New Zealand WT/TPR/S/20 Page 77 - WTO Documents Online

47

New Zealand WT/TPR/S/20 Page 77 IV. TRADE POLICIES AND PRACTICES BY SECTOR (1) Overview 1. New Zealand's trade and sectoral reforms have helped make it one of the world's most open and dynamic economies. At the time of its previous Trade Policy Review in 1990 New Zealand was in the midst of vigorous economic reform. It had removed most import licensing requirements, implemented initial tariff cuts, greatly reduced subsidies, and commercialized or privatized many State- owned enterprises. The rapid pace of reform has subsequently been maintained. Protective import licensing and other quantitative trade measures have now been abolished, whereas just over a decade ago nearly all imports required licences. Substantial reductions have brought tariffs to near the OECD average; previously, tariff levels were triple those in most other OECD countries. Direct production or trade-related assistance to agriculture and industry has been eliminated. With few exceptions, State- owned commercial operations have been placed on a commercial footing; many of these operations have been privatized, with revenues applied to the public debt. 1 2. Reforms have touched all areas of the economy, with the primary and services sectors being opened along with - and often in advance of - the industrial sector. This has positive implications for the efficient allocation of resources across sectors, but is also important because of intersectoral linkages. The increased efficiency resulting from reform in services is important to the farming industry, for example, because services such as transport and finance account for substantial shares of farm costs. 3. The most important remaining trade measures are of two types: tariffs and the single-seller export marketing boards in agriculture. The average tariff of 6.2 per cent is moderate, but the average for lines with non-zero rates exceeds the OECD average, indicating a greater unevenness in the tariff. 2 The extensive protection provided a handful of industries comes at a cost to others, particularly those with export interests. 3 New Zealand has a schedule in place to greatly reduce remaining tariffs by 2000; a review in 1998 is to determine how to move towards the elimination of tariffs under a further unilateral tariff reduction programme. 4. New Zealand's strategy for economic growth includes maintaining an open and competitive economy to increase the flow of information and ideas, to increase efficiency and to stimulate innovation. It is not clear that this strategy has been fully followed with respect to the export marketing of agricultural products, however. Marketing boards influence or control the export of some 80 per cent of the exports of agricultural products, which comprise half of merchandise exports. There are no plans to eliminate the export monopolies that have been granted to several of these boards. 1 Important domestic reforms have also been implemented, such as in the labour market and the public service, easing the move of productive resources to more profitable uses or otherwise increasing economic efficiency. 2 According to the Ministry of Commere (1994a), in 1993 New Zealand's average tariff rate for those lines subject to duty was, at 16.6 per cent, the second highest among OECD countries and well above the OECD average of 10.6 per cent. While New Zealand's rates have been cut more rapidly than those in other countries, in 1996 the average m.f.n. rate for lines subject to duty, now equal to 14.6 per cent, is still probably among the highest in the OECD. 3 Estimates cited by the authorities suggest that the 1996/97 tariff effectively imposes a tax of some 5 per cent on New Zealand's export sector (Ministry of Commerce, 1994a).

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of New Zealand WT/TPR/S/20 Page 77 - WTO Documents Online

New Zealand WT/TPR/S/20Page 77

IV. TRADE POLICIES AND PRACTICES BY SECTOR

(1) Overview

1. New Zealand's trade and sectoral reforms have helped make it one of the world's most openand dynamic economies. At the time of its previous Trade Policy Review in 1990 New Zealand wasin the midst of vigorous economic reform. It had removed most import licensing requirements,implemented initial tariff cuts, greatly reduced subsidies, and commercialized or privatized many State-owned enterprises. The rapid pace of reform has subsequently been maintained. Protective importlicensing and other quantitative trade measures have now been abolished, whereas just over a decadeago nearly all imports required licences. Substantial reductions have brought tariffs to near the OECDaverage; previously, tariff levels were triple those in most other OECD countries. Direct productionor trade-related assistance to agriculture and industry has been eliminated. With few exceptions, State-owned commercial operations have been placed on a commercial footing; many of these operationshave been privatized, with revenues applied to the public debt.1

2. Reforms have touched all areas of the economy, with the primary and services sectors beingopened along with - and often in advance of - the industrial sector. This has positive implicationsfor the efficient allocation of resources across sectors, but is also important because of intersectorallinkages. The increased efficiency resulting from reformin services is important to the farming industry,for example, because services such as transport and finance account for substantial shares of farm costs.

3. The most important remaining trade measures are of two types: tariffs and the single-sellerexport marketing boards in agriculture. The average tariff of 6.2 per cent is moderate, but the averagefor lines with non-zero rates exceeds the OECD average, indicating a greater unevenness in the tariff.2

The extensive protection provided a handful of industries comes at a cost to others, particularly thosewith export interests.3 New Zealand has a schedule in place to greatly reduce remaining tariffs by2000; a review in 1998 is to determine how to move towards the elimination of tariffs under a furtherunilateral tariff reduction programme.

4. New Zealand's strategy for economic growth includes maintaining an open and competitiveeconomy to increase the flowof information and ideas, to increase efficiencyand to stimulate innovation.It is not clear that this strategy has been fully followedwith respect to the exportmarketing of agriculturalproducts, however. Marketing boards influence or control the export of some 80 per cent of the exportsof agricultural products, which comprise half of merchandise exports. There are no plans to eliminatethe export monopolies that have been granted to several of these boards.

1Important domestic reforms have also been implemented, such as in the labour market and the public service,easing the move of productive resources to more profitable uses or otherwise increasing economic efficiency.

2According to the Ministry of Commere (1994a), in 1993 New Zealand's average tariff rate for those linessubject to duty was, at 16.6 per cent, the second highest among OECD countries and well above the OECD averageof 10.6 per cent. While New Zealand's rates have been cut more rapidly than those in other countries, in 1996the average m.f.n. rate for lines subject to duty, now equal to 14.6 per cent, is still probably among the highestin the OECD.

3Estimates cited by the authorities suggest that the 1996/97 tariff effectively imposes a tax of some 5 percent on New Zealand's export sector (Ministry of Commerce, 1994a).

WT/TPR/S/20 Trade Policy ReviewPage 78

(2) Primary Industries

5. New Zealand's economy is largely resource-based. Primary industries, including farming,fishing, forestry and mining, account for about 11 per cent of GDP and some 13 per cent ofNew Zealand's total exports of goods and services. These numbers, however, tend to understate theimportance of the sector; for example, if inputs into processed goods are taken into consideration,then primary products comprise at least a quarter of exports.4

6. Farming, the largest part of the sector, has contracted slightly in recent years, while the otherprimary industries have grown rapidly. From 1984 to 1995 the GDP share of farming fell from7.3 per cent to 5.2 per cent; however, the share of forestry and logging increased from 1.2 per centto 3.9 per cent, that of mining and quarrying increased from 0.8 per cent to 1.1 per cent, and thatof fishing increased from 0.3 per cent to 0.4 per cent. The expansion of these industries has beendriven by export demand. The export volume of forestry products, as measured by the roundwoodequivalent, increased by 22 per cent from 1991 to 1995; as the available wood supply is anticipatedto nearly double by 2005, the volume of exports is expected to continue growing. The fish sectorproduces predominantly for the export market; some 80 per cent of production was exported in 1995,accounting for about 5.5 per cent of New Zealand's merchandise exports.

7. Market-oriented reforms in the primary sector, particularly in agriculture, were at the forefrontof economywide reforms begun in the mid-1980s. The rôle of the Government in the sector has beensharply curtailed. The outstanding exception is the continued use of marketing boards for the exportof a number of important agricultural items, including apples, pears, kiwifruit and dairy products.

(i) Farming

8. Farming contributed 5.0 per cent of GDP in 1995/96, down from 6.1 per cent in 1991/92,and accounts for some 9 per cent of employment (Table IV.1).5 Farming is at the heart of the agro-industrial sector, which also encompasses farm inputs and the transport, processing, distribution andretailing of farm products. The agro-industrial sector employs 17 per cent of the labour force; itcontributes 15 per cent of GDP and 54 per cent of merchandise exports.

9. New Zealand's farming industry is primarily livestock-oriented, with animal products responsiblefor some two thirds of the value of agricultural production. Within the livestock industry, since 1991the share of dairy has increased while that of wool has declined. Dairy production accounted for31 per cent of the total value of agricultural output in 1995/96, while wool (8 per cent), sheep andlambs (9 per cent) and beef (12 per cent) also held important shares. Vegetables, fruit, nuts and otherhorticulture together added 13 per cent of total agricultural output.

