Journal of Financial and Monetary Economics - Centrul de ...

Upload

khangminh22Category

view

0download

0

Monetary EconomicsAn Integrated Approach to Credit,Money, Income, Productionand Wealth

Wynne Godley

and

Marc Lavoie

Contents

Notations Used in the Book ix

List of Tables xviii

List of Figures xx

Preface xxxiv

1 Introduction 11.1 Two paradigms 11.2 Aspiration 41.3 Endeavour 91.4 Provenance 111.5 Some links with the ‘old’ Yale school 131.6 Links with the post-Keynesian school 161.7 A sketch of the book 18A1.1 Compelling empirical failings of the neo-classical

production function 20A1.2 Stock-flow relations and the post-Keynesians 21

2 Balance Sheets, Transaction Matrices and the Monetary Circuit 232.1 Coherent stock-flow accounting 232.2 Balance sheets or stock matrices 252.3 The conventional income and expenditure matrix 332.4 The transactions flow matrix 372.5 Full integration of the balance sheet and the transactions

flow matrices 432.6 Applications of the transactions flow matrix: the monetary

circuit 47

3 The Simplest Model with Government Money 573.1 Government money versus private money 573.2 The service economy with government money and no

portfolio choice 583.3 Formalizing Model SIM 613.4 A numerical example and the standard Keynesian multiplier 683.5 Steady-state solutions 713.6 The consumption function as a stock-flow norm 743.7 Expectations mistakes in a simple stock-flow model 783.8 Out of the steady state 833.9 A graphical illustration of Model SIM 88

v

vi Contents

3.10 Preliminary conclusion 91A3.1 Equation list of Model SIM 91A3.2 Equation list of Model SIM with expectations (SIMEX ) 92A3.3 The mean lag theorem 92A3.4 Government deficits in a growing economy 95

4 Government Money with Portfolio Choice 994.1 Introduction 994.2 The matrices of Model PC 994.3 The equations of Model PC 1024.4 Expectations in Model PC 1074.5 The steady-state solutions of the model 1114.6 Implications of changes in parameter values on temporary

and steady-state income 1164.7 A government target for the debt to income ratio 124A4.1 Equation list of Model PC 126A4.2 Equation list of Model PC with expectations (PCEX) 126A4.3 Endogenous money 127A4.4 Alternative mainstream closures 129

5 Long-term Bonds, Capital Gains and Liquidity Preference 1315.1 New features of Model LP 1315.2 The value of a perpetuity 1315.3 The expected rate of return on long-term bonds 1325.4 Assessing capital gains algebraically and geometrically 1345.5 Matrices with long-term bonds 1365.6 Equations of Model LP 1375.7 The short-run and long-run impact of higher interest rates

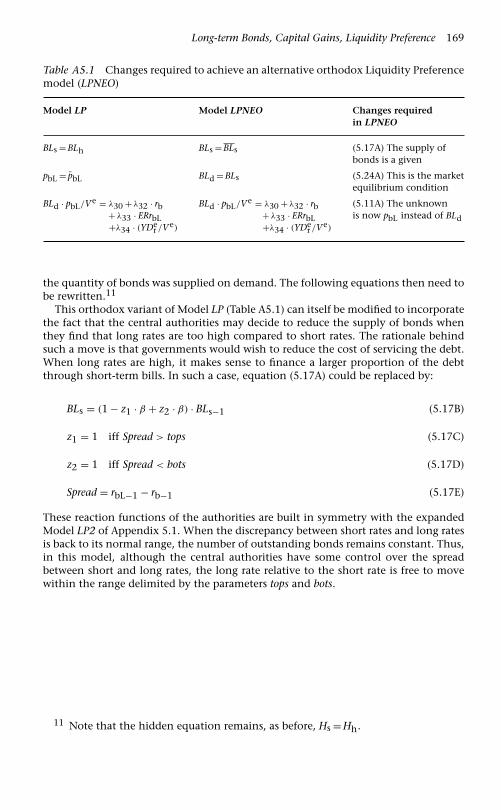

on real demand 1505.8 The effect of household liquidity preference on long rates 1535.9 Making government expenditures endogenous 160A5.1 Equations of Model LP 165A5.2 The liquidity trap 167A5.3 An alternative, more orthodox, depiction of the bond market 168

6 Introducing the Open Economy 1706.1 A coherent framework 1706.2 The matrices of a two-region economy 1716.3 The equations of a two-region economy 1736.4 The steady-state solutions of Model REG 1766.5 Experiments with Model REG 1806.6 The matrices of a two-country economy 1876.7 The equations of a two-country economy 1916.8 Rejecting the Mundell–Fleming approach and adopting

the compensation approach 194

Contents vii

6.9 Adjustment mechanisms 2016.10 Concluding thoughts 207A6.1 Equations of Model REG 209A6.2 Equations of Model OPEN 211A6.3 Historical and empirical evidence concerning the

compensation principle 213A6.4 Other institutional frameworks: the currency board 214A6.5 How to easily build an open model 215

7 A Simple Model with Private Bank Money 2177.1 Private money and bank loans 2177.2 The matrices of the simplest model with private money 2187.3 The equations of Model BMW 2227.4 The steady state 2277.5 Out-of-equilibrium values and stability analysis 2337.6 The role of the rate of interest 2407.7 A look forward 247A7.1 The equations of Model BMW 247

8 Time, Inventories, Profits and Pricing 2508.1 The role of time 2508.2 The measure of profits 2528.3 Pricing 2638.4 Numerical examples of fluctuating inventories 276A8.1 A Numerical example of inventory accounting 278

9 A Model with Private Bank Money, Inventories and Inflation 2849.1 Introduction 2849.2 The equations of Model DIS 2859.3 Additional properties of the model 2939.4 Steady-state values of Model DIS 2959.5 Dealing with inflation in (a slightly modified) Model DIS 300A9.1 Equation list of Model DIS 308A9.2 The peculiar role of given expectations 310A9.3 Equation list of Model DISINF 312

10 A Model with both Inside and Outside Money 31410.1 A model with active commercial banks 31410.2 Balance sheet and transaction matrices 31510.3 Producing firms 31810.4 Households 32210.5 The government sector and the central bank 33110.6 The commercial banking system 33310.7 Making it all sing with simulations 34210.8 Conclusion 374

viii Contents

A10.1 Overdraft banking systems 374A10.2 Arithmetical example of a change in portfolio preference 376

11 A Growth Model Prototype 37811.1 Prolegomena 37811.2 Balance sheet, revaluation and transactions-flow matrices 37911.3 Decisions taken by firms 38311.4 Decisions taken by households 39211.5 The public sector 39711.6 The banking sector 39911.7 Fiscal and monetary policies 40411.8 Households in the model as a whole 42211.9 Financial decisions in the model as a whole 43511.10 A concluding recap 441

12 A More Advanced Open Economy Model 44512.1 Introduction 44512.2 The two matrices 44612.3 Equations of the generic model 45012.4 Alternative closures 46212.5 Experiments with the main fixed exchange rate closure 46612.6 Experiments with alternative fixed exchange rate closures 47212.7 Experiments with the flexible exchange rate closure 47812.8 Lessons to be drawn 487A12.1 A fundamental and useful open-economy flow-of-funds

identity 490A12.2 An alternative flexible exchange rate closure 492

13 General Conclusion 49313.1 Unique features of the models presented here 49313.2 A summary 499

References 501

Index 514

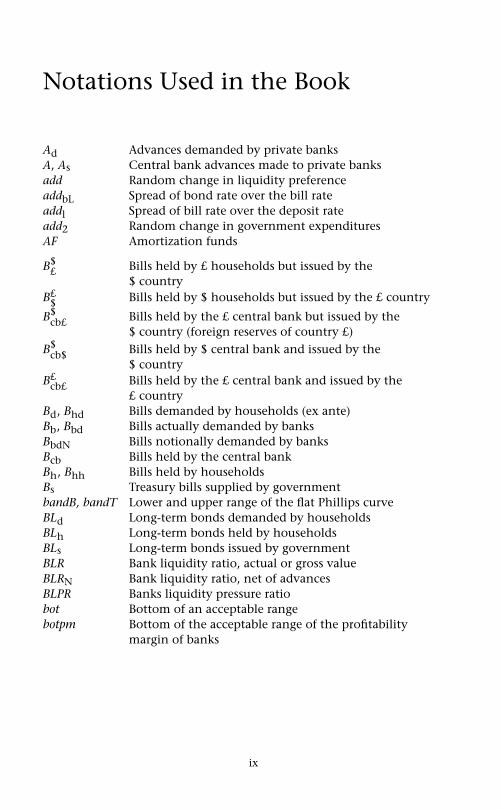

Notations Used in the Book

Ad Advances demanded by private banksA, As Central bank advances made to private banksadd Random change in liquidity preferenceaddbL Spread of bond rate over the bill rateaddl Spread of bill rate over the deposit rateadd2 Random change in government expendituresAF Amortization funds

