Oracle® iPayment - Oracle Help Center

96

Oracle® iPayment Concepts and Procedures Guide Release 11i Part No. A95477-03 April 2003

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Oracle® iPayment - Oracle Help Center

Oracle® iPaymentConcepts and Procedures Guide

Release 11i

Part No. A95477-03

April 2003

Oracle iPayment Concepts and Procedures Guide, Release 11i

Part No. A95477-03

Copyright © 1998, 2003 Oracle Corporation. All rights reserved.

Contributors: Jonathan Leybovich, Rajiv Menon, Elizabeth Newell, Aalok Shah

The Programs (which include both the software and documentation) contain proprietary information ofOracle Corporation; they are provided under a license agreement containing restrictions on use anddisclosure and are also protected by copyright, patent and other intellectual and industrial propertylaws. Reverse engineering, disassembly or decompilation of the Programs, except to the extent requiredto obtain interoperability with other independently created software or as specified by law, is prohibited.

The information contained in this document is subject to change without notice. If you find any problemsin the documentation, please report them to us in writing. Oracle Corporation does not warrant that thisdocument is error-free. Except as may be expressly permitted in your license agreement for thesePrograms, no part of these Programs may be reproduced or transmitted in any form or by any means,electronic or mechanical, for any purpose, without the express written permission of Oracle Corporation.

If the Programs are delivered to the U.S. Government or anyone licensing or using the programs onbehalf of the U.S. Government, the following notice is applicable:

Restricted Rights Notice Programs delivered subject to the DOD FAR Supplement are "commercialcomputer software" and use, duplication, and disclosure of the Programs, including documentation,shall be subject to the licensing restrictions set forth in the applicable Oracle license agreement.Otherwise, Programs delivered subject to the Federal Acquisition Regulations are "restricted computersoftware" and use, duplication, and disclosure of the Programs shall be subject to the restrictions in FAR52.227-19, Commercial Computer Software - Restricted Rights (June, 1987). Oracle Corporation, 500Oracle Parkway, Redwood City, CA 94065.

The Programs are not intended for use in any nuclear, aviation, mass transit, medical, or other inherentlydangerous applications. It shall be the licensee's responsibility to take all appropriate fail-safe, backup,redundancy, and other measures to ensure the safe use of such applications if the Programs are used forsuch purposes, and Oracle Corporation disclaims liability for any damages caused by such use of thePrograms.

Oracle is a registered trademark, and Oracle8i, Oracle9i, OracleMetaLink, Oracle Store, PL/SQL, Pro*C,SQL*Net, and SQL*Plus, are trademarks or registered trademarks of Oracle Corporation. Other namesmay be trademarks of their respective owners.

Contents

Audience for This Guide ...................................................................................................................... ixDocumentation Accessibility ............................................................................................................... ixHow To Use This Guide ........................................................................................................................ xOther Information Sources ................................................................................................................... xiDo Not Use Database Tools to Modify Oracle Applications Data ............................................... xviAbout Oracle ........................................................................................................................................ xvi

1 Understanding iPayment

New in this Document .............................................................................................................1-1Overview of Oracle iPayment .................................................................................................1-2Integration with Other Oracle Applications ............................................................................1-3iPayment Architectural Overview ...........................................................................................1-4Understanding Credit Card Transactions ................................................................................1-6Understanding Terminal-Based and Host-Based Merchants ...................................................1-8Understanding Gateway-Model and Processor-Model Payment Systems ..............................1-8Understanding Purchase Cards ...............................................................................................1-9Understanding Bank Account Transfers ...............................................................................1-13Understanding Offline and Online Payments .......................................................................1-14How the Scheduling System Works ......................................................................................1-18Scheduling Concurrent Programs .........................................................................................1-19Understanding Risk Management .........................................................................................1-20Risk Factors Shipped with iPayment .....................................................................................1-21iPayment Routing and Operation ..........................................................................................1-23Routing Rule Conditions .......................................................................................................1-25Understanding iPayment Security .........................................................................................1-26

iii

Understanding Extensibility ................................................................................................. 1-28

2 Administering iPayment

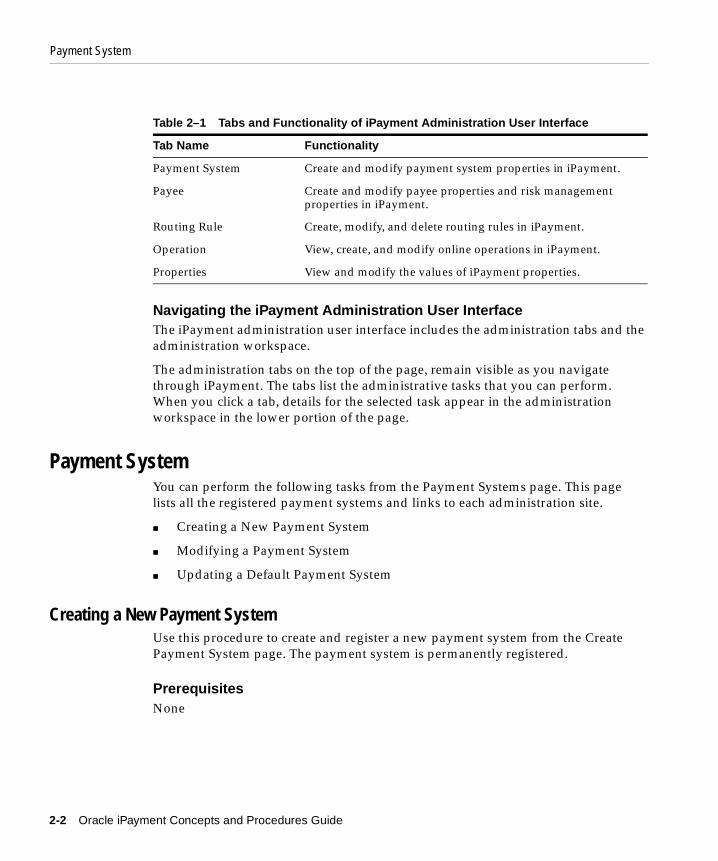

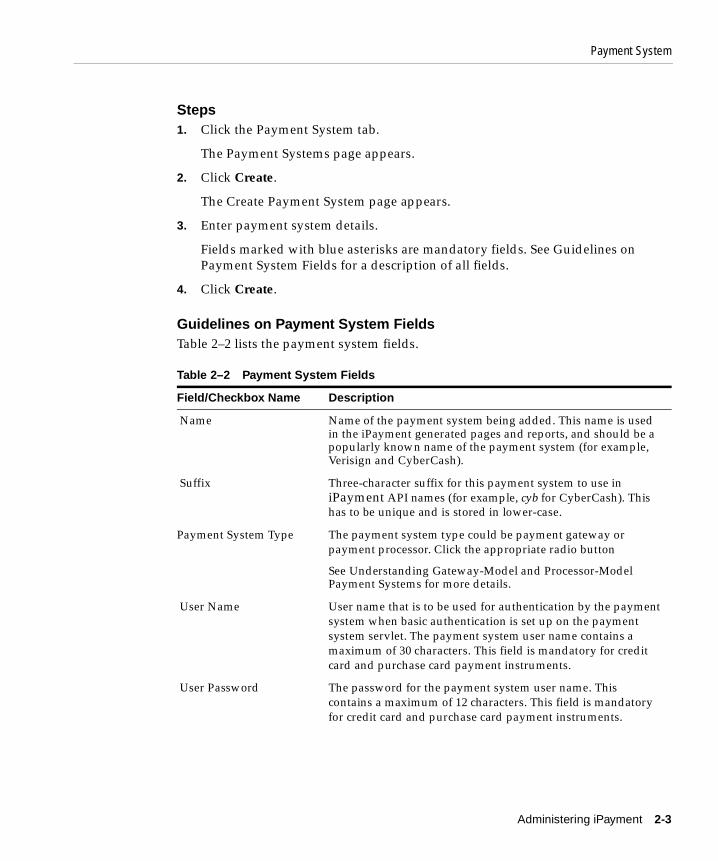

Administration Overview ....................................................................................................... 2-1iPayment Administration User Interface ......................................................................................... 2-1Payment System ................................................................................................................................... 2-2Creating a New Payment System ............................................................................................ 2-2Modifying a Payment System ................................................................................................. 2-4Updating a Default Payment System ...................................................................................... 2-5Payee .................................................................................................................................................. 2-5Creating a New Payee ............................................................................................................. 2-5Modifying a Payee .................................................................................................................. 2-7Inactivating a Payee ................................................................................................................ 2-8Updating the Risk Management Status ................................................................................... 2-8Risk Factors ............................................................................................................................. 2-9Modifying the Risk Score ...................................................................................................... 2-10Modifying the Payment Amount Limit Risk Factor .............................................................. 2-10Modifying the Payment History Risk Factor ......................................................................... 2-11Modifying the Transaction Amount Risk Factor ................................................................... 2-11Modifying the Time of Purchase Risk Factor ........................................................................ 2-12Modifying the AVS Codes Risk Factor .................................................................................. 2-13Modifying the Frequency of Purchase Risk Factor ....................................................................... 2-14Modifying Oracle Receivables Risk Codes Risk Factor ......................................................... 2-14Modifying Oracle Receivables Credit Rating Codes Risk Factor ................................................ 2-15Modifying the Risky Instruments Risk Factor ....................................................................... 2-16Modifying the Ship to/Bill to Address Risk Factor ............................................................... 2-16Modifying Oracle Receivables Transactional Credit Limit Risk Factor ................................. 2-16Modifying Oracle Receivables Overall Credit Limit Risk Factor .......................................... 2-16Risk Formula ......................................................................................................................... 2-16Creating a Risk Formula ....................................................................................................... 2-17Updating a Risk Formula ...................................................................................................... 2-18Deleting a Risk Formula ........................................................................................................ 2-18Routing Rule ......................................................................................................................... 2-19Viewing Routing Rules ......................................................................................................... 2-19Creating Routing Rules ......................................................................................................... 2-20

iv

Modifying Routing Rules ......................................................................................................2-21Deleting Routing Rules ..........................................................................................................2-22Managing Operations ............................................................................................................2-22Performing a Payment Authorization ...................................................................................2-23Searching for Transactions ....................................................................................................2-26Matching Transactions ..........................................................................................................2-27Performing a Capture Operation ..................................................................................................... 2-28Viewing Transaction Summary ....................................................................................................... 2-28iPayment Properties ..............................................................................................................2-30Modifying iPayment Properties ...................................................................................................... 2-32

