RESTRICTED WT/TPR/S/425 23 March 2022 (22-2457) Page

203

RESTRICTED WT/TPR/S/425 23 March 2022 (22-2457) Page: 1/203 Trade Policy Review Body TRADE POLICY REVIEW REPORT BY THE SECRETARIAT SWITZERLAND AND LIECHTENSTEIN This report, prepared for the sixth joint Trade Policy Review of Switzerland and Liechtenstein, has been drawn up by the WTO Secretariat on its own responsibility. The Secretariat has, as required by the Agreement establishing the Trade Policy Review Mechanism (Annex 3 of the Marrakesh Agreement Establishing the World Trade Organization), sought clarification from Switzerland and Liechtenstein on its trade policies and practices. Any technical questions arising from this report may be addressed to Mr Mark Koulen (tel. 022 739 5224), Mr Pierre Latrille (tel. 022 739 5266), Ms Katie Waters (tel. 022 739 5067), Mr Michael Kolie (tel. 022 739 5931), and Ms Takako Ikezuki (tel. 022 739 5534). Document WT/TPR/G/425 contains the policy statements submitted by Switzerland and Liechtenstein. Note: This report is subject to restricted circulation and press embargo until the end of the first session of the meeting of the Trade Policy Review Body on Switzerland and Liechtenstein. This report was drafted in English.

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of RESTRICTED WT/TPR/S/425 23 March 2022 (22-2457) Page

RESTRICTED

WT/TPR/S/425

23 March 2022

(22-2457) Page: 1/203

Trade Policy Review Body

TRADE POLICY REVIEW

REPORT BY THE SECRETARIAT

SWITZERLAND AND LIECHTENSTEIN

This report, prepared for the sixth joint Trade Policy Review of Switzerland and Liechtenstein, has been drawn up by the WTO Secretariat on its own responsibility. The Secretariat has, as required by the Agreement establishing the Trade Policy Review Mechanism (Annex 3 of the Marrakesh Agreement Establishing the World Trade Organization), sought clarification from Switzerland and Liechtenstein on its trade policies and practices.

Any technical questions arising from this report may be addressed to Mr Mark Koulen (tel. 022 739 5224), Mr Pierre Latrille (tel. 022 739 5266), Ms Katie Waters (tel. 022 739 5067), Mr Michael Kolie (tel. 022 739 5931), and Ms Takako Ikezuki (tel. 022 739 5534). Document WT/TPR/G/425 contains the policy statements submitted by Switzerland and Liechtenstein.

Note: This report is subject to restricted circulation and press embargo until the end of the first session of the meeting of the Trade Policy Review Body on Switzerland and Liechtenstein. This report

was drafted in English.

WT/TPR/S/425 • Switzerland and Liechtenstein

- 2 -

CONTENTS

SUMMARY ........................................................................................................................ 9

1 ECONOMIC ENVIRONMENT ........................................................................................ 15

1.1 Main Features of the Economy .....................................................................................15

1.1.1 Switzerland .............................................................................................................15

1.1.2 Liechtenstein ...........................................................................................................16

1.2 Recent Economic Developments ...................................................................................17

1.2.1 Switzerland .............................................................................................................17

1.2.2 Liechtenstein ...........................................................................................................19

1.2.2.1 Fiscal policy ..........................................................................................................19

1.2.2.2 Monetary policy and exchange rate .........................................................................20

1.2.2.3 Balance of payments .............................................................................................22

1.3 Structural Challenges ..................................................................................................24

1.3.1 Switzerland .............................................................................................................24

1.3.2 Liechtenstein ...........................................................................................................27

1.4 Developments in Trade and Investment ........................................................................27

1.4.1 Trends and patterns in merchandise and services trade ................................................27

1.4.2 Trends and patterns in FDI .......................................................................................33

2 TRADE AND INVESTMENT REGIMES........................................................................... 34

2.1 General Framework ....................................................................................................34

2.1.1 Switzerland .............................................................................................................34

2.1.2 Liechtenstein ...........................................................................................................36

2.2 Trade Policy Formulation and Objectives ........................................................................37

2.3 Trade Agreements and Arrangements ...........................................................................38

2.3.1 WTO ......................................................................................................................38

2.3.2 Regional trade agreements (RTAs) .............................................................................42

2.3.2.1 Switzerland and Liechtenstein Customs Union...........................................................42

2.3.2.2 European Free Trade Association (EFTA) ..................................................................43

2.3.2.3 European Economic Area (EEA) ...............................................................................45

2.3.2.4 Switzerland's bilateral agreements with the European Union.......................................47

2.3.2.5 Other agreements and arrangements ......................................................................49

2.3.3 Other agreements and arrangements .........................................................................50

2.3.3.1 Non-reciprocal preferential arrangements ................................................................50

2.4 Investment Regime and Business Environment ..............................................................50

2.4.1 Switzerland .............................................................................................................50

2.4.2 Liechtenstein ...........................................................................................................53

3 TRADE POLICIES AND PRACTICES BY MEASURE ........................................................ 55

3.1 Measures Directly Affecting Imports ..............................................................................55

3.1.1 Customs procedures, valuation, and requirements .......................................................55

3.1.2 Rules of origin .........................................................................................................58

WT/TPR/S/425 • Switzerland and Liechtenstein

- 3 -

3.1.3 Tariffs ....................................................................................................................58

3.1.3.1 Applied MFN tariff .................................................................................................58

3.1.3.2 Tariff rate quotas ..................................................................................................61

3.1.3.3 Bound duties ........................................................................................................63

3.1.3.4 Other duties and charges .......................................................................................63

3.1.3.5 Tariff exemptions and reductions ............................................................................64

3.1.3.6 Tariff preferences ..................................................................................................66

3.1.4 Import prohibitions, restrictions, and licensing ............................................................69

3.1.5 Anti-dumping, countervailing, and safeguard measures ................................................71

3.2 Measures Directly Affecting Exports ..............................................................................72

3.2.1 Customs procedures and requirements .......................................................................72

3.2.2 Taxes, charges, and levies ........................................................................................72

3.2.3 Export prohibitions, restrictions, and licensing .............................................................73

3.2.4 Export support and promotion ...................................................................................75

3.2.5 Export finance, insurance, and guarantees ..................................................................76

3.3 Measures Affecting Production and Trade .......................................................................78

3.3.1 Taxation and incentives ............................................................................................78

3.3.1.1 Corporate income tax ............................................................................................78

3.3.1.2 Indirect taxes .......................................................................................................79

3.3.1.2.1 VAT ..................................................................................................................80

3.3.1.2.2 Excises .............................................................................................................81

3.3.1.3 Incentives and other assistance ..............................................................................84

3.3.1.3.1 Switzerland .......................................................................................................84

3.3.2 Standards and other technical requirements ...............................................................87

3.3.3 Sanitary and phytosanitary requirements ....................................................................91

3.3.4 Competition policy and price controls .........................................................................94

3.3.4.1 Competition policy – Switzerland ............................................................................94

3.3.4.2 Competition policy – Liechtenstein ..........................................................................97

3.3.4.3 Price controls – Switzerland ....................................................................................97

3.3.4.4 Price controls – Liechtenstein .................................................................................98

3.3.5 State trading, state-owned enterprises, and privatization .............................................98

3.3.6 Government procurement ....................................................................................... 101

3.3.6.1 Overview ........................................................................................................... 101

3.3.6.1 Switzerland ........................................................................................................ 102

3.3.7 Intellectual property rights ...................................................................................... 104

3.3.7.1 Trade-related intellectual property rights ............................................................... 104

3.3.7.2 Economic context ................................................................................................ 106

3.3.7.3 Structure and use of the IP system ....................................................................... 107

3.3.7.4 International initiatives and WTO participation ........................................................ 108

3.3.7.5 Copyright and related rights ................................................................................. 110

