Market Trends, Marketing Spend and Sales Strategies in the Global Construction Industry

153

© Timetric. This report is a licensed product and is not to be photocopied Global Construction Industry Supplier Outlook Survey 2013–2014: Market Trends, Marketing Spend and Sales Strategies in the Global Construction Industry Reference code: CN2145SU Published: June 2013 Timetric John Carpenter House 7 Carmelite Street London EC4Y 0BS United Kingdom Tel: +44 (0)20 7936 6400 Fax: +44 (0)20 7336 6813 Website: www.timetric.com

-

Upload

independent -

Category

Documents

-

view

2 -

download

0

Transcript of Market Trends, Marketing Spend and Sales Strategies in the Global Construction Industry

© Timetric. This report is a licensed product and is not to be photocopied

Global Construction Industry Supplier

Outlook Survey 2013–2014:

Market Trends, Marketing Spend and Sales Strategies in

the Global Construction Industry

Reference code: CN2145SU

Published: June 2013

Timetric

John Carpenter House

7 Carmelite Street

London EC4Y 0BS

United Kingdom

Tel: +44 (0)20 7936 6400

Fax: +44 (0)20 7336 6813

Website: www.timetric.com

TABLE OF CONTENTS

Global Construction Supplier Industry Outlook Survey 2013–2014:

Market Trends, Marketing Spend and Sales Strategies in the Global Construction Industry Page 2

© Timetric. This product is licensed and is not to be photocopied Published: June 2013

TABLE OF CONTENTS

1 Introduction .................................................................................................................. 8

1.1 What is this report about? ...................................................................................................... 8

1.2 Definitions .............................................................................................................................. 8

1.3 Methodology .......................................................................................................................... 9

1.4 Global Construction Industry: Profile of Survey Respondents .............................................. 11

1.4.1 Global construction industry: profile of contractor and developer respondents ........................... 11

1.4.2 Global construction industry: profile of supplier respondents ...................................................... 12

2 Executive Summary ................................................................................................... 14

3 Global Construction Industry Dynamics .................................................................. 16

3.1 Revenue Growth Projections in the Global Construction Industry ........................................ 17

3.1.1 Revenue growth projections by company type ............................................................................ 19

3.1.2 Revenue growth projections by region ......................................................................................... 21

3.1.3 Revenue growth projections by turnover ..................................................................................... 22

3.1.4 Revenue growth projections by senior-level respondents ........................................................... 24

3.2 Future Developments in Business Structure in the Global Construction Industry ................. 25

3.2.1 Future developments in business structure by contractors and developers ................................ 25

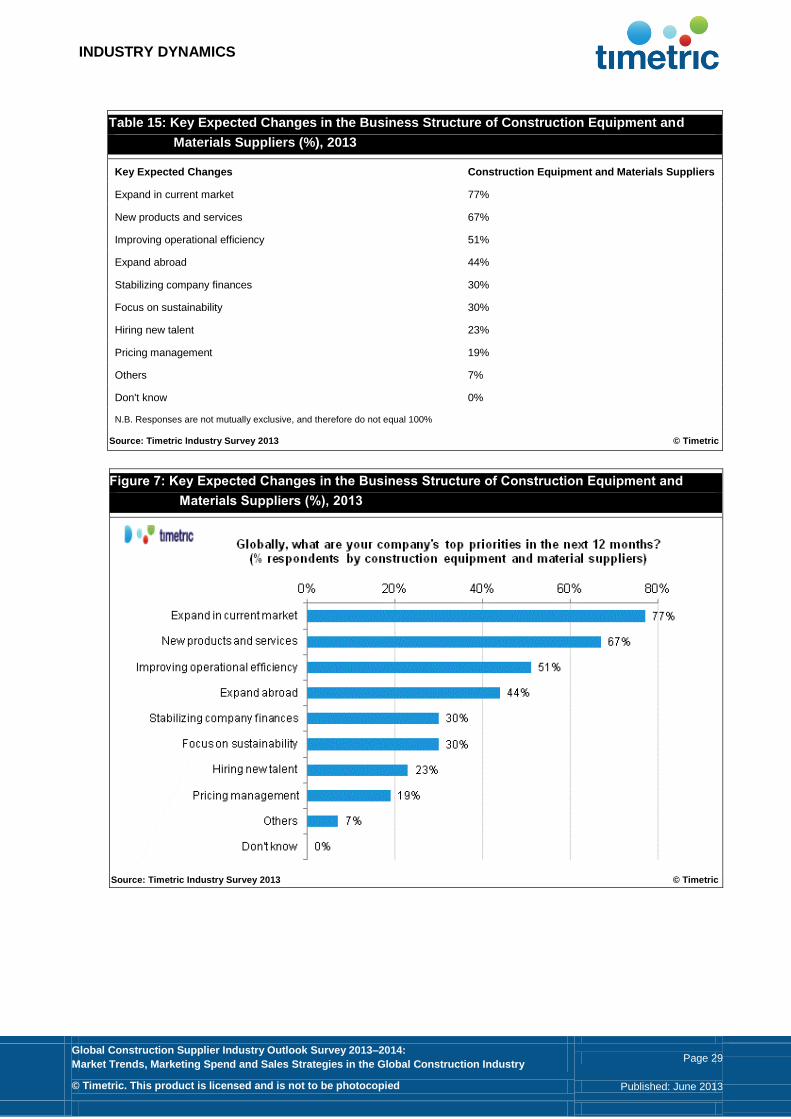

3.2.2 Future developments in business structure by suppliers ............................................................. 28

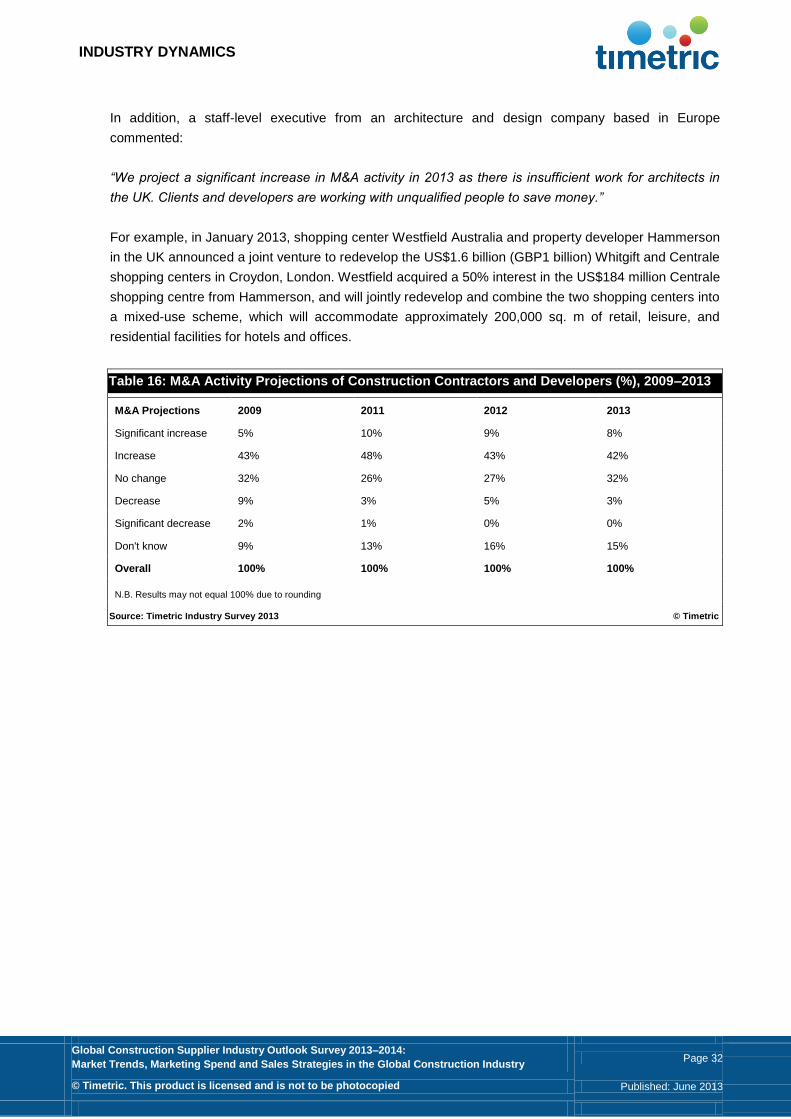

3.3 Merger and Acquisition Activity Projections in the Global Construction Industry ................... 31

3.3.1 M&A activity projections by contractors and developers ............................................................. 31

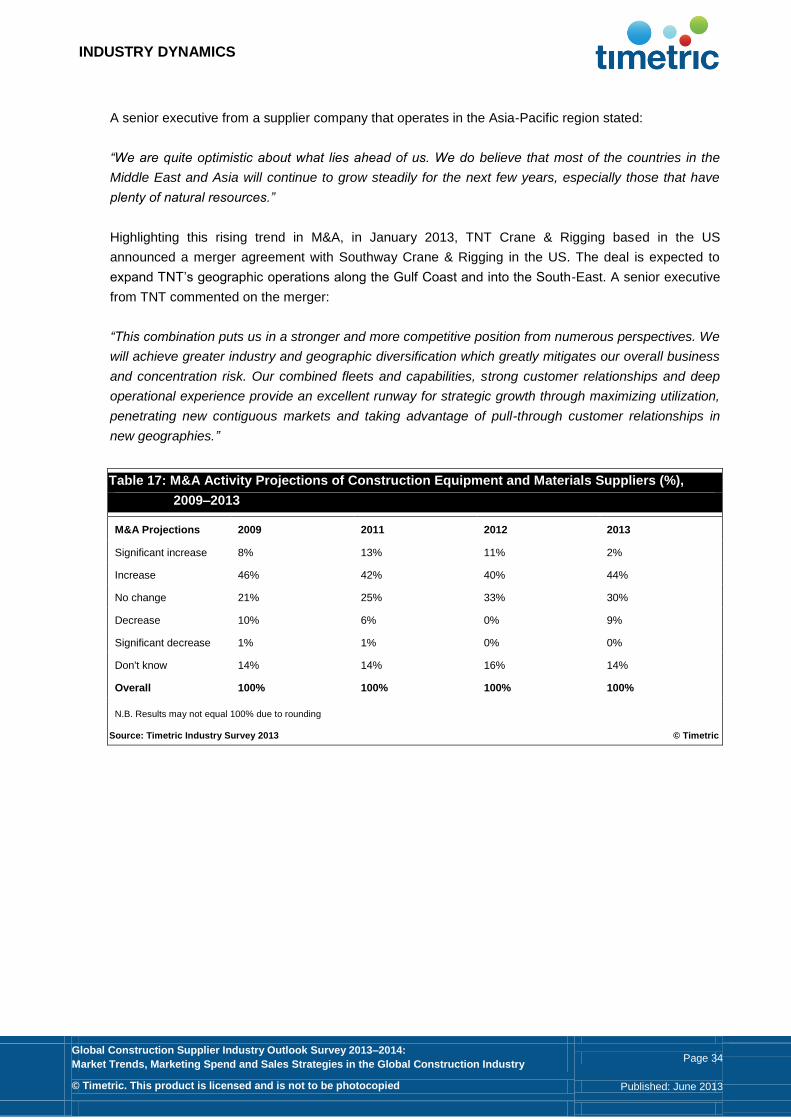

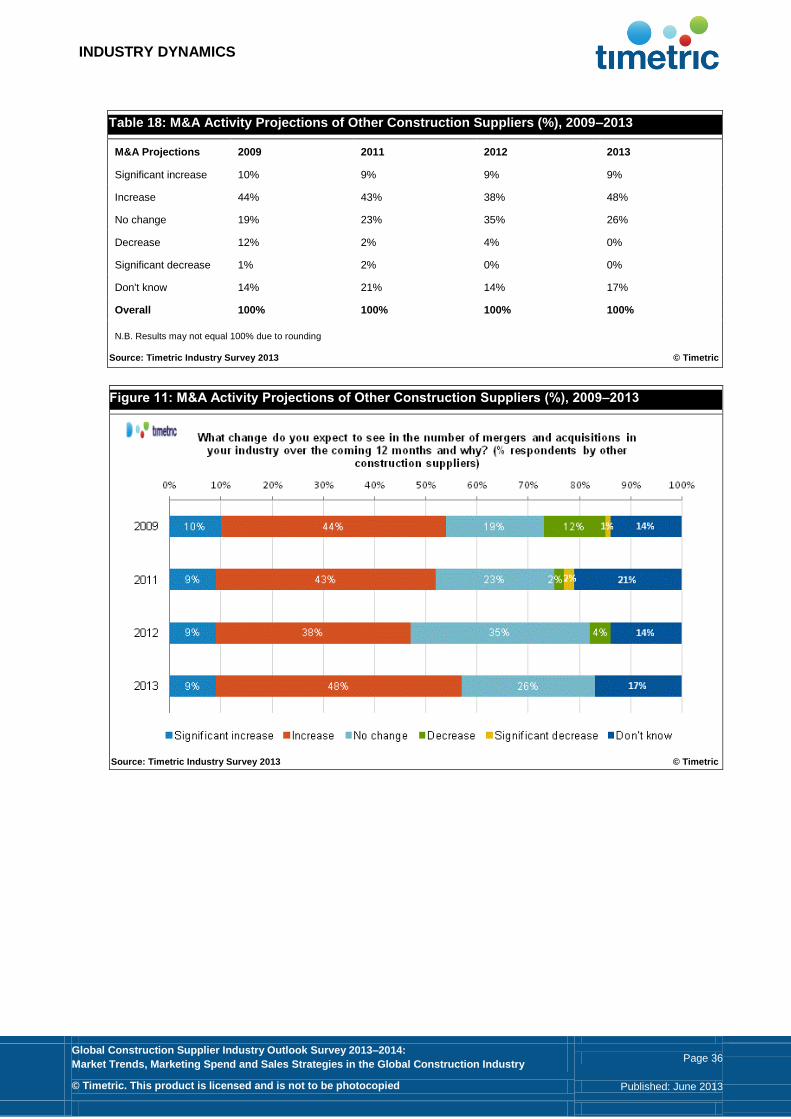

3.3.2 M&A activity projections by suppliers ........................................................................................... 33

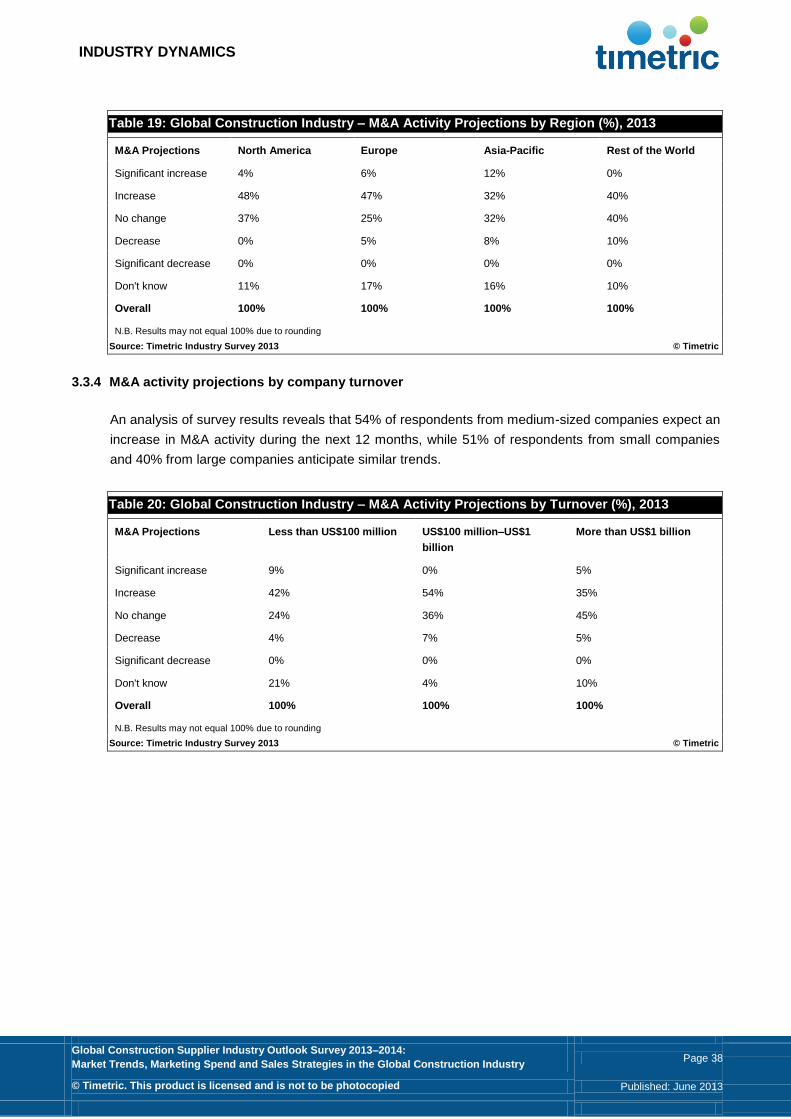

3.3.3 M&A activity projections by region ............................................................................................... 37

3.3.4 M&A activity projections by company turnover ............................................................................ 38

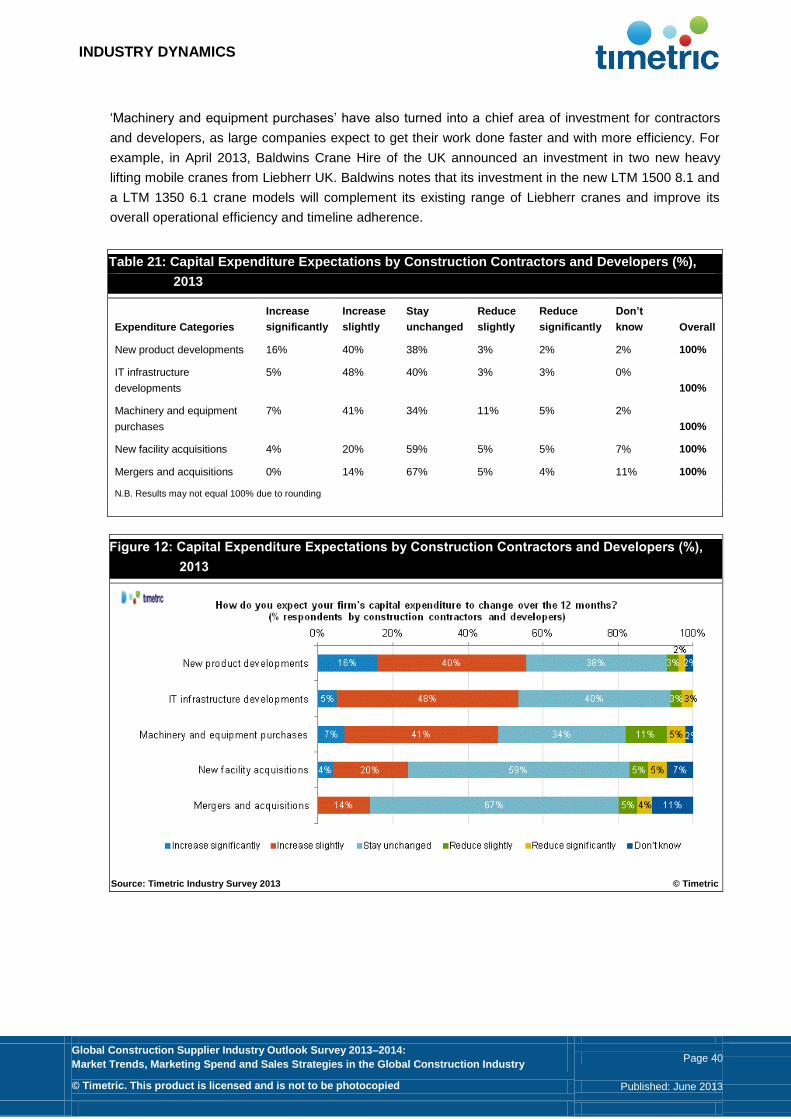

3.4 Estimation of Capital Expenditure in the Global Construction Industry ................................. 39

3.4.1 Estimation of capital expenditure by contractors and developers ................................................ 39

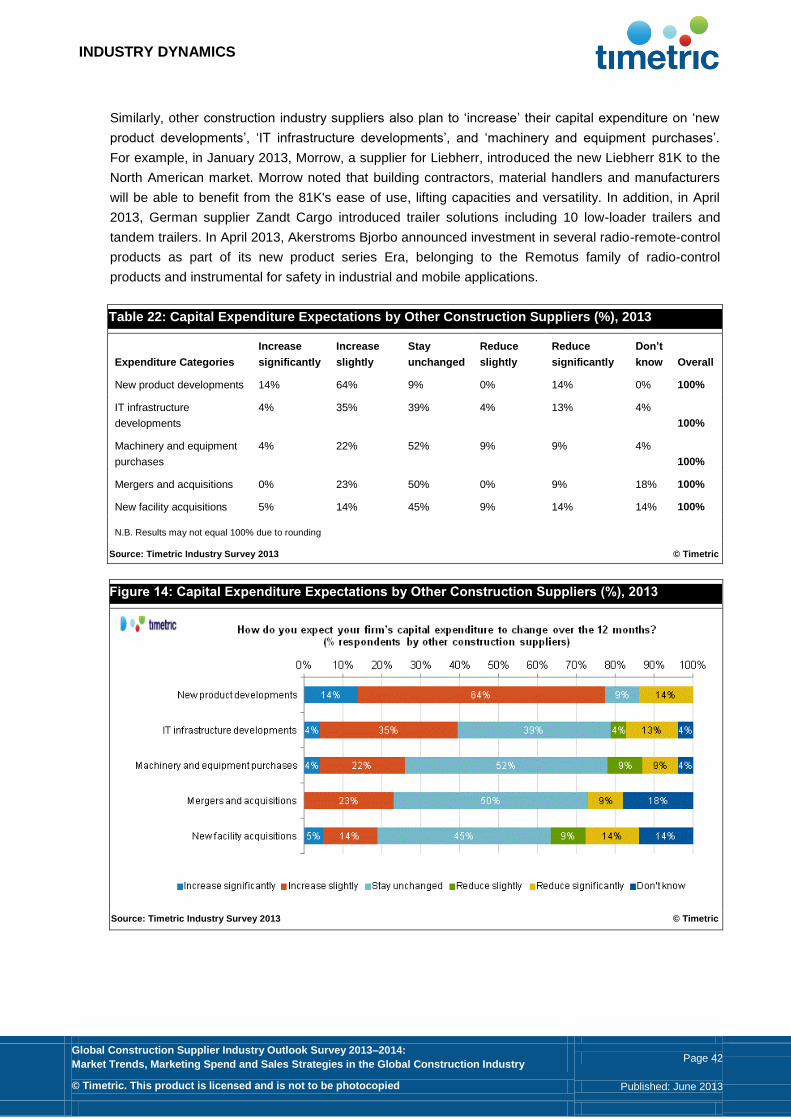

3.4.2 Estimation of capital expenditure by suppliers ............................................................................. 41

