Présentation PowerPoint - Bolloré

23

septembre 2007 2008 interim results September 1, 2008

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Présentation PowerPoint - Bolloré

1

septembre 2007

2008 interim resultsSeptember 1, 2008

2

20

40

60

80

100

120

140

160

180

Bolloré SBF 250 indexed

CHANGE IN SHARE PRICE

Bolloré (formerly Bolloré Investissement) share price

in € (monthly averages)

2008 interim results

3

ORGANISATION CHART ON JUNE 30, 2008

Delisting of Nord-Sumatra Investissements in January 2008

The squeeze-out offer that followed Bolloré’spublic bid for Nord-Sumatra Investissementsended in January 2008. The cost of purchasing the shares totalled €61m, including €16m in the first half of 2008. The Group now owns 100% of Nord-Sumatra Investissements, which has been delisted.

Increased equity stake in Bolloré

The Group once again raised its stake in Bolloré during the first half of 2008. Nord-Sumatra Investissements and Compagnie du Cambodge paid €102m for 3.4% of Bolloré’sshares. As of June 30, 2008, Financière de l’Odet controlled 79% of Bolloré’s capital.

2008 interim results

2008 INTERIM RESULTS

In short:Very good activity and excellent income in the traditional businesses:

Transportation and Logistics, Fuel Turnover

1st half 2008(in € millions)

1st half 2007(in € millions)

3,361 2,744distribution Operating income 162 129

Ongoing development costs in new sectors:

Group net income of €140m, vs. €366m in the first half 2007: financial income in the first half of 2008 includes a €358m capital gain that is almost identical to that of the first half of 2007 (€346m); however, we wrote down the Havas equity stake by €204m amidst falling equity markets.

Net debt was roughly the same: €1,401m, vs. €1,301m, but falling equity markets reduced shareholders’ equity to €3,058m. The debt-to-equity ratio was 0.46.