WT/TPR/S/425 • Switzerland and Liechtenstein

- 4 -

3.3.7.6 Trademarks ........................................................................................................ 111

3.3.7.7 Geographical indications ...................................................................................... 112

3.3.7.8 Patents .............................................................................................................. 113

3.3.7.9 Plant varieties .................................................................................................... 114

3.3.7.10 Enforcement ..................................................................................................... 114

4 TRADE POLICIES BY SECTOR ................................................................................... 116

4.1 Agriculture ............................................................................................................... 116

4.1.1 Overview and recent policy developments ................................................................. 116

4.1.2 Market access ....................................................................................................... 119

4.1.2.1 Applied MFN tariffs .............................................................................................. 119

4.1.2.1.1 Tariff escalation ............................................................................................... 119

4.1.2.1.2 Adjustable tariffs .............................................................................................. 119

4.1.2.1.3 Seasonal tariffs ................................................................................................ 120

4.1.2.1.4 Tariff quotas .................................................................................................... 121

4.1.3 Domestic support................................................................................................... 121

4.1.3.1 Direct payments ................................................................................................. 122

4.1.3.2 Market support measures ..................................................................................... 125

4.1.3.3 Milk ................................................................................................................... 125

4.1.3.4 Grains, oilseeds, and sugar .................................................................................. 126

4.1.4 Export subsidies .................................................................................................... 127

4.1.5 Evolution of support ............................................................................................... 128

4.2 Mining and Energy .................................................................................................... 129

4.2.1 Mining .................................................................................................................. 129

4.2.1.1 Switzerland ........................................................................................................ 129

4.2.1.2 Liechtenstein ...................................................................................................... 129

4.2.2 Energy ................................................................................................................. 129

4.2.2.1 Switzerland ........................................................................................................ 129

4.2.2.1.1 Economic developments .................................................................................... 129

4.2.2.1.2 Policy developments ......................................................................................... 135

4.2.2.1.2.1 Environmental issues ..................................................................................... 135

4.2.2.1.2.2 Electricity ..................................................................................................... 137

4.2.2.1.2.3 Nuclear energy .............................................................................................. 139

4.2.2.1.2.4 Renewable energies (including hydropower) ..................................................... 140

4.2.2.1.2.5 Oil ............................................................................................................... 140

4.2.2.1.2.6 Gas ............................................................................................................. 140

4.2.2.2 Liechtenstein ...................................................................................................... 141

4.3 Manufacturing .......................................................................................................... 143

4.3.1 Switzerland ........................................................................................................... 143

4.3.2 Liechtenstein ......................................................................................................... 146

4.4 Services .................................................................................................................. 147

WT/TPR/S/425 • Switzerland and Liechtenstein

- 5 -

4.4.1 Telecommunications services .................................................................................. 147

4.4.1.1 Switzerland ........................................................................................................ 147

4.4.1.2 Liechtenstein ...................................................................................................... 153

4.4.2 Financial services ................................................................................................... 156

4.4.2.1 Switzerland ........................................................................................................ 156

4.4.2.1.1 Overview of the economic evolution and of the market structure of the financial

services sector ................................................................................................................. 156

4.4.2.1.1.1 Overview of the economic evolution and of the market structure of banking services .......................................................................................................... 157

4.4.2.1.1.2 Overview of the economic evolution and of the market structure of insurance services ........................................................................................................ 158

4.4.2.1.1.3 Overview of the economic evolution and of the market structure of pension fund

services and stock exchange and securities services ............................................................. 159

4.4.2.1.2 Evolution of the overall regulatory framework ...................................................... 159

4.4.2.1.2.1 Regulatory framework for banking services ....................................................... 160

4.4.2.1.2.2 Regulatory framework for insurance services .................................................... 162

4.4.2.1.2.3 Regulatory framework for financial market infrastructures .................................. 164

4.4.2.1.2.4 Regulatory framework for pension fund services ................................................ 165

4.4.2.1.2.5 Regulatory framework for mutual fund services ................................................. 165

4.4.2.1.2.6 Regulatory framework for fintech .................................................................... 167

4.4.2.2 Liechtenstein ...................................................................................................... 167

4.4.2.2.1 Overview of economic and regulatory developments in the financial services sector ................................................................................................................. 167

4.4.2.2.1.1 Economic and regulatory developments in the asset management and investment undertakings sector ......................................................................................... 169

4.4.2.2.1.2 Economic and regulatory developments in the insurance sector ........................... 171

4.4.2.2.1.3 Economic and regulatory developments in the fintech e-payments and cryptocurrencies sector ..................................................................................................... 171

4.4.3 Transport services ................................................................................................. 173

4.4.3.1 Switzerland ........................................................................................................ 173

4.4.3.1.1 Surface transport services ................................................................................. 173

4.4.3.1.1.2 Road transport services .................................................................................. 173

4.4.3.1.1.3 Railway transport services .............................................................................. 174

4.4.3.1.1.4 Pipeline transport services .............................................................................. 175

4.4.3.1.1.5 Inland waterways transport services ................................................................ 176

4.4.3.1.1.6 Maritime transport services ............................................................................ 177

4.4.3.1.1.7 Freight forwarding and logistics services ........................................................... 178

4.4.3.1.1.8 Air transport services ..................................................................................... 178

4.4.3.2 Liechtenstein ...................................................................................................... 181

4.4.3.2.1 Road freight and passenger transport services ..................................................... 181

4.4.3.2.2 Rail transport services ...................................................................................... 181

4.4.3.2.3 Air transport services ........................................................................................ 182

5 APPENDIX TABLES .................................................................................................. 183

WT/TPR/S/425 • Switzerland and Liechtenstein

- 6 -

CHARTS Chart 1.1 Gross domestic product by economic activity for Switzerland, 2020 ...........................15

Chart 1.2 Gross domestic product by economic activity for Liechtenstein, 2019 .........................16

Chart 1.3 Federal revenues, 2020 ........................................................................................20

Chart 1.4 Product composition of merchandise trade, 2016 and 2020 .......................................30

Chart 1.5 Direction of merchandise trade, 2016 and 2020 .......................................................31

Chart 3.1 Breakdown of estimated applied MFN tariffs, 2016 and 2021 .....................................61

Chart 3.2 Breakdown of applied MFN and preferential tariffs, 2021 ...........................................67

Chart 3.3 Swiss imports by tariff regimes, 2020 .....................................................................69

Chart 3.4 The positive relationship between innovation and development................................ 105

Chart 3.5 Charges for the use of intellectual property, n.i.e, 2015-20 ..................................... 106

Chart 4.1 Level and composition of support to agricultural producers ..................................... 129

Chart 4.2 Gross energy consumption by source, 2015 and 2020 ............................................ 133

Chart 4.3 Electricity generation by source, 2015 and 2020 .................................................... 134

Chart 4.4 Total CO2 emissions, 2015-19 ............................................................................. 135

Chart 4.5 Types of plants and measures financed by the grid surcharge.................................. 138

Chart 4.6 Energy consumption, 2020 .................................................................................. 142

Chart 4.7 Production structure ........................................................................................... 144

Chart 4.8 Employment share of manufacturing, 2000-21 ...................................................... 144

Chart 4.9 Domestic and international passenger flights, January to December 2019 and 2020 ................................................................................. 179

TABLES Table 1.1 Selected macroeconomic indicators for Switzerland, 2016-20 ....................................17

Table 1.2 Selected macroeconomic indicators for Liechtenstein, 2016-20 ..................................19

Table 1.3 Balance of payments, 2016-20 ..............................................................................23

Table 1.4 Trade in services by sector and destination/origin, 2016-20 ......................................32