3.4.3 Estimation of capital expenditure by region ................................................................................. 43

3.4.4 Estimation of capital expenditure by company turnover .............................................................. 44

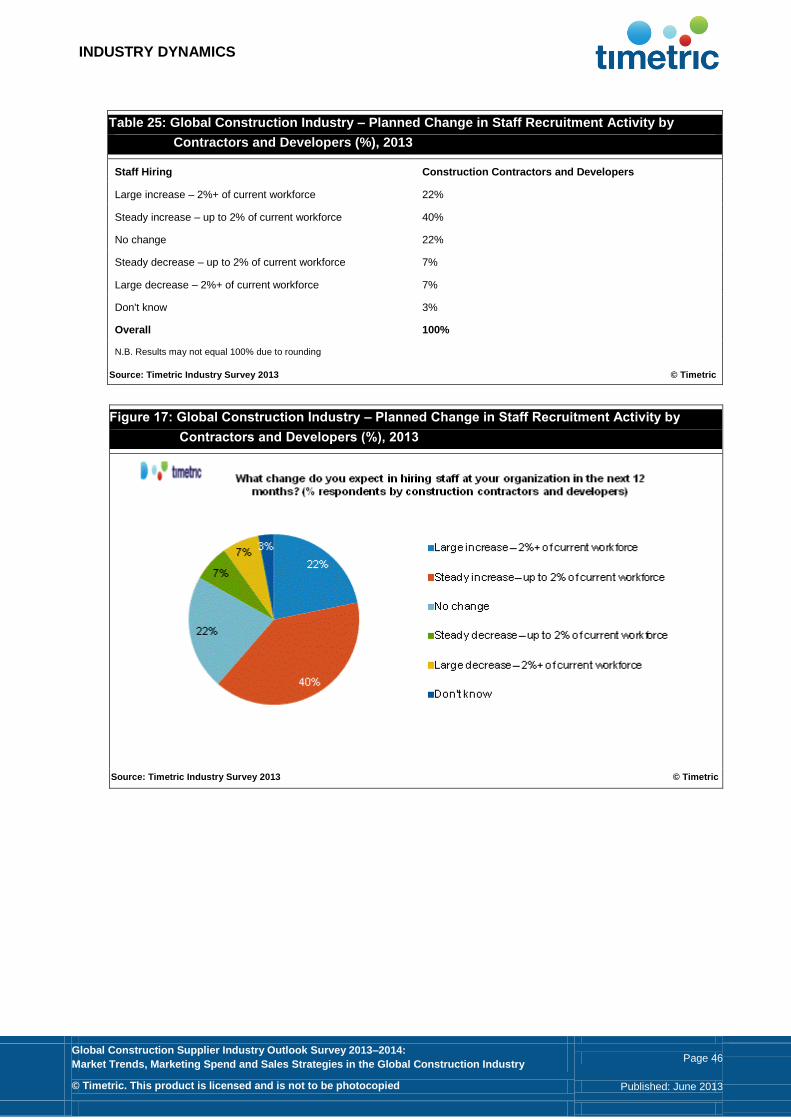

3.5 Planned Change in Staff Recruitment Activity in Global Construction Industry ..................... 45

3.5.1 Planned change in staff recruitment activity by contractors and developers ............................... 45

3.5.2 Planned change in staff recruitment activity by suppliers ............................................................ 47

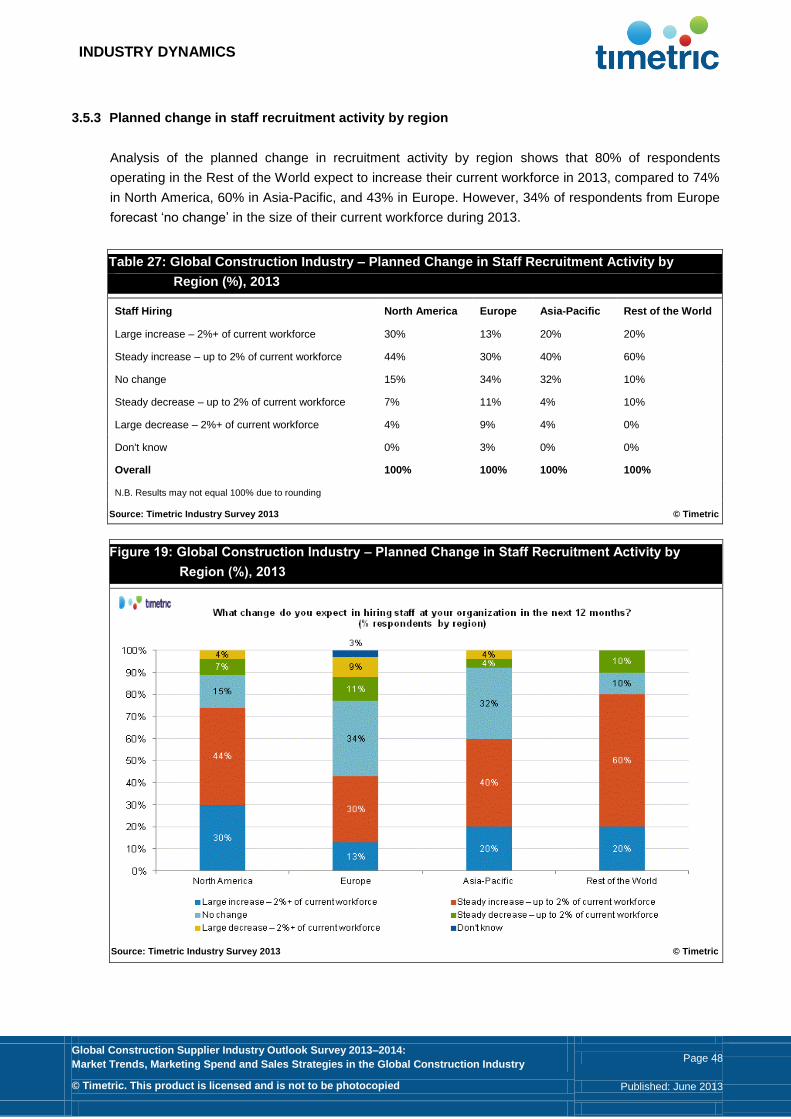

3.5.3 Planned change in staff recruitment activity by region ................................................................ 48

3.5.4 Planned change in staff recruitment activity by company turnover.............................................. 49

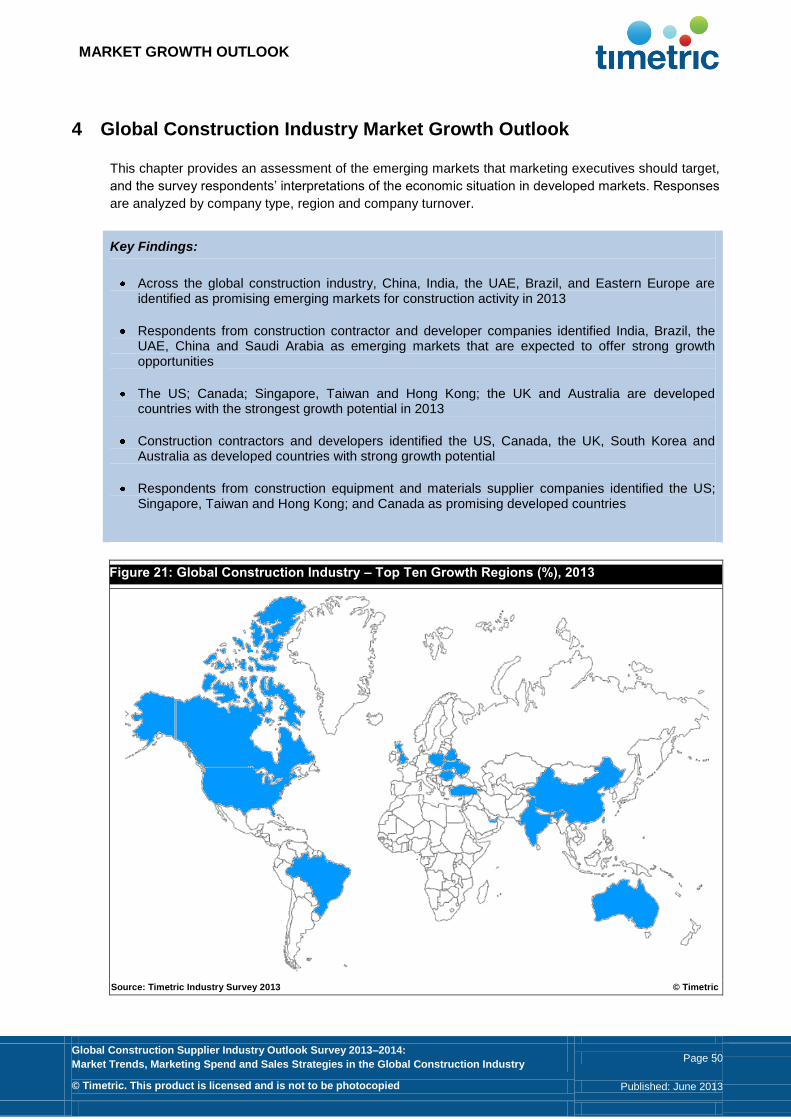

4 Global Construction Industry Market Growth Outlook ........................................... 50

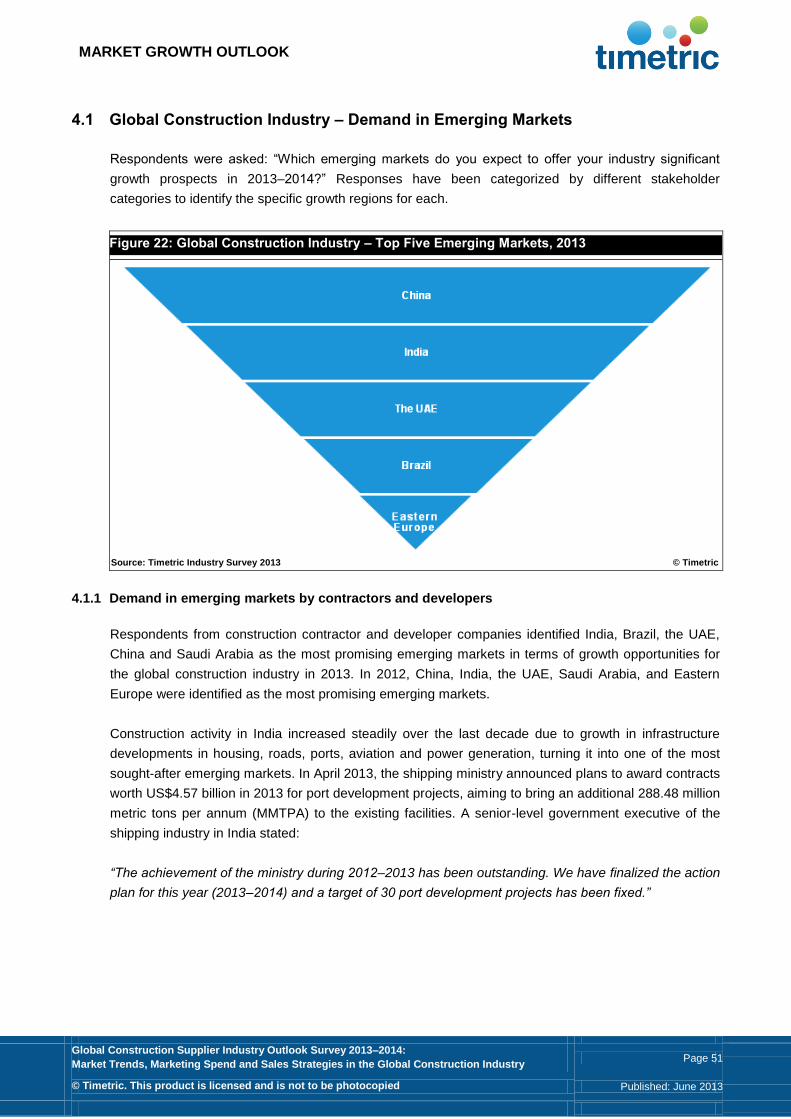

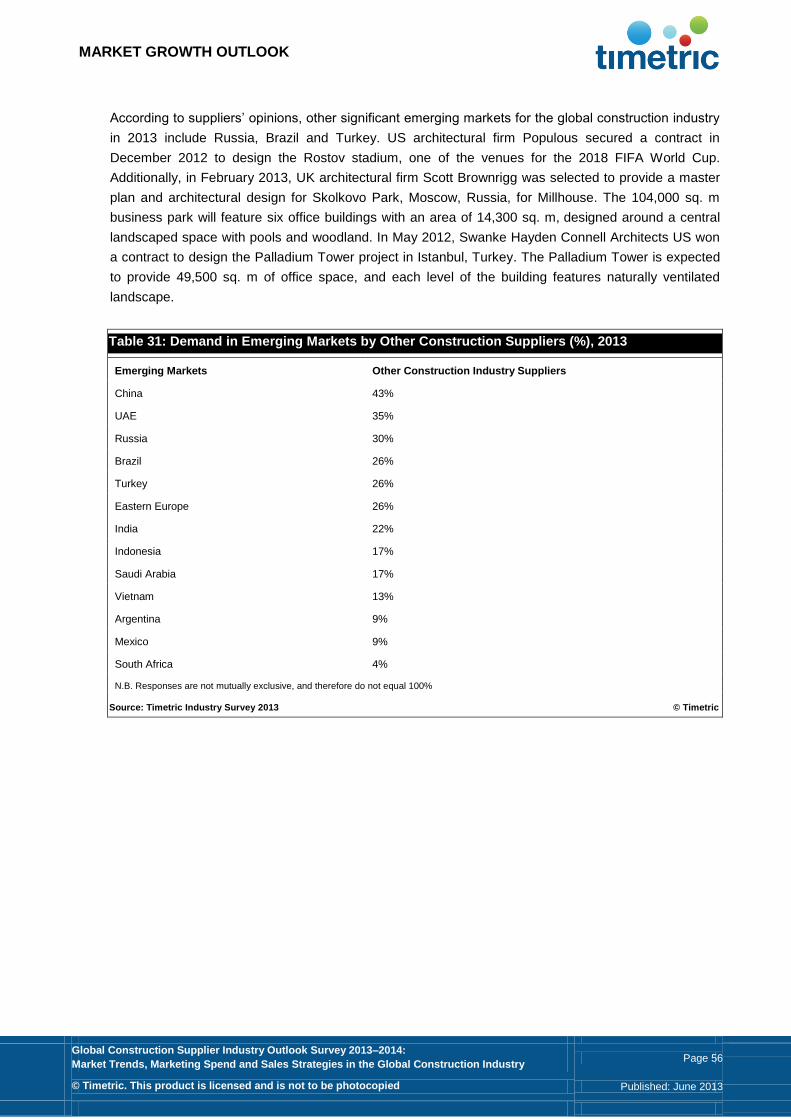

4.1 Global Construction Industry – Demand in Emerging Markets ............................................. 51

4.1.1 Demand in emerging markets by contractors and developers .................................................... 51

4.1.2 Demand in emerging markets by suppliers .................................................................................. 53

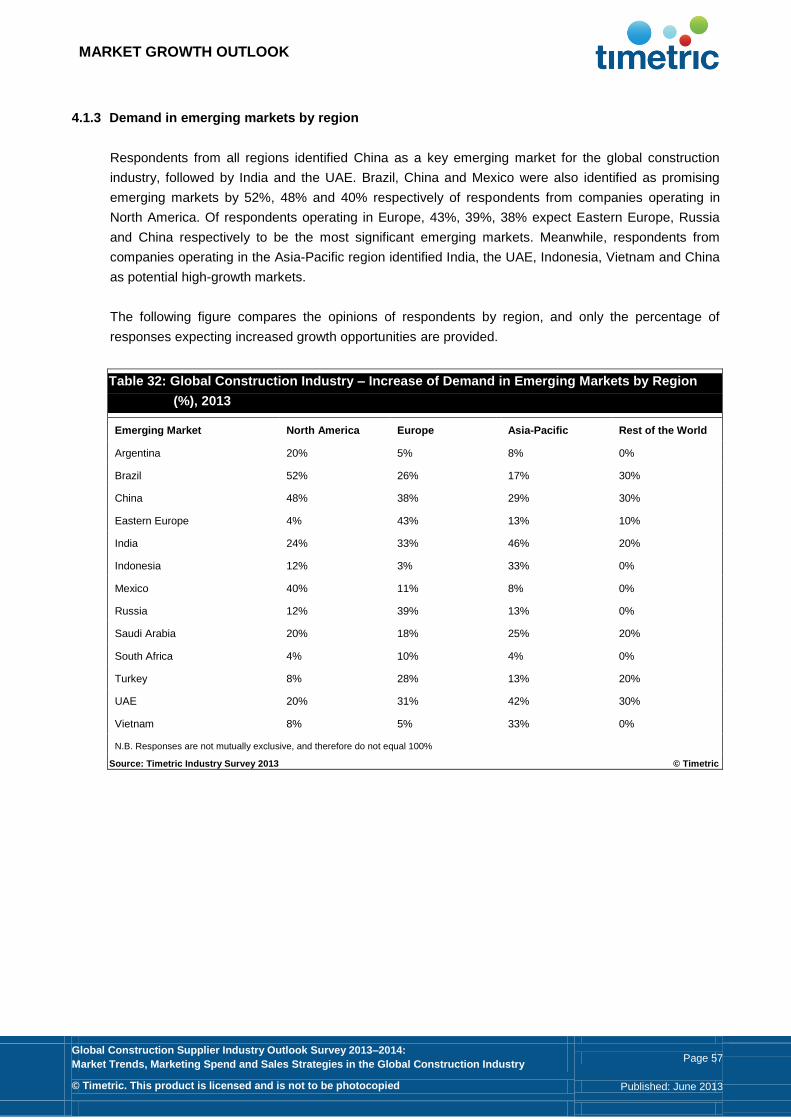

4.1.3 Demand in emerging markets by region ...................................................................................... 57

4.1.4 Demand in emerging markets by company turnover ................................................................... 58

4.2 Global Construction Industry – Growth Projections in Developed Countries ........................ 59

TABLE OF CONTENTS

Global Construction Supplier Industry Outlook Survey 2013–2014:

Market Trends, Marketing Spend and Sales Strategies in the Global Construction Industry Page 3

© Timetric. This product is licensed and is not to be photocopied Published: June 2013

4.2.1 Growth projections in developed countries by contractors and developers ................................ 60

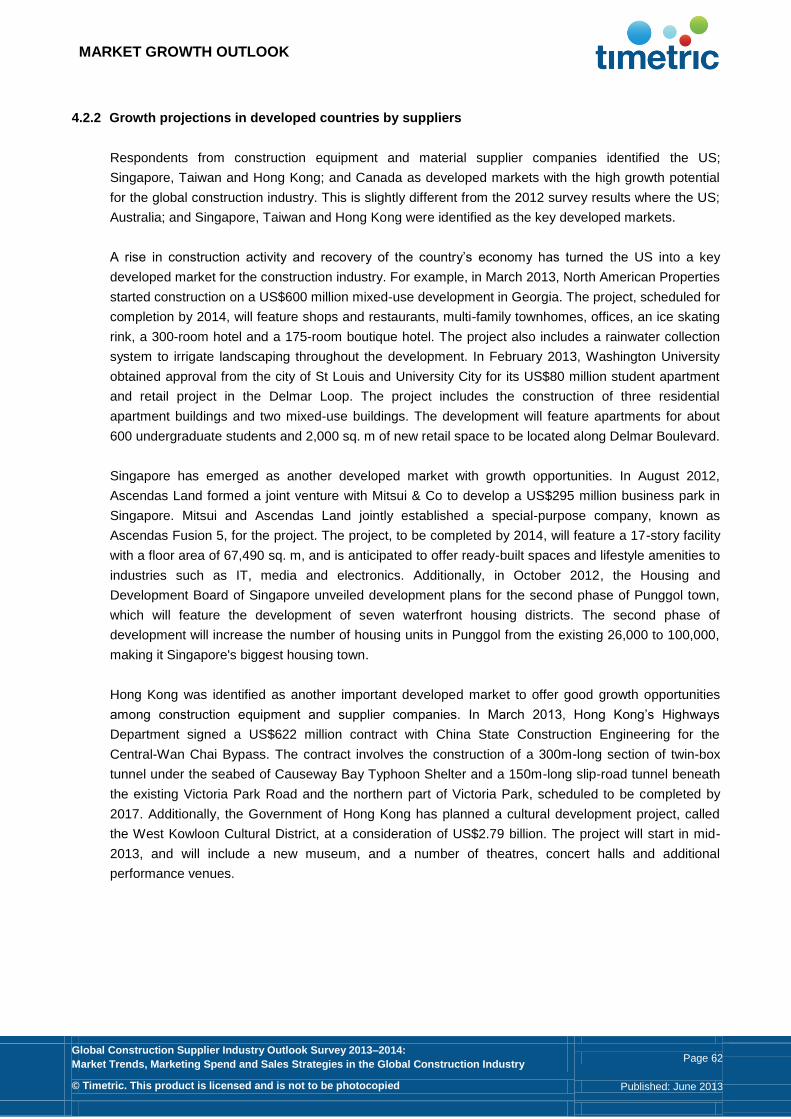

4.2.2 Growth projections in developed countries by suppliers .............................................................. 62

