Operating Guide - SAP Help Portal

123

1 SAP® Financial Consolidation 10.1, starter kit for IFRS, SP9 Operating guide

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Operating Guide - SAP Help Portal

1

SAP® Financial Consolidation 10.1, starter kit for IFRS, SP9 Operating guide

3

Copyright © 2019 SAP AG. All rights reserved. SAP, R/3, SAP NetWeaver, Duet, PartnerEdge, ByDesign, SAP Business ByDesign, and other SAP products and services mentioned herein as well as their respective logos are trademarks or registered trademarks of SAP AG in Germany and other countries. Business Objects and the Business Objects logo, BusinessObjects, Crystal Reports, Crystal Decisions, Web Intelligence, Xcelsius, and other Business Objects products and services mentioned herein as well as their respective logos are trademarks or registered trademarks of Business Objects S.A. in the United States and in other countries. Business Objects is an SAP company. All other product and service names mentioned are the trademarks of their respective companies. Data contained in this document serves informational purposes only. National product specifications may vary. These materials are subject to change without notice. These materials are provided by SAP AG and its affiliated companies ("SAP Group") for informational purposes only, without representation or warranty of any kind, and SAP Group shall not be liable for errors or omissions with respect to the materials. The only warranties for SAP Group products and services are those that are set forth in the express warranty statements accompanying such products and services, if any. Nothing herein should be construed as constituting an additional warranty.

2019-10-15

Legal No part of this starter kit may be reproduced or transmitted in any form or for any purpose Disclaimer without the express permission of SAP AG. The information contained herein may be

changed without prior notice. Some software products marketed by SAP AG and its distributors contain proprietary software components of other software vendors. The information in this starter kit is proprietary to SAP. No part of this starter kit’s content may be reproduced, copied, or transmitted in any form or for any purpose without the express prior permission of SAP AG. This starter kit is not subject to your license agreement or any other agreement with SAP. This starter kit contains only intended content, and pre-customized elements of the SAP® product and is not intended to be binding upon SAP to any particular course of business, product strategy, and/or development. Please note that this starter kit is subject to change and may be changed by SAP at any time without notice. SAP assumes no responsibility for errors or omissions in this starter kit. SAP does not warrant the accuracy or completeness of the information, text, pre-configured elements, or other items contained within this starter kit. SAP DOES NOT PROVIDE LEGAL, FINANCIAL OR ACCOUNTING ADVISE OR SERVICES. SAP WILL NOT BE RESPONSIBLE FOR ANY NONCOMPLIANCE OR ADVERSE RESULTS AS A RESULT OF YOUR USE OR RELIANCE ON THE STARTER KIT. THIS STARTER KIT IS PROVIDED WITHOUT A WARRANTY OF ANY KIND, EITHER EXPRESS OR IMPLIED, INCLUDING BUT NOT LIMITED TO THE IMPLIED WARRANTIES OF MERCHANTABILITY, FITNESS FOR A PARTICULAR PURPOSE, OR NON-INFRINGEMENT. SAP SHALL HAVE NO LIABILITY FOR DAMAGES OF ANY KIND INCLUDING WITHOUT LIMITATION DIRECT, SPECIAL, INDIRECT, OR CONSEQUENTIAL DAMAGES THAT MAY RESULT FROM THE USE OF THIS STARTER KIT. THIS LIMITATION SHALL NOT APPLY IN CASES OF INTENT OR GROSS NEGLIGENCE. The statutory liability for personal injury and defective products (under German law) is not affected. SAP has no control over the use of pre-customized elements contained in this starter kit and does not endorse your use of the starter kit nor provide any warranty whatsoever relating to third-party use of the starter kit.

5

Contents Chapter 1 Introduction ...................................................................................................................... 10

Presentation ....................................................................................................................... 10

Organization............................................................................................................... 10

Other Documentation ................................................................................................. 10

Database Structure ............................................................................................................ 10

Flow-Based Consolidation ................................................................................................. 11

List of Accounting Flows ............................................................................................ 12

Entering Data in Flows ............................................................................................... 14

Balancing Flows ......................................................................................................... 15

Chapter 2 Initializing the Consolidation .......................................................................................... 16

Section Objectives ..................................................................................................... 16

Key Points .................................................................................................................. 16

Suggested Approach ................................................................................................. 16

Documents to be kept ................................................................................................ 16

Updating Reporting Units ................................................................................................... 16

Key Concepts............................................................................................................. 16

Structure of the Reporting Unit Table ......................................................................... 17

Procedure .................................................................................................................. 17

Breakdown by Division ............................................................................................... 18

Creating Packages ............................................................................................................. 18

Creating a Reporting ID ............................................................................................. 19

Creating Reporting Sets ............................................................................................. 20

Sending Opening Packages ...................................................................................... 20

Entering and Updating Conversion Rates .......................................................................... 20

Conversion Rate Tables ............................................................................................ 20

Conversion Rate Types ............................................................................................. 21

Entering Conversion Rates ........................................................................................ 21

Chapter 3 Collecting Data ................................................................................................................. 23

Section Objectives ..................................................................................................... 23

Key Points .................................................................................................................. 23

Suggested Approach ................................................................................................. 23

Entering Data at Data Entry Site ........................................................................................ 23

Receiving Packages .................................................................................................. 23

Loading Data into Packages ...................................................................................... 24

Publishing Packages .................................................................................................. 24

Receiving, Checking and Integrating Packages ................................................................. 24

Contents

6

Receiving Packages .................................................................................................. 24

Running Package Controls ........................................................................................ 24

Integrating Packages ................................................................................................. 24

Sending a Given Package Several Times .................................................................. 24

Chapter 4 Consolidation Scope ....................................................................................................... 26

Section Objectives ..................................................................................................... 26

Key Points .................................................................................................................. 26

Suggested Approach ................................................................................................. 26

Documents to be kept ................................................................................................ 26

Concepts and Definitions ................................................................................................... 26

Definitions .................................................................................................................. 26

Defining Scopes ......................................................................................................... 28

Portfolios ............................................................................................................................ 29

Creating Portfolios and Portfolio Occurrences ........................................................... 29

Copying a Portfolio Occurrence ................................................................................. 30

Controls and Corrections ........................................................................................... 30

Printing a Portfolio Occurrence .................................................................................. 31

Scopes ............................................................................................................................... 32

Statutory and Reporting Scopes ................................................................................ 32

Creating a Scope ....................................................................................................... 32

Making Changes to a Statutory Scope Manually ....................................................... 32

Specific Cases ........................................................................................................... 33

Hierarchical Scope ..................................................................................................... 33

Printing a Scope......................................................................................................... 33

Chapter 5 Processing the Data: Key concepts ............................................................................... 34

Section Objectives ..................................................................................................... 34

Key Points .................................................................................................................. 34

Suggested Approach ................................................................................................. 34

Introduction ........................................................................................................................ 35

Manual Journal Entries ...................................................................................................... 37

Procedure .................................................................................................................. 37

Defining a Journal Entry Header ................................................................................ 37

Audit IDs .................................................................................................................... 38