3 Transaction Reporting

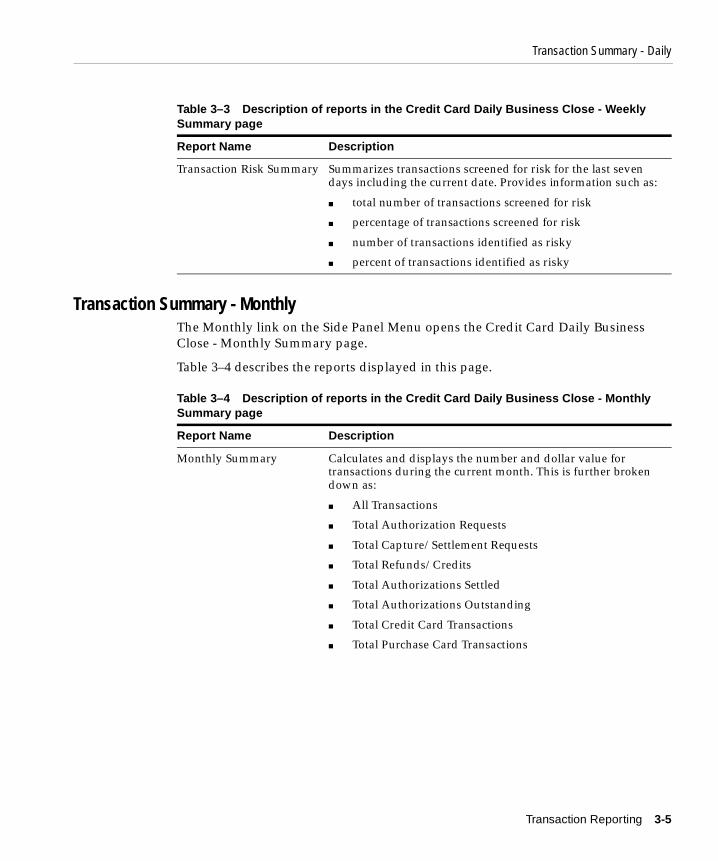

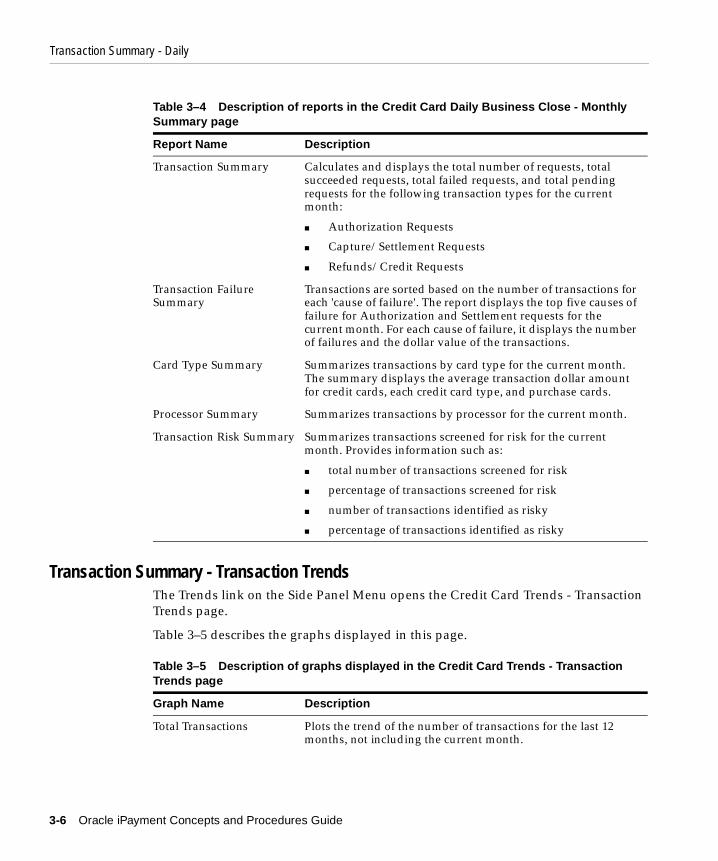

Transaction Reporting Overview ...................................................................................................... 3-1iPayment TR User Interface .....................................................................................................3-1Transaction Summary - Daily ..................................................................................................3-2Transaction Summary - Weekly ..............................................................................................3-3Transaction Summary - Monthly .............................................................................................3-5Transaction Summary - Transaction Trends ............................................................................3-6Transaction Summary - Processor Trends ...............................................................................3-7Transaction Summary - Card Type Trends .............................................................................3-7Transaction Summary - Failure Trends ...................................................................................3-7Payee Summary .......................................................................................................................3-8Daily Summary by Payee ........................................................................................................3-8Weekly Summary by Payee ...................................................................................................3-10Monthly Summary by Payee .................................................................................................3-11Transaction Summary - Transaction Trends ..........................................................................3-13Transaction Summary - Processor Trends .............................................................................3-13Transaction Summary - Card Type Trends ...........................................................................3-14Transaction Summary - Failure Trends .................................................................................3-14

v

vi

Send Us Your Comments

Oracle iPayment Concepts and Procedures Guide, Release 11i

Part No. A95477-03

Oracle Corporation welcomes your comments and suggestions on the quality and usefulness of thisdocument. Your input is an important part of the information used for revision.

■ Did you find any errors?■ Is the information clearly presented?■ Do you need more information? If so, where?■ Are the examples correct? Do you need more examples?■ What features did you like most?

If you find any errors or have any other suggestions for improvement, please indicate the documenttitle and part number, and the chapter, section, and page number (if available). You can send com-ments to us via the postal service.

■ Electronic mail: [email protected]■ FAX: (801) 659-7164 Attention: Oracle Applications Global Financials Documentation■ Postal service:

Oracle CorporationOracle Applications Global Financials Documentation500 Oracle ParkwayRedwood Shores, CA 94065USA

If you would like a reply, please give your name, address, telephone number, and (optionally) elec-tronic mail address.

If you have problems with the software, please contact your local Oracle Support Services.

vii

viii

Preface

Audience for This GuideWelcome to Release 11i of the Oracle iPayment Concepts and Procedures Guide.

This guide assumes you have a working knowledge of the following:

■ The principles and customary practices of your business area.

■ Oracle iPayment

If you have never used Oracle iPayment, Oracle suggests you attend one ormore of the Oracle iPayment training classes available through OracleUniversity.

■ The Oracle Applications graphical user interface.

To learn more about the Oracle Applications graphical user interface, read theOracle Applications User’s Guide.

See Other Information Sources for more information about Oracle Applicationsproduct information.

Documentation AccessibilityOur goal is to make Oracle products, services, and supporting documentationaccessible, with good usability, to the disabled community. To that end, ourdocumentation includes features that make information available to users ofassistive technology. This documentation is available in HTML format, and containsmarkup to facilitate access by the disabled community. Standards will continue toevolve over time, and Oracle Corporation is actively engaged with othermarket-leading technology vendors to address technical obstacles so that ourdocumentation can be accessible to all of our customers. For additional information,

ix

visit the Oracle Accessibility Program Web site athttp://www.oracle.com/accessibility/.

Accessibility of Code Examples in DocumentationJAWS, a Windows screen reader, may not always correctly read the code examplesin this document. The conventions for writing code require that closing bracesshould appear on an otherwise empty line; however, JAWS may not always read aline of text that consists solely of a bracket or brace.

Accessibility of Links to External Web Sites in DocumentationThis documentation may contain links to Web sites of other companies ororganizations that Oracle Corporation does not own or control. Oracle Corporationneither evaluates nor makes any representations regarding the accessibility of theseWeb sites.

How To Use This GuideThis document contains the information you need to understand and use OracleiPayment.

This manual contains the following two chapters:

■ Chapter 1, "Understanding iPayment"

This chapter provides overviews of the application and its components,explanations of key concepts, features, and functions, as well as theapplication’s relationships to other Oracle or third-party applications.

■ Chapter 2, "Administering iPayment"

This chapter provides process-oriented, task-based procedures for using theuser interface to set up the application and perform essential business tasks.

■ Chapter 3, "Transaction Reporting"

This chapter provides details of the pages provided for viewing the keyperformance metrics such as transaction summaries, payee summaries, andother critical performance indicators.

x

Other Information SourcesYou can choose from many sources of information, including onlinedocumentation, training, and support services, to increase your knowledge andunderstanding of Oracle iPayment.

If this guide refers you to other Oracle Applications documentation, use only theRelease 11i versions of those guides.