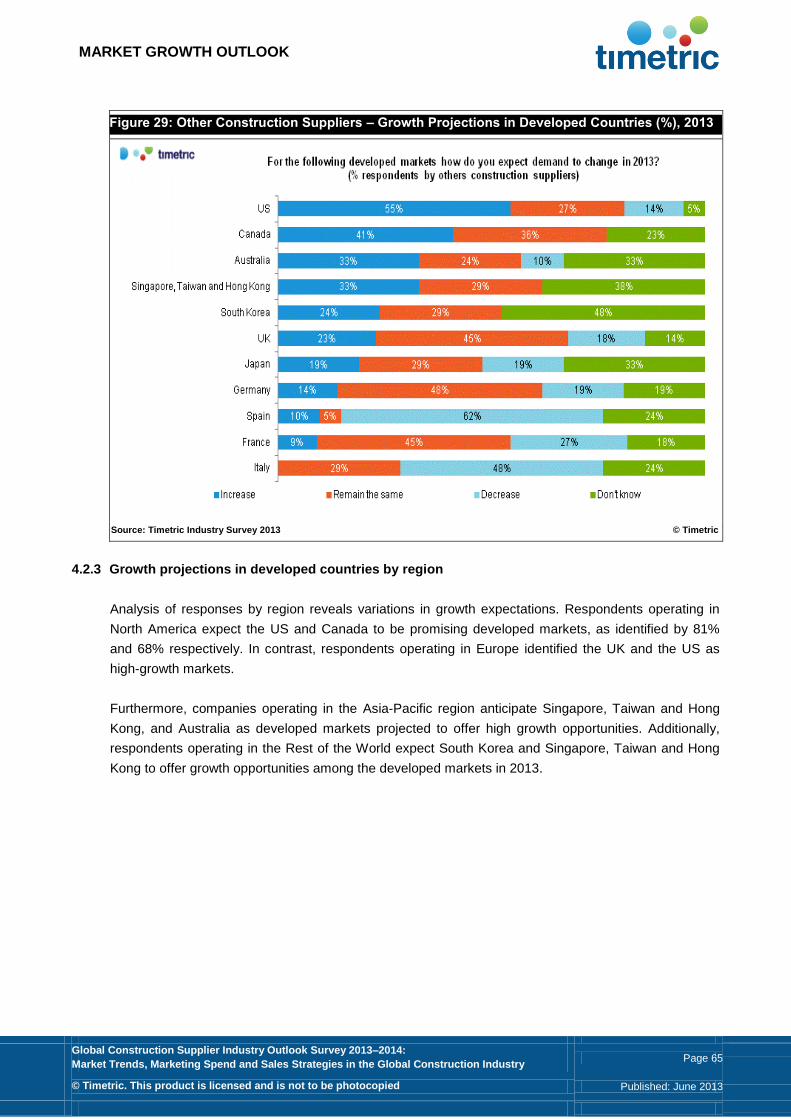

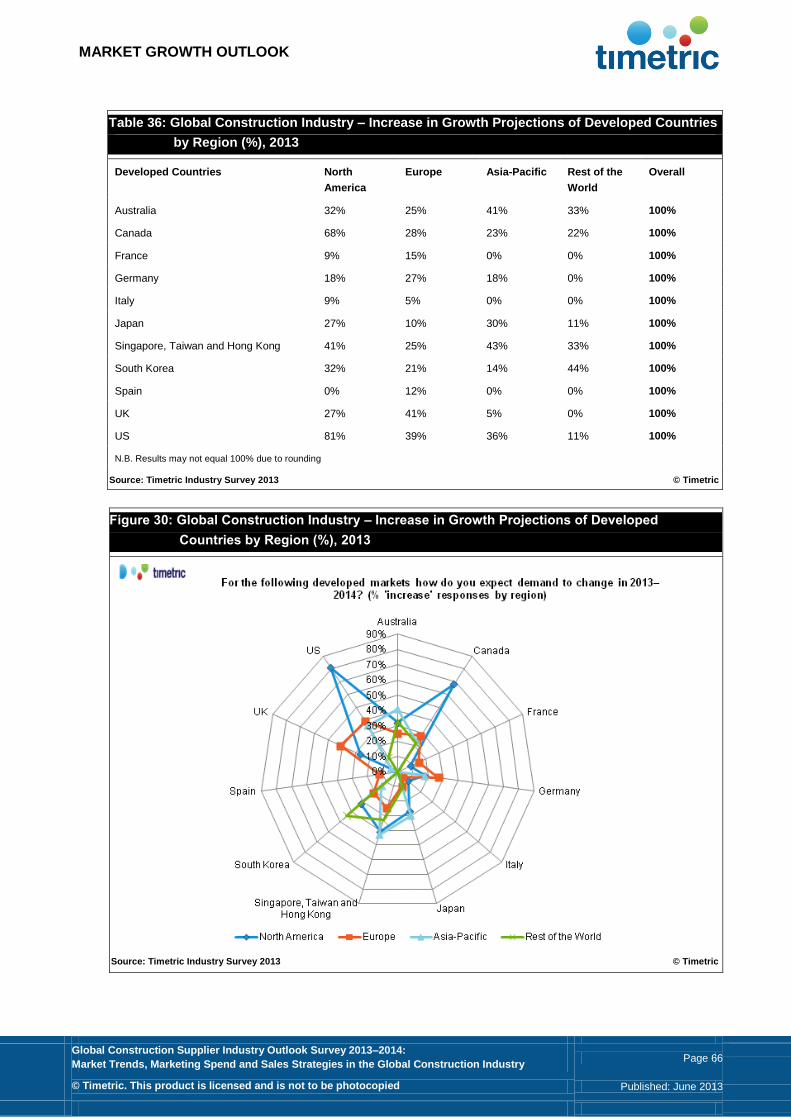

4.2.3 Growth projections in developed countries by region .................................................................. 65

4.2.4 Growth projections in developed countries by company turnover ............................................... 67

5 Threats and Opportunities for the Global Construction Industry .......................... 68

5.1 Global Construction Industry – Leading Business Concerns for 2013–2014 ........................ 69

5.1.1 Leading business concerns for 2013–2014 by company type ..................................................... 72

5.1.2 Leading business concerns for 2013–2014 by region ................................................................. 74

5.1.3 Leading business concerns for 2013–2014 by company turnover .............................................. 75

5.2 Global Construction Industry – Key Supplier Actions to Maintain and Win Buyer Business .. 76

5.2.1 Actions to maintain and secure buyer business by company type .............................................. 76

5.2.2 Actions to maintain and secure buyer business by region ........................................................... 78

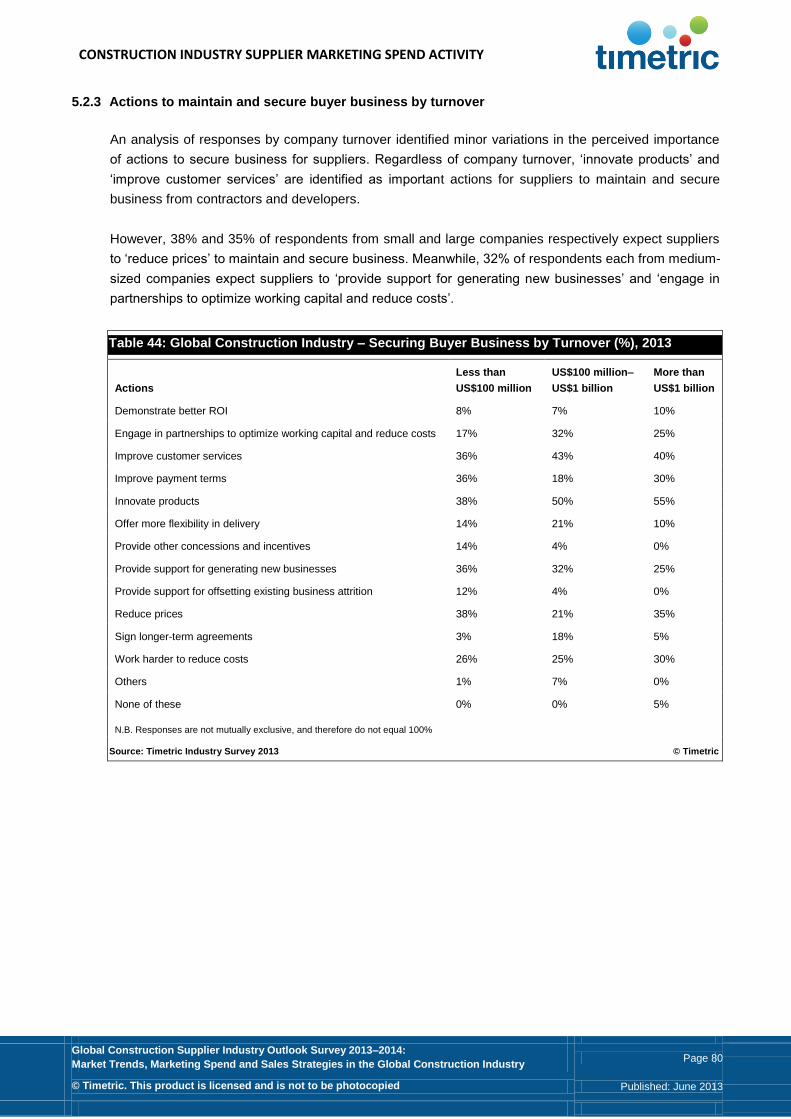

5.2.3 Actions to maintain and secure buyer business by turnover ....................................................... 80

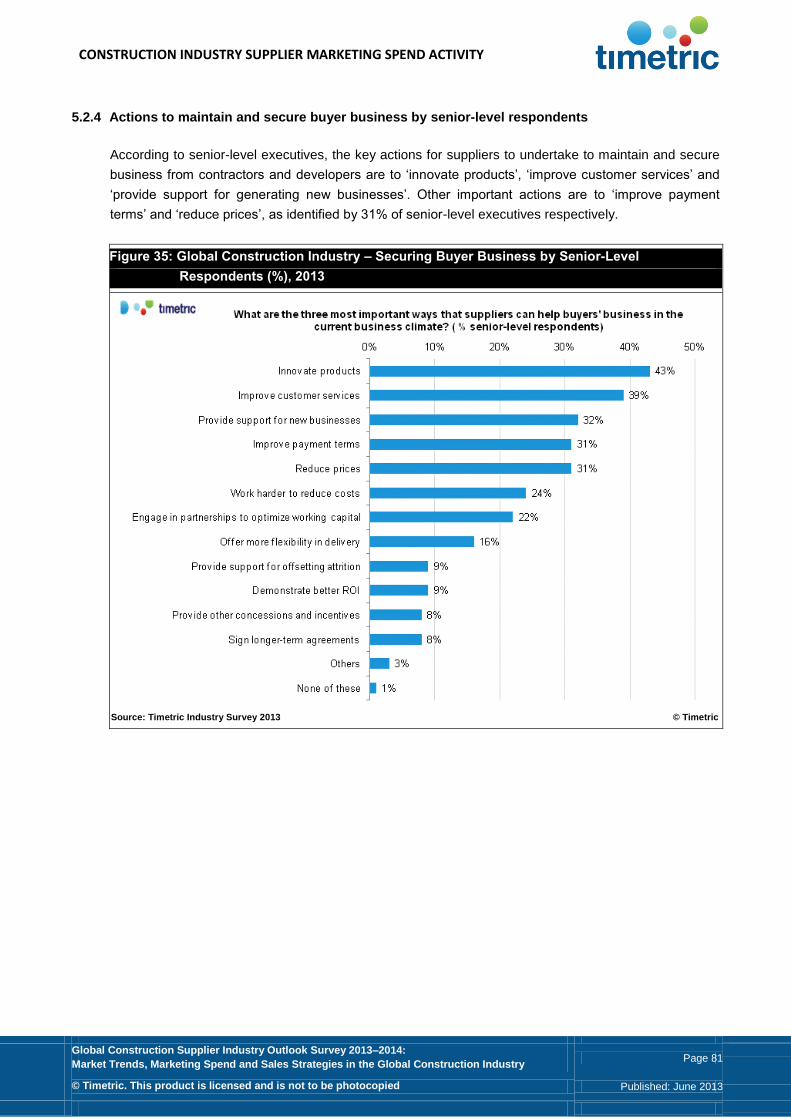

5.2.4 Actions to maintain and secure buyer business by senior-level respondents ............................. 81

5.3 Global Construction Industry – Key Variations in Operational Costs .................................... 82

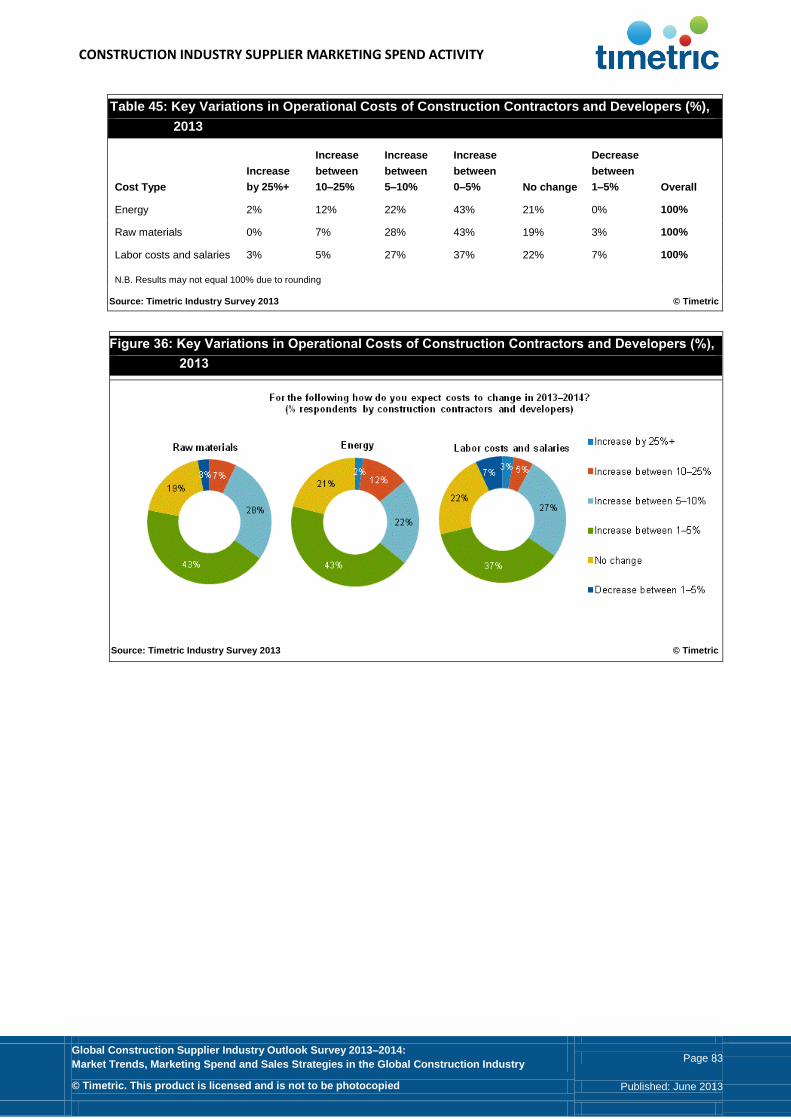

5.3.1 Key variations in operational costs by contractors and developers ............................................. 82

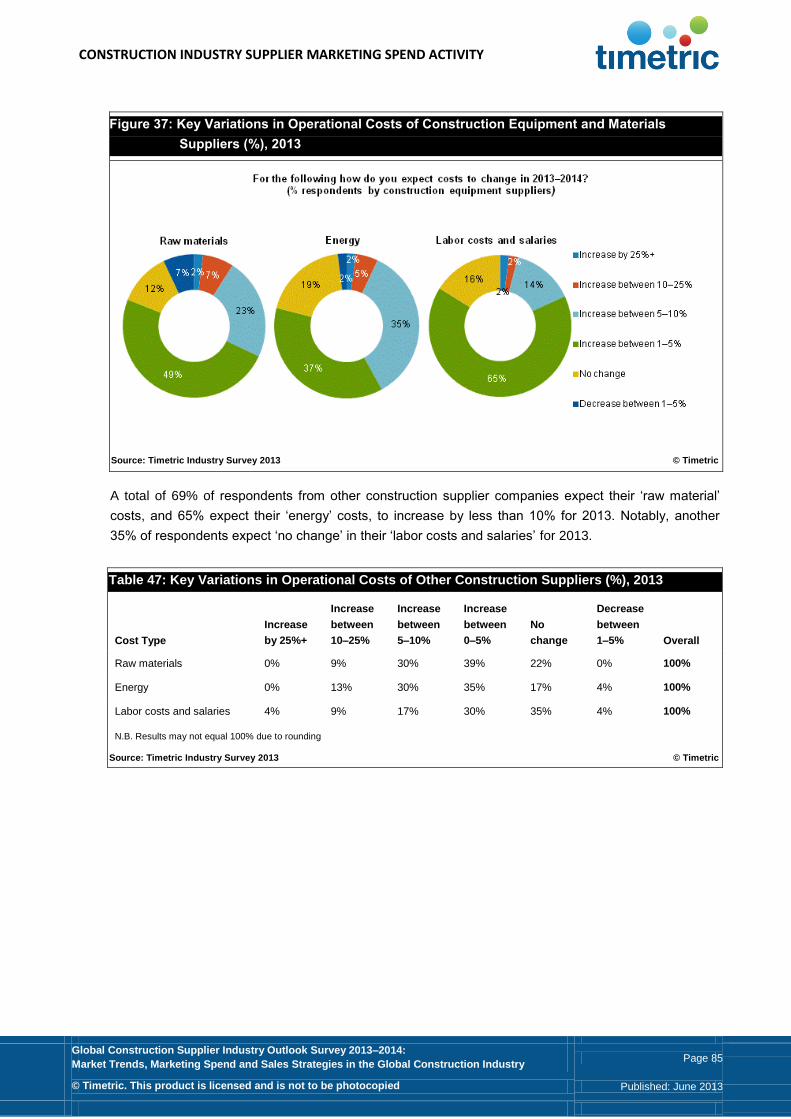

5.3.2 Key variations in operational costs by suppliers .......................................................................... 84

5.3.3 Key variations in operational costs by region ............................................................................... 86

5.3.4 Key variations in operational costs by company turnover ............................................................ 87

5.4 Global Construction Industry – Impact of Costs on Product Pricing ...................................... 88

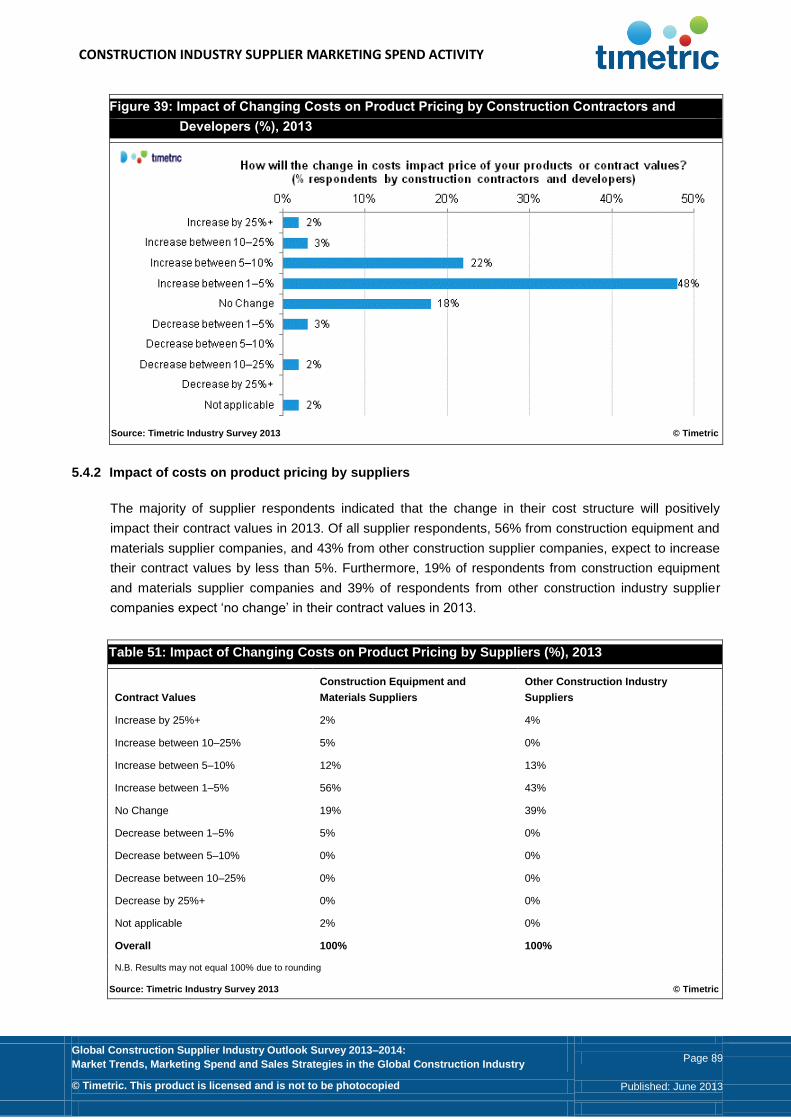

5.4.1 Impact of costs on product pricing by contractors and developers .............................................. 88

5.4.2 Impact of costs on product pricing by suppliers ........................................................................... 89

6 Global Construction Industry - Supplier Marketing Spend Activity ...................... 90

6.1 Annual Marketing Budgets – Global Construction Industry Suppliers ................................... 91

6.1.1 Annual marketing budgets by suppliers ....................................................................................... 91

6.1.2 Annual marketing budgets by region ........................................................................................... 93

6.1.3 Annual marketing budgets by company turnover ......................................................................... 94