Converting Data ................................................................................................................. 40

Main Principles........................................................................................................... 40

YTD and Periodic Conversion .................................................................................... 41

Consolidation Processing ................................................................................................... 42

Defining a Consolidation ............................................................................................ 42

Running a Consolidation Processing ......................................................................... 43

Contents

7

Retrieving and Checking Data ........................................................................................... 43

Data Retrieval Reports ............................................................................................... 43

Checking Consolidated Data ..................................................................................... 43

Chapter 6 Making adjustments to individual accounts .................................................................. 47

Section Objectives ..................................................................................................... 47

Key Points .................................................................................................................. 47

Correcting Package Data ................................................................................................... 47

Correcting Differences for Net Income N-1 ................................................................ 47

Recommended Solution: Package Processing .......................................................... 47

Other Package Corrections ........................................................................................ 51

Making Adjustments to Packages ...................................................................................... 52

Making Fair Value Adjustments ................................................................................. 52

Other Adjustments ..................................................................................................... 54

Making IFRS Adjustments .................................................................................................. 54

Chapter 7 Intercompany Transactions ............................................................................................ 57

Section Objectives ..................................................................................................... 57

Key Points .................................................................................................................. 57

Suggested Approach ................................................................................................. 57

Checking Intercompany Declarations................................................................................. 57

Running Intercompany Reconciliations ...................................................................... 57

Correcting Differences ............................................................................................... 60

Elimination of Internal Transactions ................................................................................... 62

Elimination of Reciprocal Transactions ...................................................................... 62

Dividends ................................................................................................................... 65

Provisions .................................................................................................................. 68

Gains or Losses on Internal Transfer of Assets ......................................................... 71

Chapter 8 Deferred Taxation............................................................................................................. 77

Section Objectives ..................................................................................................... 77

Key Points .................................................................................................................. 77

Overview ............................................................................................................................ 77

Identifying the Bases of Deferred Tax ........................................................................ 77

Booking Deferred Tax ................................................................................................ 77

Accounting for Deferred Tax ...................................................................................... 78

Chapter 9 Consolidation Entries ...................................................................................................... 79

Section objectives ...................................................................................................... 79

Calculation of Non-controlling Interests.............................................................................. 80

Principles ................................................................................................................... 80

Contents

8

Elimination of Investments ................................................................................................. 83

Principles ................................................................................................................... 83

Converting Consolidated Shareholders' Equity and Investments in Subsidiaries............... 88

Principles ................................................................................................................... 88

Manual Journal Entries .............................................................................................. 88

Analysing the changes in the foreign currency exchange reserve for the Group ....... 92

Optional Conversion Process on Investment and Capital/Share Premium ................ 93

Equity Method .................................................................................................................... 95

Principles ................................................................................................................... 95

Booking of Goodwill ........................................................................................................... 99

General principle ........................................................................................................ 99

Specific cases ...........................................................................................................100

Checking Goodwill of incoming companies ...............................................................101

Chapter 10 Scope Changes ...............................................................................................................104

Section Objectives ....................................................................................................104

Key Points .................................................................................................................104

Overview of the Scope Changes .......................................................................................104

Typology of Scope Changes .....................................................................................104

Scope Changes: Using the Right Flow .....................................................................105

Events Covered in this Documentation .....................................................................106

Incoming Entities ...............................................................................................................106

Preparing the Reporting Cycle ..................................................................................106

Automatic Processing ...............................................................................................107

Manual Processing ...................................................................................................108

Outgoing Entities ...............................................................................................................109

Preparing the Reporting Cycle ..................................................................................109

Automatic Processing ...............................................................................................111

Manual Processing ...................................................................................................112

Chapter 11 Completing the Consolidation .......................................................................................113

Section Objectives ....................................................................................................113

Key Points .................................................................................................................113

Checking the Statement of Comprehensive Income .........................................................113

Overview of the Statement of Comprehensive Income Reports ...............................113

Manual Journal Entries .............................................................................................114

Path between the Statement of Comprehensive Income and the Statement of Changes in Equity .....................................................................................................115

Checking the Statement of Changes in Equity ..................................................................115

Checks Specific to Certain Accounts ........................................................................115

Checking Variation Flows .........................................................................................115

Contents

9

Performing Detailed Checks for Reporting Units.......................................................117

Checking the Statement of Cash Flows ............................................................................117

Overview of the Statement of Cash Flows Reports...................................................117

Analyzing Differences ...............................................................................................118

Manual Journal Entries .............................................................................................121

Checking IFRS adoption ...................................................................................................123

Introduction

10

Introduction

Presentation

Organization

The operating guide is organized according to the steps performed in a consolidation processing.

◼ Preparing the reporting cycle: This step describes how the consolidation is initialized (see Initializing the Consolidation), how package data is collected (see Collecting Data) and how the Group structure is defined (see Consolidation Scope).

◼ Processing the data: This step describes the main concepts (see Processing the Data: Key concepts), how intercompany transactions are eliminated (see Intercompany Transactions), how deferred taxes are computed (see Deferred Taxation) and how technical consolidated journal entries are posted (see Consolidation Entries).

◼ Completing the consolidation: in this step the entire consolidation is validated on the basis of the Statement of Changes in Equity and the Cash Flow Statement (see Completing the Consolidation).

Each section presents:

◼ Key points

◼ A detailed approach with references to other sections for more information.

Other Documentation

The following documentation is available:

◼ Product Documentation: This document, available in the application, describes functions and procedures.

◼ Configuration Design Documentation: This document offers in-depth knowledge about customizing the database structure.

You should refer to this documentation to get detailed information about:

◼ using the application for operations and customization purposes.

◼ making changes to the setup of the Starter kit.

Database Structure

All of the information in the database is identified by a set of elements required for storing, processing and retrieving data. These elements are called dimensions.

The following dimensions are used in the configuration:

◼ Required dimensions

All of the data stored in the database must be identified by these dimensions.

◼ CATEGORY The configuration provides one category scenario, called A-Actual, to be used for statutory consolidations.

◼ DATA ENTRY PERIOD: The date on which the information is entered for all of the defined periods using the following format: YYYY.MM

◼ PERIOD: The same value as the data entry period in a statutory consolidation.

◼ REPORTING UNIT: The company or Business Unit whose data is being entered.

Introduction

11

◼ CURRENCY: The currency in which the data is stored.

◼ ACCOUNT: The balance sheet and income statement accounts as well as technical accounts for consolidation purposes, for example suspense accounts.

◼ FLOW (see Flow-Based Consolidation).

◼ AUDIT ID: The ID that identifies the origin of the data for packages, local adjustments, manual journal entries, and automatic journal entries.

◼ Analysis dimensions

◼ PARTNER: The reporting unit involved in an intercompany transaction.

◼ MANAGEMENT UNIT: In-built dimension not used in the starter kit

◼ PARTNER MANAGEMENT UNIT: In-built dimension not used in the starter kit.

◼ SHARE: The held company in the investment portfolios.

◼ COUNTRY: The breakdown of external sales by geographical area.