Online DocumentationAll Oracle Applications documentation is available online (HTML or PDF).

About Document - Refer to the About document for patches that you have installedto learn about new documentation that you can download. The new Aboutdocument is available on MetaLink.

Related DocumentationOracle iPayment shares business and setup information with other OracleApplications products. Therefore, you may want to refer to other productdocumentation when you set up and use Oracle iPayment.

You can read the documents online by choosing Library from the expandable menuon your HTML help window, by reading from the Oracle Applications DocumentLibrary CD included in your media pack, or by using a Web browser with a URLthat your system administrator provides.

If you require printed guides, you can purchase them from the Oracle Store athttp://oraclestore.oracle.com.

Documents Related to All Products

Oracle Applications User’s GuideThis guide explains how to enter data, query, run reports, and navigate using thegraphical user interface (GUI) available with this release of Oracle iPayment (andany other Oracle Applications products). This guide also includes information onsetting user profiles, as well as running and reviewing reports and concurrentprocesses.

You can access this user’s guide online by choosing”Getting Started with OracleApplications” from any Oracle Applications help file.

xi

Installation and System Administration

Oracle Applications ConceptsThis guide provides an introduction to the concepts, features, technology stack,architecture, and terminology for Oracle Applications Release 11i. It provides auseful first book to read before an installation of Oracle Applications. This guidealso introduces the concepts behind Applications-wide features such as BusinessIntelligence (BIS), languages and character sets, and Self-Service Web Applications.

Installing Oracle ApplicationsThis guide provides instructions for managing the installation of OracleApplications products. In Release 11i, much of the installation process is handledusing Oracle Rapid Install, which minimizes the time to install Oracle Applications,the Oracle8 technology stack, and the Oracle8i Server technology stack byautomating many of the required steps. This guide contains instructions for usingOracle Rapid Install and lists the tasks you need to perform to finish yourinstallation. You should use this guide in conjunction with individual productuser’s guides and implementation guides.

Oracle Applications Supplemental CRM Installation StepsThis guide contains specific steps needed to complete installation of a few of theCRM products. The steps should be done immediately following the tasks given inthe Installing Oracle Applications guide.

Upgrading Oracle ApplicationsRefer to this guide if you are upgrading your Oracle Applications Release 10.7 orRelease 11.0 products to Release 11i. This guide describes the upgrade process andlists database and product-specific upgrade tasks. You must be either at Release10.7 (NCA, SmartClient, or character mode) or Release 11.0, to upgrade to Release11i. You cannot upgrade to Release 11i directly from releases prior to 10.7.

Maintaining Oracle ApplicationsUse this guide to help you run the various AD utilities, such as AutoUpgrade,AutoPatch, AD Administration, AD Controller, AD Relink, License Manager, andothers. It contains how-to steps, screenshots, and other information that you need torun the AD utilities. This guide also provides information on maintaining theOracle applications file system and database.

xii

Oracle Applications System Administrator’s GuideThis guide provides planning and reference information for the Oracle ApplicationsSystem Administrator. It contains information on how to define security, customizemenus and online help, and manage concurrent processing.

Oracle Alert User’s GuideThis guide explains how to define periodic and event alerts to monitor the status ofyour Oracle Applications data.

Oracle Applications Developer’s GuideThis guide contains the coding standards followed by the Oracle Applicationsdevelopment staff. It describes the Oracle Application Object Library componentsneeded to implement the Oracle Applications user interface described in the OracleApplications User Interface Standards for Forms-Based Products. It also providesinformation to help you build your custom Oracle Forms Developer 6i forms so thatthey integrate with Oracle Applications.

Oracle Applications User Interface Standards for Forms-Based ProductsThis guide contains the user interface (UI) standards followed by the OracleApplications development staff. It describes the UI for the Oracle Applicationsproducts and how to apply this UI to the design of an application built by usingOracle Forms.

Other Implementation Documentation

Multiple Reporting Currencies in Oracle ApplicationsIf you use the Multiple Reporting Currencies feature to record transactions in morethan one currency, use this manual before implementing Oracle iPayment. Thismanual details additional steps and setup considerations for implementing OracleiPayment with this feature.

Multiple Organizations in Oracle ApplicationsThis guide describes how to set up and use Oracle iPayment with OracleApplications' Multiple Organization support feature, so you can define and supportdifferent organization structures when running a single installation of OracleiPayment.

xiii

Oracle Workflow GuideThis guide explains how to define new workflow business processes as well ascustomize existing Oracle Applications-embedded workflow processes.You also usethis guide to complete the setup steps necessary for any Oracle Applicationsproduct that includes workflow-enabled processes.

Oracle Applications Flexfields GuideThis guide provides flexfields planning, setup and reference information for theOracle iPayment implementation team, as well as for users responsible for theongoing maintenance of Oracle Applications product data. This manual alsoprovides information on creating custom reports on flexfields data.

Oracle eTechnical Reference ManualsEach eTechnical Reference Manual (eTRM) contains database diagrams and adetailed description of database tables, forms, reports, and programs for a specificOracle Applications product. This information helps you convert data from yourexisting applications, integrate Oracle Applications data with non-Oracleapplications, and write custom reports for Oracle Applications products. OracleeTRM is available on Metalink

Oracle Manufacturing APIs and Open Interfaces ManualThis manual contains up-to-date information about integrating with other OracleManufacturing applications and with your other systems. This documentationincludes APIs and open interfaces found in Oracle Manufacturing.

Oracle Order Management Suite APIs and Open Interfaces ManualThis manual contains up-to-date information about integrating with other OracleManufacturing applications and with your other systems. This documentationincludes APIs and open interfaces found in Oracle Order Management Suite.

Oracle Applications Message Reference ManualThis manual describes Oracle Applications messages. This manual is available inHTML format on the documentation CD-ROM for Release 11i.

Oracle CRM Application Foundation Implementation GuideMany CRM products use components from CRM Application Foundation. Use thisguide to correctly implement CRM Application Foundation.

xiv

Other Information SourcesFor more information, see the latest versions of the following manuals:

■ Oracle iPayment Implementation Guide

■ iPayment JavaDoc (Available on Metalink)

■ Apache Server Documentation (http://www.apache.com)

■ Oracle iStore and Oracle iMarketing Implementation Guide

■ Apache’s mod-ssl documentation (http://www.mod-ssl.org/docs).

■ Java Developer’s Guide (http://www.sun.com)

■ Merchant Connection Kit (MCK) Documentation(http://www.cybercash.com/cashregister/download.html)

Training and Support

TrainingOracle offers training courses to help you and your staff master Oracle iPaymentand reach full productivity quickly. You have a choice of educational environments.You can attend courses offered by Oracle University at any one of our manyEducation Centers, you can arrange for our trainers to teach at your facility, or youcan use Oracle Learning Network (OLN), Oracle University's online educationutility. In addition, Oracle training professionals can tailor standard courses ordevelop custom courses to meet your needs. For example, you may want to useyour organization’s structure, terminology, and data as examples in a customizedtraining session delivered at your own facility.

SupportFrom on-site support to central support, our team of experienced professionalsprovides the help and information you need to keep Oracle iPayment working foryou. This team includes your Technical Representative, Account Manager, andOracle’s large staff of consultants and support specialists with expertise in yourbusiness area, managing an Oracle8i server, and your hardware and softwareenvironment.

OracleMetaLinkOracleMetaLink is your self-service support connection with web, telephone menu,and e-mail alternatives. Oracle supplies these technologies for your convenience,available 24 hours a day, 7 days a week. With OracleMetaLink, you can obtain

xv

information and advice from technical libraries and forums, download patches,download the latest documentation, look at bug details, and create or update TARs.To use MetaLink, register at (http://metalink.oracle.com).

Alerts: You should check OracleMetaLink alerts before you begin to install orupgrade any of your Oracle Applications. Navigate to the Alerts page as follows:Technical Libraries/ERP Applications/Applications Installation andUpgrade/Alerts.

Self-Service Toolkit: You may also find information by navigating to theSelf-Service Toolkit page as follows: Technical Libraries/ERPApplications/Applications Installation and Upgrade.

Do Not Use Database Tools to Modify Oracle Applications DataOracle STRONGLY RECOMMENDS that you never use SQL*Plus, Oracle DataBrowser, database triggers, or any other tool to modify Oracle Applications dataunless otherwise instructed.

Oracle provides powerful tools you can use to create, store, change, retrieve, andmaintain information in an Oracle database. But if you use Oracle tools such asSQL*Plus to modify Oracle Applications data, you risk destroying the integrity ofyour data and you lose the ability to audit changes to your data.

Because Oracle Applications tables are interrelated, any change you make usingOracle Applications can update many tables at once. But when you modify OracleApplications data using anything other than Oracle Applications, you may change arow in one table without making corresponding changes in related tables. If yourtables get out of synchronization with each other, you risk retrieving erroneousinformation and you risk unpredictable results throughout Oracle Applications.

When you use Oracle Applications to modify your data, Oracle Applicationsautomatically checks that your changes are valid. Oracle Applications also keepstrack of who changes information. If you enter information into database tablesusing database tools, you may store invalid information. You also lose the ability totrack who has changed your information because SQL*Plus and other databasetools do not keep a record of changes.

About OracleOracle Corporation develops and markets an integrated line of software productsfor database management, applications development, decision support, and officeautomation, as well as Oracle Applications, an integrated suite of more than 160

xvi

software modules for financial management, supply chain management,manufacturing, project systems, human resources and customer relationshipmanagement.

