Output file - Department of Industry, Science, Energy and ...

317

SUBMISSION PUBLIC VERSION Case No: ADC 416 Period of Investigation: 1 April 2016 – 31 March 2017 20 October 2017 The Director Operations 1 Anti-Dumping Commission EMAIL: [email protected] Ref: Anti-Dumping Investigation No.416 of Imports of Steel Rod In Coils from Indonesia, Republic of South Korea and Vietnam Sub: Comments on the Applicant’s particular market situation claims and Request for the Use of Rod In Coils Price in Vietnam to Determine the Normal Value in the Instant Investigation. Dear Mr. Director, On behalf of Government of Vietnam (hereinafter referred to as “GOV”), we hereby submit comments on the applicant’s particular market situation claims in the on-going anti- dumping investigation against steel rod in coils imported from Vietnam. In summary of this submission as analyzed below, the GOV requests the Australia Anti-dumping Commission (hereinafter referred to as “the Commission”):

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Output file - Department of Industry, Science, Energy and ...

SUBMISSION PUBLIC VERSION

Case No: ADC 416

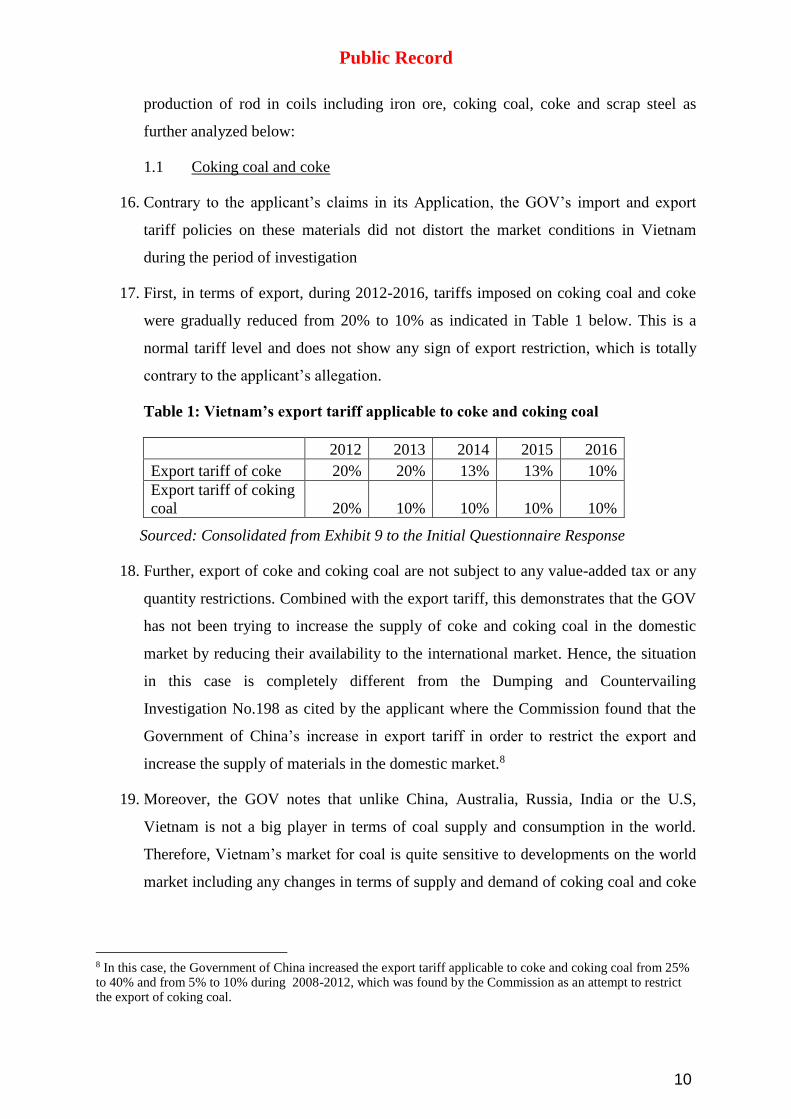

Period of Investigation: 1

April 2016 – 31 March 2017

20 October 2017

The Director

Operations 1

Anti-Dumping Commission

EMAIL: [email protected]

Ref: Anti-Dumping Investigation No.416 of Imports of Steel Rod In Coils

from Indonesia, Republic of South Korea and Vietnam

Sub: Comments on the Applicant’s particular market situation claims and

Request for the Use of Rod In Coils Price in Vietnam to Determine the

Normal Value in the Instant Investigation.

Dear Mr. Director,

On behalf of Government of Vietnam (hereinafter referred to as “GOV”), we hereby

submit comments on the applicant’s particular market situation claims in the on-going anti-

dumping investigation against steel rod in coils imported from Vietnam. In summary of this

submission as analyzed below, the GOV requests the Australia Anti-dumping Commission

(hereinafter referred to as “the Commission”):

Public Record

To reject the applicant’s claims of the existence of a particular market

situation in Vietnam and thus, to apply the rod in coils price in Vietnam’s

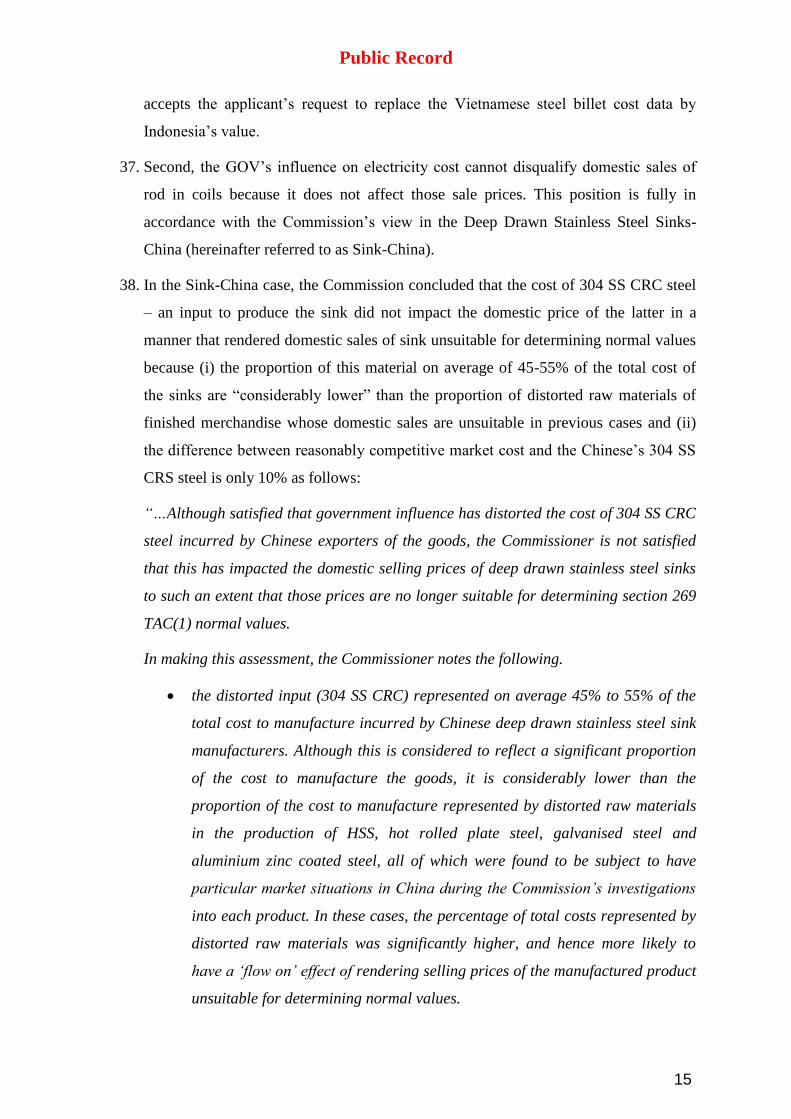

market in determining the normal value for those products originating from

Vietnam. In this case, any claim on a particular market situation in Vietnam

under Section 269 (2) (a) (ii) TAC, Custom Act 1901 is not warranted because

of insufficient evidence of the case record showing that:

(i) the rod in coils prices in Vietnam are artificially low due to the

absence of the GOV’s influence in both prices and cost of steel rod in

coils in Vietnam and

(ii) other conditions exist in Vietnam market that render the rod in coils

sales in Vietnam not suitable for use in determining the normal value

within the instant investigation.

In case of an affirmative decision on the particular market situation in

Vietnam, to implement Australia’s obligation under Article 2 of the WTO

Antidumping Agreement by using Vietnamese producers’ production cost data

to construct the normal value, instead of using Indonesian or any foreign data

as suggested by the applicant.

In addition, the GOV also notes that it has fully cooperated at its best capacity and provided

the Commission with requested response and information to the Commission’s questionnaire

in a timely manner. They are official and factual evidence to demonstrate that the GOV’s law

and policy do not intend to have or result in any distorting effects with regard to the rod in

coil industry and market in Vietnam. As an interested party to this proceeding, the GOV

requests that this position as supported by factual evidence should be carefully taken into

account by the Commission in accordance with its obligation under Article 6 of the

Agreement on Implementation of Article VI of the General Agreement on Tariffs and Trade

1994 (hereinafter referred to as “the WTO Antidumping Agreement) to which Vietnam and

Australia are both members. The GOV reserves its rights to provide additional comments on

the applicant’s allegation as well as any findings of the Commission at the later stage of this

investigation.

2

Public Record

Yours sincerely,

Dinh Anh Tuyet

IDVN Lawyers

Legal Counsel for the Government of Vietnam

3

3

Public Record

INTRODUCTION

1. At the outset, the GOV would like to note that the instant case against rod in coils is

the forth antidumping case and the second case having particular market situation

(herein after referred to as “PMS”) allegations initiated by the Commission against

Vietnamese imports only within 12 months. The first PMS investigation also targeted

the steel sector of Vietnam where the Commission sought detailed information on the

GOV’s law and policy applicable to the steel industry in general and galvanized steel

sector in particular as well as upstream producers of iron ore, coking coal, coke and

scrap steels. In its response to the Commission’s questionnaire, the GOV provided a

detailed explanation of its law and policy with supported data and legal documents

which was then reasonably and thoroughly examined by the Commission in order to

arrive at the conclusion that:

“... Additionally, the Commission did not find any evidence to support a finding that

the Government of Vietnam influenced or distorted the prices or costs of the goods in

the market, or any other conditions in the market that would support a finding of a

particular market situation in Vietnam.”1

2. This finding demonstrates an accurate and thorough understanding of the Commission

on the GOV’s law and policy with regards to the steel industry of Vietnam and should

serve as an important precedent for the Commission when considering any subsequent

PMS allegation against Vietnam, including this case on steel rod in coils. Therefore,

while the GOV is surprised and concerned with the Commission’s decision to

investigate the PMS issue within the steel sector again, it would trust that the

Commission would take a cautious approach in examining all evidence submitted by

the GOV in its response and other submissions and again reach a similar negative

conclusion on the existence of a particular market situation in Vietnam in this rod in

coil case.

3. In this case, the applicant relied entirely on its own misleading interpretation of the

GOV’s export and import tariff on raw materials to produce steel billet – the direct

input of steel rod in coils production to claim that the GOV intervened and distorted

1 Page 109-110, Final Report No.370, Alleged dumping of zinc coated (galvanized) steel exported to Australia from the Republic of India, Malaysia and the Socialist Republic of Vietnam.

4

Public Record

the prices of rod in coils on Vietnam market.2 Such claim is completely unwarranted

because neither the applicant’s submission nor factual evidence of the case record

supports the existence of any GOV’s intervention that may distort the rod in coils

price in Vietnam market. In this submission, the GOV discusses and analyzes all

factual evidence in light of Australia’s regulations and international obligations on

antidumping investigation to sustain (i) non-existence of a particular market situation

with regards to the rod in coils industry and market in Vietnam and (ii) the necessity

and suitability of using data associated with Vietnamese producers of rod in coils to

ensure a suitable determination of normal value under Article 2 of the WTO

Antidumping Agreement, instead of using Indonesian or any foreign cost benchmark

as suggested by the applicant as a result of any possible affirmation of a particular

market situation in Vietnam.