Table 2.1 Selected referenda and popular initiatives, 1 January 2017 to 31 January 2022 ...........34

Table 2.2 Main trade and investment-related laws in Switzerland, January 2022 ........................35

Table 2.3 Main trade and investment-related laws in Liechtenstein, January 2022 ......................36

Table 2.4 Notifications made by Switzerland to the WTO, 1 January 2017 to 31 January 2022 .....39

Table 2.5 Notifications made by Liechtenstein to the WTO, 1 January 2017 to 31 January 2022 ...41

Table 2.6 Switzerland's main bilateral agreements with the European Union, 2021 .....................48

Table 3.1 Main customs-related laws and regulations, January 2022 ........................................55

Table 3.2 Physical inspections on imports by customs, 2017-21 ...............................................57

Table 3.3 Structure of MFN tariffs, 2021 ...............................................................................60

Table 3.4 Preferential tariff rate quotas, by tariff regime, 2021 ................................................62

Table 3.5 Guarantee fund contributions, 2021 .......................................................................63

Table 3.6 Guarantee fund contributions, applied tariffs and bound tariffs ..................................64

Table 3.7 Suspension of customs duties in the textiles sector, 2015-19 and 2019-23 .................65

WT/TPR/S/425 • Switzerland and Liechtenstein

- 7 -

Table 3.8 Key features of tariff exemptions and reductions, 2021 .............................................65

Table 3.9 Tariffs under preferential agreements, 2021 ............................................................67

Table 3.10 Selected products subject to import prohibitions, 2021 ...........................................70

Table 3.11 Physical inspections on exports by customs, 2017-21 .............................................72

Table 3.12 Selected export controls in Switzerland and Liechtenstein, January 2022 ..................73

Table 3.13 Export finance, insurance, and guarantee products available from SERV, 2021 ..........77

Table 3.14 Liechtenstein corporate taxes and other selected taxes ...........................................79

Table 3.15 Taxation of alcoholic beverages ............................................................................84

Table 3.16 Competition enforcement statistics 2018-20 ..........................................................96

Table 3.17 Government procurement in Switzerland, 2016-20 ............................................... 103

Table 3.18 Switzerland: Applications for trademarks, industrial designs, and patents,

and patents granted, 2016-20 ........................................................................................... 108

Table 3.19 Liechtenstein: Applications for trademarks, industrial designs, and patents, and patents granted, 2016-20 ........................................................................................... 108

Table 4.1 Farms according to size classes, 2019 and 2020 .................................................... 116

Table 4.2 Direct payments, 2017-20 .................................................................................. 123

Table 4.3 Liechtenstein's direct payments, 2016-20 ............................................................. 125

Table 4.4 Market support and direct payments, 2017-20 ....................................................... 125

Table 4.5 Crop premiums 2017-19 ..................................................................................... 127

Table 4.6 OECD PSE for Switzerland, 2016-20 ..................................................................... 128

Table 4.7 Energy balance of Switzerland, 2015-20 ............................................................... 130

Table 4.8 Imports of petroleum oils, 2015-20 ...................................................................... 131

Table 4.9 Imports of gas, 2015-20 ..................................................................................... 131

Table 4.10 Imports of coal, 2015-20 .................................................................................. 132

Table 4.11 Imports of electrical energy, 2015-20 ................................................................. 132

Table 4.12 Transformation process of primary energy supply, 2020 ....................................... 133

Table 4.13 Final energy consumption, 2020......................................................................... 134

Table 4.14 Contribution to GVA of the various manufacturing subsectors, 2016-20 .................. 143

Table 4.15 Contribution to employment of the various manufacturing subsectors, 2016-21 ....... 145

Table 4.16 Structure of employment in the manufacturing sector by company size, 2020 ......... 146

Table 4.17 Evolution of the contribution of the telecommunications and ICT sectors to GVA and to total employment, 2015-20 .......................................................................... 147

Table 4.18 Telecom tariffs, 2015-20 ................................................................................... 148

Table 4.19 Access/interconnection rates, 2015-20................................................................ 148

Table 4.20 Retail mobile roaming rates, Q4 2020 ................................................................. 148

Table 4.21 ICT prices trends by type of basket, 2020 ........................................................... 149

Table 4.22 Contribution of the financial services sector and its subsectors to GVA and total employment, 2014-20 .............................................................................. 157

Table 4.23 Evolution of main indicators of the banking system, 2015-20 ................................. 168

Table 4.24 Passenger and freight traffic handled at Swiss international airports, 2015 and 2020 ................................................................................................... 178

Table 4.25 Main features of recent air transport agreements ................................................. 180

WT/TPR/S/425 • Switzerland and Liechtenstein

- 8 -

BOXES Box 2.1 Liechtenstein's Market Control and Surveillance Mechanism .........................................46

Box 4.1 Measures to reduce nitrogen and phosphorus losses through the direct payments system and the reduction of the risk associated with the use of pesticides in Switzerland .......... 124

Box 4.2 Main economic indicators of Switzerland's telecommunications sector ......................... 148

Box 4.3 Switzerland telecommunications market structure .................................................... 149

Box 4.4 Telecom sector .................................................................................................... 153

Box 4.5 Evolution of the market structure and of the main economic indicators of the banking sector ........................................................................................................... 157

Box 4.6 Evolution of the market structure and of the main economic indicators

of the insurance sector ..................................................................................................... 158

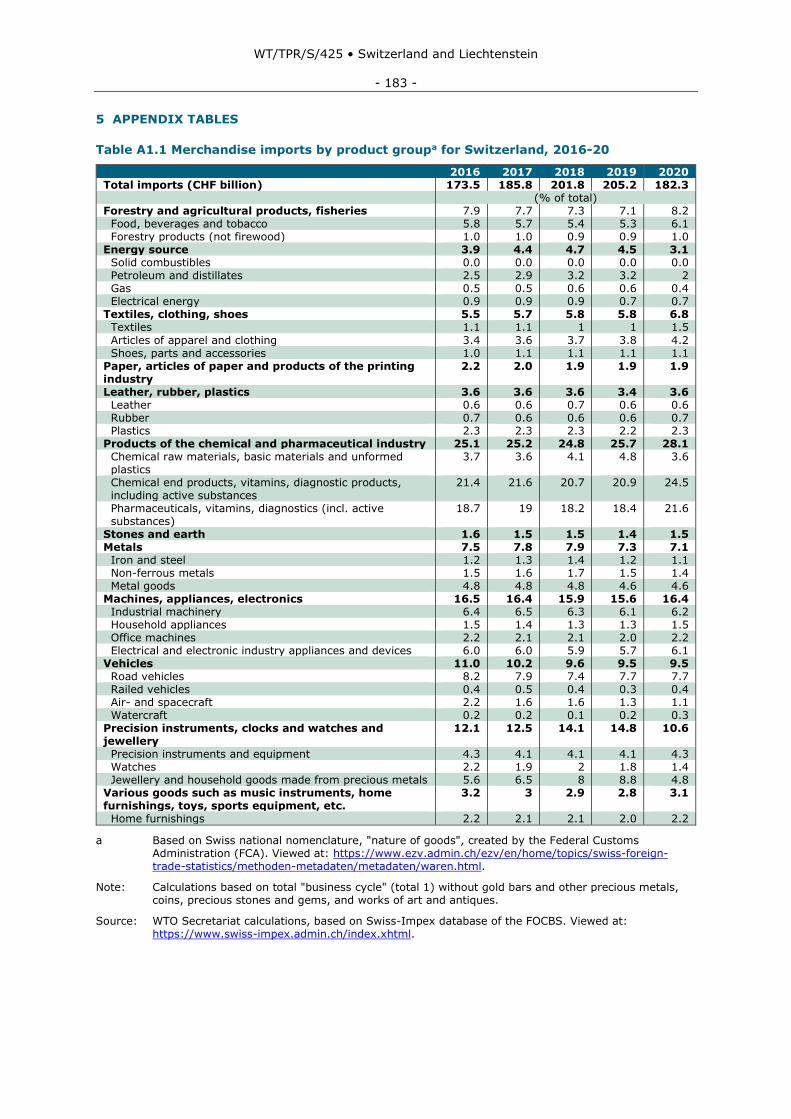

APPENDIX TABLES Table A1.1 Merchandise imports by product groupa for Switzerland, 2016-20 .......................... 183