Oracle products are available for mainframes, minicomputers, personal computers,network computers and personal digital assistants, allowing organizations tointegrate different computers, different operating systems, different networks, andeven different database management systems, into a single, unified computing andinformation resource.

Oracle is the world’s leading supplier of software for information management, andthe world’s second largest software company. Oracle offers its database, tools, andapplications products, along with related consulting, education, and supportservices, in over 145 countries around the world.

xvii

xviii

Understanding iPay

1

Understanding iPaymentThis topic group provides overviews of the application and its components,explanations of key concepts, features, and functions, as well as the application’srelationships to other Oracle or third-party applications.

New in this DocumentThe following features are available in Oracle iPayment 11i:

Processor-Model Payment SystemsOracle iPayment now supports the processor-model payment system that passespayment requests directly to a payment processor. With this enhancement, OracleiPayment can be integrated with both gateway-model and processor-modelpayment systems.

Besides supporting credit card transactions, the processor-model payment systemswill also support Electronic Fund Transfer (EFT) transactions. Thus, both thegateway and processor-model payment systems now support EFT transactions.

Multiple Payment System IdentifiersiPayment has been enhanced to include multiple payment system identifiers for apayee. Multiple payment system identifiers are required because a payee maymaintain multiple accounts at a payment system. Using Oracle iPayment, the payeecan now configure multiple payment system identifiers for a payment system androute the transactions to the appropriate account. The payment system identifiersrepresent the accounts maintained by the payee with the payment system. Thepayee is known to the payment system using the identifiers. Two payees cannothave the same identifier for one payment system.

ment 1-1

Overview of Oracle iPayment

Transaction ReportingiPayment offers an executive Transaction Reporting (TR) portal that displays keyperformance metrics such as transaction summaries, payee summaries, and othercritical performance indicators that roll up across all processors, types of cards, andtransaction types. iPayment TR users can view the information summarized on adaily, weekly or monthly basis. iPayment provides a graphical view of the variousbusiness trends and how they are changing. This helps executive users to takebusiness decisions in real time. iPayment also provides a concurrent manager-basede-mail notification system that relieves the burden of constantly monitoring criticalmeasures.

Overview of Oracle iPaymentOracle iPayment provides an integrated electronic payment solution for both ECapplications and client-server applications. It provides user-friendly access, and theapplications have the control of payment processing.

Oracle iPayment supports three electronic payment methods: credit card, purchasecard, and EFT transactions. iPayment also supports payment partners such asVerisign and Paymentech.

iPayment offers easy installation, administration, and extension capabilities. Therisk management functionality of iPayment can quantify and identify fraudulentonline transactions for both business-to-business and business-to- consumermodels.

Key Benefits of iPayment■ Integrates with many payment processing systems. This feature allows

businesses to offer several payment options to their customers and thus reduceimplementation and maintenance costs.

■ Provides rules based payment processing. This feature allows businesses toincorporate their existing business operations, rules, and procedures and lowercosts by controlling relationships with payment processing vendors.

■ Provides security through support for industry standards such as SSL.

■ Integrates with other Oracle applications, such as Oracle iStore via OrderCapture and Order Management, Oracle Receivables, and a single, openapplication programming interface (API) to integrate with any web-based, orclient-server application.

1-2 Oracle iPayment Concepts and Procedures Guide

Integration with Other Oracle Applications

■ Provides support for both single and multi site installations of electroniccommerce (EC) or client-server applications. iPayment also allows bothstand-alone businesses and internet service providers to offer electronicpayment processing.

Integration with Other Oracle ApplicationsiPayment integrates with other Oracle applications to provide payment processingacross your enterprise. Various applications send payment transaction requests toiPayment for processing. Without iPayment, each of these applications would needto build integration to back end payment (BEP) systems. iPayment saves integrationeffort by providing a single source to the Back end payment systems such asVerisign, Paymentech, and country-specific or region-specific payment systems.

Example of a Payment Processing Flow Using iPayment and OtherOracle Applications:1. Sales application (for example, iStore or TeleSales): A customer purchases a

product and decides to pay by credit card. The sales application submits theorder.

2. Order Capture or Order Management: Order Capture and Order Managementprocess the order. They use iPayment to verify if the credit card number is validand authorize the order amount. They can also perform some risk evaluation aspart of the authorization.

3. Oracle Receivables: When the order is shipped, the credit card information ispassed to Oracle Receivables and the billing and credit capture takes place.

4. Oracle Collections: When the payment is overdue and your call center beginsoutbound collection attempts, Oracle Collections uses iPayment to authorizeand capture credit card transactions.

Understanding iPayment 1-3

iPayment Architectural Overview

Figure 1–1 iPayment’s Integration with Oracle Applications

iPayment Architectural OverviewiPayment can be integrated with any EC or other sales applications. The integratediPayment component can communicate with the Oracle database and other servletsto provide payment processing.

1-4 Oracle iPayment Concepts and Procedures Guide

iPayment Architectural Overview

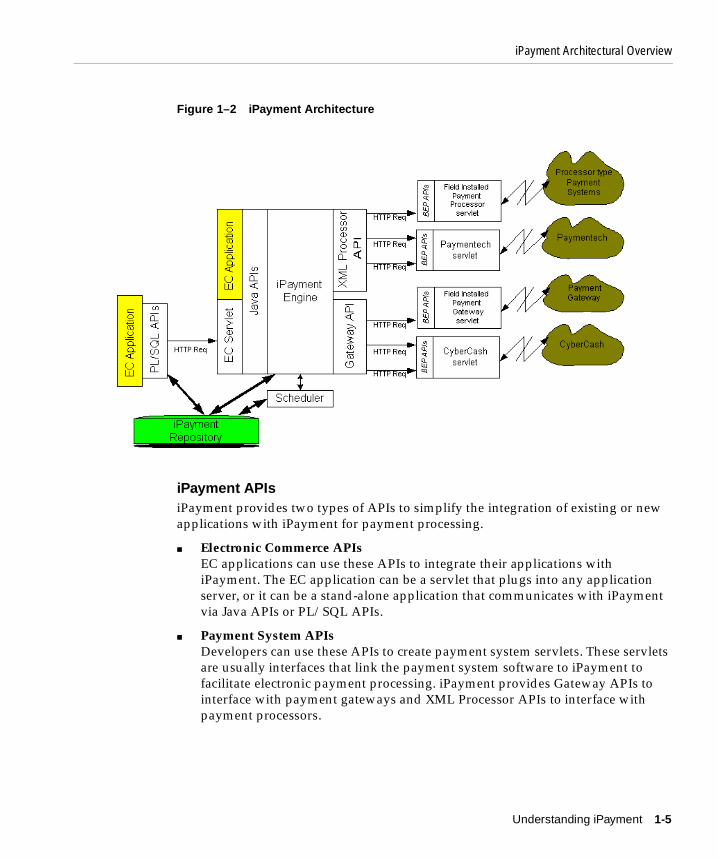

Figure 1–2 iPayment Architecture

iPayment APIsiPayment provides two types of APIs to simplify the integration of existing or newapplications with iPayment for payment processing.

■ Electronic Commerce APIsEC applications can use these APIs to integrate their applications withiPayment. The EC application can be a servlet that plugs into any applicationserver, or it can be a stand-alone application that communicates with iPaymentvia Java APIs or PL/SQL APIs.

■ Payment System APIsDevelopers can use these APIs to create payment system servlets. These servletsare usually interfaces that link the payment system software to iPayment tofacilitate electronic payment processing. iPayment provides Gateway APIs tointerface with payment gateways and XML Processor APIs to interface withpayment processors.

Understanding iPayment 1-5

Understanding Credit Card Transactions

iPayment EngineThe iPayment engine contains functionality for multi-payment method support,routing, risk management, etc. It works easily with the APIs.

iPayment ServletsiPayment consists of the following servlets:

■ ECServlet

The ECServlet provides an interface to the iPayment engine to process paymentrelated operations such as authorization, capture, and return. This servlet isprimarily used for the PL/SQL APIs provided by iPayment.

■ Payment system servlets

iPayment provides a complete payment solution, bundling payment system servletsdeveloped by Oracle and its payment system partners. The payment systemscommunicate with the payment processors and the acquirers or banks to processpayment transactions. iPayment includes payment system servlets for Paymentech,CyberCash, First Data (North) and EFS. Some payment systems, such as Verisign,have built their own iPayment servlets.

■ Field-installable servlets

iPayment supports field-installable servlets. These payment system servlets are notbundled with iPayment. This feature allows a payee to acquire a new, additional, orupgraded payment system servlet and configure it in the same way as the paymentsystem servlets bundled with iPayment.

The ability to add field-installable servlets provides payment flexibility and allowsnew releases of iPayment and the payment systems to be independent of eachother. It also enables EC applications to customize the payment system for theirspecific needs and regions.

Field-installable payment system servlets for iPayment are usually available fromOracle’s payment system partners.

Understanding Credit Card TransactionsiPayment handles credit card, purchase card, and EFT transactions. The followinginformation explains the process flow for a typical credit card transaction.

1-6 Oracle iPayment Concepts and Procedures Guide

Understanding Credit Card Transactions

Traditional Credit Card TransactionsTraditional credit card transaction processing involves a customer, a payee, anacquiring bank or processor, and an issuing bank.

A credit card transaction consists of three phases: authorization, settlement, andreconciliation.

■ Authorization

The customer purchases goods or services and sends credit card informationand payment instructions to the payee or business.