I. Any claim on the existence of a particular market situation in Vietnam

with regards to rod in coils in this case as provided under Section 269

(2)(a)(ii)TAC of Australia’s Custom Act 1901 is not warranted.

4. The GOV submits that there is no particular market situation in Vietnam regarding

rod in coils because criteria of establishing the existence of such market under Section

269(2)(a)(ii)TAC of Australia’s Custom Act 1901 and the Commission’s Dumping

and Subsidy Manual are not satisfied.

5. Pursuant to Section 269(1)TAC of Australia’s Custom Tariff 1901, a general principle

to establish the normal value of any goods exported to Australia is using “the price

paid or payable for like goods sold for home consumption in the exporting country”.

However, Section 269(2)(a)(ii) TAC provides an instance where the normal value of

goods exported to Australia cannot be ascertained by using the price paid or payable

in the exporting country because of the situation in the market of the country of export

which render the sales in that market are not suitable for use in determining a price

under subsection 1. This situation as described in Section 269(2)(a)(ii)TAC as such is

often referred to as “a particular market situation”.

6. The legislation does not define what constitutes a particular market situation that

would render domestic sales as unsuitable. However, the Commission in its Dumping

2 Page 67, Application for the publication of dumping and/or countervailing duty notices – Steel Rod in coils – exported from Republic of Indonesia, the Socialist Republic of Vietnam and the Republic of Korean, May 2017.

5

Public Record

and Subsidy Manual determines that a particular market situation exists in an

exporting country when

“(i) the prices are artificially low; or

(ii) there are other conditions in the market which render sales in that market not

suitable for use in determining prices under Subsection 269 TAC(1)” .3

7. The GOV believes that none of these factors exist in this case.

1. Insufficient evidence showing that the price of rod in coils sold in Vietnam are

artificially low

8. In the Commission’s Dumping and Subsidy Manual, in order to find “artificially low

pricing” of the subject merchandise, there must be sufficient evidence of the record

showing significant influence by the government of an exporting country that distorts

the prices or cost of that merchandise.

“…in investigating whether a market situation exists due to government influence, the

Commission will seek to determine whether the impact of the government’s

involvement in the domestic market has materially distorted competitive conditions. A

finding that competitive conditions have been materially distorted may give rise to a

finding that domestic prices are artificially low or not substantially the same as they

would be if they were determined in a competitive market. One example of

government influence distorting competitive conditions and leading to artificially low

prices may be the presence of government owned enterprises in the domestic market.

The presence of government owned enterprises, of itself, may not lead to the

conclusion that sales are unsuitable. Rather, market conditions will no longer be said

to prevail when the number of government owned enterprises, together with any

unprofitable sales by those same enterprises, has caused a significant distortion to the

prices received by private enterprises.”4

9. In the instant investigation, the GOV does not have any influence in a manner that

materially distorts competitive conditions of rod in coils on Vietnam market.

10. First, as indicated in its response to the Commission’s questionnaire, the GOV does

not have any direct ownership or representation in any rod in coil producers and

3 Page 36 Dumping and Subsidy Manual, April 2017 by the Anti-dumping Commission of Australia. 4 Page 36-37, Id.

6

Public Record

traders in Vietnam. The rod in coils industry is subject to the same set of laws and

regulations with other sectors of production and business in Vietnam. There is no

restriction or control by the GOV over the number of producers and traders or over

the private or foreign ownership in this sector or over the quantity of production and

sale in Vietnam and export markets. They are free to decide how much to produce and

at which price to sell their products in Vietnam and abroad. Being a steel rod in coil

maker or trader has never been a criterion to receive any benefit or favor under the

Vietnam’s law.

11. Second, to the extent that the Commission is concerned with the ownership of

Vietnam Steel Corporation – a state-owned company – in 05 rod in coils

producers,[INFORMATION OF ENTERPRISES] the GOV emphasizes two relevant

important factors to demonstrate that competitive market conditions still prevail in

Vietnam in this sector. Firstly, Vietnam Steel Corporation [INFORMATION OF

ENTERPRISES] did not produce and sell rod in coils during the POI but rather

operated as a holding company having equity interests and acting as shareholder in

those 05 producers,[INFORMATION OF ENTERPRISES]. Secondly, the local

private sector and foreign-invested enterprise prevail the whole rod in coils industry

when accounting for more than 75% of the total industry’s production quantity while

these 05 producers only accounted less than 25% and never exported the subject

merchandise to Australia.5 ,[INFORMATION OF ENTERPRISES] Thirdly, the only

exporter of rod in coils to Australia is a 100% private company in which both the

GOV and Vietnam Steel Corporation ,[INFORMATION OF ENTERPRISES]do not

have any ownership or equity interest.

12. Third, as responded to the Commission, steel rod in coils is not subject to any price

control measure taken by the GOV. Pursuant to Article 11 of the Law on Prices of

Vietnam6, enterprises have the right to self-determine the prices of goods or services

which they manufacture or deliver except for certain products subject to price

determination by the GOV. A list of these products is provided in Article 19 of this

Law. Rod in coils as well as all of the upstream raw materials including iron ore,

coking coal, coke, scrap steel and square billets are completely absent from such list.

5 Exhibit 1 to the GOV’s questionnaire response 6 This law is provided at Exhibit 10 to the GOV’s questionnaire response.

7

Public Record

Therefore, sale and purchase of rod in coils follow market supply and demand without

any intervention by the GOV.

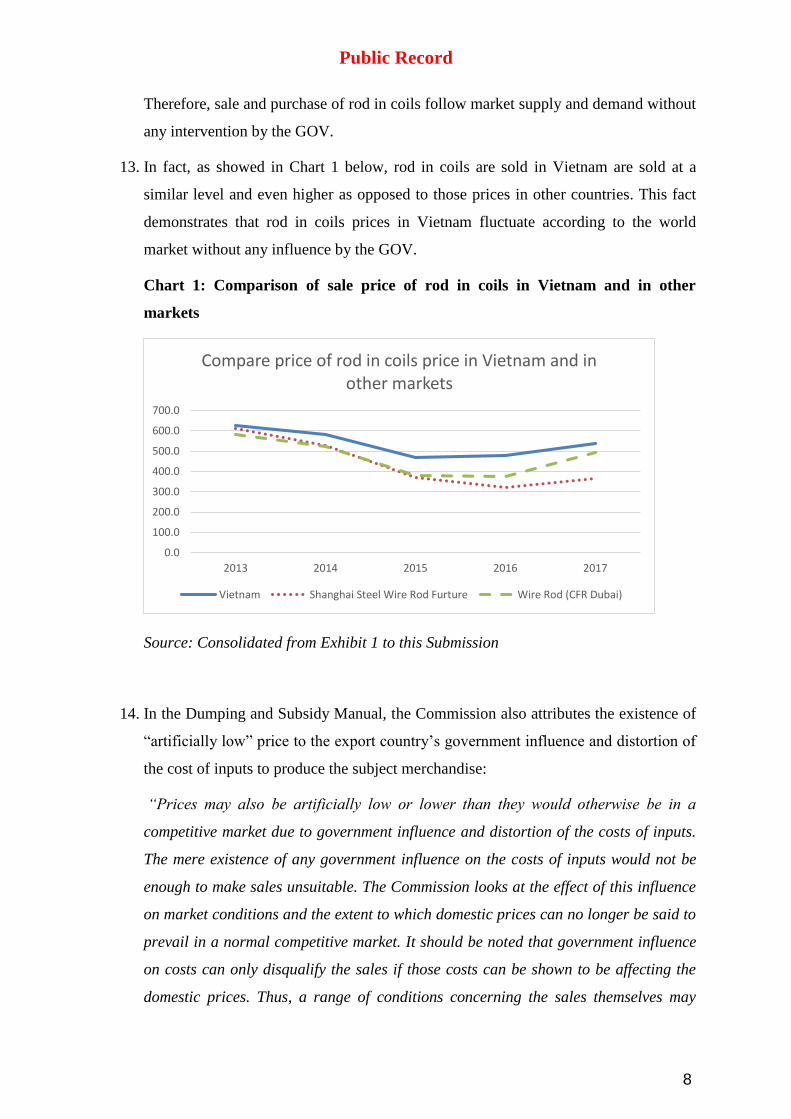

13. In fact, as showed in Chart 1 below, rod in coils are sold in Vietnam are sold at a

similar level and even higher as opposed to those prices in other countries. This fact

demonstrates that rod in coils prices in Vietnam fluctuate according to the world

market without any influence by the GOV.

Chart 1: Comparison of sale price of rod in coils in Vietnam and in other

markets

Source: Consolidated from Exhibit 1 to this Submission

14. In the Dumping and Subsidy Manual, the Commission also attributes the existence of

“artificially low” price to the export country’s government influence and distortion of

the cost of inputs to produce the subject merchandise:

“Prices may also be artificially low or lower than they would otherwise be in a

competitive market due to government influence and distortion of the costs of inputs.

The mere existence of any government influence on the costs of inputs would not be

enough to make sales unsuitable. The Commission looks at the effect of this influence

on market conditions and the extent to which domestic prices can no longer be said to

prevail in a normal competitive market. It should be noted that government influence

on costs can only disqualify the sales if those costs can be shown to be affecting the

domestic prices. Thus, a range of conditions concerning the sales themselves may

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

2013 2014 2015 2016 2017

Compare price of rod in coils price in Vietnam and in other markets

Vietnam Shanghai Steel Wire Rod Furture Wire Rod (CFR Dubai)

8

Public Record

have the effect of rendering those sales prices as being unsuitable for use in

determining prices under subsection 269TAC(1). When relevant and reasonably

reliable evidence supporting the proposition that domestic selling prices are

unsuitable for normal values is set out in the application, and an investigation is

initiated, the Commission will adopt the following procedures in order to ensure

interested parties have an opportunity to consider the claims and present evidence:

Notify the government of the country and the exporters of the claims and of the

evidence provided. Additional questions will be inserted into the exporter

questionnaire titled “Market Situation”. A ‘Market Situation’ questionnaire will

also be prepared for government.

Both questionnaires will be based upon the evidence provided by the Australian

industry that supported the decision to investigate. That is, the information

supporting the claim that the domestic prices are materially influenced by the

government of that country and are not substantially the same as they would be if

they were determined in a competitive market. Any other relevant information in

the possession of the Commission may also be taken into account when preparing

the questionnaire. The government and the exporter will be asked to respond as

specifically as possible to the questions. Accompanying letters will draw attention

to these questions.

If the government of the country or exporters fail to respond after being given a

reasonable opportunity to do so, or do not provide probative evidence in

response, all available evidence is weighed up, including the prima facie evidence

of the application. One possible outcome is that the Commission will determine

that a situation in the market has rendered domestic selling prices unsuitable for

establishing normal values.”7

15. In the Questionnaire, specific questions were raised to the GOV regarding its law and

policy regarding iron ore, coking coal, coke, scrap steels, and steel billet – raw

materials that constitute a part of production cost of the subject merchandise. The

GOV fully cooperated with the Commission by providing requested information and

data at its best capacity, which demonstrates that the GOV has not implemented any

policy to place a downward effect on the price of raw material inputs into the

7 Page 37, the Dumping and Subsidy Manual, April 2017 by the Anti-dumping Commission of Australia.

9

Public Record

production of rod in coils including iron ore, coking coal, coke and scrap steel as

further analyzed below:

1.1 Coking coal and coke

16. Contrary to the applicant’s claims in its Application, the GOV’s import and export

tariff policies on these materials did not distort the market conditions in Vietnam

during the period of investigation

17. First, in terms of export, during 2012-2016, tariffs imposed on coking coal and coke

were gradually reduced from 20% to 10% as indicated in Table 1 below. This is a

normal tariff level and does not show any sign of export restriction, which is totally

contrary to the applicant’s allegation.

