Novi Dewan Indian Life and Health Insurance Industry

182

Novi Dewan Indian Life and Health Insurance Industry

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Novi Dewan Indian Life and Health Insurance Industry

Novi Dewan

Indian Life and Health Insurance Industry

GABLER EDITION WISSENSCHAFTInternational Management ScienceEditorsMichael Frenkel, WHU – Otto Beisheim School of ManagementFrank Himpel (Managing Editor), University of MainzAnshuman Khare, Athabasca UniversityPete Nye, University of WashingtonKatharina J. Auer-Srnka, University of Vienna

Editorial Advisory BoardKlaus Bellmann, University of MainzMarc Förstemann, A.T. KearneyRené Haak, German Federal Ministry of Education and ResearchEvi Hartmann, European Business SchoolSabine T. Köszegi, University of ViennaMarkus Pütz, University of WuppertalJürgen Schröder, University of MannheimPaula M.C. Swatman, University of South AustraliaMichael Weller, Clifford ChanceJochen Wittmann, Dr Ing hc F Porsche AG

The aim of International Management Science is to promote interna-tional research and understanding of strategic issues in managementtopics. The series embraces a wide range of methodologies, approa-ches, traditions, and schools of thought. The mission of InternationalManagement Science is to meet the demands of the scholarly community sharing an interest in the management of strategic contextsin the regions of North America, Europe, Asia, and Australia.

Novi Dewan

Indian Life and Health Insurance IndustryA Marketing Approach

With forewords by Martin Fassnacht and Dirk Schmidt-Gallas

GABLER EDITION WISSENSCHAFT

Bibliographic information published by Die Deutsche NationalbibliothekDie Deutsche Nationalbibliothek lists this publication in the Deutsche Nationalbibliografie;detailed bibliographic data is available in the Internet at <http://dnb.d-nb.de>.

1st Edition 2008

All rights reserved© Betriebswirtschaftlicher Verlag Dr. Th. Gabler | GWV Fachverlage GmbH, Wiesbaden 2008

Editorial Office: Frauke Schindler / Anita Wilke

Gabler-Verlag is a company of Springer Science+Business Media.www.gabler.de

No part of this publication may be reproduced, stored in a retrieval systemor transmitted, mechanical, photocopying or otherwise without priorpermission of the copyright holder.

Registered and/or industrial names, trade names, trade descriptions etc. cited in this publica-tion are part of the law for trade-mark protection and may not be used free in any form or byany means even if this is not specifically marked.

Cover design: Regine Zimmer, Dipl.-Designerin, Frankfurt/MainPrinted on acid-free paperPrinted in Germany

ISBN 978-3-8349-0946-6

Foreword

The Indian market with its one billion plus population, presents lucrative and diverseopportunities for various industries. However, the intricacies that make up this mar-ket are not very well known to most people, particularly those living in developedcountries. India with its numerous and varied sub-cultures presents a microcosmicview of the world itself – it constitutes a small, representative system that has analo-gies to a larger world in configuration and/or development. This makes the study ofthe Indian insurance industry especially pertinent and appealing as it goes beyond theIndian market, facilitating an understanding of the dynamics of other countries/mar-kets with similar growth paths.

In her book, Novi Dewan provides an insight into the history, development, currentsituation and the emerging challenges and opportunities of the insurance industry inIndia. She methodically focuses on the marketing aspects of the life and health insur-ance industry with respect to the four Ps (product, price, place, promotion). In orderto substantiate her findings, Miss Dewan has conducted and presented the results ofan empirical study that comprises standardized interviews with decision makers ofIndian insurance companies.

The book is divided into four main sections. In the first section, the author presentsan understanding of the overall Indian Insurance Industry vis-à-vis other markets.Additionally, the rapid changes in the regulatory environment and the consequenteconomic impact on the industry are discussed. In the second and third sections,Miss Dewan systematically elaborates on the life and health insurance industry inlight of classical elements of marketing – the 4Ps and her empirical findings. Thebook ends with an outlook and prescriptive approach summarizing the best practicesfor the two industries.

It is indeed an excellent book for anyone interested in an in depth understanding ofinsurance in general, the Indian insurance industry in specific, the correspondingmarketing facets and best practices and a consequent comprehension of the insurancesector in countries with similar trajectories of growth.

Professor Martin FassnachtWHU – Otto Beisheim School of Management

Associate Dean and Holder of theOtto Beisheim Endowed Chair of Marketing and Commerce

Foreword

The heat is on. While many mature insurance markets are halting in stagnation, newand fast-growing economies are appearing on the international stage of the insurancebusiness and are offering opportunities that sometimes leave the bystanders breathless.

This has not gone unnoticed. Major players from across the globe have been joiningthe gold rush and entering promising markets such as India or China to conquer theAsia-Pacific region and reap the benefits from the enormous growth materialisingthere. Due to regulatory requirements, most of them enter partnerships to avoid settingup a distribution network from scratch or to benefit from a partner’s local experience.

India is, by all accounts, a prime target of this movement. Once a crown jewel ofthe British Empire, it is already on its way towards developing into a gem of the glob-al insurance industry.

However, the market today is still comparably small. Its gross written premiums ofabout 25 billion USD (world: 3,151 billion USD) only put it in fourth place in theAsia-Pacific, well behind Japan holding roughly 64% of the region’s market, SouthKorea (approx. 11%) and China (approx. 8%). India currently only accounts forslightly more than three percent of the region’s premium.

This market’s charm, however, stems from its enviable growth story. The potentialseems enormous. International comparisons show, for example, that only countrieslike Egypt or Mexico have a lower penetration of life insurance (India approx. 2.5%),looking meagre compared to Taiwan’s staggering 11%. More than 100 million house-holds are well aware of the life insurance concept without owning one. The potentialof those who are not yet educated about insurance seems to offer even bigger poten-tial in light of a population of over one billion.

But India is catching up at a fast pace. While the whole region has grown by lessthan four percent in 2005, India’s growth stands at 14%. New life policies havegrown by more than 35% in 2005, and privately held insurance companies (as op-posed to the public sector offering insurance) have realised an even more impressivegrowth rate of above 73%.

The outlook continues to be bold: The Indian insurance market is forecasted to havegrown by more than 60% in 2010, considerably outpacing the dynamic developmentof the Asia-Pacific region (which will have grown by 23% in the same time frame).

A brief look back into history – During its colonial aftermath, the Indian insurancemarket was private, then taken over by the government. Since 2000, more and morerights have been granted to private insurance providers.

While the public providers still hold a market share of about 80%, privately heldinsurance companies by far outpace them as mentioned above. Legal privatisation is

followed by an unstoppable factual privatisation, driven by the expertise that top-notch foreign partners inject into the partnerships with local experts to provide supe-rior products and services. While only 73% of all grievances are solved by publics,the ratio of privates stands at more than 93%.

Other markets have gone down this road already and they are vivid testimonials tothe dangers along the way. Price wars, loss-leading products without cross-sellingever materialising, a focus on growth that sacrifices profits, and returns that are hard-ly attractive to investors can be the disappointing results.

India is not immune. Since January 2007, the formerly regulated tariffs have beenopened to the free market game play. It is important, however, to understand that theIndian market is coming from much less than a balance. While fire and motor poli-cies, for example, have been very profitable, others such as health and marine insur-ance were cross-subsidised. It remains to be seen whether deregulation will lead tofire and motor prices falling and even more importantly, if the prices of health, ma-rine and others can be brought up to compensate. Increasing prices have always beenthe kingpin of all pricing measures, only mastered by few.

The current state of pricing in China warrants a word of caution, as India may fol-low a similar path. The underwriting discipline and capability of many Chinese play-ers is very low. Growth is put before profitability and the appetite for risk seems insa-tiable. Rogue pricing is used to buy market share.

Consequently in India, a well-defined appetite for risk must be underscored bysound underwriting practices that have yet to be established and costs should be con-tained by proven measures to fight fraud (such as in Indonesia, where the insurancecompany dictates the repair shop that has to be used when a motor claim is made).This is important since risk costs are the lower boundaries of price and therefore vitalfor proper tariff-setting in a market economy.

The price, however, is only the flip-side of the value provided to the customer.Hence, the challenges run deeper than can be tackled with proper underwriting andrisk-based pricing. As of April 2008, not only the prices but also the terms and condi-tions can be set freely by insurance companies in India.

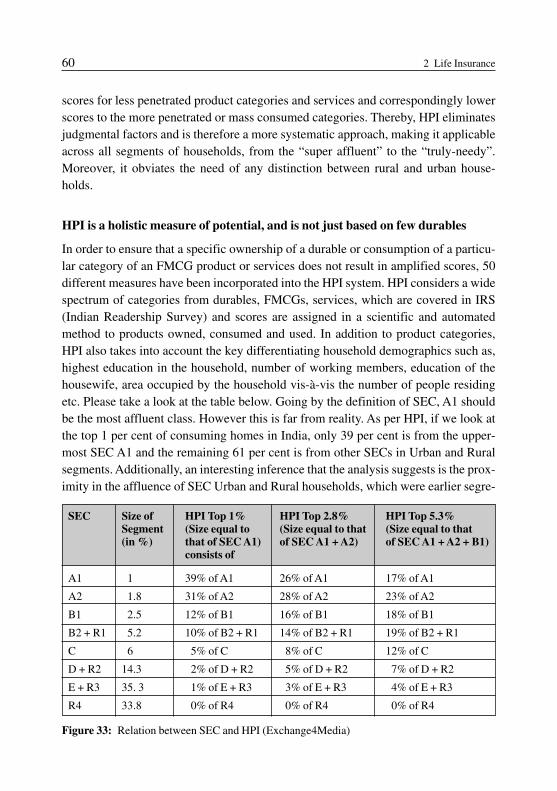

Novi Dewan’s book impressively shows that today’s insurance products in Indiaare lacking differentiation and that the customer segmentation currently used is inap-propriate, as it is mainly based on demographics or life-cycle stages. As a conse-quence, delivering real customer value that would justify profitable prices will provea daunting task.

The author also demonstrates the idiosyncratic characteristics of the Indian insur-ance market that will make the simple transfer of existing models from other parts ofthe world impossible. Among them are:

VIII Foreword

• Geography: 75% of all households in Bangalore possess life insurance, whereasthe overall penetration is less than three percent.

• Society: Despite a strong middle class, the divide between rich and poor seems towiden, calling for a multi-tiered approach to develop the market.

• Demographics: Younger generations turning their backs on rural India to pursuetheir happiness in the big cities render traditional models of retirement fundingfragile.

• Culture: The Indian consumer considers himself indestructible and therefore not inneed of insurance – behaviour well-known from other markets such as Malaysia.

Miss Dewan goes well beyond a pure description of the status quo. She uses a com-prehensive and well-proven arsenal of scientific instruments to render managerially-relevant prescriptions. She concentrates her studies on life and health insurance.These two business lines are wisely chosen: Life insurance constitutes 80% of thepresent insurance business in India and health insurance used to be a loss-leadingproduct that may well serve as the acid test of whether the free market will only serveto drive prices down or whether insurers succeed in translating product value into ahealthy bottom-line.

The author systematically develops a marketing concept for the Indian insurancemarket. Much of what she derives for the life and health markets should be conceptu-ally transferable to the general insurance arena. She includes all aspects of the classi-cal marketing mix, the 4 Ps of product, price, placement and promotion.

The scientific work is never done as a l’art pour l’art, but always yields tangiblepractical implications. This is garnished with the results from an empirical studyamong stakeholders of the Indian insurance market such as senior executives as wellas the regulator and best practices from current players.

The reader can expect three types of lessons:

1. A comprehensive description of the status quo of the Indian insurance market.2. Hands-on advice for successful insurance marketing in this environment.3. Insights for other markets that may follow a similar trajectory.

What is this book about? At the very core, it is about market excellence which I de-fine as the ability of an insurance company to

• understand customer, competitor and sales dynamics• define innovative and powerful value propositions based on this understanding• deliver exceptional value to the customer• extract this value to the benefit of the insurer by charging high prices, not low

prices.

Foreword IX

Our projects show that this skill set is largely underdeveloped in the insurance world.Our comparative studies show that many other industries are well ahead of the insur-ance sector. Even the banking industry as a very traditional industry is three to fiveyears ahead of insurers.

The insurance industry in general is inward-looking, resistant to change, sees thecustomer as a cost-driver rather than a profit-driver, poor in designing customer-ori-ented value propositions and believes that pricing should be based on risk and othercosts.

However, cost-based pricing is something that other more advanced and customer-oriented industries have abandoned decades ago. It’s the value that counts. The typi-cal excuses that insurance products allegedly are commodities that are being soldrather than bought do not carry any weight.

What does that mean for successful marketing in India? There have to be differen-tiated offerings for a polarised society with a strong middle class. Customer segmen-tation has to be done based on benefits, not demographics. Price elasticities, the rela-tionship between price adjustments and their impact on volumes have to be re-searched to allow pricing that optimises the bottom-line.

The low financial literacy of the Indian consumer makes customer perceptionsmuch more important than objective measures. Typically, the insurance industryturns a blind eye on such psychological phenomena.

Finally, the trade-off between growth and profits must be addressed early. Manymarkets have been drawn into price wars in the past by insurance executives puttinggrowth before profits hoping that as soon as a high market share has been realised,profits will follow. In most cases, this has not materialised.

India and other comparable markets offer ample opportunity for breathtaking prof-itable growth. Will insurance executives reap the benefits of this growth without de-stroying their profits?

Dr. Dirk Schmidt-GallasPartner and Global Head of Insurance,

Simon-Kucher & Partnerswww.simon-kucher.com

X Foreword

Preface

India, with a population of over 1 billion, offers magnanimous potential for insuranceby virtue of two aspects foundational to the concept of insurance: [a] risk reductionthrough pooling and [b] probability theory and law of large numbers.

India’s rapid rate of economic growth over the past decade has been one of themore significant developments in the global economy. This growth has its roots in theintroduction of economic liberalization in the early 1990s, which has allowed Indiato exploit its economic potential and raise the population’s standard of living. Insur-ance has a very important role in this process. Health insurance and pension systemsare fundamental to protecting individuals against the hazards of life. Private insur-ance systems complement social security systems and add value by matching riskand price. Accurate risk pricing is one of the most powerful tools for setting the rightincentives for the allocation of resources, a feature which is key to a fast developingcountry like India. By nature of its business, insurance is closely related to saving andinvesting. Life insurance, funded pension systems and (to a lesser extent) non-life in-surance, will accumulate huge amounts of capital over time which can be investedproductively in the economy. In developed countries (re)insurers often own morethan 25% of the capital markets. The mutual dependence of insurance and capitalmarkets can play a powerful role in channeling funds and investment expertise tosupport the development of the Indian economy. (Sinha)

The massive population, sound economic fundamentals, huge consuming middleclass, an improvement in the insurance regulatory framework and increasing aware-ness amongst Indians about the relevance of health and life insurance in India as in-struments of risk mitigation, security, tax-savings and even investment (with ULIPs),call for an understanding of the insurance industry in India.

This study forms the master thesis which is part of the 16-month MBA program atthe WHU – Otto Beisheim School of Management, in collaboration with SimonKucher and Partners. The main purpose of this study is to understand the current sta-tus of the Indian Insurance Industry in general and life and health insurance industryin specific from a marketer’s point of view. This report intends to serve as a researchinput by projecting a picture of the Indian Insurance Market and thereby helpingreaders understand the insurance paradigm of other emerging markets – like LatinAmerica and certain markets in Asia, that closely mirror India’s development pattern.

Moreover, the aim of this report is to provide a strategic marketing perspective;hence I have sought to make the report comprehensive by adopting a scientific ap-proach through – the projection of best practices, marketing methodologies and tools,mapping empirical data from latest insurance journals, magazines and specialized

books onto these tools and finally summarizing primary data which includes inter-views/surveys of insurance executives/senior management.

The study begins with an analysis of evolution of insurance in India to understandits relevance in today’s context; it then moves on to understanding the dynamic mar-ket environment owing to the changes in the Indian insurance backdrop that have beenbrought about through deregulation and now de-tariffing of the general insurancearea. An understanding of the role of the regulator (Insurance Regulatory Develop-ment Authority of India) is crucial in order to comprehend the regulator’s contributionin shaping and promoting the Indian insurance business through laws that seek to pro-tect the policyholder’s interest, enhance the competitive environment, promote inno-vation and improve the sophistication of customer service. The study then analysesthe status quo of the Indian market vis-à-vis the Asian and Global insurance market.

The study develops to analyze the life and health insurance market in depth in lieuof the elements of marketing mix; projecting best practices and empirical evidencevia the survey “Emerging Opportunities and Challenges for the Insurance Industry inIndia.” The report concludes with an outlook for the Indian insurance industry and asummary of best practices.

The report intends to provide an overview of the health and life insurance industry;the data from this report should be furthered in order to enhance research in any par-ticular facet of marketing of the two areas – life and health. Moreover, the scope ofthis research may be augmented by considering other areas of insurance in India. Fi-nally, as mentioned previously, the insights from this report can be used to serve as amodel basis for other emerging markets, thus an analysis of insurance in similar mar-kets may be developed along the lines of this study.

Acknowledgment

This study has been plausible because of the impetus, contribution and relentless helpand support of several people. I would like to thank my parents, Mr. Bhushan Dewanand Dr. (Mrs) Ranjna Dewan for their constant support and ideas even while they aremiles away in India. I would like to thank Jan Richard and Matthew Armstrong foreverything. They also re-revised my thesis and supported me during my phases of dif-ficulty. My friends and mentors – Ravi Punjabi, Zeeshan Sultan and Kabir Wadiwalafor being my strongest pillars of encouragement since I have known them. I wouldlike to thank the perfect financial services team at Simon Kucher & Partners who of-fered diligent support and guidance even though I was working from home.

Alexander Dechent, my mentor at Simon Kucher, who, despite his ongoing projectdeliveries and responsibilities at SKP, offered exceptional suggestions, precisethought process, relentless guidance, continual follow-up and an immense amount of

XII Preface

time and efforts, that played a key role in the direction and formulation of my thesis.Moreover, Vanessa Behling for her presence, Daniel Loskamp for his philanthropiccontribution to my research via an article that he sent.

I would like to thank Heidi Hoffmann, the program manager of the MBA program,for a well-designed program and the endless and kind support she offered me andseveral others in helping us integrate into the lovely environment of the school andculture, my classmates, for their exotic complementarities and attributes; that servedas a steady source of entertainment and learning. Prof. Dr. Jurgen Weigand, the Deanof the program, an exceptional professor and a constant source of rock steady inspira-tion and help. He guided, spoke, discussed and suggested each and every time hecould despite his busy schedule and endless commitments. Prof. Dr. MichaelFrenkel, the Dean of the school, one of the best professors, the kindest and most hum-ble individual with his untiring spirit for the school, the program and its students; andhis conscientious effort towards improving the school and paying attention to everylittle feedback and/or complaint.

Dr. Dieter Lauszus, SKP, who interviewed me and was very kind and approachableeven on the interview day, Dr Dirk Schmidt-Gallas, also leading the financial servic-es team at SKP, who interviewed me on business and domain knowledge and skills;and merely by his style of interviewing taught me the critical ways of addressingbusiness problems and arriving at thought-process-driven and logic-driven appropri-ate solutions in an efficient and yet meticulous way. Dr. Schmidt-Gallas was the oneresponsible for giving me this prospect to work on the “Insurance Industry in India”and integrating me in his team at Franfurt. Dr. Lauszus’ and Dr. Schmidt-Gallas’ re-search papers on insurance and pricing served contributory to several sections of mythesis. Prof. Dr. Hermann Simon, the CEO of Simon Kucher and Partners, who wasso kind to personally meet with me on my interview day and bestow me with thelovely opportunity to work with his esteemed organization. I would like to thankDr. Frank Himpel, editor, Anita Wilke, editorial office at Gabler and Mr. Baier, whoformatted the manuscript, for their incessant support and follow-up while editing thisbook. They offered me their time and insightful ideas on how to go about publishingthis study into a book. Without them this book would not be a possibility.

Last, but not the least, I would like to thank Prof. Dr. Martin Fassnacht, the Associ-ate Dean of WHU, my supervising professor. An outstanding professor, he taught usmarketing in a way that was unique, enjoyable and engaging. A meticulous mentor,who always took pains to read, made contributory suggestions, and offered hisrevered views and opinion to everything that I presented to him for advice and an un-varying teacher, who appreciated and cared for his students in his own kind way.

Novi Dewan

Preface XIII

Contents

Foreword Prof. Fassnacht . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Foreword Dr. Schmidt-Gallas . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Preface . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Table of Illustrations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

1 Insurance Industry in India . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1.1 Insurance – Introduction and History . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1.2 An Analysis of Evolution of Insurance in India . . . . . . . . . . . . . . . . . . . . .1.3 Dynamic Market Environment for Insurance in India . . . . . . . . . . . . . . . .1.4 Authorities and Regulatory Environment . . . . . . . . . . . . . . . . . . . . . . . . . .1.5 Status Quo – The Indian Market vis-à-vis other Markets . . . . . . . . . . . . . .

2 Life Insurance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2.1 Industry Outlook and Major Players . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2.2 Market Opportunities and Challenges: Empirical Results and Analysis . .2.3 Urgent Needs and Customer Segmentation . . . . . . . . . . . . . . . . . . . . . . . .2.4 Products . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2.5 Pricing Criteria . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2.6 Distribution Channels . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2.7 Communication Strategy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

3 Health Insurance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3.1 Industry Outlook and Major Players . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3.2 Market Opportunities and Challenges: Empirical Results and Analysis . .3.3 Urgent Needs and Customer Segmentation . . . . . . . . . . . . . . . . . . . . . . . .3.4 Products . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3.5 Pricing Criteria . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3.6 Distribution Channels . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3.7 Communication Strategy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

4 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4.1 Outlook for the Life and Health Insurance Market in India . . . . . . . . . . . .4.1 Summary of the Best Practices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Appendix . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Bibliography . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

About the Author . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

V

VII

XI

126

142732

4546525662707690

101102108112118126130139

143144147

151

165

169

XVII

Table of Illustrations

Fig. 1: Financial Savings of the Household Sector (Graph) . . . . . . . . . . . . . . . 6Fig. 2: Financial Savings of the Household Sector (Table) . . . . . . . . . . . . . . . . 7Fig. 3: Milestones of Evolution of Insurance before Nationalization . . . . . . . . 8 Fig. 4: Rural Share of Life Insurance Business in India . . . . . . . . . . . . . . . . . . 9Fig. 5: Milestones of Evolution of Insurance after Nationalization in 1956 . . . 11Fig. 6: Relationship between national savings and life insurance

premium, 1950–1991 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13Fig. 7: Convergence of Efficiency amongst the 4 public sector general

insurers (1997–2003) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14Fig. 8: Factors influencing the Company Marketing Strategy . . . . . . . . . . . . . 15Fig. 9: PEST Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16Fig. 10: Facets while considering effects of de-tariffing . . . . . . . . . . . . . . . . . . . 19Fig. 11: Porter’s Five Force Analysis of the Insurance Industry . . . . . . . . . . . . . 20Fig. 12: Anita McGahan’s Model for Strategies in Dynamic Environments . . . 24Fig. 13: LUDI’s Internationalization Cube . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26Fig. 14: Status of Grievances – Non-Life Insurers (2005–2006) . . . . . . . . . . . . 28Fig. 15: Status of Grievances – Life Insurers (2005–2006) . . . . . . . . . . . . . . . . 28Fig. 16: Investment Regulations for the Life Insurance Business . . . . . . . . . . . . 30Fig. 17: Investment Regulations for the General Insurance Business . . . . . . . . . 31Fig. 18: Key Highlights of Indian Insurance vis-à-vis Asia Pacific & Global