The payee accepts the authorization request and sends it to the credit cardprocessor through iPayment and the payment system.

The processor matches the information with a database maintained by the cardissuer (such as Visa or MasterCard) to determine if the customer has enoughavailable credit to cover the transaction. If so, then the processor reserves thefunds and sends back an authorization code.

■ Settlement

Settling transactions includes capturing authorized transactions, processingvoids and returns, and batch administration.

The payee issues capture, void, return, credit, and close batch functions to theprocessor through iPayment and the payment system.

The processor settles the payment with the issuing bank and causes the funds totransfer to the acquiring bank.

■ Reconciliation

Depending on the agreement between the payee and the acquiring bank, theacquiring bank sends daily, weekly, or monthly reports to the payee forreconciliation.

The payee cross-checks transaction information in the database with the bankstatement for reconciliation.

Voice AuthorizationSometimes credit card processing networks decline transactions with a referralmessage indicating that the merchant must call the cardholder’s issuing bank tocomplete the transaction. The payment information in such cases is submitted overthe phone. If the transaction is approved, the merchant is provided with an

Understanding iPayment 1-7

Understanding Terminal-Based and Host-Based Merchants

authorization code for the transaction. To facilitate follow-on transactions throughiPayment for this voice authorization (for example, capture or void), iPaymentprovides voice authorization support.

Understanding Terminal-Based and Host-Based MerchantsiPayment supports the following processing models that the financial industry usesfor credit card transactions:

■ Terminal-Based Merchant

The payee or business determines when to close batches of transactions for clearingand settlement, and is responsible to perform the close batch operations. Therefore,the payee or business has more flexibility.

■ Host-Based Merchant

In this model, the processor’s host maintains all the transactions and is usuallyresponsible for close batch operations at a predetermined frequency. The payee orbusiness does not have to perform close batch operations. Corrections, such asreturns and voids, are sent as new transactions to the host.

Why Is this Important?The choice of being a terminal-based or host-based merchant is generallydetermined by the business type, number of transactions per day, and the modelsupported by the acquiring bank. The processing model you choose affects how youperform the settlement operations. For a terminal-based merchant model, you haveto perform close batch operations periodically. Consult your inquiring bank formore information at the time of signing up.

Understanding Gateway-Model and Processor-Model Payment SystemsOracle iPayment supports both gateway-model and processor-model paymentsystems. A gateway-model is an interface between Oracle iPayment and a gateway.A payment gateway is a separate service and acts as an intermediary between theEC application and all the financial networks involved with the transaction,including the customers' credit card issuer and your merchant account. It checks forvalidity, encrypts transaction details, ensures they are sent to the correct destinationand then decrypts the responses which are sent back to the EC application viaiPayment. A processor-model is an interface that enables Oracle iPayment to passcredit card, purchase card, EFT, and Automated Clearing House (ACH) paymentrequests directly to a payment processor without going through a gateway.

1-8 Oracle iPayment Concepts and Procedures Guide

Understanding Purchase Cards

A processor-based system allows authorizations in real-time and follow-uptransactions such as captures and credits offline. Offline transactions must bebatched together and sent as a single request to the payment system. Hence, alltransactions other than authorizations are, by default, performed offline. Offlinetransactions are sent to the processor when the next batch close operation isattempted.

A batch close operation can be done manually or automatically. In a manual batchclose, a call is made to the iPayment close batch API. The iPayment schedulerperforms an automatic batch close. To determine the final statuses of all submittedtransactions in a batch close, a follow-up call to the batch query API can be made.The follow-up call may be a manual call to the API, or can be made automaticallythrough the iPayment scheduler. The follow-up call must be made some time afterthe batch is submitted. The actual period of time depends on the processor and thenumber of transactions in the batch.

Understanding Purchase CardsPurchase Cards, also known as procurement cards, are a special type of charge card.These cards possess more features, capabilities, and controls than standardconsumer credit or charge cards. Purchase cards are issued by an organisation(hereafter referred to as buyer) to its employees. The card is generally used by theemployees for purchasing corporate supplies and services. Payments are directlymade by the buyer to the merchants.

Central billing to the buyer, to which the cards are issued, is done. The merchantreceives payment a few days after submitting a transaction and the buyer pays theissuing bank for the aggregate amount of purchases made in the billing period.

A purchase card transaction can contain level II or level III data. For moreinformation on card data levels, see Purchase Card Data Levels. In a typicalbusiness-to-business scenario, level III data is used. Purchase cards providemerchants with a mechanism to eliminate the costly paper process of providing andcollecting funds for outstanding invoices.

iPayment supports purchase cards requiring level II and level III data. FromiPayment's perspective, purchase cards are similar to credit cards, except that thepayment processor gets more information in the case of purchase cards.

iPayment only supports Level III data purchase card transactions sent via OracleReceivables. For more information, please look up the credit card chapter in the'Oracle Receivables User Guide'.

Understanding iPayment 1-9

Understanding Purchase Cards

Benefits of Purchase Cards

To the Merchant■ Accepting purchase cards is crucial to increasing competitiveness. Businesses

use purchase cards to cut costs and streamline labor intensive processes toprocure goods and services. Many buyers prefer merchants that acceptpurchase cards.

■ Merchants generally receive better rates with purchase cards than with creditcards.

■ Purchase cards provide a cleaner payment collection process for merchants.Merchants have the ability to collect their funds in conjunction with thesettlement of their credit card transactions.

To the Buyer■ A reconciliation stream by providing purchase order number and additional

information.

■ Aggregation of purchases when companies receive one invoice for multiplepurchase cards.

■ Streamlining the purchase order process. Lower processing costs by simplifyingthe purchasing process, reducing paperwork, and automating controls on thespending limits.

■ Merchants accepting purchase card as a payment method help the buyer bymaking purchase information available electronically. This may help companies(buyers) comply with tax regulations, reporting requirements, and expensereconciliation.

Purchase Card Data LevelsFor a purchase card, three levels of data can be captured and sent by a merchant tothe buyer organisation. They are:

Level I:Level I transaction data consists of only basic data. A standard credit cardtransaction provides Level I data to the processor. The buyer cannot derive anyspecial benefits from purchase card usage if the merchant passes only Level I data.

1-10 Oracle iPayment Concepts and Procedures Guide

Understanding Purchase Cards

Level II:Level II transaction data consists of data such as tax amount and order number inaddition to Level I data.

Level III:Level III line item detail provides specific purchase information such as itemdescription, quantity, unit of measure and price. This information is very useful tothe buyer to help streamline accounting and business practices and to mergepayment data with electronic procurement systems.

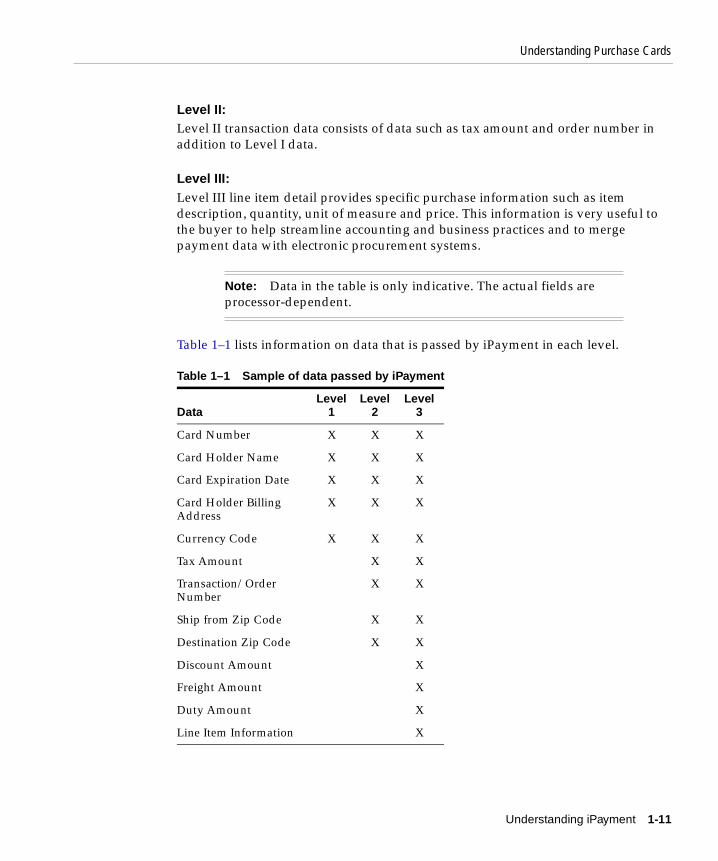

Table 1–1 lists information on data that is passed by iPayment in each level.

Note: Data in the table is only indicative. The actual fields areprocessor-dependent.

Table 1–1 Sample of data passed by iPayment

DataLevel

1Level

2Level

3

Card Number X X X

Card Holder Name X X X

Card Expiration Date X X X

Card Holder BillingAddress

X X X

Currency Code X X X

Tax Amount X X

Transaction/OrderNumber

X X

Ship from Zip Code X X

Destination Zip Code X X

Discount Amount X

Freight Amount X

Duty Amount X

Line Item Information X

Understanding iPayment 1-11

Understanding Purchase Cards

Processing Purchase Card TransactionsThe transaction phases in a purchase card transaction are the same as in a creditcard transaction. The phases are: authorization, settlement, and reconciliation. Seethe Understanding Credit Card Transactions for more information abouttransaction phases.

iPayment passes additional information to the payment system only during theclose batch operation. Authorization and other settlement operations carry the sameinformation for purchase cards as they do for credit cards.

