Measuring Environmental Strategy: Construct Development, Reliability, and Validity

46

http://bas.sagepub.com/ Business & Society http://bas.sagepub.com/content/50/1/71 The online version of this article can be found at: DOI: 10.1177/0007650310394427 2011 50: 71 Business Society Judith L. Walls, Phillip H. Phan and Pascual Berrone Reliability, and Validity Measuring Environmental Strategy: Construct Development, Published by: http://www.sagepublications.com On behalf of: International Association for Business and Society can be found at: Business & Society Additional services and information for http://bas.sagepub.com/cgi/alerts Email Alerts: http://bas.sagepub.com/subscriptions Subscriptions: http://www.sagepub.com/journalsReprints.nav Reprints: http://www.sagepub.com/journalsPermissions.nav Permissions: http://bas.sagepub.com/content/50/1/71.refs.html Citations: at Universidad de Navarra-Biblioteca on March 1, 2011 bas.sagepub.com Downloaded from

Transcript of Measuring Environmental Strategy: Construct Development, Reliability, and Validity

http://bas.sagepub.com/Business & Society

http://bas.sagepub.com/content/50/1/71The online version of this article can be found at:

DOI: 10.1177/0007650310394427

2011 50: 71Business SocietyJudith L. Walls, Phillip H. Phan and Pascual Berrone

Reliability, and ValidityMeasuring Environmental Strategy: Construct Development,

Published by:

http://www.sagepublications.com

On behalf of:

International Association for Business and Society

can be found at:Business & SocietyAdditional services and information for

http://bas.sagepub.com/cgi/alertsEmail Alerts:

http://bas.sagepub.com/subscriptionsSubscriptions:

http://www.sagepub.com/journalsReprints.navReprints:

http://www.sagepub.com/journalsPermissions.navPermissions:

http://bas.sagepub.com/content/50/1/71.refs.htmlCitations:

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

Business & Society50(1) 71 –115

© 2011 SAGE PublicationsReprints and permission: http://www.sagepub.com/journalsPermissions.nav

DOI: 10.1177/0007650310394427http://bas.sagepub.com

394427 BAS50110.1177/0007650310394427Walls et al.Business & Society© 2011 SAGE Publications

Reprints and permission: http://www.sagepub.com/journalsPermissions.nav

1Concordia University, Montreal, Quebec, Canada2The Johns Hopkins University, Baltimore, MD3University of Navarra, Madrid, Spain

Corresponding Author:Judith L. Walls, Assistant Professor, John Molson School of Business, Concordia University, 1455 de Maisonneuve Blvd. W., Montreal, Quebec, Canada H3G 1M8 Email: [email protected]

Measuring Environmental Strategy: Construct Development, Reliability, and Validity

Judith L. Walls1, Phillip H. Phan2, and Pascual Berrone3

Abstract

Inconsistent results in prior work that link environmental strategy to com-petitive advantage may be due to the empirical difficulties of marrying the theoretical connection between a firm’s resource base and its environmental strategy. The authors contribute to the field by developing a measure that is congruent with the natural resource–based view, a dominant paradigm in this line of work. This article content analyses company reports and second-ary data to develop a measure of environmental strategy grounded in the natural resource–based view. They identify six environmental capabilities that form components of a reliable, multidimensional construct of proactive environmental strategy. They also identify a measure of reactive compliance strategy. They verify reliability of their new measure through exploratory and confirmatory factor analyses, establish convergent and discriminant validity via a multitrait, multimethod matrix and demonstrate superior

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

72 Business & Society 50(1)

predictive validity of their measure compared to two others commonly used in the literature. In the conclusion, they discuss implications for research and practice.

Keywords

environmental strategy, competitive advantage, environmental capabilities, measurement, reliability, validity

Introduction

Consideration of the natural environment has become a critical element in a firm’s long-term strategy. Changes in the regulatory and institutional envi-ronment as well as more fundamental changes in managerial and consumer perception has driven many companies to shift from a reactive to proactive approach to address environmental issues (Hoffman, 1999). Accordingly, firms are building unique environmental capabilities that drive competitive advantage in the manner put forth by the natural resource–based view, or NRBV (Hart, 1995).

As research in this area has proliferated, a variety of measures of environ-mental strategy has emerged. As a result, theoretical and empirical approaches to studying environmental strategy are wide-ranging and generate inconsis-tent results. For instance, studies tend to blur the lines between environmental management and environmental performance (Claver-Cortés, Molina-Azorín, Tarí-Guilló, & López-Gamero, 2005). As a result, studies often proxy envi-ronmental strategy with environmental performance measures. Or, in the case of propriety measures, the operationalizations have not been validated. As a consequence, it has been difficult for researchers to compare results, replicate studies, and refine theory in the field.

The purpose of this article is to create a measure of environmental strategy that is consistent with theory. We focus on the construct, its definition, opera-tionalization, and measurement in a manner that is congruent with the NRBV. We develop a new measure of environmental strategy using content analysis, and assess its reliability and validity against two commonly used measures. Specifically, we identify six environmental capabilities that form a multidimen-sional construct of a firm’s “proactive” environmental strategy. In addition, we capture the dimensions of “reactive” compliance strategy via the content analysis. We establish construct reliability, convergent and discriminant valid-ities, and show that our measure has stronger predictive power than the other commonly used measures. We contribute to the environmental management

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

Walls et al. 73

literature by closing the gap between the extant empirical approaches and theoretical underpinnings of the NRBV.

Environmental StrategyA corporate environmental strategy is a set of initiatives that mitigate a firm’s impact on the natural environment. Firms achieve such a strategy by implementing products, processes, and policies that reduce energy consump-tion and waste, use ecologically sustainable resources, and employ environ-mental management systems (Bansal & Roth, 2000). To understand how environmental strategy creates value for a firm, researchers have increas-ingly turned to the natural resource–based view (NRBV) as a dominant theo-retical paradigm (Hart, 1995; Sharma & Aragón-Correa, 2005). This view is an extension of the resource-based view of the firm, which emphasizes that internal resources and capabilities, when valuable, rare, inimitable, and with-out equivalent substitutes, can lead to sustainable competitive advantage (Barney, 1991).

Sustainable competitive advantage is achieved when resources and capa-bilities are path dependent, causally ambiguous, and socially complex (Barney, 1991). In the case of environmental strategy, related capabilities can take the form of continuous improvements that lower costs, integration of stakehold-ers to preempt competition, and developing a shared vision that secures a firm’s future position (Hart, 1995). A firm may build environmental capabili-ties sequentially due to the path dependence of capability development in general (Wernerfelt, 1984), or indeed concurrently because of the social embeddedness of environmental issues specifically (Hart, 1995).

A firm’s approach to environmental strategy may lie along a continuum of “reactive” to “proactive” (Aragón-Correa, 1998; Hart, 1995; Henriques & Sadorsky, 1999; Hunt & Auster, 1990; Klassen & Whybark, 1999; Russo & Fouts, 1997; Sharma & Vredenburg, 1998; Shrivastava, 1995). Reactive environmental strategies address environmental issues when they arise as a result of the firm’s activities. Such strategies are designed to comply with environmental regulation, and usually implement so-called “end-of-pipe” solutions that are corrective and emphasize the minimization of risk, liabili-ties, and costs (Roome, 1992).

In contrast, proactive environmental strategies emphasize prevention and are a unique combination of resources through which firms develop environ-mental capabilities. There is little systematic research on how firms acquire environmental capabilities but Marcus (2005) suggests that they can be developed from internal, external, or systemwide sources of the firm. Thus,

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

74 Business & Society 50(1)

in addition to traditional resource–based perspectives in which firms generate capabilities as an incremental result of growth and expansion through under-lying skills and knowledge, environmental capabilities may also come from interfirm ties and networks (external), and public policies, values, and beliefs (systemwide; Marcus, 2005). Researchers suggest that to bestow a competi-tive advantage, proactive environmental strategies must (a) be future-oriented and go beyond regulatory compliance (Aragón-Correa, 1998); (b) implement pollution prevention technologies via product and process (re)design or adap-tation (Christmann, 2000; Marcus & Geffen, 1998); and, (c) be reflected in corporate and managerial values and integrated into management systems and business strategy (Hart, 1995; Russo & Fouts, 1997).

Whether environmental strategy indeed leads to competitive advantage is a topic that has been thoroughly studied. Evidence from several meta-analyses suggests a positive, though small, relationship between environmental and financial performance (Margolis, Elfenbein, & Walsh, 2007; Orlitzky, Schmidt, & Rynes, 2003). Yet studies that link environmental strategy to competitive advantage are often plagued with methodological problems such as omitted variables and endogeneity (Siegel, 2009). Thus the environmental strategy—competitive advantage relationship remains under much debate.