B$£ Bills held by £ households but issued by the

$ countryB£

$ Bills held by $ households but issued by the £ country

B$cb£ Bills held by the £ central bank but issued by the

$ country (foreign reserves of country £)B$

cb$ Bills held by $ central bank and issued by the$ country

B£cb£ Bills held by the £ central bank and issued by the

£ countryBd, Bhd Bills demanded by households (ex ante)Bb, Bbd Bills actually demanded by banksBbdN Bills notionally demanded by banksBcb Bills held by the central bankBh, Bhh Bills held by householdsBs Treasury bills supplied by governmentbandB, bandT Lower and upper range of the flat Phillips curveBLd Long-term bonds demanded by householdsBLh Long-term bonds held by householdsBLs Long-term bonds issued by governmentBLR Bank liquidity ratio, actual or gross valueBLRN Bank liquidity ratio, net of advancesBLPR Banks liquidity pressure ratiobot Bottom of an acceptable rangebotpm Bottom of the acceptable range of the profitability

margin of banks

ix

x Notations Used in the Book

BP Balance of paymentsBPM Bank profit marginBUR Relative burden of interest payments on loans taken by

households

c, cd Consumption goods demand by households, in realterms

Cd Consumption goods demand by households, in nominalterms

C, Cs Consumption goods supply by firms, in nominal termsCAB Current account balanceCAR Realized capital adequacy ratio of banksCF Cash flow of firmsCG Capital gainsCGe Expected capital gains of the current period

DA Depreciation allowanceDEF Government deficitDS Nominal domestic salesds Real domestic salesdxre Expected change in the exchange rate

E, Ef , Eb Value of equities, issued by firms, issued by bankseb Number of equities supplied by banksed Number of firms’ equities demanded by householdses, ef Number of equities supplied by firmsER Employment rate (the complement of the

unemployment rate)ERrbL Expected rate of return on long-term bonds

F Sum of bank and firm profitsF, Ff Realized entrepreneurial profits of production firmsFb Realized profits of banksFT

b Target profits of banksFcb Profits of central bankFe Expected entrepreneurial profits of firmsFf Realized entrepreneurial profits of production firmsFe

f Expected profits of firmsFT

f Target entrepreneurial profits of production firmsFT Total profits of firms, inclusive of interest payments on

inventoriesFnipa Profits, as measured by national accountantsFD Business dividends

Notations Used in the Book xi

FDb Dividends of banksFDf Realized dividends of production firmsFU Business retained earningsFUb Retained earnings of banksFUT

b Target retained earnings of banksFUf Realized retained earnings of production firmsFUT

f Target retained earnings of production firmsfs Real fiscal stance

g Pure government expenditures in real termsg ′ Real total government expenditures (inflation

accounted)G Pure government expenditures in nominal termsGs, Gd Services supplied to and demanded by governmentGNT Total government expenditures, including interest

payments net of taxesgd Real government debtGT Total government expenditures, inclusive of

interest payments on debtGTD Total domestic government expendituresGD Government debt (public debt), in nominal termsGL Gross flow of new loans made to the household

sectorgr Steady-state growth rate of the economygrk Growth rate of net capital accumulationgrg Growth rate of real pure government expendituresgrpr Growth rate of trend labour productivity

Hbd Reserves demanded by banksHb, Hbs Reserves supplied to banks by the central bankHd, Hhd Cash money demanded by householdsHd, Hh, Hhh Cash money held by householdsHg Cash money held by governmentHhs Cash money supplied to households by the central

bankH , Hs High-powered money, or cash money, supplied by

the central bankHC Historic costsHCe Expected historic costsHUC Historic unit costHUCe Expected historic unit costHWC Historic wage cost

xii Notations Used in the Book

id New fixed capital goods demanded by firms(investment flow), in real terms

Id New fixed capital goods demanded by firms(investment flow), in nominal terms

Ih Residential investment of householdsIs, I , If New fixed capital goods supplied by firms,

in nominal termsin Realized stock of inventories, in real termsine Short-run target level (expected level) of

inventories, in real termsinT Long-run target level of inventories, in real

termsIN Realized stock of inventories, at current unit

costsim Real importsIM Imports, in nominal termsIMT Total imports, inclusive of interest payments

made abroadINTb Interest payments paid by banksINTf Interest payments paid by firmsINTh Interest payments received by households

k, kf , kb Fixed capital stock, in real terms (number ofmachines), of firms, of banks

K, Kf , Kb, Kh Value of fixed capital stock, in nominalterms, of firms, of banks, of households

KT Targeted capital stockKABOSA Capital account balance, inclusive of the

official settlements accountKAB Capital account balance, excluding official

transactions

Ld, Lfd Loans demanded by firms from banksL, Ls, Lfs, Lf Loans supplied by banks to firmsLg Loans to government sectorLhd Loans demanded by households from banksLhs, Lh Loans supplied by banks to households

M , Mh, Mhh Money deposits actually held by householdsM1, M1h Checking account money deposits held by

households

Notations Used in the Book xiii

M1d Checking account money deposits demandedM1s Checking account money deposits suppliedM2, M2h Time or term money deposits held by

householdsM2d Time or term money deposits demandedM2s Time or term money deposits suppliedM1hN The notional amount of bank checking

account deposits that households would holdMd, Mhd Money deposits demanded by householdsMf Financial assets of firmsMg Bank deposits of governmentmh Real money balances held by householdsMs Money supplied by the government (ch. 3) or

the banksML Mean lag

N, Nd Demand for labourNfe The full-employment labour forceNe

s Expected supply of labourNs Supply of labourNT Target level of employment by firmsNAFA Net accumulation of financial assets by the

household sector (financial saving)NCAR Normal capital adequacy ratio of banks

(Cooke ratio)NHUC Normal historic unit costNL Net flow of new loans made to the household

sectornl Real amount of new personal loansnpl Proportion of non-performing loansnple Expected proportion of non-performing loansNPL Amount of non-performing loans (defaulting

loans of firms)NUC Normal unit costsNW, NWh, NWf ,NWg, NWb

Net worth (of households, firms,government, banks)

or Gold unitsOFb Own funds (equity capital) of banksOFe

b Short-run own funds target of banks

OFTb Long-run own funds target of banks

xiv Notations Used in the Book

p Price levelpbL Price of long-term bonds (perpetuities)pe

bL Expected price of long-term bonds in the nextperiod

pds Price index of domestic salespe, pef Price of firms’ equitiespeb Price of banks’ equitiespg Price of goldpk Price of fixed capital goodspm Price index of importsps Price index of salespx Price index of exportspy GDP deflatorPE Price-earnings ratioPERbL Pure expected rate of return on long-term bondspr Labour productivity, or trend labour productivityPSBR Public sector borrowing requirement (government

deficit)

q The valuation ratio of firms (Tobin’s q ratio)

REP Repayment by household borrowers (payment onprincipal)

r, rb Rate of interest on billsr, re Actual and expected yield on perpetuities

(Appendix 5.2)ra Rate of interest on central bank advancesrbL Yield on long-term bondsrk Dividend yieldrl Rate of interest on bank loansrlN Normal rate of interest on bank loans that firms use

to set the markuprm Rate of interest on depositsrrb Real rate of interest on billsrrT

b Target real bill rateRrbl Rate of return on bondsrrbL Real yield on long-term bondsrrc Real rate of interest on bank loans, deflated by the

cost of inventories indexrrl Real rate of interest on bank loansrrm Real rate of interest on term deposits

Notations Used in the Book xv

r̆ Average rate of interest payable on overallgovernment debt

Ra Random number modifying expectationss Realized real sales (in widgets)se Expected real salesS Sales in nominal termsSe Expected sales in nominal termsSA Stock appreciation (inventory valuation

adjustment IVA)SAVh, SAVf ,SAVg, SAV

Household, business, government, and overallsaving

T TaxesTh Income taxes of householdsTf Indirect taxes on firmsTd Taxes demanded by governmentTs, Te

s Taxes supplied or expected to be suppliedtop Top of a target rangetoppm Top of a target range of bank profitabilityTP Target proportion of bonds in national debt held

by households

UC Unit cost of production

v Wealth of households in real termsV , Vh Wealth of households, in nominal termsVT Target level of household wealthVe Expected wealth of households, in nominal termsVf Wealth of firms, in nominal termsVfma Wealth of households devoted to financial market

assetsVg Wealth of government, in nominal termsVnc Wealth of households, net of cashVe

nc Expected wealth of households, net of cash

W Nominal wage rateWB The wage bill, in nominal termswb Real wage bill

x Real exportsX Exports in nominal termsXT Total exports, inclusive of interest payments

received from abroad

xvi Notations Used in the Book

xr Exchange ratexr$ Dollar exchange rate: value of one dollar expressed

in poundsxr£ Sterling exchange rate: value of one pound sterling

expressed in dollarsxre Expected level of the future exchange rate

Y National income, in nominal termsYfc Full-capacity outputYT National income plus government debt serviceYD Disposable income of householdsYDe Expected disposable incomeYDhs Haig–Simons nominal disposable income

(including all capital gains)YDr Regular disposable incomeYDe

r Expected regular disposable incomeYP Nominal personal incomey Real outputyd Deflated regular incomeydhs Haig–Simons realised real disposable incomeyde Expected real disposable incomeydhse Haig–Simons expected real disposable incomeydr Realized real regular disposable incomeyde

r Expected real regular disposable income

z Dichotomic variable or some numerical parameterzm Proportional response of the money deposit rate

following a change in the bill rate

Greek Letters

α (alpha) Consumption parametersα0 Autonomous consumptionα1 Propensity to consume out of regular incomeα2 Propensity to consume out of past wealthα3 Implicit target wealth to disposable income ratio of

householdsα4 Long-run government debt to GDP ratioβ (beta) Reaction parameter related to expectationsγ (gamma) Partial adjustment function that applies to

inventories and fixed capitalδ (delta) Rate of depreciation on fixed capitalδrep Rate of amortization on personal loansε (epsilon) Another reaction parameter related to expectations

