Optimal Bidding Strategy for GENCO with Green Power in Day ...

10

Optimal Bidding Strategy for GENCO with Green Power in Day-ahead Electricity Market Xian Guo, Student Member, IEEE and Dr. Cameron A. MacKenzie 1 January 5, 2016. This paper is currently under review with a journal. Please check back for updates to the paper. Abstract—The electricity market has evolved from a regulated monopoly to a more liberalized competitive market, which allows a generating company (GENCO) to bid to provide energy. The two-period structure of the electricity market (day-ahead and real-time market) introduces a mechanism for determining the GENCO’s optimal bidding strategy. The difference between clearing prices for each period adds uncertainty to GENCO’s determination of its optimal bid. In addition, the fast growth of renewable energy sources (wind and solar power) and their increasing penetration to the power system adds uncertainty over how much energy the GENCO can actually produce in the real- time market. Based on the two-period market structure, we develop an optimization model for a single GENCO with green power to derive an optimal strategy to bid a price and quantity for the day-ahead market with the objective of maximizing its expected profit. Furthermore, we apply the optimization model with risk-aversion attitude to reduce chance of negative profits for GENCO. We fit probability distributions to historical data to reflect the uncertainties, and Monte-Carlo simulation allows us to solve the stochastic optimization problem. The optimization model and corresponding algorithm are verified in Southern California Edison, a GENCO in California ISO. Index Terms—GENCO, bidding strategy, green power, electricity market, risk-aversion, utility function, stochastic optimization NOMENCLATURE Decision variables Bid quantity for day-ahead market (MW) Bid price for day-ahead market ($/MWh) Exogenous random variables Actual generated quantity for real-time market from generation technology (MW), = , , , , 1- wind, 2-solar, 3-coal, 4-gas Total actual generated quantity for real-time market (MW), =∑ = , , Clearing price for day-head (DA) or real-time (RT) market ($/MWh), i.e., DA-price or RT-price Parameters Production costs for generation technology ($/MWh), = , , , , Curtailment costs for variable generation technology ($/MWh), = , The probability of scenario = , , … , The profit made by scenario Xian Guo and Dr. Cameron Mackenzie are with Iowa State University, Ames, IA 50010 USA (e-mail: [email protected]). I. INTRODUCTION Since the 1990s, the electricity market has evolved from a vertically integrated structure to a competitive deregulated market design. The reconstructed market is similar to an imperfect competition or oligopoly market due to the special characteristics, such as a limited number of suppliers, long construction periods of power plants and large capital investment sizes [1]. The current market structure is consisted of two separate financial settlements: day-ahead market and real- time market. The day-ahead market is a forward market, which is settled 24 hours before the operating day and allows market participants to commit selling offer or buying biddings for the next operating day. The real-time market is settled every five minutes in the specific operating day, which balances the difference between day-ahead commitments and the real-time actual production and demand. A typical energy market timeline is shown in Figure 1, which illustrates the well-organized structure of the two-period settlements in ISO-New England (Independent System Operator) [2]. Fig. 1. Electricity market timeline Under such a market setting, the supplier (generation company (GENCO), or virtual bidder) can maximize its profits by strategic bidding, and the buyers (load-serving entities) hope to pay a reasonable amount to satisfy their demand requirements. Thus, the development of optimal bidding strategy for GENCO is crucial. With the fast growth of renewable energy, especially wind and solar power, a GENCO’s optimal bidding strategy becomes more complicated and challenging. In addition to dealing with the possible load deviations, the output uncertainty from solar and wind power should also be considered when a GENCO

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Optimal Bidding Strategy for GENCO with Green Power in Day ...

Optimal Bidding Strategy for GENCO with Green

Power in Day-ahead Electricity Market

Xian Guo, Student Member, IEEE and Dr. Cameron A. MacKenzie1

January 5, 2016. This paper is currently under review with a journal. Please check back for updates to the paper.

Abstract—The electricity market has evolved from a regulated

monopoly to a more liberalized competitive market, which allows

a generating company (GENCO) to bid to provide energy. The

two-period structure of the electricity market (day-ahead and

real-time market) introduces a mechanism for determining the

GENCO’s optimal bidding strategy. The difference between

clearing prices for each period adds uncertainty to GENCO’s

determination of its optimal bid. In addition, the fast growth of

renewable energy sources (wind and solar power) and their

increasing penetration to the power system adds uncertainty over

how much energy the GENCO can actually produce in the real-

time market. Based on the two-period market structure, we

develop an optimization model for a single GENCO with green

power to derive an optimal strategy to bid a price and quantity for

the day-ahead market with the objective of maximizing its

expected profit. Furthermore, we apply the optimization model

with risk-aversion attitude to reduce chance of negative profits for

GENCO. We fit probability distributions to historical data to

reflect the uncertainties, and Monte-Carlo simulation allows us to

solve the stochastic optimization problem. The optimization model

and corresponding algorithm are verified in Southern California

Edison, a GENCO in California ISO.

Index Terms—GENCO, bidding strategy, green power,

electricity market, risk-aversion, utility function, stochastic

optimization

NOMENCLATURE

Decision variables

𝑮𝑩𝑰𝑫 Bid quantity for day-ahead market (MW)

𝝆𝑩𝑰𝑫 Bid price for day-ahead market ($/MWh)

Exogenous random variables

𝑮𝒊 Actual generated quantity for real-time market from

generation technology 𝒊 (MW), 𝒊 = 𝟏, 𝟐, 𝟑, 𝟒 , 1-

wind, 2-solar, 3-coal, 4-gas

𝑮 Total actual generated quantity for real-time market

(MW), 𝑮 = ∑ 𝑮𝒊𝟒𝒊=𝟏

𝝆𝑫𝑨, 𝝆𝑹𝑻, Clearing price for day-head (DA) or real-time (RT)

market ($/MWh), i.e., DA-price or RT-price

Parameters

𝒄𝒊 Production costs for generation technology

𝒊($/MWh), 𝒊 = 𝟏, 𝟐, 𝟑, 𝟒

𝒄𝑪𝑻,𝒊 Curtailment costs for variable generation technology

𝒊 ($/MWh), 𝒊 = 𝟏, 𝟐

𝑷𝒋 The probability of scenario 𝒋 = 𝟏, 𝟐, … , 𝟕

𝑭𝒋 The profit made by scenario 𝒋

Xian Guo and Dr. Cameron Mackenzie are with Iowa State University, Ames, IA 50010 USA (e-mail: [email protected]).

I. INTRODUCTION

Since the 1990s, the electricity market has evolved from a

vertically integrated structure to a competitive deregulated

market design. The reconstructed market is similar to an

imperfect competition or oligopoly market due to the special

characteristics, such as a limited number of suppliers, long

construction periods of power plants and large capital

investment sizes [1]. The current market structure is consisted of

two separate financial settlements: day-ahead market and real-

time market. The day-ahead market is a forward market, which

is settled 24 hours before the operating day and allows market

participants to commit selling offer or buying biddings for the

next operating day. The real-time market is settled every five

minutes in the specific operating day, which balances the

difference between day-ahead commitments and the real-time

actual production and demand. A typical energy market timeline

is shown in Figure 1, which illustrates the well-organized

structure of the two-period settlements in ISO-New England

(Independent System Operator) [2].

Fig. 1. Electricity market timeline

Under such a market setting, the supplier (generation

company (GENCO), or virtual bidder) can maximize its profits

by strategic bidding, and the buyers (load-serving entities) hope

to pay a reasonable amount to satisfy their demand requirements.

Thus, the development of optimal bidding strategy for GENCO

is crucial.

With the fast growth of renewable energy, especially wind

and solar power, a GENCO’s optimal bidding strategy becomes

more complicated and challenging. In addition to dealing with

the possible load deviations, the output uncertainty from solar

and wind power should also be considered when a GENCO

develops a bidding strategy. In particular, the GENCO should

pay for energy production deviations resulted from the

prediction error [3]. Thus, researching the optimal bidding

strategy for GENCO with green power in day-ahead electricity

market is of interest.

Prior research has modeled the optimal bidding strategy for

GENCOs ([1], [4]). The models fall into four categories: 1) a

single GENCO optimization model [5-7]; 2) game theory with

multiple GENCOs and buyers [8-10]; 3) agent-based models

[11,12] and 4) hybrid models [13,14]. Most of them focus on the

bidding strategy based on the day-ahead market, and only a few

consider the background of the real-time market [15]. Some

literature addresses the bidding strategy when relying on

renewable energy [16-18]. A mixed-integer nonlinear

programming model determines the optimal hydro scheduling

and offering strategies in the Portugal energy market [16]. A

stochastic Cournot model based on generated scenarios from the

Auto Regressive Moving Average is proposed to realize

strategic bidding for wind-dominated GENCOs [17]. Angarita

et al. [18] introduce a combined bidding strategy for wind farm

and hydro generating units, which can reduce the loss brought

by the fact that variable energy has uncertain output.

In summary, much of the foregoing research focuses on a

single market, which does not address the difference between

day-ahead market and real-time market. For most of these cases,

only a single generation technology is considered, which cannot

satisfy the real-world fact that multiple technologies (especially

green power) are available within a single GENCO. The unique

contribution of this paper is the development of an optimization

model based on a two-period market structure to determine the

optimal bidding strategy for a GENCO with green power and

multiple generation technology. The electricity prices for both

periods and the generation output for the green power are

uncertain. This type of model allows the GENCO to produce

more electricity from fossil fuel sources if the renewable energy

sources generate less electricity than anticipated. The GENCO

can determine the best way to meet its requirements based on

which generation technology costs less and produces the highest

profits. We also incorporate risk attitude into the model to

understand how the bidding strategy should change for a risk-

averse GENCO. This is another significant contribution of this

paper.

Based on a typical electricity market structure and

management rules, we develop a stochastic optimization model

in order to recommend the optimal bidding strategy for a

GENCO who wishes to maximize its expected profit or expected

utility under this two-period electricity market.

The remaining of the paper is organized as follows. Section

II introduces the market structure and management rules, which

is the foundation of our analysis. Section III details and

formulates the bidding problem and proposes the stochastic

optimization model. Section IV applies the model to Southern

California Edison (SCE, a GENCO from California ISO,

CAISO). Section V concludes the paper.

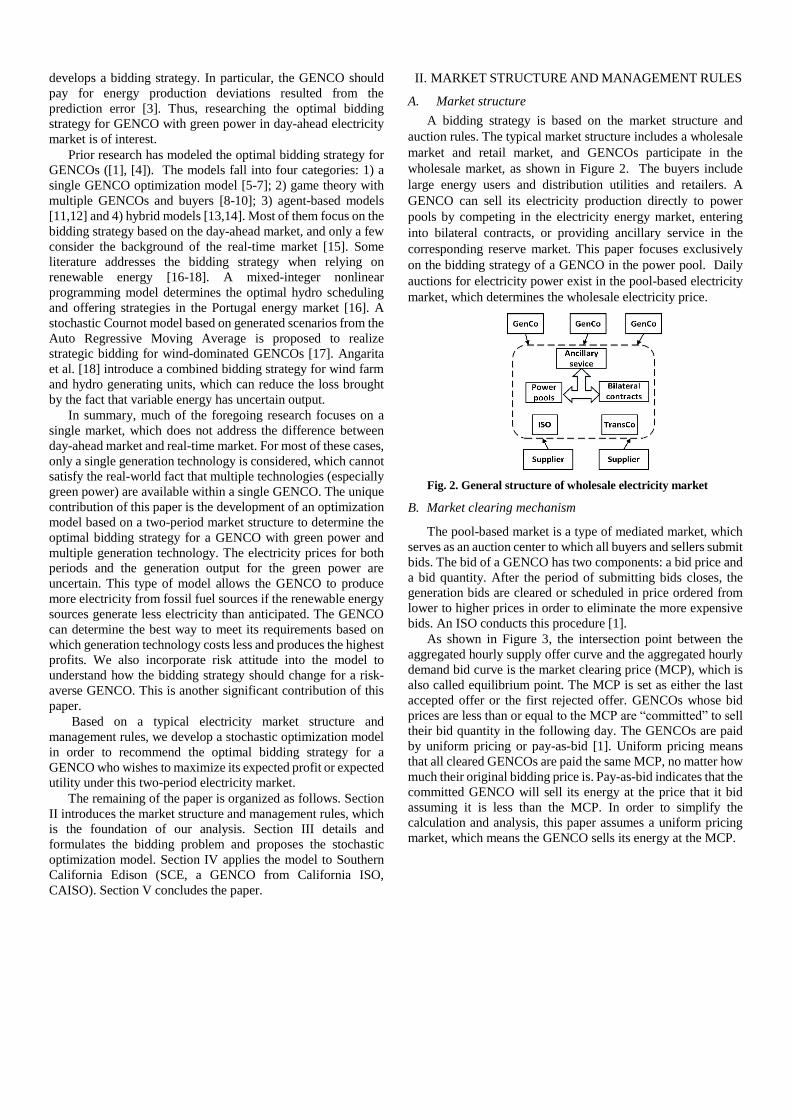

II. MARKET STRUCTURE AND MANAGEMENT RULES

A. Market structure

A bidding strategy is based on the market structure and

auction rules. The typical market structure includes a wholesale

market and retail market, and GENCOs participate in the

wholesale market, as shown in Figure 2. The buyers include

large energy users and distribution utilities and retailers. A

GENCO can sell its electricity production directly to power

pools by competing in the electricity energy market, entering

into bilateral contracts, or providing ancillary service in the

corresponding reserve market. This paper focuses exclusively

on the bidding strategy of a GENCO in the power pool. Daily

auctions for electricity power exist in the pool-based electricity

market, which determines the wholesale electricity price.

Fig. 2. General structure of wholesale electricity market

B. Market clearing mechanism

The pool-based market is a type of mediated market, which

serves as an auction center to which all buyers and sellers submit

bids. The bid of a GENCO has two components: a bid price and

a bid quantity. After the period of submitting bids closes, the

generation bids are cleared or scheduled in price ordered from

lower to higher prices in order to eliminate the more expensive

bids. An ISO conducts this procedure [1].

As shown in Figure 3, the intersection point between the

aggregated hourly supply offer curve and the aggregated hourly

demand bid curve is the market clearing price (MCP), which is

also called equilibrium point. The MCP is set as either the last

accepted offer or the first rejected offer. GENCOs whose bid

prices are less than or equal to the MCP are “committed” to sell

their bid quantity in the following day. The GENCOs are paid

by uniform pricing or pay-as-bid [1]. Uniform pricing means

that all cleared GENCOs are paid the same MCP, no matter how

much their original bidding price is. Pay-as-bid indicates that the

committed GENCO will sell its energy at the price that it bid

assuming it is less than the MCP. In order to simplify the

calculation and analysis, this paper assumes a uniform pricing

market, which means the GENCO sells its energy at the MCP.

Fig. 3. Market clearing process

C. Day-ahead market and real-time market

The day-ahead market develops schedules about unit

commitment to satisfy the forecasted load requirement. Buyers

purchase a certain amount of electricity in the day-ahead market,

but the real-time actual demand may be higher or lower than the

equilibrium quantity from the day-ahead market. A real-time

market exists in which buyers purchase electricity in real time

[2]. Two conditions can happen, detailed as follows:

When the real-time price is higher than the day-ahead price,

GENCOs whose bid prices exceed the day-ahead MCP but

are less than the real-time price will be committed in the

real-time market.

When the real-time price is less than the day-ahead price,

a committed GENCO has the option to “buy out.” A

GENCO can decide between 1) producing its bid quantity

from the day-ahead action or 2) buying the same quantity

from the real-time market. It should make this decision

based on the alternative that yields higher profits.

Uncertainty in the relationship between the day-ahead

price and real-time price plays a significant role in determining

the optimal bidding strategy for GENCOs.

III. PROBLEM FORMULATION

The GENCO’s optimization problem is to maximize its

expected profit (or utility) by bidding a paired price and quantity

in the day-ahead market. Four parameters are uncertain in the

model: the day-ahead MCP (denoted as day-ahead price), the

real-time MCP (denoted as real-time price), the actual real-time

output of wind power, and the actual real-time output of solar

power. We assume the capacity mix of the GENCO is wind

power, solar power, natural gas, and coal. To simplify the

analysis, we focus on a bidding strategy for a particular hour.

A. Uncertainty analysis

1) Day-ahead price and real-time price

The day-ahead price and the difference between the day-

ahead and real-time prices are modeled as independent random

variables. There are several studies researching price forecasting

[19], including statistical methods and optimization methods. In

this paper, we derive probability distributions for the day-ahead

price 𝜌𝐷𝐴 and the difference between the two prices in order to

preserve dependence between the day-ahead and real-time

prices. The real-time price 𝜌𝑅𝑇 equals to 𝜌𝐷𝐴 plus the difference

between the two prices. The model assumes that both prices are

determined exogenously from the GENCO’s bid price.

2) Wind output and solar output

As variable and intermittent generation, wind and solar

power have uncertain output, especially 24 hours prior to

generation. Unlike traditional gas-fired and coal-fired units,

which can produce exactly what is bid in the day-ahead market,

the output of wind and solar is challenged by over-generation or

under-generation. If solar and wind power are over generated,

the GENCO curtails the extra power with specific curtailment

costs. If solar and wind power are under generated, the GENCO

will need to buy additional power from the real-time market.

Prior research has studied forecasting the output of variable

energy [20-21]. In this paper, we adopt a similar method to the

uncertain prices by modeling wind and solar power generation

as random variables whose distributions are derived from

historical data.

The model assumes that four generation technologies are

available to the GENCO. The first two generation technologies

are wind (𝑖 = 1) and solar (𝑖 = 2) and the other two generation

technologies are coal ( 𝑖 = 3 ) and natural gas ( 𝑖 = 4 ). To

calculate the curtailment costs, the generation technology with

lower curtailment costs (Technology A) will be chosen to reduce

power output first. If reducing all available power from A still

cannot solve the problem of over-generation, the curtailment

behavior will come to technology B. The corresponding

curtailment costs is denoted as 𝑓(𝑐𝐶𝑇 , 𝐺 − 𝐺𝐵𝐼𝐷) where 𝑐𝐶𝑇 are

the curtailment costs, 𝐺 is the total amount of energy produced,

and 𝐺𝐵𝐼𝐷 is the GENCO’s bid quantity in the day-ahead market.

The GENCO submits a single bid price 𝜌𝐵𝐼𝐷 and a single

bid quantity 𝐺𝐵𝐼𝐷 , regardless of the power sources. The time

horizon is one hour, i.e., the decision variables are the GENCO’s

bidding quantity and price for a particular hour of the next day.

We assume that the GENCO can purchase as much energy as

they need from the real-time market.

B. Model formulation with expected profits-Model I

1) Objective function: maximize the expected profits.

7

1

max ,BID BID j j

j

E F G P F

(1)

where 𝑃𝑗 is the probability of each scenario, and 𝐹𝑗 is the

corresponding profit for each scenario. The scenarios are

classified based on the relationships i) between the day-ahead

price and real-time price and ii) between the actual output 𝐺 and

the bid quantity 𝐺𝐵𝐼𝐷 . The seven scenarios are detailed as

follows:

a) 𝜌𝐵𝐼𝐷 ≤ 𝜌𝐷𝐴 ≤ 𝜌𝑅𝑇 , 𝐺 ≥ 𝐺𝐵𝐼𝐷 : The GENCO is

committed in the day-ahead market and does not have the

option to “buy out” because the real-time price is more than the

bid price. The profit equals the revenue from selling electricity

in the day-ahead market minus the production costs and the

curtailment costs in which 𝐺 − 𝐺𝐵𝐼𝐷 must be curtailed.

4

1

1

,DA BID i i CT BID

i

F G c G f c G G

(2)

b) 𝜌𝐵𝐼𝐷 ≤ 𝜌𝐷𝐴 ≤ 𝜌𝑅𝑇 , 𝐺 < 𝐺𝐵𝐼𝐷 : The GENCO is

committed in the day-ahead market and does not have the

option to “buy out”. The wind and/or solar power does not

generate enough, and the GENCO should buy the additional

power from the real-time market. The profit equals the revenue

from the day-ahead market minus the production costs and the

costs for purchasing additional power in the real-time market.

4

2

1

DA BID i i RT BID

i

F G c G G G

(3)

c) 𝜌𝐵𝐼𝐷 ≤ 𝜌𝐷𝐴 , 𝜌𝐷𝐴 > 𝜌𝑅𝑇 , 𝐺 ≥ 𝐺𝐵𝐼𝐷 : The GENCO

makes decisions of “produce or buy” based on the production

costs 𝑐𝑖 and real-time price (plus curtailment costs for wind and

solar power) for each generation technology. As with the first

scenario, the surplus power 𝐺 − 𝐺𝐵𝐼𝐷 must be curtailed.

2

3 ,

1

4

3

min ,

min , ,

DA BID i RT CT i i

i

i RT i CT BID

i

F G c c G

c G f c G G

(4)

d) 𝜌𝐵𝐼𝐷 ≤ 𝜌𝐷𝐴 , 𝜌𝐷𝐴 > 𝜌𝑅𝑇 , 𝐺 < 𝐺𝐵𝐼𝐷 : The GENCO is

committed in the day-ahead market and has the option to “buy

out”, but it also needs to buy additional power from the real-

time market.

2

4 ,

1

4

3

min ,

min ,

DA BID i RT CT i i

i

i RT i RT BID

i

F G c c G

c G G G

(5)

e) 𝜌𝐷𝐴 < 𝜌𝐵𝐼𝐷 < 𝜌𝑅𝑇 , 𝐺 < 𝐺𝐵𝐼𝐷 : The GENCO is not

committed in the day-ahead market, but it will be committed in

real-time market.

4

5

1

RT BID i i RT BID

i

F G c G G G

(6)

f) 𝜌𝐷𝐴 < 𝜌𝐵𝐼𝐷 < 𝜌𝑅𝑇 , 𝐺 ≥ 𝐺𝐵𝐼𝐷 : The GENCO is

committed in the real-time market and needs to curtail extra

power produced by the green energy.

4

6

1

,RT BID i i CT BID

i

F G c G f c G G

(7)

g) All other situations: The GENCO will not be

committed but it will need to pay the curtailment costs for wind

and solar power. 2

7 ,

1

CT i i

i

F c G

(8)

2) Constraints:

The optimization model has a few constraints. One

constraint is:

_ in _ maxBID m BID BID (9)

where 𝜌𝐷𝐴_𝑚𝑖𝑛 is the minimum day-ahead price and 𝜌𝐷𝐴_𝑚𝑎𝑥 is

the maximum day-ahead price. The GENCO should not bid a

price less than the minimum day-ahead price (to avoid extreme

clearing prices) or bid more than the maximum day-ahead price.

The second constraint is that the total bid quantity should not

exceed the maximum available capacity (the capacity factor is

included):

4

_ max

1

BID i

i

G G

(10)

where 𝐺𝑖_𝑚𝑎𝑥 is the maximum amount of electricity that can be

produced by generation technology 𝑖. The model assumes the GENCO can purchase as much

electricity as it needs in the real-time market (e.g., if the wind or

solar power under generates). This is a reasonable assumption

for our case study because the GENCO only produces about 20%

of the region’s electricity. However, if the GENCO is a major

player in the market, a constraint could be added that limits how

much electricity it can purchase in the real-time market.

C. Model formulation with risk attitude-Model II

A GENCO may be risk averse, which means it may be

willing to sacrifice the possibility of higher profits in order to

avoid losing money. In order to integrate a GENCO’s risk

attitude, we propose Model II, which introduces a utility

function to describe the GENCO’s risk attitude over the

uncertain profits.

1) Utility function of GENCO

We assume an exponential utility function to represent the

GENCO’s preferences, as shown as equation (11).

/1 x RU x e (11)

where 𝑥 is the GENCO’s profit and 𝑅 represents its risk

tolerance (where both are in millions of dollars). When 𝑅 > 0,

the GENCO is risk averse, and a smaller value of 𝑅 indicates

more risk-aversion. If 𝑅 < 0, the GENCO is risk seeking and if

𝑅 → ∞, 𝑈(𝑥) becomes risk-neutral [22].

The GENCO’s risk tolerance has a direct relation to the

GENCO’s willingness to accept an uncertain deal between

earning $1 million and losing $1 million. The value of 𝑅 can be

calculated based on the probability 𝑞 for which the GENCO is

indifferent between no gain and no loss ($0) and a 𝑞 probability

of earning $1 million and 1 − 𝑞 probability of losing $1 million.

Figure 4 depicts that indifference relationship, and equation (12)

shows how to calculate 𝑅 given a value for 𝑞.

1

ln1

Rq

q

(12)

Fig.4. Assessing risk tolerance

2) Model formulation

Given a utility function, Model II calculates the utility for

each scenario as depicted in equations (2)-(8) and maximizes the

expected utility as given in equation (13). Since higher expected

profits may mean more risk, a risk-averse GENCO may choose

a bidding strategy that yields lower expected profits than a risk-

neutral GENCO.

7

1

max ,BID BID j j

j

E U F G P U F

(13)

C. Solving procedure

Monte-Carlo simulation provides an efficient alternative to

deal with the four uncertain parameters. The simulation

generates thousands of realizations of price and output

uncertainties, and an optimization algorithm determines the

optimal bidding strategy given these simulated values. The

algorithm works identically whether expected profit or expected

utility is maximized.

The solving process is detailed as follows:

Collect historical data for the day-ahead price, real-time price,

hourly wind output, and hourly solar output, and fit the

corresponding distributions;

Apply the Monte-Carlo simulation to generate price and

variable power output data;

Apply an optimization tool to solve the model and achieve the

optimal bidding strategy for a GENCO.

IV. NUMERICAL EXAMPLE

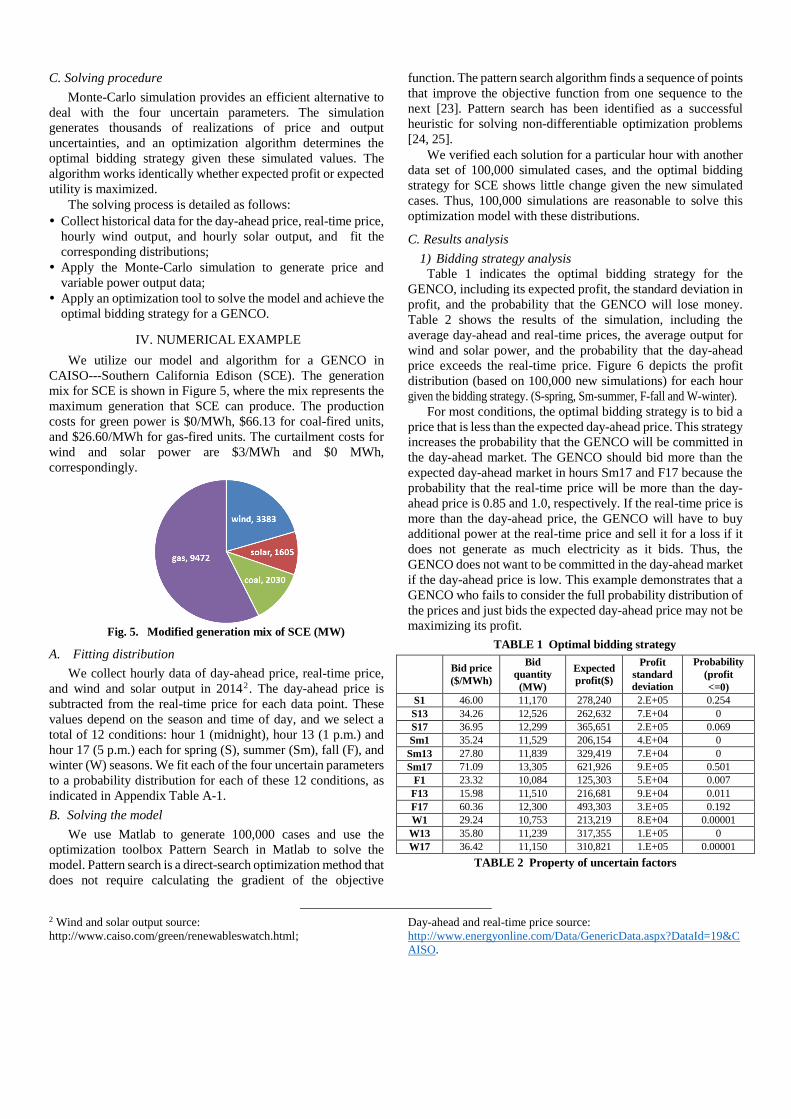

We utilize our model and algorithm for a GENCO in

CAISO---Southern California Edison (SCE). The generation

mix for SCE is shown in Figure 5, where the mix represents the

maximum generation that SCE can produce. The production

costs for green power is $0/MWh, $66.13 for coal-fired units,

and $26.60/MWh for gas-fired units. The curtailment costs for

wind and solar power are $3/MWh and $0 MWh,

correspondingly.

Fig. 5. Modified generation mix of SCE (MW)

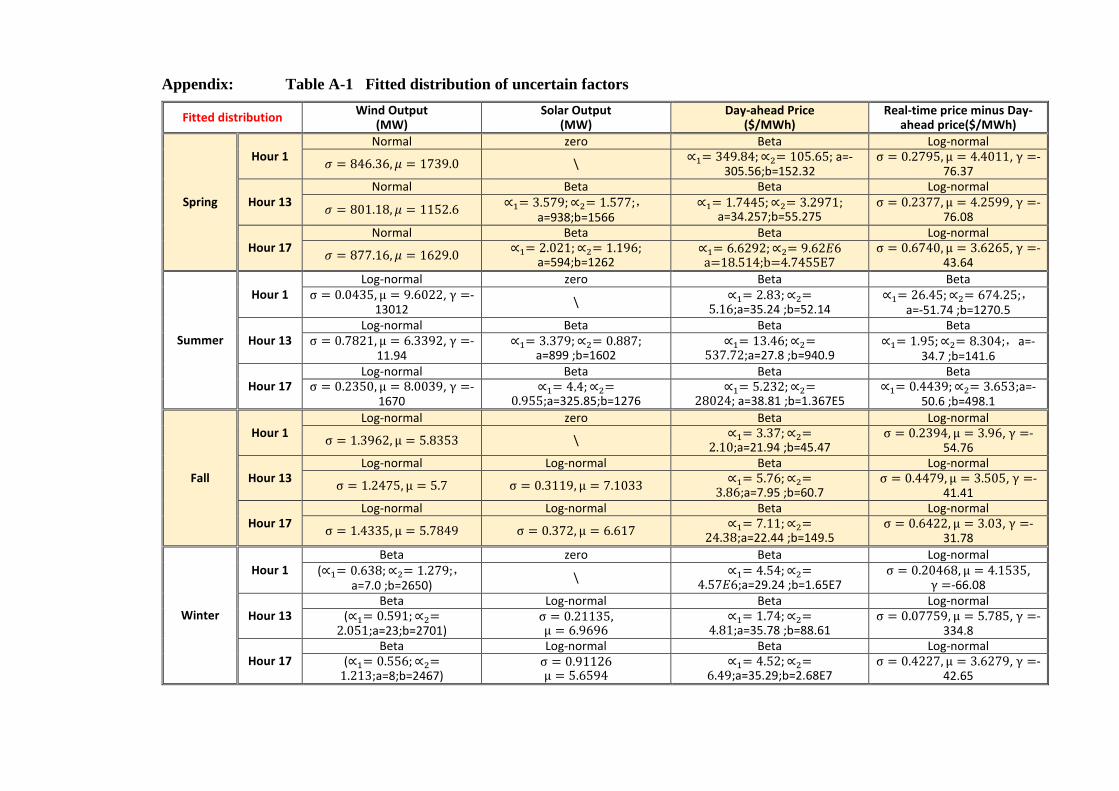

A. Fitting distribution

We collect hourly data of day-ahead price, real-time price,

and wind and solar output in 20142. The day-ahead price is

subtracted from the real-time price for each data point. These

values depend on the season and time of day, and we select a

total of 12 conditions: hour 1 (midnight), hour 13 (1 p.m.) and

hour 17 (5 p.m.) each for spring (S), summer (Sm), fall (F), and

winter (W) seasons. We fit each of the four uncertain parameters

to a probability distribution for each of these 12 conditions, as

indicated in Appendix Table A-1.

B. Solving the model

We use Matlab to generate 100,000 cases and use the

optimization toolbox Pattern Search in Matlab to solve the

model. Pattern search is a direct-search optimization method that

does not require calculating the gradient of the objective

2 Wind and solar output source:

http://www.caiso.com/green/renewableswatch.html;

function. The pattern search algorithm finds a sequence of points

that improve the objective function from one sequence to the

next [23]. Pattern search has been identified as a successful

heuristic for solving non-differentiable optimization problems

[24, 25].

We verified each solution for a particular hour with another

data set of 100,000 simulated cases, and the optimal bidding

strategy for SCE shows little change given the new simulated

cases. Thus, 100,000 simulations are reasonable to solve this

optimization model with these distributions.

C. Results analysis

1) Bidding strategy analysis

Table 1 indicates the optimal bidding strategy for the

GENCO, including its expected profit, the standard deviation in

profit, and the probability that the GENCO will lose money.

Table 2 shows the results of the simulation, including the

average day-ahead and real-time prices, the average output for

wind and solar power, and the probability that the day-ahead

price exceeds the real-time price. Figure 6 depicts the profit

distribution (based on 100,000 new simulations) for each hour

given the bidding strategy. (S-spring, Sm-summer, F-fall and W-winter).

For most conditions, the optimal bidding strategy is to bid a

price that is less than the expected day-ahead price. This strategy

increases the probability that the GENCO will be committed in

the day-ahead market. The GENCO should bid more than the

expected day-ahead market in hours Sm17 and F17 because the

probability that the real-time price will be more than the day-

ahead price is 0.85 and 1.0, respectively. If the real-time price is

more than the day-ahead price, the GENCO will have to buy

additional power at the real-time price and sell it for a loss if it

does not generate as much electricity as it bids. Thus, the

GENCO does not want to be committed in the day-ahead market

if the day-ahead price is low. This example demonstrates that a

GENCO who fails to consider the full probability distribution of

the prices and just bids the expected day-ahead price may not be

maximizing its profit.

TABLE 1 Optimal bidding strategy

Bid price

($/MWh)

Bid

quantity

(MW)

Expected

profit($)

Profit

standard

deviation

Probability

(profit

<=0)

S1 46.00 11,170 278,240 2.E+05 0.254

S13 34.26 12,526 262,632 7.E+04 0

S17 36.95 12,299 365,651 2.E+05 0.069

Sm1 35.24 11,529 206,154 4.E+04 0

Sm13 27.80 11,839 329,419 7.E+04 0

Sm17 71.09 13,305 621,926 9.E+05 0.501

F1 23.32 10,084 125,303 5.E+04 0.007

F13 15.98 11,510 216,681 9.E+04 0.011

F17 60.36 12,300 493,303 3.E+05 0.192

W1 29.24 10,753 213,219 8.E+04 0.00001

W13 35.80 11,239 317,355 1.E+05 0

W17 36.42 11,150 310,821 1.E+05 0.00001

TABLE 2 Property of uncertain factors

Day-ahead and real-time price source:

http://www.energyonline.com/Data/GenericData.aspx?DataId=19&C

AISO.

Day-

ahead

price

mean

($/MWh)

Real-

time

price

mean

($/MWh)

Actual

wind

output

mean

(MW)

Actual

solar

output

mean

(MW)

Probability

(day-ahead

price>real-time

price)

S1 46.13 55 1221 0 20.87%

S13 41.53 38 743 946 61.63%

S17 51.24 55 1,465 1,759 52.48%

Sm1 41.21 39 747 0 59.89%

Sm13 50.12 49 1,478 1,120 58.52%

Sm17 64.29 74 1,237 818 15.17%

F1 36.41 36 513 0 57.08%

F13 39.53 35 1,172 769 68.74%

F17 51.08 77 591 340 0.00%

W1 45.60 44 705 0 57.31%

W13 49.85 44 536 677 62.39%

W17 53.95 52 393 241 61.71%

Fig.6. Distribution of profits for different hours and seasons

Hour S1 is one of the few conditions when the GENCO’s

optimal bid price is close to the expected day-ahead price. The

expected day-ahead price is $46.13/MWh, and the bid price is

$46.00/MWh. At these prices, the GENCO should not generate

coal because its production cost ($66.13) is $20 more than the

mean day-ahead price. Since it is midnight, solar power is

nonexistent. The GENCO will produce natural gas because its

production cost ($22.60) is $44 less than the mean day-ahead

price. The expected output of wind power is 1221 MW. From

Table 1, the GENCO should bid to offer 11,170 MW, which is

approximately 500 MW more than the expected output from

wind (1121 MW) plus the output from natural gas (9472 MW).

The GENCO should bid a higher quantity of output in hours

13 and 17 than in hour 1 because it can depend on solar power.

The GENCO tends to generate higher profits in hour 17 because

the day-ahead and real-time prices are higher. This reflects more

demand for electricity during this hour.

Hour F1 yields the lowest expected profit, which results

from the unavailability of solar power, a low expected wind

output, and a relatively low day-ahead price.

The GENCO has the highest expected profit in hour Sm17

($621,926), and its profit could be as much a $7 or $8 million.

Both the day-ahead and real-time prices tend to be high, which

means that the GENCO should produce from its coal-fired units

and it can also sell its electricity at a high price. Both of these

conditions lead to a high expected profit.

Hour Sm17 also has the highest probability that the GENCO

will lose money during the hour, around 50%. The most it will

lose according to the simulation is $20,590, which is a lot less

than its expected profit. The potential for lost profit is due to: (i)

bidding a price greater than the day-ahead and real-time prices

so that wind power must be curtailed; (ii) bidding a quantity that

exceeds output and needing to buy additional power from the

real-time market; and (iii) producing coal to meet its bid

quantity when the day-ahead price is less than the cost of

producing coal-generated electricity.

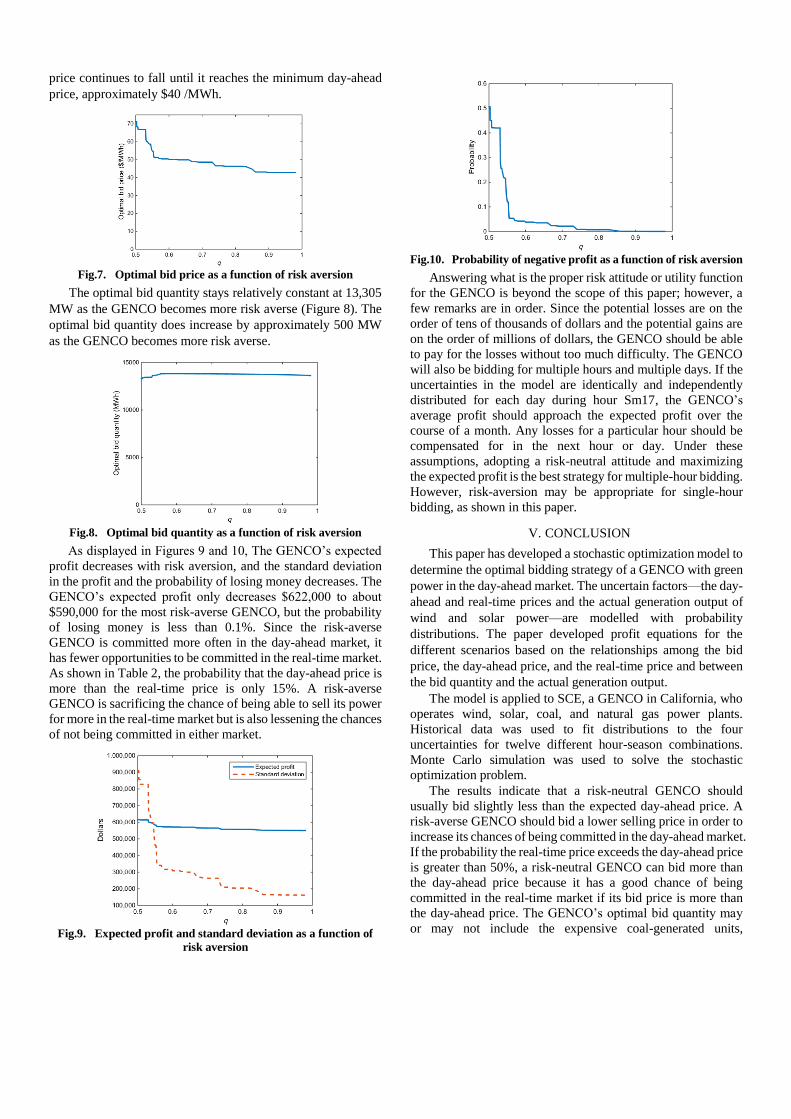

2) Risk-averse GENCO

As shown in Table 1, the possibility exists that the GENCO

could lose money, which suggests the GENCO may want to be

risk averse and seek to minimize its losses. Hour Sm17 has the

most volatile distribution for profit, and the chance that GENCO

may lose money is 50%. If the GENCO is risk averse, it may

optimal for a different bidding strategy in order to avoid

negative profits.

We apply Model II with risk attitude to hour Sm17 for

several values of 𝑞 as explained in Section 3.D. Larger values

of 𝑞 indicate more risk aversion. As depicted in Figure 7, the

optimal bid price decreases as the GENCO becomes more risk

averse. By decreasing its bid price, the GENCO is increasing

the chances that it will be committed in the day-ahead market.

This suggests that the largest profit losses are due to curtailing

wind power or buying additional power from real-time market.

Increasing the probability of being committed in the day-ahead

market also increases the probability of needing to buy

additional power from the real-time market. The optimal bid

price continues to fall until it reaches the minimum day-ahead

price, approximately $40 /MWh.

Fig.7. Optimal bid price as a function of risk aversion

The optimal bid quantity stays relatively constant at 13,305

MW as the GENCO becomes more risk averse (Figure 8). The

optimal bid quantity does increase by approximately 500 MW

as the GENCO becomes more risk averse.

Fig.8. Optimal bid quantity as a function of risk aversion

As displayed in Figures 9 and 10, The GENCO’s expected

profit decreases with risk aversion, and the standard deviation

in the profit and the probability of losing money decreases. The

GENCO’s expected profit only decreases $622,000 to about

$590,000 for the most risk-averse GENCO, but the probability

of losing money is less than 0.1%. Since the risk-averse

GENCO is committed more often in the day-ahead market, it

has fewer opportunities to be committed in the real-time market.

As shown in Table 2, the probability that the day-ahead price is

more than the real-time price is only 15%. A risk-averse

GENCO is sacrificing the chance of being able to sell its power

for more in the real-time market but is also lessening the chances

of not being committed in either market.

Fig.9. Expected profit and standard deviation as a function of

risk aversion

Fig.10. Probability of negative profit as a function of risk aversion

Answering what is the proper risk attitude or utility function

for the GENCO is beyond the scope of this paper; however, a

few remarks are in order. Since the potential losses are on the

order of tens of thousands of dollars and the potential gains are

on the order of millions of dollars, the GENCO should be able

to pay for the losses without too much difficulty. The GENCO

will also be bidding for multiple hours and multiple days. If the

uncertainties in the model are identically and independently

distributed for each day during hour Sm17, the GENCO’s

average profit should approach the expected profit over the

course of a month. Any losses for a particular hour should be

compensated for in the next hour or day. Under these

assumptions, adopting a risk-neutral attitude and maximizing

the expected profit is the best strategy for multiple-hour bidding.

However, risk-aversion may be appropriate for single-hour

bidding, as shown in this paper.

V. CONCLUSION

This paper has developed a stochastic optimization model to

determine the optimal bidding strategy of a GENCO with green

power in the day-ahead market. The uncertain factors—the day-

ahead and real-time prices and the actual generation output of

wind and solar power—are modelled with probability

distributions. The paper developed profit equations for the

different scenarios based on the relationships among the bid

price, the day-ahead price, and the real-time price and between

the bid quantity and the actual generation output.

The model is applied to SCE, a GENCO in California, who

operates wind, solar, coal, and natural gas power plants.

Historical data was used to fit distributions to the four

uncertainties for twelve different hour-season combinations.

Monte Carlo simulation was used to solve the stochastic

optimization problem.

The results indicate that a risk-neutral GENCO should

usually bid slightly less than the expected day-ahead price. A

risk-averse GENCO should bid a lower selling price in order to

increase its chances of being committed in the day-ahead market.

If the probability the real-time price exceeds the day-ahead price

is greater than 50%, a risk-neutral GENCO can bid more than

the day-ahead price because it has a good chance of being

committed in the real-time market if its bid price is more than

the day-ahead price. The GENCO’s optimal bid quantity may

or may not include the expensive coal-generated units,

depending on how the distribution on the day-ahead price

compares with the cost of generating electricity from coal.

Future work can refine the model to account for the

possibility that the GENCO may not be able to purchase

additional power on the real-time market if actual generation is

less than the bid quantity. A GENCO’s bid may also influence

the market clearing price, which would require the probability

distributions to be dependent upon the GENCO’s strategy. The

effect of including multiple GENCOs could also be included in

the model.

To our knowledge, this paper represents the first model that

incorporates two periods (day-ahead and real-time markets)

with multiple generating technologies including green power.

Modeling uncertainties with probability distributions based on

historical data allow us to develop realistic results that a

GENCO can use to make better decisions in the electricity

markets.

REFERENCES

[1] Li, G., Shi, J., & Qu, X. (2011). Modeling methods for GENCO

bidding strategy optimization in the liberalized electricity spot

market–A state-of-the-art review. Energy, 36(8), 4686-4700.

[2] Energy market introduction-introduction to wholesale electricity

markets (WEM101). [online]. http://www.iso-ne.com/static-

assets/documents/2015/05/05_wem101_april_2015_energy_

market _intro.pdf.

[3] Cormack J, Hollis A, Zareipour H, Rosehart W. The large-scale

integration of wind generation: impacts on price, reliability and

dispatchable conventional uppliers. Energy Policy

2010;38(7):3837e46.

[4] David, A. K., & Wen, F. (2000). Strategic bidding in competitive

electricity markets: a literature survey. In Power Engineering

Society Summer Meeting, 2000. IEEE (Vol. 4, pp. 2168-2173).

IEEE

[5] Borghetti, A., Frangioni, A., Lacalandra, F., Nucci, C. A., &

Pelacchi, P. (2003, June). Using of a cost-based unit commitment

algorithm to assist bidding strategy decisions. In Power Tech

Conference Proceedings, 2003 IEEE Bologna (Vol. 2, pp. 8-pp).

IEEE.

[6] Valenzuela, J., & Mazumdar, M. (2003). Commitment of electric

power generators under stochastic market prices. Operations

Research, 51(6), 880-893.

[7] Foley, A. M., Gallachóir, B. Ó., Hur, J., Baldick, R., & McKeogh,

E. J. (2010). A strategic review of electricity systems models.

Energy, 35(12), 4522-4530.

[8] Borenstein, S., & Bushnell, J. (1999). An empirical analysis of

the potential for market power in California’s electricity industry.

The Journal of Industrial Economics, 47(3), 285-323.

[9] Federico G, Rahman D. Bidding in an electricity pay-as-bid

auction. Journal of Regulatory Economics 2003;24(2):175-211.

[10] Klemperer, P. D., & Meyer, M. A. (1989). Supply function

equilibria in oligopoly under uncertainty. Econometrica: Journal

of the Econometric Society, 1243-1277.

[11] Rahimiyan, M., & Mashhadi, H. R. (2008). Supplier's optimal

bidding strategy in electricity pay-as-bid auction: Comparison of

the Q-learning and a model-based approach. Electric Power

Systems Research, 78(1), 165-175.

[12] Tesfatsion, L. (2006). Agent-based computational economics: A

constructive approach to economic theory. Handbook of

computational economics, 2, 831-880.

[13] Yamin, H. Y., & Shahidehpour, S. M. (2004). Self-scheduling

and energy bidding in competitive electricity markets. Electric

Power Systems Research, 71(3), 203-209.

[14] Azevedo, E. M., & Correia, P. B. (2006). Bidding strategies in

Brazilian electricity auctions. International Journal of Electrical

Power & Energy Systems, 28(5), 309-314.

[15] Gao, F., Sheble, G. B., Hedman, K. W., & Yu, C. N. (2015).

Optimal bidding strategy for GENCOs based on parametric

linear programming considering incomplete information.

International Journal of Electrical Power & Energy Systems, 66,

272-279.

[16] Catalao, J. P. S., Pousinho, H. M. I., & Contreras, J. (2012).

Optimal hydro scheduling and offering strategies considering

price uncertainty and risk management. Energy, 37(1), 237-244.

[17] Sharma, K. C., Bhakar, R., & Tiwari, H. P. (2014). Strategic

bidding for wind power producers in electricity markets. Energy

Conversion and Management, 86, 259-267.

[18] Angarita, J. L., Usaola, J., & Martínez-Crespo, J. (2009).

Combined hydro-wind generation bids in a pool-based electricity

market. Electric Power Systems Research, 79(7), 1038-1046.

[19] Daneshi, H., & Daneshi, A. (2008, April). Price forecasting in

deregulated electricity markets-a bibliographical survey. In

Electric Utility Deregulation and Restructuring and Power

Technologies, 2008. DRPT 2008. Third International Conference

on (pp. 657-661). IEEE.

[20] Cadogan, J., Milligan, M., Wan, Y., & Kirby, B. (2001). Short-

Term Output Variations in Wind Farms--Implications for

Ancillary Services in the United States: Preprint (No. NREL/CP-

500-29155). National Renewable Energy Lab., Golden, CO (US).

[21] Zhang, J., Hodge, B. M., Florita, A., Lu, S., Hamann, H. F., &

Banunarayanan, V. (2013). Metrics for Evaluating the Accuracy

of Solar Power Forecasting.

[22] Clemen, R. T., & Reilly, T. (2004). Making Hard Decisions with

Decision Tools Suite. Update edition. Mason, OH: Cengage

Learning.

[23]How Pattern Search Works. Mathworks. [online]

http://www.mathworks.com/help/gads/how-pattern-search-

polling-works.html.

[24] Lewis, R. M., & Torczon, V. (1999). Pattern search algorithms

for bound constrained minimization. SIAM Journal on

Optimization, 9(4), 1082-1099.

[25] Lewis, R. M., & Torczon, V. (2000). Pattern search methods for

linearly constrained minimization. SIAM Journal on

Optimization, 10(3), 917-941.

Xian Guo (S’12) received the B.S. degree from

Shanghai University of Electric Power in 2010 and M.S

degree from Shanghai Jiao Tong University in 2013,

China. Currently she is pursuing the PhD. Degree at

Iowa State University, Ames, IA, USA. She was a summer intern in Argonne National Lab

in 2014. Her research interests are power system

optimization, electricity market and risk analysis.

Cameron A. MacKenzie is currently an assistant

professor in the Department of Industrial and Manufacturing Systems Engineering at Iowa State

University, Ames. He received the B.Sc. degree in

mathematics and the B.A. degree in history from Indiana University–Purdue University at Fort Wayne,

Fort Wayne, the M.Sc. degree in management science

and engineering from Stanford University, Stanford, CA, the M.A. degree in international affairs from The

George Washington University, Washington, DC, and the Ph.D. degree in

industrial engineering from the University of Oklahoma, Norman. His research focuses on decision and risk analysis, with a particular emphasis on

modeling the business and economic impacts caused by disruptions and

building resilience within organizations.

Appendix: Table A-1 Fitted distribution of uncertain factors

Fitted distribution Wind Output

(MW) Solar Output

(MW) Day-ahead Price

($/MWh) Real-time price minus Day-

ahead price($/MWh)

Spring

Hour 1 Normal zero Beta Log-normal

𝜎 = 846.36, 𝜇 = 1739.0 \ ∝1= 349.84; ∝2= 105.65; a=-

305.56;b=152.32 σ = 0.2795, μ = 4.4011, γ =-

76.37

Hour 13 Normal Beta Beta Log-normal

𝜎 = 801.18, 𝜇 = 1152.6 ∝1= 3.579; ∝2= 1.577;,

a=938;b=1566 ∝1= 1.7445; ∝2= 3.2971;

a=34.257;b=55.275 σ = 0.2377, μ = 4.2599, γ =-

76.08

Hour 17 Normal Beta Beta Log-normal

𝜎 = 877.16, 𝜇 = 1629.0 ∝1= 2.021; ∝2= 1.196;

a=594;b=1262 ∝1= 6.6292; ∝2= 9.62𝐸6

a=18.514;b=4.7455E7 σ = 0.6740, μ = 3.6265, γ =-

43.64

Summer

Hour 1 Log-normal zero Beta Beta

σ = 0.0435, μ = 9.6022, γ =-13012

\ ∝1= 2.83; ∝2=

5.16;a=35.24 ;b=52.14 ∝1= 26.45; ∝2= 674.25;,

a=-51.74 ;b=1270.5

Hour 13 Log-normal Beta Beta Beta

σ = 0.7821, μ = 6.3392, γ =-11.94

∝1= 3.379; ∝2= 0.887; a=899 ;b=1602

∝1= 13.46; ∝2=537.72;a=27.8 ;b=940.9

∝1= 1.95; ∝2= 8.304;,a=-34.7 ;b=141.6

Hour 17 Log-normal Beta Beta Beta

σ = 0.2350, μ = 8.0039, γ =-1670

∝1= 4.4; ∝2=0.955;a=325.85;b=1276

∝1= 5.232; ∝2=28024; a=38.81 ;b=1.367E5

∝1= 0.4439; ∝2= 3.653;a=-50.6 ;b=498.1

Fall

Hour 1 Log-normal zero Beta Log-normal

σ = 1.3962, μ = 5.8353 \ ∝1= 3.37; ∝2=

2.10;a=21.94 ;b=45.47 σ = 0.2394, μ = 3.96, γ =-

54.76

Hour 13 Log-normal Log-normal Beta Log-normal

σ = 1.2475, μ = 5.7 σ = 0.3119, μ = 7.1033 ∝1= 5.76; ∝2=

3.86;a=7.95 ;b=60.7 σ = 0.4479, μ = 3.505, γ =-

41.41

Hour 17 Log-normal Log-normal Beta Log-normal

σ = 1.4335, μ = 5.7849 σ = 0.372, μ = 6.617 ∝1= 7.11; ∝2=

24.38;a=22.44 ;b=149.5 σ = 0.6422, μ = 3.03, γ =-

31.78

Winter

Hour 1 Beta zero Beta Log-normal

(∝1= 0.638; ∝2= 1.279;,a=7.0 ;b=2650)

\ ∝1= 4.54; ∝2=

4.57𝐸6;a=29.24 ;b=1.65E7 σ = 0.20468, μ = 4.1535,

γ =-66.08

Hour 13 Beta Log-normal Beta Log-normal

(∝1= 0.591; ∝2=2.051;a=23;b=2701)

σ = 0.21135, μ = 6.9696

∝1= 1.74; ∝2=4.81;a=35.78 ;b=88.61

σ = 0.07759, μ = 5.785, γ =-334.8

Hour 17 Beta Log-normal Beta Log-normal

(∝1= 0.556; ∝2=1.213;a=8;b=2467)

σ = 0.91126 μ = 5.6594

∝1= 4.52; ∝2=6.49;a=35.29;b=2.68E7

σ = 0.4227, μ = 3.6279, γ =-42.65