Table A1.2 Merchandise exports by product groupa for Switzerland, 2016-20........................... 184

Table A1.3 Merchandise imports by origin for Switzerland, 2016-20 ....................................... 185

Table A1.4 Merchandise exports by destination for Switzerland, 2016-20 ................................ 186

Table A1.5 Merchandise imports by origin for Liechtenstein, 2016-20 ..................................... 187

Table A1.6 Merchandise exports by destination for Liechtenstein, 2016-20 .............................. 188

Table A1.7 FDI by economic activity, 2016-20 ..................................................................... 189

Table A1.8 Foreign direct investment by selected trading partners, 2016-20 ........................... 191

Table A2.1 Switzerland and Liechtenstein's RTAs in force, January 2022 ................................. 193

Table A2.2 Work and residence permits: rules and procedures for EU/EFTA citizens, January 2022 .................................................................................................................. 195

Table A3.1 MFN applied tariff summary, 2021 ...................................................................... 196

Table A3.2 Swiss imports by preferential tariff regimes, 2020 ................................................ 198

Table A4.1 Switzerland's major traded agricultural products, 2016-20 .................................... 200

Table A4.2 WTO tariff quotas for agricultural products .......................................................... 202

WT/TPR/S/425 • Switzerland and Liechtenstein

- 9 -

SUMMARY

1. Switzerland and Liechtenstein are among the top high-per capita income countries in the world and are very well integrated into international trade. They both benefit from strong democratic institutions, educated populations, and a specialization in value-added production. Their fiscal situation is sound and their unemployment traditionally low. Services account for about three quarters of the Swiss economy. One particularity of the Liechtenstein economy is the importance of

manufacturing, representing 40% of GDP in 2019. During the review period, and prior to the COVID 19 pandemic, real GDP growth in Switzerland was positive, ranging from 1.2% in 2019 to 2.9% in 2018. GDP growth in Liechtenstein tends to be more volatile because of the small size of the economy. After three years of real GDP growth, Liechtenstein's GDP contracted by 2.3% in 2019. Because of the COVID 19 pandemic, real GDP growth fell by 2.4% in 2020 in Switzerland, and further in Liechtenstein. Thanks to strong financial buffers and a prompt response by the Governments, the

pandemic is not expected to have negative effects on long-term economic prospects.

2. Switzerland has recorded fiscal surpluses in most years since 2016. The application of a debt

brake rule has meant that government spending and liabilities remain far below the average OECD level. The impact of the COVID 19 pandemic resulted in a change from a fiscal surplus of 1.3% in 2019 to a fiscal deficit of 2.8% in 2020. In recent years, the Swiss National Bank pursued a very accommodative monetary policy, mainly through a negative interest rate and, where necessary, foreign exchange market interventions. It played an important role in crisis management in the

context of the COVID 19 pandemic, for example, by intervening more strongly in foreign exchange markets to counter the upward pressure on the Swiss franc. Issues that have been raised regarding Swiss monetary policy include the increasing difficulty of achieving the price stability objective and the need to address certain structural factors that account for the persistent appreciation pressures faced by the Swiss franc since the 2008-09 financial crisis.

3. While Switzerland and Liechtenstein enjoy favourable economic conditions, they also face similar challenges, including the ageing of the population, low productivity growth, adaptation to

digitalization, climate change, and risks posed by high levels of household debt.

4. Switzerland's current account remained in surplus but overall declined steadily between 2016

and 2019 and registered a very sharp decline in 2020. The long-term evolution of the structure of Swiss merchandise exports reveals a growing specialization in certain product sectors that are relatively unaffected by exchange rate movements. Chemical and pharmaceutical products now account for more than half of Swiss merchandise exports. While the trade goods balance reached a

record surplus in 2020, the services trade balance continued its long-term decline. Europe continues to account for more than 70% of Swiss merchandise imports and more than 50% of its merchandise exports, although in the long term its share in Swiss merchandise imports and exports has declined somewhat. In the case of Liechtenstein, 78% of merchandise imports (excluding trade with Switzerland) originate in Europe and 61% of merchandise exports (excluding trade with Switzerland) are destined for Europe. Switzerland ranks among the world's top 10 economies in terms of inward and outward foreign direct investment (FDI) stock, with an inward FDI stock that is heavily

concentrated in services. FDI inflows to Switzerland have fallen since 2015 and were negative in 2018-20. The recent negative FDI inflows reflect the conduit nature of Switzerland's annual FDI inflows, as FDI in Switzerland is made mainly through intermediate companies in European holding companies.

5. Given the two countries' limited domestic markets and export orientation, trade policy in both is focused on promoting and guaranteeing open markets, with an increased emphasis on sustainable development. Both countries are active members of the WTO, supporting the Buenos Aires

Declaration on Women and Trade and participating in the joint statement initiatives (JSIs) on e-commerce, MSMEs, and domestic regulation of trade in services. In addition, Switzerland participates in the JSI on investment facilitation for development. Over the review period, Switzerland was involved in one WTO dispute settlement case as complainant. Both countries maintain a solid record of notifications to the WTO, with those outstanding only in the areas of tariff quotas and domestic support, for both countries, and subsidies for Switzerland. Notifications are also pending for some

RTAs.

6. Switzerland and Liechtenstein form a customs union; they have a common currency; and their policies are aligned in various other areas. Both economies are members of the European Free Trade Association (EFTA) under the auspices of which they have concluded an extensive range of RTAs (29

WT/TPR/S/425 • Switzerland and Liechtenstein

- 10 -

RTAs with 39 economies). Liechtenstein is in a unique position due to its participation in the Customs Union with Switzerland (which covers goods) and its simultaneous membership in the European Economic Area (EEA). Over the review period, new EFTA RTAs entered into force with Georgia, the Philippines, Ecuador, and Indonesia, and existing EFTA RTAs with Israel and Turkey were revised. Switzerland concluded a new RTA with the United Kingdom (with application of goods aspects to Liechtenstein). Another RTA was concluded between EEA-EFTA members and the United Kingdom

(with non-goods aspects applying to Liechtenstein)).

7. In May 2021, Switzerland announced its decision not to sign the Institutional Framework Agreement with the European Union, largely due to concerns about wage protection and state aid. Since this Agreement was to encompass and upgrade the extensive set of bilateral agreements in place, the failure to reach agreement on the framework has raised questions about the future of those bilateral agreements, including, for example, the mutual recognition agreement between

Switzerland and the European Union-EEA.

8. Both Switzerland and Liechtenstein are open to investment, with few restrictions on FDI,

although state monopolies operate in a few areas. The Swiss Federal Council is drafting a law on the control of foreign investments, which will be published for consultations at the end of March 2022.

9. Over the review period, Switzerland and Liechtenstein launched strategies to digitally transform government services and render them more efficient and cost-effective. Switzerland is also taking steps to reform legal and regulatory processes, including through the issuance of new

regulatory impact assessment guidelines and the launch of consultations on a new Business Relief Act. Liechtenstein revised its Business Act to introduce simplified registration procedures for certain types of business activity.