◼ ANALYSIS Used to build the Statements of Cash Flows, Changes in equity, Comprehensive income and thr Country-by-Country Reporting (BEPS). Also used for data entry on a daily basis for flows F20/F40 on Investment, F40 on Issued capital/Share premium and F06 on Dividends.

Note: These dimensions do not always contain values.

◼ Dimensions specific to consolidation processing

◼ SCOPE, VARIANT and CONSOLIDATION CURRENCY: These dimensions are used to identify a consolidation definition.

◼ Technical dimensions

◼ JOURNAL ENTRY NUMBER

◼ LEDGER

◼ ORIGINAL REPORTING UNIT

◼ TECHNICAL ORIGIN

◼ GEOGRAPHICAL ORIGIN

Note: Data for these dimensions is automatically loaded by the application.

Example

Reporting unit RU1 has € 5 000 in cash at the end of the 2009 fiscal year.

This information, which originates from the data entry package, is stored as follows in the database:

Category Data Entry

Period Period

Reporting

unit Currency Account Flow Audit ID Amount

A 2009.12 2009.12 RU1 EUR A2610-Cash

on hand

F99-

Closing

PACK01-

Package Data 5 000

For more information on the database structure, see the functional design documentation.

Flow-Based Consolidation

The flow dimension is used to identify and analyze the changes between the opening and closing balances. The accuracy of automatic processing depends on whether data has been correctly entered in flows. Flows differ according to the account being analyzed.

Introduction

12

List of Accounting Flows

Types of Flow

Opening and closing balances correspond respectively to flows F00 and F99. Variation flows can be organized into the following categories:

Flows for Current Transactions

Income statement

Transactions for the income statement are posted in flow Y99.

Debt management

Movements in debt management items, made up of current assets and liabilities (excluding provisions) and the cash flow are posted in variation flow F15.

Example

You want to enter an amount of 100 € excluding VAT from the sale of goods.

In company accounts:

Account Debit Credit

Sale of goods 100

Accounts receivables 100

In the application:

Account Flow Debit Credit

P1100 Revenues Y99 100

A2210 Trade receivables, Gross F15 100

Depreciation, impairment and provisions

The balance sheet movements due to depreciation, impairment and provisions are posted using the following flows:

◼ F25 - Increase in depreciation

◼ F35 - Decrease in depreciation

Example

You want to enter a gross amount of 100 as allowances for provisions on shares.

In the accounting system:

Account Debit Credit

Depreciation on investment 100

Allowance/depreciation of investments 100

In the application:

Account Flow Debit Credit

A1812 Investments in subsidiaries, JV and associates, Impair.

F25 100

P2210 Allowances for provisions on shares Y99 100

Equity

In equity accounts, shareholders' equity is processed separately from the other items.

Introduction

13

Movements in shareholders' equity usually originate from:

◼ The distribution of dividends (posted in flow F06)

◼ The income of the current fiscal year (recorded in F10)

◼ The increase or decrease in capital (posted in F40)

◼ Movements that come under “Other comprehensive income”, for example, flow F55 on fair value reserve

◼ Other specific operations, like acquisition (flow F20) and disposal (flow F30) of treasury shares

Note: In the Equity section of the Balance sheet, there is no specific account for the Net profit of the period. This net profit must be included in account E1610-Retained earnings.

Non-current assets and liabilities

For the non-current assets and liabilities:

◼ Increases are posted in F20.

◼ Decreases are posted in F30.

◼ Investments in subsidiaries and capital subscription (increase, decrease or creation of capital) are posted in F40.

Example

You invest in the creation of Company F by subscribing 1 000 to its capital. During the year, you buy an associate’s share for 250. This investment is financed by a bank loan.

In the accounting system:

Account Debit Credit

Investments in subsidiaries 1 250

Bank loans 1 250

In the application:

Account Flow Debit Credit

A1810 Investments in subsidiaries, JV and associates F40 1 000

A1810 Investments in subsidiaries, JV and associates F20 250

L1510 Borrowings, Non current F20 1 250

Transfers between items

Transfers between balance sheet accounts are recorded in F50-Reclassification.

Adjustment to IFRS standards

Variations in fair value for financial assets and liabilities are posted in F55-Fair value.

Flows for Specific Transactions

The flows used for specific transactions are as follows:

◼ Changes in accounting policies: The impact on balance sheet items is posted in F09-Change in accounting policies, which must balance (Total Assets = Total Liabilities).

◼ Contribution to capital and merger transactions: The impact on balance sheet items, including issue of shares for capital contribution, is posted in F70-Internal mergers. Any impact on the net income for the period is recorded in account P1620-Merger result.

Introduction

14

Flows Specific to Consolidated Accounts

The flows specific to consolidated accounts are generated automatically by the application and are as follows:

◼ Effect of foreign exchange rate variations: F80

◼ Effect of variations in scope:

F01: Incoming units

F02: Change in consolidation method (old). This flow is used as the reverse opening flow for reporting units that change their consolidation method, for example from the equity method to a full or proportionate consolidation or vice versa.

F03: Change in consolidation method (new). This flow is used as the incoming flow of the new consolidation method.

F04: Change in consolidation rate. This flow records the impact of change in consolidation rate for subsidiaries consolidated using the proportionate or equity method.

F92: Change in interest rate. This flow corresponds to the impact of change in Group financial interest on the equity.

F98: Outgoing units

Entering Data in Flows

In Data Entry Packages

In the consolidation package, you must enter the closing balance in F99. Flow F15-Net variation is then automatically calculated by subtracting the sum of the opening flow and other movement flows from the closing flow (F99).

Flow F15 is used as a control flow that should be analyzed using the relevant variation flows, for all the balance sheet items except:

◼ Cash accounts

◼ Current assets/liabilities accounts, excluding depreciation, impairment and provisions, for which no detailed analysis by flow, like increase/decrease, is required to build the Statement of cash flows.

Example

Company A has assets of up to 100 at closing, as compared to 50 at opening. After entering or importing data, the assets variation table should be as follows:

ACCOUNTS CODE F00 F99 F20

Increase F30

Decrease F50

Reclass. Other

Control (F15)

Assets A11xx 50 100 50

Movements during the fiscal year correspond to an investment of 80 and a sale of 30. Data should therefore be entered in the schedule as follows:

ACCOUNTS CODE F00 F99 F20

Increase F30

Decrease F50

Reclass. Other

Control (F15)

Assets A11xx 50 100 80 -30 0

In Journal Entries

Regardless of whether they are automatic or manual journal entries, they are automatically saved in a movement flow that carries over data to the closing balance of the balance sheet.

Introduction

15

Balancing Flows

Certain flows must be balanced for assets and liabilities/equity. Others must ensure that assets - liabilities = income.

Flow Assets –Liabilities =

Equity Assets - Liabilities = Income (income statement accounts)

F00 – Opening X

F01 – Incoming units X

F03 – Change in consolidation method (new) X

F09 – Change in accounting policies X

F50 – Reclassification X

F70 – Internal mergers X (P1620)

F80 – Currency translation adjustment X

F99 – Closing X

If these principles are not respected in manual journal entries, then cash flow statements may not be balanced. Data retrieval reports are used to ensure that flows are balanced.