4

Industry, Media, Telecoms, others Turnover 216 199Operating income -104 -83

Turnover +21,5% 3,577 2,943Operating income +27% 58 46

Total

2008 interim results

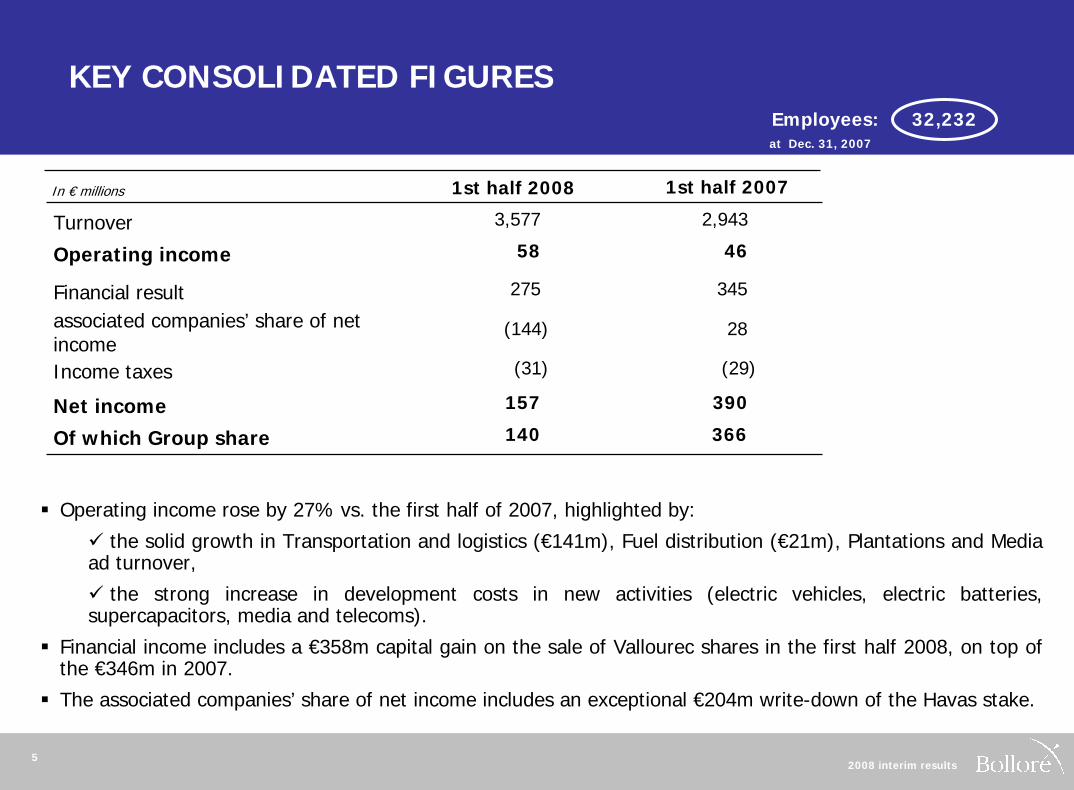

KEY CONSOLIDATED FIGURES Employees: 32,232

Turnover

Operating income

Net income

Of which Group share

In € millions 1st half 2008 1st half 2007

Financial result

3,577

275

157

140

2,943

46

390

366

345

associated companies’ share of net income

(144) 28

Income taxes (31) (29)

Operating income rose by 27% vs. the first half of 2007, highlighted by:

the solid growth in Transportation and logistics (€141m), Fuel distribution (€21m), Plantations and Media ad turnover,

the strong increase in development costs in new activities (electric vehicles, electric batteries, supercapacitors, media and telecoms).

Financial income includes a €358m capital gain on the sale of Vallourec shares in the first half 2008, on top of the €346m in 2007.

The associated companies’ share of net income includes an exceptional €204m write-down of the Havas stake.

5

58

at Dec. 31, 2007

2008 interim results

KEY CONSOLIDATED FIGURES

Capital and other equity

Net debt

Debt-to-equity ratio

In € millions At December 31, 2007

of which group share

3,515

3,269

1,301

0.37

At June 30, 2008

3,058

2,854

1,401

0.46

Capital and other equity came to €3,058m, including -€424m from the recognition at fair value of shareholdings (including a -€318m cancelling of the fair value of Vallourec shares that were sold off).

Net debt at Bolloré rose by €100m. This includes the sale of the 3.6% Vallourec stake, the purchase of listed shares (Vallourec, Bolloré, Odet, Nord-Sumatra Investissements, etc.), the recognition at fair value of financial instruments (mainly sales and acquisitions of Vallourec shares in the first half of 2008), as well as all investments in various businesses, in Transportation and logistics in Africa.

62008 interim results

7

TURNOVER

Transportation and logistics

In € millions 1st half 2008 1st half 2007

2,183 1,959

Fuel distribution 1,178 785

Industry 167 167

Media, telecoms, plantations, holdings 49 32

Turnover 3,577 2,943

Turnover rose by 21.5%, in spite of a €60m negative foreign exchange impact. On a like-for-like and constant-currency basis, turnover rose by 21.8%, thanks to a solid performance in Transportation and Logistics, sharply higher oil products prices in Fuel Distribution, and rapid growth in Media advertising revenue.

2008 interim results

OPERATING INCOME BY ACTIVITY

Transportation and logistics

Fuel distribution

Industry

Media, telecoms, plantations, holdings

Operating income

In € millions 1st half 2008 1st half 2007

141

21

(56)

(48)

58

120

9

(23)

(60)

46

Operating income rose sharply in Transportation and logistics (+17%) and Fuel distribution (+143%), on the back of a sharp rebound in sales and a heavy inventory impact.

Big improvement in results at Plantations and in Media ad turnover (x3 in one year), which partly offset costs in Media and Telecoms (Direct 8, Direct Soir, Direct Matin Plus and Bolloré Telecom).

In accordance with the Group’s strategy, operating income also includes investment in Industry, highlighted by:

- Development costs for the vehicle business launched in early 2008 (partnerships with Pininfarina and Gruau) and increased expenditure in electric batteries (Bathium, in Canada) and supercapacitors,

- Increased raw material and energy costs in industrial activities.

82008 interim results

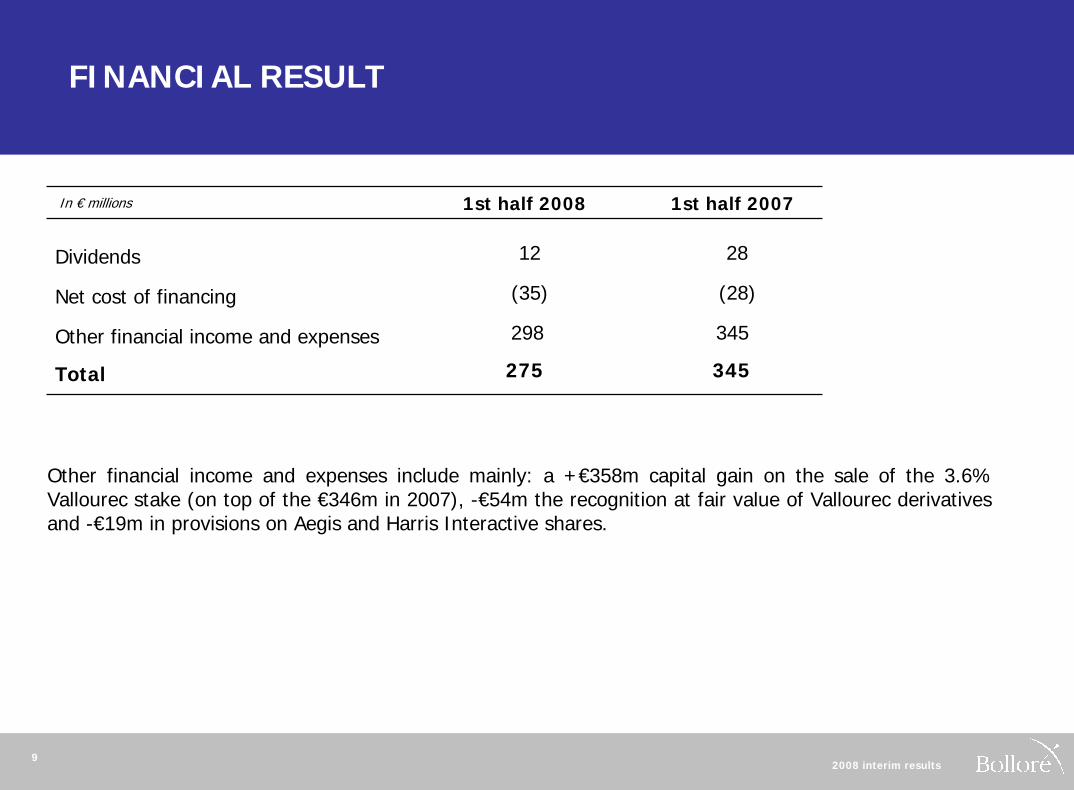

FINANCIAL RESULT

Total

Dividends

Net cost of financing

Other financial income and expenses

In € millions 1st half 2008 1st half 2007

12

(35)

298

275

28

(28)

345

345

Other financial income and expenses include mainly: a +€358m capital gain on the sale of the 3.6% Vallourec stake (on top of the €346m in 2007), -€54m the recognition at fair value of Vallourec derivatives and -€19m in provisions on Aegis and Harris Interactive shares.

92008 interim results

SHARE OF NET INCOME OF ASSOCIATED COMPANIES

associated companies’ share of net income

In € millions 1st half 2008 1st half 2007

(144) 28

The associated companies’ share of net income mainly includes:

Havas: €14m net income share prior to the €204m write-down on the shares, in spite of a 40% increase in the Group net profit of the Havas group, to €49m.

Plantations: €45m net income share, including the impact of revaluation of biological assets (IAS41).

102008 interim results

CASH FLOW

Change in WCR (+= reduction)

Net cash flow from operating activitiesNet industrial investments

In € millions

Net financial investments

Dividends paid

Change in net debt(- = increase in debt)

Cash flow

June 30, 2008

Capital gains and dividends from companies consolidated by the equity method

(73)

421

(58)

11

133

(45)

(100)

(352)

Change in fair value and other items (126)

December 31, 2007

(215)

482

(44)

69

12

(42)

113

(63)

(369)

The increase in WCR is due mainly to the sharp increase in oil product inventories in the Fuel distribution division.

112008 interim results

TRANSPORTATION AND LOGISTICS

Turnover

Operating income

In € millions

Investments (1)

1st half 2008 1st half 2007

2,183

141

75

1,959

120

117

+11%

+17%

(1) including acquisitions of White Horse in South Africa in the first half 2008 and JE Bernard in the UK in the first half of 2007

122008 interim results

INTERNATIONAL LOGISTICS

Sustained increase in activity, despite slower growth in international trade and a stronger euro.

Ongoing strategy of development and targeted acquisitions to expand the international network:

- creation of SDV Dubai, in partnership with local players in the first half of 2008,

- joint acquisition with African transportation and logistics network of SAEL, one of South Africa’s main freight forwarding agents.

All geographical regions made a positive contribution to these results:

- France: strong business, sale of Lurit’s customer base and business (a non-core business in French and international road transport),

- Europe: sharp increase in UK turnover, where reorganisation around the single brand name SDV-Bernard has generated productivity gains,

- Rest of world: accelerated expansion, with strong trade volumes, particularly in China, India and Brazil.

132008 interim results

TRANSPORTATION AND LOGISTICS IN AFRICA

New acceleration in growth in Transportation and Logistics in Africa, and further investments in harbour infrastructure and in equipment renewal and development

West Africa: very solid performance in the Ivory Coast (increased volumes handled at the SETV terminal, sustained activity in conventional handling and transit at SDV-Saga, and strengthened traffic in the Abidjan-hinterland corridor) and stability of earnings in Senegal.

Central Africa: - improved earnings in Cameroon (sustained handling activity at DIT and SDV) and Ghana, which got the full

benefit of the Tema terminal that started up in late April 2007,- strong business in Nigeria, which benefited from growth in all businesses and increased traffic at the Lagos/Tin

Can container terminal, - the start-up of Owendo container terminal operations in Libreville (a concession won in 2007) is planned for

the second half of 2008.

East Africa: expansion in hinterland transit, thanks to mining projects and increased traffic at the two dry docks, at Mombasa, Kenya, and Dar es-Salaam, Tanzania. Ongoing extension in the network via new facilities in the horn of Africa (Djibouti and Ethiopia).

Southern Africa: very good performances thanks to major regional mining projects:- excellent earnings in Angola, thanks to activity at the Luanda base and further developments at Lobito, Soyo

and Cabinda,- growth in South African transit activity, among others through the acquisition of White Horse, a benchmark

transporter in the Copper Belt corridor,- solid earnings in Madagascar, thanks to mining projects, as well as in the Democratic Republic of Congo and

handling and maritime freight.

142008 interim results

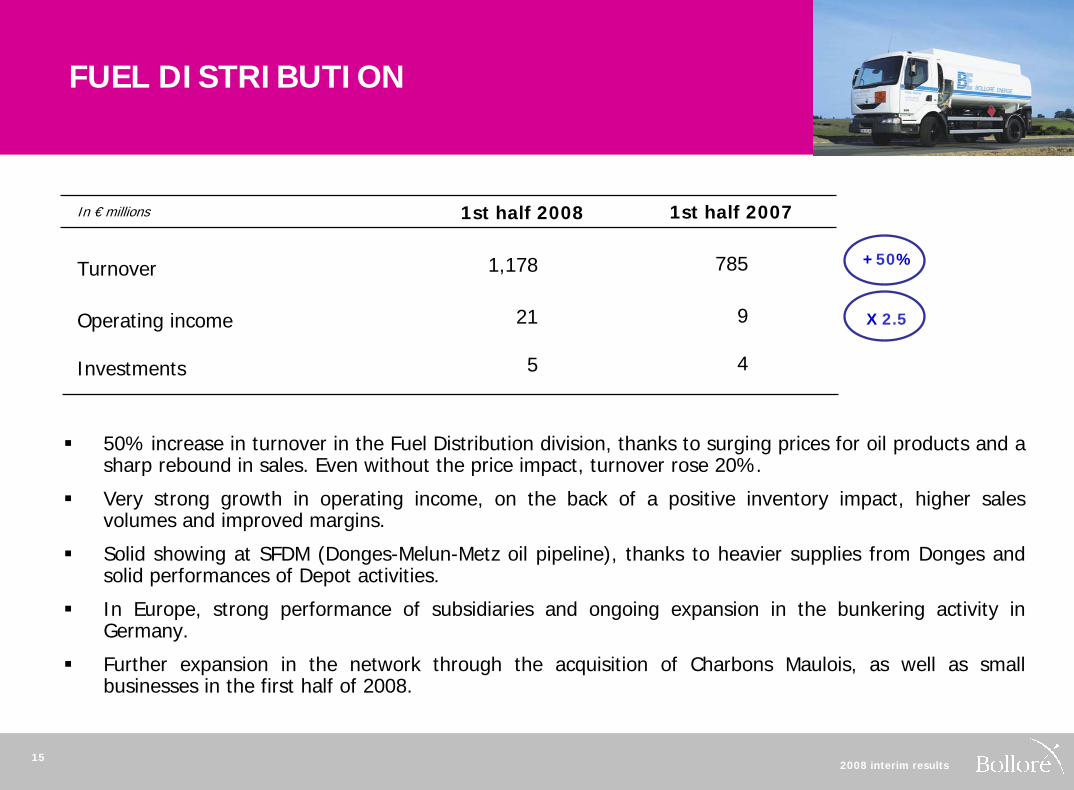

FUEL DISTRIBUTION

Turnover

Operating income

In € millions

Investments

1st half 20071st half 2008

1,178

21

5

785

9

4

+50%

X 2.5

50% increase in turnover in the Fuel Distribution division, thanks to surging prices for oil products and a sharp rebound in sales. Even without the price impact, turnover rose 20%.

Very strong growth in operating income, on the back of a positive inventory impact, higher sales volumes and improved margins.

Solid showing at SFDM (Donges-Melun-Metz oil pipeline), thanks to heavier supplies from Donges and solid performances of Depot activities.

In Europe, strong performance of subsidiaries and ongoing expansion in the bunkering activity in Germany.

Further expansion in the network through the acquisition of Charbons Maulois, as well as small businesses in the first half of 2008.

152008 interim results

INDUSTRY

Turnover

Operating income

In € millions

Investments

1st half 20071st half 2008

167

(56)

10

167

(23)

15

Increased development expenditure in new high-technology products : including electric vehicles, electric batteries and supercapacitors and consolidation of Bathium in Canada

A weak dollar and high raw material and energy prices continued to penalise traditional businesses (plastic films, thin paper and IER)

162008 interim results

17

ELECTRIC BATTERIES,SUPERCAPACITORS, ELECTRIC VEHICLES

Electric batteries / Supercapacitors / Electric vehicles:

Acceleration in R&D spending in batteries and supercapacitors.

January 2008, launch of an supercapacitor industrial production unit able to produce one million components annually (a €36m investment).

Two joint-ventures set up to develop electric vehicles:

VEPB (Véhicule Electrique Pininfarina Bolloré): 50/50 Bolloré-Pininfarina joint-venture to design and produce an electric car.

Gruau Microbus: a 50/50 Bolloré-Gruau joint-venture to produce and market microbuses using batteries and supercapacitors produced by Batscap and Bathium.

2008 interim results

18

PLASTIC FILMS, THIN PAPER,TERMINALS AND SPECIALISED SYSTEMS (IER)

Plastic films:

Increased sales of dielectric films in the first half and dip in sales of shrink wrap packaging.A weak dollar and high raw material costs continued to hit these activities hard.

Thin paper:

Flat sales in thin paper in a still-difficult economic context, marked by higher raw material and energy prices, as well as excess capacity on the world market.Higher costs passed on in sale price in the first half of 2008, to compensate costs increase.Further success of new product lines (pharmaceutical notices).

IER:

IER’s turnover was down slightly, and operating income, which includes more than €5m in R&D costs, was penalised by lower margins on printer sales and by a dip in related services.Sharp increase in sales of self-service kiosks, notably in the air transport market. Increased sales of the new multi-airline 918 self-service kiosk. Solid growth in new products (Speed Boarding Gate), which partly offset the decline in terminals, printers and readers.Access control: slight decline in sales, due to the lack of major contracts (Lyon underground in 2007).Increase in RFID sales, with a fourth production line commissioned in the first half of 2008.

2008 interim results

19

PLANTATIONS

Very good results at Plantations, which were boosted by further increases in prices of rubber (+30%) and palm oil (+51%). At June 30, 2008, CPO palm oil was at $1,200/tonne, and rubber, at $3,275/tonne

Safa Cameroon (8,500 hectares of rubber and palm trees): 22% increase in oil production (9,300 tonnes), after the production cycle trough in palm groves of 2007; 15% increase in rubber output (2,350 tonnes), as young trees began producing and through external purchases.Turnover in the first half of 2008 came to €10m (+52%), thanks to higher production and sale prices. Operating income doubled, and the operating income including IAS 41 came to €10m. Safa Cameroon was the subject of an IPO on the Douala exchange on July 6, 2008.

Groupe Socfinal (1): the Group holds almost 39% of Socfinal, which manages 135,000 hectares of plantations in Indonesia and Africa:– Socfindo, in Indonesia, (48,000 hectares of palm and rubber trees): income rose 71% to almost $48m,

thanks to the sharp increase in palm oil, – Okomu, in Nigeria, (14,400 hectares of palm and rubber trees): net income tripled, to $15.7m, on the

back of higher palm oil prices and as rubber began to be sold,– Socapalm (25,600 hectares of palm trees), in Cameroon: surge in earnings, due to the 40% increase in

palm oil sale prices and the 8% increase in yields,

(1) parent-company data before IFRS restatement

2008 interim results

20

PLANTATIONS

– Ferme Suisse (3,700 hectares of palm trees) in Cameroon: net income tripled to €3.6m, vs. €1.2m at end-June 2007,

– Lac, in Liberia, (14,200 hectares of rubber trees): 27% increase in earnings, to $6.2m,– SOGB, in the Ivory Coast, (22,000 hectares of palm and rubber trees): income more than doubled, to

€9.2m, thanks to higher sale prices for palm oil (+59%) and rubber (+15%).

Socfinal continues to expand with the recent acquisition of plantations in Cambodia and the Democratic Republic of Congo, where new trees were planted this year.

Other real-estate assets:– American farms: the three farms cover 2,900 hectares. Arable lands (cotton, maize, soy, peanuts) are

leased on a triennial basis, while pinewoods (600 hectares) are planted and maintained directly. – Vineyards: the two wine estates in southern France, Domaine de la Croix (a top-ranked, or cru classé,

wine) and Domaine de la Bastide Blanche, cover 230 hectares, plus 104 hectares of vineyard rights. Ongoing restoration of the vineyard, with 65% vines replanted and completion of building renovation works at Domaine de la Croix. Output: 350,000 bottles planned for 2008.

2008 interim results

21

Ongoing development in the communication-media sectors

Increased contribution of television and free newspapers• Direct 8: very sharp increase of the audience, to 1.6% in June 2008. The channel is watched each week

by more than 18 million viewers. • Personal Mobile Television licence obtained in the first half of the year.• Direct Matin Plus – Direct Soir: growing success of the free daily Direct Matin Plus, in partnership with

the national daily Le Monde and the network Ville Plus, and success of the redesigned Direct Soir. The two newspapers have been distributed since February 2008 in the main Paris Metro subway stations.

1.2 million copies distributed daily.• Advertising revenue tripled in one year. Media costs came to €37m, vs. €41m in the first half of 2007.

Audiovisual and cinema logistics• Euro Média Group: Bolloré has owned 22% of EMG since the merger of Euro Média Télévision with UBF.

In the first half of the year, EMG acquired the audiovisual company Transpalux, and generated turnover of €147m.

• The Group owns almost 10% of the shares in Gaumont and also owns the Mac-Mahon cinema in Paris.

COMMUNICATION, MEDIA

2008 interim results

22

COMMUNICATION, MEDIA

Investments in advertising and market studies

• Strong increase of Havas results (of which the Group owns 32.9%) in the first half of 2008: - turnover of €755m, record organic growth of +8%,- operating income of €91m, up 21%, and Group net income of €49m, up 40%,- net indebtedness down significantly: €340m at June 30, 2008, vs. €430m one year earlier.

• 29.84% stake in Aegis Group Plc, one of the top independent groups of specialised media buying and marketing services agencies, and also one of the largest market survey companies.

• Equity stake raised to 100% in the market study and survey institute CSA in July 2008. CSA generated a turnover of €13.7m in the first half of 2008, up 17%.

• Stake of about 13% in Harris Interactive, a US company specialising in Internet studies.

Expansion in telecoms

• After obtaining 12 WiMax licences in July 2006, Bolloré Telecom acquired eight new regional licences in the second half of 2008, subject to the approval of ARCEP, the French telecommunications authority. The company is preparing to roll out the network and is testing the pilot equipment offered by manufacturers. Cumulative expenditure at this point, including the costs of the licences: about €100m.

• Further roll-out of Wifirst, which equips and sells wireless high-speed Internet services, notably in student dormitories. Number of rooms equipped: 42,000.

2008 interim results

SHAREHOLDINGS

At June 30, 2008, following the sale of a portion of the Vallourec equity stake for €400m, the Group’s portfolio of listed shareholdings was worth €988m (€1,431m when including the 4.99% stake in Mediobanca, which is held at the level of Financière de l’Odet)

Update on the main equity stakes:

Vallourec: after selling 3.5% of Vallourec in 2007 for €377m (including a €346m capital gain), the Group sold another 3.6% in January 2008 for €400m, generating a €358m capital gain. Following these transactions and the fall in the share price, the Group decided to raise its Vallourec stake again, and now holds a 2.02% equity stake (acquisition of shares for €111m in 2008), some of which is hedged, thus limiting the Group’s exposure to a fall in the share price.

Havas: at June 30, 2008, Groupe Bolloré owned 32.9% of the equity in Havas, with a market value of €331m. In income from associated companies Havas accounted for €14m in the first half of 2008, prior to a €204m write-down in the value of the shares.

Aegis: Groupe Bolloré owned 29.84%(1) of the equity in Aegis at June 30, 2008, with a market value of€468m.The fall in Aegis’ share price in 2008 and in sterling generated a -€9m earnings impact (write-downs in the value of the shares).

232008 interim results

(1) of which 0.8% owned by Bolloré Participations.