10. A major customs reform initiative is ongoing in Switzerland; its objective is to meet future challenges of increased traffic and trade as well as to take advantage of digitalization opportunities. This will result in, inter alia, enhanced customs security measures and the introduction of a fully-fledged single window system (Passar) to replace the existing systems (e-dec and the New

Computerized Transit System (NCTS)). Switzerland undertakes customs clearance operations, including the collection of taxes and duties, at Liechtenstein's customs posts on its behalf.

11. The Switzerland-Liechtenstein tariff is fully composed of specific rates. The simple average tariff in 2021 was 7.2% based on AVE estimates. High tariffs prevail on agricultural products (simple average applied tariff of 25.4%, with tariffs ranging from 0% to 671.3%). Highest tariffs apply to out-of-quota imports of fresh or chilled lollo lettuce. Tariff quotas apply to a number of agricultural

products, comprising 3.7% of all tariff lines in 2021 (down from 3.8% in 2016). Seasonal tariffs apply to 95 products and are levied mostly on fruits and vegetables produced domestically, and most of which are also subject to tariff quotas. As at the time of the previous Review, applied MFN tariffs may exceed bound rates for certain goods due to fees levied on imports by compulsory stock organizations.

12. During the review period, temporary tariff reductions were granted on certain feed items, medical goods, and textiles and intermediate materials to respond to emergency situations or

respond to industry needs. The Swiss Government has announced that all duties on industrial goods will be eliminated on 1 January 2024.

13. As at the time of the previous Review, Switzerland and Liechtenstein apply import and export prohibitions and restrictions largely for reasons of security, health, and protection of the environment. Additionally, some import and export prohibitions are applied related to sanctions. Temporary export controls were introduced between March and June 2020 for certain goods related to the COVID 19 pandemic. Neither Switzerland nor Liechtenstein has any specific legislation on

contingency measures; they have no specialized authorities in place to initiate and conduct anti-dumping and countervailing investigations; and they have no anti-dumping, countervailing, or safeguard measures in place.

14. No export taxes or duties are levied. Switzerland Global Enterprise, a private non-profit association mandated by the State Secretariat for Economic Affairs, continues to help SMEs in Switzerland and Liechtenstein to export their products and services; over the review period, it

formed new partnerships and expanded its services. Swiss Export Risk Insurance (SERV) continues

WT/TPR/S/425 • Switzerland and Liechtenstein

- 11 -

to provide export finance and insurance services to companies registered in Switzerland where there is a gap in private-sector provision; in response to the COVID 19 pandemic, it simplified certain processes to assist exporters. Export finance, insurance, and guarantees are provided only by the private sector in Liechtenstein.

15. During the period under review, Switzerland and Liechtenstein implemented new reforms to comply with international standards on corporate income tax. Consequently, the European Union

withdrew both countries from its taxation grey list. While competitive corporate tax regimes have been one of the countries' strengths, both Governments raised concerns about the implementation of the future international corporate tax framework. However, they indicated that other features of their economies and additional measures will maintain their attractiveness for companies. Switzerland and Liechtenstein apply similar excise taxes on products causing a risk to human health or to the environment.

16. The mutual recognition agreement (MRA) between Switzerland and the European Union-EEA is based on harmonized technical regulations in 20 sectors. Switzerland regularly supports specific

trade concerns (STCs) in the TBT Committee to raise concerns regarding planned or adopted measures of trading partners. Neither Switzerland nor Liechtenstein was subject to an STC during the review period. Liechtenstein follows Swiss and the relevant EU technical regulations, and it does not have its own regulatory mechanism for technical regulations.

17. In June 2017, Switzerland notified to the WTO the framework of legislative acts that entered

into force along with its new food legislation, intended to harmonize Swiss law with EU law. Switzerland also applied a new regulation on plant health, which is aligned with the updated EU regulation. Under the Customs Union Treaty, Liechtenstein applies Switzerland's sanitary and phytosanitary measures. No STCs were raised during the review period regarding Switzerland's or Liechtenstein's sanitary and phytosanitary measures.

18. Switzerland amended its Cartel Law by introducing the concept of undertakings with relative market power and a new item on restrictions on procurement and amended the Law Against Unfair

Competition by introducing a prohibition on geo-blocking by private parties. As previously, Switzerland's Competition Commission prioritized the fight against hard-core horizontal and vertical

cartels as well as market foreclosures. The Government continued to consider the modernization of the Swiss system for merger control. Liechtenstein does not have a national competition law or competition authority, and it is subject to EEA competition rules that are applied by the EFTA Surveillance Authority. During the review period, no competition cases concerning Liechtenstein

were referred to the EFTA Surveillance Authority.

19. Switzerland's regime of price surveillance and prevention of abusive pricing by public and private monopolies or enterprises with market power remained unchanged. Under the Law on Price Surveillance, the Price Supervisor is responsible for observing price developments and preventing abusive price increases or abusive price maintenance in any market where the price level is not the consequence of effective competition. At the federal level, Switzerland maintains administrative prices for medicines, electricity, gas, water, basic telecommunications services, airport taxes, and

notary services. Liechtenstein maintains price controls on public transport, telecommunications, postal and medical services, and drugs and medical equipment.

20. Alcosuisse's monopoly on the importation of ethanol ended in 2019 with the liberalization of

the ethanol market. Switzerland notified the WTO Working Party on State Trading Enterprises in December 2020 that imports of ethanol and spirits are allowed without restrictions and without the need for any permit. The Swiss cantons hold a monopoly on the import and sale of various types of salt. Plans have been announced for the privatization of PostFinance Ltd., a wholly owned subsidiary

of Swiss Post, which is one of the five state-owned enterprises in Switzerland that are wholly or majority-owned by the Confederation. There were no major changes regarding state ownership and privatization in Liechtenstein.

21. Amendments to the Swiss Federal Law on Public Procurement and the implementing Ordinance that entered into force in January 2021 aimed to implement the revised Government Procurement Agreement and to achieve more harmonization of federal and cantonal laws on public procurement.

The main changes concern the increased emphasis on quality and sustainability aspects of public procurement, the definition of technical terms and scope of application, the regulation of

WT/TPR/S/425 • Switzerland and Liechtenstein

- 12 -

additional/subsequent procurement, the prevention of corruption, and the introduction of more flexible instruments, such as dialogue, framework agreements, electronic procurement, electronic auctions, and shorter timelines. An important development at the sub-federal level was the adoption and entry into force of a revised Intercantonal Agreement on Government Procurement. Liechtenstein amended its Law on Sectoral Public Procurement and its Law on Public Procurement to implement four EU directives.

22. Switzerland is one of the world's most innovative economies and a net exporter of intellectual property. During the review period, Switzerland took further steps to implement its "Swissness" legislation. It reinforced the protection of the "Swiss Made" designation through amendments to the Federal Law on the Protection of Trademarks and to the Federal Law on the Protection of Coats of Arms and Other Public Signs and by adopting ordinances that extend the scope of the Swissness regulation to additional products, including watches and food products. The Federal Law on Copyright

and Related Rights was revised to reflect technological developments and to address online piracy more effectively. In addition to FTAs with comprehensive provisions on intellectual property and an agreement on geographical indications concluded with Georgia, Switzerland became a party to the

Geneva Act of the Lisbon Agreement on Appellations of Origin and Geographical Indications (December 2021), the Marrakesh Treaty to Facilitate Access to Published Works for Persons Who Are Blind, Visually Impaired or Otherwise Print Disabled (May 2020), and the Beijing Treaty on Audiovisual Performances (May 2020). As a result of the customs union between Switzerland and

Liechtenstein, Liechtenstein's intellectual property system is deeply integrated and intertwined with the Swiss intellectual property system. Liechtenstein amended its copyright law to implement two EU directives.