Table 1: Vietnam’s export tariff applicable to coke and coking coal

2012 2013 2014 2015 2016

Export tariff of coke 20% 20% 13% 13% 10%

Export tariff of coking

coal 20% 10% 10% 10% 10%

Sourced: Consolidated from Exhibit 9 to the Initial Questionnaire Response

18. Further, export of coke and coking coal are not subject to any value-added tax or any

quantity restrictions. Combined with the export tariff, this demonstrates that the GOV

has not been trying to increase the supply of coke and coking coal in the domestic

market by reducing their availability to the international market. Hence, the situation

in this case is completely different from the Dumping and Countervailing

Investigation No.198 as cited by the applicant where the Commission found that the

Government of China’s increase in export tariff in order to restrict the export and

increase the supply of materials in the domestic market.8

19. Moreover, the GOV notes that unlike China, Australia, Russia, India or the U.S,

Vietnam is not a big player in terms of coal supply and consumption in the world.

Therefore, Vietnam’s market for coal is quite sensitive to developments on the world

market including any changes in terms of supply and demand of coking coal and coke

8 In this case, the Government of China increased the export tariff applicable to coke and coking coal from 25% to 40% and from 5% to 10% during 2008-2012, which was found by the Commission as an attempt to restrict the export of coking coal.

10

Public Record

taking place in giant players rather than to the GOV’s import or export tariff on these

materials.

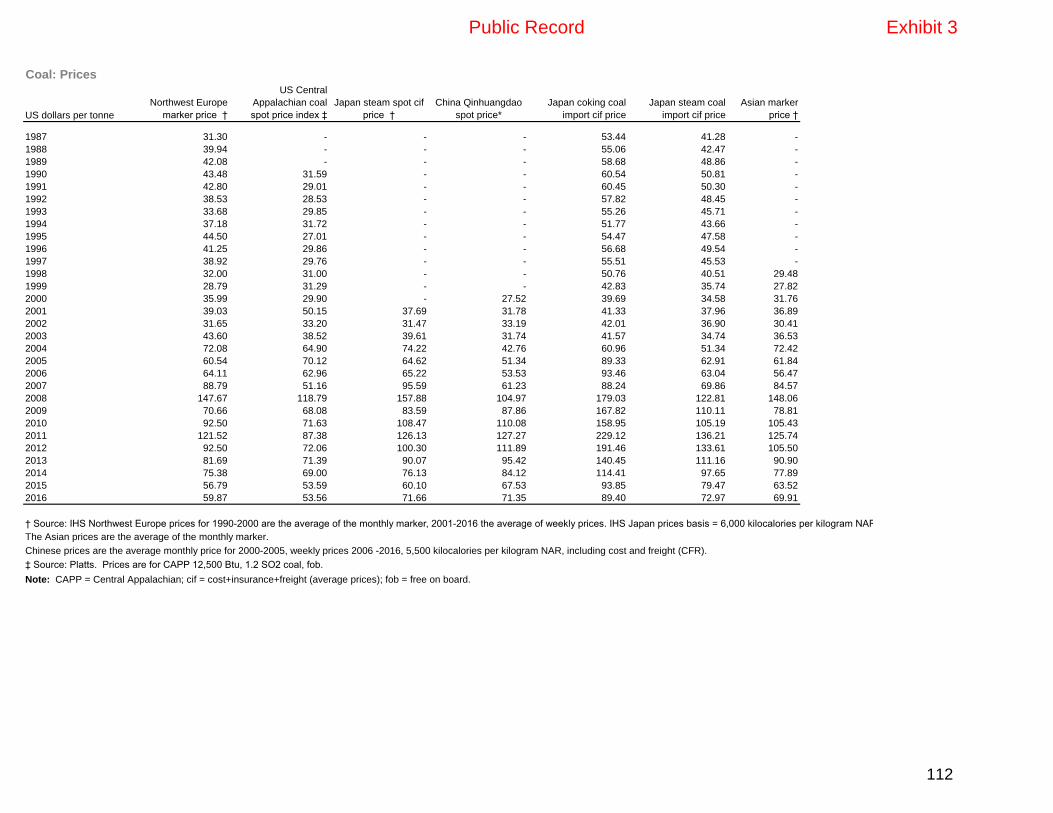

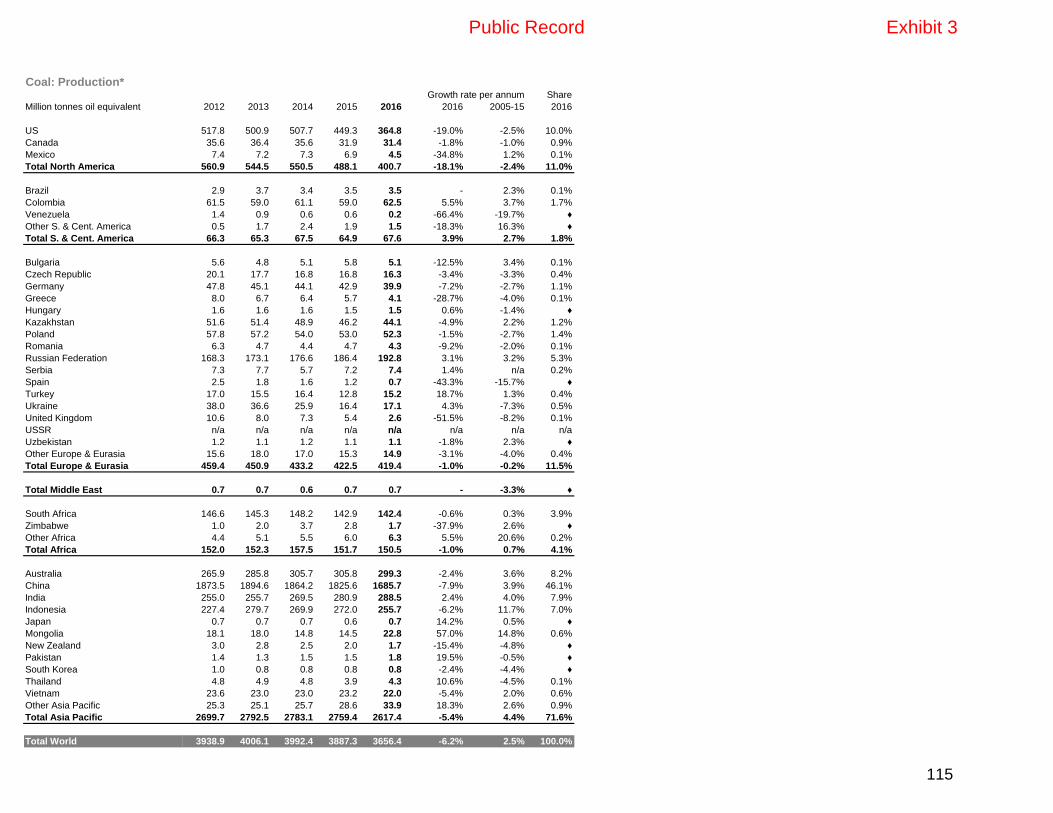

Table 2: Vietnam and other countries’ coal production and consumption

Coal: Production Unit: Million tonnes oil equivalent

Year 2012 2013 2014 2015 2016 Share (%)

US 517.79 500.87 507.70 449.34 364.82 10.0%

Russian Federation 168.29 173.12 176.59 186.38 192.77 5.3%

South Africa 146.57 145.26 148.23 142.89 142.44 3.9%

Australia 265.86 285.78 305.70 305.81 299.29 8.2%

China 1873.54 1894.59 1864.21 1825.56 1685.71 46.1%

India 255.05 255.73 269.45 280.90 288.53 7.9%

Indonesia 227.39 279.66 269.94 271.98 255.74 7.0%

Vietnam 23.57 23.00 23.01 23.23 22.04 0.6%

Coal: Consumption Unit: Million tonnes oil equivalent

Year 2012 2013 2014 2015 2016 Share (%)

US 437.92 454.57 453.53 391.82 358.43 10%

Total Europe &

Eurasia 528.06 508.05 487.26 471.34 451.56 12%

China 1927.79 1969.07 1954.48 1913.62 1887.55 51%

India 329.99 352.78 387.54 396.55 411.95 11%

Indonesia 53.02 57.01 45.12 51.16 62.70 2%

Japan 115.82 121.15 119.15 119.89 119.94 3%

Vietnam 15.04 15.83 18.94 22.25 21.33 1%

Source: Consolidated from World Energy Statistics 2017 provided at Exhibit 3 to this

Submission.

20. As can be seen from Table 2, Vietnam’s shares of the world’s coal production and

consumption account less than 1%. Indeed, Vietnam’s export of coking coal during

2012-2016 is totally inelastic to the GOV’s change in the export tariff on this

material:

Chart 2: Vietnam’s coking coal export quantity during 2012-2016

21. As can be seen, the export quantity of coking coal reached the highest level in 2012

when the export tariff was set at the highest level. When the tariff was reduced to 10%

in 2013 and maintained that level until 2016, the quantity of export did not increase

but followed a downward trend. Thus, there is no causation between the GOV’s

export tariff and the supply of coking coal to international markets.

11

Public Record

22. Similar observations can be made with regards to coke export as described in Table 3

below:

Table 3: Coke export by Vietnam and Applicable Export Tariff

23. The overall trend for both export tariff and the quantity of coke export by Vietnam is

decreasing during 2012-2016.

24. Second, in terms of import, the GOV notes that tariff levels levied on imported coking

coal and coke are not decided merely by the GOV’s discretion. Rather, they are

subject to Vietnam’s obligation under multilateral agreement (i.e. WTO) or free trade

agreements. Thus, applicable tariffs during 2012-2016 on imported coking coal and

coke from major country suppliers should be anticipated a long time before the POI

and should not be considered as an attempt of the GOV to encourage the importation

for the domestic market. For example, the fact that a decrease in the tariff of coking

coal of HS code 2704.0020 and 27.04.00.30 imported from Australia to 0% in 2016 as

cited by the applicant in the petition was in fact decided since 2009 as a Vietnam’s

obligation under the ASEAN-Australia/New Zealand Free Trade Area. Exhibit 2

provides detailed information of the import tariff on coking coal and coke into

Vietnam from 05 largest suppliers corresponding to Vietnam’s commitments under

relevant free trade agreements.

25. Import tariff rates applicable to coking coal and coke during 2012-2016 result from

the negotiation and agreement between the GOV and its counterparts in the process of

establishing free trade areas. It is the implementation of such obligations that led to

the reduction in the import tariff rates in 2016. This fact obviously contradicts the

applicant’s allegation that the GOV changed its import policy to encourage the

importation of these materials into Vietnam in order to create a favor to the

downstream value added industries such as steel billet and rod in coils.

26. In addition, the quantity of coking coal imported into Vietnam is more dependent on

prices fluctuations in the world market. For instance, as indicated in Chart 3 below,

the import volume of coking coal into Vietnam in 2016 from Australia – the largest

supplier – was completely elastic to the price market.

Chart 3: Price elasticity of Coal import into Vietnam from Australia in 2016

1.2 Iron ore and scrap steel

12

Public Record

27. First, the GOV submits that no export restriction measures in form of quota or tariff

against iron ore and scrap steel were introduced during the POI in order to reserve the

market for these products for domestic downstream users as claimed by the applicant.

It is an obvious fact that the export tariff levied by the GOV on iron core remained

unchanged during 2012-2016 while the quantity of export has increased dramatically

as shown in Table 4 below:

Table 4: Iron ore export by Vietnam and Applicable Export Tariff

28. A similar trend is observable with regards to the export of scrap steel.

Table 5: Scrap steel export by Vietnam and Applicable Export Tariff

29. Thus, there is no correlation between the GOV’s export tariff in this regard and the

so-called “export restriction” policy as claimed by the applicant.

