Monetary Economics (ECS3701) (15) The Money Supply Process

26

1 of 21 ECS 3701 Monetary Economics Errol Goetsch 078 573 5046 [email protected] Lorraine 082 770 4569 [email protected] www.facebook.com/groups/ecs3701 Boston | UNISA 2015 15: The Money Supply Process

Transcript of Monetary Economics (ECS3701) (15) The Money Supply Process

1 of 21

ECS 3701Monetary Economics

Errol Goetsch 078 573 5046 [email protected] 082 770 4569 [email protected]

www.facebook.com/groups/ecs3701

Boston | UNISA 201515: The Money Supply Process

Slide 2 of 26

Part 1 – Introduction01 Why study money, banking, financial markets02 Overview of the financial system03 What is Money?Part 2 – Financial Markets04 Understanding interest rates05 The behaviour of interest rates06 The risk and term structure of interest ratesPart 3 – Financial Institutions08 An economic analysis of financial structure09 Financial crises in advanced economies10 Financial crises in emerging economies11 Banking and management of financial institutionsPart 4 – Central banking and monetary policy14 Central banks: a global perspective15 The money supply process16 Tools of monetary policy17 The conduct of monetary policy: strategy and tacticsPart 6 – Monetary theory20 Quantity theory, inflation and demand for money21 The IS curve24 Monetary policy theory25 The role of expectations in Monetary Policy26 Transmission mechanisms of Monetary Policy

ECS3701 Monetary EconomicsParts 1, 2,3, 4 and 6

15.1 Definitions15.1.1 Definition of Money Supply15.1.2 Definition of Monetary Base15.2 4 Channels for changing the MB15.2.1 The Treasury Channel15.2.2 The Banking Channel (Open Market Operations)15.2.3 The Banking Channel (Discount Loans)15.2.4 Trading foreign reserves (Foreign Channel)15.3 Deposit Creation15.3.1 Step 1: Open Market Operation15.3.2 Step 2: Cheque deposit15.3.3 Step 3: New loan15.3.4 Step 4: Repeat15.4 The (simple) Money MultiplierThe formula15.5 The (complex) Money Multiplier15.4.1 The formula and operation15.4.2 The SARB's level of control15.4.3 The variables15.4.4 The parameters15.4.5 Its sensitivity15.6 The causal direction of the Money SupplyR => D vs. D => R

3 of 21

15.1 DefinitionsDefinition of the Money Supply = Currency + Deposits = ΔMs = ΔC + ΔD

Monetary Policy is the management of Money and Interest Rates by the SARBM1 / M2 / M3 supply – see dedefinitions of D, (we use M1 – C + Cheque Deposits)

(M)oney Supply; (C)urrency; (D)eposits; Ms = C + D

(M)onetary (B)ase; MB = C + R; (R)eserves; R = MBn + BR; Ms = m x MB

Deposits > Currency because SA has a Fractional Reserve System1. Banks hold accounts at the Reserve Bank2. SARB changes reserves of Banks (the Monetary Base)3. Borrowers apply to banks for loans4. Banks turn new Reserves into new Deposits (the Money Supply ) via new loans5. Borrowers deposit new loans at other banks6. New bank receives deposit and lends it out again; chain of deposits continuesSARB ↑Reserves (and MB) by 1 , Deposits (and MS ) ↑ by a multiple of 1

Limiting factors1. How much D↑ increases for every R1↑ (m)2. SARB's requirement for banks to hold back on loans (r)3. Bank's tendency to hold more in reserve than required (e)4. Borrower's tendency to hold some cash rather than deposit all their loan (c)

4 of 21

15.1 DefinitionsDefinition of the Monetary Base = Currency + Reserves MB = C + R

MB = SARB's liabilities

SARB Assets LiabilitiesForeign Assets (C*) + I Currency in circulation C

Loans to banks Bank Reserves R

Central Govt. and other DOther liabilities

Total Total

Bank Assets Liabilities

Deposits with the SARB R Deposits

Bank notes & coins Borrowings of bank

Securities Capital

Loans

Total Total

1

2

3

4

R↑ whenSARB buys assets from banks

SARB buys assets from pvt sector

SARB makes loans to banks

Pvt sector deposits C with banks

Govt. transfers from T&L account with SARB to T&L account with banks

SARB makes payments to pvt sector from account at SARB

Slide 5 of 26

Part 1 – Introduction01 Why study money, banking, financial markets02 Overview of the financial system03 What is Money?Part 2 – Financial Markets04 Understanding interest rates05 The behaviour of interest rates06 The risk and term structure of interest ratesPart 3 – Financial Institutions08 An economic analysis of financial structure09 Financial crises in advanced economies10 Financial crises in emerging economies11 Banking and management of financial institutionsPart 4 – Central banking and monetary policy14 Central banks: a global perspective15 The money supply process16 Tools of monetary policy17 The conduct of monetary policy: strategy and tacticsPart 6 – Monetary theory20 Quantity theory, inflation and demand for money21 The IS curve24 Monetary policy theory25 The role of expectations in Monetary Policy26 Transmission mechanisms of Monetary Policy

ECS3701 Monetary EconomicsParts 1, 2,3, 4 and 6

15.1 Definitions15.1.1 Definition of Money Supply15.1.2 Definition of Monetary Base15.2 4 Channels for changing the MB15.2.1 The Treasury Channel15.2.2 The Banking Channel (Open Market Operations)15.2.3 The Banking Channel (Discount Loans)15.2.4 Trading foreign reserves (Foreign Channel)15.3 Deposit Creation15.3.1 Step 1: Open Market Operation15.3.2 Step 2: Cheque deposit15.3.3 Step 3: New loan15.3.4 Step 4: Repeat15.4 The (simple) Money MultiplierThe formula15.5 The (complex) Money Multiplier15.4.1 The formula and operation15.4.2 The SARB's level of control15.4.3 The variables15.4.4 The parameters15.4.5 Its sensitivity15.6 The causal direction of the Money SupplyR => D vs. D => R

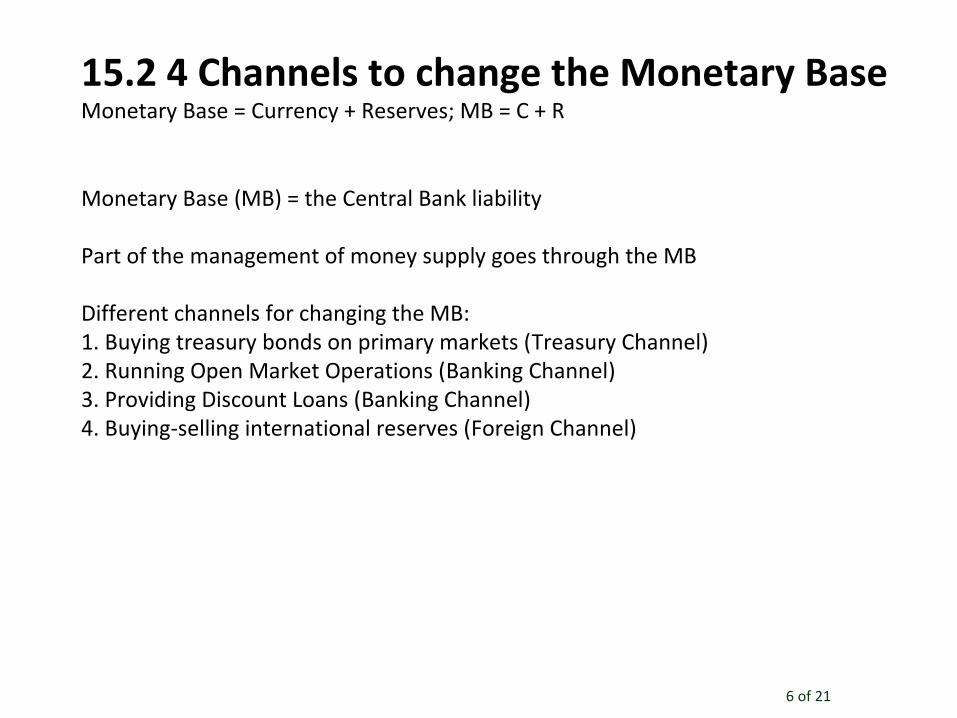

6 of 21

15.2 4 Channels to change the Monetary BaseMonetary Base = Currency + Reserves; MB = C + R

Monetary Base (MB) = the Central Bank liability

Part of the management of money supply goes through the MB

Different channels for changing the MB:1. Buying treasury bonds on primary markets (Treasury Channel)2. Running Open Market Operations (Banking Channel)3. Providing Discount Loans (Banking Channel)4. Buying-selling international reserves (Foreign Channel)

7 of 21

15.2 4 Channels to change the Monetary Base15.2.1 The Treasury Channel

Active when central banks are legally or implicitly committed to buying newly issued treasury bonds

- the government can finance any fiscal deficit, as the central bank will intervene and provide money whenever necessary

- can be a serious source of excessive inflationary pressures

- in most countries this channel is formally prohibited, for the sake of monetary policy independence: I.e separate who creates money from those who spend it

8 of 21

15.2 4 Channels to change the Monetary Base15.2.2 The Banking Channel 1 – Open Market Operations

Suppose that the central bank (SARB) buys (sells) securities from the private sector. This means that it will offer (withdraw) money in exchange

An expansionary (contractionary) monetary policy will expand (contract) the central bank balance sheet, affecting the MB. Under a monetary policy expansion, SARB buys securities and credits an equal amount on the Reserve account that the counterpart has with the SARB

A monetary policy contraction works on the other way around: SARB contracts its balance sheet. OMOs are run by central banks on a daily basis, not just for changing the monetary policy stance but also to meet the demand for reserves by the system.

Banking System SARB

Assets Liabilities Assets Liabilities

Securities -100 Securities +100 Reserves +100

Reserves +100

9 of 21

15.2 4 Channels to change the Monetary Base15.2.3 The Banking Channel 2 - Discount Loans

Commercial Banks can approach the SARB directly for loans, if they cannot or do not want to raise funds from the private sectorThis allows the SARB to inject liquidity directly towards specific institutions, instead of increasing the monetary base for the entire SystemThe downside is that an institution demanding funds directly on the discount window is a negative signal to the marketsThe reserves provided to the system with this channel are called Borrowed Reserves. The other are simply non-borrowed reserves. MB = borrowed and non-borrowed MBNote, unlike OMOs, it is the private sector that decides indirectly whether the MB will expand, as the SARB is committed to providing loans upon request at the discount rate.

Banking System SARB

Assets Liabilities Assets Liabilities

Reserves +100 Discount loans +100 Discount loans +100 Reserves +100

(borrowing from SARB)

(borrowing from SARB)

10 of 21

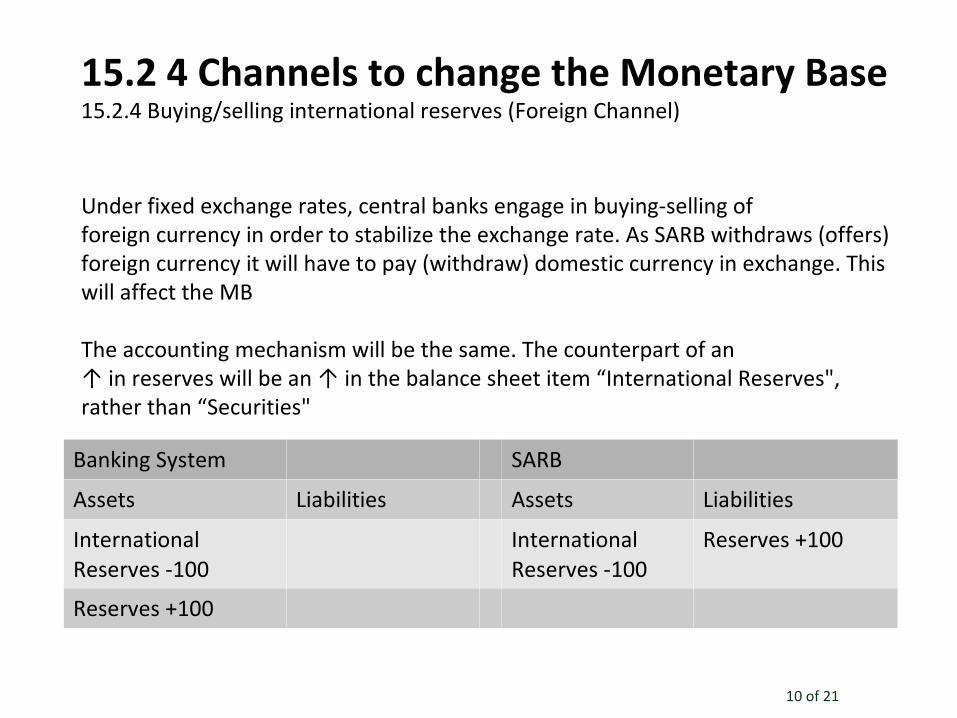

15.2 4 Channels to change the Monetary Base15.2.4 Buying/selling international reserves (Foreign Channel)

Under fixed exchange rates, central banks engage in buying-selling offoreign currency in order to stabilize the exchange rate. As SARB withdraws (offers) foreign currency it will have to pay (withdraw) domestic currency in exchange. This will affect the MB

The accounting mechanism will be the same. The counterpart of an↑ in reserves will be an ↑ in the balance sheet item “International Reserves", rather than “Securities"

Banking System SARB

Assets Liabilities Assets Liabilities

International Reserves -100

International Reserves -100

Reserves +100

Reserves +100

Slide 11 of 26

Part 1 – Introduction01 Why study money, banking, financial markets02 Overview of the financial system03 What is Money?Part 2 – Financial Markets04 Understanding interest rates05 The behaviour of interest rates06 The risk and term structure of interest ratesPart 3 – Financial Institutions08 An economic analysis of financial structure09 Financial crises in advanced economies10 Financial crises in emerging economies11 Banking and management of financial institutionsPart 4 – Central banking and monetary policy14 Central banks: a global perspective15 The money supply process16 Tools of monetary policy17 The conduct of monetary policy: strategy and tacticsPart 6 – Monetary theory20 Quantity theory, inflation and demand for money21 The IS curve24 Monetary policy theory25 The role of expectations in Monetary Policy26 Transmission mechanisms of Monetary Policy

ECS3701 Monetary EconomicsParts 1, 2,3, 4 and 6

15.1 Definitions15.1.1 Definition of Money Supply15.1.2 Definition of Monetary Base15.2 4 Channels for changing the MB15.2.1 The Treasury Channel15.2.2 The Banking Channel (Open Market Operations)15.2.3 The Banking Channel (Discount Loans)15.2.4 Trading foreign reserves (Foreign Channel)15.3 Deposit Creation15.3.1 Step 1: Open Market Operation15.3.2 Step 2: Cheque deposit15.3.3 Step 3: New loan15.3.4 Step 4: Repeat15.4 The (simple) Money MultiplierThe formula15.5 The (complex) Money Multiplier15.4.1 The formula and operation15.4.2 The SARB's level of control15.4.3 The variables15.4.4 The parameters15.4.5 Its sensitivity15.6 The causal direction of the Money SupplyR => D vs. D => R

12 of 21

15.3 Deposit CreationStep 1

ΔM = ΔC + ΔDStart from the ↑ in MB achieved through, say, OMOs

Call r = 0:10 the reserve requirement, i.e. the share of deposits that commercial banks must deposit as reserves at the SARB forprecautionary reasons

Assume that the counterpart in the OMO is the First Bank.It will receive ↑100 on its reserves. But its deposits have not ↑, so it can provide a loan for the entire amount (no excess reserves)

First BankAssets Liabilities

Securities -100

Loans +100

{Total change in money supply} = {Initial change in reserves} * {Money multiplier}

13 of 21

15.3 Deposit CreationStep 2

The firm receiving this loan from the First Bank will deposit this cheque in its own bank account, say at Bank A.

Assume that the entire amount is deposited, no cash is held.

Bank A will experience an ↑ in deposits for 100. 10 % of this will have to go in reserves, leaving 90 for new loans

Bank A Bank A

Assets Liabilities Assets Liabilities

Reserves +100 Cheque deposits +100 Reserves 10 Cheque deposits +100

Loans 90

14 of 21

15.3 Deposit CreationStep 3

But this new loan implies exactly the same mechanism: some Bank B will receive an extra deposit of 90, out which 81 will be given as new loans and the remainder held for required reserves

This mechanism multiplies the initial effect triggered by the SARB: the deposit base will ↑ by a multiple of the initial injection ofliquidity through the OMO

Bank B Bank B

Assets Liabilities Assets Liabilities

Reserves +90 Cheque deposits +90 Reserves 9 Cheque deposits +90

Loans 81

15 of 21

15.3 Deposit CreationStep 4

r = 10%

Bank ∆Deposits ∆Loans ∆Reserves

Example 0.0 100.0 0.0

A 100.0 90.0 15.0

B 90.0 81.0 9.0

C 81.0 72.9 8.1

D 72.9 65.6 7.3

E 65.6 59.0 6.6

F 59.0 53.1 5.9

G 53.1 47.8 5.3

- - - -

1,000.0 1,000.0 100.0

Slide 16 of 26

Part 1 – Introduction01 Why study money, banking, financial markets02 Overview of the financial system03 What is Money?Part 2 – Financial Markets04 Understanding interest rates05 The behaviour of interest rates06 The risk and term structure of interest ratesPart 3 – Financial Institutions08 An economic analysis of financial structure09 Financial crises in advanced economies10 Financial crises in emerging economies11 Banking and management of financial institutionsPart 4 – Central banking and monetary policy14 Central banks: a global perspective15 The money supply process16 Tools of monetary policy17 The conduct of monetary policy: strategy and tacticsPart 6 – Monetary theory20 Quantity theory, inflation and demand for money21 The IS curve24 Monetary policy theory25 The role of expectations in Monetary Policy26 Transmission mechanisms of Monetary Policy

ECS3701 Monetary EconomicsParts 1, 2,3, 4 and 6

15.1 Definitions15.1.1 Definition of Money Supply15.1.2 Definition of Monetary Base15.2 4 Channels for changing the MB15.2.1 The Treasury Channel15.2.2 The Banking Channel (Open Market Operations)15.2.3 The Banking Channel (Discount Loans)15.2.4 Trading foreign reserves (Foreign Channel)15.3 Deposit Creation15.3.1 Step 1: Open Market Operation15.3.2 Step 2: Cheque deposit15.3.3 Step 3: New loan15.3.4 Step 4: Repeat15.4 The (simple) Money MultiplierThe formula15.5 The (complex) Money Multiplier15.4.1 The formula and operation15.4.2 The SARB's level of control15.4.3 The variables15.4.4 The parameters15.4.5 Its sensitivity15.6 The causal direction of the Money SupplyR => D vs. D => R

17 of 21

15.4 The (simple) Money MultiplierΔD = 1 / r ΔR

SARB ↑ MB by 100

Deposits ↑ by 100 + (1 - r)100 + (1 - r )2100 + (1 - r )3100 + .... =

Note that 1/r is bigger than one, given that r is smaller than one.

This is not the full money multiplier, since- static - no excess reserves (e = ER / D)- no money kept as cash (c = C / D)

Slide 18 of 26

Part 1 – Introduction01 Why study money, banking, financial markets02 Overview of the financial system03 What is Money?Part 2 – Financial Markets04 Understanding interest rates05 The behaviour of interest rates06 The risk and term structure of interest ratesPart 3 – Financial Institutions08 An economic analysis of financial structure09 Financial crises in advanced economies10 Financial crises in emerging economies11 Banking and management of financial institutionsPart 4 – Central banking and monetary policy14 Central banks: a global perspective15 The money supply process16 Tools of monetary policy17 The conduct of monetary policy: strategy and tacticsPart 6 – Monetary theory20 Quantity theory, inflation and demand for money21 The IS curve24 Monetary policy theory25 The role of expectations in Monetary Policy26 Transmission mechanisms of Monetary Policy

ECS3701 Monetary EconomicsParts 1, 2,3, 4 and 6

15.1 Definitions15.1.1 Definition of Money Supply15.1.2 Definition of Monetary Base15.2 4 Channels for changing the MB15.2.1 The Treasury Channel15.2.2 The Banking Channel (Open Market Operations)15.2.3 The Banking Channel (Discount Loans)15.2.4 Trading foreign reserves (Foreign Channel)15.3 Deposit Creation15.3.1 Step 1: Open Market Operation15.3.2 Step 2: Cheque deposit15.3.3 Step 3: New loan15.3.4 Step 4: Repeat15.4 The (simple) Money MultiplierThe formula15.5 The (complex) Money Multiplier15.4.1 The formula and operation15.4.2 The SARB's level of control15.4.3 The variables15.4.4 The parameters15.4.5 Its sensitivity15.6 The causal direction of the Money SupplyR => D vs. D => R

19 of 21

15.5 The (complex) Money MultiplierThe multiplier for turning ΔReserves (i.e. ΔCash + ΔDeposits) into ΔM

r = RRR / D ratio of deposits that banks must keep as Required Reserves ≤ 1e = ER / D ratio of deposits that banks want to keep as Excess Reserves ≤ 1c =C / D proportion of deposits that borrowers want to keep as cash ≥ 0

MB = C + R = c D + r D + e D = (c + r + e) DMS = C + D = c D + D = (c + 1) DCombine the two, substitute out D, get

[C/D] + 1m = ------------------------------ RRR + [ER/D] + [C/D]

Since r + e < 1, m > 1

20 of 21

15.5.1 The (complex) Money MultiplierFormula and operation

ΔMB the ↑ in reserves after a monetary policy expansion;Bank 1 receives this extra reserve, with no extra deposits, lends it allBorrower 1 keeps c/(1 + c) ΔMB in cash + deposits 1/(1 + c) ΔMB in Bank 2C= cD so C + D = ΔMBBank 2 will provide a new loan for the amount of 1 – r – e / (1 + c) ΔMBBorrower 2 keeps c/(1 + c) ΔMB in cash + deposits 1/(1 + c) ΔMB in Bank 3and so on

21 of 21

15.5.2 The endogeneity of the Money MultiplierHow much control the SARB has

The SARB does not have full control of the MS

It partially depends on outside behaviour which depends on economic environmentCan totally controlreserve ratio r Can partly controlMB, as the discount window works at the discretion of borrowers,whenever they need fundsCan influencethe size of m by changing the RRR(if and when m changes, the SARB must make offsetting changes in MB to keep MS stable)Cannot controlc and e depends on banks, borrowers and depositors

=> MS can vary for reasons independent on the SARB

c + 1ΔMB

c + r + e

22 of 21

15.5.3 The variables affecting Money MultiplierThe multiplier for turning reserves into deposits

23 of 21

15.5.4 The Sensitivity of Money MultiplierThe parameters that affect m

m ↓ in r and e: the ↑banks keep as reserves, and provide fewer loans, the ↓m can workm ↓ in c: the ↑wealth kept as cash, ↓money is available for loans to start the m processA banking panic can reduce money supply: Increase in c and e can cause a sharp collapse in money supply, making ↑MB ineffectivem is pro-cyclical (m rises in economic upswings; m falls in recessions). the excess reserves ratio (ER/D) tends to rise during recessionsthe currency-deposit ratio (C/D) tends to rise during recessionsm is also affected by changes in interest rates

c r e m c + 1 / c + r + e

0.2 0.1 0.1 3.0 1.2 / 0.4

0.2 0.3 0.1 2.0 1.2 / 0.6

Central Bank ↑ r

0.2 0.1 0.0 4.0 1.2 / 0.3

Banks hold no excess reserves

0.2 0.1 0.4 1.7 1.2 / 0.7

Banks ↑ excess reserves

Slide 24 of 26

Part 1 – Introduction01 Why study money, banking, financial markets02 Overview of the financial system03 What is Money?Part 2 – Financial Markets04 Understanding interest rates05 The behaviour of interest rates06 The risk and term structure of interest ratesPart 3 – Financial Institutions08 An economic analysis of financial structure09 Financial crises in advanced economies10 Financial crises in emerging economies11 Banking and management of financial institutionsPart 4 – Central banking and monetary policy14 Central banks: a global perspective15 The money supply process16 Tools of monetary policy17 The conduct of monetary policy: strategy and tacticsPart 6 – Monetary theory20 Quantity theory, inflation and demand for money21 The IS curve24 Monetary policy theory25 The role of expectations in Monetary Policy26 Transmission mechanisms of Monetary Policy

ECS3701 Monetary EconomicsParts 1, 2,3, 4 and 6

15.1 Definitions15.1.1 Definition of Money Supply15.1.2 Definition of Monetary Base15.2 4 Channels for changing the MB15.2.1 The Treasury Channel15.2.2 The Banking Channel (Open Market Operations)15.2.3 The Banking Channel (Discount Loans)15.2.4 Trading foreign reserves (Foreign Channel)15.3 Deposit Creation15.3.1 Step 1: Open Market Operation15.3.2 Step 2: Cheque deposit15.3.3 Step 3: New loan15.3.4 Step 4: Repeat15.4 The (simple) Money MultiplierThe formula15.5 The (complex) Money Multiplier15.4.1 The formula and operation15.4.2 The SARB's level of control15.4.3 The variables15.4.4 The parameters15.4.5 Its sensitivity15.6 The causal direction of the Money SupplyR => D vs. D => R

25 of 21

15.6 The causal direction of the Ms ProcessR => D vs D => R

1. Cash Reserves comprise Money issued by SARB, kept as deposits by banks at the SARB2. This makes banks dependent on the SARB3. SARB must issue cash reserves as needed on day to day and lender of last resort basis4. SARB meet demand by (a) fixing cash Q and let cash P float or (b) fixing P and let Q float5. Given policy 2, SARB will always meet systemic demand for cash6. Average bank with normal cash demand will always be met7. Knowing this, banks lend out their deposits and buy (cheap) cash to fill reserve8. Changes in r, c and e affect D:

- if r (= R/D) ↑, banks need ↑ R for the D they created- if c (= C/D) ↑, SARB must create ↑R for the D the banks created- if e (= ER/D) ↑, SARB must create ↑R for the D the banks created

Confirmation1. Banks have low e (see no need to hold cash)Explanation1. P collusion means fight for market share (i.e. maximise Q)2. Banks only need to have reserve on monthly average, not daily

Slide 26 of 26

Part 1 – Introduction01 Why study money, banking, financial markets02 Overview of the financial system03 What is Money?Part 2 – Financial Markets04 Understanding interest rates05 The behaviour of interest rates06 The risk and term structure of interest ratesPart 3 – Financial Institutions08 An economic analysis of financial structure09 Financial crises in advanced economies10 Financial crises in emerging economies11 Banking and management of financial institutionsPart 4 – Central banking and monetary policy14 Central banks: a global perspective15 The money supply process16 Tools of monetary policy17 The conduct of monetary policy: strategy and tacticsPart 6 – Monetary theory20 Quantity theory, inflation and demand for money21 The IS curve24 Monetary policy theory25 The role of expectations in Monetary Policy26 Transmission mechanisms of Monetary Policy

ECS3701 Monetary EconomicsParts 1, 2,3, 4 and 6

15.1 Definitions15.1.1 Definition of Money Supply15.1.2 Definition of Monetary Base15.2 4 Channels for changing the MB15.2.1 The Treasury Channel15.2.2 The Banking Channel (Open Market Operations)15.2.3 The Banking Channel (Discount Loans)15.2.4 Trading foreign reserves (Foreign Channel)15.3 Deposit Creation15.3.1 Step 1: Open Market Operation15.3.2 Step 2: Cheque deposit15.3.3 Step 3: New loan15.3.4 Step 4: Repeat15.4 The (simple) Money MultiplierThe formula15.5 The (complex) Money Multiplier15.4.1 The formula and operation15.4.2 The SARB's level of control15.4.3 The variables15.4.4 The parameters15.4.5 Its sensitivity15.6 The causal direction of the Money SupplyR => D vs. D => R