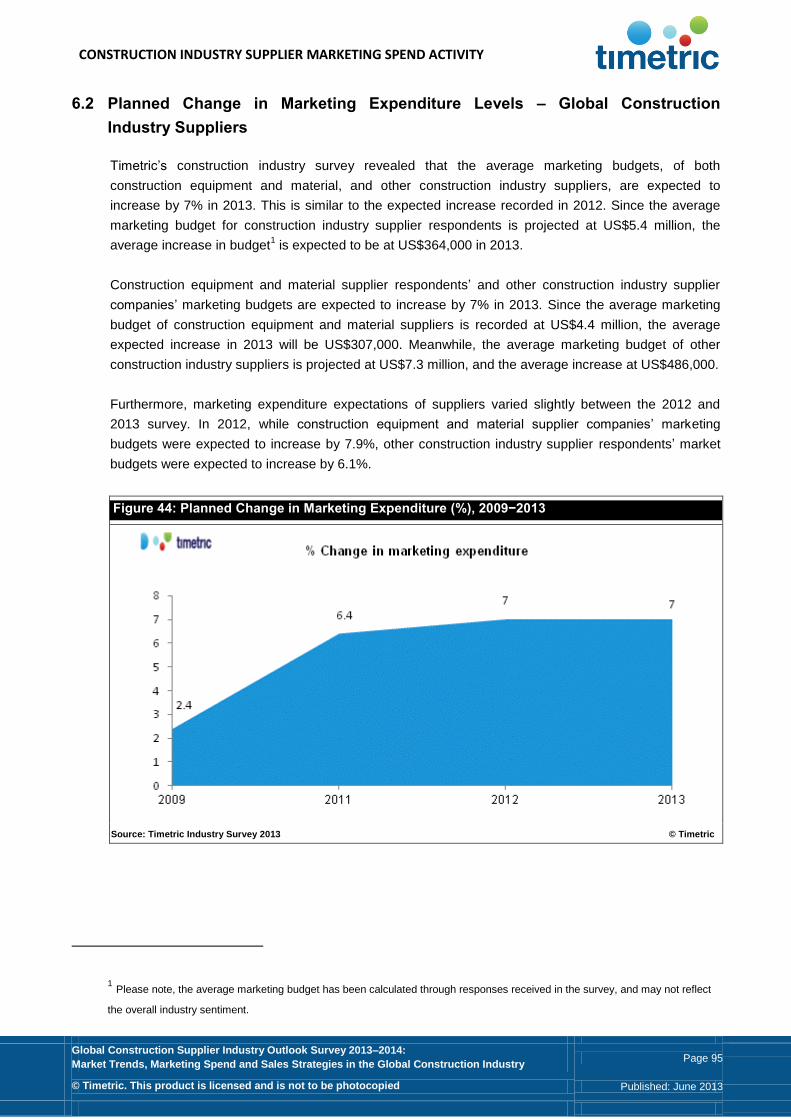

6.2 Planned Change in Marketing Expenditure Levels – Global Construction Industry Suppliers95

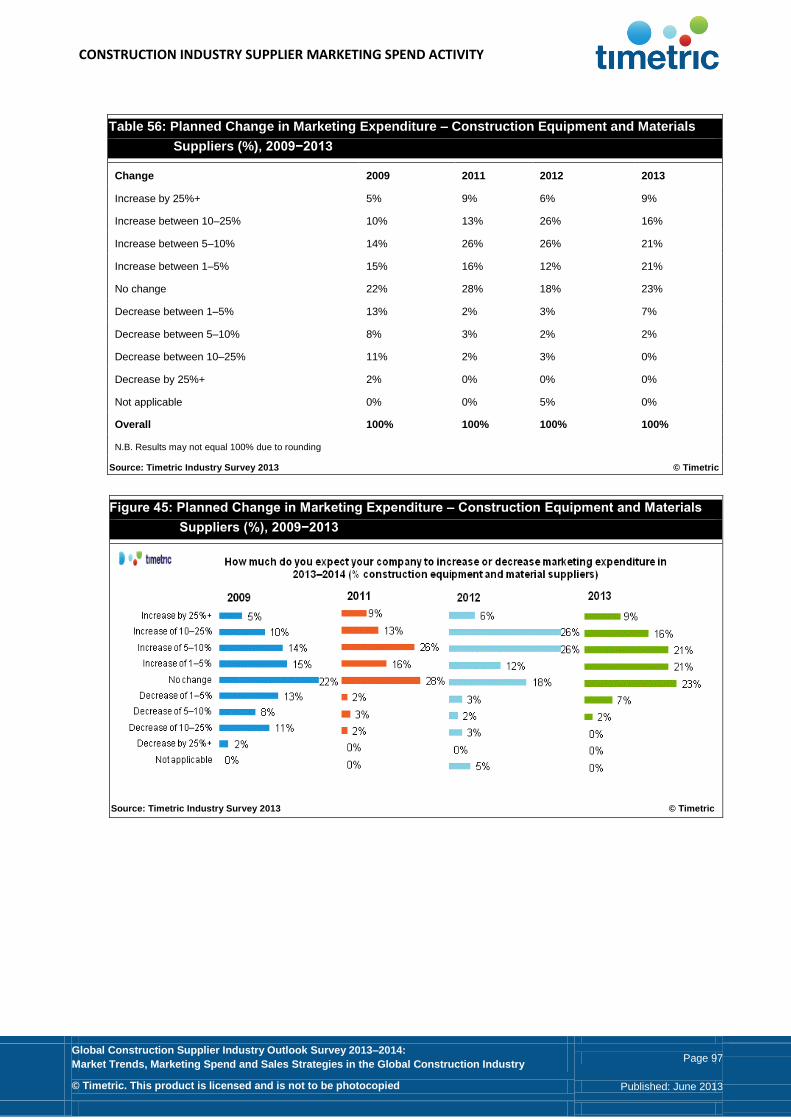

6.2.1 Planned change in marketing expenditure by suppliers .............................................................. 96

6.2.2 Planned change in marketing expenditure by region ................................................................. 100

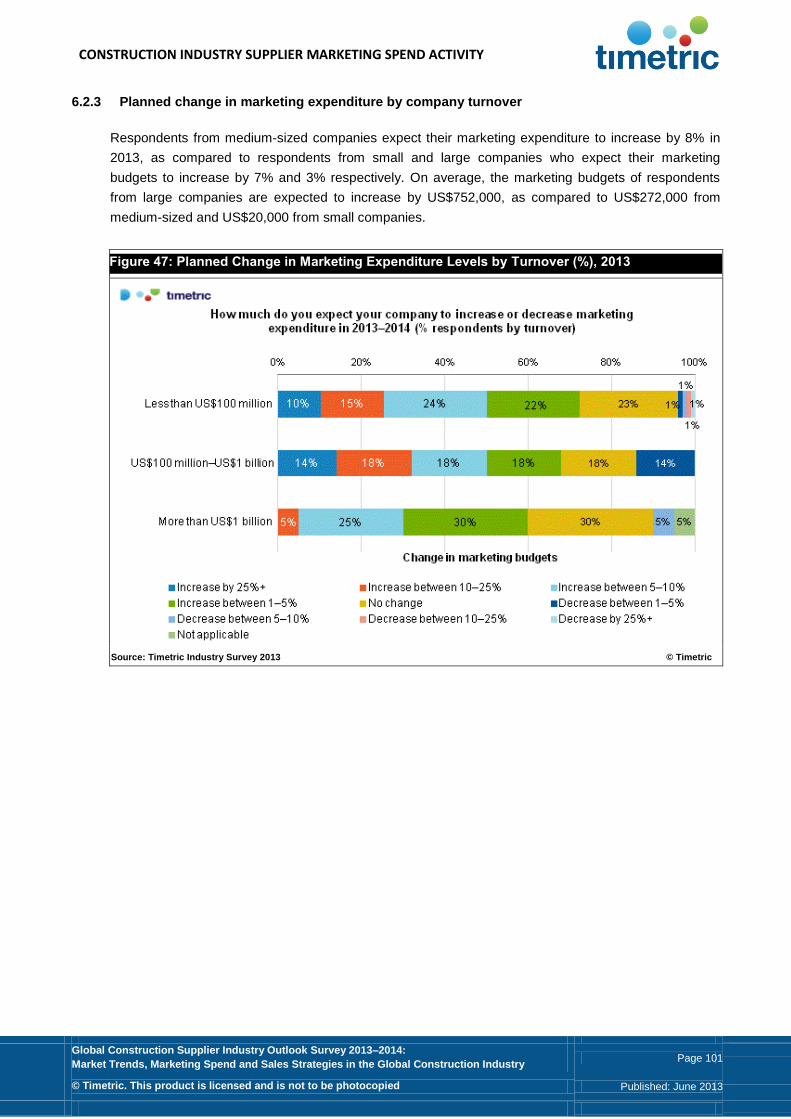

6.2.3 Planned change in marketing expenditure by company turnover .............................................. 101

6.2.4 Planned change in marketing expenditure levels by revenue growth expectations .................. 102

6.3 Future Investment in Media Channels – Global Construction Industry Suppliers ................ 103

6.3.1 Future investment in media channels by suppliers .................................................................... 103

6.3.2 Future investment in media channels by region ........................................................................ 106

6.3.3 Future investment in media channels by company turnover ..................................................... 107

6.4 Global Construction Industry Suppliers' Future Investment in Marketing and Sales Technology

108

6.4.1 Planned investment in marketing and sales technologies by suppliers ..................................... 108

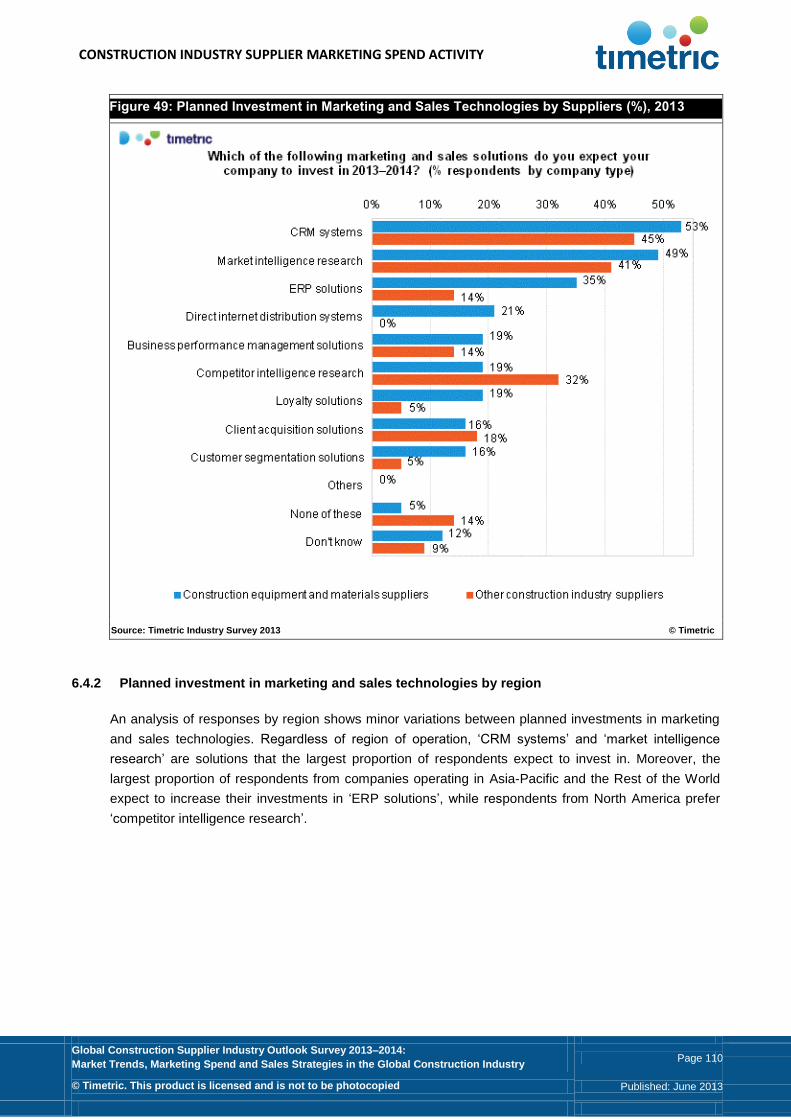

6.4.2 Planned investment in marketing and sales technologies by region ......................................... 110

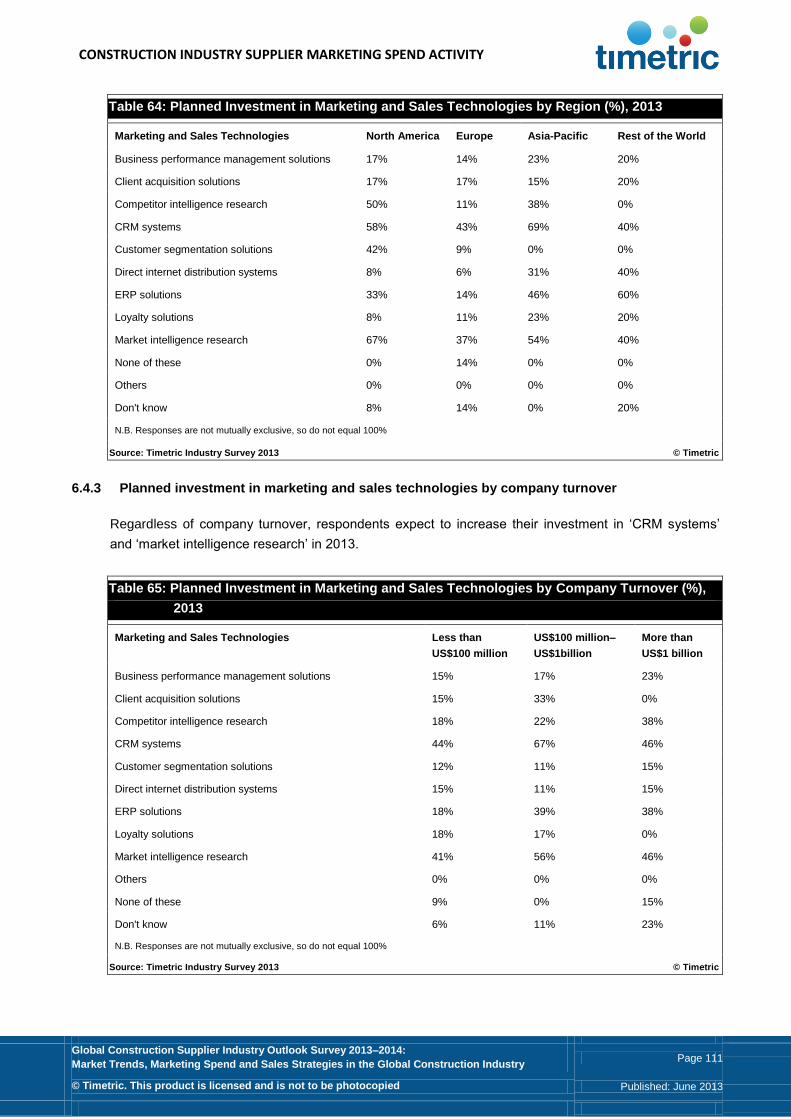

6.4.3 Planned investment in marketing and sales technologies by company turnover ...................... 111

7 Marketing and Sales Behaviors and Strategies in 2013–2014 ............................. 112

TABLE OF CONTENTS

Global Construction Supplier Industry Outlook Survey 2013–2014:

Market Trends, Marketing Spend and Sales Strategies in the Global Construction Industry Page 4

© Timetric. This product is licensed and is not to be photocopied Published: June 2013

7.1 Key Marketing Aims for 2013–2014 – Global Construction Industry ................................... 113

7.1.1 Key marketing aims by suppliers ............................................................................................... 113

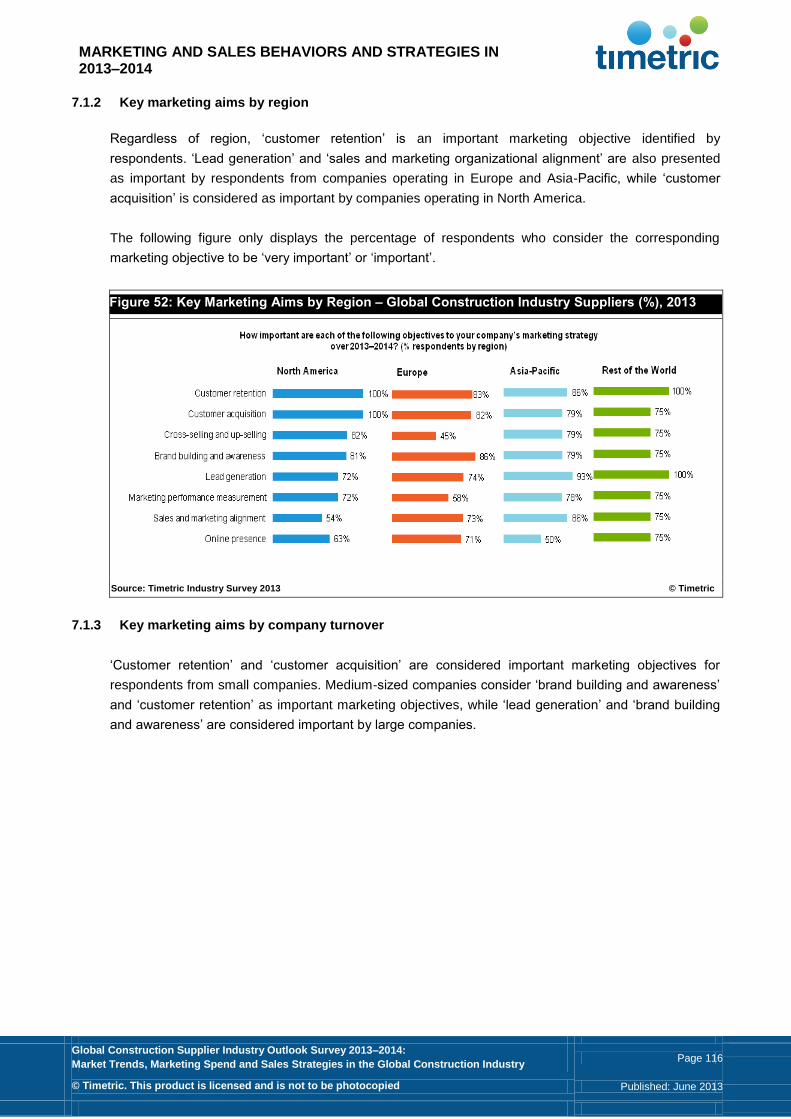

7.1.2 Key marketing aims by region .................................................................................................... 116

7.1.3 Key marketing aims by company turnover ................................................................................. 116

7.1.4 Key marketing aims by revenue growth expectations ............................................................... 117

7.2 Essential Amendments to Marketing Activities in 2013–2014 ............................................. 118

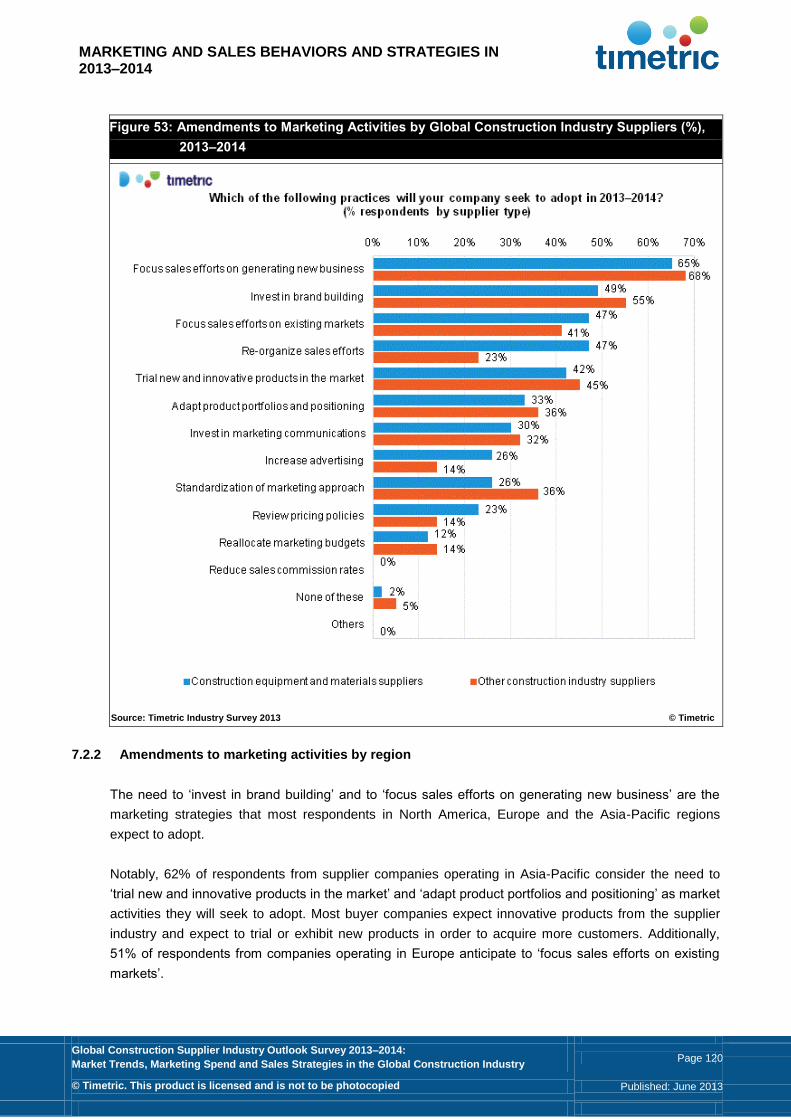

7.2.1 Amendments to marketing activities by suppliers ...................................................................... 118

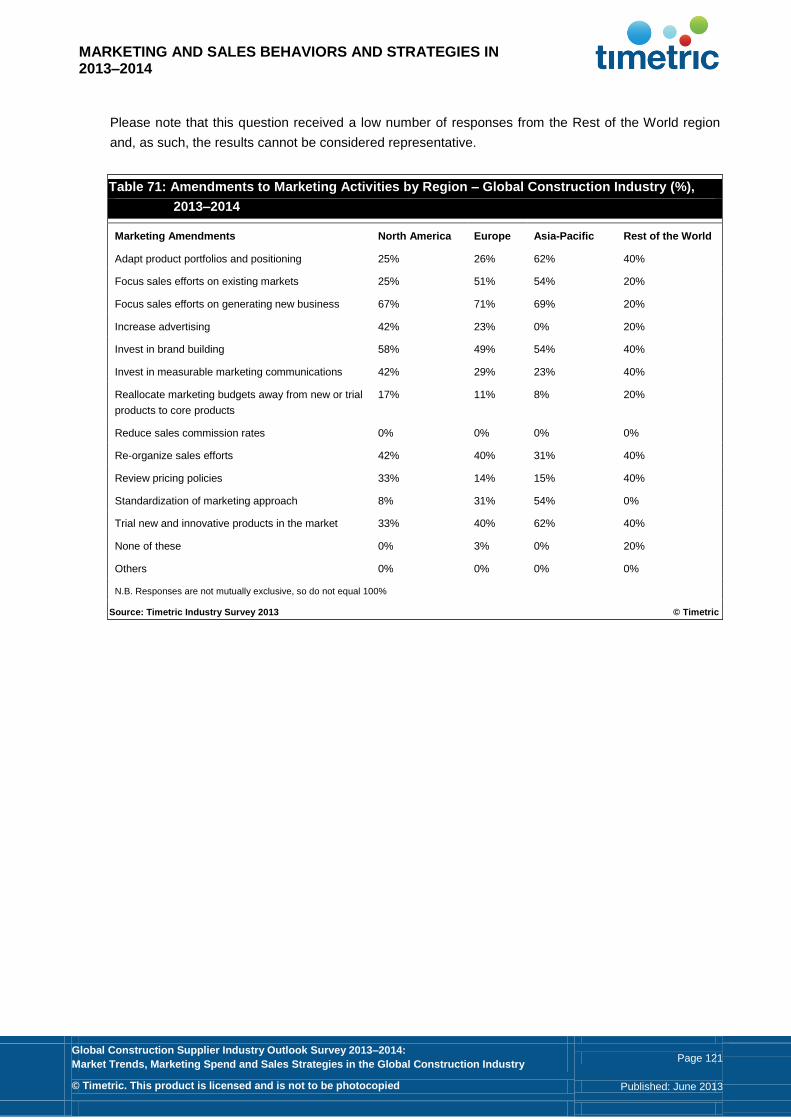

7.2.2 Amendments to marketing activities by region .......................................................................... 120