Initializing the Consolidation

16

Initializing the Consolidation

Section Objectives

To present all of the tasks required to run a new consolidation processing.

Key Points

To initialize a new consolidation processing, you should:

◼ Update the list of companies and data entry sites

◼ Create packages for the data entry period or send opening packages to the subsidiaries

◼ Enter the conversion rate for the period

Before creating packages or sending packages to subsidiaries, you should add all of the Group's incoming companies to the list of companies. You can manage the list of companies in the Dimension Builder module of the Setup domain.

You can manage the opening packages to be sent to subsidiaries and opening balances, if required, in the Reporting Organizer and RU Organizer modules of the Operation domain.

Conversion rates for the period can be entered before or after you send the packages to the subsidiaries. For the list of companies, however, you must update it first in order to determine exactly which currencies will be required for the consolidation.

Suggested Approach

1. Update the list of companies in the group and the list of data entry sites.

2. Create packages or send opening packages to subsidiaries.

3. Enter conversion rates for the period.

Documents to be kept

Printout of the conversion rate tables

Updating Reporting Units

The Reporting Unit is the elementary component of the Group’s structure. Each Reporting Unit populates a package.

In a statutory consolidation, a Reporting Unit is usually a legal entity, but it can also be a sub-group, a branch, a business unit, or a department.

Key Concepts

The reporting unit table contains all of the reporting units for which the Group has defined a code, regardless of whether or not they will be consolidated.

You can assign a code to companies that are not linked by their capital to the Group. You usually do so in the following cases:

◼ When the Group is included in the consolidated accounts of another Group, even though it consolidates data at its own level. By specifying a code for sister or parent companies, you can manage all of the data required for the top level consolidation process (for example, investments and intercompany transactions).

Initializing the Consolidation

17

◼ When the Group wants to perform breakdowns by partner (customers/suppliers) using consolidated data.

The code TP-999-Third parties corresponds to all of the reporting units that do not have a code. You should never delete it.

Structure of the Reporting Unit Table

A certain amount of information for each Reporting Unit is stored in the database. This information includes characteristics or sub-characteristics. This information is required because it enables the Reporting Unit to be correctly included in the consolidation processing.

Currency

This identifies the currency in which data is collected.

Country

This indicates the country in which the Reporting Unit's headquarters are located. This characteristic is used to produce geographical area analysis.

Company

This is the legal entity to which the Reporting Unit belongs. A Reporting Unit may be its own legal entity. This information is required when the consolidation scope is being defined.

Several business units (BUs) may correspond to the split of one legal entity. In that case, all these BUs will have the same Company (corresponding to the Head BU).

Purpose

This characteristic is used to distinguish between Legal entity, Business unit, Sub-consolidation, Archived, and Technical Reporting Units.

Division

When your consolidation definition is based on a hierarchical scope, the Division characteristic is used to eliminate intercompany transactions by distinguishing between inter/intra segment transactions during a consolidation processing.

Branch

This sub-characteristic identifies the branch for each Division. It is used to create a Reporting Unit hierarchy that can be used in the Scope Builder module.

The Division characteristic and Branch sub-characteristic share the same reference table.

Procedure

To add a Reporting Unit (Dimension Builder module, Setup domain)

1. Expand the tree structure to display Data sources > Amounts > RU-Reporting unit. Check that

the Load data mode is enabled.

Initializing the Consolidation

18

2. Select File > New.

In the General tab, enter the code, short description and long description you want to assign to the new reporting unit.

In the Properties tab, enter the characteristics and properties for the new reporting unit.

3. Translate the descriptions in the Translate tab.

If you do not translate the descriptions into other languages, then when subsidiaries open the application in a language other than English, they will not be able to see the descriptions of their partners when entering intercompany data.

4. Select File > Save.

5. Select File > Close.

Breakdown by Division

To ensure a correct breakdown by Division/Branch, you should:

◼ Create new members in the Division/Branch list.

◼ Select the Branch sub-characteristic for each of the divisions.

◼ Select the Division characteristic in the Reporting unit table for each of the reporting units.

Note: The breakdown by division as proposed in the IFRS Starter kit is based on the following principle: 1 reporting unit = 1 division = 1 branch.

If your Group holds companies corresponding to multiple divisions, you have to split the legal entity or entities into several mono-division reporting units.

To create a new Division or Branch

1. In the Dimension Builder module of the Setup domain, expand the tree structure to display Reference tables > EN-DIVISION and check that the Load data mode is enabled.

2. Select File New.

In the General tab, enter the code, short description and long description you want to assign to the new activity or branch.

3. For a new Division, enter the Branch sub-characteristic in the Properties tab.

4. Select File > Save.

5. Select File > Close.

Creating Packages

You create packages in three stages:

◼ Create a reporting ID in the Reporting Organizer module of the Operation domain.

◼ Define the list of reporting units included in the reporting ID in the RU Organizer module of the Operation domain and adapt these settings for some of the reporting units, if needed.

◼ Generate the packages on the current site or send packages to another data entry site in the RU Organizer module of the Operation domain.

Initializing the Consolidation

19

Creating a Reporting ID

A Reporting ID consists of:

◼ A category, like a type of data to be processed. For example category A for statutory consolidations.

◼ A data entry period, for example 2009.12 for the yearly consolidation on 31 December 2009.

A Reporting ID contains properties that are applied by default to all of the packages included in it, except for changes made individually to the properties of certain Reporting sets (RU Organizer module).

In the IFRS Starter kit, the following options must be considered when creating a Reporting ID:

Category Scenario

The Starter Kit comes with one category scenario: A-Actual, version C-Current.

Data Entry Folders

In the IFRS Starter kit, two package formats are available:

◼ P-A - Package for Actual

This package is used when entering data for entities consolidated using the Full or Proportionate consolidation method.

◼ P-E - Package for EM companies

This is a package dedicated to entities consolidated using the Equity method. The list of accounts to enter is much smaller, including only Equity accounts, Net Income for the period and Dividends paid.

In case an EM entity holds subsidiaries, it should be included in the group’s consolidated financial statements based on its own sub-consolidated accounts, according to IAS 28. For this reason, some consolidation flows and accounts are available in the P-E package schedules.

Note: The same folders are available for data entry via both the Windows and Web interfaces.

Sets of Controls

Two sets of controls have been defined in the starter kit, and correspond to the package formats available for data entry.

Depending on which data entry folder you choose, you have to specify the corresponding set of controls (P-A or P-E).

Control Level

Two control levels can be applied to packages:

◼ LEV1 – Balance Analysis is used to group together basic accounting controls, such as Assets – Liabilities = Equity. The controls checking the breakdown of Investments and Equity by flows also come under LEV1.

◼ LEV2 – Flow Analysis is used to check that flow analyses are complete.

Origin of Opening Balances

We recommend that you use data from consolidated tables rather than preconsolidated tables (see Processing the Data: Key concepts) so that the data used for package opening balances is consistent with data from the consolidated opening balances.