The business flow differs on the buyer’s side and for the payment system, but notfor the merchant except for the additional information that is passed. The businessflow is as follows:

■ Buyer places an order and provides payment information. Payment informationis entered in the merchant’s system. The information includes: purchase cardaccount number, card expiration date, amount of purchase, applicable sales tax,and purchase order number.

■ Buyer authorizes payment by requesting authorization through the paymentsystem and the network.

■ Card issuer verifies that the purchase is within the cardholder's authorizedspending limits. Within seconds, the merchant receives either an approval or adenial of the payment request.

■ Merchant may display a receipt summarizing the items purchased, totalamount of the sale, and any taxes paid.

■ Merchant captures the payment by issuing a capture transaction to itsprocessor.

■ Funds are transferred from the issuing bank (customer’s bank) to the acquiringbank (merchant’s bank).

■ Issues bank bills and collects payment at the end of a billing cycle. The buyerreceives a central invoice from the issuer bank for all company cardholdertransactions.

■ Buyer sends a consolidated payment to the purchase card issuer.

■ Each cardholder also receives a monthly memo statement at the end of thebilling cycle to review it for accuracy. This statement may be reconciled andapproved by management.

■ The buyer’s accounting department allocates valid expenses to appropriateprojects, cost centers, general ledger, or purchase order accounts.

1-12 Oracle iPayment Concepts and Procedures Guide

Understanding Bank Account Transfers

Understanding Bank Account TransfersiPayment supports bank account transfers for both business-to-consumer andbusiness-to-business models. Account transfer functionality facilitates electronictransfer of payment amounts from a customer’s bank account to the payee’s bankaccount. EC applications can use bank account transfers for Electronic FundTransfers (EFT) and, in the US, for Automated Clearing House (ACH) transactions.EC applications use iPayment as their interface to payment processors that provideconnectivity to appropriate clearing house networks. iPayment integrates withPaymentech and Verisign’s PayNow service to provide this feature.

The number of operations supported for EFT is less than for credit card paymentsbecause of the current practices and processes involved in processing accounttransfers. You cannot receive real time response for bank account transfers due tothe current practices in account transfer processing. The only status that can beprovided is whether the payment was submitted to the processing network or not.iPayment only supports offline payments for bank account transfers. SeeUnderstanding Offline and Online Payments for more information.

Interface with Electronic Commerce ApplicationsEC applications can use the same API for credit card, purchase card, and bankaccount payments. iPayment routes the request to the correct Back end paymentsystem.

The operations that are supported for bank account transfers are merged into thesame framework of operations that are supported for credit card payments. Thefollowing operations are supported for bank account transfers:

■ Payment request

■ Payment modification

■ Payment cancellation

■ Payment inquiry

■ Payment query transaction status

Note: Certain credit card operations are not supported for bankaccount transfers.

Understanding iPayment 1-13

Understanding Offline and Online Payments

Process Flow of a Bank Account Payment Request1. The EC application calls the iPayment API to schedule an offline bank account

transfer payment request.

2. All bank account transfer payments need some lead time before the settlementdate. At the time of an API call, iPayment determines whether the paymentrequest can be settled on the requested date or not, based on the lead time of thepayment system.

3. If it can be settled, then iPayment accepts the payment request. Otherwise,based on the API parameters, iPayment either rejects the payment request oraccepts the payment request with a different settlement date.

4. A scheduled offline payment request can either be modified or canceled beforeit is routed to the payment system.

5. Once a request is routed to the payment system, the EC application can neithermodify nor cancel the request.

6. The payment system routes the payment to the appropriate network.

7. If the payment processor is a payment gateway, then the EC application canquery iPayment to retrieve the status of the payment transaction. iPayment, inturn, queries the payment system. If there is any failure on the paymentnetwork or at the payment system site while processing the payment, then thepayment system responds with those errors.

8. Finally, iPayment updates its tables with the status of the transaction and thenreturns to the EC application the status of the payment request.

Understanding Offline and Online PaymentsiPayment supports two models of payment processing:

■ Online Payment Processing

■ Offline Payment Processing

Online Payment ProcessingOnline payment processing is the model in which payment processing request isimmediately forwarded to the Back end payment processor. The results from theprocessor are immediately returned to the EC application.

1-14 Oracle iPayment Concepts and Procedures Guide

Understanding Offline and Online Payments

Offline Payment ProcessingOffline payment processing is the model in which payment requests are notimmediately forwarded to Back end payment processors. When an EC applicationmakes a payment processing request in a scheduled mode, or if the payment ispredated, the payment information is saved in the iPayment database and is sent tothe payment processor at a later time.

The offline method uses a scheduler, a utility that functions at regular intervals. Thescheduler browses the stored requests and sends requests to the Back end paymentsystems and updates to the EC applications.

States of Offline Bank Account Payment RequestsAn offline bank account payment request in iPayment, at any given time, can be inone of the following states:

■ Pending: After the EC application makes a request and before the schedulerroutes the request to the payment system.

■ Scheduled: After routing to the payment system.

■ Submitted: Once the payment system submits the request to the bankingnetwork, for example, ACH network.

■ Canceled: When a pending payment is canceled by the EC application.

■ Failed: Failed due to technical errors.

■ Communication Error: Failed due to communication errors. Transaction maybe retried.

■ Unpaid: Insufficient funds.

The state of a payment is determined on the status of the payment request. Toobtain the status of a payment request, EC applications can call the QueryTransaction Status API.

The following diagram shows the state diagram of an offline payment request (Forbank accounts only).

Understanding iPayment 1-15

Understanding Offline and Online Payments

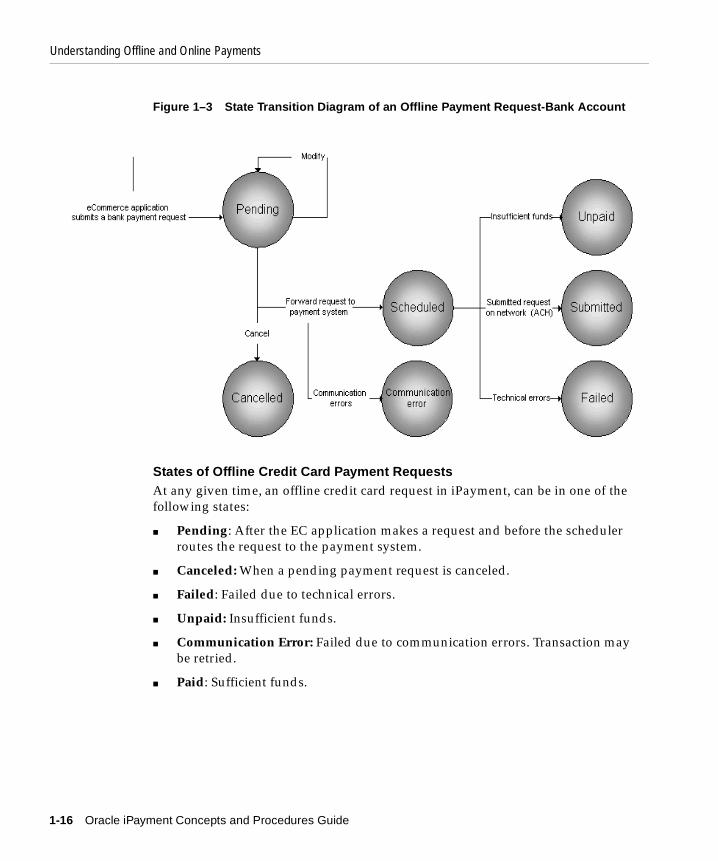

Figure 1–3 State Transition Diagram of an Offline Payment Request-Bank Account

States of Offline Credit Card Payment RequestsAt any given time, an offline credit card request in iPayment, can be in one of thefollowing states:

■ Pending: After the EC application makes a request and before the schedulerroutes the request to the payment system.

■ Canceled: When a pending payment request is canceled.

■ Failed: Failed due to technical errors.

■ Unpaid: Insufficient funds.

■ Communication Error: Failed due to communication errors. Transaction maybe retried.

■ Paid: Sufficient funds.

1-16 Oracle iPayment Concepts and Procedures Guide

Understanding Offline and Online Payments

Figure 1–4 State Transition Diagram of an Offline Payment Request-Credit Card

Understanding iPayment 1-17

How the Scheduling System Works

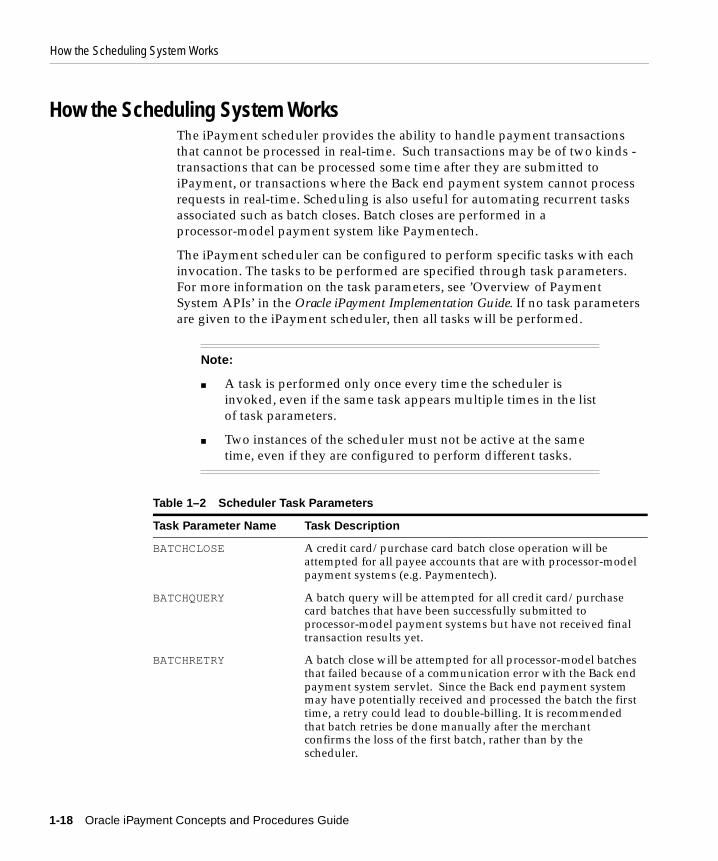

How the Scheduling System WorksThe iPayment scheduler provides the ability to handle payment transactionsthat cannot be processed in real-time. Such transactions may be of two kinds -transactions that can be processed some time after they are submitted toiPayment, or transactions where the Back end payment system cannot processrequests in real-time. Scheduling is also useful for automating recurrent tasksassociated such as batch closes. Batch closes are performed in aprocessor-model payment system like Paymentech.