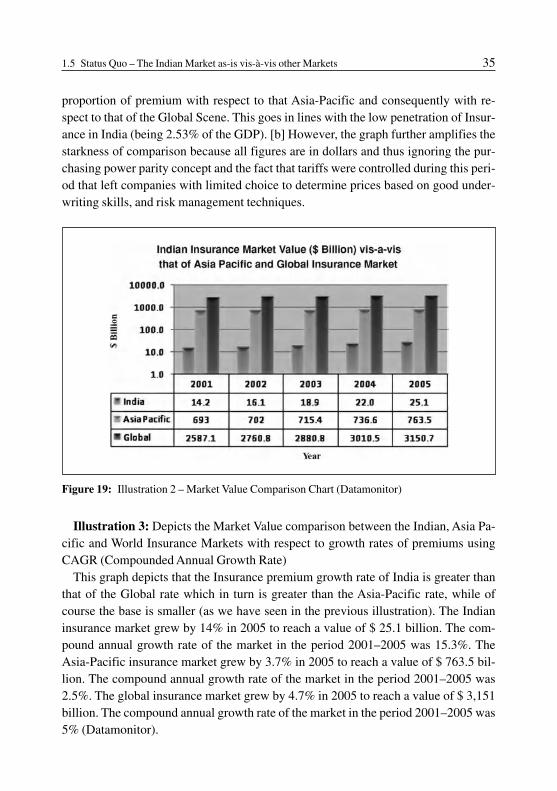

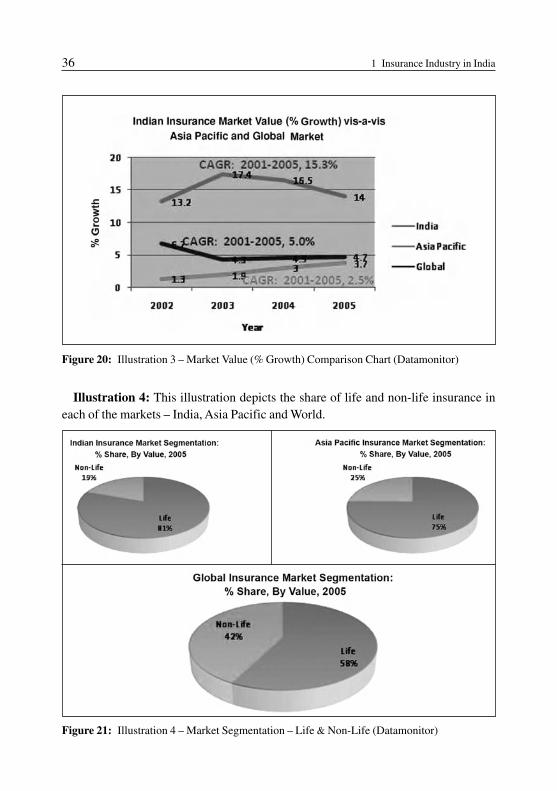

Insurance Markets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34Fig. 19: Market Value Comparison Chart . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35Fig. 20: Market Value (Growth Rate) Comparison Chart . . . . . . . . . . . . . . . . . . 36Fig. 21: Market Segmentation: Life and Non-Life . . . . . . . . . . . . . . . . . . . . . . . 36Fig. 22: Market Segmentation: By Geography . . . . . . . . . . . . . . . . . . . . . . . . . . 37Fig. 23: Market Value Forecast: 2010 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39Fig. 24: Market Value (% growth) forecast: 2010 . . . . . . . . . . . . . . . . . . . . . . . . 40Fig. 25: Insurance Penetration Comparison Chart in the Life Insurance Area . . 41Fig. 26: Insurance Penetration Comparison Chart in the Non-Life Area . . . . . . 41Fig. 27: Insurance Density Comparison Chart in the Life Insurance Area . . . . . 42Fig. 28: Insurance Density Comparison Chart in the Non-Life Insurance Area . 43Fig. 29: Market Share development for first year, renewal and total premium

for Life Insurers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47Fig. 30: New Policies Issued: Life Insurers Development and Market Share . . . 48Fig. 31: SEC for Urban India . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57Fig. 32: SEC for Rural India . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58

Fig. 33: Relation between SEC and HPI . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60Fig. 34: Pricing Levels based on Profit Potential and Professionalism . . . . . . . 72Fig. 35: New Business Underwritten through various Intermediaries in Life

Insurance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78Fig. 36: Representation of Relationships of Agents and Brokers with Insurers I 83Fig. 37: Representation of Relationships of Agents and Brokers with Insurers II 83Fig. 38: Key Differences between Brokers and Agents . . . . . . . . . . . . . . . . . . . 83Fig. 39: The Role of Service Communications in determining Marketing and

Firm Value . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91Fig. 40: IMC Audience Contact Tools . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 93Fig. 41: TV Advertisement Volumes for the year 2006 by Category . . . . . . . . . 94Fig. 42: Seasonality Trend of Advertising for the Insurance sector on TV:

2005–2006 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 94Fig. 43: Top 3 Channels contributed 52% of ad volumes in the Insurance Sector

on TV: 2006 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 95Fig. 44: Top 5 Advertisers of the Insurance Sector on TV in 2006 . . . . . . . . . . . 95Fig. 45: Options of Service Communications for making Services Tangible . . . 96Fig. 46: Approach proposed for Financing of Health Expenditure . . . . . . . . . . . 104Fig. 47: Overall Healthcare Financing Situation in India . . . . . . . . . . . . . . . . . . 104Fig. 48: Health Insurance Development (in Rupees Billion) . . . . . . . . . . . . . . . 105Fig. 49: Development of Number of Policies issued year wise . . . . . . . . . . . . . 106Fig. 50: The Stimulus-Organism-Response Model . . . . . . . . . . . . . . . . . . . . . . 112 Fig. 51: Health Matters Survey and SOR Model . . . . . . . . . . . . . . . . . . . . . . . . 113Fig. 52: Asian Attitude Comparisons to risk and insurance . . . . . . . . . . . . . . . . 114Fig. 53: Customer Segments and Segmentation Variables for Bajaj Allianz . . . 116Fig. 54: Five Patterns of Target Market Selection . . . . . . . . . . . . . . . . . . . . . . . . 117Fig. 55: Shortcomings & Innovations in the Development of the Mediclaim

Policy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 121Fig. 56: Evolution of Medical Insurance Business . . . . . . . . . . . . . . . . . . . . . . . 122Fig. 57: A Health Insurer’s Cost Sheet . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 126Fig. 58: Types of “Risks” subject to “Downstream Delegation” or Outsourcing 132Fig. 59: Workflow for the Cashless Treatment . . . . . . . . . . . . . . . . . . . . . . . . . . 133Fig. 60: Top Growing Segments of Insurance Sector for TV Advertising in the

year 2006 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 140

XVIII Table of Illustrations

Chapter 1:Insurance Industry in India

This chapter starts with an analysis of evolution of insurance in India which isessential because insurance in India commenced with a de-regulated environ-ment (or private firms), moved to a regulated/government owned environ-ment and finally completed a full circle with de-regulation in the year 2000.The next sub-chapter discusses the dynamic market environment for insur-ance in India, in lieu of the changing regulations, de-tariffing of the generalinsurance industry and discussions about increase in foreign-equity cap. Thissub-chapter examines the environmental factors from the insurer’s point ofview, de-tariffing and its consequences, the porter’s 5 forces analysis, thekind of change and trajectory that the industry is expected to undergo, thetype of internationalization strategy that a foreign player must pursue. Thenext sub-chapter details the role of the authority/regulator in shaping and pro-moting the business environment and enlists the statutory functions of the IR-DA (the regulator). The final sub-chapter examines the Indian Market as-isvis-à-vis other markets; the Asian and Global Insurance markets illustratingmarket value, market value forecast, premium share of the total market acrossgeographies and categories, insurance penetration, insurance density andcompetitive landscape comparisons.

2 1 Insurance Industry in India

1.1 Insurance – Introduction and History

Introductory Terms to Insurance

An essential commodity in terms of social security, insurance simplistically definedhas two fundamental characteristics

– Transferring or shifting risk from one individual to a group– Sharing losses, on some equitable basis, by all members of the group

From an individual’s point of view, insurance is an economic device whereby the in-dividual substitutes a small certain cost (the premium) for a large uncertain financialloss (the contingency insured against) that would exist if it were not for the insurance.The primary function of insurance is to create a counterpart of risk, which is security.

From a social point of view, insurance is an economic device for reducing andeliminating risk through the process of combining a sufficient number of homoge-nous exposures into a group to make the losses predictable for the group as a whole(Vaughan and Vaughan).

Insurance Sector Revisited

Looking back in the Time Machine

Interesting accounts of ancient commerce have revealed the initial attempts of hu-mans at insurance. Around 6000 years ago, Babylonians, whose home in the Tigris-Euphrates Valley lay at the crossroads of early world traffic, had developed businesspractices to high degrees of sophistication. Babylon, a territory where all importantland trade routes converged, became the clearing house of trade. Though Babylonbuilt up a worthy commercial system, and its people were the first to enjoy the fruitsof political economy, the travelers were exposed to risks of robbery, pirates and un-canny winds at the seas. Human ingenuity was set to work and, in course of time, apractice developed that debt of the trader, both principal and interest, should be ab-solved if certain specified contingencies occur. By 2000 BC, the Babylonians and an-cient Hindus were familiar with the essentials of the insurance contract as indicatedby the provisions included in the codes of Hammurabi and Manu; the Babyloniancontract and the code of Hammurabi applying mostly to caravans, and Manu Dhar-mashastra referring to both seaborne and overland traffic.

Better and more sophisticated insurance came of age in the 11th century, on thebeach of Hastings, when King Harold (who carried a large Personal Disability Insur-ance) was shot dead by a Norman bowman firing through a narrow slit in the defensewall. His queen immediately got in touch with the insurance company enclosing a

plan, as required on the claim form showing the path of the arrow. The insurers exam-ined the policy for a few days and grew desperate at their inability to find a way of le-gitimately escaping the deal, when a bright “employee” noticed a gap in the defenses.Keeping the defenses without gap was a policy condition and was Harold’s responsi-bility, “Here”, he said, “if the gap wasn’t there, the arrow would never have gottenthrough, so there can be no claim” and that was how the “loophole” entered the histo-ry of insurance or more precisely said the ingenuity in drafting the policy documentwith clauses and “if-conditions” (Ayyar).

Understanding Insurance

Insurance is a service, which is sought to be commoditized for better conceptualiza-tion in keeping with the other unification trends running across the world. Insurerssell a promise to pay or defray on a future date for a predefined contingency. Thefunction of insurance is to protect a few against the heavy financial impact of the ex-pected loss by dispersing the losses among many who are exposed to homogenousrisks.