23. Switzerland is a net importer of agricultural and food products. Despite the small size of its agriculture sector, both in terms of its contribution to GDP (0.7% in 2020) and total employment (2.7%), Switzerland places great importance on agriculture due to its multifunctionality in terms of, inter alia, food security, environmental protection, and the maintenance of its cultural landscapes.

In 2017, a new article was adopted in the Federal Constitution calling for a guarantee of sufficient food supplies for the Swiss population, in the long term. A complex and comprehensive set of trade instruments, including domestic support and border measures, continues to be implemented, with a view to ensuring the viability of Swiss agriculture. In 2018, the authorities decided to abolish export

subsidies for agricultural products, and the related contributions were allocated to eligible producers as a market support measure for cereals and marketed milk. In Liechtenstein, agriculture is

marginal, and Switzerland acts on its behalf on Customs Union matters, such as with respect to imports and exports of agricultural products.

24. Switzerland's Energy 2050 Strategy results from a decision taken in the early 2010s to progressively phase out nuclear energy and to promote energy efficiency and the production of renewable energy. To implement the strategy, a completely revised Federal Energy Law entered into force in January 2018 that sets out targets for energy production and consumption, defines energy efficiency standards, and provides incentives for investment in renewable energy production. As part

of an Electricity Networks Strategy, a new Federal Law on the Conversion and Expansion of the Electricity Grid was adopted; most of its provisions entered into force in June 2019, and aim to facilitate the development of electricity networks. In 2020, Switzerland updated its Nationally Determined Contribution under the Paris Agreement to commit to reduce greenhouse gas emissions by at least 50% by 2030, compared to 1990 levels, and to achieve climate neutrality by 2050. Following the rejection by the Swiss electorate in June 2021 of a comprehensive revision of the Swiss CO2 Law, the Federal Assembly in December 2021 adopted a partial amendment to temporarily

prolong some limited and unchallenged aspects of the CO2 Law during the period 2022-24. A new proposal for a comprehensive revision of the CO2 Law to continue to reduce greenhouse gas submissions beyond this period is currently the subject of consultations. Although Switzerland is closely integrated in the European electricity network, the conditions for electricity trade with the European Union are suboptimal because of the absence of a formal agreement with the European Union.

25. Liechtenstein adopted measures to increase energy efficiency, increase use of renewable energy, and reduce greenhouse gas emissions as part of its Energy Strategy 2020 originally adopted in 2012. In 2020, Liechtenstein adopted a new Energy Strategy 2030 and Energy Vision 2050, the purpose of which is to further increase the use of energy from renewable sources. Liechtenstein's CO2 Law derives directly from the Swiss CO2 Law but differs with respect to the allocation of the revenues from the CO2 tax. In its Nationally Determined Contribution under the Paris Agreement,

WT/TPR/S/425 • Switzerland and Liechtenstein

- 13 -

Liechtenstein has committed to achieve a reduction of 40% of its greenhouse gas emissions by 2030 compared to 1990 levels.

26. Switzerland and Liechtenstein have strong manufacturing sectors. The contribution to the Swiss economy (in terms of gross value added) of the manufacturing sector increased in recent years. The increase was particularly significant in the largest subsector, chemical and pharmaceutical products. Other prominent subsectors are computers, electronics, watches and clocks; machinery

and equipment; and fabricated metals. Within Swiss manufacturing, there is a long term trend towards a growing share of high-end products. The Swiss Federal Council recently reiterated its opposition to the adoption of an industrial policy to support particular industry branches. Liechtenstein's manufacturing sector accounts for a share in GDP and employment far higher than in other developed countries. The sector is very diversified with the most important subsectors being mechanical engineering; vehicle construction; food production; and basic metals and fabricated

metals. The Government recently identified research and innovation as a priority in its 2021-25 strategy.

27. Switzerland has a modern telecommunications sector using the latest technologies, including 5G. Prices of telecommunications services remain high by international standards although the gap appears to be narrowing progressively. There were no significant changes in the Swiss telecommunications services market during the review period in terms of the main actors, market shares, foreign ownership, and state ownership. The Swiss telecommunications regulatory

framework was updated to adapt it to technological evolutions and to alleviate administrative burdens on operators to facilitate market entry. A comprehensive revision of the Telecommunications Law in 2019 that entered into force in January 2021 introduces many changes, including, for example, the adoption of the principle of Internet neutrality, the abolition of the general notification requirement for all providers of telecommunications services, new and strengthened transparency provisions regarding roaming services, and new methods to measure and publicize the quality of fixed and mobile Internet access.

28. The telecommunications services sector in Liechtenstein is based on a vertical separation regime agreed between the electricity supplier, which owns, operates, and maintains a major part of the fixed communications network, and the major provider of telecommunications services. The

main changes made during the review period to the regulatory framework for telecommunications services resulted from the application of EU regulations and directives on telecommunications. These concerned, among other things, roaming services, the introduction of an obligation for the incumbent

to offer VoIP wholesale services on non-discriminatory and transparent terms, national voice call termination prices, number portability, and universal service provisions.

29. Switzerland's financial services sector is mature and sophisticated, but its share in GDP has declined since the 2008 financial crisis due to factors such as changes in the international taxation framework and the global wealth management business and low interest rates. In view of this more challenging competitive environment, the Federal Council launched a new strategy for the financial services sector in 2020 that rests on three main pillars: (i) the creation of more favourable conditions

for innovation; (ii) the promotion of international interconnectedness and open markets; and (iii) more emphasis on sustainability. The review period witnessed many changes in the general regulatory framework for financial services, with the adoption of the Financial Market Infrastructure Law, which entered into force in 2016, the Financial Services Law and the Financial Institutions Law, which both entered into force in 2020, and changes to legislation in the areas of money laundering and the financing of terrorism. In addition, there were changes in regulations that pertain more

specifically to each of the subsectors of the financial services industry. For example, in banking,

steps were taken to align Swiss legislation with the Basel III international banking standards.

30. Liechtenstein's financial services sector to a large extent faces the same challenges as the Swiss financial services sector, but its situation differs in two important respects. First, Liechtenstein's EEA membership means that the financial services sector has access to a very large market via passporting. Second, the absence of investment banking from Liechtenstein's financial services sector has made it more resistant to the low interest rate environment. Liechtenstein

reinforced its rules on money laundering and terrorist financing and adapted its domestic legislation on banking, asset management companies, and collective investment schemes to implement relevant EU directives. In 2019, Liechtenstein became the first country to adopt comprehensive legislation on trustworthy technology (TT) service providers. The Token and TT Service Provider Law,

WT/TPR/S/425 • Switzerland and Liechtenstein

- 14 -

which entered into force in January 2020, is autonomous legislation that does not derive from an EEA transposition of the EU acquis.

31. During the period under review, Switzerland continued to improve its road infrastructure to alleviate transit problems. The domestic legal framework for road transport services remained largely unchanged. With respect to railway services, Switzerland continued to align its regime with that of the European Union by implementing key elements of the EU third railway package in 2020

and 2021. These include, inter alia, the creation of an independent body responsible for the allocation of train paths, and the strengthening of passenger rights regarding delays, cancellations, liabilities, and the transport of bicycles. Inland waterways transport, transport on the Rhine, and maritime transport stricto sensu constitute a somewhat important, though often neglected, activity. Registration of seagoing commercial vessels is subject to very strict requirements. A major development was the termination in 2017 of a 60-year-old policy whereby Switzerland was providing

federal mortgage guarantees for the construction of Swiss-flagged ships. The air transport industry was severely affected by the economic consequences of the COVID 19 pandemic and was subject to several individual rescue plans for airports, airlines, and auxiliary providers both at the cantonal and

federal levels.

WT/TPR/S/425 • Switzerland and Liechtenstein

- 15 -

1 ECONOMIC ENVIRONMENT

1.1 Main Features of the Economy

1.1.1 Switzerland

1.1. Switzerland is a high-income country with a population of less than nine million. It enjoys favourable economic conditions, with strong and transparent democratic institutions that support trade and investment. The country ranks high in economic complexity1, with a specialization in value-

added production and an educated population. Main economic sectors are manufacturing (18.7% of GDP in 2020), led by the chemical and pharmaceutical sector; real estate, professional and support service activities (18.0%)2; and trade and repair of motor vehicles and motorcycles (15.1%). Aggregated, services account for more than 70% of its GDP (Chart 1.1). There was no major change in the distribution of GDP per economic activity between 2016 and 2020.3 The economy is managed with fiscal prudence, and the fiscal balance is traditionally in surplus (Table 1.1). Switzerland's

unemployment rate is low, below 3.5% during the review period. Trade accounts for over 117% of

GDP. The customs union between Switzerland and Liechtenstein is surrounded by the European Union, by far its main trade partner (Section 1.4). Due to Switzerland's close relationship with the European Union, the end of negotiations on the institutional framework agreement (Sections 2.3.2.4 and 3.3.2) raises questions on the definition of their future relationship.

Chart 1.1 Gross domestic product by economic activity for Switzerland, 2020

Note: Percentage of current GDP at basic prices.

Source: State Secretariat for Economic Affairs (SECO), Economic Situation.

1.2. Despite Switzerland being a landlocked country without any significant natural resources, it is

well integrated into international trade. According to the 2021 Foreign Economic Policy Strategy, Switzerland is one of the countries that benefit the most from globalization.4 Most imports and exports (78% and 86%, respectively, in volume) transit by land (railway and road transportation).5 Switzerland's railway density is the highest in Europe and the 4th worldwide, as the Government intends to favour rail over road transportation.6 Transport of merchandise by air grew during the

1 Switzerland ranks 2nd worldwide for economic complexity. Routley, N. (2019), "These Are the Most

Complex Economies around the Globe", WEF, 2 December. Viewed at: https://www.weforum.org/agenda/2019/12/countries-ranked-by-their-economic-complexity.

2 Including real estate, legal, accounting, management, architecture, and engineering activities, scientific research and development, scientific and technical activities, and administrative and support service activities.

3 It can be noted that in constant 2015 prices, the chemical and pharmaceutical sector's share increased from 6% to 8.2% between 2016 and 2020.

4 Federal Council (2021), Switzerland's Foreign Economic Policy Strategy. 5 Federal Office for Customs and Border Security (FOCBS), Means of Transport. Viewed at:

https://www.bazg.admin.ch/bazg/en/home/topics/swiss-foreign-trade-statistics/daten/verkehrsmittel.html. 6 Union des Transports Publics, Faits et arguments concernant les transports publics suisses 2020-2021.

Viewed at: https://www.voev.ch/fr/Services/Publications/Faits-et-arguments-concernant-les-TP-suisses.

Agriculture, forestry and fishing

0.7%

Manufacturing

18.7%

Electricity, gas, steam and air

conditioning supply

1.8%

Construction

5.1%

Trade, repair of motor vehicles

and motorcycles

15.1%

Transportation and storage;

information and communication

7.9%

Financial service activities

5.5%

Insurance service activities

4.2%

Real estate, professional,

scientific and technical

activities; administration and

support service activities

18.0%

Public administration

10.7%

Human health and social work

activities

8.0%

Other services

4.0%

Other 0.4%

Source: State Secretariat for Economic Affairs (SECO), Economic situation. Viewed at: https://www.seco.admin.ch/seco/en/home.html.

Services

73.3%

Chart 1.[CHE] Gross domestic product by economic activity, 2020

Note: Based on current prices.

WT/TPR/S/425 • Switzerland and Liechtenstein

- 16 -

past decade, and half of Switzerland's exportation (in value) leaves the country by air.7 Switzerland has efficient airport infrastructure, with most of the merchandise trade transiting through the Zurich airport. In 2020, 8% of total trade, notably crude oil and petroleum products, was transported by the Rhine river at the Basel ports.8 Switzerland tops the 2020 UNCTAD Global E-Commerce Index, thanks not only to very high Internet access and use by its population, but also due to the quality of transportation and postal services allowing for efficient delivery.9 The Universal Postal Union 2021

report confirmed that Switzerland retained the world's highest score on the Integrated Index for Postal Development.10

1.1.2 Liechtenstein

1.3. Liechtenstein is a small country with a total territory of 160 km2 and a population of less than 40,000. It has one of the highest GDP per capita in the world, second only to Monaco. However, the authorities emphasize that for comparative purposes GDP per capita is of limited relevance due to

the large number of inward cross-border commuters (since 2017, there have been more employees than inhabitants). Thus, GDP per employed person in full-time equivalents is seen as a more accurate

measure, and was estimated at CHF 186,880 in 2019. Liechtenstein benefits from stable political institutions and an exceptionally low gross public debt in relation to GDP of 0.6%.11 Its unemployment rate is also exceptionally low, below 2% over the review period. Manufacturing accounts for 40.1% of the GDP in 2019, followed by professional, scientific, and technical activities (14.1%), and financial and insurance activities (11.5%). Services represent 54.1% of the GDP

(Chart 1.2). There has been no major change in the distribution of GDP per sector between 2016 and 2019. Manufacturing as a whole gained 2 percentage points while financial and insurance services followed the opposite trend (from 13.3% to 11.5%). As a member of the European Economic Area (EEA), Liechtenstein participates in the single market among the European Union and EEA/EFTA countries, which is designed to provide for the free movement of goods, services, persons, and capital. Liechtenstein and Switzerland share the same currency, the Swiss franc (CHF), and a customs union. All international trade in goods is transported to and from Liechtenstein via the road

network.12

Chart 1.2 Gross domestic product by economic activity for Liechtenstein, 2019

Note: Percentage of current GDP at basic prices.

Source: Liechtenstein Office of Statistics, eTab. Viewed at: https://etab.llv.li/PXWeb/pxweb/en/eTab/.

7 FOCBS, Means of Transport. 8 Federal Statistical Office (FSO), Goods Transport by Air, Water and Pipeline. Viewed at:

https://www.bfs.admin.ch/bfs/en/home/statistics/mobility-transport/goods-transport/air-water-pipeline.html. 9 UNCTAD (2021), "Switzerland Climbs to Top of Global E-Commerce Index", 17 February. 10 Universal Postal Union (2021), Postal Development Report 2021, October. 11 Government of the Principality of Liechtenstein (2021), Economic and Financial Data on Liechtenstein,

data as of 24 June 2021, p. 38. Viewed at: https://www.liechtenstein-institut.li/application/files/3316/3058/6915/Economic-and-financial-data-2021-1-.pdf.

12 Information provided by the authorities.

Agriculture, forestry and

fishing, 0.1%

Mining and quarrying, 0.1%

Machinery and

equipment, 19.8%

Transport

equipment, 4.1%

Food products,

beverages and

tobacco products,

3.4%

Other

manfacturing,

12.9%

Electricity, gas, steam and air

conditioning supply,

Water supply, sewerage, waste

management and remediation

activities, 1.3%

Construction, 4.3%

Wholesale and retail trade;

repair of motor vehicles and

motorcycles, 4.9%

Financial and

insurance activities,

11.5%

Real estate activities, 6.5%

Professional, scientific and

technical activities, 14.1%

Public administration and

defence; compulsory social

security, 6.0%

Human health and social work

activities, 2.5%

Other services, 8.6%

Source: Liechtenstein Office of Statistics, eTab. Viewed at: https://etab.llv.li/PXWeb/pxweb/en/eTab/.