The iPayment scheduler can be configured to perform specific tasks with eachinvocation. The tasks to be performed are specified through task parameters.For more information on the task parameters, see ’Overview of PaymentSystem APIs’ in the Oracle iPayment Implementation Guide. If no task parametersare given to the iPayment scheduler, then all tasks will be performed.

Note:

■ A task is performed only once every time the scheduler isinvoked, even if the same task appears multiple times in the listof task parameters.

■ Two instances of the scheduler must not be active at the sametime, even if they are configured to perform different tasks.

Table 1–2 Scheduler Task Parameters

Task Parameter Name Task Description

BATCHCLOSE A credit card/purchase card batch close operation will beattempted for all payee accounts that are with processor-modelpayment systems (e.g. Paymentech).

BATCHQUERY A batch query will be attempted for all credit card/purchasecard batches that have been successfully submitted toprocessor-model payment systems but have not received finaltransaction results yet.

BATCHRETRY A batch close will be attempted for all processor-model batchesthat failed because of a communication error with the Back endpayment system servlet. Since the Back end payment systemmay have potentially received and processed the batch the firsttime, a retry could lead to double-billing. It is recommendedthat batch retries be done manually after the merchantconfirms the loss of the first batch, rather than by thescheduler.

1-18 Oracle iPayment Concepts and Procedures Guide

How the Scheduling System Works

Scheduling Concurrent ProgramsUse the following steps to schedule concurrent requests:

1. Log on to Self Service Applications. Use users - IBYADMIN or SYSADMIN(you can use any user with Payment Administrator responsibility).

2. Choose the Payment Administrator responsibility.

3. From the Main menu, select View -> Requests to open the Find Requestswindow.

4. Click Submit a New Request to open the Submit a New Request window.

5. Select the Single Request option.

6. In the Name field, select the iPayment Scheduler from the list of values.

7. Specify the list of tasks that the scheduler has to perform.

8. To define a schedule, click Schedule to open the Schedule window.

BANKACCOUNT Offline bank account transactions are submitted.

CREDITCARD Offline credit card transactions are submitted.

PURCHASECARD Offline purchase card transactions are submitted.

EFTBATCHCLOSE A batch close will be attempted for all EFT payee accounts withprocessor-model payment systems (e.g.Paymentech).

EFTBATCHRETRY A batch close will be attempted for all EFT processor-modelbatches that failed because of an error (please see below forerror types) with the Back end payment system servlet. Sincethe Back end payment system may have received andprocessed the batch the first time, a retry could potentially leadto double-billing. It is recommended that batch retries be donemanually after the merchant confirms the loss of the first batch,rather than by the scheduler. The three instances when aEFTBatchRetry could occur are:

1. A communication error occurs with the servlet or theprocessor.

2. The database fails (i.e. DB shutdown) while the scheduleris running.

3. If the number of batches per day has exceeded the limit onthat processor.

Table 1–2 Scheduler Task Parameters

Task Parameter Name Task Description

Understanding iPayment 1-19

Understanding Risk Management

Defining a schedule can be as simple as submitting as soon as possible or usinga more complex schedule.

9. Click Submit on the Submit Request window if you want to submit theconcurrent request for processing.

Understanding Risk ManagementCard transactions continue to grow in number, taking an ever-larger share of thepayment system and leading to a higher rate of stolen account numbers andsubsequent losses by banks and merchants. Improved fraud detection thus hasbecome essential to maintain the viability of the payment system and merchants.

Banks have used early fraud warning systems for some years. iPayment providessimilar risk management functionality for credit card and purchase cardtransactions for EC applications. Risk management functionality is provided forboth business-to-business and business-to-consumer models. iPayment includes anumber of built-in risk factors and provides the option to the payees to run or notrun the risk evaluation functionality for each payment operation. Payees can alsorun the risk evaluation for operations that handle amounts exceeding a specifiedamount.

A risk factor includes any information which a payee wants to use to evaluate therisk of a customer wanting to buy goods or services from the payee. Examples ofrisk factors are: address verification, time of purchase and payment amount. Theserisk factors can be configured for each payee (merchant or biller).

Risk management functionality enables payees and EC service providers to managethe risk involved in processing transactions online. It allows businesses to have anynumber of predefined risk factors to verify the identity of their customers, assesstheir customer credit rating, and risk rating in a secure environment.

Payees can associate the risk factors with different weights as a formula and defineany number of risk formulas in iPayment based on their business model. When aPayment Request API is called, the EC application can specify which formula to beused to verify the identity of their customers, assess their customer credit rating,and risk rating in a secure environment. When the EC application calls the PaymentRequest API with the risk formula specified, iPayment will evaluate the risk and inparallel send the authorization request to the payment system. After getting aresponse from the payment system, iPayment will return both the authorizationcode and the risk score to the EC application. The EC application has to now decidewhether to continue with the sales process and make a payment capture ordiscontinue the transaction.

1-20 Oracle iPayment Concepts and Procedures Guide

Risk Factors Shipped with iPayment

Alternatively, Risk API can be called independent of the Payment Request APIs.Using the Risk API separately allows merchants to evaluate risk first. Depending onthe risk score, merchants may not want to send the payment request forauthorization. This avoids the overhead of sending an authorization for apotentially risky transaction. Please note that when the EC application calls the RiskAPI separately, iPayment cannot evaluate the risk scores associated with AVS.iPayment gets the AVS codes directly from the payment system during anauthorization request. As no authorization request is send in this scenario,iPayment cannot get AVS codes from the payment system and hence cannotevaluate risks scores associated with AVS.

Risk management helps businesses in reducing manual operational overheads tohandle bad transactions and in avoiding costly penalties such as charge backs frombanks.

Risk Factors Shipped with iPaymentThe following is a list of basic risk factors shipped with the Risk Managementcomponent. These risk factors can be configured per payee.

■ Payment amount limit is the amount involved in a payment request. It variesfrom business to business and the risk factor score can be configured fordifferent amount ranges based on the business model.

■ Time of purchase is the time that a payment request is made by the customer.Site administrators can define the time duration during which the paymentrequests are high risk and assign the risk factor scores for each duration.

■ Ship to/bill to address is used to match the ship to address to the bill to addressin a payment request. A payment request is considered high risk if these twoaddresses do not match.

■ Risky payment instruments are a list of payment instruments (e.g, credit cards,bank accounts) that are considered risky by each payee. These include theinstruments that were used by customers earlier and had resulted in fraud orchargebacks. Such a list can be generated internally by the payee or obtainedfrom other sources. If these instruments are reused in a payment request, thenthe payee may again face fraud or chargeback. Risk management functionalitycan detect whether risky payment instruments are being used duringprocessing by looking at the risky instrument repository. If the instrumentbeing used for the payment is found in the repository, then the payment isconsidered a high risk payment. The Risky Instruments Upload Utility addsand deletes a list of risky instruments from the database.

Understanding iPayment 1-21

Risk Factors Shipped with iPayment

■ Transaction amount is the total amount of payments made by a customer usingthe same instrument in a specified duration of time. The duration of time issetup by the user. This is related to the payment amount limit risk factor. Acustomer can make payments in smaller amounts, which are not captured bythe payment amount limit risk factor but can be captured by the transactionamount risk factor. Transaction amount risk factor sums up the total amount ofpayments in a specific duration of time and captures the risk on that amount.The total number of payments made during a specific time period can bechecked by looking at the payment history. The site administrator can set up atime duration and a transaction amount. In evaluating this risk factor, if thetotal payment amount exceeds the transaction amount within the specified timeduration, then the payment is considered a high risk payment.

■ Payment history tracks the reliability of the payer involved in a paymentrequest. If a payer has a good history of payments over a long duration, thenpayments requested by this payer are considered to be low risk payments.

■ Address verification service (AVS) check is the risk involved on the AVS codethat is returned by the credit card network. Address verification service isprovided by MasterCard and Visa credit card networks to match the billing orshipping address with the address that is maintained for the cardholder by theissuing bank. iPayment does address verification during an authorizationrequest, by calling the payment system with the address and zipcodeinformation along with the payment transaction information. The paymentsystem then does the authorization and also returns various AVS codes toiPayment. Various AVS codes are returned based on the complete addressmatch, zipcode match, street address match, etc. A site administrator canconfigure all AVS codes returned by the payment systems and theircorresponding risk factor scores. This service is only provided in the UnitedStates of America.