30. Meanwhile, import tariff on iron ore of 0% applicable during 2012-2016 was actually

the ceiling rate under Vietnam’s WTO commitments since 2007. Obviously contrary

to the applicant’s claim, it is not the GOV’s policy to maintain a difference of 40%

between the export and import tariff rates on iron ore in order to favor the

downstream producers such as steel billet or rod in coils.

31. In addition, the increase in iron ore import volume during 2015-2016 is attributed to

the steel billet production expansion by a number of BOF projects invested with

private and foreign capital by Hoa Phat Group and Formosa Ha Tinh Steel

[INFORMATION OF ENTERPRISES]. Chart 4 shows that Vietnam’s domestic

production of iron ore hardly satisfied the demand during this period.

Chart 4: Iron ore production and consumption for steel billet production in

Vietnam

32. Similarly, the increase in scrap steel imports results from the investment in steel billet

by private sectors such as Vinakyoei Vietnam and POSCO SS Vina.

[INFORMATION OF ENTERPRISES]

13

Public Record

33. Therefore, the fact that import of iron ore and scrap steel increased significantly into

Vietnam during 2015-2016 has nothing to do with the GOV’s import tariff. Rather it

results from the capacity expansion of the billet sector by investment from the private

and foreign sectors.

1.3 Electricity

34. In its submission dated September 6, 2017, the applicant claimed that the rod in coil

prices in Vietnam is artificially low due to government influence and distortion of the

cost of electricity9 and requested the Commission to substitute the steel billet

production cost of Indonesia for that of Vietnam in order to calculate the cost of

production of rod in coils. This claim is clearly unfounded

35. First, the GOV’s influence in the electricity price – an input of steel billet production

– is not sufficient to allow a conclusion that a market situation exists in the

Vietnamese’s rod in coils market that renders the sale of rod in coils in Vietnam

unsuitable for determining normal value under Section 269TAC(1). The

Commission’s Dumping and Subsidy Manual correctly points out that:

“…The mere existence of any government influence on the costs of inputs would not

be enough to make sales unsuitable. The Commission looks at the effect of this

influence on market conditions and the extent to which domestic prices can no longer

be said to prevail in a normal competitive market. It should be noted that government

influence on costs can only disqualify the sales if those costs can be shown to be

affecting the domestic prices.”10

36. First, the GOV would note that its regulation of electricity tariff is a normal practice

that is also adopted by a number of other countries including Indonesia and Australia.

Exhibit 6 provides the applicable tariff decided by the GOV during 2012-2015 in

comparison with that of Indonesia and Australia (Queensland) where caps on

electricity tariff are also applied. Nowhere in Australia’s regulations on antidumping

and the Commission’s practice of previous cases that support an affirmative finding of

a particular market situation resulting from the government control on electricity

tariff. Further, given the fact that electricity tariffs in Vietnam and Indonesia are both

regulated by the government, it would be even more unreasonable if the Commission

9 Page 1, OneSteel Manufacturing Pty Ltd’s Submission dated 6 September 2017. 10 Page 36, the Dumping and Subsidy Manual, April 2017 by the Anti-dumping Commission of Australia

14

Public Record

accepts the applicant’s request to replace the Vietnamese steel billet cost data by

Indonesia’s value.

37. Second, the GOV’s influence on electricity cost cannot disqualify domestic sales of

rod in coils because it does not affect those sale prices. This position is fully in

accordance with the Commission’s view in the Deep Drawn Stainless Steel Sinks-

China (hereinafter referred to as Sink-China).

38. In the Sink-China case, the Commission concluded that the cost of 304 SS CRC steel

– an input to produce the sink did not impact the domestic price of the latter in a

manner that rendered domestic sales of sink unsuitable for determining normal values

because (i) the proportion of this material on average of 45-55% of the total cost of

the sinks are “considerably lower” than the proportion of distorted raw materials of

finished merchandise whose domestic sales are unsuitable in previous cases and (ii)

the difference between reasonably competitive market cost and the Chinese’s 304 SS

CRS steel is only 10% as follows:

“…Although satisfied that government influence has distorted the cost of 304 SS CRC

steel incurred by Chinese exporters of the goods, the Commissioner is not satisfied

that this has impacted the domestic selling prices of deep drawn stainless steel sinks

to such an extent that those prices are no longer suitable for determining section 269

TAC(1) normal values.

In making this assessment, the Commissioner notes the following.

the distorted input (304 SS CRC) represented on average 45% to 55% of the

total cost to manufacture incurred by Chinese deep drawn stainless steel sink

manufacturers. Although this is considered to reflect a significant proportion

of the cost to manufacture the goods, it is considerably lower than the

proportion of the cost to manufacture represented by distorted raw materials

in the production of HSS, hot rolled plate steel, galvanised steel and

aluminium zinc coated steel, all of which were found to be subject to have

particular market situations in China during the Commission’s investigations

into each product. In these cases, the percentage of total costs represented by

distorted raw materials was significantly higher, and hence more likely to

have a ‘flow on’ effect of rendering selling prices of the manufactured product

unsuitable for determining normal values.

15

Public Record

The difference between the reasonably competitive market cost determined by

the Commission for 304-SS CRC87 (see Non-Confidential Appendix 4 and

Non-Confidential Appendix 8 for discussion) and the costs actually incurred

by Chinese exporters of the goods is on average 10% (i.e. Chinese-incurred

costs are 10% lower than the reasonably competitive market cost for 304 SS

CRC). This uplift, while significant, is substantially lower than uplifts to steel

raw material costs observed by the Commission in its investigations into other

Chinese steel products.

When combined with the consideration that this is a 10% uplift to a cost that is

approximately 45 – 55% of total manufacturing costs, the Commission

considers this does not provide strong evidence that the impact of distorted

stainless steel costs has had the impact of creating a market situation in the

deep drawn stainless steel sinks market (i.e. it is likely that this distorted input

has not impacted the price of deep drawn stainless steel sinks to such an extent

that domestic prices of those goods are no longer suitable for use in

determining normal value)..”11

39. In this case, a thorough examination of Vietnam’s electricity tariff and its proportion

in the cost of billet and rod in coils production also shows a similar uplift level as in

the Deep Drawn Stainless Steel Sinks- China case.

40. First, electricity represents on average 3% to 10% of the total cost to manufacture

steel billet for BOF and EAF technologies.12 Adding to rolling stage (i.e. rolling billet

into rod in coils), total cost of electricity to manufacture long steel accounts for

around 35% and can even be more efficient.13This proportion is even much lower than

the proportion of the distorted cost of raw material in the China-Sink case.

41. Second, Vietnam’s electricity tariff during 2016 is almost at the same level with other

countries. Exhibit 6 provides the applicable tariff to electricity consumption for

production and business purpose in Vietnam and other countries including Indonesia,

11 Page 131-132, REP 238 Deep Drawn Stainless Steel Sinks- China

12 Cost of electricity to produce steel using BOF and EAF technologies can be found via

http://www.steelonthenet.com/cost-eaf.html and http://www.steelonthenet.com/cost-bof.html

13 Id.

16

Public Record

Thailand, Malaysia and Australia in 2016. Accordingly, Vietnam’s tariff is around

14% lower than the average of these countries and 9% lower than Indonesia.

42. As such, an uplift of 8%-14% to a cost that is approximately 35% of the total

manufacturing cost of rod in coils should not be considered strong evidence that

influence cost of electricity in Vietnam has had the impact of creating a market

situation in the rod in coil market.

43. In fact, electricity cost does not have any significant impact on the price of steel billet

and rod in coils in Vietnam. As indicated in Chart 5 below, fluctuations in electricity

tariffs had no correlation with the prices of steel billet in Vietnam’s market.

Chart 5: Electricity price changes and steel billet price developments in Vietnam

during 2012-2016

44. As can be seen, billet price reached its highest peak in 2012 when the electricity price

was lowest. Meanwhile, the former reduced almost by 50% when the latter reached

almost the highest level in 2015.

45. For all of reasons above, the GOV strongly requests the Commission to reject the

applicant’s position in its submission dated September 6, 2017 regarding the existence

of a particular market situation in Vietnam’s rod in coils market due to the GOV’s

influence on electricity and thus, render the applicant’s request for using Indonesia’s

billet cost of production groundless.

1.4 Steel billet

46. Regarding steel billet, as indicated in Exhibit 6 and 9 to the GOV’s Initial

Questionnaire Response, export tariff of steel billet was maintained at 0% for 2012-

2016 while import tariff for main foreign suppliers such as Japan and China were set

at various levels between 0% - 7%. In addition, steel billet is not subject to any import

or export restrictions. These are strong evidence that the GOV does not encourage the

importation and restrict the exportation of inputs to manufacture rod in coils as

alleged by the applicant.

47. In addition, as reported in the GOV’s Initial Questionnaire Response, effectively from

March 22, 2016, the GOV levied a safeguard tax of 23% on imported billet with a

17

Public Record

regular liberalization of 2% each year in order to rescue the domestic billet industry.

This, needless to say, results in increasing the price of steel billets in Vietnam.

Chart 7: Steel billet price in Vietnam after safeguard duty in 2016 in comparison

with price of Black sea areas

48. As a result, Vietnamese producers of rod in coils incurred a higher cost of production

of rod in coils given the fact that domestic production of billet did not satisfy the

consumption demand.14

49. Further, the GOV would note that all of its policy including import and export tariff

on iron ore, scrap steel, coking coal and coke were already reported to the

Commission in the Zinc Coated (Galvanized) Steel-Vietnam No 370 (hereinafter

referred to as Galvanized Steel-Vietnam), where the Commission concluded that there

is no evidence “to support a finding that the Government of Vietnam influenced or

distorted the prices or costs of the goods in the market, or any other conditions in the

market that would support a finding of a particular market situation in Vietnam.”15

Accordingly, the GOV requests the Commission to adopt the same findings as there

are no changes in terms of the GOV’s policies as reported in the Gavalnized Steel-

Vietnam case and this instant investigation.

50. As with galvanize steel producers, Vietnamese rod in coils manufacturers are totally

free from the GOV control to decide on their own production and sale price. Thus, the

GOV strongly opposes the applicant’s claim on the existence of the so-called

“artificially low” price of rod in coils sale in Vietnam market and requests the

Commission to conclude that there is no particular market situation in Vietnam that

may arise out of such claim.

2. There are no other conditions in the market rendering sales in Vietnam not

suitable for use in determining the normal value

14 As indicated in Exhibit 4 to the GOV’s Initial Questionnaire Response, total domestic supply of billet was 7.8 million tons in 2016 while the consumption quantity is more than 8.6 million tons. 15 Page 109-110, Final Report No.370, Alleged dumping of zinc coated (galvanized) steel exported to Australia from the Republic of India, Malaysia and the Socialist Republic of Vietnam.

18

Public Record

51. According the Antidumping and Subsidy Manual, other conditions in the market

which may render sales in that market not suitable for use in determining prices under

subsection 269TAC(1) may include:

differing patterns of demand in the exporter’s domestic market and the

sales to Australia (including domestic sales significantly different in

character or design features to the types exported; domestic sales

through a single sales channel (including via a related party

distributor); and unusual patterns of sales in the domestic market for

the good). Implicit in such findings is the assumption that it is not

possible to make reasonable adjustments to ensure comparability of

the domestic sales prices;

where only a single sale to one customer constitutes 5 per cent of the

sales to Australia;

significant barter trade; or

Non-commercial processing arrangements.”16

52. None of those conditions exist in this case. First, long steel products including rod in

coils are of high demand in Vietnam market due to the significant development of

infrastructure and housing construction all over the country. As estimated by the

Vietnam Steel Association, the domestic market in 2016 was in need of more than 3

million tons of rod in coils. The total production of the whole country was estimated

at around 1.3 million tons and 75%17 was served the domestic market. Thus, sales in

domestic market play a dominant proportion and are comparable to export sales for

purpose of dumping calculations.