Initially insurance business structure was architected in three dimensions:

– The cross section of people, property or interest– Pre-determinable risks– Time ambit of coverage (Mishra and Mishra)

Insurance products were designed around such dimensions. Then started the era ofclassification of such products – choices of handling the assorted products createdtwo classes of insurers – life and non-life; life meant human life.

The discovery driven insurance industry encountered the problem of size. To prunethe vertical risk size another class of insurance business evolved, which is now fa-mous as reinsurance (Mishra and Mishra).

Augmentation of the Sector

Insurance products slowly incorporated other developments in the society and eco-nomics. Monetization of economy assorted the income of people into propensity toconsume and propensity to save. Such individual savings were pooled to classes ofinvestments depending on the economies of scope, scale and prioritization for thepurpose of common social good. There was need to internalize functional efficiencyin mobilizing the savings. Functional efficiency consists of allocative and operativeefficiency. Insurance sector got the share of these savings in the equilibrating processof allocative efficiency. Thus, the insurance sector found a new way to augment itsbusiness. Insurance products packaged savings features with risk management fea-

1.1 Insurance – Introduction and History 3

4 1 Insurance Industry in India

tures. The demand for operative efficiency forced insurers to define their core com-petencies; thus called for compartmentalization of insurance activities either by dic-tates of operative efficiency or by statutory and prudential regulations.

Originally meant to be a support service, the sector proved its excellence like a sol-id sphere and developed hydra-headed growth characteristics. The possibilities werepruned by regulations and that seemed to be the only constraining factor for the all-engulfing growth possibilities of the sector; which explains, as the global thrust onderegulation and liberalization compels nations to open up doors for the insurancesector growth, there is a stampede to enter into the sector.

The cardinal attraction of the insurance sector is harnessing long term funds forlong term investments in ever expanding sectors like infrastructure, technology andR & D. The earning potential of these sectors seem almost endemic (Mishra andMishra).

Tools and Methodology

Tools and methodologies have been used in order to contextually understand the In-dian life and health insurance market through a scientifically driven approach. Theyare as follows

– Porter’s 5 Forces for Industry Analysis– The PEST Framework for Macroeconomic Environmental Analysis– Anita McGahan’s Model for evaluating the Dynamic Market Environment– Ludi’s Internationalization Cube to understand the Internationalization strategy of

foreign players in India– Ansoff’s Matrix to understand the Marketing Strategy pursued by an insurer– The 4Ps of Marketing analyzed in depth to understand the Marketing Facets for

both Life and Health Insurance in India– Certain Service Marketing Tools used, since Insurance is a service

Moreover, certain information has been “boxed” in order to bring specific issues tothe foreground

– The “Management in Action” boxes intend to depict certain strategies that insurersin India have implemented; serving as best practices or role models for the rest ofthe industry.

– “The Regulator Says” boxes throw light on the regulatory developments of conse-quential importance to the Indian Insurance scenario.

– “Critical Support Functions” boxes detail the significance of certain functions likeClaims Management, Underwriting and Risk Management.

– “Customer Management and Retention” boxes seek to discuss aspects critical tocustomer centricity and orientation like Customer Relationship Management, Sim-plicity of Insurance Contracts etc.

– “Consumer Insight” boxes detail latest survey results or studies offering a deeperunderstanding of the Indian consumer thus a subsequent enhancement of latest lo-cal market knowledge.

1.1 Insurance – Introduction and History 5

1.2 An Analysis of Evolution of Insurance in India

An account of the Indian Economy and Insurance in Context

The Indian economy has been growing rapidly and the growth impulses continuedduring 2005–2006. There has been sustained manufacturing activity and impressiveperformance of the services sector along with a reasonable recovery in the agricultur-al sector. The agricultural and allied activities registered a growth of 3.9% due to im-provement in the agricultural production. The industrial sector improved by 7.6%and the services sector maintained a higher growth of 10.3%. Thus, the growth in realGDP was 8.4% during 2005–2006 as opposed to 7.5% in 2004–2005. Within theservices sector, there has been an improved performance in finance, insurance, realestate and business services. There has been a substantial increase in the GDP ema-nating from insurance. The deregulation of the sector in 2000 has contributed to in-surance growth. GDP from insurance sector which constituted 12% of the GDP in2000–2001, has increased to 19.3% in 2004–2005. The gross domestic savings, acomponent of which is the financial savings of the household sector, as a percentageof GDP increased to 29.1% in 2004–2005.

6 1 Insurance Industry in India

Figure 1: Financial Savings of the Household Sector – Gross (IRDA)

Financial Savings as a Percentage of GDP

The financial savings of the household sector as a percentage of the GDP has in-creased from 11.9% in 2000–2001, to 16.7% in 2005–2006. Moreover, of this finan-cial savings of the household sector, insurance funds equated to 13.6% in 2000–2001,which increased to 14.2% in 2005–2006, peaking at 16% in 2004–2005. All in all, in-surance funds as a component of the financial savings formed 1% of the GDP in1991, 1.5% in 2000, 1.6% in 2001 to a 2.4% in 2006 (IRDA). Please see the illustra-tions below which elucidate a development of financial savings of the household sec-tor.

1.2 An Analysis of Evolution of Insurance in India 7

Item 2000– 2001– 2002– 2003– 2004– 2005–2001 2002 2003 2004 2005 2006

Financial savings (FS) 11,90% 12,70% 13,10% 13,80% 14,00% 16,70%as a % of GDP

Currency (as a % of FS) 6,30% 9,70% 8,90% 11,20% 8,50% 8,80%

Currency (as a % of GDP) 0,70% 1,20% 1,20% 1,50% 1,20% 1,50%

Deposits (as a % of FS) 41,00% 39,40% 40,90% 38,30% 37,00% 47,40%

Deposits (as a % of GDP) 4,90% 5,00% 5,40% 5,30% 5,20% 7,90%

Shares and Debentures 4,10% 2,70% 1,70% 0,10% 1,10% 4,90%(as a % of FS)

Shares and Debentures 0,50% 0,30% 0,20% 0,00% 0,20% 0,80%(as a % of GDP)

Claims on Governement 15,70% 17,90% 17,40% 23,00% 24,40% 14,70%(as a % of FS)

Claims on Governement 1,90% 2,30% 2,30% 3,20% 3,40% 2,50%(as a % of GDP)

Insurance Funds (as a % of FS) 13,60% 14,20% 16,10% 13,70% 16,00% 14,20%

Insurance Funds (as a % of GDP) 1,60% 1,80% 2,10% 1,90% 2,20% 2,40%

Provident and Pension Funds 19,30% 16,10% 15,00% 13,60% 12,90% 10,00%(as a % of FS)

Provident and Pension Funds 2,30% 2,00% 2,00% 1,90% 1,80% 1,70%(as a % of GDP)

Figure 2: Financial Savings of the Household Sector – Gross (IRDA)

Insurance in India has completed a full circle; from being private with minimalgovernment intervention before 1956, to the nationalization of life insurance and for-mation of a monopoly (with Life Insurance Corporation of India) in 1956, and na-tionalization of general insurance in 1972 and finally back to deregulation in 2000.

First, I will present the milestones of the insurance industry before nationalization,essentially because the denationalized structure brought back to play (in 1999) im-portant legal rules from 1938.

Milestones of the Evolution of Insurance before nationalization in 1956

The Insurance Act, 1938 was the first comprehensive piece of legislation for Insur-ance in India. It covered both life and general insurance companies and clearly de-fined what would come under the life insurance business, the fire insurance businessand so on. It covered aspects ranging from deposits, supervision of insurance compa-nies, investments, commissions of agents, directors appointed by the policyholders,among others. This act lost its significance after nationalization in 1956 (of Life In-surance) and in 1972 (of General Insurance). With the privatization in the late 20th

century, it has returned as the backbone of the current legislation of insurance compa-nies (Sinha).

8 1 Insurance Industry in India

Figure 3: Milestones of Evolution of Insurance before Nationalization (Sinha)

Rationale for Nationalization of the Life Insurance Business in 1956

The genesis of nationalization of life insurance in India came from a document pro-duced by Mr. H.D. Malaviya (on behalf of the Indian National Congress) called “In-surance Business in India”. In his document, Mr. Malaviya made four importantclaims to justify nationalization. First, he argued that insurance is a “cooperative en-terprise”, under a socialist form of government; therefore it is more suited for thegovernment to be in the insurance business on behalf of the people. Second, heclaimed that Indian insurance companies were excessively expensive. Third, he ar-gued that private competition had not improved services to the “public” or to the pol-icyholders. Preventive activities like better public health, medical check-up, hazardprevention had not improved, according to him. Fourth, he commented that the lapseratios of life policies were very high and leading to “national waste” (Sinha). Severalof his arguments that were analyzed proved to stand on rather weak grounds. For ex-ample, his claim that Indian insurance companies were very expensive was justifiedby comparing the overall expenses of life insurers in India with those of the UK andthe USA. However, the base or denominator he used for India resulted in amplifica-tion of the figures beyond credible.