When several consolidations have been run using different variants, you can choose any variant for the package opening balances, as long as the package data and corrections are identical for all variants.

When initializing a consolidation for the first time, the "Opening balance data" option should be disabled.

Initializing the Consolidation

20

Restrictions

◼ Read-only flows: When the opening flow (F00) is selected, data in opening flows cannot be changed in the package. Enable the "Read-only flows only if there is an opening balance" option in order to let incoming reporting units enter their opening balances.

◼ Read-only periods: This option is not used in the Starter Kit because category A-Actual has only one period for entering data, identical to the Reporting ID's data entry period.

◼ Data entry restrictions: The Starter Kit comes with one default data entry restriction, PACK-STD (Package – Standard), that limits the available members for the following dimensions:

◼ AC-Account: All the accounts are allowed except archived and consolidation-specific accounts.

◼ ANALYSIS (multi-purpose dimension): The reference members available are the dates, used for optional currency translation process.

This data entry restriction does not apply to reporting IDs defined with the “P-E - Package for equity method companies” folder (in that case, consolidation specific accounts should be available).

Note: If you decide to apply a Monthly or Quarterly conversion (see YTD and Periodic Conversion), you may need to use a different data entry restriction. For example, PACK-Q2 when you process the quarterly consolidation for June.

Creating Reporting Sets

When you create a Reporting ID in the Reporting Organizer module of the Operation domain, you also define the general environment for all Reporting Units. Once this is done, you should:

◼ Create a reporting set for each reporting unit required to enter data in a package.

◼ Validate or update the reporting properties for each reporting unit if required. Besides the properties from the Reporting ID defined in the Reporting Organizer module, the reporting set presents additional properties in the Roadmap tab which are used to define the data entry site, currency and users authorized to access the package in data entry.

Sending Opening Packages

Two possibilities are offered to enter data in the packages:

◼ Entering data at decentralized data entry sites in the Windows interface

Note: If you want to use this option, you must first send opening packages by creating a new send task and including the transferable object “Opening package”.

◼ Entering data in packages at central site

When data is entered in the package at central site, you do not need to create a send task.

You can make the package available directly in the RU Organizer module by right-clicking the reporting set and selecting "Generate Package at Current Site".

Note: Detailed information on sending opening packages is available in the application help.

Entering and Updating Conversion Rates

Conversion Rate Tables

Conversion rates are identified by:

◼ a rate version

◼ a period

Initializing the Consolidation

21

The rate versions enable you to specify different conversion rates for the same period and therefore simulate different consolidations. You usually use this functionality:

◼ To produce temporary accounts when the currency exchange rate is not yet known, for example when publishing data in advance for intercompany transactions.

◼ To run simulations using different currency scenarios.

In the Starter Kit, two conversion options are available, depending on whether you apply YTD or periodic (Monthly or Quarterly) exchange rates (this will be dealt with in detail in chapter YTD and Periodic Conversion). As a result, two rate versions are available by default: A-YTD and A-PER.

You can also create new conversion rate versions.

Conversion Rate Types

For a given rate version and period, the following conversion rate types are available:

◼ ARPP - Average exchange rate, prior period

◼ OR - Opening exchange rate, current period

◼ AR - Average exchange rate, current period

◼ CR - Closing exchange rate, current period

◼ Daily-specific rates

The ARPP rate type is used only if you apply Monthly or Quarterly conversion (see YTD and Periodic Conversion).

Daily-specific rates were created to enable the conversion of paid dividend (F06) at the rate of distribution. Paid dividends are entered by beneficiary and date in the package and converted by default to the average rate or at the rate of the day when entered (see Dividends).

Daily rates also enable the conversion of F20/F40 on Investment and Issued capital/Share premium, based on daily rates rather than the average rate for the period (see Optional Conversion Process on Investment and Capital/Share Premium ).

A report checks the consistency between the analysis by date entered in the package and daily rates entered in the conversion rate table.

The conversion rates entered are based on the base currency selected by users for each conversion rate table. This currency has a conversion rate equal to one for all rate types.

The choice of this base currency is not related to the currency in which the consolidation is run. However, it would be easier to choose the consolidation currency as the base currency in the case you have to enter specific rates (daily rates or specific rates for incoming and outgoing companies) for companies using the base currency. In that case, If you run consolidations with different consolidation currencies, you would have to create as many conversion rate tables as consolidation currencies.

If the consolidation currency is different from the base currency, it is also necessary to enter a specific conversion rate for reporting units using the base currency. This conversion rate should be calculated according to the consolidation currency specific exchange rate (and will not be equal to one).

Entering Conversion Rates

You can enter conversion rates in one of the following ways:

◼ Enter the different rate types in the conversion rate table.

◼ Import data from a file (see the product documentation).

Initializing the Consolidation

22

Calculation Methods

Conversion rates can be expressed as follows:

◼ Divide: The amounts entered are divided by the conversion rate for the "Certain for uncertain" calculation method.

◼ Multiply: The amounts entered are multiplied by the conversion rate for the "Uncertain for certain" calculation method.

Example

The base currency is USD. Exchange rate for USD and EUR are entered as follows, depending on the calculation method you choose:

Currency Divide Multiply

USD 1 1

EUR 0.67253 1.48692

Conversion Rates Specific to Certain Reporting Units

You can enter a conversion rate specific to one reporting unit. You use this option for incoming and outgoing companies, for example the opening rate for an incoming reporting unit is the rate applicable at the time it was included in the scope and not the rate applicable on the first day of the data entry period. This is explained in chapter Incoming Entities.

Daily Rates

To enter daily-specific rates for a given currency you should add columns in the right part of the conversion rate table. The list of additional rate types corresponds to the days of the year.

For example, if a particular consolidation event occurred on Sept 14th, first add the 09.14-September 14 rate type in the list of available columns, then enter the exchange rate for the relevant currencies at this date.

The exchange rate for the pivot currency must always be populated (with a value of 1) for any of the date-specific rate types to ensure a correct conversion process.

Besides, if the consolidation currency differs from the pivot currency, you must also populate the exchange rates of the consolidation currency for any of the date-specific rate types.

In case you apply periodic conversion, enter daily-specific rates only for the dates included in the period (month or quarter).

For example, if you use quarterly conversion, the conversion rate table for Q3 should only include rates for dates from Jul 1st to Sept 30th. Indeed, if a consolidation event occurred in Q2 and you entered specific exchange rates for the corresponding date in Q2 conversion rate table, the conversion for F20 or F40 has already been done in the consolidation for Q2 and should not be re-processed in Q3.

Collecting Data

23

Collecting Data

Section Objectives

To describe how package data is collected.

Key Points

At local data entry sites, data is loaded manually into consolidation packages by entering data, or automatically by interfacing with the accounting system or by importing data tables.

After the data is entered or imported, controls must be run on packages, which are then published and sent to the consolidation department (in the case where data entry is decentralized).

In order for the package data to be included in the consolidation, packages must be integrated into the database.