4In 1991, 14 per cent of exports were farm products embodied in processed food; processed food productscomprised 35 per cent of exports and farm-product content was 40 per cent of the cost of the products. Similarly,about 2 per cent of exports were primary products incorporated in textiles and clothing exports. Data basedon Inter-industry accounts for 1990/91 in Statistics New Zealand (1995b).

5Ministry of Agriculture (1996).

New Zealand WT/TPR/S/20Page 79

Table IV.1

Agricultural production and exports, 1990-96a

($ millions)

Product 1990 1991 1992 1993 1994 1995 1996c

Wool 1,252 832 793 737 724 933 864

Wool exports 1,424 1,044 1,173 985 1,134 1,322 1,099

Sheep and lambs 865 885 845 1,037 1,216 1,120 953

Lamb exportsMutton exports

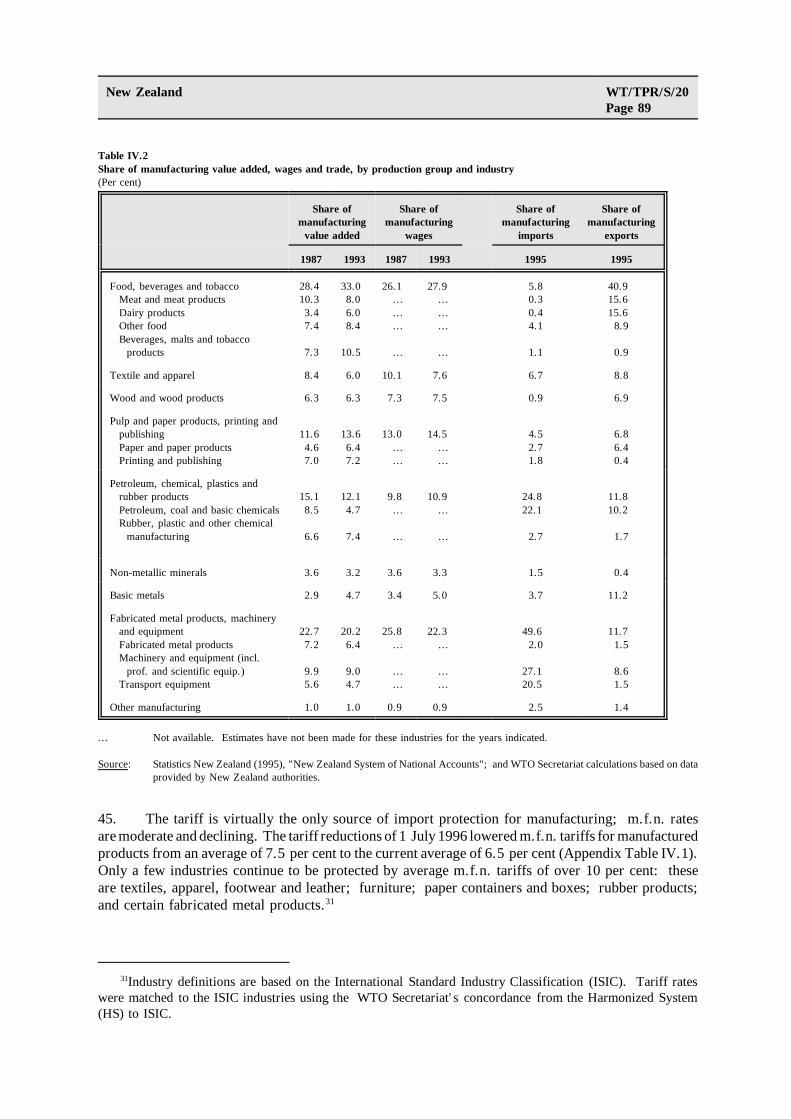

958136

978172

1,177171

1,209180

1,085166

1,044d

1531,139d

198

Cattle 1,187 1,376 1,443 1,559 1,540 1,394 1,137

Beef and veal exports 1,092 1,284 1,451 1,419 1,384 1,161 1,054

Dairy products 2,166 1,641 2,235 2,536 2,569 2,585 3,270

Dairy exports 2,534 2,485 2,897 3,369 3,563 3,473 3,717

Fruits, vegetables, nuts and otherhorticulture 1,201 1,257 1,402 1,374 1,269 1,337 1,351

Fresh kiwifruit exportsApples and pears; nashi exports

Total fruit and vegetable exports

539218

999

520305

1,069

506335

1,167

370349

1,026

381320

1,076

321491

1,195

263534

1,291

Agricultural services 731 760 807 873 950 1,006 993

Otherb 945 838 835 989 1,248 756 631

Total agricultural output 9,284 8,488 9,274 10,135 10,515 10,246 10,336

Total agricultural based exports 8,784 8,752 9,993 10,267 10,559 10,815 10,583

Agriculture's share of GDP (per cent) 6.4 5.4 6.1 5.8 5.6 5.2 5.0

Agriculture-based exports, share oftotal merchandise exports (per cent) 60.5 58.1 58.2 56.3 55.2 53.5 52.6

a For production, year ending 31 March; for exports, year ending 30 June.

b Includes change in the stock of livestock, sales of live animals and non-farm income.c Preliminary.

d Total sheepmeat.

Note: Production figures refer to farmgate values while export figures refer to processed products.

Source: Ministry of Agriculture (1996).

10. The farming industry has close economic links to other industries, particularly food manufacturingand transport. Also, as an export dependent industry producing relatively undifferentiated products,farming is influenced by the macroeconomic situation, and particularly exchange rate movements.Thus, farmers and farm groups take an active interest in trade policy and its sectoral aspects, and havebeen a force behind the Government's economic reforms. Prior to the 1984 elections the FederatedFarmers, the major farm lobby group, sought measures to "create an environment conducive to economicgrowth and sustainable low inflation with a minimum of Government intervention in the economy",including limits on export incentives, the introduction of a floating exchange rate régime, labour marketreforms, the removal of all import licence requirements, the reduction of tariffs, and liberalization

WT/TPR/S/20 Trade Policy ReviewPage 80

of the transport sector.6 During a 1994 review of tariff policy, the group called for the completeelimination of tariffs by July 1997.

11. Another matter of fundamental importance to New Zealand's farming industry, given the highshare of exports in total production, is access to foreign markets and the impact of other countries'agricultural subsidies in third markets. While the Uruguay Round Agreement on Agriculture is ofgreat value to New Zealand, substantial market access restrictions and subsidies still remain, and arelikely to do so even after full implementation of the Uruguay Round. Based on economic studies,the authorities believe that such remaining distortions will cost New Zealand the equivalent of some2 per cent of GDP annually.

(a) Agricultural policies

12. New Zealand's agricultural industry is market driven, with very liberal import and domesticpolicy régimes. This is the result of a rapid dismantling of agricultural support with the start of reformsin the mid-1980s. Agricultural subsidies as a share of GDP were reduced from 3.8 per cent in 1983to 0.9 per cent in 1987 and 0.1 per cent in 1994. New Zealand's producer subsidy equivalent (PSE),a measure of assistance to farmers, fell during this period from its peak of 33 per cent to 3 per cent,a figure much lower than that of any other OECD country.7 However, the export of a number ofproducts, including dairy products, continues to be controlled by marketing boards.

Import policies

13. Tariffs are the only means of intentional import protection for New Zealand's agriculturalproducts.8 No import licensing is used, there are no tariff quotas or similar trade-restrictive devices,and all import-related powers once held by producer boards have been eliminated.9 Tariffs are generallylow, with m.f.n. rates averaging 1.5 per cent and a maximum rate of 10.5 per cent for farm-levelagricultural and livestock products (ISIC 11) (Appendix Table IV.1). Imports of most agriculturalproducts, including live animals, beef, sheepmeat, butter, cheese, fresh fruit and most cereals, enterduty free. Moderate tariff rates remain on some manufactured food products (section 3), althoughthese are scheduled to be reduced; by 2000, all m.f.n. tariffs on primary, semi-processed or processedproducts of agriculture, forestry or fisheries will be 5 per cent or less. Although most New Zealandagricultural industries are open to international price signals as a result of this liberal import policy,sanitary requirements, which according to the authorities are justified under the WTO Agreement onSanitary and Phytosanitary Measures, have the effect of partly isolating the New Zealand markets foreggs and live, fresh and frozen poultry meat from the world markets for these products.10

6New Zealand Federated Farmers (1984).

7According to the authorities, agricultural support was granted partly to compensate farmers for protectionin other sectors of the New Zealand economy.

8Sanitary and phytosanitary measures are discussed in Chapter III(2)(vi).