53. In addition, the whole sector is majority owned by the private sector which are free to

decide what and how many to produce and who to sell. Therefore, rod in coils market

in Vietnam is an absolutely commercial market where producers are free to set up

different channels of sale including distribution and agents. Exhibit 9 provides a list of

distribution and agents of some rod in coils producers. Their sale prices in the

domestic markets show no relevance with any non-commercial arrangement or

significant barter trade or any other conditions that are sufficient to remove the

“commercial nature” out of the Vietnam market.

54. Therefore, the GOV is not aware of any other conditions in Vietnam’s rod in coils

market that may render domestic sales unsuitable for normal value determination.

16 Page 36, Dumping and Subsidy Manual 17 Total export of rod in coils by Vietnam in 2016 was 306,159 tons.

19

Public Record

II. In the event of an affirmative decision of a particular market situation in

Vietnam, the Commission is obliged to use Vietnam producers’ data of

production cost to construct the normal value.

55. Even if the Commission affirmatively determines that a particular market situation in

Vietnam exists in a manner that renders domestic sales of rod in coils in Vietnam

unsuitable for normal value calculation, it is obliged under Article 2.2 of the WTO

Antidumping Agreement to construct the normal value based on Vietnamese

producers’ data on cost of production or export sale to third countries.

56. Article 2.2 provides as below:

“ When there are no sales of the like product in the ordinary course of trade in the

domestic market of the exporting country or when, because of the particular market

situation or the low volume of the sales in the domestic market of the exporting

country(2), such sales do not permit a proper comparison, the margin of dumping

shall be determined by comparison with a comparable price of the like product when

exported to an appropriate third country, provided that this price is representative, or

with the cost of production in the country of origin plus a reasonable amount for

administrative, selling and general costs and for profits.”

57. As such, the existence of a particular market situation authorizes the Commission

only to disregard domestic sales of rod in coils in Vietnam for normal value

calculation. Either the cost of production incurred by Vietnamese producers or

representative sale prices of rod in coils to third countries must be applied to

determine normal value. Nothing in this Article further authorizes the Commission to

rely on a foreign benchmark of production cost to calculate the normal value as

requested by the applicant in this case. This interpretation is fully supported and

clarified by Article 2.2.1.1 as follows:

“For purpose of paragraph 2, costs “shall” normally be calculated on the basis of

records kept the exporter or producer under investigation, provided that such records

are in accordance with the generally accepted accounting principles of the exporting

country and reasonably reflect the costs associated with the production and sale of

the product under consideration.”

58. As long as the Vietnamese producer’s cost records comply with requirements under

Article 2.2.1.1, the Commission is obliged to calculate the cost of production based on

20

Public Record

the former’s records and data as a general principle. This Article does not require an

investigated producer’s cost to be on competitive basis in order for such cost records

to be used to construct normal value. Thus, the Commission is not authorized to use a

foreign cost benchmark to replace Vietnamese producers’ cost records merely because

the latter is not competitively based due to the existence of a particular market

situation in Vietnam.

59. The GOV’s position in this regard is supported by the WTO jurisprudence with

regards to the interpretation of Article 2.2 of the WTO Anti-dumping Agreement.

60. In EC-Tube or Pipe Fitting, the Appellate Body clearly indicated that Article 2.2.1.1

identified the records kept by the exporter or producer under investigation “to be the

preferred source for cost of production data.”18 Therefore, the Commission as the

investigation authority in this case is directed to base its calculation of costs on such

records when two conditions under this Article are met.

61. Moreover, in EU-Biodiesel – a dispute that addresses a similar situation where

Argentina challenged the EU’s departure from the Argentinian respondents’ recorded

costs of raw materials because of Argentina’s imposition of an export tax on soya-a

biodiesel input, the Appellate Body found that the EU’s departure acted inconsistently

with Article 2.2.1.1 and Article 2.2 of the WTO Anti-dumping Agreement. Therefore,

the GOV opines that the applicant’s request for substituting Indonesia’s steel billet

cost data for that of Vietnamese producers’ in this case would obviously amount to a

violation engaged by the EU in the Biodiesel case and thus, such request should be

dismissed by the Commission.

62. First, Article 2.2.1.1 of the WTO Antidumping Agreement requires the cost records to

“reasonably reflect” the cost actually incurred by the producers instead of insisting on

the reasonableness of the cost itself. In other words, this Article “requires a

comparison between the costs in the producer's or exporter's records and the costs

incurred by such producer or exporter. The object of the comparison is to establish

whether the records reasonably reflect the costs actually incurred, and not whether

they reasonably reflect some hypothetical costs that might have been incurred under a

different set of conditions or circumstances and which the investigating authority

considers more 'reasonable' than the costs actually incurred.”19 Therefore, in EU-

Biodiesel case, the mere affirmation by EU that the Argentina’s domestic prices of the

soya bean – main raw material used by biodiesel producers – were found to be

18 EC-Tube or Pipe Fittings, (DS219) AB report, para 99. 19 EU-Biodiesel, (DS473), AB report, para 6.41.

21

Public Record

artificially lower than international prices due to the distortion by Argentina

government’s export tax system “cannot serve as a sufficient basis under Article

2.2.1.1 for concluding that the producers' records do not reasonably reflect the costs

associated with the production and sale of biodiesel.20” Applying the same

interpretation in this rod in coils case, the applicant’s request for replacing

Vietnamese producers’ billet cost data with those of Indonesian by merely relying on

its alleged existence of “artificially low” prices of inputs to produce rod in coils in

Vietnam would present a violation of Article 2.2.1.1 in an exact manner with the EU

in the cited case. The GOV strongly believes that the Commission would carefully

take into account this issue in order to avoid this mistake.

63. Second, according to the Appellate Body, while Article 2.2 does not prohibit the

authority from relying on information other than that contained in the records kept by

the exporter or producer, including in-country and out-of-country evidence, this does

not mean that an investigating authority may simply substitute the costs from outside

the country of origin for the "cost of production in the country of origin" as suggested

by the applicant.21 According to the Appellate Body, Article 2.2 of the Anti-Dumping

Agreement and Article VI:1(b)(ii) of the GATT 1994 “make clear that the

determination is of the "cost of production […] in the country of origin". Thus,

whatever the information that it uses, an investigating authority has to ensure that

such information is used to arrive at the "cost of production in the country of origin.

Compliance with this obligation may require the investigating authority to adapt the

information that it collects22”. Thus, by replacing the actual cost of raw materials in

the Argentine producers’ records with the surrogate price of soybeans, the EU was

found not to adapt the information it used to arrive at the cost of production in

Argentina and thus, the arising cost was found not to represent the cost of production

in Argentina for purpose of constructing normal value as required by Article 2.2

64. In the rod in coils case, the applicant is repeating exactly the EU’s mistake when

requesting the Commission to just substitute the Vietnamese producer’s billet cost of

production data with those of Indonesia without any adapting attempt to ensure the

surrogate value may result in an arrival at the cost of production in Vietnam as

required by Article 2.2. Therefore, the GOV requests the Commission to reject the

applicant’s request for surrogate value.

20 Id, para 6.55. 21 Id, para6.73 22 Id.

22

Public Record

CONCLUSION

For the above analysis, the GOV once again urges the Commission to reject (i) the

applicant's claim on the existence of a particular market situation in Vietnam with regards to

rod in coils and (ii) its requests to replace Vietnamese producers's cost of production data

with those of Indonesia for purpose of constructing the normal value. In addition, in case

where the Commission decides to construct the normal value of rod in coils in this case, the

GOV requests the Commission to implement Australia's obligation under Article 2 of the

WTO Antidumping Agreement to ensure that the arising constructed normal value reflects

the the cost of production of rods in coils in Vietnam. The GOV also reverses its rights to

submit to the Commission additional comments in this matter within the schedule of the

authority in this investigation./

Respectfully .

IDVN Lawyers

Counsel for the Government of Vietnam

23

23

Column 1 Column 2 Column 3 Column 4 Column 5

Tariff Item Number

Description of Goods Base Rate

Category Note

2702.20.00.00.00 - Agglomerated lignite

5% B10

27.03 Peat (including peat litter), whether or not agglomerated.

2703.00.10.00.00 - Peat, whether or not compressed into bales, but not agglomerated

5% B10

2703.00.20.00.00 - Agglomerated peat

5% B10

27.04 Coke and semi-coke of coal, of lignite or of peat, whether or not agglomerated; retort carbon.

2704.00.10.00.00 - Coke and semi-coke of coal A 2704.00.20.00.00 - Coke and semi-coke of lignite or of

peat 5% B10

2704.00.30.00.00 - Retort carbon

5% B10

2705.00.00.00.00 Coal gas, water gas, producer gas and similar gases, other than petroleum gases and other gaseous hydrocarbons.

A

2706.00.00.00.00 Tar distilled from coal, from lignite or from peat, and other mineral tars, whether or not dehydrated or partially distilled, including reconstituted tars.

A

27.07 Oils and other products of the distillation of high temperature coal tar; similar products in which the weight of the aromatic constituents exceeds that of the non-aromatic constituents.

2707.10.00.00.00 - Benzol (benzene) 1% B10 2707.20.00.00.00 - Toluol (toluene) 1% B10 2707.30.00.00.00 - Xylol (xylenes) 1% B10 2707.40.00.00.00 - Naphthalene 1% B10 2707.50.00.00.00 - Other aromatic hydrocarbon mixtures of

which 65% or more by volume (including losses) distils at 250°C by the ASTM D 86 method

1% B10

- Other: 2707.91.00.00.00 - - Creosote oils 1% B10 2707.99 - - Other: 2707.99.20.00.00 - - - Carbon black feedstock 1% B10 2707.99.90.00.00 - - - Other

1% B10

27.08 Pitch and pitch coke, obtained from coal tar or from other mineral tars.

2708.10.00.00.00 - Pitch A 2708.20.00.00.00 - Pitch coke

A

27.09 Petroleum oils and oils obtained from bituminous minerals, crude.

2709.00.10.00.00 - Crude petroleum oil 15% B10 2709.00.20.00.00 - Condensates X 2709.00.90.00.00 - Other

X

Public Record Exhibit 2

24

User

Typewriter

VJEPA TARIFF SCHEDULE

HS Code Description

Base

rate

(MFN

2005)

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

2022 and

subsequent

years

Viet Nam

Schedule of Tariff Commitments

Annex 1

2621.10.00.00 - Ash and residues from the incineration of

municipal waste

10% 10% 10% 10% 7% 5% 5% 5% 0% 0% 0% 0% 0% 0% 0%

2621.90.00.00 - Other 10% 10% 10% 10% 7% 5% 5% 5% 0% 0% 0% 0% 0% 0% 0%

27 Chapter 27-Mineral fuels, mineral oils and

products of their distillation; bituminous

substances; mineral waxes

27.01 Coal; briquettes, ovoids and similar solid

fuels manufactured from coal.

- Coal, whether or not pulverised, but not

agglomerated:

2701.11.00.00 - - Anthracite 5% 5% 5% 5% 5% 5% 5% 5% 0% 0% 0% 0% 0% 0% 0%

2701.12 - - Bituminous coal:

2701.12.10.00 - - - Coking coal 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0%

2701.12.90.00 - - - Other 5% 5% 5% 5% 5% 5% 5% 5% 0% 0% 0% 0% 0% 0% 0%

2701.19.00.00 - - Other coal 5% 5% 5% 5% 5% 5% 5% 5% 0% 0% 0% 0% 0% 0% 0%

2701.20.00.00 - Briquettes, ovoids and similar solid fuels

manufactured from coal

5% 5% 5% 5% 5% 5% 5% 5% 0% 0% 0% 0% 0% 0% 0%

27.02 Lignite, whether or not agglomerated,

excluding jet.

2702.10.00.00 - Lignite, whether or not pulverised, but not

agglomerated

5% 5% 5% 5% 5% 5% 5% 5% 0% 0% 0% 0% 0% 0% 0%

2702.20.00.00 - Agglomerated lignite 5% 5% 5% 5% 5% 5% 5% 5% 0% 0% 0% 0% 0% 0% 0%

27.03 Peat (including peat litter), whether or not

agglomerated.

2703.00.10.00 - Peat, whether or not compressed into

bales, but not agglomerated

5% 5% 5% 5% 5% 5% 5% 5% 0% 0% 0% 0% 0% 0% 0%

2703.00.20.00 - Agglomerated peat 5% 5% 5% 5% 5% 5% 5% 5% 0% 0% 0% 0% 0% 0% 0%

27.04 Coke and semi-coke of coal, of lignite or

of peat, whether or not agglomerated;

retort carbon.

2704.00.10.00 - Coke and semi-coke of coal 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0%

2704.00.20.00 - Coke and semi-coke of lignite or of peat 5% 5% 5% 5% 5% 5% 5% 5% 0% 0% 0% 0% 0% 0% 0%

2704.00.30.00 - Retort carbon 5% 5% 5% 5% 5% 5% 5% 5% 0% 0% 0% 0% 0% 0% 0%

2705.00.00.00 Coal gas, water gas, producer gas and

similar gases, other than petroleum gases

and other gaseous hydrocarbons.

0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0%

AANZFTA - Annex 1 (Viet Nam)

91 / 632

Public Record Exhibit 2

25

HS Code Description

Base

rate

(MFN

2005)

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

2022 and

subsequent

years

Viet Nam

Schedule of Tariff Commitments

Annex 1

2706.00.00.00 Tar distilled from coal, from lignite or from

peat, and other mineral tars, whether or not

dehydrated or partially distilled, including

reconstituted tars.

0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0%

27.07Oils and other products of the distillation

of high temperature coal tar; similar

products in which the weight of the

aromatic constituents exceeds that of the

non-aromatic constituents.

2707.10.00.00 - Benzol (benzene) 1% 1% 1% 1% 1% 1% 1% 1% 0% 0% 0% 0% 0% 0% 0%

2707.20.00.00 - Toluol (toluene) 1% 1% 1% 1% 1% 1% 1% 1% 0% 0% 0% 0% 0% 0% 0%

2707.30.00.00 - Xylol (xylenes) 1% 1% 1% 1% 1% 1% 1% 1% 0% 0% 0% 0% 0% 0% 0%

2707.40.00.00 - Naphthalene 1% 1% 1% 1% 1% 1% 1% 1% 0% 0% 0% 0% 0% 0% 0%

2707.50.00.00 - Other aromatic hydrocarbon mixtures of

which 65% or more by volume (including

losses) distils at 250°C by the ASTM D 86

method

1% 1% 1% 1% 1% 1% 1% 1% 0% 0% 0% 0% 0% 0% 0%

- Other:

2707.91.00.00 - - Creosote oils 1% 1% 1% 1% 1% 1% 1% 1% 0% 0% 0% 0% 0% 0% 0%

2707.99 - - Other:

2707.99.20.00 - - - Carbon black feedstock 1% 1% 1% 1% 1% 1% 1% 1% 0% 0% 0% 0% 0% 0% 0%

2707.99.90.00 - - - Other 1% 1% 1% 1% 1% 1% 1% 1% 0% 0% 0% 0% 0% 0% 0%

27.08 Pitch and pitch coke, obtained from coal

tar or from other mineral tars.

2708.10.00.00 - Pitch 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0%

2708.20.00.00 - Pitch coke 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0%

27.09 Petroleum oils and oils obtained from

bituminous minerals, crude.

2709.00.10.00 - Crude petroleum oils 15% 15% 15% 10% 10% 7% 7% 5% 0% 0% 0% 0% 0% 0% 0%

2709.00.20.00 - Condensates 5% 5% 5% 5% 5% 5% 5% 5% 5% 5% 5% 5% 5% 5% 5%

2709.00.90.00 - Other 15% 15% 15% 15% 15% 15% 15% 15% 15% 15% 15% 15% 15% 15% 15%

AANZFTA - Annex 1 (Viet Nam)

92 / 632

Public Record Exhibit 2

26

2015 2016 2017 2018No CC AHTN 2012 Description Schedule

ATIGA Tariff (%)

2701.12 - - Bituminous coal:

1719 VN 2701.12.10 - - - Coking coal Sch-A 0 0 0 0

1720 VN 2701.12.90 - - - Other Sch-A 0 0 0 0

1721 VN 2701.19.00 - - Other coal Sch-A 0 0 0 0

1722 VN 2701.20.00 - Briquettes, ovoids and similar solid fuels manufactured from coal Sch-A 0 0 0 0

27.02 Lignite, whether or not agglomerated, excluding jet.

1723 VN 2702.10.00 - Lignite, whether or not pulverised, but not agglomerated Sch-A 0 0 0 0

1724 VN 2702.20.00 - Agglomerated lignite Sch-A 0 0 0 0

2703.00 Peat (including peat litter), whether or not agglomerated.

1725 VN 2703.00.10 - Peat, whether or not compressed into bales, but not agglomerated Sch-A 0 0 0 0

1726 VN 2703.00.20 - Agglomerated peat Sch-A 0 0 0 0

2704.00Coke and semi-coke of coal, of lignite or of peat, whether or not

agglomerated; retort carbon.

1727 VN 2704.00.10 - Coke and semi-coke of coal Sch-A 0 0 0 0

1728 VN 2704.00.20 - Coke and semi-coke of lignite or of peat Sch-A 0 0 0 0

1729 VN 2704.00.30 - Retort carbon Sch-A 0 0 0 0

1730 VN 2705.00.00Coal gas, water gas, producer gas and similar gases, other than petroleum

gases and other gaseous hydrocarbons.Sch-A 0 0 0 0

1731 VN 2706.00.00Tar distilled from coal, from lignite or from peat, and other mineral tars,

whether or not dehydrated or partially distilled, including reconstituted tars.Sch-A 0 0 0 0

27.07

Oils and other products of the distillation of high temperature coal tar; similar

products in which the weight of the aromatic constituents exceeds that of the

non-aromatic constituents.

1732 VN 2707.10.00 - Benzol (benzene) Sch-A 0 0 0 0

1733 VN 2707.20.00 - Toluol (toluene) Sch-A 0 0 0 0

1734 VN 2707.30.00 - Xylol (xylenes) Sch-A 0 0 0 0

1735 VN 2707.40.00 - Naphthalene Sch-A 0 0 0 0

1736 VN 2707.50.00- Other aromatic hydrocarbon mixtures of which 65% or more by volume (including

losses) distils at 250°C by the ASTM D 86 methodSch-A 0 0 0 0

- Other:

1737 VN 2707.91.00 - - Creosote oils Sch-A 0 0 0 0

2707.99 - - Other:

1738 VN 2707.99.10 - - - Carbon black feedstock Sch-A 0 0 0 0

Page 91 of 515

Public Record Exhibit 2

27

User

Typewriter

ATIGA TARIFF SCHEDULE

HS Code Description Base rate EIF 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 20262027 and subsequent

years

Viet Nam Schedule of Tariff Commitments

- Coal, whether or not pulverised, but not agglomerated:

2701.11.00 - - Anthracite 0 0 0 0 0 0 0 0 0 0 0 0 0 0

2701.12 - - Bituminous coal:

2701.12.10 - - - Coking coal 0 0 0 0 0 0 0 0 0 0 0 0 0 0

2701.12.90 - - - Other 0 0 0 0 0 0 0 0 0 0 0 0 0 0

2701.19.00 - - Other coal 0 0 0 0 0 0 0 0 0 0 0 0 0 0

2701.20.00- Briquettes, ovoids and similar solid fuels manufactured

from coal0 0 0 0 0 0 0 0 0 0 0 0 0 0

27.02 Lignite, whether or not agglomerated, excluding jet.

2702.10.00- Lignite, whether or not pulverised, but not

agglomerated0 0 0 0 0 0 0 0 0 0 0 0 0 0

2702.20.00 - Agglomerated lignite 0 0 0 0 0 0 0 0 0 0 0 0 0 0

2703.00 Peat (including peat litter), whether or not agglomerated.

2703.00.10- Peat, whether or not compressed into bales, but not

agglomerated0 0 0 0 0 0 0 0 0 0 0 0 0 0

2703.00.20 - Agglomerated peat 0 0 0 0 0 0 0 0 0 0 0 0 0 0

2704.00Coke and semi-coke of coal, of lignite or of peat, whether

or not agglomerated; retort carbon.

2704.00.10 - Coke and semi-coke of coal 3 2.5 2.0 1.5 1.0 0.5 0 0 0 0 0 0 0 0

2704.00.20 - Coke and semi-coke of lignite or of peat 3 2.5 2.0 1.5 1.0 0.5 0 0 0 0 0 0 0 0

2704.00.30 - Retort carbon 0 0 0 0 0 0 0 0 0 0 0 0 0 0

2705.00.00Coal gas, water gas, producer gas and similar gases, other

than petroleum gases and other gaseous hydrocarbons.U U U U U U U U U U U U U

2706.00.00

Tar distilled from coal, from lignite or from peat, and

other mineral tars, whether or not dehydrated or partially

distilled, including reconstituted tars.

0 0 0 0 0 0 0 0 0 0 0 0 0 0

27.07

Oils and other products of the distillation of high

temperature coal tar; similar products in which the weight

of the aromatic constituents exceeds that of the non-

aromatic constituents.

118

Public Record Exhibit 2

28

User

Typewriter

VEAEU TARIFF SCHEDULE

HS Code Description Base rate EIF 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 20262027 and subsequent

years

Viet Nam Schedule of Tariff Commitments

2707.10.00 - Benzol (benzene) 0 0 0 0 0 0 0 0 0 0 0 0 0 0

2707.20.00 - Toluol (toluene) 0 0 0 0 0 0 0 0 0 0 0 0 0 0

2707.30.00 - Xylol (xylenes) 0 0 0 0 0 0 0 0 0 0 0 0 0 0

2707.40.00 - Naphthalene 0 0 0 0 0 0 0 0 0 0 0 0 0 0

2707.50.00

- Other aromatic hydrocarbon mixtures of which 65% or

more by volume (including losses) distils at 250°C by the

ASTM D 86 method

0 0 0 0 0 0 0 0 0 0 0 0 0 0

- Other:

2707.91.00 - - Creosote oils 0 0 0 0 0 0 0 0 0 0 0 0 0 0

2707.99 - - Other:

2707.99.10 - - - Carbon black feedstock 0 0 0 0 0 0 0 0 0 0 0 0 0 0

2707.99.90 - - - Other 0 0 0 0 0 0 0 0 0 0 0 0 0 0

27.08Pitch and pitch coke, obtained from coal tar or from other

mineral tars.

2708.10.00 - Pitch 0 0 0 0 0 0 0 0 0 0 0 0 0 0

2708.20.00 - Pitch coke 0 0 0 0 0 0 0 0 0 0 0 0 0 0

2709.00Petroleum oils and oils obtained from bituminous

minerals, crude.

2709.00.10 - Crude petroleum oils 0 0 0 0 0 0 0 0 0 0 0 0 0 0

2709.00.20 - Condensates 0 0 0 0 0 0 0 0 0 0 0 0 0 0

2709.00.90 - Other 0 0 0 0 0 0 0 0 0 0 0 0 0 0

27.10

Petroleum oils and oils obtained from bituminous

minerals, other than crude; preparations not elsewhere

specified or included, containing by weight 70% or more

of petroleum oils or of oils obtained from bituminous

minerals, these oils being the basic constituents of the

preparations; waste oils.

- Petroleum oils and oils obtained from bituminous

minerals (other than crude) and preparations not

elsewhere specified or included, containing by weight 70

% or more of petroleum oils or of oils obtained from

bituminous minerals, these oils being the basic

constituents of the preparations, other than those

containing biodiesel and other than waste oils :

2710.12 - - Light oils and preparations :

- - - Motor spirit :

119

Public Record Exhibit 2

29

14

ANNEX 1

MODALITY FOR TARIFF REDUCTION AND ELIMINATION FOR TARIFF LINES PLACED IN THE NORMAL TRACK

1. Tariff lines placed by each Party in the Normal Track on its own accord shall have their respective applied MFN tariff rates gradually reduced and eliminated according to the following Schedules:

(i) ASEAN 6 and China

ACFTA Preferential Tariff Rate

(Not later than 1 January) X = Applied MFN Tariff Rate

2005* 2007 2009 2010

X > 20% 20 12 5 0

15% < x < 20% 15 8 5 0

10% < x < 15% 10 8 5 0

5% < x < 10% 5 5 0 0

X < 5% Standstill 0 0

* The first date of implementation shall be 1 July 2005. (ii) Viet Nam

ACFTA Preferential Tariff Rate

(Not later than 1 January) X = Applied MFN Tariff Rate

2005* 2006 2007 2008 2009 2011 2013 2015

X > 60% 60 50 40 30 25 15 10 0

45% < X < 60% 40 35 35 30 25 15 10 0

35% < X < 45% 35 30 30 25 20 15 5 0

30% < X < 35% 30 25 25 20 17 10 5 0

25% < X < 30% 25 20 20 15 15 10 5 0

20% < X < 25% 20 20 15 15 15 10 0-5 0

15% < X < 20% 15 15 10 10 10 5 0-5 0

10% < X < 15% 10 10 10 10 8 5 0-5 0

7% < X < 10% 7 7 7 7 5 5 0-5 0

5% < X < 7% 5 5 5 5 5 5 0-5 0

X < 5% Standstill 0

* The first date of implementation shall be 1 July 2005.

Public Record Exhibit 2

30

User

Typewriter

ACFTA TARIFF SCHEDULE

15

(iii) Cambodia, Lao PDR and Myanmar

ACFTA Preferential Tariff Rate

(Not later than 1 January) X = Applied

MFN Tariff Rate 2005* 2006 2007 2008 2009 2011 2013 2015

X > 60% 60 50 40 30 25 15 10 0

45% < X < 60% 40 35 35 30 25 15 10 0

35% < X < 45% 35 35 30 30 20 15 5 0

30% < X < 35% 30 25 25 20 20 10 5 0

25% < X < 30% 25 25 25 20 20 10 5 0

20% < X < 25% 20 20 15 15 15 10 0-5 0

15% < X < 20% 15 15 15 15 15 5 0-5 0

10% < X < 15% 10 10 10 10 8 5 0-5 0

7% < X < 10% 7** 7** 7** 7** 7** 5 0-5 0

5% < X < 7% 5 5 5 5 5 5 0-5 0

X < 5% Standstill 0

* The first date of implementation shall be 1 July 2005. ** Myanmar shall be allowed to maintain ACFTA Rates at no more than 7.5% until 2010.

2. If a Party places a tariff line in the Normal Track, that Party shall enjoy the tariff concessions other Parties have made for that tariff line as specified in and applied pursuant to the relevant Schedules either in Annex 1 or Annex 2 together with the undertakings and conditions set out therein. This right shall be enjoyed for so long as that Party adheres to its own commitments for tariff reduction and elimination for that tariff line.

3. The tariff rates specified in the relevant Schedules in paragraph 1 only set out the level of the applicable ACFTA preferential tariff rates to be applied by each Party for the tariff lines concerned in the specified year of implementation and shall not prevent any Party from unilaterally accelerating its tariff reduction or elimination at any time if it so wishes. 4. Tariff lines in the Normal Track, which are subject to specific tariff rates, shall have such tariffs reduced to zero, in equal proportions in accordance with the timeframes provided in the Schedules set out in paragraph 1 of this Annex. 5. For all tariff lines placed in the Normal Track where the applied MFN tariff rates are at 0%, they shall remain at 0%. Where they have been reduced to 0%, they shall remain at 0%. No Party shall be permitted to increase the tariff rates for any tariff line, except as otherwise provided by the Agreement.

Public Record Exhibit 2

31

16

6. As an integral part of its commitments to reduce and/or eliminate the applied MFN tariff rates in accordance with the relevant Schedules in paragraph 1, each Party hereby commits to undertake further tariff reduction and/or elimination in accordance with the following thresholds:

(a) ASEAN 6 and China

(i) Each Party shall reduce to 0-5% not later than 1 July 2005 the tariff rates for at least 40% of its tariff lines placed in the Normal Track.

(ii) Each Party shall reduce to 0-5% not later than 1 January 2007 the tariff rates for at least 60% of its tariff lines placed in the Normal Track.

(iii) Each Party shall eliminate all its tariffs for tariff lines placed in the Normal Track not later than 1 January 2010, with flexibility to have tariffs on some tariff lines, not exceeding 150 tariff lines, eliminated not later than 1 January 2012.

(iv) Each Party shall eliminate all its tariffs for tariff lines placed in the Normal Track not later than 1 January 2012.

(b) Newer ASEAN Member States

(i) Each Party shall reduce to 0-5% not later than 1 January 2009 for Viet Nam; 1 January 2010 for Lao PDR and Myanmar; and 1 January 2012 for Cambodia the tariff rates for at least 50% of its tariff lines placed in the Normal Track.

(ii) Cambodia, Lao PDR and Myanmar shall eliminate their respective tariffs not later than 1 January 2013 on 40% of its tariff lines placed in the Normal Track.

(iii) For Viet Nam, the percentage of Normal Track tariff lines to have their tariffs eliminated not later than 1 January 2013 shall be determined not later than 31 December 2004.

(iv) Each Party shall eliminate all its tariffs for tariff lines placed in the Normal Track not later than 1 January 2015, with flexibility to have tariffs on some tariff lines, not exceeding 250 tariff lines, eliminated not later than 1 January 2018.

(v) Each Party shall eliminate all its tariffs for tariff lines placed in the Normal Track not later than 1 January 2018.

7. The tariff lines listed by the Parties in Appendix 1 shall have their respective ACFTA tariffs eliminated not later than 1 January 2012 for ASEAN 6 and China, and 1 January 2018 for CLMV.

Public Record Exhibit 2

32

BP Statistical Review of World Energy 2017

BP Statistical Review of World Energy June 2017

This workbook contains information presented in the 2017 BP Statistical Review of World Energy, which can be found on the internet at:

http://www.bp.com/statisticalreview

Please use the contents or the tabs at the bottom to navigate between the tables.

Primary Energy: Consumption - Mtoe (from 1965)

Primary Energy: Consumption by fuel type - Mtoe (2015-2016)

Oil: Proved reserves

Oil: Proved reserves - Barrels (from 1980)

Oil: Production – Barrels (from 1965)

Oil: Production – Tonnes (from 1965)

Oil: Consumption – Barrels (from 1965)

Oil: Consumption – Tonnes (from 1965)

Oil: Regional consumption – by product (from 1965)

Oil: Spot crude prices

Oil: Crude prices since 1861

Oil: Refinery throughput (from 1980)

Oil: Refinery capacities (from 1965)

Oil: Regional refining margins (from 1992)

Oil: Trade movements (from 1980)

Oil: Inter-area movements

Oil: Trade 2015-2016

Gas: Proved reserves

Gas: Proved reserves - Bcm (from 1980)

Gas: Production – Bcm (from 1970)

Gas: Production – Bcf (from 1970)

Gas: Production – Mtoe (from 1970)

Gas: Consumption – Bcm (from 1965)

Gas: Consumption – Bcf (from 1965)

Gas: Consumption – Mtoe (from 1965)

Gas: Trade movements pipeline

Gas: Trade movements LNG

Gas: Trade 2015-2016

Public Record Exhibit 3

33

BP Statistical Review of World Energy 2017

Gas: Prices

Coal: Reserves

Coal: Prices

Coal: Production - Tonnes (from 1981)

Coal: Production - Mtoe (from 1981)

Coal: Consumption - Mtoe (from 1965)

Nuclear Energy – Consumption - TWh (from 1965)

Nuclear Energy – Consumption - Mtoe (from 1965)

Hydroelectricity – Consumption - TWh (from 1965)

Hydroelectricity – Consumption - Mtoe (from 1965)

Renewables - Other renewables consumption -Twh (from 1965)

Renewables - Other renewables consumption - Mtoe (from 1965)

Renewables - Solar consumption - TWh (from 1965)

Renewables - Solar consumption - Mtoe (from 1965)

Renewables - Wind consumption - TWh (from 1965)

Renewables - Wind consumption - Mtoe (from 1965)

Renewables - Geothermal, Biomass and Other - TWh (from 1965)

Renewables - Geothermal, Biomass and Other - Mtoe (from 1965)

Renewables - Biofuels production - Kboe/d (from 1990)

Renewables - Biofuels production - Ktoe (from 1990)

Electricity Generation - TWh (from 1985)

Carbon Dioxide Emissions (from 1965)

Renewable Energy - Geothermal (Installed capacity)

Renewable Energy - Solar (Installed capacity)

Renewable Energy - Wind (Installed capacity)

Approximate conversion factors

Definitions

Public Record Exhibit 3

34

BP Statistical Review of World Energy 2017

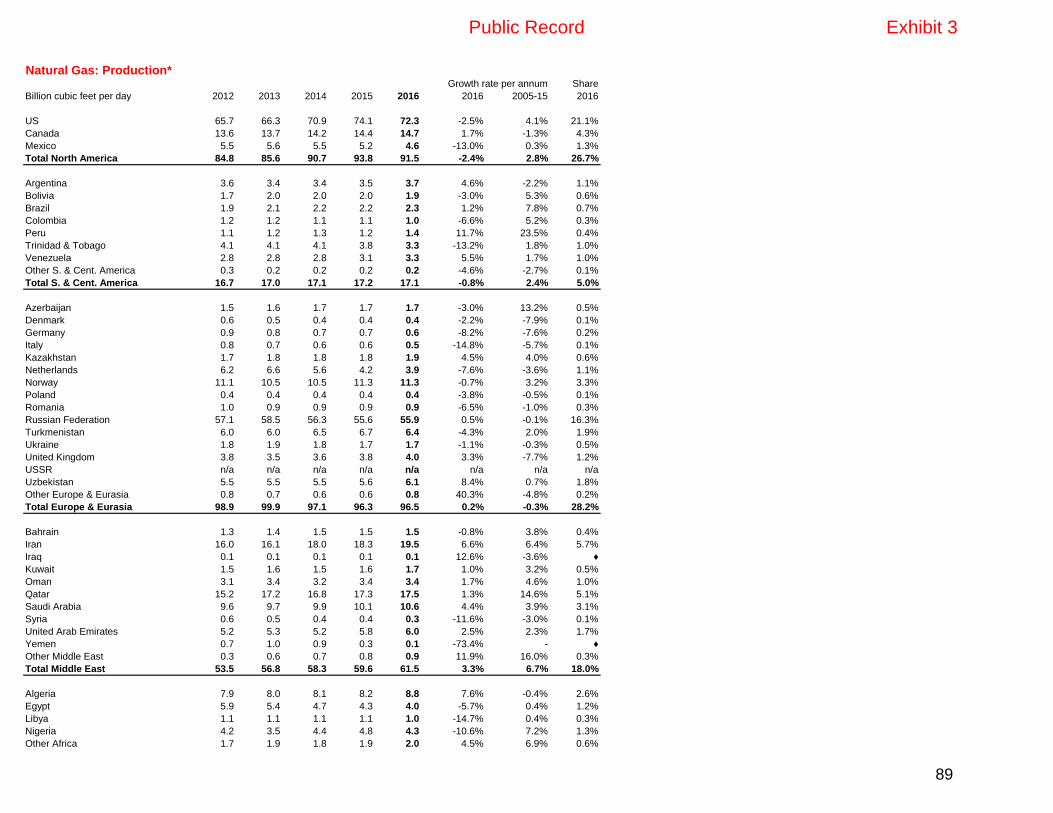

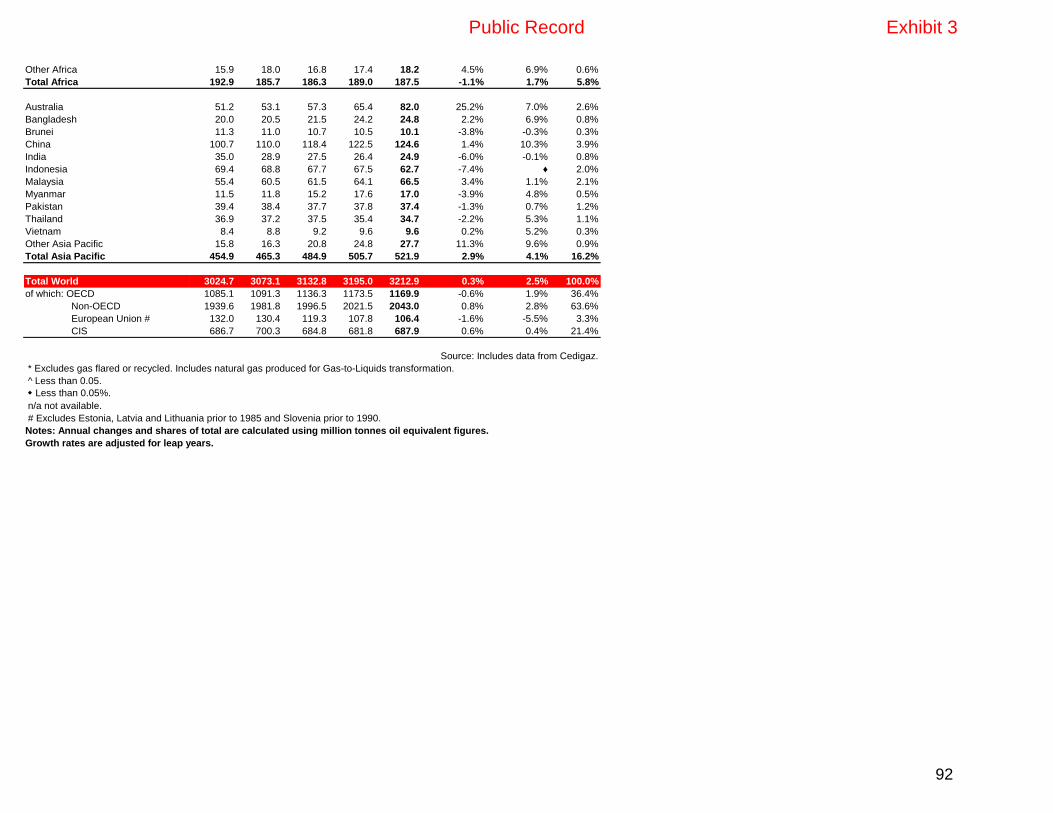

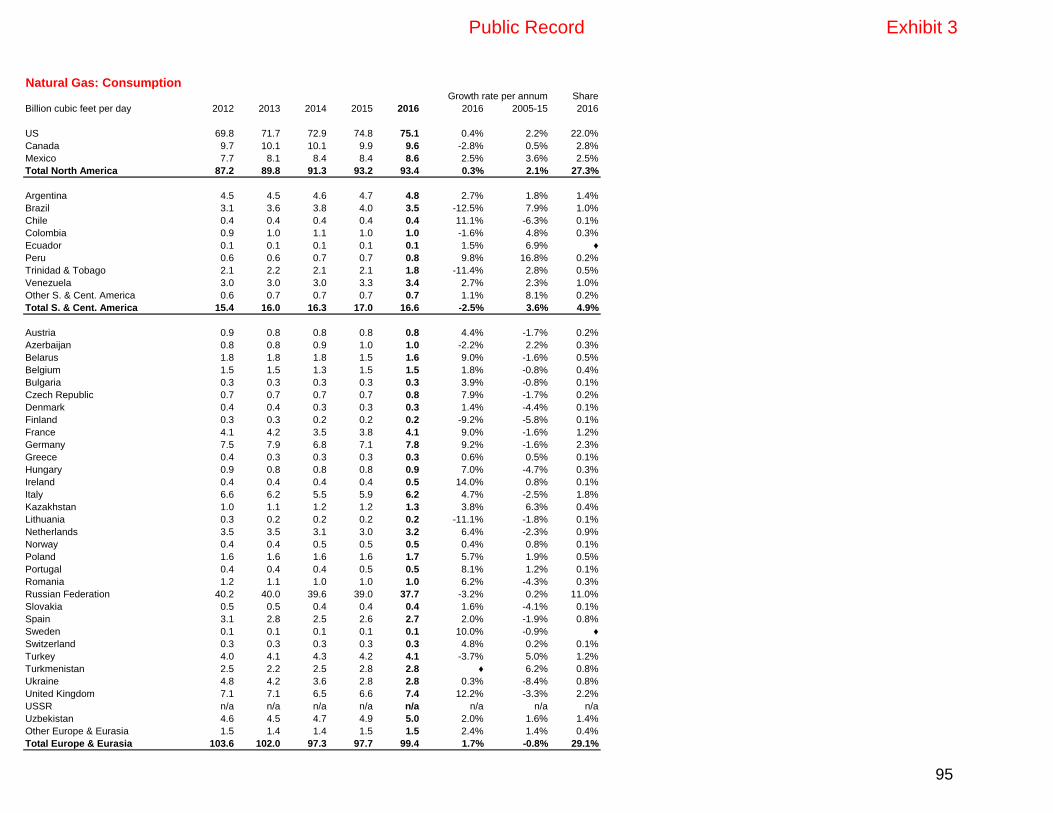

Primary Energy: Consumption*Share

Million tonnes oil equivalent 2012 2013 2014 2015 2016 2016 2005-15 2016

US 2209.3 2270.6 2296.5 2275.9 2272.7 -0.4% -0.3% 17.1%

Canada 326.5 336.1 334.3 327.7 329.7 0.3% 0.2% 2.5%

Mexico 188.5 189.1 190.4 188.8 186.5 -1.5% 1.2% 1.4%

Total North America 2724.3 2795.9 2821.2 2792.4 2788.9 -0.4% -0.2% 21.0%

Argentina 83.4 86.5 86.7 88.7 88.9 -0.1% 2.5% 0.7%

Brazil 284.8 296.8 304.9 302.6 297.8 -1.8% 3.7% 2.2%

Chile 34.1 34.4 35.4 35.9 36.8 2.0% 2.4% 0.3%

Colombia 38.4 38.2 40.3 41.0 41.1 ♦ 4.2% 0.3%

Ecuador 14.3 14.7 15.5 15.5 15.3 -1.3% 4.7% 0.1%

Peru 21.2 21.7 22.4 23.7 25.3 6.3% 5.7% 0.2%

Trinidad & Tobago 22.0 22.4 21.9 21.6 19.4 -10.7% 2.8% 0.1%

Venezuela 84.1 83.3 78.1 78.8 74.6 -5.5% 1.1% 0.6%

Other S. & Cent. America 98.7 98.7 98.9 102.6 106.2 3.3% 1.2% 0.8%

Total S. & Cent. America 680.9 696.7 704.1 710.4 705.3 -1.0% 2.8% 5.3%

Austria 35.4 35.1 33.8 33.9 35.1 3.3% -0.6% 0.3%

Azerbaijan 12.3 12.6 13.2 14.5 14.5 -0.4% 0.5% 0.1%

Belarus 27.9 24.7 25.5 22.4 23.7 5.4% -1.0% 0.2%

Belgium 58.7 60.0 55.8 56.9 61.7 8.1% -1.3% 0.5%

Bulgaria 18.1 16.7 17.9 19.0 18.1 -5.2% -0.3% 0.1%

Czech Republic 41.9 41.8 40.2 40.2 39.9 -1.0% -0.9% 0.3%

Denmark 17.1 17.9 17.4 16.9 17.1 1.1% -1.5% 0.1%

Finland 28.1 27.7 26.7 26.7 27.1 1.4% -1.2% 0.2%

France 244.8 247.2 237.6 239.4 235.9 -1.7% -0.9% 1.8%

Germany 316.4 325.5 312.1 317.8 322.5 1.2% -0.4% 2.4%

Greece 29.3 27.9 26.3 26.4 25.9 -2.2% -2.2% 0.2%

Hungary 21.1 20.1 20.0 21.2 21.9 3.2% -2.0% 0.2%

Ireland 14.0 13.7 13.7 14.5 15.2 4.1% -0.9% 0.1%

Italy 162.2 155.7 146.9 149.9 151.3 0.7% -2.1% 1.1%

Kazakhstan 59.4 60.2 66.4 62.7 63.0 0.3% 3.5% 0.5%

Lithuania 5.8 5.4 5.2 5.4 5.5 0.9% -3.7% ♦

Netherlands 88.1 85.9 80.9 82.1 84.5 2.6% -1.6% 0.6%

Norway 47.8 45.0 46.4 47.2 48.6 2.7% 0.3% 0.4%

Poland 95.7 96.0 92.4 93.4 96.7 3.2% 0.3% 0.7%

Portugal 22.4 24.5 24.6 24.6 26.0 5.5% -0.3% 0.2%

Romania 34.0 31.5 32.5 32.6 33.1 1.2% -1.8% 0.2%

Russian Federation 695.2 686.8 689.2 681.7 673.9 -1.4% 0.5% 5.1%

Slovakia 16.2 16.8 15.5 15.7 15.9 1.4% -1.9% 0.1%

Spain 142.4 134.2 132.2 134.4 135.0 0.2% -1.2% 1.0%

Sweden 54.5 51.3 51.4 52.9 52.2 -1.7% -0.5% 0.4%

Switzerland 28.8 29.7 28.5 27.9 26.4 -5.5% 0.2% 0.2%

Turkey 120.1 118.5 122.6 131.9 137.9 4.2% 4.4% 1.0%

Turkmenistan 29.7 26.8 29.5 33.1 33.2 0.2% 5.4% 0.3%

Ukraine 122.6 114.7 101.2 83.9 87.0 3.4% -4.7% 0.7%

United Kingdom 202.1 200.9 188.6 190.9 188.1 -1.7% -1.8% 1.4%

USSR n/a n/a n/a n/a n/a n/a n/a n/a

Uzbekistan 49.2 48.7 50.5 51.7 52.7 1.5% 1.1% 0.4%

Other Europe & Eurasia 95.0 97.0 93.6 94.8 97.6 2.6% 0.6% 0.7%

Total Europe & Eurasia 2936.3 2900.6 2838.3 2846.6 2867.1 0.4% -0.4% 21.6%

Iran 235.2 246.0 261.9 262.8 270.7 2.7% 4.0% 2.0%

Israel 25.2 25.2 24.5 26.0 26.4 1.5% 1.9% 0.2%

Kuwait 41.0 39.5 37.6 41.5 41.7 0.3% 3.1% 0.3%

Qatar 29.3 43.4 42.5 50.2 49.2 -2.3% 9.5% 0.4%

Saudi Arabia 235.7 237.4 252.1 260.8 266.5 1.9% 5.1% 2.0%

United Arab Emirates 95.8 97.2 99.5 108.6 113.8 4.5% 5.6% 0.9%

Other Middle East 118.7 123.6 121.9 124.7 126.8 1.4% 2.9% 1.0%

Total Middle East 780.8 812.4 840.0 874.6 895.1 2.1% 4.5% 6.7%

Algeria 45.1 47.8 51.6 55.1 55.1 -0.3% 5.4% 0.4%

Egypt 86.5 85.7 85.4 86.7 91.0 4.7% 3.4% 0.7%

South Africa 121.9 123.6 125.2 120.1 122.3 1.5% 0.8% 0.9%

Growth rate per annum

Public Record Exhibit 3

35

BP Statistical Review of World Energy 2017

Other Africa 149.3 158.3 165.6 171.7 171.8 -0.2% 3.5% 1.3%