Suggested Approach

At data entry site:

1. Receive the opening package sent by the consolidation department (if applicable).

2. Enter or import data to the package.

3. Run controls on the package.

4. Publish the package so that its data is made available to the consolidation department.

At the consolidation department:

1. Receive the packages (if applicable).

2. If there are no send conditions, check that the package sent has reached the control level required. If this is not the case, then run controls and correct the errors.

3. Integrate package data into the database.

Entering Data at Data Entry Site

Receiving Packages

To receive packages, perform the following actions:

◼ Define an inspection task so that it can detect the objects to be received. If objects are detected by this task, then a new reception task RYYMMDD.000x will be automatically created.

◼ Run the reception task.

This procedure only applies to the Windows client when the packages are filled out on a decentralized data entry site. In any other case, the packages are directly available on the current site without performing any additional action.

Collecting Data

24

Loading Data into Packages

The procedure to enter or import data into a package and to run package controls is described in detail in the Package Data Entry Guide.

Publishing Packages

After a package has been filled out, it must be published so that it will be available at the central level when the consolidation is processed.

When the data entry is done on a different site from the consolidation site, the publication of a package creates a “Send objects” task with the package.

There are several publication options. To learn more about them, refer to the application help.

Receiving, Checking and Integrating Packages

Receiving Packages

Just like at data entry sites, to receive packages, perform the following actions (see Receiving Packages):

◼ Define an inspection task so that it can detect the objects to be received. If objects are detected by this task, then a new reception task RYYMMDD.000x will be automatically created.

◼ Run the reception task.

Running Package Controls

If the "Blocking" option was checked when the packages were created or sent to the subsidiaries, then the control level set must be reached before the subsidiaries can publish or send their packages back to you.

However, the send condition is not always required for a reporting process that is carried out for the first time or for incoming entities. For these two cases, you will, however, need to know the control level reached by the package before integrating it. If the package does not comply with the control level set, you will also need to rerun controls in order to obtain details on the errors.

Integrating Packages

This step is used to integrate packages automatically in the preconsolidated table that will be used when the consolidation is processed. This step is mandatory for running the consolidation processing and must be performed:

◼ Once you have received the package and checked that its data is correct.

◼ When changes are made to a package which is then published again, if you want these changes to be included in the consolidated accounts.

Sending a Given Package Several Times

A subsidiary may need to send its package several times to central site if it incrementally corrected or completed its package data.

Collecting Data

25

If the consolidation department wants to find out which changes were made to the accounting data as compared to the previous version, it can display/print the following schedule for the relevant Reporting Unit:

Folder Book Schedule

C4 C41 C41-05 – Compare local/pre-consolidated data

An overall control report (not detailed by elementary accounts) can also be run for all the packages related to one Reporting ID:

Folder Book Schedule

C4 C41 C41-10 – Check integration by Reporting Unit

You should consult these schedules before integrating the new version of package data.

Consolidation Scope

26

Consolidation Scope

Section Objectives

To define the consolidation scope.

Key Points

The configuration proposes three ways to define your scope:

◼ An automatic mode, where you first enter data in packages, and then generate the portfolio and the scope automatically.

◼ A semi-automatic mode, where you first enter data in the portfolio manually, and then generate the scope automatically.

◼ A manual mode, where you enter data in the scope manually or copy an existing scope.

Before creating the consolidation scope, you should first have updated the list of companies in the Group (see Initializing the Consolidation). This is done in the Scope Builder module of the Operation domain.

The Starter Kit offers segment reporting capabilities, based on hierarchical scopes.

Suggested Approach

1. Create a portfolio.

2. Load data in the portfolio in one of the following ways:

◼ Initialize it using the data collected in the packages. (mode 1)

◼ Enter data manually or copy an existing portfolio. (mode 2)

3. Create a scope.

4. Load data in the scope in one of the following ways:

◼ Initialize it using the portfolio. (mode 1 and 2)

◼ Enter data manually or copy an existing scope. (mode 3)

5. Define the hierarchy to be applied for Reporting Unit Rollup calculations

Documents to be kept

◼ Printout of the portfolio

◼ Printout of the scope

Concepts and Definitions

Definitions

Portfolios

A portfolio consists of information about the direct legal investments between companies in the same corporation. It:

◼ stores the number of shares and voting rights owned by companies.

◼ stores the number of shares and voting rights held by one company in another.

Consolidation Scope

27

◼ uses shares and voting rights to calculate the direct investment, financial interest and ownership interest of one company in another (see Rates Used).

Consolidation Scope

The scope shows the following for all of the companies included in it:

◼ The consolidation method, like Not consolidated (NC), Full (FC), Proportionate consolidation (PC) and Equity method (EM).

◼ The financial interest, ownership interest and consolidation rate.

Besides this data displayed at period closing, the application also displays the data from the previous period. This enables you to identify scope changes:

◼ Incoming entities (I)

◼ Outgoing entities (O)

◼ No variation (N)

Segment Analyses

The segment reporting, especially the Revenue by segment, relies on the Reporting Unit Rollup functionality. It automatically calculates the inter-intra segment eliminations using the hierarchical scope entered in the consolidation definition. Therefore, it is mandatory to define the unit hierarchy to be applied in the Hierarchical scope step; otherwise, the reports dedicated to segment analyses will not retrieve consistent data.

Rates Used

Direct Shareholding, Financial Interest and Ownership Interest

The portfolio refers to three types of rate:

◼ Direct shareholding: This represents the percentage of shares a parent company holds in the held company.

◼ Financial interest: This represents the percentage of capital that a parent company holds directly or indirectly in the held company.

◼ Ownership interest:

◼ When one company holds another company directly, the ownership interest is the same as the shareholding percentage.

◼ When one company holds another one via intermediate companies, the ownership interest is calculated by adding together the direct shareholding percentages held by the companies in which there is an interest greater than 50% (because the default control threshold is 50%).

Example 1

60%

50%

50%

F2

F1

M

Subsidiary Parent

company Direct

shareholding Financial interest

Ownership interest

F1 M 60% 60% 60%

F2 M

F1

50%

50%

80% (1)

50%

100% (2)

50%

(1) Percentage of financial interest of M in F2 = 50% (direct) + 60% x 50% (indirect via F1) = 80% (2) Percentage of ownership interest of M in F2 = 50% (direct) + 50% (indirect via F1, as more

than 50% of F1 is held)

Consolidation Scope

28

Example 2

20%

50%

50%

F2

F1

M

Subsidiary Parent

company Direct

shareholding Financial interest

Ownership interest

F1 M 20% 20% 20%

F2 M

F1

50%

50%

60% (1)

50%

50% (2)

50%

(1) Percentage of financial interest of M in F2 = 50% (direct) + 20% x 50% (indirect via F1) = 60% (2) The percentage of F1 in F2 is not taken into account because M's interest in F1 is less than

the threshold.

Consolidation Rate

Besides the financial and ownership interests, scopes also display the consolidation rate. This rate depends on the consolidation method:

◼ For a fully consolidated company, it is 100%.

◼ For a proportionate consolidation, it represents the share of assets and liabilities (or expenses and income) included in the Group balance sheet (or income statement). It is equal to the sum of all direct shareholdings in the subsidiary held by companies in the scope, after the consolidation rates for the latter have been applied accordingly.

◼ For a company consolidated using the equity method, it represents the Group share used to calculate the consolidated value of the investments in associated undertakings. It is calculated in the same way as in a proportionate consolidation.

Example

20%

80%

F2

F1

M

Company Ownership

interest Consolidation

method Financial interest

Consolidation rate

F1 80% Full 80% 100% (1)

F2 20% Equity method 16% 20% (2)

(1) F1 fully consolidated so consolidation rate = 100% (2) Consolidation rate for F2 = direct rate via F1 (20%) x F1 consolidation rate (100%) = 20%

Initial Values/Revised Values

The number of shares as well as the rates displayed in portfolios and scopes have two different values:

◼ Initial value: This is the value calculated by the application using source data when initializing the following automatically:

◼ Portfolios (source data = preconsolidated data)

◼ Scopes (source data = portfolio)

◼ Revised value: You can enter this value manually in a scope or portfolio. If this value exists, then it will take priority over the initial value when applying rates in consolidation processing.

Defining Scopes

The configuration proposes three ways to define consolidation scopes in order to select which entities are to be consolidated, the consolidation method and rates to be used.

You must define the unit hierarchy to be applied, whichever way for defining scopes you choose. Otherwise, consolidations using a set of rules that includes a Reporting Unit Rollup rule cannot be processed.

Consolidation Scope

29

Automatically

Portfolio is automatically generated by loading data entered in consolidation packages:

◼ By the subsidiaries in schedule PA2600: This schedule outlines the distribution of capital in number of securities per shareholder (group and third party) after having entered the total amount of capital (account E1110) and the total number of shares (account XE1110).

◼ By the shareholder in schedule PA2400: This schedule analyzes the variation in investment securities held, by number (account XA1810).

The direct shareholding rate is derived from the total number of capital shares declared by the subsidiary and the number of shares held declared by the parent company or companies. The scope is then generated automatically using the portfolio.

This is the surest method because you can check that shares declared by subsidiaries and parent companies correspond, and because the rates for direct shareholding, financial interest, ownership interest and consolidation are calculated automatically.

Semi-Automatically

In this method, you enter the portfolio manually and then generate the consolidation scope automatically.

This method is often used when the consolidation department wants to build the scope before having received all the packages, assuming that legal data is available and up-to-date in the central database.

Manually

This method consists of loading data in the scope either by entering it manually , or by copying an existing scope. This method is adopted when defining pro forma accounts, or when performing simulations. It does not, however, enable you to check the consistency of the data entered.

Portfolios

Creating Portfolios and Portfolio Occurrences

You manage portfolios in the Scope Builder module of the Operation domain. You enter data in a portfolio in two stages:

◼ Create a portfolio with a code and description, and specify a number of settings for loading and calculating rates. This is only mandatory when performing the reporting cycle for the first time.

◼ Create a portfolio occurrence in order to enter data for a given data entry period.

Properties Tab

“Voting rights are proportionate to shares” Option

If you select the "Voting rights are proportionate to shares" option, then the number of shares that you enter are applied automatically to the number of voting rights, which are then used for calculating ownership interest.

Moreover, the fields displaying the number of voting rights are grayed out. You can only change this value by changing the value for the number of shares.

Therefore, this option is:

◼ to be deactivated when you initialize the portfolio with data entered in packages, which is the recommended method,

◼ only advisable when portfolio is entered manually, in order to avoid a double keying.

Consolidation Scope

30

Other Parameters

The table below indicates the manner in which you should enter the other Properties tab’s parameters when defining either a Portfolio or a Portfolio occurrence. These parameters are required only if you want to initialize the portfolio using the data collected in the packages.

Parameter Value Only available for a portfolio occurrence

Reporting ID (Category) A – Actual

Reporting ID (Data entry period)

[Data entry period of the consolidation]

X

Period [Same value as Data entry period] X

Flow F99 – Closing position

Non-group reporting unit TP-999 – Third parties

Audit ID filter AU1-S-R – Level S and R, i.e.

package origin

Initialization Tab

If you want to initialize the Portfolio occurrence using the information collected in the packages, the Initialization tab should be filled out as follows:

Parameter Value

For declaring

capital stock

Parent company SH - Share

Subsidiary RU – Reporting unit

Shares AC1-001 – Issued capital – Number of stocks

Voting rights AC1-001 – Issued capital – Number of stocks

For declaring

portfolio

Parent company RU – Reporting unit

Subsidiary SH - Share

Shares AC1-002 – Investment in subsidiaries, JV,

associates – Number of shares

Voting rights AC1-002 – Investment in subsidiaries, JV,

associates – Number of shares

Copying a Portfolio Occurrence

In the application, you can copy a list of investments from one portfolio occurrence to another, regardless of the other initialization settings.

Controls and Corrections

Controls of the Investment

Control reports are available in the software to check the consistency of portfolio data. The Control reports available are the following:

Consolidation Scope

31

Investments Greater than 100%

This report displays errors coming from stockholdings greater than 100%, for instance, when the total number of shares held is bigger than the share capital declared by the subsidiary or when the sum of direct and indirect stockholding is greater than 100%. We recommend that you print this report using revised data, which is used to generate consolidation scope from portfolio.

Missing Capital Stock

This report shows the list of reporting units that have not entered the number of shares included in their capital, on the account used for the initialization of the investment.

Revised Data/Declarations

This report shows the discrepancies between a holding and its subsidiary on revised values. The subsidiary enters in its data package the number of shares by shareholders. The holding enters the number of shares it holds. This report reconciles these two declarations.

Note: The “Control for declarations” report also shows the reconciliation, but on initial values. We recommend that you check the revised values, given that they are used for the initialization of the consolidation scope.

Initial Data/Declarations Control

The discrepancies displayed in this report between the initial value of the shares and the declared shares indicate that the pre-consolidated data (integrated data packages and manual journal entries) has been modified since the last initialization of the investment.

This report should be used only if the portfolio was initialized using the data collected in the packages.

Correcting Errors

Use one of the following methods to correct errors:

◼ Direct correction of the package data

It is the easiest way for correcting, but the following steps must strictly be performed:

1. Enter the corrections in the data package.

2. Control and save the data package.

3. Publish and integrate the package.

4. Re-initialize the investment in the portfolio occurrence. This step is critical.

When the dialog box “Do you want to save your changes” appears, click Yes if you want to keep any manual modification you might have made within to the portfolio occurrence.

◼ Manual correction of the investment

The major drawback of this solution is the fact that the corrections recorded in the investment will not be carried forward on the opening balance of the following year.

Printing a Portfolio Occurrence

You can customize the display of portfolio occurrence investments on screen or paper by adding, removing and sorting the columns displaying rates, number of shares and voting rights.

Consolidation Scope

32

Scopes

Statutory and Reporting Scopes

In the application, you can create two types of scope:

◼ Statutory scopes: These scopes must be generated using a portfolio. They cannot be changed without first changing the capital and investment rows in the portfolio.