9The last such restriction, the control of the Hop Marketing Board over imports of hops, was eliminatedon 1 January 1995; the Apple and Pear Marketing Board's control over apple and pear imports had been revokeda year earlier.

10OECD (1995a).

New Zealand WT/TPR/S/20Page 81

Domestic policies

14. New Zealand does not provide any production-linked support to farmers nor any subsidiesfor the use of agricultural inputs. The Government has progressively reduced its involvement in domesticsupport measures, and remaining public sector services are generally provided on a user-pays basis.Virtually all irrigation schemes have recently been privatized.11 Meat inspection and certification isprovided on a fully user-pays basis by the Ministry of Agriculture. Government extension andconsultancy services to farmers, and some aspects of the monitoring of farm sector performance, havebeen privatized.12 Remaining support for public sector services is limited to animal welfare and pestand disease control; Government expenditure in these areas in 1994/95 was $52 million.

15. The Government retains several agri-environmental policies and programmes with objectivesthat include sustainable development, soil conservation and water quality.13 The authorities estimatethe total cost of agricultural environment-related programmes, including the $52 million cited above,at some $140 million, with about 40 per cent of this relating purely to environmental protection andthe rest attributable to safeguarding agriculture against environmental forces, such as pests and floods.While these policies and programmes remain important, the authorities also note that the environmentalbenefits of agricultural policy reform have been substantial, and have included the reduced use offertilizer and pesticides; an increase in afforestation, due largely to planting on former farmland;and, as a result of a decline in sheep numbers, a less intensive use of hill-country pasture.

16. According to the authorities, climatic disaster relief, which is partly community-funded, isthe only potential source of direct payment to farmers. The authorities are of the view that disasterrelief programmes can encourage unsustainable land use and contribute to environmental degradation,and the Government has therefore reduced its rôle in this area.14 In general, farmers are expectedto use private insurance or manage their own risks, and the Government has reduced its commitmentaccordingly in recent years.

17. Under the Commodity Levies Act 1990, industry organizations may, following a referendum,impose compulsory levies on commodities in order to undertake certain activities or to provide fundsfor the organization. Eligible activities include research, market development, market promotion, andhealth measures, but exclude trading or commercial activities. As at July 1996, commodities and theirmaximum levy rates included: asparagus (0.15 per cent), avocados (3 per cent), eggs (5 cents perchick), export squash (0.15 per cent), fresh tomatoes (1 per cent), processing tomatoes (0.15 per cent)and winemaking grapes (1.5 per cent).

18. Two marketing boards retain active or latent powers to regulate the domestic marketing ofsome products; these powers are currently under review. The Hop Marketing Board controls the

11Among the 50 irrigation schemes, one remains under the ownership of the Crown. Negotiations on salesof the other schemes took place in 1988-90, and payments and other obligations were completed in 1996.

12The Government contracts for the provision of monitoring and policy-advice services with the firm thatit privatized. The privatization of services in 1996 was preceded by a user-pays approach initiated in 1988 andthe commercialization of a business unit within the Ministry of Agriculture in 1991. Government expenditurein this area has fallen from $28 million in 1988 to $3 million in 1996.

13OECD (1995b).

14OECD (1995b).

WT/TPR/S/20 Trade Policy ReviewPage 82

domestic (and export) marketing of hops, while the Raspberry Marketing Council has the authorityto, but does not currently, fix domestic marketing quotas or otherwise control the domestic market.No other marketing boards have active or latent powers with respect to domestic marketing.

Export policies

19. Most of New Zealand's agricultural output is exported, either directly or indirectly, makingthe export marketing structure potentially important for the national economy. For some products,particularly dairy (25 per cent) and kiwifruit (27 per cent), New Zealand accounts for substantial sharesof world trade. Its export marketing structure may thus affect parts of the world market for theseproducts.

20. New Zealand has neither agricultural export taxes or subsidies.

21. Five entities exercise export market monopolies for their products (Chapter III(3)(iii)). Theseare the Apple and Pear Marketing Board, the Dairy Board, the Hop Marketing Board, the KiwifruitMarketing Board (other than to Australia) and the Raspberry Marketing Council.15 The HorticultureExport Authority licenses exporters in accordance with export marketing strategies developed by producerand exporter groups. In addition, the Game Industry Board, the Meat Producers Board and the WoolBoard have regulatory authority that includes export marketing and licensing; however, they do notexercise their potential control over export operations.16 Each of the above bodies is a statutory entitythat, with the exception of the Horticulture Export Authority, operates without government assistanceand isdirectly or indirectlyproducer-controlled. In sum, these entities directly control, or arepotentiallyable to influence, the export of about 80 per cent of NewZealand's agricultural and horticultural exports.This export marketing structure, and especially the rôle of single-seller export marketing boards, hasbeen criticized on several grounds, particularly that of efficiency (Box IV.1)

22. In many cases the Boards' activities require exemptions from provisions of New Zealand'scompetition legislation, the Commerce Act (Chapter III(5)(ii)). This exemplifies the exceptional characterof the Boards withinNew Zealand's otherwise very competition-oriented framework. The DairyBoardAct 1961: (i) allows the Dairy Board to prohibit, restrict and control the export of any other entity;(ii) gives the Board special powers in the acquisition and marketing of dairy products for export; and(iii) sets formulae for the determination of prices paid by the Board to dairy product manufacturers.The Apple and Pear Marketing Act 1971 contains exemptions from the Commerce Act allowing theBoard: (i) to establish export standards for apples and pears; (ii) monopoly powers over the exportingof these products; and (iii) to fix prices for the apples and pears that it purchases. Export-relatedpowers of the Meat Producers Board and the Wool Board are expected to be made explicitly exemptfrom parts of the Commerce Act by the Producer Board Acts Reform Bill currently being consideredby Parliament.

15The Apple and Pear Board, Dairy Board and Kiwifruit Board can grant export consent to other entities;however, to date, exports by other entities have not accounted for a substantial share of exports of the respectiveproducts.

16The Wool Board and Meat Producers Board do, however, set export standards for their respective products,and the Meat Producers Board does control the export of meat to restricted access (tariff-quota) markets. TheProducer Board Acts Reform Bill would eliminate the export marketing powers of the Meat and Wool Boardsto acquire and sell products. The export licensing powers of the Wool Board would also be eliminated, but theMeat Board would retain its powers to restrict exports, particularly to those countries that have market accessrestrictions.

New Zealand WT/TPR/S/20Page 83

Box IV.1 New Zealand's single-exporter marketing boards

New Zealand's single-exporter marketing boards seek to maximize export returns for the benefit ofdomestic producers. Proponents of the single-seller approach argue that in the highly-distorted worldmarkets for agricultural products, a single seller able to set differential prices will be able to generatehigher revenues and to pass these on to producers.

This may be the case for a single seller exporting a product into a market protected by a bilateral tariff-rate quota. Under competition, the product would be exported from New Zealand at or near the worldmarket price. A monopsonistic exporter, however, could probably sell at a higher price; economic rents- the difference between the world market price and the distorted internal price in the protected market -could then be collected mainly by the exporting country rather than the importing country. This situationmay exist for exports of butter to the European Union (EU) and of beef to the United States, but thereare few other examples involving New Zealand. Even when this is the case, the importing country mayset the in-quota tariff at high rates, so as to effectively collect these economic rents as tariff revenue.

The single-seller approach might also be advantageous to New Zealand if it were the only, or thepredominant, exporter on the world market. New Zealand is not, however, a "large" exporter on theworld market for any broad product categories. A 1993 Ministry of Agriculture report stated thatNew Zealand's export share on world markets suggested "exporters are not in a position to influencegreatly the returns received for their primary products on world markets" (MAF, 1993). This reportnoted that other factors also determined whether New Zealand exporters could influence their prices.However, the notion that New Zealand might exercise market power to positively affect its export priceshas been challenged by many observers, and the authorities have indicated that the Dairy Board is a"price-taker" in all markets and for all products.

The advantages to New Zealand of single-seller boards may thus be doubted, while there are probablyseveral disadvantages of such boards.

First, the system can lead to allocative inefficiency. Producer returns may be based on a bundle ofproducts rather than just those products sold by the producer to the marketing board. This bundle couldconsist of several different farm-level products, or of a mix of farm-level products and elements ofmarketing, packaging, processing and other services engaged in by the board. In either instance, afarmer receives a price based on some average of the components of the bundle, rather than a price equalto the additional revenue that his production would bring. These distorted market price signals can leadfarmers to allocate their resources inefficiently.

