PRELIMINARY DECISION Energex determination 2015−16 ...

309

7-0 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20 PRELIMINARY DECISION Energex determination 2015−16 to 2019−20 Attachment 7 − Operating expenditure April 2015

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of PRELIMINARY DECISION Energex determination 2015−16 ...

7-0 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

PRELIMINARY DECISION

Energex determination 2015−16

to 2019−20

Attachment 7 − Operating

expenditure

April 2015

7-1 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

© Commonwealth of Australia 2015

This work is copyright. In addition to any use permitted under the Copyright Act 1968, all

material contained within this work is provided under a Creative Commons Attributions 3.0

Australia licence, with the exception of:

the Commonwealth Coat of Arms

the ACCC and AER logos

any illustration, diagram, photograph or graphic over which the Australian Competition and

Consumer Commission does not hold copyright, but which may be part of or contained

within this publication. The details of the relevant licence conditions are available on the

Creative Commons website, as is the full legal code for the CC BY 3.0 AU licence.

Requests and inquiries concerning reproduction and rights should be addressed to the Director,

Corporate Communications,

Australian Competition and Consumer Commission,

GPO Box 4141, Canberra ACT 2601

Inquiries about this publication should be addressed to:

Australian Energy Regulator

GPO Box 520

Melbourne Vic 3001

Tel: (03) 9290 1444

Fax: (03) 9290 1457

Email: [email protected]

7-2 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

Note

This attachment forms part of the AER's preliminary decision on Energex's 2015–20

distribution determination. It should be read with all other parts of the preliminary

decision.

The preliminary decision includes the following documents:

Overview

Attachment 1 – Annual revenue requirement

Attachment 2 – Regulatory asset base

Attachment 3 – Rate of return

Attachment 4 – Value of imputation credits

Attachment 5 – Regulatory depreciation

Attachment 6 – Capital expenditure

Attachment 7 – Operating expenditure

Attachment 8 – Corporate income tax

Attachment 9 – Efficiency benefit sharing scheme

Attachment 10 – Capital expenditure sharing scheme

Attachment 11 – Service target performance incentive scheme

Attachment 12 – Demand management incentive scheme

Attachment 13 – Classification of services

Attachment 14 – Control mechanism

Attachment 15 – Pass through events

Attachment 16 – Alternative control services

Attachment 17 – Negotiated services framework and criteria

Attachment 18 – Connection policy

7-3 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

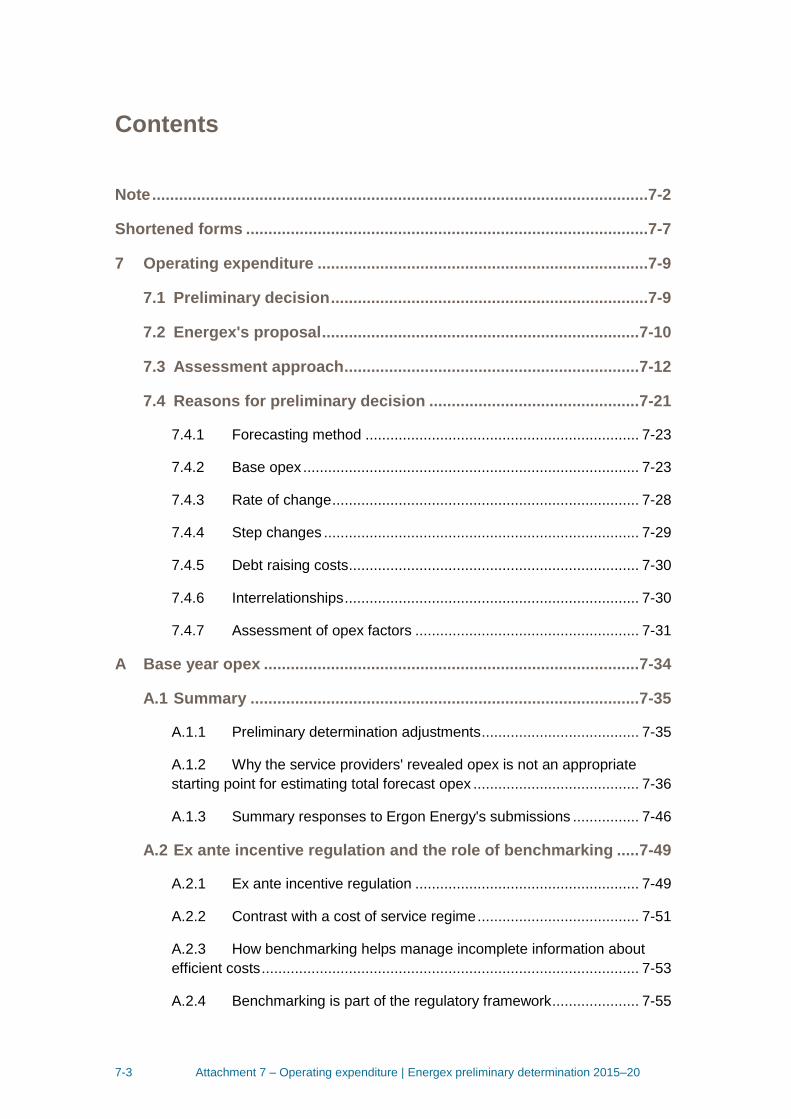

Contents

Note ...............................................................................................................7-2

Shortened forms ..........................................................................................7-7

7 Operating expenditure ..........................................................................7-9

7.1 Preliminary decision .......................................................................7-9

7.2 Energex's proposal ....................................................................... 7-10

7.3 Assessment approach .................................................................. 7-12

7.4 Reasons for preliminary decision ............................................... 7-21

7.4.1 Forecasting method .................................................................. 7-23

7.4.2 Base opex ................................................................................. 7-23

7.4.3 Rate of change .......................................................................... 7-28

7.4.4 Step changes ............................................................................ 7-29

7.4.5 Debt raising costs ...................................................................... 7-30

7.4.6 Interrelationships ....................................................................... 7-30

7.4.7 Assessment of opex factors ...................................................... 7-31

A Base year opex .................................................................................... 7-34

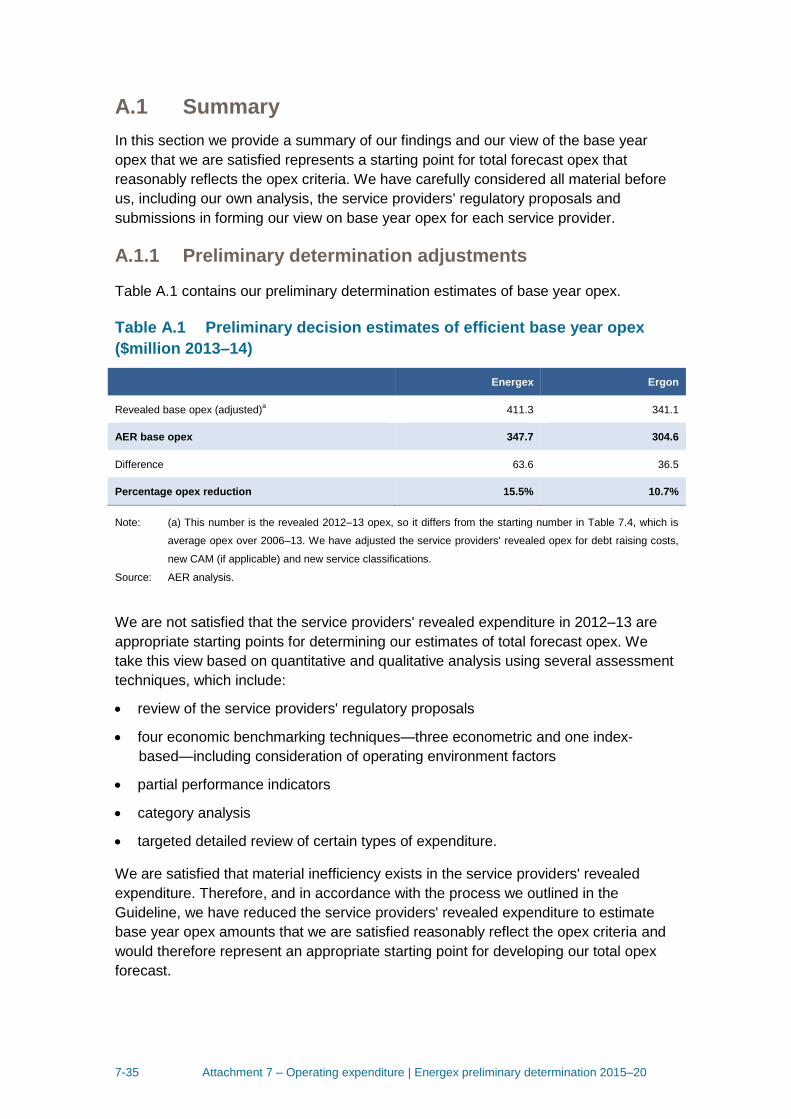

A.1 Summary ....................................................................................... 7-35

A.1.1 Preliminary determination adjustments ...................................... 7-35

A.1.2 Why the service providers' revealed opex is not an appropriate

starting point for estimating total forecast opex ........................................ 7-36

A.1.3 Summary responses to Ergon Energy's submissions ................ 7-46

A.2 Ex ante incentive regulation and the role of benchmarking ..... 7-49

A.2.1 Ex ante incentive regulation ...................................................... 7-49

A.2.2 Contrast with a cost of service regime ....................................... 7-51

A.2.3 How benchmarking helps manage incomplete information about

efficient costs ........................................................................................... 7-53

A.2.4 Benchmarking is part of the regulatory framework ..................... 7-55

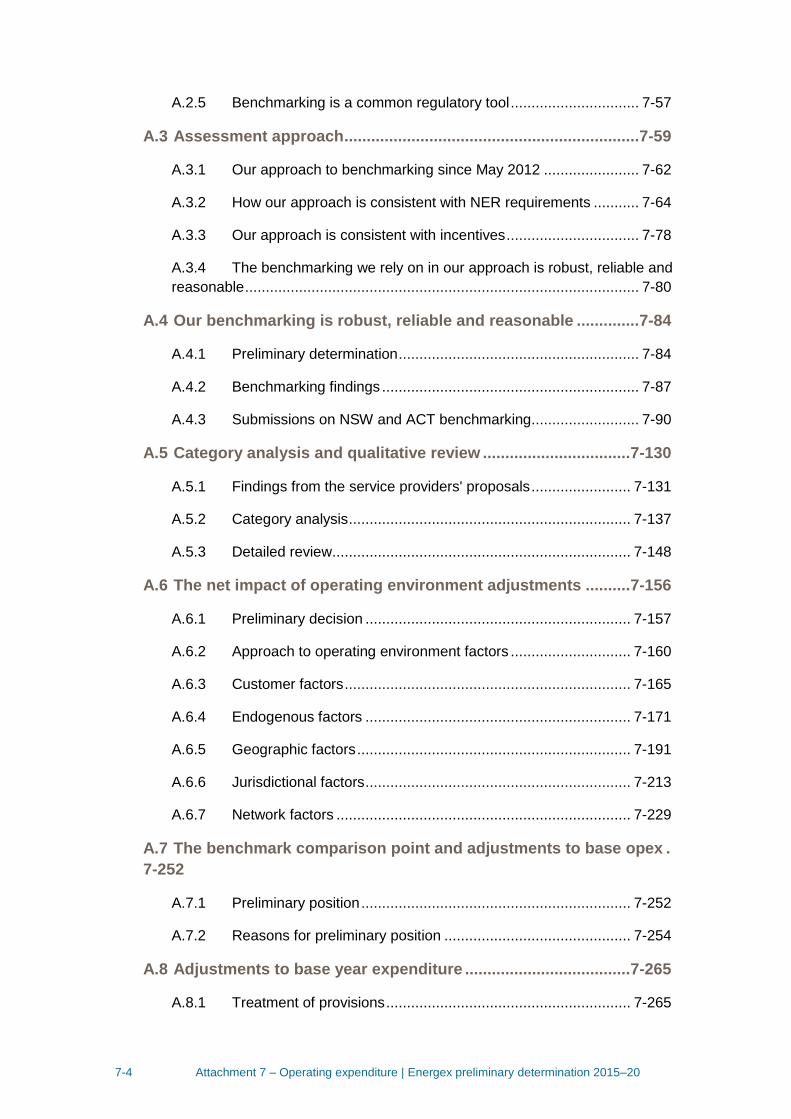

7-4 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

A.2.5 Benchmarking is a common regulatory tool ............................... 7-57

A.3 Assessment approach .................................................................. 7-59

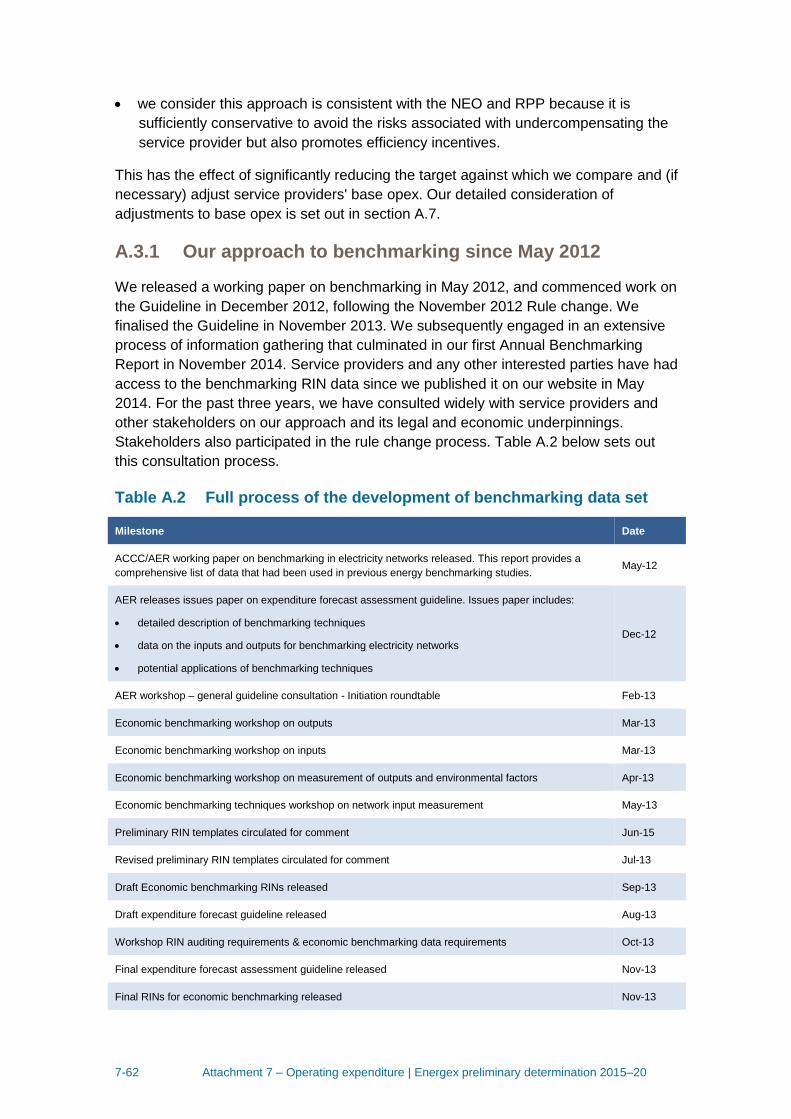

A.3.1 Our approach to benchmarking since May 2012 ....................... 7-62

A.3.2 How our approach is consistent with NER requirements ........... 7-64

A.3.3 Our approach is consistent with incentives ................................ 7-78

A.3.4 The benchmarking we rely on in our approach is robust, reliable and

reasonable ............................................................................................... 7-80

A.4 Our benchmarking is robust, reliable and reasonable .............. 7-84

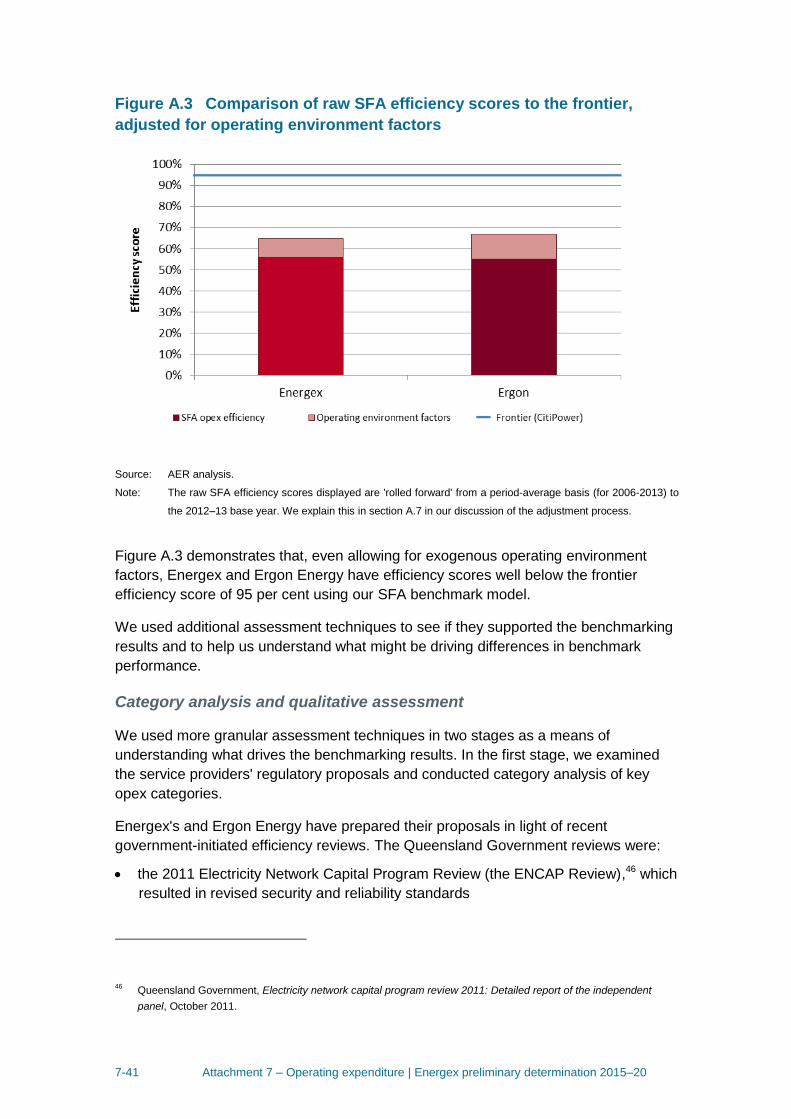

A.4.1 Preliminary determination .......................................................... 7-84

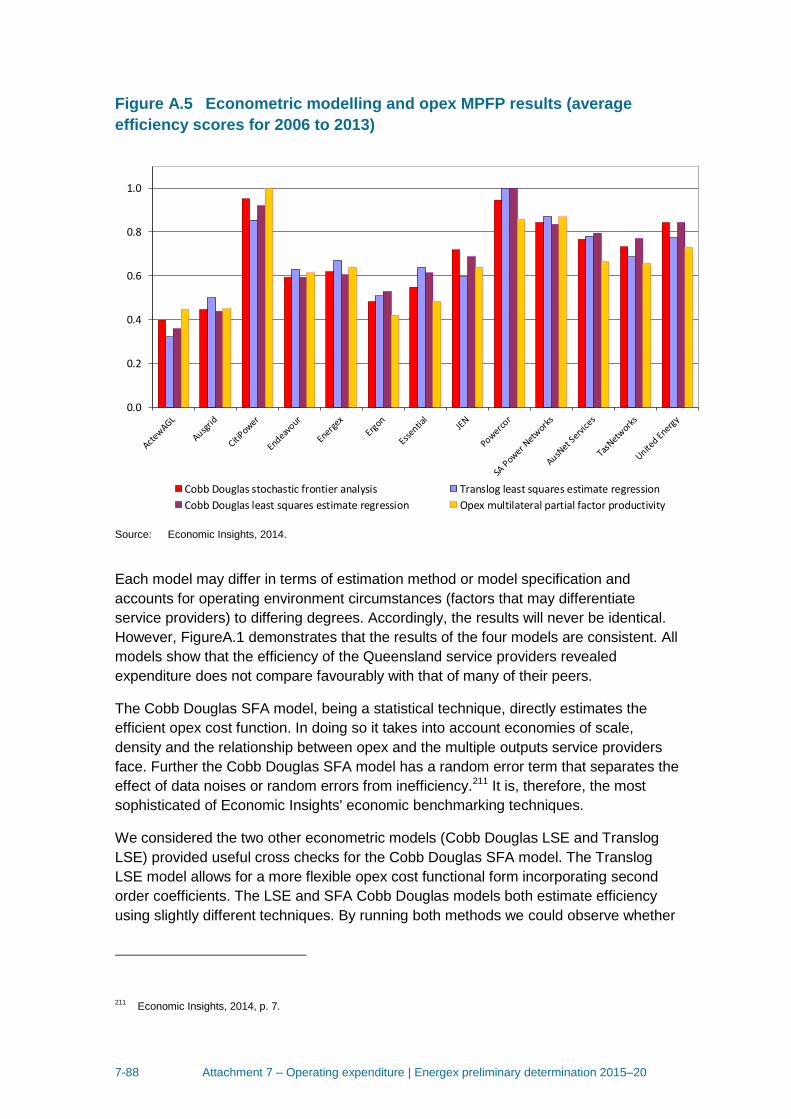

A.4.2 Benchmarking findings .............................................................. 7-87

A.4.3 Submissions on NSW and ACT benchmarking.......................... 7-90

A.5 Category analysis and qualitative review ................................. 7-130

A.5.1 Findings from the service providers' proposals ........................ 7-131

A.5.2 Category analysis .................................................................... 7-137