Moreover, empirical studies have often blurred the lines between environ-mental management and environmental performance (Claver-Cortés et al., 2005). Empirical work in this area relies on the NRBV to make an implicit assumption that environmental performance is a proxy for environmental strategy. Nevertheless, this approach conflates cause and effect and has led to a lack of consensus on the relationship between environmental strategy, envi-ronmental performance, and financial performance (Claver-Cortés et al., 2005). As a result, it has been difficult for researchers to compare studies, replicate results, and refine theoretical models in this field.

We propose that a better measure of environmental strategy is needed to address these concerns. This article is a first step toward developing a mea-sure of environmental strategy rooted in the theoretical underpinnings of the NRBV. A considerable body of work supports the notion that under some circumstances it pays to be green (Gladwin, 1993; King & Lenox, 2002; Orsata, 2006; Russo & Fouts, 1997). In particular, environmental strategy tends to pay when firms acquire green competencies (e.g., Marcus & Anderson, 2006; McEvily & Marcus, 2005). We show that our measure of environmental strategy, aligned with theoretical underpinnings of this body of work, has strong reliability and validity and better predictive validity than the extant measures.

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

Walls et al. 75

Method

We studied large U.S. firms during 2003 in industries with high level of effluent in their production processes since environmental issues for these firms are salient (Hart & Ahuja, 1996). Our sample consisted of 184 firms in the S&P 500 index, covering 22 industries from primary and manufacturing industries with SIC codes below 5,000.

Our study was conducted in three phases. First, it was our goal to establish a new, reliable measure of environmental strategy that was consistent with theory, specifically the NRBV. Second, we wanted to compare our new mea-sure to other measures commonly used by researchers to assess the reliability and validity of our measure. Last, we aimed to establish whether our new measure predicted outcomes related to competitive advantage to determine whether our measure had stronger predictive power than other measures. We describe our data collection and analytical procedure for each phase below.

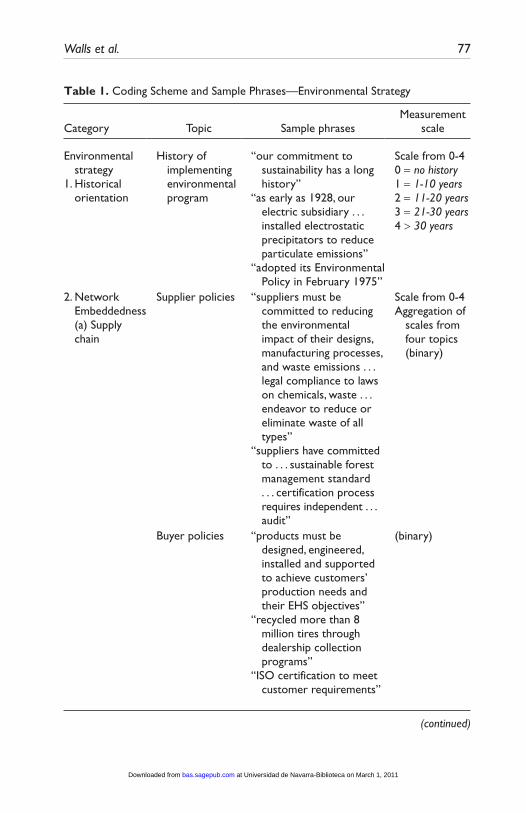

Phase I: Measuring Environmental StrategyData came from corporate environment (or social responsibility) reports, environmental pages from corporate web sites, and annual reports. Annual reports are useful to study organizational strategy because they are public, readily available, and provide comparable sets of data (e.g., Abbott & Monsen, 1979; Arndt & Bigelow, 2000; Bowman, 1984). Similarly, environ-mental reports provide comparable data on firm’s environmental activities (Morhardt, 2001), particularly with the emergence of standardized reporting systems such as the Global Reporting Initiative in 2000. We targeted reports for the year 2003. Since not all firms report annually on their environmental activities, if a report for 2003 was missing, we chose the report produced closest to that year. When an environmental report was not available or data was thin, we sourced additional information from environmental web pages and/or annual reports. In our sample, 83 firms produced environmental reports, 60 had environmental web sites and 106 stated environmental infor-mation in their annual reports.

To analyze the data, we used content analysis (Holsti, 1969; Miles & Huberman, 1994) in two stages, following the process of Arndt and Bigelow (2000). The initial stage consisted of developing a coding scheme to code text, pictures, and captions from all reports. The process was iterative, going back and forth between words/phrases in each report and topics that emerged (Glaser & Strauss, 1967; Miles & Huberman, 1994).

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

76 Business & Society 50(1)

The second stage interpreted the content in reports through the lens of the NRBV. We wanted to identify specific resources and capabilities that organi-zations had developed to address environmental issues. Guided by a holistic literature review of the NRBV and through another iterative process, we identi-fied which topics were relevant and collated them into environmental capabil-ity categories. To avoid the possibility of capturing environmental performance instead of environmental strategy, we also coded statements about outcomes of environmental strategy such as new products, designs, or technologies firms developed, emissions and other key environmental indicators, and environ-mental awards won. We explicitly excluded these from our analysis.

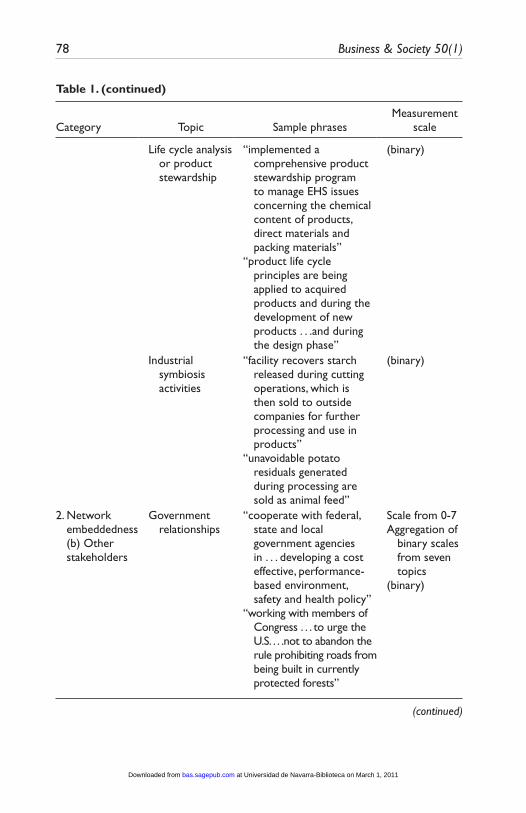

Since our goal was to develop a measure of environmental strategy, we developed a set of scales for each category that could be summed up (Abbott & Monsen, 1979). Topics were either coded as binary or converted to a sliding scale if the code referred to amounts (years, numbers, etc.) or level of inten-sity. The result was that categories were represented by scales and therefore captured the intensity and scope of a firm’s environmental capability as well as its presence. The final coding scheme consisted of 21 topics that fell into six major categories of “proactive” environmental strategy (Table 1) and one cat-egory of a “reactive” compliance strategy that contained two topics (Table 2).

We tested for reliability and validity to verify the congruence of the constructs with theoretical underpinnings of the NRBV (Hoskisson, Hitt, Johnson, & Moesel, 1993; Schwab, 1980; Venkatraman & Grant, 1986). Reliability of the content analysis and environmental strategy construct was measured in several ways. First, we assessed interrater agreement by asking a second researcher to code a random selection of reports. This procedure yielded a Cronbach’s alpha of 91.3%. Second, we established content validity by matching topics with theory through our iterative coding process (Nunnally & Bernstein, 1984). Third, we assessed construct validity by splitting our sample to conduct exploratory factor analysis on the first data set and confir-matory factor analysis on the second data set (Bollen, 1989). We used a factor-extraction method with quartimin oblique rotation to establish that the six capability categories were dimensions of an environmental strategy construct (Bartholomew, Steele, Moustaki, & Galbraith, 2002; Fabrigar, Wegener, MacCallum, & Strahan, 1999).1

Phase II: Evaluating the New Environmental Strategy MeasureTo evaluate our new environmental strategy measure, we compared it to data collected on two other measures often used as proxies for environmental

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

Walls et al. 77

Table 1. Coding Scheme and Sample Phrases—Environmental Strategy

Category Topic Sample phrasesMeasurement

scale

Environmental strategy

1. Historical orientation

History of implementing environmental program

“our commitment to sustainability has a long history”

“as early as 1928, our electric subsidiary . . . installed electrostatic precipitators to reduce particulate emissions”

“adopted its Environmental Policy in February 1975”

Scale from 0-40 = no history1 = 1-10 years2 = 11-20 years3 = 21-30 years4 > 30 years

2. Network Embeddedness (a) Supply chain

Supplier policies “suppliers must be committed to reducing the environmental impact of their designs, manufacturing processes, and waste emissions . . . legal compliance to laws on chemicals, waste . . . endeavor to reduce or eliminate waste of all types”

“suppliers have committed to . . . sustainable forest management standard . . . certification process requires independent . . . audit”

Scale from 0-4 Aggregation of

scales from four topics (binary)

Buyer policies “products must be designed, engineered, installed and supported to achieve customers’ production needs and their EHS objectives”

“recycled more than 8 million tires through dealership collection programs”

“ISO certification to meet customer requirements”

(binary)

(continued)

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

78 Business & Society 50(1)

Category Topic Sample phrasesMeasurement

scale

Life cycle analysis or product stewardship

“implemented a comprehensive product stewardship program to manage EHS issues concerning the chemical content of products, direct materials and packing materials”

“product life cycle principles are being applied to acquired products and during the development of new products . . .and during the design phase”

(binary)

Industrial symbiosis activities

“facility recovers starch released during cutting operations, which is then sold to outside companies for further processing and use in products”

“unavoidable potato residuals generated during processing are sold as animal feed”

(binary)

2. Network embeddedness (b) Other stakeholders

Government relationships

“cooperate with federal, state and local government agencies in . . . developing a cost effective, performance-based environment, safety and health policy”

“working with members of Congress . . . to urge the U.S. . . .not to abandon the rule prohibiting roads from being built in currently protected forests”

Scale from 0-7Aggregation of

binary scales from seven topics

(binary)

Table 1. (continued)

(continued)

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

Walls et al. 79

Table 1. (continued)

Category Topic Sample phrasesMeasurement

scale

NGO relationships

“pipe was donated to three different wildlife refuges in California for use in watershed habitat maintenance”

“spent nearly US$300,000 to fund the installation of hack boxes and hack tower material to reintroduce peregrine falcons to the Big River habitats”

(binary)

Business/industry associations

“participate in the Global Roundtable on Climate Change”

“member of the Business for Social Responsibility (BSR)”

“participate in conferences, industry-working groups on specific projects such as cleaner transportation”

(binary)

Community programs

“a statewide initiative to teach young people about renewable energy technologies”

“community and environmental commitment through employee volunteerism programs, corporate donation campaigns, and environmental education and curriculum development programs”

(binary)

Employee programs

“instituted programs to reduce air emissions

(binary)

(continued)

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

80 Business & Society 50(1)

Category Topic Sample phrasesMeasurement

scale

from employees’ vehicles traveling to and from work”

“more than 600 . . . environmental activities are being undertaken . . . by our employees”

“actively support employee volunteerism . . . donate US$10 for every qualifying hour of volunteer work”

Socially responsible shareholders

“proudly listed in the Dow Jones Sustainability Index, Calvert Social Index and the Domini 400 Social Index”

“met with 15 SRI firms,” “increased shareholder value through EHS commitment”

“CSR analyst meetings”

(binary)

Volunteer programs

“entered into voluntary cleanup agreements . . . with the Department of Environmental Conservation”

“joined U.S. EPA Climate Leaders Partnership to work towards a voluntary commitment to reduce greenhouse gases”

(binary)

3. Endowments

ISO certification “half of our locations are ISO14001 certified”

“all our facilities worldwide are expected to comply with our corporate

Scale from 0-5Aggregation of

scales from three topics

Table 1. (continued)

(continued)

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

Walls et al. 81

Category Topic Sample phrasesMeasurement

scale

Environmental Protection Program, which is aligned with ISO 14001”

0 = No ISO1 = some sites

have ISO2 = all sites have

ISO(binary)

Environmental management system

“we are using Six Sigma to reduce the amount of wood waste from ‘cut direct’ saws by 50%”

“environmental management system being developed at facility by facility basis”

Environmental R&D

“investing US$1.5 billion over the next several years in environmental systems that will significantly reduce emissions of SO2 and NOx at our power plants”

“US$82million in environmental spending”

“invested more than US$4 million on research in the pursuit of a ‘zero-discharge’ water-recycling technology”

0 = US$0-US$399mil

1 = US$400-US$1.6bn

2 = > US$1.6bn

4. Managerial vision

Long-term commitment to environment

“we also set key milestones to be met by 2010”

“new voluntary program to reduce carbon intensity by 2012”

“life cycle management reviews of all existing products must be completed by 2010”

Scale from 0-3Aggregation of

scales from two topics

0 = no visionary statement

1 = statement is made

2 = vision is > 5 years

Table 1. (continued)

(continued)

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

82 Business & Society 50(1)

Category Topic Sample phrasesMeasurement

scale

Global level of vision

“three regional sustainability reports were published in . . . Australia . . . Canada . . . Latin America”

“revised our sustainable forestry policies and practices to . . . promote sustainable forestry on a global level”

(binary)

5. Top management team skills

Senior environmental executive

“the vice president of the department . . . reports to our group president . . . who reports directly to Chairman and CEO”

“officers . . .Vice President-Environment, Health & Safety and Audit”

“we welcomed . . . as Vice President and Chief Sustainability Officer [reports directly to the board]”

Scale from 0-4Aggregation of

scales from two topics

(binary)

Reporting structure level

“senior managers are part of the environmental management reporting structure”

“independent assessments by external organizations”

“corporate responsibility committee at board level”

“local facilities are responsible for implementation”

0 = no reporting structure

1 = local/facility level

2 = senior management

3 = board/external auditors

Table 1. (continued)

(continued)

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

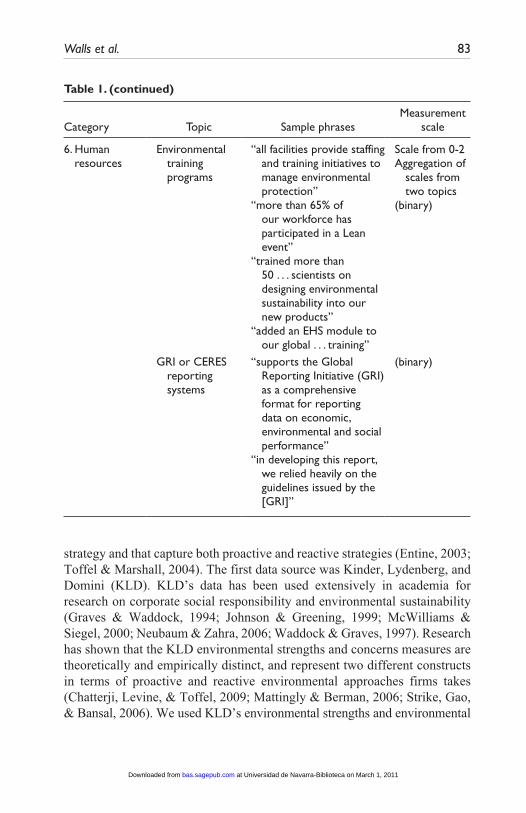

Walls et al. 83

Table 1. (continued)

Category Topic Sample phrasesMeasurement

scale

6. Human resources

Environmental training programs

“all facilities provide staffing and training initiatives to manage environmental protection”

“more than 65% of our workforce has participated in a Lean event”

“trained more than 50 . . . scientists on designing environmental sustainability into our new products”

“added an EHS module to our global . . . training”

Scale from 0-2Aggregation of

scales from two topics

(binary)

GRI or CERES reporting systems

“supports the Global Reporting Initiative (GRI) as a comprehensive format for reporting data on economic, environmental and social performance”

“in developing this report, we relied heavily on the guidelines issued by the [GRI]”

(binary)

strategy and that capture both proactive and reactive strategies (Entine, 2003; Toffel & Marshall, 2004). The first data source was Kinder, Lydenberg, and Domini (KLD). KLD’s data has been used extensively in academia for research on corporate social responsibility and environmental sustainability (Graves & Waddock, 1994; Johnson & Greening, 1999; McWilliams & Siegel, 2000; Neubaum & Zahra, 2006; Waddock & Graves, 1997). Research has shown that the KLD environmental strengths and concerns measures are theoretically and empirically distinct, and represent two different constructs in terms of proactive and reactive environmental approaches firms takes (Chatterji, Levine, & Toffel, 2009; Mattingly & Berman, 2006; Strike, Gao, & Bansal, 2006). We used KLD’s environmental strengths and environmental

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

84 Business & Society 50(1)

Table 2. Coding Scheme and Sample Phrases—Environmental Compliance

Category Topic Sample phrasesMeasurement

scale

Environmental Compliance

Violations “12 noncompliance orders for seven facilities”

“21 violations in 331 inspection”

“123 noncompliance events and accidental releases in 2003”

Scale from 0-6Aggregation of

scales from two topics

0 = no violations1 = at least 1

violation Remediation

costs and/ or fines

“[we] companies paid US$151,250 in environmental fines or penalties”

“environmental fines totaled US$16,200 for violations at five locations worldwide”

“we have determined that the recorded liability for environmental matters . . . is approximately US$337.4 million”

“[we are investigating] several current and former manufacturing facilities, in both the United States and abroad, to investigate and remediate environmental contamination resulting from past operations up to possibly US$578.8 mil”

0 = no remediation costs or fines

1 < US$100mil2 = US$100mil-

US$399mil3 = US$400mil-

US$899mil4 = US$900mil-

US$1.6bn5 = > US$1.6bn

concerns categories (appendix).2 Each category was binary to indicate whether the firm performed the activity. We aggregated the category scores for a total respective score of KLD strengths as a measure of “proactive” environmental strategy and KLD concerns as a measure of “reactive” environmental strat-egy, attributing equal weights to the categories. The maximum possible score was 6 for KLD strengths and 7 for KLD concerns. In our sample, 32.1% of firms had at least one KLD strength and 40.8% had at least one KLD con-cern. The most frequent KLD strength was for KLD’s “pollution prevention”

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

Walls et al. 85

category (12.5% of our sample) and the most frequent KLD concern was for “hazardous waste” (26.6%).

TRI data was a second oft-used measure of environmental strategy (King & Lenox, 2002; Klassen & Whybark, 1999; Russo & Harrison, 2005). TRI data consisted of toxic emissions via air, water, land, or underground injection that must be reported to the Environmental Protection Agency (EPA). To account for risks associated to human health, we weighted chemicals using the Human Toxicity Potential Factor (HTP) developed by Hertwich, Mateles, Pease, and McKone (2001), which measures toxicity in terms of benzene equivalence (for carcinogens) or toluene equivalence (for noncarcinogens). Each measure was aggregated across chemicals at facility level and then to parent company. We next calculated the predicted value of pollution by esti-mating total waste generation levels using production ratios in the prior year reported by TRI and compared these against actual levels (King & Lenox, 2000, 2002). If actual waste was lower than predicted, this pollution preven-tion measure would yield positive results. We aggregated the carcinogenic and noncarcinogenic measures (Berrone & Gomez-Mejia, 2009) to capture “proactive” environmental strategy. “Reactive” environmental strategy mea-sure was calculated in the form of end-of-pipe pollution control. This measure was calculated as a ratio of the sum of chemicals recycled, treated on-site, and transferred to other locations for further treatment divided by the total waste generated by the firm (King & Lenox, 2001, 2002, 2004; Sarkis & Cordeiro, 2001). TRI data was available for about three quarters of our sample.

While both the KLD and TRI measures clearly say something about a firm’s environmental activities, neither is rooted explicitly in theory. Yet, they are often used as proxies for environmental strategy. Therefore, we compared the KLD and TRI measures against our new environmental strategy measure, developed with theoretical alignment in mind, to test convergent and discrimi-nant validity. To do so, we used a multitrait, multimethod matrix (Campbell & Fiske, 1959). This procedure allowed us to check that correlations converged between different methods of capturing the same trait, for instance proactive environmental strategy, and that these could be discriminated from traits intended to differ, in our case reactive environmental strategy. In addition, the matrix assessed internal reliability scores for each measure.

Phase III: Environmental Strategy and Competitive AdvantageThe third phase of our analysis was to assess the relationship between our environmental strategy measure and a competitive advantage outcome for

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

86 Business & Society 50(1)

firms. Our goal was to establish the predictive validity of our new measure and compare the predictive power of our measure to other measures often used in the literature.

We considered competitive advantage in terms of two firm-level outcomes: environmental and financial. We used two different outcomes because we wanted to delineate between environmental strategy, in the form of manage-ment practices, certification, initiatives, and technologies, and environ-mental performance in the form of the impact of a firm’s activities on the natural environment (Claver-Cortés et al., 2005). Past research has largely considered the relationship of environmental performance (not strategy) with financial performance (e.g., Hart & Ahuja, 1996; King & Lenox, 2002; Russo & Fouts, 1997). Yet the relationship between environmental and finan-cial performance may be explained by environmental strategy (Claver-Cortés et al., 2005). For instance, there is evidence that firms with developed environmental capabilities in manufacturing or supplier networks have stronger environmental performance (Klassen & Whybark, 1999; Marcus & Geffen, 1998).

To avoid common method bias, data on environmental performance was collected from a source unrelated to our measures. We collected data from RiskMetrics’ Innovest Strategic Value. This database establishes ratings on firm’s environmental activities based on company data, in-depth sector anal-ysis, and interviews.3 We used Innovest’s environmental score with a 5-year lag (i.e., data from 2008) to capture future environmental performance of a firm based on its environmental strategy in 2003.

Financial performance was measured as Tobin’s Q using Compustat data (King & Lenox, 2002). Tobin’s Q captures a firm’s market value based on expectations of future cash flow, such as those gained from environmental initiatives. Therefore, we assessed Tobin’s Q in 2003 and did not use lags in the financial performance analysis.

Predictive validity on both outcomes of competitive advantage was assessed using regression analysis, as a form of criterion-related validity of a new measure (Kerlinger & Lee, 2000). To avoid omitted variable bias, we included a number of controls that are known to affect financial performance and typically used in environmental management research (McWilliams & Siegel, 2000; King & Lenox, 2002). These controls were collected using Compustat data and included firm size as a log of assets, sales growth as change of sales over the last 3 years, R&D intensity as R&D expenditure over sales, capital intensity as capital expense over sales, and leverage as total debt over total assets. We added an industry control in the form of pol-lution intensity that ranked 2-digit SIC industries by total amount of toxic

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

Walls et al. 87

emissions, from most (highest score) to least (lowest score) polluting sector (Berrone & Gomez-Mejia, 2009).

ResultsWe present our results in four sections. First, we provide a detailed overview of our findings of the content analysis, and the six environmental capabilities that emerged. We link these capabilities to the literature the NRBV and describe how we operationalized them. Next, we review the reliability of our environmental strategy construct based on these six capabilities. Third, we demonstrate the results of the multitrait, multimethod matrix analysis that compares our measures with those of KLD and TRI. Finally, we show the results of the predictive validity of the construct.

Content AnalysisEven though there is a trend toward standardized global environmental reporting, reports in our sample varied in many respects. They differed in length, type of information reported, and style; some reports emphasized pictures, others graphs and tables. Data on environmental resources and capabilities were found in various sections or aspects of reports—sometimes in formal descriptive text, other times in diagrams or stories. In spite of these differences, reports were fairly consistent in what they reported. In our sample, 83.2% contained information on proactive environmental strategy in the form of capabilities, and 34.2% contained information of reactive envi-ronmental strategy in the form of compliance issues.

In terms of proactive environmental strategy, the content analysis revealed six categories of environmental capabilities. These included historical orien-tation (52.2% of firms), network embeddedness including supply chain net-works (53.8%), and stakeholder engagement (64.7%), endowments (69.0%), managerial vision (75.0%), top management team skills (51.1%), and human resource systems (42.4%). Each capability is rooted in theoretical paradigm of the natural resource–based view and identified through the iterative coding process we described earlier. We describe the capabilities and how they were operationalized.

Historical orientation. A company’s path through time and space and the unique historical conditions of its establishment dictates how it acquires and exploits resources and therefore how well it performs in the future (Arthur, 1989; Barney, 1991). History can bestow firms with competitive advantage: preferential locations, founding conditions, scientific breakthroughs, and values

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

88 Business & Society 50(1)

and beliefs that dominate the period all contribute to the development of firm specific capabilities.

Environmental capabilities are no different. For example, the develop-ment of environmental capabilities often begins as a reflection of the institu-tional environment at a point in history with a reactive approach of pollution control that later builds up toward a proactive goal of sustainable develop-ment (Hart, 1995; Hoffman, 1999). By forming a reactive approach, firms build a foundational capability to address ongoing environmental issues. Having a “foot-in-the-door” in dealing with the natural environment makes it easier to gain support for future environmental projects, especially if past experiences were successful (Cordano & Frieze, 2000). In addition, actively seeking opportunities to improve environmental performance becomes a part of the corporate culture and identity (Sharma, 2000). Firms with a strong his-tory in environmental strategy are more likely to consider the environmental impact of new strategies, products, and processes. They are also more likely to spread environmental values throughout their supply chain in their rela-tionships with buyers, suppliers, consumers, and peers. Therefore, the longer a firm’s history of having an environmental strategy, the more likely it is to have built environmental capabilities. In our content analysis, “historical ori-entation” was coded as a scale based on the years since a firm implemented an environmental program.

Network embeddedness. A network is a set of linkages among organizations characterized by specified relationships based on (a) resource transfers such as money, information, power, commitment, or personnel or (b) interpenetra-tion of organizational boundaries through shared interest groups (Laumann, Galaskiewicz, & Marsden, 1978). Networks are strategically important because they allow firms to respond to their interdependence with the general external environment (Pfeffer & Salancik, 1978; Uzzi, 1999) by having access to the right resources, identifying opportunities, matching expectations, and gaining control over information (Burt, 1997; Lenz, 1980). The ability of organiza-tions to generate resources is partly determined by their networks (Lenz, 1980). Because networks evolve over time, they are path dependent and become a capability of the firm (Freeman & Barley, 1990; Lenz, 1980). Net-works are furthermore socially complex and difficult to imitate.

Access to networks is particularly critical for corporate environmental strategy because environmental issues are extremely complex and thus require firms to have interdisciplinary skills and coordinate their environ-mental response with others (Roome, 1992). Moreover, networks and exter-nal ties are a source of environmental capability acquisition in the form of

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

Walls et al. 89

information sharing, trust, and joint problem solving (McEvily & Marcus, 2005). In terms of environmental strategy, networks fall into two groups: firms along the product supply chain acting as suppliers and buyers, and other stakeholders such as governments, employees, NGOs, or “any group or indi-vidual who can affect or is affected by the attainment of the organization’s objectives” (Freeman, 1984, p. 46). The “supply chain network” has a direct impact on a firm’s production process and therefore also on its environmental performance through engaging with outsiders and sharing information along the product supply chain (Cerin & Karlson, 2002; Marcus & Geffen, 1998). The “other stakeholder network,” on the other hand, influences environmental strategy through social pressure and can determine the type of environmental strategy a firm pursues (Delmas & Toffel, 2008). In response to stakeholder influence, firms can develop specific environmental strategies such as eco-design and ecosystem stewardship (Sharma & Henriques, 2005). By address-ing stakeholder concerns, companies develop trust and credibility and build a good corporate reputation, an intangible resource (Sharma & Vredenburg, 1998; Russo & Fouts, 1997). Networking thus represents a socially complex environmental skill that forms a competitive advantage for environmental strategy (Delmas & Toffel, 2004; Hart, 1995; Henriques & Sadorksy, 1999). Our content analysis suggests that “supply chain network” can be measured as a reflection of companies’ engagement with suppliers, buyers, conduct product stewardship efforts, or engage in material exchange (industrial symbiosis) with other companies. In turn, the “other stakeholder network” is a reflection of a firm’s association with governments, NGOs, industry associations, communities, employees, socially responsible investors, and voluntary programs.

Endowments. Firms can build competitive advantage through the accumu-lation of assets over time. Such endowments become an asset stock for the firm when the resource flows form a consistent pattern of appropriate choices on expenditure to build resources and skills (Dierickx & Cool, 1989). This path-dependent process is usually causally ambiguous and can allow firms to achieve strategic goals more quickly than competitors. Asset stocks are also interconnected with other stocks and subject to continual reinvestment to forestall erosion (Dierickx & Cool, 1989). Endowments can appear in the form of physical assets or structures in the form of organizational slack. Organizational slack is the cushion of actual or potentially accessible resources that allows organizations to respond to pressure, initiate strategic change, champion causes, and facilitate innovative or creative behavior (Bourgeois, 1981; Singh, 1986). Slack allows firms to retain earnings for

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

90 Business & Society 50(1)

reinvestment, particularly useful if the firm wants to invest in long-term proj-ects such as environmental strategy.

An effective environmental strategy requires continual and considerable reinvestment (Darnall & Edwards, 2006). Firms that possess long-term endowments can more easily build environmental capabilities because it allows them to invest in technological leadership and exploit opportunities (Aragón-Correa, 1998). In particular, the greater the degree of discretionary slack—that which is within the latitude of managerial action—the more likely it is that managers can address environmental issues (Sharma, 2000). Slack allows flexibility and firms with slack respond in a timelier manner to changes in environmental technologies (Aragón-Correa, Matías-Reche, & Senise-Barrio, 2004). Thus, endowments and related slack allow firms to build proactive environmental strategies. “Endowments,” in our analysis, is a combination of the amount of money a firm invests in environmental research and development (scale) and supporting structures such as an environmental management system or an ISO-14001 certified environmental process that would create the necessary slack to maximize the endowment.

Managerial vision. “Visioning” is the process of projecting a desired future organizational state that, when effectively communicated, empowers follow-ers to enact the vision (see Westley & Mintzberg, 1989). Visionary leadership may result from an individual’s capacity for imagination, inspiration, insight, foresight, or sagacity and can be directed to focus on products, processes, the market, the organization, or ideals (Westley & Mintzberg, 1989). Visionary leadership benefits company performance, attitudes of followers, creates cohesion among the top management team, and has a positive influence on corporate citizenship (see Groves, 2006). Visionary leadership furthermore positively influences values of social corporate responsibility toward share-holders, stakeholders, and the community at large (Waldman et al., 2006). Managerial vision is also important for building internal interdependencies and interrelationship within organizations (Dierickx & Cool, 1989). Vision is particularly important when uncertainty is high and actions are difficult to contract, and managers with strong visions will tend to attract employees with similar beliefs (Van den Steen, 2005).

Visionary leadership is a unique capability because it is not clear if such leaders can be trained. In addition, a complex or internally interdependent organization is difficult for competitors to copy because it cannot be system-atically managed or influenced (Barney, 1991; Child, 1972). Environmental strategies require visionary leadership because the success of environmental strategies depends on long-term commitment and investment (Hart, 1995).

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

Walls et al. 91

A corporate mission that embeds social goals allows firms to develop envi-ronmental capabilities (Marcus & Andersson, 2006). Vision prioritizes the environment on the corporate agenda; managers champion and direct functional, department and production processes toward environmental goals (Andersson & Bateman, 2000). Our analysis indicates that managerial vision of environ-mental strategy can be measured in terms of the time dimension of the envi-ronmental vision (short- or long-term goals have been set) and the depth of the vision across the organization (global or not).

Top management skills. Managerial skills may be generic (transferable), industry specific, and firm specific (such as know-how) used to make opera-tional and strategic decisions that build competitive advantage (Castanias & Helfat, 1991). Superior management skills are a source of economic rent (Penrose, 1959) and difficult for competitors to imitate as they are firm-specific (Barney, 1991). The competitive advantage of top managers comes not just from within the firm but also through the managers’ connections within the business environment. Evidence suggests, for example, that the ability to network along the supply chain and stakeholders through reciprocal relationships based on trust confers competitive advantage (Tsang, 1998).

A successful environmental strategy is likely to require managerial com-petencies in combination with other firm-specific capabilities (Russo & Fouts, 1997). Implementing environmental strategic initiatives requires tight internal integration and coordination as well as stable external partnerships (Dechant & Altman, 1994), which require a talented top management team. The role of managers in environmental strategy is one of central coordina-tion, integration, and connections with others to source for talent, ideas, and technologies (Marcus & Geffen, 1998). To do so, environmental managers must have some tenure with the firm and relevant functional experience in environmental issues (Aragón-Correa et al., 2004). In our content analysis “top management team” environmental skills are assessed by whether the environmental manager is on the executive team and by the reporting level of the environmental manager (a scale of local or facility level) to senior man-agement team or the board.

Human resources. Human resources are firm-specific capabilities that can also bestow competitive advantage (Barney, 1991). Particularly, human resources can be a unique capability if a firm’s HR practices differ from most of its peers were developed through trial-and-error (path-dependent), consist of continual investment, and are highly integrated with other firm resources (socially complex), and cannot be substituted by planning systems (non-substitutable; Lee, Phan, & Chan, 2005).

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

92 Business & Society 50(1)

Human resources are an important capability for the development of envi-ronmental strategies because dealing with environmental issues requires expert knowledge and specific incentives (Wehrmeyer, 1996). Such experi-ence may not necessarily rest within the firm but can be brought in by hiring professionals or experts. Indeed, the more firms search for talent and ideas externally, the more likely they will be able to build environmental capabili-ties if they can harmonize the external learning within the firm (Marcus & Geffen, 1998). In addition, firms that evaluate managers on environmental performance criteria are more likely to develop environmental capabilities (Sharma, 2000). In our analysis, two processes that firms have in place rele-vant to “human resources” skills for environmental strategy are formal envi-ronmental training programs and formal environmental performance reporting systems.

Content was also analyzed for reactive environmental strategy. These were captured in the form of noncompliance with environmental regulation. Two topics were captured for this category that we labeled environmental compliance: an indication of violation of environmental regulation, that may or may not have involved a penalty in the form of a fine, and costs in terms of fines or remediation costs the company reported.

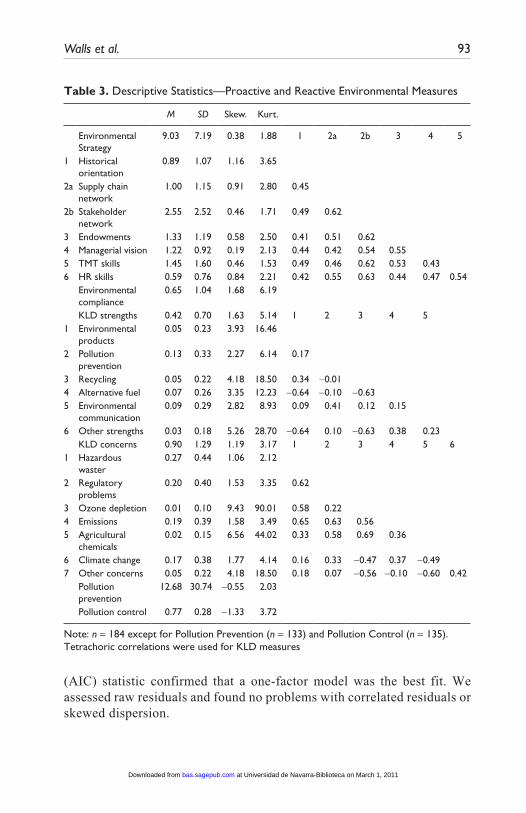

Construct ReliabilityWe assessed the reliability of our environmental strategy construct, based on six environmental capabilities using factor analysis. Table 3 indicates that all capabilities are positively correlated with one another. It appears that firms develop environmental capabilities in parallel as suggested by Hart (1995).

The reliability analysis was done using both exploratory and confirmatory factor analysis. We split the data into two random samples, one containing 122 observations and a smaller one with 62 observations, to cross-validate our model (Bollen, 1989). The larger sample was used in an exploratory fac-tor analysis using a factor extraction method, in case reliabilities were low (Fabrigar et al., 1999). We used oblique quartimin rotation, allowing factors to correlate (Fabrigar et al., 1999), based on the evidence that firms build environmental capabilities in parallel.

Results are given in Table 4 and show that all environmental capabili-ties loaded onto a single factor with loadings ranging from 0.52 to 0.81, above the 0.40 cutoff point typically used in strategic management litera-ture (e.g., Finkelstein, 1992). Loadings on additional factors were below the 0.40 cutoff point. The eigenvalue of the first factor was 3.42 (Chi-square = 355.78), and a scree plot and Akaike Information Criterion

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

Walls et al. 93

Table 3. Descriptive Statistics—Proactive and Reactive Environmental Measures

M SD Skew. Kurt.

Environmental Strategy

9.03 7.19 0.38 1.88 1 2a 2b 3 4 5

1 Historical orientation

0.89 1.07 1.16 3.65

2a Supply chain network

1.00 1.15 0.91 2.80 0.45

2b Stakeholder network

2.55 2.52 0.46 1.71 0.49 0.62

3 Endowments 1.33 1.19 0.58 2.50 0.41 0.51 0.62 4 Managerial vision 1.22 0.92 0.19 2.13 0.44 0.42 0.54 0.55 5 TMT skills 1.45 1.60 0.46 1.53 0.49 0.46 0.62 0.53 0.43 6 HR skills 0.59 0.76 0.84 2.21 0.42 0.55 0.63 0.44 0.47 0.54 Environmental

compliance 0.65 1.04 1.68 6.19

KLD strengths 0.42 0.70 1.63 5.14 1 2 3 4 5 1 Environmental

products 0.05 0.23 3.93 16.46

2 Pollution prevention

0.13 0.33 2.27 6.14 0.17

3 Recycling 0.05 0.22 4.18 18.50 0.34 −0.01 4 Alternative fuel 0.07 0.26 3.35 12.23 −0.64 −0.10 −0.63 5 Environmental

communication 0.09 0.29 2.82 8.93 0.09 0.41 0.12 0.15

6 Other strengths 0.03 0.18 5.26 28.70 −0.64 0.10 −0.63 0.38 0.23 KLD concerns 0.90 1.29 1.19 3.17 1 2 3 4 5 61 Hazardous

waster 0.27 0.44 1.06 2.12

2 Regulatory problems

0.20 0.40 1.53 3.35 0.62

3 Ozone depletion 0.01 0.10 9.43 90.01 0.58 0.22 4 Emissions 0.19 0.39 1.58 3.49 0.65 0.63 0.56 5 Agricultural

chemicals 0.02 0.15 6.56 44.02 0.33 0.58 0.69 0.36

6 Climate change 0.17 0.38 1.77 4.14 0.16 0.33 −0.47 0.37 −0.49 7 Other concerns 0.05 0.22 4.18 18.50 0.18 0.07 −0.56 −0.10 −0.60 0.42 Pollution

prevention12.68 30.74 −0.55 2.03

Pollution control 0.77 0.28 −1.33 3.72

Note: n = 184 except for Pollution Prevention (n = 133) and Pollution Control (n = 135).Tetrachoric correlations were used for KLD measures

(AIC) statistic confirmed that a one-factor model was the best fit. We assessed raw residuals and found no problems with correlated residuals or skewed dispersion.

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

94 Business & Society 50(1)

Table 4. Exploratory Factor Analysis

Variables Factor 1 Factor 2 Factor 3

1. Historical orientation 0.693 −0.039 0.1252a. Supply chain network 0.759 −0.022 −0.1602b. Stakeholder network 0.810 0.033 −0.020 3. Endowments 0.581 0.305 −0.041 4. Managerial vision 0.520 0.235 −0.003 5. TMT skills 0.655 0.014 0.207 6. Human resources 0.723 −0.152 −0.012Eigenvalues 3.42 0.68 0.10

Note: factor extraction (principal factor) method was used with oblique quartimin rotation. n = 122, Chi-square = 355.78, degrees of freedom = 21, Cronbach’s alpha = 0.86.

The single-factor construct had a high reliability score with a Cronbach’s alpha of 0.86 and a reliability coefficient Rho of 0.84, well above the 0.70 cutoff point that is considered acceptable for early stage construct validation (Nunnally & Bernstein, 1994).

We then used the smaller sample to run a confirmatory factor analysis. We used a factor extraction method but restricted the analysis to one factor. The results were closely aligned with those of the exploratory factor analysis (Table 5), indicating that our measure appeared appropriate.4

Results of the factor analyses suggest that all environmental capabilities were a component of the environmental strategy measure we developed

Table 5. Confirmatory Factor Analysis

Variables Factor 1

1. Historical orientation 0.5052a. Supply chain network 0.6462b. Stakeholder network 0.857 3. Endowments 0.761 4. Managerial vision 0.738 5. TMT skills 0.806 6. Human resources 0.804Eigenvalue 3.83

Note: factor extraction (principal factor) method was used, constrained to one factor. n = 62, Chi-square = 220.71, degrees of freedom = 21, Cronbach’s alpha = .964.

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

Walls et al. 95

through our content analysis. Thus our environmental strategy measure was a formative (aggregated) construct (Edwards, 2001) that consisted of six environmental capabilities.5

Construct Validity: The Multitrait Multimethod MatrixWe tested the validity of our environmental strategy construct using a multi-trait, multimethod matrix analysis (Table 6). This analysis provides informa-tion on internal reliabilities of the measures (in parentheses), discriminant validity between correlations of different constructs using the same measure-ment instruments (superscript “a”), convergent validity of correlations of the same constructs using different measurement instruments (superscript “b”), and discriminant validity between correlations of different constructs using different measures (Campbell & Fiske, 1959).

Internal reliability scores were calculated through Cronbach’s alpha, and were not available for the environmental compliance measure constructed in our content analysis or TRI’s pollution control measure as these were single-item constructs. Internal reliabilities were strong for our environmental strat-egy measure (0.86), KLD concerns (0.65) and TRI pollution prevention (0.63). The KLD strengths reliability score was only 0.24. Since this measure is based on an unsystematic categorization of firm’s environmental initiatives

Table 6. Multitrait Multimethod Matrix of Environmental Measures

A1 B1 A2 B2 A3 B3

Environmental strategy A1 (0.86) Environmental compliance B1 −0.06a ( )

KLD strengths A2 0.51b 0.04 (0.24) KLD concerns B2 0.17 0.11b 0.31a (0.65)

Pollution prevention A3 −0.02b 0.03 0.10b −0.03 (0.63) Pollution control B3 0.03 0.13b 0.13 −0.18b 0.38a ( )

Note: Cronbach’s alpha not available for “Compliance” and “Pollution Control.” n = 127, correlations greater than 0.16 are significant at a 5% level. Internal reliabilities of the measures are shown within parenthesesa. Discriminant validity between correlations of different constructs using the same measurement instruments.b. Convergent validity of correlations of the same constructs using different measurement instruments.

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

96 Business & Society 50(1)

without sound theoretical grounding, however, there was no a priori expecta-tion for strong internal reliability.

Discriminant validity of different constructs using the same method (hetero-trait mono-method) was marked with superscript “a”, and should have been close to zero. These correlations were between the “proactive” and “reactive” environmental strategy constructs in our content analysis, KLD, and TRI. Our environmental strategy construct had a very low correlation with envi-ronmental compliance (–0.06), suggesting strong discriminant validity. In contrast, convergent validity was less strong for KLD (0.31) and TRI (0.38) where proactive and reactive constructs correlated moderately.

Convergent validity of similar constructs measured in different ways (homo-trait hetero-method) was marked with superscript “b”. These correla-tions should have been significantly different from zero. Among the proac-tive constructs, convergent validity was strong between our measure of environmental strategy and KLD strengths (0.51). In contrast, the TRI pollu-tion prevention measure did not correlate significantly with the environmen-tal strategy nor KLD strengths.

Among the reactive constructs, convergent validity did not take place—none of the correlations were statistically significant. Qualitatively, the envi-ronmental compliance measure from our content analysis was weakly positively correlated with both KLD concerns and TRI pollution control. However, the correlation among the latter two reactive measures was signifi-cant but negative. This relationship suggests that firms that have implemented fewer pollution control techniques have higher KLD concerns. Thus, while both of these variables are considered “reactive” environmental approaches in our analysis, there appears to be a difference between them. Future research may need to reconsider “reactive” approaches along a continuum that distin-guishes between minimal compliance to environmental regulation (in the form of pollution control) versus failure to comply (in the form of KLD con-cerns). Our environmental compliance measure appears to capture both these types of reactive approaches. Furthermore, the KLD concerns measure may be artificially inflated because a firm with one environmental problem could be captured in several of the KLD concerns categories. For example, a firm that has “substantial emissions” may also have “regulatory problems” for which it would score a double hit in the KLD concerns measure. Such infla-tion could partly explain why the convergence between our environmental compliance measure and KLD concerns, although positively correlated, is not statistically significant.

A final discriminant validity check assessed correlations of different con-structs measured in different ways (hetero-trait hetero-method). In this analysis,

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

Walls et al. 97

superscript “b” diagonal values should have been higher than adjacent values in normal font. We found discriminant validity in the case of our content analysis measures and KLD measures. Evidence was inconsistent for the TRI measures. The pollution control measure could be discriminated from our content analysis measures, but the pollution prevention measure could not be. The TRI measures could also not be sufficiently discriminated from either of the KLD measures. This circumstance would suggest that TRI pollution pre-vention (a proactive construct) does not discriminate enough from reactive constructs. Again, future researchers may wish to consider different levels of proactive approaches firms take when dealing with environmental issues.

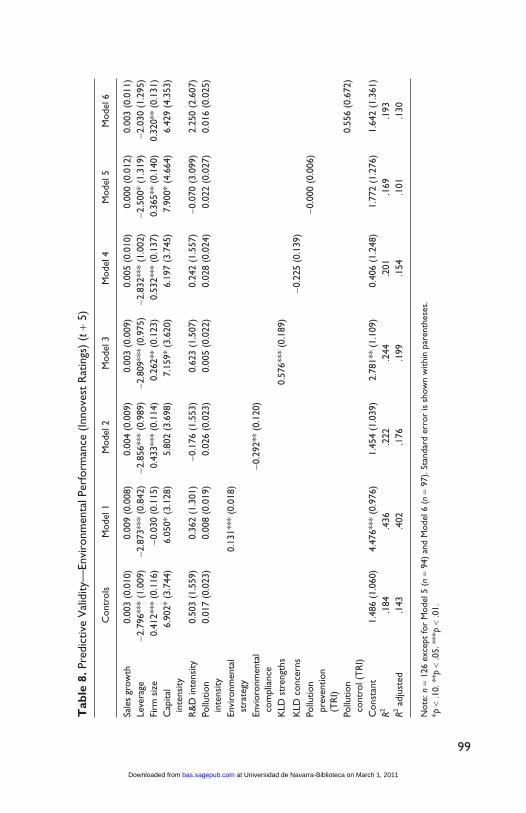

Predictive ValidityThe final stage of our analysis was to test for predictive validity. The purpose was to examine how our measure of environmental strategy, developed from content analysis and aligned with the theory of the NRBV, improved the predictability of competitive advantage outcomes. Specifically, we studied the association of all proactive and reactive environmental measures with two types of outcomes: environmental performance and financial perfor-mance. The regression models were run in stages. We first ran a base model that included only controls. Subsequently we ran models for each proactive and reactive environmental measure to separately assess the association with the performance outcome and predictive power. Table 7 shows descriptive statistics of the variables used in the regressions.

We first ran these models on the environmental performance outcome (t + 5), to assess the association of a firm’s proactive and reactive environ-mental approaches on actual environmental performance 5 years down the line (Table 8). The basic model including controls indicates that leverage is negatively associated with environmental performance. Firm size is posi-tively associated with environmental performance, as is capital intensity (weakly so). Models 1 and 2 show that our environmental strategy and envi-ronmental compliance measures predicted environmental performance. Environmental strategy is positively associated with environmental perfor-mance and environmental compliance is negatively associated. The KLD strengths measure was also positively associated with environmental perfor-mance (Model 3). In contrast, no association was found for KLD concerns or either of TRI measures. The KLD strengths measures explained an additional 5.6% of variance (adjusted R2) compared to the base model. Our environmen-tal compliance measure explained an additional 3.3% of variance. Our envi-ronmental strategy measure almost tripled explanatory power for environmental

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

98

Tab

le 7

. Des

crip

tive

Stat

istic

s—D

epen

dent

and

Inde

pend

ent

Var

iabl

es

MSD

Skew

.K

urt.

12

34

56

78

910

1112

13

1En

viro

nmen

tal

perf

orm

ance

5.20

1.51

−0.0

92.

43

2To

bin’

s Q

1.75

1.22

1.47

5.19

0.19

3

Envi

ronm

enta

l st

rate

gy9.

037.

190.

381.

880.

650.

15

4En

viro

nmen

tal

com

plia

nce

0.65

1.04

1.68

6.19

−0.2

6−0

.18−0

.07

5K

LD s

tren

gths

0.42

0.70

1.63

5.14

0.49

−0.0

90.

560.

07

6K

LD c

once

rns

0.90

1.29

1.19

3.18

0.11

−0.2

60.

200.

270.

40

7Po

llutio

n pr

even

tion

12.6

830

.74−0

.55

2.03

0.05

0.02

0.09

0.08

0.00

0.19

8Po

llutio

n co

ntro

l0.

770.

28−1

.33

3.72

0.13

0.23

0.20

0.07

0.19

0.02

0.16

9Sa

les

grow

th14

.63

15.7

31.

536.

600.

040.

01−0

.18

0.00

0.07

0.11

−0.0

80.

00

10Le

v era

ge0.

250.

150.

132.

48−0

.17−0

.38−0

.02−0

.03−0

.01

0.01

0.04

−0.2

7−0

.12

11

Firm

siz

e9.

161.

110.

363.

250.

350.

000.

480.

080.

360.

530.

290.

09−0

.05

0.00

12

Cap

ital i

nten

sity

0.06

0.05

1.77

6.37

0.28

0.32

0.14

−0.1

90.

05−0

.05

0.15

0.14

0.20

−0.1

40.

09

13R

&D

inte

nsity

0.09

0.12

3.20

16.8

00.

260.

540.

16−0

.20−0

.01−0

.16−0

.08

0.21

0.07

−0.4

20.

090.

53

14Po

llutio

n in

tens

ity17

.90

6.48

−0.1

31.

640.

150.

120.

190.

120.

250.

310.

320.

07−0

.21

0.13

0.20

0.13

0.00

Not

e: n

= 8

4.

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

99

Tab

le 8

. Pre

dict

ive

Val

idity

—En

viro

nmen

tal P

erfo

rman

ce (

Inno

vest

Rat

ings

) (t

+ 5

)

Con

trol

sM

odel

1M

odel

2M

odel

3M

odel

4M

odel

5M

odel

6

Sale

s gr

owth

0.00

3 (0

.010

)0.

009

(0.0

08)

0.00

4 (0

.009

)0.

003

(0.0

09)

0.00

5 (0

.010

)0.

000

(0.0

12)

0.00

3 (0

.011

)Le

vera

ge−2

.796

***

(1.0

09)

−2.8

73**

* (0

.842

)−2

.856

***

(0.9

89)

−2.8

09**

* (0

.975

)−2

.832

***

(1.0

02)

−2.5

00*

(1.3

19)

−2.0

30 (

1.29

5)Fi

rm s

ize

0.41

2***

(0.

116)

−0.0

30 (

0.11

5)0.

433*

** (

0.11

4)0.

262*

* (0

.123

)0.

532*

** (

0.13

7)0.

365*

* (0

.140

)0.

320*

* (0

.131

)C

apita

l i

nten

sity

6.90

2* (

3.74

4)6.

050*

(3.

128)

5.80

2 (3

.698

)7.

159*

(3.

620)

6.19

7 (3

.745

)7.

900*

(4.

664)

6.42

9 (4

.353

)

R&

D in

tens

ity0.

503

(1.5

59)

0.36

2 (1

.301

)−0

.176

(1.

553)

0.62

3 (1

.507

)0.

242

(1.5

57)

−0.0

70 (

3.09

9)2.

250

(2.6

07)

Pollu

tion

int

ensi

ty0.

017

(0.0

23)

0.00

8 (0

.019

)0.

026

(0.0

23)

0.00

5 (0

.022

)0.

028

(0.0

24)

0.02

2 (0

.027

)0.

016

(0.0

25)

Envi

ronm

enta

l s

trat

egy

0.13

1***

(0.

018)

Envi

oron

men

tal

com

plia

nce

−0.2

92**

(0.

120)

KLD

str

engt

hs0.

576*

** (

0.18

9)

KLD

con

cern

s−0

.225

(0.

139)

Po

llutio

n p

reve

ntio

n (

TR

I)

−0.0

00 (

0.00

6)

Pollu

tion

con

trol

(T

RI)

0.55

6 (0

.672

)

Con

stan

t1.

486

(1.0

60)

4.47

6***

(0.

976)

1.45

4 (1

.039

)2.

781*

* (1

.109

)0.

406

(1.2

48)

1.77

2 (1

.276

)1.

642

(1.3

61)

R2.1

84.4

36.2

22.2

44.2

01.1

69.1

93R2 a

djus

ted

.143

.402

.176

.199

.154

.101

.130

Not

e: n

= 1

26 e

xcep

t fo

r M

odel

5 (

n =

94)

and

Mod

el 6

(n

= 97

). St

anda

rd e

rror

is s

how

n w

ithin

par

enth

eses

.*p

< .1

0. *

*p <

.05.

***

p <

.01.

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

100 Business & Society 50(1)

performance increasing adjusted R2 from 14.3% to 40.2%, an additional 25.9% of variance explained. These results suggest that an environmental strategy measure developed in close alignment with the natural resource–based theoretical perspective has a much stronger predictive ability for future environmental performance, a form of competitive advantage, than other measures often used by researchers.

We next ran the environmental measures on the financial performance outcome, to assess the association of proactive and reactive environmental approaches on the (future) market value of the firm (Table 9). The base model indicates that, as in the environmental performance regression, lever-age has a significant negative association with financial performance. In addition, R&D intensity was positively associated with financial perfor-mance, as was pollution intensity (weakly so). Models 2 and 4 show that two types of reactive environmental measures were negatively associated with financial performance (environmental compliance and KLD concerns). None of the other measures were significantly associated with financial perfor-mance. Environmental compliance explained an additional 1.7% of variance (adjusted R2) over the base model, and KLD concerns explained an addi-tional 4.1% of variance. These modest predictive powers are not unexpected since many factors affect firm performance. What is surprising is that none of the proactive environmental measures appear to affect firm performance, a finding that contradicts results found in several meta-analyses (Margolis et al., 2007; Orlitzky et al., 2003). This lack of relationship may be because we included several controls such as R&D intensity, which appear to mediate the relationship between firm’s social strategies and financial performance (McWilliams & Siegel, 2000). Our results suggest that firms are not rewarded by the market for implementing more proactive types of environmental strat-egies. However, when firms fail to meet basic environmental regulatory requirements, the market appears to punish them perhaps viewing such a strategy as excessively risky.

DiscussionThis article represents a first step toward developing a measure of environ-mental strategy that is coherent with the natural resource–based view of the firm. In the past, scholars have used a variety of measures that blurred the lines between environmental strategy and environmental performance to pre-dict competitive advantage, with inconsistent results. This article addresses these concerns by using a content analysis approach to develop a measure of environmental strategy rooted in theory, a major contribution of our work.

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

101

Tab

le 9

. Pre

dict

ive

Val

idity

—Fi

nanc

ial P

erfo

rman

ce (

Tob

in’s

Q)

Con

trol

sM

odel

1M

odel

2M

odel

3M

odel

4M

odel

5M

odel

6

Sale

s gr

owth

0.00

8 (0

.006

)0.

009

(0.0

06)

0.00

9 (0

.006

)0.

008

(0.0

06)

0.01

1* (

0.00

6)0.

008

(0.0

07)

0.00

1 (0

.006

)Le

vera

ge−1

.796

** (

0.78

8)−1

.838

** (

0.78

7)−1

.862

** (

0.77

9)−1

.805

** (

0.79

1)−2

.008

***

(0.7

66)

−0.8

33 (

0.86

5)−2

.021

** (

0.84

4)Fi

rm s

ize

−0.1

17 (

0.08

8)−0

.181

* (0

.102

)−0

.105

(0.

087)

−0.1

00 (

0.09

3)0.

021

(0.0

97)

−0.0

67 (

0.08

9)−0

.040

(0.

083)

Cap

ital

int

ensi

ty−2

.104

(2.

681)

−2.2

56 (

2.67

8)−2

.918

(2.

675)

−2.1

52 (

2.69

1)−3

.087

(2.

615)

−0.4

93 (

2.76

0)1.

036

(2.5

58)

R&

D in

tens

ity6.

057*

** (

1.10

0)6.

038*

** (

1.09

8)5.

650*

** (

1.10

3)6.

030*

** (

1.10

5)5.

593*

** (

1.07

6)8.

241*

** (

1.81

6)5.

032*

** (

1.53

1)Po

llutio

n i

nten

sity

0.03

1* (

0.01

7)0.

031*

(0.

016)

0.03

8**

(0.0

17)

0.03

3* (

0.01

7)0.

046*

** (

0.01

7)0.

017

(0.0

16)

0.02

3 (0

.015

)

Envi

ronm

enta

l s

trat

egy

0.01

9 (0

.015

)

Envi

ronm

enta

l c

ompl

ianc

e−0

.179

** (

0.08

7)

KLD

str

engt

hs−0

.077

(0.

145)

K

LD c

once

rns

−0.3

06**

* (0

.102

)

Pollu

tion

pre

vent

ion

(T

RI)

0.00

3 (0

.004

)

Pollu

tion

con

trol

(T

RI)

0.12

8 (0

.389

)

Con

stan

t2.

332*

** (

0.79

3)2.

759*

** (

0.86

5)2.

315*

** (

0.78

3)2.

193*

* (0

.838

)1.

086

(0.8

73)

1.55

1* (

0.81

1)1.

613*

(0.

853)

R2.3

91.3

99.4

12.3

93.4

35.3

46.3

23R2 a

djus

ted

.360

.363

.377

.356

.401

.291

.267

Not

e: S

tand

ard

erro

r is

sho

wn

with

in p

aren

thes

es.

*p <

.10.

**p

< .0

5. *

** p

< .0

1.

at Universidad de Navarra-Biblioteca on March 1, 2011bas.sagepub.comDownloaded from

102 Business & Society 50(1)

We find that our environmental strategy measure, which captures firm’s proactive environmental initiatives, has strong reliability and validity. Our content analysis shows that firms develop up to six specific environmental capabilities. Taken together, these capabilities form a firm’s proactive environ-mental strategy that converges with another measure of proactive envi-ronmental strategy (by KLD) and can be distinguished from various measures of reactive environmental strategy in the form of noncompliance or minimal compliance. Moreover, the predictive validity of our measure is strong. Our environmental strategy measure explains an additional 25.9% of variance over a base model, and double the variance of the KLD strengths measure, to predict future environmental performance. Our reactive envi-ronmental compliance measure shows weak convergence with other reac-tive measures. Nevertheless, environmental compliance predicts both future environmental performance and future financial performance, with modest additional variance explained at 3.3% and 1.7% over base models, respec-tively. Our conclusion is that our new measure of environmental strategy, rooted in theory, is better able to capture firms’ environmental capability development and environmental noncompliance than other measures often used as proxies.