A second possible disadvantage, noted by MAF (1993), is that statutory monopolies face lesscompetition. This may reduce incentives to contain costs of preparing and processing products forexport. The influence of competition on efficiency has been an important motivation behind reforms inother areas of the economy. This factor has not, however, received widespread attention in the exportmarketing of agricultural and horticultural products.

It has also been suggested that monopolistic marketing boards, by preventing or restricting entry intoexport marketing, may suppress the use of other strategies and thus reduce innovation. Examples ofmissed marketing opportunities have been cited, although it remains difficult to assess the economic costsof reduced innovation.

Source: Hussey (1992); Kerr (1996); Ministry of Agriculture and Fisheries (1993); OECD (1996).

WT/TPR/S/20 Trade Policy ReviewPage 84

23. The objective of the Apple and Pear Marketing Board is to maximize the total long-term exportincome of the domestic apple and pear industry. Its main functions under the Apple and Pear MarketingAct 1971 are to acquire, export and market all New Zealand-grown fresh apples and pears that meetits export standards and to set the prices paid to growers for export-standard apples and pears. TheBoard sets prices for various sizes and varieties of apples and pears based largely on its expected returnfor the size and variety of the fruit on the world market. It may permit other traders to undertakeexporting; such consent is conditional on the fruit, country of destination, and sometimes the specificexport customer. In this case, charges are levied, largely based on the size of the export shipment,to recover the Board's processing and other costs, to a limit of $12,000 in charges.17

24. Under the Dairy Board Act 1961, the New Zealand Dairy Board controls almost all dairy productexports.18 Dairy exports accounted for 18 per cent of New Zealand's merchandise exports in 1995/96.While the Board may grant export permission to other entities, and guidelines for doing so have beenpublished, some 99 per cent of dairy exports are undertaken by the Board itself.19 The Board purchasesdairy products from New Zealand's several producer-owned co-operative dairy manufacturers and setsexport prices and quantities for each product and export market.20 The manufacturers purchasecompetitively from dairy farmers. The Board sets the price it pays to manufacturers as follows:quarterly, on the basis of manufacturing costs and its expected export returns from all dairy products,it calculates a guide price for fluid milk; this price is then adjusted for the cost of producing eachdairy product, and for any incentive/disincentive that the Board wishes to build-in to influence investmentor innovation.21 Annually, based upon actual receipts, a final accounting is made with each manufacturer;in practice the difference between the initial and final prices received by the manufacturers may beas high as 20 per cent, depending on movements in world prices over the season.

25. A recent OECD report notes that the Dairy Board's exclusive export control has had a clearimpact "on the structure of the existing industry and the behaviour of individual firms" because thecurrent arrangement not only restricts export marketing by domestic firms but also effectively restrictsthe ability of overseas firms to process New Zealand milk for export.22 The report notes that severalproposals have been made for reform, including: (i) the liberalization of the entitlement to export,by allowing co-operatives direct access to international markets; and (ii) privatization of the Board,with shares being allocated to existing producers. This latter approach would be relatively simple,given that the producers, through their ownership of the co-operatives, are already indirect owners.

26. The Kiwifruit Marketing Board exercises full control over kiwifruit exports, other than toAustralia. It sets export standards and acquires domestically produced kiwifruit that meets thesestandards. The prices it sets for export-standard kiwifruit are principally based on expected market

17Apple and Pear Marketing Board (1994).

18The Board's export control is limited to products with greater than 30 per cent by weight of dairy products.

19The Board has over 70 fully-owned subsidiaries, associate companies and agencies and is the world's largestmultinational dairy marketing entity (Statistics New Zealand, 1995a).

20OECD (1996).

21Thus, if the Board expects a future price rise for a particular product it may try to bring about an increasein production capacity by raising its offer price for the product.

22OECD (1996).

New Zealand WT/TPR/S/20Page 85

returns minus costs, but also on other factors, including the maintenance of stability in the industry.At the end of each season the Kiwifruit Marketing Board makes final payments to (or recoveries from)growers, thereby balancing its books for that year.

27. Horticultural producergroups formulate exportmarketingstrategies,whichmay includeplacingconditions or limitations on exports. The Horticultural Export Authority grants export licences inaccordance with the marketing strategy. Exporters that do not comply with the agreed export marketingstrategy are subject to the loss of their export licence (Chapter III(3)(ii)). The Horticulture ExportAuthority does not require an exemption from the Commerce Act.

28. The Government keeps the Boards under constant review and this has led to changes in recentyears, including inownership structures, improved accountability to farmers and producers, the removalof controls over imports, reduced controls over domestic marketing, and increased transparency ofexport consent guidelines for the Apple and Pear Marketing Board and Dairy Board. However, nosubstantial changes have been made to export-related powers and no such changes are being proposedfor the single-exporter marketing boards.

(ii) Forestry

29. Forestry is among New Zealand's fastest growing industries, with its share of GDP more thandoubling, to 2.5 per cent, in the ten years to 1993. Processing and manufacturing of forestry productsaccounted for another 2.8 per cent of GDP. Forestry and first-stage processing accounted for1.5 per cent of employment as at February 1996. Planted-production forest area grew at an annualrate of 7.5 per cent in the 1970s and 4.4 per cent a year since 1980. As a result, with these plantingscoming to maturity, production increased by some 55 per cent from 1989 to 1995.23 Supplies fromplanted production forest, which account for 97 per cent of total production, are expected to increaseby 70 per cent from 1995 to 2005.

30. Export volumes increased by 82 per cent in the period 1989 to 1995 and now account for overthree fifths of production. Primary and semi-processed forestry products accounted for 13 per centof merchandise exports in the year to December 1995, with Japan, Australia and Korea jointly accountingfor some three quarters of the total export value. With rapid increases in production and little expansionin domestic demand, the volume of forestry products exported is expected to rise sharply, perhapsdoubling by 2005. The authorities are of the view that the expected growth in global demand for woodproducts, the environmental benefits, and the advantages of land-use diversification and carbonsequestration make clear the benefit of a further expansion of planted forests, including the continuedintegration of forestry and farming.24

31. There has been substantial privatization of forestry cutting rights for planted forests. The majorreasons for the privatization of State-owned forests were the perceived conflict of interest betweenthe functions of the Forest Services. Additionally, by allowing private companies to purchase cuttingrights and thus gain more certainty over their wood supply, these vertically-integrated companies havebeen encouraged to increase their investment in processing facilities.25

23Production is measured in terms of roundwood equivalent. Data are based on the statistical releases ofthe New Zealand Ministry of Forestry; annual figures refer to years ending 31 March.

24Ministry of Agriculture and Ministry of Forestry (1994).

25Ministry of Forestry (1995).

WT/TPR/S/20 Trade Policy ReviewPage 86

32. The ownership and control structure of the forestry industry is undergoing change. About36 per cent of planted forests are owned by two public companies, 16 per cent by private companies,13 per cent by State-owned enterprises, and 33 per cent by a mix of private ownership, Maori leasesand local authorities. The State had held 48 per cent of the planted forest area in 1990 when theprivatization of forestry assets was begun; by 1995, this had declined to 19 per cent. The State'sinvolvement in the industry is now limited to the ownership of forests by four State entities, the largestof which, the Forestry Corporation of New Zealand (FCNZ), manages 12 per cent of the total plantedarea; it also has substantial processing assets.26 In August 1996, the Government announced the saleof FCNZ to a consortium for some $2.0 billion, with net proceeds of $1.6 billion, after coveringliabilities, to be used to reduce Government net foreign currency debt. A successor to the New ZealandForest Service, the New Zealand Forestry Corporation (NZFC), was established in 1987 as a State-ownedenterprise as part of a restructuring process to isolate commercial activities from non-commercialfunctions such as research, training, and regulation (Brown and Valentine, 1994). The NZFC wasrenamed Crown Forestry Management and now manages 24,000 hectares of planted forests.

33. Other than the control of some forestry assets, New Zealand has no specific forestry-relatedpolicies other than environmental measures.27 The provision of loans and grants to encourage forestryhas been discontinued, including the Forest Encouragement Grants and Loans which could be usedto clear natural forests and were discontinued in 1984. Tariffs are the only means of import protection;and m.f.n. rates are low, averaging 0.5 per cent for forestry and logging products. Tariffs on woodproducts and paper products (ISIC 33 and 34) are substantially higher, ranging to 25 per cent(Section 3(iii)).

(iii) Fishing

34. Fishing accounted for some 0.4 per cent of New Zealand GDP in 1993. Four fifths of productionis exported; seafood exports accounted for 5.5 per cent of total merchandise exports in the year endingJune 1995. Exports rose from about $10 million annually in the 1970s to $1.2 billion in 1995, andare expected by the industry to reach $2.0 billion by 2000. Australia, Japan and the United Statesare the major markets, each being the destination for about a third of New Zealand's seafood exports.However, the industry is diversifying its markets, with exports to Hong Kong, Chinese Taipei andSpain growing in importance.