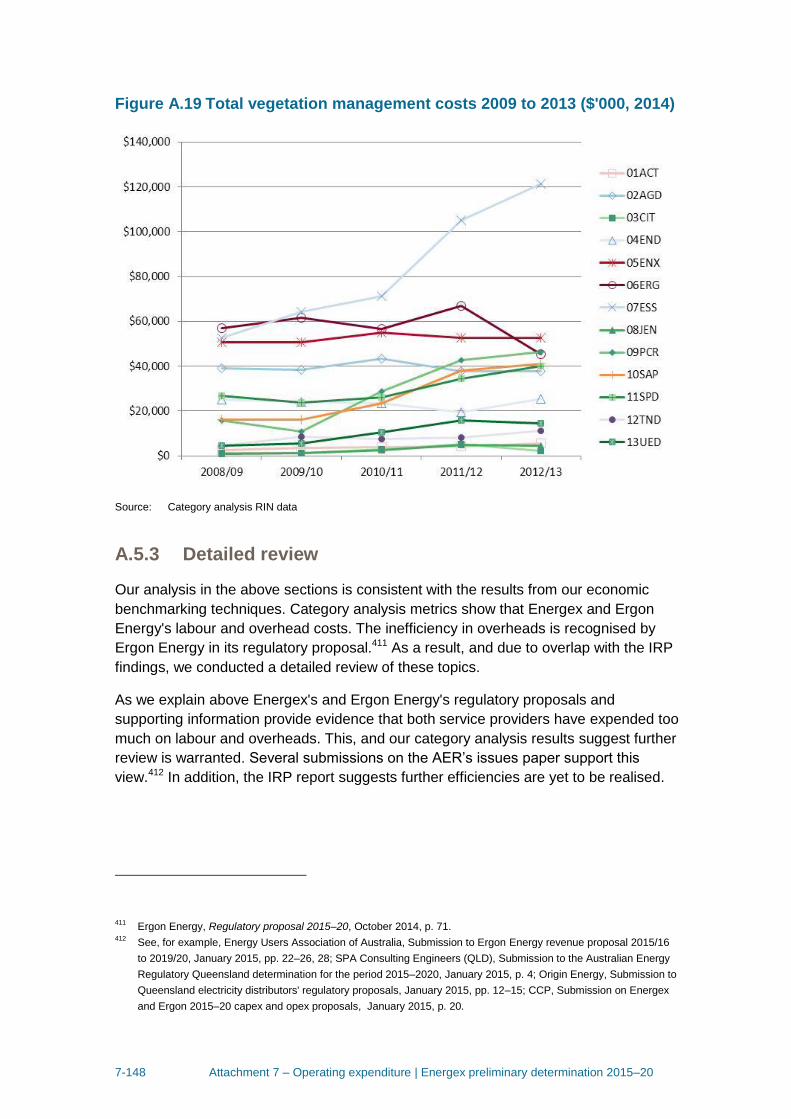

A.5.3 Detailed review........................................................................ 7-148

A.6 The net impact of operating environment adjustments .......... 7-156

A.6.1 Preliminary decision ................................................................ 7-157

A.6.2 Approach to operating environment factors ............................. 7-160

A.6.3 Customer factors ..................................................................... 7-165

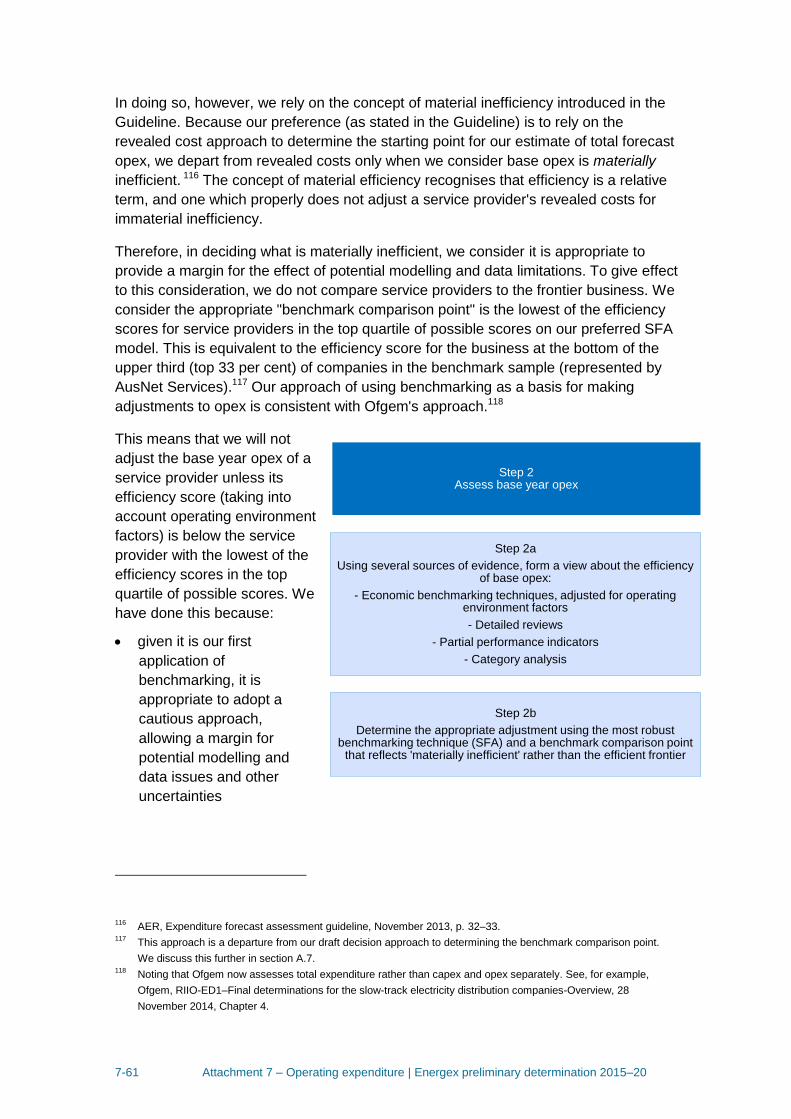

A.6.4 Endogenous factors ................................................................ 7-171

A.6.5 Geographic factors .................................................................. 7-191

A.6.6 Jurisdictional factors ................................................................ 7-213

A.6.7 Network factors ....................................................................... 7-229

A.7 The benchmark comparison point and adjustments to base opex .

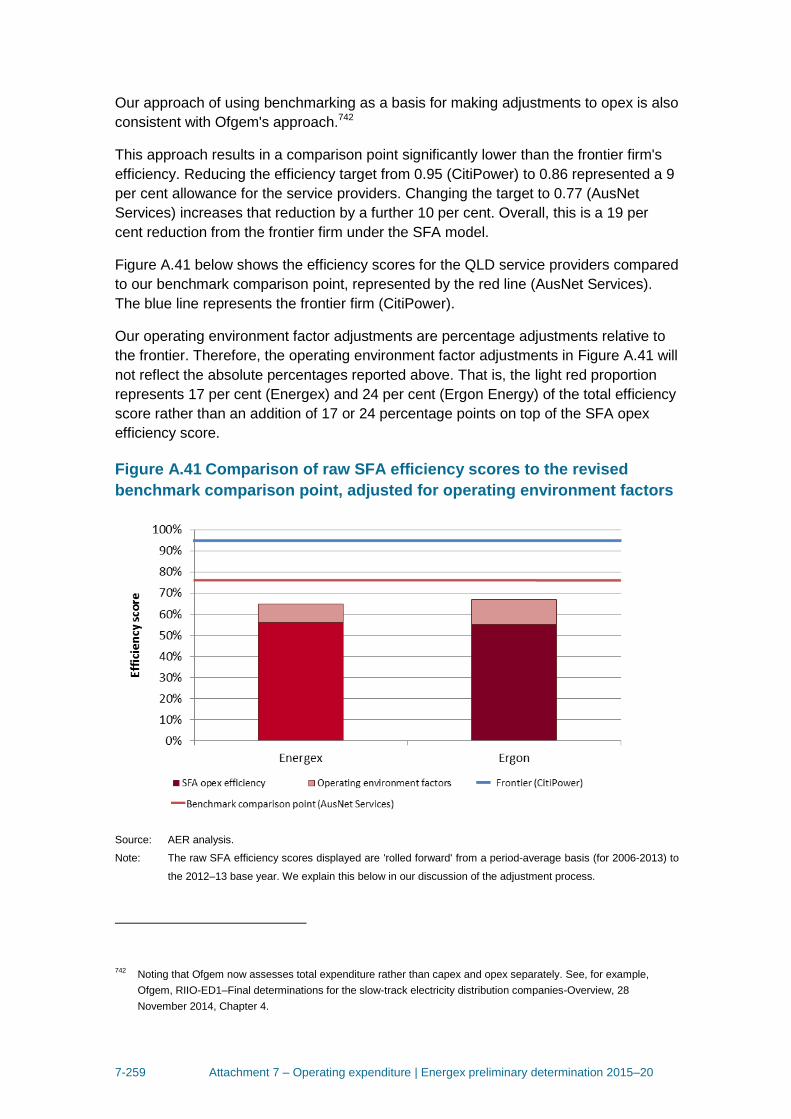

7-252

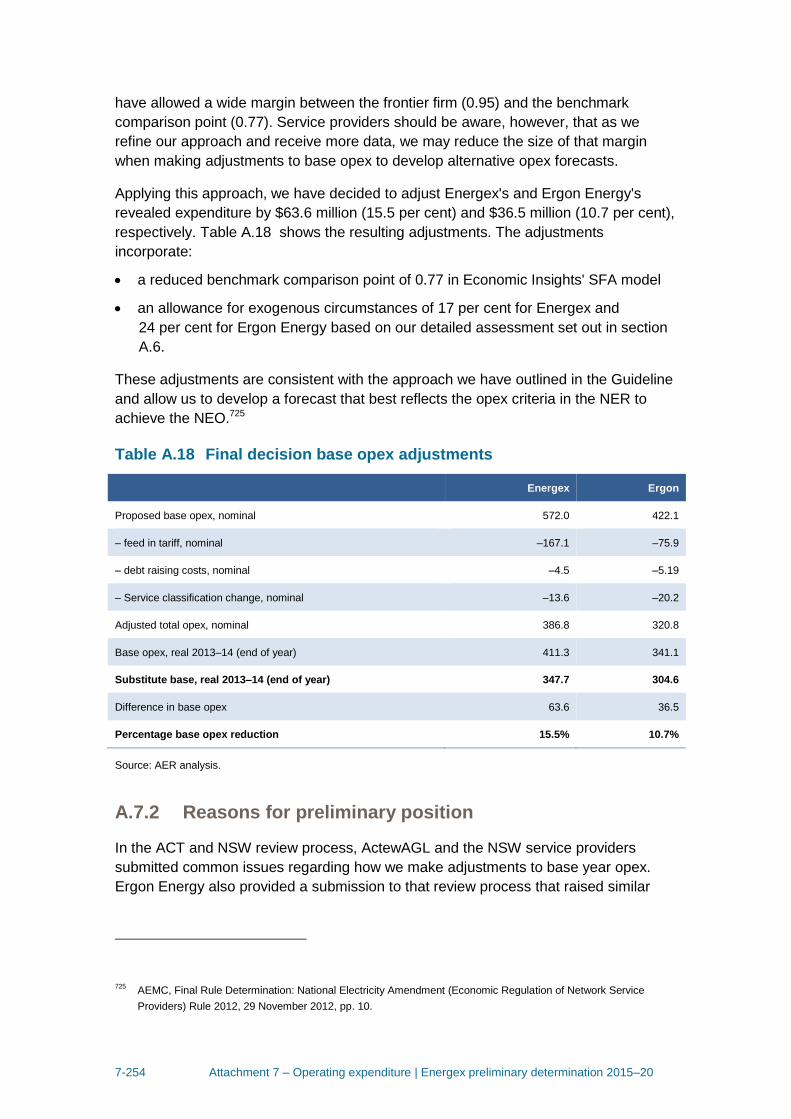

A.7.1 Preliminary position ................................................................. 7-252

A.7.2 Reasons for preliminary position ............................................. 7-254

A.8 Adjustments to base year expenditure ..................................... 7-265

A.8.1 Treatment of provisions ........................................................... 7-265

7-5 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

A.8.2 Service classification change .................................................. 7-266

A.8.3 Category specific forecasts ..................................................... 7-266

A.8.4 Non-recurrent expenditure ...................................................... 7-267

A.8.5 Step changes .......................................................................... 7-267

A.8.6 Reallocation of expenditure between functional areas ............. 7-267

A.9 Estimate of final year expenditure............................................. 7-268

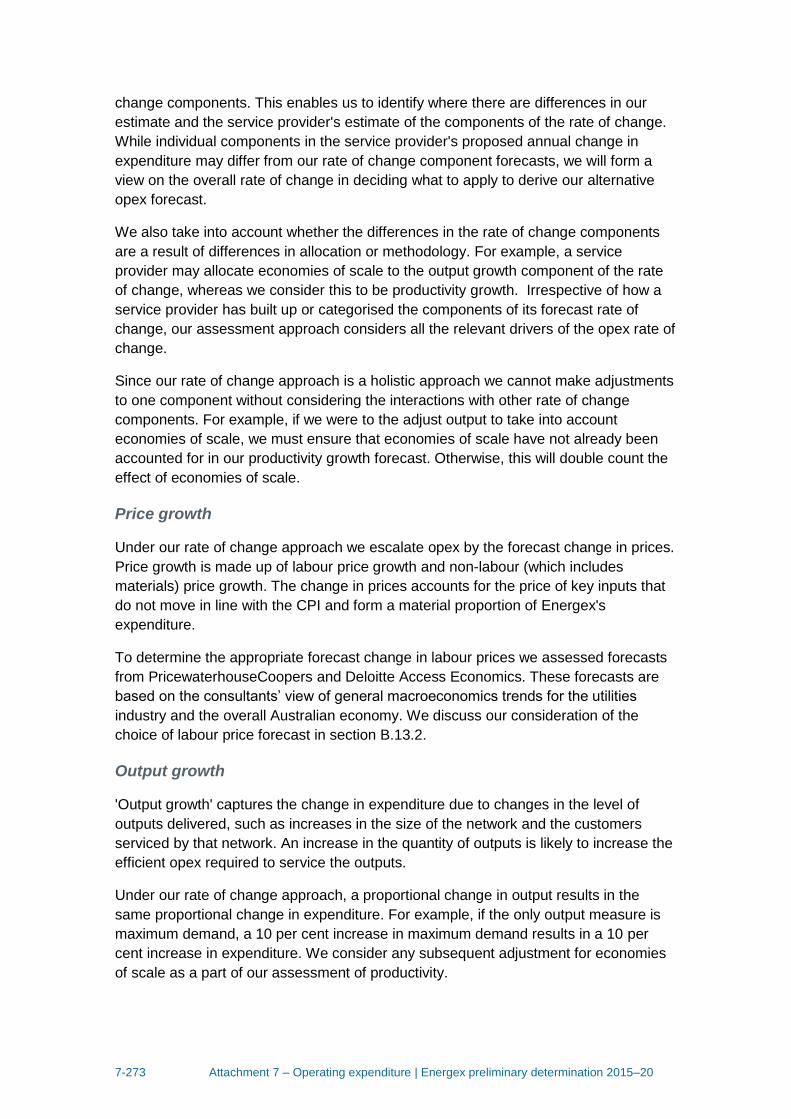

B Rate of change ................................................................................... 7-269

B.10 Position .................................................................................. 7-269

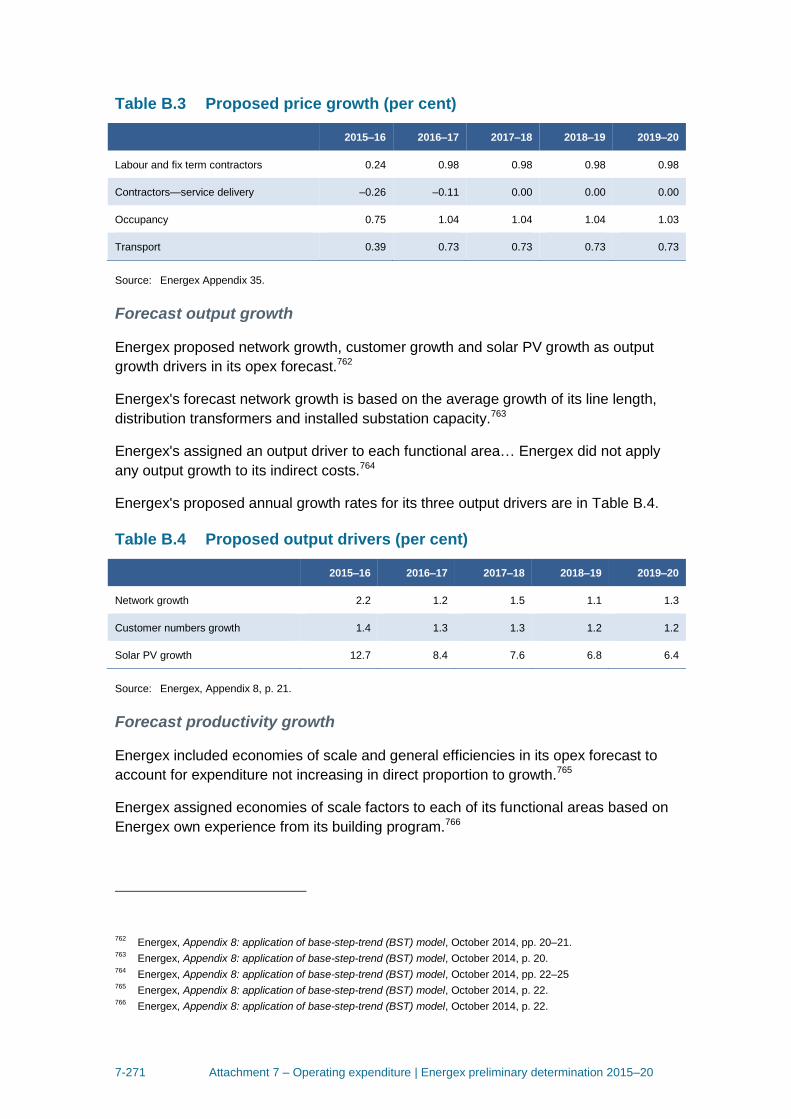

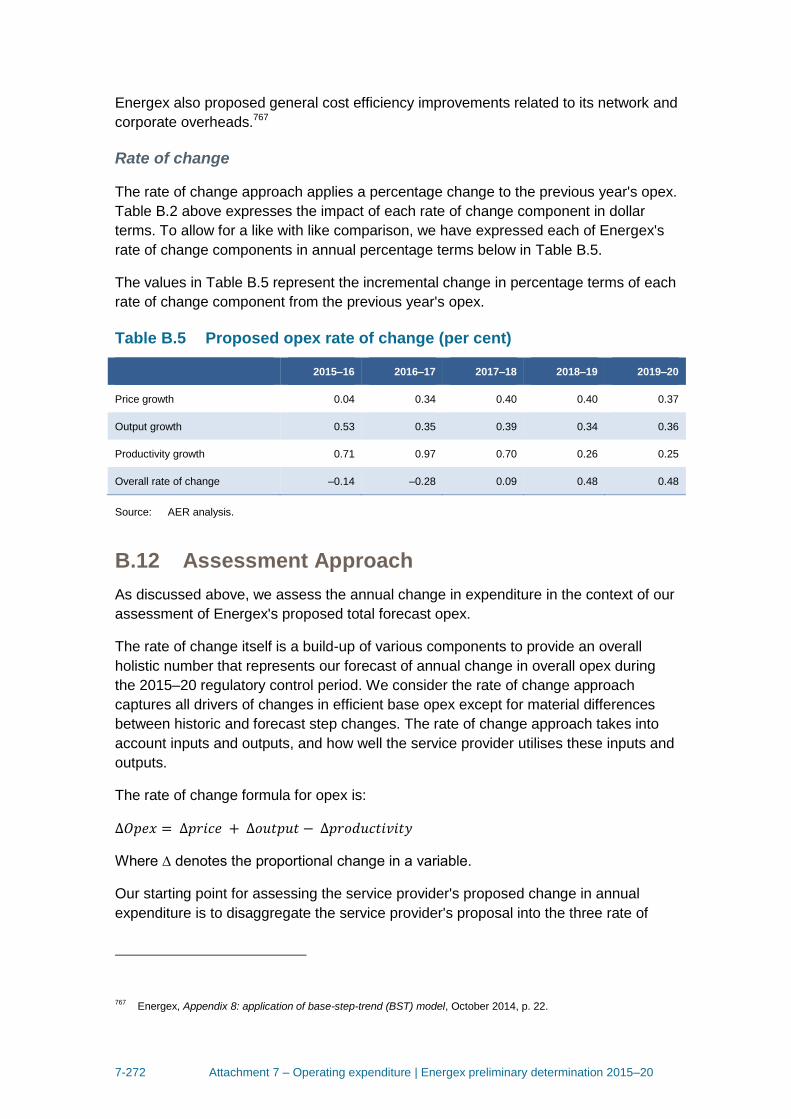

B.11 Energex proposal .................................................................. 7-270

B.12 Assessment Approach ......................................................... 7-272

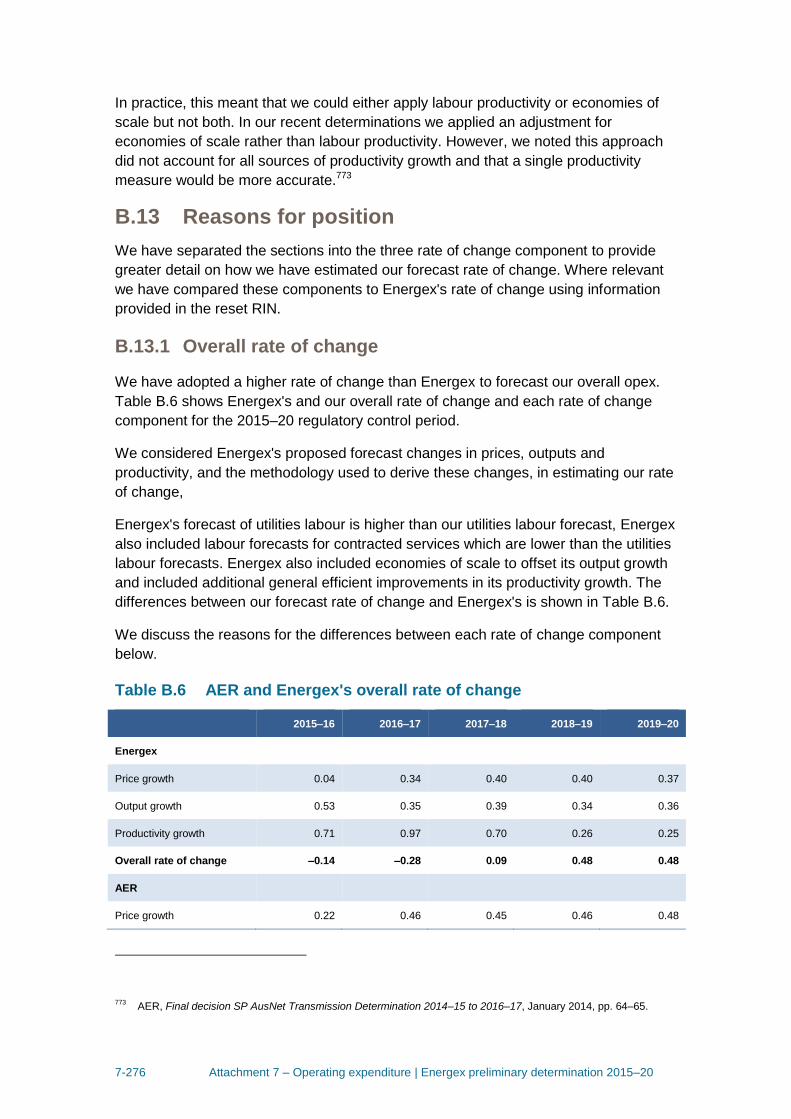

B.13 Reasons for position ............................................................ 7-276

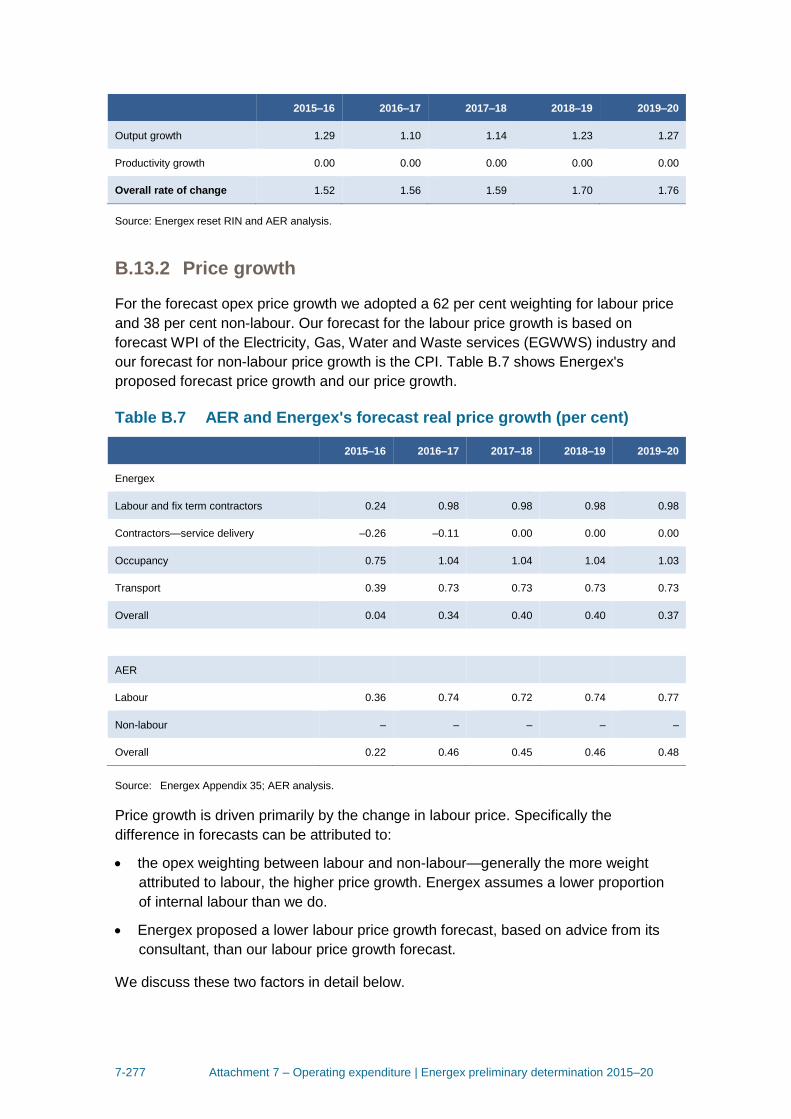

B.13.1 Overall rate of change ............................................................. 7-276

B.13.2 Price growth ............................................................................ 7-277

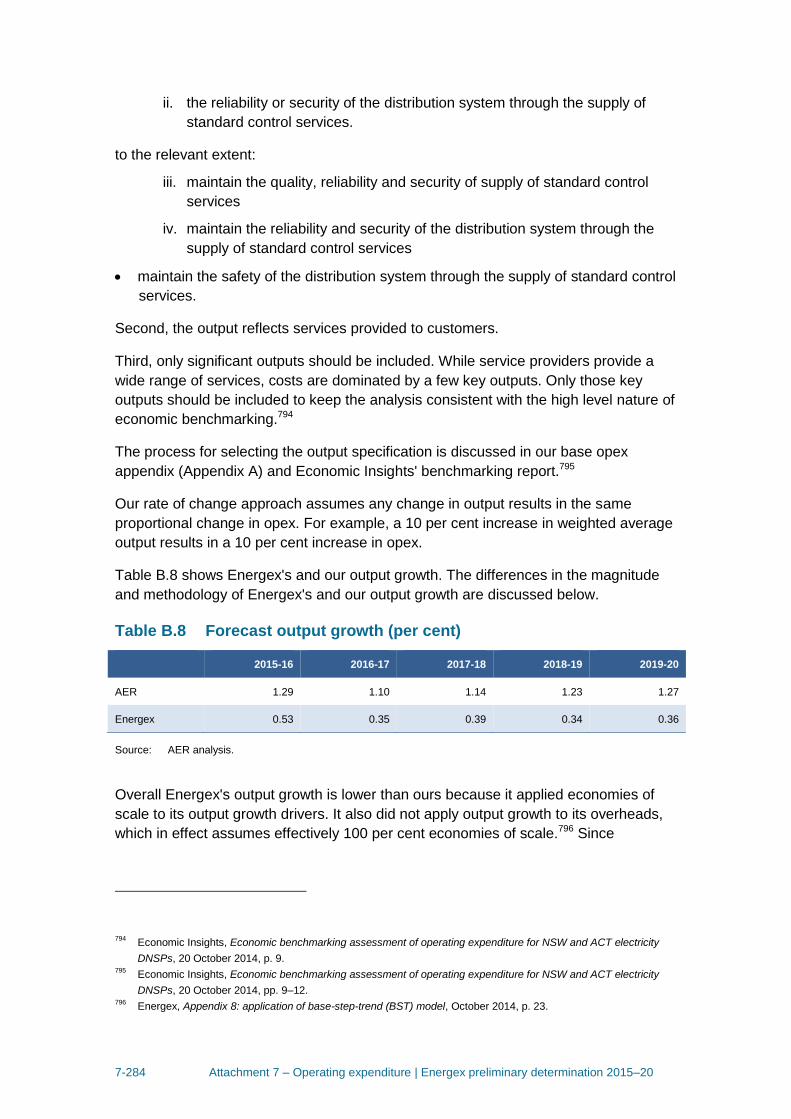

B.13.3 Output growth ......................................................................... 7-283

B.13.4 Productivity growth .................................................................. 7-286

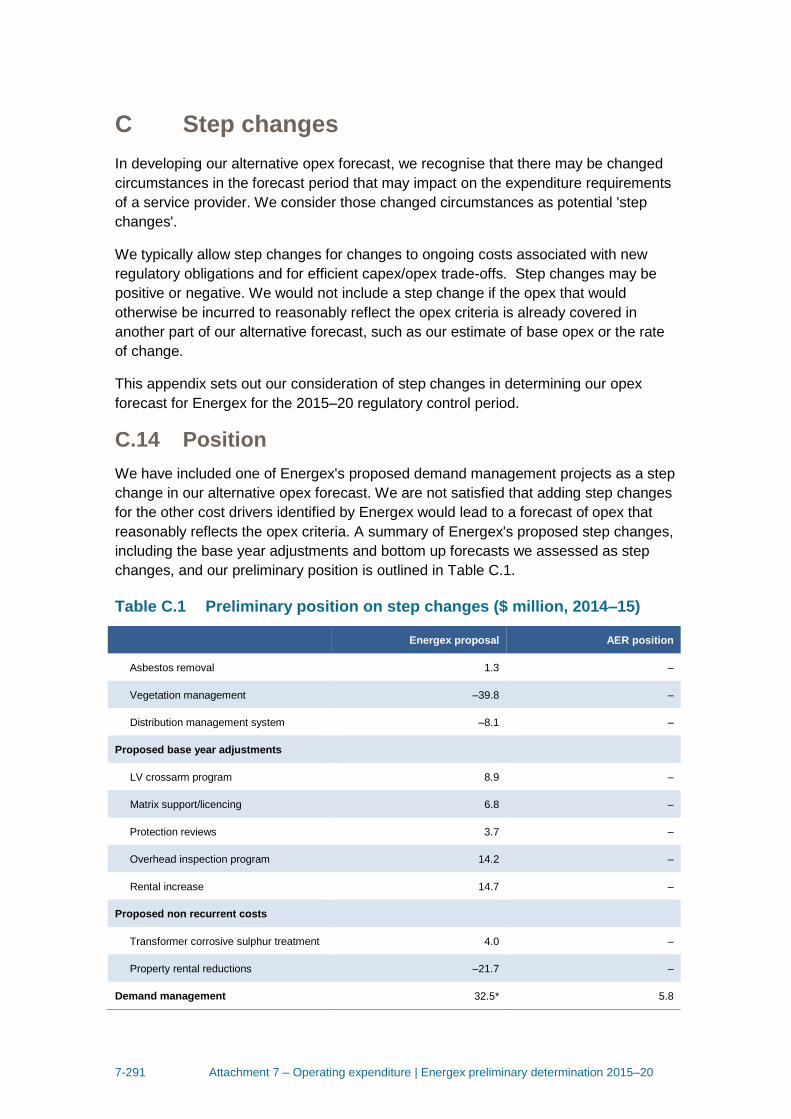

C Step changes ..................................................................................... 7-291

C.14 Position .................................................................................. 7-291

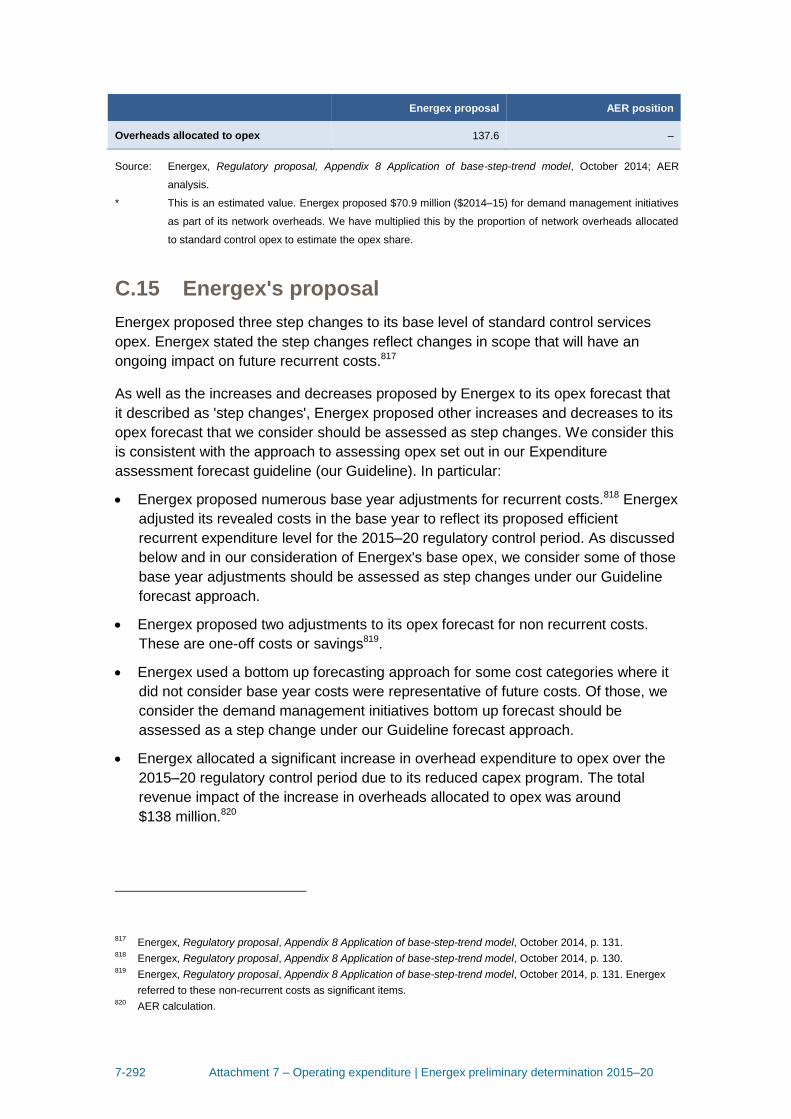

C.15 Energex's proposal ............................................................... 7-292

C.16 Assessment approach .......................................................... 7-293

C.17 Reasons for position ............................................................ 7-295

C.17.1 Proposed step changes ........................................................... 7-296

C.17.2 Proposed base year adjustments ............................................ 7-298

C.17.3 Proposed non recurrent expenditure ....................................... 7-300

C.17.4 Demand management ............................................................. 7-301

C.17.5 Increased overheads allocated to opex ................................... 7-303

D Forecasting method assessment ..................................................... 7-305

D.18 Position .................................................................................. 7-305

7-6 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

D.19 Energex's proposal ............................................................... 7-305

D.20 Assessment approach .......................................................... 7-305

D.21 Reasons for position ............................................................ 7-306

7-7 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

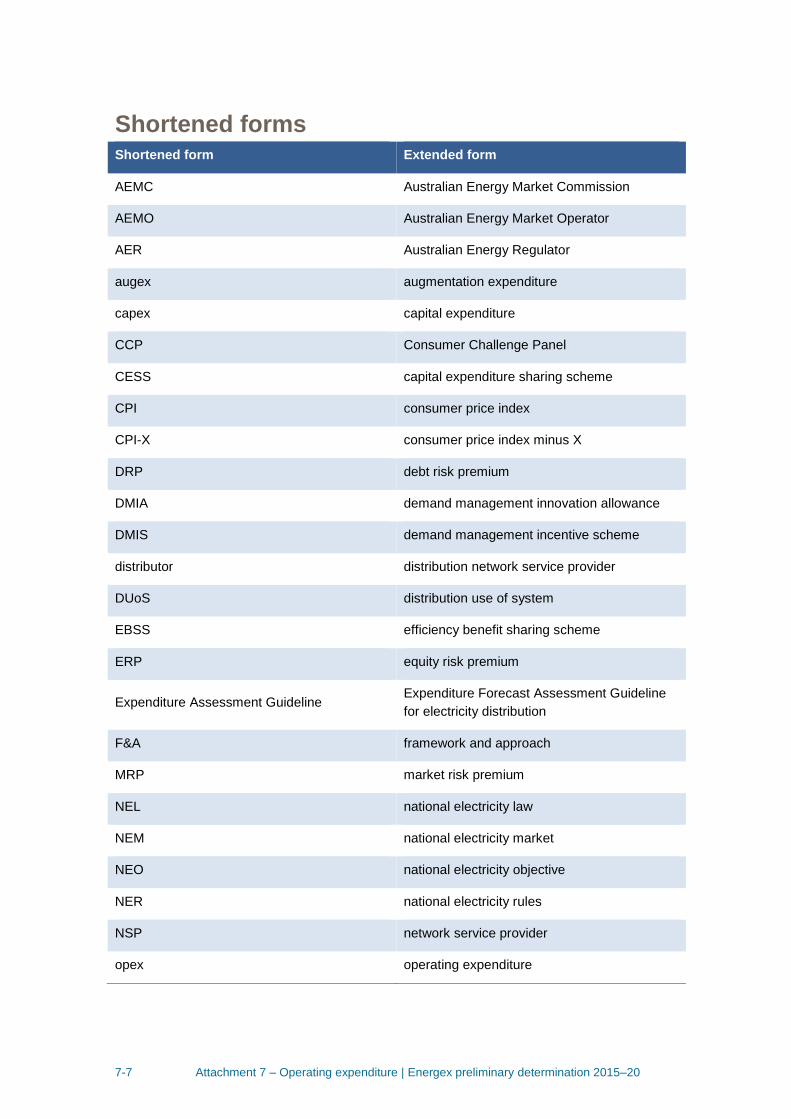

Shortened forms Shortened form Extended form

AEMC Australian Energy Market Commission

AEMO Australian Energy Market Operator

AER Australian Energy Regulator

augex augmentation expenditure

capex capital expenditure

CCP Consumer Challenge Panel

CESS capital expenditure sharing scheme

CPI consumer price index

CPI-X consumer price index minus X

DRP debt risk premium

DMIA demand management innovation allowance

DMIS demand management incentive scheme

distributor distribution network service provider

DUoS distribution use of system

EBSS efficiency benefit sharing scheme

ERP equity risk premium

Expenditure Assessment Guideline Expenditure Forecast Assessment Guideline

for electricity distribution

F&A framework and approach

MRP market risk premium

NEL national electricity law

NEM national electricity market

NEO national electricity objective

NER national electricity rules

NSP network service provider

opex operating expenditure

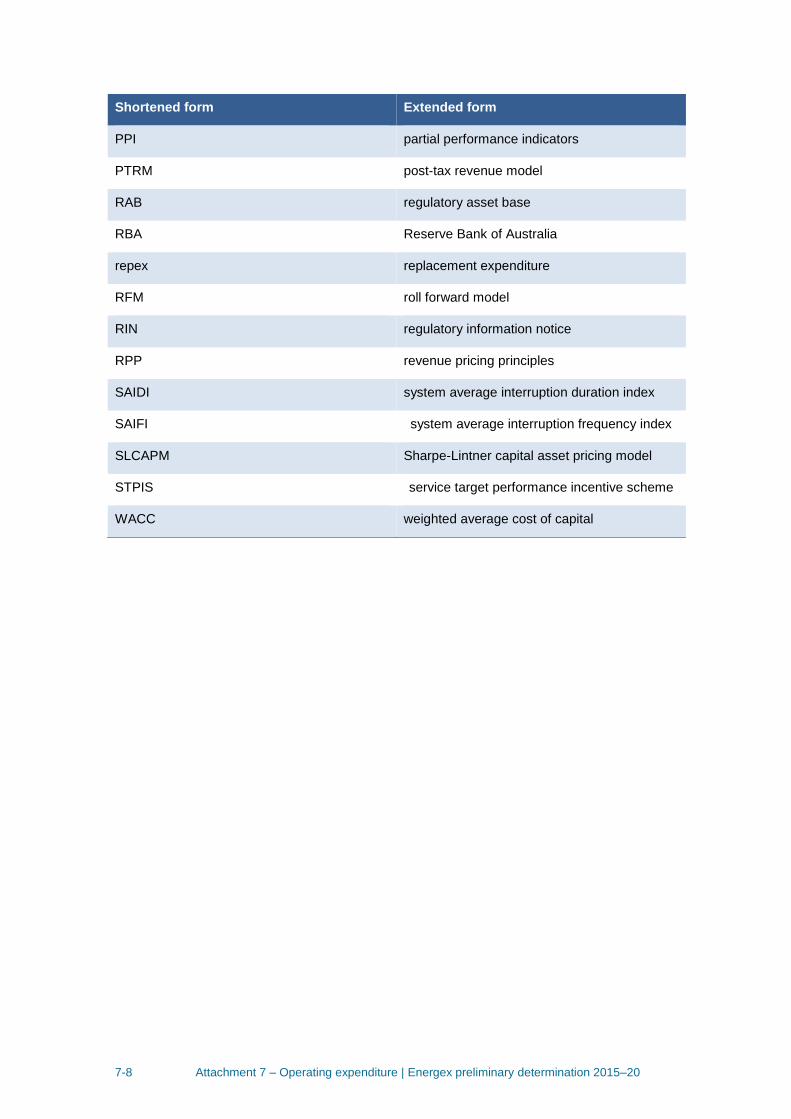

7-8 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

Shortened form Extended form

PPI partial performance indicators

PTRM post-tax revenue model

RAB regulatory asset base

RBA Reserve Bank of Australia

repex replacement expenditure

RFM roll forward model

RIN regulatory information notice

RPP revenue pricing principles

SAIDI system average interruption duration index

SAIFI system average interruption frequency index

SLCAPM Sharpe-Lintner capital asset pricing model

STPIS service target performance incentive scheme

WACC weighted average cost of capital

7-9 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

7 Operating expenditure

Operating expenditure (opex) refers to the operating, maintenance and other non-

capital expenses, incurred in the provision of network services. Forecast opex for

standard control services is one of the building blocks we use to determine a service

provider's total revenue requirement.

This attachment provides an overview of our assessment of opex. Detailed analysis of

our assessment of opex is in the following appendices:

Appendix A—Base year opex

Appendix B—Rate of change

Appendix C—Step changes

Appendix D—forecasting method assessment.

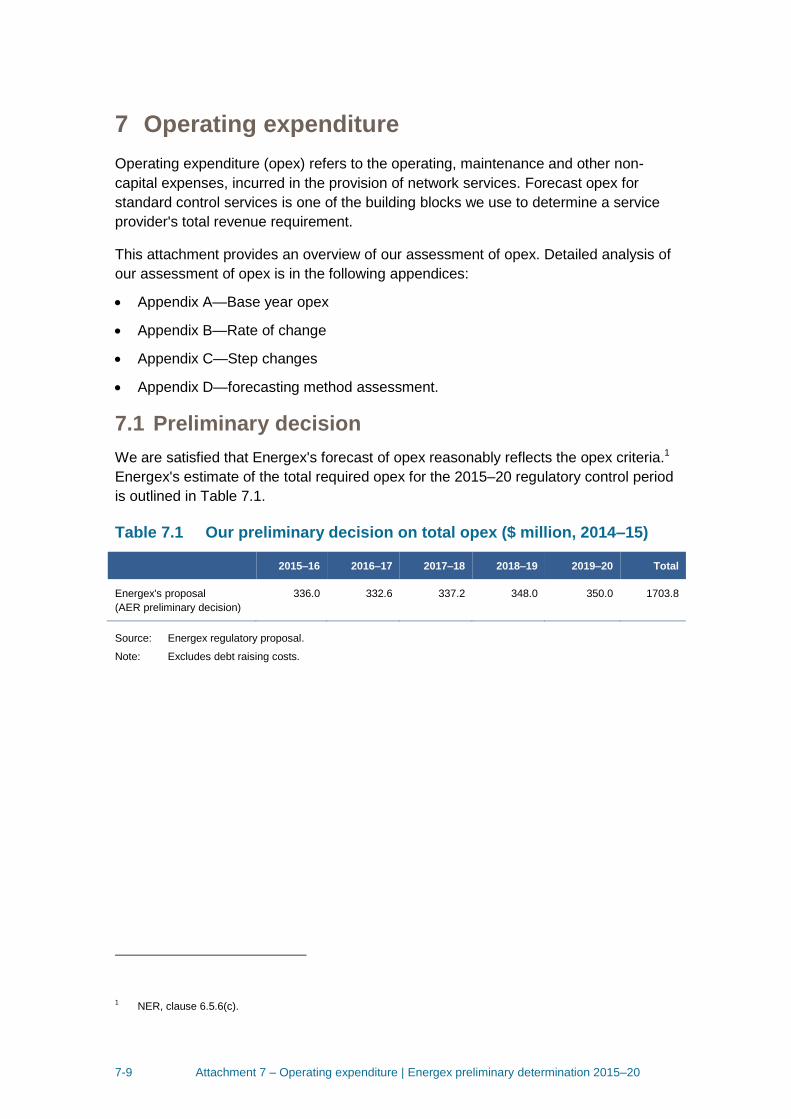

7.1 Preliminary decision

We are satisfied that Energex's forecast of opex reasonably reflects the opex criteria.1

Energex's estimate of the total required opex for the 2015–20 regulatory control period

is outlined in Table 7.1.

Table 7.1 Our preliminary decision on total opex ($ million, 2014–15)

2015–16 2016–17 2017–18 2018–19 2019–20 Total

Energex's proposal

(AER preliminary decision)

336.0 332.6 337.2 348.0 350.0 1703.8

Source: Energex regulatory proposal.

Note: Excludes debt raising costs.

1 NER, clause 6.5.6(c).

7-10 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

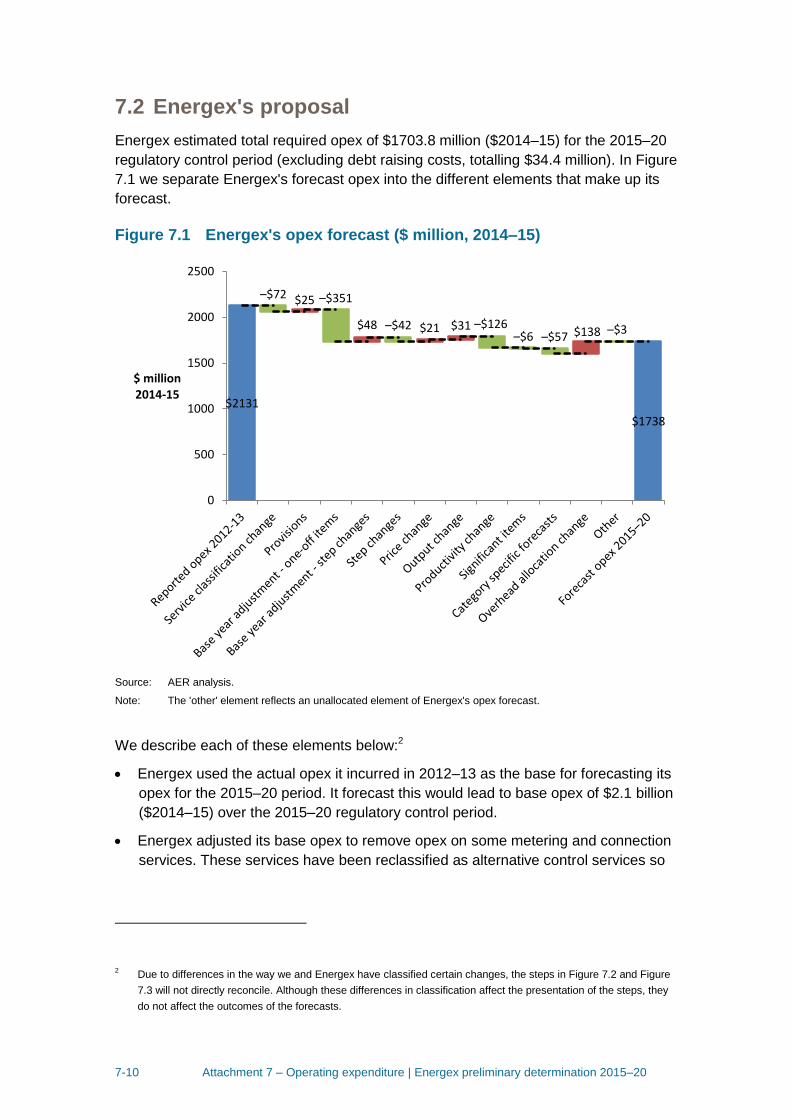

7.2 Energex's proposal

Energex estimated total required opex of $1703.8 million ($2014–15) for the 2015–20

regulatory control period (excluding debt raising costs, totalling $34.4 million). In Figure

7.1 we separate Energex's forecast opex into the different elements that make up its

forecast.

Figure 7.1 Energex's opex forecast ($ million, 2014–15)

Source: AER analysis.

Note: The 'other' element reflects an unallocated element of Energex's opex forecast.

We describe each of these elements below:2

Energex used the actual opex it incurred in 2012–13 as the base for forecasting its

opex for the 2015–20 period. It forecast this would lead to base opex of $2.1 billion

($2014–15) over the 2015–20 regulatory control period.

Energex adjusted its base opex to remove opex on some metering and connection

services. These services have been reclassified as alternative control services so

2 Due to differences in the way we and Energex have classified certain changes, the steps in Figure 7.2 and Figure

7.3 will not directly reconcile. Although these differences in classification affect the presentation of the steps, they

do not affect the outcomes of the forecasts.

$2131

$1738

$25

$48 $21 $31 $138

–$72 –$351

–$42 –$126–$6 –$57

–$3

0

500

1000

1500

2000

2500

$ million2014-15

7-11 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

need to be removed from Energex's standard control services opex. This reduced

Energex's forecast by $72 million ($2014–15).

Energex adjusted its forecast for movements in provisions in its base year. This led

to a $25 million ($2014–15) increase in its forecast opex.

Energex identified non-recurrent costs in its base year. Removing these costs

reduced its forecast opex by $351 million ($2014–15).

Energex identified step changes that occurred between the base year and the

2015–20 period. These led to an increase of $48 million ($2014–15) in Energex's

forecast of total opex.

Energex identified step changes forecast to occur during the 2015–20 period.

These led to a decrease of $42 million ($2014–15) in Energex's forecast of total

opex.

Energex accounted for forecast growth in prices related to labour price increases,

materials price increases, and contractor price decreases. This forecast of price

growth increased Energex's opex forecast by $21 million ($2014–15).

Energex forecast output growth would increase its opex forecast by $31million

($2014–15).

Energex subtracted $126 million ($2014–15) from its total opex forecast for forecast

productivity growth.

Energex identified some significant items: non-recurrent changes in costs not

included in the base year. These items led to a decrease in Energex's opex

forecast of $6 million ($2014–15).

Energex forecast some cost categories using category specific methods. The

change in these costs over the period led to a decrease of $57 million ($2014–15)

in Energex's forecast of total opex.

Energex forecast that changes in the relative shares of capex and opex in totex

would lead to an increase in the amount of overheads allocated to opex. This was

forecast to increase Energex's opex by $138 million ($2014–15).

7-12 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

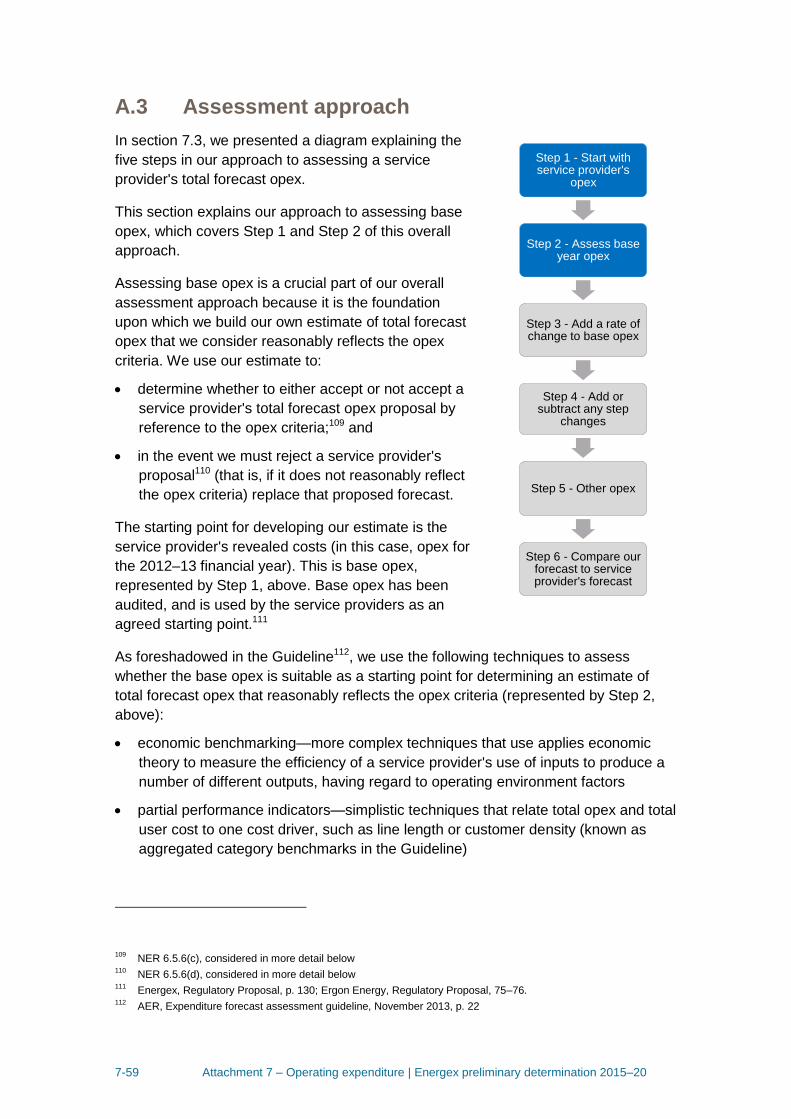

7.3 Assessment approach

Our assessment approach, outlined below, is, for the most part, consistent with the

Guideline.3 We decide whether or not to accept the service provider's total forecast

opex. We accept the service provider's forecast if we are satisfied that it reasonably

reflects the opex criteria.4 If we are not satisfied, we replace it with a total forecast of

opex that we are satisfied does reasonably reflect the opex criteria.5

It is important to note that we make our assessment about the total forecast opex and

not about particular categories or projects in the opex forecast. The Australian Energy

Market Commission (AEMC) has expressed our role in these terms:6

It should be noted here that what the AER approves in this context is

expenditure allowances, not projects.

The service provider’s forecast is intended to cover the expenditure that will be needed

to achieve the operating expenditure objectives. These objectives are:7

1. meeting or managing the expected demand for standard control services over the

regulatory control period

2. complying with all applicable regulatory obligations or requirements associated with

providing standard control services

3. where there is no regulatory obligation or requirement, maintaining the quality,

reliability and security of supply of standard control services and maintaining the

reliability and security of the distribution system

4. maintaining the safety of the distribution system through the supply of standard

control services.

We assess the proposed total forecast opex against the opex criteria set out in the

NER. The opex criteria provide that the total forecast must reasonably reflect:8

1. the efficient costs of achieving the operating expenditure objectives

2. the costs that a prudent operator would require to achieve the operating

expenditure objectives

3. a realistic expectation of the demand forecast and cost inputs required to achieve

the operating expenditure objectives.

3 We did not apply the DEA benchmarking technique. We outline the reasons why we did not apply this technique in

section A.4 of our base opex appendix. 4 NER, clause 6.5.6(c).

5 NER, clause 6.5.6(d).

6 AEMC, Final Rule Determination: National Electricity Amendment (Economic Regulation of Network Service

Providers) Rule 2012, 29 November 2012, p. vii. 7 NER, clause 6.5.6(a).

8 NER, clause 6.5.6(c).

7-13 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

The AEMC noted that '[t]hese criteria broadly reflect the NEO [National Electricity

Objective]'.9

In deciding whether or not we are satisfied the service provider's forecast reasonably

reflects the opex criteria we have regard to the opex factors.10 We attach different

weight to different factors when making our decision to best achieve the NEO. This

approach has been summarised by the AEMC as follows:11

As mandatory considerations, the AER has an obligation to take the capex and

opex factors into account, but this does not mean that every factor will be

relevant to every aspect of every regulatory determination the AER makes. The

AER may decide that certain factors are not relevant in certain cases once it

has considered them.

The opex factors we have regard to are:

the most recent annual benchmarking report that has been published under clause

6.27 and the benchmark operating expenditure that would be incurred by an

efficient distribution network service provider over the relevant regulatory control

period

the actual and expected operating expenditure of the distribution network service

provider during any preceding regulatory control periods

the extent to which the operating expenditure forecast includes expenditure to

address the concerns of electricity consumers as identified by the distribution

network service provider in the course of its engagement with electricity consumers

the relative prices of operating and capital inputs

the substitution possibilities between operating and capital expenditure

whether the operating expenditure forecast is consistent with any incentive scheme

or schemes that apply to the distribution network service provider under clauses

6.5.8 or 6.6.2 to 6.6.4

the extent the operating expenditure forecast is referable to arrangements with a

person other than the distribution network service provider that, in our opinion, do

not reflect arm’s length terms

whether the operating expenditure forecast includes an amount relating to a project

that should more appropriately be included as a contingent project under clause

6.6A.1(b)

the extent to which the distribution network service provider has considered and

made provision for efficient and prudent non-network alternatives

9 AEMC, Final Rule Determination: National Electricity Amendment (Economic Regulation of Network Service

Providers) Rule 2012, 29 November 2012, p. 113. 10

NER, clause 6.5.6(e). 11

AEMC, Final Rule Determination: National Electricity Amendment (Economic Regulation of Network Service

Providers) Rule 2012, 29 November 2012, p. 115.

7-14 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

any relevant final project assessment conclusions report published under

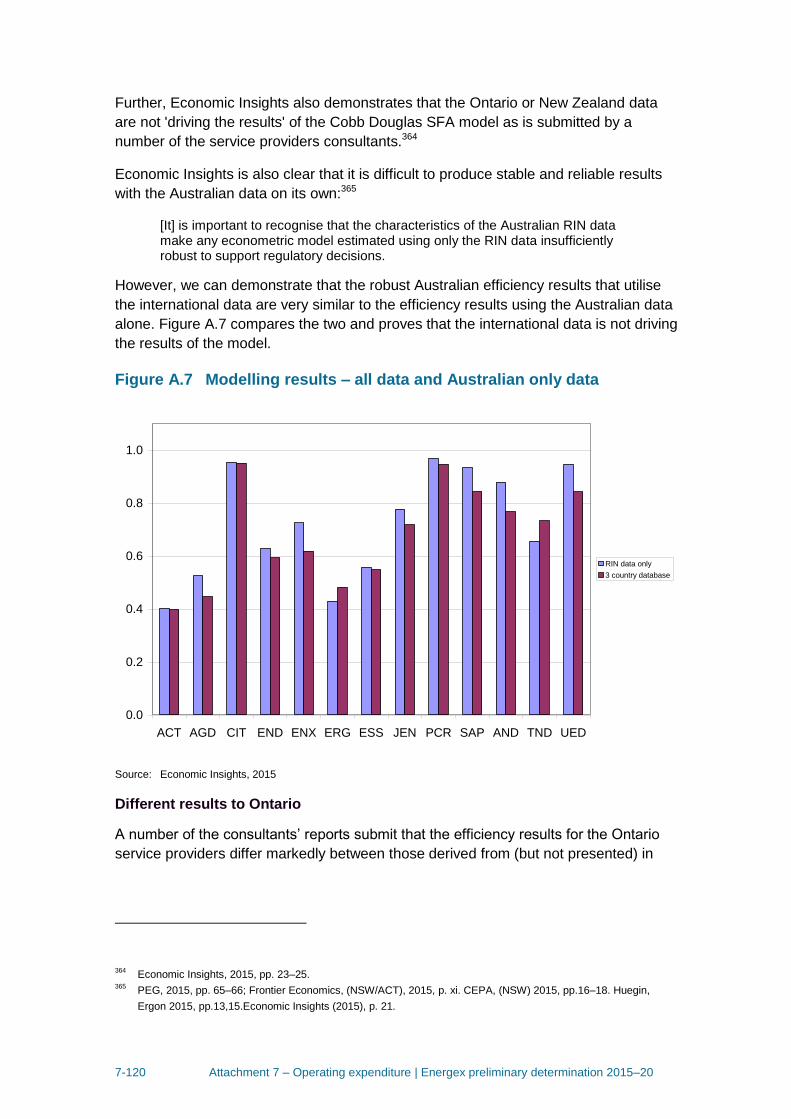

5.17.4(o),(p) or (s)

any other factor we consider relevant and which we have notified the distribution

network service provider in writing, prior to the submission of its revised regulatory

proposal under clause 6.10.3, is an operating expenditure factor.

For this determination, there are two additional operating expenditure factors that we

will take into account under the last opex factor above:

our benchmarking data sets including, but not necessarily limited to:

(a) data contained in any economic benchmarking RIN, category analysis RIN,

reset RIN or annual reporting RIN

(b) any relevant data from international sources

(c) data sets that support econometric modelling and other assessment

techniques consistent with the approach set out in the Guideline

as updated from time to time.

economic benchmarking techniques for assessing benchmark efficient expenditure

including stochastic frontier analysis and regressions utilising functional forms such

as Cobb Douglas and Translog.12

For transparency and ease of reference, we have included a summary of how we have

had regard to each of the opex factors in our assessment at the end of this attachment.

More broadly, we also note in exercising our discretion, we take into account the

revenue and pricing principles which are set out in the National Electricity Law.13

This attachment sets out our general approach to assessment. Our approach to

assessment of particular aspects of the opex forecast is also set out in more detail in

the relevant appendices.

The Expenditure Forecast Assessment Guideline

After conducting an extensive consultation process with service providers, users,

consumers and other interested stakeholders we issued the Expenditure forecast

assessment guideline (the Guideline) in November 2013 together with an explanatory

statement.14 The Guideline sets out our intended approach to assessing operating

expenditure in accordance with the NER.15

12

This is consistent with the approach we outlined in the explanatory statement to our Expenditure Forecast

Assessment Guideline. See, for example, p. 131. 13

NEL, s. 16(2); s. 7A. 14

AER, Expenditure forecasting assessment guideline - explanatory statement, November 2013. 15

NER clause 6.5.6.

7-15 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

We may depart from the approach set out in the Guideline but if we do so we give

reasons for doing so. In this determination for the most part we have not departed from

the approach set out in the Guideline. 16 In our Framework and Approach paper for

each service provider, we set out our intention to apply the Guideline approach in

making this determination.

Our approach is to compare the service provider's total forecast opex with an

alternative estimate that we develop ourselves.17 By doing this we form a view on

whether we are satisfied that the service provider's proposed total forecast opex

reasonably reflects the opex criteria. If we conclude the proposal does not reasonably

reflect the opex criteria, we use our estimate as a substitute forecast. This approach

was expressly endorsed by the AEMC in its decision on the major rule changes that

were introduced in November 2012. The AEMC stated:18

While the AER must form a view as to whether a NSP's proposal is reasonable,

this is not a separate exercise from determining an appropriate substitute in the

event the AER decides the proposal is not reasonable. For example,

benchmarking the NSP against others will provide an indication of both whether

the proposal is reasonable and what a substitute should be. Both the

consideration of "reasonable" and the determination of the substitute must be in

respect of the total for capex and opex.

Our estimate is unlikely to exactly match the service provider's forecast because the

service provider may not adopt the same forecasting method. However, if the service

provider's inputs and assumptions are reasonable, its method should produce a

forecast consistent with our estimate.

If a service provider's total forecast opex is materially different to our estimate and we

find no satisfactory explanation for this difference, we may form the view that the

service provider's forecast does not reasonably reflect the opex criteria. Conversely, if

our estimate demonstrates that the service provider's forecast reasonably reflects the

opex criteria, we will accept the forecast.19 Whether or not we accept a service

provider's forecast, we will provide the reasons for our decision.20

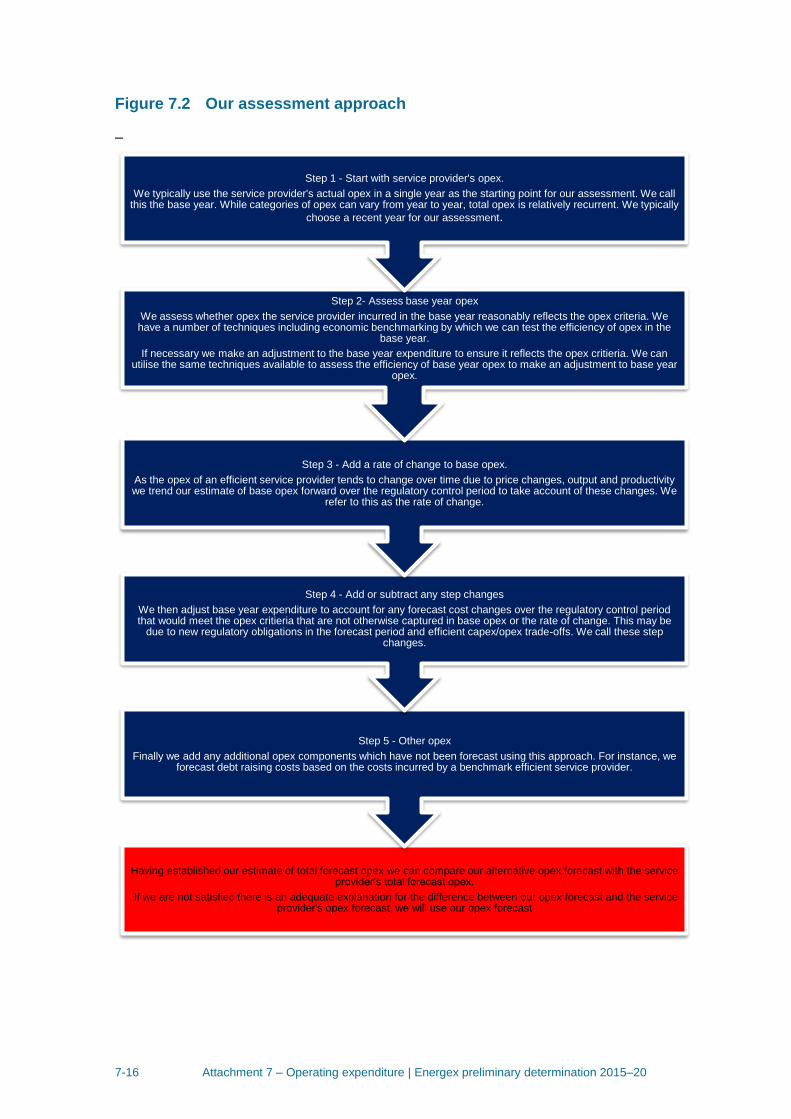

Building an alternative estimate of total forecast opex

Our approach to forming an alternative estimate of opex involves five key steps which

we outline below in Figure 7.2.

16

We did not apply the DEA benchmarking technique. We outline the reasons why we did not apply this technique in

section A.4 of our base opex appendix. 17

AER, Expenditure forecast assessment guideline, November 2013, p. 7. 18

AEMC, Final Rule Determination: National Electricity Amendment (Economic Regulation of Network Service

Providers) Rule 2012, 29 November 2012, p. 112. 19

NER, clause 6.5.6(c). 20

NER, clause 6.12.1(3)(ii).

7-16 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

Figure 7.2 Our assessment approach

–

Having established our estimate of total forecast opex we can compare our alternative opex forecast with the service provider’s total forecast opex.

If we are not satisfied there is an adequate explanation for the difference between our opex forecast and the service provider's opex forecast, we will use our opex forecast

Step 5 - Other opex

Finally we add any additional opex components which have not been forecast using this approach. For instance, we forecast debt raising costs based on the costs incurred by a benchmark efficient service provider.

Step 4 - Add or subtract any step changes

We then adjust base year expenditure to account for any forecast cost changes over the regulatory control period that would meet the opex critieria that are not otherwise captured in base opex or the rate of change. This may be

due to new regulatory obligations in the forecast period and efficient capex/opex trade-offs. We call these step changes.

Step 3 - Add a rate of change to base opex.

As the opex of an efficient service provider tends to change over time due to price changes, output and productivity we trend our estimate of base opex forward over the regulatory control period to take account of these changes. We

refer to this as the rate of change.

Step 2- Assess base year opex

We assess whether opex the service provider incurred in the base year reasonably reflects the opex criteria. We have a number of techniques including economic benchmarking by which we can test the efficiency of opex in the

base year.

If necessary we make an adjustment to the base year expenditure to ensure it reflects the opex critieria. We can utilise the same techniques available to assess the efficiency of base year opex to make an adjustment to base year

opex.

Step 1 - Start with service provider's opex.

We typically use the service provider's actual opex in a single year as the starting point for our assessment. We call this the base year. While categories of opex can vary from year to year, total opex is relatively recurrent. We typically

choose a recent year for our assessment.

7-17 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

Underlying our approach are two general assumptions:

1. the efficiency criterion and the prudence criterion in the NER are complementary

2. actual expenditure was sufficient to achieve the expenditure objectives in the past.

We have used this general approach in our past decisions. It is a well-regarded top-

down forecasting model that has been employed by a number of Australian regulators

over the last fifteen years. We refer to it as a ‘revealed cost method’ in the Guideline

(and we have sometimes referred to it as the base-step-trend method in our past

regulatory decisions).

While these general steps are consistent with our past determinations, we have

adopted a significant change in how we give effect to this approach, following the

major changes to the NER made in November 2012. Those changes placed significant

new emphasis on the use of benchmarking in our opex analysis. We will now issue

benchmarking reports annually and have regard to those reports. These benchmarking

reports provide us with one of a number of inputs for determining forecast opex.

We have set out more detail about each of the steps we follow in constructing our

forecast below.

Step 1—Starting point—base year expenditure

We prefer to use a recent year for which audited figures are available as the starting

point for our analysis. We call this the base year. This is for a number of reasons:

As total opex tends to be relatively recurrent, total opex in a recent year typically

best reflects a service provider's current circumstances.

During the past regulatory control period, we have incentives in place to reward the

service provider for making efficiency improvements by allowing it to retain a

portion of the efficiency savings it makes. Similarly, we penalise the service

provider when it is relatively less efficient. This gives us confidence that the service

provider did not spend more in the proposed base year to try to inflate its opex

forecast for the next regulatory control period.

Service providers also face many regulatory obligations in delivering services to

consumers. These regulatory obligations ensure that the financial incentives a

service provider faces to reduce its costs are balanced by obligations to deliver

services safely and reliably. In general, this gives us confidence that recent

historical opex will be at least enough to achieve the opex objectives.

In choosing a base year, we need to make a decision as to whether any categories of

opex incurred in the base year should be removed. For instance:

If a material cost was incurred in the base year that is unrepresentative of a service

provider's future opex we remove it from the base year in undertaking our

assessment. For instance, for this preliminary decision we removed metering and

ancillary network services which will be reclassified as alternative control services

in the 2015–20 regulatory control period.

7-18 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

Rather than use all opex in the base year, service providers also often forecast

specific categories of opex using different methods. We must also assess these

methods in deciding what the starting point should be. If we agree that these

categories of opex should be assessed differently, we will also remove them from

the base year.

As part of this step we also need to consider any interactions with the incentive

scheme for opex, the Efficiency Benefit Sharing Scheme (EBSS). The EBSS is

designed to achieve a fair sharing of efficiency gains and losses between a service

provider and its consumers. Under the EBSS, service providers receive a financial

reward for reducing their costs in the regulatory control period and a financial penalty

for increasing their costs. The benefits of these reductions in opex flow through to

consumers as long as base year opex is no higher than the opex incurred in that year.

Similarly, the costs of an increase in opex flow through to consumers if base year opex

is no lower than the opex incurred in that year. If the starting point is not consistent with

the EBSS, service providers could be excessively rewarded for efficiency gains or

excessively penalised for efficiency losses in the prior regulatory control period.

Step 2—Assessing base year expenditure

Regardless of the base year we choose, the service provider's actual expenditure may

not reflect the opex criteria. For example, it may not be efficient or management may

not have acted prudently in its governance and decision-making processes. We must

test whether actual expenditure in that year should be used to forecast efficient opex in

the next regulatory control period.

As we set out in the Guideline, to assess the efficiency of a service provider's actual

expenditure, we use a number of different techniques.21

For instance, we may undertake a detailed review of a service provider's actual opex.

For this preliminary decision, we have reviewed Energex’s IT and labour practices.

Benchmarking is particularly important in comparing the relative efficiency of different

service providers. The AEMC highlighted the importance of benchmarking in its

changes to the NER in November 2012:22

The Commission views benchmarking as an important exercise in assessing

the efficiency of a NSP and informing the determination of the appropriate

capex or opex allowance.

By benchmarking a service provider's expenditure we can compare its productivity

over time, and to other service providers. For this decision we have used Multilateral

21

AER, Expenditure forecast assessment guideline, November 2013, p. 22. 22

AEMC, Final Rule Determination: National Electricity Amendment (Economic Regulation of Network Service

Providers) Rule 2012, 29 November 2012, p. 97.

7-19 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

Total Factor Productivity, Partial Factor Productivity and several opex cost function

models to assess Energex’s efficiency.23

We also have regard to trends in total opex and category specific data to construct

category benchmarks. We have also used this information to inform our assessment of

the efficiency of base year expenditure. In particular, we can use this category

analysis data to identify sources of spending that are unlikely to reflect the opex criteria

over the forecast period. It may also lend support to, or identify potential

inconsistencies with, our broader benchmark modelling.

If we determine that a service provider's base year expenditure does not reasonably

reflect the opex criteria, we will not use it as our starting point for our estimate of total

forecast opex. Rather, we will adjust it so it reflects an efficient, recurrent level of opex

that does reflect the opex criteria. To arrive at an adjustment, we use the same

techniques we used to assess the service provider's efficiency.

Step 3—Rate of change

Once we have chosen a starting point that reflects the opex criteria, we apply an

annual escalator to take account of the likely ongoing changes to opex over the

forecast regulatory control period. Opex that reflects the opex criteria in the forecast

regulatory control period could reasonably differ from the starting point due to changes

in:

price growth

output growth

productivity growth.

We estimate the change by adding expected changes in prices (such as the price of

labour and materials) and outputs (such as changes in customer numbers and demand

for electricity). We then incorporate reasonable estimates of changes in productivity.

Step 4—Step changes

Next we consider if any other opex is required to achieve the opex objectives in the

forecast period. We refer to these as ‘step changes’. Step changes may be for cost

drivers such as new, changed or removed regulatory obligations, or efficient

capex/opex trade-offs. As the Guideline explains, we will typically include a step

change only if efficient base year opex and the rate of change in opex of an efficient

service provider do not already include the proposed costs.24

23

The benchmarking models are discussed in detail in Appendix A, which details our assessment of base opex. 24

AER, Expenditure forecast assessment guideline, November 2013, p. 24.

7-20 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

Step 5—Other costs that are not included in the base year

In our final step, we make any further adjustments we need for our opex forecast to

achieve the opex objectives. For instance, our approach is to forecast debt raising

costs based on a benchmarking approach rather than a service provider’s actual costs.

This is to be consistent with the forecast of the cost of debt in the rate of return building

block.

After applying these five steps, we arrive at our total opex forecast.

Comparing the service provider's proposal with our estimate

Having established our estimate of total forecast opex we can test the service

provider's proposed total forecast opex. This includes comparing our alternative total

with the service provider’s total forecast opex. However, we also assess whether the

service provider's forecasting method, assumptions, inputs and models are

reasonable, and assess the service provider's explanation of how that method results

in a prudent and efficient forecast.

The service provider may be able to adequately explain any differences between its

forecast and our estimate. We can only determine this on a case by case basis using

our judgment.

This approach is supported by the AEMC’s decision when implementing the changes

to the NER in November 2012. The Commission stated:25

the AER could be expected to approach the assessment of a NSP's

expenditure (capex or opex) forecast by determining its own forecast of

expenditure based on the material before it. Presumably this will never match

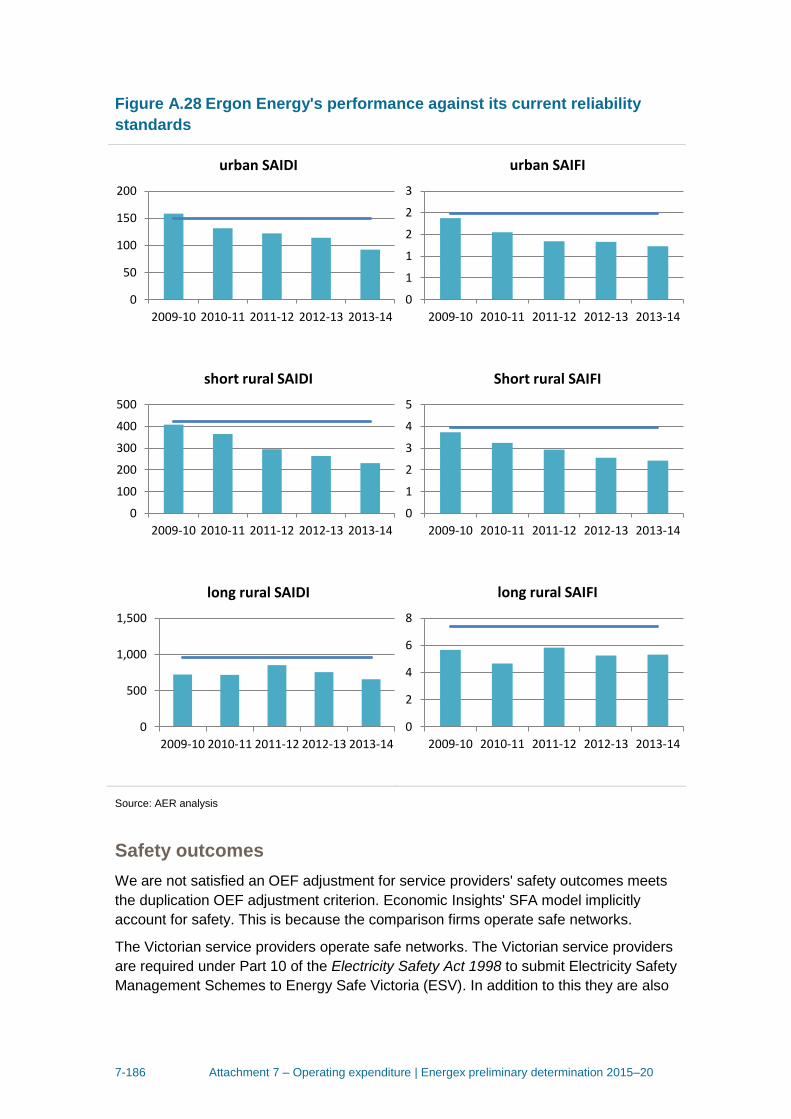

exactly the amount proposed by the NSP. However there will be a certain

margin of difference between the AER's forecast and that of the NSP within

which the AER could say that the NSP's forecast is reasonable. What the

margin is in a particular case, and therefore what the AER will accept as

reasonable, is a matter for the AER exercising its regulatory judgment.

If we are not satisfied there is an adequate explanation for the difference between our

opex forecast and the service provider's opex forecast, we will use our opex forecast in

determining a service provider's total revenue requirement.

25

AEMC, Final Rule Determination: National Electricity Amendment (Economic Regulation of Network Service

Providers) Rule 2012, 29 November 2012, p. 112.

7-21 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

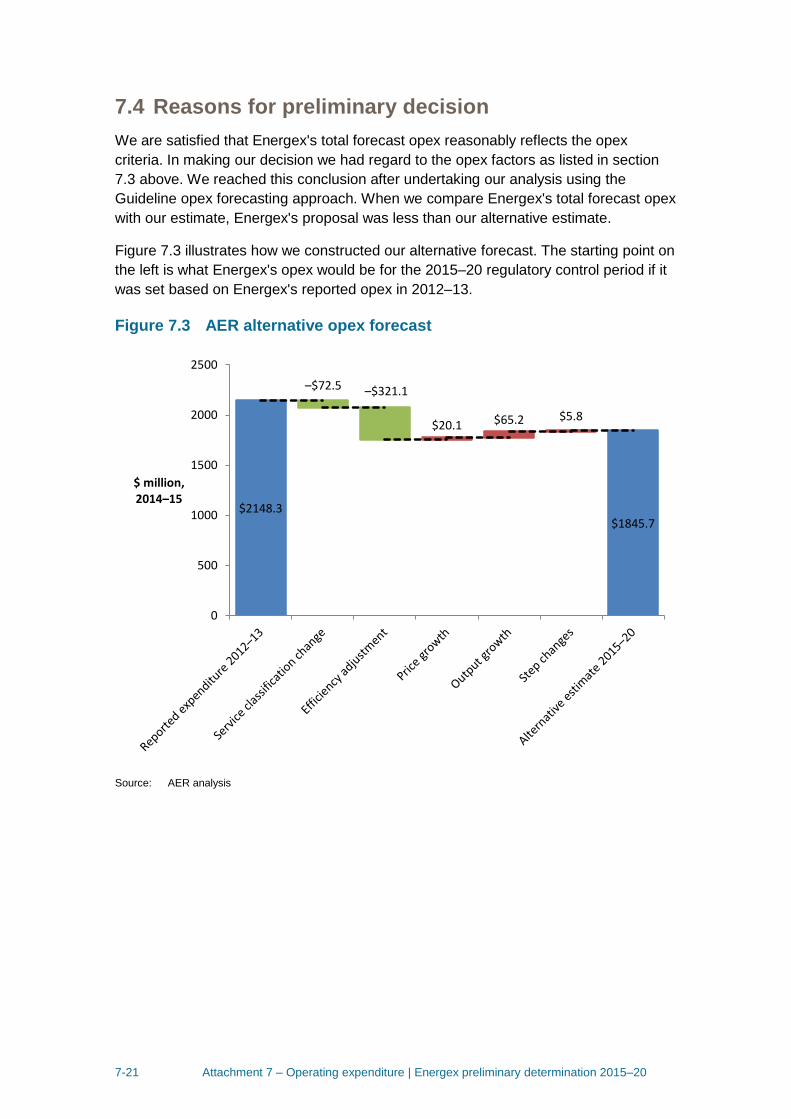

7.4 Reasons for preliminary decision

We are satisfied that Energex's total forecast opex reasonably reflects the opex

criteria. In making our decision we had regard to the opex factors as listed in section

7.3 above. We reached this conclusion after undertaking our analysis using the

Guideline opex forecasting approach. When we compare Energex's total forecast opex

with our estimate, Energex's proposal was less than our alternative estimate.

Figure 7.3 illustrates how we constructed our alternative forecast. The starting point on

the left is what Energex's opex would be for the 2015–20 regulatory control period if it

was set based on Energex's reported opex in 2012–13.

Figure 7.3 AER alternative opex forecast

Source: AER analysis

$2148.3$1845.7

$20.1 $65.2 $5.8

–$72.5 –$321.1

0

500

1000

1500

2000

2500

$ million, 2014–15

7-22 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

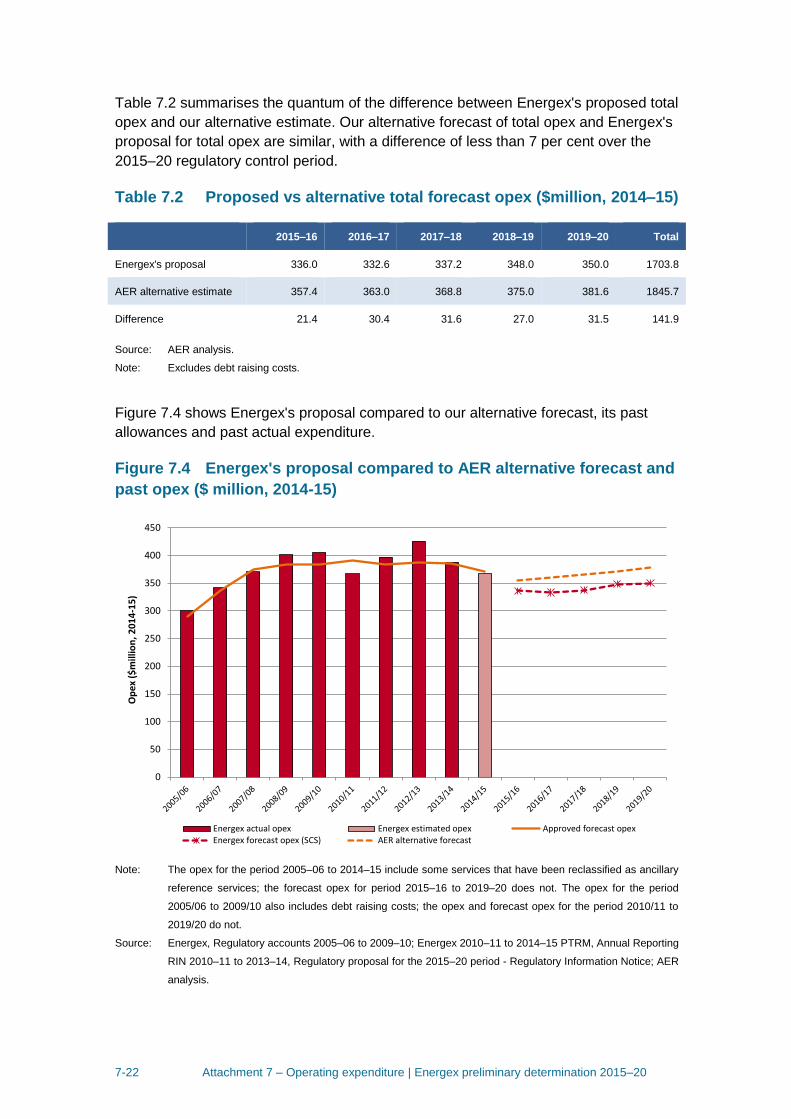

Table 7.2 summarises the quantum of the difference between Energex's proposed total

opex and our alternative estimate. Our alternative forecast of total opex and Energex's

proposal for total opex are similar, with a difference of less than 7 per cent over the

2015–20 regulatory control period.

Table 7.2 Proposed vs alternative total forecast opex ($million, 2014–15)

Source: AER analysis.

Note: Excludes debt raising costs.

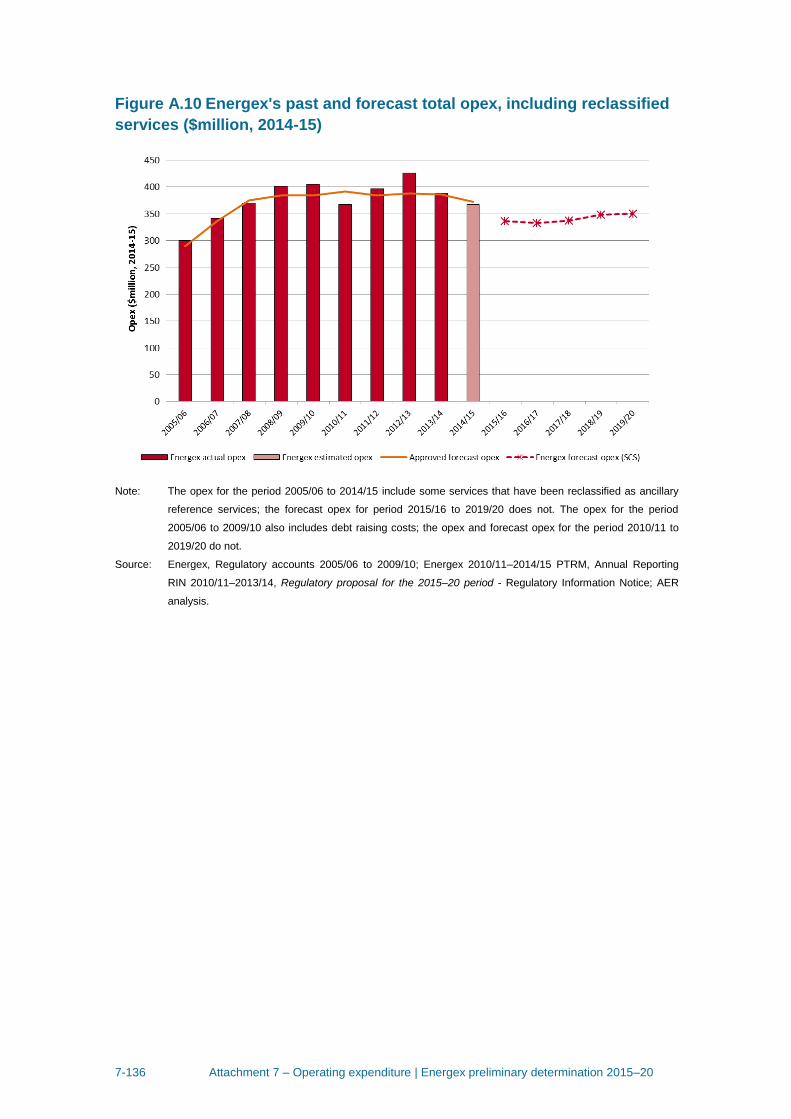

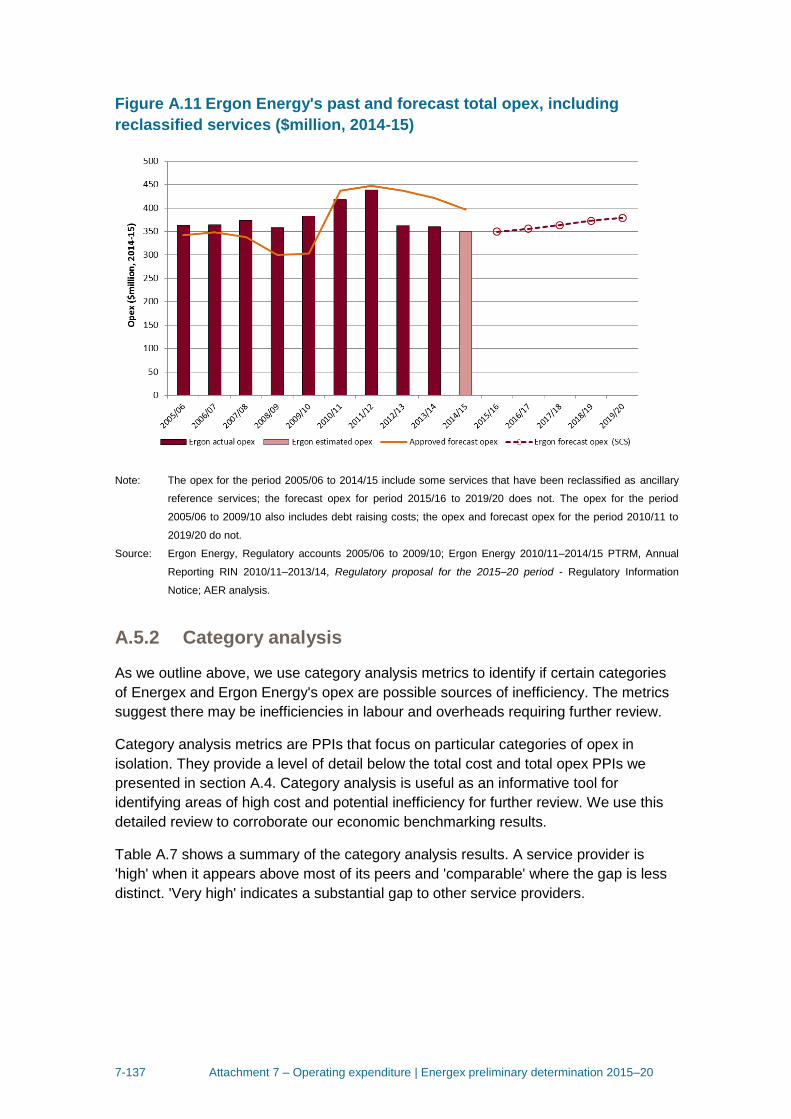

Figure 7.4 shows Energex's proposal compared to our alternative forecast, its past

allowances and past actual expenditure.

Figure 7.4 Energex's proposal compared to AER alternative forecast and

past opex ($ million, 2014-15)

Note: The opex for the period 2005–06 to 2014–15 include some services that have been reclassified as ancillary

reference services; the forecast opex for period 2015–16 to 2019–20 does not. The opex for the period

2005/06 to 2009/10 also includes debt raising costs; the opex and forecast opex for the period 2010/11 to

2019/20 do not.

Source: Energex, Regulatory accounts 2005–06 to 2009–10; Energex 2010–11 to 2014–15 PTRM, Annual Reporting

RIN 2010–11 to 2013–14, Regulatory proposal for the 2015–20 period - Regulatory Information Notice; AER

analysis.

0

50

100

150

200

250

300

350

400

450

Op

ex

($m

illio

n,

20

14

-15

)

Energex actual opex Energex estimated opex Approved forecast opexEnergex forecast opex (SCS) AER alternative forecast

2015–16 2016–17 2017–18 2018–19 2019–20 Total

Energex's proposal 336.0 332.6 337.2 348.0 350.0 1703.8

AER alternative estimate 357.4 363.0 368.8 375.0 381.6 1845.7

Difference 21.4 30.4 31.6 27.0 31.5 141.9

7-23 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

While we are satisfied that Energex's total forecast opex reasonably reflects the opex

criteria, we have taken a different view to Energex on component elements of the total

opex forecast based on our analysis.

The key elements of our alternative forecast and the areas where elements of our

forecast differs to Energex is discussed below.26

7.4.1 Forecasting method

As noted above, our estimate of total opex is unlikely to exactly match Energex's.

Broadly, differences between the two forecasts can be explained by differences in the

forecasting methods adopted and the inputs and assumptions used to apply the

method. We have reviewed Energex's forecast method to identify if and where

Energex's forecasting method departed from the method set out in the Guideline (the

guideline forecasting method). Where Energex's forecasting method did depart from

the guideline forecasting method we considered whether this departure explained the

difference between Energex's forecast of total opex and our own. We also considered

whether adopting Energex's approach was required to produce an opex forecast that

reasonably reflects the opex criteria, having regard to the opex factors.

In appendix D we set out our consideration of Energex’s forecasting methodology in

determining our alternative estimate opex for the 2015–20 regulatory control period.

Having considered the differences between the guideline forecasting method and

Energex's method, we are satisfied that the guideline forecasting method produces an

opex forecast that reasonably reflects the opex criteria. We have not used category

specific forecasting methods to separately forecast any of Energex's opex categories

other than debt raising costs in our substitute total opex forecast. We formed our

alternative estimate of total opex using the guideline forecasting method with all opex

categories other than debt raising costs included in base opex.

Energex, however, did forecast some categories of opex using category specific

methods. The change in these costs over the period reduced Energex's forecast of

total opex by $57 million ($2014–15).

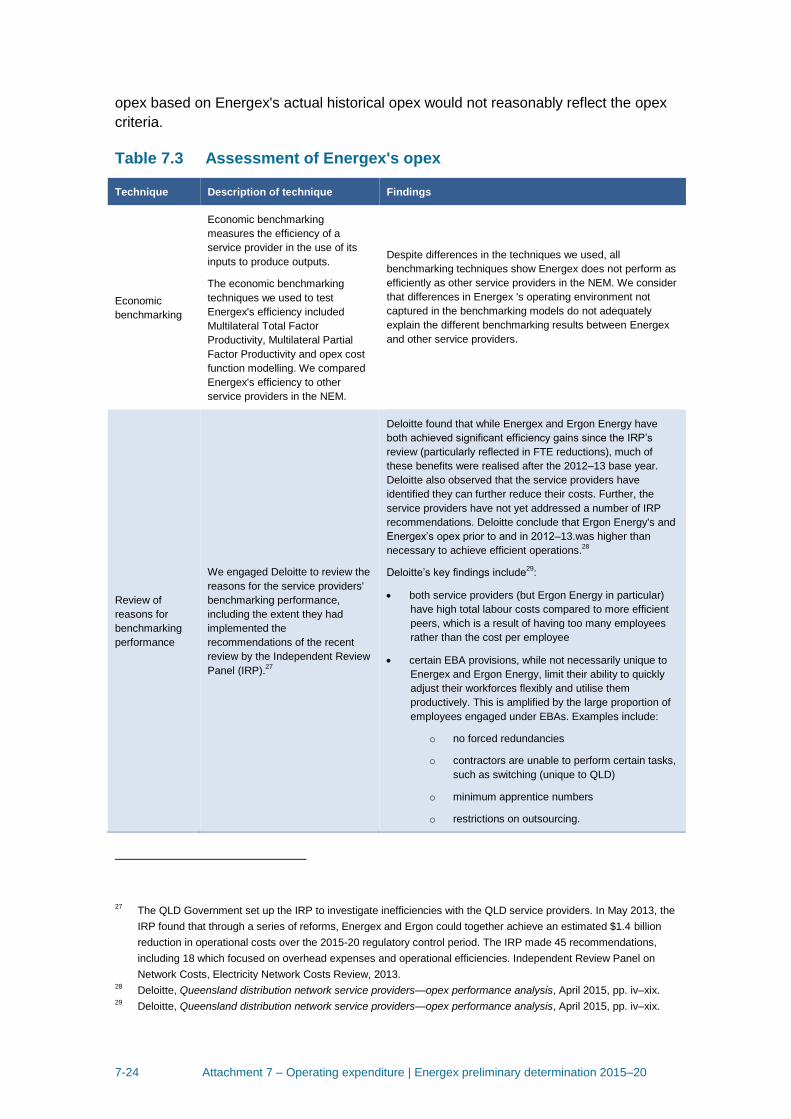

7.4.2 Base opex

We first assessed Energex's proposed base year of 2012–13. We tested Energex's

base opex in 2012–13 using overall benchmarking techniques. We then examined the

drivers of the results of these benchmarking techniques by examining key components

of opex.

The main techniques we used to test the efficiency of Energex's base opex are

outlined in Table 7.3. Our findings from our detailed review support our overall

benchmarking findings, which suggest that Energex's actual base opex is materially

inefficient. Therefore, without an efficiency adjustment, we consider a forecast base

26

For each of these parts of opex, our analysis is supported by an appendix.

7-24 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

opex based on Energex's actual historical opex would not reasonably reflect the opex

criteria.

Table 7.3 Assessment of Energex's opex

Technique Description of technique Findings

Economic

benchmarking

Economic benchmarking

measures the efficiency of a

service provider in the use of its

inputs to produce outputs.

The economic benchmarking

techniques we used to test

Energex's efficiency included

Multilateral Total Factor

Productivity, Multilateral Partial

Factor Productivity and opex cost

function modelling. We compared

Energex's efficiency to other

service providers in the NEM.

Despite differences in the techniques we used, all

benchmarking techniques show Energex does not perform as

efficiently as other service providers in the NEM. We consider

that differences in Energex 's operating environment not

captured in the benchmarking models do not adequately

explain the different benchmarking results between Energex

and other service providers.

Review of

reasons for

benchmarking

performance

We engaged Deloitte to review the

reasons for the service providers'

benchmarking performance,

including the extent they had

implemented the

recommendations of the recent

review by the Independent Review

Panel (IRP).27

Deloitte found that while Energex and Ergon Energy have

both achieved significant efficiency gains since the IRP’s

review (particularly reflected in FTE reductions), much of

these benefits were realised after the 2012–13 base year.

Deloitte also observed that the service providers have

identified they can further reduce their costs. Further, the

service providers have not yet addressed a number of IRP

recommendations. Deloitte conclude that Ergon Energy's and

Energex’s opex prior to and in 2012–13.was higher than

necessary to achieve efficient operations.28

Deloitte’s key findings include29

:

both service providers (but Ergon Energy in particular)

have high total labour costs compared to more efficient

peers, which is a result of having too many employees

rather than the cost per employee

certain EBA provisions, while not necessarily unique to

Energex and Ergon Energy, limit their ability to quickly

adjust their workforces flexibly and utilise them

productively. This is amplified by the large proportion of

employees engaged under EBAs. Examples include:

o no forced redundancies

o contractors are unable to perform certain tasks,

such as switching (unique to QLD)

o minimum apprentice numbers

o restrictions on outsourcing.

27

The QLD Government set up the IRP to investigate inefficiencies with the QLD service providers. In May 2013, the

IRP found that through a series of reforms, Energex and Ergon could together achieve an estimated $1.4 billion

reduction in operational costs over the 2015-20 regulatory control period. The IRP made 45 recommendations,

including 18 which focused on overhead expenses and operational efficiencies. Independent Review Panel on

Network Costs, Electricity Network Costs Review, 2013. 28

Deloitte, Queensland distribution network service providers—opex performance analysis, April 2015, pp. iv–xix. 29

Deloitte, Queensland distribution network service providers—opex performance analysis, April 2015, pp. iv–xix.

7-25 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

Technique Description of technique Findings

Energex and Ergon Energy have not implemented the

IRP's recommendation that they market test the ICT

services that SPARQ (a joint venture owned by the two

distributors) provides, resulting in significant

inefficiencies

Source: AER analysis.

Arriving at an alternative estimate of base opex

We are unable to use Energex's historical opex to prepare our alternative forecast of

opex because basing our forecast on Energex's historical opex would not result in a

forecast opex that would reasonably reflect the opex criteria.

We therefore need to determine a starting point that would lead to a forecast opex that

would reasonably reflect the opex criteria.

We have used the results from our preferred benchmarking model (Cobb Douglas

SFA) to adjust to Energex’s base opex to determine a starting point for our forecast of

overall opex that would reasonably reflect the criteria.30 Our preferred benchmarking

model measures the opex efficiency of all service providers in the NEM over the 2006

to 2013 period relative to a frontier service provider. The outputs in the model are

customer numbers, line length and ratcheted maximum demand.

In doing this, we have not adjusted Energex’s base opex relative to the efficiency of the

frontier service provider. This is consistent with the preference in the Guideline to rely

on revealed costs and only adjust base opex where it is materially inefficient.

Instead, we have used a benchmark comparison point that is the lowest of the

efficiency scores in the top quartile of possible scores. This is equivalent to the

efficiency score for the business at the bottom of the upper third (top 33 per cent) of

companies in the benchmark sample (represented by AusNet Services). We have

done this because:

this recognises that more than a third of the service providers in the NEM,

operating in varied environments, are able to perform at or above our benchmark

comparison point. We are confident that a firm that performs below this level is

therefore spending in a manner that does not reasonably reflect the opex criteria.

An adjustment back to this appropriately conservative point is sufficient to remove

material inefficiency while still incorporating an appropriately wide margin for

potential modelling and data errors for the purposes of forecasting

given it is our first application of benchmarking, it is appropriate to adopt a cautious

approach

30

Stochastic frontier analysis (SFA) can directly estimate efficiency scores and has superior statistical properties.

Economic Insights, Economic Benchmarking Assessment of Operating Expenditure for NSW and ACT Electricity

DNSPs, November 2014, p. v.

7-26 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

we consider this approach achieves the NEO and RPP because it is sufficiently

conservative to avoid the risks associated with undercompensating the service

provider but also promotes efficiency incentives.

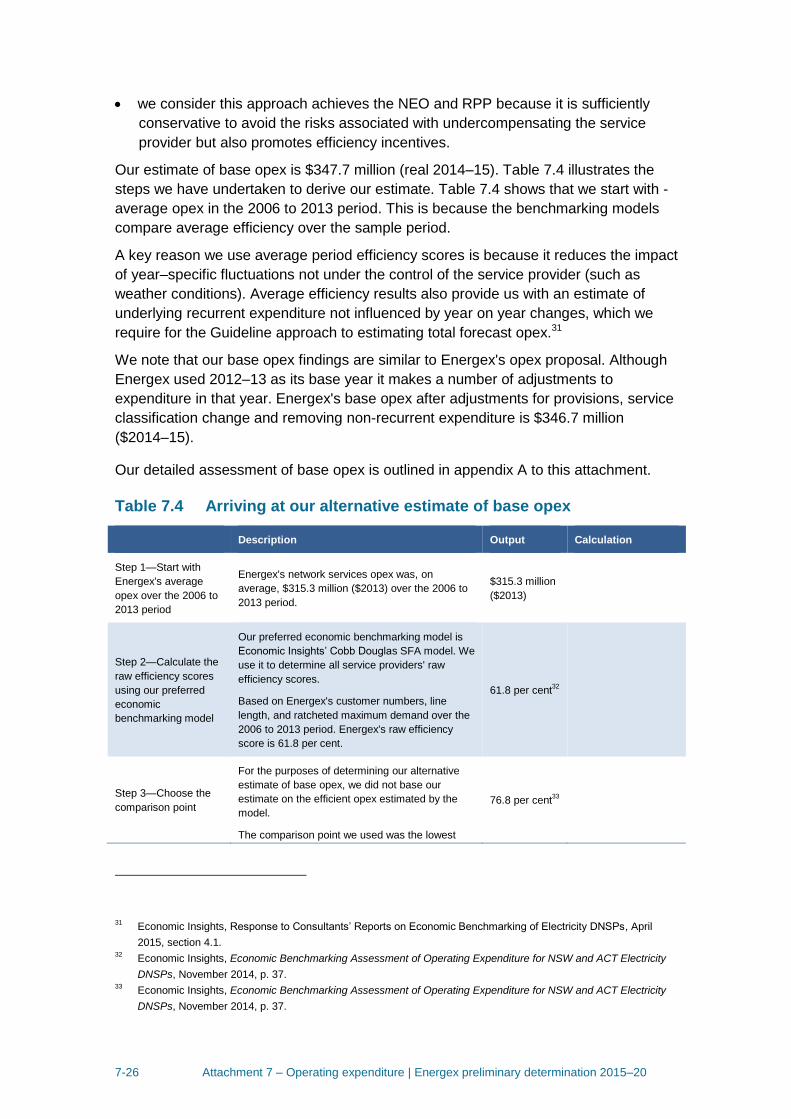

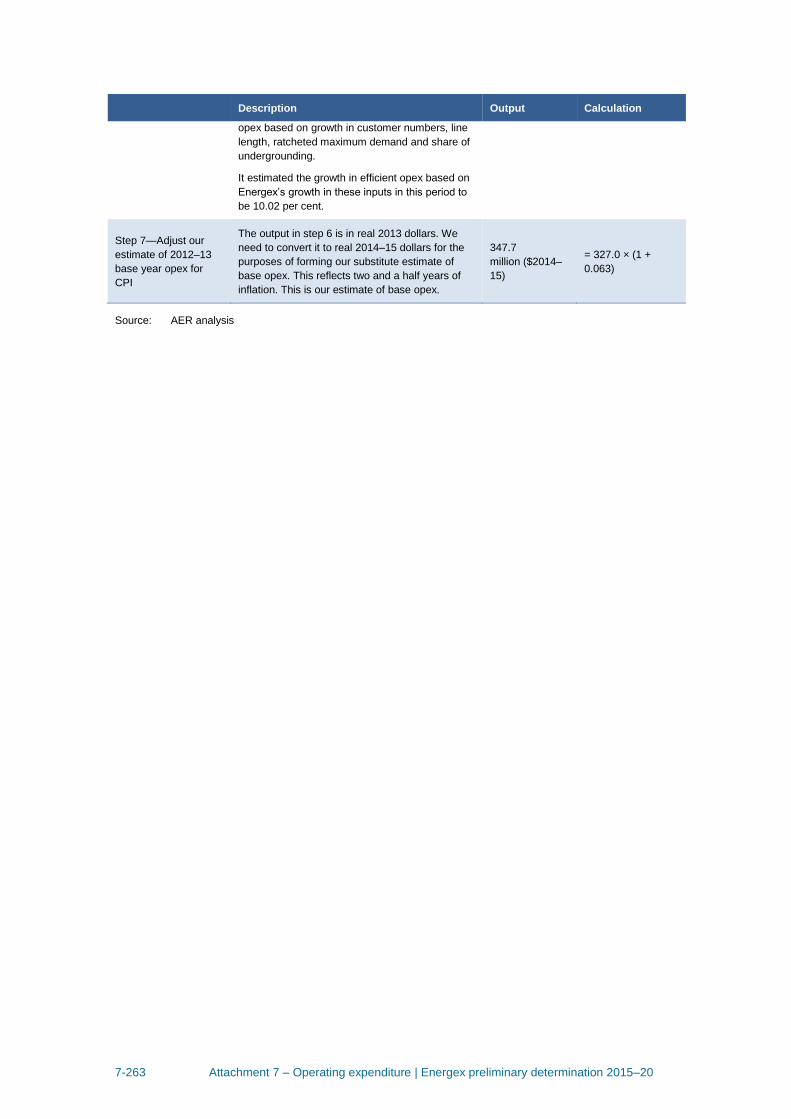

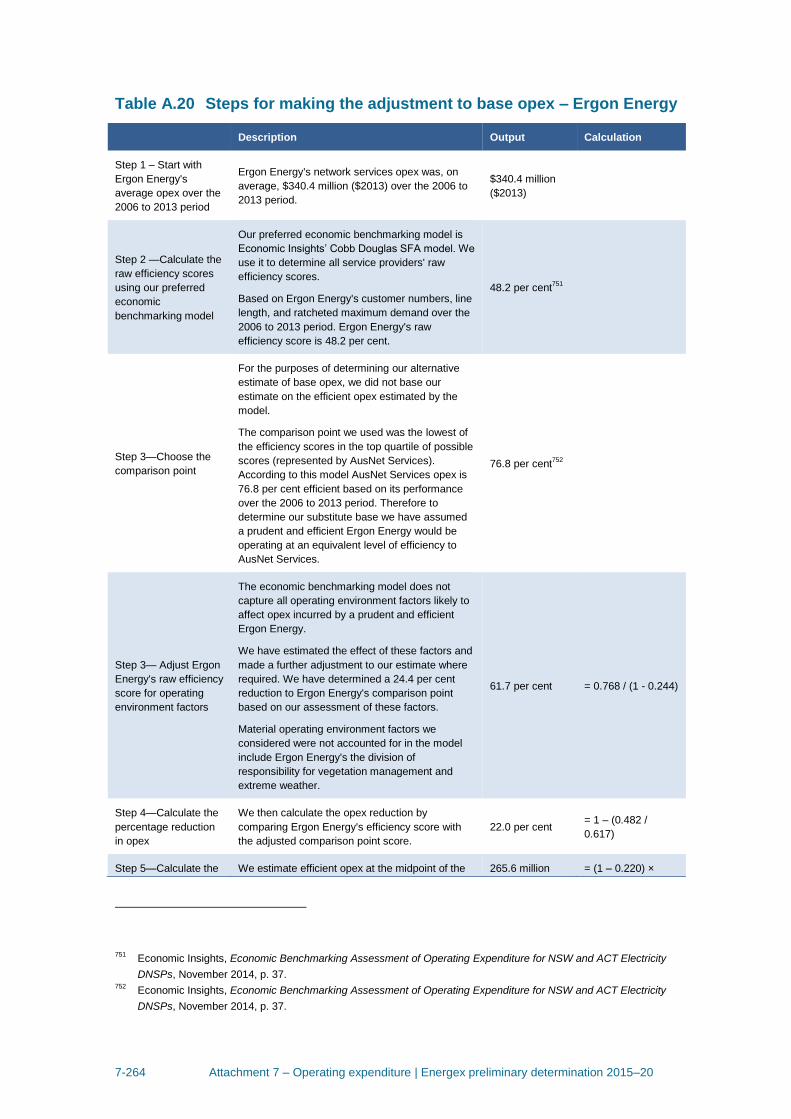

Our estimate of base opex is $347.7 million (real 2014–15). Table 7.4 illustrates the

steps we have undertaken to derive our estimate. Table 7.4 shows that we start with -

average opex in the 2006 to 2013 period. This is because the benchmarking models

compare average efficiency over the sample period.

A key reason we use average period efficiency scores is because it reduces the impact

of year–specific fluctuations not under the control of the service provider (such as

weather conditions). Average efficiency results also provide us with an estimate of

underlying recurrent expenditure not influenced by year on year changes, which we

require for the Guideline approach to estimating total forecast opex.31

We note that our base opex findings are similar to Energex's opex proposal. Although

Energex used 2012–13 as its base year it makes a number of adjustments to

expenditure in that year. Energex's base opex after adjustments for provisions, service

classification change and removing non-recurrent expenditure is $346.7 million

($2014–15).

Our detailed assessment of base opex is outlined in appendix A to this attachment.

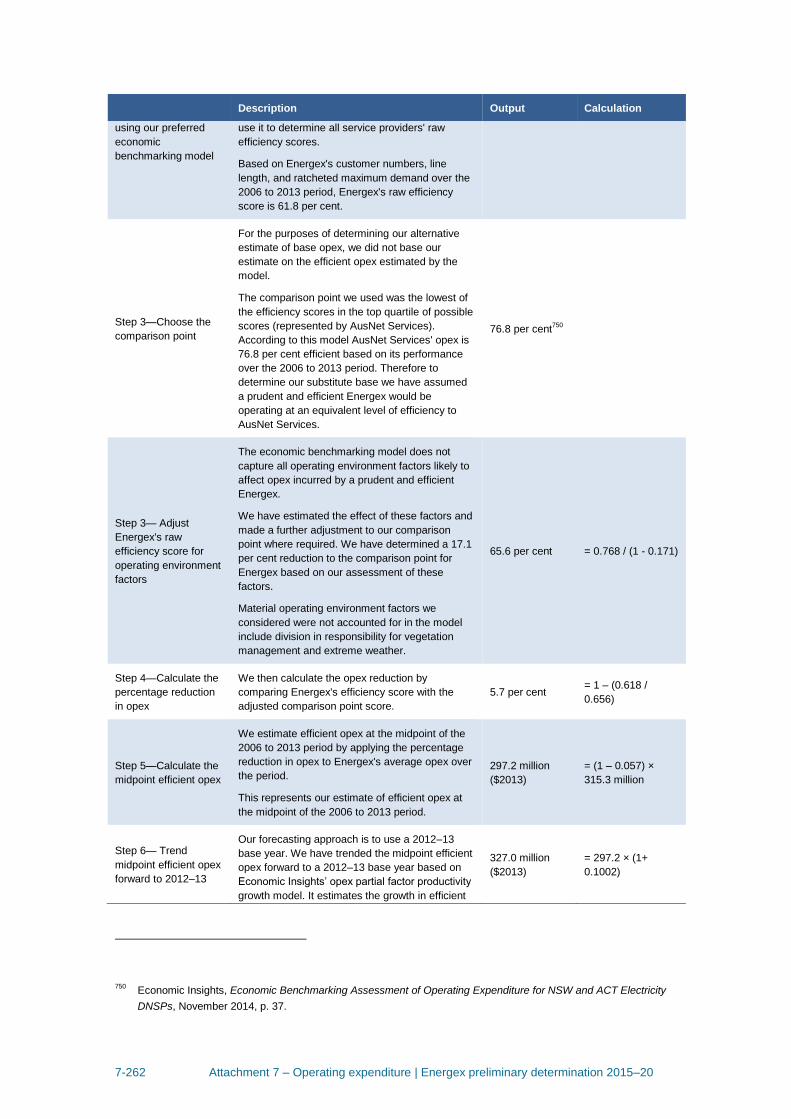

Table 7.4 Arriving at our alternative estimate of base opex

Description Output Calculation

Step 1—Start with

Energex's average

opex over the 2006 to

2013 period

Energex's network services opex was, on

average, $315.3 million ($2013) over the 2006 to

2013 period.

$315.3 million

($2013)

Step 2—Calculate the

raw efficiency scores

using our preferred

economic

benchmarking model

Our preferred economic benchmarking model is

Economic Insights’ Cobb Douglas SFA model. We

use it to determine all service providers' raw

efficiency scores.

Based on Energex's customer numbers, line

length, and ratcheted maximum demand over the

2006 to 2013 period. Energex's raw efficiency

score is 61.8 per cent.

61.8 per cent32

Step 3—Choose the

comparison point

For the purposes of determining our alternative

estimate of base opex, we did not base our

estimate on the efficient opex estimated by the

model.

The comparison point we used was the lowest

76.8 per cent33

31

Economic Insights, Response to Consultants’ Reports on Economic Benchmarking of Electricity DNSPs, April

2015, section 4.1. 32

Economic Insights, Economic Benchmarking Assessment of Operating Expenditure for NSW and ACT Electricity

DNSPs, November 2014, p. 37. 33

Economic Insights, Economic Benchmarking Assessment of Operating Expenditure for NSW and ACT Electricity

DNSPs, November 2014, p. 37.

7-27 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

Description Output Calculation

performing service provider in the top quartile of

possible efficiency scores, AusNet Services.

According to this model AusNet Services opex is

76.8 per cent efficient based on its performance

over the 2006 to 2013 period. Therefore to

determine our substitute base we have assumed

a prudent and efficient Energex would be

operating at an equivalent level of efficiency to

AusNet Services.

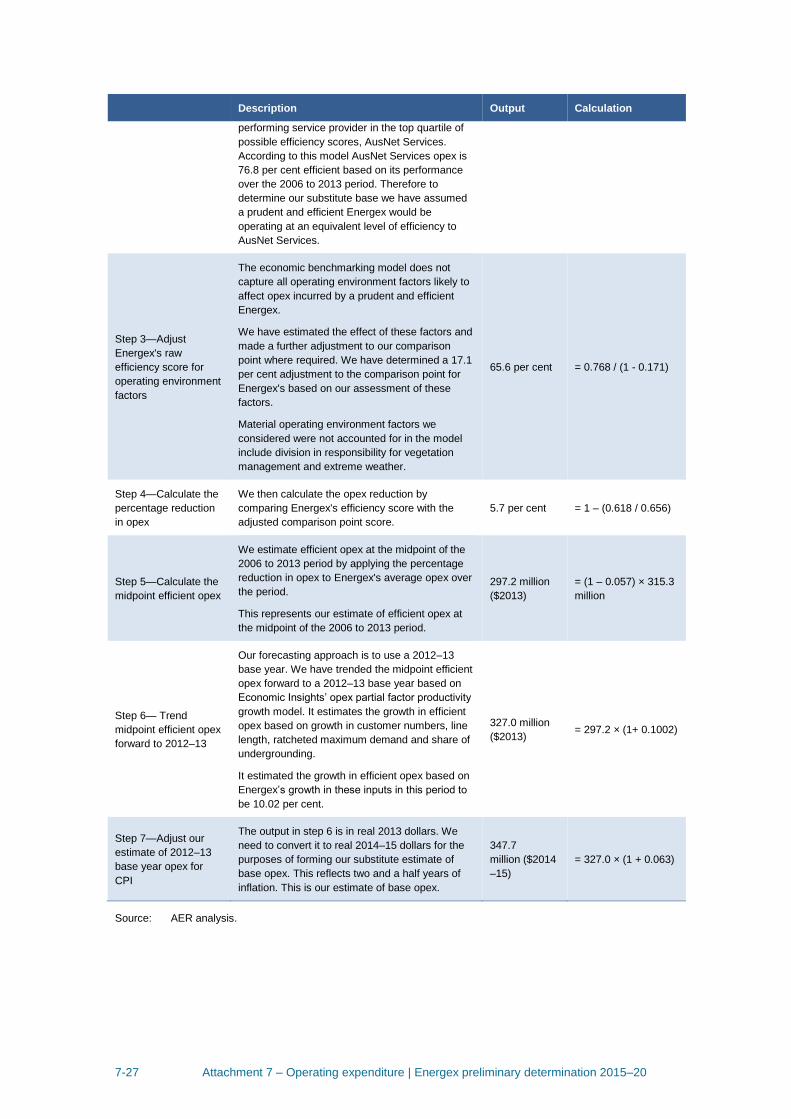

Step 3—Adjust

Energex's raw

efficiency score for

operating environment

factors

The economic benchmarking model does not

capture all operating environment factors likely to

affect opex incurred by a prudent and efficient

Energex.

We have estimated the effect of these factors and

made a further adjustment to our comparison

point where required. We have determined a 17.1

per cent adjustment to the comparison point for

Energex's based on our assessment of these

factors.

Material operating environment factors we

considered were not accounted for in the model

include division in responsibility for vegetation

management and extreme weather.

65.6 per cent = 0.768 / (1 - 0.171)

Step 4—Calculate the

percentage reduction

in opex

We then calculate the opex reduction by

comparing Energex's efficiency score with the

adjusted comparison point score.

5.7 per cent = 1 – (0.618 / 0.656)

Step 5—Calculate the

midpoint efficient opex

We estimate efficient opex at the midpoint of the

2006 to 2013 period by applying the percentage

reduction in opex to Energex's average opex over

the period.

This represents our estimate of efficient opex at

the midpoint of the 2006 to 2013 period.

297.2 million

($2013)

= (1 – 0.057) × 315.3

million

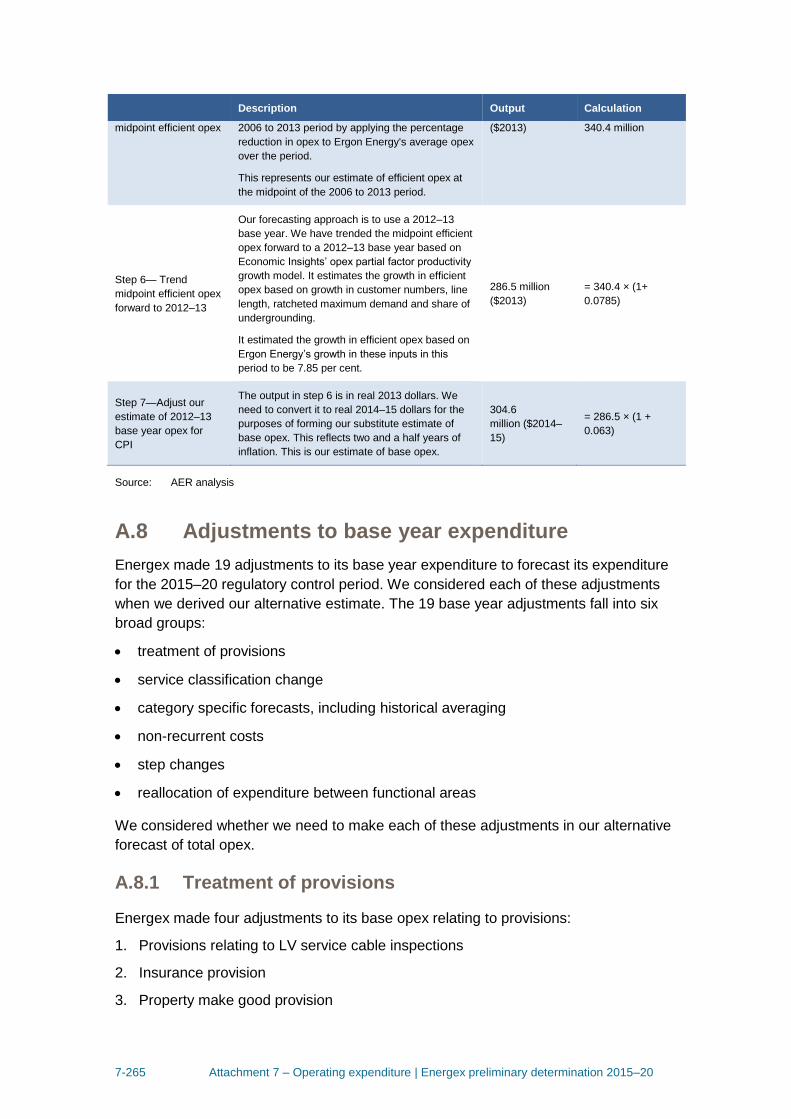

Step 6— Trend

midpoint efficient opex

forward to 2012–13

Our forecasting approach is to use a 2012–13

base year. We have trended the midpoint efficient

opex forward to a 2012–13 base year based on

Economic Insights’ opex partial factor productivity

growth model. It estimates the growth in efficient

opex based on growth in customer numbers, line

length, ratcheted maximum demand and share of

undergrounding.

It estimated the growth in efficient opex based on

Energex’s growth in these inputs in this period to

be 10.02 per cent.

327.0 million

($2013) = 297.2 × (1+ 0.1002)

Step 7—Adjust our

estimate of 2012–13

base year opex for

CPI

The output in step 6 is in real 2013 dollars. We

need to convert it to real 2014–15 dollars for the

purposes of forming our substitute estimate of

base opex. This reflects two and a half years of

inflation. This is our estimate of base opex.

347.7

million ($2014

–15)

= 327.0 × (1 + 0.063)

Source: AER analysis.

7-28 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

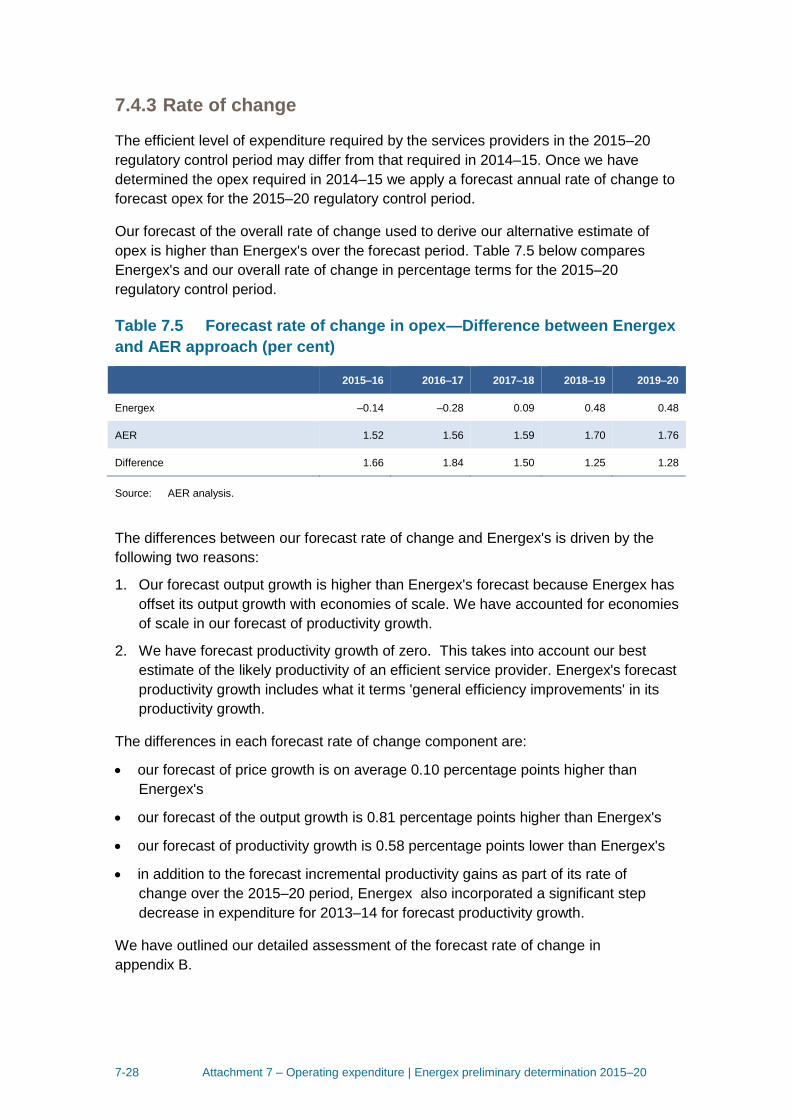

7.4.3 Rate of change

The efficient level of expenditure required by the services providers in the 2015–20

regulatory control period may differ from that required in 2014–15. Once we have

determined the opex required in 2014–15 we apply a forecast annual rate of change to

forecast opex for the 2015–20 regulatory control period.

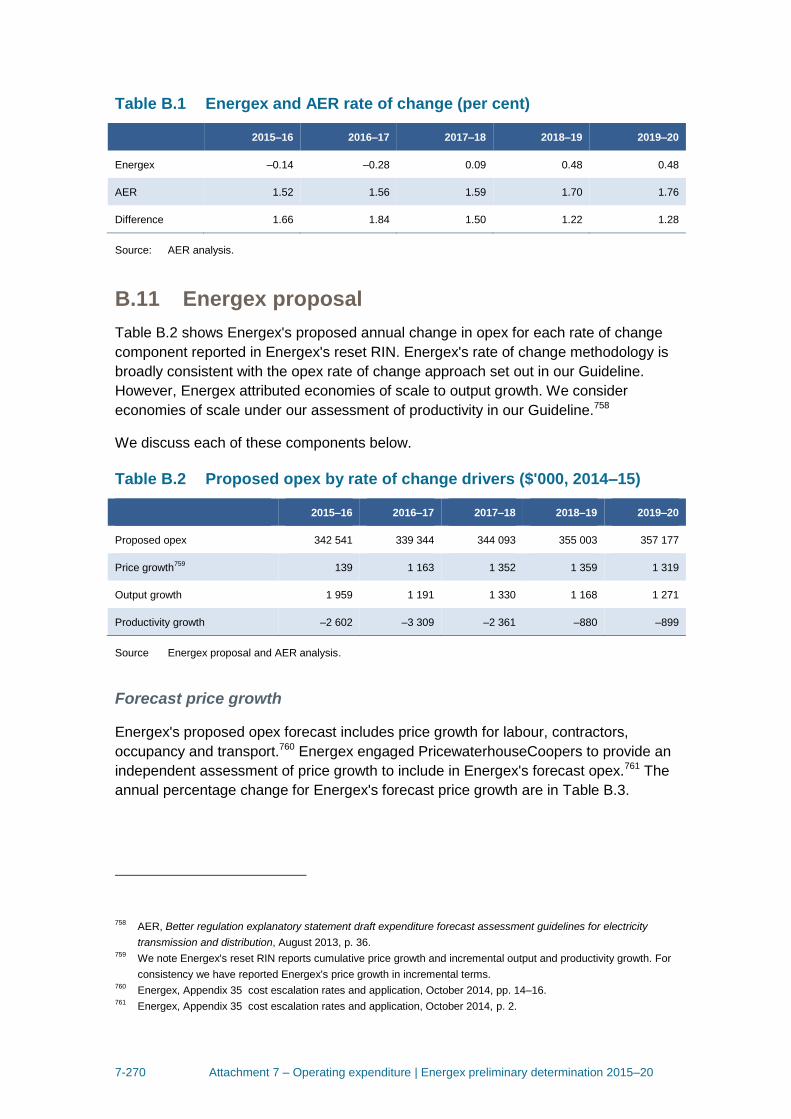

Our forecast of the overall rate of change used to derive our alternative estimate of

opex is higher than Energex's over the forecast period. Table 7.5 below compares

Energex's and our overall rate of change in percentage terms for the 2015–20

regulatory control period.

Table 7.5 Forecast rate of change in opex—Difference between Energex

and AER approach (per cent)

2015–16 2016–17 2017–18 2018–19 2019–20

Energex –0.14 –0.28 0.09 0.48 0.48

AER 1.52 1.56 1.59 1.70 1.76

Difference 1.66 1.84 1.50 1.25 1.28

Source: AER analysis.

The differences between our forecast rate of change and Energex's is driven by the

following two reasons:

1. Our forecast output growth is higher than Energex's forecast because Energex has

offset its output growth with economies of scale. We have accounted for economies

of scale in our forecast of productivity growth.

2. We have forecast productivity growth of zero. This takes into account our best

estimate of the likely productivity of an efficient service provider. Energex's forecast

productivity growth includes what it terms 'general efficiency improvements' in its

productivity growth.

The differences in each forecast rate of change component are:

our forecast of price growth is on average 0.10 percentage points higher than

Energex's

our forecast of the output growth is 0.81 percentage points higher than Energex's

our forecast of productivity growth is 0.58 percentage points lower than Energex's

in addition to the forecast incremental productivity gains as part of its rate of

change over the 2015–20 period, Energex also incorporated a significant step

decrease in expenditure for 2013–14 for forecast productivity growth.

We have outlined our detailed assessment of the forecast rate of change in

appendix B.

7-29 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

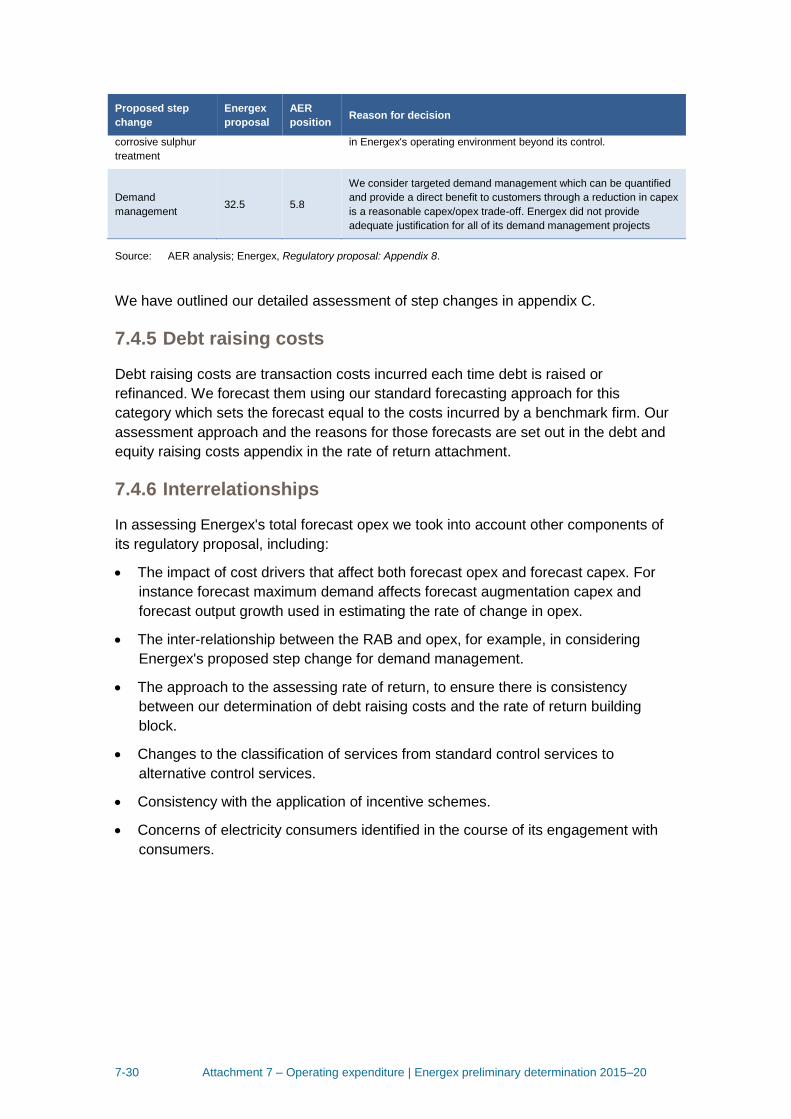

7.4.4 Step changes

We have included a step change above our estimate base level of opex for one of

Energex's demand management projects. We are satisfied that the Bromelton deferral

project is an efficient capex/opex trade-off.

As well as the opex changes proposed by Energex to its opex forecast that it described

as 'step changes', Energex proposed other changes to its opex forecast that we

consider should be assessed as step changes. We are not satisfied that other cost

changes Energex identified require a change to our estimate of base opex. We outline

all the cost changes we have assessed as step changes in Table 7.6.34

Table 7.6 Summary of AER assessment of step changes

($ million, 2014—15)

Proposed step

change

Energex

proposal

AER

position Reason for decision

LV crossarm

program 8.9 –

These step changes represent business as usual costs that an

efficient and prudent service provider would typically incur while

meeting its existing regulatory obligations. We do not consider these

step changes are necessary as our estimate of base opex already

provides sufficient funding for Energex, acting as a prudent service

provider, to efficiently deliver standard control distribution services,

given its operating environment.

Matrix

support/licencing 6.8 –

Protection reviews 3.7 –

Overhead

inspection program 14.2 –

Rental increase 14.7 –

Property rental

reductions –21.7 –

Overheads

allocated to opex 137.6 –

Vegetation

management –39.8 –

We have not included these negative step changes in our alternative

opex forecast. This is because in setting our estimate of base opex

consistent with the opex criteria, we have already factored in

efficiency savings that should be reflected in the base opex. To

provide further reductions via step changes would lead to a base

opex below that which reasonably reflects the opex criteria.

Distribution

management

system

–8.1 –

Asbestos removal 1.3 –

Our estimate of base opex already provides sufficient funding for a

prudent service provider to efficiently deliver standard control

distribution services while meeting all existing regulatory obligations.

We are not satisfied an increase in base opex is needed as asbestos

removal is an existing obligation.

Transformer 4.0 – This expenditure does not relate to a new obligation or some change

34

We note that Energex proposed some base year adjustments, a bottom-up forecast and a non-recurrent

expenditure cost increases in its opex forecast. It did this because the amount of expenditure in its base year was

not representative of its expectation of expenditure in the 2015–19 regulatory control period. Consequently, if these

adjustments were required for the opex forecast to meet the opex criteria, we assessed them as step changes.

7-30 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

Proposed step

change

Energex

proposal

AER

position Reason for decision

corrosive sulphur

treatment

in Energex's operating environment beyond its control.

Demand

management 32.5 5.8

We consider targeted demand management which can be quantified

and provide a direct benefit to customers through a reduction in capex

is a reasonable capex/opex trade-off. Energex did not provide

adequate justification for all of its demand management projects

Source: AER analysis; Energex, Regulatory proposal: Appendix 8.

We have outlined our detailed assessment of step changes in appendix C.

7.4.5 Debt raising costs

Debt raising costs are transaction costs incurred each time debt is raised or

refinanced. We forecast them using our standard forecasting approach for this

category which sets the forecast equal to the costs incurred by a benchmark firm. Our

assessment approach and the reasons for those forecasts are set out in the debt and

equity raising costs appendix in the rate of return attachment.

7.4.6 Interrelationships

In assessing Energex's total forecast opex we took into account other components of

its regulatory proposal, including:

The impact of cost drivers that affect both forecast opex and forecast capex. For

instance forecast maximum demand affects forecast augmentation capex and

forecast output growth used in estimating the rate of change in opex.

The inter-relationship between the RAB and opex, for example, in considering

Energex's proposed step change for demand management.

The approach to the assessing rate of return, to ensure there is consistency

between our determination of debt raising costs and the rate of return building

block.

Changes to the classification of services from standard control services to

alternative control services.

Consistency with the application of incentive schemes.

Concerns of electricity consumers identified in the course of its engagement with

consumers.

7-31 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

7.4.7 Assessment of opex factors

In deciding whether or not we are satisfied the service provider's forecast reasonably

reflects the opex criteria we have regard to the opex factors.35 Table 7.7 summarises

how we have taken the opex factors into account in making our preliminary decision.

Table 7.7 AER consideration of opex factors

Opex factor Consideration

The most recent annual benchmarking report that has

been published under rule 6.27 and the benchmark

operating expenditure that would be incurred by an

efficient distribution network service provider over the

relevant regulatory control period.

There are two elements to this factor. First, we must have

regard to the most recent annual benchmarking report.

Second, we must have regard to the benchmark operating

expenditure that would be incurred by an efficient

distribution network service provider over the period. The

annual benchmarking report is intended to provide an

annual snapshot of the relative efficiency of each service

provider.

The second element, that is, the benchmark operating

expenditure that would be incurred by an efficient provider

during the forecast period, necessarily provides a different

focus. This is because this second element requires us to

construct the benchmark opex that would be incurred by a

hypothetically efficient provider for that particular network

over the relevant period.

We have used several assessment techniques that

enable us to estimate the benchmark opex that an

efficient service provider would require over the forecast

period. These techniques include economic

benchmarking, opex cost function modelling, category

analysis and a detailed review of Energex's labour and

workforce practices. We have used our judgment based

on the results from all of these techniques to holistically

form a view on the efficiency of Energex's proposed total

forecast opex compared to the benchmark efficient opex

that would be incurred over the relevant regulatory control

period.

The actual and expected operating expenditure of the

Distribution Network Service Provider during any

proceeding regulatory control periods.

Our forecasting approach uses the service provider's

actual opex as the starting point. We have compared

several years of Energex's actual past opex with that of

other service providers to form a view about whether or

not its revealed expenditure is sufficiently efficient to rely

on it as the basis for forecasting required opex in the

forthcoming period.

The extent to which the operating expenditure forecast

includes expenditure to address the concerns of electricity

consumers as identified by the Distribution Network

Service Provider in the course of its engagement with

electricity consumers.

We understand the intention of this particular factor is to

require us to have regard to the extent to which service

providers have engaged with consumers in preparing their

regulatory proposals, such that they factor in the needs of

consumers.36

We have considered the concerns of electricity

consumers as identified by Energex – particularly those

expressed in the consumer-focussed overview provided

35

NER, clause 6.5.6(e). 36

AEMC, Rule Determination, 29 November 2012, pp. 101, 115.

7-32 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

Opex factor Consideration

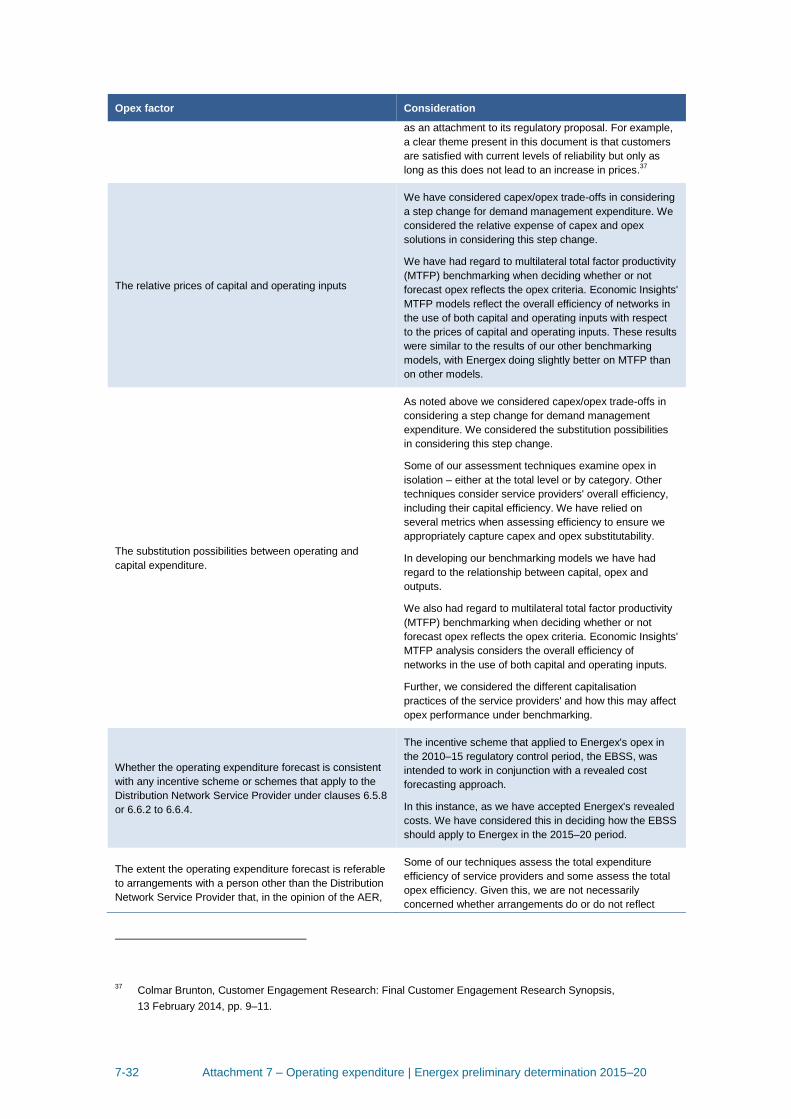

as an attachment to its regulatory proposal. For example,

a clear theme present in this document is that customers

are satisfied with current levels of reliability but only as

long as this does not lead to an increase in prices.37

The relative prices of capital and operating inputs

We have considered capex/opex trade-offs in considering

a step change for demand management expenditure. We

considered the relative expense of capex and opex

solutions in considering this step change.

We have had regard to multilateral total factor productivity

(MTFP) benchmarking when deciding whether or not

forecast opex reflects the opex criteria. Economic Insights'

MTFP models reflect the overall efficiency of networks in

the use of both capital and operating inputs with respect

to the prices of capital and operating inputs. These results

were similar to the results of our other benchmarking

models, with Energex doing slightly better on MTFP than

on other models.

The substitution possibilities between operating and

capital expenditure.

As noted above we considered capex/opex trade-offs in

considering a step change for demand management

expenditure. We considered the substitution possibilities

in considering this step change.

Some of our assessment techniques examine opex in

isolation – either at the total level or by category. Other

techniques consider service providers' overall efficiency,

including their capital efficiency. We have relied on

several metrics when assessing efficiency to ensure we

appropriately capture capex and opex substitutability.

In developing our benchmarking models we have had

regard to the relationship between capital, opex and

outputs.

We also had regard to multilateral total factor productivity

(MTFP) benchmarking when deciding whether or not

forecast opex reflects the opex criteria. Economic Insights'

MTFP analysis considers the overall efficiency of

networks in the use of both capital and operating inputs.

Further, we considered the different capitalisation

practices of the service providers' and how this may affect

opex performance under benchmarking.

Whether the operating expenditure forecast is consistent

with any incentive scheme or schemes that apply to the

Distribution Network Service Provider under clauses 6.5.8

or 6.6.2 to 6.6.4.

The incentive scheme that applied to Energex's opex in

the 2010–15 regulatory control period, the EBSS, was

intended to work in conjunction with a revealed cost

forecasting approach.

In this instance, as we have accepted Energex's revealed

costs. We have considered this in deciding how the EBSS

should apply to Energex in the 2015–20 period.

The extent the operating expenditure forecast is referable

to arrangements with a person other than the Distribution

Network Service Provider that, in the opinion of the AER,

Some of our techniques assess the total expenditure

efficiency of service providers and some assess the total

opex efficiency. Given this, we are not necessarily

concerned whether arrangements do or do not reflect

37

Colmar Brunton, Customer Engagement Research: Final Customer Engagement Research Synopsis,

13 February 2014, pp. 9–11.

7-33 Attachment 7 – Operating expenditure | Energex preliminary determination 2015–20

Opex factor Consideration

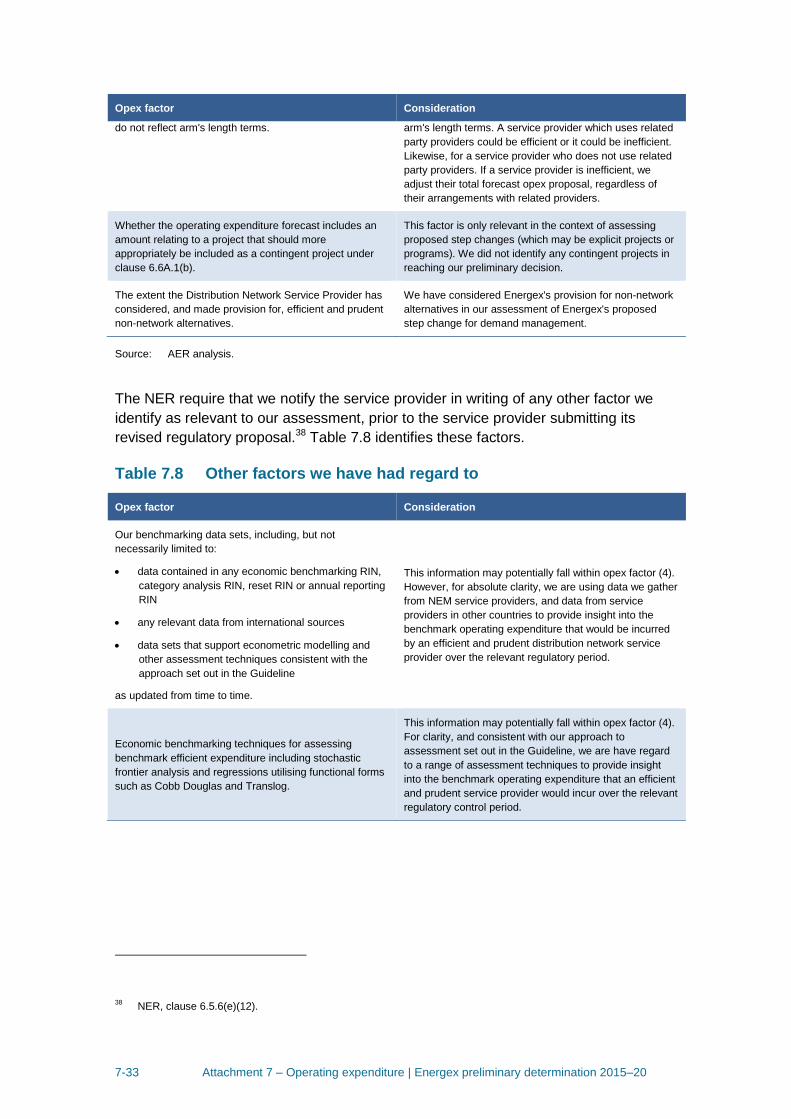

do not reflect arm's length terms. arm's length terms. A service provider which uses related

party providers could be efficient or it could be inefficient.

Likewise, for a service provider who does not use related

party providers. If a service provider is inefficient, we

adjust their total forecast opex proposal, regardless of

their arrangements with related providers.

Whether the operating expenditure forecast includes an

amount relating to a project that should more

appropriately be included as a contingent project under

clause 6.6A.1(b).

This factor is only relevant in the context of assessing

proposed step changes (which may be explicit projects or

programs). We did not identify any contingent projects in

reaching our preliminary decision.

The extent the Distribution Network Service Provider has

considered, and made provision for, efficient and prudent

non-network alternatives.

We have considered Energex's provision for non-network

alternatives in our assessment of Energex's proposed

step change for demand management.

Source: AER analysis.

The NER require that we notify the service provider in writing of any other factor we

identify as relevant to our assessment, prior to the service provider submitting its

revised regulatory proposal.38 Table 7.8 identifies these factors.

Table 7.8 Other factors we have had regard to

Opex factor Consideration