◼ Reporting scopes: These scopes can be created with or without a portfolio and all of their data can be changed directly.

The consistency between the basic information (the number of shares and voting rights) and the rates in the scope can only be guaranteed by using statutory scopes.

A statutory scope initialized with a portofolio is required for the automatic calculation of goodwill of incoming companies. Indeed, it enables to store all relationships between owner and held companies used by coefficients to generate goodwill.

Creating a Scope

There are two ways of populating a scope, depending on whether or not you want to use a portfolio.

Setting up a Scope using a Portfolio

This can be done with a Statutory scope or a Reporting scope.

You can specify the settings for the opening scope. The application uses this information to identify the incoming and outgoing reporting units and the rate variations to be used in consolidation processing.

When using the built-in unit Rollup functionality, you must define the hierarchy of the Reporting Units in the ‘hierarchical scope’ step.

Note: All reporting units belonging to the scope at opening and closing must be included in the hierarchy so that the Rollup calculations can be performed.

Setting up a Scope without a Portfolio

This can only be done with a Reporting scope.

For each Reporting Unit, all the parameters (consolidation method, rates, and so on) can be entered/modified.

You must define the Reporting Unit hierarchy if you want to retrieve consistent segment analyses.

If needed, an opening scope can be specified.

Making Changes to a Statutory Scope Manually

Adding and Deleting Companies

It is possible to add a company to the scope. To do this, the modification must be done in the Investments step of the scope. Then, in the Scope step, check the consolidation method and change it if needed.

The same method applies when you want to delete a company from the scope. In the Scope step, you need to make sure the consolidation method is “Not consolidated (NC)”.

Changing the Consolidation Method

Consolidation methods are automatically assigned according to the ownership interest threshold defined in the “Initialize using a portfolio” step in the scope editor.

Consolidation Scope

33

If you select the “Full Consolidation” method, the consolidation rate will automatically be 100%. In the other cases, for example for proportionate or equity methods, however, you must change the consolidation rate manually to ensure that the consolidated accounts are valid.

Financial Interest and Ownership Interest

In statutory scopes, you cannot change the financial and ownership interests directly. You should therefore change the number of shares and voting rights in the Investments step.

Specific Cases

Incoming Companies

By default, the processing applied to incoming companies uses the financial interest and consolidation rate at closing. You can specify intermediate rates(1) in order to process the incoming transaction in the incoming flow and one subsequent operation (purchase or partial disposal) in a variation flow.

Outgoing Companies

In the application, you can manage Reporting Units:

◼ leaving the scope at the start of the period

◼ leaving the scope during the period

◼ acquired, “merged”, at the start of the period

◼ acquired, “merged” during the period

By default, an outgoing company is considered as leaving the consolidation at the beginning of the period. To manage the other three cases, select the Incoming/Outgoing tab, and enter the following parameters:

◼ If the company is merged with another Reporting Unit in the Group, enter the code of this reporting unit.

◼ If the company is outgoing, “merged”, during the period, you can consolidate its income and expenses until the effective outgoing date. To do this, enter the data entry period corresponding to the package whose data you want to integrate.

Opening rates are applied by default to companies outgoing or acquired during the period. If you want to use different rates to calculate the non-controlling interests in the net income for the period, check the "Intermediate rate" option and enter these rates.

Hierarchical Scope

As mentioned before (see Segment Analyses), some of the segment analyses provided by the IFRS Starter Kit are based on Reporting Unit Rollup rules. Consequently, defining a hierarchical scope is required in order to retrieve consistent segment analysis data. The secondary hierarchy tab is not used in the starter kit.

Printing a Scope

The procedure is identical to the one described for printing a portfolio occurrence (see above).

(1) In the current version of Financial Consolidation, you cannot manage intermediate consolidation rates for companies consolidated using the proportionate method. Therefore, you should enter an intermediate consolidation rate that is equal to the consolidation rate at closing.

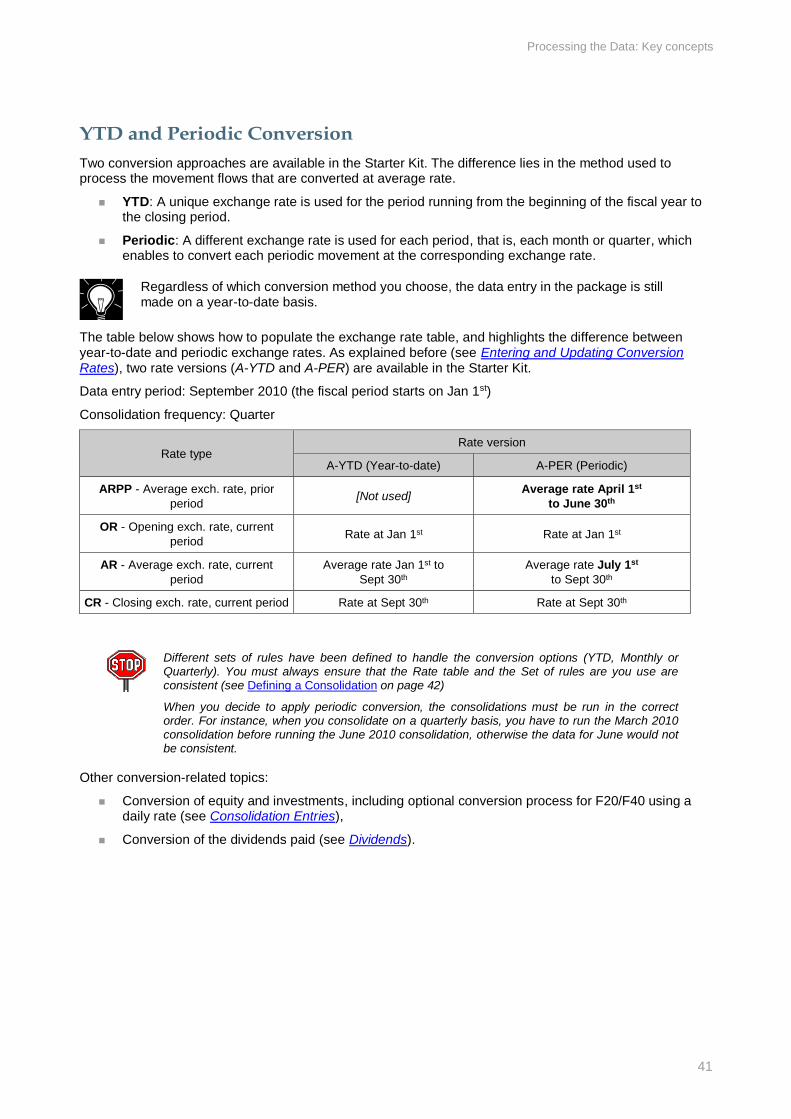

Processing the Data: Key concepts

34

Processing the Data: Key concepts

Section Objectives

This chapter is the first section that describes how data is processed. It will provide a general overview of the transition made by package data as it is processed to produce the Group's consolidated accounts.

Key Points