■ Frequency of purchase tracks the sudden surge in the use of a paymentinstrument in a short duration. For a particular payment instrument in apayment request, if the frequency of use in a duration configured is more thanthe setup value, then the payment request is considered to be a high riskpayment.

Oracle Receivables Risk FactorsFor customers who have both iPayment and Oracle Receivables installed andregistered, more risk factors are available. These risk factors are set up in OracleiPayment and the values of these risk factors are setup in Oracle Receivables. Oracle

1-22 Oracle iPayment Concepts and Procedures Guide

iPayment Routing and Operation

Receivables stores credit management information about customer accounts such ascredit rating, risk rating, etc. The following are risk factors used in risk analysis:

■ Credit limit is an overall credit limit associated with a customer’s account. If acustomer has an outstanding balance and the total amount of payment made bythe customer exceeds the overall credit limit, then the payment becomes a highrisk payment. Overall credit limit varies from business to business. It can be setup as an overall credit limit at the customer or site level through OracleReceivables.

■ Transaction credit limit is the credit limit per transaction associated with acustomer’s account. When a payment request exceeds the transaction creditlimit, it becomes a risky payment. The transaction credit limit varies frombusiness to business. It can be set up at the customer or site level throughOracle Receivables.

■ Credit rating is the information that enables payees to effectively managefinancial terms with their customers. It is useful for online financing or inevaluating purchases of a large amount by a new customer. Credit Rating is auser defined field and the information can be taken from Oracle Receivables. Apayee associates risk scores to credit rating. A higher risk score implies thatselling goods or services to the customer is risky.

■ Risk code is a user defined risk assessment field in Oracle Receivables. It isuseful for online financing or for evaluating purchases of a large amount for anew customer. The information is available from Oracle Receivables. A payeeassociates risk scores to all the risk codes. A higher risk score implies thatselling goods or services to the customer is risky.

iPayment Routing and OperationiPayment accepts payment transactions from EC applications and routes them tothe appropriate Back end payment systems. The customer uses a web browser or aclient application to exchange data with a web or server-based EC application. TheEC application sends payment requests to iPayment. Finally, iPayment routes thepayment requests to the appropriate payment systems.

What constitutes a routing rule?Every routing rule is made up of three components -

■ Basic Rule Information - This information is used to select and rank all therules that may be applicable to a payment transaction. The basic rule

Understanding iPayment 1-23

iPayment Routing and Operation

information consists of Rule Name, Payee, Payment Instrument Type, RulePriority and Status.

■ Destination Information - The destination information specifies the Back endpayment system to which the payment transaction should be routed. Thedestination information consists of Payment System and Payment SystemIdentifier.

■ Routing Rule Conditions - This specifies the conditions under which a rulebecomes applicable to a payment transaction. A rule condition is comprised of acondition name, a criterion for the condition (such as -Amount, Currency,Organization ID, Card Type, Card Number and Bank Routing Number), thetype of operation related to the criterion and the value of the criterion. Multiplerule conditions can be defined for a routing rule.

How Routing WorksRouting of a payment transaction is based on a set of routing rules set up in theiPayment user interface by the iPayment administrator. The routing engine findsthe appropriate Payment System in the following sequence:

1. The routing engine retrieves the rules associated with the Payee and InstrumentType specified in the payment request.

2. The routing rule with the highest priority is evaluated first. If the values in thetransaction match the conditions specified in the routing rule, the request isrouted to the corresponding Payment System using the specified PaymentSystem Identifier.

3. If the values in the request do not match the conditions specified, the routingrule with the next highest priority is evaluated.

4. In case the payment request values do not match any of the conditionsspecified, the transaction is routed to the default Payment System using thedefault Payment System Identifier.

Routing rules are prioritized by an administrator. During processing, the rules areevaluated in the order in which they are prioritized.

iPayment supports credit cards, purchase cards and bank account transfers. Thepayment methods available depend on the payment system that you decide to use.

Payees and businesses can customize how iPayment routes transactions to thepayment systems using routing rules based on their business rules and the availablepayment methods. For example:

1-24 Oracle iPayment Concepts and Procedures Guide

iPayment Routing and Operation

■ A business sends all electronic payment transactions to a single paymentsystem: Payment System A.

■ A business sends all small or micropayment transactions to Payment System Aand all credit card transactions to Payment System B.

■ A business sends all bank account transfers under $10 to Payment System A,and all other transactions to Payment system B.

■ A business sends all transactions using US dollars to Payment System A and alltransactions using other currencies to Payment System B.

Routing Rule ConditionsRouting rule conditions determine whether the rule is applicable to a paymenttransaction. A rule can have multiple rule conditions. A rule is applicable to apayment transaction only if the payment transaction can meet all the conditions forthe rule. For example, a payee can route all Visa credit card transactions where theOrder Amount is greater than 500 US dollars to Payment System C.

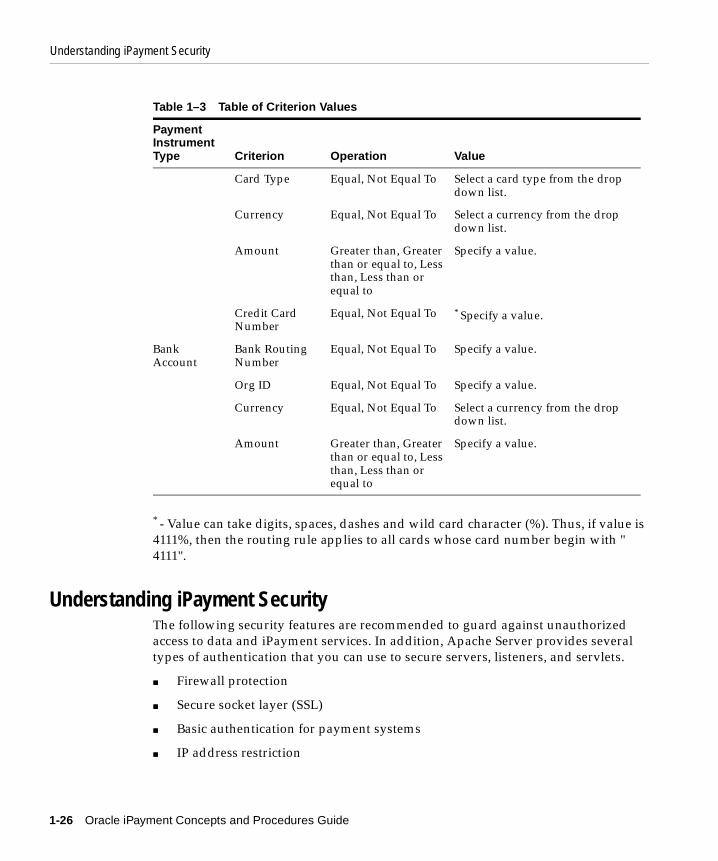

Table 1–3 lists the values in the Operation and Value fields for a selected PaymentInstrument Type and Criterion.

Table 1–3 Table of Criterion Values

PaymentInstrumentType Criterion Operation Value

PurchaseCard

Org ID Equal, Not Equal To Specify a value.(Only digitsallowed)

Card Type Equal, Not Equal To Select a card type from the dropdown list.

Currency Equal, Not Equal To Select a currency from the dropdown list.

Amount Greater than, Greaterthan or equal to, Lessthan, Less than orequal to

Specify a value.(Only digitsallowed)

Purchase CardNumber

Equal, Not Equal To * Specify a value.

Credit Card Org ID Equal, Not Equal To Specify a value.(Only digitsallowed)

Understanding iPayment 1-25

Understanding iPayment Security

* - Value can take digits, spaces, dashes and wild card character (%). Thus, if value is4111%, then the routing rule applies to all cards whose card number begin with "4111".

Understanding iPayment SecurityThe following security features are recommended to guard against unauthorizedaccess to data and iPayment services. In addition, Apache Server provides severaltypes of authentication that you can use to secure servers, listeners, and servlets.

■ Firewall protection

■ Secure socket layer (SSL)

■ Basic authentication for payment systems

■ IP address restriction

Card Type Equal, Not Equal To Select a card type from the dropdown list.

Currency Equal, Not Equal To Select a currency from the dropdown list.

Amount Greater than, Greaterthan or equal to, Lessthan, Less than orequal to

Specify a value.

Credit CardNumber

Equal, Not Equal To * Specify a value.

BankAccount

Bank RoutingNumber

Equal, Not Equal To Specify a value.

Org ID Equal, Not Equal To Specify a value.

Currency Equal, Not Equal To Select a currency from the dropdown list.

Amount Greater than, Greaterthan or equal to, Lessthan, Less than orequal to

Specify a value.

Table 1–3 Table of Criterion Values

PaymentInstrumentType Criterion Operation Value

1-26 Oracle iPayment Concepts and Procedures Guide

Understanding iPayment Security

■ Data Privacy

Firewall ProtectionOracle strongly recommends that you install iPayment and the payment systemservlets on a machine inside the Firewall.

Oracle also recommends that you use one of the following two configurationoptions to further reduce the risk of data being intercepted as it passes betweendifferent parts of iPayment:

■ Install all the following components on the same machine:

■ iPayment

■ Payment system servlet

■ EC application

■ Use Secure Socket Layer (SSL) to connect distributed components

Secure Socket LayerIf either iPayment (or its components) or the EC application is installed in adistributed environment, then Oracle recommends configuring SSL betweeniPayment and the payment system components.