35. The Government's primary policy objective for the sector is to set the framework for thesustainable use of fisheries resources. This is implemented mainly through the Quota ManagementSystem (QMS), begun in 1986. Commercial fisheries are managed under the QMS through the useof Individual Transferable Quotas (ITQs), which apply to 31 species groups in ten geographic areas

26The FCNZ was created in 1990, after the first round of asset sales, and combined seven Crown forestscovering 170,000 hectares.

27The Resource Management Act 1991 is designed to promote the sustainable management of all natural andphysical resources. The Act does not target activities but rather environmental effects, and is implemented byRegional and District Councils, which develop policies and plans for their areas. Options available to Councilsare discussed in New Zealand Forest Owners Association (1994). In addition, commercial forestry interestsand environmental and other groups have signed several agreements, including the New Zealand Forestry Accordin 1991 and the Principles for Commercial Plantation Forest Management in New Zealand in 1995. See alsoMinistry for the Environment (1991).

New Zealand WT/TPR/S/20Page 87

of New Zealand's Exclusive Economic Zone (EEZ).28 ITQs, which are fully transferable, are specifiedas a percentage of the Total Allowable Commercial Catch (TACC) for each species group and geographicarea. TACCs are set annually by the Minister of Fisheries after consultation with interested groups;179 TACCs are active. In most cases, ITQs were allocated to fishermen on the basis of demonstratedhistory anddependency on the fishery. Owners of ITQsmust beNew Zealand residents orNew Zealandcompanies that are less than 25 per cent foreign-owned.29

36. New Zealand provides no direct support to the fisheries sector. The last remaining indirectsubsidization of the fishing industry was removed in 1994 with the Fisheries Amendment Act, whichgave Government the authority to recover from the industry costs associated with providing fisheriesmanagementandconservationservices,enforcingfisheries legislation,andconductingrelevantresearch.Earlier, and particularly in the 1970s, Government loan guarantees were provided for the purchaseof fishing vessels, and to make aquacultural and processing investment. This was partly in responseto the perception that the many licensed foreign fishing vessels then working off New Zealand's coastrepresented a forgone opportunity for New Zealanders. Since then, the domestic fishing fleet has grownsubstantially and the use of foreign vessels chartered by New Zealand companies remains common.The size of licensed foreign fleets has dropped markedly. In 1983, 59,087 tonnes were harvested fromthe New Zealand EEZ by foreign licensed vessels. By 1995, this figure had dropped to 37 tonnes.

37. Foreign fleets can be licensed for New Zealand waters under New Zealand's bilateral agreements,which are in effect with Japan, Korea and Russia. In 1993/94, such access was limited to tuna species,and licensed fishing activity has been steadily falling in recent years, and is likely to be zero in 1996.

(iv) Mining

38. Mining and quarrying accounted for 1.5 per cent of New Zealand's GDP and 0.5 per centof employment in 1993. About three quarters of the sector's value added, and one quarter of itsemployment, is in the extraction of crude petroleumand, particularly, natural gas; New Zealand exportstwo thirds of its output of crude oil and condensate, but imports 80 per cent of its domestic consumption.Crude oil is exported because New Zealand's oil refinery is configured to handle crude oils heavierthan those produced domestically. The mining of minerals accounts for about a quarter of sectoraloutput, primarily gold, silver, and sand, rock and gravel. Imports of mineral products accounted for5 per cent of merchandise imports in 1993, some four fifths being crude petroleum or condensate.Exports of these products, also primarily consisting of crude petroleum or condensate, were 2 per centof New Zealand's merchandise exports.

39. Tariffs on imports of most mining products are zero and there are no other import restrictions.The only substantial tariffs are in the area of stone quarrying, clay, and sand, where m.f.n. rates average3.1 per cent; imports of these products account for 1 to 2 per cent of all mining and quarrying imports.No direct financial assistance is provided the industry. Tax concessions are offered to miners of certainminerals, including gold and silver; these allow the deduction of all exploration and developmentexpenditure in the year incurred.30 The authorities estimate that the cost of the tax concession scheme,in terms of forgone government revenue, is $7 to $10 million a year. A similar régime is provided

28New Zealand's EEZ, which was expanded in 1978 to 200 miles, is among the largest in the world.

29Under the Fisheries Act 1996, the Minister of Fisheries may allow a quota owner to have foreign ownershipof up to 40 per cent of its shares, subject to certain criteria.

30This deduction would otherwise be treated as a capital expense and be written off over a number of years.

WT/TPR/S/20 Trade Policy ReviewPage 88

for petroleum mining (allowing the immediate deduction of exploration and development expenditure),and a less generous régime is in place for coal mining (allowing the amortization of capital expenditureover the expected life of the mine). According to the authorities, the tax revenue forgone becauseof the petroleum mining scheme is small and no revenue is forgone because of the coal mining scheme.

40. The Government began in 1984 to separate its commercial activities from its policy and regulatoryfunctions in the sector. With the exception of the markets for electricity and gas, where reforms areprogressing, markets throughout the sector have been deregulated. The Coal Corporation ofNew Zealand is the only remaining State-owned enterprise involved in prospecting, exploration ormining; it operates on a commercial basis. Price controls on petroleum products were eliminatedin 1988; those on gas were among the last to be removed, having been lifted in 1993.

41. All petroleum, gold, silver and uranium inNew Zealand is owned by the Crown; othermineralsare either in Crown or private ownership. The extraction of Crown-owned minerals is controlled bypermits for prospecting, exploration and mining. Permits are allocated by the Ministry of Commerceeither non-competitively (based on an acceptable frontier offer or the first acceptable work programmeoffer) or competitively (based on staged work programme bidding or cash bonus bidding). Land owners(or occupiers) have an effective right of veto over the extraction of non-petroleum minerals, whichmay be overruled only for reasons of national interest. In the case of a permit for petroleum miningwhere the land owner and permit holder cannot reach agreement, an arbitrator may be appointed.

42. The Resource Management Act and other legislation requires certain environmental safeguardson prospecting, exploration and mining. Environmental controls are effects based, requiring all extractorsof minerals to avoid, remedy or mitigate the effects of their activities on the environment. The gas,petroleum and other mining industries are subject to the Commerce Act, including the threat ofregulation if market dominance is abused.

43. Special levies are applied on several mining and energy products. These (and the use to whichthe revenues are put) are: natural gas and coal (Energy Resources Levy (ERL), used for generalgovernment revenue); compressed natural gas and liquefied natural gas (excise tax, earmarked forthe Transport Fund, the Accident Compensation Corporation levy and the petroleum fuels monitoringlevy). Apart from the ERL, other levies and taxes listed apply to fuels sold for transportation purposes.All such levies and taxes are applied equally on domestic and imported products.

(3) Manufacturing

44. The New Zealand manufacturing sector accounted for 21 per cent of GDP and 18 per centof employment in 1995. Manufactured products comprised 86 per cent of total merchandise exportsand 96 per cent of total merchandise imports. The composition of New Zealand's manufacturing sectorand its international trade in manufactures reflects its strength in primary production. One third ofmanufacturing is in foodprocessing;manufactured food products comprise41 per centofmanufacturingexports (Table IV.2). Pulp and paper products account for 6 per cent of manufacturing value addedand 6 per cent of manufacturing exports. Imports of manufactured products are concentrated inmachinery and equipment (27 per cent), transport equipment (20 per cent), and petroleum and basicchemicals products (22 per cent).

New Zealand WT/TPR/S/20Page 89

Table IV.2

Share of manufacturing value added, wages and trade, by production group and industry(Per cent)

Share ofmanufacturing

value added

Share ofmanufacturing

wages

Share ofmanufacturing

imports

Share ofmanufacturing

exports

1987 1993 1987 1993 1995 1995

Food, beverages and tobaccoMeat and meat products

Dairy productsOther food

Beverages, malts and tobaccoproducts

28.410.3

3.47.4

7.3

33.08.0

6.08.4

10.5

26.1...

...

...

...

27.9...

...

...

...

5.80.3

0.44.1

1.1

40.915.6

15.68.9

0.9

Textile and apparel 8.4 6.0 10.1 7.6 6.7 8.8

Wood and wood products 6.3 6.3 7.3 7.5 0.9 6.9

Pulp and paper products, printing andpublishing

Paper and paper productsPrinting and publishing

11.6

4.67.0

13.6

6.47.2

13.0

...

...

14.5

...

...

4.5

2.71.8

6.8

6.40.4

Petroleum, chemical, plastics andrubber products

Petroleum, coal and basic chemicalsRubber, plastic and other chemical

manufacturing

15.1

8.5

6.6

12.1

4.7

7.4

9.8

...

...

10.9

...

...

24.8

22.1

2.7

11.8

10.2

1.7

Non-metallic minerals 3.6 3.2 3.6 3.3 1.5 0.4

Basic metals 2.9 4.7 3.4 5.0 3.7 11.2

Fabricated metal products, machineryand equipment

Fabricated metal productsMachinery and equipment (incl.

prof. and scientific equip.)Transport equipment

22.7

7.2

9.95.6

20.2

6.4

9.04.7

25.8

...

...

...

22.3

...

...

...

49.6

2.0

27.120.5

11.7

1.5

8.61.5

Other manufacturing 1.0 1.0 0.9 0.9 2.5 1.4

... Not available. Estimates have not been made for these industries for the years indicated.

Source: Statistics New Zealand (1995), "New Zealand System of National Accounts"; and WTO Secretariat calculations based on dataprovided by New Zealand authorities.

45. The tariff is virtually the only source of import protection for manufacturing; m.f.n. ratesare moderate and declining. The tariff reductions of 1 July 1996 lowered m.f.n. tariffs for manufacturedproducts from an average of 7.5 per cent to the current average of 6.5 per cent (Appendix Table IV.1).Only a few industries continue to be protected by average m.f.n. tariffs of over 10 per cent: theseare textiles, apparel, footwear and leather; furniture; paper containers and boxes; rubber products;and certain fabricated metal products.31

31Industry definitions are based on the International Standard Industry Classification (ISIC). Tariff rateswere matched to the ISIC industries using the WTO Secretariat's concordance from the Harmonized System(HS) to ISIC.

WT/TPR/S/20 Trade Policy ReviewPage 90

46. The July 1996 tariff reduction appears to have reduced tariff escalation. Rates on unprocessedproducts of the manufacturing sector fell slightly, from 1.2 to 1.0 per cent, while average tariffs onsemi-processed products fell from 4.1 to 3.6 per cent and those on processed products were reducedfrom 9.6 to 8.4 per cent. Nevertheless, tariff escalation remains important, and tends to protectprocessing activities at the expense of primary and semi-processing activities. As rates for primaryand semi-processed products are now quite low, future tariff cuts will have their greatest effect onprocessed products and will thus diminish the remaining tariff escalation (Chapter III(2)(i)(b)).

47. Future tariff cuts will also reduce the margins of preference given to imports from preferentialtrading partners, including Australia, Canada, SPARTECA countries and developing countries receivingGSP treatment (Chapter III(2)(i)(k) and (2)(ii)). As imports from Australia and SPARTECA countriesenter duty free, the average preference margin for manufactured imports from these countries equalsthe average m.f.n. tariff, 6.5 per cent. Australia accounts for 22 per cent of New Zealand'smanufactured imports and SPARTECA countries account for 0.3 per cent of imports. The averagetariff on imports from Canada, which accounts for 1.5 per cent of manufactured imports, is 2.9 per cent,3.6 percentage points less than the average m.f.n. rate. Preference margins under New Zealand's GSPscheme for developing countries are less than those for Canada; imports from least-developed countriesenter duty free.

48. New Zealand's manufacturing sector was heavily protected by import licensing and high tariffsuntil the mid-1980s. Controls on the import of most manufactured goods were eliminated during theperiod January 1987-July 1992. However, the initial tariff reductions of 1986 and 1987 affected onlygoods for which there was not an industry plan (Chapter III(2)); thus, in 1988 average m.f.n. tariffsfor pulp and paper products, textiles and apparel, footwear, machinery, transport equipment, andmiscellaneous manufactures remained above 20 per cent.32 General tariff reductions of two thirds weremade from 1988 to 1996; smaller reductions have been made for "sensitive sectors", namely textilesand apparel, footwear, motor vehicles and components, and tyres.33 In 1993, effective protection,according to estimates by the Ministry of Commerce, was highest in transport equipment, followedby apparel and footwear, and textiles. These estimates suggest that such protection came mostly atthe expense of the food processing industries; printing and publishing; petroleum refining; basicmetals industries; and professional equipment.

49. The elimination of import licensing and the reduction of tariff rates has encouraged domesticmanufacturers to bring their production patterns more into line with New Zealand's apparent comparativeadvantage. Thus, as measured by value added, between 1987 and 1993 textiles and clothing and basicchemical manufacturing contracted by 16 and 35 per cent, respectively; food, beverages and tobaccomanufacturing expanded by 37 per cent, wood and wood products by 18 per cent, and paper and paperproducts by 39 per cent. The share of manufactured output that is exported has also increased markedly.From a share of 32.7 per cent of production in 1984/85, exports rose to 42 per cent of productionin 1992/93, the last year for which data are available. Most of this growth has been in the above notedareas where value added has expanded.

32Ministry of Commerce (1994a).

33The effective protection of apparel and footwear products is actually estimated to have increased as a resultof tariff reductions made between 1990 and 1993, because tariffs on inputs were being reduced relatively morerapidly than tariffs on the products produced by these industries (Ministry of Commerce, 1994a).

New Zealand WT/TPR/S/20Page 91

(i) Food, beverages and tobacco manufacturing

50. The share of New Zealand's food manufacturing industries34 in manufacturing value addedrose from 28.4 to 33.0 per cent in the period 1987 to 1993. This was based on a 37 per cent increasein the sector's value added, led by rapid growth in dairy-product manufacturing (110 per cent), raisingits share inmanufacturing from3.4 to 6.0 per cent, andbeverage and maltmanufacturing (70 per cent).35

The share of meat and meat products in manufacturing declined slightly, but in 1995 it still accountedfor 8.0 per cent of manufacturing value added.

51. Over half the production of the food manufacturing industries is exported, including nearly90 per cent of dairy products.36 Processed food exports in 1995 totalled $8.9 billion and accountedfor 41 per cent of totalmanufacturing exports and 35 per cent of allmerchandise exports. Meat productsand dairy products each accounted for 38 per cent of the exports of food manufacturing industries,followed by fish and fish products (11 per cent) and fruit and vegetables (5 per cent). Dairy productsmay be exported only by the New Zealand Dairy Board, or entities authorized by the Board; othermarketing boards may also directly or indirectly influence exports of certain products (section 2(i)(a)and Chapter III(3)(iii)).

52. The Uruguay Round results on increased market access and reduced export subsidies onagricultural products are important to New Zealand, particularly for its dairy products.37 This isparticularly so with respect to the market access and export subsidy reduction commitments of theEuropean Union (EU) and the United States. New Zealand's country-specific tariff quota on butterinto the EU increased by almost 50 per cent, from 51,380 tonnes in 1994 to 76,667 tonnes as from1996; its in-quota tariff, however, has more than doubled, from ECU 408.6 to 868.8 per tonne. Anin-quota tariff reduces the economic rents that may accrue to New Zealand because of the quota. Ifthere was not an in-quota tariff, New Zealand's Dairy Marketing Board could sell amounts up to thequota limit at a price near the internal EU price. With the in-quota tariff, the import price could bereduced to approximately the internal EU price minus the in-quota tariff rate. This weakens one ofthe main arguments for having a "single-seller" dairy exporter (Box IV.1). The EU has also increasedits global cheese access, for which New Zealand expects to be very competitive. In addition,New Zealand has received increases in its country-specific access for cheese to the United States andbutter to Canada, and secured country-specific access for prepared edible fats to Japan. Reduced volumesof subsidized dairy exports, particularly EU cheese and United States skimmed milk powder, are alsoexpected to benefit the New Zealand dairy industry.

53. Tariff cuts on 1 July 1996 reduced New Zealand's m.f.n. tariff average for manufactured foodproducts from 5.5 per cent to 4.9 per cent. These cuts were greatest on the relatively high tariff itemsin the sector, including bakery products (from 11.5 per cent to 9.4 per cent), soft drinks (9.8 per centto 8.4 per cent) and cocoa, chocolate and sugar products (9.7 per cent to 8.1 per cent). The lowest

34ISIC 31; these industries include food products, animal feeds, beverages and manufactured tobacco.

35Rapid growth in these industries actually started in late 1986, with value added in 1987 28 per cent higherthan the previous year. Because of confidentiality concerns, the figure for beverage and malt manufacturing alsoincludes tobacco product manufacturing; however, the latter accounts for a small share of the total.

36Statistics New Zealand (1995b). Figures refer to 1990/91.

37New Zealand feels that, among its industries, "The dairy industry will probably be the largest beneficiaryof the export subsidy disciplines negotiated in the Uruguay Round" (Ministry ofForeign Affairs and Trade, 1994).

WT/TPR/S/20 Trade Policy ReviewPage 92

tariffs in these industries are those on refined sugar, imports of which are duty free.38 The July 1996tariff cuts also helped reduce tariff escalation in the industry. Rates on fully processed and semi-processed products fell from 6.2 to 5.6 per cent and 5.8 to 4.9 per cent, respectively; those onunprocessed products fell from 1.1 to 0.9 per cent. The greater reduction on highly processed itemsis important because these products account for four fifths of non-preferential imports of manufacturedfood products. Other than tariffs and sanitary and phytosanitary requirements, no border measuresapply to imports of processed food items.

(ii) Textiles, clothing and footwear

54. The textiles, clothing and footwear (TCF) industries (ISIC 32) accounted for 6 per cent ofNew Zealand's manufacturing activity in 1993, down from 8.4 per cent in 1987. According to theauthorities, these industries have faced a difficult adjustment over the past decade. Imports increasedfrom $300 million in 1988 to $1,150 million in 1993, mainly as a result of the progressive removalof import licensing. This required domestic firms to improve their competitiveness, or leave the industry.With many firms exiting, investment in the textiles sector fell from $19 million in 1988 to $3 millionin 1992, and that in clothing fell from $46 to $29 million.

55. New Zealand does not restrict imports of TCF through import licensing or other quantitativebarriers.39 Tariffs are the only means of import protection. M.f.n. tariffs, however, average12.9 per cent, nearly triple the average for all other goods, and range as high as 30 per cent.40 Tariffsare highest for wearing apparel, at 26.6 per cent, followed by products of knitting mills (23.7 per cent),carpets and rugs (21.9 per cent) and footwear (17.8 per cent). Many of the tariff lines, such as thaton leather clothing, include alternative specific rates, which are used if the duty revenue from applyingthe specific rate would exceed that from applying the ad valorem rate. This occurs most frequentlyfor relatively low-priced products, thus increasing protection for the domestically produced, competingitem.

56. Tariffs for TCF products tend to rise with, and protect, the level of processing. All unprocessedTCF products (accounting for 38 tariff lines) have m.f.n. rates of zero, while tariffs on semi-processedproducts (506 lines) average 4.4 per cent and rates on processed products (634 lines) average20.4 per cent. However, escalation will be reduced with the implementation of planned tariff cutsduring the period 1997-2000.

57. Because TCF products were subject to industry plans, tariffs on these products were not reducedin line with the general tariff reductions of 50 per cent between 1988 and 1992 and a further one thirdfrom 1993 to 1996. Rather, tariff reductions on TCF products were effected more cautiously. Tariffs

38This combination of low rates on sugar and relatively high rates on sugar-based products appears to givesubstantial effective protection to activities such as chocolate and beverages manufacturing.

39The removal of import licensing for TCF goods began with the implementation of the 1985 review of theTextile Industry Development Plan. Licensing requirements were eliminated for imports of textiles and clothingfrom Forum Island Countries in 1988 and Australia in 1989. Imports of textiles from all other countries weresubject to licensing until 1991; clothing imports from other countries were the last products subject to importlicensing, with restrictions eliminated in July 1992.

40New Zealand's average m.f.n. tariff is 6.2 per cent; excluding TCF, however, the average is 4.8 per cent.The tariff reduction of 1 July 1996 cut the average m.f.n. tariff for TCF by over one percentage point, from14.0 per cent.

New Zealand WT/TPR/S/20Page 93

on footwear remained at about 45 per cent, with some exceptions, until 1992, and were phased downto 25 per cent (children's sizes) and 30 per cent (adult sizes) by 1996.41 From 1989 to 1992, m.f.n.tariffs on clothing were reduced from a range of 40 to 65 per cent to 40 per cent; these rates weresubsequently reduced by a quarter, to 30 per cent, in the period 1993-1996. For textiles, most ratesover 30 per cent were reduced to 30 per cent in the period 1988 to 1992. Thereafter, with someexceptions, textiles became subject to the general tariff reduction programme, and rates were reducedby a third from July 1993 to July 1996.

58. As part of the 1997-2000 tariff reduction programme, m.f.n. tariffs on TCF products are tobe substantially reduced. Most rates on clothing and adult footwear will be progressively loweredfrom the 30 per cent rate introduced on 1 July 1996 to 15 per cent on 1 July 2000; rates on children'sfootwear will be cut from 25 per cent to 15 per cent. Rates on carpets will be reduced from the current23 per cent to 15 per cent; those on most textiles (including knitted and woven fabrics, twine andcordage) will be reduced from 20 per cent to 10 per cent and rates on yarns will be cut from 13 per centto 5 per cent.

(iii) Wood and paper products

59. New Zealand's wood and paper products industries (ISIC 33 and 341) accounted for 12.7 per centof manufacturing value added in 1993, up from 10.9 per cent in 1987. Much of this expansion tookplace in paper products, the share of which increased from 4.6 to 6.4 per cent. Wood and paper productsaccounted for 13.4 per cent of manufactured exports and 3.6 per cent of manufactured imports in 1995.

60. Tariffs are the only means of protection or assistance to the industry. M.f.n. tariffs are atmoderate rates, with the average tariff on imports of wood products having been reduced from 6.7 to5.5 per cent on 1 July 1996; concurrently the average tariff on paper products was cut from 9.1 to7.6 per cent. New Zealand will reduce its tariffs on pulp, paper and printed matter to zero by 2004,as part of its tariff-reduction commitments in the Uruguay Round.

61. The authorities expect particularly strong growth over the next five years in the wood productsindustry, based on increased wood production from planted forests (section 2(ii)), increased investmentin forest-based industries, and increased market access for New Zealand's exports as countries implementtheir Uruguay Round commitments. Implementation of these commitments will reduce the averagetariff applied by developed countries on imports of forestry products from 3.5 to 1.1 per cent.New Zealand may also benefit from the expanded scope of tariff bindings by many developing Asianeconomies.

(iv) Motor vehicle manufacturing

62. Motor vehicle production (ISIC 3843) contributes about 2 per cent of the manufacturing sector'svalue added.42 The industry has undergone substantial restructuring in recent years, partly as a resultof the progressive removal of import licensing and reductions in tariffs. Imports of motor vehiclesincreased by nearly 80 per cent from 1987 to 1992, reaching a value of $1.9 billion, equivalent tonearly double the domestic output. During this period, employment in motor vehicle assembly fell

41Tariffs on adult footwear were actually increased from 45 to 55 per cent for one year on 1 July 1991.

42Motor vehicle manufacturing comprises roughly half of the transport equipment manufacturing sector;this sector accounted for 4.7 per cent of manufacturing sector value added in 1993, down from 5.6 per cent in1987. Data are largely drawn from Ministry of Commerce (1994a).

WT/TPR/S/20 Trade Policy ReviewPage 94

from 4,300 to 2,300 and employment in motor vehicle component manufacturing fell from 3,000 to1,500. Investment in these areas remained steady.

63. Import licensingrequirements formotorvehicles andcomponentswereprogressivelyeliminatedbetween 1985 and 1989. Tariffs, however, remained high: m.f.n. rates on passenger cars and lightcommercial vehicles remained at 55 per cent until July 1988 and were cut to 35 per cent by July 1992.From 1988 to 1990, tariffs on commercial vehicles were reduced, and those on heavy commercialvehicles were eliminated. Tariffs on passenger vehicles were progressively reduced to 25 per centfrom July 1993 to July 1996. Tariffs on components were phased down to 35 per cent for originalequipment and 20 per cent for replacement parts by 1992. These tariffs were subsequently reducedto 25 per cent and 12.5 per cent, respectively, on 1 July 1996. With the final instalment of tariffreductions under the 1993-96 programme, on 1 July 1996 the average m.f.n. tariff in all categoriesof motor vehicles fell from 10.7 per cent to 9.8 per cent.

64. Under the 1997-2000 tariff reduction programme, tariffs on replacement parts are to beprogressively reduced from 12.5 to 10 per cent and tariffs on original equipment components are tobe reduced from 25 to 15 per cent. For passenger and commercial vehicles, tariffs will be reducedto 15 and 5 per cent, respectively.

(4) Services

65. New Zealand's services sector accounts for about 62 per cent of GDP and 65 per cent of totalemployment.43 External trade in services comprised 23 per cent of New Zealand's total trade in 1995and has increased slightly more rapidly than merchandise trade over the past five years. New Zealandis normally a small net importer of services, with net imports equivalent to 0.8 per cent of GDP inthe year ending March 1995. Services exports are equivalent to over 7 per cent of GDP, up from6 per cent in 1990.44

66. The size of the services sector gives it special economic importance: as two thirds ofNew Zealand's productive resources are employed in services, their efficiency and productivity arekey determinants in the nation's economic welfare. The sector, moreover, plays a much greater partin New Zealand's export performance than its share of total exports would suggest. Most of theeconomy, including the export of goods, intensively uses services. For example, in the foodmanufacturing industry, which accounts for one third of total exports, services comprise 40 per centof direct input costs.45 To the extent that such costs can be reduced, through open internationalcompetition and increased productivity, this will be reflected in the enhanced competitiveness of sectorssuch as food manufacturing.

67. Given this clear importance of services, the authorities placed the sector at the forefront ofNew Zealand's structural reform. In general, competition is now relied upon, with direct regulationlargely absent under what is termed the "light-handed" approach to regulation. Virtually all key State-owned enterprises have been placed on a commercial footing, and many have also been privatized.Particularly given New Zealand's relatively small market, the openness of services markets tointernational competition has been vital to establishing the desired levels of economic competition.

43New Zealand Treasury (1996b), p. 23.

44Services exports rose by 8 per cent a year from 1990 to 1995.

45Based on inter-industry transactions data for 1990/91 in Statistics New Zealand (1995b).

New Zealand WT/TPR/S/20Page 95

68. New Zealand relies on competition law in areas where market failure might arise, such as withvertically-integrated natural monopolies in basic telecommunications. Even here, New Zealand haseschewed the use of industry-specific regulation: there is, for example, no telecommunications regulatorybody. Instead there is a combination of free domestic and foreign market entry, the application ofcompetition policy, and the use of indirect regulation to enhance the operation of the market by, forexample, seeking to ensure that adequate information is made available to consumers and competitors.

(i) Commitments under the General Agreement on Trade in Services (GATS)

69. New Zealand actively participated in the Uruguay Round services negotiations. It made manycommitments in a broad range of service industries; these are summarized in Annex IV.1, as per theServices Sectoral Classification List (SSCL). New Zealand also undertook one horizontal (i.e. cross-sectoral) commitment and specified three horizontal limitations; these, and m.f.n. exemptions aredescribed below.

70. By accepting the GATS, New Zealand agreed to provide m.f.n. treatment in all GATS sectorsother than those in which it took a GATS Article II (m.f.n.) exemption. These sectors are: audiovisualservices, interpretation services, and maritime services; in addition, in all sectors, New Zealand hasan m.f.n. exemption on the right of entry of natural persons. The audiovisual services exemption relatesto a preferential measure applied to Canada, France and the United Kingdom and concerns financialand tax concessions and simplified requirements for the temporary entry of skilled personnel.46 Itsobjective is to support the domestic film industry and to share benefits with other countries with similarpolicies. The m.f.n. exemption for certain translation services reflects the policy of giving morefavourable entry conditions to Japanese nationals with the requisite skills as interpreters. Its purposeis to help develop tourism.47 The maritime services exemption, which is fully explained below(section 5(v)(a)), reflects preferential treatment for certain Commonwealth personnel. The exemptionfor the entry of natural persons for all sectors relates to New Zealand's policy of providing favourabletemporary entry conditions for 20 Kiribati and 80 Tuvalu nationals a year. The purpose is developmentassistance by providing income, job skills, on-the-job training and work experience.

71. One of New Zealand's horizontal limitations is in the area of national treatment for theestablishment of commercial presence; it concerns approval from the Overseas Investment Commissionforcertain foreigndirect investments (Chapter I(4)). NewZealand'shorizontalcommitmentguarantees,in market access, the entry and temporary stay of certain employees of service suppliers with acommercial presence in New Zealand; it is limited to the following categories of employees: executivesand senior managers; specialists or senior personnel; installers and servicers; and service sellers.New Zealand's other horizontal limitations relate to: (i) enterprises currently in State ownership, and(ii) special treatment for Maori indigenous interests.

(ii) Agreement with Australia

72. The Protocol on Trade in Services to the Australia-New Zealand Closer Economic RelationsAgreement was signed in 1988 and entered into force on 1 January 1989. The Protocol calls for freebilateral services trade for all sectors not inscribed on a negative list and is applied automatically toany new services (Chapter II(2)(iv)). The Parties' respective negative lists have been considerably

46New Zealand is willing to consider extending this preference to other countries with which cultural co-operation may be desirable and which are willing to exchange preferential treatment.

47This measure may be extended to other countries.

WT/TPR/S/20 Trade Policy ReviewPage 96

shortened since 1989. Sectors fully or partially represented are: (i) for Australia, telecommunications,airport services, domestic air services, international aviation (passenger and freight services), coastalshipping, broadcasting and television (short-wave and satellite broadcasting), basic health insuranceservices, third-party insurance, workers' compensation insurance and postal services; and (ii) forNew Zealand, airways services, telecommunications, and postal services. It is the expectation of theParties that further sectors will be removed from the negative list over time.

(iii) Telecommunications

73. The communications sector accounted for 3.3 per cent of New Zealand's GDP in 1993, upslightly from 2.9 per cent in 1987. Value added in the sector grew by some 11 per cent in the yearto June 1995, led by rapidly growing activities such as cellular services. The Government's objectiveis that the sector "establish and maintain efficient markets in telecommunications goods and services."48

74. The Telecommunications Act 1987 deregulated part of the sector and subsequent amendmentsto the Act opened the sector completely to competition in 1989. The sector now consists of two majorcompetitors, Telecom and Clear, and many smaller firms that are active in some areas, such as datatransmission. Telecom, the former State-owned enterprise, owns and operates much of the country'stelecommunications network; it is under a legal limitation not to increase basic residential rates inreal terms, a limitation made necessary, according to the authorities, by Telecom's dominant position.Clear competes with Telecom in most services areas, and has a substantial share of the long distanceand international markets.

75. Telecommunication reform came early in New Zealand's structural adjustment effort. Froma situation in 1987 with a monopoly State-owned enterprise (SOE) that covered nearly all aspects oftelecommunications, the sector progressed through corporatization of the SOE and the establishmentof Telecom, deregulation of virtually the entiremarket, and Telecom's subsequent privatization in 1990.The New Zealand approach indicates that even in sectors with considerable scale economies and othercomplexities, techniques can be found to facilitate and encourage competition.

76. The establishment of a liberal telecommunications régime appears to have brought a numberof positive results, including an improvement in the standard and range of service, the rapid introductionof new technologies, greater variety, higher productivity, and lower prices.49 Thus, Telecom greatlyincreased investment while modernizing its network during the late 1980s and early 1990s. This hasled to a high share of digital switches (98 per cent) and a commitment to be fully digitalized by 1998.On the services side, the waiting time for a new telephone connection has been reduced from six weeksto two days. While in 1988 only 76 per cent of payphones were operational at any one time, this figureis now 98 per cent. Productivity, measured by the number of lines per Telecom employee, has alsogreatly increased, moving from 86 in 1990 to 214 in 1994.50 Prices have fallen, creating businessand consumer savings; from 1990 to 1994, residential prices fell by 7 per cent in real terms and theaverage price charged per minute by Telecom for long distance calls fell 55 per cent, in nominal terms,

48Ministry of Commerce (1994e).

49de Boer and Evans (1995), Galt (1995), and Ministry of Commerce and the New Zealand Treasury (1995).

50The OECD average (based on latest available data) moved from 150 in 1990 to 168 in 1992.

New Zealand WT/TPR/S/20Page 97

from 1988 to 1994.51 Despite these price reductions, Telecom has enjoyed a moderate return on capitalin recent years and Clear is now also showing signs of a moderate return.

77. The benefits of these developments are felt beyond the telecommunications sector. For example,productivity improvements have not only brought improved service but have also facilitated lowertelecommunications prices and hence business costs. Thus, telecommunications reform has also hadan important effect on the competitive position of New Zealand's exporters and its import-competingfirms.

78. New Zealand has made GATS commitments in relation to value-added services (Annex IV.1)and is a participant in the ongoing WTO negotiations on basic telecommunications. According to theauthorities, no current policies would require change in the event that New Zealand were to make newcommitments in the sector.

Sectoral overview and the impact of reform

79. Prospective entrants intoNew Zealand's telecommunicationsmarket faceno legal restrictions.52

Prior to 1987, the New Zealand Post Office held a monopoly in public telecommunications services.53