Anyway, the nationalization of the Life Insurance business in 1956 was justified bythe government on three distinct grounds. First, the government wanted to use the re-sources for its own purpose. This clearly meant that the government was unwilling to

1.2 An Analysis of Evolution of Insurance in India 9

Figure 4: Rural Share of Life Insurance Business in India (Annual Reports of LIC for differentyears)

pay the market return on assets (otherwise they could have raised the capital whetherinsurance companies were public or private). Second it sought to increase the marketpenetration through nationalization. There can be two reasons why nationalizationwould make more sense than privatization for market penetration (Sinha). [a] Thegovernment, by virtue of being a monopoly, could generate huge economies of scaleand thereby reduce costs of operation and thus reap higher volumes, by transferringthe lower costs into lower prices for the public. [b] Through nationalization, the gov-ernment may be able to take life insurance to rural areas where it may not be possiblefor private insurers to be profitable. This goal was definitely achieved by the newlyformed monopoly to a considerable extent. Please see the illustration below “Ruralshare of Life Insurance Business”. The last reason cited for nationalization was thatthe government found the number of failures of life insurance companies to be unac-ceptable.

Thus, with the Life Insurance Corporation Act of 1956, the 245 insurance compa-nies of both Indian and foreign origin in 1956 were nationalized by the governmentacquisition of the management of the companies; and the Life Insurance Corporationof India was created on 1st September, 1956, as a result; LIC has grown to be thelargest insurance company in India as of 2007.

Rationale for the non-nationalization of the General Insurance Business in 1956

However, general insurance was not nationalized in 1956. The then Finance Ministeraddressed it in his speech as follows, “I would like to explain briefly why we have de-cided not to bring in general insurance into the public sector. The considerationwhich influenced us the most is the basic fact that general insurance is a part and par-cel of the private sector of trade and industry and functions on a year to year basis.Errors of omission and commission in the conduct of the business do not directly af-fect the individual citizen. Life Insurance Business, by contrast, directly concerns theindividual citizen whose savings, so vitally needed for economic development, maybe affected by any acts of folly or misfeasance on the part of those in control or be re-tarded by their lack of imaginative policy.”

Milestones of the Evolution of Insurance after Nationalization in 1956

The diagram below illustrates the key milestones in the evolution of insurance in In-dia from the nationalization of life insurance in 1956, to the IRDA (Insurance Regu-latory and Development Authority) act in 1999 that led to the deregulation of the in-surance industry in India.

10 1 Insurance Industry in India

Nationalization of General Insurance in 1972

General Insurance was nationalized in 1972 (with effect from January 1st, 1973).There were 107 general insurers operating at that time. These were mainly large cityoriented companies catering to the organized sector (trade and industry). They wereof different sizes, operating at different levels of sophistication and were assigned tofour different subsidiaries (roughly of equal size) of the General Insurance Corpora-tion (GIC). The four subsidiaries were [1] the National Insurance Company, [2] theNew India Assurance Company, [3] the Oriental Insurance Company, [4] the UnitedIndia Insurance Company with head offices in Calcutta (now Kolkata), Bombay(now Mumbai), New Delhi, and Madras (now Chennai) respectively, collectivelyknown as NOUN for their initials. There were several goals for setting up such astructure [a] the subsidiaries were expected to “set up standards of conduct and soundpractices in the general insurance business and render efficient customer service”, [b]the GIC would assist controlling their expense, [c] the GIC would help in the chan-neling of funds, [d] this structure would help bring general insurance in rural areas,[e] GIC was also designated as the national reinsurer, [f] finally, all four subsidiarieswere expected to compete with one another. Most of these goals remained rather elu-sive and were not achieved to a massive degree (Sinha).

1.2 An Analysis of Evolution of Insurance in India 11

Figure 5: Milestones of Evolution of Insurance after Nationalization in 1956 (Sinha)

Development of the Life Insurance Industry during the Nationalized Era

By 2000, LIC had 100 divisional offices in 7 zones with 2,048 branches. There wereover 680,000 active agents across India with a total of 117,000 employees in the LIC.I will now present facets that explicate the development of the life insurance marketin India.

The largest product category of the life insurance market in India has been individ-ual life insurance. The types of the policies sold were mainly whole life, endowmentand “money back” policies. Money back policies return a fraction of the nominal val-ue of the premium paid by the policyholder at the termination of the contract. Untilrecently, term life policies were not available in the Indian market. Note that even in2001, individual life business accounted for 92% of all life insurance market. Thenumber of new policies sold each year went from about 0.95 million a year in 1957 toaround 22.49 million in 2001. The total number of policies in force increased from5.42 million in 1957 to 125.79 million in 2001. Thus, on both counts there has been a25-fold increase in the number of policies sold. Of course, during the same period,the population has grown from 413 million in 1957 to over 1,033 million in 2001. Ona per capita basis, there were 0.0023 new policies in 1957 compared with 0.0218 newpolicies in 2001. Total policies per capita went from 0.0131 in 1957 to 0.1218 in2001. Thus, whether we examine the new policies sold or the total number of policiesin force, there has been a tenfold increase during that period. Therefore, if we exam-ine the headcount of policies as an indication of penetration, there has been a substan-tial rise. A part of this rise is directly attributable to a deliberate policy of rural expan-sion of the Life Insurance Corporation. Between 1985 and 2001, total life businesshad grown from below 18 billion rupees to over 500 billion rupees. During that peri-od, the price index increased fourfold. Thus, if there were no change in life insurancebought in real terms, it would have accounted for 78 billion rupees worth of business(Sinha).

In recent years, life insurance saving has played a bigger role in national savings.Please see the figure below.

Note: The figure is plotted with Gross Domestic Savings as a percent of GDP onthe horizontal axis and Gross Life Premium as a percent of GDP on the vertical axis.Thus, there are fifty-two data points each pair representing data for a given year.

It clearly reveals a nonlinear relationship between these two variables. Specifical-ly, at relatively lower levels of saving rate (that correspond to a lower level of in-come), a rise in saving rate does not lead to a rise in life insurance premium expressedas a fraction of GDP. However, beyond a threshold; with the threshold value of sav-ing rate being 20% for India, the life premium as a percent of GDP starts to grow rap-idly. India seems to have reached that deflection point.

12 1 Insurance Industry in India

Moreover, we have already seen earlier in this chapter that insurance savings as apercentage of financial savings has increased over the years (till 2006).

1.2 An Analysis of Evolution of Insurance in India 13

Figure 6: Relationship between national savings and life insurance premium, 1950–1991(Calculated based on data from the Central Statistical Organization Database)

Deregulation of Insurance in India with the IRDAAct, 1999

With effect from 1st, January, 2000, with the passage of the IRDA Act, the Indian In-surance Industry was privatized or deregulated. The deregulation was brought aboutwith the following objectives: to increase coverage of population, propel a choice ofbetter products with informed decisions, promote competition, encourage the en-trance and joint partnership of foreign players with the Indian insurers, boost innova-tion, advance economy of operations, enhance customer centricity and service excel-lence and improve the efficiency of the public sector companies. The Insurance Reg-ulatory and Development Authority (IRDA) was formulated as an independent bodythat would monitor and shape the insurance business in India. The IRDA has separat-ed out life, non-life and reinsurance insurance businesses and therefore a companyhas to have separate licenses for each line of business. Each license has its own capi-tal requirements (around USD 24 million for life and non-life and USD 48 million forreinsurance business). The role and the statutory functions of the IRDA will be dis-cussed in chapter 1.3 that deals with Authorities and Regulatory environment.

To illustrate the positive direct or indirect effects of deregulation of insurance in In-dia, I have presented a graph below, which represents the convergence of efficiencyof the four public sector general insurers (now independent of the GIC): [1] the Na-

tional Insurance Company, [2] the New India Assurance Company, [3] the OrientalInsurance Company, [4] the United India Insurance Company, in 2003. The technicalefficiency of each of the above is used as a parameter of comparison, with the numberof employees (labor), the number of offices (physical capital) and commission paidas the inputs, and premiums and claims as two alternative measures of outputs. Therelative efficiency was calculated using the data envelopment analysis (DEA), amathematical programming framework (Sinha)

The graph depicts that New India Insurance has consistently stayed as the companywith the highest technical efficiency. Moreover, it shows that after some initialchange the relative efficiency level among the public sector general insurance com-panies converged, in 2003.

14 1 Insurance Industry in India

Figure 7: Convergence of Efficiency amongst the four public sector general insurers1997–2003 (Sinha)

1.3 Dynamic Market Environment for Insurance in India

An Era of Change

The insurance industry has experienced significant change over the past few decades.But never before have the changes been so pronounced, the pace so rapid and thescope so broad. Insurers are in the midst of a true paradigm shift. Their governingrules are changing. Their functional bodies are blurring. Buyers are becoming moresophisticated about services and value, and are ever more demanding. This height-ened form of consumerism is spurring a new demand pressure on insurance products.

At the same time, the industry is experiencing traditional financial pressures, aswell as new competition, new market entrants, new substitutes for traditional insur-

ance offerings. The industry is responding in many ways. For example, there is an en-hanced focus on market selection, new and varied distribution channels, bundlingand unbundling of products and services, all in an effort to customize and achievegreater value while re-engineering and consolidating for efficiency.

The Dynamic Environment and the Insurer’s point of View

In view of the ever-changing landscape of the Insurance Industry in India, insurersneed to revisit the core competencies and the cardinal features of their underlyingstrategy.

The schematic diagram below illustrates the key aspects influencing the insurer’sstrategy, conducive to the marketing point of view.

1.3 Dynamic Market Environment for Insurance in India 15

Figure 8: Factors Influencing Company Marketing Strategy (Kotler and Lane)

PEST Analysis

Of the facets illustrated above, it would make logical sense to take an outside-in viewand begin by analyzing the environment, a backdrop amidst which a new firm wouldlike to enter or an existing insurer would like to relook its strategy. Thus, I have illus-trated all factors contributory to the environment via the PEST (P-Political/Legal

Factors, E- Economical Factors, S – Social/Cultural Factors, T – Technological/Phys-ical Factors) framework.

Political Factors: The regulatory aspects of the political factors will be discussedin chapter 1.3. De-tariffing, the opening up of the market to free pricing and flexiblepolicy terms and conditions (which came into effect on the 1st January, 2007), is themost essential aspect that is set to revolutionalize the face of the insurance industryby directly affecting the insurers, concerned intermediaries, customers and stake-holders; thus, a separate subsection detailing its prime characteristics will be dedicat-ed to de-tariffing.

16 1 Insurance Industry in India

Figure 9: PEST Analysis (Research and Understanding gathered from several sources andAuthor)

Economical Factors:

– Increase in contribution of insurance to the GDP: GDP from insurance sector con-stituted 12% of GDP in 2000–01, increased to 19.3% in 2004–2005.

– Gross domestic savings as a per cent of GDP increased to 29.1% in 2004–2005.Savings in the form of life insurance funds accounted for 15.1% of the gross finan-cial savings.

– A decline in the savings in the form of insurance funds was witnessed, even thoughlife insurers increased their business during the year.

Economic Factors– Increase in contribution of insurance to the GDP– Increase in gross domestic savings as a

percentage of GDP– Decline in savings in the form of insurance funds– Buoyancy in the Indian stock market– Insurance business (first year premium) grew at

47.93% in 2005–2006

Political Factors– De-tariffing of general insurance with effect

from 1st Jan, 2007– Safety valve imposed by the IRDA, of not

changing the terms and conditions of thepolicies till 31st Mar, 2008

– Investment regulations– Social and rural sector obligations

Technological Factors– Building up data warehouses– Increase in CRM solutions– Increased use of online portals for policy

purchase, renewal, claims processing etc.– Impending importance of technology to lower

costs in a de-tariffed scenario– Grievance redressal cells– Online Complaints reporting mechanisms with

the regulatory body– Using bank databases to cross sell insurance

products through bancassurance

Social Factors– Insurance penetration stood at 2.53% for life

insurance, 0.62% for non-life insurance,thus huge scope

– Huge middle class– Increase in lifestyle diseases– Higher demand for old age provisions– Increasing awareness among the population– Growth of insurance catering to certain

groups – Islamic insurance, micro insuranceetc.

PEST

– Buoyancy in the Indian stock market due to strong macroeconomic fundamentals,robust corporate results, positive investment climate and sound business outlook.

– Insurance business (first year premium) grew at 47.93% in 2005–2006, surpassingthe growth of 32.49% in 2004–2005

Technological and Social Factors: These are self-explanatory in the illustration. The“Grievance Redressal Cell” of the technological factors will be elaborated upon insection 1.3.

De-tariffing and its consequences

A tariff market is one where the premium rates, policy terms and deductibles are con-trolled and to be applied uniformly by all the underwriters. The market portfolio mixfor general insurers on tariff/non-tariff covers during the tariff regime were as fol-lows: 73.09% of the overall premiums were tariffed, and 29.91% was non-tariffed.Health formed a part of the non-tariffed portfolio which implied that insurers couldset their own prices and adopt flexible policy terms and conditions.

The primary effects of the tariffed regime were

– Cross subsidization: Profitable businesses like fire and motor which were tariffedpaid for un-profitable businesses of a company like health and marine cargo insur-ance (which were non-tariffed), thus making these (health and marine cargo insur-ance) available to customers at throw away prices. The profitable businesses, thuscross-subsidized the unprofitable businesses. This is also the core reason for theabsence of any standalone health insurance company until 2006, because such aninsurer would not be able to compete with the general insurers, for whom healthinsurance was one of the businesses that could be easily subsidized despite exorbi-tant claim-to-premium ratios at 130%.

– “Good” customers paid for “bad” customers: In a tariffed regime, where priceswere uniform, all the “good” customers, who had a better risk management historywith lower risks and thus consequently fewer claims, ended up paying for “bad”customers with higher risks. In fact the tariffed regime, induced complacency inthe customer, who had no incentive to improve their risk profile or management ashe would get reimbursed anyway.

– Underwriting skills smothered: The biggest defect of the tariffed regime was thecomplete dearth of underwriting skills. For businesses that were tariffed, under-writing was rule based rather than risk based (as it should be for insurance); and forbusinesses that weren’t tariffed, underwriting did not matter on account of depend-ency on the profitable tariffed businesses. Thus although underwriting is the core

1.3 Dynamic Market Environment for Insurance in India 17

activity defining the profitability of an insurance company, the tariffed regime nul-lified its significance.

– Complete lack of quality data: Risk profiling, customer history, data warehouse,data mining, management information systems were deemed insignificant and justinvestments with a rather negative net present value because of their irrelevance tothe pricing of an insurance product; thus subsequently leading to complete lack ofquality data available to insurers and intermediaries, and reliance on outdated in-formation that was provided by the Tariff Advisory Committee.

The movement from a tariffed to a de-tariffed regime will occur in a phased manner

In order to prevent cut-throat competition with the lifting of tariffs, the IRDA has de-cided to move from the tariffed to a de-tariffed regime in a phased manner. Thisphased process would act as a safety valve for insurers and help preserve the sanctityof the industry.

– Phase 1: • What is it? Opening up of the free market pricing policy with effect from 1st of

January, 2007. However, insurers cannot change their policy terms and condi-tions during this phase (of the businesses that belonged to the tariffed part of theportfolio mix)

• Process of Preparation in this phase includes:• – Data compilation and stratification• – Data warehousing, analysis of data and sending data to the appointed actuary

– Phase 2:• What is it? With effect from 1st April, 2008, insurers can change their policy

terms, conditions, wordings, tariff rules and regulations. This phase would in-clude launching new or redefined products.

• Process of Preparation in this phase includes:• In order to launch new products with options to choose perils and add-on covers

and considerations on “what are the most urgent requirements of the customer?”,define product concepts like [a] policies purely on first loss covers, [b] policieson selective perils basis, [c] policies considering agreed value covers etc.

Effects and Consequences of Lifting of Tariffs

In order to understand the consequences of de-tariffing, I will present its impact onvarious facets of the Indian insurance archetype that would invariably alter the trailof progression of the industry as a whole. This account of effects would also serve inunderstanding the nature of change and trajectory of industry evolution on Anita McGahan’s Model for strategies in dynamic environments.

18 1 Insurance Industry in India

Please see the illustration below depicting the various facets while considering ef-fects of de-tariffing.

1.3 Dynamic Market Environment for Insurance in India 19

Figure 10: Facets while considering the effects of de-tariffing (Author)

Please find below Porter’s 5 Forces for industry analysis, as there are several ele-ments in the 5 forces analysis that overlap with the current rage that de-tariffingbrings. Thus they will have to be discussed in congruence.

Note with respect to the Porter’s 5 Forces Illustration: All aspects related to de-tar-iffing are marked with a “D” followed by a “+” sign indicating it has a positive effecton insurers, “–” sign indicating it has a negative effect on insurers, and “+/–” sign if ithas both positive and negative effect on insurers. The points in the illustration that arenot preceded with a “D” are unrelated to the de-tariffing aspect and would have pro-gressively occurred irrespective of the de-tariffed scenario.

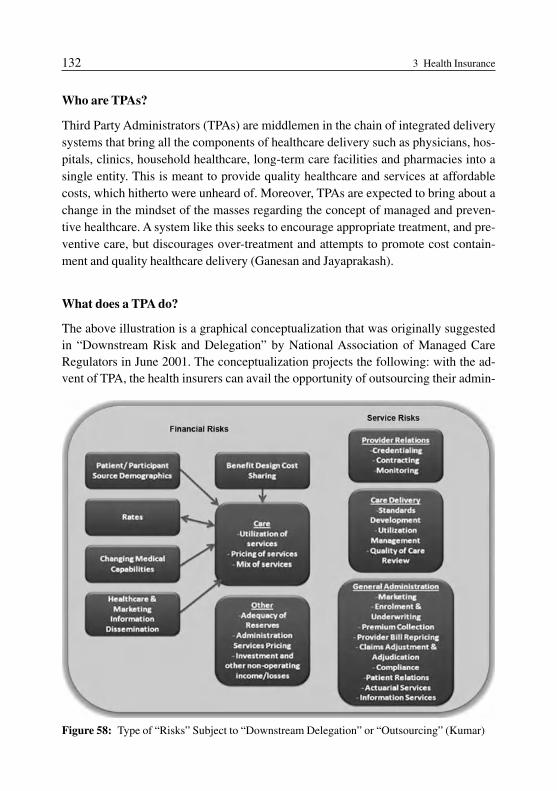

TPA = Third Part AdministratorFacets explicated

Marketing Facets

– Pricing: • Industry experts predict that fire and motor premiums would go down by

30–35% (these were part of the tariffed, thus profitable businesses). This is at-tributed to the tendency of players to undercut one another, due to free market

pricing policy, thus resulting in some type of cut-throatism and a price war. [Ini-tial ill effects of a de-tariffed scenario – Industry Rivalry, Porter’s 5 forces.]

• Health and marine premiums will have to rise due to end of cross-subsidizationby their profitable counterparts (motor and fire).

• There will be a rise of sophisticated price segmentation methods: for example,having location based pricing in place, people in cities would pay higher premi-ums than those in suburbs.

– Products:• De-tariffing will propel competition because of a need to differentiate, thus pro-

mote heightened innovation in product design; for example, there may be healthinsurance products developed for people with specific hereditary diseases whichwere not in existence earlier.

– Distribution channels:• Need of an innovative combination of distribution channels to increase the num-

ber of touch points with the customers and maximize customer reach via channeleffectiveness.

20 1 Insurance Industry in India

Figure 11: Porter’s Five Force Analysis of the Insurance Industry (Author throughaccumulated readings and research)

Buyer/Customer Power✔ D+ Widening product range

✔ D– Increasing pricesensitivity of customers

✔ D± Increased competitionin a de-tariffed scenario

✔ D– Large corporate clients✔ D– Switching costs

✔ D+ Good risk customerwill not longer subsidize bad

risk customer✔ Low penetration, thus less

number of buyers✔ Yearly renewal for non-life

products✔ Multiple distribution

✔ Sale of Bancassurance

Suppliers’ Power✔ D– Reduced commission

offered by reinsurancecompanies with de-tariffing

✔ D- Increased efficiency ofBrokers necessitated

✔ Limited actuaries in themarked

✔ Reinsurance concentration✔ Lock in & high switching

costs for firms✔ Cession to the National

Insurer✔ Dependence on IT providers

✔ Dependence on TPAs✔ Orphaned customers due

to high attribution ofagents

Barriers to Entry✔ FDI Ceiling

✔ Capital requirements✔ Experience with respect to

understanding of the market✔ Elaborate distribution requirements

✔ “Lock-in” of buyers

Threat of Substitutes✔ D– Increased competition, thus

substitutes due to de-tariffing✔ Government pension schemes

✔ Tax savings instruments✔ Emerging substitutes

✔ Switching costs of customers✔ Dependence on Children in rural

India

Industry Rivalry✔ D– Initial effects ofDetarifed scenario

✔ Industry concentration in bothlife and non-life

✔ Foreign players entering✔ Restricted competition due

to regulations✔ Solvent Margin requirements

✔ Low penetration ofinsurance

• Achieving operational efficiencies in channels would be inevitable; as priceswould go down initially and costs will have to be kept at an all time low, if thestipulated solvency margins have to be maintained.

Customers

– “Good” customers will cease to subsidize “bad” customers, as each customerwould pay premiums based on his/her risk profile [Good customers will no longersubsidize bad customers – Buying Power, Porter’s 5 Forces]

– Due to de-tariffing, competition would heighten and consequently result in newand innovative products, thus resulting in increased consumer choice and height-ened customer centricity and service. [Increased competition in a de-tariffed sce-nario – Buying Power, Porter’s 5 forces]

– Price sensitivity of customers will increase in areas where competition results in aninitial price fight. [Increasing price sensitivity of customers – Buying Power,Porter’s 5 forces]

– The obvious consequence of the de-tariffed regime is increasing customer aware-ness and aggravated premium tension.

– The moral hazard will end with high risk customers coming in the spot light asthey can no longer find “cover” under the low risk customers.

– The information asymmetry would reduce as customers would be willing to dis-close more information to get a better risk rating in case they are good customers;thus complete and furnished information from customers would be rewarded withdiscounts.

– Policyholders would be incentivized to improve their risk portfolio, as doing sowould be compensated for.

– Large corporate clients’ bargaining power would be enhanced in the fire and motorportfolio where prices will be slashed; however, corporate clients would be lost in thehealth insurance area where prices will have to be increased to ensure the profitabilityof these businesses. [Large Corporate Clients – Buying Power, Porter’s 5 forces.]

Reserving

– The IRDA (regulatory authority) has stipulated regulations with respect to the sol-vency margin that companies must adhere to; solvency margin is the extent towhich assets need to be over the liabilities for the insurer. In lieu of the same, insur-ers cannot indulge in price wars to the extent that their solvency margins will behurt, thus serving as a necessary evil. Moreover, insurers are answerable to theshareholders for their bottom line, which is why they cannot afford to let it get af-fected too drastically.

1.3 Dynamic Market Environment for Insurance in India 21

Regulations

– The IRDA (regulatory authority) has disallowed cross subsidization of businessesin light of the solvency margin argument; however, if insurers do need to crosssubsidize, they can do so by presenting a proposal to the IRDA with a justificationfor the same.

– Actuaries have been appointed to insurers to help them in their underwriting activ-ities and rate making process.

– The phased process sequenced by the IRDA acts as a safety valve (as discussedearlier).

Reinsurance

– If competition based on price increases, it would imply reduced prices, howeversame liabilities or better put, increased liability for the same price suggests that theinsurers would pass on more liabilities to the reinsurer (who in turn gives commis-sion to the insurer for the percentage of premium received and obviously even car-ries partial risk of the insurer in return). More liabilities to the reinsurer withoutcorresponding increase in premium would reduce the commissions that insurerscan get out of reinsurers. [Reduced commission offered by reinsurers in case of de-tariffing – Supplier’s Power , Porter’s 5 forces.]

Investments

– Price reduction by insurers would call for more efficient management of their in-vestment portfolio and thus cautious and conscientious pooling of resources toreap maximum returns, in order to be able to augment their bottom line and sustaintheir solvency margins.

Risk Management and Underwriters

– The switch from a tariffed to a de-tariffed regime calls for a transition from rulebased underwriting to risk profile based underwriting.

– This would imply classification of risks into class rated risks and individual ratedrisks.• Class rates: where risks of a class have similar risk factors and individual varia-

tions are not financially significant; for example motor risks in India• Individual rates: where each risk has significant variation in risk factors and the

financial magnitude justifies individual rating – for example engineering risks(Bhattacharya).

– More time and money will need to be invested in risk profiling through and datacollection.

22 1 Insurance Industry in India

– Low pricing will not be the basis for creating the best company; it will be based up-on risk acceptance, service delivery standards and commensurate remunerativepricing.

– Efforts will have to be made to overcome the steep learning curve with respect tosophistication in risk management practices.

– Underwriters will have to team up with the marketing department and rate policiesbased on claims data collected at a micro level which would include [a]productlevel knowledge per se, [b]enhanced customer domain knowledge and correspon-ding merit rating of the same

– Use of IT and innovative techniques to improve decision making via data ware-housing, data mining and other business intelligence systems augmenting microlevel data analysis will have to be used to improve efficiency and quality of deci-sion making.

Brokers