Services

54.1%

Chart 1.[LIE] Gross domestic product by economic activity, 2019

Manufacturing

40.1%

WT/TPR/S/425 • Switzerland and Liechtenstein

- 17 -

1.2 Recent Economic Developments

1.2.1 Switzerland

1.4. During the review period and prior to the COVID-19 pandemic, real GDP growth was positive, ranging from 1.2% to 2.9% from 2016 to 2019. Prior to 2020, the fiscal balance was in surplus. In December 2019, the Federal Department of Economic Affairs, Education and Research (EAER) published a report to evaluate the implementation of the 2016-2019 New Growth Policy. The three

pillars of the policy were enhancing productivity, strengthening the resilience of the economy (e.g. enhanced "too-big-to-fail" regulation), and reducing negative externalities of economic growth (e.g. climate and energy policy). Most measures were deemed as either completed or in completion. However, measures on the development of bilateral relations with the European Union were rated as unsuccessful.13

1.5. The impact of the COVID-19 pandemic on the Swiss economy led to the biggest drop in GDP

per capita registered in decades. However, comparatively, the effects of the COVID-19 pandemic

remained contained. Real GDP growth fell by 2.4% compared to 5.9% for the EU-27.14 Pre-existing financial buffers and sound economic features helped mitigate the impact. In addition to diversification between sectors, the Swiss Foreign Economic Policy Strategy noted that diversification of trade partners is key to avoid supply shortages for a medium-sized economy such as Switzerland (Section 1.4.1).15 The OECD also noted that high trust in the Government and the highly effective health system enabled less strict lockdowns than in many countries.16 In December 2021, the Swiss

National Bank (SNB) declared that GDP in the third quarter of 2021 had surpassed pre-COVID-19 GDP for the first time since the beginning of the crisis, and the SNB estimated that GDP growth will reach 3.5% in 2021 and 3% in 2022.17

1.6. Table 1.1 gives an overview of selected macroeconomic indicators for Switzerland from 2016 to 2020.

Table 1.1 Selected macroeconomic indicators for Switzerland, 2016-20

2016 2017 2018 2019 2020

Nominal GDP (CHF billion) 685.4 693.7 719.3 727.2 706.2

Nominal GDP (USD billion) 695.9 704.5 735.4 731.9 752.9

Real GDP (percentage change, reference year = 2015)

2.0 1.6 2.9 1.2 -2.4

Nominal GDP per capita (CHF '000) 81.4 81.8 84.2 84.5 81.5

Nominal GDP per capita (USD '000) 82.6 83.0 86.1 85.0 86.8

Population (million)a 8.4 8.5 8.5 8.6 8.7

Unemployment rate (annual average, %) 3.3 3.1 2.6 2.3 3.1

Men 3.5 3.2 2.6 2.4 3.3

Women 3.1 2.9 2.5 2.2 3.0

General government finances (% of GDP)b

Revenue 32.3 33.1 32.6 32.8 33.6

Expenditure 32.1 32.0 31.3 31.5 36.5

Overall fiscal balance 0.2 1.1 1.3 1.3 -2.8

Gross debt ratio as defined by the IMF 40.5 41.2 39.3 39.8 42.4

Debt ratio (Maastricht) 27.4 27.7 25.8 25.9 27.8

Tax-to-GDP ratio

General government 26.7 27.4 26.9 27.3 27.7

Confederation 9.3 9.9 9.6 9.8 9.2

Cantons 6.7 6.7 6.7 6.9 7.1

Municipalities 4.2 4.2 4.2 4.2 4.4

Social security funds 6.5 6.5 6.4 6.5 6.9

Money and credit

CPI (percentage change) -0.43 0.53 0.94 0.36 -0.73

13 EAER (2019), Rapport final du DEFR sur l'état de mise en œuvre de la politique de croissance

2016-2019, 6 December 2019. 14 Eurostat, Real GDP Growth Rate – Volume. Viewed at:

https://ec.europa.eu/eurostat/databrowser/view/tec00115/default/table?lang=en. 15 Federal Council (2021), Switzerland's Foreign Economic Policy Strategy, p. 39. 16 OECD (2022), OECD Economic Surveys: Switzerland 2022, p. 10. 17 SNB (2021), Bulletin trimestriel Q4 2021, p. 5.

WT/TPR/S/425 • Switzerland and Liechtenstein

- 18 -

2016 2017 2018 2019 2020

Broad money (M3, percentage change, end of period)

3.08 3.54 3.16 0.78 6.47

Yield on government bonds – 10 years (%)c -0.36 -0.07 0.03 -0.49 -0.52

External sector

CHF/EUR (period average) 1.09 1.11 1.15 1.11 1.07

CHF/USD (period average) 0.99 0.98 0.98 0.99 0.94

Nominal exchange rate indexd 158 157 156 159 169

Real exchange rate indexd 116 114 111 112 116

Current account (% of GDP) 8.0 6.3 6.1 5.4 2.8

Trade (goods and services, based on BoP) (% of GDP)

120.6 120.5 121.0 120.1 117.5

External debt (% GDP) 267.1 279.6 254.6 266.4 280.2

Total reserves (includes gold, USD billion) 679.6 812.2 788.3 853.5 1,082.8

n.a. Not applicable.

a Permanent resident population at the end of the period. b Based on Government Finance Statistics model. 2020 forecast. c Annual average calculated on the basis of monthly data. d Trade-weighted against 54 trading partners, January 2000 = 100. An increase means appreciation of

the Swiss franc.

Source: Federal Finance Administration (FFA), Data. Viewed at: https://www.efv.admin.ch/efv/en/home.html; SNB, Statistics. Viewed at: https://www.snb.ch/en/; and SECO, Economic Situation. Viewed at: https://www.seco.admin.ch/seco/en/home.html.

1.7. Thus, the economy had favourable pre-existing conditions to weather the worldwide disruption brought by the COVID-19 pandemic. The Government's prompt response also contributed to this overall positive assessment. In its latest Article IV Consultation Report on Switzerland, the

International Monetary Fund (IMF) commended the Government's early, strong, and sustained response.18 For 2020, the Confederation approved a total of expenditure and guarantees of 10% of GDP19, mostly aiming at avoiding job losses, and maintaining employees' wages and companies' liquidity. In practice, actual support was below the maximum approved support, and totalled CHF 15 billion in expenditure and CHF 17.5 billion in guarantees.20 Specific sectors particularly hit

by the pandemic benefited from targeted measures: professional and mass sports, culture, print media, public transport, aviation, and tourism.21 Cantons also granted additional support measures

such as funding short-time work, loan guarantees, interest-free loans, or granting more flexibility to pay utility fees.22 Together, cantons' and communes' pandemic-related expenditures totalled CHF 3 billion for 2020.23 For the year 2021, the Confederation did not grant support in the form of sureties and guarantees but only through expenditures, which amounted to CHF 14 billion.24

1.8. The authorities indicate that the New Growth Policy for 2016-2019 was the last policy of this sort (the first New Growth Policy was introduced for the period 2004-2007). Alternatively, the

Federal Council published in May 2021 its "normalization strategy" based on three phases: progressive waiving of extraordinary economic stabilization measures until April 2022; maintaining measures helping companies and individuals adapt to structural economic changes (e.g. support innovation, promote targeted tourism activities); and fostering sustainable growth enablers and revitalize the economy (e.g. digitalization, climate regulation, less administrative burden).25 The third phase intends to ensure long-term recovery of the economy after the COVID-19 pandemic. In

18 IMF (2021), Switzerland: Staff Report for the 2021 Article IV Consultation, IMF Country Report

No. 21/130, p. 23. 19 Based on GDP for 2020. 20 FFA, Covid-19: Impact on Federal Finances, as of February 2022. Viewed at:

https://www.efv.admin.ch/efv/en/home/aktuell/brennpunkt/covid19.html. 21 EAER and Federal Department of Finance, Federal Measures for the Economy. Viewed at: