditor General on the Public Accounts of Ghana – Public Boards, Corporations and Other Statutory Institutions for the year ended 31 December 2019

3. This report highlights the significant findings arising from my audit

of the financial operations of Public Boards, and Corporations and other

Statutory Institutions in accordance with Section 13 of the Audit Service Act

2000 (Act 584). This includes details of financial irregularities identified,

and resulting from breakdown of internal controls. The report also provides

recommendations, and which implementation is reasonably expected to help

rectify identified weaknesses in the financial management control systems.

4. Aware of the extent of my reliance on others to produce my report, I

would like to thank my staff and the contracted Audit Firms for the

invaluable assistance provided to enable me prepare this report.

5. I am also grateful to the Management and Staff of the various

institutions for their cooperation during the audits.

6. Finally, I would like to thank the Public Accounts Committee for their

continued support for the work of the Office of the Auditor General,

especially, in reviewing my reports and reinforcing recommendations to the

Public Boards and Corporations for purposes of prudent management of the

public purse.

Yours faithfully

JOHNSON AKUAMOAH ASIEDU

ACTING AUDITOR GENERAL

THE RT. HON. SPEAKER

OFFICE OF PARLIAMENT

PARLIAMENT HOUSE

ACCRA

v Report of the Auditor General on the Public Accounts of Ghana – Public Boards, Corporations and Other Statutory Institutions for the year ended 31 December 2019

Contributing audit firms

Benning, Anang & Partners

PriceWaterhouseCoopers

Boateng, Offei & Co.

Osei Owusu-Ansah & Associates

Kwesie And Partners Chartered Accountants

AAK Services Chartered Accountants

Gogoe & Associates

Asamoa Bonsu & Co. Chartered Accountants

Ayew Agyeman & Co. Chartered Accountant

Kwesie And Partners Chartered Accountants

Ernst & Young

James Quagraine And Associates

Asafu-Adjaye & Partners

Opoku Andoh And Co.

EAV & Associates Chartered Accountants

Kwame Asante & Associastes

Baker Tilly Andah + Andah

Opoku, Andoh & Co.

Eddie Nikoi Accounting Consultancy

Ofori Anom Consult

MGI O.A.K Chartered Accountants

A.D. & Associates Chartered Accountants

JOP Consult Chartered Accountants

1 Report of the Auditor General on the Public Accounts of Ghana – Public Boards, Corporations and Other Statutory Institutions for the year ended 31 December 2019

REPORT OF THE AUDITOR-GENERAL ON THE

PUBLIC ACCOUNTS OF GHANA-PUBLIC BOARDS,

CORPORATIONS AND OTHER STATUTORY

INSTITUTIONS FOR THE YEAR ENDED 31 DECEMBER 2019

Introduction

The audit of the accounts of Public Boards, Corporations and other

Statutory Institutions for the period ended 31 December 2019 has

been conducted in accordance with Article 187(2) of the 1992

Constitution of the Republic of Ghana.

2. The objective of the audit is to express an opinion on the

accounts submitted to me by each Public Board, Corporation and

other Statutory Institutions for my examination.

3. I also evaluated the adequacy of the system of internal

controls, compliance with relevant legislations, stated accounting

policies and applicable financial rules and regulations of these

organisations.

4. Matters raised in this report are among those which came to

my notice during the period ended 31 December 2019. The

observations and recommendations arising out of the audits were

discussed with Managements of the affected Institutions and

comments received, where appropriate, have been incorporated in

this report. The report is in three parts:

Part I provides a summary of the significant audit findings and

recommendations;

2 Report of the Auditor General on the Public Accounts of Ghana – Public Boards, Corporations and Other Statutory Institutions for the year ended 31 December 2019

Part II provides the significant findings and recommendations

according to Sector Ministries; and

Part III deals with the details of findings and recommendations

3 Report of the Auditor General on the Public Accounts of Ghana – Public Boards, Corporations and Other Statutory Institutions for the year ended 31 December 2019

PART I

SUMMARY OF SIGNIFICANT FINDINGS AND

RECOMMENDATIONS

5. Presented in table 1 is the financial impact of these

irregularities according to their nature.

Table 1: Summary of financial irregularities for the period ended 31

December 2019

NO Type of

Irregularity %

Amount (GHC)

Amount (US$)

Amount (€)

Amount (£)

Total Amount (GH¢)

1 Outstanding Debtors/Loans Recoverable 88.87 4,851,565,319 1,437,088.98 4,859,727,984

2 Cash Irregularities 3.93 212,533,506 431,506.36 4,655.00 1,564.00 215,025,782

3

Payroll

Irregularities 1.21 66,248,946 0 0 66,248,946

4 Procurement Irregularities 0.68 20,302,867 3,000,000.00 0 0 37,342,867

5 Tax Irregularities 3.65 198,721,247 0 146,094.40 0 199,651,868

6

Stores

Irregularities 0.05 1,802,905 0 148,453.00 0 2,748,551

7 Contract Irregularities 1.60 87,652,433 0 0 0 87,652,433

Sub-total ($€£)

4,868,595.34 299,202.40 1,564.00

Total 100 5,438,827,223 27,653,621.5 1,905,919.28 11,667.44 5,468,398,431

4 Report of the Auditor General on the Public Accounts of Ghana – Public Boards, Corporations and Other Statutory Institutions for the year ended 31 December 2019

6. Table 1 shows that, the total irregularities stood at

GH¢5,468,398,431which included US$ 4,868,595.34 converted into

Cedis at the prevailing exchange rate of GH¢5.68 to the US$1 as at

31 December2019, €299,202.40 converted into Cedis at the

prevailing exchange rate of GH¢6.37 to the €1 as at 31 December

2019 and £1,564.00 converted into Cedis at the prevailing exchange

rate of GH¢7.46 to £1 as at 31 December 2019.

Table 2: Comparative Analysis of Irregularities from 2015-2019 (figures

rounded to the nearest cedi)

7. The total irregularities figure of GH¢3,311,963,314 for 2015

decreased to GH¢718,085,208 in 2016. Total irregularities went up

to GH¢12,002,880,339 in 2017. However, the total irregularities

declined by GH¢8,995,621,415 from the 2017 figure of

GH¢12,002,880,339 to GH¢3,007,258,924 in 2018 and went up by

81.8% to GH¢5,468,398,431 in 2019.

No. Type of Irregularities

2015 GH¢

2016 GH¢

2017 GH¢

2018 GH¢

2019 GH¢

1.

Outstanding Debtors/Loans /Recoverable

Charges

2,705,086,348

302,233,654

11,813,109,116

1,801,416,815

4,859,727,984

2. Cash

Irregularities

222,227,944 246,015,992 149,208,182 1,087,713,932 215,025,782

3. Payroll

Irregularities

1,424,941 494,728 2,540,432 3,163,473 66,248,946

4. Procurement

Irregularities

568,322 91,506,091 6,431,451 15,121,639 37,342,867

5. Tax Irregularities 377,410,669 24,291,448 6,394,113 4,371,199 199,651,868

6. Stores

Irregularities

58,845 47,830,661 8,946,359 734,461 2,748,551

7. Contract

Irregularities

5,186,245 5,782,634 16,250,686 94,737,405 87,652,433

Total 3,311,963,314 718,085,208 12,002,880,339 3,007,258,924 5,468,398,431

5 Report of the Auditor General on the Public Accounts of Ghana – Public Boards, Corporations and Other Statutory Institutions for the year ended 31 December 2019

8. The 81.8% or GH¢2,461,139,507 jump from the 2018 total

irregularities figure of GH¢3,007,258,924 to GH¢5,468,334,006 in

2019 was occasioned mainly by a surge of GH¢3,058,438,311,169

in outstanding debtors/loans/recoverable component of the total

irregularities in 2019.

6 Report of the Auditor General on the Public Accounts of Ghana – Public Boards, Corporations and Other Statutory Institutions for the year ended 31 December 2019

GH¢ USD GH¢ EUR GBP USD GH¢ GH¢ USD GH¢ GH¢ EUR GH¢

Min is try of Health - - 35,146 - - - - - - 2,842 26,437 - -

Min is try of Lan d s & Natu ral

Res ou rces4,502,007 - 1,193,801 - - - 69,472.00 17,354 - 37,057 20,560 - -

Min is try of Ed u cation 12,811,097 1,437,089 40,476,461 - - - 3,850,992.04 10,083,654.38 3,000,000 261,969.22 329,479.14 - 86,832,909.00

Min is try of Food &

Ag ricu ltu re 7,777,626 - 13,860,374 - - - - - - - 1,060,805 - -

Min is try of Com m u n ication - - 3,275,790.11 - - 108,767 339,479.41 3,628,038 - 48,486 - - 210,300

Min is try T ou ris m , Cu ltu re

& Creative Arts - - - - - - - 138,295 - - - - 9,224

Min is try of In terior - - - - - - 138,983.18 - - - - - -

Min is try of Y ou th & S p orts 242,300 - 3,894,538.09 - - 214,484 20,732.60 - - 2,138.25 - 148,453 -

Min is try of Fin an ce 11,068,482 - 445,163 - - - - - - 365,542 - - 600,000

Min is try of En erg y 234,450,405 - 632,208 - - - 44,367,132 - - 193,755,445 365,624 - -

Min is try of Em p loym en t

an d Lab ou r Relation s 4,479,558,581 - 89,032,135 - - - 593,726 990,638 - - - - -

Min is try of T ran s p ort - - 5,000,000 - - - - 3,011,507 - 3,986,035 - - -

Min is try of T rad e an d

In d u s try 53,362,884 - 53,202,787 4,655 1,564 108,256 3,114,539 1,136,226.20 - 232,213.71 - - -

Min is try of In form ation 5,228 - 1,171,394.30 - - - 192,447.82 - - 9,319 - - -

Min is try of W orks &

Hou s in g 45,919,268 - - - - - 13,535,122 1,297,154 - - - - -

Min is try of S an itation an d

W ater Res ou rces 1,867,441 - 139,858 - - - - - - 20,200.00 - - -

Extra Min is terial Ag en cy - - 173,850 - - - 26,320 - - - - - -

T o ta l 4,851,565,319 1, 4 3 7 , 0 8 9 2 12 , 5 3 3 , 5 0 6 4 , 6 5 5 1, 5 6 4 4 3 1, 5 0 7 6 6 , 2 4 8 , 9 4 6 2 0 , 3 0 2 , 8 6 7 3 , 0 0 0 , 0 0 0 19 8 , 7 2 1, 2 4 7 1, 8 0 2 , 9 0 5 14 8 , 4 5 3 8 7 , 6 5 2 , 4 3 3

Contract

Irregularities

Table 3: Summary of Financial Irregularities According to Sector Ministries

MinistryOutstanding Debtors/

Loans RecoverableCash Irregularities

Payroll

Irregularities

Procurement

Irregularities

Tax

Irregularities

Stores

Irregularities

7 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

Outstanding Debts/ Loans Recoverable - GH¢4,859,727,984.00

9. These irregularities represent trade debtors, staff debtors and

outstanding loans. Included in this figure is an amount of

GH¢3,643,789,172.39 loans granted by SSNIT to other 16 related

institutions who have defaulted in paying back the facility and

workers contributions due from Controller and Accountant

General’s Department. Absence of effective debt collection policies,

non-existence of credit controls to retrieve the debts and

Management’s indifferent posture towards loan recovery contributed

significantly to these anomalous conditions. Also, improper

maintenance of records on debtors, the absence of debtors’ ageing

analyses, non-documentation of agreements stipulating the terms

and conditions of loans, failure to ensure that loans are repaid and

Management’s non-compliance with rules and regulations

accounted for these irregularities.

10. I recommended that Management of Public Boards,

Corporations and other Statutory Institutions should strictly adhere

to rules and regulations with regards to debts management. They

should also put in place proper policies for the management of loans

as well as ensuring that loans are repaid on due dates to avoid or

minimise the occurrence of bad debts.

Cash Irregularities - GH¢215,025,782.00

11. Cash irregularities related to the misapplication of funds, non-

retirement of imprest, payments not authenticated, payment of

Board Allowances to Council Members without Ministerial approval,

losses envisaged from projects undertaken by corporate entities and

outright cash shortages. Out of the total figure of GH¢215,025,782

cash irregularities, GH¢80,914,176.00 represented loss envisaged

by SSNIT as a result of the affordable housing projects undertaken

by SSNIT. These occurred as a result of poor oversight responsibility,

8 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

non-existent controls. Other contributory factors were finance

officers’ failure to properly file and keep records, Management’s

failure to ensure the security and safety of vital documents, non-

maintenance of returned cheque registers and management’s inertia

in complying with procedures stipulated in the Public Financial

Management Act; and poor accounting systems.

12. I therefore urged the Management of the Public Boards,

Corporations and other Statutory Institutions to strengthen

supervisory controls over their finance officers, and ensure that they

adhere to the provisions of the Public Financial Management Act

2016, (Act 921). I also recommended the authentication of all

payment vouchers, prompt payment to bank and full retirement of

accountable imprest on due dates.

Payroll Irregularities - GH¢66,248,946.00

13. These lapses were caused by the failure of Management to

exercise due diligence, and the laxity of officers in charge of payroll

validation in reviewing payment vouchers to ensure salaries were

paid to only those who were entitled as well as payroll related

irregularities. They were also caused by Management’s failure to

notify banks to stop the payment of unearned salaries. The

Controller and Accountants General’s Department also did not

promptly delete names of separated staff when notified to do so. In

other instances, Management also did not obtain financial clearance

from the Ministry of Finance before employing new staff. Contained

in the total irregularity of GH¢66,248,946.00 is an amount of

GH¢44,367,132 attributed to GRIDCO in respect of outstanding

compensation payments without the requisite documentation and

non-payments of 2017 3rd tier pensions contribution from GRIDCO

which remained unremitted as 31st December 2017.

9 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

14. I advised Management of the affected Institutions to promptly

notify the bankers of the separated staff to withhold and pay to

government chest all unearned salaries. I also recommended that

officers in charge of payroll should exercise due care in the discharge

of their duties.

Procurement Irregularities - GH¢37,342,867.00

15. These irregularities occurred as a result of Managements’ non-

compliance with the provisions of the Public Procurement Act 2003,

(Act 663). Of the total irregularities $3,000,000.00

(GH¢13,530,000) represented improper procurement of IT services

by the University of Cape Coast from KLEOS UK LTD.

16. I once again recommended that Management of the various

Institutions should undertake procurement transactions strictly in

accordance with the provisions of the Public Procurement Act.

Tax Irregularities-GH¢199,651,868.00

17. The Tax irregularities related to failure to pay statutory tax

deductions on due dates, and non-deduction of applicable taxes.

They also related to transaction of business with non-VAT registered

persons or entities.

18. I recommended that the Finance Officers should strictly

adhere to the tax laws to ensure that all tax revenues are promptly

collected and paid to the applicable revenue agencies.

Stores Irregularities - GH¢2,748,551

19. These irregularities include non-documentation of store items,

lack of awareness of officers assigned to store duties, inadequate

supervision, and non-reconciliation of fuel purchases with fuel

station records. Included in the sum of GH¢2,748,551 is an amount

10 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

of GH¢1,060,805.25 for abandoned equipment procured by Cocoa

Research Institute between 2009 and 2012.

20. I recommended the strengthening of controls over store

management and accounting and also recommended strict

adherence to Rules and Regulations that governs the effectual

conduct of public financial business.

Contract Irregularities - GH¢87,625,433

21. These mainly relates to overpayment of contract sum, absence

of signing of contract agreements, failure to comply with tendering

procedures, delay in construction, ineffective control over contracts

and the absence of transparency in the disbursement of funds, non-

recovery of mobilisation and irregular additions to existing

contracts.

22. I therefore urged Management to strengthen controls over

contracts and comply with tendering procedures.

Audit Opinion

23. The financial statements submitted for validation presented

fairly financial information in accordance with applicable statutory

provisions, and my office was satisfied in all material respect that

the financial statements complied with stated accounting policies

of Government and is in accordance with generally accepted

accounting standards and essentially consistent with that of the

preceding year.

24. In my opinion all the financial statements presented a true

and fair view of the financial positions as at 31 December 2019, and

financial performance of the organisations for the year ended.

11 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

Accounts Submission

25. All the audited entities presented their financial statements

for audit except National Sports Authority, Ghana Export Promotion

Authority and Ghana News Agency who did not submit their

financial statements for audit during the time of our reviews and as

such my office could not form an opinion on the financial statements

of these three institutions.

Conclusion

26. As part of the processes of good governance, I urged the

appointing Authorities to ensure that Board of Directors are

constituted promptly for organisations having none. The absence of

Governing Boards tends to delay the signing of the financial

statements resulting in avoidable delays.

27. The operational results and financial positions of the Public

Corporations and other Statutory Institutions during the year under

review, could have been healthier if there had been effective

supervision of schedule officers.

28. I reiterate my advice to Management to strengthen their

Internal Audit Units to ensure effective and efficient internal control

systems.

29. I also recommended that Management should establish and

strengthen the Audit Committees within the organisations in

accordance with Sections 86 to 88 of the Public Financial

Management Act 2016 (Act 921) to ensure that audit

recommendations are duly implemented.

12 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

PART II

SUMMARY OF FINDINGS AND

RECOMMENDATIONS

MINISTRY OF ENERGY

NORTHERN ELECTRICITY DISTRIBUTION COMPANY (NEDCo)

NEDCO Head Office

30. Our review of Internal Audit Reports covering the 2018

Financial Year of the Company disclosed that a total amount of

GH¢632,207.68 in respect of sales revenues collected at three (3)

Operational Areas of the Company were not lodged into the

respective bank accounts. We recommended that Management

should intensify its supervisory role over the activities of the Area

Managers, the Finance Officers and Account Assistants and also

recommended that the sum of GH¢632,207.68 being funds

embezzled should be recovered from Tsitsia Samuel and four others.

31. The E-Business Suite (Oracle) software which the Company

uses for its financial transactions has not been approved by the

Auditor-General in contravention of Section 11(3) of the Audit

Service Act, 2000 (Act 584). We recommended to Management to

seek retrospective approval from the Auditor-General.

32. Contrary to section 1.4.5 of the Public Procurement

Authority’s Manual, we found that the Company’s Entity Tender

Committee (ETC) did not submit any monthly report on its

procurement activities to the Public Procurement Authority.

13 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

33. We advised Management to strictly comply with the

provisions of the procurement laws and manual to avoid any

sanctions.

34. Contrary to Section 20(d) of the Public Procurement

(Amendment) Act, 2016 (Act 914) which legislates on meetings, we

noted that the Entity Tender Committee (ETC) met only twice, on the

13th June and 26th November, 2018 for the period under review.

35. We urged Management to ensure that the Entity Tender

Committee meets at least once every quarter as required by law.

36. Management of the NEDco procured goods and services worth

GH¢196,321.92 from non-VAT registered entities. This contravenes

Regulation 183(4) of the Financial Administration Regulations (FAR),

2004 (L. I 1802). We advised Management to comply with the

provisions of the FAR and any other applicable laws in all their

procurement transactions.

Tamale Operational Area

There was no Inventory Register at the Tamale Area Office of NEDco

to effectively monitor and control its assets contrary to Regulation

183(3) of the FAR 2004, L.I. 1802. We recommended that

Management should prepare an inventory register and our office

informed for verification failing which Section 98(2) of the Public

Financial Management Act 921 shall apply.

VOLTA RIVER AUTHORITY (VRA) 2018

37. We reviewed minutes of the VRA board as well as letters

appointing board members and found that the board consisted of

the chairperson, the Chief Executive and six other persons making

an 8-member Board instead of a 9-member Board in contravention

14 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

of Section 1 of the Volta River Development (Amendment) Act, 2005

(Act 692). We advised the Board and Management to liaise with the

appointing authority to properly constitute the Board in accordance

with Section 1 of the Volta River Development (Amendment) Act,

2005 (Act 692).

38. We noted that, 96 residential facilities of the Authority,

comprising two- and three-bedrooms units remained unoccupied

since March 2014. We urged Management to take immediate steps

to put the affected housing facilities to economic use without further

delay.

39. Management of the Authority in 2018 used “Request for

Quotation” method of procurement instead of competitive tendering

in the award of 3 contracts amounting to GH¢720,078.99. We

advised Management to regularise these contracts in accordance

with Section 50(3) of the Public Procurement (Amendment) Act, 2016

(Act 914) and inform our office for verification.

VRA RESETTLEMENT TRUST FUND (VRA/RTF)

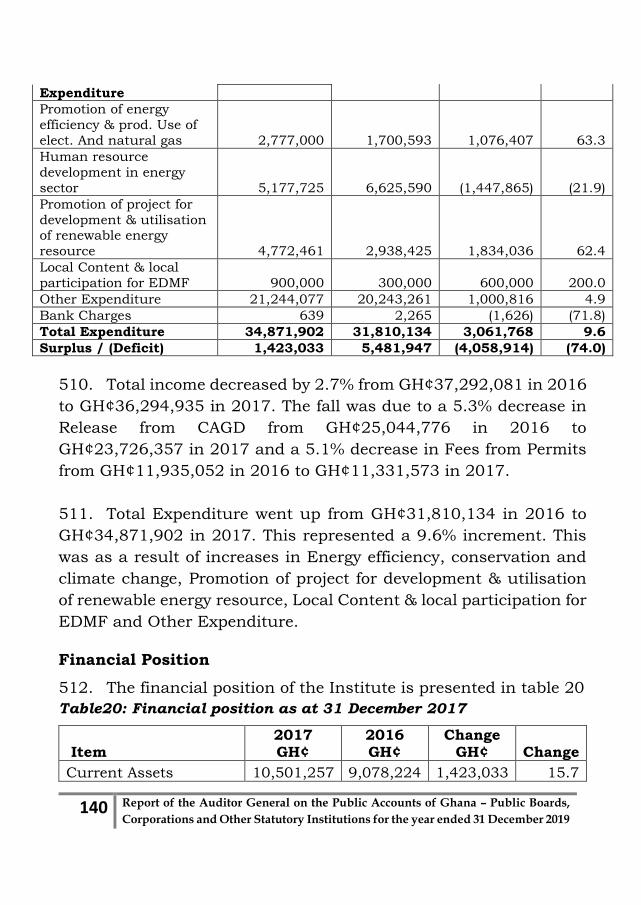

40. Our review of the financial records showed that the Board’s

Committee on Finance, over the period, invested some funds in

various financial institutions with the intention of earning returns

to complement the major sources of funds from Volta River Authority

but were not guided by any documented policy on investment. We

further noted that the managing trustees were unable to recoup the

principal and the returns amounting to GH¢1,031,184. We

recommended that Management should develope an investment

policy to take into account the unpredictability nature of the

financial markets and to minimize, where feasible, any potential

adverse effects on the Organisation's financial performance; the

focus being on capital retention rather than maximizing revenue.

15 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

Also Managing trustees should pursue collection of the lock up

funds from the affected financial institutions.

41. We noted that, based on Article 11 of the Trust Deed,

membership of the Volta River Authority Trust Fund trustees is

sixteen (16). The current re-demarcation of regions in the country,

we envisage the number of trustees would increase from the current

sixteen (16) thus making governance arrangements expensive. We

also noted that since authentication of the Trust Deed in 22 July

1996, no revisions have been carried out. We urged the Managing

Trustees to liaise with the Minister and the Authority to initiate a

process to review the trust deed to keep project delivery in the

resettlement communities efficient.

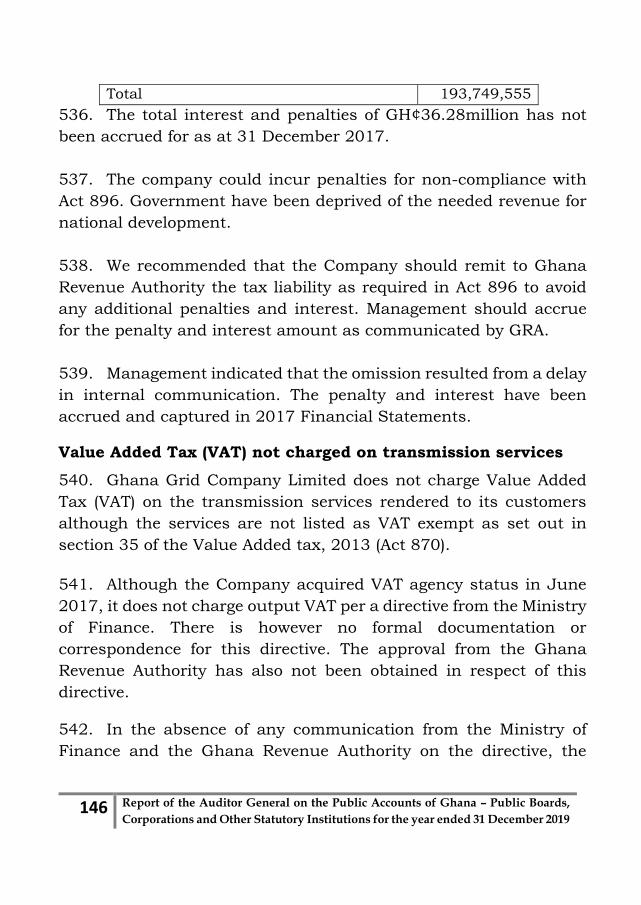

GHANA GRID COMPANY LIMITED 42. Contrary to Section 3(3) of the National Pensions Act 2008,

(Act 766) Management did not remit to the custodian, Ecobank

Ghana Limited monthly third tier pension contributions totalling

GH¢21,986,104 as at the year end 31 December. This amount is

made up of the principal contributions due of GH¢2,616,586 and

accrued interest of GH¢19,369,518, which has accrued since

August 2013. We recommended to Management to ensure that,

contributions are remitted to the appropriate custodians within the

required period as set out in Section 3(3) of Act 766 to avoid payment

of penalties.

43. Ghana Grid Company acquired VAT agency status in June

2017, however it did not charge output VAT per a directive from the

Ministry of Finance. There was however no formal documentation or

correspondence for this directive. The approval from the Ghana

Revenue Authority has also not been obtained in respect of this

directive. In order to avoid penalties from GRA, we recommended

that Management should obtain approval from the Ministry of

16 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

Finance and the Ghana Revenue Authority in respect of VAT not

charged on transmission services provided.

44. The Company did not have a signed transmission service

agreement (TSA) with 8 customers and power generators, although

its accounting and finance manual requires a contract to be in place

for transmission services rendered. Also, TSA’s for 7 customers had

expired and have not been renewed. We recommended to

Management to sign and renew all expired TSA agreements with all

its customers.

45. Contrary to Section 91(1) of the PFMA 2016, and Clause 16.1

of the GRIDCO transmission agreement with customers,

Management did not collect from 10 customers a total of

GH¢234,338,331, which has been outstanding for more than twelve

(12) months as at 31 December 2017. We recommended to

Management to assess the recoverability of these balances. In

addition, clauses in the respective transmission agreement

including clause 16.2 (reduce capacity for no-payment within 10

working days), 16.3 (termination of service) and 16.1 (application of

bank guarantees) aimed at recoverability of transmission fees should

be enforced.

46. Based on trade receivable confirmation responses received, 4

customers reference table 23 disputed amounts totalling

GH¢183,765,553 charged by the Company as regulatory levies,

ancillary charges and power infrastructure levies. We recommended

that Management should engage the Public Utilities and Regulatory

Commission (PURC) and the respective customers to resolve this

dispute.

47. There was no on-lending agreement between VRA and GRIDCo

in respect of facilities VRA borrowed funds to construct and

transferred to GRIDCO. The asset was recognised as long-term

17 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

liabilities in GRIDCO’s accounts. We advised Management to engage

VRA and the Ministry of Finance to conclude on an on-lending

agreement stating the terms of the facility.

48. Bui Power Authority responded to our trade receivable

confirmation that GRIDCo owed them GH¢28.96 million. This has

however not been recorded in the books of GRIDCo. Discussion with

Management disclosed that these amounts have not been agreed

upon. We recommended to Management that they should reconcile

these amounts with Bui Power Authority (BPA) and once an

agreement is reached, Management should recognise these

transactions.

49. Contrary to Regulation 39(2c) of FAR 2004, an amount of

GH¢22,381,028 recognised as compensation payments were not

supported with independent valuer’s report. We recommended to

Management to ensure that all compensation payments are

recognised and adequately supported. In addition, Management

should make such documents available to the audit team.

50. VRA in response to our trade payables confirmation disputed

the balance due from GRIDCo as at 31 December 2017. There was

difference of GH¢53,752,944 in favour of VRA. The variance is as a

result of different rates used in the computation of the transmission

losses. We recommended to Management to engage the Public

Utilities and Regulatory Commission (PURC) and VRA to resolve the

dispute. In addition, Management should recognise the amounts in

the general ledger once resolved.

51. GRIDCO as at 31 December 2017 breached the loan covenants

ratios with 4 of its lenders referenced in table 28. This could trigger

early repayment, non-approval of subsequent disbursement or

18 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

penalties. We advised Management to monitor loan covenants to

ensure compliance, as non-compliance may restrict access to funds.

52. In contravention of Section 91(1) of PFMA 2016, Act 921,

GH¢112,074 advanced to thirteen (13) institutions has either not

been retired or the services for which the payments were made have

not been rendered for over six months to six years. We recommended

to Management to put in place measures to recover these amounts,

if the purpose or services for which the amounts were paid are no

longer needed. We recommended to Management to investigate the

alleged stolen items and put in place controls to prevent this from

recurring.

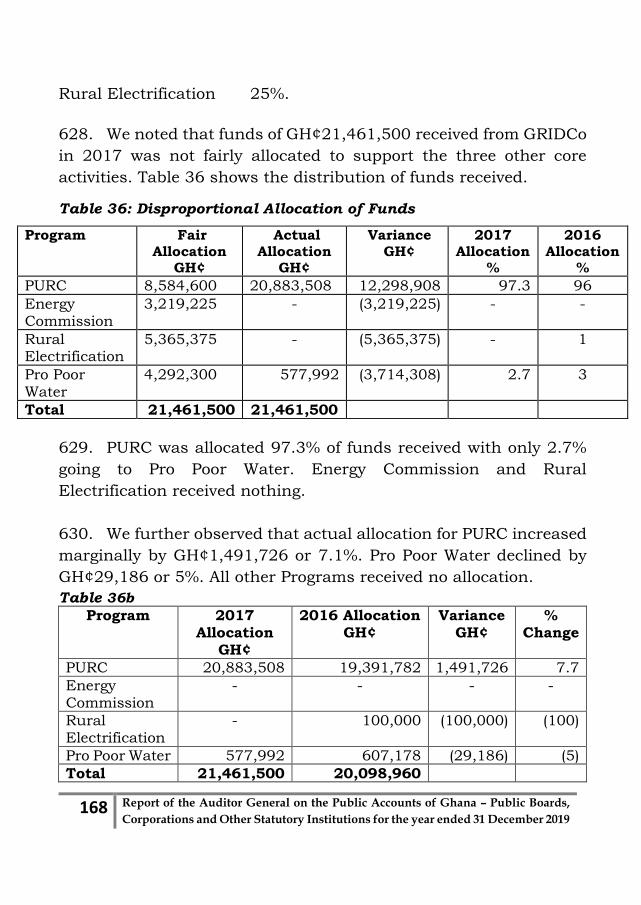

PUBLIC UTILITIES REGULATORY COMMISSION

53. The recovery rate of the fines due from Ghana Grid Company

Limited (GRIDCo) continues to deteriorate over the three-year period

from 2015 to 2017. In 2017, the percentage collected was 20.50%

compared with that of 2016 of 24.38% and 2015’s 39.71%. Also, the

Ghana National Gas Company (GNGC) remitted zero from the

amounts of GH¢137,133,529 and GH¢230,338,601 for 2016 and

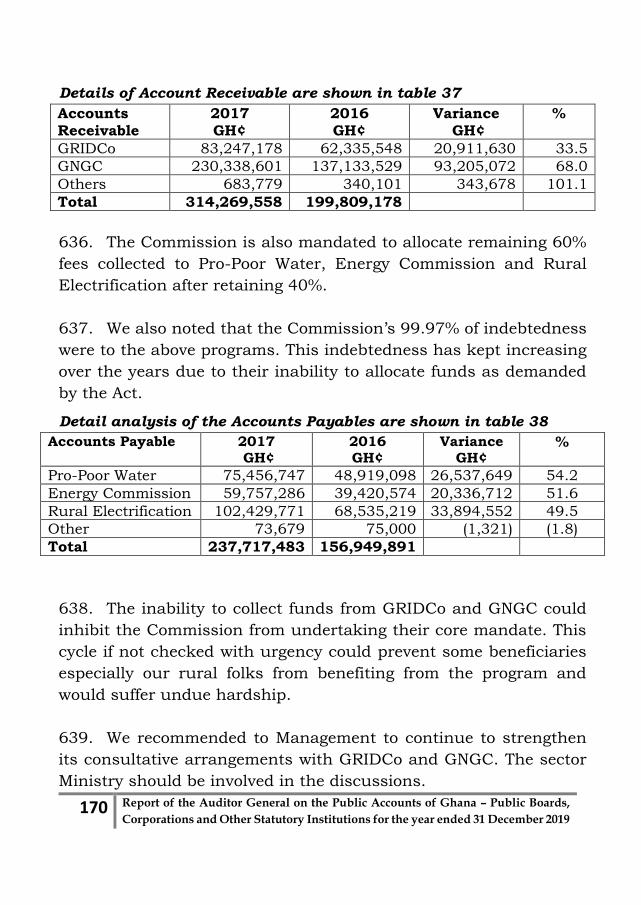

2017respectively due from them. We recommended to Management

to continue to strengthen its consultative arrangements with

GRIDCo and GNGC. The sector Ministry should be involved in the

discussions.

54. The Funds earmarked for Pro-Poor Water, Energy Commission

and Rural Electrification, may not be available to achieve the

intended objectives due to the unfair allocation of funds received.

Management has been advised to evaluate current terms of

allocating funds received aimed at ensuring, a much equitable

modality for the consideration and approval of the Commission’s

Board

19 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

NATIONAL PETROLEUM AUTHORITY

55. Management did not reconcile its Account receivable balances

as confirmation received showed conflicting balances between the

ledger balance and the amount confirmed. We advised Management

to take the necessary measures to reconcile the differences in

balances.

MINISTRY OF FINANCE

NATIONAL DEVELOPMENT PLANNING COMMISSION (NDPC) 56. We noted during the examination of payment vouchers that a

total amount of GH¢850,616.75 was spent on Consultancy fees.

There were no official receipts to acknowledge receipt of those

payment by beneficiaries. We advised that hence forth the

Accountant should demand receipts and other relevant documents

and attach them to the respective vouchers for our reviews.

Furthermore, official receipts and all relevant documentation needed

to fully account for the amount of GH¢850,616.75 should be made

available to the audit team for our verification.

57. We noted that the Commission spent GH¢45,898.00 on staff

who were admitted in various Medical centers for consumption of

poisonous food contracted by Administration for stakeholders

meeting. We advised that Management should as matter of urgency

put in place food policy to safeguard the lives of staff and other

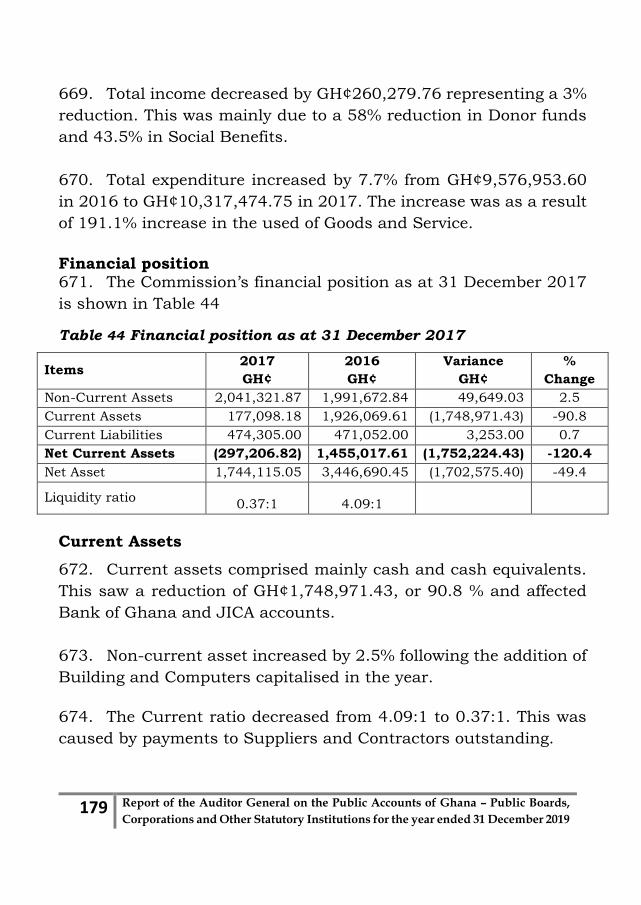

participants of various meeting at the instance of the Commission.

58. The Commission paid an amount of GH¢17,422.49 to Ms.

Veronica Baffoe who was on Korea International Cooperation Agency

(KOICA) scholarship as travel time and shipment allowance without

20 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

supporting documents. We recommended that the Finance Officer

should obtain the supporting documents to cover these payments

and inform our office accordingly, failing which we may disallow and

surcharge the authorising and paying officers with the amount

involved in accordance with Section 18 of the Audit Service Act 2000,

Act 584.

GHANA INVESTMENT FUND FOR ELECTRONIC

COMMUNICATIONS

(GIFEC)

59. The Financial Statements of GEFEC disclosed

GH¢10,900,000 as receivable from Ministry of Finance. This was

part of the debt of Ghana Telecom (GT), which government through

the Ministry of Finance agreed with Vodafone to absorb as part of

GT take over arrangement in July, 2008. We recommended to

Management of the Fund to continue to engage the Ministry of

Finance to ensure the settlement of this debt.

NATIONAL LOTTERY AUTHORITY

60. The Authority has nine legal cases with an estimated value of

GH¢160,390,000 at various Courts. The outcome of these cases may

weaken its financial position in the event that the Authority loses

the cases. We recommended to Management to ensure that the

Authority does not engage in a lot of litigations and also institute

measures to reduce its financial exposures in these legal battles.

61. Management did not renew the expired contracts for

promotion activities with four organisations with an expected

revenue of GH¢600,000. We advised Management to regularise these

contracts to avoid loss of the expected revenue and litigations.

62. Due to laxity of controls in the Management of Post of Sales

Terminal (POST) and debtors, there were slow movements in the

21 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

balances over the past four years. Management was advised to

strictly comply with the provisions in the policy to prevent increase

in its bad debts.

GHANA PUBLISHING COMPANY LIMITED

63. Management did not sign any Maintenance and Support

agreement with vendors of the accounting and payroll package.

Additionally, the dataflow software is incapable of properly exporting

or importing data to Excel seamlessly. Data so exported are in most

cases distorted. We recommended that Management sign a service

level agreement with the software vendors, and ensure that training

reports are submitted after each training programme.

64. Contrary to Section 13 of the Audit Service Act 2000, our

review of the staff debtors disclosed that, personal account for staff

was not maintained, the list of balances from payroll software did

not provide full complement of transactions between the company

and staff. Also, the total of the schedule of balance generated by the

payroll software showed a difference of GH¢47,394.14 lower than

the total of the control account of GH¢188,456. We recommended

and Management agreed to ensure that the differences are

reconciled and recovered from the identified staff of the company.

65. Bank reconciliations for the various banks were not done

timely by Management. There were differences totalling

GH¢258,099.58 between the amounts reported in the Reconciliation

Statements and the ledger balances of 3 bank accounts. Also, Bank

Reconciliation Statements were not prepared for 9 bank accounts.

We recommended to Management to put in controls to ensure that

monthly bank reconciliation statements are prepared on time.

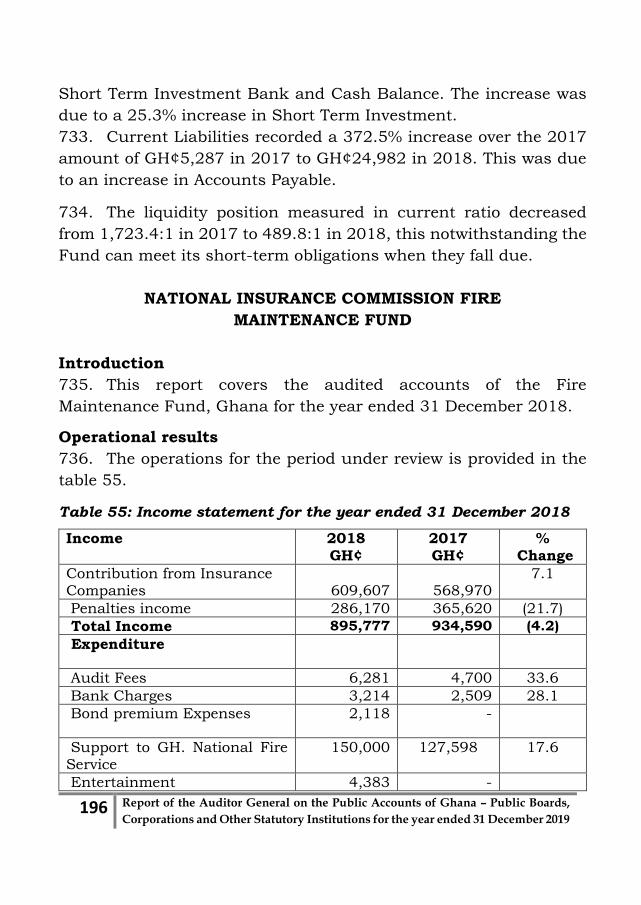

Management should investigate and rectify differences in ledger

balances and reconciliations statements.

22 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

66. Contrary to Regulation 183 (4) of the Financial Administration

Regulations 2004, (LI 1802), Management procured goods and

services totalling GH¢273,755.00 from non-VAT registered persons.

Management was advised to strictly comply with the regulations, by

procuring from VAT registered persons or entities.

67. We noted that in contravention of Regulation 19(1) of the

Value Added Tax Regulations, 1998 (L.I.1646), the company sold

goods and provided services totalling GH¢91,786.50 to 5 Institutions

without charging VAT. We recommended to Management to ensure

that the VAT laws are fully complied with.

G-PAK LIMITED

68. Management invested an amount of GH¢1,000,000 with Utrak

Savings and Loans which was expected to mature on 27th December,

2018, but Utrak released GH¢700,000 out of the accumulated value

of GH¢1,127,740.25 with GH¢427,740.25 still outstanding. We

advised Management to institute measures that would ensure that

the difference of GH¢427,740.25 is recovered.

MINISTRY OF HEALTH

NATIONAL HEALTH INSURANCE AUTHORITY

Fomena District 69. We observed that 13 payment vouchers (PVs) totalling

GH¢5,136.00 from NHIA, Fomena Office were not accounted for. We

recommended that the Accountant should as a matter of urgency

account for the said expenditures without fail by producing all the

relevant expenditure authentication documents for our audit

perusal. Failing this the expenditures should be refunded by the

approval and authorising officers, the District Manager Mr. Annan-

Turkson Thomas and Accountant-Patrick Appiah Kodua.

23 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

70. We noted that payments on 9 vouchers totalling GH¢7,575.00

made to the District Manager and the Accountant of the Authority

as claims of travel and transport (T&T) and other allowances were

without any evidence of activities undertaken. We therefore

recommended that the expense of GH¢7,575.00 should be refunded

by the Accountant Patrick Appiah Kodua and the Manager Mr.

Annan-Turkson Thomas.

71. We noted that the Fomena NHIA office could not present six

(6) payment vouchers totalling GH¢2,916.00 for audit. We therefore

recommended that the six (6) payment vouchers should be made

available for audit scrutiny, failure of which the amount of

GH¢2,916.00 should be refunded by the District Manager Mr.

Annan-Turkson Thomas and the Accountant – Patrick Appiah

Kodua jointly.

Obuasi

72. We noted that an amount of GH¢23,357.96 was used to

purchase different store items which were not receipted into the

Authority’s stores and same recorded in their ledger. We

recommended that Management should account for the stores items

in their ledgers or the amount of GH¢23,357.96 jointly refunded by

the Manager, Mr. Kwabena Kyeremanteng and the Accountant, Mr.

Domingo Adongo.

73. We observed that Management of the NHIA, Obuasi did not

account for fuel coupons worth GH¢3,080.00 procured for the

running of the Authority’s machineries. We recommended that the

Municipal Manager and the Accountant who were the custodians of

the said fuel coupons should provide justification regarding the

24 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

usage of the coupons for our audit review, failing which the amount

of GH¢3,080.00 should be refunded by them.

74. We noted that the Accountant of the Obuasi Municipal Health

Insurance Scheme, did not withhold statutory taxes totalling

GH¢2,841.98 from purchases of goods and services made between

2013 and 2015. Management however paid the tax amount out of

the coffers of the Authority following a tax audit carried out on the

outfit by the GRA. We recommended that the Municipal Manager

and Accountant should jointly and personally refund the amount of

GH¢2,841.98 to the NHIA Obuasi and recover same from the

suppliers and service providers as required by Section 117 of Income

Tax Act 2015 (Act 895) if they so wish. Evidence of the refund should

be forwarded to our office for verification.

Asawase

75. We noted during the audit that revenues collected between

July, 2018 and January, 2019 amounting to GHȼ462,207.00 was

under paid by GHȼ19,519.00. We therefore recommended that the

issue should be reported to the police and the terms and conditions

of the bond entered between the NHIA and Mr. Jones Nana Tsibu be

executed.

MINISTRY OF LANDS AND NATURAL

RESOURCES

LANDS COMMISSION (CONSOLIDATED)

Corporate Division

76. A review of ground rent ledgers for the period under review

showed that 43 lessees in Achimota residential area, Ring Road,

North Industrial Area and Roman Ridge residential area have not

25 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

been paying ground rent since 1960, to the Commission. We

recommended that the head of the ground rent unit should update

the information of the forty-three lessees and recover the rent due

from 1960 and our office informed for verification. We also

recommended that Management should commission a full and

detailed audit of the ground rent unit to address all relevant

anomalies.

77. Management of the Commission did not remit an amount of

GH¢1,163,470.17 in respect of rent collection on behalf of the Office

of the Administrator of Stool Lands to the Administrator for the

period under review. We recommended to Management to remit

same to the Office of the Administrator of Stool lands without further

delay.

78. Management of the Commission did not comply with the

Ministry of Finance’s directive on the On-site/Daily collection

Programme as a mechanism for the collection of government revenue

by banks on behalf of Ministries, Departments and Agencies (MDAs).

Universal Merchant Bank was contracted for this revenue collection,

but received cash payment of GH¢3,247,375.00 and cheque

payments of GH¢6,554,041.00 on purchase of government lands at

Borteyman. We recommended that Management should comply with

the contract agreement between the Ministry of Finance and the on-

site Bank on behalf of the MDAs to enhance financial discipline.

79. A review of vehicle files of the Commission for the period under

review indicated that, the Commission did not have legal title to

seven vehicles as these vehicles were in the names of Toyota Ghana,

CFAO, Stelin Automobile or other individuals. We advised

Management to ensure that legal title to seven vehicles revert to the

Commission.

26 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

80. Management of the Commission did not provide the audit

team with records on the allocation of Government Lands at

Borteyman to enable the team establish and confirm the debtors

figure in the financial statements for the period under review. We

recommended that, Management should make the records on

Borteyman government lands available to the team without further

delay.

Public and Vested Lands Management Division 81. Contrary to Stores Regulation 0502, stores purchased

totalling GH¢20,560.00 were not accounted for in the store records.

We therefore recommended that the items in question be accounted

for failing which the amount should be recovered from the

authorising and approving officers.

82. Our review of payment procedures, disclosed that an amount

of GH¢700.00 was paid in respect of fuel and lunch was not

supported with receipts. We recommended that the payment should

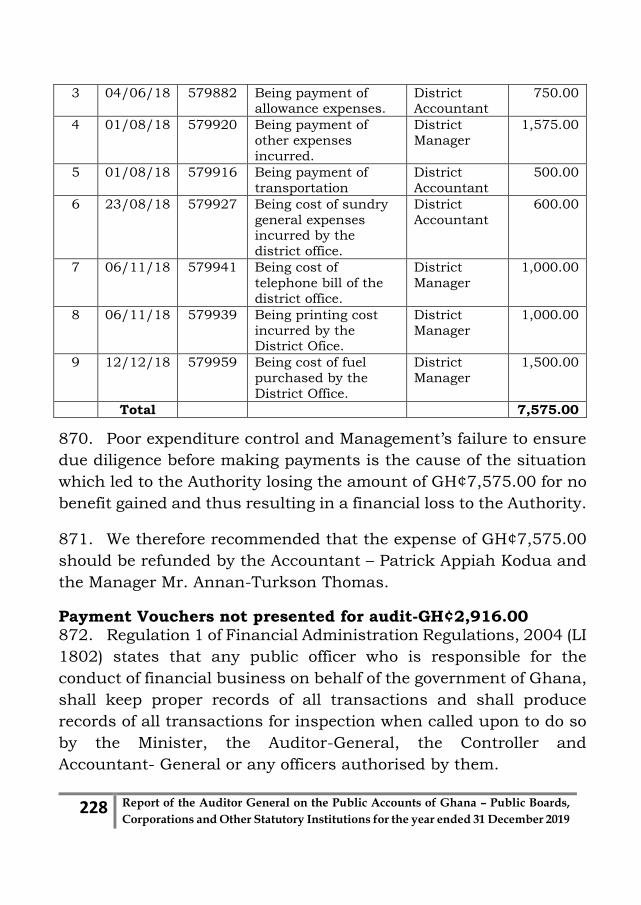

be supported with the relevant receipts, failure of which the amount

should be recovered from the signatories to the account.

Survey and Mapping Division

83. We observed that 15 staff members had their names appearing

in the payment vouchers after their separation from the

establishment by way of retirement, resignation and death for the

years under review, resulting in a total unearned salary of

GH¢54,957.26. The unearned salary was GH¢10,150.91 and

GH¢44,806.35 for 2016 and 2017 respectively. We recommended to

Management to recover the total unearned salaries of

GH¢54,957.26, and pay same to Government chest and produce the

Treasury Receipt supporting the payment, for our verification.

84. Our examination of payment vouchers disclosed that 13

payments totalling GH¢37,057.30 were made to various payees

27 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

without deduction of withholding tax. We recommended that

Management takes steps to ensure that the due tax component on

the amount of GH¢37,057.30 is recovered from the affected payees

and paid to Ghana Revenue Authority (GRA).

85. We noted that instead of an amount of GH¢26,150.00

budgeted and approved for ‘Jubilee Gate Fieldwork’ that is, the

demarcation and Survey of the Jubilee Gate Site (Nungua farms) an

amount of GH¢53,781.00 was spent on the project resulting in an

excess expenditure of GH¢27,631.00. We recommended to

Management to produce approval to justify the excess expenditure

of GH¢27,631.00 for our inspection.

86. Our review of sampled payments to temporary staff indicated

that a total amount of GH¢1,160.50 deducted in respect of

employees Social Security contribution was not supported with

evidence of remittance to SSNIT. We recommended that

Management should ensure that all contributions deducted but not

remitted be paid to SSNIT as required by law.

Land Valuation Division 87. During our physical inspection of assets, we noted that two

official vehicles belonging to Land Valuation Division were grounded

between 1½ to 2 years. We advised Management either to dispose of

them in accordance with prescribed legislation or repair them to

avoid further deterioration.

88. Contrary to Regulation 297 of FAR L.I 1802, we observed

during the examination of the Electronic Salary Payment Vouchers

that one separated staff who retired on 3 May 2016 was paid

unearned salary totalling GH¢4,312.89. We recommended that

Management should make strenuous effort to retrieve the amount

and pay same to government chest.

28 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

Land Registration Division

89. Contrary to Section 8.3(b) of the Staff Training and

Development Policy of the Lands Commission Nana Kojo Esilfie, a

Land Administration Officer was granted a year study leave with pay

to pursue a professional Law course at the Ghana School of Law,

Accra for the 2016/2017 academic year. Though the academic year

ended in August 2017. The officer has since not reported to work

resulting in unearned salary payment of GH¢9,041.25 and has also

failed to comply with the bond condition governing the study leave

with pay.

We recommended to Management to ensure that the officer refunds

the amount of GH¢9,041.25 paid to him with interest at the

prevailing Bank of Ghana interest rate and our office informed for

verification.

MINISTRY OF EDUCATION

CHARTERED INSTITUTE OF TAXATION

90. Accountable imprest and other payments for various activities

of the Institute totalling GH¢25,170.08 had not been retired as at

the end of the financial year. We advised the Spending Officer to

ensure that the amount is properly accounted for.

91. In violation of Section 43 (1) of the Public Procurement Act,

Management purchased office equipment and stationery and other

services totalling GH¢414,690.03 without obtaining alternative

quotations. Management was advised to comply with the Act.

NATIONAL BOARD FOR PROFESSIONAL AND TECHNICIAN EXAMINATIONS (NABPTEX)

92. Due to inaccurate data kept by NABPTEX on three (3)

Technical Universities and one (1) Polytechnic, revenue amounting

to GH¢165,240.00 was not collected. We recommended to

29 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

Management to ensure that the above stated amount is collected

from the Institutions involved, while necessary steps are taken to

put the right system in place for gathering accurate data on all the

institutions to help in collecting all the revenue due from them.

93. We observed that the Accounts Office collected revenue in

cash ranging from GH¢100.00 to GH¢5,000.00 as examination,

affiliation, expert review and other fees during the year under

review, contrary to Regulation 48(2) of the FAR. We advised

Management to ensure that, with the exception of the sale of past

questions which are in small amounts, all other revenue should be

collected in cheque or bankers’ draft.

94. MAK-EDU Consult Limited did not develop and implement a

student information management system and E-learning solutions

for NABPTEX as required in a Contract agreement. Part payments of

GH¢215,695.00 out of Contract price of GH¢345,356.00 had been

made to him. The Board should pursue MAK- EDU to refund GHC

215,695.00 or develop and implement all the modules as stated in

the Contract.

95. The Governing Council of NABPTEX did not comply with the

judgement of the Supreme Court of Ghana dated 9th May, 2018

quashing the termination of appointments of Mr. Francis Owusu-

Mensah and Mr. Stephen Onwona Adjapong. The Council should in

consultation with the Minister of Education and relevant institutions

ensure compliance with the judgement of the Supreme Court of

Ghana.

96. The Board over spent its budgets for 2017 and 2018 by

GH¢1,641,185.28 and GH¢2,220,595.70 respectively. We urged

Management to use the appropriated estimate from Parliament to

control disbursement of funds.

30 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

NATIONAL ACCREDITATION BOARD 2015 - 2016

97. Contrary to Regulations 2(b), 5(4), 22(2) and 23(4) of LI 1984

(2010) of the National Accreditation Board Regulations, the Board

reviewed its service charges at the 92nd Board meeting without

parliamentary approval. We recommended that Management should

take steps to get parliamentary approval in order to avoid any legal

challenges.

98. We observed that the Board did not take any action on those

who flouted the law by advertising, operating and running of

unaccredited Institutions and Programmes. We recommended that

the Board should ensure compliance with the Act and persons found

culpable should be dealt with in accordance with the law.

NATIONAL COUNCIL FOR TERTIARY EDUCATION

99. We noted that an amount of GH¢2,974,914.76 was disbursed

from the Council’s Trust Funds (feeding grant and others) without

approval from Ministry of Finance. We urged Management to

transfer the GH¢2,653,887.76 back to the Trust Funds, failing

which the authorising and paying officers shall be sanctioned in

accordance with Section 98(1)(d) & (2)(b) of the Public Financial

Management Act (PFM).

100. An accounting software named, Tally ERP 9 was purchased off

the counter in the year 2012. However, the Council did not seek for

prior approval from the Auditor-General before implementation.

Going forward we urged Management to ensure that approval is

sought from the Auditor-General before the purchase and usage of

anaccounting software.

31 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

UNIVERSITY OF PROFFESSIONAL STUDIES ACCRA (UPSA)

101. We noted that out of a total amount of GH¢2,302,369.67

released to some officers of UPSA to transact official business on

behalf of the University, only GH¢353,279.43 was accounted for

with the necessary supporting documents leaving a difference of

GH¢1,949,090.24 to be accounted for, though the activities for

which the funds were released had been conducted long ago. We

recommended that; the amount be adjusted to the personal advance

accounts in the names of individual imprest holders in line with

Regulation 288(1) of the Financial Administration Regulations.

102. We noted during our review that, Management of UPSA, Accra,

signed a retainer agreement dated 16th March 2014 and paid an

amount of GH¢263,670.00 to Lithur Brew and Company a law firm

as a retainer fees without evidence of the provision of any legal

services to the University. We also noted that Lithur Brew and

Company was appointed through sole sourcing without recourse to

the provisions of the Public Procurement (Amendment) Act, 2016

(Act 914).

103. We advised that, the former Vice Chancellor; Prof. Joshua

Alabi and Lithur Brew and company be made to refund the amount

with an interest at the prevailing Bank of Ghana interest rate. We

further advised that, Management sets up a legal directorate that

shall facilitate all legal matters for the University through the

Attorney General’s department.

NATIONAL SERVICE SCHEME

104. Management authorised and paid salaries amounting to

GH¢688,132.06 to four (4) Government appointees from IGF instead

of government subvention. We recommended that the amount paid

32 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

to these appointees should be recovered when their salary arrears

are paid to them.

105. We noted that a total amount of GH¢908,644.05 paid to

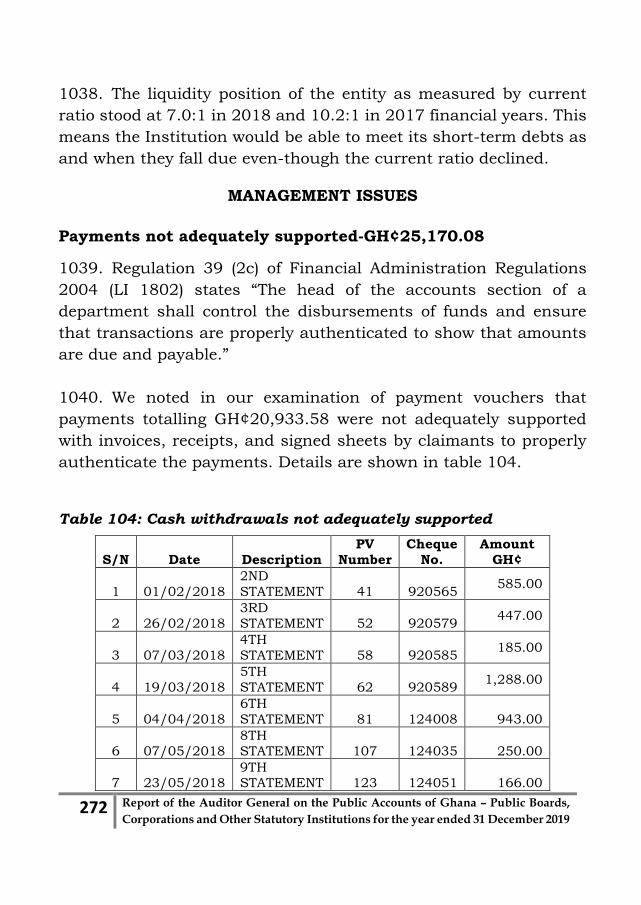

various companies were not covered with official receipts to

authenticate payments. Management should ensure that original

receipts from the payees are attached to the payment vouchers for

our verification.

UNIVERSITY OF CAPE COAST

106. Contrary to Regulation 15 (1) of the Financial Administration

Regulations, 2004 (L.I. 1802) Mr. Kwame Fenyi a Senior

Administrative Assistant of the University’s Accra Office and Mr.

Francis Arthur of UCC Enterprises did not account for total revenue

of GH¢55,557.60 collected between June 2017 and April 2018. We

recommended that the total amount of GH¢55,557.60 should be

recovered from Mr Kwame Fenyi and Mr. Francis Arthur and paid to

the University’s account for our verification.

107. Our audit disclosed that the University paid an amount of

GH¢113,116.56 to Top Express Freight Handling Ltd to clear 3600

MIFIs and 8000 U Sim Chip from KLM Airlines for Bolte

Communication Limited a private company. We however noted that

after the clearance, Bolte Communication Limited took delivery of

the goods from the University Stores on 20/8/18 preventing the

University access to the MIFIs and the U Sim Chips for use. We

recommended that the total amount of GH¢113,116.56 should be

recovered from Bolte Communication Limited with interest, failing

which the total amount of GH¢113,116.56 should be recovered from

the Vice Chancellor, Professor Ghartey Ampiah with interest.

33 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

108. Contrary to Regulation 39(2)(c) & (d) of the Financial

Administration Regulations 2004 (L.I. 1802) our vouching disclosed

that the University made a part payment of GH¢451,530.00 to

KLEOS Technology for information and communication services

without justification. We recommended that KLEOS Technology, the

Council and the University Director of ICT services Dr. Regina

Gyampoh-Vidogah should provide evidence that 20,000 students

and officers of the University did use the KLEOS services, the basis

of the invoice and payment of GH¢451,530.00 to KLEOS Technology,

failing which all payments to KLEOS Technology should stop and

the amount of GH¢451,530.00 ($100,000.00) recovered from KLEOS

Technology, the Council, and the Director of ICT services Dr. Regina

Gyampoh-Vidogah.

109. We noted during our audit that, the University granted loans

amounting to GH¢9,234,190.00 to Student Representative Council

(SRC) and UCC Alumni but recovered only GH¢679,119.84 leaving

a difference of GH¢8,555,070.47 unrecovered as at 31/12/18. We

recommended that Management should recover the outstanding

loans of GH¢8,555,070.47 from SRC and UCC Alumni or take over

the facilities based on which the loan was contracted. Again, the

Council in future should conduct financial feasibility studies before

providing guarantee to loan facilities.

110. Our audit disclosed that GOIL Ghana Ltd deducted an amount

of GH¢15,570.00 from fuel revenue due UCC Enterprise without

justification. Out of total revenue of GH¢676,000.00 due UCC

Enterprise as commission on sale of fuel, GOIL Ghana Ltd deducted

an amount of GH¢15,570.00 for generator, electrical works and

others without agreement or approval from UCC Enterprise and paid

only GH¢659,380.00 to the University. We recommended to

Management to obtain justification from GOIL Ghana Ltd for the

34 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

deductions, failure of which the University should demand from

GOIL Ghana Ltd an amount of GH¢15,570.00 to the University.

111. Contrary to Regulation 2(d) of the Financial Administration

Regulations, 2004 (L.I. 1802) we noted that forty-four (44) affiliated

institutions owed the University an amount of US$1,401,185.64 in

respect of unpaid affiliation fees as at the 31 December 2018. We

recommended to Management to recover the US$1,401,185.64 from

the affected Institutions, including legal actions where necessary.

112. Ten (10) corporate institutions occupying the University’s

Lands and Office Spaces owed the University unpaid rent amounting

to GH¢305,927.16 and US$35,903.34 as at 31 December 2018. We

recommended to Management to recover the outstanding rent of

GH¢305,927.16 and US$35,903.34 from the tenants without

further delay.

113. Contrary to Regulation 227 of Financial Administration

Regulations, 2004 (L.I.1802) the University paid a total amount of

GH¢9,449.50 for replacement of stolen items from the School of

Business Guest House without any form of investigation by the

security agencies. There was no Police or Investigation report to

ascertain the cause and who should be held liable. We recommended

that the Guest House Manager who has responsibility for the

security of guests and assets at the facility should be made to pay

for the cost of the stolen items. Furthermore, Management should

put in place adequate security measures including CCTV cameras

at vantage points within the periphery of the guest house. However,

the matter should be taken up with the police.

A creditor’s balance of GH¢187,500.00 shown in the University’s

financial statements payable to Jay K Industries and Investment

Limited as at 31 December 2018 had no supporting documents such

35 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

as invoices, store received vouchers and others to authenticate that

Jay K Industries and Investment Limited had made any supplies to

the University. We recommended to the University Printing Press

accounts officer to provide documentary evidence to authenticate

the payable amount of GH¢187,500.00, failing which the entries

should be reversed.

114. Contrary to Financial and Stores Regulations, we noted

descrepancies between book balances and physical stock balances

at the University Printing Press during stock count. The value of the

shortage noted was GH¢15,443.44. We recommended that the

storekeeper should produce evidence of usage or physically produce

the items for verification, failing, the total amount of GH¢15,443.44

should be recovered from the storekeeper.

115. Contrary to Section 5 (c) of the Retention of Funds Act, 2007,

(Act 735) we noted that Management paid an amount of

GH¢4,223,294.40 from Internally Generated Funds (IGF) to one

hundred and two (102) retired staff as end of service benefit for the

year 2018. We recommended that Management should stop using

Internally Generated Funds to pay end of service benefits to avoid

future sanctions.

116. Contrary to Section 16.1 of the Conditions of Service for Senior

Members of Public Universities of Ghana, 2011, we noted that the

University granted study leave with pay amounting to

GH¢1,868,638.72 to eight (8) staff members but the officers did not

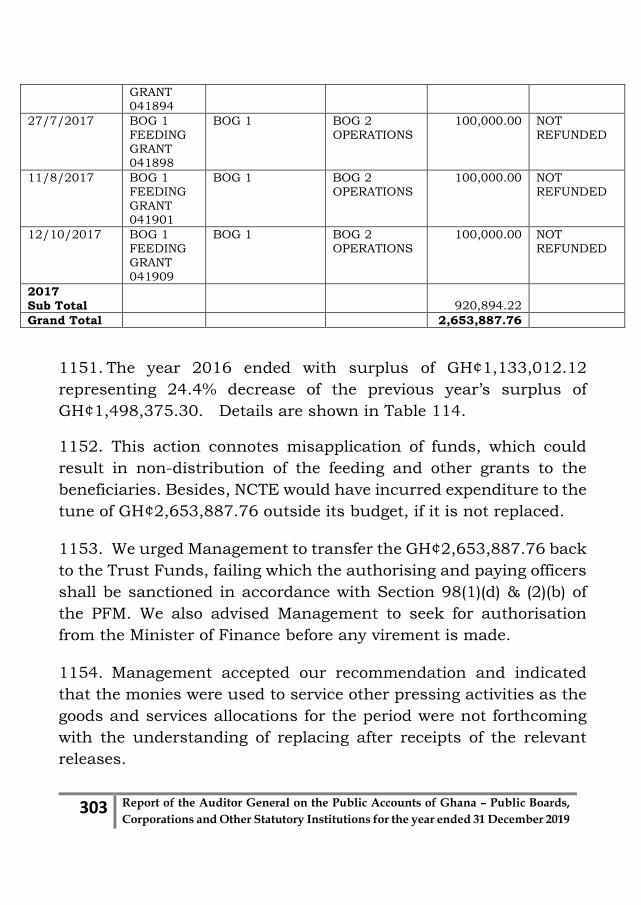

return to serve the University as required. We recommended that

Management should pursue the affected officers and their

guarantors to refund the total amount of GH¢1,868,638.72 to the

University.

117. Three (3) officers who were granted sabbatical leave, drew

salary of GH¢128,826.29 from the University of Cape Coast and took

36 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

same from the sister Universities and Government departments

leading to central government paying double salary to the affected

officers. We recommended that the officers involved should refund

the double salary of GH¢128,826.29 paid to them. We also

recommended that the University should endeavour to communicate

with other sister institutions where its officers undertake their

sabbatical leave to prevent double payment of salaries by central

government.

118. Our audit disclosed that the University engaged in single

source procurements activities amounting to GH¢435,796.63. This

was however without approval from Public Procurement Authority.

We urged Management to ensure compliance with the provisions of

the Public Procurement Act, Act 914.

119. We noted that the University paid KLEOS UK Ltd an amount

of GH¢451,530.00 without recourse to the Public Procurement Act.

The Vice Chancellor Professor Ghartey Ampiah entered into an

international contract on behalf of the University with KLEOS UK

Ltd a company incorporated in United Kingdom for the provision of

Information and Communication Technology (ICT) services to the

University. We recommended that the Vice Chancellor should

forward the Build, Own, Operate and Transfer (BOOT) Agreement

entered into with KLEOS UK Ltd to the University Council, Minister

of Education and Minster of Finance for ratification, failing which

the agreement should be suspended and all cost incurred recovered

from the Vice Chancellor. Again, the University should seek

concurrent approval of same from the Public Procurement Authority.

120. We noted that the Vice Chancellor, Professor Ghartey Ampiah

entered into a 10 year Build, Own, Operate and Transfer Agreement

with KLEOS UK Ltd for the provision of information and

37 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

communication technology (ICT) services at a cost of $300,000.00

per year totalling $3,000,000.00 for the contract period without

seeking approval from the University Council, the Minister of

Education and Public Procurement before committing the University

to such financial obligation. The contract signed by the Vice

Chancellor was only witnessed by the Director of ICT services Dr.

Regina Gyampoh-Vidogah. We recommended that the Vice

Chancellor should submit the Build, Own, Operate and Transfer

Agreement (BOOT) with KLEOS UK Ltd to the University Council,

Minister of Education and Public Procurement Authority for

approval, failing which the sanctions in section 92 (1) of the Public

Procurement Act shall be applied.

121. Contrary to Section 35 (1) of the Public Procurement Act, 2003

(Act 663) we noted that the College of Distance Education and

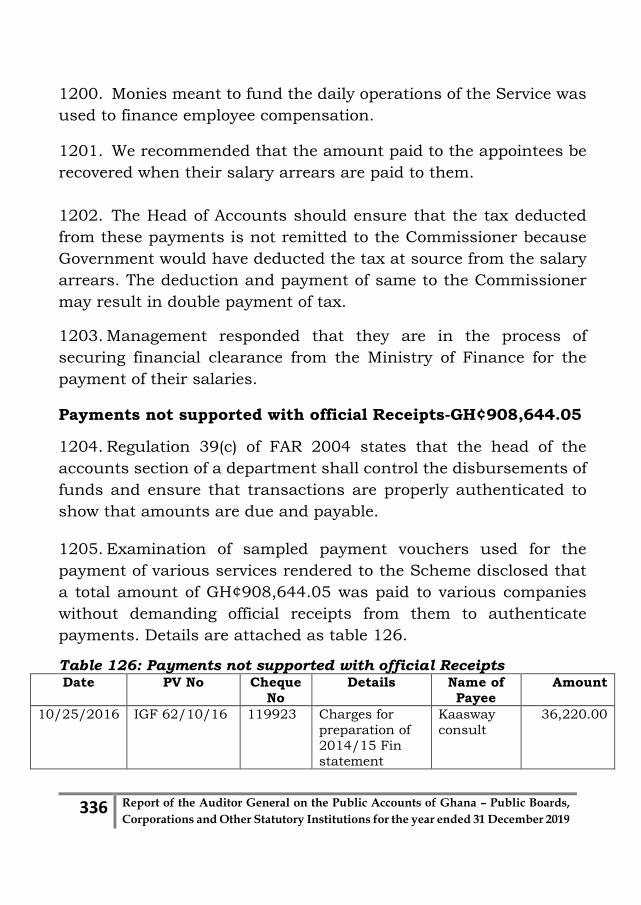

Central Administration procured Information Technology Service

from Vertebra Limited amounting to GH¢397,602.00 without

recourse to the Public Procurement Act. We recommended that the

Vice Chancellor and the Provost of College of Distance Education

should be sanctioned per section 92 (1) of the Public Procurement

Act, 2003 (Act 663) as amended.

122. Our audit disclosed that College of Distance Education

granted advances amounting to GH¢21,298,853.44 without any

agreement whatsoever to four (4) contractors for the execution of

various projects but recovered only GH¢6,345,578.70 leaving a

difference of GH¢14,953,274.74 unrecovered as at 31/12/18. The

advances were granted since 2013 and 2016 financial years from

Internally Generated Fund of the University. We recommended that

Management should recover the total outstanding advance of

GH¢14,953,274.74 from the affected contractors with interest using

Bank of Ghana interest rate, failing which the total amount of

38 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

GH¢14,953,274.74 should be recovered from the officers who

authorised the payment.

123. Our review of contract management disclosed that the College

of Distance Education paid an amount of GH¢394,500.00 to Wilkado

Construction Works Ltd for the supply of Nissan Patrol Vehicle for

the Construction of Regional Study Center- WA project since

15/01/2014 but the vehicle was not supplied as at 31/12/18. We

recommended that the contractor should supply the vehicle to the

University, failing which the total amount of GH¢394,500.00 should

be recovered from the contractor with interest using Bank of Ghana

prevailing interest rate.

124. Contrary to Section 35 (1) of the Public Procurement Act, 2003

(Act 663) we noted that the College of Distance Education paid a

total amount of GH¢18,225,418.54 to two (2) contractors for various

construction works without recourse to the Public Procurement Act.

We recommended that the Vice Chancellor, Director of Development

and the Head of Procurement should produce the procurement

documents if any to the audit team, failing which the Vice

Chancellor, Director of Development and the Head of Procurement

should be sanctioned per Section 92 (1) of the Public Procurement

Act, 2003 (Act 663) as amended.

125. Our project inspection disclosed that the College of Distance

Education paid a total amount of GH¢8,187,762.77 to three (3)

contractors for additional works but no works according to our

review was carried out on the said projects. We recommended that

the contractors and Director of Development should produce

documentary and physical evidence of additional works done on the

projects involved to justify the payment of the amount, failing which

the total amount of GH¢8,187,762.77 should be recovered from the

39 Report of the Auditor General on the Public Accounts of Ghana – Public Boards,

Corporations and Other Statutory Institutions for the year ended 31 December 2019

affected contractors and the Director of Development sanctioned for

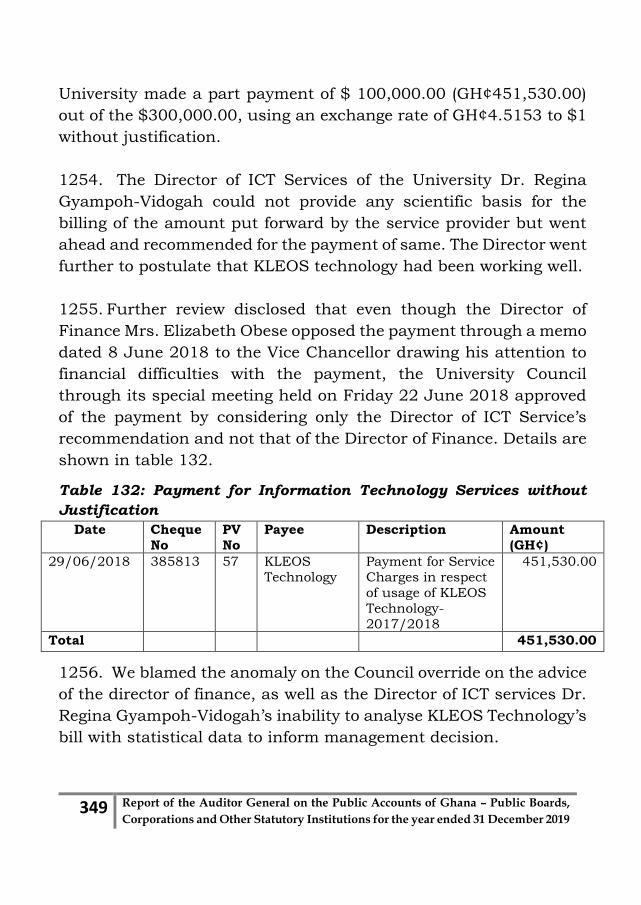

certifying the interim payment certificates and assisting the

contractors to claim such amount from the University for no work

done.

126. Contrary to Section 66 of the Public Procurement Act, 2003

(Act 663) as amended, our audit disclosed that the College of

Distance Education paid a total amount of GH¢1,587,369.10 to

Phase 2-Consultancy for consultancy services on various

construction works without recourse to the Public Procurement

Authority Acts. We recommended that the Director of Development

and Head of Procurement should explain the basis for contracting

the consultancy services without recourse to provisions of the Public

Procurement Law, failing which the Director of Development, Head

of Procurement should be sanctioned per Section 96(1) (a) of Public

Financial Management Act, 2016 (Act 921).

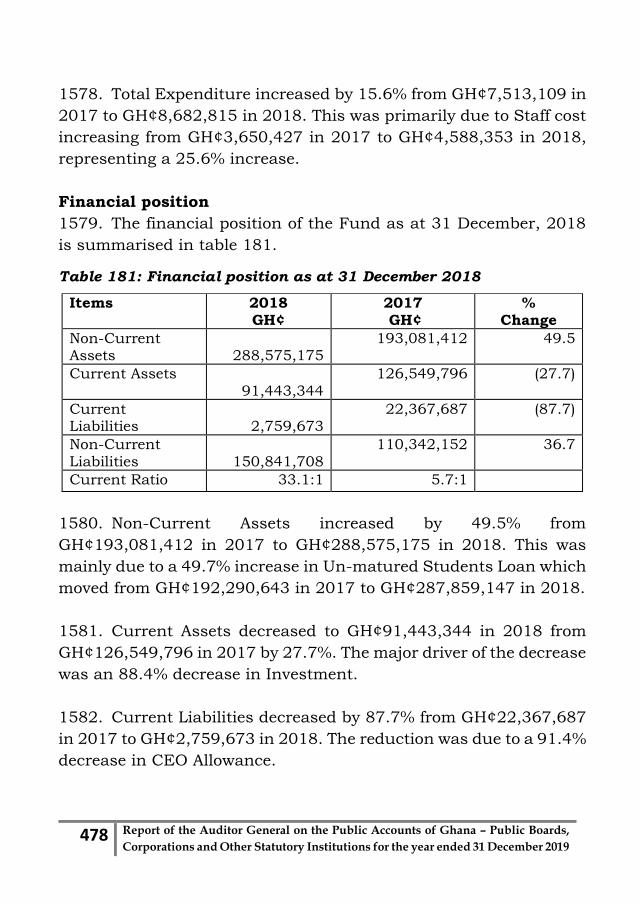

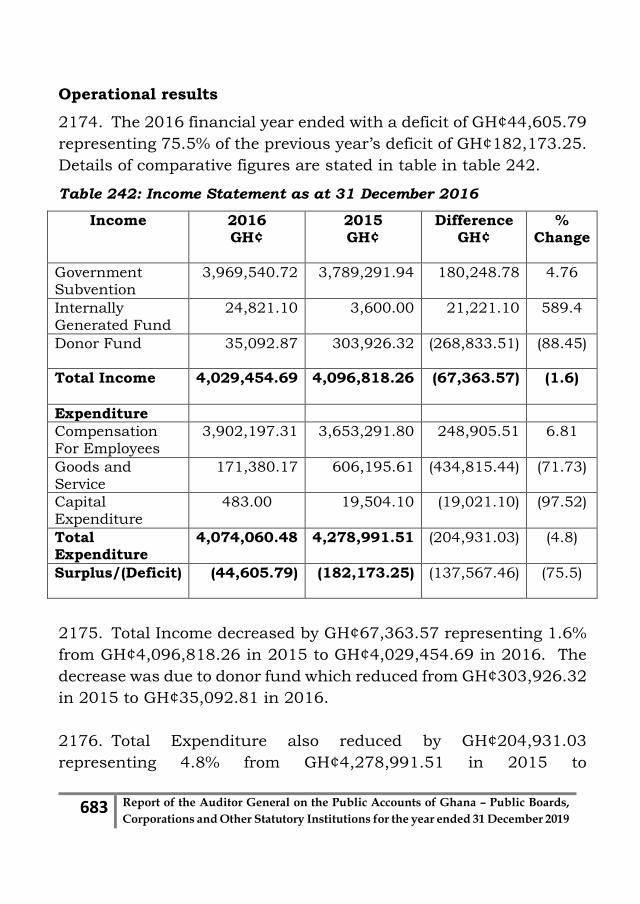

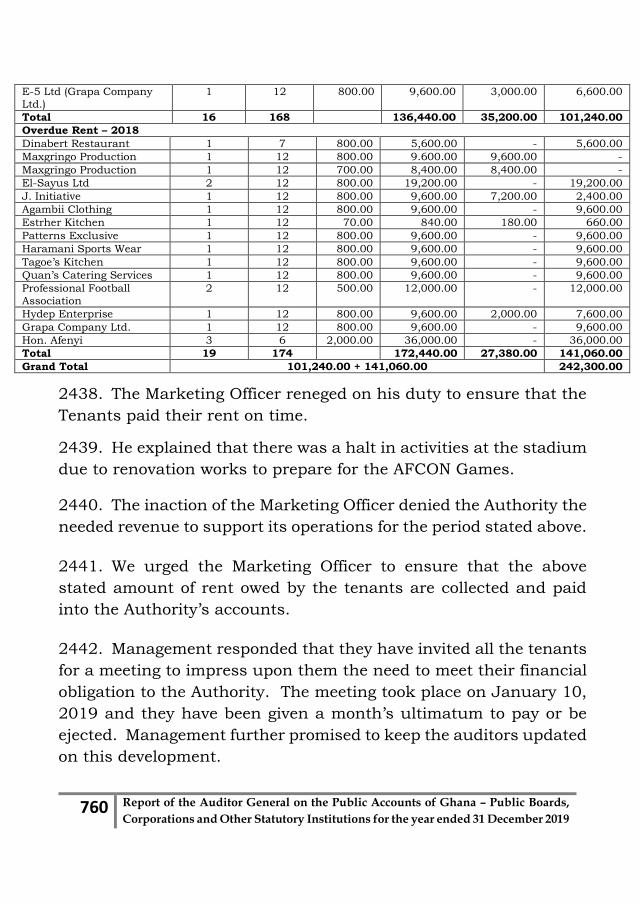

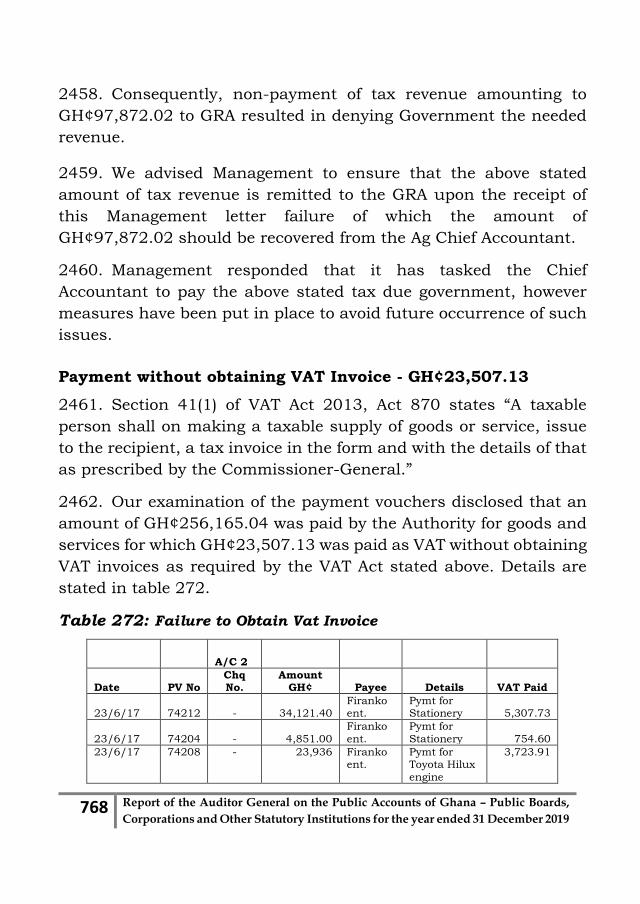

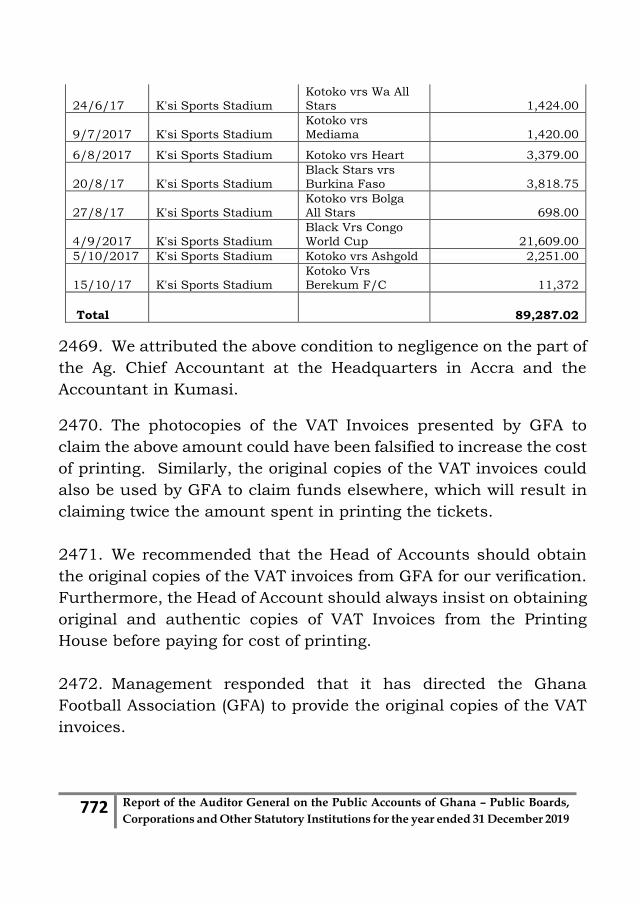

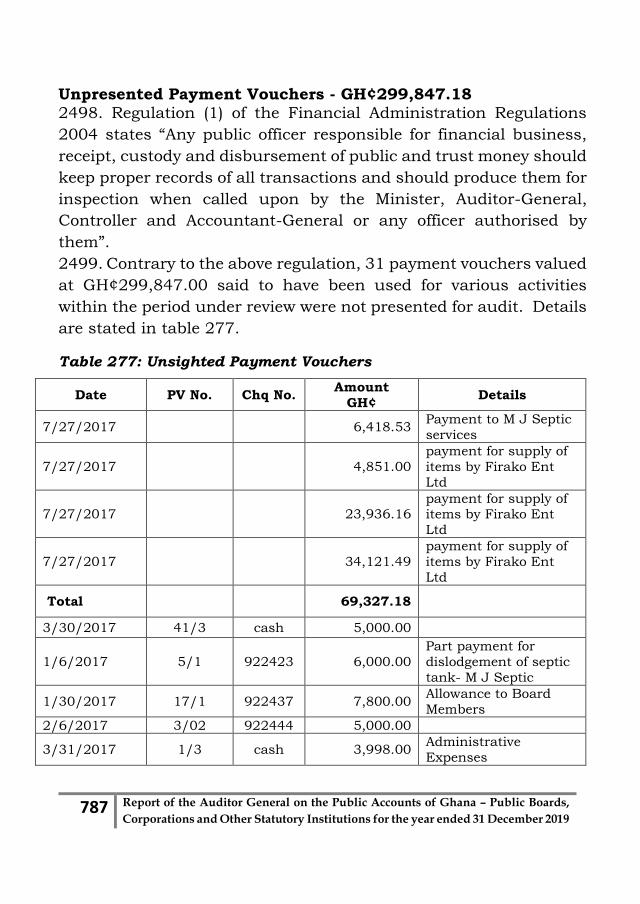

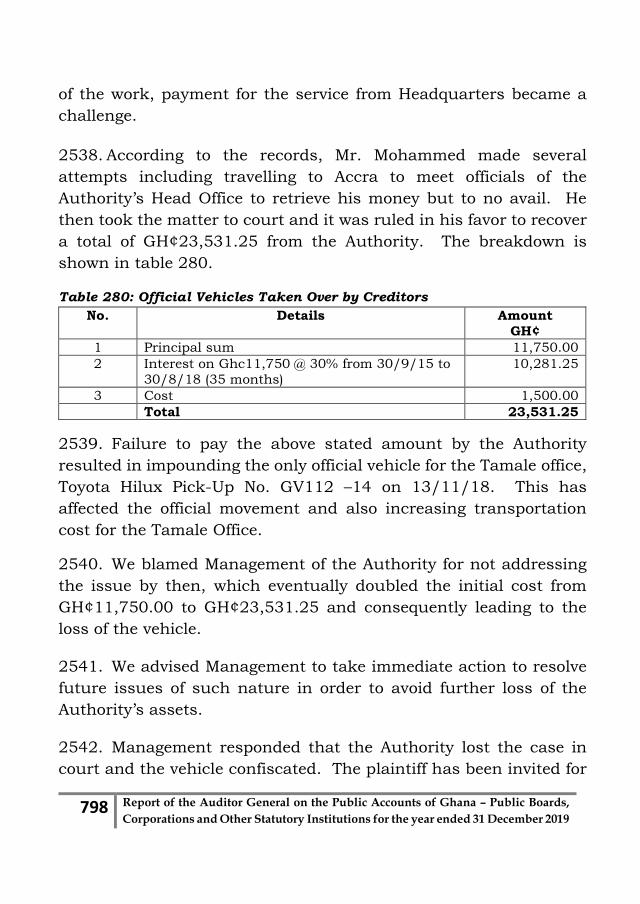

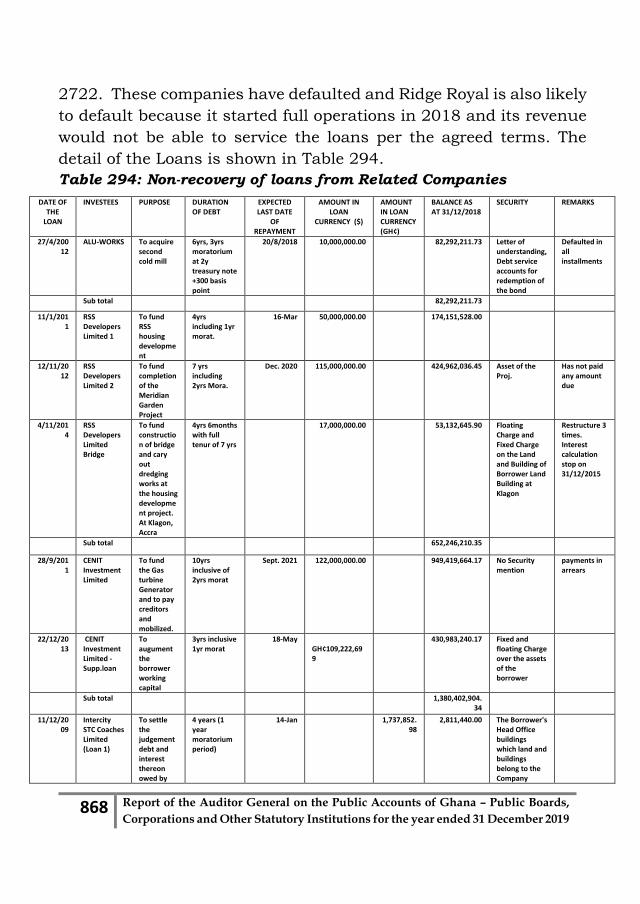

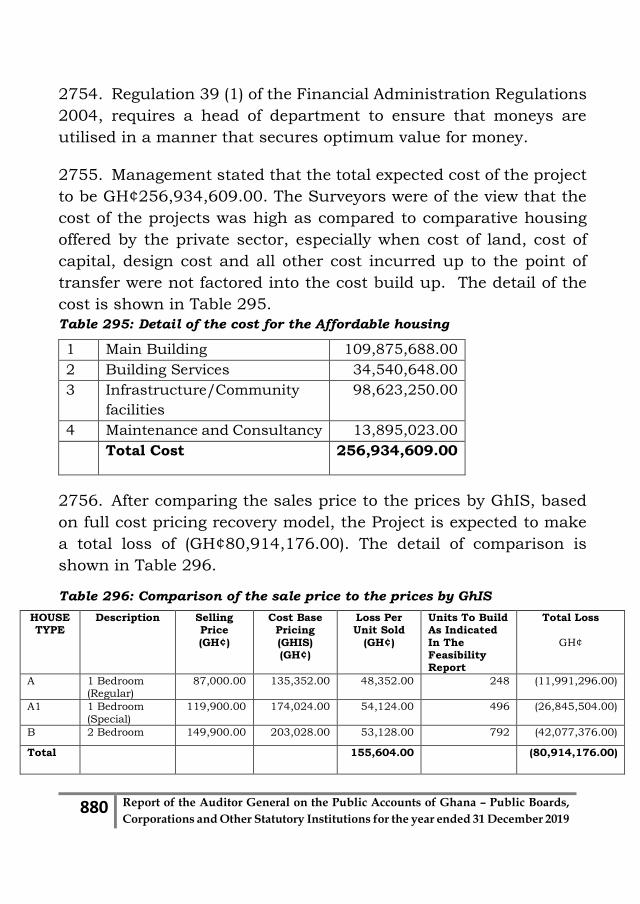

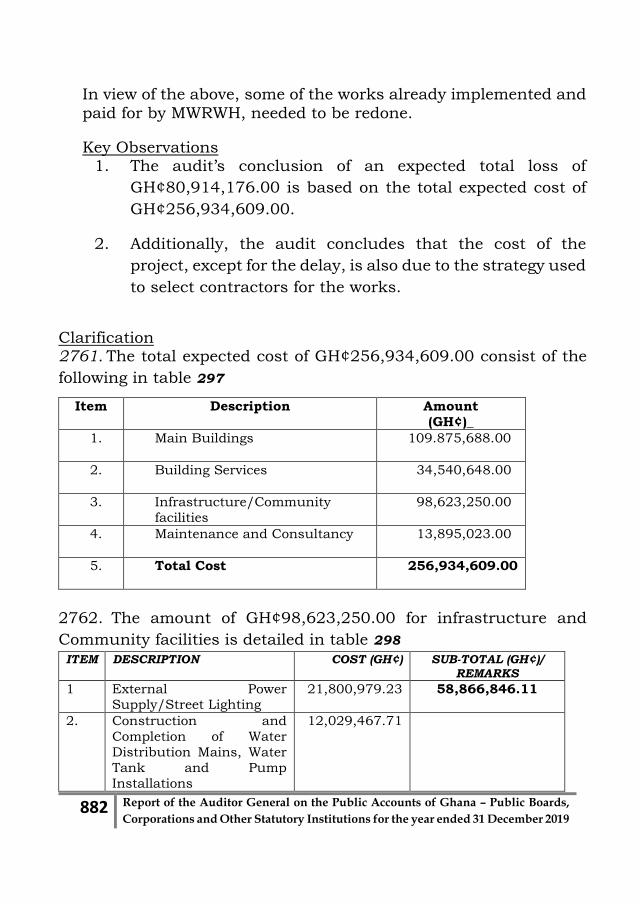

127. Contrary to Regulation 16(1)(a) of the Financial