Export parameter of a country

Notations Used in the Book xvii

ζ (zeta) Reaction parameter related to changes ininterest rates

η (eta) New loans to personal income ratioθ (theta) Personal income tax rateθ ′ Taxes to GDP ratioι (iota) Parameter tied to the impact of interest rates

on the propensity to consumeκ (kappa) Target fixed capital to output ratioλ (lambda) Reaction parameters in the portfolio choice of

householdsλc Cash to consumption ratioμ (mu) Import propensity or parameterv (nu) Parameter tied to import pricesξ (xi) Reaction parameter tied to changes in interest

rateso (omicron)π (pi) Price inflation rateπc Inflation rate of unit costsρ (ro) Compulsory reserve ratios on bank depositsσ (sigma) Various measures of inventories to output (or

sales) ratioσs Realized (past period) inventories to sales

ratioσse Expected (past period) inventories to sales

ratioσN Normal (past period) inventories to sales ratioσT Target (current) inventories to sales ratioτ (tau) Sales tax rateυ (upsilon) Parameter tied to export pricesϕ (phi) Costing margin in pricingϕT Ideal costing marginϕ′/(1 + ϕ′) Realized share of entrepreneurial profits in

salesχ (chi) Weight of conviction in expected bond pricesψ (psi) Target retained earnings to lagged investment

ratioω (omega) Real wage rateωT Real wage target� (OMEGA) Reaction parameters related to real wage

targeting(hebrew letter) = �p/p (nearly price inflation, but not quite)

$ dollar£ pound sterling

List of Tables

1.1 Standard textbook simplified national income matrix 51.2 Transactions-flow matrix 71.3 Balance-sheet matrix 81.4 Suggested reading sequence 202.1 Household balance sheet 262.2 Balance sheet of production firms at market prices, with

equities as a liability 282.3 Balance sheet of production firms at market prices, without

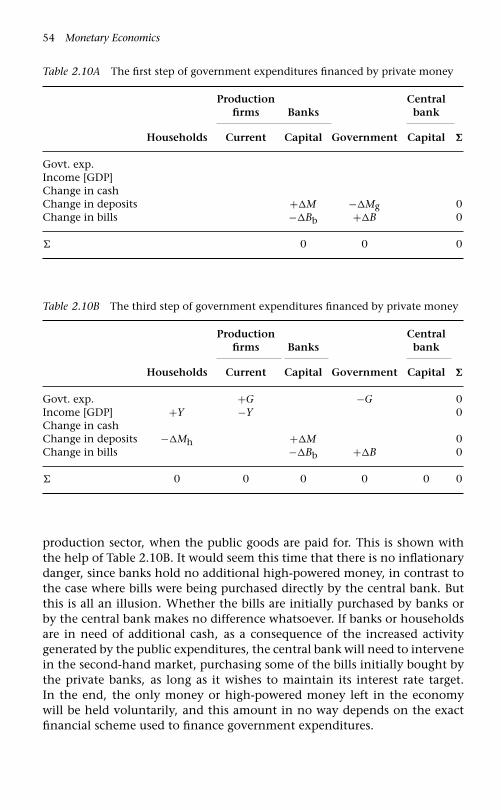

equities as a liability 312.4 A simplified sectoral balance sheet matrix 322.5 Conventional Income and expenditure matrix 332.6 Transactions-flow matrix 392.7 Full-integration matrix 442.8A First step of the monetary circuit with private money 482.8B The second step of the monetary circuit with private money 492.9A The first step of government expenditures financed by

central bank money 522.9B The second step of government expenditures financed by

central bank money 522.9C The third step of government expenditures financed by

central bank money 532.10A The first step of government expenditures financed by

private money 542.10B The third step of government expenditures financed by

private money 542.11A First step of government expenditures in overdraft system 552.11B Second step of government expenditures in overdraft system 553.1 Balance sheet of Model SIM 593.2 Accounting (transactions) matrix for Model SIM 603.3 Behavioural (transactions) matrix for Model SIM 623.4 The impact of $20 of government expenditures, with perfect

foresight 693.5 Behavioural (transactions) matrix for Model SIM, with

mistaken expectations 803.6 The impact of $20 of government expenditures, with

mistaken expectations 814.1 Balance sheet of Model PC 1004.2 Transactions-flow matrix of Model PC 1015.1 Balance sheet of Model LP 137

xviii

List of Tables xix

5.2 Transactions-flow matrix of Model LP 1385.3 Integration of household flow and stock accounts, within

Model LP 139A5.1 Changes required to achieve an alternative orthodox

Liquidity Preference model (LPNEO) 1696.1 Balance sheet of two-region economy (Model REG) 1716.2 Transactions-flow matrix of two-region economy (Model REG) 1726.3 Balance sheet of two-country economy (Model OPEN) 1886.4 Transactions-flow matrix of two-country economy (Model

OPEN) 1906.5 First-period effect of the jump in imports on the balance

sheet of the South central bank 2007.1 Balance sheet of Model BMW 2197.2 The accounting transactions-flow matrix of Model BMW 2207.3 The behavioural transactions matrix of Model BMW 2217.4 Stability conditions 2378.1 The operations of production firms in a simplified setting 2538.2 Starting from scratch: all produced goods enter inventories 2548.3 A numerical example of varying sales, without inflation 2778.4 A numerical example of varying sales, with cost inflation 278A8.1 A numerical example with inventories 279A8.2 A numerical example of the national accounts 2829.1 Balance sheet of Model DIS 2859.2 The transactions-flow matrix of Model DIS 28510.1 The balance sheet of Model INSOUT 31510.2 Transactions matrix of Model INSOUT 316A10.1 Arithmetical example of a change in portfolio preference 37611.1 The balance sheet of Model GROWTH 37911.2 Revaluation matrix of Model GROWTH: Changes in assets

arising from revaluation gains 38011.3 Transactions matrix of Model GROWTH 38212.1 Balance sheets of the two economies 44712.2 Transactions-flow matrix of the two economies 449

List of Figures

2.1 Total internal funds (including IVA) to gross investment ratio,USA, 1946–2005 35

3.1 Impact on national income Y and the steady state solutionY∗, following a permanent increase in governmentexpenditures (�G = 5) 72

3.2 Disposable income and consumption starting from scratch(Table 3.4) 73

3.3 Wealth change and wealth level, starting from scratch(Table 3.4) 75

3.4 Evolution of wealth, target wealth, consumption anddisposable income following an increase in governmentexpenditures (�G = 5) – Model SIM . 76

3.5 Disposable income and expected disposable income startingfrom scratch with delayed expectations (Table 3.6) – ModelSIMEX 82

3.6 Impact on national income Y and the steady state solutionY∗, following an increase in government expenditures(�G = 5), when expected disposable income remains fixed 84

3.7 Evolution of wealth, consumption and disposable incomefollowing an increase in government expenditures (�G = 5),when expected disposable income remains fully fixed 84

3.8 Evolution of consumption, disposable income and wealthfollowing an increase in the propensity to consume out ofcurrent income (α1 moves from 0.6 to 0.7) 86

3.9 The stability of the dynamic process 883.10 Temporary versus stationary equilibria 89A3.1 The mean lag theorem: speed at which the economy adjusts 94A3.2 Adjustment of national income on different assumptions

about the marginal propensity to consume out of currentincome (MPC), for a given target wealth to disposableincome ratio 95

A3.3 The transition from a stationary to a growing economy:impact on the government debt to GDP ratio (continuouscurve) and on the government deficit to GDP ratio (dottedcurve) 97

A3.4 Discrepancy between the target wealth to income ratio andthe realized wealth to income ratio with economic growth 98

4.1 Money demand and held money balances, when theeconomy is subjected to random shock 110

xx

List of Figures xxi

4.2 Changes in money demand and in money balances held (firstdifferences), when the economy is subjected to random shocks 110

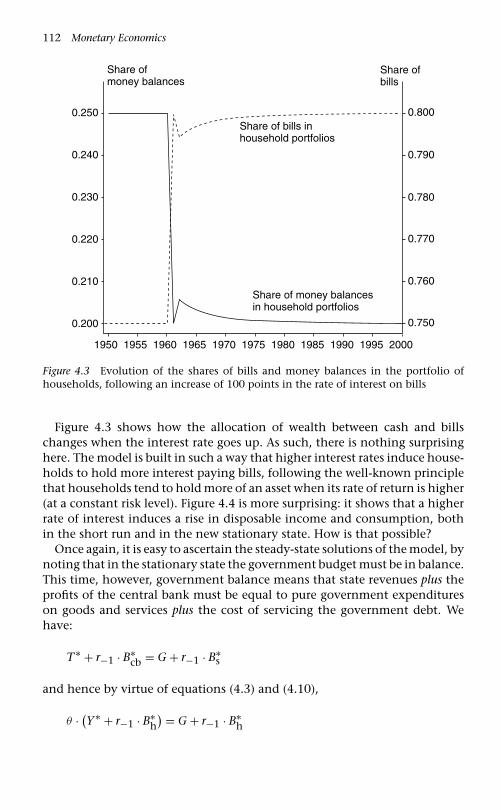

4.3 Evolution of the shares of bills and money balances in theportfolio of households, following an increase of 100 pointsin the rate of interest on bills 112

4.4 Evolution of disposable income and household consumptionfollowing an increase of 100 points in the rate of intereston bills 113

4.5 Rise and fall of national income (GDP) following an increasein the propensity to consume out of expected disposableincome (α1) 118

4.6 Evolution of consumption, expected disposable income andlagged wealth, following an increase in the propensity toconsume out of expected disposable income (α1) 119

4.7 Short-run effect of an increase in the interest rate 1204.8 Short-run effect of a fall in the propensity to consume 1214.9 Evolution of GDP, disposable income, consumption and

wealth, following an increase of 100 points in the rate ofinterest on bills, in Model PCEX2 where the propensity toconsume reacts negatively to higher interest rates 123

4.10 Evolution of tax revenues and government expendituresincluding net debt servicing, following an increase of 100points in the rate of interest on bills, in Model PCEX2 wherethe propensity to consume reacts negatively to higherinterest rates 123

A4.1 Evolution of the rate of interest on bills, following a stepdecrease in the amount of Treasury bills held by the centralbank (Model PCNEO) 129

5.1 The Ostergaard diagram 1355.2 Evolution of the wealth to disposable income ratio, following

an increase in both the short-term and long-term interestrates, with Model LP1 152

5.3 Evolution of household consumption and disposable income,following an increase in both the short-term and long-terminterest rates, with Model LP1 152

5.4 Evolution of the bonds to wealth ratio and the bills to wealthratio, following an increase from 3% to 4% in the short-terminterest rate, while the long-term interest rate moves from 5%to 6.67%, with Model LP1 153

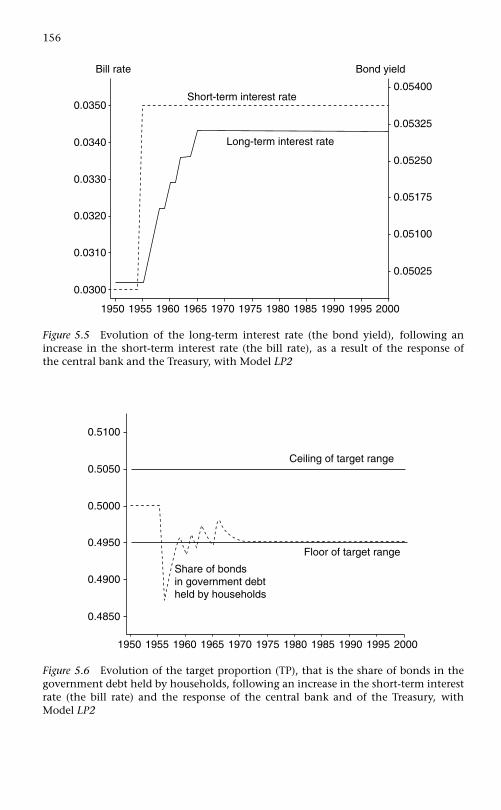

5.5 Evolution of the long-term interest rate (the bond yield),following an increase in the short-term interest rate (the billrate), as a result of the response of the central bank and theTreasury, with Model LP2 156

xxii List of Figures

5.6 Evolution of the target proportion (TP), that is the share ofbonds in the government debt held by households, followingan increase in the short-term interest rate (the bill rate) andthe response of the central bank and of the Treasury, withModel LP2 156

5.7 Evolution of the long-term interest rate, following ananticipated fall in the price of bonds, as a consequence of theresponse of the central bank and of the Treasury, with ModelLP2 157

5.8 Evolution of the expected and actual bond prices, followingan anticipated fall in the price of bonds, as a consequence ofthe response of the central bank and of the Treasury, withModel LP2 158

5.9 Evolution of the target proportion (TP), that is the share ofbonds in the government debt held by households, followingan anticipated fall in the price of bonds, as a consequence ofthe response of the central bank and of the Treasury, withModel LP2 158

5.10 Evolution of national income (GDP), following a sharpdecrease in the propensity to consume out of current income,with Model LP1 163

5.11 Evolution of national income (GDP), following a sharpdecrease in the propensity to consume out of current income,with Model LP3 163

5.12 Evolution of pure government expenditures and of thegovernment deficit to national income ratio (the PSBR toGDP ratio), following a sharp decrease in the propensity toconsume out of current income, with Model LP3 164

6.1 Evolution of GDP in the North and the South regions,following an increase in the propensity to import of theSouth region 181

6.2 Evolution of the balances of the South region – netacquisition of financial assets by the household sector,government budget balance, trade balance – following anincrease in the propensity to import of the South region 182

6.3 Evolution of GDP in the South and the North regions,following an increase in the government expenditures in theSouth region 184

6.4 Evolution of the balances of the South region – netacquisition of financial assets by the household sector,government budget balance, trade balance – following anincrease in the government expenditures in the South region 184

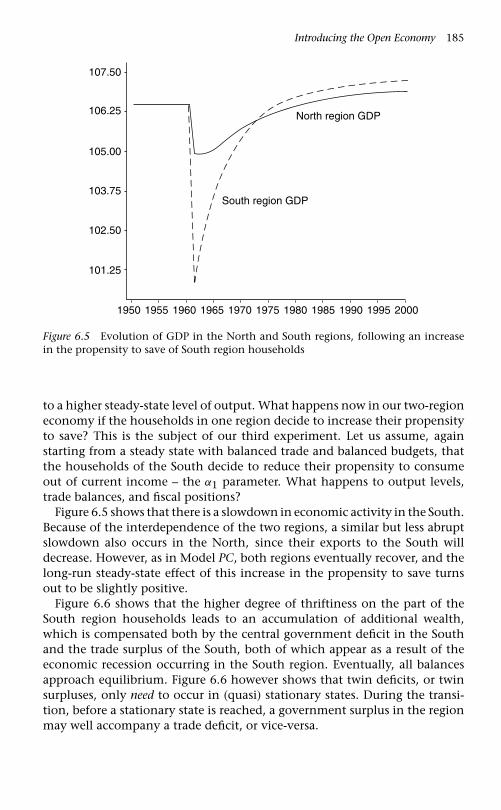

6.5 Evolution of GDP in the North and South regions, followingan increase in the propensity to save of South regionhouseholds 185

List of Figures xxiii

6.6 Evolution of the balances of the South region – netacquisition of financial assets by the household sector,government budget balance, trade balance – following anincrease in the propensity to save of South regionhouseholds 186

6.7 Evolution of the balances of the South region – netacquisition of financial assets by the household sector,government budget balance, trade balance – following adecrease in the liquidity preference of South region households 187

6.8 Evolution of GDP in the North and in the South countries,following an increase in the South propensity to import 194

6.9 Evolution of the balances of the South country – netacquisition of financial assets by the household sector,government budget balance, trade balance – following anincrease in the South propensity to import 195

6.10 Evolution of the three components of the balance sheet of theSouth central bank – gold reserves, domestic Treasury billsand money – following an increase in the South propensity toimport 198

6.11 Evolution of the components of the balance sheet of theSouth central bank, following an increase in the Southpropensity to consume out of current income 201

6.12 Evolution of the balances of the South country – netacquisition of financial assets by the household sector,government budget balance, trade balance – following anincrease in the South propensity to import, with fiscal policyreacting to changes in gold reserves 204

6.13 Evolution of GDP in the South and the North countries,following an increase in the South propensity to consume,with fiscal policy reacting to changes in gold reservess 204

6.14 Evolution of interest rates, following an increase in the Southpropensity to import, with monetary rules based on changesin gold reserves 206

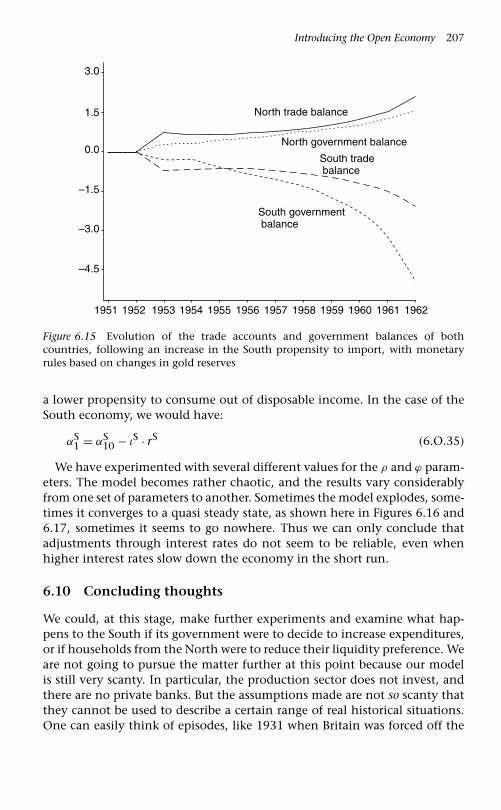

6.15 Evolution of the trade accounts and government balances ofboth countries, following an increase in the South propensityto import, with monetary rules based on changes in goldreserves 207

6.16 Evolution of interest rates, following an increase in the Southpropensity to import, with interest rates acting onpropensities to consume and reacting to changes in goldreserves 208

6.17 Evolution of trade accounts and government balances,following an increase in the South propensity to import, withinterest rates acting on propensities to consume and reactingto changes in gold reserves 208

xxiv List of Figures

7.1 Evolution of household disposable income and consumption,following an increase in autonomous consumptionexpenditures, in Model BMW 231

7.2 Evolution of gross investment and disposable investment,following an increase in autonomous consumptionexpenditures, in Model BMW 231

7.3 Evolution of household disposable income and consumption,following an increase in the propensity to save out ofdisposable income, in Model BMW 232

7.4 Evolution of the output to capital ratio (Y/K−1), following anincrease in the propensity to save out of disposable income,in Model BMW 240

7.5 Evolution of the real wage rate (W), following an increase inthe propensity to save out of disposable income, in Model BMW 242

7.6 The relationship between the real wage and the interest rateon loans 242

7.7 The maximum capital to output ratio that can be attainedduring the transition, for a given interest rate on loans 243

7.8 Evolution of Gross Domestic Income (Y), following anincrease in the interest rate, in Model BMWK 247

8.1 Evolution of price inflation and the inventories to expectedsales ratio, following a decrease in autonomous demand 269

9.1 Evolution of (Haig–Simons) real disposable income and ofreal consumption, following a one-shot increase in thecosting margin 296

9.2 Evolution of (Haig–Simons) real disposable income and ofreal consumption, following an increase in the targetinventories to sales ratio 299

9.3 Evolution of the desired increase in physical inventories andof the change in realized inventories, following an increase inthe target inventories to sales ratio 299

9.4 Evolution of (Haig–Simons) real disposable income and ofreal consumption, following an increase in the rate ofinflation, in a variant where households are blind to thecapital losses inflicted by price inflation 306

9.5 Evolution of real wealth, following an increase in the rate ofinflation, in a variant where households are blind to thecapital losses inflicted by price inflation 306

9.6 Evolution of the rate of price inflation, following a one-shotincrease in the target real wage of workers 307

A9.1 Evolution of real output and real sales following a permanentupward shift in the level of expected real sales 311

A9.2 Convergence of the overestimate of real sales with the desiredreduction in physical inventories following a permanentupward shift in the level of expected sales 311

List of Figures xxv

10.1A Evolution of inventories (and hence bank loans), followingan increase in the target inventories to sales ratio 344

10.1B Evolution of real output and real consumption, relative totheir initial steady state values, following an increase in thetarget inventories to sales ratio 344

10.1C Evolution of household wealth and of its variouscomponents, relative to their initial steady state values,during the first periods that follow an increase in the targetinventories to sales ratio 345

10.1D Evolution of the interest rate on term deposits, following anincrease in the target inventories to sales ratio 346

10.1E Evolution of the various components of the balance sheetof commercial banks, relative to their initial steady statevalues, during the first periods that follow an increase in thetarget inventories to sales ratio 346

10.1F Evolution of the net bank liquidity ratio, relative to itstarget range, following an increase in the target inventoriesto sales ratio 347

10.1G Evolution of the bank profitability margin, relative to itstarget range, following an increase in the target inventoriesto sales ratio 348

10.1H Evolution of the government budget balance, relative to itsinitial steady state value, following an increase in the targetinventories to sales ratio 349

10.1I Evolution of the stock of Treasury bills held by the centralbank, following an increase in the target inventories to salesratio 349

10.2A Evolution of household real wealth, real disposable incomeand real consumption, following a one-step permanentincrease in real government expenditures 350

10.2B Evolution of the public sector borrowing requirement,deflated by the price level, following a one-step permanentincrease in real government expenditures 351

10.2C Evolution the price inflation rate, following a one-steppermanent increase in real government expenditures 352

10.2D Evolution of the real government budget balance, takinginto account the capital gains due to the erosion of thepublic debt by price inflation, following aone-step permanent increase in real governmentexpenditures 353

10.2E Evolution of the debt to GDP ratio, following a one-steppermanent increase in real government expenditures 353

xxvi List of Figures

10.2F Evolution of interest rates on bank loans and term deposits,relative to short and long-term rates on governmentsecurities, following a one-step permanent increase in realgovernment expenditures 354

10.2G Evolution of the various components of the balance sheetof private banks, relative to their initial steady state values,during the first periods that follow an increase in the realgovernment expenditures 354

10.2H Evolution of the net bank liquidity ratio, relative to itstarget range, following a one-step permanent increase inreal government expenditures 355

10.2I Evolution of the bank profitability margin, relative to itstarget range, following a one-step permanent increase inreal government expenditures 355

10.2J Period-by-period changes in the stock of Treasury bills heldby the central bank and in the advances granted tocommercial banks, following a one-step permanent increasein real government expenditures 356

10.3A Evolution of the various components of the balance sheetof commercial banks, relative to their initial steady statevalues, during the first periods that follow an increase in thecompulsory reserve ratios 357

10.3B Evolution of the net bank liquidity ratio, following anincrease in the compulsory reserve ratios 358

10.3C Evolution of the interest rate on deposits and the interestrate on loans, for a given interest rate on bills, following anincrease in the compulsory reserve ratios 359

10.3D Evolution of the bank profitability margin, following anincrease in the compulsory reserve ratios 359

10.3E Evolution of the stock of money deposits, following anincrease in the compulsory reserve ratios 360

10.4A Evolution of the bank liquidity ratio, following an increasein the liquidity preference of banks, proxied by an upwardshift of the liquidity ratio target range 361

10.4B Evolution of the interest rates on deposits and loans,following an increase in the liquidity preference of banks,proxied by an upward shift of the liquidity ratio target range 362

10.4C Evolution of the bank profitability margin, following anincrease in the liquidity preference of banks, proxied by anupward shift of the liquidity ratio target range 362

10.4D Evolution of the various components of the balance sheetof commercial banks, relative to their initial steady statevalues, following an increase in the liquidity preference ofbanks, proxied by an upward shift of the liquidity ratiotarget range 363

List of Figures xxvii

10.5A Evolution of real regular disposable income and of realconsumption, following a decrease in the propensity toconsume out of (expected) real regular disposableincome 364

10.5B Evolution of the real government budget balance, followinga decrease in the propensity to consume out of (expected)real regular disposable income 364

10.6A Evolution of the rate of price inflation, following a one-stepincrease in the target real wage rate 365

10.6B Evolution of real sales and real output following a one-stepincrease in the target real wage that generates an increase inthe rate of inflation 366

10.6C Evolution of the public sector borrowing requirement,deflated by the price level, following a one-step increase inthe target real wage that generates an increase in the rate ofinflation 366

10.6D Evolution of the real government budget deficit, taking intoaccount the capital gains due to the erosion of the publicdebt by price inflation, following a one-step increase in thetarget real wage that generates an increase in the rate ofinflation 367

10.7A Evolution of real sales and real output following a one-stepincrease in the target real wage that generates an increase inthe rate of inflation, accompanied by an increase innominal interest rates that approximately compensates forthe increase in inflation 372

10.7B Evolution of real household debt and real government debtfollowing a one-step increase in the target real wage thatgenerates an increase in the rate of inflation, accompaniedby an increase in nominal interest rates that approximatelycompensates for the increase in inflation 372

10.7C Evolution of the deflated government budget balance,adjusted and unadjusted for inflation gains, following aone-step increase in the target real wage that generates anincrease in the rate of inflation, accompanied by an increasein nominal interest rates that approximately compensatesfor the increase in inflation 373

11.1 Phillips curve with horizontal mid-rangesegment 387

11.2A Evolution of wage inflation and price inflation, followingan autonomous increase in the target real wage 406

11.2B Evolution of real gross fixed investment, real output andreal consumption, all relative to the base line solution,following an autonomous increase in the target realwage 406

xxviii List of Figures

11.2C Evolution of the real interest rate on bills, following anautonomous increase in inflation, when the nominal billrate is set so as to ensure a long-run real rate which is nodifferent from the real rate of the base line solution 407

11.2D Evolution of real output, relative to the base line solution,following an autonomous increase in inflation, when thenominal bill rate rate is set so as to ensure a long-run realrate which is no different from the real rate of the base linesolution 408

11.3A Evolution of real output and real consumption, relative tothe base line solution, following an increase in the rate ofgrowth of real pure government expenditures for only oneyear 409

11.3B Evolution of the employment rate, assumed to be at unityin the base line solution, following an increase in the rate ofgrowth of real pure government expenditures for only oneyear 409

11.3C Evolution of the government deficit to GDP ratio and of thegovernment debt to GDP ratio, relative to the base linesolution, following an increase in the rate of growth of realpure government expenditures for only one year 410

11.3D Evolution of the bank liquidity ratio and of the loans toinventories ratio of firms, relative to the base line solution,following an increase in the rate of growth of real puregovernment expenditures for only one year 411

11.3E Evolution of real consumption and real output, relative tothe base line solution, following a permanent one-shotdecrease in the income tax rate 412

11.4A Evolution of the employment rate and of the inflation rate,with the growth rate of real pure government expendituresbeing forever higher than in the base line solution 413

11.4B Evolution of the real rate of capital accumulation and of thegrowth rate of real output, with the growth rate of real puregovernment expenditures being forever higher than in thebase line solution 413

11.4C Evolution of the government deficit to GDP ratio and of thegovernment debt to GDP ratio, with the growth rate of realpure government expenditures being forever higher than inthe base line solution 414

11.5A Evolution of the lending rate, the deposit rate, and thebond rate, when the (nominal) bill rate is being hiked up insteps and then kept at this higher level 415

List of Figures xxix

11.5B Evolution of real consumption and real output, relative tothe base line solution, when the (nominal) bill rate is set ata higher level 416

11.5C Evolution of the government debt to GDP ratio, when the(nominal) bill rate is set at a higher level 416

11.5D Evolution of the personal loans to regular disposableincome ratio, when the (nominal) bill rate is set at a higherlevel 417

11.5E Evolution of the burden of personal debt (the weight ofinterest payments and principal repayment, as a fraction ofpersonal income), when the (nominal) bill rate is set at ahigher level 418

11.6A Evolution of the growth rate of real output, with the growthrate of real pure government expenditures being foreverhigher than in the base line solution, when the centralbank attempts to keep the real interest rate on bills at aconstant level, but with a partial adjustmentfunction 419

11.6B Evolution of the nominal bill rate, with the growth rate ofreal pure government expenditures being forever higherthan in the base line solution, when the central bankattempts to keep the real interest rate on bills at a constantlevel, but with a partial adjustment function 420

11.6C Evolution of real pure government expenditures and of theemployment rate, relative to the base line solution, with thegrowth rate of real pure government expenditures beingforever higher than in the base line solution, when thecentral bank attempts to keep the employment rate at aconstant level in a forward-looking manner 421

11.6D Evolution of the lending rate, the bill rate and the depositrate, with the growth rate of real pure governmentexpenditures being forever higher than in the base linesolution, when the central bank attempts to keep theemployment rate at a constant level in a forward-lookingmanner 421

11.7A Evolution of real consumption and real output, relative tothe base line solution, following a one-step permanentincrease in the propensity to consume out of regularincome 423

11.7B Evolution of real household wealth, relative to the base linesolution, following a one-step permanent increase in thepropensity to consume out of regular income 424

xxx List of Figures

11.7C Evolution of the inflation rate, relative to the base linesolution, following a one-step permanent increase in thepropensity to consume out of regular income 424

11.7D Evolution of the costing margin of firms and of theirnormal historic unit costs, relative to the base line solution,following a one-step permanent increase in the propensityto consume out of regular income 425

11.7E Evolution of the retained earnings to gross fixed investmentratio and of real inventories, relative to the base linesolution, following a one-step permanent increase in thepropensity to consume out of regular income 426

11.7F Evolution of government deficit to GDP ratio and of thegovernment debt to GDP ratio, relative to the base linesolution, following a one-step permanent increase in thepropensity to consume out of regular income 426

11.7G Evolution of Tobin’s q ratio and of the price-earnings ratio,relative to the base line solution, following a one-steppermanent increase in the propensity to consume out ofregular income 427

11.8A Evolution of the personal loans to personal income ratioand of the burden of personal debt, following an increase inthe gross new loans to personal income ratio 428

11.8B Evolution of real output and real consumption, relative tothe base line solution, following an increase in the grossnew loans to personal income ratio 429

11.8C Evolution of the bank capital adequacy ratio and of thebank liquidity ratio, relative to the base line solution,following an increase in the gross new loans to personalincome ratio 430

11.8D Evolution of the lending rate set by banks, following anincrease in the gross new loans to personal income ratio 430

11.8E Evolution of the government deficit to GDP ratio and of thegovernment debt to GDP ratio, relative to the base linesolution, following an increase in the gross new loans topersonal income ratio 431

11.9A Evolution of Tobin’s q ratio, the price-earnings ratio and theshare of equities in household wealth held in the form offinancial market assets, all relative to the base line solution,following an increase in the household desire to hold stockmarket equities 432

11.9B Evolution of real wealth, real consumption, real output andreal gross investment, all relative to the base line solution,following an increase in the household desire to hold stockmarket equities 433

List of Figures xxxi

11.9C Evolution of the lending rate and the deposit rate,following an increase in the household desire to hold stockmarket equities, when this desire is offset by a drop in thedesire to hold bank deposits 434

11.9D Evolution of the lending rate and the deposit rate,following an increase in the household desire to hold stockmarket equities, when this desire is offset by a drop in thedesire to hold bills and bonds 434

11.10A Evolution of the costing margin of firms, following anincrease in the target proportion of gross investment beingfinanced by gross retained earnings 436

11.10B Evolution of the wage inflation rate, following an increasein the target proportion of gross investment being financedby gross retained earnings 436

11.10C Evolution of the employment rate and of real consumption,relative to the base line solution, following an increase inthe target proportion of gross investment being financed bygross retained earnings 437

11.10D Evolution of Tobin’s q ratio and of the price earnings ratio,relative to the base line solution, following an increase inthe target proportion of gross investment being financed bygross retained earnings, which also corresponds to adecrease in the proportion of investment being financed bynew equity issues 438

11.10E Evolution of the deflated averaged growth rate of theentrepreneurial profits of firms and of the deflated growthrate of equity prices, following an increase in the targetproportion of gross investment being financed by grossretained earnings and no new equity issues 438

11.11A Evolution of the actual bank capital adequacy ratio,following an increase the percentage of non performingloans (defaulting loans) 439

11.11B Evolution of the lending rate and deposit rate, relative tothe base line solution, following an increase thepercentage of non-performing loans (defaultingloans) 440

11.11C Evolution of the actual bank capital adequacy ratio,following a one-time permanent increase in the normalcapital adequacy ratio 440

11.11D Evolution of the interest rate on loans set bybanks, following a one-time permanent increase in thenormal capital adequacy ratio 441

xxxii List of Figures

12.1A Effect of an increase in the US propensity to import on UKvariables, within a fixed exchange rate regime withendogenous foreign reserves: net accumulation of financialassets, current account balance, trade balance andgovernment budget balance 467

12.1B Effect of an increase in the US propensity to import, withina fixed exchange rate regime with endogenous foreignreserves, on the UK current account balance and elementsof the balance sheet of the Bank of England (the UK centralbank): change in foreign reserves, stock of money, holdingsof domestic Treasury bills 468

12.1C Effect of an increase in the US propensity to import on theUS debt to GDP ratio and on the UK debt to income ratio,within a fixed exchange rate regime with endogenousforeign reserves 471

12.2A Effect of an increase in the UK propensity to import, withina fixed exchange rate regime with endogenous UK interestrates, on UK variables: capital account balance, tradebalance, and current account balance 473

12.2B Effect of an increase in the UK propensity to import, withina fixed exchange rate regime with endogenous UK interestrates, on the UK interest rate and on the UK debt to GDP ratio 473

12.3A Effect of an increase in the UK propensity to import, withina fixed exchange rate regime with endogenous UKgovernment expenditures, on the US and UK real GDP 474

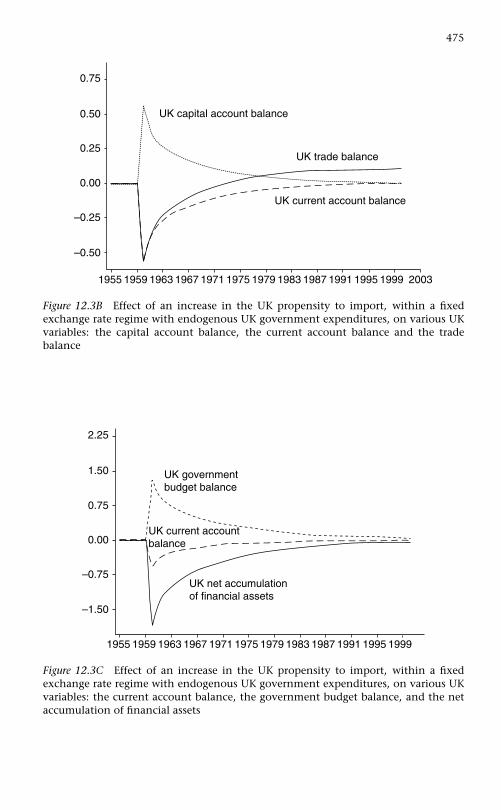

12.3B Effect of an increase in the UK propensity to import, withina fixed exchange rate regime with endogenous UKgovernment expenditures, on various UK variables: thecapital account balance, the current account balance andthe trade balance 475

12.3C Effect of an increase in the UK propensity to import, withina fixed exchange rate regime with endogenous UKgovernment expenditures, on various UK variables: thecurrent account balance, the government budget balance,and the net accumulation of financial assets 475

12.3D Effect of an increase in the UK propensity to import, withina fixed exchange rate regime with endogenous UKgovernment expenditures, on the UK and US debt to GDPratios 476

12.4A Effect on the UK current account balance and trade balanceof a successful one-step devaluation of the sterling pound,following an increase in the UK propensity to import,within a fixed exchange rate regime with endogenousforeign reserves 477

List of Figures xxxiii

12.4B Effect of a successful one-step devaluation of the sterlingpound on UK real GDP, following an increase in the UKpropensity to import, within a fixed exchange rate regimewith endogenous foreign reserves 477

12.5A Effect of a decrease in the UK propensity to export, within aflexible exchange rate regime, on various UK variables:current account balance, trade balance and governmentbudget deficit 479

12.5B Effect on the sterling exchange rate of a decrease in the UKpropensity to export, within a flexible exchange rate regime 479

12.5C Effect of a decrease in the UK propensity to export, within aflexible exchange rate regime, over various UK price indices:export prices, import prices, and domestic sales prices 480

12.5D Effect of a decrease in the UK propensity to export, within aflexible exchange rate regime, on the UK and US real GDP 480

12.6A Effect of a step increase in real US governmentexpenditures, within a flexible exchange rate regime, on theUS and UK real GDP 482

12.6B Effect of a step increase in real US governmentexpenditures, within a flexible exchange rate regime, on themain US balances: net accumulation of financial assets,government budget deficit, current account balance 482

12.6C Effect of a step increase in real US government expenditures,within a flexible exchange rate regime, on the share of thewealth of UK residents held in the form of US Treasury bills,when denominated in dollars and then in sterling 483

12.6D Effect on the dollar exchange rate of a step increase in realUS government expenditures, within a flexible exchangerate regime 483

12.7A Effect on the dollar exchange rate of an increase in thedesire to hold US Treasury bills, within a flexible exchangerate regime 485

12.7B Effect of an increase in the desire to hold US Treasury bills,within a flexible exchange rate regime, on the share of thewealth of UK residents held in the form of US Treasury bills,when denominated in dollars and then in sterling 485

12.7C Effect on UK and US real GDP of an increase in the desire tohold US Treasury bills, within a flexible exchange rate regime 486

12.7D Effect of an increase in the desire to hold US Treasury bills,within a flexible exchange rate regime, on various USvariables: net accumulation of financial assets, governmentbudget deficit, current account balance and trade balance 487

Preface

The premises underlying this book are, first, that modern industrialeconomies have a complex institutional structure comprising productionfirms, banks, governments and households and, second, that the evolutionof economies through time is dependent on the way in which these insti-tutions take decisions and interact with one another. Our aspiration is tointroduce a new way in which an understanding can be gained as to howthese very complicated systems work as a whole.

Our method is rooted in the fact that every transaction by one sectorimplies an equivalent transaction by another sector (every purchase implies asale), while every financial balance (the difference between a sector’s incomeand its outlays) must give rise to an equivalent change in the sum of itsbalance-sheet (or stock) variables, with every financial asset owned by onesector having a counterpart liability owed by some other. Provided all thesectoral transactions are fully articulated so that ‘everything comes fromsomewhere and everything goes somewhere’ such an arrangement of con-cepts will describe the activities and evolution of the whole economic system,with all financial transactions (including changes in the money supply) fullyintegrated, at the level of accounting, into the processes which generate factorincome, expenditure and production.

As any model which includes the whole range of economic activitiesdescribed in the national income and flow-of-funds accounts must beextremely complicated, we start off by imagining economies which haveunrealistically simplified institutions, and explore how these would work.Then, in stages, we add more and more realistic features until, by the end,the economies we describe bear a fair resemblance to the modern economieswe know. In the text we shall employ the narrative method of expositionwhich Keynes and his followers used, trying to infuse with intuition ourconclusions about how particular mechanisms (say the consumption or assetdemand functions) work, one at a time, and how they relate to other partsof the economic system. But our underlying method is completely different.Each of our models, before we started to write it up, was set up with its ownstock and flow transactions so comprehensively articulated that, howeverlarge or small the model, the nth equation was always logically implied bythe other n − 1 equations. The way in which the system worked as a wholewas then explored via computer simulation, by first solving the model inquestion for its steady state and then discovering its properties by changingassumptions about exogenous variables and parameters.

xxxiv

Preface xxxv

The text which follows can do no more than provide a narrative supple-mented with equations, but we believe that readers’ understanding will beenhanced, if not transformed, if they reproduce the simulations for them-selves and put each model through its paces as we go along. It should be easyto download each model complete with data and solution routine.1

In Chapters 3–5 we present very elementary models, with drasticallysimplified institutional structures, which will illustrate some basic prin-ciples regarding the functioning of dynamic stock-flow consistent (SFC)models, and which incorporate the creation of ‘outside’ money into theincome–expenditure process.

Chapter 6 introduces the open economy, which is developed seamlessly outof a model describing the evolution of two regions within a single country.

Chapters 7–9 present models with progressively more realistic featureswhich, in particular, introduce commercial banks and discuss the role ofcredit and ‘inside’ money.

The material in Chapters 10–11 constitutes a break, in terms of com-plexity and reality, with everything that has gone before. We first presentmodels which describe how inside money and outside money interact, howfirms’ pricing decisions determine the distribution of the national incomeand how the financial sector makes it possible for firms and households tooperate under conditions of uncertainty. The Chapter 11 model includes arepresentation of growth, investment, equity finance and inflation.

Finally, in Chapter 12, we return to the open economy (always conceivedas a closed system comprising two economies trading merchandise and assetswith one another) and flesh-out the Chapter 6 model with additional realisticfeatures.

It has taken many years to generate the material presented here. But weare painfully aware that this is only a beginning which leaves everything toplay for.

W.G. and M.L.

Background memories (by W.G.)

My first significant memory as an economist was the moment in 1944 whenP.W.S Andrews, my brilliant teacher at Oxford, got me to extrude a questionfrom my mind: Is output determined by the intersection of marginal revenuewith marginal cost curves or is it determined by aggregate demand? Thus Iwas vouchsafed a precocious vision of the great divide which was to obsessme for years.

1 At http.gennaro.zezza.it/software/models.

xxxvi Preface

My apprenticeship was served in the British Treasury, where, from 1956to 1970, I mainly worked on the conjuncture2 and short-term forecasting.This was the heyday of ‘stop–go’ policies, when we tried to forecast whatwould happen during the following 18 months and then design a budgetwhich would rectify anything likely to go wrong. Forecasting consisted ofscratching together estimates of the component parts of real GDP and addingthem up using, so far as we could, a crude version of the Keynesian multiplier.I now think the theoretical and operational principles we used were seriouslydefective, but the whole experience was instructive and extremely exciting.The main thing I derived from this work was an expertise with statisticalconcepts and sources while gathering a considerable knowledge of stylizedfacts – for instance concerning the (non) response of prices to fluctuationsin demand (Godley 1959; Godley and Gillion 1965) and the response ofunemployment to fluctuations in output (Godley and Shepherd 1964). I alsogot a lot of contemporary history burned into my mind – what kind of year1962 was and so on – and, always waiting for the next figure to come out,I learned to think of the economy as an organism which evolves throughtime, with each period having similarities as well as differences from previousperiods. I came to believe that advances in macro-economic theory couldusefully take place only in tandem with an improved knowledge of whatwas actually happening in the real world – an endless process of iterationbetween algebra and statistics. My perspective was very much enlarged bymy close friendship with Nicholas Kaldor, who worked in the Treasury fromthe mid-sixties. Kaldor was touched by genius and, contrary to what onemight suppose, he had an open mind, being prepared to argue any questionthrough with anyone at any time on its merits and even, very occasionally,to admit that he was wrong.

In 1970 I moved to Cambridge, where, with Francis Cripps, I foundedthe Cambridge Economic Policy Group (CEPG). I remember a damascenemoment when, in early 1974 (after playing round with concepts devised inconversation with Nicky Kaldor and Robert Neild), I first apprehended thestrategic importance of the accounting identity which says that, measured atcurrent prices, the government’s budget deficit less the current account deficitis equal, by definition, to private saving net of investment. Having alwaysthought of the balance of trade as something which could only be analysed interms of income and price elasticities together with real output movements at

2 I believe myself, perhaps wrongly, to have coined this word and its variants in1967 when I was working on devaluation. Bryan Hopkin had given me a cutting froma French newspaper describing the work of a ‘conjoncturiste’, adding ‘This is whatyou are.’

Preface xxxvii

home and abroad, it came as a shock to discover that if only one knows whatthe budget deficit and private net saving are, it follows from that informationalone, without any qualification whatever, exactly what the balance of pay-ments must be. Francis Cripps and I set out the significance of this identityas a logical framework both for modelling the economy and for the formula-tion of policy in the London and Cambridge Economic Bulletin in January 1974(Godley and Cripps 1974). We correctly predicted that the Heath Barber boomwould go bust later in the year at a time when the National Institute was infull support of government policy and the London Business School (i.e. JimBall and Terry Burns) were conditionally recommending further reflation! Wealso predicted that inflation could exceed 20% if the unfortunate threshold(wage indexation) scheme really got going interactively. This was importantbecause it was later claimed that inflation (which eventually reached 26%)was the consequence of the previous rise in the ‘money supply’, while othersput it down to the rising pressure of demand the previous year.

However, far more important than any predictions we then made wasour suggestion that an altogether different set of principles for managingthe economy should be adopted, which did not rely nearly so much onshort-term forecasting. Our system of thought, dubbed ‘New Cambridge’by Richard Kahn and Michael Posner (1974), turned on our view that inthe medium term there were limits to the extent to which private net sav-ing would fluctuate and hence that there was a medium-term functionalrelationship between private disposable income and private expenditure.Although this view encountered a storm of protest at the time it has graduallygained some acceptance and is treated as axiomatic in, for example, Garrattet al. (2003).

We had a bad time in the mid-1970s because we did not then understandinflation accounting, so when inflation took off in 1975, we underestimatedthe extent to which stocks of financial assets would rise in nominal terms.We made some bad projections which led people to conclude that New Cam-bridge had been confuted empirically and decisively. But this was neithercorrect nor fair because nobody else at that time seems to have understoodinflation accounting. Our most articulate critic, perhaps, was John Bispham(1975), then editor of the National Institute Economic Review, who wrote anarticle claiming that the New Cambridge equation had ‘broken down mas-sively’. Yet the National Institute’s own consumption function under-forecastthe personal saving rate in 1975 by 6 percentage points of disposable income!And no lesser authority than Richard Stone (1973) made the same mistakebecause in his definition of real income he did not deduct the erosion, due toinflation, of the real value of household wealth. But no one concluded thatthe consumption function had ‘broken down’ terminally if at all.

It was some time before we finally got the accounting quite right. We gotpart of the way with Cripps and Godley (1976), which described the CEPG’s

xxxviii Preface

empirical model and derived analytic expressions which characterized itsmain properties, and which included an early version of the conflictual,‘target real wage’ theory of inflation. Eventually our theoretical model wasenlarged to incorporate inflation accounting and stocks as well as flows andthe results were published in Godley and Cripps (1983)3 with some furtherrefinements regarding inflation accounting in Coutts, Godley and Gudgin(1985). Through the 1970s we gave active consideration to the use of importcontrols to reverse the adverse trends in trade in accordance with principlesset out in Godley and Cripps (1978). And around 1984 James Tobin spent apleasant week in Cambridge (finding time to play squash and go to the opera)during which he instructed us in the theory of asset allocation, particularlyBackus et al. (1980), which thenceforth was incorporated in our work.

In 1979 Mrs Thatcher came to power largely on the grounds that, withunemployment above one million, ‘Labour [wasn’t] working’, and Britainwas subjected to the monetarist experiment. We contested the policies andthe theory underlying them with all the rhetoric we could muster, predict-ing that there would be an extremely severe recession with unprecedentedunemployment. The full story of the Thatcher economic policies (taking theperiod 1979–92) has yet to be told. Certainly the average growth rate was byfar the lowest and least stable of the post-war period while unemploymentrose to at least four million, once the industrial workers in Wales and theNorth who moved from unemployment to invalidity benefit are counted in.

In 1983 the CEPG and several years of work were destroyed, and discreditedin the minds of many people, by the ESRC decision to decimate our funding,which they did without paying us a site visit or engaging in any significantconsultation.

Still, ‘sweet are the uses of adversity’, and deprived of Francis Cripps (per-haps the cleverest economist I have so far encountered) and never havingtouched a computer before, I was forced to spend the hours (and hours) nec-essary to acquire the modelling skills with which I invented prototypes ofmany of the models in this book.

In 1992, I was invited to join the Treasury’s panel of Independent Forecast-ers (the ‘Six Wise Men’). In my contributions I wrongly supposed that thedevaluation of 1992 would be insufficient to generate export-led growth fora time. But I did steadfastly support the policies pursued by Kenneth Clarke(the UK Chancellor of the Exchequer) between 1993 and 1997 – perhapsthe best time for macro-economic management during the post-war period.Unfortunately a decision was made not to make any attempt to explain,

3 A rhetorically adverse and unfair review of this book, by Maurice Peston (1983),appeared in the Times simultaneously with its publication.

Preface xxxix

let alone reconcile, the divergent views of the Wise Men, with the result thattheir reports, drafted by the Treasury, were cacophonous and entirely withoutvalue.

Through most of the 1990s I worked at the Levy Economics Institute ofBard College, in the United States, where I spent about half my time build-ing a simple ‘stock-flow consistent’ model of the United States – with a greatdeal of help from Gennaro Zezza – and writing a number of papers on thestrategic problems facing the United States and the world economies. Wecorrectly argued (Godley and McCarthy 1998; Godley 1999c), slap contraryto the view held almost universally at the time, that US fiscal policy wouldhave to be relaxed to the tune of several hundred billion dollars if a majorrecession was to be avoided. And in Godley and Izurieta (2001), as well as insubsequent papers, we forecast correctly that if US output were to rise enoughto recover full employment, there would be, viewed ex ante, a balance of pay-ments deficit of about 6% of GDP in 2006 – and that this would pose hugestrategic problems both for the US government and for the world. The otherhalf of my time was spent developing the material contained in this book.In 2002 I returned to the United Kingdom where I continued doing simi-lar work, initially under the benign auspices of the Cambridge Endowmentfor Research in Finance, and more recently with the financial support ofWarren Mosler, who has also made penetrating comments on drafts ofthis book.

My friendship with Marc Lavoie started with an email which he sent meout of the blue saying that he could not penetrate one of the equations in apaper I had written called ‘Money and Credit in a Keynesian Model of IncomeDetermination’ which was published by the Cambridge Journal of Economicsin 1999. The reason, I could immediately explain, was that the equationcontained a lethal error! And so our collaboration began. Marc brought to theenterprise a superior knowledge of how the monetary system works, togetherwith scholarship and a knowledge of the literature which I did not possessand without which this book would never have been written. Unfortunately,we have not been able to spend more than about two weeks physically in oneanother’s presence during the past five years – and this is one of the reasonsit has taken so long to bring the enterprise to fruition.

Joint authorship background (by M.L.)

The present book is the culminating point of a long collaboration that startedin December 1999, when Wynne Godley made a presentation of his 1999Cambridge Journal of Economics paper at the University of Ottawa, followingmy invitation. I had been an avid reader of Godley and Cripps’s innovative

xl Preface

book, Macroeconomics, when it came out in 1983, but had been put off some-what by some of its very difficult inflation accounting sections, as well as bymy relative lack of familiarity with stock-flow issues. Nonetheless, the bookclearly stood out in my mind as being written in the post-Keynesian tra-dition, being based on effective demand, normal-cost pricing, endogenousmoney, interest rate targeting by the monetary authorities and bank financeof production and inventories. I could also see ties with the French circuittheory, as I soon pointed out (Lavoie 1987: 77). Indeed, I was later to dis-cover that Wynne Godley himself felt very much in sync with the theoryof the monetary circuit and its understanding of Keynes’s finance motive, aspropounded by Augusto Graziani (1990, 2003). A great regret of mine is thatduring my three-week stint at the University of Cambridge in 1985, under thetutelage of Geoff Harcourt, I did not take up the opportunity to meet WynneGodley then. This led to a long span during which I more or less forgot aboutWynne’s work, although it is cited and even quoted in my post-Keynesiantextbook (Lavoie 1992).

As an aside, it should be pointed out that Wynne Godley himself hasalways seen his work as being part of the Cambridge school of Keynesianeconomics. This was not always very clear to some of his readers, especiallyin the 1970s or 1980s.4 For instance, Robert Dixon (1982–83: 291) arguedthat the ideas defended by the New Cambridge School, of which Godley wasa leading figure, were virtually tantamount to a monetarist vision of incomedistribution, concluding that ‘Doctrines associated with the New CambridgeSchool represent a dramatic break with the ideas of Keynes. New Cambridgetheory seems to be more pertinent to long-run equilibrium than the worldin which we have our being’ (1982–83: 294). In addition, during a discus-sion of Godley (1983), two different conference participants claimed thatGodley’s model ‘had a real whiff of monetarism about it’ (in Worswick andTrevithick, 1983: 174), so that Francis Cripps, Godley’s co-author, felt obligedto state that ‘what they were doing was Keynesian monetary economics; itwas not neoclassical let alone general equilibrium monetary economics’ (inWorswick and Trevithick, 1983: 176). In retrospect, the confusion arose, soit seems, as a result of the insistence of New Cambridge School membersupon stock-flow consistency and the long-run relationships or medium-runconsequences that this required coherence possibly entailed. It is this focuson possible long-run results that led some readers to see some parallels withmonetarism. But as is clearly explained by Keith Cuthbertson (1979), New

4 And even more recently, as Godley is virtually omitted from King’s (2003) historyof post-Keynesianism. By contrast, Hamouda and Harcourt (1988: 23–4) do devote afull page to his work.

Preface xli

Cambridge authors were opposed to monetarists on just about every policyissue, and the underlying structure of their model was clearly of Keynesianpedigree. Godley himself, more than once, made very clear that he associ-ated himself with the post-Keynesian school. For instance, in a paper thatcan be considered to be the first draft of Chapter 10 of the present book,Godley (1997: 48) claimed ‘to have made, so far as I know for the first time,a rigorous synthesis of the theory of credit and money creation with that ofincome determination in the (Cambridge) Keynesian tradition. My belief isthat nothing the paper contains would have been surprising or new to, sayKaldor, Hicks, Joan Robinson or Kahn’.5

In the late 1990s Anwar Shaikh, who had been working at the Levy Insti-tute, brought my attention to a working paper that had been written thereby Wynne Godley (1996), saying that this was innovative work that was ofutmost importance, although hard to follow. I did get a copy of the workingpaper, and remember discussing it with my long-time friend and colleagueat the University of Ottawa – Mario Seccareccia – and arguing that this wasthe kind of work that we ought to be doing if we wanted to move ahead withcircuit theory and post-Keynesian monetary economics, which at the timeseemed to me to be in a sort of an impasse with its endless and inconclusivedebates. When a substantially revised version of the working paper came outin June 1999 in the Cambridge Journal of Economics, I was now ready to diginto it and put it on the programme of the four-person monthly seminar thatwe had set up in the autumn of that year, with Mario Seccareccia, Tom Rymes(TK), Colin Rogers (visiting from Adelaide), and myself. From this came outthe invitation for Wynne to give a formal presentation at the end of 1999.

Wynne himself looked quite excited that some younger scholars wouldonce more pay attention to his work. What I found stimulating was thatWynne’s working paper and published article had managed to successfullyintegrate the flow aspects of production and bank credit with the stock fea-tures of portfolio choice and money balances – an integration that had alwaysevaded my own efforts – while offering a definite post-Keynesian model,which I felt was in the spirit of one of my favourite authors – NicholasKaldor. Indeed, in contrast to other readers of the 1999 article, I thoughtthat Godley’s model gave substantial (but indirect) support to the so-calledKaldor–Moore accommodationist or horizontalist position, of which I wasone of the few supporters at the time, as I have tried to explain in great detailrecently (Lavoie 2006a).

5 Elsewhere, in Godley (1993: 63), when presenting what I believe to be a prelimi-nary version of his 1999 Cambridge Journal of Economics article, Wynne mentions thathis new work is based on his ‘eclectic understanding’ of Sylos Labini, Graziani, Hicks,Keynes, Kaldor, Pasinetti, Tobin and Adrian Wood.

xlii Preface

Around that time I was working on improving Kaldor’s (1966) well-knownneo-Pasinetti growth model, in which corporate firms keep retained earn-ings and issue stock market shares. I had successfully managed to incorporateexplicit endogenous rates of capacity utilization (Lavoie 1998), but was expe-riencing difficulties in introducing money balances into the model, whiletaking care adequately of capital gains on the stock market. These accountingintricacies were child’s play for Wynne, who offered to help out and build amodel that would provide simulations of this modified Kaldorian model. Thisbecame our first published joint effort – the Lavoie and Godley (2001–2) paperin the Journal of Post Keynesian Economics. This gave rise to a very neat ana-lytical formalization, with a variety of possible regimes, provided by LanceTaylor (2004b: 272–8, 303–5), another keen admirer of the methodologypropounded by Wynne Godley. In my view, these two papers taken together,along with the extension by Claudio Dos Santos and Gennaro Zezza (2005),offer a very solid basis for those who wish to introduce debt and stock marketquestions in demand-led models, allowing them, for instance to tackle theissues brought up by Hyman Minsky with his financial fragility hypothesis.