7.2.3 Amendments to marketing activities by company turnover ....................................................... 122

7.3 Best Uses of New Media for Business Prospects – Global Construction Industry .............. 123

7.3.1 Best uses of new media by suppliers ......................................................................................... 123

7.3.2 Best uses of new media by region ............................................................................................. 125

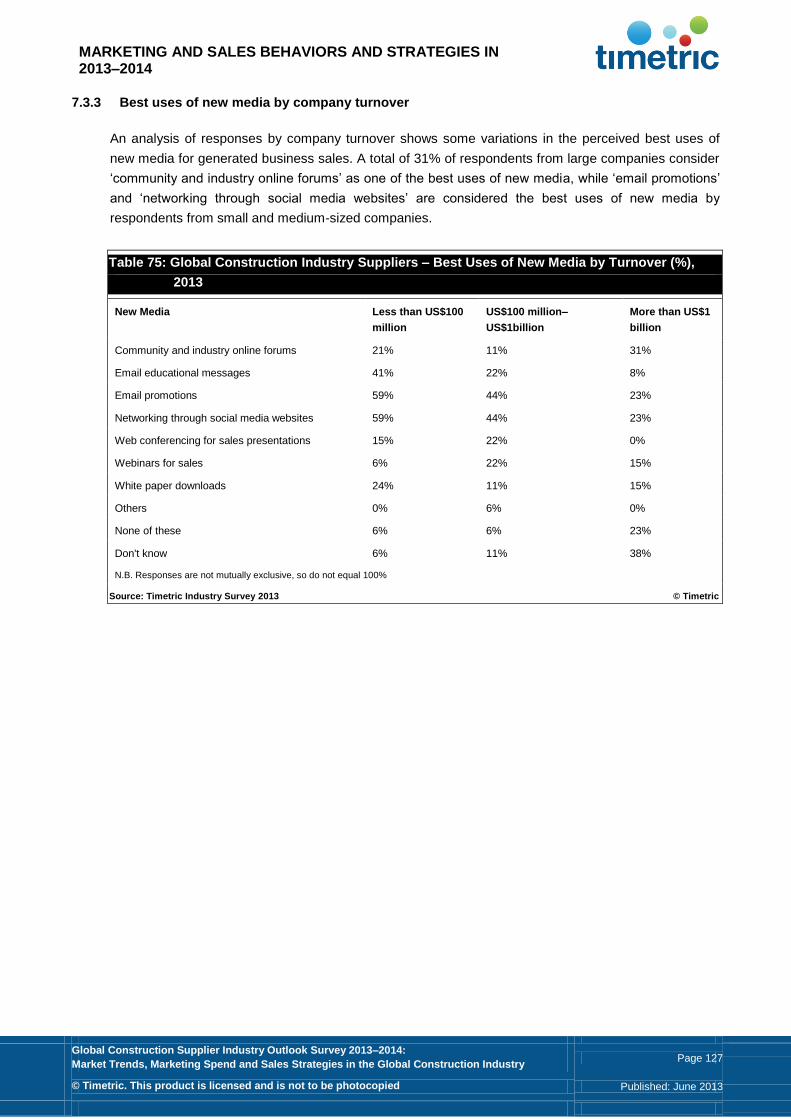

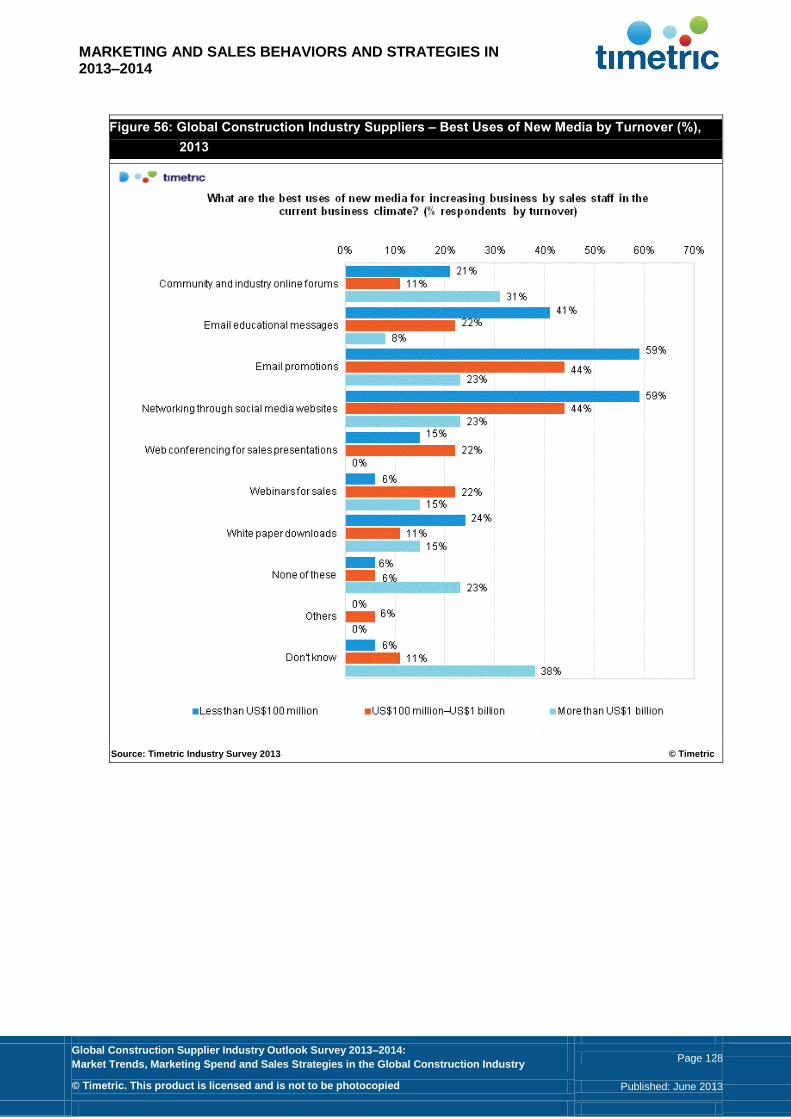

7.3.3 Best uses of new media by company turnover .......................................................................... 127

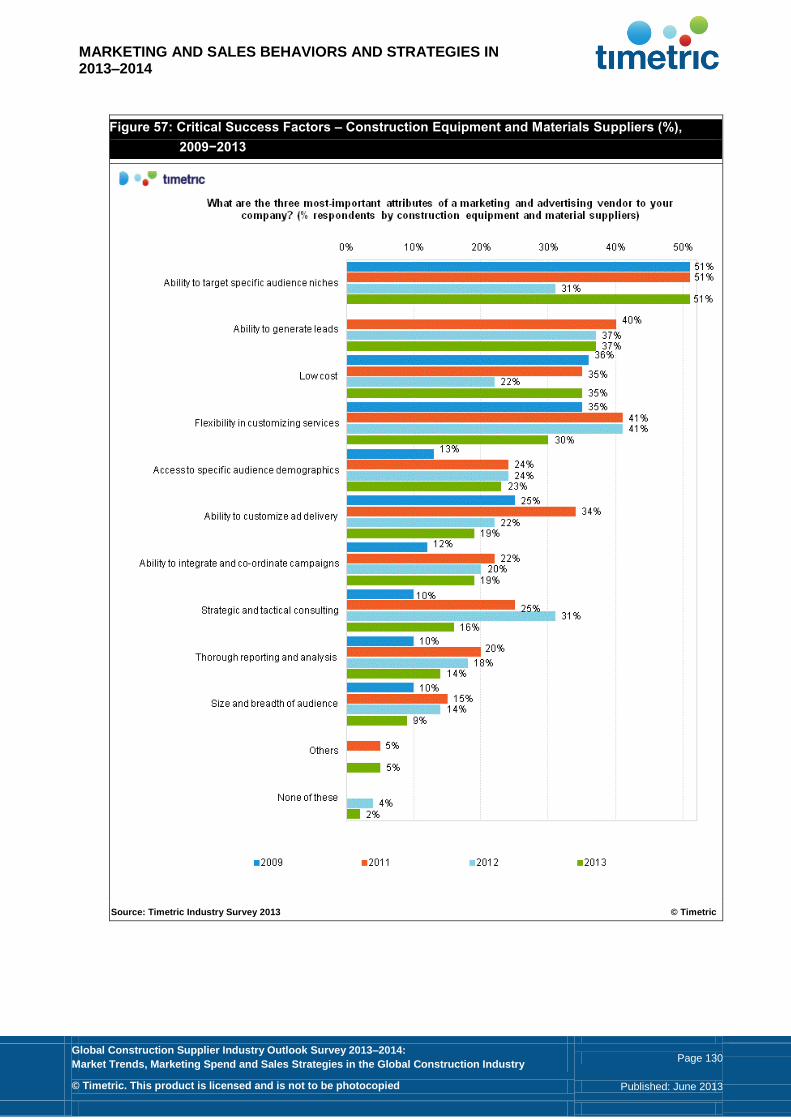

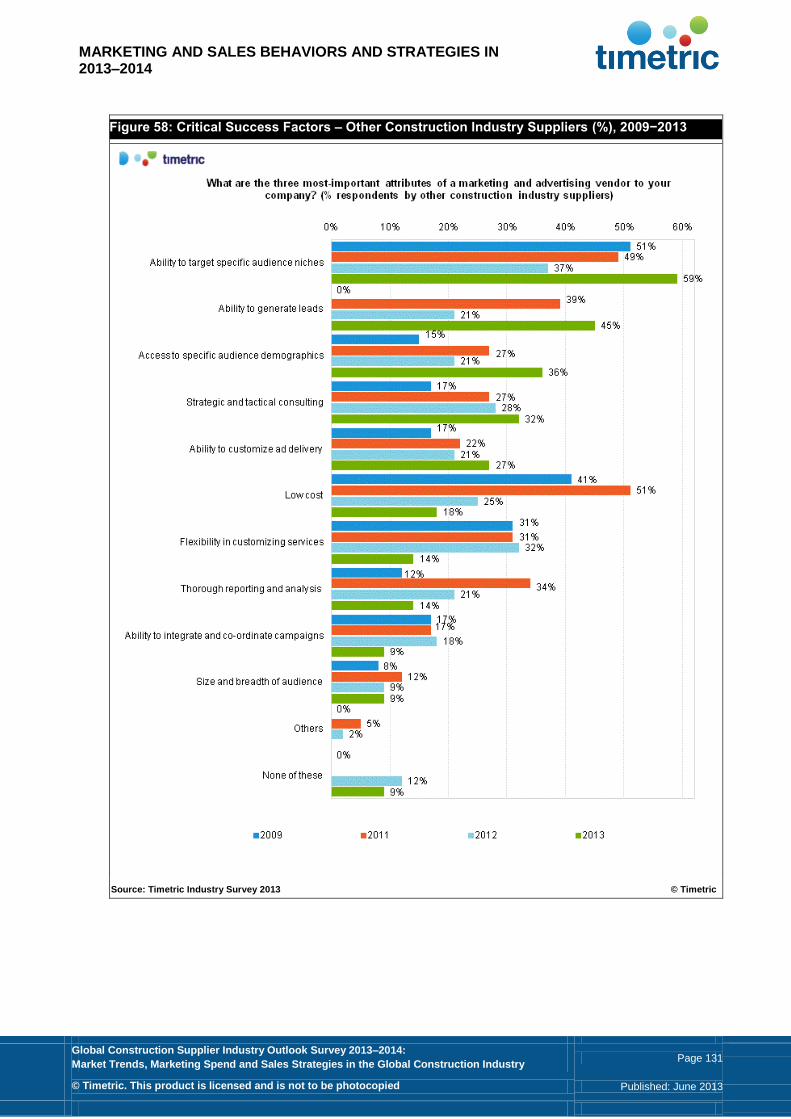

7.4 Critical Success Factors for Choosing a Marketing Agency ............................................... 129

7.4.1 Critical success factors by suppliers .......................................................................................... 129

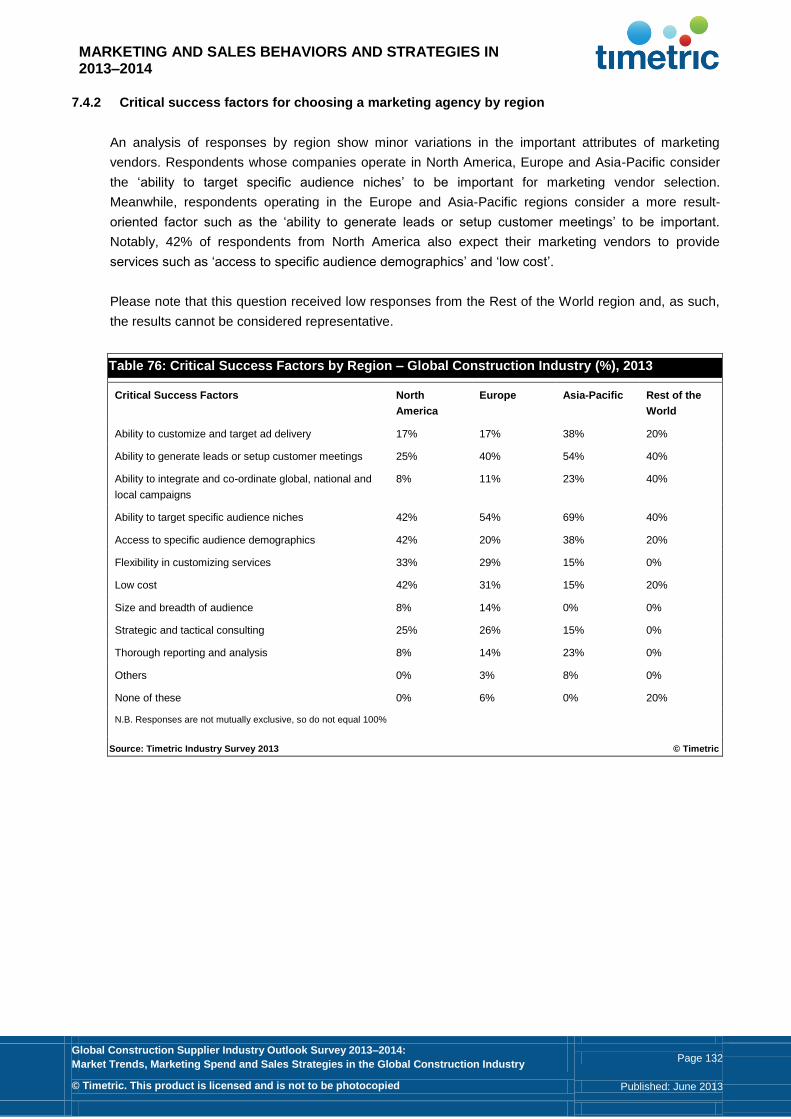

7.4.2 Critical success factors for choosing a marketing agency by region ......................................... 132

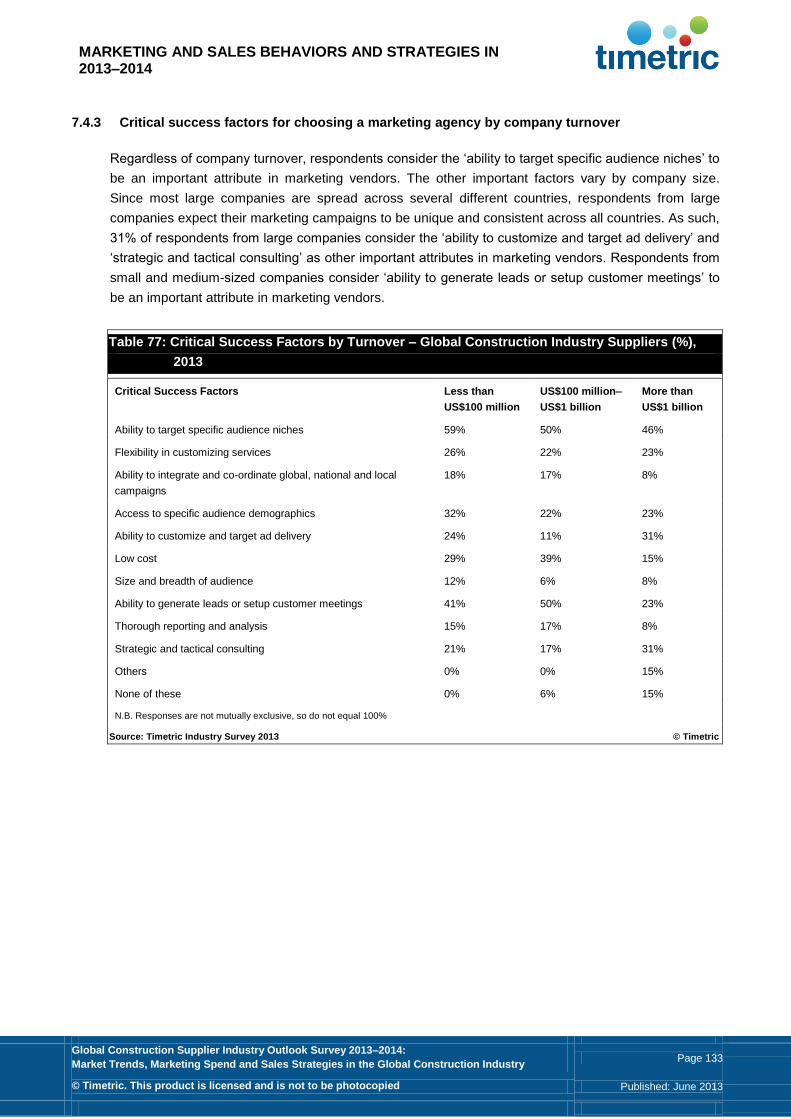

7.4.3 Critical success factors for choosing a marketing agency by company turnover ...................... 133

8 Appendix ................................................................................................................... 134

8.1 Survey Results – Closed Questions ................................................................................... 134

8.2 Methodology ...................................................................................................................... 152

8.3 Contact Us ......................................................................................................................... 152

8.4 About Timetric.................................................................................................................... 152

8.5 Disclaimer .......................................................................................................................... 153

TABLE OF CONTENTS

Global Construction Supplier Industry Outlook Survey 2013–2014:

Market Trends, Marketing Spend and Sales Strategies in the Global Construction Industry Page 5

© Timetric. This product is licensed and is not to be photocopied Published: June 2013

LIST OF FIGURES

Figure 1: Revenue Growth Optimism in the Global Construction Industry (%), 2009–2013 ......................................................................18 Figure 2: Revenue Growth Optimism in the Global Construction Industry by Company Type (%), 2009–2013 .........................................21 Figure 3: Revenue Growth Optimism in the Global Construction Industry by Region (%), 2013 ...............................................................22 Figure 4: Revenue Growth Optimism in the Global Construction Industry by Turnover (%), 2013 ............................................................23 Figure 5: Revenue Growth Optimism by Senior-Level Respondents (%), 2013 ........................................................................................24 Figure 6: Key Expected Changes in the Business Structure of Construction Contractors and Developers (%), 2013 ...............................27 Figure 7: Key Expected Changes in the Business Structure of Construction Equipment and Materials Suppliers (%), 2013 ....................29 Figure 8: Key Expected Changes in the Business Structure of Other Construction Suppliers (%), 2013 ..................................................30 Figure 9: M&A Activity Projections of Construction Contractors and Developers (%), 2009–2013 ............................................................33 Figure 10: M&A Activity Projections of Construction Equipment and Materials Suppliers (%), 2009–2013 ...............................................35 Figure 11: M&A Activity Projections of Other Construction Suppliers (%), 2009–2013 .............................................................................36 Figure 12: Capital Expenditure Expectations by Construction Contractors and Developers (%), 2013 .....................................................40 Figure 13: Capital Expenditure Expectations by Construction Equipment and Materials Suppliers (%), 2013 ..........................................41 Figure 14: Capital Expenditure Expectations by Other Construction Suppliers (%), 2013.........................................................................42 Figure 15: Global Construction Industry – Increase in Capital Expenditure by Region (%), 2013 .............................................................43 Figure 16: Global Construction Industry – Increase in Capital Expenditure by Turnover (%), 2013 ..........................................................44 Figure 17: Global Construction Industry – Planned Change in Staff Recruitment Activity by Contractors and Developers (%), 2013 .......46 Figure 18: Global Construction Industry – Planned Change in Staff Recruitment Activity by Suppliers (%), 2013 ....................................47 Figure 19: Global Construction Industry – Planned Change in Staff Recruitment Activity by Region (%), 2013 ........................................48 Figure 20: Global Construction Industry – Planned Change in Staff Recruitment Activity by Company Turnover (%), 2013 .....................49 Figure 21: Global Construction Industry – Top Ten Growth Regions (%), 2013 ........................................................................................50 Figure 22: Global Construction Industry – Top Five Emerging Markets, 2013 ..........................................................................................51 Figure 23: Demand in Emerging Markets by Construction Contractors and Developers (%), 2013...........................................................53 Figure 24: Demand in Emerging Markets by Construction Equipment and Materials Suppliers (%), 2013 ................................................55 Figure 25: Global Construction Industry – Increase of Demand in Emerging Markets by Company Turnover (%), 2013 ..........................58 Figure 26: Global Construction Industry – Top Five Developed Regions by Growth (%), 2013 ................................................................59 Figure 27: Construction Contractors and Developers – Growth Projections in Developed Countries (%), 2013 ........................................61 Figure 28: Construction Equipment and Materials Suppliers – Growth Projections in Developed Countries (%), 2013 .............................63 Figure 29: Other Construction Suppliers – Growth Projections in Developed Countries (%), 2013 ...........................................................65 Figure 30: Global Construction Industry – Increase in Growth Projections of Developed Countries by Region (%), 2013 .........................66 Figure 31: Global Construction Industry – Top Five Leading Business Concerns, 2013–2014 .................................................................70 Figure 32: Global Construction Industry – Leading Business Concerns (%), 2009–2013 .........................................................................71 Figure 33: Global Construction Industry – Securing Buyer Business: Buyer vs. Supplier Responses (%), 2013 .......................................77 Figure 34: Global Construction Industry – Securing Buyer Business by Region (%), 2013 .......................................................................79 Figure 35: Global Construction Industry – Securing Buyer Business by Senior-Level Respondents (%), 2013 .........................................81 Figure 36: Key Variations in Operational Costs of Construction Contractors and Developers (%), 2013 ..................................................83 Figure 37: Key Variations in Operational Costs of Construction Equipment and Materials Suppliers (%), 2013 ........................................85 Figure 38: Key Variations in Operational Costs of Other Construction Suppliers (%), 2013 ......................................................................86 Figure 39: Impact of Changing Costs on Product Pricing by Construction Contractors and Developers (%), 2013 ...................................89 Figure 40: Annual Marketing Budgets – Construction Equipment and Materials Suppliers (%), 2009−2013 .............................................92 Figure 41: Annual Marketing Budgets – Other Construction Industry Suppliers (%), 2009−2013 .............................................................92 Figure 42: Annual Marketing Budgets by Region – Global Construction Industry Suppliers (%), 2013 .....................................................93 Figure 43: Annual Marketing Budgets by Company Turnover – Global Construction Industry Suppliers (%), 2013 ..................................94 Figure 44: Planned Change in Marketing Expenditure (%), 2009−2013 ...................................................................................................95 Figure 45: Planned Change in Marketing Expenditure – Construction Equipment and Materials Suppliers (%), 2009−2013 ....................97 Figure 46: Planned Change in Marketing Expenditure – Other Construction Industry Suppliers (%), 2009−2013 .....................................99 Figure 47: Planned Change in Marketing Expenditure Levels by Turnover (%), 2013 ............................................................................ 101 Figure 48: Future Investment in Media Channels by Region (% ‘Increase’ Responses), 2013 ............................................................... 106 Figure 49: Planned Investment in Marketing and Sales Technologies by Suppliers (%), 2013 ............................................................... 110 Figure 50: Key Marketing Aims – Construction Equipment and Materials Suppliers (%), 2013 ............................................................... 114 Figure 51: Key Marketing Aims – Other Construction Industry Suppliers (%), 2013 ............................................................................... 115 Figure 52: Key Marketing Aims by Region – Global Construction Industry Suppliers (%), 2013 ............................................................. 116 Figure 53: Amendments to Marketing Activities by Global Construction Industry Suppliers (%), 2013–2014 .......................................... 120 Figure 54: Best Uses of New Media – Global Construction Industry Suppliers (%), 2013 ....................................................................... 124 Figure 55: Global Construction Industry Suppliers – Best Uses of New Media by Region (%), 2013 ...................................................... 126 Figure 56: Global Construction Industry Suppliers – Best Uses of New Media by Turnover (%), 2013 ................................................... 128 Figure 57: Critical Success Factors – Construction Equipment and Materials Suppliers (%), 2009−2013 .............................................. 130 Figure 58: Critical Success Factors – Other Construction Industry Suppliers (%), 2009−2013 ............................................................... 131

TABLE OF CONTENTS

Global Construction Supplier Industry Outlook Survey 2013–2014:

Market Trends, Marketing Spend and Sales Strategies in the Global Construction Industry Page 6

© Timetric. This product is licensed and is not to be photocopied Published: June 2013

LIST OF TABLES

Table 1: Global Construction Industry Survey Respondents by Company Type, 2013 .............................................................................11 Table 2: Global Construction Industry Contractor and Developer Respondents by Job Role (%), 2013 ...................................................11 Table 3: Global Construction Industry Contractor and Developer Respondents by Company Turnover (%), 2013 ...................................12 Table 4: Global Construction Industry Contractor and Developer Respondents by Region (%), 2013 ......................................................12 Table 5: Global Construction Industry Supplier Respondents by Job Role (%), 2013 ...............................................................................13 Table 6: Global Construction Industry Supplier Respondents by Company Turnover (%), 2013 ...............................................................13 Table 7: Global Construction Industry Supplier Respondents by Region (%), 2013 .................................................................................13 Table 8: Revenue Growth Optimism in the Global Construction Industry (%), 2009–2013 .......................................................................18 Table 9: Revenue Growth Optimism in the Global Construction Industry by Contractors and Developers (%), 2009–2013 ......................20 Table 10: Revenue Growth Optimism in the Global Construction Industry by Suppliers (%), 2009–2013 .................................................20 Table 11: Revenue Growth Optimism in the Global Construction Industry by Region (%), 2013 ..............................................................22 Table 12: Revenue Growth Optimism in the Global Construction Industry by Turnover (%), 2013 ...........................................................23 Table 13: Revenue Growth Optimism by Senior-Level Respondents (%), 2013 .......................................................................................24 Table 14: Key Expected Changes in the Business Structure of Construction Contractors and Developers (%), 2013 ..............................26 Table 15: Key Expected Changes in the Business Structure of Construction Equipment and Materials Suppliers (%), 2013 ...................29 Table 16: M&A Activity Projections of Construction Contractors and Developers (%), 2009–2013 ...........................................................32 Table 17: M&A Activity Projections of Construction Equipment and Materials Suppliers (%), 2009–2013 ................................................34 Table 18: M&A Activity Projections of Other Construction Suppliers (%), 2009–2013 ..............................................................................36 Table 19: Global Construction Industry – M&A Activity Projections by Region (%), 2013 .........................................................................38 Table 20: Global Construction Industry – M&A Activity Projections by Turnover (%), 2013 ......................................................................38 Table 21: Capital Expenditure Expectations by Construction Contractors and Developers (%), 2013 ......................................................40 Table 22: Capital Expenditure Expectations by Other Construction Suppliers (%), 2013 ..........................................................................42 Table 23: Global Construction Industry – Increase in Capital Expenditure by Region (%), 2013 ..............................................................43 Table 24: Global Construction Industry – Increase in Capital Expenditure by Turnover (%), 2013 ...........................................................44 Table 25: Global Construction Industry – Planned Change in Staff Recruitment Activity by Contractors and Developers (%), 2013.........46 Table 26: Global Construction Industry – Planned Change in Staff Recruitment Activity by Suppliers (%), 2013 ......................................47 Table 27: Global Construction Industry – Planned Change in Staff Recruitment Activity by Region (%), 2013 .........................................48 Table 28: Global Construction Industry – Planned Change in Staff Recruitment Activity by Company Turnover (%), 2013 ......................49 Table 29: Demand in Emerging Markets by Construction Contractors and Developers (%), 2013 ............................................................52 Table 30: Demand in Emerging Markets by Construction Equipment and Materials Suppliers (%), 2013 .................................................54 Table 31: Demand in Emerging Markets by Other Construction Suppliers (%), 2013 ...............................................................................56 Table 32: Global Construction Industry – Increase of Demand in Emerging Markets by Region (%), 2013 ..............................................57 Table 33: Construction Contractors and Developers – Growth Projections in Developed Countries (%), 2013 .........................................61 Table 34: Construction Equipment and Materials Suppliers – Growth Projections in Developed Countries (%), 2013 ..............................63 Table 35: Other Construction Suppliers – Growth Projections in Developed Countries (%), 2013 ............................................................64 Table 36: Global Construction Industry – Increase in Growth Projections of Developed Countries by Region (%), 2013 ..........................66 Table 37: Global Construction Industry – Increase in Growth Projections of Developed Countries by Turnover (%), 2013 .......................67 Table 38: Global Construction Industry – Leading Business Concerns (%), 2009–2013...........................................................................71 Table 39: Leading Business Concerns by Company Type (%), 2013–2014 .............................................................................................73 Table 40: Global Construction Industry – Leading Business Concerns by Region (%), 2013–2014 ..........................................................74 Table 41: Global Construction Industry – Leading Business Concerns by Turnover (%), 2013–2014 .......................................................75 Table 42: Global Construction Industry – Securing Buyer Business: Buyer vs. Supplier Responses (%), 2013 ........................................77 Table 43: Global Construction Industry – Securing Buyer Business by Region (%), 2013 ........................................................................78 Table 44: Global Construction Industry – Securing Buyer Business by Turnover (%), 2013 .....................................................................80 Table 45: Key Variations in Operational Costs of Construction Contractors and Developers (%), 2013 ...................................................83 Table 46: Key Variations in Operational Costs of Construction Equipment and Materials Suppliers (%), 2013 .........................................84 Table 47: Key Variations in Operational Costs of Other Construction Suppliers (%), 2013 .......................................................................85 Table 48: Key Variations in Operational Costs by Region (%), 2013 ........................................................................................................86 Table 49: Key Variations in Operational Costs by Company Turnover (%), 2013 .....................................................................................87 Table 50: Impact of Changing Costs on Product Pricing by Construction Contractors and Developers (%), 2013 ....................................88 Table 51: Impact of Changing Costs on Product Pricing by Suppliers (%), 2013 ......................................................................................89 Table 52: Annual Marketing Budgets – Construction Equipment and Materials Suppliers (%), 2009−2013 ..............................................91 Table 53: Annual Marketing Budgets – Other Construction Industry Suppliers (%), 2009−2013 ...............................................................92 Table 54: Annual Marketing Budgets by Region – Global Construction Industry Suppliers (%), 2013 ......................................................93 Table 55: Annual Marketing Budgets by Company Turnover – Global Construction Industry Suppliers (%), 2013 ...................................94 Table 56: Planned Change in Marketing Expenditure – Construction Equipment and Materials Suppliers (%), 2009−2013 .....................97 Table 57: Planned Change in Marketing Expenditure – Other Construction Industry Suppliers (%), 2009−2013 ......................................99 Table 58: Planned Change in Marketing Expenditure Levels by Region (%), 2013 ................................................................................ 100 Table 59: Planned Change in Marketing Expenditure Levels by Revenue Growth Expectations (%), 2013 ............................................ 102 Table 60: Future Investment in Media Channels – Construction Equipment and Materials Suppliers (%), 2013 ..................................... 104 Table 61: Future Investment in Media Channels – Other Construction Industry Suppliers (%), 2013 ..................................................... 105 Table 62: Future Investment in Media Channels by Turnover (% ‘Increase’ Responses), 2013 .............................................................. 107 Table 63: Planned Investment in Marketing and Sales Technologies by Suppliers (%), 2013 ................................................................ 109

TABLE OF CONTENTS

Global Construction Supplier Industry Outlook Survey 2013–2014:

Market Trends, Marketing Spend and Sales Strategies in the Global Construction Industry Page 7

© Timetric. This product is licensed and is not to be photocopied Published: June 2013

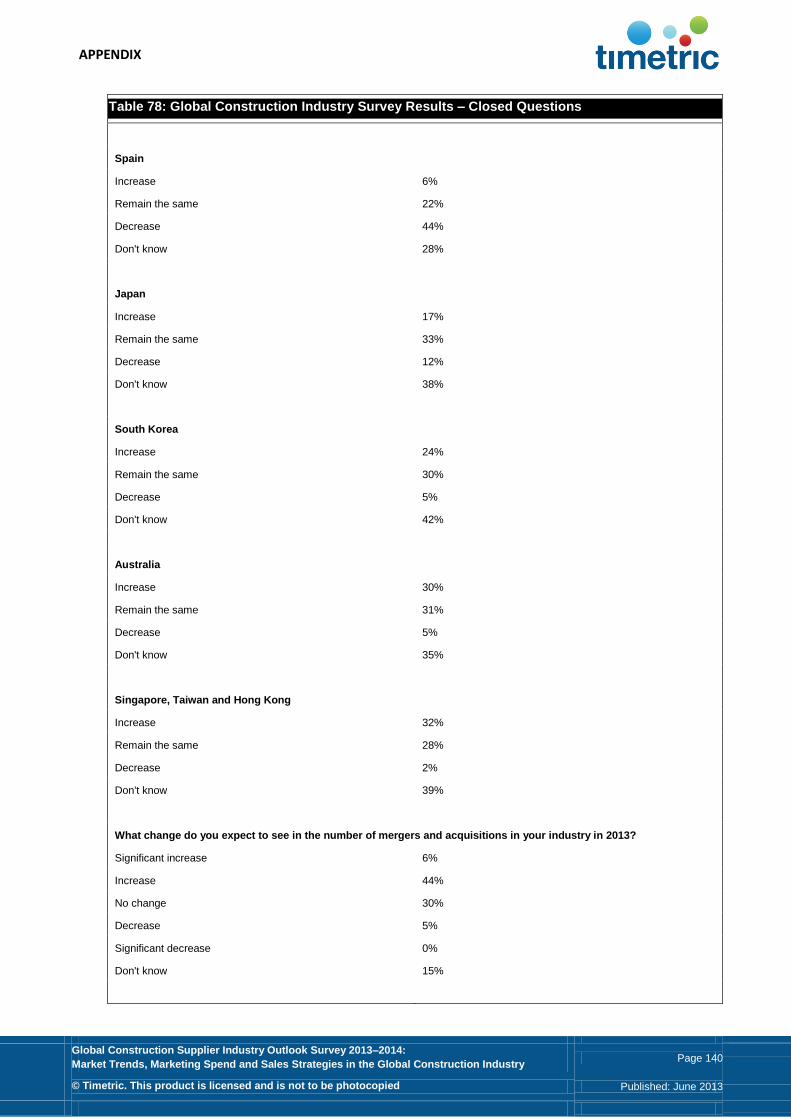

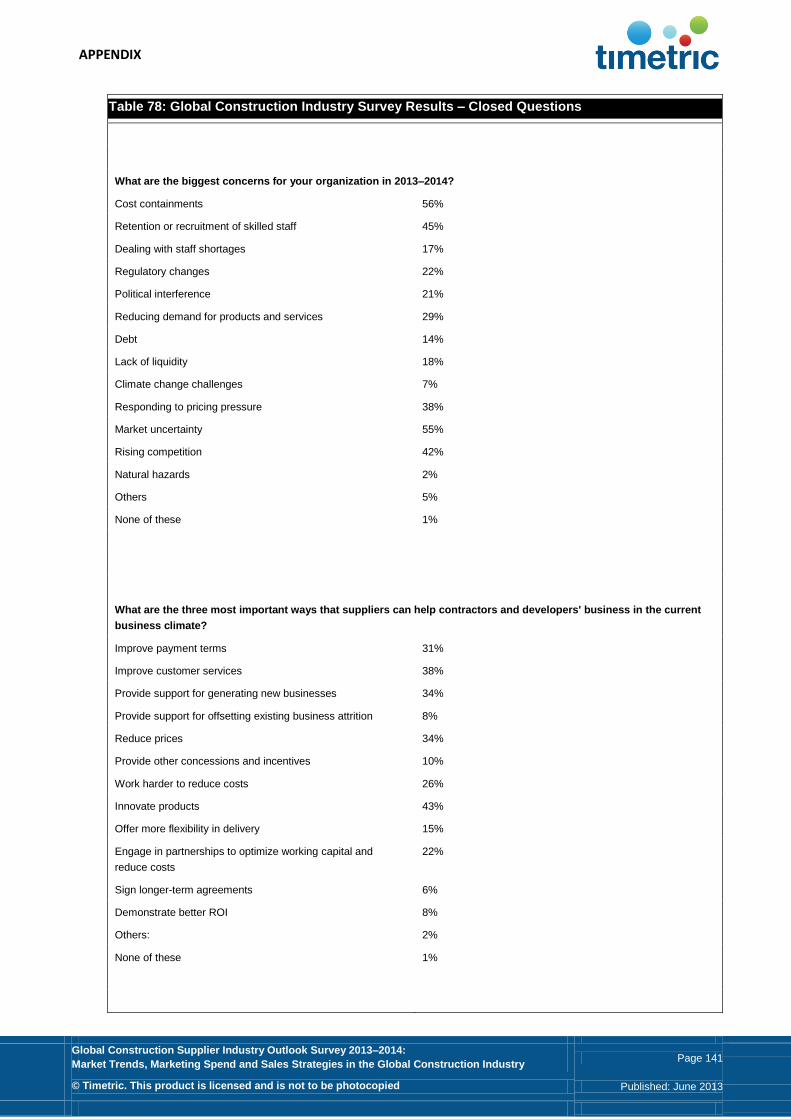

Table 64: Planned Investment in Marketing and Sales Technologies by Region (%), 2013 .................................................................... 111 Table 65: Planned Investment in Marketing and Sales Technologies by Company Turnover (%), 2013 ................................................. 111 Table 66: Key Marketing Aims – Construction Equipment and Materials Suppliers (%), 2013 ................................................................ 114 Table 67: Key Marketing Aims – Other Construction Industry Suppliers (%), 2013................................................................................. 115 Table 68: Key Marketing Aims by Turnover – Global Construction Industry Suppliers (%), 2013 ........................................................... 117 Table 69: Key Marketing Aims by Revenue Growth Expectations (%), 2013 .......................................................................................... 117 Table 70: Amendments to Marketing Activities by Global Construction Industry Suppliers (%), 2013–2014 ........................................... 119 Table 71: Amendments to Marketing Activities by Region – Global Construction Industry (%), 2013–2014 ............................................ 121 Table 72: Amendments to Marketing Activities by Turnover – Global Construction Industry (%), 2013–2014 ......................................... 122 Table 73: Best Uses of New Media – Global Construction Industry Suppliers (%), 2013 ........................................................................ 124 Table 74: Global Construction Industry Suppliers – Best Uses of New Media by Region (%), 2013 ....................................................... 125 Table 75: Global Construction Industry Suppliers – Best Uses of New Media by Turnover (%), 2013 .................................................... 127 Table 76: Critical Success Factors by Region – Global Construction Industry (%), 2013........................................................................ 132 Table 77: Critical Success Factors by Turnover – Global Construction Industry Suppliers (%), 2013 ..................................................... 133 Table 78: Global Construction Industry Survey Results – Closed Questions .......................................................................................... 134

INTRODUCTION

Global Construction Supplier Industry Outlook Survey 2013–2014:

Market Trends, Marketing Spend and Sales Strategies in the Global Construction Industry Page 8

© Timetric. This product is licensed and is not to be photocopied Published: June 2013

1 Introduction

1.1 What is this report about?

This report is the result of an extensive survey drawn from Timetric’s exclusive panel of leading

construction industry companies. This report provides the reader with a definitive analysis of the global

construction industry outlook, and explores how business opportunities and demands are expected to

change in 2013–2014. This report not only provides access to the opinions and strategies of business

decision makers and competitors, but also examines the actions surrounding business priorities. The

report provides respondent information by region, company type and size.

The report also examines:

Revenue growth expectations: projects the revenue growth expectations of major stakeholders of

the industry

Market-specific growth opportunities: identifies the main growth prospects in order to provide

assistance for companies in effectively allocating their marketing activities and budgets

M&A: expectations surrounding M&A activity and core influencing factors

Leading business concerns: identifies leading business concerns and subsequent efforts to

negate them

Marketing expenditure trends: tracks the marketing budgets of supplier companies and forecasts

possible changes to expenditure

Key factors for marketing agency selection: provides insights into the marketing needs of

competitors among supplier companies

1.2 Definitions

Construction contractors and developers (buyer): includes construction contractors or

subcontractors, private-sector project sponsors, developers or investors, and public-sector project

sponsors and developers.

Construction equipment and material suppliers (supplier 1): includes construction equipment

suppliers; building merchants or products distributors; construction materials or building products

manufacturers; furniture, fittings or interior products manufacturers; and other suppliers for raw

materials, logistics and factory equipment.

Other construction industry suppliers (supplier 2): includes architecture and design companies,

planning; surveying or civil engineering companies; trade bodies; academia or industry observers;

government or public-sector organizations; and other suppliers of technology and consultancy

services.

INTRODUCTION

Global Construction Supplier Industry Outlook Survey 2013–2014:

Market Trends, Marketing Spend and Sales Strategies in the Global Construction Industry Page 9

© Timetric. This product is licensed and is not to be photocopied Published: June 2013

Email marketing: It is defined as directly marketing a business message to a group of customers

using email.

Customer relationship management (CRM): It involves using technology to organize, automate,

and synchronize sales, marketing, customer service, and technical support.

Company turnover: companies with turnover of less than US$100 million are identified in the

report as small companies. In addition, companies with turnover between US$100 million–US$1

billion are referred to as medium-sized companies, and companies with turnover of more than US$1

billion as large companies.

1.3 Methodology

All Timetric reports are rigorously sourced and created according to a comprehensive four-stage

methodology:

1) Online survey

The research source in this report is based on the surveyed opinions and expectations of senior

industry professionals. Timetric conducted an extensive online survey in March-April 2013, which was

taken by 126 senior global industry executives worldwide; the respondents include C-level executives,

directors, and managers.

The survey’s respondents are drawn from the Timetric Industry Insight Panel, an exclusive industry

panel covering over 2 million business professionals worldwide. Respondents represent a dedicated

professional community where participants are surveyed ‘in context’, drawn from industry magazine and

media communities including the readership of Blueprint, designbuild-network.com, Tunnels &

Tunneling International and Cranes Today, as well as delegate relationships across Timetric’s global

industry conference and forum events. These business communities are made up of qualified

professionals who rely on Timetric’s flagship media brands, enabling Timetric to access informed

industry opinions.

INTRODUCTION

Global Construction Supplier Industry Outlook Survey 2013–2014:

Market Trends, Marketing Spend and Sales Strategies in the Global Construction Industry Page 10

© Timetric. This product is licensed and is not to be photocopied Published: June 2013

2) Secondary research

Collection of the latest market-specific data from a wide variety of respected third-party industry

sources:

Government statistics

Industry associations

Company filings

Broker reports

International organizations

Industry news websites

Industry reports

3) Data analysis and report writing

The results of this research have been analyzed and evaluated by Timetric’s industry-specific in-house

analysts. The analysts’ research and expertise, pedigree in marketing, market research, consulting

backgrounds in their industry, and ongoing education on leading economic and industry news have

shaped their analytical judgments and conclusions of the opinions gathered.

4) Quality control

Detailed process manuals

Standardized report templates and accompanying style guides

Advanced data analysis and survey programming tools

QC checklists

Randomized spot checks on data integrity

Peer review

Senior-level QC

INTRODUCTION

Global Construction Supplier Industry Outlook Survey 2013–2014:

Market Trends, Marketing Spend and Sales Strategies in the Global Construction Industry Page 11

© Timetric. This product is licensed and is not to be photocopied Published: June 2013

1.4 Global Construction Industry: Profile of Survey Respondents

Timetric’s in-depth industry survey was completed by 126 respondents, employed by the organizations

shown in the table below:

Table 1: Global Construction Industry Survey Respondents by Company Type, 2013

Company Type Number of Respondents

Construction contractors and developers 60

Construction equipment and materials suppliers 43

Other construction industry suppliers 23

Overall 126

Source: Timetric Industry Survey 2013 © Timetric

1.4.1 Global construction industry: profile of contractor and developer respondents

The contractors and developers in the global construction industry include construction contractors or

subcontractors; private-sector project sponsors, developers or investors; and public-sector project

sponsors and developers. Of the survey’s total respondents, 48% were from construction contracting

and developer companies.

Of all contractor and developer respondents, 12% belong to organizations with a turnover of more than

US$1 billion, and 72% belong to organizations with a turnover of less than US$100 million. In addition,

71% of all contractor and developer respondents are C-level or director-level executives, while the

remaining 29% are managers and professionals with technical backgrounds. Furthermore, 48% of

contractor and developer respondents are from companies in Europe, 25% are from companies in

North America and 18% are from companies in the Asia-Pacific.

Table 2: Global Construction Industry Contractor and Developer Respondents by Job Role (%),

2013

Role Percentage of Operator Respondents

CEO / president / MD / board member / C-level executive 22%

Director / VP / SVP 25%

Head of business unit 7%

Head of department 17%

Manager 12%

Professional and technical staff (e.g. lawyer, engineer, architect) 13%

Staff 5%

Overall 100%

N.B. Results may not equal 100% due to rounding

Source: Timetric Industry Survey 2013 © Timetric

INTRODUCTION

Global Construction Supplier Industry Outlook Survey 2013–2014:

Market Trends, Marketing Spend and Sales Strategies in the Global Construction Industry Page 12

© Timetric. This product is licensed and is not to be photocopied Published: June 2013

Table 3: Global Construction Industry Contractor and Developer Respondents by Company

Turnover (%), 2013

Turnover Percentage of Operator Respondents

Less than US$100 million 72%

US$100 million–US$1 billion 17%

More than US$1 billion 12%

Overall 100%

N.B. Results may not equal 100% due to rounding

Source: Timetric Industry Survey 2013 © Timetric

Table 4: Global Construction Industry Contractor and Developer Respondents by Region (%),

2013

Region Percentage of Operator Respondents

North America 25%

Europe 48%

Asia-Pacific 18%

Rest of the World 9%

Overall 100%

Source: Timetric Industry Survey 2013 © Timetric

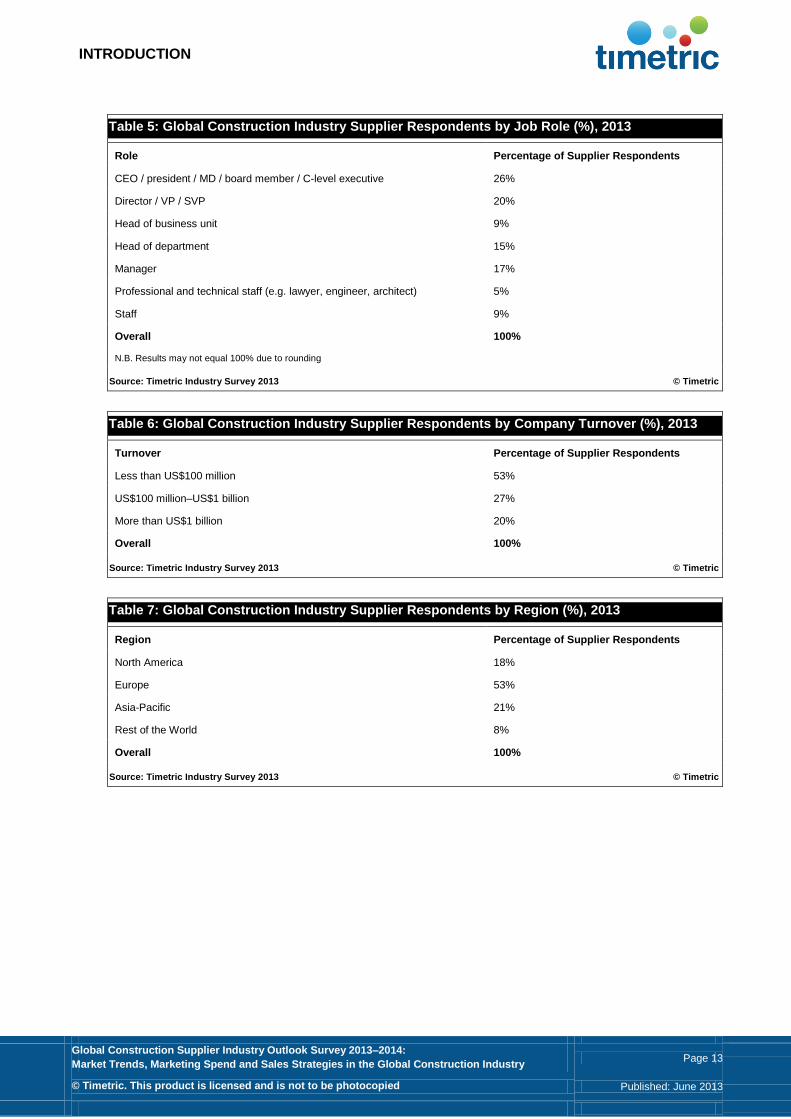

1.4.2 Global construction industry: profile of supplier respondents

Suppliers to the global construction industry include construction equipment and materials suppliers,

and other construction industry suppliers. Construction equipment and materials suppliers include

construction equipment suppliers; building merchants or products distributors; construction materials or

building products manufacturers; furniture, fittings or interior products manufacturers; and other

suppliers for raw materials, logistics and factory equipment. Other construction industry suppliers

include architecture and design companies; planning, surveying or civil engineering companies; trade

bodies; academia or industry observers; government or public-sector organizations; and other suppliers

of technology and consultancy services. Of all survey respondents, 34% are from construction

equipment and materials supplier companies, while 18% are from other construction industry supplier

companies.

Of all supplier respondents, 20% belong to organizations with a turnover of more than US$1 billion, and

53% belong to organizations with turnover of less than US$100 million. In addition, 70% of all supplier

respondents are C-level or director-level executives, while the remaining 30% represent managers and

professionals with technical backgrounds.

INTRODUCTION

Global Construction Supplier Industry Outlook Survey 2013–2014:

Market Trends, Marketing Spend and Sales Strategies in the Global Construction Industry Page 13

© Timetric. This product is licensed and is not to be photocopied Published: June 2013

Table 5: Global Construction Industry Supplier Respondents by Job Role (%), 2013

Role Percentage of Supplier Respondents

CEO / president / MD / board member / C-level executive 26%

Director / VP / SVP 20%

Head of business unit 9%

Head of department 15%

Manager 17%

Professional and technical staff (e.g. lawyer, engineer, architect) 5%

Staff 9%

Overall 100%

N.B. Results may not equal 100% due to rounding

Source: Timetric Industry Survey 2013 © Timetric

Table 6: Global Construction Industry Supplier Respondents by Company Turnover (%), 2013

Turnover Percentage of Supplier Respondents

Less than US$100 million 53%

US$100 million–US$1 billion 27%

More than US$1 billion 20%

Overall 100%

Source: Timetric Industry Survey 2013 © Timetric

Table 7: Global Construction Industry Supplier Respondents by Region (%), 2013

Region Percentage of Supplier Respondents

North America 18%

Europe 53%

Asia-Pacific 21%

Rest of the World 8%

Overall 100%

Source: Timetric Industry Survey 2013 © Timetric

EXECUTIVE SUMMARY

Global Construction Supplier Industry Outlook Survey 2013–2014:

Market Trends, Marketing Spend and Sales Strategies in the Global Construction Industry Page 14

© Timetric. This product is licensed and is not to be photocopied Published: June 2013

2 Executive Summary

Overall, respondents are optimistic about revenue growth in 2013

Of the survey respondents across the global construction industry, 53% are ‘more optimistic’ about

revenue growth for their companies in 2013, due to increased investments in IT infrastructure and other

public and private-sector construction projects, and growing demand for sustainable construction. The

key expected changes for 2013 are ‘expand in current market’ and ‘improving operational efficiency’,

while in 2012, the emphasis was on ‘improving operational efficiency’, ‘expand operations in domestic

market’, ‘stabilize company finances’ and ‘manage pricing strategies’.

Mergers and acquisitions in the global construction industry expected to increase in 2013

Executives from the global construction industry expect to see increased levels of consolidation, with

50% of respondents anticipating either a significant increase or an increase in M&A activity in 2013.

Slow recovery in the global economy and weak market conditions, a growing desire for large

construction companies to increase their global presence, and increased pressure of rising costs on

small and medium-sized construction companies are considered the key drivers for participating in M&A

activity. Respondents across the global construction industry anticipate a considerable increase in

capital expenditure on ‘new product developments’, ‘IT infrastructure developments’ and ‘machinery

and equipment purchases’. Respondents also anticipate increases in their current workforce in 2013.

China, India, the UAE, Brazil, and Eastern Europe are considered key emerging markets in 2013

Respondents from construction contractor and developer companies identified India, Brazil, the UAE,

China and Saudi Arabia as promising emerging markets for 2013. Construction activity in India has

increased steadily due to growth in infrastructure development in housing, roads, ports, aviation

infrastructure and power generation, leading the country to become one of the emerging markets in the

global construction industry. Additionally, the US, Canada, Singapore, Australia and the UK were

identified as chief growth regions among developed countries. France, Italy and Spain are expected to

offer low growth potential.

Companies face key challenges due to ‘cost containments’, market uncertainty’, ‘retention or

recruitment of skilled staff’ and ‘rising competition’

‘Cost containments’ will be a leading challenge for the global construction industry in 2013–2014, as

expressed by 56% of industry respondents, while 55% identified ‘market uncertainty’ as important.

Regardless of company size, global construction industry companies consider ‘market uncertainty’ and

‘cost containments’ as leading business concerns. As a result, the key objectives for suppliers were

identified as ‘provide support for generating new businesses’ and the adoption of practices to ‘innovate

product’ and ‘improve customer services’, as identified by construction contractors and developers.

EXECUTIVE SUMMARY

Global Construction Supplier Industry Outlook Survey 2013–2014:

Market Trends, Marketing Spend and Sales Strategies in the Global Construction Industry Page 15

© Timetric. This product is licensed and is not to be photocopied Published: June 2013

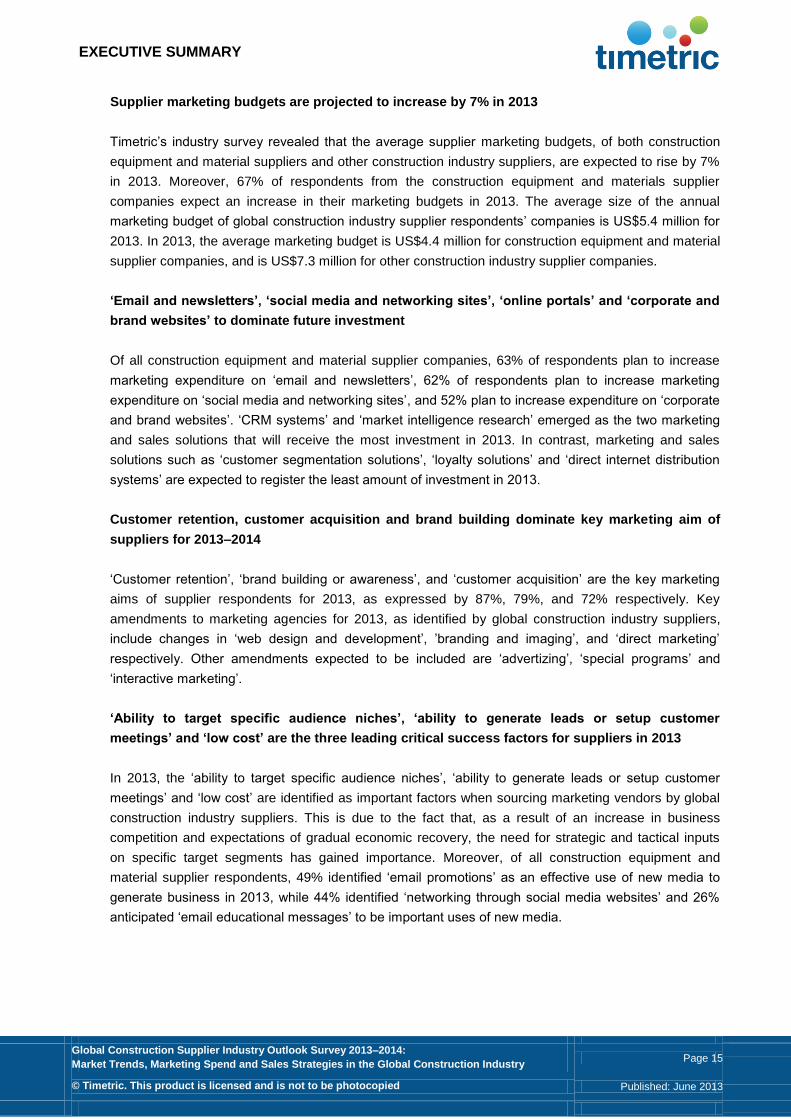

Supplier marketing budgets are projected to increase by 7% in 2013

Timetric’s industry survey revealed that the average supplier marketing budgets, of both construction

equipment and material suppliers and other construction industry suppliers, are expected to rise by 7%

in 2013. Moreover, 67% of respondents from the construction equipment and materials supplier

companies expect an increase in their marketing budgets in 2013. The average size of the annual

marketing budget of global construction industry supplier respondents’ companies is US$5.4 million for

2013. In 2013, the average marketing budget is US$4.4 million for construction equipment and material

supplier companies, and is US$7.3 million for other construction industry supplier companies.

‘Email and newsletters’, ‘social media and networking sites’, ‘online portals’ and ‘corporate and

brand websites’ to dominate future investment

Of all construction equipment and material supplier companies, 63% of respondents plan to increase

marketing expenditure on ‘email and newsletters’, 62% of respondents plan to increase marketing

expenditure on ‘social media and networking sites’, and 52% plan to increase expenditure on ‘corporate

and brand websites’. ‘CRM systems’ and ‘market intelligence research’ emerged as the two marketing

and sales solutions that will receive the most investment in 2013. In contrast, marketing and sales

solutions such as ‘customer segmentation solutions’, ‘loyalty solutions’ and ‘direct internet distribution

systems’ are expected to register the least amount of investment in 2013.

Customer retention, customer acquisition and brand building dominate key marketing aim of

suppliers for 2013–2014

‘Customer retention’, ‘brand building or awareness’, and ‘customer acquisition’ are the key marketing

aims of supplier respondents for 2013, as expressed by 87%, 79%, and 72% respectively. Key

amendments to marketing agencies for 2013, as identified by global construction industry suppliers,

include changes in ‘web design and development’, ’branding and imaging’, and ‘direct marketing’

respectively. Other amendments expected to be included are ‘advertizing’, ‘special programs’ and

‘interactive marketing’.

‘Ability to target specific audience niches’, ‘ability to generate leads or setup customer

meetings’ and ‘low cost’ are the three leading critical success factors for suppliers in 2013

In 2013, the ‘ability to target specific audience niches’, ‘ability to generate leads or setup customer

meetings’ and ‘low cost’ are identified as important factors when sourcing marketing vendors by global

construction industry suppliers. This is due to the fact that, as a result of an increase in business

competition and expectations of gradual economic recovery, the need for strategic and tactical inputs

on specific target segments has gained importance. Moreover, of all construction equipment and

material supplier respondents, 49% identified ‘email promotions’ as an effective use of new media to

generate business in 2013, while 44% identified ‘networking through social media websites’ and 26%

anticipated ‘email educational messages’ to be important uses of new media.

INDUSTRY DYNAMICS

Global Construction Supplier Industry Outlook Survey 2013–2014:

Market Trends, Marketing Spend and Sales Strategies in the Global Construction Industry Page 16

© Timetric. This product is licensed and is not to be photocopied Published: June 2013

3 Global Construction Industry Dynamics

In this chapter, survey respondents in the global construction industry detail the future growth

expectations of their companies, and provide insights into mergers and acquisitions (M&A) and

business structure in the global construction industry. This chapter provides an overview of the

business outlook for the global construction industry, including the overall change in organizations’

capital expenditure and staff recruitment activity. Industry trends in this area are also analyzed in

comparison with the results of the 2009, 2011 and 2012 construction industry surveys, providing an

opportunity to follow changes in respondents’ attitudes.

Key Findings:

Of all respondents across the global construction industry, 53% are ‘more optimistic’ about revenue growth in 2013 as compared with the previous 12 months

A total of 62% of contractor and developer respondents are ‘more optimistic’ about revenue growth in 2013

Respondents from companies operating in the Rest of the World and North America are more

optimistic about revenue growth in 2013

‘Expand in current market’ and ‘improving operational efficiency’ are the key priorities for

construction contractors and developers in 2013

In total, 50% of construction contractors anticipate either a ‘significant increase’ or ‘increase’ in

M&A activity during 2013

Survey results reveal that 46% of construction industry supplier respondents expect either a

‘significant increase’ or ‘increase’ in M&A activity in 2013

‘New product developments’, ‘IT infrastructure developments’, and ‘machinery and equipment

purchases’ are expected to increase significantly in 2013

A total of 40% of respondents from construction contractor and developer companies anticipate a

maximum 2% increase of their current workforce in 2013

INDUSTRY DYNAMICS

Global Construction Supplier Industry Outlook Survey 2013–2014:

Market Trends, Marketing Spend and Sales Strategies in the Global Construction Industry Page 17

© Timetric. This product is licensed and is not to be photocopied Published: June 2013

3.1 Revenue Growth Projections in the Global Construction Industry

Within the global construction industry, 53% of survey respondents are ‘more optimistic’ about revenue

growth expectations in 2013 as compared to the previous 12 months. Meanwhile, 24% of respondents

are ‘less optimistic’ about revenue growth, while 22% expect ‘no change’ whatsoever. Increased

investments in IT infrastructure and other public and private-sector construction projects, in tandem with

growing demand for sustainable construction, are considered key drivers of revenue-growth optimism

for 2013. For example, according to a press release from Singapore’s Building and Construction

Authority (BCA) in January 2013, construction demand in Singapore is forecast to register a growth of

53%, totaling US$26–32 billion for 2013. The BCA notes that growth is expected due to the sector’s

healthy performance in 2012, and strong growth potential generated from the public sector and rail

construction. The key public-sector projects in Singapore which are likely to be awarded in 2013, as

projected by the BCA, include:

Construction of undergraduate halls in Nanyang Technological University

Construction of storage tanks at Jurong Island

Construction of Jurong Town Corporation’s large floating oil storage structure at Pulau Sebarok

Construction contracts for the Thomson Mass Rapid Transit Line

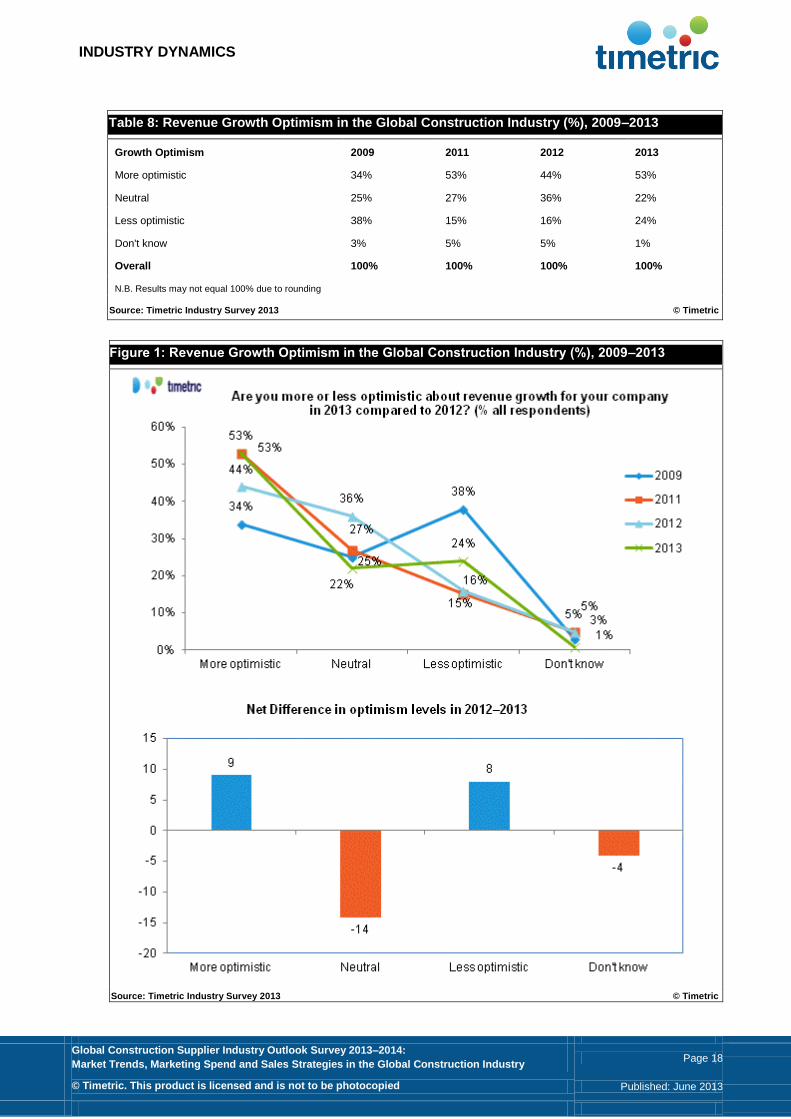

Furthermore, according to the 2013 Timetric Research survey results, revenue growth optimism levels

increased by nine percentage points in comparison to 2012, though optimism levels remained similar to

2011’s survey results. This indicates that the construction sector is forecast to perform well in 2013 as

compared with 2012, mainly due to the growing number of projects in the pipeline that are expected to

benefit global construction companies and stakeholders. For example, Primoris Services Corporation, a

contractor and engineering company serving the US power and energy sectors, secured new contracts

worth US$322.7 million between January 2013 and March 2013. These contracts are spread across

power, pipeline, gas utility, water, wastewater treatment and highway infrastructure projects throughout

the US.

Similarly, in January 2013, Manchester City Council UK announced the selection of Solutions 4

Brunswick (S4B) consortium as its preferred developer for the US$118 million Brunswick regeneration

scheme. The project includes the renovation of 650 council homes, construction of 500 new homes for

rent or sale, as well as new road layouts and open spaces. A senior executive from Brunswick S4B

commented:

“The area deserves and needs substantial investment to bring the homes and environment up to decent

modern homes’ standards set by the government.”

INDUSTRY DYNAMICS

Global Construction Supplier Industry Outlook Survey 2013–2014:

Market Trends, Marketing Spend and Sales Strategies in the Global Construction Industry Page 18

© Timetric. This product is licensed and is not to be photocopied Published: June 2013

Table 8: Revenue Growth Optimism in the Global Construction Industry (%), 2009–2013

Growth Optimism 2009 2011 2012 2013

More optimistic 34% 53% 44% 53%

Neutral 25% 27% 36% 22%

Less optimistic 38% 15% 16% 24%

Don't know 3% 5% 5% 1%

Overall 100% 100% 100% 100%

N.B. Results may not equal 100% due to rounding

Source: Timetric Industry Survey 2013 © Timetric

Figure 1: Revenue Growth Optimism in the Global Construction Industry (%), 2009–2013

Source: Timetric Industry Survey 2013 © Timetric

INDUSTRY DYNAMICS

Global Construction Supplier Industry Outlook Survey 2013–2014:

Market Trends, Marketing Spend and Sales Strategies in the Global Construction Industry Page 19

© Timetric. This product is licensed and is not to be photocopied Published: June 2013

3.1.1 Revenue growth projections by company type

In total, 62% of contractors and developers are ‘more optimistic’ about revenue growth in 2013 as

compared to the previous 12 months. The improvement is expected to be driven by gradual recovery in

both the residential and non-residential construction markets, and expansion in the real estate industry

in several countries, including the US, one of the largest construction markets. For example, in

February 2013, project development and construction group, Skanska, secured a US$48 million

contract for the Green Court Bucharest office project in Bucharest, Romania.

Furthermore, a total of 51% of construction equipment and materials suppliers, and 35% of other

construction industry suppliers are ‘more optimistic’ about revenue growth in 2013, primarily driven by

increases in construction contracts. For example, in March 2013, crane dealer Manitex US announced

an increase in its overall revenue by 44% from US$142.3 million in 2011 to US$205.2 million in 2012.

The company notes that the increase in sales was due to the higher level of penetration of products

specifically targeting construction projects in the energy and power line distribution sectors. Moreover,

the company expects healthy returns for 2013 with a set target of US$350 million by 2015. Emphasizing

this point, a senior executive from the company noted:

“We have 25% of our current sales coming from products that we've recently introduced into the

markets. We've considered that trend by introducing into the fourth quarter a 15-ton Badger crane,

which we believe will show some positive returns in the not-too-distant future. And we are very excited

about seven new products which we will be introducing this year.”

Similarly, engineering services provider, Sparrows Group, from Scotland secured contracts worth

US$285 million in the first quarter of 2013, from clients such as Shell, CNR, ConocoPhillips, Perenco,

and Wood Group in the North Sea. The company also won orders and contracts worth US$60 million in

the US, the Middle East, and Asia. It also secured renewals of agreements to work with BP in Angola

and CNR in Gabon and Côte d’Ivoire. The company notes that its new contract wins for 2013 succeed

favorable results in 2012, when its revenues grew by 10% from 2011. A senior executive from Sparrows

commented:

“We will be reporting robust results for 2012 later this year and, with these latest contract wins, are well

on course to deliver exceptional results for 2013. Our focus is firmly on excelling in delivery for our

clients. We have a strong reputation for delivering on our promises and this is underlined by the amount

of renewals we are securing.”

Notably, 28% and 22% of respondents respectively from the two supplier categories expressed neutral

sentiments about revenue growth, while 43% from other construction industry suppliers are ‘less

optimistic’ about revenue growth in 2013. The recent deceleration in the growth rate of several

economies due to the impact of the European sovereign debt crisis may have adversely affected some

construction companies due to unforeseen delays and postponements.

INDUSTRY DYNAMICS

Global Construction Supplier Industry Outlook Survey 2013–2014:

Market Trends, Marketing Spend and Sales Strategies in the Global Construction Industry Page 20

© Timetric. This product is licensed and is not to be photocopied Published: June 2013

Table 9: Revenue Growth Optimism in the Global Construction Industry by Contractors and

Developers (%), 2009–2013

Growth Optimism 2009 2011 2012 2013

More optimistic 35% 53% 40% 62%

Neutral 25% 21% 37% 18%

Less optimistic 36% 23% 21% 18%

Don't know 4% 3% 3% 2%

Overall 100% 100% 100% 100%

N.B. Results may not equal 100% due to rounding

Source: Timetric Industry Survey 2013 © Timetric

Table 10: Revenue Growth Optimism in the Global Construction Industry by Suppliers (%), 2009–

2013

Growth Optimism Construction Equipment and Materials Suppliers Other Construction Industry Suppliers

2009 2011 2012 2013 2009 2011 2012 2013

More optimistic 32% 56% 56% 51% 35% 45% 43% 35%

Neutral 20% 10% 33% 28% 25% 13% 35% 22%

Less optimistic 46% 30% 10% 21% 36% 30% 10% 43%

Don't know 1% 4% 1% 0% 4% 13% 12% 0%

Overall 100% 100% 100% 100% 100% 100% 100% 100%

N.B. Results may not equal 100% due to rounding

Source: Timetric Industry Survey 2013 © Timetric

INDUSTRY DYNAMICS

Global Construction Supplier Industry Outlook Survey 2013–2014:

Market Trends, Marketing Spend and Sales Strategies in the Global Construction Industry Page 21

© Timetric. This product is licensed and is not to be photocopied Published: June 2013

Figure 2: Revenue Growth Optimism in the Global Construction Industry by Company Type (%),

2009–2013

Source: Timetric Industry Survey 2013 © Timetric

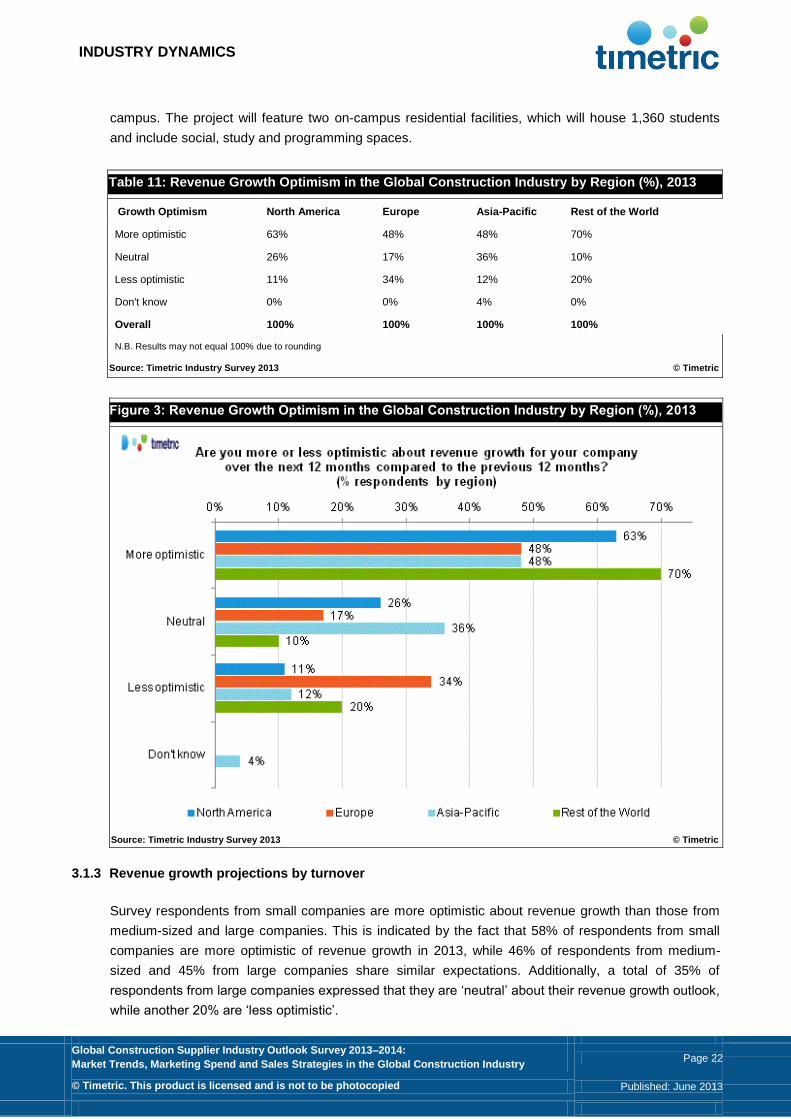

3.1.2 Revenue growth projections by region

Of all survey respondents, 70% from companies that operate in the Rest of the World and 63% from

companies operating in North America are optimistic about revenue growth in 2013. Meanwhile, 48% of

respective respondents from companies operating in Europe and Asia-Pacific are optimistic about

revenue growth in 2013.

Interestingly, a significant percentage of respondents from companies operating in the Rest of the

World anticipate increased optimism for revenue growth due to the rising number of infrastructure

projects in several countries. For example, in March 2013, construction equipment manufacturer

Liebherr Group, based in Germany, opened a new sales and service subsidiary in Mexico. This unit will

initially handle sales and servicing of Liebherr mobile cranes in Mexico and other neighboring countries

in Central America. The company noted that the move to establish a Mexican subsidiary was in

response to the growing importance of this market for Liebherr, as large-scale investments in Mexico’s

energy sector and infrastructure have contributed for increased demand for mobile and crawler cranes.

The reason respondents from companies operating in North America are more optimistic about revenue

growth is because the US construction industry has started to recover alongside the country’s

improving GDP. In reference to the trend, in March 2013, Howard University in Washington, DC

partnered with Campus Apartments for a US$107 million residential expansion at its Northwest DC

INDUSTRY DYNAMICS

Global Construction Supplier Industry Outlook Survey 2013–2014:

Market Trends, Marketing Spend and Sales Strategies in the Global Construction Industry Page 22

© Timetric. This product is licensed and is not to be photocopied Published: June 2013

campus. The project will feature two on-campus residential facilities, which will house 1,360 students

and include social, study and programming spaces.

Table 11: Revenue Growth Optimism in the Global Construction Industry by Region (%), 2013

Growth Optimism North America Europe Asia-Pacific Rest of the World

More optimistic 63% 48% 48% 70%

Neutral 26% 17% 36% 10%

Less optimistic 11% 34% 12% 20%

Don't know 0% 0% 4% 0%

Overall 100% 100% 100% 100%

N.B. Results may not equal 100% due to rounding

Source: Timetric Industry Survey 2013 © Timetric

Figure 3: Revenue Growth Optimism in the Global Construction Industry by Region (%), 2013

Source: Timetric Industry Survey 2013 © Timetric

3.1.3 Revenue growth projections by turnover

Survey respondents from small companies are more optimistic about revenue growth than those from

medium-sized and large companies. This is indicated by the fact that 58% of respondents from small

companies are more optimistic of revenue growth in 2013, while 46% of respondents from medium-

sized and 45% from large companies share similar expectations. Additionally, a total of 35% of

respondents from large companies expressed that they are ‘neutral’ about their revenue growth outlook,

while another 20% are ‘less optimistic’.

INDUSTRY DYNAMICS

Global Construction Supplier Industry Outlook Survey 2013–2014:

Market Trends, Marketing Spend and Sales Strategies in the Global Construction Industry Page 23

© Timetric. This product is licensed and is not to be photocopied Published: June 2013

Table 12: Revenue Growth Optimism in the Global Construction Industry by Turnover (%), 2013

Growth Optimism Less than US$100 million US$100 million–US$1 billion More than US$1 billion

More optimistic 58% 46% 45%

Neutral 18% 25% 35%

Less optimistic 23% 29% 20%

Don't know 1% 0% 0%

Overall 100% 100% 100%

N.B. Results may not equal 100% due to rounding

Source: Timetric Industry Survey 2013 © Timetric

Figure 4: Revenue Growth Optimism in the Global Construction Industry by Turnover (%), 2013

Source: Timetric Industry Survey 2013 © Timetric

INDUSTRY DYNAMICS

Global Construction Supplier Industry Outlook Survey 2013–2014:

Market Trends, Marketing Spend and Sales Strategies in the Global Construction Industry Page 24

© Timetric. This product is licensed and is not to be photocopied Published: June 2013

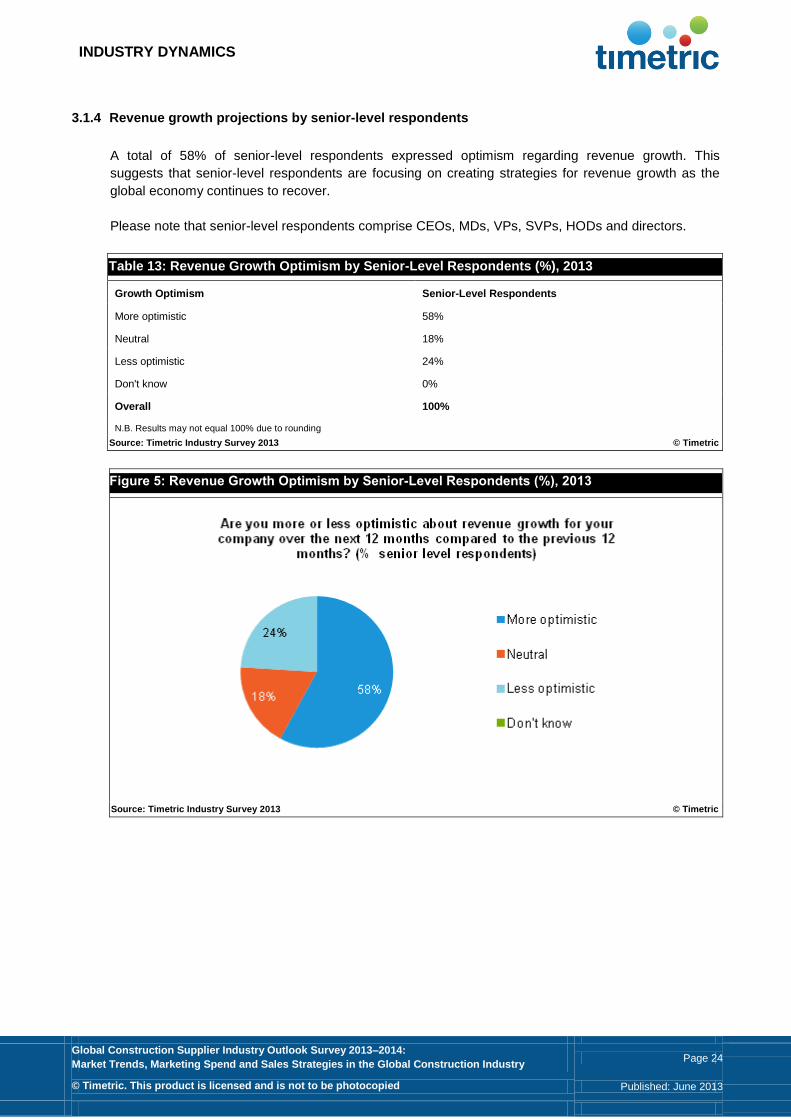

3.1.4 Revenue growth projections by senior-level respondents

A total of 58% of senior-level respondents expressed optimism regarding revenue growth. This

suggests that senior-level respondents are focusing on creating strategies for revenue growth as the

global economy continues to recover.

Please note that senior-level respondents comprise CEOs, MDs, VPs, SVPs, HODs and directors.

Table 13: Revenue Growth Optimism by Senior-Level Respondents (%), 2013

Growth Optimism Senior-Level Respondents

More optimistic 58%

Neutral 18%

Less optimistic 24%

Don't know 0%

Overall 100%

N.B. Results may not equal 100% due to rounding

Source: Timetric Industry Survey 2013 © Timetric

Figure 5: Revenue Growth Optimism by Senior-Level Respondents (%), 2013

Source: Timetric Industry Survey 2013 © Timetric

INDUSTRY DYNAMICS

Global Construction Supplier Industry Outlook Survey 2013–2014:

Market Trends, Marketing Spend and Sales Strategies in the Global Construction Industry Page 25

© Timetric. This product is licensed and is not to be photocopied Published: June 2013

3.2 Future Developments in Business Structure in the Global Construction Industry

Construction companies across the world are being forced to adjust their business structures due to the

changing economic conditions. As a result, construction companies are focusing more on the business

structures that affect their future developments. Respondents were asked what their top priorities are in

developing their company's business structure in 2013. Respondents were also asked if they will be

expanding or diversifying into specific regions or product types. The answers have been analyzed into

different groups, which identify the apparent changes anticipated across the industry and provide an

insight into general global construction industry dynamics.

3.2.1 Future developments in business structure by contractors and developers

Overall, the key anticipated changes in business structure for construction contractors and developers

have not changed considerably from those identified in the 2012 Timetric construction survey. The main

priorities identified by construction contractors and developers for 2013 are the need to ‘expand in

current market’ and ‘improving operational efficiency’. The priorities indentified in the 2012 survey were

‘improving operational efficiency’, to ‘expand operations in domestic market’, ‘stabilize company

finances’, and ‘manage pricing strategies’.

‘Expand operations in domestic market’ has emerged as an important business priority for construction

contractors and developers. With the gradual recovery of the global construction industry, these

companies are looking to shift their focus from survival to growth. For example, in March 2013, London-

based construction services firm, Morgan Sindall, won a contract to build a new US$36 million office

building in Glasgow as part of the Clyde Gateway regeneration project. Morgan Sindall will redevelop

the vacant land on the banks of the River Clyde into 11,000 sq. m of office accommodation in a new

five-story building by October 2014. Similarly, in February 2013, Australian property development firm,

Stockland, selected Brookfield Multiplex as the preferred contractor for its US$125 million

redevelopment of the Stockland Wetherill Park shopping centre in south-west Sydney. Commenting on

the agreement, a senior executive from Brookfield Multiplex said:

“We have forged a strong relationship in recent years, having been involved in the redevelopment of

Stockland Merrylands, completed in October 2012, as well as Stockland Shellharbour which we're set

to hand over mid this year.”

For ‘improving operational efficiency’, several construction companies have started to implement

advanced IT technologies such as building information modeling (BIM). A company’s operational

efficiency directly affects its profit margins, and construction contractors and developers are

increasingly employing technological initiatives to improve their operational efficiency. In April 2013,

radio systems developer HBC-radiomatic, based in Germany, announced the introduction of Spectrum

E, a new radio control system, which has space for a large number of operating elements and features.

The device is suited for applications with large function ranges, such as bucket excavators, special

transport vehicles, and drilling machines, and also features a newly developed live video transmission

and user identification with the HBC data logger.

INDUSTRY DYNAMICS

Global Construction Supplier Industry Outlook Survey 2013–2014:

Market Trends, Marketing Spend and Sales Strategies in the Global Construction Industry Page 26

© Timetric. This product is licensed and is not to be photocopied Published: June 2013

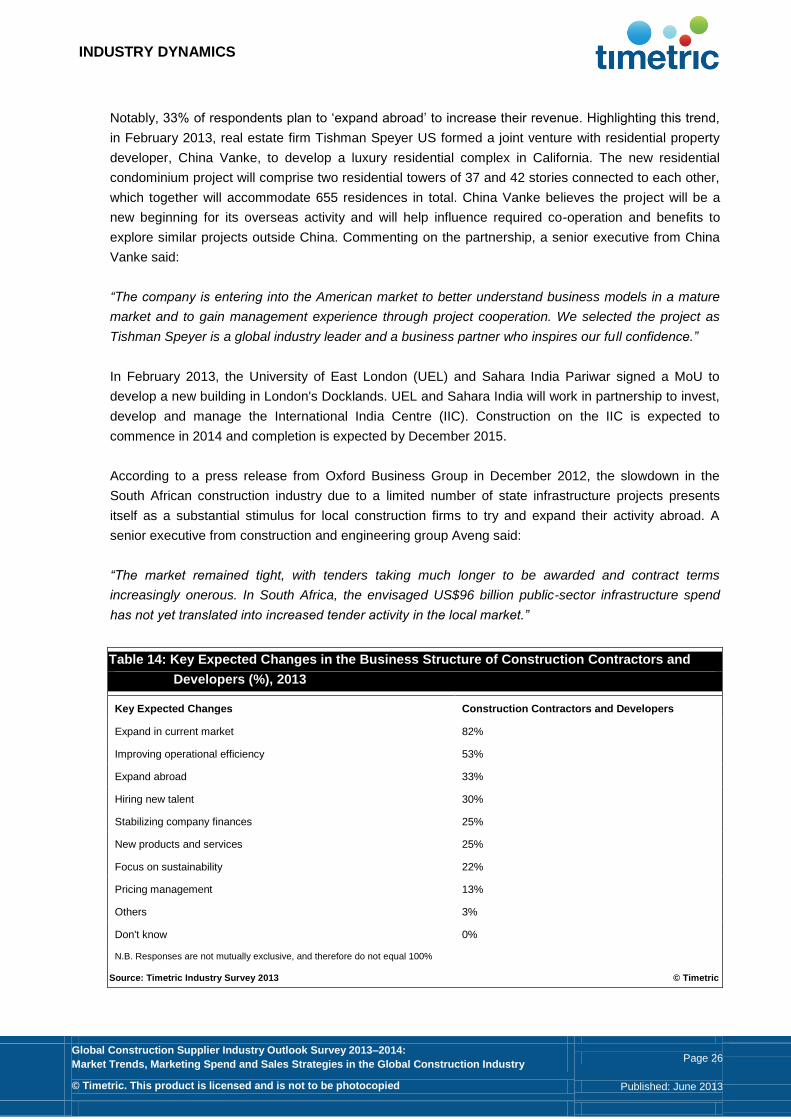

Notably, 33% of respondents plan to ‘expand abroad’ to increase their revenue. Highlighting this trend,

in February 2013, real estate firm Tishman Speyer US formed a joint venture with residential property

developer, China Vanke, to develop a luxury residential complex in California. The new residential

condominium project will comprise two residential towers of 37 and 42 stories connected to each other,

which together will accommodate 655 residences in total. China Vanke believes the project will be a

new beginning for its overseas activity and will help influence required co-operation and benefits to

explore similar projects outside China. Commenting on the partnership, a senior executive from China

Vanke said:

“The company is entering into the American market to better understand business models in a mature

market and to gain management experience through project cooperation. We selected the project as

Tishman Speyer is a global industry leader and a business partner who inspires our full confidence.”

In February 2013, the University of East London (UEL) and Sahara India Pariwar signed a MoU to

develop a new building in London's Docklands. UEL and Sahara India will work in partnership to invest,

develop and manage the International India Centre (IIC). Construction on the IIC is expected to

commence in 2014 and completion is expected by December 2015.

According to a press release from Oxford Business Group in December 2012, the slowdown in the

South African construction industry due to a limited number of state infrastructure projects presents

itself as a substantial stimulus for local construction firms to try and expand their activity abroad. A

senior executive from construction and engineering group Aveng said: